UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06431

AMG Funds II

(Exact name of registrant as specified in charter)

680 Washington Boulevard, Suite 500, Stamford, Connecticut 06901

(Address of principal executive offices) (Zip code)

AMG Funds LLC

680 Washington Boulevard, Suite 500, Stamford, Connecticut 06901

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2022 – DECEMBER 31, 2022

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

| | |

| | ANNUAL REPORT |

| | |

| | | AMG Funds December 31, 2022 |

| | |

| | |

|

| | |

| | | AMG GW&K ESG Bond Fund |

| | |

| | | Class N: MGFIX | Class I: MGBIX |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund |

| | |

| | | Class N: MFDAX | Class I: MFDSX | Class Z: MFDYX |

| | |

| | | AMG GW&K High Income Fund |

| | |

| | | Class N: MGGBX | Class I: GWHIX |

| | |

| | | AMG GW&K Municipal Bond Fund |

| | |

| | | Class N: GWMTX | Class I: GWMIX |

| | |

| | | AMG GW&K Municipal Enhanced Yield Fund |

| | |

| | | Class N: GWMNX | Class I: GWMEX | Class Z: GWMZX |

| | |

| | | |

| | |

| | | |

| | | | |

| amgfunds.com | | | | 123122 AR088 |

| | |

| | | AMG Funds Annual Report — December 31, 2022 |

| | | | | | |

| | | |

| | | | | | | |

| | | TABLE OF CONTENTS | | PAGE | |

| | | | |

| | | LETTER TO SHAREHOLDERS | | | 2 | |

| | | |

| | | ABOUT YOUR FUND’S EXPENSES | | | 3 | |

| | | |

| | | PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | |

| | | |

| | | AMG GW&K ESG Bond Fund | | | 4 | |

| | | |

| | | AMG GW&K Enhanced Core Bond ESG Fund | | | 14 | |

| | | |

| | | AMG GW&K High Income Fund | | | 23 | |

| | | |

| | | AMG GW&K Municipal Bond Fund | | | 31 | |

| | | |

| | | AMG GW&K Municipal Enhanced Yield Fund | | | 40 | |

| | | |

| | | FINANCIAL STATEMENTS | | | | |

| | | |

| | | Statement of Assets and Liabilities | | | 48 | |

| | | |

| | | Balance sheets, net asset value (NAV) per share computations and cumulative distributable earnings (loss) | | | | |

| | | |

| | | Statement of Operations | | | 50 | |

| | | |

| | | Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | |

| | | |

| | | Statements of Changes in Net Assets | | | 51 | |

| | | |

| | | Detail of changes in assets for the past two fiscal years | | | | |

| | | |

| | | Financial Highlights | | | 53 | |

| | | |

| | | Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | |

| | | |

| | | Notes to Financial Statements | | | 65 | |

| | | |

| | | Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | |

| | | |

| | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 74 | |

| | | |

| | | OTHER INFORMATION | | | 75 | |

| | | |

| | | TRUSTEES AND OFFICERS | | | 76 | |

| | | | | | | |

|

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds Family of Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. | |

| | |

| |

| | Letter to Shareholders |

| | | |

| | | |

| | | |

Dear Shareholder:

We are pleased to provide this annual report for your investment with AMG Funds. Our foremost goal is to provide investment solutions that help our shareholders successfully achieve their long-term investment goals. We appreciate the privilege of providing you with investment tools.

The past year was a challenging period for investors, as uncertainties about high inflation, tighter financial conditions, and the Russian invasion of Ukraine led to significant volatility. Global equity and bond markets fell in tandem amid sharply higher interest rates and eroding investor confidence as worries of an impending recession lingered most of the year. A global commodity shock caused by the war in Ukraine only made matters worse. The S&P 500® Index slipped into a bear market with the Index falling more than (24)% from its peak earlier in the year. The abrupt shift in markets this year has reset expectations around future growth, as the U.S. Federal Reserve (the Fed) and other global central banks have taken aggressive policy action to bring down inflation. While the outlook is uncertain given recent negative returns across many asset classes, global stock and bond valuations are now far more attractive entering 2023 compared to a year ago.

There was very wide dispersion in S&P 500® Index sector performance. Energy significantly outperformed all other sectors with a gain of 65.72% as the price of oil surged during the period. The defensive-oriented sectors also outperformed, although utilities was the only other sector with a positive return, gaining 1.54%. Consumer staples and health care were slightly negative with returns of (0.62)% and (1.95)%, respectively. High-growth technology and mega cap internet-related companies underperformed during the period, and real estate was impacted by higher interest rates. Communications services fell the most with a (39.93)% return during the year, followed by declines of (37.03)% for consumer discretionary, (28.14)% for information technology and (26.13)% for real estate. Value stocks held up much better than growth stocks as the Russell 1000® Value Index returned (7.54)% compared to the (29.14)% return for the Russell 1000® Growth Index. Small cap stocks struggled as the Russell 2000® Index lost (20.44)%. Outside the U.S., foreign developed markets were negative with a (14.45)% return for the MSCI EAFE Index, however a very strong fourth quarter rally drove international equity returns ahead of their U.S. counterparts for the year.

The 10-year Treasury yield more than doubled during the year, surging to the highest levels since before the Great Financial Crisis. Rapidly rising rates from a very low base led to historic negative performance for bonds as the Bloomberg U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance, lost (13.01)% over the period. Investment-grade corporate bonds underperformed, returning (15.76)% for the year. High yield bonds held up better with a (11.19)% return as measured by the return of the Bloomberg U.S. Corporate High Yield Bond

Index. Municipal bonds were also negative, but outperformed the broader market with a (8.53)% return for the Bloomberg Municipal Bond Index.

AMG Funds provides access to a distinctive array of actively managed return-oriented investment strategies. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit. For more information about AMG Funds’ wide range of products and resources, please visit www.amgfunds.com. We thank you for your investment and continued trust in AMG Funds.

Respectfully,

Keitha Kinne

President

AMG Funds

| | | | | | | | | | | | | | |

| | | | | Periods ended | |

| Average Annual Total Returns | | December 31, 2022* | |

| | | | |

| Stocks: | | | | 1 Year | | | 3 Years | | | 5 Years | |

| | | | |

Large Cap | | (S&P 500® Index) | | | (18.11 | )% | | | 7.66 | % | | | 9.42 | % |

| | | | |

Small Cap | | (Russell 2000® Index) | | | (20.44 | )% | | | 3.10 | % | | | 4.13 | % |

| | | | |

International | | (MSCI ACWI ex USA) | | | (16.00 | )% | | | 0.07 | % | | | 0.88 | % |

| | | | |

Bonds: | | | | | | | | | | | | | | |

| | | | |

Investment Grade | | (Bloomberg U.S. Aggregate Bond Index) | | | (13.01 | )% | | | (2.71 | )% | | | 0.02 | % |

| | | | |

High Yield | | (Bloomberg U.S. Corporate High Yield Bond Index) | | | (11.19 | )% | | | 0.05 | % | | | 2.31 | % |

| | | | |

Tax-exempt | | (Bloomberg Municipal Bond Index) | | | (8.53 | )% | | | (0.77 | )% | | | 1.25 | % |

| | | | |

Treasury Bills | | (ICE BofAML U.S. 6-Month Treasury Bill Index) | | | 1.34 | % | | | 0.82 | % | | | 1.39 | % |

*Source: FactSet. Past performance is no guarantee of future results.

