UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

(Exact name of registrant as specified in charter)

680 Washington Boulevard, Suite 500, Stamford, Connecticut 06901

(Address of principal executive offices) (Zip code)

AMG Funds LLC

680 Washington Boulevard, Suite 500, Stamford, Connecticut 06901

(Name and address of agent for service)

Registrant's telephone number, including area code:

Date of reporting period:

November 01, 2023 - October 31, 2024

(Annual Shareholder Report)

Item 1. Reports to Shareholders

(a)

AMG Frontier Small Cap Growth Fund

Class N/MSSVX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Frontier Small Cap Growth Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Frontier Small Cap Growth Fund

(Class N/MSSVX) | $152 | 1.30% |

Management's Discussion of Fund Performance

PERFORMANCE OVERVIEW

• The Fund’s Class N shares returned 33.53% for the fiscal year that ended October 31, 2024, underperforming the Russell 2000® Growth Index, which returned 36.49% for the period. The S&P 500® Index returned 38.02% for the period.

• The first eight months of the fiscal year were defined by a shifting market sentiment towards declining interest rates as inflation cooled. During this time, technology stocks, specifically those related to artificial intelligence (AI), led the market and contributed meaningfully to the Fund’s performance.

• The last four months were defined by the market realization that interest rates would not be lowered as quickly as anticipated, a decline in tech stocks, but an overall broadening of the market’s performance.

TOP CONTRIBUTORS AND DETRACTORS

• The industrials sector was a positive contributor with several strong performers in the commercial aerospace and building product markets, including FTAI Aviation (+264%) and Granite Construction (+109%).

• The materials sector was a positive contributor due to strength from Carpenter Technology (+140%) and Eagle Materials (+86%).

• Technology stocks contributed strongly to performance through the first half of the year, but declined in the third quarter as the technology sector overall, and especially our semiconductor-related stocks, sold off. Top contributors included Coherent (+212%) and Pure Storage (+51%). Top detractors included indie Semiconductor (-32%) and MaxLinear (-15%).

• The consumer discretionary sector was the top detractor as the Fund’s 11% return could not keep pace with the 35% return for the Russell 2000® Growth Index. The top detractor in the sector was Xponential Fitness (-26%). The Fund exited its position in Xponential Fitness during the period.

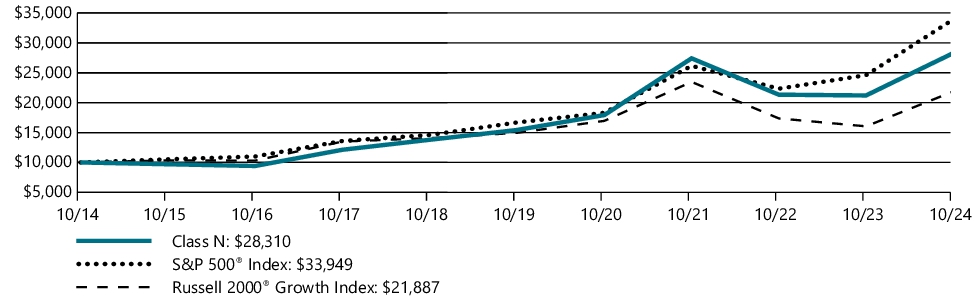

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class N | 33.53% | 12.92% | 10.97% |

| S&P 500® Index | 38.02% | 15.27% | 13.00% |

| Russell 2000® Growth Index | 36.49% | 7.92% | 8.15% |

Effective October 31, 2024, the S&P 500® Index was added as a broad measure of market performance in accordance with recent changes to regulatory disclosure requirements. The Fund continues to use the Russell 2000® Growth Index as an additional benchmark that reflects the market segment(s) in which the Fund invests.

The S&P Index is proprietary data of Standard & Poor’s, a division of McGraw-Hill Companies, Inc. All rights reserved.

The Russell Index is a trademark of the London Stock Exchange Group companies.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $78,712,660 |

| Total number of portfolio holdings | 122 |

| Net advisory fees paid | $347,097 |

| Portfolio turnover rate as of the end of the reporting period | 234% |

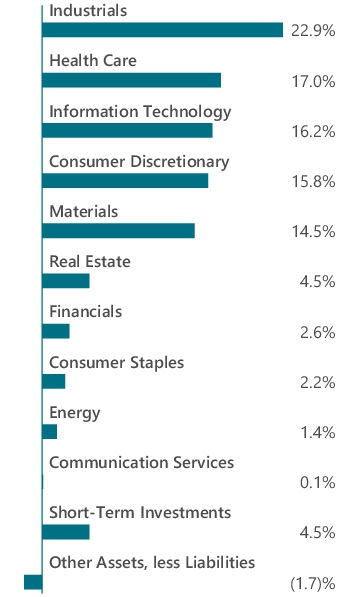

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund.

| Summit Materials, Inc., Class A | 4.1% |

| Eagle Materials, Inc. | 3.8% |

| Lithia Motors, Inc. | 3.8% |

| United Therapeutics Corp. | 3.2% |

| Beacon Roofing Supply, Inc. | 3.2% |

| Viking Therapeutics, Inc. | 3.1% |

| Caesars Entertainment, Inc. | 3.1% |

| Granite Construction, Inc. | 3.1% |

| Credo Technology Group Holding, Ltd. | 2.8% |

| ATI, Inc. | 2.3% |

| Top Ten as a Group | 32.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG Frontier Small Cap Growth Fund

Class I/MSSCX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Frontier Small Cap Growth Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Frontier Small Cap Growth Fund

(Class I/MSSCX) | $116 | 0.99% |

Management's Discussion of Fund Performance

PERFORMANCE OVERVIEW

• The Fund’s Class I shares returned 33.86% for the fiscal year that ended October 31, 2024, underperforming the Russell 2000® Growth Index, which returned 36.49% for the period. The S&P 500® Index returned 38.02% for the period.

• The first eight months of the fiscal year were defined by a shifting market sentiment towards declining interest rates as inflation cooled. During this time, technology stocks, specifically those related to artificial intelligence (AI), led the market and contributed meaningfully to the Fund’s performance.

• The last four months were defined by the market realization that interest rates would not be lowered as quickly as anticipated, a decline in tech stocks, but an overall broadening of the market’s performance.

TOP CONTRIBUTORS AND DETRACTORS

• The industrials sector was a positive contributor with several strong performers in the commercial aerospace and building product markets, including FTAI Aviation (+264%) and Granite Construction (+109%).

• The materials sector was a positive contributor due to strength from Carpenter Technology (+140%) and Eagle Materials (+86%).

• Technology stocks contributed strongly to performance through the first half of the year, but declined in the third quarter as the technology sector overall, and especially our semiconductor-related stocks, sold off. Top contributors included Coherent (+212%) and Pure Storage (+51%). Top detractors included indie Semiconductor (-32%) and MaxLinear (-15%).

• The consumer discretionary sector was the top detractor as the Fund’s 11% return could not keep pace with the 35% return for the Russell 2000® Growth Index. The top detractor in the sector was Xponential Fitness (-26%). The Fund exited its position in Xponential Fitness during the period.

