UNITEDSTATES

SECURITIESANDEXCHANGECOMMISSION

Washington,D.C.20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-06499

Name of Fund: BlackRock MuniYield California Fund, Inc. (MYC)

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock

MuniYield California Fund, Inc., 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 07/31/2011

Date of reporting period: 07/31/2011

Item 1 – Report to Stockholders

Annual Report

BlackRock Muni New York Intermediate Duration Fund, Inc. (MNE)

BlackRock MuniYield Arizona Fund, Inc. (MZA)

BlackRock MuniYield California Fund, Inc. (MYC)

BlackRock MuniYield Investment Fund (MYF)

BlackRock MuniYield New Jersey Fund, Inc. (MYJ)

Not FDIC Insured • No Bank Guarantee • May Lose Value

| |

| Table of Contents | |

| | Page |

| Dear Shareholder | 3 |

| Annual Report: | |

| Municipal Market Overview | 4 |

| Fund Summaries | 5 |

| The Benefits and Risks of Leveraging | 10 |

| Derivative Financial Instruments | 11 |

| Financial Statements: | |

| Schedules of Investments | 12 |

| Statements of Assets and Liabilities | 28 |

| Statements of Operations | 29 |

| Statements of Changes in Net Assets | 30 |

| Statements of Cash Flows | 33 |

| Financial Highlights | 34 |

| Notes to Financial Statements | 39 |

| Report of Independent Registered Public Accounting Firm | 46 |

| Important Tax Information | 47 |

| Disclosure of Investment Advisory Agreements and Sub-Advisory Agreements | 48 |

| Automatic Dividend Reinvestment Plan | 52 |

| Officers and Directors | 53 |

| Additional Information | 56 |

| | |

| 2 | ANNUAL REPORT | JULY 31, 2011 |

Dear Shareholder

Financial markets have been extremely volatile in the wake of the Standard & Poor’s downgrade of

US Treasury debt. While the August 5 announcement was the catalyst for the market turmoil, weaker-

than-expected economic data and Europe’s deepening financial crisis further compounded investor

uncertainty as the future direction of the global economy became increasingly questionable. Although

markets remain highly volatile and conditions are highly uncertain, BlackRock remains focused on

finding opportunities in this environment.

The pages that follow reflect your mutual fund’s reporting period ended July 31, 2011. Accordingly,

the below discussion is intended to provide you with additional perspective on the performance of

your investments during that period.

During the summer of 2010, investors were in “risk-off” mode as the global economy was sputtering

and the sovereign debt crisis was spreading across Europe. But markets were revived toward the end

of the summer on positive economic news and robust corporate earnings. The global economy had

finally gained traction and fear turned to optimism with the anticipation of a second round of quan-

titative easing (“QE2”) from the US Federal Reserve (the “Fed”). Stock markets rallied even though

the European debt crisis continued and inflationary pressures loomed over emerging markets. Fixed

income markets, however, saw yields move sharply upward (pushing prices down) especially on the

long end of the historically steep yield curve. While high yield bonds benefited from the risk rally, most

fixed income sectors declined in the fourth quarter. The tax-exempt municipal market faced additional

headwinds as it became evident that the Build America Bond program would not be extended and

municipal finance troubles abounded.

The new year brought spikes of volatility as political turmoil swept across the Middle East/North Africa

region and as prices of oil and other commodities soared. Natural disasters in Japan disrupted indus-

trial supply chains and concerns mounted over US debt and deficit issues. Equities quickly rebounded

as investors chose to focus on the continuing stream of strong corporate earnings and positive eco-

nomic data. Credit markets were surprisingly resilient in this environment and yields regained relative

stability in 2011. The tax-exempt market saw relief from its headwinds and steadily recovered from its

fourth-quarter lows. Equities, commodities and high yield bonds outpaced higher-quality assets as

investors increased their risk tolerance.

However, longer-term headwinds had been brewing. Inflationary pressures intensified in emerging

economies, many of which were overheating, and the European debt crisis continued to escalate.

Markets were met with a sharp reversal in May when political unrest in Greece pushed the nation closer

to defaulting on its debt.This development rekindled fears about the broader debt crisis and its further

contagion among peripheral European countries. Concurrently, it became evident that the pace of global

economic growth had slowed. Higher oil prices and supply chain disruptions finally showed up in eco-

nomic data. In the final month of the reporting period, the prolonged debt ceiling debate in Washington,

DC led to a loss of confidence in policymakers. Stocks generally declined from May through the end of

the period, but 6- and 12-month returns through the end of July remained in positive territory. In bond

markets, yields were volatile but generally moved lower for the period as a whole (pushing prices up).

Continued low short-term interest rates kept yields on money market securities near their all-time lows.

“Although markets remain highly

volatile and conditions are highly

uncertain, BlackRock remains

focused on finding opportunities in

this environment.”

Rob Kapito

President, BlackRock Advisors, LLC

| | |

| Total Returns as of July 31, 2011 | |

| | 6-month | 12-month |

| US large cap equities | 1.46% | 19.65% |

| (S&P 500® Index) | | |

| US small cap equities | 2.63 | 23.92 |

| (Russell 2000® Index) | | |

| International equities | 0.93 | 17.17 |

| (MSCI Europe, Australasia, | | |

| Far East Index) | | |

| Emerging market | 3.23 | 17.45 |

| equities (MSCI Emerging | | |

| Markets Index) | | |

| 3-month Treasury | 0.07 | 0.14 |

| bill (BofA Merrill Lynch | | |

| 3-Month Treasury | | |

| Bill Index) | | |

| US Treasury securities | 6.93 | 4.53 |

| (BofA Merrill Lynch 10- | | |

| Year US Treasury Index) | | |

| US investment grade | 4.23 | 4.44 |

| bonds (Barclays | | |

| Capital US Aggregate | | |

| Bond Index) | | |

| Tax-exempt municipal | 6.27 | 3.24 |

| bonds (Barclays Capital | | |

| Municipal Bond Index) | | |

| US high yield bonds | 3.90 | 12.89 |

| (Barclays Capital US | | |

| Corporate High Yield 2% | | |

| Issuer Capped Index) | | |

Past performance is no guarantee of future results. Index performance is

shown for illustrative purposes only. You cannot invest directly in an index.

| |

| THIS PAGE NOT PART OF YOUR FUND REPORT | 3 |

Municipal Market Overview

For the 12-Month Period Ended July 31, 2011

At the outset of the 12-month period, investor concerns were focused on the possibility of deflation and a double-dip in the US economy thus leading to a

flatter municipal yield curve at that time as compared to July 31, 2011. From July through September 2010, rates moved lower (and prices higher) across

the curve, reaching historic lows in August when the yield on 5-year issues touched 1.06%, the 10-year reached 2.18%, and the 30-year closed at 3.67%.

However, the market took a turn in October amid a “perfect storm” of events that ultimately resulted in the worst quarterly performance for municipals since

the Fed tightening cycle of 1994. Treasury yields lost support due to concerns over the US deficit and municipal valuations suffered a quick and severe

setback as it became evident that the Build America Bond (“BAB”) program would expire at the end of 2010. The BAB program opened the taxable market

to municipal issuers, which had successfully alleviated supply pressure in the traditional tax-exempt marketplace, bringing down yields in that space.

Towards the end of the fourth quarter 2010, news about municipal finance troubles mounted and damaged confidence among retail investors. From

mid-November through year end, weekly outflows from municipal mutual funds averaged over $2.5 billion. Political uncertainty surrounding the midterm

elections and tax policies along with the expiration of the BAB program exacerbated the situation. These conditions combined with seasonal illiquidity

sapped willful market participation from the trading community. December brought declining demand with no comparable reduction in supply as issuers

rushed their deals to market before the BAB program was retired. This supply-demand imbalance led to wider quality spreads and higher yields.

Demand is usually strong at the beginning of a new year, but retail investors continued to move away from municipal mutual funds in 2011. From

mid-November, outflows persisted for 29 consecutive weeks, totaling $35.1 billion before the trend finally broke in June. Weak demand has been counter-

balanced by lower supply in 2011. According to Thomson Reuters, year-to-date through July, new issuance was down 40% compared to the same period

last year. Issuers have been reluctant to bring new deals to the market due to higher interest rates, fiscal policy changes and a reduced need for municipal

borrowing. In this positive technical environment, the S&P/Investortools Main Municipal Bond Index gained 4.22% for the second quarter of 2011, its

best second-quarter performance since 1992, and municipals outperformed most other fixed income asset classes for the quarter.

Municipals displayed an impressive degree of resiliency throughout the month of July as Moody’s Investors Service signaled that its potential downgrade of

US government debt could also result in downgrades of a number of triple A-rated states and nearly 200 local general obligation issues. July also brought

weaker US economic data. The housing market remained sluggish, fewer jobs were created and consumer confidence declined. US Treasury yields moved

lower, dragging municipal yields down, which pushed bond prices up.

