UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE YEAR ENDED DECEMBER 31, 2008 |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report _____________________

For the year ended December 31, 2008

Commission File Number: 0-20420

CALCITECH LTD.

(Exact name of Registrant as specified in its charter)

A CORPORATION FORMED UNDER THE LAWS OF BERMUDA

(Jurisdiction of Incorporation or Organization)

10 route de l’aeroport

1215 Geneva, Switzerland

(Address of principal executive offices)

Roger A. Leopard

President and Chief Executive Officer

CalciTech Ltd.

10 route de l’aeroport

1215 Geneva, Switzerland

Telephone: + 41 22 7104020

Fax: + 41 22 7883092

(Name, Telephone, E-mail and/or Facsimile number

and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act: NONE

| Title of each class | | Name of exchange on which registered |

| | | |

| NONE | | |

| | | |

Securities registered or to be registered pursuant to Section 12(g) of the Act

Common Shares

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

126,588,812

Indicate by check mark if the Company is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the Company is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

x Yes ¨ No

Indicate by check mark whether the Company (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the Company has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

¨ Yes x No

Indicate by check mark whether the Company is a large accelerated filer, an accelerated filer or a non-accelerated filer.

Large accelerated filer ¨ | | Accelerated filer ¨ | | Non-accelerated filer x |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ¨ | International Financial Reporting Standards as issued By the International Accounting Standards Board x | | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

x Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the Company is a shell company (as defined in Rule 12b-2 of the Exchange Act.

¨ Yes x No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the Company has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

NOT APPLICABLE ¨ Yes ¨ No

TABLE OF CONTENTS

| | | | | Page |

| | | | 1 |

| Item 1. | | Identity of Directors, Senior Management and Advisors | | 1 |

| Item 2. | | Offer Statistics and Expected Timetable | | 1 |

| Item 3. | | Key Information | | 1 |

| 3A. | | Selected Financial Data | | 1 |

| 3B. | | Capitalization and Indebtedness | | 2 |

| 3C. | | Reasons for the Offer and Use of Proceeds | | 2 |

| 3D. | | Risk Factors | | 2 |

| Item 4. | | Information on the Company | | 5 |

| 4A. | | History and Development of the Company | | 5 |

| 4B. | | Business Overview | | 6 |

| 4C. | | Organizational Structure | | 18 |

| 4D. | | Property, Plants and Equipment | | 18 |

| | Unresolved Staff Comments | | 19 |

| Item 5. | | Operating and Financial Review and Prospects | | 19 |

| 5A. | | Operating Results | | 19 |

| 5B. | | Liquidity and Capital Resources | | 21 |

| 5C. | | Research and Development, Patents and Licenses, etc. | | 23 |

| 5D. | | Trend Information | | 23 |

| 5E. | | Off Balance Sheet Arrangements | | 23 |

| 5F. | | Tabular Disclosure of Contractual Obligations | | 23 |

| Item 6. | | Directors, Senior Management and Employees | | 24 |

| 6A. | | Directors, Senior Management | | 24 |

| 6B. | | Compensation | | 25 |

| 6C. | | Board Practices | | 26 |

| 6D. | | Employees | | 26 |

| 6E. | | Share Ownership | | 26 |

| Item 7. | | Major Shareholders and Related Party Transactions | | 27 |

| 7A. | | Major Shareholders | | 27 |

| 7B. | | Related Party Transactions | | 28 |

| 7C. | | Interest of Experts and Counsel. | | 28 |

| Item 8. | | Financial Statements | | 28 |

| 8A. | | Consolidated Statements and Other Financial Information | | 28 |

| 8B. | | Significant Changes | | 29 |

| Item 9. | | The Offer and Listing | | 29 |

| 9A. | | Price History of Stock | | 29 |

| 9B. | | Plan of Distribution | | 31 |

| 9C. | | Markets | | 31 |

| 9D. | | Selling Shareholders | | 31 |

| 9E. | | Dilution | | 31 |

| 9F. | | Expenses of the Issue | | 31 |

| Item 10. | | Additional Information | | 31 |

| 10A. | | Share Capital | | 31 |

| 10B. | | Memorandum and Articles of Association | | 31 |

| 10C. | | Material Contracts | | 32 |

| 10D. | | Exchange Controls | | 33 |

| 10E. | | Taxation | | 34 |

| 10F. | | Dividends and Paying Agents. | | 37 |

| 10G. | | Statement of Experts. | | 37 |

| 10H. | | Documents on Display. | | 37 |

| 10I. | | Subsidiary Information | | 38 |

| Item 11. | | Quantitative and Qualitative Disclosures About Market Risk | | 38 |

| Item 12. | | Description of Securities Other than Equity Securities | | 38 |

| Item 13. | | Defaults, Dividend Arrearages and Delinquencies | | 38 |

| Part II | | | | 38 |

| Item 14. | | Material Modifications to the Rights of Security Holders and Use of Proceeds | | 38 |

| Item 15T. | | Controls and Procedures. | | 38 |

| Item 16. | | [Reserved] | | 39 |

| Item 16A | | Audit Committee Financial Report | | 39 |

| Item 16B | | Code of Ethics | | 40 |

| Item 16C | | Principal Accountant Fees and Services | | 40 |

| Item 16D | | Exemptions From The Listing Standards For Audit Committees | | 41 |

| Item 16E | | Purchases Of Equity Securities By The Issuer And Affiliated Purchasers | | 41 |

| Part III | | | | 41 |

| Item 17. | | Financial Statements | | 41 |

| Item 18. | | Financial Statements | | 41 |

| Item 19. | | Exhibits | | 41 |

| SIGNATURES | | 43 |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | | F |

PART I

The following discussion contains forward-looking statements regarding events and financial trends, which may affect CalciTech Ltd’s (“CalciTech,” the “Company,” “we,” “our” or “us”) future operating results and financial position. Such statements are subject to risks and uncertainties that could cause our actual results and financial position to differ materially from those anticipated in forward-looking statements. These factors include, but are not limited to, the fact that we are in the development stage, will need additional financing to build our proposed plants and will be subject to certain technological risks associated with scaling up production to a commercial level, all of which factors are set forth in more detail in the section entitled “Risk Factors” in Item 3.D. and “Operating and Financial Review and Prospects” at Item 5.

Item 1. Identity of Directors, Senior Management and Advisors

Not Applicable.

Item 2. Offer Statistics and Expected Timetable

Not Applicable.

Item 3. Key Information

3A. Selected Financial Data

The following tables set forth selected financial data regarding our operating results and financial position prepared in accordance with International Financial Reporting Standards (IFRS). This data has been derived from our financial statements for the year ended December 31, 2008, the year ended December 31, 2007, and the ten (10) months ended December 31, 2006. The following table sets forth selected financial data with respect to the Company and is qualified in its entirety by, and should be read in conjunction with, the financial statements and notes thereto for the fiscal year ended December 31, 2008, the year ended December 31, 2007, and the ten (10) months ended December 31, 2006. Historical information for periods prior to the ten (10) months ended December 31, 2006 are derived from restated financial statements, not included herein. The financial data for fiscal years 2008 and 2007 are presented on a consolidated basis.

