UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03833

MAINSTAY VP FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

169 Lackawanna Avenue

Parsippany, NJ 07054

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 576-7000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

FORM N-CSR

Item 1. Reports to Stockholders.

MainStay VP Funds Trust

Message from the President and Annual Report

December 31, 2012

Message from the President

Most stock and bond investors enjoyed positive total returns for 2012. Several major U.S., international and world stock market indexes provided double-digit returns during the reporting period.

The stock market’s progress, however, was far from uniform. Stocks began the year buoyed by signs that systemic risk in Europe was coming under control. The European Central Bank’s Long Term Financing Operations helped ease market concerns and provide needed liquidity. During the second quarter, however, stocks tumbled as investors again focused on major risk factors, including missed budget targets, contentious elections and slowing economic growth.

Stocks began to rise again at the end of May and reached their high point for the year in mid-September. The remainder of the year was relatively volatile but ended on an up note, as investors weighed in on the U.S. presidential election and the continued debate about how best to address the fiscal cliff.

Much of the market’s advance during the year can be attributed to central bank actions designed to calm investor concerns. In July, European Central Bank President Mario Draghi pledged to do “whatever it takes” to support the euro. Later, he outlined a plan for direct purchases of government bonds across Europe.

Throughout the year, the Federal Reserve held the federal funds rate in a range near zero. It also continued to extend the average maturity of its U.S. Treasury holdings in an effort to put downward pressure on longer-term interest rates, provide broad easing in financial market conditions and contribute to an economic recovery. In September, the Federal Open Market Committee agreed to increase policy accommodation by purchasing an additional $40 billion per month in agency mortgage-backed securities.

In the bond market, the prospect of continued low interest rates led yield-hungry investors to lengthen

maturities and lower their aversion to risk. During 2012, higher-risk fixed-income securities tended to outperform those with lower risk. As an asset class, high-yield bonds were the top performers, providing strong double-digit returns. They were followed by convertible securities, leveraged loans, and high-grade corporate bonds. U.S. government securities provided positive total returns in the low single digits. It is important to note, however, that past performance is no guarantee of future results.

While most investors are pleased when markets advance, the portfolio managers of MainStay VP Funds know that long-term results depend on more than short-term market movements. They also depend on the consistent application of well-defined investment strategies and risk-management techniques over longer periods.

At MainStay VP Funds, we believe that a long-term perspective can help investors as well. Rather than focus on daily or weekly market movements, we invite you to consider the long-term potential that can come from getting invested, staying invested and adding to your investments over time.

The following pages contain more specific information on the market events, investment decisions and securities that affected your MainStay VP Portfolio(s) during the 12 months ended December 31, 2012. We encourage you to read the information carefully and use it as part of your ongoing Portfolio evaluation and investment review.

Sincerely,

Stephen P. Fisher

President

Not part of the Annual Report

This page intentionally left blank

Table of Contents

Investors should refer to the MainStay VP Funds Trust Prospectus dated May 1, 2012, as supplemented, for a discussion of each Portfolio’s investment objectives, strategies and risks. You may obtain copies of the Prospectus and the relevant Statement of Additional Information free of charge, upon request, by calling toll-free 800-598-2019, or by writing to New York Life Insurance and Annuity Corporation, 51 Madison Avenue, Room 251, New York, New York 10010. These documents are also available at mainstayinvestments.com.

| | | | |

| mainstayinvestments.com | | | M-1 | |

Index Definitions

The information below is an explanation of the various indices and reference rates cited throughout the Portfolio Investment and Performance Comparisons and the Portfolio Management Discussion and Analysis sections that follow from page M-4 through page M-435. Please use this as a reference.

Please note that you cannot make an investment directly in an index. Past performance is no guarantee of future results. Results for securities indices assume reinvestment of all income and capital gains but do not reflect fees, expenses or taxes. Securities in each Portfolio may not precisely match those in a related index, and as a result, performance of the Portfolio may differ.

Balanced Composite Index is an unmanaged index that consists of the Russell Midcap® Value Index (60% weighted) and the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index (40% weighted).

Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index is a market-capitalization-weighted index including U.S. government and fixed-coupon domestic investment-grade corporate bonds.

Bank of America Merrill Lynch All U.S. Convertible Index is a market-capitalization-weighted index of domestic corporate convertible securities. To be included in the Index, bonds and preferred stocks must be convertible only to common stock.

Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S. dollar denominated, fixed-rate taxable bond market, including Treasurys, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid adjustable-rate mortgage pass-throughs), asset-backed securities and commercial mortgage-backed securities.

Barclays U.S. Government Bond Index is an unmanaged index that consists of publicly issued debt of the U.S. Treasury and government agencies.

Barclays U.S. TIPS Index includes all publicly issued, U.S. Treasury Inflation-Protected Securities that have at least one year remaining to maturity and are rated investment grade.

Barclays U.S. Government/Credit Bond Index includes investment-grade corporate debt issues as well as debt issues of U.S. government agencies and the U.S. Treasury, with maturities of at least one year.

Credit Suisse High Yield Index is an unmanaged market-weighted index that includes publicly traded bonds rated below BBB by Standard & Poor’s and below Baa by Moody’s.

Credit Suisse Leveraged Loan Index is an unmanaged index that represents tradable, senior-secured, U.S. dollar denominated non-investment-grade loans.

Dow Jones Global Utilities Index is a free float market-capitalization-weighted index that measures the performance of utility companies in developed and emerging markets.

Income Builder Composite Index consists of the MSCI World Index and the Barclays U.S. Aggregate Bond Index weighted 50%/50%, respectively.

Janus Balanced Composite Index is an unmanaged index that consists of the S&P 500® Index (55% weighted) and the Barclays U.S. Aggregate Bond Index (45% weighted).

LIBOR—London InterBank Offered Rate is a composite of interest rates at which banks borrow from one another in the London market, and it is a widely used benchmark for short-term interest rates.

Lipper Inc. is an independent monitor of fund performance. Results are based on total returns with all dividend and capital-gain distributions reinvested. More information about the Lipper peer group for an individual Portfolio can be found in the Portfolio’s Investment and Performance Comparison.

MSCI ACWI® Ex U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets, excluding the United States.

MSCI EAFE® Index is an unmanaged index that consists of international stocks representing the developed world outside of North America.

MSCI Emerging Markets Index is a free float-adjusted market-capitalization-weighted index that is designed to measure equity market performance in the global emerging markets.

MSCI World Index is a free float-adjusted market- capitalization-weighted index that is designed to measure the equity market performance of developed markets.

Russell 1000® Index is an unmanaged index that measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000® Index represents approximately 92% of the U.S. market.

Russell 1000® Growth Index is an unmanaged index that measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® Index companies with higher price- to-book ratios and higher forecasted growth values.

Russell 1000® Value Index is an unmanaged index that measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® Index companies with lower price-to-book ratios and lower expected growth values.

Russell 2000® Growth Index is an unmanaged Index that measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® Index companies with higher price-to-book ratios and higher forecasted growth values.

Russell 2500™ Index is an unmanaged index that measures the performance of the small- to mid-cap segment of the U.S. equity universe, commonly referred to as “smid” cap. The Russell 2500™ Index is a subset of the Russell 3000® Index. It includes approximately 2,500 of the smallest securities based on a combination of their market cap and current index membership.

Russell 3000® Index is an unmanaged index that measures the performance of the largest 3,000 U.S. companies.

Russell Midcap® Index is an unmanaged index that measures the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap® Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market

cap and current index membership. The Russell Midcap® Index represents approximately 31% of the total market capitalization of the Russell 1000® companies.

Russell Midcap® Value Index is an unmanaged index that measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with lower price-to-book ratios and lower forecasted growth values.

S&P 500® is a registered trademark of the McGraw-Hill Companies, Inc.

S&P 500® Index is an unmanaged index and is widely regarded as the standard index for measuring large-cap U.S. stock-market performance.

S&P North American Natural Resources Sector Index is a modified capitalization-weighted index designed as a benchmark for U.S. traded natural resource-related stocks. The natural resource sector includes mining, energy, paper and forest products, and plantation-owning companies.

| | | | |

| mainstayinvestments.com | | | M-3 | |

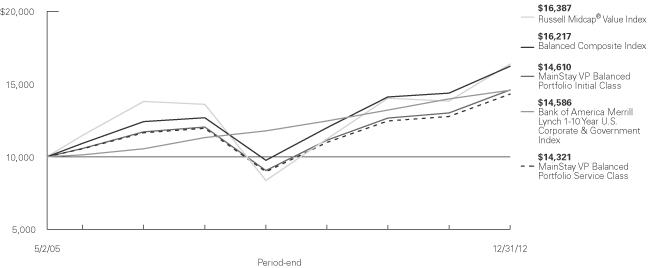

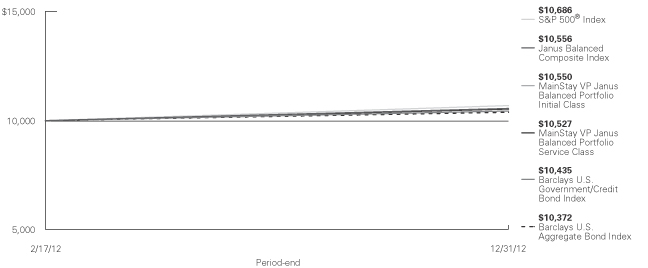

MainStay VP Balanced Portfolio

Investment and Performance Comparison1 (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The performance table and graph do not reflect any deduction of sales charges, mortality and expense charges, contract charges or administrative charges. Please refer to the Performance Summary appropriate for your policy. For performance information current to the most recent month-end, please call 800-598-2019 or visit www.newyorklife.com.