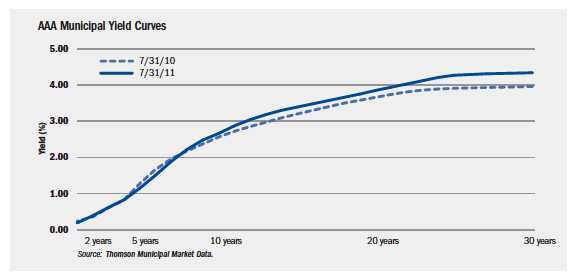

Overall, the municipal yield curve steepened during the period from July 31, 2010 to July 31, 2011. As measured by Thomson Municipal Market Data, yields

on AAA quality-rated 30-year municipals rose 38 basis points (“bps”) to 4.35%, while yields for 5-year maturities rallied by 13 bps to 1.16%, and 10-year

maturities increased by 10 bps to 2.67%. With the exception of the 2- to 5-year range, the yield spread between maturities increased over the

past year, with the greatest increase seen in the 5- to 30-year range, where the spread widened by 51 bps, while overall the slope between 2- and

30-year maturities increased by 35 bps to 3.95%.

The fundamental picture for municipalities is improving as most states began their new fiscal year with a balanced budget. Austerity is the general theme

across the country, while a small number of states continue to rely on the “kick the can” approach, using aggressive revenue projections and accounting

gimmicks to close their shortfalls. As long as economic growth stays positive, tax receipts for states should continue to rise and lead to better credit

fundamentals. BlackRock maintains a constructive view of the municipal market, recognizing that careful credit research and security selection remain

imperative amid uncertainty in the economic environment.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

| | |

| 4 | ANNUAL REPORT | JULY 31, 2011 |

Fund Summary as of July 31, 2011 BlackRock Muni New York Intermediate Duration Fund, Inc.

Fund Overview

BlackRock Muni New York Intermediate Duration Fund, Inc.’s (MNE) (the “Fund”) investment objective is to provide shareholders with high current income

exempt from federal income tax and New York State and New York City personal income taxes. The Fund seeks to achieve its investment objective by

investing at least 80% of its assets in municipal obligations exempt from federal income tax (except that the interest may be subject to the federal

alternative minimum tax) and New York State and New York City personal income taxes. Under normal market conditions, the Fund invests at least 75%

of its assets in municipal obligations that are investment grade quality at the time of investment. Under normal market conditions, the Fund invests at least

80% of its assets in municipal obligations with a duration of three to ten years. The Fund may invest directly in such securities or synthetically through the

use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Performance

For the 12 months ended July 31, 2011, the Fund returned 1.26% based on market price and 5.71% based on net asset value (“NAV”). For the same

period, the closed-end Lipper Intermediate Municipal Debt Funds category posted an average return of 0.75% based on market price and 4.58% based on

NAV. All returns reflect reinvestment of dividends. The Fund's discount to NAV, which widened during the period, accounts for the difference between perform-

ance based on price and performance based on NAV. The following discussion relates to performance based on NAV. Although tax-free yields on the long end

of the municipal yield curve were higher at the close of the period than where they started, performance was strong in the intermediate range of the curve as

investors preferred the slightly lower volatility associated with shorter maturities while capturing most of the yield on the long end. From a sector perspective,

the Fund’s positive performance came mostly from its exposure to higher-yielding sectors including housing, health care and corporate/industrial develop-

ment bonds. The Fund also benefited from its exposure to lower-quality bonds, which, in addition to offering higher embedded yields, experienced some price

appreciation due to spread compression during the period. The Fund was most heavily invested in tax-backed credits, where performance was moderately

positive during the period. Low exposure to the short end of the yield curve and high-quality pre-refunded bonds proved beneficial as performance was weak

in those issues. Detracting from performance was the Fund’s allocation to Puerto Rico credits, which underperformed New York issues during the period. Low

exposure to tobacco, the strongest performing sector, was a disadvantage. The Fund’s holdings of higher education bonds hindered returns; however, we

increased exposure to the sector despite its recent underperformance as these holdings help diversify the portfolio and we believe they will benefit the Fund

during periods of scarce new-issue supply. For most of the period, the Fund maintained a slightly long duration bias, which also detracted from performance.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These

views are not intended to be a forecast of future events and are no guarantee of future results.

Fund Information

| |

| Symbol on New York Stock Exchange (“NYSE”) | MNE |

| Initial Offering Date | August 1, 2003 |

| Yield on Closing Market Price as of July 31, 2011 ($12.98)1 | 5.64% |

| Tax Equivalent Yield2 | 8.68% |

| Current Monthly Distribution per Common Share3 | $0.061 |

| Current Annualized Distribution per Common Share3 | $0.732 |

| Leverage as of July 31, 20114 | 34% |

1 Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results.

2 Tax equivalent yield assumes the maximum federal tax rate of 35%.

3 The distribution rate is not constant and is subject to change.

4 Represents Auction Market Preferred Shares (“AMPS”) and tender option bond trusts (“TOBs”) as a percentage of total managed assets, which is the total assets of the Fund,

including any assets attributable to AMPS and TOBs, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and

Risks of Leveraging on page 10.

The table below summarizes the changes in the Fund’s market price and NAV per share:

| | | | | |

| | 7/31/11 | 7/31/10 | Change | High | Low |

| Market Price | $12.98 | $13.54 | (4.14)% | $14.26 | $12.05 |

| Net Asset Value | $14.51 | $14.50 | 0.07% | $15.03 | $13.35 |

The following charts show the sector and credit quality allocations of the Fund’s long-term investments:

| | |

| Sector Allocations | | |

| | 7/31/11 | 7/31/10 |

| Transportation | 16% | 14% |

| County/City/Special District/School District | 15 | 16 |

| Health | 14 | 14 |

| Housing | 11 | 13 |

| State | 11 | 13 |

| Corporate | 11 | 9 |

| Education | 11 | 10 |

| Utilities | 10 | 10 |

| Tobacco | 1 | 1 |

| | |

| Credit Quality Allocations5 | | |

| | 7/31/11 | 7/31/10 |

| AAA/Aaa | 5% | 13% |

| AA/Aa | 41 | 29 |

| A | 25 | 31 |

| BBB/Baa | 18 | 13 |

| BB/Ba | 6 | 5 |

| CCC/Caa | 2 | 3 |

| Not Rated6 | 3 | 6 |

5 Using the higher of Standard & Poor’s (“S&P’s”) or Moody’s Investors Service

(“Moody’s”) ratings.

6 The investment advisor has deemed certain of these non-rated securities to be of

investment grade quality. As of July 31, 2011 and July 31, 2010, the market value of

these securities was $2,875,100, representing 3%, and $1,690,946, representing

2%, respectively, of the Fund’s long-term investments.

| | |

| ANNUAL REPORT | JULY 31, 2011 | 5 |

Fund Summary as of July 31, 2011 BlackRock MuniYield Arizona Fund, Inc.

Fund Overview

BlackRock MuniYield Arizona Fund, Inc.’s (MZA) (the “Fund”) investment objective is to provide shareholders with as high a level of current income exempt

from federal and Arizona income taxes as is consistent with its investment policies and prudent investment management. The Fund seeks to achieve its invest-

ment objective by investing at least 80% of its assets in municipal obligations exempt from federal income taxes (except that the interest may be subject to

the federal alternative minimum tax) and Arizona income taxes. Under normal market conditions, the Fund expects to invest at least 75% of its assets in

municipal obligations that are investment grade quality at the time of investment. The Fund may invest directly in such securities or synthetically through the

use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Performance

For the 12 months ended July 31, 2011, the Fund returned 0.09% based on market price and 3.92% based on NAV. For the same period, the closed-end

Lipper Other States Municipal Debt Funds category posted an average return of (3.65)% based on market price and 3.25% based on NAV. All returns reflect

reinvestment of dividends. The Fund's discount to NAV, which widened during the period, accounts for the difference between performance based on price

and performance based on NAV. The following discussion relates to performance based on NAV. The Fund’s exposure to bonds with shorter maturities and

shorter durations (lower sensitivity to interest rate movements) contributed positively to performance as yields on the short and intermediate parts of the

municipal curve increased to a smaller degree than on the long end. Holdings of premium coupon bonds, which tend to be less sensitive to changes in

interest rates, also had a positive impact. Conversely, the Fund’s overall long duration stance detracted from performance as interest rates increased for the

period as a whole. Further, the Fund’s exposure to longer maturity bonds had a negative impact as the long end of the yield curve steepened during the

period (i.e., long-term interest rates increased more than short and intermediate rates). Additionally, the Fund’s exposure to various Puerto Rico-domiciled

issuers hurt returns as these securities generally underperformed other states and territories.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These

views are not intended to be a forecast of future events and are no guarantee of future results.

| |

| Fund Information | |

| Symbol on NYSE Amex | MZA |

| Initial Offering Date | October 29, 1993 |

| Yield on Closing Market Price as of July 31, 2011 ($12.83)1 | 6.50% |

| Tax Equivalent Yield2 | 10.00% |

| Current Monthly Distribution per Common Share3 | $0.0695 |

| Current Annualized Distribution per Common Share3 | $0.8340 |

| Leverage as of July 31, 20114 | 40% |

1 Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results.

2 Tax equivalent yield assumes the maximum federal tax rate of 35%.

3 The distribution rate is not constant and is subject to change.

4 Represents Variable Rate Demand Preferred Shares (“VRDP Shares”) and TOBs as a percentage of total managed assets, which is the total assets of the Fund, including any assets

attributable to VRDP Shares and TOBs, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and Risks of

Leveraging on page 10.

