UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06686

JPMorgan China Region Fund, Inc.

(Exact name of registrant as specified in charter)

One Beacon Street, 18th Floor

Boston, MA 02108

(Address of principal executive offices) (Zip code)

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 441-9800

Date of fiscal year end: December 31

Date of reporting period: January 1, 2014 through December 31, 2014

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

[INSERT— JPMorgan China Region Fund, Inc. annual report 12/31/14]

This report, including the financial statements herein, is sent to the stockholders of the Fund for their information. It is not a prospectus, circular or representation intended for use in the purchase or sale of shares of the Fund or of any securities mentioned in this report.

Annual Report

December 31, 2014

CONTENTS

OBJECTIVES (Unaudited)

JPMorgan China Region Fund, Inc. (the ‘Fund’) seeks to achieve long-term capital appreciation through investments primarily in equity securities of companies with substantial assets in, or revenues derived from, the People’s Republic of China (‘China’), Hong Kong, Taiwan and Macau — collectively, the ‘China Region’.

The Fund provides investors with an opportunity to participate in the growing economies of the China Region where the economies of China, Hong Kong, Taiwan and Macau have become increasingly linked over recent years. Hong Kong enterprises have made substantial investments in China, particularly where labor and land prices are lower than in Hong Kong. Similarly, many Chinese companies have Hong Kong based subsidiaries with securities listed on the Hong Kong Stock Exchange (H-shares). Renminbi denominated China A-shares, which are listed in China, are available for acquisition by the Fund by direct investment up to $20m and by indirect investment up to 10% of the Fund’s total assets through exposure to China A-share investment companies. It is intended that the Fund will maintain a $20m direct investment in China A-shares. Further details on China A-shares are provided in note 7(iii) of the Notes to Financial Statements on page 25.

The Fund invests to take advantage of the many opportunities that result from this linkage among the markets of the China Region.

MANAGEMENT (Unaudited)

JF International Management Inc. (‘JFIMI’) is the investment management company appointed to advise and manage the Fund’s portfolio (the ‘Investment Advisor’). JFIMI is part of JPMorgan Chase & Co. (‘JPMC’), one of the world’s premier financial services institutions. In asset management, JPMC operates globally under the name of J.P. Morgan Asset Management (‘JPMAM’). Funds under management for the global asset management business of JPMAM were US$1.7 trillion as of December 31, 2014.

The Fund’s lead portfolio manager is Emerson Yip, a Senior Portfolio Manager within JPMAM’s Greater China investment team in Hong Kong.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 1 | |

FORWARD-LOOKING STATEMENTS (Unaudited)

This report contains certain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. Forward-looking statements include statements regarding the goals, beliefs, plans or current expectations of the Fund and JFIMI and their respective representatives, taking into account the information currently available to them. Forward-looking statements include all statements that do not relate solely to current or historical fact. For example, forward-looking statements include the use of words such as ‘anticipate,’ ‘estimate,’ ‘intend,’ ‘expect,’ ‘believe,’ ‘plan,’ ‘may,’ ‘should,’ ‘would,’ or other words that convey uncertainty of future events or outcomes. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the Fund to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Factors that could materially and negatively affect the results, performance or achievements of the Fund include changes in economic, political, legal and regulatory conditions in the China Region and elsewhere, changes in interest and exchange rates and related policies and other risks. When evaluating the information included in this report, you are cautioned not to place undue reliance on these forward-looking statements, which reflect the judgment of the Fund, JFIMI or its respective representatives only as of the date hereof. The Fund, JFIMI and their respective representatives undertake no obligation to publicly revise or update these forward-looking statements to reflect events and circumstances that arise after the date hereof.

|

| MARKET INFORMATION |

The Fund is listed on the New York Stock Exchange (symbol JFC). The share price is published in • The Wall Street Journal (daily online at www.WSJ.com/Free) |

The estimated net asset value is published in • The Wall Street Journal under “Closed-End Funds” (every Saturday) • www.jpmchinaregionfund.com |

| | | | | | |

| | | |

| 2 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

HIGHLIGHTS (unaudited, except as indicated)

| | | | | | | | |

| | | DECEMBER 31, 2014

US$ | | | DECEMBER 31, 2013

US$ | |

Net Assets (Audited) | | | $125.0 million | | | | $111.4 million | |

Net Asset Value Per Share (Audited) | | | $19.39 | | | | $17.28 | |

| | |

Market Data | | | | | | | | |

Share Price on the New York Stock Exchange | | | $16.91 | | | | $15.16 | |

Discount to Net Asset Value Per Share | | | 12.8% | | | | 12.3% | |

| | |

Total Return for the Year Ended December 31, 2014 | | | | | | | | |

Net Asset Value | | | | | | | +13.0% | |

Share Price | | | | | | | +12.5% | |

| | |

JFC Benchmark Index* | | | | | | | +16.1% | |

MSCI Hong Kong Index | | | | | | | +5.1% | |

MSCI China Index | | | | | | | +8.3% | |

MSCI Taiwan Index | | | | | | | +10.1% | |

CSI 300 Index | | | | | | | +51.6% | |

|

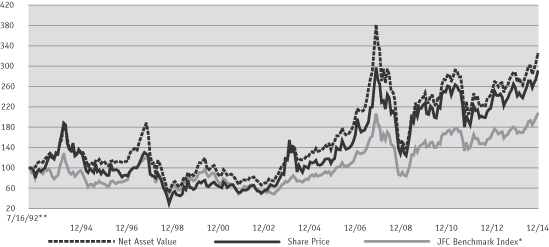

Net Asset Value and Share Price vs. Benchmark Index | |

| * | | JFC Benchmark Index: 80% MSCI Golden Dragon Index (Net) 20% CSI 300 Index (Net). Prior to October 1, 2013, 80% MSCI Golden Dragon Index (GDR) +20% CSI 300 Index (Total). Prior to April 13, 2012, the MSCI Golden Dragon Index (Total). At December 31, 2011 the MSCI Golden Dragon Index (Total) comprised 24.1% of the MSCI Hong Kong Index (Total), 42.7% of the MSCI China Index (Total) and 33.2% of the MSCI Taiwan Index (Total). Prior to March 2001, 25% Taiwan Weighted Index, 20% BNP Paribas China Index, 50% MSCI Hong Kong, 5% HSBC; Prior to March 1999, 60% Hong Kong All Ordinaries, 30% Credit Lyonnais Securities Asia All China B Index, 10% Taiwan Weighted Index. Prior to January 1997, Peregrine Greater China Index. |

| ** | | Commencement of operations. |

Source: J.P. Morgan Asset Management.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 3 | |

CHAIRMAN‘S STATEMENT

DECEMBER 31, 2014 (Unaudited)

Dear Fellow Stockholder

Performance

During the year ended December 31, 2014 the Fund’s total return on net asset value was +13.0% compared to a total return of +16.1% for the composite benchmark. Over the same period, the Fund’s share price total return was +12.5% as the discount at which the share trades to its NAV widened slightly from 12.3% to 12.8%. At the portfolio level, the Fund’s underperformance was largely due to stock selection in Hong Kong and Macau.

China A-shares

The Fund has $20m of China A-share quota which provides exposure to an investment universe otherwise restricted to foreign investors. This serves as a differentiating factor for the Fund when compared to its peer group of other New York listed Greater China region closed ended funds. As at December 31, 2014, the Fund held 24.6% of its total assets in China A-share investments. Overall, 2014 was a strong year for China A-shares, with most of the performance coming in the later part of the calendar year after the surprise interest rate cut by the People’s Bank of China.

Leverage

The Fund renewed its $17.5m credit facility with Scotiabank (Ireland) Ltd for a further two year period on February 25, 2015. The facility expires on February 24, 2017 at which point the Board will consider another credit facility. Under this arrangement, Scotiabank provides a secured, committed credit facility which can be utilized at any time. This financing arrangement gives the Investment Advisor the flexibility to tactically manage borrowed monies at its discretion under the scrutiny of the Board. During the year to December 31, 2014, the Fund’s

leverage ranged from 8.7% to 12.9% and at the time of writing is 11.6%, reflecting the Investment Advisor’s positive view on the market. The Investment Advisor does not receive a management fee on any cash held when borrowings are drawn under the leverage facility.

Total Expense Ratio

The Board monitors closely the Fund’s expenses. For the year ended December 31, 2014, the Fund’s ratio of total expenses to average net assets (excluding interest expense) was 1.94% (2013: 2.06%).

Share Repurchases and Discount Management

The Board currently has authority to repurchase up to 644,763 shares (equal to 10% of the Fund’s issued share capital). Although there have been no share repurchases since January 2003, the Board continues to believe that the power to repurchase shares is of ongoing benefit to shareholders. Share repurchases are a useful tool for decreasing discount volatility and this approach will be used when considered to be appropriate by the Board.

Board Succession

As mentioned in last year’s report, the Board through its Nomination Committee, considered succession planning and the need to refresh its Board and Committees. As a result, it has discussed the retirement of two Directors in 2016. The Board intends to recruit two new Directors in place of those retiring and will ensure it maintains an appropriate balance of skills.