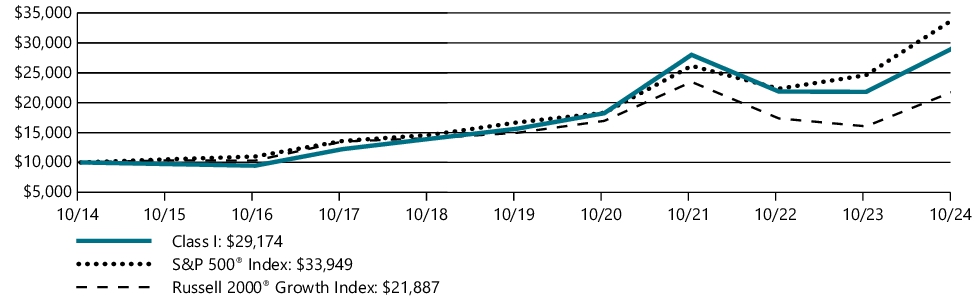

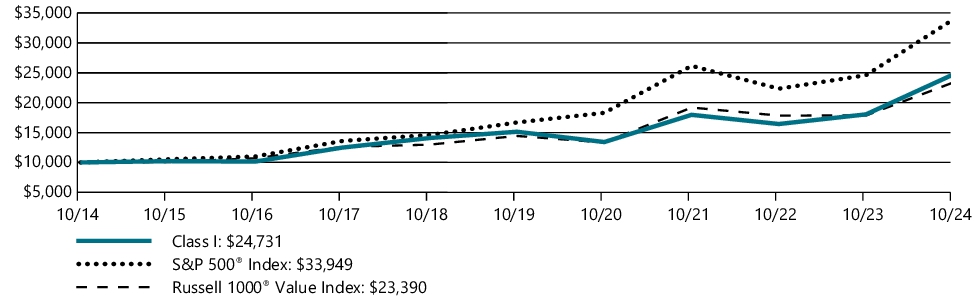

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class I | 33.86% | 13.30% | 11.30% |

| S&P 500® Index | 38.02% | 15.27% | 13.00% |

| Russell 2000® Growth Index | 36.49% | 7.92% | 8.15% |

Effective October 31, 2024, the S&P 500® Index was added as a broad measure of market performance in accordance with recent changes to regulatory disclosure requirements. The Fund continues to use the Russell 2000® Growth Index as an additional benchmark that reflects the market segment(s) in which the Fund invests.

The S&P Index is proprietary data of Standard & Poor’s, a division of McGraw-Hill Companies, Inc. All rights reserved.

The Russell Index is a trademark of the London Stock Exchange Group companies.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $78,712,660 |

| Total number of portfolio holdings | 122 |

| Net advisory fees paid | $347,097 |

| Portfolio turnover rate as of the end of the reporting period | 234% |

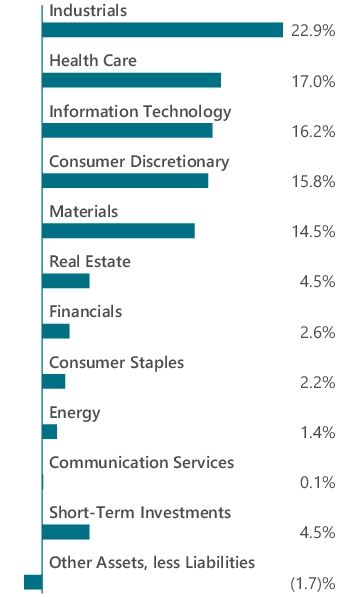

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund.

| Summit Materials, Inc., Class A | 4.1% |

| Eagle Materials, Inc. | 3.8% |

| Lithia Motors, Inc. | 3.8% |

| United Therapeutics Corp. | 3.2% |

| Beacon Roofing Supply, Inc. | 3.2% |

| Viking Therapeutics, Inc. | 3.1% |

| Caesars Entertainment, Inc. | 3.1% |

| Granite Construction, Inc. | 3.1% |

| Credo Technology Group Holding, Ltd. | 2.8% |

| ATI, Inc. | 2.3% |

| Top Ten as a Group | 32.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG Frontier Small Cap Growth Fund

Class Z/MSSYX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Frontier Small Cap Growth Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Frontier Small Cap Growth Fund

(Class Z/MSSYX) | $105 | 0.90% |

Management's Discussion of Fund Performance

PERFORMANCE OVERVIEW

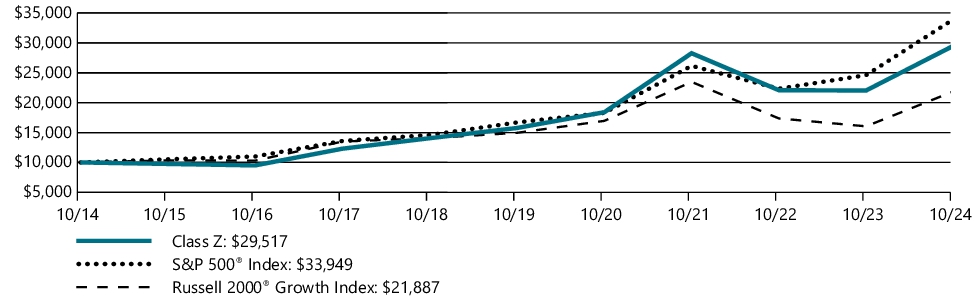

• The Fund’s Class Z shares returned 34.01% for the fiscal year that ended October 31, 2024, underperforming the Russell 2000® Growth Index, which returned 36.49% for the period. The S&P 500® Index returned 38.02% for the period.

• The first eight months of the fiscal year were defined by a shifting market sentiment towards declining interest rates as inflation cooled. During this time, technology stocks, specifically those related to artificial intelligence (AI), led the market and contributed meaningfully to the Fund’s performance.

• The last four months were defined by the market realization that interest rates would not be lowered as quickly as anticipated, a decline in tech stocks, but an overall broadening of the market’s performance.

TOP CONTRIBUTORS AND DETRACTORS

• The industrials sector was a positive contributor with several strong performers in the commercial aerospace and building product markets, including FTAI Aviation (+264%) and Granite Construction (+109%).

• The materials sector was a positive contributor due to strength from Carpenter Technology (+140%) and Eagle Materials (+86%).

• Technology stocks contributed strongly to performance through the first half of the year, but declined in the third quarter as the technology sector overall, and especially our semiconductor-related stocks, sold off. Top contributors included Coherent (+212%) and Pure Storage (+51%). Top detractors included indie Semiconductor (-32%) and MaxLinear (-15%).

• The consumer discretionary sector was the top detractor as the Fund’s 11% return could not keep pace with the 35% return for the Russell 2000® Growth Index. The top detractor in the sector was Xponential Fitness (-26%). The Fund exited its position in Xponential Fitness during the period.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class Z | 34.01% | 13.37% | 11.43% |

| S&P 500® Index | 38.02% | 15.27% | 13.00% |

| Russell 2000® Growth Index | 36.49% | 7.92% | 8.15% |

Effective October 31, 2024, the S&P 500® Index was added as a broad measure of market performance in accordance with recent changes to regulatory disclosure requirements. The Fund continues to use the Russell 2000® Growth Index as an additional benchmark that reflects the market segment(s) in which the Fund invests.

The S&P Index is proprietary data of Standard & Poor’s, a division of McGraw-Hill Companies, Inc. All rights reserved.

