Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 1

| x | Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the Fiscal Year Ended December 31, 2012

| ¨ | Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File No. 1-13726

Chesapeake Energy Corporation

(Exact name of registrant as specified in its charter)

| Oklahoma | 73-1395733 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

6100 North Western Avenue Oklahoma City, Oklahoma | 73118 | |

| (Address of principal executive offices) | (Zip Code) | |

(405) 848-8000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.01 | New York Stock Exchange | |

| 7.625% Senior Notes due 2013 | New York Stock Exchange | |

| 9.5% Senior Notes due 2015 | New York Stock Exchange | |

| 6.25% Senior Notes due 2017 | New York Stock Exchange | |

| 6.5% Senior Notes due 2017 | New York Stock Exchange | |

| 6.875% Senior Notes due 2018 | New York Stock Exchange | |

| 7.25% Senior Notes due 2018 | New York Stock Exchange | |

| 6.775% Senior Notes due 2019 | New York Stock Exchange | |

| 6.625% Senior Notes due 2020 | New York Stock Exchange | |

| 6.875% Senior Notes due 2020 | New York Stock Exchange | |

| 6.125% Senior Notes due 2021 | New York Stock Exchange | |

| 2.75% Contingent Convertible Senior Notes due 2035 | New York Stock Exchange | |

| 2.5% Contingent Convertible Senior Notes due 2037 | New York Stock Exchange | |

| 2.25% Contingent Convertible Senior Notes due 2038 | New York Stock Exchange | |

| 4.5% Cumulative Convertible Preferred Stock | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES x NO ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | x | Accelerated Filer | ¨ | |||

| Non-accelerated Filer | ¨ | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO x

The aggregate market value of our common stock held by non-affiliates on June 30, 2012 was approximately $12.2 billion. At February 21, 2013, there were 667,567,791 shares of our $0.01 par value common stock outstanding.

Table of Contents

CHESAPEAKE ENERGY CORPORATION AND SUBSIDIARIES

2012 ANNUAL REPORT ON FORM 10-K/A

| Page | ||||

| PART III | ||||

Item 10. Directors, Executive Officers and Corporate Governance | 4 | |||

| 9 | ||||

| 45 | ||||

Item 13. Certain Relationships and Related Transactions, and Director Independence | 48 | |||

| 52 | ||||

| PART IV | ||||

| 53 | ||||

Table of Contents

EXPLANATORY NOTE

Chesapeake Energy Corporation filed its Form 10-K for the year ended December 31, 2012 (the “2012 Form 10-K”) with the Securities and Exchange Commission on March 1, 2013. Pursuant to General Instruction G(3) to Form 10-K, the Company incorporated by reference the information required by Part III of Form 10-K from our definitive proxy statement for the 2013 Annual Meeting of Shareholders (the “2013 Proxy Statement”) that we expected to file with the Commission not later than 120 days after the end of the fiscal year covered by the 2012 Form 10-K. Because the definitive 2013 Proxy Statement will not be filed with the Commission before such date, the Company is filing this Amendment No. 1 to the 2012 Form 10-K (the “Form 10-K/A”) to provide the additional information required by Part III of Form 10-K. This Form 10-K/A does not change the previously reported financial statements or any of the other disclosures contained in Part I, Part II or Part IV, other than to provide an updated list of our executive officers in Item 10 and to add new Exhibits 31.3 and 31.4 under Item 15(a)(3). Some of the information provided in this Form 10-K/A may be superseded by the information provided in the definitive 2013 Proxy Statement to be filed with the Commission. References to “Chesapeake,” “us,” “we,” “Company” and “our” in this report refer to Chesapeake Energy Corporation, together with its subsidiaries.

Table of Contents

Item 10.Directors, Executive Officers and Corporate Governance

Board of Directors

The Company’s Board of Directors has changed significantly over the past year. In June 2012, after extensive discussions with the Company’s major shareholders, the Board appointed Archie W. Dunham as the Company’s independent, non-executive Chairman of the Board and Aubrey K. McClendon, our co-founder and then-CEO, stepped down as Chairman. The Board also appointed four other new independent directors, Bob G. Alexander, Vincent J. Intrieri, R. Brad Martin and Frederic M. Poses, to replace four directors in office at that time. The Board also recently appointed Louis A. Raspino to serve as a director of the Company. Since the Board’s reconstitution, the Board has appointed new members and new chairman to each of its committees, including Mr. Raspino, who replaced V. Burns Hargis as the chairman of the Audit Committee.

On April 1, 2013, Mr. McClendon ceased serving as President, CEO and a director of the Company. On March 29, 2013, the Board established a three-person Office of the Chairman while the Board continues its search for the Company’s next CEO. The Office of the Chairman consists of Mr. Dunham, Steven C. Dixon, the Company’s Acting CEO and Chief Operating Officer, and Domenic J. Dell’Osso, Jr., the Company’s Executive Vice President and Chief Financial Officer. The Office of the Chairman provides oversight of strategic, operational and financial matters as well as certain day-to-day management responsibilities.

Board Committees

The Company currently has three standing committees: an Audit Committee, a Compensation Committee and a Nominating, Governance and Social Responsibility Committee or Nominating Committee. Each committee has a charter which can be found on our website atwww.chk.com in the Corporate Governance sub-section of the section entitled “About”. A biographical overview of the members of our committees can be found beginning on page 5.

Name and Members(1) | Primary Responsibilities | Meetings | ||

Audit Committee(2) Louis A. Raspino (Chair) R. Brad Martin Merrill A. (“Pete”) Miller, Jr. | • Oversee the integrity of the Company’s financial statements and disclosure • Oversee the Company’s compliance with legal and regulatory requirements • Oversee the Company’s internal audit function • Appoint and oversee the independent auditor • Oversee the Company’s enterprise risk management program • Oversee the Employee and Vendor Hotline for anonymous reporting of questionable activity | 5 meetings in person 7 telephonic meetings | ||

Compensation Committee Merrill A. (“Pete”) Miller (Chair) Bob G. Alexander R. Brad Martin | • Establish compensation policies that effectively attract, retain and motivate executive officers • Establish goals and objectives relevant to CEO compensation, evaluate CEO performance and set CEO compensation levels • Periodically evaluate succession plans for executive officers • Evaluate and recommend to the Board compensation of directors and other executive officers • Oversee and administer the Company’s compensation plans • Establish and monitor compliance with stock ownership guidelines | 3 meetings in person 4 telephonic meetings | ||

Nominating Committee Louis A. Simpson (Chair) Archie W. Dunham Vincent J. Intrieri Frederic M. Poses | • Establish criteria for Board and committee membership and selection of new directors • Evaluate and recommend nominees for Board service • Periodically assess and advise the Board on sufficiency of the size and diversity of the Board • Periodically evaluate the Company’s Corporate Governance Principles and make recommendations to the Board on corporate governance matters • Oversee compliance by the Board and management with the Company’s Corporate Governance Principles and its Code of Business Conduct and Ethics • Oversee policies, programs and practices respecting corporate social responsibility | 3 meetings in person 1 telephonic meeting |

| (1) | All committee members are independent as determined by the Board in accordance with the NYSE corporate governance listing standards. |

| (2) | Messrs. Raspino, Martin and Miller are all independent, as determined by the Board in accordance with Section 10A of the Securities Exchange Act of 1934 (the “Exchange Act”), and each has been designated by the Board as an “audit committee financial expert”, as defined in Item 407(d) of Regulation S-K. For the relevant experience of Messrs. Raspino, Martin and Miller, please refer to their respective biographies on pages 6-7. |

-4-

Table of Contents

Code of Business Conduct and Ethics

The Board has adopted a Code of Business Conduct and Ethics applicable to all directors, officers and employees of the Company, including our principal executive officer, principal financial officer and principal accounting officer. The Code of Business Conduct and Ethics is posted on the Company’s website atwww.chk.com in the Corporate Governance sub-section of the section entitled “About”. Waivers of provisions of the Code as to any director or executive officer and amendments to the Code must be approved by the Audit Committee of the Board. We will post on our website required disclosure about any such waiver or amendment within four business days of such approval.