Average Annual Total Returns for the Period Ended December 31, 2012

| | | | | | | | | | |

| Class | | One Year | | Five Years | | Since Inception (5/2/05) | | Gross Expense Ratio2 | |

| Initial Class Shares | | 12.32% | | 3.94% | | 5.06% | | | 0.84% | |

| Service Class Shares | | 12.04 | | 3.68 | | 4.79 | | | 1.09 | |

| | | | | | | | | | | | |

| Benchmark Performance | | One

Year | | | Five

Years | | | Since Inception

(5/2/05) | |

Russell Midcap® Value Index3 | | | 18.51 | % | | | 3.79 | % | | | 6.65 | % |

Balanced Composite Index3 | | | 12.74 | | | | 5.04 | | | | 6.50 | |

Bank of America Merrill Lynch 1-10 Year U.S. Corporate & Government Index3 | | | 4.24 | | | | 5.19 | | | | 5.05 | |

Average Lipper Variable Products Mixed-Asset Target Allocation Growth Portfolio4 | | | 13.50 | | | | 1.93 | | | | 5.20 | |

| 1. | Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been different. For information on current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect the Portfolio’s “Total Annual Portfolio Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |

| 3. | Please refer to pages M-2 and M-3 for additional explanations and disclosure regarding the Portfolios, their benchmark indices and other indices mentioned in the reports. |

| 4. | The Average Lipper Variable Products Mixed-Asset Target Allocation Growth Portfolio is representative of portfolios that, by portfolio practice, maintain a mix of between 60%-80% equity securities, with the remainder invested in bonds, cash, and cash equivalents. Lipper Inc. is an independent monitor of fund performance. Results are based on total returns with all dividend and capital gain distributions reinvested. |

| | |

| M-4 | | MainStay VP Balanced Portfolio |

Cost in Dollars of a $1,000 Investment in MainStay VP Balanced Portfolio (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from July 1, 2012 to December 31, 2012, and the impact of those costs on your investment.

Example

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Portfolio expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other Portfolios. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from July 1, 2012, to December 31, 2012. Shares are only sold in connection with variable life and annuity contracts and the example does not reflect any contract level or transactional fees or expenses. If these costs had been included, your costs would have been higher.

This example illustrates your Portfolio’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended

December 31, 2012. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled ‘‘Expenses Paid During Period’’ to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Portfolio with the ongoing costs of investing in other Portfolios. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other Portfolios.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Share Class | | Beginning

Account

Value

7/1/12 | | | Ending Account

Value (Based

on Actual

Returns and

Expenses)

12/31/12 | | | Expenses

Paid

During

Period1 | | | Ending Account

Value (Based

on Hypothetical

5% Annualized

Return and

Actual Expenses)

12/31/12 | | | Expenses

Paid

During

Period1 | |

| | | | | |

| Initial Class Shares | | $ | 1,000.00 | | | $ | 1,061.00 | | | $ | 4.04 | | | $ | 1,021.20 | | | $ | 3.96 | |

| | | | | |

| Service Class Shares | | $ | 1,000.00 | | | $ | 1,059.70 | | | $ | 5.33 | | | $ | 1,020.00 | | | $ | 5.23 | |

| 1. | Expenses are equal to the Portfolio’s annualized expense ratio of each class (0.78% for Initial Class and 1.03% for Service Class) multiplied by the average account value over the period, divided by 366 and multiplied by 184 (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

| | | | |

| mainstayinvestments.com | | | M-5 | |

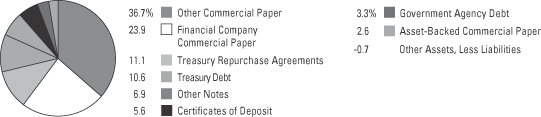

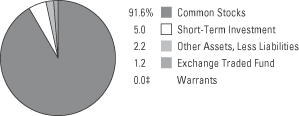

Portfolio Composition as of December 31, 2012 (Unaudited)

See Portfolio of Investments beginning on page M-10 for specific holdings within these categories.

Top Ten Holdings or Issuers Held as of December 31, 2012 (excluding short-term investments) (Unaudited)

| 1. | United States Treasury Notes, 0.125%–2.25%, due 9/30/14–11/15/22 |

| 2. | S&P Midcap 400 Index—Midcap SPDR Trust Series 1 |

| 3. | Federal Home Loan Mortgage Corporation, 0.50%–1.75%, due 11/25/14–8/1/19 |

| 4. | Federal National Mortgage Association, 0.375%–2.75%, due 3/13/14–12/28/17 |

| 5. | S&P 500 Index—SPDR Trust Series 1 |

| 9. | Marathon Petroleum Corp. |

| | |

| M-6 | | MainStay VP Balanced Portfolio |

Portfolio Management Discussion and Analysis (Unaudited)

Answers to the questions reflect the views of portfolio managers Jae S. Yoon, CFA, Thomas J. Girard, Donald F. Serek, CFA, and George S. Cherpelis of New York Life Investments,1 the Portfolio’s Manager, and Harvey J. Fram, CFA, of Madison Square Investors LLC,2 the Portfolio’s Subadvisor.

��

How did MainStay VP Balanced Portfolio perform relative to its peers and its benchmarks during the 12 months ended December 31, 2012?

For the 12 months ended December 31, 2012, MainStay VP Balanced Portfolio returned 12.32% for Initial Class shares and 12.04% for Service Class shares. Over the same period both share classes underperformed the 13.50% return of the average Lipper3 Variable Products Mixed-Asset Target Allocation Growth Portfolio, the 18.51% return of the Russell Midcap® Value Index3 and the 12.74% return of the Balanced Composite Index.3 Both share classes outperformed the 4.24% return of the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index3 for the 12 months ended December 31, 2012. The Russell Midcap® Value Index is the Portfolio’s broad-based securities-market index. The Balanced Composite Index is the secondary benchmark for the Portfolio. The Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index is an additional benchmark for the Portfolio.

Were there any changes to the Portfolio during the reporting period?

At a meeting held on December 10–12, 2012, the Portfolio’s Board of Trustees approved, effective February 28, 2013, a change in the Portfolio’s Principal Investment Strategy and the addition of Andrew Ver Planck as a portfolio manager of the Portfolio. For more information on these changes, see the Supplement dated December 17, 2012, to the Prospectus dated May 1, 2012, as supplemented.

What factors affected the Portfolio’s relative performance during the reporting period?

In the equity portion of the Portfolio, the most important factor affecting relative performance was that many stocks started 2012 at unprecedentedly low valuation levels. By the end of the year, almost all of them had not only survived but had seen their multiples expand. The best example of this is in the energy sector, where refinery stocks were particularly strong contributors. (Contributions take weightings and total returns into account.) The turnaround in the housing market also affected relative performance. The price of PulteGroup shares almost tripled, and the

equity portion of the Portfolio held an overweight position in the stock.

Throughout the majority of the year, the fixed-income portion of the Portfolio held overweight positions in corporate bonds, mortgage-backed securities, commercial mortgage-backed securities and asset-backed securities. These sectors performed extremely well during the reporting period and added to the Portfolio’s relative performance. Corporate bonds made the most significant positive contributions.

During the second quarter of 2012, the fixed-income portion of the Portfolio reduced its overall exposure to risk assets. As we reduced allocations to corporate bonds and mortgage-backed securities, we also decreased the degree to which the fixed-income portion of the Portfolio was underweight in U.S. Treasury and agency securities. We maintained an overweight position in commercial mortgage-backed securities and slightly increased the allocation to asset-backed securities in the fixed-income portion of the Portfolio. The repositioning resulted in positive performance for the reporting period, as security selection within spread4 assets was accretive to performance.

Which sectors were the strongest positive contributors to relative performance in the equity portion of the Portfolio, and which sectors were particularly weak?

In the equity portion of the Portfolio, financials, energy and materials made the strongest positive contributions to excess returns relative to the Russell Midcap® Value Index. The standout stock among financials was Bank of America, whose stock price more than doubled for the year as much of the uncertainty about the company’s mortgage-related problems dissipated. In energy, refinery stocks such as Tesoro and Phillips 66 outperformed the Index after starting the year at valuations that we felt were extremely attractive. In materials, stocks such as chemicals company LyondellBasell Industries benefited from low raw material costs and from sales growth in many areas, including automobiles and housing.

| 1. | “New York Life Investments” is a service mark used by New York Life Investment Management LLC. |

| 2. | Effective on or about January 25, 2013, Madison Square Investors LLC changed its name to Cornerstone Capital Management Holdings LLC. |

| 3. | Please refer to pages M-2 and M-3 for additional explanations and disclosure regarding the Portfolios, their benchmark indices and service providers mentioned in the reports. |

| 4. | The terms “spread” and “yield spread” may refer to the difference in yield between a security or type of security and comparable U.S. Treasury issues. The terms may also refer to the difference in yield between two specific securities or types of securities at a given time. |

| | | | |

| mainstayinvestments.com | | | M-7 | |

The sectors that made the weakest contributions to performance in the equity portion of the Portfolio were industrials, information technology and consumer staples. Poor stock selection in industrials and consumer staples hurt performance. In the equity portion of the Portfolio, information technology also detracted from relative performance, largely because of overweight positions in Hewlett-Packard and Dell.

During the reporting period, which individual stocks made the strongest positive contributions to absolute performance in the equity portion of the Portfolio and which stocks detracted the most?

In the equity portion of the Portfolio, the best contributions to the Portfolio’s absolute performance came from refiners Marathon Petroleum and Valero Energy and from financial company Bank of America. Refiners were among the stocks that started the year at extremely attractive valuations and saw their multiples expand over the year as profitability improved. Bank of America advanced as mortgage-related concerns dissipated.