The Russell Index is a trademark of the London Stock Exchange Group companies.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $78,712,660 |

| Total number of portfolio holdings | 122 |

| Net advisory fees paid | $347,097 |

| Portfolio turnover rate as of the end of the reporting period | 234% |

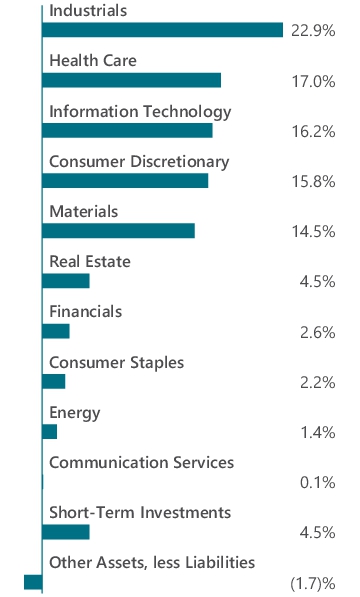

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund.

| Summit Materials, Inc., Class A | 4.1% |

| Eagle Materials, Inc. | 3.8% |

| Lithia Motors, Inc. | 3.8% |

| United Therapeutics Corp. | 3.2% |

| Beacon Roofing Supply, Inc. | 3.2% |

| Viking Therapeutics, Inc. | 3.1% |

| Caesars Entertainment, Inc. | 3.1% |

| Granite Construction, Inc. | 3.1% |

| Credo Technology Group Holding, Ltd. | 2.8% |

| ATI, Inc. | 2.3% |

| Top Ten as a Group | 32.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG GW&K Core Bond ESG Fund

Class N/MBGVX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG GW&K Core Bond ESG Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG GW&K Core Bond ESG Fund

(Class N/MBGVX) | $93 | 0.88% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class N shares returned 10.70% for the fiscal year that ended October 31, 2024, outperforming the Bloomberg U.S. Aggregate Bond Index, which returned 10.55% during the period.

• The fixed income market generated strong returns during the past fiscal year, as interest rates fell and credit spreads narrowed amidst a decrease in the pace of inflation and a solid economy.

Top Contributors and Detractors

• The primary driver of this outperformance was the Fund’s overweight position to corporates.

• An overweight position to the securitized debt sector and allocation decisions also contributed positively, particularly the Fund’s focus on higher coupon mortgage-backed securities (MBS).

• Security selection within MBS played a significant role in the Fund’s outperformance.

• An out-of-benchmark allocation to preferreds further enhanced overall performance.

Positioning Update

• The Fund is generally neutral duration and is focused on the intermediate part of the yield curve where we find the best risk-adjusted value in the spread sectors.

• The Fund is overweight corporate bonds, and its allocation is expressed in higher-quality issuers with strong cash flows and solid balance sheets. Corporates continue to benefit from the strong fundamental environment supported by solid balance sheets and resilient earnings. Conversely, spreads are historically tight and further moves lower from here are likely limited.

• MBS valuations look attractive at these levels, but interest rate volatility has been a headwind.

• Asset-backed securities (ABS) has proven to be a good diversifier in the securitized space, with less correlation to rate volatility versus the MBS sector, and market demand remains strong.

• Preferred securities potentially offer attractive income and diversification.

• The Fund is overweight taxable municipal bonds given strong fundamentals and the recession-resistant characteristics offered by the asset class.

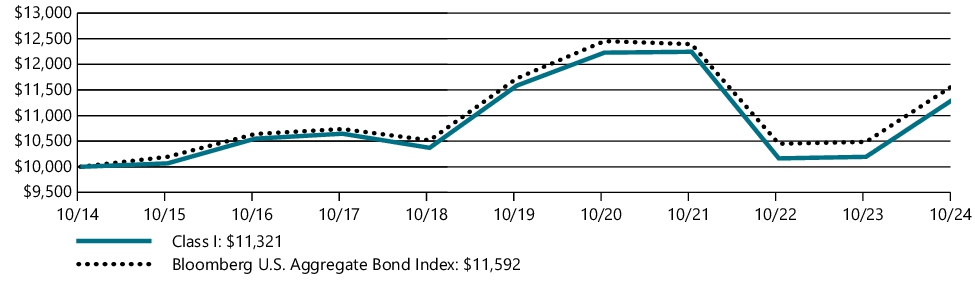

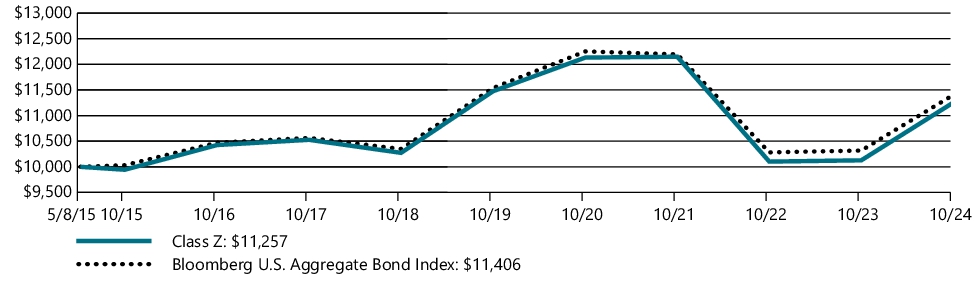

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted since the class's inception on May 08, 2015, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-year and five-year periods and the period from the class's inception through October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | Since Inception |

| Class N | 10.70% | (0.78%) | 0.85% |

| Bloomberg U.S. Aggregate Bond Index | 10.55% | (0.23%) | 1.40% |

"Bloomberg®" and any Bloomberg index described herein are service marks of Bloomberg Finance L. P. and its affiliates, including Bloomberg Index Services Limited ("BISL"), the administrator of the index (collectively, "Bloomberg") and have been licensed for use for certain purposes by AMG Funds LLC. Bloomberg is not affiliated with AMG Funds LLC, and Bloomberg does not approve, endorse, review, or recommend the fund described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to such fund.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $118,779,576 |

| Total number of portfolio holdings | 121 |

| Net advisory fees paid | $194,655 |

| Portfolio turnover rate as of the end of the reporting period | 34% |

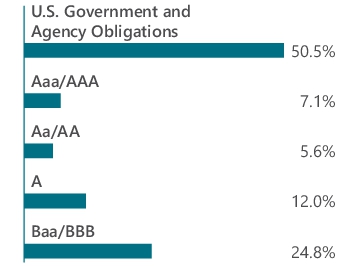

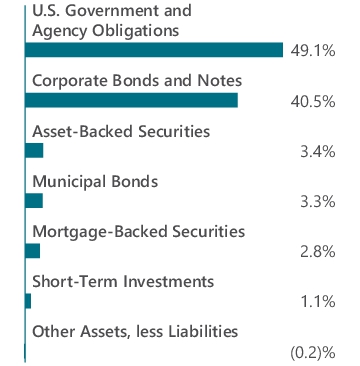

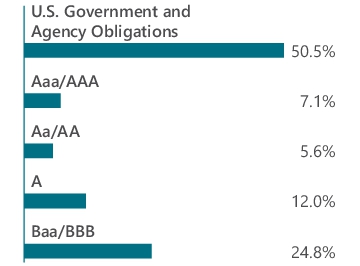

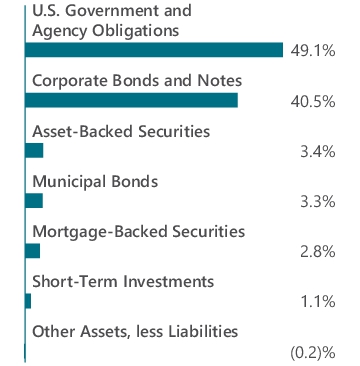

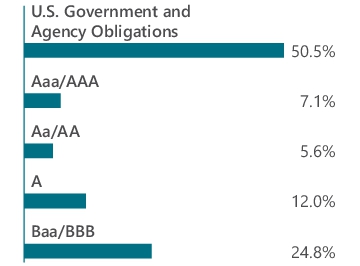

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and ratings are shown as a percentage of total long-term investments of the Fund.

| U.S. Treasury Bonds, 2.250%, 05/15/41 | 4.4% |

| U.S. Treasury Bonds, 3.125%, 05/15/48 | 2.9% |

| FHLMC, 3.500%, 10/01/45 | 2.4% |

| U.S. Treasury Bonds, 3.500%, 02/15/39 | 2.3% |

| FHLMC, 5.500%, 06/01/53 | 2.0% |

| FHLMC, 3.000%, 11/01/49 | 2.0% |

| U.S. Treasury Bonds, 1.875%, 02/15/51 | 1.8% |

| FNMA, 4.500%, 06/01/41 | 1.6% |

| FHLMC, 2.500%, 10/01/34 | 1.6% |

| California State General Obligation, School Improvements, Build America Bonds, 7.550%, 04/01/39 | 1.5% |

| Top Ten as a Group | 22.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG GW&K Core Bond ESG Fund

Class I/MBDFX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG GW&K Core Bond ESG Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG GW&K Core Bond ESG Fund

(Class I/MBDFX) | $58 | 0.55% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class I shares returned 11.06% for the fiscal year that ended October 31, 2024, outperforming the Bloomberg U.S. Aggregate Bond Index, which returned 10.55% during the period.

