UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06400

The Advisors’ Inner Circle Fund

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 446-3863

Date of fiscal year end: October 31, 2022

Date of reporting period: October 31, 2022

Item 1. Reports to Stockholders.

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

The Advisors’ Inner Circle Fund

Loomis Sayles Full Discretion Institutional Securitized Fund

ANNUAL REPORT

OCTOBER 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| 1 | ||||

| 7 | ||||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 24 | ||||

| 39 | ||||

| 42 | ||||

| 50 | ||||

| 52 | ||||

| 53 | ||||

| 57 | ||||

The Fund files its complete schedule of portfolio holdings with the SEC (the “SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Form N-PORT reports (and its predecessor form, Form N-Q) are available on the SEC’s website at www.sec.gov, and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-343-2029; and (ii) on the Commission’s website at https://www.sec.gov.

Letter to Shareholders (Unaudited)

Loomis Sayles Full Discretion Institutional Securitized Fund

Portfolio Objective

The investment objective of the Loomis Sayles Full Discretion Institutional Securitized Fund (the fund) is to provide current income and the potential for total return. The Manager seeks to achieve this objective through a diversified credit exposure to securitized assets, including asset-backed securities (ABS), commercial mortgage-backed securities (CMBS), non-agency residential mortgage-backed securities (RMBS), and collateralized loan obligations (CLOs)

In purchasing securities for the fund, the Manager uses a fundamental, top-down approach to evaluate sectors in the securitized market to make sector and capital structure allocation decisions. The Manager utilizes a bottom-up approach for individual security selection that is focused on the risk/return profile of each security.

Market Review

The fixed-income markets experienced significant, broad-based weakness in the 12-month period that ended on October 31, 2022. Inflation, which had already been increasing throughout 2021, took another leg higher in February 2022 after Russia’s invasion of Ukraine created additional supply-chain pressures and led to a spike in commodity prices. Consumer price inflation remained elevated long after the conflict began. Inflation has seemingly peaked at 9.1% in June, though still has yet to meaningfully recover.

The U.S. Federal Reserve (Fed) responded with an aggressive series of interest-rate increases, bringing its benchmark fed funds rate to a range of 3.0% to 3.25% from 0% to 0.25% at the start of 2022. This marked the largest move in such a short interval since 1980. Perhaps even more important for the markets, investors continued to ratchet up their expectations for the “terminal rate” in 2023; or in other words, the level at which the Fed was likely to stop raising rates.

Tighter Fed policy not only led to a rise in prevailing yields, but also fueled an increase in investors’ aversion to risk more generally. As a result, more volatile asset categories that trade based on their yield advantage (or “spread”) over Treasurys faced an additional headwind. US Treasurys endured one of their worst stretches of performance in over 40 years as the yield curve inverted significantly (meaning that short-term yields traded above those on longer-term debt). In late September, in fact, the yield curve moved to its largest inversion since 1982.

Amidst rising inflation, geopolitical instability, and a broad selloff in rates and risk markets, securitized credit markets have generally produced negative total and excess returns over the past 12 months. Down in credit CLOs have suffered the most as prices on underlying bank loans have dropped significantly. Sectors like consumer ABS with lower interest rate sensitivity and less direct impact from geopolitical instability have underperformed less. Sectors

| | 1 |

Letter to Shareholders (Unaudited)

Loomis Sayles Full Discretion Institutional Securitized Fund

like commercial ABS, namely aircraft, have been negatively impacted. Pockets of the CMBS market have held in relatively well amidst a longer term recovery from COVID-19 related shocks. Senior tranches of RMBS have provided positive excess returns while subordinates have sold off. Agency mortgage backed securities (MBS) produced significantly negative excess returns versus US treasuries. Agency MBS has experienced massive interest rate volatility and the impact of concerns related to quantitative tightening.

Portfolio Performance Discussion

The ICE BofA Merrill Lynch ABS & CMBS Index (the index), a broad measure of the securitized credit market, posted a total return of -9.07% and a negative excess return of -1.96% over duration-matched Treasurys for the year ended October 31, 2022. Over the same time period, the fund generated a return of -6.36%, outperforming its benchmark by 267 basis points.

FUND PERFORMANCE AS OF OCTOBER 31, 2022:

| CUMULATIVE | AVERAGE ANNUALIZED RETURN | |||||||||||||

| TOTAL RETURN | ||||||||||||||

| 3 MONTH | YTD | 1 YEAR | 3 YEAR | 5 YEAR | 10 YEAR | SINCE INCEPTION | ||||||||

FUND | -2.60% | -6.53% | -6.36% | -0.03% | 2.13% | 4.35% | 6.07% | |||||||

INDEX | -4.21% | -8.85% | -9.07% | -1.45% | 0.68% | 1.39% | 1.86% | |||||||

Performance data shown represents past performance and is no guarantee of future results. Investment return and value will vary and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. Performance for multi-year periods is annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The fund’s inception date is 12/15/2011.

All indexes are unmanaged and do not incur fees. You may not invest directly in an index.

Spread and specific contribution was negative for the period given the funds deeper credit exposure relative to the benchmark. Duration and yield curve positioning benefitted the portfolio significantly on a benchmark-relative basis.

On a benchmark relative basis, CLOs, Commercial ABS, and RMBS underperformed. CMBS, Consumer ABS, and agency multifamily outperformed. Lower mezzanine CLO led underperformance within the subsectors, followed by aircraft-related commercial ABS. On the positive side relative to the benchmark, exposures to CMBS Conduit Subs and ABS personal consumer loans were additive. A lack of exposure to agency CMBS was also positive.

2 | |

Letter to Shareholders (Unaudited)

Loomis Sayles Full Discretion Institutional Securitized Fund

The fund’s effective duration as of October 31, 2022 was 1.74, approximately 1.17 years shorter than that of the index. The funds relative duration decreased over the period as rates rose, leading to a large positive contribution.

Outlook

Consumer ABS fundamentals are mixed given the employment picture remains very strong and consumer balance sheets are healthy but delinquencies have now risen back to pre-COVID levels. This recent deterioration in performance has almost exclusively been driven by non-prime consumers. Inflation remains a top concern for lower income consumers, particularly due to rising costs of food, energy, and childcare. We will be watching to see how consumer behavior may change after the expected federal student loan forgiveness plan and the resumption of student loan payments in June 2023.

Commercial ABS fundamentals has been mostly positive during 2H2022. Among Whole Business deals, quick service restaurant operators have normalized same store sales growth after strong sales growth through COVID. Timeshare companies posted strong earnings in recent months due to the recovery of U.S. leisure travel and we expect earnings to fully recover back to pre COVID levels this year. Fundamentals in the aviation sector have improved due to strong consumer demand for travel in the U.S., Western Europe, and Latin America, and lower expected supply of new aircraft due to significant delays in production and shortages of engines. As a result, we expect the percentage of aircraft currently off-lease to continue moving down toward pre-COVID levels and the performance of Aircraft ABS to improve.

After broadly widening in 2022 around ‘hard landing’ fears and decrease in bank loan prices, CLO spreads have rallied somewhat as the market saw the greater potential for a ‘soft landing’ amidst the Fed’s continuation of rate hikes into restrictive levels. The full impact of rising costs (goods, labor, and debt service) will likely take time to play out but we expect near-term loan market defaults to increase to historical average levels. Weakened loan covenants are concerning but we remain confident in the structural protection provided by CLOs. Yields on CLO IG bonds provide investors with opportunities for price appreciation. Overall, the team’s positive view on IG tranches of CLOs (specifically AAAs through As) is rooted in our expectations of manageable bank loan downgrades and defaults, robust CLO structural protections, and attractive valuations.

We maintain our cautiously positive outlook on CMBS for the remainder of 2022 given recent macro volatility, a pickup in hiring freezes, and a softening of net absorption. CMBS LCF AAAs spreads have widened less then IG Corporates so far this year. The Green Street all property index declined in 2022 but is still at pre-COVID levels. We expect cap rates to increase with Fed tightening, a headwind to real estate price appreciation.

| | 3 |

Letter to Shareholders (Unaudited)

Loomis Sayles Full Discretion Institutional Securitized Fund

We maintain a positive outlook for RMBS despite the potential for weakening housing prices in the short run. Already, home sales have softened as buyers have stepped back purchases, leading to an increase in inventories. This has been balanced by a material slowdown in new listings in many markets. Given the secular tailwinds of deficient housing supply and strong underwriting, we anticipate the softening of prices to be controlled and manageable, particularly in the context of the structures we prefer. In addition, we are not forecasting a wave of distressed sales given the strong equity position of most borrowers and historically high quality credit. Within RMBS, we remain confident in the protections provided in the deals’ structures to prevent losses from impacting held positions. New issue RMBS supply has fallen meaningfully as most sponsors have dramatically reduced loan acquisition activity in line with the broader housing market, increasing the probability of a technical-driven rally in the sector in the near term.

Outlook as presented in this material reflects subjective judgments and assumptions of the portfolio team and does not necessarily reflect the views of Loomis, Sayles & Company, L.P. There is no assurance that developments will transpire as stated. Opinions expressed will evolve as future events unfold.

