UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-06351

Green Century Funds

114 State Street

Suite 200

Boston, MA 02109

(Address of principal executive offices)

Green Century Capital Management, Inc.

114 State Street

Suite 200

Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 482-0800

Date of fiscal year end: July 31

Date of reporting period: January 31, 2016

Item 1. Reports to Stockholders

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

| SEMI-ANNUAL REPORT Green Century Balanced Fund Green Century Equity Fund January 31, 2016 | |

| An investment for your future.® | 114 State Street, Boston, Massachusetts 02109 | |

For information on the Green Century Funds®, call 1-800-93-GREEN. For information on how to open an account and account services, call 1-800-221-5519 8:00 am to 6:00 pm Eastern Time, Monday through Friday. For daily share price information twenty-four hours a day, visit www.greencentury.com.

Dear Green Century Funds Shareholder:

Whether you are a new investor with Green Century—or one who has been with us over the decades—we appreciate the trust that you have placed in us. For this Semi-Annual Report, we are focusing on our overall investment strategy, saving for retirement through IRAs and a recent improvement that Green Century secured as part of our work to curb climate change and promote clean energy.

Investing In Today’s Market

Even if you don’t follow the stock market regularly, you have no doubt been aware of the recent market swings since our last update. Green Century and the subadvisors for our Funds are keeping a watchful eye on key factors while we maintain a long term horizon in mind. As a reminder, Green Century believes that sustainable and responsible companies can enjoy competitive advantages, such as liability reductions and

access to expanding growth markets, and seeks to invest in well managed companies that strive to maximize their environmental advantages and minimize their environmental risks. In this update, we also have included our discussion and analysis of the Green Century Balanced Fund’s and Green Century Equity Fund’s performance through January 31, 2016. If you are interested in more frequent updates, please sign up for our e-newsletter at www.greencentury.com.

Investing for Your Retirement—Upcoming April 18th IRA Deadline

It is never too early or too late to start planning for your retirement—and the upcoming IRA deadline is a good reminder to do so. If you have not made your 2015 contribution to an IRA, there is good news: contributions for 2015 can be made until April 18, 2016. If you have made your 2015 contribution, you can also make your 2016 contribution now and cross it off your “to do” list.

Sometimes the hardest part is getting started, which is why Green Century can help you if you have questions along the way. Whether you want to open a new IRA or transfer an

Green Century believes that environmentally and socially responsible companies may enjoy competitive advantages.

existing IRA to Green Century, there are clear steps available on our website or by calling us at 1-800-93-GREEN (or 1-800-934-7336) Monday through Friday from 9am to 6pm Eastern Time.

Making Companies More Sustainable

A key way that you make an impact with a Green Century investment is through the direct work that we do to make companies more sustainable. While our Forest Protection Campaign has captured most of the headlines for its successes in preserving rainforests, reducing carbon emissions and protecting endangered species like the orangutan, we want to share another recent success.

In response to a shareholder proposal filed by the Green Century Balanced Fund, Hologic,1 a manufacturer and supplier of diagnostic and medical imaging systems used for women’s health care, has agreed to reduce its greenhouse gas emissions. The company has adopted quantitative, time-bound goals for reducing the company’s greenhouse gas emissions by September 2016. A company typically reduces emissions by employing energy efficiency measures or sourcing clean energy. As with all of our successful advocacy, Green Century will follow up with Hologic to ensure that it maintains its commitment to this important change.

For more information about how Green Century presses companies to become more sustainable, please visit www.greencentury.com and “Why Choose Green Century.” If you want to receive breaking news about our advocacy work, simply join our email list.

Fossil Fuel Free Investing Continues to Grow

The financial and moral case to avoid investing in coal, oil and gas companies has led thousands of people and a growing number of institutions to cut financial ties to the fossil fuel industry. Around the Paris COP21 climate negotiations this fall, environmental activist and actor Leonardo DiCaprio announced his pledge, raising global visibility around the role of investors in tackling climate change.

As the first family of diversified and responsible fossil fuel free funds, Green Century is proud to play a role in supporting the transition to a cleaner economy. To learn more about the increasing concerns about stranded assets or to download our free Guide to Personal Divestment, please visit our updated Fossil Fuel Free Investing page at www.greencentury.com/fossil-fuel-free.

Leonardo DiCaprio 2014 by Christopher William Adach from London, UKCC BY-SA 2.0 via Commons

2

We want to hear from you and stay in touch. If you are not receiving our e-newsletter with up to date impact stories and more, please visit www.greencentury.com, email us at info@greencentury.com or call us at 1-800-93-GREEN.

Respectfully,

Green Century Capital Management

3

THE GREEN CENTURY EQUITY FUND

The Green Century Equity Fund invests essentially all of its assets in the stocks which make up the MSCI KLD 400 Social ex Fossil Fuels Index (the KLD 400 Index or the Index), comprised primarily of large capitalization U.S. companies selected based on comprehensive social and environmental sustainability criteria. The Equity Fund seeks to provide shareholders with a long-term total return that matches that of the Index.

Average Annual Return* Total expense ratio: 1.25% | One Year | Three Years | Five Years | Ten Years | ||||||||||||||

| December 31, 2015 | Green Century Equity Fund | 0.94% | 15.23% | 11.47% | 6.34% | |||||||||||||

| S&P 500® Index2 | 1.38% | 15.13% | 12.57% | 7.31% | ||||||||||||||

| January 31, 2016 | Green Century Equity Fund | –1.32% | 10.96% | 9.94% | 5.56% | |||||||||||||

| S&P 500® Index2 | –0.67% | 11.30% | 10.91% | 6.48% | ||||||||||||||

* The performance data quoted represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information as of the most recent month-end, call 1-800-93-GREEN. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder might pay on Fund distributions or the redemption of Fund shares. A redemption fee of 2.00% may be imposed on redemptions or exchanges of shares you have owned for 60 days or less. Please see the Prospectus for more information.

The Green Century Equity Fund, which closely tracks the KLD 400 Index, returned –6.48% for the six month period ended January 31, 2016, while the S&P 500® Index (the S&P 500®) returned –6.77% during the same period.

The difference in performance of the Equity Fund relative to the S&P 500® was largely due to differences in sector allocation and stock selection criteria between the two portfolios. The materials sector was the worst performing sector in the S&P 500® during the period, losing more than 14%. As a function of becoming fossil fuel free on April 1, 2014, the Equity Fund did not hold any stocks in the traditional energy sector during the period, contributing to its outperformance versus the S&P 500®. However, the Equity Fund’s performance relative to the S&P 500® was hurt by stock selection in the industrials sector.

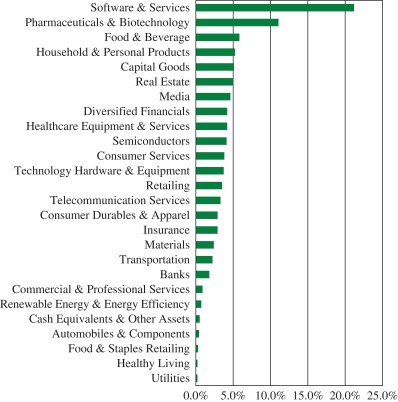

GREEN CENTURY EQUITY FUND

INVESTMENT BY INDUSTRY

4

According to an analysis by the Equity Fund’s portfolio managers, U.S. equities experienced negative returns in the third quarter, with increased volatility seen in August. Three events are attributable to the heightened volatility in U.S. equity markets during this quarter, including China’s stock market crash, concerns over global growth, and the U.S. Federal Reserve’s (the Fed’s) indecision on raising interest rates. The Chinese stock market’s bull run was interrupted in July prompting the Chinese government to devalue the renminbi in hopes of driving the economy and the market up despite indicators of weaker growth in China.

The strong U.S. dollar abroad negatively impacted sectors with a greater reliance on non-U.S. revenues. The Fed decided to not raise rates in its September meeting; however, Fed officials stated that they were still on track to raise rates in 2015. The U.S. stock market responded poorly to this decision, falling more than 3% from September 17th to September 30th.

The Fund’s portfolio managers believe that U.S. equities experienced positive returns in the fourth quarter, driven largely by a market rebound in October, while U.S. markets were generally flat in the final two months of the year. In October, Federal Reserve officials signaled a looming rate hike which would eventually occur in December. The market’s positive reaction to this, along with the announcement of an expansion of the European Central Bank’s bond buying program, helped support the rally of global equity markets in October. During the fourth quarter, crude oil prices plummeted roughly 20%, continuing the downward trend seen throughout the year. Falling oil prices have negatively impacted sectors with a greater reliance on oil, the energy sector being most significant. As a reminder, the Equity Fund is fossil fuel free, which has positively contributed to its outperformance versus the S&P 500® recently. Economic data was mostly positive in the fourth quarter; however, there were some signs suggesting slowing growth in the U.S.

The Equity Fund, like other mutual funds invested primarily in stocks, carries the risk of investing in the stock market. The large companies in which the Equity Fund is invested may perform worse than the stock market as a whole. The Equity Fund will not shift concentration from one industry to another or from stocks to bonds or cash, in order to defend against a falling stock market.

THE GREEN CENTURY BALANCED FUND

The Green Century Balanced Fund seeks capital growth and income from a diversified portfolio of stocks and bonds that meet Green Century’s standards for corporate environmental performance. The portfolio managers of the Balanced Fund avoid fossil fuel companies and aim to invest in companies that are in the business of solving environmental problems or that are committed to reducing their environmental impact.

Average Annual Return* Total expense ratio: 1.48% | One Year | Three Years | Five Years | Ten Years | ||||||||||||||

| December 31, 2015 | Green Century Balanced Fund | –1.35% | 9.36% | 8.16% | 4.95% | |||||||||||||

| Custom Balanced Fund Index3 | 1.29% | 9.35% | 8.60% | 6.37% | ||||||||||||||

| January 31, 2016 | Green Century Balanced Fund | –4.63% | 6.22% | 6.78% | 4.41% | |||||||||||||

| Custom Balanced Fund Index3 | –0.23% | 7.33% | 7.72% | 5.90% | ||||||||||||||

* The performance data quoted represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information as of the most recent month-end, call 1-800-93-GREEN. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder might pay on Fund distributions or the redemption of Fund shares. A redemption fee of 2.00% may be imposed on redemptions or exchanges of shares you have owned for 60 days or less. Please see the Prospectus for more information.

