UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | | | | | | | | | | | | | | | | | | | |

| Investment Company Act file number | 811-06441 |

| |

| AMERICAN CENTURY INTERNATIONAL BOND FUNDS |

| (Exact name of registrant as specified in charter) |

| |

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 |

| (Address of principal executive offices) | (Zip Code) |

| |

JOHN PAK

4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 |

| (Name and address of agent for service) |

| |

| Registrant’s telephone number, including area code: | 816-531-5575 |

| |

| Date of fiscal year end: | 10-31 |

| |

| Date of reporting period: | 10-31-2021 |

ITEM 1. REPORTS TO STOCKHOLDERS.

(a) Provided under separate cover.

| | | | | |

| |

| Annual Report |

| |

| October 31, 2021 |

| |

| Emerging Markets Debt Fund |

| Investor Class (AEDVX) |

| I Class (AEHDX) |

| Y Class (AEYDX) |

| A Class (AEDQX) |

| C Class (AEDHX) |

| R Class (AEDWX) |

| R5 Class (AEDJX) |

| R6 Class (AEXDX) |

| G Class (AEDGX) |

| | | | | |

| President’s Letter | |

| Performance | |

| Portfolio Commentary | |

| Fund Characteristics | |

| Shareholder Fee Example | |

| Schedule of Investments | |

| Statement of Assets and Liabilities | |

| Statement of Operations | |

| Statement of Changes in Net Assets | |

| Notes to Financial Statements | |

| Financial Highlights | |

| Report of Independent Registered Public Accounting Firm | |

| Management | |

| Approval of Management Agreement | |

| |

| |

| Additional Information | |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Jonathan Thomas

Jonathan Thomas

Dear Investor:

Thank you for reviewing this annual report for the period ended October 31, 2021. Annual reports help convey important information about fund returns, including market factors that affected performance. For additional investment insights, please visit americancentury.com.

Economic, Earnings Gains Fueled Rally Among Risk-On Assets

Stocks and other risk-on assets rallied for the 12-month period, despite lingering pandemic-related challenges. Upbeat data on U.S. manufacturing, employment and housing, along with central bank and federal government support and positive vaccine developments, helped boost corporate earnings and promote investor optimism. Outside the U.S., most economies recovered, but generally at a slower pace. Virus outbreaks and slower vaccine rollouts, particularly in emerging markets, led to lingering lockdowns in some regions.

As the period progressed, steady economic gains combined with ongoing monetary and fiscal support, rising energy prices and severe supply chain disruptions pushed global interest rates and inflation higher. In the U.S., year-over-year headline inflation climbed to 6.2% in October 2021, the largest 12-month increase in nearly 31 years.

Late in the period, the Federal Reserve (Fed) confirmed it would start tapering its bond buying in November. Yet despite inflation’s surge, the Fed left short-term interest rates unchanged. Central banks in Europe and the U.K. maintained their supportive interest rate and bond-buying programs as inflation ticked higher.

Overall, stocks delivered stellar performance for the 12-month period, highlighted by the S&P 500 Index’s gain of nearly 43%. Assets offering inflation-fighting potential, including real estate investment trusts, fared even better. Meanwhile, global bonds retreated as interest rates rose. However, emerging markets bonds largely advanced, benefiting from risk-on sentiment.

Several Factors Shaping Market Dynamics

The return to pre-pandemic life is progressing, albeit somewhat cautiously due to COVID-19’s lingering effects. As the economy and markets respond to this fluid backdrop, investors will face opportunities and ongoing challenges. Economic growth, inflation, the virus’s trajectory, supply chain normalization and fiscal and monetary policy likely will sway market dynamics.

We appreciate your confidence in us during these extraordinary times. Our firm has a long history of helping clients weather unpredictable markets, and we’re confident we will continue to meet today’s challenges.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

| | | | | | | | | | | | | | | | | | |

| Total Returns as of October 31, 2021 |

| | | | | | |

| | | | Average Annual Returns | |

| | Ticker Symbol | | 1 year | 5 years | Since Inception | Inception Date |

| Investor Class | AEDVX | | 5.29% | 4.16% | 4.39% | 7/29/14 |

| JPMorgan Corporate Emerging Market Bond (CEMBI) Broad Diversified Index | — | | 5.27% | 5.11% | 4.98% | — |

| I Class | AEHDX | | 5.30% | — | 4.22% | 4/10/17 |

| Y Class | AEYDX | | 5.40% | — | 4.32% | 4/10/17 |

| A Class | AEDQX | | | | | 7/29/14 |

| No sales charge | | | 5.03% | 3.88% | 4.13% | |

| With sales charge | | | 0.27% | 2.92% | 3.47% | |

| C Class | AEDHX | | 4.25% | 3.11% | 3.35% | 7/29/14 |

| R Class | AEDWX | | 4.67% | 3.63% | 3.86% | 7/29/14 |

| R5 Class | AEDJX | | 5.49% | 4.38% | 4.60% | 7/29/14 |

| R6 Class | AEXDX | | 5.56% | 4.40% | 4.65% | 7/29/14 |

| G Class | AEDGX | | 6.20% | — | 5.01% | 11/14/17 |

G Class returns would have been lower if a portion of the fees had not been waived.

C Class shares will automatically convert to A Class shares after being held for approximately eight years. C Class average annual returns do not reflect this conversion.

Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 4.50% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

| | |

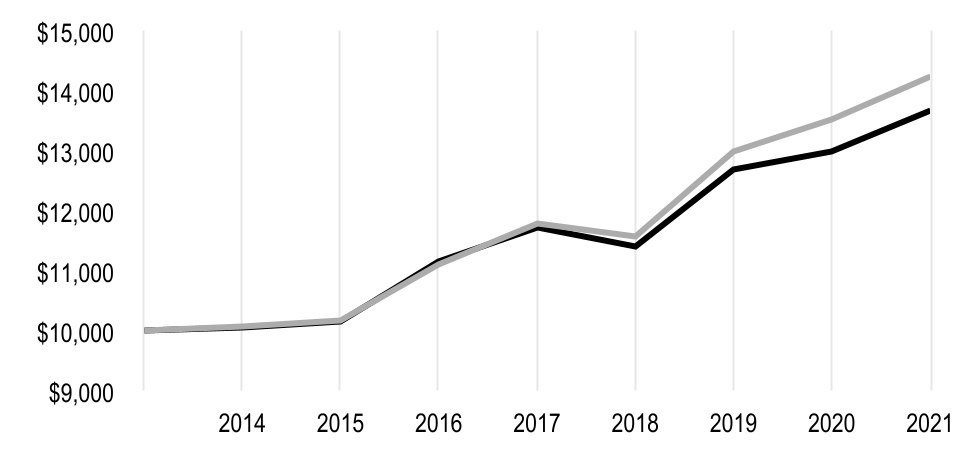

| Growth of $10,000 Over Life of Class |

| $10,000 investment made July 29, 2014 |

| Performance for other share classes will vary due to differences in fee structure. |

| | | | | |

| Value on October 31, 2021 |

| Investor Class — $13,662 |

|

| JPMorgan CEMBI Broad Diversified Index — $14,229 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total Annual Fund Operating Expenses | |

| Investor Class | I Class | Y Class | A Class | C Class | R Class | R5 Class | R6 Class | G Class |

| 0.98% | 0.88% | 0.78% | 1.23% | 1.98% | 1.48% | 0.78% | 0.73% | 0.73% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

Portfolio Managers: John Lovito, Thomas Youn and Alessandra Alecci

Brian Howell, Vice President and Senior Portfolio Manager, left the fund’s portfolio management team August 1, 2021. He is retiring, effective December 31, 2021.

Performance Summary

Emerging Markets Debt returned 5.29%* for the fiscal year ended October 31, 2021. By comparison, the JPMorgan Corporate Emerging Markets Bond (CEMBI) Broad Diversified Index rose 5.27% over the same time period. Fund returns reflect operating expenses, while index returns do not.

Market Review

Emerging markets bonds generally outperformed those from developed economies during the 12-month period. Encouraging signs regarding the world’s recovery from pandemic-related challenges stoked higher risk appetites. The period wasn’t without obstacles, however, as surging economic activity sent inflation soaring, while recurring spikes in infection rates selectively tempered enthusiasm.

The reporting period opened boldly as encouraging news around COVID-19 vaccines heartened investors in late 2020 and contributed to gains in emerging markets debt. Improving economic expectations supported a rally in commodity prices, which also benefited from a declining U.S. dollar.

The landscape changed dramatically during the first quarter of 2021. U.S. lawmakers approved $2.2 trillion in fiscal stimulus, and U.S. Treasury yields rose swiftly and sharply. These events, along with a faster-than-expected U.S. rollout of COVID-19 vaccines, fueled sizable upgrades in U.S. economic outlooks. The U.S. dollar also surged. Rising yields and falling bond prices triggered fears of financial stress among many emerging markets governments and corporations with strained balance sheets.

However, Treasury yields eased through much of the second and third quarters, restoring demand for emerging markets bonds. Although the U.S. dollar continued to outperform most other global currencies, commodity prices, which tend to falter as the dollar gains, largely advanced. Improving global growth expectations aided oil and metals prices, while copper and silver also drew support from green technologies. Protection from rising inflation further aided the asset class.

Due in part to soaring inflation, the Federal Reserve (Fed) started preparing the financial markets for the tapering of the bond-buying program it implemented after the pandemic’s onset. It also indicated it may raise its key lending rate sooner than previously anticipated.

