| Filed by: Voya Mutual Funds | |

| (SEC File Nos.: 033-56094; 811-07428) | |

| pursuant to Rule 425 under the | |

| Securities Act of 1933, as amended, | |

| and deemed filed pursuant to Rule 14a-12 | |

| under the Securities Exchange Act of 1934, as amended. | |

| Subject Company: The Advisors’ Inner Circle Fund, on behalf of its CBRE Clarion Long /Short Fund. | |

| (SEC File Nos.: 033-42484; 811-06400) |

May 1, 2017

Voya Investment Management

ClientTalking Points

Voya CBRE Long / Short Fund

Voya Investment Management has announced the following changes:

| Upcoming Change | Effective Date (on or about) | Merging Fund Name | Surviving Fund Name |

| Reorganization | June 26, 2017 | CBRE Clarion Long/Short Fund | Voya CBRE Long/Short Fund |

The respective Board of Trustees for the CBRE Clarion Long/Short Fund (“CBRE Long/Short Fund”), a series of The Advisors’ Inner Circle Fund (the “AICF Trust”), and the Voya CBRE Long/Short Fund (“Voya Long/Short Fund”), a newly created series of Voya Mutual Funds (“VMF”), have approved an Agreement and Plan of Reorganization (“Reorganization Plan”) providing for the reorganization of CBRE Long/Short Fund with and into Voya Long/Short Fund (the “Reorganization”). The approval of shareholders of CBRE Long/Short Fund is required before the Reorganization may take place. CBRE Long/Short Fund and Voya Long/Short Fund are referred to herein collectively as the “Funds” and individually as a “Fund.”

Client Talking Points

| § | What is happening? |

| o | On January 26, 2017 the AICF Trust announced that the Board of Trustees of the AICF Trust had approved the Reorganization Agreement to reorganize CBRE Long/Short Fund into Voya Long/Short Fund. |

| o | Voya Long/Short Fund was created specifically for the purpose of acquiring the assets and liabilities of CBRE Long/Short Fund. |

| o | Pending shareholder approval, the Reorganization is expected to close on or about June 26, 2017 (the “Closing Date”). |

| o | A proxy statement/prospectus (the “Proxy Statement/Prospectus”) seeking shareholder approval of the Reorganization is expected to be mailed to shareholders on or about May 15, 2017. |

| § | How will the Reorganization work? |

| o | If shareholders of CBRE Long/Short Fund approve the Reorganization, each owner of Investor Class and Institutional Class shares of CBRE Long/Short Fund would become a shareholder of the Class A and Class I shares, respectively, of Voya Long/Short Fund. |

| o | Each shareholder of CBRE Long/Short Fund will hold, immediately after the close of the Reorganization, shares of Voya Long/Short Fund having an aggregate value equal to the aggregate value of the shares of CBRE Long/Short Fund held by that shareholder as of the close of business on the Closing Date. |

| § | How do the Investment Objectives compare? |

| CBRE Long/Short Fund | Voya Long/Short Fund | |

| Investment Objective | CBRE Long/Short Fund seeks to provide total return, consisting of capital appreciation and current income, while attempting to preserve capital and mitigate risk by employing hedging strategies, primarily short selling. | Voya Long/Short Fund seeks total return including capital appreciation and current income. |

| § | What is the experience of the CBRE Investment Management Team? |

| o | As of December 31, 2016, CBRE Clarion Securities, LLC (“CBRE Clarion”), the investment adviser of CBRE Long/Short Fund, had approximately $17.5 billion in assets under management. |

| o | T. Ritson Ferguson, Steven D. Burton, and Joseph P. Smith are jointly responsible for the day-to-day management of CBRE Long/Short Fund and, if the Reorganization is approved by shareholders, for the day-to-day management of the Voya Long/Short Fund. |

| o | Mr. Ferguson is one of the three founding members of CBRE Clarion. He serves as the Chief Executive Officer and leads the firm’s Management Committee. Mr. Ferguson is Global Chief Investment Officer and Senior Portfolio Manager, as well as a member of the firm’s Global Infrastructure Allocation Committee. He has been employed with CBRE Clarion and its predecessor firms since 1992. |