4 | |

Letter to Shareholders (Unaudited)

Loomis Sayles Full Discretion Institutional Securitized Fund

Definition of Comparative Index

The ICE BofA Merrill Lynch US ABS & CMBS Index tracks the performance of US dollar denominated investment grade fixed and floating rate asset backed securities and fixed rate commercial mortgage backed securities publicly issued in the US domestic market. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P, and Fitch) at least one year remaining term to final stated maturity and at least one month to the last expected cash flow. 144a securities qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date. Inverse floating rate, interest only and principal only tranches of qualifying deals are excluded from the Index as are all tranches of re-securitized and agency deals. Qualifying asset backed securities must have a fixed or floating rate coupon, an original deal size for the collateral group of at least $250 million, a current outstanding deal size for the collateral group greater than or equal to 10% of the original deal size and a minimum outstanding tranche size of $50 million for senior tranches and $10 million for mezzanine and subordinated tranches. Qualifying commercial mortgage backed securities must have a fixed coupon schedule, an original deal size for the collateral group of at least $250 million, a current outstanding deal size for the collateral group that is greater than or equal to 10% of the original deal size and at least $50 million current amount outstanding for senior tranches and $25 million current amount outstanding for mezzanine and subordinated tranches. Fixed- to- floating rate securities qualify provided they are callable within the fixed rate period and are at least one year from the last call prior to the date the bond transitions from a fixed to a floating rate security. Floating rate securities are excluded.

| | 5 |

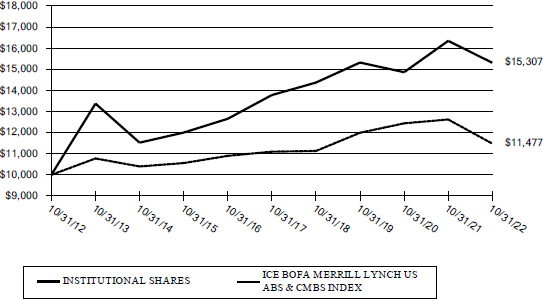

Growth of a $10,000 Investment (Unaudited)

Loomis Sayles Full Discretion Institutional Securitized Fund

TOTAL RETURN FOR THE PERIOD ENDED OCTOBER 31, 2022* | ||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | Annualized Inception to Date** | |||||||

Loomis Sayles Full Discretion Institutional | ||||||||||||

Securitized Fund | -6.36% | -0.03% | 2.13% | 4.35% | 6.07% | |||||||

ICE BofA Merrill Lynch US ABS & | ||||||||||||

CMBS Index | -9.07% | -1.45% | 0.68% | 1.39% | 1.86% | |||||||

* If the Adviser had not limited certain expenses, the Fund’s total return would have been lower.

** The Fund commenced operations on December 15, 2011.

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost.

Past performance is no guarantee of future performance and should not be considered as a representation of the future results of the Fund.

The Fund’s performance assumes the reinvestment of all dividends and all capital gains. Index returns assume reinvestment of dividends and, unlike a Fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities.

Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

See definition of comparative index on page 5.

6 | |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Asset-Backed Securities — 54.0% | ||||||||||

| 522 Funding CLO, Series 2021-6A, Class A1R | ||||||||||

$ | 2,265,000 | 5.475%, ICE LIBOR USD 3 Month + 1.150%, 10/23/34 (A)(B) | $ | 2,164,031 | ||||||

| AASET, Series 2022-1A, Class A | ||||||||||

| 2,774,573 | 6.000%, 05/16/47 (A) | 2,563,550 | ||||||||

| Accelerated Assets, Series 2018-1, Class B | ||||||||||

| 448,807 | 4.510%, 12/02/33 (A) | 426,377 | ||||||||

| Adams Outdoor Advertising, Series 2018-1, Class C | ||||||||||

| 5,200,000 | 7.356%, 11/15/48 (A) | 4,620,053 | ||||||||

| AGL CLO, Series 2020-3A, Class D | ||||||||||

| 2,100,000 | 7.379%, ICE LIBOR USD 3 Month + 3.300%, 01/15/33 (A)(B) | 1,868,633 | ||||||||

| AGL CLO, Series 2021-1A, Class DR | ||||||||||

| 1,000,000 | 7.293%, ICE LIBOR USD 3 Month + 3.050%, 10/20/34 (A)(B) | 875,382 | ||||||||

| AGL CLO, Series 2021-7A, Class ER | ||||||||||

| 2,345,000 | 10.429%, ICE LIBOR USD 3 Month + 6.350%, 07/15/34 (A)(B) | 1,928,340 | ||||||||

| AIG CLO, Series 2021-2A, Class E | ||||||||||

| 2,500,000 | 10.743%, ICE LIBOR USD 3 Month + 6.500%, 07/20/34 (A)(B) | 2,067,820 | ||||||||

| AIG CLO, Series 2021-1A, Class ER | ||||||||||

| 1,000,000 | 10.843%, ICE LIBOR USD 3 Month + 6.600%, 04/20/32 (A)(B) | 865,211 | ||||||||

| AIMCO CLO Series, Series 2021-AA, Class DR | ||||||||||

| 665,000 | 7.393%, ICE LIBOR USD 3 Month + 3.150%, 04/20/34 (A)(B) | 583,494 | ||||||||

| Allegro CLO VI, Series 2018-2A, Class D | ||||||||||

| 250,000 | 6.829%, ICE LIBOR USD 3 Month + 2.750%, 01/17/31 (A)(B) | 219,584 | ||||||||

| American Homes 4 Rent, Series 2015-SFR1, Class F | ||||||||||

| 3,966,000 | 5.885%, 04/17/52 (A) | 3,836,894 | ||||||||

| Anchorage Capital CLO, Series 2017-1A, Class CR | ||||||||||

| 250,000 | 7.141%, ICE LIBOR USD 3 Month + 3.200%, 10/13/30 (A)(B) | 226,326 | ||||||||

| Atrium XV, Series 15A, Class D | ||||||||||

| 845,000 | 7.325%, ICE LIBOR USD 3 Month + 3.000%, 01/23/31 (A)(B) | 757,112 | ||||||||

| Avis Budget Rental Car Funding AESOP, Series 2021-1A, Class D | ||||||||||

| 5,000,000 | 3.710%, 08/20/27 (A) | 4,128,081 | ||||||||

| Avis Budget Rental Car Funding AESOP, Series 2022-3A, Class A | ||||||||||

| 2,815,000 | 4.620%, 02/20/27 (A) | 2,720,015 | ||||||||

| Bain Capital Credit CLO, Series 2018-2A, Class A1 | ||||||||||

| 2,220,000 | 5.307%, ICE LIBOR USD 3 Month + 1.080%, 07/19/31 (A)(B) | 2,168,745 | ||||||||

| Bain Capital Credit CLO, Series 2021-2A, Class AR | ||||||||||

| 2,220,000 | 5.179%, ICE LIBOR USD 3 Month + 1.100%, 10/17/32 (A)(B) | 2,141,634 | ||||||||

| Ballyrock CLO, Series 2018-1A, Class C | ||||||||||

| 250,000 | 7.393%, ICE LIBOR USD 3 Month + 3.150%, 04/20/31 (A)(B) | 217,631 | ||||||||

| Barings CLO, Series 2018-2A, Class C | ||||||||||

| 620,000 | 6.779%, ICE LIBOR USD 3 Month + 2.700%, 04/15/30 (A)(B) | 558,132 | ||||||||

| Battalion CLO XVI, Series 2021-16A, Class ER | ||||||||||

| 830,000 | 10.843%, ICE LIBOR USD 3 Month + 6.600%, 12/19/32 (A)(B) | 661,041 | ||||||||

| BHG Securitization Trust, Series 2022-C, Class E | ||||||||||

| 1,890,000 | 9.730%, 10/17/35 (A) | 1,814,626 | ||||||||

The accompanying notes are an integral part of the financial statements.

| | 7 |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Asset-Backed Securities — 54.0% (continued) | ||||||||||

| Business Jet Securities, Series 2021-1A, Class C | ||||||||||

| $ | 754,517 | 5.067%, 04/15/36 (A) | $ | 656,445 | ||||||

| CAL Funding IV, Series 2020-1A, Class B | ||||||||||

| 847,604 | 3.500%, 09/25/45 (A) | 738,060 | ||||||||

| CarVal CLO IV, Series 2021-1A, Class A1A | ||||||||||

| 1,850,000 | 5.423%, ICE LIBOR USD 3 Month + 1.180%, 07/20/34 (A)(B) | 1,768,483 | ||||||||

| Carvana Auto Receivables Trust, Series 2022-P1, Class A3 | ||||||||||

| 3,230,000 | 3.350%, 02/10/27 | 3,117,146 | ||||||||

| Carvana Auto Receivables Trust, Series 2022-P2, Class B | ||||||||||

| 2,382,000 | 5.080%, 04/10/28 | 2,257,431 | ||||||||

| Castlelake Aircraft Structured Trust, Series 2021-1A, Class A | ||||||||||

| 519,375 | 3.474%, 01/15/46 (A) | 441,469 | ||||||||

| Castlelake Aircraft Structured Trust, Series 2021-1R, Class B | ||||||||||

| 529,359 | 3.924%, 08/15/41 (A) | 418,199 | ||||||||

| CIFC Funding, Series 2017-5A, Class C | ||||||||||

| 500,000 | 6.929%, ICE LIBOR USD 3 Month + 2.850%, 11/16/30 (A)(B) | 453,867 | ||||||||

| CIFC Funding, Series 2018-1A, Class D | ||||||||||

| 365,000 | 6.844%, ICE LIBOR USD 3 Month + 2.650%, 04/18/31 (A)(B) | 313,300 | ||||||||

| CIG Auto Receivables Trust, Series 2021-1A, Class E | ||||||||||

| 2,550,000 | 4.450%, 05/12/28 (A) | 2,314,701 | ||||||||

| CIM TRUST, Series 2022-R2, Class A1 | ||||||||||

| 1,012,284 | 3.750%, 12/25/61 (A)(B) | 942,192 | ||||||||

| CLI Funding VI, Series 2020-3A, Class B | ||||||||||

| 801,500 | 3.300%, 10/18/45 (A) | 699,498 | ||||||||

| Connecticut Avenue Securities Trust, Series 2021-R01, Class 1B1 | ||||||||||

| 730,000 | 6.097%, SOFR30A + 3.100%, 10/25/41 (A)(B) | 659,390 | ||||||||

| CoreVest American Finance Trust, Series 2017-1, Class D | ||||||||||

| 136,107 | 4.358%, 10/15/49 (A) | 135,730 | ||||||||

| CoreVest American Finance Trust, Series 2019-1, Class E | ||||||||||

| 575,000 | 5.606%, 03/15/52 (A)(B) | 505,688 | ||||||||

| CoreVest American Finance Trust, Series 2020-2, Class D | ||||||||||

| 1,211,000 | 4.598%, 05/15/52 (A)(B) | 1,021,657 | ||||||||

| Diamond Resorts Owner Trust, Series 2018-1, Class C | ||||||||||

| 405,580 | 4.530%, 01/21/31 (A) | 395,615 | ||||||||

| Dryden Senior Loan Fund, Series 2018-45A, Class ER | ||||||||||

| 575,000 | 9.929%, ICE LIBOR USD 3 Month + 5.850%, 10/15/30 (A)(B) | 476,361 | ||||||||