2

| | |

| | |

| | | About Your Fund’s Expenses |

| | | |

| | | |

| | | |

| | | | | | | | |

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below. ACTUAL EXPENSES The first line of the following table provides information about the actual account values and | | | | actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period. HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s | | | | actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| | | | | | | | |

| | | | | | | | | | |

Six Months Ended December 31, 2022 | | Expense

Ratio for

the Period | | Beginning

Account

Value

07/01/22 | | Ending

Account

Value

12/31/22 | | | Expenses

Paid

During

the Period* |

AMG GW&K ESG Bond Fund |

|

Based on Actual Fund Return |

Class N | | 0.68% | | $1,000 | | | $981 | | | $3.40 |

Class I | | 0.48% | | $1,000 | | | $982 | | | $2.40 |

|

Based on Hypothetical 5% Annual Return |

Class N | | 0.68% | | $1,000 | | | $1,022 | | | $3.47 |

Class I | | 0.48% | | $1,000 | | | $1,023 | | | $2.45 |

AMG GW&K Enhanced Core Bond ESG Fund |

|

Based on Actual Fund Return |

Class N | | 0.73% | | $1,000 | | | $971 | | | $3.63 |

Class I | | 0.56% | | $1,000 | | | $970 | | | $2.78 |

Class Z | | 0.48% | | $1,000 | | | $972 | | | $2.39 |

|

Based on Hypothetical 5% Annual Return |

Class N | | 0.73% | | $1,000 | | | $1,022 | | | $3.72 |

Class I | | 0.56% | | $1,000 | | | $1,022 | | | $2.85 |

Class Z | | 0.48% | | $1,000 | | | $1,023 | | | $2.45 |

AMG GW&K High Income Fund |

|

Based on Actual Fund Return |

Class N | | 0.87% | | $1,000 | | | $1,040 | | | $4.47 |

Class I | | 0.67% | | $1,000 | | | $1,041 | | | $3.45 |

|

Based on Hypothetical 5% Annual Return |

Class N | | 0.87% | | $1,000 | | | $1,021 | | | $4.43 |

Class I | | 0.67% | | $1,000 | | | $1,022 | | | $3.41 |

| | | | | | | | | | |

Six Months Ended December 31, 2022 | | Expense

Ratio for

the Period | | Beginning

Account

Value

07/01/22 | | Ending

Account

Value

12/31/22 | | | Expenses

Paid

During

the Period* |

AMG GW&K Municipal Bond Fund |

|

Based on Actual Fund Return |

Class N | | 0.73% | | $1,000 | | | $1,016 | | | $3.71 |

Class I | | 0.39% | | $1,000 | | | $1,019 | | | $1.98 |

|

Based on Hypothetical 5% Annual Return |

Class N | | 0.73% | | $1,000 | | | $1,022 | | | $3.72 |

Class I | | 0.39% | | $1,000 | | | $1,023 | | | $1.99 |

AMG GW&K Municipal Enhanced Yield Fund |

|

Based on Actual Fund Return |

Class N | | 0.99% | | $1,000 | | | $984 | | | $4.95 |

Class I | | 0.64% | | $1,000 | | | $985 | | | $3.20 |

Class Z | | 0.59% | | $1,000 | | | $985 | | | $2.95 |

|

Based on Hypothetical 5% Annual Return |

Class N | | 0.99% | | $1,000 | | | $1,020 | | | $5.04 |

Class I | | 0.64% | | $1,000 | | | $1,022 | | | $3.26 |

Class Z | | 0.59% | | $1,000 | | | $1,022 | | | $3.01 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

3

| | |

| | |

| | | AMG GW&K ESG Bond Fund Portfolio Manager’s Comments (unaudited) |

| | | |

| | | |

| | | |

| | | | | | | | |

THE YEAR IN REVIEW AMG GW&K ESG Bond Fund Class N (the “Fund”) shares returned (13.17)% for the year ended December 31, 2022, compared with the (13.01)% return for its current benchmark, the Bloomberg U.S. Aggregate Bond Index (the “Index”). MARKET OVERVIEW In the first quarter of 2022, fixed income markets experienced their worst quarter in more than four decades amid an extraordinary confluence of economic and geopolitical shocks. Core inflation jumped to 5.4%, its highest level since 1983, on a broad-based rise in consumer prices. The U.S. Federal Reserve (the Fed) responded in kind, intensifying its hawkish rhetoric and laying out an aggressive course of hikes to bring inflation back to target. And in addition to exacting a tragic human toll, Russia’s invasion of Ukraine exacerbated already strained supply chains and commodity markets, threatening acute and prolonged shortages of materials vital to the basic functioning of the global economy. But for all this uncertainty and turmoil, there was a notable divergence between the performance of rates and credit; the former extended a historically severe downdraft, while the latter continued to enjoy a remarkably benign trading environment. How this disconnect eventually would resolve itself was a central question before investors, though policy uncertainty and heightened tensions seemed unlikely to subside anytime soon. More volatility followed in the second quarter, as bonds traded in a wide range and struggled to commit to a consistent narrative. The central question revolved around how persistent inflation would be and what policy measures would be necessary to quell it. A natural deceleration would allow the Fed to pursue less aggressive policy and possibly achieve a soft landing; more recalcitrant price pressure would require the Fed to mount a harsher response and invite a potential recession. The implications of these two different paths were at odds, leading to a broad lack of conviction with no clear market direction. Similarly, puzzling was a consumer with a strong proclivity to spend but a deeply pessimistic outlook and a corporate sector earning solid profits but starting to announce layoffs. Additionally, China offered a potential bright spot as it emerged from recent shutdowns, but the Ukraine conflict lingered as a major threat to global energy and commodity markets. An imminent resolution to any of these tensions seemed unlikely, so disciplined risk management and careful analysis of relative value were of particular importance for the months ahead. | | | | Fixed income markets were under extraordinary pressure in the third quarter as investors continued to adapt to restrictive monetary policy after more than a decade of accommodation. Stubbornly rising prices, hawkish central banks, and various geopolitical forces combined to tighten financial conditions and raise the cost of borrowing around the world. Defying expectations that it had peaked, inflation remained elevated and manifested across a broader and more entrenched collection of goods and services. The Fed also confounded expectations, projecting a more cautious outlook and a more aggressive path of hikes than most economists had anticipated. International pressures escalated as well, as currency market dislocations, political leadership changes in Europe and Asia, and multiple energy crises collectively drove a heightened sense of uncertainty. The variety and momentum of these forces suggested no near-term end to volatility, especially against a backdrop of increasingly expensive capital. Bonds rebounded in the fourth quarter amid growing confidence that central banks have succeeded in slowing inflation and will soon be able to pursue less restrictive policy. This modest rally nevertheless ended up being too little, too late to help the bond market avoid its worst annual performance on record and an unprecedented second consecutive year of losses. Sentiment among both investors and consumers may have reached an inflection point, but data continue to justify some measure of caution: inflation is still stubbornly above the Fed’s target, the labor market shows few signs of loosening and corporations have yet to see a meaningful deterioration in earnings. Only the rate-sensitive housing market really stands out as a casualty of the Fed’s tightening campaign to this point. Whether the end of the cycle is imminent is likely to remain an open question, especially as investors await the realization of the “long and variable lag” that has yet to be fully reflected across so many segments of the economy. FUND REVIEW The Fund slightly underperformed the Index during the fiscal year. Yield curve positioning was a relative positive, given the Fund’s shorter relative duration in a period of rising rates. Our overweight allocation to corporates had a negative impact to performance amid the heightened spread volatility. Our preference for lower-rated securities within the investment grade corporate space also had a negative effect. On | | | | the positive side, being slightly underweight mortgage-backed securities (MBS) within Securitized and our bias to higher coupon mortgages were helpful to relative performance. Our out-of-benchmark allocation to high yield had little incremental impact on relative performance. ESG (Environmental, Social, and Governance) remained an important area of focus for the corporate bond market in what could be viewed as a transition year in 2022. A growing list of companies have moved beyond publishing sustainability reports to set emissions reduction and net zero targets over the past year. Investors shook off an overall difficult market environment, from geopolitical turmoil to interest rate volatility, to demonstrate continued strong interest in ESG. This was also a landmark year for global sustainability regulation, with regulators across Europe, North America, and Asia introducing new rules and proposals related to reporting for both corporations and investors. In the U.S., the Inflation Reduction Act is poised to provide policy support for many companies of interest to ESG investors. We continue to integrate ESG as a core part of our fundamental investment process, while monitoring regulatory and policy actions that could influence the ESG investing landscape in the coming years. OUTLOOK The disconnect between the Fed’s projections and market pricing has widened following the most recent Summary of Economic Projections (SEP). The median estimate of Federal Open Market Committee (FOMC) participants for the overnight rate at the end of 2023 is 5.125%, up from 4.625% in September; the Fed Funds futures market sees a terminal rate of nearly 5.0% in June of 2023, and then two cuts by year end. There has also been a small but not insignificant chorus of economists calling for the FOMC to raise its target inflation to 3.0% from 2.0%, prompting objections that this would undermine the Fed’s hard-earned credibility. These are just two sources of tension in the rates market, and their resolution could have significant implications for both the level and the shape of the yield curve. We don’t believe investors are being sufficiently compensated for these risks, so duration and curve positioning is positioned relatively neutral to the benchmark. Our fundamental view of credit is broadly constructive, and we believe balance sheets in general are sound and liquidity is sufficient. But we recognize the potential for macroeconomic forces to |

