UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06351

Green Century Funds

114 State Street

Suite 200

Boston, MA 02109

(Address of principal executive offices)

Green Century Capital Management, Inc.

114 State Street

Suite 200

Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 482-0800

Date of fiscal year end: July 31

Date of reporting period: January 31, 2023

Item 1. Reports to Stockholders.

| (a) | The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). |

| | |

| | SEMI-ANNUAL REPORT Green Century Balanced Fund Green Century Equity Fund Green Century MSCI International Index Fund January 31, 2023 |

| |

| An investment for your future.® | | 114 State Street, Boston, Massachusetts 02109 |

For information on the Green Century Funds®, call 1-800-93-GREEN. For information on how to open an account and account services, call 1-800-221-5519 8:00 am to 6:00 pm Eastern Time, Monday through Friday. For daily share price information twenty-four hours a day, visit www.greencentury.com.

Dear Green Century Funds Shareholder:

Thank you for putting your trust in the Green Century Funds°. Every day our team works to provide opportunities for you to invest in alignment with your environmental values and make an impact through the dollars you are saving for the future. I’m excited to share some of our highlights in this letter.

But first I want to acknowledge that 2022 was a challenging year for investors in both equities and bonds. Faced with rising inflation, interest rate hikes and recessionary fears, the S&P 500® recorded its worst year since 2008. In moments like this, some investors may abandon the market and move to cash holdings. While there might be good reasons for changing an investment strategy, acting on emotion may compromise a portfolio’s long-term return potential and I encourage you to consult with a financial advisor before you make any substantial changes.

In addition to our investment strategy, a key way that the Green Century Funds helps you make a difference is through our shareholder advocacy program. Our team of dedicated advocates worked with 80 companies last year to achieve new environmental policies with 20 major corporations. I’m pleased to share some highlights.

Negotiated a commitment with Lowe’s1 that resulted in four new industry-leading commitments to protect forests around the world, including the Canadian boreal.

Persuaded Jack in the Box1 to only purchase pork raised without the use of cruel gestation crates, which improves animal welfare and helps reduce the harmful effects of factory farming.

Won majority shareholder votes at Sysco1 (92%) and General Mills1 (55%) requesting that the companies measure their plastic use as the first step toward reducing it to protect ocean wildlife and public health.

I am proud of Green Century’s achievements in an unprecedented and challenging year, and I am eager to see what we are able to accomplish as we move forward. Our work to protect the environment and protect public health is far from finished—and none of it would be possible without investors like you.

If you have enjoyed this update and are not yet part of our enews community, I invite you to send your email address to info@greencentury.com or sign up on our website www.greencentury.com.

Thank you for choosing Green Century to help save for your future.

Sincerely,

Leslie Samuelrich, President

Green Century Funds

° Green Century Capital Management, Inc. (Green Century) is the investment advisor to the Green Century Funds (The Funds).

Green Century on the Web

E-News. For more regular updates on the Green Century Funds and on our advocacy efforts, please consider signing up for our e-newsletter. Call 1-800-934-7336, visit www.greencentury.com, or email info@greencentury.com.

Online Access. Information on your account is available on our website at www.greencentury.com. From the home page, click on Access My Account. Shareholders may also perform online transactions on the site. While there, please consider registering for e-delivery of your statements and other Fund documents.

Website. Visit www.greencentury.com to get quarterly performance, our impact stories, and more.

The Green Century Funds’ proxy voting guidelines and a record of the Funds’ proxy votes for the year ended June 30, 2022 are available without charge, upon request, (i) at www.greencentury.com, (ii) by calling 1-800-934-7336, (iii) by sending an e-mail to info@greencentury.com, and (iv) on the Securities and Exchange Commission’s website at www.sec.gov.

The Green Century Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of the year on Form N-PORT, Part F. The Green Century Funds’ Forms N-PORT, Part F are available on the EDGAR database on the SEC’s website at www.sec.gov. Copies may be obtained upon payment of a duplicating fee, by writing the SEC’s Public Reference Section, Washington DC 20549-0102 or by electronic request at the following e-mail address: publicinfo@sec.gov. The information on Form N-PORT, Part F may also be obtained by calling us at 1-800-934-7336, or by e-mailing a request to info@greencentury.com

2

THE GREEN CENTURY BALANCED FUND

The Green Century Balanced Fund seeks capital growth and income from a portfolio of stocks and bonds that meet Green Century’s standards for environmentally responsible and sustainable investing. The portfolio managers of the Balanced Fund avoid fossil fuel companies and other environmentally harmful industries and consider environmental, social, and governance data in their decision making.

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | CUMULATIVE

RETURNS* | | | AVERAGE ANNUAL RETURNS* | |

| | | | | Six Months | | | One Year | | | Three Years | | | Five Years | | | Ten Years | |

| December 31, 2022 | | Green Century Balanced Fund — Individual Investor Share Class | | | 1.84% | | | | –16.21% | | | | 4.19% | | | | 6.00% | | | | 7.60% | |

| | | Green Century Balanced Fund — Institutional Share Class** | | | 2.03% | | | | –15.93% | | | | 4.42% | | | | 6.14% | | | | 7.67% | |

| | | Custom Balanced Fund Index2 | | | 1.19% | | | | –13.70% | | | | 4.44% | | | | 6.12% | | | | 8.04% | |

| January 31, 2023 | | Green Century Balanced Fund — Individual Investor Share Class | | | 0.05% | | | | –7.35% | | | | 6.10% | | | | 6.51% | | | | 7.76% | |

| | | Green Century Balanced Fund — Institutional Share Class** | | | 0.21% | | | | –7.08% | | | | 6.33% | | | | 6.65% | | | | 7.83% | |

| | | Custom Balanced Fund Index2 | | | –0.27% | | | | –6.15% | | | | 5.90% | | | | 6.48% | | | | 8.20% | |

The Individual Investor Share Class total expense ratio of the Fund is 1.46% and the Institutional Share Class total expense ratio of the Fund is 1.16% as of the most recent prospectus.

* The performance data quoted represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information as of the most recent month-end, call 1-800-93-GREEN. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder might pay on Fund distributions or the redemption of Fund shares. A redemption fee of 2.00% may be imposed on redemptions or exchanges of shares you have owned for 60 days or less. Please see the Prospectus for more information.

** Institutional Shares were offered as of November 28, 2020. The Institutional Share Class performance prior to November 28, 2020 reflects the performance of the Fund’s Individual Investor Share Class.

During the six month period ended January 31, 2023, the Balanced Fund outperformed the Custom Balanced Index, with the Balanced Fund returning 0.21% and the Custom Balanced index returning –0.27%. For the one year period ending January 31, 2023, the Balanced Fund returned –7.08%, while the Custom Balanced Index returned –6.15%. The Fund’s equity holdings that most positively contributed to relative performance during the twelve months ended January 31, 2023 included: First Solar1, SolarEdge Technologies1, LPL Financial Holdings1, Travelers Companies1 and TJX Companies1. Holdings detracting from performance included Alphabet1, SVB Financial1, Paypal Holdings1, Baxter International1 and Bright Horizons1.

Equity markets saw heightened volatility over the last six months as markets reacted to increasing inflation numbers and expectations for corresponding faster tightening by the Federal Reserve (“Fed”) and other global central banks. Inflation numbers in certain areas such as housing and lumber have started to cool, but the economy continues to post strong labor and wage numbers that may prompt the Fed to stay higher for longer. Federal Reserve Chair Powell and the members of the Federal Reserve Board of Governors continue to assert that they will do “whatever it takes” to tame inflation. Instead, after Core Consumer Price Inflation readings showed signs of moderating in September, investors opted to use their rose-colored glasses to view

3

indicators of both stronger and weaker economic trends as good news, bidding up share prices for value stocks and for the highly cyclical companies in the Energy, Industrials, Materials, and Financials sectors. Yields on longer-dated Treasuries declined through early December, as investors chose to believe that the Fed’s announced intention to slow the pace of rate increases meant that the Fed was reversing course and would reduce the terminal rate and quickly cut rates thereafter. This despite the Fed publicly indicating the contrary. The portfolio managers do not believe that the Fed has lowered its terminal rate or decreased the length of time it intends to hold the Funds rate at that higher terminal rate level. The Fed’s increases in the Funds rate this cycle have been breathtakingly aggressive; furthermore, the Fed’s rate increases have been accompanied by significant quantitative tightening. The Fed has repeatedly expressed its concern that a too-hasty return to normal will allow inflation to rekindle. Other Central Banks have also instituted record amounts of monetary restraint, the most significant since 1980. This synchronized monetary tightening has initiated the predictable chain of events.

The frequently articulated concern of worldwide Central Banks, including the Fed, with breaking any established embedded inflationary pattern, seems very likely to lengthen the period of monetary restriction, which will lengthen the duration of decreasing employment and make an extended recession ever more likely. Indeed, the Federal Reserve noted in December that “it would take substantially more evidence of progress to be confident that inflation was on a sustained downward path” and “No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023.” While the bond market continues to predict that Fed Fund rates will begin to drop in July, 2023, the portfolio managers disagree. Federal Reserve Chair Jerome Powell has repeatedly referenced the 1979 to 1982 experience, when the Fed believes that it prematurely eased monetary policy after slightly softer inflation readings, only to have to quickly raise rates again when inflation persisted at unacceptably high levels. The portfolio managers

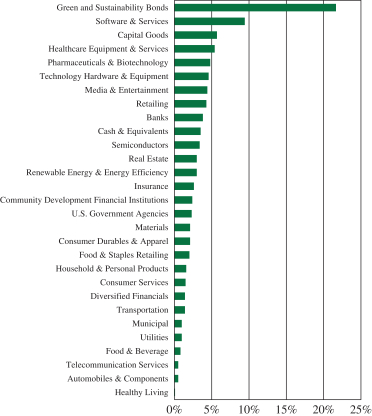

GREEN CENTURY BALANCED FUND

INVESTMENT BY INDUTRY (unaudited)

4

expect the interest rate hikes to continue until the Fed is persuaded by several consecutive readings of much softer core inflation, much softer growth in unit labor costs and average hourly earnings, and a substantial rise in unemployment. They also expect that the Fed will be quite reluctant to cut rates until both the employment cost index and the broad personal consumption expenditure deflator measure of inflation are clearly headed back to acceptable levels. The country has now entered the time where every aspect of the economy will begin to feel the effects of the prior tightening; it will show up in wage growth, unemployment, falling housing prices, discretionary income, and spending.

