Exhibit (a)(5)(F)

| David E. Bower (SBN 119546) MONTEVERDE & ASSOCIATES PC 600 Corporate Pointe, Suite 1170 Culver City, CA 90230 Tel: (213) 446-6652 Fax: (212) 202-7880 Attorneys for Plaintiffs conformed copy original filed superior court of California County of Los Angeles July 25 2017 SUPERIOR COURT OF THE STATE OF CALIFORNIA IN AND FOR THE COUNTY OF LOS ANGELES RAVINDRAN CHELVARATNAM, individually Case No. BC 669740 and on behalf of all others similarly situated, Plaintiffs, CLASS ACTION V. COMPLAINT FOR BREACHES OF FIDUCIARY DUTY KEN TRAUB, MARK J. BONNEY, ROBERT PONS, JEANNIE H. DIEFENDERFER, BRIAN BELLINGER, and JEFFREY TUDER, DEMAND FOR JURY TRIAL Assigned to Judge Ann Jones Defendants. Dept. 308 Plaintiff Ravindran Chelvaratnam (“Plaintiff’),by his attorneys, alleges upon information and belief, except for his own acts, which are alleged on personal knowledge, as follows: SUMMARY OF THE ACTION 1. This is a stockholder class action brought by plaintiff on behalf of all holders of MRV Communications, Inc. (“MRV” or the “Company”) common stock against the members of MRV’s board of directors (the “Board” or the “Defendants”). This action seeks to enjoin Defendants from further breaching their fiduciary duties in their pursuit of a sale of the Company at an unfair price and through an unfair and self-serving process to ADVA NA Holdings, Inc. (“ADVA”). 2. MRV is a Delaware corporation and maintains its headquaiters at 20520 Nordhoff Street, Chatsworth, California. The Company enables service providers, data center operators and COMPLAINT FOR BREACHES OF FIDUCIARY DUTY |

| enterprises to make their networks smarter, faster, and easier to operate. MRV’s end-to-end portfolio includes innovative packet, optical, and software platforms designed for flexibility and reliability. MRV’s common stock trades on the NASDAQ under the ticker symbol “MRVC”. 3. On July 2, 2017, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with ADVA. 4. Pursuant to the Merger Agreement, on July 17, 2017, a wholly owned subsidiary of ADVA (“Merger Sub”) commenced a tender offer (the “Tender Offer”) to purchase all the outstanding shares of MRV common stock for $10.00 per share (the “Offer Price”). The Tender Offer is scheduled to expire at 12:00 midnight, Eastern time, at the end of the day on August 11, 2017. Upon the successful completion of the Tender Offer, Merger Sub will merge with and into MRV, with MRV continuing as the surviving corporation and a wholly owned subsidiary of ADVA (the “Proposed Transaction”). 5. The Offer Price undervalues MRV and provides a grossly insufficient premium to MRV stockholders. 6. Compounding the failure to provide adequate consideration, the sales and negotiation process leading up to the consummation of the Merger Agreement was fundamentally flawed. 7. Moreover, Defendants agreed to lock-up the Proposed Transaction with preclusive deal protection devices. Pursuant to the Merger Agreement, Defendants agreed to: (i) a strict no-solicitation provision that prevents the Company from soliciting other potential acquirers and continuing discussions and negotiations with potential acquirers; (ii) a matching rights provision that requires the Company to disclose confidential information about competing bids to ADVA within 48 hours; (iii) a provision that provides ADVA with five (5) business days to match any competing proposal in the event one is made; and (iv) a prohibitively large combined termination fee of up to $3,410,000. 8. Additionally, certain members of the Company’s Board and officers of the Company, along with affiliates of MRV stockholder Raging Capital Management, LLC (“Raging Capital”), have 3 COMPLAINT FOR BREACHES OF FIDUCIARY |

| signed Tender and Support Agreements covering all shares beneficially owned by such individuals. These agreements provide that the signatory will fully support the Tender Offer and oppose any alternative acquisition proposal. 9. These deal protection provisions and Support Agreements, particularly when considered collectively, substantially and improperly limit the Board’s ability to act with respect to investigating and pursuing superior proposals and alternatives, including a sale of all or part of MRV. 10. On July 17, 2017, MRV filed with the U.S. Securities and Exchange Commission (“SEC”) a materially incomplete and misleading Solicitation/Recommendation Statement on Schedule 14D-9 (the “Recommendation Statement”). The Recommendation Statement provides materially misleading information and omits material information related to the Tender Offer, including the financial analyses conducted by the Board’s financial advisor, Cowen and Company, LLC (“Cowen”), in support of its fairness opinion. 