4

| | |

| | |

| | | AMG GW&K ESG Bond Fund Portfolio Manager’s Comments (continued) |

| | | |

| | | |

| | | |

| | | | | | | | |

alter this landscape and we don’t believe all these risks are adequately reflected in valuations. Consequently, our allocation to corporate credit is at the lower end of its historical range. Within the space, we see the best value at the front end, where higher quality credits in less rate-sensitive sectors offer attractive yields and compelling breakevens. | | | | We have also been able to identify names that we believe can improve their credit profiles independently of a challenging macro backdrop. Our exposure to mortgages is neutral, as we believe the benefits of lower originations and potentially lower rate volatility are offset by event risks surrounding quantitative tightening and middling spread levels. | | | | The views expressed represent the opinions of GW&K Investment Management, LLC as of December 31, 2022, and are not intended as a forecast or guarantee of future results, and are subject to change without notice. |

5

| | |

| | |

| | | AMG GW&K ESG Bond Fund Portfolio Manager’s Comments (continued) |

| | | |

| | | |

| | | |

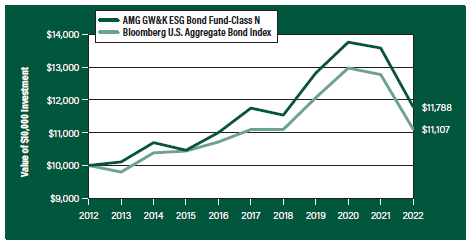

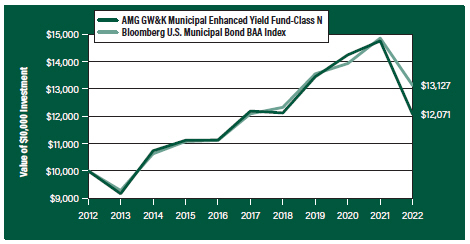

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG GW&K ESG Bond Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The graph compares a hypothetical $10,000 investment made in the AMG GW&K ESG Bond Fund’s Class N shares on December 31, 2012, to a $10,000 investment made in the Bloomberg U.S. Aggregate Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG GW&K ESG Bond Fund and the Bloomberg U.S. Aggregate Bond Index for the same time periods ended December 31, 2022.

| | | | | | | | | | | | | | | | | | | | |

| | | One | | | Five | | | Ten | | | Since | | | Inception | |

| Average Annual Total Returns1 | | Year | | | Years | | | Years | | | Inception | | | Date | |

AMG GW&K ESG Bond Fund2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12 | |

| | | | | |

Class N | | | (13.17%) | | | | 0.07% | | | | 1.66% | | | | 7.11% | | | | 06/01/84 | |

| | | | | |

Class I | | | (12.99%) | | | | 0.26% | | | | — | | | | 1.68% | | | | 04/01/13 | |

| | | | | |

Bloomberg U.S. Aggregate Bond Index13 | | | (13.01%) | | | | 0.02% | | | | 1.06% | | | | 6.40% | | | | 06/01/84 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2022. All returns are in U.S. Dollars($). |

|

2 As of March 19, 2021, the Fund’s subadvisor was changed to GW&K Investment Management, LLC. Prior to March 19, 2021, the Fund was known as the AMG Managers Loomis Sayles Bond Fund and had different principal investment strategies and corresponding risks. Performance shown for periods prior to March 19, 2021, reflects the performance and investment strategies of the Fund’s previous subadvisor, Loomis, Sayles & Company, L.P. The Fund’s past performance would have been different if the Fund were managed by the current subadvisor and strategy, and the Fund’s prior performance record might be less pertinent for investors considering whether to purchase shares of the Fund. 3 From time to time, the Fund’s investment manager has waived fees and/or absorbed Fund expenses, which has resulted in higher returns. 4 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 5 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. 6 High-yield bonds (also known as “junk bonds”) may be subject to greater levels of interest rate, credit, and liquidity risk than investments in higher rated securities. These securities are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. The issuers of the Fund’s holdings may be involved in bankruptcy proceedings, reorganizations, or financial restructurings, and are not as strong financially as higher-rated issuers. 7 Obligations of certain government agencies are not backed by the full faith and credit of the U.S. government. If one of these agencies defaulted on a loan, there is no guarantee that the U.S. government would provide financial support. Additionally, debt securities of the U.S. government may be affected by changing interest rates and subject to prepayment risk. 8 Market prices of investments held by the Fund may fall rapidly or unpredictably due to a variety of economic or political factors, market conditions, disasters or public health issues, or in response to events that affect particular industries or companies. 9 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in |

6

| | |

| | |

| | | AMG GW&K ESG Bond Fund Portfolio Manager’s Comments (continued) |

| | | |

| | | |

| | | |

| | | | |

significant market fluctuations. These risks are magnified in emerging markets. 10 Applying the Fund’s ESG investment criteria may result in the selection or exclusion of securities of certain issuers for reasons other than performance, and the Fund may underperform funds that do not utilize an ESG investment strategy. The application of his strategy may affect the Fund’s exposure to certain companies, sectors, regions, countries or types of investments, which could negatively impact the Fund’s performance depending on whether such investments are in or out of favor. Applying ESG criteria to investment decisions is qualitative and subjective by nature, and there is no guarantee that the criteria utilized by the subadviser or any judgment exercised by the | | subadviser will reflect the beliefs or values of any particular investor. 11 Because exchange-traded funds (ETFs) incur their own costs, investing in them could result in a higher cost to the investor. Additionally, the fund will be indirectly exposed to all the risks of securities held by the ETFs. 12 Factors unique to the municipal bond market may negatively affect the value in municipal bonds. 13 The Bloomberg U.S. Aggregate Bond Index an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds. Unlike the Fund, the Bloomberg U.S. Aggregate Bond Index is unmanaged, is not available for investment and does not incur expenses. | | “Bloomberg®” and any Bloomberg index described herein are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by AMG Funds LLC. Bloomberg is not affiliated with AMG Funds LLC, and Bloomberg does not approve, endorse, review, or recommend the fund described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to such fund. Not FDIC insured, nor bank guaranteed. May lose value. |

7

| | |

| | |

| | | AMG GW&K ESG Bond Fund Fund Snapshots (unaudited) December 31, 2022 |

| | | |

| | | |

| | | |

PORTFOLIO BREAKDOWN

| | |

| Category | | % of Net Assets |

| | |

Corporate Bonds and Notes | | 51.4 |

| | |

U.S. Government and Agency Obligations | | 40.5 |

| | |

Municipal Bonds | | 5.9 |

| | |

Foreign Government Obligations | | 0.9 |

| | |

Short-Term Investments | | 2.1 |

| | |

Other Assets, less Liabilities | | (0.8) |

| | |

| Rating | | % of Market Value1 |

| | |

U.S. Government and Agency Obligations | | 41.0 |

| | |

Aaa/AAA | | 2.2 |

| | |

Aa/AA | | 8.6 |

| | |

A | | 7.0 |

| | |

Baa/BBB | | 23.7 |

| | |

Ba/BB | | 16.4 |

| | |

B | | 1.1 |

| 1 | Includes market value of long-term fixed-income securities only. |

TOP TEN HOLDINGS

| | |

| Security Name | | % of Net Assets |

| | |

U.S. Treasury Bonds, 2.250%, 05/15/41 | | 3.0 |

| | |

FHLMC, 3.000%, 04/01/51 | | 3.0 |

| | |

FNMA, 3.500%, 02/01/35 | | 2.2 |

| | |

FNMA, 3.500%, 08/01/49 | | 2.1 |

| | |

FNMA, 2.000%, 04/01/51 | | 2.1 |

| | |

U.S. Treasury Bonds, 1.875%, 02/15/51 | | 2.1 |

| | |

FNMA, 3.500%, 02/01/47 | | 2.0 |

| | |

U.S. Treasury Bonds, 3.125%, 05/15/48 | | 1.9 |

| | |

FHLMC, 3.500%, 02/01/50 | | 1.8 |

| | |

U.S. Treasury Bonds, 5.000%, 05/15/37 | | 1.8 |

| | | |

| | |

Top Ten as a Group | | 22.0 |

| | |

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB- or higher. Below investment grade ratings are credit ratings of BB+ or lower. Investments designated N/R are not rated by any of the rating agencies. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