In the near term, declining business confidence and consumer confidence will likely translate into reduced corporate earnings, which may well initiate another down leg for equity markets. While the portfolio managers anticipate a recession and some earnings declines, they expect that the decline in earnings will be fairly modest. Even with the price-to-earnings compression that we have already experienced, they judge that further market downside is possible. In addition, consumer confidence tracks inversely with inflation; as inflation eases, this should support consumer confidence. Consumer confidence, housing starts, and equity market bottoms are all closely associated, so improving consumer confidence may limit the downside. Recovery from bear markets is usually sudden and sharp, so that attempts to time the market are usually unsuccessful. Overall, the portfolio managers conclude that the Fund is appropriately positioned for a modestly more risk-off equity market. In either a slowing growth or a recessionary environment, they expect that the focus on quality, lower-leverage, profitable companies with steadier earnings and revenues will be protective.

The growing environmental, social, and policy challenges facing the world make it increasingly imperative that shareholders demand that companies create the transition to a lower-carbon economy and recognize the human rights and dignity of their workers. The portfolio managers expect companies held within the portfolio to act with integrity and purpose, and to take leading roles in creating alternative mechanisms, through legislation or internal policies, to protect the needs and concerns of their employees, communities, and planet.

The Green Century Balanced Fund invests in the stocks and bonds of environmentally responsible corporations of various sizes, including small, medium, and large companies. The Green Century Balanced Fund does not invest in fossil fuels though most other diversified mutual funds do.

The value of the stocks held in the Balanced Fund will fluctuate in response to factors that may affect a single issuer, industry, or sector of the economy or may affect the market as a whole. Bonds are subject to a variety of risks including interest rate, credit, and inflation risk.

5

THE GREEN CENTURY EQUITY FUND

The Green Century Equity Fund invests essentially all of its assets in the stocks which make up the MSCI KLD 400 Social ex Fossil Fuels Index (the KLD 400 Index or the Index),3 comprised primarily of large capitalization U.S. companies selected based on comprehensive environmental, social and governance sustainability criteria. The Equity Fund seeks to provide shareholders with a long-term total return that matches that of the Index.

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | CUMULATIVE

RETURNS* | | | AVERAGE ANNUAL RETURNS* | |

| | | | | Six Months | | | One Year | | | Three Years | | | Five Years | | | Ten Years | |

| December 31, 2022 | | Green Century Equity Fund — Individual Investor Share Class | | | –0.12% | | | | –23.04% | | | | 6.85% | | | | 8.89% | | | | 12.00% | |

| | | Green Century Equity Fund — Institutional Share Class | | | 0.02% | | | | –22.81% | | | | 7.17% | | | | 9.20% | | | | 12.15% | |

| | | S&P 500 Index4 | | | 2.31% | | | | –18.11% | | | | 7.66% | | | | 9.42% | | | | 12.56% | |

| January 31, 2023 | | Green Century Equity Fund — Individual Investor Share Class | | | –1.58% | | | | –11.87% | | | | 9.02% | | | | 9.05% | | | | 12.07% | |

| | | Green Century Equity Fund — Institutional Share Class | | | –1.41% | | | | –11.59% | | | | 9.35% | | | | 9.36% | | | | 12.24% | |

| | | S&P 500 Index4 | | | –0.44% | | | | –8.22% | | | | 9.88% | | | | 9.54% | | | | 12.68% | |

The Individual Investor Share Class total expense ratio of the Fund is 1.25% and the Institutional Share Class total expense ratio of the Fund is 0.95% as of the most recent prospectus.

* The performance data quoted represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information as of the most recent month-end, call 1-800-93-GREEN. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder might pay on Fund distributions or the redemption of Fund shares. A redemption fee of 2.00% may be imposed on redemptions or exchanges of shares you have owned for 60 days or less. Please see the Prospectus for more information.

As of April 1, 2014, the Equity Fund invests in the common stocks which make up the MSCI KLD 400 Social ex Fossil Fuel Index; prior to April 1, 2014, the Fund invested in the common stocks which made up the MSCI KLD 400 Social Index.

For the six month period ended January 31, 2023, the Green Century Equity Fund, which closely tracks the KLD 400 Index, underperformed the S&P 500® Index (“benchmark”) by 114 basis points in the Individual Investor Share Class and by 97 basis points in the Institutional Share Class. The Equity Fund returned –1.58% in the Individual Investor Share Class and –1.41% in the Institutional Share Class for the six month period ended January 31, 2023, while the benchmark returned –0.44% during the same period.

As the MSCI KLD 400 Social ex Fossil Fuels Index does not include all of the stocks in the benchmark and includes some stocks not included in the benchmark, the performance of the Equity Fund can be expected to differ from the performance of the broader benchmark. The difference in performance of the Equity Fund relative to the benchmark was influenced by differences in sector allocation and stock selection criteria between the Fund and the benchmark.

6

The Energy sector was the best performing sector of the benchmark, returning 17.78%. The Equity Fund does not have an allocation to this sector, while the sector has a 5.08% weight in the benchmark. The performance of the Fund, relative to the benchmark, was positively impacted by stock selection within the Consumer Discretionary, Health Care and Industrials sectors. The relative performance of the Fund was negatively impacted by stock selection within the Communication Services, Financials and Materials sectors.

According to an analysis by the Fund’s portfolio managers, the strongest performing sectors in the Equity Fund were Financials, Industrials and Health Care, which returned 8.79%, 8.46%, and 7.94%, respectively. The worst performing sectors were Communication Services and Consumer Discretionary, which returned –11.43% and –7.83%, respectively, for the six month period.

Within the benchmark, Energy and Materials were the strongest performing sectors, gaining 17.78% and 9.71%, respectively. The worst performing sectors were Consumer Discretionary and Real Estate, which returned –9.35% and –6.34%, respectively, for the six month period.

The Equity Fund, like other mutual funds invested primarily in stocks, carries the risk of investing in the stock market. The large companies in which the Equity Fund is invested may perform worse than the stock market as a whole. The Equity Fund will not shift concentration from one industry to another or from stocks to bonds or cash, in order to defend against a falling stock market.

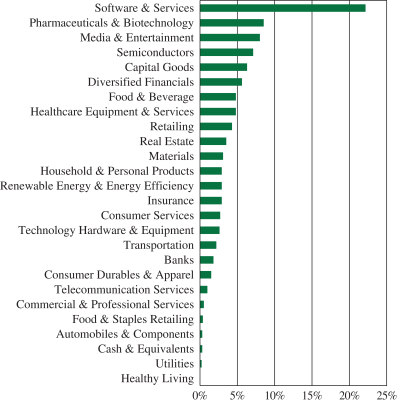

GREEN CENTURY EQUITY FUND

INVESTMENT BY INDUSTRY (unaudited)

7

THE GREEN CENTURY MSCI INTERNATIONAL INDEX FUND

The Green Century MSCI International Index Fund (the International Fund) invests in the stocks which make up the MSCI World ex USA SRI ex Fossil Fuels Index (the Index),5 comprised primarily of foreign companies selected based on comprehensive environmental, social and governance (ESG) sustainability criteria. The International Fund seeks to provide shareholders with a long-term total return that matches that of the Index.

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | CUMULATIVE

RETURNS* | | | AVERAGE ANNUAL RETURNS* | |

| | Six Months | | | One Year | | | Three Years | | | Five Years | | | Since

Inception | |

| December 31, 2022 | | Green Century International Index Fund — Individual Investor Share Class | | | 3.95% | | | | –21.35% | | | | –0.24% | | | | 1.24% | | | | 3.99% | |

| | | Green Century International Index Fund — Institutional Share Class | | | 4.18% | | | | –21.11% | | | | 0.05% | | | | 1.55% | | | | 4.29% | |

| | | MSCI World ex USA Index6 | | | 5.50% | | | | –14.29% | | | | 1.27% | | | | 1.79% | | | | 4.95% | |

| January 31, 2023 | | Green Century International Index Fund — Individual Investor Share Class | | | 6.97% | | | | –8.50% | | | | 3.17% | | | | 2.17% | | | | 5.31% | |

| | | Green Century International Index Fund — Institutional Share Class | | | 7.12% | | | | –8.25% | | | | 3.50% | | | | 2.48% | | | | 5.62% | |

| | | MSCI World ex USA Index6 | | | 8.74% | | | | –2.98% | | | | 4.64% | | | | 2.47% | | | | 6.19% | |

The Individual Investor Share Class total expense ratio of the Fund is 1.28% and the Institutional Share Class total expense ratio of the Fund is 0.98% as of the most recent prospectus.

* The performance data quoted represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information as of the most recent month-end, call 1-800-93-GREEN. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder might pay on Fund distributions or the redemption of Fund shares. A redemption fee of 2.00% may be imposed on redemptions or exchanges of shares you have owned for 60 days or less. Please see the Prospectus for more information.

The Green Century MSCI International Index Fund closely tracks the MSCI World ex USA SRI ex Fossil Fuels Index. The International Fund’s Individual Investor Share Class returned 6.97% and the International Fund’s Institutional Share Class returned 7.12% for the six month period ended January 31, 2023, underperforming the MSCI World ex USA Index (“Benchmark”), the Fund’s benchmark, which returned 8.74% during the same period.

The MSCI World ex USA Index is not a values-based or SRI screened index and may invest in fossil fuels, nuclear weapons, and producers of genetically modified organisms. The difference in performance of the International Fund relative to the benchmark was largely due to differences in sector allocation and stock selection criteria between the Fund and the benchmark.

According to an analysis by the Fund’s portfolio managers, the strongest performing sectors in the International Fund were Financials, Information Technology and Consumer Discretionary, which returned 14.76%, 14.17% and 10.84%, respectively. The worst performing sectors were Real Estate and Communication Services, which returned –0.65% and –0.46%, respectively, for the six month period.

8

Within the benchmark, Materials and Financials were the strongest performing sectors, gaining 19.12% and 16.84%, respectively. The worst performing sectors were Real Estate and Utilities, which returned –2.16% and 0.89%, respectively, for the six month period.

