UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the Appropriate Box:

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☐ | Definitive Proxy Statement | |

| ☒ | Definitive Additional Materials | |

| ☐ | Soliciting Material Under Rule 14a-12 | |

MID PENN BANCORP, INC.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials: | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

2020 ANNUAL REPORT TO SHAREHOLDERS

A LET TER FROM Robert C. Grubic, our Chair, and Rory G. Ritrievi, our President and CEO DEAR FELLOW SHAREHOLDERS: As we write this letter to you in early March, 2021, the COVID-19 public health crisis and the nation’s response to handling that crisis continues. Our principal thoughts remain with all those who have lost a loved one to this coronavirus and to those individuals and businesses who have been harmed financially with the loss of a job or business income. While there appears to be some encouraging signs with vaccine distribution, there is clearly work to be done to get our communities and our country safely back to normal. Your Board of Directors continues to oversee Mid Penn Bancorp, Inc.’s (“Mid Penn” or the “Corporation”) effort to help those who have been most affected, both within our company and throughout our communities. While markets were roiling throughout 2020, we remained steadfast in our commitment to help as many customers as possible secure the loans or payment deferrals they needed, or to grant them access to the liquidity they needed. We believe those commitments were instrumental in helping individuals and preserving many businesses throughout Pennsylvania. Through those efforts, we are pleased to report solid performance for the Corporation for the year 2020 in many different respects. We had record levels of organic asset growth, core deposit growth, revenues, net income, and earnings per share. The Board and Management Team are pleased to deliver those results to you despite a difficult year for so many. Allow us to highlight a few of those financial and non-financial successes for you. ... continued on next page.

A LET TER FROM Robert C. Grubic, our Chair, and Rory G. Ritrievi, our President and CEO UNIQUE CULTURE/UNIQUE STRATEGY In the first few months of 2020 as COVID-19 began to grip the country, it became apparent to us that the work we had done in 2019 formulating a 2020 strategic plan was almost all for naught. Starting in late February 2020, our Management Team, under the close supervision of the Board, began to develop a new strategic plan crafted in the early hours of each day and evaluated for adjustments at the end of each long day. We focused our commitments on protecting our employees and customers and on creating an environment where the employees could continue to provide world class customer service in a way never before done, supporting the needs of our customer base when they needed it most. When the Commonwealth of Pennsylvania went into shutdown mode, we transitioned 80% of our employees to work from home virtually overnight. We were able to do that as a result of our diligent disaster recovery planning in the years leading up to 2020. We did not allow the employees to become isolated though, as we developed a Community Portal for them to stay connected with each other and to the Management Team. It also enabled each of those employees to take care of job #1: ensuring their own and their families’ health and welfare. While we believe that we have always had a strong culture throughout Mid Penn, we put that belief to the test in 2020 by entering the American Banker “Best Banks To Work For” contest. The ranking that results from that is, in essence, an employee morale gauge. Of the over 5,000 banks eligible to participate, we placed as the 20th Best Bank To Work For in the country and the best in Pennsylvania. We take a great deal of pride in that accomplishment as it is the strength of our morale -the basis of our culture- that enabled us to deliver on our uniquely designed daily strategic plans, the results of which were meaningful to our customers and instrumental to our performance. ORGANIC GROWTH Over the five years leading up to 2020, as we acquired Phoenix Bancorp, Inc. (Schuylkill and Luzerne counties), The Scottdale Bank and Trust Company (Westmoreland and Fayette counties) and First Priority Bank (Chester, Bucks, Montgomery and Berks counties), while growing in our existing counties of Dauphin and Cumberland and adding Lancaster organically, we built a footprint of demographic diversity that we felt would accelerate organic growth on both sides of the balance sheet regardless of the circumstances in the external environment. That was proven in 2020. In a year where many financial institutions were unable or reticent to provide liquidity to the marketplace, we originated nearly $1.2 billion in commercial, consumer and residential loans. That was a record level of production for us and it led to a near best-in-class 13% organic loan growth. In providing that liquidity to borrowers, we were also able to deepen our relationships with depositors. Throughout 2020, we grew our core deposit portfolio by 29%, with 50% of that in the form of noninterest-bearing deposits. That growth allowed us to decrease our cost of deposits by 75 basis points which helped to preserve our net interest margin at a level above most banks in our regional peer group. We also had a record level of growth and performance in our Trust and Wealth Management business as revenues topped $1 million for the first time in our history, despite the challenges for members of our Trust and Wealth Management calling team to meet with their customers and prospects for most of the year. RECORD REVENUES/RECORD EARNINGS With that organic growth success on both sides of the balance sheet, we had, for the first time in our history, over $100 million in revenues. While doing our best to control expenses, and despite a loan loss provision expense that was more than triple that of the previous year, we were able to convert those revenues into a record level of net earnings available to common shareholders of $26 million (up from $17 million in 2019) and a record level of earnings per share of $3.11 (up from $2.09 in 2019). With that earnings success, we were able to deliver our highest level of dividend distribution in 12 years while still increasing our book value by 8% and tangible book value by 12%. While the market for financial stocks, including Mid Penn, was severely depressed in 2020 due to concerns over potential asset quality fallout, we are extremely happy to deliver this type of improvement in measurable shareholder value. ASSET QUALITY We clearly take great pride in the organic growth we delivered in 2020; however, we are even more encouraged by our asset quality performance and the overall state of our asset quality, even during a state-wide and country-wide economic crisis. We added over $4 million to our reserve for loan losses in 2020 (the second highest level of annual provisioning in our history), but experienced only $332,905 in net charge-offs. Consequently, our overall loan loss reserve ratio increased from 0.54% in 2019 to 0.67% in 2020. This is encouraging for a company with the level of loan growth (both organic and acquired) we have had over the last six years as aggregate net charge-offs over that six year period amount of just over $1 million. Management’s key asset quality metric (an aggregation of the net charge-off ratio + less than 90-day delinquency + non-performing asset ratio compared to total loans) remained steady around 1% throughout the year. We are very pleased with that result. The success we had in asset quality in 2020 is attributed to the strength