11. For these reasons and as set forth in detail herein, Plaintiff seeks to enjoin Defendants from closing the Tender Offer and taking any further steps to consummate the Proposed Transaction, or, in the event the Proposed Transaction is consummated, to recover damages resulting from the Defendants’ violations of their fiduciary duties of loyalty, good faith, and due care. JURISDICTION AND VENUE 12. This Court has jurisdiction over the cause of action asserted herein pursuant to the California Constitution, art. VI, §10, because the cause of action is not given by statute to other trial courts. 13. This Court has personal jurisdiction over Defendants because they conduct business in and have sufficient minimum contacts with California, including maintaining their Company headquarters at 20520 Nordhoff St., Chatsworth, CA 91311. 14. Venue is proper in this Court because the conduct at issue took place and had an effect in this County. THE PARTIES 4 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 15. Plaintiff is, and has been at all relevant times, a stockholder of MRV. 16. Defendant Ken Traub is director of MRV and is the Chairman of the Board. In December 2015, Traub agreed to serve as a Managing Partner of Raging Capital, the Company’s largest stockholder, with obligations to Raging Capital effective immediately. 17. Defendant Mark J. Bonney is a director of MRV and is the President and Chief Executive Officer of the Company. 18. Defendant Robert Pons is, and has been at all relevant times, a director of the Company. 19. Defendant Jeannie H. Diefenderfer is, and has been at all relevant times, a director of the Company. 20. Defendant Brian Bellinger is, and has been at all relevant times, a director of the Company. Bellinger is also a Senior Analyst at Raging Capital. 21. Defendant Jeffrey Tuder is, and has been at all relevant times, a director of the Company. 22. The parties listed in paragraph 16-21 are referred to collectively as “Defendants”. THE DEFENDANTS’ FIDUCIARY DUTIES 23. By reason of the Defendants’ positions with the Company as officers and/or directors, said individuals are in a fiduciary relationship with Plaintiff and the other stockholders of MRV and owe Plaintiff and the other members of the Class (defined herein) the duties of good faith, fair dealing, candor, and loyalty. 24. By virtue of their positions as directors and/or officers of MRV, the Defendants, at all relevant times, had the power to control and influence, and did control, influence, and cause MRV to engage in the practices complained of herein. 25. Each of the Defendants is required to act in good faith, in the best interests of the Company’s stockholders, and with such care, including reasonable inquiry, as would be expected of an ordinarily prudent person. In a situation where the directors of a publicly traded company undertake a transaction that may result in a change in corporate control, the directors must take all steps 5 COMPLAINT FOR BREACHES OF FIDUCIARY |

| reasonably required to maximize the value stockholders will receive rather than use a change of control to benefit themselves. To diligently comply with this duty, the directors of a corporation may not take any action that: (a) adversely affects the value provided to the corporation’s stockholders; (b) contractually prohibits them from complying with or carrying out their fiduciary duties; (c) discourages or inhibits alternative offers to purchase control of the corporation or its assets; (d) will otherwise adversely affect their duty to search for and secure the best value reasonably available under the circumstances for the corporation’s stockholders; or (e) will provide the directors and/or officers with preferential treatment at the expense of, or separate from, the public stockholders. 26. Plaintiff alleges herein that the Defendants, separately and together, in connection with the Proposed Transaction, violated duties owed to Plaintiff and the other stockholders of MRV, including their duties of loyalty, good faith, due care, candor, and independence, insofar as they, inter alia: (i) failed to obtain the best price possible under the circumstances before entering into the Merger Agreement; (ii) engaged in self-dealing and obtained for themselves personal benefits, including personal financial benefits, not shared equally by Plaintiff or the other stockholders of MRV common stock; and (iii) caused the materially incomplete and misleading Recommendation Statement to be disseminated to the Company’s shareholders. CLASS ACTION ALLEGATIONS 27. Plaintiff brings this action pursuant to California Code of Civil Procedure §382, individually and on behalf of the stockholders of MRV common stock who are being and will be harmed by defendants’ actions described herein (the “Class”). The Class specifically excludes Defendants herein, and any person, firm, trust, corporation or other entity related to, or affiliated with, any of the Defendants. 