Despite the Fed’s hawkish tone, Treasury yields remained near historic lows, which generally led to sustained demand for higher-yielding emerging markets bonds. Growth expectations remained largely healthy for most emerging markets countries. However, China’s prospects faded late in the period amid potential high-profile defaults in the real estate industry.

Broadly speaking, high-yield securities benefited from elevated risk tolerances and largely outperformed higher-quality securities. Gains among corporate bonds generally topped those from sovereign securities, which ended on a weak note amid the Fed’s posturing.

*All fund returns referenced in this commentary are for Investor Class shares. Performance for other share classes will vary due to differences in fee structure; when Investor Class performance exceeds that of the fund’s index, other share classes may not. See page 3 for returns for all share classes.

Asset Allocation Bolstered Performance

An underweight position relative to the index in China lifted relative returns. China’s property crisis, global supply chain issues and energy shortage eroded the nation’s growth outlook. An overweight stake in Ghana enhanced gains, as oil and gas sector holdings benefited from rising energy prices. Our underweight position in investment-grade bonds proved advantageous amid the high-yield rally. From a sector perspective, underweight exposure to the real estate and financials sectors supplied a lift.

Conversely, an underweight stake in the lowest quality high-yield names hindered performance, most notably in Argentina, where many corporate issues are rated CCC or lower. An underweight to corporate bonds in Turkey, where we preferred sovereign securities, detracted, as did hedges in Mexico and Brazil.

Security Selection, Duration Mixed

Investments in Mexico aided relative results, most notably in the financials and oil and gas sectors. Holdings among shipping port and renewable energy entities lifted our exposure in India. Security selection among chemicals and petrochemicals companies and in the metals and mining sector further boosted performance, as did investments in higher-rated, high-yield securities.

Alternatively, investments in the technology, media and telecommunications sector diminished results amid the Chinese government’s continued pressure on major technology firms. Our security selection within Ghana’s advancing oil and gas sector also detracted from relative returns. Our duration positioning underperformed, especially holdings in the intermediate portion of the U.S. Treasury curve that slumped as the curve steepened.

Positioning for the Future

Although comprehensive COVID-19 vaccination programs have proven problematic, we believe emerging markets hold greater recovery potential than developed markets. We are wary, however, of potential complications in China. We largely hold a positive view of Latin American countries outside of Brazil, where posturing around the 2022 presidential election has already begun.

We expect longer-maturity Treasury yields to move higher amid solid economic growth, higher inflation and massive government spending. However, a hawkish shift by the Fed may prove challenging, given slowing growth in China and the rising possibility of accommodative measures by the Chinese government. Nevertheless, the real interest rate differential continues to favor emerging markets, given early moves by several central banks to contain nascent inflation. Recent strength in the U.S. dollar may prove to be short lived as longer-maturity yields rise. Additionally, we believe the specter of sustained inflation will continue to make commodity-tied assets attractive as an inflation hedge.

Against this backdrop, our overweight in high-yield exposure was largely focused on higher-quality names at period-end. We also increased exposure to the defensive utilities and technology, media and telecommunications sectors. Our duration remained short but closer to neutral by period-end. As always, we remain focused on select, bottom-up opportunities.

| | | | | |

| OCTOBER 31, 2021 |

| Types of Investments in Portfolio | % of net assets |

| Corporate Bonds | 86.8% |

| Sovereign Governments and Agencies | 4.2% |

| Preferred Stocks | 2.5% |

| U.S. Treasury Securities | 1.3% |

| Exchange-Traded Funds | 0.1% |

| Temporary Cash Investments | 4.2% |

| Temporary Cash Investments - Securities Lending Collateral | 2.8% |

| Other Assets and Liabilities | (1.9)% |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from May 1, 2021 to October 31, 2021.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or I Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not through a financial intermediary or employer-sponsored retirement plan account), American Century Investments may charge you a $25.00 annual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $25.00 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments brokerage accounts, you are currently not subject to this fee. If you are subject to the account maintenance fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | |

| Beginning

Account Value

5/1/21 | Ending

Account Value

10/31/21 | Expenses Paid During Period(1) 5/1/21 - 10/31/21 | Annualized Expense Ratio(1) |

| Actual | | | | |

| Investor Class | $1,000 | $1,006.00 | $4.90 | 0.97% |

| I Class | $1,000 | $1,005.60 | $4.40 | 0.87% |

| Y Class | $1,000 | $1,006.10 | $3.89 | 0.77% |

| A Class | $1,000 | $1,004.80 | $6.16 | 1.22% |

| C Class | $1,000 | $1,000.90 | $9.94 | 1.97% |

| R Class | $1,000 | $1,003.50 | $7.42 | 1.47% |

| R5 Class | $1,000 | $1,007.00 | $3.90 | 0.77% |

| R6 Class | $1,000 | $1,007.30 | $3.64 | 0.72% |

| G Class | $1,000 | $1,009.90 | $0.05 | 0.01% |

| Hypothetical | | | | |

| Investor Class | $1,000 | $1,020.32 | $4.94 | 0.97% |

| I Class | $1,000 | $1,020.82 | $4.43 | 0.87% |

| Y Class | $1,000 | $1,021.32 | $3.92 | 0.77% |

| A Class | $1,000 | $1,019.06 | $6.21 | 1.22% |

| C Class | $1,000 | $1,015.28 | $10.01 | 1.97% |

| R Class | $1,000 | $1,017.80 | $7.48 | 1.47% |

| R5 Class | $1,000 | $1,021.32 | $3.92 | 0.77% |

| R6 Class | $1,000 | $1,021.58 | $3.67 | 0.72% |

| G Class | $1,000 | $1,025.16 | $0.05 | 0.01% |

(1)Expenses are equal to the class's annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 184, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. Annualized expense ratio reflects actual expenses, including any applicable fee waivers or expense reimbursements and excluding any acquired fund fees and expenses.

OCTOBER 31, 2021 | | | | | | | | |

| Shares/

Principal Amount | Value |

| CORPORATE BONDS — 86.8% |

|

|

| Argentina — 0.2% | | |

| YPF SA, 8.50%, 7/28/25 | $ | 500,000 | | $ | 405,380 | |

YPF SA, 4.00%, 2/12/26(1) | 168,000 | | 144,895 | |

YPF SA, 1.50%, 9/30/33(1) | 1,200,000 | | 671,226 | |

| | 1,221,501 | |

| Austria — 0.6% | | |

Iochpe-Maxion Austria GmbH / Maxion Wheels de Mexico S de RL de CV, 5.00%, 5/7/28(1) | 4,050,000 | | 3,951,463 | |

| Brazil — 10.7% | | |

| Azul Investments LLP, 5.875%, 10/26/24 | 3,000,000 | | 2,787,675 | |

Azul Investments LLP, 7.25%, 6/15/26(1)(2) | 2,000,000 | | 1,858,310 | |

B2W Digital Lux Sarl, 4.375%, 12/20/30(1) | 3,800,000 | | 3,539,054 | |

Banco BTG Pactual SA, 4.50%, 1/10/25(1) | 1,400,000 | | 1,424,500 | |

| Banco BTG Pactual SA, 4.50%, 1/10/25 | 500,000 | | 508,750 | |

CSN Inova Ventures, 6.75%, 1/28/28(1) | 4,900,000 | | 5,209,925 | |

| CSN Resources SA, 7.625%, 4/17/26 | 1,500,000 | | 1,580,265 | |

Embraer Netherlands Finance BV, 6.95%, 1/17/28(1) | 6,000,000 | | 6,665,040 | |

| Embraer Overseas Ltd., 5.70%, 9/16/23 | 2,000,000 | | 2,110,820 | |

FS Luxembourg Sarl, 10.00%, 12/15/25(1) | 1,000,000 | | 1,104,130 | |

Gol Finance SA, 8.00%, 6/30/26(1) | 1,000,000 | | 968,225 | |

| GTL Trade Finance, Inc., 7.25%, 4/16/44 | 1,700,000 | | 2,257,192 | |

Guara Norte Sarl, 5.20%, 6/15/34(1) | 7,268,946 | | 7,134,398 | |

GUSAP III LP, 4.25%, 1/21/30(1)(2) | 5,000,000 | | 5,265,825 | |

Itau Unibanco Holding SA, VRN, 4.50%, 11/21/29(1) | 4,000,000 | | 3,995,040 | |

Itau Unibanco Holding SA, VRN, 3.875%, 4/15/31(1) | 400,000 | | 384,940 | |

| JBS USA Food Co., 5.75%, 1/15/28 | 1,900,000 | | 1,983,144 | |

JSM Global Sarl, 4.75%, 10/20/30(1) | 3,000,000 | | 2,861,280 | |

Klabin Austria GmbH, 5.75%, 4/3/29(2) | 2,000,000 | | 2,180,000 | |

MARB BondCo plc, 3.95%, 1/29/31(1) | 4,650,000 | | 4,428,916 | |

MC Brazil Downstream Trading SARL, 7.25%, 6/30/31(1) | 3,371,000 | | 3,286,725 | |

| NBM US Holdings, Inc., 7.00%, 5/14/26 | 1,000,000 | | 1,059,750 | |

| NBM US Holdings, Inc., 6.625%, 8/6/29 | 2,000,000 | | 2,180,020 | |

| Petrobras Global Finance BV, 6.875%, 1/20/40 | 3,000,000 | | 3,264,810 | |

| Petrobras Global Finance BV, 5.50%, 6/10/51 | 2,800,000 | | 2,462,656 | |

Simpar Europe SA, 5.20%, 1/26/31(1) | 3,800,000 | | 3,661,965 | |

| Suzano Austria GmbH, 3.125%, 1/15/32 | 1,000,000 | | 946,135 | |

Tupy Overseas SA, 4.50%, 2/16/31(1) | 2,000,000 | | 1,890,120 | |

| | 76,999,610 | |

| Chile — 3.5% | | |

Alfa Desarrollo SpA, 4.55%, 9/27/51(1) | 2,900,000 | | 2,837,839 | |

| Celulosa Arauco y Constitucion SA, 4.25%, 4/30/29 | 2,000,000 | | 2,125,070 | |