Communications to the Board

Shareholders and other interested parties may communicate with the Board, either individually or as a group, through one of the processes outlined on the Company’s website atwww.chk.com in the Corporate Governance sub-section of the section entitled “About”.

Director Criteria, Qualifications and Experience

The Nominating Committee periodically assesses the skills and the experience needed for the Board to properly oversee the business and affairs of the Company. The Committee then compares those skills to the skills of the current directors and potential director candidates. The Committee conducts targeted efforts to identify and recruit individuals who have the qualifications identified through this process. The Committee has used third party consultants to assist in identifying potential director nominees. The Committee considers director candidates recommended by shareholders and, in the past, has nominated appropriate candidates recommended pursuant to the foregoing process.

Chesapeake is a large, vertically integrated exploration and production company. As such, the Committee looks for its current and potential directors collectively to have a diverse mix of skills, qualifications and experience, some of which are described below:

• business leadership | • government/public policy | |

• corporate governance | • international | |

• energy production/distribution | • legal | |

• energy services | • risk management | |

• financial expertise | • technology |

The Committee seeks a mix of directors with the qualities that will achieve the ultimate goal of a well-rounded, diverse Board that thinks critically yet functions effectively by reaching informed decisions. The Committee’s charter was recently amended to ensure that diverse candidates were included in all director searches, taking into account race, gender, age, culture, thought, leadership and geography. The Committee and the Board believe that a boardroom with a wide array of talents and perspectives leads to innovation, critical thinking and enhanced discussion. Additionally, the Committee expects each of the Company’s directors to have proven leadership, sound judgment, integrity and a commitment to the success of the Company.

In evaluating director candidates and considering incumbent directors for nomination to the Board, the Committee considers a variety of factors. These include each nominee’s independence, financial literacy, personal and professional accomplishments and experience in light of the needs of the Company. For incumbent directors, the factors also include past performance on the Board and contributions to their respective committees. Along with each director’s biography, we have included below an assessment of the skills and experience of such director.

Directors

Archie W. Dunham, 74, has been the non-executive Chairman of our Board of Directors since June 2012, and has served as a member of the Company’s three-person Office of the Chairman since March 2013. Mr. Dunham served as Chairman of ConocoPhillips (NYSE:COP) from 2002 until his retirement in 2004. Prior to that, he served as Chairman, President and Chief Executive Officer of Conoco Inc. from 1999 to 2002, after being elected President and Chief Executive Officer in 1996. Mr. Dunham currently serves on the Board of Directors of Union Pacific Corporation (NYSE:UNP) and Louisiana-Pacific Corporation (NYSE:LPX). Mr. Dunham was a director of Phelps Dodge Corporation from 1998 to 2007 and Pride International, Inc. from 2005 until May 2011. Mr. Dunham is currently a member of Deutsche Bank’s Americas Advisory Board and is the past Chairman of the National Association of Manufacturers, the United States Energy Association and the National Petroleum Council. The Board believes Mr. Dunham’s experience as Chief Executive Officer of Conoco Inc. and Chairman of ConocoPhillips and service on multiple public company boards qualifies him to serve on the Board.

-5-

Table of Contents

Bob G. Alexander, 79, has been a member of our Board of Directors since June 2012. Mr. Alexander, a founder of Alexander Energy Corporation, served as Chairman of the Board, President and Chief Executive Officer of Alexander Energy from 1980 to 1996. Alexander Energy merged with National Energy Group, Inc., an oil and gas property management company, in 1996 and Mr. Alexander served as President and Chief Executive Officer from 1998 to 2006. From 1976 to 1980, Mr. Alexander served as Vice President and General Manager of the Northern Division of Reserve Oil, Inc. and President of Basin Drilling Corporation, both subsidiaries of Reserve Oil and Gas Company of Denver, Colorado. He currently serves on the Board of Directors of TransAtlantic Petroleum Ltd. (AMEX:TAT) and CVR Energy, Inc. (NYSE:CVI). Mr. Alexander also served as a director of Quest Resource Corporation from June to August 2008. Mr. Alexander has served on numerous committees with the Independent Petroleum Association of America, the Oklahoma Independent Petroleum Association and the State of Oklahoma Energy Commission. The Board believes Mr. Alexander’s experience as Chief Executive Officer of two public energy companies and current service as a director of two public energy companies qualifies him to serve on the Board.

Vincent J. Intrieri, 56, has been a member of our Board of Directors since June 2012. Mr. Intrieri has been employed by Icahn-related entities since October 1998 in various investment related capacities. Since January 2008, Mr. Intrieri has served as Senior Managing Director of Icahn Capital LP, the entity through which Carl C. Icahn manages private investment funds. In addition, since November 2004, Mr. Intrieri has been a Senior Managing Director of Icahn Onshore LP, the general partner of Icahn Partners LP, and Icahn Offshore LP, the general partner of Icahn Partners Master Fund LP, Icahn Partners Master Fund II LP and Icahn Partners Master Fund III LP, entities through which Mr. Icahn invests in securities. Mr. Intrieri has been a director of CVR Refining GP, LLC, the general partner of CVR Refining, LP (NYSE:CVRR), an independent downstream energy limited partnership, since January 2013; Navistar International Corporation (NYSE:NAV), a truck and engine manufacturer, since October 2012; CVR Energy, Inc. (NYSE:CVI), an independent petroleum refiner and marketer of high value transportation fuels, since May 2012; and Federal-Mogul Corporation (NYSE:FDML), a supplier of automotive powertrain and safety components, since December 2007. Mr. Intrieri was previously a director of Icahn Enterprises G.P. Inc., the general partner of Icahn Enterprises L.P. (NASDAQ:IEP), a diversified holding company engaged in a variety of businesses, including investment, automotive, energy, gaming, railcar, food packaging, metals, real estate and home fashion, from July 2006 to September 2012, and was Senior Vice President of Icahn Enterprises G.P. Inc. from October 2011 to September 2012; a director of Dynegy Inc. (NYSE:DYN), a company primarily engaged in the production and sale of electric energy, capacity and ancillary services, from March 2011 to September 2012; chairman of the board and a director of PSC Metals Inc., a metal recycling company, from December 2007 to April 2012; a director of Motorola Solutions, Inc. (NYSE:MSI), a provider of communication products and services, from January 2011 to March 2012; a director of XO Holdings, Inc., a telecommunications company, from February 2006 to August 2011; a director of National Energy Group, Inc., a company that was engaged in the business of managing the exploration, production and operations of natural gas and oil properties, from December 2006 to June 2011; a director of American Railcar Industries, Inc. (NASDAQ:AEII), a railcar manufacturing company, from August 2005 to March 2011, and was a Senior Vice President, the Treasurer and the Secretary of American Railcar Industries from March 2005 to December 2005; a director of WestPoint International, Inc., a manufacturer and distributor of home fashion consumer products, from November 2005 to March 2011; chairman of the board and a director of Viskase Companies, Inc., a meat casing company, from April 2003 to March 2011; a director of WCI Communities, Inc., a homebuilding company, from August 2008 to September 2009; a director of Lear Corporation (NYSE:LEA), a global supplier of automotive seating and electrical power management systems and components, from November 2006 to November 2008; and President and Chief Executive Officer of Philip Services Corporation, an industrial services company, from April 2005 to September 2008. CVR Refining, CVR Energy, Federal-Mogul, PSC Metals, XO Holdings, National Energy Group, American Railcar Industries, WestPoint, Viskase Companies and Philip Services each are or previously were indirectly controlled by Carl C. Icahn. Mr. Icahn also has or previously had a non-controlling interest in Chesapeake, Navistar, Dynegy, Motorola Solutions, WCI Communities and Lear, in each case, through the ownership of securities. Mr. Intrieri was a certified public accountant. The Board believes Mr. Intrieri’s vast executive experience and service on multiple public company boards qualifies him to serve on the Board.

