Item 1: Report to Shareholders| Mid-Cap Growth Fund | June 30, 2007 |

The views and opinions in this report were current as of June 30, 2007. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our E-mail Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

The celebration continued on Wall Street during the past six months, even as the mood on Main Street was somewhat subdued. While the slumping housing sector, rising interest rates, and high energy prices caused the U.S. economy to slow considerably, the stock market extended its winning streak into year five. Corporate profits continued to advance—if a bit more slowly—thanks in part to better growth overseas. Corporations repurchased their shares at unprecedented rates, and private-equity investors supported valuations by continuing to draw on generous pools of cheap capital to finance their acquisitions of public companies. Our fund benefited from these and other factors, and we are pleased to report results that nicely outpaced the solid returns of our benchmarks. As we will explain, however, we are managing the portfolio with the belief that Main Street and Wall Street will eventually intersect—and only companies well grounded in the real economy will prosper over the longer term.

HIGHLIGHTS

• Robust economic growth overseas, stock buybacks, and an active takeover market helped stock prices rise in the first half of 2007, and larger-cap shares outpaced small-caps.

• The fund recorded a strong return in this environment that surpassed its benchmarks, and our longer-term relative performance remains strong.

• The fund’s technology and energy holdings led its returns in the period, and results also benefited from the announcement of takeovers of several holdings.

• We are cautious about how the aging credit cycle might impact takeover activity and therefore stock prices, but we remain enthusiastic about the attractive valuations of many high-quality growth companies.

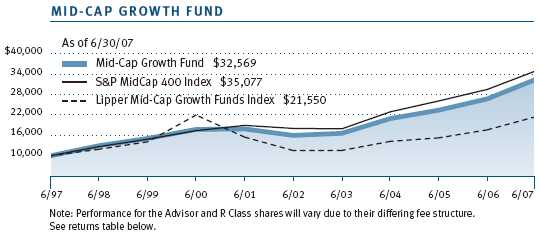

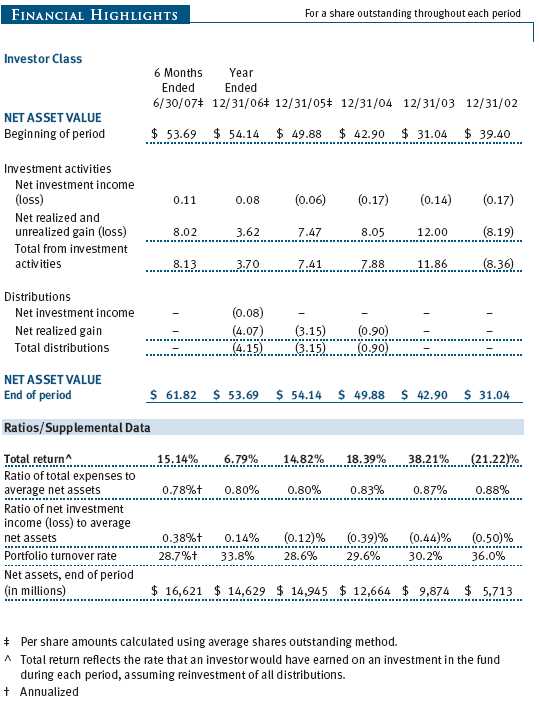

The Mid-Cap Growth Fund returned 15.14% during the past six months and 21.46% for the 12-month period ended June 30, 2007. (Returns for Advisor and R Class shares were lower due to their different fee structure.) The favorable results relative to our benchmarks reflected some of the very factors that hindered our performance last year, namely our focus on technology firms and other fast-growing companies.

In both good and bad periods of relative performance, our focus is always on how we fare over longer time frames. These comparisons remain solid. The fund ranked in the top 23% of its category for the three-year period ended June 30, within the top 14% for the five-year period, and within the top 5% for the 10-year period. (Based on cumulative total return, Lipper ranked the Mid-Cap Growth Fund 195 out of 608, 107 out of 485, 53 out of 383, and 7 out of 159 funds in the category for the 1-, 3-, 5-, and 10-year periods ended June 30, 2007. Results will vary for other time periods. Past performance cannot guarantee future results.)

MARKET ENVIRONMENT

After five years of expansion, the U.S. economy entered 2007 in deceleration mode. Growth in gross domestic product slowed to a paltry 0.7% in the first quarter, its worst showing in over four years. The housing sector was undeniably responsible for much of the malaise. Home prices and new home construction continued to decline, putting pressure on a whole panoply of related sectors, from homebuilders to housing goods retailers to finance firms. While this was reasonably predictable after the speculative frenzy that characterized the final stages of the 15-year housing expansion, it was cold comfort to those losing jobs in housing-related industries or needing to sell a home. Those who had taken out adjustable-rate mortgages felt a particular pinch as their loans began to be reset to higher rates.

Indeed, a troublesome new development for housing arrived in the near-collapse of the subprime mortgage market this spring. As defaults rose on a number of loans made with questionable documentation or collateral, numerous and prominent subprime lenders went out of business. The full fallout of the subprime breakdown remains unknown, however. Many institutional investors purchased these loans after they were bundled into esoteric securities by Wall Street intermediaries. Because these securities are not actively traded, no one knows exactly what they are now worth or to what extent the problems will be duplicated in other sectors of the debt markets.