Hewlett-Packard, Dell and Humana were the worst absolute performers in the equity portion of the Portfolio. Facing strong competition from tablet devices, Hewlett-Packard and Dell continued to see PC sales decline. Humana came under pressure after the Patient Protection and Affordable Care Act, commonly known as Obamacare, was upheld by the Supreme Court.

Did the equity portion of the Portfolio make any significant purchases or sales during the reporting period?

Among the stocks the equity portion of the Portfolio purchased in 2012, two household durables companies—home builder PulteGroup and home appliance manufacturer Whirlpool—were noteworthy. Both stocks benefited from the recovery in the U.S. housing market.

During 2012, the equity portion of the Portfolio reduced its weighing in mortgage finance real estate investment trust (REIT) Annaly Capital Management and steel producer Nucor. Despite having a high dividend yield, Annaly Capital Management had become relatively expensive on a cash flow basis as demand for high-yield stocks rose in 2011. Nucor’s stock price weakened as steel prices declined.

How did sector weightings change in the equity portion of the Portfolio during the reporting period?

The equity portion of the Portfolio increased its sector weightings relative to the Russell Midcap® Value Index in consumer staples and financials. Despite the increase in financials, the equity portion of the Portfolio was underweight relative to the Index. During the reporting period, we decreased relative exposure to the energy and information technology sectors in the equity portion of the Portfolio. It should be noted that sector weightings in the Russell Midcap® Value Index can change substantially from year to year when the Index is reconstituted. In 2012, the Index weighting in energy saw a substantial increase, and the Index weighting in consumer staples saw a substantial decrease.

How was the equity portion of the Portfolio positioned at the end of the reporting period?

As of December 31, 2012, the sectors in the equity portion of the Portfolio that were most substantially overweight relative to the Russell Midcap® Value Index were health care and consumer staples. As of the same date, the most substantially underweight sectors in the equity portion of the Portfolio were financials and utilities. We typically seek to keep sector deviations from the Russell Midcap® Value Index at moderate levels. As of December 31, 2012, however, the deviation in financials was fairly large.

What was the duration strategy of the fixed-income portion of the Portfolio during the reporting period?

The duration of the fixed-income portion of the Portfolio varied over the course of the reporting period. In general, the duration was close to that of the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index. There were, however, two instances when the duration of the fixed-income portion of the Portfolio was modestly shorter or longer. The first instance was during the first half of the reporting period, when the duration of the fixed-income portion of the Portfolio was shorter than that of the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index. The second instance was in the second half of the reporting period, when the duration of the fixed-income portion of the Portfolio was longer than that of this Index. Overall duration positioning had a modestly negative impact on the Portfolio’s performance during the reporting period.

| | |

| M-8 | | MainStay VP Balanced Portfolio |

What specific factors, risks or market forces prompted significant decisions for the fixed-income portion of the Portfolio during the reporting period?

There were three periods where specific factors, risks and market forces prompted asset allocation decisions for the Portfolio during the reporting period. The Portfolio started the reporting period with an overweight position in spread assets. This positioning was adopted because we anticipated that funding pressures in Europe would abate and the U.S. economy would improve. This allocation decision contributed positively to the Portfolio’s performance. Toward the start of the second quarter of 2012, however, an upward swing in global economic risks and rising systemic risk from Europe prompted us to reduce spread-asset exposure to levels that were more neutral. This allocation decision was defensive, and the Portfolio’s performance during this portion of the reporting period was neutral to the benchmark. In the third quarter of 2012, aggressive central bank actions led us to once again view spread assets favorably. We increased the allocation to spread assets, maintaining overweight positions in them until the end of the reporting period. These allocation decisions were accretive to performance, as spread assets generated positive excess returns.

During the reporting period, which market segments were the strongest contributors to performance in the fixed-income portion of the Portfolio and which market segments were particularly weak?

During the reporting period, overweight positions relative to the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index in corporate bonds, asset-backed securities, mortgage-backed securities and commercial mortgage-backed securities were all strong contributors to performance in the fixed-income portion of the Portfolio. Within the fixed-income portion of the Portfolio, corporate bonds—specifically overweight positions in financials, industrials and utilities—made the most substantial contribution to performance.

In the fixed-income portion of the Portfolio, an underweight position relative to the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index in U.S. Treasury securities was the most substantial detractor from performance. The negative impact of U.S. Treasury securities, however, was more than offset by the returns on spread assets. Duration positioning had a modestly negatively impact on performance.

Did the fixed-income portion of the Portfolio make any significant purchases or sales during the reporting period?

Outside of its normal operating parameters, the fixed-income portion of the Portfolio did not make any significant purchases or sales.

During the reporting period, how did sector weightings change in the fixed-income portion of the Portfolio?

As previously noted, we modified exposure to spread assets throughout the year in response to risk factors and perceived reward potential. We funded overweight positions in spread assets by lowering allocations to U.S. Treasury and agency securities.

How was the fixed-income portion of the Portfolio positioned at the end of the reporting period?

As of December 31, 2012, the fixed-income portion of the Portfolio held overweight positions relative to the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index in spread assets. The largest overweight was in U.S. corporate bonds, followed by mortgage-backed securities. In addition, the fixed-income portion of the Portfolio held overweight positions relative to this Index in asset-backed securities and commercial mortgage-backed securities. As of the same date, the fixed-income portion of the Portfolio held an underweight position relative to this Index in U.S. Treasurys. As of December 31, 2012, the duration of the fixed-income portion of the Portfolio was neutral in relation to the Bank of America Merrill Lynch 1–10 Year U.S. Corporate & Government Index.

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

Not all MainStay VP Portfolios and/or share classes are available under all policies.

| | | | |

| mainstayinvestments.com | | | M-9 | |

Portfolio of Investments December 31, 2012

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Long-Term Bonds 34.3%†

Asset-Backed Securities 1.0% | |

Automobile 0.6% | |

Ally Auto Receivables Trust

Series 2012-1, Class A3

0.93%, due 2/16/16 | | $ | 90,000 | | | $ | 90,561 | |

Ford Credit Auto Owner Trust

Series 2012-A, Class A3

0.84%, due 8/15/16 | | | 150,000 | | | | 150,783 | |

Huntington Auto Trust

Series 2012-2, Class A3

0.51%, due 4/17/17 | | | 200,000 | | | | 199,925 | |

Hyundai Auto Receivables Trust

Series 2012-A, Class A3

0.72%, due 3/15/16 | | | 156,000 | | | | 156,541 | |

Mercedes-Benz Auto Receivables Trust | | | | | | | | |

Series 2012-1, Class A3

0.47%, due 10/17/16 | | | 300,000 | | | | 299,885 | |

Series 2009-1, Class A3

1.67%, due 1/15/14 | | | 11,030 | | | | 11,040 | |

USAA Auto Owner Trust

Series 2012-1, Class A3

0.43%, due 8/15/16 | | | 100,000 | | | | 99,928 | |

Volkswagen Auto Loan Enhanced Trust

Series 2012-1, Class A3

0.85%, due 8/22/16 | | | 150,000 | | | | 150,879 | |

World Omni Automobile Lease Securitization Trust

Series 2012-A, Class A3

0.93%, due 11/16/15 | | | 100,000 | | | | 100,626 | |

| | | | | | | | |

| | | | | | | 1,260,168 | |

| | | | | | | | |

Credit Cards 0.1% | |

Discover Card Master Trust

Series 2012-A1, Class A1

0.81%, due 8/15/17 | | | 86,000 | | | | 86,649 | |

| | | | | | | | |

|

Other ABS 0.3% | |

CNH Equipment Trust

Series 2012-C, Class A3

0.57%, due 12/15/17 | | | 200,000 | | | | 200,031 | |

John Deere Owner Trust | | | | | | | | |

Series 2012-B, Class A3

0.53%, due 7/15/16 | | | 200,000 | | | | 200,146 | |

Series 2012-A, Class A3

0.75%, due 3/15/16 | | | 200,000 | | | | 200,689 | |

| | | | | | | | |

| | | | | | | 600,866 | |

| | | | | | | | |

Total Asset-Backed Securities

(Cost $1,942,909) | | | | | | | 1,947,683 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Corporate Bonds 11.6% | |

Aerospace & Defense 0.4% | |

General Dynamics Corp. | | | | | | | | |

2.25%, due 7/15/16 | | $ | 50,000 | | | $ | 52,403 | |

2.25%, due 11/15/22 | | | 250,000 | | | | 244,646 | |

Northrop Grumman Corp.

1.85%, due 11/15/15 | | | 100,000 | | | | 102,679 | |

United Technologies Corp.

1.80%, due 6/1/17 | | | 300,000 | | | | 308,808 | |

| | | | | | | | |

| | | | | | | 708,536 | |

| | | | | | | | |

Auto Manufacturers 0.1% | |

Daimler Finance North America LLC

3.875%, due 9/15/21 (a) | | | 150,000 | | | | 161,816 | |

| | | | | | | | |

|

Banks 2.2% | |

¨Bank of America Corp. | | | | | | | | |

3.70%, due 9/1/15 | | | 50,000 | | | | 52,857 | |

4.50%, due 4/1/15 | | | 450,000 | | | | 479,667 | |

5.65%, due 5/1/18 | | | 375,000 | | | | 436,291 | |

BB&T Corp.

