Exhibit (a)(5)(E)

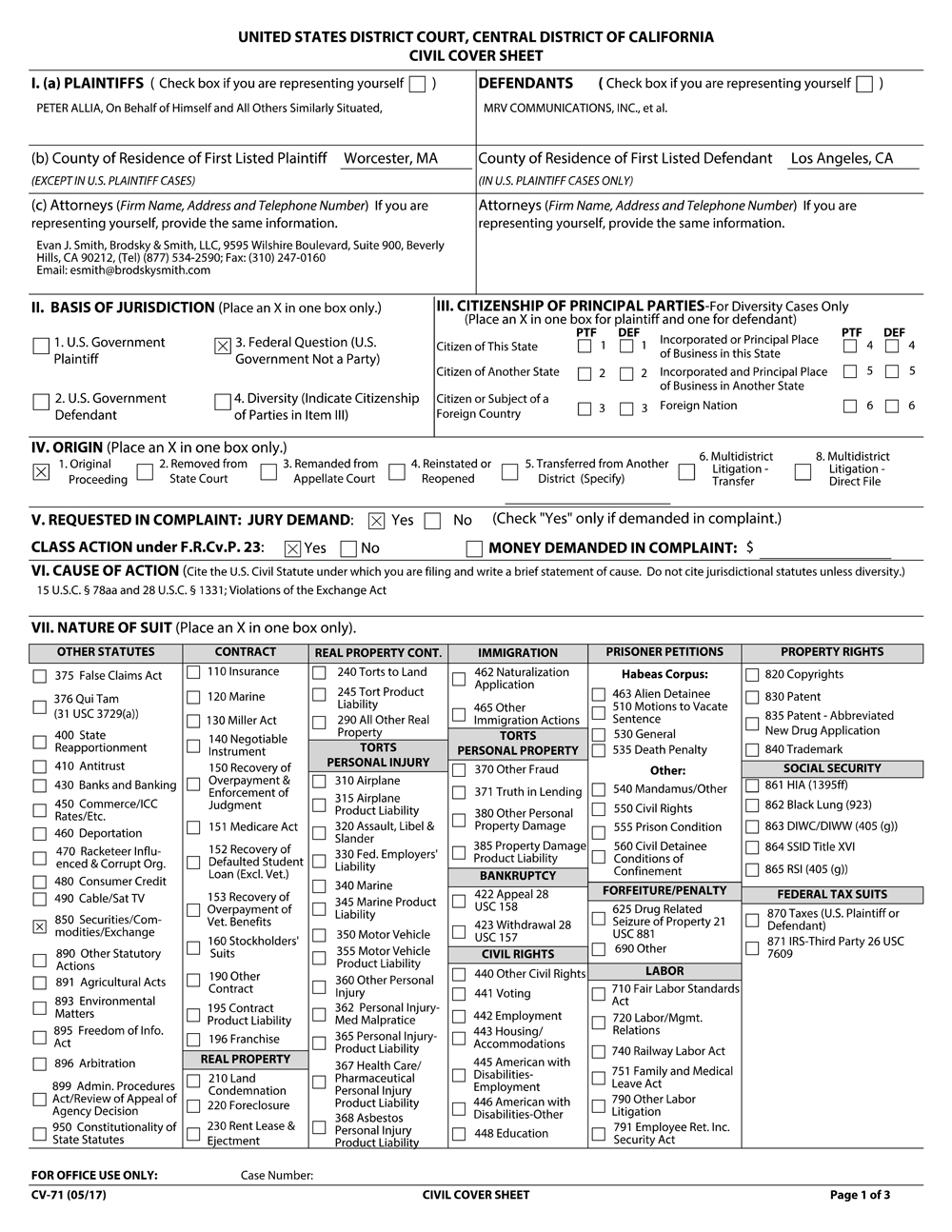

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 1 of 27 Page ID #:1 BRODSKY & SMITH, LLC Evan J. Smith, Esquire 9595 Wilshire Boulevard, Suite 900 Beverly Hills, CA 90212 Phone: (877) 534-2590 Facsimile: (610) 667-9029 esmith@brodskysmith.com Attorneys for Plaintiff IN THE UNITED STATES DISTRICT COURT CENTRAL DISTRICT OF CALIFORNIA PETER ALLIA, On Behalf of Himself and All Others Similarly Situated, Plaintiff, v. MRV COMMUNICATIONS, INC., KEN TRAUB, ROBERT PONS, MARK J. BONNEY, JEANNIE H. DIEFENDERFER, BRIAN BELLINGER, JEFFREY TUDER, ADVA NA HOLDINGS, INC., and GOLDEN ACQUISITION CORPORATION, Defendants. : : : : : : : : : : : : : : : : : : : : Case No.: CLASS ACTION COMPLAINT FOR: (1) Violation of § 14(e) of the Securities Exchange Act of 1934 (2) Violation of § 20(a) of the Securities Exchange Act of 1934 (3) Breach of Fiduciary Duties JURY DEMAND Plaintiff Peter Allia ("Plaintiff"), by his attorneys, on behalf of himself and those similarly situated, files this action against the defendants, and alleges upon information and belief, except for those allegations that pertain to him, which are alleged upon personal knowledge, as follows: SUMMARY OF THE ACTION 1. Plaintiff brings this stockholder class action on behalf of himself and all other public stockholders of MRV Communications, Inc. ("MRVC" or the "Company"), against MRVC, and the Company's Board of Directors (the "Board" or the "Individual Defendants," and collectively with MRVC, the "Defendants") for violations of Sections 14(e) and 20(a) of the Securities and Exchange Act of 1934 (the "Exchange Act"), and for breaches of fiduciary duty as a result of Defendants' efforts to sell the Company as a result of an unfair process, and for an unfair price. Also named as defendants are ADVA NA Holdings, Inc. ("Parent") and Parent's wholly - 1 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 2 of 27 Page ID #:2 owned subsidiary, Golden Acquisition Corporation ("Merger Sub," and together with Parent, "ADVA NA"). This action seeks to enjoin a tender offer currently scheduled to expire at 12:00 midnight, Eastern time, at the end of the day on August 11, 2017 (the "Tender Offer" or "Offer"), upon the successful completion of which ADVA NA shall acquire each outstanding share of MRVC common stock for $10.00 per share in cash (the "Proposed Transaction" or "Merger"). 2. The terms of the Proposed Transaction were memorialized in a July 3, 2017 filing with the Securities and Exchange Commission ("SEC") on Form 8-K attaching the definitive Agreement and Plan of Merger (the "Merger Agreement"). Notably, the terms of the Merger Agreement require that stockholders tender only one share more than 50% of the sum of the total number of shares of MRVC stock then outstanding at the time of the expiration of the Offer (the "Minimum Condition"). 3. Significantly, in connection with the Offer and Merger, and concurrently with entering into the Merger Agreement, Parent and Merger Sub entered into Tender and Support Agreements, dated as of July 2, 2017 (the "Support Agreements"), with Raging Capital Management, LLC ("RCM"), and Kenneth H. Traub, Robert M. Pons, Mark J. Bonney, Brian Bellinger, Jeannie H. Diefenderfer, Jeffrey Tuder, Stephen G. Krulik, and Adam L.A. Scheer (each, a "Supporting Stockholder"). The Support Agreements obligate the Supporting Stockholders to tender their shares of Company common stock into the Offer and otherwise support the transactions contemplated by the Merger Agreement. RCM beneficially owned, as of July 2, 2017, 2,136,864 shares of MRVC common stock, which represent approximately 31.37% of the outstanding shares of MRVC common stock. Messrs. Traub, Pons, Bonney, Bellinger, Tuder, Krulik, Scheer and Mrs. Diefenderfer beneficially owned, as of July 2, 2017, an aggregate of 386,258 shares of MRVC common stock which represent approximately 5.67% of the shares of MRVC common stock that are issued and outstanding. As such, approximately 37% of all MRVC common stock currently issued and outstanding has been pledged in support of the Merger and the Offer thereby making consummation of the Proposed Transaction a fait accompli. - 2 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 3 of 27 Page ID #:3 4. On July 17, 2017, MRVC filed a Solicitation/Recommendation Statement on Schedule 14D-9 (the "14D-9") with the Securities and Exchange Commission (the "SEC") in support of the Proposed Transaction. 5. Defendants breached their fiduciary duties to the Company's stockholders by agreeing to a transaction that undervalues MRVC and is the result of a flawed sales process. Post-closure, MRVC stockholders will be frozen out of seeing the return on their investment of any and all future profitability of MRVC. 6. Further, pursuant to the terms of the Merger Agreement, upon the consummation of the Proposed Transaction, the Individual Defendants and executive officers of MRVC will be able to exchange large, illiquid blocks of Company stock for massive payouts, in addition to receiving cash in exchange for certain outstanding and unvested options and/or other types of restricted stock units. Moreover, certain Directors and other insiders will also be the recipients of lucrative change-in-control agreements, triggered upon the termination of their employment as a consequence of the consummation of the Proposed Transaction. All stated, Company insiders stand to reap hundreds of thousands of dollars in personal profits as a result of the Proposed Transaction. Such large paydays upon the consummation of the Proposed Transaction, have clearly tainted the motivations of the Board in approving it. 7. Finally, in violation of sections 14(e) and 20(a) of the Exchange Act and their fiduciary duties, Defendants caused to be filed the materially deficient 14D-9 in an effort to solicit stockholders to tender their MRVC shares in favor of the Proposed Transaction. The 14D-9 is materially deficient and deprives MRVC stockholders of the information they need to make an intelligent, informed and rational decision of whether to tender their shares in favor of the Proposed Transaction. As detailed below, the 14D-9 omits and/or misrepresents material information concerning, among other things: (a) the Company's financial projections; (b) the sales process of the Company; and (b) the data and inputs underlying the financial valuation analyses that purport to support the fairness opinions provided by the Company's financial advisor Cowen and Company, LLC ("Cowen"); and (c) the financial analyses performed by Cowen in support of the Proposed Transaction. - 3 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 4 of 27 Page ID #:4 8. Absent judicial intervention, the merger will be consummated, resulting in irreparable injury to Plaintiff and the Class. This action seeks to enjoin the Proposed Transaction or, in the event the Proposed Transaction is consummated, to recover damages resulting from violation of the federal securities laws by Defendants. PARTIES 9. Plaintiff is an individual citizen of the State of Massachusetts. He is, and at all times relevant hereto, has been a MRVC stockholder. 10. Defendant MRVC is a Delaware corporation and maintains its principal executive offices at 20520 Nordhoff Street, Chatsworth, CA 91311. MRVC's common stock is traded on the Nasdaq under the ticker symbol "MRVC." 11. Defendant Ken Traub ("Traub") has been a director at all relevant times and is Chairman of the Board. 12. Defendant Robert Pons ("Pons") has been a director at all relevant times and is Vice-Chairman of the Board. 13. Defendant Mark J. Bonney has been a director at all relevant times. He is also President and Chief Executive Officer ( "CEO") of the Company. 14. Defendant Jeannie H. Diefenderfer ("Diefenderfer") has been a director at all relevant times. 15. Defendant Brian Bellinger ("Bellinger") has been a director at all relevant times. 16. Defendant Jeffrey Tuder ("Tuder") has been a director at all relevant times. 17. The defendants identified in paragraphs 12 through 17 are collectively referred to herein as the "Director Defendants" or the "Individual Defendants." 18. Defendant Parent is a Delaware corporation and a party to the Merger Agreement. 19. Defendant Merger Sub is a Delaware corporation, a wholly-owned subsidiary of Parent, and a party to the Merger Agreement. JURISDICTION AND VENUE 20. This Court has subject matter jurisdiction pursuant to Section 27 of the Exchange Act (15 U.S.C. § 78aa) and 28 U.S.C. § 1331 (federal question jurisdiction) as Plaintiff alleges - 4 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 5 of 27 Page ID #:5 violations of Sections 14(e) and Section 20(a) of the Exchange Act. This action is not a collusive one to confer jurisdiction on a court of the United States, which it would not otherwise have. The Court has supplemental jurisdiction over any claims arising under state law pursuant to 28 U.S.C. § 1367. 21. Personal jurisdiction exists over each defendant either because the defendant conducts business in or maintains operations in this District, or is an individual who is either present in this District for jurisdictional purposes or has sufficient minimum contacts with this District as to render the exercise of jurisdiction over defendant by this Court permissible under traditional notions of fair play and substantial justice. 22. Venue is proper in this District pursuant to 28 U.S.C. § 1391, because MRVC has its principal offices in this District, and each of the Individual Defendants, as Company officers or directors, has extensive contacts within this District. CLASS ACTION ALLEGATIONS 23. Plaintiff brings this action pursuant to Federal Rule of Civil Procedure 23, individually and on behalf of the stockholders of MRVC's common stock who are being and will be harmed by Defendants' actions described herein (the "Class"). The Class specifically excludes Defendants herein, and any person, firm, trust, corporation or other entity related to, or affiliated with, any of the Defendants. 24. This action is properly maintainable as a class action because: (a) The Class is so numerous that joinder of all members is impracticable. According to the Company's most recent 10-Q, as of April 27, 2017, there were more than 6.8 million common shares of MRVC outstanding. The actual number of public stockholders of MRVC will be ascertained through discovery; (b) There are questions of law and fact which are common to the Class, including inter alia, the following: (i) Whether Defendants have violated the federal securities laws; - 5 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 6 of 27 Page ID #:6 (ii) Whether Defendants made material misrepresentations and/or omitted material facts in the 14D-9; (iii) Whether Defendants have breached their fiduciary duties; and (iv) Whether Plaintiff and the other members of the Class have and will continue to suffer irreparable injury if the Proposed Transaction is consummated. (c) Plaintiff is an adequate representative of the Class, has retained competent counsel experienced in litigation of this nature and will fairly and adequately protect the interests of the Class; (d) Plaintiff's claims are typical of the claims of the other members of the Class and Plaintiff does not have any interests adverse to the Class; (e) The prosecution of separate actions by individual members of the Class would create a risk of inconsistent or varying adjudications with respect to individual members of the Class which would establish incompatible standards of conduct for the party opposing the Class; (f) Plaintiff anticipates that there will be no difficulty in the management of this litigation and, thus, a class action is superior to other available methods for the fair and efficient adjudication of this controversy; and (g) Defendants have acted on grounds generally applicable to the Class with respect to the matters complained of herein, thereby making appropriate the relief sought herein with respect to the Class as a whole. THE INDIVIDUAL DEFENDANTS' FIDUCIARY DUTIES 25. By reason of the Individual Defendants' positions with the Company as officers and/or directors, said individuals are in a fiduciary relationship with MRVC and owe the Company the duties of due care, loyalty, and good faith. 