of our overall loan team. We are confident that our team of lenders, credit administration professionals and loan operations specialists develop, underwrite and administer loan growth in a manner that is consistent with our objective of pristine asset quality. Additionally, throughout 2020 as our borrowing community was challenged given the pandemic’s effect on the economy, we did everything possible to stabilize that community. We held daily forums throughout the year where we evaluated loan payment deferral requests and implemented those approvals in an efficient and secure manner. When the Paycheck Protection Program was implemented, we did it as well as any bank in the country which really helped to stabilize borrowers in our portfolio. And, of course, even though we were unable to meet with borrowers face to face, we made the commitment to continue strong communications with them throughout the year. Those actions all attributed to delivering solid asset quality performance for the year. PAYCHECK PROTECTION PROGRAM The Corporation had a solid year of performance partially aided by Mid Penn Bank’s participation in the Paycheck Protection Program (PPP), a small business recovery program implemented by the federal government in late March of 2020. Throughout that first round of PPP, we worked to deliver over 4,100 PPP loans totaling over $630 million, helping to protect over 55,000 paychecks for employees throughout our market. The success we had, which ranked us in the top tier of performance nationally, was the result of leveraging our SBA and technology expertise in building a solid processing environment that was staffed around the clock for several months by a core group of employees, including each of our named executives. There was, of course, an immediate and positive impact to the Corporation in generating almost $21 million of origination fees on those loans, but there was also a longer-term positive impact. In working so efficiently to get those loans approved for businesses that so desperately needed them to survive and in establishing communications that eased the stress of those applicants, we generated a significant amount of goodwill with both existing customers and customers new to us through the PPP process. The responses we received from those customers—existing and new—was so overwhelming that we decided to memorialize it all in a book. You will see a few of those comments displayed later in this annual report. Throughout the remainder of the year, our team of calling professionals throughout the company utilized that goodwill to develop even deeper relationships with pre-PPP customers and to establish non-PPP relationships with those new to us. That effort was instrumental in our ability to deliver the organic growth numbers identified above. YOUR BOARD The Board of Mid Penn delivered oversight and guidance to the Corporation’s Management Team and mission in a manner of which we as shareholders can be proud. While there were very few face-to-face meetings, through the use of technology, we had more Board and Board-related meetings than in any previous year. Through that oversight and guidance, the Corporation was able to deliver record results of operations, a record level of organic growth, PPP production that positioned us at the top of banks nationally, and the placement of $27 million of subordinated debt to increase our capital position at no cost to the shareholders. The Board was focused on keeping the entire Management Team intact and motivated to deliver record results. Each and every member of our Board was instrumental in getting that done. Our Board also grew and continued to demonstrate its commitment to increase diversity. Late in 2020, we welcomed Brian Hudson to the team. Brian has long term, statewide financial executive experience as a retired CEO of the Pennsylvania Housing Finance Agency. As a Certified Public Accountant, Brian becomes the third Independent “Financial Expert” on the Board and Audit Committee. We are confident that our shareholders will be pleased with Brian’s appointment. The Nominating and Corporate Governance Committee has developed a multi-year succession and diversity plan that we feel will keep this Board energetic, engaged and a driving factor for successfully propelling our organization into the future. OUR VIEW OF 2021 On February 18, 2021, we issued a Form 8-K and press release that announced that we had already funded over 2,100 Round 2 PPP loans for over $290 million which helped to save over 26,000 paychecks. We are once again distinguishing ourselves as being the PPP bank of choice for many businesses in need throughout Pennsylvania and surrounding states. The sense of satisfaction we get in completing this process on behalf of our business customers and their employees makes all the work we do very worthwhile. With another round of PPP success, continued strong business development throughout the state in our loan, deposit, trust and wealth management business lines, as well as a great start in MPB Financial Service’s wealth and insurance lines, we are cautiously optimistic that 2021 will be another great year. We thank you for your investment in Mid Penn Bancorp, Inc. and wish you and yours all the very best of health, happiness and prosperity throughout the year. Rory G. Ritrievi Robert C. Grubic President and CEO Chair of the Board

