FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of March, 2020

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

Banco Santander, S.A.

TABLE OF CONTENTS

| 2019 Pillar 3 Disclosures |

| Index | |||||

| Pillar 3 - Disclosures Report | |||||

| Pillar 3 | |||||

| Image omitted | |||||

5 |

| 2019 Pillar 3 Disclosures |

| Image omitted | ||||

Introduction (Ch.1) | Capital (Ch.2) | ||||

| Capital | |||||

| Pillar 1 - Regulatory Capital | |||||

| Pillar 2 - Economic Capital | |||||

Risks (Ch. 3, 4, 5, 6, 7 and 8) | Santander Group (Ch. 9 and 10) | ||||

Other appendices available on the Santander Group website. Pillar 3 editable format tables. | |||||

| Image omitted | |||||

6 |

| 2019 Pillar 3 Disclosures |

| Navigability Enhancements | ||||||

| Image omitted | ||||||

7 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| Image omitted | ||||

| Bookmarks (web version of the Report) | |

| The inclusion of bookmarks for the different sections allow improved navigability across the Pillar 3 Disclosures Report | ||

| Excel tables | ||

| Every table disclosed in the Pillar 3 Report is published in Excel format (editable) for further analysis | ||

QR Codes (written version of the Report) | ||

| QR codes are included in the Report to facilitate further consultation on other relevant documents of Santander Group | ||

| CRR Cross references | ||

| Incorporation of an Appendix containing all disclosures required under part VIII of the Capital Requirements Regulation (CRR) and their locations in the Pillar 3 Disclosures Report | ||

8 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| 1 | ||||||

| Introduction | ||||||

| Image omitted | ||||||

9 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| Image omitted | ||||

10 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

1.Introduction

1.1. Executive summary

Santander is one of the largest banks in the eurozone. As at end December 2019, our market capitalisation was EUR 61,986 million, and had approximately four million shareholders. We have a EUR 1,522,695 million of assets on our balance sheet and control EUR 1,050,765 million of total funds.

Our main purpose is to help people and businesses prosper. We do not merely meet our legal and regulatory obligations, but we aspire to exceed people's expectations. As such, we focus on the areas where, as a Group, our activity can have the greatest impact, helping more people and businesses prosper, in an inclusive and sustainable way.

This means that the Group engages in all types of activities, operations and services that are typical of the banking business in general. Our scale, business model and diversification enable us to aim to be the best open digital financial services platform, acting responsibly and earning the lasting loyalty of our stakeholders (customers, shareholders, people and communities).

We have close to 200,000 employees who serve more than 145 million customers worldwide, including individuals, private banking clients, SMEs, businesses and large corporates, whenever, wherever and however the customer needs. To do this, our strategy focuses on continuing to strengthen loyalty and digitalisation.

We interact with our customers through a global network of 11,952 branches, the largest branch network among international banks. The distribution network has both universal offices as well as specialised ones aimed at certain customer segments and new collaborative spaces with increased digital capabilities. Examples of these are the Work Café branches, SmartBank and Ágil branches.

As well as the branch network, we have contact centres which have received various awards for their quality of service.

In addition, our progress in the digitalisation process which combines our commercial network strength with that of our technology, is key to increasing our number of customers and improving their experience.

As a result, our loyal and digital customers continued to grow this year. The number of loyal customers reached 21.6 million (+9% in the year), with an increase in both individuals and corporates. Digital customers rose 15% in the year to close to 37 million.

On average, our customers accessed digital touchpoints five times per week and digital sales increased to 36% of total sales. We also aim to be one of the top three banks for customer satisfaction in our main countries.

In April 2019, we presented our strategic plan for the medium term to drive growth and increase profitability by accelerating digitalisation, improving operational performance and continuing to improve capital allocation. We will invest over EUR 20 billion in digital transformation and technology over the next four years with the aim of improving and personalising customer experience and, as a consequence, increasing trust and loyalty while at the same time reducing costs.

In this strategic plan, we laid out a new organisational structure, three geographical regions and a new reporting unit segment, Santander Global Platform (SGP), which will enable us to accelerate our commercial and digital transformation, while making progress towards our financial and non-financial objectives.

This new simplified management structure for Europe, North America and South America, together with a management committee with increased business focus will allow better and more agile execution throughout the Group.

Europe primarily includes Spain, the United Kingdom, Portugal, Poland and Santander Consumer Finance (SCF). The latter also plays a significant role in consumer finance in 15 European countries.

Given the current environment characterised by lower for longer interest rates, we are progressing toward a common organisational structure under which we can take advantage of the strengths, innovation and leadership of each market, applying what we learn in one country to the rest and avoiding overlaps.

North America includes the United States and Mexico. Both countries are increasing coordination with each other and capturing new opportunities, reducing cost duplication and improving efficiency.

South America includes Brazil, Chile, Argentina, Uruguay and Andean Region (Peru and Colombia).

The focus is to accelerate profitable growth and lead the retail financial industry. To this end, we have a strategy that seeks to strengthen a more connected regional network and facilitate the expansion of successful businesses to other countries in the region.

Finally, with the creation of SGP we are taking another step forward in our digital transformation, which combines our experience in banking and technology. Our goal is to extend the benefits of the talent and scale of the Group to the payments and digital businesses with the highest growth potential. We are building platforms only once to be used by all countries, which will allow us to be best-in-class, and provide faster and better digital banking and global payment solutions to individuals and SMEs.

In addition, we have two transversal global businesses which add value to our local businesses: Santander Corporate and Investment Banking (SCIB) and Wealth Management and Insurance (WM&I).

11 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

SCIB is the global business division for corporate and institutional customers who require a tailored service and value-added wholesale products suited to their complexity and sophistication. It is a business with high levels of profitability and with resilient returns through the economic cycle.

WM&I includes the asset management, private banking and insurance businesses. It is a very capital efficient business with significant growth potential and high returns.