R. Brad Martin, 61, has been a member of our Board of Directors since June 2012. Mr. Martin is the Chairman of RBM Venture Company, a private investment company, and was recently named interim president of the University of Memphis effective July 1, 2013. He was Chairman and Chief Executive Officer of Saks Incorporated (NYSE:SKS) from 1989 to January 2006, and remained Chairman until his retirement in May 2007. Mr. Martin currently serves as a director of FedEx Corporation (NYSE:FDX), First Horizon National Corporation (NYSE:FHN) and Dillard’s Inc. (NYSE:DDS), although he has notified Dillard’s that he will not stand for re-election at its annual meeting of stockholders in May 2013. He was previously a director of Caesars Entertainment Corporation (NASDAQ:CZR) (formerly Harrah’s Entertainment, Inc.), lululemon athletica inc. (NASDAQ:LULU), Gaylord Entertainment Company (now Ryman Hospitality Properties, Inc. (NYSE:RHP)) and Ruby Tuesday, Inc. (NYSE:RT). The Board believes Mr. Martin’s experience as Chief Executive Officer of a publicly traded company for nearly 20 years and service on multiple public company boards qualifies him to serve on the Board.

-6-

Table of Contents

Merrill A. (“Pete”) Miller, Jr., 62, has been a member of our Board of Directors since 2007 and was our Lead Independent Director from March 2010 to June 2012. Mr. Miller is Chairman, President and Chief Executive Officer of National Oilwell Varco, Inc. (NYSE:NOV), a supplier of oilfield services, equipment and components to the worldwide oil and natural gas industry. Mr. Miller joined NOV in 1996 as Vice President of Marketing, Drilling Systems and was promoted in 1997 to President of the company’s products and technology group. He was named President and Chief Operating Officer in 2000, elected President and Chief Executive Officer in 2001 and also elected Chairman of the Board in 2002. Mr. Miller served as President of Anadarko Drilling Company from 1995 to 1996. Prior to his service at Anadarko, Mr. Miller spent fifteen years at Helmerich & Payne International Drilling Company (NYSE:HP) in Tulsa, Oklahoma, serving in various senior management positions, including Vice President, U.S. Operations. Mr. Miller serves on the Board of Directors for the Offshore Energy Center, Petroleum Equipment Suppliers Association and Spindletop International, and is a member of the National Petroleum Council. The Board believes Mr. Miller’s more than 30 years of management and executive experience in the energy industry and service as Chairman, President and Chief Executive Officer of NOV qualifies him to serve on the Board.

Frederic M. Poses, 70, has been a member of our Board of Directors since June 2012. Mr. Poses is the Chief Executive Officer of Ascend Performance Materials, a private company. Previously, he was Chairman and Chief Executive Officer of Trane Inc. (formerly American Standard Companies, Inc.), a subsidiary of Ingersoll-Rand plc (NYSE:IR), from 1999 to 2008. He previously spent 30 years at AlliedSignal, Inc. and predecessor companies from 1969 to 1999, most recently as President and Chief Operating Officer. He currently serves as non-executive Chairman of the Board of Directors of TE Connectivity Ltd. (NYSE:TEL) and a director of Raytheon Company (NYSE:RTN). He is a former director of Centex Corporation (now a part of PulteGroup, Inc. (NYSE:PHM)) and WABCO Holdings Inc. (NYSE:WBC). The Board believes Mr. Poses’ experience as Chief Executive Officer of publicly traded and private companies and service on multiple public company boards qualifies him to serve on the Board.

Louis A. Raspino, 60, has been a member of our Board of Directors since March 2013 when he was appointed to the vacancy created by the retirement of V. Burns Hargis. Mr. Raspino was President and Chief Executive Officer of Pride International Inc., an international provider of contract drilling and related services to oil and natural gas companies, from June 2005 until the sale of the company in May 2011. He was the Executive Vice President and Chief Financial Officer of Pride International Inc. from December 2003 until June 2005. Before joining Pride International in December 2003, he was Senior Vice President and Chief Financial Officer of Grant Prideco, Inc., a manufacturer of drilling and completion products supplying the energy industry, from July 2001 until December 2003. Previously, he was Vice President of Finance for Halliburton Company (NYSE:HAL), Senior Vice President and Chief Financial Officer of The Louisiana Land & Exploration Company and began his career with Ernst & Young. He has been a director of Dresser-Rand Group, Inc. (NYSE:DRC) since 2005 and a director of Forum Energy Technologies, Inc. (NYSE:FET) since 2012. Mr. Raspino is a certified public accountant. The Board believes Mr. Raspino’s over 35 years experience in the oil and gas industry, including serving as Chief Executive Officer of Pride International, Inc., Chief Financial Officer of three public companies and 20 years experience in the exploration and production industry, and service on multiple public company boards qualifies him to serve on the Board.

Louis A. Simpson, 76, has been a member of our Board of Directors since June 2011. He is the Chairman of SQ Advisors, LLC, a private investment company. Mr. Simpson served as President and Chief Executive Officer, Capital Operations, of GEICO Corporation (a subsidiary of Berkshire Hathaway Corporation (NYSE:BRK.A)) from 1993 until his retirement on December 31, 2010. From 1985 to 1993, he served as Vice Chairman of the Board of GEICO. Mr. Simpson joined GEICO in 1979 as Senior Vice President and Chief Investment Officer. Prior to joining GEICO, Mr. Simpson was President and Chief Executive Officer of Western Asset Management, a subsidiary of the Los Angeles, California-based Western Bancorporation. Previously, Mr. Simpson was a partner at Stein Roe and Farnham, a Chicago, Illinois investment firm, and an instructor of economics at Princeton University. Mr. Simpson has also served as a director of VeriSign, Inc. (NASDAQ:VRSN) since 2005 and served as a director of SAIC, Inc. (NYSE:SAI) from 2006 to June 2012. He was previously a director of Western Asset Funds Inc. and Western Asset Income Fund and a trustee of Western Asset Premier Bond Fund until 2006. The Board believes Mr. Simpson’s experience as Chief Executive Officer, Capital Operations, of GEICO and service on multiple public company boards provides a unique blend of experience and qualifies him to serve on the Board.

Executive Officers

Steven C. Dixon, 54, was named Acting CEO effective April 1, 2013, and has served as a member of the Company’s three-person Office of the Chairman since March 2013. In addition, he has served as Executive Vice President—Operations and Geosciences and Chief Operating Officer since February 2010. Mr. Dixon served as Executive Vice President-Operations and Chief Operating Officer from 2006 to February 2010 and as Senior Vice President—Production from 1995 to 2006. He also served as Vice President-Exploration from 1991 to 1995.

-7-

Table of Contents

Domenic J. (“Nick”) Dell’Osso, Jr., 36, has served as Executive Vice President and Chief Financial Officer since November 2010, and has served as a member of the Company’s three-person Office of the Chairman since March 2013. Mr. Dell’Osso has also served as a director of the general partner of ACMP since June 2011. Mr. Dell’Osso served as Vice President—Finance of the Company and Chief Financial Officer of Chesapeake’s wholly owned midstream subsidiary, Chesapeake Midstream Development, L.P., from August 2008 to November 2010.

Douglas J. Jacobson, 59, has served as Executive Vice President—Acquisitions and Divestitures since 2006. He served as Senior Vice President—Acquisitions and Divestitures from 1999 to 2006.

Jeffrey A. Fisher, 53, has served as Executive Vice President—Production since December 2012. He served as Senior Vice President—Production from 2006 to December 2012. Mr. Fisher served as Vice President—Operations for the Company’s Southern Division from 2005 to 2006 and served as Operations Manager from 2003 to 2005.

Martha A. Burger, 60, has served as Senior Vice President—Human and Corporate Resources since 2007. She served as Treasurer from 1995 to 2007 and as Senior Vice President—Human Resources since 2000. She was the Company’s Vice President—Human Resources from 1998 until 2000, Human Resources Manager from 1996 to 1998 and Corporate Secretary from 1999 to 2000. From 1994 to 1995, she served in various accounting positions with the Company, including Assistant Controller—Operations.