6 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 28. This action is properly maintainable as a class action because: (a) The Class is so numerous that joinder of all members is impracticable. According to the Merger Agreement, as of the close of business on July 2, 2017, there were approximately 6.8 million shares of MRV common stock issued and outstanding. The actual number of public stockholders of MRV will be ascertained through discovery; (b) There are questions of law and fact which are common to the Class, including inter alia, the following: i. whether the Defendants have breached their fiduciary duties of undivided loyalty, independence, due care, and candor with respect to Plaintiff and the other members of the Class in connection with the Proposed Transaction; ii. whether Defendants are engaging in self-dealing in connection with the Proposed Transaction; iii. whether the Defendants have breached their fiduciary duty to secure and obtain the best price reasonable under the circumstances for the benefit of Plaintiff and the other members of the Class in connection with the Proposed Transaction; iv. whether Defendants are unjustly enriching themselves and other insiders or affiliates of MRV and/or ADVA; v. whether the Defendants, in bad faith and for improper motives, have impeded or erected barriers to discourage other offers for the Company or its assets; and vi. whether Plaintiff and the other members of the Class would suffer irreparable injury were the Proposed Transaction complained of herein consummated. (c) Plaintiff is an adequate representative of the Class, has retained competent counsel experienced in litigation of this nature and will fairly and adequately protect the interests of the Class; 7 COMPLAINT FOR BREACHES OF FIDUCIARY |

| (d) Plaintiff’s claims are typical of the claims of the other members of the Class and Plaintiff does not have any interests adverse to the Class; (e) The prosecution of separate actions by individual members of the Class would create a risk of inconsistent or varying adjudications with respect to individual members of the Class which would establish incompatible standards of conduct for the party opposing the Class; (f) Plaintiff anticipates that there will be no difficulty in the management of this litigation and, thus, a class action is superior to other available methods for the fair and efficient adjudication of this controversy; and (g) Defendants have acted on grounds generally applicable to the Class with respect to the matters complained of herein, thereby making appropriate the relief sought herein with respect to the Class as a whole. THE OFFER PRICE UNDERVALUES MRV 29. MRV, incorporated on March 9, 1992, is a supplier of communications solutions to telecommunications service providers, enterprises, and governments throughout the world. The Company’s products enable customers to provide high-bandwidth data, video services, and mobile communications services. The Company operates through Network Equipment segment. Its Network Equipment segment designs, manufactures, sells, and services equipment used by commercial customers, governments, and telecommunications service providers. Its products include switches, optical transport platforms, physical layer products, out-of-band management products, and specialized networking products. MRV markets and sells its products, through a variety of channels, which include a direct sales force, manufacturers’ representatives, value-added-resellers, distributors, and systems integrators. 30. The Offer Price is grossly inadequate given MRV’s recent financial performance and strong growth prospects. In the six months leading up to the Merger Agreement, MRV’s stock price 8 COMPLAINT FOR BREACHES OF FIDUCIARY |

| increased approximately 24%, going from $7.95 on January 2, 2017 to $9.85 on June 30, 2017, as illustrated by the chart below: 31. At the time of the announcement of the Tender Offer, NCI stock was trading almost equal to the Offer Price. Typically, in merger situations the target company receives a substantial premium from the acquirer. Here, there is virtually no premium. On July 3, 2017, the day the Tender Offer was announced, MRV stock was trading at $9.90 per share. This means that the Offer Price represented a paltry 1% premium. The July 3rd stock price cannot be attributed to deal rumors, because there were no rumors prior to the announcement. The average price for the 12 months leading up to the announcement of the Proposed Transaction was also $9.90 per share. 