(Exact Name of Registrant as Specified in Charter)

Federated Investors Funds

4000 Ericsson Drive

Warrendale, Pennsylvania 15086-7561

(Address of Principal Executive Offices)

(412) 288-1900

(Registrant's Telephone Number)

John W. McGonigle, Esquire

Federated Investors Tower

1001 Liberty Avenue

Pittsburgh, Pennsylvania 15222-3779

(Name and Address of Agent for Service)

(Notices should be sent to the Agent for Service)

Date of Fiscal Year End: 09/30/2012

Date of Reporting Period: 09/30/2012

Item 1. Reports to Stockholders

Annual Shareholder Report

September 30, 2012

Share Class

Ticker

A

FMUUX

Institutional

FMUSX

Federated Municipal Ultrashort Fund

Fund Established 2000

A Portfolio of Federated Fixed Income Securities, Inc.

Dear Valued Shareholder,

I am pleased to present the Annual Shareholder Report for your fund covering the period from October 1, 2011 through September 30, 2012. This report includes Management's Discussion of Fund Performance, a complete listing of your fund's holdings, performance information and financial statements along with other important fund information.

In addition, our website, FederatedInvestors.com, offers easy access to Federated resources that include timely fund updates, economic and market insights from our investment strategists, and financial planning tools. We invite you to register to take full advantage of its capabilities.

Thank you for investing with Federated. I hope you find this information useful and look forward to keeping you informed.

Sincerely,

J. Christopher Donahue, President

Not FDIC Insured • May Lose Value • No Bank Guarantee

Management's Discussion of Fund Performance (unaudited)

The Fund's total return, based on net asset value, for the 12-month reporting period ended September 30, 2012, was 0.59% for the Class A Shares and 1.05% for the Institutional Shares. The total return of the Barclays 1-Year Municipal Bond Index (B1MB),1 the Fund's broad-based securities market index, was 0.94%, and the total return of the Lipper Tax-Exempt Money Market Funds Classification Average (LTEMMFCA),2 a peer group average for the Fund, was 0.01% during the same period. The Fund's total return for the most recently completed fiscal year reflected actual cash flows, transaction costs and other expenses that were not reflected in the total return of the B1MB.

During the reporting period, the Fund's investment strategy focused on: (a) the effective duration3 of its portfolio (which indicates the portfolio's price sensitivity to interest rates);4 (b) the selection of securities with different maturities (expressed by a yield curve showing the relative yield of securities with different maturities); (c) the allocation of the portfolio among securities of similar issuers (referred to as “sectors”); and (d) the credit quality and ratings of the portfolio securities (which indicates the risk that securities may default). These were the most significant factors affecting the Fund's performance relative to the B1MB.

The following discussion will focus on the Fund's Institutional Shares. The Fund's Institutional Shares 1.05% total return for the reporting period consisted entirely of tax-exempt dividend income, as the net asset value of the Fund finished the reporting period unchanged at $10.05 per share.5

MARKET OVERVIEW

During the 12-month reporting period, tax-exempt municipal bond yields dropped significantly, raising the values of existing bonds. At the very beginning of the reporting period, the tax-exempt bond market experienced a sharp technical sell-off, as supply outweighed demand after an extensive summer rally. During the rally, fund flows were sharply positive, as investors fled the equity and risk-based markets in favor of Treasuries and the attractive tax-exemption of municipal bond income. However, by late 2011 and well into 2012, tax-exempt municipal bond fund flows were once again consistently positive, particularly in the short and short-intermediate municipal portion of the yield curve. A lengthy rally in the tax-exempt municipal bond market received additional support from the “January Effect” at the beginning of 2012, which consisted of significant money being reinvested into the tax-exempt municipal bond market from bonds maturing and being called by issuers. Also, the amount of tax-exempt municipal bond issuance during the first quarter of 2012 was muted, which created a favorable technical environment (supply/demand imbalance) within the tax-exempt municipal bond market. This trend largely continued

throughout 2012 so that by the end of September, 2012, tax-exempt municipal bond fund inflows were consistently positive for 43 consecutive weeks and totaled over $44 billion during that period.

Treasury yields also declined significantly during the 12-month reporting period, and this powerful rally spilled over into the tax-exempt municipal bond market. The ten-year United States Treasury bond declined from a high of 2.40% in October of 2011 to a low of 1.39% in July of 2012 and ended the reporting period at 1.63%. In an attempt to support a stronger economic recovery, the Federal Reserve (Fed) maintained a highly accommodative monetary policy stance during the reporting period. Developments in Europe continued to be a central focus for investors, as concerns persisted about the prospects for a durable solution to the European fiscal and financial difficulties, which indirectly affected interest rate levels in the tax-exempt municipal bond market. The overriding positives for the tax-exempt municipal bond market during the reporting period were the sharp decline in Treasury yields, light tax-exempt new issue supply, the Fed maintaining its near-zero interest rate policy and the extremely low rate of municipal defaults despite persistent budget pressures for municipal issuers and headlines in the press to the contrary.

At the Fed's meeting in September 2012, in response to weak conditions, the Federal Open Market Committee (FOMC) continued to keep the target range for the federal funds rate at 0.0% to 0.25% and reiterated that economic conditions – including decelerating economic growth, strains in the global financial markets and a weak labor market –were likely to warrant exceptionally low levels for the federal funds rate at least through mid-2015. The Fed also announced open-end plans to purchase mortgage-backed securities to foster economic recovery and exert downward pressure on long-term interest rates. In Europe, the European Central Bank announced plans to purchase troubled peripheral nation sovereign debt to restrain market yields for countries willing to submit to fiscal constraints. On the municipal front, state and local governments continued to feel the stress of the weak recovery, property tax revenues that did not yet show the results of a nascent housing recovery and rising health care and pension costs for employees.

DURATION

The Fund is an ultrashort tax-exempt municipal bond fund and pursues a low volatility strategy. As such, during the 12-month reporting period, the Fund's typical dollar-weighted average duration generally ranged from six months to one year. As determined at the end of the reporting period, the Fund's dollar-weighted average duration was 0.90 years and the Fund's average dollar-weighted portfolio duration during the reporting period was approximately 0.85 years. The duration of the B1MB (which contains only bonds with maturities from one to two years) was 1.42 years at the end of the reporting period.

Because the Fund has a structural duration range and prospectus limit that is shorter than the duration of the B1MB, when interest rates decline, the Fund's net asset value will likely benefit less than the B1MB. The duration of the Fund relative to the B1MB slightly detracted from Fund performance during the reporting period, but helped the Fund significantly relative to the LTEMMFCA.

MATURITY/YIELD CURve

During the 12-month reporting period, the yield curve flattened as a result of yields on longer maturity bonds declining more than bonds with shorter maturities. Tax-exempt bonds with short-intermediate maturities (three to seven years) had more yield decline and better total return performance than those bonds with maturities from one to three years and zero to one year. Because the Fund continued to pursue a low volatility ultrashort duration strategy, and in order to provide a high degree of liquidity, the Fund was managed with an intention of maintaining a barbell structure consisting of: (a) a 45% to 55% weighting in very short-term maturity securities such as tax-exempt weekly reset municipal variable rate demand notes (MVRDNs), weekly reset municipal floating rate notes (MFRNs) and 90-day or less municipal commercial paper; and (b) a 45% to 55% weighting in tax-exempt fixed-rate municipal bonds with maturities generally from three months to five years.

The B1MB contains only bonds with maturities greater than one but less than two years and does not contain any bonds with less than one year remaining to maturity, nor does it include any MVRDNs or most MFRNs. The Fund's portfolio weighting in liquid MVRDNs and MFRNs of 40% to 50% slightly detracted from Fund performance relative to the B1MB, as these instruments slightly underperformed the positive price performance and total return of bonds contained in the B1MB. Many of the MVRDNs and MFRNs provided above-average tax-exempt income due to credit spread but none of the price gain of the one to two year fixed-rate bonds in the B1MB. The Fund also had significant weightings in tax-exempt, municipal bonds maturing from one to two years and two to five years and these holdings helped Fund performance relative to the B1MB.