Outlook

The Investment Advisor expects the macroeconomic environment to gradually recover from the post-financial crisis lows, underpinned by an improving property sector outlook and continued government

For more information please refer to the Fund’s website at www.jpmchinaregionfund.com

| | | | | | |

| | | |

| 4 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

support on infrastructure projects. The Investment Advisor also expects favourable liquidity conditions should continue to support China A-shares in the medium term, but anticipates more short term volatility after the strong rally and rising percentage of leveraged trades.

The Investment Advisor believes that expectations for regional growth are increasingly divergent with investors generally more confident of U.S. growth prospects, but concerned about stagnation in Europe, and a potentially sharp slowdown in China. The fall in oil prices however is expected to be a positive for China. Monetary policy globally is also mixed with the US expected to raise rates this year or next, but with central banks in Europe, China and Japan expected to ease further.

China’s reform program may cause stock market volatility (as it involves both de-leveraging and substantial policy changes), but ultimately the Investment Advisor believes this should result in a positive re-rating of the market. Furthermore, the People’s Bank of China has embarked on monetary easing which should be supportive of liquidity. Taiwan corporate performance should improve as trade continues to pick up and as the U.S. dollar strengthens. In contrast, we see less opportunities in Hong Kong given that the valuations of many of the companies will be adversely impacted by rising U.S. interest rates due to the Hong Kong dollar currency peg.

Respectfully submitted

The Rt. Hon. The Earl of Cromer

Chairman

February 27, 2015

For more information please refer to the Fund’s website at www.jpmchinaregionfund.com

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 5 | |

INVESTMENT ADVISOR’S REPORT (Unaudited)

Over the 12-month period ending December 2014, the Company achieved a total return, based on net asset value, of +13.0% underperforming the benchmark return of +16.1% by 3.1%.

The major drivers on the upside to the Fund’s performance included our overweight position in internet stocks such as Alibaba and JD.Com which we felt offered us the best way to gain exposure to Chinese consumption spending. In addition, we were correctly overweight in Chinese financials such as broker Haitong Securities, banks such as China Minsheng Bank and insurance companies such as Ping An Insurance. These stocks re-rated later in the year following the surprise cut in interest rates in China. On the negative side, we were hurt by our overweight position in Macau casino stocks which detracted from performance as the stocks fell on negative earnings revisions. Several of our renewable energy names such as Huaneng Renewables corrected in 2014 as growth slowed from 2013 levels.

China Review (including A-shares)

Chinese equities fell in the first quarter, with offshore-listed equities down 5.8% and domestic A-shares (CSI 300) down 7.9%. Most of the decline took place in January when the US Federal Reserve’s announcement of the tapering of its quantitative easing programme renewed concerns about emerging market currencies. The gradual decline in interbank rates from their fourth-quarter high did not alleviate market concerns over slowing growth, cases of trust/bond defaults and lack of evidence for solid structural reforms. Economic-sensitive sectors such as financials, consumer discretionary and commodities/industrials lagged, while structural growth sectors such as internet and health care outperformed.

In the second quarter Chinese equities rose, with offshore-listed equities up 3.4% and domestic A-shares (CSI 300) up 0.9%. Again, markets were volatile, with initial weakness in April due to weak

macro data, followed by a series of mini policy stimulus measures, which sparked a recovery. Economic-sensitive sectors such as banks, brokerage and autos outperformed, while defensives such as staples and health care lagged. Internet stocks rebounded due to strong earnings visibility, after a sharp global style shift led the sector lower in March/April.

Chinese equities diverged in the third quarter, with offshore-listed equities almost flat, returning 0.5%, and domestic A-shares (CSI 300) up strongly, returning 13%. The strong return for the A-share market was driven by the government’s continued mini policy stimulus, potential liquidity inflows from Shanghai-Hong Kong Stock Connect, further structural reform from the upcoming 4th Plenum, and a series of stock market reforms, such as increasing the scope of stocks eligible for financial leverage. Offshore markets rose first on better economic data and lagged performance status among emerging markets. Weak macroeconomic data for August, along with market worries about the Federal Reserve’s first rate rise, triggered an 8% market correction from early-September’s high. Reform beneficiaries, such as telecoms, along with cyclical recovery proxy properties, outperformed. Growth sectors such as technology, media & telecommunications (‘TMT’), gas and consumer-related sectors lagged.

Finally, in the fourth quarter, Chinese equities rallied with offshore-listed equities up 7% and domestic A-shares (CSI 300) rising sharply, up 44%, accounting for the bulk of the full-year gains for both markets. The key catalysts were the rate cut in late November — the first cut since 2012 — coupled with a steady recovery in property transactions and further progress on structural reforms (such as local government financing vehicle (‘LGFV’) debt). The rise was led almost solely by financial sectors, which benefited from the avoidance of a hard landing, rate sensitivity and attractive valuations.

| | | | | | |

| | | |

| 6 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

China Outlook

We expect the macroeconomic environment to gradually recover from the post-financial crisis lows, underpinned by an improving property sector outlook and continued government support on infrastructure projects. We believe there should be further interest rate and reserve ratio requirement (‘RRR’) cuts as real interest rates are still too high to ensure a smooth deleveraging process. We do not expect any major stimulus policies as the government continues its structural reforms.

On the structural reform front, we have seen good progress. The China Banking Regulatory Commission (‘CBRC’) circular 43 has largely resolved the LGFV concerns with its implicit guarantee of qualified local government debt from the central government, relieving a key market concern. We believe 2015 will be a critical year for the implementation of structural reforms, such as state-owned enterprise and fiscal reforms, following a lot of initial planning in 2014.

The market’s valuation at 9.2x forward one-year price to earnings, with earnings growth in the high single digits, is undemanding (vs. mid-cycle 12x). We believe the market will continue to re-rate as the macroeconomic environment stabilises and as there is further evidence of structural reform being carried out.

Hong Kong Review

The Hong Kong market was weighed down early in the year due to a correction in Macau gaming stocks. Hong Kong equities rebounded sharply in the second quarter, due to a confluence of positive factors, including economic stabilisation in China, the announcement of the mutual market access agreement with the Shanghai stock exchange and a surprising drop in long-term US Treasury yields. Hong Kong equities outperformed Chinese equities as well as regional and global stock markets for the quarter.

Hong Kong equities suffered a sharp correction in September due to slowing economic momentum in China. This correction more than erased the strong start to the quarter, which was aided by incremental targeted loosening. In late September, sentiment suffered a major hit as student pro-democracy protests rolled into an earlier-than-expected start to the Occupy Central campaign. The early use of tear gas for crowd control purposes garnered international headlines and galvanised the population, leading to more participants joining the demonstrations.

Despite a massive rally in the domestic Chinese equity market, Hong Kong equities managed only a modest gain in the fourth quarter, held back by substantial weakness in the Macau gaming sector. The highly-anticipated Shanghai-Hong Kong Stock Connect scheme commenced with disappointing volumes, especially on the southbound route. Institutional investors were likely not ready to participate in the scheme, while retail investors were more interested in their own domestic market. Meanwhile, the student-led pro-democracy protests were cleared up without much further incident due to waning public support. However, the aftermath of these protests may result in further political gridlock, affecting the ability of the government to move forward with its economic policy initiatives.

Hong Kong Outlook

With the pro-democracy protests having wound down peacefully and interest rate rise expectations being dampened, the prospects for equities have turned more positive for the medium term. Moreover, as the Shanghai-Hong Kong Stock Connect programme matures, with potential scope for expansion, this could spur further buying interest in Hong Kong equities.

The residential property market looks stable in the near term, since the supply situation remains attractive relative to growing demand. While the risk of

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 7 | |

INVESTMENT ADVISOR’S REPORT (Unaudited) (continued)

further government policy tightening remains present, this is likely only if price growth becomes excessive, which is not currently expected. Office property is also benefiting from tight supply conditions amid modest demand growth. However, retail property is facing more challenging conditions given slowing retail sales growth, especially in the high end, as mainland tourists continue to diversify their travels and spending outside of Hong Kong.

The policy risks on Macau remain heightened, especially given the more explicit attention and focus from Beijing. This scrutiny has dampened the potential for increased demand arising from monetary loosening and revived activity in the property sector in China.

Taiwan Review

After shrugging off several market shocks, including the collapse of Ukraine’s government, US Federal Reserve chair Janet Yellen’s indication of a possible rate rise in six months and home-grown protests over a trade deal with China, the Taiwan Stock Exchange Weighted Index (‘TWSE’) hit new yearly highs, to close with a 2.8% gain from the fourth quarter of 2013. Among the major losers were finance stocks, down 5.5% quarter on quarter, as students continued to occupy Taiwan’s parliament, demanding the withdrawal of the services pact. This is expected to boost access of Taiwanese firms to China’s financial markets.