The International Fund, like other mutual funds invested primarily in stocks, carries the risk of investing in the stock market. The developed ex-U.S. equities in which the International Fund is invested may perform worse than the stock market as a whole. The International Fund will not shift concentration from one industry to another or from stocks to bonds or cash, in order to defend against a falling stock market.

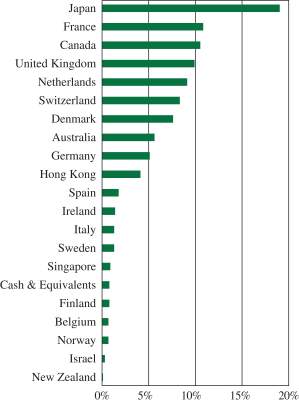

GREEN CENTURY MSCI INTERNATIONAL INDEX FUND

INVESTMENT BY COUNTRY (unaudited)

9

1 As of January 31, 2023, the following companies comprised the listed percentages of each of the Green Century Funds:

| | | | | | | | | | | | |

| Portfolio Holdings | | GREEN

CENTURY

BALANCED

FUND | | | GREEN

CENTURY

EQUITY

FUND | | | GREEN

CENTURY

INTERNATIONAL

INDEX FUND | |

Lowe’s Companies Inc. | | | 0.00 | % | | | 0.71 | % | | | 0.00 | % |

Jack in the Box Inc. | | | 0.00 | % | | | 0.01 | % | | | 0.00 | % |

Sysco Corporation | | | 0.61 | % | | | 0.22 | % | | | 0.00 | % |

General Mills Inc. | | | 0.00 | % | | | 0.26 | % | | | 0.00 | % |

First Solar Inc. | | | 0.87 | % | | | 0.00 | % | | | 0.00 | % |

SolarEdge Technologies Inc. | | | 0.94 | % | | | 0.00 | % | | | 0.00 | % |

LPL Financial Holdings, Inc. | | | 0.92 | % | | | 0.00 | % | | | 0.00 | % |

| | | | | | | | | | | | |

| Portfolio Holdings | | GREEN

CENTURY

BALANCED

FUND | | | GREEN

CENTURY

EQUITY

FUND | | | GREEN

CENTURY

INTERNATIONAL

INDEX FUND | |

Travelers Companies Inc. | | | 1.51 | % | | | 0.25 | % | | | 0.00 | % |

TJX Companies Inc. | | | 1.34 | % | | | 0.01 | % | | | 0.00 | % |

Alphabet Inc. | | | 3.50 | % | | | 6.33 | % | | | 0.00 | % |

SVB Financial Group | | | 0.52 | % | | | 0.10 | % | | | 0.00 | % |

Paypal Holdings, Inc. | | | 0.53 | % | | | 0.49 | % | | | 0.00 | % |

Baxter International, Inc. | | | 0.34 | % | | | 0.00 | % | | | 0.00 | % |

Bright Horizons Family Solutions, Inc. | | | 0.50 | % | | | 0.00 | % | | | 0.00 | % |

Portfolio composition will change due to ongoing management of the Funds. Please refer to the Green Century Funds website for current information regarding the Funds’ portfolio holdings. Note that some of the holdings discussed above may not have been held by any Fund during the six-month period ended January 31, 2023, or may have been held by a Fund for a portion of the period, or may have been held by a Fund for the entire period. These holdings are subject to risk as described in the Funds’ prospectus. References to specific investments should not be construed as a recommendation of the securities by the Funds, their administrator, or their distributor.

2 The Custom Balanced Index is comprised of a 60% weighting in the S&P 1500 Index and a 40% weighting in the BofA Merrill Lynch 1-10 Year US Corporate & Government Index (the BofA Merrill Lynch Index). The S&P Supercomposite 1500 Index is an unmanaged broad-based capitalization-weighted index comprising 1500 stocks of large-cap, mid-cap, and small-cap U.S. companies. The BofA Merrill Lynch Index tracks the performance of U.S. dollar-denominated investment grade government and corporate public debt issued in the U.S. domestic bond market with at least 1 year and less than 10 years remaining maturity, including U.S. treasury, U.S. agency, foreign government, supranational and corporate securities. It is not possible to invest directly in the Custom Balanced Index, the S&P Supercomposite 1500 Index, or the BofA Merrill Lynch Index.

3 The MSCI KLD 400 Social ex Fossil Fuels Index (the KLD400 ex Fossil Fuels Index) is a custom index calculated by MSCI Inc. and is comprised of the common stocks of the approximately 400 companies in the MSCI KLD 400 Social Index (the KLD400 Index), minus the stocks of the companies that explore for, extract, produce, manufacture or refine coal, oil or gas or produce or transmit electricity derived from fossil fuels or transmit natural gas or have carbon reserves included in the KLD400 Index. The KLD400 Index is a free float-adjusted market capitalization index designed to provide exposure to U.S. companies that have positive Environmental, Social and Governance (ESG) characteristics and consists of approximately 400 companies selected from the MSCI USA Investable Market Index. It is not possible to invest directly in an index.

4 The S&P 500 Index is an unmanaged index of 500 selected common stocks, most of which are listed on the New York Stock Exchange. The S&P 500 Index is heavily weighted toward stocks with large market capitalization and represents approximately two-thirds of the total market value of all domestic stocks. It is not possible to invest directly in the S&P 500 Index.

5 The World ex USA SRI ex Fossil Fuels Index is a custom index calculated by MSCI Inc. The World ex USA SRI ex Fossil Fuels Index is comprised of the common stocks of the companies in the MSCI World ex USA SRI Index (the World ex USA SRI Index), minus the stocks of the companies that explore for, extract, produce, manufacture or refine coal, oil or gas or produce or transmit electricity derived from fossil fuels or transmit natural gas or have carbon reserves included in the World ex USA SRI (Socially Responsible Investment) Index. The World ex USA SRI Index includes large and mid-cap stocks from approximately 22 developed market countries (excluding the U.S.). The World ex USA SRI Index is a capitalization weighted index that provides exposure to companies with what MSCI calculates to have outstanding ESG ratings and excludes companies whose products have negative social or environmental impacts. It is not possible to invest directly in an index.

6 The MSCI World ex USA Index is a custom index calculated by MSCI Inc. The MSCI World ex USA Index includes large and mid-cap stocks across 22 of 23 Developed Markets countries and excludes the United States. With 1,023 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI World ex USA Index is a free float-adjusted market capitalization index. It is not possible to invest directly in the MSCI World ex USA Index.

10

The Funds’ environmental criteria limit the investments available to the Funds compared to mutual funds that do not use environmental criteria.

This information has been prepared from sources believed reliable. The views expressed are as of the date of publication and are those of the Advisor to the Funds.

This material must be preceded or accompanied by a current Prospectus.

Distributor: UMB Distribution Services, LLC 2/23

The Green Century Equity Fund and the Green Century MSCI International Index Fund (the “Funds”) are not sponsored, endorsed, or promoted by MSCI, its affiliates, information providers or any other third party involved in, or related to, compiling, computing or creating the MSCI indices (the “MSCI Parties”), and the MSCI Parties bear no liability with respect to the Funds or any index on which a Fund is based. The MSCI Parties are not sponsors of the Funds and are not affiliated with the Funds in any way. The Statement of Additional Information contains a more detailed description of the limited relationship the MSCI Parties have with Green Century Capital Management and the Funds.

11

GREEN CENTURY FUNDS EXPENCE EXAMPLE

For the six months ended January 31, 2023 (unaudited)

As a shareholder of the Green Century Funds (the “Funds”), you incur two types of costs: (1) transaction costs, including redemption fees on certain redemptions; and (2) ongoing costs, including management fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from August 1, 2022 to January 31, 2023 (the “period”).

Actual Expenses The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 equals 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the actual return of either of the Funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5%hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees on shares held for 60 days or less. Therefore, the second line of the table is useful in comparing the ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs could have been higher.

| | | | | | | | | | | | |

| | | BEGINNING

ACCOUNT VALUE

AUGUST 1, 2022 | | | ENDING

ACCOUNT VALUE

JANUARY 31, 2023 | | | EXPENSES

PAID DURING

THE PERIOD1 | |

| | | |

Balanced Fund | | | | | | | | | | | | |

Actual Expenses — Individual Investor Class | | $ | 1,000.00 | | | $ | 1,000.50 | | | $ | 7.37 | |

Actual Expenses — Institutional Class | | | 1,000.00 | | | | 1,002.10 | | | | 5.87 | |

Hypothetical Example, assuming a 5% return before expenses — Individual Investor Class | | | 1,000.00 | | | | 1,017.63 | | | | 7.44 | |

Hypothetical Example, assuming a 5% return before expenses — Institutional Class | | | 1,000.00 | | | | 1,019.14 | | | | 5.92 | |

12

| | | | | | | | | | | | |

| | | BEGINNING

ACCOUNT VALUE

AUGUST 1, 2022 | | | ENDING

ACCOUNT VALUE

JANUARY 31, 2023 | | | EXPENSES

PAID DURING

THE PERIOD1 | |

| | | |

Equity Fund | | | | | | | | | | | | |

Actual Expenses — Individual Investor Class | | $ | 1,000.00 | | | $ | 984.20 | | | $ | 6.25 | |

Actual Expenses — Institutional Class | | | 1,000.00 | | | | 985.90 | | | | 4.75 | |

Hypothetical Example, assuming a 5% return before expenses — Individual Investor Class | | | 1,000.00 | | | | 1,018.70 | | | | 6.36 | |

Hypothetical Example, assuming a 5% return before expenses — Institutional Class | | | 1,000.00 | | | | 1,020.21 | | | | 4.84 | |

| | | |

| | | BEGINNING

ACCOUNT VALUE

AUGUST 1, 2022 | | | ENDING

ACCOUNT VALUE

JANUARY 31, 2023 | | | EXPENSES

PAID DURING

THE PERIOD1 | |

| | | |

MSCI International Index Fund | | | | | | | | | | | | |

Actual Expenses — Individual Investor Class | | $ | 1,000.00 | | | $ | 1,069.70 | | | $ | 6.68 | |

Actual Expenses — Institutional Class | | | 1,000.00 | | | | 1,071.20 | | | | 5.12 | |

