QuickLinks -- Click here to rapidly navigate through this document

Exhibit 99.2(c)(ii) to Form 18-K

2002-2003 Budget Update

2002-03

Budget Update

Presented by:

The Honourable John Brumby, M.P.

Treasurer of the State of Victoria

For the information of Honourable Members

| TABLE OF CONTENTS |

| Budget update highlights | |||

Chapter 1: Financial policy objectives and strategies | |||

| Financial strategy, objectives and priorities | |||

Chapter 2: Budget position and outlook | |||

| Forward estimates outlook 2002-03 to 2005-06 | |||

| Reconciliation of forward estimates to previously published estimates | |||

| Summary Statement of Financial Position | |||

| Other budget indicators | |||

| Use of cash resources | |||

Chapter 3: Economic conditions and outlook | |||

| The economy since the Budget | |||

| Economic outlook | |||

| Economic risks | |||

Chapter 4: Estimated Financial Statements and Notes | |||

| Introduction | |||

| Estimated Financial Statements for the Victorian general government sector | |||

| Notes to the Estimated Financial Statements | |||

Chapter 5: Statement of risks | |||

| Economic risks | |||

| Sensitivity of the Budget to economic conditions | |||

| Fiscal risks | |||

| Contingent liabilities | |||

Appendix A: Specific policy initiatives affecting the budget position | |||

| Output and asset initiatives | |||

| Revenue initiatives | |||

Appendix B: General government sector year-to-date actuals | |||

| Revenue | |||

| Expenses | |||

Appendix C: Accrual uniform presentation of government finance statistics | |||

| The accrual GFS presentation | |||

| Institutional sectors | |||

Appendix D: Tax expenditures | |||

Appendix E: Requirements of the Financial Management Act 1994 | |||

- •

- A revised 2002-03 general government operating surplus of $594 million, up from the $522 million 2002-03 Budget estimate primarily as a result of stronger than expected taxation and other revenue, partly offset by an increase in superannuation expense. Operating surpluses expected to average $505 million per annum in the following three years.

- •

- Output policy decisions taken since the 2002-03 Budget worth $181 million in 2002-03, and an average of $161 million per annum over the following three years. This includes an $82 million package of initiatives in 2002-03 to assist drought-affected farmers.

- •

- Output initiative election commitments published in Labor's Financial Statement 2002 total approximately $140 million in 2003-04, $240 million in 2004-05 and $290 million in 2005-06.

- •

- Increased operating surplus since the publication of the Pre-Election Budget Update of $52 million in 2002-03, and $27 million per annum on average over the remainder of the forward estimates period.

- •

- Net financial liabilities, as a percentage of gross state product (GSP), to decline from 8.6 per cent at 30 June 2002, to 7.5 per cent at 30 June 2006 (excluding the Growing Victoria infrastructure reserve).

- •

- Net debt to fall from $2.4 billion (1.3 per cent of GSP) at 30 June 2002 to $1.7 billion (0.8 per cent of GSP) at 30 June 2006 (excluding the Growing Victoria infrastructure reserve).

- •

- Expenditure on fixed assets to average $2.2 billion per annum over the four years to 2005-06.

- •

- A projected increase in net assets from $21.8 billion at 30 June 2002 to $26.2 billion by 30 June 2006.

- •

- Economic growth forecast to moderate from 4.9 per cent in 2001-02 to 3.25 per cent in 2002-03 (down slightly from budget time reflecting a worse than expected drought impact and sluggish world economy) and to between 3.5 and 3.75 per cent in later years.

CHAPTER 1: FINANCIAL POLICY OBJECTIVES AND STRATEGIES

- •

- The Government is committed to maintaining a substantial operating surplus of at least $100 million in each year.

- •

- The Government is committed to providing capital works that enhance social and economic infrastructure, with expenditure on strategic infrastructure projects boosted by funding from the Growing Victoria infrastructure reserve.

- •

- Improved services will be delivered to all Victorians, with the key priorities being education, health and community safety.

- •

- The Government is committed to providing a fair and competitive tax system to Victorian businesses and households through the continued implementation of reforms announced in the Better Business Taxes and Building Tomorrow's Businesses Today packages.

- •

- The Government will maintain state government net financial liabilities at prudent levels and Victoria's triple-A credit rating.

