LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

Investors have many reasons to remain cautious. The challenges in the Euro area continue to cast a shadow over global economies and financial markets. The political support for addressing fiscal issues is eroding as the economic and social impacts become more visible. Despite strong action by the European Central Bank, member nations appear unwilling to surrender sufficient sovereignty to unify the Euro area financial system or strengthen its banks. The gains made in reducing deficits, and the hard-won progress on winning popular acceptance of the need for economic austerity, are at risk. To their credit, European political leaders press on to find compromise solutions, but there is increasing concern that time is running out.

In the U.S., the extended period of increasing corporate earnings that enabled the equity markets to withstand the downward pressures coming from weakening job creation and slower economic growth appears to be coming to an end. The Fed remains committed to low interest rates and announced a third phase of quantitative easing (QE3) scheduled to continue until mid-2015. The recent election results have removed a major element of uncertainty in the U.S. political picture, but it remains to be seen whether the outcome will reduce the highly partisan atmosphere in Congress and enable progress on the many pressing fiscal and budgetary issues that must be resolved in the coming months.

During the last twelve months, U.S. investors have experienced a solid recovery in the domestic equity markets with increasing volatility as the ‘fiscal cliff’ approaches. The experienced investment teams at Nuveen keep their eye on a longer time horizon and use their practiced investment disciplines to negotiate through market peaks and valleys to achieve long-term goals for investors. Experienced professionals pursue investments that will weather short-term volatility and at the same time, seek opportunities that are created by markets that overreact to negative developments. Monitoring this process is an important consideration for the Fund Board as it oversees your Nuveen Fund on your behalf.

As always, I encourage you to contact your financial consultant if you have any questions about your investment in a Nuveen Fund. On behalf of the other members of your Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Robert P. Bremner

Portfolio managers Tom Spalding and Scott Romans examine key investment strategies and the six-month performance of the Nuveen Select Portfolios. Tom has managed the three national Portfolios since 1999. Scott, who joined Nuveen in 2000, has managed NXC since 2003 and NXN since January 2011.

What key strategies were used to manage the Nuveen Select Portfolios during the six-month reporting period ended September 30, 2012?

During this reporting period, municipal bond prices generally rallied, as strong demand and tight supply combined to create favorable market conditions for municipal bonds. Although the total volume of tax-exempt supply improved over that of the same six-month period a year earlier, the issuance pattern remained light compared with long-term historical trends. This supply/demand dynamic served as a key driver of performance. Concurrent with rising prices, yields continued to decline across most maturities, especially at the longer end of the municipal yield curve and the yield curve flattened. During this period, we saw an increased number of borrowers come to market seeking to take advantage of the low rate environment through refunding activity, with approximately 60% of new municipal paper issued by borrowers that were calling existing debt and refinancing at lower rates.

In this environment, we continued to take a bottom-up approach to discovering sectors that appeared undervalued as well as individual credits that we believe the potential to perform well over the long-term. The national Portfolios, NXP, NXQ and NXR, were generally well-positioned going into the period and had only modest turnover during these six months. Our main goal was the reinvestment of proceeds from this turnover across a range of sectors to keep these Portfolios fully invested.

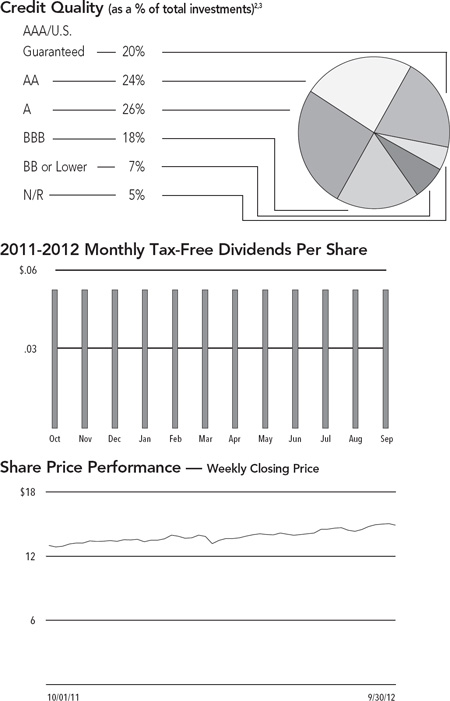

During this period, NXC found value in several areas of the market, including health care, tobacco and California state general obligation (GO) bonds. The purchase of state GOs rather than local GOs helped to minimize NXC’s exposure to some of the fiscal problems faced by local governments in California, including local real estate valuations and Proposition 13’s constraints on property taxes, as well as pension issues. NXC also continued to add exposure to redevelopment agency (RDA) bonds in the secondary

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

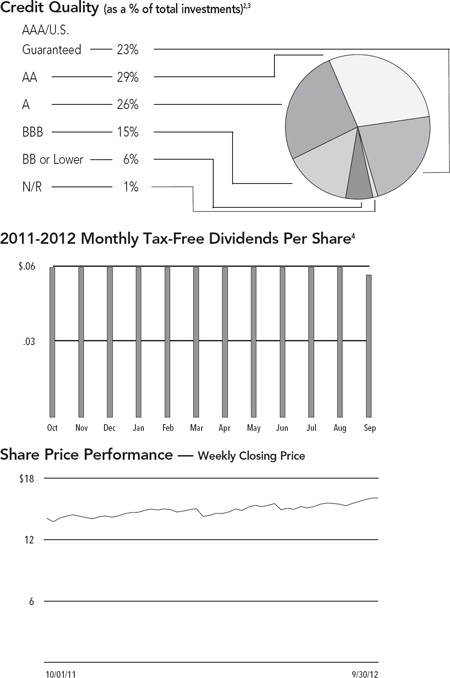

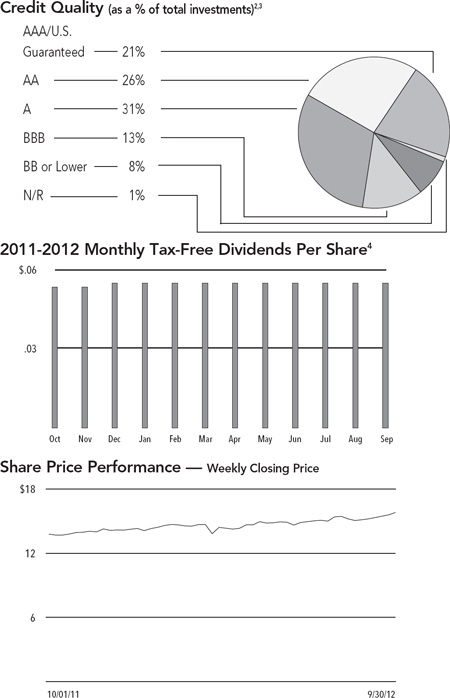

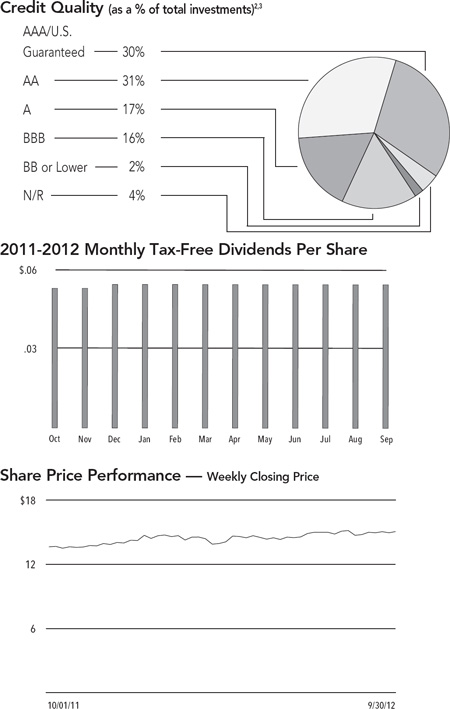

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

market. Because of recent changes to the RDA program, we remained very selective in our purchases in this area, evaluating issuers on a case by case basis. (In 2011, as part of cost saving measures to close gaps in the California state budget, all 400 RDAs in the state were ordered to dissolve by February 1, 2012, and successor agencies and oversight boards were created to manage obligations that were in place prior to the dissolution and take title to the RDAs’ housing and other assets.)

In NXN, we added to our positions in New York City GOs. In general, issuance in New York tends to be concentrated in a few major issuers. During this period, we actively sought to diversify our holdings by purchasing bonds with more unusual structures from other strong issuers, for example, bonds with higher coupons and shorter calls. We also took advantage of short-term market opportunities created by supply/demand dynamics in the municipal market. While demand for tax-exempt paper remained consistently strong throughout the period, supply fluctuated widely. We found that periods of substantial supply provided good short-term buying opportunities not only because of the increased number of issues available, but also because some investors became more hesitant in their buying as supply grew, causing spreads to widen temporarily. At times when supply was more plentiful, we focused on anticipating cashflows from bond calls and maturing bonds and closely monitored opportunities for reinvestment.

