EXHIBIT 13

COLOR YOUR WORLD TANDY BRANDS ACCESSORIES, INC. ANNUAL REPORT 2004

COLOR Inspiring Tandy Brands’ bold, expressive, trend-right fashions. This year it’s all about color. Throughout the pages of this report, we explore the many ways that colors communicate — each has its own distinct personality. Our company’s fashion-forward brands also have distinct personalities. And all are responding to the trend toward bright, bold colors. As a fashion industry leader, Tandy Brands Accessories, Inc. is using fiery oranges, brilliant yellows and eye-popping reds to create a bright 2005 for our shareholders.

financial highlights Tandy Brands Acessories, Inc. and Subsidiaries (dollars in thousands, except per share amounts)20042003 2002 Total Revenues ........................................................$215,420$224,487 $205,769 Gross Profit ................................................................75,28578,088 72,063 Operating Income ......................................................13,71115,371 13,385 Net Income (1) ..............................................................7,0377,136 6,293 Diluted Earnings Per Share ........................................1.101.18 1.08 Working Capital ..........................................................81,63589,282 78,217 Total Assets .................................................................135,574147,986 132,778 Stockholders’ Equity ....................................................99,89990,054 80,664 Book Value Per Share (2) .............................................15.8414.96 13.67 (1) Includes cumulative effect of accounting change for SFAS No. 142 of ($581), or ($.10) per diluted share, in 2003. See Note 8 for effect on net income for 2002 due to change to non-amortization of goodwill. (2) Book value per share is total stockholders’ equity divided by the number of shares of stock issued and outstanding at that date.

Fiscal 2004 Consolidated Product Line Sales Mens Product Line Womens Product Line

letter to shareholders

Dear Shareholders:

We are pleased to share with you the highlights and challenges of this past year, as well as some exciting opportunities for the company in 2005. Throughout the pages of this report, we’ll also take a look at the way different colors can affect our moods, our thinking and our interaction with the things around us. Colors, specifically strong, bold, fashion colors, should certainly inspire and benefit our business this coming year.

Profitable and Financially Strong

Tandy Brands continues to be very profitable and financially stable. Our debt is at its lowest point since 1994 — only $10 million. During the past year, we reduced debt by $20 million as we generated $23 million in cash flow from the operations of the company.

Fashion trends and their impact on the marketplace drive the business of Tandy Brands Accessories. As we saw in fiscal 2003, when fashion accessory trends are strong, our sales accelerate. In fiscal 2004, the fashion trends for women’s accessories weakened, which led to a decrease in sales compared to 2003. This decrease was offset in part by

strong sales in our men’s accessories for the year. Based on the strong fashion color trends for accessories this season, we anticipate that women’s fashion accessories will return to normalized sales levels during 2005.

Cash Dividend Initiated

The board of directors and company management continue to seek ways to increase shareholder value. Because of the company’s strong cash flow, the board initiated payment of the company’s first quarterly cash dividends. As a result, shareholders received $0.10 per share over the past year. We are pleased to announce that the board has increased the September quarterly dividend to $0.0275 per share, a 10 percent increase over the same quarter last year.

Competitive Advantage Through Technology

During fiscal 2004, we invested over $3 million in systems and equipment to enhance our operating and manufacturing efficiencies. Our superior service capabilities allow us to continue to gain various competitive advantages. We have been recognized by Wal-Mart for being among the first group of suppliers to begin using the new Radio Frequency Identification (RFID) technology. Additionally, our superior distribution capabilities earned Target’s Operational Vendor of the Year Award.

target award

2

New Products

Each year we look for new opportunities to increase market share. We are very enthusiastic about two new product categories to be introduced this next year.

As men’s dress fashion-accessory trends strengthened, we saw new opportunity in the men’s jewelry business. Focusing primarily on cufflinks and tie accessories in exciting colors and styles, we recently obtained significant placement for our new products in a wide variety of department stores for 2005.

We have also introduced men’s neckwear to our product offerings. We have a talented sales and product team to create and promote a great line of neckwear, but a new aspect of this business will be in its delivery. We will be producing and shipping this product directly to our customers from offshore factories so that our pricing is very competitive as compared to established neckwear suppliers.

Gift Business Acquisition

On the first day of fiscal 2005, we acquired Superior Merchandise Company and opened up an entirely new product category — gift accessories. Selling under the totes®, ETON® and a variety of private-label brands, we expect to generate sales of over $12 million this year.

This acquisition strengthens our position in the department store channel and provides excellent growth opportunities for the future.

Looking Ahead to a Colorful 2005

We are excited about the upcoming year. The new, bright, color trends in men’s and women’s fashion accessories, which you can see throughout this annual report, are generating strong customer interest in our product lines. We are enthusiastic about the growth opportunities for Tandy Brands Accessories in 2005, and we are confident that our recent new product introductions and gift business acquisition will provide increased sales and increased earnings for the company. Finally, because of our financial strength and strong cash flow, the company is well-positioned to take advantage of future growth opportunities to increase shareholder value.

Thank you for continuing to support Tandy Brands. We hope you enjoy this colorful look at fiscal 2004.

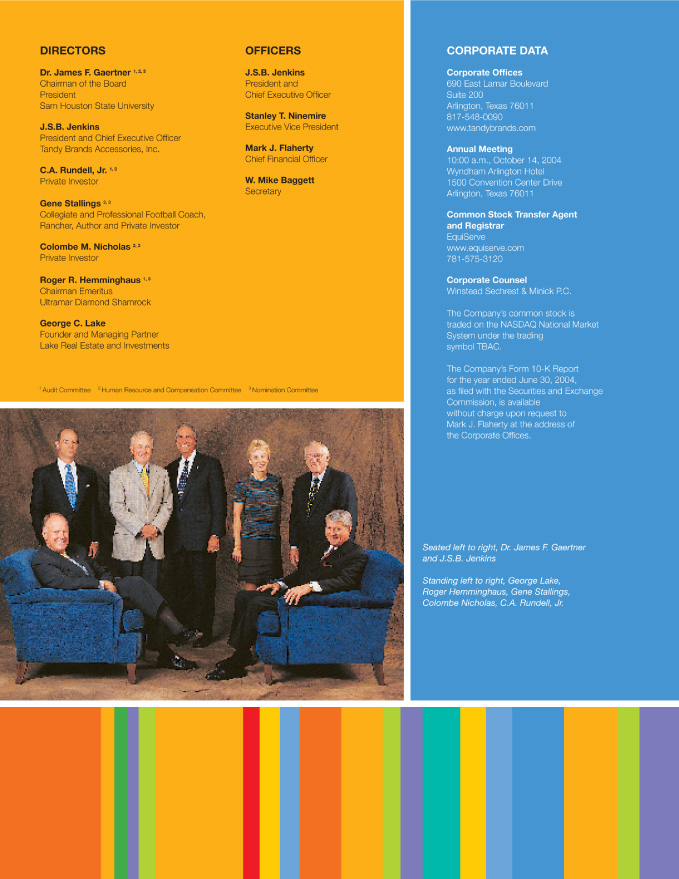

James F. Gaertner

Chairman of the Board

J.S.B. Jenkins

President and Chief Executive Officer

3

rolfs

Orange the color of friendship In nature, orange works closely with other colors to create f ire, autumn leaves and sunsets. It’s a team player and yet it commands its own attention. Orange makes people smile. It is deliciously appetizing. In fashion, orange turns accent pieces into exclamation points.

LEVI’S

PINK Pink is a close cousin to red. It shares the excitement, but adds a touch of sweetness. It’s a color of many moods. In vivid tones, pink can be shocking. It can be fresh, or it can remind us of the pastel ‘50s. Pink is as fashionable and versatile as the Tandy Brands products it colors. the color of caring & sharing

DOCKERS WOMEN

green Green is the official color of nature — from the stunning array of greens in a forest to the cool blue-green of a peaceful lake. Foods that are good for you, like spinach and broccoli, are green. In the wrong hands, green can become an avocado refrigerator. In the right hands, it can be a refreshing development in fashion. the color of life

JONES NEW YORK

brown It’s no accident that many wallets are brown. But the richness of brown is deeper and more meaningful. Brown is down-to -earth, lasting. It’s the color of the family dining table and your favorite old reading chair. As a color, brown is an anchor that allows other colors to go wild. the color of richness

ACCESSORY DESIGN GROUP

red What can we say about red that red doesn’t say for itself. It’s the color of stop signs and Valentine roses. It’s brash, warm, it arouses the senses. You can almost taste red. In fashion, red can be loud or it can be classic. It can be an underline or it can be the message. the color of passion

