111 Wagaraw Road

Hawthorne, New Jersey 07506

September 22, 2004

Dear Stockholder:

On September 13, 2004, Craft Retail Acquisition Corp. ("Purchaser") purchased from certain of our officers, directors and stockholders approximately 55.7% of the issued and outstanding shares of Rag Shops, Inc. common stock for cash at $4.30 per share. Simultaneously with that transaction, Rag Shops, Inc. entered into an Agreement and Plan of Merger with Purchaser and its parent corporation. Pursuant to that agreement, Purchaser has commenced an offer to purchase each share of Rag Shops common stock not owned by it for $4.30, net to the seller in cash. The offer will be followed by a merger in which each share of Rag Shops common stock not purchased in the offer will be converted into the right to receive the same amount of cash that is being paid in the offer. The offer and the merger are subject to conditions that are explained in the attached Offer to Purchase.

YOUR BOARD OF DIRECTORS HAS DETERMINED THAT THE OFFER AND THE MERGER ARE ADVISABLE, FAIR TO AND IN THE BEST INTERESTS OF RAG SHOPS AND ITS STOCKHOLDERS, AND HAS APPROVED THE OFFER, THE MERGER AND THE AGREEMENT AND PLAN OF MERGER AND THE TRANSACTIONS CONTEMPLATED THEREBY, AND RECOMMENDS THAT RAG SHOPS' STOCKHOLDERS ACCEPT THE OFFER AND TENDER THEIR SHARES OF RAG SHOPS COMMON STOCK PURSUANT TO THE OFFER. THE ACTIONS OF THE BOARD WERE UNANIMOUS, WITH STANLEY BERENZWEIG AND JEFFREY C. GERSTEL ABSTAINING DUE TO THEIR INTEREST IN THE TRANSACTIONS.

In arriving at its recommendation, the board of directors considered a number of factors, as described in the attached Schedule 14D-9, including the written opinion of the investment banking firm of SunTrust Robinson Humphrey, a division of SunTrust Capital Markets, Inc., that as of the date of such opinion, from a financial point of view, the consideration to be received by the holders of shares of Rag Shops common stock pursuant to the Agreement and Plan of Merger is fair to Rag Shops' stockholders. A copy of SunTrust Robinson Humphrey's written opinion, which sets forth the assumptions made, procedures followed and matters considered by them in rendering their opinion, can be found in Annex A to the Schedule 14D-9. You should read the opinion carefully and in its entirety. Enclosed are Purchaser's Offer to Purchase, dated as of the date of this letter, Letter of Transmittal and related documents. These documents set forth the terms and conditions of the offer and provide information on how to tender your Rag Shops shares to Purchaser. The Schedule 14D-9 describes in more detail the reasons for your board's conclusions and contains other information relating to the offer. We urge you to consider this information carefully.

| Very truly yours, |

| /s/ Jeffrey C. Gerstel |

| Jeffrey C. Gerstel President and Chief Operating Officer |

___________________________________________________________________________________________

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

____________________________________

SCHEDULE 14D-9

(RULE 14d-101)

SOLICITATION/RECOMMENDATION STATEMENT

UNDER SECTION 14(d)(4) OF THE

SECURITIES EXCHANGE ACT OF 1934

Rag Shops, Inc.

(Name of Subject Company)

Rag Shops, Inc.

(Name of Person(s) Filing Statement)

COMMON STOCK, $0.01 PAR VALUE

(Title of Class of Securities)

750624108

(Cusip Number of Class of Securities)

Jeffrey C. Gerstel

President & Chief Operating Officer

111 Wagaraw Road

Hawthorne, NJ 07506-2711

(973) 423-1303

(Name, Address And Telephone Number Of Person Authorized To Receive Notices And Communications On Behalf Of The Person(s) Filing Statement)

Copies To:

Steven R. Kamen, Esq.

Sills Cummis Epstein & Gross P.C.

One Riverfront Plaza

Newark, New Jersey 07102-5400

(973) 643-7000

[ ] Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer.

Item 1. Subject Company Information

The name of the subject company to which this Solicitation/Recommendation Statement on Schedule 14D-9 relates is Rag Shops, Inc., a Delaware corporation which we refer to as "Rag Shops". The address of our principal executive offices is 111 Wagaraw Road, Hawthorne, New Jersey 07506-2711. The telephone number of our principal executive offices is (973) 423-1303.

The title of the class of equity securities to which this Schedule 14D-9 relates is our common stock, par value $0.01 per share (the "Shares"). As of September 13, 2004, there were 4,797,983 Shares issued and outstanding.

Item 2. Identity And Background Of Filing Person

Name and Address

The filing person of this Schedule 14D-9 (the "Statement") is the subject company, Rag Shops. Our address and telephone number are set forth in Item 1 above.

This Statement relates to the tender offer by Crafts Retail Acquisition Corp., a Delaware corporation ("Purchaser") , a wholly-owned subsidiary of Crafts Retail Holding Corp. (the "Parent") and an affiliate of Sun Capital Partners, Inc. ("Sun"), to purchase all of the outstanding Shares, other than Shares owned by Purchaser, at a price of $4.30 per Share, net to the seller in cash, without interest thereon and less any required withholding taxes (the "Offer Price"). The tender offer is being made upon the terms and subject to the conditions set forth in the Purchaser's Offer to Purchase dated September 22, 2004 (the "Offer to Purchase") and the related Letter of Transmittal (which, as may be amended from time to time, together constitute the "Offer"), copies of which are filed as Exhibits (a)(1)(A) and (a)(1)(B) to this Statement. The Offer is described in a Tender Offer Statement on Schedule TO (as amended or supplemented from time to time, the "Schedule TO") filed by Purchaser with the United States Securities and Exchange Commission (the "SEC") on September 22, 2004. We urge you to read the Schedule TO, including the Offer to Purchase, in conjunction with this Statement because they each contain important additional information regarding the Offer.

The Offer is being made pursuant to an Agreement and Plan of Merger (the "Acquisition Agreement"), dated as of September 13, 2004, by and among Parent, Purchaser and Rag Shops. The Acquisition Agreement provides that, among other things, after the satisfaction or, if permissible, waiver of the conditions set forth in the Acquisition Agreement, including the purchase of Shares pursuant to the Offer (sometimes referred to herein as the "consummation" or "completion" of the Offer), Purchaser may be merged with and into Rag Shops (the "Merger"). Following the consummation of the Merger, Rag Shops will continue as the surviving corporation and will be a wholly-owned subsidiary of Parent. The purpose of the Offer and the Merger is to facilitate the acquisition by Parent of all of the Shares for cash and thereby enable Parent, after giving effect to the transactions contemplated by the Stock Purchase Agreement (as described below), to own 100% of the issued and outstanding Shares. In connection with entering into the Acquisition Agreement, Purchaser also entered into a Stock Purchase Agreement with certain of our stockholders and as a result Parent now owns approximately 55.7% of the Shares which is sufficient for Parent to control the stockholder voting power of Rag Shops. However, if certain conditions are not met Parent is not obligated to consummate the Offer and/or the Merger (the Merger, but not the Offer, is conditioned on, among other things, the ownership by Parent and Purchaser of at least 90% of the Shares on a fully-diluted basis). We incorporate by reference the summary of the material provisions of the Acquisition Agreement with Parent and Purchaser and a statement of the material conditions to the Offer and the Merger which are included in Sections 14 and 11, respectively, of the Offer to Purchase.

If all of the conditions set forth in the Acquisition Agreement are met or waived by Parent and the Merger is consummated, at the effective time of the Merger (the "Effective Time"), each Share issued and outstanding immediately prior to the Effective Time held by the stockholders of Rag Shops (other than shares held by us as treasury stock, and shares held by Parent, Purchaser and any other wholly-owned subsidiary of Parent) will be canceled and, subject to appraisal rights of dissenting

2

stockholders under the Delaware General Corporation Law ("DGCL"), converted automatically into the right to receive $4.30 in cash or, in the event any higher price is paid in the Offer, such higher price, without interest thereon. If the Merger is not consummated, and you have not tendered in the Offer the Shares held by you, you will not be entitled to receive the Offer Price. We incorporate by reference the summary of the material provisions of the Acquisition Agreement with Parent and Purchaser and a statement of the material conditions to the Offer and the Merger which are included in Sections 14 and 11, respectively, of the Offer to Purchase. Assuming all of the conditions to the Merger are satisfied or waived and the Merger is consummated, stockholders who hold their Shares at the time of the Merger and who fully comply with the statutory dissenters' procedures set forth in the DGCL will be entitled to dissent from the Merger and have the fair value of their Shares (which may be more than, equal to, or less than the consideration received in the Merger) judicially determined and paid to them in cash pursuant to the procedures prescribed by the DGCL.

