UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06310

Legg Mason Partners Variable Income Trust

(Exact name of registrant as specified in charter)

55 Water Street, New York, NY 10041

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code:

Funds Investor Services 1-800-822-5544

or

Institutional Shareholder Services 1-888-425-6432

Date of fiscal year end: December 31

Date of reporting period: June 30, 2010

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

June 30, 2010

Semi-Annual Repor t

Legg Mason

Western Asset

Variable Diversified

Strategic Income

Portfolio

INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

| | |

| II | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio |

Portfolio objective

The Portfolio seeks high current income.

Portfolio name change

Prior to November 2, 2009, the Portfolio was known as Legg Mason Partners Variable Diversified Strategic Income Portfolio. There was no change in the Portfolio’s investment objective or investment policies as a result of the name change.

| | |

| Letter from the chairman | |  |

Dear Shareholder,

We are pleased to provide the semi-annual report of Legg Mason Western Asset Variable Diversified Strategic Income Portfolio for the six-month reporting period ended June 30, 2010.

Please read on for Portfolio performance information and a detailed look at prevailing economic and market conditions during the Portfolio’s reporting period. Important information with regard to recent regulatory developments that may affect the Portfolio is contained in the Notes to Financial Statements included in this report.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.leggmason.com/individualinvestors. Here you can gain immediate access to market and investment information, including:

| Ÿ | | Market insights and commentaries from our portfolio managers and |

| Ÿ | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

July 30, 2010

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio | | III |

Investment commentary

Economic review

While the overall U.S. economy continued to expand over the six months ended June 30, 2010, several economic data points weakened toward the end of the reporting period. This, in combination with sovereign debt woes in Europe, caused investor sentiment to turn negative and had significant implications for the financial markets.

Looking back, the U.S. Department of Commerce reported that U.S. gross domestic product (“GDP”)i contracted four consecutive quarters, beginning in the third quarter of 2008 through the second quarter of 2009. Economic conditions then began to improve in the third quarter of 2009, as GDP growth was 1.6%. A variety of factors helped the economy to regain its footing, including the government’s $787 billion stimulus program. Economic growth then accelerated during the fourth quarter of 2009, as GDP growth was 5.0%. A slower drawdown in business inventories and renewed consumer spending were contributing factors spurring the economy’s higher growth rate. While the recovery continued during the first half of 2010, it did so at a more modest pace, as GDP growth was 3.7% during the first quarter of 2010 and an estimated 2.4% during the second quarter. The slower pace of growth in the second quarter was due, in part, to slower consumer spending, which rose an annualized 1.6% during the quarter, versus a 1.9% gain over the first three months of the year.

Even before GDP growth turned positive, there were signs that the economy was on the mend. The manufacturing sector, as measured by the Institute for Supply Management’s PMIii, rose to 52.8 in August 2009, the first time it surpassed 50 since January 2008 (a reading below 50 indicates a contraction, whereas a reading above 50 indicates an expansion). While June 2010’s PMI reading of 56.2 was lower than May’s reading of 59.7, manufacturing has now expanded eleven consecutive months according to PMI data. The manufacturing sector’s growth remained fairly broad-based with thirteen of the eighteen industries tracked by the Institute for Supply Management expanding during June.

After experiencing sharp job losses in 2009, the U.S. Department of Labor reported that over one million new positions were added during the first five months of 2010. Included in that total, however, were 700,000 temporary government jobs tied to the 2010 Census. In June, 225,000 of these temporary positions were eliminated, offsetting private sector growth and resulting in a net loss of 125,000 jobs for the month. However, the unemployment rate fell to 9.5% in June, versus 9.7% and 9.9% in May and April, respectively.

There was mixed news in the housing market during the period. According to the National Association of Realtors, existing home sales increased 7.0% and 8.0% in March and April, respectively, after sales had fallen for the period from December 2009 through February 2010. The rebound was largely attributed to people rushing to take advantage of the government’s $8,000 tax credit for first-time home buyers that expired at the end of April. However, with the end of the tax credit, existing home sales then declined 2.2% and 5.1% in May and June, respectively. In addition, the inventory of unsold homes increased 2.5% to 3.99 million in June. Looking at home prices, the S&P/Case-Shiller Home Price Indexiii indicated that month-to-month U.S. home prices rose 1.3% in May. This marked the second straight monthly increase following six consecutive months of declining prices.

Financial market overview

During the first half of the reporting period, the financial markets were largely characterized by healthy investor risk appetite and solid results by lower-quality bonds. However, the market experienced a sharp sell-off during the second half of the reporting period, during which risk aversion returned and investors flocked to the relative safety of U.S. Treasury securities.

Given certain pockets of weakness in the economy, including elevated unemployment in the U.S., the Federal Reserve Board (“Fed”)iv remained cautious. At its meeting in June 2010, the Fed said it “will maintain the target range for the federal funds ratev at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

However, the Fed took several steps in reversing its accommodative monetary stance. On February 18, 2010, the Fed raised the discount rate, the interest rate it charges banks for temporary loans, from 1/2 to 3/4 percent. The Fed also concluded its $1.25 trillion mortgage securities purchase program at the end of the first quarter of 2010. However, the Fed left the door open for future stimulus measures if needed. In the minutes of its June meeting that were released on July 14th (after the reporting period ended), the Fed said, “In addition to continuing to develop and test instruments to exit from the period of unusually accommodative monetary policy, the Committee would need to consider whether further policy stimulus might become appropriate if the outlook were to worsen appreciably.”

| | |

| IV | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio |

Investment commentary (cont’d)

Fixed-income market review

Continuing the trend that began in the second quarter of 2009, nearly every spread sector (non-Treasury) outperformed equal-durationvi Treasuries during the first half of the reporting period. Over that time, investor confidence was high given encouraging economic data, continued low interest rates, benign inflation and rebounding corporate profits. However, robust investor appetite was replaced with heightened risk aversion toward the end of April and during the month of May. This was due to the escalating sovereign debt crisis in Europe, uncertainties regarding new financial reforms in the U.S. and some worse-than-expected economic data. Most spread sectors then produced positive absolute returns in June, as investor demand for these securities began to again increase.

Both short- and long-term Treasury yields fluctuated during the period but generally moved lower. When the period began, two- and ten-year Treasury yields were 1.14% and 3.85%, respectively. Two- and ten-year Treasury yields initially rose, reaching as high as 1.18% and 4.01%, respectively, in early April. Yields then largely declined amid the investor “flight to quality.” On June 30, 2010, two- and ten-year Treasury yields reached their lows for the reporting period: 0.61% and 2.97%, respectively. Over the six-month reporting period, the yield curvevii flattened, with longer-term Treasury yields declining more than their shorter-term counterparts. For the six months ended June 30, 2010, the Barclays Capital U.S. Aggregate Indexviii returned 5.33%.

While the high-yield bond market could not escape the negative impact of the investor flight to quality, it still was able to produce strong results during the reporting period. The asset class posted positive returns during each month except for May 2010 when risk aversion reached extremely elevated levels. The high-yield market was supported by better-than-expected corporate profits and overall strong investor demand. All told, the Barclays Capital U.S. High Yield – 2% Issuer Cap Indexix returned 4.45% for the six months ended June 30, 2010.

Emerging market debt prices rallied over the reporting period, also posting positive returns each month during the period except for May 2010. This impressive performance was triggered by strong economic growth in many emerging market countries, solid domestic demand and generally robust investor demand for the asset class. The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”)x returned 5.37% over the six months ended June 30, 2010.

Performance review

For the six months ended June 30, 2010, Legg Mason Western Asset Variable Diversified Strategic Income Portfolio1 returned 7.23%. The Portfolio’s unmanaged benchmark, the Barclays Capital U.S. Aggregate Index, returned 5.33% over the same time frame. The Lipper Variable General Bond Funds Category Average2 returned 4.77% for the same period.

| | | |

| Performance Snapshot as of June 30, 2010 (unaudited) | |

| | | 6 months | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio1 | | 7.23 | % |

| Barclays Capital U.S. Aggregate Index | | 5.33 | % |

| Lipper Variable General Bond Funds Category Average | | 4.77 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value, investment returns and yields will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

Portfolio returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

The 30-Day SEC Yield for the period ended June 30, 2010 was 3.53%. The 30-Day SEC Yield is the average annualized net investment income per share for the 30-day period indicated and is subject to change.

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| 2 | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the six-month period ended June 30, 2010, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 71 funds in the Portfolio’s Lipper category. |

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio | | V |

|

| Total Annual Operating Expenses (unaudited) |

As of the Portfolio’s most current prospectus dated April 30, 2010, the gross total operating expense ratio for the Portfolio was 0.95%.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Portfolio expense ratios are more likely to increase when markets are volatile.

As always, thank you for your confidence in our stewardship of your assets.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

July 30, 2010

RISKS: As interest rates rise, bond prices fall, reducing the value of the Portfolio’s share price. High-yield bonds involve greater credit and liquidity risks than investment grade bonds. Investing in foreign securities is subject to certain risks not associated with domestic investing, such as currency fluctuations, and changes in political and economic conditions. These risks are magnified in emerging or developing markets. The Portfolio may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Portfolio performance. Please see the Portfolio’s prospectus for more information on these and other risks.