| Elmwood CLO VIII, Series 2021-1A, Class D1 | ||||||||||

| 715,000 | 7.243%, ICE LIBOR USD 3 Month + 3.000%, 01/20/34 (A)(B) | 645,333 | ||||||||

| Elmwood CLO XI, Series 2021-4A, Class E | ||||||||||

| 1,250,000 | 10.243%, ICE LIBOR USD 3 Month + 6.000%, 10/20/34 (A)(B) | 1,090,834 | ||||||||

| Falcon Aerospace, Series 2017-1, Class A | ||||||||||

| 601,132 | 4.581%, 02/15/42 (A) | 545,066 | ||||||||

| First Investors Auto Owner Trust, Series 2019-2A, Class E | ||||||||||

| 2,620,000 | 3.880%, 01/15/26 (A) | 2,516,732 | ||||||||

The accompanying notes are an integral part of the financial statements.

8 | |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Asset-Backed Securities — 54.0% (continued) | ||||||||||

| First Investors Auto Owner Trust, Series 2021-1A, Class E | ||||||||||

| $ | 660,000 | 3.350%, 04/15/27 (A) | $ | 595,964 | ||||||

| First Investors Auto Owner Trust, Series 2022-2A, Class D | ||||||||||

| 750,000 | 8.710%, 10/16/28 (A) | 749,833 | ||||||||

| FirstKey Homes Trust, Series 2020-SFR2, Class F1 | ||||||||||

| 2,450,000 | 3.017%, 10/19/37 (A) | 2,098,275 | ||||||||

| FirstKey Homes Trust, Series 2020-SFR1, Class F2 | ||||||||||

| 2,305,000 | 4.284%, 08/17/37 (A) | 2,026,559 | ||||||||

| Foursight Capital Automobile Receivables Trust, Series 2022-2, Class D | ||||||||||

| 2,745,000 | 7.090%, 10/15/29 (A) | 2,602,363 | ||||||||

| Galaxy XXVI CLO, Series 2018-26A, Class E | ||||||||||

| 400,000 | 8.834%, ICE LIBOR USD 3 Month + 5.850%, 11/22/31 (A)(B) | 322,726 | ||||||||

| Gilbert Park CLO, Series 2017-1A, Class D | ||||||||||

| 707,000 | 7.029%, ICE LIBOR USD 3 Month + 2.950%, 10/15/30 (A)(B) | 630,974 | ||||||||

| GLS Auto Receivables Issuer Trust, Series 2021-4A, Class E | ||||||||||

| 2,550,000 | 4.430%, 10/16/28 (A) | 2,126,854 | ||||||||

| Goldentree Loan Management US CLO, Series 2017-2A, Class D | ||||||||||

| 250,000 | 6.893%, ICE LIBOR USD 3 Month + 2.650%, 11/28/30 (A)(B) | 225,131 | ||||||||

| Greenwood Park CLO, Series 2018-1A, Class D | ||||||||||

| 285,000 | 6.579%, ICE LIBOR USD 3 Month + 2.500%, 04/15/31 (A)(B) | 242,632 | ||||||||

| Harbor Park CLO, Series 2018-1A, Class D | ||||||||||

| 400,000 | 7.143%, ICE LIBOR USD 3 Month + 2.900%, 01/20/31 (A)(B) | 352,591 | ||||||||

| Hertz Vehicle Financing III, Series 2022-3A, Class D | ||||||||||

| 1,065,000 | 6.310%, 03/25/25 (A) | 1,016,167 | ||||||||

| Hertz Vehicle Financing III, Series 2022-1A, Class D | ||||||||||

| 1,040,000 | 4.850%, 06/25/26 (A) | 906,056 | ||||||||

| Hilton Grand Vacations Trust, Series 2018-AA, Class C | ||||||||||

| 144,428 | 4.000%, 02/25/32 (A) | 137,544 | ||||||||

| Hilton Grand Vacations Trust, Series 2022-2A, Class C | ||||||||||

| 687,520 | 5.570%, 01/25/37 (A) | 656,556 | ||||||||

| Home Partners of America Trust, Series 2021-1, Class F | ||||||||||

| 607,499 | 3.325%, 09/17/41 (A) | 478,648 | ||||||||

| Home Partners of America Trust, Series 2021-2, Class F | ||||||||||

| 2,482,865 | 3.799%, 12/17/26 (A) | 2,063,527 | ||||||||

| JPMorgan Chase Bank, Series 2021-1, Class F | ||||||||||

| 1,000,000 | 4.280%, 09/25/28 (A) | 928,791 | ||||||||

| JPMorgan Chase Bank, Series 2021-2, Class F | ||||||||||

| 1,200,000 | 4.393%, 12/26/28 (A) | 1,101,656 | ||||||||

| Kestrel Aircraft Funding, Series 2018-1A, Class A | ||||||||||

| 2,180,114 | 4.250%, 12/15/38 (A) | 1,836,936 | ||||||||

| KKR CLO, Series 2018-23, Class F | ||||||||||

| 840,000 | 12.093%, ICE LIBOR USD 3 Month + 7.850%, 10/20/31 (A)(B) | 612,122 | ||||||||

| KKR CLO, Series 2019-24, Class E | ||||||||||

| 860,000 | 10.623%, ICE LIBOR USD 3 Month + 6.380%, 04/20/32 (A)(B) | 733,779 | ||||||||

The accompanying notes are an integral part of the financial statements.

| | 9 |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Asset-Backed Securities — 54.0% (continued) | ||||||||||

| Lehman XS Trust, Series 2006-2N, Class 1A1 | ||||||||||

| $ | 491,173 | 4.106%, ICE LIBOR USD 1 Month + 0.520%, 02/25/46 | $ | 425,429 | ||||||

| Madison Park Funding XLVI, Series 2021-46A, Class ER | ||||||||||

| 2,140,000 | 10.329%, ICE LIBOR USD 3 Month + 6.250%, 10/15/34 (A)(B) | 1,802,469 | ||||||||

| Magnetite XXIX, Series 2021-29A, Class E | ||||||||||

| 850,000 | 9.829%, ICE LIBOR USD 3 Month + 5.750%, 01/15/34 (A)(B) | 725,298 | ||||||||

| MAPS, Series 2018-1A, Class B | ||||||||||

| 1,076,808 | 5.193%, 05/15/43 (A) | 694,412 | ||||||||

| Med Trust, Series MDLN, Class A | ||||||||||

| 530,000 | 4.363%, ICE LIBOR USD 1 Month + 0.950%, 11/15/38 (A)(B) | 504,784 | ||||||||

| Mercury Financial Credit Card Master Trust, Series 2021-1A, Class C | ||||||||||

| 4,000,000 | 4.210%, 03/20/26 (A) | 3,590,008 | ||||||||

| Mercury Financial Credit Card Master Trust, Series 2022-1A, Class C | ||||||||||

| 2,500,000 | 5.200%, 09/21/26 (A) | 2,256,893 | ||||||||

| MVW, Series 2022-1A, Class A | ||||||||||

| 2,569,154 | 4.150%, 11/21/39 (A) | 2,454,597 | ||||||||

| Neuberger Berman Loan Advisers CLO 37, Series 2021-37A, Class AR | ||||||||||

| 2,570,000 | 5.213%, ICE LIBOR USD 3 Month + 0.970%, 07/20/31 (A)(B) | 2,504,971 | ||||||||

| Oaktree CLO, Series 2019-4A, Class E | ||||||||||

| 265,000 | 11.473%, ICE LIBOR USD 3 Month + 7.230%, 10/20/32 (A)(B) | 218,776 | ||||||||

| OCP CLO, Series 2018-15A, Class D | ||||||||||

| 645,000 | 10.093%, ICE LIBOR USD 3 Month + 5.850%, 07/20/31 (A)(B) | 530,031 | ||||||||

| OCP CLO, Series 2021-17A, Class ER | ||||||||||

| 1,000,000 | 10.743%, ICE LIBOR USD 3 Month + 6.500%, 07/20/32 (A)(B) | 803,515 | ||||||||

| Octagon Investment Partners, Series 2018-3A, Class E | ||||||||||

| 280,000 | 9.993%, ICE LIBOR USD 3 Month + 5.750%, 10/20/30 (A)(B) | 232,354 | ||||||||

| OHA Credit Funding, Series 2021-8A, Class D | ||||||||||

| 1,880,000 | 7.044%, ICE LIBOR USD 3 Month + 2.850%, 01/18/34 (A)(B) | 1,663,042 | ||||||||

| OHA Credit Funding, Series 2021-4A, Class ER | ||||||||||

| 2,355,000 | 10.725%, ICE LIBOR USD 3 Month + 6.400%, 10/22/36 (A)(B) | 2,011,648 | ||||||||

| OHA Credit Funding, Series 2021-2A, Class ER | ||||||||||

| 445,000 | 10.638%, ICE LIBOR USD 3 Month + 6.360%, 04/21/34 (A)(B) | 377,161 | ||||||||

| OHA Credit Funding, Series 2021-3A, Class ER | ||||||||||

| 2,415,000 | 10.493%, ICE LIBOR USD 3 Month + 6.250%, 07/02/35 (A)(B) | 2,068,892 | ||||||||

| OHA Credit Funding 2, Series 2021-2A, Class AR | ||||||||||

| 2,300,000 | 5.428%, ICE LIBOR USD 3 Month + 1.150%, 04/21/34 (A)(B) | 2,224,864 | ||||||||

| OHA Credit Partners XVI, Series 2021-16A, Class D | ||||||||||

| 2,185,000 | 7.044%, ICE LIBOR USD 3 Month + 2.850%, 10/18/34 (A)(B) | 1,908,862 | ||||||||

| OneMain Financial Issuance Trust, Series 2018-2A, Class A | ||||||||||

| 329,000 | 3.570%, 03/14/33 (A) | 321,637 | ||||||||

| OneMain Financial Issuance Trust, Series 2020-1A, Class C | ||||||||||

| 2,565,000 | 5.810%, 05/14/32 (A) | 2,534,047 | ||||||||

| Orange Lake Timeshare Trust, Series 2019-A, Class D | ||||||||||

| 898,887 | 4.930%, 04/09/38 (A) | 826,436 | ||||||||

The accompanying notes are an integral part of the financial statements.