Even as the housing sector faltered, U.S. employment remained strong. Wages grew moderately as businesses competed more for workers. This helped keep consumer confidence steady despite the burden of $3 per gallon of gasoline on family budgets. Due in part to energy prices, incomes for many Americans remained stagnant after accounting for inflation.

Economic conditions overseas were far more buoyant. Economists had worried early in the decade that the U.S was shouldering too much of the burden of driving the world’s economy. In the last couple of years, however, emerging markets in Asia and Latin America, along with developed markets in Europe, have come charging back. Indeed, many emerging economies are booming, propelled by high natural resource prices and healthy domestic conditions. Robust growth abroad, and the continuing decline of the dollar, have provided a strong boost to U.S. exporters.

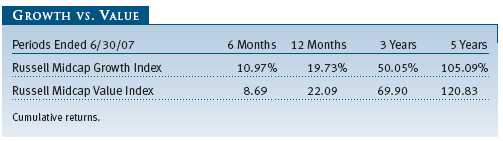

The market rewarded all major asset classes in the year’s first half. Two trends were notable, however, as they appear to have reversed long-term tendencies. First, both large- and mid-cap stocks outpaced small-caps. To some extent, this pattern may reflect the fact that larger companies tend to derive more of their revenues overseas, while smaller firms rely more on the spending habits of the American consumer. Second, shares of growth companies outperformed their value counterparts across all market capitalizations, with the trend the most pronounced among smaller firms. Growth stocks may come back into vogue as investors begin to differentiate secular from cyclical growth as the economy slows; however, the strong relative performance of growth shares to date has helped them recapture only a very small portion of the ground they had lost on value stocks since the start of the decade. As shown in the table, value maintained a substantial longer-term lead over growth.

PORTFOLIO REVIEW

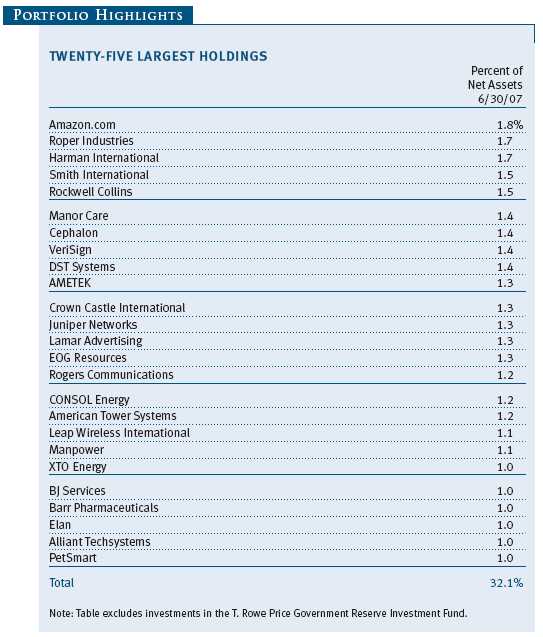

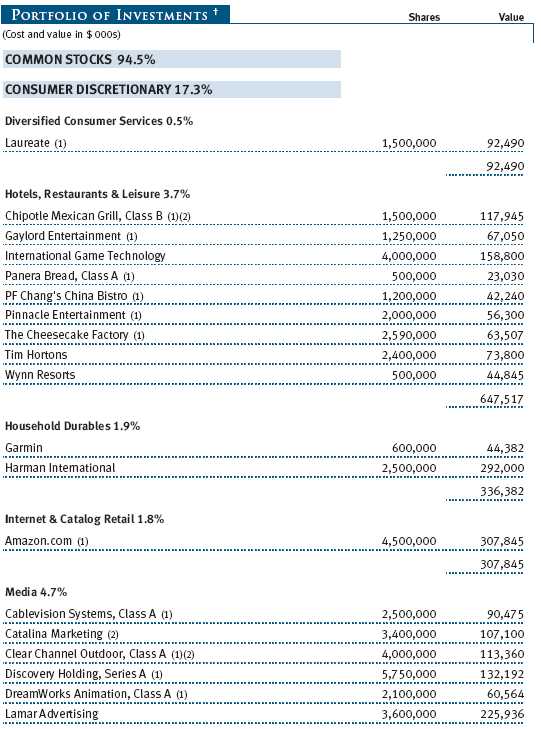

For a couple of years, the fund has had a large weighting in technology companies, and three of the top 10 contributors to results in the first half of the year were from that sector. Our leading contributor was aQuantive, which we mentioned as a new holding only a year ago. Microsoft announced plans to acquire this online advertising technology firm at a stunning 85% premium. Internet infrastructure firm VeriSign was also a strong performer as investors reacted favorably to its decision to emphasize profitability and rationalize its lines of business. (Please see the portfolio of investments for a complete listing of holdings and the amount each represents in the portfolio.)

While energy and technology stocks have often been at two ends of the market’s seesaw, both sectors rose in the period. Energy shares climbed as oil prices remained elevated and encouraged further investment in new production. CONSOL Energy, a coal company with a significant interest in gas as well, moved almost steadily higher throughout the period as demand for its output remained sturdy. Equipment and services firm Smith International also had substantial gains. Valuations in the sector have bounced up and down with energy prices lately, and it is worthwhile to note that energy was the sole area of the market to detract from returns in the previous six-month period.