All investments are subject to risk including the possible loss of principal. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| i | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| ii | The Institute for Supply Management’s PMI is based on a survey of purchasing executives who buy the raw materials for manufacturing at more than 350 companies. It offers an early reading on the health of the manufacturing sector. |

| iii | The S&P/Case-Shiller Home Price Index measures the residential housing market, tracking changes in the value of the residential real estate market in twenty metropolitan regions across the United States. |

| iv | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| v | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| vi | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| vii | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

| viii | The Barclays Capital U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| ix | The Barclays Capital U.S. High Yield – 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Barclays Capital U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. |

| x | The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds and local market instruments. |

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 1 |

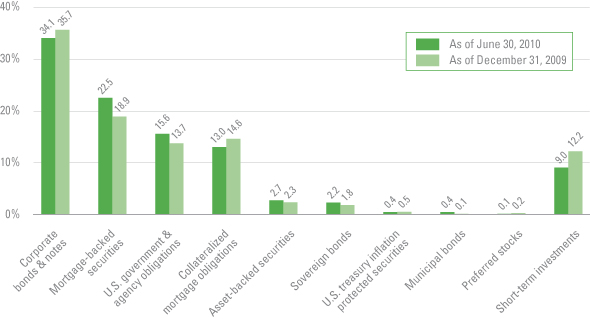

Portfolio at a glance† (unaudited)

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of June 30, 2010 and December 31, 2009 and does not include derivatives. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

| 2 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Portfolio expenses (unaudited)

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on January 1, 2010 and held for the six months ended June 30, 2010.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Based on actual total return1 | | | | Based on hypothetical total return1 |

Actual Total

Return2 | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period3 | | | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period3 |

| 7.23% | | $ | 1,000.00 | | $ | 1,072.30 | | 0.96 | % | | $ | 4.93 | | | | 5.00 | % | | $ | 1,000.00 | | $ | 1,020.03 | | 0.96 | % | | $ | 4.81 |

| 1 | For the six months ended June 30, 2010. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total return does not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total return. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Expenses are equal to the Portfolio’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181), then divided by 365. |

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 3 |

Schedule of investments (unaudited)

June 30, 2010

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

| Corporate Bonds & Notes — 37.5% | | | | | | | | | | | | |

| Consumer Discretionary — 2.4% | | | | | | | | | | | | |

Automobiles — 0.1% | | | | | | | | | | | | |

Motors Liquidation Co., Senior Debentures | | 8.250 | % | | 7/15/23 | | $ | 155,000 | | $ | 47,662 | (a) |

Hotels, Restaurants & Leisure — 0.2% | | | | | | | | | | | | |

Boyd Gaming Corp., Senior Subordinated Notes | | 6.750 | % | | 4/15/14 | | | 10,000 | | | 8,800 | |

MGM MIRAGE Inc., Notes | | 6.750 | % | | 9/1/12 | | | 65,000 | | | 60,775 | |

Station Casinos Inc., Senior Notes | | 7.750 | % | | 8/15/16 | | | 50,000 | | | 3,406 | (a)(b) |

Total Hotels, Restaurants & Leisure | | | | | | | | | | | 72,981 | |

Media — 2.0% | | | | | | | | | | | | |

Cengage Learning Acquisitions Inc., Senior Notes | | 10.500 | % | | 1/15/15 | | | 10,000 | | | 9,350 | (c) |

Comcast Cable Communications LLC, Notes | | 8.875 | % | | 5/1/17 | | | 80,000 | | | 100,467 | |

Comcast Corp., Notes | | 6.500 | % | | 1/15/15 | | | 120,000 | | | 137,866 | |

Comcast Corp., Notes | | 5.875 | % | | 2/15/18 | | | 10,000 | | | 11,144 | |

CSC Holdings Inc., Senior Notes | | 6.750 | % | | 4/15/12 | | | 50,000 | | | 52,000 | |

DISH DBS Corp., Senior Notes | | 6.625 | % | | 10/1/14 | | | 10,000 | | | 10,025 | |

DISH DBS Corp., Senior Notes | | 7.750 | % | | 5/31/15 | | | 40,000 | | | 41,400 | |

News America Inc., Senior Notes | | 6.200 | % | | 12/15/34 | | | 20,000 | | | 21,132 | |

News America Inc., Senior Notes | | 6.650 | % | | 11/15/37 | | | 10,000 | | | 11,260 | |

Reed Elsevier Capital Inc., Notes | | 8.625 | % | | 1/15/19 | | | 50,000 | | | 63,755 | |

Time Warner Cable Inc., Senior Notes | | 8.750 | % | | 2/14/19 | | | 20,000 | | | 25,275 | |

Time Warner Cable Inc., Senior Notes | | 8.250 | % | | 4/1/19 | | | 170,000 | | | 209,406 | |

Time Warner Cable Inc., Senior Notes | | 6.750 | % | | 6/15/39 | | | 40,000 | | | 44,337 | |

Time Warner Inc., Senior Notes | | 7.625 | % | | 4/15/31 | | | 50,000 | | | 60,319 | |

Total Media | | | | | | | | | | | 797,736 | |

Multiline Retail — 0.1% | | | | | | | | | | | | |

Neiman Marcus Group Inc., Senior Notes | | 9.000 | % | | 10/15/15 | | | 21,750 | | | 21,913 | (d) |

Total Consumer Discretionary | | | | | | | | | | | 940,292 | |

| Consumer Staples — 1.5% | | | | | | | | | | | | |

Beverages — 0.4% | | | | | | | | | | | | |

Anheuser-Busch InBev Worldwide Inc., Senior Notes | | 5.375 | % | | 1/15/20 | | | 80,000 | | | 86,369 | |

Anheuser-Busch InBev Worldwide Inc., Senior Notes | | 5.000 | % | | 4/15/20 | | | 10,000 | | | 10,475 | (c) |

Diageo Finance BV | | 3.250 | % | | 1/15/15 | | | 50,000 | | | 51,482 | |

Total Beverages | | | | | | | | | | | 148,326 | |

Food & Staples Retailing — 0.5% | | | | | | | | | | | | |

CVS Caremark Corp., Senior Notes | | 6.600 | % | | 3/15/19 | | | 70,000 | | | 81,596 | |

CVS Pass-Through Trust, Secured Notes | | 6.943 | % | | 1/10/30 | | | 123,442 | | | 136,515 | |

Total Food & Staples Retailing | | | | | | | | | | | 218,111 | |

Food Products — 0.3% | | | | | | | | | | | | |

Kraft Foods Inc., Senior Notes | | 5.625 | % | | 11/1/11 | | | 5,000 | | | 5,263 | |

Kraft Foods Inc., Senior Notes | | 5.375 | % | | 2/10/20 | | | 100,000 | | | 107,357 | |

Total Food Products | | | | | | | | | | | 112,620 | |

Tobacco — 0.3% | | | | | | | | | | | | |

Altria Group Inc., Senior Notes | | 8.500 | % | | 11/10/13 | | | 40,000 | | | 46,729 | |

Reynolds American Inc., Senior Notes | | 7.250 | % | | 6/1/12 | | | 50,000 | | | 53,781 | |

Total Tobacco | | | | | | | | | | | 100,510 | |

Total Consumer Staples | | | | | | | | | | | 579,567 | |

See Notes to Financial Statements.

| | |

| 4 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Schedule of investments (unaudited) (cont’d)

June 30, 2010

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

| Energy — 4.3% | | | | | | | | | | | | |

Energy Equipment & Services — 0.1% | | | | | | | | | | | | |

Complete Production Services Inc., Senior Notes | | 8.000 | % | | 12/15/16 | | $ | 40,000 | | $ | 39,300 | |

Oil, Gas & Consumable Fuels — 4.2% | | | | | | | | | | | | |

Anadarko Petroleum Corp., Senior Notes | | 8.700 | % | | 3/15/19 | | | 40,000 | | | 37,822 | |

BP Capital Markets PLC, Guaranteed Notes | | 5.250 | % | | 11/7/13 | | | 80,000 | | | 73,595 | |

BP Capital Markets PLC, Senior Notes | | 3.125 | % | | 3/10/12 | | | 20,000 | | | 18,498 | |

Chesapeake Energy Corp., Senior Notes | | 6.625 | % | | 1/15/16 | | | 100,000 | | | 102,125 | |

Chesapeake Energy Corp., Senior Notes | | 6.250 | % | | 1/15/18 | | | 50,000 | | | 50,750 | |

Compagnie Generale de Geophysique SA, Senior Notes | | 7.500 | % | | 5/15/15 | | | 10,000 | | | 9,575 | |

Compagnie Generale de Geophysique SA, Senior Notes | | 7.750 | % | | 5/15/17 | | | 45,000 | | | 42,862 | |

ConocoPhillips Holding Co., Senior Notes | | 6.950 | % | | 4/15/29 | | | 105,000 | | | 129,224 | |

CONSOL Energy Inc., Senior Notes | | 8.250 | % | | 4/1/20 | | | 30,000 | | | 31,425 | (c) |

El Paso Corp., Medium-Term Notes | | 7.375 | % | | 12/15/12 | | | 50,000 | | | 52,609 | |

El Paso Corp., Medium-Term Notes | | 7.800 | % | | 8/1/31 | | | 22,000 | | | 21,853 | |

Hess Corp., Notes | | 8.125 | % | | 2/15/19 | | | 160,000 | | | 199,772 | |

Kerr-McGee Corp., Notes | | 7.875 | % | | 9/15/31 | | | 95,000 | | | 87,241 | |

Kinder Morgan Energy Partners LP, Notes | | 6.750 | % | | 3/15/11 | | | 100,000 | | | 103,533 | |

Kinder Morgan Energy Partners LP, Senior Notes | | 5.850 | % | | 9/15/12 | | | 20,000 | | | 21,454 | |

Noble Energy Inc., Senior Notes | | 8.250 | % | | 3/1/19 | | | 60,000 | | | 72,732 | |

Pemex Project Funding Master Trust, Senior Bonds | | 6.625 | % | | 6/15/35 | | | 15,000 | | | 15,503 | |

Petrobras International Finance Co., Senior Notes | | 6.125 | % | | 10/6/16 | | | 26,000 | | | 27,731 | |

Petrobras International Finance Co., Senior Notes | | 5.750 | % | | 1/20/20 | | | 32,000 | | | 32,386 | |

SandRidge Energy Inc., Senior Notes | | 9.875 | % | | 5/15/16 | | | 35,000 | | | 35,700 | (c) |