5

As of January 31, 2016, the Balanced Fund underperformed the Custom Balanced Index over various time periods. According to an analysis by the Fund’s portfolio managers, the bond holdings in the Balanced Fund held up well, but the stock performance was disappointing for the one year period ending January 31, 2016. The Fund’s equity holdings that positively contributed to its performance during the twelve months ended January 31, 2016 included: Alphabet Inc.,1 Palo Alto Networks,1 Cigna Corporation,1 Microsoft Corporation,1 First Solar, Inc.,1 and Ormat Technologies.1 Poor performers included United Natural Foods, Inc.,1 Men’s Wearhouse, Inc.,1 Wisdomtree Investments, Inc.,1 BorgWarner Inc.,1 Biogen Inc.,1 and Whole Foods Market, Inc.1

In the view of the Balanced Fund’s portfolio managers, during the twelve months ended January 31, 2016, investors increasingly focused on perceived risks. These risks include a weakening global economy, geopolitical risks, and the risks of a policy error by the U.S. Federal Reserve, which began to raise interest rates in late 2015, while the European Central Bank and the Bank of Japan were still easing monetary policy.

The Fund’s portfolio managers believe that overall, 2015 was a year of contradictions and noise, along with a highly concentrated and narrowly-focused market, and January 2016 continued this trend with a discouraging start to the year. Oil prices dropped throughout the year, with West Texas Intermediate oil at $37 per barrel on December 31, down 18% for the fourth calendar quarter, extending the 23% decline in the third quarter, and down 39% during the full year of 2015. Oil continued to drop in January, ending at $34 on January 31. This steep decline in energy prices both reflects slower economic growth and has further slowed economic growth in oil-exporting countries, compounding the growth decline. While the Balanced Fund does not invest in fossil-fuel companies, the steep decline in oil prices also hurt the sales of clean-technology companies involved in wind and solar power and also companies selling highly efficient engines or energy conservation technology.

GREEN CENTURY BALANCED FUND

INVESTMENT BY INDUSTRY

6

The strength in the U.S. dollar continued to be a headwind for U.S. multinational companies. In addition to the dollar strength and oil price weakness, investors focused on slowing Chinese growth and the implications of falling growth in China for oil and commodity prices. The portfolio managers believe that the markets’ reactions to these concerns are overblown for the United States.

The Balanced Fund’s portfolio managers believe the Fund is positioned to benefit from the moderate economic growth expected for the U.S. in 2016, and continue to emphasize stocks of the U.S. and other developed markets over bonds, believing that the balance of risk and return for 2016 favors developed market stocks over bonds and cash. The Fund’s equity holdings are slightly weighted toward more cyclical sectors such as industrials stocks, and the Fund’s bond holdings are weighted toward short to intermediate maturity and high quality bonds.

The Green Century Balanced Fund invests in the stocks and bonds of environmentally responsible corporations of various sizes, including small, medium, and large companies. The Green Century Balanced Fund does not invest in fossil fuels though most other diversified mutual funds do.

The value of the stocks held in the Balanced Fund will fluctuate in response to factors that may affect a single issuer, industry, or sector of the economy or may affect the market as a whole. Bonds are subject to a variety of risks including interest rate, credit, and inflation risk.

The Green Century Funds’ proxy voting guidelines and a record of the Funds’ proxy votes for the year ended June 30, 2015 are available without charge, upon request, (i) at www.greencentury.com, (ii) by calling 1-800-93-GREEN, (iii) sending an e-mail to info@greencentury.com, and (iv) on the Securities and Exchange Commission’s website at www.sec.gov.

The Green Century Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of the year on Form N-Q. The Green Century Funds’ Forms N-Q are available on the EDGAR database on the SEC’s website at www.sec.gov. These Forms may also be reviewed and copied at the SEC’s Public Reference Room in Washington D.C. Information about the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The information on Form N-Q may also be obtained by calling 1-800-93-GREEN, or by e-mailing a request to info@greencentury.com.

1 As of January 31, 2016, the following companies comprised the listed percentages of each of the Green Century Funds:

7

| Portfolio Holding | GREEN CENTURY BALANCED FUND | GREEN CENTURY EQUITY FUND | ||||||

Hologic | 0.85 | % | 0.12 | % | ||||

Alphabet, Inc. | 2.19 | % | 6.36 | % | ||||

Palo Alto Networks | 0.86 | % | 0.00 | % | ||||

Cigna Corporation | 1.79 | % | 0.49 | % | ||||

Microsoft Corporation | 0.83 | % | 5.91 | % | ||||

First Solar, Inc. | 0.57 | % | 0.00 | % | ||||

Ormat Technologies | 0.74 | % | 0.02 | % | ||||

United Natural Foods, Inc. | 1.14 | % | 0.03 | % | ||||

Men’s Wearhouse, Inc. | 0.29 | % | 0.00 | % | ||||

Wisdomtree Investments, Inc. | 0.58 | % | 0.00 | % | ||||

BorgWarner Inc. | 0.52 | % | 0.09 | % | ||||

Biogen, Inc. | 0.88 | % | 0.91 | % | ||||

Whole Foods Market, Inc. | 0.92 | % | 0.15 | % | ||||

Portfolio composition will change due to ongoing management of the Funds. Please refer to the Green Century Funds website for current information regarding the Funds’ portfolio holdings. These holdings are subject to risk as described in the Funds’ Prospectus. References to specific investments should not be construed as a recommendation of the securities by the Funds, their administrator, or their distributor.

2 The S&P 500® Index is an unmanaged index of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The S&P 500® Index is heavily weighted toward stocks with large market capitalization and represents approximately two-thirds of the total market value of all domestic stocks. It is not possible to invest directly in the S&P 500® Index.

3 The Custom Balanced Index is comprised of a 60% weighting in the S&P 1500 Index and a 40% weighting in the BofA Merrill Lynch 1-10 Year US Corporate & Government Index (the BofA Merrill Lynch Index). The S&P Supercomposite 1500 Index is an unmanaged broad-based capitalization-weighted index comprising 1500 stocks of large-cap, mid-cap, and small-cap U.S. companies. The BofA Merrill Lynch Index tracks the performance of U.S. dollar-denominated investment grade government and corporate public debt issued in the U.S. domestic bond market with at least 1 year and less than 10 years remaining maturity, including U.S. treasury, U.S. agency, foreign government, supranational and corporate securities. It is not possible to invest directly in the Custom Balanced Index, the S&P Supercomposite 1500 Index, or the BofA Merrill Lynch Index.

The Funds’ environmental criteria limit the investments available to the Funds compared to mutual funds that do not use environmental criteria.

This information has been prepared from sources believed reliable. The views expressed are as of the date of publication and are those of the Advisor to the Funds.

This material must be preceded or accompanied by a current Prospectus.

Distributor: UMB Distribution Services, LLC, 3/16

The Green Century Equity Fund (the “Fund”) is not sponsored, endorsed, or promoted by MSCI, its affiliates, information providers or any other third party involved in, or related to, compiling, computing or creating the MSCI indices (the “MSCI Parties”), and the MSCI Parties bear no liability with respect to the Fund or any index on which the Fund is based. The MSCI Parties are not sponsors of the Fund and are not affiliated with the Fund in any way. The Statement of Additional Information contains a more detailed description of the limited relationship the MSCI Parties have with Green Century Capital Management and the Fund.

8

GREEN CENTURY FUNDS EXPENSE EXAMPLE

For the six months ended January 31, 2016 (unaudited)

As a shareholder of the Green Century Funds (the “Funds”), you incur two types of costs: (1) transaction costs, including redemption fees on certain redemptions; and (2) ongoing costs, including management fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from August 1, 2015 to January 31, 2016 (the “period”).

Actual Expenses The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 equals 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the actual return of either of the Funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees on shares held for 60 days or less. Therefore, the second line of the table is useful in comparing the ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs could have been higher.

| BEGINNING ACCOUNT VALUE AUGUST 1, 2015 | ENDING ACCOUNT VALUE JANUARY 31, 2016 | EXPENSES PAID DURING THE PERIOD1 | ||||||||||

Balanced Fund | ||||||||||||

Actual Expenses | $ | 1,000.00 | $ | 893.60 | $ | 7.04 | ||||||

Hypothetical Example, assuming a 5% return before expenses | 1,000.00 | 1,017.56 | 7.50 | |||||||||

Equity Fund | ||||||||||||

Actual Expenses | 1,000.00 | 935.20 | 6.08 | |||||||||

Hypothetical Example, assuming a 5% return before expenses | 1,000.00 | 1,018.72 | 6.34 | |||||||||

1 Expenses are equal to the Funds’ annualized expense ratios (1.48% for the Balanced Fund and 1.25% for the Equity Fund), multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