Empresa Nacional de Telecomunicaciones SA, 3.05%, 9/14/32(1) | 2,700,000 | | 2,639,115 | |

Engie Energia Chile SA, 3.40%, 1/28/30(1) | 2,000,000 | | 2,012,530 | |

Falabella SA, 3.375%, 1/15/32(1) | 1,800,000 | | 1,788,750 | |

Interchile SA, 4.50%, 6/30/56(1) | 1,000,000 | | 1,055,940 | |

Kenbourne Invest SA, 6.875%, 11/26/24(1) | 3,750,000 | | 3,914,062 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

Kenbourne Invest SA, 4.70%, 1/22/28(1) | $ | 2,800,000 | | $ | 2,789,500 | |

VTR Comunicaciones SpA, 4.375%, 4/15/29(1) | 2,000,000 | | 2,019,400 | |

VTR Finance NV, 6.375%, 7/15/28(1) | 4,000,000 | | 4,268,800 | |

| | 25,451,006 | |

| China — 2.8% | | |

| Country Garden Holdings Co. Ltd., 3.875%, 10/22/30 | 2,000,000 | | 1,840,381 | |

| Huarong Finance 2019 Co. Ltd., MTN, 2.50%, 2/24/23 | 1,500,000 | | 1,449,375 | |

| Logan Group Co. Ltd., 6.90%, 6/9/24 | 1,450,000 | | 1,416,729 | |

Meituan, 2.125%, 10/28/25(1)(2) | 5,300,000 | | 5,113,412 | |

| Shimao Group Holdings Ltd., 4.75%, 7/3/22 | 1,000,000 | | 966,419 | |

Tencent Holdings Ltd., MTN, 3.24%, 6/3/50(2) | 2,000,000 | | 1,943,716 | |

| Vanke Real Estate Hong Kong Co. Ltd., MTN, 5.35%, 3/11/24 | 1,000,000 | | 1,072,819 | |

| Vanke Real Estate Hong Kong Co. Ltd., MTN, 3.50%, 11/12/29 | 400,000 | | 398,462 | |

| Weibo Corp., 3.375%, 7/8/30 | 6,100,000 | | 6,030,446 | |

| | 20,231,759 | |

| Colombia — 5.8% | | |

| AI Candelaria Spain SLU, 7.50%, 12/15/28 | 3,000,000 | | 3,232,500 | |

Banco GNB Sudameris SA, VRN, 7.50%, 4/16/31(1) | 4,050,000 | | 4,106,821 | |

| Bancolombia SA, VRN, 4.625%, 12/18/29 | 1,500,000 | | 1,530,000 | |

| Ecopetrol SA, 6.875%, 4/29/30 | 3,200,000 | | 3,700,512 | |

Ecopetrol SA, 4.625%, 11/2/31(3) | 1,060,000 | | 1,053,529 | |

| Ecopetrol SA, 5.875%, 5/28/45 | 3,150,000 | | 3,193,943 | |

Ecopetrol SA, 5.875%, 11/2/51(3) | 900,000 | | 894,632 | |

| Geopark Ltd., 6.50%, 9/21/24 | 3,014,000 | | 3,107,886 | |

Geopark Ltd., 5.50%, 1/17/27(1)(2) | 6,918,000 | | 6,882,199 | |

| Grupo de Inversiones Suramericana SA, 5.50%, 4/29/26 | 2,700,000 | | 2,920,752 | |

| Millicom International Cellular SA, 6.25%, 3/25/29 | 1,800,000 | | 1,959,750 | |

Millicom International Cellular SA, 4.50%, 4/27/31(1) | 3,000,000 | | 3,082,560 | |

Oleoducto Central SA, 4.00%, 7/14/27(1) | 3,800,000 | | 3,892,283 | |

Promigas SA ESP / Gases del Pacifico SAC, 3.75%, 10/16/29(1) | 2,000,000 | | 1,992,140 | |

| | 41,549,507 | |

| Ghana — 1.5% | | |

Kosmos Energy Ltd., 7.125%, 4/4/26(1)(2) | 4,092,000 | | 4,088,542 | |

Kosmos Energy Ltd., 7.50%, 3/1/28(1)(2) | 2,800,000 | | 2,748,634 | |

Tullow Oil plc, 10.25%, 5/15/26(1) | 3,500,000 | | 3,692,133 | |

| | 10,529,309 | |

| Hong Kong — 0.2% | | |

CK Hutchison International 20 Ltd., 2.50%, 5/8/30(1) | 1,500,000 | | 1,511,400 | |

| India — 6.9% | | |

Adani Electricity Mumbai Ltd., 3.95%, 2/12/30(1) | 2,000,000 | | 1,983,780 | |

Adani Green Energy Ltd., 4.375%, 9/8/24(1) | 1,800,000 | | 1,824,483 | |

| Adani Ports & Special Economic Zone Ltd., 4.00%, 7/30/27 | 2,800,000 | | 2,881,557 | |

Adani Ports & Special Economic Zone Ltd., 4.20%, 8/4/27(1) | 3,900,000 | | 4,039,487 | |

Adani Ports & Special Economic Zone Ltd., 3.10%, 2/2/31(1) | 2,000,000 | | 1,908,435 | |

Adani Ports & Special Economic Zone Ltd., 3.83%, 2/2/32(1) | 2,000,000 | | 1,984,600 | |

Adani Transmission Ltd., 4.25%, 5/21/36(1) | 2,992,000 | | 3,041,086 | |

Azure Power Solar Energy Pvt Ltd., 5.65%, 12/24/24(1) | 1,050,000 | | 1,105,125 | |

Continuum Energy Levanter Pte Ltd., 4.50%, 2/9/27(1) | 4,267,750 | | 4,385,113 | |

Delhi International Airport Ltd., 6.45%, 6/4/29(1) | 3,000,000 | | 2,978,580 | |

| GMR Hyderabad International Airport Ltd., 5.375%, 4/10/24 | 2,000,000 | | 2,060,397 | |

GMR Hyderabad International Airport Ltd., 4.75%, 2/2/26(1) | 800,000 | | 808,231 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

Greenko Dutch BV, 3.85%, 3/29/26(1) | $ | 2,167,000 | | $ | 2,191,162 | |

Greenko Investment Co., 4.875%, 8/16/23(1) | 3,300,000 | | 3,335,064 | |

| Greenko Solar Mauritius Ltd., 5.95%, 7/29/26 | 1,000,000 | | 1,057,102 | |

| ICICI Bank Ltd., MTN, 4.00%, 3/18/26 | 3,625,000 | | 3,882,400 | |

Indian Railway Finance Corp. Ltd., 2.80%, 2/10/31(1) | 3,000,000 | | 2,900,579 | |

ReNew Wind Energy AP2 / ReNew Power Pvt Ltd. other 9 Subsidiaries, 4.50%, 7/14/28(1) | 1,000,000 | | 1,017,186 | |

Vedanta Resources Finance II plc, 8.95%, 3/11/25(1) | 6,000,000 | | 6,099,060 | |

| | 49,483,427 | |

| Indonesia — 5.3% | | |

| Cikarang Listrindo Tbk PT, 4.95%, 9/14/26 | 6,901,000 | | 7,068,349 | |

| Indika Energy Capital III Pte Ltd., 5.875%, 11/9/24 | 1,000,000 | | 1,016,750 | |

Indika Energy Capital IV Pte Ltd., 8.25%, 10/22/25(1) | 5,000,000 | | 5,309,375 | |

Indonesia Asahan Aluminium Persero PT, 5.45%, 5/15/30(1) | 5,000,000 | | 5,721,900 | |

Indonesia Asahan Aluminium Persero PT, 5.80%, 5/15/50(1) | 3,250,000 | | 3,807,245 | |

Medco Bell Pte Ltd., 6.375%, 1/30/27(1) | 2,500,000 | | 2,564,375 | |

| Medco Oak Tree Pte Ltd., 7.375%, 5/14/26 | 1,500,000 | | 1,610,625 | |

| Medco Platinum Road Pte Ltd., 6.75%, 1/30/25 | 2,700,000 | | 2,819,894 | |

Perusahaan Perseroan (Persero) PT Perusahaan Listrik Negara, 6.25%, 1/25/49(2) | 1,000,000 | | 1,254,145 | |