26. By virtue of their positions as directors and/or officers of MRVC, the Individual Defendants, at all relevant times, had the power to control and influence, and did control and influence and cause MRVC to engage in the practices complained of herein. - 6 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 7 of 27 Page ID #:7 27. Each of the Individual Defendants are required to act with due care, loyalty, good faith and in the best interests of the Company. To diligently comply with these duties, directors of a corporation must: (a) act with the requisite diligence and due care that is reasonable under the circumstances; (b) act in the best interest of the company; (c) use reasonable means to obtain material information relating to a given action or decision; (d) refrain from acts involving conflicts of interest between the fulfillment of their roles in the company and the fulfillment of any other roles or their personal affairs; (e) avoid competing against the company or exploiting any business opportunities of the company for their own benefit, or the benefit of others; and (f) disclose to the Company all information and documents relating to the company's affairs that they received by virtue of their positions in the company. 28. In accordance with their duties of loyalty and good faith, the Individual Defendants, as directors and/or officers of MRVC, are obligated to refrain from: (a) participating in any transaction where the directors' or officers' loyalties are divided; (b) participating in any transaction where the directors or officers are entitled to receive personal financial benefit not equally shared by the Company or its public stockholders; and/or (c) unjustly enriching themselves at the expense or to the detriment of the Company or its stockholders. - 7 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 8 of 27 Page ID #:8 29. Plaintiff alleges herein that the Individual Defendants, separately and together, in connection with the Proposed Transaction, violated, and are violating, the fiduciary duties they owe to MRVC, Plaintiff and the other public stockholders of MRVC, including their duties of loyalty, good faith, and due care. 30. As a result of the Individual Defendants' divided loyalties, Plaintiff and Class members will not receive adequate, fair or maximum value for their MRVC common stock in the Proposed Transaction. SUBSTANTIVE ALLEGATIONS Company Background 31. MRVC, incorporated on March 9, 1992, is a supplier of communications solutions to telecommunications service providers, enterprises and governments throughout the world. The Company's products enable customers to provide high-bandwidth data, and video services and mobile communications services. 32. The Company operates through its Network Equipment segment which designs, manufactures, sells and services equipment used by commercial customers, governments and telecommunications service providers. Its products include switches, optical transport platforms, physical layer products and out-of-band management products, and specialized networking products. MRVC markets and sells its products, through a variety of channels, which include a direct sales force, manufacturers' representatives, value-added-resellers, distributors and systems integrators. 33. The Network Equipment business includes two business units: Optical Communications Systems division ("OCS") and Appointech, Inc. ("Appointech"). 34. OCS provides a portfolio of packet and optical solutions enabling the access, aggregation, transport and management of various communications traffic for fixed line, cable, content delivery, cloud-based and mobile communications networks leveraging both direct and channel sales through third party channel partners. 35. Appointech is a Taiwan-based provider of design and manufacturing of fiber optic modules for the fiber-optic communications industry. - 8 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 9 of 27 Page ID #:9 36. The Company's products and services include optical transport products; packet/carrier Ethernet products; network management products, and infrastructure management product. Its OptiDriver is an advanced optical transport network element. OptiDriver is engineered to support the advances in optical technologies, including intelligent optical automated Reconfigurable Optical Add Drop Multiplexer (ROADM) networks and 100 gigabits per second (Gbps) transport. Its Fiber Driver optical multi-service access product line provides a range of services, including demarcation, media conversion, signal repeating and fiber-optimization solutions 37. The Company's OptiSwitch Carrier Ethernet service demarcation series delivers capabilities that enable carriers and service providers to deliver assured service-level agreement (SLA) services. OptiSwitch CE 2.0 solution consists of Pro-Vision, which is a service provisioning and management software that enables carriers to simplify Ethernet service delivery and accelerate time-to-market for new applications, and provides centralized service visibility, intelligence along with substantial operating expense (OPEX) reductions. Pro-Vision is a service orchestration platform that gives service providers the automated tools to design, provision, manage, diagnose, visualize and optimize both packet and optical access networks. It automates the provisioning, orchestration and management of a range of network elements and a range of services. 38. The Company's Media Cross Connect is an optical/electrical/optical (OEO) switch used for data rates and media till approximately 10 Gbps. The Optical Cross Connect is an all optical (OOO) switch for single mode fiber rates till approximately 100 Gbps. 39. The Company's LX product line provides secure remote service port access and remote power control to devices in a networks and infrastructures, including data centers, remote sites and test labs. 40. MRVC has shown sustained solid financial performance. For example, a March 9, 2017 press release issued by the Company reporting its Fourth-Quarter and Full-Year 2016 financial results, revenue grew 13% year-over year to $20.9 MM. In addition to the quarterly revenue growth, in the words of Defendant Bonney, MRVC's President and CEO, MRVC also - 9 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 10 of 27 Page ID #:10 "… accomplished several important product development milestones and completed the transition of all packet and optical manufacturing to a single world-class manufacturing partner." There was additional, and notable, MRVC achievements mentioned by Bonney in the press release that are, as follows: (a) Executed on the go-to-market strategy, adding new customers in the regional service provider and carrier natural provider target market segments and significantly expanding relationships with existing Tier One accounts; two new programs for existing Tier One customers began shipping in 2016 and two more programs are expected to start shipping production units in the third quarter of 2017; (b) Increased OptiDriver® customer count to 134 at December 31, 2016, including several new customers in the data center segment, growing the number of cumulative customers by 58% during the year. During 2016, the Company added 49 new OptiDriver customers of which 34 were new optical transport customers for MRVC; (c) Completed the move of all packet and optical product manufacturing into a single, world-class, manufacturing partner lowering manufacturing overhead costs by approximately $1 million annually; (d) Implemented cost reduction actions, including the reduction of approximately 10% of headcount, expected to lower operating costs by approximately $5 million on an annualized basis beginning in the first quarter of 2017 without impacting the product roadmap or customer engagements; (e) Released a new enhancement to the field-proven OptiSwitch® product line the OS-V Series - a portfolio of MEF CE 2.0-Compliant modular and programmable 1GbE and 10GbE CPEs; (f) Demonstrated the Company's commitment to supporting network administrators in their battle against cyber threats by achieving FIPS 140-2 Certification for the LX Series Out-of-Band Networking Solution; and (g) Received several accolades and numerous awards for the OptiPacket® OPX-1 including the 2016 TMC Labs Innovation Award and the 2016 TMC - 10 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 11 of 27 Page ID #:11 Communications Solutions Product of the Year Award for MRV Communication's 100G CE aggregation capability. 41. Speaking on these positive results, Company COO Adam Scheer noted "With most of the heavy lifting associated with our product refresh behind us, the timing was right to streamline our cost structure. The team is now in a stronger position to drive profitable growth. In 2017, we are executing on a number of strategic development activities that include the release of new 100G and 200G products for optical transport, the launch of variants of the OS V-Series for a specific customer, and continued enhancements of our Pro-Vision® service orchestration platform. With these growth initiatives, and with a lower cost structure, we are well positioned for profitable growth going forward." 42. As of December 31, 2016, the Company remained debt free with cash and investments of $25.4 million. 43. Additionally, Defendant Bonney spoke positively about the Company's future prospects, noting that, "We are excited to see strong validation of our strategy with customer wins in our target markets and continued momentum behind our newly released product lines. With customer momentum building, as well as a streamlined cost structure, we are confident that we have positioned our company to deliver sustainable profitable growth." 44. MRVC next reported financial results on May 3, 2017, for the three-months ended March 31, 2017. Similar to the Fourth-Quarter 2016 and Year-End 2016 financial results, MRVC's quarter one reporting was positive and encouraging. Revenue was $21.2 million, compared to $18.9 million in Q1 2016, up 12.1%, and driven by strong growth of packet and optical products; GAAP gross margin remained robust at 50.6%; and GAAP operating expenses were $11.5 million, down from $13.4 million from Q1 the previous year. As of March 31, 2017, the Company continued to remain debt free, and flush with significant cash and investments. 45. "MRVC's investments in new product development over the past few years has enabled us to deepen our relationships with our major customers while broadening our market opportunities and customer base," said Defendant Bonney, MRV's president and CEO. "We increased our revenue 12%, a second consecutive quarter of double digit year-over-year growth. - 11 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 12 of 27 Page ID #:12 Packet and optical revenue grew 17% year-over-year, with OptiDriver® and OptiSwitch® platforms increasing both quarter-over-quarter and year-over-year. In the quarter, we added 15 new OptiDriver customers. In addition, 13 customers have now purchased our new OptiSwitch V Series of enhanced packet switches. With the lower cost structure resulting from the initiatives we announced last quarter coupled with our increased momentum with both existing and new customers, we have built a strong foundation for sustainable, profitable growth." 