In general during this period, we emphasized bonds with longer maturities. This enabled us to take advantage of more attractive yields at the longer end of the municipal yield curve and also provided some protection for the Portfolios’ duration and yield curve positioning. We also purchased lower rated bonds when we found attractive opportunities, especially in NXN, as we believed these bonds continued to offer relative value. Our opportunities in these areas were somewhat constrained by the structure of bonds typically issued as part of refinancing deals, which tended to be characterized by higher quality and shorter maturities.

Cash for new purchases during this period was generated primarily by the proceeds from an increased number of bond calls resulting from the increase in refinancings. During this period, we worked to redeploy these proceeds as well as those from maturing bonds to keep the Portfolios as fully invested as possible. Overall, selling was minimal because the bonds in our portfolios generally offered higher yields than those available in the current marketplace.

As of September 30, 2012, all five of these Portfolios continued to use inverse floating rate securities. We employ inverse floaters for a variety of reasons, including duration management, income enhancement and total return enhancement.

Individual results for the Nuveen Select Portfolios, as well as for relevant index and peer group information, are presented in the accompanying table.

For the six months ended September 30, 2012, the cumulative returns on net asset value (NAV) for all five Select Portfolios exceeded the returns for their respective S&P Municipal Bond Index. For this same period, NXP and NXR performed in line with the average return for the Lipper General and Insured Unleveraged Municipal Debt Funds Classification Average, while NXQ trailed this Lipper average. Both NXC and NXN underperformed their respective state Lipper averages. One of the reasons behind the underperformance of NXC and NXN relative to their Lipper averages was the fact that these Portfolios do not use regulatory leverage (however, they may use effective leverage), while the majority of funds in the Lipper California and New York classifications are leveraged.

Key management factors that influenced the Portfolios’ returns during this period included yield curve and duration positioning, credit exposure and sector allocation.

In an environment of declining rates and flattening yield curve, municipal bonds with longer maturities generally outperformed those with shorter maturities during this period. Overall, credits at the longest end of the municipal yield curve posted the strongest returns, while bonds at the shortest end produced the weakest results. For this period, duration and yield curve positioning was a positive contributor to the performance of these Portfolios, with the net impact varying according to each Portfolio’s individual weightings along the yield curve. For example, NXQ had the shortest duration among the

three national Portfolios, which impacted its performance, while NXN’s performance was hurt by its overweighting of bonds at the shortest end of the yield curve. All five of the Portfolios benefited from their overweighting in zero coupon bonds, which generally outperformed the market during this period due to their longer durations.

Credit exposure was another important factor in the Portfolios’ performance during these six months, as lower quality bonds generally outperformed higher quality bonds. This outperformance was due in part to the greater demand for lower rated bonds as investors looked for investment vehicles offering higher yields. As investors became more comfortable taking on additional investment risk, credit spreads, or the difference in yield spreads between U.S. Treasury securities and comparable investments such as municipal bonds, narrowed through a variety of rating categories. As a result of this spread compression, the Portfolios generally benefited from their holdings of lower rated credits, with good weightings of bonds rated A and BBB across the board. In NXN, this was offset to some degree by a heavier weighting in bonds rated AAA and AA.

During this period, revenue bonds as a whole outperformed the general municipal market. Holdings that generally made positive contributions to the Portfolios’ returns included health care (together with hospitals), education, transportation, and water and sewer bonds. Appropriation and dedicated tax bonds also exceeded the overall market return. NXP, NXQ, NXR and NXN all had strong contributions from their overweighting in health care, while NXC benefited from its overweighting in appropriation and dedicated tax bonds. Tobacco credits backed by the 1998 master tobacco settlement agreement also performed very well, helped in part by their longer effective durations. These bonds also benefited from market developments, including increased demand for higher yielding investments by investors who had become less risk averse. In addition, based on recent data showing that cigarette sales had fallen less steeply than anticipated, the 46 states participating in the agreement, including California and New York, stand to receive increased payments from the tobacco companies. As of September 30, 2012, all of the Portfolios held tobacco credits, which benefited their performance as tobacco bonds rallied.

In contrast, pre-refunded bonds, which are often backed by U.S. Treasury securities, were the poorest performing market segment during this period. The underperformance of these bonds can be attributed primarily to their shorter effective maturities and higher credit quality. As of September 30, 2012, the three national Portfolios were overweight in pre-refunded bonds relative to the market average, which detracted from their investment performance. NXC and NXN held smaller amounts of pre-refunded bonds, which lessened the negative impact. General obligation (GO) bonds and utilities and housing credits slightly lagged the performance of the general municipal market for this period. Although GOs generally tended to trail the market during this period, bonds issued by the states of California and Illinois, which represented the two largest state holdings in the national Portfolios, performed well as they benefited from the spread compression discussed earlier. This in turn benefited the performance of the three national Portfolios as well as NXC.

Fund shares are not guaranteed or endorsed by any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation. Past performance is no guarantee of future results. Fund common shares are subject to a variety of risks, including:

During the six-month reporting period ended September 30, 2012, NXP had one monthly dividend reduction, while the dividends of NXQ, NXR, NXC and NXN remained stable.

All of these Portfolios seek to pay stable dividends at rates that reflect each Portfolio’s past results and projected future performance. During certain periods, each Portfolio may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Portfolio during the period. If a Portfolio has cumulatively earned more than it has paid in dividends, it holds the excess in reserve as undistributed net investment income (UNII) as part of the Portfolio’s NAV. Conversely, if a Portfolio has cumulatively paid dividends in excess of its earnings, the excess constitutes negative UNII that is likewise reflected in the Portfolio’s NAV. Each Portfolio will, over time, pay all of its net investment income as dividends to shareholders. As of September 30, 2012, all of the Portfolios in this report had positive UNII balances, based upon our best estimate, for tax purposes and positive UNII balances for financial reporting purposes.

Since the inception of the Portfolios’ repurchase programs, the Portfolios have not repurchased any of their outstanding shares.

As of September 30, 2012, and during the six-month reporting period, the share prices of the Portfolios were trading at (+)premiums and/or (-) discounts to their NAVs as shown in the accompanying table.

| | | Statement of |

| | | Assets & Liabilities |

September 30, 2012 (Unaudited)

| | | | Select | | | Select | | | Select | | | California | | | New York | |

| | | Tax-Free | | Tax-Free 2 | | Tax-Free 3 | | Select Tax-Free | | Select Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Assets | | | | | | | | | | | | | | | | |

| Investments, at value (cost $218,015,911, $228,682,480, $170,525,522, $87,266,210 and $54,548,487, respectively) | | $ | 242,258,028 | | $ | 245,643,785 | | $ | 187,180,997 | | $ | 98,293,255 | | $ | 58,993,504 | |

| Cash | | | 4,759,981 | | | 1,127,533 | | | 2,785,684 | | | — | | | 157,560 | |

| Receivables: | | | | | | | | | | | | | | | | |

| Interest | | | 2,656,736 | | | 3,095,301 | | | 2,150,108 | | | 1,119,601 | | | 768,624 | |

| Investments sold | | | — | | | 4,926,070 | | | 4,750,000 | | | 1,000,000 | | | — | |

| Other assets | | | 45,933 | | | 48,304 | | | 36,136 | | | 19,239 | | | 13,030 | |

| Total assets | | | 249,720,678 | | | 254,840,993 | | | 196,902,925 | | | 100,432,095 | | | 59,932,718 | |

| Liabilities | | | | | | | | | | | | | | | | |

| Cash overdraft | | | — | | | — | | | — | | | 798,595 | | | — | |

| Floating rate obligations | | | — | | | 1,000,000 | | | — | | | 1,540,000 | | | 1,005,000 | |

| Payables: | | | | | | | | | | | | | | | | |

| Dividends | | | 863,985 | | | 876,439 | | | 679,579 | | | 317,567 | | | 201,380 | |

| Investments purchased | | | — | | | — | | | 1,575,686 | | | — | | | — | |

| Accrued expenses: | | | | | | | | | | | | | | | | |

| Management fees | | | 43,299 | | | 54,308 | | | 42,104 | | | 21,471 | | | 12,903 | |

| Trustees fees | | | 50,243 | | | 52,774 | | | 38,690 | | | 19,099 | | | 11,854 | |

| Other | | | 87,973 | | | 92,343 | | | 74,472 | | | 45,130 | | | 37,100 | |

| Total liabilities | | | 1,045,500 | | | 2,075,864 | | | 2,410,531 | | | 2,741,862 | | | 1,268,237 | |

| Net assets | | $ | 248,675,178 | | $ | 252,765,129 | | $ | 194,492,394 | | $ | 97,690,233 | | $ | 58,664,481 | |

| Shares outstanding | | | 16,558,966 | | | 17,706,419 | | | 13,038,998 | | | 6,268,833 | | | 3,919,031 | |

| Net asset value per share outstanding | | $ | 15.02 | | $ | 14.28 | | $ | 14.92 | | $ | 15.58 | | $ | 14.97 | |

| Net assets consist of: | | | | | | | | | | | | | | | | |

| Shares, $.01 par value per share | | $ | 165,590 | | $ | 177,064 | | $ | 130,390 | | $ | 62,688 | | $ | 39,190 | |

| Paid-in surplus | | | 230,186,697 | | | 247,027,665 | | | 179,437,451 | | | 87,291,285 | | | 53,769,405 | |

| Undistributed (Over-distribution of) net investment income | | | 1,284,246 | | | 927,988 | | | 1,110,405 | | | 282,058 | | | 174,910 | |

| Accumulated net realized gain (loss) | | | (7,203,472 | ) | | (12,328,893 | ) | | (2,841,327 | ) | | (972,843 | ) | | 235,959 | |

| Net unrealized appreciation (depreciation) | | | 24,242,117 | | | 16,961,305 | | | 16,655,475 | | | 11,027,045 | | | 4,445,017 | |

| Net assets | | $ | 248,675,178 | | $ | 252,765,129 | | $ | 194,492,394 | | $ | 97,690,233 | | $ | 58,664,481 | |

| Authorized shares | | | Unlimited | | | Unlimited | | | Unlimited | | | Unlimited | | | Unlimited | |