Jennifer M. Grigsby, 44, has served as Senior Vice President and Treasurer since 2007 and as Corporate Secretary since 2000. She served as Vice President from 2006 to 2007 and as Assistant Treasurer from 1998 to 2007. From 1995 to 1998, Ms. Grigsby served in various accounting positions with the Company.

Michael A. Johnson, 47, has served as Senior Vice President—Accounting, Controller and Chief Accounting Officer since 2000. He served as Vice President of Accounting and Financial Reporting from 1998 to 2000 and as Assistant Controller from 1993 to 1998.

James R. Webb, 45, has served as Senior Vice President—Legal and General Counsel since October 2012. Prior to joining the Company, Mr. Webb was an attorney with the law firm of McAfee & Taft from February 1995 to October 2012.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934 requires our directors and executive officers and persons who beneficially own more than 10% of the Company’s common stock to file reports of ownership and subsequent changes with the Securities and Exchange Commission (the “SEC”). Based only on a review of copies of such reports and written representations delivered to the Company by such persons, the Company believes that there were no late filings under Section 16(a) by any such persons during 2012.

-8-

Table of Contents

Item 11.Executive Compensation

Compensation Discussion and Analysis

In this section, we describe the material components of our executive compensation system for the Company’s named executive officers listed below, whose compensation is set forth in the 2012 Summary Compensation Table and other compensation tables contained in this Item 11.

Aubrey K. McClendon | President and Chief Executive Officer, or CEO; co-founded the Company in 1989(1) | |

Steven C. Dixon | Acting Chief Executive Officer, or Acting CEO, Executive Vice President – Operations and Geosciences and Chief Operating Officer; has been with the Company for 22 years(2)(3) | |

Domenic J. (“Nick”) Dell’Osso, Jr. | Executive Vice President and Chief Financial Officer, or CFO; has been with the Company for four years(3) | |

Douglas J. Jacobson | Executive Vice President—Acquisitions and Divestitures; has been with the Company for 14 years | |

Jeffrey A. Fisher | Executive Vice President—Production; has been with the Company for 10 years |

| (1) | Mr. McClendon ceased serving as President and CEO of the Company on April 1, 2013. |

| (2) | Mr. Dixon was named Acting CEO effective April 1, 2013. |

| (2) | Messrs. Dixon and Dell’Osso, along with the Company’s independent, non-executive Chairman Mr. Dunham, were named to the Office of the Chairman upon its formation on March 29, 2013. |

We present our Compensation Discussion and Analysis in the following sections:

| 1. | Say-on-Pay Response and Compensation Highlights. In this section, we discuss the response of the Compensation Committee of our Board to the 2012 shareholder advisory vote on named executive officer compensation and highlight aspects of our redesigned executive compensation system. |

| 2. | Executive Compensation System. In this section, we describe the Company’s executive compensation philosophy and the material components of our executive compensation system, including certain important changes the Compensation Committee recently implemented. |

| 3. | 2012 Named Executive Officer Compensation. In this section, we detail the Company’s 2012 named executive officer compensation and explain how and why the Compensation Committee arrived at specific compensation decisions. |

| 4. | Other Executive Compensation Matters. In this section, we provide a brief overview of policies related to minimum stock ownership, prohibition of margining and derivative or speculative transactions involving Company stock and executive compensation clawbacks. We also review the risks associated with our compensation programs and accounting and tax treatment of compensation. |

| 5. | Actions Related to 2013 Executive Compensation. In this section, we provide an overview of certain Compensation Committee executive compensation decisions for 2013. |

| 6. | Mr. McClendon’s Separation; Mr. Dixon’s Appointment as Acting CEO. In this section, we provide details with regard to compensatory arrangements related to Mr. McClendon’s separation from the Company and Mr. Dixon’s appointment as Acting CEO. |

Say-on-Pay Response and Compensation Highlights

Response to 2012 Shareholder Advisory Vote on Named Executive Officer Compensation

At our 2012 annual meeting of shareholders, approximately 80% of shares were cast “against” our named executive officer compensation. Shortly thereafter, in June 2012, the Board appointed five new independent directors, including an independent, non-executive Chairman of the Board. The Compensation Committee, comprised of entirely new members, considered the results of the advisory vote and believed it conveyed our shareholders’ dissatisfaction with the Company’s executive compensation in light of performance. The Compensation Committee engaged in a comprehensive review of the Company’s executive compensation system, considering the outcome from the 2012 annual meeting, with a goal of ensuring that the Company’s compensation programs appropriately tie executive pay to Company performance. To assist in its review, the Compensation Committee engaged Frederic W. Cook & Co., Inc., or F.W. Cook, as its independent compensation consultant. The Company discussed its 2012 compensation program with many of its major shareholders. In addition, the Company’s largest shareholder, representing 13.7% of the Company’s common stock, recommended two directors who currently serve on our Compensation Committee.

-9-

Table of Contents

The Compensation Committee implemented substantial changes to the Company’s executive compensation system in 2012, including implementing annual and long-term incentive programs that are based on objective performance criteria and that are designed to tie pay to performance. In response to shareholder feedback emphasizing the importance of incorporating both total shareholder return, or TSR, and operational performance goals in order to provide named executive officers with effective incentives associated with the Company’s long-term growth and performance, the Company included operational metrics as part of the performance-based component of its long-term incentive program for 2012. The Compensation Committee’s decisions with regard to the Company’s executive compensation system for 2012 included the following:

| • | Adopted a formal compensation philosophy that emphasizes pay for performance and targets peer median compensation levels. |

| • | Exercised downward discretion to further reduce payouts calculated based on a formulaic assessment of Company performance under the annual incentive program in 2012 to an average of approximately 50% of 2011 annual incentive payouts for the named executive officers and, after considering Mr. McClendon’s recommendation to such effect, awarded no annual incentive compensation to Mr. McClendon. |

| • | Held base salaries flat in 2012 for the majority of our named executive officers. Only Messrs. Dell’Osso and Fisher received base salary increases in 2012, which were driven by competitive positioning and internal pay equity considerations. The salaries of Messrs. Dixon and Jacobson were not increased in 2012, and remained at levels set for each in July 2008. Similarly, Mr. McClendon’s salary remained at $975,000, reflecting no increase since 2006. We increased Mr. Dixon’s salary to $975,000 in connection with his appointment as Acting CEO effective April 1, 2013. See “—Mr. McClendon’s Separation; Mr. Dixon’s Appointment as Acting CEO” on page 28. |

| • | Significantly reduced perquisites for executive officers, including eliminating, or further limiting in the case of Mr. McClendon, personal use of fractionally owned Company aircraft by named executive officers. |

The connection between pay and performance is further reflected in decisions of the Compensation Committee for 2013 executive compensation, including:

| • | Entered into new executive employment agreements that contain substantial changes from the Company’s previous executive employment agreements, including the elimination of “single-trigger” change-of-control cash payments and cash payments upon death or disability. |

| • | Maintained base salary levels for the named executive officers at 2012 levels, other than for Mr. Dixon, whose base salary was increased upon his appointment as Acting CEO. |

| • | Implemented a new Annual Incentive Plan and based annual incentive opportunities on the Company’s performance relative to eleven pre-established objective operational and financial performance goals. Target annual incentive opportunities remained flat for named executive officers. |

| • | Reduced target long-term incentive awards for named executive officers by approximately 10% from 2012 target levels. |

At the 2013 annual meeting of shareholders, we will again hold an advisory vote to approve named executive officer compensation, in accordance with the shareholders’ advisory vote in 2011 in favor of annual advisory votes on executive compensation. The Compensation Committee will consider the results from this year’s and future advisory votes on executive compensation.