The Acquisition Agreement also provides that upon execution of the Acquisition Agreement, and from time to time, thereafter, Parent is entitled to designate for election as directors of Rag Shops such number of directors, rounded up to the next whole number, as is equal to the product of (1) the total number of directors of Rag Shops constituting our whole board of directors (giving effect to any increase in the number of directors in order to comply with this provision) and (2) the percentage that the voting power of our Shares beneficially owned by Parent and Purchaser (including shares paid for pursuant to the Offer and pursuant to the Stock Purchase Agreement) bears to the total voting power of Shares then outstanding. As a result of the transactions contemplated by the Stock Purchase Agreement, Parent already owns approximately 55.7% of the issued and outstanding Shares. Therefore, we have filed an information statement (the "Information Statement"), attached as Annex B hereto, pursuant to Rule 14f-1 of the Securities Exchange Act of 1934, as amended (the "Exchange Act") to permit not fewer than four nominees of Parent to be elected to our board of directors as soon as permitted by the rules of the SEC. Such directors will constitute a majority of our board. We are required under the Acquisition Agreement to take all action necessary, including the filing of the Information Statement (which is being filed as Annex B to this Statement), to cause Purchaser's designees to be elected or appointed to our board of directors, including, without limitation, increasing the number of directors and seeking and accepting resignations of incumbent directors; provided, however, that our board of directors must at all times until the effective time of the Merger have at least three directors, or such greater number as may be required by the rules of the Nasdaq Stock Market, Inc., who are not stockholders or affiliates of Parent or Purchaser and who are otherwise considered independent directors within the meaning of the rules of the Nasdaq Stock Market, Inc.

In addition, the independent directors shall form a committee consisting of three members that prior to the Effective Time or the expiration or termination of the Acquisition Agreement shall have sole power and authority, by majority vote, on behalf of Rag Shops to, among other things, amend or terminate the Acquisition Agreement and, except as set forth in the Acquisition Agreement, approve any amendment or modification to the Offer or take any other action under or in connection with the Acquisition Agreement, the Offer or the Merger if such action materially and adversely affects holders of Shares other than Parent or Purchaser.

Attached hereto as Annex B is the Information Statement that sets forth the persons designated by Purchaser to serve on our board of directors and also contains information required by the SEC to be transmitted to stockholders as if such persons were nominees for election as directors at a meeting of stockholders. The persons listed in the Information Statement as the directors designees of Parent are Rodger R. Krouse, Marc J. Leder, Clarence E. Terry and T. Scott King.

With respect to all information described in this Statement as contained in the Schedule TO and the Offer and all information regarding Purchaser, Rag Shops takes no responsibility for the accuracy or completeness of such information or for any failure by Purchaser to disclose events or circumstances that may affect the significance, completeness or accuracy of any such information.

According to the Schedule TO, the address of the principal executive offices of the Purchaser and Parent is c/o Sun Capital Partners, Inc. 5200 Town Center Circle Suite 470, Boca Raton FL 33486.

3

Item 3. Past Contacts, Transactions, Negotiations And Agreements

Certain contracts, agreements, arrangements or understandings between Rag Shops or its affiliates and certain of its directors and executive officers and between Rag Shops and Parent and Purchaser are, except as noted below, described in the Information Statement that is attached as Annex B to this Statement and incorporated herein by reference. Except as set forth in this Item 3 or in the Information Statement or as incorporated by reference to the Information Statement and this Statement, to our knowledge, as of the date hereof, there are no material agreements, arrangements or understandings and no actual or potential conflicts of interest between Rag Shops or its affiliates and (1) Rag Shops or its executive officers, directors or affiliates or (2) Parent, Purchaser, or their respective executive officers, directors or affiliates.

The Acquisition Agreement

We incorporate by reference the summary of the material provisions of the Acquisition Agreement with Parent and Purchaser and a statement of the material conditions to the Offer which are included in Sections 11 and 14, respectively, of the Offer to Purchase. The summary of the Acquisition Agreement is qualified in its entirety by reference to the Acquisition Agreement, which is filed as Exhibit (e)(1) hereto, and we incorporate it herein by reference. The summary may not contain all of the information that is important to you. Accordingly, you should carefully read the Acquisition Agreement in its entirety for a more complete description of the matters summarized in the Offer to Purchase.

Stock Purchase Agreement

As an inducement to enter into the Acquisition Agreement, Stanley Berenzweig, Doris Berenzweig, The Doris and Stanley Berenzweig Charitable Foundation Inc., Mona Adelson, Gail Loia, Steven Barnett and Judith Lombardo concurrently executed a Stock Purchase Agreement with the Parent and the Purchaser on the date of the Acquisition Agreement (the "Stock Purchase Agreement") pursuant to which they have, among other things, sold all of the shares of Common Stock owned by them to the Purchaser at purchase price of $4.30 per share in cash. Prior to the execution of the Stock Purchase Agreement, Mr. Berenzweig was the chairman of our board and our chief executive officer and Mrs. Berenzweig, his spouse was our secretary. Ms. Adelson and Ms. Loia are the daughters of Mr. and Mrs. Berenzweig. Mrs. Lombardo is our senior vice-president and Mr. Barnett is our executive vice president and treasurer. A total of 2,671,199 shares of our Common Stock was acquired by the Purchaser pursuant to the Stock Purchase Agreement, which represents approximately 55.7% of the total issued and outstanding shares of Common Stock of Rag Shops, for a total purchase price of $11,486,155.70.

Each selling stockholder agreed to (1) during the period commencing on September 13, 2004, and ending on the earlier of (x) two years after the termination of the Acquisition Agreement in accordance with its terms and (y) consummation of the Merger, such stockholder will not acquire any securities or assets of Rag Shops (except for shares acquired upon the exercise of Rag Shops stock options ("Stock Options")), and (2) with respect to any shares of Common Stock issuable upon the exercise of Stock Options that are not cancelled pursuant to the Acquisition Agreement, each selling stockholder agrees to validly tender in accordance with the terms of the Offer, all such shares unless the Acquisition Agreement is validly terminated in accordance with its terms.

Prior to the Effective Time, Rag Shops, and from and after the Effective Time, we have agreed to indemnify each selling stockholder under the Stock Purchase Agreement against any losses, claims, damages, liabilities, costs, expenses and the like in connection with any threatened or actual claim in which such selling stockholder is, or is threatened to be, made a party as a result of the Stock Purchase Agreement.

The summary of the Stock Purchase Agreement is qualified in its entirety by reference to the Acquisition Agreement, which is filed as Exhibit (e)(2) hereto, and we incorporate it herein by reference.

4

Agreements Between Rag Shops and Our Executive Officers and Other Employees

Effect of the Merger On Employee Benefit Plans and Stock Plans

For a period of three months following the Effective Time, Parent will, or will cause the surviving corporation to provide to each of our employees employed by us prior to the Merger that remains an employee of Rag Shops after the Effective Time, with employee benefits that are substantially similar, in the aggregate, to the benefits currently provided to our employees. Parent may, or may cause the surviving corporation to, comply with the prior sentence by either (1) retaining Rag Shops' benefit plans in their form or, in Parent's discretion, amending such plans as provided therein, or (2) terminating such plans and enabling our employees to participate in its employee benefit plans, if any. To the extent permitted pursuant to Parent's benefit plans, Parent will, or will cause the surviving corporation to: (1) waive all limitations as to preexisting conditions, exclusions and waiting periods with respect to participation and coverage requirements applicable to the employees under any welfare plan that the employees may be eligible to participate in after the Effective Time to the extent waived or satisfied under the applicable corresponding benefit plan immediately prior to the Effective Time; (2) provide each employee with credit for purposes of satisfying any applicable deductible or out-of-pocket requirements under any welfare plans that such employee is eligible to participate in after the Effective Time for any co-payments and deductibles paid under a corresponding benefit plan for the year in which the Effective Time occurs; and (3) provide each employee with credit for all purposes for all service with us and our affiliates under each employee benefit plan, program, or arrangement of the Parent or its affiliates in which such employee is eligible to participate to the extent such service was credited for similar purposes under similar benefit plans; provided, however, that in no event shall the employees be entitled to any credit (A) under any defined benefit pension plan of Parent or its subsidiaries (other than the surviving corporation and its subsidiaries) or (B) to the extent that it would result in a duplication of benefits with respect to the same period of service.