| 2 |

Client Talking Points

| o | Mr. Burton is a Managing Director of CBRE Clarion. He is a Co-Chief Investment Officer and a Senior Portfolio Manager, as well as a member of the firm’s Global Investment Policy Committee. He has been employed by CBRE Clarion and its predecessor firms since 1995. |

| o | Mr. Smith is a Managing Director of CBRE Clarion. He is a Co-Chief Investment Officer and a Senior Portfolio Manager, as well as a member of the firm’s Global Investment Policy Committee. He has been employed by CBRE Clarion and its predecessor firms since 1997. |

| § | How do the principal investment strategies compare? |

| o | The Funds have substantially identical principal investment strategies. Both Funds seek to achieve their investment objective by taking long and short positions in equity securities of companies that are principally engaged in the real estate industry. |

| o | CBRE Clarion will use the same multi-step investment process for constructing Voya Long/Short Fund’s investment portfolio as is currently used to construct CBRE Long/Short Fund’s investment portfolio. The following chart compares the principal investment strategies of CBRE Long/Short Fund and Voya Long/Short Fund. The differences between the principal investment strategies as described below do not reflect a material difference in the manner in which each Fund is managed, except that Voya Long/Short Fund, as a fund in the Voya family of funds, will be permitted to participate in the Voya securities lending program. |

| CBRE Long/Short Fund | Voya Long/Short Fund | |

| Investment Strategies | The Fund seeks to achieve its objective by taking long and short positions in equity securities of companies that are principally engaged in the real estate industry (‘real estate companies”). The adviser (“Adviser”) defines a real estate company as a company that derives its intrinsic value from owning, operating, leasing, developing, managing, brokering and/or selling commercial or residential real estate, land or infrastructure. Real estate companies include, for example, real estate investment trusts. To take a long position, the Fund purchases a security outright; with a short position, the Fund sells a security that it has borrowed. When the Fund sells a security short, it borrows the security from a third party and sells it at the then current market price. The Fund is then obligated to buy the security on a later date so that it can return the security to the lender. Short positions may be used either to hedge long positions or to seek positive returns in instances where the Adviser believes a security’s price will decline. The Fund will either realize a profit or incur a loss from a short position, depending on whether the value of the underlying stock decreases or increases, respectively, between the time it is sold and the time when the Fund replaces the borrowed security. The Fund may reinvest the proceeds of its short sales by taking additional long positions, thus allowing the Fund to maintain long positions in excess of 100% of its | The Fund seeks to achieve its investment objective by taking long and short positions in equity securities of companies that are principally engaged in the real estate industry (“real estate companies”). The sub-adviser (“Sub-Adviser”) defines a real estate company as a company that derives its intrinsic value from owning, operating, leasing, developing, managing, brokering and/or selling commercial or residential real estate, land or infrastructure. Real estate companies include, for example, real estate investment trusts.

When the Fund sells a security short, it borrows the security from a third party and sells it at the then current market price. The Fund is then obligated to buy the security on a later date so that it can return the security to the lender. The Fund will either realize a profit or incur a loss from a short position, depending on whether the value of the underlying security decreases or increases, respectively, between the time it is sold and the time when the Fund replaces the borrowed security. Short positions may be used either to eliminate or reduce investment or risk exposures within the Fund’s portfolio or to seek positive returns in instances where the Sub-Adviser believes a security’s price will decline.

There is no limit on the amount of the Fund’s short exposure, and it is possible that the Fund’s short exposure may equal or exceed the value of |

| 3 |

Client Talking Points

| CBRE Long/Short Fund | Voya Long/Short Fund | |

net assets. The Adviser varies the Fund’s long and short exposures over time, based on its assessment of market conditions and other factors, but expects the Fund to maintain net-long exposure over multi-year periods.