The table below summarizes the changes in the Fund’s market price and NAV per share:

| | | | | |

| | 7/31/11 | 7/31/10 | Change | High | Low |

| Market Price | $12.83 | $13.67 | (6.14)% | $14.25 | $11.50 |

| Net Asset Value | $13.38 | $13.73 | (2.55)% | $14.26 | $12.05 |

The following charts show the sector and credit quality allocations of the Fund’s long-term investments:

| | |

| Sector Allocations | | |

| | 7/31/11 | 7/31/10 |

| County/City/Special District/School District | 34% | 37% |

| State | 19 | 14 |

| Utilities | 15 | 21 |

| Health | 11 | 8 |

| Education | 10 | 9 |

| Transportation | 5 | 5 |

| Corporate | 3 | — |

| Housing | 3 | 6 |

| | |

| Credit Quality Allocations5 | | |

| | 7/31/11 | 7/31/10 |

| AAA/Aaa | 17% | 27% |

| AA/Aa | 44 | 31 |

| A | 25 | 31 |

| BBB/Baa | 9 | 8 |

| BB/Ba | 1 | 1 |

| B | 1 | 1 |

| Not Rated | 36 | 1 |

5 Using the higher of S&P’s or Moody’s ratings.

6 The investment advisor has deemed certain of these non-rated securities to be of

investment grade quality. As of July 31, 2011, the market value of these securities

was $2,615,595, representing 3% of the Fund's long-term investments.

| | |

| 6 | ANNUAL REPORT | JULY 31, 2011 |

Fund Summary as of July 31, 2011 BlackRock MuniYield California Fund, Inc.

Fund Overview

BlackRock MuniYield California Fund, Inc.’s (MYC) (the “Fund”) investment objective is to provide shareholders with as high a level of current income

exempt from federal and California income taxes as is consistent with its investment policies and prudent investment management. The Fund seeks to

achieve its investment objective by investing at least 80% of its assets in municipal obligations exempt from federal income taxes (except that the interest

may be subject to the federal alternative minimum tax) and California income taxes. Under normal market conditions, the Fund invests primarily in long-

term municipal obligations that are investment grade quality at the time of investment. The Fund may invest directly in such securities or synthetically

through the use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Performance

For the 12 months ended July 31, 2011, the Fund returned (1.49)% based on market price and 4.28% based on NAV. For the same period, the closed-end

Lipper California Municipal Debt Funds category posted an average return of (1.84)% based on market price and 3.16% based on NAV. All returns reflect

reinvestment of dividends. The Fund's discount to NAV, which widened during the period, accounts for the difference between performance based on price

and performance based on NAV. The following discussion relates to performance based on NAV. The Fund’s slightly long duration posture benefited perform-

ance as bonds with longer maturities experienced the greatest price appreciation as the yield curve flattened amid the investor flight-to-quality in the latter

half of the period. Increased exposure to inverse floating rate instruments (tender option bonds) while the municipal yield curve was historically steep

boosted the Fund’s income accrual. Holdings of higher quality essential service revenue bonds had a positive impact on performance as investors favored

these securities versus general obligation bonds and school district credits, which lagged due to budget concerns in California. Conversely, some widening of

credit spreads, especially among California school district and health care issues, had a negative impact on returns. In addition, the Fund’s cash reserves

detracted as cash underperformed longer maturity, coupon bonds as yields fell and spreads tightened. The Fund held short-call, high-coupon bonds, which

have good defensive characteristics, but proved a drag on returns when rates fell.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These

views are not intended to be a forecast of future events and are no guarantee of future results.

| |

| Fund Information | |

| Symbol on NYSE | MYC |

| Initial Offering Date | February 28, 1992 |

| Yield on Closing Market Price as of July 31, 2011 ($13.29)1 | 7.13% |

| Tax Equivalent Yield2 | 10.97% |

| Current Monthly Distribution per Common Share3 | $0.079 |

| Current Annualized Distribution per Common Share3 | $0.948 |

| Leverage as of July 31, 20114 | 41% |

1 Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results.

2 Tax equivalent yield assumes the maximum federal tax rate of 35%.

3 The distribution rate is not constant and is subject to change.

4 Represents VRDP Shares and TOBs as a percentage of total managed assets, which is the total assets of the Fund, including any assets attributable to VRDP Shares and TOBs,

minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and Risks of Leveraging on page 10.

The table below summarizes the changes in the Fund’s market price and NAV per share:

| | | | | |

| | 7/31/11 | 7/31/10 | Change | High | Low |

| Market Price | $13.29 | $14.44 | (7.96)% | $15.00 | $12.27 |

| Net Asset Value | $14.38 | $14.76 | (2.57)% | $15.41 | $12.65 |

The following charts show the sector and credit quality allocations of the Fund’s long-term investments:

| | |

| Sector Allocations | | |

| | 7/31/11 | 7/31/10 |

| County/City/Special District/School District | 43% | 35% |

| Utilities | 24 | 26 |

| Health | 10 | 8 |

| Education | 7 | 14 |

| Corporate | 6 | 7 |

| Transportation | 5 | 3 |

| State | 4 | 6 |

| Housing | 1 | 1 |

| | |

| Credit Quality Allocations5 | | |

| | 7/31/11 | 7/31/10 |

| AAA/Aaa | 7% | 27% |

| AA/Aa | 66 | 46 |

| A | 18 | 24 |

| BBB/Baa | 9 | 2 |

| Not Rated | — | 16 |

5 Using the higher of S&P’s or Moody’s ratings.

6 The investment advisor has deemed certain of these non-rated securities to be of

investment grade quality. As July 31, 2010, the market value of these securities was

$2,416,739, representing 1% of the Fund's long-term investments.

| | |

| ANNUAL REPORT | JULY 31, 2011 | 7 |

Fund Summary as of July 31, 2011 BlackRock MuniYield Investment Fund

Fund Overview

BlackRock MuniYield Investment Fund’s (MYF) (the “Fund”) investment objective is to provide shareholders with as high a level of current income exempt

from federal income taxes as is consistent with its investment policies and prudent investment management. The Fund seeks to achieve its investment objective

by investing at least 80% of its assets in municipal obligations exempt from federal income taxes (except that the interest may be subject to the federal alter-

native minimum tax). Under normal market conditions, the Fund primarily invests in municipal bonds that are investment grade quality at the time of invest-

ment. The Fund may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Performance

For the 12 months ended July 31, 2011, the Fund returned (2.45)% based on market price and 2.97% based on NAV. For the same period, the closed-end

Lipper General & Insured Municipal Debt Funds (Leveraged) category posted an average return of (2.24)% based on market price and 4.19% based on

NAV. All returns reflect reinvestment of dividends. The Fund moved from a premium to NAV to a discount by period end, which accounts for the difference

between performance based on price and performance based on NAV. The following discussion relates to performance based on NAV. The Fund’s holdings in

spread sectors, including housing and health care bonds, enhanced performance as these sectors provided a relatively high degree of incremental income

in the low interest rate environment. In addition, the Fund’s holdings of premium coupon bonds (6% or higher) and shorter-duration bonds (bonds with

lower sensitivity to interest rate movements) performed well as long-term interest rates climbed toward the end of 2010 and into the early part of 2011.

Conversely, the Fund’s exposure to bonds with longer duration (greater sensitivity to interest rate movements) and bonds with longer-dated maturities

detracted from performance as the municipal yield curve steepened over the 12-month period. The surprise non-extension of the BAB program at the end of

2010 put additional upward pressure on the long end of the yield curve, where most of the BAB supply was issued. US Treasury financial futures contracts

used to hedge interest rate risk in the portfolio had a negative impact on performance.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These

views are not intended to be a forecast of future events and are no guarantee of future results.

| |

| Fund Information | |

| Symbol on NYSE | MYF |

| Initial Offering Date | February 28, 1992 |

| Yield on Closing Market Price as of July 31, 2011 ($13.08)1 | 7.11% |

| Tax Equivalent Yield2 | 10.94% |

| Current Monthly Distribution per Common Share3 | $0.0775 |

| Current Annualized Distribution per Common Share3 | $0.9300 |

| Leverage as of July 31, 20114 | 39% |

1 Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results.

2 Tax equivalent yield assumes the maximum federal tax rate of 35%.

3 The distribution rate is not constant and is subject to change.

4 Represents VRDP Shares and TOBs as a percentage of total managed assets, which is the total assets of the Fund, including any assets attributable to VRDP Shares and TOBs,

minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and Risks of Leveraging on page 10.

The table below summarizes the changes in the Fund’s market price and NAV per share:

| | | | | |

| | 7/31/11 | 7/31/10 | Change | High | Low |

| Market Price | $13.08 | $14.36 | (8.91)% | $15.10 | $11.73 |

| Net Asset Value | $13.71 | $14.26 | (3.86)% | $14.78 | $12.16 |

The following charts show the sector and credit quality allocations of the Fund’s long-term investments:

| | |

| Sector Allocations | | |

| | 7/31/11 | 7/31/10 |

| County/City/Special District/School District | 25% | 22% |

| Transportation | 22 | 21 |

| Health | 17 | 20 |

| Utilities | 16 | 15 |

| Education | 7 | 7 |

| State | 5 | 7 |

| Housing | 4 | 4 |

| Corporate | 3 | 4 |

| Tobacco | 1 | — |

| | |

| Credit Quality Allocations5 | | |

| | 7/31/11 | 7/31/10 |

| AAA/Aaa | 10% | 16% |

| AA/Aa | 56 | 52 |

| A | 25 | 26 |

| BBB/Baa | 7 | 4 |

| Not Rated6 | 2 | 2 |

5 Using the higher of S&P’s or Moody’s ratings.

6 The investment advisor has deemed certain of these non-rated securities to be of

investment grade quality. As of July 31, 2011 and July 31, 2010, the market value of

these securities was $5,683,625, representing 2%, and $635,244, representing 1%,

respectively, of the Fund's long-term investments.

| | |

| 8 | ANNUAL REPORT | JULY 31, 2011 |

Fund Summary as of July 31, 2011 BlackRock MuniYield New Jersey Fund, Inc.