Consolidated Statements of Income Tandy Brands Accessories, Inc. and Subsidiaries(Dollars in thousands, except per share amounts)

| | | | | | | | | | | | | |

| | | Year Ended June 30,

|

| | | 2004

| | 2003

| | 2002

|

| Net sales | | $ | 215,420 | | | $ | 224,487 | | | $ | 205,769 | |

| Cost of goods sold | | | 140,135 | | | | 146,399 | | | | 133,706 | |

| | | |

| | | |

| | | |

| |

| Gross margin | | | 75,285 | | | | 78,088 | | | | 72,063 | |

| Selling, general and administrative expenses | | | 57,519 | | | | 58,450 | | | | 53,297 | |

| Depreciation and amortization | | | 4,055 | | | | 4,267 | | | | 5,381 | |

| | | |

| | | |

| | | |

| |

| Total operating expenses | | | 61,574 | | | | 62,717 | | | | 58,678 | |

| | | |

| | | |

| | | |

| |

| Operating income | | | 13,711 | | | | 15,371 | | | | 13,385 | |

| Interest expense | | | (2,357 | ) | | | (2,833 | ) | | | (3,152 | ) |

| Royalty and other income | | | 128 | | | | 101 | | | | 70 | |

| | | |

| | | |

| | | |

| |

| Income before provision for income taxes and cumulative effect of accounting change | | | 11,482 | | | | 12,639 | | | | 10,303 | |

| Provision for income taxes | | | 4,445 | | | | 4,922 | | | | 4,010 | |

| | | |

| | | |

| | | |

| |

| Net income before cumulative effect of accounting change | | | 7,037 | | | | 7,717 | | | | 6,293 | |

| Cumulative effect of accounting change for SFAS No. 142, net of income taxes of $369,000 | | | — | | | | (581 | ) | | | — | |

| | | |

| | | |

| | | |

| |

| Net income | | $ | 7,037 | | | $ | 7,136 | | | $ | 6,293 | |

| | | |

| | | |

| | | |

| |

| Earnings per common share: | | | | | | | | | | | | |

| Before cumulative effect of accounting change | | $ | 1.13 | | | $ | 1.30 | | | $ | 1.09 | |

| Cumulative effect of accounting change | | | — | | | | (.10 | ) | | | — | |

| | | |

| | | |

| | | |

| |

| | | $ | 1.13 | | | $ | 1.20 | | | $ | 1.09 | |

| | | |

| | | |

| | | |

| |

| Earnings per common share — assuming dilution: | | | | | | | | | | | | |

| Before cumulative effect of accounting change | | $ | 1.10 | | | $ | 1.28 | | | $ | 1.08 | |

| Cumulative effect of accounting change | | | — | | | | (.10 | ) | | | — | |

| | | |

| | | |

| | | |

| |

| | | $ | 1.10 | | | $ | 1.18 | | | $ | 1.08 | |

| | | |

| | | |

| | | |

| |

| Dividends declared per share | | $ | 0.10 | | | $ | — | | | $ | — | |

| | | |

| | | |

| | | |

| |

| Common shares outstanding | | | 6,229 | | | | 5,952 | | | | 5,779 | |

| | | |

| | | |

| | | |

| |

| Common shares outstanding — assuming dilution | | | 6,389 | | | | 6,046 | | | | 5,833 | |

| | | |

| | | |

| | | |

| |

| | | |

| 14 | | The accompanying notes are an integral part of these consolidated financial statements. |

Consolidated Balance Sheets Graphic Tandy Brands Accessories, Inc. and Subsidiaries(Dollars in thousands)

| | | | | | | | | |

| | | June 30,

|

| | | 2004

| | 2003

|

Assets | | | | | | | | |

| Current assets: | | | | | | | | |

| Cash and cash equivalents | | $ | 6,086 | | | $ | 3,814 | |

| Accounts receivable, net of allowances of $1,142 and $1,745 | | | 33,427 | | | | 41,672 | |

| Inventories | | | 57,086 | | | | 62,156 | |

| Deferred income taxes | | | 4,009 | | | | 4,757 | |

| Other current assets | | | 1,613 | | | | 1,250 | |

| | | |

| | | |

| |

| Total current assets | | | 102,221 | | | | 113,649 | |

| | | |

| | | |

| |

| Property, plant and equipment, at cost: | | | | | | | | |

| Buildings | | | 8,243 | | | | 7,925 | |

| Leasehold improvements | | | 1,661 | | | | 1,560 | |

| Machinery and equipment | | | 24,677 | | | | 22,400 | |

| | | |

| | | |

| |

| | | | 34,581 | | | | 31,885 | |

| Accumulated depreciation | | | (20,206 | ) | | | (17,261 | ) |

| | | |

| | | |

| |

| Net property, plant and equipment | | | 14,375 | | | | 14,624 | |

| | | |

| | | |

| |

| Other assets: | | | | | | | | |

| Goodwill, net of accumulated amortization of $7,143 | | | 11,655 | | | | 11,641 | |

| Other intangibles, net of accumulated amortization of $4,240 and $3,874 | | | 4,534 | | | | 4,900 | |

| Supplemental Executive Retirement Plan intangible asset | | | 1,255 | | | | 1,456 | |

| Other noncurrent assets | | | 1,534 | | | | 1,716 | |

| | | |

| | | |

| |

| Total other noncurrent assets | | | 18,978 | �� | | | 19,713 | |

| | | |

| | | |

| |

| | | $ | 135,574 | | | $ | 147,986 | |

| | | |

| | | |

| |

Liabilities and Stockholders’ Equity | | | | | | | | |

| Current liabilities: | | | | | | | | |

| Accounts payable | | $ | 14,224 | | | $ | 14,522 | |

| Accrued payroll and bonuses | | | 3,804 | | | | 4,193 | |

| Accrued expenses | | | 2,558 | | | | 5,652 | |

| | | |

| | | |

| |

| Total current liabilities | | | 20,586 | | | | 24,367 | |

| | | |

| | | |

| |

| Other liabilities: | | | | | | | | |

| Notes payable | | | 10,000 | | | | 30,000 | |

| Deferred income taxes | | | 2,066 | | | | 1,776 | |

| Supplemental Executive Retirement Plan liability | | | 1,721 | | | | 1,607 | |

| Other noncurrent liabilities | | | 1,302 | | | | 182 | |

| | | |

| | | |

| |

| Total other liabilities | | | 15,089 | | | | 33,565 | |

| | | |

| | | |

| |

| Commitments and contingencies (Note 7) | | | | | | | | |

| Stockholders’ equity: | | | | | | | | |

| Preferred stock, $1 par value; 1,000,000 shares authorized; none issued | | | — | | | | — | |

| Common stock, $1 par value; 10,000,000 shares authorized; 6,305,886 shares and 6,019,286 shares issued and outstanding as of June 30, 2004 and 2003, respectively | | | 6,306 | | | | 6,019 | |

| Additional paid in capital | | | 26,765 | | | | 23,802 | |

| Retained earnings | | | 67,843 | | | | 61,429 | |

| Cumulative other comprehensive income | | | (121 | ) | | | (1,196 | ) |

| Shares held by Benefit Restoration Plan Trust | | | (894 | ) | | | — | |

| | | |

| | | |

| |

| Total stockholders’ equity | | | 99,899 | | | | 90,054 | |

| | | |

| | | |

| |

| | | $ | 135,574 | | | $ | 147,986 | |

| | | |

| | | |

| |

| | | | | |

The accompanying notes are an integral part of these consolidated financial statements. | | | 15 | |

Consolidated Statements of Cash Flows Tandy Brands Accessories, Inc. and Subsidiaries(Dollars in thousands)

| | | | | | | | | | | | | |

| | | 2004

| | 2003

| | 2002

|

| Cash flows from operating activities: | | | | | | | | | | | | |

| Net income | | $ | 7,037 | | | $ | 7,136 | | | $ | 6,293 | |

| Adjustments to reconcile net income to net cash provided by (used for) operating activities: | | | | | | | | | | | | |

| Depreciation | | | 3,863 | | | | 3,677 | | | | 3,774 | |

| Amortization | | | 366 | | | | 503 | | | | 1,523 | |

| Amortization of debt origination costs | | | 116 | | | | 269 | | | | 219 | |

| Deferred taxes | | | 392 | | | | (95 | ) | | | (388 | ) |

| Income tax benefit of exercise of employee stock options | | | 257 | | | | — | | | | — | |

| Cumulative effect of accounting change, net of tax | | | — | | | | 581 | | | | — | |

| Other | | | 90 | | | | 100 | | | | (674 | ) |

| Change in assets and liabilities, net of effects from acquisitions: | | | | | | | | | | | | |

| Accounts receivable | | | 8,245 | | | | (7,973 | ) | | | 996 | |

| Inventories | | | 5,070 | | | | (9,338 | ) | | | 9,761 | |

| Other assets | | | (655 | ) | | | (122 | ) | | | (548 | ) |

| Accounts payable | | | (298 | ) | | | 1,767 | | | | 3,347 | |

| Accrued expenses | | | (1,470 | ) | | | 1,503 | | | | 1,963 | |

| | | |

| | | |

| | | |

| |

| Net cash provided by (used for) operating activities | | | 23,013 | | | | (1,992 | ) | | | 26,266 | |