See accompanying notes to financial statements.

| | Six Months Ended September 30, 2012 |

| | (Unaudited) |

| | | | Select | | | Select | | | Select | | | California | | | New York | |

| | | Tax-Free | | Tax-Free 2 | | Tax-Free 3 | | Select Tax-Free | | Select Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Investment Income | | $ | 6,279,218 | | $ | 6,252,701 | | $ | 4,769,807 | | $ | 2,368,764 | | $ | 1,392,674 | |

| Expenses | | | | | | | | | | | | | | | | |

| Management fees | | | 264,558 | | | 331,899 | | | 256,462 | | | 131,143 | | | 78,807 | |

| Shareholders servicing agent fees and expense | | | 10,620 | | | 9,815 | | | 8,223 | | | 3,123 | | | 2,849 | |

| Interest expense on floating rate obligations | | | — | | | 3,511 | | | — | | | 4,673 | | | 2,343 | |

| Custodian’s fees and expenses | | | 23,111 | | | 23,865 | | | 18,037 | | | 11,115 | | | 7,681 | |

| Trustees fees and expenses | | | 3,269 | | | 3,330 | | | 2,552 | | | 1,289 | | | 767 | |

| Professional fees | | | 11,391 | | | 11,511 | | | 10,243 | | | 8,153 | | | 7,352 | |

| Shareholder reporting expenses | | | 20,540 | | | 22,439 | | | 17,960 | | | 9,111 | | | 10,622 | |

| Stock exchange listing fees | | | 4,257 | | | 4,231 | | | 4,235 | | | 4,227 | | | 4,227 | |

| Investor relations expense | | | 14,843 | | | 15,340 | | | 11,277 | | | 5,119 | | | 3,407 | |

| Other expenses | | | 7,399 | | | 7,658 | | | 4,560 | | | 4,758 | | | 4,163 | |

| Total expenses before custodian fee credit | | | 359,988 | | | 433,599 | | | 333,549 | | | 182,711 | | | 122,218 | |

| Custodian fee credit | | | (3,272 | ) | | (2,986 | ) | | (3,476 | ) | | (446 | ) | | (409 | ) |

| Net expenses | | | 356,716 | | | 430,613 | | | 330,073 | | | 182,265 | | | 121,809 | |

| Net investment income (loss) | | | 5,922,502 | | | 5,822,088 | | | 4,439,734 | | | 2,186,499 | | | 1,270,865 | |

| Realized and Unrealized Gain (Loss) | | | | | | | | | | | | | | | | |

| Net realized gain (loss) from investments | | | 375,313 | | | 402,856 | | | 205,117 | | | (259,609 | ) | | 62,419 | |

| Change in net unrealized appreciation (depreciation) of investments | | | 7,254,829 | | | 6,251,528 | | | 6,009,858 | | | 3,436,088 | | | 1,414,974 | |

| Net realized and unrealized gain (loss) | | | 7,630,142 | | | 6,654,384 | | | 6,214,975 | | | 3,176,479 | | | 1,477,393 | |

| Net increase (decrease) in net assets from operations | | $ | 13,552,644 | | $ | 12,476,472 | | $ | 10,654,709 | | $ | 5,362,978 | | $ | 2,748,258 | |

See accompanying notes to financial statements.

| | | Statement of |

| | | Changes in Net Assets (Unaudited) |

| | | Select Tax-Free (NXP) | | Select Tax-Free 2 (NXQ) | | Select Tax-Free 3 (NXR) | |

| | | | Six Months | | | Year | | | Six Months | | | Year | | | Six Months | | | Year | |

| | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | | 9/30/12 | | | 3/31/12 | | | 9/30/12 | | | 3/31/12 | | | 9/30/12 | | | 3/31/12 | |

| Operations | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | $ | 5,922,502 | | $ | 12,041,194 | | $ | 5,822,088 | | $ | 11,722,663 | | $ | 4,439,734 | | $ | 8,989,157 | |

| Net realized gain (loss) from investments | | | 375,313 | | | (7,139,651 | ) | | 402,856 | | | (10,714,709 | ) | | 205,117 | | | (2,503,311 | ) |

| Change in net unrealized appreciation (depreciation) of investments | | | 7,254,829 | | | 22,982,613 | | | 6,251,528 | | | 27,951,803 | | | 6,009,858 | | | 14,571,245 | |

| Net increase (decrease) in net assets from operations | | | 13,552,644 | | | 27,884,156 | | | 12,476,472 | | | 28,959,757 | | | 10,654,709 | | | 21,057,091 | |

| Distributions to Shareholders | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (5,859,046 | ) | | (11,856,344 | ) | | (5,576,326 | ) | | (11,255,497 | ) | | (4,301,697 | ) | | (8,498,394 | ) |

| From accumulated net realized gains | | | — | | | — | | | — | | | — | | | — | | | (560,019 | ) |

| Decrease in net assets from distributions to shareholders | | | (5,859,046 | ) | | (11,856,344 | ) | | (5,576,326 | ) | | (11,255,497 | ) | | (4,301,697 | ) | | (9,058,413 | ) |

| Capital Share Transactions | | | | | | | | | | | | | | | | | | | |

| Net proceeds from shares issued to shareholders due to reinvestment of distributions | | | 290,195 | | | 395,626 | | | 80,896 | | | 64,229 | | | 129,433 | | | 165,224 | |

| Net increase (decrease) in net assets from capital share transactions | | | 290,195 | | | 395,626 | | | 80,896 | | | 64,229 | | | 129,433 | | | 165,224 | |

| Net increase (decrease) in net assets | | | 7,983,793 | | | 16,423,438 | | | 6,981,042 | | | 17,768,489 | | | 6,482,445 | | | 12,163,902 | |

| Net assets at the beginning of period | | | 240,691,385 | | | 224,267,947 | | | 245,784,087 | | | 228,015,598 | | | 188,009,949 | | | 175,846,047 | |

| Net assets at the end of period | | $ | 248,675,178 | | $ | 240,691,385 | | $ | 252,765,129 | | $ | 245,784,087 | | $ | 194,492,394 | | $ | 188,009,949 | |

| Undistributed (Over-distribution of) net investment income at the end of period | | $ | 1,284,246 | | $ | 1,220,790 | | $ | 927,988 | | $ | 682,226 | | $ | 1,110,405 | | $ | 972,368 | |

See accompanying notes to financial statements.

| | | California Select Tax-Free (NXC) | | New York Select Tax-Free (NXN) | |

| | | | Six Months | | | Year | | | Six Months | | | Year | |

| | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | | 9/30/12 | | | 3/31/12 | | | 9/30/12 | | | 3/31/12 | |

| Operations | | | | | | | | | | | | | |

| Net investment income (loss) | | $ | 2,186,499 | | $ | 4,370,484 | | $ | 1,270,865 | | $ | 2,583,551 | |

| Net realized gain (loss) from investments | | | (259,609 | ) | | (403,104 | ) | | 62,419 | | | 279,185 | |

| Change in net unrealized appreciation (depreciation) of investments | | | 3,436,088 | | | 10,548,676 | | | 1,414,974 | | | 3,092,158 | |

| Net increase (decrease) in net assets from operations | | | 5,362,978 | | | 14,516,056 | | | 2,748,258 | | | 5,954,894 | |

| Distributions to Shareholders | | | | | | | | | | | | | |

| From net investment income | | | (2,143,633 | ) | | (4,268,024 | ) | | (1,281,124 | ) | | (2,498,852 | ) |

| From accumulated net realized gains | | | — | | | — | | | — | | | — | |

| Decrease in net assets from distributions to shareholders | | | (2,143,633 | ) | | (4,268,024 | ) | | (1,281,124 | ) | | (2,498,852 | ) |

| Capital Share Transactions | | | | | | | | | | | | | |

| Net proceeds from shares issued to shareholders due to reinvestment of distributions | | | 23,823 | | | — | | | 27,204 | | | 8,959 | |

| Net increase (decrease) in net assets from capital share transactions | | | 23,823 | | | — | | | 27,204 | | | 8,959 | |

| Net increase (decrease) in net assets | | | 3,243,168 | | | 10,248,032 | | | 1,494,338 | | | 3,465,001 | |

| Net assets at the beginning of period | | | 94,447,065 | | | 84,199,033 | | | 57,170,143 | | | 53,705,142 | |

| Net assets at the end of period | | $ | 97,690,233 | | $ | 94,447,065 | | $ | 58,664,481 | | $ | 57,170,143 | |

| Undistributed (Over-distribution of) net investment income at the end of period | | $ | 282,058 | | $ | 239,192 | | $ | 174,910 | | $ | 185,169 | |