• The fixed income market generated strong returns during the past fiscal year, as interest rates fell and credit spreads narrowed amidst a decrease in the pace of inflation and a solid economy.

Top Contributors and Detractors

• The primary driver of this outperformance was the Fund’s overweight position to corporates.

• An overweight position to the securitized debt sector and allocation decisions also contributed positively, particularly the Fund’s focus on higher coupon mortgage-backed securities (MBS).

• Security selection within MBS played a significant role in the Fund’s outperformance.

• An out-of-benchmark allocation to preferreds further enhanced overall performance.

Positioning Update

• The Fund is generally neutral duration and is focused on the intermediate part of the yield curve where we find the best risk-adjusted value in the spread sectors.

• The Fund is overweight corporate bonds, and its allocation is expressed in higher-quality issuers with strong cash flows and solid balance sheets. Corporates continue to benefit from the strong fundamental environment supported by solid balance sheets and resilient earnings. Conversely, spreads are historically tight and further moves lower from here are likely limited.

• MBS valuations look attractive at these levels, but interest rate volatility has been a headwind.

• Asset-backed securities (ABS) has proven to be a good diversifier in the securitized space, with less correlation to rate volatility versus the MBS sector, and market demand remains strong.

• Preferred securities potentially offer attractive income and diversification.

• The Fund is overweight taxable municipal bonds given strong fundamentals and the recession-resistant characteristics offered by the asset class.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class I | 11.06% | (0.46%) | 1.25% |

| Bloomberg U.S. Aggregate Bond Index | 10.55% | (0.23%) | 1.49% |

"Bloomberg®" and any Bloomberg index described herein are service marks of Bloomberg Finance L. P. and its affiliates, including Bloomberg Index Services Limited ("BISL"), the administrator of the index (collectively, "Bloomberg") and have been licensed for use for certain purposes by AMG Funds LLC. Bloomberg is not affiliated with AMG Funds LLC, and Bloomberg does not approve, endorse, review, or recommend the fund described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to such fund.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $118,779,576 |

| Total number of portfolio holdings | 121 |

| Net advisory fees paid | $194,655 |

| Portfolio turnover rate as of the end of the reporting period | 34% |

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and ratings are shown as a percentage of total long-term investments of the Fund.

| U.S. Treasury Bonds, 2.250%, 05/15/41 | 4.4% |

| U.S. Treasury Bonds, 3.125%, 05/15/48 | 2.9% |

| FHLMC, 3.500%, 10/01/45 | 2.4% |

| U.S. Treasury Bonds, 3.500%, 02/15/39 | 2.3% |

| FHLMC, 5.500%, 06/01/53 | 2.0% |

| FHLMC, 3.000%, 11/01/49 | 2.0% |

| U.S. Treasury Bonds, 1.875%, 02/15/51 | 1.8% |

| FNMA, 4.500%, 06/01/41 | 1.6% |

| FHLMC, 2.500%, 10/01/34 | 1.6% |

| California State General Obligation, School Improvements, Build America Bonds, 7.550%, 04/01/39 | 1.5% |

| Top Ten as a Group | 22.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG GW&K Core Bond ESG Fund

Class Z/MBDLX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG GW&K Core Bond ESG Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG GW&K Core Bond ESG Fund

(Class Z/MBDLX) | $51 | 0.48% |

Management's Discussion of Fund Performance

Performance Overview

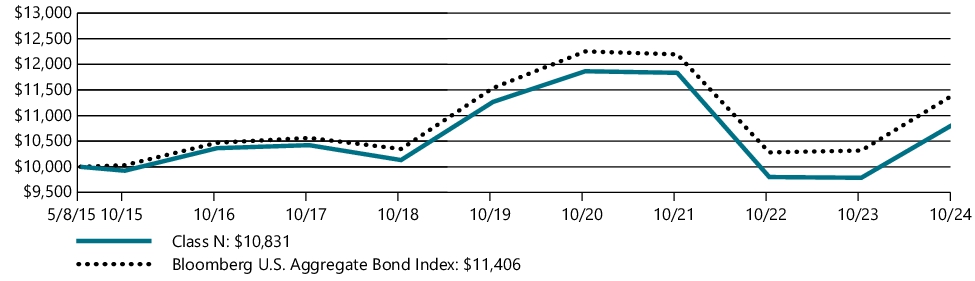

• The Fund’s Class Z shares returned 11.15% for the fiscal year that ended October 31, 2024, outperforming the Bloomberg U.S. Aggregate Bond Index, which returned 10.55% during the period.

• The fixed income market generated strong returns during the past fiscal year, as interest rates fell and credit spreads narrowed amidst a decrease in the pace of inflation and a solid economy.

Top Contributors and Detractors

• The primary driver of this outperformance was the Fund’s overweight position to corporates.

• An overweight position to the securitized debt sector and allocation decisions also contributed positively, particularly the Fund’s focus on higher coupon mortgage-backed securities (MBS).

• Security selection within MBS played a significant role in the Fund’s outperformance.

• An out-of-benchmark allocation to preferreds further enhanced overall performance.

Positioning Update

• The Fund is generally neutral duration and is focused on the intermediate part of the yield curve where we find the best risk-adjusted value in the spread sectors.

• The Fund is overweight corporate bonds, and its allocation is expressed in higher-quality issuers with strong cash flows and solid balance sheets. Corporates continue to benefit from the strong fundamental environment supported by solid balance sheets and resilient earnings. Conversely, spreads are historically tight and further moves lower from here are likely limited.

• MBS valuations look attractive at these levels, but interest rate volatility has been a headwind.

• Asset-backed securities (ABS) has proven to be a good diversifier in the securitized space, with less correlation to rate volatility versus the MBS sector, and market demand remains strong.

• Preferred securities potentially offer attractive income and diversification.

• The Fund is overweight taxable municipal bonds given strong fundamentals and the recession-resistant characteristics offered by the asset class.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted since the class's inception on May 08, 2015, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-year and five-year periods and the period from the class's inception through October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | Since Inception |

| Class Z | 11.15% | (0.39%) | 1.26% |

| Bloomberg U.S. Aggregate Bond Index | 10.55% | (0.23%) | 1.40% |

"Bloomberg®" and any Bloomberg index described herein are service marks of Bloomberg Finance L. P. and its affiliates, including Bloomberg Index Services Limited ("BISL"), the administrator of the index (collectively, "Bloomberg") and have been licensed for use for certain purposes by AMG Funds LLC. Bloomberg is not affiliated with AMG Funds LLC, and Bloomberg does not approve, endorse, review, or recommend the fund described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to such fund.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $118,779,576 |

| Total number of portfolio holdings | 121 |

| Net advisory fees paid | $194,655 |

| Portfolio turnover rate as of the end of the reporting period | 34% |

Graphical Representation of Holdings (as of October 31, 2024)

