Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934 (Amendment No. 1)

Filed by the Registrantx Filed by a Party Other than the Registrant¨

Check the appropriate box:

| x | Preliminary Proxy Statement |

| ¨ | Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to Section 240.14a-12 |

RENTECH, INC.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ | No fee required. |

| x | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): |

| The filing fee of $16,112 was determined pursuant to Rule 0-11(c)(1) under the Securities Exchange Act of 1934 by multiplying 1/50 of 1% by $80,560,000, which is equal to the currently estimated aggregate amount of consideration to be paid pursuant to the transaction. The underlying transaction value on which the filing is calculated is comprised of: (i) the cash payment of $50,000,000 to acquire all of the outstanding capital stock Royster-Clark Nitrogen, Inc.; (ii) the estimated cash payment of $30,000,000 for the closing net working capital of Royster-Clark Nitrogen, Inc.; and (iii) estimated transaction costs of $560,000. |

| (4) | Proposed maximum aggregate value of transaction: |

$80,560,000

| (5) | Total fee paid: |

$16,112

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

1

Table of Contents

PRELIMINARY MATERIALS

RENTECH, INC.

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

TO BE HELD MARCH __, 2006

You are cordially invited to attend the annual meeting of shareholders of Rentech, Inc. to be held at the Magnolia Ballroom, 817 17th Street, Denver, Colorado, on , March __, 2006 at 9:00 a.m. (local time) for the following purposes:

| 1. | To elect two directors for terms of three years each; |

| 2. | To vote upon a proposal to purchase Royster-Clark Nitrogen, Inc.; |

| 3. | To vote upon a proposal for the potential issuance of 20% or more of Rentech’s outstanding common stock at prices below market value; |

| 4. | To vote upon a proposal to adopt the 2006 Incentive Award Plan; and |

| 5. | To transact such other business as may properly come before the meeting or any adjournments or postponements of the meeting. |

Accompanying this notice is a form of proxy and a proxy statement, including a copy of Rentech’s annual report on Form 10-K for the fiscal year ended September 30, 2005 (excluding exhibits).

Only holders of record of the common stock of Rentech at the close of business on February __, 2006 will be entitled to notice of and to vote at the meeting and any adjournments or postponements of the meeting.

By Order of the Board of Directors, | ||

Amanda M. Darby | ||

| Secretary | ||

Denver, Colorado

Date: February __, 2006

2

Table of Contents

YOUR VOTE IS IMPORTANT

This proxy statement is furnished in connection with the solicitation of proxies by Rentech, on behalf of the Board of Directors, for the 2006 annual meeting of shareholders. The proxy statement and the related proxy form are first being distributed to shareholders on or about February __, 2006. You can vote your shares using one of the following methods:

| • | Vote through the Internet at the website shown on the proxy card. |

| • | Vote by telephone using the toll-free number shown on the proxy card. |

| • | Complete and return a written proxy card. |

| • | Attend Rentech’s 2006 annual meeting of shareholders and vote. |

Votes submitted through the Internet or by telephone must be received by 11:59 p.m. Eastern Time, on March __, 2006. Internet and telephone voting are available 24 hours per day. If you vote via Internet or telephone, you do not need to return a proxy card.

You are invited to attend the meeting; however, to ensure your representation at the meeting, you are urged to vote via the Internet or telephone, or mark, sign, date and return the enclosed proxy card as promptly as possible in the postage-prepaid envelope enclosed for that purpose. Any shareholder attending the meeting may vote in person even if he or she has voted via the Internet or telephone, or returned a proxy card.

3

Table of Contents

i

Table of Contents

| 29 | ||||

Adoption of the 2006 Stock Incentive Incentive Award Plan (Proxy Item 4) | 30 | |||

| 30 | ||||

| 31 | ||||

| 31 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 33 | ||||

| 34 | ||||

| 34 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

Annexes | ||||

B Historical Financial Statements of Royster-Clark Nitrogen, Inc. | ||||

C Unaudited Condensed Consolidated Pro Forma Combined Financial Statements | ||||

ii

Table of Contents

Date, Time and Place.March __, 2006, at 9:00 a.m.(MST), at the Magnolia Ballroom, 817 17th Street, Denver, Colorado.

Record Date; Quorum.Only holders of record of Rentech common stock on February __, 2006, will be entitled to notice of, and to vote at, the annual meeting; a majority of the outstanding shares of common stock present in person or by proxy will constitute a quorum.

Vote Required for Approval.The two directors that receive the most votes cast in their favor will be elected. The acquisition of Royster-Clark Nitrogen, Inc., the potential issuance of 20% or more of our outstanding common stock at prices below market value, and the 2006 Incentive Award Plan may be approved by the vote of a majority of votes represented by shares present in person or by proxy and entitled to vote at the annual meeting.

Recommendation of the Board of Directors.The Board of Directors unanimously recommends a vote FOR its nominees for elections as directors, Messrs. Ramsbottom and Washburn, FOR approval of the acquisition of Royster-Clark Nitrogen, Inc., FOR approval of the potential issuance of more than 20% of our outstanding common stock at prices below market value, and FOR approval of the 2006 Incentive Award Plan.

| Item 1. | Election of Directors |

The two nominees for election to the Board of Directors, for terms of three years ending 2009 are Messrs. Ramsbottom and Washburn. Each person nominated for election has agreed to serve if elected and management has no reason to believe that any of the nominees will be unable to serve.

In the event that any nominee should be unexpectedly unavailable for election, such shares shall be voted for the election of such substitute nominee as the Nominating Committee of the Board may propose and the Board approve.

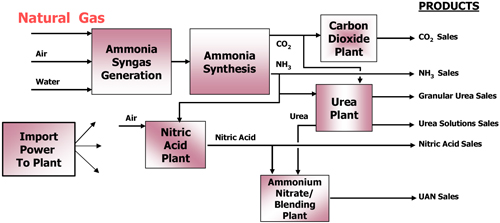

| Item 2. | Purchase of Royster-Clark Nitrogen, Inc. |

Purchase Agreement. We have entered into an agreement to purchase Royster-Clark Nitrogen, Inc. (“RCN”) for $50 million for the stock, plus an amount equal to RCN’s net working capital, as defined in the agreement, at the closing, subject to shareholder approval and other conditions. As of 2/2/06, our estimate of what RCN’s net working capital will be is approximately $30 million at closing. RCN owns and operates an 830 ton per day, natural gas fed, ammonia plant in East Dubuque, Illinois, which is used to make nitrogen fertilizer products. We currently have a commitment of $35 million of debt financing to finance a portion of the purchase price, and intend to raise the remaining portion of the purchase price and net working capital for RCN through a combination of debentures, cash on hand, additional equity issuance(s), and a working capital facility that has not yet been obtained. Some or all of the securities proposed to be offered to finance the purchase of RCN have not been registered under the Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements.

Background of the Transaction.We identified RCN as the ideal vehicle with which to execute our business strategy and entered into an agreement to purchase it in 2004. The agreement expired on March 18, 2005. We continued to discuss with the seller using our technology at the RCN plant, and, eventually, another agreement to purchase RCN.

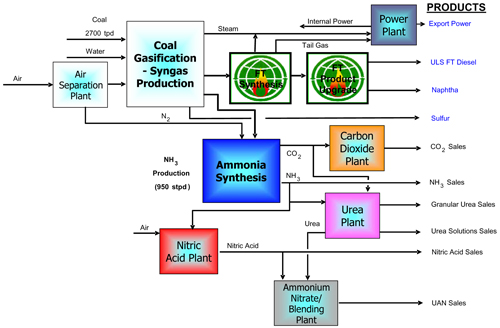

Purpose of the Transaction.We intend to commercialize our proprietary Fischer-Tropsch technology by initially converting the East Dubuque facility to coal as a feedstock and then deploying our technology for the co-production of liquid hydrocarbon products (principally diesel fuel) and electrical power.