Shell International Finance BV, Senior Notes | | 4.375 | % | | 3/25/20 | | | 90,000 | | | 93,220 | |

Stone Energy Corp., Senior Subordinated Notes | | 6.750 | % | | 12/15/14 | | | 55,000 | | | 47,025 | |

Tennessee Gas Pipeline Co., Debentures | | 7.625 | % | | 4/1/37 | | | 50,000 | | | 55,532 | |

Whiting Petroleum Corp., Senior Subordinated Notes | | 7.000 | % | | 2/1/14 | | | 25,000 | | | 25,625 | |

Williams Cos. Inc., Debentures | | 7.500 | % | | 1/15/31 | | | 22,000 | | | 23,465 | |

Williams Cos. Inc., Notes | | 7.875 | % | | 9/1/21 | | | 44,000 | | | 50,525 | |

Williams Cos. Inc., Senior Notes | | 7.750 | % | | 6/15/31 | | | 52,000 | | | 56,015 | |

Williams Cos. Inc., Senior Notes | | 8.750 | % | | 3/15/32 | | | 8,000 | | | 9,360 | |

XTO Energy Inc., Senior Notes | | 7.500 | % | | 4/15/12 | | | 30,000 | | | 33,418 | |

XTO Energy Inc., Senior Notes | | 5.500 | % | | 6/15/18 | | | 30,000 | | | 34,361 | |

XTO Energy Inc., Senior Notes | | 6.500 | % | | 12/15/18 | | | 50,000 | | | 60,778 | |

Total Oil, Gas & Consumable Fuels | | | | | | | | | | | 1,655,714 | |

Total Energy | | | | | | | | | | | 1,695,014 | |

| Financials — 17.2% | | | | | | | | | | | | |

Capital Markets — 1.7% | | | | | | | | | | | | |

Credit Suisse Guernsey Ltd., Junior Subordinated Notes | | 5.860 | % | | 5/15/17 | | | 80,000 | | | 71,000 | (e)(f) |

Goldman Sachs Group Inc., Notes | | 6.600 | % | | 1/15/12 | | | 10,000 | | | 10,580 | |

Goldman Sachs Group Inc., Notes | | 5.450 | % | | 11/1/12 | | | 20,000 | | | 21,080 | |

Goldman Sachs Group Inc., Notes | | 4.750 | % | | 7/15/13 | | | 10,000 | | | 10,448 | |

Goldman Sachs Group Inc., Notes | | 5.250 | % | | 10/15/13 | | | 20,000 | | | 21,098 | |

Goldman Sachs Group Inc., Senior Notes | | 3.625 | % | | 8/1/12 | | | 10,000 | | | 10,192 | |

Goldman Sachs Group Inc., Senior Notes | | 5.375 | % | | 3/15/20 | | | 260,000 | | | 257,390 | |

Kaupthing Bank HF, Senior Notes | | 7.625 | % | | 2/28/15 | | | 370,000 | | | 90,650 | (a)(b)(c) |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 5 |

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

Capital Markets — continued | | | | | | | | | | | | |

Lehman Brothers Holdings Capital Trust VII, Medium-Term Notes | | 5.857 | % | | 5/31/12 | | $ | 90,000 | | $ | 234 | (a)(e)(f) |

Lehman Brothers Holdings E-Capital Trust I, Notes | | 6.155 | % | | 8/19/65 | | | 60,000 | | | 156 | (a)(e) |

Lehman Brothers Holdings Inc., Medium-Term Notes, Senior Notes | | 5.250 | % | | 2/6/12 | | | 50,000 | | | 10,125 | (a) |

Merrill Lynch & Co. Inc., Notes | | 6.875 | % | | 4/25/18 | | | 20,000 | | | 21,368 | |

Morgan Stanley, Medium-Term Notes | | 5.625 | % | | 1/9/12 | | | 100,000 | | | 104,093 | |

Morgan Stanley, Medium-Term Notes | | 0.754 | % | | 10/18/16 | | | 50,000 | | | 43,557 | (e) |

Total Capital Markets | | | | | | | | | | | 671,971 | |

Commercial Banks — 5.0% | | | | | | | | | | | | |

Barclays Bank PLC, Senior Notes | | 5.200 | % | | 7/10/14 | | | 100,000 | | | 105,631 | |

Commonwealth Bank of Australia, Senior Notes | | 3.750 | % | | 10/15/14 | | | 50,000 | | | 51,452 | (c) |

Commonwealth Bank of Australia, Senior Notes | | 5.000 | % | | 10/15/19 | | | 20,000 | | | 20,799 | (c) |

Credit Agricole SA, Subordinated Notes | | 8.375 | % | | 10/13/19 | | | 120,000 | | | 114,000 | (c)(e)(f) |

Glitnir Banki HF, Notes | | 6.330 | % | | 7/28/11 | | | 150,000 | | | 39,750 | (a)(b)(c) |

Glitnir Banki HF, Subordinated Notes | | 6.693 | % | | 6/15/16 | | | 130,000 | | | 488 | (a)(b)(c) |

ICICI Bank Ltd., Subordinated Bonds | | 6.375 | % | | 4/30/22 | | | 100,000 | | | 92,125 | (c)(e) |

Landsbanki Islands HF, Senior Notes | | 6.100 | % | | 8/25/11 | | | 260,000 | | | 30,550 | (a)(b)(c) |

Lloyds TSB Bank PLC, Bonds | | 4.375 | % | | 1/12/15 | | | 100,000 | | | 96,443 | (c) |

Lloyds TSB Bank PLC, Notes | | 5.800 | % | | 1/13/20 | | | 100,000 | | | 94,558 | (c) |

Nordea Bank AB, Senior Notes | | 3.700 | % | | 11/13/14 | | | 100,000 | | | 101,973 | (c) |

Nordea Bank AB, Senior Notes | | 4.875 | % | | 1/27/20 | | | 100,000 | | | 102,900 | (c) |

Resona Preferred Global Securities Cayman Ltd., Junior Subordinated Bonds | | 7.191 | % | | 7/30/15 | | | 120,000 | | | 110,537 | (c)(e)(f) |

Royal Bank of Scotland Group PLC, Senior Notes | | 6.400 | % | | 10/21/19 | | | 100,000 | | | 101,540 | |

Royal Bank of Scotland Group PLC, Subordinated Notes | | 5.000 | % | | 11/12/13 | | | 20,000 | | | 19,421 | |

Royal Bank of Scotland Group PLC, Subordinated Notes | | 5.000 | % | | 10/1/14 | | | 50,000 | | | 46,957 | |

Royal Bank of Scotland Group PLC, Subordinated Notes | | 5.050 | % | | 1/8/15 | | | 40,000 | | | 37,395 | |

Santander Issuances SA Unipersonal, Subordinated Notes | | 5.805 | % | | 6/20/16 | | | 120,000 | | | 116,225 | (c)(e) |

Shinsei Finance Cayman Ltd., Junior Subordinated Bonds | | 6.418 | % | | 7/20/16 | | | 130,000 | | | 83,663 | (c)(e)(f) |

SunTrust Capital, Trust Preferred Securities | | 6.100 | % | | 12/15/36 | | | 60,000 | | | 45,803 | (e) |

Wachovia Corp., Subordinated Notes | | 5.250 | % | | 8/1/14 | | | 420,000 | | | 445,182 | |

Wells Fargo Capital X, Capital Securities | | 5.950 | % | | 12/15/36 | | | 100,000 | | | 89,191 | |

Total Commercial Banks | | | | | | | | | | | 1,946,583 | |

Consumer Finance — 2.6% | | | | | | | | | | | | |

American Express Co., Subordinated Debentures | | 6.800 | % | | 9/1/66 | | | 100,000 | | | 96,000 | (e) |

American Express Credit Corp., Senior Notes | | 5.125 | % | | 8/25/14 | | | 60,000 | | | 64,613 | |

Ford Motor Credit Co., LLC, Senior Notes | | 5.787 | % | | 6/15/11 | | | 131,000 | | | 132,801 | (e) |

GMAC Inc., Notes | | 1.750 | % | | 10/30/12 | | | 100,000 | | | 101,793 | |

GMAC Inc., Senior Notes | | 6.625 | % | | 5/15/12 | | | 62,000 | | | 62,620 | |

GMAC Inc., Senior Notes | | 7.500 | % | | 12/31/13 | | | 51,000 | | | 51,382 | |

GMAC Inc., Senior Notes | | 6.750 | % | | 12/1/14 | | | 92,000 | | | 89,930 | |

SLM Corp., Medium-Term Notes | | 5.000 | % | | 10/1/13 | | | 105,000 | | | 100,450 | |

SLM Corp., Medium-Term Notes | | 5.375 | % | | 5/15/14 | | | 225,000 | | | 205,904 | |

SLM Corp., Medium-Term Notes | | 5.050 | % | | 11/14/14 | | | 30,000 | | | 26,856 | |

SLM Corp., Medium-Term Notes, Senior Notes | | 5.625 | % | | 8/1/33 | | | 25,000 | | | 18,400 | |

SLM Corp., Senior Notes | | 3.934 | % | | 4/1/14 | | | 30,000 | | | 25,714 | (e) |

SLM Corp., Senior Notes | | 8.000 | % | | 3/25/20 | | | 30,000 | | | 26,388 | |

Total Consumer Finance | | | | | | | | | | | 1,002,851 | |

See Notes to Financial Statements.

| | |

| 6 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Schedule of investments (unaudited) (cont’d)

June 30, 2010

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

Diversified Financial Services — 6.3% | | | | | | | | | | | | |

Bank of America Corp., Senior Notes | | 4.500 | % | | 4/1/15 | | $ | 210,000 | | $ | 212,476 | |

Bank of America Corp., Senior Notes | | 5.625 | % | | 7/1/20 | | | 20,000 | | | 20,197 | |