Despite local protests over free-trade agreement talks with China, protests in Vietnam impacting some Taiwanese companies, and issues in Ukraine, the TWSE finished the second quarter up 6% from the first quarter. A surge of liquidity into Taiwan pushed the TWSE to its highest level since 2007, as enthusiasm grew over local technology companies and a recovering economy boosted corporate earnings. The technology sector outperformed, whilst the construction sector closed down for the quarter as the government announced expanded measures to

control rocketing housing prices by reducing the amount of money banks can lend to home buyers.

The Taiwan Capitalization Weighted Stock Index (‘TAIEX’) ended the third quarter down by over 4% quarter on quarter. The market peaked in early July as a surge of cash into Taiwan pushed the TAIEX to its highest level since 2007 on signs of a recovering economy and stronger corporate earnings. The Taiex looked to retest its July highs in late August with technology stocks leading the way, as the launch of new models by several global electronics brands, such as Apple and Samsung, were expected to boost local suppliers’ shipments. However, the index sold off all through September, with low trading volumes on weak sentiment and net foreign institutional selling.

The TWSE ended the fourth quarter with an almost 4% quarter-on-quarter gain, with a late year-end rally. The quarter was initially hampered by weak sentiment ahead of the 9-in-1 election. There were a number of negative factors, such as technology seasonality, unhappiness over the government’s plan to implement a tax on large retail investors (big player tax), concerns over Ebola, and the Kuomintang’s potential weak showing in the November election. Alongside the election, a food scandal dominated the news. Ting Hsin International Group was found to mix lard oil meant for animal feed in edible oil, which it then sold to the public. The other overriding influence for the period was the decline in the oil price, which led to airlines and shipping names outperforming massively. Concurrently, the currency weakened, following the continued quantitative easing attempts in Japan and Europe and the general US dollar strength vs. Asian currencies.

Taiwan Outlook

With Taiwan’s municipal elections out of the way and the presidential election not due until 2016, president Ma Ying-jeou could use this window wisely

| | | | | | |

| | | |

| 8 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

to win back confidence for the Kuomintang party. Several factors should support a decent first half to 2015. The positive effect from the iPhone 6 will carry over into the first half of the year, and the cheaper oil price will bolster disposable incomes, lending a boost to retailers. Tourism will be a bright spot, further supporting domestic consumption. The three-year delay to the big player tax should help retail sentiment and participation. However, macroeconomic uncertainty, especially from Europe, and a weak New Taiwan dollar could weigh on the market.

Overall, the market’s risk/reward prospects continue to look favourable given sustained growth into 2015. Fundamentals remain strong and valuations are still modest. We remain an overweight position in technology, industrial and consumption, and an underweight position in telecommunications and petrochemicals.

Greater China Outlook

2015 should be another positive year for Greater China markets. However, we expect continued volatility in the near-term given the strong rally in equity markets last year paired with the continued tapering of Fed stimulus. China’s reform program may cause stock market volatility (as it involves both de-leveraging and substantial policy changes), but ultimately this should result in a re-rating of the market. Furthermore, the People’s Bank of China has embarked on monetary easing which should be supportive of liquidity. Taiwan corporate performance should improve as trade continues to pick up and as the U.S. dollar strengthens. In contrast, we see fewer opportunities in Hong Kong given its sensitivity to expectations in U.S. interest rates.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 9 | |

TOP TEN HOLDINGS

AT DECEMBER 31, 2014 (Unaudited)

| | | | |

| | | % OF

NET ASSETS | |

Taiwan Semiconductor Manufacturing Co., Ltd. (‘TSMC’) | | | 6.2 | |

| Manufactures and markets integrated circuits. The company provides the following services: wafer manufacturing, wafer probing, assembly and testing, mask production and design services. The company’s integrated circuits are used in computer, communication, consumer electronics, automotive and industrial equipment industries. | | | | |

| |

Tencent Holdings Ltd. | | | 4.9 | |

| Provides internet, mobile, and telecommunication value-added services in China. The company has an instant messaging community in China. Tencent also provides online advertising services. | | | | |

| |

China Construction Bank Corp. ‘A’ ‘H’ | | | 4.6 | |

| Provides a complete range of banking services and other financial services to individual and corporate customers. The bank’s services include retail banking, international settlement, project finance and credit card services. | | | | |

| |

Ping An Insurance Group Co. Ltd. ‘A’ ‘H’ | | | 4.5 | |

| Provides a variety of insurance service in China. The Company writes property, casualty, and life insurance. Ping An Insurance also offers financial services. | | | | |

| |

AIA Group Ltd. | | | 3.7 | |

| Offers insurance and financial services. The company writes life insurance for individuals and businesses, accident and health insurance, retirement planning, and wealth management services. | | | | |

| |

Agricultural Bank of China Ltd. ‘A’ ‘H’ | | | 3.3 | |

| Provides a full range of commercial banking services. The Banks services includes RMB and foreign currency deposit, loan, international and domestic settlement, bill discount, currency trading, bank guarantee, and treasury bill underwriting. | | | | |

| |

China Minsheng Banking Corp., Ltd. ‘A’ ‘H’ | | | 3.2 | |

| Provides deposit, loan, settlement, discount, financial bond issuance, government bond underwriting and trading, letter of credit, bank guarantee, and other related financial services. | | | | |

| |

China Vanke Co., Ltd. ‘A’ ‘H’ | | | 2.4 | |

| A Property development company. The Company mainly develops residential properties in Shenzhen, Shanghai, Beijing, Tianjin, Tangshan, Nanjing, and other big cities in China. | | | | |

| |

China Pacific Insurance Group Co., Ltd. ‘A’ ‘H’ | | | 2.2 | |

| Provides integrated insurance services. The Company offers life and property insurance products through its subsidiaries. | | | | |

| |

China Telecom Corp., Ltd. | | | 2.0 | |

| Provides wireline telephone, data, and Internet, as well as leased line services in China through its subsidiaries. | | | | |

| | | | | | |

| | | |

| 10 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

INVESTMENT PORTFOLIO

AT DECEMBER 31, 2014

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

COMMON STOCK (unless otherwise noted) | | | | | |

CHINA (66.2%) | | | | | |

Aerospace & Defense (0.3%) | | | | | |

AVIC Aircraft Co., Ltd., ‘A’ | | | 39,200 | | | | 119,673 | |

China Avic Electronics Co., Ltd., ‘A’ | | | 46,006 | | | | 205,336 | |

| | | | | | | | |

| | | | | | | 325,009 | |

| | | | | | | | |

Airlines (0.2%) | | | | | |

China Eastern Airlines Corp., Ltd. (a) | | | 624,000 | | | | 299,340 | |

| | | | | | | | |

Auto Components (0.6%) | | | | | |

Fuyao Glass Industry Group Co., Ltd., ‘A’ | | | 91,200 | | | | 178,461 | |

Huayu Automotive Systems Co., Ltd., ‘A’ | | | 129,900 | | | | 324,122 | |

Minth Group Ltd. | | | 140,000 | | | | 290,664 | |

| | | | | | | | |

| | | | | | | 793,247 | |

| | | | | | | | |

Automobiles (1.4%) | | | | | |

Chongqing Changan Automobile Co., Ltd., ‘A’ | | | 78,902 | | | | 208,955 | |

Chongqing Changan Automobile Co., Ltd., ‘B’ | | | 449,619 | | | | 1,018,139 | |

FAW CAR Co., Ltd., ‘A’ | | | 45,800 | | | | 111,769 | |

Jiangling Motors Corp., Ltd., ‘A’ | | | 19,452 | | | | 95,002 | |

SAIC Motor Corp., Ltd., ‘A’ | | | 107,200 | | | | 370,984 | |

| | | | | | | | |

| | | | | | | 1,804,849 | |

| | | | | | | | |

Banks (15.1%) | | | | | |

Agricultural Bank of China Ltd. | | | 6,639,000 | | | | 3,356,035 | |

Agricultural Bank of China Ltd., ‘A’ | | | 1,220,700 | | | | 729,980 | |

Bank of Communications Co., Ltd., ‘A’ | | | 875,000 | | | | 959,059 | |

China Construction Bank Corp. | | | 6,077,000 | | | | 4,991,907 | |

China Construction Bank Corp., ‘A’ | | | 664,400 | | | | 720,731 | |

China Everbright Bank Co., Ltd., ‘A’ | | | 430,000 | | | | 338,233 | |

China Merchants Bank Co., Ltd., ‘A’ | | | 428,000 | | | | 1,144,507 | |

China Merchants Bank Co., Ltd. | | | 208,500 | | | | 523,223 | |

China Minsheng Banking Corp., Ltd. | | | 2,156,900 | | | | 2,837,057 | |

China Minsheng Banking Corp., Ltd., ‘A’ | | | 655,000 | | | | 1,148,678 | |

Industrial Bank Co., Ltd., ‘A’ | | | 279,000 | | | | 742,021 | |

Ping An Bank Co., Ltd., ‘A’ | | | 340,264 | | | | 868,759 | |

Shanghai Pudong Development Bank Co., Ltd., ‘A’ | | | 220,000 | | | | 556,383 | |

| | | | | | | | |

| | | | | | | 18,916,573 | |

| | | | | | | | |

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

Beverages (0.4%) | | | | | |

Jiangsu Yanghe Brewery Joint-Stock Co., Ltd., ‘A’ | | | 17,805 | | | | 226,867 | |

