UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07384

NICHOLAS-APPLEGATE INSTITUTIONAL FUNDS

(Exact name of registrant as specified in charter)

600 WEST BROADWAY, 30th FLOOR, SAN DIEGO, CA 92101

(Address of principal executive offices) (Zip Code)

Charles H. Field, Jr.

c/o Nicholas-Applegate Capital Management, LLC

600 West Broadway, 30th Floor

San Diego, CA 92101

(Name and address of agent for service)

Copy to:

Deborah A. Wussow-Hammalian

c/o Nicholas-Applegate Capital Management, LLC

600 West Broadway, 30th Floor

San Diego, CA 92101

Registrant's telephone number, including area code: (619) 687-2988

Date of fiscal year end: March 31

Date of reporting period: September 30, 2009

Item 1. Reports to Stockholders.

September 30, 2009 Semi Annual Report (Unaudited)

Class I, II, III & IV Shares

U.S. Ultra Micro Cap

U.S. Micro Cap

U.S. Emerging Growth

U.S. Small to Mid Cap Growth

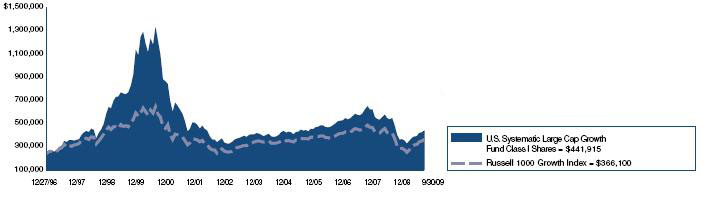

U.S. Systematic Large Cap Growth

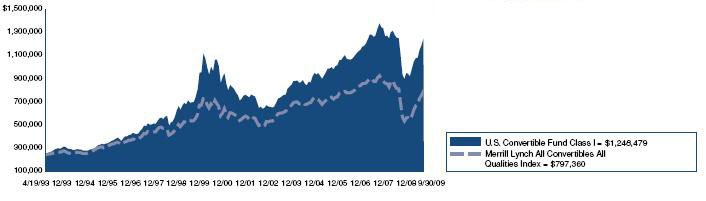

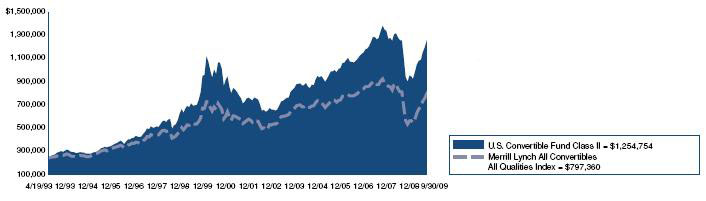

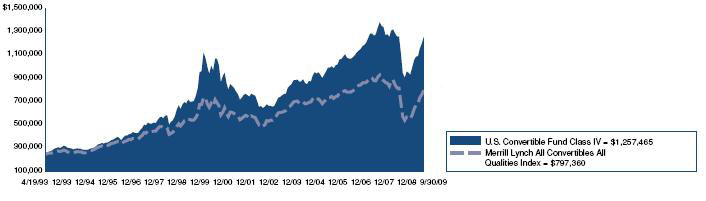

U.S. Convertible

Global Select

International Growth

International Growth Opportunities

Emerging Markets

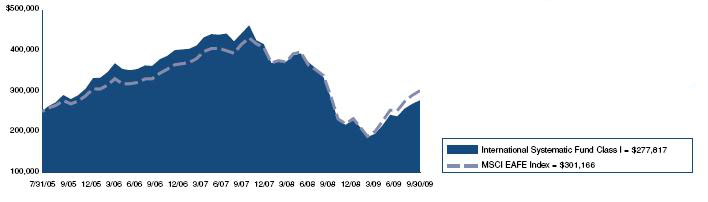

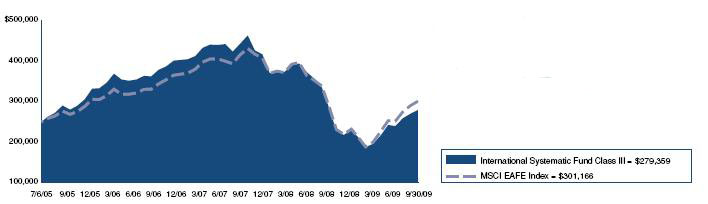

International Systematic

U.S. High Yield Bond

LETTER TO SHAREHOLDERS

Dear Fellow Shareholder,

Following the most severe correction since the 1930s, the global equity market came roaring back during the six months ended September 30, 2009. Stock markets around the world posted dramatic gains, as monetary and fiscal stimulus helped thaw the credit markets and stabilize the global economy.

In this semi-annual report, we review the performance of the financial markets and our mutual funds from April 1 through September 30, 2009. We also share our perspective on the dynamics shaping the investment environment and our outlook for the future.

In the United States, the S&P 500 Index rose 34.0%. The Federal Reserve held short-term interest rates near zero and continued to flood the credit markets with liquidity by making loans and asset purchases. As investors gained confidence in the financial system, borrowers had easier and cheaper access to credit. In addition, some of the $787 billion stimulus package made its way into the economy through tax credits, the “cash for clunkers” vehicle trade-in program and other initiatives. Economic data released during the period showed that policymakers’ efforts were paying off. GDP declined at an annual rate of 0.7% in the second quarter of 2009, after having fallen 6.4% in the first quarter. More recent indicators suggested that the economy might be growing again, despite persistent weakness in the labor market. Corporate earnings were another source of optimism. While earnings for S&P 500 companies continued to decline, they were better than anticipated, supported by cost-cutting measures.

Stock markets in developed countries outside the United States also performed well. The MSCI EAFE Index gained 34.8% in local currencies and 50.4% in dollar terms. The U.S. dollar fell 8.7% versus a basket of currencies on expectations that the Federal Reserve would not raise interest rates any time soon. Like the Fed, central bankers in Europe and Japan held interest rates at record lows and continued with the special liquidity programs they had established during the financial crisis. However, demand for some of these programs was waning, testament to the improvement in the credit markets. Several developed countries came out of recession in the second quarter of 2009, including Japan whose economy grew at an annual pace of 2.3%. The German and French economies expanded as well, although GDP for the entire euro region dropped 4.8%, weighed down by weakness in Spain and Italy.

Equities in emerging countries delivered the strongest gains, with the MSCI Emerging Markets Index rising 45.7% in local currencies and 63.2% in U.S. dollars. As the global economy stabilized, investors rotated out of more defensive assets into higher-risk areas, such as emerging markets. Emerging markets further benefited from the relative strength of developing economies and rising commodity prices. For example, Chinese GDP grew at an annual rate of 7.1% in the first half of the year, helped by a surge in bank lending. Russia, whose main export is oil, was one of the best-performing equity markets this period amid a 42% spike in oil prices.

Against this favorable backdrop, all of the Nicholas-Applegate funds generated significant gains. That said, a number of our funds struggled to keep up with their benchmarks in the rapidly rising market. We believe this was because the rally was driven more by sentiment than company fundamentals. As the panic of last fall and winter subsided, relieved investors jumped back into the market, buying securities rather indiscriminately. A sentiment-driven rally is not unusual to see coming out of a severe correction. Nonetheless, it was a headwind for the funds given our focus on company fundamentals.

The volatile investment environment has underscored the importance of risk management, which remains a top priority at Nicholas-Applegate.

Our risk management program has been in place for more than a decade and has become increasingly sophisticated over the years. Today, we produce approximately 1,600 charts, tables and reports that our investment teams use to evaluate a wide range of risk metrics. We also have a risk management program that supports our entire business. This effort is guided by Nicholas-Applegate’s World Class Execution Committee (WCEC). The goal of the WCEC is to ensure a standard of excellence in all that we do to provide shareholders with world-class investment solutions. Its mandate encompasses everything from operations to compliance to the introduction of new products.

Looking forward, we expect the U.S. recovery to be more muted than past recoveries, given the high unemployment rate and continued tightness in certain segments of the credit markets. Foreign developed nations should recover more quickly than the United States, but real growth is also likely to remain subpar. Prices of gold, commodities and inflation-protected securities are telling us disinflation is coming to an end, and that inflation is in our future. We believe stock selection will be very important, as investors look for companies that will benefit from an environment of potentially slow growth, high unemployment and inflation. This bodes well for the fundamentally driven, bottom-up investment processes that we use to manage the funds.

On behalf of everyone at the firm, thank you for your participation in the Nicholas-Applegate Institutional Funds. We appreciate the trust that you have placed in us and look forward to serving your investment needs throughout the coming years.

Horacio A. Valeiras, CFA

President and Chief Investment Officer

September 30, 2009

TABLE OF CONTENTS

| The Funds’ Review and Outlook, Performance and Schedules of Investments: | |

| U.S. Ultra Micro Cap | 1 |

| U.S. Micro Cap | 4 |

| U.S. Emerging Growth | 9 |

| U.S. Small to Mid Cap Growth | 13 |

| U.S. Systematic Large Cap Growth | 17 |

| U.S. Convertible | 20 |

| Global Select | 25 |

| International Growth | 29 |

| International Growth Opportunities | 33 |

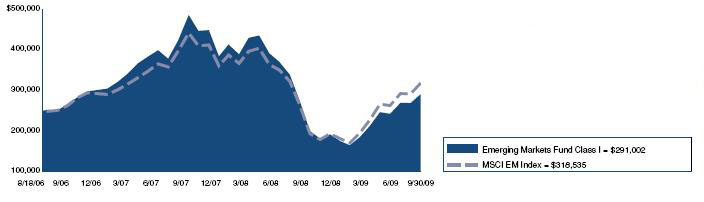

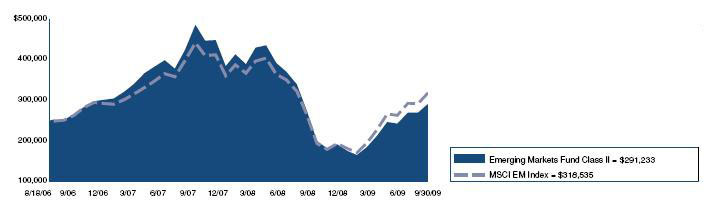

| Emerging Markets | 37 |

| International Systematic | 41 |

| U.S. High Yield Bond | 45 |

| The Funds’: | |

| Financial Highlights | 50 |

| Statements of Assets and Liabilities | 58 |

| Statements of Operations | 60 |

| Statements of Changes in Net Assets | 62 |

| Notes to Financial Statements | 66 |

| Shareholder Expense Example | 76 |

| Supplementary Information | 78 |

This report is authorized for distribution to shareholders and to others only when preceded or accompanied by a currently effective prospectus for Nicholas-Applegate Institutional Funds Class I, II, III & IV Shares. Distributor: Nicholas-Applegate Securities.

U.S. ULTRA MICRO CAP FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Ultra Micro Cap Fund seeks to maximize long-term capital appreciation by investing primarily in U.S. companies with market capitalizations below the weighted average of the Russell Microcap Growth Index at time of purchase.

Market Overview: During the six months ended September 30, 2009, the U.S. stock market continued to rebound from multi-year lows set in March. All of the major indexes climbed sharply higher in response to improvement in the credit markets and economy, with small- and micro-cap growth stocks turning in some of the best results.