See accompanying notes to financial statements.

| | | Financial |

| | | Highlights (Unaudited) |

| | | |

| | Selected data for a Common share outstanding throughout each period: |

| | | | | Investment Operations | | Less Distributions | | | | | |

| | | Beginning Net Asset Value | | Net Investment Income (Loss) | | Net Realized/ Unrealized Gain (Loss) | | Total | | Net Investment Income | | Capital Gains | | Total | | Ending Net Asset Value | | Ending Market Value | |

| Select Tax-Free (NXP) | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended 3/31: | | | | | | | | | | | | | | | | | | | | | | | | |

| 2013(d) | | $ | 14.55 | | $ | .36 | | $ | .46 | | $ | .82 | | $ | (.35 | ) | $ | — | | $ | (.35 | ) | $ | 15.02 | | $ | 16.06 | |

| 2012 | | | 13.58 | | | .73 | | | .96 | | | 1.69 | | | (.72 | ) | | — | | | (.72 | ) | | 14.55 | | | 14.57 | |

| 2011 | | | 14.19 | | | .71 | | | (.61 | ) | | .10 | | | (.71 | ) | | — | | | (.71 | ) | | 13.58 | | | 13.25 | |

| 2010 | | | 13.52 | | | .73 | | | .66 | | | 1.39 | | | (.72 | ) | | — | | | (.72 | ) | | 14.19 | | | 14.74 | |

| 2009 | | | 14.30 | | | .71 | | | (.81 | ) | | (.10 | ) | | (.68 | ) | | — | | | (.68 | ) | | 13.52 | | | 13.67 | |

| 2008 | | | 14.72 | | | .70 | | | (.44 | ) | | .26 | | | (.68 | ) | | — | | | (.68 | ) | | 14.30 | | | 14.24 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Select Tax-Free 2 (NXQ) | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended 3/31: | | | | | | | | | | | | | | | | | | | | | | | | |

| 2013(d) | | | 13.89 | | | .33 | | | .38 | | | .71 | | | (.32 | ) | | — | | | (.32 | ) | | 14.28 | | | 14.88 | |

| 2012 | | | 12.89 | | | .66 | | | .98 | | | 1.64 | | | (.64 | ) | | — | | | (.64 | ) | | 13.89 | | | 13.63 | |

| 2011 | | | 13.53 | | | .64 | | | (.61 | ) | | .03 | | | (.67 | ) | | — | | | (.67 | ) | | 12.89 | | | 12.40 | |

| 2010 | | | 12.63 | | | .68 | | | .89 | | | 1.57 | | | (.67 | ) | | — | | | (.67 | ) | | 13.53 | | | 13.81 | |

| 2009 | | | 13.93 | | | .67 | | | (1.30 | ) | | (.63 | ) | | (.67 | ) | | — | | | (.67 | ) | | 12.63 | | | 13.14 | |

| 2008 | | | 14.60 | | | .66 | | | (.69 | ) | | (.03 | ) | | (.64 | ) | | — | | | (.64 | ) | | 13.93 | | | 13.79 | |

| | | | Ratios/Supplemental Data |

| | Total Returns | | | | Ratios to Average Net Assets(b) | | | |

| | Based on Market Value | (a) | Based on Net Asset Value | (a) | Ending Net Assets (000) | | Expenses | (c) | Net Investment Income (Loss) | | Portfolio Turnover Rate | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | 12.85 | % | | 5.71 | % | $ | 248,675 | | | .29 | %* | | 4.82 | %* | | 12 | % |

| | | 15.72 | | | 12.72 | | | 240,691 | | | .31 | | | 5.18 | | | 19 | |

| | | (5.40 | ) | | .69 | | | 224,268 | | | .32 | | | 5.05 | | | 6 | |

| | | 13.45 | | | 10.45 | | | 233,869 | | | .32 | | | 5.20 | | | 3 | |

| | | .89 | | | (.65 | ) | | 222,114 | | | .33 | | | 5.12 | | | 11 | |

| | | .61 | | | 1.83 | | | 234,494 | | | .32 | | | 4.83 | | | 4 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | 11.61 | | | 5.12 | | | 252,765 | | | .35 | * | | 4.65 | * | | 11 | |

| | | 15.32 | | | 12.97 | | | 245,784 | | | .35 | | | 4.94 | | | 20 | |

| | | (5.56 | ) | | .13 | | | 228,016 | | | .39 | | | 4.81 | | | 6 | |

| | | 10.45 | | | 12.62 | | | 239,100 | | | .37 | | | 5.12 | | | 4 | |

| | | .24 | | | (4.63 | ) | | 222,771 | | | .39 | | | 5.08 | | | 6 | |

| | | 2.69 | | | (.24 | ) | | 245,244 | | | .40 | | | 4.58 | | | 7 | |

| (a) | Total Return Based on Market Value is the combination of changes in the market price per share and the effect of reinvested dividend income and reinvested capital gains distributions, if any, at the average price paid per share at the time of reinvestment. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending market price. The actual reinvestment for the last dividend declared in the period may take place over several days, and in some instances may not be based on the market price, so the actual reinvestment price may be different from the price used in the calculation. Total returns are not annualized. |

| | Total Return Based on Net Asset Value is the combination of changes in net asset value, reinvested dividend income at net asset value and reinvested capital gains distributions at net asset value, if any. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending net asset value. The actual reinvest price for the last dividend declared in the period may often be based on the Fund’s market price (and not its net asset value), and therefore may be different from the price used in the calculation. Total returns are not annualized. |

| (b) | Ratios do not reflect the effect of custodian fee credits earned on the Fund’s net cash on deposit with the custodian bank, where applicable. |

| (c) | The expense ratios reflect, among other things, the interest expense deemed to have been paid by the Fund on the floating rate certificates issued by the special purpose trusts for the self-deposited inverse floaters held by the Fund, where applicable, as described in Footnote 1 – General Information and Significant Accounting Policies, Inverse Floating Rate Securities as follows: |

| Select Tax-Free (NXP) | | | | |

| Year Ended 3/31: | | | | |

| 2013(d) | | | — | % |

| 2012 | | | — | |

| 2011 | | | — | |

| 2010 | | | — | |

| 2009 | | | — | |

| 2008 | | | — | |

| | | | | |

| Select Tax-Free 2 (NXQ) | | | | |

| Year Ended 3/31: | | | | |

| 2013(d) | | | — | %*** |

| 2012 | | | — | ** |

| 2011 | | | — | |

| 2010 | | | — | |

| 2009 | | | .01 | |

| 2008 | | | .04 | |

| (d) | For the six months ended September 30, 2012. |

| * | Annualized. |

| ** | Rounds to less than .01%. |

| *** | Rounds to less than .01% annualized. |

See accompanying notes to financial statements.

