UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07384

NICHOLAS-APPLEGATE INSTITUTIONAL FUNDS

(Exact name of registrant as specified in charter)

600 WEST BROADWAY, 30TH FLOOR, SAN DIEGO, CA 92101

(Address of principal executive offices) (Zip Code)

Charles H. Field, Jr.

c/o Nicholas-Applegate Capital Management, LLC

600 West Broadway, 30th Floor

San Diego, CA 92101

(Name and address of agent for service)

Copy to:

Deborah A. Wussow

c/o Nicholas-Applegate Capital Management, LLC

600 West Broadway, 30th Floor

San Diego, CA 92101

Registrant's telephone number, including area code: (619) 687-2988

Date of fiscal year end: March 31

Date of reporting period: September 30, 2008

ITEM 1. REPORTS TO STOCKHOLDERS.

September 30, 2008 Semi-Annual Report (Unaudited)

Class I, II, III & IV Shares

U.S. Micro Cap

U.S. Emerging Growth

U.S. Ultra Micro Cap

U.S. Systematic Large Cap Growth

U.S. Small to Mid Cap Growth

U.S. Convertible

Global Equity 130/30

Global Select

International Growth

International Growth Opportunities

Emerging Markets

International Systematic

International All Cap Growth

U.S. High Yield Bond

LETTER TO SHAREHOLDERS

Dear Fellow Shareholder,

The six-month period ended September 30, 2008 was a challenging time for investors. The problems in the credit markets that began in 2007 intensified, dimming the outlook for the global economy and sending stock prices lower around the world.

In this semi-annual report, we review the performance of the financial markets and our mutual funds from April 1, 2008 through September 30, 2008. We also share our outlook for the months ahead.

In the United States, the S&P 500 Index declined 10.9% in the face of significant headwinds. S&P 500 companies posted a fourth straight quarter of negative earnings growth, the economy appeared to be faltering and a deepening of the credit crisis transformed Wall Street in September. Crippled by mortgage losses, one major financial institution after another faced insolvency, causing risk aversion to skyrocket, lending to dry up and stock prices to fall. The Federal Reserve flooded the banking system with extra liquidity but held the target funds rate at 2% after having lowered it 0.25% in April. The U.S. Treasury proposed a $700 billion program to buy up bad mortgage securities, the terms of which were being negotiated by Congress on September 30.

The crisis in the United States spread overseas, where a handful of large European financial institutions were rescued by their respective governments. The turmoil in the credit markets, along with signs of a sharp economic slowdown in Europe and Japan, contributed to the 13.4% loss in the MSCI EAFE Index in local currencies. The index shed 22.0% in U.S. dollar terms, as the euro, pound and yen fell 10.7%, 10.2% and 6.4%, respectively, versus the dollar on concerns about the deterioration in international economies. Monetary policy in developed non-U.S. countries was mixed. Like the Fed, the Bank of England eased in April but subsequently kept rates at 5% amid rising inflation. The European Central Bank tightened in July to combat inflation but then held rates at 4.25%, while the Bank of Japan maintained its 0.5% target rate throughout the period. Nonetheless, these and other central banks around the world joined the Fed in injecting liquidity into the credit markets.

Stocks in developing countries registered the biggest losses, with the MSCI Emerging Markets Index falling 22.0% in local currencies and 27.5% in U.S. dollars. The sell-off was triggered by rising risk aversion, fears of a global recession and a steep decline in commodity prices, as energy and materials companies represent nearly a third of the index’s market value. After rising 19.6% during the first half of the period, the Reuters/Jefferies CRB Index of nineteen commodities plunged 25.3% from July through September on worries about softening demand. Policymakers in emerging countries shifted their focus from curbing inflation, which showed signs of easing, to stabilizing their financial markets. For example, Chinese officials cut stock-trading taxes, bought shares of large local banks and lowered the country’s benchmark lending rate for the first time since 2002.

While investment returns were disappointing in absolute terms, we are pleased that the majority of our funds outperformed their benchmarks in the volatile environment. In addition, most of the funds that lagged did so by a modest amount, including Global Equity 130/30, a new fund we opened April 1 that has the flexibility to short stocks. The timing of the Fund’s launch turned out to be challenging, but we remain excited about its long-term prospects. Global Equity 130/30 seeks to deliver more alpha than similar long-only approaches — without a commensurate increase in risk — and capitalizes on our expertise in fundamental research, quantitative analysis and short selling.

Just as we are committed to providing innovative investment solutions, we are committed to continually strengthening our organization. During the period, we welcomed several highly qualified analysts to both our traditional and systematic investment teams. We are enhancing our global trading platform by implementing the latest in trade order management technology — technology that will enable faster, better execution. By fine-tuning our trading capabilities, we hope to more fully capture the value of our investment decisions in the funds.

As the end of 2008 draws near, the outlook for the financial markets is uncertain. We believe that many developed economies will slip into recession early next year, if they have not already, and that emerging economies will slow. Now that inflation is yesterday’s problem, we expect the Federal Reserve and other central banks to cut interest rates, which may help unfreeze the credit markets and stimulate growth. Beyond monetary policy, governments have intervened to shore up their banking systems and economies; however, the effectiveness of their actions is yet to be seen.

Since Nicholas-Applegate was founded in 1984, the markets have experienced periods of volatility, spanning both peaks and valleys. Throughout them all, we have maintained our disciplined, long-term approach to investing. As difficult as the current situation may seem, this too shall pass. Meanwhile, we will continue to faithfully adhere to our investment philosophy and process, which we believe will produce strong performance in the funds over time.

On behalf of everyone at the firm, thank you for your participation in the Nicholas-Applegate Institutional Funds. We appreciate the trust you have placed in us.

Best Regards,

Horacio A. Valeiras, CFA

President and Chief Investment Officer

September 30, 2008

TABLE OF CONTENTS

The Funds’ Review and Outlook, Performance and Schedules of Investments:

| U.S. Micro Cap | 1 |

| U.S. Emerging Growth | 5 |

| U.S. Ultra Micro Cap | 9 |

| U.S. Systematic Large Cap Growth | 12 |

| U.S. Small to Mid Cap Growth | 16 |

| U.S. Convertible | 20 |

| Global Equity 130/30 | 25 |

| Global Select | 28 |

| International Growth | 32 |

| International Growth Opportunities | 36 |

| Emerging Markets | 40 |

| International Systematic | 44 |

| International All Cap Growth | 48 |

| U.S. High Yield Bond | 52 |

The Funds’:

| Financial Highlights | 56 |

| Statements of Assets and Liabilities | 64 |

| Statements of Operations | 66 |

| Statements of Changes in Net Assets | 68 |

| Statement of Cash Flows | 72 |

| Notes to Financial Statements | 73 |

| Shareholder Expense Example | 80 |

| Supplementary Information | 82 |

This report is authorized for distribution to shareholders and to others only when preceded or accompanied by a currently effective prospectus for Nicholas-Applegate Institutional Funds Class I, II, III & IV Shares. Distributor: Nicholas-Applegate Securities.

U.S. MICRO CAP FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Micro Cap Fund seeks to maximize long-term capital appreciation by investing primarily in U.S. companies with market capitalizations similar to the Russell Microcap Growth Index at time of purchase.

Market Overview: The Russell Microcap Growth Index fell from April 1 to September 30, 2008 in what was a volatile six months in the U.S. equity market. Major factors influencing stock prices were:

| · | Acceleration in the unwinding of leverage in the economy, which left several large financial firms at or near the brink of collapse and caused the credit markets to seize up |

| · | Dramatic swings in the prices of oil and other raw materials, with a key commodity index rising 19.6% through June then sliding 25.3% over the remainder of the period |

| · | Continued weakness in the housing market, including a record number of foreclosure filings and a 16.3% year-over-year drop in home prices in 20 large cities |

While GDP grew at an annual rate of 2.8% in the second quarter, more recent data suggested that the problems in the housing and credit markets were taking a severe toll on the broader economy. For example, the unemployment rate surged to a five-year high, and consumer spending lost steam due to the fading impact of $90 billion in tax rebate checks mailed between April and July. U.S. officials acted aggressively to shore up the financial system and economy, including drafting legislation that would allow the government to buy bad mortgage debt from financial firms.

Performance: The Fund’s Class I shares lost 2.84% from April 1 through September 30, 2008, outperforming the Russell Microcap Growth Index, which declined 5.76%.

Portfolio Specifics: Consistent with our bottom-up investment process, the Fund’s outperformance was due to stock selection, which was particularly strong in the industrials sector. Two of our best-performing holdings were Axsys Technologies, a manufacturer of surveillance cameras and imaging systems, and Team, Inc., a provider of maintenance and repair services for high-pressure piping systems. Axsys reported two quarters of better-than-expected earnings, boosted by strong sales in its high-margin surveillance business. Team benefited from healthy demand from its oil refinery customers, whose facilities are operating at near capacity and need continuous attention. Stock selection was also strong in the consumer discretionary sector, where restaurant chain Buffalo Wild Wings was a top performer. The company’s attractive menu prices helped drive robust revenue growth in the difficult consumer environment, and lower chicken costs contributed to margin improvement.

Areas of relative weakness in the Fund included stock selection in the information technology and energy sectors. An underweight in the defensive health care sector also detracted. Health care was one of the best-performing groups in the index, as anxious investors sought safe-haven assets.

Market Outlook: The stock market is likely to remain volatile over the coming months as investors measure the impact of the government rescue package and other policy steps aimed at stabilizing the financial system and economy. While it may take time for the environment to improve, it is worth noting that equities have recovered from significant shocks in the past.

In this dynamic environment, we believe that our focus on micro-cap stocks exhibiting positive and sustainable change will continue to benefit the Fund.