FINANCIAL STRATEGY, OBJECTIVES AND PRIORITIES

This chapter sets out the Government's financial policy objectives and strategies as required by the Financial Management (Financial Responsibility) Act 2000. The Act includes a set of sound financial management principles. These are to:

- •

- manage financial risks faced by the State prudently, having regard to economic circumstances;

- •

- pursue spending and taxation policies that are consistent with a reasonable degree of stability and predictability in the level of the tax burden;

- •

- maintain the integrity of the Victorian tax system;

- •

- ensure that government policy decisions have regard to their financial effects on future generations; and

- •

- provide full, accurate and timely disclosure of financial information relating to the activities of the Government and its agencies.

These financial management principles underpin the Government's financial policy objectives and strategies.

The broad strategic priority remains to provide a sound and stable financial basis, from which growth can be promoted across the whole State. This is achieved through delivering a substantial operating surplus of at least $100 million in each year, ensuring that net financial liabilities remain at prudent levels, and maintaining Victoria's triple-A credit rating. This sound financial position allows the Government to provide capital works to enhance social and economic infrastructure, and improve quality, access and equity in key services across the whole State, particularly in education, health and community safety.

The Government's financial responsibility legislation requires a statement of its short and long-term financial objectives in the Budget Update. It is also a necessary element of the financial management principle of providing full, accurate and timely disclosure of financial information relating to the activities of the Government and its agencies.

Consistent with this, the Government has a number of short and long-term financial objectives, as shown in Table 1.1.

Table 1.1: 2002-03 Financial objectives

| Long-term | Short-term | |

|---|---|---|

| Maintain a substantial budget operating surplus | Operating surplus of at least $100 million in each year | |

Provide capital works to enhance social and economic infrastructure throughout Victoria | Implement strategic infrastructure projects, including those funded from the Growing Victoria infrastructure reserve | |

Provide improved service delivery to all Victorians | Expenditure priority on education, health and community safety | |

Ensure competitive and fair taxes and charges to Victorian businesses and households | Implement reforms to Victoria's business taxation system | |

Maintain state government net financial liabilities at prudent levels | Maintain a triple-A credit rating |

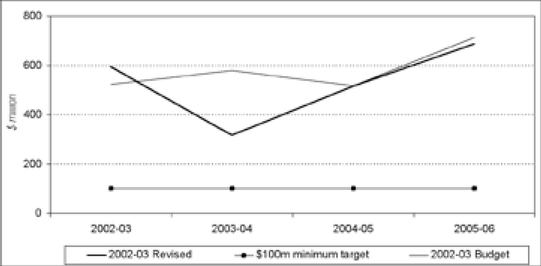

Operating surplus

The Government's long-term objective is to maintain a substantial budget operating surplus. In the short term, its objective is to maintain an operating surplus of at least $100 million in each year. This is the Government's key financial measure. The revised outlook for the budget surplus remains consistent with this objective, as can be seen in Chart 1.1. Following a general government surplus of $273 million in 2001-02, the operating surplus is now forecast to be $594 million in 2002-03 and to average $505 million per annum in the following three years.

Chart 1.1: General government sector operating surplus(a)

Source: Department of Treasury and Finance

Note:

- (a)

- The 'general government sector operating surplus' is equivalent to the 'net result' in the statement of financial performance in Chapter 4, Estimated Financial Statements and Notes.

The operating surplus objective is in accord with the financial management principle of pursuing expenditure and taxation policies that allow reasonable stability and predictability in tax burden levels. Thus, businesses and households can have confidence that tax rates and the level of service delivery will not need to be adjusted markedly and unexpectedly at some future date to retrieve the State's financial position. The substantial operating surplus is also an important funding source for the Government's strong capital investment program.

Given the continued uncertainties in the world economy (see Chapter 3, Economic Conditions and Outlook), the Government is maintaining a buffer over its $100 million minimum operating surplus target. This will ensure the achievement of the Government's key financial target in the event of a moderate deterioration in the national and world economies and asset markets. For a more detailed discussion of economic and other risks, and the sensitivity of the operating surplus to changes in economic conditions, see Chapter 5, Statement of Risks.