Perusahaan Perseroan (Persero) PT Perusahaan Listrik Negara, 4.875%, 7/17/49(2) | 4,000,000 | | 4,251,280 | |

| Perusahaan Perseroan (Persero) PT Perusahaan Listrik Negara, MTN, 3.00%, 6/30/30 | 2,000,000 | | 1,988,090 | |

| Star Energy Geothermal Wayang Windu Ltd., 6.75%, 4/24/33 | 838,700 | | 938,509 | |

| | 38,350,537 | |

| Ireland — 0.1% | | |

Aragvi Finance International DAC, 8.45%, 4/29/26(1) | 1,000,000 | | 1,034,117 | |

| Israel — 3.8% | | |

| Altice Financing SA, 5.00%, 1/15/28 | 2,000,000 | | 1,929,740 | |

Altice Financing SA, 5.00%, 1/15/28(1) | 5,500,000 | | 5,306,785 | |

Energean Israel Finance Ltd., 4.50%, 3/30/24(1) | 9,907,000 | | 10,132,409 | |

Leviathan Bond Ltd., 5.75%, 6/30/23(1) | 3,500,000 | | 3,639,305 | |

| Teva Pharmaceutical Finance Netherlands III BV, 2.80%, 7/21/23 | 2,950,000 | | 2,975,223 | |

| Teva Pharmaceutical Finance Netherlands III BV, 6.00%, 4/15/24 | 2,000,000 | | 2,100,000 | |

| Teva Pharmaceutical Finance Netherlands III BV, 7.125%, 1/31/25 | 1,500,000 | | 1,612,035 | |

| | 27,695,497 | |

| Jamaica — 0.4% | | |

Digicel International Finance Ltd. / Digicel International Holdings Ltd., 8.75%, 5/25/24(1) | 3,000,000 | | 3,116,250 | |

| Kazakhstan — 0.6% | | |

| KazMunayGas National Co. JSC, 4.75%, 4/19/27 | 2,500,000 | | 2,779,234 | |

| KazMunayGas National Co. JSC, 5.75%, 4/19/47 | 1,500,000 | | 1,814,239 | |

| | 4,593,473 | |

| Kuwait — 0.3% | | |

Equate Petrochemical BV, 2.625%, 4/28/28(1) | 1,000,000 | | 1,000,111 | |

| Kuwait Projects Co. SPC Ltd., 5.00%, 3/15/23 | 1,350,000 | | 1,353,794 | |

| | 2,353,905 | |

| Luxembourg — 0.6% | | |

Petrorio Luxembourg Sarl, 6.125%, 6/9/26(1) | 4,300,000 | | 4,337,625 | |

| Macau — 2.3% | | |

Melco Resorts Finance Ltd., 5.75%, 7/21/28(1) | 5,500,000 | | 5,486,250 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

| Sands China Ltd., 5.125%, 8/8/25 | $ | 3,300,000 | | $ | 3,511,695 | |

| Sands China Ltd., 5.40%, 8/8/28 | 2,000,000 | | 2,163,000 | |

Studio City Finance Ltd., 5.00%, 1/15/29(1) | 5,000,000 | | 4,534,225 | |

Wynn Macau Ltd., 5.50%, 1/15/26(1) | 500,000 | | 470,945 | |

Wynn Macau Ltd., 5.625%, 8/26/28(1) | 700,000 | | 654,731 | |

| | 16,820,846 | |

| Mauritius — 0.4% | | |

India Toll Roads, 5.50%, 8/19/24(1) | 3,000,000 | | 2,970,180 | |

| Mexico — 10.6% | | |

Axtel SAB de CV, 6.375%, 11/14/24(1) | 4,759,000 | | 4,914,905 | |

BBVA Bancomer SA, VRN, 5.125%, 1/18/33(1) | 7,000,000 | | 7,229,915 | |

BBVA Bancomer SA, VRN, 5.875%, 9/13/34(1) | 2,700,000 | | 2,940,259 | |

Braskem Idesa SAPI, 6.99%, 2/20/32(1) | 3,200,000 | | 3,280,000 | |

| Cemex SAB de CV, 5.45%, 11/19/29 | 2,000,000 | | 2,168,900 | |

Cemex SAB de CV, 3.875%, 7/11/31(1) | 5,000,000 | | 5,024,750 | |

Cemex SAB de CV, VRN, 5.125%, 6/8/26(1) | 4,000,000 | | 4,137,696 | |

Cometa Energia SA de CV, 6.375%, 4/24/35(1) | 2,921,750 | | 3,323,505 | |

Comision Federal de Electricidad, 3.875%, 7/26/33(1) | 4,300,000 | | 4,157,842 | |

FEL Energy VI Sarl, 5.75%, 12/1/40(1) | 7,519,305 | | 7,452,232 | |

Fresnillo plc, 4.25%, 10/2/50(1)(2) | 800,000 | | 819,152 | |

Industrias Penoles SAB de CV, 4.75%, 8/6/50(1)(2) | 1,750,000 | | 1,901,384 | |

| Infraestructura Energetica Nova SAB de CV, 4.875%, 1/14/48 | 1,500,000 | | 1,535,978 | |

Infraestructura Energetica Nova SAB de CV, 4.75%, 1/15/51(1) | 4,300,000 | | 4,397,051 | |

| Infraestructura Energetica Nova SAB de CV, 4.75%, 1/15/51 | 500,000 | | 511,285 | |

Minera Mexico SA de CV, 4.50%, 1/26/50(1) | 2,650,000 | | 2,899,074 | |

Operadora de Servicios Mega SA de CV Sofom ER, 8.25%, 2/11/25(1) | 3,750,000 | | 3,682,387 | |

Petroleos Mexicanos, 6.875%, 10/16/25(1) | 850,000 | | 929,713 | |

| Petroleos Mexicanos, 6.49%, 1/23/27 | 2,200,000 | | 2,341,680 | |

| Petroleos Mexicanos, 6.50%, 3/13/27 | 3,300,000 | | 3,522,354 | |

| Petroleos Mexicanos, 5.35%, 2/12/28 | 2,000,000 | | 1,998,950 | |

| Petroleos Mexicanos, 5.95%, 1/28/31 | 2,000,000 | | 1,971,650 | |

| Petroleos Mexicanos, 6.50%, 6/2/41 | 3,400,000 | | 3,084,140 | |

| Sigma Finance Netherlands BV, 4.875%, 3/27/28 | 2,000,000 | | 2,237,520 | |

| | 76,462,322 | |

| Morocco — 1.0% | | |

| OCP SA, 6.875%, 4/25/44 | 5,900,000 | | 7,101,765 | |

| Nigeria — 2.0% | | |

| IHS Netherlands Holdco BV, 7.125%, 3/18/25 | 4,000,000 | | 4,145,000 | |

IHS Netherlands Holdco BV, 8.00%, 9/18/27(1) | 6,000,000 | | 6,390,000 | |

SEPLAT Energy plc, 7.75%, 4/1/26(1) | 4,000,000 | | 4,126,000 | |

| | 14,661,000 | |

| Panama — 2.5% | | |

AES Panama Generation Holdings SRL, 4.375%, 5/31/30(1) | 2,000,000 | | 2,064,860 | |

C&W Senior Financing DAC, 6.875%, 9/15/27(1) | 9,095,000 | | 9,595,225 | |

Cable Onda SA, 4.50%, 1/30/30(1) | 5,950,000 | | 6,179,819 | |

| | 17,839,904 | |

| Peru — 4.5% | | |

| Banco Internacional del Peru SAA Interbank, 3.25%, 10/4/26 | 1,000,000 | | 1,025,450 | |

| Banco Internacional del Peru SAA Interbank, VRN, 6.625%, 3/19/29 | 200,000 | | 213,776 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

Banco Internacional del Peru SAA Interbank, VRN, 4.00%, 7/8/30(1) | $ | 2,000,000 | | $ | 2,022,200 | |

| Fenix Power Peru SA, 4.32%, 9/20/27 | 1,487,647 | | 1,515,593 | |

| Inkia Energy Ltd., 5.875%, 11/9/27 | 8,700,000 | | 9,060,093 | |

Intercorp Financial Services, Inc., 4.125%, 10/19/27(1) | 4,960,000 | | 4,976,566 | |

| Kallpa Generacion SA, 4.875%, 5/24/26 | 2,000,000 | | 2,135,110 | |

| Kallpa Generacion SA, 4.125%, 8/16/27 | 2,904,000 | | 3,020,349 | |

Minsur SA, 4.50%, 10/28/31(1) | 600,000 | | 592,785 | |

Nexa Resources SA, 5.375%, 5/4/27(2) | 1,500,000 | | 1,595,655 | |

| Petroleos del Peru SA, 4.75%, 6/19/32 | 1,000,000 | | 1,058,065 | |

Petroleos del Peru SA, 5.625%, 6/19/47(1) | 2,900,000 | | 2,947,473 | |

SAN Miguel Industrias Pet SA / NG PET R&P Latin America SA, 3.50%, 8/2/28(1) | 2,000,000 | | 1,969,760 | |

| | 32,132,875 | |

| Qatar — 0.4% | | |

Nakilat, Inc., 6.07%, 12/31/33(1) | 974,151 | | 1,194,411 | |

| Nakilat, Inc., 6.27%, 12/31/33 | 526,455 | | 655,337 | |

Ooredoo International Finance Ltd., 2.625%, 4/8/31(1) | 400,000 | | 404,570 | |

| Ooredoo International Finance Ltd., MTN, 5.00%, 10/19/25 | 300,000 | | 341,594 | |

| | 2,595,912 | |

| Russia — 2.2% | | |

| Gazprom PJSC Via Gaz Capital SA, 4.95%, 3/23/27 | 1,600,000 | | 1,764,216 | |

| Gazprom PJSC Via Gaz Capital SA, MTN, 7.29%, 8/16/37 | 1,450,000 | | 1,961,292 | |

Gazprom PJSC via Gaz Finance plc, 3.25%, 2/25/30(1) | 3,700,000 | | 3,663,374 | |