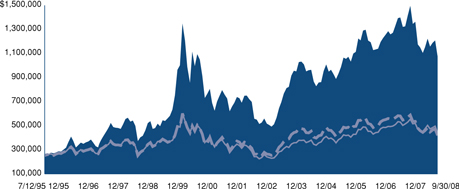

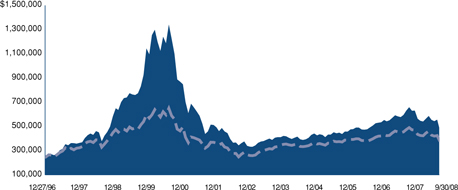

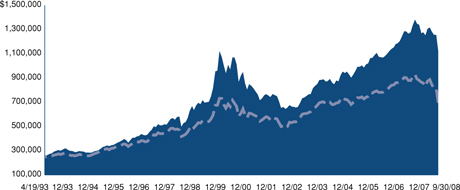

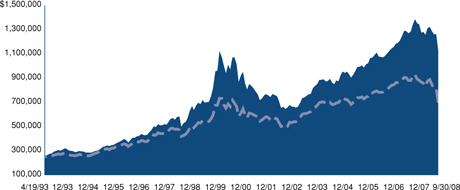

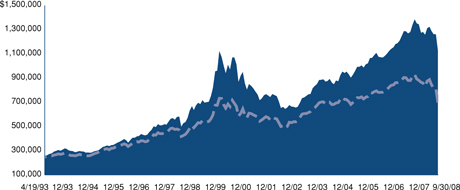

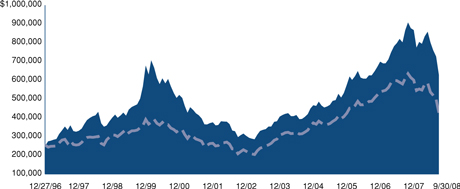

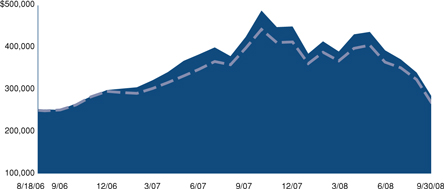

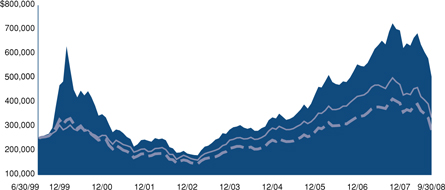

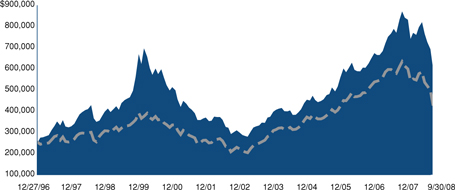

Comparison of Change in Value of a $250,000 Investment in U.S. Micro Cap Fund Class I Shares with the Russell 2000 Growth/Russell Microcap Growth Blend Index and Russell 2000 Growth Index.

| Annualized Total Returns As of 9/30/08 | |||

1 Year | 5 Years | 10 Years | |

| U.S. Micro Cap Fund Class I | -24.18% | 5.44% | 10.28% |

Russell 2000 Growth/Russell Microcap Growth Index | -26.46% | 1.40% | 4.17% |

| Russell 2000 Growth Index | -17.08% | 6.63% | 4.67% |

The graph above shows the value of a hypothetical $250,000 investment in the Fund’s Class I shares compared with the Russell 2000 Growth Index and a blended index comprised of the Russell 2000 Growth Index/Russell Microcap Growth Index. The Fund’s Class I shares calculate their performance based upon the historical performance of their corresponding series of Nicholas-Applegate Mutual Funds (renamed ING Mutual Funds), adjusted to reflect all fees and expenses applicable to Class I shares. The Nicholas-Applegate Institutional Funds’ Class I shares were first available on May 7, 1999. Average annual total return figures include changes in principal value, reinvestment dividends, and capital gain distributions. The total returns shown above do not show the effects of income taxes on an individual’s investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

The Russell 2000 Growth Index is an unmanaged index comprised of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Growth Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The Russell Microcap Index isolates the smallest 1,000 securities in the Russell 2000 Index plus the next 1,000 securities. The Russell Microcap Growth Index isolates the securities in the Russell Microcap Index with purely growth characteristics. The Russell 2000 Growth/Russell Microcap Growth Blend Index is a combination of the Russell 2000 Growth Index and the Russell Microcap Growth Index. The blended index exhibits Russell 2000 Growth performance from the inception of the Fund until August 2000, and Russell Microcap Growth performance thereafter. The Fund created the blended index because Russell Microcap Growth performance incepted in August 2000.

The Indexes differ from the Fund in composition, do not pay management fees or expenses and include reinvested dividends. One cannot invest directly in an index. Since markets can go down as well as up, investment return and principal value will fluctuate with market conditions. You may have a gain or loss when you sell your shares.

1

U.S. MICRO CAP FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Common Stock - 98.6% | |||||||

Aerospace/Defense-Equipment - 0.4% | |||||||

| National Presto Industries, Inc. | 3,700 | $ | 275,650 | ||||

Alternative Waste Technology - 1.4% | |||||||

| Calgon Carbon Corp.** | 43,860 | 892,990 | |||||

Apparel Manufacturers - 0.7% | |||||||

| Maidenform Brands, Inc.* | 31,900 | 462,869 | |||||

Applications Software - 0.9% | |||||||

| EPIQ Systems, Inc.** | 39,070 | 531,352 | |||||

Auto Repair Centers - 1.0% | |||||||

| Monro Muffler, Inc. | 25,700 | 592,642 | |||||

Auto/Truck Parts & Equipment-Original - 1.1% | |||||||

| Titan International, Inc. | 19,917 | 424,630 | |||||

| Wonder Auto Technology, Inc.* | 39,200 | 251,272 | |||||

| 675,902 | |||||||

Batteries/Battery Systems - 0.9% | |||||||

| Greatbatch, Inc.* | 21,500 | 527,610 | |||||

Chemicals-Plastics - 0.5% | |||||||

| Metabolix, Inc.** | 25,700 | 279,616 | |||||

Coffee - 0.9% | |||||||

| Green Mountain Coffee Roasters, Inc.* | 14,500 | 570,430 | |||||

Commercial Services - 2.9% | |||||||

| HMS Holdings Corp.* | 28,961 | 693,905 | |||||

| Medifast, Inc.* | 66,600 | 453,546 | |||||

| Team, Inc.* | 18,206 | 657,601 | |||||

| 1,805,052 | |||||||

Commercial Services-Finance - 2.0% | |||||||

| Cardtronics, Inc.* | 38,900 | 305,754 | |||||

| CBIZ, Inc.* | 54,300 | 458,835 | |||||

| TNS, Inc.* | 26,000 | 503,620 | |||||

| 1,268,209 | |||||||

Communications Software - 0.8% | |||||||

| Seachange International, Inc.* | 51,900 | 501,354 | |||||

Computer Services - 1.7% | |||||||

| Furmanite Corp.* | 49,600 | 512,864 | |||||

| Ness Technologies, Inc.* | 47,900 | 549,413 | |||||

| 1,062,277 | |||||||

Computer Software - 0.7% | |||||||

| Double-Take Software, Inc.* | 41,100 | 408,945 | |||||

Computers-Integrated Systems - 1.7% | |||||||

| Netscout Systems, Inc.* | 52,300 | 556,472 | |||||

| Super Micro Computer, Inc.* | 53,200 | 479,332 | |||||

| 1,035,804 | |||||||

Computers-Peripheral Equipment - 1.4% | |||||||

| Compellent Technologies, Inc.* | 39,200 | 486,080 | |||||

| Transact Technologies, Inc.* | 44,400 | 353,424 | |||||

| 839,504 | |||||||

Consulting Services - 0.7% | |||||||

| Hill International, Inc.* | 30,100 | 416,885 | |||||

Disposable Medical Products - 0.9% | |||||||

| Merit Medical Systems, Inc.** | 30,600 | 574,362 | |||||

Distribution/Wholesale - 0.8% | |||||||

| MWI Veterinary Supply, Inc.* | 12,800 | 502,912 | |||||

Electronic Components-Semiconductors - 1.4% | |||||||

| Ceva, Inc.* | 40,200 | 333,660 | |||||

| Monolithic Power Systems, Inc.* | 30,100 | 522,837 | |||||

| 856,497 | |||||||

Electronic Measure Instruments - 1.4% | |||||||

| Axsys Technologies, Inc.* | 14,758 | 869,837 | |||||

Energy-Alternate Sources - 0.6% | |||||||

| Canadian Solar, Inc.** | 18,500 | 361,305 | |||||

Engineering/R & D Services - 1.3% | |||||||

| Stanley, Inc.* | 21,400 | 789,874 | |||||

Enterprise Software/Services - 1.9% | |||||||

| Opnet Technologies, Inc.* | 49,000 | 596,820 | |||||

| Taleo Corp. Cl. A* | 30,548 | 607,600 | |||||

| 1,204,420 | |||||||

Finance-Investment Bankers/Brokers - 1.6% | |||||||

| Penson Worldwide, Inc.* | 22,000 | 305,140 | |||||

| SWS Group, Inc. | 34,300 | 691,488 | |||||

| 996,628 | |||||||

Food-Miscellaneous/Diversified - 1.7% | |||||||

| American Italian Pasta Co.* | 24,300 | 403,380 | |||||

| Diamond Foods, Inc. | 23,900 | 669,917 | |||||

| 1,073,297 | |||||||

Food-Wholesale/Distribution - 2.4% | |||||||

| Nash Finch Co. | 14,700 | 633,864 | |||||

| Spartan Stores, Inc.* | 33,770 | 840,198 | |||||

| 1,474,062 | |||||||

Footwear & Related Apparel - 0.9% | |||||||

| Steven Madden, Ltd.* | 21,800 | 540,204 | |||||

Hazardous Waste Disposal - 0.8% | |||||||

| American Ecology Corp. | 17,400 | 481,458 | |||||

Human Resources - 1.0% | |||||||

| On Assignment, Inc.* | 76,100 | 599,668 | |||||

Insurance Brokers - 1.3% | |||||||

| Life Partners Holdings, Inc.* | 22,001 | 791,376 | |||||

Internet Applications Software - 3.2% | |||||||

| Cybersource Corp.* | 40,870 | 658,416 | |||||

| S1 Corp.* | 86,370 | 528,584 | |||||

| Vocus, Inc.* | 24,160 | 820,474 | |||||

| 2,007,474 | |||||||

Internet Infrastructure Software - 1.1% | |||||||

| AsiaInfo Holdings, Inc.* | 74,600 | 684,828 | |||||

Internet Security - 0.7% | |||||||

| Vasco Data Security International, Inc.* | 39,200 | 406,112 | |||||

Machinery-General Industry - 1.2% | |||||||

| DXP Enterprises, Inc.* | 8,500 | 453,135 | |||||

| Intevac, Inc.* | 28,700 | 305,368 | |||||

| 758,503 | |||||||

Medical Imaging Systems - 1.1% | |||||||

| IRIS International, Inc.* | 38,700 | 692,730 | |||||

Medical Instruments - 2.0% | |||||||

| Kensey Nash Corp.* | 18,600 | 585,156 | |||||

| Natus Medical, Inc.* | 30,100 | 682,066 | |||||

| 1,267,222 | |||||||

See Accompanying Notes to Financial Statements.