Bank of America Corp., Subordinated Notes | | 7.400 | % | | 1/15/11 | | | 60,000 | | | 61,787 | |

Bank of America Corp., Subordinated Notes | | 5.420 | % | | 3/15/17 | | | 90,000 | | | 89,791 | |

Boeing Capital Corp., Senior Notes | | 4.700 | % | | 10/27/19 | | | 30,000 | | | 32,315 | |

Citigroup Inc., Notes | | 6.500 | % | | 8/19/13 | | | 160,000 | | | 170,549 | |

Citigroup Inc., Notes | | 6.000 | % | | 12/13/13 | | | 110,000 | | | 115,492 | |

Citigroup Inc., Senior Notes | | 6.010 | % | | 1/15/15 | | | 50,000 | | | 52,496 | |

Citigroup Inc., Senior Notes | | 6.875 | % | | 3/5/38 | | | 150,000 | | | 157,858 | |

Citigroup Inc., Subordinated Notes | | 5.000 | % | | 9/15/14 | | | 180,000 | | | 180,205 | |

El Paso Performance-Linked Trust Certificates, Senior Notes | | 7.750 | % | | 7/15/11 | | | 220,000 | | | 227,872 | (c) |

General Electric Capital Corp., Senior Notes | | 6.875 | % | | 1/10/39 | | | 260,000 | | | 288,020 | |

General Electric Capital Corp., Subordinated Debentures | | 6.375 | % | | 11/15/67 | | | 220,000 | | | 205,975 | (e) |

JPMorgan Chase & Co., Subordinated Notes | | 5.125 | % | | 9/15/14 | | | 400,000 | | | 427,255 | |

JPMorgan Chase & Co., Subordinated Notes | | 6.125 | % | | 6/27/17 | | | 110,000 | | | 120,515 | |

MUFG Capital Finance 1 Ltd., Preferred Securities | | 6.346 | % | | 7/25/16 | | | 100,000 | | | 96,868 | (e)(f) |

Total Diversified Financial Services | | | | | | | | | | | 2,459,671 | |

Insurance — 1.4% | | | | | | | | | | | | |

American International Group Inc., Junior Subordinated Debentures | | 6.250 | % | | 3/15/37 | | | 110,000 | | | 75,350 | |

American International Group Inc., Medium-Term Notes, Senior Notes | | 5.850 | % | | 1/16/18 | | | 20,000 | | | 17,975 | |

Berkshire Hathaway Inc., Senior Notes | | 3.200 | % | | 2/11/15 | | | 70,000 | | | 72,164 | |

MetLife Inc., Junior Subordinated Debentures | | 6.400 | % | | 12/15/36 | | | 190,000 | | | 168,150 | |

MetLife Inc., Senior Notes | | 6.750 | % | | 6/1/16 | | | 60,000 | | | 67,965 | |

Teachers Insurance & Annuity Association of America — College Retirement Equity Fund, Notes | | 6.850 | % | | 12/16/39 | | | 60,000 | | | 70,125 | (c) |

Travelers Cos. Inc., Junior Subordinated Debentures | | 6.250 | % | | 3/15/37 | | | 100,000 | | | 93,962 | (e) |

Total Insurance | | | | | | | | | | | 565,691 | |

Real Estate Management & Development — 0.2% | | | | | | | | | | | | |

Realogy Corp., Senior Notes | | 10.500 | % | | 4/15/14 | | | 110,000 | | | 93,775 | |

Total Financials | | | | | | | | | | | 6,740,542 | |

| Health Care — 2.4% | | | | | | | | | | | | |

Health Care Equipment & Supplies — 0.1% | | | | | | | | | | | | |

Medtronic Inc., Senior Notes | | 4.450 | % | | 3/15/20 | | | 30,000 | | | 32,031 | |

Health Care Providers & Services — 1.5% | | | | | | | | | | | | |

Community Health Systems Inc., Senior Notes | | 8.875 | % | | 7/15/15 | | | 30,000 | | | 31,012 | |

DaVita Inc., Senior Notes | | 6.625 | % | | 3/15/13 | | | 39,000 | | | 39,244 | |

HCA Inc., Senior Notes | | 6.300 | % | | 10/1/12 | | | 10,000 | | | 10,000 | |

HCA Inc., Senior Notes | | 6.250 | % | | 2/15/13 | | | 58,000 | | | 57,275 | |

HCA Inc., Senior Secured Notes | | 9.625 | % | | 11/15/16 | | | 1,000 | | | 1,073 | (d) |

Tenet Healthcare Corp., Senior Notes | | 7.375 | % | | 2/1/13 | | | 75,000 | | | 75,375 | |

UnitedHealth Group Inc., Senior Notes | | 6.000 | % | | 2/15/18 | | | 30,000 | | | 33,502 | |

WellPoint Health Networks Inc., Notes | | 6.375 | % | | 1/15/12 | | | 300,000 | | | 320,941 | |

WellPoint Inc., Notes | | 5.875 | % | | 6/15/17 | | | 10,000 | | | 11,157 | |

Total Health Care Providers & Services | | | | | | | | | | | 579,579 | |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 7 |

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

Pharmaceuticals — 0.8% | | | | | | | | | | | | |

Abbott Laboratories, Senior Notes | | 5.125 | % | | 4/1/19 | | $ | 140,000 | | $ | 156,486 | |

Pfizer Inc., Senior Notes | | 6.200 | % | | 3/15/19 | | | 90,000 | | | 107,141 | |

Wyeth, Notes | | 5.950 | % | | 4/1/37 | | | 70,000 | | | 79,573 | |

Total Pharmaceuticals | | | | | | | | | | | 343,200 | |

Total Health Care | | | | | | | | | | | 954,810 | |

| Industrials — 2.4% | | | | | | | | | | | | |

Aerospace & Defense — 0.5% | | | | | | | | | | | | |

Boeing Co., Senior Notes | | 6.000 | % | | 3/15/19 | | | 40,000 | | | 47,190 | |

Boeing Co., Senior Notes | | 4.875 | % | | 2/15/20 | | | 20,000 | | | 22,064 | |

L-3 Communications Corp., Senior Subordinated Notes | | 5.875 | % | | 1/15/15 | | | 125,000 | | | 124,062 | |

Total Aerospace & Defense | | | | | | | | | | | 193,316 | |

Airlines — 0.6% | | | | | | | | | | | | |

Delta Air Lines Inc., Pass-Through Certificates | | 6.821 | % | | 8/10/22 | | | 168,540 | | | 166,433 | |

Northwest Airlines Corp., Pass-Through Certificates | | 7.575 | % | | 3/1/19 | | | 31,575 | | | 31,890 | |

United Airlines, Pass-Through Trust, Secured Notes | | 9.750 | % | | 1/15/17 | | | 30,000 | | | 32,025 | |

Total Airlines | | | | | | | | | | | 230,348 | |

Industrial Conglomerates — 1.2% | | | | | | | | | | | | |

Tyco International Group SA, Notes | | 6.000 | % | | 11/15/13 | | | 420,000 | | | 470,469 | |

Road & Rail — 0.1% | | | | | | | | | | | | |

Kansas City Southern de Mexico, Senior Notes | | 12.500 | % | | 4/1/16 | | | 20,000 | | | 24,000 | |

RailAmerica Inc., Senior Secured Notes | | 9.250 | % | | 7/1/17 | | | 40,000 | | | 42,100 | |

Total Road & Rail | | | | | | | | | | | 66,100 | |

Total Industrials | | | | | | | | | | | 960,233 | |

| Information Technology — 0.0% | | | | | | | | | | | | |

Semiconductors & Semiconductor Equipment — 0.0% | | | | | | | | | | | | |

National Semiconductor Corp., Senior Notes | | 6.600 | % | | 6/15/17 | | | 10,000 | | | 11,219 | |

| Materials — 0.9% | | | | | | | | | | | | |

Chemicals — 0.2% | | | | | | | | | | | | |

FMC Finance III SA, Senior Notes | | 6.875 | % | | 7/15/17 | | | 60,000 | | | 60,900 | |

Containers & Packaging — 0.1% | | | | | | | | | | | | |

Ball Corp., Senior Notes | | 6.750 | % | | 9/15/20 | | | 40,000 | | | 40,600 | |

Radnor Holdings Inc., Senior Notes | | 11.000 | % | | 3/15/11 | | | 25,000 | | | 0 | (a)(b)(g) |

Total Containers & Packaging | | | | | | | | | | | 40,600 | |

Metals & Mining — 0.6% | | | | | | | | | | | | |

Freeport-McMoRan Copper & Gold Inc., Senior Notes | | 8.375 | % | | 4/1/17 | | | 60,000 | | | 66,086 | |

Rio Tinto Finance USA Ltd., Notes | | 6.500 | % | | 7/15/18 | | | 30,000 | | | 34,246 | |

Rio Tinto Finance USA Ltd., Senior Notes | | 5.875 | % | | 7/15/13 | | | 10,000 | | | 10,964 | |

Steel Dynamics Inc., Senior Notes | | 6.750 | % | | 4/1/15 | | | 35,000 | | | 35,306 | |

Teck Resources Ltd., Senior Secured Notes | | 9.750 | % | | 5/15/14 | | | 5,000 | | | 5,914 | |

Teck Resources Ltd., Senior Secured Notes | | 10.250 | % | | 5/15/16 | | | 5,000 | | | 5,907 | |

Teck Resources Ltd., Senior Secured Notes | | 10.750 | % | | 5/15/19 | | | 5,000 | | | 6,136 | |

Vale Overseas Ltd., Notes | | 6.875 | % | | 11/21/36 | | | 70,000 | | | 73,151 | |

Total Metals & Mining | | | | | | | | | | | 237,710 | |

Total Materials | | | | | | | | | | | 339,210 | |

See Notes to Financial Statements.