Kweichow Moutai Co., Ltd., ‘A’ | | | 10,500 | | | | 320,924 | |

| | | | | | | | |

| | | | | | | 547,791 | |

| | | | | | | | |

Biotechnology (0.1%) | | | | | |

Beijing SL Pharmaceutical Co., Ltd., ‘A’ | | | 15,000 | | | | 95,745 | |

| | | | | | | | |

Capital Markets (4.7%) | | | | | |

China Cinda Asset Management Co., Ltd. (a) | | | 1,696,000 | | | | 826,714 | |

China Merchants Securities Co., Ltd., ‘A’ | | | 89,200 | | | | 406,461 | |

CITIC Securities Co., Ltd., ‘A’ | | | 334,937 | | | | 1,830,169 | |

Founder Securities Co., Ltd., ‘A’ (a) | | | 113,000 | | | | 256,636 | |

GF Securities Co., Ltd., ‘A’ | | | 132,700 | | | | 555,056 | |

Haitong Securities Co., Ltd. | | | 381,600 | | | | 960,563 | |

Haitong Securities Co., Ltd., ‘A’ | | | 197,000 | | | | 763,994 | |

Huatai Securities Co., Ltd., ‘A’ | | | 65,000 | | | | 256,375 | |

| | | | | | | | |

| | | | | | | 5,855,968 | |

| | | | | | | | |

Chemicals (0.3%) | | | | | |

Qinghai Salt Lake Industry Co., Ltd., ‘A’ | | | 74,249 | | | | 259,704 | |

Shandong Hualu Hengsheng Chemical Co., Ltd., ‘A’ | | | 45,000 | | | | 79,352 | |

| | | | | | | | |

| | | | | | | 339,056 | |

| | | | | | | | |

Construction & Engineering (1.5%) | | | | | |

China Communications Construction Co., Ltd., ‘A’ | | | 165,700 | | | | 370,982 | |

China Railway Construction Corp., Ltd., ‘A’ | | | 289,700 | | | | 712,576 | |

China State Construction Engineering Corp., Ltd., ‘A’ | | | 587,000 | | | | 688,807 | |

Power Construction Corp of China Ltd., ‘A’ | | | 62,200 | | | | 84,518 | |

| | | | | | | | |

| | | | | | | 1,856,883 | |

| | | | | | | | |

Construction Materials (0.1%) | | | | | |

Anhui Conch Cement Co., Ltd., ‘A’ | | | 45,000 | | | | 160,155 | |

| | | | | | | | |

Diversified Consumer Services (0.5%) | | | | | |

China Maple Leaf Educational Systems Ltd. (a) | | | 1,776,000 | | | | 558,818 | |

| | | | | | | | |

Diversified Financial Services (0.2%) | | | | | |

Avic Capital Co., Ltd., ‘A’ | | | 76,000 | | | | 219,155 | |

| | | | | | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 11 | |

INVESTMENT PORTFOLIO

AT DECEMBER 31, 2014 (continued)

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

COMMON STOCK — continued | |

Diversified Telecommunication Services (2.2%) | |

China Telecom Corp., Ltd. | | | 4,300,000 | | | | 2,517,457 | |

Dr Peng Telcom & Media Group Co., Ltd., ‘A’ | | | 66,600 | | | | 193,016 | |

| | | | | | | | |

| | | | | | | 2,710,473 | |

| | | | | | | | |

Electrical Equipment (0.1%) | | | | | |

Henan Pinggao Electric Co., Ltd., ‘A’ | | | 56,600 | | | | 135,387 | |

| | | | | | | | |

Electronic Equipment, Instruments & Components (1.4%) | |

AAC Technologies Holdings, Inc. | | | 236,000 | | | | 1,264,506 | |

Hangzhou Hikvision Digital Technology Co., Ltd., ‘A’ | | | 100,380 | | | | 361,944 | |

Shenzhen O-film Tech Co., Ltd., ‘A’ | | | 36,000 | | | | 110,019 | |

| | | | | | | | |

| | | | | | | 1,736,469 | |

| | | | | | | | |

Food & Staples Retailing (0.4%) | | | | | |

Jointown Pharmaceutical Group Co., Ltd., ‘A’ | | | 24,802 | | | | 72,239 | |

Shanghai Bailian Group Co., Ltd., ‘A’ | | | 75,800 | | | | 218,579 | |

Yonghui Superstores Co., Ltd., ‘A’ | | | 128,000 | | | | 179,703 | |

| | | | | | | | |

| | | | | | | 470,521 | |

| | | | | | | | |

Food Products (2.1%) | | | | | |

Beijing Dabeinong Technology Group Co., Ltd., ‘A’ | | | 102,000 | | | | 220,638 | |

Gansu Yasheng Industrial Group Co., ‘A’ | | | 101,000 | | | | 152,054 | |

Henan Shuanghui Investment & Development Co., Ltd., ‘A’ | | | 25,500 | | | | 129,678 | |

Inner Mongolia Yili Industrial Group Co., Ltd., ‘A’ | | | 96,654 | | | | 446,035 | |

Tingyi Cayman Islands Holding Corp. | | | 346,000 | | | | 790,638 | |

Want Want China Holdings Ltd. | | | 717,000 | | | | 944,948 | |

| | | | | | | | |

| | | | | | | 2,683,991 | |

| | | | | | | | |

Health Care Equipment & Supplies (0.1%) | |

Shinva Medical Instrument Co., Ltd., ‘A’ | | | 26,000 | | | | 131,299 | |

| | | | | | | | |

Health Care Providers & Services (1.9%) | |

Aier Eye Hospital Group Co., Ltd., ‘A’ | | | 43,411 | | | | 192,775 | |

iKang Healthcare Group, Inc. ADR (a) | | | 49,779 | | | | 748,676 | |

Phoenix Healthcare Group Co., Ltd. | | | 532,000 | | | | 981,037 | |

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

Health Care Providers & Services — continued | |

Shanghai Pharmaceuticals Holding Co., Ltd., ‘A’ | | | 157,000 | | | | 417,553 | |

| | | | | | | | |

| | | | | | | 2,340,041 | |

| | | | | | | | |

Hotels, Restaurants & Leisure (0.1%) | | | | | |

China International Travel Service Corp. Ltd., ‘A’ | | | 25,050 | | | | 179,275 | |

| | | | | | | | |

Household Durables (1.3%) | | | | | |

Gree Electric Appliances, Inc. of Zhuhai, ‘A’ | | | 46,001 | | | | 275,235 | |

Midea Group Co., Ltd., ‘A’ | | | 99,000 | | | | 437,872 | |

Ozner Water International Holding Ltd. (a) (e) | | | 1,195,000 | | | | 459,221 | |

Qingdao Haier Co., Ltd., ‘A’ | | | 135,000 | | | | 403,869 | |

| | | | | | | | |

| | | | | | | 1,576,197 | |

| | | | | | | | |

Independent Power & Renewable Electricity Producers (1.8%) | |

CGN Power Co., Ltd. (a) (e) | | | 1,426,000 | | | | 619,708 | |

China Longyuan Power Group Corp., Ltd. | | | 664,000 | | | | 691,002 | |

China Yangtze Power Co., Ltd., ‘A’ | | | 209,000 | | | | 359,451 | |

GD Power Development Co., Ltd., ‘A’ | | | 200,000 | | | | 149,259 | |

Huaneng Power International, Inc., ‘A’ | | | 172,000 | | | | 244,803 | |

SDIC Power Holdings Co., Ltd., ‘A’ | | | 118,100 | | | | 217,773 | |

| | | | | | | | |

| | | | | | | 2,281,996 | |

| | | | | | | | |

Insurance (6.9%) | | | | | |

China Life Insurance Co., Ltd., ‘A’ | | | 50,000 | | | | 275,226 | |

China Pacific Insurance Group Co., Ltd. | | | 470,000 | | | | 2,387,986 | |

China Pacific Insurance Group Co., Ltd., ‘A’ | | | 65,000 | | | | 338,411 | |

Ping An Insurance Group Co. of China Ltd. | | | 386,500 | | | | 3,942,428 | |

Ping An Insurance Group Co. of China Ltd., ‘A’ | | | 141,776 | | | | 1,707,299 | |

| | | | | | | | |

| | | | | | | 8,651,350 | |

| | | | | | | | |

Internet & Catalog Retail (0.2%) | | | | | |

JD.com, Inc. ADR (a) | | | 10,006 | | | | 231,539 | |

| | | | | | | | |

Internet Software & Services (6.9%) | | | | | |

Alibaba Group Holding Ltd. ADR (a) | | | 16,701 | | | | 1,735,902 | |

Leju Holdings Ltd. ADR (a) | | | 3,757 | | | | 40,424 | |

Tencent Holdings Ltd. | | | 422,800 | | | | 6,133,739 | |

YY, Inc. ADR (a) | | | 12,006 | | | | 748,454 | |

| | | | | | | | |

| | | | | | | 8,658,519 | |

| | | | | | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 12 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