All financial information is presented in U.S. dollars, unless indicated otherwise.

| | | year to | | | year to | | | 10 months to | | | Year to | | | year to | |

| | | Dec 31, 2008 | | | Dec 31, 2007 | | | Dec 31, 2006 | | | Feb 28, 2006 | | | Feb 28, 2005 | |

| | | | | | | | | | | | | | | | |

| | | $ | | | $ | | | $ | | | $ | | | $ | |

| Operations Data | | | | | | | | | | | | | | | | | | | | |

| Revenue | | | 0 | | | | 58,291 | | | | 47,649 | | | | 59,805 | | | | 75,000 | |

| Income (loss) from operations | | | (1,234,000 | ) | | | (314,000 | ) | | | (394,000 | ) | | | (1,438,000 | ) | | | (1,319,000 | ) |

| Net loss | | | (2,025,000 | ) | | | (678,000 | ) | | | (620,000 | ) | | | (1,858,000 | ) | | | (1,668,000 | ) |

| Number of shares | | | 126,588,812 | | | | 99,998,665 | | | | 88,899,675 | | | | 88,899,675 | | | | 79,899,675 | |

| Loss per Common Share | | | (0.016 | ) | | | (0.007 | ) | | | (0.07 | ) | | | (0.02 | ) | | | (0.03 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Balance Sheet Data | | | | | | | | | | | | | | | | | | | | |

| Cumulative Deferred | | | | | | | | | | | | | | | | | | | | |

| Development Expenditure | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Total Assets | | | 7,157,000 | | | | 5,450,000 | | | | 3,244,000 | | | | 2,507,000 | | | | 1,481,000 | |

| Long Term Obligations | | | 5,545,000 | | | | 1,782,000 | | | | 1,993,000 | | | | 847,000 | | | | 1,577,000 | |

| Capital stock | | | 1,846,000 | | | | 1,824,000 | | | | 1,813,000 | | | | 1,813,000 | | | | 1,805,000 | |

| Total Stockholders’ Equity/ (Deficiency) | | | 609,000 | | | | 2,267,000 | | | | (77,000 | ) | | | (730,000 | ) | | | (1,141,000 | ) |

For further information on this selected financial data, please see our Consolidated Financial Statements.

| 3B. | Capitalization and Indebtedness |

Not Applicable.

| 3C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

In addition to the other information presented in this Annual Report, the following should be considered carefully in evaluating us and our business. This Annual Report contains forward-looking statements that involve risk and uncertainties. Our actual results may differ materially from the results discussed in the forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed below and elsewhere in this Annual Report.

Notwithstanding the foregoing, our future success will be affected by many factors that are frequently associated with the development of a new business, which include, but are not limited to, the following:

Risks Related to Our Business.

We Have Incurred Net Losses Since Our Inception and Expect Losses to Continue. Except for net income of $732,000 for fiscal year ended February 28, 1996, we have not been profitable since our inception. Historically and since fiscal year ended February 29, 2004, we have earned some revenues from the limited sale of our Synthetic Calcium Carbonate (“SCC”) samples. However, for the year ended December 31, 2008, we had no sales of Synthetic Calcium Carbonate (“SCC”) samples since the samples were produced to test non-paper applications. In addition, no revenues were earned during the period commencing with the fiscal year ended February 28, 1999 up to the fiscal year ended February 29, 2004. For the year ended December 31, 2008, we had a net loss of U.S. $2,025,000 and an accumulated deficit of U.S. $46,393,000. The report of independent auditors on our December 31, 2008 financial statements includes an explanatory paragraph assuming the Company will continue as a going concern. Lack of operating funds may result in staff reductions and curtailing the construction currently planned. See Risk Factor entitled "If We Are Unable to Raise Funds Our Growth May Be Adversely Affected" below.

If We Are Unable to Raise Funds Our Growth May Be Adversely Affected. Historically, we have had to seek capital for research and development of our SCC products due to lack of revenues. Based on the available amount of $26,000 in cash and together with the restructuring of its debt in order to facilitate the arrangement of on-going working capital in early 2009, and the continuing control of expenses, the Company has sufficient working capital to meet its obligations up to the next 12 months following the date of the approval of our consolidated financial statements for the fiscal year ended December 31, 2008.

In an effort to build our planned 100,000 tonnes per annum plant in Sachsen Anhalt, Germany, we tried to applied for a grant from the European Regional Structural Fund using a house bank in Germany to secure 50% of the capital expenditure. Unfortunately, we have failed to secure the endorsement of a house bank in Germany to cover the 50% of the capital expenditure requirements of our planned 100,000 tonnes per annum plant in Sachsen Anhalt, Germany. This recently has been largely due to the difficulties in the banking sector in Germany, particularly affected by sub-prime debt and more recently the collapse of the credit markets. Although we have determined to seek a strategic partner , there is no assurance in the current economic climate that such a partner will participate in the total projected capital expenditures, which are now estimated at €45 million.

We believe that due to the environmental aspect of our technology, substantial grants and loans will be available for future projects. However, in the event that there is a cash shortage and we are unable to obtain a debt financing or grants, additional equity financing will be required. The proposed plants in Germany will also require additional funds, if our revenues or grants are unable to cover the building expenses. For information on the dilution of our current stockholders in the event of subsequent equity financing, please see the Risk Factor entitled “If we have to raise capital by selling securities in the future, the rights of our stockholders and the value of their investment in the Company could be reduced.”

Our Inability to Protect Our Patents and Other Proprietary Rights Could Adversely Impact Our Competitive Position. We believe that our patents and other proprietary rights are important to our success and our competitive position. Accordingly, we devote substantial resources to the establishment and protection of our patents and proprietary rights. We currently hold patents for processes and have patents pending for additional processes that we intend to use to market our SCC technology. However, our actions to establish and protect our patents and other proprietary rights may be inadequate to prevent others from using our process outside of the jurisdiction of our patent or to prevent others from claiming violations of their patents and proprietary rights by us. If our processes are challenged as infringing upon patents of other parties, we will be required to modify our processes, obtain a license or litigate the issue, all of which may have an adverse effect on our business.

Failure to Protect Our Trade Secrets May Assist Our Competitors. We protect our trade secrets and proprietary know-how for our processes by various methods, including the use of confidentiality agreements with employees and strategic partners. However, such methods may not provide complete protection and there can be no assurance that others will not obtain our know-how or independently develop the same or similar technology. We prepare and file for patent protection on aspects of our technology, which we think will be integrated into final processes early in research phases, thereby limiting the potential risks.

We Have Never Produced SCC on a Commercial Scale. We operated a 10 kg per hour pilot plant based in Norway, which was moved to Leuna in Germany in 2002. The equipment has now been scaled up on a ratio of approximately 60:1 but still requires to be scaled up on a ratio of approximately 20:1 for the commercial plant. Although specialist suppliers of filtration and drying equipment have conducted trials for us and found the scale up ratio to be within acceptable limits, there are no guarantees that the technology will operate as planned or that costs for additional modifications will not occur. In addition, if we are unable to produce SCC on a commercial scale we will be unable to successfully commercialise our SCC technology as planned in our business plan.

Our Competitors May Develop a Competing Technology. One of our competitive advantages depends on our ability to use waste lime, which is a waste product available at little or no cost. If competitors are able to develop a competing technology, we may no longer have the free or low cost source of raw material.

Our SCC Product is at Initial Market Introduction and We Are Not Sure the Market Will Accept it. We intend to target our SCC products in the following markets: paper; food and pharmaceutical, plastic, sealants and adhesives industries. The market acceptance of SCC products produced by our process for use in pharmaceutical and food additives will depend upon consumers and regulatory authorities accepting them. Moreover, although our process can produce pure SCC from waste lime and letters of intent from paper and other industrial producers for the supply from the first commercial plant have been signed, there is no assurance that we will be able to convince customers to convert these to contracts of purchase, limiting the number of potential customers for our product to paper or chemical producers. Failure to achieve market share in these industries could have material adverse effects on our long-term business, financial condition and results of operation.

All of our operations are located outside of the United States, substantially all of our sales from samples are generated outside of the United States and all of our assets are located outside of the United States, subjecting us to risks associated with international operations. Our operations are in Europe and we have no operations in the United States. To the extent that we have sales from our SCC samples, currently 100% of our revenue from our samples was generated from outside of the United States. The international nature of our business subjects us to the laws and regulations of the jurisdictions in which we operate and sell our products. In addition, we are subject to risks inherent in international business activities, including:

| | · | difficulties in collecting accounts receivable and longer collection periods, |

| | · | changes in overseas economic conditions, |

| | · | fluctuations in currency exchange rates, |

| | · | potentially weaker intellectual property protections, |

| | · | changing and conflicting local laws and other regulatory requirements, |

| | · | political and economic instability, |

| | · | war, acts of terrorism or other hostilities, |

| | · | potentially adverse tax consequences, |

| | · | difficulties in staffing and managing foreign operations, or |

| | · | tariffs or other trade regulations and restrictions. |

Our results of operations may be adversely impacted by currency fluctuations. Our revenue is in currencies other than United States dollars, primarily in Euros. Because our financial statements are reported in United States dollars, fluctuations in Euros against the United States dollar may cause us to recognise foreign currency transaction gains and losses, which may be material to our operations and impact our reported financial condition and results of operations.