8

| | |

| | |

| | | AMG GW&K ESG Bond Fund Schedule of Portfolio Investments December 31, 2022 |

| | | |

| | | |

| | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| |

Corporate Bonds and Notes - 51.4% | | | | | |

| |

Financials - 12.2% | | | | | |

| | |

AerCap Ireland Capital DAC/AerCap Global Aviation Trust (Ireland) | | | | | | | | |

1.650%, 10/29/24 | | | $5,450,000 | | | | $5,027,082 | |

| | |

Aircastle, Ltd. (Bermuda) | | | | | | | | |

5.250%, 08/11/251 | | | 2,282,000 | | | | 2,194,686 | |

| | |

American Express Co. | | | | | | | | |

(3.550% to 09/15/26 then U.S. Treasury Yield Curve CMT 5 year + 2.854%), 3.550%, 09/15/262,3,4 | | | 1,195,000 | | | | 981,693 | |

| | |

American Tower Corp. | | | | | | | | |

4.400%, 02/15/265 | | | 1,900,000 | | | | 1,851,418 | |

| | |

Bank of America Corp. | | | | | | | | |

(3.559% to 04/23/26 then 3 month LIBOR + 1.060%), 3.559%, 04/23/272,4 | | | 2,850,000 | | | | 2,670,080 | |

MTN, (4.330% to 03/15/49 then 3 month LIBOR + 1.520%), 4.330%, 03/15/502,4 | | | 2,775,000 | | | | 2,276,024 | |

| | |

The Bank of New York Mellon Corp. | | | | | | | | |

Series G, (4.700% to 09/20/25 then U.S. Treasury Yield Curve CMT 5 year + 4.358%), 4.700%, 09/20/252,3,4 | | | 4,300,000 | | | | 4,128,559 | |

| | |

The Charles Schwab Corp. | | | | | | | | |

Series I, (4.000% to 06/01/26 then U.S. Treasury Yield Curve CMT 5 year + 3.168%), 4.000%, 06/01/262,3,4 | | | 4,400,000 | | | | 3,817,000 | |

| | |

Crown Castle, Inc. | | | | | | | | |

4.000%, 03/01/27 | | | 2,300,000 | | | | 2,193,392 | |

| | |

First-Citizens Bank & Trust Co. | | | | | | | | |

6.125%, 03/09/28 | | | 2,825,000 | | | | 2,870,967 | |

| | |

The Goldman Sachs Group, Inc. | | | | | | | | |

6.750%, 10/01/37 | | | 1,850,000 | | | | 1,973,993 | |

| | |

JPMorgan Chase & Co. | | | | | | | | |

(1.470% to 09/22/26 then SOFR + 0.765%), 1.470%, 09/22/272,4 | | | 3,104,000 | | | | 2,687,328 | |

| | |

Morgan Stanley | | | | | | | | |

3.950%, 04/23/27 | | | 2,200,000 | | | | 2,077,664 | |

(4.431% to 01/23/29 then 3 month LIBOR + 1.628%), 4.431%, 01/23/302,4 | | | 2,948,000 | | | | 2,743,714 | |

| | |

Owl Rock Capital Corp. | | | | | | | | |

4.250%, 01/15/26 | | | 2,300,000 | | | | 2,111,443 | |

| | |

SBA Communications Corp. | | | | | | | | |

3.875%, 02/15/27 | | | 3,700,000 | | | | 3,343,000 | |

| | |

SLM Corp. | | | | | | | | |

3.125%, 11/02/26 | | | 3,365,000 | | | | 2,861,764 | |

4.200%, 10/29/25 | | | 838,000 | | | | 766,733 | |

| | |

Starwood Property Trust, Inc. | | | | | | | | |

4.750%, 03/15/25 | | | 1,700,000 | | | | 1,622,224 | |

| | |

Truist Financial Corp. | | | | | | | | |

Series P, (4.950% to 12/01/25 then U.S. Treasury Yield Curve CMT 5 year + 4.605%), 4.950%, 09/01/252,3,4 | | | 3,400,000 | | | | 3,250,740 | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| | |

VICI Properties LP/VICI Note Co., Inc. | | | | | | | | |

3.500%, 02/15/251 | | | $1,900,000 | | | | $1,791,377 | |

| | |

Wells Fargo & Co., MTN | | | | | | | | |

(2.879% to 10/30/29 then 3 Month Term SOFR + 1.432%), 2.879%, 10/30/302,4 | | | 3,435,000 | | | | 2,917,705 | |

| | |

Weyerhaeuser Co. | | | | | | | | |

6.875%, 12/15/33 | | | 2,600,000 | | | | 2,788,953 | |

| | |

Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp. | | | | | | | | |

5.500%, 03/01/251 | | | 1,250,000 | | | | 1,186,682 | |

| | |

Total Financials | | | | | | | 60,134,221 | |

| |

Industrials - 37.2% | | | | | |

| | |

Advocate Health & Hospitals Corp. | | | | | | | | |

4.272%, 08/15/48 | | | 1,700,000 | | | | 1,443,252 | |

| | |

AECOM | | | | | | | | |

5.125%, 03/15/27 | | | 1,650,000 | | | | 1,588,125 | |

| | |

Air Products and Chemicals, Inc. | | | | | | | | |

2.700%, 05/15/40 | | | 2,450,000 | | | | 1,822,883 | |

| | |

Alcoa Nederland Holding, B.V. (Netherlands) | | | | | | | | |

4.125%, 03/31/291 | | | 5,750,000 | | | | 5,101,162 | |

| | |

Amazon.com, Inc. | | | | | | | | |

4.600%, 12/01/255 | | | 5,053,000 | | | | 5,040,560 | |

| | |

Anglo American Capital PLC (United Kingdom) | | | | | | | | |

2.875%, 03/17/311,5 | | | 3,554,000 | | | | 2,901,876 | |

| | |

Anheuser-Busch InBev Worldwide, Inc. | | | | | | | | |

4.375%, 04/15/38 | | | 2,200,000 | | | | 1,966,603 | |

| | |

Aramark Services, Inc. | | | | | | | | |

5.000%, 02/01/281,5 | | | 3,220,000 | | | | 3,004,051 | |

| | |

Ardagh Metal Packaging Finance USA LLC/Ardagh Metal Packaging Finance PLC | | | | | | | | |

3.250%, 09/01/281 | | | 3,500,000 | | | | 2,973,058 | |

| | |

Ashtead Capital, Inc. | | | | | | | | |

1.500%, 08/12/261 | | | 3,536,000 | | | | 3,017,590 | |

| | |

AT&T, Inc. | | | | | | | | |

4.300%, 02/15/30 | | | 2,200,000 | | | | 2,071,513 | |

| | |

Ball Corp. | | | | | | | | |

2.875%, 08/15/30 | | | 3,875,000 | | | | 3,092,715 | |

| | |

Broadcom Corp./Broadcom Cayman Finance, Ltd. | | | | | | | | |

3.875%, 01/15/27 | | | 3,019,000 | | | | 2,855,642 | |

| | |

CCO Holdings LLC/CCO Holdings Capital Corp. | | | | | | | | |

5.500%, 05/01/261 | | | 2,000,000 | | | | 1,936,201 | |

| | |

Celanese US Holdings LLC | | | | | | | | |

6.050%, 03/15/25 | | | 5,085,000 | | | | 5,065,216 | |

| | |

Centene Corp. | | | | | | | | |

3.375%, 02/15/305 | | | 3,650,000 | | | | 3,085,601 | |

| | |

Cisco Systems, Inc. | | | | | | | | |

5.500%, 01/15/40 | | | 1,650,000 | | | | 1,716,999 | |

| | |

Clearwater Paper Corp. | | | | | | | | |

4.750%, 08/15/281 | | | 1,950,000 | | | | 1,713,418 | |

The accompanying notes are an integral part of these financial statements.

