UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-6653

The Jensen Portfolio, Inc.

(Exact name of registrant as specified in charter)

5300 Meadows Road, Suite 250

Lake Oswego, OR 97035

(Address of principal executive offices) (Zip code)

Robert McIver

5300 Meadows Road, Suite 250

Lake Oswego, OR 97035

(Name and address of agent for service)

(800) 221-4384

Registrant's telephone number, including area code

Date of fiscal year end: May 31

Date of reporting period: November 30, 2012

Item 1. Reports to Stockholders.

Letter from The Investment Adviser

Dear Fellow Shareholders,

The Jensen Quality Growth Fund (the “Fund”) -- Class J Shares – returned 8.14 % for the six months ended November 30, 2012, compared to a return of 9.32% over this period for the Standard & Poor’s 500 Index. Please see pages 3 through 5 of this report for complete standardized performance information for the Fund.

Market Perspective

Despite an economic backdrop characterized by economic headwinds and uncertainty, we remain pleased with the underlying business performance from the companies held in the Fund. While earnings growth for these companies has been muted relative to our long-term expectations, they have held up well relative to that of the broader market. Average earnings for companies held in the portfolio are up 6.28% on a year-over-year basis through 9/30/12, which compares favorably to a 0% increase for the S&P 500 Index. In the most recently reported quarter, the average organic revenue growth for companies held in the portfolio was nearly 5.0%, showing the kind of resilient growth that we expect from these businesses.

Unfortunately, as noted earlier, relative stock price performance during this period paints a somewhat different picture. While we are disappointed that the Quality Growth Fund lagged the index during this period, we believe that relative performance must be viewed in the context of the strong market rally in 2012.

The Effect at Jensen

The Fund’s relative underperformance during this period was due in part to 1) the lower-quality nature of this period’s rally and 2) security selection in the Healthcare sector. Offsetting this to a degree was 1) positive security selection in the Information Technology sector and 2) an absence of holdings in the Utilities and Telecommunications Services sectors.

Leading contributors to performance during the period were Oracle, Procter & Gamble and Cognizant Technology Solutions. Leading detractors during the period, Nike and Microsoft, suffered from difficult market reactions to earnings results and performance expectations, respectively, stemming from the economy, and in the case of Microsoft, concerns over new product introductions – primarily related to the launch of the Windows 8 operating system. These reactions and concerns caused detraction from the Fund’s overall performance although we continue to believe that the long-term prospects for both businesses are positive and our investment theses for each are very much intact.

Portfolio Changes

Jensen sold Paychex and C.R. Bard during this period, and began the sale of Stryker at the end of the period.

We believe the impact of the difficult economy continues to hamper the primary growth engine for Paychex, that being small business formation and expansion. As such, we have concluded that the company’s largest competitor, and another Fund holding, Automatic Data Processing, merits our investment focus at this time as we continue to believe that the advantages of technology and scale in the provision of payroll outsourcing and related services are strong and compelling.

The liquidation decisions of C.R. Bard and Stryker were made after careful review of a combination of company-specific issues and our view on the negative macro forces that are impacting the broader healthcare sector. In particular, we believe that the traditional growth engine for both these companies – innovation and new product development – will face increasing headwinds due to heightened cost sensitivity by healthcare systems in developed economies. With our remaining holdings in healthcare, we are emphasizing companies that we believe have opportunities in emerging markets (where healthcare system dynamics have generally improved) and companies that can take advantage of higher volumes by leveraging manufacturing scale.

United Parcel Service (UPS), which was added to the Fund in July, is a package delivery company that provides transportation, logistics, and freight services worldwide. In 2011, UPS shipped an average of over 15 million packages a day to more than 220 countries and territories around the world. The company generates about 74% of its $53 billion in sales in the United States, where we believe they will benefit from the ongoing shift toward online consumer purchases. Additionally, while most of UPS’s total sales are from package delivery, about 17% are generated by supply chain and freight services, including logistics, brokerage, import/export financing, and UPS retail stores. UPS’s stock performance this period reacted to lowered guidance from competitors and short term growth concerns. We believe UPS is a solid quality growth company that is well positioned to provide long term shareholder value.

In September, Accenture (ACN) was added to the Fund’s portfolio. Accenture is a global business services firm that provides management consulting, technology services and outsourcing worldwide. It is the largest consulting firm in the world servicing clients in approximately 120 countries. Accenture interfaces at the upper management level of large multinational companies and currently serves 94 of the Fortune Global 100. We believe their growth is fueled by multiple factors including globalization, technology adoption, and the ever increasing demand from clients to improve efficiency. Accenture enjoys high client retention, which we believe is based on their ability to deliver superior service to their clients. Retention for its highest level clients,

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 1 |

those that generate more than $100 million in revenue per year, was 99 out of the top 100 for the last 5 years and 92 out of the top 100 for the last ten years. We believe this quality growth company is well positioned to provide long term shareholder value, and we were able to add it at an attractive valuation.

A position in TJX Companies (TJX) was added at the end of the period. TJX is the largest off-price retailer in the world. The company operates over 2,900 stores throughout the U.S. and in five other countries. Well known store concepts operated by TJX include T.J. Maxx, Marshalls, and HomeGoods. In each of these concepts, the company offers name-brand apparel and merchandise at everyday prices that are generally 20% to 60% below prices for similar goods at department and specialty stores. TJX’s buying operation consists of over 700 buyers that work with more than 15,000 vendors in over 60 countries throughout the world. Size is an important factor in TJX’s off-price buying in that it creates bargaining power with apparel manufacturers. Additionally, size often gives TJX’s buyers the important “first call” from potential suppliers that allows them to have the first look at available merchandise. Importantly, we believe that the scale and scope of TJX’s buying operation would be difficult to replicate for a potential new entrant.

TJX’s business model has produced strong and resilient historical results, and we expect that steady growth to continue into the future for TJX as a result of new store openings and continued same-store-sales growth. However TJX does face competition from a variety of existing and emerging competitive threats, perhaps the most dynamic of these potential threats is the emergence of e-commerce. At present, there are a variety of e-commerce sites that attempt to create an on-line version of off-price retailing; however, we remain skeptical that the off-price business model can flourish on-line on a standalone basis. Although TJX’s stock price has been strong this year, we are optimistic about the future prospects for the company and believe that the stock is attractively valued even when using conservative estimates in our valuation models.

The Jensen Outlook

Certainly, there are headwinds that remain that will likely cause ongoing volatility within the markets. As of this writing, the “fiscal cliff” has been temporarily averted due to agreement regarding the raising of additional revenues by the federal government. At the same time, a new stalemate appears even more likely and difficult related to the spending side of the economic equation, potentially affecting the debt ceiling, debt ratings and industries that could be hit directly by spending cuts. These issues will require fiscal statesmanship – something that seems in short supply. Regardless, businesses must continue to execute their strategies or get left behind in a competitive marketplace.

As we look forward to 2013, our crystal ball remains a bit foggy but we believe that investment in quality growth businesses remains an important component to every investor’s portfolio. Many of these businesses have continued to post consistent growth in revenue, earnings, and free cash flow in spite of what feels like perpetually uncertain global economic landscape. We believe the ongoing actions taken by the companies in the Jensen Quality Growth Fund are an appropriate response to the uncertain times. We remain committed to our belief that long term ownership of quality growth businesses is a sound decision and, importantly, we believe that patient investors in these businesses should be rewarded if this consistent growth eventually becomes reflected in share prices.