1.45%, due 1/12/18 | | | 100,000 | | | | 100,447 | |

Capital One Financial Corp. | | | | | | | | |

1.00%, due 11/6/15 | | | 200,000 | | | | 199,324 | |

2.15%, due 3/23/15 | | | 150,000 | | | | 153,111 | |

¨Citigroup, Inc. | | | | | | | | |

4.587%, due 12/15/15 | | | 160,000 | | | | 174,680 | |

5.375%, due 8/9/20 | | | 100,000 | | | | 117,845 | |

5.50%, due 10/15/14 | | | 450,000 | | | | 482,778 | |

6.00%, due 8/15/17 | | | 100,000 | | | | 117,815 | |

6.01%, due 1/15/15 | | | 25,000 | | | | 27,318 | |

Goldman Sachs Group, Inc. (The) | | | | | | | | |

3.625%, due 2/7/16 | | | 75,000 | | | | 79,389 | |

5.375%, due 3/15/20 | | | 125,000 | | | | 143,254 | |

6.00%, due 6/15/20 | | | 100,000 | | | | 118,821 | |

HSBC USA, Inc.

1.625%, due 1/16/18 | | | 250,000 | | | | 250,227 | |

¨JPMorgan Chase & Co. | | | | | | | | |

3.25%, due 9/23/22 | | | 225,000 | | | | 231,701 | |

4.35%, due 8/15/21 | | | 400,000 | | | | 447,295 | |

KeyCorp

6.50%, due 5/14/13 | | | 275,000 | | | | 280,902 | |

Morgan Stanley

5.50%, due 1/26/20 | | | 100,000 | | | | 112,179 | |

Wachovia Bank

4.80%, due 11/1/14 | | | 440,000 | | | | 472,276 | |

| | | | | | | | |

| | | | | | | 4,478,177 | |

| | | | | | | | |

| † | Percentages indicated are based on Portfolio net assets. |

| ¨ | | Among the Portfolio’s 10 largest holdings or issuers held, as of December 31, 2012, excluding short-term investments. May be subject to change daily. |

| | | | |

| M-10 | | MainStay VP Balanced Portfolio | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Corporate Bonds (continued) | |

Beverages 0.3% | |

Anheuser-Busch InBev Worldwide, Inc. | | | | | | | | |

1.375%, due 7/15/17 | | $ | 250,000 | | | $ | 252,633 | |

4.375%, due 2/15/21 | | | 75,000 | | | | 87,269 | |

SABMiller Holdings, Inc.

2.45%, due 1/15/17 (a) | | | 250,000 | | | | 260,599 | |

| | | | | | | | |

| | | | | | | 600,501 | |

| | | | | | | | |

Building Materials 0.1% | |

CRH America, Inc.

4.125%, due 1/15/16 | | | 100,000 | | | | 104,120 | |

| | | | | | | | |

|

Chemicals 0.4% | |

Dow Chemical Co. (The) | | | | | | | | |

3.00%, due 11/15/22 | | | 200,000 | | | | 199,555 | |

5.70%, due 5/15/18 | | | 150,000 | | | | 178,391 | |

Eastman Chemical Co.

2.40%, due 6/1/17 | | | 75,000 | | | | 77,493 | |

Ecolab, Inc. | | | | | | | | |

1.45%, due 12/8/17 | | | 125,000 | | | | 124,432 | |

4.35%, due 12/8/21 | | | 125,000 | | | | 139,523 | |

| | | | | | | | |

| | | | | | | 719,394 | |

| | | | | | | | |

Commercial Services 0.1% | |

Western Union Co. (The)

2.875%, due 12/10/17 | | | 150,000 | | | | 148,627 | |

| | | | | | | | |

|

Computers 0.3% | |

Hewlett-Packard Co. | | | | | | | | |

2.35%, due 3/15/15 | | | 425,000 | | | | 426,893 | |

4.65%, due 12/9/21 | | | 125,000 | | | | 125,486 | |

| | | | | | | | |

| | | | | | | 552,379 | |

| | | | | | | | |

Cosmetics & Personal Care 0.0%‡ | |

Procter & Gamble Co. (The)

1.45%, due 8/15/16 | | | 50,000 | | | | 50,948 | |

| | | | | | | | |

|

Diversified Financial Services 0.3% | |

General Electric Capital Corp. | | | | | | | | |

2.10%, due 12/11/19 | | | 175,000 | | | | 175,495 | |

2.30%, due 4/27/17 | | | 250,000 | | | | 259,220 | |

6.00%, due 8/7/19 | | | 225,000 | | | | 273,727 | |

| | | | | | | | |

| | | | | | | 708,442 | |

| | | | | | | | |

Electric 1.3% | |

American Electric Power Co., Inc.

1.65%, due 12/15/17 | | | 200,000 | | | | 200,701 | |

Commonwealth Edison Co.

1.95%, due 9/1/16 | | | 100,000 | | | | 103,165 | |

Consumers Energy Co.

2.85%, due 5/15/22 | | | 50,000 | | | | 51,681 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Electric (continued) | |

Entergy Louisiana LLC | | | | | | | | |

1.875%, due 12/15/14 | | $ | 25,000 | | | $ | 25,543 | |

3.30%, due 12/1/22 | | | 50,000 | | | | 50,058 | |

Entergy Mississippi, Inc.

3.10%, due 7/1/23 | | | 50,000 | | | | 49,354 | |

Great Plains Energy, Inc. | | | | | | | | |

2.75%, due 8/15/13 | | | 250,000 | | | | 252,592 | |

4.85%, due 6/1/21 | | | 55,000 | | | | 60,595 | |

5.292%, due 6/15/22 (b) | | | 45,000 | | | | 50,569 | |

Kansas City Power & Light Co.

7.15%, due 4/1/19 | | | 250,000 | | | | 319,538 | |

NextEra Energy Capital Holdings, Inc.

1.20%, due 6/1/15 | | | 100,000 | | | | 100,711 | |

Niagara Mohawk Power Corp.

2.721%, due 11/28/22 (a) | | | 100,000 | | | | 99,439 | |

Nisource Finance Corp.

4.45%, due 12/1/21 | | | 100,000 | | | | 109,502 | |

NSTAR Electric Co.

2.375%, due 10/15/22 | | | 150,000 | | | | 149,076 | |

Pepco Holdings, Inc.

2.70%, due 10/1/15 | | | 100,000 | | | | 103,512 | |

PPL Capital Funding, Inc. | | | | | | | | |

3.50%, due 12/1/22 | | | 100,000 | | | | 101,790 | |

4.20%, due 6/15/22 | | | 100,000 | | | | 107,540 | |

Progress Energy, Inc.

6.05%, due 3/15/14 | | | 250,000 | | | | 265,326 | |

Westar Energy, Inc.

6.00%, due 7/1/14 | | | 300,000 | | | | 321,260 | |

| | | | | | | | |

| | | | | | | 2,521,952 | |

| | | | | | | | |

Electronics 0.2% | |

Thermo Fisher Scientific, Inc.

1.85%, due 1/15/18 | | | 400,000 | | | | 405,477 | |

| | | | | | | | |

|

Engineering & Construction 0.1% | |

ABB Finance USA, Inc.

2.875%, due 5/8/22 | | | 100,000 | | | | 102,384 | |

| | | | | | | | |

|

Finance—Auto Loans 0.1% | |

Ford Motor Credit Co. LLC

4.25%, due 9/20/22 | | | 200,000 | | | | 211,477 | |

| | | | | | | | |

|

Finance—Commercial 0.1% | |

Caterpillar Financial Services Corp.

2.05%, due 8/1/16 | | | 225,000 | | | | 232,912 | |

| | | | | | | | |

|

Finance—Consumer Loans 0.2% | |

John Deere Capital Corp. | | | | | | | | |

1.70%, due 1/15/20 | | | 200,000 | | | | 197,952 | |

2.80%, due 9/18/17 | | | 50,000 | | | | 53,376 | |

5.75%, due 9/10/18 | | | 75,000 | | | | 91,458 | |

| | | | | | | | |

| | | | | | | 342,786 | |

| | | | | | | | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | M-11 | |

Portfolio of Investments December 31, 2012 (continued)

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Corporate Bonds (continued) | |

Finance—Credit Card 0.1% | |

American Express Co.

5.50%, due 9/12/16 | | $ | 250,000 | | | $ | 285,815 | |

| | | | | | | | |

|

Finance—Leasing Companies 0.0%‡ | |

Boeing Capital Corp.

2.90%, due 8/15/18 | | | 50,000 | | | | 53,908 | |

| | | | | | | | |

|

Finance—Other Services 0.2% | |

Aon Corp.

3.125%, due 5/27/16 | | | 75,000 | | | | 78,958 | |

National Rural Utilities Cooperative Finance Corp. | | | | | | | | |

1.90%, due 11/1/15 | | | 100,000 | | | | 103,152 | |

3.05%, due 2/15/22 | | | 100,000 | | | | 104,907 | |

5.45%, due 4/10/17 | | | 100,000 | | | | 117,152 | |

| | | | | | | | |

| | | | | | | 404,169 | |

| | | | | | | | |

Food 0.4% | |

General Mills, Inc.

3.15%, due 12/15/21 | | | 200,000 | | | | 209,058 | |

Ingredion, Inc.

1.80%, due 9/25/17 | | | 75,000 | | | | 74,507 | |

Kellogg Co.

1.75%, due 5/17/17 | | | 75,000 | | | | 76,218 | |

Mondelez International, Inc.

4.125%, due 2/9/16 | | | 375,000 | | | | 408,564 | |

Unilever Capital Corp.

0.85%, due 8/2/17 | | | 100,000 | | | | 98,992 | |

| | | | | | | | |

| | | | | | | 867,339 | |

| | | | | | | | |

Forest Products & Paper 0.1% | |

International Paper Co.

4.75%, due 2/15/22 | | | 150,000 | | | | 169,730 | |

| | | | | | | | |

|

Gas 0.0%‡ | |

Sempra Energy

2.30%, due 4/1/17 | | | 75,000 | | | | 77,878 | |

| | | | | | | | |

|

Hand & Machine Tools 0.0%‡ | |

Stanley Black & Decker, Inc.