Health care was not an ebullient stock market sector in 2007’s first half, but the portfolio benefited handsomely from the acquisition of MedImmune, a longtime biotechnology holding, by London-based pharmaceutical giant AstraZeneca at a substantial premium to market. We have long thought that MedImmune’s uneven execution of its business strategy was obscuring a valuable vaccine franchise, and perhaps it will be better off within a larger company. On the other side of the health care ledger, Sepracor notably disappointed in the period. Medicare reduced reimbursement for its key asthma drug, and investors worried about the future of the firm’s Lunesta sleep medication after a slow market launch.

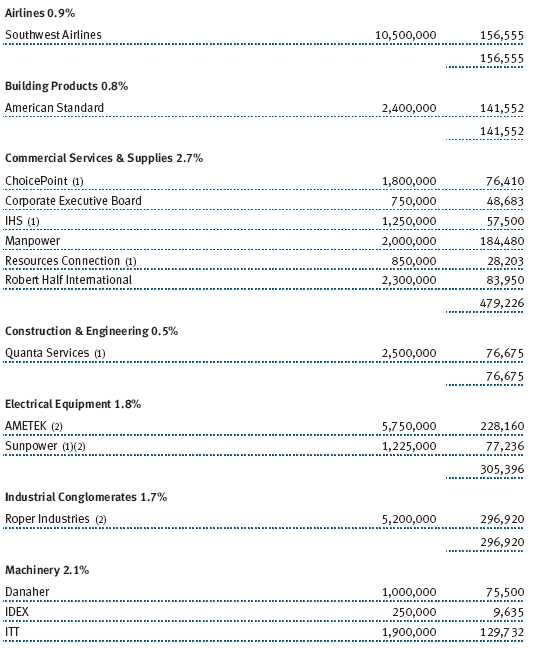

Our wide range of industrial holdings once again provided good results, although no single position stood out. Aerospace holdings benefited from the rapid growth in airliner orders overseas and defense business at home. Machinery, electrical equipment, and commercial services firms also performed well.

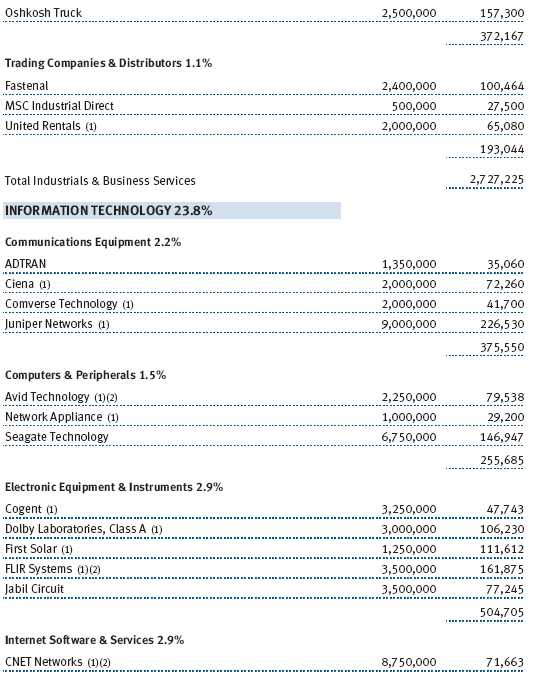

Finally, two outstanding performers deserve mention. We have long had a philosophical interest in alternative energy. Until recently, however, there have been few mid-cap ways to play the sector. In late 2006, we purchased a small position in First Solar, a leader in thin film solar technology. The stock astounded us by more than tripling as investors reacted to strong yields from its factories, significant new contracts, and earnings that were far higher than anticipated. Amazon.com was also a stellar performer in the period as sales growth accelerated and margins began to turn upward. This company has enormous earnings potential, in our opinion, based on a strong brand and best-in-class technology, and this began to be recognized by the market.

Apart from Amazon, many of our other consumer-related holdings lagged during the period. XM Satellite Radio Holdings was a significant detractor. Even though the company narrowed its operating losses and signed up more subscribers, investors turned a skeptical eye toward its proposed merger with competing satellite broadcaster Sirius and bid shares down. Organic foods marketer Whole Foods Market also fell as its earnings suffered from an acceleration of its new store expansion concurrent with a modest slowdown in its same-store sales growth. Retail overall has weakened, which may not bode well for the consumer-driven American economy.

INVESTMENT STRATEGY AND OUTLOOK

As we begin the second half of 2007, the ebullient financial environment makes us a touch nervous. It contrasts with the pronounced slowdown of the U.S. economy in recent months, which itself stands in sharp contradiction to the boom conditions in most of the rest of the world, particularly in emerging markets such as China. Given the central role of the United States within the global economy, we doubt that this divergence can persist for long.

The bull market in equities, now about five years old, has endured far longer than most, and signs of excess have begun to appear. While lower-and middle-class Americans are being squeezed by higher energy and interest costs, in New York City, condominiums are selling to hedge fund managers for unfathomable sums; 28-year-old investment bankers are buying Maseratis; and parking spaces are being auctioned for $250,000 apiece. Meanwhile, private-equity magnates, who made their careers proselytizing the merits of taking companies private, are suddenly pining to sell stakes in their own firms to the public. Caveat emptor!