2

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Medical Labs & Testing Services - 2.1% | |||||||

| Bio-Reference Labs, Inc.* | 23,760 | $ | 686,664 | ||||

| Life Sciences Research, Inc.* | 18,200 | 637,000 | |||||

| 1,323,664 | |||||||

Medical Laser Systems - 0.7% | |||||||

| Cynosure, Inc. Cl. A* | 25,710 | 461,237 | |||||

Medical Products - 3.3% | |||||||

| Exactech, Inc.* | 28,000 | 622,720 | |||||

| Hanger Orthopedic Group, Inc.* | 30,000 | 523,500 | |||||

| Synovis Life Technologies, Inc.* | 46,960 | 883,787 | |||||

| 2,030,007 | |||||||

Medical-Biomedical/Genetics - 4.3% | |||||||

| CryoLife, Inc.* | 61,700 | 809,504 | |||||

| Omrix Biopharmaceuticals, Inc.** | 31,700 | 568,698 | |||||

| RTI Biologics, Inc.* | 80,121 | 749,131 | |||||

| Seattle Genetics, Inc.* | 52,900 | 566,030 | |||||

| 2,693,363 | |||||||

Medical-Drugs - 2.1% | |||||||

| Array Biopharma, Inc.* | 62,200 | 477,696 | |||||

| Pharmasset, Inc.* | 21,800 | 434,910 | |||||

| Vivus, Inc.* | 50,000 | 397,000 | |||||

| 1,309,606 | |||||||

Medical-Nursing Homes - 1.1% | |||||||

| Sun Healthcare Group, Inc.* | 47,100 | 690,486 | |||||

Medical-Outpatient/Home Medical Care - 2.2% | |||||||

| Almost Family, Inc.* | 21,800 | 862,190 | |||||

| LHC Group, Inc.* | 17,400 | 495,552 | |||||

| 1,357,742 | |||||||

MRI/Medical Diagnostic Imaging Centers - 1.4% | |||||||

| Alliance Imaging, Inc.* | 63,100 | 648,037 | |||||

| RadNet, Inc.** | 58,100 | 232,981 | |||||

| 881,018 | |||||||

Networking Products - 1.6% | |||||||

| Extreme Networks* | 151,600 | 510,892 | |||||

| Switch & Data Facilities Co., Inc.* | 36,300 | 451,935 | |||||

| 962,827 | |||||||

Oil Companies-Exploration & Production - 1.7% | |||||||

| Gasco Energy, Inc.** | 149,100 | 271,362 | |||||

| GMX Resources, Inc.** | 10,000 | 478,000 | |||||

| NGAS Resources, Inc.** | 61,000 | 289,750 | |||||

| 1,039,112 | |||||||

Oil Field Machinery & Equipment - 0.8% | |||||||

| Mitcham Industries, Inc.* | 26,500 | 267,385 | |||||

| Natural Gas Services Group, Inc.* | 14,600 | 255,062 | |||||

| 522,447 | |||||||

Oil-Field Services - 1.4% | |||||||

| Boots & Coots International Control, Inc.* . | 143,900 | 277,727 | |||||

| Matrix Service Co.* | 29,340 | 560,394 | |||||

| 838,121 | |||||||

Patient Monitoring Equipment - 1.0% | |||||||

| CardioNet, Inc.* | 23,600 | 589,056 | |||||

Physical Practice Management - 0.9% | |||||||

| IPC The Hospitalist Co., Inc.* | 22,100 | 567,970 | |||||

Power Conversion/Supply Equipment - 1.7% | |||||||

| C&D Technologies, Inc.** | 59,600 | 338,528 | |||||

| Powell Industries, Inc.* | 17,600 | 718,256 | |||||

| 1,056,784 | |||||||

Private Corrections - 1.0% | |||||||

| Cornell Cos., Inc.* | 21,800 | 592,524 | |||||

Property/Casualty Insurance - 1.0% | |||||||

| Meadowbrook Insurance Group, Inc. | 85,900 | 606,454 | |||||

Research & Development - 2.1% | |||||||

| Exponent,Inc.* | 20,400 | 675,036 | |||||

| Kendle International, Inc.* | 14,600 | 652,766 | |||||

| 1,327,802 | |||||||

Retail-Apparel/Shoe - 4.4% | |||||||

| Cache, Inc.* | 33,900 | 232,893 | |||||

| HOT Topic, Inc.* | 81,500 | 538,715 | |||||

| JOS. A Bank Clothiers, Inc.** | 16,400 | 551,040 | |||||

| New York & Co., Inc.* | 53,900 | 514,206 | |||||

| Shoe Carnival, Inc.* | 26,500 | 434,070 | |||||

| The Wet Seal, Inc. Cl. A* | 128,700 | 467,181 | |||||

| 2,738,105 | |||||||

Retail-Computer Equipment - 0.5% | |||||||

| PC Mall, Inc.* | 47,400 | 323,742 | |||||

Retail-Convenience Store - 0.9% | |||||||

| Pantry, Inc.* | 25,600 | 542,464 | |||||

Retail-Discount - 0.6% | |||||||

| Citi Trends, Inc.* | 22,900 | 373,041 | |||||

Retail-Miscellaneous/Diversified - 0.7% | |||||||

| Titan Machinery, Inc.** | 19,500 | 405,795 | |||||

Retail-Pet Food & Supplies - 0.8% | |||||||

| PetMed Express, Inc.* | 29,900 | 469,430 | |||||

Retail-Restaurants - 1.0% | |||||||

| Buffalo Wild Wings, Inc.** | 15,600 | 627,744 | |||||

Savings & Loans/Thrifts-Eastern US - 1.6% | |||||||

| Flushing Financial Corp. | 30,700 | 537,250 | |||||

| OceanFirst Financial Corp. | 26,200 | 474,744 | |||||

| 1,011,994 | |||||||

Semiconductor Components-Integrated Circuits - 1.6% | |||||||

| O2Micro International, Ltd. - ADR* | 62,870 | 228,218 | |||||

| Pericom Semiconductor Corp.* | 37,000 | 388,500 | |||||

| Techwell, Inc.* | 37,800 | 356,454 | |||||

| 973,172 | |||||||

Semiconductor Equipment - 1.3% | |||||||

| Amtech Systems, Inc.* | 43,200 | 402,192 | |||||

| Ultratech, Inc.* | 31,600 | 382,360 | |||||

| 784,552 | |||||||

Telecommunication Equipment-Fiber Optics - 0.8% | |||||||

| Oplink Communications, Inc.* | 40,000 | 482,800 | |||||

Textile-Apparel - 0.8% | |||||||

| Perry Ellis International, Inc.* | 31,700 | 472,647 | |||||

Therapeutics - 0.9% | |||||||

| Allos Therapeutics, Inc.* | 25,600 | 189,696 | |||||

| Cypress Bioscience, Inc.* | 50,800 | 373,380 | |||||

| 563,076 | |||||||

See Accompanying Notes to Financial Statements.

3

U.S. MICRO CAP FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Transport-Services - 1.2% | |||||||

| Pacer International, Inc. | 17,700 | $ | 291,519 | ||||

| Vitran Corp., Inc.* | 32,300 | 435,081 | |||||

| 726,600 | |||||||

Transport-Truck - 0.9% | |||||||

| Saia, Inc.* | 40,300 | 535,184 | |||||

Ultra Sound Imaging Systems - 0.9% | |||||||

| SonoSite, Inc.** | 17,100 | 536,940 | |||||

Veterinary Diagnostics - 0.8% | |||||||

| Neogen Corp.* | 17,400 | 490,332 | |||||

Water Treatment Systems - 0.8% | |||||||

| Energy Recovery, Inc.** | 48,900 | 468,951 | |||||

Web Hosting/Design - 0.8% | |||||||

| Terremark Worldwide, Inc.** | 74,900 | 514,563 | |||||

Wireless Equipment - 0.6% | |||||||

| Globecomm Systems, Inc.* | 41,950 | 366,643 | |||||

| Total Common Stock (Cost: $61,920,085) | 61,337,855 | ||||||

Principal Amount | |||||||

Short Term Investments - | |||||||

Repurchase Agreement | |||||||

BNP Paribas Securities Corp., 0.150% dated 9/30/08, to be repurchased at $6,983,236 on 10/1/08 | $ | 6,983,207 | 6,983,207 | ||||

Time Deposit - 13.8% | |||||||

Bank of America London 3.470%, 10/01/08 | 1,621,498 | 1,621,498 | |||||

| Total Short Term Investments (Cost: $8,604,705) | 8,604,705 | ||||||

| Total Investments - 112.4% (Cost: $70,524,790) | 69,942,560 | ||||||

| Liabilities In Excess of Other Assets - (12.4)% | (7,733,984 | ) | |||||

| Net Assets - 100.0% | $ | 62,208,576 | |||||

** | All or a portion of the Fund’s holdings in this security was on loan as of September 30, 2008. |

* | Non-income producing securities. |

ADR - American Depository Receipt

SCHEDULE OF INVESTMENTS BY SECTOR

as of September 30, 2008

| Sector | Percent of Net Assets | |||

| Consumer, Non-cyclical | 40.2 | % | ||

| Industrial | 14.8 | |||

| Consumer, Cyclical | 13.1 | |||

| Technology | 12.4 | |||

| Communications | 8.7 | |||

| Financial | 5.5 | |||

| Energy | 3.9 | |||

| Short Term Investments | 13.8 | |||

| Total Investments | 112.4 | |||

| Liabilities in excess of other assets | (12.4 | ) | ||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

4

U.S. EMERGING GROWTH FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Emerging Growth Fund seeks to maximize long-term capital appreciation through investments primarily in U.S. companies with market capitalizations similar to the Russell 2000 Growth Index at time of purchase.

Market Overview: The Russell 2000 Growth Index declined in the six months ended September 30, 2008. However, small-cap growth stocks were much more resilient than large caps, due in part to better earnings from smaller companies.

The Russell 2000 Growth Index shook off weakness in June to end the first five months of the period with a nearly 10% gain. Returns were especially strong in April and May when the Federal Reserve made its seventh in a series of interest rate cuts, and small companies outside of financials reported healthy first quarter profits.

September turned out to be an exceptionally weak and volatile month, and small-cap growth stocks gave back all of their earlier gains and then some. During September, a number of bellwether U.S. financial institutions became overwhelmed by mortgage-related losses, including one that was forced into bankruptcy. Policymakers sprang into action, effectively nationalizing the largest U.S. mortgage lenders, providing a loan to one of the world’s biggest insurance companies and orchestrating the sale of two major banks. In addition, the Federal Reserve pumped liquidity into the financial system and expanded its emergency bank lending programs. Despite these efforts to stabilize the markets, investors shunned riskier assets, credit dried up and equity prices plummeted. The month ended on hopes that Congress would pass a $700 billion financial rescue package.

Performance: During the six months ended September 30, 2008, the Fund’s Class I shares posted a 7.25% loss and the Russell 2000 Growth Index fell 2.83%.

Portfolio Specifics: Overall, the Fund’s sector exposures positively impacted relative results. An underweight in materials — one of the worst-performing sectors in the index — was helpful, as deterioration in the outlook for the global economy sent commodity prices sharply lower from July through September. An overweight in health care was another plus, as health care was the best-performing sector in the benchmark. Investors typically favor this defensive group when the market is volatile, and this period was no exception.

In the risk-averse climate, investors also favored the larger-cap stocks in the Russell 2000 Growth Index. This was a headwind for the Fund, since the types of fast-growing companies that we like to own tend to be on the smaller side of small cap. In terms of sectors, stock selection among industrials and information technology companies subtracted the most from relative results.