10| |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Asset-Backed Securities — 54.0% (continued) | ||||||||||

| Palmer Square CLO, Series 2021-1A, Class CR | ||||||||||

$ | 1,000,000 | 5.955%, ICE LIBOR USD 3 Month + 3.050%, 11/14/34 (A)(B) | $ | 868,519 | ||||||

| Palmer Square CLO, Series 2021-1A, Class CR4 | ||||||||||

| 1,740,000 | 5.834%, ICE LIBOR USD 3 Month + 2.850%, 05/21/34 (A)(B) | 1,521,395 | ||||||||

| Palmer Square CLO, Series 2021-4A, Class E | ||||||||||

| 1,875,000 | 10.129%, ICE LIBOR USD 3 Month + 6.050%, 10/15/34 (A)(B) | 1,625,190 | ||||||||

| Palmer Square Loan Funding, Series 2021-1A, Class D | ||||||||||

| 750,000 | 10.243%, ICE LIBOR USD 3 Month + 6.000%, 04/20/29 (A)(B) | 661,671 | ||||||||

| Pikes Peak CLO, Series 2018-1A, Class D | ||||||||||

| 510,000 | 7.475%, ICE LIBOR USD 3 Month + 3.150%, 07/24/31 (A)(B) | 432,225 | ||||||||

| Pikes Peak CLO, Series 2021-4A, Class ER | ||||||||||

| 1,990,000 | 10.689%, ICE LIBOR USD 3 Month + 6.610%, 07/15/34 (A)(B) | 1,613,639 | ||||||||

| Prestige Auto Receivables Trust, Series 2019-1A, Class E | ||||||||||

| 1,415,000 | 3.900%, 05/15/26 (A) | 1,381,348 | ||||||||

| Prestige Auto Receivables Trust, Series 2020-1A, Class E | ||||||||||

| 2,740,000 | 3.670%, 02/15/28 (A) | 2,651,205 | ||||||||

| Progress Residential Trust, Series 2020-SFR3, Class F | ||||||||||

| 645,000 | 2.796%, 10/17/27 (A) | 557,201 | ||||||||

| Progress Residential Trust, Series 2021-SFR3, Class F | ||||||||||

| 905,000 | 3.436%, 05/17/26 (A) | 760,053 | ||||||||

| Progress Residential Trust, Series 2021-SFR2, Class F | ||||||||||

| 2,450,000 | 3.395%, 04/19/38 (A) | 2,040,214 | ||||||||

| Progress Residential Trust, Series 2021-SFR4, Class F | ||||||||||

| 2,175,000 | 3.407%, 05/17/38 (A) | 1,828,252 | ||||||||

| Progress Residential Trust, Series 2021-SFR1, Class F | ||||||||||

| 360,000 | 2.757%, 04/17/38 (A) | 297,103 | ||||||||

| PRPM, Series 2020-4, Class A2 | ||||||||||

| 1,290,000 | 3.436%, 10/25/25 (A) | 1,231,881 | ||||||||

| PRPM, Series 2021-1, Class A2 | ||||||||||

| 1,055,000 | 3.720%, 01/25/26 (A)(B) | 912,843 | ||||||||

| PRPM, Series 2021-2, Class A2 | ||||||||||

| 980,000 | 3.770%, 03/25/26 (A)(B) | 836,947 | ||||||||

| PRPM, Series 2021-4, Class A2 | ||||||||||

| 555,000 | 3.474%, 04/25/26 (A) | 436,511 | ||||||||

| PRPM, Series 2022-5, Class A1 | ||||||||||

| 1,975,000 | 6.900%, 09/27/27 (A) | 1,947,775 | ||||||||

| Rockford Tower CLO, Series 2017-3A, Class D | ||||||||||

| 250,000 | 6.893%, ICE LIBOR USD 3 Month + 2.650%, 10/20/30 (A)(B) | 216,546 | ||||||||

| Rockland Park CLO, Series 2021-1A, Class E | ||||||||||

| 2,450,000 | 10.493%, ICE LIBOR USD 3 Month + 6.250%, 04/20/34 (A)(B) | 1,996,868 | ||||||||

| RR, Series 2018-3A, Class CR2 | ||||||||||

| 250,000 | 6.579%, ICE LIBOR USD 3 Month + 2.500%, 01/15/30 (A)(B) | 200,558 | ||||||||

| Santander Bank - SBCLN, Series 2021-1A, Class E | ||||||||||

| 700,000 | 6.171%, 12/15/31 (A) | 618,083 | ||||||||

The accompanying notes are an integral part of the financial statements.

| |11 |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Asset-Backed Securities — 54.0% (continued) | ||||||||||

| SCF Equipment Leasing, Series 2021-1A, Class E | ||||||||||

$ | 755,000 | 3.560%, 08/20/32 (A) | $ | 678,520 | ||||||

| Sierra Timeshare, Series 2020-2A, Class D | ||||||||||

| 336,743 | 6.590%, 07/20/37 (A) | 321,085 | ||||||||

| Sierra Timeshare, Series 2021-1A, Class D | ||||||||||

| 628,583 | 3.170%, 11/20/37 (A) | 573,287 | ||||||||

| S-Jets, Series 2017-1, Class A | ||||||||||

| 942,866 | 3.967%, 08/15/42 (A) | 705,962 | ||||||||

| S-Jets, Series 2017-1, Class B | ||||||||||

| 651,509 | 5.682%, 08/15/42 (A) | 381,178 | ||||||||

| Sound Point Clo XIV, Series 2021-3A, Class B1R | ||||||||||

| 2,470,000 | 5.825%, ICE LIBOR USD 3 Month + 1.500%, 01/23/29 (A)(B) | 2,409,695 | ||||||||

| Textainer Marine Containers VII, Series 2021-1A, Class B | ||||||||||

| 604,180 | 2.520%, 02/20/46 (A) | 496,407 | ||||||||

| Thayer Park CLO, Series 2021-1A, Class DR | ||||||||||

| 650,000 | 10.493%, ICE LIBOR USD 3 Month + 6.250%, 04/20/34 (A)(B) | 545,373 | ||||||||

| THL Credit Wind River, Series 2018-3A, Class D | ||||||||||

| 280,000 | 7.193%, ICE LIBOR USD 3 Month + 2.950%, 01/20/31 (A)(B) | 242,088 | ||||||||

| Trestles CLO II, Series 2018-2A, Class D | ||||||||||

| 415,000 | 10.108%, ICE LIBOR USD 3 Month + 5.750%, 07/25/31 (A)(B) | 325,934 | ||||||||

| Tricon American Homes Trust, Series 2020-SFR1, Class F | ||||||||||

| 160,000 | 4.882%, 07/17/38 (A) | 140,475 | ||||||||

| VOLT XCIV, Series 2021-NPL3, Class A2 | ||||||||||

| 1,630,000 | 4.949%, 02/27/51 (A) | 1,300,690 | ||||||||

| VOLT XCVI, Series 2021-NPL5, Class A2 | ||||||||||

| 640,000 | 4.826%, 03/27/51 (A) | 524,986 | ||||||||

| WAVE, Series 2017-1A, Class A | ||||||||||

| 1,960,646 | 3.844%, 11/15/42 (A) | 1,419,135 | ||||||||

| Welk Resorts, Series 2019-AA, Class D | ||||||||||

| 267,622 | 4.030%, 06/15/38 (A) | 256,669 | ||||||||

| Willis Engine Structured Trust IV, Series 2018-A, Class A | ||||||||||

| 2,270,366 | 4.750%, 09/15/43 (A) | 1,637,148 | ||||||||

| Willis Engine Structured Trust V, Series 2020-A, Class A | ||||||||||

| 1,060,088 | 3.228%, 03/15/45 (A) | 836,314 | ||||||||

|

|

| ||||||||

| Total Asset-Backed Securities (Cost $167,439,357) | 150,082,692 | |||||||||

|

|

| ||||||||

Commercial Mortgage-Backed Obligations — 26.7% | ||||||||||

| BANK, Series BN34, Class A5 | ||||||||||

| 1,000,000 | 2.438%, 06/15/63 | 779,885 | ||||||||

| BBCMS Mortgage Trust, Series BID, Class A | ||||||||||

| 2,885,000 | 5.552%, ICE LIBOR USD 1 Month + 2.140%, 10/15/37 (A)(B) | 2,824,660 | ||||||||

| BB-UBS Trust, Series 2012-TFT, Class C | ||||||||||

| 2,000,000 | 3.419%, 06/05/30 (A)(B) | 1,689,367 | ||||||||

The accompanying notes are an integral part of the financial statements.