FOCUSING ON EDUCATION AND DEVELOPMENT Although 2020 provided many challenges, Mid Penn University found ways to persevere and continued to deliver on its commitment to provide the best education and development opportunities for all Mid Penn Bank employees. Leveraging recent investments in classroom and meeting technologies, the University transitioned to a fully-virtual environment in early 2020, converting 100% of offered classes to online availability. Despite this pivot, 2020 saw the highest enrollment in Mid Penn University history with 2,250 students enrolled in 292 classes. The Summer Intern Program was in full swing over the summer of last year as ten college students were onboarded into various business units, learning valuable skills and getting to know how business operates. Each intern met with senior executives and leaders around the Bank and were exposed to multiple facets of our operation. The University supported 40 mentorship pairs in 2020 that help facilitate the growth and development of emerging leaders and foster an inclusive and collaborative environment. Mid Penn Bank’s mentor program helps employees gain confidence, provides professional development opportunities and exposes them to new and different ways of thinking. We believe strongly that mentorships are a great talent builder and serve to develop a pipeline of future leaders that understand our business and the Mid Penn Bank culture. 2020 EDUCATION & DEVELOPMENT HIGHLIGHTS 200% 100% 165% 160 10 INCREASE IN OF UNIVERSITY CLASSES INCREASE IN THE NUMBER OF EMPLOYEES ENROLLED IN COLLEGE CLASSES HELD TRANSFORMED FROM CLASSROOM MENTORSHIPS SUPPORTED CERTIFICATION PROGRAMS; INTERNS TO VIRTUAL DELIVERY IN 2 MONTHS AT THE UNIVERSITY 28 GRADUATES