Hypothetical Example, assuming a 5% return before expenses — Individual Investor Class | | | 1,000.00 | | | | 1,018.55 | | | | 6.51 | |

Hypothetical Example, assuming a 5% return before expenses — Institutional Class | | | 1,000.00 | | | | 1,020.06 | | | | 4.99 | |

1 Expenses are equal to the Funds’ annualized expense ratios (1.46% for the Balanced Fund Individual Investor Class, 1.16% for the Balanced Fund Institutional Class, 1.25% for the Equity Fund Individual Investor Class, 0.95% for the Equity Fund Institutional Class, 1.28% for the International Index Fund Individual Investor Class and 0.98% for the International Index Fund Institutional Class), multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

13

| | |

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | |

| | | | | | | | |

COMMON STOCKS — 64.2% | |

| | | SHARES | | | VALUE | |

Software & Services — 7.7% | |

Adobe, Inc. (a) | | | 9,207 | | | $ | 3,409,720 | |

Autodesk, Inc. (a) | | | 11,965 | | | | 2,574,389 | |

Mastercard, Inc., Class A | | | 18,404 | | | | 6,820,523 | |

Microsoft Corporation | | | 53,091 | | | | 13,156,481 | |

Paycom Software, Inc. (a) | | | 7,024 | | | | 2,275,355 | |

PayPal Holdings, Inc. (a) | | | 25,725 | | | | 2,096,330 | |

| | | | | | | | |

| | | | | | | 30,332,798 | |

| | | | | | | | |

Healthcare Equipment & Services — 5.3% | |

Alcon, Inc. (b) | | | 35,019 | | | | 2,633,779 | |

Baxter International, Inc. | | | 28,987 | | | | 1,324,416 | |

CVS Health Corp. | | | 31,621 | | | | 2,789,605 | |

Elevance Health, Inc. | | | 14,251 | | | | 7,125,357 | |

Medtronic PLC | | | 22,868 | | | | 1,913,823 | |

Stryker Corporation | | | 12,760 | | | | 3,238,616 | |

West Pharmaceutical Services, Inc. | | | 7,437 | | | | 1,975,267 | |

| | | | | | | | |

| | | | | | | 21,000,863 | |

| | | | | | | | |

Capital Goods — 4.9% | |

Deere & Company | | | 7,381 | | | | 3,120,982 | |

Eaton Corporation PLC | | | 21,989 | | | | 3,566,835 | |

Illinois Tool Works, Inc. | | | 11,220 | | | | 2,648,369 | |

Rockwell Automation, Inc. | | | 8,926 | | | | 2,517,400 | |

Trane Technologies PLC | | | 15,557 | | | | 2,786,570 | |

Westinghouse Air Brake Technologies Corporation | | | 27,643 | | | | 2,869,620 | |

Xylem, Inc. | | | 15,837 | | | | 1,647,206 | |

| | | | | | | | |

| | | | | | | 19,156,982 | |

| | | | | | | | |

Pharmaceuticals & Biotechnology — 4.8% | |

AstraZeneca PLC ADR (b) | | | 80,933 | | | | 5,290,590 | |

IQVIA Holdings, Inc. (a) | | | 15,895 | | | | 3,646,472 | |

Merck & Company, Inc. | | | 27,300 | | | | 2,932,293 | |

Roche Holding AG ADR | | | 92,577 | | | | 3,624,390 | |

Thermo Fisher Scientific, Inc. | | | 5,889 | | | | 3,358,673 | |

| | | | | | | | |

| | | | | | | 18,852,418 | |

| | | | | | | | |

Technology Hardware & Equipment — 4.6% | |

Apple, Inc. | | | 108,052 | | | | 15,590,823 | |

Palo Alto Networks, Inc. (a) | | | 15,612 | | | | 2,476,688 | |

| | | | | | | | |

| | | | | | | 18,067,511 | |

| | | | | | | | |

Retailing — 4.3% | |

Home Depot, Inc. (The) | | | 11,443 | | | | 3,709,478 | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Retailing — (continued) | |

Target Corporation | | | 26,209 | | | $ | 4,511,617 | |

TJX Companies, Inc. (The) | | | 63,991 | | | | 5,238,303 | |

Tractor Supply Company | | | 14,712 | | | | 3,354,189 | |

| | | | | | | | |

| | | | | | | 16,813,587 | |

| | | | | | | | |

Banks — 3.8% | |

East West Bancorp, Inc. | | | 43,189 | | | | 3,391,200 | |

First Republic Bank | | | 23,150 | | | | 3,261,372 | |

KeyCorp. | | | 161,925 | | | | 3,107,341 | |

PNC Financial Services Group, Inc. (The) | | | 19,684 | | | | 3,256,324 | |

SVB Financial Group (a) | | | 6,707 | | | | 2,028,465 | |

| | | | | | | | |

| | | | | | | 15,044,702 | |

| | | | | | | | |

Media & Entertainment — 3.6% | |

Alphabet, Inc., Class A (a) | | | 105,940 | | | | 10,471,110 | |

Walt Disney Company (The) (a) | | | 32,150 | | | | 3,487,953 | |

| | | | | | | | |

| | | | | | | 13,959,063 | |

| | | | | | | | |

Semiconductors — 3.4% | |

Analog Devices, Inc. | | | 19,593 | | | | 3,359,612 | |

ASML Holding NV (b) | | | 5,655 | | | | 3,737,050 | |

NVIDIA Corporation | | | 20,293 | | | | 3,964,643 | |

Wolfspeed, Inc. (a) . | | | 29,189 | | | | 2,247,845 | |

| | | | | | | | |

| | | | | | | 13,309,150 | |

| | | | | | | | |

Renewable Energy & Energy Efficiency — 3.0% | |

First Solar, Inc. (a) | | | 19,182 | | | | 3,406,723 | |

Hannon Armstrong Sustainable Infrastructure Capital, Inc. REIT | | | 41,772 | | | | 1,541,805 | |

Ormat Technologies, Inc. | | | 19,664 | | | | 1,819,903 | |

SolarEdge Technologies, Inc. (a) | | | 11,498 | | | | 3,669,357 | |

Sunrun, Inc. (a) | | | 47,155 | | | | 1,239,233 | |

| | | | | | | | |

| | | | | | | 11,677,021 | |

| | | | | | | | |

Insurance — 2.3% | |

Aflac, Inc. | | | 56,782 | | | | 4,173,477 | |

Travelers Companies, Inc. (The) | | | 25,349 | | | | 4,844,701 | |

| | | | | | | | |

| | | | | | | 9,018,178 | |

| | | | | | | | |

Real Estate — 2.1% | |

American Tower Corporation REIT | | | 14,574 | | | | 3,255,686 | |

AvalonBay Communities, Inc. REIT | | | 10,785 | | | | 1,913,690 | |

14

| | |

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | continued |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Real Estate — (continued) | |

Jones Lang LaSalle, Inc. (a) | | | 9,787 | | | $ | 1,809,323 | |

Prologis, Inc. REIT | | | 10,930 | | | | 1,413,030 | |

| | | | | | | | |

| | | | | | | 8,391,729 | |

| | | | | | | | |

Materials — 2.1% | |

Ball Corporation | | | 58,571 | | | | 3,411,175 | |

Ingevity Corporation (a) | | | 30,562 | | | | 2,519,531 | |

International Flavors & Fragrances, Inc. | | | 20,248 | | | | 2,277,090 | |

| | | | | | | | |

| | | | | | | 8,207,796 | |

| | | | | | | | |

Consumer Durables & Apparel — 2.1% | |

Levi Strauss & Company, Class A | | | 129,446 | | | | 2,381,806 | |

Lululemon Athletica, Inc. (a) | | | 7,754 | | | | 2,379,548 | |

NIKE, Inc., Class B | | | 26,195 | | | | 3,335,409 | |

| | | | | | | | |

| | | | | | | 8,096,763 | |

| | | | | | | | |

Food & Staples Retailing — 2.0% | |

Costco Wholesale Corporation | | | 10,528 | | | | 5,381,282 | |

Sysco Corporation | | | 30,845 | | | | 2,389,254 | |

| | | | | | | | |

| | | | | | | 7,770,536 | |

| | | | | | | | |

Household & Personal Products — 1.6% | |

Procter & Gamble Company (The) | | | 17,374 | | | | 2,473,710 | |

Unilever PLC ADR (b) | | | 74,953 | | | | 3,830,099 | |

| | | | | | | | |

| | | | | | | 6,303,809 | |

| | | | | | | | |

Consumer Services — 1.5% | |

Bright Horizons Family Solutions, Inc. (a) | | | 25,343 | | | | 1,945,836 | |

Starbucks Corporation | | | 35,086 | | | | 3,829,286 | |

| | | | | | | | |

| | | | | | | 5,775,122 | |

| | | | | | | | |

Transportation — 1.4% | |

J.B. Hunt Transport Services, Inc. . | | | 15,948 | | | | 3,014,969 | |

United Parcel Service, Inc., Class B | | | 14,085 | | | | 2,608,965 | |

| | | | | | | | |

| | | | | | | 5,623,934 | |

| | | | | | | | |

Utilities — 1.0% | |

American Water Works Company, Inc. | | | 24,572 | | | | 3,845,272 | |

| | | | | | | | |

Diversified Financials — 0.9% | |

LPL Financial Holdings, Inc. | | | 15,259 | | | | 3,618,214 | |

| | | | | | | | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Food & Beverage — 0.8% | |

McCormick & Company, Inc. | | | 39,734 | | | $ | 2,984,818 | |

| | | | | | | | |

Telecommunication Services — 0.5% | |

Verizon Communications, Inc. | | | 49,228 | | | | 2,046,408 | |

| | | | | | | | |

Automobiles & Components — 0.5% | |

Aptiv PLC (a) | | | 15,823 | | | | 1,789,423 | |

| | | | | | | | |

Total Common Stocks

(Cost $146,346,586) | | | | | | | 251,686,097 | |

| | | | | | | | |

| | | PRINCIPAL

AMOUNT | | | | |

|

BONDS & NOTES — 32.3% | |

Green and Sustainability Bonds — 21.6% | |

Apple, Inc.

