Table of Contents

Amendment No. 1 to Pricing Supplement No. 337 to theProspectus dated April 6, 2009, | Filed Pursuant to Rule 424(b)(3) Registration Statement No. 333-154173 |

The Goldman Sachs Group, Inc. Medium-Term Notes, Series D $156,772,000 Autocallable Underlier-Linked Notes due 2011 (Linked to a Weighted Basket Consisting of the Dow Jones EURO STOXX 50® Index, the FTSE® 100 Index and the TOPIX® Index) |

General

Your notes do not bear interest.The amount that you will be paid on your notes will be based on the performance of a weighted basket (which we refer to as the basket) comprised of the Dow Jones EURO STOXX 50® Index, the FTSE® 100 Index and the TOPIX® Index (which we refer to as the basket underliers),subject to some very significant conditions which are described below.

If, as measured on any call observation date (every Wednesday of each week commencing on April 14, 2010 and ending on the determination date (April 20, 2011), each subject to adjustment), the basket closing level has increased by 7% or more from the initial basket level of 100 on any of the call observation dates, your notes will be automatically called and three business days after the call observation date we will pay you a cash settlement amount of $1,070 for each $1,000 face amount of your notes. As a result of this weekly call feature, the return on your notes is capped and the maximum payment you could receive with respect to a $1,000 face amount note is $1,070.

If the basket closing level has declined, as compared to the initial basket level, by more than the knock-out amount of 20% on any day during the measurement period (every day which is a trading day for all three basket underliers from but excluding the trade date (April 1, 2010) to and including the determination date), which we refer to as a knock-out event, and your notes havenot been called, at stated maturity the return on your notes will equal the performance of the basket (subject to a maximum increase of 7%) from the trade date through the determination date.

If a knock-out event hasnot occurred and your notes havenot been called, the return on your notes will be the contingent minimum return of 0% if the final basket level (the basket closing level on the determination date) has remained the same or declined 20% or less from the initial basket level (a decline of more than 20% will result in a knock-out event). If the final basket level is greater than the initial basket level, but not greater than 107% of the initial basket level, your return on your notes will be equal to such increase (if the basket level increases by 7% or more, your notes will be called).

If your notes arenot called, on the stated maturity date, for each $1,000 face amount of your notes we will pay you an amount in cash equal to the cash settlement amount. We will determine the cash settlement amount by first calculating the percentage increase or decrease in the basket, which we refer to as the basket return. The basket return will be determined as follows: First, we will subtract the initial basket level from the final basket level. Then, we will divide the result by the initial basket level and express the resulting fraction as a percentage.

If the notes arenot called, the cash settlement amount for each note will be an amount in cash equal to:

• if a knock-out event occurs, thesum of (i) $1,000plus (ii) the product of the basket returnmultiplied by $1,000;

• if a knock-out event doesnot occur:

• if the basket return is zero or negative (the final basket level isequal to orless than the initial basket level), $1,000;

• if the basket return is positive (the final basket level isgreaterthan the initial basket level), thesum of$1,000plus theproduct of the basket returnmultiplied by $1,000.

Therefore, you will receive less than the face amount of your notes on the stated maturity date and you could lose all or a substantial portion of your investment in the notes if there is a knock-out event and the final basket level is less than the initial basket level. The maximum return on your notes is 7%. In addition, as a result of the knock-out feature, a small change in the basket level could result in a significant decrease in the return on your notes.

Because we have provided only a brief summary of the terms of your notes above, you should read the detailed description of the terms of the offered notes found in “Summary Information” on page PS-2 in this pricing supplement and the general terms of the notes found in “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes” on page S-60 of the accompanying prospectus supplement no. 209.

Your investment in the notes involves certain risks. In particular, assuming no changes in market conditions or our creditworthiness and other relevant factors, the value of your notes on the trade date (as determined by reference to pricing models used by Goldman, Sachs & Co. and taking into account our credit spreads) is, and the price you may receive for your notes may be, significantly less than the original issue price. The value or quoted price of your notes at any time will reflect many factors and cannot be predicted; however, the price at which Goldman, Sachs & Co. would initially buy or sell notes (if Goldman, Sachs & Co. makes a market) and the value that Goldman, Sachs & Co. will initially use for account statements and otherwise will significantly exceed the value of your notes using such pricing models. The amount of the excess will decline on a straight line basis over the period from the date hereof through September 28, 2010. We encourage you to read “Additional Risk Factors Specific to the Non-Principal Protected Underlier-Linked Autocallable Notes” on page S-46 of the accompanying prospectus supplement no. 209 and “Additional Risk Factors Specific to Your Notes” on page PS-10 of this pricing supplement so that you may better understand those risks.

Original issue date: | April 7, 2010 | Original issue price: | 100% of the face amount* | |||

Underwriting discount: | 1.33% of the face amount | Net proceeds to the issuer: | 98.67% of the face amount |

* The notes will be sold at variable prices. Accounts of certain national banks, acting as purchase agents for such accounts, have agreed with the purchase agents to pay a purchase price of 98.77% of the face amount, and as a result of such agreements, the agents with respect to sales to be made to such accounts will not receive any portion of the underwriting discount from Goldman, Sachs & Co.

The issue price, underwriting discount and net proceeds listed above relate to the notes we sell initially. We may decide to sell additional notes after the date of this pricing supplement but prior to the settlement date, at an issue price, underwriting discount and net proceeds that differ from the amounts set forth above.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this pricing supplement. Any representation to the contrary is a criminal offense.

The notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

Goldman Sachs may use this pricing supplement in the initial sale of the notes. In addition, Goldman, Sachs & Co., or any other affiliate of Goldman Sachs may use this pricing supplement in a market-making transaction in a note after its initial sale.Unless Goldman Sachs or its agent informs the purchaser otherwise in the confirmation of sale, this pricing supplement is being used in a market-making transaction.

Goldman, Sachs & Co. JPMorgan |

Placement Agent

Pricing Supplement dated April 1, 2010.

The Dow Jones EURO STOXX 50® Index is the intellectual property of (including registered trademarks) STOXX Limited, Zurich, Switzerland and/or Dow Jones & Company, Inc., a Delaware corporation, New York, USA, (the “Licensors”), which is used under license. The notes based on the index are in no way sponsored, endorsed, sold or promoted by the Licensors and neither of the Licensors shall have any liability with respect thereto.

“FTSE®”, “FT-SE” and “Footsie” are trademarks of The London Stock Exchange PLC and The Financial Times Ltd. and are used by FTSE International Ltd. under license. The notes are not issued, endorsed, sponsored, sold or otherwise promoted by FTSE International Ltd. or by the London Stock Exchange PLC or by The Financial Times Ltd., and none of them makes any representation regarding the advisability of investing in the notes.

The copyright of TOPIX and other intellectual property rights related to “TOPIX”, “TOPIX Index” and “TOPIX Sector Index” (each, a “TSE Index”) belong solely to the Tokyo Stock Exchange (“TSE”). No transactions relating to a TSE Index are in any way sponsored, endorsed or promoted by the TSE and the TSE makes no warranty or representation whatsoever, express or implied, either as to the results to be obtained as to the use of any TSE Index or the figure at which any TSE Index stands on any particular day or otherwise. Each TSE Index is compiled and calculated solely by the TSE. However, the TSE shall not be liable to any person for any error in any TSE Index and the TSE shall not be under any obligation to advise any person, including a purchaser or vendor of any transactions, of any error therein. The TSE gives no assurance regarding any modification or change in any methodology used in calculating any TSE Index and the TSE is under no obligation to continue the calculation, publication and dissemination of any TSE Index.

Table of Contents

We refer to the notes we are offering by this pricing supplement as the “notes”. Each of the notes, including your notes, has the terms described below. Please note that in this pricing supplement, references to “The Goldman Sachs Group, Inc.”, “we”, “our” and “us” mean only The Goldman Sachs Group, Inc. and do not include its consolidated subsidiaries. Also, references to the “accompanying prospectus” mean the accompanying prospectus, dated April 6, 2009, as supplemented by the accompanying prospectus supplement, dated April 6, 2009, of The Goldman Sachs Group, Inc. relating to the Medium-Term Notes, Series D program of The Goldman Sachs Group, Inc., and references to the “accompanying prospectus supplement no. 209” mean the accompanying prospectus supplement no. 209, dated October 27, 2009, of The Goldman Sachs Group, Inc., to the accompanying prospectus. This section is meant as a summary and should be read in conjunction with the section entitled “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes” on page S-60 of the accompanying prospectus supplement no. 209.