We Are Subject To the Laws, Regulations and Taxes of Various Jurisdictions. The Company is a Bermuda company and has subsidiaries in Denmark, Germany, Switzerland and Norway, as well as a new subsidiary in the United Kingdom. As such, the Company is subject to numerous national, state and local governmental regulations, including environmental, labor, waste management, health and safety matters and product specifications. It is subject to laws and regulations governing its relationship with its employees, including: wage and hour requirements, working and safety conditions, citizenship requirements, work permits and travel restrictions. These include local labor laws and regulations, which may require substantial resources for compliance.

Additionally, the Company is subject to the tax regimes of the countries listed above. Any change in tax laws and regulation or the interpretation or application thereof, either internally in one of those jurisdictions or as between those jurisdictions, may adversely affect our profitability and tax liabilities.

Potential litigation or environmental exposure may have a material adverse effect on our financial condition or results of operation. Our operations are subject to international, federal, state and local governmental, tax and other laws and regulations, and potentially to claims for various legal, environmental and tax matters. While we carry liability insurance, which we believe to be appropriate to our business, an unanticipated liability, arising out of such a litigation matter or a tax or environmental proceeding could have a material adverse effect on our financial condition or results of operations.

Risks Related to Our Common Shares.

Penny stock rules may make it more difficult to trade our common shares. The Securities and Exchange Commission has adopted regulations which generally define a “penny stock” to be any equity security that has a market price, as defined, less than U.S. $5.00 per share or an exercise price of less than U.S. $5.00 per share, subject to certain exceptions. Our securities may be covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and accredited investors such as, institutions with assets in excess of U.S. $5,000,000 or an individual with net worth in excess of U.S. $1,000,000 or annual income exceeding U.S. $200,000 or U.S. $300,000 jointly with his or her spouse. For transactions covered by this rule, the broker-dealers must make a special suitability determination for the purchase and receive the purchaser’s written agreement of the transaction prior to the sale. Consequently, the rule may affect the ability of broker-dealers to sell our securities and also affect the ability of our investors to sell their shares in the secondary market.

If we have to raise capital by selling securities in the future, the rights of our stockholders and the value of their investment in the Company could be reduced. If we issue debt securities, the lenders would have a claim to our assets that would be superior to the stockholders’ rights. Interest on the debt would increase costs and negatively impact operating results. If we issue more stock, our current stockholders’ percentage of ownership will decrease and their stock may experience additional dilution. It is likely that we will sell our securities in the future. The terms of such future transactions presently are not determinable.

If the market for our common share is illiquid in the future, our stockholders could encounter difficulty if they try to sell their stock. Our stock trades on the “OTCBB” but it is not actively traded. If there is no active trading market, our stockholders may not be able to resell their shares at any price, if at all. It is possible that the trading market in the future will continue to be "thin" or "illiquid," which could result in increased price volatility. Prices may be influenced by investors' perceptions of us and general economic conditions, as well as the market for energy companies generally. Until our financial performance indicates substantial success in executing our business plan, it is unlikely that there will be coverage by stock market analysts. Without such coverage, institutional investors are not likely to buy the stock. Until such time, if ever, as such coverage by analysts and wider market interest develops, the market may have a limited capacity to absorb significant amounts of trading.

We may be classified as a passive foreign investment company, which could result in adverse United States federal income tax consequences to U.S. holders. We believe that we were not a “passive foreign investment company”, or PFIC, for U.S. federal income tax purposes for our taxable year ending on December 31, 2008, and we do not expect to become one for our current taxable year or in the future, although there can be no assurance in this regard. A non-U.S. corporation will be considered a PFIC for any taxable year if either (1) at least 75.0% of its gross income is passive income or (2) at least 50.0% of the value of its assets (based on an average of the quarterly values of the assets during a taxable year) is attributable to assets that produce or are held for the production of passive income. The market value of our assets may be determined in large part by the market price of our common shares, which is likely to fluctuate. In addition, the composition of our income and assets will be affected by how, and how quickly, we spend the cash we receive. If we are treated as a PFIC for any taxable year during which U.S. holders hold our shares, certain adverse United States federal income tax consequences could apply to U.S. holders. See “Special United States Federal Income Tax Considerations - Passive Foreign Investment Company.”

| Item 4. | Information on the Company |

| 4A. | History and Development of the Company |

CalciTech Ltd., a Bermuda Company, has developed a new process for manufacturing high quality Synthetic Calcium Carbonate (“SCC”). Our process produces SCC from waste lime and air polluting carbon dioxide. SCC is a white pigment. It is also a calcium source for pharmaceuticals and food. As of the date of this report, we do not have facilities to commence production of SCC on a full commercial scale.

Originally, we were formed on November 9, 1978, under the laws of British Columbia, Canada with the name Cornwall Petroleum & Resources Ltd. We then changed our name to Rexplore Resources International Limited and which was engaged in petroleum and resource development. In December of 1987, we were restructured and the prior management replaced in connection with the acquisition of a license to develop Trylene Gas. In July 1994, we changed our domicile from British Columbia, Canada to Bermuda and changed our name from Kemgas Sydney Ltd. to Kemgas Ltd. On July 25, 2000, we changed our name from Kemgas Ltd. to our present name, CalciTech Ltd., to better reflect our change in business to the production and sale of SCC. Our resident agent in Bermuda is Consolidated Services Ltd., located at Par La Ville Place, 14 Par-La-Ville Road, Hamilton, Bermuda.

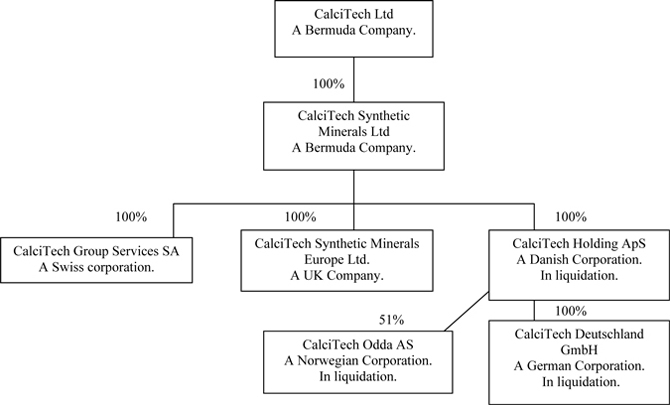

For the purpose of commercialising our technology, we established CalciTech Synthetic Minerals Ltd, a Bermuda company that is wholly owned by us. On February 1, 2003, we transferred all of our entire SCC intellectual property rights and associated business activity to CalciTech Synthetic Minerals Ltd. CalciTech Synthetic Minerals Ltd has three wholly owned companies, CalciTech Group Services SA, a Swiss corporation, CalciTech Holdings ApS, a Danish corporation us, and a newly formed subsidiary, as of April, 2009, CalciTech Synthetic Minerals Europe Ltd., a UK company. We also own through CalciTech Holdings ApS, a 51% interest in CalciTech Odda A.S., a Norwegian corporation (now in liquidation) and a 100% interest in CalciTech Deutschland GmbH, a German corporation (now in liquidation).

Our administration headquarters are located at World Trade Centre, 10 Route de l’Aeroport, Geneva, Switzerland. We currently do not have full-scale commercial plants. We are currently engaged in the commercialisation and project development stage using sample material produced by a small-scale production plant located in Leuna, Germany. This plant produced bulk samples to support the limited sales activity to place the first 100,000 tonnes per annum plant production under letters of intent. However, for year ended December 31, 2008, we had no sales of SCC samples since the samples were produced to test non-paper applications. Construction and commissioning are expected to take eighteen (18) months from the conclusion of the project finance.