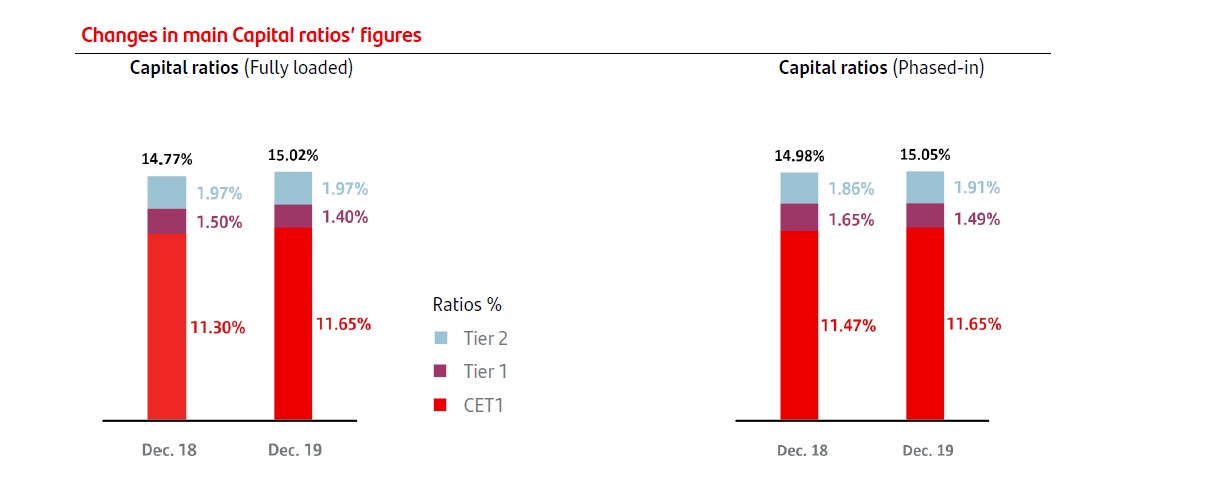

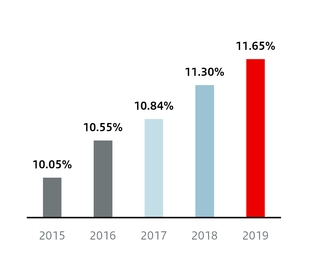

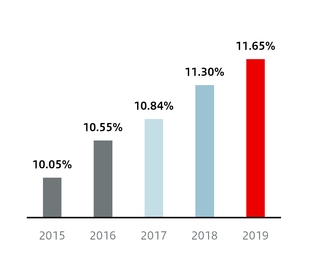

The Group’s CET1 capital ratio increased to 11.65%

| Fully loaded | Phased-in | ||||||||

| Millon euros | Dec-2019 | Dec-2018 | Dec-2019 | Dec-2018 | |||||

| Common Equity (CET1) | 70,497 | 66,904 | 70,497 | 67,962 | |||||

| Tier 1 | 78,964 | 75,838 | 79,536 | 77,716 | |||||

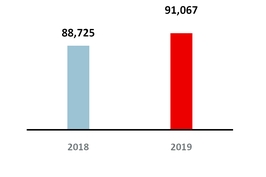

| Total capital | 90,937 | 87,506 | 91,067 | 88,725 | |||||

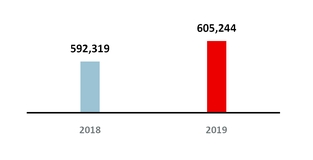

| Risk weighted assets | 605,244 | 592,319 | 605,244 | 592,319 | |||||

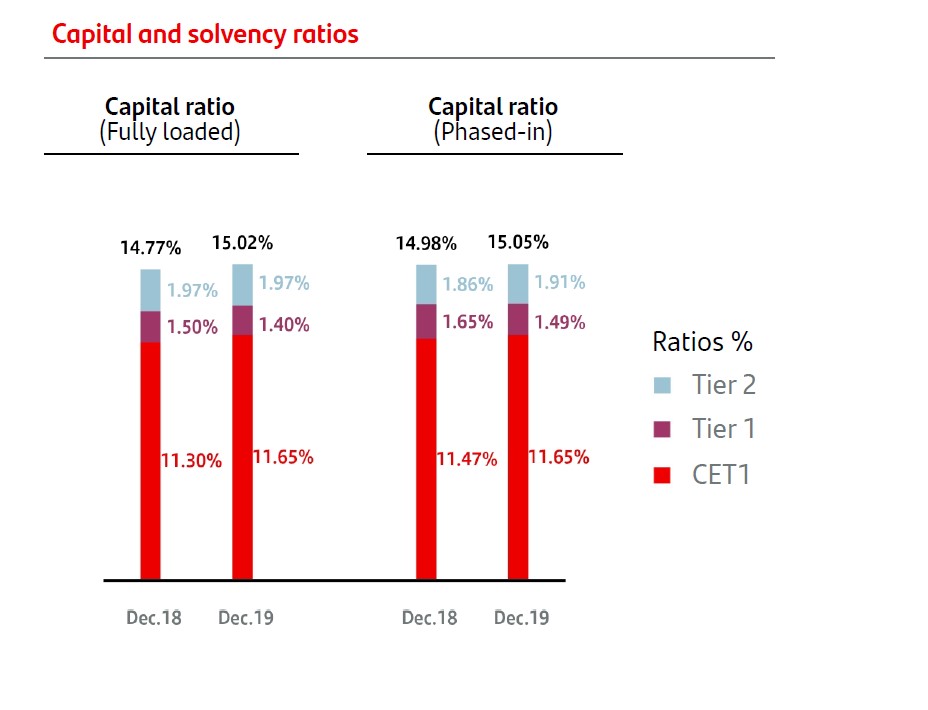

| CET1 Ratio | 11.65 | % | 11.30 | % | 11.65 | % | 11.47 | % | |

| Tier 1 Ratio | 13.05 | % | 12.80 | % | 13.14 | % | 13.12 | % | |

| Total capital ratio | 15.02 | % | 14.77 | % | 15.05 | % | 14.98 | % | |

| Leverage Ratio | 5.11 | % | 5.10 | % | 5.15 | % | 5.22 | % | |

2018 and 2019 data has been calculated under application of IFRS 9 transitional arrangements, unless otherwise indicated.

Note: this English version is a translation of the original in Spanish for information purposes only. In the event of discrepancy, the original Spanish-language version prevails.

| 12 | 2019 Pillar 3 Disclosures Report | ||

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

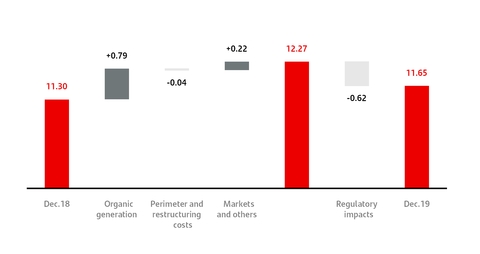

2019 a record-high year in terms of gross capital generation, partially offset by regulatory headwinds

| 2019 Fully Loaded CET1 evolution |

| % |

| +35bps |

13 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

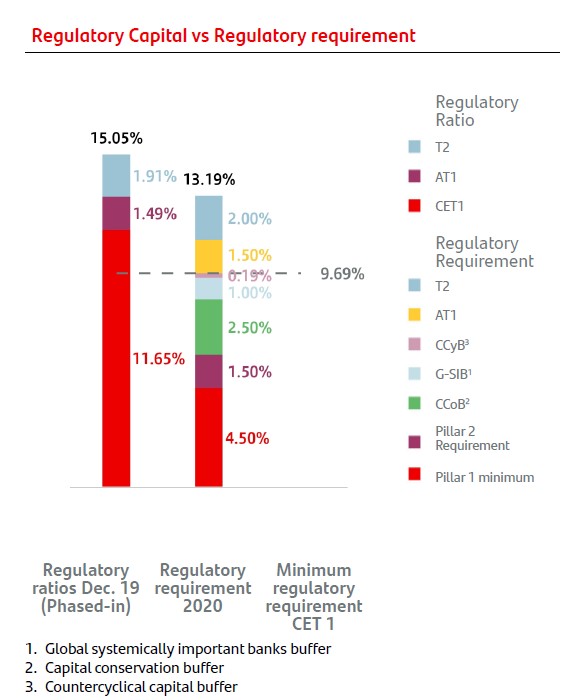

We comfortably met the minimum ratios set by the ECB on a consolidated basis

| Regulatory Capital vs Regulatory requirement | |

| Regulatory ratio | |

| n | T2 |

| n | AT1 |

| n | CET1 |

| Regulatory requirement | |

| n | T2 |

| n | AT1 |

| n | CCyB3 |

| n | G-SIB1 |

| n | CCoB2 |

| n | Pillar 2 Requirement |

| n | Pillar 1 minimum |

Regulatory ratios Dec. 19 (Phased-in) | Regulatory requirement 2020 | Minimum regulatory requirement CET 1 |

| 1. | Global systemically important banks buffer |

| 2. | Capital conservation buffer |

| 3. | Countercyclical capital buffer |

1.2. Santander Group Pillar 3 report overview

1.2.1. Background information on Santander Group

Banco Santander, S.A. is a private-law company, subject to the rules and regulations applicable to banks operating in Spain. In addition to its own activities, Banco Santander is the parent of a group of subsidiaries engaged in a variety of activities, which together make up Santander Group. The CRR and CRD IV and their transposition in Spain through Bank of Spain Circular 2/2016, on supervision and solvency, apply on a consolidated level across the entire Santander Group.

Santander Group does not make use of the exemption contemplated in article 49 of the CRR, therefore the disclosure of table INS1 (Non-deducted participations in insurance undertakings) does not apply.

As of 31 December 2019, under article 7 and 9 of the CRR, the subsidiaries Santander Leasing S.A. EFC and Santander Factoring y Confirming S.A. EFC are exempt from the minimum capital requirements, the limit on large exposures and the internal corporate governance obligations. No use of the exemptions under the applicable regulations has been made for any other Santander Group subsidiaries.

Santander Group is one of the banks that have not required state aid in any of the countries in which it operates.

For all those aspects for which disclosure is required under Part Eight of the CRR and which are not applicable to Santander Group, see Appendix II – CRR Mapping – , where they are reported as “N/A” (not applicable).

As of 31 December 2019, none of the financial institutions included consolidated in Santander Group had less than the minimum capital required under applicable regulation.

| 14 | 2019 Pillar 3 Disclosures Report | ||

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

1.2.2. Governance: approval and publication

Pursuant to the official disclosure policy, Santander Group publishes its annual Pillar 3 disclosures report following board approval. Prior to the board of directors’ approval on 27 February 2020, the report was reviewed by the risk supervision, regulation and compliance committee at a meeting held on 17 February, and also by the capital committee at a meeting held on 21 January 2020.

Additionally, on 24 February 2020, the report was reviewed by the audit committee.

Furthermore, a set of quarterly information has been published since March 2015 in compliance with the EBA’s Guidelines on materiality, proprietary and confidentiality and on disclosure frequency, pursuant to article 432, sections 1 and 2 and article 433 of Regulation (EU) 575/2013.

No exceptions have been made to the publication of information considered proprietary or confidential.

Appendix II contains a list showing the location of the information disclosed in accordance with the relevant articles of Part Eight of the Regulation.

The information contained in this report has been subject to review by the external auditor (PwC), who did not find any issue with regard to the reasonableness of the disclosures and compliance with the reporting requirements established in the CRD IV and the CRR.

Governing bodies’ certification

The board of directors of Santander Group certifies that the publication of the Pillar 3 disclosures report is compliant with the guidelines of Part Eight of Regulation (EU) 575/2013 and consistent with the “Pillar 3 Disclosures Policy” adopted by the board of directors.

The Pillar 3 Disclosures Report relies on a range of processes relating to the internal control framework, with duties and responsibilities having been defined for review and certification of the information set out in the report at several levels of the organisation.

Further information on Santander Group's internal control model (ICM) can be found in section VIII of the chapter on Corporate governance of the 2019 Annual Report.

In addition, the external auditors carry out an ex ante review, and the work plans for recurring reviews by internal audit also cover this report.

The Pillar 3 disclosures report is available in the Shareholders and Investors section of the Santander Group website (www.santander.com), under “Financial and Economic Information”.

Disclosures of Santander Group subsidiaries

In addition to the information contained in this report, Santander Group subsidiaries that are considered to have significant importance for their local market, pursuant to article 13 of the CRR (Application of disclosure requirements on a consolidated basis), publish information at individual level on their websites in relation to: own funds, capital requirements, capital buffers, credit risk adjustments, remuneration policy and the application of credit risk mitigation techniques.

1.2.3. Transparency enhancements

In recent years, Santander Group has taken note of the recommendations issued by different international bodies with the aim of improving the transparency of the information published each year in the Pillar 3 disclosures report.

In December 2016, the European Banking Association (EBA) published its final guidelines on disclosure requirements under Part Eight of the Capital Requirements Regulation. These guidelines provide guidance to financial institutions on how to comply with applicable regulations.

Further, in March 2017 and December 2018 the Basel Committee published the second and third phase of its Revised Pillar 3 Disclosure Requirements.

Santander Group has now incorporated all of this year’s applicable enhancements. Appendix II provides a list showing the location of the information required under the different articles of Part Eight of the CRR, while the Santander Group website includes a file containing all of the tables shown in this document in editable format to facilitate their treatment.