In previous reports, we have discussed the prodigious quantities of liquidity washing through global financial markets. The sources of this liquidity are severalfold. Corporate balance sheets became underleveraged in the wake of the collapse of the Internet bubble as executives chose to hoard cash rather than invest in new capital projects. Large current account surpluses in countries such as Saudi Arabia and China—resulting from high oil prices and the migration of U.S. manufacturing overseas—were also sources of liquidity. Finally, the continued movement by institutions and wealthy individuals from equities into alternative investments, which often incorporate significant leverage, also added to liquidity.

The willingness of the banks and credit markets to lend on easy terms has been the rocket fuel that has powered this market. Indeed, it has seemed to us that creditors have collectively underpriced risk by relaxing underwriting standards, dispensing with traditional loan covenants, and demanding interest rates that seem too low. We believe that the world’s central banks are aware of this phenomenon, and it is not surprising that these institutions have been gradually raising short-term rates for almost two years. Slowly but surely, they are taking away the proverbial punch bowl.

Within our portfolio, this global surfeit of liquidity has manifested itself in a significant number of announced deals to acquire companies we own. In fact, 10 companies, comprising almost 10% of our fund, were the recipients of offers in the last six months. This accounted for approximately one-third of our relative performance over the period. Many of the offers came from private-equity firms in conjunction with managements. These bids typically offered measly premiums of about 20% to previous, sometimes depressed, trading prices for these stocks. We have discussed this phenomenon at length in previous shareholder reports. Typically, management teams, with much to gain from the transaction, are aided by cadres of investment bankers and lawyers in structuring deals that make opposition difficult. Boards of directors, whose charge is to protect shareholders, have too often been toothless bystanders. It is worth reiterating that we have opposed a number of these transactions as we believe the prices we are being offered do not reflect the long-term values of these businesses. We would rather suffer a one-day decline in a stock when a deal is rebuffed than allow these companies to be taken from the public realm at insufficient prices.

We believe it is telling that, in contrast to the typical 20% premiums to market of private-equity-led transactions, we have had three companies acquired by other companies in strategic deals at very attractive premiums relative to recent trading. Investors Financial Services was purchased by State Street at a 38% premium; MedImmune was bought by AstraZeneca at an 80% premium to the price at which it was trading before buyout speculation began in mid-March; and aQuantive is about to be acquired by Microsoft at an 85% premium.

As plentiful as liquidity appears at the moment, it is dependent on market psychology that can change abruptly. As we write, credit markets appear to be starting to price risk back into the system. In the last several months, we have witnessed significant dislocation in the subprime mortgage market leading to the demise of several overly leveraged hedge funds. The spectacle of these entities vaporizing their investors’ entire stakes may be enough to reintroduce the notion of risk into the credit market’s vocabulary. This should be a healthy process, but if it happens too suddenly, it could have significant unforeseen consequences.

Within the equity markets, it has been popular for institutional investors, and sometimes activist investors and hedge funds, to implore managements to lever their balance sheets by repurchasing shares, issuing extraordinary dividends and, in some cases, initiating leveraged recapitalizations or management-led buyouts. Investors’ disdain for cash reminds us of other frothy periods when the mantra was also “cash is trash.” But the pendulum swings through the credit cycle, and company managements should beware that many of these same investors will be part of a chorus questioning their business acumen for compromising their corporate balance sheets when credit conditions tighten. A wise investor told us very early in our career that balance sheets don’t matter 98% of the time, but when they do matter, they’re the only thing that matters. This sage advice is a lesson that is learned, usually by a new set of managers and investors, each and every credit cycle.

This fund is constructed stock by stock. Generally, we seek to buy well-managed, growing, medium-sized companies that have sustainable competitive advantages and sound financial footings. While the mid-cap growth sector is one of the riskiest in the equity market, we try to moderate our risk profile through diversification and a degree of valuation sensitivity in our purchases and sales. We like to buy good companies and hold them for years. Our average holding period is about three years, though we have a number of holdings that we have owned for a decade, and two, Danaher and Smith International, which we have owned since the inception of the fund 15 years ago. Though our style is more successful in some markets than others, the market’s short-term focus of the last several years has provided good opportunities to buy premier companies at good prices. Similarly, at times investors become overly enthusiastic about an event or data point and provide liquidity into which we can harvest positions.

While we focus on individual stocks, we do have views on sectors and the market environment, and they are reflected to some extent in the composition of the fund. In this vein, we continue to be leery about residential housing, and derivatively the American consumer, as we have written at length for a couple of years. Residential housing had an extremely long upcycle, approximately 15 years, and the speculation toward the end of the cycle is now legendary. Housing is by nature a leveraged asset, which implies that the hangover in this market may last for several years. While we are hopeful that the correction in the housing market will be gradual, allowing homeowners and markets to adjust more easily, there is a lower-probability scenario of a serious unwinding with significant repercussions for the economy. We own no housing stocks though we do own a handful of companies, such as retailers Williams-Sonoma and Best Buy, that are related somewhat to the health of the sector.