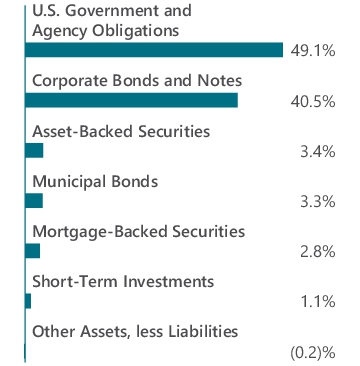

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and ratings are shown as a percentage of total long-term investments of the Fund.

| U.S. Treasury Bonds, 2.250%, 05/15/41 | 4.4% |

| U.S. Treasury Bonds, 3.125%, 05/15/48 | 2.9% |

| FHLMC, 3.500%, 10/01/45 | 2.4% |

| U.S. Treasury Bonds, 3.500%, 02/15/39 | 2.3% |

| FHLMC, 5.500%, 06/01/53 | 2.0% |

| FHLMC, 3.000%, 11/01/49 | 2.0% |

| U.S. Treasury Bonds, 1.875%, 02/15/51 | 1.8% |

| FNMA, 4.500%, 06/01/41 | 1.6% |

| FHLMC, 2.500%, 10/01/34 | 1.6% |

| California State General Obligation, School Improvements, Build America Bonds, 7.550%, 04/01/39 | 1.5% |

| Top Ten as a Group | 22.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG River Road Large Cap Value Select Fund

Class N/FQUAX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG River Road Large Cap Value Select Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG River Road Large Cap Value Select Fund

(Class N/FQUAX) | $112 | 0.95% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class N shares returned 36.62% for the fiscal year that ended October 31, 2024, underperforming the S&P 500® Index, which returned 38.02% for the period.

Top Contributors and Detractors

• Stock selection was positive, while sector allocation was negative.

• The sectors with the highest contribution to relative return were industrials and materials. Industrials benefited from positive stock selection and an underweight allocation. Materials benefited from positive stock selection, partially offset by an overweight allocation.

• The holdings with the highest contribution to active return were KKR, Talen Energy, and CRH.

• The sectors with the lowest contribution to relative return were information technology and consumer discretionary. Information technology suffered from lack of exposure. Consumer discretionary suffered from negative stock selection, partially offset by an overweight allocation.

• The holdings with the lowest contribution to active return were Nestle, LKQ, and Valaris Limited.

Positioning

• As of October 31, 2024, the Fund is meaningfully overweight (greater than 5%) in four sectors and meaningfully underweight (greater than -5%) in two. The largest overweight allocations were consumer staples and financials. The largest underweight allocations were information technology and communication services.

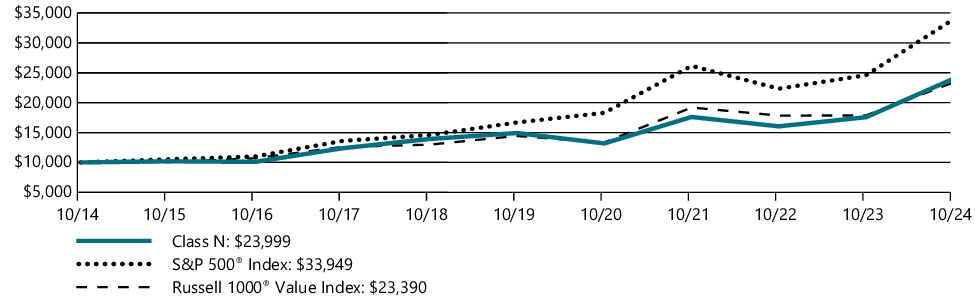

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class N | 36.62% | 9.97% | 9.15% |

| S&P 500® Index | 38.02% | 15.27% | 13.00% |

| Russell 1000® Value Index | 30.98% | 10.14% | 8.87% |

Effective October 31, 2024, the S&P 500® Index was added as a broad measure of market performance in accordance with recent changes to regulatory disclosure requirements. The Fund continues to use the Russell 1000® Value Index as an additional benchmark that reflects the market segment(s) in which the Fund invests.

As of March 22, 2021, the Fund's Subadviser was changed to River Road Asset Management, LLC. Prior to March 22, 2021, the Fund had different principal investment strategies and corresponding risks. The Fund's performance before March 22, 2021, might be less pertinent for investors considering whether to purchase shares of the Fund.

The S&P Index is proprietary data of Standard & Poor’s, a division of McGraw-Hill Companies, Inc. All rights reserved.

The Russell Index is a trademark of the London Stock Exchange Group companies.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $46,111,504 |

| Total number of portfolio holdings | 28 |

| Net advisory fees paid | $58,846 |

| Portfolio turnover rate as of the end of the reporting period | 106% |

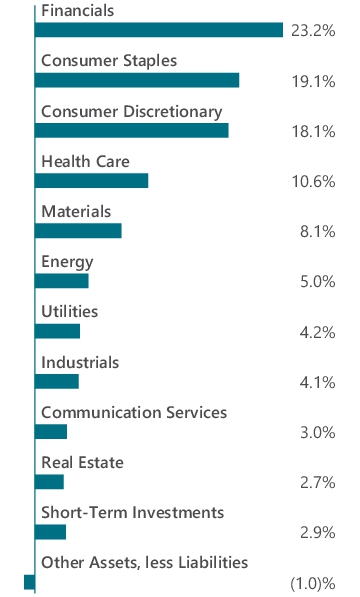

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund.

| CRH PLC | 8.1% |

| BJ's Wholesale Club Holdings, Inc. | 6.3% |

| Willis Towers Watson PLC (United Kingdom) | 6.0% |

| Fairfax Financial Holdings, Ltd. (Canada) | 5.7% |

| Lululemon Athletica, Inc. (Canada) | 5.1% |

| The Kroger Co. | 5.0% |

| Labcorp Holdings, Inc. | 4.9% |

| Lennar Corp., Class A | 4.6% |

| KKR & Co., Inc. | 4.5% |

| Casey's General Stores, Inc. | 4.3% |

| Top Ten as a Group | 54.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG River Road Large Cap Value Select Fund

Class I/MEQFX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG River Road Large Cap Value Select Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG River Road Large Cap Value Select Fund

(Class I/MEQFX) | $75 | 0.63% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class I shares returned 37.06% for the fiscal year that ended October 31, 2024, underperforming the S&P 500® Index, which returned 38.02% for the period.

Top Contributors and Detractors

• Stock selection was positive, while sector allocation was negative.

• The sectors with the highest contribution to relative return were industrials and materials. Industrials benefited from positive stock selection and an underweight allocation. Materials benefited from positive stock selection, partially offset by an overweight allocation.

• The holdings with the highest contribution to active return were KKR, Talen Energy, and CRH.

• The sectors with the lowest contribution to relative return were information technology and consumer discretionary. Information technology suffered from lack of exposure. Consumer discretionary suffered from negative stock selection, partially offset by an overweight allocation.

• The holdings with the lowest contribution to active return were Nestle, LKQ, and Valaris Limited.

Positioning

• As of October 31, 2024, the Fund is meaningfully overweight (greater than 5%) in four sectors and meaningfully underweight (greater than -5%) in two. The largest overweight allocations were consumer staples and financials. The largest underweight allocations were information technology and communication services.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of (i) a broad based index and (ii) an additional index reflecting the market segment(s) in which the Fund invests over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class I | 37.06% | 10.32% | 9.47% |

| S&P 500® Index | 38.02% | 15.27% | 13.00% |

| Russell 1000® Value Index | 30.98% | 10.14% | 8.87% |

Effective October 31, 2024, the S&P 500® Index was added as a broad measure of market performance in accordance with recent changes to regulatory disclosure requirements. The Fund continues to use the Russell 1000® Value Index as an additional benchmark that reflects the market segment(s) in which the Fund invests.

As of March 22, 2021, the Fund's Subadviser was changed to River Road Asset Management, LLC. Prior to March 22, 2021, the Fund had different principal investment strategies and corresponding risks. The Fund's performance before March 22, 2021, might be less pertinent for investors considering whether to purchase shares of the Fund.

