FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of July, 2020

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

BANCO SANTANDER, S.A.

________________________

TABLE OF CONTENTS

PART 1. INTERIM CONSOLIDATED DIRECTORS' REPORT

| Interim Consolidated Directors' Report | 2020 | ||||

| First half | |||||

Index

| RESPONSE TO THE COVID-19 CRISIS | |||||

| BUSINESS MODEL | |||||

Key consolidated data

| BALANCE SHEET (EUR million) | Jun-20 | Mar-20 | % | Jun-20 | Jun-19 | % | Dec-19 | |||||||||||||||||||||||||||||||||||||

| Total assets | 1,572,881 | 1,540,359 | 2.1 | 1,572,881 | 1,512,096 | 4.0 | 1,522,695 | |||||||||||||||||||||||||||||||||||||

| Loans and advances to customers | 934,796 | 935,407 | (0.1) | 934,796 | 908,235 | 2.9 | 942,218 | |||||||||||||||||||||||||||||||||||||

| Customer deposits | 846,832 | 815,459 | 3.8 | 846,832 | 814,751 | 3.9 | 824,365 | |||||||||||||||||||||||||||||||||||||

| Total funds | 1,039,996 | 1,006,948 | 3.3 | 1,039,996 | 1,032,769 | 0.7 | 1,050,765 | |||||||||||||||||||||||||||||||||||||

| Total equity | 91,859 | 106,113 | (13.4) | 91,859 | 109,985 | (16.5) | 110,659 | |||||||||||||||||||||||||||||||||||||

| Note: Total funds includes customer deposits, mutual funds, pension funds and managed portfolios | ||||||||||||||||||||||||||||||||||||||||||||

| INCOME STATEMENT (EUR million) | Q2'20 | Q1'20 | % | H1'20 | H1'19 | % | 2019 | |||||||||||||||||||||||||

| Net interest income | 7,715 | 8,487 | (9.1) | 16,202 | 17,636 | (8.1) | 35,283 | |||||||||||||||||||||||||

| Total income | 10,459 | 11,809 | (11.4) | 22,268 | 24,436 | (8.9) | 49,229 | |||||||||||||||||||||||||

| Net operating income | 5,341 | 6,220 | (14.1) | 11,561 | 12,849 | (10.0) | 25,949 | |||||||||||||||||||||||||

| Profit before tax | (8,301) | 1,891 | — | (6,410) | 6,531 | — | 12,543 | |||||||||||||||||||||||||

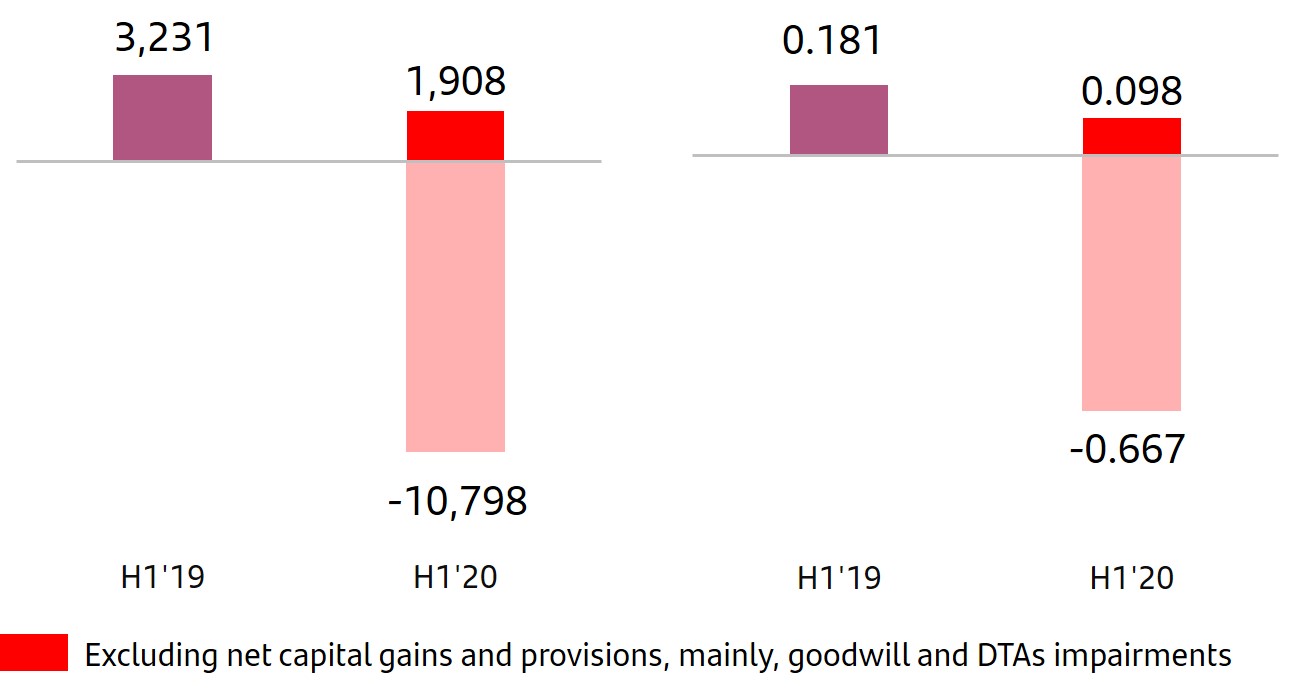

| Attributable profit to the parent | (11,129) | 331 | — | (10,798) | 3,231 | — | 6,515 | |||||||||||||||||||||||||

| Changes in constant euros: | ||||||||||||||||||||||||||||||||

| Q2'20 / Q1'20: NII: -1.9%; Total income: -4.6%; Net operating income: -6.1%; Attributable profit: +/- | ||||||||||||||||||||||||||||||||

| H1'20 / H1'19: NII: -0.2%; Total income: -1.1%; Net operating income: -0.9%; Attributable profit: +/- | ||||||||||||||||||||||||||||||||

| EPS, PROFITABILITY AND EFFICIENCY (%) | Q2'20 | Q1'20 | % | H1'20 | H1'19 | % | 2019 | ||||||||||||||||

| EPS (euros) | (0.679) | 0.012 | — | (0.667) | 0.181 | — | 0.362 | ||||||||||||||||

| RoE | (7.06) | 1.47 | (9.28) | 7.41 | 6.62 | ||||||||||||||||||

| RoTE | 5.19 | 2.04 | 1.73 | 10.51 | 11.44 | ||||||||||||||||||

| RoA | (0.38) | 0.18 | (0.51) | 0.60 | 0.54 | ||||||||||||||||||

| RoRWA | (1.02) | 0.45 | (1.34) | 1.48 | 1.33 | ||||||||||||||||||

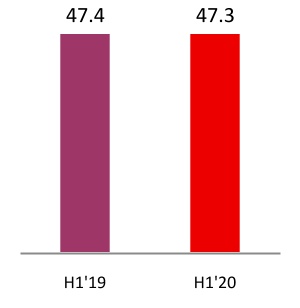

| Efficiency ratio | 47.4 | 47.2 | 47.3 | 47.4 | 47.0 | ||||||||||||||||||

UNDERLYING INCOME STATEMENT (1) (EUR million) | Q2'20 | Q1'20 | % | H1'20 | H1'19 | % | 2019 | |||||||||||||||||||||||||

| Net interest income | 7,715 | 8,487 | (9.1) | 16,202 | 17,636 | (8.1) | 35,283 | |||||||||||||||||||||||||

| Total income | 10,704 | 11,814 | (9.4) | 22,518 | 24,436 | (7.8) | 49,494 | |||||||||||||||||||||||||

| Net operating income | 5,628 | 6,237 | (9.8) | 11,865 | 12,849 | (7.7) | 26,214 | |||||||||||||||||||||||||

| Profit before tax | 1,885 | 1,956 | (3.6) | 3,841 | 7,579 | (49.3) | 14,929 | |||||||||||||||||||||||||

| Attributable profit to the parent | 1,531 | 377 | 306.1 | 1,908 | 4,045 | (52.8) | 8,252 | |||||||||||||||||||||||||

| Changes in constant euros: | ||||||||||||||||||||||||||||||||

| Q2'20 / Q1'20: NII: -1.9%; Total income: -2.5%; Net operating income: -1.6%; Attributable profit: +420.9% | ||||||||||||||||||||||||||||||||

| H1'20 / H1'19: NII: -0.2%; Total income: 0.0%; Net operating income: +1.7%; Attributable profit: -47.5% | ||||||||||||||||||||||||||||||||

UNDERLYING EPS AND PROFITABILITY (1) (%) | Q2'20 | Q1'20 | % | H1'20 | H1'19 | % | 2019 | ||||||||||||||||

| Underlying EPS (euros) | 0.084 | 0.014 | 487.4 | 0.098 | 0.231 | (57.5) | 0.468 | ||||||||||||||||

| Underlying RoE | 6.62 | 1.52 | 3.98 | 8.24 | 8.38 | ||||||||||||||||||

| Underlying RoTE | 8.93 | 2.11 | 5.44 | 11.68 | 11.79 | ||||||||||||||||||

| Underlying RoA | 0.43 | 0.18 | 0.31 | 0.66 | 0.65 | ||||||||||||||||||

| Underlying RoRWA | 1.14 | 0.46 | 0.80 | 1.62 | 1.61 | ||||||||||||||||||

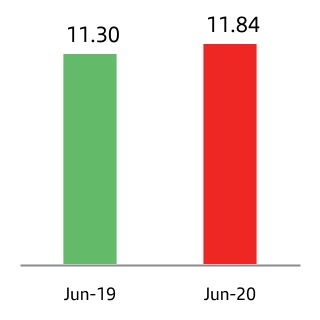

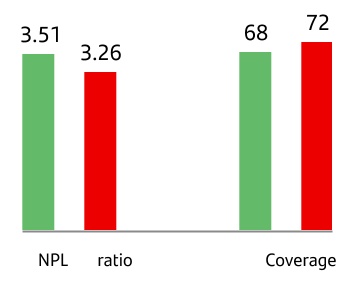

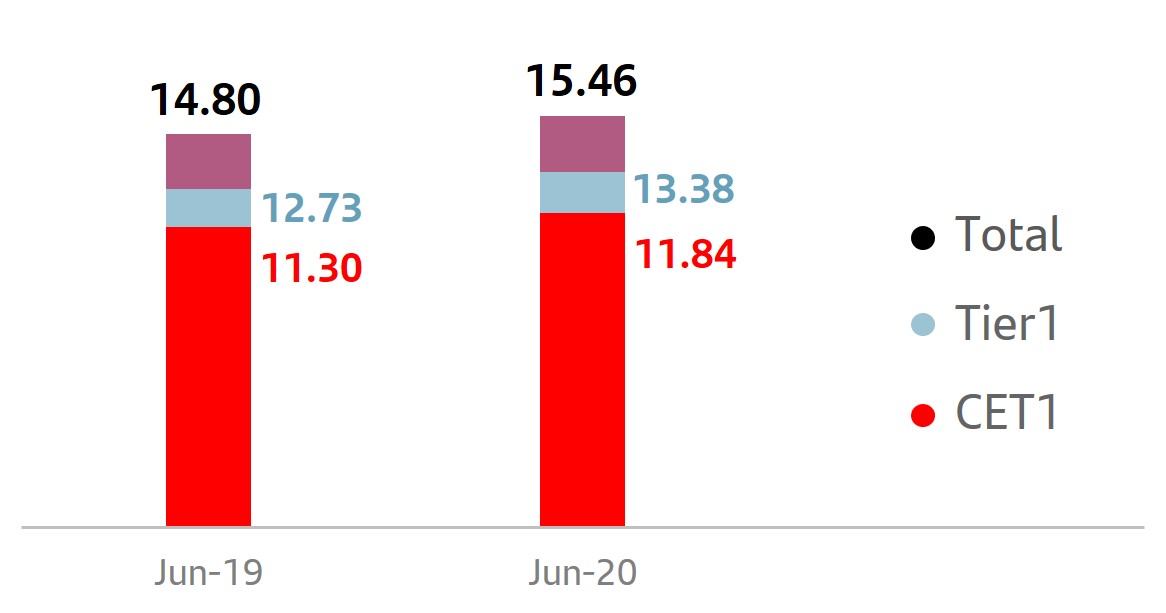

SOLVENCY (2) AND NPL RATIOS (%) | Jun-20 | Mar-20 | Jun-20 | Jun-19 | Dec-19 | ||||||||||||||||||

| CET1 | 11.84 | 11.58 | 11.84 | 11.30 | 11.65 | ||||||||||||||||||

| Fully loaded Total capital ratio | 15.46 | 15.08 | 15.46 | 14.80 | 15.02 | ||||||||||||||||||

| NPL ratio | 3.26 | 3.25 | 3.26 | 3.51 | 3.32 | ||||||||||||||||||

| Coverage ratio | 72 | 71 | 72 | 68 | 68 | ||||||||||||||||||

| MARKET CAPITALISATION AND SHARES | Jun-20 | Mar-20 | % | Jun-20 | Jun-19 | % | Dec-19 | ||||||||||||||||

| Shares (millions) | 16,618 | 16,618 | 0.0 | 16,618 | 16,237 | 2.3 | 16,618 | ||||||||||||||||

| Share price (euros) | 2.175 | 2.218 | (2.0) | 2.175 | 4.081 | (46.7) | 3.730 | ||||||||||||||||

| Market capitalisation (EUR million) | 36,136 | 36,859 | (2.0) | 36,136 | 66,253 | (45.5) | 61,986 | ||||||||||||||||