For several years, we have thought that the credit cycle could get no better, and have been reluctant to own financial stocks that have significant credit risk. We own just one bank, for instance, and we have only a moderate overall weighting in the sector. While delinquencies have sharply increased in the residential mortgage sector in the last year, commercial and corporate credit has remained solid. Nevertheless, given the lowering of credit standards in recent years, we think it is only a matter of time before problems begin to assert themselves more broadly. We do not foresee a crisis, but conditions are not benign for many financial stocks.

Conversely, we have been bullish on technology stocks for several years, and, in spite of better performance thus far in 2007, we have been wrong. We had theorized that the dearth of capital spending in the aftermath of the crash of the Internet bubble would subside by 2005 and 2006, and companies would begin to spend again on productivity-enhancing technology. Companies have spent, but the real focus of capital flows this cycle has been in manufacturing and commodities, sectors that have benefited enormously from the exceptional growth occurring in developing markets, particularly China. We continue to like the technology sector, where we are finding companies with global competitive advantages and strong financial characteristics at reasonable valuations.

Finally, we may sound like a broken record, but we believe the largest anomaly in the domestic stock market is that growth is very cheap relative to value. Investors are according historically small premiums to companies that we believe can grow their earnings at the highest rates throughout an economic cycle. We have gradually skewed the average growth rate of the portfolio’s holdings higher over the last couple of years. While large-cap growth companies currently appear, to us, to be the most attractive sector, we believe mid-cap companies are structurally situated at the sweet spot of the corporate lifecycle, leaving us confident that we will continue to deliver good returns over the long term.

Respectfully submitted,

Brian W.H. Berghuis

President of the fund and chairman of its Investment Advisory Committee

John F. Wakeman

Executive vice president of the fund

July 20, 2007

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

RISKS OF STOCK INVESTING

As with all stock and bond mutual funds, the fund’s share price can fall because of weakness in the stock or bond markets, a particular industry, or specific holdings. The financial markets can decline for many reasons, including adverse political or economic developments, changes in investor psychology, or heavy institutional selling. The prospects for an industry or company may deteriorate because of a variety of factors, including disappointing earnings or changes in the competitive environment. In addition, the investment manager’s assessment of companies held in a fund may prove incorrect, resulting in losses or poor performance even in rising markets. The stocks of mid-cap companies entail greater risk and are usually more volatile than the shares of larger companies. In addition, growth stocks can be volatile for several reasons. Since they usually reinvest a high proportion of earnings in their own businesses, they may lack the dividends usually associated with value stocks that can cushion their decline in a falling market. Also, since investors buy these stocks because of their expected superior earnings growth, earnings disappointments often result in sharp price declines.

GLOSSARY

Lipper indexes: Fund benchmarks that consist of a small number of the largest mutual funds in a particular category as tracked by Lipper Inc.

Russell Midcap Growth Index: An unmanaged index that measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values.

Russell Midcap Index: An unmanaged index that tracks the performance of the 800 smallest companies in the Russell 1000 Index.

Russell Midcap Value Index: An unmanaged index that measures the performance of those Russell Midcap companies with lower price-to-book ratios and lower forecasted growth values.

S&P 500 Stock Index: An unmanaged index that tracks the stocks of 500 primarily large-cap U.S. companies.

S&P MidCap 400 Index: An unmanaged index that tracks the stocks of 400 U.S. mid-cap companies.

Performance and Expenses

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

This table shows how the fund would have performed each year if its actual (or cumulative) returns had been earned at a constant rate.

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

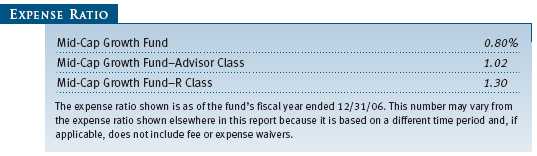

Please note that the fund has three share classes: The original share class (“investor class”) charges no distribution and service (12b-1) fee; Advisor Class shares are offered only through unaffiliated brokers and other financial intermediaries and charge a 0.25% 12b-1 fee; R Class shares are available to retirement plans serviced by intermediaries and charge a 0.50% 12b-1 fee. Each share class is presented separately in the table.

Actual Expenses

The first line of the following table (“Actual”) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (“Hypothetical”) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual small-account maintenance fee of $10, generally for accounts with less than $2,000 ($500 for UGMA/UTMA). The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $25,000 or more, accounts employing automatic investing, and IRAs and other retirement plan accounts that utilize a prototype plan sponsored by T. Rowe Price (although a separate custodial or administrative fee may apply to such accounts). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

The accompanying notes are an integral part of these financial statements.

Unaudited

| NOTES TO FINANCIAL STATEMENTS |

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

T. Rowe Price Mid-Cap Growth Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund seeks to provide long-term capital appreciation by investing in mid-cap stocks with potential for above-average earnings growth. The fund has three classes of shares: the Mid-Cap Growth Fund original share class, referred to in this report as the Investor Class, offered since June 30, 1992; the Mid-Cap Growth Fund—Advisor Class (Advisor Class), offered since March 31, 2000; and the Mid-Cap Growth Fund—R Class (R Class), offered since September 30, 2002. Advisor Class shares are sold only through unaffiliated brokers and other unaffiliated financial intermediaries, and R Class shares are available to retirement plans serviced by intermediaries. The Advisor Class and R Class each operate under separate Board-approved Rule 12b-1 plans, pursuant to which each class compensates financial intermediaries for distribution, shareholder servicing, and/or certain administrative services. Each class has exclusive voting rights on matters related solely to that class, separate voting rights on matters that relate to all classes, and, in all other respects, the same rights and obligations as the other classes.