Compensation Highlights

Our redesigned executive compensation system has the following attributes:

Compensation System | Description | |

Compensation philosophy* | Adopted formal compensation philosophy that emphasizes pay for performance and targets peer median compensation levels | |

Objective long-term performance measures* | Over 50% of long-term compensation is subject to achievement of objective pre-determined performance goals tied to operational and strategic objectives and the creation of long-term shareholder value | |

Objective annual incentive program with pre-determined performance measures* | Annual incentive compensation based on achievement of pre-determined objective operational and financial performance goals | |

2012 CEO compensation reduced* | Reduced 2012 CEO total compensation by $1 million, including no 2012 annual incentive compensation, following an earlier 2011 reduction of total compensation of over $3 million |

-10-

Table of Contents

No tax gross-ups for executive officers | No tax gross-ups for executive officers | |

Historical and expected future use of tally sheets | Tally sheets allow the Compensation Committee to analyze both the individual elements of compensation (including the compensation mix) and the aggregate total amount of actual and projected compensation | |

Minimum stock ownership guidelines* | Enhanced minimum stock ownership guidelines for all named executive officers | |

Margining and speculative transactions prohibited* | Full prohibition on margining, derivative or speculative transactions, such as hedges, pledges and margin accounts, by executive officers | |

Incentive plans designed to qualify for Section 162(m) tax deductibility | Performance share unit (PSU) awards are intended to qualify as performance-based compensation under Section 162(m); we are asking that shareholders approve the 2013 annual incentive plan, which will permit 2013 and future annual incentive compensation to so qualify | |

Substantially all perquisites ended* | Ended substantially all perquisites for named executive officers, including personal use of Company aircraft, except in the case of Mr. McClendon, who agreed to increase his reimbursement to the Company for personal travel in excess of $250,000 | |

Double trigger upon change of control* | Effective January 1, 2013, new employment agreements with our named executive officers eliminated “single-trigger” change-of-control cash payments | |

Clawback policy* | Implemented a compensation recovery policy to recapture unearned incentive payments in the event of material noncompliance with any financial reporting requirement under the law that leads to an accounting restatement | |

Representative and relevant peer group* | The Compensation Committee worked with its independent compensation consultant to increase the number of companies in the peer group from five to 11 while satisfying other important peer group criteria such as comparable size and relevance to the Company’s industry | |

No cash payments on death and disability* | Effective January 1, 2013, new employment agreements with our named executive officers other than the CEO eliminated lump sum payments of 52 weeks of base salary in the event of death and 26 weeks of base salary in the event of a disability |

| * | Indicates item has been implemented or further enhanced by the Compensation Committee since the beginning of 2012. |

Executive Compensation System

Philosophy and Objectives of our Executive Compensation System

In 2012, to guide its review and future compensation decisions, the Compensation Committee adopted a formal compensation philosophy. The philosophy reflects the Compensation Committee’s intent to generally set all elements of target compensation (e.g., base salary, target annual incentive award opportunity and target long-term incentive award opportunity) at the median of similarly situated executives among the Company’s peer group or other relevant industry benchmarks. The competitive positioning of target compensation levels for individuals may vary above or below the median based on executive-specific factors such as tenure, experience, proficiency in role or criticality to the organization. The Compensation Committee’s objective is to have a program that:

| • | Attracts and retains high performing executives; |

| • | Pays for performance and thus has a meaningful portion of pay tied to business performance; |

| • | Aligns compensation with shareholder interests while rewarding long-term value creation; |

| • | Discourages excessive risk by rewarding both short-term and long-term performance; |

| • | Reinforces high ethical conduct, environmental awareness and safety; and |

| • | Maintains flexibility to better respond to the dynamic and cyclical energy industry. |

Unliketarget compensation levels, which are set by the Compensation Committee near the beginning of the year,actualcompensation is a function of the Company’s operational, financial and stock price performance, as reflected through annual incentive payouts, performance share payouts and the value of all other long-term incentive awards at vesting. Actual compensation is intended to vary above or below target levels commensurate with Company performance.

Elements of our Executive Compensation System

The purpose and key characteristics of each element of our 2012 executive compensation system are summarized below:

-11-

Table of Contents

Element | Purpose | Key Characteristics | ||

Base salary | Reflects each named executive officer’s base level of responsibility, leadership, tenure, qualifications and contribution to the success and profitability of the Company and the competitive marketplace for executive talent specific to our industry. | Fixed compensation that is reviewed annually and adjusted if and when appropriate. | ||

Annual incentive award | Motivates named executive officers to achieve our short-term business objectives that drive long-term performance while providing flexibility to respond to opportunities and changing market conditions. | Variable performance-based annual cash award. Awards were based on corporate performance compared to pre-established performance goals. Adjusted downward for all named executive officers in 2012. | ||

PSU award | Motivates named executive officers to achieve our business objectives by tying incentives to our financial and key operational metrics over the performance period while continuing to reinforce the link between the interests of our named executive officers and our shareholders. | Variable performance-based long-term award. The ultimate number of units earned is based on the achievement of relative and absolute total shareholder return and production and proved reserve growth performance goals. | ||

Restricted stock award | Motivates named executive officers to achieve our business objectives by tying incentives to the performance of our common stock over the long term; reinforces the link between the interests of our named executive officers and our shareholders; motivates our named executive officers to remain with the Company by mitigating swings in incentive values during periods of high commodity price volatility. | Long-term restricted stock award with a ratable vesting period over four years. The ultimate value realized varies with our common stock price. | ||

Other compensation | Provides benefits that promote employee health and work-life balance, which assists in attracting and retaining our named executive officers. | Indirect compensation element consisting of health and welfare plans and minimal perquisites. | ||

2012 Named Executive Officer Compensation

2012 Process for Determining Executive Compensation

Role of the Compensation Committee

In determining compensation, the Compensation Committee makes an overall assessment of the performance of the named executive officer team and the role and relative contribution of each of its members. In 2012, the Compensation Committee transitioned to conducting performance and compensation reviews of our named executive officers on an annual basis instead of on a semi-annual basis. In 2012, the Compensation Committee’s approach consisted of both subjective consideration of each named executive officer’s performance and overall role in the organization and objective consideration of the Company’s performance relative to predetermined metrics as more fully described beginning on page 15 under “—2012 Named Executive Officer Compensation Elements”. In its assessment of the performance of each named executive officer in 2012, the Compensation Committee considered the following:

Individual Performance | Company Performance | Intangibles | ||

• Named executive officer’s contributions to the development and execution of the Company’s business plans and strategies (including contributions that are expected to provide substantial benefit to the Company in future periods)

• Performance of the named executive officer’s department or functional unit

• Level of responsibility

• Longevity with the Company | • Overall performance of the Company, including progress made with respect to production, reserves, operating costs, drilling results, risk management activities and asset monetizations

• Financial performance as measured by cash flow, net income, cost of capital, general and administrative costs, progress towards debt reduction goals and common stock price performance | • Leadership ability

• Demonstrated commitment to the Company

• Motivational skills

• Attitude

• Work ethic |

Role of the Compensation Consultant

The Compensation Committee has the sole authority for the appointment, compensation and oversight of the Company’s outside compensation consultant. Our Compensation Committee set out to redesign our executive compensation system and, from the second half of 2011 through June 2012, retained Cogent Compensation Partners, an independent compensation consulting firm with extensive experience in the energy industry, to provide recommendations to the Compensation Committee for the Company’s 2012 executive compensation system. At the request of the Compensation Committee, Cogent conducted a peer group benchmarking analysis and assessed all elements of the Company’s executive compensation system and practices and designed and proposed new program elements, including a performance-based annual

-12-

Table of Contents

incentive program and a mix of long-term incentives consisting of over half PSUs. The Compensation Committee formally adopted the proposed program elements, as discussed in detail below under “—2012 Named Executive Officer Compensation Elements”. The compensation services provided also included advising on director compensation.

In support of the comprehensive review of the Company’s executive compensation system initiated by the Compensation Committee following the 2012 annual meeting, the Compensation Committee retained F.W. Cook as its independent compensation consultant to replace Cogent. F.W. Cook provided an objective analysis of, and counsel on, the Company’s executive compensation system, attending meetings of the Compensation Committee upon request and communicating with the chairman of the Compensation Committee between meetings. Both Cogent and F.W. Cook reported directly to the Compensation Committee and neither provided additional services to the Company.