9 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 32. Indeed, on March 9, 2017, the Company announced positive financial results for the 2016 fourth quarter and full fiscal year. The Company beat earnings projections for both the quarter and the year. CEO Bonney noted: “In the fourth quarter, we grew revenue 13% year-over year delivering revenue of $20.9 million, despite continued temporary softness in orders from two of our largest customers. In the quarter, we accomplished several important product development milestones and completed the transition of all packet and optical manufacturing to a single world-class manufacturing partner. Also, we implemented a cost reduction program that reduces our future operating costs by approximately $5 million per year while preserving our capability to execute on our product roadmap, support all of our customers and grow the business.” 33. As a result of the positive earnings report, MRV stock skyrocketed. The week after the earnings release, their stock was trading at $10.95 per share, up approximately 55%. 34. Financial analysts had long noted that MRV was trading at a very low multiple, and any deal, based on underlying value, would likely result in a large premium. Multiple analysts arrived at the same figure of 75% upside. More recently, financial analysts placed a price target for MRV at $13.50. This represents a significant premium to the Offer Price of $10. It is important to note that price targets are a predictive valuation of what the stock is worth on its own.1 They do not account for premiums associated with a merger or takeover. A “take-out price”, or the price that analysts predict in the event a merger or takeover, would include those premiums and be significantly higher. 35. In sum, the $10.00 per share Merger Consideration significantly undervalues MRV, especially given its recent financial performance. Having failed to maximize the sale price for the Company, Defendants breached the fiduciary duties they owe to the Company’s public stockholders, as the Company has been improperly valued and public stockholders will not receive adequate or fair value for their MRV common stock. THE BOARD CONDUCTED A FLAWED PROCESS THAT FAILED TO MAXIMIZE STOCKHOLDER VALUE 1 See http://www.investopedia.com/terms/p/pricetarget.asp 10 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 36. The Board conducted an unnecessarily desperate and flawed sales process that failed to maximize stockholder value. 37. In 2010, MRV began selling off the Company piece-by-piece. Now they have decided to hastily sell the entirety of MRV for an unfair price. The Board’s desire for the procession of the deal trumped the duty they owed to maximize stockholder value. 38. In October 2010, MRV completed the sale of its former wholly-owned subsidiaries Source Photonics, Inc. and Source Photonics Santa Clara, Inc. 39. In September 2011, MRV publicly announced that it retained investment bankers to assist it in exploring strategic alternatives with respect to its Network Equipment segment, including its Optical Communications Systems division and Creative Electronics Systems SA., its Swiss subsidiary in the aerospace and defense industry (“CES”). 40. On October 20, 2011, MRV announced a special cash dividend of approximately $75 million in the aggregate. 41. In March 2012, MRV completed the sale of CES to CES Holding SA. 42. On May 2, 2012, MRV announced a special cash dividend of approximately $48.6 million in the aggregate. 43. In October 2012, MRV sold two of the three businesses within its Network Integration segment. MRV sold all of the issued and outstanding capital stock of its former wholly-owned operating subsidiary, Alcadon-MRV AB based in Sweden. Also in October 2012, MRV sold all of the issued and outstanding capital stock of its former wholly-owned subsidiary, Pedrena Enterprises B.V., the parent company of Interdata, a wholly-owned operating subsidiary, based in France. 44. On December 3, 2012, MRV announced a special cash dividend of approximately $11 million in the aggregate and a share repurchase plan for up to $10 million of the then issued and outstanding shares of MRV’s common stock. 11 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 45. In December 2015, MRV sold the remainder of its Network Integration segment, which consisted of one business unit in Italy, Tecnonet S.p.A., that provided consulting, installation and support, and managed services for fixed line, cable, and mobile communications networks. 46. In the middle of 2016, the Board decided to sell the remainder of MRV. In June 2016, the Board engaged Cowen to act as its financial advisor throughout the Company’s sales process. 