We are also evaluating new product developments for new market applications and testing various feedstocks. It is intended that the small-scale plant will continue to produce and sell our sample material to support other projects in other regions. We are also engaged in the preliminary stage of planning and developing proposed full-scale commercial plants located elsewhere in Europe. See “4B. Business Overview – Business Activity.” No assurance can be given that the planned plants will be economically or technically feasible. We have generated no cash flows from our operations, other than those generated through limited sample sales. See “Item 3D. Risk Factors.”

Synthetic Calcium Carbonate (“SCC”)

Since June 1999, we have actively pursued our plan to develop and commercialize SCC from waste lime using our own proprietary process. Acutely aware of the industrial waste created from the production of acetylene gas, one of our former businesses, we have moved forward to develop a method to extract a commercial product from what is considered to be waste product: waste lime. Waste lime is generated from (i) the production of acetylene gas, (ii) manufacture of dicyandiamide from calcium cyanamide and (iii) the manufacture of other chemical and mineral processes. In our pursuit to turn an environmental problem into a commercially viable business, we have developed our proprietary process to extract and produce quality SCC from waste lime. SCC is a white filler pigment and is used for paper filling and coating, as well as in, for example paint, polymers, food and pharmaceuticals.

Currently, we are in discussions with industrial partner(s) to establish our first full scale commercial plant and are engaged in sales activity within the paper, polymer, food, pharmaceutical and cosmetic industries to seek commitment from potential customers to purchase SCC products from this first full scale commercial plant. In addition, we will have to seek industrial partner(s) or raise additional funds through loans from business partners, debt or equity financing and/or through environmental grants from authorities to build our initial plants. Assuming we have the capital to proceed, we intend to build a further thirteen (13) to fifteen (15) commercial plants over the next three (3) to four (4) years, some through joint ventures with financial or industry partners.

Below is a discussion of our proprietary SCC process, conventional Precipitated Calcium Carbonate (“PCC”) production, our products and a summary of our current activities by site. We refer to the PCC produced by our technology as Synthetic Calcium Carbonate, SCC.

Our SCC Process

Our SCC process can utilise most grades of lime, including low quality lime or industrial waste lime such as carbide lime. In our process, the waste lime is mixed with a solution of water and a proprietary promoter in a digester, which selectively dissolves the calcium and leaves the impurities behind as insoluble solids, which are readily removed by subsequent flocculation. The clear calcium solution is then pumped into a reactor into which carbon dioxide from any industrial emission source is passed to produce synthetic calcium carbonate by precipitation. After the SCC product is filtered off, the promoter solution is recycled back into the digester. The SCC can be supplied directly as slurry or dried and bagged for market.

By the use of this process, we reduce waste lime and carbon dioxide emissions into the environment. Carbide lime in particular is a waste problem in many countries. Currently, this waste lime is stored in large ponds with no or very limited disposal processes available. Its high pH has potential pollution impacts to soil and ground water. This is a common environmental problem in the former Eastern Block countries, including the eastern section of Germany and Slovakia and remains a problem in other industrial nations. Many of these governments have regulations for the clean up of these ponds, which gives us the opportunity to have sources of free or low cost waste lime. Many private companies are also willing to supply waste lime at little or no cost because they have limited storage for the waste lime. Additionally, each year over half a million tonnes of waste lime is created as a by-product of on-going acetylene plants alone. Although availability of new waste carbide lime from acetylene production will reduce in the future, we expect to utilise other available waste lime sources.

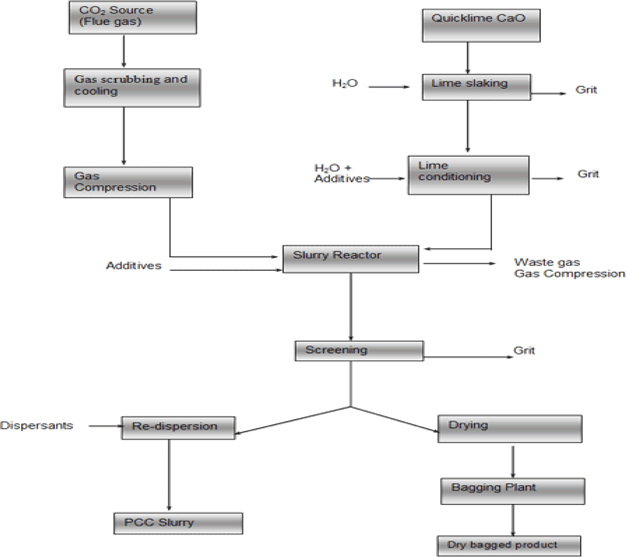

Conventional PCC Process

Other PCC producers must use the conventional method for producing their PCC starting from high-grade limestone. High-grade limestone deposits are found in quarries that must be mined, creating dust and noise pollution and leaving scars on the land. The conventional process involves calcining high quality white limestone to produce high purity quicklime. The quicklime is slaked with water to create milk of lime. PCC is produced by sparging carbon dioxide through a batch reactor containing the milk of lime, then the PCC is filtered and sold dried or as slurry.

SCC Versus PCC Production Process

Below are figures, which describe the differences between the SCC process and the PCC process.

The SCC Process

Conventional PCC Production

As shown above, there are a number of ways in which the SCC process differs from the conventional process. The advantages resulting from the differences between the SCC process and the PCC process are as follows:

| | · | The SCC process does not require lime slaking and classification steps. This gives us significant advantages in both quality and cost effectiveness. |

| | · | The SCC process includes a digester circuit that facilitates the use of any waste lime, such as carbide lime, thereby removing the need to purchase lime as is required in the conventional process. |

| | · | The SCC process includes a promoter recycle loop to enhance the process economics. Any impurities in the lime feed are rejected as insolubles in the digester resulting in a final SCC product of the highest purity. SCC is less dependent on the purity of the starting material and is always superior to that of the starting material. |

| | · | In the SCC process, the total lime content is present in solution whereas in the conventional process the lime is present in suspension (milk-of-lime). The reaction times in the SCC process are therefore much shorter than in the conventional process as the SCC process eliminates the slow lime dissolution step. This advantage allows for the use of smaller equipment as well as providing a much higher degree of control over the process. The SCC solution process is therefore more flexible and easier controlled than the conventional suspension process enabling a narrower particle size distribution. Additionally, the higher level of control enables us to tailor make SCC products to serve a wide range of markets. |

Patents

We first applied to patent our process of transforming waste lime into high quality SCC in 1998 and subsequently a patent was granted the United Kingdom. An international application was filed under the European Patent Cooperation Treaty in December of 1999 to expand the protection of our intellectual property on an international level. The patent examination was completed in May 2001 and patents were granted on July 31, 2003 in 13 European countries. Since then, patents have also been granted in Eurasia (Russia and the independent states formerly part of the Soviet Union), South Africa, Hong Kong, Indonesia, China, Republic of Korea, Slovakia, Australia, New Zealand and Poland. During 2008 further patents were granted in the United States, Canada, Brazil, Czech Republic, Hungary and India. Patent registration is still pending in a number of other countries, including Japan and Norway.

Development of the SCC Technology

The research and development of our SCC process began in 1994 with J.W. Bunger & Associates, a technical research company based in Salt Lake City, USA. This led to a research project associated with the Swiss Federal Institute of Technology in Lausanne, Switzerland and University of Lyon in France. We began a pilot project in Manchester, England, which ran between September 1998 and November 1999. During the pilot project, we were successful in converting waste-lime into high quality SCC. The Recherche et Valorisation des Mineraux (“RVM”) of Paris, France confirmed the application as a superior quality paper coating pigment, a market currently dominated by GCC and kaolin. The pilot plant was moved to the site of an industrial partner at Odda in Norway, where the SCC development program continued.