During 2012, Pay Governance LLC was retained by Company management to provide services related to the Company’s compensation program, policies and processes, including consulting on the Company’s executive compensation system. On occasion, the Compensation Committee obtained the advice of Pay Governance through meetings in which F.W. Cook also participated. The Compensation Committee further directed F.W. Cook to review and coordinate with Pay Governance on the delivery of any work product by Pay Governance to the Committee, to perform an independent, objective analysis of market and other data provided by Pay Governance and to generally counsel the Committee as to the advice obtained from Pay Governance.

The Compensation Committee evaluated whether conflicts of interest were created by the retention of any of the advisors providing compensation consulting services in 2012, considering the following factors: (1) other services provided to the Company by the advisor; (2) past fees paid to the advisor as a percentage of total revenue of the advisor; (3) conflicts of interest policies of the advisor; (4) relationships between the advisor and members of the Board; (5) company stock owned by employees of the advisor; and (6) relationships between the advisor and any executive of the Company. As a result of this assessment, the Compensation Committee concluded that (i) no conflicts of interest exist with respect to F.W. Cook and (ii) Pay Governance is not independent from management given the reporting relationship with management, the responsibility of management for the oversight of Pay Governance’s work product and the services provided. The Compensation Committee concluded that any potential conflict posed by the Compensation Committee’s receipt of advice from Pay Governance was sufficiently mitigated by the direct involvement of F.W. Cook and the Compensation Committee’s own examination and assessment of the objectivity of Pay Governance’s advice.

Benchmarking

In 2011, at the request of the Compensation Committee, Cogent conducted a peer group benchmarking analysis. The objective of this analysis was to understand the competitiveness of the named executive officers’ total direct compensation, consisting of base salary, annual incentive compensation and the value of long-term incentive awards, relative to our compensation peer group companies. The peer group consisted of certain exploration and production peer companies which are similar to the Company in size, scope and nature of business operations. Cogent collected and analyzed the benchmark data based on publicly disclosed information and presented its analysis to the Compensation Committee. The analysis indicated that total direct compensation for our CEO and each of the other named executive officers in 2011 generally ranged from the median to the seventy-fifth percentile of benchmark data as compared to our peer group. These results informed the Compensation Committee’s decisions with respect to setting 2012 executive compensation, including establishing the targets for the newly implemented performance-based annual incentive award program and PSU component of the Company’s long-term incentive program for named executive officers. Our 2011 industry peer group consisted of the following companies: Anadarko Petroleum Corporation, Apache Corporation, Devon Energy Corporation, EOG Resources, Inc. and Occidental Petroleum Corporation.

During 2012, F.W. Cook was asked by the Compensation Committee to review the Company’s peer group in support of the Committee’s comprehensive review of the Company’s executive compensation system following the 2012 annual meeting of shareholders. In 2012, following F.W. Cook’s review, the Compensation Committee enlarged the peer group to better align it with typical market practice in terms of the number of peers and the Company’s relative size. Peer group candidates were drawn from the relevant Global Industry Classification Standard group and narrowed based on size criteria, primarily revenue and market capitalization. Marathon Oil Corporation and Noble Energy, Inc. satisfied the size, scope and nature of business operations criteria and were added to the peer group. Within the exploration and production industry, there are a small number of companies that closely resemble us in size, scope and nature of business operations. Enlarging our peer group also required that the Compensation Committee broaden its industry screen to include integrated oil and gas companies that also satisfied the revenue and market capitalization criteria, which resulted in adding Hess Corporation and Murphy Oil Corporation to the Company’s peer group. These companies are also considered peers by other companies in our peer group. Finally, the Compensation Committee added Continental Resources, Inc. and SandRidge Energy, Inc. to the peer group as they are Oklahoma-based exploration and production companies that are direct competitors with the Company for local talent.

-13-

Table of Contents

Our resulting industry peer group contains companies in our industry that are both larger and smaller in size and scope. With the exception of the integrated oil and gas companies discussed above, all of the peer companies are independent exploration and production companies. We considered companies that compete in our industry, but are significantly larger than we are, and companies that compete in unrelated industries within the energy sector such as the mining or coal industries but did not include such companies in our peer group.

We compete with the companies in our compensation peer group for talent and the Compensation Committee believes the selected companies are currently the most appropriate for use in executive compensation benchmarking. The differences and similarities between us and the companies in our industry peer group are taken into consideration when referencing benchmarks for named executive officer compensation decisions. As discussed above under “—Executive Compensation System—Philosophy and Objectives of Our Executive Compensation System”, the Compensation Committee intends to generally set all elements of target compensation at the median of similarly situated executives among the Company’s peer group and may also consider other relevant industry benchmarks in making compensation decisions. The Compensation Committee directed F.W. Cook to conduct a peer group benchmarking analysis using the new peer group companies and determined that, relative to the new peer group companies, target total cash compensation for our CEO and other named executive officers was near the median of the Company’s peer group target total cash compensation. Target total direct compensation for our CEO and other named executive officers, however, exceeded the median, falling around the 75% percentile, suggesting the stronger than necessary competitive positioning of target long-term incentive grants. This determination became one factor in the Compensation Committee’s determination to reduce the long-term incentive as detailed below under “—Actions Related to 2013 Executive Compensation”.

CEO and Management Role in Executive Compensation Process

Mr. McClendon generally met with the chairman of the Compensation Committee in 2012 and, as appropriate, made recommendations and participated in discussions in order to provide information to the Compensation Committee regarding the compensation of the other named executive officers. On occasion, Mr. McClendon attended Compensation Committee meetings; however, the Compensation Committee met in executive session without Mr. McClendon throughout the year. Following such recommendations, the Compensation Committee discussed the compensation of each named executive officer and approved the final named executive officer compensation amounts, subject to such modifications as it deemed appropriate. Following such approval, the Compensation Committee made a report to the Board of Directors for discussion and ratification. Mr. McClendon, not being a member of the Compensation Committee, did not vote at Compensation Committee meetings, and he did not participate in the Board’s vote on the acceptance and approval of the Compensation Committee’s recommendations or reports with respect to his compensation.

In addition, our CEO, CFO, COO, Senior Vice President—Human and Corporate Resources and Senior Vice President, Treasurer and Corporate Secretary typically provide the Compensation Committee and its advisors with detailed analyses and recommendations regarding each element of named executive officer compensation to facilitate the Compensation Committee’s annual review of named executive officer compensation.

Use of Tally Sheets in Executive Compensation Process

The information provided to the Compensation Committee has historically included tally sheets detailing for each named executive officer:

| • | the components of the named executive officer’s current compensation, including cash compensation, equity-based compensation, accumulated 401(k) and deferred compensation balances and perquisites; |

| • | potential payouts under the termination of employment and change of control provisions under the named executive officer’s employment agreement and applicable equity compensation plans; and |

| • | projected wealth accumulation from the named executive officer’s outstanding equity compensation awards assuming 0%, 5% and 10% appreciation and depreciation in the price of the Company’s common stock over the next five years. |

The tally sheets bring together in one place all of the elements of actual and potential future compensation of the named executive officers, as well as information about their wealth accumulation. This allows the Compensation Committee to analyze both the individual elements of compensation (including the compensation mix) and the aggregate total amount of actual and projected compensation. In light of the comprehensive review of executive compensation in 2012 conducted with the assistance of Pay Governance and F.W. Cook, the Committee did not incorporate the use of tally sheets. However, the Compensation Committee intends to use tally sheets in the future.

2012 Corporate Performance Highlights

2012 was a period of transition and provided many challenges for our Company. We are the second-largest producer of natural gas, a top 11 producer of liquids and the most active driller of wells in the U.S. The natural gas commodities environment of 2012 placed significant stress on our financial performance and weighed heavily on the Company’s TSR, along with other financial performance measures.