3.40%, due 12/1/21 | | | 50,000 | | | | 52,192 | |

| | | | | | | | |

|

Health Care—Products 0.2% | |

Becton Dickinson and Co.

3.125%, due 11/8/21 | | | 200,000 | | | | 213,699 | |

CR Bard, Inc.

1.375%, due 1/15/18 | | | 75,000 | | | | 75,396 | |

Medtronic, Inc.

3.125%, due 3/15/22 | | | 75,000 | | | | 79,630 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Health Care—Products (continued) | |

Zimmer Holdings, Inc.

1.40%, due 11/30/14 | | $ | 100,000 | | | $ | 100,752 | |

| | | | | | | | |

| | | | | | | 469,477 | |

| | | | | | | | |

Health Care—Services 0.4% | |

Aetna, Inc.

1.75%, due 5/15/17 | | | 50,000 | | | | 50,754 | |

Laboratory Corp. of America Holdings

2.20%, due 8/23/17 | | | 100,000 | | | | 102,644 | |

Roche Holdings, Inc.

5.00%, due 3/1/14 (a) | | | 291,000 | | | | 305,683 | |

UnitedHealth Group, Inc.

2.75%, due 2/15/23 | | | 100,000 | | | | 100,900 | |

WellPoint, Inc.

1.875%, due 1/15/18 | | | 150,000 | | | | 151,863 | |

| | | | | | | | |

| | | | | | | 711,844 | |

| | | | | | | | |

Insurance 0.4% | |

MetLife, Inc.

1.756%, due 12/15/17 | | | 150,000 | | | | 152,361 | |

Metropolitan Life Global Funding I | | | | | | | | |

2.00%, due 1/9/15 (a) | | | 175,000 | | | | 179,722 | |

5.125%, due 6/10/14 (a) | | | 225,000 | | | | 239,198 | |

Principal Financial Group, Inc.

8.875%, due 5/15/19 | | | 90,000 | | | | 120,766 | |

Prudential Financial, Inc.

4.50%, due 11/16/21 | | | 100,000 | | | | 112,464 | |

| | | | | | | | |

| | | | | | | 804,511 | |

| | | | | | | | |

Machinery—Diversified 0.1% | |

Roper Industries, Inc.

6.625%, due 8/15/13 | | | 150,000 | | | | 155,342 | |

| | | | | | | | |

|

Media 0.4% | |

COX Communications, Inc. | | | | | | | | |

3.25%, due 12/15/22 (a) | | | 100,000 | | | | 103,126 | |

5.45%, due 12/15/14 | | | 64,000 | | | | 69,797 | |

DIRECTV Holdings LLC / DIRECTV Financing Co., Inc.

3.50%, due 3/1/16 | | | 75,000 | | | | 79,456 | |

NBC Universal Media LLC

5.15%, due 4/30/20 | | | 125,000 | | | | 148,182 | |

Reed Elsevier Capital, Inc.

7.75%, due 1/15/14 | | | 100,000 | | | | 107,082 | |

Time Warner Cable, Inc.

6.75%, due 7/1/18 | | | 100,000 | | | | 124,918 | |

Viacom, Inc.

1.25%, due 2/27/15 | | | 100,000 | | | | 100,976 | |

| | | | | | | | |

| | | | | | | 733,537 | |

| | | | | | | | |

Metal Fabricate & Hardware 0.0%‡ | |

Precision Castparts Corp.

2.50%, due 1/15/23 | | | 100,000 | | | | 100,641 | |

| | | | | | | | |

| | | | |

| M-12 | | MainStay VP Balanced Portfolio | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Corporate Bonds (continued) | |

Miscellaneous—Manufacturing 0.1% | |

Eaton Corp.

1.50%, due 11/2/17 (a) | | $ | 150,000 | | | $ | 150,307 | |

General Electric Co.

2.70%, due 10/9/22 | | | 50,000 | | | | 50,965 | |

| | | | | | | | |

| | | | | | | 201,272 | |

| | | | | | | | |

Oil & Gas 0.2% | |

Marathon Oil Corp.

0.90%, due 11/1/15 | | | 275,000 | | | | 275,222 | |

Phillips 66

2.95%, due 5/1/17 (a) | | | 125,000 | | | | 132,479 | |

| | | | | | | | |

| | | | | | | 407,701 | |

| | | | | | | | |

Oil & Gas Services 0.0%‡ | |

Cameron International Corp.

1.60%, due 4/30/15 | | | 50,000 | | | | 50,513 | |

| | | | | | | | |

|

Packaging & Containers 0.1% | |

Bemis Co., Inc.

5.65%, due 8/1/14 | | | 215,000 | | | | 230,149 | |

| | | | | | | | |

|

Pharmaceuticals 0.4% | |

AbbVie, Inc.

1.75%, due 11/6/17 (a) | | | 300,000 | | | | 303,263 | |

Cardinal Health, Inc.

1.90%, due 6/15/17 | | | 50,000 | | | | 50,931 | |

Express Scripts Holding Co.

2.10%, due 2/12/15 (a) | | | 250,000 | | | | 254,664 | |

Merck & Co., Inc.

2.40%, due 9/15/22 | | | 150,000 | | | | 150,049 | |

Watson Pharmaceuticals, Inc.

3.25%, due 10/1/22 | | | 125,000 | | | | 127,606 | |

| | | | | | | | |

| | | | | | | 886,513 | |

| | | | | | | | |

Pipelines 0.5% | |

Energy Transfer Partners, L.P.

5.20%, due 2/1/22 | | | 175,000 | | | | 199,625 | |

Enterprise Products Operating LLC

1.25%, due 8/13/15 | | | 100,000 | | | | 100,614 | |

ONEOK Partners, L.P.

2.00%, due 10/1/17 | | | 50,000 | | | | 50,416 | |

Plains All American Pipeline, L.P. / PAA Finance Corp.

8.75%, due 5/1/19 | | | 200,000 | | | | 272,082 | |

Texas Eastern Transmission, L.P.

2.80%, due 10/15/22 (a) | | | 175,000 | | | | 175,056 | |

Williams Cos., Inc. (The)

3.70%, due 1/15/23 | | | 150,000 | | | | 151,298 | |

| | | | | | | | |

| | | | | | | 949,091 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Real Estate 0.1% | |

WEA Finance LLC / WT Finance Aust Pty, Ltd.

5.75%, due 9/2/15 (a) | | $ | 100,000 | | | $ | 111,646 | |

| | | | | | | | |

|

Real Estate Investment Trusts 0.8% | |

Brandywine Operating Partnership, L.P.

5.70%, due 5/1/17 | | | 300,000 | | | | 339,714 | |

DDR Corp.

4.75%, due 4/15/18 | | | 200,000 | | | | 221,655 | |

Hospitality Properties Trust

6.30%, due 6/15/16 | | | 170,000 | | | | 187,473 | |

National Retail Properties, Inc.

6.25%, due 6/15/14 | | | 200,000 | | | | 213,779 | |

Prologis, L.P.

6.625%, due 5/15/18 | | | 325,000 | | | | 392,543 | |

Realty Income Corp.

2.00%, due 1/31/18 | | | 150,000 | | | | 149,875 | |

Simon Property Group, L.P.

2.75%, due 2/1/23 | | | 150,000 | | | | 149,916 | |

| | | | | | | | |

| | | | | | | 1,654,955 | |

| | | | | | | | |

Retail 0.1% | |

Costco Wholesale Corp.

1.70%, due 12/15/19 | | | 150,000 | | | | 151,021 | |

Home Depot, Inc. (The)

4.40%, due 4/1/21 | | | 125,000 | | | | 147,424 | |

| | | | | | | | |

| | | | | | | 298,445 | |

| | | | | | | | |

Semiconductors 0.1% | |

Samsung Electronics America, Inc.

1.75%, due 4/10/17 (a) | | | 200,000 | | | | 202,350 | |

| | | | | | | | |

|

Special Purpose Entity 0.0%‡ | |

MassMutual Global Funding II

2.50%, due 10/17/22 (a) | | | 100,000 | | | | 98,322 | |

| | | | | | | | |

|

Telecommunications 0.6% | |

AT&T, Inc. | | | | | | | | |

1.70%, due 6/1/17 | | | 100,000 | | | | 101,425 | |

2.40%, due 8/15/16 | | | 200,000 | | | | 208,714 | |

2.625%, due 12/1/22 | | | 150,000 | | | | 150,247 | |

Cellco Partnership / Verizon Wireless Capital LLC

5.55%, due 2/1/14 | | | 300,000 | | | | 314,923 | |

Qwest Corp.