Cordially,

The Jensen Investment Committee

This discussion and analysis of the Fund is as of November 30, 2012 and is subject to change, and any forecasts made cannot be guaranteed and should not be considered investment advice. Past performance is no guarantee of future results. Fund holdings and sector weightings are subject to change and are not recommendations to buy or sell any security. For more complete information regarding performance and holdings, please refer to the financial statements and schedule of investments headings of this report. Current and future portfolio holdings are subject to risk. The S&P 500 Stock Index is an unmanaged but commonly used measure of common stock total return performance. One cannot invest directly in an index. Mutual fund investing involves risk, and principal loss is possible. The Fund is non-diversified, meaning that it may concentrate its assets in fewer individual holdings than a diversified fund and is therefore more exposed to individual stock volatility than a diversified fund. Earnings growth is not a measure of the Fund’s future performance. Free Cash Flow: Is equal to the after-tax net income of a company plus depreciation and amortization less capital expenditures. Earnings Per Share (EPS): Is the net income of a company divided by the total number of shares it has outstanding. Earnings Per Share Growth (EPS Growth): Is the year-over-year percent change in a company’s earnings per share. For use only when preceded or accompanied by a current prospectus for the Fund. The Jensen Quality Growth Fund is distributed by Quasar Distributors, LLC. |

| | |

| 2 | Jensen Quality Growth Fund | Semi-Annual Report |

Jensen Quality Growth Fund - Class J (Unaudited)

Total Returns vs. The S&P 500

| Average Annual – For periods ended November 30, 2012 | | 1 year | | | 3 years | | | 5 years | | | 10 years | |

| Jensen Quality Growth Fund - Class J | | 11.80% | | | 8.29% | | | 2.30% | | | 4.87% | |

| S&P 500 Stock Index | | 16.13% | | | 11.25% | | | 1.34% | | | 6.36% | |

The S&P 500 Stock Index is an unmanaged but commonly used measure of common stock total return performance. This chart assumes an initial gross investment of $10,000 made on November 30, 2002 for Class J, the original share class of the fund. Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data shown represents past performance; Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance shown. Performance data current to the most recent month end may be obtained by calling 1-800-992-4144 or by visiting www.jenseninvestment.com.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 3 |

Jensen Quality Growth Fund - Class R (Unaudited)

Total Returns vs. The S&P 500

| Average Annual – For periods ended November 30, 2012 | | 1 year | | | 3 years | | | 5 years | | | Since Inception | |

| | | | | | | | | | | July 30, 2003 | |

| Jensen Quality Growth Fund - Class R | | 11.50% | | | 8.07% | | | 2.08% | | | 4.96% | |

| S&P 500 Stock Index | | 16.13% | | | 11.25% | | | 1.34% | | | 6.08% | |

The S&P 500 Stock Index is an unmanaged but commonly used measure of common stock total return performance. This chart assumes an initial gross investment of $10,000 made on July 30, 2003, the inception date for Class R shares. Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data shown represents past performance; Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance shown. Performance data current to the most recent month end may be obtained by calling 1-800-992-4144 or by visiting www.jenseninvestment.com.

| | |

| 4 | Jensen Quality Growth Fund | Semi-Annual Report |

Jensen Quality Growth Fund - Class I (Unaudited)

Total Returns vs. The S&P 500

| Average Annual – For periods ended November 30, 2012 | | 1 year | | | 3 years | | | 5 years | | | Since Inception | |

| | | | | | | | | | | July 30, 2003 | |

| Jensen Quality Growth Fund - Class I | | 12.15% | | | 8.63% | | | 2.61% | | | 5.46% | |

| S&P 500 Stock Index | | 16.13% | | | 11.25% | | | 1.34% | | | 6.08% | |

The S&P 500 Stock Index is an unmanaged but commonly used measure of common stock total return performance. This chart assumes an initial gross investment of $1,000,000 made on July 30, 2003, the inception date for Class I shares. Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data shown represents past performance; Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance shown. Performance data current to the most recent month end may be obtained by calling 1-800-992-4144 or by visiting www.jenseninvestment.com.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 5 |

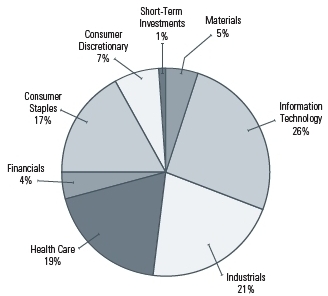

Investments by Sector as of November 30, 2012

(as a Percentage of Total Investments) (Unaudited)

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

| | |

| 6 | Jensen Quality Growth Fund | Semi-Annual Report |

Statement of Assets & Liabilities

November 30, 2012 (Unaudited)

| Assets: | |

| Investment, at value (cost $2,951,997,613) | $3,881,735,830 |

| Income receivable | 6,563,917 |

| Receivables for investments sold | 119,097,888 |

| Receivable for capital stock issued | 2,688,726 |

| Other Assets | 114,715 |

| Total Assets | 4,010,201,076 |

| |

| Liabilities: | |

| Payable to Investment Adviser | 1,617,656 |

| Payable to Custodian | 48,795 |

| Payable for investments purchased | 101,612,559 |

| Payable for capital stock redeemed | 2,900,033 |

| Accrued distribution fees | 891,601 |

| Accrued director fees | 43,306 |

| Accrued expenses and other liabilities | 863,133 |

| Total Liabilities | 107,977,083 |

| Net Assets | $3,902,223,993 |

| |

| Net Assets Consist of: | |

| Capital stock | $2,983,514,058 |

| Accumulated undistributed net investment income | 7,919,330 |

| Accumulated net realized loss | (18,947,612) |

| Unrealized appreciation on investments | 929,738,217 |

| Total Net Assets | $3,902,223,993 |

| |

| Net Assets Consist of: | |

| Class J Shares | |

| Net Assets | $2,255,656,424 |

| Shares outstanding | 76,706,531 |

| Net Asset Value Per Share (2,000,000,000 shares authorized, $.001 par value) | $29.41 |

| |

| Class R Shares | |

| Net Assets | $42,907,970 |

| Shares outstanding | 1,464,925 |

| Net Asset Value Per Share (1,000,000,000 shares authorized, $.001 par value) | $29.29 |

| |

| Class I Shares | |

| Net Assets | $1,603,659,599 |

| Shares outstanding | 54,497,243 |

| Net Asset Value Per Share (1,000,000,000 shares authorized, $.001 par value) | $29.43 |

The accompanying notes are an integral part of these financial statements.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 7 |

Schedule of Investments

November 30, 2012 (Unaudited) (showing percentage of total net assets)