Stock Options

We maintain the following stock option plans: (1) the Rag Shops, Inc. 1991 Stock Option Plan, (2) the Rag Shops, Inc. 1999 Stock Incentive Award Plan and (3) the Rag Shops Inc. 2002 Stock Option Plan. Our board of directors has adopted such resolutions and will in the future take such other actions (if any), as may be required to: (a) permit the exercise of each stock option outstanding as of the date of this Acquisition Agreement (whether or not vested and exercisable); and (b) cause the cancellation of each stock option outstanding at the consummation of the Offer. In addition, we may seek the consent of each holder of a stock option to amend such stock option in order to provide that it will, without further action of the holder thereof, be cancelled upon consummation of he Offer and converted into the right to receive an amount in cash determined by multiplying (x) the excess, if any, of $4.30 over the applicable exercise price of such stock option by with an exercise price less than the $4.30 by (y) the total number of shares of our Common Stock subject to such stock option (whether or not vested or exercisable); and we shall, and Purchaser shall advance funds to us to, pay such amount promptly after such consummation to the holder of each such stock option. Assuming that each outstanding stock option with an exercise price in excess of $4.30 is cancelled and the holder thereof receives the amount to which it is entitled under the Acquisition Agreement, Purchaser shall pay to those holders an aggregate amount equal to $214,194.30, of which approximately $82,000 is payable to Jeffrey C. Gerstel, $29,400 is payable to Steven B. Barnett and $29,400 is payable to Judith Lombardo.

Retention Bonuses

In February and March of 2004, a committee consisting of our compensation committee members and our audit committee members established a pool of $838,500 for bonuses to employees as a means of retaining the services of those employees who are instrumental in the successful completion of the Offer and Merger. From this pool, Jeffrey C. Gerstel, Steven B. Barrett, Judith Lombardo, Bruce Miller, Leonard M. Settanni, Patricia Dahlem and John Alberto will receive lump sum payments equal to $100,000, $145,000, $10,000, $50,000, $30,000 and $30,000, respectively, if the terms

5

set forth in their respective change in control agreements are met. More information regarding the foregoing may be found in our Information Statement attached hereto as Annex B.

Arrangements with Respect to Our Board of Directors

Indemnification, Exculpation and Insurance

The Acquisition Agreement provides that the surviving corporation shall, and Parent shall cause the surviving corporation to, indemnify, to the full extent permitted under applicable law, the present and former directors and officers of Rag Shops and its subsidiaries in respect of actions taken prior to and including the Effective Time in connection with their duties as directors or officers of Rag Shops or its subsidiaries (including in connection with the Offer and the Merger). The Acquisition Agreement also provides that for at least six years after the Effective Time, the surviving corporation will, and Parent shall cause the surviving corporation to, maintain in effect directors' and officers' liability insurance covering the persons who are currently covered by the existing directors' and officers' liability insurance of Rag Shops with respect to actions that have taken place prior to or at the Effective Time, on terms and conditions (including coverage amount) no less favorable to such persons than those in effect under the existing directors' and officers' liability insurance of Rag Shops.

Pursuant to the Acquisition Agreement, prior to the date of this Statement, Rag Shops purchased a "tail" policy with a premium equal to $108,524.

Agreements with Sun or its Affiliates

Management Services Agreement

Concurrent with the execution of the Acquisition Agreement, we entered into a Management Services Agreement (the "Management Agreement") with Sun Capital Partners Management III, LLC ("Sun Management"), an affiliate of the Parent and the Purchaser, pursuant to which Sun Management will render management and consulting services to us regarding our business and such other services relating to the us as our board of directors or our executive officers may from time to time request. The term of the Management Agreement will commence on September 13, 2004, and shall continue until the tenth anniversary of that date. However, the Management Agreement may be earlier terminated by us if the percentage of our outstanding equity owned by Parent, Purchaser, Sun Management or any affiliate of such parties (taken as a group) falls below 30%. In exchange for their services, we will pay Sun Management a fee in quarterly installments equal to the greater of (i) $400,000 or (ii) 6% of the Company's EBITDA, determined without taking into consideration the fees payable pursuant to the Management Agreement, as determined by our independent auditors with respect to each fiscal year. On the date of the Acquisition Agreement, we paid to Sun Management in cash a fee equal to $83,516, representing the pro rata portion of the Management fee for the quarter ending November 29, 2004. In addition, we will reimburse Sun Management for its reasonable out-of-pocket fees and expenses incurred in the performance of their services. We will also pay Sun Management a consulting fee, in cash, equal to 1% of the aggregate consideration paid to or by us, our subsidiaries or our stockholders in connection with events such as acquisitions, mergers, consolidations, business combinations and the like. This fee was payable in connection with the execution of the Acquisition Agreement and the Stock Purchase Agreement.

We incorporate by reference the full text of the management services agreement which we filed as Exhibit (e)(3) to this Statement.

Confidentiality Agreement

On May 13, 2004, our financial advisors, SunTrust, a division of SunTrust Capital Markets, Inc. ("SunTrust"), executed as our agent a confidentiality agreement with Sun. The confidentiality agreement contains customary provisions pursuant to which, among other things, Sun agreed on behalf of itself and its representatives, subject to limited exceptions, to maintain the confidentiality of

6

nonpublic, confidential or proprietary information furnished to it and to use the confidential information solely in connection with evaluating a business combination with us. In addition, Sun agreed not to disclose to any third parties the fact that negotiations were taking place.

We incorporate by reference the full text of the confidentiality agreement which we filed as Exhibit (e)(4) to this Statement.

Letter of Intent

On August 3, 2004, we entered into a non-binding letter of intent with Sun. The letter of intent contains customary provisions pursuant to which, among other things, we agreed that for a period of 30 days not we, nor our any of our subsidiaries or affiliates, nor any of their respective directors, officers, managers, employees, agents advisors or representatives will solicit offers for, or discuss, a possible sale, merger combination, consolidation, restructuring, recapitalization, refinancing or other disposition of all or any material part of us, or our subsidiaries or any of our or our subsidiaries assets or issued or unissued capital stock with any other party other than Sun, or provide any information to any party other than Sun in that connection, subject to limited, but customary, exceptions.

On September 10, 2004, we executed a letter with Sun extending Sun's exclusivity period set forth in the letter of intent through and including September 17, 2004.

We incorporate the full text of the letter of intent and the extension letter which we filed as Exhibit (e)(5) and Exhibit (e)(6), respectively, to this Statement.

Mutual Releases, Funding Agreement and Escrow Agreement

Stanley Berenzweig and Doris Berenzweig resigned as executive officers of Rag Shops (and Mr. Berenzweig resigned as a director of Rag Shops), effective immediately prior to the execution of the Acquisition Agreement. In connection with Mr. and Mrs. Berenzweig's resignations, Rag Shops and each of Mr. and Mrs. Berenzweig executed a general release on the date of the Acquisition Agreement that covered all claims except for, among other things, claims arising under or related to the Stock Purchase Agreement, the Acquisition Agreement, any indemnification arrangement between the company and either of them. We incorporate the full text of each mutual release which are filed as Exhibit (e)(7) and (e)(8) to this Statement, respectively.

In addition, concurrent with the execution of the Acquisition Agreement and as a condition to the willingness of Rag Shops to enter into a mutual release, Mr. Berenzweig entered into a funding agreement with Rag Shops (the "Funding Agreement"), pursuant to which Mr. Berenzweig agreed to fund certain expenses, up to $750,000, incurred from time to time by the company or any of its direct or indirect subsidiaries. In connection with the Funding Agreement, Mr. Berenzweig agreed to deposit, pursuant to an escrow agreement (the "Escrow Agreement") among himself, Rag Shops and Hughes Hubbard & Reed LLP, as escrow agent, $750,000, to be held in escrow, to satisfy any of Mr. Berenzweig's obligations under the Funding Agreement.