SECTOR ALLOCATION

During the 12-month reporting period, as compared to the B1MB, the Fund allocated more of its portfolio to (i.e., was overweight in) securities in revenue bond yield sectors backed by hospitals, electric and gas, industrial development/pollution control projects, education, public power and transportation. Overall, revenue debt outperformed general obligation debt during the reporting period as state and local government budgets started to show renewed signs of strain due to weak economic, housing and employment conditions. Select revenue sectors were significant outperformers, namely hospitals and industrial development bonds backed by corporate obligors. The Fund allocated less of the portfolio to (i.e. was underweight in) general obligation bonds and pre-refunded

bonds (bonds for which principal and interest payments are secured or guaranteed by cash or U.S. Treasury securities held in an escrow account) compared to the B1MB.

These allocations helped the Fund's performance due to narrowing of credit spreads within several of the overweight revenue sectors during the reporting period. Also, the Fund's significant underweight in general obligation bonds, which makes up a large portion of the B1MB, helped Fund performance relative to the B1MB because revenue debt generally outperformed general obligation debt during the reporting period. Because of the demand for short maturity yield paper in an ultra-low yield environment, “AAA” rated pre-refunded bonds (and unrated bonds of comparable quality) lagged the overall B1MB return, so the Fund's underweight allocation helped the Fund's relative performance.

CREDIT QUALITY6

During the 12-month reporting period, risk-taking was rewarded for investors as absolute yields in the market place reached new lows and investors attempted to add income by reaching into lower credit quality categories. Headline risk concerning municipal credit quality dampened, although the risks of a high profile municipal issuer becoming distressed continued to increase as local municipalities struggled. This strong investor demand for “yield paper” and credit spread contraction resulted in outperformance of bonds rated “A” or “BBB” (or unrated bonds of comparable quality) relative to bonds rated in the higher rating categories (or unrated bonds of comparable quality). During the reporting period, the Fund increased its exposure to “A”-rated paper while decreasing its exposure to “AA”-rated paper. Allocations to “AAA” and “BBB”-rated paper remained relatively unchanged during the reporting period. The Fund was significantly overweight “A” and “BBB”-rated paper and significantly underweight “AAA” and “AA”-rated paper during the reporting period relative to the B1MB.

With the decline in credit spreads during the reporting period, and the reduction of credit spreads to a lesser extent for “AAA” and “AA”-rated debt (or unrated bonds of comparable quality), the Fund's significant overweight position, relative to the B1MB, in “A” and “BBB”-rated debt (or unrated bonds of comparable quality) during the reporting period substantially helped the Fund's performance, as the yield on “A” and “BBB”-rated debt (or unrated bonds of comparable quality) decreased to a greater extent than for other investment-grade securities.

The Fund also had a slight weighting, less than 0.5%, in high yield (noninvestment-grade) municipal debt, which outperformed during the reporting period and added to the performance of the Fund relative to the B1MB.

Barclays Capital changed the name of the B1MB from “Barclays Capital 1-Year Municipal Bond Index” to “Barclays 1-Year Municipal Bond Index.” Please see the footnotes to the line graphs under “Fund Performance and Growth of a $10,000 Investment” below for the definition of, and more information about, the B1MB.

2

Please see the footnotes to the line graphs under “Fund Performance and Growth of a $10,000 Investment” below for the definition of, and more information about, the LTEMMFCA.

3

Duration is a measure of a security's price sensitivity to changes in interest rates. Securities with longer durations are more sensitive to changes in interest rates than securities with shorter durations. For purposes of this Management's Discussion of Fund Performance, duration is determined using a third-party analytical system.

4

Bond prices are sensitive to changes in interest rates and a rise in interest rates can cause a decline in their prices.

5

Income may be subject to the federal alternative minimum tax, as well as state and local taxes.

6

Investment-grade securities and noninvestment-grade securities may either be: (a) rated by a nationally recognized statistical ratings organization or rating agency; or (b) unrated securities that the Fund's investment adviser (“Adviser”) believes are of comparable quality. The rating agencies that provided the ratings for rated securities include Standard & Poor's, Moody's Investor Services, Inc. and Fitch Rating Service. When ratings vary, the highest rating is used. Credit ratings of “AA” or better are considered to be high credit quality; credit ratings of “A” are considered high or medium/good quality; and credit ratings of “BBB” are considered to be medium/good credit quality, and the lowest category of investment-grade securities; credit ratings of “BB” and below are lower-rated, noninvestment-grade securities or junk bonds; and credit ratings of “CCC” or below are noninvestment-grade securities that have high default risk. Any credit quality breakdown does not give effect to the impact of any credit derivative investments made by the Fund. Credit ratings are an indication of the risk that a security will default. They do not protect a security from credit risk. Lower rated bonds typically offer higher yields to help compensate investors for the increased risk associated with them. Among these risks are lower creditworthiness, greater price volatility, more risk to principal and income than with higher rated securities and increased possibilities of default.

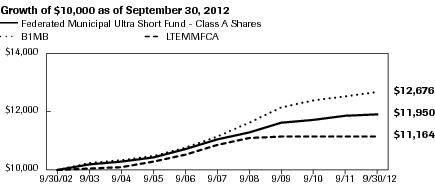

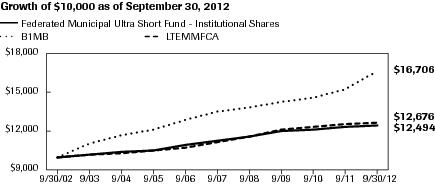

FUND PERFORMANCE AND GROWTH OF A $10,000 INVESTMENT

The Average Annual Total Return table below shows returns for each class averaged over the stated periods. The graphs below illustrate the hypothetical investment of $10,0001 in the Federated Municipal Ultrashort Fund (the “Fund”) from September 30, 2002 to September 30, 2012, compared to the Barclays 1-Year Municipal Bond Index (B1MB)2 and the Lipper Tax-Exempt Money Market Funds Classification Average (LTEMMFCA).3

Average Annual Total Returns for the Period Ended 9/30/2012

(returns reflect all applicable sales charges as specified below in footnote #1)

Share Class

1 Year

5 Years

10 Years

A

-1.46%

1.18%

1.58%

Institutional

1.05%

2.04%

2.25%

Performance data quoted represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Mutual fund performance changes over time and current performance may be lower or higher than what is stated. For current to the most recent month-end performance and after-tax returns, visit FederatedInvestors.com or call 1-800-341-7400. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured.

Growth of a $10,000 Investment - InStitutional Shares

Federated Municipal Ultra Short Fund -

Institutional Shares

B1MB

LTEMMFCA

9/30/2002

10,000

10,000

10,000

9/30/2003

10,243

10,233

10,065

9/30/2004

10,366

10,349

10,115

9/30/2005

10,561

10,469

10,269

9/30/2006

10,916

10,762

10,542

9/30/2007

11,294

11,160

10,867

9/30/2008

11,603

11,629

11,097

9/30/2009

12,029

12,176

11,157

9/30/2010

12,180

12,392

11,161

9/30/2011

12,364

12,558

11,163

9/30/2012

12,494

12,676

11,164

41 graphic description end -->

1

Represents a hypothetical investment of $10,000. Effective February 14, 2003, a maximum sales charge of 2.00% ($10,000 investment minus $200 sales charge = $9,800) for newly purchased Class A Shares was implemented. The line graphs above reflect any front-end sales charge, as applicable, as of the date of the initial investment. The Average Annual Total Returns reflect the current sales charge applicable to each class, if any. The Fund's performance assumes the reinvestment of all dividends and distributions. The B1MB and the LTEMMFCA have been adjusted to reflect reinvestment of dividends on securities in the index and the average.

2

Barclays Capital changed the name of the B1MB from “Barclays Capital 1-Year Municipal Bond Index” to “Barclays 1-Year Municipal Bond Index.” The B1MB is the one-year (1-2) component of the Barclays Municipal Bond Index. The Barclays Municipal Bond Index is an unmanaged index of tax-exempt municipal bonds issued after December 31, 1990, with a minimum credit rating of at least Baa3 or BBB-, which have been issued as part of a deal of at least $75 million, have a minimum maturity value of at least $7 million and mature in at least one, but not more than two years. The B1MB also includes both zero coupon bonds and bonds subject to the alternative minimum tax (AMT). The B1MB is not adjusted to reflect sales charges, expenses or other fees that the Securities and Exchange Commission requires to be reflected in the Fund's performance. The Fund is not a money market fund and is not subject to the special regulatory requirements (including maturity and credit quality constraints) designed to enable money market funds to maintain a stable share price. The B1MB is unmanaged, and unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an index.