2.85%, due 2/23/23 (c) | | $ | 3,000,000 | | | | 2,997,210 | |

Apple, Inc.

3.00%, due 6/20/27 (c) | | | 2,000,000 | | | | 1,913,356 | |

Asian Development Bank

2.125%, due 3/19/25 (b) | | | 1,000,000 | | | | 957,083 | |

Asian Development Bank

3.125%, due 9/26/28 (b) | | | 4,000,000 | | | | 3,854,312 | |

Bank of America Corporation

2.456% (3-Month USD Libor+87 basis points), due 10/22/25 (c) | | | 4,000,000 | | | | 3,824,068 | |

BlueHub Loan Fund, Inc.

2.89%, due 1/1/27 (d) | | | 2,000,000 | | | | 1,781,720 | |

Boston Properties LP

4.50%, due 12/1/28 (c) | | | 5,000,000 | | | | 4,793,275 | |

Bridge Housing Corporation

3.25%, due 7/15/30 (c) | | | 4,500,000 | | | | 4,054,365 | |

Century Housing Corporation

0.60%, due 2/15/24 | | | 2,500,000 | | | | 2,389,395 | |

Citigroup, Inc.

1.678% (SOFR Rate+166.7 basis points), due 5/15/24 (c) | | | 5,000,000 | | | | 4,950,590 | |

City & County of San Francisco CA Community Facilities District No. 2014-1

2.75%, due 9/1/23 | | | 650,000 | | | | 643,152 | |

City of San Francisco CA Public Utilities Commission Water Revenue

2.806%, due 11/1/23 | | | 2,000,000 | | | | 1,977,012 | |

15

| | |

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | continued |

| | | | | | | | |

| | | PRINCIPAL

AMOUNT | | | VALUE | |

Green and Sustainability Bonds — (continued) | |

European Investment Bank

2.50%, due 10/15/24 (b) | | $ | 2,000,000 | | | $ | 1,939,198 | |

European Investment Bank

2.125%, due 4/13/26 (b) | | | 500,000 | | | | 472,107 | |

International Bank for Reconstruction & Development

2.125%, due 3/3/25 (b) | | | 2,000,000 | | | | 1,915,454 | |

International Finance Corporation

2.125%, due 4/7/26 (b) | | | 500,000 | | | | 472,837 | |

Johnson Controls International plc / Tyco Fire & Security Finance SCA

1.75%, due 9/15/30 (b)(c) | | | 2,000,000 | | | | 1,653,864 | |

National Australia Bank Ltd.

3.625%, due 6/20/23 (b) | | | 2,000,000 | | | | 1,991,840 | |

Nederlandse Waterschapsbank NV

2.375%, due 3/24/26 (b)(e) | | | 1,000,000 | | | | 947,714 | |

New Jersey Infrastructure Bank

3.00%, due 9/1/31 | | | 2,500,000 | | | | 2,226,393 | |

NXP BV / NXP Funding LLC / NXP USA, Inc.

5.00%, due 1/15/33 (b)(c) | | | 4,500,000 | | | | 4,403,961 | |

PNC Financial Services Group, Inc. (The)

2.20%, due 11/1/24 (c) | | | 5,000,000 | | | | 4,811,530 | |

Preservation Of Affordable Housing, Inc.

4.479%, due 12/1/32 (c) | | | 3,000,000 | | | | 2,812,491 | |

Prologis LP

1.25%, due 10/15/30 (c) | | | 4,500,000 | | | | 3,549,123 | |

Regency Centers LP

3.75%, due 6/15/24 (c) | | | 2,000,000 | | | | 1,947,076 | |

San Francisco Bay Area Rapid Transit District

2.622%, due 8/1/29 | | | 2,000,000 | | | | 1,812,122 | |

Starbucks Corporation

2.45%, due 6/15/26 (c) | | | 4,500,000 | | | | 4,223,124 | |

United States International Development Finance Corporation

3.43%, due 6/1/33 | | | 195,198 | | | | 185,916 | |

United States International Development Finance Corporation

3.05%, due 6/15/35 | | | 1,233,900 | | | | 1,145,440 | |

| | | | | | | | |

| | | PRINCIPAL

AMOUNT | | | VALUE | |

Green and Sustainability Bonds — (continued) | |

United States International Development Finance Corporation

2.58%, due 7/15/38 | | $ | 2,851,082 | | | $ | 2,513,828 | |

Verizon Communications, Inc.

3.875%, due 2/8/29 (c) | | | 3,500,000 | | | | 3,365,533 | |

Visa, Inc.

0.75%, due 8/15/27 (c) | | | 5,000,000 | | | | 4,360,230 | |

Xylem, Inc.

2.25%, due 1/30/31 (c) | | | 4,500,000 | | | | 3,770,640 | |

| | | | | | | | |

| | | | | | | 84,655,959 | |

| | | | | | | | |

Community Development Financial Institutions — 2.4% | |

Capital Impact Partners

1.00%, due 9/15/25 (c) | | | 1,500,000 | | | | 1,340,055 | |

Enterprise Community Loan Fund, Inc.

4.152%, due 11/1/28 (c) | | | 3,000,000 | | | | 2,884,122 | |

Local Initiatives Support Corporation

1.00%, due 11/15/25 | | | 2,000,000 | | | | 1,753,734 | |

Local Initiatives Support Corporation

3.782%, due 3/1/27 (c) | | | 2,000,000 | | | | 1,919,720 | |

Reinvestment Fund, Inc. (The)

3.78%, due 2/15/26 | | | 1,400,000 | | | | 1,339,265 | |

| | | | | | | | |

| | | | | | | 9,236,896 | |

| | | | | | | | |

U.S. Government Agencies — 2.3% | |

Federal Farm Credit Banks Funding Corporation

2.26%, due 11/13/24 | | | 500,000 | | | | 482,685 | |

Federal Farm Credit Banks Funding Corporation

1.82%, due 12/18/25 | | | 3,000,000 | | | | 2,826,633 | |

Federal Farm Credit Banks Funding Corporation

2.80%, due 11/12/27 | | | 3,000,000 | | | | 2,868,363 | |

Federal Home Loan Banks

0.75%, due 12/14/23 (c) | | | 3,000,000 | | | | 2,894,931 | |

| | | | | | | | |

| | | | | | | 9,072,612 | |

| | | | | | | | |

Software & Services — 1.6% | |

Adobe, Inc.

3.25%, due 2/1/25 (c) | | | 3,500,000 | | | | 3,416,819 | |

16

| | |

GREEN CENTURY BALANCED FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | concluded |

| | | | | | | | |

| | | PRINCIPAL

AMOUNT | | | VALUE | |

Software & Services — (continued) | |

Salesforce, Inc.

3.70%, due 4/11/28 (c) | | $ | 3,000,000 | | | $ | 2,932,557 | |

| | | | | | | | |

| | | | | | | 6,349,376 | |

| | | | | | | | |

Municipal — 1.0% | |

Commonwealth of Massachusetts

4.11%, due 7/15/31 (c) | | | 4,000,000 | | | | 3,954,760 | |

| | | | | | | | |

Real Estate — 0.9% | |

National Community Renaissance of California

3.27%, due 12/1/32 (c) | | | 4,000,000 | | | | 3,406,820 | |

| | | | | | | | |

Capital Goods — 0.8% | |

Trane Technologies Luxembourg Finance SA

3.80%, due 3/21/29 (c) | | | 3,500,000 | | | | 3,327,142 | |

| | | | | | | | |

Media & Entertainment — 0.8% | |

Alphabet, Inc.

1.998%, due 8/15/26 (c) | | | 3,500,000 | | | | 3,255,098 | |

| | | | | | | | |

Diversified Financials — 0.5% | |

State Street Corporation

3.10%, due 5/15/23 | | | 2,000,000 | | | | 1,989,770 | |

| | | | | | | | |

Insurance — 0.3% | |

Travelers Property Casualty Corporation

7.75%, due 4/15/26 | | | 1,000,000 | | | | 1,095,369 | |

| | | | | | | | |

Healthy Living — 0.1% | |

Whole Foods Market, Inc.

5.20%, due 12/3/25 (c)(e) | | | 500,000 | | | | 505,827 | |

| | | | | | | | |

Total Bonds & Notes

(Cost $137,196,773) | | | | | | | 126,849,629 | |

| | | | | | | | |

| | | | | | | | |

SHORT-TERM INVESTMENTS — 3.3% | |

| | | PRINCIPAL

AMOUNT | | | VALUE | |

UMB Money Market Fiduciary Account, 0.01% (f)

(Cost $12,979,209) | | | | | | $ | 12,979,209 | |

| | | | | | | | |

Total Short-term Investments

(Cost $12,979,209) | | | | | | | 12,979,209 | |

| | | | | | | | |

TOTAL INVESTMENTS (g) — 99.8% | |

(Cost $296,522,568) | | | | | | | 391,514,935 | |

Other Assets Less

Liabilities — 0.2% | | | | | | | 714,303 | |

| | | | | | | | |

NET ASSETS — 100.0% | | | | | | $ | 392,229,238 | |

| | | | | | | | |

| PLC | – Public Limited Company |

| ADR | – American Depository Receipt |

| REIT | – Real Estate Investment Trusts |

| LLC | – Limited Liability Company |

| (a) | Non-income producing security. |

| (b) | Securities whose value are determined or significantly influenced by trading in markets other than the United States or Canada. |

| (d) | Level 3 securities fair valued under procedures established by the Board of Trustees, represents 0.5% of Net Assets. The total value of these securities is $1,781,720. |

| (e) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration to qualified institutional buyers. The total value of these securities is $1,453,541. |

| (f) | The rate quoted is the annualized seven-day yield of the fund at the period end. |

| (g) | The cost of investments for federal income tax purposes is $296,229,352 resulting in gross unrealized appreciation and depreciation of $112,396,258 and $17,110,675 respectively, or net unrealized appreciation of $95,285,583. |