Common Stocks - 98.59%

| shares | Aerospace & Defense - 4.52% | | value |

| 2,204,000 | United Technologies Corporation | $176,562,440 |

| |

| shares | Air Freight & Logistics - 5.34% | | value |

| 1,442,000 | CH Robinson Worldwide, Inc. | $89,029,080 |

| 1,630,000 | United Parcel Service, Inc. | $119,169,300 |

| | $208,198,380 |

| |

| shares | Beverages - 7.82% | | value |

| 2,568,000 | The Coca-Cola Company | $97,378,560 |

| 2,960,000 | PepsiCo, Inc. | $207,821,600 |

| | $305,200,160 |

| |

| shares | Capital Markets - 3.49% | | value |

| 2,106,000 | T. Rowe Price Group, Inc. | $136,195,020 |

| |

| shares | Chemicals - 4.81% | | value |

| 937,000 | Ecolab, Inc. | $67,538,960 |

| 1,121,000 | Praxair, Inc. | $120,182,410 |

| | $187,721,370 |

| |

| shares | Electrical Equipment - 3.43% | | value |

| 2,666,100 | Emerson Electric Company | $133,918,203 |

| |

| Electronic Equipment, Instruments & | |

| shares | Components - 2.90% | | value |

| 1,826,000 | Amphenol Corporation Class A | $113,065,920 |

| |

| Health Care Equipment & Supplies - | |

| shares | 9.06% | | value |

| 1,469,606 | Becton Dickinson & Company | $112,674,692 |

| 2,175,400 | Medtronic, Inc. | $91,606,094 |

| 1,126,479 | Stryker Corporation | $61,010,103 |

| 1,274,000 | Varian Medical Systems, Inc. (a) | $88,109,840 |

| | $353,400,729 |

| |

| Health Care Providers & Services - | |

| shares | 2.17% | | value |

| 1,000,000 | Laboratory Corporation of America Holdings (a) | $84,590,000 |

| | | |

| shares | Household Products - 9.35% | | value |

| 1,473,000 | Colgate-Palmolive Company | $159,820,500 |

| 2,936,000 | The Procter & Gamble Company | $205,020,880 |

| | $364,841,380 |

| |

| shares | Industrial Conglomerates - 4.86% | | value |

| 2,086,500 | 3M Company | $189,767,175 |

| |

| shares | IT Services - 10.38% | | value |

| 1,960,000 | Accenture PLC (b) | $133,123,200 |

| 2,580,000 | Automatic Data Processing, Inc. | $146,440,800 |

| 1,864,000 | Cognizant Technology Solutions Corporation | |

| Class A (a) | $125,316,720 |

| | $404,880,720 |

| |

| shares | Life Sciences Tools & Services - 3.33% | | value |

| 1,539,000 | Waters Corporation (a) | $130,122,450 |

| |

| shares | Media - 3.77% | | value |

| 2,959,000 | Omnicom Group, Inc. | $147,180,660 |

| |

| shares | Pharmaceuticals - 4.37% | | value |

| 2,625,000 | Abbott Laboratories | $170,625,000 |

| |

| shares | Professional Services - 2.68% | | value |

| 2,043,000 | Equifax, Inc. | $104,683,320 |

| |

| shares | Software - 12.68% | | value |

| 4,228,000 | Adobe Systems, Inc. (a) | $146,331,080 |

| 5,552,000 | Microsoft Corporation | $147,794,240 |

| 6,253,000 | Oracle Corporation | $200,721,300 |

| $494,846,620 |

| |

| shares | Specialty Retail - 0.89% | | value |

| 785,500 | TJX Companies, Inc. | $34,829,070 |

The accompanying notes are an integral part of these financial statements.

| | |

| 8 | Jensen Quality Growth Fund | Semi-Annual Report |

Schedule of Investments continued

| Textiles, Apparel & Luxury Goods - | |

| shares | 2.74% | | value |

| 1,095,000 | NIKE, Inc. | $106,740,600 |

| |

| Total Common Stocks | | value |

| (Cost $2,917,631,000) | $3,847,369,217 |

| |

| Short-Term Investments - 0.88% | |

| |

| shares | Money Market Fund - 0.88% | | value |

| 34,366,613 | Fidelity Institutional Government Portfolio - |

| Class I, 0.01% (c) | $34,366,613 |

| |

| Total Short-Term Investments | | value |

| (Cost $34,366,613) | $34,366,613 |

| |

| Total Investments | | value |

| (Cost $2,951,997,613) - 99.47% | $3,881,735,830 |

| Other Assets in Excess of Liabilities - 0.53% | $20,488,163 |

| TOTAL NET ASSETS - 100.00% | $3,902,223,993 |

| (a) | Non-income producing security. |

| (b) | Foreign issued security. Foreign concentration (including ADRs) was as follows: Ireland 3.41%. |

| (c) | Variable rate security. The rate listed is as of November 30, 2012. |

The accompanying notes are an integral part of these financial statements.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 9 |

Statement of Operations

Six Months Ended November 30, 2012 (Unaudited)

| Investment Income: | |

| Dividend income | $37,549,966 |

| Interest income | 2,538 |

| | 37,552,504 |

| Expenses: | |

| Investment advisory fees | 9,835,039 |

| 12b-1 - Class J | 2,880,266 |

| Sub-transfer agent expenses - Class J | 880,944 |

| Administration fees | 666,891 |

| Shareholder servicing fees - Class I | 311,513 |

| Custody fees | 149,969 |

| Transfer agent fees - Class J | 138,015 |

| Fund accounting fees | 116,455 |

| Reports to shareholders - Class J | 114,139 |

| 12b-1 fees - Class R | 105,238 |

| Federal and state registration fees | 96,771 |

| Directors’ fees and expenses | 77,822 |

| Professional fees | 57,885 |

| Transfer agent expenses | 56,840 |

| Other | 29,498 |

| Reports to shareholders - Class I | 15,783 |

| Shareholder servicing fees - Class R | 13,484 |

| Transfer agent fees - Class I | 10,886 |

| Reports to shareholders - Class R | 1,647 |

| Transfer agent fees - Class R | 626 |

| Total expenses | 15,559,711 |

| |

| Net Investment Income | 21,992,793 |

| |

| Realized and Unrealized Gain on Investments: | |

| Net realized gain on investment transactions | 73,169,748 |

| Change in unrealized appreciation on investments | 211,160,928 |

| Net gain on investments | 284,330,676 |

| |

| Net Increase in Net Assets Resulting | |

| from Operations | $306,323,469 |

Statements of Changes in Net Assets

| | six months | | | | |

| | ended | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Operations: | | (Unaudited) | | | May 31, 2012 | |

| Net investment income | | $21,992,793 | | | $50,634,979 | |

| Net realized gain (loss) on investment | | | | | | |

| transactions | | 73,169,748 | | | (14,044,213) | |

| Change in unrealized appreciation | | | | | | |

| (depreciation) on investments | | 211,160,928 | | | (244,497,502) | |

| Net increase (decrease) in net assets | | | | | | |

| resulting from operations | | 306,323,469 | | | (207,906,736) | |

| | | | | | |

| | six months | | | | |

| | ended | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Capital Share Transactions: | | (Unaudited) | | | May 31, 2012 | |

| Shares sold - Class J | | 150,881,449 | | | 551,017,487 | |

| Shares sold - Class R | | 5,754,281 | | | 23,392,591 | |

| Shares sold - Class I | | 222,981,669 | | | 437,900,081 | |

| Shares issued in reinvestment of | | | | | | |

| dividends - Class J | | 11,235,980 | | | 26,136,633 | |

| Shares issued in reinvestment of | | | | | | |

| dividends - Class R | | 165,540 | | | 342,922 | |

| Shares issued in reinvestment of | | | | | | |

| dividends - Class I | | 9,468,631 | | | 18,408,431 | |

| Shares redeemed - Class J | | (383,245,120) | | | (703,077,911) | |

| Shares redeemed - Class R | | (6,275,456) | | | (10,936,093) | |

| Shares redeemed - Class I | | (190,949,129) | | | (463,057,910) | |

| Net decrease | | (179,982,155) | | | (119,873,769) | |

| | | | | | |

| | six months | | | | |

| | ended | | | | |

| Dividends and Distributions to | | Nov. 30, 2012 | | | year ended | |

| Shareholders: | | (Unaudited) | | | May 31, 2012 | |

| Net investment income - Class J | | (11,528,417) | | | (26,852,375) | |

| Net investment income - Class R | | (165,540) | | | (343,136) | |

| Net investment income - Class I | | (10,501,943) | | | (21,225,862) | |

| Total dividends and distributions | | (22,195,900) | | | (48,421,373) | |

| | | | | | |

| | six months | | | | |

| | ended | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Increase (Decrease) in Net Assets | | (Unaudited) | | | May 31, 2012 | |

| | 104,145,414 | | | (376,201,878) | |

| | | | | | |

| | | six months | | | | |

| | ended | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Net Assets: | | (Unaudited) | | | May 31, 2012 | |

| Beginning of period | | 3,798,078,579 | | | 4,174,280,457 | |

| End of period (including undistributed net | | | | | | |

| investment income of $7,919,330 and | | | | | | |

| $8,122,437, respectively) | | $3,902,223,993 | | | $3,798,078,579 | |

The accompanying notes are an integral part of these financial statements.