COMMON STOCK — continued | |

Machinery (2.5%) | | | | | |

China CNR Corp., Ltd., ‘A’ | | | 212,900 | | | | 243,648 | |

China Conch Venture Holdings Ltd. | | | 513,000 | | | | 1,118,000 | |

China Shipbuilding Industry Co., Ltd., ‘A’ | | | 493,600 | | | | 732,762 | |

Guangxi Liugong Machinery Co., Ltd., ‘A’ | | | 75,000 | | | | 152,079 | |

Sany Heavy Industry Co., Ltd., ‘A’ | | | 203,000 | | | | 326,554 | |

Siasun Robot & Automation Co., Ltd., ‘A’ | | | 12,500 | | | | 79,364 | |

Weichai Power Co., Ltd., ‘A’ | | | 50,660 | | | | 222,842 | |

Zoomlion Heavy Industry Science and Technology Co., Ltd., ‘A’ | | | 210,000 | | | | 238,975 | |

| | | | | | | | |

| | | | | | | 3,114,224 | |

| | | | | | | | |

Media (0.0%) | | | | | |

China South Publishing & Media Group Co., Ltd., ‘A’ | | | 20,000 | | | | 53,514 | |

| | | | | | | | |

Metals & Mining (0.7%) | | | | | |

Baoshan Iron & Steel Co., Ltd., ‘A’ | | | 212,000 | | | | 239,542 | |

China Minmetals Rare Earth Co., Ltd., ‘A’ (a) | | | 30,000 | | | | 145,019 | |

Inner Mongolia Baotou Steel Rare-Earth Hi-Tech Co., Ltd., ‘A’ | | | 35,000 | | | | 146,003 | |

Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd., ‘A’ | | | 191,000 | | | | 292,165 | |

| | | | | | | | |

| | | | | | | 822,729 | |

| | | | | | | | |

Multiline Retail (0.6%) | | | | | |

Intime Retail Group Co., Ltd. | | | 810,500 | | | | 587,391 | |

Wuhan Department Store Group Co., Ltd., ‘A’ (a) | | | 64,535 | | | | 164,562 | |

| | | | | | | | |

| | | | | | | 751,953 | |

| | | | | | | | |

Oil, Gas & Consumable Fuels (2.8%) | | | | | |

China Petroleum & Chemical Corp. | | | 2,553,400 | | | | 2,057,959 | |

China Shenhua Energy Co., Ltd., ‘A’ | | | 69,000 | | | | 225,662 | |

CNOOC Ltd. | | | 739,000 | | | | 994,908 | |

Jizhong Energy Resources Co., Ltd., ‘A’ | | | 139,000 | | | | 186,857 | |

| | | | | | | | |

| | | | | | | 3,465,386 | |

| | | | | | | | |

Pharmaceuticals (2.3%) | | | | | |

CSPC Pharmaceutical Group Ltd. | | | 1,154,000 | | | | 1,017,887 | |

Jiangsu Hengrui Medicine Co., Ltd., ‘A’ | | | 50,745 | | | | 306,564 | |

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

Pharmaceuticals — continued | | | | | |

Luye Pharma Group Ltd. (a) | | | 852,000 | | | | 1,097,597 | |

Tasly Pharmaceutical Group Co., Ltd., ‘A’ | | | 59,447 | | | | 393,822 | |

| | | | | | | | |

| | | | | | | 2,815,870 | |

| | | | | | | | |

Real Estate Management & Development (4.6%) | |

Beijing Capital Development Co., Ltd., ‘A’ | | | 165,000 | | | | 268,085 | |

China Vanke Co., Ltd. (a) | | | 811,300 | | | | 1,809,945 | |

China Vanke Co., Ltd., ‘A’ | | | 559,000 | | | | 1,252,434 | |

E-House China Holdings Ltd. ADR | | | 75,138 | | | | 543,999 | |

Poly Real Estate Group Co., Ltd., ‘A’ | | | 294,450 | | | | 513,532 | |

Sunac China Holdings Ltd. | | | 1,293,000 | | | | 1,315,568 | |

| | | | | | | | |

| | | | | | | 5,703,563 | |

| | | | | | | | |

Road & Rail (0.8%) | | | | | |

CAR, Inc. (a) | | | 642,000 | | | | 862,662 | |

Daqin Railway Co., Ltd., ‘A’ | | | 64,980 | | | | 111,651 | |

| | | | | | | | |

| | | | | | | 974,313 | |

| | | | | | | | |

Semiconductors & Semiconductor Equipment (0.4%) | |

Hua Hong Semiconductor Ltd. (a) (e) | | | 420,000 | | | | 554,609 | |

| | | | | | | | |

Software (0.2%) | | | | | |

Aisino Co., Ltd., ‘A’ | | | 53,000 | | | | 260,643 | |

Yonyou Software Co., Ltd., ‘A’ | | | 12,000 | | | | 45,435 | |

| | | | | | | | |

| | | | | | | 306,078 | |

| | | | | | | | |

Specialty Retail (0.2%) | |

Pang Da Automobile Trade Co., Ltd., ‘A’ (a) | | | 137,300 | | | | 131,679 | |

Suning Commerce Group Co., Ltd., ‘A’ (a) | | | 96,200 | | | | 139,555 | |

| | | | | | | | |

| | | | | | | 271,234 | |

| | | | | | | | |

Transportation Infrastructure (0.3%) | |

Shanghai International Airport Co., Ltd., ‘A’ | | | 73,000 | | | | 230,861 | |

Sichuan Haite High-tech Co., Ltd., ‘A’ | | | 38,900 | | | | 137,943 | |

| | | | | | | | |

| | | | | | | 368,804 | |

| | | | | | | | |

TOTAL CHINA | | | | | | | 82,761,923 | |

| | | | | | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 13 | |

INVESTMENT PORTFOLIO

AT DECEMBER 31, 2014 (continued)