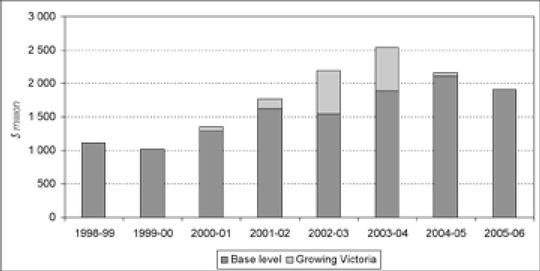

Infrastructure

The Government is committed to delivering world-class infrastructure in order to drive economic growth and improve the delivery of key services across the whole State. This commitment is reflected in the significant increase in infrastructure spending since 1999-2000 (see Chart 1.2). Over the period 2002-03 to 2005-06, annual expenditure on fixed assets will average $2.2 billion, which far outstrips depreciation of around $1.0 billion per annum, leading to an increase in the real per capita capital stock.

Chart 1.2 shows past actual expenditure on fixed assets, together with projections provided for in the forward estimates.

Chart 1.2: General government sector net infrastructure investment

Source: Department of Treasury and Finance

The significant boost to Victoria's infrastructure over the medium term has been made possible by Victoria's strong financial position, indicated by the affirmation of its triple-A credit rating. The substantial forecast operating surpluses over the next four years, together with the Growing Victoria infrastructure reserve, has enabled the Government to pursue its program of significantly upgrading and modernising infrastructure.

In the 2002-03 Budget, $3.0 billion (total estimated investment) was allocated for the commencement of new infrastructure projects. Since the Budget, the Government has approved further infrastructure investments including:

- •

- $52 million associated with the consolidation of the Department of Human Services' accommodation to a building to be constructed at 50 Lonsdale Street, Melbourne;

- •

- $35 million, extending beyond the forward estimates period, for the provision of 200 social housing households as part of the Commonwealth Games Athletes' Village;

- •

- $32 million over three years to assist in transforming the State's three zoos into centres of wildlife experience, conservation, education and research; and

- •

- $10 million, as part of the Government's counter-terrorism initiatives, to purchase equipment for Victoria Police, and to establish a new State Crisis Centre that links key Federal and emergency services agencies to ensure effective communications.

Implementation of the Government's election commitments as outlined in Labor's Financial Statement 2002 will also improve infrastructure provision across the State. Initiatives announced (total estimated investment) include $475 million for Linking Victoria (including $190 million for the Geelong Bypass), $190 million for the Royal Women's Hospital redevelopment, $180 million for new schools, and $114 million for continued police station construction.

Service delivery

The Government continues to build on last year's service delivery initiatives by adopting medium to long-term strategies to improve quality, access and equity in the delivery of services across the State, particularly in health, education, community safety and transport. Since the 2002-03 Budget, additional funding has been provided for new output policy initiatives of $181 million in 2002-03, and an average of $161 million per annum over the following three years.

The Government is providing an $82 million package of initiatives in 2002-03 to assist drought-affected farmers. This includes cash grants up to a maximum of $20 000 per farm, rural financial counselling, community support activities, and new and maintained community water bores. Other specific post-budget initiatives include:

- •

- $310 million over five years, which will be targeted to innovation projects across a number of departments. As part of this package, around $50 million has been allocated for capital investment expenditure;

- •

- $109 million, extending beyond the forward estimates period, for the development of an Athletes' Village at Parkville for the Commonwealth Games;

- •

- $77 million contribution towards the redevelopment of the Northern Stand of the Melbourne Cricket Ground;

- •

- $57 million for the Electricity Network Tariff Rebate scheme to address the structural cost disadvantage faced by rural domestic and small business electricity customers;

- •

- $47 million as part of the Interim Operating Agreements signed by the Government with public transport franchise operators Connex and Yarra Trams, to guarantee services until 31 December 2003;

- •

- $22 million to establish a new Counter Terrorism Coordination Unit, and bolster Special Operations Group resources, to enhance the Government's planning and response capabilities; and

- •

- $22 million under the Disabilities and Impairments program to meet increased demand growth for support services provided to government school students with special educational needs.

Implementation of the Government's election commitments as outlined in Labor's Financial Statement 2002 will also improve service delivery in Victoria. Initiatives announced include:

- •

- over $100 million in 2003-04 and an average of around $260 million over the following three years for the Hospital Demand Strategy;

- •

- approximately $25 million in 2003-04 rising to over $100 million by 2006-07 for education; and

- •

- approximately $10 million in 2003-04 rising to around $60 million in 2006-07 for more police resources.