Key Terms

Issuer: | The Goldman Sachs Group, Inc. | |||||||

Basket: | Basket Underliers | Bloomberg Ticker | Weighting Percentage | Initial Basket Underlier Level | ||||||

Dow Jones EURO STOXX 50® Index | SX5E | 52.00% | 2,978.50 | |||||||

FTSE®100 Index | UKX | 24.00% | 5,744.89 | |||||||

TOPIX® Index | TPX | 24.00% | 985.26 |

Specified currency: | U.S. dollars (“$”) | |||||||

| Terms to be specified in accordance with the accompanying prospectus supplement no. 209: |

• type of notes: notes linked to a basket of underliers • exchange rates: not applicable • averaging dates: not applicable • buffer level: not applicable • knock-out event: yes, as described below • interest: not applicable • coupon: not applicable • redemption right or price dependent redemption right: yes, as described below • cap level: not applicable • contingent minimum return: yes, as described below | |||||||

Face amount: | each note will have a face amount of $1,000; $156,772,000 in the aggregate for all the offered notes; the aggregate face amount of the offered notes may be increased if the issuer, at its sole option, decides to sell an additional amount of the offered notes on a date subsequent to the date of this pricing supplement but prior to the settlement date | |||||||

Minimum denomination: | $10,000 and integral multiples of $1,000 in excess thereof | |||||||

| Cash settlement amount (on any call observation date): | • if your notes are automatically called, $1,070 (thesum of (i) $1,000plus (ii) the product of $1,000multiplied by the call premium amount (7.00%)), for each $1,000 face amount of your notes | |||||||

| Cash settlement amount (on the stated maturity date): |

• if your notes are not automatically called, for each $1,000 face amount of your notes • if a knock-out event occurs during the measurement period, thesum of (i) $1,000plus (ii) theproduct of the basket returnmultiplied by $1,000; and • if a knock-out event does not occur during the measurement period, • if the basket return is zero or negative (the final basket level isequal to orless than the initial basket level), $1,000 (thesum of (i) $1,000plus (ii) theproduct of $1,000 multiplied by the contingent minimum return (0%)); and • if the basket return is positive (the final basket level isgreater than the initial basket level) thesum of (i) $1,000plus(ii) theproduct of the basket return multiplied by $1,000 | |||||||

| Initial basket level: | 100 | |||||||

Final basket level: | the basket closing level on the determination date, except in the limited circumstances described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Payment of Principal on Stated Maturity Date or Call Payment Dates, if Applicable — Consequences of a Market Disruption Event or a Non-Trading Day” on page S-79 of the accompanying prospectus supplement no. 209 and subject to adjustment as provided under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Discontinuance or Modification of an Underlier ” on page S-82 of the accompanying prospectus supplement no. 209 | |||||||

PS-2

Table of Contents

Basket return: | thequotientof (1) the final basket levelminusthe initial basket leveldividedby (2) the initial basket level, expressed as a percentage | |||||||

Weighting percentage: | 52.00%, with respect to the Dow Jones EURO STOXX® 50 Index; 24.00%, with respect to the FTSE® 100 Index; and 24.00% with respect to the TOPIX® Index | |||||||

Weighting multiplier: | 0.017458452, with respect to the Dow Jones EURO STOXX® 50 Index; .004177626, with respect to the FTSE® 100 Index; and 0.024359052, with respect to the TOPIX® Index; subject to adjustment as provided under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Discontinuance or Modification of an Underlier” on page S-82 of the accompanying prospectus supplement no. 209 | |||||||

| Initial basket underlier level: | with respect to each basket underlier, as set forth in the table above | |||||||

Basket closing level: | for any given trading day, thesum of theproducts, as calculated for each basket underlier, of the closing level for each basket underlier on such trading daymultiplied by the weighting multiplier for each such basket underlier | |||||||

Upside participation rate: | 100.00% | |||||||

Call level: | 107.00% of the initial basket level | |||||||

Call premium amount: | 7.00% | |||||||

Call observation dates: | for each basket underlier and for your notes, every Wednesday of each week (or if Wednesday is not a trading day for all three basket underliers, the originally scheduled call observation date for such week shall be the first following day which is a scheduled trading day for all three basket underliers), commencing on April 14, 2010 and ending on April 20, 2011, subject to adjustment as described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Payment of Principal on Stated Maturity Date or Call Payment Dates, if Applicable — Call Observation Dates” on page S-76 of the accompanying prospectus supplement no. 209 | |||||||

Call payment dates: | three business days after each originally scheduled call observation date, each subject to postponement as described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Payment of Principal on Stated Maturity Date or Call Payment Dates, if Applicable — Call Payment Dates” on page S-74 of the accompanying prospectus supplement no. 209 | |||||||

Knock-out event: | the basket closing level has declined, as compared to the initial basket level, by more than the knock-out amount during the measurement period | |||||||

Knock-out amount: | 20% | |||||||

Measurement period: | every day which is a trading day for all three basket underliers from but excluding the trade date to and including the determination date, subject to adjustment as described in “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Payment of Principal on Stated Maturity Date or Call Payment Dates, if Applicable — Measurement Periods” on page S-77 of the accompanying prospectus supplement no. 209 | |||||||

Contingent minimum return: | 0% | |||||||

Trade date: | April 1, 2010 | |||||||

Original issue date (settlement date): | April 7, 2010 | |||||||

Stated maturity date: | the final call payment date (April 25, 2011), subject to adjustment as described under “—Call payment dates” above | |||||||

PS-3

Table of Contents

Determination date: | the final call observation date (April 20, 2011), subject to adjustment as described under “—Call observation dates” above | |

No interest: | the offered notes do not bear interest | |

No listing: | the offered notes will not be listed on any securities exchange or interdealer quotation system | |

Redemption: | as described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Redemption of Your Notes” on page S-61 of the accompanying prospectus supplement no. 209 | |

Calculation agent: | Goldman, Sachs & Co. | |

Closing level: | with respect to the FTSE® 100 Index and the TOPIX® Index, as described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Special Calculation Provisions — Closing Level” on page S-85 of the accompanying prospectus supplement no. 209; with respect to the Dow Jones EURO STOXX 50® Index, the official closing level of the Dow Jones EURO STOXX 50® Index or any successor underlier published by the underlier sponsor on the relevant trading day | |

Business day: | as described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Special Calculation Provisions — Business Day” on page S-84 of the accompanying prospectus supplement no. 209 | |

Trading day: | with respect to the FTSE® 100 Index and the TOPIX® Index, as described under “General Terms of the Non-Principal Protected Underlier-Linked Autocallable Notes — Special Calculation Provisions — Trading Day” on page S-84 of the accompanying prospectus supplement no. 209; with respect to the Dow Jones EURO STOXX 50® Index, each day on which the Dow Jones EURO STOXX® Index is calculated and published by the underlier sponsor | |

Fixed income CUSIP no.: | 38143UHL8 | |

ISIN: | US38143UHL89 | |

Use of proceeds and hedging: | as described under “Use of Proceeds and Hedging” on page S-90 of the accompanying prospectus supplement no. 209 | |

| Supplemental discussion of federal income tax consequences: | as described under “Supplemental Discussion of Federal Income Tax Consequences” on page PS-19 of this pricing supplement | |

ERISA: | as described under “Employee Retirement Income Security Act” on page S-98 of the accompanying prospectus supplement no. 209 |

PS-4

Table of Contents

Conflicts of interest: | Goldman, Sachs & Co. is an affiliate of The Goldman Sachs Group, Inc. and, as such, has a "conflict of interest" in this offering within the meaning of NASD Rule 2720. Consequently, the offering is being conducted in compliance with the provisions of Rule 2720. Goldman, Sachs & Co. is not permitted to sell notes in this offering to an account over which it exercises discretionary authority without the prior specific written approval of the account holder | |

FDIC: | the notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation (the “FDIC”) or any other governmental agency, nor are they obligations of, or guaranteed by, a bank. In addition, the notes are not guaranteed under the FDIC’s Temporary Liquidity Guarantee Program |

PS-5

Table of Contents

Additional Terms Specific to Your Notes

You should read this pricing supplement together with the prospectus dated April 6, 2009, the prospectus supplement dated April 6, 2009, and the prospectus supplement no. 209 dated October 27, 2009. You may access these documents on the SEC website atwww.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Prospectus dated April 6, 2009: |

http://www.sec.gov/Archives/edgar/data/886982/000095012309006141/y74641p3posasr.htm

| • | Prospectus supplement dated April 6, 2009 |

http://www.sec.gov/Archives/edgar/data/886982/000095012309006143/y75395ae424b2.htm

| • | Prospectus supplement no. 209 dated October 27, 2009: |

http://www.sec.gov/Archives/edgar/data/886982/000119312509214499/d424b2.htm

PS-6

Table of Contents

The following table is provided for purposes of illustration only. It should not be taken as an indication or prediction of future investment results and is intended merely to illustrate the impact that the various hypothetical basket closing levels on the determination date and the call observation dates could have on the cash settlement amount assuming all other variables remain constant.