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

COMMON STOCK — continued | |

HONG KONG (24.7%) | |

Banks (3.0%) | |

BOC Hong Kong Holdings Ltd. | | | 640,000 | | | | 2,141,683 | |

Dah Sing Financial Holdings Ltd. | | | 213,769 | | | | 1,247,387 | |

HSBC Holdings plc | | | 38,444 | | | | 366,858 | |

| | | | | | | | |

| | | | | | | 3,755,928 | |

| | | | | | | | |

Commercial Services & Supplies (1.2%) | |

China Everbright International Ltd. | | | 1,021,000 | | | | 1,519,390 | |

| | | | | | | | |

Distributors (0.3%) | |

Dah Chong Hong Holdings Ltd. | | | 646,000 | | | | 349,047 | |

| | | | | | | | |

Diversified Financial Services (0.5%) | |

Hong Kong Exchanges and Clearing Ltd. | | | 29,100 | | | | 644,319 | |

| | | | | | | | |

Diversified Telecommunication Services (1.1%) | |

China Unicom Hong Kong Ltd. | | | 976,000 | | | | 1,308,944 | |

| | | | | | | | |

Electric Utilities (0.1%) | |

Cheung Kong Infrastructure Holdings Ltd. | | | 11,000 | | | | 81,422 | |

| | | | | | | | |

Gas Utilities (0.7%) | |

China Resources Gas Group Ltd. | | | 358,000 | | | | 930,242 | |

| | | | | | | | |

Hotels, Restaurants & Leisure (1.6%) | |

Melco Crown Entertainment Ltd. ADR | | | 26,426 | | | | 671,221 | |

REXLot Holdings Ltd. | | | 2,773,240 | | | | 225,302 | |

Sands China Ltd. | | | 230,000 | | | | 1,131,515 | |

| | | | | | | | |

| | | | | | | 2,028,038 | |

| | | | | | | | |

Industrial Conglomerates (1.9%) | |

Hutchison Whampoa Ltd. | | | 132,000 | | | | 1,519,217 | |

Shun Tak Holdings Ltd. | | | 1,892,000 | | | | 875,898 | |

| | | | | | | | |

| | | | | | | 2,395,115 | |

| | | | | | | | |

Insurance (3.7%) | |

AIA Group Ltd. | | | 823,600 | | | | 4,582,843 | |

| | | | | | | | |

Marine (0.9%) | |

Orient Overseas International Ltd. | | | 199,500 | | | | 1,166,697 | |

| | | | | | | | |

Multiline Retail (0.9%) | |

Lifestyle International Holdings Ltd. | | | 502,000 | | | | 1,056,481 | |

| | | | | | | | |

Pharmaceuticals (0.7%) | |

Sino Biopharmaceutical Ltd. | | | 1,004,000 | | | | 910,179 | |

| | | | | | | | |

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

Real Estate Investment Trusts (REITs) (1.0%) | |

Champion REIT | | | 1,310,000 | | | | 608,151 | |

Yuexiu Real Estate Investment Trust | | | 1,201,000 | | | | 602,463 | |

| | | | | | | | |

| | | | | | | 1,210,614 | |

| | | | | | | | |

Real Estate Management & Development (4.4%) | |

Cheung Kong Holdings Ltd. | | | 122,000 | | | | 2,049,944 | |

Hang Lung Properties Ltd. | | | 410,000 | | | | 1,149,955 | |

Hongkong Land Holdings Ltd. | | | 207,000 | | | | 1,399,320 | |

New World Development Co., Ltd. | | | 607,207 | | | | 698,457 | |

Wharf Holdings Ltd. (The) | | | 33,000 | | | | 238,309 | |

| | | | | | | | |

| | | | | | | 5,535,985 | |

| | | | | | | | |

Specialty Retail (0.9%) | |

Chow Tai Fook Jewellery Group Ltd. | | | 815,600 | | | | 1,093,826 | |

| | | | | | | | |

Textiles, Apparel & Luxury Goods (0.7%) | |

Samsonite International S.A. | | | 308,100 | | | | 913,813 | |

| | | | | | | | |

Water Utilities (1.1%) | |

Beijing Enterprises Water Group Ltd. (a) | | | 1,980,000 | | | | 1,350,699 | |

| | | | | | | | |

TOTAL HONG KONG | | | | | | | 30,833,582 | |

| | | | | | | | |

|

TAIWAN (20.1%) | |

Banks (1.1%) | |

E.Sun Financial Holding Co., Ltd. | | | 2,131,044 | | | | 1,325,075 | |

| | | | | | | | |

Chemicals (0.5%) | |

China Steel Chemical Corp. | | | 123,000 | | | | 603,285 | |

| | | | | | | | |

Diversified Financial Services (2.6%) | |

Chailease Holding Co., Ltd. | | | 398,000 | | | | 992,418 | |

Fubon Financial Holding Co., Ltd. | | | 1,429,989 | | | | 2,294,173 | |

| | | | | | | | |

| | | | | | | 3,286,591 | |

| | | | | | | | |

Electronic Equipment, Instruments & Components (2.5%) | |

Delta Electronics, Inc. | | | 279,000 | | | | 1,664,182 | |

Largan Precision Co., Ltd. | | | 20,000 | | | | 1,515,727 | |

| | | | | | | | |

| | | | | | | 3,179,909 | |

| | | | | | | | |

Food & Staples Retailing (0.9%) | |

President Chain Store Corp. | | | 143,000 | | | | 1,106,370 | |

| | | | | | | | |

Health Care Equipment & Supplies (0.3%) | |

St Shine Optical Co., Ltd. | | | 24,000 | | | | 396,431 | |

| | | | | | | | |

Internet Software & Services (0.6%) | |

PChome Online, Inc. | | | 66,917 | | | | 725,241 | |

| | | | | | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 14 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

| | | | | | | | |

| DESCRIPTION | | HOLDINGS

(IN SHARES) | | | VALUE

(IN US$) | |

COMMON STOCK — continued | |

Leisure Products (0.6%) | |

Johnson Health Tech Co., Ltd. | | | 180,288 | | | | 407,904 | |

Merida Industry Co., Ltd. | | | 47,950 | | | | 325,463 | |

| | | | | | | | |

| | | | | | | 733,367 | |

| | | | | | | | |

Real Estate Management & Development (0.5%) | |

Ruentex Development Co., Ltd. | | | 394,992 | | | | 629,947 | |

| | | | | | | | |

Semiconductors & Semiconductor Equipment (9.5%) | |

Advanced Semiconductor Engineering, Inc. | | | 1,156,802 | | | | 1,394,664 | |

Chipbond Technology Corp. | | | 374,000 | | | | 686,412 | |

MediaTek, Inc. | | | 108,000 | | | | 1,578,887 | |

Powertech Technology, Inc. (a) | | | 292,000 | | | | 500,804 | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | | 1,737,057 | | | | 7,750,302 | |

| | | | | | | | |

| | | | | | | 11,911,069 | |

| | | | | | | | |

Technology Hardware, Storage & Peripherals (0.9%) | |

Asustek Computer, Inc. | | | 104,000 | | | | 1,140,307 | |

| | | | | | | | |

Textiles, Apparel & Luxury Goods (0.1%) | |

Pou Chen Corp. | | | 108,000 | | | | 131,403 | |

| | | | | | | | |

TOTAL TAIWAN | | | | | | | 25,168,995 | |

| | | | | | | | |

TOTAL INVESTMENTS

(111.0% of Net Assets)

(Cost $110,900,213) | | | | | | | 138,764,500 | |

| | | | | | | | |

Liabilities in excess of other assets

(-11.0% of Net Assets) | | | | (13,742,193 | ) |

| | | | | | | | |

NET ASSETS (100.0%) | | | | | | | 125,022,307 | |

| | | | | | | | |

| | | | |

As of December 31, 2014, aggregate cost for Federal income tax purposes was $111,279,676. The aggregate unrealized gain for all securities is as follows: | |

Excess of value over cost | | | 31,529,533 | |

Excess of cost over value | | | (4,044,709 | ) |

| | | | |

Net unrealized gain | | | 27,484,824 | |

| | | | |

NOTES TO SCHEDULE OF PORTFOLIO INVESTMENTS:

| ADR – | American Depositary Receipt |

| (a) | Non-income producing security. |

| (e) | Security is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. Unless otherwise indicated, this security has been determined to be liquid under procedures established by the Board of Directors and may be resold in transactions exempt from registration, normally to qualified institutional buyers. |

| A | China A shares (See Note 7.iii on page 25) |

| B | China B shares (See Note 7.iii on page 25) |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 15 | |

STATEMENT OF ASSETS AND LIABILITIES

AT DECEMBER 31, 2014

| | | | |

| | | (in US$) | |

ASSETS: | | | | |

Investments in non-affiliates, at value (cost $110,900,213) | | | 138,764,500 | |

Cash | | | 1,106,048 | |

Foreign currency, at value (cost $1,160,677) | | | 1,162,989 | |

Deposits at broker (See Note 7.iii.) | | | 28,431 | |

Receivable for securities sold | | | 860,373 | |

Dividends receivable | | | 49,228 | |

| | | | |

Total Assets | | | 141,971,569 | |

| | | | |

| |

LIABILITIES: | | | | |

Loan payable to bank (See Note 6) | | | 15,000,000 | |

Payables | | | | |

Payable for securities purchased | | | 1,109,948 | |

Accrued Liabilities | | | | |

Deferred China capital gains tax | | | 496,421 | |

Custodian and accounting fees | | | 91,829 | |

Administration fees | | | 59,200 | |

Investment advisory fees | | | 34,557 | |

Interest on loan | | | 16,430 | |

Directors’ fees and expenses | | | 6,849 | |

Other | | | 134,028 | |

| | | | |

Total Liabilities | | | 16,949,262 | |

| | | | |

Net Assets | | | 125,022,307 | |

| | | | |

| |

| Net assets consist of: | | | | |

Common stock, $0.01 par value

(100,000,000 shares authorized; 6,447,637 shares issued and outstanding) | | | 64,476 | |

Paid-in capital | | | 98,994,144 | |

Undistributed net investment income | | | 1,491,587 | |

Accumulated realized loss on investments and foreign currency transactions | | | (3,393,798 | ) |

Accumulated net unrealized appreciation on investments, foreign currency holdings, and other

assets and liabilities denominated in foreign currencies | | | 27,865,898 | |

| | | | |

Net Assets | | | 125,022,307 | |

| | | | |

Net Asset Value Per Share ($125,022,307 ÷ 6,447,637) | | | 19.39 | |

| | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 16 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

STATEMENT OF OPERATIONS

FOR THE YEAR ENDED DECEMBER 31, 2014

| | | | |

| | | (in US$) | |

INVESTMENT INCOME: | | | | |

Dividends from non-affiliates (net of foreign withholding tax of $291,822) | | | 3,273,820 | |

Interest income from non-affiliates | | | 5,895 | |

Interest income from affiliates | | | 465 | |

| | | | |

Total Investment Income | | | 3,280,180 | |

| | | | |

| |

EXPENSES: | | | | |

Investment advisory fees | | | 1,206,369 | |

Directors’ fees and expenses | | | 366,189 | |

Interest expense to non-affiliates (See Note 6) | | | 225,281 | |

Custodian and accounting fees | | | 185,931 | |

Legal fees | | | 89,018 | |

Administration fees | | | 88,367 | |

Audit fees | | | 71,942 | |

Insurance fees | | | 41,493 | |

Shareholder service fees | | | 30,846 | |

NYSE listing fees | | | 25,430 | |

Shareholder report fees | | | 11,322 | |

Interest expense to affiliates | | | 2 | |

Other expenses | | | 30,553 | |

| | | | |

Total Expenses | | | 2,372,743 | |

| | | | |

Net Investment Income | | | 907,437 | |

| | | | |

| |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, FOREIGN CURRENCY

HOLDINGS AND OTHER ASSETS AND LIABILITIES DENOMINATED IN FOREIGN CURRENCIES: | | | | |

Net realized gain (loss) | | | | |

Investments in non-affiliates (net of China tax of $138,405 on realized gain) | | | 7,467,309 | |