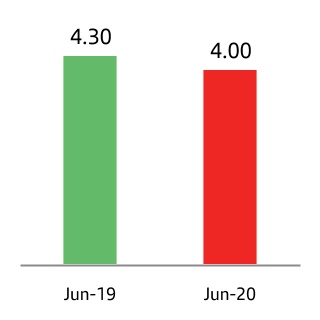

| Tangible book value per share (euros) | 4.00 | 4.21 | 4.00 | 4.30 | 4.36 | ||||||||||||||||||

| Price / Tangible book value per share (X) | 0.54 | 0.53 | 0.54 | 0.95 | 0.86 | ||||||||||||||||||

| OTHER DATA | Jun-20 | Mar-20 | % | Jun-20 | Jun-19 | % | Dec-19 | ||||||||||||||||

| Number of shareholders | 4,080,201 | 4,043,974 | 0.9 | 4,080,201 | 4,054,208 | 0.6 | 3,986,093 | ||||||||||||||||

| Number of employees | 194,284 | 194,948 | (0.3) | 194,284 | 201,804 | (3.7) | 196,419 | ||||||||||||||||

| Number of branches | 11,847 | 11,902 | (0.5) | 11,847 | 13,081 | (9.4) | 11,952 | ||||||||||||||||

| (1) In addition to financial information prepared in accordance with International Financial Reporting Standards (IFRS) and derived from our consolidated financial statements, this report contains certain financial measures that constitute alternative performance measures (APMs) as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority (ESMA) on 5 October 2015 and other non-IFRS measures, including the figures related to “underlying” results, as they are recorded in the separate line of “net capital gains and provisions”, above the line of attributable profit to the parent. Further details are provided on page 14 of this report. For further details of the APMs and non-IFRS measures used, including its definition or a reconciliation between any applicable management indicators and the financial data presented in the consolidated financial statements prepared under IFRS, please see 2019 Annual Financial Report, published in the CNMV on 28 February 2020, our 20-F report for the year ending 31 December 2019 registered with the SEC in the United States as well as the “Alternative performance measures” section of the annex to this report. | ||

| (2) Data applying the IFRS 9 transitional arrangements. | ||

January - June 2020 |  | 3 | ||||||

Response to the COVID-19 crisis | ||||||||||||||||||||||||||

| Response to COVID-19 crisis | ||||||||||||||||||||||||||

In order to support the global effort being made to combat COVID-19, Grupo Santander is implementing various measures to protect our stakeholders. The most relevant measures are detailed below, focused on six main dimensions:

| Contingency plan |  | Health of our employees | ||||||||||||||||||||

Preserving our business and critical functions in stress conditions is essential to providing our services to customers to our usual high standards. Consequently, the Group has the necessary contingency plans, which incorporate simulations of stress scenarios, that have enabled us to face the current situation with suitable preparation and knowledge. In February, in line with our Special Situations Management Framework, the highest level Corporate Special Situation Committees were activated to ensure an early and coordinated response in all geographic areas, where Local Committees were also activated according to the spread of the pandemic and local government responses. The contingency plans were implemented through these committees including the participation of local senior management (Country Heads, Local Special Situations Management Directors, Local Directors, etc.). Our Contingency Plans ensured the operational continuity of business in all geographic areas, identifying their critical businesses and, among other measures, segregating teams and technological infrastructures, establishing shifts between critical employees and their back-ups, as well as increasing the capacity of systems and lines, carried out by the Technology and Operations area. Consequently, none of our units' operational continuity was compromised, nor did they record any relevant incidents. At the same time, we continued to serve our customers with the utmost attention. | Our priority was to safeguard the health and safety of our employees. During the different phases of the confinement, both tightening and relaxing of measures, in which some countries still find themselves: •We have provided all our employees special safety and protection measures: –We redefined our way of working to adapt to remote working, reaching more than 110,000 employees working from home. –We ensured the physical and mental well-being of the employees who continued to work in our offices, or face to face with customers. These measures included providing masks, gloves and protective screens, as well as the reorganisation of physical space to ensure the recommended social distance, combined with strict personal hygiene measures. –Financial well-being was also covered, offering various financial support measures to help employees who are experiencing financial difficulties, such as flexible loans or salary advances. •On the other hand, our training and development programmes were adapted to a new online format. In particular, those related to project management, leadership and remote working efficiency attracted great interest. •Lastly, we started to gradually return to the usual workplaces in some countries at the end of May, always following the recommendations of local governments, respecting the individual needs of each employee and based on three pillars: development and implementation of health and safety protocols, prioritisation and monitoring the health status of our employees, and tracking and tracing (through health apps). | ||||||||||||||||||||||

|  | ||||||||||||||||||||||

| 4 | | January - June 2020 | ||||||

Response to the COVID-19 crisis | ||||||||||||||||||||||||||

| Response to COVID-19 crisis | ||||||||||||||||||||||||||

| Customers |  | Business, liquidity and risks | ||||||||||||||||||||

Santander has implemented measures to ensure the health and safety of its customers and foster their economic resilience during the crisis in all countries. Of note were: •Provide liquidity and credit facilities for businesses facing hardship. •Facilitate payment deferrals and payment holidays in many of our markets. •Temporary option to increase credit card and overdraft limits. •Proactive support for vulnerable customers trying to cover their needs. •Temporary reduction and suspension of fees (withdrawals from ATMs, interest free online purchases, bank transfers, etc.). •Ensure COVID-19 health insurance coverage. •Specialised teams to advise customers facing financial difficulties. We are continuously adapting the branch network, ensuring the continuity of service in the branch network. Currently, around 90% of our branches are open. On the other hand, we strengthened our contact centres' capabilities, which has enabled us to increase the volume of services by 16% on average compared to normal times. The Group is actively supporting our customers through various relief programmes, especially those that are more vulnerable, monitoring their performance and payment capacity as well as ensuring that business continuity plans remain effective so that we can keep serving our clients under the highest quality standards. The Bank is reassessing the situation as the pandemic evolves in each market, and taking action according to the specific needs of every country. | In the second quarter, business performance continued its growth trajectory recorded in the previous quarter. Group loans and advances to customers excluding the exchange rate impact increased 6% and customer funds 7% year-on-year. During the second quarter, the recovery of pre-COVID-19 new business levels in the individuasl segment (mortgages and consumer finance) began, mainly in Europe and the US. On the other hand, activity in large corporates stood at more normal levels, following the sharp increase recorded in March, and SMEs and corporates reflected the state-guaranteed programmes. Since the beginning of the crisis, liquidity has been closely monitored in the parent bank and our subsidiaries, and preventive management measures were carried out to strengthen its position. Our liquidity position has remained solid at all times. The Group's LCR ratio was 175%, the parent bank's was 193% and all our subsidiaries stood above 130%, at the end of the first half. In addition, central banks have adopted measures to provide significant liquidity to the system. Regarding risks, the main indicators are also continuously monitored, and maintain a robust credit quality supported by mitigation measures and volume increases. In the first half of the year, we recorded provisions amounting to EUR 7,027 million, 63% more than in the same period of 2019 (+78% excluding the exchange rate impact). In addition, due to the deterioration of the economic outlook, the Bank has adjusted the valuation of its goodwill ascribed to several subsidiaries and deferred tax assets for EUR 12.6 billion. This adjustment has no impact on the Bank's liquidity or market and credit risk position, and is neutral in CET1 capital. | ||||||||||||||||||||||

|  | ||||||||||||||||||||||

January - June 2020 | | 5 | ||||||

Response to the COVID-19 crisis | ||||||||||||||||||||||||||

| Response to COVID-19 crisis | ||||||||||||||||||||||||||

| Society |  | Information for stakeholders | ||||||||||||||||||||

One of our main priorities is to contribute to the well-being of society as a whole. We have implemented actions and mobilised resources together with governments and institutions to help society combat the health crisis. Santander All. Together. Now. is the motto that brings together the Group's collective efforts around the world to stand beside the people who need it the most at this time. This effort has succeeded in mobilising more than EUR 100 million dedicated to solidarity initiatives to fight COVID-19. The main initiatives adopted are: •Creation of a solidarity fund to acquire medical equipment and materials, and to support organisations in the fight against COVID-19. This fund is primarily financed by contributions from senior management, employees and the Group's subsidiaries, as well as contributions from third parties. As a starting point, the Executive Chairman and the CEO, have renounced 50% of their total compensation in 2020 and non-executive directors 20% of their total remuneration. The Group has created employee funds in most of the countries where it operates. •Supporting different projects and social initiatives to protect the vulnerable groups most impacted by the effects of the pandemic. •Santander Universidades reallocated funds to support collaboration projects with universities to face the health and educational challenges arising from the COVID-19 crisis, scholarships to foster online education during the confinement period and support the most disadvantaged students. The Bank also launched Santander X Tomorrow Challenge, with the aim of supporting creativity and and entrepreneurs' capacity to contribute the best solutions to the major post-COVID-19 challenges. •Launch of Overcome Together, an open and accessible space for individuals and companies, both customers and non-customers, which contains information and resources to help overcome the situation arising from COVID-19. It is available in Spain, Portugal, Mexico, Brazil, Uruguay, Chile, Poland, Argentina, the UK and Openbank. •Santander, together with another financial entity, developed and provided the Mexican Government the free use of a digital platform that will help the population to generate a COVID-19 self-diagnosis (personal and for a family), where relevant information about the pandemic is available. We will continue to monitor the situation in order to continue to contribute to minimise the impact of COVID-19 on society. | Based on transparency and anticipation, the Group continued to be proactive in keeping our people, customers, shareholders and investors informed at all times. We followed various initiatives during the different phases of the pandemic: •To stay close to all our employees, we sent out newsletters in most of our markets including updates on the health crisis. We reported on measures, policies and recommendations related to prevention and protection. Advice was also given on how to reconcile work and family life, as well as different proposals for leisure and health-related activities. •We continued to issue communications to customers encouraging the use of digital channels, cybersecurity tips, new branch opening hours and functionality and all information regarding the public and the Bank's own support measures. •In order to protect the health of our shareholders, Santander held its first ever general shareholder's meeting via remote channels from Ciudad Grupo Santander. Clear, regular communication is very important for us as a Group. The Bank's senior management (Group executive chairman, Group CEO, Heads of Division and Country Heads) have been in regular contact with all teams. Of note were the five Ask Ana events held to report on the Group's situation and answer questions from employees. The main measures announced by each country can be found on the Group's website (www.santander.com). Santander’s outstanding COVID-19 response and support to SMEs was recognised by Euromoney: •Euromoney has praised Santander's response to the COVID-19 crisis in Europe (Western and Central and Eastern Europe) with an “Excellence in Leadership” award. The magazine commended Santander for the way it managed the health and economic crisis for its employees, clients, business and the society in general. •Euromoney also recognised the valuable support that Santander is providing to SMEs during the crisis and more generally with the Best Bank for SMEs in Western Europe and Latin America awards. Furthermore, the magazine’s editors acknowledged Santander as Best Bank in Spain and Portugal, and Best Investment Bank in Portugal. | ||||||||||||||||||||||

|  | ||||||||||||||||||||||

| 6 | | January - June 2020 | ||||||

Business model | Group financial information | Financial information by segments | Responsible banking Corporate governance Santander share | Appendix | ||||||||||||||||||||||

| Business model | ||||||||||||||||||||||||||

Our business model is based on three pillars

1. Our scale Local scale and global reach | 2. Customer focus Unique personal banking relationships strengthen customer loyalty | 3. Diversification Our geographic and business diversification makes us more resilient under adverse circumstances | ||||||||||||||||||

•Local scale based on three geographic regions, where we maintain a leadership position in our 10 core markets. •Global reach backed by our global businesses, enabling greater collaboration across the Group to generate higher revenue and efficiencies. | •We serve 146 million customers, in markets with a total population of more than one billion people. •We have over 100,000 people talking to our customers every day in our c.12,000 branches and contact centres. | •Geographic diversification in three regions, with a good balance between mature and developing markets. •Global businesses that strengthen our local franchises. •Santander Global Platform supports the digital transformation across the Group. | ||||||||||||||||||

|  |  | ||||||||||||||||||

| 1. Market share in lending as of March 2020 including only privately-owned banks. UK benchmark refers to the mortgage market. | 2. NPS – Customer Satisfaction internal benchmark of active customers’ experience and satisfaction audited by Stiga / Deloitte. | Note. Underlying attributable profit contribution by region, excluding Santander Global Platform and Corporate Centre. | ||||||||||||||||||

Our corporate culture: Santander Way

The Santander Way reflects our purpose, our aim, and how we do business. It is the bedrock on which we are building a more responsible bank.