9

| | |

| | |

| | | AMG GW&K ESG Bond Fund Schedule of Portfolio Investments (continued) |

| | | |

| | | |

| | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| | |

Industrials - 37.2% (continued) | | | | | | | | |

| | |

The Coca-Cola Co. | | | | | | | | |

2.500%, 06/01/40 | | | $2,400,000 | | | | $1,748,822 | |

| | |

Cogent Communications Group, Inc. | | | | | | | | |

3.500%, 05/01/261 | | | 3,365,000 | | | | 3,056,909 | |

| | |

CommonSpirit Health | | | | | | | | |

3.347%, 10/01/29 | | | 1,950,000 | | | | 1,696,984 | |

| | |

Crown Americas LLC/Crown Americas Capital Corp. V | | | | | | | | |

4.250%, 09/30/265 | | | 3,350,000 | | | | 3,194,493 | |

| | |

Dell International LLC/EMC Corp. | | | | | | | | |

8.100%, 07/15/36 | | | 972,000 | | | | 1,089,241 | |

| | |

Dell, Inc. | | | | | | | | |

7.100%, 04/15/28 | | | 2,950,000 | | | | 3,145,746 | |

| | |

Delta Air Lines, Inc. | | | | | | | | |

7.375%, 01/15/265 | | | 3,100,000 | | | | 3,167,394 | |

| | |

Discovery Communications LLC | | | | | | | | |

3.950%, 03/20/285 | | | 2,047,000 | | | | 1,816,889 | |

| | |

FMG Resources August 2006 Pty, Ltd. (Australia) | | | | | | | | |

4.500%, 09/15/271 | | | 3,000,000 | | | | 2,767,500 | |

| | |

The Ford Foundation | | | | | | | | |

Series 2020, 2.415%, 06/01/50 | | | 2,725,000 | | | | 1,714,252 | |

| | |

Freeport-McMoRan, Inc. | | | | | | | | |

4.625%, 08/01/305 | | | 2,961,000 | | | | 2,757,859 | |

| | |

The Goodyear Tire & Rubber Co. | | | | | | | | |

4.875%, 03/15/275 | | | 500,000 | | | | 457,365 | |

| | |

Graphic Packaging International LLC | | | | | | | | |

3.500%, 03/01/291 | | | 2,850,000 | | | | 2,428,279 | |

| | |

Hanesbrands, Inc. | | | | | | | | |

4.875%, 05/15/261,5 | | | 3,250,000 | | | | 2,904,106 | |

| | |

Hasbro, Inc. | | | | | | | | |

3.900%, 11/19/29 | | | 3,425,000 | | | | 3,043,744 | |

| | |

HB Fuller Co. | | | | | | | | |

4.250%, 10/15/28 | | | 3,400,000 | | | | 3,009,000 | |

| | |

HCA, Inc. | | | | | | | | |

3.500%, 09/01/30 | | | 3,050,000 | | | | 2,630,553 | |

| | |

Hilton Domestic Operating Co., Inc. | | | | | | | | |

4.875%, 01/15/30 | | | 3,600,000 | | | | 3,262,356 | |

| | |

The Home Depot, Inc. | | | | | | | | |

5.875%, 12/16/36 | | | 1,600,000 | | | | 1,711,065 | |

| | |

Howmet Aerospace, Inc. | | | | | | | | |

6.875%, 05/01/25 | | | 2,000,000 | | | | 2,052,340 | |

| | |

KB Home | | | | | | | | |

4.800%, 11/15/29 | | | 1,222,000 | | | | 1,062,639 | |

6.875%, 06/15/275 | | | 1,751,000 | | | | 1,761,418 | |

| | |

Lamar Media Corp. | | | | | | | | |

4.875%, 01/15/295 | | | 3,250,000 | | | | 2,984,075 | |

| | |

Merck & Co., Inc. | | | | | | | | |

1.900%, 12/10/28 | | | 7,010,000 | | | | 6,018,509 | |

| | |

Meritage Homes Corp. | | | | | | | | |

6.000%, 06/01/25 | | | 485,000 | | | | 482,666 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| | |

MGM Resorts International | | | | | | | | |

5.750%, 06/15/25 | | | $1,175,000 | | | | $1,141,954 | |

| | |

Microsoft Corp. | | | | | | | | |

2.525%, 06/01/50 | | | 2,450,000 | | | | 1,612,220 | |

| | |

MSCI, Inc. | | | | | | | | |

3.250%, 08/15/331 | | | 2,015,000 | | | | 1,556,101 | |

| | |

Mueller Water Products, Inc. | | | | | | | | |

4.000%, 06/15/291 | | | 3,000,000 | | | | 2,636,250 | |

| | |

Murphy Oil USA, Inc. | | | | | | | | |

4.750%, 09/15/29 | | | 3,250,000 | | | | 2,973,848 | |

| | |

Newell Brands, Inc. | | | | | | | | |

4.450%, 04/01/266 | | | 3,400,000 | | | | 3,198,704 | |

| | |

Novelis Corp. | | | | | | | | |

3.250%, 11/15/261 | | | 3,175,000 | | | | 2,846,419 | |

| | |

Owens Corning | | | | | | | | |

7.000%, 12/01/36 | | | 1,800,000 | | | | 1,904,913 | |

| | |

Parker-Hannifin Corp. | | | | | | | | |

3.250%, 06/14/29 | | | 1,900,000 | | | | 1,696,696 | |

| | |

Penske Automotive Group, Inc. | | | | | | | | |

3.500%, 09/01/255 | | | 2,000,000 | | | | 1,856,119 | |

| | |

Prime Security Services Borrower LLC/Prime Finance, Inc. | | | | | | | | |

5.750%, 04/15/261 | | | 3,250,000 | | | | 3,128,125 | |

| | |

PulteGroup, Inc. | | | | | | | | |

6.000%, 02/15/35 | | | 2,050,000 | | | | 1,960,131 | |

| | |

SK Hynix, Inc. (South Korea) | | | | | | | | |

2.375%, 01/19/311 | | | 3,000,000 | | | | 2,199,494 | |

| | |

Sonoco Products Co. | | | | | | | | |

2.850%, 02/01/32 | | | 3,682,000 | | | | 2,992,949 | |

| | |

Sysco Corp. | | | | | | | | |

2.400%, 02/15/30 | | | 4,475,000 | | | | 3,719,568 | |

| | |

Teleflex, Inc. | | | | | | | | |

4.250%, 06/01/281 | | | 3,350,000 | | | | 3,058,081 | |

| | |

Tenet Healthcare Corp. | | | | | | | | |

4.875%, 01/01/261 | | | 3,350,000 | | | | 3,167,903 | |

| | |

Toll Brothers Finance Corp. | | | | | | | | |

4.875%, 03/15/27 | | | 3,250,000 | | | | 3,103,212 | |

| | |

Travel + Leisure Co. | | | | | | | | |

5.650%, 04/01/246 | | | 2,700,000 | | | | 2,659,368 | |

| | |

Twilio, Inc. | | | | | | | | |

3.625%, 03/15/29 | | | 600,000 | | | | 487,440 | |

3.875%, 03/15/315 | | | 2,694,000 | | | | 2,137,298 | |

| | |

United Parcel Service, Inc. | | | | | | | | |

6.200%, 01/15/38 | | | 1,500,000 | | | | 1,658,363 | |

| | |

United Rentals North America, Inc. | | | | | | | | |

3.875%, 02/15/31 | | | 3,650,000 | | | | 3,059,759 | |

| | |

Verizon Communications, Inc. | | | | | | | | |

3.875%, 02/08/295 | | | 3,460,000 | | | | 3,246,398 | |

| | |

VF Corp. | | | | | | | | |

2.950%, 04/23/305 | | | 2,100,000 | | | | 1,744,175 | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

10

| | |

| | |

| | | AMG GW&K ESG Bond Fund Schedule of Portfolio Investments (continued) |

| | | |

| | | |

| | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| | |

Industrials - 37.2% (continued) | | | | | | | | |

| | |

VMware, Inc. | | | | | | | | |

3.900%, 08/21/27 | | | $3,400,000 | | | | $3,173,153 | |

| | |

Walgreens Boots Alliance, Inc. | | | | | | | | |

4.800%, 11/18/44 | | | 2,520,000 | | | | 2,109,022 | |

| | |

Walmart, Inc. | | | | | | | | |

4.050%, 06/29/48 | | | 1,850,000 | | | | 1,641,798 | |

| | |

WESCO Distribution, Inc. | | | | | | | | |

7.125%, 06/15/251 | | | 1,600,000 | | | | 1,620,019 | |

| | |

Western Digital Corp. | | | | | | | | |

4.750%, 02/15/26 | | | 1,916,000 | | | | 1,804,336 | |

| | |

Yum! Brands, Inc. | | | | | | | | |

3.625%, 03/15/31 | | | 3,550,000 | | | | 2,976,675 | |

| | |

Total Industrials | | | | | | | 183,431,160 | |

| |

Utilities - 2.0% | | | | | |

| | |

Dominion Energy, Inc. | | | | | | | | |

Series B, (4.650% to 12/15/24 then U.S. Treasury Yield Curve CMT 5 year + 2.993%), 4.650%, 12/15/242,3,4 | | | 3,950,000 | | | | 3,456,250 | |