| | | |

| | | |

| | | |

| |

| Cash flows from investing activities: | | | | | | | | | | | | |

| Purchases of property and equipment | | | (3,118 | ) | | | (2,444 | ) | | | (2,716 | ) |

| Purchase of assets of AA&E Leathercraft, Inc. | | | — | | | | — | | | | (995 | ) |

| | | |

| | | |

| | | |

| |

| Net cash used for investing activities | | | (3,118 | ) | | | (2,444 | ) | | | (3,711 | ) |

| | | |

| | | |

| | | |

| |

| Cash flows from financing activities: | | | | | | | | | | | | |

| Sale of stock to Stock Purchase Program | | | 1,640 | | | | 1,381 | | | | 1,131 | |

| Exercise of employee stock options | | | 1,203 | | | | 363 | | | | 141 | |

| Dividends | | | (466 | ) | | | — | | | | — | |

| Proceeds from borrowings | | | 36,950 | | | | 66,145 | | | | 65,432 | |

| Payments under borrowings | | | (56,950 | ) | | | (66,145 | ) | | | (82,832 | ) |

| | | |

| | | |

| | | |

| |

| Net cash provided by (used for) financing activities | | | (17,623 | ) | | | 1,744 | | | | (16,128 | ) |

| | | |

| | | |

| | | |

| |

| Net increase (decrease) in cash and cash equivalents | | | 2,272 | | | | (2,692 | ) | | | 6,427 | |

| Cash and cash equivalents at beginning of period | | | 3,814 | | | | 6,506 | | | | 79 | |

| | | |

| | | |

| | | |

| |

| Cash and cash equivalents at end of period | | $ | 6,086 | | | $ | 3,814 | | | $ | 6,506 | |

| | | |

| | | |

| | | |

| |

| Supplemental disclosures of cash flow information: | | | | | | | | | | | | |

| Cash paid during the year for: | | | | | | | | | | | | |

| Interest | | $ | 2,686 | | | $ | 2,560 | | | $ | 2,720 | |

| Income taxes | | | 4,717 | | | | 4,662 | | | | 3,602 | |

| | | |

| 16 | | The accompanying notes are an integral part of these consolidated financial statements. |

Consolidated Statements of Stockholders’ Equity Tandy Brands Accessories, Inc. and Subsidiaries(Dollars in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Common Stock

| | Additional

Paid in | | Retained | | Cumulative

Other

Comprehensive | | Shares Held

by Benefit

Restoration | | Treasury Stock

| | Total

Stockholders' |

| | | Shares

| | Amount

| | Capital

| | Earnings

| | Loss

| | Plan Trust

| | Shares

| | Amount

| | Equity

|

| Balance at June 30, 2001 | | | 5,882,926 | | | $ | 5,883 | | | $ | 22,572 | | | $ | 48,000 | | | $ | (670 | ) | | | — | | | | (212,011 | ) | | $ | (1,650 | ) | | $ | 74,135 | |

| Comprehensive income: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income | | | — | | | | — | | | | — | | | | 6,293 | | | | — | | | | — | | | | — | | | | — | | | | 6,293 | |

| Other comprehensive income, net of tax: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Currency translation adjustments, net of tax of $3 | | | — | | | | — | | | | — | | | | — | | | | 5 | | | | — | | | | — | | | | — | | | | 5 | |

| Fair value of interest rate swap, net of tax of $659 | | | — | | | | — | | | | — | | | | — | | | | (1,041 | ) | | | — | | | | — | | | | — | | | | (1,041 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 5,257 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Sale of stock to the Tandy Brands Accessories, Inc. Stock Purchase Program | | | — | | | | — | | | | (7 | ) | | | — | | | | — | | | | — | | | | 145,751 | | | | 1,138 | | | | 1,131 | |

| Sale of unissued common stock to employees for exercise of stock options | | | 12,958 | | | | 13 | | | | 101 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 114 | |

| Sale of unissued common stock to directors for exercise of stock options | | | 3,289 | | | | 3 | | | | 24 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 27 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| Balance at June 30, 2002 | | | 5,899,173 | | | | 5,899 | | | | 22,690 | | | | 54,293 | | | | (1,706 | ) | | | — | | | | (66,260 | ) | | | (512 | ) | | | 80,664 | |

| Comprehensive income: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income | | | — | | | | — | | | | — | | | | 7,136 | | | | — | | | | — | | | | — | | | | — | | | | 7,136 | |

| Other comprehensive income, net of tax: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Currency translation adjustments, net of tax of $332 | | | — | | | | — | | | | — | | | | — | | | | 488 | | | | — | | | | — | | | | — | | | | 488 | |

| Fair value of interest rate swap, net of tax of $13 | | | — | | | | — | | | | — | | | | — | | | | 22 | | | | — | | | | — | | | | — | | | | 22 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 7,646 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Sale of stock to the Tandy Brands Accessories, Inc. Stock Purchase Program | | | 72,941 | | | | 73 | | | | 796 | | | | — | | | | — | | | | — | | | | 66,260 | | | | 512 | | | | 1,381 | |

| Sale of unissued common stock to employees for exercise of stock options | | | 44,587 | | | | 44 | | | | 298 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 342 | |

| Sale of unissued common stock to directors for exercise of stock options | | | 2,585 | | | | 3 | | | | 18 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 21 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| Balance at June 30, 2003 | | | 6,019,286 | | | | 6,019 | | | | 23,802 | | | | 61,429 | | | | (1,196 | ) | | | — | | | | — | | | | — | | | | 90,054 | |

| Comprehensive income: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income | | | — | | | | — | | | | — | | | | 7,037 | | | | — | | | | — | | | | — | | | | — | | | | 7,037 | |

| Other comprehensive income, net of tax: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Currency translation adjustments, net of tax of $39 | | | — | | | | — | | | | — | | | | — | | | | 57 | | | | — | | | | — | | | | — | | | | 57 | |

| Fair value of interest rate swap, net of tax of $646 | | | — | | | | — | | | | — | | | | — | | | | 1,018 | | | | — | | | | — | | | | — | | | | 1,018 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Comprehensive income | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 8,112 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Dividends | | | — | | | | — | | | | — | | | | (623 | ) | | | — | | | | — | | | | — | | | | — | | | | (623 | ) |

| Shares held by Benefit Restoration Plan Trust | | | — | | | | — | | | | — | | | | — | | | | — | | | | (894 | ) | | | — | | | | — | | | | (894 | ) |

| Sale of stock to the Tandy Brands Accessories, Inc. Stock Purchase Program | | | 117,299 | | | | 118 | | | | 1,522 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 1,640 | |

| Restricted stock issued to officers | | | 22,800 | | | | 23 | | | | 252 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 275 | |

| Restricted stock issued to directors | | | 3,720 | | | | 4 | | | | 54 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 58 | |

| Unearned compensation on restricted stock | | | — | | | | — | | | | (183 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (183 | ) |

| Sale of unissued common stock to employees for exercise of stock options | | | 140,320 | | | | 140 | | | | 1,296 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 1,436 | |

| Sale of unissued common stock to directors for exercise of stock options | | | 2,461 | | | | 2 | | | | 22 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 24 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| Balance at June 30, 2004 | | | 6,305,886 | | | $ | 6,306 | | | $ | 26,765 | | | $ | 67,843 | | | $ | (121 | ) | | $ | (894 | ) | | | — | | | $ | — | | | $ | 99,899 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| | | | | |

The accompanying notes are an integral part of these consolidated financial statements. | | | 17 | |

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 1 — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Company and Basis of Presentation

Tandy Brands Accessories, Inc. (the “Company”) designs, manufactures and markets fine leather goods, handbags and fashion accessories for men, women and children. We sell our products through all major retail distribution channels throughout the United States and Canada, including mass merchants, national chain stores, department stores, men’s and women’s specialty stores, catalog retailers, grocery stores, drug stores, golf pro shops, sporting goods stores and the retail exchange operations of the United States military.

The preparation of our consolidated financial statements in accordance with accounting principles generally accepted in the United States requires the use of estimates that affect the reported value of assets, liabilities, revenues and expenses. These estimates are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis for our conclusions. We continually evaluate the information used to make these estimates as the business and economic environment changes. Actual results may differ from these estimates under different assumptions or conditions.

The consolidated financial statements include the accounts of the Company and its subsidiaries, all of which are wholly owned. All significant intercompany accounts and transactions have been eliminated in consolidation.

Reclassifications

Certain prior year amounts have been reclassified to conform to the fiscal 2004 presentation.

Cash and Cash Equivalents

We consider cash on hand, deposits in banks and short-term investments with original maturities of less than three months as cash and cash equivalents.

Inventories

Inventories are stated at the lower of cost (principally standard cost, which approximates actual cost on a first-in, first-out basis) or market. Cost includes materials, direct and indirect labor and factory overhead. Market, with respect to raw materials, is replacement cost; and for work-in-process and finished goods, it is net realizable value.