| | |

| 10 | Jensen Quality Growth Fund | Semi-Annual Report |

Financial Highlights

Class J

| | six months | | | | | | | | | | | | | | | | |

| | ended | | | | | | | | | | | | | | | | |

| | Nov. 30, 2012 | | | year ended | | | year ended | | | year ended | | | year ended | | | year ended | |

| Per Share Data: | | (Unaudited) | | | May 31, 2012 | | | May 31, 2011 | | | May 31, 2010 | | | May 31, 2009 | | | May 31, 2008 | |

| Net asset value, beginning of period | | $27.33 | | | $29.11 | | | $23.86 | | | $19.47 | | | $26.91 | | | $28.53 | |

| Income from investment operations: | | | | | | | | | | | | | | | | | | |

| Net investment income | | 0.15 | | | 0.32 | | | 0.27 | | | 0.24 | | | 0.30 | | | 0.27 | |

| Net realized and unrealized gains (losses) | | | | | | | | | | | | | | | | | | |

| on investments | | 2.07 | | | (1.80) | | | 5.25 | | | 4.39 | | | (6.78) | | | (1.42) | |

| Total from investment operations | | 2.22 | | | (1.48) | | | 5.52 | | | 4.63 | | | (6.48) | | | (1.15) | |

| Less distributions: | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | (0.14) | | | (0.30) | | | (0.27) | | | (0.24) | | | (0.31) | | | (0.26) | |

| Distributions from net realized capital gains | | — | | | — | | | — | | | — | | | (0.65) | | | (0.21) | |

| Total distributions | | (0.14) | | | (0.30) | | | (0.27) | | | (0.24) | | | (0.96) | | | (0.47) | |

| Net asset value, end of period | | $29.41 | | | $27.33 | | | $29.11 | | | $23.86 | | | $19.47 | | | $26.91 | |

| Total return(1) | | 8.14% | | | -5.04% | | | 23.31% | | | 23.85% | | | -23.90% | | | -4.08% | |

| Supplemental data and ratios: | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | | $2,255,656 | | | $2,307,634 | | | $2,593,128 | | | $1,776,091 | | | $1,340,826 | | | $1,706,765 | |

| Ratio of expenses to average net assets(2) | | 0.91% | | | 0.91% | | | 0.92% | | | 0.92% | | | 0.86% | | | 0.85% | |

| Ratio of net investment income to average net assets(2) | | 1.00% | | | 1.18% | | | 1.07% | | | 1.04% | | | 1.47% | | | 0.95% | |

| Portfolio turnover rate(1) | | 10.97% | | | 15.80% | | | 6.84% | | | 12.33% | | | 23.59% | | | 8.25% | |

| (1) | Not annualized for the six months ended November 30, 2012. |

| (2) | Annualized for the six months ended November 30, 2012. |

The accompanying notes are an integral part of these financial statements.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 11 |

Financial Highlights

Class R

| | | six months | | | | | | | | | | | | | | | | |

| | | ended | | | | | | | | | | | | | | | | |

| | | Nov. 30, 2012 | | | year ended | | | year ended | | | year ended | | | year ended | | | year ended | |

| Per Share Data: | | | (Unaudited) | | | May 31, 2012 | | | May 31, 2011 | | | May 31, 2010 | | | May 31, 2009 | | | May 31, 2008 | |

| Net asset value, beginning of period | | | $27.22 | | | $29.01 | | | $23.78 | | | $19.40 | | | $26.81 | | | $28.43 | |

| Income from investment operations: | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.11 | | | 0.26 | | | 0.23 | | | 0.20 | | | 0.23 | | | 0.22 | |

| Net realized and unrealized gains (losses) | | | | | | | | | | | | | | | | | | | |

| on investments | | | 2.07 | | | (1.79) | | | 5.23 | | | 4.37 | | | (6.75) | | | (1.44) | |

| Total from investment operations | | | 2.18 | | | (1.53) | | | 5.46 | | | 4.57 | | | (6.52) | | | (1.22) | |

| Less distributions: | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.11) | | | (0.26) | | | (0.23) | | | (0.19) | | | (0.24) | | | (0.19) | |

| Distributions from net realized capital gains | | | — | | | — | | | — | | | — | | | (0.65) | | | (0.21) | |

| Total distributions | | | (0.11) | | | (0.26) | | | (0.23) | | | (0.19) | | | (0.89) | | | (0.40) | |

| Net asset value, end of period | | | $29.29 | | | $27.22 | | | $29.01 | | | $23.78 | | | $19.40 | | | $26.81 | |

| Total return(1) | | | 8.02% | | | -5.26% | | | 23.08% | | | 23.59% | | | -24.10% | | | -4.34% | |

| Supplemental data and ratios: | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | | | $42,908 | | | $40,216 | | | $29,077 | | | $12,533 | | | $7,562 | | | $18,662 | |

| Ratio of expenses to average net assets(2) | | | 1.14% | | | 1.12% | | | 1.10% | | | 1.12% | | | 1.13% | | | 1.10% | |

| Ratio of net investment income to average net assets(2) | | | 0.77% | | | 0.96% | | | 0.87% | | | 0.83% | | | 1.18% | | | 0.70% | |

| Portfolio turnover rate(1) | | | 10.97% | | | 15.80% | | | 6.84% | | | 12.33% | | | 23.59% | | | 8.25% | |

| (1) | Not annualized for the six months ended November 30, 2012. |

| (2) | Annualized for the six months ended November 30, 2012. |

The accompanying notes are an integral part of these financial statements.

| | |

| 12 | Jensen Quality Growth Fund | Semi-Annual Report |

Financial Highlights

Class I

| | six months | | | | | | | | | | | | | | | | |

| | ended | | | | | | | | | | | | | | | | |

| | Nov. 30, 2012 | | | year ended | | | year ended | | | year ended | | | year ended | | | year ended | |

| Per Share Data: | | (Unaudited) | | | May 31, 2012 | | | May 31, 2011 | | | May 31, 2010 | | | May 31, 2009 | | | May 31, 2008 | |

| Net asset value, beginning of period | | $27.35 | | | $29.14 | | | $23.88 | | | $19.48 | | | $26.91 | | | $28.53 | |

| Income from investment operations: | | | | | | | | | | | | | | | | | | |

| Net investment income | | 0.19 | | | 0.40 | | | 0.37 | | | 0.34 | | | 0.37 | | | 0.30 | |

| Net realized and unrealized gains (losses) | | | | | | | | | | | | | | | | | | |

| on investments | | 2.08 | | | (1.80) | | | 5.24 | | | 4.36 | | | (6.80) | | | (1.38) | |

| Total from investment operations | | 2.27 | | | (1.40) | | | 5.61 | | | 4.70 | | | (6.43) | | | (1.08) | |

| Less distributions: | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | (0.19) | | | (0.39) | | | (0.35) | | | (0.30) | | | (0.35) | | | (0.33) | |

| Distributions from net realized capital gains | | — | | | — | | | — | | | — | | | (0.65) | | | (0.21) | |

| Total distributions | | (0.19) | | | (0.39) | | | (0.35) | | | (0.30) | | | (1.00) | | | (0.54) | |

| Net asset value, end of period | | $29.43 | | | $27.35 | | | $29.14 | | | $23.88 | | | $19.48 | | | $26.91 | |

| Total return(1) | | 8.31% | | | -4.76% | | | 23.72% | | | 24.21% | | | -23.71% | | | -3.86% | |

| Supplemental data and ratios: | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000’s) | | $1,603,660 | | | $1,450,228 | | | $1,552,075 | | | $831,505 | | | $303,557 | | | $343,250 | |

| Ratio of expenses to average net assets(2) | | 0.61% | | | 0.60% | | | 0.60% | | | 0.61% | | | 0.61% | | | 0.61% | |

| Ratio of net investment income to average net assets(2) | | 1.30% | | | 1.49% | | | 1.39% | | | 1.33% | | | 1.72% | | | 1.20% | |

| Portfolio turnover rate(1) | | 10.97% | | | 15.80% | | | 6.84% | | | 12.33% | | | 23.59% | | | 8.25% | |

| (1) | Not annualized for the six months ended November 30, 2012. |

| (2) | Annualized for the six months ended November 30, 2012. |

The accompanying notes are an integral part of these financial statements.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 13 |

Notes to the Financial Statements

November 30, 2012 (Unaudited)

1. Organization and Significant Accounting Policies

The Jensen Portfolio, Inc., doing business as Jensen Quality Growth Fund (the “Fund”), was organized as an Oregon Corporation on April 17, 1992, and is registered as an open-end, nondiversified management investment company under the Investment Company Act of 1940 (the “1940 Act”). The Fund commenced operations on August 3, 1992. The Fund is authorized to issue 5,000,000,000 shares of common stock. The Fund currently offers three different classes of shares. Effective July 30, 2003, the Fund issued two new classes of shares, Class R and Class I, and renamed the existing class as Class J. Class J shares are subject to a 0.25% 12b-1 fee and a sub-transfer agency fee, Class R shares are subject to a 0.50% 12b-1 fee and up to a 0.25% shareholder servicing fee, and Class I shares are subject to a shareholder servicing fee up to 0.10%, as described in each Class’ prospectus. Each class of shares has identical rights and privileges except with respect to the 12b-1 fees, sub-transfer agency fees and shareholder servicing fees, and voting rights on matters affecting a single class of shares. The principal investment objective of the Fund is long-term capital appreciation.