Lukoil Capital DAC, 3.60%, 10/26/31(1) | 896,000 | | 895,074 | |

| Lukoil Securities BV, 3.875%, 5/6/30 | 2,000,000 | | 2,078,500 | |

Lukoil Securities BV, 3.875%, 5/6/30(1) | 1,500,000 | | 1,558,875 | |

VEON Holdings BV, 3.375%, 11/25/27(1) | 4,000,000 | | 4,016,460 | |

| | 15,937,791 | |

| Saudi Arabia — 3.2% | | |

| Dar Al-Arkan Sukuk Co. Ltd., 6.875%, 3/21/23 | 3,800,000 | | 3,964,251 | |

| Dar Al-Arkan Sukuk Co. Ltd., 6.875%, 2/26/27 | 1,000,000 | | 1,051,307 | |

| Dar Al-Arkan Sukuk Co. Ltd., MTN, 6.875%, 4/10/22 | 1,000,000 | | 1,019,734 | |

SA Global Sukuk Ltd., 2.69%, 6/17/31(1) | 1,290,000 | | 1,294,386 | |

SABIC Capital II BV, 4.50%, 10/10/28(1) | 4,300,000 | | 4,892,510 | |

Saudi Arabian Oil Co., 3.50%, 4/16/29(1) | 2,700,000 | | 2,887,183 | |

| Saudi Arabian Oil Co., MTN, 4.25%, 4/16/39 | 4,200,000 | | 4,719,523 | |

| Saudi Electricity Global Sukuk Co. 4, 4.72%, 9/27/28 | 2,900,000 | | 3,374,389 | |

| | 23,203,283 | |

| Singapore — 0.7% | | |

| BOC Aviation Ltd., MTN, 2.625%, 9/17/30 | 1,000,000 | | 981,651 | |

BOC Aviation USA Corp., 1.625%, 4/29/24(1) | 2,000,000 | | 2,004,125 | |

United Overseas Bank Ltd., VRN, 2.00%, 10/14/31(1) | 2,000,000 | | 1,990,690 | |

| | 4,976,466 | |

| South Africa — 3.4% | | |

| AngloGold Ashanti Holdings plc, 6.50%, 4/15/40 | 2,000,000 | | 2,434,940 | |

Liquid Telecommunications Financing plc, 5.50%, 9/4/26(1) | 1,500,000 | | 1,563,540 | |

| MTN Mauritius Investments Ltd., 4.76%, 11/11/24 | 3,125,000 | | 3,277,962 | |

Prosus NV, 3.68%, 1/21/30(1) | 6,950,000 | | 7,151,415 | |

| Prosus NV, 3.83%, 2/8/51 | 2,000,000 | | 1,816,853 | |

| SASOL Financing USA LLC, 5.875%, 3/27/24 | 3,000,000 | | 3,174,750 | |

| Sasol Financing USA LLC, 5.50%, 3/18/31 | 5,000,000 | | 5,142,750 | |

| | 24,562,210 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

| South Korea — 0.1% | | |

Shinhan Financial Group Co. Ltd., VRN, 3.34%, 2/5/30(1) | $ | 1,000,000 | | $ | 1,033,858 | |

| Spain — 0.8% | | |

EnfraGen Energia Sur SA / EnfraGen Spain SA / Prime Energia SpA, 5.375%, 12/30/30(1) | 6,000,000 | | 5,754,090 | |

| Tanzania, United Republic Of — 1.0% | | |

HTA Group Ltd., 7.00%, 12/18/25(1) | 6,700,000 | | 7,029,774 | |

| Thailand — 0.4% | | |

Thaioil Treasury Center Co. Ltd., 3.50%, 10/17/49(1) | 3,000,000 | | 2,666,924 | |

| Turkey — 0.9% | | |

| KOC Holding AS, 5.25%, 3/15/23 | 3,300,000 | | 3,373,550 | |

| Turk Telekomunikasyon AS, 4.875%, 6/19/24 | 1,500,000 | | 1,535,359 | |

Turkiye Sise ve Cam Fabrikalari AS, 6.95%, 3/14/26(1) | 1,700,000 | | 1,841,957 | |

| | 6,750,866 | |

| Ukraine — 2.3% | | |

Kernel Holding SA, 6.50%, 10/17/24(1) | 1,850,000 | | 1,966,045 | |

Kernel Holding SA, 6.75%, 10/27/27(1) | 1,250,000 | | 1,330,132 | |

Metinvest BV, 7.65%, 10/1/27(1) | 2,000,000 | | 2,202,370 | |

Metinvest BV, 7.75%, 10/17/29(1) | 2,000,000 | | 2,183,200 | |

| MHP Lux SA, 6.95%, 4/3/26 | 1,000,000 | | 1,066,064 | |

MHP SE, 7.75%, 5/10/24(1) | 3,200,000 | | 3,460,819 | |

| VF Ukraine PAT via VFU Funding plc, 6.20%, 2/11/25 | 4,000,000 | | 4,146,262 | |

| | 16,354,892 | |

| United Arab Emirates — 0.5% | | |

Abu Dhabi National Energy Co. PJSC, 2.00%, 4/29/28(1) | 240,000 | | 239,391 | |

Abu Dhabi National Energy Co. PJSC, 4.875%, 4/23/30(1) | 2,000,000 | | 2,380,100 | |

DP World Ltd., 4.70%, 9/30/49(1) | 1,000,000 | | 1,083,569 | |

| | 3,703,060 | |

| United Arab Emirates — 1.9% | | |

DAE Funding LLC, 1.55%, 8/1/24(1) | 3,150,000 | | 3,111,412 | |

| DP World Crescent Ltd., MTN, 4.85%, 9/26/28 | 1,600,000 | | 1,802,284 | |

| DP World Crescent Ltd., MTN, 3.875%, 7/18/29 | 4,600,000 | | 4,902,681 | |

Galaxy Pipeline Assets Bidco Ltd., 2.625%, 3/31/36(1) | 3,000,000 | | 2,929,970 | |

Galaxy Pipeline Assets Bidco Ltd., 2.94%, 9/30/40(1) | 1,150,000 | | 1,133,065 | |

| | 13,879,412 | |

| United Kingdom — 0.1% | | |

Endeavour Mining plc, 5.00%, 10/14/26(1) | 1,000,000 | | 1,010,950 | |

| United States — 1.0% | | |

JBS Finance Luxembourg Sarl, 3.625%, 1/15/32(1) | 1,500,000 | | 1,483,005 | |

LCPR Senior Secured Financing DAC, 6.75%, 10/15/27(1) | 1,000,000 | | 1,051,250 | |

SierraCol Energy Andina LLC, 6.00%, 6/15/28(1) | 5,000,000 | | 4,913,550 | |

| | 7,447,805 | |

| Zambia — 1.3% | | |

First Quantum Minerals Ltd., 6.50%, 3/1/24(1) | 3,200,000 | | 3,252,000 | |

| First Quantum Minerals Ltd., 6.875%, 3/1/26 | 4,500,000 | | 4,691,250 | |

First Quantum Minerals Ltd., 6.875%, 10/15/27(1) | 1,000,000 | | 1,068,750 | |

| | 9,012,000 | |

TOTAL CORPORATE BONDS (Cost $617,315,015) | | 626,318,571 | |

| SOVEREIGN GOVERNMENTS AND AGENCIES — 4.2% |

|

|

| Brazil — 0.5% | | |

| Brazilian Government International Bond, 3.875%, 6/12/30 | 2,000,000 | | 1,880,080 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

| Brazilian Government International Bond, 4.75%, 1/14/50 | $ | 2,000,000 | | $ | 1,712,880 | |

| | 3,592,960 | |

| Colombia — 0.5% | | |

| Colombia Government International Bond, 3.125%, 4/15/31 | 500,000 | | 469,140 | |

| Colombia Government International Bond, 6.125%, 1/18/41 | 3,000,000 | | 3,341,235 | |

| | 3,810,375 | |

| Dominican Republic — 0.5% | | |

| Dominican Republic International Bond, 5.95%, 1/25/27 | 2,500,000 | | 2,793,775 | |

Dominican Republic International Bond, 4.50%, 1/30/30(1) | 1,000,000 | | 1,015,010 | |

| | 3,808,785 | |

| El Salvador — 0.1% | | |

| El Salvador Government International Bond, 6.375%, 1/18/27 | 1,100,000 | | 852,500 | |

| India — 0.2% | | |

| Export-Import Bank of India, 3.375%, 8/5/26 | 613,000 | | 645,896 | |

| Export-Import Bank of India, 3.875%, 2/1/28 | 400,000 | | 429,228 | |

| | 1,075,124 | |

Jordan† | | |

Jordan Government International Bond, 7.375%, 10/10/47(1) | 200,000 | | 207,464 | |

| Nigeria — 0.5% | | |

| Nigeria Government International Bond, MTN, 6.50%, 11/28/27 | 3,100,000 | | 3,180,755 | |

| Oman — 0.6% | | |

| Oman Government International Bond, MTN, 6.00%, 8/1/29 | 1,000,000 | | 1,075,885 | |

Oman Sovereign Sukuk Co., 4.875%, 6/15/30(1) | 2,800,000 | | 2,985,808 | |

| | 4,061,693 | |

| Saudi Arabia — 0.3% | | |

Saudi Government International Bond, 2.25%, 2/2/33(1) | 2,500,000 | | 2,416,748 | |

| Turkey — 0.9% | | |

| Turkey Government International Bond, 5.60%, 11/14/24 | 1,600,000 | | 1,614,846 | |

| Turkey Government International Bond, 4.875%, 10/9/26 | 2,000,000 | | 1,901,564 | |

| Turkey Government International Bond, 5.125%, 2/17/28 | 1,000,000 | | 940,995 | |

| Turkey Government International Bond, 6.875%, 3/17/36 | 2,000,000 | | 1,941,404 | |

| | 6,398,809 | |

| Ukraine — 0.1% | | |

Ukraine Government International Bond, 7.25%, 3/15/33(1) | 750,000 | | 765,683 | |