The examples below are based on a range of final basket levels that are entirely hypothetical; no one can predict what the basket level will be on any day throughout the life of your notes, and no one can predict what the closing levels of the basket underliers or the final basket level will be on the determination date. The basket underliers have been highly volatile in the past — meaning that the basket underlier levels have changed considerably in relatively short periods — and their performance cannot be predicted for any future period.

The information in the following examples reflects hypothetical rates of return on the offered notes assuming that they are purchased on the original issue date and held to the stated maturity date or automatically called on one of the call payment dates. If you sell your notes in a secondary market prior to the stated maturity date, your return will depend upon the market value of your notes at the time of sale, which may be affected by a number of factors that are not reflected in the table below such as interest rates and the volatility of the basket underliers.

In addition, assuming no changes in market conditions or our creditworthiness and other relevant factors, the value of your notes on the trade date (as determined by reference to pricing models used by Goldman, Sachs & Co. and taking into account our credit spreads) is, and the price you may receive for your notes may be, significantly less than the issue price. For more information on the value of your notes in the secondary market, see “Additional Risk Factors Specific to the Non-Principal Protected Underlier-Linked Autocallable Notes — Assuming No Changes in Market Conditions or any Other Relevant Factors, the Market Value of Your Notes on the Date of Any Applicable Pricing Supplement (as Determined By Reference to Pricing Models Used by Goldman, Sachs & Co.) Will, and the Price You May Receive for Your Notes May, Be Significantly Less Than the Issue Price” on page S-47 of the accompanying prospectus supplement no. 209 and “Additional Risk Factors Specific to Your Notes” on page PS-10 of this pricing supplement.

The information in the table also reflects the key terms and assumptions in the box below.

| Key Terms and Assumptions | ||

Face amount | $1,000 | |

Upside participation rate | 100% | |

Contingent minimum return | 0% | |

Knock-out amount | 20% | |

Call level | 107% of the initial basket level | |

Call premium amount | 7% | |

• Neither a market disruption event nor a non-trading day occurs with respect to any basket underlier on the originally scheduled determination date or on any call observation date | ||

• No change in or affecting any of the basket underliers or the method by which each underlier sponsor calculates the relevant basket underlier | ||

• Notes purchased on original issue date and held to the stated maturity date or automatically called on a call payment date | ||

For these reasons, the actual performance of the basket underliers over the life of your notes, as well as the amount payable on a call payment date or at maturity, if any, may bear little relation to the hypothetical examples shown below or to the historical basket underlier levels shown elsewhere in this pricing supplement. For information about the historical levels of the basket underliers during recent periods, see “The Basket and the Basket Underliers — Historical High, Low and Closing Levels of the Basket Underliers and Historical Basket Levels ” below. Before investing in the offered notes, you should consult publicly available information to determine the levels of the basket underliers between the date of this pricing supplement and the date of your purchase of the offered notes.

Also, the hypothetical examples shown below do not take into account the effects of applicable taxes. Because of the U.S. tax treatment applicable to your notes, tax liabilities could affect the after-tax rate of return on your notes to a comparatively greater extent than the after-tax return on the basket underlier stocks.

The levels in the first (the leftmost) column of the table below represent hypothetical final basket levels on the determination date and are expressed as percentages of the initial basket level. The amounts in the second column represent the hypothetical cash settlement amounts, as percentages of the face amount of each note, based on the corresponding hypothetical final basket levels, assuming thatthe notes have not been automatically called on or prior to the determination date and a knock-out event has not occurred (i.e., the closing level of the basket has not been equal to or greater than the call level on each of the call observation dates on or prior to the determination date and the basket closing level has not declined, as compared to the initial basket level, by more than the knock-out amount during the measurement period). The amounts in the third column represent the hypothetical cash settlement amounts, as percentages of the face amount of each note, based on the corresponding hypothetical final basket levels, assuming thatthe notes have not been automatically called on or prior to the determination date and a knock-out event has occurred (i.e., the basket closing level has not been equal to or greater than the call level on each of the call observation dates on or prior to the determination date and the basket closing level has declined, as compared to the initial basket level, by more than the knock-out amount during the measurement period). A hypothetical cash settlement amount of 100% means that the value of the cash payment that we would deliver for each $1,000 of the outstanding face amount of the offered notes on the stated maturity date would equal 100% of the face amount of a note.

This table assumes that your notes have not been automatically called on or prior to the determination date and reflects hypothetical cash settlements that you could receive on the stated maturity date. Ifyour notes are automatically called, the cash settlement amount that we would deliver on your notes on the call payment date would be 107% of the face amount of your notes. Therefore, you would not benefit from any increase in the final basket level over 107% of the initial basket level.

PS-7

Table of Contents

Hypothetical Final Basket Level on the Determination Date (as Percentage of Initial Basket Level) | Hypothetical Cash Settlement Amount at Maturity (as Percentage of Face Amount) | |||

A knock-out event has not occurred | A knock-out event has occurred | |||

150% | N/A | N/A | ||

130% | N/A | N/A | ||

110% | N/A | N/A | ||

107% | N/A | N/A | ||

105% | 105% | 105% | ||

103% | 103% | 103% | ||

101% | 101% | 101% | ||

100% | 100% | 100% | ||

90% | 100% | 90% | ||

80% | 100% | 80% | ||

60% | N/A | 60% | ||

50% | N/A | 50% | ||

30% | N/A | 30% | ||

10% | N/A | 10% | ||

0% | N/A | 0% | ||

If, for example,the notes have not been automatically called on or prior to the determination date and a knock-event has not occurred and the final basket level were determined to be 90% of the initial basket level, the cash settlement amount that we would deliver on your notes at maturity would be 100% of the face amount of your notes, as shown in the table above. Because a knock-out event has not occurred and the hypothetical return of -10% is less than the contingent minimum return of 0%, the cash settlement amount that we would deliver on your notes at maturity would be 100% of the face amount of your notes, as shown in the table above.

If, for example,the notes have not been automatically called on or prior to the determination date and a knock-out event has occurred and the final basket level were determined to be 90% of the initial basket level, the cash settlement amount that we would deliver on your notes at maturity would be 90% of the face amount of your notes, as shown in the table above. As a result, if you purchased your notes on the original issue date and held them to the stated maturity date, you would lose 10% of your investment. In addition, if the final basket level were determined to be 60% of the initial basket level, the cash settlement amount that we would deliver on your notes at maturity would be 60% of the face amount of your notes, as shown in the table above.

PS-8

Table of Contents

The cash settlement amounts shown above are entirely hypothetical; they are based on basket closing levels that may not be achieved on any trading day during the measurement period, or on any call observation date (including the determination date) and on assumptions that may prove to be erroneous. The actual market value of your notes on the stated maturity date or at any other time, including any time you may wish to sell your notes, may bear little relation to the hypothetical cash settlement amounts shown above, and these amounts should not be viewed as an indication of the financial return on an investment in the offered notes. Please read “Additional Risk Factors Specific to the Non-Principal Protected Underlier-Linked Autocallable Notes — The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” on page S-52 of the accompanying prospectus supplement no. 209.