| | |

| 8 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Schedule of investments (unaudited) (cont’d)

June 30, 2010

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

| Telecommunication Services — 3.5% | | | | | | | | | | | | |

Diversified Telecommunication Services — 2.8% | | | | | | | | | | | | |

AT&T Inc., Global Notes | | 5.500 | % | | 2/1/18 | | $ | 100,000 | | $ | 110,756 | |

AT&T Inc., Global Notes | | 6.550 | % | | 2/15/39 | | | 50,000 | | | 56,196 | |

Deutsche Telekom International Finance BV, Senior Notes | | 5.750 | % | | 3/23/16 | | | 155,000 | | | 169,800 | |

Intelsat Corp., Senior Notes | | 9.250 | % | | 8/15/14 | | | 20,000 | | | 20,550 | |

Intelsat Jackson Holdings Ltd., Senior Notes | | 9.500 | % | | 6/15/16 | | | 5,000 | | | 5,275 | |

Intelsat Jackson Holdings Ltd., Senior Notes | | 8.500 | % | | 11/1/19 | | | 10,000 | | | 10,150 | (c) |

Koninklijke KPN NV, Senior Notes | | 8.000 | % | | 10/1/10 | | | 160,000 | | | 162,559 | |

Qwest Communications International Inc., Senior Notes | | 7.500 | % | | 2/15/14 | | | 50,000 | | | 50,375 | |

Telecom Italia Capital S.p.A., Senior Notes | | 5.250 | % | | 10/1/15 | | | 140,000 | | | 141,455 | |

Telefonica Emisiones SAU, Senior Notes | | 5.134 | % | | 4/27/20 | | | 80,000 | | | 80,337 | |

Verizon Communications Inc., Senior Notes | | 8.950 | % | | 3/1/39 | | | 20,000 | | | 28,422 | |

Verizon Global Funding Corp., Notes | | 7.375 | % | | 9/1/12 | | | 80,000 | | | 89,925 | |

Verizon New York Inc., Senior Debentures | | 6.875 | % | | 4/1/12 | | | 120,000 | | | 129,722 | |

Windstream Corp., Senior Notes | | 8.625 | % | | 8/1/16 | | | 40,000 | | | 40,500 | |

Total Diversified Telecommunication Services | | | | | | | | | | | 1,096,022 | |

Wireless Telecommunication Services — 0.7% | | | | | | | | | | | | |

America Movil SAB de CV, Senior Notes | | 5.625 | % | | 11/15/17 | | | 30,000 | | | 32,944 | |

Rogers Communications Inc., Senior Notes | | 6.800 | % | | 8/15/18 | | | 30,000 | | | 35,520 | |

Sprint Capital Corp., Senior Notes | | 8.375 | % | | 3/15/12 | | | 200,000 | | | 210,750 | |

Total Wireless Telecommunication Services | | | | | | | | | | | 279,214 | |

Total Telecommunication Services | | | | | | | | | | | 1,375,236 | |

| Utilities — 2.9% | | | | | | | | | | | | |

Electric Utilities — 1.4% | | | | | | | | | | | | |

Duke Energy Corp., Senior Notes | | 5.625 | % | | 11/30/12 | | | 70,000 | | | 76,614 | |

Exelon Corp., Bonds | | 5.625 | % | | 6/15/35 | | | 165,000 | | | 160,385 | |

FirstEnergy Corp., Notes | | 7.375 | % | | 11/15/31 | | | 205,000 | | | 216,744 | |

Pacific Gas & Electric Co., First Mortgage Bonds | | 6.050 | % | | 3/1/34 | | | 70,000 | | | 78,357 | |

Total Electric Utilities | | | | | | | | | | | 532,100 | |

Gas Utilities — 0.1% | | | | | | | | | | | | |

Southern Natural Gas Co., Notes | | 5.900 | % | | 4/1/17 | | | 20,000 | | | 21,289 | (c) |

Southern Natural Gas Co., Senior Notes | | 8.000 | % | | 3/1/32 | | | 25,000 | | | 28,453 | |

Total Gas Utilities | | | | | | | | | | | 49,742 | |

Independent Power Producers & Energy Traders — 1.1% | | | | | | | | | | | | |

AES Corp., Senior Notes | | 7.750 | % | | 10/15/15 | | | 40,000 | | | 40,700 | |

Calpine Construction Finance Co. LP and CCFC Finance Corp., Senior Secured Notes | | 8.000 | % | | 6/1/16 | | | 35,000 | | | 35,962 | (c) |

Edison Mission Energy, Senior Notes | | 7.625 | % | | 5/15/27 | | | 20,000 | | | 11,450 | |

Energy Future Holdings Corp., Senior Notes | | 11.250 | % | | 11/1/17 | | | 440,901 | | | 288,790 | (d) |

NRG Energy Inc., Senior Notes | | 7.250 | % | | 2/1/14 | | | 25,000 | | | 25,406 | |

NRG Energy Inc., Senior Notes | | 7.375 | % | | 2/1/16 | | | 35,000 | | | 34,913 | |

Total Independent Power Producers & Energy Traders | | | | | | | | | | | 437,221 | |

Multi-Utilities — 0.3% | | | | | | | | | | | | |

Dominion Resources Inc., Senior Notes | | 8.875 | % | | 1/15/19 | | | 90,000 | | | 119,066 | |

Total Utilities | | | | | | | | | | | 1,138,129 | |

Total Corporate Bonds & Notes (Cost — $15,337,243) | | | | | | | | | | | 14,734,252 | |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 9 |

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

| Asset-Backed Securities — 3.0% | | | | | | | | | | | | |

| Financials — 3.0% | | | | | | | | | | | | |

Automobiles — 0.5% | | | | | | | | | | | | |

AESOP Funding II LLC, 2010-3A A | | 4.640 | % | | 5/20/16 | | $ | 100,000 | | $ | 103,735 | (c) |

Hertz Vehicle Financing LLC, 2009-2A A2 | | 5.290 | % | | 3/25/16 | | | 80,000 | | | 86,660 | (c) |

Total Automobiles | | | | | | | | | | | 190,395 | |

Home Equity — 2.3% | | | | | | | | | | | | |

Accredited Mortgage Loan Trust, 2005-3 A1 | | 0.587 | % | | 9/25/35 | | | 76,021 | | | 69,232 | (e) |

ACE Securities Corp., 2006-SL2 A | | 0.517 | % | | 1/25/36 | | | 382,985 | | | 23,320 | (e) |

Bear Stearns Asset-Backed Securities Trust, 2004-BO1 1A2 | | 0.697 | % | | 9/25/34 | | | 71,023 | | | 70,369 | (e) |

Countrywide Asset-Backed Certificates, 2004-5 M4 | | 1.597 | % | | 6/25/34 | | | 83,405 | | | 20,872 | (e) |

Countrywide Home Equity Loan Trust, 2006-RES 4Q1B | | 0.650 | % | | 12/15/33 | | | 301,675 | | | 64,196 | (c)(e) |

First Horizon ABS Trust, 2006-HE1 A | | 0.507 | % | | 10/25/34 | | | 264,851 | | | 135,114 | (e) |

GSRPM Mortgage Loan Trust, 2006-1 A1 | | 0.647 | % | | 3/25/35 | | | 281,971 | | | 226,031 | (c)(e) |

Indymac Home Equity Loan Asset-Backed Trust, 2006-H1 A | | 0.517 | % | | 4/25/36 | | | 219,872 | | | 58,064 | (e) |

Lehman XS Trust, 2006-14N 1A1B | | 0.557 | % | | 9/25/46 | | | 418,874 | | | 181,581 | (e) |

SACO I Trust, 2006-4 A1 | | 0.517 | % | | 2/25/34 | | | 233,874 | | | 47,472 | (e) |

Sail Net Interest Margin Notes, 2003-3 A | | 7.750 | % | | 4/27/33 | | | 7,825 | | | 0 | (b)(c) |

Total Home Equity | | | | | | | | | | | 896,251 | |

Student Loan — 0.2% | | | | | | | | | | | | |

Education Funding Capital Trust, 2003-3 A6 | | 1.520 | % | | 12/15/42 | | | 50,000 | | | 47,500 | (e) |

Education Funding Capital Trust, 2003-3 A7 | | 2.430 | % | | 12/15/42 | | | 50,000 | | | 46,813 | (e) |

Total Student Loan | | | | | | | | | | | 94,313 | |

Total Asset-Backed Securities (Cost — $2,618,397) | | | | | | | | | | | 1,180,959 | |

| Collateralized Mortgage Obligations — 14.3% | | | | | | | | | | | | |

American Home Mortgage Investment Trust, 2005-1 6A | | 2.749 | % | | 6/25/45 | | | 364,801 | | | 297,214 | (e) |

Banc of America Mortgage Securities, 2005-H 2A1 | | 4.787 | % | | 9/25/35 | | | 266,590 | | | 225,882 | (e) |

Commercial Mortgage Pass-Through Certificates, 2001-J2A A1 | | 5.447 | % | | 7/16/34 | | | 218,802 | | | 222,844 | (c) |

Countrywide Alternative Loan Trust, 2003-20CB 1A1 | | 5.500 | % | | 10/25/33 | | | 31,450 | | | 32,392 | |

Countrywide Alternative Loan Trust, 2005-72 A1 | | 0.617 | % | | 1/25/36 | | | 364,385 | | | 221,183 | (e) |

Countrywide Alternative Loan Trust, 2006-OA6 1A1A | | 0.557 | % | | 7/25/46 | | | 415,290 | | | 215,477 | (e) |

Countrywide Home Loan Mortgage Pass-Through Trust, 2004-23 A | | 2.454 | % | | 11/25/34 | | | 257,630 | | | 153,202 | (e) |