47. After contacting 78 parties, engaging in 21 non-disclosure agreements, meeting for 7 management presentations, and receiving 5 non-binding proposal letters, the Board was not happy with any of the offers. The sales process should have ended there, but it continued. The Board pressed on with negotiations with two of the parties to see if they could reach a better offer price, but failed to do so. Again, the sales process should have ended there, but it continued. 48. On October 6, 2016, ADVA indicated that they were not interested in pursuing a transaction with MRV at that time. ADVA further indicated that although they were not interested at that time, MRV could approach ADVA again once MRV had exhausted all prospects with other potential buyers. Sure enough, on February 21, 2017, MRV arranged and held a call with ADVA, during which MRV updated ADVA regarding the strategic merits of a combination between the two companies, and ADVA indicated that it would reconsider a potential acquisition. ADVA indicated that it would take two weeks to formulate a proposal. 49. After months of negotiating with ADVA, during a time which MRV saw their stock price climb higher and higher, the Board failed to receive an offer price they felt was fair. This is evinced by their repeated requests for ADVA to increase their Offer Price above $10.00. On June 27, 2017, ADVA indicated that they were completely unwilling to offer a price higher than $10.00, and that they might terminate the negotiations altogether. Finally, and conclusively, this should have ended the sales process, but it did not. Instead the Board agreed to a deal with ADVA for a derisory 1% premium. 50. As a result of the Proposed Transaction, all restricted stock units and options owned by the Board and MRV’s named executive officers will immediately vest and become due when the 12 COMPLAINT FOR BREACHES OF FIDUCIARY |

| Tender Offer is consummated. This places the Board’s interest in completing the transaction separate from stockholders generally. This is especially true for CEO and director Bonney, perhaps the single most important and influential Board member. Based solely upon the Merger Agreement and consummation of the Tender Offer, Bonney stands to receive over $4.5 million in new money. That figure does not include previously owned equity, or any of the compensation due with respect to his status as managing partner at Raging Capital. 51. In sum, the Board allowed itself to be taken advantage of by ADVA, which used the Company’s unrelenting desire to make a deal to drastically reduce the value of its offer. Rather than properly accounting for MRV’s recent financial performance, the Board inexplicably decided to accept ADVA’s substantially reduced offer. The Board, after the conclusion of a hastily run sales process, has thus agreed to sell the Company at an inopportune time and at a price that fails to adequately compensate MRV’s stockholders in light of the Company’s future prospects. THE MERGER AGREEMENT UNFAIRLY DETERS COMPETITIVE OFFERS AND IS UNDULY BENEFICIAL TO ADVA 52. The Proposed Transaction is also unfair because, as part of the Merger Agreement, Defendants agreed to certain onerous and preclusive deal protection devices that operate conjunctively to make the Tender Offer a fait accompli and ensure that no competing offers will emerge for the Company. 53. First, Section 6.3 of the Merger Agreement explicitly prohibits MRV or any of its affiliates from soliciting or proactively seeking a competing or better offer, as Section 6.3(a) states that the Company and its representatives shall not: (i) solicit, initiate, knowingly encourage or knowingly facilitate any Takeover Proposal or the making or consummation thereof or the making of any inquiry, offer or proposal that would reasonably be expected to lead to any Takeover Proposal, (ii) enter into, engage in or otherwise participate in any discussions (except to notify such Person of the existence of the provisions of this Section 6.3) or negotiations regarding, or furnish to any Person any non-public information in connection with, any Takeover Proposal, or otherwise cooperate in any way with, or knowingly assist, participate in, facilitate or encourage any effort by, any third party that is seeking to make, or has made, any 13 COMPLAINT FOR BREACHES OF FIDUCIARY |