Fund Overview

BlackRock MuniYield New Jersey Fund, Inc.’s (MYJ) (the “Fund”) investment objective is to provide shareholders with as high a level of current income

exempt from federal income taxes and New Jersey personal income tax as is consistent with its investment policies and prudent investment management.

The Fund seeks to achieve its investment objective by investing at least 80% of its assets in municipal obligations exempt from federal income taxes (except

that the interest may subject to the federal alternative minimum tax) and New Jersey personal income taxes. Under normal market conditions, the Fund invests

primarily in long-term municipal obligations that are investment grade quality at the time of investment. The Fund may invest directly in such securities or

synthetically through the use of derivatives.

No assurance can be given that the Fund’s investment objective will be achieved.

Performance

For the 12 months ended July 31, 2011, the Fund returned (5.28)% based on market price and 3.55% based on NAV. For the same period, the closed-end

Lipper New Jersey Municipal Debt Funds category posted an average return of (3.20)% based on market price and 3.20% based on NAV. All returns reflect

reinvestment of dividends. The Fund's discount to NAV, which widened during the period, accounts for the difference between performance based on price

and performance based on NAV. The following discussion relates to performance based on NAV. The Fund’s holdings in spread sectors, including housing,

health care and corporate-backed municipal bonds, enhanced performance as these sectors provided a relatively high degree of incremental income in the

low interest rate environment. In addition, the Fund’s holdings of premium coupon bonds (6% or higher) and shorter-duration bonds (bonds with lower sen-

sitivity to interest rate movements) performed well as long-term interest rates climbed toward the end of 2010 and into the early part of 2011. Conversely,

the Fund’s exposure to bonds with longer duration (greater sensitivity to interest rate movements) and bonds with longer-dated maturities detracted from

performance as the municipal yield curve steepened over the 12-month period. The surprise non-extension of the BAB program at the end of 2010 put

additional upward pressure on the long end of the yield curve, where most of the BAB supply was issued.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These

views are not intended to be a forecast of future events and are no guarantee of future results.

| |

| Fund Information | |

| Symbol on NYSE | MYJ |

| Initial Offering Date | May 1, 1992 |

| Yield on Closing Market Price as of July 31, 2011 ($13.53)1 | 6.43% |

| Tax Equivalent Yield2 | 9.89% |

| Current Monthly Distribution per Common Share3 | $0.0725 |

| Current Annualized Distribution per Common Share3 | $0.8700 |

| Leverage as of July 31, 20114 | 35% |

1 Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results.

2 Tax equivalent yield assumes the maximum federal tax rate of 35%.

3 The distribution rate is not constant and is subject to change.

4 Represents VRDP Shares and TOBs as a percentage of total managed assets, which is the total assets of the Fund, including any assets attributable to VRDP Shares and TOBs,

minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Fund, please see The Benefits and Risks of Leveraging on page 10.

The table below summarizes the changes in the Fund’s market price and NAV per share:

| | | | | |

| | 7/31/11 | 7/31/10 | Change | High | Low |

| Market Price | $13.53 | $15.19 | (10.93)% | $15.97 | $12.59 |

| Net Asset Value | $14.84 | $15.24 | (2.62)% | $15.75 | $13.49 |

The following charts show the sector and credit quality allocations of the Fund’s long-term investments:

| | |

| Sector Allocations | | |

| | 7/31/11 | 7/31/10 |

| State | 24% | 26% |

| Transportation | 20 | 14 |

| Education | 14 | 12 |

| County/City/Special District/School District | 12 | 15 |

| Health | 11 | 12 |

| Housing | 11 | 12 |

| Corporate | 4 | 3 |

| Utilities | 3 | 4 |

| Tobacco | 1 | 2 |

| | |

| Credit Quality Allocations5 | | |

| | 7/31/11 | 7/31/10 |

| AAA/Aaa | 10% | 23% |

| AA/Aa | 38 | 32 |

| A | 40 | 31 |

| BBB/Baa | 12 | 9 |

| BB/Ba | — | 2 |

| Not Rated | — | 36 |

5 Using the higher of S&P’s or Moody’s ratings.

6 The investment advisor has deemed certain of these non-rated securities to be of

investment grade quality. As of July 31, 2010, the market value of these securities

was $8,311,633, representing 3% of the Fund's long-term investments.

| | |

| ANNUAL REPORT | JULY 31, 2011 | 9 |

The Benefits and Risks of Leveraging

The Funds may utilize leverage to seek to enhance the yield and NAV of

their common shares (“Common Shares”). However, these objectives can-

not be achieved in all interest rate environments.

To leverage, the Funds issue AMPS or VRDP Shares (collectively, “Preferred

Shares”), which pay dividends at prevailing short-term interest rates, and

invest the proceeds in long-term municipal bonds. In general, the concept

of leveraging is based on the premise that the financing cost of assets to

be obtained from leverage, which will be based on short-term interest rates,

will normally be lower than the income earned by each Fund on its longer-

term portfolio investments. To the extent that the total assets of each Fund

(including the assets obtained from leverage) are invested in higher-yielding

portfolio investments, each Fund’s holders of Common Shares (“Common

Shareholders”) will benefit from the incremental net income.

To illustrate these concepts, assume a Fund’s Common Shares capitalization

is $100 million and it issues Preferred Shares for an additional $50 million,

creating a total value of $150 million available for investment in long-term

municipal bonds. If prevailing short-term interest rates are 3% and long-

term interest rates are 6%, the yield curve has a strongly positive slope.

In this case, the Fund pays dividends on the $50 million of Preferred

Shares based on the lower short-term interest rates. At the same time,

the securities purchased by the Fund with assets received from the

Preferred Shares issuance earn income based on long-term interest rates.

In this case, the dividends paid to holders of Preferred Shares (“Preferred

Shareholders”) are significantly lower than the income earned on the

Fund’s long-term investments, and therefore the Common Shareholders

are the beneficiaries of the incremental net income.

If short-term interest rates rise, narrowing the differential between short-term

and long-term interest rates, the incremental net income pickup on the

Common Shares will be reduced or eliminated completely. Furthermore, if

prevailing short-term interest rates rise above long-term interest rates, the

yield curve has a negative slope. In this case, the Fund pays dividends to

Preferred Shareholders on the higher short-term interest rates whereas the

Fund’s total portfolio earns income based on lower long-term interest rates.

Furthermore, the value of the Funds’ portfolio investments generally varies

inversely with the direction of long-term interest rates, although other factors

can influence the value of portfolio investments. In contrast, the redemption

value of the Funds’ Preferred Shares does not fluctuate in relation to inter-

est rates. As a result, changes in interest rates can influence the Funds’

NAV positively or negatively in addition to the impact on Fund performance

from leverage from Preferred Shares discussed above.

The Funds may also leverage their assets through the use of TOBs, as

described in Note 1 of the Notes to Financial Statements. TOB investments

generally will provide the Funds with economic benefits in periods of

declining short-term interest rates, but expose the Funds to risks during

periods of rising short-term interest rates similar to those associated with

Preferred Shares issued by the Funds, as described above. Additionally,

fluctuations in the market value of municipal bonds deposited into the

TOB trust may adversely affect each Fund’s NAV per share.

The use of leverage may enhance opportunities for increased income to the

Funds and Common Shareholders, but as described above, it also creates

risks as short- or long-term interest rates fluctuate. Leverage also will gener-

ally cause greater changes in the Funds’ NAVs, market prices and dividend

rates than comparable portfolios without leverage. If the income derived

from securities purchased with assets received from leverage exceeds the

cost of leverage, the Funds’ net income will be greater than if leverage had

not been used. Conversely, if the income from the securities purchased is

not sufficient to cover the cost of leverage, each Fund’s net income will be

less than if leverage had not been used, and therefore the amount available

for distribution to Common Shareholders will be reduced. Each Fund may

be required to sell portfolio securities at inopportune times or at distressed

values in order to comply with regulatory requirements applicable to the use

of leverage or as required by the terms of leverage instruments, which may

cause a Fund to incur losses. The use of leverage may limit each Fund’s

ability to invest in certain types of securities or use certain types of hedging

strategies, such as in the case of certain restrictions imposed by ratings

agencies that rate the Preferred Shares issued by the Funds. Each Fund will

incur expenses in connection with the use of leverage, all of which are borne

by Common Shareholders and may reduce income to the Common Shares.