January - June 2020 | | 7 | ||||||

GROWTH

GROWTHIn the quarter, the Group continued to provide significant financial support to customers to help them overcome the consequences of the pandemic

We are starting to see signs of normalisation in lending trends with mortgage and consumer lending recovering in June. The SME and corporate segments, backed by government-guaranteed programmes, and CIB decreased from the peak in April.

On a year-on-year basis, strong negative exchange rate impact (-5/-6 pp). In constant euros, gross loans and advances to customers (excluding reverse repos) grew 6% and customer funds (excluding repos) rose 7%, both with the 10 core markets growing, except customer funds in Spain.

| Activity Jun-20 / Jun-19 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| % change in constant euros | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individuals | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +11% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +11% | Demand | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SMEs and corporates | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +6% | +1% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +7% | Time | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| +14% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CIB and institutions | -1% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mutual funds | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gross loans and advances to customers excl. reverse repos | Customer deposits excl. repos + mutual funds | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

In the current environment, digital penetration is accelerating. We reached almost 40 million digital customers (+15% year-on-year), mobile customers exceeded 32 million (+5.8 million in 12 months) and digital sales represented 47% of total sales in the quarter (36% in 2019).

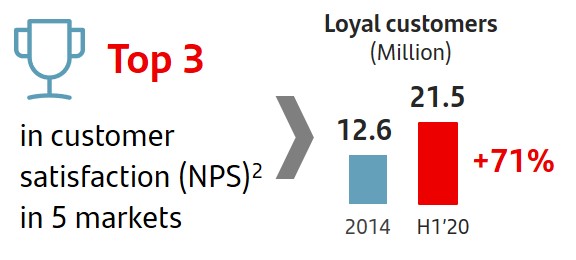

Loyal customers rose nearly 1 million year-on-year, with growth both in individuals and corporates.

| Digital customers | Digital sales | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Million | % of total sales | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 39.9 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 47 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 34.8 | +15% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 36 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Jun-19 | Jun-20 | 2019 | Q2'20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

PROFITABILITY

PROFITABILITYDespite these difficult circumstances, our operating performance has been strong...

In the first half of the year, results were affected by the deterioration of the economic environment derived from the health crisis and the sharp exchange rate depreciation that distort the year-on-year comparison.

Excluding the exchange rate impact, the underlying performance of the business was strong, supported by resilient customer revenue, cost reductions and robust credit quality.

Net interest income and customer revenue remained stable year-on-year, as the fall in activity and lower interest rates were offset by higher volumes, good market volatility management and the reduction in the cost of deposits.

On the other hand, cost reductions were ahead of plan, as costs fell 5% in real terms and excluding the FX impact, due to the optimisation plans carried out in recent years, together with the additional savings measures adopted from the beginning of the crisis.

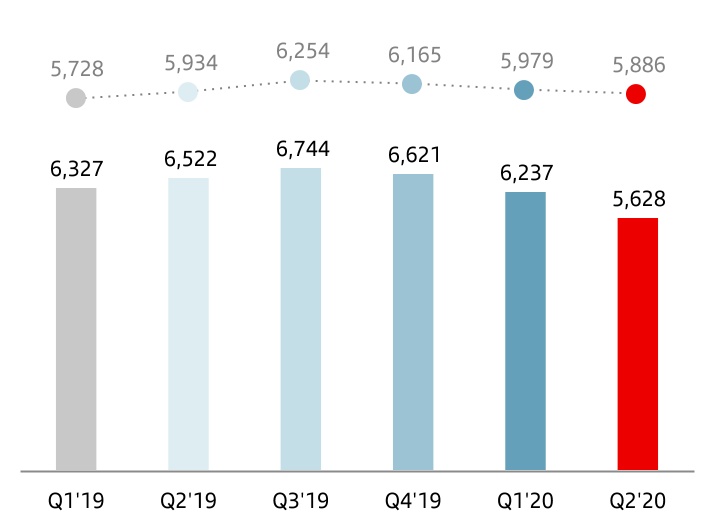

As a result, net operating income increased 2% to EUR 11,865 million, primarily driven by the positive performance in Latin America, Santander Corporate & Investment Banking and Wealth Management & Insurance.

The efficiency ratio stood at around 47%, one of the best among our peers.

| Efficiency ratio | ||

| % | ||

| 8 | | January - June 2020 | ||||||

PROFITABILITY… and profit affected by higher loan-loss provisions and valuation adjustments

Loan-loss provisions rose significantly to EUR 7,027 million, driven by lending growth and the expected macro-economic deterioration.

In addition, as a result of the economic outlook, lower for longer interest rates and the increase of discount rates, the Bank has adjusted the valuation of its goodwill ascribed to several units and deferred tax assets for a total of EUR 12.6 billion.

This adjustment has no impact on the Bank's liquidity or market and credit risk position, is neutral in CET1 capital and do not change the strategic importance of any of the Group's markets. The Group remains confident in the potential for the long-term value creation in each of its regions and markets.

This results in an attributable loss of EUR 10,798 million.

| Attr. profit to the parent | Earnings per share | |||||||||||||

| EUR million | EUR | |||||||||||||

| ||||||||||||||

Before these adjustments and restructuring costs, underlying attributable profit was EUR 1,908 million, 53% lower year-on-year (-48% excluding the exchange rate impact).

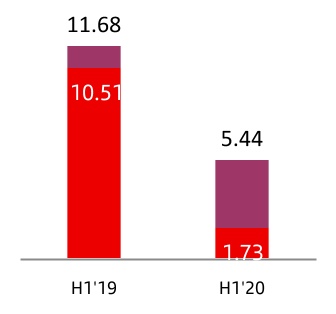

Underlying RoTE was 5.4% and underlying RoRWA 0.80%.

| RoTE | |||||||||||||||||

| % | |||||||||||||||||

n Total n Underlying* | |||||||||||||||||

(*) Excluding net capital gains and provisions

STRENGTH

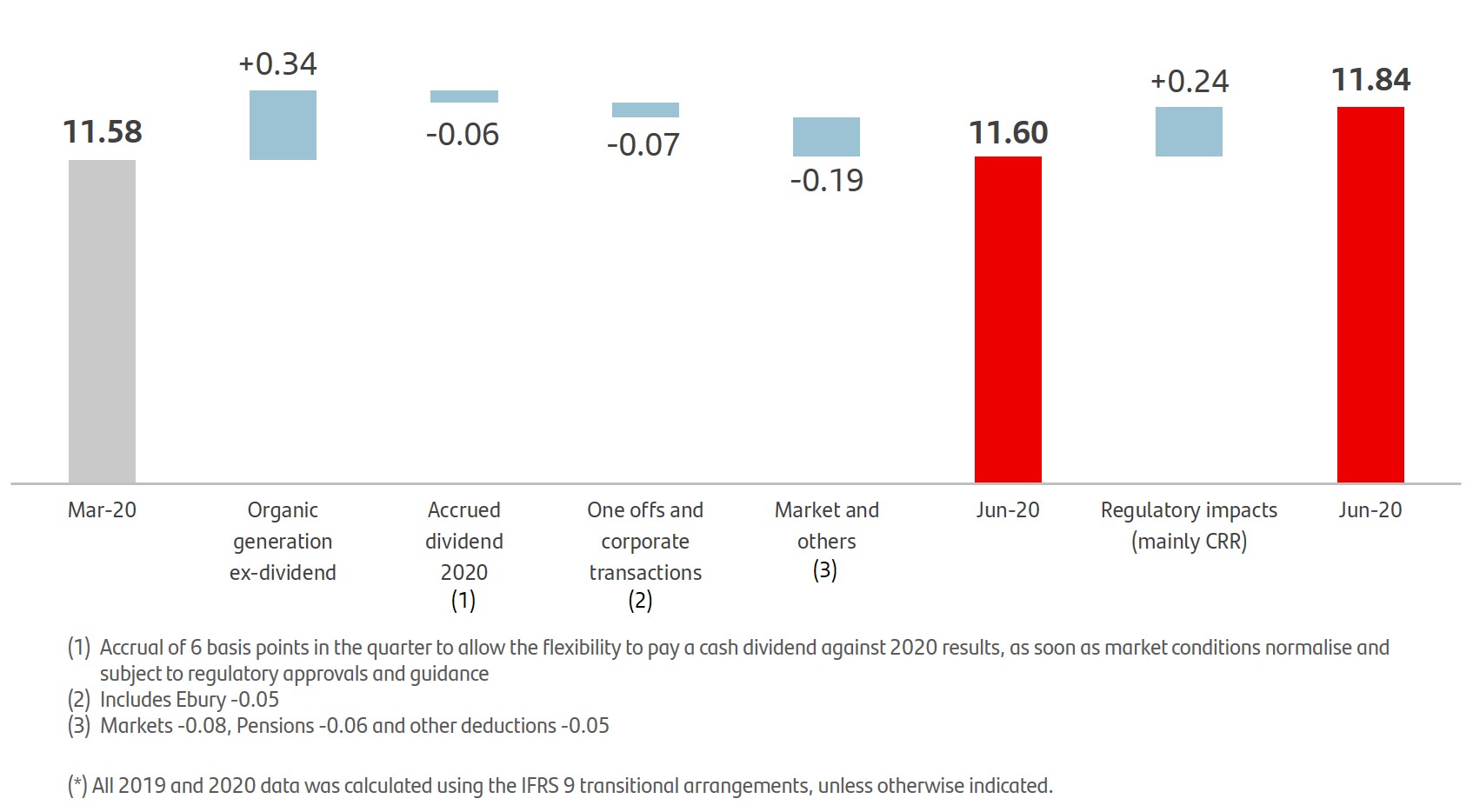

STRENGTHCET1 ratio at the top end of our target range and cost of credit in line with our 140-150 bps year-end expectation

The CET1 ratio increased 26 bps in the quarter to 11.84%, driven by the net impact from the strong organic generation, a positive regulatory impact (mainly CRR2 quick fix) and a negative impact primarily from corporate operations pensions and markets. This results in a Group CET1 management buffer of 298 bps post- COVID-19 compared to 189 bps pre-COVID-19.

Net tangible equity per share (TNAV) in June 2020 was EUR 4.00 and declined 5% since March, due to the net effect from the adjustment of deferred tax assets, exchange rates and markets, partially offset by the organic generation in the quarter.

| CET1* | TNAV per share | |||||||

| % | Euros | |||||||

(*) Using the IFRS 9 transitional arrangement

Risk management remained focused on minimising the impacts arising from the health crisis.