12| |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Commercial Mortgage-Backed Obligations — 26.7% (continued) | ||||||||||

| Benchmark Mortgage Trust, Series B31, Class A5 | ||||||||||

$ | 1,000,000 | 2.669%, 12/15/54 | $ | 784,864 | ||||||

| Benchmark Mortgage Trust, Series B11, Class A5 | ||||||||||

| 943,000 | 3.542%, 05/15/52 | 829,029 | ||||||||

| BPR Trust, Series 2021-NRD, Class F | ||||||||||

| 2,545,000 | 10.286%, TSFR1M + 6.870%, 12/15/23 (A)(B) | 2,344,114 | ||||||||

| BPR Trust, Series 2022-SSP, Class A | ||||||||||

| 2,920,000 | 6.376%, TSFR1M + 3.000%, 05/15/39 (A)(B) | 2,897,069 | ||||||||

| BPR Trust, Series 2022-SSP, Class D | ||||||||||

| 2,170,000 | 10.007%, TSFR1M + 6.631%, 05/15/39 (A)(B) | 2,113,945 | ||||||||

| BPR Trust, Series STAR, Class A | ||||||||||

| 1,530,000 | 6.608%, TSFR1M + 3.232%, 08/15/24 (A)(B) | 1,507,041 | ||||||||

| CG-CCRE Commercial Mortgage Trust, Series 2014-FL2, Class COL1 | ||||||||||

| 965,730 | 6.912%, ICE LIBOR USD 1 Month + 3.500%, 11/15/31 (A)(B) | 806,771 | ||||||||

| CG-CCRE Commercial Mortgage Trust, Series 2014-FL2, Class COL2 | ||||||||||

| 2,351,552 | 7.912%, ICE LIBOR USD 1 Month + 4.500%, 11/15/31 (A)(B) | 1,654,081 | ||||||||

| Citigroup Commercial Mortgage Trust, Series 2014-GC21, Class D | ||||||||||

| 2,555,000 | 4.945%, 05/10/47 (A)(B) | 2,263,509 | ||||||||

| COMM Mortgage Trust, Series 2012-LC4, Class C | ||||||||||

| 17,000 | 5.278%, 12/10/44 (B) | 15,302 | ||||||||

| COMM Mortgage Trust, Series 2012-LC4, Class D | ||||||||||

| 1,605,000 | 5.278%, 12/10/44 (A)(B) | 1,139,753 | ||||||||

| COMM Mortgage Trust, Series 2012-CCRE3, Class D | ||||||||||

| 1,005,000 | 4.728%, 10/15/45 (A)(B) | 733,650 | ||||||||

| COMM Mortgage Trust, Series 2012-CR2, Class E | ||||||||||

| 1,000,000 | 4.905%, 08/15/45 (A)(B) | 847,368 | ||||||||

| COMM Mortgage Trust, Series 2014-UBS4, Class AM | ||||||||||

| 762,000 | 3.968%, 08/10/47 | 724,545 | ||||||||

| COMM Mortgage Trust, Series 2014-CR21, Class AM | ||||||||||

| 330,000 | 3.987%, 12/10/47 | 312,939 | ||||||||

| CSMC OA, Series 2014-USA, Class C | ||||||||||

| 895,000 | 4.336%, 09/15/37 (A) | 733,867 | ||||||||

| CSMC OA, Series 2014-USA, Class E | ||||||||||

| 5,475,000 | 4.373%, 09/15/37 (A) | 3,629,911 | ||||||||

| CSMC Trust, Series 2021-RPL1, Class A2 | ||||||||||

| 1,850,000 | 3.937%, 09/27/60 (A) | 1,724,055 | ||||||||

| Extended Stay America Trust, Series 2021-ESH, Class F | ||||||||||

| 2,899,291 | 7.113%, ICE LIBOR USD 1 Month + 3.700%, 07/15/38 (A)(B) | 2,710,551 | ||||||||

| GS Mortgage Securities Trust, Series 2011-GC5, Class C | ||||||||||

| 100,000 | 5.155%, 08/10/44 (A)(B) | 79,533 | ||||||||

| GS Mortgage Securities Trust, Series 2011-GC5, Class D | ||||||||||

| 4,972,728 | 5.155%, 08/10/44 (A)(B) | 2,105,302 | ||||||||

| GS Mortgage Securities Trust, Series 2013-GC13, Class C | ||||||||||

| 610,000 | 4.074%, 07/10/46 (A)(B) | 517,040 | ||||||||

The accompanying notes are an integral part of the financial statements.

| |13 |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Commercial Mortgage-Backed Obligations — 26.7% (continued) |

| |||||||||

| GS Mortgage Securities Trust, Series 2014-GC20, Class C | ||||||||||

$ | 2,625,000 | 5.001%, 04/10/47 (B) | $ | 2,310,145 | ||||||

| GS Mortgage Securities Trust, Series GC22, Class D | ||||||||||

| 3,000,000 | 4.687%, 06/10/47 (A)(B) | 2,657,417 | ||||||||

| Hudsons Bay Simon JV Trust, Series 2015-HB10, Class A10 | ||||||||||

| 3,375,000 | 4.155%, 08/05/34 (A) | 2,923,401 | ||||||||

| JPMBB Commercial Mortgage Securities Trust, Series C24, Class AS | ||||||||||

| 230,000 | 3.914%, 11/15/47 (B) | 215,134 | ||||||||

| JPMorgan Chase Commercial Mortgage Securities Trust, Series 2013- LC11, Class C | ||||||||||

| 945,000 | 3.958%, 04/15/46 (B) | 893,804 | ||||||||

| JPMorgan Chase Commercial Mortgage Securities Trust, Series C3, Class C | ||||||||||

| 2,490,000 | 5.360%, 02/15/46 (A)(B) | 2,316,284 | ||||||||

| JPMorgan Mortgage Trust, Series 2004-S1, Class 2A1 | ||||||||||

| 967,503 | 6.000%, 09/25/34 | 906,757 | ||||||||

| Legacy Mortgage Asset Trust, Series 2021-GS2, Class A2 | ||||||||||

| 520,000 | 3.500%, 04/25/61 (A) | 473,624 | ||||||||

| Lehman Mortgage Trust, Series 2007-9, Class 1A1 | ||||||||||

| 161,267 | 6.000%, 10/25/37 | 208,671 | ||||||||

| Morgan Stanley Bank of America Merrill Lynch Trust, Series C11, Class B | ||||||||||

| 3,330,000 | 4.350%, 08/15/46 (B) | 2,295,464 | ||||||||

| Morgan Stanley Capital I Trust, Series 2011-C2, Class E | ||||||||||

| 2,930,000 | 5.211%, 06/15/44 (A)(B) | 2,326,605 | ||||||||

| Morgan Stanley Capital I Trust, Series 2013-ALTM, Class E | ||||||||||

| 2,500,000 | 3.705%, 02/05/35 (A)(B) | 1,784,375 | ||||||||

| Morgan Stanley Capital I Trust, Series C4, Class D | ||||||||||

| 645,951 | 5.164%, 03/15/45 (A)(B) | 597,505 | ||||||||

| Morgan Stanley Mortgage Loan Trust, Series 2005-7, Class 7A5 | ||||||||||

| 119,164 | 5.500%, 11/25/35 | 106,703 | ||||||||

| MSBAM Commercial Mortgage Securities Trust, Series 2012-CKSV, Class C | ||||||||||

| 830,000 | 4.280%, 10/15/30 (A)(B) | 598,638 | ||||||||

| MSBAM Commercial Mortgage Securities Trust, Series 2012-CKSV, Class D | ||||||||||

| 400,000 | 4.280%, 10/15/30 (A)(B) | 200,000 | ||||||||

| RBS Commercial Funding Trust, Series 2013-SMV, Class F | ||||||||||

| 2,000,000 | 3.584%, 03/11/31 (A)(B) | 1,797,582 | ||||||||

| Starwood Retail Property Trust, Series 2014-STAR, Class A | ||||||||||

| 375,160 | 4.883%, ICE LIBOR USD 1 Month + 1.470%, 11/15/27 (A)(B) | 256,508 | ||||||||

| Starwood Retail Property Trust, Series 2014-STAR, Class E | ||||||||||

| 3,185,000 | 7.813%, ICE LIBOR USD 1 Month + 4.400%, 11/15/27 (A)(B)(C) | 338,406 | ||||||||

| Starwood Retail Property Trust, Series 2014-STAR, Class F | ||||||||||

| 3,785,000 | 7.107%, ICE LIBOR USD 1 Month + 3.694%, 11/15/27 (A)(B)(C) | 344,642 | ||||||||

| Towd Point Mortgage Trust, Series 2018-4, Class A2 | ||||||||||

| 1,100,000 | 3.000%, 06/25/58 (A)(B) | 855,363 | ||||||||

The accompanying notes are an integral part of the financial statements.

