Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-154173

Amendment No. 1 to Prospectus Supplement No. 520 to theProspectus dated April 6, 2009 and

theProspectus Supplement dated April 6, 2009

| The Goldman Sachs Group, Inc. | ||||||||

| Medium-Term Notes, Series D | ||||||||

| ||||||||

| $879,000 | ||||||||

| Equity Index-Linked Notes due 2017 | ||||||||

| (Linked to the Dow Jones Industrial Average®) | ||||||||

| ||||||||

The notes do not bear interest. The amount that you will be paid on your notes on the stated maturity date (August 31, 2017, subject to adjustment) is based on the performance of the Dow Jones Industrial Average® (which we refer to as the index or underlier) as measured from the trade date (August 26, 2010) through the determination date (August 28, 2017, subject to adjustment). The Dow Jones Industrial Average® is described more fully beginning on page S-20.If the index return (defined below) is negative you will receive the outstanding face amount of your notes.

To determine your payment at maturity, we will first calculate the percentage increase or decrease in the final index level (which will be the closing level of the index on the determination date) from the initial index level of 9,985.81, which we refer to as the index return. The index return may reflect a positive return (based on any increase in the index level over the life of the notes) or a negative return (based on any decrease in the index level over the life of the notes). On the stated maturity date, for each $1,000 face amount of your notes:

| • | if the index return ispositive (the final index level isgreater than the initial index level), you will receive an amount in cash equal to thesum of (i) $1,000plus (ii) theproduct of the index returntimes $1,000; or |

| • | if the index return iszero ornegative (the final index level isequal to orless than the initial index level), you will receive $1,000. |

The notes do not pay interest, and no other payments on your notes will be made prior to the stated maturity date.

Because we have provided only a brief summary of the terms of your notes above, you should read the detailed description of the terms of the notes found in “Summary Information” on page S-2 and “Specific Terms of Your Notes” on page S-13.

Your investment in the notes involves certain risks. In particular, assuming no changes in market conditions or our creditworthiness and any other relevant factors, the value of your notes on the trade date (as determined by reference to pricing models used by Goldman, Sachs & Co. and taking into account our credit spreads) is, and the price you may receive for your notes may be, significantly less than the original issue price. The value or quoted price of your notes at any time will reflect many factors and cannot be predicted; however, the price at which Goldman, Sachs & Co. would initially buy or sell notes (if Goldman, Sachs & Co. makes a market) and the value that Goldman, Sachs & Co. will initially use for account statements and otherwise will significantly exceed the value of your notes using such pricing models. The amount of the excess will decline on a straight line basis over the period from the date hereof through February 26, 2014. We encourage you to read “Additional Risk Factors Specific to Your Notes” on page S-7 of this prospectus supplement so that you may better understand those risks.

| Original issue date (settlement date): | August 31, 2010 | Original issue price: | 100% of the face amount | |||||

| Underwriting discount: | 4.90% of the face amount | Net proceeds to the issuer: | 95.10% of the face amount |

The issue price, underwriting discount and net proceeds listed above relate to the notes we sell initially. We may decide to sell additional notes after the date of this prospectus supplement, at issue prices, underwriting discounts and net proceeds that differ from the amounts set forth above.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus supplement. Any representation to the contrary is a criminal offense.

The notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

Goldman Sachs may use this prospectus supplement in the initial sale of the notes. In addition, Goldman, Sachs & Co., or any other affiliate of Goldman Sachs may use this prospectus supplement in a market-making transaction in a note after its initial sale.Unless Goldman Sachs or its agent informs the purchaser otherwise in the confirmation of sale, this prospectus supplement is being used in a market-making transaction.

“Dow Jones,” and “Dow Jones Industrial Average®” are service marks of Dow Jones & Company, Inc. (“Dow Jones”) and have been licensed for use for certain purposes by The Goldman Sachs Group, Inc. The Goldman Sachs Group, Inc. notes linked to the Dow Jones Industrial Average® are not sponsored, endorsed, sold or promoted by Dow Jones, and Dow Jones makes no representation regarding the advisability of investing in such notes.

Goldman, Sachs & Co.

Prospectus Supplement dated August 26, 2010.

Table of Contents

We refer to the notes we are offering by this prospectus supplement as the “notes”. Each of the notes, including your notes, has the terms described below and under “Specific Terms of Your Notes” on page S-13. Please note that in this prospectus supplement, references to “The Goldman Sachs Group, Inc.”, “we”, “our” and “us” mean only The Goldman Sachs Group, Inc. and do not include its consolidated subsidiaries. Also, references to the “accompanying prospectus” mean the accompanying prospectus, dated April 6, 2009, as supplemented by the accompanying prospectus supplement, dated April 6, 2009, of The Goldman Sachs Group, Inc. relating to the Medium-Term Notes, Series D program of The Goldman Sachs Group, Inc. References to the “indenture” in this prospectus supplement mean the senior debt indenture, dated July 16, 2008, between The Goldman Sachs Group, Inc. and The Bank of New York Mellon, as trustee.

Key Terms

Issuer: The Goldman Sachs Group, Inc.

Index: the Dow Jones Industrial Average® (Bloomberg ticker “INDU”), as published by Dow Jones & Company, Inc.; see “The Index” on page S-20

Specified currency: U.S. dollars (“$”)

Face amount:each note will have a face amount equal to $1,000, or integral multiples of $1,000 in excess thereof; $879,000 in the aggregate for all the offered notes; the aggregate face amount of the offered notes may be increased if the issuer, at its sole option, decides to sell an additional amount of the offered notes on a date subsequent to the date of this prospectus supplement

Payment amount: on the stated maturity date, we will pay, for each $1,000 face amount of notes, an amount in cash equal to:

| • | if the final index level isgreater than the initial index level, thesumof (1) the $1,000 face amountplus(2) theproductof (i) the $1,000 face amounttimes(ii) the index return; or |

| • | if the final index level isequal to orless than the initial index level, the $1,000 face amount |

Minimum settlement amount: $1,000

Initial index level: 9,985.81

Stated maturity date: August 31, 2017, subject to postponement as described under “Specific Terms of Your Notes — Payment of Principal on Stated Maturity Date — Stated Maturity Date” on page S-14

Determination date: August 28, 2017, subject to adjustment as described under “Specific Terms of

Your Notes — Payment of Principal on Stated Maturity Date — Determination Date” on page S-14

Final index level: the closing level of the index on the determination date, except in the limited circumstances described under “Specific Terms of Your Notes — Payment of Principal on Stated Maturity Date — Consequences of a Market Disruption Event or a Non-Trading Day” on page S-14 and subject to adjustment as provided under “Specific Terms of Your Notes — Payment of Principal on Stated Maturity Date — Discontinuance or Modification of the Index” on page S-14

Closing level of the index:the official closing level of the index or any successor index published by the index sponsor at the regular weekday close of trading on the relevant exchanges on the relevant trading day

Index return: thequotient of (i) the final index levelminusthe initial index leveldividedby (ii) the initial index level, expressed as a positive or negative percentage

Trade date:August 26, 2010

Original issue date: August 31, 2010

No interest: the notes do not bear interest

No listing: the notes will not be listed on any securities exchange or interdealer market quotation system

No redemption: the notes will not be subject to redemption right or price dependent redemption right

Market disruption event:as described under “Specific Terms of Your Notes — Special

S-2

Table of Contents

Calculation Provisions — Market Disruption Event” on page S-17

Calculation agent: Goldman, Sachs & Co.