In the first half of the period, equities soared as measures of investor fear and credit risk recovered to levels unseen since Lehman Brothers failed in September 2008. Various liquidity programs implemented by the Treasury and Federal Reserve helped unlock the credit markets, giving more borrowers access to cash. Although the economy remained weak, data suggested that it was deteriorating at a slower pace. This was confirmed in July, when the government reported that second-quarter GDP fell at an annual rate of 1.0% after having fallen 6.4% in the first quarter. The second-quarter figure was later revised to a 0.7% decline.

Equities maintained their upward momentum in the last half of the period, buoyed by better-than-expected earnings and generally upbeat economic data. Home prices appeared to have stabilized, the manufacturing sector expanded for the first time since early 2008 and retail sales posted their biggest monthly increase in over three years. In September, Fed Chairman Ben Bernanke said that it was “very likely” the recession had ended but warned that the unemployment rate could continue to rise.

Performance: The Fund’s Class I shares gained 62.11% from April 1, 2009 to September 30, 2009 outperforming the Russell Microcap Growth Index, which rose 53.87%.

Portfolio Specifics: The Fund’s outperformance was due to stock selection, which was strongest in the information technology, materials and consumer discretionary sectors. Three of the best-performing names in the portfolio were Terremark Worldwide, a provider of IT infrastructure services that is experiencing robust demand; Boise, a paper manufacturer that strengthened its balance sheet; and Carrols Restaurant Group, a fast-food chain with expanding operating margins. Stock selection also added value in the energy, industrials and consumer staples sectors. Gulfport Energy, an oil and gas producer, was another top performer in the Fund. The company ramped up drilling activity in response to strong oil prices and lower oilfield service costs.

The main area of relative weakness in the portfolio was stock selection in the health care sector. One of our biggest detractors was a supplier of diagnostic systems that reported disappointing earnings.

Market Outlook: While it is widely believed that the recession is over, we think that the economic recovery will be muted due to the high unemployment rate and large federal deficit. That said, several factors could fuel additional gains in the stock market over the months ahead, including:

| • | Expectations for a strong rebound in corporate earnings in 2010 |

| • | Potential for investors to move some of the $3.4 trillion sitting in low-yielding money market funds into equities |

| • | Indications from the Fed that it plans to keep interest rates low for an extended period of time |

Whatever direction the broad market takes, we believe that the Fund will continue to benefit from our focus on company-specific fundamentals.

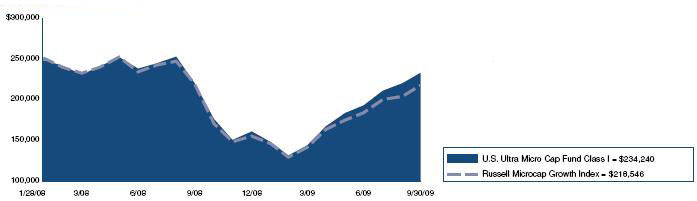

Comparison of Change in Value of a $250,000 Investment in U.S. Ultra Micro Cap Fund Class I Shares with the Russell Microcap Growth Index.

Annualized Total Returns As of 9/30/09 | ||

| 1 Year | Since Inception | |

| U.S. Ultra Micro Cap Fund Class I | 6.00% | –3.81% |

| Russell Microcap Growth Index | 6.72% | –7.73% |

The graph above shows the value of a hypothetical $250,000 investment in the Fund’s Class I shares with the Russell Microcap Growth Index for the periods indicated. Average annual total return figures include changes in principal value, reinvested dividends, and capital gain distributions. The Class I shares commenced operations on January 28, 2008. The total returns shown above do not show the effects of income taxes on an individuals’ investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

The Russell Microcap Index measures performance of the microcap segment, representing less than 3% of the U.S. equity market. The Russell Microcap Index includes the smallest 1,000 securities in the small-cap Russell 2000 Index plus the next 1,000 securities. The Russell Microcap Growth Index isolates the securities in the Russell Microcap Index with purely growth characteristics. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index. Since markets can go down as well as up, investment return and principal value will fluctuate with market conditions. You may have a gain or loss when you sell shares.

1

U.S. ULTRA MICRO CAP FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2009

| Number of | ||||||||

| Shares | Value | |||||||

| Common Stock - 97.9% | ||||||||

| Applications Software - 2.5% | ||||||||

| China TransInfo Technology Corp.* | 2,900 | $ | 27,434 | |||||

| inContact, Inc.* | 5,950 | 17,731 | ||||||

| 45,165 | ||||||||

| Auto/Truck Parts & Equipment-Original - 1.2% | ||||||||

| Wonder Auto Technology, Inc.* | 1,800 | 21,600 | ||||||

| Broadcast Services/Programming - 1.0% | ||||||||

| Acacia Research - Acacia Technologies* | 2,000 | 17,420 | ||||||

| Chemicals-Specialty - 4.8% | ||||||||

| ICO, Inc.* | 5,600 | 26,152 | ||||||

| KMG Chemicals, Inc. | 2,200 | 24,574 | ||||||

| Omnova Solutions, Inc.* | 3,300 | 21,384 | ||||||

| Penford Corp. | 2,300 | 16,491 | ||||||

| 88,601 | ||||||||

| Commercial Services - 1.1% | ||||||||

| StarTek, Inc.* | 2,400 | 20,832 | ||||||

| Commercial Services-Finance - 0.9% | ||||||||

| PRG-Schultz International, Inc.* | 3,000 | 16,800 | ||||||

| Communications Software - 1.3% | ||||||||

| Incredimail, Ltd. | 2,800 | 23,688 | ||||||

| Computer Services - 1.0% | ||||||||

| Virtusa Corp.* | 1,900 | 18,031 | ||||||

| Computers-Integrated Systems - 1.2% | ||||||||

| Radiant Systems, Inc.* | 2,080 | 22,339 | ||||||

| Computers-Memory Devices - 2.7% | ||||||||

| Dot Hill Systems Corp.* | 10,900 | 18,966 | ||||||

| Xyratex, Ltd.* | 3,300 | 31,383 | ||||||

| 50,349 | ||||||||

| Computers-Peripheral Equipment - 0.5% | ||||||||

| iGO, Inc.* | 7,500 | 8,175 | ||||||

| Consumer Products-Miscellaneous - 1.1% | ||||||||

| Summer Infant, Inc.* | 4,100 | 20,418 | ||||||

| Direct Marketing - 1.5% | ||||||||

| APAC Customer Services, Inc.* | 4,700 | 27,777 | ||||||

| Disposable Medical Products - 1.0% | ||||||||

| Medical Action Industries, Inc.* | 1,500 | 18,105 | ||||||

| Distribution/Wholesale - 1.0% | ||||||||

| Navarre Corp.* | 8,700 | 19,140 | ||||||

| Diversified Manufacturing Operations - 1.4% | ||||||||

| Park-Ohio Holdings Corp.* | 3,000 | 26,160 | ||||||

| Drug Delivery Systems - 0.7% | ||||||||

| Depomed, Inc.* | 3,100 | 13,547 | ||||||

| E-Commerce/Products - 0.9% | ||||||||

| 1-800-FLOWERS.COM, Inc.* | 4,700 | 16,215 | ||||||

| Electronic Components-Miscellaneous - 2.5% | ||||||||

| NVE Corp.* | 400 | 21,264 | ||||||

| Stoneridge, Inc.* | 3,600 | 25,488 | ||||||

| 46,752 | ||||||||

| Electronic Components-Semiconductors - 2.2% | ||||||||

| Ceva, Inc.* | 1,992 | 21,414 | ||||||

| MIPS Technologies, Inc. Cl. A* | 5,200 | 19,604 | ||||||

| 41,018 | ||||||||

| Electronic Measure Instruments - 1.4% | ||||||||

| Measurement Specialties, Inc.* | 2,600 | 26,546 | ||||||

| Hazardous Waste Disposal - 1.0% | ||||||||

| Sharps Compliance Corp.* | 1,800 | 17,730 | ||||||

| Health Care Cost Containment - 1.5% | ||||||||

| Integramed America, Inc.* | 2,840 | 26,980 | ||||||

| Human Resources - 1.2% | ||||||||

| Hudson Highland Group, Inc.* | 6,950 | 21,128 | ||||||

| Industrial Audio & Video Products - 0.7% | ||||||||

| SRS Labs, Inc.* | 1,800 | 13,158 | ||||||

| Instruments-Controls - 0.7% | ||||||||

| Spectrum Control, Inc.* | 1,573 | 13,355 | ||||||

| Insurance Brokers - 0.6% | ||||||||

| Life Partners Holdings, Inc. | 652 | 11,671 | ||||||

| Internet Applications Software - 1.8% | ||||||||

| Clicksoftware Technologies, Ltd.* | 2,100 | 13,209 | ||||||

| interCLICK, Inc.* | 9,000 | 18,990 | ||||||

| 32,199 | ||||||||

| Internet Content-Information/News - 1.1% | ||||||||

| Health Grades, Inc.* | 4,200 | 20,790 | ||||||

| Internet Infrastructure Software - 1.2% | ||||||||

| RADVision, Ltd.* | 2,400 | 21,264 | ||||||

| Machinery-General Industry - 1.1% | ||||||||

| Intevac, Inc.* | 1,500 | 20,160 | ||||||

| Medical Instruments - 2.1% | ||||||||

| Endologix, Inc.* | 3,400 | 21,046 | ||||||

| Vascular Solutions, Inc.* | 2,020 | 16,705 | ||||||

| 37,751 | ||||||||

| Medical Products - 2.0% | ||||||||

| ATS Medical, Inc.* | 7,735 | 20,730 | ||||||

| HealthTronics, Inc.* | 6,800 | 16,728 | ||||||

| 37,458 | ||||||||

| Medical-Biomedical/Genetics - 1.2% | ||||||||

| Repligen Corp.* | 2,000 | 10,020 | ||||||

| Transcept Pharmaceuticals, Inc.* | 800 | 11,064 | ||||||

| 21,084 | ||||||||

| Medical-Drugs - 1.5% | ||||||||

| Biospecifics Technologies Corp.* | 300 | 9,603 | ||||||

| Sciclone Pharmaceuticals, Inc.* | 4,400 | 18,744 | ||||||

| 28,347 | ||||||||

| Medical-Outpatient/Home Medical Care - 4.3% | ||||||||

| Almost Family, Inc.* | 500 | 14,875 | ||||||

| America Service Group, Inc. | 1,420 | 23,487 | ||||||

| Continucare Corp.* | 6,100 | 18,422 | ||||||

| NovaMed, Inc.* | 4,770 | 21,608 | ||||||

| 78,392 | ||||||||

| Networking Products - 2.3% | ||||||||

| Hypercom Corp.* | 8,400 | 26,040 | ||||||

| Silicom, Ltd.* | 1,800 | 16,884 | ||||||

| 42,924 | ||||||||

| Oil Companies-Exploration & Production - 3.6% | ||||||||

| GeoMet, Inc.* | 8,300 | 14,027 | ||||||

| Gulfport Energy Corp.* | 3,400 | 29,716 | ||||||

| Rex Energy Corp.* | 2,700 | 22,545 | ||||||

| 66,288 | ||||||||

See Accompanying Notes to Financial Statements.