Investments in affiliates | | | 885,684 | |

Foreign currency transactions | | | (31,963 | ) |

| | | | |

Net realized gain (loss) | | | 8,321,030 | |

| | | | |

Net change in unrealized appreciation/depreciation | | | | |

Investments in non-affiliates (net of a reduction in China tax of $170,734 on unrealized appreciation) | | | 5,402,471 | |

Investments in affiliates | | | (221,422 | ) |

Foreign currency translations | | | (3,956 | ) |

| | | | |

Change in net unrealized appreciation/depreciation | | | 5,177,093 | |

| | | | |

Net realized and unrealized gain (loss) on investments, foreign currency holdings and other assets and liabilities denominated in foreign currencies | | | 13,498,123 | |

| | | | |

Net increase in net assets resulting from operations | | | 14,405,560 | |

| | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 17 | |

STATEMENTS OF CHANGES IN NET ASSETS

FOR THE PERIODS INDICATED

| | | | | | | | |

| | | Year Ended

December 31, 2014

(in US$) | | | Year Ended

December 31, 2013

(in US$) | |

INCREASE IN NET ASSETS: | | | | | | | | |

Operations | | | | | | | | |

Net investment income | | | 907,437 | | | | 641,115 | |

Net realized gain (loss) on investment transactions | | | 8,321,030 | | | | 5,738,325 | |

Net change in unrealized appreciation (depreciation) on investments, foreign currency holdings and other assets and liabilities denominated in foreign currencies | | | 5,177,093 | | | | 6,159,859 | |

| | | | | | | | |

Net increase (decrease) in net assets resulting from operations | �� | | 14,405,560 | | | | 12,539,299 | |

| | | | | | | | |

| | |

DISTRIBUTIONS TO STOCKHOLDERS: | | | | | | | | |

Net investment income | | | (818,850 | ) | | | (831,745 | ) |

| | | | | | | | |

Total distributions to shareholders | | | (818,850 | ) | | | (831,745 | ) |

| | | | | | | | |

Total increase (decrease) in net assets | | | 13,586,710 | | | | 11,707,554 | |

| | | | | | | | |

| | |

NET ASSETS: | | | | | | | | |

Beginning of period | | | 111,435,597 | | | | 99,728,043 | |

| | | | | | | | |

End of period (including undistributed net investment income of $1,491,587 and $534,460, respectively) | | | 125,022,307 | | | | 111,435,597 | |

| | | | | | | | |

| | |

SHARE TRANSACTIONS | | | | | | | | |

Opening number of shares | | | 6,447,637 | | | | 6,447,637 | |

| | | | | | | | |

Closing number of shares | | | 6,447,637 | | | | 6,447,637 | |

| | | | | | | | |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 18 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2014

| | | | |

| | | (in US$) | |

INCREASE (DECREASE) IN CASH | | | | |

Cash flows provided (used) by operating activities: | | | | |

Net increase/decrease in net assets from operations | | | 14,405,560 | |

Adjustments to reconcile net increase/decrease in net assets

from operations to net cash provided (used) by operating activities: | | | | |

Purchase of investment securities | | | (107,376,521 | ) |

Proceeds from disposition of investment securities | | | 107,954,750 | |

Change in unrealized (appreciation)/depreciation on investments | | | (5,181,049 | ) |

Net realized (gain)/loss on investments | | | (8,352,993 | ) |

Decrease in deposits at broker | | | 704 | |

Increase in dividends receivable | | | (48,449 | ) |

Increase in accrued expenses and other liabilities | | | 169,264 | |

| | | | |

Net cash provided (used) by operating activities | | | 1,571,266 | |

| | | | |

| |

Cash flows provided (used) by financing activities: | | | | |

Cash distributions paid to shareholders | | | (818,850 | ) |

| | | | |

Net cash provided (used) by financing activities | | | (818,850 | ) |

| | | | |

Net increase/decrease in cash | | | 752,416 | |

| | | | |

| |

Cash: | | | | |

Beginning of period (including foreign currency of $1,497,939) | | | 1,516,621 | |

| | | | |

End of period (including foreign currency of $1,162,989) | | | 2,269,037 | |

| | | | |

Supplemental disclosure of cash flow information:

During 2014, the Fund paid $213,568 in interest expense, including $2 to affiliates.

For purposes of reporting the Statement of Cash Flows, the Fund considers all cash accounts that are not subject to withdrawal restrictions or penalties to be cash equivalents.

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 19 | |

FINANCIAL HIGHLIGHTS

FOR THE PERIODS INDICATED

| | | | | | | | | | | | | | | | | | | | |

| | | For the

Year Ended

December 31,

2014

(in US$) | | | For the

Year Ended

December 31,

2013

(in US$) | | | For the

Year Ended

December 31,

2012

(in US$) | | | For the

Year Ended

December 31,

2011

(in US$) | | | For the

Year Ended

December 31,

2010

(in US$) | |

For a share outstanding throughout each year: | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | | 17.28 | | | | 15.47 | | | | 12.75 | | | | 17.41 | | | | 15.27 | |

| | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.14 | | | | 0.10 | | | | 0.08 | | | | 0.14 | | | | 0.05 | |

Net realized and unrealized gain (loss) | | | 2.10 | | | | 1.84 | | | | 2.74 | | | | (4.70 | ) | | | 2.11 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 2.24 | | | | 1.94 | | | | 2.82 | | | | (4.56 | ) | | | 2.16 | |

| | | | | | | | | | | | | | | | | | | | |

Dividends from net investment income | | | (0.13 | ) | | | (0.13 | ) | | | (0.10 | ) | | | (0.10 | ) | | | (0.02 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | | 19.39 | | | | 17.28 | | | | 15.47 | | | | 12.75 | | | | 17.41 | |

| | | | | | | | | | | | | | | | | | | | |

Market value, end of period | | | 16.91 | | | | 15.16 | | | | 14.00 | | | | 11.02 | | | | 15.79 | |

| | | | | | | | | | | | | | | | | | | | |

Total Investment Return | | | | | | | | | | | | | | | | | | | | |

Per share market value* | | | 12.5 | % | | | 9.2 | % | | | 28.2 | % | | | (29.6 | )% | | | 14.7 | % |

| | | | | |

RATIOS/SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period | | | 125,022,307 | | | | 111,435,597 | | | | 99,728,043 | | | | 82,226,478 | | | | 112,248,790 | |

Ratios of total expenses to average net assets | | | 2.14 | % | | | 2.26 | % | | | 2.11 | % | | | 1.89 | % | | | 1.99 | % |

Ratios of total expenses to average net assets, excluding interest expense | | | 1.94 | % | | | 2.05 | % | | | 2.04 | % | | | 1.89 | % | | | 1.99 | % |

Ratios of net investment income to average net assets | | | 0.82 | % | | | 0.61 | % | | | 0.54 | % | | | 0.87 | % | | | 0.32 | % |

Portfolio turnover rate | | | 86.7 | % | | | 66.6 | % | | | 85.8 | % | | | 66.8 | % | | | 76.1 | % |

Number of shares outstanding at end of period (in thousands) | | | 6,448 | | | | 6,448 | | | | 6,448 | | | | 6,448 | | | | 6,448 | |

| * | The total investment return excludes the effect of commissions. Dividends and distributions, if any, are assumed for the purpose of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan or if specified in accordance with the terms of the distribution. |

SEE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 20 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

NOTES TO FINANCIAL STATEMENTS

AT DECEMBER 31, 2014

1. Organization and Capital

JPMorgan China Region Fund, Inc. (the ‘Fund’) was incorporated in the State of Maryland on May 22, 1992, and is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940 (‘1940 Act’). The Fund commenced operations on July 16, 1992.

The Fund seeks to achieve long-term capital appreciation through investments primarily in equity securities of companies with substantial assets in, or revenues derived from, the People’s Republic of China (‘China’), Hong Kong, Taiwan and Macau — collectively, the ‘China Region’.

2. Significant Accounting Policies

The following significant accounting policies, which are in conformity with U.S. generally accepted accounting principles (‘GAAP’), are consistently followed by the Fund in the preparation of its financial statements.

The Fund is an investment company and, accordingly, follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board Accounting Standards Codification Topic 946 — Investment Companies, which is part of GAAP.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reported period. Actual results could differ from these estimates.

i) Security Valuation — All securities for which market quotations are readily available are valued at the last sales price prior to the time of determination or, if no sales price is available at that time, at the mean between the last current bid and ask prices. Securities that are traded over-the-counter are valued, if bid and ask quotations are available, at the mean between the current bid and ask prices. Certain investments of the Fund may, depending upon market conditions, trade in relatively thin markets and/or in markets that experience significant volatility. As a result of these conditions, the prices used by the Fund to value securities may differ from the value that would be realized if these securities were sold and the differences could be material. All other securities and assets are valued at fair value as determined in good faith by the Board of Directors. It is possible that the estimated values may differ significantly from the values that would have been used had a ready market for the investments existed, and such differences could be material. In valuing the Fund’s assets, quotations of foreign securities in a foreign currency are translated to United States (‘U.S.’) dollar equivalents at the prevailing exchange rate in effect on the valuation date. Investments in open ended mutual funds are valued at current day’s closing net asset value per share (‘NAV’).