Business day: as described on page S-16

Trading day: as described on page S-16

CUSIP no.: 38143UKX8

ISIN no.: US38143UKX80

Conflicts of interest:Goldman, Sachs & Co. is an affiliate of The Goldman Sachs Group, Inc. and, as such, has a “conflict of interest” in this offering

within the meaning of NASD Rule 2720. Consequently, the offering is being conducted in compliance with the provisions of Rule 2720. Goldman, Sachs & Co. is not permitted to sell notes in this offering to an account over which it exercises discretionary authority without the prior specific written approval of the account holder

FDIC:the notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank

S-3

Table of Contents

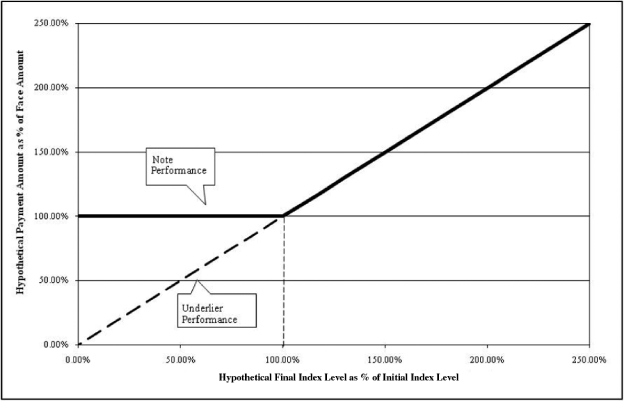

The following table and chart are provided for purposes of illustration only. They should not be taken as an indication or prediction of future investment results and are intended merely to illustrate the impact that the various hypothetical final index levels on the determination date could have on the payment amount at maturity assuming all other variables remain constant.

The information in the table reflects hypothetical rates of return on the offered notes assuming that they are purchased on the original issue date and held to the stated maturity date. If you sell your notes prior to the stated maturity date, your return will depend upon the market value of your notes at the time of sale, which may be affected by a number of factors that are not reflected in the examples shown below. In addition, assuming no changes in market conditions or our creditworthiness and other relevant factors, the value of your notes on the trade date (as determined by reference to pricing models used by Goldman, Sachs & Co. and taking into account our credit spreads) is, and the price you may receive for your notes may be, significantly less than the original issue price. For more information on the value of your notes in the secondary market, see “Additional Risk Factors Specific to Your Notes — Assuming No Changes in Market Conditions or Any Other Relevant Factors, the Value of Your Notes on the Trade Date (As Determined by Reference to Pricing Models Used by Goldman, Sachs & Co.) Will, and the Price You May Receive for Your Notes May, Be Significantly Less Than the Original Issue Price” on page S-7 and “— The Market Value of Your Notes May Be Influenced by Many Factors That Are Unpredictable and Interrelated in Complex Ways” on page S-8. The information in the table also reflects the key terms and assumptions in the box below.

Key Terms and Assumptions

Face amount | $1,000 |

Minimum settlement amount | $1,000.00 | |

Neither a market disruption event nor a non-trading day occurs on the originally scheduled determination date

No change in or affecting any of the index stocks or the method by which the index sponsor calculates the index

Notes purchased on original issue date and held to the stated maturity date

The examples below are based on a range of final index levels that are entirely hypothetical; no one can predict what the index level will be on the determination date.

The index has been highly volatile — meaning that the level of the index has changed substantially in relatively short periods — in the past, and its future performance cannot be predicted.

Also, the hypothetical examples shown below do not take into account the effects of applicable taxes. Because of the U.S. tax treatment applicable to your notes, tax liabilities could affect the after-tax rate of return on your notes to a comparatively greater extent than the after-tax return on the index stocks.

For these reasons, the actual performance of the index over the life of the offered notes, as well as the payment amount at maturity, may bear little or no relation to the hypothetical examples shown below or to the historical closing levels of the index shown elsewhere in this prospectus supplement. For information about the closing level of the index during recent periods, see “The Index — Historical Quarterly High, Low and Closing Levels of the Index” on page S-21.

Any rate of return you may earn on an investment in the notes may be lower than that which you could earn on a comparable investment in the index stocks. Among other things, the return on the notes will not reflect any dividends that may be paid on the index stocks.

S-4

Table of Contents

The table below shows the hypothetical payment amounts that we would deliver on the stated maturity date in exchange for each $1,000 face amount of the notes if the final index level (expressed as a percentage of the initial index level) were any of the hypothetical levels shown in the left column.

The levels in the left column of the table below represent hypothetical final index levels and are expressed as percentages of the initial index level. The amounts in the right column represent the hypothetical payment amounts, based on the

corresponding hypothetical final index level (expressed as a percentage of the initial index level), and are expressed as percentages of the face amount of a note (rounded to the nearest one-hundredth of a percent). Thus, a hypothetical payment amount of 100.00% means that the value of the cash payment that we would deliver for each $1,000 of the outstanding face amount of the offered notes on the stated maturity date would equal 100.00% of the face amount of a note, based on the corresponding hypothetical final index level (expressed as a percentage of the initial index level) and the assumptions noted above.

Hypothetical Final Index | Hypothetical Payment Amount (as Percentage of Face Amount) | |

| 150.00% | 150.00% | |

| 125.00% | 125.00% | |

| 100.00% | 100.00% | |

| 75.00% | 100.00% | |

| 50.00% | 100.00% | |

| 25.00% | 100.00% | |

| 0.00% | 100.00% |

If, for example, the final index level were determined to be 25.00% of the initial index level, the payment amount that we would deliver on your notes at maturity would be 100.00% of the face amount of your notes, as shown in the table above. As a result, if you purchased your notes on the original issue date and held them to the stated maturity date, you would receive no return on your investment. In addition, if the final index level were determined to be 125.00% of the initial index level, the payment amount that we would deliver on your notes at maturity would be 125.00% of the face amount of your notes, as shown in the table above. As a result, if you purchased your notes on the original issue date and held them to the stated maturity date, you would benefit from any increase

in the final index level over 100.00% of the initial index level.

The following chart also shows a graphical illustration of the hypothetical payment amounts (expressed as a percentage of the face amount of your notes) that we would pay on your notes on the stated maturity date, if the final index level (expressed as a percentage of the initial index level) were any of the hypothetical levels shown on the horizontal axis. The chart shows that any hypothetical final index level (expressed as a percentage of the initial index level) of less than 100.00% (the section left of the 100.00% marker on the horizontal axis) would result in a hypothetical payment amount of 100.00% of the face amount of your notes.

S-5

Table of Contents

The payment amounts shown above are entirely hypothetical; they are based on market prices for the index stocks that may not be achieved on the determination date and on assumptions that may prove to be erroneous. The actual market value of your notes on the stated maturity date or at any other time, including any time you may wish to sell your notes, may bear little relation to the hypothetical payment amounts shown above, and these amounts should not be viewed as an indication of the financial return on an investment in the offered notes. Please read “Additional Risk Factors Specific to Your Notes — The Market Value of Your Notes May Be Influenced by Many Factors

That Are Unpredictable and Interrelated in Complex Ways” on page S-8.

Payments on the notes are economically equivalent to the amounts that would be paid on a combination of other instruments. For example, payments on the notes are economically equivalent to the amounts that would be paid on a combination of an interest-bearing bond bought, and an option bought, by the holder (with an implicit option premium paid over time by the holder). The discussion in this paragraph does not modify or affect the terms of the notes or the United States income tax treatment of the notes, as described elsewhere in this prospectus supplement and the accompanying prospectus.