A detail of the applicable enhancements can be found in the Appendix I.

15 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

1.2.4. Disclosure criteria used in this report

This report has been prepared in accordance with the applicable European Capital Requirements Regulation (CRR).

Below are the details of the type of information that best reflects the discrepancies between the regulatory information shown in this report, and the information shown in the Annual Report and the accounting information:

| • | The measures of credit risk exposure used for calculating regulatory capital requirements include: |

| • | Not only current exposures, but also potential future risk exposures arising from future commitments (contingent liabilities and commitments) or changes in market risk factors (derivative instruments). |

| • | The mitigating factors of these exposures (netting agreements and collateral agreements for derivative exposures, and collateral and personal guarantees for on-balance-sheet exposures). |

| • | Criteria used when classifying defaulted exposures in portfolios subject to advanced approaches for calculation of regulatory capital are more conservative than those used for preparing the disaggregated information provided in the Annual Report. |

1.3. Scope of consolidation

Santander Group companies included in the scope of consolidation for the purposes of calculating the capital adequacy ratio under the CRR are the same as those included in the scope of consolidation for accounting purposes under Bank of Spain Circular 2/2018.

1.3.1. Differences between the consolidation method for accounting purposes and the consolidation method for regulatory capital calculation purposes

In application of Part I (General Provisions) of the CRR, certain Santander Group companies are consolidated using a different method to that used for accounting consolidation.

The companies for which a different consolidation method is used, based on the regulations applied are listed in Appendix V of the 2019 Pillar 3 Appendix document available on the Santander Group website. To this day, both the participations in significant financial institutions and insurance companies are exempt from deductions under CRR article 48.

For the purposes of calculating the capital adequacy ratio based on the nature of their business activities, Santander Group units included in the prudential scope of consolidation are consolidated using the full consolidation method, with the exception of jointly controlled entities, which uses proportionate consolidation. All companies that cannot be consolidated based on their business activities are accounted for using the equity method and so are treated as equity exposures.

The basis of the information used for accounting purposes differs from that used for the calculation of regulatory capital requirements. The measures of risk exposure may differ depending on the purpose for which they are calculated, such as financial reporting, regulatory capital reporting or management information. The exposure data included in the quantitative disclosures in this document are used for calculating regulatory capital.

The following table shows the relationship between the various categories of the financial statements and the risk categories in accordance with prudential requirements.

| 16 | 2019 Pillar 3 Disclosures Report | ||

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| Table 1. Differences between accounting and regulatory scopes of consolidation and mapping of financial statements categories with regulatory risk categories (LI1) | ||||||||||||||

| Million euros | ||||||||||||||

| 31 Dec. 2019 | ||||||||||||||

| Carrying values as reported in published financial statements | Carrying values under scope of regulatory consolidation | Carrying values of items: | ||||||||||||

| Subject to credit risk framework | Subject to the CCR framework | Subject to securitisation framework | Subject to market risk framework | Not subject to capital requirements or subject to deduction from capital | ||||||||||

| Assets | ||||||||||||||

| Cash and cash balances at central banks | 101,067 | 101,204 | 101,204 | — | — | 0 | — | |||||||

| Financial assets held for trading | 108,230 | 108,226 | — | 63,415 | 97 | 108,128 | — | |||||||

| Financial assets designated at fair value through profit or loss | 66,980 | 63,716 | 1,081 | 40,055 | 588 | 55,574 | — | |||||||

| Financial assets at fair value through other comprehensive income | 125,708 | 110,824 | 107,325 | — | 3,499 | — | — | |||||||

| Financial assets at amortised cost | 995,482 | 999,334 | 957,670 | 38,644 | 2,940 | — | 79 | |||||||

| Derivatives - Hedge accounting | 7,216 | 7,216 | — | 7,216 | — | — | — | |||||||

| Fair value changes of the hedged items in portfolio hedge of interest rate risk | 1,702 | 1,702 | — | — | — | — | 1,702 | |||||||

| Investments in subsidiaries, joint ventures and associates | 8,772 | 9,647 | 7,783 | — | — | — | 1,864 | |||||||

| Reinsurance assets | 292 | — | — | — | — | — | — | |||||||

| Tangible assets | 35,235 | 32,643 | 32,643 | — | — | — | — | |||||||

| Intangible assets | 27,687 | 27,929 | — | — | — | — | 27,929 | |||||||

| Tax assets | 29,585 | 29,637 | 26,213 | — | — | — | 3,424 | |||||||

| Other assets | 10,138 | 10,441 | 9,539 | — | — | — | 903 | |||||||

| Non-current assets and disposal groups classified as held for sale | 4,601 | 4,753 | 4,740 | — | — | 12 | 1 | |||||||

| Total assets | 1,522,695 | 1,507,272 | 1,248,198 | 149,330 | 7,125 | 163,714 | 35,902 | |||||||

| Liabilities | ||||||||||||||

| Financial liabilities held for trading | (77,139 | ) | (77,164 | ) | — | (63,041 | ) | — | (77,164 | ) | — | |||

| Financial liabilities designated at fair value through profit or loss | (60,995 | ) | (40,268 | ) | — | (19,125 | ) | — | (40,268 | ) | — | |||

| Financial liabilities measured at amortised cost | (1,230,745 | ) | (1,237,314 | ) | — | — | — | — | (1,237,314 | ) | ||||

| Derivatives – Hedge accounting | (6,048 | ) | (6,071 | ) | — | (6,071 | ) | — | — | — | ||||

| Fair value changes of the hedged items in portfolio hedge of interest rate risk | (269 | ) | (269 | ) | — | — | — | — | — | |||||

| Liabilities under insurance contracts | (739 | ) | — | — | — | — | — | — | ||||||

| Provisions | (13,987 | ) | (13,980 | ) | (739 | ) | — | — | — | (13,241 | ) | |||

| Tax liabilities | (9,322 | ) | (9,185 | ) | — | — | — | — | (9,185 | ) | ||||

| Other liabilities | (12,792 | ) | (12,386 | ) | — | — | — | — | (12,655 | ) | ||||

| Total liabilities | (1,412,036 | ) | (1,396,637 | ) | (739 | ) | (88,238 | ) | — | (117,433 | ) | (1,272,395 | ) | |

17 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

Shown below are the main differences between the carrying amounts appearing on the financial statements and the exposures for prudential purposes:

| Table 2. Main sources of differences between regulatory exposure amounts and carrying values in financial statements (LI2) | |||||||||||

| Million euros | |||||||||||

| 31 Dec. 2019 | |||||||||||

| Total | Items subject to: | ||||||||||

| Credit risk framework | CCR framework | Securitisation frameweork | Market risk framework | ||||||||

| Asset carrying value amount under scope of regulatory consolidation (as per template EU LI1) | 1,568,368 | 1,248,198 | 149,330 | 7,125 | 163,714 | ||||||

| Liabilities carrying value amount under regulatory scope of consolidation (as per template EU LI1) | (206,410 | ) | (739 | ) | (88,238 | ) | — | (117,433 | ) | ||

| Total net amount under regulatory scope of consolidation | 1,361,959 | 1,247,459 | 61,093 | 7,125 | 46,282 | ||||||

| Off-balance sheet amounts | 300,792 | 300,791 | 1 | — | |||||||

| Regulatory Add-on | 54,032 | — | 54,032 | — | — | ||||||

| Differences in valuations | — | — | — | — | |||||||

| Differences due to different netting rules, other than those already included in row 2 | (84,811 | ) | — | (38,529 | ) | — | (46,282 | ) | |||

| Non-eligibility of the balances corresponding to accounting hedges (derivatives) | (7,216 | ) | — | (7,216 | ) | — | — | ||||

| Securitisations with risk transfer | (3,837 | ) | (39,090 | ) | — | 35,254 | — | ||||

| Other | (16,942 | ) | (18,220 | ) | — | 1,278 | — | ||||

| Differences due to consideration of provisions | 8,332 | 8,388 | — | (56 | ) | — | |||||

| Differences due to CRMs | (38,617 | ) | (7,839 | ) | (30,778 | ) | — | — | |||

| Differences due to CCFs | (219,003 | ) | (219,003 | ) | — | — | — | ||||

| Exposure amounts considered for regulatory purposes (EAD) | 1,354,689 | 1,272,485 | 38,601 | 43,602 | — | ||||||

The reconciliation of public and non-public balance sheets is shown in Appendix VI on the Santander Group website.

1.3.2. Substantial amendments due to a change in perimeter and corporate transactions

For more information on the main acquisitions and disposals of stakes in other companies, and other major corporate transactions by Santander Group last year, see section 3 of Auditor’s Report and Financial Statements available in the 2019 Annual Report.

1.4. Regulatory framework

On 26 June 2013 the Basel III legal framework was incorporated in the European legal order via Directive 2013/36 (CRD IV), which repeals Directives 2006/48 and 2006/49, and Regulation 575/2013 on prudential requirements for credit institutions and investment firms (the CRR).

CRD IV was introduced into Spanish law through Law 10/2014 on the regulation, supervision and solvency of credit institutions, and its subsequent regulatory implementation via Royal Decree 84/2015 and Circular 2/2016 of the Bank of Spain, which completes its adaptation to the Spanish system of laws.

The CRR, which is immediately applicable in all European countries, includes a calendar for the phase-in period that will allow institutions to adapt gradually to the new requirements in the European Union in relation to AT1 and T2 equity instruments. These calendars have been introduced into Spanish regulations through the Bank of Spain Circular 2/2014, which affects both the new deductions and those issues and elements of own funds that cease to be eligible as such under this new regulation.