We cannot predict the actual final basket level or what the market value of your notes will be on any particular trading day or call observation date, nor can we predict the relationship between the basket level and the market value of your notes at any time prior to the stated maturity date. The actual amount that you will receive, if any, at maturity and the rate of return on the offered notes will depend on whether or not a knock-out event has occurred, whether the notes are called, the actual basket closing level on any call observation date, the actual basket closing level on any trading day during the measurement period and the final basket level determined by the calculation agent as described above. Moreover, the assumptions on which the hypothetical returns are based may turn out to be inaccurate. Consequently, the amount of cash to be paid in respect of your notes, if any, on the stated maturity date may be very different from the information reflected in the table above. |

PS-9

Table of Contents

Additional Risk Factors Specific to Your Notes

An investment in your notes is subject to the risks described below, as well as the risks described under “Considerations Relating to Indexed Securities” in the accompanying prospectus dated April 6, 2009, and “Additional Risk Factors Specific to the Non-Principal Protected Underlier-Linked Autocallable Notes” in the accompanying prospectus supplement no. 209. Your notes are a riskier investment than ordinary debt securities. Also, your notes are not equivalent to investing directly in the basket underlier stocks, i.e., the stocks comprising the basket underliers to which your notes are linked. You should carefully consider whether the offered notes are suited to your particular circumstances.

| • | ASSUMING NO CHANGES IN MARKET CONDITIONS OR ANY OTHER RELEVANT FACTORS, THE MARKET VALUE OF YOUR NOTES ON THE TRADE DATE (AS DETERMINED BY REFERENCE TO PRICING MODELS USED BY GOLDMAN, SACHS & CO.) IS, AND THE PRICE YOU MAY RECEIVE FOR YOUR NOTES MAY BE, SIGNIFICANTLY LESS THAN THE ISSUE PRICE |

The price at which Goldman, Sachs & Co. would initially buy or sell notes (if Goldman, Sachs & Co. makes a market) and the value that Goldman, Sachs & Co. will initially use for account statements and otherwise will significantly exceed the value of your notes using such pricing models. The amount of the excess will decline on a straight line basis over the period from the date hereof through September 28, 2010. After September 28, 2010, the price at which Goldman, Sachs & Co. would buy or sell notes will reflect the value determined by reference to the pricing models, plus our customary bid and asked spread. In addition to the factors discussed above, the value or quoted price of your notes at any time, however, will reflect many factors and cannot be predicted. If Goldman, Sachs & Co. makes a market in the notes, the price quoted by Goldman, Sachs & Co. would reflect any changes in market conditions and other relevant factors, including a deterioration in our creditworthiness or perceived creditworthiness whether measured by our credit ratings or other credit measures. These changes may adversely affect the market price of your notes, including the price you may receive for your notes in any market making transaction. In addition, even if our creditworthiness does not decline, the value of your notes on the trade date is significantly less than the original issue price taking into account our credit spreads on that date. The quoted price (and the value of your notes that Goldman, Sachs & Co. will use for account statements or otherwise) could be higher or lower than the original issue price, and may be higher or lower than the value of your notes as determined by reference to pricing models used by Goldman, Sachs & Co. If at any time a third party dealer quotes a price to purchase your notes or otherwise values your notes, that price may be significantly different (higher or lower) than any price quoted by Goldman, Sachs & Co. You should read “Additional Risk Factors Specific to the Non-Principal Protected Underlier-Linked Autocallable Notes — The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” on page S-52 of the accompanying prospectus supplement no. 209. Furthermore, if you sell your notes, you will likely be charged a commission for secondary market transactions, or the price will likely reflect a dealer discount. There is no assurance that Goldman, Sachs & Co. or any other party will be willing to purchase your notes and, in this regard, Goldman, Sachs & Co. is not obligated to make a market in the notes. See “Additional Risk Factors Specific to the Non-Principal Protected Underlier-Linked Autocallable Notes — Your Notes May Not Have an Active Trading Market” on page S-51 of the accompanying prospectus supplement no. 209.

| • | YOU MAY LOSE YOUR ENTIRE INVESTMENT IN THE NOTES |

You can lose all or substantially all of your investment in the notes. The cash payment on your notes, if any, on the stated maturity date will be based on the performance of the basket as measured from the initial basket level of 100 to the basket closing level on the determination date. If a knock-out event has occurred and the final basket level for your notes is less than the initial basket level, the amount in cash you will receive on your notes on the stated maturity date, if any, will be less than the face amount of your notes. Thus, you may lose your entire investment in the notes. Also, the market price of your notes prior to the stated maturity date may be significantly lower than the purchase price you paid for your notes. Consequently, if you sell your notes before the stated maturity date, you may receive far less than the amount of your investment in the notes.

| • | THE RETURN ON YOUR NOTES MAY DECREASE SIGNIFICANTLY DESPITE ONLY A SMALL CHANGE IN THE BASKET LEVEL |

If a knock-out event occurs at any time during the measurement period and the final basket level is less than the initial basket level, you will receive less than the face amount of your notes and you could lose all or a substantial portion of your investment in the notes. This means that while a basket decline of 19.99% will not result in a loss of principal on the notes (so long as a knock-out event does not occur), a basket decline of more than 20% of the initial basket level during the measurement period may result in a loss of a significant portion of the principal amount of the notes despite only a small change in the basket level.

| • | THE POTENTIAL FOR THE VALUE OF YOUR NOTES TO INCREASE IS LIMITED |

The maximum payment that you may receive per $1,000 face amount of your notes is $1,070. Your ability to participate in any increase in the value of the basket over the life of your notes will be limited by the weekly call feature, by which your notes will be automatically called if the basket closing level has increased by 7.00% or more from the initial basket level on any of the call observation dates. The call level will limit the amount in cash you may receive for each of your notes, no matter how much the level of the basket may rise beyond the call level over the life of your notes. Accordingly, the amount payable for each of your notes may be significantly less than it would have been had you invested directly in the basket underliers.

| • | YOUR NOTES DO NOT BEAR INTEREST |

You will not receive any interest payments on your notes. As a result, even if the amount payable for each of your notes on the stated maturity date exceeds the face amount of your notes, the overall return you earn on your notes may be less than you would have earned by investing in a non-underliered debt security of comparable maturity that bears interest at a prevailing market rate.

| • | THE POTENTIAL TO RECEIVE THE CONTINGENT MINIMUM RETURN MAY TERMINATE AT ANY TIME DURING THE LIFE OF YOUR NOTES |

If during the measurement period the basket closing level has declined, as compared to the initial basket level, by more than the knock-out amount of 20%, you will not be entitled to receive the protection provided by the contingent minimum return on the notes. Under these circumstances, you may lose some or all of your investment at maturity and will be fully exposed to any decline in the level of the basket.

PS-10

Table of Contents

| • | YOUR NOTES ARE SUBJECT TO AUTOMATIC REDEMPTION |

We will call and automatically redeem all, but not part, of your notes on the call payment dates, if the closing level of the underlier on any of the call observation dates is greater than or equal to the call level (107.00% of the initial basket level). Therefore, the term for your notes may be reduced to as short as one week. You may not be able to reinvest the proceeds from an investment in the notes at a comparable return for a similar level of risk in the event the notes are called prior to maturity.

| • | THE LOWER PERFORMANCE OF ONE BASKET UNDERLIER MAY OFFSET AN INCREASE IN THE OTHER UNDERLIERS IN THE BASKET |

Declines in the level of one basket underlier may offset increases in the levels of the other underliers in the basket. As a result, any return on the basket — and thus on your notes — may be reduced or eliminated, which will have the effect of reducing the amount payable in respect of your notes at maturity. In addition, because the basket underliers are not equally weighted, increases in the lower weighted basket underliers may be offset by even a small decrease in the more heavily weighted basket underlier.

| • | AN INVESTMENT IN THE OFFERED NOTES IS SUBJECT TO RISKS ASSOCIATED WITH FOREIGN SECURITIES MARKETS |

You should be aware that investments in securities linked to the value of foreign equity securities involve particular risks. The foreign securities markets whose stocks comprise the underlying indices may have less liquidity and may be more volatile than U.S. or other securities markets and market developments may affect foreign markets differently from U.S. or other securities markets. Direct or indirect government intervention to stabilize the foreign securities markets, as well as cross-shareholdings in foreign companies, may affect trading prices and volumes in those markets. Also, there is generally less publicly available information about foreign companies than about those U.S. companies that are subject to the reporting requirements of the U.S. Securities and Exchange Commission, and foreign companies are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. reporting companies.