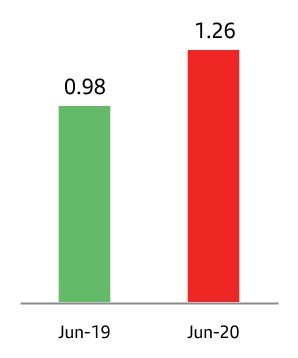

The cost of credit in the first half was in line with out year-en expectation of 140-150 bps and credit quality benefited from mitigation measures and volume increases, reflected in the 25 bp fall year-on-year (+1 bp in the quarter) of the NPL ratio and higher coverage (72%, +4 pp year-on-year).

| Cost of credit | NPL ratio and coverage | ||||||||||||||||||||||

| % | % | ||||||||||||||||||||||

n Jun-19 n Jun-20 | |||||||||||||||||||||||

January - June 2020 | | 9 | ||||||

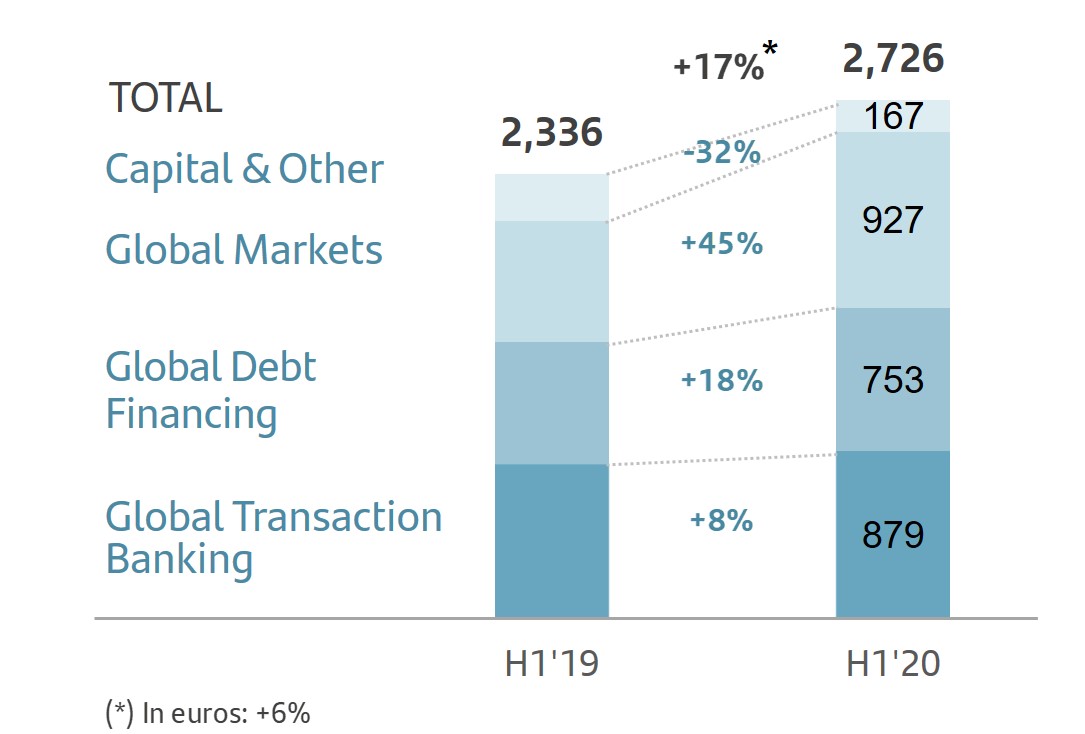

GRUPO SANTANDER RESULTS

•The Group's results were affected by the health crisis caused by the spread of COVID-19, which is reflected in a weaker economic environment, lower for longer interest rates and a sharp depreciation of some currencies.

•Total income fell, affected by exchange rates. Excluding their impact, it remained stable as the decrease in activity and lower interest rates were offset by higher volumes, sound management of market volatility and the lower cost of deposits.

•Acceleration in cost reductions, ahead of schedule in the optimisation plans implemented in recent years, along with additional measures adopted since the start of the crisis.

•Greater loan-loss provisions, amounting to EUR 7,027 million due to credit growth, the expected deterioration in economic conditions due to the pandemic and its impact on the deterioration of the portfolio’s credit quality.

•In addition, as a result of the worsening economic outlook, adjustments to the goodwill ascribed to some units and to deferred tax assets have been made totalling EUR 12,600 million, which results in an attributable profit to the Group of negative EUR 10,798 million.

•Excluding the above adjustments and restructuring costs, attributable profit to the parent would have been EUR 1,908 million, with net operating income of EUR 11,865 million, 2% more in constant euros than at the end of the first half of 2019.

| Grupo Santander. Summarised income statement | ||||||||||||||||||||||||||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Change | Change | |||||||||||||||||||||||||||||||||||||||||||||||||

| Q2'20 | Q1'20 | % | % excl. FX | H1'20 | H1'19 | % | % excl. FX | |||||||||||||||||||||||||||||||||||||||||||

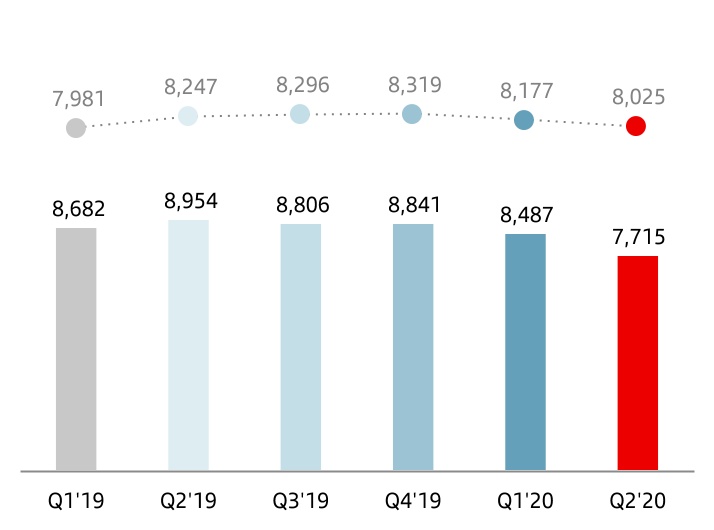

| Net interest income | 7,715 | 8,487 | (9.1) | (1.9) | 16,202 | 17,636 | (8.1) | (0.2) | ||||||||||||||||||||||||||||||||||||||||||

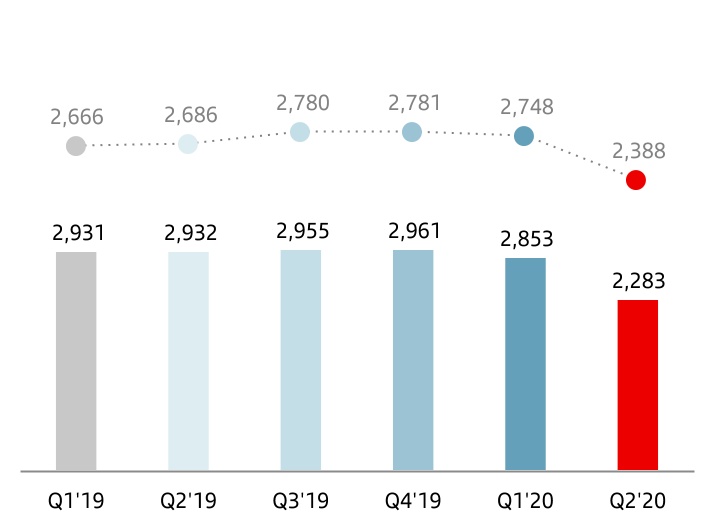

| Net fee income (commission income minus commission expense) | 2,283 | 2,853 | (20.0) | (13.1) | 5,136 | 5,863 | (12.4) | (4.0) | ||||||||||||||||||||||||||||||||||||||||||

| Gains or losses on financial assets and liabilities and exchange differences (net) | 786 | 287 | 173.9 | 174.8 | 1,073 | 511 | 110.0 | 137.6 | ||||||||||||||||||||||||||||||||||||||||||

| Dividend income | 208 | 57 | 264.9 | 265.4 | 265 | 361 | (26.6) | (26.1) | ||||||||||||||||||||||||||||||||||||||||||

| Share of results of entities accounted for using the equity method | (233) | 98 | — | — | (135) | 306 | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Other operating income / expenses | (300) | 27 | — | — | (273) | (241) | 13.3 | 72.7 | ||||||||||||||||||||||||||||||||||||||||||

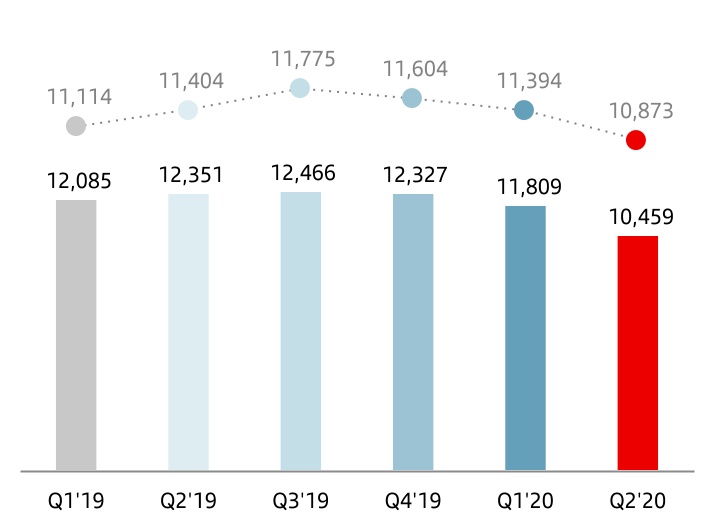

| Total income | 10,459 | 11,809 | (11.4) | (4.6) | 22,268 | 24,436 | (8.9) | (1.1) | ||||||||||||||||||||||||||||||||||||||||||

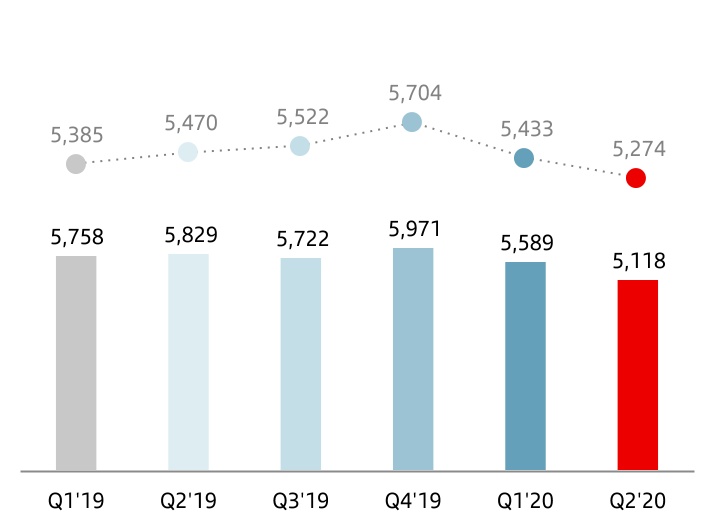

| Operating expenses | (5,118) | (5,589) | (8.4) | (2.9) | (10,707) | (11,587) | (7.6) | (1.4) | ||||||||||||||||||||||||||||||||||||||||||

| Administrative expenses | (4,428) | (4,860) | (8.9) | (3.4) | (9,288) | (10,110) | (8.1) | (1.9) | ||||||||||||||||||||||||||||||||||||||||||

| Staff costs | (2,571) | (2,899) | (11.3) | (6.5) | (5,470) | (6,080) | (10.0) | (4.7) | ||||||||||||||||||||||||||||||||||||||||||

| Other general administrative expenses | (1,857) | (1,961) | (5.3) | 1.2 | (3,818) | (4,030) | (5.3) | 2.3 | ||||||||||||||||||||||||||||||||||||||||||

| Depreciation and amortisation | (690) | (729) | (5.3) | 0.4 | (1,419) | (1,477) | (3.9) | 2.6 | ||||||||||||||||||||||||||||||||||||||||||

| Provisions or reversal of provisions | (240) | (374) | (35.8) | (31.0) | (614) | (1,916) | (68.0) | (67.5) | ||||||||||||||||||||||||||||||||||||||||||

| Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net) | (3,096) | (3,934) | (21.3) | (15.4) | (7,030) | (4,368) | 60.9 | 76.3 | ||||||||||||||||||||||||||||||||||||||||||