On 27 December 2017, Regulation 2017/2395 was published which modified CRR in relation to the transitory provisions to mitigate the impact of the introduction of IFRS 9, which took place on 1 January 2018. The calendar envisages a five-year gradual phase-in period, and the applicable factor for the current year (2020) will be 0.7.

| 18 | 2019 Pillar 3 Disclosures Report | ||

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

In addition, on 28 December 2017, Regulations 2017/2401 and 2017/2402 were published, which include the new securitisations framework. The first of these regulations, establishes a new calculation methodology of capital requirements for securitisations and a transition period which ended on 31 December 2019; while the second one defines an STS (simple, transparent and standardised) securitisation, which because of its characteristics of simplicity, being used to finance the real economy, etc., receives preferential treatment in terms of lower capital requirements.

Regulations have been published with respect to non-performing exposures (NPEs), with the aim of applying the "Action plan to tackle non-performing loans in Europe" released by the European Council in July 2017. The most significant of which are:

| • | ECB supervisory expectations to deal with the NPEs stock through provisioning. |

| • | The European Central Bank Guidance on non-performing loans for credit institutions, published in March 2017: Calendars with quantitative supervisory expectations for the provisioning of this type of exposure are established in the addendum to this guidance, published in March 2018. Applicable to exposures originating before 26 April 2019 and which have been converted into NPE from 1 April 2018 and their non-compliance might imply a higher Pillar 2 charge. |

| • | Amendment of the CRR through Regulation 2019/630 as regards minimum loss coverage for non-performing exposures (prudential backstop), published in April 2019: This regulation includes calendars of quantitative requirements for the minimum provisioning of NPEs. It applies to NPEs originating after 26 April 2019 and their non-compliance would cause a CET1 deduction of the entities. |

On 20 May 2019, the new regulatory package was approved, which consisted of Regulation 2019/876 (CRR II) and the Directive 2019/878 (CRD V).

As a general rule, it is established that CRR II will come into force from 28 June 2021, except for certain exceptions which will come into force over a period of time, which started on 1 January 2019 and ends on 28 June 2023.

Of particular note among these exceptions are the entry into force on 27 June 2019, of the main changes in own funds, capital deductions, standard credit risk and IRB, and authorisations.

CRD V came into force on 27 June, but has not yet been applied, as the member states have until 28 December 2020 to transpose it into their domestic systems of laws. CRD V includes significant changes such as those to Pillar 2 guidance (P2G).

The regulatory package published in June 2019, sees the inclusion in CRR II of the principles established in the TLAC term sheet, set internationally by the FSB (Financial Stability Board), as a Pillar 1 minimum requirement for own funds and eligible liabilities for G-SIBs.

This package of changes also includes the substitution of the Bank Recovery and Resolution Directive (BRRD) by BRRD II, which establishes Pillar 2 MREL requirements for all resolution entities, whether systemically important or not, in which the resolution authority will decide the requirements on a case-by-case basis. For the G-SIBs, the CRR II introduces the minimum requirement established in the TLAC term sheet (16%/18%) which will have to be made up of subordinated liabilities, except for a certain percentage of senior debt (2.5%/3.5%). BRRD II sets a minimum subordination requirement of the higher of 13.5% of risk-weighted assets or 5% of the leverage ratio exposure measure for large banks (defined as those with total assets over EUR 100,000 million), or other institutions which, without being large, the resolution authority considers may be systemically important. For all other institutions, the subordinated requirement will be determined by the resolution authority on a case-by-case basis.

1.4.1. Regulatory changes in 2019

The most notable milestone in 2019 is the approval of capital and resolution regulations in Europe after more than two years of intensive negotiations. After the 2017 Basel accord, supplemented by the market risk framework agreement in January 2019, the next milestone will be its implementation in the various jurisdictions. Also of note is the European legislative agenda in relation to climate change and sustainable financing, which has progressed significantly during the year. Finally, the digital agenda, including the possibility of adopting new technologies, and discussions about the supervisory and regulatory framework that needs to be applied to non-banking players, have also occupied a large part of the current regulatory environment.

International framework

In 2019, the Basel Committee continued to work on, among other issues, the following:

| • | Market risk. The final standard on the Minimum capital requirements for market risk was published in January. |

| • | Consolidated Basel framework. In April, the Basel Committee launched a new section of its website that sets out a consolidated version of its Global standards for the regulation and supervision of banks. |

| • | Leverage ratio. In June, the final document on the Leverage ratio treatment of client cleared derivatives was published, with the aim of aligning it with the standardised approach to measuring counterparty credit risk (SA-CCR). |

| • | Margin requirements for non-centrally cleared derivatives. The Basel Committee and the International Organisation of Securities Commissions reviewed the Margin requirements for non-centrally cleared derivatives framework and extended its implementation deadline. |

| • | Interaction and cooperation between prudential and anti-money laundering/countering financing of terrorism supervision. In November, the Basel Committee launched a consultative document on the Introduction of guidelines on interaction and cooperation between prudential and AML/CFT Supervision. The deadline for comments is 6 February 2020. |

19 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| • | Pillar 3 disclosure requirements. In June, the Committee published its final text on Revisions to leverage ratio disclosure requirements, establishing additional disclosure requirements for this ratio as calculated using daily averages of securities financing transactions. In November, the Basel Committee launched two consultative documents asking for comments on: (i) Sovereign exposures disclosure templates, the implementation of which is voluntary, unless requested by national supervisors; (ii) Revisions to market risk exposures disclosure templates, to reflect the changes introduced by the final standard on the Minimum capital requirements for market risk. The deadline for comments was 14 February 2020. |

| • | Sectoral countercyclical capital buffer. In November, the Basel Committee issued the Guiding principles for the operationalisation of a sectoral countercyclical capital buffer, which are intended to support the implementation of the Basel III countercyclical capital buffer on a consistent basis across jurisdictions. |

| • | Credit valuation adjustment (CVA) risk. The Basel Committee launched a consultative document in December, on a set of adjustments to the CVA risk framework published in December 2017, with the aim of aligning it with the final standard on the Minimum capital requirements for market risk and the Capital requirements for bank exposures to central counterparties. The deadline for comments was 25 February 2020. |

With respect to crisis management framework, the Financial Stability Board (FSB) issued a report in 2019 on the implementation of the Total Loss Absorbing Capacity (TLAC) process in the different jurisdictions and concluded that no changes were necessary. The FSB will continue to monitor the implementation of TLAC in the various jurisdictions, including the volume of issuances of TLAC instruments. It is expected that progress in these aspects will be subject to at least annual review.

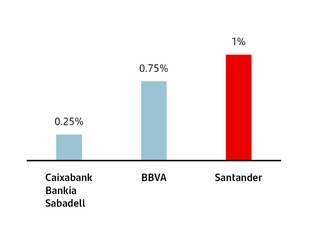

In November 2019, the FSB updated the list of G-SIBs for 2020. Santander remains within the least systemically important group of banks and is subject to the minimum additional capital buffer for global systemically important banks (1%).

In the digital arena, the fintech phenomenon and the need to review the regulatory and supervisory framework are increasingly pressing points on the agendas of international authorities. The most important in 2019 are those published by the various authorities (FSB, BIS) on the consequences of the entry of Bigtechs into financial services, both directly (as banking services providers) or indirectly (as technology services providers on which the banks are dependant, such as cloud services). Various ideas have been proposed, such as allowing all types of financial services operators greater access to data, and not only banks; the need to review the suitability of the regulatory and supervisory framework; the potential risks for financial stability resulting from the use of the cloud by financial institutions and the small number of major global players.

Also in the digital arena, the OECD is leading the multilateral initiatives to address the tax challenges resulting from the digitalisation of the economy to ensure that digital companies pay tax wherever they have consumers and their activities generate profits. This year, two consultative documents have been published and an agreement is expected to be reached in 2020.

European regulation

June 2019, saw the publication of the final texts reviewing the capital framework and the resolution framework (review of the CRR/CRD/BRRD). This package implements a set of factors agreed in the Basel Committee and the FSB, among them the net stable funding ratio (NSFR); the total loss absorbing capacity (TLAC) requirement for global systemically important banks; the revised standards on large exposures; counterparty credit risk; the leverage ratio; investment fund units; disclosure requirements and the new market risk reporting framework.

The following is of particular note within the new CRR II/CRD V capital framework: the extension of the scope of the support factor for the funding of SMEs; the introduction of a support factor for infrastructure financing; the recognition in the European Union of the issuance of capital from third countries in the calculation of consolidated capital; and the possible exemption of certain intangible software assets from deduction from own funds under certain circumstances to be determined by the EBA.

The EBA has published a set of roadmaps in which it outlines its action plan to deliver on the mandates resulting from this new capital and resolution framework for each of the issues. One of these mandates is the drafting of the technical standards to develop the new prudential treatment of the banks' software assets.

The implementation process in the European Union of the final Basel III framework, approved in December 2017, has continued during 2019.

In compliance with the mandate given to it by the European Commission in 2018, the EBA has issued two advisory reports on the implementation of Basel III, which include the impact on capital requirements for European banks with some policy recommendations

In October 2019, the European Commission launched the consultative document, "Implementing the final Basel III reforms in the EU", with a deadline for comments of 3 January 2020, which also includes other issues other than Basel III standards. The European Commission is expected to issue a legislative proposal for the review of CRR/CRD in 2020.