3

Lipper figures represent the average of the total returns reported by all the mutual funds designated by Lipper, Inc. as falling into the respective categories indicated. They do not reflect sales charges.

Portfolio of Investments Summary Table (unaudited)

At September 30, 2012, the Fund's sector composition1 was as follows:

Sector Composition

Percentage of Total Net Assets

General Obligation—State

15.2%

Hospital

14.6%

General Obligation—Local

12.4%

Industrial Development Bond/Pollution Control Revenue

11.9%

Electric & Gas

10.5%

Transportation

9.9%

Public Power

4.5%

Education

4.3%

Special Tax

4.0%

Water & Sewer

2.9%

Other2

10.0%

Other Assets and Liabilities—Net3

(0.2)%

TOTAL

100.0%

1

Sector classifications, and the assignment of holdings to such sectors, are based upon the economic sector and/or revenue source of the underlying obligor, as determined by the Fund's Adviser. For securities that have been enhanced by a third-party, including bond insurers and banks, sector classifications are based upon the economic sector and/or revenue source of the underlying obligor, as determined by the Fund's Adviser.

2

For purposes of this table, sector classifications constitute 90.2% of the Fund's total net assets. Remaining sectors have been aggregated under the designation “Other.”

3

Assets, other than investments in securities, less liabilities. See Statement of Assets and Liabilities.

Connecticut State, UT GO SIFMA Index Bonds (Series 2012A), 0.58%, 4/15/2015

$4,501,125

5,000,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012A), 0.71%, 4/15/2016

5,006,350

4,000,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012A), 0.86%, 4/15/2017

4,010,280

4,500,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012A), 1.06%, 4/15/2018

4,514,355

3,500,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012D), 0.46%, 9/15/2015

3,501,505

3,000,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012D), 0.60%, 9/15/2016

3,000,660

1,875,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012D), 0.69%, 9/15/2017

1,881,750

2,500,000

Connecticut State, UT GO SIFMA Index Bonds (Series 2012D), 0.94%, 9/15/2018

2,511,575

2,050,000

West Haven, CT, 3.00% BANs, 5/30/2013

2,070,377

600,000

West Haven, CT, UT GO Bonds, 3.00% (Assured Guaranty Municipal Corp. INS), 8/1/2015

616,446

2,000,000

West Haven, CT, UT GO Bonds, 4.00% (Assured Guaranty Municipal Corp. INS), 8/1/2017

2,158,800

1,000,000

West Haven, CT, UT GO Bonds, 4.00%, 8/1/2013

1,018,440

500,000

West Haven, CT, UT GO Bonds, 4.00%, 8/1/2014

519,375

2,500,000

West Haven, CT, UT GO Bonds, 5.00% (Assured Guaranty Municipal Corp. INS), 8/1/2016

2,766,500

TOTAL

78,615,464

District of Columbia—1.6%

10,000,000

District of Columbia Income Tax Revenue, Income Tax Secured Revenue Refunding Bonds (Series 2011B), 0.78%, 12/1/2015

10,000,400

13,285,000

District of Columbia Income Tax Revenue, Income Tax Secured Revenue Refunding Bonds (Series 2011B), 0.93%, 12/1/2017

13,286,328

10,000,000

District of Columbia Income Tax Revenue, Income Tax Secured Revenue Refunding Bonds (Series 2011E), 0.78%, 12/1/2015

10,000,400

3,000,000

District of Columbia Revenue, University Refunding Revenue Bonds (Series 2009A), 5.00% (Georgetown University), 4/1/2013

3,071,190

15,150,000

District of Columbia Water & Sewer Authority, Public Utility Subordinate Lien Multimodal Revenue Bonds (Series 2012B-1), 0.66% TOBs, Mandatory Tender 6/1/2015

15,151,212

12,000,000

District of Columbia Water & Sewer Authority, Public Utility Subordinate Lien Multimodal Revenue Bonds (Series 2012B-2), 0.76% TOBs, Optional Tender 6/1/2016

Cleveland, OH Public Power System, Revenue Refunding Bonds (Series 2010), 5.00%, 11/15/2014

$5,421,350

8,000,000

Ohio State Air Quality Development Authority, Air Quality Revenue Refunding Bonds (Series 2009A), 3.875% TOBs (Columbus Southern Power Company), Mandatory Tender 6/1/2014

8,248,160

25,890,000

Ohio State Air Quality Development Authority, PCR Refunding Bonds (Series 2006A), 2.25% TOBs (FirstEnergy Solutions Corp.), Mandatory Tender 6/3/2013

26,059,062

20,000,000

Ohio State Air Quality Development Authority, PCR Refunding Bonds (Series 2009D), 2.25% TOBs (FirstEnergy Solutions Corp.), Mandatory Tender 9/15/2016

Canadian County Educational Facilities Authority, OK, Educational Facilities Lease Revenue Bonds (Series 2012), 3.50% (Mustang Public Schools), 9/1/2017

$1,172,128

1,390,000

Canadian County Educational Facilities Authority, OK, Educational Facilities Lease Revenue Bonds (Series 2012), 4.00% (Mustang Public Schools), 9/1/2018

1,568,615

1,000,000

Oklahoma County, OK Finance Authority, Educational Facilities Lease Revenue Bonds (Series 2010), 4.00% (Putnam City Public Schools), 3/1/2013

1,013,280

1,205,000

Oklahoma County, OK Finance Authority, Educational Facilities Lease Revenue Bonds (Series 2012), 2.00% (Midwest City-Del City Public Schools), 3/1/2013

1,212,712

1,000,000

Oklahoma County, OK Finance Authority, Educational Facilities Lease Revenue Bonds (Series 2012), 2.00% (Midwest City-Del City Public Schools), 3/1/2014

1,018,550

1,500,000

Oklahoma County, OK Finance Authority, Educational Facilities Lease Revenue Bonds (Series 2012), 2.00% (Midwest City-Del City Public Schools), 3/1/2015

1,540,950

4,390,000

Oklahoma County, OK Finance Authority, Educational Facilities Lease Revenue Bonds (Series 2012), 3.00% (Midwest City-Del City Public Schools), 3/1/2017

4,698,266

5,345,000

Oklahoma County, OK Finance Authority, Educational Facilities Lease Revenue Bonds (Series 2012), 4.00% (Midwest City-Del City Public Schools), 3/1/2016

West Virginia University Board of Governors, University Improvement Revenue Bonds (Series 2011B), 4.00% (West Virginia University), 10/1/2015

$412,425

800,000

West Virginia University Board of Governors, University Improvement Revenue Bonds (Series 2011B), 5.00% (West Virginia University), 10/1/2014

871,256

700,000

West Virginia University Board of Governors, University Improvement Revenue Bonds (Series 2011B), 5.00% (West Virginia University), 10/1/2015

790,678

21,225,000

West Virginia University Board of Governors, University Improvement Variable Rate Revenue Bonds (Series 2011C), 0.83% TOBs (West Virginia University), Mandatory Tender 10/1/2014

21,229,033

TOTAL

65,824,375

Wisconsin—0.7%

12,000,000

Wisconsin Health & Educational Facilities Authority, Revenue Bonds (Series 2009B), 4.75% TOBs (Aurora Health Care, Inc.), Mandatory Tender 8/15/2014

Gulf Shores, AL Medical Clinic Board, (Series 2007) Weekly VRDNs (Colonial Pinnacle MOB, LLC)/(Regions Bank, Alabama LOC), 0.80%, 10/4/2012

$5,960,000

TOTAL

13,035,000

Arkansas—0.2%

6,400,000

Pulaski County, AR Public Facilities Board, (Series 2005: Markham Oaks and Indian Hills Apartments) Weekly VRDNs (Bailey Properties, LLC)/(Regions Bank, Alabama LOC), 1.10%, 10/4/2012

6,400,000

Colorado—1.0%

15,250,000

Denver (City & County), CO, (Series 2007G-1) Daily VRDNs (Denver, CO City & County Airport Authority)/(Assured Guaranty Corp. INS)/(Morgan Stanley Bank, N.A. LIQ), 0.23%, 10/1/2012