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by fund management. Fund management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the fund ultimately realizes upon sale of the securities.

Valuation The fund values its investments and computes its net asset value per share at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day that the NYSE is open for business. Equity securities listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made, except for OTC Bulletin Board securities, which are valued at the mean of the latest bid and asked prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the latest bid and asked prices for domestic securities and the last quoted sale price for international securities.

Investments in mutual funds are valued at the mutual fund’s closing net asset value per share on the day of valuation.

Other investments, including restricted securities, and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors.

Most foreign markets close before the close of trading on the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, which in turn will affect the fund’s share price, the fund will adjust the previous closing prices to reflect the fair value of the securities as of the close of the NYSE, as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors. A fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. In deciding whether to make fair value adjustments, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund uses outside pricing services to provide it with closing market prices and information used for adjusting those prices. The fund cannot predict when and how often it will use closing prices and when it will adjust those prices to reflect fair value. As a means of evaluating its fair value process, the fund routinely compares closing market prices, the next day’s opening prices in the same markets, and adjusted prices.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Class Accounting The Advisor Class and R Class each pay distribution, shareholder servicing, and/or certain administrative expenses in the form of Rule 12b-1 fees, in an amount not exceeding 0.25% and 0.50%, respectively, of the class’s average daily net assets. Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to all classes, investment income, and realized and unrealized gains and losses are allocated to the classes based upon the relative daily net assets of each class.

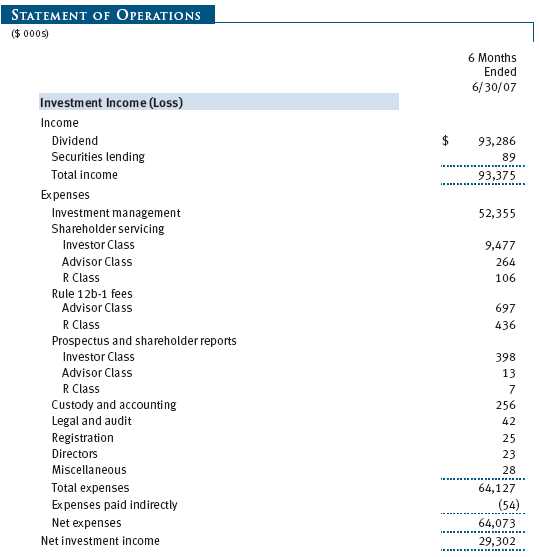

Rebates and Credits Subject to best execution, the fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the fund in cash. Commission rebates are reflected as realized gain on securities in the accompanying financial statements and totaled $181,000 for the six months ended June 30, 2007. Additionally, the fund earns credits on temporarily uninvested cash balances at the custodian that reduce the fund’s custody charges. Custody expense in the accompanying financial statements is presented before reduction for credits, which are reflected as expenses paid indirectly.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Any income tax-related interest and penalties would be classified as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared and paid by each class on an annual basis. Capital gain distributions, if any, are declared and paid by the fund, typically on an annual basis.

New Accounting Pronouncements Effective June 29, 2007, the fund adopted Financial Accounting Standards Board (“FASB”) Interpretation No. 48 (“FIN 48”), Accounting for Uncertainty in Income Taxes, a clarification of FASB Statement No. 109, Accounting for Income Taxes. FIN 48 establishes financial accounting and disclosure requirements for recognition and measurement of tax positions taken or expected to be taken on an income tax return. The adoption of FIN 48 had no impact on the fund’s net assets or results of operations.

In September 2006, the FASB released the Statement of Financial Accounting Standard No. 157 (“FAS 157”), Fair Value Measurements. FAS 157 clarifies the definition of fair value and establishes the framework for measuring fair value, as well as proper disclosure of this methodology in the financial statements. It will be effective for the fund’s fiscal year beginning January 1, 2008. Management is evaluating the effects of FAS 157; however, it is not expected to have a material impact on the fund’s net assets or results of operations.