We cannot predict the actual final index level or what the market value of your notes will be on any particular trading day, nor can we predict the relationship between the index level and the market value of your notes at any time prior to the stated maturity date. The actual amount that you will receive at maturity and the rate of return on the offered notes will depend on the actual final index level determined by the calculation agent as described above. Moreover, the assumptions on which the hypothetical returns are based may turn out to be inaccurate. Consequently, the amount of cash to be paid in respect of your notes on the stated maturity date may be very different from the information reflected in the table and chart above.

S-6

Table of Contents

ADDITIONAL RISK FACTORS SPECIFIC TO YOUR NOTES

An investment in your notes is subject to the risks described below, as well as the risks described under “Considerations Relating to Indexed Securities” in the accompanying prospectus dated April 6, 2009. Your notes are a riskier investment than ordinary debt securities. Also, your notes are not equivalent to investing directly in the index stocks, i.e., the stocks comprising the index to which your notes are linked. You should carefully consider whether the offered notes are suited to your particular circumstances.

Assuming No Changes in Market Conditions or Any Other Relevant Factors, the Value of Your Notes on the Trade Date (As Determined by Reference to Pricing Models Used By Goldman, Sachs & Co.) Is, and the Price You May Receive for Your Notes May Be, Significantly Less than the Original Issue Price

The price at which Goldman, Sachs & Co. would initially buy or sell notes (if Goldman, Sachs & Co. makes a market) and the value that Goldman, Sachs & Co. will initially use for account statements and otherwise will significantly exceed the value of your notes using such pricing models. The amount of the excess will decline on a straight line basis over the period from the date hereof through February 26, 2014. After February 26, 2014, the price at which Goldman, Sachs & Co. would buy or sell notes will reflect the value determined by reference to the pricing models, plus our customary bid and asked spread.

The value or quoted price of your notes at any time will reflect many factors and cannot be predicted. If Goldman Sachs makes a market in the offered notes, the price quoted by us or our affiliates for the offered notes would reflect any changes in market conditions and other relevant factors, including a deterioration in our creditworthiness or perceived creditworthiness whether measured by our credit ratings or other credit measures. These changes may adversely affect the market price of your notes, including the price you may receive for your notes in any market making transaction. In addition, even if our creditworthiness does not decline, the value of your notes on the trade date is significantly less than the original issue price taking into account our credit spreads on that date. The quoted price (and the value of your notes that Goldman, Sachs & Co. will use for account statements or otherwise) could be higher or lower than the original issue price, and may be higher or lower than the value of your notes as determined by

reference to pricing models used by Goldman, Sachs & Co.

If at any time a third party dealer quotes a price to purchase your notes or otherwise values your notes, that price may be significantly different (higher or lower) than any price quoted by Goldman, Sachs & Co. See “— The Market Value of Your Notes May Be Influenced by Many Factors That Are Unpredictable and Interrelated in Complex Ways” below.

Furthermore, if you sell your notes, you will likely be charged a commission for secondary market transactions, or the price will likely reflect a dealer discount.

There is no assurance that Goldman, Sachs & Co. or any other party will be willing to purchase your notes and, in this regard, Goldman, Sachs & Co. is not obligated to make a market in the notes. See “— Your Notes May Not Have an Active Trading Market” below.

Your Notes Do Not Bear Interest

You will not receive any interest payments on your notes. Even if the payment amount on your notes on the stated maturity date exceeds the face amount of your notes, the overall return you earn on your notes may be less than you would have earned by investing in a non-indexed debt security of comparable maturity that bears interest at a prevailing market rate.

The Small Number of Stocks in the Index and the Selection Criteria Used to Select Them May Result in Larger Declines in Value of the Index Than That Experienced by The U.S. Markets As a Whole

The index is comprised of 30 stocks of U.S. companies selected by the editors ofThe Wall Street Journal. The editors make the selections using subjective criteria that may vary over time and that are not disclosed, except that the stocks are

S-7

Table of Contents

selected to reflect the broader U.S. market. Because of the limited number of stocks in the index, the index may experience large swings in value (including declines) that are larger than those experienced by the U.S. equity market as a whole. Also, a particular stock that is selected to represent a certain sector of the U.S. market may, for non-sector related reasons, experience a much larger decline than that sector of the U.S. economy as a whole. Finally, because the selection criteria consists of an exercise of subjective judgment on the part of the editors, they may select a company that is ultimately not representative of the sector as a whole and may experience greater losses than its sector as a whole. For the foregoing reasons, the index may not be an accurate reflection of the U.S. market as a whole, and your notes will not experience the same return as they would if they were linked to a larger index or to the U.S. equities market as a whole.

The Amount Payable on Your Notes Is Not Linked to the Level of the Index at Any Time Other than the Determination Date

The final index level will be based on the closing level of the index on the determination date (subject to adjustment as described elsewhere in this prospectus supplement). Therefore, if the closing level of the index dropped precipitously on the determination date, the payment amount for your notes may be significantly less than it would have been had the payment amount been linked to the closing level of the index prior to such drop in the level of the index. Although the actual level of the index on the stated maturity date or at other times during the life of your notes may be higher than the final index level, you will not benefit from the closing level of the index at any time other than on the determination date.

Past Index Performance is No Guide to Future Performance

The actual performance of the index over the life of the notes, as well as the amount payable at maturity, may bear little relation to the historical closing level of the index or to the hypothetical return examples set forth elsewhere in this prospectus supplement. We cannot predict the future performance of the index.

We May Sell an Additional Aggregate Face Amount of the Notes at a Different Issue Price

At our sole option, we may decide to sell an additional aggregate face amount of the notes subsequent to the date of this prospectus supplement but prior to the settlement date. The issue price of the notes in the subsequent sale may differ substantially (higher or lower) from the original issue price you paid as provided on the cover of this prospectus supplement.

The Return on Your Notes Will Not Reflect Any Dividends Paid on the Index Stocks

The index sponsor calculates the level of the index by reference to the prices of the common stocks included in the index, without taking account of the value of dividends paid on those stocks. As a result, the return on your notes will not reflect the return you would realize if you actually owned the stocks included in the index and received the dividends paid on those stocks. You will not receive any dividends that may be paid on any of the index stocks by the index stock issuers. See “— You Have No Shareholder Rights or Rights to Receive Any Stock” below for additional information.

The Market Value of Your Notes May Be Influenced by Many Factors That Are Unpredictable and Interrelated in Complex Ways

When we refer to the market value of your notes, we mean the value that you could receive for your notes if you chose to sell them in the open market before the stated maturity date. A number of factors, many of which are beyond our control, will influence the market value of your notes, including:

| • | the level of the index; |

| • | the volatility — i.e., the frequency and magnitude of changes — in the level of the index; |

| • | the dividend rates of the stocks underlying the index; |

| • | economic, financial, legislative, regulatory and political, military or other events that affect the stock markets generally and the |

S-8

Table of Contents

stocks underlying the index, and which may affect the level of the index; |

| • | other interest rate and yield rates in the market; |

| • | the time remaining until your notes mature; and |

| • | our creditworthiness, whether actual or perceived, and including actual or anticipated upgrades or downgrades in our credit ratings or changes in other credit measures. |

These factors will influence the price you will receive if you sell your notes before maturity, including the price you may receive for your notes in any market making transaction. If you sell your notes before maturity, you may receive less than the face amount of your notes.

You cannot predict the future levels of the index based on its historical fluctuations. The actual level of the index over the life of the notes may bear little or no relation to the historical closing level of the index or to the hypothetical examples shown elsewhere in this prospectus supplement.