In 2007, worldwide PCC capacity was 13 million tonnes, of which two thirds was utilised by the paper industry. Sales of PCC totalled approximately U.S. $1.3 billion. However, the entire pigments for paper market totalled 27 million tonnes per annum worth approximately U.S. $5 billion. Within the paper industry, SCC is aimed at the coatings sector, currently dominated by Kaolin and GCC. In Western Europe, consumption of kaolin and GCC for coating was 2.6 million tonnes and 3.7 million tonnes respectively in 2002, representing around U.S. $1.5 billion in sales.

On July 8, 2002, we announced that we had commissioned and fine-tuned our Synthetic Calcium Carbonate “SCC” small scale production plant at Leuna, Germany. Presentations were held at Leuna in September 2002 to introduce the new small plant and our SCC technology to a variety of interested parties, including potential project partners, financial institutions and those from the region that may be involved with the project. A laboratory facility was also installed adjacent to the plant. Confirmation and fine-tuning of the key operational parameters of this plant was necessary as a result of the large scale-up from the original pilot plant. The plant has been used to test raw materials from various other sites located around the world in order to ascertain not only their suitability to the SCC process but also the quality of SCC that can be produced and for the ongoing production of samples for sales purposes and product developments with certain customers.

This plant has consistently produced a range of SCC products primarily in the sub micron range, all with a brightness of over 96% ISO and a steep particle size distribution. The SCC process produces particles of uniform size and shape, tailor made to the needs of our end markets. For the paper industry this means that a new pigment will be available that addresses key issues such as quality and runnability improvements.

In October 2002, we completed trials at the Centre Technique du Papier at Grenoble in France and with a paper manufacturer. These results met our expectations and led to the design and launch in February 2003 of our first two SCC products: CalciLSTM and CalciSGTM.

Development and Marketing of SCC Product

The SCC products manufactured by the use of our SCC process involves the selective dissolution of calcium from industrial waste and its subsequent precipitation from solution with waste CO2 into pure calcium carbonate. The high calcium selectivity at the initial dissolution step guarantees the final purity of the product at a unique level. The solution environment assures the exceptional uniformity of the final precipitate with easy control of the desired particle size, particle size distribution and crystal morphology.

We initially developed SCC products for the paper industry. However, since the introduction of our SCC products to the paper industry in February 2003, we have developed three non-paper SCC products targeting the food, pharmaceutical and cosmetic industry, and the plastic, sealant, rubber and adhesives industries.

Paper Industry

We currently have three SCC products targeting the paper industry: CalciLSTM, CalciSGTM and CalciRGTM. All three are directed at the high value end of the paper pigment market.

CalciLSTM Products. CalciLSTM is designed to maximize light scattering. CalciLSTM is targeted to partially replace and extend costly Titanium Dioxide “TiO2”, Aluminium TriHydrate “ATH” and Precipitated Silica “PS” and substitute calcined clay in fine paper applications and Super Calendered A+ (“SCA+”) on a cost effective basis. Examples of such applications are Bible paper, security paper, laminating paper, auto-adhesive labels, flexible packaging etc. Several trial runs on various applications confirmed the high performance of CalciLSTM. Using CalciLSTM in pre-coating, allows board producers to totally replace calcined clay, while finished product quality remains at the high levels required. CalciLSTM used as filler in SCA+ grades shows similar impressive results. Brightness increases of around 2.5 units can be expected, while opacity is maintained at levels reached with standard PCC filler. Porosity, a very important parameter for this type of paper grade, will also improve significantly.

CalciLSTM is also very suitable for pigmentation applications. Adding CalciLSTM to a starch based formulation helps the papermaker to increase brightness and opacity. The low binder demand due to the absence of fines will maintain paper dusting levels at normal levels.

CalciSGTM Products. CalciSGTM, is designed to provide a super gloss coating for premium grade printing and writing papers including both Ultra Light Weight Coated (“ULWC”) and Light Weight Coated (“LWC”) and coated folding boxboard. In the latter application, CalciSGTM allows for a reduction in calendaring nips to improve bulk at no loss in gloss.

CalciRGTM Products. In October 2004, we launched our third product, CalciRGTM for the paper coatings market. CalciRGTM is a performance-enhancing additive aimed at the rotogravure market. For the launch of this product, we worked closely with our potential customers to identify specific needs. CalciRGTM was designed and developed in collaboration with these customers, and thoroughly tested in commercial trials, showing the unique properties of our SCC based products.

Rotogravure is a printing method used, among others, for LWC and ULWC. These paper grades are predominantly aimed at the highly competitive catalogue and magazine markets, where bulk is an important factor contributing to costs. Lightweight papers typically consist of approximately 30% coating material. The worldwide market for LWC and ULWC papers is estimated to be around 10 million tonnes of which approximately 7 million tonnes is produced in Europe, with the US and Japan accounting for the balance. This market segment of the paper industry is intensely competitive. Other market segments using rotogravure are super calendared papers and lightweight papers for flexible packaging.

First commercial tests have shown that substituting as little as 10% of the original coatings mix with CalciRGTM show a significant improvement in opacity, a very important quality parameter in this segment due to the thinness of the paper and the demands for high quality prints. Other characteristics such as brightness, roughness reduction, and smoothness also showed a significant improvement in performance.

In addition to the normal quality parameters, CalciRGTM has the same rheological characteristics as our other SCC related products. With typical machine speeds for these paper types of around 1,200 m/min (45 mph), rheology of the coatings mix is extremely important. Using CalciRGTM as an additive to an existing coating product for the LWC and ULWC can provide a paper producer and its supplier of coating material with important cost and quality related competitive advantages.

In November 2004, we announced the results of the most exhaustive trial programme to date of our SCC based products, carried out by BASF. BASF is the dominant supplier to the paper coating industry for various additives. These additives do not have a pigment related function such as SCC but impart certain properties on the coatings mix and typically contribute up to 15%. A good example of this group of additives is a binding agent. BASF approached us in order to ascertain whether its additives would be compatible with SCC based products.

In the trials our SCC product was benchmarked against leading products in the mineral pigments for paper industry. It was shown that our SCC:

| | · | Is the only product to show consistent low viscosity at all shear levels: applying our SCC in a coatings mix will positively influence the running behaviour of the paper producing machinery, leading to increased productivity and lower costs. |

| | · | Imparts superior whiteness and brightness: these are essential product quality parameters, required to produce high quality high-end paper. |

| | · | Leads to greater opacity: another very important quality parameter, especially important for light-weight papers. |

| | · | Has superior print gloss: this parameter greatly determines the quality of the printed product. Our SCC imparts a higher gloss on the coated paper, but over and above that, the contrast between the print and background shows superiority as well. |

| | · | Gives slow ink settling: this leads to lower ink consumption and hence significant cost savings for the printer. |

| | · | Provides superior rotogravure printability. |

Following these tests using CalciSGTM, we developed our latest product, CalciRGTM for the rotogravure market as a high-end additive to Kaolin. In total, over twenty trials have been conducted with both scientific institutions and commercial paper producers, varying from lab scale to pilot machine trials.

In April 2003, we appointed GUSCO Handel as our sole sales representative to the paper and board industry for our SCC products: CalciLSTM and CalciSGTM. GUSCO Handel is a subsidiary of family owned G. Schürfeld Group, founded in 1937 and is active as an accredited agency in the marketing and sales of forest products (pulp, paper, board and timber). The broad experience of GUSCO Handel in the paper industry gained from its wide customer relations developed over many years, made them spot the unique growth opportunity presented by our SCC. GUSCO Handel was appointed as our sole European sales representative for paper to commence pre sales and reservation for the planned production from its proposed first commercial plant in Germany. We built a small scale plant at Leuna, Germany, and we also retained the services of W S Atkins plc of Stockport, UK, as consulting engineers for our first large scale commercial plant, which resulted in their production of an in-depth feasibility study and technical due diligence report. In September 2007, the Company received all the permitting document for the planned plant.