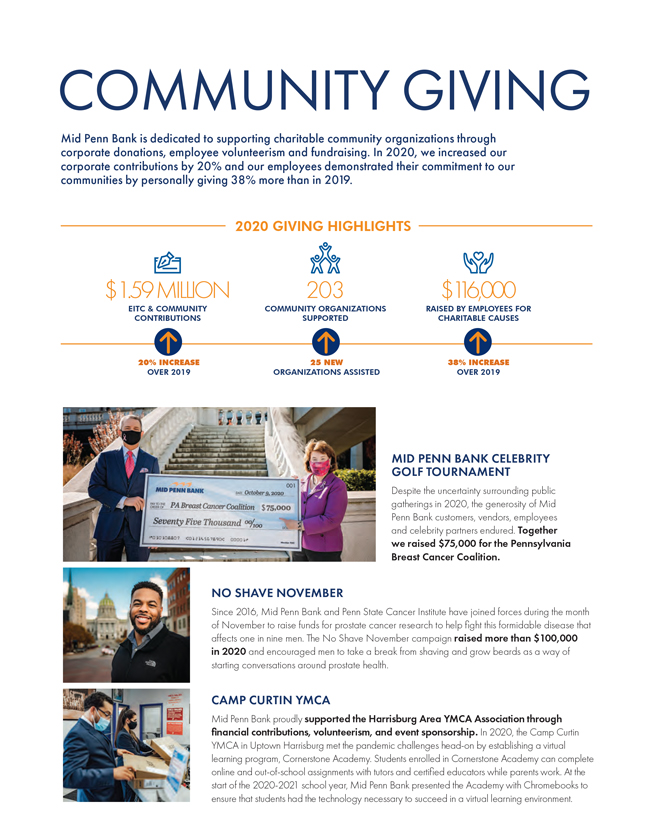

COMMUNITY GIVING Mid Penn Bank is dedicated to supporting charitable community organizations through corporate donations, employee volunteerism and fundraising. In 2020, we increased our corporate contributions by 20% and our employees demonstrated their commitment to our communities by personally giving 38% more than in 2019. 2020 GIVING HIGHLIGHTS $1.59 MILLION 203 $ 16,000 EITC & COMMUNITY COMMUNITY ORGANIZATIONS RAISED BY EMPLOYEES FOR CONTRIBUTIONS SUPPORTED CHARITABLE CAUSES 20% INCREASE 25 NEW 38% INCREASE OVER 2019 ORGANIZATIONS ASSISTED OVER 2019 MID PENN BANK CELEBRITY GOLF TOURNAMENT Despite the uncertainty surrounding public gatherings in 2020, the generosity of Mid Penn Bank customers, vendors, employees and celebrity partners endured. Together we raised $75,000 for the Pennsylvania Breast Cancer Coalition. NO SHAVE NOVEMBER Since 2016, Mid Penn Bank and Penn State Cancer Institute have joined forces during the month of November to raise funds for prostate cancer research to help fight this formidable disease that affects one in nine men. The No Shave November campaign raised more than $100,000 in 2020 and encouraged men to take a break from shaving and grow beards as a way of starting conversations around prostate health. CAMP CURTIN YMCA Mid Penn Bank proudly supported the Harrisburg Area YMCA Association through financial contributions, volunteerism, and event sponsorship. In 2020, the Camp Curtin YMCA in Uptown Harrisburg met the pandemic challenges head-on by establishing a virtual learning program, Cornerstone Academy. Students enrolled in Cornerstone Academy can complete online and out-of-school assignments with tutors and certified educators while parents work. At the start of the 2020-2021 school year, Mid Penn Bank presented the Academy with Chromebooks to ensure that students had the technology necessary to succeed in a virtual learning environment.

