Exhibit (17)(c)

ANNUAL REPORT / DECEMBER 31, 2008

Legg Mason Partners

Capital and Income Fund

| | |

| Managed by | | CLEARBRIDGE ADVISORS |

| | |

| | WESTERN ASSET |

INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

Fund objective

The Fund seeks total return (that is, a combination of income and long-term capital appreciation).

What’s inside

Legg Mason Partners Fund Advisor, LLC (“LMPFA”) is the Fund’s investment manager. ClearBridge Advisors, LLC (“ClearBridge”), Western Asset Management Company (“Western Asset”) and Western Asset Management Company Limited (“Western Asset Limited”) are the Fund’s subadvisers. LMPFA, ClearBridge, Western Asset and Western Asset Limited are wholly-owned subsidiaries of Legg Mason, Inc.

Letter from the chairman

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

The U.S. economy weakened significantly during the 12-month reporting period ended December 31, 2008. Looking back, U.S. gross domestic product (“GDP”)i contracted 0.2% in the fourth quarter of 2007. This was due to continued weakness in the housing market, an ongoing credit crunch and soaring oil and food prices. The economy then expanded 0.9% and 2.8% during the first and second quarters of 2008, respectively. Contributing to this rebound were rising exports that were buoyed by a weakening U.S. dollar. In addition, consumer spending accelerated, aided by the government’s tax rebate program. However, the dollar’s rally and the end of the rebate program, combined with other strains on the economy, caused GDP to take a step backward during the second half of 2008. According to the U.S. Department of Commerce, third quarter 2008 GDP declined 0.5% and its advance estimate for fourth quarter GDP decline was 3.8%, the latter being the worst quarterly reading since 1982.

While there were increasing signs that the U.S. was headed for a recession, the speculation ended in December 2008. At that time, the National Bureau of Economic Research (“NBER”) — which has the final say on when one begins and ends — announced that a recession had begun in December 2007. The NBER determined that a recession had already started using its definition, which is based on “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in production, employment, real income and other indicators.”

Regardless of how one defines a recession, it felt like we were in the midst of an economic contraction for much of 2008. Consumer spending, which represents approximately two-thirds of GDP, has been disappointing. According to the International Council of Shopping Centers, retail sales rose a tepid 1% in 2008, the weakest level in at least 38 years. In terms of the job market, the U.S. Department of Labor reported that payroll employment declined in each of the 12 months of 2008. During 2008 as a whole, 2.6 million jobs were lost, the largest annual decline since World War II ended in 1945. In addition, at the end of 2008, the unemployment rate had risen to 7.2%, its highest level since January 1993.

| | |

| Legg Mason Partners Capital and Income Fund | | I |

Letter from the chairman continued

Ongoing issues related to the housing and subprime mortgage markets and seizing credit markets prompted the Federal Reserve Board (“Fed”)ii to take aggressive and, in some cases, unprecedented actions. When 2008 began, the federal funds rateiii was 4.25%. This was quickly brought down to 3.00% by the end of January 2008, on the back of two Fed rate cuts. The Fed continued to lower the federal funds rate to 2.00% by the end of April 2008, but then left rates on hold for several months. This was due to growing inflationary pressures as a result of soaring oil and commodity prices, coupled with the sagging U.S. dollar. However, as inflation receded along with oil prices and the global financial crisis escalated, the Fed cut rates twice in October to 1.00%. Then, in mid-December 2008, it reduced the federal funds rate to a range of zero to 0.25%, an historic low. In conjunction with its December meeting, the Fed stated that it “will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time.”

In addition to the interest rate cuts, the Fed took several actions to improve liquidity in the credit markets. In March 2008, it established a new lending program allowing certain brokerage firms, known as primary dealers, to also borrow from its discount window. Also in March, the Fed played a major role in facilitating the purchase of Bear Stearns by JPMorgan Chase. In mid-September 2008, it announced an $85 billion rescue plan for ailing AIG and pumped $70 billion into the financial system as Lehman Brothers’ bankruptcy and mounting troubles at other financial firms roiled the markets.

The U.S. Department of the Treasury has also taken an active role in attempting to stabilize the financial system, as it orchestrated the government’s takeover of mortgage giants Fannie Mae and Freddie Mac in September 2008. In addition, on October 3, 2008, the Treasury’s $700 billion Troubled Asset Relief Program (“TARP”) was approved by Congress and signed into law by President Bush. As part of TARP, the Treasury had planned to purchase bad loans and other troubled financial assets. However, in November 2008, Treasury Secretary Paulson said, “Our assessment at this time is that this is not the most effective way to use TARP funds, but we will continue to examine whether targeted forms of asset purchase can play a useful role, relative to other potential uses of TARP resources, in helping to strengthen our financial system and support lending.”

The U.S. stock market was extremely volatile and generated very poor results during the 12 months ended December 31, 2008. Stock prices declined during each of the first three months of the reporting period. This was due, in part, to the credit crunch, weakening corporate profits, rising inflation and fears of an impending recession. The market then reversed course and posted positive returns in April and May 2008. The market’s

| | |

| II | | Legg Mason Partners Capital and Income Fund |

gains were largely attributed to hopes that the U.S. would skirt a recession and that corporate profits would rebound as the year progressed. However, given the escalating credit crisis and the mounting turmoil in the financial markets, stock prices moved lower during five of the last seven months of the reporting period, including S&P 500 Indexiv (the “Index”) returns of -8.91%, -16.79% and -7.18% in September, October and November 2008, respectively. While the Index rallied approximately 20% from its low on November 20, 2008 through the end of the year, it was too little, too late. All told, the Index returned -37.00% in 2008, its third worst year ever and the biggest calendar year loss since 1937.

Turning to the fixed-income markets, both short- and long-term Treasury yields experienced periods of extreme volatility during the 12-month reporting period ended December 31, 2008. Investors were initially focused on the subprime segment of the mortgage-backed market. These concerns broadened, however, to include a wide range of financial institutions and markets. As a result, other fixed-income instruments also experienced increased price volatility. This unrest triggered several “flights to quality,” causing Treasury yields to move lower (and their prices higher), while riskier segments of the market saw their yields move higher (and their prices lower). This was particularly true toward the end of the reporting period, as the turmoil in the financial markets and sharply falling stock prices caused investors to flee securities that were perceived to be risky, even high-quality corporate bonds and high-grade municipal bonds. On several occasions, the yield available from short-term Treasuries fell to nearly zero, as investors were essentially willing to forgo any return potential in order to access the relative safety of government-backed securities. During the 12 months ended December 31, 2008, two-year Treasury yields fell from 3.05% to 0.76%. Over the same time frame, 10-year Treasury yields moved from 4.04% to 2.25%. Looking at the 12-month period as a whole, the overall bond market, as measured by the Barclays Capital U.S. Aggregate Indexv, returned 5.24%.

A special note regarding increased market volatility

In recent months, we have experienced a series of events that have impacted the financial markets and created concerns among both novice and seasoned investors alike. In particular, we have witnessed the failure and consolidation of several storied financial institutions, periods of heightened market volatility, and aggressive actions by the U.S. federal government to steady the financial markets and restore investor confidence. While we hope that the worst is over in terms of the issues surrounding the credit and housing crises, it is likely that the fallout will continue to impact the financial markets and the U.S. economy well into 2009.

Like all asset management firms, Legg Mason has not been immune to these difficult and, in some ways, unprecedented times. However, today’s

| | |

| Legg Mason Partners Capital and Income Fund | | III |

Letter from the chairman continued

challenges have only strengthened our resolve to do everything we can to help you reach your financial goals. Now, as always, we remain committed to providing you with excellent service and a full spectrum of investment choices. And rest assured, we will continue to work hard to ensure that our investment managers make every effort to deliver strong long-term results.

We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our enhanced website, www.leggmason.com/individualinvestors. Here you can gain immediate access to many special features to help guide you through difficult times, including:

| • | | Fund prices and performance, |

| • | | Market insights and commentaries from our portfolio managers, and |

| • | | A host of educational resources. |

During periods of market unrest, it is especially important to work closely with your financial advisor and remember that reaching one’s investment goals unfolds over time and through multiple market cycles. Time and again, history has shown that, over the long run, the markets have eventually recovered and grown.

Information about your fund

As you may be aware, several issues in the mutual fund industry have come under the scrutiny of federal and state regulators. Affiliates of the Fund’s manager have, in recent years, received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund is not in a position to predict the outcome of these requests and investigations.

Please read on for a more detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

Important information with regard to recent regulatory developments that may affect the Fund is contained in the Notes to Financial Statements included in this report.

| | |

| IV | | Legg Mason Partners Capital and Income Fund |

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

January 30, 2009

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| ii | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| iv | The S&P 500 Index is an unmanaged index of 500 stocks and is generally representative of the performance of larger companies in the U.S. |

| v | The Barclays Capital (formerly Lehman Brothers) U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| | |

| Legg Mason Partners Capital and Income Fund | | V |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund seeks total return (a combination of income and long-term capital appreciation) by investing in both equities and fixed-income securities of both U.S. and foreign issuers. The Fund seeks to generate income and appreciation by allocating Fund assets to income and non-income producing equity and equity-related securities, including common stocks, real estate investment trusts (“REITs”)i and convertible securities. To generate income and enhance exposure to the equity markets, the Fund may purchase investment grade and high-yield fixed-income securities or unrated securities of equivalent quality along with options on securities indexes. Fixed-income securities may be of any maturity.