| | |

National Rural Utilities Cooperative Finance Corp. | | | | | | | | |

1.350%, 03/15/31 | | | 4,750,000 | | | | 3,509,956 | |

| | |

Northern States Power Co. | | | | | | | | |

2.900%, 03/01/50 | | | 3,800,000 | | | | 2,599,065 | |

| | |

Total Utilities | | | | | | | 9,565,271 | |

| |

Total Corporate Bonds and Notes | | | | | |

(Cost $288,413,877) | | | | | | | 253,130,652 | |

| | |

Municipal Bonds - 5.9% | | | | | | | | |

| | |

California Health Facilities Financing Authority | | | | | | | | |

4.190%, 06/01/37 | | | 3,500,000 | | | | 3,126,553 | |

| | |

California State General Obligation, School Improvements Build America Bonds, 7.550%, 04/01/39 | | | 2,300,000 | | | | 2,878,754 | |

| | |

Commonwealth of Massachusetts | | | | | | | | |

Series B, 4.110%, 07/15/31 | | | 3,660,000 | | | | 3,533,621 | |

| | |

Dallas Fort Worth International Airport, Series A | | | | | | | | |

4.507%, 11/01/51 | | | 1,000,000 | | | | 898,819 | |

| | |

JobsOhio Beverage System, Series A | | | | | | | | |

2.833%, 01/01/38 | | | 3,700,000 | | | | 2,890,756 | |

| | |

Los Angeles Unified School District, School Improvements

5.750%, 07/01/34 | | | 3,225,000 | | | | 3,368,776 | |

| | |

Massachusetts School Building Authority | | | | | | | | |

Series B, 1.753%, 08/15/30 | | | 4,500,000 | | | | 3,673,920 | |

| | |

New Jersey Economic Development Authority, Pension Funding, Series A (National Insured) | | | | | | | | |

7.425%, 02/15/29 | | | 3,550,000 | | | | 3,821,584 | |

| | |

Port Authority of New York & New Jersey | | | | | | | | |

6.040%, 12/01/29 | | | 2,000,000 | | | | 2,109,782 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| | |

University of California, Series BI | | | | | | | | |

1.697%, 05/15/29 | | | $3,650,000 | | | | $2,996,395 | |

| | |

Total Municipal Bonds | | | | | | | | |

(Cost $34,814,883) | | | | | | | 29,298,960 | |

| |

| U.S. Government and Agency Obligations - 40.5% | | | | | |

| | |

Fannie Mae - 17.2% | | | | | | | | |

| | |

FNMA | | | | | | | | |

2.000%, 04/01/51 | | | 12,427,952 | | | | 10,147,515 | |

2.500%, 11/01/50 | | | 5,079,053 | | | | 4,326,132 | |

3.500%, 02/01/35 to 02/01/51 | | | 39,894,854 | | | | 37,465,019 | |

4.000%, 07/01/44 to 01/01/51 | | | 24,014,213 | | | | 22,930,759 | |

4.500%, 05/01/48 to 06/01/49 | | | 6,969,461 | | | | 6,872,502 | |

5.000%, 05/01/50 | | | 3,240,435 | | | | 3,248,364 | |

| | |

Total Fannie Mae | | | | | | | 84,990,291 | |

| | |

Freddie Mac - 8.4% | | | | | | | | |

| | |

FHLMC | | | | | | | | |

2.000%, 03/01/36 | | | 8,784,509 | | | | 7,835,185 | |

3.000%, 04/01/51 | | | 16,670,090 | | | | 14,676,474 | |

3.500%, 02/01/50 | | | 9,647,506 | | | | 8,898,566 | |

4.500%, 10/01/48 to 12/01/48 | | | 10,081,490 | | | | 9,887,915 | |

| | |

Total Freddie Mac | | | | | | | 41,298,140 | |

| | |

U.S. Treasury Obligations - 14.9% | | | | | | | | |

| | |

U.S. Treasury Bonds | | | | | | | | |

1.250%, 05/15/50 | | | 4,625,000 | | | | 2,489,009 | |

1.875%, 02/15/51 | | | 15,912,000 | | | | 10,112,822 | |

2.250%, 05/15/41 | | | 19,759,000 | | | | 14,853,982 | |

2.500%, 02/15/46 | | | 2,096,000 | | | | 1,568,234 | |

3.125%, 05/15/48 | | | 11,143,000 | | | | 9,364,908 | |

3.500%, 02/15/39 | | | 7,852,000 | | | | 7,375,052 | |

5.000%, 05/15/37 | | | 7,846,000 | | | | 8,762,388 | |

6.750%, 08/15/26 | | | 2,579,000 | | | | 2,800,431 | |

| | |

U.S. Treasury Notes | | | | | | | | |

0.250%, 03/15/24 | | | 5,868,000 | | | | 5,562,910 | |

0.500%, 02/28/26 | | | 3,270,000 | | | | 2,913,749 | |

2.500%, 01/31/25 | | | 3,450,000 | | | | 3,319,008 | |

2.625%, 02/15/29 | | | 4,763,000 | | | | 4,402,054 | |

| | |

Total U.S. Treasury Obligations | | | | | | | 73,524,547 | |

| | |

Total U.S. Government and Agency Obligations | | | | | | | | |

(Cost $237,183,222) | | | | | | | 199,812,978 | |

| |

Foreign Government Obligation - 0.9% | | | | | |

| | |

The Korea Development Bank (South Korea)

0.500%, 10/27/23

(Cost $4,552,913) | | | 4,550,000 | | | | 4,394,653 | |

| |

Short-Term Investments - 2.1% | | | | | |

| |

Joint Repurchase Agreements - 1.5%7 | | | | | |

| | |

Bank of America Securities, Inc., dated 12/30/22,due 01/03/23, 4.300% total to be received $1,761,488 (collateralized by various U.S. Government Agency Obligations, 1.500% - 6.500%, 05/01/37 - 05/01/58, totaling $1,795,860) | | | 1,760,647 | | | | 1,760,647 | |

| | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

11

| | |

| | |

| | | AMG GW&K ESG Bond Fund Schedule of Portfolio Investments (continued) |

| | | |

| | | |

| | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

Joint Repurchase Agreements - 1.5%7 | | | | | |

(continued) | | | | | | | | |

| | |

Citigroup Global Markets, Inc., dated 12/30/22, due 01/03/23, 4.250% total to be received $369,995 (collateralized by various U.S. Treasuries, 0.000% - 4.500%, 04/11/23 - 10/31/29, totaling $377,216) | | | $369,820 | | | | $369,820 | |

| | |

MUFG Securities America, Inc., dated 12/30/22, due 01/03/23, 4.300% total to be received $1,761,488 (collateralized by various U.S. Government Agency Obligations, 2.000% - 5.500%, 08/01/24 - 01/01/53, totaling $1,795,860) | | | 1,760,647 | | | | 1,760,647 | |

| | |

National Bank Financial, dated 12/30/22, due 01/03/23, 4.340% total to be received $1,761,496 (collateralized by various U.S. Treasuries, 0.000% - 4.435%, 01/03/23 - 09/09/49, totaling $1,795,860) | | | 1,760,647 | | | | 1,760,647 | |

| | |

RBC Dominion Securities, Inc., dated 12/30/22, due 01/03/23, 4.300% total to be received $1,761,488 (collateralized by various U.S. Government Agency Obligations, 2.000% - 6.000%, 09/01/24 - 10/20/52, totaling $1,795,860) | | | 1,760,647 | | | | 1,760,647 | |

| | |

Total Joint Repurchase Agreements | | | | | | | 7,412,408 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

Repurchase Agreements - 0.6% | | | | | | | | |

| | |

Fixed Income Clearing Corp., dated 12/30/22 due 01/03/23, 4.150% total to be received $3,071,416 (collateralized by a U.S. Treasury, 0.125%, 01/15/32, totaling $3,131,490) | | | $3,070,000 | | | | $3,070,000 | |

| |

Total Short-Term Investments | | | | | |

(Cost $10,482,408) | | | | 10,482,408 | |

| |

Total Investments - 100.8% | | | | | |

(Cost $575,447,303) | | | | 497,119,651 | |

| |

Other Assets, less Liabilities - (0.8)% | | | | (4,113,005 | ) |

| |

Net Assets - 100.0% | | | | $493,006,646 | |

| | | | | |

| 1 | Security exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified institutional buyers. At December 31, 2022, the value of these securities amounted to $57,189,287 or 11.6% of net assets. |

| 2 | Fixed to variable rate investment. The rate shown reflects the fixed rate in effect at December 31, 2022. Rate will reset at a future date. |

| 3 | Perpetuity Bond. The date shown represents the next call date. |

| 4 | Variable rate security. The rate shown is based on the latest available information as of December 31, 2022. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| 5 | Some of these securities, amounting to $25,458,950 or 5.2% of net assets, were out on loan to various borrowers and are collateralized by cash and various U.S. Treasury Obligations. See Note 4 of Notes to Financial Statements. |

| 6 | Step Bond: A debt instrument with either deferred interest payments or an interest rate that resets at specific times during its term. |

| 7 | Cash collateral received for securities lending activity was invested in these joint repurchase agreements. |

| | |

| CMT | | Constant Maturity Treasury |

| FHLMC | | Freddie Mac |

| FNMA | | Fannie Mae |

| LIBOR | | London Interbank Offered Rate |

| MTN | | Medium-Term Note |

| National Insured | | National Public Finance Guarantee Corp. |

| SOFR | | Secured Overnight Financing Rate |

The accompanying notes are an integral part of these financial statements.