Taxation

The Government is committed to ensuring a fair and competitive tax system in Victoria, in order to foster a business environment conducive to investment and job creation.

The Government's tax reform package of 26 April 2001, Better Business Taxes: Lower, Fewer, Simpler, announced tax cuts totalling $774 million over four years, through reducing the burden of payroll tax, cuts to the number of state business taxes, and reducing paperwork and red tape.

As a result of the Government's strong financial position, further business tax cuts worth $262 million to 2005-06 were announced as part of the Building Tomorrow's Businesses Today statement, released on 22 April 2002. The reforms announced in these packages result in tax cuts of over $1.0 billion, and have further ensured a competitive tax regime for Victorian businesses that provides an environment which promotes jobs and growth in Victoria.

Under the Government's Better Business Taxes package, stamp duty on mortgages will be abolished from 1 July 2004. Further, the Government's last instalment of payroll tax initiatives announced in Building Tomorrow's Businesses Today will take effect on 1 July 2003 when the payroll tax rate is scheduled to be reduced from 5.35 per cent to 5.25 per cent. From 1 January 2003 the Government will provide payroll tax exemptions to employers for voluntary maternity leave payments.

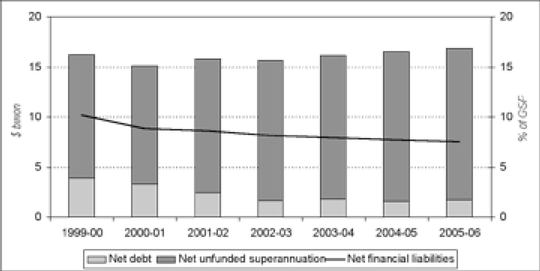

Net financial liabilities

The Government is committed to maintaining the State's net financial liabilities at prudent levels in order to achieve its short-term objective of maintaining Victoria's triple-A credit rating.

Victoria's triple-A long-term local currency debt rating was affirmed by Standard & Poor's on 7 October 2002 and by Moody's on 29 October 2002. Both rating agencies cited Victoria's low debt levels, strong fiscal position and strong financial performance in recent years as key reasons behind their affirmations. Moody's also upgraded the State's foreign currency rating to triple-A, to reflect the raising of Australia's foreign currency country ceiling.

The 2002-03 revised budget outlook reinforces these positive factors as:

- •

- substantial operating surpluses are projected for 2002-03 ($594 million) and the remainder of the forward estimates period ($505 million per annum on average);

- •

- general government net financial liabilities (excluding the Growing Victoria infrastructure reserve) were 10.9 per cent of GSP ($16.3 billion) at 30 June 1999. As a proportion of GSP, net financial liabilities are expected to fall from 8.6 per cent at 30 June 2002 to 7.5 per cent at 30 June 2006 (see Chart 1.3). In nominal terms, they are projected to rise from $15.8 billion to $16.9 billion over this period, where the increase reflects growth in the unfunded superannuation liability resulting from the increasing present value of members' accrued benefit entitlements;

- •

- net debt (excluding the Growing Victoria infrastructure reserve), as a component of net financial liabilities, was $4.9 billion (3.3 per cent of GSP) at 30 June 1999. Net debt is forecast to fall from $2.4 billion (1.3 per cent of GSP) at 30 June 2002 to a low $1.7 billion (0.8 per cent of GSP) by 30 June 2006; and

- •

- Victoria's net financial liabilities position (incorporating net debt) is expected to remain comparable with other triple-A jurisdictions.

Chart 1.3: General government net financial liabilities excluding Growing Victoria(a) (b)

Source: Department of Treasury and Finance

Note:

- (a)

- General government net financial liabilities are calculated as the sum of net debt and net unfunded superannuation liabilities.

- (b)

- Net debt is calculated as gross debt less liquid financial assets. Growing Victoria investments are excluded as an offset to gross debt on grounds that these investments are earmarked for infrastructure projects and are therefore not available to redeem gross debt.

CHAPTER 2: BUDGET POSITION AND OUTLOOK

- •

- The 2002-03 operating surplus is projected to be $594 million, an increase of $72 million from the result projected in the 2002-03 Budget. This movement mainly reflects higher than projected taxation and other revenue, partly offset by an increase in superannuation expense.

- •

- Over the remainder of the forward estimates period the operating surplus is projected to average $505 million per annum.