Inventories consist of the following:

| | | | | | | | | |

| | | June 30,

|

| | | 2004

| | 2003

|

| Raw materials | | $ | 3,776,000 | | | $ | 4,789,000 | |

| Work-in-process | | | 1,204,000 | | | | 1,032,000 | |

| Finished goods | | | 52,106,000 | | | | 56,335,000 | |

| | | |

| | | |

| |

| | | $ | 57,086,000 | | | $ | 62,156,000 | |

| | | |

| | | |

| |

Property and Equipment

Property and equipment are carried at cost less accumulated depreciation. Depreciation is primarily calculated at the following rates using the straight-line method:

| | | |

| Buildings | | 3% |

| Leasehold improvements | | The lesser of the life of the lease or asset |

| Machinery and equipment | | 10% to 50% |

Maintenance and repairs are charged to expense as incurred. Renewals and betterments which materially prolong the useful lives of the assets are capitalized. The cost and the related accumulated depreciation of property retired or sold are removed from the accounts, and gains or losses from retirements and sales are recognized in the consolidated statements of income.

Impairment of Long-Lived Assets

We review long-lived assets and certain identifiable intangibles for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset is impaired. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to its estimated fair value, based on future net cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value of the assets.

18

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 1 — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Fair Values of Financial Instruments

Our financial instruments consist primarily of cash, trade receivables, trade payables, debt instruments and interest rate swaps. The carrying values of cash, trade receivables and trade payables are considered to be representative of their respective fair values. The potential impact of market conditions on the fair value of our indebtedness is not expected to be material. Given that such lines of credit bear interest at floating market interest rates, the fair value of amounts borrowed approximates carrying value. See Note 5 for information regarding our interest rate swap agreement, which expired on June 27, 2004.

Goodwill and Other Intangibles

Effective July 1, 2002, we adopted Statement of Financial Accounting Standards (“SFAS”) No. 142, “Goodwill and Other Intangible Assets.” This Statement changed the accounting for goodwill and indefinite-lived intangible assets from an amortization approach to an impairment-only approach. During the first quarter of fiscal 2003, we recorded a transitional goodwill impairment charge of $950,000 ($581,000, net of tax), presented as a cumulative effect of an accounting change. The charge related to our women’s accessories segment of products. Prior to the adoption of SFAS No. 142, we amortized goodwill and other intangible assets using the straight-line method over their estimated useful lives, which range from three to forty years. We continue to amortize finite-lived intangibles, primarily trade names, over their useful lives. See Note 8.

Foreign Currency Translation

The functional currency for our Canadian subsidiary is the Canadian dollar. The assets and liabilities of the subsidiary are translated into U.S. dollars at the exchange rates in effect at each balance sheet date, and resulting translation gains or losses are accumulated in other comprehensive income (loss) as a separate component of stockholders’ equity. Revenue and expenses are translated at the monthly average exchange rates occurring during each year. Cumulative other comprehensive loss included currency translation adjustments of ($121,000), ($177,000) and ($665,000), net of tax of ($82,000), ($120,000) and ($453,000) at June 30, 2004, 2003 and 2002, respectively.

Revenues

We recognize revenue when merchandise is shipped and title to the goods has passed to the customer. We record allowances, including cash discounts, in-store customer allowances, cooperative advertising allowances and customer returns, at the time the revenue is recognized based upon historical experience, current trends in the retail industry and individual customer and product experience.

We perform periodic credit evaluations of our customers’ financial condition and reserve against accounts deemed uncollectible based upon historical losses and customer specific events. After all collection efforts are exhausted and the account is deemed uncollectible, it is written off against the reserve for doubtful accounts. Credit losses have historically been within management’s expectations and we generally do not require collateral. During the second quarter of fiscal 2004, we recorded a bad debt recovery of approximately $651,000 arising from a customer’s bankruptcy court settlement and receipt of payment of accounts receivable previously reserved by the Company.

Major Customers

Consolidated net sales to Wal-Mart accounted for approximately 37%, 36% and 39% of our sales in fiscal 2004, 2003 and 2002, respectively. Both men’s and women’s accessories sales include revenues from Wal-Mart. Additionally, consolidated net sales to Target accounted for approximately 14%, 15% and 13% of our sales in fiscal 2004, 2003 and 2002, respectively. Women’s accessories sales include revenues from Target. No other customers accounted for 10% or more of our total revenues.

Advertising Costs

We expense advertising costs as they are incurred. Advertising costs were $1,786,000, $2,079,000 and $2,224,000 in fiscal 2004, 2003 and 2002, respectively, consisting primarily of shows and conventions as well as display and print advertising.

19

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 1 — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Stock-Based Compensation

We may, with the approval of our Board of Directors, grant stock options for a fixed number of shares to employees with an exercise price equal to the fair value of the shares at the date of grant. We account for stock option grants using the intrinsic value method in accordance with APB Opinion No. 25, “Accounting for Stock Issued to Employees,” and, accordingly, we recognize no compensation expense for the stock option grants. The following table reflects the impact on net income if we had applied the fair value recognition provisions of SFAS No. 123, “Accounting for Stock-Based Compensation,” to stock-based employee compensation for fiscal 2004, 2003 and 2002 (dollars in thousands, except per share amounts):

| | | | | | | | | | | | | |

| | | 2004

| | 2003

| | 2002

|

| Net income: | | | | | | | | | | | | |

| As reported | | $ | 7,037 | | | $ | 7,136 | | | $ | 6,293 | |

| Stock-based compensation expense | | | 150 | | | | — | | | | — | |

| | | |

| | | |

| | | |

| |

| Net income | | $ | 7,187 | | | $ | 7,136 | | | $ | 6,293 | |

| Compensation expense per SFAS No. 123 | | | (625 | ) | | | (496 | ) | | | (562 | ) |

| | | |

| | | |

| | | |

| |

| Pro forma | | $ | 6,562 | | | $ | 6,640 | | | $ | 5,731 | |

| | | |

| | | |

| | | |

| |

| Earnings per share: | | | | | | | | | | | | |

| As reported | | $ | 1.13 | | | $ | 1.20 | | | $ | 1.09 | |

| Pro forma | | $ | 1.05 | | | $ | 1.12 | | | $ | 0.99 | |

| Earnings per share — assuming dilution: | | | | | | | | | | | | |

| As reported | | $ | 1.10 | | | $ | 1.18 | | | $ | 1.08 | |

| Pro forma | | $ | 1.03 | | | $ | 1.10 | | | $ | 0.98 | |

Pro forma information regarding net income and earnings per share is required by SFAS No. 123, “Accounting for Stock-Based Compensation,” and has been determined as if we had accounted for our stock options under the fair value method of SFAS No. 123. The fair value for these options was estimated at the date of grant using the Black-Scholes option-pricing model with the following weighted-average assumptions for fiscal 2004, 2003 and 2002: dividend yield of 1.0% for 2004 and 0.0% for 2003 and 2002; expected volatility of 0.238%, 0.270% and 0.334% for fiscal 2004, 2003 and 2002, respectively; a risk-free interest rate of 5.25%, 5.25% and 6.50% for fiscal 2004, 2003 and 2002, respectively; and an expected holding period of seven years. Using these assumptions for the options granted during fiscal 2004, 2003 and 2002, the weighted-average fair value of such options on the date of grant was $4.76, $4.76 and $2.76, respectively.

The Black-Scholes valuation models are used in estimating the fair value of traded options that have no vesting restrictions and are fully transferable. In addition, option valuation models require the input of highly subjective assumptions, including the expected stock price volatility and the average life of options. Because our stock options have characteristics significantly different from those of traded options, and because changes in the subjective input assumptions can materially affect the fair value estimate, in management’s opinion the existing models do not necessarily provide a reliable single measure of the fair value of our stock options.

Derivative Instruments and Hedging Activities

Our risk management policy as it relates to derivative investments is to mitigate, subject to market conditions, against interest rate risk. We do not enter into any derivative investments for the purpose of speculative investment. Our overall risk management philosophy is re-evaluated as business conditions change. For information regarding our interest rate swap, which expired during fiscal 2004, see Note 5.

Impact of Recently Issued Accounting Standards

In December 2003, the Financial Accounting Standards Board (“FASB”) issued SFAS No. 132R, “Employers’ Disclosures about Pensions and Other Postretirement Benefits.” This Statement amends the disclosure requirements of SFAS No. 132 to require additional disclosures about plan assets and obligations, cash flows, investment policy and measurement dates. The required disclosures have been included in Notes 9 and 10.