While the Fund expects to invest primarily in common stock, it may also invest in other equity securities including depositary receipts with characteristics similar to common stock, preferred stocks, shares of exchange-traded funds (“ETFs”), convertible securities, and rights or warrants to buy common stocks. The Fund may also create short positions in ETFs. In addition, the Fund may invest in exchange-traded options (i) as tools in the management of portfolio assets, (ii) to hedge various investments for risk management and/or (iii) for income enhancement, which is also known as speculation.

The Fund may invest in securities of companies of any market capitalization and, as a general matter, the Fund expects its investments to be primarily in equity securities issued by U.S. companies. However, the Fund may invest up to 50% of its assets in securities of non-U.S. issuers, including emerging market issuers, denominated in U.S. dollars, non-U.S. currencies or multinational currency units. The Fund may utilize forward contracts and create short positions in currency-related ETFs to hedge its currency exposure. The Fund is non-diversified, meaning that it may invest a large percentage of its assets in a single issuer or a relatively small number of issuers.

The Adviser utilizes a multi-step investment process for constructing the Fund’s investment portfolio that combines top-down region and sector allocation with bottom-up individual stock selection. The Adviser first selects property sectors and geographic regions in which to invest, and determines the degree of representation of such sectors and regions, through a systematic evaluation of listed and direct real estate market trends and conditions. The Adviser then uses an in-house valuation process to identify investments that it believes demonstrate superior current income and growth potential relative to their peers. The Adviser’s in-house valuation process examines several factors, including the value and quality of a company’s properties, its capital structure, its strategy and the ability of its management team. Short positions are an important part of the Fund’s investment strategy. Short selling is expected to contribute to performance as well as to help preserve capital during declines in the real estate securities | the Fund’s net assets. The Fund may invest the proceeds of its short sales in additional long positions, thus allowing the Fund to maintain long positions in excess of 100% of its net assets. The Fund’s use of short sales, and its investment of the short proceeds in additional long positions, will create investment leverage in the portfolio. The Fund may lose money on both the long positions in its portfolio and on its short positions at the same time. The Sub-Adviser varies the Fund’s long and short exposures over time, based on its assessment of market conditions and other factors, but expects the Fund to maintain net-long exposure over multi-year periods.

Under normal circumstances, the Fund invests primarily in equity securities including common stocks, preferred stocks, convertible securities, rights or warrants to buy common or preferred stocks, and depositary receipts providing indirect exposures to common or preferred stocks. The Fund may invest in initial public offerings. The Fund may invest up to 50% of its total assets in securities of non-U.S. issuers, including securities of issuers located in developed and emerging market countries. Securities may be denominated in U.S. dollars, non-U.S. currencies, or multinational currency units. The Fund may, but will not necessarily, hedge its currency exposure to securities denominated in non-U.S. currencies. The Fund may invest in pooled vehicles that hold non-U.S. currency to hedge its currency exposure or to enhance returns. The Fund may invest in securities of companies of any market capitalization. The Fund is non-diversified, which means it may invest a significant portion of its assets in a single issuer.

The Fund may invest in other investment companies, including exchange-traded funds (“ETFs”) and inverse ETFs, to the extent permitted under the Investment Company Act of 1940, as amended, and the rules, regulations, and exemptive orders thereunder (“1940 Act”). The Fund may invest also create short positions in ETFs.

The Fund may invest in derivative instruments including options and forwards. The Fund typically uses derivatives to seek to reduce exposure or other risks such as interest rate or currency risk, as a substitute for taking a position in the underlying asset, and/or in an effort to enhance returns in the Fund.

The Sub-Adviser utilizes a multi-step investment process for constructing the Fund’s investment |

| 4 |

Client Talking Points

| CBRE Long/Short Fund | Voya Long/Short Fund | |

| market. Companies that are valued unfavorably using the Adviser’s in-house process are considered for short positions, although the Adviser also considers a company’s size relative to its property sector or geographic region, as well as its liquidity. The Fund may buy and sell investments frequently, which could result in a high portfolio turnover rate. | portfolio that combines top-down geographic region and property sector allocation with bottom-up individual stock selection. The Sub-Adviser first selects property sectors and geographic regions in which to invest, and determines the degree of representation in the portfolio of such sectors and regions, through a systematic evaluation of real estate market trends and conditions. The Sub-Adviser then uses a proprietary valuation process to identify real estate companies that it believes exhibit superior current income and/or growth potential relative to their peers. The Sub-Adviser’s proprietary valuation process examines several factors, including the value and quality of a company’s properties, its capital structure, its strategy and the ability of its management team.