46. Despite this upward trajectory and glowing pronouncements by management, the Individual Defendants have caused MRVC to enter into the Proposed Transaction, thereby depriving Plaintiff and other public stockholders of the Company the opportunity to reap the benefits of MRVC's present and future success. The Flawed Sales Process 47. The process deployed by the Individual Defendants was flawed and inadequate, and conducted out of the self-interest of the Individual Defendants 48. During the period between June and September 2016, Cowen contacted 78 potential strategic and financial buyers (collectively, the "Identified Parties"). Of the Identified Parties contacted, 21 signed non-disclosure agreements and were granted access to a virtual data room to perform due diligence regarding MRVC, and nine attended presentations by the MRVC management team. 49. In November and December 2016, Cowen sent process letters to seven of the Identified Parties who attended management presentations asking that they provide final written acquisition proposals regarding MRVC by the end of January 2017. 50. Five Identified Parties, including Parent, submitted non-binding proposal letters outlining a potential transaction involving MRVC or one of its product lines. Two of said proposals was dismissed due to inadequate value and/or lack of cash and financing ability. MRVC engaged in negotiations with the other three Identified Parties, which were Parent, Other Strategic Interested Party, and PE-Backed Strategic Party. 51. Between August 24, 2016 and April 19, 2017, MRVC negotiated with PE-Backed Strategic Party, and PE-Backed Strategic Party performed due diligence with respect to an - 12 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 13 of 27 Page ID #:13 acquisition of MRVC. Initially, PE-Backed Strategic Party drafted and sent to MRVC a nonbinding letter of intent indicating a valuation range of $10 - $10.50/share to acquire MRVC's outstanding common stock. Later, in February 2017, PE-Backed Strategic Party would revise downward the letter of intent to $10/share, before ultimately indicating on April 19, 2017 that it was no longer interested in pursuing a transaction with MRVC. Based on this, MRVC discontinued negotiations with PE-Backed Strategic Party. 52. Between August 25, 2016 and April 11, 2017, MRVC negotiated with Other Strategic Interested Party. On December 5, 2016, MRVC received a non-binding letter of intent from Other Strategic Interested Party to acquire MRVC at an enterprise value of $40,000,000, excluding net operating losses and cash. However, the publicly available information relating to Other Strategic Interested Party led MRVC to conclude that Other Strategic Interested Party did not have sufficient available cash or borrowing capacity to acquire MRVC, and its proposal included a financing contingency. On Mach 31, 2017, Other Strategic Interested Party announced an acquisition of another company. Following this announcement, on April 11, 2017, Other Strategic Interested Party informed MRVC that, while it was still potentially interested in a roll-up acquisition of MRVC following the closing of the other acquisition, any potential transaction with MRVC could not take place until summer of 2018, at the earliest. The Board and MRVC management did not consider such a transaction in 2018 to be a realistic prospect. 53. After executing a confidentiality agreement with Parent in August 2016, Parent advised MRVC in October 2016 that is was not interested in pursuing a transaction with the Company at that time. Parent further indicated, however, that although it was not interested at this time, MRVC could approach Parent again once the Company had exhausted all prospects with other potential buyers. 54. On February 21, 2017, MRVC contacted Parent to discuss the strategic merits of a combination between the two companies. Thereafter, on April 26, 2017 MRVC received a letter of intent from Parent providing for an offer price range of between $9.85 and $10/share. On April 30, 2017, MRVC received an updated non-binding letter of intent from Parent with a revised value - 13 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 14 of 27 Page ID #:14 range of between $10 and $10.50/share, the receipt of which motivated the Board to commence a non-exclusive, 45-day due diligence period with Parent. 55. During the due diligence period, MRVC granted to Parent meetings with key MRVC employees, and permitted Parent a site visit to MRVC's Israel facility with the hope that such acquiescence would convince ADVA to submit an offer at the higher end of the value range stated in the Parent's letter of intent. All the while, Parent continued to communicate to MRVC that it was having difficulty justifying a price above $10/share. 56. During the month of June, MRVC attempted to persuade Parent to offer greater than $10/share, and each attempt was rebuffed. On June 28, 2017, Parent advised MRVA that the Parent board of directors was not comfortable with a price above $10/share and that Parent might terminate negotiations altogether. Later that day, the Board authorized MRVC management to accept Parent's offer of $10/share. The Proposed Transaction 57. On July 3, 2017, the Company issued a press release announcing that MRVC had agreed to be acquired by ADVA NA in the Proposed Transaction. The press release states in relevant part: CHATSWORTH, California and MUNICH, July 3, 2017 /PRNewswire/ - MRV Communications, Inc. (NASDAQ: MRVC), a provider of innovative network solutions for data center operators, service providers, and enterprises, today announced that ADVA Optical Networking (FSE: ADV) has agreed to acquire MRV. Under the terms of the agreement, ADVA Optical Networking will make a tender offer of $10.00 per share for all the outstanding common stock of MRV. The agreement has been approved and unanimously recommended by both the board of directors of ADVA Optical Networking and the board of directors of MRV. The acquisition is subject to customary closing conditions, including the tender of at least a majority of MRV Communications, Inc. outstanding shares of common stock. "The network equipment markets that we serve continue to be highly competitive. In this environment, we concluded that the best course of action for MRV's shareholders was to undertake a review of strategic alternatives. At the conclusion of this review, we have determined that the agreement we have reached to be acquired by ADVA Optical Networking provides the best alternative for MRV and its shareholders. We see a very natural fit between ADVA Optical Networking and MRV as both companies have been long-standing suppliers to the Carrier Ethernet and Optical Transport markets. With so much in common technically and culturally but with relatively little overlap among customers, the combined company will be - 14 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 15 of 27 Page ID #:15 in a stronger position to support the evolving needs of its target markets," said Mark Bonney, CEO of MRV. Cowen and Company, LLC is acting as financial adviser to MRV Communications, Inc. Norton Rose Fulbright LLP is serving as MRV Communications, Inc.'s legal adviser. Hogan Lovells is serving as ADVA Optical Networking's legal adviser. The Inadequate Merger Consideration 58. Significantly, analyst expectations, the Company's strong market position, extraordinary growth, positive future outlook, and synergistic benefits with ADVA NA establish the inadequacy of the merger consideration. 59. First, the compensation afforded under the Proposed Transaction to Company stockholders significantly undervalues the Company. The proposed valuation does not adequately reflect the intrinsic value of the Company. Moreover, the valuation does not adequately take into consideration how the Company is performing, considering increases in revenues reported by the Company recent quarters of the past financial year. 60. Notably, analyst coverage indicates a high target above the deal price, with analysts at Northland Securities, valuing the Company at $14.00 per share as recently as July of 2017, a value that is 40% greater than the valuation offered to Plaintiff and other public stockholders in the Proposed Transaction. 61. Furthermore, the consideration offered in the Proposed Transaction does not take into account the considerable synergies afforded to ADVA NA. Notably, Brian Protiva, CEO of Parent, stated in the press release announcing the Proposed Transaction that, "[…] Over 29 years, [MRVC] has driven some key innovations and played an important role in shaping our industry. That's why we signed a definitive agreement to acquire it today. We believe there's a strong synergy between our two companies. MRV Communications, Inc.'s technology and talent will strengthen our own product set and help us to deliver even more value to our customers. Our combined teams present the marketplace with an incredibly compelling skill set and technology base." 62. Uli Dopfer, CFO of Parent stated, "The networking industry is experiencing one of the most exciting and tumultuous phases in its history. The pace of innovation has never been - 15 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 16 of 27 Page ID #:16 faster or more demanding. To continue to exceed customer expectations and outperform network demands, we must use every possible advantage. Our acquisition of MRV Communications, Inc. will help us to do this. It not only strengthens our cloud access portfolio, but it also opens the door to new customers. There can be no question that this acquisition will present many new business opportunities, especially for communication service providers who are seeking to explore the possibilities of virtualized network services. Together, ADVA Optical Networking and MRV Communications, Inc. present an exciting networking force." 63. Finally, the inadequacy of the proposed merger consideration is further evident when the $10 acquisition price is compared to recent and historical trading prices for MRVC stock. Significantly, MRVC stock traded as high as $10.50/share on July 12, 2017; and as high as $10.95/share on March 21, 2017. Moreover, the proposed merger consideration is significantly below the Company's 52-week trading high of $13.09/share. 64. Obviously, the opportunity to invest in such Company in order to strengthen its market presence is a great coup for ADVA NA, however it undercuts the foresight and investment of Plaintiff and all other public stockholders who have done the same. 65. Moreover, post-closure, MRVC stockholders will be completely cashed out from any and all ownership interest in the Company, forever foreclosing them from receiving any future benefit in their investment as MRVC continues on its upward financial trajectory. 66. It is clear from these statements and the facts set forth herein that this deal is designed to maximize benefits for ADVA NA at the expense of MRVC and MRVC's stockholders, which clearly indicates that MRVC stockholders were not an overriding concern in the formation of the Proposed Transaction. Preclusive Deal Mechanisms 67. The Merger Agreement contains certain provisions that unduly benefit ADVA NA by making an alternative transaction either prohibitively expensive or otherwise impossible. Significantly, the Merger Agreement contains a termination fee provision that requires MRVC to pay up to $2.41 million to ADVA NA if the Merger Agreement is terminated under certain circumstances. Moreover, under one circumstance, MRVC must pay this termination fee even if - 16 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 17 of 27 Page ID #:17 it consummates any Takeover Proposal (as defined in the Merger Agreement) within 12 months following the termination of the Merger Agreement. The termination fee will make the Company that much more expensive to acquire for potential purchasers. The termination fee in combination with other preclusive deal protection devices will all but ensure that no competing offer will be forthcoming. 68. The Merger Agreement also contains a "No Solicitation" provision that restricts MRVC from considering alternative acquisition proposals by, inter alia, constraining MRVC's ability to solicit or communicate with potential acquirers or consider their proposals. Specifically, the provision prohibits the Company from directly or indirectly soliciting, initiating, proposing or inducing any alternative proposal, but permits the Board to consider a Takeover Proposal only if it constitutes or is reasonably calculated to lead to a "Superior Proposal" as defined in the Merger Agreement. 