NOTE 2 — ACQUISITIONS

On April 12, 2002, we acquired certain assets of AA&E Leathercraft, Inc. (“AA&E”) for approximately $995,000 in cash. The cash purchase price was provided by drawing on our existing credit facility. The assets included, but were not limited to, wholesale accounts receivable, wholesale inventory, certain machinery and equipment, and a 10,000-square-foot building located in Yoakum, Texas. AA&E is a manufacturer and distributor of leather sporting goods accessories. We combined AA&E with existing product offerings in our men’s accessories segment. See Note 13. We used the purchase method of accounting for this acquisition which resulted in goodwill of approximately $164,000. Other intangibles related to the consideration given for non-compete agreements of approximately $75,000 are being amortized over 7 years. The pro forma effects of this acquisition are not material.

20

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 2 — ACQUISITIONS (continued)

On June 3, 2004, we announced an agreement to purchase all of the equity interest in Superior Merchandise Company (“Superior”) for approximately $10,000,000 in cash and the retirement of all of Superior’s debt. Based in New Orleans, Superior, which also operates under the name ETON®, is a gift accessory company that sells under both the ETON® and the licensed totes® brands. The pro forma effects of this acquisition are not expected to be material. We completed this transaction on July 1, 2004. See Note 16.

NOTE 3 — EARNINGS PER SHARE

The following sets forth the computation of basic and diluted earnings per share (dollars in thousands, except per share amounts):

| | | | | | | | | | | | | |

| | | Year Ended June 30,

|

| | | 2004

| | 2003

| | 2002

|

| Numerator for basic and diluted earnings per share: | | | | | | | | | | | | |

| Net income before cumulative effect of accounting change | | $ | 7,037 | | | $ | 7,717 | | | $ | 6,293 | |

| Cumulative effect of accounting change for SFAS No. 142, net of income taxes | | | — | | | | (581 | ) | | | — | |

| | | |

| | | |

| | | |

| |

| Net income | | $ | 7,037 | | | $ | 7,136 | | | $ | 6,293 | |

| | | |

| | | |

| | | |

| |

| Denominator: | | | | | | | | | | | | |

| Weighted-average shares outstanding | | | 6,208 | | | | 5,934 | | | | 5,765 | |

| Contingently issuable shares | | | 21 | | | | 18 | | | | 14 | |

| | | |

| | | |

| | | |

| |

| Denominator for basic earnings per share — weighted-average shares | | | 6,229 | | | | 5,952 | | | | 5,779 | |

| Effect of dilutive securities: | | | | | | | | | | | | |

| Employee stock options | | | 132 | | | | 78 | | | | 46 | |

| Director stock options | | | 28 | | | | 16 | | | | 8 | |

| | | |

| | | |

| | | |

| |

| Dilutive potential common shares | | | 160 | | | | 94 | | | | 54 | |

| Denominator for earnings per share — assuming dilution — adjusted weighted-average shares | | | 6,389 | | | | 6,046 | | | | 5,833 | |

| | | |

| | | |

| | | |

| |

| Earnings per common share: | | | | | | | | | | | | |

| Before cumulative effect of accounting change | | $ | 1.13 | | | $ | 1.30 | | | $ | 1.09 | |

| Cumulative effect of accounting change | | | — | | | | (.10 | ) | | | — | |

| | | |

| | | |

| | | |

| |

| | | $ | 1.13 | | | $ | 1.20 | | | $ | 1.09 | |

| | | |

| | | |

| | | |

| |

| Earnings per share — assuming dilution: | | | | | | | | | | | | |

| Before cumulative effect of accounting change | | $ | 1.10 | | | $ | 1.28 | | | $ | 1.08 | |

| Cumulative effect of accounting change | | | — | | | | (.10 | ) | | | — | |

| | | |

| | | |

| | | |

| |

| | | $ | 1.10 | | | $ | 1.18 | | | $ | 1.08 | |

| | | |

| | | |

| | | |

| |

Options to purchase approximately 265,000 shares of common stock at prices ranging from $13.38-$17.75 per share were outstanding during fiscal year 2004 but were not included in the computation of earnings per share - assuming dilution because the options’ exercise prices were greater than the average market price of the common shares and therefore, the effect would be antidilutive.

NOTE 4 — STOCK REPURCHASE PROGRAM

On September 10, 1999, our Board of Directors approved a plan to repurchase, from time to time in the open market or through privately negotiated transactions, shares of our common stock at an aggregate purchase price of up to $2,000,000, and on October 17, 2000, our Board increased the plan by up to an additional $2,000,000. On April 21, 2001, our Board determined to temporarily discontinue any purchases under the stock repurchase plan. Since such time, the Board has not authorized management to resume repurchases under the plan. As a result, no shares were repurchased during fiscal 2004, 2003 or 2002. During fiscal 2004, no treasury shares were reissued to our employee Stock Purchase Program. During 2003 and 2002, 66,260 and 145,751 shares of treasury stock, respectively, were reissued to our employee Stock Purchase Program.

21

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 5 — CREDIT ARRANGEMENTS

On June 26, 2003, we amended our committed secured revolving credit facility (“credit facility”) with certain financial institutions. The amendment to the credit facility extended the expiration of the agreement from June 27, 2004, to November 30, 2006, and reduced the facility from $80,000,000 to $60,000,000. Of this amount, $10,000,000 was a sub-limit of the credit facility (“swing line”) which could be used for same-day advances to be provided solely by the administrative agent (a financial institution) of the credit facility. Both the credit facility and swing line bore interest at variable rates with short-term durations. The credit facility could be used for borrowings and letters of credit. The credit facility was guaranteed by substantially all of our subsidiaries, was secured by substantially all of our assets and the assets of our subsidiaries, and required the maintenance of certain financial covenants which, if not met, could adversely impact our liquidity. Our credit facility permitted the payment of dividends and did not require us to enter into a new interest rate swap agreement (see below) against the borrowings under the credit facility. The credit facility also included a commitment fee based on certain financial performance objectives ranging from 25 to 37.5 basis points on the unused balance. Principal payments on the credit facility are due on the expiration date. At June 30, 2004, we had borrowings under the credit facility of $10,000,000 bearing interest at 2.82%. Our interest rate swap agreement (see description below) expired on June 27, 2004, and is not included in our effective interest rate on that date. As of June 30, 2003, we had borrowings under the credit facility of $30,000,000 bearing interest at 5.60%, including the interest rate swap agreement that was in effect at that time. At June 30, 2004 and 2003, we had no borrowings under the swing line. Given that our credit facility bears interest at floating market interest rates, the fair value of amounts borrowed approximate carrying value. On August 26, 2004, we amended our credit facility. See Note 16 for additional information regarding this subsequent event.

At June 30, 2004 and 2003, we had outstanding letters of credit under the credit facility of $4,447,000 and $7,352,000, respectively, which were used in conjunction with merchandise procurement.

We also have a Canadian line of credit for approximately $746,000 secured by a letter of credit from a U.S. bank. At June 30, 2004 and 2003, there were no borrowings under this line of credit.

We are subject to interest rate risk on our long-term debt. We manage our exposure to changes in interest rates. We hedged our exposure to changes in interest rates on a portion of our variable debt by entering into an interest rate swap agreement to lock in a fixed interest rate for a portion of these borrowings. On July 1, 2001, we entered into a three-year interest rate swap agreement with the administrative agent of our credit facility converting $30,000,000 of outstanding indebtedness from a variable to a fixed interest rate. The average receive rate was based on a 90-day LIBOR rate. At June 30, 2003, the receive and pay rates related to the interest rate swap were 1.29% and 5.60%, respectively. Interest differentials paid or received under the swap agreement are reflected as an adjustment to interest expense when paid. Prior to June 26, 2003, the interest rate swap agreement represented a valid cash flow hedge investment under SFAS No. 133. As such, during fiscal 2003, changes in the fair value of the interest rate swap were recognized in other comprehensive income. As of June 27, 2004, the interest rate swap agreement expired and is therefore not reflected on our balance sheet at June 30, 2004. The fair value of the swap agreement at June 30, 2003, was approximately ($1,665,000), and was included in accrued liabilities at June 30, 2003. At June 30, 2003 and 2002, the balance in other comprehensive income, related to the swap agreement, was approximately ($1,019,000), net of tax of $646,000, and ($1,041,000), net of tax of $659,000, respectively. We do not expect the potential impact of market conditions on the fair value of our indebtedness to be material.

In conjunction with the amendment to our credit facility during fiscal 2003, we discontinued hedge accounting on this swap. The change in the fair value of the swap agreement and balance in other comprehensive income was charged to interest expense during 2004, for the remaining term of the swap. We held the swap until two days before maturity on June 27, 2004. At that time, we canceled the swap with no penalty, and on June 28, 2004, we paid $20,000,000 on the outstanding debt.

At June 30, 2004, we had credit availability under our credit facility and our Canadian line of credit as follows:

| | | | | |

| | | June 30, 2004

|

| Total credit facility | | $ | 60,746,000 | |

| Less: | | | | |

| Debt outstanding | | | 10,000,000 | |

| Outstanding letters of credit | | | 4,447,000 | |

| Canadian standby letter of credit | | | 746,000 | |

| | | |

| |

| Credit available | | $ | 45,553,000 | |

| | | |

| |

Under the credit facilities described above, future payments required for debt maturities will be $10,000,000 in fiscal year 2007.