12

| | |

| | |

| | | AMG GW&K ESG Bond Fund Schedule of Portfolio Investments (continued) |

| | | |

| | | |

| | | |

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of December 31, 2022:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | | | |

Investments in Securities | | | | | | | | | | | | | | | | |

| | | | |

Corporate Bonds and Notes† | | | — | | | | $253,130,652 | | | | — | | | | $253,130,652 | |

| | | | |

Municipal Bonds† | | | — | | | | 29,298,960 | | | | — | | | | 29,298,960 | |

| | | | |

U.S. Government and Agency Obligations† | | | — | | | | 199,812,978 | | | | — | | | | 199,812,978 | |

| | | | |

Foreign Government Obligation† | | | — | | | | 4,394,653 | | | | — | | | | 4,394,653 | |

| | | | |

Short-Term Investments | | | | | | | | | | | | | | | | |

| | | | |

Joint Repurchase Agreements | | | — | | | | 7,412,408 | | | | — | | | | 7,412,408 | |

| | | | |

Repurchase Agreements | | | — | | | | 3,070,000 | | | | — | | | | 3,070,000 | |

| | | | | | | | | | | | | | | | |

| | | | |

Total Investments in Securities | | | — | | | | $497,119,651 | | | | — | | | | $497,119,651 | |

| | | | | | | | | | | | | | | | |

| † | All corporate bonds and notes, municipal bonds, U.S. government and agency obligations and foreign government obligations held in the Fund are Level 2 securities. For a detailed breakout of corporate bonds and notes, municipal bonds, U.S. government and agency obligations and foreign government obligations by major industry or agency classification, please refer to the Fund’s Schedule of Portfolio Investments. |

The following table below is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value at December 31, 2022:

| | | | |

| | | Asset-Backed Securities | |

| |

Balance as of December 31, 2021 | | | $2,475,909 | |

| |

Accrued discounts (premiums) | | | 2,490 | |

| |

Realized gain (loss) | | | (207,677 | ) |

| |

Change in unrealized appreciation/depreciation | | | 4,633,827 | |

| |

Sales | | | (1,670,846 | ) |

| |

Paydown | | | (5,233,703 | ) |

| |

Transfers in to Level 3 | | | — | |

| |

Transfers out of Level 3 | | | — | |

| |

Balance as of December 31, 2022 | | | $0 | |

| |

| | | | |

| |

Net change in unrealized appreciation/depreciation on investments still held at December 31, 2022 | | | — | |

The accompanying notes are an integral part of these financial statements.

13

| | |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund Portfolio Manager’s Comments (unaudited) |

| | | |

| | | |

| | | |

| | | | |

THE YEAR IN REVIEW AMG GW&K Enhanced Core Bond ESG Fund (the “Fund”) Class N shares returned (14.17)% for the year ended December 31, 2022, compared to the return of (13.01)% for the Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index. MARKET OVERVIEW In the first quarter of 2022 fixed income markets experienced their worst quarter in more than four decades amid an extraordinary confluence of economic and geopolitical shocks. Core inflation jumped to 5.4%, its highest level since 1983, on a broad-based rise in consumer prices. The U.S. Federal Reserve (the Fed) responded in kind, intensifying their hawkish rhetoric and laying out an aggressive course of hikes to bring inflation back to target. And—in addition to exacting a tragic human toll—Russia’s invasion of Ukraine exacerbated already strained supply chains and commodity markets, threatening acute and prolonged shortages of materials vital to the basic functioning of the global economy. But for all this uncertainty and turmoil, there was a notable divergence between the performance of rates and credit; the former extended a historically severe downdraft, while the latter continued to enjoy a remarkably benign trading environment. How this disconnect eventually would resolve itself was a central question before investors, though policy uncertainty and heightened tensions seemed unlikely to subside anytime soon. More volatility followed in the second quarter, as bonds traded in a wide range and struggled to commit to a consistent narrative. The central question revolved around how persistent inflation would be and what policy measures would be necessary to quell it. A natural deceleration would allow the Fed to pursue less aggressive policy and possibly achieve a soft landing; more recalcitrant price pressure would require the Fed to mount a harsher response and invite a potential recession. The implications of these two different paths were at odds, leading to a broad lack of conviction with no clear market direction. Similarly, puzzling was a consumer with a strong proclivity to spend but a deeply pessimistic outlook and a corporate sector earning solid profits but starting to announce layoffs. Additionally, China offered a potential bright spot as it emerged from recent shutdowns, but the Ukraine conflict lingered as a major threat to global energy and commodity markets. An imminent resolution to any of these tensions seemed unlikely, so disciplined risk management and careful analysis of relative value were of particular importance for the months ahead. | | Fixed income markets were under extraordinary pressure in the third quarter as investors continued to adapt to restrictive monetary policy after more than a decade of accommodation. Stubbornly rising prices, hawkish central banks, and various geopolitical forces combined to tighten financial conditions and raise the cost of borrowing around the world. Defying expectations that it had peaked, inflation remained elevated and manifested across a broader and more entrenched collection of goods and services. The Fed also confounded expectations, projecting a more cautious outlook and a more aggressive path of hikes than most economists had anticipated. International pressures escalated as well, as currency market dislocations, political leadership changes in Europe and Asia, and multiple energy crises collectively drove a heightened sense of uncertainty. The variety and momentum of these forces suggested no near-term end to volatility, especially against a backdrop of increasingly expensive capital. Bonds rebounded in the fourth quarter amid growing confidence that central banks have succeeded in slowing inflation and will soon be able to pursue less restrictive policy. This modest rally nevertheless ended up being too little, too late to help the bond market avoid its worst annual performance on record and an unprecedented second consecutive year of losses. Sentiment among both investors and consumers may have reached an inflection point, but data continue to justify some measure of caution: inflation is still stubbornly above the Fed’s target, the labor market shows few signs of loosening, and corporations have yet to see a meaningful deterioration in earnings. Only the rate-sensitive housing market really stands out as a casualty of the Fed’s tightening campaign to this point. Whether the end of the cycle is imminent is likely to remain an open question, especially as investors await the realization of the “long and variable lag” that has yet to be fully reflected across so many segments of the economy. FUND REVIEW The Fund underperformed the Index during the fiscal year. Yield curve positioning was a relative positive, given the Fund’s shorter relative duration in a period of rising rates. Our overweight allocation to corporates had a negative impact on performance amid the heightened spread volatility. Our preference for lower-rated securities within the investment grade corporate space also had a negative effect. On | | the positive side, our bias to higher coupon mortgages was helpful to relative performance. Our out-of-benchmark allocation to high yield had an incrementally positive influence on overall corporate security selection. ESG (Environmental, Social, and Governance) remained an important area of focus for the corporate bond market in what could be viewed as a transition year in 2022. A growing list of companies have moved beyond publishing sustainability reports to set emissions reduction and net zero targets over the past year. Investors shook off an overall difficult market environment, from geopolitical turmoil to interest rate volatility, to demonstrate continued strong interest in ESG. This was also a landmark year for global sustainability regulation, with regulators across Europe, North America, and Asia introducing new rules and proposals related to reporting for both corporations and investors. In the U.S., the Inflation Reduction Act is poised to provide policy support for many companies of interest to ESG investors. We continue to integrate ESG as a core part of our fundamental investment process, while monitoring regulatory and policy actions that could influence the ESG investing landscape in the coming years. OUTLOOK The disconnect between the Fed’s projections and market pricing has widened following the most recent Summary of Economic Projections (SEP). The median estimate of Federal Open Market Committee (FOMC) participants for the overnight rate at the end of 2023 is 5.125%, up from 4.625% in September; the Fed Funds futures market sees a terminal rate of nearly 5% in June of 2023, and then two cuts by year end. There has also been a small but not insignificant chorus of economists calling for the FOMC to raise its target inflation to 3.0% from 2.0%, prompting objections that this would undermine the Fed’s hard-earned credibility. These are just two sources of tension in the rates market, and their resolution could have significant implications for both the level and the shape of the yield curve. We don’t believe investors are being sufficiently compensated for these risks, so duration and curve positioning is relatively neutral relative to its benchmark. Our fundamental view of credit is broadly constructive, and we believe balance sheets in general are sound and liquidity is sufficient. But we recognize the potential for macroeconomic forces to alter this landscape and we don’t believe all these |