| Takeover Proposal, (iii) approve or recommend, or make any public statement approving or recommending, a Takeover Proposal, (iv) enter into any letter of intent, merger agreement or other agreement providing for a Takeover Proposal, (v) submit any Takeover Proposal to a vote of the stockholders of the Company, (vi) amend or grant any waiver or release under any standstill or similar agreement with respect to any class of equity securities of the Company or any of its Subsidiaries, (vii) approve any transaction under, or any third party becoming an “interested stockholder” under, Section 203 of the DGCL or (viii) resolve or agree to do any of the foregoing. 54. Furthermore, Section 6.3(c) grants ADVA recurring and unlimited matching rights, which gives MRV 48 hours to provide unfettered access to confidential, non-public information about competing proposals from third parties to ADVA. Additionally, Section 6.3 grants ADVA five (5) business days to negotiate with MRV, amend the terms of the Merger Agreement, and make a counter-offer that matches the superior offer. 55. The matching rights provision essentially ensures that no superior bidder will emerge. Any potential suitor will be unlikely to expend the time, cost, and effort to perform due diligence and make a superior proposal while knowing that MRV must inform ADVA of the terms and details of any superior proposal and allow ADVA five days to match. As a result, the matching rights provision unreasonably favors ADVA, to the detriment of MRV’s public stockholders. 56. Finally, Section 8.3 of the Merger Agreement requires the Company to pay ADVA a termination fee of $2,410,000 in the event the Company decides to pursue any alternative offer. The Merger Agreement also requires MRV to reimburse ADVA up to $ $1,000,000 in expenses under certain circumstances. Based on a transaction value of $68 million, this coercive termination fee of over 5% would require any competing bidder to agree to pay a naked premium simply for the right to provide MRV’s stockholders a superior offer. 57. Compounding matters, Raging Capital, Kenneth H. Traub, Robert M. Pons, Mark J. Bonney, Brian Bellinger, Jeannie H. Diefenderfer, Jeffrey Tuder, Stephen G. Krulik, and Adam L.A. Scheer (each, a “Supporting Stockholder”) entered into Tender and Support Agreements in connection with the Merger Agreement. The Support Agreements obligate the Supporting Stockholders to tender their shares of Company stock and otherwise support the transactions contemplated by the Merger 14 COMPLAINT FOR BREACHES OF FIDUCIARY |

| Agreement. Raging Capital beneficially owns 2,136,864 shares of MRV stock, which represents approximately 31.37% of the outstanding shares. Traub, Pons, Bonney, Bellinger, Tuder, Krulik, Scheer, and Diefenderfer beneficially own an aggregate of 386,258 shares of MRV stock, which represent approximately 5.67% of the shares of Common Stock. Together, as a result of the Support Agreements, over 37% of the outstanding shares of MRV stock have already been tendered in favor of the merger. These Support Agreements make it a near certainty that Tender Offer will consummate, and, therefore, are materially unfair to MRV stockholders generally. 58. Ultimately, these preclusive deal protection provisions impoperly restrain the Company’s ability to solicit or engage in negotiations with any third party regarding a proposal to acquire all or a significant interest in the Company. Accordingly, Plaintiff seeks injunctive and other equitable relief to prevent the irreparable injury that the Company’s stockholders will continue to suffer absent judicial intervention. THE MATERIALLY INCOMPLETE AND MISLEADING RECOMMENDATION STATEMENT 59. The Defendants further breached their fiduciary duties to MRV’s stockholders by causing the materially incomplete and misleading Recommendation Statement to be filed with the SEC on July 17, 2017. As discussed below, the Recommendation Statement omits material information that must be disclosed to enable MRV’s stockholders to make an informed decision with respect to the Tender Offer. 60. While the Recommendation Statement discloses certain information regarding the financial analyses Cowen performed to support its fairness opinion, the information is incomplete and misleading to stockholders because critical material information that was considered by Defendants has been omitted. 61. In connection with the Selected Companies and Selected Transactions Analyses, the Recommendation Statement fails to disclose the individual multiples the advisors utilized for each of the companies and transactions included in their analyses. A fair summary of these analyses requires 15 COMPLAINT FOR BREACHES OF FIDUCIARY |