We incorporate the full text of the Funding Agreement and the Escrow Agreement which are filed as Exhibit (e)(9) and (e)(10) to this Statement, respectively.

As of the date of this Statement, none of our executive officers has received, or has any arrangement or agreement to receive, any equity or other similar interest in Rag Shops following the consummation of the transactions contemplated by our Acquisition Agreement and the Stock Purchase Agreement.

Item 4. The Solicitation Or Recommendation

At a meeting held on September 7, 2004, our board of directors unanimously (with Stanley Berenzweig and Jeffrey C. Gerstel abstaining):

| • | determined that the terms of the Acquisition Agreement, the Offer and the Merger were fair to, and in the best interests of, Rag Shops and its stockholders, and declared that the Offer and the Merger are advisable; |

7

| • | approved the Acquisition Agreement and the transactions contemplated by the Acquisition Agreement, including the Offer and the Merger; |

| • | approved the Stock Purchase Agreement and the transactions contemplated by the Stock Purchase Agreement; |

| • | approved the Management Services Agreement and the transactions contemplated by the Management Services Agreement; |

| • | resolved to increase the size of the board of directors to seven members; and |

| • | resolved to recommend (subject to the further exercise of its fiduciary duties) that our stockholders accept the offer and tender their shares of our common stock pursuant to the Offer and, if necessary under the DGCL, approve and adopt the Acquisition Agreement and the Merger. |

THE BOARD RECOMMENDS THAT THE STOCKHOLDERS ACCEPT THE OFFER AND TENDER THEIR SHARES OF PURSUANT TO THE OFFER.

Background of the Offer; Contacts with Sun

In early 2004, certain of our executive officers and members of our board discussed our financial condition and determined that it would be advisable to engage an investment banking firm to serve as our financial advisor to explore our strategic alternatives.

During February 2004, certain members our board interviewed several investment banking firms to act as its financial advisor. On February 24, 2004, SunTrust Robinson Humphey, a division of SunTrust Capital Markets, Inc., or SunTrust, met with our board of directors and presented a number of strategic alternatives for the company, including maintaining the status quo, raising capital in the public and private markets, acquiring other businesses and a sale of the company. SunTrust also summarized its expertise in the retail sector and its bank affiliation and reviewed our present situation.

Our board determined to negotiate an engagement agreement with SunTrust, after considering relative to the other firms interviewed, among other things, SunTrust's national reputation, fees, depth of experience in the retail sector and SunTrust's ability to conduct a fairness analysis of any proposed transaction.

An engagement agreement with SunTrust was executed on February 24, 2004. Under the engagement agreement, SunTrust was engaged as the board's exclusive financial advisor to assist the board in considering various strategic alternatives, including, determining whether a sale of the company was advisable and, if so, identify opportunities for such sale, to assist the board in negotiating the financial aspects and facilitate the consummation of any such acquisition and, if requested, to render an opinion with respect to the fairness, from a financial point of view, to our stockholders of the consideration to be received in any such acquisition. The engagement agreement is more fully discussed below under "—Persons Retained, Employed, Compensated or Used". At the February 24, 2004 meeting, the board also considered the risk that members of management might decide to terminate their employment with us if the board chose to proceed with a sale of the company. The board believed that there was a risk to our business and to our ability to maximize the value to our stockholders upon a sale of our company if we were unable to retain the services and cooperation of our management and that it would be necessary to consider ways to properly provide assurances to management so that they would be in a position to assist the board in maximizing stockholder value in a transaction. Accordingly, the board, after discussion and deliberation, decided to grant retention bonuses in connection with a change in control of our company to promote the retention of key members of our management team through the sale process.

Later that same day we issued a press release stating that we had retained SunTrust to provide financial advisory services and review possible strategic alternatives for us, including a sale, merger or other corporate transaction in an effort to maximize stockholder value. Our board determined, after weighing a number of factors, including our depressed stock price, our inability to further leverage the company and our lack of a management succession plan, that the sale of the company was our best

8

alternative. SunTrust was then authorized by the board to prepare a confidential offering memorandum, to conduct a market check by identifying and contacting potential strategic and financial buyers, to provide informational materials regarding our company (subject to the execution of a confidentiality agreement) and to negotiate with parties that express interest in acquiring us.

Between March 5, 2004, and April 13, 2004, SunTrust conducted a preliminary analysis of our company and prepared, with our assistance, a confidential memorandum which contained a brief discussion of our business as well as certain financial information.

SunTrust also promptly commenced the process of identifying and contacting potential strategic and financial buyers. From April 2004 through June 2004, SunTrust contacted or was contacted by 115 potential bidders, including 29 strategic buyers (some of whom are direct competitors of ours) and 86 financial buyers, including Parent, about the possibility of acquiring us or entering into another strategic transaction with us.

Of the 115 potential buyers contacted by SunTrust, 36 signed confidentiality agreements (of which 4 were strategic buyers and 32 were financial buyers), providing them with access to the confidential offering memorandum and additional information about us.

On May 13, 2004, Sun executed a confidentiality agreement with SunTrust, who executed the agreement on our behalf. Representatives of SunTrust and Sun had numerous conferences over the next several weeks with respect to the company.

During the week of June 3, 2004, SunTrust received initial indications of interest from 7 potential bidders, all of whom were financial buyers. Meetings between our management, SunTrust and 6 of the potential bidders, including Sun, were held between June 14, 2004 and July 13, 2004.

On July 13, 2004, SunTrust sent out process letters, together with a draft of the Acquisition Agreement prepared by Sills Cummis Epstein & Gross P.C., our legal counsel, to 6 of the potential bidders. The process letters asked the potential bidders to submit a non-binding proposal to acquire the company by July 22, 2004. SunTrust also requested that any proposal be accompanied by the bidder's comments to the Acquisition Agreement and specify any conditions to which the proposal would be subject.

In response to the process letters, SunTrust received 4 non-binding written acquisition proposals by the close of business on July 27, 2004: the proposal from Sun and 3 from other financial buyers.

On July 27, 2004, Sun sent SunTrust its non-binding proposal to acquire all of the fully-diluted outstanding shares of our common stock by means of a cash tender offer or merger at a price of $4.17 per share plus the assumption of our debt as of the closing date. The proposal was subject to certain conditions, including the satisfactory completion of Sun's due diligence investigation and the negotiation and execution of definitive documents. In addition, the proposal requested a 60 day exclusivity period and assumed a normalized level of working capital. Sun also sent to SunTrust its preliminary comments to the Acquisition Agreement. SunTrust engaged in preliminary discussions with Sun with respect to its proposals. During this time, SunTrust also continued discussions with each of the other bidders concerning their proposals.

On July 29, 2004, our board of directors met to discuss, among other things, the status of discussions with parties potentially interested in strategic transactions with us, including Sun. Also in attendance were representatives of Sills Cummis and SunTrust. SunTrust reviewed in detail the process that resulted in the expression of interest from Parent (and the expressions of interest from others) and indicated that it had substantially completed the process of soliciting proposals. SunTrust then highlighted for the board the 4 proposals received by SunTrust. Sills Cummis then discussed the details of the proposals in greater depth. At the conclusion of the meeting, the board instructed SunTrust to provide additional information to the bidders and to solicit final and best proposals from each bidder.

Following the meeting of our board, SunTrust contacted the bidders. Over the next few days, our board of directors met several times to discuss the status of negotiations.

On August 2, 2004, SunTrust contacted Sun and asked Sun to raise its proposed offer price to $4.30 per share, to eliminate the normalized working capital assumption, to assume the payment of

9

the outstanding stock options and to reduce the exclusivity period from 60 days to 30 days. Sun agreed to these terms telephonically, with an additional condition that the 30 day exclusivity period would be extended by 15 days if Sun still needed more information from the Rag Shops. SunTrust also contacted each of the other bidders and asked them to raise their proposed offer price by noon on August 3, 2004.