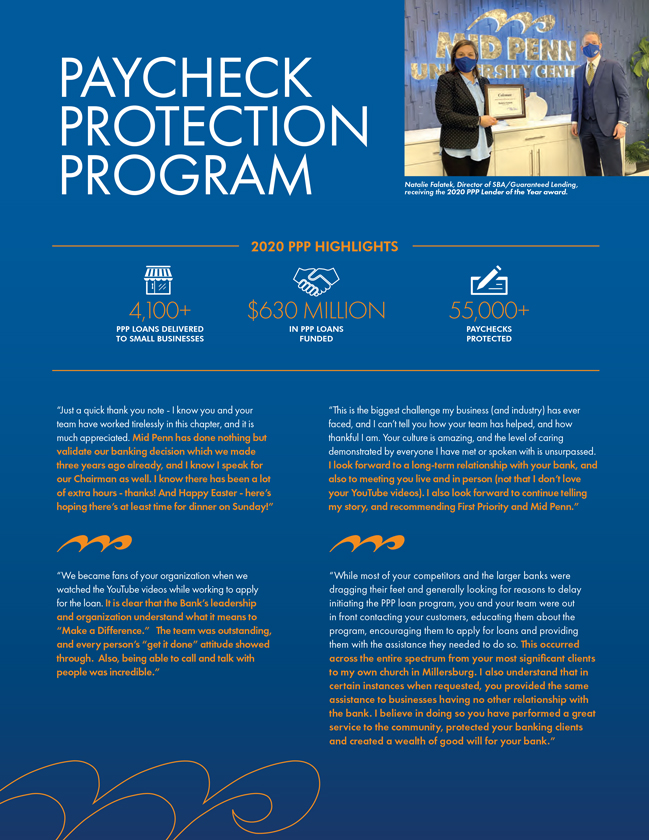

PAYCHECK PROTECTION PROGRAM receiving Natalie Falatek, the 2020 Director PPP Lender of SBA/Guaranteed of the Year award Lending, . 2020 PPP HIGHLIGHTS 4,100+ $630 MILLION 55,000+ PPP LOANS DELIVERED IN PPP LOANS PAYCHECKS TO SMALL BUSINESSES FUNDED PROTECTED “Just a quick thank you note—I know you and your team have worked tirelessly in this chapter, and it is much appreciated. Mid Penn has done nothing but validate our banking decision which we made three years ago already, and I know I speak for our Chairman as well. I know there has been a lot of extra hours—thanks! And Happy Easter—here’s hoping there’s at least time for dinner on Sunday!” “We became fans of your organization when we watched the YouTube videos while working to apply for the loan. It is clear that the Bank’s leadership and organization understand what it means to “Make a Difference.” The team was outstanding, and every person’s “get it done” attitude showed through. Also, being able to call and talk with people was incredible.” “This is the biggest challenge my business (and industry) has ever faced, and I can’t tell you how your team has helped, and how thankful I am. Your culture is amazing, and the level of caring demonstrated by everyone I have met or spoken with is unsurpassed. I look forward to a long-term relationship with your bank, and also to meeting you live and in person (not that I don’t love your YouTube videos). I also look forward to continue telling my story, and recommending First Priority and Mid Penn.” “While most of your competitors and the larger banks were dragging their feet and generally looking for reasons to delay initiating the PPP loan program, you and your team were out in front contacting your customers, educating them about the program, encouraging them to apply for loans and providing them with the assistance they needed to do so. This occurred across the entire spectrum from your most significant clients to my own church in Millersburg. I also understand that in certain instances when requested, you provided the same assistance to businesses having no other relationship with the bank. I believe in doing so you have performed a great service to the community, protected your banking clients and created a wealth of good will for your bank.”