NOTE 2 - INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

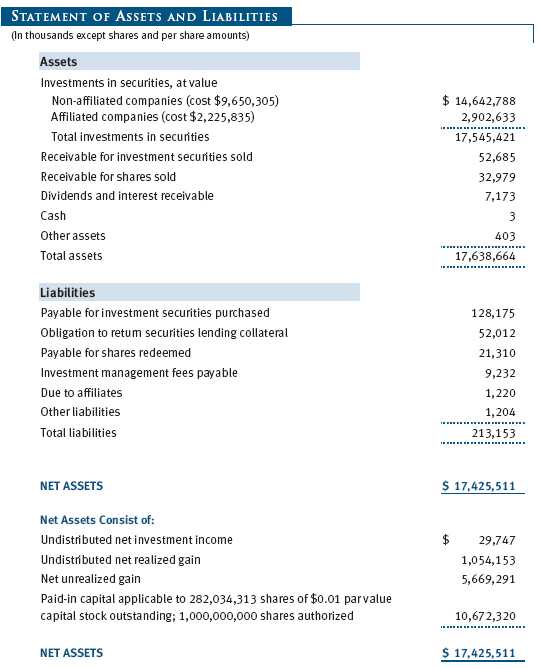

Securities Lending The fund lends its securities to approved brokers to earn additional income. It receives as collateral cash and U.S. government securities valued at 102% to 105% of the value of the securities on loan. Cash collateral is invested in a money market pooled trust managed by the fund’s lending agent in accordance with investment guidelines approved by fund management. Collateral is maintained over the life of the loan in an amount not less than the value of loaned securities, as determined at the close of fund business each day; any additional collateral required due to changes in security values is delivered to the fund the next business day. Although risk is mitigated by the collateral, the fund could experience a delay in recovering its securities and a possible loss of income or value if the borrower fails to return the securities. Securities lending revenue recognized by the fund consists of earnings on invested collateral and borrowing fees, net of any rebates to the borrower and compensation to the lending agent. At June 30, 2007, the value of loaned securities was $50,701,000; aggregate collateral consisted of $52,012,000 in the money market pooled trust.

Other Purchases and sales of portfolio securities, other than short-term securities, aggregated $2,236,287,000 and $2,835,725,000, respectively, for the six months ended June 30, 2007.

NOTE 3 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Federal income tax regulations differ from generally accepted accounting principles; therefore, distributions determined in accordance with tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character. Financial records are not adjusted for temporary differences. The amount and character of tax-basis distributions and composition of net assets are finalized at fiscal year-end; accordingly, tax-basis balances have not been determined as of June 30, 2007.

At June 30, 2007, the cost of investments for federal income tax purposes was $11,876,140,000. Net unrealized gain aggregated $5,669,282,000 at period-end, of which $5,964,854,000 related to appreciated investments and $295,572,000 related to depreciated investments.

NOTE 4 - ACQUISITION

On June 19, 2006, the fund acquired substantially all of the assets of the Preferred Mid-Cap Growth Fund (the acquired fund), pursuant to the Agreement and Plan of Reorganization dated February 15, 2006, and approved by shareholders of the acquired fund on June 9, 2006. The acquisition was accomplished by a tax-free exchange of 317,307 shares of the fund (with a value of $17,008,000) for all 1,615,268 shares of the acquired fund outstanding on June 16, 2006 with the same value. The net assets of the acquired fund at that date included $995,000 of unrealized depreciation. Net assets of the acquired fund were combined with those of the fund, resulting in aggregate net assets of $14,974,367,000 immediately after the acquisition.

NOTE 5 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (the manager or Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. The investment management agreement between the fund and the manager provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.35% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.285% for assets in excess of $220 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At June 30, 2007, the effective annual group fee rate was 0.30%.

In addition, the fund has entered into service agreements with Price Associates and two wholly owned subsidiaries of Price Associates (collectively, Price). Price Associates computes the daily share prices and provides certain other administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend disbursing agent. T. Rowe Price Retirement Plan Services, Inc., provides subaccounting and recordkeeping services for certain retirement accounts invested in the Investor Class and R Class. For the six months ended June 30, 2007, expenses incurred pursuant to these service agreements were $62,000 for Price Associates, $1,672,000 for T. Rowe Price Services, Inc., and $3,711,000 for T. Rowe Price Retirement Plan Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

Additionally, the fund is one of several mutual funds in which certain college savings plans managed by Price Associates may invest. As approved by the fund’s Board of Directors, shareholder servicing costs associated with each college savings plan are borne by the fund in proportion to the average daily value of its shares owned by the college savings plan. For the six months ended June 30, 2007, the fund was charged $101,000 for shareholder servicing costs related to the college savings plans, of which $90,000 was for services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At June 30, 2007, approximately 1% of the outstanding shares of the Investor Class were held by college savings plans.

The fund is also one of several mutual funds sponsored by Price Associates (underlying Price funds) in which the T. Rowe Price Retirement Funds (Retirement Funds) may invest. The Retirement Funds do not invest in the underlying Price funds for the purpose of exercising management or control. Pursuant to a special servicing agreement, expenses associated with the operation of the Retirement Funds are borne by each underlying Price fund to the extent of estimated savings to it and in proportion to the average daily value of its shares owned by the Retirement Funds. Expenses allocated under this agreement are reflected as shareholder servicing expense in the accompanying financial statements. For the six months ended June 30, 2007, the fund was allocated $1,123,000 of Retirement Funds’ expenses, of which $882,000 related to services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At June 30, 2007, approximately 7% of the outstanding shares of the Investor Class were held by the Retirement Funds.

The fund may invest in the T. Rowe Price Reserve Investment Fund and the T. Rowe Price Government Reserve Investment Fund (collectively, the T. Rowe Price Reserve Investment Funds), open-end management investment companies managed by Price Associates and affiliates of the fund. The T. Rowe Price Reserve Investment Funds are offered as cash management options to mutual funds, trusts, and other accounts managed by Price Associates and/or its affiliates, and are not available for direct purchase by members of the public. The T. Rowe Price Reserve Investment Funds pay no investment management fees.