See Notes to Financial Statements

17

| | |

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | |

| | | | | | | | |

COMMON STOCKS — 99.7% | | | | | | | | |

| | | SHARES | | | VALUE | |

Software & Services — 22.1% | | | | | | | | |

Accenture PLC, Class A (a) | | | 17,580 | | | $ | 4,905,699 | |

Adobe, Inc. (b) | | | 13,010 | | | | 4,818,123 | |

ANSYS, Inc. (b) | | | 2,437 | | | | 649,119 | |

Autodesk, Inc. (b) | | | 6,035 | | | | 1,298,491 | |

Automatic Data Processing, Inc. | | | 11,550 | | | | 2,608,106 | |

Cadence Design Systems, Inc. (b). | | | 7,610 | | | | 1,391,336 | |

Cognizant Technology Solutions Corporation, Class A | | | 14,393 | | | | 960,733 | |

Fidelity National Information Services, Inc. | | | 16,875 | | | | 1,266,300 | |

Fortinet, Inc. (b) | | | 18,567 | | | | 971,797 | |

Gen Digital, Inc | | | 16,649 | | | | 383,094 | |

International Business Machines Corporation. | | | 25,093 | | | | 3,380,780 | |

Intuit, Inc. | | | 7,443 | | | | 3,145,933 | |

Mastercard, Inc., Class A | | | 24,000 | | | | 8,894,400 | |

Microsoft Corporation. | | | 197,131 | | | | 48,851,033 | |

Okta, Inc., Class A (b) | | | 4,237 | | | | 311,886 | |

Oracle Corporation | | | 44,502 | | | | 3,936,647 | |

Paycom Software, Inc. (b) | | | 1,428 | | | | 462,586 | |

PayPal Holdings, Inc. (b) | | | 30,599 | | | | 2,493,513 | |

PTC, Inc. (b) | | | 3,122 | | | | 421,095 | |

salesforce, Inc. (b) | | | 27,788 | | | | 4,667,550 | |

ServiceNow, Inc. (b) | | | 5,609 | | | | 2,552,824 | |

Splunk, Inc. (b) | | | 4,515 | | | | 432,402 | |

Teradata Corporation (b) | | | 2,946 | | | | 102,756 | |

Visa, Inc., Class A | | | 45,485 | | | | 10,471,102 | |

VMware, Inc., Class A (b) | | | 5,911 | | | | 723,920 | |

Western Union Company (The) | | | 10,613 | | | | 150,386 | |

Workday, Inc., Class A (b) | | | 5,594 | | | | 1,014,919 | |

ZoomInfo Technologies, Inc. (b) | | | 7,367 | | | | 207,970 | |

| | | | | | | | |

| | | | | | | 111,474,500 | |

| | | | | | | | |

Pharmaceuticals & Biotechnology — 8.5% | |

AbbVie, Inc. | | | 49,215 | | | | 7,271,516 | |

Agilent Technologies, Inc. | | | 8,218 | | | | 1,249,793 | |

Amgen, Inc | | | 14,889 | | | | 3,757,984 | |

Biogen, Inc. (b) | | | 4,029 | | | | 1,172,036 | |

BioMarin Pharmaceutical, Inc. (b) | | | 5,176 | | | | 597,052 | |

Bio-Techne Corporation | | | 4,416 | | | | 351,779 | |

Bristol-Myers Squibb Company | | | 59,370 | | | | 4,313,231 | |

Danaher Corporation | | | 19,209 | | | | 5,078,475 | |

Gilead Sciences, Inc. | | | 34,818 | | | | 2,922,623 | |

Illumina, Inc. (b) | | | 4,352 | | | | 932,198 | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Pharmaceuticals & Biotechnology — (continued) | |

IQVIA Holdings, Inc. (b) | | | 5,190 | | | $ | 1,190,638 | |

Jazz Pharmaceuticals PLC (a)(b) | | | 1,735 | | | | 271,805 | |

Merck & Company, Inc. | | | 70,486 | | | | 7,570,901 | |

Mettler-Toledo International, Inc. (b) | | | 623 | | | | 955,009 | |

Vertex Pharmaceuticals, Inc. (b) | | | 7,145 | | | | 2,308,550 | |

Waters Corporation (b) | | | 1,676 | | | | 550,700 | |

Zoetis, Inc. | | | 13,033 | | | | 2,156,831 | |

| | | | | | | | |

| | | | | | | 42,651,121 | |

| | | | | | | | |

Media & Entertainment — 8.0% | |

Alphabet, Inc., Class A (b) | | | 166,767 | | | | 16,483,250 | |

Alphabet, Inc., Class C (b) | | | 154,263 | | | | 15,406,246 | |

Electronic Arts, Inc. | | | 7,708 | | | | 991,865 | |

John Wiley & Sons, Inc., Class A | | | 1,277 | | | | 58,487 | |

Liberty Global PLC, Series A (a)(b) | | | 4,718 | | | | 102,333 | |

Liberty Global PLC, Series C (a)(b) | | | 7,830 | | | | 175,001 | |

New York Times Company (The), Class A | | | 4,670 | | | | 162,703 | |

Omnicom Group, Inc. | | | 5,726 | | | | 492,379 | |

Scholastic Corporation | | | 806 | | | | 35,657 | |

Walt Disney Company (The) (b) | | | 50,671 | | | | 5,497,297 | |

Warner Bros Discovery, Inc. (b) | | | 64,515 | | | | 956,112 | |

| | | | | | | | |

| | | | | | | 40,361,330 | |

| | | | | | | | |

Semiconductors — 7.1% | |

Advanced Micro Devices, Inc. (b) | | | 44,841 | | | | 3,369,801 | |

Analog Devices, Inc. | | | 14,325 | | | | 2,456,308 | |

Applied Materials, Inc. | | | 23,961 | | | | 2,671,412 | |

Intel Corporation | | | 114,064 | | | | 3,223,449 | |

Lam Research Corporation | | | 3,808 | | | | 1,904,381 | |

Microchip Technology, Inc. | | | 15,304 | | | | 1,187,896 | |

NVIDIA Corporation | | | 69,245 | | | | 13,528,396 | |

NXP Semiconductors NV (a) | | | 7,314 | | | | 1,348,043 | |

ON Semiconductor Corporation (b) | | | 12,119 | | | | 890,140 | |

Skyworks Solutions, Inc. | | | 4,465 | | | | 489,677 | |

Texas Instruments, Inc. | | | 25,414 | | | | 4,503,615 | |

| | | | | | | | |

| | | | | | | 35,573,118 | |

| | | | | | | | |

Capital Goods — 6.3% | |

3M Company . | | | 15,412 | | | | 1,773,613 | |

A.O. Smith Corporation | | | 3,506 | | | | 237,356 | |

AGCO Corporation | | | 1,756 | | | | 242,556 | |

Air Lease Corporation, Class A | | | 2,900 | | | | 130,413 | |

18

| | |

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | continued |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Capital Goods — (continued) | | | | | | | | |

Allegion PLC (a) . | | | 2,423 | | | $ | 284,824 | |

Applied Industrial Technologies, Inc. | | | 1,062 | | | | 152,089 | |

Builders FirstSource, Inc. (b) | | | 4,366 | | | | 347,970 | |

Carrier Global Corporation | | | 23,430 | | | | 1,066,768 | |

Caterpillar, Inc. | | | 14,667 | | | | 3,700,337 | |

Cummins, Inc. . | | | 3,902 | | | | 973,705 | |

Deere & Company . | | | 8,066 | | | | 3,410,627 | |

Dover Corporation | | | 4,018 | | | | 610,053 | |

Eaton Corporation PLC | | | 11,073 | | | | 1,796,151 | |

EMCOR Group, Inc. | | | 1,379 | | | | 204,437 | |

Fastenal Company | | | 16,075 | | | | 812,591 | |

Ferguson PLC (a) | | | 5,828 | | | | 829,558 | |

Flowserve Corporation | | | 3,598 | | | | 123,843 | |

Fortive Corporation | | | 9,452 | | | | 643,020 | |

Fortune Brands Innovations, Inc. . | | | 3,624 | | | | 233,784 | |

Graco, Inc. | | | 4,675 | | | | 319,396 | |

Granite Construction, Inc. | | | 1,169 | | | | 49,776 | |

IDEX Corporation . | | | 2,113 | | | | 506,444 | |

Illinois Tool Works, Inc. | | | 8,619 | | | | 2,034,429 | |

Lennox International, Inc. | | | 886 | | | | 230,909 | |

Lincoln Electric Holdings, Inc. | | | 1,548 | | | | 258,315 | |

Masco Corporation | | | 6,312 | | | | 335,798 | |

MDU Resources Group, Inc. | | | 5,639 | | | | 174,302 | |

Middleby Corporation (The) (b) | | | 1,417 | | | | 220,273 | |

Owens Corning . | | | 2,694 | | | | 260,375 | |

PACCAR, Inc. | | | 9,625 | | | | 1,052,109 | |

Parker-Hannifin Corporation | | | 3,571 | | | | 1,164,146 | |

Quanta Services, Inc | | | 4,000 | | | | 608,760 | |

Rockwell Automation, Inc | | | 3,193 | | | | 900,522 | |

Roper Technologies, Inc | | | 2,954 | | | | 1,260,620 | |

Sensata Technologies Holding NV | | | 4,217 | | | | 214,435 | |

Snap-on, Inc. | | | 1,491 | | | | 370,856 | |

Stanley Black & Decker, Inc. | | | 4,138 | | | | 369,565 | |

Tennant Company | | | 469 | | | | 32,891 | |

Timken Company (The) | | | 1,836 | | | | 151,195 | |

Trane Technologies PLC (a) | | | 6,453 | | | | 1,155,861 | |

United Rentals, Inc. (b) | | | 1,958 | | | | 863,380 | |

W.W. Grainger, Inc. | | | 1,280 | | | | 754,534 | |

Westinghouse Air Brake Technologies Corporation | | | 4,833 | | | | 501,714 | |

Xylem, Inc. | | | 5,038 | | | | 524,002 | |

| | | | | | | | |

| | | | | | | 31,888,302 | |

| | | | | | | | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Diversified Financials — 5.5% | |