In March 2019, the European Commission recognised the equivalence of the prudential supervision and regulatory framework of Argentina. This decision permits certain categories of exposures to this country to benefit from preferential treatment in terms of capital requirements.

| 20 | 2019 Pillar 3 Disclosures Report | ||

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

With respect to supervision, the supervisory activity conducted by the Single Supervisory Mechanism (SSM) within the framework of the Supervisory Review and Evaluation Process (SREP) is notable. In this area, Banco Santander’s Joint Supervisory Team (JST) from the European Central Bank worked tirelessly in 2019, holding over 100 meetings with the Bank, most of which were related to its inspection and monitoring activities.

Along with a busy supervisory agenda, in 2019 the SSM continued to make great strides towards the harmonisation of supervisory policies across countries, and improving the transparency of their expectations.

Europe also continues to make progress in the implementation of the crisis management framework. The Single Resolution Mechanism (SRM), the second pillar of the Banking Union after the Single Supervisory Mechanism, has been operational since 1 January 2016. The Single Resolution Board, together with the national resolution authorities, have defined the framework for establishing MREL (minimum requirement for own funds and eligible liabilities) and continue to work towards ensuring the effectiveness of the resolution framework.

Turning to the Single Resolution Fund managed by the Single Resolution Board, the period of gradual mutualisation will allow for a transition from the national resolution funds to the Single Resolution Fund, which will be fully implemented by 2024. The funding target of the Single Resolution Fund is 1% of covered deposits in 2024.

In 2019, the main features were agreed for the creation of a backstop for the Single Resolution Fund, after an agreement was reached on the design and allocation for funds for the European Stability Mechanism (ESM), which will act as the backstop. A final agreement is expected to be signed in the first quarter of 2020. However, the issue of the provision of liquidity on resolution remains unresolved.

Negotiations on Pillar 3 of the banking union, the European Deposit Insurance Scheme (EDIS), for which the European Commission already submitted a proposal in 2015, are making very slow progress. For this purpose, a high-level work group was set up at the end of 2018, with the aim of moving the proposal forward. At the end of 2019, the work group set out a roadmap for 2020 with the goal of continuing to work on completing Banking Union.

Further, in March 2018, the Commission published a raft of measures to address the high rates of non-performing loans (NPLs). Along these same lines, in March 2019, the Commission published a regulation in relation to minimum loss coverage for non-performing exposures. The European Banking Authority (EBA) has issued a draft of proposed new guidelines on loan origination and monitoring. One of the objectives of these guidelines is to clarify internal governance and control framework for the credit granting, set out requirements for information and data collection from borrowers, along with documentation and requirements for their creditworthiness assessment. The guidelines also include environmental, social and governance, anti-money laundering and counter-terrorist financing, and technological innovation factors.

In the digital area, the Commission continued to roll out its fintech action plan, in which developments to facilitate the adoption of new technologies particularly stand out. A particular highlight was the publication in April of the Ethics guidelines for trustworthy artificial intelligence (including an assessment survey, the final version of which will be published in early 2020), the results of the workgroup on regulatory barriers to financial innovation

In addition, there have been changes in the following areas:

| • | In addition, the authorities, especially the competition authorities, have shown interest in opening up data access. Of particular note in this area is the report, "Competition policy for the digital era", published by the European Commission, along with other similar reports in the United Kingdom and Germany. |

| • | With regard to infrastructure access, a number of competition cases have been opened against large platforms in relation to data use or blocking of access by competitors. In addition, a regulation has been approved in Germany which requires payment technology infrastructures to allow access to other operators. |

| • | In the area of platforms, the Regulation on platform-to-business relations was approved in July 2019, with the aim of ensuring fairness and transparency for business users. At the same time, the European Commission created an Observatory on the online platform economy to monitor this economic area. |

| • | In the area of provider management, in February 2019, the EBA published its Guidelines on outsourcing agreements, which specify the internal governance systems, including adequate risk management, that must be applied in the outsourcing of functions, including the use of the cloud. The guidelines entered into force on 30 September of 2019. |

The Commission has also decided to strengthen the anti-money laundering and counter-terrorist financing framework. In July 2019, the Commission published a Communication calling for a better implementation of the EU’s regulatory and supervisory framework. Among the options considered are the creation of a European Supervisory Authority (or to grant these powers to an already existing authority) and, if necessary, a European regulation that avoids the inconsistencies generated by a directives-based framework. Along this same line, in July 2019 the EBA issued an Opinion highlighting the importance of also considering anti-money laundering and counter-terrorist financing risks from a prudential perspective, and invited the prudential supervisors to notify the financial institutions that AML/CFT supervisors' assessments will be factored into the prudential supervisory process.

The legislative agenda in relation to climate change and sustainable financing has progressed significantly. Specifically, the following have been approved as part of the European Commission Action Plan:

| • | The Disclosure Regulation, which clarifies asset managers’ and institutional investors’ duties to consider sustainability in the investment process and strengthen disclosure requirements. |

21 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| • | The review of the non-binding guidelines on reporting of non-financial information focused on information about climate change, which aims to increase the transparency of corporate reports. The guidelines include the conclusions of the FSB Task Force on Climate-related Financial Disclosures. |

| • | Changes to the Benchmarks Regulation, which includes the development of climate change benchmarks: the EU Paris-aligned benchmarks and the information related to sustainability in these benchmarks. To ensure that these benchmarks are reliable, only asset managers that meet the requirements of this regulation will be able to use these labels when marketing their benchmarks in the EU. |

| • | In addition, a preliminary political agreement has been reached between the European Parliament and Council in the taxonomy framework, to establish a unified classification system for sustainable assets and the technical criteria for their identification. |

The EBA continues to carry out the mandates relating to sustainable financing received through the review of the CRD and CRR: the possibility of including environmental, social and corporate governance risks (ESG) in the SREP; greater transparency for companies with regard to ESG risk and the mandate enabling the EBA to carry out an analysis to assess the viability of recalibrating the capital requirements for banks (green/brown factor). In relation to this, in December 2019 the EBA published a roadmap with the 2019 -2025 work plan in relation to the sustainability agenda.

Santander Group holds and passes on the views from corporate and local level on the matters being discussed in the financial sector where these may affect its activities. The corporate and local Public Policy function, in coordination with the business and support units concerned in each case, identifies the regulatory alerts and establishes the position of Santander Group.

The main courses of action taken along these lines are as follows:

| • | Santander Group has been a keen participant in the main banking associations worldwide and in Europe, and in the main markets in which we operate, providing responses to existing regulatory consultations. |

| • | Santander Group maintains proactive and constructive dialogue with policy-makers through the existing channels (public hearings, consultations, forums and conferences) and sends individual replies to official consultations on issues considered relevant to Santander Group. |

| • | Santander Group particularly defends the recognition of the strength of our organisational model through autonomous subsidiaries with control of their own capital and liquidity, the benefits of our geographic diversification and of our equivalence in the jurisdictions of third countries where we operate. |

| • | Santander also maintains that the regulatory framework should enable banks to play an active role in the new digital economy, and implement their transformation so that they can continue to respond to changing consumer needs. |

| 22 | 2019 Pillar 3 Disclosures Report | ||

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| 2 | |||||

| Capital | |||||

| Image omitted | |||||

23 |

| INTRODUCTION 2019 Pillar 3 Disclosures Report |

| Image omitted | |||||

24 |

| CAPITAL 2019 Pillar 3 Disclosures Report |

2. Capital

| Table 3. Main capital figures and capital adequacy ratios | |||||||||

| Million euros | |||||||||

| Fully loaded | Phased-in | ||||||||

| Dec-2019 | Dec-2018 | Dec-2019 | Dec-2019 | ||||||

| Common Equity (CET1) | 70,497 | 66,904 | 70,497 | 67,962 | |||||

| Tier 1 | 78,964 | 75,838 | 79,536 | 77,716 | |||||

| Total capital | 90,937 | 87,506 | 91,067 | 88,725 | |||||

| Risk weighted assets | 605,244 | 592,319 | 605,244 | 592,319 | |||||

| CET1 Ratio | 11.65 | % | 11.30 | % | 11.65 | % | 11.47 | % | |

| Tier 1 Ratio | 13.05 | % | 12.80 | % | 13.14 | % | 13.12 | % | |

| Total capital ratio | 15.02 | % | 14.77 | % | 15.05 | % | 14.98 | % | |

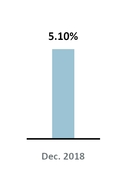

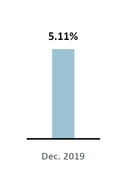

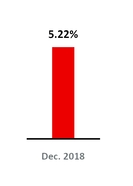

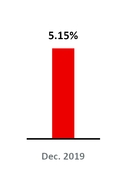

| Leverage Ratio | 5.11 | % | 5.10 | % | 5.15 | % | 5.22 | % | |

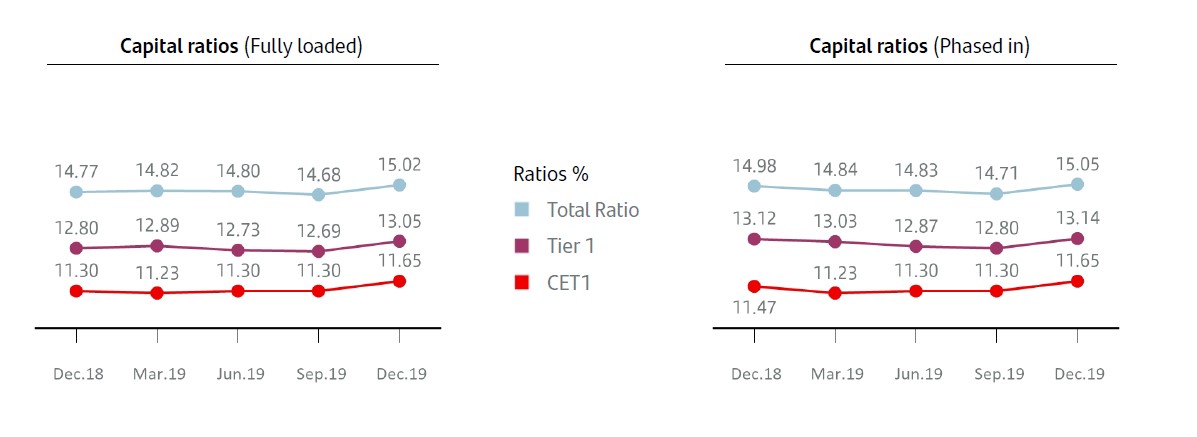

| Fully loaded CET1 Capital evolution | |

| % | |

Note: 2018 and 2019 figures are calculated applying the transitional arrangements of IFRS 9 unless specified otherwise.