The following is a summary of significant accounting policies consistently followed by the Fund. The policies are in conformity with accounting principles generally accepted in United States of America (“GAAP”).

a) Investment Valuation – Securities that are listed on United States stock exchanges or the Nasdaq Stock Market are valued at the last sale price on the day the securities are valued or, if there has been no sale on that day, at their current bid price. Investments in open-end and closed-end registered investment companies, including money market funds, that do not trade on an exchange are valued at the end of day net asset value per share. Quotations are taken from the market in which the security is primarily traded. Over-the-counter securities are valued at the current bid price in the absence of a closing price. Securities for which market quotations are not readily available are valued at fair value as determined by Jensen Investment Management, Inc. (the “Investment Adviser”) at or under the direction of the Fund’s Board of Directors.

There is no definitive set of circumstances under which the Fund may elect to use fair value procedures to value a security. Although the Fund only invests in publicly traded securities, the large majority of which are large capitalization, highly liquid securities, they nonetheless may become securities for which market quotations are not readily available, such as in instances where the market quotation for a security has become stale, sales of a security have been infrequent, trading in the security has been suspended, or where there is a thin market in the security. Securities for which market quotations are not readily available will be valued at their fair value as determined under the Fund’s fair valuation procedures established by the Board of Directors. The Fund is prohibited from investing in restricted securities (securities issued in private placement transactions that may not be offered or sold to the public without registration under the securities laws); therefore, fair value pricing considerations for restricted securities are generally not applicable to the Fund.

Fair Value Measurement – The Fund has adopted authoritative fair valuation accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion of changes in valuation techniques and related inputs during the period. The three levels of the fair value hierarchy are as follows:

| Level 1 | | Inputs that reflect unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access at the measurement date. |

| | | |

| Level 2 | | Inputs other than quoted prices that are observable for the asset or liability either directly or indirectly, including inputs in markets that are not considered to be active and prices for similar securities, interest rates, credit risk, etc. |

| | |

| Level 3 | | Inputs that are unobservable (including the Fund’s own assumptions in determining the fair value of investments). |

Inputs refer broadly to the assumptions that market participants use to make valuation decisions, including assumptions about risk. Inputs may include price information, volatility statistics, specific and broad credit data, liquidity statistics, and other factors. A financial instrument’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. However, the determination of what constitutes “observable” requires significant judgment by the Fund. The Fund considers observable data to be that market data which is readily available, regularly distributed or updated, reliable and verifiable, not proprietary, and provided by independent sources that are actively involved in the relevant market. The categorization of a financial instrument within the hierarchy is based upon the pricing transparency of the instrument and does not necessarily correspond to the Fund’s perceived risk of that instrument.

Investments whose values are based on quoted market prices in active markets, include common stocks and certain money market securities, and are classified within Level 1. Investments that trade in markets that are not considered to be active, but are valued based on quoted market

| | |

| 14 | Jensen Quality Growth Fund | Semi-Annual Report |

prices, dealer quotations or alternative pricing sources supported by observable inputs are classified within Level 2. Investments classified within Level 3 have significant unobservable inputs, as they trade infrequently or not at all.

The following is a summary of the inputs used, as of November 30, 2012, to value the Fund’s investments carried at fair value. The inputs and methodology used for valuing securities may not be an indication of the risk associated with investing in those securities.

| Investments at Value | | Total | | | Level 1 | | Level 2 | Level 3 |

| Total Common | | | | | | | | | | | | | | |

| Stocks* | | $3,847,369,217 | | | $3,847,369,217 | | | $ | — | | | $ | — | |

| Total Money | | | | | | | | | | | | | | |

| Market Fund | | 34,366,613 | | | 34,366,613 | | | | — | | | | — | |

| Total Investments | | $3,881,735,830 | | | $3,881,735,830 | | | $ | — | | | $ | — | |

* For further information regarding security characteristics and industry classifications, please see the Schedule of Investments.

The Fund did not hold any investments during the period ended November 30, 2012 with significant unobservable inputs which would be classified as Level 3. There were no transfers of securities between levels during the reporting period. It is the Fund’s policy to record transfers between levels as of the end of the reporting period. The Fund did not hold any derivative instruments during the reporting period.

b) Federal Income Taxes – No provision has been made for Federal income taxes since the Fund has elected to be taxed as a “regulated investment company” and intends to distribute substantially all net investment company taxable income and net capital gains to its shareholders and otherwise comply with the provision of the Internal Revenue Code applicable to regulated investment companies.

The Fund has reviewed all open tax years and major jurisdictions and concluded that there is no tax liability resulting from unrecognized tax benefits relating to uncertain income tax positions taken or expected to be taken as of and for the year ended May 31, 2012. The Fund recognizes interest and penalties, if any, related to uncertain tax benefits in the Statement of Operations. During the year, the Fund did not incur any interest or penalties. Open tax years are those that are open for exam by taxing authorities. As of May 31, 2012, open Federal tax years include the tax years ended May 31, 2009 through 2012. The Fund has no examination in progress. The Fund is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

c) Distributions to Shareholders – Dividends to shareholders are recorded on the ex-dividend date. Dividends from net investment income are declared and paid quarterly by the Fund. Distributions of net realized capital gains, if any, will be declared and paid at least annually. Income and capital gain distributions are determined in accordance with income tax regulations which may differ from GAAP. Additionally, GAAP requires that certain components of net assets relating to permanent differences be reclassified between the components of net assets. These reclassifications have no effect on net assets or net asset value per share. For the year ended May 31, 2012, there were no reclassifications made.

d) Use of Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

e) Guarantees and Indemnifications – Under the Fund’s organizational documents, each Director, officer, employee or other agent of the Fund is indemnified, to the extent permitted by the 1940 Act, against certain liabilities that may arise out of performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, the Fund has not had prior claims or losses pursuant to these contracts and believes the risk of loss to be remote.

f) Allocation of Income, Expenses and Gains/Losses – Income, expenses (other than those deemed attributable to a specific share class), and gains and losses of the Fund are allocated daily to each class of shares based upon the ratio of net assets represented by each class as a percentage of the net assets of the Fund. Expenses deemed directly attributable to a class of shares are recorded by the specific class. Most Fund expenses are allocated by class based on relative net assets. Transfer agent fees and reports to shareholders are allocated based on the number of shareholder accounts in each class. Sub-transfer agency fees are expensed to the Class J shares based on the actual number of shareholder accounts held and serviced by certain financial intermediaries as described in the Class J shares’ prospectus. 12b-1 fees are expensed at 0.25% of average daily net assets of Class J shares and 0.50% of average daily net assets of Class R shares. Shareholder servicing fees are expensed at up to 0.10% and up to 0.25% of the average daily net assets of Class I shares and Class R shares, respectively.

g) Other – Investment and shareholder transactions are recorded on trade date. Gains or losses from investment transactions are determined on the basis of identified carrying value using the specific identification method. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 15 |