| | | Financial |

| | | Highlights (Unaudited) (continued) |

| | | |

| | Selected data for a Common share outstanding throughout each period: |

| | | | | Investment Operations | | Less Distributions | | | | | |

| | | Beginning Net Asset Value | | Net Investment Income (Loss) | | Net Realized/ Unrealized Gain (Loss) | | Total | | Net Investment Income | | Capital Gains | | Total | | Ending Net Asset Value | | Ending Market Value | |

| Select Tax-Free 3 (NXR) | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended 3/31: | | | | | | | | | | | | | | | | | | | | | | | | |

| 2013(d) | | $ | 14.43 | | $ | .34 | | $ | .48 | | $ | .82 | | $ | (.33 | ) | $ | — | | $ | (.33 | ) | $ | 14.92 | | $ | 15.82 | |

| 2012 | | | 13.51 | | | .69 | | | .92 | | | 1.61 | | | (.65 | ) | | (.04 | ) | | (.69 | ) | | 14.43 | | | 14.34 | |

| 2011 | | | 14.06 | | | .66 | | | (.57 | ) | | .09 | | | (.64 | ) | | — | ** | | (.64 | ) | | 13.51 | | | 13.03 | |

| 2010 | | | 13.38 | | | .67 | | | .65 | | | 1.32 | | | (.64 | ) | | — | ** | | (.64 | ) | | 14.06 | | | 14.22 | |

| 2009 | | | 13.98 | | | .66 | | | (.62 | ) | | .04 | | | (.64 | ) | | — | | | (.64 | ) | | 13.38 | | | 13.57 | |

| 2008 | | | 14.42 | | | .64 | | | (.44 | ) | | .20 | | | (.64 | ) | | — | | | (.64 | ) | | 13.98 | | | 13.75 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| California Select Tax-Free (NXC) | | | | | | | | | | | | | | | | | | | | | |

| Year Ended 3/31: | | | | | | | | | | | | | | | | | | | | | | | | |

| 2013(d) | | | 15.07 | | | .35 | | | .50 | | | .85 | | | (.34 | ) | | — | | | (.34 | ) | | 15.58 | | | 15.98 | |

| 2012 | | | 13.43 | | | .70 | | | 1.62 | | | 2.32 | | | (.68 | ) | | — | | | (.68 | ) | | 15.07 | | | 14.80 | |

| 2011 | | | 13.97 | | | .68 | | | (.55 | ) | | .13 | | | (.67 | ) | | — | | | (.67 | ) | | 13.43 | | | 12.59 | |

| 2010 | | | 13.24 | | | .67 | | | .73 | | | 1.40 | | | (.67 | ) | | — | | | (.67 | ) | | 13.97 | | | 13.08 | |

| 2009 | | | 14.09 | | | .66 | | | (.84 | ) | | (.18 | ) | | (.67 | ) | | — | | | (.67 | ) | | 13.24 | | | 12.00 | |

| 2008 | | | 14.73 | | | .66 | | | (.65 | ) | | .01 | | | (.64 | ) | | (.01 | ) | | (.65 | ) | | 14.09 | | | 14.08 | |

| | | | Ratios/Supplemental Data |

| | Total Returns | | | | Ratios to Average Net Assets(b) | | | |

| | Based on Market Value | (a) | Based on Net Asset Value | (a) | Ending Net Assets (000) | | Expenses | (c) | Net Investment Income (Loss) | | Portfolio Turnover Rate | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | 12.79 | % | | 5.73 | % | $ | 194,492 | | | .35 | %* | | 4.62 | %* | | 17 | % |

| | | 15.69 | | | 12.23 | | | 188,010 | | | .38 | | | 4.94 | | | 16 | |

| | | (3.98 | ) | | .62 | | | 175,846 | | | .37 | | | 4.75 | | | 4 | |

| | | 9.70 | | | 10.05 | | | 182,779 | | | .38 | | | 4.81 | | | 3 | |

| | | 3.51 | | | .34 | | | 173,678 | | | .39 | | | 4.83 | | | 5 | |

| | | 2.91 | | | 1.42 | | | 181,288 | | | .38 | | | 4.49 | | | 2 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | 10.40 | | | 5.70 | | | 97,690 | | | .38 | * | | 4.53 | * | | 9 | |

| | | 23.56 | | | 17.64 | | | 94,447 | | | .42 | | | 4.87 | | | 11 | |

| | | 1.18 | | | .83 | | | 84,199 | | | .38 | | | 4.89 | | | 8 | |

| | | 14.71 | | | 10.71 | | | 87,548 | | | .41 | | | 4.87 | | | 4 | |

| | | (10.34 | ) | | (1.30 | ) | | 82,953 | | | .43 | | | 4.85 | | | 12 | |

| | | 3.68 | | | .05 | | | 88,224 | | | .44 | | | 4.52 | | | 8 | |

| (a) | Total Return Based on Market Value is the combination of changes in the market price per share and the effect of reinvested dividend income and reinvested capital gains distributions, if any, at the average price paid per share at the time of reinvestment. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending market price. The actual reinvestment for the last dividend declared in the period may take place over several days, and in some instances may not be based on the market price, so the actual reinvestment price may be different from the price used in the calculation. Total returns are not annualized. |

| | Total Return Based on Net Asset Value is the combination of changes in net asset value, reinvested dividend income at net asset value and reinvested capital gains distributions at net asset value, if any. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending net asset value. The actual reinvest price for the last dividend declared in the period may often be based on the Fund’s market price (and not its net asset value), and therefore may be different from the price used in the calculation. Total returns are not annualized. |

| (b) | Ratios do not reflect the effect of custodian fee credits earned on the Fund’s net cash on deposit with the custodian bank, where applicable. |

| (c) | The expense ratios reflect, among other things, the interest expense deemed to have been paid by the Fund on the floating rate certificates issued by the special purpose trusts for the self-deposited inverse floaters held by the Fund, where applicable, as described in Footnote 1 – General Information and Significant Accounting Policies, Inverse Floating Rate Securities as follows: |

| Select Tax-Free 3 (NXR) | | | | |

| Year Ended 3/31: | | | | |

| 2013(d) | | | — | % |

| 2012 | | | — | |

| 2011 | | | — | |

| 2010 | | | — | |

| 2009 | | | — | |

| 2008 | | | .02 | |

| | | | | |

| California Select Tax-Free (NXC) | | | | |

| Year Ended 3/31: | | | | |

| 2013(d) | | | .01 | %* |

| 2012 | | | .01 | |

| 2011 | | | .01 | |

| 2010 | | | .02 | |

| 2009 | | | .02 | |

| 2008 | | | .06 | |

| (d) | For the six months ended September 30, 2012. |

| * | Annualized. |

| ** | Rounds to less than $.01 per share. |

See accompanying notes to financial statements.

| | | Financial |

| | | Highlights (Unaudited) (continued) |

| | | |

| | Selected data for a Common share outstanding throughout each period: |

| | | | | Investment Operations | | Less Distributions | | | | | |

| | | Beginning Net Asset Value | | Net Investment Income (Loss) | | Net Realized/ Unrealized Gain (Loss) | | Total | | Net Investment Income | | Capital Gains | | Total | | Ending Net Asset Value | | Ending Market Value | |

| New York Select Tax-Free (NXN) | | | | | | | | | | | | | | | | | | | | | |

| Year Ended 3/31: | | | | | | | | | | | | | | | | | | | | | | | | |

| 2013(d) | | $ | 14.59 | | $ | .32 | | $ | .39 | | $ | .71 | | $ | (.33 | ) | $ | — | | $ | (.33 | ) | $ | 14.97 | | $ | 15.07 | |

| 2012 | | | 13.71 | | | .66 | | | .86 | | | 1.52 | | | (.64 | ) | | — | | | (.64 | ) | | 14.59 | | | 14.10 | |

| 2011 | | | 14.06 | | | .64 | | | (.38 | ) | | .26 | | | (.61 | ) | | — | | | (.61 | ) | | 13.71 | | | 13.06 | |

| 2010 | | | 13.37 | | | .62 | | | .68 | | | 1.30 | | | (.61 | ) | | — | | | (.61 | ) | | 14.06 | | | 13.80 | |

| 2009 | | | 13.79 | | | .62 | | | (.43 | ) | | .19 | | | (.61 | ) | | — | | | (.61 | ) | | 13.37 | | | 13.08 | |

| 2008 | | | 14.28 | | | .62 | | | (.49 | ) | | .13 | | | (.61 | ) | | (.01 | ) | | (.62 | ) | | 13.79 | | | 13.79 | |

| | | | Ratios/Supplemental Data |

| | Total Returns | | | | Ratios to Average Net Assets(b) | | | |

| | Based on Market Value | (a) | Based on Net Asset Value | (a) | Ending Net Assets (000) | | Expenses | (c) | Net Investment Income (Loss) | | Portfolio Turnover Rate | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | 9.27 | % | | 4.89 | % | $ | 58,664 | | | .42 | %* | | 4.38 | %* | | 13 | % |

| | | 13.05 | | | 11.25 | | | 57,170 | | | .50 | | | 4.62 | | | 19 | |

| | | (1.08 | ) | | 1.84 | | | 53,705 | | | .41 | | | 4.55 | | | 3 | |

| | | 10.31 | | | 9.89 | | | 55,007 | | | .44 | | | 4.50 | | | 1 | |

| | | (.57 | ) | | 1.47 | | | 52,268 | | | .47 | | | 4.57 | | | 1 | |

| | | 2.06 | | | .94 | | | 53,908 | | | .46 | | | 4.35 | | | 20 | |

| (a) | Total Return Based on Market Value is the combination of changes in the market price per share and the effect of reinvested dividend income and reinvested capital gains distributions, if any, at the average price paid per share at the time of reinvestment. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending market price. The actual reinvestment for the last dividend declared in the period may take place over several days, and in some instances may not be based on the market price, so the actual reinvestment price may be different from the price used in the calculation. Total returns are not annualized. |

| | Total Return Based on Net Asset Value is the combination of changes in net asset value, reinvested dividend income at net asset value and reinvested capital gains distributions at net asset value, if any. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending net asset value. The actual reinvest price for the last dividend declared in the period may often be based on the Fund’s market price (and not its net asset value), and therefore may be different from the price used in the calculation. Total returns are not annualized. |

| (b) | Ratios do not reflect the effect of custodian fee credits earned on the Fund’s net cash on deposit with the custodian bank, where applicable. |

| (c) | The expense ratios reflect, among other things, the interest expense deemed to have been paid by the Fund on the floating rate certificates issued by the special purpose trusts for the self-deposited inverse floaters held by the Fund, where applicable, as described in Footnote 1 – General Information and Significant Accounting Policies, Inverse Floating Rate Securities as follows: |

| New York Select Tax-Free (NXN) | | | | |

| Year Ended 3/31: | | | | |

| 2013(d) | | | .01 | %* |

| 2012 | | | .01 | |

| 2011 | | | .01 | |

| 2010 | | | .02 | |

| 2009 | | | .02 | |

| 2008 | | | .03 | |

| (d) | For the six months ended September 30, 2012. |

| * | Annualized. |

See accompanying notes to financial statements.