15,250,000

6,000,000

Denver (City & County), CO, (Series 2007G-2) Daily VRDNs (Denver, CO City & County Airport Authority)/(Assured Guaranty Corp. INS)/(Morgan Stanley Bank, N.A. LIQ), 0.23%, 10/1/2012

Miami, FL Health Facilities Authority, (Series 2005) Weekly VRDNs (Miami Jewish Home and Hospital for the Aged, Inc.)/(SunTrust Bank LOC), 0.37%, 10/3/2012

11,230,000

4,000,000

Orange County, FL IDA, (Series 2000) Weekly VRDNs (Central Florida Kidney Centers, Inc.)/(SunTrust Bank LOC), 0.37%, 10/3/2012

4,000,000

3,105,000

Orange County, FL IDA, (Series 2004) Weekly VRDNs (UCF Hospitality School Student Housing Foundation)/(SunTrust Bank LOC), 0.37%, 10/3/2012

3,105,000

8,135,000

Orange County, FL, Health Facilities Authority, (Series 2008) Weekly VRDNs (Lakeside Behavioral Healthcare, Inc.)/(SunTrust Bank LOC), 0.37%, 10/3/2012

8,135,000

15,080,000

Pinellas County, FL Health Facility Authority, (Series 2004) Daily VRDNs (Bayfront Obligated Group)/(SunTrust Bank LOC), 0.25%, 10/1/2012

15,080,000

TOTAL

51,065,000

Georgia—2.7%

43,345,000

Albany-Dougherty County, GA Hospital Authority, (Series 2008A) Daily VRDNs (Phoebe Putney Memorial Hospital)/(SunTrust Bank LOC), 0.25%, 10/1/2012

43,345,000

14,200,000

Albany-Dougherty County, GA Hospital Authority, (Series 2008B) Daily VRDNs (Phoebe Putney Memorial Hospital)/(Regions Bank, Alabama LOC), 0.50%, 10/1/2012

Clayton County, GA Housing Authority, (Series 2004: Ashton Walk Apartments) Weekly VRDNs (Ashton Forest Park LP)/(Regions Bank, Alabama LOC), 1.10%, 10/4/2012

$7,970,000

10,950,000

Clayton County, GA Housing Authority, (Series 2006) Weekly VRDNs (Provence Place Apartments)/(Regions Bank, Alabama LOC), 1.05%, 10/4/2012

10,950,000

3,760,000

Fulton County, GA IDA, (Series 2005) Weekly VRDNs (Phoenix Stamping Group LLC)/(Federal Home Loan Bank of Atlanta LOC), 0.38%, 10/4/2012

3,760,000

15,880,000

5,6

Metropolitan Atlanta Rapid Transit Authority, GA, P-FLOATs (Series PT-4042) Weekly VRDNs (Dexia Credit Local LIQ)/(Dexia Credit Local LOC), 0.68%, 10/4/2012

15,880,000

12,900,000

Walker, Dade & Catoosa Counties, GA Hospital Authority, (Series 2008) Weekly VRDNs (Hutcheson Medical Center, Inc.)/(Regions Bank, Alabama LOC), 0.80%, 10/4/2012

12,900,000

TOTAL

109,005,000

Illinois—0.3%

11,250,000

5,6

Illinois Finance Authority, ROCs (Series 11503) Weekly VRDNs (Resurrection Health Care Corp.)/(Assured Guaranty Municipal Corp. INS)/(Citibank NA, New York LIQ), 0.43%, 10/4/2012

11,250,000

Indiana—0.6%

22,250,000

Indiana State Finance Authority Environmental Revenue, (Series 2006) Weekly VRDNs (Mittal Steel USA, Inc.)/(Banco Bilbao Vizcaya Argentaria SA LOC), 0.85%, 10/3/2012

New Jersey EDA, (Series 2003B) Weekly VRDNs (Port Newart Container Terminal LLC)/(Sovereign Bank LOC), 2.00%, 10/4/2012

$26,200,000

TOTAL

46,050,000

New York—1.7%

16,600,000

New York City, NY, (Fiscal 2008 Subseries J-7) Weekly VRDNs (Landesbank Baden-Wurttemberg LOC), 0.65%, 10/4/2012

16,600,000

6,000,000

New York City, NY, (Series 1994A-5) Daily VRDNs (KBC Bank N.V. LOC), 0.33%, 10/1/2012

6,000,000

32,900,000

New York State HFA, (Series 2008A: Related 42nd & 10th) Weekly VRDNs (42nd and 10th Associates, LLC)/(Landesbank Baden-Wurttemberg LOC), 0.48%, 10/3/2012

32,900,000

11,400,000

New York State HFA, (Series 2010A) Weekly VRDNs (42nd and 10th Associates, LLC)/(Landesbank Baden-Wurttemberg LOC), 0.48%, 10/3/2012

11,400,000

TOTAL

66,900,000

North Carolina—0.4%

14,045,000

5,6

North Carolina Eastern Municipal Power Agency, P-FLOATs (Series PT-4112) Weekly VRDNs (Dexia Credit Local LIQ)/(Dexia Credit Local LOC), 0.88%, 10/4/2012

14,045,000

Ohio—2.1%

71,370,000

Ohio HFA, Mortgage-Backed Securities Program (Series 2010B) Weekly VRDNs (GNMA COL)/(KBC Bank N.V. LIQ), 0.60%, 10/3/2012

71,370,000

14,575,000

Ohio HFA, Mortgage-Backed Securities Program (Series 2010C) Weekly VRDNs (GNMA COL)/(KBC Bank N.V. LIQ), 0.60%, 10/3/2012

14,575,000

TOTAL

85,945,000

Pennsylvania—1.0%

39,300,000

Luzerne County, PA, (Series A of 2006) Weekly VRDNs (Assured Guaranty Municipal Corp. INS)/(JPMorgan Chase Bank, N.A. LIQ), 0.39%, 10/4/2012

39,300,000

Rhode Island—0.1%

2,935,000

Rhode Island State Health and Educational Building Corp., (Series 2005A: Catholic School Pool Program Issue) Daily VRDNs (RBS Citizens Bank N.A. LOC), 0.21%, 10/1/2012

2,935,000

Tennessee—0.5%

13,000,000

Blount County, TN Public Building Authority, Local Government Public Improvement Bonds (Series E-3-A) Daily VRDNs (Cumberland County, TN)/(KBC Bank N.V. LOC), 0.55%, 10/1/2012

Sevier County, TN Public Building Authority, Local Government Public Improvement Bonds (Series VII-A-4) Daily VRDNs (Sevier County, TN)/(KBC Bank N.V. LOC), 0.55%, 10/1/2012

Sevier County, TN Public Building Authority, Local Government Public Improvement Bonds (Series VII-A-5) Daily VRDNs (Bradley County, TN)/(KBC Bank N.V. LOC), 0.55%, 10/1/2012

$4,340,000

TOTAL

20,795,000

Texas—1.7%

56,400,000

Oakbend, TX HFDC, (Series 2008) Daily VRDNs (Oakbend Medical Center)/(Regions Bank, Alabama LOC), 0.58%, 10/1/2012

Albemarle County, VA IDA, (Series 2007) Weekly VRDNs (Jefferson Scholars Foundation)/(SunTrust Bank LOC), 0.37%, 10/3/2012

16,000,000

21,550,000

Halifax, VA IDA, MMMs, PCR (Series 1992), 1.15% CP (Virginia Electric & Power Co.), Mandatory Tender 10/19/2012

21,550,215

TOTAL

37,550,215

West Virginia—0.1%

3,000,000

Grant County, WV County Commission, PCRB (Series 1994), 0.40% CP (Virginia Electric & Power Co.), Mandatory Tender 11/2/2012

3,000,000

TOTAL SHORT-TERM MUNICIPALS (IDENTIFIED COST $934,700,000)

934,701,481

TOTAL MUNICIPAL INVESTMENTS—100.2% (IDENTIFIED COST $3,993,732,877)8

4,016,562,377

OTHER ASSETS AND LIABILITIES - NET—(0.2)%9

(6,582,550)

TOTAL NET ASSETS—100%

$4,009,979,827

Securities that are subject to the federal alternative minimum tax (AMT) represent 11.1% of the portfolio as calculated based upon total market value (percentage is unaudited).