2

SCHEDULE OF INVESTMENTS (Unaudited)

| As of September 30, 2009 |

| Number of | ||||||||

| Shares | Value | |||||||

| Oil Field Machine & Equipment - 1.9% | ||||||||

| Gulf Island Fabrication, Inc. | 800 | $ | 14,992 | |||||

| T-3 Energy Services, Inc.* | 1,030 | 20,291 | ||||||

| 35,283 | ||||||||

| Oil-Field Services - 0.8% | ||||||||

| Trico Marine Services, Inc.* | 2,000 | 15,440 | ||||||

| Paper & Related Products - 3.2% | ||||||||

| Boise, Inc.* | 7,200 | 38,016 | ||||||

| KapStone Paper & Packaging Corp.* | 2,500 | 20,350 | ||||||

| 58,366 | ||||||||

| Pharmacy Services - 1.1% | ||||||||

| BioScrip, Inc.* | 3,100 | 20,956 | ||||||

| Physical Therapy/Rehabilitation Centers - 1.2% | ||||||||

| US Physical Therapy, Inc.* | 1,510 | 22,756 | ||||||

| Power Conversion/Supply Equipment - 1.4% | ||||||||

| PowerSecure International, Inc.* | 3,700 | 25,086 | ||||||

| Recycling - 1.4% | ||||||||

| Metalico, Inc.* | 5,990 | 24,978 | ||||||

| Retail-Apparel/Shoe - 0.6% | ||||||||

| Destination Maternity Corp.* | 600 | 10,878 | ||||||

| Retail-Automobile - 1.4% | ||||||||

| America’s Car-Mart, Inc.* | 1,085 | 25,986 | ||||||

| Retail-Drug Store - 1.0% | ||||||||

| Allion Healthcare, Inc.* | 3,269 | 19,124 | ||||||

| Retail-Restaurants - 5.7% | ||||||||

| AFC Enterprises, Inc.* | 2,430 | 20,461 | ||||||

| Caribou Coffee Co., Inc.* | 2,900 | 20,938 | ||||||

| Carrols Restaurant Group, Inc.* | 3,400 | 25,704 | ||||||

| Einstein Noah Restaurant Group, Inc.* | 2,083 | 25,079 | ||||||

| Famous Dave’s Of America, Inc.* | 2,100 | 12,285 | ||||||

| 104,467 | ||||||||

| Retirement/Aged Care - 1.2% | ||||||||

| Five Star Quality Care, Inc.* | 6,100 | 22,326 | ||||||

| Semiconductor Components-Integrated Circuits - 2.1% | ||||||||

| Anadigics, Inc.* | 3,600 | 16,956 | ||||||

| Techwell, Inc.* | 1,986 | 21,806 | ||||||

| 38,762 | ||||||||

| Semiconductor Equipment - 1.4% | ||||||||

| Nanometrics, Inc.* | 3,900 | 25,623 | ||||||

| Steel-Producers - 1.4% | ||||||||

| Olympic Steel, Inc. | 900 | 25,821 | ||||||

| Telecommunication Equipment - 1.0% | ||||||||

| Anaren, Inc.* | 1,120 | 19,040 | ||||||

| Telecommunication Equipment-Fiber Optics - 1.0% | ||||||||

| Oplink Communications, Inc.* | 1,300 | 18,876 | ||||||

| Textile-Apparel - 1.8% | ||||||||

| Perry Ellis International, Inc.* | 2,100 | 33,684 | ||||||

| Transport-Marine - 1.2% | ||||||||

| CAI International, Inc.* | 3,100 | 22,847 | ||||||

| Transport-Services - 0.7% | ||||||||

| Vitran Corp., Inc.* | 1,404 | 12,664 | ||||||

| Transport-Truck - 3.1% | ||||||||

| Celadon Group, Inc.* | 1,926 | 21,783 | ||||||

| Quality Distribution, Inc.* | 5,350 | 18,029 | ||||||

| Saia, Inc.* | 1,045 | 16,804 | ||||||

| 56,616 | ||||||||

| Web Hosting/Design - 1.5% | ||||||||

| Terremark Worldwide, Inc.* | 4,300 | 26,746 | ||||||

| Wire & Cable Products - 1.1% | ||||||||

| Fushi Copperweld, Inc.* | 2,390 | 20,219 | ||||||

| Wireless Equipment - 0.9% | ||||||||

| WPCS International, Inc.* | 4,500 | 17,100 | ||||||

| Total Common Stock (Cost: $1,309,321) | 1,803,001 | |||||||

| Limited Partnerships - 1.0% | ||||||||

| Transport-Marine - 1.0% | ||||||||

| Navios Maritime Partners LP (Cost $13,444) | 1,600 | 19,120 | ||||||

| Principal | ||||||||

| Amount | ||||||||

| Short Term Investments - 1.1% | ||||||||

| Time Deposit - 1.1% | ||||||||

| Citibank London 0.030%, 10/01/09 | ||||||||

| (Cost: $20,183) | $ | 20,183 | 20,183 | |||||

| Total Investments - 100.0% (Cost: $1,342,948) | 1,842,304 | |||||||

| Other Assets in Excess of Liabilities - 0.0% | 430 | |||||||

| Net Assets - 100.0% | $ | 1,842,734 | ||||||

* Non-income producing securities.

SCHEDULE OF INVESTMENTS BY SECTOR | ||||

| as of September 30, 2009 | ||||

| Percent of | ||||

| Sector | Net Assets | |||

| Consumer, Non-cyclical | 23.0 | % | ||

| Industrial | 18.7 | |||

| Technology | 14.9 | |||

| Communications | 14.2 | |||

| Consumer, Cyclical | 12.7 | |||

| Basic Materials | 8.5 | |||

| Energy | 6.3 | |||

| Financial | 0.6 | |||

| Short Term Investments | 1.1 | |||

| Total Investments | 100.0 | |||

| Other assets in excess of liabilities | 0.0 | |||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

3

U.S. MICRO CAP FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Micro Cap Fund seeks to maximize long-term capital appreciation by investing primarily in U.S. companies with market capitalizations similar to the Russell Microcap Growth Index at time of purchase.

Market Overview: U.S. equities delivered significant gains during the six months ended September 30, 2009. While the rally was broad-based, micro-cap growth stocks did particularly well.

The following themes contributed to stocks’ strong performance:

| • | Improvement in the credit markets, with the London interbank offer rate for three-month dollars (Libor) — a proxy for financial stress — falling to record lows |

| • | Extremely inexpensive valuations following the dramatic sell-off in equities that occurred last fall and winter |

| • | Signs the recession was coming to an end, including the first monthly increase in a key index of home prices in nearly three years |

Government programs, such as the $8,000 new homebuyer tax credit, contributed to the improvement in the economy. In addition, the Federal Reserve kept interest rates at an all-time low of 0.00% to 0.25%. Because conditions in the financial markets had stabilized, the central bank cut back some of its emergency liquidity programs or let them expire. However, concerns about job losses and tighter consumer credit made the Fed cautious about shrinking its balance sheet too quickly, especially since inflation remained in check.

Performance: The Fund’s Class I shares gained 45.78%, from April 1 through September 30, 2009. The Russell Microcap Growth Index advanced 53.87%.

Portfolio Specifics: Stock selection in the information technology, energy and materials sectors had the largest positive impact on results versus the index. Top-performing holdings included Taleo, a software provider on the cusp of a new product cycle; Stone Energy, an energy exploration and production company that announced its first deepwater discovery; and Omnova Solutions, a chemical producer that benefited from lower manufacturing and raw material costs.

Within the Russell Microcap Growth Index, the smallest market-cap stocks and those with the lowest stock prices generated the highest returns, which was consistent with rising risk appetites. This had a negative impact on the Fund’s relative performance, since our investment style generally leads to under-representation in these segments of the benchmark. From a sector perspective, stock selection in health care and information technology subtracted the most from results versus the index.

Market Outlook: While it is widely believed that the recession is over, we think that the economic recovery will be muted due to the high unemployment rate and large federal deficit. That said, several factors could fuel additional gains in the stock market over the months ahead, including:

| • | Expectations for a strong rebound in corporate earnings in 2010 |

| • | Potential for investors to move some of the $3.4 trillion sitting in low-yielding money market funds into equities |

| • | Indications from the Fed that it plans to keep interest rates low for an extended period of time |

As events unfold, we are confident that our bottom-up investment process will identify exciting growth opportunities for the Fund.

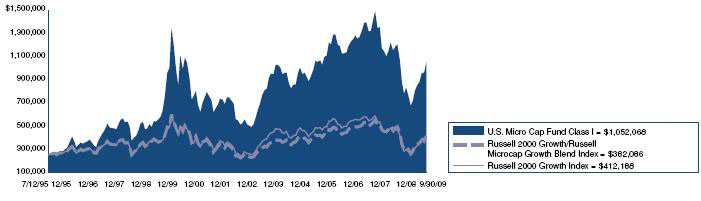

Comparison of Change in Value of a $250,000 Investment in U.S. Micro Cap Fund Class I Shares with the Russell 2000 Growth/Russell Microcap Growth Blend Index and Russell 2000 Growth Index

Annualized Total Returns As of 9/30/09 | |||

1 Year | 5 Years | 10 Years | |

| U.S. Micro Cap Fund Class I | –1.91% | 4.13% | 6.09% |

| Russell 2000 Growth/Russell | |||

| Microcap Growth Blend Index | 22.35% | 0.01% | 1.20% |

| Russell 2000 Growth Index | –6.32% | 2.91% | 1.10% |

The graph above shows the value of a hypothetical $250,000 investment in the Fund’s Class I shares compared with the Russell 2000 Growth Index and a blended index comprised of the Russell 2000 Growth Index/Russell Microcap Growth Index. The Fund’s Class I shares calculate their performance based upon the historical performance of their corresponding series of Nicholas-Applegate Mutual Funds (renamed ING Mutual Funds), adjusted to reflect all fees and expenses applicable to Class I shares. The Nicholas-Applegate Institutional Funds’ Class I shares were first available on May 7, 1999. Average annual total return figures include changes in principal value, reinvestment of dividends, and capital gain distributions. The total returns shown above do not show the effects of income taxes on an individual’s investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

4

U.S. MICRO CAP FUND

The Russell 2000 Growth Index is an unmanaged index comprised of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Growth Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The Russell Microcap Growth Index isolates the smallest 1,000 securities in the Russell 2000 Index plus the next 1,000 securities. The Russell Microcap Growth Index isolates the securities in the Russell Microcap Index with purely growth characteristics. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. The Russell 2000 Growth/Russell Microcap Growth Blend Index is a combination of the Russell 2000 Growth Index and the Russell Microcap Growth Index. The blended index exhibits Russell 2000 Growth performance from the inception of the Fund until August 2000, and Russell Microcap Growth performance thereafter. The Fund created the blended index because Russell Microcap Growth performance incepted in August 2000.

One cannot invest directly in an index. Since markets can go down as well as up, investment return and principal value will fluctuate with market conditions. You may have a gain or loss when you sell your shares.