22

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 6 — INCOME TAXES

Significant components of our deferred tax assets and liabilities as of June 30, 2004 and 2003, are as follows:

| | | | | | | | | |

| | | 2004

| | 2003

|

| Deferred tax assets: | | | | | | | | |

| Accounts receivable valuation | | $ | 386,000 | | | $ | 601,000 | |

| Inventory valuation | | | 2,340,000 | | | | 2,399,000 | |

| Interest rate swap | | | — | | | | 646,000 | |

| Foreign interest income | | | 951,000 | | | | 866,000 | |

| Other, net | | | 332,000 | | | | 245,000 | |

| | | |

| | | |

| |

| Total deferred tax assets | | | 4,009,000 | | | | 4,757,000 | |

| | | |

| | | |

| |

| Deferred tax liabilities: | | | | | | | | |

| Goodwill and other intangibles | | | (1,142,000 | ) | | | (950,000 | ) |

| Depreciation | | | (924,000 | ) | | | (826,000 | ) |

| | | |

| | | |

| |

| Total deferred tax liabilities | | | (2,066,000 | ) | | | (1,776,000 | ) |

| | | |

| | | |

| |

| Net deferred tax asset | | $ | 1,943,000 | | | $ | 2,981,000 | |

| | | |

| | | |

| |

Significant components of the provision (benefit) for income taxes are as follows:

| | | | | | | | | | | | | |

| | | 2004

| | 2003

| | 2002

|

| Current: | | | | | | | | | | | | |

| Federal | | $ | 3,341,000 | | | $ | 4,189,000 | | | $ | 4,215,000 | |

| Foreign | | | 118,000 | | | | 53,000 | | | | (88,000 | ) |

| State and local | | | 594,000 | | | | 406,000 | | | | 271,000 | |

| | | |

| | | |

| | | |

| |

| | | | 4,053,000 | | | | 4,648,000 | | | | 4,398,000 | |

| | | |

| | | |

| | | |

| |

| Deferred: | | | | | | | | | | | | |

| Federal | | | 373,000 | | | | 249,000 | | | | (369,000 | ) |

| State and local | | | 19,000 | | | | 25,000 | | | | (19,000 | ) |

| | | |

| | | |

| | | |

| |

| | | | 392,000 | | | | 274,000 | | | | (388,000 | ) |

| | | |

| | | |

| | | |

| |

| Income tax provision | | $ | 4,445,000 | | | $ | 4,922,000 | | | $ | 4,010,000 | |

| | | |

| | | |

| | | |

| |

The following table reconciles the statutory federal income tax rate to the effective income tax rate:

| | | | | | | | | | | | | |

| | | 2004

| | 2003

| | 2002

|

| Statutory rate | | | 34.0 | % | | | 34.0 | % | | | 34.0 | % |

| State and local taxes, net of federal income tax benefit | | | 3.4 | % | | | 3.5 | % | | | 2.5 | % |

| Other, net | | | 1.3 | % | | | 1.4 | % | | | 2.4 | % |

| | | |

| | | |

| | | |

| |

| | | | 38.7 | % | | | 38.9 | % | | | 38.9 | % |

| | | |

| | | |

| | | |

| |

23

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 7 — COMMITMENTS

We lease property, which includes office, manufacturing and warehouse facilities, under operating leases expiring through the year 2010 with varying renewal and escalation clauses. Total rental expense for all of our leased properties for fiscal 2004, 2003 and 2002 totaled $2,237,000, $2,165,000 and $2,251,000, respectively.

We have entered into licensing agreements with other companies for the purpose of using their trademarks on our products. Royalty expense related thereto for fiscal 2004, 2003 and 2002 totaled $1,429,000, $1,821,000 and $1,960,000, respectively.

Future minimum rental and royalty commitments as of June 30, 2004, are as follows:

| | | | | |

Fiscal Year

| | Amount

|

| 2005 | | $ | 3,609,000 | |

| 2006 | | | 3,342,000 | |

| 2007 | | | 2,342,000 | |

| 2008 | | | 1,542,000 | |

| 2009 | | | 1,554,000 | |

| Thereafter | | | 560,000 | |

| | | |

| |

| | | $ | 12,949,000 | |

| | | |

| |

NOTE 8 — GOODWILL

Effective July 1, 2002, we adopted SFAS No. 142, “Goodwill and Other Intangible Assets.” This Statement changed the accounting for goodwill from an amortization approach to an impairment-only approach. The SFAS No. 142 goodwill impairment model is a two-step process. The first step compares the fair value of a reporting unit that has goodwill assigned to its carrying value. We estimated the fair value of a reporting unit using a discounted cash flow analysis. If the fair value of the reporting unit is determined to be less than its carrying value, a second step is performed to compute the amount of goodwill impairment, if any. Step two allocates the fair value of the reporting unit to the reporting unit’s net assets other than goodwill. The excess of the fair value of the reporting unit over the amounts assigned to its net assets other than goodwill is considered the implied fair value of the reporting unit’s goodwill. The implied fair value of the reporting unit’s goodwill is then compared to the carrying value of its goodwill. Any shortfall represents the amount of goodwill impairment.

Using the SFAS No. 142 approach described above, we recorded a transitional goodwill impairment charge during the first quarter of fiscal 2003 of $950,000 ($581,000, net of tax), presented as a cumulative effect of accounting change. This charge related to our women’s accessories segment of products.

The following table illustrates the gross carrying amount and accumulated amortization of our acquired intangible assets as of June 30, 2004, compared to the previous year (in thousands):

| | | | | | | | | |

| | | 2004

| | 2003

|

| Amortized intangible assets (various, principally trade names): | | | | | | | | |

| Gross carrying amount | | $ | 8,774 | | | $ | 8,774 | |

| Accumulated amortization | | | (4,240 | ) | | | (3,874 | ) |

| | | |

| | | |

| |

| Net amortized intangible assets | | $ | 4,534 | | | $ | 4,900 | |

| | | |

| | | |

| |

Amortization expense for acquired finite-lived intangible assets during the year ended June 30, 2004, was $366,000. The following table illustrates our estimated amortization expense through June 30, 2009:

| | | | | |

| Estimated amortization expense: | | | | |

| Fiscal year ending 6/30/05 | | $ | 361,000 | |

| Fiscal year ending 6/30/06 | | | 361,000 | |

| Fiscal year ending 6/30/07 | | | 361,000 | |

| Fiscal year ending 6/30/08 | | | 361,000 | |

| Fiscal year ending 6/30/09 | | | 359,000 | |

24

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 8 — GOODWILL (continued)

The following table reconciles net income, earnings per common share and earnings per share — assuming dilution, adjusted to exclude amortization expense recognized in such periods related to goodwill (dollars in thousands, except per share amounts):

| | | | | | | | | | | | | |

| | | Year Ended June 30,

|

| | | 2004

| | 2003

| | 2002

|

| Reported net income before cumulative effect of accounting change | | $ | 7,037 | | | $ | 7,717 | | | $ | 6,293 | |

| Add back after-tax amounts: | | | | | | | | | | | | |

| Goodwill amortization | | | — | | | | — | | | | 622 | |

| | | |

| | | |

| | | |

| |

| Adjusted net income before cumulative effect of accounting change | | $ | 7,037 | | | $ | 7,717 | | | $ | 6,915 | |

| | | |

| | | |

| | | |

| |

| Earnings per common share before cumulative effect of accounting change: | | | | | | | | | | | | |

| Reported net income | | $ | 1.13 | | | $ | 1.30 | | | $ | 1.09 | |

| Goodwill amortization | | | — | | | | — | | | | .11 | |

| | | |

| | | |

| | | |

| |

| Adjusted basic earnings per common share before cumulative effect of accounting change | | $ | 1.13 | | | $ | 1.30 | | | $ | 1.20 | |

| | | |

| | | |

| | | |

| |

| Earnings per share — assuming dilution before cumulative effect of accounting change: | | | | | | | | | | | | |

| Reported net income | | $ | 1.10 | | | $ | 1.28 | | | $ | 1.08 | |

| Goodwill amortization | | | — | | | | — | | | | .11 | |

| | | |

| | | |

| | | |

| |

| Adjusted earnings per share — assuming dilution before cumulative effect of accounting change | | $ | 1.10 | | | $ | 1.28 | | | $ | 1.19 | |

| | | |

| | | |

| | | |

| |

The following table illustrates the changes in the carrying amount of goodwill by reportable segment for the year ended June 30, 2004:

| | | | | | | | | | | | | |

| | | Men's | | Women's | | |

| | | Accessories

| | Accessories

| | Total

|

June 30, 2002 | | $ | 9,733 | | | $ | 2,734 | | | $ | 12,467 | |

| Impairment losses | | | — | | | | (950 | ) | | | (950 | ) |

| Other (1) | | | 124 | | | | — | | | | 124 | |

| | | |

| | | |

| | | |

| |

June 30, 2003 | | $ | 9,857 | | | $ | 1,784 | | | $ | 11,641 | |

| | | |

| | | |

| | | |

| |

| Other (1) | | | 14 | | | | — | | | | 14 | |

| | | |

| | | |

| | | |

| |

June 30, 2004 | | $ | 9,871 | | | $ | 1,784 | | | $ | 11,655 | |

| | | |

| | | |

| | | |

| |

| | (1) | | Difference due to foreign currency translation adjustments. |

25

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 9 — STOCK OPTIONS

Employee Stock Options

Our officers and key management employees are eligible to receive options to purchase shares of our common stock under the Tandy Brands Accessories, Inc. 2002 Omnibus Plan (see description below). In addition, many of our officers and key management employees have received options under our prior stock option plans. All options are granted at the market price as of the date of grant and have a contractual life of ten years. Options are generally exercisable annually at a rate of one-third per year beginning one year after the grant date. The following table reflects employee stock option activity from June 30, 2001, to June 30, 2004:

| | | | | | | | | |

| | | Number | | Weighted-Average |

| | | of Shares

| | Exercise Price

|

| Outstanding at June 30, 2001 | | | 755,928 | | | $ | 12.94 | |

| Options granted | | | 180,000 | | | $ | 5.63 | |

| Options exercised | | | (12,958 | ) | | $ | 8.70 | |

| Options canceled or expired | | | (80,956 | ) | | $ | 11.13 | |

| | | |

| | | | | |

| Outstanding at June 30, 2002 | | | 842,014 | | | $ | 11.62 | |

| Options granted | | | 179,000 | | | $ | 11.67 | |

| Options exercised | | | (44,587 | ) | | $ | 7.68 | |

| Options canceled or expired | | | (97,900 | ) | | $ | 15.02 | |

| | | |

| | | | | |

| Outstanding at June 30, 2003 | | | 878,527 | | | $ | 11.40 | |

| Options granted | | | 149,350 | | | $ | 12.07 | |

| Options exercised | | | (140,320 | ) | | $ | 8.40 | |

| Options canceled or expired | | | (35,750 | ) | | $ | 19.75 | |

| | | |

| | | | | |

| Outstanding at June 30, 2004 | | | 851,807 | | | $ | 11.66 | |

| | | |

| | | | | |

| Exercisable on June 30, 2004 | | | 534,352 | | | $ | 12.19 | |

| | | |

| | | | | |

The following table segregates outstanding options granted to employees into groups based on price ranges of less than and greater than $10 per share as of June 30, 2004:

| | | | | | | | | |

| | | $5.63-$9.25

| | $11.67-$17.56

|

| All outstanding options: | | | | | | | | |

| Number of shares | | | 272,918 | | | | 578,889 | |

| Weighted-average exercise price | | $ | 6.90 | | | $ | 13.91 | |

| Weighted-average remaining contractual life | | 6.6 years | | 7.4 years |

| Exercisable options: | | | | | | | | |

| Number of shares | | | 216,365 | | | | 317,987 | |

| Weighted-average exercise price | | $ | 7.23 | | | $ | 15.56 | |

Omnibus Plan

The Tandy Brands Accessories, Inc. 2002 Omnibus Plan (the “Omnibus Plan”) was approved by our stockholders on October 16, 2002. The purpose of the Omnibus Plan is to attract and retain the services of key management employees and Board members through the granting of incentive stock options, non-qualified stock options, performance units, stock appreciation rights or restricted stock. All grants under the Omnibus Plan have a maximum contractual life of ten years. Any grants under the Omnibus Plan will be made at the fair market value of our common stock and specific vesting terms will be addressed in each award. All shares available for grant under our prior option plans on October 16, 2002, were transferred to the Omnibus Plan and are authorized and reserved for issuance under the Omnibus Plan. All shares of common stock presently authorized and reserved for issuance on the exercise of outstanding stock options under our prior stock option plans will, on the cancellation or expiration of any such stock options, automatically be authorized and reserved for issuance in connection with the Omnibus Plan.

At June 30, 2004 and 2003, the number of shares available for grant under the Omnibus Plan was 395,031 and 514,840, respectively.

26

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 9 — STOCK OPTIONS (continued)

Non-Employee Director Stock Options

Our non-employee directors are also eligible for awards under the Omnibus Plan. The Omnibus Plan provides that, when a non-employee director is first elected or appointed to the Board, he or she will be granted a non-qualified stock option to purchase 5,000 shares of our common stock or, if the Board so elects, an alternative form of award (other than an incentive stock option) with a value substantially equivalent to the value of such non-qualified stock option. The Omnibus Plan also provides that concurrently with each regular annual election of the Board of Directors, each continuing non-employee director (other than our Chairman) will receive a non-qualified stock option to purchase 2,500 shares of our common stock and our Chairman will receive a non-qualified stock option to purchase 4,425 shares of our common stock. If the Board so elects, non-employee directors and our Chairman may receive an alternative form of award (other than an incentive stock option) with a value substantially equivalent to the value of a non-qualified stock option to purchase 2,500 and 4,425 shares of our common stock, respectively.

On October 15, 2003, each of our non-employee directors, other than the Chairman of the Board, was granted a stock option to purchase 1,500 shares of common stock at an exercise price of $15.60 and 645 shares of restricted stock. Our Chairman was granted a stock option to purchase 2,657 shares of common stock at an exercise price of $15.60 per share and 1,140 shares of restricted stock. The options became fully vested six months after the date of grant. The restricted stock awards will become fully vested on October 15, 2006, with one-third of the shares vesting on each anniversary of the date of the grant. Generally, upon the death, disability, resignation or termination of a non-employee director, that director’s shares become fully vested. These shares of stock, while not transferable, bear rights of ownership, including voting and dividend rights, during the vesting period.

Compensation expense of $58,000 related to the restricted stock awards granted to our non-employee directors was recorded during fiscal 2004.

Many of our non-employee directors have also received options to purchase shares of our common stock under our prior stock option plans. The options are generally exercisable beginning six months after the date of grant. During fiscal 2004, 2003 and 2002, our non-employee directors exercised options to purchase 2,461, 2,585 and 3,289 shares of our common stock, respectively.

The following table reflects non-employee director stock option transactions from June 30, 2001, to June 30, 2004:

| | | | | | | | | |

| | | Number | | Weighted-Average |

| | | of Shares

| | Exercise Price

|

| Outstanding at June 30, 2001 | | | 95,258 | | | $ | 11.57 | |

| Options granted | | | 45,282 | | | $ | 6.09 | |

| Options exercised | | | (3,289 | ) | | $ | 8.13 | |

| Options canceled or expired | | | — | | | | — | |

| | | |

| | | | | |

| Outstanding at June 30, 2002 | | | 137,251 | | | $ | 10.25 | |

| Options granted | | | 14,425 | | | $ | 9.23 | |

| Options exercised | | | (2,585 | ) | | $ | 8.13 | |

| Options canceled or expired | | | (19,618 | ) | | $ | 13.37 | |

| | | |

| | | | | |

| Outstanding at June 30, 2003 | | | 129,473 | | | $ | 9.71 | |

| Options granted | | | 8,657 | | | $ | 15.60 | |

| Options exercised | | | (2,461 | ) | | $ | 9.88 | |

| Options canceled or expired | | | (6,000 | ) | | $ | 19.00 | |

| | | |

| | | | | |

| Outstanding at June 30, 2004 | | | 129,669 | | | $ | 9.67 | |

| | | |

| | | | | |

| Exercisable on June 30, 2004 | | | 129,669 | | | $ | 9.67 | |

| | | |

| | | | | |

27

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 9 — STOCK OPTIONS (continued)

The following table segregates outstanding options granted to non-employee directors into groups based on price ranges of less than $10 or greater than or equal to $10 per share as of June 30, 2004:

| | | | | | | | | |

| | | $6.09-$9.23

| | $10.00-$17.75

|

| All outstanding options: | | | | | | | | |

| Number of shares | | | 84,827 | | | | 44,842 | |

| Weighted-average exercise price | | $ | 7.13 | | | $ | 14.47 | |

| Weighted-average remaining contractual life | | 6.4 years | | 5.1 years |

| Exercisable options: | | | | | | | | |

| Number of shares | | | 84,827 | | | | 44,842 | |

| Weighted-average exercise price | | $ | 7.13 | | | $ | 14.47 | |

Other Non-Employee Director Stock Plans

In fiscal 1995, our stockholders adopted the Tandy Brands Accessories, Inc. 1995 Stock Deferral Plan for Non-Employee Directors (the “Deferral Plan”). The Deferral Plan was established to provide non-employee directors an equity interest in the Company in order to attract and retain well-qualified individuals to serve as non-employee directors and to enhance the identity of interests between the non-employee directors and our stockholders. The Deferral Plan provides the directors with an election to defer the receipt of their annual and committee chair retainer fees until a future date determined by each director. The payment of such fees will be in the form of phantom stock units which will ultimately be settled in shares of our common stock. All amounts deferred are credited to a bookkeeping reserve account we maintain in phantom stock units which are equivalent in value to our common stock. The phantom stock units representing shares are calculated by dividing the deferred cash amount by the average closing price of the stock for each day of the period during which such cash amount would have been paid but for the deferral election. We record compensation expense for the amount of the directors’ retainer fees. We benefit from cash retained when directors elect to defer their retainer fees and receive phantom stock units. The Deferral Plan, which became active in 1996, provides for the issuance of up to 50,000 shares of our common stock to non-employee directors. During fiscal 2004, 2003 and 2002, 2,885, 3,411 and 4,030 phantom stock units, respectively, were issued under the Deferral Plan. Amounts recorded as compensation expense related to the Deferral Plan for fiscal 2004, 2003 and 2002 were $40,096, $34,150 and $31,470, respectively.