1

Non-income producing security.

2

Floating rate note with current rate shown.

3

Security in default.

4

Principal amount and interest were not paid upon final maturity.

5

Denotes a restricted security that either: (a) cannot be offered for public sale without first being registered, or being able to take advantage of an exemption from registration, under the Securities Act of 1933; or (b) is subject to a contractual restriction on public sales. At September 30, 2012, these restricted securities amounted to $92,877,750, which represented 2.3% of total net assets.

6

Denotes a restricted security that may be resold without restriction to “qualified institutional buyers” as defined in Rule 144A under the Securities Act of 1933 and that the Fund has determined to be liquid under criteria established by the Fund's Board of Directors (the “Directors”). At September 30, 2012, these liquid restricted securities amounted to $92,877,750, which represented 2.3% of total net assets.

7

Current rate and next reset date shown for Variable Rate Demand Notes.

8

The cost of investments for federal tax purposes amounts to $3,993,630,435.

9

Assets, other than investments in securities, less liabilities. See Statement of Assets and Liabilities.

Note: The categories of investments are shown as a percentage of total net assets at September 30, 2012.

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1—quoted prices in active markets for identical securities, including investment companies with daily net asset values, if applicable.

Level 2—other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Also includes securities valued at amortized cost.

Level 3—significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

As of September 30, 2012, all investments of the Fund utilized Level 2 inputs in valuing the Fund's assets carried at fair value.

Net realized and unrealized gain (loss) on investments

0.002

0.01

0.02

0.10

(0.11)

TOTAL FROM INVESTMENT OPERATIONS

0.06

0.11

0.08

0.31

0.22

Less Distributions:

Distributions from net investment income

(0.06)

(0.10)

(0.06)

(0.21)

(0.32)

Net Asset Value, End of Period

$10.05

$10.05

$10.04

$10.02

$9.92

Total Return3

0.59%

1.06%

0.81%

3.21%

2.27%

Ratios to Average Net Assets:

Net expenses

0.79%4

0.80%

0.80%

0.80%4

0.80%4

Net investment income

0.58%

0.95%

0.61%

1.77%

3.12%

Expense waiver/reimbursement5

0.44%

0.41%

0.42%

0.44%

0.45%

Supplemental Data:

Net assets, end of period (000 omitted)

$2,198,969

$1,797,275

$1,982,542

$2,543,523

$566,536

Portfolio turnover

66%

92%

37%

44%

123%

1

Beginning with the year ended September 30, 2010, the Fund was audited by KPMG LLP. The previous years were audited by another independent registered public accounting firm.

2

Represents less than $0.01.

3

Based on net asset value, which does not reflect the sales charge, redemption fee or contingent deferred sales charge, if applicable.

4

The net expense ratio is calculated without reduction for expense offset arrangements. The net expense ratios are 0.79%, 0.80% and 0.80% for the years ended September 30, 2012, 2009 and 2008, respectively, after taking into account these expense reductions.

5

This expense decrease is reflected in both the net expense and net investment income ratios shown above.

See Notes which are an integral part of the Financial Statements

Net realized and unrealized gain (loss) on investments

0.002

0.01

0.02

0.10

(0.10)

TOTAL FROM INVESTMENT OPERATIONS

0.10

0.15

0.13

0.36

0.27

Less Distributions:

Distributions from net investment income

(0.10)

(0.14)

(0.11)

(0.26)

(0.37)

Net Asset Value, End of Period

$10.05

$10.05

$10.04

$10.02

$9.92

Total Return3

1.05%

1.51%

1.26%

3.67%

2.73%

Ratios to Average Net Assets:

Net expenses

0.34%4

0.35%

0.35%

0.35%4

0.35%4

Net investment income

1.02%

1.40%

1.06%

2.25%

3.64%

Expense waiver/reimbursement5

0.40%

0.36%

0.37%

0.39%

0.40%

Supplemental Data:

Net assets, end of period (000 omitted)

$1,811,011

$1,245,370

$1,195,878

$875,235

$194,720

Portfolio turnover

66%

92%

37%

44%

123%

1

Beginning with the year ended September 30, 2010, the Fund was audited by KPMG LLP. The previous years were audited by another independent registered public accounting firm.

2

Represents less than $0.01.

3

Based on net asset value.

4

The net expense ratio is calculated without reduction for expense offset arrangements. The net expense ratios are 0.34%, 0.35% and 0.35% for the years ended September 30, 2012, 2009 and 2008, respectively, after taking into account these expense reductions.

5

This expense decrease is reflected in both the net expense and net investment income ratios shown above.

See Notes which are an integral part of the Financial Statements

Federated Fixed Income Securities, Inc. (the “Corporation”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company. The Corporation consists of two portfolios. The financial statements included herein are only those of Federated Municipal Ultrashort Fund (the “Fund”), a diversified portfolio. The financial statements of the other portfolio are presented separately. The assets of each portfolio are segregated and a shareholder's interest is limited to the portfolio in which shares are held. Each portfolio pays its own expenses. The Fund offers two classes of shares: Class A Shares and Institutional Shares. All shares of the Fund have equal rights with respect to voting, except on class-specific matters. The investment objective of the Fund is to provide current income exempt from federal regular income tax. Interest income from the Fund's investments may be subject to the federal AMT for individuals and corporations and state and local taxes.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. These policies are in conformity with U.S. generally accepted accounting principles (GAAP).

Investment Valuation

In calculating its net asset value (NAV), the Fund generally values investments as follows:

■

Fixed-income securities acquired with remaining maturities greater than 60 days are fair valued using price evaluations provided by a pricing service approved by the Directors.

■

Fixed-income securities acquired with remaining maturities of 60 days or less are valued at their cost (adjusted for the accretion of any discount or amortization of any premium), which approximates market value.

■

Shares of other mutual funds are valued based upon their reported NAVs.

■

Derivative contracts listed on exchanges are valued at their reported settlement or closing price.

■

Over-the-counter (OTC) derivative contracts are fair valued using price evaluations provided by a pricing service approved by the Directors.

■

For securities that are fair valued in accordance with procedures established by and under the general supervision of the Directors, certain factors may be considered such as: the purchase price of the security, information obtained by contacting the issuer, analysis of the issuer's financial statements or other available documents, fundamental analytical data, the nature and duration of restrictions on disposition, the movement of the market in which the security is normally traded and public trading in similar securities of the issuer or comparable issuers.

If the Fund cannot obtain a price or price evaluation from a pricing service for an investment, the Fund may attempt to value the investment based upon the mean of bid and asked quotations or fair value the investment based on price evaluations, from one or more dealers. If any price, quotation, price evaluation or other pricing source is not readily available when the NAV is calculated, the Fund uses the fair value of the investment determined in accordance with the procedures described below. There can be no assurance that the Fund could purchase or sell an investment at the price used to calculate the Fund's NAV.

The Directors have appointed a Valuation Committee comprised of officers of the Fund, Federated Investment Management Company (“Adviser”) and the Adviser's affiliated companies to determine fair value of securities and in overseeing the calculation of the NAV. The Directors have also authorized the use of pricing services recommended by the Valuation Committee to provide fair value evaluations of the current value of certain investments for purposes of calculating the NAV. The Valuation Committee employs various methods for reviewing third-party pricing service evaluations including periodic reviews of third-party pricing services' policies, procedures and valuation methods (including key inputs and assumptions), transactional back-testing, comparisons of evaluations of different pricing services and review of price challenges by the Adviser based on recent market activity. In the event that market quotations and price evaluations are not available for an investment, the Valuation Committee determines the fair value of the investment in accordance with procedures adopted by the Directors. The Directors periodically review and approve the fair valuations made by the Valuation Committee and any changes made to the procedures. Factors considered by pricing services in evaluating an investment include the yields or prices of investments of comparable quality, coupon, maturity, call rights and other potential prepayments, terms and type, reported transactions, indications as to values from dealers and general market conditions. Some pricing services provide a single price evaluation reflecting the bid-side of the market for an investment (a “bid” evaluation). Other pricing services offer both bid evaluations and price evaluations indicative of a price between the prices bid and asked for the investment (a “mid” evaluation). The Fund normally uses bid evaluations for U.S. Treasury and Agency securities and municipal securities. The Fund normally uses mid evaluations for other types of fixed-income securities and OTC derivative contracts. In the event that market quotations and price evaluations are not available for an investment, the fair value of the investment is determined in accordance with procedures adopted by the Directors.