-14-

Table of Contents

The period was also one of substantial accomplishment. In that time, the Company continued its transition to an operational focus on asset development, concluding its leasehold acquisition phase and exiting ancillary businesses that were no longer integral parts of our overall business strategy. Further, lower natural gas prices in 2012 and early 2013 have confirmed the Company’s strategy, initiated in 2011, to focus leasehold acquisitions and production activities on increasing liquids production, which includes oil and natural gas liquids. In 2012, the Company executed value-creating asset sales of approximately $12 billion of assets and had one of the best liquids growth stories in the industry, with liquids production up approximately 54% on average relative to 2011.

In 2012, Chesapeake delivered the following major accomplishments:

| • | Continued Growth Through the Drillbit. We believe that our most distinctive characteristic is our commitment and ability to grow production and proved reserves organically through the drillbit at a low cost in areas with large unconventional accumulations of natural gas and liquids. We are currently utilizing 83 operated drilling rigs and 31 non-operated drilling rigs to conduct the most active drilling program in the U.S. We are active in most of the nation’s major unconventional plays, where we drill more horizontal wells than any other company in the industry. For many years, we have invested large amounts of capital in undeveloped leasehold, three dimensional (3-D) seismic information and human resources to take full advantage of our capacity to grow through the drillbit. As a result of those investments, we have been able to increase production for 23 consecutive years. Our daily production for 2012 averaged 3.89 bcfe, an increase of 614 mmcfe, or 19%, over the 3.272 bcfe of daily production for 2011, and consisted of 3.08 bcf of natural gas (80% on a natural gas equivalent basis), approximately 85,420 bbls of oil (13% on a natural gas equivalent basis) and approximately 48,130 bbls of natural gas liquids (7% on a natural gas equivalent basis). Our natural gas production in 2012 grew by 12%, or 333 mmcf per day; our oil production increased by 84%, or approximately 38,950 bbls per day; and our natural gas liquids production increased by 19%, or approximately 7,820 bbls per day. |

| • | Increased Liquids Production. In recognition of the value gap between liquids and natural gas prices that has widened to historic levels in the last five years, we directed a significant portion of our technological and leasehold acquisition expertise to identify, secure and commercialize new unconventional liquids-rich plays. This transition results in a more balanced and likely more profitable portfolio between natural gas and liquids. To date, we have established production in multiple liquids-rich plays on approximately 6.4 million net acres. Our production of liquids averaged approximately 133,550 bbls per day during 2012, a 54% increase over the average during 2011, as a result of the increased development of our unconventional liquids-rich plays. In 2012, approximately 85% of our drilling and completion expenditures were allocated to liquids-rich plays, compared to 50% in 2011 and 30% in 2010. |

| • | Continued to Focus our Operations in the “Core of the Core” of our Leasehold. We have made significant acquisitions of leasehold inventory and necessary investments in infrastructure, oilfield services, seismic data and human resources that have allowed us to drill wells more successfully and at a lower cost. Recently, we have shifted our focus to the development of the 10 plays in which we have a #1 or #2 ownership position. In an effort to optimize our portfolio around our core natural gas and oil properties, during 2012 we completed sales of natural gas and oil properties, midstream and other assets for proceeds of approximately $12 billion (including $1.25 billion from the sale of a preferred security in a subsidiary). By concentrating on the “core of the core” of our assets, we believe we can leverage our past investments to prioritize our drilling program around our highest-return assets and enhance returns on capital. |

We believe this is an excellent series of accomplishments in a very tough year for the industry as natural gas prices reached 10-year lows in early 2012 and remained depressed throughout the year.

2012 Named Executive Officer Compensation Elements

In December 2011, the Compensation Committee adopted substantial changes which are reflected in our 2012 executive compensation system. As shown below, our 2012 system continued to utilize base salary and restricted stock awards and also featured the following new performance-based components: (1) annual incentive awards based on objective pre-established performance goals and (2) PSUs under our Amended and Restated Long Term Incentive Plan, or LTIP.

-15-

Table of Contents

Base Salary

Base salaries reflect each named executive officer’s base level of responsibility, leadership, tenure and contribution to the success and profitability of the Company and the competitive marketplace for executive talent specific to our industry. With the exception of Messrs. Dell’Osso and Fisher, base salaries for named executives remained flat for 2012.

Annual Incentive Compensation

The annual incentive component of our executive compensation system is intended to motivate and reward named executive officers for achieving our short-term business objectives that we believe drive the overall performance of the Company over the long term. In 2012, the Compensation Committee focused heavily on redesigning the annual incentive program, implementing a formulaic approach to awarding annual incentives based on an evaluation of the Company’s performance relative to seven pre-established, objective operational and financial goals. The Company proposed the 2012 Annual Incentive Plan at the 2012 annual meeting of shareholders, which failed to receive shareholder approval. In response to that vote and the Company’s 2012 say on pay vote, the Compensation Committee reformulated the 2012 annual incentive program using the proposed 2012 Annual Incentive Plan as a framework and establishing a formulaic methodology for determining annual incentive awards based on the Company’s achievement of performance goals based on the original performance goals established by the Compensation Committee in 2011 and communicated to shareholders in the 2012 proxy statement. In doing so, the Compensation Committee removed any ability to exercise upward discretion; however, the Compensation Committee retained the ability to reduce payouts below the amounts calculated by the formula based on qualitative factors.

Calculating Annual Incentive Awards. The following formula was used to calculate the maximum payment that could be awarded to a named executive officer under the reformulated 2012 annual incentive program:

Base Salary X Target Percentage of Base Salary X Payout Factor (0 - 200%)

The Compensation Committee used the base salary in effect on the last day of 2012 in calculating the annual incentive payments. The Compensation Committee established the target percentage of base salary of 150% for the CEO, 125% for EVPs and 100% for SVPs to provide an annual incentive opportunity that is competitive with our peers. Following the end of 2012, the Compensation Committee determined the payout factor based on the Company’s achievement of pre-established threshold, target and maximum performance levels and the corresponding payout opportunities of 50%, 100% and 200% of the target percentage of base salary (using linear interpolation for performance levels falling in between threshold and target and between target and maximum) with no payment for performance not achieving the minimum 50% threshold performance level, as discussed below. The following chart shows the range of annual incentive award opportunities expressed as a percentage of salary for the named executive officers by title, based on the target percentage of base salary multiplied by the above-listed threshold, target and maximum payout opportunities.

Executive Level | Threshold | Target | Maximum | |||||||||

CEO | 75 | % | 150 | % | 300 | % | ||||||

EVP | 62.5 | % | 125 | % | 250 | % | ||||||

SVP | 50 | % | 100 | % | 200 | % | ||||||

-16-

Table of Contents

The 2012 annual incentive awards payable to certain named executive officers were further subject to limitations previously imposed under the executives’ employment agreements. Given the outcome of the formulaic analysis described below and the Compensation Committee’s further reduction of annual incentive payouts, in 2012, the annual incentive payments did not exceed the limitations prescribed by any of our named executive officers’ employment agreements.

Calculation of Payout Factor. In reformulating the 2012 annual incentive program, the Compensation Committee established the performance goals detailed in the table below based on the annual incentive performance goals previously disclosed in the Company’s 2012 proxy statement, which it believed appropriately reflected factors that positively impact shareholder value. The table below also details the Company’s level of achievement with respect to each performance goal and the final payout factor to be applied to each named executive officer’s target annual incentive award opportunity calculated using linear interpolation as described above.