2.1. Capital

Capital management and control at Santander Group is a fully transversal process that seeks to guarantee the Bank’s capital adequacy, while complying with regulatory requirements and maximising profitability. It is determined by the strategic objectives and by risk appetite set by the board of directors. To achieve this, the following policies have been established to shape the approach that the Group applies to capital management:

| • | Establish adequate capital planning, so as to meet current needs and provide the necessary resources to meet the needs of the business plans, regulatory requirements and the associated risks in the short and medium term, while maintaining the risk profile approved by the board. |

| • | Ensure that the Group and its companies maintain sufficient capital to cover requirements during stress scenarios due to the increase in risks as the macroeconomic climate deteriorates. |

| • | Optimise capital use through appropriate allocation of capital among the businesses, based on the relative return on regulatory and economic capital and taking the risk appetite, growth and strategic objectives into account. |

Santander Group maintains a very comfortable capital adequacy position, well above the levels required by applicable regulations and by the European Central Bank.

Santander Group’s solvency ratios at 31 December 2019 are as shown in table 3. Phased-in ratios are calculated applying the transitory schedules for implementation of Basel III, whereas fully loaded ratios are calculated without applying any schedules, hence, using the final regulation.

IFRS 9 became effective on 1 January 2019, implying changes in accounting that affect capital ratios. Santander decided to apply the transitional arrangements, implying a five-year transitional period.

25 |

| CAPITAL 2019 Pillar 3 Disclosures Report |

Had it not applied the IFRS 9 transitional arrangements, the total impact on the fully loaded CET 1 ratio at December would have been -24 bps. For further details, see Appendix XII.

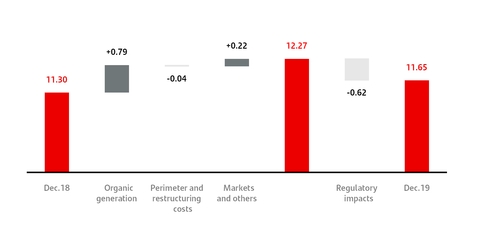

In fully-loaded terms CET1 in December stood at 11.65%, increasing by 35 bps during the year and reaching the goal at year-end which was announced at the beginning of the year. The fully-loaded capital ratio was 15.02%, up 25 bps during the year.

| 2019 Fully Loaded CET1 evolution | |

| +35bps |

The 35 basis point increase in the year was mainly due to underlying profit generation and proactive RWA management, resulting in an organic generation of 79 bps.

Additionally, there was a favourable evolution from markets (+22 bps) due to recovery in the Held to Collect & Sell portfolios (driven by falls in interest rates) and a positive 11 basis point perimeter impact (mainly related to increased minority interests in Mexico and the incorporation of the custody business), in part offset by the negative impact from restructuring costs (-15 bps).

As a result, there was a 97 basis point increase in the year, bringing the fully-loaded CET1 ratio to 12.27% in December before accounting and regulatory impacts (-62 bps, primarily due to IFRS 16 and TRIM).

From a qualitative perspective, Grupo Santander has solid ratios that are suited to its business model, the structure balance sheet and its risk profile. Santander Group exceeds 186 basis points over the minimum regulatory requirement for the total ratio for 2020 taking into account the shortfalls in AT1 and T2.

| ¤ | For further information, see section 2.1.5. |

| 26 | 2019 Pillar 3 Disclosures Report | ||

| CAPITAL 2019 Pillar 3 Disclosures Report |

| Strategic principles of the capital function |

• Autonomy. The Group’s corporate structure is based on a legally independent subsidiary model, each responsible for its own capital and liquidity. This provides advantages when raising funds and limits the risk of contagion, thus reducing systemic risk. Under this structure, subsidiaries are subject to two tiers of supervision and internal control: local and global. Each unit must raise and manage its own financial resources accordingly in order to maintain the required levels of capital at all times. Local units must have the necessary capital to carry on their activity autonomously and meet local regulatory requirements and the expectations of their local market. | • Solvency. The Group and its subsidiaries must ensure at all times that the structure and level of their capital is suitable in view of the risks to which they are exposed. Capital must be allocated accordingly so as to ensure the effective management of the risks assumed within the subsidiaries and it must be assigned proportionately among all those risks. | • Efficiency. The Group and its subsidiaries must roll out mechanisms to actively seek and promote an efficient use of capital and to ensure that the value created by an investment exceeds at least the cost of the capital invested. Capital is a scarce commodity that must be used as efficiently as possible, given the high cost of generating capital, whether organically or through the markets. Subsidiaries must have on - going monitoring mechanisms in place to optimise their capital consumption. | ||||

• Centralised monitoring. The capital management model must ensure a holistic view, through a corporate environment of global coordination and review (every business, every geography). The first level of monitoring, by the local units themselves, is supplemented by the monitoring activity of the corporate units. One of the main ways the Group achieves this is by defining and applying standard policies, metrics, methodologies and tools across the Group, though these may be adapted accordingly to bring them in line with local regulations and supervisory requirements and to reflect the degree of progress made by each subsidiary. | ||||||

2.1.1. Capital function

The core principles establish the basic guidelines governing the actions of Santander Group entities in capital management, monitoring and control processes.

2.1.1.1. Organisation

The organisational structure has been defined with the aim of guaranteeing compliance with the core principles in relation to capital and ensuring that the relationship between the subsidiaries and the corporate centre is maintained. This function allows twin objectives to be met: comply with the subsidiary’s financial autonomy while at the same time retaining coordinated monitoring at Group level.

Santander Group’s risk management and control model is based on three lines of defence. The first line comprises the business functions or activities that assume or generate exposure to risk. Risks undertaken or generated within the first line of defence must be compatible with the risk appetite and limits in place. To carry out its function, the first line of defence must have the resources to identify, measure, address and report the risks assumed. The second line of defence comprises the function of controlling and supervising risk, along with the Compliance function. This second line of defence is charged with effective control of risks and ensures that they are managed in accordance with the established risk appetite.

Internal Audit is the third line of defence and the last layer of control, and regularly assesses policies, methods and procedures to ensure they are suitable, and also checks they are operational.

The risk control function, the compliance function and the internal audit function are sufficiently separate and independent from each other and also regarding the other functions they control and supervise when carrying out their tasks. They likewise have access to the board of directors and/or to its committees at the highest level.