Break Fee. In the event we fail to close by reason of our failure to obtain financing, shareholder approval or the American Stock Exchange listing of any shares to be issued to finance the acquisition, we will forfeit $2.5 million to the seller.

iii

Table of Contents

| Item 3. | Potential Issuance of Common Stock Representing 20% or More of Our Outstanding Common Stock at Prices Below Market Value |

In order to commercialize our technology by acquiring or constructing process plants, converting them to the use of our technology, and operating them in the future, as well as to conduct our normal operations until such time (if ever) as we attain profitability, it will be necessary for us to raise capital, including by the sale of our common stock, or securities convertible into or exercisable or exchangeable for our common stock, sometimes at a discount to the then current market price. Under the rules of the American Stock Exchange, where our common stock is listed and traded, shareholder approval is required for the sale, issuance or potential issuance of common stock (or securities convertible into or exercisable or exchangeable for common stock) equal to 20% or more of presently outstanding stock for less than the greater of book or market value. We therefore propose that the shareholders authorize our issuing up to 40,000,000 shares of our common stock (or securities convertible into or exercisable for common stock) for up to an aggregate of $200,000,000 in gross proceeds, at a discount of up to 30% from the market price at the time of issuance and sale, for a period of up to one year from the date that our shareholders approve the proposal (or until the next annual meeting, if longer), the proceeds of which would be used for the general purposes outlined above.

| Item 4. | 2006 Incentive Award Plan |

The Board of Directors has adopted, subject to shareholder approval, the Rentech, Inc. 2006 Incentive Award Plan (the “2006 Plan”). The 2006 Plan provides for grants of a wide range of equity and other incentive awards to members of the Board, employees and consultants of Rentech and its subsidiaries, which awards may be subject to various restrictions and vesting terms. An aggregate of [ ] shares of common stock are available for grant pursuant to the 2006 Plan. The maximum number of shares of common stock that may be subject to one or more awards to a participant pursuant to the 2006 Plan during any rolling three calendar-year period is . To the extent that an award terminates, expires or lapses for any reason, any shares subject to the award may be used again for new grants under the 2006 Plan; however, shares tendered or withheld to satisfy the grant or exercise price or tax withholding obligations arising in connection with any awards may not be used for grants under the 2006 Plan. The 2006 Plan may be terminated, amended or modified at any time; provided, that shareholder approval will be obtained for any amendment to the extent necessary and desirable to comply with any applicable law, regulation or stock exchange rule

The consummation of the transactions proposed in this proxy statement will involve risks that are described in more detail in Item 1A of our annual report on Form 10-K for the fiscal year ended September 30, 2005, included in Annex A to this proxy statement. These risks include:

| • | If we do not succeed in acquiring RCN, we may be forced to pay a substantial break-up fee, will incur considerable transactional expenses, and our business and future prospects may be damaged. |

| • | If we succeed in acquiring RCN, and convert it to use our technology to make alternative fuels, we will be required to issue substantial equity, resulting in substantial dilution to existing shareholders, and incur substantial indebtedness, leaving us a highly leveraged enterprise. There is no assurance we will be able to secure the needed financing or pay any indebtedness so incurred. |

| • | We have never converted any chemical process plant to use our technology to make alternative fuels, nor has anyone else; the conversion may not occur within the times or at the cost we presently project, and may not be economic or operable when done. |

| • | We have never operated a nitrogen fertilizer business, which is highly seasonal in nature, has a history of losses, and is subject to material environmental and other risks; our lack of experience or intrinsic risks of the business may result in substantial losses. |

| • | We are attempting to acquire rights to land and certain existing facilities in Natchez, Mississippi in order to develop process plants using our and other technologies, which if successful will involve further risks of the sort described above and others. |

| • | We have limited liquidity and capital resources, and cash flows from operations that do not cover our expenses; we must raise additional capital to execute our business plans, and to maintain our current operations. |

iv

Table of Contents

Summary Selected Historical Financial Data

Rentech

The following consolidated selected financial data has been derived from our historical consolidated financial statements and should be read in conjunction with Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” Item 8, “Financial Statements and Supplementary Data,” our consolidated financial statements and notes, and Item 1A “Risk Factors,” in our annual report on Form-10-K for the fiscal year ended September 30, 2005, included as Annex A to this proxy statement.

Rentech, Inc. and Subsidiaries

| Years Ended September 30 | ||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||||||||||

CONSOLIDATED STATEMENT OF OPERATIONS DATA | ||||||||||||||||||||

Revenues | $ | 7,185,485 | $ | 5,706,280 | $ | 4,496,011 | $ | 4,731,744 | $ | 5,605,570 | ||||||||||

Cost of Sales | $ | 5,213,092 | $ | 4,035,779 | $ | 2,940,022 | $ | 2,385,784 | $ | 4,867,832 | ||||||||||

Gross Profit | $ | 1,972,393 | $ | 1,670,501 | $ | 1,555,989 | $ | 2,345,960 | $ | 737,738 | ||||||||||

Loss from Continuing Operations | $ | (14,369,273 | ) | $ | (6,492,558 | ) | $ | (8,812,320 | ) | $ | (4,939,418 | ) | $ | (6,773,360 | ) | |||||

Net Loss | $ | (14,358,897 | ) | $ | (7,210,693 | ) | $ | (9,535,405 | ) | $ | (5,332,613 | ) | $ | (6,770,707 | ) | |||||

Loss Applicable to Common Stock | $ | (23,700,372 | ) | $ | (7,210,693 | ) | $ | (9,535,405 | ) | $ | (5,469,545 | ) | $ | (7,254,306 | ) | |||||

BASIC AND DILUTED LOSS PER SHARE(1) | ||||||||||||||||||||

Loss from Continuing Operations Per Common Share | $ | (.26 | ) | $ | (.08 | ) | $ | (.12 | ) | $ | (.07 | ) | $ | (.11 | ) | |||||

Loss Per Common Share | $ | (.26 | ) | $ | (.08 | ) | $ | (.13 | ) | $ | (.08 | ) | $ | (.11 | ) | |||||

Cash dividend declared per common share | — | — | — | — | — | |||||||||||||||

| (1) | The weighted average number of shares of common stock outstanding during the fiscal years ended September 30, 2005, 2004, 2003, 2002 and 2001 were 92,918,545, 85,932,544, 73,907,041, 69,987,685 and 64,807,168, respectively. |

CONSOLIDATED BALANCE SHEET DATA | ||||||||||||||||||||

Working Capital | $ | 32,031,397 | $ | (1,081,487 | ) | $ | (1,571,738 | ) | $ | 775,686 | $ | 1,412,195 | ||||||||

Total Assets | $ | 43,491,949 | $ | 9,379,288 | $ | 11,187,114 | $ | 16,163,228 | $ | 16,115,455 | ||||||||||

Total Long-Term Liabilities | $ | 2,849,943 | $ | 3,018,795 | $ | 3,223,994 | $ | 3,269,044 | $ | 1,157,927 | ||||||||||

Total Liabilities | $ | 9,220,767 | $ | 6,341,424 | $ | 8,005,734 | $ | 7,422,576 | $ | 4,069,122 | ||||||||||

Accumulated Deficit | $ | (62,008,636 | ) | $ | (47,649,739 | ) | $ | (40,439,046 | ) | $ | (30,903,641 | ) | $ | (25,571,028 | ) |

Royster-Clark Nitrogen, Inc.

The following consolidated selected financial data has been derived from RCN’s historical financial statements and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations of RCN” and “RCN Financial Statements,” included as Annex B to this proxy statement

v

Table of Contents

and Item 1A “Risk Factors - Risks Related to Possible Inability to Complete Acquisitions and the Financing Required for the Acquisitions and Subsequent Operations” and “Risks Related to Our Operations after Acquisitions” included in our annual report on Form 10-K for the fiscal year ended September 30, 2005, included as Annex A to this proxy statement. As discussed in note 1 to the RCN Financial Statements for September 30, 2005, the nine month period ended September 30, 2005 includes a 202-day period ended July 21, 2005 and a 71-day period ended September 30, 2005, and are using a different cost basis of certain assets and are therefore not comparable to financial statements for other periods. In the opinion of RCN’s management, the nine months unaudited information reflects all adjustments and consists only of normal recurring adjustments necessary for a fair presentation. Historical results are not necessarily indicative of results to be reported in future periods.

| Nine Months ended September 30, | Year ended December 31, | ||||||||||||||||||||||||||

| 2005 | 2004 | 2004 | 2003 | 2002 | 2001 | 2000 | |||||||||||||||||||||

STATEMENT OF OPERATIONS DATA | |||||||||||||||||||||||||||

Net sales | $ | 67,629,095 | $ | 69,135,376 | $ | 97,294,329 | $ | 68,465,617 | $ | 61,643,392 | $ | 50,227,340 | $ | 59,297,630 | |||||||||||||

Gross profit (loss) | $ | 2,764,354 | $ | 3,705,455 | $ | 7,320,015 | $ | (2,281,991 | ) | $ | (2,597,165 | ) | $ | (1,724,483 | ) | $ | 8,439,104 | ||||||||||

Operating income (loss) | $ | 1,483,571 | $ | 2,583,353 | $ | 5,545,289 | $ | (4,070,056 | ) | $ | (4,533,443 | ) | $ | (3,331,252 | ) | $ | 6,491,241 | ||||||||||

Net income (loss) | $ | (2,742,424 | ) | $ | (1,315,539 | ) | $ | 425,375 | $ | (23,021,056 | ) | $ | (4,368,254 | ) | $ | (4,796,457 | ) | $ | 7,050,953 | ||||||||

Net income (loss) applicable to common stock | $ | (2,742,424 | ) | $ | (1,315,539 | ) | $ | 425,375 | $ | (23,021,056 | ) | $ | (4,368,254 | ) | $ | (4,796,457 | ) | $ | 7,050,953 | ||||||||