5

U.S. MICRO CAP FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2009

| Number of | ||||||||

| Shares | Value | |||||||

| Common Stock - 97.9% | ||||||||

| Agricultural Operations - 0.7% | ||||||||

| The Andersons, Inc. | 12,100 | $ | 425,920 | |||||

| Apparel Manufacturers - 0.9% | ||||||||

| Maidenform Brands, Inc.* | 33,800 | 542,828 | ||||||

| Applications Software - 2.8% | ||||||||

| China TransInfo Technology Corp.* | 58,600 | 554,356 | ||||||

| Ebix, Inc.* | 13,500 | 747,360 | ||||||

| inContact, Inc.* | 103,700 | 309,026 | ||||||

| 1,610,742 | ||||||||

| Auto/Truck Parts & Equipment-Original - 1.7% | ||||||||

| Titan International, Inc. | 49,200 | 437,880 | ||||||

| Wonder Auto Technology, Inc.* | 46,200 | 554,400 | ||||||

| 992,280 | ||||||||

| Batteries/Battery Systems - 0.7% | ||||||||

| Greatbatch, Inc.* | 17,400 | 390,978 | ||||||

| Broadcast Services/Programming - 1.5% | ||||||||

| Acacia Research - Acacia Technologies* | 50,800 | 442,468 | ||||||

| DG FastChannel, Inc.* | 20,800 | 435,552 | ||||||

| 878,020 | ||||||||

| Building-Heavy Construction - 0.9% | ||||||||

| Orion Marine Group, Inc.* | 25,000 | 513,500 | ||||||

| Casino Services - 1.0% | ||||||||

| Shuffle Master, Inc.* | 59,500 | 560,490 | ||||||

| Chemicals-Diversified - 1.0% | ||||||||

| Innospec, Inc.* | 38,800 | 572,300 | ||||||

| Chemicals-Plastics - 0.8% | ||||||||

| Spartech Corp.* | 40,300 | 434,031 | ||||||

| Chemicals-Specialty - 1.3% | ||||||||

| Omnova Solutions, Inc.* | 111,700 | 723,816 | ||||||

| Coal - 0.7% | ||||||||

| James River Coal Co.* | 20,600 | 393,666 | ||||||

| Collectibles - 0.8% | ||||||||

| RC2 Corp.* | 31,800 | 453,150 | ||||||

| Commercial Services - 0.8% | ||||||||

| StarTek, Inc.* | 52,500 | 455,700 | ||||||

| Commercial Services-Finance - 0.8% | ||||||||

| Dollar Financial Corp.* | 27,300 | 437,346 | ||||||

| Communications Software - 1.5% | ||||||||

| Seachange International, Inc.* | 40,500 | 303,750 | ||||||

| Smith Micro Software, Inc.* | 44,700 | 552,492 | ||||||

| 856,242 | ||||||||

| Computer Services - 2.8% | ||||||||

| LivePerson, Inc.* | 96,900 | 488,376 | ||||||

| Ness Technologies, Inc.* | 67,800 | 534,942 | ||||||

| VanceInfo Technologies, Inc. - ADR* | 29,000 | 563,760 | ||||||

| 1,587,078 | ||||||||

| Computers-Integrated Systems - 2.1% | ||||||||

| Netscout Systems, Inc.* | 44,000 | 594,440 | ||||||

| Radiant Systems, Inc.* | 55,700 | 598,218 | ||||||

| 1,192,658 | ||||||||

| Computers-Memory Devices - 1.1% | ||||||||

| Xyratex, Ltd.* | 67,500 | 641,925 | ||||||

| Computers-Peripheral Equipment - 0.8% | ||||||||

| Compellent Technologies, Inc.* | 24,300 | 438,615 | ||||||

| Cosmetics & Toiletries - 0.9% | ||||||||

| Elizabeth Arden, Inc.* | 42,000 | $ | 494,340 | |||||

| Direct Marketing - 0.9% | ||||||||

| APAC Customer Services, Inc.* | 90,700 | 536,037 | ||||||

| Disposable Medical Products - 2.1% | ||||||||

| ICU Medical, Inc.* | 11,400 | 420,204 | ||||||

| Medical Action Industries, Inc.* | 30,900 | 372,963 | ||||||

| Merit Medical Systems, Inc.* | 22,900 | 396,857 | ||||||

| 1,190,024 | ||||||||

| Distribution/Wholesale - 1.2% | ||||||||

| MWI Veterinary Supply, Inc.* | 11,400 | 455,430 | ||||||

| Rentrak Corp.* | 13,800 | 246,468 | ||||||

| 701,898 | ||||||||

| Drug Delivery Systems - 0.8% | ||||||||

| Depomed, Inc.* | 105,500 | 461,035 | ||||||

| Electric Products-Miscellaneous - 1.7% | ||||||||

| Harbin Electric, Inc.* | 31,100 | 524,968 | ||||||

| SmartHeat, Inc.* | 39,700 | 471,239 | ||||||

| 996,207 | ||||||||

| Electronic Components-Miscellaneous - 0.8% | ||||||||

| NVE Corp.* | 8,800 | 467,808 | ||||||

| Electronic Components-Semiconductors - 0.7% | ||||||||

| Ceva, Inc.* | 38,600 | 414,950 | ||||||

| Enterprise Software/Services - 1.8% | ||||||||

| Opnet Technologies, Inc. | 42,500 | 464,525 | ||||||

| Taleo Corp. Cl. A* | 25,348 | 573,879 | ||||||

| 1,038,404 | ||||||||

| Finance-Consumer Loans - 1.0% | ||||||||

| Portfolio Recovery Associates, Inc.* | 12,600 | 571,158 | ||||||

| Food-Canned - 0.8% | ||||||||

| Seneca Foods Corp. Cl. A* | 16,700 | 457,580 | ||||||

| Insurance Brokers - 0.7% | ||||||||

| Life Partners Holdings, Inc. | 21,376 | 382,630 | ||||||

| Internet Incubators - 0.7% | ||||||||

| Internet Capital Group, Inc.* | 48,400 | 404,624 | ||||||

| Internet Infrastructure Software - 0.7% | ||||||||

| TeleCommunication Systems, Inc. Cl. A* | 50,300 | 420,508 | ||||||

| Machinery-General Industry - 2.1% | ||||||||

| Albany International Corp. Cl. A | 31,000 | 601,400 | ||||||

| Intevac, Inc.* | 43,300 | 581,952 | ||||||

| 1,183,352 | ||||||||

| Medical Imaging Systems - 1.3% | ||||||||

| Given Imaging, Ltd.* | 21,300 | 317,583 | ||||||

| Merge Healthcare, Inc.* | 103,700 | 426,207 | ||||||

| 743,790 | ||||||||

| Medical Information Systems - 1.3% | ||||||||

| AMICAS, Inc.* | 89,800 | 323,280 | ||||||

| Computer Programs & Systems, Inc. | 9,500 | 393,395 | ||||||

| 716,675 | ||||||||

| Medical Instruments - 1.7% | ||||||||

| Endologix, Inc.* | 80,700 | 499,533 | ||||||

| Symmetry Medical, Inc.* | 45,900 | 475,983 | ||||||

| 975,516 | ||||||||

| Medical Labs & Testing Services - 1.0% | ||||||||

| Bio-Reference Labs, Inc.* | 17,460 | 600,624 | ||||||

See Accompanying Notes to Financial Statements.

6

SCHEDULE OF INVESTMENTS (Unaudited)