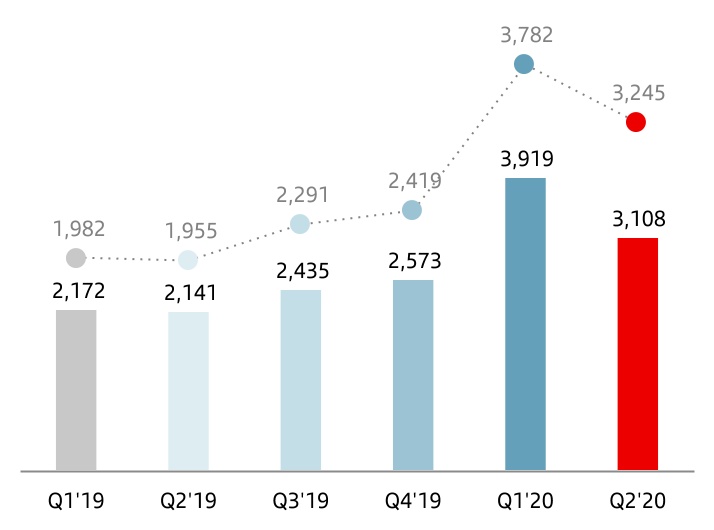

| o/w: net loan-loss provisions | (3,108) | (3,919) | (20.7) | (14.4) | (7,027) | (4,313) | 62.9 | 78.5 | ||||||||||||||||||||||||||||||||||||||||||

| Impairment on other assets (net) | (10,227) | (14) | — | — | (10,241) | (27) | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Gains or losses on non financial assets and investments, net | 9 | 18 | (50.0) | (50.0) | 27 | 250 | (89.2) | (89.2) | ||||||||||||||||||||||||||||||||||||||||||

| Negative goodwill recognised in results | 6 | — | — | — | 6 | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Gains or losses on non-current assets held for sale not classified as discontinued operations | (94) | (25) | 276.0 | 276.0 | (119) | (257) | (53.7) | (53.1) | ||||||||||||||||||||||||||||||||||||||||||

| Profit or loss before tax from continuing operations | (8,301) | 1,891 | — | — | (6,410) | 6,531 | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Tax expense or income from continuing operations | (2,684) | (1,244) | 115.8 | 126.4 | (3,928) | (2,449) | 60.4 | 82.7 | ||||||||||||||||||||||||||||||||||||||||||

| Profit from the period from continuing operations | (10,985) | 647 | — | — | (10,338) | 4,082 | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Profit or loss after tax from discontinued operations | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Profit for the period | (10,985) | 647 | — | — | (10,338) | 4,082 | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Attributable profit to non-controlling interests | (144) | (316) | (54.4) | (51.4) | (460) | (851) | (45.9) | (41.4) | ||||||||||||||||||||||||||||||||||||||||||

| Attributable profit to the parent | (11,129) | 331 | — | — | (10,798) | 3,231 | — | — | ||||||||||||||||||||||||||||||||||||||||||

| EPS (euros) | (0.679) | 0.012 | — | (0.667) | 0.181 | — | ||||||||||||||||||||||||||||||||||||||||||||

| Diluted EPS (euros) | (0.677) | 0.011 | — | (0.666) | 0.180 | — | ||||||||||||||||||||||||||||||||||||||||||||

| Memorandum items: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Average total assets | 1,558,854 | 1,536,725 | 1.4 | 1,548,851 | 1,492,954 | 3.7 | ||||||||||||||||||||||||||||||||||||||||||||

| Average stockholders' equity | 92,528 | 99,221 | (6.7) | 95,803 | 98,191 | (2.4) | ||||||||||||||||||||||||||||||||||||||||||||

| 10 | | January - June 2020 | ||||||

è Evolution of results compared to the first half of 2019

The main lines of the profit and loss account are detailed below.

The Group presents, both at the total level and for each of the business units, the real changes in euros produced in the income statement, as well as variations excluding the exchange rate effect (FX), on the understanding that the latter provide a better analysis of the Group’s management. For the Group as a whole, the exchange rate impact was -8 percentage points in revenue and -6 percentage points in costs.

u Revenue

Revenue totalled EUR 22,268 million in the first half, down 9%. If the FX impact is taken out, total income remained resilient, in line with last year, due to customer relationships and the strength that our geographical and business diversification provides. Net interest income and net fee income accounted for over 95% of total revenue. By line:

•Net interest income amounted to EUR 16,202 million, 8% less than in the same period of 2019. Stripping out the exchange rate impact, it remained stable (-0.2%), the net effect of the increase in revenue from higher lending and deposit volumes and the reduction in revenue from lower interest rates in many markets, regulatory impacts (mainly in Brazil and Poland) and increased liquidity buffer costs.

| Net interest income | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

Net interest income was very heterogeneous among units. On the one hand, there were increases in SCF, Mexico and Brazil, due to higher volumes, Chile, due to higher inflation, and Argentina, due to the placement of excess liquidity. There were decreases in Portugal and Spain due to lower interest rates, on top of the lower average volumes and smaller ALCO portfolio in Spain, the UK, impacted by the base rate cut and SVR attrition, Poland, due to a one-off provision for the CJEU judgement on consumer loans, and the United States, driven by lower interest rates which cancelled out growth in average volumes.

•Net fee income fell 12% to EUR 5,136 million. Excluding the exchange rate impact, it was down 4% compared to the first six months of 2019. This item has been the most affected by the health crisis, reflecting lower client transactionality. Our strategy remains focused on increasing our customer loyalty and growth in higher value-added services and products.

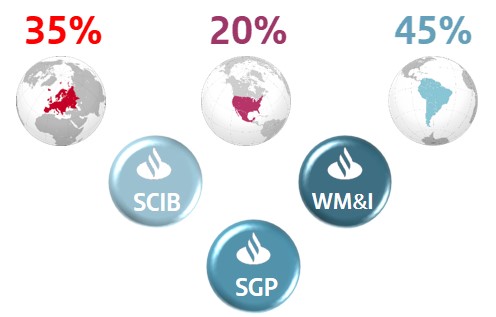

By business, of note was the 20% growth in Santander Corporate & Investment Banking and the 1% increase in Wealth Management & Insurance ( the latter including fees ceded to the branch network). Overall, together the businesses now account for 47% of the Group’s total (SCIB: 16%; WM&I 31%).

By region, there were declines in North and South America (-2% in both cases) and, especially in Europe (-8%), with generalised declines due to lower activity volumes, along with regulatory changes affecting net fee income in Santander Consumer Finance and the UK. On the other hand, "Other Europe", which includes the wholesale banking business in the region, increased net fee income by 58%.

| Net fee income | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

January - June 2020 | | 11 | ||||||

•Gains on financial transactions, accounted for 5% of total income and stood at EUR 1,073 million, double the figure for the first half of 2019 (+138% excluding the exchange rate effect) due to the favourable impact from foreign currency hedging, portfolio sales and market volatility.

•Dividend income was EUR 265 million in the first six months of 2020, 27% lower than in the same period of 2019 (-26% excluding exchange rate effect). This item was affected by the delay or cancellation of dividend payments by several companies.

•The results of entities accounted for using the equity method reflect the lower contribution from the entities associated to the Group.

•Other operating income recorded a loss of EUR 273 million (loss of EUR 241 million in the first half of 2019) due to the greater contribution to the Single Resolution Fund (SRF).

u Costs

Operating costs amounted to EUR 10,707 million, 8% lower year-on-year. Excluding the exchange rate impact, costs fell 2%.

In real terms (excluding inflation) costs were down 5%, reflecting the successful management over the last three years, as well as the first impacts of additional savings measures adopted since the beginning of the crisis.

The efficiency ratio was 47.3%, in line with last year, which has enabled Santander to remain one of the most efficient global banks in the world.

| Total income | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

The Group's objective is still to improve our operational capacity while also managing our costs more efficiently and adapted to each region. Therefore, for a better comparison, the trends by region and market are detailed below:

•In Europe, costs strongly reflect the synergies from the recent integrations and additional savings, decreasing 5.9% in nominal terms and 6.8% in real terms, with falls across all markets. There were reductions in Poland (-10.9%), Spain (-10.1%) and Portugal (-5.2%) due to the optimisation efforts, in the UK (-6.3%) due to the savings from our transformation programme, and in Santander Consumer Finance (-4.5%) driven by efficiency projects carried out in several countries and absorbing the perimeter effect.

The cost reduction plan in Europe is ahead of schedule, having already reached 75% of the total expected for the year as a whole.

•In North America, costs fell 0.8% in nominal terms, affected by inflation, as in real terms they were down 2.9% (US -3.8%, Mexico -0.8%). The efficiency ratio in the region declined to 41.5%.

•Finally, in South America, the increase in costs was greatly distorted by the very high inflation in Argentina. Excluding it, costs rose 2.4% in nominal terms but decreased 0.9% in real terms (Brazil: -1.4% and Chile: -0.4%). Efficiency improved in all markets (35.2% for the region as a whole, improving by 1.1 percentage points).

We believe that this management by region and the lessons learnt from the management of the pandemic will enable us to accelerate our transformation in the future and, consequently, further optimise costs while improving customer experience.

| Operating expenses | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

| 12 | | January - June 2020 | ||||||

u Provisions or reversal of provisions

Provisions (net of provisions reversals) amounted to EUR 614 million (EUR 1,916 million in the first half of 2019). This line item includes charges for restructuring costs.

u Impairment or reversal of impairment of financial assets not measured at fair value through profit or loss (net)

Impairment or reversal of impairment on financial assets not measured at fair value through profit or loss (net) was EUR 7,030 million, up 61% year-on-year in euros and 76% in constant euros.

Loan-loss provisions included in this item amounted to EUR 7,027 million, 63% more than in the same period last year. Stripping out the effect of exchange rates, the increase was 78%, heavily impacted by the effects of the COVID-19 and growth in credit volumes. This includes the provisions overlay of EUR 1,600 million which was recorded in the first quarter and which was been allocated by business unit.

Accordingly, the Group’s cost of credit, calculated as the ratio of loan-loss provisions over the last twelve months to the average investment in the period, increased to 1.26% (1.46% considering the annualised year-to-date provisions).

u Impairment on other assets (net)

Every year, usually during the last quarter, the Group evaluates whether an adjustment to the goodwill generated in the acquisition of the subsidiaries is necessary. The accounting rules require this analysis to be carried out earlier should any trigger events occur, which happened in the second quarter of this year, given that the global economic environment has been significantly affected by the COVID-19 crisis.

| Net loan-loss provisions | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

Specifically, the trigger events for this exercise were as follows:

•Changes in the economic environment where a decrease of the GDP is expected in all countries this year and where recovery will take 2 or 3 years.

•A generalised reduction in interest rates, which is expected to last longer than expected before the crisis began.

•The increase of discount rates to reflect greater volatility and risk premiums.

This analysis has resulted in an adjustment in the valuation of goodwill of EUR 10,100 million (Santander UK: EUR 6,101 million; Santander US: EUR 2,330 million; Santander Bank Polska: EUR 1,192 million; Santander Consumer Nordics: 277 million and Other: 200 million). This adjustment does not affect cash generation and has no impact on the Group’s CET1 ratios or tangible net value per share (TNAV).

Consequently, the impairment of other assets (net) in the first half of 2020 amounted to EUR 10,241 million. In the first half of 2019, this line was EUR 27 million.

u Gains or losses on non-financial assets and investments (net)

Net gains on non-financial assets and investments were EUR 27 million in the first half of 2020, compared to EUR 250 million in the same period of 2019, when capital gains from the sale of 51% of our stake in Prisma Medios de Pago S.A. and the revaluation of the remaining stake (49%) were recorded.

u Gains or losses on non-current assets held for sale not classified as discontinued operations

This item, which mainly includes impairment of foreclosed assets recorded and the sale of properties acquired upon foreclosure, totalled EUR -119 million in the six months to June 2020, compared to EUR -257 million in the first half of 2019.

u Profit before tax

Profit before tax was EUR -6,410 million, affected by the adjustment in the valuation of goodwill, compared to EUR 6,531 million posted in the first half of 2019.

u Income tax

As with goodwill, and due to the impact that the crisis arising from COVID-19 may have on the current and future performance of our businesses, an adjustment of EUR 2,500 million has been made to deferred tax assets of the Spanish consolidated fiscal group in the first half of the year. As a result, the total corporate income tax was EUR 3,928 million (EUR 2,449 million in the first half of 2019).

January - June 2020 | | 13 | ||||||

u Attributable profit to non-controlling interests

Attributable profit to non-controlling interests amounted to EUR 460 million, down 46% year-on-year (-41% excluding the exchange rate impact), due to lower profit obtained by Group companies, on top of the share buyback in Mexico last year and the increased stake in SC USA.

u Attributable profit to the parent

Profit attributable to the parent amounted to EUR -10,798 million in the first half of 2020, compared with EUR 3,231 million in the first six months of 2019. RoTE stood at 1.73% and earnings per share stood at EUR -0.667.

u Underlying attributable profit to the parent

The attributable profit to the parent recorded in the first six months was affected, in 2020 and 2019, by results (net of tax) that are outside the ordinary course performance of our business and distort the year-on-year comparison, and are detailed below:

•In the first half of 2020, the valuation adjustment of goodwill ascribed to various Group units of EUR -10,100 million, with the previously detailed breakdown in Impairment on other assets (net), the valuation adjustment to deferred tax assets of the Spanish consolidated fiscal group with an impact of EUR -2,500 million and restructuring costs and other provisions with a net impact of EUR -106 million, of which EUR -46 million were recognised in the first quarter. The total amount of these results was EUR -12,706 million.

•In the first half of 2019, capital gains from the sale of 51% of our stake in the Argentinian entity Prisma Medios de Pago S.A. and the revaluation of the remaining 49% (EUR 150 million), capital losses related to real estate assets in Spain (EUR -180 million), PPI provisions to cover potential claims in the UK (EUR -80 million) and restructuring costs (EUR -704 million). The combined amount of all these totalled EUR -814 million.

Excluding these results from the various P&L lines where they are recorded, and incorporating them separately in the net capital gains and provisions line, the adjusted or underlying attributable profit to the parent was EUR 1,908 million in the first half of 2020 and EUR 4,045 million in the first half of 2019, 53% lower year-on-year (-48% excluding the FX impact), strongly conditioned by the rise in provisions, mostly related to COVID-19.