9

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) |

COMMON STOCKS — 66.0% |

| |||||||

| SHARES | VALUE | |||||||

Software & Services — 7.1% |

| |||||||

Adobe Systems, Inc. (a) | 15,064 | $ | 1,342,654 | |||||

Alphabet, Inc., Class A (a) | 4,940 | 3,761,069 | ||||||

ANSYS, Inc. (a) | 20,362 | 1,795,725 | ||||||

eBay, Inc. (a) | 37,211 | 872,970 | ||||||

MasterCard, Inc., Class A | 10,709 | 953,422 | ||||||

Microsoft Corporation | 25,877 | 1,425,564 | ||||||

PayPal Holdings, Inc. (a) | 38,711 | 1,399,016 | ||||||

Zendesk, Inc. (a) | 29,651 | 652,618 | ||||||

|

| |||||||

| 12,203,038 | ||||||||

|

| |||||||

Capital Goods — 5.5% |

| |||||||

A.O. Smith Corporation | 13,091 | 914,406 | ||||||

ABB Ltd. American Depositary Receipt (b) | 82,310 | 1,423,963 | ||||||

Hexcel Corporation | 29,452 | 1,218,724 | ||||||

Illinois Tool Works, Inc. | 20,368 | 1,834,546 | ||||||

Lincoln Electric Holdings, Inc. | 11,594 | 617,265 | ||||||

Middleby Corporation (The) (a) | 6,045 | 546,226 | ||||||

Wabtec Corporation | 25,034 | 1,600,924 | ||||||

Xylem, Inc. | 34,923 | 1,255,482 | ||||||

|

| |||||||

| 9,411,536 | ||||||||

|

| |||||||

Healthcare Equipment & Services — 5.5% |

| |||||||

Cigna Corporation | 23,011 | 3,074,270 | ||||||

DENTSPLY International, Inc. | 22,414 | 1,319,960 | ||||||

Hologic, Inc. (a) | 43,098 | 1,462,746 | ||||||

Medtronic PLC (b) | 15,184 | 1,152,769 | ||||||

Omnicell, Inc. (a) | 34,317 | 960,533 | ||||||

Zimmer Biomet Holdings, Inc. | 14,215 | 1,410,981 | ||||||

|

| |||||||

| 9,381,259 | ||||||||

|

| |||||||

Pharmaceuticals & Biotechnology — 5.1% |

| |||||||

Amgen, Inc. | 6,709 | 1,024,666 | ||||||

Biogen, Inc. (a) | 5,551 | 1,515,756 | ||||||

Gilead Sciences, Inc. | 22,048 | 1,829,984 | ||||||

Merck & Company, Inc. | 22,135 | 1,121,580 | ||||||

Novartis A.G. American Depositary Receipt (b) | 19,568 | 1,525,717 | ||||||

Shire PLC American Depositary Receipt (b) | 10,557 | 1,776,743 | ||||||

|

| |||||||

| 8,794,446 | ||||||||

|

| |||||||

| SHARES | VALUE | |||||||

Technology Hardware & Equipment — 5.0% |

| |||||||

Apple, Inc. | 28,238 | $ | 2,748,687 | |||||

Cisco Systems, Inc. | 69,115 | 1,644,245 | ||||||

F5 Networks, Inc. (a) | 21,846 | 2,048,718 | ||||||

Palo Alto Networks, Inc. (a) | 9,906 | 1,480,848 | ||||||

SanDisk Corporation | 10,147 | 717,393 | ||||||

|

| |||||||

| 8,639,891 | ||||||||

|

| |||||||

Banks — 4.8% |

| |||||||

East West Bancorp, Inc. | 23,205 | 752,306 | ||||||

Fifth Third Bancorp | 59,794 | 944,745 | ||||||

First Republic Bank | 19,347 | 1,315,596 | ||||||

PNC Financial Services Group, Inc. (The) | 17,774 | 1,540,117 | ||||||

SVB Financial Group (a) | 12,259 | 1,242,082 | ||||||

Umpqua Holdings Corporation | 74,742 | 1,082,264 | ||||||

Wells Fargo & Company | 26,213 | 1,316,679 | ||||||

|

| |||||||

| 8,193,789 | ||||||||

|

| |||||||

Renewable Energy & Energy Efficiency — 4.2% |

| |||||||

8point3 Energy Partners LP | 78,780 | 1,295,931 | ||||||

Acuity Brands, Inc. | 5,572 | 1,127,940 | ||||||

EnerNOC, Inc. (a) | 48,289 | 253,517 | ||||||

First Solar, Inc. (a) | 14,364 | 986,232 | ||||||

Hannon Armstrong Sustainable Infrastructure Capital, Inc. | 33,080 | 593,786 | ||||||

Johnson Controls, Inc. | 34,178 | 1,225,965 | ||||||

Ormat Technologies, Inc. | 35,670 | 1,262,718 | ||||||

SolarCity Corporation (a) | 12,216 | 435,501 | ||||||

|

| |||||||

| 7,181,590 | ||||||||

|

| |||||||

Retailing — 3.9% |

| |||||||

Home Depot, Inc. (The) | 14,029 | 1,764,287 | ||||||

Men’s Wearhouse, Inc. (The) | 36,409 | 499,168 | ||||||

Priceline Group, Inc. (The) (a) | 856 | 911,614 | ||||||

Target Corporation | 22,043 | 1,596,354 | ||||||

TJX Companies, Inc. (The) | 26,928 | 1,918,351 | ||||||

|

| |||||||

| 6,689,774 | ||||||||

|

| |||||||

Semiconductors — 3.2% |

| |||||||

Analog Devices, Inc. | 17,124 | 922,299 | ||||||

ARM Holdings PLC American Depositary Receipt (b) | 18,970 | 817,228 | ||||||

ASML Holding NV (b) | 10,584 | 972,034 | ||||||

NXP Semiconductors NV (a)(b) | 23,571 | 1,762,639 | ||||||

Xilinx, Inc. | 19,926 | 1,001,680 | ||||||

|

| |||||||

| 5,475,880 | ||||||||

|

| |||||||

10

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | continued |

| SHARES | VALUE | |||||||

Healthy Living — 2.9% |

| |||||||

United Natural Foods, Inc. (a) | 55,789 | $ | 1,953,731 | |||||

WhiteWave Foods Company (The) (a) | 50,608 | 1,910,452 | ||||||

Whole Foods Market, Inc. | 36,822 | 1,079,253 | ||||||

|

| |||||||

| 4,943,436 | ||||||||

|

| |||||||

Consumer Durables & Apparel — 2.8% |

| |||||||

Deckers Outdoor Corporation (a) | 23,260 | 1,150,440 | ||||||

Jarden Corporation (a) | 20,524 | 1,088,798 | ||||||

lululemon athletica, Inc. (a) | 21,622 | 1,342,077 | ||||||

NIKE, Inc., Class B | 20,092 | 1,245,905 | ||||||

|

| |||||||

| 4,827,220 | ||||||||

|

| |||||||

Insurance — 2.8% |

| |||||||

Aflac, Inc. | 34,928 | 2,024,427 | ||||||

Lincoln National Corporation | 28,123 | 1,109,733 | ||||||

Reinsurance Group of America, Inc. | 19,460 | 1,639,116 | ||||||

|

| |||||||

| 4,773,276 | ||||||||

|

| |||||||

Diversified Financials — 2.1% |

| |||||||

Charles Schwab Corporation (The) | 39,975 | 1,020,562 | ||||||

Stifel Financial Corporation (a) | 45,527 | 1,523,333 | ||||||

WisdomTree Investments, Inc. | 82,543 | 990,516 | ||||||

|

| |||||||

| 3,534,411 | ||||||||

|

| |||||||

Materials — 1.7% |

| |||||||

Minerals Technologies, Inc. | 20,706 | 848,739 | ||||||

Owens-Illinois, Inc. (a) | 35,318 | 457,015 | ||||||

Sealed Air Corporation | 39,637 | 1,606,487 | ||||||

|

| |||||||

| 2,912,241 | ||||||||

|

| |||||||

Transportation — 1.5% |

| |||||||

J.B. Hunt Transport Services, Inc. | 15,976 | 1,161,455 | ||||||

United Parcel Service, Inc., Class B | 14,699 | 1,369,947 | ||||||

|

| |||||||

| 2,531,402 | ||||||||

|

| |||||||

Food & Staples Retailing — 1.4% |

| |||||||

Costco Wholesale Corporation | 8,613 | 1,301,597 | ||||||

CVS Health Corporation | 12,100 | 1,168,739 | ||||||

|

| |||||||

| 2,470,336 | ||||||||

|

| |||||||

| SHARES | VALUE | |||||||

Real Estate — 1.4% |

| |||||||

CBRE Group, Inc., Class A (a) | 55,564 | $ | 1,554,125 | |||||

Forest City Realty Trust, Inc., Class A (a) | 43,881 | 864,456 | ||||||

|

| |||||||

| 2,418,581 | ||||||||

|

| |||||||

Telecommunication Services — 1.1% |

| |||||||

BT Group PLC American Depositary Receipt (b) | 26,508 | 924,069 | ||||||

SBA Communications Corporation, Class A (a) | 10,189 | 1,011,564 | ||||||

|

| |||||||

| 1,935,633 | ||||||||

|

| |||||||

Food & Beverage — 1.1% |

| |||||||

General Mills, Inc. | 300 | 16,953 | ||||||

Unilever NV American Depositary Receipt (b) | 41,260 | 1,832,357 | ||||||

|

| |||||||

| 1,849,310 | ||||||||

|

| |||||||

Media — 1.0% |

| |||||||

Discovery Communications, Inc., Class A (a) | 24,137 | 665,940 | ||||||

IMAX Corporation (a) | 31,470 | 977,458 | ||||||

|

| |||||||

| 1,643,398 | ||||||||

|

| |||||||

Consumer Services — 0.7% |

| |||||||

Panera Bread Company, Class A (a) | 6,231 | 1,208,814 | ||||||

Starbucks Corporation | 550 | 33,423 | ||||||

|

| |||||||

| 1,242,237 | ||||||||

|

| |||||||

Automobiles & Components — 0.5% |

| |||||||

BorgWarner, Inc. | 30,369 | 891,634 | ||||||

|

| |||||||

Commercial & Professional Services — 0.4% |

| |||||||

Interface, Inc. | 37,859 | 639,439 | ||||||

|

| |||||||

Household & Personal Products — 0.3% |

| |||||||

Church & Dwight Company, Inc. | 7,283 | 611,772 | ||||||

|

| |||||||

Total Common Stocks | 113,195,529 | |||||||

|

| |||||||

11

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | continued |

BONDS & NOTES — 29.2% |

| |||||||

| PRINCIPAL AMOUNT | VALUE | |||||||

Green Bonds, Renewable Energy & Energy Efficiency — 14.9% |

| |||||||

African Development Bank | $ | 1,000,000 | $ | 1,000,661 | ||||

Asian Development Bank | 1,000,000 | 1,003,751 | ||||||

Bank of America Corporation | 1,500,000 | 1,500,352 | ||||||

Digital Realty Trust LP | 2,000,000 | 2,030,210 | ||||||

European Investment Bank | 2,000,000 | 2,064,118 | ||||||

Export-Import Bank of Korea | 1,000,000 | 1,001,094 | ||||||

International Bank for Reconstruction & Development | 500,000 | 506,053 | ||||||

International Bank for Reconstruction & Development | 2,000,000 | 2,005,304 | ||||||