| | | Notes to |

| | | Financial Statements (Unaudited) |

1. General Information and Significant Accounting Policies

General Information

The funds covered in this report and their corresponding New York Stock Exchange (“NYSE”) symbols are Nuveen Select Tax-Free Income Portfolio (NXP), Nuveen Select Tax-Free Income Portfolio 2 (NXQ), Nuveen Select Tax-Free Income Portfolio 3 (NXR), Nuveen California Select Tax-Free Income Portfolio (NXC) and Nuveen New York Select Tax-Free Income Portfolio (NXN) (each a “Fund” and collectively, the “Funds”). The Funds are registered under the Investment Company Act of 1940, as amended, as closed-end registered investment companies.

Each Fund seeks to provide current income and stable dividends, exempt from regular federal and designated state income taxes, where applicable, consistent with the preservation of capital by investing primarily in a portfolio of municipal obligations.

Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Funds in the preparation of their financial statements in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”).

Investment Valuation

Prices of municipal bonds are provided by a pricing service approved by the Funds’ Board of Trustees. These securities are generally classified as Level 2 for fair value measurement purposes. The pricing service establishes a security’s fair value using methods that may include consideration of the following: yields or prices of investments of comparable quality, type of issue, coupon, maturity and rating, market quotes or indications of value from security dealers, evaluations of anticipated cash flows or collateral, general market conditions and other information and analysis, including the obligor’s credit characteristics considered relevant. In pricing certain securities, particularly less liquid and lower quality securities, the pricing service may consider information about a security, its issuer, or market activity, provided by Nuveen Fund Advisors, Inc. (the “Adviser”), a wholly-owned subsidiary of Nuveen Investments, Inc. (“Nuveen”). These securities are generally classified as Level 2 or Level 3 depending on the priority of the significant inputs.

Certain securities may not be able to be priced by the pre-established pricing methods as described above. Such securities may be valued by the Funds’ Board of Trustees or its designee at fair value. These securities generally include, but are not limited to, restricted securities (securities which may not be publicly sold without registration under the Securities Act of 1933, as amended) for which a pricing service is unable to provide a market price; securities whose trading has been formally suspended; debt securities that have gone into default and for which there is no current market quotation; a security whose market price is not available from a pre-established pricing source; a security with respect to which an event has occurred that is likely to materially affect the value of the security after the market has closed but before the calculation of a Fund’s net asset value (as may be the case in non-U.S. markets on which the security is primarily traded) or make it difficult or impossible to obtain a reliable market quotation; and a security whose price, as provided by the pricing service, is not deemed to reflect the security’s fair value. As a general principle, the fair value of a security would appear to be the amount that the owner might reasonably expect to receive for it in a current sale. A variety of factors may be considered in determining the fair value of such securities, which may include consideration of the following: yields or prices of investments of comparable quality, type of issue, coupon, maturity and rating, market quotes or indications of value from security dealers, evaluations of anticipated cash flows or collateral, general market conditions and other information and analysis, including the obligor’s credit characteristics considered relevant. These securities are generally classified as Level 2 or Level 3 depending on the priority of the significant inputs. Regardless of the method employed to value a particular security, all valuations are subject to review by the Funds’ Board of Trustees or its designee.

Refer to Footnote 2 – Fair Value Measurements for further details on the leveling of securities held by the Funds as of the end of the reporting period.

Investment Transactions

Investment transactions are recorded on a trade date basis. Realized gains and losses from transactions are determined on the specific identification method, which is the same basis used for federal income tax purposes. Investments purchased on a when-issued/delayed delivery basis may have extended settlement periods. Any investments so purchased are subject to market fluctuation during this period. The Funds have instructed the

custodian to earmark securities in the Funds’ portfolio with a current value at least equal to the amount of the when-issued/delayed delivery purchase commitments. At September 30, 2012, NXR had outstanding delayed delivery purchase commitments of $1,575,686. There were no such outstanding purchase commitments in any of the other Funds.

Investment Income

Investment income, which reflects the amortization of premiums and includes accretion of discounts for financial reporting purposes, is recorded on an accrual basis. Investment income also reflects paydown gains and losses, if any.

Professional Fees

Professional fees presented on the Statement of Operations consist of legal fees incurred in the normal course of operations, audit fees, tax consulting fees and, in some cases, workout expenditures. Workout expenditures are incurred in an attempt to protect or enhance an investment, or to pursue other claims or legal actions on behalf of Fund shareholders.

Income Taxes

Each Fund is a separate taxpayer for federal income tax purposes. Each Fund intends to distribute substantially all of its net investment income and net capital gains to shareholders and to otherwise comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies. Therefore, no federal income tax provision is required. Furthermore, each Fund intends to satisfy conditions that will enable interest from municipal securities, which is exempt from regular federal and designated state income taxes, to retain such tax-exempt status when distributed to shareholders of the Funds. Net realized capital gains and ordinary income distributions paid by the Funds are subject to federal taxation.

For all open tax years and all major taxing jurisdictions, management of the Funds has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Open tax years are those that are open for examination by taxing authorities (i.e., generally the last four tax year ends and the interim tax period since then). Furthermore, management of the Funds is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Dividends and Distributions to Shareholders

Dividends from net investment income are declared monthly. Net realized capital gains and/or market discount from investment transactions, if any, are distributed to shareholders at least annually. Furthermore, capital gains are distributed only to the extent they exceed available capital loss carryforwards.

Distributions to shareholders of net investment income, net realized capital gains and/or market discount, if any, are recorded on the ex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP.

Inverse Floating Rate Securities

Each Fund is authorized to invest in inverse floating rate securities. An inverse floating rate security is created by depositing a municipal bond, typically with a fixed interest rate, into a special purpose trust created by a broker-dealer. In turn, this trust (a) issues floating rate certificates, in face amounts equal to some fraction of the deposited bond’s par amount or market value, that typically pay short-term tax-exempt interest rates to third parties, and (b) issues to a long-term investor (such as one of the Funds) an inverse floating rate certificate (sometimes referred to as an “inverse floater”) that represents all remaining or residual interest in the trust. The income received by the inverse floater holder varies inversely with the short-term rate paid to the floating rate certificates’ holders, and in most circumstances the inverse floater holder bears substantially all of the underlying bond’s downside investment risk and also benefits disproportionately from any potential appreciation of the underlying bond’s value. The price of an inverse floating rate security will be more volatile than that of the underlying bond because the interest rate is dependent on not only the fixed coupon rate of the underlying bond but also on the short-term interest paid on the floating rate certificates, and because the inverse floating rate security essentially bears the risk of loss of the greater face value of the underlying bond.

A Fund may purchase an inverse floating rate security in a secondary market transaction without first owning the underlying bond (referred to as an “externally-deposited inverse floater”), or instead by first selling a fixed-rate bond to a broker-dealer for deposit into the special purpose trust and receiving in turn the residual interest in the trust (referred to as a “self-deposited inverse floater”). The inverse floater held by a Fund gives the Fund the right (a) to cause the holders of the floating rate certificates to tender their notes at par, and (b) to have the broker transfer the fixed-rate bond held by the trust to the Fund, thereby collapsing the trust. An investment in an externally-deposited inverse floater is identified in the Portfolio of Investments as “(IF) – Inverse floating rate investment.” An investment in a self-deposited inverse floater is accounted for as a financing transaction. In such instances, a fixed-rate bond deposited into a special purpose trust is identified in the Portfolio of Investments as “(UB) – Underlying bond of an inverse floating rate trust reflected as a financing transaction,” with the Fund accounting for the short-term floating rate certificates issued by the trust as “Floating rate obligations” on the Statement of Assets and Liabilities. In addition, the Fund reflects in “Investment Income” the entire earnings of

| | | Notes to |

| | | Financial Statements (Unaudited) (continued) |

the underlying bond and the related interest paid to the holders of the short-term floating rate certificates as a component of “Interest expense and amortization of offering costs” on the Statement of Operations.