If the Level of the Index Changes, the Market Value of Your Notes May Not Change in the Same Manner

Your notes may trade quite differently from the performance of the index. Changes in the level of the index may not result in a comparable change in the market value of your notes. Even if the level of the index increases above the initial index level during the life of the notes, the market value of your notes may not increase by the same amount. We discuss some of the reasons for this disparity under “— The Market Value of Your Notes May Be Influenced by Many Factors That Are Unpredictable and Interrelated in Complex Ways” above.

Trading and Other Transactions by Goldman Sachs in Instruments Linked to the Index or Index Stocks May Impair the Value of Your Notes

As we describe under “Use of Proceeds and Hedging” below, we, through Goldman, Sachs & Co. or one or more of our other affiliates, have hedged or expect to hedge our obligations under the notes by purchasing futures and/or other

instruments linked to the index or the stocks comprising the index, which we refer to as the index stocks. We also have adjusted or expect to adjust our hedge by, among other things, purchasing or selling any of the foregoing, and perhaps other instruments linked to the index or index stocks at any time and from time to time, and to unwind the hedge by selling any of the foregoing, on or before the determination date for your notes. We may also enter into, adjust and unwind hedging transactions relating to other index-linked notes whose returns are linked to changes in the level of the index or one or more of the index stocks. Any of these hedging activities may adversely affect the level of the index — directly or indirectly by affecting the price of the index stocks — and therefore the market value of your notes and the amount we will pay on your notes at maturity. It is possible that we, through our affiliates, could receive substantial returns with respect to our hedging activities while the value of your notes may decline. See “Use of Proceeds and Hedging” on page S-19 for a further discussion of transactions in which we or one or more of our affiliates may engage.

Goldman, Sachs & Co. and our other affiliates have engaged or may engage in trading in one or more of the index stocks or instruments whose returns are linked to the index or index stocks for their proprietary accounts, for other accounts under their management or to facilitate transactions, including block transactions, on behalf of customers. Any of these activities of Goldman, Sachs & Co. or our other affiliates could adversely affect the level of the index — directly or indirectly by affecting the price of the index stocks — and therefore, the market value of your notes and the amount we will pay on your notes at maturity. We may also issue, and Goldman, Sachs & Co. and our other affiliates may also issue or underwrite, other securities or financial or derivative instruments with returns linked to changes in the level of the index or one or more of the index stocks. By introducing competing products into the marketplace in this manner, we or our affiliates could adversely affect the market value of your notes and the amount we will pay on your notes at maturity.

You Have No Shareholder Rights or Rights to Receive Any Stock

Investing in your notes will not make you a holder of any of the index stocks. Neither you nor

S-9

Table of Contents

any other holder or owner of your notes will have any voting rights, any right to receive dividends or other distributions or any other rights with respect to the index stocks. Your notes will be paid in cash, and you will have no right to receive delivery of any index stocks.

Our Business Activities May Create Conflicts of Interest Between Your Interests in the Notes and Us

As we have noted above, Goldman, Sachs & Co. and our other affiliates have owned or expect to own securities of, and have engaged or expect to engage in trading activities related to the index and the index stocks that are not for your account or on your behalf. These trading activities may present a conflict between your interest in your notes and the interests Goldman, Sachs & Co. and our other affiliates will have in their proprietary accounts, in facilitating transactions, including block trades, for their customers and in accounts under their management. These trading activities, if they influence the level of the index, could be adverse to your interests as a beneficial owner of your notes.

Goldman, Sachs & Co. and our other affiliates may, at present or in the future, engage in business with the issuers of the index stocks, including making loans to or equity investments in those companies or providing advisory services to those companies. These services could include merger and acquisition advisory services. These activities may present a conflict between the obligations of Goldman, Sachs & Co. or another affiliate of Goldman Sachs and your interests as a beneficial owner of your notes. Moreover, one or more of our affiliates may have published and in the future expect to publish research reports with respect to the index and some or all of the issuers of the index stocks. Any of these activities by any of our affiliates may affect the level of the index and, therefore, the market value of your notes and the amount we will pay on your notes at maturity.

As Calculation Agent, Goldman, Sachs & Co. Will Have the Authority to Make Determinations that Could Affect the Value of Your Notes, When Your Notes Mature and the Amount You Receive at Maturity

As of the date of this prospectus supplement, we have appointed Goldman, Sachs & Co. as the calculation agent for your notes. As calculation agent for your notes, Goldman, Sachs & Co. will

have discretion in making various determinations that affect your notes, including determining the final index level on the determination date, which we will use to determine the amount we must pay on the stated maturity date; market disruption events; non-trading days; the determination date; the stated maturity date; the default amount and any amount payable on your notes. See “Specific Terms of Your Notes” below. The calculation agent also has discretion in making certain adjustments relating to a discontinuation or modification of the index. See “Specific Terms of Your Notes — Discontinuance or Modification of the Index” below. The exercise of this discretion by Goldman, Sachs & Co. could adversely affect the value of your notes and may present Goldman, Sachs & Co. with a conflict of interest of the kind described under “— Our Business Activities May Create Conflicts of Interest Between Your Interests in the Notes and Us” above. We may change the calculation agent at any time without notice and Goldman, Sachs & Co. may resign as calculation agent at any time upon 60 days’ written notice to Goldman Sachs.

The Policies of the Index Sponsor and Changes That Affect the Index or the Index Stocks Could Affect the Payment Amount on Your Notes and Their Market Value

The policies of the index sponsor concerning the calculation of the level of the index, additions, deletions or substitutions of index stocks and the manner in which changes affecting the index stocks or their issuers, such as stock dividends, reorganizations or mergers, are reflected in the level of the index could affect the level of the index and, therefore, the payment amount on your notes on the stated maturity date and the market value of your notes before that date. The payment amount on your notes and their market value could also be affected if the index sponsor changes these policies, for example, by changing the manner in which it calculates the level of the index or if the index sponsor discontinues or suspends calculation or publication of the level of the index, in which case it may become difficult to determine the market value of your notes. If events such as these occur, or if the closing level of the index is not available on the determination date because of a market disruption event or for any other reason, the calculation agent — which initially will be Goldman, Sachs & Co., our affiliate — may determine the closing level of the index on the determination date — and thus the payment amount on the stated

S-10

Table of Contents

maturity date — in a manner it considers appropriate, in its sole discretion. We describe the discretion that the calculation agent will have in determining the closing level of the index on the determination date and the payment amount on your notes more fully under “Specific Terms of Your Notes — Discontinuance or Modification of the Index” and “— Role of Calculation Agent” below.

There Is No Affiliation Between the Index Stock Issuers or the Index Sponsor and Us, and We Are Not Responsible for Any Disclosure by Any of the Other Index Stock Issuers or the Index Sponsor

Goldman Sachs is not affiliated with the issuers of the index stocks or the index sponsor. As we have told you above, however, we or our affiliates may currently or from time to time in the future own securities of, or engage in business with, the index sponsor of the index stock issuers. Nevertheless, neither we nor any of our affiliates assumes any responsibility for the accuracy or the completeness of any information about the index or any of the other index stock issuers. You, as an investor in your notes, should make your own investigation into the index and the index stock issuers. See “The Index” below for additional information about the index.

Neither the index sponsor nor any of the other index stock issuers are involved in this offering of your notes in any way and none of them have any obligation of any sort with respect to your notes. Thus, neither the index sponsor nor any of the index stock issuers have any obligation to take your interests into consideration for any reason, including in taking any corporate actions that might affect the value of your notes.

Your Notes May Not Have an Active Trading Market

Your notes will not be listed or displayed on any securities exchange or included in any interdealer market quotation system, and there may be little or no secondary market for your notes. Even if a secondary market for your notes develops, it may not provide significant liquidity and we expect that transaction costs in any secondary market would be high. As a result, the difference between bid and asked prices for your notes in any secondary market could be substantial.