Short positions are an important part of the Fund’s investment strategy. The Sub-Adviser seeks to use short-selling to contribute to the Fund's performance and to help preserve capital during declines in the real estate securities market. Securities that are valued unfavorably using the Sub-Adviser’s in-house process are considered for short positions, although the Sub-Adviser will consider various other factors, such as a company’s size relative to its property sector or geographic region, as well as a security’s liquidity, in determining whether to short a security. The Fund may buy and sell investments frequently, which could result in a high portfolio turnover rate.

The Sub-Adviser may sell securities for a variety of reasons, such as to secure gains, limit losses, or redeploy assets into opportunities believed to be more promising, among others.

The Fund may lend portfolio securities on a short-term or long-term basis, up to 33 1⁄3% of its total assets. |

| § | How do the Total Annual Fund Expenses after reductions and waivers compare? |

| o | These tables below describe the fees and expense that you may pay if you buy and hold shares of the Funds. |

| o | Pro Forma fees and expenses, which are the estimated fees and expenses of Voya Long/Short Fund after giving effect to the Reorganization, assume the Reorganization occurred on October 31, 2016. |

| o | Shareholders of CBRE Long/Short Fund will not pay any sales charges or redemption fees in connection with the Reorganization. In addition, Voya Long/Short Fund’s Class A shares sales |

| 5 |

Client Talking Points

charges (including front-end sales charges and contingent deferred sales charges) will not apply to investors who held Investor Class shares of CBRE Long/Short Fund prior to the date of the Reorganization and received Class A shares of Voya Long/Short Fund as a result of the Reorganization, including with respect to additional purchases of Class A shares by the same account.

Shareholder Fees Fees paid directly from your investment | |||

| Maximum sales charge (load) as a % of offering price | Maximum deferred sales charge as a % of purchase or sales price, whichever is less | Redemption Fee as a % | |

| CBRE Long/Short Fund – Investor Class | None | None | 2.001 |

| Voya Long/Short Fund – Class A | 5.75 | None2 | N/A |

| CBRE Long/Short Fund – Institutional Class | None | None | 2.001 |

| Voya Long/Short Fund –Class I | None | None | N/A |

Annual Fund Operating Expenses3 Expenses you pay each year as a % of the value of your investment | |||||

| CBRE Long/Short Fund | Voya Long/Short Pro Forma | ||||

| Investor Class | Class A | ||||

| Management Fees | % | 1.25 | 1.35 | ||

| Distribution and/or Shareholder Services (12b-1) Fees | % | 0.25 | 0.25 | ||

| Other Expenses | % | 2.86 | 2.71 | ||

| Dividend, Interest and Stock Loan Expense on Securities Sold Short | % | 2.58 | 2.58 | ||

| Shareholder Servicing Fees | % | 0.10 | None | ||

| Other Operating Expenses | % | 0.18 | 0.135 | ||

| Total Annual Fund Operating Expenses | % | 4.36 | 4.31 | ||

| Less Fee Reductions and/or Expense Reimbursements | % | None4 | None6 | ||

| Total Annual Fund Operating Expenses after Fee Reductions and/or Expense Reimbursements | % | 4.36 | 4.31 | ||

| Institutional Class | Class I | ||||

| Management Fees | % | 1.25 | 1.35 | ||

| Distribution and/or Shareholder Services (12b-1) Fees | % | None | None | ||

| Other Expenses | % | 2.82 | 2.68 | ||

| Dividend, Interest and Stock Loan Expense on Securities Sold Short | % | 2.58 | 2.58 | ||