By investing in a combination of equity and fixed-income securities, the Fund seeks to produce a pattern of total return that moves with the S&P 500 Indexii (the “Index”), while generating high income. In addition, the Fund may use options, futures and options on futures to increase exposure to part or all of the market or to hedge against adverse changes in the market value of the Fund’s securities.

Mr. Gendelman, the Fund’s lead portfolio manager at ClearBridge Advisors, LLC, one of the Fund’s subadvisers, oversees the Fund’s allocation between equity and fixed-income securities, as well as the Fund’s equity investments in general. He manages the equity side of the Fund with a “bottom-up” approach focused on the risk and reward of each investment opportunity. A portfolio management team at Western Asset Management Company, one of the Fund’s subadvisers, manages the fixed-income portion of the Fund. Their focus is on portfolio structure, including allocation, durationiii weighting and term-structure decisions.

Q. What were the overall market conditions during the Fund’s reporting period?

A. During the fiscal year, the stock market experienced periods of heightened volatility. The overall stock market, as measured by the Index, fell 37% in 2008, its worst calendar year performance since 1937. Stock prices stumbled out of the gate in 2008, due to concerns over the economy and the outlook for corporate profits. By the end of the first quarter of 2008, the Index had fallen 9.44%. After rallying in April and May, stock prices again weakened and continued to fall during much of the last seven months of the year. Frozen credit markets, the ongoing bursting of the housing bubble, upheaval in the financial markets and expectations for a deep and prolonged recession were some of the factors driving stock prices sharply lower.

Economic numbers deteriorated significantly in the fourth quarter of the year. The unemployment rate rose to 7.2% and threatened to move far higher. During the Christmas season, retail sales fell 2.6%, the worst since 1970. Auto sales collapsed to a 10.5 million seasonally adjusted annual rate,

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 1 |

Fund overview continued

the lowest level since the early 1980s. Chrysler and GM are teetering on the edge of bankruptcy. Housing starts and permits hit new lows. Home prices fell sharply and have not yet stabilized, while inventories remain elevated.

The stock market in September and in the fourth quarter reeled from blow after blow to the U.S. financial system. On Monday, September 14, 2008, the Department of the U.S. Treasury and the Federal Reserve Board (“Fed”)iv decided to allow Lehman Brothers to declare bankruptcy, without interfering to protect creditors as they had with Bear Stearns in March. Their lack of action led to panic in the U.S. credit markets. The U.S. Congress compounded what we believe was the Treasury’s mistake by fumbling its first attempt to pass a $700 billion bailout package.

Only in November, when the Fed announced a plan to purchase mortgage-backed securities, did the markets start to settle. Since early November, numerous signs of credit improvement appeared. Mortgage rates fell below 5%, London Interbank Offered Rate (“LIBOR”)v fell back to pre-crisis levels and high-quality bond spreads fell enough that several large companies issued debt in late December. The stock market responded to the signs of credit easing by rallying more than 20% between the bottom on November 20th and the end of the year.

In terms of the bond market, changing perceptions regarding the economy, inflation and future Fed monetary policy caused bond prices to fluctuate. Two- and 10-year Treasury yields began the reporting period at 3.05% and 4.04%, respectively. Treasury yields moved lower — and their prices moved higher — during the first quarter of 2008, as concerns regarding the subprime mortgage market and a severe credit crunch caused a “flight to quality.” During this period, investors were drawn to the relative safety of Treasuries, while increased risk aversion caused other segments of the bond market to falter. Treasury yields then moved higher in April, May and early June 2008, as the economy performed better than expected and inflation moved higher. Over this period, riskier fixed-income asset classes, such as high-yield bonds and emerging market debt, rallied. However, the credit crunch resumed in mid-June, resulting in another flight to quality. Investors’ risk aversion then intensified from September through November given the severe disruptions in the global financial markets. During this time, virtually every asset class, with the exception of short-term Treasuries, performed poorly. At the end of the fiscal year, two- and 10-year Treasury yields were 0.76% and 2.25%, respectively. Aided by the strong performance in the Treasury market, the overall U.S. bond market, as measured by the Barclays Capital U.S. Aggregate Indexvi, gained 5.24% during the 12 months ended December 31, 2008.

Q. How did we respond to these changing market conditions?

A. We entered the fiscal year concerned about the health of the overall financial system and positioned the equity side of the portfolio with what we

| | |

| 2 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

felt was an appropriately defensive posture. During the fiscal year, we made two strategic changes to the portfolio. First, we increased its allocation to fixed-income from a low 20% to a high 20% range. Second, within the fixed-income portion of the portfolio, we increased exposure to high-yield fixed-income securities as credit spreads expanded and, therefore, made high-yield securities a more attractive investment in our view.

Performance review

For the 12 months ended December 31, 2008, Class A shares of Legg Mason Partners Capital and Income Fund, excluding sales charges, returned -35.59%. The Fund’s unmanaged benchmarks, the S&P 500 Index and the Barclays Capital U.S. Aggregate Index, returned -37.00% and 5.24%, respectively, for the same period. The Lipper Mixed-Asset Target Allocation Growth Funds Category Average1 returned -29.85% over the same time frame.

| | | | |

| PERFORMANCE SNAPSHOT as of December 31, 2008 (excluding sales charges) (unaudited) |

| | | 6 MONTHS | | 12 MONTHS |

| Capital and Income Fund — Class A Shares | | -31.26% | | -35.59% |

| S&P 500 Index | | -28.48% | | -37.00% |

| Barclays Capital U.S. Aggregate Index | | 4.07% | | 5.24% |

| Lipper Mixed-Asset Target Allocation Growth Funds Category Average1 | | -24.04% | | -29.85% |

| | | | |

| The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, please visit our website at www.leggmason.com/individualinvestors. |

| Excluding sales charges, Class B shares returned -31.46%, Class C shares returned -31.52%, Class R shares returned -31.26% and Class I shares returned -31.12% over the six months ended December 31, 2008. Excluding sales charges, Class B shares returned -35.96%, Class C shares returned -36.09% and Class I shares returned -35.37% over the 12 months ended December 31, 2008. All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Returns have not been adjusted to include sales charges that may apply when shares are purchased or the deduction of taxes that a shareholder would pay on Fund distributions. |

| Performance figures reflect expense reimbursements and/or fee waivers, without which the performance would have been lower. |

| Performance information for the 12-month period is not provided for Class R shares as this share class commenced operations on April 30, 2008. |

| TOTAL ANNUAL OPERATING EXPENSES (unaudited) |

| As of the Fund’s most current prospectus dated April 28, 2008, the gross total operating expense ratios for Class A, Class B, Class C, Class R and Class I shares were 1.07%, 1.64%, 1.82%, 1.42% and 0.77%, respectively. |

| 1 | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the period ended December 31, 2008, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 702 funds for the six-month period and among the 689 funds for the 12-month period in the Fund’s Lipper category, and excluding sales charges. |

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 3 |

Fund overview continued

Q. What were the leading contributors to performance?

A. For the equity portion of the portfolio, overall sector allocation contributed to performance relative to the Index. In particular, an overweight to the Energy sector and underweights to the Financials, Information Technology (“IT”) and Health Care sectors, as well as our use of derivatives, helped relative performance. Stock selection in the Materials and IT sectors also contributed to relative performance for the year. In terms of individual holdings, leading contributors to performance for the year included positions in Newmont Mining Corp. and Barrick Gold Corp., both in the Materials sector, Fidelity National Financial Inc. in the Financials sector, QUALCOMM Inc. in the IT sector and Schlumberger Ltd. in the Energy sector, as well as several derivatives and exchange-traded-fund positions.

In the fixed-income portion of the portfolio, our tactically-driven duration and yield curvevii positioning were contributors to performance as interest rates fell during the 12-month reporting period.

Q. What were the leading detractors from performance?

A. For the equity portion of the portfolio, overall stock selection detracted from relative performance for the period, specifically in the Energy, Consumer Discretionary, Financials, Utilities, Industrials and Health Care sectors. The Fund’s overweights to the Industrials and Consumer Discretionary sectors and underweights to the Consumer Staples, Materials and Telecommunication Services (“Telecom”) sectors also hurt relative performance for the year. In terms of individual Fund holdings, leading detractors from performance for the year included positions in Crosstex Energy Inc. and El Paso Corp., both in the Energy sector, General Electric Co. in the Industrials sector, American International Group Inc., Och-Ziff Capital Management Group and Invesco Ltd., all in the Financials sector, Lamar Advertising Co. (Class A Shares) and Liberty Media Corp. Series A Liberty Entertainment, both in the Consumer Discretionary sector.