The Calculation Agent Can Postpone the Determination Date If a Market Disruption Event or a Non-Trading Day Occurs

If the calculation agent determines that, on the date that would otherwise be the determination date, a market disruption event has occurred or is continuing or that day is not a trading day, the determination date will be postponed until the first following trading day on which the market disruption event for the index has ceased. In no cases, however, will such applicable date be postponed to a date later than the originally scheduled stated maturity date or, if the originally scheduled stated maturity date is not a business day, later than the first business day after the originally scheduled stated maturity date. Moreover, if the determination date is postponed to the last possible day, but the market disruption event has not ceased by that day or that day is not a trading day, that day will nevertheless be the determination date. In such a case, the calculation agent will determine the final index level based on the procedures described under “Specific Terms of Your Notes — Consequences of a Market Disruption Event or a Non-Trading Day” below.

Certain Considerations for Insurance Companies and Employee Benefit Plans

Any insurance company or fiduciary of a pension plan or other employee benefit plan that is subject to the prohibited transaction rules of the Employee Retirement Income Security Act of 1974, as amended, which we call “ERISA”, or the Internal Revenue Code of 1986, as amended, including an IRA or a Keogh plan (or a governmental plan to which similar prohibitions apply), and that is considering purchasing the offered notes with the assets of the insurance company or the assets of such a plan, should consult with its counsel regarding whether the purchase or holding of the offered notes could become a “prohibited transaction” under ERISA, the Internal Revenue Code or any substantially similar prohibition in light of the representations a purchaser or holder in any of the above categories is deemed to make by purchasing and holding the offered notes. This is discussed in more detail under “Employee Retirement Income Security Act” below.

S-11

Table of Contents

Your Notes Will Be Treated as Debt Instruments Subject to Special Rules Governing Contingent Payment Debt Obligations for United States Federal Income Tax Purposes

The notes will be treated as debt instruments subject to special rules governing contingent payment debt obligations for United States federal income tax purposes. If you are a U.S. individual or taxable entity, you generally will be required to pay taxes on ordinary income from the notes over their term based on the comparable yield for the notes, even though you will not receive any payments from us until maturity. This comparable yield is

determined solely to calculate the amount on which you will be taxed prior to maturity and is neither a prediction nor a guarantee of what the actual yield will be. In addition, any gain you may recognize on the sale or maturity of the notes will be taxed as ordinary interest income. If you are a secondary purchaser of the notes, the tax consequences to you may be different. Please see “Supplemental Discussion of Federal Income Tax Consequences” below for a more detailed discussion. Please also consult your own tax advisor concerning the U.S. federal income tax and any other applicable tax consequences to you of owning your notes in your particular circumstances.

S-12

Table of Contents

We refer to the notes we are offering by this prospectus supplement as the “offered notes” or the “notes”. Please note that in this prospectus supplement, references to “The Goldman Sachs Group, Inc.”, “we”, “our” and “us” mean only The Goldman Sachs Group, Inc. and do not include its consolidated subsidiaries. Also, references to the “accompanying prospectus” mean the accompanying prospectus, dated April 6, 2009, as supplemented by the accompanying prospectus supplement, dated April 6, 2009, in each case relating to the Medium-Term Notes, Series D, of The Goldman Sachs Group, Inc. Please note that in this section entitled “Specific Terms of Your Notes”, references to “holders” mean those who own notes registered in their own names, on the books that we or the trustee maintain for this purpose, and not those who own beneficial interests in notes registered in street name or in notes issued in book-entry form through The Depository Trust Company. Please review the special considerations that apply to owners of beneficial interests in the accompanying prospectus, under “Legal Ownership and Book-Entry Issuance”.

The offered notes are part of a series of debt securities, entitled “Medium-Term Notes, Series D”, that we may issue under the indenture from time to time as described in the accompanying prospectus and accompanying prospectus supplement. The offered notes are also “indexed debt securities”, as defined in the accompanying prospectus.

This prospectus supplement summarizes specific financial and other terms that apply to the offered notes, including your notes; terms that apply generally to all Series D medium-term notes are described in “Description of Notes We May Offer” in the accompanying prospectus supplement. The terms described here supplement those described in the accompanying prospectus supplement and the accompanying prospectus and, if the terms described here are inconsistent with those described there, the terms described here are controlling.

In addition to those terms described on the first three pages of this prospectus supplement, the following terms will apply to your notes:

No interest:we will not pay interest on your notes

Specified currency:

| • | U.S. dollars (“$”) |

Form of note:

| • | global form only: yes, at DTC |

| • | non-global form available: no |

Denominations:each note registered in the name of a holder must have a face amount of $1,000 or integral multiples of $1,000 in excess thereof

Defeasance applies as follows:

| • | full defeasance: no |

| • | covenant defeasance: no |

Other terms:

| • | the default amount will be payable on any acceleration of the maturity of your notes as described under “— Special Calculation Provisions” below |

| • | a business day for your notes will not be the same as a business day for our other Series D medium-term notes, as described under “— Special Calculation Provisions” below |

| • | a trading day for your notes will be as described under “— Special Calculation Provisions” below |

Please note that the information about the settlement date or trade date, issue price, underwriting discount and net proceeds to The Goldman Sachs Group, Inc. on the front cover page or elsewhere in this prospectus supplement relates only to the initial issuance and sale of the notes. We may decide to sell additional notes on one or more dates after the date of this prospectus supplement, at issue prices, underwriting discounts and net proceeds that differ from the amounts set forth on

S-13

Table of Contents

the front cover page or elsewhere in this prospectus supplement. If you have purchased your notes in a market-making transaction after the initial issuance and sale of the notes, any such relevant information about the sale to you will be provided in a separate confirmation of sale.

We describe the terms of your notes in more detail below.

Index, Index Sponsor and Index Stocks

In this prospectus supplement, when we refer to the index, we mean the index specified on the front cover page, or any successor index, as it may be modified, replaced or adjusted from time to time as described under “— Payment of Principal on Stated Maturity Date — Discontinuance or Modification of the Index” below. When we refer to the index sponsor as of any time, we mean the entity, including any successor sponsor, that determines and publishes the index as then in effect. When we refer to the index stocks as of any time, we mean the stocks that comprise the index as then in effect, after giving effect to any additions, deletions or substitutions.

Payment of Principal on Stated Maturity Date

The payment amount for each $1,000 face amount of notes outstanding on the stated maturity date will be an amount in cash equal to:

| • | if the final index level isgreater than the initial index level, thesumof (1) the $1,000 face amountplus(2) theproductof (i) the $1,000 face amounttimes (ii) the index return; or |

| • | if the final index level isequal to orless than the initial index level, the $1,000 face amount. |

The initial index level is 9,985.81. The calculation agent will determine the final index level, which will be the closing level of the index on the determination date as calculated and published by the index sponsor, subject to adjustment in certain circumstances described under “— Consequences of a Market Disruption Event or a Non-Trading Day” and “— Discontinuance or Modification of the Index” below.

The index return will equal thequotientof (1) the final index levelminusthe initial index leveldividedby (2) the initial index level, expressed as a percentage.

The amount payable on your notes on the stated maturity date will be based on the closing level of the index on the determination date, which we call the final index level. If the final index level is greater than the initial index level, – i.e., the index return is positive due to an increase in the level of the index, you will participate in any such increase on a one-for-one basis. If the final index level is less than the initial index level, – i.e., the index return is negative due to a decrease in the level of the index, you will receive 100% of your investment. As a result, if the index declines below the initial index level, the payment you would receive at maturity for each of your notes would be equal to 100% of each $1,000 face amount of a note (or $1,000).