Investment Income, Gains and Losses, Expenses and Distributions

Investment transactions are accounted for on a trade-date basis. Realized gains and losses from investment transactions are recorded on an identified-cost basis. Interest income and expenses are accrued daily. Distributions to shareholders are recorded on the ex-dividend date. Distributions of net investment income are declared daily and paid monthly. Non-cash dividends included in dividend income, if any, are recorded at fair value. Investment income, realized and unrealized gains and losses and certain fund-level expenses are allocated to each class based on relative average daily net assets, except that Class A Shares and Institutional Shares may bear account administration fees, distribution services fees and shareholder services fees unique to those classes. For the year ended September 30, 2012, account administration fees for the Fund were as follows:

Account Administration Fees Incurred

Class A Shares

$12,715

Dividends are declared separately for each class. No class has preferential dividend rights; differences in per share dividend rates are generally due to differences in separate class expenses.

The Bank of New York Mellon, the Fund's custodian and portfolio accounting agent, voluntarily agreed to waive all fees due from the Fund for the year ended September 30, 2012. This level of waiver is not expected to occur in the future.

Premium and Discount Amortization

All premiums and discounts on fixed-income securities are amortized/accreted using the effective interest rate method.

Federal Taxes

It is the Fund's policy to comply with the Subchapter M provision of the Internal Revenue Code (the “Code”) and to distribute to shareholders each year substantially all of its income. Accordingly, no provision for federal income tax is necessary. As of and during the year ended September 30, 2012, the Fund did not have a liability for any uncertain tax positions. The Fund recognizes interest and penalties, if any, related to tax liabilities as income tax expense in the Statement of Operations. As of September 30, 2012, tax years 2009 through 2012 remain subject to examination by the Fund's major tax jurisdictions, which include the United States of America, the state of Maryland and the Commonwealth of Pennsylvania.

Other Taxes

As an open-end management investment company incorporated in the state of Maryland but domiciled in the Commonwealth of Pennsylvania, the Fund is subject to the Pennsylvania Franchise Tax. This franchise tax is assessed annually on the value of the Fund, as represented by average net assets for the tax year.

When-Issued and Delayed Delivery Transactions

The Fund may engage in when-issued or delayed delivery transactions. The Fund records when-issued securities on the trade date and maintains security positions such that sufficient liquid assets will be available to make payment for the securities purchased. Securities purchased on a when-issued or delayed delivery basis are marked to market daily and begin earning interest on the settlement date. Losses may occur on these transactions due to changes in market conditions or the failure of counterparties to perform under the contract.

Restricted Securities

The Fund may purchase securities which are considered restricted. Restricted securities are securities that either: (a) cannot be offered for public sale without first being registered, or being able to take advantage of an exemption from registration, under the Securities Act of 1933; or (b) are subject to contractual restrictions on public sales. In some cases, when a security cannot be offered for public sale without first being registered, the issuer of the restricted security has agreed to register such securities for resale, at the issuer's expense, either upon demand by the Fund or in connection with another registered offering of the securities. Many such restricted securities may be resold in the secondary market in transactions exempt from registration. Restricted securities may be determined to be liquid under criteria established by the Directors. The Fund will not incur any registration costs upon such resales. The Fund's restricted securities are valued at the price provided by dealers in the secondary market or, if no market prices are available, at the fair value as determined in accordance with procedures established by and under the general supervision of the Directors.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts of assets, liabilities, expenses and revenues reported in the financial statements. Actual results could differ from those estimated.

3. Capital Stock

The following tables summarize capital stock activity:

Year Ended September 30

2012

2011

Class A Shares:

Shares

Amount

Shares

Amount

Shares sold

190,923,524

$1,918,181,698

143,913,183

$1,443,617,031

Shares issued to shareholders in payment of distributions declared

1,119,990

11,251,266

1,499,307

15,036,578

Shares redeemed

(152,192,310)

(1,529,162,655)

(163,939,435)

(1,643,735,508)

NET CHANGE RESULTING FROM CLASS A SHARE TRANSACTIONS

39,851,204

$400,270,309

(18,526,945)

$(185,081,899)

Year Ended September 30

2012

2011

Institutional Shares:

Shares

Amount

Shares

Amount

Shares sold

173,960,443

$1,747,814,747

130,889,300

$1,313,000,702

Shares issued to shareholders in payment of distributions declared

985,854

9,905,297

768,733

7,709,573

Shares redeemed

(118,760,190)

(1,193,194,531)

(126,787,408)

(1,271,247,228)

NET CHANGE RESULTING FROM INSTITUTIONAL SHARE TRANSACTIONS

56,186,107

$564,525,513

4,870,625

$49,463,047

NET CHANGE RESULTING FROM TOTAL FUND SHARE TRANSACTIONS

96,037,311

$964,795,822

(13,656,320)

$(135,618,852)

4. Federal Tax Information

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP. These differences are due to differing treatments for discount accretion/premium amortization on debt securities and expiration of capital loss carryforwards.

For the year ended September 30, 2012, permanent differences identified and reclassified among the components of net assets were as follows:

Increase (Decrease)

Paid-In Capital

Undistributed Net Investment Income (Loss)

Accumulated Net Realized Gain (Loss)

$(59,924)

$(13,257)

$73,181

Net investment income (loss), net realized gains (losses), and net assets were not affected by this reclassification.

The tax character of distributions as reported on the Statement of Changes in Net Assets for the years ended September 30, 2012 and 2011, was as follows:

As of September 30, 2012, the components of distributable earnings on a tax basis were as follows:

Distribution in excess of tax-exempt income

$ (318,325)

Net unrealized appreciation

$ 22,921,751

Capital loss carryforwards

$ (5,198,873)

The difference between book-basis and tax-basis net unrealized appreciation/depreciation is attributable to differing treatments for discount accretion/premium amortization on debt securities.

At September 30, 2012, the cost of investments for federal tax purposes was $3,993,630,435. The net unrealized appreciation of investments for federal tax purposes was $22,931,942. This consists of net unrealized appreciation from investments for those securities having an excess of value over cost of $23,439,212 and net unrealized depreciation from investments for those securities having an excess of cost over value of $507,270.

At September 30, 2012, the Fund had a capital loss carryforward of $5,198,873 which will reduce the Fund's taxable income arising from future net realized gains on investments, if any, to the extent permitted by the Code, thereby reducing the amount of distributions to shareholders which would otherwise be necessary to relieve the Fund of any liability for federal income tax. Pursuant to the Code, a net capital loss incurred in taxable years beginning on or before December 22, 2010, is characterized as short-term and may be carried forward for a maximum of eight tax years (“Carryforward Limit”), whereas a net capital loss incurred in taxable years beginning after December 22, 2010, retains its character as either short-term or long-term, does not expire and is required to be utilized prior to the losses which have a Carryforward Limit.

The following schedule summarizes the Fund's capital loss carryforwards and expiration years:

Expiration Year

Short-Term

Long-Term

Total

No expiration

$26

$624

$650

2013

$884,421

NA

$884,421

2014

$978,739

NA

$978,739

2015

$631,311

NA

$631,311

2016

$148,172

NA

$148,172

2017

$1,306,058

NA

$1,306,058

2018

$1,242,780

NA

$1,242,780

2019

$6,742

NA

$6,742

Capital loss carryforwards of $59,924 expired during the year ended September 30, 2012.

5. Investment Adviser Fee and Other Transactions WITH AFFILIATES

Investment Adviser Fee

The advisory agreement between the Fund and the Adviser provides for an annual fee equal to 0.60% of the Fund's average daily net assets. Subject to the terms described in the Expense Limitation note, the Adviser may voluntarily choose to waive any portion of its fee. For the year ended September 30, 2012, the Adviser voluntarily waived $13,908,969 of its fee.