International Finance Corporation | 1,000,000 | 998,930 | ||||||

KFW | 1,500,000 | 1,519,515 | ||||||

Morgan Stanley | 1,500,000 | 1,512,114 | ||||||

Nordic Investment Bank | 1,500,000 | 1,545,864 | ||||||

Overseas Private Investment Corporation | 800,000 | 833,233 | ||||||

Overseas Private Investment Corporation | 243,304 | 254,077 | ||||||

Overseas Private Investment Corporation | 249,911 | 263,626 | ||||||

Regency Centers LP | 2,000,000 | 2,045,740 | ||||||

Sumitomo Mitsui Bank | 2,000,000 | 2,016,736 | ||||||

Svensk Exportkredit AB | 1,500,000 | 1,517,730 | ||||||

| PRINCIPAL AMOUNT | VALUE | |||||||

Green Bonds, Renewable Energy & Energy Efficiency — (continued) |

| |||||||

Vornado Realty LP | $ | 2,000,000 | $ | 1,981,908 | ||||

|

| |||||||

| 25,601,016 | ||||||||

|

| |||||||

U.S. Government Agencies — 3.0% |

| |||||||

Federal Farm Credit Bank | 500,000 | 513,019 | ||||||

Federal Farm Credit Bank | 200,000 | 203,273 | ||||||

Federal Farm Credit Bank | 1,000,000 | 1,006,096 | ||||||

Federal Home Loan Bank | 1,000,000 | 1,018,990 | ||||||

Federal Home Loan Bank | 550,000 | 591,856 | ||||||

Federal Home Loan Bank | 1,000,000 | 1,001,319 | ||||||

Federal Home Loan Mortgage Corporation | 500,000 | 540,758 | ||||||

Federal Home Loan Mortgage Corporation | 200,000 | 187,347 | ||||||

|

| |||||||

| 5,062,658 | ||||||||

|

| |||||||

Software & Services — 2.5% |

| |||||||

International Business Machines Corporation | 500,000 | 617,462 | ||||||

Oracle Corporation | 500,000 | 501,560 | ||||||

Oracle Corporation | 1,000,000 | 1,109,722 | ||||||

Oracle Corporation | 500,000 | 494,837 | ||||||

Symantec Corporation | 1,500,000 | 1,563,258 | ||||||

|

| |||||||

| 4,286,839 | ||||||||

|

| |||||||

Banks — 1.9% |

| |||||||

HSBC Bank USA N.A. | 500,000 | 531,166 | ||||||

HSBC Holdings PLC | 1,500,000 | 1,670,371 | ||||||

12

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | concluded |

| PRINCIPAL AMOUNT | VALUE | |||||||

Banks — (continued) |

| |||||||

JPMorgan Chase & Company | $ | 1,000,000 | $ | 1,071,151 | ||||

|

| |||||||

| 3,272,688 | ||||||||

|

| |||||||

Diversified Financials — 1.2% |

| |||||||

Bank of New York Mellon Corporation (The) | 1,000,000 | 1,054,253 | ||||||

Citigroup, Inc. | 500,000 | 506,207 | ||||||

Morgan Stanley | 500,000 | 503,559 | ||||||

|

| |||||||

| 2,064,019 | ||||||||

|

| |||||||

Pharmaceuticals & Biotechnology — 1.1% |

| |||||||

Amgen, Inc. | 1,250,000 | 1,387,840 | ||||||

Thermo Fisher Scientific, Inc. | 500,000 | 503,425 | ||||||

|

| |||||||

| 1,891,265 | ||||||||

|

| |||||||

Capital Goods — 0.9% |

| |||||||

Koninklijke Philips NV | 1,500,000 | 1,610,251 | ||||||

|

| |||||||

Telecommunication Services — 0.8% |

| |||||||

America Movil SAB de C.V. | 750,000 | 817,548 | ||||||

Verizon Communications, Inc. | 500,000 | 565,142 | ||||||

|

| |||||||

| 1,382,690 | ||||||||

|

| |||||||

Media — 0.7% |

| |||||||

Discovery Communications LLC | 1,150,000 | 1,258,678 | ||||||

|

| |||||||

Healthcare Equipment & Services — 0.6% |

| |||||||

Baxter International, Inc. | 500,000 | 499,270 | ||||||

Stryker Corporation | 500,000 | 497,576 | ||||||

|

| |||||||

| 996,846 | ||||||||

|

| |||||||

Real Estate — 0.6% |

| |||||||

HCP, Inc. | 1,000,000 | 979,201 | ||||||

|

| |||||||

| PRINCIPAL AMOUNT | VALUE | |||||||

Technology Hardware & Equipment — 0.4% |

| |||||||

EMC Corporation | $ | 700,000 | $ | 669,622 | ||||

|

| |||||||

Food & Staples Retailing — 0.3% |

| |||||||

CVS Health Corporation | 500,000 | 503,991 | ||||||

|

| |||||||

Healthy Living — 0.3% |

| |||||||

Whole Foods Market, Inc. | 500,000 | 501,756 | ||||||

|

| |||||||

Total Bonds & Notes | 50,081,520 | |||||||

|

| |||||||

CERTIFICATES OF DEPOSIT — 0.1% |

| |||||||

Self Help Credit Union Environmental Certificate of Deposit | 95,000 | 95,000 | ||||||

|

| |||||||

Total Certificates Of Deposit | 95,000 | |||||||

|

| |||||||

SHORT-TERM INVESTMENT — 4.5% |

| |||||||

UMB Money Market Fiduciary Account, 0.01% (d) | 7,793,543 | |||||||

|

| |||||||

Total Short-term Investment | 7,793,543 | |||||||

|

| |||||||

TOTAL INVESTMENTS (e) — 99.8% |

| |||||||

(Cost $165,186,062) | 171,165,592 | |||||||

Other Assets Less Liabilities — 0.2% |

| 428,123 | ||||||

|

| |||||||

NET ASSETS — 100.0% | $ | 171,593,715 | ||||||

|

| |||||||

| (a) | Non-income producing security. |

| (b) | Securities whose values are determined or significantly influenced by trading in markets other than the United States or Canada. |

| (c) | Step rate bond. Rate shown is currently in effect at January 31, 2016 |

| (d) | The rate quoted is the annualized seven-day yield of the Fund at the period end. |

| (e) | The cost of investments for federal income tax purposes is $165,159,442 resulting in gross unrealized appreciation and depreciation of $18,711,510 and $12,705,360 respectively, or net unrealized appreciation of $6,006,150. |

See Notes to Financial Statements

13

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) |

COMMON STOCKS — 99.5% |

| |||||||

| SHARES | VALUE | |||||||

Software & Services — 21.1% |

| |||||||

Accenture PLC, Class A (a) | 12,534 | $ | 1,322,838 | |||||

Adobe Systems, Inc. (b) | 10,010 | 892,191 | ||||||

Alphabet, Inc., Class A (b) | 5,824 | 4,434,102 | ||||||

Alphabet, Inc., Class C (b) | 6,219 | 4,620,406 | ||||||

ANSYS, Inc. (b) | 1,803 | 159,007 | ||||||

Autodesk, Inc. (b) | 4,626 | 216,589 | ||||||

Automatic Data Processing, Inc. | 9,381 | 779,467 | ||||||

CA, Inc. | 6,594 | 189,446 | ||||||

Citrix Systems, Inc. (b) | 3,196 | 225,190 | ||||||

Cognizant Technology Solutions Corporation, Class A (b) | 12,268 | 776,687 | ||||||