While the portfolio generated a decline, there were a number of individual holdings that performed well. The Fund’s top contributors included Jos. A. Bank Clothiers, an apparel retailer; Alexion Pharmaceuticals, a biotechnology firm; and NuVasive, a medical device company.

Market Outlook: The stock market is likely to remain volatile over the coming months as investors measure the impact of the government rescue package and other policy steps aimed at stabilizing the financial system and economy. While it may take time for the environment to improve, it is worth noting that equities have recovered from significant shocks in the past.

Regardless of which direction the broad stock market takes, we believe that consistent application of our investment process will lead us to fast-growing small-cap companies for the Fund.

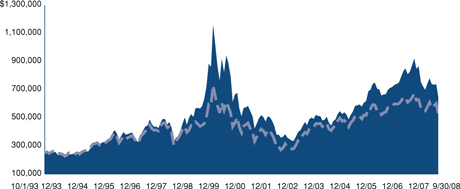

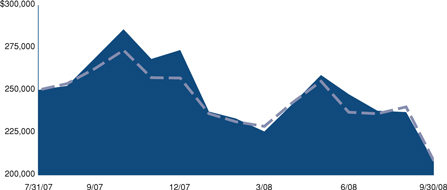

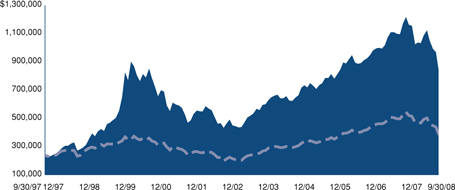

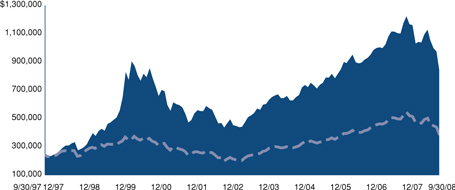

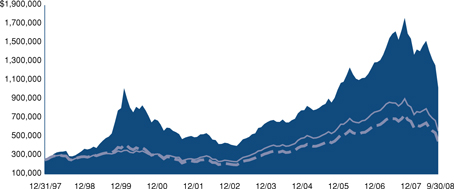

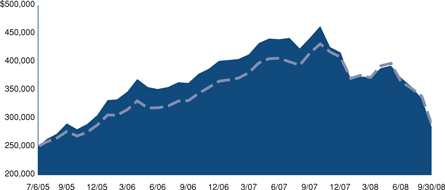

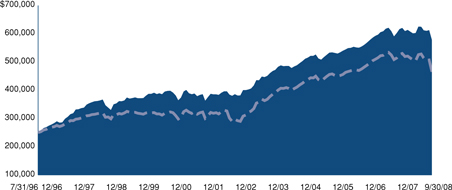

Comparison of Change in Value of a $250,000 Investment in U.S. Emerging Growth Fund Class I Shares with the Russell 2000 Growth Index.

| Annualized Total Returns As of 9/30/08 | |||

1 Year | 5 Years | 10 Years | |

| U.S. Emerging Growth Fund Class I | -25.58% | 7.68% | 6.07% |

| Russell 2000 Growth Index | -17.08% | 6.63% | 4.67% |

The graph above shows the value of a hypothetical $250,000 investment in the Fund’s Class I shares compared with the Russell 2000 Growth Index for the periods indicated. The Fund calculates performance based upon the historical performance of a corresponding series of Nicholas-Applegate Mutual Funds (renamed ING Mutual Funds), adjusted to reflect all fees and expenses applicable to Class I shares. The Nicholas-Applegate Institutional Funds’ Class I shares were first available on May 7, 1999. Average annual total return figures include changes in principal value, reinvested dividends, and capital gain distributions. The total returns shown above do not show the effects of income taxes on an individual’s investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

The Russell 2000 Growth Index is an unmanaged index comprised of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. The unmanaged Index differs from the Fund in composition, does not pay management fees or expenses and includes reinvested dividends. One cannot invest directly in an index.

Since markets can go down as well as up, investment return and principal value will fluctuate with market conditions. You may have a gain or loss when you sell your shares.

5

U.S. EMERGING GROWTH FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Common Stock - 100.7% | |||||||

Aerospace/Defense-Equipment - 3.7% | |||||||

| BE Aerospace, Inc.* | 3,100 | $ | 49,073 | ||||

| Curtiss-Wright Corp. | 1,400 | 63,630 | |||||

| Moog, Inc. Cl. A* | 1,900 | 81,472 | |||||

| National Presto Industries, Inc. | 700 | 52,150 | |||||

| Orbital Sciences Corp.* | 4,300 | 103,071 | |||||

| Triumph Group, Inc. | 1,000 | 45,710 | |||||

| 395,106 | |||||||

Airlines - 0.9% | |||||||

| Hawaiian Holdings, Inc.* | 9,900 | 91,872 | |||||

Apparel Manufacturers - 1.7% | |||||||

| G-III Apparel Group, Ltd.* | 5,600 | 104,776 | |||||

| Jones Apparel Group, Inc. | 4,500 | 83,295 | |||||

| 188,071 | |||||||

Applications Software - 0.7% | |||||||

| Compuware Corp.* | 7,300 | 70,737 | |||||

Auto/Truck Parts & Equipment-Original - 0.5% | |||||||

| Titan International, Inc. | 2,500 | 53,300 | |||||

Batteries/Battery Systems - 0.8% | |||||||

| Greatbatch, Inc.* | 3,300 | 80,982 | |||||

Beverages-Wine/Spirits - 0.7% | |||||||

| Central European Distribution Corp.* | 1,600 | 72,656 | |||||

Chemicals-Diversified - 0.6% | |||||||

| Olin Corp. | 3,400 | 65,960 | |||||

Chemicals-Plastics - 0.4% | |||||||

| Metabolix, Inc.* | 4,400 | 47,872 | |||||

Coffee - 0.6% | |||||||

| Green Mountain Coffee Roasters, Inc.* | 1,700 | 66,878 | |||||

Commercial Banks-Western US - 0.6% | |||||||

| SVB Financial Group* | 1,200 | 69,504 | |||||

Commercial Services - 1.4% | |||||||

| HMS Holdings Corp.* | 2,700 | 64,692 | |||||

| Team, Inc.* | 2,400 | 86,688 | |||||

| 151,380 | |||||||

Commercial Services-Finance - 0.7% | |||||||

| TNS, Inc.* | 3,900 | 75,543 | |||||

Computer Aided Design - 0.5% | |||||||

| Parametric Technology Corp.* | 3,100 | 57,040 | |||||

Computer Services - 0.5% | |||||||

| Ness Technologies, Inc.* | 5,100 | 58,497 | |||||

Computer Software - 0.7% | |||||||

| Double-Take Software, Inc.* | 7,200 | 71,640 | |||||

Computers-Integrated Systems - 0.7% | |||||||

| Netscout Systems, Inc.* | 6,800 | 72,352 | |||||

Consulting Services - 3.7% | |||||||

| Forrester Research, Inc.* | 2,700 | 79,164 | |||||

| FTI Consulting, Inc.* | 1,100 | 79,464 | |||||

| Gartner, Inc. Cl. A* | 3,400 | 77,112 | |||||

| Navigant Consulting, Inc.* | 4,100 | 81,549 | |||||

| Watson Wyatt Worldwide, Inc. Cl. A | 1,600 | 79,568 | |||||

| 396,857 | |||||||

Consumer Products-Miscellaneous - 0.6% | |||||||

| Jarden Corp.* | 2,800 | 65,660 | |||||

Containers-Paper/Plastic - 0.7% | |||||||

| Rock-Tenn Co. Cl. A | 1,800 | 71,964 | |||||

Cosmetics & Toiletries - 0.9% | |||||||

| Elizabeth Arden, Inc.* | 4,900 | 96,187 | |||||

Disposable Medical Products - 0.7% | |||||||

| Merit Medical Systems, Inc.* | 3,900 | 73,203 | |||||

Distribution/Wholesale - 1.2% | |||||||

| Fossil, Inc.* | 2,100 | 59,283 | |||||

| LKQ Corp.* | 4,400 | 74,668 | |||||

| 133,951 | |||||||

Diversified Operations - 0.7% | |||||||

| Compass Diversified Holdings | 5,600 | 78,064 | |||||

Electronic Components-Semiconductors - 3.2% | |||||||

| Macrovision Solutions Corp.* | 4,400 | 67,672 | |||||

| Monolithic Power Systems, Inc.* | 4,600 | 79,902 | |||||

| ON Semiconductor Corp.* | 11,400 | 77,064 | |||||

| PMC - Sierra, Inc.* | 10,400 | 77,168 | |||||

| Renesola Ltd. - ADR* | 4,600 | 48,254 | |||||

| 350,060 | |||||||

Electronic Design Automations - 0.8% | |||||||

| Mentor Graphics Corp.* | 7,800 | 88,530 | |||||

Electronic Measure Instruments - 0.7% | |||||||

| Itron, Inc.* | 900 | 79,677 | |||||

Energy-Alternate Sources - 0.5% | |||||||

| Canadian Solar, Inc.* | 2,600 | 50,778 | |||||

Engineering/R & D Services - 0.8% | |||||||

| EMCOR Group, Inc.* | 3,200 | 84,224 | |||||

Enterprise Software/Services - 2.9% | |||||||

| Concur Technologies, Inc.* | 1,700 | 65,042 | |||||

| Lawson Software, Inc.* | 10,400 | 72,800 | |||||

| Mantech International Corp. Cl. A* | 2,000 | 118,580 | |||||

| Taleo Corp. Cl. A* | 2,800 | 55,692 | |||||

| 312,114 | |||||||

E-Services/Consulting - 1.3% | |||||||

| GSI Commerce, Inc.* | 5,100 | 78,948 | |||||

| Websense, Inc.* | 2,500 | 55,875 | |||||

| 134,823 | |||||||

Finance-Consumer Loans - 0.7% | |||||||

| Portfolio Recovery Associates, Inc.* | 1,500 | 72,945 | |||||

Finance-Investment Bankers/Brokers - 2.6% | |||||||

| Knight Capital Group, Inc. Cl. A* | 4,800 | 71,328 | |||||

| Raymond James Financial, Inc. | 3,000 | 98,940 | |||||

| SWS Group, Inc. | 5,400 | 108,864 | |||||

| 279,132 | |||||||

Food-Miscellaneous/Diversified - 0.8% | |||||||

| Diamond Foods, Inc. | 3,200 | 89,696 | |||||

Food-Wholesale/Distribution - 1.8% | |||||||

| Spartan Stores, Inc. | 4,000 | 99,520 | |||||

| United Natural Foods, Inc.* | 3,600 | 89,964 | |||||

| 189,484 | |||||||

Footwear & Related Apparel - 1.4% | |||||||

| Skechers U.S.A, Inc. Cl. A* | 3,200 | 53,856 | |||||

| Steven Madden, Ltd.* | 3,800 | 94,164 | |||||

| 148,020 | |||||||

Hazardous Waste Disposal - 0.7% | |||||||

| American Ecology Corp. | 2,600 | 71,942 | |||||

Industrial Automation/Robotics - 0.5% | |||||||

| Cognex Corp. | 2,600 | 52,416 | |||||

See Accompanying Notes to Financial Statements.