| Shareholder Servicing Fees | % | 0.06 | None | ||

| Other Operating Expenses | % | 0.18 | 0.105 | ||

| Total Annual Fund Operating Expenses | % | 4.07 | 4.03 | ||

| Less Fee Reductions and/or Expense Reimbursements | % | None4 | None6 | ||

| 6 |

Client Talking Points

Annual Fund Operating Expenses3 Expenses you pay each year as a % of the value of your investment | |||||

| CBRE Long/Short Fund | Voya Long/Short Pro Forma | ||||

| Total Annual Fund Operating Expenses after Fee Reductions and/or Expense Reimbursements | % | 4.07 | 4.03 | ||

| 1. | A 2.00% redemption fee will be charged on the redemption of shares held less than 60 days. The redemption fee will not apply to shares purchased with reinvested dividends or distributions. |

| 2. | A contingent deferred sales charge of 1.00% is assessed on certain redemptions of Class A shares made within 18 months after purchase where no initial sales charge was paid at the time of purchase as part of an investment of $1 million or more. |

| 3. | Expense ratios have been adjusted to reflect current contractual rates. |

| 4. | CBRE Clarion has contractually agreed to reduce fees and reimburse expenses to the extent necessary to keep Total Annual Fund Operating Expenses after Fee Reductions and/or Expense Reimbursements (excluding Dividend, Interest and Stock Loan Expense on Securities Sold Short, interest, taxes, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses (collectively, “excluded expenses”)) from exceeding 1.99% and 1.64% of CBRE Long/Short Fund’s Investor Class shares’ average daily net assets and CBRE Long/Short Fund’s Institutional Class shares’ average daily net assets, respectively, until February 28, 2018 (the “contractual expense limit”). In addition, if at any point Total Annual Fund Operating Expenses (not including excluded expenses) are below the contractual expense limit, CBRE Clarion may receive from CBRE Long/Short Fund the difference between the Total Annual Fund Operating Expenses (not including excluded expenses) and the contractual expense limit to recover all or a portion of its fee reductions or expense reimbursements made during the preceding three-year period during which this agreement (or any prior agreement) was in place. This agreement may be terminated: (i) by the AICF Board, for any reason at any time, or (ii) by CBRE Clarion, upon ninety (90) days’ prior written notice to the AICF Trust, effective as of the close of business on February 28, 2018. |

| 5. | Other Expenses are based on estimated amounts for the current fiscal year. |

| 6. | Voya Investments, LLC (“VIL”), the investment adviser of Voya Long/Short Fund, is contractually obligated to limit the expenses to 1.89% and 1.64% for Class A and Class I shares, respectively, through March 1, 2019. The limitations do not extend to interest, taxes, investment-related costs, leverage expenses, extraordinary expenses, Dividend, Interest and Stock Loan Expense on Securities Sold Short, and Acquired Fund Fees and Expenses. Amounts waived or reimbursed pursuant to these limitations are subject to possible recoupment by VIL within 36 months of the waiver or reimbursement, subject to the expense limitation in effect at the time of such waiver or reimbursement or at the time of recoupment, whichever is lower. Termination or modification of these obligations requires approval by the VMF Board. |

| § | Who will pay for the expenses of the Reorganization? |

| o | The expenses of the Reorganization will be paid by CBRE Clarion or VIL or their affiliates. |

| o | The expenses of the Reorganization are estimated to be approximately $410,000 and do not include the transition costs described below. |

| § | What are the expected Portfolio Transitioning costs? |

| o | As discussed above, the Funds have substantially identical principal investment strategies. As a result, CBRE Clarion does not anticipate that it will need to sell a significant portion of CBRE Long/Short Fund’s holdings if the Reorganization is approved by shareholders. |

| 7 |

Client Talking Points

| § | How does CBRE Long/Short Fund performance compare to Voya Long/Short Fund? |

| o | No performance information is included here for Voya Long/Short Fund since the Fund has not yet commenced investment operations. Voya Long/Short Fund will assume the performance history of CBRE Long/Short Fund at the closing of the Reorganization. |