A | B | C | D | E= D/C | F (a function of E) | G = F x B | ||||||||||||||

Goal | Weighting | Performance | Performance | Achievement Level | Individual Payout Factor | Weighted Payout Factor | ||||||||||||||

Operating cash flow(a) | 10.0 | % | $4.691 billion | $4.053 billion | 86 | % | 72 | % | 7.2 | % | ||||||||||

Adjusted EBITDA(b) | 10.0 | % | $4.6 billion | $3.754 billion | 82 | % | 64 | % | 6.4 | % | ||||||||||

Long-term debt reduction | 10.0 | % | $1.126 billion | ($1.531 billion) | 0 | % | 0 | % | 0.0 | % | ||||||||||

Adjusted net income(c) | 10.0 | % | $2.064 billion | $0.285 billion | 14 | % | 0 | % | 0.0 | % | ||||||||||

Liquids production (% of production mix) | 20.0 | % | 20% | 20% | 100 | % | 100 | % | 20.0 | % | ||||||||||

2012 production (bcfe) (d) | 20.0 | % | 1,294 | 1,477 | 114 | % | 156 | % | 31.2 | % | ||||||||||

Organic proved reserves added | 20.0 | % | 3.5 | 3.62 | 103 | % | 112 | % | 22.4 | % | ||||||||||

FINAL PAYOUT FACTOR: 87.2% |

| |||||||||||||||||||

| (a) | Operating cash flow represents net cash provided by operating activities before changes in assets and liabilities. For 2012, operating cash flow was $4.053 billion. |

| (b) | EBITDA represents net income (loss) before income tax expense, interest expense and depreciation, depletion and amortization expense. Adjusted EBITDA excludes certain items that management believes affect the comparability of operating results, including unrealized gains and losses on natural gas, oil and natural gas liquids derivatives, impairments, gains and losses on sales of fixed assets and investments, and losses on purchases of debt. For 2012, adjusted EBITDA was $3.754 billion. |

| (c) | Adjusted net income available to common stockholders represents net income available to common stockholders, excluding certain items that management believes affect the comparability of operating results, including unrealized gains and losses on derivatives, impairments, gains and losses on sales of fixed assets and investments, losses on purchases/exchanges of debt. For 2012, adjusted net income available to common stockholders was $285 million. |

| (d) | The production target is measured against full-year Company performance ignoring production gains/losses associated with asset sales and purchases. The Compensation Committee believes this adjustment is appropriate in light of the Company’s strategic goal of divesting non-core assets. |

| (e) | The proved reserves growth target is an organic growth goal and ignores changes in proved reserves caused by changes in oil and natural gas prices and asset sales and purchases. The Compensation Committee believes these adjustments are appropriate in light of the Company’s strategic goal of divesting non-core assets and promoting organic proved reserves growth through the drillbit. |

Summary of Payments for 2012. The annual incentive analysis under the reformulated annual incentive program yielded below target payouts for all executives. In light of the Company’s performance in 2012, the Compensation Committee exercised negative discretion to further reduce the payouts otherwise calculated by the formula above, resulting in average year-over-year reductions to named executive officers’ annual incentive compensation of approximately 50% and, after considering Mr. McClendon’s recommendation to such effect, awarded him no annual incentive compensation for 2012. The following table shows how the formula was applied and the actual amounts awarded under the 2012 annual incentive program.

Name | Base Salary(a) | Target Annual Incentive(b) | Target Value of Annual Incentive | Potential Payments at Grant Date(c) | Payout Factor | Range of Payments based on 2012 Performance | 2012 Actual Award | 2011 Cash Bonus Award | Percentage Change | |||||||||||||||||||||||||||

Aubrey K. McClendon | $ | 975,000 | 150 | % | $ | 1,462,500 | $ | 0 – $1,951,000 | 87.2 | % | $ | 0 – $1,275,300 | $ | 0 | $ | 1,950,000 | -100.0 | % | ||||||||||||||||||

Steven C. Dixon | 860,000 | 125 | % | 1,075,000 | 0 – 1,361,000 | 87.2 | % | 0 – 937,400 | 775,000 | 1,360,000 | -43.01 | |||||||||||||||||||||||||

Domenic J. (“Nick”) Dell’Osso, Jr. | 725,000 | 125 | % | 906,250 | 0 – 1,812,500 | 87.2 | % | 0 – 790,250 | 750,000 | 1,025,000 | -26.83 | |||||||||||||||||||||||||

-17-

Table of Contents

Douglas J. Jacobson | 800,000 | 125 | % | 1,000,000 | 0 – 1,201,000 | 87.2 | % | 0 – 872,000 | 700,000 | 1,200,000 | -41.67 | |||||||||||||||||||||||

Jeffrey A. Fisher | 725,000 | 125 | % | 906,250 | 0 – 1,812,500 | 87.2 | % | 0 – 790,250 | 575,000 | 965,000 | -40.41 |

| (a) | As of December 31, 2012. |

| (b) | Reflected as a percentage of base salary. |

| (c) | Maximum amounts for Messrs. McClendon, Dixon and Jacobson reflect contractual caps on annual cash bonus payments pursuant to their employment agreements with the Company effective through 2012. See “—Executive Compensation Tables—Grants of Plan-based Awards Table for 2012” for more details. |

The Compensation Committee has continued to improve the annual incentive program applicable to our named executive officers for 2013 as discussed in more detail under “—Actions Related to 2013 Executive Compensation” on page 25 below.

Long-Term Incentive Compensation

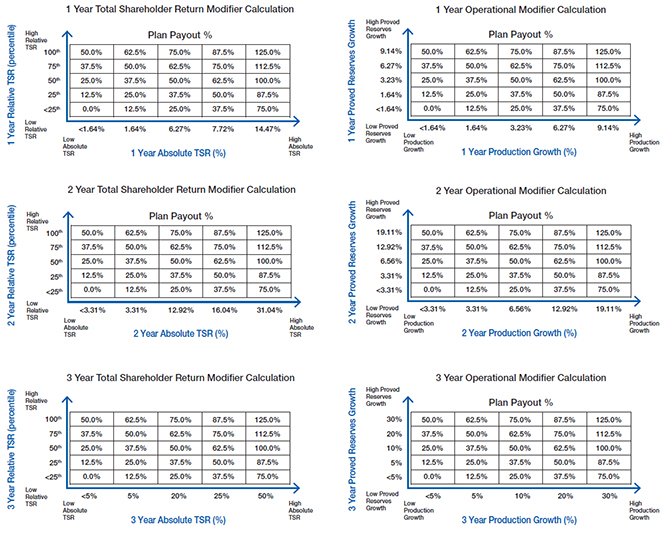

Long-term incentive compensation aligns the interests of the named executive officers with our shareholders, consistent with our goal of shareholder value creation. In 2012, the Compensation Committee and the Board approved significant modifications to our long-term incentive compensation program, incorporating PSU awards under the LTIP into the mix of long-term incentive compensation. Total compensation for the named executive officers is weighted heavily toward long-term incentive compensation, and for 2012 a substantial majority of each named executive officer’s total incentive compensation consisted of the grant of restricted stock and PSUs. For 2012, the Compensation Committee determined that long-term incentive compensation that consists of approximately half restricted stock and half performance-based incentives best met our compensation objectives. This approach is intended to motivate our named executive officers to achieve our business objectives by tying incentives to the achievement of our key financial and operational performance objectives and continuing to reinforce the link between the interests of our named executive officers and our shareholders.

2012 Restricted Stock Awards.Since 2004, the Company has provided long-term incentive compensation in the form of restricted stock granted under the LTIP. On the first trading day of January 2012, the Compensation Committee awarded shares of restricted stock, with a ratable vesting period of four years, in an amount equal to approximately half of the aggregate long-term incentive award value intended for such officer. The Compensation Committee continues to believe that restricted stock grants to named executive officers play an important role in accomplishing the objectives of the executive compensation system, in particular, retention and alignment with shareholder interest. Further, in 2012, the Compensation Committee approved the right of holders of unvested outstanding and future restricted stock awards to receive dividends on restricted shares.

2012 PSU Awards. On the first trading day of January 2012, the Compensation Committee awarded PSUs to each named executive officer in an amount equal to approximately half of the aggregate long-term incentive award value intended for such officer. The final number and value of the PSUs paid to a named executive officer depends on the Company’s performance relative to objective performance goals following the end of the performance periods. The Compensation Committee established the performance goals in early 2012, based on performance measures enumerated in the LTIP and, if met, each PSU awarded entitles a named executive officer to a cash payment based on the price per share of the Company’s common stock. No dividend equivalents are paid on PSUs.