69. Moreover, the Agreement further reduces the possibility of a topping offer from an unsolicited purchaser. Here, the Individual Defendants agreed to provide ADVA NA information in order to match any other offer, thus providing ADVA NA access to the unsolicited bidder's financial information and giving ADVA NA the ability to top the superior offer. Thus, a rival bidder is not likely to emerge with the cards stacked so much in favor of ADVA NA. 70. Finally certain of the Individual Defendants and other members of Company management have agreed to enter into Tender and Support agreements, locking up a significant portion of the Company's stock to tender in support of the Proposed Transaction, further constraining a rival bidder from being able to make an effective bid for the Company. According to the Merger Agreement, the Supporting Stockholders entered into the Support Agreements which obligate them to tender their shares of Company common stock into the Offer and otherwise support the transactions contemplated by the Merger Agreement. As such, approximately 37% of all MRVC common stock currently issued and outstanding has been pledged in support of the Merger and the Offer thereby making consummation of the Proposed Transaction a fait accompli. 71. Accordingly, the Company's true value is compromised by the consideration offered in the Proposed Transaction. - 17 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 18 of 27 Page ID #:18 Potential Conflicts of Interest 72. There is strong evidence that the Proposed Transaction may be tainted by the self-interest of the Individual Defendants. Certain insiders stand to receive massive financial benefits as a result of the Proposed Transaction, as the large, illiquid chunks of shares currently held by certain Defendants and Company insiders will be exchanged for cash. 73. In addition, under the terms of the Merger Agreement, upon the consummation of the Proposed Transaction, each outstanding Company option, equity award, restricted stock unit, or other right to purchase Company stock will vest and be cancelled in exchange for the right to receive the merger consideration, instantly converting additional large, illiquid holdings of many of the Individual Defendants and other Company insiders into cash. 74. For example, the following table sets forth the approximate amount of the payments that each of MRVC's directors and executive officers is entitled to receive in connection with the consummation of the Merger pursuant to their shares and MRVC compensatory awards held as of July 14, 2017: Name Shares Held (#)(1) Value of Shares Held ($)(2) Shares Underlying Vested Options (#)(3) Value of Vested Options ($)(4) Shares Underlying Accelerating MRV Compensatory Awards (#)(5) Value of Shares Underlying Accelerating MRV Compensatory Awards ($)(6) Aggregate Value for Equity ($) Kenneth H. Traub 33,831 338,310 26,103 7,881 9,070 35,120 381,311 Robert M. Pons 28,649 286,490 26,103 7,881 9,070 35,120 329,491 Mark J. Bonney 36,663 366,630 86,746 21,616 190,749 401,346 789,592 Brian Bellinger - - 14,083 2,711 9,070 35,120 37,831 Jeannie H. Diefenderfer 7,045 70,450 16,534 3,691 9,070 35,120 109,261 Jeffrey Tuder 3,657 36,570 6,165 - 9,070 35,120 71,690 Stephen G. Krulik 8,167 81,670 16,334 4,074 48,499 107,866 193,610 Adam L.A. Scheer 3,560 35,600 11,667 - 112,333 178,000 213,600 75. Furthermore, certain employment agreements with several MRVC officers or directors are entitled to severance packages should their employment be terminated under certain circumstances. These 'golden parachute' packages are significant, and will grant each director or - 18 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 19 of 27 Page ID #:19 officer entitled to them at the very least, hundreds of thousands of dollars, compensation not shared by MRVC's common stockholders. The following table sets forth the Golden Parachute compensation for certain MRVC directors and officers, as well as their estimated value payable: Name Cash ($)(1) Equity ($)(2) Perquisites/ Benefits ($)(3) All Other Compensation(4) Total ($) Mark J. Bonney 1,200,465 789,592 27,826 39,246 2,057,129 Stephen G. Krulik 298,200 193,610 14,731 23,045 529,586 Adam L.A. Scheer 468,600 213,600 19,642 22,304 724,146 76. Thus, while the Proposed Transaction is not in the best interests of MRVC's public stockholders, it will produce lucrative benefits for the Company's officers and directors. The Materially Misleading and/or Incomplete 14D-9 77. On July 17, 2017, MRVC filed with the SEC a materially misleading and incomplete 14D-9 that failed to provide the Company's stockholders with material information and/or provides them with materially misleading information critical to the total mix of information available to the Company's stockholders concerning the financial and procedural fairness of the Proposed Transaction. Omissions and/or Material Misrepresentations Concerning MRVC's Financial Projections 78. The 14D-9 fails to provide material information concerning financial projections provided by MRVC's management, reviewed with MRVC's and relied upon by Cowen in its analyses. Courts have uniformly stated that "projections … are probably among the most highlyprized disclosures by investors. Investors can come up with their own estimates of discount rates or [] market multiples. What they cannot hope to do is replicate management's inside view of the company's prospects." In re Netsmart Techs., Inc. S'holders Litig., 924 A.2d 171, 201-203 (Del. Ch. 2007). 79. With respect to the "Bidder Projections," the 14D-9 fails to disclose the following line items, (a) Taxes (or tax rate), (b) Capital expenditures, (c) Changes in net working capital; (d) - 19 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 20 of 27 Page ID #:20 Stock-based compensation expense, (e) EBITDA, (f) Interest Expense, (g) Non-recurring items, (h) Depreciation and amortization, (i) Earnings; and (j) Net operating profit. 80. Significantly, the 14D-9 fails to provide a reconciliation of all non-GAAP to GAAP financial metrics for CY2019 through CY 2022. When a company discloses information in a proxy that includes non-GAAP financial metrics, such as Adjusted EBITDA and Unlevered Free Cash Flow, the company must also disclose comparable GAAP metrics and a quantitative reconciliation of the non-GAAP metrics to GAAP metrics. See 17 C.F.R. § 244.100 (requiring that the disclosure of material non-GAAP financial measures be accompanied by an identification and presentation of the most directly comparable GAAP measure, and a reconciliation of the non- GAAP measure to the comparable GAAP measure by a clearly understandable method). Indeed, the SEC has repeatedly emphasized that disclosure of unreconciled non-GAAP projections is inherently misleading, and has heightened its scrutiny of the use of such projections. 81. Additionally, the 14D-9 also fails to disclose when the projections were prepared during the strategic alternative process, other than to state, "[t]he MRV Projections were prepared early in the process of consideration of strategic alternatives and were not updated." (14D-9 at 37.) The 14D-9 should disclose why the projections were not updated. 82. Further, the 14D-9 does not disclose why Parent was only supplied the Bidder Projections and why such projections only covered 2017-2018. 83. Without accurate projection data presented in the 14D-9, Plaintiff and other stockholders of MRVC are unable to properly evaluate the Company's true worth, the accuracy of Cowen's financial analyses, or make an informed decision whether to tender their Company stock in the Proposed Transaction. Omissions and/or Material Misrepresentations Concerning the Sales Process leading up to the Proposed Transaction 84. Specifically, the 14D-9 fails to provide material information concerning the process conducted by the Company and the events leading up to the Proposed Transaction. In particular, the 14D-9 fails to disclose: - 20 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 21 of 27 Page ID #:21 (a) The specific nature of any standstills provisions, including details related to any corresponding Don't Ask, Don't Waive ("DADW") provisions or fall-away provisions therein, entered into as part of NDA agreements between the Company on the one hand and the seven (7) identified parties who attended management presentations, and whether those standstills or NDAs are still in effect and were different in any way from one another; (b) The reasons communicated by PE-Backed Strategic Party for no longer having interest in pursuing a transaction with MRVC; (c) With respect to the December 5, 2016 non-binding letter of intent from the Other Strategic Interested Party that indicated an enterprise value of $40,000,000, excluding net operating losses and cash, what the value of the offer equated to on a per-share basis; (d) The reason that MRVC did not consider Other Strategic Party's potential interest in a roll-up acquisition in the summer of 2018 to be a "realistic prospect"; (e) What were the "technical items" that "required clarification internally relating to integration" that Parent needed to consider in February 2017; and (f) Why were no other interested parties permitted a site inspection of MRVC's Israel facility; and (g) The timing and nature of communications regarding future employment and/or directorship of MRVC's officers and directors, including who participated in all such communications. Omissions and/or Material Misrepresentations Concerning the Financial Analyses Performed by Cowen 85. In the 14D-9, Cowen describe its fairness opinions and the various valuation analyses performed to render its opinion. However, the descriptions fail to include necessary underlying data, support for conclusions, or the existence of, or basis for, underlying assumptions. Without this information, one cannot replicate the analyses, confirm the valuations or evaluate the fairness opinions. - 21 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 22 of 27 Page ID #:22 86. For example, the 14D-9 does not disclose material details concerning the analyses performed by Cowen in connection with the Proposed Transaction, including (among other things): a. Selected Publicly Traded Companies: With respect to Cowen's Selected Publicly Traded Companies Analysis, the 14D- 9 fails to disclose: i. The objective selection criteria and the observed company-by-company pricing multiples and financial metrics examined; ii. whether Cowen performed any benchmarking analysis in relation to the other publicly traded companies; and iii. The appropriateness of analyzing Implied Enterprise Value as a multiple of CY2017 Adjusted EBITDA given that the multiples for Calix, Inc. and Infinera Corp. were excluded and multiples for DASAN Zhone Solutions, Inc. and UTStarcom were not available; and iv. The appropriateness of analyzing for price as a multiple of CY2017E Non-GAAP EPS given that the multiples for four (4) of the six (6) identified companies were negative and therefore deemed not meaningful. b. Discounted Cash Flow Analyses: With respect to Cowen's Discounted Cash Flow analysis, the 14D-9 fails to disclose: i. the estimated future unlevered free cash flows of the Company used by Cowen in its analysis; ii. the definition of unlevered free cash flow; iii. Cowen's basis for utilizing a discount rate range of 16.0%-20.0%, including MRVC's cost of capital; and iv. Cowen's basis for utilizing terminal multiples of 6.0x-8.0x; - 22 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 23 of 27 Page ID #:23 v. The basis for Cowen performing a DCF which excluded "MRV's estimated United States federal net operating loss carryforwards; and vi. The basis for Cowen utilizing a discount rate of 18% in calculating the Company's net operating loss carryforwards. c. Selected Transactions With respect to Cowen's Selected Companies Analysis, the 14D-9 fails to disclose: i. The objective selection criteria and the observed company-by-company pricing multiples and financial metrics examined; and ii. The value for each selected transaction. 