| | | | |

14

| | |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund Portfolio Manager’s Comments (continued) |

| | | |

| | | |

| | | |

| | | | |

risks are adequately reflected in valuations. Consequently, our allocation to corporate credit is at the lower end of its historical range. Within the space, we see the best value at the front end, where higher quality credits in less rate-sensitive sectors offer attractive yields and compelling breakevens. We have also been able to identify names that we | | believe can improve their credit profiles independently of a challenging macro backdrop. Our exposure to mortgages is neutral, as we believe the benefits of lower originations and potentially lower rate volatility are offset by event risks surrounding quantitative tightening and middling spread levels. | | The views expressed represent the opinions of GW&K Investment Management, LLC as of December 31, 2022, and are not intended as a forecast or guarantee of future results, and are subject to change without notice. |

| | | | |

15

| | |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund Portfolio Manager’s Comments (continued) |

| | | |

| | | |

| | | |

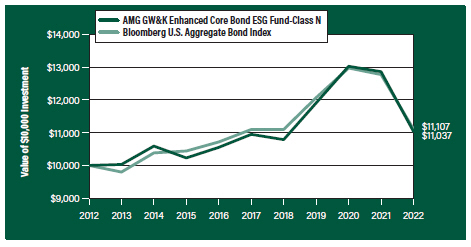

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG GW&K Enhanced Core Bond ESG Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The graph compares a hypothetical $10,000 investment made in the AMG GW&K Enhanced Core Bond ESG Fund’s Class N shares on December 31, 2012, to a $10,000 investment made in the Bloomberg U.S. Aggregate Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG GW&K Enhanced Core Bond ESG Fund and the Bloomberg U.S. Aggregate Bond Index for the same time periods ended December 31, 2022.

| | | | | | | | | | | | |

| Average Annual Total Returns1 | | One Year | | | Five Years | | | Ten Years | |

|

AMG GW&K Enhanced Core Bond ESG Fund2, 3, 4, 5, 6, 7, 8, 9 | |

| | | |

Class N | | | (14.17% | ) | | | 0.16% | | | | 0.99% | |

| | | |

Class I | | | (14.07% | ) | | | 0.32% | | | | 1.16% | |

| | | |

Class Z | | | (14.00% | ) | | | 0.41% | | | | 1.24% | |

| | | |

Bloomberg U.S. Aggregate Bond Index10 | | | (13.01% | ) | | | 0.02% | | | | 1.06% | |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2022. All returns are in U.S. Dollars ($). |

|

2 From time to time, the Fund’s investment manager has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 4 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. 5 High-yield bonds (also known as “junk bonds”) may be subject to greater levels of interest rate, credit, and liquidity risk than investments in higher rated securities. These securities are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. The issuers of the Fund’s holdings may be involved in bankruptcy proceedings, reorganizations, or financial restructurings, and are not as strong financially as higher-rated issuers. 6 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. These risks are magnified in emerging markets. 7 Market prices of investments held by the Fund may fall rapidly or unpredictably due to a variety of economic or political factors, market conditions, disasters or public health issues, or in response to events that affect particular industries or companies. 8 Obligations of certain government agencies are not backed by the full faith and credit of the U.S. government. If one of these agencies defaulted on a loan, there is no guarantee that the U.S. government would provide financial support. Additionally, debt securities of the U.S. government may be affected by changing interest rates and subject to prepayment risk. 9 Applying the Fund’s ESG investment criteria may result in the selection or exclusion of securities of certain issuers for reasons other than performance, and the Fund may underperform funds that do not utilize an ESG investment strategy. The application of this strategy may affect the Fund’s exposure to certain companies, sectors, regions, countries or types of investments, which could negatively impact the Fund’s performance depending on whether such investments are in or out of favor. Applying ESG criteria to investment decisions is qualitative and subjective by nature, and there is no guarantee that the criteria utilized by the |

| |

16

| | |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund Portfolio Manager’s Comments (continued) |

| | | |

| | | |

| | | |

| | | | |

Subadviser or any judgment exercised by the Subadviser will reflect the beliefs or values of any particular investor. 10 The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds. Unlike the Fund, the Bloomberg U.S. Aggregate Bond Index is unmanaged, is not available for investment and does not incur expenses. | | “Bloomberg®” and any Bloomberg index described herein are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by AMG Funds LLC. Bloomberg is not affiliated with AMG Funds LLC, and Bloomberg does not approve, endorse, review, or recommend the fund described herein. Bloomberg | | does not guarantee the timeliness, accurateness, or completeness of any data or information relating to such fund. Not FDIC insured, nor bank guaranteed. May lose value. |

| | | | |

17

| | |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund Fund Snapshots (unaudited) December 31, 2022 |

| | | |

| | | |

| | | |

PORTFOLIO BREAKDOWN

| | |

| Category | | % of Net Assets |

| | |

U.S. Government and Agency Obligations | | 48.3 |

| | |

Corporate Bonds and Notes | | 42.5 |

| | |

Municipal Bonds | | 6.4 |

| | |

Foreign Government Obligations | | 0.8 |

| | |

Short-Term Investments | | 3.7 |

| | |

Other Assets, less Liabilities | | (1.7) |

| | |

| Rating | | % of Market Value1 |

| | |

U.S. Government and Agency Obligations | | 49.2 |

| | |

Aaa/AAA | | 3.3 |

| | |

Aa/AA | | 7.0 |

| | |

A | | 8.1 |

| | |

Baa/BBB | | 22.6 |

| | |

Ba/BB | | 9.3 |

| | |

B | | 0.5 |

| 1 | Includes market value of long-term fixed-income securities only. |

TOP TEN HOLDINGS

| | | | |

| Security Name | | | | % of Net Assets |

| | | |

U.S. Treasury Bonds, 3.500%, 02/15/39 | | | | 3.5 |

| | | |

FNMA, 4.000%, 10/01/43 | | | | 2.2 |

| | | |

U.S. Treasury Bonds, 1.875%, 02/15/51 | | | | 2.0 |

| | | |

FNMA, 4.500%, 09/01/46 | | | | 2.0 |

| | | |

U.S. Treasury Bonds, 2.250%, 05/15/41 | | | | 2.0 |

| | | |

FNMA, 3.500%, 02/01/47 | | | | 1.9 |

| | | |

FHLMC, 3.000%, 03/01/51 | | | | 1.7 |

| | | |

U.S. Treasury Bonds, 3.125%, 05/15/48 | | | | 1.7 |

| | | |

California State General Obligation, School Improvements, , 7.550%, 04/01/39 | | | | 1.6 |

| | | |

FNMA, 3.500%, 07/01/50 | | | | 1.6 |

| | | |

Top Ten as a Group | | | | 20.2 |

| | | | |

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB- or higher. Below investment grade ratings are credit ratings of BB+ or lower. Investments designated N/R are not rated by any of the rating agencies. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

18

| | |

| | |

| | | AMG GW&K Enhanced Core Bond ESG Fund Schedule of Portfolio Investments December 31, 2022 |

| | | |

| | | |

| | | |

| | | | | | | | |

| | | Principal Amount | | | Value | |

| |

Corporate Bonds and Notes - 42.5% | | | | | |

| |

Financials - 12.0% | | | | | |

| | |

AerCap Ireland Capital DAC/AerCap Global Aviation Trust (Ireland) 1.650%, 10/29/24 | | | $450,000 | | | | $415,080 | |

| | |