6

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Internet Applications Software - 0.7% | |||||||

| Cybersource Corp.* | 4,800 | $ | 77,328 | ||||

Internet Security - 0.6% | |||||||

| Vasco Data Security International, Inc.* | 5,900 | 61,124 | |||||

Machinery-General Industry - 2.0% | |||||||

| Altra Holdings, Inc.* | 5,300 | 78,228 | |||||

| DXP Enterprises, Inc.* | 1,200 | 63,972 | |||||

| Wabtec Corp. | 1,400 | 71,722 | |||||

| 213,922 | |||||||

Medical Instruments - 4.9% | |||||||

| Bruker Corp.* | 7,100 | 94,643 | |||||

| Integra LifeSciences Holdings Corp.* | 1,700 | 74,851 | |||||

| Kensey Nash Corp.* | 2,800 | 88,088 | |||||

| Natus Medical, Inc.* | 4,300 | 97,438 | |||||

| NuVasive, Inc.* | 1,600 | 78,928 | |||||

| Thoratec Corp.* | 3,400 | 89,250 | |||||

| 523,198 | |||||||

Medical Labs & Testing Services - 1.8% | |||||||

| Bio-Reference Labs, Inc.* | 3,500 | 101,150 | |||||

| Icon PLC - ADR* | 2,300 | 87,975 | |||||

| 189,125 | |||||||

Medical Laser Systems - 0.5% | |||||||

| Cynosure, Inc. Cl. A* | 2,800 | 50,232 | |||||

Medical Products - 4.5% | |||||||

| American Medical Systems Holdings, Inc.* | 3,800 | 67,488 | |||||

| China Medical Technologies, Inc. - ADR | 2,300 | 74,934 | |||||

| Exactech, Inc.* | 3,200 | 71,168 | |||||

| Haemonetics Corp.* | 1,500 | 92,580 | |||||

| Wright Medical Group, Inc.* | 3,200 | 97,408 | |||||

| Zoll Medical Corp.* | 2,500 | 81,800 | |||||

| 485,378 | |||||||

Medical-Biomedical/Genetics - 5.2% | |||||||

| Alexion Pharmaceuticals, Inc.* | 2,600 | 102,180 | |||||

| Medicines Co.* | 3,800 | 88,236 | |||||

| Myriad Genetics, Inc.* | 1,300 | 84,344 | |||||

| OSI Pharmaceuticals, Inc.* | 1,900 | 93,651 | |||||

| Regeneron Pharmaceuticals, Inc.* | 2,700 | 58,941 | |||||

| Savient Pharmaceuticals, Inc.* | 2,600 | 38,766 | |||||

| United Therapeutics Corp.* | 900 | 94,653 | |||||

| 560,771 | |||||||

Medical-Drugs - 1.8% | |||||||

| Eurand NV* | 4,100 | 74,456 | |||||

| Pharmasset, Inc.* | 2,800 | 55,860 | |||||

| Rigel Pharmaceuticals, Inc.* | 2,800 | 65,380 | |||||

| 195,696 | |||||||

Medical-Nursing Homes - 0.7% | |||||||

| Sun Healthcare Group, Inc.* | 5,400 | 79,164 | |||||

Medical-Outpatient/Home Medical Care - 0.6% | |||||||

| LHC Group, Inc.* | 2,100 | 59,808 | |||||

Networking Products - 0.8% | |||||||

| Polycom, Inc.* | 3,500 | 80,955 | |||||

Oil Companies-Exploration & Production - 1.7% | |||||||

| EXCO Resources, Inc.* | 4,000 | 65,280 | |||||

| GMX Resources, Inc.* | 1,500 | 71,700 | |||||

| Venoco, Inc.* | 3,700 | 48,100 | |||||

| 185,080 | |||||||

Oil-Field Services - 3.0% | |||||||

| Cal Dive International, Inc.* | 7,700 | 81,620 | |||||

| Hornbeck Offshore Services, Inc.* | 1,300 | 50,206 | |||||

| Matrix Service Co.* | 4,000 | 76,400 | |||||

| Tetra Technologies, Inc.* | 4,200 | 58,170 | |||||

| Willbros Group, Inc.* | 2,100 | 55,650 | |||||

| 322,046 | |||||||

Pharmacy Services - 0.9% | |||||||

| HealthExtras, Inc* | 3,500 | 91,420 | |||||

Physical Practice Management - 0.6% | |||||||

| IPC The Hospitalist Co., Inc.* | 2,500 | 64,250 | |||||

Power Conversion/Supply Equipment - 1.2% | |||||||

| Energy Conversion Devices, Inc.* | 900 | 52,425 | |||||

| Powell Industries, Inc.* | 1,800 | 73,458 | |||||

| 125,883 | |||||||

Private Corrections - 0.8% | |||||||

| Cornell Cos., Inc.* | 3,000 | 81,540 | |||||

Property/Casualty Insurance - 0.6% | |||||||

| Amtrust Financial Services, Inc. | 4,600 | 62,514 | |||||

Research & Development - 1.6% | |||||||

| Kendle International, Inc.* | 2,100 | 93,891 | |||||

| Parexel International Corp.* | 2,900 | 83,114 | |||||

| 177,005 | |||||||

Retail-Apparel/Shoe - 4.6% | |||||||

| Aeropostale, Inc.* | 2,300 | 73,853 | |||||

| Brown Shoe Co., Inc. | 4,200 | 68,796 | |||||

| Collective Brands, Inc.* | 5,100 | 93,381 | |||||

| Dress Barn, Inc.* | 5,000 | 76,450 | |||||

| JOS. A Bank Clothiers, Inc.* | 1,900 | 63,840 | |||||

| Phillips-Van Heusen Corp. | 1,700 | 64,447 | |||||

| The Childrens Place Retail Stores, Inc.* | 1,700 | 56,695 | |||||

| 497,462 | |||||||

Retail-Convenience Store - 0.8% | |||||||

| Pantry, Inc.* | 3,900 | 82,641 | |||||

Retail-Miscellaneous/Diversified - 0.5% | |||||||

| Pricesmart, Inc. | 3,200 | 53,568 | |||||

Retail-Perfume & Cosmetics - 0.7% | |||||||

| Ulta Salon Cosmetics & Fragrance, Inc.* | 6,000 | 79,680 | |||||

Retail-Restaurants - 2.5% | |||||||

| Buffalo Wild Wings, Inc.* | 2,100 | 84,504 | |||||

| CBRL Group, Inc. | 2,600 | 68,380 | |||||

| CKE Restaurants, Inc. | 6,600 | 69,960 | |||||

| Jack in the Box, Inc.* | 2,300 | 48,530 | |||||

| 271,374 | |||||||

Seismic Data Collection - 0.7% | |||||||

| ION Geophysical Corp.* | 5,300 | 75,207 | |||||

Semiconductor Components - Integrated Circuits - 1.6% | |||||||

| O2Micro International, Ltd. - ADR* | 8,100 | 29,403 | |||||

| Pericom Semiconductor Corp.* | 6,600 | 69,300 | |||||

| TriQuint Semiconductor, Inc.* | 16,000 | 76,640 | |||||

| 175,343 | |||||||

Telecommuications Services - 1.7% | |||||||

| NTELOS Holdings Corp. | 3,300 | 88,737 | |||||

| Premiere Global Services, Inc.* | 6,500 | 91,390 | |||||

| 180,127 | |||||||

See Accompanying Notes to Financial Statements.

7

U.S. EMERGING GROWTH FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Telecommunication Equipment - 0.3% | |||||||

| Arris Group, Inc.* | 4,300 | $ | 33,239 | ||||

Telecommunication Equipment-Fiber Optics - 0.8% | |||||||

| IPG Photonics Corp.* | 4,400 | 85,844 | |||||

Textile-Apparel - 0.5% | |||||||

| Perry Ellis International, Inc.* | 3,500 | 52,185 | |||||

Theaters - 0.1% | |||||||

| Cinemark Holdings, Inc. | 400 | 5,440 | |||||

Therapeutics - 0.9% | |||||||

| Alnylam Pharmaceuticals, Inc.* | 1,800 | 52,110 | |||||

| Medarex, Inc.* | 7,100 | 45,937 | |||||

| 98,047 | |||||||

Transport-Air Freight - 0.7% | |||||||

| Atlas Air Worldwide Holdings, Inc.* | 1,900 | 76,589 | |||||

Transport-Equipment & Leasing - 1.1% | |||||||

| GATX Corp. | 1,400 | 55,398 | |||||

| TAL International Group, Inc. | 3,100 | 64,542 | |||||

| 119,940 | |||||||

Transport-Marine - 0.6% | |||||||

| Gulfmark Offshore, Inc.* | 1,400 | 62,832 | |||||

Transport-Rail - 0.8% | |||||||

| Genesee & Wyoming, Inc. Cl. A* | 2,200 | 82,544 | |||||

Transport-Services - 0.5% | |||||||

| Pacer International, Inc. | 3,200 | 52,704 | |||||

Transport-Truck - 2.0% | |||||||

| Con-way, Inc. | 1,800 | 79,398 | |||||

| Old Dominion Freight Line, Inc.* | 2,500 | 70,850 | |||||

| Saia, Inc.* | 4,700 | 62,416 | |||||

| 212,664 | |||||||

Ultra Sound Imaging Systems - 0.7% | |||||||

| SonoSite, Inc.* | 2,300 | 72,220 | |||||

Vitamins & Nutrition Products - 1.4% | |||||||

| Herbalife, Ltd. | 1,900 | 75,088 | |||||

| NBTY, Inc.* | 2,500 | 73,800 | |||||

| 148,888 | |||||||

Water Treatment Systems - 0.5% | |||||||

| Energy Recovery, Inc.* | 6,100 | 58,499 | |||||

| Total Common Stock (Cost: $11,431,122) | 10,872,593 | ||||||

| Total Investments - 100.7% (Cost: $11,431,122) | 10,872,593 | ||||||

| Liabilities In Excess of Other Assets - (0.7%) | (77,564 | ) | |||||

| Net Assets - 100.0% | $ | 10,795,029 | |||||

* Non-income producing securities.

ADR - American Depository Receipt

SCHEDULE OF INVESTMENTS BY SECTOR

as of September 30, 2008

| Sector | Percent of Net Assets | |||

| Consumer, Non-cyclical | 38.4 | % | ||

| Industrial | 18.0 | |||

| Consumer, Cyclical | 15.4 | |||

| Technology | 11.6 | |||

| Communications | 6.1 | |||

| Energy | 5.4 | |||

| Financial | 4.5 | |||

| Diversified | 0.7 | |||

| Basic Materials | 0.6 | |||

| Total Investments | 100.7 | |||

| Liabilities in excess of other assets | (0.7 | ) | ||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

8

U.S. ULTRA MICRO CAP FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Ultra Micro Cap Fund seeks to maximize long-term capital appreciation by investing primarily in U.S. companies with market capitalizations below the median of the Russell Microcap Growth Index at time of purchase.