87. Without the omitted information identified above, MRVC's public stockholders are missing critical information necessary to evaluate whether the proposed consideration truly maximizes stockholder value and serves their interests. Moreover, without the key financial information and related disclosures, MRVC's public stockholders cannot gauge the reliability of the fairness opinion and the Board's determination that the Proposed Transaction is in their best interests. FIRST COUNT Claim for Breach of Fiduciary Duties (Against the Individual Defendants) 88. Plaintiff repeats all previous allegations as if set forth in full herein. 89. The Individual Defendants have violated their fiduciary duties of care, loyalty and good faith owed to Plaintiff and the Company's public stockholders. 90. By the acts, transactions and courses of conduct alleged herein, Defendants, individually and acting as a part of a common plan, are attempting to unfairly deprive Plaintiff and other members of the Class of the true value of their investment in MRVC. 91. As demonstrated by the allegations above, the Individual Defendants failed to exercise the care required, and breached their duties of loyalty and good faith owed to the stockholders of MRVC by entering into the Proposed Transaction through a flawed and unfair process and failing to take steps to maximize the value of MRVC to its public stockholders. - 23 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 24 of 27 Page ID #:24 92. Indeed, Defendants have accepted an offer to sell MRVC at a price that fails to reflect the true value of the Company, thus depriving stockholders of the reasonable, fair and adequate value of their shares. 93. Moreover, the Individual Defendants breached their duty of due care and candor by failing to disclose to Plaintiff and the Class all material information necessary for them to make an informed decision on whether to tender their shares in support of the Proposed Transaction. 94. The Individual Defendants dominate and control the business and corporate affairs of MRVC, and are in possession of private corporate information concerning MRVC's assets, business and future prospects. Thus, there exists an imbalance and disparity of knowledge and economic power between them and the public stockholders of MRVC which makes it inherently unfair for them to benefit their own interests to the exclusion of maximizing stockholder value. 95. By reason of the foregoing acts, practices and course of conduct, the Individual Defendants have failed to exercise due care and diligence in the exercise of their fiduciary obligations toward Plaintiff and the other members of the Class. 96. As a result of the actions of the Individual Defendants, Plaintiff and the Class will suffer irreparable injury in that they have not and will not receive their fair portion of the value of MRVC's assets and have been and will be prevented from obtaining a fair price for their common stock. 97. Unless the Individual Defendants are enjoined by the Court, they will continue to breach their fiduciary duties owed to Plaintiff and the members of the Class, all to the irreparable harm of the Class. 98. Plaintiff and the members of the Class have no adequate remedy at law. Only through the exercise of this Court's equitable powers can Plaintiff and the Class be fully protected from the immediate and irreparable injury which Defendants' actions threaten to inflict. SECOND COUNT Violations of Section 14(e) of the Exchange Act (Against All Defendants) 99. Plaintiff repeats all previous allegations as if set forth in full herein. - 24 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 25 of 27 Page ID #:25 100. Defendants have disseminated the 14D-9 with the intention of soliciting stockholders to tender their shares in favor of the Proposed Transaction. 101. Section 14(e) of the Exchange Act provides that in the solicitation of shares in a tender offer, "[i]t shall be unlawful for any person to make any untrue statement of a material fact or omit to state any material fact necessary in order to make the statements made, in the light of the circumstances under which they are made, not misleading[.]" 102. The 14D-9 was prepared in violation of Section 14(e) because it is materially misleading in numerous respects and omits material facts, including those set forth above. Moreover, in the exercise of reasonable care, Defendants knew or should have known that the 14D-9 is materially misleading and omits material facts that are necessary to render them non-misleading. 103. The Individual Defendants had actual knowledge or should have known of the misrepresentations and omissions of material facts set forth herein. 104. The Individual Defendants were at least negligent in filing a 14D-9 that was materially misleading and/or omitted material facts necessary to make the 14D-9 not misleading. 105. The misrepresentations and omissions in the 14D-9 are material to Plaintiff and the Class, and Plaintiff and the Class will be deprived of his entitlement to decide whether to tender his shares on the basis of complete information if such misrepresentations and omissions are not corrected prior to the expiration of the tender offer period regarding the Proposed Transaction. THIRD COUNT Violations of Section 20(a) of the Exchange Act (Against all Individual Defendants and ADVA NA Holdings, Inc.) 106. Plaintiff repeats all previous allegations as if set forth in full herein. 107. The Individual Defendants and ADVA NA were privy to non-public information concerning the Company and its business and operations via access to internal corporate documents, conversations and connections with other corporate officers and employees, - 25 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 26 of 27 Page ID #:26 attendance at management and Board meetings and committees thereof and via reports and other information provided to them in connection therewith. Because of their possession of such information, the Individual Defendants and ADVA NA knew or should have known that the 14D- 9 was materially misleading to Company stockholders. 108. The Individual Defendants and ADVA NA were involved in drafting, producing, reviewing and/or disseminating the materially false and misleading statements complained of herein. The Individual Defendants and ADVA NA were aware or should have been aware that materially false and misleading statements were being issued by the Company in the 14D-9 and nevertheless approved, ratified and/or failed to correct those statements, in violation of federal securities laws. The Individual Defendants and ADVA NA were able to, and did, control the contents of the 14D-9. The Individual Defendants and ADVA NA were provided with copies of, reviewed and approved, and/or signed the 14D-9 before its issuance and had the ability or opportunity to prevent its issuance or to cause it to be corrected. 109. The Individual Defendants and ADVA NA also were able to, and did, directly or indirectly, control the conduct of MRVC' business, the information contained in its filings with the SEC, and its public statements. Because of their positions and access to material non-public information available to them but not the public, the Individual Defendants and ADVA NA knew or should have known that the misrepresentations specified herein had not been properly disclosed to and were being concealed from the Company's stockholders and that the 14D-9 was misleading. As a result, the Individual Defendants and ADVA NA are responsible for the accuracy of the 14D- 9 and are therefore responsible and liable for the misrepresentations contained herein. 110. The Individual Defendants acted as controlling persons of MRVC within the meaning of Section 20(a) of the Exchange Act. By reason of their position with the Company, the Individual Defendants had the power and authority to cause MRVC to engage in the wrongful conduct complained of herein. The Individual Defendants controlled MRVC and all of its employees. Additionally, ADVA NA also had direct supervisory control over the composition of the 14D-9 and the information disclosed therein, as well as the information that was omitted and/or misrepresented in the 14D-9. As alleged above, MRVC is a primary violator of Section 14 of the - 26 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1 Filed 07/24/17 Page 27 of 27 Page ID #:27 Exchange Act and SEC Rule 14d-9. By reason of their conduct, the Individual Defendants are liable pursuant to section 20(a) of the Exchange Act. WHEREFORE, Plaintiff demands injunctive relief, in his favor and in favor of the Class, and against the Defendants, as follows: A. Ordering that this action may be maintained as a class action and certifying Plaintiff as the Class representatives and Plaintiff's counsel as Class counsel; B. Enjoining the Proposed Transaction; C. In the event defendants consummate the Proposed Transaction, rescinding it and setting it aside or awarding rescissory damages to Plaintiff and the Class; D. Declaring and decreeing that the Merger Agreement was agreed to in breach of the fiduciary duties of the Individual Defendants and is therefore unlawful and unenforceable; E. Directing the Individual Defendants to exercise their fiduciary duties to commence a sale process that is reasonably designed to secure the best possible consideration for MRVC and obtain a transaction which is in the best interests of MRVC and its stockholders; F. Directing defendants to account to Plaintiff and the Class for damages sustained because of the wrongs complained of herein; G. Awarding Plaintiff the costs of this action, including reasonable allowance for Plaintiff's attorneys' and experts' fees; and H. Granting such other and further relief as this Court may deem just and proper. DEMAND FOR JURY TRIAL Plaintiff hereby demands a jury on all issues which can be heard by a jury. Dated: July 24, 2017 BRODSKY & SMITH, LLC By: /s/ Evan J. Smith Evan J. Smith (SBN242352) 9595 Wilshire Boulevard, Suite 900 Beverly Hills, CA 90212 Telephone: (877) 534-2590 Facsimile: (310) 247-0160 Attorneys for Plaintiff - 27 - CLASS ACTION COMPLAINT