Before the recording of loan-loss provisions, net operating income (total income less operating expenses) of Grupo Santander was EUR 11,865 million, an 8% decrease year-on-year, though this becomes a 2% increase excluding the FX impact, with the following performance by line and region:

By line:

•Total income remained unchanged driven by net interest income stability and higher gains on financial transactions, offsetting the fall in net fee income and other operating income (lower dividends, lower results of entities accounted for by the equity method and greater contribution to the SRF).

•Costs were 2% lower, with broad-based declines across countries, mainly in Europe, where cost reductions are ahead of schedule as previously mentioned.

By region:

•Europe decreased 10% with falls in most markets (except SCF).

•In North America, net operating income was 2% higher versus 2019. By country, the US fell 3% and Mexico increased 11%.

•In South America, 8% growth with rises of 5% in Brazil, 9% in Chile and 64% in Argentina.

In the first half of 2020, the Group’s underlying RoTE was 5.44%, underlying RoRWA was 0.80% and underlying earnings per share EUR 0.098 (11.68%, 1.62% and EUR 0.231, respectively in the same period of 2019).

| 14 | | January - June 2020 | ||||||

| Summarised underlying income statement | ||||||||||||||||||||||||||||||||||||||||||||||||||

| EUR million | Change | Change | ||||||||||||||||||||||||||||||||||||||||||||||||

| Q2'20 | Q1'20 | % | % excl. FX | H1'20 | H1'19 | % | % excl. FX | |||||||||||||||||||||||||||||||||||||||||||

| Net interest income | 7,715 | 8,487 | (9.1) | (1.9) | 16,202 | 17,636 | (8.1) | (0.2) | ||||||||||||||||||||||||||||||||||||||||||

| Net fee income | 2,283 | 2,853 | (20.0) | (13.1) | 5,136 | 5,863 | (12.4) | (4.0) | ||||||||||||||||||||||||||||||||||||||||||

Gains (losses) on financial transactions (1) | 781 | 292 | 167.5 | 174.8 | 1,073 | 511 | 110.0 | 137.6 | ||||||||||||||||||||||||||||||||||||||||||

| Other operating income | (75) | 182 | — | — | 107 | 426 | (74.9) | (78.0) | ||||||||||||||||||||||||||||||||||||||||||

| Total income | 10,704 | 11,814 | (9.4) | (2.5) | 22,518 | 24,436 | (7.8) | 0.0 | ||||||||||||||||||||||||||||||||||||||||||

| Administrative expenses and amortisations | (5,076) | (5,577) | (9.0) | (3.5) | (10,653) | (11,587) | (8.1) | (1.9) | ||||||||||||||||||||||||||||||||||||||||||

| Net operating income | 5,628 | 6,237 | (9.8) | (1.6) | 11,865 | 12,849 | (7.7) | 1.7 | ||||||||||||||||||||||||||||||||||||||||||

| Net loan-loss provisions | (3,118) | (3,909) | (20.2) | (14.2) | (7,027) | (4,313) | 62.9 | 78.5 | ||||||||||||||||||||||||||||||||||||||||||

| Other gains (losses) and provisions | (625) | (372) | 68.0 | 79.3 | (997) | (957) | 4.2 | 11.6 | ||||||||||||||||||||||||||||||||||||||||||

| Profit before tax | 1,885 | 1,956 | (3.6) | 8.8 | 3,841 | 7,579 | (49.3) | (43.8) | ||||||||||||||||||||||||||||||||||||||||||

| Tax on profit | (208) | (1,260) | (83.5) | (79.7) | (1,468) | (2,679) | (45.2) | (39.0) | ||||||||||||||||||||||||||||||||||||||||||

| Profit from continuing operations | 1,677 | 696 | 140.9 | 183.0 | 2,373 | 4,900 | (51.6) | (46.4) | ||||||||||||||||||||||||||||||||||||||||||

| Net profit from discontinued operations | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Consolidated profit | 1,677 | 696 | 140.9 | 183.0 | 2,373 | 4,900 | (51.6) | (46.4) | ||||||||||||||||||||||||||||||||||||||||||

| Non-controlling interests | (146) | (319) | (54.2) | (51.1) | (465) | (855) | (45.6) | (41.1) | ||||||||||||||||||||||||||||||||||||||||||

| Net capital gains and provisions | (12,660) | (46) | — | — | (12,706) | (814) | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Attributable profit to the parent | (11,129) | 331 | — | — | (10,798) | 3,231 | — | — | ||||||||||||||||||||||||||||||||||||||||||

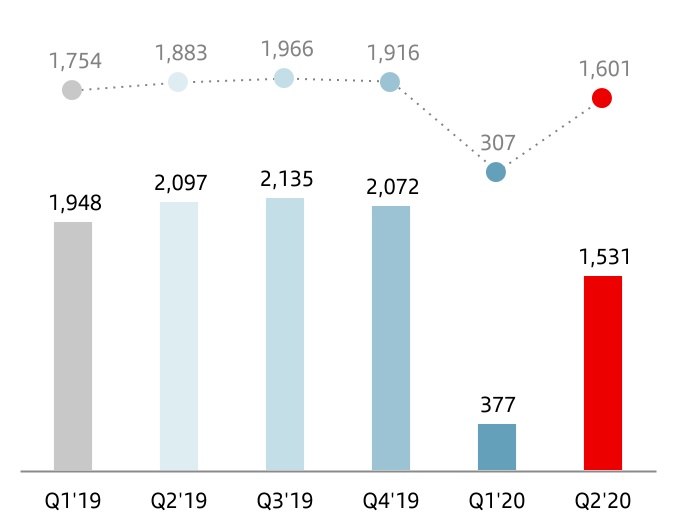

Underlying attributable profit to the parent (2) | 1,531 | 377 | 306.1 | 420.9 | 1,908 | 4,045 | (52.8) | (47.5) | ||||||||||||||||||||||||||||||||||||||||||

(1) Includes exchange differences. (2) Excludes net capital gains and provisions, mainly goodwill and DTA impairments.

è Second quarter results compared to the first quarter of 2020

Attributable profit to the parent in the second quarter of 2020 amounted to EUR -11,129 million (EUR 331 million in the first quarter).

Excluding net capital gains and provisions in both periods (EUR -12,660 million in the second quarter and EUR -46 million in the first quarter, as previously detailed), underlying attributable profit to the parent in the second quarter stood at EUR 1,531 million (EUR 377 million in the first quarter), with the following performance by line without the impact of exchange rates, which had a negative impact on the quarterly comparison of -7 percentage points in income and -6 percentage points in costs:

• Total income was down 2%, mostly net fee income, which fell 13% due to the lower activity caused by the impact of COVID-19 and the contribution to the Single Resolution Fund. On the positive side, there were increases in dividend income (seasonally higher in the second quarter) and better gains on financial transactions particularly from SCIB. Net interest income remained relatively strong, falling just 2%.

• Costs were down 3%, falling 6% in Europe and 4% in North America. In South America, a slight increase of 1%.

• Loan-loss provisions fell by 14% due to the high level of provisions relating to the health crisis in the first quarter.

| Net operating income | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

| Underlying attributable profit to the parent* | ||||||||

| EUR million | ||||||||

| constant euros | |||||||

(*) Excluding net capital gains and provisions.

January - June 2020 | | 15 | ||||||

| Response to the COVID-19 crisis Business model | ||||||||||||||||||||||||||

| Balance sheet | ||||||||||||||||||||||||||

| Grupo Santander. Condensed balance sheet | ||||||||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||||||||

| Change | ||||||||||||||||||||||||||||||||

| Assets | Jun-20 | Jun-19 | Absolute | % | Dec-19 | |||||||||||||||||||||||||||

| Cash, cash balances at central banks and other demand deposits | 138,266 | 104,104 | 34,162 | 32.8 | 101,067 | |||||||||||||||||||||||||||

| Financial assets held for trading | 124,145 | 102,574 | 21,571 | 21.0 | 108,230 | |||||||||||||||||||||||||||

| Debt securities | 32,062 | 33,343 | (1,281) | (3.8) | 32,041 | |||||||||||||||||||||||||||

| Equity instruments | 7,782 | 11,133 | (3,351) | (30.1) | 12,437 | |||||||||||||||||||||||||||

| Loans and advances to customers | 289 | 300 | (11) | (3.7) | 355 | |||||||||||||||||||||||||||

| Loans and advances to central banks and credit institutions | 6 | — | 6 | — | — | |||||||||||||||||||||||||||

| Derivatives | 84,006 | 57,798 | 26,208 | 45.3 | 63,397 | |||||||||||||||||||||||||||

| Financial assets designated at fair value through profit or loss | 97,270 | 78,813 | 18,457 | 23.4 | 66,980 | |||||||||||||||||||||||||||

| Loans and advances to customers | 35,421 | 23,407 | 12,014 | 51.3 | 31,147 | |||||||||||||||||||||||||||

| Loans and advances to central banks and credit institutions | 54,815 | 46,915 | 7,900 | 16.8 | 28,122 | |||||||||||||||||||||||||||

| Other (debt securities an equity instruments) | 7,034 | 8,491 | (1,457) | (17.2) | 7,711 | |||||||||||||||||||||||||||

| Financial assets at fair value through other comprehensive income | 122,560 | 118,062 | 4,498 | 3.8 | 125,708 | |||||||||||||||||||||||||||

| Debt securities | 112,041 | 111,891 | 150 | 0.1 | 118,405 | |||||||||||||||||||||||||||

| Equity instruments | 2,228 | 2,789 | (561) | (20.1) | 2,863 | |||||||||||||||||||||||||||

| Loans and advances to customers | 8,291 | 3,382 | 4,909 | 145.2 | 4,440 | |||||||||||||||||||||||||||

| Loans and advances to central banks and credit institutions | — | — | — | — | — | |||||||||||||||||||||||||||

| Financial assets measured at amortised cost | 976,298 | 981,046 | (4,748) | (0.5) | 995,482 | |||||||||||||||||||||||||||

| Debt securities | 27,167 | 39,382 | (12,215) | (31.0) | 29,789 | |||||||||||||||||||||||||||

| Loans and advances to customers | 890,795 | 881,146 | 9,649 | 1.1 | 906,276 | |||||||||||||||||||||||||||

| Loans and advances to central banks and credit institutions | 58,336 | 60,518 | (2,182) | (3.6) | 59,417 | |||||||||||||||||||||||||||

| Investments in subsidiaries, joint ventures and associates | 8,668 | 7,788 | 880 | 11.3 | 8,772 | |||||||||||||||||||||||||||

| Tangible assets | 33,271 | 33,755 | (484) | (1.4) | 35,235 | |||||||||||||||||||||||||||

| Intangible assets | 15,946 | 28,794 | (12,848) | (44.6) | 27,687 | |||||||||||||||||||||||||||

| Goodwill | 12,595 | 25,613 | (13,018) | (50.8) | 24,246 | |||||||||||||||||||||||||||

| Other intangible assets | 3,351 | 3,181 | 170 | 5.3 | 3,441 | |||||||||||||||||||||||||||

| Other assets | 56,457 | 57,160 | (703) | (1.2) | 53,534 | |||||||||||||||||||||||||||

| Total assets | 1,572,881 | 1,512,096 | 60,785 | 4.0 | 1,522,695 | |||||||||||||||||||||||||||

| Liabilities and shareholders' equity | ||||||||||||||||||||||||||||||||

| Financial liabilities held for trading | 97,700 | 74,187 | 23,513 | 31.7 | 77,139 | |||||||||||||||||||||||||||

| Customer deposits | — | — | — | — | — | |||||||||||||||||||||||||||

| Debt securities issued | — | — | — | — | — | |||||||||||||||||||||||||||

| Deposits by central banks and credit institutions | — | — | — | — | — | |||||||||||||||||||||||||||

| Derivatives | 84,202 | 58,341 | 25,861 | 44.3 | 63,016 | |||||||||||||||||||||||||||

| Other | 13,498 | 15,846 | (2,348) | (14.8) | 14,123 | |||||||||||||||||||||||||||

| Financial liabilities designated at fair value through profit or loss | 59,619 | 60,237 | (618) | (1.0) | 60,995 | |||||||||||||||||||||||||||

| Customer deposits | 36,346 | 37,849 | (1,503) | (4.0) | 34,917 | |||||||||||||||||||||||||||

| Debt securities issued | 4,386 | 3,117 | 1,269 | 40.7 | 3,758 | |||||||||||||||||||||||||||

| Deposits by central banks and credit institutions | 18,887 | 19,141 | (254) | (1.3) | 22,194 | |||||||||||||||||||||||||||

| Other | — | 130 | (130) | (100.0) | 126 | |||||||||||||||||||||||||||

| Financial liabilities measured at amortised cost | 1,283,581 | 1,224,194 | 59,387 | 4.9 | 1,230,745 | |||||||||||||||||||||||||||