14| |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Commercial Mortgage-Backed Obligations — 26.7% (continued) |

| |||||||||

| Towd Point Mortgage Trust, Series 2018-5, Class M1 | ||||||||||

$ | 505,000 | 3.250%, 07/25/58 (A)(B) | $ | 361,479 | ||||||

| Towd Point Mortgage Trust, Series 2019-2, Class M1 | ||||||||||

| 890,000 | 3.750%, 12/25/58 (A)(B) | 671,349 | ||||||||

| Towd Point Mortgage Trust, Series 2020-4, Class M1 | ||||||||||

| 2,300,000 | 2.875%, 10/25/60 (A) | 1,726,485 | ||||||||

| UBS Commercial Mortgage Trust, Series 2018-C14, Class C | ||||||||||

| 1,885,000 | 5.258%, 12/15/51 (B) | 1,528,870 | ||||||||

| UBS-Barclays Commercial Mortgage Trust, Series 2012-C2, Class E | ||||||||||

| 866,000 | 4.720%, 05/10/63 (A)(B) | 29,271 | ||||||||

| Wells Fargo Commercial Mortgage Trust, Series 2014-LC16, Class C | ||||||||||

| 1,485,000 | 4.458%, 08/15/50 | 912,179 | ||||||||

| Wells Fargo Commercial Mortgage Trust, Series 2016-C34, Class C | ||||||||||

| 2,902,000 | 5.067%, 06/15/49 (B) | 2,480,892 | ||||||||

| Wells Fargo Commercial Mortgage Trust, Series C36, Class C | ||||||||||

| 500,000 | 4.135%, 11/15/59 (B) | 380,960 | ||||||||

| WFRBS Commercial Mortgage Trust, Series 2011-C3, Class D | ||||||||||

| 2,609,443 | 5.378%, 03/15/44 (A)(B) | 1,072,481 | ||||||||

| WFRBS Commercial Mortgage Trust, Series 2011-C4, Class D | ||||||||||

| 722,000 | 4.843%, 06/15/44 (A)(B) | 645,535 | ||||||||

| WFRBS Commercial Mortgage Trust, Series 2011-C4, Class E | ||||||||||

| 1,680,000 | 4.843%, 06/15/44 (A)(B) | 1,344,000 | ||||||||

| WFRBS Commercial Mortgage Trust, Series 2012-C7, Class C | ||||||||||

| 82,696 | 4.694%, 06/15/45 (B) | 58,921 | ||||||||

| WFRBS Commercial Mortgage Trust, Series 2012-C7, Class D | ||||||||||

| 1,483,000 | 4.694%, 06/15/45 (A)(B) | 548,710 | ||||||||

| WFRBS Commercial Mortgage Trust, Series 2012-C7, Class E | ||||||||||

| 3,846,032 | 4.694%, 06/15/45 (A)(B) | 293,837 | ||||||||

| WFRBS Commercial Mortgage Trust, Series C24, Class C | ||||||||||

| 255,000 | 4.290%, 11/15/47 (B) | 208,242 | ||||||||

| WFRBS Commercial Mortgage Trust, Series C10, Class C | ||||||||||

| 2,130,000 | 4.298%, 12/15/45 (B) | 1,919,070 | ||||||||

|

|

| ||||||||

Total Commercial Mortgage-Backed Obligations (Cost $91,455,868) | 74,357,460 | |||||||||

|

|

| ||||||||

Residential Mortgage-Backed Obligations — 9.2% |

| |||||||||

| Alternative Loan Trust, Series 2004-J3, Class 1A1 | ||||||||||

| 266,003 | 5.500%, 04/25/34 | 240,802 | ||||||||

| Alternative Loan Trust, Series 2004-J10, Class 2CB1 | ||||||||||

| 600,534 | 6.000%, 09/25/34 | 561,231 | ||||||||

| Alternative Loan Trust, Series 2004-28CB, Class 5A1 | ||||||||||

| 133,260 | 5.750%, 01/25/35 | 122,541 | ||||||||

| Alternative Loan Trust, Series 2005-J1, Class 2A1 | ||||||||||

| 50,783 | 5.500%, 02/25/25 | 48,708 | ||||||||

The accompanying notes are an integral part of the financial statements.

| |15 |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Residential Mortgage-Backed Obligations — 9.2% (continued) |

| |||||||||

| Banc of America Alternative Loan Trust, Series 2003-8, Class 1CB1 | ||||||||||

$ | 360,826 | 5.500%, 10/25/33 | $ | 336,135 | ||||||

| Banc of America Funding Trust, Series 2005-7, Class 3A1 | ||||||||||

| 340,546 | 5.750%, 11/25/35 | 328,984 | ||||||||

| Banc of America Funding Trust, Series 2007-4, Class 5A1 | ||||||||||

| 88,204 | 5.500%, 11/25/34 | 77,095 | ||||||||

| CHL Mortgage Pass-Through Trust, Series 2004-12, Class 8A1 | ||||||||||

| 232,239 | 4.079%, 08/25/34 (B) | 211,228 | ||||||||

| Citigroup Mortgage Loan Trust, Series 2005-3, Class 2A3 | ||||||||||

| 556,938 | 3.692%, 08/25/35 (B) | 444,167 | ||||||||

| Citigroup Mortgage Loan Trust, Series 2009-10, Class 6A2 | ||||||||||

| 150,078 | 4.020%, 09/25/34 (A)(B) | 146,400 | ||||||||

| Citigroup Mortgage Loan Trust, Series 2010-9, Class 2A2 | ||||||||||

| 297,290 | 6.470%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 2.400%, 11/25/35 (A) | 279,147 | ||||||||

| Citigroup Mortgage Loan Trust, Series 2019-RP1, Class M3 | ||||||||||

| 1,005,000 | 4.000%, 01/25/66 (A)(B) | 798,718 | ||||||||

| Countrywide Alternative Loan Trust, Series 2004-14T2, Class A11 | ||||||||||

| 182,397 | 5.500%, 08/25/34 | 166,827 | ||||||||

| Deutsche Mortgage Securities Mortgage Loan Trust, Series 2004-1, Class 3A5 | ||||||||||

| 1,201,938 | 6.160%, 12/25/33 | 1,114,075 | ||||||||

| Deutsche Mortgage Securities Mortgage Loan Trust, Series 2004-4, Class 7AR1 | ||||||||||

| 142,346 | 3.936%, ICE LIBOR USD 1 Month + 0.350%, 06/25/34 | 123,885 | ||||||||

| FHLMC STACR REMIC Trust, Series 2020-DNA3, Class B1 | ||||||||||

| 818,847 | 8.686%, ICE LIBOR USD 1 Month + 5.100%, 06/25/50 (A)(B) | 843,563 | ||||||||

| FHLMC STACR REMIC Trust, Series 2020-DNA4, Class B1 | ||||||||||

| 1,500,000 | 9.586%, ICE LIBOR USD 1 Month + 6.000%, 08/25/50 (A)(B) | 1,567,259 | ||||||||

| FHLMC STACR REMIC Trust, Series 2020-DNA6, Class B1 | ||||||||||

| 2,000,000 | 5.997%, SOFR30A + 3.000%, 12/25/50 (A)(B) | 1,835,033 | ||||||||

| FHLMC STACR REMIC Trust, Series 2021-DNA3, Class B1 | ||||||||||

| 2,000,000 | 6.497%, SOFR30A + 3.500%, 10/25/33 (A)(B) | 1,710,852 | ||||||||

| FHLMC STACR REMIC Trust, Series 2022-DNA7, Class M1B | ||||||||||

| 1,845,000 | 7.997%, SOFR30A + 5.000%, 03/25/52 (A)(B) | 1,921,438 | ||||||||

| GSR Mortgage Loan Trust, Series 2005-AR4, Class 4A1 | ||||||||||

| 25,679 | 3.375%, 07/25/35 (B) | 24,133 | ||||||||

| IndyMac Index Mortgage Loan Trust, Series 2004-AR6, Class 4A | ||||||||||

| 751,225 | 3.811%, 10/25/34 (B) | 687,993 | ||||||||

| IndyMac Index Mortgage Loan Trust, Series 2005-AR11, Class A3 | ||||||||||

| 1,024,656 | 3.190%, 08/25/35 (B) | 825,407 | ||||||||

| IndyMac Index Mortgage Loan Trust, Series 2006-AR2, Class 2A1 | ||||||||||

| 2,608,692 | 4.006%, ICE LIBOR USD 1 Month + 0.420%, 02/25/46 | 1,898,518 | ||||||||

| MASTR Adjustable Rate Mortgages Trust, Series 2005-2, Class 3A1 | ||||||||||

| 922,599 | 2.927%, 03/25/35 (B) | 836,028 | ||||||||

The accompanying notes are an integral part of the financial statements.

16| |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| Principal Amount | Description | Value | ||||||||

Residential Mortgage-Backed Obligations — 9.2% (continued) |

| |||||||||

| MASTR Adjustable Rate Mortgages Trust, Series 2005-2, Class 4A1 | ||||||||||

$ | 1,704,277 | 2.668%, 03/25/35 (B) | $ | 1,408,348 | ||||||

| MASTR Adjustable Rate Mortgages Trust, Series 2006-2, Class 1A1 | ||||||||||

| 383,404 | 2.648%, 04/25/36 (B) | 350,869 | ||||||||

| MASTR Alternative Loan Trust, Series 2003-9, Class 4A1 | ||||||||||

| 249,926 | 5.250%, 11/25/33 | 232,502 | ||||||||

| MASTR Alternative Loan Trust, Series 2004-2, Class 8A4 | ||||||||||

| 2,054,984 | 5.500%, 03/25/34 | 1,757,268 | ||||||||

| MASTR Alternative Loan Trust, Series 2004-5, Class 1A1 | ||||||||||

| 207,924 | 5.500%, 06/25/34 | 196,282 | ||||||||

| MASTR Alternative Loan Trust, Series 2004-5, Class 2A1 | ||||||||||

| 321,012 | 6.000%, 06/25/34 | 305,068 | ||||||||

| MASTR Alternative Loan Trust, Series 2004-8, Class 2A1 | ||||||||||

| 692,482 | 6.000%, 09/25/34 | 643,332 | ||||||||

| Mill City Mortgage Loan Trust, Series 2021-NMR1, Class M3 | ||||||||||

| 730,000 | 2.500%, 11/25/60 (A)(B) | 557,956 | ||||||||

| RFMSI Series Trust, Series 2005-SA1, Class 1A1 | ||||||||||

| 1,763,483 | 3.690%, 03/25/35 (B) | 960,113 | ||||||||

| Structured Adjustable Rate Mortgage Loan Trust, Series 2005-14, Class A1 | ||||||||||

| 2,985,191 | 3.896%, ICE LIBOR USD 1 Month + 0.310%, 07/25/35 | 1,912,569 | ||||||||

|

|

| ||||||||

Total Residential Mortgage-Backed Obligations (Cost $28,323,557) | 25,474,474 | |||||||||

|

|

| ||||||||

Corporate Obligation — 1.0% | ||||||||||

| PG&E Wildfire Recovery Funding | ||||||||||

| 3,000,000 | 4.263%, 06/01/36 | 2,700,688 | ||||||||

|

|

| ||||||||

Total Corporate Obligation (Cost $2,999,880) | 2,700,688 | |||||||||

|

|

| ||||||||

Other Investment — 0.0% | ||||||||||

| ECAF I BLOCKER Ltd. | ||||||||||

| 900 | 03/15/40 (C)(D) | 61,425 | ||||||||

|

|

| ||||||||

Total Other Investment (Cost $9,000,000) | 61,425 | |||||||||

|

|

| ||||||||

| Shares |

| |||||||||

Short-Term Investment — 8.8% | ||||||||||

| 24,368,258 | First American Treasury Obligation Fund, 3.060% (E) | 24,368,258 | ||||||||

|

|

| ||||||||

Total Short-Term Investment (Cost $24,368,258) | 24,368,258 | |||||||||

|

|

| ||||||||

Total Investments — 99.7% (Cost $323,586,920) | 277,044,997 | |||||||||

| Other Assets and Liabilities, net — 0.3% | 785,365 | |||||||||

|

|

| ||||||||

| Net Assets — 100.0% | $ | 277,830,362 | ||||||||

|

|

| ||||||||

The accompanying notes are an integral part of the financial statements.