In the fixed-income portion on the portfolio, our high-yield positions significantly underperformed over the past year. In particular, our high-yield Industrials issues and bank loans, especially those of lower-rated quality, were hit hard by the credit crisis and declining commodity prices. Our investment grade Financials suffered from a series of bankruptcies, government conservatorships and mergers. Non-agency mortgage-backed securities reached new lows amid all the market turmoil and the ongoing fallout from the housing slowdown.

Q. Were there any significant changes to the Fund during the reporting period?

A. On the equity side of the Fund’s portfolio, at the start of the period we held overweight positions in the Financials, Energy and Consumer

| | |

| 4 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

Discretionary sectors, with no holdings in the Materials sector. The balance of the equity portfolio was focused in, what we believed to be, high-quality companies with relatively defensive fundamental business characteristics. Over the course of the year, we reduced our overweight positions in Financials, Energy and Consumer Discretionary to underweights, while increasing our allocations to the Materials, Industrials, Consumer Staples and Health Care sectors.

During the fiscal year, we established a number of new positions, including those in Total SA (ADR) and El Paso Corp., both in the Energy sector, Consumer Staples sector holdings Kimberly-Clark Corp., Kraft Foods Inc. (Class A Shares) and Procter & Gamble Co., Health Care sector holdings HLTH Corp. (which we consider to be an IT holding), Wyeth and Novartis AG (ADR), as well as L-3 Communications Holdings Inc. in the Industrials sector. We also closed a number of existing positions, including Altria Group, Inc. in the Consumer Staples sector, Bank of America Corp., American International Group Inc., American Express Co. and UBS AG, all in the Financials sector, Dover Corp. in the Industrials sector, Liberty Media Corp. in the Consumer Discretionary sector, as well as SBA Communications Corp. and Crown Castle International Corp., both in the Telecom sector.

As of the close of the fiscal year, we maintained a preference for the existing holdings in the Energy sector and other, what we believed to be, high-quality companies, even though they may have not performed significantly better than the overall market in the recent difficult economic environment.

In terms of the fixed-income portion of the portfolio, in addition to the previously discussed changes, we gradually reduced our positions in agency mortgage-backed securities and added to the investment grade credit sector.

Thank you for your investment in Legg Mason Partners Capital and Income Fund. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

| | |

| | |

Robert Gendelman Lead Portfolio Manager ClearBridge Advisors, LLC (Fund Allocation and Equity Portion) | | Western Asset Management Company |

| | (Fixed-Income Portion) |

| | |

January 20, 2009

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 5 |

Fund overview continued

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of December 31, 2008 and are subject to change and may not be representative of the portfolio managers’ current or future investments. The Fund’s top 10 holdings (as a percentage of net assets) as of this date were: Covanta Holding Corp. (3.4%), Total SA, ADR (2.7%), General Electric Co. (2.4%), Assa Abloy AB (2.3%), Time Warner Inc. (2.3%), United Technologies Corp. (2.1%), Kimberly-Clark Corp. (2.1%), EI Paso Corp. (1.9%), Kraft Foods Inc., Class A Shares (1.8%) and HLTH Corp. (1.7%). Please refer to pages 12 through 42 for a list and percentage breakdown of the Fund’s holdings.

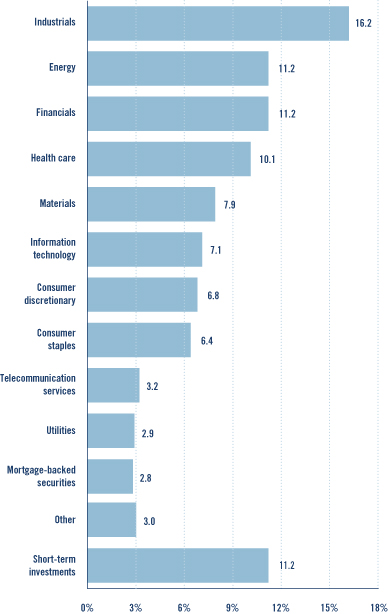

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2008 were: Industrials (16.2%), Energy (11.2%), Financials (11.2%), Health Care (10.1%) and Materials (7.9%). The Fund’s portfolio composition is subject to change at any time.

RISKS: Stock and bond prices are subject to fluctuation. As interest rates rise, bond prices fall, reducing the value of the Fund’s share price. High-yield securities are rated below investment grade and involve greater credit and liquidity risk than higher-rated securities. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. The Fund is subject to certain risks of overseas investing not associated with domestic investing, including currency fluctuations and changes in political and economic conditions. Please see the Fund’s prospectus for more information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | Real estate investment trusts (“REITs”) invest in real estate or loans secured by real estate and issue shares in such investments, which can be illiquid. |

| ii | The S&P 500 Index is an unmanaged index of 500 stocks and is generally representative of the performance of larger companies in the U.S. |

| iii | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| iv | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| v | The London Interbank Offered Rate (“LIBOR”) is the interest rate offered by a specific group of London banks for U.S. dollar deposits of a stated maturity. LIBOR is used as a base index for setting rates of some adjustable rate financial instruments, including Adjustable Rate Mortgages (“ARMs”). |

| vi | The Barclays Capital (formerly Lehman Brothers) U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| vii | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

| | |

| 6 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

Fund at a glance (unaudited)

|

| INVESTMENT BREAKDOWN (%) As a percent of total investments — December 31, 2008 |

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 7 |

Fund expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments, and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on July 1, 2008 and held for the six months ended December 31, 2008.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

| | | | | | | | | | | | | | | |

| BASED ON ACTUAL TOTAL RETURN1 |

| | | ACTUAL TOTAL

RETURN

WITHOUT

SALES

CHARGES2 | | | BEGINNING

ACCOUNT

VALUE | | ENDING

ACCOUNT

VALUE | | ANNUALIZED

EXPENSE

RATIO3 | | | EXPENSES

PAID DURING

THE PERIOD4 |

| Class A | | (31.26 | )% | | $ | 1,000.00 | | $ | 687.40 | | 1.13 | % | | $ | 4.79 |

| Class B | | (31.46 | ) | | | 1,000.00 | | | 685.40 | | 1.71 | | | | 7.24 |

| Class C | | (31.52 | ) | | | 1,000.00 | | | 684.80 | | 1.94 | | | | 8.22 |

| Class R | | (31.26 | ) | | | 1,000.00 | | | 687.40 | | 1.31 | | | | 5.56 |

| Class I | | (31.12 | ) | | | 1,000.00 | | | 688.80 | | 0.78 | | | | 3.31 |

| 1 | For the six months ended December 31, 2008. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Class B and Class C shares. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | The expense ratios include dividend expense related to securities sold short and not subject to a contractual expense limitation. |

| 4 | Expenses (net of fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

| | |

| 8 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | |

| BASED ON HYPOTHETICAL TOTAL RETURN1 | | | | | |

| | | HYPOTHETICAL

ANNUALIZED

TOTAL

RETURN | | | BEGINNING

ACCOUNT

VALUE | | ENDING

ACCOUNT

VALUE | | ANNUALIZED

EXPENSE

RATIO2 | | | EXPENSES

PAID DURING

THE PERIOD3 |

| Class A | | 5.00 | % | | $ | 1,000.00 | | $ | 1,019.46 | | 1.13 | % | | $ | 5.74 |

| Class B | | 5.00 | | | | 1,000.00 | | | 1,016.54 | | 1.71 | | | | 8.67 |

| Class C | | 5.00 | | | | 1,000.00 | | | 1,015.38 | | 1.94 | | | | 9.83 |

| Class R | | 5.00 | | | | 1,000.00 | | | 1,018.55 | | 1.31 | | | | 6.65 |

| Class I | | 5.00 | | | | 1,000.00 | | | 1,021.22 | | 0.78 | | | | 3.96 |

| 1 | For the six months ended December 31, 2008. |

| 2 | The expense ratios include dividend expense related to securities sold short and not subject to a contractual expense limitation. |

| 3 | Expenses (net of fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 366. |