Ally Financial, Inc | | | 8,641 | | | $ | 280,746 | |

American Express Company | | | 17,753 | | | | 3,105,532 | |

Ameriprise Financial, Inc. | | | 3,001 | | | | 1,050,710 | |

Bank of New York Mellon Corporation (The) | | | 21,260 | | | | 1,075,118 | |

BlackRock, Inc. | | | 4,188 | | | | 3,179,572 | |

Charles Schwab Corporation (The) | | | 40,395 | | | | 3,127,381 | |

CME Group, Inc. | | | 9,995 | | | | 1,765,717 | |

Equitable Holdings, Inc. | | | 10,511 | | | | 337,088 | |

FactSet Research Systems, Inc. | | | 1,059 | | | | 447,893 | |

Franklin Resources, Inc. | | | 8,275 | | | | 258,180 | |

Intercontinental Exchange, Inc. | | | 15,527 | | | | 1,669,929 | |

Invesco Ltd. | | | 9,662 | | | | 178,844 | |

Moody’s Corporation | | | 4,587 | | | | 1,480,454 | |

Morgan Stanley . | | | 35,772 | | | | 3,481,689 | |

Nasdaq, Inc. | | | 9,612 | | | | 578,546 | |

Northern Trust Corporation. | | | 5,555 | | | | 538,668 | |

S&P Global, Inc. | | | 9,465 | | | | 3,548,807 | |

State Street Corporation . | | | 10,168 | | | | 928,643 | |

T. Rowe Price Group, Inc. | | | 6,316 | | | | 735,625 | |

Voya Financial, Inc. | | | 2,740 | | | | 191,170 | |

| | | | | | | | |

| | | | | | | 27,960,312 | |

| | | | | | | | |

Food & Beverage — 4.8% | |

Archer-Daniels-Midland Company | | | 15,579 | | | | 1,290,720 | |

Bunge Ltd | | | 4,263 | | | | 422,463 | |

Campbell Soup Company . | | | 5,891 | | | | 305,920 | |

Coca-Cola Company (The) | | | 114,219 | | | | 7,003,909 | |

Conagra Brands, Inc | | | 13,358 | | | | 496,784 | |

Darling Ingredients, Inc. (b) | | | 4,475 | | | | 296,648 | |

General Mills, Inc. | | | 16,545 | | | | 1,296,466 | |

Hormel Foods Corporation | | | 8,326 | | | | 377,251 | |

Ingredion, Inc. | | | 1,861 | | | | 191,311 | |

JM Smucker Company (The) | | | 2,982 | | | | 455,650 | |

Kellogg Company . | | | 7,026 | | | | 481,843 | |

Keurig Dr Pepper, Inc. | | | 21,636 | | | | 763,318 | |

Kraft Heinz Company (The) | | | 20,573 | | | | 833,824 | |

Lamb Weston Holdings, Inc. | | | 4,019 | | | | 401,458 | |

McCormick & Company, Inc. | | | 7,025 | | | | 527,718 | |

Mondelez International, Inc., Class A | | | 38,178 | | | | 2,498,368 | |

PepsiCo, Inc. | | | 38,380 | | | | 6,563,747 | |

| | | | | | | | |

| | | | | | | 24,207,398 | |

| | | | | | | | |

19

| | |

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | continued |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Healthcare Equipment & Services — 4.7% | |

Align Technology, Inc. (b) | | | 2,077 | | | $ | 560,229 | |

AmerisourceBergen Corporation . | | | 4,349 | | | | 734,807 | |

Becton, Dickinson and Company . | | | 7,916 | | | | 1,996,574 | |

Cardinal Health, Inc | | | 7,623 | | | | 588,877 | |

Centene Corporation (b) | | | 15,875 | | | | 1,210,310 | |

Cigna Corporation | | | 8,473 | | | | 2,683,145 | |

Cooper Cos., Inc. (The) | | | 1,373 | | | | 479,081 | |

DaVita, Inc. (b) | | | 1,534 | | | | 126,386 | |

DENTSPLY SIRONA, Inc. | | | 6,103 | | | | 224,773 | |

DexCom, Inc. (b) | | | 10,916 | | | | 1,168,994 | |

Edwards Lifesciences | | | | | | | | |

Corporation (b) | | | 17,219 | | | | 1,320,697 | |

Elevance Health, Inc | | | 6,675 | | | | 3,337,433 | |

HCA Healthcare, Inc. | | | 6,382 | | | | 1,627,857 | |

Henry Schein, Inc. (b) | | | 3,810 | | | | 328,232 | |

Hologic, Inc. (b) | | | 6,929 | | | | 563,813 | |

Humana, Inc. | | | 3,527 | | | | 1,804,766 | |

IDEXX Laboratories, Inc. (b) | | | 2,306 | | | | 1,108,033 | |

Insulet Corporation (b) | | | 1,939 | | | | 557,113 | |

Laboratory Corporation of America Holdings | | | 2,530 | | | | 637,864 | |

Patterson Companies, Inc. | | | 2,363 | | | | 71,339 | |

Pediatrix Medical Group, Inc. (b) . | | | 2,345 | | | | 35,996 | |

Quest Diagnostics, Inc. | | | 3,264 | | | | 484,639 | |

ResMed, Inc. | | | 4,060 | | | | 927,182 | |

Select Medical Holdings Corporation | | | 2,929 | | | | 85,146 | |

STERIS PLC | | | 2,791 | | | | 576,369 | |

Teladoc Health, Inc. (b) | | | 4,537 | | | | 133,388 | |

West Pharmaceutical Services, Inc. | | | 2,072 | | | | 550,323 | |

| | | | | | | | |

| | | | | | | 23,923,366 | |

| | | | | | | | |

Retailing — 4.3% | |

AutoNation, Inc. (b) . | | | 1,017 | | | | 128,874 | |

Best Buy Company, Inc. | | | 5,647 | | | | 501,002 | |

Booking Holdings, Inc. (b) | | | 1,105 | | | | 2,689,680 | |

Buckle, Inc. (The) | | | 773 | | | | 34,012 | |

CarMax, Inc. (b) | | | 4,437 | | | | 312,587 | |

Foot Locker, Inc | | | 2,366 | | | | 102,945 | |

GameStop Corporation, Class A (b) | | | 7,256 | | | | 158,689 | |

Gap, Inc. (The) | | | 5,660 | | | | 76,806 | |

Home Depot, Inc. (The) | | | 28,466 | | | | 9,227,823 | |

Kohl’s Corporation | | | 3,615 | | | | 117,018 | |

LKQ Corporation | | | 7,286 | | | | 429,583 | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Retailing — (continued) | | | | | | | | |

Lowe’s Companies, Inc. | | | 17,245 | | | $ | 3,591,271 | |

Nordstrom, Inc. | | | 3,112 | | | | 60,808 | |

ODP Corporation (The) (b) | | | 1,210 | | | | 62,436 | |

Pool Corporation | | | 1,107 | | | | 426,870 | |

Signet Jewelers Ltd | | | 1,332 | | | | 102,311 | |

Target Corporation | | | 12,814 | | | | 2,205,802 | |

Tractor Supply Company | | | 3,104 | | | | 707,681 | |

Ulta Beauty, Inc. (b) | | | 1,432 | | | | 735,991 | |

| | | | | | | | |

| | | | | | | 21,672,189 | |

| | | | | | | | |

Real Estate — 3.5% | |

American Tower Corporation REIT | | | 12,932 | | | | 2,888,879 | |

Anywhere Real Estate, Inc. (b) | | | 3,345 | | | | 28,366 | |

AvalonBay Communities, Inc. REIT | | | 3,884 | | | | 689,177 | |

Boston Properties, Inc. REIT | | | 4,135 | | | | 308,223 | |

CBRE Group, Inc., Class A (b) | | | 8,990 | | | | 768,735 | |

Corporate Office Properties Trust REIT | | | 3,020 | | | | 84,771 | |

Digital Realty Trust, Inc. REIT | | | 8,018 | | | | 919,023 | |

Equinix, Inc. REIT | | | 2,532 | | | | 1,868,945 | |

Equity Residential REIT | | | 9,921 | | | | 631,472 | |

Federal Realty Investment Trust REIT | | | 2,054 | | | | 229,083 | |

Healthpeak Properties, Inc. REIT . | | | 15,017 | | | | 412,667 | |

Host Hotels & Resorts, Inc. REIT . | | | 19,655 | | | | 370,497 | |

Iron Mountain, Inc. REIT | | | 8,096 | | | | 441,880 | |

Jones Lang LaSalle, Inc. (b) | | | 1,342 | | | | 248,095 | |

Macerich Company (The) REIT | | | 5,952 | | | | 81,780 | |

PotlatchDeltic Corporation REIT . | | | 2,268 | | | | 111,019 | |

Prologis, Inc. REIT | | | 25,639 | | | | 3,314,610 | |

SBA Communications Corporation, Class A REIT | | | 2,985 | | | | 888,127 | |

Simon Property Group, Inc. REIT | | | 9,110 | | | | 1,170,271 | |

UDR, Inc. REIT. | | | 9,139 | | | | 389,230 | |

Ventas, Inc. REIT . | | | 11,193 | | | | 579,909 | |

Welltower, Inc. REIT | | | 12,825 | | | | 962,388 | |

| | | | | | | | |

| | | | | | | 17,387,147 | |

| | | | | | | | |

Materials — 3.1% | |

Air Products & Chemicals, Inc | | | 6,167 | | | | 1,976,585 | |

Albemarle Corporation . | | | 3,277 | | | | 922,312 | |

Amcor PLC (a) | | | 41,645 | | | | 502,239 | |

Avery Dennison Corporation | | | 2,271 | | | | 430,218 | |

20

| | |

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | continued |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Materials — (continued) | | | | | | | | |