| Customer deposits | 810,486 | 776,902 | 33,584 | 4.3 | 789,448 | |||||||||||||||||||||||||||

| Debt securities issued | 254,398 | 251,672 | 2,726 | 1.1 | 258,219 | |||||||||||||||||||||||||||

| Deposits by central banks and credit institutions | 189,214 | 160,808 | 28,406 | 17.7 | 152,969 | |||||||||||||||||||||||||||

| Other | 29,483 | 34,812 | (5,329) | (15.3) | 30,109 | |||||||||||||||||||||||||||

| Liabilities under insurance contracts | 2,246 | 731 | 1,515 | 207.3 | 739 | |||||||||||||||||||||||||||

| Provisions | 11,948 | 14,571 | (2,623) | (18.0) | 13,987 | |||||||||||||||||||||||||||

| Other liabilities | 25,928 | 28,191 | (2,263) | (8.0) | 28,431 | |||||||||||||||||||||||||||

| Total liabilities | 1,481,022 | 1,402,111 | 78,911 | 5.6 | 1,412,036 | |||||||||||||||||||||||||||

| Shareholders' equity | 112,899 | 122,006 | (9,107) | (7.5) | 124,239 | |||||||||||||||||||||||||||

| Capital stock | 8,309 | 8,118 | 191 | 2.4 | 8,309 | |||||||||||||||||||||||||||

| Reserves | 117,050 | 110,657 | 6,393 | 5.8 | 111,077 | |||||||||||||||||||||||||||

| Attributable profit to the Group | (10,798) | 3,231 | (14,029) | — | 6,515 | |||||||||||||||||||||||||||

| Less: dividends | (1,662) | — | (1,662) | — | (1,662) | |||||||||||||||||||||||||||

| Other comprehensive income | (30,637) | (23,377) | (7,260) | 31.1 | (24,168) | |||||||||||||||||||||||||||

| Minority interests | 9,597 | 11,356 | (1,759) | (15.5) | 10,588 | |||||||||||||||||||||||||||

| Total equity | 91,859 | 109,985 | (18,126) | (16.5) | 110,659 | |||||||||||||||||||||||||||

| Total liabilities and equity | 1,572,881 | 1,512,096 | 60,785 | 4.0 | 1,522,695 | |||||||||||||||||||||||||||

| 16 | | January - June 2020 | ||||||

| Response to the COVID-19 crisis Business model | ||||||||||||||||||||||||||

| Balance sheet | ||||||||||||||||||||||||||

GRUPO SANTANDER BALANCE SHEET

•Strong negative exchange rate impact on a year-on-year basis (-5 pp in loans and -6 pp in customer funds).

•Excluding this impact, the following movements were recorded in the quarter:

–Gross loans and advances to customers excluding reverse repos rose 1% driven by the overall increase in corporates, as activity of individuals remained stable in the quarter.

–Customer funds increased 5%, with 5% growth both in deposits excluding repos and mutual funds, following the sharp reduction of the latter in the first quarter.

•Compared to June 2019:

–Gross loans and advances to customers excluding reverse repos rose 6% year-on-year in constant euros with the 10 core markets growing, particularly in South America (+18%) and North America (+11%).

–Customer funds (excluding repos) increased 7% in constant euros, driven by deposits excluding repos, which rose 9%. Growth in nine of our 10 core markets.

è Loans and advances to customers

Gross loans and advances to customers rose to EUR 934,796 million in June 2020. The Group uses gross loans and advances to customers excluding reverse repos for the purpose of analysing traditional commercial banking loans.

•In the quarter, gross loans and advances to customers excluding reverse repos remained unchanged. Without the exchange rate impact, growth was 1%, mostly derived from the impact of the health crisis in activity and the need for funding of the different segments, which varies across countries depending on the spread of the pandemic. This was reflected in a strong growth in loans to SMEs and in the stability of the lending activity of individuals.

Volumes grew across all markets except Mexico, Poland and Santander Consumer Finance, although it began to recover the levels of new lending prior to the halt in consumer activity due to COVID-19 in June. This recovery in new lending in the consumer business could also be observed in the US, driven by Fiat Chrysler prime production incentive programmes. On the other hand, the mortgage business also started to recover in Europe, while the large corporate business returned to more normal levels of activity, following the strong increases recorded in March. Lastly, the South American countries have reflected the different evolution of COVID-19 over time.

Compared to June 2019, gross loans and advances to customers excluding reverse repos increased 1%. Excluding the exchange rate impact, 6% growth, with the following detail by region:

In Europe, 4% growth with all markets increasing. Poland rose 4%, as well as Portugal, consolidating the shift in trend in March, and the UK, driven by strong residential mortgage activity early this year and the government programmes for corporate customers. Santander Consumer Finance rose 3%. Lastly, Spain grew 1% following the 6% increase in the quarter, which shifted the trend of previous quarters. Other Europe, which includes most of the wholesale banking business in the region, increased 19%.

In North America, the US grew 11% driven by auto loans and commercial banking and Mexico 9% due to corporates and SCIB, leading to an 11% increase in the region.

Growth in South America was 18%, with Argentina growing 39%, Brazil +18% with positive performance in all segments and Chile +13% driven by increased new lending to corporates and large corporates in the quarter.

Gross loans and advances to customers excluding reverse repos maintained a balanced structure: individuals (45%), consumer credit (17%), SMEs and corporates (25%) and SCIB (13%).

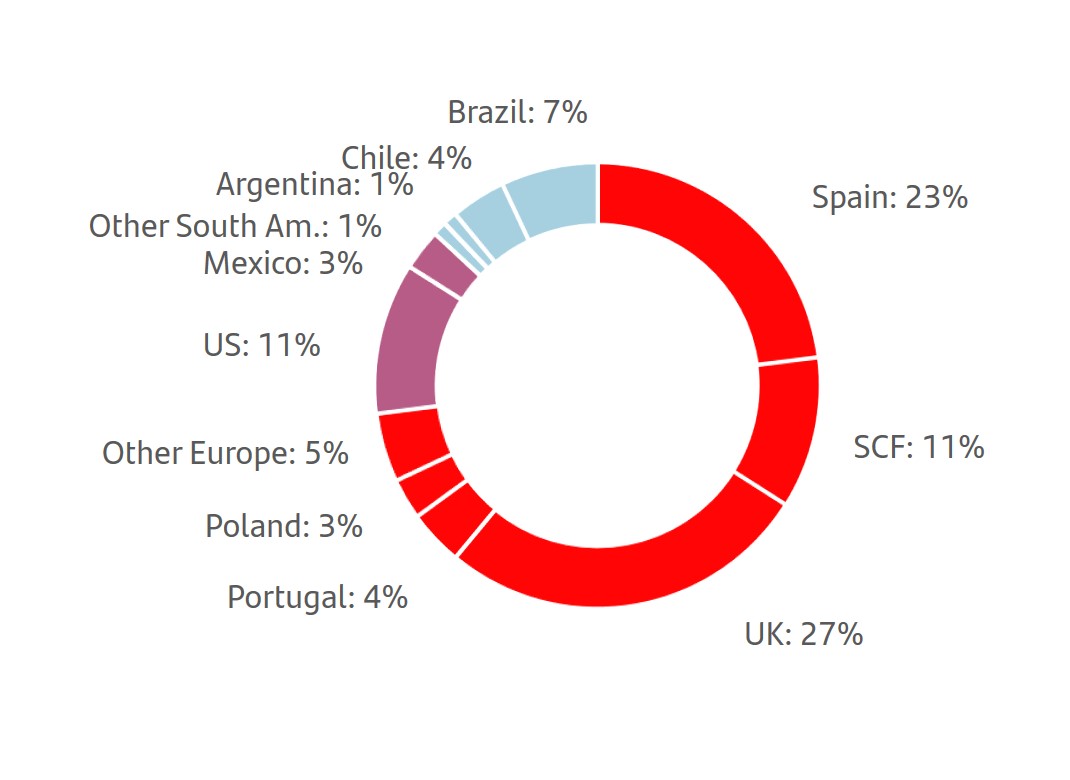

| Gross loans and advances to customers (excl. reverse repos) | Gross loans and advances to customers (excl. reverse repos) | |||||||||||||||||||

| EUR billion | % operating areas. June 2020 | |||||||||||||||||||

|  | |||||||||||||||||||

(*) In constant EUR: +6%

January - June 2020 | | 17 | ||||||

| Response to the COVID-19 crisis Business model | ||||||||||||||||||||||||||

| Balance sheet | ||||||||||||||||||||||||||

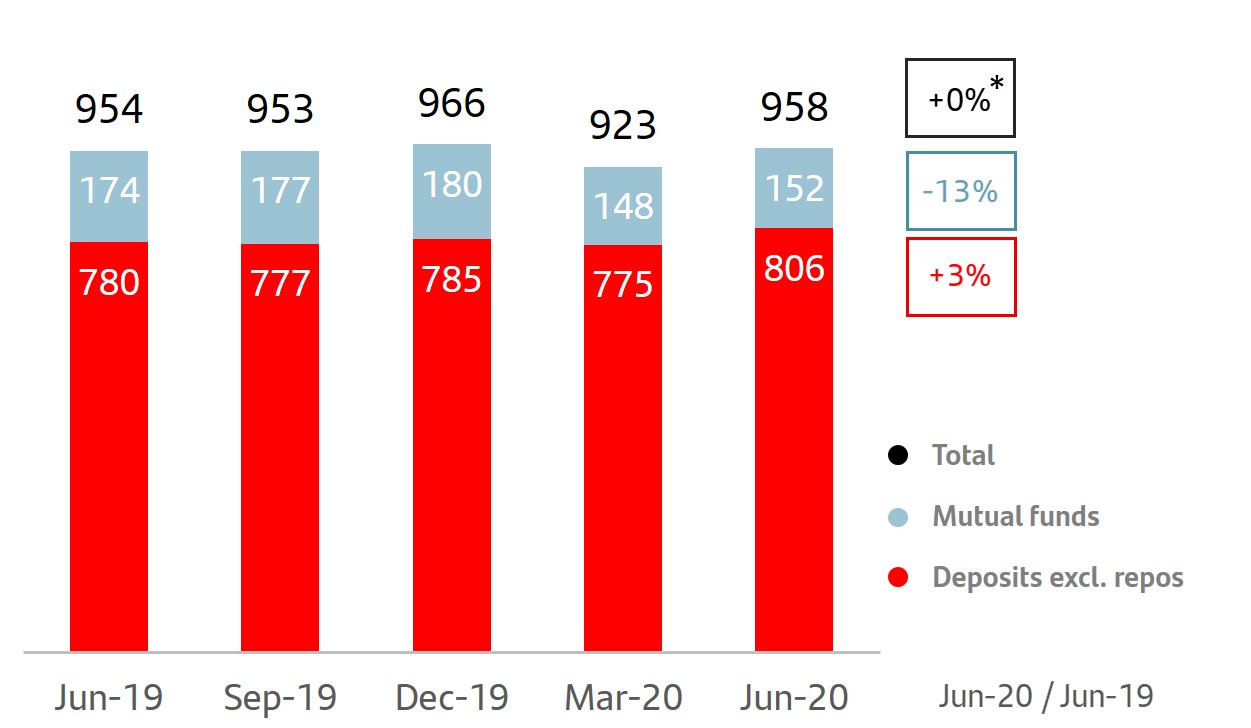

è Customer funds

Customer deposits amounted to EUR 846,832 million. The Group uses customer funds (customer deposits excluding repos, plus including mutual funds) for the purpose of analysing traditional retail banking funds.

•In the second quarter, customer funds were 4% higher. Excluding exchange rate impacts, growth was 5%:

–By product: customer deposits excluding repos rose 5%, boosted by demand deposits (+7%) whilst time deposits remained stable. Mutual funds increased 5% following the sharp fall in the previous quarter.

–Broad-based growth by market, ranging from 14% in Argentina to 3% in Portugal (falls only recorded in SCF: -1%, and Mexico remained flat). By region, increases in Europe (+5%), North America (+6%) and South America (+7%).

•Compared to June 2019, customer funds had no material change. Excluding the exchange rate impact, increases of 7%, as follows:

–By product, deposits excluding repos rose 9%. Demand deposits (+11%) increased in the ten core markets and time deposits grew 1% as the strong growth recorded in the Americas was offset by the falls in all European countries. Mutual funds dropped 1%, due to market volatility in the first quarter of 2020, with decreases in most European countries and increases in the Americas (except Brazil and Mexico).