BASIC AND DILUTED INCOME (LOSS) PER SHARE | |||||||||||||||||||||||||||

Net income (loss) per share based on 985 shares | $ | (2,784.19 | ) | $ | (1,335.57 | ) | $ | 431.85 | $ | (23,371.63 | ) | $ | (4,434.78 | ) | $ | (4,869.50 | ) | $ | 7,158.33 | ||||||||

Cash dividend declared per common share | — | — | — | — | — | — | — | ||||||||||||||||||||

BALANCE SHEET DATA | |||||||||||||||||||||||||||

Working capital | $ | 11,376,858 | $ | 5,795,895 | $ | 2,912,671 | $ | 8,371,105 | $ | 5,731,295 | $ | 6,830,928 | $ | 12,195,661 | |||||||||||||

Total assets | $ | 74,861,704 | $ | 38,696,452 | $ | 35,205,451 | $ | 44,136,163 | $ | 55,196,168 | $ | 59,998,154 | $ | 66,192,162 | |||||||||||||

Total long-term liabilities | $ | 54,625,691 | $ | 64,462,464 | $ | 58,765,253 | $ | 67,992,824 | $ | 56,413,091 | $ | 54,376,411 | $ | 54,294,283 | |||||||||||||

Total liabilities | $ | 61,092,849 | $ | 67,180,469 | $ | 61,948,554 | $ | 71,304,641 | $ | 59,343,590 | $ | 59,777,323 | $ | 61,174,873 | |||||||||||||

Total retained earnings (accumulated deficit) | $ | (3,544,653 | ) | $ | (28,484,017 | ) | $ | (26,743,103 | ) | $ | (27,168,478 | ) | $ | (4,147,422 | ) | $ | 220,831 | $ | 5,017,289 | ||||||||

Selected Unaudited Condensed Consolidated Pro Forma Combined Financial Data

The unaudited condensed consolidated pro forma combined financial data presented below gives effect to the acquisition of the outstanding shares of RCN for an aggregate purchase price of approximately $66,460,000, using the purchase method of accounting. The unaudited condensed consolidated pro forma combined results of operations data for the twelve months ended September 30, 2005 gives effect to the acquisition of RCN and related financing as of the beginning of the period presented. The unaudited condensed consolidated pro forma combined balance sheet data gives effect to the acquisition RCN and related financing as of September 30, 2005. The unaudited condensed pro forma combined financial data is presented for comparative purposes only and is not necessarily indicative of the financial position or results of operations that would have been realized had the acquisition occurred at the beginning of the period presented or results that may be achieved in the future. The unaudited condensed consolidated pro forma combined financial data has been derived from the historical financial statements of Rentech and RCN appearing in Annexes A and B in this proxy statement, and should be read in conjunction with them and with the unaudited condensed consolidated pro forma combined financial statements included in Annex C to this proxy statement.

vi

Table of Contents

| Twelve Months ended September 30, 2005 | ||||

INCOME STATEMENT DATA | ||||

Net sales | $ | 110,629,718 | ||

Gross loss | $ | 13,416,065 | ||

Loss from Operations | $ | (1,049,444 | ) | |

Net loss | $ | (10,809,008 | ) | |

Loss applicable to common stock | $ | (20,150,483 | ) | |

BASIC AND DILUTED LOSS PER SHARE | ||||

Net loss per share based on 101,907,116 shares | $ | (0.198 | ) | |

Cash dividend declared per common share | — | |||

BALANCE SHEET DATA | ||||

Working capital | $ | 43,408,255 | ||

Total assets | $ | 116,359,928 | ||

Total long-term liabilities | $ | 37,849,943 | ||

Total liabilities | $ | 50,687,925 | ||

Total accumulated deficit | $ | (62,008,636 | ) | |

vii

Table of Contents

RENTECH, INC.

1331 17th Street, Suite 720

Denver, Colorado 80202

PROXY STATEMENT

ANNUAL MEETING OF SHAREHOLDERS

TO BE HELD MARCH , 2006

This proxy statement is furnished to shareholders in connection with the solicitation by the Board of Directors of Rentech, Inc. of proxies for use at the annual meeting of shareholders to be held at the Magnolia Ballroom, 817 17th Street, Denver, Colorado, on , March , 2006 at 9:00 a.m., local time, and at any adjournments or postponements of the meeting.

Rentech anticipates that this proxy statement and the accompanying form of proxy will be first sent or given to shareholders on or about February , 2006.

VOTING SECURITIES AND VOTING RIGHTS

Only shareholders of record at the close of business on February , 2006 are entitled to notice of and to vote at the annual meeting or any adjournments or postponements of the meeting. On that date, shares of common stock were outstanding held by shareholders of record. Each share of common stock outstanding on that date entitles the holder to one vote on each matter submitted to a vote at the meeting. Cumulative voting is not allowed.

Shareholders may vote in person or by proxy at the annual meeting. All properly executed proxies received prior to the commencement of voting at the meeting, and which have not been revoked, will be voted in accordance with the directions given. If no specific instructions are given for a matter to be voted upon, the proxy holders will vote the shares covered by proxies received by them (i) FOR the election of the two nominees to the Board of Directors; (ii) FOR the purchase of Royster-Clark Nitrogen, Inc; (iii) FOR the potential issuance of 20% or more of Rentech’s outstanding common stock at prices below market value; and (iv) FOR approval of the proposal to adopt the 2006 Incentive Award Plan.

A quorum for the transaction of business at the meeting requires the presence at the annual meeting, in person or by proxy, of the holders of a majority of the shares entitled to vote at the meeting. If a quorum is present, the two nominees for election as directors who receive the greatest number of votes cast for the election of directors at the meeting will be elected. The proposals (a) to purchase Royster-Clark Nitrogen, Inc., (b) to potentially issue 20% or more of Rentech’s outstanding common stock at prices below market value, and (c) to approve adoption of the 2006 Incentive Award Plan and any other matters submitted to a vote of the shareholders will be approved if they receive the affirmative vote of the holders of a majority of shares of common stock present in person or by proxy and entitled to vote on the matter. If brokers have not received any instruction from their customers on how to vote the customer’s shares on a particular proposal, the brokers are allowed to vote on routine matters but not on non-routine proposals. The absence of votes by brokers on non-routine matters are “broker non-votes.” Abstentions and broker non-votes will be counted as present for purposes of establishing a quorum, but will have no effect on the election of directors. Abstentions and broker non-votes will have the effect of a vote against the proposals to approve the purchase of Royster-Clark Nitrogen, Inc., to potentially issue 20% or more of Rentech’s outstanding common stock at prices below market value, and to approve the 2006 Incentive Award Plan.

Any shareholder giving a proxy pursuant to the present solicitation has the power to revoke it at any time before it is exercised. It may be revoked by giving a subsequent proxy or by mailing to our principal executive offices at 1331 17th Street, Suite 720, Denver, Colorado 80202, Attn: Secretary, an instrument of revocation. If you

1

Table of Contents

vote electronically via the Internet or telephone, a proxy may be revoked by the submission of a later electronic proxy. A proxy may also be revoked by attending the meeting and giving our Secretary a vote in person (subject to the restriction that a shareholder holding shares in street name must bring to the meeting a legal proxy from the broker, bank or other nominee holding that shareholder’s shares which confirms that shareholder’s beneficial ownership of the shares and gives the shareholder the right to vote the shares).

Rentech will bear the cost of solicitation of proxies, including expenses in connection with preparing and mailing this proxy statement. We will furnish copies of solicitation materials to brokerage houses, fiduciaries, and custodians to forward to beneficial owners of our common stock held in their names. In addition, we will reimburse brokerage firms and other persons representing beneficial owners of stock for their expenses in forwarding solicitation materials to such beneficial owners. Original solicitation of proxies by mail may be supplemented by telephone, facsimile and personal solicitation by our directors, officers and other employees. No additional compensation will be paid to our directors, officers or other employees for these services.

The purposes of the meeting and the matters to be acted upon are set forth in the foregoing attached Notice of Annual Meeting. As of the date of this proxy statement, management knows of no other business that will be presented for consideration at the meeting. However, if any such other business shall properly come before the meeting, votes will be cast pursuant to said proxies in respect of any such other business in accordance with the best judgment of the persons acting under said proxies.

2

Table of Contents

(Proxy Item 1)

There are currently eight positions on Rentech’s Board of Directors. The board currently is divided into three classes two of which include two directors and one of which currently includes four directors. The directors in each class are elected for three years and until the election and qualification of their successors. Director Erich W. Tiepel, whose term expires in 2006, has elected not to seek an additional term following the annual meeting of shareholders.