The S&P Index is proprietary data of Standard & Poor’s, a division of McGraw-Hill Companies, Inc. All rights reserved.

The Russell Index is a trademark of the London Stock Exchange Group companies.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $46,111,504 |

| Total number of portfolio holdings | 28 |

| Net advisory fees paid | $58,846 |

| Portfolio turnover rate as of the end of the reporting period | 106% |

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund.

| CRH PLC | 8.1% |

| BJ's Wholesale Club Holdings, Inc. | 6.3% |

| Willis Towers Watson PLC (United Kingdom) | 6.0% |

| Fairfax Financial Holdings, Ltd. (Canada) | 5.7% |

| Lululemon Athletica, Inc. (Canada) | 5.1% |

| The Kroger Co. | 5.0% |

| Labcorp Holdings, Inc. | 4.9% |

| Lennar Corp., Class A | 4.6% |

| KKR & Co., Inc. | 4.5% |

| Casey's General Stores, Inc. | 4.3% |

| Top Ten as a Group | 54.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG Veritas China Fund

Class N/MMCFX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Veritas China Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Veritas China Fund

(Class N/MMCFX) | $115 | 1.15% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class N shares delivered a positive return of 0.36% for the fiscal year that ended October 31, 2024, but underperformed the MSCI China Index, which returned 21.75% for the period.

• For much of the year, China’s equity markets lagged behind regional peers like India, South Korea, and Taiwan, despite high initial optimism post-COVID-19.

• Investor sentiment was dampened by a slower-than-expected economic recovery and weak consumer spending. However, signs of stabilisation began to surface midway through the year, and a market rebound ensued after China’s extensive stimulus measures boosted market confidence.

Relative Performance

• The Fund’s largest detractors were in consumer discretionary, with notable weaknesses in Meituan, China’s major food delivery platform, and New Oriental, a leading private education provider.

• Alibaba showed signs of recovery toward the end of the period, while Tencent delivered strong returns, backed by diversified revenues in gaming, advertising, and strategic investments.

Positioning and Outlook

• September’s policy easing by President Xi’s administration marked a shift from China’s previous moderate stance. Increased corporate buybacks suggest improved governance and shareholder returns, potentially translating to stronger earnings per share growth.

• With Chinese equities trading at attractive valuations relative to global and Emerging Markets, we are optimistic that these policies will support sustained recovery and strengthen market confidence.

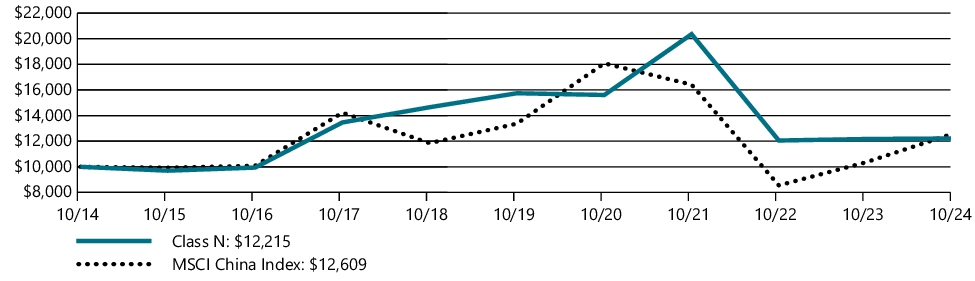

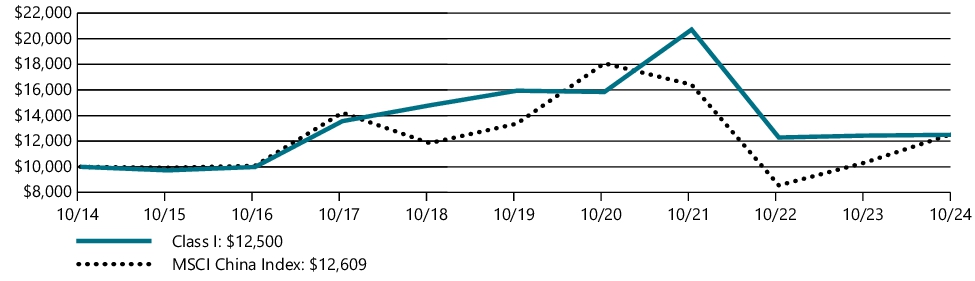

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class N | 0.36% | (4.95%) | 2.02% |

| MSCI China Index | 21.75% | (1.17%) | 2.35% |

As of May 21, 2021, the Fund's Subadviser was changed to Veritas Asset Management LLP. Prior to May 21, 2021, the Fund had different principal investment strategies and corresponding risks. The Fund's performance before May 21, 2021, might be less pertinent for investors considering whether to purchase shares of the Fund.

All MSCI data is provided "as is". The products described herein are not sponsored or endorsed and have not been reviewed or passed on by MSCI. In no event shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data or the products described herein. Copying or redistributing the MSCI data is strictly prohibited.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $43,196,442 |

| Total number of portfolio holdings | 36 |

| Net advisory fees paid | $168,265 |

| Portfolio turnover rate as of the end of the reporting period | 100% |

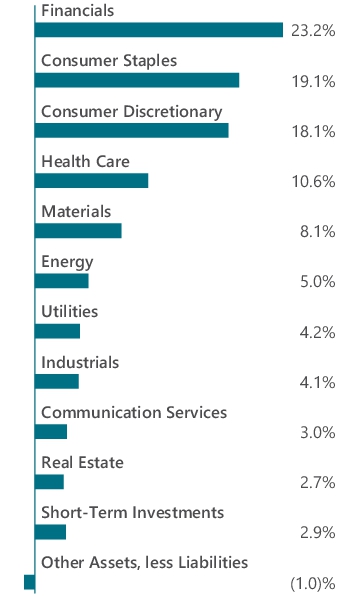

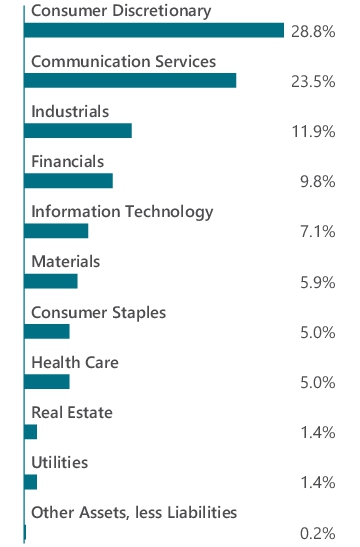

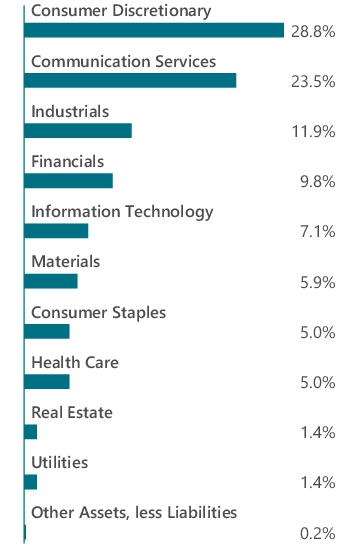

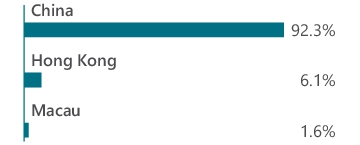

Graphical Representation of Holdings (as of October 31, 2024)

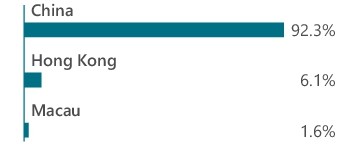

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and country allocation is shown as a percentage of total long-term investments of the Fund.

| Tencent Holdings, Ltd. (China) | 19.4% |

| Alibaba Group Holding, Ltd. (China) | 9.5% |

| Zijin Mining Group Co., Ltd., Class H (China) | 4.9% |

| NARI Technology Co., Ltd., Class A (China) | 4.8% |

| Meituan, Class B (China) | 4.4% |

| Contemporary Amperex Technology Co., Ltd., Class A (China) | 4.0% |

| BYD Co., Ltd., Class A (China) | 3.8% |

| PDD Holdings, Inc., ADR (China) | 3.7% |

| NetEase, Inc. (China) | 3.1% |

| Tsingtao Brewery Co., Ltd., Class H (China) | 2.9% |

| Top Ten as a Group | 60.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

AMG Veritas China Fund

Class I/MIMFX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Veritas China Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Veritas China Fund

(Class I/MIMFX) | $94 | 0.94% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class I shares delivered a positive return of 0.53% for the fiscal year that ended October 31, 2024, but underperformed the MSCI China Index, which returned 21.75% for the period.