Market Overview: The Russell Microcap Growth Index posted a loss between April 1 and September 30, 2008. The market environment was volatile, as four months of strong gains in the index were eclipsed by sharp declines in June and September.

The period started on a positive note, with the Federal Reserve cutting interest rates 0.25% in April, and smaller companies reporting healthy first quarter earnings growth, excluding financials. Stock prices subsequently retreated in June on concerns about rising inflation and news of credit write-downs by banks. Downbeat news on the economy contributed to the selling pressure, including the largest spike in the unemployment rate since 1986.

Stocks regained their footing over the summer, as falling oil prices, some encouraging economic data and hopes for a bottom in the housing market lifted investor confidence. However, that confidence was shattered in September, when a dramatic series of events in the financials sector triggered a broad sell-off in equities. Mortgage-related losses impaired the ability of several large financial institutions to access the capital markets, and they were taken over by the government, sold or, in one case, forced into bankruptcy. Unsure of which firm might be next, risk aversion soared and lending tightened up. As September drew to a close, Congress was negotiating the terms of a $700 billion bank rescue package — the largest proposed federal market intervention since Franklin Roosevelt’s New Deal.

Performance: During the six months ended September 30, 2008, the Fund’s Class I shares declined 4.74% but outperformed the Russell Microcap Growth Index, which fell 5.76%.

Portfolio Specifics: The Fund’s outperformance was driven by stock selection in the industrials, consumer discretionary and financials sectors. Top-performing holdings included DXP Enterprises, a distributor of pumps that saw strong demand from customers in the food/beverage and energy markets; G-III Apparel, a sportswear manufacturer that was recognized for the growth potential of its national and private-label brands; and Life Partners, a provider of life settlement transactions that benefited from increasing awareness of its industry. NCI, a supplier of Web management services to government entities, was another top contributor, helped by its high percentage of recurring revenue.

Overall, the Fund’s sector exposures, which are a byproduct of our bottom-up investment decisions, negatively impacted relative results. For example, an overweight in consumer discretionary stocks and an underweight in health care were unfavorable. Consumer discretionary was one of the worst-performing sectors in the index, as high food and gasoline prices cut into spending on non-essential items. Health care was one of the few sectors to generate a gain, supported by a general preference for companies with stable demand characteristics in the turbulent investment environment.

Market Outlook: The stock market is likely to remain volatile over the coming months as investors measure the impact of the government rescue package and other policy steps aimed at stabilizing the financial system and economy. While it may take time for the environment to improve, it is worth noting that equities have recovered from significant shocks in the past.

As events unfold, we believe our research-driven investment process will continue to identify stocks for the Fund that are poised to outperform.

9

U.S. ULTRA MICRO CAP FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Common Stock - 98.3% | |||||||

Air Pollution Control Equipment - 1.2% | |||||||

| Met-Pro Corp. | 1,256 | $ | 18,325 | ||||

Apparel Manufacturers - 1.8% | |||||||

| G-III Apparel Group, Ltd.* | 1,487 | 27,822 | |||||

Applications Software - 1.7% | |||||||

| Ebix, Inc.* | 274 | 25,745 | |||||

Chemicals-Specialty - 1.2% | |||||||

| American Pacific Corp.* | 1,362 | 17,788 | |||||

Commercial Banks-Western US - 1.2% | |||||||

| Center Financial Corp. | 1,400 | 17,878 | |||||

Commercial Services - 1.1% | |||||||

| Medifast, Inc.* | 2,500 | 17,025 | |||||

Communications Software - 1.3% | |||||||

| Seachange International, Inc.* | 2,100 | 20,286 | |||||

Computer Services - 1.4% | |||||||

| Furmanite Corp.* | 2,049 | 21,187 | |||||

Computer Software - 1.0% | |||||||

| Double-Take Software, Inc.* | 1,554 | 15,462 | |||||

Computers-Integrated Systems - 2.0% | |||||||

| NCI, Inc. Cl. A* | 1,088 | 30,986 | |||||

Computers-Memory Devices - 0.8% | |||||||

| Datalink Corp.* | 2,900 | 12,644 | |||||

Computers-Peripheral Equipment - 2.4% | |||||||

| iCAD, Inc.* | 5,300 | 16,907 | |||||

| Transact Technologies, Inc.* | 2,469 | 19,653 | |||||

| 36,560 | |||||||

Cosmetics & Toiletries - 0.9% | |||||||

| Parlux Fragrances, Inc.* | 2,727 | 14,017 | |||||

Data Processing/Management - 0.7% | |||||||

| Versant Corp.* | 551 | 10,667 | |||||

Diagnostic Equipment - 0.8% | |||||||

| Home Diagnostics, Inc.* | 1,290 | 12,487 | |||||

Distribution/Wholesale - 1.0% | |||||||

| FGX International Holdings, Ltd.* | 1,400 | 15,498 | |||||

Electric Products-Miscellaneous - 0.8% | |||||||

| Harbin Electric, Inc.* | 1,034 | 12,253 | |||||

Electronic Components-Miscellaneous - 0.8% | |||||||

| Chyron International Corp.* | 2,818 | 11,554 | |||||

Electronic Components-Semiconductors - 0.9% | |||||||

| Ceva, Inc.* | 1,662 | 13,795 | |||||

Electronic Security Devices - 1.1% | |||||||

| Digital Ally, Inc.* | 2,385 | 16,385 | |||||

Engineering/R & D Services - 1.0% | |||||||

| Argan, Inc.* | 1,000 | 15,480 | |||||

Enterprise Software/Services - 1.1% | |||||||

| Opnet Technologies, Inc.* | 1,400 | 17,052 | |||||

Food-Miscellaneous/Diversified - 2.9% | |||||||

| American Italian Pasta Co.* | 1,720 | 28,552 | |||||

| Overhill Farms, Inc.* | 3,193 | 16,444 | |||||

| 44,996 | |||||||

Hazardous Waste Disposal - 0.8% | |||||||

| Heritage-Crystal Clean, Inc.* | 940 | 12,690 | |||||

Health Care Cost Containment - 1.1% | |||||||

| Integramed America, Inc.* | 2,400 | 17,040 | |||||

Heart Monitors - 1.6% | |||||||

| Cardiac Science Corp.* | 2,358 | 24,429 | |||||

Human Resources - 1.3% | |||||||

| On Assignment, Inc.* | 2,536 | 19,984 | |||||

Industrial Automation/Robotics - 0.8% | |||||||

| Adept Technology, Inc. Cl. A* | 1,409 | 12,315 | |||||

Instruments-Controls - 0.7% | |||||||

| Spectrum Control, Inc.* | 1,353 | 10,107 | |||||

Insurance Brokers - 1.6% | |||||||

| Life Partners Holdings, Inc. | 688 | 24,747 | |||||

Machinery Tools & Relative Products - 0.9% | |||||||

| K-Tron International, Inc.* | 110 | 14,171 | |||||

Machinery-General Industry - 1.0% | |||||||

| DXP Enterprises, Inc.* | 288 | 15,353 | |||||

Medical Imaging Systems - 1.7% | |||||||

| IRIS International, Inc.* | 1,436 | 25,704 | |||||

Medical Instruments - 1.8% | |||||||

| AtriCure, Inc.* | 1,511 | 15,140 | |||||

| SenoRx, Inc.* | 2,686 | 13,269 | |||||

| 28,409 | |||||||

Medical Labs & Testing Services - 1.5% | |||||||

| Bio-Imaging Technologies, Inc.* | 2,979 | 22,998 | |||||

Medical Laser Systems - 0.8% | |||||||

| Cynosure, Inc. Cl. A* | 649 | 11,643 | |||||

Medical Products - 8.0% | |||||||

| Alphatec Holdings, Inc.* | 3,587 | 16,500 | |||||

| Atrion Corp. | 206 | 21,224 | |||||

| ATS Medical, Inc.* | 7,025 | 20,302 | |||||

| Exactech, Inc.* | 978 | 21,751 | |||||

| Synovis Life Technologies, Inc.* | 1,143 | 21,512 | |||||

| Vnus Medical Technologies, Inc.* | 1,054 | 22,060 | |||||

| 123,349 | |||||||

Medical-Biomedical/Genetics - 3.6% | |||||||

| Avigen, Inc.* | 3,800 | 15,200 | |||||

| CryoLife, Inc.* | 1,692 | 22,199 | |||||

| RTI Biologics, Inc.* | 1,972 | 18,438 | |||||

| 55,837 | |||||||

Medical-Drugs - 0.8% | |||||||

| Santarus, Inc.* | 5,700 | 11,571 | |||||

Medical-Outpatient/Home Medical Care - 3.5% | |||||||

| Allied Healthcare International, Inc.* | 7,542 | 14,330 | |||||

| Almost Family, Inc.* | 600 | 23,730 | |||||

| NovaMed, Inc.* | 3,400 | 16,116 | |||||

| 54,176 | |||||||

MRI/Medical Diagnostic Imaging Centers - 0.5% | |||||||

| RadNet, Inc.* | 2,014 | 8,076 | |||||

Oil Companies-Exploration & Production - 2.4% | |||||||

| Double Eagle Petroleum Co.* | 1,051 | 15,008 | |||||

| Meridian Resource Corp.* | 5,300 | 9,752 | |||||

| NGAS Resources, Inc.* | 2,516 | 11,951 | |||||

| 36,711 | |||||||

Oil Field Machinery & Equipment - 0.6% | |||||||

| Mitcham Industries, Inc.* | 936 | 9,444 | |||||

Oil-Field Services - 0.7% | |||||||

| Boots & Coots International Control, Inc.* | 5,564 | 10,739 | |||||

See Accompanying Notes to Financial Statements.