D. Hunt Ramsbottom and Halbert S. Washburn have been nominated for election as directors for a term of three years each and until their successors are elected and have qualified. The two nominees are presently members of the Board of Directors. All other members of the Board of Directors will continue in office until the expiration of their respective terms at the 2007 or 2008 annual meetings of shareholders.

If your vote is properly submitted, it will be voted for the election of the nominees, unless contrary instructions are specified. Each nominee has consented to serve if elected. Although the Board of Directors has no reason to believe that either of the nominees will be unable to serve as a director, should that occur, the persons appointed as proxies in the accompanying proxy card will vote, unless the number of nominees or directors is reduced by the Board of Directors, for such other nominee or nominees as the Board of Directors may designate.

Information Regarding Nominees for Election to the Board of Directors:

D. Hunt Ramsbottom, Chief Executive Officer, President and Director - Mr. Ramsbottom, age 48, was appointed President and Director of Rentech on September 13, 2005 and Chief Executive Officer on December 15, 2005. Mr. Ramsbottom was recommended for membership to the Board of Directors by Dennis L. Yakobson. Mr. Ramsbottom had been serving as a consultant to Rentech since August 5, 2005 under the terms of a Management Consulting Agreement with Management Resource Center, Inc. Mr. Ramsbottom has over 25 years of business experience. Prior to accepting his position at Rentech, Mr. Ramsbottom held various key management positions including: Principal and Managing Director of Circle Funding Group LLC, a value added partner which leverages relationships between senior lenders, equity sponsors, investment banks and management teams; Chief Executive Officer and Chairman of M2 Automotive, 1997-2004, an operator of automotive collision facilities in California, where he developed customer service systems and technology enhancements that have become widely used in the industry; and Chief Executive Officer of Thompson PBE, 1989-1997, which became the largest US distributor of auto body paint and supplies before being acquired by FinishMaster, Inc. in 1997. In April 2005, M2 Automotive completed an assignment for the benefit of its creditors. Mr. Ramsbottom holds a Bachelor of Science degree from Plymouth State College.

Halbert S. Washburn, Director – age 45, was appointed Director of Rentech on December 15, 2005. D. Hunt Ramsbottom the company’s Chief Executive Officer, President and a director recommended Mr. Washburn for election. Mr. Washburn has over 20 years of experience in the energy industry. Mr. Washburn is the co-founder and Chief Executive Officer of BreitBurn Energy Company LP (USA), a subsidiary of Provident Energy Trust. Mr. Washburn is responsible for BreitBurn’s oil and gas operations and co-manages BreitBurn’s acquisition and capital formation activities. In this capacity, he has managed capital structures ranging in size from a private equity placement of $30 million to a senior credit facility of $400 million. Mr. Washburn currently serves on the Executive Committee of the Board of Directors of the California Independent Petroleum Association. He also served as Chairman of the Stanford University Petroleum Investments Committee and as Secretary and Chairman of the Wildcat Committee. Mr. Washburn holds a Bachelor of Science degree in Petroleum Engineering from Stanford University.

3

Table of Contents

THE BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS A VOTE FOR ELECTION

OF THE NOMINEES.

Information Regarding Continuing Directors with Terms Expiring in 2007:

Ronald C. Butz, Director - Mr. Butz, age 68, has served as a director of Rentech since 1984. In October 1989, Mr. Butz was appointed Vice President of Rentech, in June 1990 he was appointed Secretary, and in May 1998 he became Chief Operating Officer. In December 2005, he resigned from his position as Chief Operating Officer, Vice President and Secretary and currently serves as a director. From 1984 to 1989, Mr. Butz was employed as President of Capital Growth, Inc., a privately-held Colorado corporation providing investment services and venture capital consulting. From 1982 to 1983, Mr. Butz was a shareholder, Vice President and Chief Operating Officer of World Agricultural Systems, Ltd., a privately-held Colorado corporation specializing in the international marketing of commodity storage systems. From 1966 to 1982, Mr. Butz was a practicing attorney in Denver, Colorado with the law firm of Grant, McHendrie, Haines and Crouse, P.C. He received a Bachelor of Science degree in Civil Engineering from Cornell University in 1961 and a Juris Doctor degree from the University of Denver in 1965.

Michael R. Ray, Director - Mr. Ray, age 52, was appointed a member of our Board of Directors effective May 11, 2005. Mr. Ray founded and has served as President of ThioSolv, LLC since 2001. ThioSolv, LLC is in the business of developing and licensing technology. From 1995 to 2001, Mr. Ray served as Vice President of Business Development for Coastal Catalyst and Chemicals Division. Mr. Ray worked for Coastal Chem, Inc. as President from 1990 to 1995 and Vice President of Corporate Development and Administration from 1986 to 1990. From 1985 to 1986, Mr. Ray served as Vice President of Carbon Dioxide Marketing. Mr. Ray worked for Liquid Carbonic Corporation as Regional Operations Manager from 1981 to 1985 and Plant Manager from 1980 to 1981. Mr. Ray received his Bachelor of Science in Industrial Technology from Western Washington University and his Masters of Business Administration from Houston Baptist University. Mr. Ray previously served as a member of the Board of Directors of Coastal Chem, Inc., Cheyenne LEADS and Wyoming Heritage Society. Mr. Ray also served on Nitrogen Fertilizer Industry Ad Hoc Committee, University of Wyoming EPSCOR Steering Committee and Wyoming Governor’s committee for evaluating state employee compensation.

Information Regarding Continuing Director with Term Expiring in 2008:

Thomas L. Bury, Director - Mr. Bury, age 63, was appointed a member of our Board of Directors effective November 12, 2004. He was a founding shareholder and served as Chief Financial Officer of Tecta America Corp., a member of the construction industry supplying aggregate building materials, from its organization in 1998 until completion in September 2000 of its merger that consolidated ten businesses in the construction industry. Since then he has advised investors on business valuations and acquisition strategies. Mr. Bury has over 30 years of experience as a financial officer, including financial disciplines in multi-division companies and development of planning and financial systems. He has extensive knowledge of treasury, banking, acquisitions, divestitures and corporate planning, as well as company and strategy valuation methods. Prior to founding Tecta America Corp., he was Chief Financial Officer of Redland PLC’s aggregate businesses in North America, and had responsibility for its financial functions from 1987 through 1998. From 1972 through 1987, Mr. Bury worked for Fischbach Corporation, primarily serving as Chief Financial Officer of its subsidiary, Natkin & Company, a $500 million nationwide mechanical contractor. He received his Bachelor of Science degree in Business Administration from Bowling Green State University. After serving in the U.S. Army in Vietnam, he received his Masters of Business Administration degree from Syracuse University.

Dennis L. Yakobson, Director and Chairman of the Board - Mr. Yakobson, age 69, has served as a director of Rentech and Chairman of the Board since 1983 and is one of the founders. In December 2005, he resigned from his position as Chief Executive Officer and currently serves as a director. He was employed as Vice President of Administration and Finance of Nova Petroleum Corporation, Denver, Colorado, from 1981 to 1983. From 1979 to 1983, he served as a director and Secretary of Nova Petroleum Corporation, Denver, Colorado. He resigned from those positions in November 1983 to become a director and assume the presidency of Rentech. From 1976 to 1981 he served as a director, Secretary and Treasurer of Power Resources Corporation, Denver, a mineral exploration company, and was employed by it as Vice President-Land. From 1975 to 1976 he was employed by Wyoming Mineral Corporation in Denver as a contract administrator. From 1971 through 1975 he was employed by Martin Marietta Corporation, Denver, as marketing engineer in space systems. From 1969 to 1971 he was employed by Martin Marietta in a similar position. From 1960 to 1969 he was employed by Grumman Aerospace Corporation, his final position with it being contract administrator with responsibility for negotiation of prime contracts with governmental agencies. He is a director of GTL Energy Pty Ltd., a private company based in Adelaide, Australia.

4

Table of Contents

He received a Bachelor of Science degree in Civil Engineering from Cornell University in 1959 and a Masters in Business Administration degree from Adelphi University in 1963.

Executive Officers and Other Key Managers

Information concerning the business experience of Mr. Ramsbottom, who serves as President and Chief Executive Officer, is provided under “Information Regarding Nominees for Election to the Board of Directors.”

Charles B. Benham, Vice President-Research and Development - Dr. Benham, age 69, is one of our founders and has been an officer of Rentech since our inception in 1981. He served as our President until 1983 and as one of our directors from inception until 1996. From 1977 to 1981, Dr. Benham worked at the Solar Energy Research Institute in Golden, Colorado, on thermal and chemical processes for converting agricultural crop residues to diesel fuel, on thermochemical transport of solar energy using ammonia decomposition and steam reforming of methane, and on high temperature applications of solar energy. He was employed at the Naval Weapons Center, China Lake, California, from 1958 through 1977 where he was engaged in research and development on thermal and chemical processes for converting municipal solid wastes to liquid hydrocarbon fuels, thermochemical analyses of solid-fueled and ramjet engines, combustor modeling, rocket motor thrust vector control, rocket motor thrust augmentation, catalyst behavior in carbon monoxide oxidation, and in liquid hydrocarbon fuels for ramjet applications. Dr. Benham is the author of several published articles in the fields of liquid fuel production from organic waste, catalyst pellet behavior and rocket propulsion. He received a Bachelor of Science degree in Mechanical Engineering from the University of Colorado in 1958, and a Master of Science degree in Engineering in 1964 and a Ph.D. in Engineering (energy and kinetics) in 1970, both from the University of California, Los Angeles.