Case 2:17-cv-05434 Document 1-1 Filed 07/24/17 Page 1 of 3 Page ID #:28 UNITED STATES DISTRICT COURT, CENTRAL DISTRICT OF CALIFORNIA CIVIL COVER SHEET I. (a) PLAINTIFFS ( Check box if you are representing yourself) PETER ALLIA, On Behalf of Himself and All Others Similarly Situated, (b) County of Residence of First Listed Plaintiff Worcester, MA (EXCEPT IN U.S. PLAINTIFF CASES) (c) Attorneys (Firm Name, Address and Telephone Number) If you are representing yourself, provide the same information. Evan J. Smith, Brodsky & Smith, LLC, 9595 Wilshire Boulevard, Suite 900, Beverly Hills, CA 90212, (Tel) (877) 534-2590; Fax: (310) 247-0160 Email: esmith@brodskysmith.com DEFENDANTS (Check box if you are representing yourself) MRV COMMUNICATIONS, INC., et al. County of Residence of First Listed Defendant Los Angeles, CA (IN U.S. PLAINTIFF CASES ONLY) Attorneys (Firm Name, Address and Telephone Number) If you are representing yourself, provide the same information. II. BASIS OF JURISDICTION (Place an X in one box only.) 1. U.S. Government Plaintiff 3. Federal Question (U.S. Government Not a Party) 2. U.S. Government Defendant 4. Diversity (Indicate Citizenship of Parties in Item III) III. CITIZENSHIP OF PRINCIPAL PARTIES-For Diversity Cases Only (Place an X in one box for plaintiff and one for defendant) PTF DEF PTF DEF Citizen of This State 1 1 incorporated or Principal Place 4 4 of Business in this State Citizen of Another State 2 2 Incorporated and Principal Place 5 5 of Business in Another State Citizen or Subject of a Foreign Country 3 3 Foreign Nation 6 6 IV. ORIGIN (Place an X in one box only.) 1. Original proceeding 2. Removed from State Court 3. Remanded from Appellate Court 4. Reinstated or Reopened 5. Transferred from Another District (Specify) 6. Multidistrict Litigation - Transfer 8. Multidistrict Litigation - Direct File V. REQUESTED IN COMPLAINT: JURY DEMAND: Yes No (Check "Yes" only if demanded in complaint.) CLASS ACTION under F.R.Cv.P. 23: Yes No MONEY DEMANDED IN COMPLAINT: $VI. CAUSE OF ACTION (Cite the U.S. Civil Statute under which you are filing and write a brief statement of cause. Do not cite jurisdictional statutes unless diversity.) 15 U.S.C. § 78aa and 28 U.S.C. § 1331; Violations of the Exchange Act VII. NATURE OF SUIT (Place an X in one box only). OTHER STATUTES 375 False Claims Act 376 QuiTam (31 USC 3729(a)) 400 State Reapportionment 410 Antitrust 430 Banks and Banking 450 Commerce/ICC Rates/Etc. 460 Deportation 470 Racketeer Influ- enced & Corrupt Org. 480 Consumer Credit 490 Cable/Sat TV 850 Securities/Com- modities/Exchange 890 Other Statutory Actions 891 Agricultural Acts 893 Environmental Matters 895 Freedom of Info. Act 896 Arbitration 899 Admin. Procedures Act/Review of Appeal of Agency Decision 950 Constitutionality of State Statutes CONTRACT 110 Insurance 120 Marine 130 Miller Act 140 Negotiable Instrument 150 Recovery of Overpayment & Enforcement of Judgment 151 Medicare Act 152 Recovery of Defaulted Student Loan (Excl. Vet.) 153 Recovery of Overpayment of Vet. Benefits 160 Stockholders' Suits 190 Other Contract 195 Contract Product Liability 196 Franchise REAL PROPERTY 210 Land Condemnation 220 Foreclosure 230 Rent Lease & Ejectment REAL PROPERTY CONT. 240 Torts to Land 245 Tort Product Liability 290 All Other Real Property TORTS PERSONAL INJURY 310 Airplane 315 Airplane Product Liability 320 Assault, Libel & Slander 330 Fed. Employers' Liability 340 Marine 345 Marine Product Liability 350 Motor Vehicle 355 Motor Vehicle Product Liability 360 Other Personal Injury 362 Personal Injury- Med Malpratice 365 Personal Injury- Product Liability 367 Health Care/ Pharmaceutical Personal Injury Product Liability 368 Asbestos Personal Injury Product Liability IMMIGRATION 462 Naturalization Application 465 Other Immigration Actions TORTS PERSONAL PROPERTY 370 Other Fraud 371 Truth in Lending 380 Other Personal Property Damage 385 Property Damage Product Liability BANKRUPTCY 422 Appeal 28 USC 158 423 Withdrawal 28 USC 157 CIVIL RIGHTS 440 Other Civil Rights 441 Voting 442 Employment 443 Housing/ Accommodations 445 American with Disabilities- Employment 446 American with Disabilities-Other 448 Education PRISONER PETITIONS Habeas Corpus: 463 Alien Detainee 510 Motions to Vacate Sentence 530 General 535 Death Penalty Other: 540 Mandamus/Other 550 Civil Rights 555 Prison Condition 560 Civil Detainee Conditions of Confinement FORFEITURE/PENALTY 625 Drug Related Seizure of Property 21 USC 881 690 Other LABOR 710 Fair Labor Standards Act 720 Labor/Mgmt. Relations 740 Railway Labor Act 751 Family and Medical Leave Act 790 Other Labor Litigation 791 Employee Ret. Inc. Security Act PROPERTY RIGHTS 820 Copyrights 830 Patent 835 Patent - Abbreviated New Drug Application 840 Trademark SOCIAL SECURITY 861 HIA (1395ff) 862 Black Lung (923) 863 DIWC/DIWW (405 (g)) 864 SSID Title XVI 865 RSI (405 (g)) FEDERAL TAX SUITS 870 Taxes (U.S. Plaintiff or Defendant) 871 IRS-Third Party 26 USC 7609 FOR OFFICE USE ONLY: Case Number: CV-71 (05/17) CIVIL COVER SHEET Page 1 of 3

Case 2:17-cv-05434 Document 1-1 Filed 07/24/17 Page 2 of 3 Page ID #:29 UNITED STATES DISTRICT COURT, CENTRAL DISTRICT OF CALIFORNIA CIVIL COVER SHEET VIII. VENUE: Your answers to the questions below will determine the division of the Court to which this case will be initially assigned. This initial assignment is subject to change, in accordance with the Court's General Orders, upon review by the Court of your Complaint or Notice of Removal. QUESTION A: Was this case removed from state court? Yes No If "no," skip to Question B. If "yes," check the box to the right that applies, enter the corresponding division in response to Question E, below, and continue from there. STATE CASE WAS PENDING IN THE COUNTY OF: INITIAL DIVISION IN CACD IS: Los Angeles, Ventura, Santa Barbara, or San Luis Obispo Western Orange Southern Riverside or San Bernardino Eastern QUESTION B: Is the United States, or one of its agencies or employees, a PLAINTIFF in this action? Yes No If "no," skip to Question C. If "yes," answer Question B.1, at right. B.1. Do 50% or more of the defendants who reside in the district reside in Orange Co.? check one of the boxes to the right B.2. Do 50% or more of the defendants who reside in the district reside in Riverside and/or San Bernardino Counties? (Consider the two counties together.) check one of the boxes to the right YES. Your case will initially be assigned to the Southern Division. Enter "Southern" in response to Question E, below, and continue from there. NO. Continue to Question B.2. YES. Your case will initially be assigned to the Eastern Division. Enter "Eastern" in response to Question E, below, and continue from there. NO. Your case will initially be assigned to the Western Division. Enter "Western" in response to Question E, below, and continue from there. QUESTION C: Is the United States, or one of its agencies or employees, a DEFENDANT in this action? Yes No If "no," skip to Question D. If "yes," answer Question C.1, at right. C.1. Do 50% or more of the plaintiffs who reside in the district reside in Orange Co.? check one of the boxes to the right C.2. Do 50% or more of the plaintiffs who reside in the district reside in Riverside and/or San Bernardino Counties? (Consider the two counties together.) check one of the boxes to the right YES. Your case will initially be assigned to the Southern Division. Enter "Southern" in response to Question E, below, and continue from there. NO. Continue to Question C.2. YES. Your case will initially be assigned to the Eastern Division. Enter "Eastern" in response to Question E, below, and continue from there. NO. Your case will initially be assigned to the Western Division. Enter "Western" in response to Question E, below, and continue from there. QUESTION D: Location of plaintiffs and defendants? Indicate the location(s) in which 50% or more of plaintiffs who reside in this district reside. (Check up to two boxes, or leave blank if none of these choices apply.) Indicate the location(s) in which 50% or more of defendants who reside in this district reside. (Check up to two boxes, or leave blank if none of these choices apply.) A. Orange County B. Riverside or San Bernardino County C. Los Angeles, Ventura, Santa Barbara, or San Luis Obispo County D.1. Is there at least one answer in Column A? Yes No If "yes," your case will initially be assigned to the SOUTHERN DIVISION. Enter "Southern" in response to Question E, below, and continue from there. If "no," go to question D2 to the right. D.2. Is there at least one answer in Column B? Yes No If "yes," your case will initially be assigned to the EASTERN DIVISION. Enter "Eastern" in response to Question E, below. If "no," your case will be assigned to the WESTERN DIVISION. Enter "Western" in response to Question E, below. QUESTION E: Initial Division? INITIAL DIVISION IN CACD Enter the initial division determined by Question A, B, C, or D above: WESTERN QUESTION F: Northern Counties? Do 50% or more of plaintiffs or defendants in this district reside in Ventura, Santa Barbara, or San Luis Obispo counties? Yes No CV-71 (05/17) CIVIL COVER SHEET Page 2 of 3

Case 2:17-cv-05434 Document 1-1 Filed 07/24/17 Page 3 of 3 Page ID #:30 UNITED STATES DISTRICT COURT, CENTRAL DISTRICT OF CALIFORNIA CIVIL COVER SHEET IX(a). IDENTICAL CASES: Has this action been previously filed in this court? NO YES If yes, list case number(s): IX(b). RELATED CASES: Is this case related (as defined below) to any civil or criminal case(s) previously filed in this court? NO YES If yes, list case number(s): Civil cases are related when they (check all that apply): A. Arise from the same or a closely related transaction, happening, or event; B. Call for determination of the same or substantially related or similar questions of law and fact; or C. For other reasons would entail substantial duplication of labor if heard by different judges. Note: That cases may involve the same patent, trademark, or copyright is not, in itself, sufficient to deem cases related. A civil forfeiture case and a criminal case are related when they (check all that apply): A. Arise from the same or a closely related transaction, happening, or event; B. Call for determination of the same or substantially related or similar questions of law and fact; or C. Involve one or more defendants from the criminal case in common and would entail substantial duplication of labor if heard by different judges. X. SIGNATURE OF ATTORNEY (OR SELF-REPRESENTED LITIGANT): /s/Evan J. Smith DATE: July 24,2017 Notice to Counsel/Parties: The submission of this Civil Cover Sheet is required by Local Rule 3-1. This Form CV-71 and the information contained herein neither replaces nor supplements the filing and service of pleadings or other papers as required by law, except as provided by local rules of court. For more detailed instructions, see separate instruction sheet (CV-071 A). Key to Statistical codes relating to Social Security Cases: Nature of Suit Code Abbreviation Substantive Statement of Cause of Action 861 HIA All claims for health insurance benefits (Medicare) under Title 18, Part A, of the Social Security Act, as amended. Also, include claims by hospitals, skilled nursing facilities, etc., for certification as providers of services under the program. (42 U.S.C. 1935FF(b)) 862 BL All claims for "Black Lung" benefits under Title 4, Part B, of the Federal Coal Mine Health and Safety Act of 1969. (30 U.S.C. 923) 863 DIWC All claims filed by insured workers for disability insurance benefits under Title 2 of the Social Security Act, as amended; plus all claims filed for child's insurance benefits based on disability. (42 U.S.C. 405 (g)) 863 DIWW All claims filed for widows or widowers insurance benefits based on disability under Title 2 of the Social Security Act, as amended. (42 U.S.C. 405 (g)) 864 SSID All claims for supplemental security income payments based upon disability filed under Title 16 of the Social Security Act, as amended. 865 RSI All claims for retirement (old age) and survivors benefits under Title 2 of the Social Security Act, as amended. (42 U.S.C. 405(g)) CV-71 (05/17) CIVIL COVER SHEET Page 3 of 3

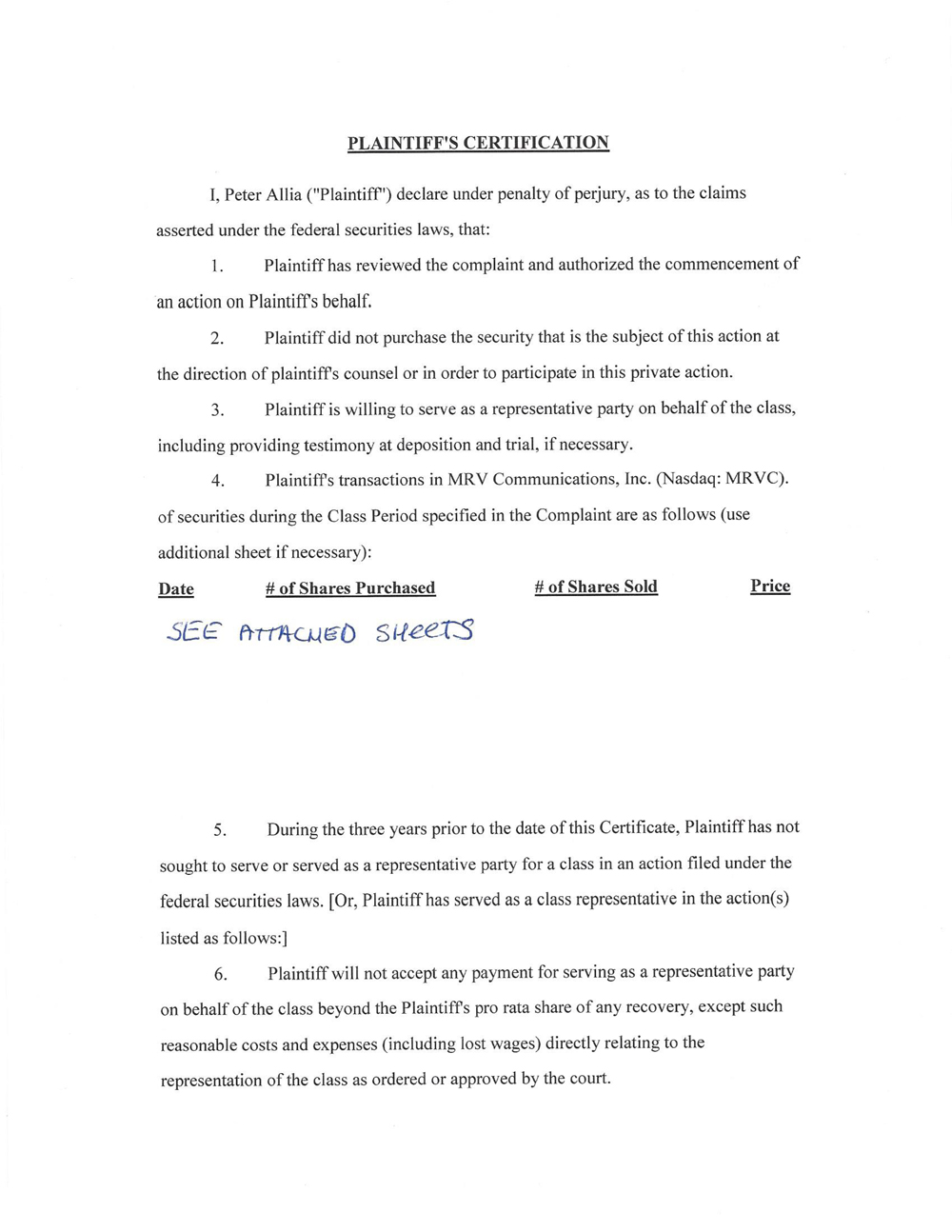

Case 2:17-cv-05434 Document 1-2 Filed 07/24/17 Page 1 of 4 Page ID #:31 PLAINTIFF'S CERTIFICATION I, Peter Allia ("Plaintiff") declare under penalty of perjury, as to the claims asserted under the federal securities laws, that: 1. Plaintiff has reviewed the complaint and authorized the commencement of an action on Plaintiffs behalf. 2. Plaintiff did not purchase the security that is the subject of this action at the direction of plaintiffs counsel or in order to participate in this private action. 3. Plaintiff is willing to serve as a representative party on behalf of the class, including providing testimony at deposition and trial, if necessary. 4. Plaintiffs transactions in MRV Communications, Inc. (Nasdaq: MRVC). of securities during the Class Period specified in the Complaint are as follows (use additional sheet if necessary): Date # of Shares Purchased # of Shares Sold Price SEE ATTACHED SHEETS 5. During the three years prior to the date of this Certificate, Plaintiff has not sought to serve or served as a representative party for a class in an action filed under the federal securities laws. [Or, Plaintiff has served as a class representative in the action(s) listed as follows:] 6. Plaintiff will not accept any payment for serving as a representative party on behalf of the class beyond the Plaintiffs pro rata share of any recovery, except such reasonable costs and expenses (including lost wages) directly relating to the representation of the class as ordered or approved by the court.