2.1.1.2. Capital governance

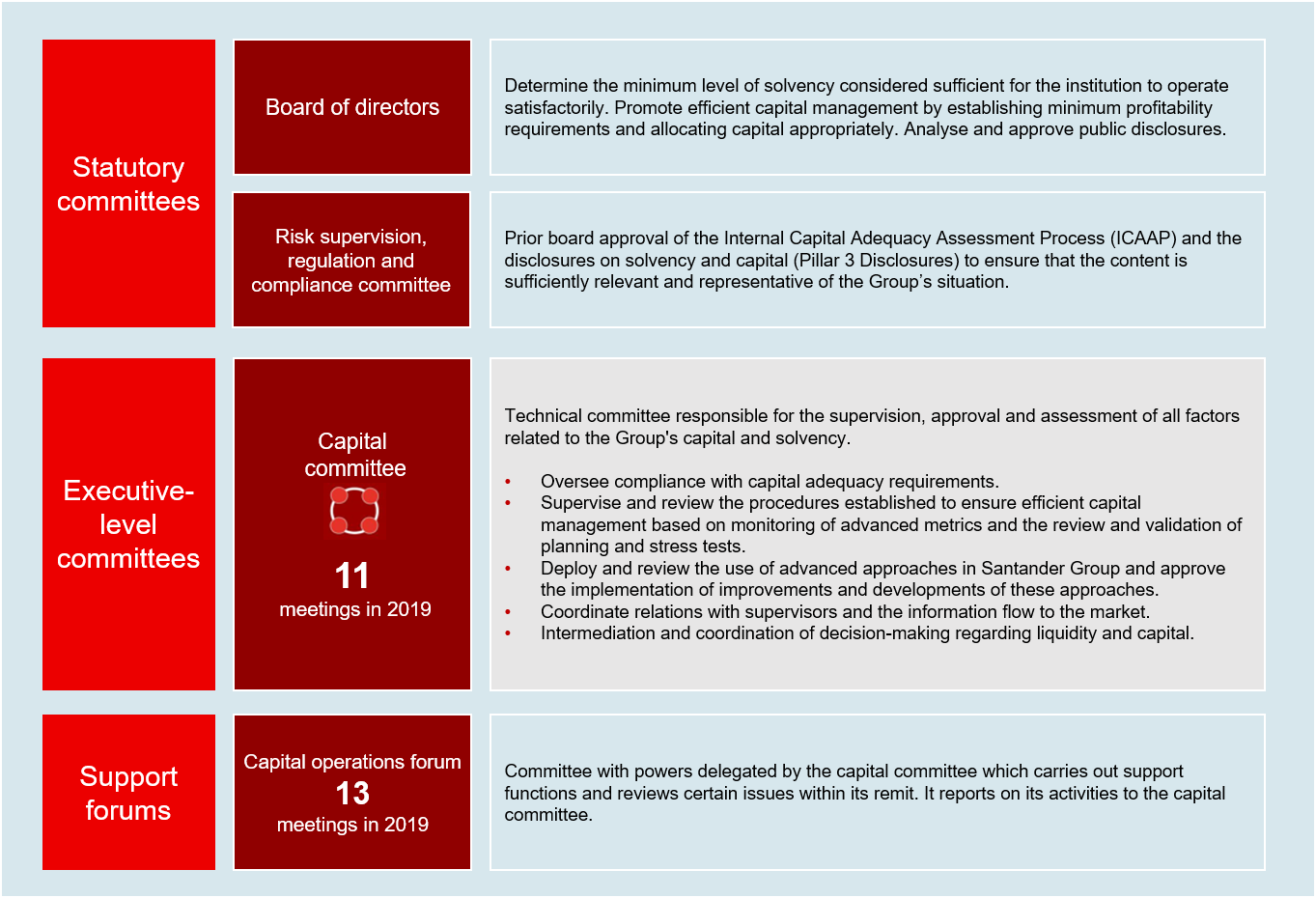

To ensure the Capital function operates properly when it comes to both decision-making and supervision and control, Santander Group has developed a structure of agile and efficient governing bodies which ensure the involvement of all the areas concerned and the necessary involvement of senior management. Because of Santander Group’s characteristic subsidiary-based structure, the governance structure of the capital function must be adapted to preserve the subsidiaries’ capital autonomy, while allowing centralised monitoring and coordinated management at Group level. There are also various committees that have responsibilities at regional level and also for coordination at Group level. The local committees must report to the corporate committees in due time and proper form on any relevant aspects of their activity that may affect capital so as to ensure proper coordination between the subsidiaries and the corporate centre.

27 |

| CAPITAL 2019 Pillar 3 Disclosures Report |

| Governance of the Capital function |

2.1.2. Capital management and adequacy

The aim of capital management and adequacy at Santander Group is to guarantee the entity’s solvency and maximise its profitability, while ensuring compliance with internal capital targets and regulatory requirements. Capital management is a fundamental strategic tool for decision making at both local and corporate level and serves to create a common framework of action by establishing uniform definitions of capital management criteria, policies, functions, metrics and processes.

| 28 | 2019 Pillar 3 Disclosures Report | ||

| CAPITAL 2019 Pillar 3 Disclosures Report |

| Key capital figures | ||||||

| The Group works with the following variables relating to the concept of capital: | ||||||

| Regulatory capital | Return on risk-adjusted capital (RoRAC) | |||||

• Capital requirements: The minimum amount of capital the supervisory authority requires the entity to hold to safeguard its solvency, based on the amount of risk assumed, in terms of credit, market and operational risk.• Eligible capital: The capital the regulator considers eligible to meet capital requirements. The main components of eligible capital are accounting capital and reserves. | The return (understood as net profit after tax) on internally required economic capital, Therefore, the higher the economic capital, the lower the RoRAC. For this reason, the Bank must demand a higher return from transactions or business units that consume more capital. RoRAC takes the investment risk into account and so provides a risk-adjusted measure of return. The use of RoRAC allows the Bank to better manage its activities, assess the real risk-adjusted return of businesses and be more efficient in decision-making relating to investments. | |||||

| Economic capital | ||||||

• Internal capital requirements: The minimum amount of capital that the Group needs with a specified level of probability to absorb unexpected losses deriving from its current exposure to all risks taken on by the entity (including risks additional to those contemplated under the regulatory capital requirements).• Available capital: The amount of capital the Group itself considers eligible, on management criteria, to meet capital needs. | Return on Risk Weighted Asset (RoRWA) | |||||

Defined as the return (understood as net profit after tax) on a business’ risk-weighted assets. The use of RoRWA allows the Bank to set up strategies to allocate regulatory capital and ensure the maximum return is obtained. | ||||||

| Cost of Capital | Value creation | |||||

| The minimum return required by investors (shareholders) as compensation for the opportunity cost incurred and the risk assumed on investing their capital in the entity. This cost of capital represents a “cut-off rate” or “minimum return” to be achieved and allows comparisons to be made between the different business units and their efficiency to be assessed. | Any profit generated above and beyond the cost of economic capital. The Bank will create value when the risk-adjusted return, measured by RoRAC, is higher than its cost of capital. Otherwise value will be destroyed. It measures the risk-adjusted return in absolute terms (monetary units), supplementing the RoRAC result. | |||||

| Leverage ratio | Expected loss | |||||

| Regulatory measure that monitors the financial solidity and strength of the Entity by linking size and capital. This ratio is calculated dividing the Tier 1 by the leverage exposure, which takes into account the balance sheet exposure and adjustments due to derivatives, secured financing transactions (SFTs) and off-balance sheet items. | Average NPL losses expected by the entity over the course of an economic cycle. From the point of view of expected loss, defaults are considered a “cost” that could be eliminated or reduced through appropriate selection of borrowers. | |||||

The Group’s Capital function is carried out on two levels:

| • | Regulatory capital: regulatory capital management is based on an analysis of the capital base, the solvency ratios as defined by applicable regulations and the scenarios used in capital planning. The objective is for the capital structure to be as efficient as possible, in terms of both cost and compliance with regulatory requirements. Active capital management includes strategies for the allocation of capital and its efficient use in business units, securitisations, asset sales and issuances of equity instruments (capital and subordinated debt hybrids). |

| • | Economic capital: the objective of the economic capital model is to ensure that the Group has adequately allocated its available capital to cover all the risks to which it is exposed as a result of its activity and risk appetite. It also aims to optimise value creation in the Group and all of the business units that comprise it. |

The real economic measurement of the capital needed for an activity, together with its return, enables value creation to be optimised by selecting those activities that maximise the return on capital. This allocation is carried out under different economic scenarios, both expected as well as unlikely but plausible, and with the level of solvency set by Santander Group.

29 |

| CAPITAL 2019 Pillar 3 Disclosures Report |

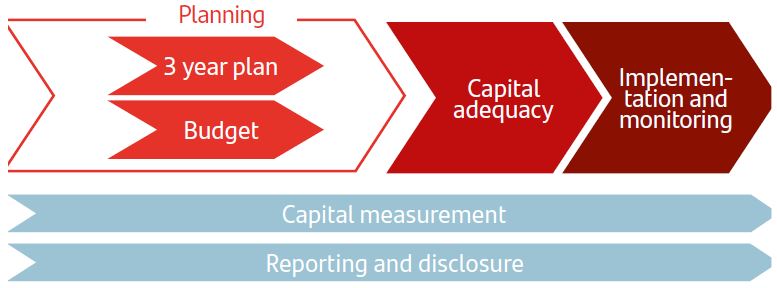

2.1.3. Capital management priorities 2019

The Group’s most notable capital management activities are:

| • | Establishing solvency and capital contributions targets aligned with the minimum regulatory requirements and internal policies, in order to guarantee a solid level of capital, consistent with the Group’s risk profile, and an efficient use of capital to maximise shareholder value. |

| • | Developing a capital plan to meet those objectives consistent with the strategic plan. Capital planning is an essential part of executing the three-year strategic plan. |

| • | Assessing capital adequacy in order to ensure that the capital plan is consistent with the Group’s risk profile and the risk appetite framework in stress scenarios. |

| • | Developing the annual capital budget as part of the Group’s budgetary process. |

| • | Monitoring and controlling budget execution and drawing up action plans to correct any deviation from the budget. |

| • | Calculating capital metrics |

| • | Preparing internal capital reports, as well as reports for the supervisory authorities and the market. |

Details of the most significant actions undertaken in 2019 are set out below:

Issuances of financial instruments

In February 2019, Banco Santander S.A. made one issue of contingent convertible bonds (CoCos) for USD 1,200 million to replace the early repayment of an issuance in dollars for a similar amount made in 2014.

After the removal of the need for pre-approval for the inclusion of third-country issuances (through Royal Decree 309/2019), the Group’s total capital includes EUR 800 million corresponding to T2 issuances of Chile and Mexico that meet the eligibility requirements.

Dividend policy*

For 2019, as stated in the material fact published on 26 February 2019, in order to align ourselves with our European peers' current practice, it is the board’s intention to set a pay-out ratio of 40-50% in the mid-term, increasing it from the 30-40% of 2018; that the proportion of dividend paid in cash is not lower than that of the last year; and, as was announced in the 2018 AGM, to make two payments against the results of 2019.

In December 2015, the European Central Bank issued a recommendation on the distribution of dividends policy applicable to all eurozone credit entities as at 2016. The recommendation calls for conservative dividend policies and prudent assumptions and has been fully observed by Banco Santander, S.A.

Finally, in some geographies, restrictions on the payment of dividends have been implemented. These include Poland, where the competent national authority (KNF) has imposed stricter minimum restrictions on the payment of dividends, with additional limits for entities with large mortgage exposures in foreign currency; and Argentina, where, in its “A6464" communication issued in 2018, the BCRA amended the rules on the distribution of profits and coupons on perpetual instruments, making them more restrictive.