Claude C. Corkadel, III, Vice President-Strategic Programs - Mr. Corkadel, age 56, was appointed Vice President – Strategic Programs of Rentech, effective January 1, 2004. For 28 years, from 1972 to 2000, Mr. Corkadel worked for Mobil Oil Corporation in various management positions. These offices included President and Country Manager of Mobil Philippines, Planning Manager for Mobil Nigeria, Strategic Planning Manager for the Alternative Energy Division (including coal, uranium, oil shale and synthetic fuels projects), Global Director for Mobil’s special products business and a member of the transition team for Africa under the ExxonMobil merger. His responsibilities in these positions included developing market entry strategies, technical product & business development, and strategic planning. After retiring from Mobil in January 2000, he worked as a special consultant for several small entrepreneurial businesses, and held executive positions during key development periods. During 2000 and early 2001, he was President of Nova Lending, an online mortgage company in Colorado Springs, Colorado. In later 2001 and 2002, he was President and Chief Executive Officer of WellDog, Inc, of Laramie, Wyoming, a technology development company working on cutting edge down-hole sensing devices for the oil and gas industry. He consulted exclusively for Rentech starting February 2003. Mr. Corkadel is a graduate of Colorado School of Mines with a Bachelor of Science degree in Metallurgical Engineering and a minor in Mineral Economics. He obtained a Master in Business Administration degree in Finance from Drexel University in 1981.

Amanda M. Darby, General Counsel and Secretary – Ms. Darby, age 38, was appointed our General Counsel in April 2005 and Secretary in January 2006. Ms. Darby is licensed to practice law in the states of California and Colorado. Ms. Darby previously served as Assistant Corporate Counsel and Assistant Secretary to The First American Corporation/First American Title Insurance Company (NYSE: FAF). Prior to working at First American, Ms. Darby practiced law for Stepp & Beauchamp, LLP and Jackson & Wallace LLP. Ms. Darby worked as a law clerk in the Business Group of Luce, Forward, Hamilton & Scripps LLP. Ms. Darby received a Bachelor of Arts degree in Communications from the University of Colorado, Boulder in 1991 and a Juris Doctor degree from California Western School of Law in 1997.

Geoffrey S. Flagg, Chief Accounting Officer - Mr. Flagg, age 35, was appointed our Chief Accounting Officer in January 2006. Mr. Flagg served as our Chief Financial Officer from January 2004 to January 2006. Mr. Flagg is a Certified Public Accountant and has been involved in auditing and accounting of publicly traded companies since 1996. From September 1996 through June 2000, he was an Audit Associate at the national accounting firm of BDO Seidman, L.L.P. While there, he was responsible for planning, performing and managing financial statement audits for a variety of public and private companies, including our annual audit and quarterly reviews. From June 2000 through January 2001, he was the controller of Wholetree.com, a software

5

Table of Contents

development company. From January 2001 through December 2003, Mr. Flagg served as our corporate controller. He received a Bachelor of Science degree in Accounting from the University of Colorado at Denver in 1996.

Jim D. Fletcher, President and General Manager, Petroleum Mud Logging, Inc. - Mr. Fletcher, age 60, has served as President of Petroleum Mud Logging, Inc. since August 1999. Mr. Fletcher has been employed in the mud logging services industry since 1973. From 1995 to August 1999, Mr. Fletcher was employed by Penson Well Logging as its general manager and marketing officer. From 1988 through 1994, Mr. Fletcher worked for Petroleum Mud Logging, Inc. of Oklahoma City, as a mud logging technician. This corporation sold its assets to Rentech, Inc. in 1999, which is continuing the business. After the purchase by Rentech, Petroleum Mud Logging then named Mr. Fletcher as its General Manager, and he continues in that position. From 1981 to 1988, Mr. Fletcher was employed by OFT Exploration in Oklahoma City as a well site geologist, and also worked as a consulting geologist. His first work experience was with Dresser Industries in 1973 to 1974 as a mud logger. Mr. Fletcher obtained a Bachelor of Science degree in Business Administration and a minor in Geology and Economics from Southwestern State College of Oklahoma in 1974.

Douglas M. Miller, Chief Operating Officer and Executive Vice President – Mr. Miller, age 46, has served as Chief Operating Officer and Executive Vice President of the Company since January 20, 2006. Mr. Miller was employed by Unocal Corporation since 1991 through its acquisition by Chevron Corporation in October 2005, and for more than five years prior to the acquisition, a corporate officer, as Vice President, Corporate Development.

Peter S. Pedersen, Vice President of Technology - Mr. Pedersen, age 51, was appointed Vice President of Technology in September 2005 and has been employed by Rentech since May 2000 in an engineering capacity. He has been the company’s lead engineer in the design for several of Rentech’s gas-to-liquids feasibility studies and, including Rentech’s feasibility study on a 10,000 barrel per day coal-to-liquids facility in the Powder River Basin of Wyoming that was supported by the Wyoming Business Council and the state of Wyoming governor’s office. Mr. Pedersen has more than 25 years of experience in a combination of chemical process engineering and operations, as well as marketing and business management within the syngas, petrochemical, refining and offshore oil and gas related industries. Mr. Pedersen received his Bachelor of Science degree in Chemical Engineering from the Technical University of Denmark, Lyngby, Denmark in 1979. Since that time, he was employed by Haldor Topsoe, Maersk Oil and Gas AS, and Howe-Baker Engineers in various high level engineering and marketing capacities.

Richard O. Sheppard, Vice President, Marketing and President, Rentech Development Corporation - Mr. Sheppard, age 57, joined us in January 1998 as Director of Sales and Marketing of our Rentech Process, and was appointed as President of Rentech Development Corporation in April 2004. Prior to joining Rentech, he was engaged in the project development of independent electrical power plants ranging in size from 25 megawatts to 250 megawatts in the United States, South America, and Central America. He held positions as Vice President Development with Flatiron Constructors from 1996 to 1999, Wellhead Electric Co. from 1992 to 1996, and Ultrasystems Power Corporation and Engineers from 1988 to 1992. Previous employers were Kaiser Power Corporation from 1983 to 1988, and Merck Chemical (Calgon) International from 1974 to 1983. Mr. Sheppard was a Lieutenant in the United States Navy from 1969 to 1974. He obtained a Bachelor of Science degree in Chemical Engineering from the University of Idaho in 1969 and earned a Master of Business Administration degree in Finance and Marketing from St. Mary College, California, in 1980.

Kevin M. Smith, Chief Financial Officer and Executive Vice President - Mr. Smith, age 47, has served as Chief Financial Officer and Executive Vice President of the Company since January 20, 2006. Prior to joining the Company, Mr. Smith was Senior Vice President and Chief Financial Officer of Edison Mission Energy from May 1999 to March 2005. Mr. Smith also served as Treasurer of Edison Mission Energy from September 1992 to February 2000 and from May 2002 until June 2004. Prior to joining Edison Mission Energy in 1986, Mr. Smith served in various positions in the venture group, marketing research and process engineering departments at Fluor Corporation from 1980 to 1986. Mr. Smith earned a Bachelor of Science degree in Chemical Engineering from the University of California, Berkeley in 1980 and a Masters of Business Administration from the University of California, Irvine in 1985.

There are no family relationships among the executive officers, directors and nominees. There are no arrangements or understandings between any officer, director or nominee and any other person pursuant to which that person was selected.