During the six months ended September 30, 2012, each Fund invested in externally deposited inverse floaters and/or self-deposited inverse floaters.

Each Fund may also enter into shortfall and forbearance agreements (sometimes referred to as a “recourse trust” or “credit recovery swap”) (such agreements referred to herein as “Recourse Trusts”) with a broker-dealer by which a Fund agrees to reimburse the broker-dealer, in certain circumstances, for the difference between the liquidation value of the fixed-rate bond held by the trust and the liquidation value of the floating rate certificates issued by the trust plus any shortfalls in interest cash flows. Under these agreements, a Fund’s potential exposure to losses related to or on inverse floaters may increase beyond the value of a Fund’s inverse floater investments as a Fund may potentially be liable to fulfill all amounts owed to holders of the floating rate certificates. At period end, any such shortfall is recognized as “Unrealized depreciation on Recourse Trusts” on the Statement of Assets and Liabilities.

At September 30, 2012, each Fund’s maximum exposure to externally-deposited Recourse Trusts was as follows:

| | | | | | | | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Maximum exposure to Recourse Trusts | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 2,000,000 | |

The average floating rate obligations outstanding and average annual interest rate and fees related to self-deposited inverse floaters for the following Funds during the six months ended September 30, 2012, were as follows:

| | | | | | | | | | | |

| | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | |

| | | | Tax-Free 2 | | | Tax-Free | | | Tax-Free | |

| | | | (NXQ | ) | | (NXC | ) | | (NXN | ) |

| Average floating rate obligations outstanding | | $ | 1,000,000 | | $ | 1,540,000 | | $ | 1,005,000 | |

| Average annual interest rate and fees | | | .70 | % | | .61 | % | | .46 | % |

Derivative Financial Instruments

Each Fund is authorized to invest in certain derivative instruments, including foreign currency forwards, futures, options and swap contracts. Although the Funds are authorized to invest in such derivative instruments, and may do so in the future, they did not make any such investments during the six months ended September 30, 2012.

Market and Counterparty Credit Risk

In the normal course of business each Fund may invest in financial instruments and enter into financial transactions where risk of potential loss exists due to changes in the market (market risk) or failure of the other party to the transaction to perform (counterparty credit risk). The potential loss could exceed the value of the financial assets recorded on the financial statements. Financial assets, which potentially expose each Fund to counterparty credit risk, consist principally of cash due from counterparties on forward, option and swap transactions, when applicable. The extent of each Fund’s exposure to counterparty credit risk in respect to these financial assets approximates their carrying value as recorded on the Statement of Assets and Liabilities. Futures contracts, when applicable, expose a Fund to minimal counterparty credit risk as they are exchange traded and the exchange’s clearinghouse, which is counterparty to all exchange traded futures, guarantees the futures contracts against default.

Each Fund helps manage counterparty credit risk by entering into agreements only with counterparties the Adviser believes have the financial resources to honor their obligations and by having the Adviser monitor the financial stability of the counterparties. Additionally, counterparties may be required to pledge collateral daily (based on the daily valuation of the financial asset) on behalf of each Fund with a value approximately equal to the amount of any unrealized gain above a pre-determined threshold. Reciprocally, when each Fund has an unrealized loss, the Funds have instructed the custodian to pledge assets of the Funds as collateral with a value approximately equal to the amount of the unrealized loss above a pre-determined threshold. Collateral pledges are monitored and subsequently adjusted if and when the valuations fluctuate, either up or down, by at least the predetermined threshold amount.

Zero Coupon Securities

Each Fund is authorized to invest in zero coupon securities. A zero coupon security does not pay a regular interest coupon to its holders during the life of the security. Income to the holder of the security comes from accretion of the difference between the original purchase price of the security at issuance and the par value of the security at maturity and is effectively paid at maturity. The market prices of zero coupon securities generally are more volatile than the market prices of securities that pay interest periodically.

Custodian Fee Credit

Each Fund has an arrangement with the custodian bank whereby certain custodian fees and expenses are reduced by net credits earned on each Fund’s cash on deposit with the bank. Such deposit arrangements are an alternative to overnight investments. Credits for cash balances may be offset by charges for any days on which a Fund overdraws its account at the custodian bank.

Indemnifications

Under the Funds’ organizational documents, their officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Funds. In addition, in the normal course of business, the Funds enter into contracts that provide general indemnifications to other parties. The Funds’ maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Funds that have not yet occurred. However, the Funds have not had prior claims or losses pursuant to these contracts and expect the risk of loss to be remote.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results may differ from those estimates.

2. Fair Value Measurements

Fair value is defined as the price that the Funds would receive upon selling an investment or transferring a liability in an orderly transaction to an independent buyer in the principal or most advantageous market for the investment. A three-tier hierarchy is used to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability. Observable inputs are based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability. Unobservable inputs are based on the best information available in the circumstances. The following is a summary of the three-tiered hierarchy of valuation input levels.

| Level 1 – | Inputs are unadjusted and prices are determined using quoted prices in active markets for identical securities. |

| Level 2 – | Prices are determined using other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). |

| Level 3 – | Prices are determined using significant unobservable inputs (including management’s assumptions in determining the fair value of investments). |

The inputs or methodologies used for valuing securities are not an indication of the risks associated with investing in those securities. The following is a summary of each Fund’s fair value measurements as of the end of the reporting period:

| | | | | | | | | | | | | | |

| Select Tax-Free (NXP) | | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Long-Term Investments*: | | | | | | | | | | | | | |

| Municipal Bonds | | $ | — | | $ | 242,258,028 | | $ | — | | $ | 242,258,028 | |

| | | | | | | | | | | | | | |

| Select Tax-Free 2 (NXQ) | | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Long-Term Investments*: | | | | | | | | | | | | | |

| Municipal Bonds | | $ | — | | $ | 245,643,785 | | $ | — | | $ | 245,643,785 | |

| | | | | | | | | | | | | | |

| Select Tax-Free 3 (NXR) | | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Long-Term Investments*: | | | | | | | | | | | | | |

| Municipal Bonds | | $ | — | | $ | 187,180,997 | | $ | — | | $ | 187,180,997 | |

| | | | | | | | | | | | | | |

| California Select Tax-Free (NXC) | | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Long-Term Investments*: | | | | | | | | | | | | | |

| Municipal Bonds | | $ | — | | $ | 98,293,255 | | $ | — | | $ | 98,293,255 | |

| | | | | | | | | | | | | | |

| New York Select Tax-Free (NXN) | | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Long-Term Investments*: | | | | | | | | | | | | | |

| Municipal Bonds | | $ | — | | $ | 58,993,504 | | $ | — | | $ | 58,993,504 | |

* Refer to the Fund’s Portfolio of Investments for industry/state classifications.

The Nuveen funds’ Board of Directors/Trustees is responsible for the valuation process and has delegated the oversight of the daily valuation process to the Adviser’s Valuation Committee. The Valuation Committee, pursuant to the valuation policies and procedures adopted by the Board of Directors/Trustees, is responsible for making fair value determinations, evaluating the effectiveness of the funds’ pricing policies, and reporting to the

| | | Notes to |

| | | Financial Statements (Unaudited) (continued) |

Board of Directors/Trustees. The Valuation Committee is aided in its efforts by the Adviser’s dedicated Securities Valuation Team, which is responsible for administering the daily valuation process and applying fair value methodologies as approved by the Valuation Committee. When determining the reliability of independent pricing services for investments owned by the funds, the Valuation Committee, among other things, conducts due diligence reviews of the pricing services and monitors the quality of security prices received through various testing reports conducted by the Securities Valuation Team.

The Valuation Committee will consider pricing methodologies it deems relevant and appropriate when making fair value determinations. Examples of possible methodologies include, but are not limited to, multiple of earnings; discount from market of a similar freely traded security; discounted cash-flow analysis; book value or a multiple thereof; risk premium/yield analysis; yield to maturity; and/or fundamental investment analysis. The Valuation Committee will also consider factors it deems relevant and appropriate in light of the facts and circumstances. Examples of possible factors include, but are not limited to, the type of security; the issuer’s financial statements; the purchase price of the security; the discount from market value of unrestricted securities of the same class at the time of purchase; analysts’ research and observations from financial institutions; information regarding any transactions or offers with respect to the security; the existence of merger proposals or tender offers affecting the security; the price and extent of public trading in similar securities of the issuer or comparable companies; and the existence of a shelf registration for restricted securities.

For each portfolio security that has been fair valued pursuant to the policies adopted by the Board of Directors/Trustees, the fair value price is compared against the last available and next available market quotations. The Valuation Committee reviews the results of such testing and fair valuation occurrences are reported to the Board of Directors/Trustees.

3. Derivative Instruments and Hedging Activities

The Funds record derivative instruments at fair value, with changes in fair value recognized on the Statement of Operations, when applicable. Even though the Funds’ investments in derivatives may represent economic hedges, they are not considered to be hedge transactions for financial reporting purposes. The Funds did not invest in derivative instruments during the six months ended September 30, 2012.