For further information, see chapter on Corporate governance (section 3.3) of the 2019 Annual report.

| (*) | Dividends charged to 2019 results are subject to the approval of the general shareholders' meeting. So far, Santander's board has only approved the first dividend charged to 2019 results for EUR 0.10 per share. |

| 30 | 2019 Pillar 3 Disclosures Report | ||

| CAPITAL 2019 Pillar 3 Disclosures Report |

2.1.4. Capital targets

Santander Group is working towards a fully loaded CET1 ratio from 11% to 12% in the medium term.

| Fully loaded CET1 Capital evolution | |

The continuous improvement in the capital ratios reflects Santander Group's profitable growth strategy and a culture of active capital management at all levels of the organisation.

Highlights:

| • | The reinforcement of teams dedicated to capital management and greater coordination with the corporate centre and local teams. |

| • | All countries and business units have developed individual capital plans focused on achieving a business that maximises the return on capital. |

| • | A higher weighting of capital management in incentives. Certain aspects relating to capital management and returns are now taken into account when setting the variable remuneration payable to members of the senior management: |

| • | The relevant metrics include the Group’s fully-loaded CET1, the capital contribution of the countries to the Group ratio or the return on tangible equity (RoTE). |

| • | The qualitative aspects considered include the proper management of regulatory changes affecting capital, effective management of capital relating to business decisions, capital generation sustainable over time and an effective capital allocation. |

At the same time, the Group continues to develop a programme of action to ensure the ongoing improvement of infrastructure, processes and methodologies that support all aspects relating to capital, with the aim of encouraging ever more active capital management, enabling the Group to respond in a more agile way to the numerous and growing number of regulatory requirements and carrying out all associated activities more efficiently.

2.1.5. Capital buffers and eligible capital requirements

Santander Group must comply, at all times, with the combined capital buffer requirement, defined as the total CET1 capital necessary to meet the following obligations:

| • | Capital conservation buffer (CCoB): mandatory for all entities and to be phased-in from 1 January 2016. The buffer for banks in 2019 was 2.5%. |

| • | Buffers for systemically important banks (G-SIB and D-SIB): Applicable from 1 January 2016 to the most systemically important institutions. There are two types with their corresponding methodologies, which classifies the financial institutions into buckets. These buckets determine their systemic risk (either global or domestic) and the buffer rate applicable. Where an institution is subject to both buffers on the same basis of consolidation, the higher of the two shall apply. The different types are: |

| i) | G-SIB buffer (global systemically important banks): Common methodology following the Basel framework. Applicable at consolidated level. |

| ii) | D-SIB buffer (domestic systemically important banks): Common methodology following EBA guidelines. May be required at consolidated, sub-consolidated or individual level |

| • | Systemic risk buffer (SRB):The competent national authority may require this to mitigate counter-cyclical systemic risks which are not covered by the systemically important institutions buffer and that could trigger a disturbance in the financial system with serious consequences for both it and the real economy. Its application by the authorities is discretionary, with a buffer being required for the entire financial sector or one or more of its sub-sectors (domestic, business, etc.). |

If the SRB is required for the whole financial sector, the highest of the three systemic buffer rates will be applied. If the SRB applies to one or more sectors, the SRB buffer will be added to the greater of the other two systemic buffers (G-SIB or D-SIB).

| • | Countercyclical capital buffer (CCyB): This will be applied when the national authorities consider that lending is growing excessively in a certain jurisdiction and with the aim of constraining it. This buffer is specifically calculated for each entity or group and consists of the weighted average of the countercyclical buffer rates applied in regions in which the bank’s major exposures are located. As with the other buffers, it has also been applicable since 1 January 2016. In November 2019, the Basel Committee issued the guiding principles which would offer the competent authorities the possibility of applying this capital buffer to individual sectors in their jurisdiction. |

31 |

| CAPITAL 2019 Pillar 3 Disclosures Report |

The table below summarises the required regulatory rates based on the different capital buffers to be applied and Banco Santander’s position in 2020:

| Application | Buffers (% RWAs) | 2020 | |||

| All entities | Conservation (CCoB) | 2.5 | % | ||

| Designated entities | G-SIB entities (1%-3.5%) (1) | 100% of the buffer | |||

D-SIB entities (2) | 100% of the buffer | ||||

| At the discretion of competent national authority | Systemic risk (SRB) (3) | 0%-5% | |||

Countercyclical (CCyB) (4) | 0% - 2.5% | ||||

| Consolidated combined buffer | CCoB + CCyB + Max (5) (G-SIB, D-SIB, SRB) | ||||

(1) Bank of Spain requires a 1% buffer from Santander Group for 2020

(2) Bank of Spain requires a 1% buffer from Santander Group for 2020

(3) This requirement is 0% for Santander Group

(4) % countercyclical buffer applicable during 2020 according to data from the European Systemic Risk Board (ESRB):

| a) | Exposures to customers resident in Spain: 0%, according to Bank of Spain data for the first quarter of 2020 |

| b) | Exposures to customers resident in the United Kingdom: from 1% to 2% (from 16 December) |

| c) | Exposures to customers resident in Belgium: from 0% to 0.5% (from 1 July) |

| d) | Exposures to customers resident in Bulgaria: from 0.5% to 1% (from 1 April) |

| e) | Exposures to customers resident in the Czech Republic: from 1.75% to 2% (from 1 July) |

| f) | Exposures to customers resident in Denmark: from 1% to 1.5% (from 30 June) to 2% (from 30 December) |

| g) | Exposures to customers resident in France: 0.25% to 0.5% (from 2 April) |

| h) | Exposures to customers resident in Norway: 2.5% |

| i) | Exposures to customers resident in Germany: from 0% to 0.25% (from 1 July) |

| j) | Exposures to customers resident in Iceland: from 1.75% to 2% (from 1 February) |

| k) | Exposures to customers resident in Ireland: 1% |

| l) | Exposures to customers resident in Lithuania: 1% |

| m) | Exposures to customers resident in Luxembourg: 0.25% |

| n) | Exposures to customers resident in Slovakia: from 1.5% to 2% (from 1 August) |

| o) | Exposures to customers resident in Sweden: 2.5% |

(5) The highest of the three buffers applies if the SRB buffer covers all exposures. Otherwise, the higher of G-SIB and D-SIB plus the SRB buffer applies.

The geographic distribution of relevant lending exposures for calculating the countercyclical capital buffer is available in Appendix XI on the Santander Group website.

Eligible capital requirements

The decision on capital resulting from the Supervisory Review and Evaluation Process (SREP) under the European Central Bank’s (ECB) Single Supervisory Mechanism comprises a Pillar 2 Requirement (Pillar 2R) and Pillar 2 Guidance (Pillar 2G). Pillar 2R is binding, and failure to comply may have direct consequences for banks. Pillar 2G is not directly binding, and failure to comply has no bearing on the maximum distributable amount (MDA) threshold. Moreover, Pillar 2G does not automatically trigger action by the ECB. However, the ECB does expect compliance with Pillar 2G at all times. If a bank is not compliant with Pillar 2G, the ECB will give careful consideration to the reasons and circumstances and may define additional supervisory control measures.

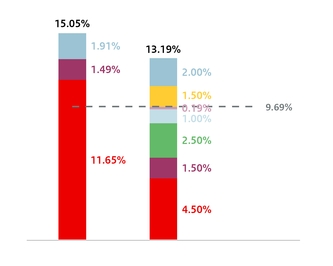

Pursuant to notification received from the ECB, on 10 December 2019, Santander Group must report a Common Equity Tier 1 (CET1) ratio of at least 9.69% at consolidated level during 2020. This requirement includes the Pillar 1 requirement (4.5%); the Pillar 2 requirement (1.5%); the capital conservation buffer (2.5%) and the requirement deriving from its status as a global systemically important institution (1%). In addition, the countercyclical capital buffer requirement of various competent authorities is 0.19% of CET1 in Santander Group. Santander Group must also maintain a minimum capital ratio of 11.19% for T1 and a minimum total ratio of 13.19%.

At 31 December 2019, Banco Santander had a CET1 regulatory capital ratio of 11.65% and a total ratio of 15.05% in application of IFRS 9 transitional arrangements.

| 32 | 2019 Pillar 3 Disclosures Report | ||

| CAPITAL 2019 Pillar 3 Disclosures Report |

As of 31 December 2019, Santander Group meets all the minimum capital requirements under current regulations.

2.1.5.1. Global systemically important institutions

Santander Group is one of 30 entities designated as global systemically important institutions (G-SIIs) in 2019.

The position of a global systemically important institutions may pose a risk to financial stability.

The insolvency of a systemically important institution, or even just the expectation that it might become insolvent, is difficult to predict but could certainly undermine the financial system and even the real economy.

This warrants special prudential treatment, which has led to the introduction of specific capital buffer requirements for both global (G-SIB) and domestic (D-SIB) systemically important banks.

This designation requires Santander Group to meet additional requirements mainly relating to the following:

| • | Its capital buffer (Santander Group is included in the group of banks with the smallest capital buffer, 1%) |

| • | TLAC (total loss-absorbing capacity) requirements |

| • | The requirement to publish relevant information more often than other banks |

| • | Stricter regulatory requirements for internal control bodies |

| • | Special supervision |

| • | Requirement to submit special reports to the supervisors. |

The Basel Committee and the Financial Stability Board jointly decide which banks qualify as global systemically important institutions, using a method based on five indicators: size, cross-jurisdiction activity, interconnectedness with other financial institutions, substitutability of financial services/infrastructure and complexity (with each category given an equal weighting of 20%).

This methodology has been changed and will come into effect from January 2021. The main changes in the methodology are as follows: change in the definition of cross-jurisdiction indicators, inclusion of a trading volume indicator modifying the weighting of the remaining indicators in the substitutability category and inclusion of insurance companies in the reporting scope.

| Indicators for systemically important institutions | ||

| Category | Individual indicator | Supervisor jurisdiction |