| the disclosure of the individual multiples for each transaction and company utilized. Merely providing the range that a banker applied to render the implied per share value is insufficient, as stockholders are unable to assess whether the banker applied appropriate multiples, or, instead, applied unreasonably low multiples in order to drive down the implied valuation of the Company. The omission of the individual multiples renders the summary of these analyses set forth on pages 32-35 of the Recommendation Statement materially incomplete and misleading. 62. Additionally, in connection with the Discounted Cash Flow Analysis, the Recommendation Statement fails to disclose the following key components used in their analysis: (i) the inputs and assumptions underlying the calculation of the discount rate range of 16.0% to 20.0%; (ii) the inputs and assumptions underlying the selection of the terminal multiple range of 6.0x to 8.0x; (iii) the terminal value calculated utilizing the terminal multiple range; (iv) the value of MRV’s estimated United States federal net operating loss carry forwards that Cowen used to adjust the cash flows; and (v) the inputs and assumptions underlying the selection of the 18% discount rate applied to the estimated United States federal net operating loss carry forwards. 63. These key inputs are material to MRV stockholders, and their omission renders the summary of Cowen’s Discounted Cash Flow Analysis on page 35 of the Recommendation Statement incomplete and misleading. As a highly-respected professor explained in one of the most thorough law review articles regarding the fundamental flaws with the valuation analyses bankers perform in support of fairness opinions in a discounted cash flow analysis a banker takes management’s forecasts, and then makes several key choices “each of which can significantly affect the final valuation.” Steven M. Davidoff, Fairness Opinions, 55 Am. U.L. Rev. 1557, 1576 (2006). Such choices include “the appropriate discount rate, and the terminal value...” Id. As Professor Davidoff explains: There is substantial leeway to determine each of these, and any change can markedly affect the discounted cash flow value. For example, a change in the discount rate by one percent on a stream of cash flows in the billions of dollars can change the discounted cash flow value by tens if not hundreds of millions of dollars....This issue arises not only with a discounted cash flow analysis, but with each of the other valuation 16 COMPLAINT FOR BREACHES OF FIDUCIARY |

| techniques. This dazzling variability makes it difficult to rely, compare, or analyze the valuations underlying a fairness opinion unless full disclosure is made of the various inputs in the valuation process, the weight assigned for each, and the rationale underlying these choices. The substantial discretion and lack of guidelines and standards also makes the process vulnerable to manipulation to arrive at the “right” answer for fairness. This raises a further dilemma in light of the conflicted nature of the investment banks who often provide these opinions. Id. at 1577-78. 64. Each of the above-referenced omissions are material because without this information, the Company’s stockholders are unable to fully understand Cowen’s analysis and, thus, are unable to decide what weight, if any, to place on its fairness opinion in determining whether to tender their shares. The Company’s stockholders are entitled to the missing material information in order to make a fully informed decision concerning the Tender Offer. 65. In sum, by failing to engage in a reasonable and fair sales process, the Defendants have breached their fiduciary duties owed to MRV’s stockholders. The Board failed to obtain reasonable consideration for MRV’s stockholders, agreed to onerous deal protection devices that will undoubtedly prevent the emergence of a superior offer, put their personal interests and/or the interests of Raging Capital ahead of MRV’s other stockholders while negotiating the terms of the Merger Agreement, and caused the materially incomplete and misleading Recommendation Statement to be filed with the SEC. 66. The Board has thus prevented Plaintiff and the Class from being adequately compensated for their MRV shares. Accordingly, Plaintiff seeks injunctive and other equitable relief to prevent the irreparable injury that Company stockholders will continue to suffer absent judicial intervention. COUNT I Breach of Fiduciary Duties (Against All Defendants) 67. Plaintiff incorporates by reference and realleges each and every allegation contained above, as though fully set forth herein. 17 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 68. The Defendants have violated fiduciary duties of care, loyalty, and good owed to the stockholders of MRV, and as a result the Defendants have failed to maximize shareholder value. 