6.75%, due 12/1/21 | | | 75,000 | | | | 87,898 | |

Verizon Communications, Inc. | | | | | | | | |

2.00%, due 11/1/16 | | | 100,000 | | | | 103,493 | |

2.45%, due 11/1/22 | | | 175,000 | | | | 175,058 | |

| | | | | | | | |

| | | | | | | 1,141,758 | |

| | | | | | | | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | M-13 | |

Portfolio of Investments December 31, 2012 (continued)

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Corporate Bonds (continued) | |

Transportation 0.1% | |

Burlington Northern Santa Fe LLC

4.70%, due 10/1/19 | | $ | 125,000 | | | $ | 144,095 | |

| | | | | | | | |

Total Corporate Bonds

(Cost $22,282,574) | | | | | | | 23,313,121 | |

| | | | | | | | |

| | |

| Foreign Government Bonds 0.4% | | | | | | | | |

Regional (State & Province) 0.4% | |

Province of Manitoba Canada

2.625%, due 7/15/15 | | | 75,000 | | | | 79,050 | |

Province of Ontario

1.10%, due 10/25/17 | | | 425,000 | | | | 425,468 | |

Province of Quebec

3.50%, due 7/29/20 | | | 200,000 | | | | 222,140 | |

| | | | | | | | |

| | | | | | | 726,658 | |

| | | | | | | | |

Sovereign 0.0%‡ | |

Poland Government International Bond

5.00%, due 3/23/22 | | | 50,000 | | | | 59,050 | |

| | | | | | | | |

Total Foreign Government Bonds

(Cost $772,749) | | | | | | | 785,708 | |

| | | | | | | | |

|

| Mortgage-Backed Securities 0.6% | |

Commercial Mortgage Loans (Collateralized Mortgage Obligations) 0.4% | |

JP Morgan Chase Commercial Mortgage Securities Corp. | | | | | | | | |

Series 2012-C6, Class A2

2.206%, due 5/15/45 | | | 100,000 | | | | 104,631 | |

Series 2006-CB15, Class A4

5.814%, due 6/12/43 (c) | | | 150,000 | | | | 171,165 | |

LB-UBS Commercial Mortgage Trust

Series 2006-C7, Class A3

5.347%, due 11/15/38 | | | 200,000 | | | | 229,831 | |

Morgan Stanley Capital I, Inc.

Series 2007-T25, Class A3

5.514%, due 11/12/49 (c) | | | 200,000 | | | | 231,995 | |

| | | | | | | | |

| | | | | | | 737,622 | |

| | | | | | | | |

Whole Loan Collateral (Collateralized Mortgage Obligations) 0.2% | |

Fosse Master Issuer PLC

Series 2011-1A, Class A5

1.825%, due 10/18/54 (a)(c) | | | 200,000 | | | | 206,320 | |

Holmes Master Issuer PLC

Series Reg S

1.99%, due 10/15/54 (a)(c) | | | 175,000 | | | | 179,170 | |

| | | | | | | | |

| | | | | | | 385,490 | |

| | | | | | | | |

Total Mortgage-Backed Securities

(Cost $1,093,305) | | | | | | | 1,123,112 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| U.S. Government & Federal Agencies 16.7% | |

Federal Home Loan Bank 0.1% | |

1.375%, due 5/28/14 | | $ | 300,000 | | | $ | 305,130 | |

| | | | | | | | |

|

¨Federal Home Loan Mortgage Corporation 1.4% | |

0.50%, due 4/17/15 | | | 550,000 | | | | 552,248 | |

0.50%, due 9/25/15 | | | 100,000 | | | | 100,070 | |

0.53%, due 11/20/15 | | | 150,000 | | | | 150,183 | |

0.55%, due 2/27/15 | | | 220,000 | | | | 220,152 | |

0.60%, due 5/22/15 | | | 200,000 | | | | 200,301 | |

0.75%, due 11/25/14 | | | 480,000 | | | | 484,357 | |

0.75%, due 1/12/18 | | | 200,000 | | | | 198,645 | |

1.00%, due 9/27/17 | | | 75,000 | | | | 75,243 | |

1.25%, due 8/1/19 | | | 200,000 | | | | 200,277 | |

1.75%, due 9/10/15 | | | 300,000 | | | | 310,991 | |

1.75%, due 5/30/19 | | | 325,000 | | | | 336,200 | |

| | | | | | | | |

| | | | | | | 2,828,667 | |

| | | | | | | | |

Federal Home Loan Mortgage Corporation

(Mortgage Pass-Through Security) 0.2% | |

3.50%, due 1/1/42 TBA (d) | | | 300,000 | | | | 319,008 | |

| | | | | | | | |

|

¨Federal National Mortgage Association 1.1% | |

0.375%, due 3/16/15 | | | 400,000 | | | | 400,532 | |

0.75%, due 12/19/14 | | | 400,000 | | | | 403,549 | |

0.875%, due 12/20/17 | | | 200,000 | | | | 200,391 | |

1.00%, due 12/28/17 | | | 100,000 | | | | 99,873 | |

1.25%, due 1/30/17 | | | 230,000 | | | | 235,788 | |

1.375%, due 11/15/16 | | | 850,000 | | | | 875,661 | |

2.75%, due 3/13/14 | | | 100,000 | | | | 103,038 | |

| | | | | | | | |

| | | | | | | 2,318,832 | |

| | | | | | | | |

Federal National Mortgage Association

(Mortgage Pass-Through Security) 0.3% | |

3.50%, due 1/1/42 TBA (d) | | | 500,000 | | | | 533,066 | |

| | | | | | | | |

|

¨United States Treasury Notes 13.6% | |

0.125%, due 12/31/14 | | | 700,000 | | | | 698,250 | |

0.25%, due 9/30/14 | | | 1,875,000 | | | | 1,875,439 | |

0.25%, due 10/31/14 | | | 720,000 | | | | 720,169 | |

0.25%, due 5/15/15 | | | 1,460,000 | | | | 1,458,175 | |

0.25%, due 8/15/15 | | | 1,010,000 | | | | 1,008,185 | |

0.25%, due 9/15/15 | | | 1,375,000 | | | | 1,371,992 | |

0.25%, due 12/15/15 | | | 1,050,000 | | | | 1,046,883 | |

0.375%, due 4/15/15 | | | 2,910,000 | | | | 2,915,229 | |

0.375%, due 11/15/15 | | | 1,520,000 | | | | 1,521,426 | |

0.50%, due 7/31/17 | | | 200,000 | | | | 198,797 | |

0.625%, due 11/30/17 | | | 1,010,000 | | | | 1,006,607 | |

0.75%, due 10/31/17 | | | 1,820,000 | | | | 1,825,971 | |

0.75%, due 12/31/17 | | | 1,400,000 | | | | 1,402,297 | |

1.00%, due 6/30/19 | | | 1,200,000 | | | | 1,196,437 | |

1.00%, due 8/31/19 | | | 200,000 | | | | 198,828 | |

| | | | |

| M-14 | | MainStay VP Balanced Portfolio | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| U.S. Government & Federal Agencies (continued) | |

¨United States Treasury Notes (continued) | |

1.00%, due 9/30/19 | | $ | 275,000 | | | $ | 273,109 | |

1.00%, due 11/30/19 | | | 350,000 | | | | 346,609 | |

1.125%, due 5/31/19 | | | 500,000 | | | | 503,164 | |

1.375%, due 9/30/18 | | | 840,000 | | | | 863,494 | |

1.50%, due 8/31/18 | | | 2,600,000 | | | | 2,692,017 | |

1.625%, due 11/15/22 | | | 400,000 | | | | 395,625 | |

2.25%, due 7/31/18 | | | 3,600,000 | | | | 3,877,592 | |

| | | | | | | | |

| | | | | | | 27,396,295 | |

| | | | | | | | |

Total U.S. Government & Federal Agencies

(Cost $33,280,056) | | | | | | | 33,700,998 | |

| | | | | | | | |

|

| Yankee Bonds 4.0% (e) | |

Aerospace & Defense 0.1% | |

BAE Systems PLC

3.50%, due 10/11/16 (a) | | | 100,000 | | | | 105,437 | |

| �� | | | | | | | |

|

Auto Manufacturers 0.1% | |

Volkswagen International Finance N.V.

1.625%, due 3/22/15 (a) | | | 100,000 | | | | 101,364 | |

| | | | | | | | |

|

Banks 1.6% | |

Bank of Montreal

1.95%, due 1/30/18 (a) | | | 325,000 | | | | 338,520 | |

Bank of Nova Scotia

1.95%, due 1/30/17 (a) | | | 250,000 | | | | 260,400 | |

BNP Paribas S.A.

2.375%, due 9/14/17 | | | 150,000 | | | | 152,152 | |

Commonwealth Bank of Australia

1.95%, due 3/16/15 | | | 250,000 | | | | 256,535 | |

Cooperatieve Centrale Raiffeisen-Boerenleenbank B.A. | | | | | | | | |

3.375%, due 1/19/17 | | | 200,000 | | | | 214,857 | |

3.875%, due 2/8/22 | | | 100,000 | | | | 107,613 | |

3.95%, due 11/9/22 | | | 250,000 | | | | 256,009 | |

HSBC Bank PLC

3.50%, due 6/28/15 (a) | | | 250,000 | | | | 265,175 | |

Korea Development Bank

3.875%, due 5/4/17 | | | 200,000 | | | | 216,224 | |

Landwirtschaftliche Rentenbank

2.50%, due 2/15/16 | | | 100,000 | | | | 105,870 | |

Royal Bank of Scotland Group PLC

2.55%, due 9/18/15 | | | 200,000 | | | | 204,682 | |

Societe Generale S.A.

2.75%, due 10/12/17 | | | 250,000 | | | | 254,306 | |

Svenska Handelsbanken AB

2.875%, due 4/4/17 | | | 250,000 | | | | 264,150 | |

UBS A.G.

2.25%, due 1/28/14 | | | 250,000 | | | | 253,610 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Banks (continued) | |

Westpac Banking Corp.

1.125%, due 9/25/15 | | $ | 100,000 | | | $ | 100,926 | |

| | | | | | | | |

| | | | | | | 3,251,029 | |

| | | | | | | | |

Beverages 0.1% | |

Diageo Capital PLC

1.50%, due 5/11/17 | | | 100,000 | | | | 101,414 | |

| | | | | | | | |

|

Electric 0.1% | |

GDF Suez

1.625%, due 10/10/17 (a) | | | 75,000 | | | | 74,982 | |

Hydro-Quebec

2.00%, due 6/30/16 | | | 150,000 | | | | 156,300 | |

| | | | | | | | |

| | | | | | | 231,282 | |

| | | | | | | | |

Finance—Investment Banker/Broker 0.1% | |

BNP Paribas Home Loan Covered Bonds S.A.