- •

- It is projected that election commitments published in Labor's Financial Statement 2002 will total approximately $140 million in 2003-04, $240 million in 2004-05 and $290 million in 2005-06.

- •

- Changes since the publication of the Pre-Election Budget Update have increased the projected 2002-03 operating surplus by $52 million. Over the remainder of the forward estimates period there is a projected increase in the operating surplus of approximately $27 million per annum on average.

- •

- Net debt (excluding the Growing Victoria infrastructure reserve) is projected to decline from $2.4 billion (1.3 per cent of gross state product (GSP)) at 30 June 2002 to $1.7 billion (0.8 per cent of GSP) at 30 June 2006.

- •

- Net financial liabilities (excluding the Growing Victoria infrastructure reserve) is projected to increase from $15.8 billion (8.6 per cent of GSP) at 30 June 2002 to $16.9 billion (7.5 per cent of GSP) at 30 June 2006.

This chapter provides an overview of the projected budget position for the period 2002-03 to 2005-06. It is important to note that the general government sector financial statements as presented in this section do not take into account the Government's 2002 election commitments that are yet to be implemented. The cost of funding output initiative election commitments is estimated to total approximately $140 million in 2003-04, $240 million in 2004-05 and $290 million in 2005-06. The cost of funding capital investment commitments is estimated to total approximately $2.0 billion. These costings are published in Labor's Financial Statement 2002. When formally approved by the Government, the impact of these election commitments will be incorporated in the budget estimates.

The projections, or forward estimates, are based on the economic projections outlined in Chapter 3, Economic Conditions and Outlook and reflect the accounting policies and assumptions documented in Chapter 4, Estimated Financial Statements and Notes. The estimates take into account the financial impacts of all policy decisions taken by the Government, Commonwealth Government funding revisions and data available regarding other factors affecting the projected general government sector financial statements as at 31 December 2002. Specific policy decisions taken since the 2002-03 Budget that have an effect on the budget position are summarised in Appendix A, Specific Policy Initiatives Affecting the Budget Position.

The forward estimates represent planning projections based on maintaining these policy and other assumptions unchanged through the forecast period. Outcomes will differ from these projections for many reasons, including realisation of the risks described in Chapter 5, Statement of Risks.

FORWARD ESTIMATES OUTLOOK 2002-03 TO 2005-06

Table 2.1 sets out the projected aggregate budget outlook over the forward estimates period 2002-03 to 2005-06. A more detailed statement of financial performance for the forward estimates period is provided in Chapter 4, Estimated Financial Statements and Notes.

Table 2.1 shows an operating surplus of $594 million is projected for 2002-03. The operating surplus is then projected to decline to $317 million in 2003-04, mainly reflecting a projected decline in revenue, before increasing to $684 million in 2005-06.

Table 2.1: Summary statement of financial performance 2002-03 to 2005-06

| | 2002-03 Budget | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||||

| Taxation | 8 802.7 | 9 213.5 | 9 123.5 | 9 375.3 | 9 564.2 | |||||

| Investment income | 1 061.6 | 1 164.4 | 946.6 | 996.9 | 1 158.3 | |||||

| Grants | 11 753.5 | 11 794.0 | 11 965.0 | 12 464.3 | 13 027.1 | |||||

| Sales of goods and services | 2 049.9 | 2 086.6 | 2 084.0 | 2 115.3 | 2 148.8 | |||||

| Other revenue(a) | 1 614.0 | 1 775.5 | 1 718.5 | 1 797.0 | 1 742.5 | |||||

| Total revenue | 25 281.7 | 26 034.0 | 25 837.7 | 26 748.9 | 27 641.0 | |||||

| % change | -0.8 | 3.5 | 3.3 | |||||||

| Superannuation | 1 713.1 | 2 368.4 | 1 819.3 | 1 856.4 | 1 910.4 | |||||

| Depreciation | 952.2 | 959.2 | 1 008.5 | 1 072.5 | 1 120.6 | |||||

| Borrowing costs | 495.2 | 493.4 | 485.9 | 477.6 | 469.0 | |||||

| Employee benefits | 9 041.5 | 9 275.5 | 9 566.4 | 9 875.8 | 10 215.6 | |||||

| Supplies and services | 8 299.9 | 7 887.2 | 8 451.1 | 8 708.8 | 8 978.8 | |||||

| Other expenses(b) | 4 258.1 | 4 456.4 | 4 189.9 | 4 242.4 | 4 262.5 | |||||

| Total expenses | 24 760.0 | 25 440.1 | 25 521.1 | 26 233.5 | 26 956.8 | |||||

| % change | 0.3 | 2.8 | 2.8 | |||||||

| Operating surplus | 521.8 | 593.9 | 316.6 | 515.4 | 684.1 | |||||

Source: Department of Treasury and Finance

Notes:

- (a)

- Comprises regulatory fees and fines, fair value of assets received free of charge, gains/losses on disposal of physical assets, capital asset charge revenue and other miscellaneous revenue.