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 9 |

Fund performance (unaudited)

| | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS1 | | | | |

| | | WITHOUT SALES CHARGES2 | |

| | | CLASS A | | | CLASS B | | | CLASS C | | | CLASS R | | | CLASS I | |

| Twelve Months Ended 12/31/08 | | (35.59 | )% | | (35.96 | )% | | (36.09 | )% | | N/A | | | (35.37 | )% |

| Five Years Ended 12/31/08 | | (2.02 | ) | | (2.56 | ) | | (2.77 | ) | | N/A | | | (1.65 | ) |

| Ten Years Ended 12/31/08 | | 1.43 | | | 0.90 | | | 0.66 | | | N/A | | | 1.80 | |

| Inception* through 12/31/08 | | 6.37 | | | 7.97 | | | 0.66 | | | (32.82 | )%† | | 5.00 | |

| |

| | | WITH SALES CHARGES3 | |

| | | CLASS A | | | CLASS B | | | CLASS C | | | CLASS R | | | CLASS I | |

| Twelve Months Ended 12/31/08 | | (39.30 | )% | | (39.03 | )% | | (36.70 | )% | | N/A | | | (35.37 | )% |

| Five Years Ended 12/31/08 | | (3.18 | ) | | (2.70 | ) | | (2.77 | ) | | N/A | | | (1.65 | ) |

| Ten Years Ended 12/31/08 | | 0.84 | | | 0.90 | | | 0.66 | | | N/A | | | 1.80 | |

| Inception* through 12/31/08 | | 5.98 | | | 7.97 | | | 0.66 | | | (32.82 | )%† | | 5.00 | |

| | | | | | | | | | | | | | | |

| CUMULATIVE TOTAL RETURNS1 | | | | | | | |

| | | |

| | | WITHOUT SALES CHARGES2 | |

| Class A (12/31/98 through 12/31/08) | | 15.30 | % |

| Class B (12/31/98 through 12/31/08) | | 9.38 | |

| Class C (12/31/98 through 12/31/08) | | 6.81 | |

| Class R (Inception date of 4/30/08 through 12/31/08) | | (32.82 | ) |

| Class I (12/31/98 through 12/31/08) | | 19.49 | |

| 1 | All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charge with respect to Class A shares or the applicable CDSC with respect to Class B and Class C shares. |

| 3 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. In addition, Class A shares reflect the deduction of the maximum initial sales charge of 5.75%; Class B shares reflect the deduction of a 5.00% CDSC, which applies if shares are redeemed within one year from purchase payment and declines thereafter by 1.00% per year until no CDSC is incurred; Class C shares also reflect the deduction of a 1.00% CDSC, which applies if shares are redeemed within one year from purchase payment. |

| * | Inception dates for Class A, Class B, Class C, Class R and Class I shares are November 6, 1992, September 16, 1985, June 15, 1998, April 30, 2008 and February 7, 1996, respectively. |

| | |

| 10 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

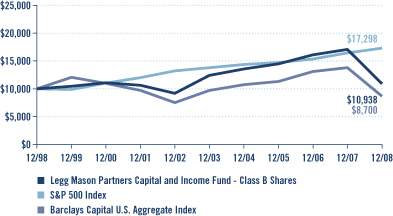

Historical performance (unaudited)

|

VALUE OF $10,000 INVESTED IN CLASS B SHARES OF LEGG MASON PARTNERS CAPITAL AND INCOME

FUND VS. S&P 500 INDEX AND BARCLAYS CAPITAL U.S. AGGREGATE INDEX† —

December 1998 - December 2008 |

| † | Hypothetical illustration of $10,000 invested in Class B shares of Legg Mason Partners Capital and Income Fund on December 31, 1998, assuming the reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2008. The S&P 500 Index is an unmanaged index of 500 stocks and is generally representative of the performance of larger companies in the U.S. The Barclays Capital (formerly Lehman Brothers) U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. The Indexes are unmanaged and are not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. The performance of the Fund’s other classes may be greater or less than the Class B shares’ performance indicated on this chart, depending on whether higher or lower sales charges and fees were incurred by shareholders investing in the other classes. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment, which will fluctuate so that an investor’s share, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 11 |

Schedule of investments

December 31, 2008

| | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

| SHARES | | SECURITY | | VALUE |

| | | | | |

| COMMON STOCKS — 60.3% | | | |

| CONSUMER DISCRETIONARY — 4.0% | | | |

| | | Household Durables — 0.0% | | | |

| 2,330,496 | | Home Interiors & Gifts Inc.(a)(b)* | | $ | 2 |

| | | Media — 4.0% | | | |

| 857,110 | | Lamar Advertising Co., Class A Shares* | | | 10,765,302 |

| 404,600 | | Thomson Reuters PLC(a) | | | 8,948,708 |

| 3,956,720 | | Time Warner Inc. | | | 39,804,603 |

| 3,142,800 | | Warner Music Group Corp. | | | 9,491,256 |

| | | Total Media | | | 69,009,869 |

| | | TOTAL CONSUMER DISCRETIONARY | | | 69,009,871 |

| CONSUMER STAPLES — 5.6% | | | |

| | | Food & Staples Retailing — 0.0% | | | |

| 28,868 | | FHC Delaware Inc.(a)(b)* | | | 0 |

| | | Food Products — 1.8% | | | |

| 1,948 | | Aurora Foods Inc.(a)(b)* | | | 0 |

| 1,163,700 | | Kraft Foods Inc., Class A Shares | | | 31,245,345 |

| | | Total Food Products | | | 31,245,345 |

| | | Household Products — 3.8% | | | |

| 671,970 | | Kimberly-Clark Corp. | | | 35,439,698 |

| 479,530 | | Procter & Gamble Co. | | | 29,644,544 |

| | | Total Household Products | | | 65,084,242 |

| | | TOTAL CONSUMER STAPLES | | | 96,329,587 |

| ENERGY — 8.0% | | | |

| | | Energy Equipment & Services — 1.9% | | | |

| 836,605 | | Halliburton Co. | | | 15,209,479 |

| 711,160 | | National-Oilwell Varco Inc.* | | | 17,380,750 |

| | | Total Energy Equipment & Services | | | 32,590,229 |

| | | Oil, Gas & Consumable Fuels — 6.1% | | | |

| 2,259,616 | | Crosstex Energy Inc. | | | 8,812,503 |

| 271,310 | | Devon Energy Corp. | | | 17,827,780 |

| 4,218,600 | | El Paso Corp. | | | 33,031,638 |

| 829,320 | | Total SA, ADR | | | 45,861,396 |

| | | Total Oil, Gas & Consumable Fuels | | | 105,533,317 |

| | | TOTAL ENERGY | | | 138,123,546 |

| EXCHANGE TRADED FUND — 0.4% | | | |

| 106,000 | | UltraShort S&P500 ProShares | | | 7,517,096 |

| FINANCIALS — 5.9% | | | |

| | | Capital Markets — 3.2% | | | |

| 1,575,300 | | Charles Schwab Corp. | | | 25,472,601 |

See Notes to Financial Statements.

| | |

| 12 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

| | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

| SHARES | | SECURITY | | VALUE |

| | | | | |

| | | Capital Markets — 3.2% continued | | | |

| 1,602,460 | | Invesco Ltd. | | $ | 23,139,523 |

| 1,207,429 | | Och-Ziff Capital Management Group | | | 6,218,259 |

| | | Total Capital Markets | | | 54,830,383 |

| | | Commercial Banks — 1.4% | | | |

| 851,700 | | Wells Fargo & Co. | | | 25,108,116 |

| | | Diversified Financial Services — 1.3% | | | |

| 703,900 | | JPMorgan Chase & Co. | | | 22,193,967 |

| | | TOTAL FINANCIALS | | | 102,132,466 |

| HEALTH CARE — 8.6% | | | |

| | | Health Care Equipment & Supplies — 2.0% | | | |

| 150,850 | | Alcon Inc. | | | 13,454,312 |

| 649,070 | | Medtronic Inc. | | | 20,393,779 |

| | | Total Health Care Equipment & Supplies | | | 33,848,091 |

| | | Health Care Technology — 1.8% | | | |

| 2,879,869 | | HLTH Corp.* | | | 30,123,430 |

| | | Pharmaceuticals — 4.8% | | | |

| 443,900 | | Johnson & Johnson | | | 26,558,537 |

| 549,350 | | Novartis AG, ADR | | | 27,335,656 |

| 785,000 | | Wyeth | | | 29,445,350 |

| | | Total Pharmaceuticals | | | 83,339,543 |

| | | TOTAL HEALTH CARE | | | 147,311,064 |

| INDUSTRIALS — 14.2% | | | |

| | | Aerospace & Defense — 2.4% | | | |

| 378,050 | | L-3 Communications Holdings Inc. | | | 27,892,529 |

| 419,778 | | TransDigm Group Inc.* | | | 14,091,948 |

| | | Total Aerospace & Defense | | | 41,984,477 |

| | | Building Products — 2.4% | | | |

| 3,564,150 | | Assa Abloy AB(a) | | | 40,440,521 |

| | | Commercial Services & Supplies — 3.5% | | | |

| 2,707,741 | | Covanta Holding Corp.* | | | 59,461,992 |

| | | Industrial Conglomerates — 5.2% | | | |

| 2,522,590 | | General Electric Co. | | | 40,865,958 |

| 1,270,100 | | McDermott International Inc.* | | | 12,548,588 |

| 690,380 | | United Technologies Corp. | | | 37,004,368 |

| | | Total Industrial Conglomerates | | | 90,418,914 |

| | | Road & Rail — 0.7% | | | |

| 360,420 | | CSX Corp. | | | 11,702,838 |

| | | TOTAL INDUSTRIALS | | | 244,008,742 |

See Notes to Financial Statements.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 13 |