Countrywide Home Loan Mortgage Pass-Through Trust, 2005-9 1A1 | | 0.647 | % | | 5/25/35 | | | 265,504 | | | 153,245 | (e) |

CS First Boston Mortgage Securities Corp., 2005-C6 A4 | | 5.230 | % | | 12/15/40 | | | 500,000 | | | 530,085 | (e) |

Deutsche ALT-A Securities Inc. Mortgage Loan Trust, 2005-AR1 2A1 | | 4.844 | % | | 8/25/35 | | | 134,091 | | | 102,579 | (e) |

Downey Savings & Loan Association Mortgage Loan Trust, 2005-AR2 2A1A | | 0.558 | % | | 3/19/45 | | | 232,181 | | | 132,277 | (e) |

Downey Savings & Loan Association Mortgage Loan Trust, 2006-AR1 1A1A | | 1.333 | % | | 3/19/46 | | | 326,721 | | | 156,083 | (e) |

GS Mortgage Securities Corp. II, 2001-1285 C | | 6.712 | % | | 8/15/18 | | | 40,000 | | | 41,308 | (c) |

GSR Mortgage Loan Trust, 2005-AR5 1A1 | | 3.464 | % | | 10/25/35 | | | 366,324 | | | 268,956 | (e) |

Harborview Mortgage Loan Trust, 2004-11 3A1A | | 0.698 | % | | 1/19/35 | | | 273,797 | | | 145,435 | (e) |

Harborview Mortgage Loan Trust, 2004-8 2A4A | | 0.748 | % | | 11/19/34 | | | 242,966 | | | 147,570 | (e) |

Harborview Mortgage Loan Trust, 2004-8 3A2 | | 0.748 | % | | 11/19/34 | | | 101,421 | | | 55,148 | (e) |

Indymac Index Mortgage Loan Trust, 2005-AR1 1A1 | | 3.247 | % | | 3/25/35 | | | 149,587 | | | 107,990 | (e) |

Indymac Index Mortgage Loan Trust, 2006-AR4 A1A | | 0.557 | % | | 5/25/46 | | | 494,097 | | | 258,007 | (e) |

Indymac Index Mortgage Loan Trust, 2007-AR15 2A1 | | 5.534 | % | | 8/25/37 | | | 248,829 | | | 131,848 | (e) |

JPMorgan Chase Commercial Mortgage Securities Corp., 2007-LD11 A3 | | 5.983 | % | | 6/15/49 | | | 200,000 | | | 205,241 | (e) |

JPMorgan Mortgage Trust, 2005-S3 1A1 | | 6.500 | % | | 1/25/36 | | | 128,909 | | | 85,279 | |

See Notes to Financial Statements.

| | |

| 10 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Schedule of investments (unaudited) (cont’d)

June 30, 2010

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity Date | | Face

Amount | | Value | |

| Collateralized Mortgage Obligations — continued | | | | | | | | | | | | |

MASTR Adjustable Rate Mortgages Trust, 2007-R5 A1 | | 5.571 | % | | 11/25/35 | | $ | 130,403 | | $ | 74,729 | (c)(e) |

Merrill Lynch Mortgage Investors Trust, 2004-A3 4A3 | | 5.055 | % | | 5/25/34 | | | 112,726 | | | 114,223 | (e) |

Morgan Stanley Mortgage Loan Trust, 2006-3AR 2A3 | | 4.962 | % | | 3/25/36 | | | 454,373 | | | 275,112 | (e) |

RBSGC Mortgage Pass-Through Certificates, 2007-B 1A4 | | 0.797 | % | | 1/25/37 | | | 140,036 | | | 77,786 | (e) |

Structured Adjustable Rate Mortgage Loan Trust, 2005-21 1A | | 5.615 | % | | 11/25/35 | | | 142,155 | | | 76,493 | (e) |

Structured Asset Mortgage Investments Inc., 2006-AR5 2A1 | | 0.557 | % | | 5/25/46 | | | 236,419 | | | 128,043 | (e) |

Voyager Dwnys Delaware Trust, 2009-1 UGL2 | | 1.361 | % | | 3/20/47 | | | 329,500 | | | 28,008 | (b)(c)(e)(g) |

Washington Mutual Inc. Mortgage Pass-Through Certificates,

2005-AR17 A1A1 | | 0.617 | % | | 12/25/45 | | | 387,253 | | | 291,790 | (e) |

Washington Mutual Inc. Mortgage Pass-Through Certificates,

2005-AR19 A1A2 | | 0.637 | % | | 12/25/45 | | | 220,154 | | | 147,327 | (e) |

Washington Mutual Inc. Mortgage Pass-Through Certificates,

2006-AR10 1A1 | | 5.890 | % | | 9/25/36 | | | 184,817 | | | 144,737 | (e) |

Wells Fargo Mortgage Backed Securities Trust, 2005-AR16 6A3 | | 3.981 | % | | 10/25/35 | | | 311,239 | | | 278,394 | (e) |

Wells Fargo Mortgage Backed Securities Trust, 2006-AR8 2A3 | | 4.759 | % | | 4/25/36 | | | 88,952 | | | 81,952 | (e) |

Total Collateralized Mortgage Obligations (Cost — $7,923,492) | | | | | | | | | | | 5,607,839 | |

| Mortgage-Backed Securities — 24.8% | | | | | | | | | | | | |

FHLMC — 9.9% | | | | | | | | | | | | |

Federal Home Loan Mortgage Corp. (FHLMC) | | 5.383 | % | | 2/1/36 | | | 169,902 | | | 178,390 | (e) |

Federal Home Loan Mortgage Corp. (FHLMC) | | 5.799 | % | | 2/1/37 | | | 36,244 | | | 38,680 | (e) |

Federal Home Loan Mortgage Corp. (FHLMC) | | 6.062 | % | | 3/1/37 | | | 216,158 | | | 231,049 | (e) |

Federal Home Loan Mortgage Corp. (FHLMC) | | 5.751 | % | | 5/1/37 | | | 86,671 | | | 92,558 | (e) |

Federal Home Loan Mortgage Corp. (FHLMC) | | 5.805 | % | | 5/1/37 | | | 105,988 | | | 112,968 | (e) |

Federal Home Loan Mortgage Corp. (FHLMC) | | 4.500 | % | | 8/12/40 | | | 300,000 | | | 309,750 | (h) |

Federal Home Loan Mortgage Corp. (FHLMC), Gold | | 7.000 | % | | 2/1/15-5/1/16 | | | 42,385 | | | 46,022 | |

Federal Home Loan Mortgage Corp. (FHLMC), Gold | | 6.500 | % | | 9/1/31 | | | 140,109 | | | 155,967 | |

Federal Home Loan Mortgage Corp. (FHLMC), Gold | | 5.500 | % | | 11/1/35-4/1/38 | | | 349,315 | | | 375,488 | |

Federal Home Loan Mortgage Corp. (FHLMC), Gold | | 5.000 | % | | 11/1/36 | | | 710,054 | | | 753,131 | |

Federal Home Loan Mortgage Corp. (FHLMC), Gold | | 6.000 | % | | 12/1/36-2/1/37 | | | 455,562 | | | 495,648 | |

Federal Home Loan Mortgage Corp. (FHLMC), Gold | | 6.000 | % | | 8/12/40 | | | 1,000,000 | | | 1,082,344 | (h) |

Total FHLMC | | | | | | | | | | | 3,871,995 | |

FNMA — 7.6% | | | | | | | | | | | | |

Federal National Mortgage Association (FNMA) | | 6.500 | % | | 3/1/16-11/1/36 | | | 844,033 | | | 928,552 | |

Federal National Mortgage Association (FNMA) | | 5.500 | % | | 12/1/16-11/1/36 | | | 109,917 | | | 118,610 | |

Federal National Mortgage Association (FNMA) | | 4.500 | % | | 8/17/25-8/12/40 | | | 700,000 | | | 726,953 | (h) |

Federal National Mortgage Association (FNMA) | | 7.500 | % | | 2/1/30-7/1/31 | | | 36,876 | | | 42,088 | |

Federal National Mortgage Association (FNMA) | | 7.000 | % | | 7/1/30-4/1/32 | | | 274,513 | | | 310,904 | |

Federal National Mortgage Association (FNMA) | | 6.000 | % | | 3/1/32-4/1/32 | | | 398,603 | | | 439,767 | |

Federal National Mortgage Association (FNMA) | | 5.000 | % | | 6/1/35 | | | 205,014 | | | 217,900 | |

Federal National Mortgage Association (FNMA) | | 4.000 | % | | 8/12/40 | | | 200,000 | | | 201,969 | (h) |

Total FNMA | | | | | | | | | | | 2,986,743 | |

GNMA — 7.3% | | | | | | | | | | | | |

Government National Mortgage Association (GNMA) | | 7.000 | % | | 6/15/28-7/15/29 | | | 33,400 | | | 37,972 | |

Government National Mortgage Association (GNMA) | | 6.500 | % | | 9/15/28-2/15/31 | | | 146,753 | | | 164,590 | |

Government National Mortgage Association (GNMA) | | 5.000 | % | | 1/15/40 | | | 595,977 | | | 636,597 | |

Government National Mortgage Association (GNMA) | | 4.500 | % | | 7/21/40 | | | 400,000 | | | 416,750 | (h) |

Government National Mortgage Association (GNMA) | | 5.000 | % | | 7/21/40-9/21/40 | | | 700,000 | | | 742,972 | (h) |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 11 |

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

GNMA — continued | | | | | | | | | | | | |

Government National Mortgage Association (GNMA) | | 5.500 | % | | 7/21/40 | | $ | 400,000 | | $ | 431,502 | (h) |

Government National Mortgage Association (GNMA) | | 6.000 | % | | 7/21/40 | | | 400,000 | | | 436,061 | (h) |