| As of September 30, 2009 | ||||||||

| Number of | ||||||||

| Shares | Value | |||||||

| Medical Products - 2.5% | ||||||||

| ATS Medical, Inc.* | 100,100 | $ | 268,268 | |||||

| Cantel Medical Corp.* | 26,000 | 391,560 | ||||||

| Exactech, Inc.* | 25,700 | 404,518 | ||||||

| Hanger Orthopedic Group, Inc.* | 28,500 | 395,295 | ||||||

| 1,459,641 | ||||||||

| Medical-Biomedical/Genetics - 2.5% | ||||||||

| Affymax, Inc.* | 7,000 | 167,230 | ||||||

| Arena Pharmaceuticals, Inc.* | 48,000 | 214,560 | ||||||

| Immunogen, Inc.* | 34,400 | 278,984 | ||||||

| Immunomedics, Inc.* | 43,200 | 238,464 | ||||||

| Micromet, Inc.* | 29,300 | 195,138 | ||||||

| Novavax, Inc.* | 35,500 | 140,580 | ||||||

| NPS Pharmaceuticals, Inc.* | 45,500 | 182,910 | ||||||

| 1,417,866 | ||||||||

| Medical-Drugs - 2.3% | ||||||||

| Hi-Tech Pharmacal Co., Inc.* | 20,300 | 455,532 | ||||||

| Sciclone Pharmaceuticals, Inc.* | 96,900 | 412,794 | ||||||

| Vivus, Inc.* | 42,000 | 438,900 | ||||||

| 1,307,226 | ||||||||

| Medical-Outpatient/Home Medical Care - 1.3% | ||||||||

| Almost Family, Inc.* | 12,800 | 380,800 | ||||||

| America Service Group, Inc. | 21,000 | 347,340 | ||||||

| 728,140 | ||||||||

| MRI/Medical Diagnostic Imaging Centers - 0.9% | ||||||||

| Nighthawk Radiology Holdings, Inc.* | 68,000 | 491,640 | ||||||

| Networking Products - 2.4% | ||||||||

| Extreme Networks* | 144,500 | 404,600 | ||||||

| Hypercom Corp.* | 161,800 | 501,580 | ||||||

| Switch & Data Facilities Co., Inc.* | 34,600 | 470,906 | ||||||

| 1,377,086 | ||||||||

| Non-Ferrous Metals - 2.0% | ||||||||

| Brush Engineered Materials, Inc.* | 21,800 | 533,228 | ||||||

| Horsehead Holding Corp.* | 51,900 | 608,268 | ||||||

| 1,141,496 | ||||||||

| Office Supplies & Forms - 1.2% | ||||||||

| ACCO Brands Corp.* | 94,100 | 679,402 | ||||||

| Oil Companies-Exploration & Production - 4.1% | ||||||||

| Carrizo Oil & Gas, Inc.* | 12,100 | 296,329 | ||||||

| Clayton Williams Energy, Inc.* | 14,400 | 433,728 | ||||||

| Gulfport Energy Corp.* | 81,500 | 712,310 | ||||||

| Stone Energy Corp.* | 54,400 | 887,264 | ||||||

| 2,329,631 | ||||||||

| Oil Field Machine & Equipment - 1.3% | ||||||||

| Gulf Island Fabrication, Inc. | 16,100 | 301,714 | ||||||

| T-3 Energy Services, Inc.* | 23,800 | 468,860 | ||||||

| 770,574 | ||||||||

| Oil-Field Services - 1.6% | ||||||||

| Hornbeck Offshore Services, Inc.* | 19,200 | 529,152 | ||||||

| Trico Marine Services, Inc.* | 52,900 | 408,388 | ||||||

| 937,540 | ||||||||

| Paper & Related Products - 2.9% | ||||||||

| Boise, Inc.* | 159,800 | 843,744 | ||||||

| Clearwater Paper Corp.* | 11,500 | 475,295 | ||||||

| KapStone Paper & Packaging Corp.* | 45,400 | 369,556 | ||||||

| 1,688,595 | ||||||||

| Pharmacy Services - 1.6% | ||||||||

| BioScrip, Inc.* | 68,500 | 463,060 | ||||||

| Clarient, Inc.* | 106,000 | 446,260 | ||||||

| 909,320 | ||||||||

| Physical Practice Management - 1.6% | ||||||||

| American Dental Partners, Inc.* | 33,400 | 467,600 | ||||||

| IPC The Hospitalist Co., Inc.* | 14,800 | 465,460 | ||||||

| 933,060 | ||||||||

| Property/Casualty Insurance - 1.0% | ||||||||

| Meadowbrook Insurance Group, Inc. | 79,000 | 584,600 | ||||||

| Recycling - 1.0% | ||||||||

| Metalico, Inc.* | 137,500 | 573,375 | ||||||

| Retail-Automobile - 0.8% | ||||||||

| America’s Car-Mart, Inc.* | 19,500 | 467,025 | ||||||

| Retail-Restaurants - 3.4% | ||||||||

| AFC Enterprises, Inc.* | 54,300 | 457,206 | ||||||

| Caribou Coffee Co., Inc.* | 56,700 | 409,374 | ||||||

| Carrols Restaurant Group, Inc.* | 53,200 | 402,192 | ||||||

| Einstein Noah Restaurant Group, Inc.* | 39,500 | 475,580 | ||||||

| O’Charleys, Inc.* | 22,700 | 212,699 | ||||||

| 1,957,051 | ||||||||

| Retail-Sporting Goods - 0.9% | ||||||||

| Big 5 Sporting Goods Corp. | 32,400 | 489,240 | ||||||

| Satellite Telecommunications - 1.1% | ||||||||

| Hughes Communications, Inc.* | 20,200 | 612,868 | ||||||

| Semiconductor Components-Integrated Circuits - 3.9% | ||||||||

| Anadigics, Inc.* | 89,900 | 423,429 | ||||||

| Cirrus Logic, Inc.* | 82,700 | 459,812 | ||||||

| O2Micro International, Ltd. - ADR* | 80,170 | 420,893 | ||||||

| Pericom Semiconductor Corp.* | 35,700 | 350,217 | ||||||

| Techwell, Inc.* | 52,700 | 578,646 | ||||||

| 2,232,997 | ||||||||

| Semiconductor Equipment - 0.3% | ||||||||

| Nanometrics, Inc.* | 23,500 | 154,395 | ||||||

| Steel-Producers - 1.0% | ||||||||

| Olympic Steel, Inc. | 20,400 | 585,276 | ||||||

| Telecommunication Equipment - 0.8% | ||||||||

| Anaren, Inc.* | 26,300 | 447,100 | ||||||

| Textile-Apparel - 1.2% | ||||||||

| Perry Ellis International, Inc.* | 43,100 | 691,324 | ||||||

| Therapeutics - 0.4% | ||||||||

| Inspire Pharmaceuticals, Inc.* | 41,600 | 217,152 | ||||||

| Transactional Software - 0.8% | ||||||||

| Bottomline Technologies, Inc.* | 35,700 | 460,530 | ||||||

| Transport-Air Freight - 0.7% | ||||||||

| Atlas Air Worldwide Holdings, Inc.* | 12,700 | 406,019 | ||||||

| Transport-Marine - 1.5% | ||||||||

| Safe Bulkers, Inc. | 62,300 | 505,876 | ||||||

| Star Bulk Carriers Corp. | 98,200 | 341,736 | ||||||

| 847,612 | ||||||||

| Transport-Services - 0.7% | ||||||||

| Vitran Corp., Inc.* | 41,700 | 376,134 | ||||||

| Transport-Truck - 0.7% | ||||||||

| Saia, Inc.* | 26,200 | 421,296 | ||||||

See Accompanying Notes to Financial Statements.

7

U.S. MICRO CAP FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2009

| Number of | ||||||||

| Shares | Value | |||||||

| Water Treatment Systems - 0.9% | ||||||||

| RINO International Corp.* | 23,800 | $ | 503,132 | |||||

| Web Hosting/Design - 0.9% | ||||||||

| Terremark Worldwide, Inc.* | 81,900 | 509,418 | ||||||

| Wire & Cable Products - 0.8% | ||||||||

| Fushi Copperweld, Inc.* | 56,000 | 473,760 | ||||||

| Total Common Stock (Cost: $44,950,480) | 56,039,966 | |||||||

| Principal | ||||||||

| Amount | ||||||||

| Short Term Investments - 1.9% | ||||||||

| Time Deposit - 1.9% | ||||||||

| Citibank London 0.030%, 10/01/09 | ||||||||

| (Cost: $1,121,915) | $ | 1,121,915 | 1,121,915 | |||||

| Total Investments - 99.8% (Cost: $46,072,395) | 57,161,881 | |||||||

| Other Assets in Excess of Liabilities - 0.2% | 101,250 | |||||||

| Net Assets - 100.0% | $ | 57,263,131 | ||||||

| * Non-income producing securities. | ||

| ADR - American Depository Receipt |

SCHEDULE OF INVESTMENTS BY SECTOR | ||||

| as of September 30, 2009 | ||||

| Percent of | ||||

| Sector | Net Assets | |||

| Consumer, Non-cyclical | 25.2 | % | ||

| Technology | 19.9 | |||

| Industrial | 12.5 | |||

| Consumer, Cyclical | 11.9 | |||

| Basic Materials | 9.0 | |||

| Communications | 9.0 | |||

| Energy | 7.7 | |||

| Financial | 2.7 | |||

| Short Term Investments | 1.9 | |||

| Total Investments | 99.8 | |||

| Other assets in excess of liabilities | 0.2 | |||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

8

U.S. EMERGING GROWTH FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Emerging Growth Fund seeks to maximize long-term capital appreciation through investments primarily in U.S. companies with market capitalizations similar to the Russell 2000 Growth Index at time of purchase.

Market Overview: U.S. equities registered substantial gains during the six months ended September 30, 2009. Signs that the worst of the recession had passed helped lift stocks higher across sectors, styles and capitalization ranges. Small-cap stocks did especially well, supported by strong inflows into small-cap funds.

The credit markets thawed considerably, thanks in large part to the aggressive actions taken by the Treasury and Federal Reserve last fall and winter. As confidence in the financial system grew, companies had easier and cheaper access to credit. They took advantage of the more favorable conditions, issuing approximately $700 billion of debt in the first nine months of 2009 — a 38% increase over the same period the previous year.

Households seemed more intent on paring back borrowing and spending, and consumer credit fell by a record $21.5 billion in July. A driving force behind the decline was the rising unemployment rate, which reached a twenty-six year high. However, unemployment is a lagging indicator, and less backward-looking statistics suggested that the economy was on the mend. New home sales picked up, industrial production increased and second-quarter GDP contracted at a better-than-expected 0.7% annual rate. As the period drew to a close — almost exactly one year after the credit crisis had erupted — economists were expecting that GDP would grow by approximately 3% in the third quarter.

Performance: During the six months ended September 30, 2009, the Fund’s Class I shares gained 57.06%, outperforming the 43.06% increase in the Russell 2000 Growth Index.

Portfolio Specifics: The Fund’s outperformance was due to stock selection, which added value in nearly every sector. Stock selection was strongest in energy, where top-performing holdings included Massey Energy and Helix Energy Solutions. Massey, a coal producer, is seeing strong demand from India, which is increasing its steelmaking capacity. Helix, a diversified energy firm, benefited from an improved liquidity position and favorable production outlook. Stock selection was also especially strong in the information technology, industrials and materials sectors. For example, TriQuint Semiconductor was another top performer in the Fund. The company makes radio frequency modules used in wireless handsets and is winning business in the fast-growing smartphone market.

Areas of relative weakness included stock selection in the health care sector. One notable detractor was a medical device manufacturer facing lower payments from insurance companies.

Market Outlook: While it is widely believed that the recession is over, we think that the economic recovery will be muted due to the high unemployment rate and large federal deficit. That said, several factors could fuel additional gains in the stock market over the months ahead, including:

• Expectations for a strong rebound in corporate earnings in 2010

• Potential for investors to move some of the $3.4 trillion sitting in low-yielding money market funds into equities

• Indications from the Fed that it plans to keep interest rates low for an extended period of time

By consistently applying our bottom-up investment process in this environment, we believe we will continue to add value to the benchmark.

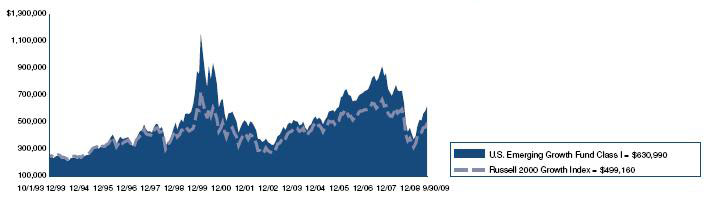

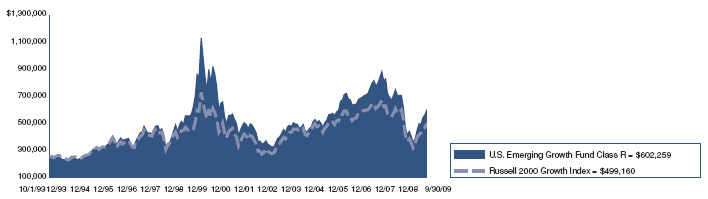

Comparison of Change in Value of a $250,000 Investment in U.S. Emerging Growth Fund Class I Shares with the Russell 2000 Growth Index.

Annualized Total Returns As of 9/30/09 | |||

| 1 Year | 5 Years | 10 Years | |

| U.S. Emerging Growth Fund Class I | –2.54% | 5.78% | 0.81% |

| Russell 2000 Growth Index | –6.32% | 2.91% | 1.10% |

The graph above shows the value of a hypothetical $250,000 investment in the Fund’s Class I shares compared with the Russell 2000 Growth Index for the periods indicated. The Fund calculates performance based upon the historical performance of a corresponding series of Nicholas-Applegate Mutual Funds (renamed ING Mutual Funds), adjusted to reflect all fees and expenses applicable to Class I shares. The Nicholas-Applegate Institutional Funds’ Class I shares were first available on May 7, 1999. Average annual total return figures include changes in principal value, reinvested dividends, and capital gain distributions. The total returns shown above do not show the effects of income taxes on an individual’s investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

The Russell 2000 Growth Index is an unmanaged index comprised of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. Index returns include reinvestment of dividends. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expense of investing. One cannot invest directly in an index.