By the end of February 2005 we received Letters of Intent (“LOI”) from various German companies in the paper industry for our SCC products: CalciLSTM and CalciSGTM. These LOIs are subject to a definitive agreement that is to be executed upon the completion of a full-scale production plant in Sachsen Anhalt, Germany. If and when these LOI are converted into definitive contracts, we believe that approximately 80% of the projected revenue for our first planned merchant facility in Germany could be derived from these definitive contracts. The customers who have signed the LOIs are a cross section of major German companies in the paper industry. Each customer has signed confidentiality agreements and tested, at their own expense, our SCC sample product in their manufacturing process. The sample product has been purchased by GUSCO Handel as part of our agreement with GUSCO Handel and GUSCO Handel has the right to recover the sample cost in the event that any sale revenue is generated from the definitive agreements. Furthermore, GUSCO Handel has undertaken to collect all revenues earned on our behalf and guarantee our customer payments for an additional fee.

Food, Pharmaceutical and Cosmetic Industries

CalciSPTM Product. In October 2005, we launched our first product following the implementation of our diversification strategy. This product, CalciSPTM, is our first non-paper product that is aimed at the food, pharmaceutical and cosmetics industries. We launched this product following tests by the Geneva Institute of Technology, certifying that CalciSPTM shows extreme high purity, especially regarding heavy metals content. With the target industries for this product moving increasingly towards higher purity products, we expect that both the purity and processibility characteristics of CalciSPTM will contribute to advantageous competitive characteristics.

The first tests carried out on CalciSPTM show that the product has certain characteristics that make it very suitable for use in bakery and cacao products. Further tests are currently being conducted on other applications within the target markets. Since its introduction in October 2005, we have been marketing this product in trade shows and assessing different opportunities for the distribution of this product.

Plastic, Sealant, Rubber and Adhesives Industry

CalciRCTM Product. In January 2006, we launched our latest product, CalciRCTM. This product is aimed at polymer applications such as plastics, sealants, rubber and adhesives. Initial trials within the plastics industries have shown that CalciRCTM significantly improves certain strength characteristics of the finished product. When trialled in PVC profiles, significant improvements in gloss, brightness and lifetime were measured. Due to the rheological properties of the SCC, higher filler loadings can be achieved which reduce the amount of polymer resin used with consequent cost savings. Further trials are currently being conducted into the processibility characteristics of the product.

Paint Industry

SCC products are currently being developed and are expected to be launched in due course to serve the water based decorative paint market. SCC brings benefits of brightness and opacity that enables the producer to reduce the amount of expensive titanium dioxide in the formulation. While paint overall is growing at a rate of two percent (2%) annually, water based emulsion paint is growing at nine percent (9%) driven by environmental considerations and generally carries a premium price over paper industry products.

Business Activity: Small scale production plant

We have been operating a small-scale production plant in Leuna, Germany. The small-scale production plant, while not a full size commercial plant, is, nevertheless, a commercial plant in that the products manufactured (high grade SCC, in particular) can be sold. High grade PCC for the pharmaceutical industry is often sold in relatively small amounts and command prices in excess of EU 800 per ton. We intend to manufacture and sell high-grade product in these specialist areas where supplies are not available to meet such demands.

Business Activity: Germany

We have finalized our plans to build our first full scale commercial SCC plant in Germany, on which our financing negotiations are based. The commercial plant will produce 100,000 tonnes of SCC per year.

The commercial plant will utilise burnt lime as its raw material, whereas for future plant development, we signed an agreement with the German government agency, Mitteldeutsche Sanierungs - und Entsorgungsgesellschaft mbH (“MDSE”), on March 2, 2000, giving us exclusive access to the carbide lime stored in a portion of MDSE’s waste dump in Schkopau, Germany and an option to purchase an additional waste pond. In May 2004, we executed a further agreement with the MDSE in Germany for the exclusive access to a further 2.5 million tonnes of carbide lime waste at the Schkopau site near Leuna.

Following these transactions, we have access to over 3.5 million tonnes of carbide lime, but the original agreements will require re-negotiation for economic reasons for the material to be used in any future plant. MDSE is the government agency responsible for the management of the Environmental Legacy of Eastern Germany. When we use this historical waste lime it will form part of MDSE’s plan for landscape recovery.

In December 2006, we filed for a grant from the European Regional Structural Fund in order to finance the initial capital expenditures for the commercial plant. While waiting for the German house bank’s endorsement of the grant application, we were advised by the authorities to withdraw the original application and re-apply for the 2007 grant since the benefits and conditions were more favourable. The more favourable 2007 grant would contribute up to 50% of the capital costs of the commercial plant. During the first half of 2007 our house bank informed us that the due diligence requirements would substantially change in seeking credit committee approval and that they were aware that the State guarantee was under review in Brussels and it was unlikely we would continue to qualify for this guarantee, under which circumstances credit approval was unlikely. In addition, we learned from the State of Sachsen Anhalt that a guarantee may be available up to 80% of the project finance portion, and that we should apply for this support with our grant application.

By the autumn of 2007 it was still unclear as to whether we would have access to the State guarantee and thus a new house bank was appointed, one of several recommended by the State of Sachsen Anhalt, who were prepared to fund 100% of our project finance without a State guarantee. This bank, an Austrian bank, conducted and concluded its due diligence in early 2008 and secured credit committee approval for the project. However, due to deterioration in the credit markets and financial conditions of the house bank, the house bank had to withdraw, and a consortium of lenders was proposed and assembled by late summer 2008. A consortium bank was later appointed in the role of house bank, but this mandate was cancelled shortly after execution in view of acquisition of the house bank by a third party German bank.

In view of the difficulties in the financial markets and the inability of the house bank to provided the necessary funding, we concluded that we should seek a strategic partner to assist with the capital and funding of our project along the original lines conceived. We are now advised that a company at our stage of development could now qualify for the State guarantee we had previously understood was withdrawn. We are currently evaluating our options in terms of how to best proceed given the new information provided and the current turmoil in the credit market. We anticipate securing the financing for our commercial 100,000 tonnes per annum plant in Sachsen Anhalt, Germany by:

| | · | A grant from European Structural Fund: up to 50% of the capital expenditure for the first plant, |

| | · | 20% of capital expenditure arranged by us and a planned industrial partner, and |

| | · | 30% of capital expenditure by the operating subsidiary company’s house bank. |

We intend to produce slurry and dry products for sale in Germany and neighboring countries. Germany is currently the largest producer of coated paper with 4.75 million tonnes and a further 1.25 million tonnes of coated board in 2003. Both applications currently use a mix of kaolin and GCC in their production.

Business Activity: Republic of Slovakia

We originally signed a memorandum of understanding with Novaky Chemical Company (“Novaky”) to form a joint venture company to produce SCC from Novaky's waste lime. A joint venture agreement was signed on March 23, 2004. Novaky currently has over 1.5 million tonnes of waste lime in temporary storage and continues to produce more in its ongoing acetylene production. Following the granting of our patent in the Slovak Republic in February 2005, we commenced the technical, financial and marketing feasibility of a large production facility plant to serve the Central European market.

Under the terms of the memorandum of understanding, we will control the joint venture. We expect the project to qualify for environmental and investment incentives from The Republic of Slovakia, which is an early entrant to the European Union enlargement. Following the granting of our patent in Slovakia in 2006, we are now actively working on developing this project.

Novaky, a renowned chemical conglomerate with a turnover of around U.S. $170 million, was founded in 1940. The company manufactures intermediate products such as electrolysis products, basic organic chemicals, vinyl chloride as well as end products manufactured from these intermediates and from polyvinyl chloride (“PVC”). Products are sold on both the domestic and the wider European market. Previously a state company, Novaky was partially privatized in 2001 when Canadian company Exall Resources was selected by the Slovak National Property Fund to buy a 40.97% stake in the company. With the entrance of the Slovak Republic into the EU, compliance with environmental standards has become critical. It was, therefore, the company that approached us for use of our proprietary technology in solving their carbide lime related environmental problems.