Convergys Corporation | 1,981 | 48,416 | ||||||

FleetCor Technologies, Inc. (b) | 1,561 | 191,753 | ||||||

International Business Machines Corporation | 18,688 | 2,332,075 | ||||||

Intuit, Inc. | 5,302 | 506,394 | ||||||

Microsoft Corporation | 152,678 | 8,411,031 | ||||||

NetSuite, Inc. (b) | 775 | 53,762 | ||||||

Oracle Corporation | 69,702 | 2,530,880 | ||||||

Rackspace Hosting, Inc. (b) | 2,337 | 47,231 | ||||||

salesforce.com, Inc. (b) | 12,529 | 852,724 | ||||||

Symantec Corporation | 13,963 | 277,026 | ||||||

Teradata Corporation (b) | 3,039 | 73,969 | ||||||

Western Union Company (The) | 10,195 | 181,879 | ||||||

Workday, Inc., Class A (b) | 2,210 | 139,252 | ||||||

Xerox Corporation | 20,873 | 203,512 | ||||||

Yahoo!, Inc. (b) | 18,019 | 531,741 | ||||||

|

| |||||||

| 29,997,568 | ||||||||

|

| |||||||

Pharmaceuticals & Biotechnology — 11.0% |

| |||||||

Affymetrix, Inc. (b) | 1,528 | 21,438 | ||||||

Agilent Technologies, Inc. | 6,618 | 249,168 | ||||||

Amgen, Inc. | 15,245 | 2,328,369 | ||||||

Bio-Techne Corporation | 722 | 59,702 | ||||||

Biogen, Inc. (b) | 4,731 | 1,291,847 | ||||||

BioMarin Pharmaceutical, Inc. (b) | 3,217 | 238,122 | ||||||

Bristol-Myers Squibb Company | 33,520 | 2,083,603 | ||||||

Celgene Corporation (b) | 15,901 | 1,595,188 | ||||||

Cepheid (b) | 1,404 | 41,348 | ||||||

Fluidigm Corporation (b) | 492 | 3,301 | ||||||

Gilead Sciences, Inc. | 29,498 | 2,448,334 | ||||||

Merck & Company, Inc. | 56,591 | 2,867,466 | ||||||

Mettler-Toledo International, Inc. (b) | 556 | 173,945 | ||||||

| SHARES | VALUE | |||||||

Pharmaceuticals & Biotechnology — (continued) |

| |||||||

PAREXEL International Corporation (b) | 1,098 | $ | 70,228 | |||||

Quintiles Transnational Holdings, Inc. (b) | 1,849 | 112,475 | ||||||

Thermo Fisher Scientific, Inc. | 8,030 | 1,060,442 | ||||||

Vertex Pharmaceuticals, Inc. (b) | 4,930 | 447,397 | ||||||

Waters Corporation (b) | 1,629 | 197,451 | ||||||

Zoetis, Inc. | 9,544 | 410,869 | ||||||

|

| |||||||

| 15,700,693 | ||||||||

|

| |||||||

Food & Beverage — 5.8% |

| |||||||

Bunge Ltd. | 2,963 | 183,736 | ||||||

Campbell Soup Company | 3,710 | 209,281 | ||||||

Coca-Cola Enterprises, Inc. | 4,414 | 204,898 | ||||||

Darling Ingredients, Inc. (b) | 3,345 | 30,071 | ||||||

Dr. Pepper Snapple Group, Inc. | 3,838 | 360,158 | ||||||

General Mills, Inc. | 12,025 | 679,533 | ||||||

Hormel Foods Corporation | 2,969 | 238,737 | ||||||

JM Smucker Company (The) | 2,264 | 290,516 | ||||||

Kellogg Company | 5,313 | 390,187 | ||||||

Keurig Green Mountain, Inc. | 2,362 | 210,808 | ||||||

Kraft Heinz Company (The) | 12,182 | 950,927 | ||||||

McCormick & Company, Inc. | 2,312 | 203,387 | ||||||

Mondelez International, Inc., Class A | 32,388 | 1,395,923 | ||||||

PepsiCo, Inc. | 29,449 | 2,924,286 | ||||||

|

| |||||||

| 8,272,448 | ||||||||

|

| |||||||

Household & Personal Products — 5.2% |

| |||||||

Avon Products, Inc. | 8,642 | 29,297 | ||||||

Clorox Company (The) | 2,567 | 331,271 | ||||||

Colgate-Palmolive Company | 17,176 | 1,159,895 | ||||||

Edgewell Personal Care Company | 1,300 | 96,213 | ||||||

Estee Lauder Companies, Inc. (The), Class A | 4,521 | 385,415 | ||||||

Kimberly-Clark Corporation | 7,340 | 942,603 | ||||||

Procter & Gamble Company (The) | 54,479 | 4,450,390 | ||||||

|

| |||||||

| 7,395,084 | ||||||||

|

| |||||||

Capital Goods — 5.1% |

| |||||||

3M Company | 12,569 | 1,897,919 | ||||||

A.O. Smith Corporation | 1,576 | 110,084 | ||||||

AGCO Corporation | 1,346 | 65,644 | ||||||

Air Lease Corporation | 1,934 | 49,820 | ||||||

American Science & Engineering, Inc. | 117 | 4,199 | ||||||

14

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | continued |

| SHARES | VALUE | |||||||

Capital Goods — (continued) |

| |||||||

Applied Industrial Technologies, Inc. | 691 | $ | 26,562 | |||||

Builders FirstSource, Inc. (b) | 1,508 | 12,109 | ||||||

Caterpillar, Inc. | 11,564 | 719,743 | ||||||

CLARCOR, Inc. | 987 | 46,251 | ||||||

Cummins, Inc. | 3,390 | 304,727 | ||||||

Deere & Company | 6,278 | 483,469 | ||||||

Dover Corporation | 3,101 | 181,253 | ||||||

EMCOR Group, Inc. | 1,243 | 56,805 | ||||||

Fastenal Company | 5,483 | 222,390 | ||||||

Flowserve Corporation | 2,812 | 108,656 | ||||||

Graco, Inc. | 1,147 | 83,364 | ||||||

Granite Construction, Inc. | 756 | 29,204 | ||||||

H&E Equipment Services, Inc. | 568 | 6,617 | ||||||

Illinois Tool Works, Inc. | 6,626 | 596,804 | ||||||

Ingersoll-Rand PLC | 5,423 | 279,122 | ||||||

Lincoln Electric Holdings, Inc. | 1,450 | 77,198 | ||||||

Masco Corporation | 6,868 | 181,247 | ||||||

Meritor, Inc. (b) | 1,653 | 11,290 | ||||||

Middleby Corporation (The) (b) | 1,155 | 104,366 | ||||||

Owens Corning | 2,184 | 100,879 | ||||||

Parker Hannifin Corporation | 2,760 | 268,162 | ||||||

Quanta Services, Inc. (b) | 3,953 | 73,921 | ||||||

Rockwell Automation, Inc. | 2,676 | 255,745 | ||||||

Snap-on, Inc. | 1,157 | 186,925 | ||||||

Tennant Company | 321 | 17,369 | ||||||

Timken Company (The) | 1,548 | 41,099 | ||||||

United Rentals, Inc. (b) | 1,918 | 91,891 | ||||||

W.W. Grainger, Inc. | 1,182 | 232,488 | ||||||

WABCO Holdings, Inc. (b) | 1,111 | 99,601 | ||||||

Wabtec Corporation | 1,949 | 124,639 | ||||||

Xylem, Inc. | 3,647 | 131,110 | ||||||

|

| |||||||

| 7,282,672 | ||||||||

|

| |||||||

Real Estate — 5.0% |

| |||||||

American Tower Corporation | 8,513 | 803,116 | ||||||

AvalonBay Communities, Inc. | 2,669 | 457,707 | ||||||

Boston Properties, Inc. | 3,080 | 357,927 | ||||||

CBRE Group, Inc., Class A (b) | 5,940 | 166,142 | ||||||

Corporate Office Properties Trust | 1,930 | 43,039 | ||||||

Digital Realty Trust, Inc. | 2,782 | 222,783 | ||||||

Duke Realty Corporation | 7,140 | 143,728 | ||||||

Equinix, Inc. | 1,338 | 415,543 | ||||||

Equity Residential | 7,314 | 563,836 | ||||||

Federal Realty Investment Trust | 1,380 | 208,145 | ||||||

| SHARES | VALUE | |||||||

Real Estate — (continued) |

| |||||||

Forest City Realty Trust, Inc., Class A (b) | 4,811 | $ | 94,777 | |||||

HCP, Inc. | 9,274 | 333,307 | ||||||

Host Hotels & Resorts, Inc. | 15,399 | 213,276 | ||||||

Iron Mountain, Inc. | 3,993 | 109,967 | ||||||

Jones Lang LaSalle, Inc. | 901 | 126,789 | ||||||

Liberty Property Trust | 3,046 | 89,309 | ||||||

Macerich Company (The) | 2,698 | 210,363 | ||||||

Plum Creek Timber Company, Inc. | 3,605 | 146,038 | ||||||

Potlatch Corporation | 740 | 21,342 | ||||||

Prologis, Inc. | 10,510 | 414,830 | ||||||

Realogy Holdings Corporation (b) | 2,948 | 96,694 | ||||||

Simon Property Group, Inc. | 6,211 | 1,156,985 | ||||||

UDR, Inc. | 5,218 | 185,709 | ||||||

Vornado Realty Trust | 3,389 | 299,791 | ||||||

Weyerhaeuser Company | 10,288 | 263,476 | ||||||

|

| |||||||

| 7,144,619 | ||||||||

|

| |||||||

Media — 4.6% |

| |||||||

Charter Communications, Inc., Class A (b) | 1,681 | 288,056 | ||||||

Discovery Communications, Inc., Class A (b) | 2,927 | 80,756 | ||||||

Discovery Communications, Inc., Class C (b) | 5,493 | 149,464 | ||||||

DreamWorks Animation SKG, Inc., Class A (b) | 1,526 | 39,127 | ||||||

John Wiley & Sons, Inc., Class A | 922 | 38,540 | ||||||

Liberty Global PLC, Class A (a)(b) | 5,035 | 173,254 | ||||||

Liberty Global PLC, Series C (a)(b) | 12,313 | 410,146 | ||||||

New York Times Company (The), Class A | 2,693 | 35,601 | ||||||

Scholastic Corporation | 424 | 14,556 | ||||||

Scripps Networks Interactive, Inc., Class A | 1,530 | 93,284 | ||||||

Time Warner Cable, Inc. | 5,690 | 1,035,637 | ||||||

Time Warner, Inc. | 16,400 | 1,155,216 | ||||||

Walt Disney Company (The) | 32,230 | 3,088,279 | ||||||

|

| |||||||

| 6,601,916 | ||||||||

|

| |||||||

Diversified Financials — 4.2% |

| |||||||