Total GNMA | | | | | | | | | | | 2,866,444 | |

Total Mortgage-Backed Securities (Cost — $9,300,044) | | | | | | | | | | | 9,725,182 | |

| Municipal Bonds — 0.4% | | | | | | | | | | | | |

California — 0.1% | | | | | | | | | | | | |

California State, GO, Build America Bonds | | 7.300 | % | | 10/1/39 | | | 40,000 | | | 41,684 | |

Georgia — 0.1% | | | | | | | | | | | | |

Municipal Electric Authority, GA, Build America Bonds, Plant Vogtle Units 3&4 Project J | | 6.637 | % | | 4/1/57 | | | 30,000 | | | 29,083 | |

Municipal Electric Authority, GA, Build America Bonds, Plant Vogtle Units 3&4 Project M | | 6.655 | % | | 4/1/57 | | | 10,000 | | | 9,656 | |

Total Georgia | | | | | | | | | | | 38,739 | |

Texas — 0.2% | | | | | | | | | | | | |

North Texas Higher Education Authority Inc., Student Loan Revenue | | 1.460 | % | | 7/1/30 | | | 80,000 | | | 79,626 | (e) |

Total Municipal Bonds (Cost — $160,327) | | | | | | | | | | | 160,049 | |

| Sovereign Bonds — 2.4% | | | | | | | | | | | | |

Italy — 0.9% | | | | | | | | | | | | |

Region of Lombardy | | 5.804 | % | | 10/25/32 | | | 350,000 | | | 350,619 | |

Japan — 0.5% | | | | | | | | | | | | |

Japan Finance Corp., Guaranteed Bonds | | 2.875 | % | | 2/2/15 | | | 190,000 | | | 195,506 | |

Mexico — 0.4% | | | | | | | | | | | | |

United Mexican States, Medium-Term Notes | | 5.875 | % | | 1/15/14 | | | 140,000 | | | 159,250 | |

Russia — 0.6% | | | | | | | | | | | | |

Russian Foreign Bond-Eurobond | | 11.000 | % | | 7/24/18 | | | 175,000 | | | 242,156 | (c) |

Total Sovereign Bonds (Cost — $916,917) | | | | | | | | | | | 947,531 | |

| U.S. Government & Agency Obligations — 17.2% | | | | | | | | | | | | |

U.S. Government Agencies — 1.9% | | | | | | | | | | | | |

Farmer Mac, Guaranteed Trust | | 5.125 | % | | 4/19/17 | | | 300,000 | | | 328,365 | (c) |

Federal Home Loan Bank (FHLB), Bonds | | 1.500 | % | | 1/16/13 | | | 50,000 | | | 50,664 | |

Federal National Mortgage Association (FNMA) | | 0.000 | % | | 10/9/19 | | | 100,000 | | | 61,962 | |

Federal National Mortgage Association (FNMA) | | 6.250 | % | | 5/15/29 | | | 100,000 | | | 124,099 | |

Federal National Mortgage Association (FNMA), Senior Notes | | 7.125 | % | | 1/15/30 | | | 90,000 | | | 122,864 | |

Tennessee Valley Authority, Notes | | 5.250 | % | | 9/15/39 | | | 40,000 | | | 44,392 | |

Total U.S. Government Agencies | | | | | | | | | | | 732,346 | |

U.S. Government Obligations — 15.3% | | | | | | | | | | | | |

U.S. Treasury Bonds | | 8.000 | % | | 11/15/21 | | | 80,000 | | | 116,362 | |

U.S. Treasury Bonds | | 3.500 | % | | 2/15/39 | | | 919,000 | | | 853,809 | |

U.S. Treasury Bonds | | 4.250 | % | | 5/15/39 | | | 600,000 | | | 634,500 | |

U.S. Treasury Bonds | | 4.500 | % | | 8/15/39 | | | 440,000 | | | 484,688 | |

U.S. Treasury Bonds | | 4.375 | % | | 11/15/39 | | | 960,000 | | | 1,036,501 | |

U.S. Treasury Notes | | 0.625 | % | | 6/30/12 | | | 230,000 | | | 230,054 | |

U.S. Treasury Notes | | 2.125 | % | | 5/31/15 | | | 30,000 | | | 30,520 | |

U.S. Treasury Notes | | 2.750 | % | | 11/30/16 | | | 480,000 | | | 492,188 | |

U.S. Treasury Notes | | 3.125 | % | | 1/31/17 | | | 210,000 | | | 219,663 | |

U.S. Treasury Notes | | 2.750 | % | | 5/31/17 | | | 230,000 | | | 234,888 | |

U.S. Treasury Notes | | 2.500 | % | | 6/30/17 | | | 600,000 | | | 602,719 | |

See Notes to Financial Statements.

| | |

| 12 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Schedule of investments (unaudited) (cont’d)

June 30, 2010

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

U.S. Government Obligations — continued | | | | | | | | | | | | |

U.S. Treasury Notes | | 3.375 | % | | 11/15/19 | | $ | 790,000 | | $ | 818,329 | |

U.S. Treasury Notes | | 3.500 | % | | 5/15/20 | | | 240,000 | | | 251,212 | |

Total U.S. Government Obligations | | | | | | | | | | | 6,005,433 | |

Total U.S. Government & Agency Obligations (Cost — $6,361,955) | | | | | | | | | | | 6,737,779 | |

| U.S. Treasury Inflation Protected Security — 0.5% | | | | | | | | | | | | |

U.S. Treasury Bonds, Inflation Indexed (Cost — $162,454) | | 2.500 | % | | 1/15/29 | | | 162,456 | | | 184,121 | |

| | | | |

| | | | | | | | Shares | | | |

| Common Stock — 0.0% | | | | | | | | | | | | |

| Energy — 0.0% | | | | | | | | | | | | |

Oil, Gas & Consumable Fuels — 0.0% | | | | | | | | | | | | |

SemGroup Corp., Class A Shares (Cost — $773) | | | | | | | | 25 | | | 656 | *(g) |

| Preferred Stocks — 0.2% | | | | | | | | | | | | |

| Financials — 0.2% | | | | | | | | | | | | |

Diversified Financial Services — 0.2% | | | | | | | | | | | | |

Citigroup Capital XII | | 8.500 | % | | | | | 2,450 | | | 61,403 | |

Thrifts & Mortgage Finance — 0.0% | | | | | | | | | | | | |

Federal Home Loan Mortgage Corp. (FHLMC) | | 8.375 | % | | | | | 7,000 | | | 2,380 | *(e) |

Federal National Mortgage Association (FNMA) | | 7.000 | % | | | | | 300 | | | 180 | *(e) |

Federal National Mortgage Association (FNMA) | | 8.250 | % | | | | | 5,300 | | | 1,802 | *(e) |

Total Thrifts & Mortgage Finance | | | | | | | | | | | 4,362 | |

Total Preferred Stocks (Cost — $384,722) | | | | | | | | | | | 65,765 | |

| | | | |

| | | | | | Expiration

Date | | Warrants | | | |

| Warrants — 0.0% | | | | | | | | | | | | |

SemGroup Corp. (Cost — $0) | | | | | 11/30/14 | | | 27 | | | 148 | * |

| | | | |

| | | | | | | | Contracts | | | |

| Purchased Options — 0.0% | | | | | | | | | | | | |

U.S. Treasury 10-Year Notes Futures, Call @ $119.50 | | | | | 8/27/10 | | | 2 | | | 6,875 | |

U.S. Treasury 10-Year Notes Futures, Call @ $121.50 | | | | | 8/27/10 | | | 4 | | | 7,813 | |

Total Purchased Options (Cost — $7,754) | | | | | | | | | | | 14,688 | |

Total Investments Before Short-Term Investments (Cost — $43,174,078) | | | | | | | | | | | 39,358,969 | |

| | | | |

| | | | | | Maturity

Date | | Face

Amount | | | |

| Short-Term Investments — 9.9% | | | | | | | | | | | | |

U.S. Government Agency — 0.2% | | | | | | | | | | | | |

Federal National Mortgage Association (FNMA), Discount Notes (Cost — $91,976) | | 0.180 | % | | 8/23/10 | | $ | 92,000 | | | 91,976 | (i)(j) |

U.S. Treasury Bills — 3.8% | | | | | | | | | | | | |

U.S. Treasury Bills (Cost — $1,488,974) | | 0.177 | % | | 11/18/10 | | | 1,490,000 | | | 1,488,985 | (j) |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 13 |

Legg Mason Western Asset Variable Diversified Strategic Income Portfolio

| | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | Face

Amount | | Value | |

Repurchase Agreement — 5.9% | | | | | | | | | | | | |

Morgan Stanley tri-party repurchase agreement dated 6/30/10; Proceeds at maturity — $2,300,001; (Fully collateralized by U.S. government agency obligations, 3.000% due 5/26/15; Market value — $2,354,680) (Cost — $2,300,000) | | 0.020 | % | | 7/1/10 | | $ | 2,300,000 | | $ | 2,300,000 | |

Total Short-Term Investments (Cost — $3,880,950) | | | | | | | | | | | 3,880,961 | |

Total Investments — 110.2% (Cost — $47,055,028#) | | | | | | | | | | | 43,239,930 | |

Liabilities in Excess of Other Assets — (10.2)% | | | | | | | | | | | (4,016,304 | ) |