Case 2:17-cv-05434 Document 1-2 Filed 07/24/17 Page 2 of 4 Page ID #:32 I declare under penalty of perjury that the foregoing is true and correct. Executed this 12th day of July, 2017. Sign Name: Peter Allia Print Name: Peter Allia Address: 9 Powerline Drive State, Zip Code: Grafton, MA 01519 County: Worcester

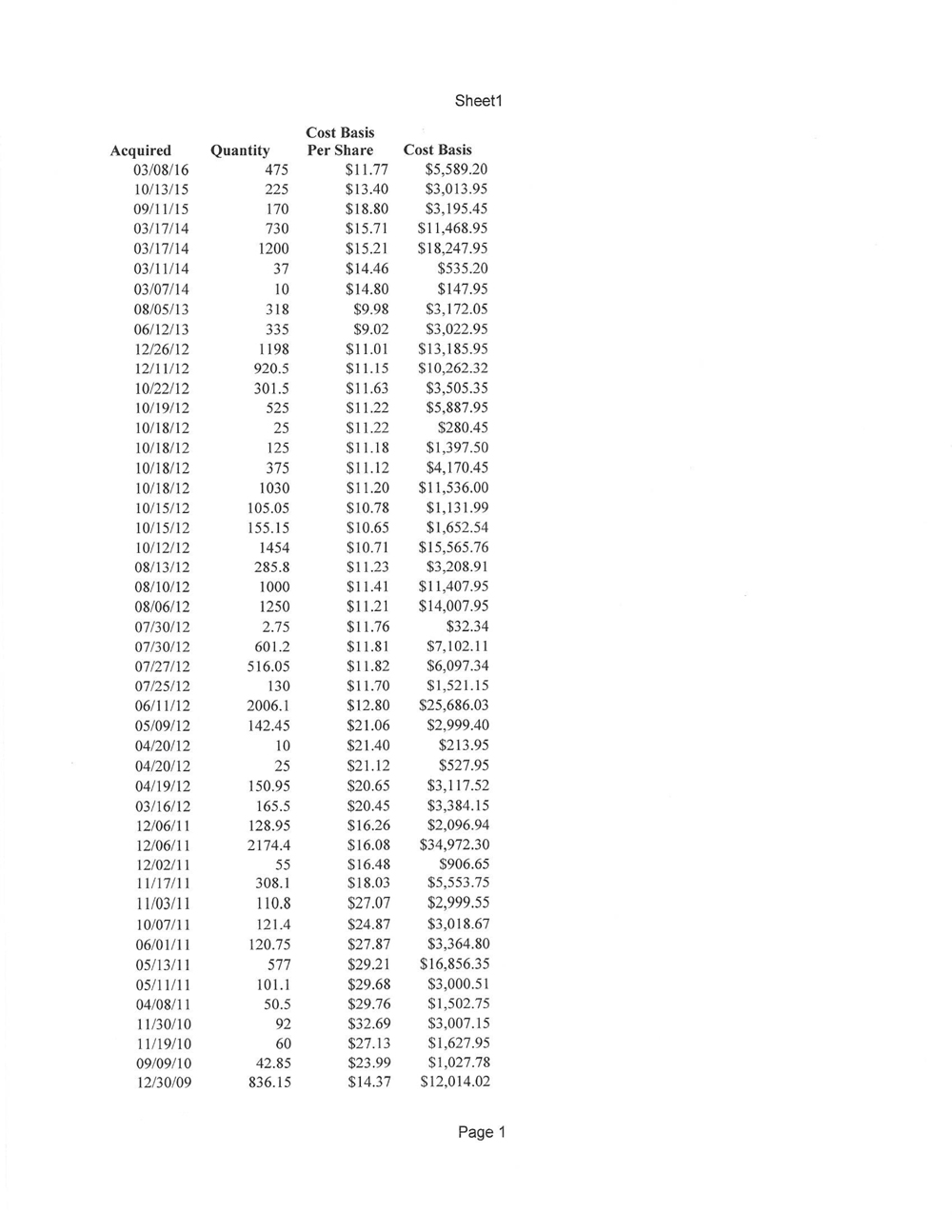

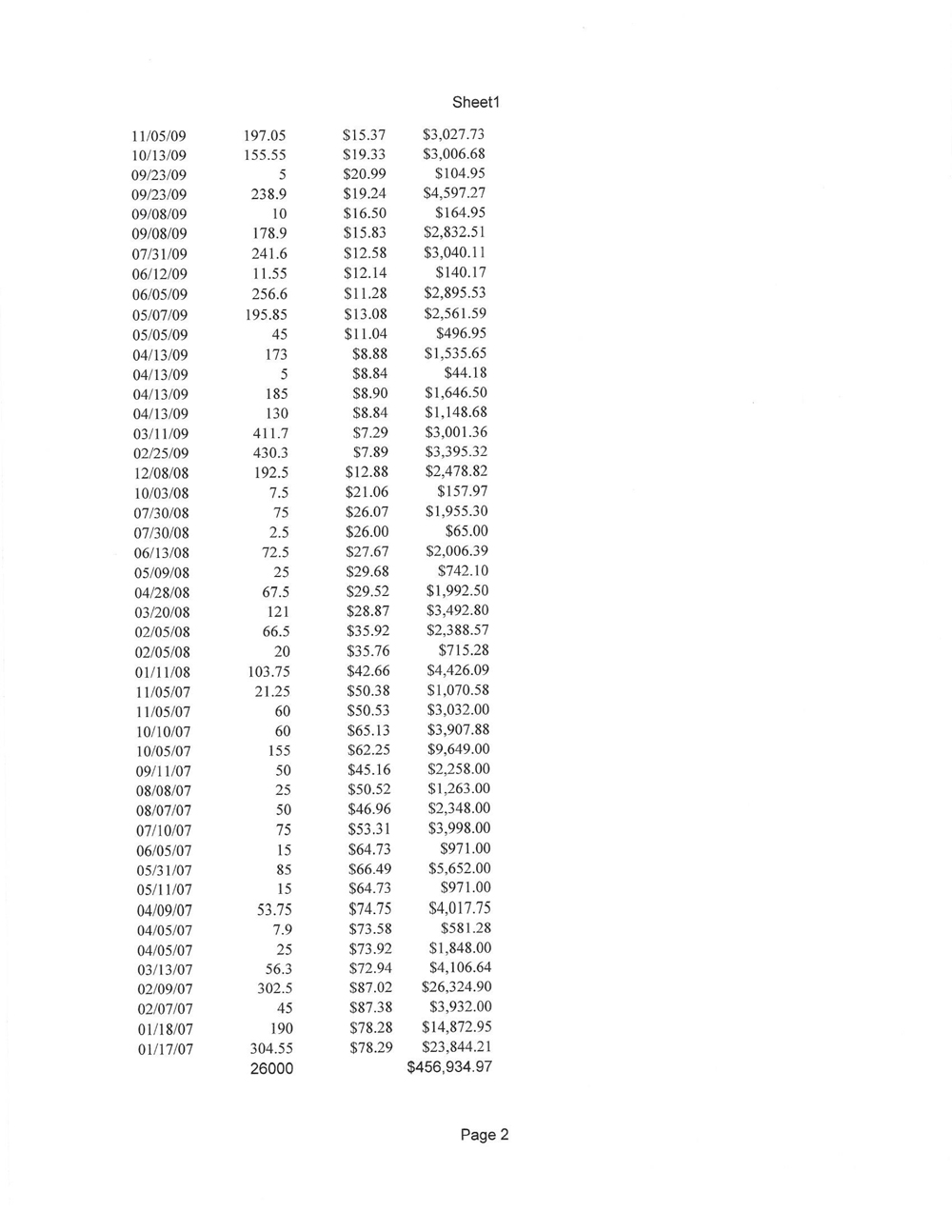

Case 2:17-cv-05434 Document 1-2 Filed 07/24/17 Page 3 of 4 Page ID #:33 Sheetl Cost Basis Acquired Quantity Per Share Cost Basis 03/08/16 475 $11.77 $5,589.20 10/13/15 225 $13.40 $3,013.95 09/11/15 170 $18.80 $3,195.45 03/17/14 730 $15.71 $11,468.95 03/17/14 1200 $15.21 $18,247.95 03/11/14 37 $14.46 $535.20 03/07/14 10 $14.80 $147.95 08/05/13 318 $9.98 $3,172.05 06/12/13 335 $9.02 $3,022.95 12/26/12 1198 $11.01 $13,185.95 12/11/12 920.5 $11.15 $10,262.32 10/22/12 301.5 $11.63 $3,505.35 10/19/12 525 $11.22 $5,887.95 10/18/12 25 $11.22 $280.45 10/18/12 125 $11.18 $1,397.50 10/18/12 375 $11.12 $4,170.45 10/18/12 1030 $11.20 $11,536.00 10/15/12 105.05 $10.78 $1,131.99 10/15/12 155.15 $10.65 $1,652.54 10/12/12 1454 $10.71 $15,565.76 08/13/12 285.8 $11.23 $3,208.91 08/10/12 1000 $11.41 $11,407.95 08/06/12 1250 $11.21 $14,007.95 07/30/12 2.75 $11.76 $32.34 07/30/12 601.2 $11.81 $7,102.11 07/27/12 516.05 $11.82 $6,097.34 07/25/12 130 $11.70 $1,521.15 06/11/12 2006.1 $12.80 $25,686.03 05/09/12 142.45 $21.06 $2,999.40 04/20/12 10 $21.40 $213.95 04/20/12 25 $21.12 $527.95 04/19/12 150.95 $20.65 $3,117.52 03/16/12 165.5 $20.45 $3,384.15 12/06/11 128.95 $16.26 $2,096.94 12/06/11 2174.4 $16.08 $34,972.30 12/02/11 55 $16.48 $906.65 11/17/11 308.1 $18.03 $5,553.75 11/03/11 110.8 $27.07 $2,999.55 10/07/11 121.4 $24.87 $3,018.67 06/01/11 120.75 $27.87 $3,364.80 05/13/11 577 $29.21 $16,856.35 05/11/11 101.1 $29.68 $3,000.51 04/08/11 50.5 $29.76 $1,502.75 11/30/10 92 $32.69 $3,007.15 11/19/10 60 $27.13 $1,627.95 09/09/10 42.85 $23.99 $1,027.78 12/30/09 836.15 $14.37 $12,014.02