Under the Investment Company Act of 1940, the Funds are permitted to

issue Preferred Shares in an amount of up to 50% of their total managed

assets at the time of issuance. Under normal circumstances, each Fund

anticipates that the total economic leverage from Preferred Shares and/or

TOBs will not exceed 50% of its total managed assets at the time such

leverage is incurred. As of July 31, 2011, the Funds had economic leverage

from Preferred Shares and/or TOBs as a percentage of their total managed

assets as follows:

| |

| | Percent of |

| | Leverage |

| MNE | 34% |

| MZA | 40% |

| MYC | 41% |

| MYF | 39% |

| MYJ | 35% |

| | |

| 10 | ANNUAL REPORT | JULY 31, 2011 |

Derivative Financial Instruments

The Funds may invest in various derivative financial instruments, including

financial futures contracts as specified in Note 2 of the Notes to Financial

Statements, which may constitute forms of economic leverage. Such deriva-

tive financial instruments are used to obtain exposure to a market without

owning or taking physical custody of securities or to hedge market and/or

interest rate risks. Derivative financial instruments involve risks, including

the imperfect correlation between the value of a derivative financial instru-

ment and the underlying asset, possible default of the counterparty to the

transaction or illiquidity of the derivative financial instrument. The Funds’

ability to use a derivative financial instrument successfully depends on the

investment advisor’s ability to predict pertinent market movements accu-

rately, which cannot be assured. The use of derivative financial instruments

may result in losses greater than if they had not been used, may require a

Fund to sell or purchase portfolio investments at inopportune times or for

distressed values, may limit the amount of appreciation a Fund can realize

on an investment, may result in lower dividends paid to shareholders or

may cause a Fund to hold an investment that it might otherwise sell. The

Funds’ investments in these instruments are discussed in detail in the

Notes to Financial Statements.

| | |

| ANNUAL REPORT | JULY 31, 2011 | 11 |

BlackRock Muni New York Intermediate Duration Fund, Inc. (MNE)

Schedule of Investments July 31, 2011 (Unaudited)

(Percentages shown are based on Net Assets)

| | |

| | Par | |

| Municipal Bonds | (000) | Value |

| New York — 124.8% | | |

| Corporate — 13.8% | | |

| Essex County Industrial Development Agency, | | |

| Refunding RB, International Paper, Series A, AMT, | | |

| 5.20%, 12/01/23 | $ 1,000 | $ 979,260 |

| Jefferson County Industrial Development Agency | | |

| New York, Refunding RB, Solid Waste, Series A, AMT, | | |

| 5.20%, 12/01/20 | 500 | 493,065 |

| New York City Industrial Development Agency, RB, AMT: | | |

| 1990 American Airlines Inc. Project, Mandatory | | |

| Put Bonds, 5.40%, 7/01/20 | 1,500 | 1,219,635 |

| British Airways Plc Project, 7.63%, 12/01/32 | 1,000 | 1,012,080 |

| Continental Airlines Inc., Mandatory Put Bonds, | | |

| Project, 8.38%, 11/01/16 | 1,000 | 1,028,960 |

| New York City Industrial Development Agency, Refunding | | |

| RB, Terminal One Group Association Project, AMT: | | |

| 5.50%, 1/01/18 | 1,000 | 1,079,550 |

| 5.50%, 1/01/24 | 1,000 | 1,028,350 |

| New York State Energy Research & Development Authority, | | |

| Refunding RB: | | |

| Brooklyn Union Gas/Keyspan, Series A, AMT (FGIC), | | |

| 4.70%, 2/01/24 | 500 | 507,805 |

| Rochester Gas & Electric Corp., Series C (NPFGC), | | |

| 5.00%, 8/01/32 (a) | 1,000 | 1,085,630 |

| | | 8,434,335 |

| County/City/Special District/School District — 20.9% | | |

| Amherst Development Corp., RB, University at Buffalo | | |

| Foundation Faculty-Student Housing Corp., Series A | | |

| (AGM), 4.00%, 10/01/24 | 1,000 | 969,530 |

| City of New York, New York, GO: | | |

| Series E, 5.00%, 8/01/24 | 1,000 | 1,086,550 |

| Series J (NPFGC), 5.25%, 5/15/18 | 1,455 | 1,600,122 |

| Series J (NPFGC), 5.25%, 5/15/18 (b) | 45 | 50,870 |

| Sub-Series I-1, 5.50%, 4/01/21 | 1,500 | 1,743,285 |

| Sub-Series I-1, 5.13%, 4/01/25 | 750 | 813,997 |

| City of New York, New York, GO, Refunding: | | |

| Series A, 5.00%, 8/01/24 | 500 | 542,380 |

| Series E, 5.00%, 8/01/27 | 600 | 642,366 |

| New York City Industrial Development Agency, RB, Queens | | |

| Baseball Stadium, PILOT (AMBAC), 5.00%, 1/01/31 | 1,500 | 1,348,275 |

| New York City Industrial Development Agency, | | |

| Refunding RB, Terminal One Group Association | | |

| Project, AMT, 5.50%, 1/01/21 (a) | 250 | 262,263 |

| New York City Transitional Finance Authority, RB: | | |

| Fiscal 2007, Series S-1 (NPFGC), 5.00%, 7/15/24 | 500 | 532,350 |

| Fiscal 2009, Series S-3, 5.00%, 1/15/23 | 575 | 623,300 |

| New York Liberty Development Corp., Refunding RB, | | |

| Second Priority, Bank of America Tower at One Bryant | | |

| Park Project, 5.63%, 7/15/47 | 1,000 | 1,011,710 |

| United Nations Development Corp. New York, Refunding | | |

| RB, Series A, 4.25%, 7/01/24 | 1,500 | 1,515,555 |

| | | 12,742,553 |

| | | |

| | | Par | |

| Municipal Bonds | | (000) | Value |

| New York (continued) | | | |

| Education — 14.7% | | | |

| Dutchess County Industrial Development Agency New York, | | |

| Refunding RB, Bard College Civic Facility, Series A-1, | | |

| 5.00%, 8/01/22 | $ 750 | $ 789,773 |

| Nassau County Industrial Development Agency, | | | |

| Refunding RB, New York Institute of Technology Project, | | |

| Series A, 5.00%, 3/01/21 | | 1,000 | 1,058,040 |

| New York City Industrial Development Agency, RB, | | | |

| Lycee Francais De New York Project, Series A (ACA), | | | |

| 5.50%, 6/01/15 | | 500 | 522,840 |

| New York City Industrial Development Agency, | | | |

| Refunding RB, Polytechnic University Project (ACA), | | | |

| 4.70%, 11/01/22 | | 1,000 | 981,930 |

| New York State Dormitory Authority, RB: | | | |

| Convent of the Sacred Heart (AGM), | | | |

| 4.00%, 11/01/18 | | 880 | 922,962 |

| Convent of the Sacred Heart (AGM), | | | |

| 5.00%, 11/01/21 | | 120 | 129,990 |

| Fordham University, Series A, 5.25%, 7/01/25 | | 500 | 543,495 |

| Master BOCES Program Lease (AGM), | | | |

| 3.50%, 8/15/25 | | 250 | 231,320 |

| Mount Sinai School of Medicine, 5.50%, 7/01/25 | 1,000 | 1,061,880 |

| Mount Sinai School of Medicine, Series A (NPFGC), | | |

| 5.15%, 7/01/24 | | 250 | 260,870 |

| The New School, 5.25%, 7/01/24 | | 750 | 795,457 |

| Schenectady County Industrial Development Agency, | | | |

| Refunding RB, Union College Project, 5.00%, 7/01/26 | 1,000 | 1,028,630 |

| Suffolk County Industrial Development Agency, | | | |

| Refunding RB, New York Institute of Technology Project, | | |

| 5.25%, 3/01/21 | | 600 | 621,006 |

| | | | 8,948,193 |

| Health — 20.2% | | | |

| Dutchess County Industrial Development Agency, RB: | | | |

| St. Francis Hospital, Series B, 7.25%, 3/01/19 | | 325 | 323,811 |

| Vassar Brothers Medical Center (AGC), | | | |

| 5.00%, 4/01/21 | | 215 | 232,871 |

| Dutchess County Local Development Corp., Refunding RB, | | |

| Health Quest System Inc., Series A (AGC), | | | |

| 5.25%, 7/01/25 | | 1,000 | 1,041,890 |

| Erie County Industrial Development Agency, RB, Episcopal | | |

| Church Home, Series A, 5.88%, 2/01/18 | | 905 | 904,900 |

| Genesee County Industrial Development Agency New York, | | |

| Refunding RB, United Memorial Medical Center Project, | | |

| 4.75%, 12/01/14 | | 280 | 268,876 |

| Monroe County Industrial Development Corp., RB, Unity | | |

| Hospital of Rochester Project (FHA), 4.20%, 8/15/25 | 500 | 518,700 |

| New York City Industrial Development Agency, RB, | | | |

| PSCH Inc. Project, 6.20%, 7/01/20 | | 1,415 | 1,332,590 |

| New York State Dormitory Authority, RB: | | | |

| NYU Hospital Center, Series A, 5.00%, 7/01/22 | | 1,000 | 1,044,600 |

| NYU Hospital Center, Series B, 5.25%, 7/01/24 | | 430 | 450,227 |

| | | | | |

| Portfolio Abbreviations | | | | |

| To simplify the listings of portfolio holdings in the | BOCES | Board of Cooperative Educational Services | IDA | Industrial Development Authority |

| Schedules of Investments, the names and descriptions of | CAB | Capital Appreciation Bonds | ISD | Independent School District |

| many of the securities have been abbreviated according | CIFG | CDC IXIS Financial Guaranty | LRB | Lease Revenue Bonds |

| to the following list: | COP | Certificates of Participation | MRB | Mortgage Revenue Bonds |

| | | EDA | Economic Development Authority | NPFGC | National Public Finance Guarantee Corp. |

| ACA | ACA Financial Guaranty Corp. | ERB | Education Revenue Bonds | PILOT | Payment in Lieu of Taxes |

| AGC | Assured Guaranty Corp. | FGIC | Financial Guaranty Insurance Co. | Radian | Radian Group, Inc. |

| AGM | Assured Guaranty Municipal Corp. | FHA | Federal Housing Administration | RB | Revenue Bonds |

| AMBAC | American Municipal Bond Assurance Corp. | GO | General Obligation Bonds | S/F | Single-Family |

| AMT | Alternative Minimum Tax (subject to) | HFA | Housing Finance Agency | SONYMA | State of New York Mortgage Agency |

| | | HRB | Housing Revenue Bonds | Syncora | Syncora Guarantee |

| See Notes to Financial Statements. | | | | |

| | |

| 12 | ANNUAL REPORT | JULY 31, 2011 |

BlackRock Muni New York Intermediate Duration Fund, Inc. (MNE)