Administrative Fee

Federated Administrative Services (FAS), under the Administrative Services Agreement, provides the Fund with administrative personnel and services. The fee paid to FAS is based on the average aggregate daily net assets of certain Federated funds as specified below, plus certain out-of-pocket expenses:

Administrative Fee

Average Aggregate Daily Net Assets of the Federated Funds

0.150%

on the first $5 billion

0.125%

on the next $5 billion

0.100%

on the next $10 billion

0.075%

on assets in excess of $20 billion

Prior to September 1, 2012, the administrative fee received during any fiscal year was at least $150,000 per portfolio and $40,000 per each additional class of Shares. Subject to the terms described in the Expense Limitation note, FAS may voluntarily choose to waive any portion of its fee. For the year ended September 30, 2012, FAS waived $62,792 of its fee. The net fee paid to FAS was 0.076% of average daily net assets of the Fund.

Distribution Services Fee

The Fund has adopted a Distribution Plan (the “Plan”) pursuant to Rule 12b-1 under the Act. Under the terms of the Plan, the Fund will compensate Federated Securities Corp. (FSC), the principal distributor, from the daily net assets of the Fund's Class A Shares to finance activities intended to result in the sale of these shares. The Plan provides that the Fund may incur distribution expenses at 0.25% of average daily net assets, annually, to compensate FSC.

Subject to the terms described in the Expense Limitation note, FSC may voluntarily choose to waive any portion of its fee. For the year ended September 30, 2012, distribution services fees for the Fund were as follows:

Distribution Services Fees Incurred

Distribution Services Fees Waived

Class A Shares

$5,186,909

$(1,031,016)

When FSC receives fees, it may pay some or all of them to financial intermediaries whose customers purchase shares. For the year ended September 30, 2012, FSC retained $2,090,884 of fees paid by the Fund.

Front-end sales charges and contingent deferred sales charges (CDSC) do not represent expenses of the Fund. They are deducted from the proceeds of sales of Fund shares prior to investment or from redemption proceeds prior to remittance, as applicable. For the year ended September 30, 2012, FSC did not retain any sales charges from the sale of Class A Shares.

Shareholder Services Fee

The Fund may pay fees (“Service Fees”) up to 0.25% of the average daily net assets of the Fund's Class A Shares to financial intermediaries or to Federated Shareholder Services Company (FSSC) for providing services to shareholders and maintaining shareholder accounts. Subject to the terms described in the Expense Limitation note, FSSC may voluntarily reimburse the Fund for Service Fees. For the year ended September 30, 2012, Service Fees for the Fund were as follows:

Service Fees Incurred

Class A Shares

$5,165,628

For the year ended September 30, 2012, FSSC received $2,918 of Service Fees paid by the Fund.

Interfund Transactions

During the year ended September 30, 2012, the Fund engaged in purchase and sale transactions with funds that have a common investment adviser (or affiliated investment advisers), common Directors/Trustees and/or common Officers. These purchase and sale transactions complied with Rule 17a-7 under the Act and amounted to $931,820,000 and $1,746,165,000, respectively.

Expense Limitation

The Adviser and its affiliates (which may include FSC, FAS and FSSC) have voluntarily agreed to waive their fees and/or reimburse expenses so that the total annual fund operating expenses (as shown in the financial highlights) paid by the Fund's Class A Shares and Institutional Shares (after the voluntary waivers and reimbursements) will not exceed 0.80% and 0.35% (the “Fee Limit”), respectively, up to but not including the later of (the “Termination Date”): (a) December 1, 2013; or (b) the date of the Fund's next effective Prospectus. While the Adviser and its affiliates currently do not anticipate terminating or increasing these arrangements prior to the Termination Date, these arrangements may only be terminated or the Fee Limit increased prior to the Termination Date with the agreement of the Directors.

General

Certain Officers and Directors of the Fund are Officers and Directors or Trustees of the above companies.

6. Investment Transactions

Purchases and sales of investments, excluding long-term U.S. government securities and short-term obligations, for the year ended September 30, 2012, were as follows:

The Fund participates in a $100,000,000 unsecured, uncommitted revolving line of credit (LOC) agreement with PNC Bank. The LOC was made available for extraordinary or emergency purposes, primarily for financing redemption payments. Borrowings are charged interest at a rate offered to the Fund by PNC Bank at the time of the borrowing. As of September 30, 2012, there were no outstanding loans. During the year ended September 30, 2012, the Fund did not utilize the LOC.

8. Interfund Lending

Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the Fund, along with other funds advised by subsidiaries of Federated Investors, Inc., may participate in an interfund lending program. This program provides an alternative credit facility allowing the Fund to borrow from other participating affiliated funds. As of September 30, 2012, there were no outstanding loans. During the year ended September 30, 2012, the program was not utilized.

9. FEDERAL TAX INFORMATION (UNAUDITED)

For the fiscal year ended September 30, 2012, 99.9% of the distributions from net investment income is exempt from federal income tax, other than the federal AMT.

Report of Independent Registered Public Accounting Firm

TO THE BOARD OF directors OF federated fixed income seCURITIES, inc., AND SHAREHOLDERS OF federated municipal ultrashort fund:

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of the Federated Municipal Ultrashort Fund (the “Fund”), a portfolio of Federated Fixed Income Securities, Inc., as of September 30, 2012 and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the three-year period then ended. These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights for the periods presented prior to October 1, 2009, were audited by other independent registered public accountants whose report thereon dated November 24, 2009, expressed an unqualified opinion on those statements.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2012, by correspondence with the custodian, transfer agent and brokers, or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Federated Municipal Ultrashort Fund as of September 30, 2012 and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the three-year period then ended, in conformity with U.S. generally accepted accounting principles.

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase or redemption payments; and (2) ongoing costs, including management fees and to the extent applicable, distribution (12b-1) fees and/or shareholder services fees and other Fund expenses. This Example is intended to help you to understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. It is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2012 to September 30, 2012.

ACTUAL EXPENSES

The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses attributable to your investment during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. Thus, you should not use the hypothetical account values and expenses to estimate the actual ending account balance or your expenses for the period. Rather, these figures are required to be provided to enable you to compare the ongoing costs of investing in the Fund with other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) on purchase or redemption payments. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Beginning Account Value 4/1/2012

Ending Account Value 9/30/2012

Expenses Paid During Period1

Actual:

Class A Shares

$1,000.00

$1,003.50

$3.91

Institutional Shares

$1,000.00

$1,005.80

$1.602

Hypothetical (assuming a 5% return before expenses):

Class A Shares

$1,000.00

$1,021.10

$3.94

Institutional Shares

$1,000.00

$1,023.40

$1.622

1

Expenses are equal to the Fund's annualized net expense ratios, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half-year period). The annualized net expense ratios are as follows:

Class A Shares

0.78%

Institutional Shares

0.32%

2

Actual and Hypothetical expenses paid during the period utilizing the Fund's Institutional Shares current Fee Limit of 0.35% (as reflected in the Notes to Financial Statements, Note 5 under Expense Limitation), multiplied by the average account value over the period, multiplied by 183/366 (to reflect current expenses as if they had been in effect throughout the most recent one-half-year period) would be $1.76 and $1.77, respectively.

The Board of Directors is responsible for managing the Corporation business affairs and for exercising all the Corporation powers except those reserved for the shareholders. The following tables give information about each Director and the senior officers of the Fund. Where required, the tables separately list Directors who are “interested persons” of the Fund (i.e., “Interested” Directors) and those who are not (i.e., “Independent” Directors). Unless otherwise noted, the address of each person listed is Federated Investors Tower, 1001 Liberty Avenue, Pittsburgh, PA 15222. The address of all Independent Directors listed is 4000 Ericsson Drive, Warrendale, PA 15086-7561; Attention: Mutual Fund Board. As of December 31, 2011, the Corporation comprised two portfolio(s), and the Federated Fund Family consisted of 43 investment companies (comprising 134 portfolios). Unless otherwise noted, each Officer is elected annually. Unless otherwise noted, each Director oversees all portfolios in the Federated Fund Family and serves for an indefinite term. The Fund's Statement of Additional Information includes additional information about Corporation Directors and is available, without charge and upon request, by calling 1-800-341-7400.