2. Capital Share Transactions

Transactions in shares of the Fund were as follows:

| | six months | | | | | |

| | ended | | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Class J | | (Unaudited) | | | May 31, 2012 | |

| Shares sold | | 5,262,978 | | | | 20,335,876 | | |

| Shares issued in reinvestment | | | | | | | | |

| of dividends | | 390,031 | | | | 978,439 | | |

| Shares redeemed | | (13,396,557 | ) | | | (25,946,957 | ) | |

| Net decrease | | (7,743,548 | ) | | | (4,632,642 | ) | |

| Shares outstanding: | | | | | | | | |

| Beginning of period | | 84,450,079 | | | | 89,082,721 | | |

| End of period | | 76,706,531 | | | | 84,450,079 | | |

| | | | | | | | |

| | six months | | | | | |

| | ended | | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Class R | | (Unaudited) | | | May 31, 2012 | |

| Shares sold | | 201,617 | | | | 869,353 | | |

| Shares issued in reinvestment | | | | | | | | |

| of dividends | | 5,766 | | | | 12,887 | | |

| Shares redeemed | | (219,898 | ) | | | (407,094 | ) | |

| Net increase (decrease) | | (12,515 | ) | | | 475,146 | | |

| Shares outstanding: | | | | | | | | |

| Beginning of period | | 1,477,440 | | | | 1,002,294 | | |

| End of period | | 1,464,925 | | | | 1,477,440 | | |

| | | | | | | | |

| | six months | | | | | |

| | ended | | | | | |

| | Nov. 30, 2012 | | | year ended | |

| Class I | | (Unaudited) | | | May 31, 2012 | |

| Shares sold | | 7,786,104 | | | | 16,216,920 | | |

| Shares issued in reinvestment | | | | | | | | |

| of dividends | | 328,281 | | | | 687,878 | | |

| Shares redeemed | | (6,650,999 | ) | | | (17,136,856 | ) | |

| Net increase (decrease) | | 1,463,386 | | | | (232,058 | ) | |

| Shares outstanding: | | | | | | | | |

| Beginning of period | | 53,033,857 | | | | 53,265,915 | | |

| End of period | | 54,497,243 | | | | 53,033,857 | | |

3. Investment Transactions

The aggregate purchases and aggregate sales of securities, excluding short-term investments, by the Fund for the period ended November 30, 2012, were $423,174,536 and $621,197,653, respectively.

4. Income Taxes

The cost of investments differ for financial statement and tax purposes primarily due to the deferral of losses on wash sales.

The distributions of $48,421,373 and $37,509,831 paid during the years ended May 31, 2012 and 2011, respectively, were classified as ordinary income for tax purposes. There were no long-term capital gain distributions paid during the years ended May 31, 2012 and 2011.

At May 31, 2012, the cost of investments, net unrealized appreciation (depreciation) and undistributed ordinary income and undistributed long term capital gains for income tax purposes were as follows:

| Cost of investments | | $3,071,514,497 |

| Gross unrealized appreciation | | $783,751,662 |

| Gross unrealized depreciation | | (65,538,777) |

| Net unrealized appreciation | | 718,212,885 |

| Undistributed ordinary income | | 8,122,437 |

| Undistributed long-term capital gain | | — |

| Total distributable earnings | | 8,122,437 |

| Other accumulated losses | | (91,752,956) |

| Total accumulated gains | | $634,582,366 |

At May 31, 2012, the Fund had total tax basis capital losses of $91,752,956 which may be used to offset future capital gains. Of the total capital losses, $77,761,993 was incurred prior to the effective date of the RIC Modernization Act provisions (See Note 9), and will expire on May 31, 2018. The remaining balance of capital losses amounting to $13,990,963 is characterized as short-term capital losses and may be carried forward indefinitely. The post-RIC Modernization Act capital losses are required to be utilized prior to the capital losses incurred in pre-enactment years, which may expire unused.

On December 20, 2012, the Fund declared and paid a distribution from ordinary income of $8,581,269, $139,921 and $7,358,794 for Class J, Class R, and Class I, respectively, to shareholders of record as of December 19, 2012.

5. Line of Credit

The Fund has a $250 million revolving credit facility for temporary emergency purposes, including the meeting of redemption requests that otherwise might require the untimely disposition of securities. The unsecured line of credit has a one year term and is reviewed annually by the Board of Directors. The current agreement ran through December 21, 2012 and has subsequently been renewed for another year at the same terms. The interest rate on the outstanding principal amount is equal to the prime rate less 1%. As of November 30, 2012, the rate on the Fund’s line of credit was 2.25%. The fund did not borrow on the line of credit as of and during the six months ended November 30, 2012.

| | |

| 16 | Jensen Quality Growth Fund | Semi-Annual Report |

6. Investment Advisory Agreement

The Fund has an Investment Advisory and Service Contract with Jensen Investment Management, Inc. Pursuant to the advisory agreement and breakpoint fee schedule, the Investment Adviser is entitled to receive a fee, calculated daily and payable monthly, at the annual rate of 0.50% as applied to the Fund’s average daily net assets of $4 billion or less, 0.475% as applied to the Fund’s average daily net assets of more than $4 billion and up to $8 billion, 0.45% as applied to the Fund’s average daily net assets of more than $8 billion and up to $12 billion, and 0.425% as applied to the Fund’s average daily net assets of more than $12 billion.

Certain officers of the Fund are also officers and directors of the Investment Adviser.

7. Distribution and Shareholder Servicing

The Fund has adopted a distribution and shareholder servicing plan pursuant to Rule 12b-1 under the 1940 Act (the “12b-1 Plan”), which provides that the Fund make payments to the Fund’s distributor at an annual rate of 0.25% of average daily net assets attributable to Class J shares and 0.50% of the average daily net assets attributable to Class R shares. The Fund’s distributor may then make payments to financial intermediaries or others at an annual rate of up to 0.25% of the average daily net assets attributable to Class J shares and up to 0.50% of the average daily net assets attributable to Class R shares. Payments under the 12b-1 Plan shall be used to compensate the Fund’s distributor or others for services provided and expenses incurred in connection with the sale and/or servicing of shares.

In addition, the Fund has adopted a Shareholder Servicing Plan for Class I shares under which the Fund can pay for shareholder support services from the Fund’s assets pursuant to a Shareholder Servicing Agreement in an amount not to exceed 0.10% of the Fund’s average daily net assets attributable to Class I shares.

The Fund has also adopted a Shareholder Servicing Plan for the Class R shares. Under the Shareholder Servicing Plan, the Fund can pay for shareholder support services, which include the recordkeeping and administrative services provided by retirement plan administrators to retirement plans (and their participants) that are shareholders of the class. Payments will be made pursuant to a Shareholder Servicing Agreement in an amount not to exceed 0.25% of the Fund’s average daily net assets attributable to Class R shares.

8. Beneficial Ownership

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of the Fund, under Section 2(a)(9) of the 1940 Act. At November 30, 2012, Charles Schwab & Co., Inc., for the benefit of its customers, held 42.50% and 31.09% of the outstanding shares of the Class J and Class I share classes, respectively. At November 30, 2012, Great-West Life & Annuity Insurance Company and Great-West Trust Company, for the benefit of their customers, owned 25.52% and 29.88%, respectively, of the outstanding shares of the Class R share class.

9. New Tax Law

On December 22, 2010, The Regulated Investment Company Modernization Act of 2010 (the “Modernization Act”) was signed into law. The Modernization Act is the first major piece of legislation affecting regulated investment companies (“RICs”) since 1986 and it modernizes several of the federal income and excise tax provisions related to RICs. Some highlights of the enacted provisions are as follows:

New capital losses may now be carried forward indefinitely, and retain the character of the original loss. Under pre-enactment law, capital losses could be carried forward for eight years, and carried forward as short-term capital losses, irrespective of the character of the original loss.

The Modernization Act contains simplification provisions, which are aimed at preventing disqualification of a RIC for “inadvertent” failures of the asset diversification and/or qualifying income tests. Additionally, the Modernization Act exempts RICs from the preferential dividend rule, and repealed the 60-day designation requirement for certain types of pay-through income and gains.

Finally, the Modernization Act contains several provisions aimed at preserving the character of distributions made by a RIC during the portion of its taxable year ending after October 31 or December 31, reducing the circumstances under which a RIC might be required to file amended Forms 1099 to restate previously reported distributions.

The provisions related to the RIC Modernization Act for qualification testing were effective for the May 31, 2011 taxable year. The effective date for changes in the treatment of capital losses is May 31, 2012 taxable year.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 17 |

Expense Example - November 30, 2012 (Unaudited)

As a shareholder of Jensen Quality Growth Fund, you incur ongoing costs, including investment advisory fees, distribution and/or shareholder servicing fees, and other Fund expenses, which are indirectly paid by shareholders. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six month period (June 1, 2012–November 30, 2012).