On August 3, 2004, Sun submitted a revised non-binding written proposal to acquire all of the fully-diluted outstanding shares of our common stock by means of a cash tender offer or merger at a price of $4.30 per share plus the assumption of debt and agreed and to shorten the exclusivity period to 30 days so long as there was an option to extend the exclusivity period by 15 days if we have not timely provided Sun with the information it reasonably needs to complete its evaluation of us. This proposal superceded Sun's July 27, 2004, proposal. The proposal was subject to certain conditions, including the satisfactory completion of Sun's due diligence investigation and the negotiation and preparation of definitive agreements. Sun also agreed to remove the assumption that there be a normalized level of working capital. No other revised proposals were received from the other bidders.

On August 3, 2004, our board of directors held a meeting for the purpose of evaluating the revised proposals. In attendance were all of the members of our board, representatives of SunTrust and representatives of Sills Cummis. SunTrust presented a comparative analysis of the bids and discussed the bids in detail with the board. Sills Cummis then reviewed the proposals in greater depth. At the conclusion of the discussions, the board determined that it should enter into exclusive discussions with Sun, a condition precedent to Sun's willingness to proceed. The determination was based on a consideration of Sun's proposed purchase price of $4.30 per share, which represented a premium over the next highest bid, as well as a consideration of the terms, conditions and contingencies of the bid (including, among other things, the fact that Sun's proposal did not have any financing contingency), Sun's proposed timeline for due diligence and negotiation, Sun's proven record of successfully completing similar transactions, Sun's financial commitment and level of effort at this point in the process and the assessment of the likelihood that the proposed transaction would be successfully completed. The board was particularly impressed with Sun's interest in completing the Offer and Merger as soon as possible. At that meeting, the board approved Sun's proposal and executed a non-binding letter of intent.

Following that meeting, SunTrust contacted the remaining bidders and informed them that we had executed a non-binding letter of intent with another party.

On August 5, 2004, in furtherance of Sun's due diligence investigation of us, representatives of Sun visited our offices and facilities and met with members of our management. Sun's accountants, insurance advisors and benefits advisors also visited our facilities in connection with their due diligence investigation of us.

During the month of August, in furtherance of Sun's due diligence investigation of us, Hughes Hubbard & Reed LLP, legal counsel to Sun, Parent and Purchaser, held multiple telephonic meetings with Sills Cummis and us to discuss legal due diligence items.

On August 10, 2004, Sills Cummis sent a memo to Hughes Hubbard in response to Sun's comments to the Acquisition Agreement. The parties then engaged in negotiations of the specific terms of the Acquisition Agreement. Negotiations continued through the month of August until September 7, 2004. Among the more significant issues negotiated were the termination provisions, the representations and warranties to be made by us and the conditions to the consummation of the offer and the merger.

On or about August 29, 2004, Hughes Hubbard sent to Sills Cummis a draft of the Stock Purchase Agreement among Parent and certain of our stockholders pursuant to which they agreed to sell to Purchaser approximately 55.7% of our outstanding common stock at a price per share equal to $4.30. Counsel for the selling stockholders, Wolff & Samson PC, and Hughes Hubbard proceeded to negotiate the stock purchase agreement through the remainder of August through September 7, 2004.

On September 7, 2004, our board of directors convened a meeting for the purpose of determining whether to approve the Acquisition Agreement and the Stock Purchase Agreement. At that meeting,

10

prior to any board action, Sills Cummis reviewed the board's fiduciary duties and the material terms of the Acquisition Agreement, including the termination provisions and break-up fees. SunTrust rendered to the board an oral opinion (which opinion was confirmed by the delivery of a written opinion, dated September 13, 2004) to the effect that, as of the date of the opinion, and based upon and subject to certain matters stated in the opinion, the $4.30 net per share cash consideration to be received in the Offer and the Merger was fair, from a financial point of view, to our stockholders. After further discussion and the evaluation of a number of factors, including those described below under "—Board's Recommendations", our board of directors, with Stanley Berenzweig and Jeffrey Gerstel abstaining, unanimously approved the Acquisition Agreement, the stock purchase agreement and other related agreements.

The same day Parent advised us that its board of directors acted by unanimous consent to approve the Offer and the Merger, subject to resolution of outstanding issues and finalization of definitive documentation.

On September 10, 2004, we were informed by Parent that it was not in a position to execute the Acquisition Agreement, the Stock Purchase Agreement and the related documents because Hurricane Ivan was expected to make landfall in Florida on September 11 or 12 and Parent was afraid of the impact Hurricane Ivan could have on our business by destroying one or more of our stores. Later that same day, we signed a letter with Sun extending Sun's exclusivity period set forth in the letter of intent through and including September 17, 2004.

The Acquisition Agreement, the Stock Purchase Agreement and other related agreements were executed, effective as of September 13, 2004, and the transaction was announced publicly through a press release issued by us on September 13, 2004.

On September 22, 2004, in accordance with the Acquisition Agreement, the Purchaser commenced the Offer.

Neither Sun, Parent nor Purchaser assumes responsibility for the accuracy or completeness of any information contained herein regarding Rag Shops discussions with any person, other than Sun, Parent, Purchaser, and their representatives, or regarding any matters involving Rag Shops or its board of directors, other than matters in which Sun, Parent, Purchaser or their representatives directly participated. All such information has been provided to Sun, Parent and Purchaser by Rag Shops for inclusion herein.

Basis for SunTrust's Fairness Opinion

The full text of SunTrust's written fairness opinion, dated September 13, 2004, which sets forth the assumptions made, procedures followed, other matters considered and limitations of the review undertaken, is attached as Annex A to this Statement. Rag Shops shareholders are urged to read this opinion and SunTrust's presentation to the board of directors, attached hereto as Exhibit (a)(7), in their entirety. SunTrust's opinion was directed only to the fairness, from a financial point of view, of the consideration to be paid by Purchaser to the holders of Rag Shops common stock pursuant to the Acquisition Agreement and Stock Purchase Agreement. SunTrust's opinion was delivered in conjunction with its presentation to the Rag Shops board of directors, and was for the information of the Rag Shops board of directors and does not constitute a recommendation as to how any stockholder should act in connection with the Offer and the Merger. This summary of the fairness opinion of SunTrust is qualified in its entirety by reference to the full text of such opinion which is filed as Exhibit (a)(6) hereto and the basis for the fairness opinion is qualified in its entirety by reference to the full text of the presentation to the board of directors which is filed as Exhibit (a)(7), and we incorporate such text herein by reference.

In preparing its opinion, SunTrust performed a variety of financial and comparative analyses, a summary of which are described below. The summary is not a complete description of the analyses underlying SunTrust's opinion. The preparation of a fairness opinion is a complex analytic process involving various determinations as to the most appropriate and relevant methods of financial analysis and the application of those methods to the particular circumstances and, therefore, is not readily susceptible to summary description. Accordingly, SunTrust believes that its analyses must be

11

considered as an integrated whole and that selecting portions of its analyses and factors, without considering all analyses and factors, could create a misleading or incomplete view of the processes underlying such analyses and SunTrust's opinion.

In performing its analyses, SunTrust made numerous assumptions with respect to Rag Shops, industry performance and general business, economic, market and financial conditions, many of which are beyond the control of Rag Shops. The estimates contained in these analyses and the valuation ranges resulting from any particular analysis are not necessarily indicative of actual values or predictive of future results or values, which may be significantly more or less favorable than those suggested by such analyses. In addition, analyses relating to the value of businesses or securities do not purport to be appraisals or to reflect the prices at which businesses or securities actually may be sold. Accordingly, these analyses and estimates are inherently subject to substantial uncertainty.

The following is a summary of the material financial and comparative analyses presented by SunTrust in connection with its opinion to the Rag Shops Board.