Following a change of management at Novacky and in view of delays with our project in Germany with the credit market turmoil, we determined to delay matters until our phased roll out program.

Business Activity: Americas

In August 2002, we appointed Charles Kunesh, formerly research director of Specialty Minerals Inc. in America, to represent our program to identify suitable waste deposits for possible SCC manufacture. This has led to a number of discussions and we announced in April 2003 an agreement to conduct feasibility studies for such a project with Carbide Industries LLC of Louisville, Kentucky. We are not pursuing this project or any other North American project at the present time until commencement of our roll out program.

Bubbletube

To address the problems associated with scaling up of reactors in the chemical industry from a small pilot plant to full-scale production, we worked with the Swiss Federal Institute of Technology in Lausanne, Switzerland in a project sponsored by the European Commission called the “Bubbletube.” Scaling up can take about a third of the time it takes to bring a product to market and often affects its quality and yield.

In November 2000, we received the European patent for the Bubbletube followed in January 2003 by the grant of the US patent. The Bubbletube is a new tubular segmented plug flow reactor for the synthesis of fine powders by precipitation. The technology uses two non-miscible fluids to generate micro reactors in which the precipitation reagents are thoroughly mixed. The micro-reactors yield precipitated particles that are uniform, small with a controlled morphology. Although this technology may have future uses for PCC, it is not expected to have uses in the SCC technology we are currently bringing in to use. Our participation with Ecole Polytechnique Fédérale de Lausanne (“EPFL”) led to its acquisition of patent rights with the agreement to license certain fields, particularly in the area of Ceramics, back to EPFL. We had been the financial coordinator of a development program consisting of seven participating organizations funded by a three million Euro grant from the European Union. We participated in the market research element of this development. This program ceased on January 1, 2002 and certain participants are continuing to develop the technology to the next stage. However, we are not participating in this stage.

We decided the technology had no value in relation to our SCC technology, nor as a stand-alone product for development warranting further investment and decided to cease spending technology development funds on this initiative. In December of 2004, we assigned the patents relating to the intellectual property rights for CHF 35,000, the amount of the direct patenting costs, to TechPowder SA of Lausanne, Switzerland, a spin off of the original consortium.

No value was previously assigned to the Bubbletube patent in our financial statements.

Other Products, Patents and Licenses

We hold licenses to develop, produce and sell Trylene Gas, which is an acetylene based fuel gas. We also hold a Canadian patent covering certain processes producing Calcium Carbonates (No. 1179138). Our Canadian patent No. 1145113 expired on April 27, 2000 and patent No. 11791138 expires on December 11, 2001. We also hold a license to a U.S. patent on an acetylene gas process. Currently, we are not exploiting these patents or licenses, which were not assigned any value in the financial statements.

We first applied to patent our process of transforming waste lime into high quality SCC in 1998 and subsequently a patent was granted the United Kingdom. An international application was filed under the European Patent Cooperation Treaty in December of 1999 to expand the protection of our intellectual property on an international level. The patent examination was completed in May 2001 and patents were granted on July 31, 2003 in 13 European countries. Since then, patents have also been granted in Eurasia (Russia and the independent states formerly part of the Soviet Union), South Africa, Hong Kong, China, Indonesia, Slovakia, Australia, New Zealand, The United States, Brazil, Canada, Czech Republic, Hungary, India, Korea and Poland. We have implemented patent registration in an extensive number of countries worldwide, including Japan and Poland.

We have no registered trademarks and no pending trademark applications.

Financing

During February 2004, our 6% convertible debentures with a value of $4,402,000 were re-negotiated by their retirement against the issue of new 5% debentures with a value of $4,642,000 to December 28, 2007. At maturity these were extended until December 31, 2009. All terms of the convertible debentures remain unchanged from the original debenture notes. During June 2004, holders were offered a proposal to amend the terms of their notes. The notes were amended to change (i) the conversion date to December 31, 2007 and (ii) the conversion price to $1.75 per share. All other terms and conditions of the 5% convertible debenture remained the same. As of this date, all of the 5% convertible debentures have been amended. In December 2008, following negotiations with the debenture holders, an agreement was reached whereby all the debenture holders agreed to convert 50% of their notes, plus accrued interest to December 31, 2008, into common shares of the Company at a price of $0.095 per share. This resulted in the issuance of 26,590,147 common shares, and a reduction of the note, to $2,526,064. The notes now carry an interest rate of 1.75% and a new conversion price of $0.75 per share. These notes have since been amended to extend the maturity date to December 31, 2010. The Company has the right, upon ten (10) business days prior written notice, without penalty, to repay all or any portion of the outstanding principal.

On January 26, 2005, we concluded a private placement for a total of U.S. $2,250,000. The placement consisted of the issuing of 9,000,000 units, each unit consisting of one common share priced at U.S. $0.25, with one full common share purchase warrant for twelve months priced at U.S. $0.35 and one half warrant for twenty four months priced at U.S. $0.25. The placement was conducted pursuant to an exemption from the registration requirements of the Securities Act of 1933, as amended, provided for in Regulation S promulgated thereunder, as a placement made exclusively to persons who are not “U.S. Persons” as defined in the exemption. The proceeds of the placement were used in part towards upgrading our small-scale production plant in Germany from a batch process to a more fully integrated operation, thereby increasing our production capacity; completion of worldwide patent applications; further development of our new premium additive product, CalciRGTM, and for general working capital purposes.

On January 26, 2006 warrant holders exercised their right to convert 9,000,000 warrants to ordinary shares at a cost of U.S. $0.35 per share, raising U.S. $3,150,000. The proceeds were used to further the Company's commercial projects, working capital and reduction of convertible short-term debt.

On January 24, 2007, we announced that the Directors of the Company had agreed to extend its U.S. $0.50 warrants, originally to mature on January 25, 2007, by one month, the new maturity date being February 25, 2007. The extended warrants were not covered and have now lapsed. The Company has no further warrants outstanding.

We are currently financed through a credit facility, up to U.S. $3,000,000, from Epsom Asset Management Ltd. (“Epsom”). The credit facility was originally issued by Epsom Investment Services, N.V., but was assigned to Epsom Asset Management Ltd. in November 2008 following a reorganization of the Epsom Group. In September 2007, Epsom Investment Services N.V. agreed to convert U.S. $2,001,000 of the balance due under the loan facility into our common shares on the basis of one share for each U.S. $0.29 of note. This conversion resulted in the issue of 6,900,000 common shares. In addition, in December 2007, Epsom Investment Services N.V. agreed to convert a further U.S. $1,259,697 of the balance due under the loan facility into our common shares on the basis of one share for each U.S. $0.30 of note. This conversion resulted in the issue of 4,198,990 common shares. The credit facility was temporarily extended to U.S. $5,000,000 during 2008 to December 31, 2008. Epsom has extended the credit facility to August 30, 2010 and the balance as at December 31, 2008 stood at U.S. $5,436,000.

In the first quarter of 2009, we successfully concluded a restructuring of our debt under the credit facility agreement. Epsom agreed to convert all of the outstanding debt under the credit facility into an aggregate amount of 57,222,053 common shares of which 27,305,844 shares were to be placed with Epsom’s clients and the other remaining common shares were placed with new investors outside of the United States by Epsom. Proceeds from the sale of the shares by Epsom will be made available to us under the terms of the current credit facility for working capital purposes with interest charged at a rate of 1.75% per annum, payable quarterly.

On April 24, 2009, we issued 1,828,221 common shares, at $0.095 per share, to eight (8) creditors located in Europe in exchange for extinguishing certain debt owed to the creditors totaling $173,681. The shares were issued pursuant to an exemption from registration requirements provided by Regulation S.

Revenue

During the fiscal year ended December 31, 2008 and the year ended December 31, 2007, we received revenues totaling U.S. $NIL and U.S. $58,000 respectively from the sale of SCC samples. Please see the Consolidated Statement of Income and Item 8, Selected Financial Data, and Item 9, Management’s Discussion and Analysis of Financial Condition and Results of Operations, for more information.