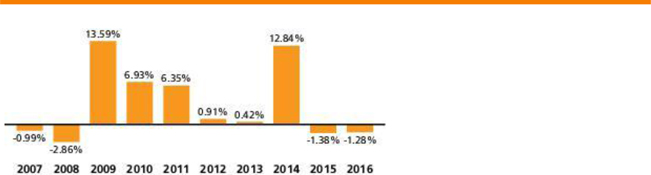

| o | The Annual Performance bar chart and Average Annual Total Returns table below illustrate the risks and volatility of an investment in CBRE Long/Short Fund by showing changes in CBRE Long/Short Fund’s Investor Class shares’ performance from year to year and by showing how CBRE Long/Short Fund’s Investor Class shares’ and Institutional Class shares’ average annual total returns for 1, 5 and 10 years and since inception compare with those of a broad measure of market performance. |

| o | Best quarter: 13.87%, 09/30/2009 and Worst quarter (6.85)%, 06/30/2015 |

CBRE Long/Short Fund – Investor Class Shares

(as of December 31 of each year)

| o | The Average Annual Total Returns table below compares CBRE Long/Short Fund’s average total returns for the periods ended December 31, 2016 to those of an appropriate broad based index. In addition, the table shows how CBRE’s average annual total returns compare with the returns of an index designed to represent the performance of the long/short hedge fund market and an index designed to represent the performance of the U.S. equity REIT market. |

Average Annual Total Returns

(for periods ended December 31, 2016)

| 1 Year | 5 Year | 10 Year | Since Inception1 | Inception Date | ||

| Investor Class before taxes | % | (1.28) | 2.17 | 3.27 | 7.84 | 11/20/00 |

| After taxes on Distributions | % | (2.05) | 1.53 | N/A | N/A | |

| After Taxes on Distributions and Sale of Fund Shares | % | (0.09) | 1.65 | N/A | N/A | |

| S&P 500 Index (reflects no deduction for fees, expenses or taxes) | % | 11.96 | 14.66 | 6.95 | 5.28 | |

| MSCI US REIT Index (reflect no deduction for fees, expenses or taxes) | % | 8.60 | 11.86 | 4.96 | 11.34 | |

| HFRX Equity Hedge Index (reflects no deduction for fees, expenses or taxes) | % | 0.10 | 2.92 | (1.20) | 0.92 | |

| Institutional Class before taxes | % | (0.98) | 2.40 | 3.39 | 7.92 | 11/20/00 |

| S&P 500 Index (reflects no deduction for fees, expenses or taxes) | % | 11.96 | 14.66 | 6.95 | 5.28 | |

| MSCI US REIT Index (reflect no deduction for fees, expenses or taxes) | % | 8.60 | 11.86 | 4.96 | 11.34 | |

| 8 |

Client Talking Points

| 1 Year | 5 Year | 10 Year | Since Inception1 | Inception Date | ||

| HFRX Equity Hedge Index (reflects no deduction for fees, expenses or taxes) | % | 0.10 | 2.92 | (1.20) | 0.92 | |

The performance quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. The investment return and principal value of an investment in the Voya CBRE Long/Short Fund will fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. You may obtain performance information current to the most recent month end by visitingwww.voyainvestments.com

| 1. | Performance information for CBRE Long/Short Fund, the S&P 500 Index and the MSCI US REIT Index is calculated from November 20, 2000, CBRE Long/Short’s inception date. Performance information for the HFRX Equity Hedge Index is calculated from April 30, 2003, the index’s inception date. |

| o | Of course, CBRE Long/Short Fund’s past performance (before and after taxes) does not necessarily indicate how CBRE Long/Short Fund or Voya Long/Short Fund will perform in the future. |