Analysis of Rag Shops

Stock Price Trading History

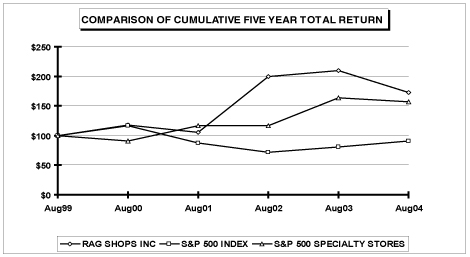

SunTrust examined the trading history of Rag Shops' common stock relative to the Offer Price. For the period beginning February 24, 2003, and ending February 24, 2004, the last business day immediately prior to the date on which Rag Shops announced that it had engaged SunTrust to provide investment banking advice and services to Rag Shops stock in connection with its review and analysis of various strategic alternatives, including a potential sale of Rag Shops. The highest daily closing price of Rag Shops common stock on the Nasdaq SmallCap Market was $4.74 and lowest daily closing price of Rag Shops was $2.98. The closing price for Rag Shops' common stock on February 24, 2004 was $3.65. For the 52-week period ending August 30, 2004, the highest daily closing price of Rag Shops was $4.74 and lowest daily closing price of Rag Shops was $3.11 The closing price of Rag Shops' common stock on the Nasdaq Small Cap Market on August 30, 2004 was $3.61.

Analysis of Selected Publicly-Traded Reference Companies

SunTrust compared selected financial data and market information for Rag Shops to the corresponding financial data and market information for two groups of public companies selected by SunTrust. The first group consisted of craft and celebration retailers and included A.C. Moore Arts & Crafts, Inc., Hancock Fabrics, Inc., Jo-Ann Stores, Inc., Michaels Stores, Inc. and Party City Corporation ("Craft & Celebration Retailers"). The second group consisted of the Craft & Celebration Retailers, as well as a group of discount retailers that included 99 Cents Only Stores, Big Lots, Inc., Dollar General Corporation, Dollar Tree Stores, Inc., Family Dollar Stores, Inc. and Fred's, Inc. ("Craft, Celebration & Discount Retailers"). The Craft & Celebration Retailers were selected by SunTrust as companies that were representative, in its opinion, of the particular segment of the retail craft and fabrics industry in which Rag Shops operates and which have similar financial characteristics to Rag Shops.

For each of the selected publicly-traded reference companies, SunTrust analyzed, among other things, the firm value of the company, defined as its market capitalization plus debt outstanding, based on publicly reported financial results as of the date of the opinion, less cash and cash equivalents on hand, based on publicly reported financial results as of the date of the opinion, as a multiple of (i) the company's revenue for the latest twelve month ("LTM") period, based on publicly reported financial results as of September 13, 2004, the date of the fairness opinion, and projections for the 2004 fiscal year; (ii) the company's earnings before interest, taxes, depreciation and amortization ("EBITDA") for the LTM period, based on publicly reported financial results as of September 13, 2004, the date of the fairness opinion and projections for the 2004 and 2005 fiscal years; and (iii) the company's earnings before interest and taxes ("EBIT") for the LTM period, based on publicly reported financial results as of September 13, 2004, the date of the fairness opinion, and projections for the 2004 fiscal year. SunTrust also analyzed the stock price of each of the selected publicly-traded reference companies as

12

a multiple of the company's (i) book value, based on publicly reported financial results as of the date of the opinion; and (ii) earnings per share ("EPS") for the LTM period, based on publicly reported financial results as of and projections for the 2004 and 2005 fiscal and/or calendar years. All multiples were based on closing stock prices of Rag Shops' common stock on the Nasdaq Small Cap Market as of August 30, 2004. Projected revenue, EBITDA and EBIT for the reference companies were based on Bloomberg consensus estimates. Bloomberg is an information provider that publishes a compilation of estimates of projected financial performance for publicly-traded companies produced by equity research analysts at leading investment banking firms. Projected EPS for the reference companies was based on First Call data. First Call is an equity/industry research service. It provides research notes, earnings estimates and fundamental analyses from the top investment firms on thousands of U.S. and international publicly-traded companies. The following table sets forth the mean and median multiples indicated by the market analysis of the two selected groups of publicly-traded reference companies:

| Craft & Celebration Retailers | Craft, Celebration & Discount Retailers | |||||||||||||||||||||

| Mean | Median | Mean | Median | |||||||||||||||||||

| Firm Value to: | ||||||||||||||||||||||

| LTM Revenue | 0.67 | x | 0.54 | x | 0.70 | x | 0.83 | x | ||||||||||||||

| 2004 Revenue | 0.64 | 0.54 | 0.66 | 0.72 | ||||||||||||||||||

| LTM EBITDA | 8.1 | 9.3 | 8.1 | 8.3 | ||||||||||||||||||

| 2004 EBITDA | 6.5 | 5.9 | 7.1 | 7.0 | ||||||||||||||||||

| 2005 EBITDA | 6.3 | 6.4 | 6.4 | 6.4 | ||||||||||||||||||

| LTM EBIT | 11.0 | 11.9 | 11.2 | 11.9 | ||||||||||||||||||

| 2004 EBIT | 9.2 | 9.9 | 10.5 | 10.4 | ||||||||||||||||||

| Equity Value to: | ||||||||||||||||||||||

| LTM Net Income | 19.0 | x | 20.7 | x | 18.7 | x | 18.8 | x | ||||||||||||||

| Net Income 2004 | 18.6 | 19.2 | 18.2 | 18.1 | ||||||||||||||||||

| Net Income 2005 | 14.1 | 14.4 | 14.6 | 14.6 | ||||||||||||||||||

| Book Value | 2.2 | 2.4 | 2.4 | 2.4 | ||||||||||||||||||

Based upon the mean and median multiples derived by SunTrust from this analysis for the Craft & Celebration Retailers, Rag Shops' LTM results for the period ended May 29, 2004, and projected 2004 and 2005 results, SunTrust calculated a range of implied equity values for Rag Shops between $15.50 and $0.00 per share using the reference companies' mean multiples and a range of implied equity values for Rag Shops between $12.45 and $0.00 per share using the reference companies' median multiples. The weighted average and median implied equity values derived from this analysis using the Craft & Celebration Retailers' mean multiples, Rag Shops' LTM results ended May 29, 2004 and projected 2004 and 2005 results were $2.64 and $0.00 per share, respectively. The weighted average and median implied equity values derived from this analysis using the Craft & Celebration Retailers' median multiples, Rag Shops' LTM results ended May 29, 2004 and projected 2004 and 2005 results were $2.42 and $0.00 per share, respectively.

Based upon the mean and median multiples derived from this analysis for the Craft, Celebration & Discount Retailers, Rag Shops' LTM results ended May 29, 2004 and projected 2004 and 2005 results, SunTrust calculated a range of implied equity values for Rag Shops between $16.19 and $0.00 per share using the reference companies' mean multiples and a range of implied equity values for Rag Shops between $19.27 and $0.00 per share using the reference companies' median multiples. The weighted average and median implied equity values derived from this analysis using the Craft, Celebration & Discount Retailers' mean multiples, Rag Shops' LTM results ended May 29, 2004 and projected 2004 and 2005 results were $2.76 and $0.00 per share, respectively. The weighted average and median implied equity values derived from this analysis using the Craft, Celebration & Discount Retailers' median multiples, Rag Shops' LTM results ended May 29, 2004 and projected 2004 and 2005 results were $2.99 and $0.00 per share, respectively.

SunTrust compared the implied equity values per share from each of these analyses to the Offer Price.

13

SunTrust noted that none of the companies used in the market analysis of selected publicly-traded reference companies was identical to Rag Shops and that, accordingly, the analysis necessarily involves complex considerations and judgments concerning differences in financial and operating characteristics of the companies reviewed and other factors that would affect the market values of the selected publicly-traded companies and Rag Shops.

Analysis of Selected Merger and Acquisition Transactions

SunTrust performed an analysis of selected completed and pending reference transactions involving retail companies announced between January 1, 1999 and August 30, 2004, that it deemed relevant.