69. By the acts, transactions and courses of conduct alleged herein, the Defendants, individually and acting as a part of a common plan, are attempting to unfairly deprive Plaintiff and other members of the Class of the true value of their investment in MRV. 70. As demonstrated by the allegations above, the Defendants failed to exercise the care required, and breached their duties of loyalty, good faith, and care owed to the stockholders of MRV because, among other reasons, they failed to take reasonable steps to obtain and/or ensure that MRV stockholders receive adequate and fair value for their shares. 71. Further, the Defendants have caused materially misleading and incomplete information concerning the Proposed Transaction to be disseminated to the Company’s public stockholders. The Defendants have an obligation to be complete and accurate in their disclosures concerning the Proposed Transaction. The Recommendation Statement fails to disclose material information, including financial information and information necessary to prevent the statements contained therein from being misleading. Because of the Defendants’ failure to provide full and fair disclosure of material information concerning the Proposed Transaction, Plaintiff and the Class will be unable to make an informed decision with respect to the Tender Offer, and thus are damaged thereby. 72. The Defendants dominate and control the business and corporate affairs of MRV both through their positions within the Company and on the Board, and are in possession of private corporate information concerning MRV assets, business and future prospects. Thus, there exists an imbalance and disparity of knowledge and economic power between them and the public stockholders of MRV which makes it inherently unfair for them to benefit their own interests to the exclusion of maximizing stockholder value. 73. By reason of the foregoing acts, practices and course of conduct, the Defendants have failed to exercise ordinary care and diligence in the exercise of their fiduciary obligations toward Plaintiff and the other members of the Class. 18 COMPLAINT FOR BREACHES OF FIDUCIARY |

| 74. As a result of the Defendants’ actions, Plaintiff and the Class will suffer irreparable injury in that they have not and will not receive their fair portion of the value of MRV assets and businesses, have been and will be prevented from obtaining a fair price for their common stock, and will be forced to make an uniformed decagons regarding whether to tender their shares. 75. Unless the Defendants are enjoined by the Court, they will continue to breach their fiduciary duties owed to Plaintiff and the members of the Class, all to the irreparable harm of the members of the Class. 76. Plaintiff and the members of the Class have no adequate remedy at law. Only through the exercise of this Court’s equitable powers can Plaintiff and the Class be fully protected from the immediate and irreparable injury which the Defendants’ actions threaten to inflict. PRAYER FOR RELIEF WHEREFORE, Plaintiff demands injunctive relief in his favor and in favor of the Class and against Defendants as follows: A. Declaring that this action is properly maintainable as a class action and certifying Plaintiff as Class representative; B. Preliminarily and permanently enjoining Defendants and their counsel, agents, employees and all persons acting under, in concert with, or for them, from proceeding with, consummating, or closing the Proposed Transaction, unless and until the Company adopts and implements a procedure or process to obtain an agreement providing fair and reasonable terms and consideration to Plaintiff and the Class, and disclose the material information omitted from the Recommendation Statement detailed above; C. Rescinding, to the extent already implemented, the Merger Agreement or any of the terms thereof, or granting Plaintiff and the Class rescissory damages; D. Directing the Defendants to account to Plaintiff and the Class for all damages suffered as a result of the Defendants wrongdoing; 19 COMPLAINT FOR BREACHES OF FIDUCIARY |

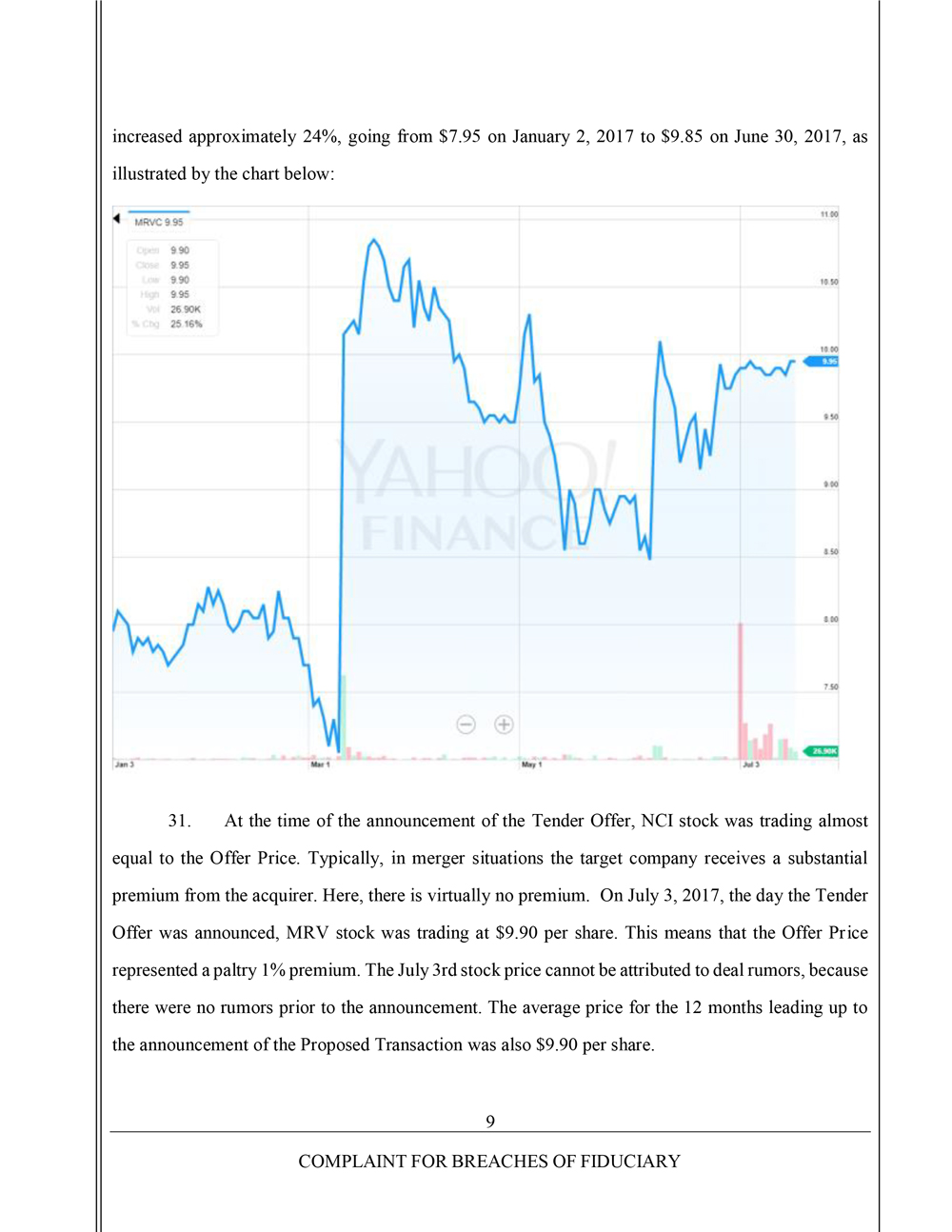

| E. Awarding Plaintiff the costs and disbursements of this action, including reasonable attorneys’ and experts’ fees; and F. Granting such other and further equitable relief as this Court may deem just and proper. DATED: July 24, 2017 Respectfully submitted David E. Bower OF COUNSEL MONTEVERDE & ASSOCIATES PC Juan E. Monteverde David E. Bower SBN 119546 The Empire State Building MONTEVERDE & ASSOCIATES PC 350 Fifth Avenue, Suite 4405 600 Corporate Pointe, Suite 1170 New York, New York 10118 Culver City, CA 90230 Tel: 212-971-1341 Tel: (310) 446-6652 Fax: 212-202-7880 Fax: (212) 202-7880 Email: dbower@monteverdelaw.com Email: jmonteverde@monteverdelaw.com Attorneys for Plaintiff Attorneys for Plaintiff 20 COMPLAINT FOR BREACHES OF FIDUCIARY |