Securities prices in foreign countries are subject to political, economic, financial and social factors that apply in those geographical regions. These factors, which could negatively affect those securities markets, include the possibility of recent or future changes in a foreign government’s economic and fiscal policies, the possibility of outbreaks of hostility and political instability and the possibility of natural disaster or adverse public health development in the region. Moreover, foreign economies may differ favorably or unfavorably from the U.S. economy in important respects such as growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency.

| • | THE NOTES ARE SUBJECT TO THE CREDIT RISK OF GOLDMAN SACHS |

Although the return on the notes will be based on the performance of the basket, the payment of any amount due on the notes is subject to the credit risk of Goldman Sachs. Investors are dependent on our ability to pay all amounts due on the notes, and therefore investors are subject to our credit risk and to changes in the market’s view of our creditworthiness. In addition, any decline in our credit ratings or any increase in our credit spreads is likely to adversely affect the market value of the notes prior to maturity.

| • | WE MAY SELL AN ADDITIONAL AGGREGATE FACE AMOUNT OF THE NOTES AT A DIFFERENT ISSUE PRICE |

At our sole option, we may decide to sell an additional aggregate face amount of the notes subsequent to the date of this pricing supplement but prior to the settlement date. The issue price of the notes in the subsequent sale may differ substantially (higher or lower) from the issue price you paid as provided on the cover of this pricing supplement.

| • | THE RETURN ON YOUR NOTES WILL NOT REFLECT ANY DIVIDENDS PAID ON THE UNDERLIER STOCKS |

Each underlier sponsor calculates the level of the applicable basket underlier by reference to the prices of the stocks included in the such basket underlier, without taking account of the value of dividends paid on those stocks. As a result, the return on your notes will not reflect the return you would realize if you actually owned the stocks included in the basket underliers and received the dividends paid on those stocks. You will not receive any dividends that may be paid on any of the basket underlier stocks by the underlier stock issuers.

| • | YOU HAVE NO SHAREHOLDER RIGHTS OR RIGHTS TO RECEIVE ANY STOCK |

Investing in your notes will not make you a holder of any of stocks included in the basket underliers. Neither you nor any other holder or owner of your notes will have any voting rights, any right to receive dividends or other distributions or any other rights with respect to the underlier stocks. Your notes will be paid in cash, and you will have no right to receive delivery of any underlier stocks.

| • | YOUR NOTES MAY BE SUBJECT TO AN ADVERSE CHANGE IN TAX TREATMENT IN THE FUTURE |

The Internal Revenue Service announced on December 7, 2007 that it is considering the proper Federal income tax treatment of an instrument such as your notes that are currently characterized as prepaid derivative contracts, which could adversely affect the tax treatment and the value of your notes. Among other things, the Internal Revenue Service may decide to require the holders to accrue ordinary income on a current basis and recognize ordinary income on payment at maturity, and could subject non-US investors to withholding tax. Moreover, in 2007, legislation was introduced in Congress that, if enacted, would have required holders that acquired such notes after the bill was enacted to accrue interest income over the term of such notes even though there may be no interest payments over the term of such notes. It is not possible to predict whether a similar or identical bill will be enacted in the future, or whether any such bill would affect the tax treatment of such notes. We describe these developments in more detail under “Supplemental Discussion of Federal Income Tax Consequences” on page PS-19 of this pricing supplement. You should consult your own tax advisor about this matter. Except to the extent otherwise provided by law, The Goldman Sachs Group, Inc. intends to continue treating the offered notes as described under “Supplemental Discussion of Federal Income Tax Consequences” on page PS-19 of this pricing supplement unless and until such time as Congress, the Treasury Department or the Internal Revenue Service determine that some other treatment is more appropriate.

PS-11

Table of Contents

The Basket and the Basket Underliers

| • | The Basket |

The basket is comprised of three equity indices with the following weighting percentages within the basket: the Dow Jones EURO STOXX 50® Index (52.00%), the FTSE® 100 Index (24.00%) and the TOPIX® Index (24.00%).

| • | The Dow Jones EURO STOXX 50® Index |

The Dow Jones EURO STOXX 50® Index, which we refer to as the Euro STOXX 50 Index, is a capitalization-weighted index of 50 European blue-chip stocks and was created by STOXX Limited, a joint venture between Deutsche Boerse AG, Dow Jones & Company, Inc. and SWX Swiss Exchange. Publication of the Euro STOXX 50 Index began on February 28, 1998, based on an initial index value of 1,000 at December 31, 1991. The Euro STOXX 50 Index is published in The Wall Street Journal and disseminated on the STOXX Limited website:http://www.stoxx.com. STOXX Limited is under no obligation to continue to publish the Euro STOXX 50 Index and may discontinue publication of the Euro STOXX 50 Index at any time.

The top ten constituent stocks of the Euro STOXX 50 Index as of March 29, 2010, by weight, are: Total (5.73%); BCO Santander (5.04%); Telefonica (4.51%); Siemens (3.94%); Sanofi-Aventis (3.75%); BNP Paribas (3.56%); E.ON (3.31%); Nokia (2.63%); Eni (2.60%) and Allianz (2.58%); constituent weightings may be found at http://www.stoxx.com/indices/download.html?symbol=SX5E under “General Information — Index Factsheet” and are updated periodically.

As of February 26, 2010, the 18 industry sectors which comprise the Euro STOXX 50 Index represent the following weights in the index: banks (19.6%); utilities (10.8%); insurance (9.5%); oil & gas (9.5%); telecommunications (9.5%); chemicals (6.7%); food and beverage (5.7%); industrial goods and services (5.4%); technology (4.4%); personal and household goods (4.0%); health care (3.8%); construction and materials (3.1%); automobiles and parts (1.8%); basic resources (1.7%); media (1.5%); retail (1.4%); real estate (0.9%) and financial services (0.7%); industry weightings may be found at http://www.stoxx.com/indices/download.html?symbol=SX5E under “General Information — Index Factsheet” and are updated periodically.Percentages may not sum to 100% due to rounding. Sector designations are determined by the index sponsor using criteria it has selected or developed. Index sponsors may use very different standards for determining sector designations. In addition, many companies operate in a number of sectors, but are listed in only one sector and the basis on which that sector is selected may also differ. As a result, sector comparisons between indices with different index sponsors may reflect differences in methodology as well as actual differences in the sector composition of the indices.

As of February 26, 2010, the 9 countries which comprise the Euro STOXX 50 Index represent the following weights in the index: France (36.3%); Germany (26.1%); Spain (14.7%); Italy (10.5%); the Netherlands (5.8%); Finland (2.5%); Belgium (1.7%); Luxembourg (1.7%) and Ireland (0.8%); country weightings may be found at http://www.stoxx.com/indices/download.html?symbol=SX5E under “General Information — Index Factsheet” and are updated periodically.

Where any index component stock price is unavailable on any trading day, the index sponsor will generally use the last reported price for such component stock; further information may be found athttp://www.stoxx.com/indices/download.html?symbol=SX5E under “General Information — Index Guide”.

The above information supplements the description of the Dow Jones EURO STOXX 50® found in the accompanying prospectus supplement no. 209. For more details about the Dow Jones EURO STOXX 50®, the underlier sponsor and license agreement between the underlier sponsor and the issuer, see “The Underliers — Dow Jones EURO STOXX 50®” on page A-2 of the accompanying prospectus supplement no. 209.

| • | The FTSE® 100 Index |

The FTSE® 100 Index is a capitalization-weighted index of the 100 most highly capitalized U.K.-domiciled blue chip companies traded on the London Stock Exchange. The index was developed with a base level of 1,000 as of January 3, 1984. The FTSE® 100 Index is calculated, published and disseminated by FTSE (“FTSE”), a company owned equally by the London Stock Exchange Plc (the “Exchange”) and The Financial Times Limited (“FT”). Additional information on the FTSE® 100 Index is available on the FTSE website:http://www.ftse.com. FTSE is under no obligation to continue to publish the FTSE 100 Index and may discontinue publication of the FTSE® 100 Index at any time.