For the selected transactions, SunTrust analyzed, among other things, the consideration paid in such transactions, including the assumption of debt by the acquiring company, of the selling company, as a multiple of LTM Revenue, EBITDA and EBIT, as well as the consideration paid in such transactions for the equity of the selling company as a multiple of net income. Revenue, EBITDA, EBIT and net income were based on historical financial information available in public filings and press releases of the selling company related to the selected transactions. The following table sets forth the multiples indicated by this analysis:

| All Reference Transactions | ||||||||||||||||||

| Mean | Median | |||||||||||||||||

| Firm Value to: | ||||||||||||||||||

| LTM Revenue | 0.60 | 0.51 | ||||||||||||||||

| LTM EBITDA | 8.9 | x | 8.7 | x | ||||||||||||||

| LTM EBIT | 13.2 | 12.0 | ||||||||||||||||

| Equity Value to: | ||||||||||||||||||

| Net Income | 20.3 | x | 22.5 | x | ||||||||||||||

Based upon the multiples derived from this analysis and Rag Shops' results for the LTM period ended May 29, 2004, SunTrust calculated a range of implied equity values for Rag Shops between $0.00 and $13.76 per share using the mean multiples for the reference transactions and a range of implied equity values for Rag Shops between $0.00 and $11.52 using the median multiples from the reference transactions. The weighted average and median implied equity values derived from this analysis using the mean multiples from the reference transactions and Rag Shops' LTM ended May 29, 2004 results were $0.00 and $2.06 per share, respectively. The weighted average and median implied equity values derived from this analysis using the median multiples from the reference transactions and Rag Shops LTM ended May 29, 2004 results were $0.00 and $1.73 per share, respectively. SunTrust compared these implied equity values per share to the Offer Price.

Premiums Paid Analysis

SunTrust performed an analysis of the premiums paid in three groups of selected merger and acquisition transactions which, in SunTrust's judgment, were deemed to be relevant to the proposed transaction for purposes of this analysis. The first group consisted of acquisitions of public companies from January 1, 2004 to August 30, 2004, with an aggregate transaction value of between $10 and $100 million and in which the purchaser purchased 50% or more of the selling company ("Recent Similar-Sized Transactions"). This group included 150 transactions. The second group consisted of acquisitions of public retail companies from January 1, 2002 to August 30, 2004 in which the purchaser purchased 50% or more of the selling company ("Retail Transactions"). This group included 93 transactions. The third group consisted of acquisitions of public specialty retail companies from January 1, 2002 to August 30, 2004 in which the purchaser purchased 50% or more of the selling company ("Specialty Retail Transactions"). This group included 32 transactions. For each group, SunTrust reviewed the percentage premium paid in such transactions for the equity of the selling company relative to the selling company's closing price of its common stock one day, five days and 30 days prior to public announcement of the transaction. The table below summarizes the range of premiums paid for each of the three groups of transactions described above.

14

| Purchase Price Premium Prior to Announcement | ||||||||||||||

| 1 Day | 5 Days | 30 Days | ||||||||||||

| Recent Similar-Sized Transactions | ||||||||||||||

| Mean Premium | 26.9 | % | 28.8 | % | 29.6 | % | ||||||||

| Median Premium | 13.5 | 16.0 | 17.5 | |||||||||||

| Retail Transactions | ||||||||||||||

| Mean Premium | 28.3 | % | 37.1 | % | 45.1 | % | ||||||||

| Median Premium | 21.0 | 29.0 | 36.0 | |||||||||||

| Specialty Retail Transactions | ||||||||||||||

| Mean Premium | 22.3 | % | 24.7 | % | 28.8 | % | ||||||||

| Median Premium | 21.0 | 22.5 | 26.0 | |||||||||||

Based upon the premiums paid on the Recent Similar-Sized Transactions, SunTrust calculated a range of implied equity values for Rag Shops between $4.58 and $4.68 per share using the mean premiums for the selected transactions and a range of implied equity values for Rag Shops between $4.10 and $4.24 per share using the median premiums for the selected transactions. The mean and median implied equity values derived from this analysis using the mean premiums from the Recent Similar-Sized Transactions and Rag Shops' closing stock price on August 30, 2004, were $4.64 and $4.65 per share, respectively. The mean and median implied equity values derived from this analysis using the median premiums from the Recent Similar-Sized Transactions and Rag Shops' closing stock price on August 30, 2004 were $4.18 and $4.19 per share, respectively.

Based upon the premiums paid on the Retail Transactions, SunTrust calculated a range of implied equity values for Rag Shops between $4.63 and $5.24 per share using the mean premiums for the selected transactions and a range of implied equity values for Rag Shops between $4.37 and $4.91 per share using the median premiums for the selected transactions. The mean and median implied equity values derived from this analysis using the mean premiums from the Retail Transactions and Rag Shops' closing stock price on August 30, 2004 were $4.94 and $4.95 per share, respectively. The mean and median implied equity values derived from this analysis using the median premiums from the Retail Transactions and Rag Shops' closing stock price on August 30, 2004 were $4.64 and $4.66 per share, respectively.

Based upon the premiums paid on the Speciality Retail Transactions, SunTrust calculated a range of implied equity values for Rag Shops between $4.41 and $4.65 per share using the mean premiums for the selected transactions and a range of implied equity values for Rag Shops between $4.37 and $4.55 per share using the median premiums for the selected transactions. The mean and median implied equity values derived from this analysis using the mean premiums from the Specialty Retail Transactions and Rag Shops' closing stock price on August 30, 2004 were $4.50 and $4.52 per share, respectively. The mean and median implied equity values derived from this analysis using the median premiums from the Specialty Retail Transactions and Rag Shops' closing stock price on August 30, 2004 were $4.42 and $4.45 per share, respectively.

SunTrust compared the implied equity values per share from each of these analyses to the Offer Price.

Discounted Cash Flow Analysis

SunTrust performed a discounted cash flow analysis of Rag Shops to estimate the net present equity value per share of Rag Shops. The discounted cash flow analysis was based upon projections provided by Rag Shops' management for fiscal years 2005 through 2009. SunTrust calculated a range of net present firm values for Rag Shops based on its free cash flow over the projected time period using a weighted average cost of capital for Rag Shops ranging from 15% to 25% and terminal value multiples of Rag Shops' fiscal year 2009 EBITDA of 5.5x to 7.5x. The analysis indicated a range of implied equity values for Rag Shops between $2.30 and $5.09 per share. SunTrust compared these implied equity values per share to the Offer Price.

15

Other Responses and Proposals

SunTrust also took into consideration various other factors including the responses and proposals that resulted from the discussions that SunTrust and Rag Shops' senior management held with various parties that were interested either in acquiring or merging with Rag Shops. Approximately 115 parties were contacted by or contacted SunTrust regarding their interest in Rag Shops. Seven of these parties submitted written, non-binding indications of value. Of these parties, 6 conducted meetings with Rag Shops' senior management and conducted further due diligence. After concluding due diligence, no party made a definitive offer to acquire or merge with Rag Shops at a price equal to or greater than the $4.30 per share value offered by Sun.

Reasons for the Board's Recommendation

In approving the Acquisition Agreement and the transactions contemplated by it, including the Stock Purchase Agreement, the Offer and the Merger (the "Transaction"), and recommending that all holders of our common stock to accept the offer and tender their shares of our common stock pursuant to the Offer, the board considered a number of factors, including:

| • | the financial condition, results of operations and businesses of Rag Shops, on both a historical and prospective basis; |

| • | our future prospects and alternatives available to us as a stand-alone enterprise; |

| • | our inability to grow the business through acquisitions due to our depressed stock price and our inability to purchase another business with cash; |

| • | our lack of a management succession plan; |

| • | current industry, economic and market conditions and historical market prices; |

| • | price-to-earnings multiples and recent trading patterns of our common stock, including the lack of liquidity and trading volume of our common stock and our common stock's decrease in price; |

| • | our lack of institutional ownership and lack of research analyst coverage; |

| • | market prices and financial data relative to other companies engaged in the same or similar businesses as ours, and the prices and other terms of recent acquisition transactions in our industry; |

| • | our financial advisor contacted or was contacted by 115 potential bidders over a five month period and received only 4 favorable bids after performing a thorough market check; |

| • | certain challenges facing Rag Shops, including competition in each part of our business from other industry participants and our position in the industry relative to our competitors; |

| • | the relationship of the Offer to the historical market prices of our common stock, including (1) that the Offer Price represents a premium of approximately 23% over the closing price of our common stock on the trading day immediately preceding the announcement of the Transaction, (2) that the Offer Price represents a premium of approximately 18% over the median trading price of our common stock during the 30 calendar days immediately preceding the announcement of the Transaction, (3) that the Offer Price represents a premium of approximately 19% over the average closing price for our common stock of $3.60 during the 12-month period ended September 10, 2004 and (4) that no other bidder offered a price per Share as high as the Offer Price; |

| • | presentations by, and discussions with, our senior management and representatives of our financial and legal advisors regarding the Merger; |

| • | the fact that the Acquisition Agreement provides for a prompt cash tender offer for all outstanding shares of our common stock which may be followed by the Merger at the same cash price per share, thereby enabling our stockholders to obtain the benefits of the Transaction at the earliest possible time, and thereby reduce the risk of intervening events; |