Valuations reflected in this report are as of the report date. As a result, changes in valuation due to market events and/or issuer related events after the report date and prior to issuance of the report are not reflected herein.

The various inputs that are used in determining the fair value of the Fund’s investments are summarized into the three broad levels listed below.

| • | | Level 1 — quoted prices in active markets for identical securities |

| • | | Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| • | | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input, both individually and in the aggregate, that is significant to the fair value measurement. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 21 | |

NOTES TO FINANCIAL STATEMENTS

AT DECEMBER 31, 2014 (continued)

The following table represents each valuation input as presented on the Investment Portfolio:

| | | | | | | | | | | | | | | | |

| | | Level 1

Quoted prices | | | Level 2

Other significant

observable inputs | | | Level 3 Significant

unobservable inputs | | | Total | |

Total Investments in Securities (a) | | $ | 138,599,938 | | | $ | 164,562 | | | $ | — | | | $ | 138,764,500 | |

| | | | | | | | | | | | | | | | |

| (a) | All portfolio holdings are designated as Level 1 with the exception of Wuhan Department Store Group Co., Ltd., ‘A’ which has been designated as Level 2. Please refer to the Investment Portfolio for industry specifics of portfolio holdings. |

ii) Foreign Currency Translation — The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the mid-market price of such currencies against U.S. dollars as follows:

| • | | investments, other assets, and liabilities at the prevailing rates of exchange on the valuation date; |

| • | | investment transactions and investment income at the prevailing rates of exchange on the dates of such transactions. |

Although the net assets of the Fund are presented at the foreign exchange rates and market values at the close of the period, the Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the fluctuations arising from changes in the market prices of the securities held. Similarly, the Fund does not isolate the effect of changes in foreign exchange rates from the fluctuations arising from changes in the market prices of securities sold during the period. Accordingly, realized and unrealized foreign currency gains (losses) are included in the reported net unrealized appreciation/depreciation on investments. The Fund does isolate the effect of changes in foreign exchange rates from fluctuations when determining realized gain or loss for sales of fixed income securities.

Unrealized currency gains (losses) resulting from valuing foreign currency denominated assets and liabilities at period-end exchange rates are reflected as a component of accumulated net unrealized gain (loss) on investments, foreign currency holdings, and other assets and liabilities denominated in foreign currencies.

iii) Restricted and Illiquid Securities — Certain securities held by the Fund may be subject to legal or contractual restrictions on resale or are illiquid. Restricted securities generally may be resold in transactions exempt from registration under the Securities Act of 1933 (the ‘Securities Act’). Illiquid securities are securities which cannot be disposed of promptly (within seven days) and in the usual course of business at approximately its fair value and include, but are not limited to, repurchase agreements maturing in excess of seven days, time deposits with a withdrawal penalty, non-negotiable instruments and instruments for which no market exists. Disposal of these securities may involve time-consuming negotiations and expense. Prompt sale at the current valuation may be difficult and could adversely affect the net assets of the Fund.

iv) Distribution of Income and Gains — The Fund intends to distribute to stockholders, at least annually, substantially all of its net investment income and expects to distribute annually any net long-term capital gains in excess of net short-term capital losses.

Income and capital gain distributions are determined in accordance with Federal income tax regulations and may differ from those determined in accordance with GAAP.

v) Other — Security transactions are accounted for on trade date. Realized gains and losses on the sale of investment securities are determined on the identified cost basis. Interest income is recognized on the accrual basis. Dividend income, net of foreign taxes withheld, if any, is recorded on the ex-dividend date or when the Fund first learns of the dividend.

vi) Foreign Taxes — The Fund may be subject to foreign taxes on income, gains on investments or currency purchases/repatriation, a portion of which may be recoverable. The Fund will accrue such taxes and recoveries as applicable, based upon its current interpretation of tax rules and regulations that exist in the markets in which it invests.

| | | | | | |

| | | |

| 22 | | | | JPMORGAN CHINA REGION FUND, INC. | | DECEMBER 31, 2014 |

NOTES TO FINANCIAL STATEMENTS

AT DECEMBER 31, 2014 (continued)

As described in Note 7.iii, the Fund invests in China A-shares, which are separately identified in the Investment Portfolio.

On November 14, 2014, the People’s Republic of China (‘PRC’) Ministry of Finance, State Administration of Taxation and China Securities Regulatory Commission jointly issued notices confirming that they would no longer seek to claim 10% capital gains tax (‘CGT’) on foreign institutional investors who trade China A-shares. The Fund’s policy has been to accrue 100% of the contingent CGT liability for all realized and unrealized gains in A Shares and B Shares.

Further to these announcements and in accordance with J.P. Morgan’s recommendation, the Fund’s Board approved the following PRC tax provisioning policy with effect from November 17, 2014:

| | 1. | PRC income tax will no longer be provided for gains realized from sale of China A-shares on or after November 17, 2014. |

| | 2. | PRC income tax will not be provided for unrealized gains of China A-shares. |

| | 3. | Full provision (10%) CGT will be provided for all realized and unrealized gains (no netting against losses) for China B-shares, bonds (corporate and government), futures, index futures and exchange traded funds. |

| | 4. | Full provision of the 10% withholding tax for all dividends (on A-shares, B-shares and H-shares) and PRC sourced interest income (except interest derived from PRC government bonds which are tax exempt). |

Based on its current interpretation of PRC tax rules, the Fund has maintained its accrual for CGT on gains realized from the sale of China A-shares prior to November 17, 2014. The announcements referred to above confirmed that such gains were taxable; however, the PRC tax authorities have not issued guidance on how such tax would be collected.

3. Investment Transactions

During the year ended December 31, 2014, the Fund made purchases of $108,330,687 and sales of $108,187,210 of investment securities other than short-term investments. There were no purchases or sales of U.S. Government securities.

4. Related party, Other Service Provider Transactions and Directors

i) JF International Management Inc. (the Investment ‘Advisor’), an indirect wholly-owned subsidiary of JPMorgan Chase & Co. (‘JPMorgan’) provides investment advisory services to the Fund under the terms of an investment advisory agreement. The Advisor is paid a fee, computed weekly and payable monthly, at the annual rate of 1.00% of the Fund’s weekly managed gross assets. Investments in funds on which the Advisor or its affiliates charges a management fee are excluded from the calculation. The Advisor has agreed to waive its entitlement to a management fee on any cash held when borrowings are drawn under a borrowing facility.

ii) During the year ended December 31, 2014, the Fund did not pay any brokerage commissions to JPMorgan companies or affiliated brokers/dealers.

iii) Other Service Providers — Pursuant to an Administration Agreement, JPMorgan Chase Bank, N.A. (‘JPMCB’), an indirect, wholly-owned subsidiary of JPMorgan (the ‘Administrator’), provides certain administration services to the Fund. For the year ended December 31, 2014, the Fund paid an administration fee of $88,367 in respect of tax, compliance, financial reporting and regulatory services.

JPMCB provides portfolio custody and accounting services for the Fund. The amounts paid directly to JPMCB by the Fund for custody and accounting services are included in Custodian and accounting fees in the Statement of Operations. In consideration of the accounting services, JPMCB receives a fee accrued daily and paid monthly at the annual rate of 0.02% of the first $12.5 billion of the average daily net assets of all funds in the JPMorgan International Fund Complex and 0.0175% of the average daily net assets in excess of $12.5 billion of all such funds subject to a minimum annual fee of $35,000. The custodian fees are split between safekeeping and transaction charges and vary by market.

| | | | | | | | |

| | | |

| DECEMBER 31, 2014 | | JPMORGAN CHINA REGION FUND, INC. | | | | | 23 | |

NOTES TO FINANCIAL STATEMENTS

AT DECEMBER 31, 2014 (continued)

iv) Directors — The Fund pays each of its Directors who is not a director, officer or employee of the Advisor, Administrator or any affiliate thereof, an annual fee of $24,100, the Audit Committee Chairman $28,500 and the Chairman $35,000 plus a $3,300 attendance fee for each Board meeting, Management Engagement Committee meeting and Audit Committee meeting attended. A per diem allowance of $2,000 per day, or $1,000 per half day, is paid to Directors in respect of time spent by Directors on Fund business outside normal Board and Committee meetings. The per diem allowance is subject to Board approval in advance. In addition, the Fund reimburses all Directors for travel and out-of-pocket expenses incurred in connection with Board of Directors meetings. Under normal circumstances, in order to minimize expenses, the Board expects to hold two meetings a year by telephone.

v) As of December 31, 2014, the Fund had two shareholders, each holding more than 5% of the Fund’s outstanding shares, who held in aggregate approximately 63.6% of the Fund’s outstanding shares.

5. Capital Share Transactions

On September 4, 2014, the Board of Directors renewed an authority for the Fund to purchase shares of its common stock from Fund stockholders, as described below. When shares trade at a discount to NAV, any purchase of shares by the Fund has the effect of increasing the NAV of the Fund’s remaining shares outstanding. All shares purchased by the Fund are thereafter considered authorized and unissued.