FTSE 100® Index

Index Stock Weighting by Sector as of March 29, 2010

Sector:* | Percentage (%)** | |||

Oil & Gas | 20.22% | |||

Basic Materials | 13.89% | |||

Industrials | 4.45% | |||

Consumer Goods | 11.87% | |||

Health Care | 8.46% | |||

Consumer Services | 8.52% | |||

Telecommunications | 6.58% | |||

Utilities | 3.58% | |||

Financials | 21.52% | |||

Technology | 0.92% |

| * | Sector designations are determined by the index sponsor using criteria it has selected or developed. Index sponsors may use very different standards for determining sector designations. In addition, many companies operate in a number of sectors, but are listed in only one sector and the basis on which that sector is selected may also differ. As a result, sector comparisons between indices with different index sponsors may reflect differences in methodology as well as actual differences in the sector composition of the indices. |

| ** | Information provided by FTSE. Percentages may not sum to 100% due to rounding. |

PS-12

Table of Contents

If there is a system problem or situation in the market that is judged to affect the quality of the constituent prices at any time when an index is being calculated, the index will be declared indicative (e.g. normally where a “fast market” exists in the equity market). The message “IND” will be displayed against the index value calculated by FTSE. The FTSE Europe Regional Committee must be satisfied that an accurate and reliable price for the purposes of determining the market value of a company exists. The FTSE Europe Regional Committee may exclude a security from the FTSE® 100 Index should it consider that an “accurate and reliable” price is not available.

If a constituent is suspended from the London Stock Exchange, it may remain in the FTSE® 100 Index, at the price at which it is suspended, for up to 10 business days. During this time, on advice from FTSE, the Chairman and Deputy Chairman of the Europe Regional Committee may agree to delete the constituent immediately either at its suspension price, or at zero. Where a suspension of a constituent lasts beyond noon on the tenth business day (and the option to remove the constituent has not been exercised), the constituent will normally be deleted from the FTSE® 100 Index on the eleventh trading day at zero or the suspension price. Where suspension is for a reason not to the detriment of the constituent, it may be retained or removed at its suspension price with the approval of the Chairman and Deputy Chairman of the Europe Regional Committee. If the suspended company is deleted from the FTSE 100® Index, it will be replaced with the highest ranking company on the Reserve List eligible to be included in the indices as at the close of the index calculation on the day preceding the inclusion of the replacement company. This change will be effected after the close of the index calculation and prior to the start of the index calculation on the following day.

The above information supplements the description of the FTSE® 100 Index found in the accompanying prospectus supplement no. 209. For more details about the FTSE® 100 Index, the underlier sponsor and the license agreement between the underlier sponsor and the issuer, see “The Underliers — FTSE® 100 Index” on page A-5 of the accompanying prospectus supplement no. 209.

| • | The TOPIX® Index |

The TOPIX® Index, also known as the Tokyo Price Index, is a capitalization weighted index of all the domestic common stocks listed on the First Section of the Tokyo Stock Exchange, Inc., which we refer to as the TSE. Domestic stocks admitted to the TSE are assigned either to the TSE First Section Index, the TSE Second Section Index or the TSE Mothers Index. Stocks listed in the First Section, which number approximately 1,700, are among the most actively traded stocks on the TSE. The TOPIX® Index is supplemented by the subbasket components of the 33 industry sectors and was developed with a base index value of 100 as of January 4, 1968. The TOPIX® Index is calculated and published by TSE. Additional information about the TOPIX® Index is available on the following website:http://www.tse.or.jp/english/market/topix/index.html.

TOPIX®Index Composition and Maintenance. The TOPIX® Index is composed of all domestic common stocks listed on the TSE First Section, excluding temporary issues and preferred stocks. Companies scheduled to be delisted or newly listed companies that are still in the waiting period are excluded from the indices. The TOPIX® Index has no constituent review. The number of constituents will change according to new listings and delistings.

TOPIX® Index

Index Stock Weighting by Sector as of February 26, 2010

Sector:* | Percentage (%)** | |||

Fishery, Agriculture & Forestry | 0.09% | |||

Mining | 0.40% | |||

Construction | 2.00% | |||

Foods | 3.37% | |||

Textiles & Apparels | 0.87% | |||

Pulp & Paper | 0.37% | |||

Chemicals | 5.85% | |||

Pharmaceutical | 4.33% | |||

Oil & Coal Products | 0.68% | |||

Rubber Products | 0.58% | |||

Glass & Ceramics Products | 1.22% | |||

Iron & Steel | 2.57% | |||

Nonferrous Metals | 1.20% | |||

Metal Products | 0.69% | |||

Machinery | 4.54% | |||

Electric Appliances | 14.60% | |||

Transportation Equipments | 9.74% | |||

Precision Instruments | 1.57% | |||

Other Products | 2.23% | |||

Electric Power & Gas | 5.28% | |||

Land Transportation | 3.89% | |||

Marine Transportation | 0.55% |

PS-13

Table of Contents

Sector:* | Percentage (%)** | |||

Air Transportation | 0.32% | |||

Warehousing & Harbor Transportation Services | 0.23% | |||

Information & Communication | 5.60% | |||

Wholesale Trade | 5.12% | |||

Retail Trade | 3.55% | |||

Banks | 9.82% | |||

Securities & Commodity Futures | 1.85% | |||

Insurance | 2.18% | |||

Other Financing Business | 0.71% | |||

Real Estate | 2.26% | |||

Services | 1.59% |

| * | Sector designations are determined by the index sponsor using criteria it has selected or developed. Index sponsors may use very different standards for determining sector designations. In addition, many companies operate in a number of sectors, but are listed in only one sector and the basis on which that sector is selected may also differ. As a result, sector comparisons between indices with different index sponsors may reflect differences in methodology as well as actual differences in the sector composition of the indices. |

| ** | Information provided by TSE. Percentages may not sum to 100% due to rounding. |

TOPIX®Index Calculation. The TOPIX® Index is a free-float adjusted market capitalization-weighted index, which reflects movements in the market capitalization from a base market value of 100 set on the base date of January 4, 1968.

The TOPIX® Index is calculated by multiplying the base point of 100 by the figure obtained from dividing the current free float adjusted market value by the base market value. The resulting value is not expressed in Japanese yen but presented in terms of points rounded off to the nearest one hundredth. The formula for calculating the TOPIX® Index value can be expressed as follows:

Index value = Base point of 100 ×

| Current free float adjusted market value | |

| Base market value |

The current free float adjusted market value is thesum of theproducts of the price and the number of free float adjusted shares for index calculation of each component stock.

The number of free float adjusted shares for index calculation is the number of listed sharesmultiplied by free-float weight. The number of listed shares for index calculation is determined by TSE. The number of listed shares for index calculation normally coincides with that of listed shares. However, in case of a stock split, the number of listed shares increases at the additional listing date which comes after such stock split becomes effective; on the other hand, the number of listed shares for index calculation increases at the ex-rights date.

Free-float weight is a weight of listed shares deemed to be available for trading in the market and is determined and calculated by TSE for each listed company for index calculation. The free float weight of Company A may be different from that of Company B. Free-float weight is reviewed once a year in order to reflect the latest distribution of share ownership. The timing of the yearly free float weight review is different according to the settlement terms of listed companies. In addition to the yearly review, extraordinary reviews are conducted in the following cases: allocation of new shares to a third party, strategic exercise of preferred shares or equity warrants, company spin-off, merger, stock-swap, take-over bid and other events TSE judges as appropriate reasons to review.

In the event of any increase or decrease in the current free float adjusted market value due to reasons other than fluctuations in the stock market, such as public offerings or changes in the number of constituents in the TSE First Section, necessary adjustments are made to the base market value in order to maintain the continuity of the TOPIX® Index. Adjustments are made as follows:

Event | Implementation of Adjustment (After close of trading) | Price used for adjustments | ||||

| Addition | Company to be listed on the TSE First Section by initial public offering or via another stock exchange | One business day before the last business day of the next month of listing | Price on the adjustment date | |||

| Addition | New Listing Parent company established through stock-swap or similar transaction (including merger through establishing new company and company spin-off) to be promptly listed on the TSE First Section after the de-listing of the stocks in TOPIX® Index (the company will be included not in the TOPIX® Index, but in the TOPIX® New Series Index to which the de-listed company with the highest liquidity and the largest free-float adjusted market capitalization belonged) | One business day before the listing or one business day after the listing if the business day before is a holiday | “Kijun Nedan” (base price used to decide the daily price limit), or the price defined by TSE | |||

| Addition | Transfer to the TSE First Section from the Second Section | One business day before the last business day of the next month of transfer (a free float weight of 0.00 is used from the transfer date to the adjustment date and thus the number of shares to be used for calculation will be 0.00 during such period) | Price on the adjustment date | |||

PS-14

Table of Contents

Event | Implementation of Adjustment (After close of trading) | Price used for adjustments | ||||

| Addition | Transfer to the TSE First Section from Mothers | One business day before the last business day of the next month of transfer (a free float weight of 0.00 is used from the transfer date to the adjustment date and thus the number of shares to be used for calculation will be 0.00 during such period) | Price on the adjustment date | |||

| Deletion | De-listing Company to be de-listed due to a stock-swap and the like while newly established companies promptly list its shares | One business day before listing of newly established company (Normally it is four business days after de-listing) | Price one business day before the de-listing date (the price used for adjustments is frozen after close of trading one business day before de-listing, to the exclusion date for index calculation purpose) | |||

| Deletion | Company to be de-listed due to other reason described above (merger and stock-swap with non-surviving company included in the TOPIX® Index) | One business day before de-listing | Price on the adjustment date | |||

| Deletion | Transfer to the TSE Second Section from the TSE First Section | One business day before transfer | Price on the adjustment date | |||

| Deletion | Designation of securities to be delisted | Four business days after the designation of securities to be delisted (one business day after designation if the day of designation is a holiday) | Price on the adjustment date | |||

If trading in a certain constituent is suspended, it is regarded as having no change in its share price for purposes of calculating the TOPIX® Index. In the event of unforeseen circumstances, or if TSE decides it is impossible to use its existing methods to calculate the TOPIX® Index, TSE may use an alternate method of index calculation as it deems valid.