American Express Company | 18,116 | 969,206 | ||||||

Ameriprise Financial, Inc. | 3,597 | 326,068 | ||||||

Bank of New York Mellon Corporation (The) | 22,363 | 809,988 | ||||||

15

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | continued |

| SHARES | VALUE | |||||||

Diversified Financials — (continued) |

| |||||||

BlackRock, Inc. | 2,475 | $ | 777,794 | |||||

Charles Schwab Corporation (The) | 23,887 | 609,835 | ||||||

CME Group, Inc. | 6,465 | 580,880 | ||||||

FactSet Research Systems, Inc. | 785 | 118,300 | ||||||

Franklin Resources, Inc. | 7,981 | 276,622 | ||||||

Invesco Ltd. | 8,580 | 256,799 | ||||||

Legg Mason, Inc. | 1,942 | 59,464 | ||||||

Northern Trust Corporation | 4,278 | 265,578 | ||||||

State Street Corporation | 8,244 | 459,438 | ||||||

T. Rowe Price Group, Inc. | 5,143 | 364,896 | ||||||

TD Ameritrade Holding Corporation | 5,399 | 148,904 | ||||||

|

| |||||||

| 6,023,772 | ||||||||

|

| |||||||

Healthcare Equipment & Services — 4.2% |

| |||||||

AmerisourceBergen Corporation | 4,119 | 368,898 | ||||||

Becton, Dickinson and Company | 4,229 | 614,770 | ||||||

Cardinal Health, Inc. | 6,589 | 536,147 | ||||||

Centene Corporation (b) | 2,236 | 138,766 | ||||||

Cerner Corporation (b) | 6,227 | 361,228 | ||||||

Cigna Corporation | 5,178 | 691,781 | ||||||

Cooper Companies, Inc. (The) | 985 | 129,183 | ||||||

DENTSPLY International, Inc. | 2,801 | 164,951 | ||||||

Edwards Lifesciences Corporation (b) | 4,306 | 336,772 | ||||||

Envision Healthcare Holdings, Inc. (b) | 3,670 | 81,107 | ||||||

HCA Holdings, Inc. (b) | 6,700 | 466,186 | ||||||

Henry Schein, Inc. (b) | 1,707 | 258,508 | ||||||

Hologic, Inc. (b) | 4,938 | 167,596 | ||||||

Humana, Inc. | 2,982 | 485,440 | ||||||

IDEXX Laboratories, Inc. (b) | 1,818 | 127,514 | ||||||

Laboratory Corporation of America Holdings (b) | 2,018 | 226,722 | ||||||

MEDNAX, Inc. (b) | 1,883 | 130,793 | ||||||

Molina Healthcare, Inc. (b) | 838 | 46,015 | ||||||

Patterson Companies, Inc. | 1,731 | 73,498 | ||||||

Quest Diagnostics, Inc. | 2,958 | 194,252 | ||||||

ResMed, Inc. | 2,879 | 163,239 | ||||||

Select Medical Holdings Corporation | 1,670 | 15,915 | ||||||

Team Health Holdings, Inc. (b) | 1,416 | 57,872 | ||||||

Varian Medical Systems, Inc. (b) | 1,974 | 152,255 | ||||||

|

| |||||||

| 5,989,408 | ||||||||

|

| |||||||

| SHARES | VALUE | |||||||

Semiconductors — 4.1% |

| |||||||

Advanced Micro Devices, Inc. (b) | 12,277 | $ | 27,009 | |||||

Analog Devices, Inc. | 6,276 | 338,025 | ||||||

Applied Materials, Inc. | 24,112 | 425,577 | ||||||

Intel Corporation | 95,598 | 2,965,450 | ||||||

Lam Research Corporation | 3,231 | 231,954 | ||||||

Microchip Technology, Inc. | 4,198 | 188,112 | ||||||

NVIDIA Corporation | 10,758 | 315,102 | ||||||

Skyworks Solutions, Inc. | 3,836 | 264,377 | ||||||

Texas Instruments, Inc. | 20,662 | 1,093,640 | ||||||

|

| |||||||

| 5,849,246 | ||||||||

|

| |||||||

Consumer Services — 3.8% |

| |||||||

Aramark | 4,542 | 145,117 | ||||||

Choice Hotels International, Inc. | 768 | 33,577 | ||||||

Darden Restaurants, Inc. | 2,296 | 144,786 | ||||||

DeVry Education Group, Inc. | 1,114 | 22,169 | ||||||

Hilton Worldwide Holdings, Inc. | 9,845 | 175,339 | ||||||

Jack in the Box, Inc. | 736 | 57,143 | ||||||

Marriott International, Inc., Class A | 4,351 | 266,629 | ||||||

McDonald’s Corporation | 18,909 | 2,340,556 | ||||||

Royal Caribbean Cruises Ltd. | 3,512 | 287,843 | ||||||

Starbucks Corporation | 29,836 | 1,813,134 | ||||||

Vail Resorts, Inc. | 724 | 90,500 | ||||||

|

| |||||||

| 5,376,793 | ||||||||

|

| |||||||

Technology Hardware & Equipment — 3.7% |

| |||||||

Calix, Inc. (b) | 639 | 4,908 | ||||||

Cisco Systems, Inc. | 102,225 | 2,431,933 | ||||||

Corning, Inc. | 24,630 | 458,364 | ||||||

EMC Corporation | 38,641 | 957,138 | ||||||

Flextronics International Ltd. (b) | 11,792 | 123,580 | ||||||

HP, Inc. | 36,213 | 351,628 | ||||||

Lexmark International, Inc. | 1,250 | 35,262 | ||||||

Motorola Solutions, Inc. | 3,270 | 218,338 | ||||||

Plantronics, Inc. | 704 | 31,560 | ||||||

Super Micro Computer, Inc. (b) | 851 | 25,343 | ||||||

TE Connectivity Ltd. (a) | 8,074 | 461,510 | ||||||

Trimble Navigation Ltd. (b) | 5,052 | 97,453 | ||||||

|

| |||||||

| 5,197,017 | ||||||||

|

| |||||||

Retailing — 3.5% |

| |||||||

Bed Bath & Beyond, Inc. (b) | 3,402 | 146,864 | ||||||

Best Buy Company, Inc. | 6,336 | 176,965 | ||||||

Blue Nile, Inc. (b) | 189 | 6,575 | ||||||

16

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | continued |

| SHARES | VALUE | |||||||

Retailing — (continued) |

| |||||||

Buckle, Inc. (The) | 529 | $ | 15,034 | |||||

Caleres Inc. | 907 | 24,380 | ||||||

CarMax, Inc. (b) | 4,152 | 183,435 | ||||||

Foot Locker, Inc. | 2,785 | 188,155 | ||||||

GameStop Corporation, Class A | 2,082 | 54,569 | ||||||

Gap, Inc. (The) | 4,927 | 121,795 | ||||||

Genuine Parts Company | 3,086 | 265,921 | ||||||

HSN, Inc. | 729 | 34,307 | ||||||

Kohl’s Corporation | 3,955 | 196,761 | ||||||

LKQ Corporation (b) | 6,085 | 166,729 | ||||||

Lowe’s Companies, Inc. | 18,588 | 1,332,016 | ||||||

Netflix, Inc. (b) | 8,138 | 747,394 | ||||||

Nordstrom, Inc. | 2,900 | 142,390 | ||||||

Nutrisystem, Inc. | 535 | 10,598 | ||||||

Office Depot, Inc. (b) | 9,830 | 50,625 | ||||||

Pier 1 Imports, Inc. | 1,662 | 6,681 | ||||||

Pool Corporation | 853 | 72,079 | ||||||

Shutterfly, Inc. (b) | 783 | 32,612 | ||||||

Signet Jewelers Ltd. | 1,510 | 175,160 | ||||||

Staples, Inc. | 12,907 | 115,130 | ||||||

Tiffany & Company | 2,663 | 170,006 | ||||||

Tractor Supply Company | 2,786 | 246,032 | ||||||

Ulta Salon, Cosmetics & Fragrance, Inc. (b) | 1,244 | 225,376 | ||||||

Weyco Group, Inc. | 120 | 3,216 | ||||||

|

| |||||||

| 4,910,805 | ||||||||

|

| |||||||

Telecommunication Services — 3.3% |

| |||||||

CenturyLink, Inc. | 11,351 | 288,543 | ||||||

Cincinnati Bell, Inc. (b) | 3,478 | 11,269 | ||||||

Level 3 Communications, Inc. (b) | 6,056 | 295,593 | ||||||

Sprint Corporation (b) | 15,556 | 46,979 | ||||||

Verizon Communications, Inc. | 81,672 | 4,081,150 | ||||||

|

| |||||||

| 4,723,534 | ||||||||

|

| |||||||

Consumer Durables & Apparel — 2.9% |

| |||||||

Callaway Golf Company | 1,289 | 11,227 | ||||||

Columbia Sportswear Company | 513 | 28,307 | ||||||

CSS Industries, Inc. | 156 | 4,370 | ||||||

Deckers Outdoor Corporation (b) | 593 | 29,330 | ||||||

Ethan Allen Interiors, Inc. | 443 | 11,828 | ||||||

Hanesbrands, Inc. | 8,229 | 251,560 | ||||||

Hasbro, Inc. | 2,252 | 167,279 | ||||||

Jarden Corporation (b) | 3,995 | 211,935 | ||||||

La-Z-Boy, Inc. | 961 | 20,604 | ||||||

| SHARES | VALUE | |||||||

Consumer Durables & Apparel — (continued) |

| |||||||

Mattel, Inc. | 6,792 | $ | 187,391 | |||||

Meritage Homes Corporation (b) | 789 | 26,045 | ||||||

Michael Kors Holdings Ltd. (a)(b) | 3,870 | 154,413 | ||||||

Mohawk Industries, Inc. (b) | 1,251 | 208,179 | ||||||

Newell Rubbermaid, Inc. | 5,493 | 213,019 | ||||||

NIKE, Inc., Class B | 27,230 | 1,688,532 | ||||||

PVH Corporation | 1,663 | 122,031 | ||||||

Tupperware Brands Corporation | 979 | 45,455 | ||||||

Under Armour, Inc., Class A (b) | 3,679 | 314,297 | ||||||

VF Corporation | 6,849 | 428,747 | ||||||

Wolverine World Wide, Inc. | 2,115 | 35,765 | ||||||

|

| |||||||

| 4,160,314 | ||||||||

|

| |||||||

Insurance — 2.9% |

| |||||||

Aflac, Inc. | 8,668 | 502,397 | ||||||

Chubb Ltd. (a) | 9,270 | 1,048,159 | ||||||

Hartford Financial Services Group, Inc. | 8,312 | 333,976 | ||||||

Marsh & McLennan Companies, Inc. | 10,682 | 569,671 | ||||||

PartnerRe Ltd. (a) | 958 | 134,503 | ||||||

Principal Financial Group, Inc. | 5,890 | 223,820 | ||||||

Progressive Corporation (The) | 11,737 | 366,781 | ||||||