Since markets can go down as well as up, investment returns and principal value will fluctuate with market conditions. You may have a gain or loss when you sell your shares

9

U.S. EMERGING GROWTH FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2009

| Number of | ||||||||

| Shares | Value | |||||||

| Common Stock - 96.8% | ||||||||

| Aerospace/Defense - 0.5% | ||||||||

| Cubic Corp. | 2,000 | $ | 78,940 | |||||

| Aerospace/Defense-Equipment - 1.3% | ||||||||

| AAR Corp.* | 4,900 | 107,506 | ||||||

| BE Aerospace, Inc.* | 5,400 | 108,756 | ||||||

| 216,262 | ||||||||

| Agricultural Operations - 0.7% | ||||||||

| The Andersons, Inc. | 3,300 | 116,160 | ||||||

| Airlines - 0.5% | ||||||||

| Hawaiian Holdings, Inc.* | 9,700 | 80,122 | ||||||

| Apparel Manufacturers - 1.8% | ||||||||

| Carter’s, Inc.* | 3,600 | 96,120 | ||||||

| Jones Apparel Group, Inc. | 6,400 | 114,752 | ||||||

| Quiksilver, Inc.* | 32,300 | 88,825 | ||||||

| 299,697 | ||||||||

| Applications Software - 1.5% | ||||||||

| Compuware Corp.* | 11,500 | 84,295 | ||||||

| Ebix, Inc.* | 3,100 | 171,616 | ||||||

| 255,911 | ||||||||

| Auto/Truck Parts & Equipment-Original - 1.6% | ||||||||

| American Axle & Manufacturing | ||||||||

| Holdings, Inc.* | 15,200 | 107,616 | ||||||

| ArvinMeritor, Inc.* | 11,600 | 90,712 | ||||||

| Titan International, Inc. | 9,200 | 81,880 | ||||||

| 280,208 | ||||||||

| Batteries/Battery Systems - 0.5% | ||||||||

| Greatbatch, Inc.* | 4,100 | 92,127 | ||||||

| Beverages-Wine/Spirits - 0.5% | ||||||||

| Central European Distribution Corp.* | 2,400 | 78,624 | ||||||

| Broadcast Services/Programming - 1.1% | ||||||||

| DG FastChannel, Inc.* | 3,600 | 75,384 | ||||||

| Liberty Media Corp. - Capital* | 5,600 | 117,152 | ||||||

| 192,536 | ||||||||

| Building-Heavy Construction - 1.8% | ||||||||

| Chicago Bridge & Iron Co. Cl. Y* | 5,900 | 110,212 | ||||||

| Orion Marine Group, Inc.* | 4,700 | 96,538 | ||||||

| Tutor Perini Corp.* | 5,000 | 106,500 | ||||||

| 313,250 | ||||||||

| Casino Services - 0.7% | ||||||||

| Bally Technologies, Inc.* | 2,900 | 111,273 | ||||||

| Chemicals-Specialty - 0.7% | ||||||||

| Ashland, Inc. | 2,900 | 125,338 | ||||||

| Coal - 0.6% | ||||||||

| James River Coal Co.* | 5,600 | 107,016 | ||||||

| Commercial Banks-Central US - 0.7% | ||||||||

| MB Financial, Inc. | 5,500 | 115,335 | ||||||

| Commercial Services - 1.3% | ||||||||

| AerCap Holdings NV* | 12,200 | 110,654 | ||||||

| DynCorp International, Inc. Cl. A* | 5,700 | 102,600 | ||||||

| 213,254 | ||||||||

| Commercial Services-Finance - 3.8% | ||||||||

| Coinstar, Inc.* | 3,100 | 102,238 | ||||||

| Deluxe Corp. | 6,100 | 104,310 | ||||||

| Dollar Financial Corp.* | 6,000 | 96,120 | ||||||

| Global Cash Access Holdings, Inc.* | 9,700 | 70,907 | ||||||

| Net 1 UEPS Technologies, Inc.* | 4,400 | 92,224 | ||||||

| TNS, Inc.* | 3,700 | 101,380 | ||||||

| Wright Express Corp.* | 2,600 | 76,726 | ||||||

| 643,905 | ||||||||

| Computer Aided Design - 0.4% | ||||||||

| Parametric Technology Corp.* | 4,800 | 66,336 | ||||||

| Computers-Integrated Systems - 0.6% | ||||||||

| Netscout Systems, Inc.* | 7,800 | 105,378 | ||||||

| Computers-Memory Devices - 0.4% | ||||||||

| STEC, Inc.* | 2,500 | 73,475 | ||||||

| Consumer Products-Miscellaneous - 1.6% | ||||||||

| Jarden Corp. | 5,400 | 151,578 | ||||||

| Tupperware Brands Corp. | 3,100 | 123,752 | ||||||

| 275,330 | ||||||||

| Containers-Metal/Glass - 0.7% | ||||||||

| Greif, Inc. Cl. A | 2,300 | 126,615 | ||||||

| Containers-Paper/Plastic - 0.8% | ||||||||

| Rock-Tenn Co. Cl. A | 2,800 | 131,908 | ||||||

| Disposable Medical Products - 0.5% | ||||||||

| Merit Medical Systems, Inc.* | 5,200 | 90,116 | ||||||

| Distribution/Wholesale - 0.7% | ||||||||

| Brightpoint, Inc.* | 14,200 | 124,250 | ||||||

| Diversified Manufacturing Operations - 0.6% | ||||||||

| Koppers Holdings, Inc. | 3,400 | 100,810 | ||||||

| Diversified Operations - 0.3% | ||||||||

| Compass Diversified Holdings | 5,200 | 54,444 | ||||||

| Drug Delivery Systems - 0.9% | ||||||||

| Nektar Therapeutics* | 16,400 | 159,736 | ||||||

| E-Commerce/Services - 0.5% | ||||||||

| IAC/InterActiveCorp* | 4,300 | 86,817 | ||||||

| Electric Products-Miscellaneous - 0.6% | ||||||||

| GrafTech International, Ltd.* | 6,600 | 97,020 | ||||||

| Electronic Components-Miscellaneous - 0.7% | ||||||||

| Sanmina-SCI Corp.* | 14,600 | 125,560 | ||||||

| Electronic Components-Semiconductors - 3.1% | ||||||||

| Amkor Technology, Inc.* | 16,800 | 115,584 | ||||||

| Fairchild Semiconductor | ||||||||

| International, Inc. Cl. A* | 10,300 | 105,369 | ||||||

| Omnivision Technologies, Inc.* | 6,600 | 107,448 | ||||||

| Rovi Corp.* | 3,100 | 104,160 | ||||||

| Skyworks Solutions, Inc.* | 7,800 | 103,272 | ||||||

| 535,833 | ||||||||

| Electronic Design Automations - 0.8% | ||||||||

| Mentor Graphics Corp.* | 14,000 | 130,340 | ||||||

| Enterprise Software/Services - 2.7% | ||||||||

| Informatica Corp.* | 4,200 | 94,836 | ||||||

| JDA Software Group, Inc.* | 5,000 | 109,700 | ||||||

| Lawson Software, Inc.* | 12,800 | 79,872 | ||||||

| Mantech International Corp. Cl. A* | 1,500 | 70,740 | ||||||

| Taleo Corp. Cl. A* | 4,600 | 104,144 | ||||||

| 459,292 | ||||||||

| Entertainment Software - 0.5% | ||||||||

| Take-Two Interactive Software, Inc.* | 7,100 | 79,591 | ||||||

See Accompanying Notes to Financial Statements.

10

SCHEDULE OF INVESTMENTS (Unaudited)