• For much of the year, China’s equity markets lagged behind regional peers like India, South Korea, and Taiwan, despite high initial optimism post-COVID-19.

• Investor sentiment was dampened by a slower-than-expected economic recovery and weak consumer spending. However, signs of stabilisation began to surface midway through the year, and a market rebound ensued after China’s extensive stimulus measures boosted market confidence.

Relative Performance

• The Fund’s largest detractors were in consumer discretionary, with notable weaknesses in Meituan, China’s major food delivery platform, and New Oriental, a leading private education provider.

• Alibaba showed signs of recovery toward the end of the period, while Tencent delivered strong returns, backed by diversified revenues in gaming, advertising, and strategic investments.

Positioning and Outlook

• September’s policy easing by President Xi’s administration marked a shift from China’s previous moderate stance. Increased corporate buybacks suggest improved governance and shareholder returns, potentially translating to stronger earnings per share growth.

• With Chinese equities trading at attractive valuations relative to global and Emerging Markets, we are optimistic that these policies will support sustained recovery and strengthen market confidence.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class I | 0.53% | (4.74%) | 2.26% |

| MSCI China Index | 21.75% | (1.17%) | 2.35% |

As of May 21, 2021, the Fund's Subadviser was changed to Veritas Asset Management LLP. Prior to May 21, 2021, the Fund had different principal investment strategies and corresponding risks. The Fund's performance before May 21, 2021, might be less pertinent for investors considering whether to purchase shares of the Fund.

All MSCI data is provided "as is". The products described herein are not sponsored or endorsed and have not been reviewed or passed on by MSCI. In no event shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data or the products described herein. Copying or redistributing the MSCI data is strictly prohibited.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $43,196,442 |

| Total number of portfolio holdings | 36 |

| Net advisory fees paid | $168,265 |

| Portfolio turnover rate as of the end of the reporting period | 100% |

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and country allocation is shown as a percentage of total long-term investments of the Fund.

| Tencent Holdings, Ltd. (China) | 19.4% |

| Alibaba Group Holding, Ltd. (China) | 9.5% |

| Zijin Mining Group Co., Ltd., Class H (China) | 4.9% |

| NARI Technology Co., Ltd., Class A (China) | 4.8% |

| Meituan, Class B (China) | 4.4% |

| Contemporary Amperex Technology Co., Ltd., Class A (China) | 4.0% |

| BYD Co., Ltd., Class A (China) | 3.8% |

| PDD Holdings, Inc., ADR (China) | 3.7% |

| NetEase, Inc. (China) | 3.1% |

| Tsingtao Brewery Co., Ltd., Class H (China) | 2.9% |

| Top Ten as a Group | 60.5% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

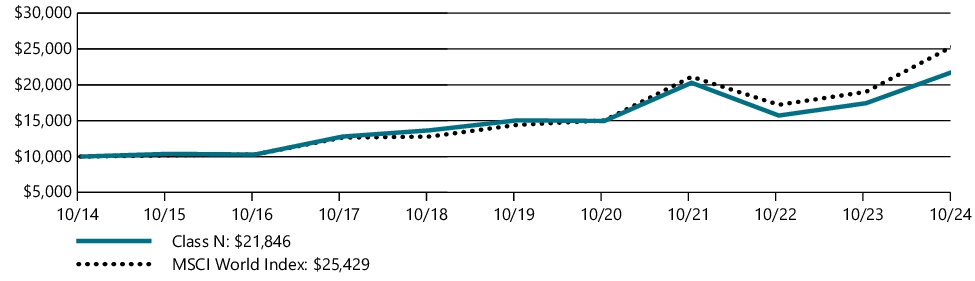

AMG Veritas Global Focus Fund

Class N/MFQAX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Veritas Global Focus Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Veritas Global Focus Fund

(Class N/MFQAX) | $127 | 1.13% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class N shares delivered strong absolute returns of 25.27% for the fiscal year that ended October 31, 2024, but underperformed the MSCI World Index, which returned 33.68% for the period.

Relative Performance

• The primary detractor to relative performance was the underweight in information technology. The Fund held Amazon, Alphabet, and Microsoft, but not NVIDIA, Apple, Meta, or Tesla, which has been a drag to relative performance.

• Without an outsized position in these select few securities, the odds have been stacked against beating the market. Being underweight, these securities were in hindsight a significant risk to relative returns, and the more concentrated and levered you were to them the better.

• Another large detractor was Charter Communications. The company’s shares fell after its Q4 results due to a 61,000 drop in broadband subscribers, impacted by a dispute with Disney and rising competition from fiber and fixed wireless access (FWA). Charter’s long-term prospects remain positive, with plans to upgrade its network for faster, multigigabit speeds, providing a competitive edge over FWA.

• Another key detractor was Diageo where there has been fear that growth has stalled due to a weak economic environment in the U.S., their single largest market. Weak consumer demand in China, along with uncertainty around GLP-1 weight loss drugs—which reportedly reduce alcohol consumption—has also driven weak sentiment.

Positioning and Outlook

• As we know, market participants are drawn to what works, like moths are drawn to flames. The more concentrated the focus, the greater the number is of excellent businesses dumped unceremoniously by the wayside. We recently had the chance to invest in several such opportunities, and when the flame burns out for other market participants, we believe our pipeline of new ideas will ignite.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class N | 25.27% | 7.74% | 8.13% |

| MSCI World Index | 33.68% | 12.03% | 9.78% |

As of May 21, 2021, the Fund's subadviser was changed to Veritas Asset Management LLP. Prior to May 21, 2021, the Fund had different principal investment strategies and corresponding risks. The Fund's performance before May 21, 2021, might be less pertinent for investors considering whether to purchase shares of the Fund.