TOTAL SOVEREIGN GOVERNMENTS AND AGENCIES

(Cost $30,819,621) | | 30,170,896 | |

| PREFERRED STOCKS — 2.5% |

|

|

| Brazil — 0.4% | | |

| Banco do Brasil SA, 6.25% | 3,000,000 | | 2,953,710 | |

| India — 0.4% | | |

Network i2i Ltd., 3.98%(1) | 3,000,000 | | 3,030,255 | |

| Mexico — 1.3% | | |

| Banco Mercantil del Norte SA, 6.875% | 1,855,000 | | 1,886,303 | |

Banco Mercantil del Norte SA, 8.375%(1) | 6,100,000 | | 7,139,196 | |

| | 9,025,499 | |

| Russia — 0.2% | | |

| Gazprom PJSC via Gaz Finance plc, 4.60% | 1,000,000 | | 1,040,000 | |

| United Arab Emirates — 0.2% | | |

| DP World Salaam, 6.00% | 1,500,000 | | 1,643,040 | |

TOTAL PREFERRED STOCKS (Cost $17,046,735) | | 17,692,504 | |

| | | | | | | | |

| Shares/

Principal Amount | Value |

| U.S. TREASURY SECURITIES — 1.3% |

|

|

| U.S. Treasury Bonds, 2.00%, 8/15/51 | $ | 2,000,000 | | $ | 2,029,062 | |

U.S. Treasury Notes, 2.875%, 8/15/28(4) | 3,885,000 | | 4,249,902 | |

| U.S. Treasury Notes, 1.25%, 8/15/31 | 3,000,000 | | 2,915,625 | |

TOTAL U.S. TREASURY SECURITIES (Cost $9,339,678) | | 9,194,589 | |

| EXCHANGE-TRADED FUNDS — 0.1% |

|

|

Energy Select Sector SPDR Fund (Cost $451,837) | 16,000 | | 919,520 | |

TEMPORARY CASH INVESTMENTS(5) — 4.2% |

|

|

| Repurchase Agreement, BMO Capital Markets Corp., (collateralized by various U.S. Treasury obligations, 2.00%, 11/15/26, valued at $6,861,336), in a joint trading account at 0.01%, dated 10/29/21, due 11/1/21 (Delivery value $6,718,635) | | 6,718,629 | |

| Repurchase Agreement, Fixed Income Clearing Corp., (collateralized by various U.S. Treasury obligations, 4.75%, 2/15/41, valued at $22,846,084), at 0.01%, dated 10/29/21, due 11/1/21 (Delivery value $22,398,019) | | 22,398,000 | |

| State Street Institutional U.S. Government Money Market Fund, Premier Class | 1,549,327 | | 1,549,327 | |

TOTAL TEMPORARY CASH INVESTMENTS (Cost $30,665,956) | | 30,665,956 | |

TEMPORARY CASH INVESTMENTS - SECURITIES LENDING COLLATERAL(6) — 2.8% |

State Street Navigator Securities Lending Government Money Market Portfolio (Cost $20,479,520) | 20,479,520 | | 20,479,520 | |

TOTAL INVESTMENT SECURITIES — 101.9% (Cost $726,118,362) |

| 735,441,556 | |

| OTHER ASSETS AND LIABILITIES — (1.9)% |

| (13,767,022) | |

| TOTAL NET ASSETS — 100.0% |

| $ | 721,674,534 | |

| | | | | | | | | | | | | | |

| FUTURES CONTRACTS PURCHASED |

| Reference Entity | Contracts | Expiration

Date | Notional

Amount | Unrealized

Appreciation

(Depreciation)^ |

| U.S. Treasury 2-Year Notes | 243 | December 2021 | $ | 53,277,750 | | $ | (254,794) | |

| U.S. Treasury 5-Year Notes | 201 | December 2021 | 24,471,750 | | (375,697) | |

| U.S. Treasury Long Bonds | 1 | December 2021 | 160,844 | | (2,558) | |

| | | $ | 77,910,344 | | $ | (633,049) | |

^Amount represents value and unrealized appreciation (depreciation).

| | | | | | | | | | | | | | |

| FUTURES CONTRACTS SOLD |

| Reference Entity | Contracts | Expiration

Date | Notional

Amount | Unrealized

Appreciation

(Depreciation)^ |

| U.S. Treasury 10-Year Notes | 382 | December 2021 | $ | 49,928,594 | | $ | 1,073,630 | |

| U.S. Treasury 10-Year Ultra Notes | 281 | December 2021 | 40,753,781 | | 846,843 | |

| U.S. Treasury Ultra Bonds | 46 | December 2021 | 9,034,688 | | 67,173 | |

| | | $ | 99,717,063 | | $ | 1,987,646 | |

^Amount represents value and unrealized appreciation (depreciation).

| | | | | | | | | | | | | | | | | | | | | | | |

| CENTRALLY CLEARED CREDIT DEFAULT SWAP AGREEMENTS |

| Reference Entity | Type | Fixed Rate

Received

(Paid)

Quarterly | Termination

Date | Notional

Amount | Premiums Paid

(Received) | Unrealized

Appreciation

(Depreciation) | Value^ |

| Markit CDX North America High Yield Index Series 34 | Buy | (5.00)% | 6/20/25 | $ | 4,968,000 | | $ | (155,800) | | $ | (289,442) | | $ | (445,242) | |

^The value for credit default swap agreements serves as an indicator of the current status of the payment/performance risk and represent the likelihood of an expected liability or profit at the period end. Increasing values in absolute terms when compared to the notional amount of the credit default swap agreement represent a deterioration of the referenced entity's credit soundness and an increased likelihood or risk of a credit event occurring as defined in the agreement.

| | | | | | | | | | | | | | | | | | | | | | | |

| CREDIT DEFAULT SWAP AGREEMENTS |

Counterparty/ Reference Entity | Type | Fixed Rate Received (Paid) Quarterly | Termination Date | Notional Amount | Premiums Paid

(Received) | Unrealized Appreciation (Depreciation) | Value^ |

| Morgan Stanley/ Brazilian Government International Bond | Buy | (1.00)% | 12/20/26 | $ | 32,800,000 | | $ | 1,580,727 | | $ | 663,641 | | $ | 2,244,368 | |

| Morgan Stanley/ Colombia Government International Bond | Buy | (1.00)% | 12/20/26 | $ | 11,400,000 | | 276,789 | | 53,783 | | 330,572 | |

| Morgan Stanley/ Mexico Government International Bond | Buy | (1.00)% | 12/20/26 | $ | 50,300,000 | | (49,737) | | 70,209 | | 20,472 | |

| $ | 1,807,779 | | $ | 787,633 | | $ | 2,595,412 | |

^The value for credit default swap agreements serves as an indicator of the current status of the payment/performance risk and represent the likelihood of an expected liability or profit at the period end. Increasing values in absolute terms when compared to the notional amount of the credit default swap agreement represent a deterioration of the referenced entity's credit soundness and an increased likelihood or risk of a credit event occurring as defined in the agreement.

| | | | | | | | |

| NOTES TO SCHEDULE OF INVESTMENTS |

| CDX | - | Credit Derivatives Indexes |

| MTN | - | Medium Term Note |

| VRN | - | Variable Rate Note. The rate adjusts periodically based upon the terms set forth in the security’s offering documents. The rate shown is effective at the period end and the reference rate and spread, if any, is indicated. The security's effective maturity date may be shorter than the final maturity date shown. |

†Category is less than 0.05% of total net assets.

(1)Security was purchased pursuant to Rule 144A or Section 4(2) under the Securities Act of 1933 and may be sold in transactions exempt from registration, normally to qualified institutional investors. The aggregate value of these securities at the period end was $420,727,347, which represented 58.3% of total net assets.

(2)Security, or a portion thereof, is on loan. At the period end, the aggregate value of securities on loan was $19,831,427. The amount of securities on loan indicated may not correspond with the securities on loan identified because securities with pending sales are in the process of recall from the brokers.

(3)When-issued security. The issue price and yield are fixed on the date of the commitment, but payment and delivery are scheduled for a future date.

(4)Security, or a portion thereof, has been pledged at the custodian bank or with a broker for collateral requirements on futures contracts and/or swap agreements. At the period end, the aggregate value of securities pledged was $1,716,488.

(5)Category includes collateral received at the custodian bank for collateral requirements on swap agreements. At the period end, the aggregate value of cash deposits received was $2,300,000.

(6)Investment of cash collateral from securities on loan. At the period end, the aggregate value of the collateral held by the fund was $20,479,520.