Dependence on Customers and Suppliers

We are not dependent upon a single or a few customers or suppliers for revenues for our operations.

Project and Product Development

During the year ended December 31, 2007 and continuing through the fiscal year ended December 31, 2008, we moved out of the research and development stage and into the commercialization stage, and project and product development. Accordingly, we no longer expense qualifying project nor qualifying research and development expenses. U.S. $2,431,000 spent in the year on project and product development appears on the Balance Sheet as an intangible asset.

We expensed U.S. $NIL on research and development in the year ended December 31, 2008, U.S. $NIL in the year ended December 31, 2007, and U.S. $NIL in the ten months ended December 31, 2006.

4C. Organizational Structure: The following is our organizational chart:

4D. Property, Plant and Equipment

We hold a lease on our administrative service office facility in Switzerland, expiring in October 2010. After October 2010, we intend to continue to locate our principal facility in Switzerland, but will reassess our need for future expansion to meet our business plan.

We maintain a Synthetic Calcium Carbonate “SCC” small scale production plant at Leuna, Germany. This small plant has a maximum capacity of 800 tonnes per annum. A suitably equipped laboratory facility has also been installed adjacent to the plant, in the same building. No additional land or rental is involved.

Construction of the 100,000 tonnes per annum SCC plant in Germany has been delayed due to the current financial climate and is expected to commence in the fourth quarter of 2009 and is pending partner and financing arrangements. The cost of the construction is estimated at Euros 45 million. Construction and commissioning are expected to take 18 months.

Item 4(A). Unresolved Staff Comments

Not Applicable.

Item 5. Operating and Financial Review and Prospects

Overview

We are currently in the process of commercialising our SCC based products. An important aspect of this commercialisation has been the building and commissioning of our small-scale production plant in Leuna, Germany. This facility has mainly been producing samples for potential clients to assess the desirability for their use in the production of coated paper. The trials conducted, varying from bench-scale testing to full machine trials, have been successful. We have received responses from paper producers indicating their interest to acquire substantial quantities of our SCC based products once the first full-scale commercial-scale plant has been commissioned.

More recently, we have provided sample material from the small-scale plant in dried form to non-paper companies. These trials, in the plastics, food and other industry sectors, have been successful and have led us to add a drying facility onto the planned large-scale plant in Sachsen Anhalt, Germany, in order to be able to serve this part of the market.

We are currently attempting to secure financing for our commercial 100,000 tonnes per annum plant in Sachsen Anhalt, Germany. Please see “Item 4B. Business Overview- Business Activity,” above, for more information.

We are currently financed through our credit facility with Epsom. For more information on this facility, please see “Item 4B. Business Overview- Financing,” above.

Critical accounting policies

The significant accounting policies that we believe are the most critical to aid in fully understanding and evaluating our reported financial results include the following:

Going concern

The financial statements have been prepared assuming we will continue as a going concern. Under the going concern assumption, an entity is ordinarily viewed as continuing in business for the foreseeable future with neither the intention nor the necessity of liquidation, ceasing trading or seeking protection from creditors pursuant to laws or regulations. In assessing whether the going concern assumption is appropriate, management takes into account all available information for the foreseeable future, in particular for the twelve (12) months from the approval of the financial statements.

Assets and liabilities are recorded on the basis that we will be able to realize our assets and discharge our liabilities in the normal course of business. Accordingly, the financial statements do not include any adjustments to the carrying values of assets and liabilities that might be necessary should we be unable to continue as a going concern.

5A. Operating Results

The following discussion and analysis relates to items that have affected our results of operations for the years ended December 31, 2008, December 31, 2007, and ten months ended December 31, 2006. During 2006, we changed our fiscal year end from February 28 to December 31, effective December 31, 2006. The information contained in the table below should be read in conjunction with our consolidated financial statements and accompanying notes included in this Annual Report on Form 20-F.

| | | Year Ended December 31, 2008 | | | Year Ended December 31, 2007 | | | 10 Months Ended December 31, 2006 | |

| OPERATING REVENUE | | $ | NIL | | | $ | 58,000 | | | $ | 48,000 | |

| COST OF REVENUES | | $ | (37,000 | ) | | $ | (60,000 | ) | | $ | (32,000 | ) |

| GROSS MARGIN | | $ | (37,000 | ) | | $ | (2,000 | ) | | $ | 16,000 | |

| Research and development expenses | | $ | -0- | | | $ | -0- | | | $ | -0- | |

| Project development expenses | | $ | -0- | | | $ | -0- | | | $ | -0- | |

| Product development expenses | | $ | -0- | | | $ | -0- | | | $ | -0- | |

| General and administrative expenses | | $ | 1,197,000 | | | $ | 313,000 | | | $ | 410,000 | |

| OPERATING LOSS | | $ | (1,234,000 | ) | | $ | (314,000 | ) | | $ | (394,000 | ) |

| LOSS BEFORE INCOME TAXES | | $ | (2,025,000 | ) | | $ | (656,000 | ) | | $ | (622,000 | ) |

| PROVISION FOR INCOME TAXES | | $ | (NIL | ) | | $ | (22,000 | ) | | $ | 2,000 | |

| NET LOSS | | $ | (2,025,000 | ) | | $ | (678,000 | ) | | $ | (620,000 | ) |

December 31, 2008 compared to December 31, 2007.

Revenue. We had revenues totalling U.S. $NIL for the year ended December 31, 2008 compared to U.S. $58,000 for the year ended December 31, 2007. Whilst the small-scale production plant in Leuna, Germany continued to produce samples, no further sales have been generated as these have been mainly smaller sample sizes for the non-paper applications. Revenues are derived from sales of SCC samples produced at the small-scale production facility in Leuna, Germany.

Expenses. Product development and project development costs remained at $NIL. Product development and project development expenditures of U.S. $2,431,000 (December 31, 2007: U.S. $1,020,000) were capitalized as an intangible asset. During 2008, we continued to contain and reduce overhead costs. Despite this, general and administrative expenditures increased from $313,000 to $1,197,000 due to factors outside the control of the management such as the down turn in the world economy. The majority of the increase was as a result of a currency loss of $145,520 during the year caused by the average decline of the U.S. Dollar against the Euro and Pound Sterling against a currency gain in 2007 of $370,442. Professional and legal fees increased from $40,000 to $355,000 and $37,000 to $113,000 respectively during the year. These increases were mainly due to the project financing efforts and due diligence requirements. Interest charges have increased substantially from $341,000 to $791,000. This is due to a failure of a planned share placement during the year requiring additional bridge facilities to year-end. We are rearranging our debt and expect interest charges to be considerably reduced for the fiscal year ending December 31, 2009.

Net Loss. The net loss in year ended December 31, 2008 increased to U.S. $2,025,000 from $678,000 in the year ended December 31, 2007.

December 31, 2007 compared to December 31, 2006 .

Revenue. We had revenues totalling U.S. $58,000 for the period ended December 31, 2007 compared to U.S. $48,000 for December 31, 2006. Revenues are derived from sales of samples produced at the small-scale production facility in Leuna, Germany.

Expenses. Product development remained at U.S. $NIL, and project development costs remained at U.S. $NIL. Project Development expenditure of U.S. $1,020,000 was capitalised as an intangible asset. General and administrative expenses decreased U.S. $97,000 to U.S. $313,000. This is explained by expenditure that was incurred on the Commercial Plant and which has been included in Intangible Assets in the Balance Sheet. Even though we are now in the commercialisation stage, project and product development continue but are recorded as Intangible Assets.

Net Loss. The net loss in fiscal year 2007 increased to U.S. $678,000 from U.S. $620,000 in 2006.

Foreign Currency Exchange Rates

A significant portion of our business is conducted in currencies other than the United States dollar. As a result, we are subject to exposure from movements in foreign currency exchange rates. We do not currently engage in hedging transactions designed to manage currency fluctuation risks.

Inflation