| |17 |

Portfolio of Investments — as of October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

| (A) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” The total value of these securities at October 31, 2022, was $210,428,136, representing 75.7% of Net Assets of the Portfolio. All securities are considered liquid unless otherwise noted. |

| (B) | Variable or floating rate security. The rate shown is the effective interest rate as of period end. The rates on certain securities are not based on published reference rates and spreads and are either determined by the issuer or agent based on current market conditions; by using a formula based on the rates of underlying loans; or by adjusting periodically based on prevailing interest rates. |

| (C) | Level 3 security in accordance with fair value hierarchy. |

| (D) | No interest rate available. |

| (E) | The rate shown is the 7-day effective yield as of October 31, 2022. |

CLO — Collateralized Loan Obligation

FHLMC — Federal Home Loan Mortgage Corporation

ICE — Intercontinental Exchange

LIBOR — London Interbank Offered Rate

Ltd. — Limited

REMIC — Real Estate Mortgage Investment Conduit

USD — United States Dollar

The following is a summary of the inputs used to value the Fund’s investments as of October 31, 2022, at value:

| Investments in Securities | Level 1 | Level 2 | Level 3(1) | Total | ||||||||||||

Asset-Backed Securities | $ | — | $ | 150,082,692 | $ | — | $ | 150,082,692 | ||||||||

Commercial Mortgage-Backed Obligations | — | 73,674,412 | 683,048 | 74,357,460 | ||||||||||||

Residential Mortgage-Backed Obligations | — | 25,474,474 | — | 25,474,474 | ||||||||||||

Corporate Obligation | — | 2,700,688 | — | 2,700,688 | ||||||||||||

Other Investment | — | — | 61,425 | 61,425 | ||||||||||||

Short-Term Investment | 24,368,258 | — | — | 24,368,258 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||

Total Investments in Securities | $ | 24,368,258 | $ | 251,932,266 | $ | 744,473 | $ | 277,044,997 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||

(1) A reconciliation of Level 3 investments and disclosures of significant unobservable inputs are presented when the Fund has a significant amount of Level 3 investments at the end of the period in relation to Net Assets. Management has concluded that Level 3 investments are not material in relation to Net Assets.

For the year ended October 31, 2022, there have been no significant changes to the Fund’s fair value methodologies.

Amounts designated as “—” are $0 or have been rounded to $0.

The accompanying notes are an integral part of the financial statements.

18| |

Statement of Assets and Liabilities

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

ASSETS | ||||

Investments at cost | $ | 323,586,920 | ||

|

|

| ||

Investments at value | $ | 277,044,997 | ||

Interest receivable | 977,819 | |||

Receivable for securities sold | 659,305 | |||

Receivable from Investment Adviser | 25,274 | |||

Prepaid expenses | 4,164 | |||

|

|

| ||

TOTAL ASSETS | 278,711,559 | |||

|

|

| ||

LIABILITIES | ||||

Payable for securities purchased | 749,951 | |||

Administration fees payable | 28,417 | |||

Trustees’ fees payable | 8,392 | |||

Chief Compliance Officer fees payable | 3,359 | |||

Other accounts payable and accrued expenses | 91,078 | |||

|

|

| ||

TOTAL LIABILITIES | 881,197 | |||

|

|

| ||

NET ASSETS | $ | 277,830,362 | ||

|

|

| ||

NET ASSETS CONSIST OF: | ||||

Paid-in capital | $ | 320,994,046 | ||

Total accumulated loss | (43,163,684 | ) | ||

|

|

| ||

NET ASSETS | $ | 277,830,362 | ||

|

|

| ||

Institutional Class: | ||||

Net assets | $ | 277,830,362 | ||

|

|

| ||

Outstanding shares of beneficial interest (unlimited authorization - no par value) | 29,841,198 | |||

|

|

| ||

Net asset value, offering and redemption price per share | $ | 9.31 | ||

|

|

| ||

The accompanying notes are an integral part of the financial statements.

| |19 |

For the year ended October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

INVESTMENT INCOME | ||||

Interest | $ | 13,070,437 | ||

|

|

| ||

Total Income | 13,070,437 | |||

|

|

| ||

Expenses | ||||

Administration fees | 322,282 | |||

Trustees’ fees | 33,460 | |||

Chief Compliance Officer fees | 8,620 | |||

Pricing fees | 100,317 | |||

Transfer agent fees | 78,899 | |||

Audit fees | 56,900 | |||

Legal fees | 50,210 | |||

Registration fees | 30,510 | |||

Custodian fees | 16,420 | |||

Shareholder reporting fees | 9,183 | |||

Other expenses | 27,615 | |||

|

|

| ||

Total expenses | 734,416 | |||

|

|

| ||

Less: | ||||

Waiver of expenses (Refer to note 5) | (197,327 | ) | ||

|

|

| ||

Net Expenses | 537,089 | |||

|

|

| ||

Net investment income | 12,533,348 | |||

|

|

| ||

NET REALIZED AND UNREALIZED LOSS | ||||

Net realized loss | (299,931 | ) | ||

Net change in unrealized depreciation | (30,211,145 | ) | ||

|

|

| ||

Net realized and unrealized loss | (30,511,076 | ) | ||

|

|

| ||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (17,977,728 | ) | |

|

|

| ||

The accompanying notes are an integral part of the financial statements.

20| |

Statements of Changes in Net Assets

Loomis Sayles Full Discretion Institutional Securitized Fund

| Year Ended | Year Ended | |||||||

| October 31, 2022 | October 31, 2021 | |||||||

|

| |||||||

FROM OPERATIONS: | ||||||||

Net investment income | $ | 12,533,348 | $ | 12,949,434 | ||||

Net realized gain/(loss) | (299,931 | ) | 955,890 | |||||

Net change in unrealized appreciation/(depreciation) | (30,211,145 | ) | 9,410,530 | |||||

|

| |||||||

Net increase/(decrease) in net assets resulting from operations | (17,977,728 | ) | 23,315,854 | |||||

|

| |||||||

DISTRIBUTIONS: | (15,868,912 | ) | (13,142,717) | |||||

|

| |||||||

CAPITAL SHARE TRANSACTIONS:(1) | ||||||||

Issued | 103,974,003 | – | ||||||

Reinvestment of distributions | 15,868,912 | 13,142,716 | ||||||

Redeemed | (62,968,109 | ) | (4,288,747) | |||||

|

| |||||||

Net increase in net assets from capital share transactions | 56,874,806 | 8,853,969 | ||||||

|

| |||||||

Net increase in net assets | 23,028,166 | 19,027,106 | ||||||

|

| |||||||

NET ASSETS: | ||||||||

Beginning of the year | 254,802,196 | 235,775,090 | ||||||

|

| |||||||

End of the year | $ | 277,830,362 | $ | 254,802,196 | ||||

|

| |||||||

(1) For share transactions, see Note 6 in Notes to Financial Statements.

Amounts designated as “-” are $0 or have been rounded to $0.

The accompanying notes are an integral part of the financial statements.

| |21 |

For a share outstanding throughout the years

Loomis Sayles Full Discretion Institutional Securitized Fund

| Net asset value, beginning of the year | Net investment | Net realized gain/(loss) | Total from investment operations | Dividends from net investment income | Distributions from net realized capital gains | Return of capital | ||||||||||||

10/31/22 | $10.55 | $0.46 | $(1.11) | $(0.65) | $(0.49) | $(0.10) | $– | |||||||||||

10/31/21 | 10.12 | 0.55 | 0.44 | 0.99 | (0.47) | (0.09) | – | |||||||||||

10/31/20 | 11.03 | 0.54 | (0.87) | (0.33) | (0.56) | (0.02) | – | |||||||||||

10/31/19 | 10.89 | 0.57 | 0.13 | 0.70 | (0.56) | — | – | |||||||||||

10/31/18 | 11.51 | 0.61 | (0.15) | 0.46 | (0.83) | (0.23) | (0.02) | |||||||||||

| (a) | Per share net investment income has been calculated using the average shares outstanding during the year. |

| (b) | Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Had certain expenses not been waived/reimbursed during the year, if applicable, total returns would have been lower. |

Amounts designated as “-” are $0 or have been rounded to $0.