Schedule of Investments (continued)

(Percentages shown are based on Net Assets)

| | | |

| | | Par | |

| Municipal Bonds | | (000) | Value |

| New York (continued) | | | |

| Health (concluded) | | | |

| New York State Dormitory Authority, RB (concluded): | | | |

| New York State Association for Retarded Children Inc., | | |

| Series A, 5.30%, 7/01/23 | $ 450 | $ 484,308 |

| North Shore-Long Island Jewish Health System, | | | |

| Series A, 5.25%, 5/01/25 | | 780 | 790,187 |

| New York State Dormitory Authority, Refunding RB: | | | |

| Lenox Hill Hospital Obligation Group, 5.75%, 7/01/17 | 500 | 505,510 |

| Mount Sinai Hospital, Series A, 4.25%, 7/01/23 | | 250 | 252,305 |

| North Shore-Long Island Jewish Health System, | | | |

| Series E, 5.00%, 5/01/22 | | 650 | 688,044 |

| Saratoga County Industrial Development Agency New York, | | |

| Refunding RB, The Saratoga Hospital Project, Series A | | |

| (Radian), 4.38%, 12/01/13 | | 365 | 385,013 |

| Suffolk County Industrial Development Agency New York, | | |

| Refunding RB, Jeffersons Ferry Project, 4.63%, 11/01/16 | 800 | 837,152 |

| Westchester County Industrial Development Agency | | | |

| New York, MRB, Kendal on Hudson Project, Series A, | | |

| 6.38%, 1/01/24 | | 1,000 | 992,580 |

| Westchester County Industrial Development Agency | | | |

| New York, RB, Special Needs Facilities Pooled Program, | | |

| Series D-1, 6.80%, 7/01/19 | | 515 | 507,646 |

| Yonkers Industrial Development Agency New York, RB, | | | |

| Sacred Heart Associations Project, Series A, AMT | | | |

| (SONYMA), 4.80%, 10/01/26 | | 750 | 737,257 |

| | | | 12,298,467 |

| Housing — 13.3% | | | |

| New York City Housing Development Corp., RB, | | | |

| Series H-2-A, AMT, 5.00%, 11/01/30 | | 780 | 746,468 |

| New York Mortgage Agency, Refunding MRB, 44th Series, | | |

| AMT, 4.00%, 10/01/21 | | 500 | 489,135 |

| New York Mortgage Agency, Refunding RB, AMT: | | | |

| Homeowner Mortgage, Series 130, 4.75%, 10/01/30 | 2,500 | 2,402,475 |

| Series 133, 4.95%, 10/01/21 | | 395 | 402,161 |

| Series 143, 4.85%, 10/01/27 | | 500 | 479,925 |

| New York State Urban Development Corp., RB, Subordinate | | |

| Lien, Corporate Purpose, Series A, 5.13%, 7/01/19 | | 2,000 | 2,119,460 |

| Yonkers Economic Development Corp., Refunding RB, | | | |

| Riverview II (Freddie Mac), 4.50%, 5/01/25 | | 1,500 | 1,499,910 |

| | | | 8,139,534 |

| State — 13.8% | | | |

| Buffalo & Erie County Industrial Land Development | | | |

| Corp., RB, Buffalo State College Foundation Housing, | | |

| 6.00%, 10/01/31 | | 1,000 | 1,085,460 |

| New York State Dormitory Authority, ERB, Series F, | | | |

| 5.00%, 3/15/30 | | 1,290 | 1,337,949 |

| New York State Dormitory Authority, LRB, Municipal Health | | |

| Facilities, Sub-Series 2-4, 5.00%, 1/15/27 | | 600 | 621,408 |

| New York State Dormitory Authority, RB, Education, | | | |

| Series D, 5.00%, 3/15/31 | | 500 | 520,365 |

| New York State Dormitory Authority, Refunding RB, | | | |

| Department of Health, Series A (CIFG), 5.00%, 7/01/25 | 1,500 | 1,559,430 |

| New York State Thruway Authority, Refunding RB, | | | |

| Series A-1, 5.00%, 4/01/22 | | 1,000 | 1,118,520 |

| New York State Urban Development Corp., RB, State | | | |

| Personal Income Tax, State Facilities, Series A-1 | | | |

| (NPFGC), 5.00%, 3/15/24 | | 485 | 521,021 |

| New York State Urban Development Corp., Refunding RB, | | |

| Service Contract, Series B, 5.00%, 1/01/21 | | 1,500 | 1,670,355 |

| | | | 8,434,508 |

| Tobacco — 1.7% | | | |

| Tobacco Settlement Financing Corp. New York, RB, | | | |

| Asset-Backed, Asset-Backed, Series B-1C, | | | |

| 5.50%, 6/01/22 | | 1,000 | 1,067,730 |

| | |

| | Par | |

| Municipal Bonds | (000) | Value |

| New York (concluded) | | |

| Transportation — 15.7% | | |

| Metropolitan Transportation Authority, RB: | | |

| Series A (NPFGC), 5.00%, 11/15/24 | $ 2,000 | $ 2,131,600 |

| Series B (NPFGC), 5.25%, 11/15/19 | 860 | 991,287 |

| Sub-Series B-1, 5.00%, 11/15/24 | 460 | 514,041 |

| Sub-Series B-4, 5.00%, 11/15/24 | 300 | 335,244 |

| Metropolitan Transportation Authority, Refunding RB: | | |

| Series A (NPFGC), 5.00%, 11/15/25 | 2,000 | 2,028,460 |

| Series B, 5.25%, 11/15/25 | 750 | 819,450 |

| Port Authority of New York & New Jersey, RB: | | |

| Consolidated 152nd Series, AMT, 5.00%, 11/01/24 | 1,000 | 1,038,520 |

| JFK International Air Terminal, 5.00%, 12/01/20 | 1,000 | 999,930 |

| Port Authority of New York & New Jersey, Refunding RB, | | |

| AMT, Consolidated: | | |

| 152nd Series, 5.00%, 11/01/23 | 500 | 518,430 |

| 155th Series, 4.75%, 12/01/30 | 205 | 202,688 |

| | | 9,579,650 |

| Utilities — 10.7% | | |

| Long Island Power Authority, Refunding RB: | | |

| General, Series D (NPFGC), 5.00%, 9/01/25 | 3,000 | 3,155,130 |

| Series A, 5.50%, 4/01/24 | 875 | 964,268 |

| New York City Municipal Water Finance Authority, RB: | | |

| Second General Resolution HH, 5.00%, 6/15/32 | 800 | 843,328 |

| Series DD, 5.00%, 6/15/32 | 500 | 520,020 |

| New York State Environmental Facilities Corp., RB, | | |

| NYC Municipal Water, 5.00%, 6/15/31 | 1,000 | 1,066,590 |

| | | 6,549,336 |

| Total Municipal Bonds in New York | | 76,194,306 |

| Guam — 2.5% | | |

| County/City/Special District/School District — 0.5% | | |

| Territory of Guam, RB, Section 30, Series A, | | |

| 5.38%, 12/01/24 | 325 | 328,959 |

| State — 0.3% | | |

| Territory of Guam, GO, Series A, 6.00%, 11/15/19 | 185 | 183,753 |

| Utilities — 1.7% | | |

| Guam Government Waterworks Authority, Refunding RB, | | |

| Water, 6.00%, 7/01/25 | 1,000 | 1,000,290 |

| Total Municipal Bonds in Guam | | 1,513,002 |

| Puerto Rico — 13.6% | | |

| Education — 0.7% | | |

| Puerto Rico Industrial Tourist Educational Medical | | |

| & Environmental Control Facilities Financing Authority, | | |

| RB, University Plaza Project, Series A (NPFGC), | | |

| 5.00%, 7/01/33 | 500 | 454,160 |

| Housing — 3.5% | | |

| Puerto Rico Housing Finance Authority, Refunding RB, | | |

| Subordinate, Capital Fund Modernization, | | |

| 5.13%, 12/01/27 | 2,070 | 2,108,502 |

| State — 0.9% | | |

| Puerto Rico Public Buildings Authority, Refunding RB, | | |

| Government Facilities, Series M-3 (NPFGC), | | |

| 6.00%, 7/01/28 | 500 | 526,840 |

| Transportation — 8.5% | | |

| Puerto Rico Highway & Transportation Authority, RB: | | |

| Series Y (AGM), 6.25%, 7/01/21 | 3,000 | 3,411,810 |

| Subordinate (FGIC), 5.75%, 7/01/21 | 1,500 | 1,550,010 |

| Puerto Rico Highway & Transportation Authority, | | |

| Refunding RB, Series AA-1 (AGM), 4.95%, 7/01/26 | 250 | 252,867 |

| | | 5,214,687 |

| Total Municipal Bonds in Puerto Rico | | 8,304,189 |

See Notes to Financial Statements.