Axalta Coating Systems Ltd. (b) | | | 6,060 | | | $ | 182,406 | |

Ball Corporation. | | | 8,792 | | | | 512,046 | |

Compass Minerals International, Inc. | | | 974 | | | | 45,447 | |

Ecolab, Inc. | | | 7,104 | | | | 1,099,912 | |

H.B. Fuller Company | | | 1,443 | | | | 99,711 | |

International Flavors & Fragrances, Inc. . | | | 7,135 | | | | 802,402 | |

Linde PLC (a) | | | 13,850 | | | | 4,583,519 | |

Minerals Technologies, Inc. | | | 847 | | | | 58,824 | |

Mosaic Company (The) | | | 9,658 | | | | 478,457 | |

Newmont Corporation . | | | 22,010 | | | | 1,164,989 | |

PPG Industries, Inc | | | 6,575 | | | | 856,986 | |

Schnitzer Steel Industries, Inc., Class A | | | 743 | | | | 25,143 | |

Sealed Air Corporation | | | 4,092 | | | | 224,078 | |

Sherwin-Williams Company (The) | | | 6,844 | | | | 1,619,222 | |

Sonoco Products Company | | | 2,725 | | | | 166,525 | |

| | | | | | | | |

| | | | | | | 15,751,021 | |

| | | | | | | | |

Household & Personal Products — 2.9% | |

Clorox Company (The) | | | 3,440 | | | | 497,734 | |

Colgate-Palmolive Company | | | 22,097 | | | | 1,646,889 | |

Estee Lauder Companies, Inc. (The), Class A | | | 6,444 | | | | 1,785,504 | |

Kimberly-Clark Corporation | | | 9,407 | | | | 1,223,004 | |

Procter & Gamble Company (The) | | | 66,346 | | | | 9,446,343 | |

| | | | | | | | |

| | | | | | | 14,599,474 | |

| | | | | | | | |

Renewable Energy & Energy Efficiency — 2.9% | |

Acuity Brands, Inc. | | | 915 | | | | 172,496 | |

Itron, Inc. (b) | | | 1,270 | | | | 72,987 | |

Johnson Controls International, PLC | | | 19,183 | | | | 1,334,561 | |

Ormat Technologies, Inc. | | | 1,232 | | | | 114,021 | |

Tesla, Inc. (b) | | | 74,062 | | | | 12,829,020 | |

| | | | | | | | |

| | | | | | | 14,523,085 | |

| | | | | | | | |

Insurance — 2.9% | |

Allstate Corporation (The) . | | | 7,482 | | | | 961,213 | |

Arthur J. Gallagher & Company . | | | 5,857 | | | | 1,146,332 | |

Chubb Ltd. (a) | | | 11,634 | | | | 2,646,619 | |

Hartford Financial Services Group, Inc. (The) . | | | 9,046 | | | | 702,060 | |

Lincoln National Corporation | | | 4,513 | | | | 159,896 | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Insurance — (continued) | | | | | | | | |

Loews Corporation | | | 5,737 | | | $ | 352,711 | |

Marsh & McLennan Companies, Inc. | | | 13,855 | | | | 2,423,378 | |

Principal Financial Group, Inc. | | | 6,970 | | | | 645,073 | |

Progressive Corporation (The) | | | 16,295 | | | | 2,221,823 | |

Prudential Financial, Inc. | | | 10,331 | | | | 1,084,135 | |

Travelers Companies, Inc. (The) | | | 6,604 | | | | 1,262,156 | |

Willis Towers Watson PLC (a) | | | 3,077 | | | | 782,143 | |

| | | | | | | | |

| | | | | | | 14,387,539 | |

| | | | | | | | |

Consumer Services — 2.7% | |

Aramark | | | 6,406 | | | | 285,259 | |

Choice Hotels International, Inc. | | | 1,023 | | | | 125,716 | |

Darden Restaurants, Inc. | | | 3,433 | | | | 507,981 | |

Domino’s Pizza, Inc. | | | 1,003 | | | | 354,059 | |

Hilton Worldwide Holdings, Inc. | | | 7,630 | | | | 1,107,037 | |

Jack in the Box, Inc | | | 583 | | | | 44,296 | |

Marriott International, Inc., Class A | | | 7,683 | | | | 1,338,225 | |

McDonald’s Corporation | | | 20,450 | | | | 5,468,330 | |

Royal Caribbean Cruises Ltd. (b) . | | | 6,412 | | | | 416,395 | |

Starbucks Corporation | | | 31,876 | | | | 3,478,947 | |

Vail Resorts, Inc. | | | 1,126 | | | | 295,395 | |

| | | | | | | | |

| | | | | | | 13,421,640 | |

| | | | | | | | |

Technology Hardware & Equipment — 2.6% | |

Cisco Systems, Inc. | | | 115,102 | | | | 5,602,014 | |

Cognex Corporation | | | 4,899 | | | | 268,171 | |

CommScope Holding Company, Inc. (b) | | | 5,878 | | | | 49,375 | |

Corning, Inc. | | | 22,469 | | | | 777,652 | |

Dell Technologies, Inc., Class C | | | 7,431 | | | | 301,847 | |

F5, Inc. (b) | | | 1,665 | | | | 245,854 | |

Flex Ltd. (b) | | | 12,749 | | | | 297,689 | |

Hewlett Packard Enterprise Company | | | 36,025 | | | | 581,083 | |

HP, Inc. | | | 28,932 | | | | 843,079 | |

Keysight Technologies, Inc. (b) | | | 5,013 | | | | 899,082 | |

Motorola Solutions, Inc. | | | 4,638 | | | | 1,192,012 | |

TE Connectivity Ltd. (a) | | | 8,880 | | | | 1,129,092 | |

Trimble, Inc. (b) | | | 6,927 | | | | 402,182 | |

Xerox Holdings Corporation | | | 3,252 | | | | 53,268 | |

Zebra Technologies Corporation, Class A (b) | | | 1,449 | | | | 458,145 | |

| | | | | | | | |

| | | | | | | 13,100,545 | |

| | | | | | | | |

21

| | |

GREEN CENTURY EQUITY FUND PORTFOLIO OF INVESTMENTS January 31, 2023 (unaudited) | | continued |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Transportation — 2.1% | |

ArcBest Corporation . | | | 682 | | | $ | 56,913 | |

Avis Budget Group, Inc. (b) | | | 872 | | | | 174,435 | |

C.H. Robinson Worldwide, Inc. | | | 3,466 | | | | 347,189 | |

CSX Corporation | | | 59,536 | | | | 1,840,853 | |

Delta Air Lines, Inc. (b) | | | 4,419 | | | | 172,783 | |

Expeditors International of Washington, Inc | | | 4,575 | | | | 494,786 | |

Ryder System, Inc. | | | 1,433 | | | | 135,290 | |

Southwest Airlines Company | | | 4,118 | | | | 147,301 | |

U-Haul Holding Company | | | 2,430 | | | | 150,150 | |

Union Pacific Corporation | | | 17,350 | | | | 3,542,696 | |

United Parcel Service, Inc., Class B | | | 20,334 | | | | 3,766,467 | |

| | | | | | | | |

| | | | | | | 10,828,863 | |

| | | | | | | | |

Banks — 1.8% | |

Bank of Hawaii Corporation | | | 1,083 | | | | 82,839 | |

Cathay General Bancorp | | | 1,913 | | | | 84,095 | |

Citizens Financial Group, Inc. | | | 13,872 | | | | 600,935 | |

Comerica, Inc | | | 3,662 | | | | 268,461 | |

First Republic Bank | | | 5,118 | | | | 721,024 | |

Heartland Financial USA, Inc | | | 1,213 | | | | 60,007 | |

Huntington Bancshares, Inc. | | | 40,229 | | | | 610,274 | |

International Bancshares Corporation. | | | 1,580 | | | | 74,055 | |

KeyCorp | | | 26,010 | | | | 499,132 | |

M&T Bank Corporation | | | 4,916 | | | | 766,896 | |

New York Community Bancorp, Inc. | | | 19,014 | | | | 189,950 | |

Old National Bancorp. | | | 8,040 | | | | 140,700 | |

PNC Financial Services Group, Inc. (The) | | | 11,418 | | | | 1,888,880 | |

Regions Financial Corporation | | | 26,168 | | | | 615,995 | |

SVB Financial Group (b) | | | 1,658 | | | | 501,446 | |

Truist Financial Corporation | | | 36,909 | | | | 1,822,935 | |

Umpqua Holdings Corporation | | | 5,772 | | | | 105,050 | |

Zions Bancorp NA | | | 4,145 | | | | 220,348 | |

| | | | | | | | |

| | | | | | | 9,253,022 | |

| | | | | | | | |

Consumer Durables & Apparel — 1.5% | |

Capri Holdings Ltd. (a)(b) | | | 3,853 | | | | 256,186 | |

Columbia Sportswear Company | | | 976 | | | | 93,598 | |

Deckers Outdoor Corporation (b) | | | 746 | | | | 318,900 | |

Ethan Allen Interiors, Inc. | | | 671 | | | | 19,285 | |

Garmin Ltd. (a) | | | 4,306 | | | | 425,777 | |

Hanesbrands, Inc. | | | 9,732 | | | | 82,138 | |

| | | | | | | | |

| | | SHARES | | | VALUE | |

Consumer Durables & Apparel — (continued) | |

Hasbro, Inc | | | 3,620 | | | $ | 214,196 | |

La-Z-Boy, Inc. | | | 1,082 | | | | 30,761 | |

Mattel, Inc. (b) | | | 9,824 | | | | 200,999 | |

Meritage Homes Corporation (b) . | | | 1,000 | | | | 107,690 | |

Mohawk Industries, Inc. (b) | | | 1,428 | | | | 171,446 | |

Newell Brands, Inc. | | | 10,893 | | | | 173,852 | |

NIKE, Inc., Class B | | | 35,117 | | | | 4,471,448 | |

PVH Corporation | | | 1,838 | | | | 165,236 | |

Topgolf Callaway Brands Corporation (b) | | | 3,876 | | | | 94,923 | |

Under Armour, Inc., Class A (b) | | | 5,256 | | | | 65,122 | |

Under Armour, Inc., Class C (b) | | | 5,022 | | | | 54,740 | |

VF Corporation | | | 9,129 | | | | 282,451 | |

Whirlpool Corporation | | | 1,522 | | | | 236,808 | |

Wolverine World Wide, Inc | | | 2,254 | | | | 36,357 | |

| | | | | | | | |

| | | | | | | 7,501,913 | |

| | | | | | | | |

Telecommunication Services — 1.0% | |

Lumen Technologies Inc. | | | 26,155 | | | | 137,314 | |

Verizon Communications, Inc. | | | 116,720 | | | | 4,852,050 | |

| | | | | | | | |

| | | | | | | 4,989,364 | |

| | | | | | | | |

Commercial & Professional Services — 0.5% | |

ACCO Brands Corporation | | | 2,536 | | | | 16,104 | |

ASGN, Inc. (b) | | | 1,433 | | | | 130,331 | |