Stated Maturity Date

The stated maturity is August 31, 2017, unless that day is not a business day, in which case the stated maturity date will be the next following business day. If the determination date is postponed as described under “— Determination date” below, the stated maturity date will be postponed by the same number of business day(s) from but excluding the originally scheduled determination date to and including the postponed determination date.

Determination date

The determination date is August 28, 2017, unless the calculation agent determines that a market disruption event with respect to the index occurs or is continuing on that day or that day is otherwise not a trading day. In that event, the determination date will be the first following trading day on which the calculation agent determines that no market disruption event occurs or is continuing. In no event, however, will the determination date be postponed to a date later than the originally scheduled stated maturity date or, if the originally scheduled stated maturity date is not a business day, later than the first business day after the originally scheduled stated maturity date. If the determination date is postponed to the last possible day, but a market disruption event occurs or is continuing on that day or that day is not a trading day, that day will nevertheless be the determination date.

Consequences of a Market Disruption Event or a Non-Trading Day

If a market disruption event occurs or is continuing on a day that would otherwise be the determination date or such day is not a trading day, then the determination date will be postponed as described under “— Determination Date” above.

S-14

Table of Contents

If the calculation agent determines that the final index level is not available on the determination date because of a market disruption event, a non-trading day or for any other reason (other than as described under “— Discontinuance or Modification of the Index” below), the calculation agent will nevertheless determine the level of the index based on its assessment, made in its sole discretion, of the level of the index at the applicable time on that day.

Discontinuance or Modification of the Index

If the index sponsor discontinues publication of the index and the index sponsor or anyone else publishes a substitute index that the calculation agent determines is comparable to the index, then the calculation agent will determine the payment amount on the stated maturity date by reference to the substitute index. We refer to any substitute index approved by the calculation agent as a successor index.

If the calculation agent determines on the determination date that the publication of the index is discontinued and there is no successor index, the calculation agent will determine the payment amount on the stated maturity date by a computation methodology that the calculation agent determines will as closely as reasonably possible replicate the index.

If the calculation agent determines that the index, the stocks comprising the index or the method of calculating the index is changed at any time in any respect — including any split or reverse split and any addition, deletion or substitution and any reweighting or rebalancing of the index or of the index stocks and whether the change is made by the index sponsor under its existing policies or following a modification of those policies, is due to the publication of a successor index, is due to events affecting one or more of the index stocks or their issuers or is due to any other reason — then the calculation agent will be permitted (but not required) to make such adjustments in the index or the method of its calculation as it believes are appropriate to ensure that the levels of the index used to determine the payment amount on the stated maturity date is equitable.

All determinations and adjustments to be made by the calculation agent with respect to the index may be made by the calculation agent in its sole discretion. The calculation agent is not obligated to make any such adjustments.

Default Amount on Acceleration

If an event of default occurs and the maturity of your notes is accelerated, we will pay the default amount in respect of the principal of your notes at the maturity, instead of the payment amount on the stated maturity date as described earlier. We describe the default amount under “— Special Calculation Provisions” below.

For the purpose of determining whether the holders of our Series D medium-term notes, which include your notes, are entitled to take any action under the indenture, we will treat the outstanding face amount of your notes as the outstanding principal amount of that note. Although the terms of the offered notes differ from those of the other Series D medium-term notes, holders of specified percentages in principal amount of all Series D medium-term notes, together in some cases with other series of our debt securities, will be able to take action affecting all the Series D medium-term notes, including your notes, except with respect to certain Series D medium-term notes if the terms of such notes specify that the holders of specified percentages in the principal amount of all such notes must also consent to such action. This action may involve changing some of the terms that apply to the Series D medium-term notes, accelerating the maturity of the Series D medium-term notes after a default or waiving some of our obligations under the indenture. In addition, certain changes to the indenture and the notes that only affect certain debt securities may be made with the approval of holders of a majority of the principal amount of such affected debt securities. We discuss these matters in the accompanying prospectus under “Description of Debt Securities We May Offer — Default, Remedies and Waiver of Default” and “— Modification of the Debt Indentures and Waiver of Covenants”.

Manner of Payment

Any payment on your notes at maturity will be made to an account designated by the holder of your notes and approved by us, or at the office of the trustee in New York City, but only when your notes are surrendered to the trustee at that office. We also may make any payment in accordance with the applicable procedures of the depositary.

S-15

Table of Contents

Modified Business Day

As described in the accompanying prospectus, any payment on your notes that would otherwise be due on a day that is not a business day may instead be paid on the next day that is a business day, with the same effect as if paid on the original due date. For your notes, however, the term business day may have a different meaning than it does for other Series D medium-term notes. We discuss this term under “— Special Calculation Provisions” below.

Role of Calculation Agent

The calculation agent in its sole discretion will make all determinations regarding the index, market disruption events, business days, trading days, the index return, the final index level, the determination date, the default amount and the payment amount on your notes at maturity. Absent manifest error, all determinations of the calculation agent will be final and binding on you and us, without any liability on the part of the calculation agent.

Please note that Goldman, Sachs & Co., our affiliate, is currently serving as the calculation agent as of the original issue date of your notes. We may change the calculation agent for your notes at any time after the original issue date without notice and Goldman, Sachs & Co. may resign as calculation agent at any time upon 60 days’ written notice to Goldman Sachs.

Special Calculation Provisions

Business Day

When we refer to a business day with respect to your notes, we mean a day that is a New York Business Day as described under “Description of Debt Securities We May Offer — Payment Mechanics for Debt Securities — Business Days” on page 28 in the accompanying prospectus.

Trading Day

When we refer to a trading day with respect to your notes, we mean a day on which the respective principal securities markets for all of the index stocks are open for trading, the index sponsor is open for business and the index is calculated and published by the index sponsor.

Default Amount

The default amount for your notes on any day will be an amount, in the specified currency for the

principal of your notes, equal to the cost of having a qualified financial institution, of the kind and selected as described below, expressly assume all of our payment and other obligations with respect to your notes as of that day and as if no default or acceleration had occurred, or to undertake other obligations providing substantially equivalent economic value to you with respect to your notes. That cost will equal:

| • | the lowest amount that a qualified financial institution would charge to effect this assumption or undertaking,plus |

| • | the reasonable expenses, including reasonable attorneys’ fees, incurred by the holder of your notes in preparing any documentation necessary for this assumption or undertaking. |

During the default quotation period for your notes, which we describe below, the holder and/or we may request a qualified financial institution to provide a quotation of the amount it would charge to effect this assumption or undertaking. If either party obtains a quotation, it must notify the other party in writing of the quotation. The amount referred to in the first bullet point above will equal the lowest — or, if there is only one, the only — quotation obtained, and as to which notice is so given, during the default quotation period. With respect to any quotation, however, the party not obtaining the quotation may object, on reasonable and significant grounds, to the assumption or undertaking by the qualified financial institution providing the quotation and notify the other party in writing of those grounds within two business days after the last day of the default quotation period, in which case that quotation will be disregarded in determining the default amount.

Default Quotation Period

The default quotation period is the period beginning on the day the default amount first becomes due and ending on the third business day after that day, unless:

| • | no quotation of the kind referred to above is obtained, or |

| • | every quotation of that kind obtained is objected to within five business days after the day the default amount first becomes due. |

If either of these two events occurs, the default quotation period will continue until the third business day after the first business day on which prompt notice of a quotation is given as described

S-16

Table of Contents

above. If that quotation is objected to as described above within five business days after that first business day, however, the default quotation period will continue as described in the prior sentence and this sentence.