10

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

Number of Shares | Value | ||||||

Optical Supplies - 1.0% | |||||||

| Staar Surgical Co.* | 3,297 | $ | 14,804 | ||||

Patient Monitoring Equipment - 1.4% | |||||||

| Somanetics Corp.* | 1,018 | 22,264 | |||||

Physical Therapy/Rehabilitation Centers - 1.5% | |||||||

| US Physical Therapy, Inc.* | 1,290 | 22,394 | |||||

Power Conversion/Supply Equipment - 1.1% | |||||||

| C&D Technologies, Inc.* | 3,052 | 17,335 | |||||

Private Corrections - 1.3% | |||||||

| Cornell Cos., Inc.* | 715 | 19,434 | |||||

Property/Casualty Insurance - 1.3% | |||||||

| Meadowbrook Insurance Group, Inc. | 2,867 | 20,241 | |||||

Research & Development - 1.1% | |||||||

| Exponent,Inc.* | 515 | 17,041 | |||||

Retail-Apparel/Shoe - 4.4% | |||||||

| Cache, Inc.* | 932 | 6,403 | |||||

| HOT Topic, Inc.* | 3,902 | 25,792 | |||||

| Shoe Carnival, Inc.* | 1,252 | 20,508 | |||||

| The Wet Seal, Inc. Cl. A* | 3,993 | 14,494 | |||||

| 67,197 | |||||||

Retail-Automobile - 0.9% | |||||||

| America’s Car-Mart, Inc.* | 775 | 14,407 | |||||

Retail-Computer Equipment - 0.6% | |||||||

| PC Mall, Inc.* | 1,379 | 9,419 | |||||

Retail-Discount - 1.1% | |||||||

| Citi Trends, Inc.* | 1,048 | 17,072 | |||||

Retail-Drug Store - 1.1% | |||||||

| Allion Healthcare, Inc.* | 2,929 | 17,428 | |||||

Retail-Miscellaneous/Diversified - 0.9% | |||||||

| Titan Machinery, Inc.* | 635 | 13,214 | |||||

Retail-Restaurants - 2.2% | |||||||

| Einstein Noah Restaurant Group, Inc.* | 1,563 | 15,755 | |||||

McCormick & Schmick’s Seafood Restaurants, Inc.* | 1,864 | 18,155 | |||||

| 33,910 | |||||||

Savings & Loans/Thrifts-Eastern US - 2.9% | |||||||

| OceanFirst Financial Corp. | 1,101 | 19,950 | |||||

| United Financial Bancorp, Inc. | 1,647 | 24,458 | |||||

| 44,408 | |||||||

Semiconductor Components - Integrated Circuits - 0.9% | |||||||

| Techwell, Inc.* | 1,396 | 13,164 | |||||

Semiconductor Equipment - 2.2% | |||||||

| Amtech Systems, Inc.* | 1,435 | 13,360 | |||||

| Ultra Clean Holdings* | 1,864 | 9,394 | |||||

| Ultratech, Inc.* | 966 | 11,689 | |||||

| 34,443 | |||||||

Textile-Apparel - 1.0% | |||||||

| Perry Ellis International, Inc.* | 1,048 | 15,626 | |||||

Transactional Software - 1.2% | |||||||

| Yucheng Technologies, Ltd.* | 1,829 | 18,564 | |||||

Transport-Marine - 0.8% | |||||||

| CAI International, Inc.* | 1,107 | 12,243 | |||||

Transport-Services - 0.9% | |||||||

| Vitran Corp., Inc.* | 1,004 | 13,524 | |||||

Transport-Truck - 3.2% | |||||||

| Celadon Group, Inc.* | 1,606 | 18,421 | |||||

| Saia, Inc.* | 1,425 | 18,924 | |||||

| USA Truck, Inc.* | 747 | 11,915 | |||||

| 49,260 | |||||||

Wireless Equipment - 1.0% | |||||||

| Globecomm Systems, Inc.* | 1,748 | 15,278 | |||||

| Total Common Stock (Cost: $1,547,154) | 1,518,055 | ||||||

Principal Amount | |||||||

Short Term Investments - 3.3% | |||||||

Time Deposit - 3.3% | |||||||

| Brown Brothers Harriman & Co. - Grand Cayman 3.470%, 10/01/08 (Cost: $50,577) | $ | 50,577 | 50,577 | ||||

| Total Investments - 101.6% (Cost: $1,597,731) | 1,568,632 | ||||||

| Liabilities In Excess of Other Assets - (1.6%) | (24,874 | ) | |||||

| Net Assets - 100.0% | $ | 1,543,758 | |||||

* Non-income producing securities.

SCHEDULE OF INVESTMENTS BY SECTOR

as of September 30, 2008

| Sector | Percent of Net Assets | |||

| Consumer, Non-cyclical | 37.8 | % | ||

| Industrial | 17.4 | |||

| Technology | 16.2 | |||

| Consumer, Cyclical | 14.0 | |||

| Financial | 7.0 | |||

| Energy | 3.7 | |||

| Basic Materials | 1.2 | |||

| Communications | 1.0 | |||

| Short Term Investments | 3.3 | |||

| Total Investments | 101.6 | |||

| Liabilities in excess of other assets | (1.6 | ) | ||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

11

U.S. SYSTEMATIC LARGE CAP GROWTH FUND

Management Team: James Li, Ph.D., CFA, Portfolio Manager; Jane Edmondson, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Systematic Large Cap Growth Fund seeks to maximize long-term capital appreciation by investing primarily in stocks from a universe of large U.S. companies with market capitalizations similar to the Russell 1000 Growth Index at time of purchase.

Market Overview: The Russell 1000 Growth Index, a barometer of U.S. large-cap growth stocks, posted a loss during the six months ended September 30, 2008. The decline was part of a broad sell-off in the market that pressured equities across styles and capitalization ranges.

The period began on a positive note, with the index generating strong gains in April and May amid optimism the emergency steps taken by the Federal Reserve in March would ease strains in the credit markets. An interest rate cut from the Fed on April 30, as well as some encouraging reports on the economy, further boosted investor sentiment.

Gains from the spring subsequently gave way to steep losses, which were driven by:

| • | Further deterioration in mortgage-linked assets that led to the bankruptcy, sale or government takeover of several large financial institutions |

| • | Seizing up of the credit markets, as uncertainty about which institution might be next to fail made banks afraid to lend, even to each other |

| • | Worsening outlook for the economy and weak corporate earnings, with second quarter profits for S&P 500 companies down more than 22% |

At the end of September, investors were awaiting the fate of legislation that would allow the Treasury to buy up to $700 billion of illiquid mortgage securities from financial firms.

Performance: The Fund’s Class I shares lost 9.44% between April 1 and September 30, 2008 but outperformed the Russell 1000 Growth Index, which fell 11.23%.

Portfolio Specifics: The Fund’s outperformance was driven by stock selection, which was strongest in the energy, consumer discretionary and industrials sectors. Areas of relative weakness included stock selection in the financials sector and an overweight in consumer discretionary companies, which lagged the broad market amid high food and gas prices.

At the individual stock level, some of our best-performing holdings were Amgen, Wal-Mart Stores and McDonald’s, which all generated double-digit gains. Optimistic business prospects and better-than-expected earnings growth boosted biotechnology firm Amgen. Wal-Mart, a defensive name in the consumer staples sector, continued to post solid same-store sales growth in a difficult retail environment. Fast food chain McDonald’s benefited from positive sales trends outside the United States and resilience in its U.S. business.

Holdings remained well-diversified throughout the period, consistent with our risk-controlled approach to portfolio construction. On September 30, the Fund’s largest overweights versus the Russell 1000 Growth Index were in the health care (+3.1%) and energy (+2.8%) sectors. The largest underweights were in financials (-3.4%) and information technology (-2.3%).

Market Outlook: Our process evaluates investment opportunities on a relative basis and is required to remain fully invested. As such, the process neither utilizes nor results in a forecast or outlook on the overall market, but expects to perform equally well versus the Russell 1000 Growth Index in both up and down markets.

Through consistent application of our systematic, model-driven process, we believe that the Fund will continue to add value to the benchmark.

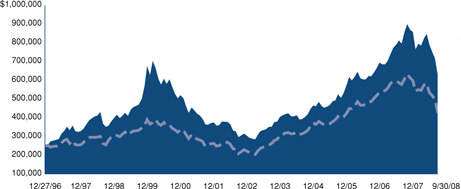

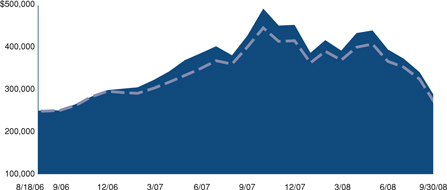

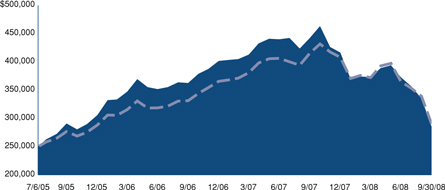

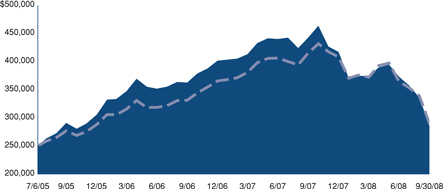

Comparison of Change in Value of a $250,000 Investment in U.S. Systematic Large Cap Growth Fund Class I and II Shares with the Russell 1000 Growth Index.

| Annualized Total Returns As of 9/30/08 | ||||||||||

1 Year | 5 Years | 10 Years | ||||||||

U.S. Systematic Large Cap Growth Fund Class I | -22.40% | 4.00% | 1.12% | |||||||

| Russell 1000 Growth Index | -20.88% | 3.74% | 0.59% | |||||||

12

U.S. SYSTEMATIC LARGE CAP GROWTH FUND

| Annualized Total Returns As of 9/30/08 | ||||||||||

1 Year | 5 Years | 10 Years | ||||||||

U.S. Systematic Large Cap Growth Fund Class II | -22.27% | 4.77% | 1.50% | |||||||

| Russell 1000 Growth Index | -20.88% | 3.74% | 0.59% | |||||||

The graphs above show the value of a hypothetical $250,000 investment in the Fund’s Class I and II shares compared with the Russell 1000 Growth Index for the periods indicated. The Fund’s Class I and II shares calculate their performance based upon the historical performance of a corresponding series of Nicholas-Applegate Mutual Funds (renamed ING Mutual Funds), adjusted to reflect all fees and expenses applicable to the Fund’s Class I and II shares. The Nicholas-Applegate Institutional Funds’ Class I shares were first available on May 7, 1999 and Class II shares on September 30, 2005. The historical performance of Class II shares includes the performance of Class I shares for periods prior to the inception of Class II. Average annual total return figures include changes in principal value, reinvested dividends, and capital gain distributions. The total returns shown above do not show the effects of income taxes on an individual’s investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

Russell 1000 Growth Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Index consists of the 1,000 largest securities in the Russell 3000 Index, which represents approximately 90% of the total market capitalization of the Russell 3000 Index. It is a large-cap, market-oriented index and is highly correlated with the S&P 500 Index. The unmanaged Index differs from the Fund in composition, does not pay management fees or expenses and includes reinvested dividends. One cannot invest directly in an index.

Since markets can go down as well as up, investment return and principal value will fluctuate with market conditions. You may have a gain or loss when you sell your shares.