NOTE 10 — EMPLOYEE BENEFIT PLANS

The Tandy Brands Accessories, Inc. Employees Investment Plan Trust (the “401(k) Plan”) is open to substantially all full-time employees who have completed one year of service. Under the 401(k) Plan, an eligible employee may contribute up to 10% of his or her annual compensation to the 401(k) Plan on a pre-tax basis. We, at our discretion, match 100% of employee contributions up to 5% of compensation. The 401(k) Plan allows participants to direct the investment of both employee and matching employer contributions from a variety of investment alternatives, one of which is our common stock. All contributions made to the 401(k) Plan prior to July 1, 2002, are fully vested and are held in a fund invested primarily in our common stock.

The Tandy Brands Accessories, Inc. Stock Purchase Program (the “Program”) is open to all full-time employees who are enrolled in the 401(k) Plan. Under the Program, participants may contribute 5% or 10% of their earnings and we match 25% or 50% of each participant’s contribution depending on their length of employment. The Program purchases treasury stock, if available (see Note 4), or unissued common stock directly from the Company at monthly average market prices. The participant’s shares are fully vested upon purchase and the participant may withdraw from the Program at any time. The shares purchased under the Program are distributed to participants annually.

The Tandy Brands Accessories, Inc. Benefit Restoration Plan Trust (the “BRP”) is a non-qualified plan of deferred compensation, the purpose of which is to restore retirement benefits on behalf of a select group of our management and highly compensated employees who are eligible to make contributions to the 401(k) Plan, the amount of which is reduced due to limitations imposed by Sections 401(a)(17) and 402(g) of the Internal Revenue Code of 1986, as amended. For any plan year, a participant may elect to defer, on a pre-tax basis, 5% of his gross salary and wages otherwise payable to him by us during such plan year, reduced by the total contributions he made during such plan year to the 401(k) Plan. Participants may direct the investment of their contributions in various investment alternatives, including our common stock. We make quarterly matching contributions in cash to the BRP on the participant’s behalf equal to 150% of the amount the participant deferred during such calendar quarter. Our matching contributions are required to be invested only in our common stock. All payments of benefits from the BRP will be made solely in cash in either a single, lump-sum distribution or in monthly installments over a certain period, not to exceed 10 years. The liability associated with the BRP of $1,087,000 is included in other noncurrent liabilities.

28

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 10 — EMPLOYEE BENEFIT PLANS (continued)

Our total contributions to these plans were approximately $1,162,000, $1,211,000 and $917,000 in fiscal 2004, 2003 and 2002, respectively.

On July 1, 2003, our executive officers were awarded a total of 22,800 shares of restricted stock, which will become fully vested on July 1, 2006. These shares of stock, while not transferable, bear rights of ownership, including voting and dividend rights, during the three-year vesting period. There are no performance requirements related to vesting, only continued employment through the vesting date. Compensation expense in the amount of approximately $92,000 related to the restricted stock awards granted to our executive officers was recorded during fiscal 2004. At June 30, 2004, the Company had unearned compensation recorded in the amount of $183,000 relating to these shares, which will be recorded as compensation expense in the amount of approximately $23,000 per quarter through June 30, 2006.

On January 1, 2003, we adopted the Tandy Brands Accessories, Inc. Supplemental Executive Retirement Plan (the “SERP”) for a select group of our executive officers. The SERP provides that at normal retirement (age 65) a participant will receive, in the form of a 100% joint and survivor annuity, an annual benefit (or actuarially equivalent lump-sum at the time of retirement in lieu of such joint and survivor annuity) which will generally be equal to 2% of the average of the participant’s highest annual gross salary and bonus (without reduction for any deductions) for three complete fiscal years over the last 10 fiscal years of the participant’s employment, multiplied by the participant’s years of service up to a maximum of 30 years, and reduced by the participant’s Social Security retirement benefits and the participant’s benefits under the Tandy Brands Accessories, Inc. Employees Investment Plan when expressed in the form of a single-life annuity commencing with the participant’s normal retirement age. If the participant has at least 15 years of service with the Company and retires at or after age 55 but before age 65, the benefit would be reduced by 5% for each year the participant’s retirement precedes age 65. A participant is also eligible for a benefit if the participant becomes disabled or if the participant terminates service with us after completing 15 years of service and the participant’s termination of service is not as a result of normal retirement, early retirement or disability. If the participant begins receiving a disability benefit or a termination benefit at or after age 55 but before age 65, the benefit would be reduced by 5% for each year the benefit distribution precedes age 65. The SERP also provides for a pre-retirement death benefit if the participant dies after reaching normal retirement or early retirement age but before receiving distributions under the SERP.

29

Notes To Consolidated Financial Statements Tandy Brands Accessories, Inc. and Subsidiaries

NOTE 10 — EMPLOYEE BENEFIT PLANS (continued)

For the year ended June 30, 2004 and 2003, we recorded expenses related to the SERP of approximately $266,000 and $151,000, respectively. This plan is not currently funded and therefore has no plan assets. Measurement of obligations under the SERP is calculated as of each fiscal year-end. The discount rate used to determine the actuarial present value of the projected benefit obligation under the SERP was 7.5% as of June 30, 2004 and 2003, and the assumed weighted-average rate increase in future compensation levels was 4.0% as of June 30, 2004 and 2003. We anticipate that there will be no SERP benefits paid during the next five years. Contributions to the SERP during fiscal 2005 are expected to be approximately $400,000.

The following table provides a reconciliation of benefit obligations and funded status of the SERP as of June 30, 2004 and 2003 (dollars in thousands):

| | | | | | | | | |

| | | 2004

| | 2003

|

| Change in projected benefit obligation: | | | | | | | | |

| Projected benefit obligation, beginning of year | | $ | 2,134 | | | $ | — | |

| Service cost | | | 15 | | | | 7 | |

| Interest cost | | | 160 | | | | 74 | |

| Actuarial loss/(gain) | | | (24 | ) | | | — | |

| Plan amendments | | | — | | | | 2,053 | |

| | | |

| | | |

| |

| Projected benefit obligation, end of year | | $ | 2,285 | | | $ | 2,134 | |

| | | |

| | | |

| |

| Reconciliation of funded status: | | | | | | | | |

| Funded status | | $ | (2,285 | ) | | $ | (2,134 | ) |

| Unrecognized prior service cost | | | 1,843 | | | | 1,983 | |

| Unrecognized prior net loss/(gain) | | | (24 | ) | | | — | |

| | | |

| | | |

| |

| Accrued benefit liability | | $ | (466 | ) | | $ | (151 | ) |

| | | |

| | | |

| |

| Amounts recognized in the balance sheet: | | | | | | | | |

| Accrued benefit liability | | $ | (1,721 | ) | | $ | (1,607 | ) |

| Intangible asset | | | 1,255 | | | | 1,456 | |

| | | |

| | | |

| |

| Net amount recognized | | $ | (466 | ) | | $ | (151 | ) |

| | | |

| | | |

| |

| Components of net periodic benefit cost: | | | | | | | | |

| Service cost | | $ | 15 | | | $ | 7 | |

| Interest cost | | | 160 | | | | 74 | |

| Amortization of prior service cost | | | 140 | | | | 70 | |

| | | |

| | | |

| |

| | $ | 315 | | | $ | 151 | |

| | | |

| | | |

| |

| Additional information for SERP: | | | | | | | | |

| Accumulated benefit obligation | | $ | 1,721 | | | $ | 1,607 | |

| | | |

| | | |

| |

At June 30, 2004, we had 1,725,503 shares authorized and reserved for future issuance under all of our stock incentive plans, including outstanding options under the Omnibus Plan and our prior stock option plans.

NOTE 11 — DIVIDENDS

During fiscal 2004, we declared dividends as set forth in the following table:

| | | | | | | | | |

Declaration Date

| | Record Date

| | Payable Date

| | Dividend per Share

|