Actual Expenses

The first line of the table below for each share class of the Fund provides information about actual account values and actual expenses. However, the table does not include shareholder specific fees, such as the $15.00 fee charged to IRA accounts, or the $15.00 fee charged for wire redemptions. The table also does not include portfolio trading commissions and related trading costs. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the actual expense ratios for each share class of the Fund and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees which, although not charged by the Fund, may be charged by other funds. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| | |

| 18 | Jensen Quality Growth Fund | Semi-Annual Report |

Expense Example Tables

| | | | | | | | | | | | | | Expenses Paid During |

| | Beginning Account Value | | | Ending Account Value | | | Period* June 1, 2012 |

| Jensen Quality Growth Fund – Class J | | June 1, 2012 | | | November 30, 2012 | | | – November 30, 2012 |

| Actual | | | $ | 1,000.00 | | | | | $ | 1,081.40 | | | | | $ | 4.75 | |

| Hypothetical (5% annual return before expenses) | | | | 1,000.00 | | | | | | 1,020.51 | | | | | | 4.61 | |

| | |

| * Expenses are equal to the Fund’s annualized six-month expense ratio of 0.91%, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. | |

| | |

| | | | | | | | | | | | | | Expenses Paid During |

| | Beginning Account Value | | | Ending Account Value | | | Period* June 1, 2012 |

| Jensen Quality Growth Fund – Class R | | June 1, 2012 | | | November 30, 2012 | | | – November 30, 2012 |

| Actual | | | $ | 1,000.00 | | | | | $ | 1,080.20 | | | | | $ | 5.94 | |

| Hypothetical (5% annual return before expenses) | | | | 1,000.00 | | | | | | 1,019.35 | | | | | | 5.77 | |

| | |

| * Expenses are equal to the Fund’s annualized six-month expense ratio of 1.14%, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. | |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | Expenses Paid During |

| | Beginning Account Value | | | Ending Account Value | | | Period* June 1, 2012 |

| Jensen Quality Growth Fund – Class I | | June 1, 2012 | | | November 30, 2012 | | | – November 30, 2012 |

| Actual | | | $ | 1,000.00 | | | | | $ | 1,083.10 | | | | | $ | 3.19 | |

| Hypothetical (5% annual return before expenses) | | | | 1,000.00 | | | | | | 1,022.01 | | | | | | 3.09 | |

* Expenses are equal to the Fund’s annualized six-month expense ratio of 0.61%, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 19 |

Additional Information (Unaudited)

1. Investment Advisory Agreement Disclosure

Section 15(c) under the 1940 Act requires that a registered investment company’s board of directors, including a majority of independent directors voting separately, approve any new investment advisory contract for the fund and thereafter to review and approve the terms of the fund’s investment advisory agreement on an annual basis. In addition, Section 15(a) of the 1940 Act requires that any new investment advisory agreement be approved by the fund’s shareholders.

In their most recent deliberations concerning whether to renew the Fund’s Investment Advisory and Service Contract with the Adviser (the “Agreement”), the Board of Directors (the “Board”), including the Fund’s independent directors (“Independent Directors”), conducted the review and made the determinations that are described below. During its deliberations, the Board requested from the Adviser, and the Adviser furnished, all information reasonably necessary for it to evaluate the renewal of the Fund’s Agreement.

The entire Board first met on April 18, 2012 to consider the information provided by the Adviser in connection with the renewal of the Agreement. After the April 18 meeting, the Independent Directors met separately with their legal counsel to consider the information provided by the Adviser and identify additional information they needed to evaluate the Agreement. The entire Board then met again on July 18, 2012 to consider the continuation of the Agreement. During those meetings, the Board evaluated the factors and reached the conclusions described below, among others. The Board did not identify any single factor as controlling. Moreover, not every factor was given the same weight by each Director.

Nature, Extent and Quality of Services

The Board considered the nature, extent and quality of services provided to the Fund by the Adviser under the Agreement. The Board reviewed the terms of the Agreement, as well as the history of the Adviser and its investment discipline, its investment performance, and its day-to-day management of the Fund. The Board noted the Adviser’s focus on the business of the Fund, the compliance and other servicing aspects of the Fund, and the Adviser’s oversight of the Fund’s service providers.

The Board considered the Adviser’s business continuity plans, its organizational and ownership structure, including the impact of changes in management and ownership, and the composition of its investment committee, which makes all investment decisions for the Fund. The Board also considered the Adviser’s approach to risk management. Based on these and other factors, including the additional factors described below, the Board concluded that the services provided to the Fund under the Agreement continued to be satisfactory.

Investment Performance

The Board examined the investment performance of the Fund compared to the S&P 500 Index and Russell 1000 Growth Index and to the Lipper Large Cap Core Funds and Morningstar Large Cap Growth Funds categories. Performance over one-, three-, five-, ten- and fifteen-year periods for the Fund against the indices, and against its Lipper and Morningstar categories for similar periods, were provided. The Board noted the favorable performance of the Fund for the five- and fifteen-year periods compared to the S&P 500 Index and the favorable performance against the Russell 1000 Growth Index for the fifteen-year period. The Board also noted the Fund’s favorable performance for the five-year period compared to its Lipper category and its four-star Morningstar rating for the same five-year period, and the Fund’s overall three-star Morningstar rating. The Board also noted the Fund’s underperformance compared to its indices and Lipper and Morningstar categories for the three- and ten-year periods. In particular, the Board observed that the three-year period underperformance compared to its indices was attributable to the performance of lower quality companies which the Fund is not permitted to purchase and from company selection that detracted from returns in certain market sectors. The Board observed that the Adviser appeared to have adhered to its strict investment discipline. As a result of these and other factors, the Board concluded that the overall long-term investment performance of the Fund continued to be satisfactory.

Advisory Fee and Expense Ratio

The Board compared the Fund’s advisory fee with those of other comparable mutual funds in the Fund’s Lipper category. The Board noted that the Fund’s advisory fee of 0.50% (before the effect of breakpoints above $4 billion in net assets) continued to be below the median and the average for its category at similar asset levels, excluding passively managed funds and funds that have no share classes that are offered to retail investors. The Board also noted the Adviser’s adoption in October 2010 of breakpoints in the Fund’s advisory fee schedule for net assets of $4 billion, at which point the advisory fee drops to 0.475% with additional fee breakpoints at higher net asset levels. The Board also noted that while the Adviser employs a relatively straightforward investment discipline, the Fund appeared to be an efficiently run operation with a high service component for shareholders.

The Board compared the fees charged to the Fund with the advisory fees charged to the non-Fund advisory clients of the Adviser. The Board observed that, with the exception of a small number of institutional separate account clients where the Adviser believes the competitive market required a lower fee, the Adviser charges its separate accounts a minimum fee of 0.50% for individual investors

| | |

| 20 | Jensen Quality Growth Fund | Semi-Annual Report |

and 0.45% for institutional investors but also noted the limitations of such comparisons due to the different services required by separate account clients compared to the Fund. The Board also noted the Adviser’s consideration of entering into sub-advisory agreements, where advisory fees are typically lower than the schedule for a directly advised separate account. Separate accounts, the Board observed, are subject to less regulation and generally do not require the same level of administrative services as the Fund.

The Board considered the Fund’s expense ratio and the expense ratios of other comparable mutual funds in the Fund’s Lipper and Morningstar categories. The Board noted that the Fund’s expense ratio was higher than the average but lower than the median of all funds with comparable net assets in its Lipper categories but also noted that, when compared to retail class shares of actively managed funds, the Fund’s expense ratio was lower than the median and the average. Compared to retail class shares of actively managed funds in the Fund’s Morningstar category, the Board noted that the Fund’s expense ratio was below the average. The Board also noted that the Fund had a relatively low turnover rate, reducing the Fund’s transaction costs, which are not included in the Fund’s expense ratio but are deducted from the Fund’s net asset value. The Board acknowledged that, with the payment by the Fund of the sub transfer agency recordkeeping and shareholder servicing expenses and fees for certain of the Fund’s omnibus accounts (“Sub TA Fees”), the Fund’s expense ratio had increased during the fiscal year ended May 31, 2010 and remained unchanged during fiscal 2011, but decreased slightly to 91 basis points for the fiscal year ended Mary 31, 2012 due to increases in overall net assets. The Board further acknowledged that it expected the expense ratio to remain lower than the Lipper and Morningstar averages for retail-class shares of actively managed funds. Based on these considerations and other factors, the Board concluded that the Fund’s advisory fee and expense ratio were reasonable relative to the Fund’s peer groups.