Travelers Companies, Inc. (The) | 6,269 | 671,034 | ||||||

Willis Towers Watson PLC (a) | 2,606 | 298,308 | ||||||

|

| |||||||

| 4,148,649 | ||||||||

|

| |||||||

Materials — 2.4% |

| |||||||

Air Products & Chemicals, Inc. | 4,110 | 520,778 | ||||||

Albemarle Corporation | 2,255 | 118,703 | ||||||

Avery Dennison Corporation | 1,829 | 111,368 | ||||||

Axalta Coating Systems Ltd. (b) | 2,801 | 66,692 | ||||||

Ball Corporation | 2,595 | 173,424 | ||||||

Compass Minerals International, Inc. | 661 | 49,476 | ||||||

Domtar Corporation | 1,275 | 41,119 | ||||||

Ecolab, Inc. | 5,349 | 576,997 | ||||||

H.B. Fuller Company | 1,090 | 40,570 | ||||||

International Flavors & Fragrances, Inc. | 1,598 | 186,902 | ||||||

Minerals Technologies, Inc. | 691 | 28,324 | ||||||

Mosaic Company (The) | 6,626 | 159,686 | ||||||

Praxair, Inc. | 5,782 | 578,200 | ||||||

Schnitzer Steel Industries, Inc., Class A | 531 | 7,142 | ||||||

17

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | continued |

| SHARES | VALUE | |||||||

Materials — (continued) |

| |||||||

Sealed Air Corporation | 4,126 | $ | 167,227 | |||||

Sherwin-Williams Company (The) | 1,588 | 406,004 | ||||||

Sonoco Products Company | 1,982 | 78,309 | ||||||

Valspar Corporation (The) | 1,517 | 118,826 | ||||||

|

| |||||||

| 3,429,747 | ||||||||

|

| |||||||

Transportation — 2.2% |

| |||||||

ArcBest Corporation | 399 | 8,192 | ||||||

Avis Budget Group, Inc. (b) | 2,042 | 53,643 | ||||||

C.H. Robinson Worldwide, Inc. | 2,820 | 182,651 | ||||||

CSX Corporation | 19,847 | 456,878 | ||||||

Echo Global Logistics, Inc. (b) | 441 | 9,706 | ||||||

Expeditors International of Washington, Inc. | 3,788 | 170,915 | ||||||

Genesee & Wyoming, Inc., Class A (b) | 1,060 | 52,555 | ||||||

Hertz Global Holdings, Inc. (b) | 7,687 | 69,798 | ||||||

Kansas City Southern | 2,207 | 156,432 | ||||||

Norfolk Southern Corporation | 6,062 | 427,371 | ||||||

Ryder System, Inc. | 1,037 | 55,137 | ||||||

Southwest Airlines Company | 3,248 | 122,190 | ||||||

United Parcel Service, Inc., Class B | 14,106 | 1,314,679 | ||||||

Wesco Aircraft Holdings, Inc. (b) | 1,552 | 17,522 | ||||||

|

| |||||||

| 3,097,669 | ||||||||

|

| |||||||

Banks — 1.8% |

| |||||||

Bank of Hawaii Corporation | 902 | 54,057 | ||||||

Cathay General Bancorp | 1,559 | 43,652 | ||||||

CIT Group, Inc. | 3,621 | 106,276 | ||||||

Citizens Financial Group, Inc. | 10,447 | 221,999 | ||||||

Comerica, Inc. | 3,672 | 125,950 | ||||||

Heartland Financial USA, Inc. | 292 | 8,745 | ||||||

International Bancshares Corporation | 1,025 | 23,770 | ||||||

KeyCorp | 16,689 | 186,249 | ||||||

M&T Bank Corporation | 2,882 | 317,539 | ||||||

New York Community Bancorp, Inc. | 9,709 | 150,295 | ||||||

Old National Bancorp | 2,554 | 31,465 | ||||||

People’s United Financial, Inc. | 6,504 | 93,463 | ||||||

PHH Corporation (b) | 1,219 | 14,969 | ||||||

PNC Financial Services Group, Inc. (The) | 10,381 | 899,514 | ||||||

Popular, Inc. (a) | 2,052 | 51,587 | ||||||

Signature Bank (b) | 1,019 | 141,987 | ||||||

Umpqua Holdings Corporation | 4,304 | 62,322 | ||||||

|

| |||||||

| 2,533,839 | ||||||||

|

| |||||||

| SHARES | VALUE | |||||||

Commercial & Professional Services — 0.9% |

| |||||||

ACCO Brands Corporation (b) | 1,919 | $ | 11,648 | |||||

CEB, Inc. | 663 | 39,104 | ||||||

Copart, Inc. (b) | 2,301 | 77,106 | ||||||

Deluxe Corporation | 994 | 55,565 | ||||||

Dun & Bradstreet Corporation (The) | 725 | 71,354 | ||||||

Essendant, Inc. | 715 | 21,350 | ||||||

Exponent, Inc. | 485 | 24,885 | ||||||

Heidrick & Struggles International, Inc. | 327 | 8,620 | ||||||

HNI Corporation | 907 | 30,856 | ||||||

ICF International, Inc. (b) | 342 | 11,700 | ||||||

IHS, Inc., Class A (b) | 1,369 | 143,225 | ||||||

Interface, Inc. | 1,229 | 20,758 | ||||||

Kelly Services, Inc. | 596 | 9,882 | ||||||

Knoll, Inc. | 925 | 16,974 | ||||||

ManpowerGroup, Inc. | 1,544 | 117,884 | ||||||

Navigant Consulting, Inc. (b) | 1,102 | 17,400 | ||||||

On Assignment, Inc. (b) | 973 | 37,606 | ||||||

R.R. Donnelley & Sons Company | 4,576 | 63,927 | ||||||

Resources Connection, Inc. | 655 | 9,897 | ||||||

Robert Half International, Inc. | 2,808 | 122,906 | ||||||

RPX Corporation (b) | 998 | 11,557 | ||||||

Steelcase, Inc. | 1,843 | 23,517 | ||||||

Team, Inc. (b) | 364 | 8,736 | ||||||

Tetra Tech, Inc. | 1,288 | 34,119 | ||||||

TrueBlue, Inc. (b) | 796 | 18,181 | ||||||

Tyco International PLC | 8,456 | 290,802 | ||||||

|

| |||||||

| 1,299,559 | ||||||||

|

| |||||||

Renewable Energy & Energy Efficiency — 0.7% |

| |||||||

Itron, Inc. (b) | 719 | 23,698 | ||||||

Johnson Controls, Inc. | 13,112 | 470,328 | ||||||

Ormat Technologies, Inc. | 783 | 27,718 | ||||||

SunPower Corporation (b) | 1,075 | 27,348 | ||||||

Tesla Motors, Inc. (b) | 1,952 | 373,222 | ||||||

|

| |||||||

| 922,314 | ||||||||

|

| |||||||

Automobiles & Components — 0.4% |

| |||||||

Autoliv, Inc. (a) | 1,806 | 185,621 | ||||||

BorgWarner, Inc. | 4,484 | 131,650 | ||||||

Harley-Davidson, Inc. | 4,243 | 169,720 | ||||||

|

| |||||||

| 486,991 | ||||||||

|

| |||||||

18

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2016 (unaudited) | concluded |

| SHARES | VALUE | |||||||

Food & Staples Retailing — 0.3% |

| |||||||

Sysco Corporation | 11,930 | $ | 474,933 | |||||

|

| |||||||

Healthy Living — 0.2% | ||||||||

Hain Celestial Group, Inc. (The) (b) | 2,097 | 76,289 | ||||||

United Natural Foods, Inc. (b) | 1,044 | 36,561 | ||||||

Whole Foods Market, Inc. | 7,114 | 208,511 | ||||||

|

| |||||||

| 321,361 | ||||||||

|

| |||||||

Utilities — 0.2% |

| |||||||

American Water Works Company, Inc. | 3,688 | 239,388 | ||||||

|

| |||||||

Total Common Stocks | 141,580,339 | |||||||

|

| |||||||

SHORT-TERM INVESTMENT — 0.5% |

| |||||||

UMB Money Market Fiduciary Account, 0.01% (c) | 722,186 | |||||||

|

| |||||||

TOTAL INVESTMENTS (d) — 100.0% |

| |||||||

(Cost $118,084,704) | 142,302,525 | |||||||

| Other Assets Less Liabilities — 0.0% | 34,051 | |||||||

|

| |||||||

NET ASSETS — 100.0% | $ | 142,336,576 | ||||||

|

| |||||||

| (a) | Securities whose values are determined or significantly influenced by trading in markets other than the United States or Canada. |

| (b) | Non-income producing security. |

| (c) | The rate quoted is the annualized seven-day yield of the Fund at the period end. |

| (d) | The cost of investments for federal income tax purposes is $120,508,870 resulting in gross unrealized appreciation and depreciation of $30,367,079 and $8,573,424 respectively, or net unrealized appreciation of $21,793,655. |

See Notes to Financial Statements

19

GREEN CENTURY FUNDS STATEMENTS OF ASSETS AND LIABILITIES

January 31, 2016

(unaudited)

| BALANCED FUND | EQUITY FUND | |||||||

ASSETS: | ||||||||

Investments, at value (cost $165,186,062 and $118,084,704, respectively) | $ | 171,165,592 | $ | 142,302,525 | ||||

Receivables for: | ||||||||

Capital stock sold | 230,717 | 134,828 | ||||||

Interest | 423,025 | 10 | ||||||

Dividends | 39,662 | 169,082 | ||||||

|

|

|

| |||||

Total assets | 171,858,996 | 142,606,445 | ||||||

|

|

|

| |||||

LIABILITIES: | ||||||||

Payable for capital stock repurchased | 50,379 | 121,207 | ||||||

Accrued expenses | 214,902 | 148,662 | ||||||

|

|

|

| |||||

Total liabilities | 265,281 | 269,869 | ||||||

|

|

|

| |||||

NET ASSETS | $ | 171,593,715 | $ | 142,336,576 | ||||

|

|

|

| |||||

NET ASSETS CONSIST OF: | ||||||||

Paid-in capital | $ | 164,824,233 | $ | 120,077,546 | ||||

Undistributed net investment income/accumulated net investment loss | (115,532 | ) | 114,469 | |||||

Accumulated net realized gains/(losses) on investments | 905,484 | (2,073,260 | ) | |||||