License Agreement between TSE and The Goldman Sachs Group, Inc.

We, or Goldman, Sachs & Co., expect to enter into non-exclusive license agreements with TSE, whereby we, in exchange for a fee, will be permitted to use the TOPIX® Index in connection with the offer and sale of the notes. We are not affiliated with TSE; the only relationship between TSE and us is the licensing of the use of the TOPIX® Index and trademarks relating to the TOPIX® Index.

Neither The Goldman Sachs Group, Inc. nor any of its affiliates accepts any responsibility for the calculation, maintenance or publication of the TOPIX® Index or any successor index.

TSE is under no obligation to continue the calculation and dissemination of the TOPIX® Index. The notes are not sponsored, endorsed or promoted by TSE. No inference should be drawn from the information contained in this pricing supplement that TSE makes any representation or warranty, implied or express, to The Goldman Sachs Group, Inc., any holder of the notes or any member of the public regarding the advisability of investing in securities generally or in the notes in particular or the ability of the TOPIX® Index to track general stock market performance.

TSE determines, composes and calculates the TOPIX® Index without regard to the notes. TSE has no obligation to take into account your interest, or that of anyone else having an interest, in the notes in determining, composing or calculating the TOPIX® Index. TSE is not responsible for and has not participated in the determination of the terms, prices or amount of the notes and will not be responsible for or participate in any determination or calculation regarding the principal amount of nonprincipal protected underlier-linked notes payable at the stated maturity date or upon redemption. TSE has no obligation or liability in connection with the administration, marketing or trading of non-principal protected underlier-linked notes.

Neither The Goldman Sachs Group, Inc. nor any of its affiliates accepts any responsibility for the calculation, maintenance or publication of the TOPIX® Index or any successor index. TSE disclaims all responsibility for any errors or omissions in the calculation and dissemination of the TOPIX® Index or the manner in which the TOPIX® Index is applied in determining any initial index level or final index level or any amount payable upon maturity or redemption of the notes.

THE TOPIX® INDEX VALUE AND THE TOPIX TRADEMARKS ARE SUBJECT TO THE INTELLECTUAL PROPERTY RIGHTS OWNED BY THE TOKYO STOCK EXCHANGE, INC. AND THE TOKYO STOCK EXCHANGE, INC. OWNS ALL RIGHTS RELATING TO THE TOPIX® INDEX SUCH AS CALCULATION, PUBLICATION AND USE OF THE TOPIX® INDEX VALUE AND RELATING TO THE TOPIX TRADEMARKS.

THE TOKYO STOCK EXCHANGE, INC. SHALL RESERVE THE RIGHTS TO CHANGE THE METHODS OF CALCULATION OR PUBLICATION, TO CEASE THE CALCULATION OR PUBLICATION OF THE TOPIX® INDEX VALUE OR TO CHANGE THE TOPIX TRADEMARKS OR CEASE THE USE THEREOF.

PS-15

Table of Contents

THE TOKYO STOCK EXCHANGE, INC. MAKES NO WARRANTY OR REPRESENTATION WHATSOEVER, EITHER AS TO THE RESULTS STEMMED FROM THE USE OF THE TOPIX® INDEX VALUE AND THE TOPIX TRADEMARKS OR AS TO THE FIGURE AT WHICH THE TOPIX®INDEX VALUE STANDS ON ANY PARTICULAR DAY.

THE TOKYO STOCK EXCHANGE, INC. GIVES NO ASSURANCE REGARDING ACCURACY OR COMPLETENESS OF THE TOPIX® INDEX VALUE AND DATA CONTAINED THEREIN. FURTHER, THE TOKYO STOCK EXCHANGE, INC. SHALL NOT BE LIABLE FOR THE MISCALCULATION, INCORRECT PUBLICATION, DELAYED OR INTERRUPTED PUBLICATION OF THE TOPIX® INDEX VALUE.

THE NOTES ARE NOT IN ANY WAY SPONSORED, ENDORSED OR PROMOTED BY THE TOKYO STOCK EXCHANGE, INC.

THE TOKYO STOCK EXCHANGE, INC. SHALL NOT BEAR ANY OBLIGATION TO GIVE AN EXPLANATION OF THE NOTES OR ANY ADVISE ON INVESTMENTS TO ANY PURCHASER OF THE NOTES OR TO THE PUBLIC.

THE TOKYO STOCK EXCHANGE, INC. NEITHER SELECTS SPECIFIC STOCKS OR GROUPS THEREOF NOR TAKES INTO ACCOUNT ANY NEEDS OF THE ISSUING COMPANY OR ANY PURCHASER OF THE NOTES, FOR CALCULATION OF THE TOPIX® INDEX VALUE.

THE TOKYO STOCK EXCHANGE, INC. SHALL NOT BE RESPONSIBLE FOR ANY DAMAGE RESULTING FROM THE ISSUE AND SALE OF THE NOTES.

| • | Historical High, Low and Closing Levels of the Basket Underliers and Historical Basket Levels |

The respective closing levels of the basket and the basket underlies have fluctuated in the past and may, in the future, experience significant fluctuations. Any historical upward or downward trend in the level of the basket or the basket underliers during any period shown below is not an indication that the basket or the basket underliers are more or less likely to increase or decrease at any time during the life of your notes.

| • | You should not take the historical levels of the basket or the basket underliers as an indication of the future performance of the basket or the basket underliers |

We cannot give you any assurance that the future performance of the basket underliers or the underlier stocks will result in your receiving an amount greater than the outstanding face amount of your notes on the stated maturity date. In light of the increased volatility currently being experienced by the financial services sector and U.S. and global securities markets and recent market declines, it may be substantially more likely that you could lose all or a substantial portion of your investment in the notes.During the period from January 4, 2007 to April 1, 2010, assuming that the basket level was 100 on January 4, 2007, there were 830 full 12-month periods, the first of which began on January 4, 2007 and the last of which ended on April 1, 2010. In 557 of such 12-month periods, approximately 66.10%, if you had owned notes with a 107% call level and call observation terms similar to these notes, your notes would have been called on one of the call observation dates. In 410 of such 12-month periods, the basket closing level on any trading day during such period has declined, as compared to the initial basket level, by more than 20%. Therefore, during approximately 49.40% of such 12-month periods, if you had owned notes with terms similar to these notes, a knock-out event with respect to your notes would have occurred. (We calculated these figures using fixed 12-month periods and did not take into account holidays or non-business days.)

Neither we nor any of our affiliates make any representation to you as to the performance of the basket or the basket underliers. The actual performance of the basket or the basket underliers over the life of the offered notes, as well as the amount payable at maturity may bear little relation to the historical levels shown below. The table below shows the high, low and final closing levels of the underlier for each of the four calendar quarters in 2007, 2008, 2009 and the first and second calendar quarters of 2010 (through April 1, 2010). We obtained the closing levels listed in the table below from Bloomberg Financial Services, without independent verification.