| As of September 30, 2009 | ||||||||

| Number of | ||||||||

| Shares | Value | |||||||

| Finance-Consumer Loans - 1.2% | ||||||||

| Ocwen Financial Corp.* | 7,800 | $ | 88,296 | |||||

| Portfolio Recovery Associates, Inc.* | 2,400 | 108,792 | ||||||

| 197,088 | ||||||||

| Finance-Investment Bankers/Brokers - 0.6% | ||||||||

| MF Global, Ltd.* | 13,900 | 101,053 | ||||||

| Food-Canned - 0.7% | ||||||||

| Seneca Foods Corp. Cl. A* | 4,200 | 115,080 | ||||||

| Food-Miscellaneous/Diversified - 1.1% | ||||||||

| Lance, Inc. | 3,400 | 87,788 | ||||||

| M&F Worldwide Corp.* | 4,800 | 97,152 | ||||||

| 184,940 | ||||||||

| Footwear & Related Apparel - 1.0% | ||||||||

| Deckers Outdoor Corp.* | 1,300 | 110,305 | ||||||

| Iconix Brand Group, Inc.* | 5,200 | 64,844 | ||||||

| 175,149 | ||||||||

| Hospital Beds/Equipment - 0.7% | ||||||||

| Hill-Rom Holdings, Inc. | 5,200 | 113,256 | ||||||

| Human Resources - 0.6% | ||||||||

| Emergency Medical Services Corp. Cl. A* | 2,200 | 102,300 | ||||||

| Instruments-Scientific - 0.6% | ||||||||

| FEI Co.* | 4,200 | 103,530 | ||||||

| Insurance Brokers - 0.6% | ||||||||

| CNinsure, Inc. - ADR | 4,300 | 98,728 | ||||||

| Internet Applications Software - 0.5% | ||||||||

| Cybersource Corp.* | 5,600 | 93,352 | ||||||

| Internet Connectivity Services - 0.8% | ||||||||

| AboveNet, Inc.* | 2,800 | 136,528 | ||||||

| Internet Infrastructure Equipment - 0.7% | ||||||||

| Avocent Corp.* | 5,900 | 119,593 | ||||||

| Internet Infrastructure Software - 1.2% | ||||||||

| AsiaInfo Holdings, Inc.* | 5,200 | 103,844 | ||||||

| TeleCommunication Systems, Inc. Cl. A* | 12,000 | 100,320 | ||||||

| 204,164 | ||||||||

| Intimate Apparel - 0.7% | ||||||||

| The Warnaco Group, Inc.* | 2,600 | 114,036 | ||||||

| Life/Health Insurance - 0.6% | ||||||||

| Delphi Financial Group, Inc. Cl. A | 4,800 | 108,624 | ||||||

| Machinery-Construction & Mining - 0.5% | ||||||||

| Bucyrus International, Inc. Cl. A | 2,300 | 81,926 | ||||||

| Machinery-General Industry - 0.8% | ||||||||

| Albany International Corp. Cl. A | 7,300 | 141,620 | ||||||

| Marine Services - 0.8% | ||||||||

| Aegean Marine Petroleum Network, Inc. | 5,700 | 128,250 | ||||||

| Medical Instruments - 0.5% | ||||||||

| NuVasive, Inc.* | 2,000 | 83,520 | ||||||

| Medical Labs & Testing Services - 0.4% | ||||||||

| Bio-Reference Labs, Inc.* | 1,800 | 61,920 | ||||||

| Medical Products - 3.6% | ||||||||

| Exactech, Inc.* | 4,700 | 73,978 | ||||||

| Haemonetics Corp.* | 1,500 | 84,180 | ||||||

| Hanger Orthopedic Group, Inc.* | 7,900 | 109,573 | ||||||

| Invacare Corp. | 4,600 | 102,488 | ||||||

| Orthofix International NV* | 4,100 | 120,499 | ||||||

| PSS World Medical, Inc.* | 5,400 | 117,882 | ||||||

| 608,600 | ||||||||

| Medical Sterilize Product - 0.7% | ||||||||

| STERIS Corp. | 3,700 | 112,665 | ||||||

| Medical-Biomedical/Genetics - 2.7% | ||||||||

| Human Genome Sciences, Inc.* | 5,400 | 101,628 | ||||||

| Incyte Corp., Ltd.* | 12,200 | 82,350 | ||||||

| Martek Biosciences Corp.* | 2,900 | 65,511 | ||||||

| Regeneron Pharmaceuticals, Inc.* | 4,200 | 81,060 | ||||||

| Seattle Genetics, Inc.* | 9,800 | 137,494 | ||||||

| 468,043 | ||||||||

| Medical-Drugs - 1.0% | ||||||||

| Eurand NV* | 6,000 | 90,840 | ||||||

| Hi-Tech Pharmacal Co., Inc.* | 3,800 | 85,272 | ||||||

| 176,112 | ||||||||

| Medical-HMO - 0.5% | ||||||||

| WellCare Health Plans, Inc.* | 3,800 | 93,670 | ||||||

| Medical-Outpatient/Home Medical Care - 0.5% | ||||||||

| Almost Family, Inc.* | 2,700 | 80,325 | ||||||

| Metal-Aluminum - 0.4% | ||||||||

| Century Aluminum Co.* | 7,900 | 73,865 | ||||||

| Multi-line Insurance - 0.8% | ||||||||

| Unitrin, Inc. | 6,900 | 134,481 | ||||||

| Oil & Gas Drilling - 1.2% | ||||||||

| Atlas Energy, Inc. | 4,000 | 108,280 | ||||||

| Atwood Oceanics, Inc.* | 2,700 | 95,229 | ||||||

| 203,509 | ||||||||

| Oil Companies-Exploration & Production - 3.5% | ||||||||

| ATP Oil & Gas Corp.* | 8,400 | 150,276 | ||||||

| Berry Petroleum Co. Cl. A | 3,700 | 99,086 | ||||||

| Gran Tierra Energy, Inc.* | 21,300 | 88,608 | ||||||

| Mariner Energy, Inc.* | 6,200 | 87,916 | ||||||

| Stone Energy Corp.* | 8,500 | 138,635 | ||||||

| W&T Offshore, Inc. | 2,600 | 30,446 | ||||||

| 594,967 | ||||||||

| Oil-Field Services - 3.0% | ||||||||

| Global Industries, Ltd.* | 13,100 | 124,450 | ||||||

| Helix Energy Solutions Group, Inc.* | 7,500 | 112,350 | ||||||

| Hercules Offshore, Inc.* | 13,300 | 65,303 | ||||||

| Hornbeck Offshore Services, Inc.* | 3,800 | 104,728 | ||||||

| Tetra Technologies, Inc.* | 10,500 | 101,745 | ||||||

| 508,576 | ||||||||

| Paper & Related Products - 3.0% | ||||||||

| Boise, Inc.* | 34,000 | 179,520 | ||||||

| Clearwater Paper Corp.* | 3,100 | 128,123 | ||||||

| Domtar Corp.* | 3,500 | 123,270 | ||||||

| Schweitzer-Mauduit International, Inc. | 1,600 | 86,976 | ||||||

| 517,889 | ||||||||

| Pharmacy Services - 0.5% | ||||||||

| Catalyst Health Solutions, Inc.* | 2,800 | 81,620 | ||||||

| Physical Practice Management - 0.6% | ||||||||

| IPC The Hospitalist Co., Inc.* | 3,100 | 97,495 | ||||||

| Physical Therapy/Rehabilitation Centers - 0.5% | ||||||||

| RehabCare Group, Inc.* | 4,200 | 91,098 | ||||||

| Property/Casualty Insurance - 0.6% | ||||||||

| Amtrust Financial Services, Inc. | 8,900 | 101,549 | ||||||

See Accompanying Notes to Financial Statements.

11

U.S. EMERGING GROWTH FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2009

| Number of | ||||||||

| Shares | Value | |||||||

| Publishing-Books - 0.6% | ||||||||

| Scholastic Corp. | 4,000 | $ | 97,360 | |||||

| Real Estate Management/Service - 1.2% | ||||||||

| E-House China Holdings, Ltd. - ADR* | 5,300 | 113,208 | ||||||

| Jones Lang LaSalle, Inc. | 2,000 | 94,740 | ||||||

| 207,948 | ||||||||

| Recreational Centers - 0.7% | ||||||||

| Life Time Fitness, Inc.* | 4,000 | 112,200 | ||||||

| Reinsurance - 0.5% | ||||||||

| Maiden Holdings, Ltd. | 12,500 | 90,875 | ||||||

| Rental Auto/Equipment - 0.8% | ||||||||

| United Rentals, Inc.* | 13,500 | 139,050 | ||||||

| Retail-Apparel/Shoe - 4.6% | ||||||||

| AnnTaylor Stores Corp.* | 8,200 | 130,298 | ||||||

| Collective Brands, Inc.* | 6,200 | 107,446 | ||||||

| Genesco, Inc.* | 4,800 | 115,536 | ||||||

| Guess ?, Inc. | 2,600 | 96,304 | ||||||

| Hanesbrands, Inc.* | 5,000 | 107,000 | ||||||

| Phillips-Van Heusen Corp. | 2,700 | 115,533 | ||||||

| The Finish Line, Inc. Cl. A | 10,600 | 107,696 | ||||||

| 779,813 | ||||||||

| Retail-Office Supplies - 0.7% | ||||||||

| OfficeMax, Inc.* | 9,100 | 114,478 | ||||||

| Retail-Perfume & Cosmetics - 0.5% | ||||||||

| Sally Beauty Holdings, Inc.* | 12,200 | 86,742 | ||||||

| Retail-Restaurants - 1.4% | ||||||||

| Buffalo Wild Wings, Inc.* | 1,800 | 74,898 | ||||||

| CKE Restaurants, Inc. | 8,400 | 88,116 | ||||||

| Cracker Barrel Old Country Store, Inc. | 2,400 | 82,560 | ||||||

| 245,574 | ||||||||

| Retail-Sporting Goods - 0.5% | ||||||||

| Big 5 Sporting Goods Corp. | 5,300 | 80,030 | ||||||

| Rubber-Tires - 0.8% | ||||||||

| Cooper Tire & Rubber Co. | 7,300 | 128,334 | ||||||

| Satellite Telecommunications - 0.6% | ||||||||

| GeoEye, Inc.* | 3,800 | 101,840 | ||||||

| Semiconductor Components-Integrated Circuits - 2.7% | ||||||||

| Cirrus Logic, Inc.* | 18,000 | 100,080 | ||||||

| Himax Technologies, Inc. - ADR | 23,000 | 76,590 | ||||||

| Integrated Device Technology, Inc.* | 14,300 | 96,668 | ||||||

| Pericom Semiconductor Corp.* | 9,400 | 92,214 | ||||||

| TriQuint Semiconductor, Inc.* | 13,400 | 103,448 | ||||||

| 469,000 | ||||||||

| Semiconductor Equipment - 0.5% | ||||||||

| Tessera Technologies, Inc.* | 2,900 | 80,881 | ||||||

| Telecommunication Equipment - 0.9% | ||||||||

| ADC Telecommunications, Inc.* | 11,100 | 92,574 | ||||||

| CommScope, Inc.* | 2,300 | 68,839 | ||||||

| 161,413 | ||||||||

| Telecommunication Equipment-Fiber Optics - 0.5% | ||||||||

| Finisar Corp.* | 9,400 | 90,992 | ||||||

| Therapeutics - 0.4% | ||||||||

| Onyx Pharmaceuticals, Inc.* | 2,500 | 74,925 | ||||||

| Transactional Software - 0.6% | ||||||||

| Solera Holdings, Inc. | 3,400 | 105,774 | ||||||

| Transport-Air Freight - 0.8% | ||||||||

| Atlas Air Worldwide Holdings, Inc.* | 4,200 | 134,274 | ||||||

| Transport-Marine - 0.7% | ||||||||

| Genco Shipping & Trading, Ltd.* | 5,800 | 120,524 | ||||||

| Transport-Rail - 0.5% | ||||||||

| Kansas City Southern* | 3,400 | 90,066 | ||||||

| Transport-Truck - 0.5% | ||||||||

| Saia, Inc.* | 4,800 | 77,184 | ||||||

| Web Portals/ISP - 0.5% | ||||||||

| United Online, Inc. | 11,600 | 93,264 | ||||||

| Wire & Cable Products - 0.5% | ||||||||

| Fushi Copperweld, Inc.* | 10,800 | 91,368 | ||||||

| Wireless Equipment - 1.1% | ||||||||

| InterDigital, Inc.* | 3,600 | 83,376 | ||||||

| RF Micro Devices, Inc.* | 18,200 | 98,826 | ||||||

| 182,202 | ||||||||

| Total Common Stock (Cost: $13,339,096) | 16,508,041 | |||||||

| Limited Partnerships - 0.6% | ||||||||

| Pipelines - 0.6% | ||||||||

| Targa Resources Partners LP | ||||||||

| (Cost $78,695) | 5,600 | 105,056 | ||||||

| Principal | ||||||||

| Amount | ||||||||

| Short Term Investments - 3.2% | ||||||||

| Time Deposit - 3.2% | ||||||||

| Citibank Nassau 0.030%, 10/01/09 | ||||||||

| (Cost: $544,711) | $ | 544,711 | 544,711 | |||||

| Total Investments - 100.6% (Cost: $13,962,502) | 17,157,808 | |||||||

| Liabilities in Excess of Other Assets - (0.6%) | (95,199 | ) | ||||||

| Net Assets - 100.0% | $ | 17,062,609 | ||||||

| * Non-income producing securities. | ||

| ADR - American Depository Receipt |

SCHEDULE OF INVESTMENTS BY SECTOR | ||||

| as of September 30, 2009 | ||||

| Percent of | ||||

| Sector | Net Assets | |||

| Consumer, Non-cyclical | 25.9 | % | ||

| Consumer, Cyclical | 16.2 | |||

| Technology | 13.8 | |||

| Industrial | 12.4 | |||

| Communications | 9.0 | |||

| Energy | 8.9 | |||

| Financial | 6.8 | |||

| Basic Materials | 4.1 | |||

| Diversified | 0.3 | |||

| Short Term Investments | 3.2 | |||

| Total Investments | 100.6 | |||

| Liabilities in excess of other assets | (0.6 | ) | ||

| Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

12

U.S. SMALL TO MID CAP GROWTH FUND

Management Team: John C. McCraw, Portfolio Manager; Robert S. Marren, Portfolio Manager

Chief Investment Officer: Horacio A. Valeiras, CFA

Goal: The U.S. Small to Mid Cap Growth Fund seeks to maximize long-term capital appreciation by investing primarily in stocks from a universe of U.S. companies with small to mid (SMID) market capitalizations similar to the Russell 2500 Growth Index at time of purchase.

Market Overview: The rally in the U.S. equity market that began in March continued throughout the six months ended September 30, 2009. The rebound was broad-based, although small- and mid-caps outpaced large caps and value stocks beat growth stocks. The outperformance of value stocks was driven by the strong performance of financials, which have a higher weight in the value indexes.

Some of the key factors fueling the market’s gains were:

| • | Recovery in the credit markets, illustrated by the 9.1% narrowing in spreads between yields on Treasury securities and high-yield bonds |

| • | Evidence that the economy was coming out of the recession, including the first expansion in manufacturing activity in 19 months |

| • | Better-than-expected earnings for mid- and large-cap stocks, albeit off low expectations |

Within the small- and mid-cap growth segment of the market, as measured by the Russell 2500 Growth Index, every sector posted a substantial gain. Energy stocks delivered the best results, supported by a 42% increase in the price of oil. Information technology was the second-best performing sector. Tech firms receive a relatively large percentage of revenues from abroad, and are benefiting from foreign growth prospects, the decline in the U.S. dollar and global inventory restocking.