2.20%, due 11/2/15 (a) | | | 175,000 | | | | 180,320 | |

| | | | | | | | |

|

Iron & Steel 0.1% | |

ArcelorMittal

4.25%, due 2/25/15 | | | 100,000 | | | | 101,006 | |

| | | | | | | | |

|

Mining 0.4% | |

BHP Billiton Finance USA, Ltd.

1.875%, due 11/21/16 | | | 150,000 | | | | 154,661 | |

Rio Tinto Finance USA PLC

1.625%, due 8/21/17 | | | 100,000 | | | | 101,248 | |

Rio Tinto Finance USA, Ltd.

2.25%, due 9/20/16 | | | 275,000 | | | | 285,293 | |

Teck Resources, Ltd.

3.75%, due 2/1/23 | | | 250,000 | | | | 256,420 | |

| | | | | | | | |

| | | | | | | 797,622 | |

| | | | | | | | |

Miscellaneous—Manufacturing 0.0%‡ | |

Tyco Electronics Group S.A.

1.60%, due 2/3/15 | | | 50,000 | | | | 50,740 | |

| | | | | | | | |

|

Oil & Gas 0.6% | |

BP Capital Markets PLC | | | | | | | | |

1.375%, due 11/6/17 | | | 150,000 | | | | 150,132 | |

1.846%, due 5/5/17 | | | 75,000 | | | | 76,671 | |

3.561%, due 11/1/21 | | | 175,000 | | | | 189,103 | |

Petrobras International Finance Co.—Pifco

2.875%, due 2/6/15 | | | 150,000 | | | | 153,914 | |

Petroleos Mexicanos

4.875%, due 3/15/15 | | | 150,000 | | | | 161,625 | |

Shell International Finance B.V. | | | | | | | | |

1.125%, due 8/21/17 | | | 150,000 | | | | 150,704 | |

2.25%, due 1/6/23 | | | 150,000 | | | | 148,190 | |

Statoil ASA

2.45%, due 1/17/23 | | | 100,000 | | | | 99,766 | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | M-15 | |

Portfolio of Investments December 31, 2012 (continued)

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Yankee Bonds (continued) | |

Oil & Gas (continued) | |

Total Capital International S.A. | | | | | | | | |

1.55%, due 6/28/17 | | $ | 100,000 | | | $ | 101,542 | |

2.875%, due 2/17/22 | | | 125,000 | | | | 130,478 | |

| | | | | | | | |

| | | | | | | 1,362,125 | |

| | | | | | | | |

Pharmaceuticals 0.4% | |

Novartis Securities Investment, Ltd.

5.125%, due 2/10/19 | | | 125,000 | | | | 149,397 | |

Sanofi S.A. | | | | | | | | |

2.625%, due 3/29/16 | | | 150,000 | | | | 157,878 | |

4.00%, due 3/29/21 | | | 125,000 | | | | 142,479 | |

Teva Pharmaceutical Finance Co. B.V. | | | | | | | | |

2.40%, due 11/10/16 | | | 100,000 | | | | 104,212 | |

2.95%, due 12/18/22 | | | 175,000 | | | | 177,023 | |

Teva Pharmaceutical Finance IV B.V.

3.65%, due 11/10/21 | | | 150,000 | | | | 160,535 | |

| | | | | | | | |

| | | | | | | 891,524 | |

| | | | | | | | |

Telecommunications 0.3% | |

America Movil SAB de CV

3.125%, due 7/16/22 | | | 200,000 | | | | 203,290 | |

British Telecommunications PLC

5.15%, due 1/15/13 | | | 100,000 | | | | 100,138 | |

France Telecom S.A.

2.75%, due 9/14/16 | | | 100,000 | | | | 104,972 | |

Telefonica Emisiones SAU

2.582%, due 4/26/13 | | | 125,000 | | | | 125,437 | |

Vivendi S.A.

2.40%, due 4/10/15 (a) | | | 100,000 | | | | 101,997 | |

Vodafone Group PLC

1.25%, due 9/26/17 | | | 100,000 | | | | 99,698 | |

| | | | | | | | |

| | | | | | | 735,532 | |

| | | | | | | | |

Transportation 0.1% | |

Canadian National Railway Co.

1.45%, due 12/15/16 | | | 125,000 | | | | 127,193 | |

| | | | | | | | |

Total Yankee Bonds

(Cost $7,789,230) | | | | | | | 8,036,588 | |

| | | | | | | | |

Total Long-Term Bonds

(Cost $67,160,823) | | | | | | | 68,907,210 | |

| | | | | | | | |

| | |

| | | | | | | | |

| | |

Shares | | | | |

| Common Stocks 62.9% | |

Aerospace & Defense 1.5% | |

Alliant Techsystems, Inc. | | | 2,079 | | | | 128,815 | |

Boeing Co. (The) | | | 5,688 | | | | 428,648 | |

General Dynamics Corp. | | | 7,125 | | | | 493,549 | |

Huntington Ingalls Industries, Inc. | | | 10,651 | | | | 461,614 | |

L-3 Communications Holdings, Inc. | | | 849 | | | | 65,050 | |

| | | | | | | | |

| | |

Shares | | | Value | |

| | | | | | | | |

Aerospace & Defense (continued) | |

Lockheed Martin Corp. | | | 4,648 | | | $ | 428,964 | |

Northrop Grumman Corp. | | | 7,147 | | | | 482,994 | |

Raytheon Co. | | | 8,386 | | | | 482,698 | |

Spirit Aerosystems Holdings, Inc. Class A (f) | | | 1,064 | | | | 18,056 | |

| | | | | | | | |

| | | | | | | 2,990,388 | |

| | | | | | | | |

Agriculture 0.7% | |

Altria Group, Inc. | | | 11,158 | | | | 350,584 | |

Archer-Daniels-Midland Co. | | | 13,827 | | | | 378,722 | |

Philip Morris International, Inc. | | | 4,186 | | | | 350,117 | |

Reynolds American, Inc. | | | 10,037 | | | | 415,833 | |

| | | | | | | | |

| | | | | | | 1,495,256 | |

| | | | | | | | |

Airlines 0.6% | |

Copa Holdings S.A. Class A | | | 3,455 | | | | 343,600 | |

Delta Air Lines, Inc. (f) | | | 46,789 | | | | 555,385 | |

Southwest Airlines Co. | | | 38,148 | | | | 390,636 | |

| | | | | | | | |

| | | | | | | 1,289,621 | |

| | | | | | | | |

Auto Manufacturers 0.6% | |

Ford Motor Co. | | | 32,577 | | | | 421,872 | |

General Motors Co. (f) | | | 16,995 | | | | 489,966 | |

Oshkosh Corp. (f) | | | 8,065 | | | | 239,127 | |

PACCAR, Inc. | | | 431 | | | | 19,486 | |

| | | | | | | | |

| | | | | | | 1,170,451 | |

| | | | | | | | |

Auto Parts & Equipment 0.2% | |

Johnson Controls, Inc. | | | 13,043 | | | | 400,420 | |

WABCO Holdings, Inc. (f) | | | 121 | | | | 7,888 | |

| | | | | | | | |

| | | | | | | 408,308 | |

| | | | | | | | |

Banks 4.6% | |

¨Bank of America Corp. | | | 46,013 | | | | 533,751 | |

Bank of New York Mellon Corp. (The) | | | 20,022 | | | | 514,565 | |

BB&T Corp. | | | 13,149 | | | | 382,767 | |

Capital One Financial Corp. | | | 7,471 | | | | 432,795 | |

CapitalSource, Inc. | | | 26,762 | | | | 202,856 | |

¨Citigroup, Inc. | | | 10,027 | | | | 396,668 | |

Comerica, Inc. | | | 8,306 | | | | 252,004 | |

Commerce Bancshares, Inc. | | | 96 | | | | 3,366 | |

East West Bancorp, Inc. | | | 6,401 | | | | 137,558 | |

Fifth Third Bancorp | | | 24,677 | | | | 374,844 | |

Goldman Sachs Group, Inc. (The) | | | 3,187 | | | | 406,534 | |

Huntington Bancshares, Inc. | | | 81,222 | | | | 519,009 | |

¨JPMorgan Chase & Co. | | | 11,494 | | | | 505,391 | |

KeyCorp | | | 72,107 | | | | 607,141 | |

M&T Bank Corp. | | | 20 | | | | 1,969 | |

Morgan Stanley | | | 21,923 | | | | 419,168 | |

Northern Trust Corp. | | | 10,382 | | | | 520,761 | |

PNC Financial Services Group, Inc. | | | 8,703 | | | | 507,472 | |

Regions Financial Corp. | | | 89,894 | | | | 640,045 | |

State Street Corp. | | | 10,821 | | | | 508,695 | |

SunTrust Banks, Inc. | | | 11,147 | | | | 316,017 | |

SVB Financial Group (f) | | | 6,563 | | | | 367,331 | |

| | | | |

| M-16 | | MainStay VP Balanced Portfolio | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| | | | | | | | |

| | |

Shares | | | Value | |

| | | | | | | | |

| Common Stocks (continued) | |

Banks (continued) | |

U.S. Bancorp | | | 11,689 | | | $ | 373,347 | |

Wells Fargo & Co. | | | 11,283 | | | | 385,653 | |

| | | | | | | | |

| | | | | | | 9,309,707 | |

| | | | | | | | |

Beverages 0.3% | |

Coca-Cola Enterprises, Inc. | | | 2,470 | | | | 78,373 | |

Constellation Brands, Inc. Class A (f) | | | 14,984 | | | | 530,284 | |

| | | | | | | | |

| | | | | | | 608,657 | |

| | | | | | | | |

Biotechnology 0.2% | |

Charles River Laboratories International, Inc. (f) | | | 9,924 | | | | 371,852 | |