- (b)

- Includes grants and transfer payments and amortisation expense.

Operating revenue

Total revenue is projected to be $26 034 million in 2002-03. Based on the 2002-03 Budget projections this represents an increase of $752 million, due largely to stronger than projected taxation revenue.

Over the remainder of the forward estimates period, total revenue is projected to decline by around 0.8 per cent or $196 million in 2003-04, before growing again at approximately 3.4 per cent per annum on average.

In 2003-04 it is expected taxation revenue will decline by 1.0 per cent. However, it is projected that taxation revenue will grow by 2.4 per cent per annum on average over the remainder of the forward estimates period. The decline in 2003-04 and low average growth rate reflect the combined impact of a number of factors, including:

- •

- an expected decline in property market activity, resulting in a reduction in property market related stamp duties collected;

- •

- implementation of tax cuts announced by the Government, including the reduction in the payroll tax rate from 5.35 per cent to 5.25 per cent in 2003-04 and abolition of stamp duty on mortgages from 2004-05; and

- •

- the expected abolition of bank accounts debits tax from 2005-06, consistent with the Intergovernmental Agreement on the Reform of Commonwealth-State Financial Relations.

Investment income also reduces in 2003-04, with a projected decline of 18.7 per cent or $217 million. Over the remaining forecast period growth of 10.6 per cent per annum on average is projected. Factors contributing to this pattern include:

- •

- the impact of a one-off increased dividend in 2002-03 from the gas sector as a result of the delayed introduction of full retail contestability in gas markets;

- •

- the completion in 2002-03 of the payment of a series of special dividends by the Transport Accident Commission to fund the Accident Blackspot Program; and

- •

- increased dividends in 2002-03 from the metropolitan water sector, mainly reflecting additional dividends from certain water companies to reinforce the commercial focus of the businesses and ensure appropriate financial ratios are maintained.

Revenue from Commonwealth grants is projected to increase on average by 3.4 per cent per annum with growth boosted by an expected increase in Commonwealth Budget Balancing Assistance payments following the abolition of debits tax from 2005-06.

Sales of goods and services revenue is projected to increase by approximately 1.0 per cent per annum on average or $62 million over the forward estimates period, in line with the projections in the 2002-03 Budget.

Operating expenses

Total expenses are projected to be $25 440 million in 2002-03, representing an increase of $680 million or 2.8 per cent on projected expenses in the 2002-03 Budget. The projected increase is due largely to an increase in superannuation expense, reflecting the impact of weak equity market performance early in the financial year.

In 2003-04 total expenses are projected to increase by only 0.3 per cent, reflecting the offset between a 2.7 per cent increase in all other expense categories and a projected 23.2 per cent decline in superannuation expense. Total expenses are then projected to increase by 2.8 per cent per annum on average over the remaining forecast period.

The projected decline in superannuation expense in 2003-04 reflects the one-off impact of poor equity market performance on superannuation expense in 2002-03. Between 2003-04 and 2005-06 growth in superannuation expense is projected to average 2.5 per cent per annum.

In line with the significant level of new capital investment in infrastructure, depreciation expense is projected to increase on average by 5.3 per cent per annum.

The increase in depreciation expense is partly offset by the decline in borrowing costs. Over the forward estimates period borrowing costs are projected to decline by 1.7 per cent per annum on average. The decline largely reflects the impact of lower interest rates on the debt portfolio as it matures and is refinanced.

The projected increase in employee benefits of 3.3 per cent per annum on average, over the forward estimates period, reflects a number of wage increases and the implementation of output initiatives announced by the Government up to and since the 2002-03 Budget.