In any event, if the default quotation period and the subsequent two business day objection period have not ended before the determination date, then the default amount will equal the principal amount of your notes.

Qualified Financial Institutions

For the purpose of determining the default amount at any time, a qualified financial institution must be a financial institution organized under the laws of any jurisdiction in the United States of America, Europe or Japan, which at that time has outstanding debt obligations with a stated maturity of one year or less from the date of issue and is rated either:

| • | A-1 or higher by Standard & Poor’s Ratings Group or any successor, or any other comparable rating then used by that rating agency, or |

| • | P-1 or higher by Moody’s Investors Service, Inc. or any successor, or any other comparable rating then used by that rating agency. |

Market Disruption Event

Any of the following will be a market disruption event:

| • | a suspension, absence or material limitation of trading in index stocks constituting 20% or more, by weight, of the index on their respective primary markets, in each case for more than two hours of trading or during the one half hour before the close of trading in that market, as determined by the calculation agent in its sole discretion, |

| • | a suspension, absence or material limitation of trading in option or futures contracts relating to the index or to index stocks constituting 20% or more, by weight, of the index, if available, in the respective primary markets for those contracts, in each case for more than two hours of trading or during the one-half hour before the close of trading in that market, as determined by the calculation agent in its sole discretion, or |

| • | index stocks constituting 20% or more, by weight, of the index, or option or futures contracts relating to the index or to index stocks constituting 20% or more, by weight, of the index, if available, are not trading on what were the respective primary markets for those index stocks or contracts, as determined by the calculation agent in its sole discretion, |

and, in the case of any of these events, the calculation agent determines in its sole discretion that the event could materially interfere with the ability of The Goldman Sachs Group, Inc. or any of its affiliates or a similarly situated party to unwind all or a material portion of a hedge that could be effected with respect to the offered notes. For more information about hedging by The Goldman Sachs Group, Inc. and/or any of its affiliates, see “Use of Proceeds and Hedging” below.

The following events will not be market disruption events:

| • | a limitation on the hours or numbers of days of trading, but only if the limitation results from an announced change in the regular business hours of the relevant market, and |

| • | a decision to permanently discontinue trading in the option or futures contracts relating to the index or to any index stock. |

For this purpose, an “absence of trading” in the primary securities market on which an index stock, or on which option or futures contracts relating to the index or an index stock are traded will not include any time when that market is itself closed for trading under ordinary circumstances. In contrast, a suspension or limitation of trading in an index stock or in option or futures contracts relating to the index or an index stock, if available, in the primary market for that stock or those contracts, by reason of:

| • | a price change exceeding limits set by that market, |

| • | an imbalance of orders relating to that index stock or those contracts, or |

| • | a disparity in bid and ask quotes relating to that index stock or those contracts, |

will constitute a suspension or material limitation of trading in that stock or those contracts in that market.

As is the case throughout this prospectus supplement, references to the index in this description of market disruption events includes

S-17

Table of Contents

the index and any successor index as it may be modified, replaced or adjusted from time to time.

S-18

Table of Contents

We expect to use the net proceeds we receive from the sale of the offered notes for the purposes we describe in the accompanying prospectus under “Use of Proceeds”. We or our affiliates may also use those proceeds in transactions intended to hedge our obligations under the offered notes as described below.

In anticipation of the sale of the offered notes, we and/or our affiliates have entered or expect to enter into hedging transactions involving purchases of futures and other instruments linked to the index on or before the trade date. In addition, from time to time after we issue the offered notes, we and/or our affiliates have entered or may enter into additional hedging transactions and to unwind those we have entered into, in connection with the offered notes and perhaps in connection with other index-linked notes we issue, some of which may have returns linked to the index or the index stocks. Consequently, with regard to your notes, from time to time, we and/or our affiliates:

| • | expect to acquire, or dispose of positions in listed or over-the-counter options, futures or other instruments linked to the index or some or all of the index stocks, |

| • | may take or dispose of positions in the securities of the index stock issuers themselves, |

| • | may take or dispose of positions in listed or over-the-counter options or other instruments based on indices designed to track the performance of the New York Stock Exchange or other components of the U.S. equity market, and /or |

| • | may take short positions in the index stocks or other securities of the kind described above — i.e., we and/or our affiliates may sell securities of the kind that we do not own or that we borrow for delivery to purchaser. |

We and/or our affiliates may acquire a long or short position in securities similar to your notes from time to time and may, in our or their sole discretion, hold or resell those securities.

In the future, we and/or our affiliates expect to close out hedge positions relating to the offered notes and perhaps relating to other notes with returns linked to the index or the index stocks. We expect these steps to involve sales of instruments linked to the index on or shortly before the determination date. These steps may also involve sales and/or purchases of some or all of the index stocks, or listed or over-the-counter options, futures or other instruments linked to the index, some or all of the index stocks or indices designed to track the performance of the New York Stock Exchange or other components of the U.S. equity market.

The hedging activity discussed above may adversely affect the market value of your notes from time to time and the amount we will pay on your notes at maturity. See “Additional Risk Factors Specific to Your Notes — Trading and Other Transactions by Goldman Sachs in Instruments Linked to the Index or Index Stocks May Impair the Value of Your Notes” and “— Our Business Activities May Create Conflicts of Interest Between Your Interests in the Notes and Us” above for a discussion of these adverse effects.

S-19

Table of Contents

We have derived all information regarding the Dow Jones Industrial Average® Index contained in this prospectus supplement, including, without limitation, its composition, methods of calculation and changes in its components, from publicly available information. Such information reflects the policies of, and is subject to change by the index sponsors. We make no representation or warranty as to the accuracy or completeness of such information. The index sponsors have no obligation to continue to publish, and may discontinue publication of, the index. Additional information concerning the DJIA may be found outhttp://www.djindexes.com. We are not incorporating any material on that website into this prospectus supplement.

The Dow Jones Industrial Average® Index, which we refer to as the DJIA, is a price-weighted index composed of 30 common stocks selected at the discretion of an Averages Committee comprised of the Managing Editor ofThe Wall Street Journal (the “WSJ”), the head of Dow Jones Indexes research and the head of CME Group research. The Averages Committee was created in March 2010, when Dow Jones Indexes became part of CME Group Index Services, LLC, a joint venture company owned 90% by CME Group Inc. and 10% by Dow Jones & Company, Inc, which we refer to as Dow Jones. Dow Jones publishesThe Wall Street Journal.The Averages Committee selects the index components as the largest and leading stocks of the sectors that are representative of the U.S. equity market. The index does not include producers of goods and services in the transportation and utilities industries. The DJIA is reported by Bloomberg under the ticker symbol “INDU <Index>”. Dow Jones is under no obligation to continue to publish the DJIA and may discontinue publication of the DJIA at any time.

There are no pre-determined criteria for selection of a component stock except that component companies represented by the DJIA should be established U.S. companies that are leaders in their industries. The DJIA serves as a measure of the entire U.S. market, including such sectors as financial services, technology, retail, entertainment and consumer goods and is not limited to traditionally defined industrial stocks. Changes in the composition of the DJIA are made by the editors of the WSJ without consultation with the component companies represented in the DJIA,

any stock exchange, any official agency or us. In order to maintain continuity, changes to the index stocks included in the DJIA tend to be made infrequently and generally occur only after a component company goes through a major change, such as a shift in its main line of business, acquisition by another company, or bankruptcy. Index reviews do not occur on any established or regular schedule, but only when corporate events with respect to a constituent stock require it. When one component stock is replaced, the entire index is reviewed. As a result, multiple component changes are often implemented simultaneously. The component stocks of the DJIA may be changed at any time for any reason. Where any index component stock price is unavailable on any trading day, the index sponsor will generally use the last reported price for such component stock.