Schedule of investments continued

December 31, 2008

| | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

| SHARES | | SECURITY | | VALUE |

| | | | | |

| INFORMATION TECHNOLOGY — 5.2% | | | |

| | | Communications Equipment — 1.9% | | | |

| 1,237,200 | | Nokia Oyj, ADR | | $ | 19,300,320 |

| 70,139 | | Nortel Networks Corp.* | | | 18,236 |

| 389,230 | | QUALCOMM Inc. | | | 13,946,111 |

| | | Total Communications Equipment | | | 33,264,667 |

| | | Computers & Peripherals — 1.2% | | | |

| 2,028 | | Axiohm Transaction Solutions Inc.(a)(b)* | | | 0 |

| 1,921,610 | | EMC Corp.* | | | 20,119,257 |

| | | Total Computers & Peripherals | | | 20,119,257 |

| | | Software — 2.1% | | | |

| 725,320 | | Autodesk Inc.* | | | 14,252,538 |

| 1,272,990 | | Oracle Corp.* | | | 22,570,112 |

| | | Total Software | | | 36,822,650 |

| | | TOTAL INFORMATION TECHNOLOGY | | | 90,206,574 |

| MATERIALS — 6.1% | | | |

| | | Chemicals — 3.2% | | | |

| 458,130 | | Air Products & Chemicals Inc. | | | 23,030,195 |

| 913,200 | | Celanese Corp., Series A Shares | | | 11,351,076 |

| 301,320 | | Monsanto Co. | | | 21,197,862 |

| | | Total Chemicals | | | 55,579,133 |

| | | Metals & Mining — 2.9% | | | |

| 380,500 | | Barrick Gold Corp. | | | 13,990,985 |

| 1,099,580 | | Commercial Metals Co. | | | 13,052,015 |

| 345,880 | | Freeport-McMoRan Copper & Gold Inc., Class B Shares | | | 8,453,307 |

| 340,800 | | Newmont Mining Corp. | | | 13,870,560 |

| | | Total Metals & Mining | | | 49,366,867 |

| | | TOTAL MATERIALS | | | 104,946,000 |

| TELECOMMUNICATION SERVICES — 1.3% | | | |

| | | Wireless Telecommunication Services — 1.3% | | | |

| 766,750 | | American Tower Corp., Class A Shares* | | | 22,481,110 |

| UTILITIES — 1.0% | | | |

| | | Gas Utilities — 1.0% | | | |

| 552,740 | | National Fuel Gas Co. | | | 17,317,344 |

| | | TOTAL COMMON STOCKS (Cost — $1,607,756,341) | | | 1,039,383,400 |

| CONVERTIBLE PREFERRED STOCKS — 1.1% | | | |

| ENERGY — 0.7% | | | |

| | | Oil, Gas & Consumable Fuels — 0.7% | | | |

| 18,600 | | El Paso Corp., 4.990%(a) | | | 12,280,650 |

See Notes to Financial Statements.

| | |

| 14 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

| SHARES | | SECURITY | | VALUE |

| | | | | | |

| | MATERIALS — 0.4% | | | |

| | | | Metals & Mining — 0.4% | | | |

| | 9,720 | | Freeport-McMoRan Copper & Gold Inc., 5.500% | | $ | 5,977,800 |

| | | | TOTAL CONVERTIBLE PREFERRED STOCKS

(Cost — $18,173,226) | | | 18,258,450 |

| | PREFERRED STOCKS — 0.0% | | | |

| | FINANCIALS — 0.0% | | | |

| | | | Consumer Finance — 0.0% | | | |

| | 1,580 | | Preferred Blocker Inc., 9.000%(c) | | | 474,000 |

| | | | Diversified Financial Services — 0.0% | | | |

| | | | TCR Holdings Corp.: | | | |

| | 321 | | Class B Shares(a)(b)* | | | 0 |

| | 177 | | Class C Shares(a)(b)* | | | 0 |

| | 466 | | Class D Shares(a)(b)* | | | 0 |

| | 964 | | Class E Shares(a)(b)* | | | 0 |

| | | | Total Diversified Financial Services | | | 0 |

| | | | Thrifts & Mortgage Finance — 0.0% | | | |

| | 74,600 | | Federal Home Loan Mortgage Corp. (FHLMC), 8.375%(d)* | | | 29,094 |

| | 2,800 | | Federal National Mortgage Association (FNMA), 7.000%(d)(e)* | | | 2,100 |

| | 54,025 | | Federal National Mortgage Association (FNMA), 8.250%(d)* | | | 44,841 |

| | | | Total Thrifts & Mortgage Finance | | | 76,035 |

| | | | TOTAL PREFERRED STOCKS (Cost — $3,800,531) | | | 550,035 |

FACE

AMOUNT | | | | |

| | ASSET-BACKED SECURITIES — 0.7% | | | |

| | FINANCIALS — 0.7% | | | |

| | | | Automobiles — 0.1% | | | |

| $ | 1,050,000 | | ARG Funding Corp., 4.290% due 4/20/11(c) | | | 944,194 |

| | | | Diversified Financial Services — 0.0% | | | |

| | 2,750,745 | | Airplanes Pass-Through Trust, Subordinated Notes,

10.875% due 3/15/19(a)(b)(f) | | | 0 |

| | | | Home Equity — 0.6% | | | |

| | 177,977 | | ACE Securities Corp., 0.641% due 1/25/36(e) | | | 24,972 |

| | | | Bear Stearns Asset-Backed Securities Trust: | | | |

| | 137,433 | | 0.821% due 9/25/34(e) | | | 129,578 |

| | 398,330 | | 0.751% due 2/25/36(e) | | | 337,582 |

| | 349,152 | | Centex Home Equity Loan Trust, 3.735% due 2/25/32 | | | 291,123 |

| | 106,718 | | Cityscape Home Equity Loan Trust, 3.045% due 7/25/28(e) | | | 55,266 |

| | 135,920 | | Countrywide Asset-Backed Certificates, 1.721% due 6/25/34(e) | | | 56,251 |

| | | | Countrywide Home Equity Loan Trust: | | | |

| | 410,531 | | 1.485% due 12/15/33(e) | | | 270,659 |

| | 576,752 | | 1.515% due 3/15/34(e) | | | 164,074 |

See Notes to Financial Statements.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 15 |

Schedule of investments continued

December 31, 2008

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | Home Equity — 0.6% continued | | | |

| $ | 648,135 | | 1.415% due 11/15/35(a)(e) | | $ | 190,272 |

| | 709,325 | | 1.425% due 2/15/36(e) | | | 376,176 |

| | 2,070,000 | | Credit-Based Asset Servicing & Securitization LLC, 5.704% due 12/25/36 | | | 1,357,762 |

| | 353,840 | | CS First Boston Mortgage Securities Corp.,

2.021% due 2/25/31(e) | | | 156,699 |

| | 73,417 | | Finance America Net Interest Margin Trust,

5.250% due 6/27/34(b)(c)(f) | | | 73 |

| | 179,230 | | First Horizon ABS Trust, 0.631% due 10/25/34(e) | | | 84,662 |

| | 159,058 | | Fremont Home Loan Trust, 2.121% due 2/25/34(e) | | | 51,826 |

| | 2,150,000 | | Green Tree, 8.960% due 4/25/38(c)(e) | | | 1,721,703 |

| | 146,028 | | Green Tree Financial Corp., 7.070% due 1/15/29 | | | 124,249 |

| | | | GSAA Home Equity Trust: | | | |

| | 2,460,000 | | 0.771% due 3/25/37(e) | | | 736,663 |

| | 4,800,000 | | 0.771% due 5/25/47(e) | | | 979,801 |

| | 61,620 | | GSAMP Trust, 0.571% due 1/25/36(e) | | | 10,617 |

| | 120,556 | | Indymac Home Equity Loan Asset-Backed Trust,

0.641% due 4/25/36(e) | | | 26,054 |

| | | | Option One Mortgage Loan Trust: | | | |

| | 126,454 | | 1.311% due 2/25/33(e) | | | 86,441 |

| | 269,549 | | 2.121% due 7/25/33(e) | | | 123,212 |

| | 697,692 | | 1.521% due 5/25/34(e) | | | 529,374 |

| | | | RAAC Series: | | | |

| | 126,956 | | 0.741% due 5/25/36(c)(e) | | | 95,390 |

| | 1,931,411 | | 0.851% due 10/25/46(a)(c)(e) | | | 865,401 |

| | 330,859 | | Renaissance Home Equity Loan Trust, 2.371% due 3/25/34(e) | | | 148,048 |

| | 141,114 | | SACO I Trust, 0.641% due 3/25/36(e) | | | 30,131 |

| | | | Sail Net Interest Margin Notes: | | | |

| | 141,210 | | 7.750% due 4/27/33(b)(c)(f) | | | 16 |

| | 35,690 | | 5.500% due 3/27/34(b)(c)(f) | | | 4 |

| | 218,785 | | Saxon Asset Securities Trust, 8.640% due 12/25/32 | | | 145,449 |

| | 1,342,778 | | Structured Asset Securities Corp., 0.721% due 11/25/37(e) | | | 973,783 |

| | 268,188 | | WMC Mortgage Loan Pass-Through Certificates, 3.445% due 10/15/29(e) | | | 89,403 |

| | | | Total Home Equity | | | 10,232,714 |

| | | | Student Loan — 0.0% | | | |

| | 990,000 | | Nelnet Student Loan Trust, 5.015% due 4/25/24(e) | | | 804,428 |

| | | | TOTAL ASSET-BACKED SECURITIES

(Cost — $22,354,966) | | | 11,981,336 |

See Notes to Financial Statements.