See Notes to Financial Statements.

| | |

| Statement of Assets and Liabilities |

| | | | | |

| OCTOBER 31, 2021 | |

| Assets | |

| Investment securities, at value (cost of $705,638,842) — including $19,831,427 of securities on loan | $ | 714,962,036 | |

| Investment made with cash collateral received for securities on loan, at value (cost of $20,479,520) | 20,479,520 | |

| Total investment securities, at value (cost of $726,118,362) | 735,441,556 | |

| Receivable for investments sold | 30,045 | |

| Receivable for capital shares sold | 1,027,545 | |

| Receivable for variation margin on swap agreements | 10,430 | |

| Swap agreements, at value (including net premiums paid (received) of $1,807,779) | 2,595,412 | |

| Interest and dividends receivable | 8,191,187 | |

| Securities lending receivable | 5,633 | |

| 747,301,808 | |

| |

| Liabilities | |

| Payable for collateral received for securities on loan | 20,479,520 | |

| Payable for collateral received for swap agreements | 2,300,000 | |

| Payable for investments purchased | 2,279,853 | |

| Payable for capital shares redeemed | 402,345 | |

| Payable for variation margin on futures contracts | 53,547 | |

| Accrued management fees | 110,746 | |

| Distribution and service fees payable | 158 | |

| Dividends payable | 1,105 | |

| 25,627,274 | |

| |

| Net Assets | $ | 721,674,534 | |

| |

| Net Assets Consist of: | |

| Capital paid in | $ | 722,219,379 | |

| Distributable earnings | (544,845) | |

| $ | 721,674,534 | |

| | | | | | | | | | | |

| Net Assets | Shares Outstanding | Net Asset Value Per Share |

| Investor Class | $103,625,588 | 9,892,513 | $10.48 |

| I Class | $12,356,147 | 1,179,802 | $10.47 |

| Y Class | $26,538,687 | 2,533,663 | $10.47 |

| A Class | $270,896 | 25,885 | $10.47* |

| C Class | $36,316 | 3,476 | $10.45 |

| R Class | $161,434 | 15,430 | $10.46 |

| R5 Class | $8,259 | 788 | $10.48 |

| R6 Class | $350,337 | 33,439 | $10.48 |

| G Class | $578,326,870 | 55,214,050 | $10.47 |

*Maximum offering price $10.96 (net asset value divided by 0.955).

See Notes to Financial Statements.

| | | | | |

| YEAR ENDED OCTOBER 31, 2021 |

| Investment Income (Loss) | |

| Income: | |

| Interest (net of foreign taxes withheld of $6,293) | $ | 31,396,059 | |

| Dividends | 130,112 | |

| Securities lending, net | 58,615 | |

| 31,584,786 | |

| |

| Expenses: | |

| Management fees | 4,987,660 | |

| Distribution and service fees: | |

| A Class | 897 | |

| C Class | 399 | |

| R Class | 779 | |

| Trustees' fees and expenses | 44,350 | |

| Other expenses | 3,127 | |

| 5,037,212 | |

| Fees waived - G Class | (3,779,286) | |

| 1,257,926 | |

| |

| Net investment income (loss) | 30,326,860 | |

| |

| Realized and Unrealized Gain (Loss) | |

| Net realized gain (loss) on: | |

| Investment transactions | 8,224,176 | |

| Futures contract transactions | 343,491 | |

| Swap agreement transactions | (3,711,146) | |

| 4,856,521 | |

| |

| Change in net unrealized appreciation (depreciation) on: | |

| Investments | (2,325,154) | |

| Futures contracts | 960,169 | |

| Swap agreements | 1,324,911 | |

| (40,074) | |

| |

| Net realized and unrealized gain (loss) | 4,816,447 | |

| |

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ | 35,143,307 | |

See Notes to Financial Statements.

| | |

| Statement of Changes in Net Assets |

| | | | | | | | |

| YEARS ENDED OCTOBER 31, 2021 AND OCTOBER 31, 2020 |

| Increase (Decrease) in Net Assets | October 31, 2021 | October 31, 2020 |

| Operations | | |

| Net investment income (loss) | $ | 30,326,860 | | $ | 18,169,864 | |

| Net realized gain (loss) | 4,856,521 | | (6,157,533) | |

| Change in net unrealized appreciation (depreciation) | (40,074) | | (787,549) | |

| Net increase (decrease) in net assets resulting from operations | 35,143,307 | | 11,224,782 | |

| | |

| Distributions to Shareholders | | |

| From earnings: | | |

| Investor Class | (3,602,033) | | (3,226,082) | |

| I Class | (261,282) | | (204,981) | |

| Y Class | (900,693) | | (539,319) | |

| A Class | (12,117) | | (11,442) | |

| C Class | (1,048) | | (1,203) | |

| R Class | (4,869) | | (3,820) | |

| R5 Class | (307) | | (288) | |

| R6 Class | (56,731) | | (328,277) | |

| G Class | (24,414,299) | | (13,127,583) | |

| Decrease in net assets from distributions | (29,253,379) | | (17,442,995) | |

| | |

| Capital Share Transactions | | |

| Net increase (decrease) in net assets from capital share transactions (Note 5) | 167,932,843 | | 171,319,312 | |

| | |

| Net increase (decrease) in net assets | 173,822,771 | | 165,101,099 | |

| | |

| Net Assets | | |

| Beginning of period | 547,851,763 | | 382,750,664 | |

| End of period | $ | 721,674,534 | | $ | 547,851,763 | |

See Notes to Financial Statements.

| | |

| Notes to Financial Statements |

OCTOBER 31, 2021

1. Organization

American Century International Bond Funds (the trust) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Massachusetts business trust. Emerging Markets Debt Fund (the fund) is one fund in a series issued by the trust. The fund’s investment objective is to seek total return.

The fund offers the Investor Class, I Class, Y Class, A Class, C Class, R Class, R5 Class, R6 Class and G Class. The A Class may incur an initial sales charge. The A Class and C Class may be subject to a contingent deferred sales charge.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The fund is an investment company and follows accounting and reporting guidance in accordance with accounting principles generally accepted in the United States of America. This may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates. Management evaluated the impact of events or transactions occurring through the date the financial statements were issued that would merit recognition or disclosure.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value (NAV) per share at the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open. The Board of Trustees has adopted valuation policies and procedures to guide the investment advisor in the fund’s investment valuation process and to provide methodologies for the oversight of the fund’s pricing function.

Fixed income securities are valued at the evaluated mean as provided by independent pricing services or at the mean of the most recent bid and asked prices as provided by investment dealers. Corporate bonds, U.S. Treasury and Government Agency securities, and sovereign governments and agencies are valued using market models that consider trade data, quotations from dealers and active market makers, relevant yield curve and spread data, creditworthiness, trade data or market information on comparable securities, and other relevant security specific information.

Equity securities that are listed or traded on a domestic securities exchange are valued at the last reported sales price or at the official closing price as provided by the exchange. Equity securities traded on foreign securities exchanges are generally valued at the closing price of such securities on the exchange where primarily traded or at the close of the NYSE, if that is earlier. If no last sales price is reported, or if local convention or regulation so provides, the mean of the latest bid and asked prices may be used. Securities traded over-the-counter are valued at the mean of the latest bid and asked prices, the last sales price, or the official closing price.

Hybrid securities are valued at the evaluated mean as provided by independent pricing services or at the mean of the most recent bid and asked prices as provided by investment dealers. Preferred stocks and convertible preferred stocks with perpetual maturities are valued using market models that consider trade data, quotations from dealers and active market makers, relevant yield curve and spread data, creditworthiness, trade data or market information on comparable securities, and other relevant security specific information.

Open-end management investment companies are valued at the reported NAV per share. Repurchase agreements are valued at cost, which approximates fair value. Exchange-traded futures contracts are valued at the settlement price as provided by the appropriate exchange. Swap agreements are valued at an evaluated mean as provided by independent pricing services or independent brokers.

If the fund determines that the market price for an investment is not readily available or the valuation methods mentioned above do not reflect an investment’s fair value, such investment is valued as determined in good faith by the Board of Trustees or its delegate, in accordance with policies and procedures adopted by the Board of Trustees. In its determination of fair value, the fund may review several factors including, but not limited to, market information regarding the specific investment or comparable investments and correlation with other investment types, futures indices or general market indicators. Circumstances that may cause the fund to use these procedures to value an investment include, but are not limited to: an investment has been declared in default or is distressed; trading in a security has been suspended during the trading day or a security is not actively trading on its principal exchange; prices received from a regular pricing source are deemed unreliable; or there is a foreign market holiday and no trading occurred.

The fund monitors for significant events occurring after the close of an investment’s primary exchange but before the fund’s NAV per share is determined. Significant events may include, but are not limited to: corporate announcements and transactions; governmental action and political unrest that could impact a specific investment or an investment sector; or armed conflicts, natural disasters and similar events that could affect investments in a specific country or region. The fund also monitors for significant fluctuations between domestic and foreign markets, as evidenced by the U.S. market or such other indicators that the Board of Trustees, or its delegate, deems appropriate. The fund may apply a model-derived factor to the closing price of equity securities traded on foreign securities exchanges. The factor is based on observable market data as provided by an independent pricing service.

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Interest income less foreign taxes withheld, if any, is recorded on the accrual basis and includes paydown gain (loss) and accretion of discounts and amortization of premiums. Inflation adjustments related to inflation-linked debt securities are reflected as interest income. Dividend income less foreign taxes withheld, if any, is recorded as of the ex-dividend date. Distributions received on securities that represent a return of capital or long-term capital gain are recorded as a reduction of cost of investments and/or as a realized gain. The fund may estimate the components of distributions received that may be considered nontaxable distributions or long-term capital gain distributions for income tax purposes. Securities lending income is net of fees and rebates earned by the lending agent for its services.

Repurchase Agreements — The fund may enter into repurchase agreements with institutions that American Century Investment Management, Inc. (ACIM) (the investment advisor) has determined are creditworthy pursuant to criteria adopted by the Board of Trustees. The fund requires that the collateral, represented by securities, received in a repurchase transaction be transferred to the custodian in a manner sufficient to enable the fund to obtain those securities in the event of a default under the repurchase agreement. ACIM monitors, on a daily basis, the securities transferred to ensure the value, including accrued interest, of the securities under each repurchase agreement is equal to or greater than amounts owed to the fund under each repurchase agreement.