Security Ownership of Certain Beneficial Owners and Management

The following table sets forth certain information as of January 25, 2006 by (i) all persons who own of record or are known to Rentech to beneficially own more than 5% of the issued and outstanding shares of Rentech’s common stock and (ii) by each director, each director nominee, each of the executive officers named in the tables under “Executive Compensation,” and by all executive officers and directors as a group:

Directors and Executive Officers (1)(2) | Amount and Nature of Beneficial Ownership(3) | Percent of Class | ||

Charles B. Benham | 912,407 | * | ||

Mark S. Bohn (4)(5) | 233,126 | * | ||

Thomas L. Bury | 81,000 | * | ||

Ronald C. Butz (6)(7)(8) | 1,027,199 | * |

6

Table of Contents

Claude C. Corkadel, III | 211,316 | * | |||

Amanda M. Darby | 65,000 | * | |||

Geoffrey S. Flagg | 156,236 | * | |||

Jim D. Fletcher | 25,000 | * | |||

Douglas M. Miller | 0 | * | |||

Peter S. Pedersen | 105,800 | * | |||

D. Hunt Ramsbottom (9) | 1,575,000 | 1.3 | % | ||

Michael F. Ray | 231,985 | * | |||

Richard O. Sheppard (10) | 259,500 | * | |||

Kevin M. Smith | 0 | * | |||

Erich W. Tiepel | 670,725 | * | |||

Halbert S. Washburn (11) | 0 | * | |||

Dennis L. Yakobson (12)(13) | 97,975 | * | |||

All Directors and Executive Officers as a Group (17 persons) | 6,534,048 | 5.5 | % | ||

Beneficial Owners of More than 5% | Amount and Nature of Beneficial Ownership | Percent of Class | |||

C. David Callaham (14) | 9,370,169 | 8.1 | % | ||

Wellington Management Company, LLP (15)(16) | 7,272,600 | 6.1 | % | ||

| * | Less than 1%. |

| (1) | Except as otherwise noted and subject to applicable community property laws, each shareholder has sole voting and investment power with respect to the shares beneficially owned. The business address of each director and executive officer is c/o Rentech, Inc., 1331 17th Street, Suite 720, Denver, CO 80202. |

| (2) | Shares of common stock subject to options that are exercisable within 60 days of January 25, 2006 are deemed outstanding for purposes of computing the percentage ownership of such person, but are not deemed outstanding for purposes of computing the percentage ownership of any other person. The following shares of common stock subject to stock options or convertible promissory notes issued to evidence deferred salary are included in the table: |

| • | Charles B. Benham – 170,000 under options and 91,087 under note; |

| • | Thomas L. Bury – 80,000 under options; |

| • | Ronald C. Butz – 75,000 under options and 102,168 under note; |

| • | Claude C. Corkadel, III – 85,000 under options; |

| • | Amanda M. Darby – 65,000 under options; |

| • | Geoffrey S. Flagg – 135,000 under options; |

| • | Jim D. Fletcher – 25,000 under options; |

| • | Peter S. Pedersen – 104,000 under options; |

| • | D. Hunt Ramsbottom – includes 1,575,000 under warrant; |

| • | Michael F. Ray – 60,000 under options and 82,248 under warrant; |

| • | Richard O. Sheppard – 160,000 under options and 25,000 under warrant; |

| • | Erich W. Tiepel – 160,000 under options; |

| • | Halbert S. Washburn – 20,000 under options; and |

| • | Dennis L. Yakobson – 115,000 under options and 151,687 under note. |

| (3) | Information with respect to beneficial ownership is based upon information furnished by each shareholder or contained in filings with the Securities and Exchange Commission. |

| (4) | Includes 31,187 shares owned by a trust of which Mr. Bohn is one of the trustees with shared investment power. |

| (5) | Mr. Bohn retired from the company effective September 30, 2005. |

| (6) | Excludes 75,000 shares owned by his spouse, as to which Mr. Butz disclaims beneficial ownership. |

7

Table of Contents

| (7) | Mr. Butz owns 320,000 shares under options which will not be exercisable until the company’s 2006 Incentive Award Plan is approved by the shareholders at the annual meeting of shareholders. Accordingly, these shares are not reflected in the table above. |

| (8) | Mr. Butz retired from the company effective December 31, 2005. Mr. Butz remains a member of the Board of Directors through his term which will expire at the annual meeting of shareholders in 2007. |

| (9) | Mr. Ramsbottom is a partner and has sole investment and voting power in East Cliff Advisors, LLC. East Cliff Advisors, LLC holds a warrant for 3.5 million shares of which 1,575,000 shares have vested. The remaining 1,925,000 will vest as follows: 875,000 shares when the company’s stock price reaches $4.25; and 1,050,000 shares when the company’s stock price reaches $5.25. The company’s stock price must be reached and close at or above such price for twelve consecutive trading days. |

| (10) | Includes 75,000 shares owned by a trust of which Mr. Sheppard is a trustee with shared investment power. |

| (11) | Mr. Washburn owns 20,000 shares under options which will not be exercisable until the company’s 2006 Incentive Award Plan is approved by the shareholders at the annual meeting of shareholders. Accordingly, these shares are not reflected in the table above. |

| (12) | Mr. Yakobson owns 455,000 shares under options which will not be exercisable until the company’s 2006 Incentive Award Plan is approved by the shareholders at the annual meeting of shareholders. Accordingly, these shares are not reflected in the table above. |

| (13) | Mr. Yakobson retired from his position as Chief Executive Officer effective December 15, 2005. Mr. Yakobson remained as an employee in a non-executive officer capacity through December 31, 2005. Mr. Yakobson will remain as Chairman of the Board of Directors of the Company through his term which will expire at the annual meeting of shareholders in 2008. |

| (14) | Mr. Callaham’s address is 10804 N.E. Highway 99, Vancouver, Washington 98686. This information is based on records available to us, including shares underlying Rentech’s convertible promissory notes and stock purchase warrants that are subject to exercise by him. |

| (15) | Shares reported by Wellington Management Company, LLP (“Wellington”) with respect to which Wellington reported to have shared voting power. Excludes 13,776,400 shares with respect to which Wellington reported to have shared dispositive power. |

| (16) | Wellington Management Company, LLP’s address is 75 State Street, Boston, Massachusetts 02109. |

Section 16(A) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934, as amended, requires Rentech’s executive officers and directors, and persons who own more than ten percent of a registered class of the Rentech’s equity securities (collectively, “Insiders”), to file initial reports of ownership and reports of changes in ownership with the Securities and Exchange Commission (the “SEC”). Insiders are required by SEC regulations to furnish Rentech with copies of all Section 16(a) forms they file. To Rentech’s knowledge, based solely on its review of the copies of such reports furnished to Rentech or written representations from certain Insiders that they were not required to file a Form 5 to report previously unreported ownership or changes in ownership, we believe that, during our fiscal year ending September 30, 2005, the Insiders complied with all such filing requirements, except as follows: Dennis L. Yakobson and Ronald C. Butz were late in reporting exercises of stock options in September 2005.

Meetings and Committees of the Board of Directors

The Board of Directors held eighteen meetings during the fiscal year ended September 30, 2005. Actions were also taken during the year by the unanimous written resolutions of the directors. Each of our directors attended at least 75% of the meetings of the Board of Directors held during the period for which he has been a director or of the meetings of committees of the Board of Directors on which he served during the period that he served. Each director attended the annual meeting of shareholders held in 2005 and is reimbursed for his expenses incurred in

8

Table of Contents

attending meetings. Directors who are employees of Rentech are not paid fees for their services. Nonemployee directors were granted shares of Rentech’s common stock as payment during the last fiscal year, at the rate of 40,000 shares each for a year of service as a director.

The Board of Directors has three standing committees, an Audit Committee, a Compensation Committee and a Nominating Committee. The Board of Directors has determined that the members of our Board of Directors other than Messrs. Ramsbottom, Yakobson and Butz are “independent” within the meaning of the listing standards of the American Stock Exchange. The Board of Directors has also determined that each member of the Audit Committee is “independent” within the meaning of the rules of the Securities and Exchange Commission. Each of our Audit Committee, Compensation Committee and Nominating Committee are comprised of independent directors.

The charters of our Audit Committee and Nominating Committee are available on the Corporate Governance section of our website at http://www.rentechinc.com. The Board of Directors regularly reviews developments in corporate governance and modifies these policies and charters as warranted. Modifications are reflected on our website at the address previously given.

The Audit Committee of the Board of Directors has been delegated responsibility for reviewing with the independent auditors the plans and results of the audit engagement; reviewing the adequacy, scope and results of the internal accounting controls and procedures; reviewing the degree of independence of the auditors; reviewing the auditors’ fees; and recommending the engagement of the auditors to the full Board of Directors. During fiscal 2005, the Audit Committee consisted of Douglas L. Sheeran (through May 11, 2005), Dr. Erich W. Tiepel, David P. Zimel and Thomas L. Bury. Mr. Zimel resigned from the Board and the Audit Committee effective January 24, 2006. The Board elected Mr. Washburn to the Board in December 2005 and the Audit Committee in January 2006 and, in connection with Dr. Tiepel’s departure from the Board of Directors after the annual meeting of shareholders, the Board intends to appoint an additional independent director to the Audit Committee. During fiscal 2005, the Audit Committee met seven times.

The Audit Committee currently consists of Mr. Bury, Mr. Washburn and Dr. Tiepel. The Board of Directors has determined that a member of the Audit Committee of the Board of Directors, Thomas L. Bury, qualifies as an “audit committee financial expert” as defined in Item 401(h) of Regulation S-K, and that he is “independent” as that term is used in Item 7(d)(3)(iv) of Schedule 14A under the Securities Exchange Act of 1934, as amended.