| | |

| 16 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | COLLATERALIZED MORTGAGE OBLIGATIONS — 1.8% | | | |

| $ | 380,000 | | American Home Mortgage Investment Trust,

1.271% due 11/25/45(e) | | $ | 42,210 |

| | 1,800,000 | | Banc of America Commercial Mortgage Inc.,

5.372% due 9/10/45(e) | | | 1,445,890 |

| | 1,483,609 | | Banc of America Funding Corp., 4.123% due 6/20/35(e) | | | 667,245 |

| | 142,628 | | Banc of America Mortgage Securities, 4.802% due 9/25/35(e) | | | 106,397 |

| | 727,548 | | Bayview Commercial Asset Trust, 0.741% due 4/25/36(c)(e) | | | 527,472 |

| | 1,899,032 | | Bear Stearns ARM Trust, 5.786% due 2/25/36(e) | | | 976,221 |

| | 1,555,958 | | Bear Stearns Structured Products Inc.,

2.036% due 9/27/37(a)(c)(e) | | | 1,513,141 |

| | 1,030,575 | | Citigroup Mortgage Loan Trust Inc., 4.900% due 12/25/35(e) | | | 745,690 |

| | | | Countrywide Alternative Loan Trust: | | | |

| | 1,620,599 | | 0.761% due 5/25/34(e) | | | 909,920 |

| | 182,617 | | 1.783% due 11/20/35(e) | | | 91,703 |

| | 1,133,089 | | 0.741% due 1/25/36(e) | | | 534,438 |

| | 150,403 | | 0.671% due 5/25/36(e) | | | 61,034 |

| | 180,043 | | 0.681% due 7/25/46(e) | | | 63,643 |

| | | | Countrywide Home Loan, Mortgage Pass-Through Trust: | | | |

| | 99,359 | | 0.801% due 2/25/35(e) | | | 48,180 |

| | 134,919 | | 0.771% due 5/25/35(e) | | | 63,035 |

| | 1,800,000 | | Credit Suisse Mortgage Capital Certificates,

5.552% due 2/15/39(e) | | | 1,466,937 |

| | 120,476 | | Deutsche ALT-A Securities Inc. Mortgage Loan Trust, 4.938% due 8/25/35(e) | | | 96,682 |

| | | | Downey Savings & Loan Association Mortgage Loan Trust: | | | |

| | 442,923 | | 1.001% due 9/19/44(e) | | | 172,691 |

| | 125,474 | | 0.791% due 3/19/45(e) | | | 60,241 |

| | 147,041 | | 3.176% due 3/19/46(e) | | | 44,112 |

| | 147,041 | | 3.176% due 3/19/47(e) | | | 33,544 |

| | | | Federal Home Loan Mortgage Corp. (FHLMC): | | | |

| | 62,764 | | 6.000% due 3/15/34(d)(e) | | | 57,107 |

| | 516,050 | | PAC, 6.000% due 4/15/34(d)(e) | | | 494,638 |

| | | | GSMPS Mortgage Loan Trust: | | | |

| | 3,573,460 | | 5.911% due 6/25/34(c)(e) | | | 1,977,622 |

| | 2,436,437 | | 0.821% due 3/25/35(c)(e) | | | 1,864,032 |

| | 123,440 | | GSR Mortgage Loan Trust, 5.252% due 10/25/35(e) | | | 72,384 |

| | | | Harborview Mortgage Loan Trust: | | | |

| | 122,582 | | 0.981% due 11/19/34(e) | | | 61,613 |

| | 140,083 | | 0.931% due 1/19/35(e) | | | 70,938 |

| | 73,615 | | Indymac Index Mortgage Loan Trust, 5.777% due 3/25/35(e) | | | 33,127 |

See Notes to Financial Statements.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 17 |

Schedule of investments continued

December 31, 2008

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | COLLATERALIZED MORTGAGE OBLIGATIONS — 1.8% continued | | | |

| $ | 250,000 | | JPMorgan Chase Commercial Mortgage Securities Corp., 5.814% due 6/12/43(e) | | $ | 193,142 |

| | | | JPMorgan Mortgage Trust: | | | |

| | 1,740,401 | | 4.587% due 6/25/34(e) | | | 1,344,356 |

| | 2,120,000 | | 5.889% due 6/25/37(e) | | | 891,990 |

| | 4,807,667 | | Lehman XS Trust, 0.691% due 4/25/46(e) | | | 1,895,968 |

| | 80,620 | | Luminent Mortgage Trust, 0.711% due 4/25/36(e) | | | 32,801 |

| | 630,000 | | Merrill Lynch Mortgage Trust, 5.657% due 5/12/39(e) | | | 515,004 |

| | | | MLCC Mortgage Investors Inc.: | | | |

| | 295,264 | | 1.391% due 4/25/29(e) | | | 116,234 |

| | 351,932 | | 1.351% due 5/25/29(e) | | | 312,662 |

| | | | Structured ARM Loan Trust: | | | |

| | 224,324 | | 4.920% due 3/25/34(e) | | | 139,743 |

| | 54,740 | | 5.041% due 6/25/34(e) | | | 37,387 |

| | 1,316,576 | | 5.370% due 5/25/35(e) | | | 689,957 |

| | 1,853,273 | | 5.891% due 5/25/36(e) | | | 963,058 |

| | 107,875 | | Structured Asset Mortgage Investments Inc.,

0.681% due 5/25/46(e) | | | 46,399 |

| | | | Structured Asset Securities Corp.: | | | |

| | 1,143,643 | | 5.500% due 3/25/19 | | | 1,007,863 |

| | 354,014 | | 1.571% due 2/25/28(e) | | | 336,529 |

| | 211,703 | | 1.471% due 3/25/28(e) | | | 181,076 |

| | | | Thornburg Mortgage Securities Trust: | | | |

| | 2,237,208 | | 6.203% due 9/25/37(e) | | | 1,719,141 |

| | 2,340,913 | | 6.216% due 9/25/37(e) | | | 1,663,636 |

| | | | WaMu Mortgage Pass-Through Certificates: | | | |

| | 627,154 | | 0.791% due 1/25/45(e) | | | 316,934 |

| | 3,864,689 | | 3.006% due 6/25/47(e) | | | 1,545,875 |

| | | | Washington Mutual Inc.: | | | |

| | 96,872 | | 5.930% due 9/25/36(e) | | | 56,141 |

| | 681,373 | | 0.831% due 10/25/45(e) | | | 229,395 |

| | 210,147 | | 0.741% due 12/25/45(e) | | | 99,170 |

| | 115,504 | | 0.761% due 12/25/45(e) | | | 53,465 |

| | 731,680 | | Washington Mutual Mortgage Pass-Through Certificates, 0.811% due 1/25/45(e) | | | 343,338 |

| | 127,811 | | Washington Mutual Pass-Through Certificates,

0.751% due 11/25/45(e) | | | 62,986 |

| | 2,195,826 | | Wells Fargo Alternative Loan Trust, 0.901% due 6/25/37(e) | | | 834,307 |

| | 112,466 | | Wells Fargo Mortgage Backed Securities Trust,

5.240% due 4/25/36(e) | | | 81,701 |

See Notes to Financial Statements.

| | |

| 18 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | | | |

| | COLLATERALIZED MORTGAGE OBLIGATIONS — 1.8% continued | | | |

| $ | 110,616 | | Zuni Mortgage Loan Trust, 0.601% due 8/25/36(e) | | $ | 104,911 |

| | | | TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS

(Cost — $45,583,743) | | | 30,117,056 |

| | COLLATERALIZED SENIOR LOANS — 2.4% | | | |

| | CONSUMER DISCRETIONARY — 0.8% | | | |

| | | | Auto Components — 0.1% | | | |

| | 1,947,742 | | Allison Transmission Inc., Term Loan B,

4.913% due 8/7/14(e) | | | 1,097,691 |

| | 1,000,000 | | Visteon Corp., Term Loan, Tranch B, 7.750% due 6/20/13(e) | | | 255,833 |

| | | | Total Auto Components | | | 1,353,524 |

| | | | Diversified Consumer Services — 0.0% | | | |

| | 990,000 | | Thomson Learning Hold, Term Loan B,

3.940% due 7/5/14(e) | | | 650,650 |

| | | | Hotels, Restaurants & Leisure — 0.2% | | | |

| | | | Aramark Corp.: | | | |

| | 58,426 | | Letter of Credit Facility Deposits, 1.875% due 1/31/14(e) | | | 48,402 |

| | 919,664 | | Term Loan, 4.676% due 1/31/14(e) | | | 761,885 |

| | | | Golden Nugget Inc.: | | | |

| | 363,636 | | Delayed Draw Term Loan, 5.457% due 6/8/14(e) | | | 105,455 |

| | 636,364 | | First Lien Term Loan, 4.470% due 6/14/14(e) | | | 184,546 |

| | 997,494 | | Harrahs Operating Co. Inc., Term Loan,

6.536% due 12/28/15(e) | | | 584,088 |

| | 1,033,131 | | Las Vegas Sands LLC, Term Loan, 5.520% due 5/8/14(e) | | | 477,535 |

| | 987,342 | | MGM MIRAGE Inc., Term Loan B, 7.012% due 4/8/11(e) | | | 422,089 |