| | |

| ANNUAL REPORT | JULY 31, 2011 | 13 |

BlackRock Muni New York Intermediate Duration Fund, Inc. (MNE)

Schedule of Investments (concluded)

(Percentages shown are based on Net Assets)

| | |

| | Par | |

| Municipal Bonds | (000) | Value |

| U.S. Virgin Islands — 3.3% | | |

| Corporate — 1.6% | | |

| United States Virgin Islands, Refunding RB, Senior | | |

| Secured, Hovensa Coker Project, AMT, 6.50%, 7/01/21 $ 500 | $ 494,190 |

| Virgin Islands Public Finance Authority, Refunding RB, | | |

| Senior Secured, Hovensa Coker Project, AMT, | | |

| 6.50%, 7/01/21 | 500 | 493,830 |

| | | 988,020 |

| State — 1.7% | | |

| Virgin Islands Public Finance Authority, RB, Senior Lien, | | |

| Matching Fund Loan Note, Series A, 5.25%, 10/01/24 | 1,000 | 1,009,950 |

| Total Municipal Bonds in the U.S. Virgin Islands | | 1,997,970 |

| Total Municipal Bonds — 144.2% | | 88,009,467 |

| Municipal Bonds Transferred to | | |

| Tender Option Bond Trusts (c) | | |

| New York — 3.9% | | |

| County/City/Special District/School District — 1.4% | | |

| City of New York New York, GO, Sub-Series B-1, | | |

| 5.25%, 9/01/22 | 750 | 841,245 |

| Utilities — 2.5% | | |

| New York City Municipal Water Finance Authority, | | |

| Refunding RB, Series A, 4.75%, 6/15/30 | 1,500 | 1,542,510 |

| Total Municipal Bonds Transferred to | | |

| Tender Option Bond Trusts — 3.9% | | 2,383,755 |

| Total Long-Term Investments | | |

| (Cost — $87,708,903) — 148.1% | | 90,393,222 |

| Short-Term Securities | Shares | |

| BIF New York Municipal Money Fund, 0.00% (d)(e) | 760,684 | 760,684 |

| Total Short-Term Securities | | |

| (Cost — $760,684) — 1.3% | | 760,684 |

| Total Investments (Cost — $88,469,587*) — 149.4% | | 91,153,906 |

| Other Assets Less Liabilities — 1.0% | | 623,180 |

| Liability for TOB Trust Certificates, Including Interest | | |

| Expense and Fees Payable — (1.8)% | | (1,125,653) |

| AMPS, at Redemption Value — (48.6)% | | (29,632,153) |

| Net Assets Applicable to Common Shares — 100.0% | | $ 61,019,280 |

| | |

| * The cost and unrealized appreciation (depreciation) of investments as of July 31, |

| 2011, as computed for federal income tax purposes, were as follows: | |

| Aggregate cost | $ 87,173,206 |

| Gross unrealized appreciation | $ 3,459,165 |

| Gross unrealized depreciation | | (603,465) |

| Net unrealized appreciation | $ 2,855,700 |

(a) Variable rate security. Rate shown is as of report rate.

(b) US government securities, held in escrow, are used to pay interest on this security,

as well as to retire the bond in full at the date indicated, typically at a premium

to par.

(c) Securities represent bonds transferred to a TOB in exchange for which the Fund

acquired residual interest certificates. These securities serve as collateral in a

financing transaction. See Note 1 of the Notes to Financial Statements for details

of municipal bonds transferred to TOBs.

(d) Investments in companies considered to be an affiliate of the Fund during the year,

for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as

amended, were as follows:

| | | | |

| | Shares Held | | Shares Held | |

| | at July 31, | Net | at July 31, | |

| Affiliate | 2010 | Activity | 2011 | Income |

| BIF New York | | | | |

| Municipal | | | | |

| Money Fund | 1,976,046 | (1,215,362) | 760,684 | $ 42 |

(e) Represents the current yield as of report date.

• Financial futures contracts sold as of July 31, 2011 were as follows:

| | | | |

| | | | Notional | Unrealized |

| Contracts Issue | Exchange | Expiration | Value | Depreciation |

| 10-Year US | Chicago Board | September | | |

| 20 Treasury Note | of Trade | 2011 | $ 2,452,150 | $ (61,601) |

• For Fund compliance purposes, the Fund’s sector classifications refer to any one

or more of the sector sub-classifications used by one or more widely recognized

market indexes or rating group indexes, and/or as defined by fund management.

These definitions may not apply for purposes of this report, which may combine

such sector sub-classifications for reporting ease.

• Fair Value Measurements — Various inputs are used in determining the fair value

of investments and derivative financial instruments. These inputs are categorized in

three broad levels for financial statement purposes as follows:

• Level 1 — price quotations in active markets/exchanges for identical assets

and liabilities

• Level 2 — other observable inputs (including, but not limited to: quoted prices for

similar assets or liabilities in markets that are active, quoted prices for identical

or similar assets or liabilities in markets that are not active, inputs other than

quoted prices that are observable for the assets or liabilities (such as interest

rates, yield curves, volatilities, prepayment speeds, loss severities, credit risks and

default rates) or other market-corroborated inputs)

• Level 3 — unobservable inputs based on the best information available in the

circumstances, to the extent observable inputs are not available (including the

Fund’s own assumptions used in determining the fair value of investments and

derivative financial instruments)

The categorization of a value determined for investments and derivative financial

instruments is based on the pricing transparency of the investment and derivative

financial instrument and does not necessarily correspond to the Fund’s perceived

risk of investing in those securities. For information about the Fund’s policy regarding

valuation of investments and derivative financial instruments and other significant

accounting policies, please refer to Note 1 of the Notes to Financial Statements.

The following tables summarize the inputs used as of July 31, 2011 in determining

the fair valuation of the Fund’s investments and derivative financial instruments:

| | | | |

| Valuation Inputs | Level 1 | Level 2 | Level 3 | Total |

| Assets: | | | | |

| Investments: | | | | |

| Long-Term | | | | |

| Investments1 | — | $ 90,393,222 | — | $ 90,393,222 |

| Short-Term | | | | |

| Securities | $ 760,684 | — | — | 760,684 |

| Total | $ 760,684 | $ 90,393,222 | — | $ 91,153,906 |

1 See above Schedule of Investments for values in each sector.

| | | | | |

| Valuation Inputs | Level 1 | Level 2 | Level 3 | Total |

| Derivative Financial Instruments2 | | | |

| Liabilities: | | | | | |

| Interest rate | | | | | |

| contracts | $ (61,601) | — | — | $ (61,601) |

2 Derivative financial instruments are financial futures contracts, which are valued

at the unrealized appreciation/depreciation on the instrument.

See Notes to Financial Statements.

| | |

| 14 | ANNUAL REPORT | JULY 31, 2011 |

BlackRock MuniYield Arizona Fund, Inc. (MZA)

Schedule of Investments July 31, 2011

(Percentages shown are based on Net Assets)