All MSCI data is provided "as is". The products described herein are not sponsored or endorsed and have not been reviewed or passed on by MSCI. In no event shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data or the products described herein. Copying or redistributing the MSCI data is strictly prohibited.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $32,420,249 |

| Total number of portfolio holdings | 31 |

| Net advisory fees paid | $109,693 |

| Portfolio turnover rate as of the end of the reporting period | 42% |

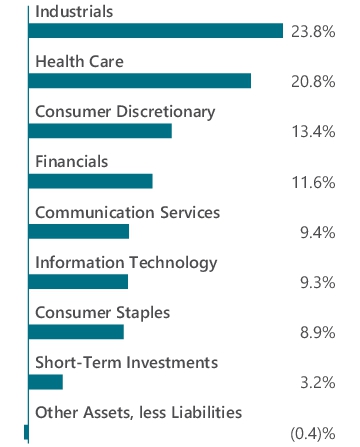

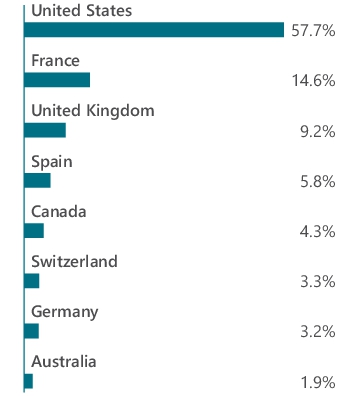

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and country allocation is shown as a percentage of total long-term investments of the Fund.

| Amazon.com, Inc. (United States) | 6.7% |

| Alphabet, Inc., Class A (United States) | 6.3% |

| Diageo PLC (United Kingdom) | 4.6% |

| Aon PLC, Class A (United States) | 4.6% |

| UnitedHealth Group, Inc. (United States) | 4.5% |

| Unilever PLC (United Kingdom) | 4.3% |

| Airbus SE (France) | 4.2% |

| Safran SA (France) | 4.2% |

| Canadian Pacific Kansas City, Ltd. (Canada) | 4.2% |

| Microsoft Corp. (United States) | 4.0% |

| Top Ten as a Group | 47.6% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

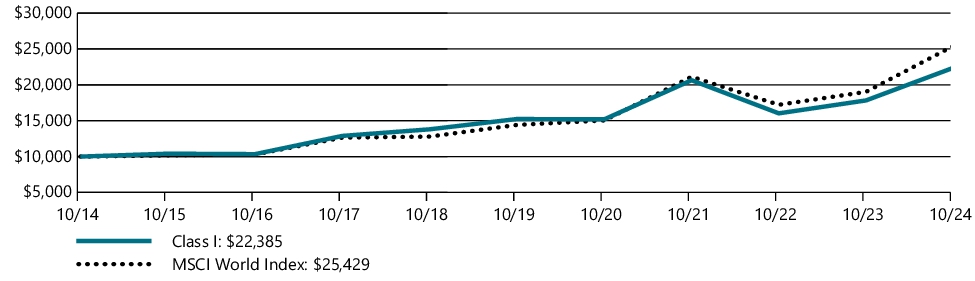

AMG Veritas Global Focus Fund

Class I/MFQTX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about AMG Veritas Global Focus Fund (the “Fund”) for the period of November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Fund Expenses

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

AMG Veritas Global Focus Fund

(Class I/MFQTX) | $99 | 0.88% |

Management's Discussion of Fund Performance

Performance Overview

• The Fund’s Class I shares delivered strong absolute returns of 25.58% for the fiscal year that ended October 31, 2024, but underperformed the MSCI World Index, which returned 33.68% for the period.

Relative Performance

• The primary detractor to relative performance was the underweight in information technology. The Fund held Amazon, Alphabet, and Microsoft, but not NVIDIA, Apple, Meta, or Tesla, which has been a drag to relative performance.

• Without an outsized position in these select few securities, the odds have been stacked against beating the market. Being underweight, these securities were in hindsight a significant risk to relative returns, and the more concentrated and levered you were to them the better.

• Another large detractor was Charter Communications. The company’s shares fell after its Q4 results due to a 61,000 drop in broadband subscribers, impacted by a dispute with Disney and rising competition from fiber and fixed wireless access (FWA). Charter’s long-term prospects remain positive, with plans to upgrade its network for faster, multigigabit speeds, providing a competitive edge over FWA.

• Another key detractor was Diageo where there has been fear that growth has stalled due to a weak economic environment in the U.S., their single largest market. Weak consumer demand in China, along with uncertainty around GLP-1 weight loss drugs—which reportedly reduce alcohol consumption—has also driven weak sentiment.

Positioning and Outlook

• As we know, market participants are drawn to what works, like moths are drawn to flames. The more concentrated the focus, the greater the number is of excellent businesses dumped unceremoniously by the wayside. We recently had the chance to invest in several such opportunities, and when the flame burns out for other market participants, we believe our pipeline of new ideas will ignite.

Fund Performance

The performance line graph below shows the performance of a hypothetical $10,000 investment in the class of shares noted over a ten year period, as compared to the performance of a broad based index. The performance table below shows the average annual total returns of the class of shares noted for the past one-, five-, and ten-year periods ended as of October 31, 2024. It also shows the average total returns of a broad based index over the same periods.

Performance for other share classes will vary. The Fund’s past performance is not a good predictor of the Fund’s future performance.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

GROWTH OF $10,000

| AVERAGE ANNUAL TOTAL RETURNS | 1 Year | 5 Years | 10 Years |

| Class I | 25.58% | 8.00% | 8.39% |

| MSCI World Index | 33.68% | 12.03% | 9.78% |

As of May 21, 2021, the Fund's subadviser was changed to Veritas Asset Management LLP. Prior to May 21, 2021, the Fund had different principal investment strategies and corresponding risks. The Fund's performance before May 21, 2021, might be less pertinent for investors considering whether to purchase shares of the Fund.

All MSCI data is provided "as is". The products described herein are not sponsored or endorsed and have not been reviewed or passed on by MSCI. In no event shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data or the products described herein. Copying or redistributing the MSCI data is strictly prohibited.

For updated Fund performance information, please visit: https://wealth.amg.com/.

Key Fund Statistics (as of October 31, 2024)

| Fund net assets | $32,420,249 |

| Total number of portfolio holdings | 31 |

| Net advisory fees paid | $109,693 |

| Portfolio turnover rate as of the end of the reporting period | 42% |

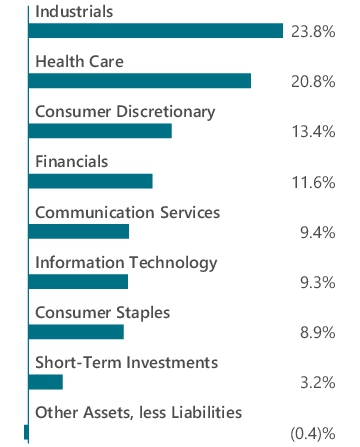

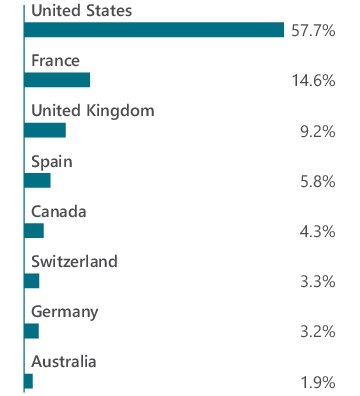

Graphical Representation of Holdings (as of October 31, 2024)

Top ten holdings and portfolio breakdown are shown as a percentage of net assets of the Fund and country allocation is shown as a percentage of total long-term investments of the Fund.

| Amazon.com, Inc. (United States) | 6.7% |

| Alphabet, Inc., Class A (United States) | 6.3% |

| Diageo PLC (United Kingdom) | 4.6% |

| Aon PLC, Class A (United States) | 4.6% |

| UnitedHealth Group, Inc. (United States) | 4.5% |

| Unilever PLC (United Kingdom) | 4.3% |

| Airbus SE (France) | 4.2% |

| Safran SA (France) | 4.2% |

| Canadian Pacific Kansas City, Ltd. (Canada) | 4.2% |

| Microsoft Corp. (United States) | 4.0% |

| Top Ten as a Group | 47.6% |

Availability of Additional Information

You can find additional information about the Fund such as the prospectus, financial information, fund holdings and proxy voting information at https://wealth.amg.com/resources/order-literature. You can also request this information by contacting us at 800.548.4539.

Householding

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communication to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 800.548.4539 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

For additional information, please navigate to the additional material at https://wealth.amg.com/resources/order-literature.

(b) Not applicable.

Item 2. CODE OF ETHICS