22| |

Total distributions | Net asset value, end of the year | Total return (%) (b) | Net assets, end of (000’s) | Ratio of expenses to | Ratio of expenses and fees paid | Ratio of net investment income to average net assets (%) | Portfolio (%) | |||||||

$(0.59) | $9.31 | (6.36) | $277,830 | 0.20 | 0.27 | 4.67 | 19 | |||||||

(0.56) | 10.55 | 10.01 | 254,802 | 0.20 | 0.26 | 5.28 | 42 | |||||||

(0.58) | 10.12 | (3.00) | 235,775 | 0.20 | 0.26 | 5.20 | 32 | |||||||

(0.56) | 11.03 | 6.62 | 310,258 | 0.20 | 0.20 | 5.23 | 19 | |||||||

(1.08) | 10.89 | 4.29 | 425,815 | 0.18 | 0.18 | 5.55 | 53 |

The accompanying notes are an integral part of the financial statements.

| |23 |

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

1. Organization. The Advisors’ Inner Circle Fund (the “Trust”) is organized as a Massachusetts business trust under an Amended and Restated Agreement and Declaration of Trust dated February 18, 1997. The Trust is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company with 28 funds. The financial statements herein are those of the Loomis Sayles Full Discretion Institutional Securitized Fund (the “Fund”). The Fund is non-diversified and its investment objective is to provide current income and the potential for total return. The Fund commenced operations on December 15, 2011. The financial statements of the remaining funds of the Trust are presented separately. The assets of each fund of the Trust are segregated, and a shareholder’s interest is limited to the fund of the Trust in which shares are held.

2. Significant Accounting Policies. The following are significant accounting policies, which are consistently followed in the preparation of the financial statements of the Fund. The Fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board (“FASB”).

a. Use of Estimates. The preparation of financial statements in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) requires management to make estimates and assumptions that affect the fair value of assets, the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates and such differences could be material.

b. Security Valuation. Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ), including securities traded over the counter, are valued at the last quoted sale price on an exchange or market (foreign or domestic) on which they are traded on valuation date (or at approximately 4:00 pm ET if a security’s primary exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing Price will be used. If available, debt securities are priced based upon valuations provided by independent, third-party pricing agents. Such values generally reflect the last reported sales price if the security is actively traded. The third-party pricing agents may also value debt securities at an evaluated bid price by employing methodologies that utilize actual market transactions, broker-supplied valuations, or other methodologies designed to identify the market value for such securities. Such methodologies generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations. On the first day a new debt security purchase is recorded, if a price is not

24| |

Notes to Financial Statements

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

available on the automated pricing feeds from our primary and secondary pricing vendors nor is it available from an independent broker, the security may be valued at its purchase price. Each day thereafter, the debt security will be valued according to the Trusts’ Fair Value Procedures until an independent source can be secured. Debt obligations with remaining maturities of sixty days or less may be valued at their amortized cost, which approximates market value provided that it is determined the amortized cost continues to approximate fair value. Should existing credit, liquidity or interest rate conditions in the relevant markets and issuer specific circumstances suggest that amortized cost does not approximate fair value, then the amortized cost method may not be used.

Investments in open-end and closed-end registered investment companies that do not trade on an exchange are valued at the end of day net asset value per share. Investments in open-end and closed-end registered investment companies that trade on an exchange are valued at the last sales price or official closing price as of the close of the customary trading session on the exchange where the security is principally traded.

Securities for which market prices are not “readily available” are required to be fair valued under the 1940 Act.

In December 2020, the SEC adopted Rule 2a-5 under the 1940 Act, establishing requirements to determine fair value in good faith for purposes of the 1940 Act. The rule permits fund boards to designate a fund’s investment adviser to perform fair-value determinations, subject to board oversight and certain other conditions. The rule also defines when market quotations are “readily available” for purposes of the 1940 Act and requires a fund to fair value a portfolio investment when a market quotation is not readily available. The SEC also adopted new Rule 31a-4 under the 1940 Act, which sets forth recordkeeping requirements associated with fair-value determinations. The compliance date for Rule 2a-5 and Rule 31a-4 was September 8, 2022.

Effective September 8, 2022, and pursuant to the requirements of Rule 2a-5, the Trust’s Board of Trustees (the “Board”) designated the Adviser as the Board’s valuation designee to perform fair-value determinations for the Fund through a Fair Value Committee (the “Committee”) established by the Adviser and approved new Adviser Fair Value Procedures for the Fund. Prior to September 8, 2022, fair-value determinations were performed in accordance with the Trust’s Fair Value Procedures established by the Board and were implemented through a Fair Value Committee designated by the Board.

Some of the more common reasons that may necessitate that a security be valued using fair value procedures include: the security’s trading has been halted or suspended; the security has been de-listed from a national exchange; the security’s primary trading market is temporarily

| |25 |

Notes to Financial Statements

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

closed at a time when under normal conditions it would be open; the security has not been traded for an extended period of time; the security’s primary pricing source is not able or willing to provide a price; or trading of the security is subject to local government-imposed restrictions. When a security is valued in accordance with the fair value procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee.

In accordance with the authoritative guidance on fair value measurement under U.S. GAAP, the Fund discloses the fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between willing market participants at the measurement date (an exit price). Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). The three levels of the fair value hierarchy are described below:

| • | Level 1 — Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

| • | Level 2 — Other significant observable inputs (includes quoted prices for similar securities, interest rates, prepayment speeds, credit risk, referenced indices, quoted prices in inactive markets, adjusted quoted prices in inactive markets, etc.); and |

| • | Level 3 — Prices, inputs or exotic modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity). |

c. Federal and Foreign Income Taxes. It is the Fund’s intention to continue to qualify as a regulated investment company for Federal income tax purposes by complying with the appropriate provisions of Subchapter M of the Internal Revenue Code of 1986, as amended. Accordingly, no provisions for Federal income taxes have been made in the financial statements.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current period. The Fund did not record any tax provision in the current period. However, management’s conclusions

26| |

Notes to Financial Statements

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to, examination by tax authorities (i.e., the last 3 open tax year ends, as applicable), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

As of and during the year ended October 31, 2022, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year the Fund did not incur any significant interest or penalties.

d. Security Transactions and Investment Income. Security transactions are accounted for on trade date. Costs used in determining realized gains and losses on the sale of investment securities are based on the specific identification method. Dividend income is recorded on the ex-dividend date, interest income is recognized on the accrual basis from settlement date and includes the amortization of premiums and the accretion of discount. Realized gains (losses) on paydowns of mortgage-backed and asset-backed securities are recorded as an adjustment to interest income.

e. Expenses. Most expenses of the Trust can be directly attributed to a particular fund. Expenses which cannot be directly attributed to a particular fund are apportioned among the funds of the Trust based on the number of funds and/or relative net assets.

f. Dividends and Distributions to Shareholders. The Fund declares its dividends monthly and distributes its net investment income, if any, at least monthly and makes distributions of its net realized capital gains, if any, at least annually. All distributions are recorded on ex-dividend date.

g. Illiquid Securities. A security is considered illiquid if it cannot be sold or disposed of in the ordinary course of business within seven days or less for its approximate carrying value on the books of a Fund. Valuations of illiquid securities may differ significantly from the values that would have been used had an active market value for these securities existed.

3. Transactions with Affiliates. Certain officers of the Trust are also employees of SEI Investments Global Funds Services (the “Administrator”), a wholly owned subsidiary of SEI Investments Company, and/or SEI Investments Distribution Co. (the “Distributor”). Such officers are paid no fees by the Trust, other than the Chief Compliance Officer (“CCO”) as described below, for serving as officers of the Trust.

A portion of the services provided by the CCO and his staff, whom are employees of the Administrator, are paid for by the Trust as incurred. The services include regulatory oversight

| |27 |

Notes to Financial Statements

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

of the Trust’s Advisors and service providers as required by SEC regulations. The CCO’s services have been approved by and are reviewed by the Board.

4. Administration, Distribution, Transfer Agent and Custodian Agreements. The Fund and the Administrator are parties to an Administration Agreement, under which the Administrator provides management and administrative services to the Fund. For these services, the Administrator is paid an asset based fee, which will vary depending on the number of share classes and the average daily net assets of the Fund. For year ended October 31, 2022, the Fund paid $322,282 for these services.

The Trust and the Distributor are parties to a Distribution Agreement. The Distributor receives no fees under the Agreement.

DST Asset Manager Solutions, Inc. (“DST”) serves as transfer agent for the Fund under the transfer agency agreement with the Trust.

U.S. Bank, N.A. serves as custodian (the “Custodian”) for the Fund. The Custodian plays no role in determining the investment policies of the Fund or which securities are to be purchased or sold by the Fund.

5. Investment Advisory Agreement. Loomis, Sayles & Company, L.P. (“Loomis Sayles”) serves as investment adviser (the “Adviser”) to the Fund. Under the terms of the management agreement, the Fund does not pay a management fee. Shares of the Fund are only available to institutional advisory clients of the Adviser. The institutional advisory clients of the Adviser pay the Adviser or its affiliates a fee for their investment advisory services outside of the Fund. If advisory fee were charged within the Fund, the total return would have been lower.

The Adviser has contractually agreed to reduce fees and reimburse expenses in order to keep total annual fund operating expenses after fee reductions and/or expense reimbursements (excluding interest, taxes, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses) from exceeding 0.20% of the Fund’s Institutional Class Shares’ average daily net assets. This Agreement may only be terminated by the Board. Refer to waiver of expenses on the Statement of Operations for fees waived for the year ended October 31, 2022.

28| |

Notes to Financial Statements

October 31, 2022

Loomis Sayles Full Discretion Institutional Securitized Fund

6. Capital Shares.

| Year Ended | Year Ended | |||||||

| October 31, 2022 | October 31, 2021 | |||||||

SHARE TRANSACTIONS: | ||||||||

Issued | 10,244,468 | — | ||||||

Reinvestment of distributions | 1,596,119 | 1,266,108 | ||||||

Redeemed | (6,140,663) | (417,945) | ||||||

|

| |||||||

Net share transactions | 5,699,924 | 848,163 | ||||||

|

| |||||||

7. Investment Transactions. The cost of security purchases and proceeds from security sales, other than short-term securities, for the year ended October 31, 2022, were as follows:

| U.S. | ||||||||

| Government | Other | |||||||

Purchases | $ | 1,845,548 | $ | 64,114,567 | ||||

Sales | $ | 181,701 | $ | 45,736,903 | ||||