Interested DIRECTORS Background

Name Birth Date Positions Held with Corporation Date Service Began

Principal Occupation(s) for Past Five Years, Other Directorships Held and Previous Position(s)

John F. Donahue* Birth Date: July 28, 1924 Director Began serving: October 1991

Principal Occupations: Director or Trustee of the Federated Fund Family; Chairman and Director, Federated Investors, Inc.; Chairman of the Federated Fund Family's Executive Committee. Previous Positions: Chairman of the Federated Fund Family; Trustee, Federated Investment Management Company; Chairman and Director, Federated Investment Counseling.

J. Christopher Donahue* Birth Date: April 11, 1949 President and Director Began serving: January 2000

Principal Occupations: Principal Executive Officer and President of the Federated Fund Family; Director or Trustee of some of the Funds in the Federated Fund Family; President, Chief Executive Officer and Director, Federated Investors, Inc.; Chairman and Trustee, Federated Investment Management Company; Trustee, Federated Investment Counseling; Chairman and Director, Federated Global Investment Management Corp.; Chairman, Federated Equity Management Company of Pennsylvania and Passport Research, Ltd. (investment advisory subsidiary of Federated); Trustee, Federated Shareholder Services Company; Director, Federated Services Company. Previous Positions: President, Federated Investment Counseling; President and Chief Executive Officer, Federated Investment Management Company, Federated Global Investment Management Corp. and Passport Research, Ltd.

*

Family relationships and reasons for “interested” status: John F. Donahue is the father of J. Christopher Donahue; both are “interested” due to their beneficial ownership of shares of Federated Investors, Inc. and the positions they hold with Federated and its subsidiaries.

Name Birth Date Positions Held with Corporation Date Service Began

Principal Occupation(s) for Past Five Years, Other Directorships Held, Previous Position(s) and Qualifications

Nicholas P. Constantakis, CPA Birth Date: September 3, 1939 Director Began serving: February 1998

Principal Occupation: Director or Trustee of the Federated Fund Family. Other Directorship Held: Director, Chairman of the Audit Committee, and member of the Compensation Committee, Michael Baker Corporation (architecture, engineering and construction services). Previous Position: Partner, Andersen Worldwide SC. Qualifications: Public accounting and director experience.

John F. Cunningham Birth Date: March 5, 1943 Director Began serving: January 1999

Principal Occupation: Director or Trustee of the Federated Fund Family. Other Directorships Held: Chairman, President and Chief Executive Officer, Cunningham & Co., Inc. (strategic business consulting); Trustee Associate, Boston College. Previous Positions: Director, Redgate Communications and EMC Corporation (computer storage systems); Chairman of the Board and Chief Executive Officer, Computer Consoles, Inc.; President and Chief Operating Officer, Wang Laboratories; Director, First National Bank of Boston; Director, Apollo Computer, Inc. Qualifications: Business management and director experience.

Maureen Lally-Green Birth Date: July 5, 1949 Director Began serving: August 2009

Principal Occupations: Director or Trustee of the Federated Fund Family; Director, Office of Church Relations, Diocese of Pittsburgh; Adjunct Professor of Law, Duquesne University School of Law. Other Directorships Held: Director, Auberle; Member, Pennsylvania State Board of Education; Director, Saint Vincent College; Director, Ireland Institute of Pittsburgh; Chair and Director, UPMC Mercy Hospital; Regent, St. Vincent Seminary; Director, Epilepsy Foundation of Western and Central Pennsylvania; Director, Saint Thomas More Society, Allegheny County; Director, Our Campaign for the Church Alive, Inc. Previous Position: Pennsylvania Superior Court Judge. Qualifications: Legal and director experience.

Peter E. Madden Birth Date: March 16, 1942 Director Began serving: October 1991

Principal Occupation: Director or Trustee, and Chairman of the Board of Directors or Trustees, of the Federated Fund Family. Previous Positions: Representative, Commonwealth of Massachusetts General Court; President, Chief Operating Officer and Director, State Street Bank and Trust Company and State Street Corporation (retired); Director, VISA USA and VISA International; Chairman and Director, Massachusetts Bankers Association; Director, Depository Trust Corporation; Director, The Boston Stock Exchange. Qualifications: Business management, mutual fund services and director experience.

Name Birth Date Positions Held with Corporation Date Service Began

Principal Occupation(s) for Past Five Years, Other Directorships Held, Previous Position(s) and Qualifications

Charles F. Mansfield, Jr. Birth Date: April 10, 1945 Director Began serving: January 1999

Principal Occupations: Director or Trustee of the Federated Fund Family; Management Consultant. Previous Positions: Chief Executive Officer, PBTC International Bank; Partner, Arthur Young & Company (now Ernst & Young LLP); Chief Financial Officer of Retail Banking Sector, Chase Manhattan Bank; Senior Vice President, HSBC Bank USA (formerly Marine Midland Bank); Vice President, Citibank; Assistant Professor of Banking and Finance, Frank G. Zarb School of Business, Hofstra University; Executive Vice President, DVC Group, Inc. (marketing, communications and technology). Qualifications: Banking, business management, education and director experience.

Thomas M. O'Neill Birth Date: June 14, 1951 Director Began serving: October 2006

Principal Occupations: Director or Trustee, Vice Chairman of the Audit Committee of the Federated Fund Family; Sole Proprietor, Navigator Management Company (investment and strategic consulting). Other Directorships Held: Board of Overseers, Children's Hospital of Boston; Visiting Committee on Athletics, Harvard College; Board of Directors, Medicines for Humanity; Board of Directors, The Golisano Children's Museum of Naples, Florida. Previous Positions: Chief Executive Officer and President, Managing Director and Chief Investment Officer, Fleet Investment Advisors; President and Chief Executive Officer, Aeltus Investment Management, Inc.; General Partner, Hellman, Jordan Management Co., Boston, MA; Chief Investment Officer, The Putnam Companies, Boston, MA; Credit Analyst and Lending Officer, Fleet Bank; Director and Consultant, EZE Castle Software (investment order management software); Director, Midway Pacific (lumber). Qualifications: Business management, mutual fund, director and investment experience.

John S. Walsh Birth Date: November 28, 1957 Director Began serving: January 1999

Principal Occupations: Director or Trustee, Chairman of the Audit Committee of the Federated Fund Family; President and Director, Heat Wagon, Inc. (manufacturer of construction temporary heaters); President and Director, Manufacturers Products, Inc. (distributor of portable construction heaters); President, Portable Heater Parts, a division of Manufacturers Products, Inc. Previous Position: Vice President, Walsh & Kelly, Inc. Qualifications: Business management and director experience.

Name Birth Date Positions Held with Corporation Date Service Began

Principal Occupation(s) for Past Five Years and Previous Position(s)

John W. McGonigle Birth Date: October 26, 1938 EXECUTIVE VICE PRESIDENT AND SECRETARY Officer since: November 1991

Principal Occupations: Executive Vice President and Secretary of the Federated Fund Family; Vice Chairman, Executive Vice President, Secretary and Director, Federated Investors, Inc. Previous Positions: Trustee, Federated Investment Management Company and Federated Investment Counseling; Director, Federated Global Investment Management Corp., Federated Services Company and Federated Securities Corp.

Richard A. Novak Birth Date: December 25, 1963 TREASURER Officer since: January 2006

Principal Occupations: Principal Financial Officer and Treasurer of the Federated Fund Family; Senior Vice President, Federated Administrative Services; Financial and Operations Principal for Federated Securities Corp., Edgewood Services, Inc. and Southpointe Distribution Services, Inc. Previous Positions: Controller of Federated Investors, Inc.; Vice President, Finance of Federated Services Company; held various financial management positions within The Mercy Hospital of Pittsburgh; Auditor, Arthur Andersen & Co.

Richard B. Fisher Birth Date: May 17, 1923 VICE CHAIRMAN Officer since: August 2002

Principal Occupations: Vice Chairman or Vice President of some of the Funds in the Federated Fund Family; Vice Chairman, Federated Investors, Inc.; Chairman, Federated Securities Corp. Previous Positions: President and Director or Trustee of some of the Funds in the Federated Fund Family; Executive Vice President, Federated Investors, Inc.; Director and Chief Executive Officer, Federated Securities Corp.

Peter J. Germain Birth Date: September 3, 1959 CHIEF LEGAL OFFICER Officer since: January 2005