Joint Trading Account — Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the fund, along with certain other funds in the American Century Investments family of funds, may transfer uninvested cash balances into a joint trading account. These balances are invested in one or more repurchase agreements that are collateralized by U.S. Treasury or Agency obligations.

Segregated Assets — In accordance with the 1940 Act, the fund segregates assets on its books and records to cover certain types of investment securities and other financial instruments. ACIM monitors, on a daily basis, the securities segregated to ensure the fund designates a sufficient amount of liquid assets, marked-to-market daily. The fund may also receive assets or be required to pledge assets at the custodian bank or with a broker for collateral requirements.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. Accordingly, no provision has been made for income taxes. The fund files U.S. federal, state, local and non-U.S. tax returns as applicable. The fund's tax returns are subject to examination by the relevant taxing authority until expiration of the applicable statute of limitations, which is generally three years from the date of filing but can be longer in certain jurisdictions. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income, if any, are declared daily and paid monthly. Distributions from net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

Securities Lending — Securities are lent to qualified financial institutions and brokers. State Street Bank & Trust Co. serves as securities lending agent to the fund pursuant to a Securities Lending Agreement. The lending of securities exposes the fund to risks such as: the borrowers may fail to return the loaned securities, the borrowers may not be able to provide additional collateral, the fund may experience delays in recovery of the loaned securities or delays in access to collateral, or the fund may experience losses related to the investment collateral. To minimize certain risks, loan counterparties pledge collateral in the form of cash and/or securities. The lending agent has agreed to indemnify the fund in the case of default of any securities borrowed. Cash collateral received is invested in the State Street Navigator Securities Lending Government Money Market Portfolio, a money market mutual fund registered under the 1940 Act. The loans may also be secured by U.S. government securities in an amount at least equal to the market value of the securities loaned, plus accrued interest and dividends, determined on a daily basis and adjusted accordingly. By lending securities, the fund seeks to increase its net investment income through the receipt of interest and fees. Such income is reflected separately within the Statement of Operations. The value of loaned securities and related collateral outstanding at period end, if any, are shown on a gross basis within the Schedule of Investments and Statement of Assets and Liabilities.

The following table reflects a breakdown of transactions accounted for as secured borrowings, the gross obligation by the type of collateral pledged, and the remaining contractual maturity of those transactions as of October 31, 2021.

| | | | | | | | | | | | | | | | | |

| Remaining Contractual Maturity of Agreements |

| Overnight and

Continuous | <30 days | Between 30 & 90 days | >90 days | Total |

Securities Lending Transactions(1) | | | | |

| Corporate Bonds | $ | 20,479,520 | | — | | — | | — | | $ | 20,479,520 | |

| Gross amount of recognized liabilities for securities lending transactions | $ | 20,479,520 | |

(1)Amount represents the payable for cash collateral received for securities on loan. This will generally be in the Overnight and Continuous column as the securities are typically callable on demand.

3. Fees and Transactions with Related Parties

Certain officers and trustees of the trust are also officers and/or directors of American Century Companies, Inc. (ACC). The trust's investment advisor, ACIM, the trust's distributor, American Century Investment Services, Inc. (ACIS), and the trust's transfer agent, American Century Services, LLC, are wholly owned, directly or indirectly, by ACC. Various funds issued by American Century Asset Allocation Portfolios, Inc. own, in aggregate, 54% of the shares of the fund. Related parties do not invest in the fund for the purpose of exercising management or control.

Management Fees — The trust has entered into a management agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that ACIM will pay all expenses of managing and operating the fund, except brokerage expenses, taxes, interest, fees and expenses of the independent trustees (including legal counsel fees), extraordinary expenses, and expenses incurred in connection with the provision of shareholder services and distribution services under a plan adopted pursuant to Rule 12b-1 under the 1940 Act. The fee is computed and accrued daily based on each class's daily net assets and paid monthly in arrears. The difference in the fee among the classes is a result of their separate arrangements for non-Rule 12b-1 shareholder services. It is not the result of any difference in advisory or custodial fees or other expenses related to the management of the fund’s assets, which do not vary by class. The investment advisor agreed to waive the G Class's management fee in its entirety. The investment advisor expects this waiver to remain in effect permanently and cannot terminate it without the approval of the Board of Trustees.

The annual management fee for each class is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investor Class | I Class | Y Class | A Class | C Class | R Class | R5 Class | R6 Class | G Class |

| 0.96% | 0.86% | 0.76% | 0.96% | 0.96% | 0.96% | 0.76% | 0.71% | 0.00%(1) |

(1)Annual management fee before waiver was 0.71%.

Distribution and Service Fees — The Board of Trustees has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, C Class and R Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay ACIS an annual distribution and service fee of 0.25%. The plans provide that the C Class will pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The plans provide that the R Class will pay ACIS an annual distribution and service fee of 0.50%. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the period ended October 31, 2021 are detailed in the Statement of Operations.

Trustees’ Fees and Expenses — The Board of Trustees is responsible for overseeing the investment advisor’s management and operations of the fund. The trustees receive detailed information about the fund and its investment advisor regularly throughout the year, and meet at least quarterly with management of the investment advisor to review reports about fund operations. The fund’s officers do not receive compensation from the fund.

Interfund Transactions — The fund may enter into security transactions with other American Century Investments funds and other client accounts of the investment advisor, in accordance with the 1940 Act rules and procedures adopted by the Board of Trustees. The rules and procedures require, among other things, that these transactions be effected at the independent current market price of the security. There were no interfund transactions during the period.

4. Investment Transactions

Purchases of investment securities, excluding short-term investments, for the period ended October 31, 2021 totaled $486,926,901, of which $10,497,813 represented U.S. Treasury and Government Agency obligations.

Sales of investment securities, excluding short-term investments, for the period ended October 31, 2021 totaled $320,556,641, of which $2,088,906 represented U.S. Treasury and Government Agency obligations.

5. Capital Share Transactions

Transactions in shares of the fund were as follows (unlimited number of shares authorized):

| | | | | | | | | | | | | | |

| Year ended

October 31, 2021 | Year ended

October 31, 2020 |

| Shares | Amount | Shares | Amount |

| Investor Class | | | | |

| Sold | 1,580,485 | | $ | 16,761,176 | | 1,463,383 | | $ | 14,801,160 | |

| Issued in reinvestment of distributions | 337,339 | | 3,587,451 | | 315,642 | | 3,211,040 | |

| Redeemed | (701,297) | | (7,442,116) | | (1,958,287) | | (19,638,937) | |

| 1,216,527 | | 12,906,511 | | (179,262) | | (1,626,737) | |

| I Class | | | | |

| Sold | 1,212,272 | | 12,908,117 | | 2,012,193 | | 20,492,202 | |

| Issued in reinvestment of distributions | 24,645 | | 261,265 | | 18,815 | | 193,373 | |

| Redeemed | (239,991) | | (2,552,321) | | (2,032,840) | | (20,693,388) | |

| 996,926 | | 10,617,061 | | (1,832) | | (7,813) | |

| Y Class | | | | |

| Sold | 823,073 | | 8,761,698 | | 764,976 | | 7,764,614 | |

| Issued in reinvestment of distributions | 84,742 | | 900,693 | | 53,070 | | 539,319 | |

| Redeemed | (164,975) | | (1,753,520) | | (116,235) | | (1,174,160) | |

| 742,840 | | 7,908,871 | | 701,811 | | 7,129,773 | |

| A Class | | | | |

| Sold | 6,350 | | 67,960 | | 12,868 | | 133,795 | |

| Issued in reinvestment of distributions | 1,140 | | 12,117 | | 1,124 | | 11,422 | |

| Redeemed | (16,816) | | (177,342) | | (8,966) | | (91,228) | |

| (9,326) | | (97,265) | | 5,026 | | 53,989 | |

| C Class | | | | |

| Issued in reinvestment of distributions | 99 | | 1,048 | | 119 | | 1,203 | |

| Redeemed | (587) | | (6,245) | | (668) | | (6,905) | |

| (488) | | (5,197) | | (549) | | (5,702) | |

| R Class | | | | |

| Sold | 5,285 | | 56,103 | | 9,188 | | 92,668 | |

| Issued in reinvestment of distributions | 436 | | 4,629 | | 373 | | 3,782 | |

| Redeemed | (3,819) | | (40,719) | | (4,477) | | (44,403) | |

| 1,902 | | 20,013 | | 5,084 | | 52,047 | |

| R5 Class | | | | |

| Sold | 14 | | 157 | | — | | — | |

| Issued in reinvestment of distributions | 29 | | 307 | | 29 | | 288 | |

| 43 | | 464 | | 29 | | 288 | |

| R6 Class | | | | |

| Sold | 4,227 | | 44,826 | | 216,660 | | 2,216,101 | |

| Issued in reinvestment of distributions | 4,806 | | 51,264 | | 32,163 | | 326,412 | |

| Redeemed | (165,343) | | (1,762,393) | | (1,036,586) | | (10,571,471) | |

| (156,310) | | (1,666,303) | | (787,763) | | (8,028,958) | |

| G Class | | | | |

| Sold | 12,229,586 | | 130,092,657 | | 20,040,002 | | 207,455,864 | |

| Issued in reinvestment of distributions | 2,296,537 | | 24,414,299 | | 1,287,138 | | 13,127,491 | |

| Redeemed | (1,524,902) | | (16,258,268) | | (4,548,550) | | (46,830,930) | |

| 13,001,221 | | 138,248,688 | | 16,778,590 | | 173,752,425 | |

| Net increase (decrease) | 15,793,335 | | $ | 167,932,843 | | 16,521,134 | | $ | 171,319,312 | |

6. Fair Value Measurements