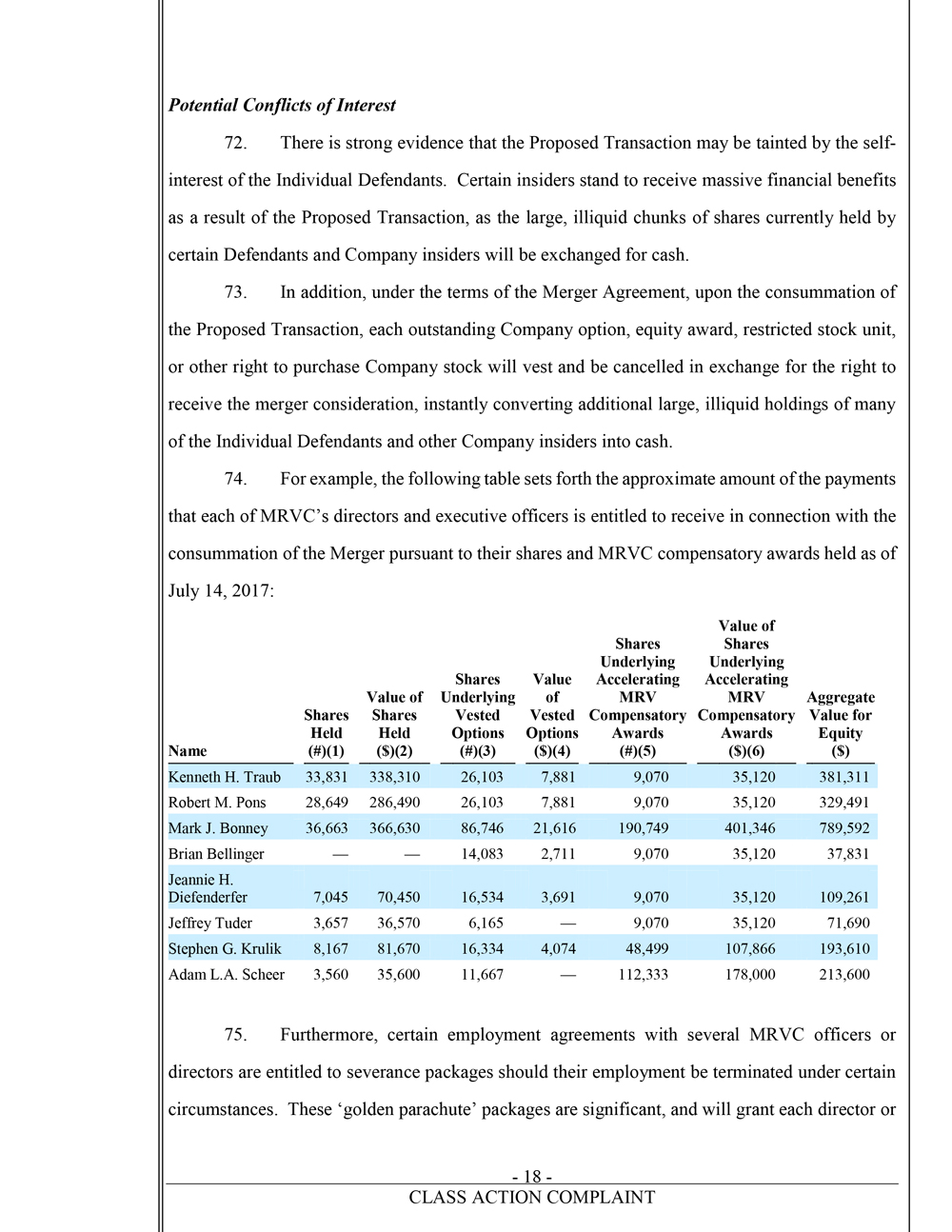

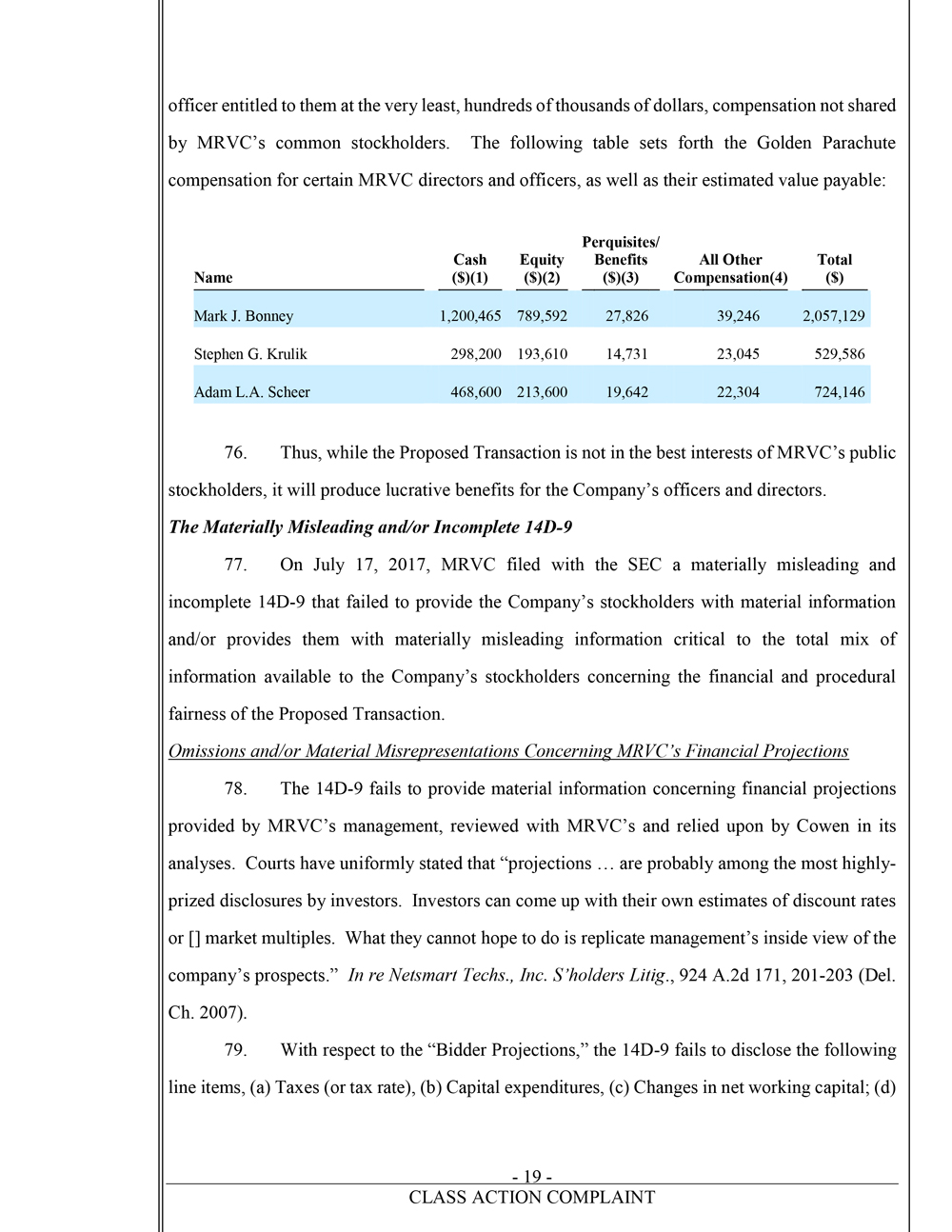

Case 2:17-cv-05434 Document 1-2 Filed 07/24/17 Page 4 of 4 Page ID #:34 Sheetl 11/05/09 197.05 S15.37 $3,027.73 10/13/09 155.55 $19.33 $3,006.68 09/23/09 5 $20.99 $104.95 09/23/09 238.9 $19.24 $4,597.27 09/08/09 10 $16.50 $164.95 09/08/09 178.9 $15.83 $2,832.51 07/31/09 241.6 $12.58 $3,040.11 06/12/09 11.55 $12.14 $140.17 06/05/09 256.6 $11.28 $2,895.53 05/07/09 195.85 $13.08 $2,561.59 05/05/09 45 $11.04 $496.95 04/13/09 173 $8.88 $1,535.65 04/13/09 5 $8.84 $44.18 04/13/09 185 $8.90 $1,646.50 04/13/09 130 $8.84 $1,148.68 03/11/09 411.7 $7.29 $3,001.36 02/25/09 430.3 $7.89 $3,395.32 12/08/08 192.5 $12.88 $2,478.82 10/03/08 7.5 $21.06 $157.97 07/30/08 75 $26.07 $1,955.30 07/30/08 2.5 $26.00 $65.00 06/13/08 72.5 $27.67 $2,006.39 05/09/08 25 $29.68 $742.10 04/28/08 67.5 $29.52 $1,992.50 03/20/08 121 $28.87 $3,492.80 02/05/08 66.5 $35.92 $2,388.57 02/05/08 20 $35.76 $715.28 01/11/08 103.75 $42.66 $4,426.09 11/05/07 21.25 $50.38 $1,070.58 11/05/07 60 $50.53 $3,032.00 10/10/07 60 $65.13 $3,907.88 10/05/07 155 $62.25 $9,649.00 09/11/07 50 $45.16 $2,258.00 08/08/07 25 $50.52 $1,263.00 08/07/07 50 $46.96 $2,348.00 07/10/07 75 $53.31 $3,998.00 06/05/07 15 $64.73 $971.00 05/31/07 85 $66.49 $5,652.00 05/11/07 15 $64.73 $971.00 04/09/07 53.75 $74.75 $4,017.75 04/05/07 7.9 $73.58 $581.28 04/05/07 25 $73.92 $1,848.00 03/13/07 56.3 $72.94 $4,106.64 02/09/07 302.5 $87.02 $26,324.90 02/07/07 45 $87.38 $3,932.00 01/18/07 190 $78.28 $14,872.95 01/17/07 304.55 $78.29 $23,844.21 26000 $456,934.97