Performance: The Fund’s Class I shares gained 48.52% from April 1 to September 30, 2009. The Fund outperformed the Russell 2500 Growth Index, which rose 42.70%.

Portfolio Specifics: Consistent with our bottom-up investment process, the Fund’s outperformance was due to stock selection. Stock selection was particularly strong in the information technology, energy and materials sectors. Top-performing positions included STEC, a supplier of data storage devices that has posted healthy revenue growth throughout the recession; Global Industries, an offshore oilfield construction firm demonstrating good cost control; and Ashland, a diversified chemical and transportation company with significant free cash flow. Tupperware Brands, a direct seller of household products, was another strong performer. Tupperware benefited from a positive growth outlook, especially in emerging markets where it derives 50% of its revenues.

The primary area of relative weakness was stock selection in the health care sector, where a biotech firm that missed sales expectations detracted.

Market Outlook: While it is widely believed that the recession is over, we think that the economic recovery will be muted due to the high unemployment rate and large federal deficit. That said, several factors could fuel additional gains in the stock market over the months ahead, including:

| • | Expectations for a strong rebound in corporate earnings in 2010 |

| • | Potential for investors to move some of the $3.4 trillion sitting in low-yielding money market funds into equities |

| • | Indications from the Fed that it plans to keep interest rates low for an extended period of time |

As events unfold, we are confident that our research-driven approach will continue to identify interesting growth companies to own in the Fund.

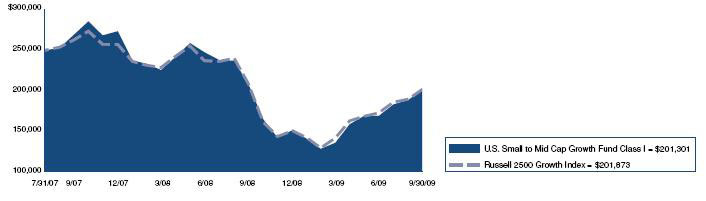

Comparison of Change in Value of a $250,000 Investment in U.S. Small to Mid Cap Growth Fund Class I Shares with the Russell 2500 Growth Index.

Annualized Total Returns As of 9/30/09 | ||

| Since | ||

| 1 Year | Inception | |

| U.S. Small to Mid Cap Growth | ||

| Fund Class I | –3.13% | –9.51% |

| Russell 2500 Growth Index | –3.08% | –9.40% |

The graph above shows the value of a hypothetical $250,000 investment in the Fund’s Class I shares with the Russell 2500 Growth Index for the periods indicated. Average annual total return figures include changes in principal value, reinvested dividends, and capital gain distributions. The Class I shares commenced operations on July 31, 2007. The total returns shown above do not show the effects of income taxes on an individuals’ investment. In most cases, taxes may reduce your actual investment returns on income or gains paid by the Fund or any gains you may realize if you sell your shares. Past performance cannot guarantee future results.

The Russell 2500 Growth Index is an unmanaged index comprised of those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2500 Index is an unmanaged index generally representative of the 2,500 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. Unless otherwise noted, index returns reflect the reinvestment of income, dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing.

Investors may not make direct investments into any index. Since markets can go down as well as up, investment return and principal value will fluctuate with market conditions. You may have a gain or loss when you sell shares.

13

U.S. SMALL TO MID CAP GROWTH FUND

SCHEDULE OF INVESTMENTS (Unaudited)

As of September 30, 2009

| Number of | ||||||||

| Shares | Value | |||||||

| Common Stock - 98.4% | ||||||||

| Agricultural Operations - 0.6% | ||||||||

| The Andersons, Inc. | 800 | $ | 28,160 | |||||

| Apparel Manufacturers - 1.2% | ||||||||

| Jones Apparel Group, Inc. | 1,700 | 30,481 | ||||||

| Quiksilver, Inc.* | 9,000 | 24,750 | ||||||

| 55,231 | ||||||||

| Applications Software - 4.1% | ||||||||

| China TransInfo Technology Corp.* | 4,300 | 40,678 | ||||||

| Compuware Corp.* | 4,230 | 31,006 | ||||||

| Ebix, Inc.* | 1,000 | 55,360 | ||||||

| Nuance Communications, Inc.* | 1,970 | 29,471 | ||||||

| Red Hat, Inc.* | 1,100 | 30,404 | ||||||

| 186,919 | ||||||||

| Auto/Truck Parts & Equipment-Original - 1.2% | ||||||||

| American Axle & Manufacturing | ||||||||

| Holdings, Inc.* | 3,700 | 26,196 | ||||||

| ArvinMeritor, Inc.* | 3,700 | 28,934 | ||||||

| 55,130 | ||||||||

| Auto-Medium & Heavy Duty Trucks - 0.4% | ||||||||

| Navistar International Corp.* | 500 | 18,710 | ||||||

| Batteries/Battery Systems - 0.7% | ||||||||

| Energizer Holdings, Inc.* | 500 | 33,170 | ||||||

| Broadcast Services/Programming - 2.0% | ||||||||

| Acacia Research - Acacia Technologies* | 3,800 | 33,098 | ||||||

| DG FastChannel, Inc.* | 1,300 | 27,222 | ||||||

| Liberty Media Corp. - Capital* | 1,600 | 33,472 | ||||||

| 93,792 | ||||||||

| Building-Heavy Construction - 0.6% | ||||||||

| Chicago Bridge & Iron Co. Cl. Y* | 1,600 | 29,888 | ||||||

| Casino Services - 0.7% | ||||||||

| Bally Technologies, Inc.* | 800 | 30,696 | ||||||

| Cellular Telecommunications - 0.6% | ||||||||

| Cellcom Israel, Ltd. | 900 | 27,387 | ||||||

| Chemicals-Specialty - 0.8% | ||||||||

| Ashland, Inc. | 900 | 38,898 | ||||||

| Coal - 1.8% | ||||||||

| James River Coal Co.* | 1,400 | 26,754 | ||||||

| Massey Energy Co. | 1,000 | 27,890 | ||||||

| Walter Energy, Inc. | 500 | 30,030 | ||||||

| 84,674 | ||||||||

| Commercial Services - 2.7% | ||||||||

| AerCap Holdings NV* | 3,800 | 34,466 | ||||||

| Alliance Data Systems Corp.* | 500 | 30,540 | ||||||

| DynCorp International, Inc. Cl. A* | 1,700 | 30,600 | ||||||

| StarTek, Inc.* | 3,500 | 30,380 | ||||||

| 125,986 | ||||||||

| Commercial Services-Finance - 3.4% | ||||||||

| Deluxe Corp. | 1,600 | 27,360 | ||||||

| Dollar Financial Corp.* | 2,000 | 32,040 | ||||||

| Global Cash Access Holdings, Inc.* | 3,200 | 23,392 | ||||||

| Net 1 UEPS Technologies, Inc.* | 1,200 | 25,152 | ||||||

| TNS, Inc.* | 1,100 | 30,140 | ||||||

| Wright Express Corp.* | 700 | 20,657 | ||||||

| 158,741 | ||||||||

| Computers-Memory Devices - 1.3% | ||||||||

| STEC, Inc.* | 700 | 20,573 | ||||||

| Xyratex, Ltd.* | 3,900 | 37,089 | ||||||

| 57,662 | ||||||||

| Consumer Products-Miscellaneous - 2.4% | ||||||||

| Jarden Corp. | 1,700 | 47,719 | ||||||

| Scotts Miracle-Gro Co. Cl. A | 700 | 30,065 | ||||||

| Tupperware Brands Corp. | 800 | 31,936 | ||||||

| 109,720 | ||||||||

| Containers-Metal/Glass - 0.8% | ||||||||

| Greif, Inc. Cl. A | 700 | 38,535 | ||||||

| Containers-Paper/Plastic - 0.7% | ||||||||

| Rock-Tenn Co. Cl. A | 710 | 33,448 | ||||||

| Diagnostic Kits - 0.7% | ||||||||

| Inverness Medical Innovations, Inc.* | 800 | 30,984 | ||||||

| Direct Marketing - 0.7% | ||||||||

| APAC Customer Services, Inc.* | 5,600 | 33,096 | ||||||

| Disposable Medical Products - 0.6% | ||||||||

| ICU Medical, Inc.* | 750 | 27,645 | ||||||

| Distribution/Wholesale - 0.8% | ||||||||

| Brightpoint, Inc.* | 4,200 | 36,750 | ||||||

| Diversified Manufacturing Operations - 1.3% | ||||||||

| Koppers Holdings, Inc. | 900 | 26,685 | ||||||

| Textron, Inc. | 1,700 | 32,266 | ||||||

| 58,951 | ||||||||

| E-Commerce/Services - 1.3% | ||||||||

| IAC/InterActiveCorp* | 1,400 | 28,266 | ||||||

| Liberty Media Corp. - Interactive* | 2,800 | 30,716 | ||||||

| 58,982 | ||||||||

| Electric Products-Miscellaneous - 0.6% | ||||||||

| GrafTech International, Ltd.* | 1,800 | 26,460 | ||||||

| Electronic Components-Miscellaneous - 0.7% | ||||||||

| Sanmina-SCI Corp.* | 3,900 | 33,540 | ||||||

| Electronic Components-Semiconductors - 3.2% | ||||||||

| Amkor Technology, Inc.* | 4,500 | 30,960 | ||||||

| Fairchild Semiconductor | ||||||||

| International, Inc. Cl. A* | 2,900 | 29,667 | ||||||

| LSI Corp.* | 5,210 | 28,603 | ||||||

| Rovi Corp.* | 970 | 32,592 | ||||||

| Skyworks Solutions, Inc.* | 1,940 | 25,686 | ||||||

| 147,508 | ||||||||

| Electronic Design Automations - 0.6% | ||||||||

| Mentor Graphics Corp.* | 3,000 | 27,930 | ||||||

| Engineering/R & D Services - 1.2% | ||||||||

| KBR, Inc. | 1,100 | 25,619 | ||||||

| McDermott International, Inc.* | 1,100 | 27,797 | ||||||

| 53,416 | ||||||||

| Enterprise Software/Services - 1.8% | ||||||||

| Informatica Corp.* | 1,300 | 29,354 | ||||||

| Mantech International Corp. Cl. A* | 450 | 21,222 | ||||||

| Sybase, Inc.* | 800 | 31,120 | ||||||

| 81,696 | ||||||||

| Finance-Consumer Loans - 1.3% | ||||||||

| Ocwen Financial Corp.* | 3,200 | 36,224 | ||||||

| Portfolio Recovery Associates, Inc.* | 550 | 24,932 | ||||||

| 61,156 | ||||||||

See Accompanying Notes to Financial Statements.

14

SCHEDULE OF INVESTMENTS (Unaudited)

| As of September 30, 2009 | ||||||||

| Number of | ||||||||

| Shares | Value | |||||||

| Finance-Investment Bankers/Brokers - 0.6% | ||||||||

| MF Global, Ltd.* | 3,800 | $ | 27,626 | |||||

| Food-Canned - 0.7% | ||||||||

| Seneca Foods Corp. Cl. A* | 1,200 | 32,880 | ||||||

| Food-Miscellaneous/Diversified - 1.3% | ||||||||

| Lance, Inc. | 1,200 | 30,984 | ||||||