4. Fund Shares

Since the inception of the Funds’ repurchase programs, the Funds have not repurchased any of their outstanding shares. Transactions in shares were as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | | Select | | | Select | | | Select | |

| | | | Tax-Free (NXP) | | | Tax-Free 2 (NXQ) | | | Tax-Free 3 (NXR) | |

| | | | Six Months | | | Year | | | Six Months | | | Year | | | Six Months | | | Year | |

| | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | | 9/30/12 | | | 3/31/12 | | | 9/30/12 | | | 3/31/12 | | | 9/30/12 | | | 3/31/12 | |

| Shares issued to shareholders due to reinvestment of distributions | | | 19,636 | | | 27,913 | | | 5,706 | | | 4,774 | | | 8,824 | | | 11,716 | |

| | | | | | | | | | California Select | | | New York Select | |

| | | | | | | | | | Tax-Free (NXC) | | | Tax-Free (NXN) | |

| | | | | | | | | | Six Months | | | Year | | | Six Months | | | Year | |

| | | | | | | | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | | | | | | | | 9/30/12 | | | 3/31/12 | | | 9/30/12 | | | 3/31/12 | |

| Shares issued to shareholders due to reinvestment of distributions | | | | | | | | | 1,542 | | | — | | | 1,832 | | | 607 | |

5. Investment Transactions

Purchases and sales (including maturities but excluding short-term investments, where applicable) during the six months ended September 30, 2012, were as follows:

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Purchases | | $ | 27,764,903 | | $ | 25,467,493 | | $ | 31,104,979 | | $ | 9,501,419 | | $ | 8,341,034 | |

| Sales and maturities | | | 29,774,250 | | | 28,934,250 | | | 31,574,225 | | | 8,327,415 | | | 7,400,664 | |

6. Income Tax Information

The following information is presented on an income tax basis. Differences between amounts for financial statement and federal income tax purposes are primarily due to timing differences in recognizing taxable market discount, timing differences in recognizing certain gains and losses on investment transactions and the treatment of investments in inverse floating rate securities reflected as financing transactions, if any. To the extent that differences arise that are permanent in nature, such amounts are reclassified within the capital accounts as detailed below. Temporary differences do not require reclassification. Temporary and permanent differences do not impact the net asset values of the Funds.

At September 30, 2012, the cost and unrealized appreciation (depreciation) of investments, as determined on a federal income tax basis, were as follows:

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Cost of investments | | $ | 217,309,126 | | $ | 227,233,502 | | $ | 169,971,771 | | $ | 85,708,150 | | $ | 53,536,585 | |

| Gross unrealized: | | | | | | | | | | | | | | | | |

| Appreciation | | $ | 25,228,072 | | $ | 18,501,966 | | $ | 17,607,320 | | $ | 11,303,308 | | $ | 4,510,790 | |

| Depreciation | | | (279,170 | ) | | (1,091,683 | ) | | (398,094 | ) | | (262,991 | ) | | (55,038 | ) |

| Net unrealized appreciation (depreciation) of investments | | $ | 24,948,902 | | $ | 17,410,283 | | $ | 17,209,226 | | $ | 11,040,317 | | $ | 4,455,752 | |

Permanent differences, primarily due to federal taxes paid and taxable market discount, resulted in reclassifications among the Funds’ components of net assets at March 31, 2012, the Funds’ last tax year end, as follows:

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Paid-in-surplus | | $ | (293 | ) | $ | 3,433 | | $ | 459 | | $ | — | | $ | — | |

| Undistributed (Over-distribution of) net investment income | | | (24,482 | ) | | (43,172 | ) | | (16,790 | ) | | (550 | ) | | (4,027 | ) |

| Accumulated net realized gain (loss) | | | 24,775 | | | 39,739 | | | 16,331 | | | 550 | | | 4,027 | |

The tax components of undistributed net tax-exempt income, net ordinary income and net long-term capital gains at March 31, 2012, the Funds’ last tax year end, were as follows:

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Undistributed net tax-exempt income* | | $ | 1,435,740 | | $ | 1,198,377 | | $ | 1,277,071 | | $ | 588,588 | | $ | 386,521 | |

| Undistributed net ordinary income** | | | 7,724 | | | 26,267 | | | 411 | | | — | | | — | |

| Undistributed net long-term capital gains | | | — | | | — | | | — | | | — | | | 167,392 | |

| * | Undistributed net tax-exempt income (on a tax basis) has not been reduced for the dividend declared on March 1, 2012, paid on April 2, 2012. |

| ** | Net ordinary income consists of taxable market discount income and net short-term capital gains, if any. |

The tax character of distributions paid during the Funds’ last tax year ended March 31, 2012, was designated for purposes of the dividends paid deduction as follows:

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | California | | | New York | |

| | | | Select | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) | | (NXN | ) |

| Distributions from net tax-exempt income | | $ | 11,795,179 | | $ | 11,308,334 | | $ | 8,418,313 | | $ | 4,258,623 | | $ | 2,485,111 | |

| Distributions from net ordinary income ** | | | 59,504 | | | — | | | 60,476 | | | — | | | — | |

| Distributions from net long-term capital gains | | | — | | | — | | | 559,452 | | | — | | | — | |

| ** | Net ordinary income consists of taxable market discount income and net short-term capital gains, if any. |

| | | Notes to |

| | | Financial Statements (Unaudited) (continued) |

At March 31, 2012, the Funds’ last tax year end, the following Funds had unused capital loss carryforwards available for federal income tax purposes to be applied against future capital gains, if any. If not applied, the carryforwards will expire as follows:

| | | | | | | | | | | |

| | | | | | | | | | California | |

| | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXC | ) |

| Expiration: | | | | | | | | | | |

| March 31, 2015 | | $ | 260,316 | | $ | 862,250 | | $ | — | |

| March 31, 2016 | | | — | | | 7,597 | | | 29,942 | |

| March 31, 2017 | | | — | | | 400,800 | | | 107,619 | |

| March 31, 2019 | | | — | | | 335,742 | | | 173,121 | |

| Total | | $ | 260,316 | | $ | 1,606,389 | | $ | 310,682 | |

During the Funds’ last tax year ended March 31, 2012, the following Funds utilized their capital loss carryforwards as follows:

| | | | | | | | | | | |

| | | | | | | | | | New York | |

| | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXN | ) |

| Utilized capital loss carryforwards | | $ | 205,014 | | $ | 455,309 | | $ | 92,679 | |

Under the Regulated Investment Company Modernization Act of 2010 (the “Act”), capital losses incurred by the Funds after December 31, 2010 will not be subject to expiration. Capital losses incurred that will be carried forward under the provisions of the Act are as follows:

| | | | California | |

| | | | Select | |

| | | | Tax-Free | |

| | | | (NXC | ) |

| Post-enactment losses: | | | | |

| Short-term | | $ | — | |

| Long-term | | | 148,537 | |

The Funds have elected to defer losses incurred from November 1, 2011 through March 31, 2012, the Funds’ last tax year end, in accordance with federal income tax rules. These losses are treated as having arisen on the first day of the current fiscal year. The following Funds have elected to defer losses as follows:

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | California | |

| | | | Select | | | Select | | | Select | | | Select | |

| | | | Tax-Free | | | Tax-Free 2 | | | Tax-Free 3 | | | Tax-Free | |

| | | | (NXP | ) | | (NXQ | ) | | (NXR | ) | | (NXC | ) |

| Post-October capital losses | | $ | 7,319,890 | | $ | 11,130,279 | | $ | 3,046,588 | | $ | 254,017 | |

| Late-year ordinary losses | | | — | | | — | | | — | | | — | |

7. Management Fees and Other Transactions with Affiliates

Each Fund’s management fee consists of two components – a fund-level fee, based only on the amount of assets within the Fund, and a complex-level fee, based on the aggregate amount of all eligible fund assets managed by the Adviser. This pricing structure enables Fund shareholders to benefit from growth in the assets within their respective Fund as well as from growth in the amount of complex-wide assets managed by the Adviser.

The annual fund-level fee for each Fund, payable monthly, is calculated according to the following schedule:

| | | | Select Tax-Free 2 (NXQ) |

| | | | Select Tax-Free 3 (NXR) |

| | | | California Select Tax-Free (NXC) |

| | Select Tax-Free (NXP) | New York Select Tax-Free (NXN) |

| Average Daily Managed Assets* | Fund-Level Fee Rate | Fund-Level Fee Rate |

| For the first $125 million | .0500 | % | .1000 | % |

| For the next $125 million | .0375 | | .0875 | |

| For the next $250 million | .0250 | | .0750 | |

| For the next $500 million | .0125 | | .0625 | |

The annual complex-level fee for each Fund, payable monthly, is calculated according to the following schedule:

| Complex-Level Managed Asset Breakpoint Level* | Effective Rate at Breakpoint Level |