| | 500,000 | | Six Flags, Term Loan B, 4.150% due 5/31/13(e) | | | 297,500 |

| | | | Total Hotels, Restaurants & Leisure | | | 2,881,500 |

| | | | Media — 0.3% | | | |

| | 1,985,000 | | Charter Communications, Term Loan B,

5.470% due 3/15/14(e) | | | 1,468,900 |

| | 1,000,000 | | Citadel Broadcasting Corp., Term Loan A,

5.241% due 6/12/13(e) | | | 430,000 |

| | 989,493 | | CMP Susquehanna Corp., Term Loan, 4.997% due 6/7/13(e) | | | 232,531 |

| | 1,000,000 | | Dex Media West LLC, Term Loan, 7.133% due 10/13/14(e) | | | 425,000 |

| | 1,485,505 | | Idearc Inc., Term Loan B, Senior Notes,

5.670% due 11/1/14(e) | | | 468,995 |

| | 1,214,375 | | LodgeNet Entertainment Corp., Term Loan B,

4.810% due 4/4/14(e) | | | 479,678 |

| | 989,899 | | Regal Cinemas Corp., Term Loan B,

5.262% due 10/19/10(e) | | | 728,126 |

| | 1,000,000 | | Univision Communications Inc., Term Loan B,

3.686% due 9/15/14(e) | | | 411,111 |

See Notes to Financial Statements.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 19 |

Schedule of investments continued

December 31, 2008

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | Media — 0.3% continued | | | |

| $ | 1,000,000 | | UPC Broadband Holding BV, Term Loan N,

5.470% due 3/30/14(e) | | $ | 675,000 |

| | | | Total Media | | | 5,319,341 |

| | | | Multiline Retail — 0.1% | | | |

| | 1,000,000 | | Dollar General Corp., Term Loan B,

5.649% due 7/15/14(e) | | | 777,500 |

| | 1,500,000 | | Neiman Marcus Group Inc., Term Loan B,

4.422% due 3/13/13(e) | | | 962,727 |

| | | | Total Multiline Retail | | | 1,740,227 |

| | | | Specialty Retail — 0.1% | | | |

| | 989,950 | | Amscan Holdings Inc., Term Loan B,

4.557% due 5/1/13(e) | | | 655,842 |

| | 987,406 | | Michaels Stores Inc., Term Loan B,

4.140% due 10/31/13(e) | | | 518,635 |

| | 989,924 | | PETCO Animal Supplies Inc., Term Loan B,

5.943% due 11/15/13(e) | | | 623,652 |

| | | | Total Specialty Retail | | | 1,798,129 |

| | | | TOTAL CONSUMER DISCRETIONARY | | | 13,743,371 |

| | CONSUMER STAPLES — 0.2% | | | |

| | | | Beverages — 0.1% | | | |

| | 999,316 | | Constellation Brands Inc., Term Loan, 4.056% due 6/5/13(e) | | | 887,517 |

| | | | Food Products — 0.1% | | | |

| | | | Dole Food Co.: | | | |

| | 98,447 | | Credit-Linked Deposit, 2.658% due 4/12/13(e) | | | 69,200 |

| | | | Term Loan: | | | |

| | 174,488 | | 5.396% due 4/12/13(e) | | | 122,651 |

| | 650,093 | | 6.239% due 4/12/13(e) | | | 456,961 |

| | 1,000,000 | | Wm. Wrigley Jr. Co., Term Loan, 7.750% due 9/30/14(e) | | | 959,167 |

| | | | Total Food Products | | | 1,607,979 |

| | | | Household Products — 0.0% | | | |

| | 927,909 | | Yankee Candle, Term Loan B, 5.731% due 1/15/14(e) | | | 476,945 |

| | | | TOTAL CONSUMER STAPLES | | | 2,972,441 |

| | ENERGY — 0.1% | | | |

| | | | Energy Equipment & Services — 0.0% | | | |

| | 997,475 | | Hercules Offshore LLC, Term Loan, 5.640% due 7/11/13(e) | | | 658,333 |

| | | | Oil, Gas & Consumable Fuels — 0.1% | | | |

| | | | Ashmore Energy International: | | | |

| | 95,952 | | Synthetic Revolving Credit Facility, 4.730% due 3/30/14(e) | | | 58,531 |

| | 864,936 | | Term Loan, 6.762% due 3/30/14(e) | | | 493,014 |

See Notes to Financial Statements.

| | |

| 20 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | Oil, Gas & Consumable Fuels — 0.1% continued | | | |

| $ | 1,981,200 | | Brand Energy and Infrastructure Services Inc., Term Loan B,

5.949% due 2/7/14(e) | | $ | 1,040,130 |

| | | | Total Oil, Gas & Consumable Fuels | | | 1,591,675 |

| | | | TOTAL ENERGY | | | 2,250,008 |

| | FINANCIALS — 0.1% |

| | | | Diversified Financial Services — 0.1% | | | |

| | 987,500 | | Chrysler Financial, Term Loan B, 6.820% due 8/3/12(e) | | | 519,142 |

| | 940,664 | | Iconix, Term Loan B, 6.020% due 5/1/14(e) | | | 681,981 |

| | 987,425 | | Sally Holdings LLC, Term Loan B, 4.605% due 11/15/13(e) | | | 707,655 |

| | | | Total Diversified Financial Services | | | 1,908,778 |

| | | | Thrifts & Mortgage Finance — 0.0% | | | |

| | 989,924 | | GM, Term Loan B, 5.795% due 12/15/13(e) | | | 455,012 |

| | | | TOTAL FINANCIALS | | | 2,363,790 |

| | HEALTH CARE — 0.3% |

| | | | Health Care Equipment & Supplies — 0.0% | | | |

| | | | Bausch & Lomb Inc.: | | | |

| | 797,189 | | Term Loan, 7.012% due 4/11/15(e) | | | 546,643 |

| | 200,803 | | Term Loan B, 4.709% due 4/11/15(e) | | | 137,694 |

| | | | Total Health Care Equipment & Supplies | | | 684,337 |

| | | | Health Care Providers & Services — 0.2% | | | |

| | | | Community Health Systems Inc.: | | | |

| | 59,526 | | Delayed Draw Term Loan, 4.631% due 7/2/14(e) | | | 46,639 |

| | 893,901 | | Term Loan B, 4.854% due 7/2/14(e) | | | 700,372 |

| | 987,437 | | HCA Inc., Term Loan B, 6.012% due 11/1/13(e) | | | 780,693 |

| | 942,994 | | Health Management Association, Term Loan B,

5.512% due 1/16/14 (e) | | | 585,329 |

| | | | IASIS Healthcare LLC, Term Loan: | | | |

| | 239,971 | | 3.431% due 6/15/14(e) | | | 172,629 |

| | 693,515 | | 5.118% due 6/15/14(e) | | | 398,771 |

| | 64,153 | | 5.704% due 6/15/14(e) | | | 36,888 |

| | 985,358 | | Manor Care Inc., Term Loan B, 5.719% due 11/15/14(e) | | | 683,181 |

| | | | Total Health Care Providers & Services | | | 3,404,502 |

| | | | Pharmaceuticals — 0.1% | | | |

| | 26,742 | | Leiner Health Products Group, Term Loan B,

8.750% due 5/26/11(e) | | | 26,073 |

| | 989,950 | | Royalty Pharma, Term Loan B, 6.012% due 5/15/14(e) | | | 881,055 |

| | | | Total Pharmaceuticals | | | 907,128 |

| | | | TOTAL HEALTH CARE | | | 4,995,967 |

| | INDUSTRIALS — 0.2% | | | |

| | | | Aerospace & Defense — 0.1% | | | |

| | 713,882 | | Dubai Aerospace Enterprise, Term Loan, 6.550% due 7/31/14(e) | | | 374,788 |

See Notes to Financial Statements.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 21 |