–By market, customer funds rose in all of them except Spain (-2%), due to the falls in time deposits and mutual funds. Of note were Argentina (+44%), the US (+23%), Chile (+22%), Brazil (+14%), Mexico (+9%) and Poland (+9%). The UK recorded more moderate growth (+5%) as well as Santander Consumer Finance and Portugal, both of which increased 3%.

With this performance, the weight of demand deposits as a percentage of total customer funds rose 5 pp in the last 12 months to 65%, to the detriment of time deposits (-3 pp to 19%) and mutual funds (-2 pp to 16%).

In addition to capturing customer deposits, Grupo Santander, for strategic reasons, maintains a selective policy of issuing securities in the international fixed income markets and strives to adapt the frequency and volume of its market operations to the structural liquidity needs of each unit, as well as to the receptiveness of each market.

• In the first half of 2020, the Group issued:

Medium- and long-term covered bonds placed in the market of EUR 6,517 million and senior debt amounting to EUR 8,796 million.

There were EUR 6,604 million of securitisations placed in the market and maturities were extended by EUR 1 bn.

Issuances to meet the TLAC (Total Loss-Absorbing Capacity) requirement amounting to EUR 10,914 million, in order to strengthen the Group’s situation (senior non-preferred: EUR 9,063 million, preferred: EUR 1,500 million, subordinated debt: EUR 351 million), including a EUR 1 billion senior non-preferred green bond issuance.

Maturities of medium- and long-term debt of EUR 19,496 million.

The net loan-to-deposit ratio was 110% (115% in March 2020 and 111% in June 2019). The ratio of deposits plus medium- and long-term funding to the Group’s loans was 115%, underscoring the comfortable funding structure.

During the first half of the year, the three main rating agencies reviewed their ratings and outlook for Spain's sovereign debt, the banking system and, in Fitch's case, Banco Santander S.A.'s. Regarding the latter, Fitch confirmed its ratings (long-term debt at A- and short-term at F2), as did Moody's and S&P until the next revision in the second half of the quarter. Fitch and S&P changed the outlook from stable to negative due to the economic consequences that the COVID-19 crisis could have on the ratings in the long term. Moody's, on the other hand, maintained its ratings at A2 and P-1, with a stable outlook.

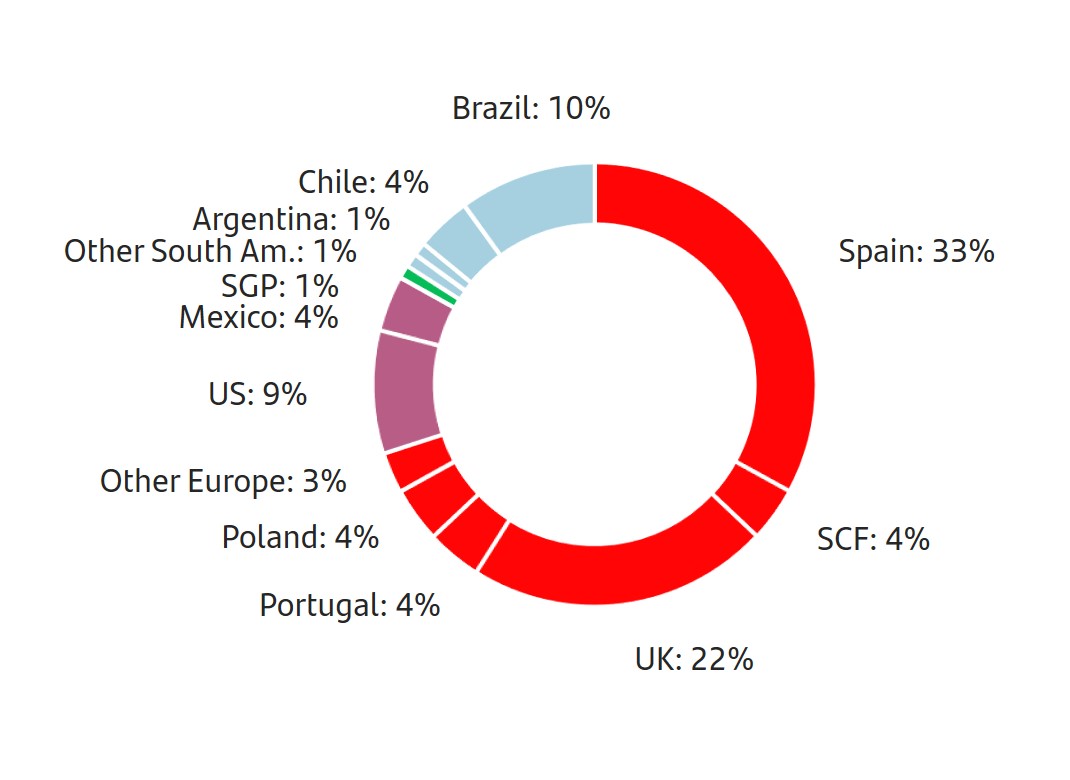

| Customer funds | Customer funds | |||||||||||||||||||

| EUR billion | % operating areas. June 2020 | |||||||||||||||||||

|  | |||||||||||||||||||

(*) In constant EUR: +7%

| 18 | | January - June 2020 | ||||||

SOLVENCY RATIOS

•At the end of June, the CET1 ratio rose 26 bps in the quarter to 11.84%. The organic generation and the anticipation of the measures expected in the European regulation of capital requirements, led to an increase of 52 bps, partially offset by corporate operations, pensions and markets performance.

•Tangible equity per share was EUR 4.00, 5% lower quarter-on-quarter.

•The fully loaded leverage ratio was 4.8%.

At the end of the quarter, the total phased-in capital ratio stood at 15.48% and the CET1 ratio (phased-in and fully loaded) at 11.84%, after increasing 26 bps in the quarter. We have a strong capital base, comfortably meeting the minimum levels required by the European Central Bank on a consolidated basis (13.02% for the total capital ratio and 8.86% for the CET1 ratio), after the recent measures adopted by regulators of reducing the Pillar 2 R and countercyclical buffer. This results in a CET1 management buffer of 298 bps, compared to the pre-COVID-19 buffer of 189 bps.

In the quarter, we continued to generate capital organically, increasing 34 bps due to underlying profit, management of risk weighted assets and increased securitisations. Additionally, 6 bp dividend accrual to allow the flexibility to pay a cash dividend against 2020 results, as soon as market conditions normalise and subject to regulatory approvals and guidance.

These, together with the positive regulatory impact mainly from bringing forward the expected European regulation of capital requirements (CRR2 quick fix) measures, led to a total increase of 52 bps.

On the other hand, there were several non-recurring impacts in the quarter, such as corporate transactions, which had a negative impact of 7 bps (mainly related to Ebury), together with other negative impacts from pensions and markets.

Had the IFRS 9 transitional arrangement not been applied, the total impact on the CET1 would have been -38 bps, of which 13 bps correspond to the second quarter due to the application of the dynamic phased-in.

| Eligible capital. June 2020* | Fully-loaded capital ratio* | |||||||||||||||||||

| EUR million | % | |||||||||||||||||||

| Phased-in | Fully-loaded |  | ||||||||||||||||||

| CET1 | 67,192 | 67,192 | ||||||||||||||||||

| Basic capital | 76,476 | 75,920 | ||||||||||||||||||

| Eligible capital | 87,837 | 87,750 | ||||||||||||||||||

| Risk-weighted assets | 567,446 | 567,446 | ||||||||||||||||||

| CET1 capital ratio | 11.84 | 11.84 | ||||||||||||||||||

| T1 capital ratio | 13.48 | 13.38 | ||||||||||||||||||

| Total capital ratio | 15.48 | 15.46 | ||||||||||||||||||

| CET1 evolution* | ||

| % | ||

| ||

January - June 2020 | | 19 | ||||||

RISK MANAGEMENT

•Santander’s Risk management in Q2 focused on protecting our stakeholders in an environment that has been, and still is, characterised by the disruption arising from COVID-19. The Group is actively supporting our customers through various relief programmes, especially those that are more vulnerable, monitoring their performance and payment capacity as well as ensuring that business continuity plans remain effective so that we keep serving our clients under the highest quality standards.

•The NPL ratio was 3.26% as of the end of June in line with the first quarter and lower on an annual basis, explained by loan growth and containment of our customers’ credit quality deterioration through the aforementioned relief programmes. Cost of credit increased to 1.26% due to the additional provisions that have been recorded to face the potential consequences of the pandemic. As a result, coverage increased to 72%, rising 1 pp compared to the previous quarter.

•Our market risk exposure in the second quarter maintained its low profile, with low VaR levels after the market volatility spike caused by the COVID-19 situation in previous months.

•The operational risk profile remained stable, with a similar distribution of losses by category as in the previous quarter, despite the exceptional circumstances. In addition to reinforcing existing controls, new ones were launched to avoid the increase of operational risk levels.

u COVID-19 risk management

Santander’s priority is to protect the health of our employees, customers and shareholders but also to help mitigate the economic and financial impact that the health crisis could have.

In this respect, several work streams were activated to find the best possible outcome for our customers as well as to preserve the Bank’s strength and solvency:

•Identification of vulnerable customers, collectives and sectors that are affected or could be affected by the effects of the pandemic.

•Close monitoring of their situation and needs in light of the most recent pandemic and market developments.

•Scenario analysis to assess potential impacts and define action plans in case they are needed.

•Assessment of the risk control framework, risk appetite statement, management limits and policies to ensure their appropriateness under the current circumstances.

•Strengthening of the recoveries teams in all our geographies.

Continuous interaction and coordination among our local units and Group is a key asset. The experience gained in fighting the health crisis across all our geographies enable us to share best practices and quickly implement actions and strategies adapted to each local market.

The Group's business contingency plans remain active across all our markets to ensure that all our processes and functions are preserved so that we keep serving our customers under the highest quality standards in these difficult times.

The additional governance activated, which includes the Special Situation Committees, has been critical to address and closely monitor the current situation and its potential negative effects.

The board and senior management, in order to facilitate the decision-making process, are regularly updated with the continuous monitoring of the key risk indicators.

In order to minimise the medium- and long-term economic impacts of the efforts taken to contain the COVID-19 pandemic, Santander implemented a set of support measures following regulatory and supervisory recommendations, that, in many cases, were materialised through moratoria on payments of credit obligations or government guaranteed loans, with the aim of supporting the economic and financial challenges faced by borrowers.

To support our customers and foster their economic resilience during the crisis and help them overcome its consequences, different measures have been implemented. Of note:

•Provide liquidity and credit facilities for individuals and businesses through government programmes. Around 630,000 operations were formalised which amounted to more than EUR 25 billion, 3% of the portfolio. Of note were the ICO (Instituto de Crédito Oficial) loans granted in Spain.

•As for payment holidays and moratoria, 5.4 million operations have been formalised for a total of EUR 116 billion (12% of the portfolio), of which 1.9 million operations correspond to government programmes, which account for EUR 72 billion (7% of the portfolio), and 3.5 million operations correspond to non-government programmes, which account for EUR 44 billion (5% of the portfolio).

The main features of the moratoria are:

–Circa 60% correspond to residential mortgages, mainly in the United Kingdom, and mostly under short-term government programmes (3 months, extendable for another 3). Santander UK's mortgage portfolio has an average LTV of around 41%.

| 20 | | January - June 2020 | ||||||

–Around 65% of consumer loans are secured (auto loans). They are mainly booked in our subsidiaries specialised in that business; Santander Consumer Finance and SC USA.

–The corporate and SME portfolio is, in percentage terms, the one that has least resorted to moratorium measures. This is partly due to the accessibility of this kind of company to other types of support measures, such the aforementioned liquidity lines and credit facilities.

–Most moratoria are short term. About 90% will expire in 2020 (less than 6 months of residual maturity). Some governments and institutions are re-extending the term of the initial moratoria, especially those that were launched in the initial phases of the pandemic, with less visibility of the potential duration of the crisis. However, these re-extensions are also short term. Circa 25% of moratoria have already expired, and although it is early to have full visibility of their performance once the support measure is over, as of the end of June the performance of expiring moratoria is similar to that of the portfolio which has not required this kind of measures. 98% of expired moratoria remain performing status.

u Credit risk management

The Group’s NPL ratio in June increased by 1 bp to 3.26% (-25 bps year-on-year) favoured by the COVID-19 public and private customer support programmes (liquidity lines, ICO in Spain, CBILS and CLBILC in the UK, etc), which were reflected in the loan growth of the SME and Corporate segments.

Regarding credit risk performance, non-performing loans amounted to EUR 32,782 million in June, a 1% increase compared to the previous quarter, in constant euros.

| Credit risk | ||||||||||||||||||||||||||

| EUR million | ||||||||||||||||||||||||||

| Jun-20 | Jun-19 | Chg (%) | Dec-19 | |||||||||||||||||||||||