| o | CBRE Long/Short Fund acquired substantially all of the assets of another fund after the close of business on December 30, 2011. The performance shown in the bar chart and the performance table above includes the performance of that predecessor fund for periods prior to December 30, 2011. The predecessor fund was managed by CBRE Clarion using investment policies, objectives, guidelines and restrictions that were in all material respects equivalent to the management of CBRE Long/Short Fund. However, the predecessor fund was not a registered mutual fund and so it was not subject to the same investment and tax restrictions as CBRE Long/Short Fund. If it had been, the predecessor fund’s performance may have been lower. The performance information in the bar chart and table for periods prior to December 30, 2011 reflects all fees and expenses, including a performance fee, incurred by the predecessor fund. The performance information for periods prior to December 30, 2011 has not been adjusted to reflect the expenses of the Investor Class or Institutional Class shares expenses. If the performance had been adjusted to reflect Investor Class or Institutional Class shares’ expenses, the performance may have been higher or lower for a given period depending on the expenses incurred by the predecessor fund for that period. The predecessor fund’s expenses varied from year to year, primarily depending on whether a performance fee was incurred. |

| o | Updated performance information is available on CBRE Long/Short Fund’s website atwww.cbreclarion.comor by calling (855) 520-4227. |

| § | Tax Considerations |

| o | The Reorganization is intended to qualify for federal income tax purposes as a tax-free reorganization under Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”). Accordingly, pursuant to this treatment, neither CBRE Long/Short Fund nor its shareholders, nor Voya Long/ Short Fund nor its shareholders, are expected to recognize any gain or loss for federal income tax purposes from the transactions contemplated by the Reorganization Agreement. |

| o | As a condition to each Fund’s obligation to consummate the Reorganization, the Funds will receive an opinion from tax counsel to the effect that, on the basis of existing provisions of the Code, U.S. Treasury Regulations promulgated thereunder, current administrative rules, |

| 9 |

Client Talking Points

pronouncements and court decisions, and subject to certain qualifications, the Reorganization will qualify as a tax-free reorganization for federal income tax purposes.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and the after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. In some cases the after-tax returns may exceed the return before taxes due to an assumed tax benefit from any losses on the sale of Fund shares at the end of the measurement period.

The foregoing is not an offer to sell, nor a solicitation of an offer to buy, shares of any portfolio, nor is it a solicitation of any proxy. For information regarding the Voya CBRE Long/Short Fund, please call Voya Investment Management toll free at 1-800-992-0180.

For information regarding any of the Funds discussed in this Talking Points, please call Voya Investment Management toll free at 1-800-992-0180. To receive a free copy of a Proxy Statement/Prospectus relating to the proposed Reorganization of the Voya Long/Short Fund that was created specifically for the purpose of acquiring the assets and liabilities of the CBRE Long/Short Fund, please call Voya Investment Management toll free at 1-800-992-0180. This “Client Talking Points” is qualified in its entirety by reference to the Proxy Statement/ Prospectus, and supersedes any prior Client Talking Points. The Proxy Statement/Prospectus contains important information about fund objectives, strategies, fees, expenses and risk considerations, and therefore you are advised to read it. The Proxy Statement/Prospectus and shareholder reports and other information are or will also be available for free on the SEC’s website (www.sec.gov ). Please read the Proxy Statement/Prospectus carefully before making any decision to invest or to approve the Reorganization.

This information is proprietary and cannot be reproduced or distributed. Certain information may be received from sources Voya Investment Management considers reliable; Voya Investment Management does not represent that such information is accurate or complete. Certain statements contained herein may constitute "projections," "forecasts" and other "forward-looking statements" which do not reflect actual results and are based primarily upon applying retroactively a hypothetical set of assumptions to certain historical financial data. Actual results, performance or events may differ materially from those in such statements. Any opinions, projections, forecasts and forward looking statements presented herein are valid only as of the date of this document and are subject to change. Nothing contained herein should be construed as: (i) an offer to buy any security; or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Voya Investment Management assumes no obligation to update any forward-looking information. Past performance is no guarantee of future results.

You should consider the investment objectives, risks, charges and expenses of Voya CBRE Long/Short Fund carefully before investing. For a free copy of the proxy statement/prospectus, which contains this and other information, please call CBRE Long/Short Fund’s proxy solicitor, toll free at (800) 769-7666. If you have any questions about voting procedures, please call the number listed on your proxy card. Representatives will be available Monday through Friday from 9:00 a.m. to 10:00 p.m., Eastern Time. Please read the prospectus carefully before investing.

CID# IM0306-31745-0318

| 10 |