Schedule of investments continued

December 31, 2008

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | Aerospace & Defense — 0.1% continued | | | |

| $ | 1,000,000 | | Transdigm Inc., Term Loan, 5.210% due 7/1/12(e) | | $ | 806,500 |

| | | | Total Aerospace & Defense | | | 1,181,288 |

| | | | Airlines — 0.0% | | | |

| | 1,421,552 | | United Airlines Inc., Term Loan B, 3.309% due 1/12/14(e) | | | 692,296 |

| | | | Commercial Services & Supplies — 0.1% | | | |

| | 989,905 | | Nielson Finance, Term Loan B, 4.388% due 8/15/13(e) | | | 673,754 |

| | 987,469 | | US Investigations Services Inc., Term Loan B,

4.275% due 2/21/15(e) | | | 718,383 |

| | | | Total Commercial Services & Supplies | | | 1,392,137 |

| | | | Electrical Equipment — 0.0% | | | |

| | 989,873 | | Sensata Technologies, Term Loan, 5.115% due 4/27/13(e) | | | 509,785 |

| | | | TOTAL INDUSTRIALS | | | 3,775,506 |

| | INFORMATION TECHNOLOGY — 0.1% |

| | | | IT Services — 0.1% | | | |

| | 1,940,400 | | First Data Corp., Term Loan, 4.338% due 10/15/14(e) | | | 1,257,795 |

| | | | Semiconductors & Semiconductor Equipment — 0.0% | | | |

| | 992,443 | | Freescale Semiconductor Inc., Term Loan, Tranch B,

4.221% due 12/1/13(e) | | | 581,131 |

| | | | TOTAL INFORMATION TECHNOLOGY | | | 1,838,926 |

| | MATERIALS — 0.2% |

| | | | Chemicals — 0.0% | | | |

| | 997,494 | | Lyondell Chemical Co., Term Loan, 7.000% due 12/20/14(e)† | | | 382,372 |

| | | | Containers & Packaging — 0.1% | | | |

| | 985,453 | | Graphic Packaging International, Term Loan C,

5.977% due 5/16/14(e) | | | 736,626 |

| | | | Paper & Forest Products — 0.1% | | | |

| | 1,329,502 | | Georgia-Pacific Corp., Term Loan, 4.441% due 12/23/13(e) | | | 1,092,408 |

| | 992,500 | | NewPage Corp., Term Loan, Tranche B, 7.156% due 11/5/14(e) | | | 636,441 |

| | | | Total Paper & Forest Products | | | 1,728,849 |

| | | | TOTAL MATERIALS | | | 2,847,847 |

| | TELECOMMUNICATION SERVICES — 0.3% |

| | | | Diversified Telecommunication Services — 0.2% | | | |

| | 1,974,619 | | Cablevision Systems Corp., Term Loan B,

4.214% due 3/30/13(e) | | | 1,694,060 |

| | 675,000 | | Insight Midwest, Term Loan B, 4.470% due 4/10/14(e) | | | 508,500 |

| | 500,000 | | Intelsat Corp., Term Loan, 5.288% due 6/30/13(e) | | | 381,785 |

| | 1,000,000 | | Level 3 Communications Inc., Term Loan, 7.000% due 3/1/14(e) | | | 612,500 |

| | | | Total Diversified Telecommunication Services | | | 3,196,845 |

See Notes to Financial Statements.

| | |

| 22 | | Legg Mason Partners Capital and Income Fund 2008 Annual Report |

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | Wireless Telecommunication Services — 0.1% | | | |

| $ | 496,250 | | ALLTEL Communications Inc., Term Loan,

5.550% due 5/15/15(e) | | $ | 488,682 |

| | 997,455 | | MetroPCS Wireless Inc., Term Loan, 4.843% due 2/20/14(e) | | | 805,445 |

| | 66,778 | | Telesat Canada, Delayed Draw Term Loan, Tranch B,

5.670% due 10/15/14(e) | | | 46,149 |

| | 926,102 | | Telesat Ganada, Term Loan B, 5.800% due 10/15/14(e) | | | 640,002 |

| | | | Total Wireless Telecommunication Services | | | 1,980,278 |

| | | | TOTAL TELECOMMUNICATION SERVICES | | | 5,177,123 |

| | UTILITIES — 0.1% |

| | | | Electric Utilities — 0.1% | | | |

| | 1,237,519 | | TXU Corp., Term Loan B, 6.303% due 10/10/14(e) | | | 863,686 |

| | | | Independent Power Producers & Energy Traders — 0.0% | | | |

| | 997,487 | | Calpine Corp., Term Loan, Senior Notes, 6.645% due 3/29/09(e) | | | 739,922 |

| | | | TOTAL UTILITIES | | | 1,603,608 |

| | | | TOTAL COLLATERALIZED SENIOR LOANS

(Cost — $63,656,041) | | | 41,568,587 |

| | CORPORATE BONDS & NOTES — 17.5% | | | |

| | CONSUMER DISCRETIONARY — 2.0% | | | |

| | | | Auto Components — 0.1% | | | |

| | 730,000 | | Allison Transmission Inc., Senior Notes,

11.250% due 11/1/15(c)(g) | | | 292,000 |

| | 865,000 | | Keystone Automotive Operations Inc., Senior Subordinated Notes, 9.750% due 11/1/13 | | | 333,025 |

| | | | Visteon Corp., Senior Notes: | | | |

| | 2,584,000 | | 8.250% due 8/1/10 | | | 813,960 |

| | 3,210,000 | | 12.250% due 12/31/16(c) | | | 786,450 |

| | | | Total Auto Components | | | 2,225,435 |

| | | | Automobiles — 0.1% | | | |

| | | | Ford Motor Co.: | | | |

| | 95,000 | | Debentures, 8.875% due 1/15/22 | | | 23,275 |

| | 2,645,000 | | Notes, 7.450% due 7/16/31 | | | 753,825 |

| | 6,725,000 | | General Motors Corp., Senior Debentures, 8.250% due 7/15/23 | | | 1,143,250 |

| | | | Total Automobiles | | | 1,920,350 |

| | | | Diversified Consumer Services — 0.0% | | | |

| | | | Education Management LLC/Education Management

Finance Corp.: | | | |

| | 195,000 | | Senior Notes, 8.750% due 6/1/14 | | | 149,175 |

| | 785,000 | | Senior Subordinated Notes, 10.250% due 6/1/16 | | | 573,050 |

| | | | Total Diversified Consumer Services | | | 722,225 |

See Notes to Financial Statements.

| | |

| Legg Mason Partners Capital and Income Fund 2008 Annual Report | | 23 |

Schedule of investments continued

December 31, 2008

| | | | | | |

| LEGG MASON PARTNERS CAPITAL AND INCOME FUND |

FACE

AMOUNT | | SECURITY | | VALUE |

| | | | | | |

| | | | Hotels, Restaurants & Leisure — 0.5% | | | |

| $ | 640,000 | | Buffets Inc., Senior Notes, 12.500% due 11/1/14(b)(f) | | $ | 4,400 |

| | 1,680,000 | | Caesars Entertainment Inc., Senior Subordinated Notes,

8.125% due 5/15/11 | | | 831,600 |

| | 620,000 | | Denny’s Holdings Inc., Senior Notes, 10.000% due 10/1/12 | | | 432,450 |

| | 520,000 | | El Pollo Loco Inc., Senior Notes, 11.750% due 11/15/13 | | | 387,400 |

| | 140,000 | | Mandalay Resort Group, Senior Subordinated Debentures,

7.625% due 7/15/13 | | | 44,100 |

| | 1,700,000 | | McDonald’s Corp., Medium Term Notes, 5.350% due 3/1/18 | | | 1,769,127 |

| | | | MGM MIRAGE Inc.: | | | |

| | 1,500,000 | | Senior Notes, 7.625% due 1/15/17 | | | 975,000 |

| | 1,670,000 | | Senior Subordinated Notes, 8.375% due 2/1/11 | | | 1,002,000 |

| | 300,000 | | Mohegan Tribal Gaming Authority, Senior Subordinated Notes, 6.875% due 2/15/15 | | | 153,000 |

| | 1,620,000 | | River Rock Entertainment Authority, Senior Secured Notes, 9.750% due 11/1/11 | | | 1,352,700 |

| | 590,000 | | Sbarro Inc., Senior Notes, 10.375% due 2/1/15 | | | 312,700 |

| | | | Station Casinos Inc., Senior Notes: | | | |

| | 300,000 | | 6.000% due 4/1/12† | | | 61,500 |

| | 1,205,000 | | 7.750% due 8/15/16† | | | 234,975 |

| | 250,000 | | Turning Stone Casino Resort Enterprise, Senior Notes, 9.125% due 12/15/10(c) | | | 211,250 |

| | | | Total Hotels, Restaurants & Leisure | | | 7,772,202 |

| | | | Household Durables — 0.2% | | | |

| | 200,000 | | Holt Group Inc., Senior Notes, 9.750% due 1/15/06(a)(b)(f) | | | 0 |

| | 600,000 | | K Hovnanian Enterprises Inc., Senior Notes,

8.625% due 1/15/17 | | | 153,000 |

| | 1,495,000 | | Norcraft Cos. LP/Norcraft Finance Corp., Senior Subordinated Notes, 9.000% due 11/1/11 | | | 1,278,225 |

| | 3,000,000 | | Norcraft Holdings LP/Norcraft Capital Corp., Senior Discount Notes, 9.750% due 9/1/12 | | | 2,250,000 |

| | | | Total Household Durables | | | 3,681,225 |

| | | | Internet & Catalog Retail — 0.0% | | | |

| | 105,000 | | Expedia Inc., Senior Notes, 8.500% due 7/1/16(c) | | | 78,750 |

| | | | Media — 0.9% | | | |

| | | | Affinion Group Inc.: | | | |

| | 1,030,000 | | Senior Notes, 10.125% due 10/15/13 | | | 757,050 |

| | 250,000 | | Senior Subordinated Notes, 11.500% due 10/15/15 | | | 151,563 |

| | 5,754,000 | | CCH I LLC/CCH I Capital Corp., Senior Secured Notes, 11.000% due 10/1/15 | | | 1,035,720 |

| | 2,249,000 | | CCH II LLC/CCH II Capital Corp., Senior Notes,

10.250% due 10/1/13 | | | 820,885 |

See Notes to Financial Statements.

| | |