16

| • | the form of consideration to be paid to our stockholders pursuant to the Offer and the Merger, and the certainty of value of cash consideration; |

| • | the financial presentation of SunTrust and the written opinion dated September 13, 2004, as to the fairness, from a financial point of view and as of such date, of the $4.30 per share cash consideration to be received in the Transaction by holders of our common stock. The full text of SunTrust's written opinion, dated September 13, 2004, which sets forth the assumptions made, procedures followed, matters considered and limitations on the review undertaken by SunTrust, is attached hereto as Annex A and is incorporated herein by reference; |

| • | that the Offer and the Merger would be taxable to Rag Shops stockholders and the cash paid to them pursuant to the Offer or the Merger could be used to satisfy any tax liability resulting from the Offer or the Merger; |

| • | that the costs of remaining a public company, including the costs of complying with the rules and regulations of the SEC, the Sarbanes-Oxley Act of 2002 and the rules and regulations of the Nasdaq SmallCap Market, which represents a significant financial drain on our resources and which is eroding stockholder value; |

| • | that the Acquisition Agreement permits the board to withdraw or modify its recommendation of the Transaction to the extent that the board determines that the failure to withdraw or modify such recommendation would be inconsistent with its fiduciary duties under applicable law; |

| • | that the withdrawal or modification of the board's recommendation of the Transaction would not alter its approval of the Acquisition Agreement for purposes of Section 203 of the DGCL; |

| • | that the Acquisition Agreement permits Rag Shops to participate in discussions or negotiations with, or furnish information to, any person that delivers a Takeover Proposal that, in the good faith judgment of the board, is, or is reasonably likely to, lead to a Superior Proposal; |

| • | that neither the commencement nor the consummation of the Offer is subject to the Parent's ability to secure financing commitments; |

| • | the fact that the offer is not contingent upon a minimum percentage of shares being tendered; |

| • | the likelihood of obtaining required regulatory approvals; and |

| • | the ability of Rag Shops stockholders who object to the Merger to obtain "fair value" for their shares of our common stock if they exercise and perfect their appraisal rights under Delaware law. |

The foregoing discussion of information and factors considered and given weight by the board is not intended to be exhaustive, but is believed to include all of the material factors, both positive and negative, considered by the board. In evaluating the Transaction, the members of the board considered their knowledge of the business, financial condition and prospects of Rag Shops, and the views of our management and its financial and legal advisors. In view of the wide variety of factors considered in connection with its evaluation of the Transaction, the board did not find it practicable to, and did not, quantify or otherwise assign relative weights to the specific factors considered in reaching its determinations and recommendations. In addition, individual members of the board may have given different weights to different factors.

The board recognized that, while the Transaction gives our stockholders the opportunity to realize a significant premium over the price at which the shares of our common stock were traded prior to the public announcement of the Transaction, adopting the Acquisition Agreement would eliminate the opportunity for our stockholders to participate in the future growth and profits of Rag Shops. The board believed that the loss of the opportunity to participate in the growth and profits of Rag Shops following the Offer are reflected in the $4.30 per share price offered by Parent in the Offer. The board also recognized that, as a result of the transactions contained in the Stock Purchase Agreement, Parent already owns approximately 55.7% of the Shares and, thus, controls the affairs of the company.

17

Intent to Tender

To the best of our knowledge, except as set forth in the following sentence, each executive officer, director, affiliate or subsidiary of Rag Shops who owns shares of our common stock intends to tender all issued and outstanding shares of our common stock held of record by such person to Purchaser in the Offer. In addition, Stanley Berenzweig, Doris Berenzweig, The Doris and Stanley Berenzweig Charitable Foundation Inc., Mona Adelson, Gail Loia, Steven Barnett and Judith Lombardo (of whom Mr. Berenzweig, Mrs. Berenzweig, Mr. Barnett and Ms. Lombardo are or were executive officers of Rag Shops) sold all of the Shares owned by them for $4.30 per share pursuant to the Stock Purchase Agreement. Such persons owned 2,671,199 shares of our outstanding common stock (approximately 55.7% of our outstanding shares), not including shares issuable upon exercise of options. Our remaining executive officers, directors, affiliates or subsidiaries own, in the aggregate, less than 1% of the issued and outstanding shares of our common stock.

Item 5. Persons, Retained, Employed, Compensated Or Used

Pursuant to the terms of the engagement agreement, dated February 24, 2004, between SunTrust and Rag Shops, Rag Shops engaged SunTrust to act as financial advisor to the board in connection with the consideration of acquisition offers. As part of its role as financial advisor, SunTrust executed and delivered an opinion with respect to the fairness, from a financial point of view, to our stockholders of the consideration to be received in any such acquisition and received a fee for such services and additional fees pursuant to the engagement agreement. For such services, SunTrust is due aggregate fees equal to $620,000, of which a portion has already been paid.

SunTrust is an institutional investment banking firm and, as part of its investment banking activities, is regularly engaged in the evaluation of businesses and their securities in connection with mergers and acquisitions, negotiated underwritings, competitive bids, secondary distributions of listed and unlisted securities, private placements and valuations for corporate and other purposes. The board of directors selected SunTrust to serve as its financial advisor because of its national reputation, fees, depth of experience in the retail sector and its ability to conduct a fairness analysis of any proposed transaction.

Except as described above, neither SunTrust, nor any member of the board of directors, nor any person acting on behalf of any of them, has or currently intends to employ, retain or compensate any person to make solicitations or recommendations with respect to the Offer or the Merger.

Except as set forth above, neither Rag Shops nor any person acting on its behalf has employed or retained or will compensate any person or class of persons to make solicitations or recommendations on its behalf with respect to the Offer.

Item 6. Interest In Securities Of The Subject Company

To our knowledge, no transactions in the Shares have been effected during the past 60 days by Rag Shops or its executive officers, directors, affiliates or subsidiaries, by Purchaser or its executive officers, directors, affiliates or subsidiaries or by any pension, profit-sharing or similar plan of Rag Shops.

Item 7. Purposes Of The Transaction And Plans Or Proposals

Except as set forth in this Statement and the Offer to Purchase, Rag Shops is not undertaking or engaged in any negotiations in response to the Offer that relate to:

| • | a tender offer for or other acquisition of our securities by Rag Shops, any subsidiary of Rag Shops or any other person; |

| • | any extraordinary transaction, such as a merger, reorganization or liquidation, involving Rag Shops or any subsidiary of Rag Shops; |

| • | any purchase, sale, or transfer of a material amount of assets of Rag Shops or any subsidiary of Rag Shops; or |

18

| • | any material change in the present dividend rate or policy, or indebtedness or capitalization of Rag Shops. |

Except as set forth in this Statement or the Offer to Purchase, there are no transactions, resolutions of the board, agreements in principle, or signed contracts in response to the Offer that relate to one or more of the events referred to in this Item 7.

Item 8. Additional Information

Section 14(f) Information Statement

The Information Statement attached as Annex B hereto and filed herewith is being furnished in connection with the designation by Parent, pursuant to the Acquisition Agreement, of certain persons to be appointed to the board other than at a meeting of our stockholders.

Anti-Takeover Statute

As Rag Shops is a Delaware corporation, the provisions of Section 203 of the DGCL by their terms apply to the approval of the Offer and the Merger. The description of these provisions and their applicability to the approval of the Offer and the Merger is contained in Section 15, "Certain Legal Matters and Regulatory Approvals" of the Offer to Purchase, which is designated as Exhibit (a)(1)(A) and incorporated herein by reference. At its meeting held on September 7, 2004, the board approved the Transaction Agreements and the transactions contemplated thereby, which approval rendered Section 203 of the DGCL inapplicable to the Transaction Agreements and the transactions contemplated thereby, including the Offer and the Merger.

Appraisal Rights