Net unrealized appreciation on investments | 5,979,530 | 24,217,821 | ||||||

|

|

|

| |||||

NET ASSETS | $ | 171,593,715 | $ | 142,336,576 | ||||

|

|

|

| |||||

SHARES OUTSTANDING (UNLIMITED NUMBER OF SHARES AUTHORIZED @ $0.01 PAR VALUE) | 7,885,287 | 4,720,751 | ||||||

|

|

|

| |||||

NET ASSET VALUE, REDEMPTION PRICE AND OFFERING PRICE PER SHARE | $ | 21.76 | $ | 30.15 | ||||

|

|

|

| |||||

GREEN CENTURY FUNDS STATEMENTS OF OPERATIONS

For the six months ended January 31, 2016

(unaudited)

| BALANCED FUND | EQUITY FUND | |||||||

INVESTMENT INCOME (LOSS): | ||||||||

Interest income | $ | 628,098 | $ | 40 | ||||

Dividend and other income (net of $5,045 and $0 foreign withholding taxes, respectively) | 646,618 | 1,448,560 | ||||||

|

|

|

| |||||

Total investment income | 1,274,716 | 1,448,600 | ||||||

|

|

|

| |||||

EXPENSES: | ||||||||

Administrative services fee | 735,060 | 708,866 | ||||||

Investment advisory fee | 575,970 | 169,789 | ||||||

|

|

|

| |||||

Total expenses | 1,311,030 | 878,655 | ||||||

|

|

|

| |||||

NET INVESTMENT INCOME (LOSS) | (36,314 | ) | 569,945 | |||||

|

|

|

| |||||

NET REALIZED AND UNREALIZED GAIN (LOSS): | ||||||||

Net realized gain (loss) on investments | 910,445 | (282,331 | ) | |||||

Change in net unrealized depreciation on investments | (20,664,422 | ) | (9,507,526 | ) | ||||

|

|

|

| |||||

NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | (19,753,977 | ) | (9,789,857 | ) | ||||

|

|

|

| |||||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (19,790,291 | ) | $ | (9,219,912 | ) | ||

|

|

|

| |||||

See Notes to Financial Statements

20

GREEN CENTURY FUNDS STATEMENTS OF CHANGES IN NET ASSETS

| BALANCED FUND | EQUITY FUND | |||||||||||||||

FOR THE SIX MONTHS ENDED JANUARY 31, 2016 (UNAUDITED) | FOR THE YEAR ENDED JULY 31, 2015 | FOR THE SIX MONTHS ENDED JANUARY 31, 2016 (UNAUDITED) | FOR THE YEAR ENDED JULY 31, 2015 | |||||||||||||

INCREASE (DECREASE) IN NET ASSETS: | ||||||||||||||||

| From operations: | ||||||||||||||||

Net investment income (loss) | $ | (36,314 | ) | $ | 39,868 | $ | 569,945 | $ | 819,772 | |||||||

Net realized gain (loss) on investments | 910,445 | 5,338,868 | (282,331 | ) | 1,232,879 | |||||||||||

Change in net unrealized appreciation (depreciation) on investments | (20,664,422 | ) | 8,672,667 | (9,507,526 | ) | 9,208,142 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Net increase (decrease) in net assets resulting from operations | (19,790,291 | ) | 14,051,403 | (9,219,912 | ) | 11,260,793 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| Dividends and distributions to shareholders: | ||||||||||||||||

From net investment income | — | (128,866 | ) | (533,961 | ) | (751,235 | ) | |||||||||

From net realized gains | (5,191,912 | ) | (6,321,658 | ) | (1,678,100 | ) | (1,274,236 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total dividends and distributions | (5,191,912 | ) | (6,450,524 | ) | (2,212,061 | ) | (2,025,471 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

| Capital share transactions: | ||||||||||||||||

Proceeds from sales of shares | 30,123,637 | 58,560,918 | 24,648,247 | 46,622,245 | ||||||||||||

Reinvestment of dividends and distributions | 5,058,189 | 6,310,894 | 2,162,005 | 1,981,663 | ||||||||||||

Payments for shares redeemed | (18,320,292 | ) | (14,665,190 | ) | (11,444,379 | ) | (14,794,680 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net increase in net assets resulting from capital share transactions | 16,861,534 | 50,206,622 | 15,365,873 | 33,809,228 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total increase (decrease) in net assets | (8,120,669 | ) | 57,807,501 | 3,933,900 | 43,044,550 | |||||||||||

NET ASSETS: | ||||||||||||||||

Beginning of period | 179,714,384 | 121,906,883 | 138,402,676 | 95,358,126 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

End of period | $ | 171,593,715 | $ | 179,714,384 | $ | 142,336,576 | $ | 138,402,676 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Undistributed net investment income/accumulated net investment loss at end of period | (115,532 | ) | (79,218 | ) | 114,469 | 78,485 | ||||||||||

See Notes to Financial Statements

21

GREEN CENTURY BALANCED FUND FINANCIAL HIGHLIGHTS

| SIX MONTHS ENDED JANUARY 31, 2016 | FOR THE YEARS ENDED JULY 31, | |||||||||||||||||||||||

| (UNAUDITED) | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||||||

Net Asset Value, beginning of period | $ | 25.07 | $ | 23.74 | $ | 21.43 | $ | 18.06 | $ | 17.50 | $ | 15.76 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Income from investment operations: | ||||||||||||||||||||||||

Net investment income | — | 0.01 | 0.09 | 0.13 | 0.10 | 0.13 | ||||||||||||||||||

Net realized and unrealized gain (loss) on investments | (2.63 | ) | 2.51 | 2.31 | 3.37 | 0.56 | 1.75 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total increase (decrease) from investment operations | (2.63 | ) | 2.52 | 2.40 | 3.50 | 0.66 | 1.88 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Less dividends: | ||||||||||||||||||||||||

Dividends from net investment income | — | (0.02 | ) | (0.09 | ) | (0.13 | ) | (0.10 | ) | (0.14 | ) | |||||||||||||

Distributions from net realized gains | (0.68 | ) | (1.17 | ) | — | — | — | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total decrease from dividends | (0.68 | ) | (1.19 | ) | (0.09 | ) | (0.13 | ) | (0.10 | ) | (0.14 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net Asset Value, end of period | $ | 21.76 | $ | 25.07 | $ | 23.74 | $ | 21.43 | $ | 18.06 | $ | 17.50 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total return | (10.64 | )%(a) | 10.84 | % | 11.20 | % | 19.44 | % | 3.81 | % | 11.92 | % | ||||||||||||

| Ratios/Supplemental data: | ||||||||||||||||||||||||

Net assets, end of period (in 000’s) | $ | 171,594 | $ | 179,714 | $ | 121,907 | $ | 85,650 | $ | 58,798 | $ | 58,410 | ||||||||||||

Ratio of expenses to average net assets | 1.48 | %(b) | 1.48 | % | 1.48 | % | 1.48 | % | 1.45 | % | 1.38 | % | ||||||||||||

Ratio of net investment income (loss) to average net assets | (0.04 | )%(b) | 0.03 | % | 0.44 | % | 0.66 | % | 0.58 | % | 0.72 | % | ||||||||||||

Portfolio turnover | 9 | %(a) | 30 | % | 42 | % | 31 | % | 58 | % | 70 | % | ||||||||||||

| (a) | Not annualized. |

| (b) | Annualized. |

GREEN CENTURY EQUITY FUND FINANCIAL HIGHLIGHTS

| SIX MONTHS ENDED JANUARY 31, 2016 | FOR THE YEARS ENDED JULY 31, | |||||||||||||||||||||||

| (UNAUDITED) | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||||||

Net Asset Value, beginning of period | $ | 32.73 | $ | 30.11 | $ | 26.30 | $ | 20.81 | $ | 19.99 | $ | 17.44 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||||||

Net investment income | 0.12 | 0.20 | 0.19 | 0.21 | 0.19 | 0.18 | ||||||||||||||||||

Net realized and unrealized gain (loss) on investments | (2.21 | ) | 2.96 | 3.79 | 5.48 | 0.83 | 2.57 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total increase (decrease) from investment operations | (2.09 | ) | 3.16 | 3.98 | 5.69 | 1.02 | 2.75 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Less dividends: | ||||||||||||||||||||||||

Dividends from net investment income | (0.12 | ) | (0.19 | ) | (0.17 | ) | (0.20 | ) | (0.20 | ) | (0.20 | ) | ||||||||||||

Distributions from net realized gains | (0.37 | ) | (0.35 | ) | — | — | — | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total decrease from dividends | (0.49 | ) | (0.54 | ) | (0.17 | ) | (0.20 | ) | (0.20 | ) | (0.20 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net Asset Value, end of period | $ | 30.15 | $ | 32.73 | $ | 30.11 | $ | 26.30 | $ | 20.81 | $ | 19.99 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total return | (6.48 | )%(a) | 10.54 | % | 15.16 | % | 27.49 | % | 5.14 | % | 15.77 | % | ||||||||||||

| Ratios/Supplemental data: | ||||||||||||||||||||||||

Net assets, end of period (in 000’s) | $ | 142,337 | $ | 138,403 | $ | 95,358 | $ | 66,809 | $ | 50,972 | $ | 53,363 | ||||||||||||

Ratio of expenses to average net assets | 1.25 | %(b) | 1.25 | % | 1.25 | % | 1.25 | % | 1.16 | % | 0.95 | % | ||||||||||||

Ratio of net investment income to average net assets | 0.81 | %(b) | 0.68 | % | 0.72 | % | 0.92 | % | 0.97 | % | 0.92 | % | ||||||||||||

Portfolio turnover | 12 | %(a) | 13 | % | 32 | % | 17 | % | 14 | % | 13 | % | ||||||||||||

| (a) | Not annualized. |

| (b) | Annualized. |

See Notes to Financial Statements

22

GREEN CENTURY FUNDS NOTES TO FINANCIAL STATEMENTS (unaudited) |

NOTE 1 — Organization and Significant Accounting Policies

Green Century Funds (the “Trust”) is a Massachusetts business trust which offers two separate series, the Green Century Balanced Fund (the “Balanced Fund”) and the Green Century Equity Fund (the “Equity Fund”), each a “Fund” and collectively, the “Funds”. The Trust is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end, diversified management investment company. The Trust accounts separately for the assets, liabilities and operations of each series. The Balanced Fund commenced operations on March 18, 1992 and the Equity Fund commenced operations on September 13, 1995.