PS-16

Table of Contents

Quarterly High, Low and Closing Levels of the Dow Jones EURO STOXX 50® Index

High | Low | Close | ||||||||||

2007 | �� | |||||||||||

Quarter ended March 31 | 4,272.32 | 3,906.15 | 4,181.03 | |||||||||

Quarter ended June 30 | 4,556.97 | 4,189.55 | 4,489.77 | |||||||||

Quarter ended September 30 | 4,557.57 | 4,062.33 | 4,381.71 | |||||||||

Quarter ended December 31 | 4,489.79 | 4,195.58 | 4,399.72 | |||||||||

2008 | ||||||||||||

Quarter ended March 31 | 4,339.23 | 3,431.82 | 3,628.06 | |||||||||

Quarter ended June 30 | 3,882.28 | 3,340.27 | 3,352.81 | |||||||||

Quarter ended September 30 | 3,445.66 | 3,000.83 | 3,038.20 | |||||||||

Quarter ended December 31 | 3,113.82 | 2,165.91 | 2,447.62 | |||||||||

2009 | ||||||||||||

Quarter ended March 31 | 2,578.43 | 1,809.98 | 2,071.13 | |||||||||

Quarter ended June 30 | 2,537.35 | 2,097.57 | 2,401.69 | |||||||||

Quarter ended September 30 | 2,899.12 | 2,281.47 | 2,872.63 | |||||||||

Quarter ended December 31 | 2,992.08 | 2,712.30 | 2,964.96 | |||||||||

2010 | ||||||||||||

Quarter ended March 31 | 3,017.85 | 2,631.64 | 2,931.16 | |||||||||

Quarter ending June 30 (through April 1, 2010) | 2,978.50 | 2,978.50 | 2,978.50 |

Quarterly High, Low and Closing Levels of the FTSE® 100 Index

High | Low | Close | ||||||||||

2007 | ||||||||||||

Quarter ended March 31 | 6,444.40 | 6,000.70 | 6,308.00 | |||||||||

Quarter ended June 30 | 6,732.40 | 6,315.50 | 6,607.90 | |||||||||

Quarter ended September 30 | 6,716.70 | 5,858.90 | 6,466.80 | |||||||||

Quarter ended December 31 | 6,730.70 | 6,070.90 | 6,456.90 | |||||||||

2008 | ||||||||||||

Quarter ended March 31 | 6,479.40 | 5,414.40 | 5,702.10 | |||||||||

Quarter ended June 30 | 6,376.50 | 5,518.20 | 5,625.90 | |||||||||

Quarter ended September 30 | 5,636.60 | 4,818.77 | 4,902.45 | |||||||||

Quarter ended December 31 | 4,980.25 | 3,780.96 | 4,434.17 | |||||||||

2009 | ||||||||||||

Quarter ended March 31 | 4,638.92 | 3,512.09 | 3,926.14 | |||||||||

Quarter ended June 30 | 4,506.19 | 3,925.52 | 4,249.21 | |||||||||

Quarter ended September 30 | 5,172.89 | 4,127.17 | 5,133.90 | |||||||||

Quarter ended December 31 | 5,437.61 | 4,988.70 | 5,412.88 | |||||||||

2010 | ||||||||||||

Quarter ended March 31 | 5,727.65 | 5,060.92 | 5,679.64 | |||||||||

Quarter ending June 30 (through April 1, 2010) | 5,744.89 | 5,744.89 | 5,744.89 |

PS-17

Table of Contents

Quarterly High, Low and Closing Levels of the TOPIX® Index

High | Low | Close | ||||||||||

2007 | ||||||||||||

Quarter ended March 31 | 1,816.97 | 1,656.72 | 1,713.61 | |||||||||

Quarter ended June 30 | 1,789.38 | 1,682.49 | 1,774.88 | |||||||||

Quarter ended September 30 | 1,792.23 | 1,480.39 | 1,616.62 | |||||||||

Quarter ended December 31 | 1,677.52 | 1,437.38 | 1,475.68 | |||||||||

2008 | ||||||||||||

Quarter ended March 31 | 1,424.29 | 1,149.65 | 1,212.96 | |||||||||

Quarter ended June 30 | 1,430.47 | 1,230.49 | 1,320.10 | |||||||||

Quarter ended September 30 | 1,332.57 | 1,087.41 | 1,087.41 | |||||||||

Quarter ended December 31 | 1,101.13 | 746.46 | 859.24 | |||||||||

2009 | ||||||||||||

Quarter ended March 31 | 888.25 | 700.93 | 773.66 | |||||||||

Quarter ended June 30 | 950.54 | 793.82 | 929.67 | |||||||||

Quarter ended September 30 | 975.59 | 852.42 | 909.84 | |||||||||

Quarter ended December 31 | 915.87 | 811.01 | 907.59 | |||||||||

2010 | ||||||||||||

Quarter ended March 31 | 979.58 | 881.57 | 978.81 | |||||||||

Quarter ending June 30 (through April 1) | 985.26 | 985.26 | 985.26 |

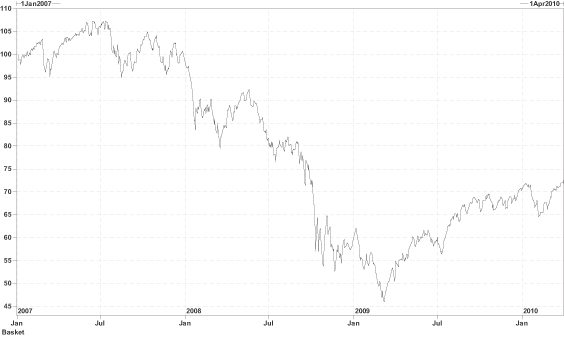

Historical Basket Levels

The following chart is based on the basket level for the period from January 1, 2007 through April 1, 2010 assuming that the basket level was 100 on January 1, 2007. The basket level can increase or decrease due to changes in the levels of the basket underliers.

PS-18

Table of Contents

Supplemental Discussion of Federal Income Tax Consequences

The following section supplements the discussion of U.S. federal income taxation in the accompanying prospectus supplement and the accompanying prospectus supplement No. 209.

The following section is the opinion of Sullivan & Cromwell LLP, counsel to The Goldman Sachs Group, Inc. In addition, it is the opinion of Sullivan & Cromwell LLP that the characterization of the notes for U.S. federal income tax purposes that will be required under the terms of the notes, as discussed below, is a reasonable interpretation of current law.

United States Holders

This section applies to you only if you are a United States holder that holds your notes as a capital asset for tax purposes. You are a United States holder if you are a beneficial owner of each of your notes and you are:

| • | a citizen or resident of the United States; |

| • | a domestic corporation; |

| • | an estate whose income is subject to United States federal income tax regardless of its source; or |

| • | a trust if a United States court can exercise primary supervision over the trust’s administration and one or more United States persons are authorized to control all substantial decisions of the trust. |

This section does not apply to you if you are a member of a class of holders subject to special rules, such as:

| • | a dealer in securities or currencies; |

| • | a trader in securities that elects to use a mark-to-market method of accounting for your securities holdings; |

| • | a bank; |

| • | a life insurance company; |

| • | a tax exempt organization; |

| • | a regulated investment company; |

| • | a common trust fund; |

| • | a person that owns a note as a hedge or that is hedged against interest rate or currency risks; |

| • | a person that owns a note as part of a straddle or conversion transaction for tax purposes; or |

| • | a United States holder whose functional currency for tax purposes is not the U.S. dollar. |

Although this section is based on the U.S. Internal Revenue Code of 1986, as amended, its legislative history, existing and proposed regulations under the Internal Revenue Code, published rulings and court decisions, all as currently in effect, no statutory, judicial or administrative authority directly addresses how your notes should be treated for U.S. federal income tax purposes, and as a result, the U.S. federal income tax consequences of your investment in your notes are uncertain. Moreover, these laws are subject to change, possibly on a retroactive basis.

You should consult your own tax advisor concerning the U.S. federal income tax and any other applicable tax consequences of your investments in the notes, including the application of state, local or other tax laws and the possible effects of changes in federal or other tax laws. |

You will be obligated pursuant to the terms of the notes — in the absence of an administrative determination or judicial ruling to the contrary — to characterize each note for all tax purposes as a prepaid derivative contract in respect of the basket of underliers. Except as otherwise noted below, the discussion herein assumes that the notes will be so treated.

Upon the sale, exchange, redemption or maturity of your notes, you should recognize capital gain or loss equal to the difference, if any, between the amount of cash you receive at such time and your tax basis in your notes. Your tax basis in the notes will generally be equal to the amount that you paid for the note. If you hold your notes for more than one year, the gain or loss generally will be long-term capital gain or loss. If you hold your notes for one year or less, the gain or loss generally will be short-term capital gain or loss.