As of June 30, 2007, T. Rowe Price Group, Inc., and/or its wholly owned subsidiaries owned 62,712 shares of the Investor Class, representing less than 1% of the fund’s net assets.

| INFORMATION ON PROXY VOTING POLICIES, PROCEDURES, AND RECORDS |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information, which you may request by calling 1-800-225-5132 or by accessing the SEC’s Web site, www.sec.gov. The description of our proxy voting policies and procedures is also available on our Web site, www.troweprice.com. To access it, click on the words “Company Info” at the top of our homepage for individual investors. Then, in the window that appears, click on the “Proxy Voting Policy” navigation button in the top left corner.

Each fund’s most recent annual proxy voting record is available on our Web site and through the SEC’s Web site. To access it through our Web site, follow the directions above, then click on the words “Proxy Voting Record” at the bottom of the Proxy Voting Policy page.

| HOW TO OBTAIN QUARTERLY PORTFOLIO HOLDINGS |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s Web site (www.sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 450 Fifth St. N.W., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| APPROVAL OF INVESTMENT MANAGEMENT AGREEMENT |

On March 7, 2007, the fund’s Board of Directors (Board) unanimously approved the investment advisory contract (Contract) between the fund and its investment manager, T. Rowe Price Associates, Inc. (Manager). The Board considered a variety of factors in connection with its review of the Contract, also taking into account information provided by the Manager during the course of the year, as discussed below:

Services Provided by the Manager

The Board considered the nature, quality, and extent of the services provided to the fund by the Manager. These services included, but were not limited to, management of the fund’s portfolio and a variety of related activities, as well as financial and administrative services, reporting, and communications. The Board also reviewed the background and experience of the Manager’s senior management team and investment personnel involved in the management of the fund. The Board concluded that it was satisfied with the nature, quality, and extent of the services provided by the Manager.

Investment Performance of the Fund

The Board reviewed the fund’s average annual total return over the 1-, 3-, 5-, and 10-year periods as well as the fund’s year-by-year returns and compared these returns with previously agreed upon comparable performance measures and market data, including those supplied by Lipper and Morningstar, which are independent providers of mutual fund data. On the basis of this evaluation and the Board’s ongoing review of investment results, the Board concluded that the fund’s performance was satisfactory.

Costs, Benefits, Profits, and Economies of Scale

The Board reviewed detailed information regarding the revenues received by the Manager under the Contract and other benefits that the Manager (and its affiliates) may have realized from its relationship with the fund, including research received under “soft dollar” agreements. The Board noted that soft dollars were not used to pay for third-party, non-broker research. The Board also received information on the estimated costs incurred and profits realized by the Manager and its affiliates from advising T. Rowe Price mutual funds, as well as estimates of the gross profits realized from managing the fund in particular. The Board concluded that the Manager’s profits were reasonable in light of the services provided to the fund. The Board also considered whether the fund or other funds benefit under the fee levels set forth in the Contract from any economies of scale realized by the Manager. Under the Contract, the fund pays a fee to the Manager composed of two components—a group fee rate based on the aggregate assets of certain T. Rowe Price mutual funds (including the fund) that declines at certain asset levels and an individual fund fee rate that is assessed on the assets of the fund. The Board concluded that the advisory fee structure for the fund continued to provide for a reasonable sharing of benefits from any economies of scale with the fund’s investors.

Fees

The Board reviewed the fund’s management fee rate, operating expenses, and total expense ratio (for the Investor Class, Advisor Class, and R Class) and compared them with fees and expenses of other comparable funds based on information and data supplied by Lipper. The information provided to the Board indicated that the fund’s management fee rate for all three classes and expense ratio for the Investor Class and Advisor Class were at or below the median for comparable funds and that the expense ratio for the R Class was above the median for comparable funds. The Board also reviewed the fee schedules for comparable privately managed accounts of the Manager and its affiliates. Management informed the Board that the Manager’s responsibilities for privately managed accounts are more limited than its responsibilities for the fund and other T. Rowe Price mutual funds that it or its affiliates advise. On the basis of the information provided, the Board concluded that the fees paid by the fund under the Contract were reasonable.

Approval of the Contract

As noted, the Board approved the continuation of the Contract. No single factor was considered in isolation or to be determinative to the decision. Rather, the Board concluded, in light of a weighting and balancing of all factors considered, that it was in the best interests of the fund to approve the continuation of the Contract, including the fees to be charged for services thereunder.

Item 2. Code of Ethics.

A code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions is filed as an exhibit to the registrant’s annual Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the registrant’s most recent fiscal half-year.

Item 3. Audit Committee Financial Expert.

Disclosure required in registrant’s annual Form N-CSR.

Item 4. Principal Accountant Fees and Services.

Disclosure required in registrant’s annual Form N-CSR.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Schedule of Investments.

Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is filed with the registrant’s annual Form N-CSR.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

| | |

SIGNATURES |

| |

| | Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment |

| Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the |

| undersigned, thereunto duly authorized. |

| |

| T. Rowe Price Mid-Cap Growth Fund, Inc. |

| |

| |

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date | August 17, 2007 |

| |

| |

| |

| | Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment |

| Company Act of 1940, this report has been signed below by the following persons on behalf of |

| the registrant and in the capacities and on the dates indicated. |

| |

| |

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date | August 17, 2007 |

| |

| |

| |

| By | /s/ Joseph A. Carrier |

| | Joseph A. Carrier |

| | Principal Financial Officer |

| |

| Date | August 17, 2007 |