The Compensation Committee is currently comprised of Mr. Michael F. Ray, Mr. Halbert S. Washburn and Dr. Erich W. Tiepel. Neither of them is or has been an employee of Rentech. The Compensation Committee reviews and approves executive officer compensation and stock option grants, administers Rentech’s stock option plans and establishes compensation philosophy for executive officers. During fiscal 2005, the Compensation Committee consisted of Douglas L. Sheeran (through May 11, 2005), Michael F. Ray and Dr. Erich W. Tiepel. The Board elected Mr. Washburn to the Board in December 2005 and the Compensation Committee in January 2006. The committee met three times during the last fiscal year.

The Nominating Committee currently consists of Mr. Bury, Mr. Ray, and Dr. Tiepel. The primary duty of the Committee is to make recommendations to the Board of Directors regarding recruitment of new directors and re-election of incumbent directors. During fiscal 2005, the Nominating Committee consisted of Douglas L. Sheeran (through May 11, 2005), Thomas Bury, Michael F. Ray, David P. Zimel and Dr. Erich W. Tiepel. Mr. Zimel resigned from the Board and the Nominating Committee effective January 24, 2006. The Board elected Mr. Washburn to the Board in December 2005 and the Compensation Committee in January 2006 and, in connection with Dr. Tiepel’s departure from the Board of Directors after the annual meeting of shareholders, the Board intends to appoint an additional independent director to the Nominating Committee. The committee met two times during fiscal 2005.

9

Table of Contents

Compensation

The following tables and accompanying notes show the compensation paid by us or any of our subsidiaries during the fiscal years indicated, to our chief executive officer and our four most highly compensated executive officers other than the chief executive officer.

Summary Compensation Table

Annual Compensation | Long-Term Compensation Awards | Payouts | ||||||||||||||||

Name and Principal Position | Year | Salary | Bonus | (7) Other Annual | Restricted Stock Award(s) | Securities Underlying Options/ SARs | LTIP Payouts | (8) All Other | ||||||||||

| ($) | ($) | ($) | ($) | ($) | ($) | ($) | ||||||||||||

Dennis L. Yakobson | 2005 | $ | 263,798 | — | $ | 23,012 | — | 645,000 | — | 901,086 | ||||||||

Chief Executive | 2004 | $ | 256,497 | — | $ | 24,650 | — | 25,000 | — | — | ||||||||

Officer (1) | 2003 | $ | 247,322 | — | $ | 29,935 | — | — | — | — | ||||||||

Ronald C. Butz | 2005 | $ | 233,821 | — | $ | 22,963 | — | 470,000 | — | 660,736 | ||||||||

Chief Operating | 2004 | $ | 227,350 | — | $ | 14,677 | — | 25,000 | — | — | ||||||||

Officer (2) | 2003 | $ | 219,218 | — | $ | 20,263 | — | — | — | — | ||||||||

Charles B. Benham | 2005 | $ | 167,041 | — | $ | 16,383 | — | 40,000 | — | — | ||||||||

Vice President - | 2004 | $ | 162,418 | — | $ | 15,854 | — | 20,000 | — | — | ||||||||

Research & Development (3) | 2003 | $ | 156,609 | — | $ | 17,060 | — | — | — | — | ||||||||

Mark S. Bohn | 2005 | $ | 167,041 | — | $ | 16,905 | — | 40,000 | — | — | ||||||||

Vice President - | 2004 | $ | 162,418 | — | $ | 15,458 | — | 20,000 | — | — | ||||||||

Engineering (4)(5) | 2003 | $ | 156,609 | — | $ | 15,733 | — | — | — | — | ||||||||

Richard O. Sheppard | 2005 | $ | 156,825 | — | $ | 16,025 | — | 35,000 | — | — | ||||||||

Vice President - | 2004 | $ | 129,150 | — | $ | 14,961 | — | 65,000 | — | — | ||||||||

Marketing (6) | 2003 | $ | 111,000 | — | $ | 15,043 | — | — | — | — | ||||||||

| (1) | Of the salary amounts, $9,380, $5,903 and $29,061, were non-funded deferred compensation as of September 30, 2005, 2004, and 2003, respectively, with a balance of non-funded deferred compensation as of September 30, 2005, 2004 and 2003 of $196,358, $244,455 and $238,551, respectively. Of the salary amounts, $0, $65,468 and $28,504 were non-funded notes payable to a related party with a balance of $80,518, $74,819 and $32,082 as of September 30, 2005, 2004 and 2003, respectively, including accrued interest. Mr. Yakobson’s salary amount for fiscal 2005 reflects compensation earned and does not reflect payment pursuant to the retirement package dated September 30, 2005 which will be paid out during the fiscal years ended September 30, 2006 and 2007. Of the other annual compensation amounts, $9,000 were for an auto allowance for all three years, $6,699, $8,450 and $6,928 were for reimbursed medical expenses and $7,313, $7,200 and $14,007 were for employer 401(k) match for the years ended September 30, 2005, 2004 and 2003, respectively. |

| (2) | Of the salary amounts, $8,314, $781 and $22,769, were non-funded deferred compensation as of September 30, 2005, 2004, and 2003, respectively, with a balance of non-funded deferred compensation as of September 30, 2005, 2004 and 2003 of $130,149, $180,196 and $179,415, respectively. Of the salary amounts, $0, $37,376 and $4,443 were non-funded notes payable to a related party with a balance of $46,745, $43,492 and $7,233 as of September 30, 2005, 2004 and 2003, respectively, including accrued interest. Mr. Butz’ salary amount for fiscal 2005 reflects compensation earned and does not reflect payment pursuant to the retirement package dated September 30, 2005 which will be paid out during the fiscal years ended September 30, 2006 and 2007. Of the other annual compensation amounts, $9,000 were for an auto allowance for all three years, $6,113, $3,372 and $3,189 were for reimbursed medical expenses and $7,850, $2,305 and $8,074 were for employer 401(k) match for the years ended September 30, 2005, 2004 and 2003, respectively. |

10

Table of Contents

| (3) | Of the salary amounts, $0, $0 and $0 were non-funded deferred compensation as of September 30, 2005, 2004 and 2003, respectively, with a balance of non-funded deferred compensation as of September 30, 2005, 2004 and 2003 of $0, $0 and $9,996, respectively. Of the salary amounts, $0, $26,833 and $0 were non-funded notes payable to a related party with a balance of $33,753, $31,418 and $1,104 as of September 30, 2005, 2004 and 2003, respectively, including accrued interest. Of the other annual compensation amounts, $9,000 were for an auto allowance for all three years, $0, $1,025 and $1,126 were for reimbursed medical expenses and $7,383, $5,829, and $6,934 were for employer 401(k) match for the years ended September 30, 2005, 2004 and 2003, respectively. |

| (4) | Of the salary amounts, $0, $0 and $0 were non-funded deferred compensation as of September 30, 2005, 2004 and 2003, respectively, with a balance of non-funded deferred compensation as of September 30, 2005, 2004 and 2003 of $0, $9,996 and $9,996, respectively. Of the salary amounts, $0, $30,509 and $2,953 were non-funded notes payable to a related party with a balance of $38,093, $35,437 and $4,805 as of September 30, 2005, 2004 and 2003, respectively, including accrued interest. Of the other annual compensation amounts, $9,000 were for an auto allowance for all three years, $0, $0 and $0 were for reimbursed medical expenses and $7,905, $6,458, and $6,733 were for employer 401(k) match for the years ended September 30, 2005, 2004 and 2003, respectively. |

| (5) | Mr. Bohn retired from the company effective September 30, 2005. |

| (6) | Of the other annual compensation amounts, $9,000 were for an auto allowance for all three years, $0, $0 and $1,014 were for reimbursed medical expenses and $7,025, $5,961, and $5,029 were for employer 401(k) match for the years ended September 30, 2005, 2004 and 2003, respectively. |

| (7) | Beginning in fiscal 2005, the company has included employer matching contributions in Other Annual Compensation. In prior years, the employer matching contributions were not included, and therefore total other annual compensation did not exceed 10% of an employee’s salary or $50,000. |

| (8) | Refer to Section Certain Relationships and Related Party Transactions for details of these amounts. |

Option/SAR Grants

The following table sets forth information with respect to the named executives concerning the grant of stock options and/or limited SARs during the last fiscal year. All the options were granted at the fair market value on the date of grant as determined by the Board of Directors.