Profitability of the Adviser

The Board considered the profitability of the Agreement to the Adviser, including an analysis of the Adviser’s profitability for 2011 and the methodology used to calculate that profitability, and compared the Adviser’s profitability to that of selected publicly traded mutual fund advisers. Even after adjustments for certain marketing revenues and compensation expenses were made, it appeared that the Adviser’s pre-tax profit was higher than the average pre-tax profit margin of the group of publicly traded investment advisory firms. It was noted that the Adviser’s adjustment to its compensation expense was made because its profitability may have been overstated due to the relatively low salaries and bonuses paid to its principals, who may receive distributions of the Adviser’s profits on account of their equity ownership in the Adviser. The Board considered the fact that the Adviser pays certain administrative expenses of the Fund, including the cost of the Fund’s Chief Compliance Officer, though it noted that under the Agreement the Fund is authorized, subject to prior Board approval, to pay for certain costs of the Fund’s compliance personnel in the future. The Board acknowledged the entrepreneurial risk taken by the Adviser when it established the Fund and the Adviser’s subsidization of the Fund during the early years of the Fund’s existence. Finally, the Board observed the increase in net assets for the Fund that contributed to higher margins for the Adviser in 2011.

The Board also examined the Adviser’s profitability from the Fund against the Adviser’s profitability from its separate account advisory business and found that the Fund provided a higher profit margin to the Adviser. The Board understood that the administrative services the Adviser provides to the Fund are, on balance, more extensive than those it provides to its separate accounts, but also noted that economies of scale are realized with respect to managing one mutual fund compared to managing between 350 - 400 separate accounts. The Board also understood that in calculating its profitability from the Fund, the Adviser had been conservative in its method of allocating expenses to its Fund business relative to other acceptable allocation methodologies.

The Board acknowledged the inherent limitations of profitability analyses, including the use of comparative data that is incomplete or dissimilar, such as financial information of publicly traded mutual fund advisers which have more diversified business lines and different cost structures than those of the Adviser, and the uncertainty of the various cost allocations and other assumptions used. Based on this and other information, the Board concluded that profits earned by the Adviser were not excessive.

Economies of Scale

The Board considered whether there have been economies of scale with respect to the management of the Fund, whether the Fund has benefited from any such economies, and whether the implementation of breakpoints in the Fund’s advisory fee was appropriate. The Board observed that, during a period of rapid Fund growth, the Fund’s expense ratio (for the Class J shares) had fallen from about 1% for the fiscal year ended May 31, 2002 to 0.92% for the fiscal year ended May 31, 2011 and declined to 0.91% for the fiscal year ended May 31, 2012. Regarding the issue of breakpoints, the Board noted the Adviser’s implementation of a breakpoint fee schedule in October 2010. The Board also observed that with net asset levels over $4 billion during part of 2012, Fund shareholders were beginning to realize the effect of the first fee breakpoint. The Board and also noted that many comparable funds with breakpoints at lower levels had higher overall advisory fees at the same asset level as the current asset level of the Fund. Based on the data presented, the Board concluded that additional breakpoints in the Fund’s advisory fee were not warranted at this time.

| | |

| Semi-Annual Report | Jensen Quality Growth Fund | 21 |

Other Benefits

The Board considered the potential fall-out benefits realized by the Adviser from services as investment manager of the Fund. The Board noted that the Adviser has no affiliated entities that provide services to the Fund and that the Adviser prohibits the receipt of third-party research for “soft dollars”. The Board understood that the Adviser maintained a separate account advisory business and managed another mutual fund. The Board noted that, while the Adviser’s non-Fund business might benefit from any favorable publicity received by the Fund, any such benefit was difficult to quantify.

Other Factors and Considerations

The Board periodically reviews and considers other material information throughout the year relating to the quality of services provided to the Fund, such as the allocation of Fund brokerage, the marketing, administration and compliance program of the Fund, the Adviser’s management of its relationship with the Fund’s administrator, custodian, transfer agent and other service providers, and the expenses paid to those service providers. At its regular meetings, the Board also reviews detailed information relating to the Fund’s portfolio and performance against various metrics, and participates in discussions with the Fund’s portfolio managers.

Based on its evaluation of all the relevant factors and the information provided to it, the Board, including all of the Independent Directors, voted unanimously to renew the Agreement for a one-year period until July 31, 2013.

2. Shareholder Notification of Federal Tax Status

The Fund designates 100% of dividends declared during the fiscal year ended May 31, 2012 as dividends qualifying for the dividends received deduction available to corporate shareholders.

The Fund designates 100% of dividends declared from net investment income during the fiscal year ended May 31, 2012 as qualified dividend income under the Jobs and Growth Tax Relief Reconciliation Act of 2003.

The Fund designates as a long-term capital gain dividend, pursuant to the Internal Revenue Code Section 852(b)(3), the amount necessary to reduce earnings and profits of the Fund related to net capital gain to zero for the fiscal year ended May 31, 2012.

Additional Information Applicable to Foreign Shareholders Only:

The Fund designates 0.10% of ordinary income distributions as interest-related dividends under Internal Revenue Code Section 871(k)(1)(c).

3. Availability of Proxy Voting Information

Information regarding how the Fund votes proxies relating to portfolio securities is available without charge, upon request by calling toll-free, 1-800-221-4384, or by accessing the SEC’s website at www.sec.gov.

4. Portfolio Holdings

The Jensen Quality Growth Fund will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q will be available on the EDGAR database on the SEC’s website at www.sec.gov. These Forms may also be reviewed and copied at the SEC’s Public Reference Room in Washington D.C. Information about the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

| | |

| 22 | Jensen Quality Growth Fund | Semi-Annual Report |

5. Additional Disclosure Regarding Fund Directors and Officers

Independent Directors

| Name, Age and Address | Position(s)

Held with

the Company | Term of Office and

Length of Time

Served** | Principal Occupation During

Past Five Years | # of Portfolios

in Fund

Complex

Overseen

by Director | Other Directorships

Held by Director |

| | | | | | |

Roger A. Cooke J.D.

Jensen Quality Growth Fund

5300 Meadows Road

Suite 250

Lake Oswego, OR 97035

Year of Birth: 1948 | Independent

Director | Indefinite Term; since June 1999. | Senior Vice President, General Counsel and Secretary of Precision Castparts Corp., a diversified manufacturer of complex metal products, (2000 – present); Executive Vice President – Regulatory and Legal Affairs of Fred Meyer, Inc., a retail grocery and general merchandise company, (1992 – 2000). | 1 | None |

| | | | | | |

Robert E. Harold

Jensen Quality Growth Fund

5300 Meadows Road

Suite 250

Lake Oswego, OR 97035

Year of Birth: 1947 | Independent

Director | Indefinite Term; since September 2000. | Retired. Senior Director of Financial Planning of Nike, Inc., a footwear and apparel company (2001 – 2002); Global Brand Controller for Nike, Inc. (1996, 1997, 2000 – 2001); Interim Chief Financial Officer for Nike, Inc. (1998 – 1999); Interim Chief Executive Officer for Laika, Inc. (formerly Will Vinton Studios), an animation studio (March 2005 – October 2005). | 1 | Director of St. Mary’s Academy, a non-profit high school (2000 – present); Director of Laika, Inc. (formerly Will Vinton Studios), an animation studio (2002 – present); Director of The Sisters of the Holy Names Foundation (2004 – 2012). |

| | | | | | |

Thomas L. Thomsen, Jr.

Jensen Quality Growth Fund

5300 Meadows Road

Suite 250