13

U.S. SYSTEMATIC LARGE CAP GROWTH FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

As of September 30, 2008

| Number of | |||||||

| Shares | Value | ||||||

Common Stock - 98.6% | |||||||

Aerospace/Defense - 2.8% | |||||||

| Boeing Co. | 3,000 | $ | 172,050 | ||||

| Northrop Grumman Corp. | 1,500 | 90,810 | |||||

| 262,860 | |||||||

Agricultural Chemicals - 2.0% | |||||||

| CF Industries Holdings, Inc. | 700 | 64,022 | |||||

| Monsanto Co. | 1,200 | 118,776 | |||||

| 182,798 | |||||||

Apparel Manufacturers - 1.8% | |||||||

| VF Corp. | 2,100 | 162,351 | |||||

Applications Software - 5.2% | |||||||

| Microsoft Corp. | 18,100 | 483,089 | |||||

Beverages-Non-alcoholic - 1.8% | |||||||

| PepsiCo, Inc. | 2,400 | 171,048 | |||||

Building-Residential/Commercial - 1.3% | |||||||

| Pulte Homes, Inc. | 8,600 | 120,142 | |||||

Cable TV - 0.8% | |||||||

| DISH Network Corp. Cl. A * | 3,300 | 69,300 | |||||

Chemicals-Diversified - 1.0% | |||||||

| Celanese Corp. Cl. A | 3,400 | 94,894 | |||||

Coal - 0.8% | |||||||

| Foundation Coal Holdings, Inc. | 1,000 | 35,580 | |||||

| Walter Industries, Inc. | 800 | 37,960 | |||||

| 73,540 | |||||||

Commercial Services - 1.0% | |||||||

| Alliance Data Systems Corp.* | 1,500 | 95,070 | |||||

Commercial Services-Finance - 0.4% | |||||||

| Mastercard, Inc. Cl. A | 200 | 35,466 | |||||

Computers - 6.6% | |||||||

| Hewlett-Packard Co. | 6,500 | 300,560 | |||||

| International Business Machines Corp. | 2,700 | 315,792 | |||||

| 616,352 | |||||||

Computers-Integrated Systems - 1.0% | |||||||

| NCR Corp.* | 4,200 | 92,610 | |||||

Computers-Memory Devices - 0.8% | |||||||

| Western Digital Corp.* | 3,300 | 70,356 | |||||

Cosmetics & Toiletries - 1.0% | |||||||

| Procter & Gamble Co. | 1,375 | 95,824 | |||||

Diversified Manufacturing Operations - 0.9% | |||||||

| Tyco International, Ltd. | 2,500 | 87,550 | |||||

Electronic Components-Semiconductors - 1.1% | |||||||

| Intel Corp. | 3,200 | 59,936 | |||||

| MEMC Electronic Materials, Inc.* | 1,400 | 39,564 | |||||

| 99,500 | |||||||

Energy-Alternate Sources - 0.6% | |||||||

| First Solar, Inc.* | 300 | 56,673 | |||||

Engineering/R & D Services - 1.3% | |||||||

| Fluor Corp. | 1,600 | 89,120 | |||||

| The Shaw Group, Inc.* | 900 | 27,657 | |||||

| 116,777 | |||||||

Engines-Internal Combust - 1.2% | |||||||

| Cummins, Inc. | 2,500 | 109,300 | |||||

Internet Security - 1.3% | |||||||

| Symantec Corp.* | 6,200 | 121,396 | |||||

Linen Supply & Relative Items - 1.3% | |||||||

| Cintas Corp. | 4,200 | 120,582 | |||||

Machinery-Construction & Mining - 1.3% | |||||||

| Bucyrus International, Inc. Cl. A | 2,600 | 116,168 | |||||

Medical Instruments - 3.9% | |||||||

| Boston Scientific Corp.* | 8,200 | 100,614 | |||||

| Medtronic, Inc. | 3,300 | 165,330 | |||||

| St. Jude Medical, Inc.* | 2,300 | 100,027 | |||||

| 365,971 | |||||||

Medical Products - 1.8% | |||||||

| Johnson & Johnson | 2,400 | 166,272 | |||||

Medical-Biomedical/Genetics - 2.8% | |||||||

| Amgen, Inc.* | 3,300 | 195,591 | |||||

| Celgene Corp.* | 1,000 | 63,280 | |||||

| 258,871 | |||||||

Medical-Drugs - 4.0% | |||||||

| Eli Lilly & Co. | 2,800 | 123,284 | |||||

| Forest Laboratories, Inc.* | 5,600 | 158,368 | |||||

| Merck & Co., Inc. | 2,800 | 88,368 | |||||

| 370,020 | |||||||

Medical-HMO - 1.0% | |||||||

| Aetna, Inc. | 2,500 | 90,275 | |||||

Medical-Hospitals - 1.0% | |||||||

| Community Health Systems, Inc.* | 3,000 | 87,930 | |||||

Metal-Diversified - 1.0% | |||||||

| Freeport-McMoRan Copper & Gold, Inc. | 1,700 | 96,645 | |||||

Metal-Iron - 0.3% | |||||||

| Cleveland-Cliffs, Inc. | 500 | 26,470 | |||||

Multi-line Insurance - 1.1% | |||||||

| ACE, Ltd. | 1,900 | 102,847 | |||||

Networking Products - 4.6% | |||||||

| Cisco Systems, Inc.* | 19,000 | 428,640 | |||||

Office Automation & Equipment - 1.1% | |||||||

| Pitney Bowes, Inc. | 3,100 | 103,106 | |||||

Oil & Gas Drilling - 3.6% | |||||||

| Diamond Offshore Drilling, Inc. | 1,500 | 154,590 | |||||

| ENSCO International, Inc. | 3,100 | 178,653 | |||||

| 333,243 | |||||||

Oil Companies-Exploration & Production - 4.1% | |||||||

| Apache Corp. | 1,800 | 187,704 | |||||

| Occidental Petroleum Corp. | 1,600 | 112,720 | |||||

| Southwestern Energy Co.* | 2,600 | 79,404 | |||||

| 379,828 | |||||||

Oil Companies-Integrated - 3.0% | |||||||

| Exxon Mobil Corp. | 3,000 | 232,980 | |||||

| Hess Corp. | 500 | 41,040 | |||||

| 274,020 | |||||||

Oil Field Machine & Equipment - 0.9% | |||||||

| National Oilwell Varco, Inc.* | 1,600 | 80,368 | |||||

Pharmacy Services - 2.9% | |||||||

| Medco Health Solutions, Inc.* | 2,500 | 112,500 | |||||

| Omnicare, Inc. | 5,300 | 152,481 | |||||

| 264,981 | |||||||

See Accompanying Notes to Financial Statements.

14

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2008

As of September 30, 2008

| Number of | |||||||

| Shares | Value | ||||||

Retail-Apparel/Shoe - 2.2% | |||||||

| Limited Brands, Inc. | 3,900 | $ | 67,548 | ||||

| Polo Ralph Lauren Corp. Cl. A | 2,000 | 133,280 | |||||

| 200,828 | |||||||

Retail-Discount - 4.2% | |||||||

| Wal-Mart Stores, Inc. | 6,500 | 389,285 | |||||

Retail-Restaurants - 2.8% | |||||||

| McDonald’s Corp. | 2,700 | 166,590 | |||||

| Panera Bread Co. Cl. A* | 1,900 | 96,710 | |||||

| 263,300 | |||||||

Semiconductor Components-Integrated Circuits - 0.6% | |||||||

| Integrated Device Technology, Inc.* | 7,600 | 59,128 | |||||

Telephone-Integrated - 0.9% | |||||||

| Verizon Communications, Inc. | 2,700 | 86,643 | |||||

Tobacco - 5.3% | |||||||

| Altria Group, Inc. | 12,400 | 246,016 | |||||

| Philip Morris International, Inc. | 5,200 | 250,120 | |||||

| 496,136 | |||||||

Transport-Marine - 0.7% | |||||||

| Frontline Ltd. | 1,400 | 67,298 | |||||

Transport-Rail - 3.5% | |||||||

| CSX Corp. | 3,500 | 190,995 | |||||

| Norfolk Southern Corp. | 1,200 | 79,452 | |||||

| Union Pacific Corp. | 700 | 49,812 | |||||

| 320,259 | |||||||

Vitamins & Nutrition Products - 0.5% | |||||||

| Herbalife, Ltd. | 1,100 | 43,472 | |||||

Web Portals/ISP - 2.6% | |||||||

| Google, Inc. Cl. A* | 300 | 120,156 | |||||

| Sohu.com, Inc.* | 2,200 | 122,650 | |||||

| 242,806 | |||||||

Wireless Equipment - 1.1% | |||||||

| QUALCOMM, Inc. | 2,400 | 103,128 | |||||

| Total Common Stock (Cost: $9,601,811) | 9,155,416 | ||||||

| Principal | |||||||

| Amount | |||||||

Short Term Investments - 1.4% | |||||||

Time Deposit - 1.4% | |||||||

| Citibank London | |||||||

| 3.470%, 10/01/08 | |||||||

| (Cost: $126,505) | $ | 126,505 | 126,505 | ||||

| Total Investments - 100.0% (Cost: $9,728,316) | 9,281,921 | ||||||

| Other Assets In Excess Of Liabilities - 0.0% | 4,224 | ||||||

| Net Assets - 100.0% | $ | 9,286,145 | |||||

* Non-income producing securities.

SCHEDULE OF INVESTMENTS BY SECTOR

as of September 30, 2008

| Sector | Percent of Net Assets | |||

| Consumer, Non-cyclical | 27.5 | % | ||

| Technology | 16.4 | |||

| Energy | 12.9 | |||

| Consumer, Cyclical | 12.8 | |||

| Industrial | 11.6 | |||

| Communications | 11.3 | |||

| Basic Materials | 4.3 | |||

| Financial | 1.1 | |||

| Consumer Non-cyclical | 0.7 | |||

| Short Term Investments | 1.4 | |||

| Total Investments | 100.0 | |||

| Other assets in excess of liabilities | 0.0 | |||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

15

U.S. SMALL TO MID CAP GROWTH FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Small to Mid Cap Growth Fund seeks to maximize long-term capital appreciation by investing primarily in stocks from a universe of U.S. companies with small to mid (SMID) market capitalizations similar to the Russell 2500 Growth Index at time of purchase.

Market Overview: The small- to mid-cap growth segment of the U.S. stock market, as measured by the Russell 2500 Growth Index, registered a decline from April 1 to September 30, 2008. Losses were concentrated in September, when deteriorating mortgage-related assets threatened the solvency of several major financial institutions. The fourth-largest U.S. securities firm ended up in bankruptcy, while others were considered too big to fail and received help from the government. Against this uncertain backdrop:

| • | Banks became afraid to lend, even to each other, and the short-term credit markets slowed to a near standstill |

| • | Investors withdrew nearly $250 billion from money market accounts in a ten-day period after one fund’s value fell below $1 per share |

| • | A widely followed measure of stock market volatility spiked to a record high |

Policymakers moved quickly to try and calm the markets. For example, the Federal Reserve injected huge amounts of liquidity into the financial system, and the Treasury unveiled a $50 billion insurance plan for money market funds and a $700 billion bank rescue package. The period ended on hopes that Congress would approve the $700 billion package after voting it down on September 29.

Performance: The Fund’s Class I shares posted a 7.87% decline between April 1 and September 30, 2008, outperforming the Russell 2500 Growth Index, which lost 8.91%.