| | | | | | | | |

| | |

Chemicals 1.9% | | | | | | | | |

Air Products & Chemicals, Inc. | | | 4,485 | | | | 376,830 | |

CF Industries Holdings, Inc. | | | 3,299 | | | | 670,225 | |

Dow Chemical Co. (The) | | | 14,036 | | | | 453,643 | |

Huntsman Corp. | | | 28,329 | | | | 450,431 | |

LyondellBasell Industries, N.V., Class A | | | 8,944 | | | | 510,613 | |

Mosaic Co. (The) | | | 8,941 | | | | 506,329 | |

W.R. Grace & Co. (f) | | | 5,848 | | | | 393,161 | |

Westlake Chemical Corp. | | | 5,351 | | | | 424,334 | |

| | | | | | | | |

| | | | | | | 3,785,566 | |

| | | | | | | | |

Coal 0.0%‡ | |

Peabody Energy Corp. | | | 731 | | | | 19,452 | |

| | | | | | | | |

| | |

Commercial Services 1.0% | | | | | | | | |

ADT Corp. (The) | | | 10,748 | | | | 499,675 | |

Booz Allen Hamilton Holding Corp. | | | 13,776 | | | | 191,762 | |

CoreLogic, Inc. (f) | | | 17,336 | | | | 466,685 | |

Equifax, Inc. | | | 3,367 | | | | 182,222 | |

H&R Block, Inc. | | | 2,790 | | | | 51,810 | |

Hertz Global Holdings, Inc. (f) | | | 13,416 | | | | 218,278 | |

Total System Services, Inc. | | | 17,779 | | | | 380,826 | |

| | | | | | | | |

| | | | | | | 1,991,258 | |

| | | | | | | | |

Computers 1.2% | |

Brocade Communications Systems, Inc. (f) | | | 47,486 | | | | 253,100 | |

Computer Sciences Corp. | | | 9,522 | | | | 381,356 | |

Dell, Inc. | | | 40,418 | | | | 409,434 | |

Hewlett-Packard Co. | | | 26,336 | | | | 375,288 | |

Lexmark International, Inc. Class A | | | 5,276 | | | | 122,351 | |

NetApp, Inc. (f) | | | 12,252 | | | | 411,055 | |

Synopsys, Inc. (f) | | | 141 | | | | 4,489 | |

Western Digital Corp. | | | 9,108 | | | | 386,999 | |

| | | | | | | | |

| | | | | | | 2,344,072 | |

| | | | | | | | |

Cosmetics & Personal Care 0.4% | |

Colgate-Palmolive Co. | | | 3,491 | | | | 364,949 | |

Procter & Gamble Co. (The) | | | 5,310 | | | | 360,496 | |

| | | | | | | | |

| | | | | | | 725,445 | |

| | | | | | | | |

| | | | | | | | |

| | |

Shares | | | Value | |

| | | | | | | | |

Electric 3.8% | |

AES Corp. (The) | | | 36,807 | | | $ | 393,835 | |

Ameren Corp. | | | 20,199 | | | | 620,513 | |

American Electric Power Co., Inc. | | | 9,906 | | | | 422,788 | |

Consolidated Edison, Inc. | | | 6,651 | | | | 369,397 | |

Dominion Resources, Inc. | | | 7,228 | | | | 374,410 | |

DTE Energy Co. | | | 11,162 | | | | 670,278 | |

Duke Energy Corp. | | | 5,797 | | | | 369,849 | |

Edison International | | | 14,848 | | | | 670,981 | |

Entergy Corp. | | | 7,344 | | | | 468,180 | |

Exelon Corp. | | | 12,543 | | | | 373,029 | |

FirstEnergy Corp. | | | 8,975 | | | | 374,796 | |

NextEra Energy, Inc. | | | 5,392 | | | | 373,072 | |

NRG Energy, Inc. | | | 24,739 | | | | 568,750 | |

NV Energy, Inc. | | | 2,017 | | | | 36,588 | |

PG&E Corp. | | | 9,122 | | | | 366,522 | |

Pinnacle West Capital Corp. | | | 3,323 | | | | 169,407 | |

PPL Corp. | | | 4,366 | | | | 124,999 | |

Public Service Enterprise Group, Inc. | | | 14,278 | | | | 436,907 | |

Southern Co. (The) | | | 8,537 | | | | 365,469 | |

Xcel Energy, Inc. | | | 5,009 | | | | 133,790 | |

| | | | | | | | |

| | | | | | | 7,683,560 | |

| | | | | | | | |

Electrical Components & Equipment 0.6% | |

Emerson Electric Co. | | | 8,385 | | | | 444,069 | |

Energizer Holdings, Inc. | | | 6,696 | | | | 535,546 | |

General Cable Corp. (f) | | | 6,714 | | | | 204,173 | |

| | | | | | | | |

| | | | | | | 1,183,788 | |

| | | | | | | | |

Electronics 0.5% | |

Tech Data Corp. (f) | | | 682 | | | | 31,051 | |

Thermo Fisher Scientific, Inc. | | | 6,631 | | | | 422,925 | |

Tyco International, Ltd. | | | 16,987 | | | | 496,870 | |

| | | | | | | | |

| | | | | | | 950,846 | |

| | | | | | | | |

Engineering & Construction 0.5% | |

AECOM Technology Corp. (f) | | | 11,675 | | | | 277,865 | |

Chicago Bridge & Iron Co. N.V. | | | 7,702 | | | | 356,988 | |

Engility Holdings, Inc. (f) | | | 11,606 | | | | 223,531 | |

Shaw Group, Inc. (The) (f) | | | 1,983 | | | | 92,428 | |

| | | | | | | | |

| | | | | | | 950,812 | |

| | | | | | | | |

Entertainment 0.1% | |

Regal Entertainment Group Class A | | | 14,975 | | | | 208,901 | |

| | | | | | | | |

| | |

Environmental Controls 0.2% | | | | | | | | |

Waste Management, Inc. | | | 14,166 | | | | 477,961 | |

| | | | | | | | |

| | |

Finance—Credit Card 0.4% | | | | | | | | |

American Express Co. | | | 7,570 | | | | 435,123 | |

Discover Financial Services | | | 11,925 | | | | 459,709 | |

| | | | | | | | |

| | | | | | | 894,832 | |

| | | | | | | | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | M-17 | |

Portfolio of Investments December 31, 2012 (continued)

| | | | | | | | |

| | |

Shares | | | Value | |

| | | | | | | | |

| Common Stocks (continued) | |

Finance—Investment Banker/Broker 0.4% | |

Charles Schwab Corp. (The) | | | 36,376 | | | $ | 522,359 | |

Interactive Brokers Group, Inc. Class A | | | 12,457 | | | | 170,412 | |

Jefferies Group, Inc. | | | 193 | | | | 3,584 | |

TD Ameritrade Holding Corp. | | | 11,419 | | | | 191,954 | |

| | | | | | | | |

| | | | | | | 888,309 | |

| | | | | | | | |

Finance—Other Services 0.2% | |

CME Group, Inc. | | | 6,897 | | | | 349,747 | |

| | | | | | | | |

| | |

Food 2.5% | | | | | | | | |

ConAgra Foods, Inc. | | | 2,438 | | | | 71,921 | |

Dean Foods Co. (f) | | | 22,896 | | | | 378,013 | |

General Mills, Inc. | | | 10,478 | | | | 423,416 | |

Hillshire Brands Co. | | | 14,118 | | | | 397,280 | |

Ingredion, Inc. | | | 7,641 | | | | 492,310 | |

J.M. Smucker Co. (The) | | | 307 | | | | 26,476 | |

Kellogg Co. | | | 6,643 | | | | 371,012 | |

Kraft Foods Group, Inc. | | | 9,693 | | | | 440,741 | |

Mondelez International, Inc. Class A | | | 18,749 | | | | 477,537 | |

Ralcorp Holdings, Inc. (f) | | | 1,642 | | | | 147,205 | |

Safeway, Inc. | | | 22,034 | | | | 398,595 | |

Smithfield Foods, Inc. (f) | | | 21,437 | | | | 462,396 | |

Sysco Corp. | | | 11,752 | | | | 372,068 | |

Tyson Foods, Inc. Class A | | | 28,097 | | | | 545,082 | |

| | | | | | | | |

| | | | | | | 5,004,052 | |

| | | | | | | | |

Forest Products & Paper 0.5% | |

Domtar Corp. | | | 5,840 | | | | 487,757 | |

International Paper Co. | | | 14,148 | | | | 563,656 | |

| | | | | | | | |

| | | | | | | 1,051,413 | |

| | | | | | | | |

Gas 0.5% | |

CenterPoint Energy, Inc. | | | 23,200 | | | | 446,600 | |

Sempra Energy | | | 1,797 | | | | 127,479 | |

UGI Corp. | | | 14,998 | | | | 490,585 | |

Vectren Corp. | | | 1,177 | | | | 34,604 | |

| | | | | | | | |

| | | | | | | 1,099,268 | |

| | | | | | | | |

Health Care—Products 1.9% | |

Alere, Inc. (f) | | | 7,329 | | | | 135,586 | |

Baxter International, Inc. | | | 6,559 | | | | 437,223 | |

Becton, Dickinson & Co. | | | 5,544 | | | | 433,485 | |

Boston Scientific Corp. (f) | | | 109,616 | | | | 628,100 | |