Total Net Assets — 100.0% | | | | | | | | | | $ | 39,223,626 | |

| * | Non-income producing security. |

| (a) | The coupon payment on these securities is currently in default as of June 30, 2010. |

| (c) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees, unless otherwise noted. |

| (d) | Payment-in-kind security for which part of the income earned may be paid as additional principal. |

| (e) | Variable rate security. Interest rate disclosed is that which is in effect at June 30, 2010. |

| (f) | Security has no maturity date. The date shown represents the next call date. |

| (g) | Security is valued in good faith at fair value in accordance with procedures approved by the Board of Trustees (See Note 1). |

| (h) | This security is traded on a to-be-announced (“TBA”) basis (See Note 1). |

| (i) | All or a portion of this security is held at the broker as collateral for open futures contracts. |

| (j) | Rate shown represents yield-to-maturity. |

| # | Aggregate cost for federal income tax purposes is substantially the same. |

| | |

Abbreviation used in this schedule: |

| GO | | — General Obligation |

| | | | | | | | | | |

| Schedule of Written Options | | | | | | | | |

| Security | | Expiration

Date | | Strike

Price | | Contracts | | Value |

| Eurodollar Futures, Call | | 9/13/10 | | $ | 99.25 | | 9 | | $ | 3,769 |

| U.S. Treasury 10-Year Notes Futures, Call | | 8/27/10 | | | 121.00 | | 4 | | | 9,125 |

| U.S. Treasury 10-Year Notes Futures, Call | | 8/27/10 | | | 123.50 | | 2 | | | 1,875 |

| U.S. Treasury 10-Year Notes Futures, Put | | 8/27/10 | | | 115.00 | | 4 | | | 250 |

| Total Written Options (Premiums received — $10,876) | | | | | | | | | $ | 15,019 |

See Notes to Financial Statements.

| | |

| 14 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Statement of assets and liabilities (unaudited)

June 30, 2010

| | | |

| |

| Assets: | | | |

Investments, at value (Cost — $47,055,028) | | $ | 43,239,930 |

Foreign currency, at value (Cost — $33,541) | | | 32,592 |

Cash | | | 604 |

Receivable for securities sold | | | 9,832,891 |

Interest receivable | | | 369,714 |

Unrealized appreciation on forward currency contracts | | | 53,133 |

Principal paydown receivable | | | 25,553 |

Total Assets | | | 53,554,417 |

| |

| Liabilities: | | | |

Payable for securities purchased | | | 14,150,027 |

Payable for Portfolio shares repurchased | | | 72,450 |

Unrealized depreciation on forward currency contracts | | | 30,430 |

Investment management fee payable | | | 20,921 |

Written options, at value (premiums received $10,876) | | | 15,019 |

Payable to broker — variation margin on open futures contracts | | | 4,989 |

Trustees’ fees payable | | | 2,851 |

Accrued expenses | | | 34,104 |

Total Liabilities | | | 14,330,791 |

| Total Net Assets | | $ | 39,223,626 |

| |

| Net Assets: | | | |

Par value (Note 5) | | $ | 47 |

Paid-in capital in excess of par value | | | 46,680,108 |

Undistributed net investment income | | | 707,428 |

Accumulated net realized loss on investments, futures contracts, written options and foreign currency transactions | | | (4,343,666) |

Net unrealized depreciation on investments, futures contracts, written options and foreign currencies | | | (3,820,291) |

| Total Net Assets | | $ | 39,223,626 |

| Shares Outstanding | | | 4,679,422 |

| Net Asset Value | | | $8.38 |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 15 |

Statement of operations (unaudited)

For the Six Months Ended June 30, 2010

| | | |

| |

| Investment Income: | | | |

Interest | | $ | 984,606 |

Dividends | | | 2,978 |

Total Investment Income | | | 987,584 |

| |

| Expenses: | | | |

Investment management fee (Note 2) | | | 129,826 |

Shareholder reports | | | 38,920 |

Audit and tax | | | 12,392 |

Transfer agent fees | | | 3,402 |

Legal fees | | | 3,115 |

Custody fees | | | 1,942 |

Insurance | | | 932 |

Trustees’ fees | | | 243 |

Miscellaneous expenses | | | 1,410 |

Total Expenses | | | 192,182 |

Less: Compensating balance arrangements (Note 1) | | | (159) |

Net Expenses | | | 192,023 |

| Net Investment Income | | | 795,561 |

| |

Realized and Unrealized Gain (Loss) on Investments, Futures Contracts, Written Options

and Foreign Currency Transactions (Notes 1, 3 and 4): | | | |

Net Realized Gain (Loss) From: | | | |

Investment transactions | | | (57,576) |

Futures contracts | | | 110,896 |

Written options | | | 16,542 |

Foreign currency transactions | | | 62,673 |

Net Realized Gain | | | 132,535 |

Change in Net Unrealized Appreciation/Depreciation From: | | | |

Investments | | | 1,890,399 |

Futures contracts | | | 5,279 |

Written options | | | (7,697) |

Foreign currencies | | | 21,616 |

Change in Net Unrealized Appreciation/Depreciation | | | 1,909,597 |

| Net Gain on Investments, Futures Contracts, Written Options and Foreign Currency Transactions | | | 2,042,132 |

| Proceeds from Settlement of a Regulatory Matter (Note 7) | | | 8,502 |

| Increase in Net Assets from Operations | | $ | 2,846,195 |

See Notes to Financial Statements.

| | |

| 16 | | Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report |

Statements of changes in net assets

| | | | | | |

For the Six Months Ended June 30, 2010 (unaudited)

and the Year Ended December 31, 2009 | | 2010 | | 2009 |

| | |

| Operations: | | | | | | |

Net investment income | | $ | 795,561 | | $ | 2,162,550 |

Net realized gain (loss) | | | 132,535 | | | (752,371) |

Change in net unrealized appreciation/depreciation | | | 1,909,597 | | | 5,927,730 |

Proceeds from settlement of a regulatory matter (Note 7) | | | 8,502 | | | — |

Increase in Net Assets From Operations | | | 2,846,195 | | | 7,337,909 |

| | |

| Distributions to Shareholders From (Note 1): | | | | | | |

Net investment income | | | (75,002) | | | (2,050,000) |

Decrease in Net Assets From Distributions to Shareholders | | | (75,002) | | | (2,050,000) |

| | |

| Portfolio Share Transactions (Note 5): | | | | | | |

Net proceeds from sale of shares | | | 293,994 | | | 664,343 |

Reinvestment of distributions | | | 75,002 | | | 2,050,000 |

Cost of shares repurchased | | | (4,397,710) | | | (8,106,122) |

Decrease in Net Assets From Portfolio Share Transactions | | | (4,028,714) | | | (5,391,779) |

Decrease in Net Assets | | | (1,257,521) | | | (103,870) |

| | |

| Net Assets: | | | | | | |

Beginning of period | | | 40,481,147 | | | 40,585,017 |

End of period* | | $ | 39,223,626 | | $ | 40,481,147 |

* Includes undistributed and (overdistributed) net investment income, respectively, of: | | | $707,428 | | | $(21,633) |

See Notes to Financial Statements.

| | |

| Legg Mason Western Asset Variable Diversified Strategic Income Portfolio 2010 Semi-Annual Report | | 17 |

Financial highlights

| | | | | | | | | | | | | | | | | | |

| For a share of beneficial interest outstanding throughout each year ended December 31, unless otherwise noted: | |

| | | 20101,2 | | | 20092 | | | 20082 | | | 20072 | | | 20062 | | | 20052 | |

| | | | | | |

| Net asset value, beginning of period | | $ 7.83 | | | $ 6.88 | | | $ 8.62 | | | $ 8.93 | | | $ 9.01 | | | $ 9.30 | |

| | | | | | |

| Income (loss) from operations: | | | | | | | | | | | | | | | | | | |

Net investment income | | 0.16 | | | 0.40 | | | 0.44 | | | 0.47 | | | 0.48 | | | 0.46 | |

Net realized and unrealized gain (loss) | | 0.41 | | | 0.96 | | | (1.65) | | | (0.30) | | | 0.01 | | | (0.22) | |

Total income (loss) from operations | | 0.57 | | | 1.36 | | | (1.21) | | | 0.17 | | | 0.49 | | | 0.24 | |

| | | | | | |

| Less distributions from: | | | | | | | | | | | | | | | | | | |

Net investment income | | (0.02) | | | (0.41) | | | (0.53) | | | (0.48) | | | (0.54) | | | (0.53) | |

Net realized gains | | — | | | — | | | — | | | — | | | (0.03) | | | — | |

Total distributions | | (0.02) | | | (0.41) | | | (0.53) | | | (0.48) | | | (0.57) | | | (0.53) | |

| | | | | | |

| Net asset value, end of period | | $8.38 | | | $7.83 | | | $6.88 | | | $8.62 | | | $8.93 | | | $9.01 | |

Total return3 | | 7.23 | % | | 19.84 | % | | (13.98) | % | | 1.98 | % | | 5.39 | % | | 2.56 | % |

| | | | | | |

| Net assets, end of period (000s) | | $39,224 | | | $40,481 | | | $40,585 | | | $62,667 | | | $76,178 | | | $89,522 | |

| | | | | | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | |

Gross expenses | | 0.96 | %4 | | 0.95 | % | | 1.07 | % | | 0.85 | % | | 0.75 | %5 | | 0.77 | % |

Net expenses6 | | 0.96 | 4 | | 0.95 | | | 1.07 | | | 0.85 | | | 0.74 | 5,7 | | 0.77 | |

Net investment income | | 3.98 | 4 | | 5.33 | | | 5.43 | | | 5.23 | | | 5.24 | | | 4.87 | |

| | | | | | |

| Portfolio turnover rate8 | | 70 | % | | 53 | % | | 29 | % | | 67 | % | | 224 | % | | 83 | % |

| 1 | For the six months ended June 30, 2010 (unaudited). |

| 2 | Per share amounts have been calculated using the average shares method. |

| 3 | Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Total returns do not reflect expenses associated with the separate accounts such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total return for all periods shown. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| 5 | Included in the expense ratios are certain non-recurring restructuring (and reorganization, if applicable) fees that were incurred by the Portfolio during the period. Without these fees, the gross and net expense ratios would have been 0.73% and 0.72%, respectively. |

| 6 | The impact of compensating balance arrangements, if any, was less than 0.01%. |

| 7 | Reflects fee waivers and/or expense reimbursements. |