“Hope all is well. We worked with Mid Penn on our PPP and were very impressed with your ability to get things done quickly and efficiently (our own bank wasn’t ready to move quickly enough!). Please pass along my gratitude to Rory, and let him know that I will look for additional opportunities to send business your way!” “How you helped us and our business back in PPP round 1 was simply amazing. It saved our company and kept our employees working. The way you have prepared and are handling round 2 is simply amazing. I have my app fully submitted and the thought of receiving another forgivable 6 figure loan literately brings tears to my eyes. I’m not sure if you all fully understand how impactful what your doing is for us business owners. It is saving jobs and the company my wife and I have killed ourselves for, for the past 15 years. Thank you to all your team for the tireless work they are doing. We are with you and eternally grateful for all your help, support and guidance. Thank you, thank you, thank you.” “I just wanted to let you know that phone call you made to me 8 months ago and the support you showed in getting me the PPP money was a game changer and one of the best things to happen to me in 2020. Thanks for the support. You are one of the main reasons my company will survive this pandemic and be stronger when we are on the other side.” “I just want to thank you and the amazing staff at Mid Penn Bank for your extraordinary service to our businesses. Rory’s video messages are terrific. Your service has been nothing short of spectacular. I have been working with several banks on PPPs for various enterprises in West Virginia. No other bank holds a candle to Mid Penn Bank. You are a true partner in support of our businesses. Please send my greetings and heartfelt thanks to Rory.” “The word is out! You guys hit this out of the ballpark! Why would anyone in the Central PA area choose any other bank? TRULY RELATIONSHIP BANKING!! Congratulations on the job you did for you and your customers!!” “I wanted to send a quick note to commend you for the extremely efficient and professional manner in which Mid Penn Bank has handled the application process for the PPP. I applied for my loan and had the funds in my account in six days! I was kept updated by the branch in Conyngham, PA, as well as through your YouTube videos. I could not be more pleased with how expeditiously my application was processed and funded. I have spoken to many other State Farm Agents throughout the country as well as numerous other small business owners, and many, many of these business owners did not have very favorable experiences with this program. This is certainly the case with those who applied through the large national banks as opposed to the small community lenders. I appreciate Mid Penn Bank’s efforts very much and plan to be a long-time customer.” “What you did for us you went above and beyond and you have a customer for life.” “Thank you all for the hard work. I am glad all my business is with you guys. After watching all these videos, I know I am with the right bank and I know that when times like this come around I can count on you guys.” “I wanted to take a minute and thank you for the superior customer service Mid Penn provided with regard to the PPP loan process. Waking up this morning to see the funds sitting in my account allows me to breathe a little easier. Our experience with your team was nothing but positive. You proactively provided guidance to make the process both efficient and effective. You were quick to respond and found new ways to do so. At every point, I knew what was going on. Mid Penn has been a great partner to my business over the years both in good times and in bad. This latest challenge has given me yet another reason to be glad I bank with such a great team.”

Officers RORY G. RITRIEVI MICHAEL D. PEDUZZI President and CEO Chief Financial Officer Executive Team RORY G. RITRIEVI MICHAEL D. PEDUZZI President and CEO Chief Financial Officer SCOTT W. MICKLEWRIGHT JUSTIN T. WEBB Chief Revenue Officer Chief Operating Officer JOAN E. DICKINSON JOSEPH L. PAESE Chief of Staff Director of Trust and Wealth Management Board of Directors ROBERT C. GRUBIC BRIAN A. HUDSON, SR. Chairman, Mid Penn Bancorp, Inc. Former Executive Director and CEO and Mid Penn Bank; Chairman and CEO Pennsylvania Housing Finance Agency Herbert, Rowland & Grubic, Inc. GREGORY M. KERWIN WILLIAM A. SPECHT, III Senior Partner, Kerwin & Kerwin, LLP Vice Chairman, Mid Penn Bancorp, Inc. and Mid Penn Bank; President and CEO DONALD F. KIEFER Seal Glove Mfg. & Ark Safety Former Chairman, President and CEO The Scottdale Bank & Trust Company; RORY G. RITRIEVI Partner, Lawrence Keister & Co. President and CEO, Mid Penn Bancorp, Inc. and Mid Penn Bank THEODORE W. MOWERY Founding Partner, Gunn Mowery, LLC ROBERT A. ABEL Principal and Shareholder JOHN E. NOONE Brown Schultz Sheridan & Fritz President, Shamrock Investments, LLC KIMBERLY J. BRUMBAUGH NOBLE C. QUANDEL, JR. Founder and CEO Executive Chairman Brumbaugh Wealth Management, LLC Quandel Enterprises, Inc. MATTHEW G. DESOTO DAVID E. SPARKS President and CEO Founder, Former Chairman and CEO MI Windows and Doors, LLC First Priority Financial Corp. and First Priority Bank

MISSION: TO REWARD ALL OF OUR SHAREHOLDERS, SERVE ALL OF OUR CUSTOMERS, VALUE ALL OF OUR EMPLOYEES AND SUPPORT ALL OF OUR COMMUNITIES. Mid Penn Bank is committed to creating an environment for all employees that is diverse, equitable, and inclusive. 349 Union Street, Millersburg, PA 17061 | 1-866-642-7736 MIDPENNBANK.COM