| | |

| | Par | |

| Municipal Bonds | (000) | Value |

| Arizona — 137.1% | | |

| County/City/Special District/School District — 52.3% | | |

| City of Glendale Arizona, RB (NPFGC), 5.00%, 7/01/25 $ | 2,305 | $ 2,413,635 |

| City of Tucson Arizona, COP: | | |

| Series A (NPFGC), 5.00%, 7/01/20 | 1,500 | 1,584,210 |

| (AGC), 5.00%, 7/01/29 | 1,000 | 1,031,630 |

| County of Pinal Arizona, COP: | | |

| 5.00%, 12/01/26 | 1,250 | 1,257,550 |

| 5.00%, 12/01/29 | 1,250 | 1,239,550 |

| Gila County Unified School District No. 10-Payson | | |

| Arizona, GO, School Improvement Project of 2006, | | |

| Series A (AMBAC), 5.25%, 7/01/27 (a) | 500 | 521,400 |

| Gilbert Public Facilities Municipal Property Corp. Arizona, | | |

| RB, 5.50%, 7/01/27 | 2,000 | 2,161,020 |

| Gladden Farms Community Facilities District, GO, | | |

| 5.50%, 7/15/31 | 750 | 677,625 |

| Greater Arizona Development Authority, RB, Santa Cruz | | |

| County Jail, Series 2, 5.25%, 8/01/31 | 1,155 | 1,155,000 |

| Marana Municipal Property Corp., RB, Series A, | | |

| 5.00%, 7/01/28 | 2,500 | 2,563,100 |

| Maricopa County Community College District Arizona, | | |

| GO, Series C, 3.00%, 7/01/22 | 1,000 | 998,600 |

| Maricopa County Public Finance Corp., RB, Series A | | |

| (AMBAC), 5.00%, 7/01/24 | 2,500 | 2,618,575 |

| Maricopa County Unified School District No. 89-Dysart | | |

| Arizona, GO, School Improvement Project of 2006, | | |

| Series C, 6.00%, 7/01/28 | 1,000 | 1,103,330 |

| Mohave County Unified School District No. 20 Kingman, | | |

| GO, School Improvement Project of 2006, Series C | | |

| (AGC), 5.00%, 7/01/26 | 1,000 | 1,063,800 |

| Phoenix Civic Improvement Corp., RB, Subordinate, | | |

| Civic Plaza Expansion Project, Series A (NPFGC), | | |

| 5.00%, 7/01/35 | 3,325 | 3,344,850 |

| Queen Creek Improvement District No. 1, Special | | |

| Assessment Bonds, 5.00%, 1/01/32 | 1,000 | 955,600 |

| Scottsdale Municipal Property Corp. Arizona, RB, | | |

| Water & Sewer Development Project, Series A, | | |

| 5.00%, 7/01/24 | 1,500 | 1,633,365 |

| State of Arizona, RB, Series A (AGM), 5.00%, 7/01/29 | 1,930 | 1,999,692 |

| Vistancia Community Facilities District Arizona, GO: | | |

| 6.75%, 7/15/22 | 1,275 | 1,306,926 |

| 5.75%, 7/15/24 | 750 | 785,588 |

| Yuma County Library District, GO (Syncora), | | |

| 5.00%, 7/01/26 | 1,465 | 1,523,497 |

| | | 31,938,543 |

| Corporate — 5.1% | | |

| Maricopa County Pollution Control Corp., Refunding RB, | | |

| Southern California Edison Co., Series A, | | |

| 5.00%, 6/01/35 | 3,100 | 3,119,623 |

| Education — 15.9% | | |

| Arizona State University, RB, Series 2008-C: | | |

| 6.00%, 7/01/25 | 970 | 1,095,014 |

| 6.00%, 7/01/26 | 745 | 838,602 |

| 6.00%, 7/01/27 | 425 | 477,028 |

| 6.00%, 7/01/28 | 400 | 446,916 |

| Glendale IDA, Refunding RB, Midwestern University, | | |

| 5.00%, 5/15/35 | 1,000 | 939,050 |

| Maricopa County IDA Arizona, RB, Arizona Charter | | |

| Schools Project, Series A, 6.63%, 7/01/20 | 700 | 542,885 |

| Pima County IDA, RB, Arizona Charter Schools Project, | | |

| Series C: | | |

| 6.70%, 7/01/21 | 710 | 710,831 |

| 6.75%, 7/01/31 | 985 | 955,086 |

| | | |

| | | Par | |

| Municipal Bonds | | (000) | Value |

| Arizona (continued) | | | |

| Education (concluded) | | | |

| Pima County IDA, Refunding RB: | | | |

| Arizona Charter Schools Project, Series O, | | | |

| 5.00%, 7/01/26 | $ 975 | $ 810,400 |

| Charter Schools II, Series A, 6.75%, 7/01/21 | | 560 | 560,773 |

| University of Arizona, COP, University of Arizona | | | |

| Projects (AMBAC): | | | |

| Series A, 5.13%, 6/01/29 | | 905 | 917,697 |

| Series B, 5.00%, 6/01/28 | | 1,400 | 1,417,570 |

| | | | 9,711,852 |

| Health — 18.3% | | | |

| Arizona Health Facilities Authority, Refunding RB, Banner | | |

| Health Series D: | | | |

| 6.00%, 1/01/30 | | 1,500 | 1,526,040 |

| 5.50%, 1/01/38 | | 1,300 | 1,325,272 |

| Maricopa County IDA Arizona, Refunding RB: | | | |

| Catholic Healthcare West, Series A, 5.50%, 7/01/26 | 1,850 | 1,870,776 |

| Samaritan Health Services, Series A (NPFGC), | | | |

| 7.00%, 12/01/16 (b) | | 1,000 | 1,200,180 |

| Maricopa County IDA, RB, Catholic Healthcare West, | | | |

| Series A, 6.00%, 7/01/39 | | 170 | 174,512 |

| Scottsdale IDA, RB, Scottsdale Healthcare, Series C | | | |

| (AGM), 5.00%, 9/01/35 | | 1,800 | 1,789,938 |

| University Medical Center Corp. Arizona, RB (GOCORP): | | |

| 6.00%, 7/01/39 (c) | | 1,000 | 987,930 |

| 6.50%, 7/01/39 | | 500 | 514,600 |

| Yavapai County IDA Arizona, RB, Yavapai Regional Medical | | |

| Center, Series A, 6.00%, 8/01/33 | | 1,800 | 1,780,488 |

| | | | 11,169,736 |

| Housing — 4.3% | | | |

| Maricopa County & Phoenix Industrial Development | | | |

| Authorities, Refunding RB, AMT (Ginnie Mae), S/F: | | | |

| Series A-1, 5.75%, 5/01/40 | | 405 | 407,130 |

| Series A-2, 5.80%, 7/01/40 | | 300 | 305,907 |

| Maricopa County IDA Arizona, RB, Series 3-B, AMT | | | |

| (Ginnie Mae), 5.25%, 8/01/38 | | 600 | 634,618 |

| Phoenix & Pima County IDA, RB, Series 1A, AMT | | | |

| (Ginnie Mae), 5.65%, 7/01/39 | | 229 | 230,279 |

| Phoenix & Pima County IDA, Refunding RB, | | | |

| Series 2007-1, AMT (Ginnie Mae), 5.25%, 8/01/38 | 509 | 512,341 |

| Phoenix IDA Arizona, Refunding RB, Series 2007-2, AMT | | |

| (Ginnie Mae), 5.50%, 12/01/38 | | 548 | 551,800 |

| | | | 2,642,075 |

| State — 16.5% | | | |

| Arizona School Facilities Board, COP: | | | |

| 5.13%, 9/01/21 | | 1,000 | 1,055,980 |

| 5.75%, 9/01/22 | | 2,000 | 2,161,160 |

| Arizona Sports & Tourism Authority, RB, Multipurpose | | | |

| Stadium Facilities, Series A (NPFGC), 5.00%, 7/01/31 | 1,000 | 902,900 |

| Arizona State Transportation Board, RB, Series B, | | | |

| 5.00%, 7/01/30 | | 4,000 | 4,234,680 |

| Greater Arizona Development Authority, RB, Series B | | | |

| (NPFGC), 5.00%, 8/01/30 | | 1,700 | 1,709,792 |

| | | | 10,064,512 |

| Transportation — 5.9% | | | |

| Phoenix Civic Improvement Corp., RB: | | | |

| Junior Lien, Series A, 5.00%, 7/01/40 | | 1,000 | 970,210 |

| Senior Lien, Series A, 5.00%, 7/01/33 | | 1,000 | 1,018,110 |

| Senior Lien, Series B AMT (NPFGC), 5.75%, 7/01/17 | 1,000 | 1,028,780 |

| Senior Lien, Series B AMT (NPFGC), 5.25%, 7/01/32 | 600 | 600,240 |

| | | | 3,617,340 |

See Notes to Financial Statements.

| | |

| ANNUAL REPORT | JULY 31, 2011 | 15 |

BlackRock MuniYield Arizona Fund, Inc. (MZA)

Schedule of Investments (continued)

(Percentages shown are based on Net Assets)

| | | |

| | | Par | |

| Municipal Bonds | | (000) | Value |

| Arizona (concluded) | | | |

| Utilities — 18.8% | | | |

| County of Pima Arizona, RB, System (AGM), | | | |

| 5.00%, 7/01/25 | $ 1,000 | $ 1,067,040 |

| Gilbert Water Resource Municipal Property Corp., RB, | | | |

| Subordinate Lien (NPFGC), 5.00%, 10/01/29 | | 900 | 921,042 |

| Phoenix Civic Improvement Corp., RB, Junior Lien | | | |

| (NPFGC), 5.50%, 7/01/20 | | 2,500 | 2,598,625 |

| Phoenix Civic Improvement Corp., Refunding RB, | | | |

| Senior Lien, 5.50%, 7/01/22 | | 2,000 | 2,277,560 |

| Pima County IDA, RB, Tucson Electric Power Co., Series A, | | |

| 5.25%, 10/01/40 | | 1,000 | 919,820 |

| Pinal County IDA Arizona, RB, San Manuel Facility Project, | | |

| AMT, 6.25%, 6/01/26 | | 500 | 445,205 |

| Salt River Project Agricultural Improvement & Power | | | |

| District, RB, Series A: | | | |

| 5.00%, 1/01/24 | | 1,000 | 1,089,780 |

| 5.00%, 1/01/38 | | 660 | 674,883 |

| Salt River Project Agricultural Improvement & Power | | | |

| District, Refunding RB, Salt River Project, Series A, | | | |

| 5.00%, 1/01/35 | | 1,500 | 1,529,715 |

| | | | 11,523,670 |

| Total Municipal Bonds in Arizona | | | 83,787,351 |

| Guam — 1.6% | | | |

| Utilities — 1.6% | | | |