The top ten constituent stocks of the DJIA as of July 30, 2010, by weight, are:International Business Machines Corp. (9.29%), 3M Co. (6.19%), Chevron Corp. (5.51%), United Technologies Corp. (5.14%), Caterpillar Inc. (5.04%), McDonald’s Corp. (5.04%), Boeing Co. (4.93%), Procter & Gamble Co. (4.42%), Exxon Mobil Corp. (4.32%) and Johnson & Johnson (4.20%). The 30 common stocks included in the DJIA include nine sectors based on the ten industries defined by the Industry Classification Benchmark. As of July 30, 2010, the Industry Classification Benchmark sectors include (with the number of percentage currently included in such sectors indicated in parentheses): Basic Materials (3.83%), Consumer Goods (10.52%), Consumer Services (13.24%), Financials (10.82%), Health Care (7.78%), Industrials (22.46%), Oil & Gas (9.75%), Technology (17.64%) and Telecommunications (3.98%). Constituent weightings and sector allocations may be found at http://www.djindexes.com/mdsidx/downloads/fact_ info/Dow_Jones_Industrial_Average_Fact_Sheet.pdf under “Top Components” and “Sector Allocation,” respectively. Sector designations are determined by the index sponsor, or by the sponsor of the classification system, using criteria it has selected or developed. Index and classification system sponsors may use very different standards for determining sector designations. In addition, many companies operate in a number of sectors, but are listed in only one sector and the basis on which that sector is selected may also differ. As a result, sector comparisons between indices with different sponsors may reflect differences in methodology as

S-20

Table of Contents

well as actual differences in the sector composition of the indices

The DJIA is price weighted rather than market capitalization weighted. Therefore, the component stock weightings are affected only by changes in the stocks’ prices, in contrast with the weightings of other indices that are affected by both price changes and changes in the number of shares outstanding. The value of the DJIA is thesum of the primary exchange prices of each of the 30 common stocks included in the DJIA,divided by a divisor. The divisor is changed in accordance with a mathematical formula to adjust for stock dividends, stock splits, spin-offs and other corporate actions. The current divisor of the DJIA is published daily in the WSJ and other publications. As of August 3, 2010, the divisor was 0.132129493. While this methodology reflects current practice in calculating the DJIA, no assurance can be given that Dow Jones will not modify or change this methodology in a manner that may affect the return on your notes.

The current formula used to calculate divisor adjustments is as follows: the new divisor (i.e., the divisor on the next trading session) is equal to (1) the divisor on the current trading session,times (2) thequotientof (a) the sum of the adjusted (for stock dividends, splits, spin-offs and other applicable corporate actions) closing prices of the DJIA components on the current trading session and (b) the sum of the unadjusted closing prices of the DJIA components on the current trading session.

| New Divisor | = | Current Divisor | x | Adjusted Sum of | ||||

| Unadjusted Sum of Prices |

Historical Quarterly High, Low and Closing Levels of the Index

The closing level of the index has fluctuated in the past and may, in the future, experience significant fluctuations. Any historical upward or downward trend in the closing level of the index during any period shown below is not an indication that the index is more or less likely to increase or decrease at any time during the life of your notes.

You should not take the historical closing levels of the index as an indication of the future performance of the index. We cannot give you any assurance that the future performance of the

index or the index stocks will result in your receiving an amount greater than the outstanding face amount of your notes on the stated maturity date. In light of the increased volatility currently being experienced by U.S. and global securities markets and recent market declines, the trend reflected in the historical performance of the index may be less likely to be indicative of the performance of the index during the period from the trade date to the determination date and of the final index level than would otherwise have been the case.

Neither we nor any of our affiliates make any representation to you as to the performance of the index. Before investing in the offered notes, you should consult publicly available information to determine the relevant index levels between the date of this prospectus supplement and the date of your purchase of the offered notes. The actual performance of the index over the life of the offered notes, as well as the payment amount at maturity, may bear little relation to the historical levels shown below.

The table below shows the high, low and final closing levels of the index for each of the four calendar quarters in 2007, 2008 and 2009 and the first three calendar quarters of 2010 (through August 26, 2010). We obtained the levels listed in the table below from Bloomberg Financial Services, without independent verification.

S-21

Table of Contents

Historical Quarterly High, Low and Closing Levels of the Index

| High | Low | Close | ||||

2007 | ||||||

Quarter ended March 31 | 12,786.64 | 12,050.41 | 12,354.35 | |||

Quarter ended June 30 | 13,676.32 | 12,382.30 | 13,408.62 | |||

Quarter ended September 30 | 14,000.41 | 12,845.78 | 13,895.63 | |||

Quarter ended December 31 | 14,164.53 | 12,743.44 | 13,264.82 | |||

2008 | ||||||

Quarter ended March 31 | 13,056.72 | 11,740.15 | 12,262.89 | |||

Quarter ended June 30 | 13,058.20 | 11,346.51 | 11,350.01 | |||

Quarter ended September 30 | 11,782.35 | 10,365.45 | 10,850.66 | |||

Quarter ended December 31 | 10,831.07 | 7,552.29 | 8,776.39 | |||

2009 | ||||||

Quarter ended March 31 | 9,034.69 | 6,547.05 | 7,608.92 | |||

Quarter ended June 30 | 8,799.26 | 7,761.60 | 8,447.00 | |||

Quarter ended September 30 | 9,829.87 | 8,146.52 | 9,712.28 | |||

Quarter ended December 31 | 10,548.51 | 9,487.67 | 10,428.00 | |||

2010 | ||||||

Quarter ended March 31 | 10,907.42 | 9,908.39 | 10,856.60 | |||

Quarter ended June 30 | 11,205.03 | 9,774.02 | 9,774.02 | |||

Quarter ending September 30 (through August 26, 2010) | 10,674.38 | 9,686.48 | 10,674.38 | |||

License Agreement

Dow Jones and The Goldman Sachs Group, Inc. have entered into a non-transferable, nonexclusive license agreement granting The Goldman Sachs Group, Inc. and its affiliates, in exchange for a fee, the right to use the Dow Jones Industrial Average® in connection with the issuance of certain securities, including the offered notes.

The offered notes are not sponsored, endorsed, sold or promoted by Dow Jones. Dow Jones does not make any representations regarding the advisability of investing in the offered notes. Dow Jones makes no representation or warranty, express or implied, to the owners of the offered notes or any member of the public regarding the advisability of investing in securities generally or in the offered notes particularly or the ability of the Dow Jones Industrial Average® to track general stock market performance. Dow Jones’ only relationship to The Goldman Sachs Group, Inc. is the licensing of certain trademarks and trade names of Dow Jones’ and of the use of the Dow Jones Industrial Average® which is determined, composed and calculated by Dow Jones without regard to The Goldman Sachs Group, Inc. or the offered notes.

Dow Jones has no obligation to take the needs of The Goldman Sachs Group, Inc. or the owners of the offered notes into consideration in determining, composing or calculating the index Dow Jones is not responsible for and has not participated in the determination of the timing of, prices at, or quantities of the offered notes to be issued or in the determination or calculation of the equation by which the offered notes are to be exchanged into cash. Dow Jones has no obligation or liability in connection with the administration, marketing or trading of the offered notes.