Option/SAR Grants in Last Fiscal Year

| Individual Grants | Grant Date Value | |||||||||||||

Name | Number of Securities Underlying Options/SARs Granted (#) | % of Total Options/SARs Granted to Employees in Fiscal Year | Exercise or Base Price ($/Sh) | Expiration Date | Grant Date Present Value (1) | |||||||||

Dennis L. Yakobson | 25,000 50,000 570,000 | (2) (2) (3) | 1.1 2.2 25.3 | % % % | $ $ $ | 1.06 1.85 2.53 | 11/11/2009 7/26/2010 9/29/2007 | $ $ $ | 12,160 53,421 557,620 | |||||

Ronald C. Butz | 25,000 50,000 395,000 | (2) (2) (4) | 1.1 2.2 17.6 | % % % | $ $ $ | 1.06 1.85 2.53 | 11/11/2009 7/26/2010 9/29/2007 | $ $ $ | 12,160 53,421 386,421 | |||||

Charles B. Benham | 40,000 | (2) | 1.8 | % | $ | 1.85 | 7/26/2010 | $ | 42,736 | |||||

Mark S. Bohn | 40,000 | (2) | 1.8 | % | $ | 1.85 | 7/26/2010 | $ | 42,736 | |||||

Richard O. Sheppard | 35,000 | (2) | 1.6 | % | $ | 1.85 | 7/26/2010 | $ | 37,394 | |||||

| (1) | Calculated using the Black-Scholes Option-Pricing model with the following weighted average assumptions used for grants in 2005: dividend yield of 0 percent; expected volatility of 48 to 66 percent; risk free interest rates of 3.53 to 4.11 percent; and expected lives of 5 years. |

| (2) | The options were subject to exercise on the date of grant. |

| (3) | Includes 455,000 shares under options which will not be exercisable until the company’s 2006 Incentive Award Plan is approved by the shareholders at the annual meeting of shareholders. |

| (4) | Includes 320,000 shares under options which will not be exercisable until the company’s 2006 Incentive Award Plan is approved by the shareholders at the annual meeting of shareholders. |

The following table sets forth information with respect to the named executives, concerning the exercise of options and limited SARs during the last fiscal year and unexercised options and limited SARs held as of the end of the last fiscal year.

11

Table of Contents

Aggregated Option/SAR Exercises in Last Fiscal Year and FY-End Option/SAR Values:

Name | Shares Acquired on Exercise (#) | Value Realized ($) | Number of Securities Underlying Unexercised Options/SARs at FY-End(#) Exercisable/ Unexercisable | Value of Unexercised In-the-Money Options/SARs at FY-End Exercisable/ Unexercisable ($) | ||||||||

Dennis L. Yakobson | 35,000 | $ | 58,713 | 335,000(1) /455,000 | (2) | $ | 347,400(1)(3) / $0 | (2)(3) | ||||

Ronald C. Butz | 35,000 | $ | 58,713 | 295,000(1) /320,000 | (2) | $ | 347,400(1)(3) / $0 | (2)(3) | ||||

Charles B. Benham | 0 | $ | 0 | 200,000 | (1) | $ | 322,225 | (1)(3) | ||||

Mark S. Bohn | 0 | $ | 0 | 150,000 | (1) | $ | 216,225 | (1)(3) | ||||

Richard O. Sheppard | 0 | $ | 0 | 160,000 | (1) | $ | 248,550 | (1)(3) | ||||

| (1) | Exercisable. |

| (2) | Unexercisable. |

| (3) | Computed based upon the difference between the stock option prices and $2.53, the closing price of the company’s common stock on September 30, 2005. |

The following table provides information as of September 30, 2005 with respect to our compensation plans, including individual compensation arrangements, under which our equity securities are authorized for issuance.

Plan category | Number of securities upon exercise of | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans | |||||

Equity compensation plans approved by security holders | 3,247,000 | (1) | $ | 1.54 | 0 | |||

Equity compensation plans not approved by security holders | 13,525,952 | $ | 1.39 | 0 | ||||

Total | 16,772,952 | $ | 1.42 | 0 | ||||

| (1) | Includes 455,000 shares under options held by Dennis L. Yakobson and 320,000 shares under options held by Ronald C. Butz under our proposed Incentive Award Plan which has been submitted for shareholder approval as Proxy Item 4 to this proxy statement. If the plan is not approved by the shareholders, the options will be void. |

The equity securities issued as compensation without shareholder approval consist of stock options and stock purchase warrants. These securities have exercise prices equal to the closing market prices of our common stock, as reported by the American Stock Exchange, on the date the securities were granted. The options and warrants may be exercised for a term of five years after the date they were granted. For a narrative description of the material terms of the equity compensation plans and other compensation arrangements summarized in the above table, please see the section entitled “Stock Options and Stock Warrants” in note 11 to our consolidated financial statements included in our annual report on 10-K for the fiscal year ended September 30, 2005, included as Annex A to this proxy statement.

Executive officers generally are elected at the annual director meeting immediately following the annual shareholder meeting. Any officer or agent elected or appointed by the Board of Directors may be removed by the Board whenever in its judgment our best interests will be served thereby, without prejudice to contractual rights, if any, of the person so removed.

12

Table of Contents

We have entered into employment agreements with Dr. Benham and Messrs. Rambsbottom, Miller and Smith, which are described below.

On January 20, 2006, we entered into an employment agreement with D. Hunt Ramsbottom to serve as the Chief Executive Officer and President of our Company. The term of the employment agreement is for three years from December 15, 2005, subject to automatic renewal unless we or Mr. Ramsbottom give prior notice. The agreement provides for base compensation of $370,000 per year, subject to annual cost of living adjustments, provides Mr. Ramsbottom with the opportunity to earn an annual cash bonus, and provides for his participation in our standard benefit programs and the reimbursement of specified expenses. Also in connection with the agreement, we agreed to grant Mr. Ramsbottom 450,000 restricted stock units that are to be settled in shares of common stock of the Company. These restricted stock units will vest over a three-year period such that one-third will vest on each of Mr. Ramsbottom’s one year, two year and three year anniversary dates of his vesting commencement date of December 15, 2005, subject to partial or complete acceleration under certain circumstances, including termination without cause, termination for good reason or upon a change in control (in each case as defined in the agreement). If Mr. Ramsbottom is terminated without cause, terminated for good reason or we fail to offer to renew this agreement on competitive terms, we will be obligated to pay Mr. Ramsbottom severance including base salary continuation for 24-months, a target bonus for the year of termination equal to his then-applicable base salary, continuation of his health care benefits, and acceleration of the vesting of a portion of the restricted stock unit grant. If a termination entitling Mr. Ramsbottom to severance occurs during the period of three months prior and two years after a change in control, the severance payment will be made in a lump sum, the bonus component will be increased to the extent the most recent prior actual annual bonus earned by Mr. Ramsbottom exceeded his then applicable annual base salary, and the full restricted stock unit grant will vest. In addition, in the event any federal excise tax is payable with respect to any payment due to Mr. Ramsbottom upon a change in control, we have agreed to pay such excise tax, including a grossup payment. Subject to the severance obligations contained in the agreement, we may terminate Mr. Ramsbottom’s employment at any time. Mr Ramsbottom also executed a corporate confidentiality and proprietary rights agreement.

On January 20, 2006, we entered into an employment agreement with Douglas M. Miller to serve as the Chief Operating Officer and an Executive Vice President of our Company. The term of the employment agreement is for three years from January 20, 2006, subject to automatic renewal unless we or Mr. Miller give prior notice. The agreement provides for base compensation of $300,000 per year, subject to annual cost of living adjustments, provides Mr. Miller with the opportunity to earn an annual cash bonus, and provides for his participation in our standard benefit programs and the reimbursement of specified expenses. Also in connection with the agreement, we agreed to grant Mr. Miller 375,000 restricted stock units that are to be settled in shares of common stock of the Company. These restricted stock units will vest over a three-year period such that one-third will vest on each of Mr. Miller’s one year, two year and three year anniversary dates of his vesting commencement date of January 20, 2006, subject to partial or complete acceleration under certain circumstances, including termination without cause, termination for good reason or upon a change in control (in each case as defined in the agreement). If Mr. Miller is terminated without cause, terminated for good reason or we fail to offer to renew this agreement on competitive terms, we will be obligated to pay Mr. Miller severance including base salary continuation for 12-months, a target bonus for the year of termination equal to his then-applicable base salary, continuation of his health care benefits, and acceleration of the vesting of a portion of the restricted stock unit grant. If a termination entitling Mr. Miller to severance occurs during the period of three months prior and two years after a change in control, the severance payment will be made in a lump sum, the bonus component will be increased to the extent the most recent prior actual annual bonus earned by Mr. Miller exceeded his then applicable annual base salary, and the full restricted stock unit grant will vest. In addition, in the event any federal excise tax is payable with respect to any payment due to Mr. Miller upon a change in control, we have agreed to pay such excise tax, including a gross-up payment. Subject to the severance obligations contained in the agreement, we may terminate Mr. Miller’s employment at any time. Mr. Miller also executed a corporate confidentiality and proprietary rights agreement.