RECONCILIATION OF FORWARD ESTIMATES TO PREVIOUSLY PUBLISHED ESTIMATES

Table 2.2 compares the revised outlook for the operating surplus for the period 2002-03 to 2005-06 to the estimates published in the 2002-03 Budget.

Table 2.2: Reconciliation of estimates to 2002-03 Budget

| | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | ||||

|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||

| General government sector operating surplus — 2002-03 Budget | 521.8 | 580.0 | 517.3 | 711.9 | ||||

| Plus: Revenue variations since 2002-03 Budget | ||||||||

| Economic/demographic effects | ||||||||

| Taxation revenue | 401.8 | 177.6 | 248.4 | 257.5 | ||||

| Investment income | 102.8 | -45.3 | -20.8 | 101.5 | ||||

| Other economic/demographic effects | 35.0 | — | — | — | ||||

| Total economic/demographic variations | 539.7 | 132.3 | 227.6 | 358.9 | ||||

| Policy decisions | ||||||||

| Taxation initiatives | -0.4 | -1.0 | -1.1 | -1.1 | ||||

| Other initiatives affecting revenue | 9.4 | 21.3 | 31.3 | 33.5 | ||||

| Total policy variations | 9.0 | 20.3 | 30.2 | 32.4 | ||||

| Commonwealth funding revisions | ||||||||

| General purpose grants | 9.0 | -89.8 | -15.6 | -3.4 | ||||

| Specific purpose payments | 31.6 | -17.5 | 17.4 | -40.4 | ||||

| Total Commonwealth funding variations | 40.5 | -107.3 | 1.8 | -43.8 | ||||

| Total administrative variations (a) | 163.2 | 103.7 | 110.9 | 120.9 | ||||

| Total variation in operating revenue since 2002-03 Budget | 752.3 | 149.0 | 370.5 | 468.4 | ||||

| | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | ||||

|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||

| Less: Operating expenses variations since 2002-03 Budget | ||||||||

| Economic/demographic effects | ||||||||

| Superannuation revisions | 655.3 | 94.0 | 90.5 | 106.1 | ||||

| Total economic/demographic variations | 655.3 | 94.0 | 90.5 | 106.1 | ||||

| Policy decisions | ||||||||

| Output policy decisions (d) | 180.6 | 219.2 | 141.5 | 121.0 | ||||

| Total policy variations | 180.6 | 219.2 | 141.5 | 121.0 | ||||

| Commonwealth funding revisions | 24.6 | -1.2 | 7.3 | 4.3 | ||||

| Administrative variations | ||||||||

| Wage growth contingency variations | 95.8 | 102.0 | 130.6 | |||||

| Expenditure reclassification (b) | -115.2 | 28.9 | -17.6 | -22.4 | ||||

| Other administrative variations (c) | -65.1 | -24.2 | 48.7 | 156.6 | ||||

| Total administrative variations | - 180.3 | 100.5 | 133.1 | 264.8 | ||||

| Total variation in operating expenses since 2002-03 Budget | 680.2 | 412.4 | 372.4 | 496.3 | ||||

| General government sector operating surplus — 2002-03 Budget Update | 593.9 | 316.6 | 515.4 | 684.1 | ||||

Source: Department of Treasury and Finance

Notes:

- (a)

- Includes revenue impacts flowing from finalisation of Partnerships Victoria contracts and revised forecasts of commercial revenue of outer budget sector agencies.

- (b)

- Made up of transfers and accounting reclassifications of expenditure between operating and capital expenditure.

- (c)

- Includes variations in operating expenses attributable to output delivery timing changes and changes in activity funded from third party revenue sources net of Treasurer's contingency funding in 2002-03 for output decisions.

- (d)

- Output policy decisions reflect the total cost of decisions. The total expenditure for each year may differ to Appendix A, Specific Policy Initiatives Affecting the Budget Position for certain initiatives due to savings and/or revenue being netted off against expenditure.

Operating revenue

In 2002-03 total revenue is $752 million higher than the 2002-03 Budget estimates and is projected to be $329 million per annum higher on average over the remainder of the forward estimates period.

Taxation revenue is projected to be $271 million per annum on average higher than estimates in the 2002-03 Budget. Increases in taxation revenue are largely the result of stronger than expected property market sales and prices, resulting in higher revenue from land tax and conveyancing and mortgage stamp duties. Offsetting these increases were reductions in gambling tax estimates of $99 million in 2002-03, $52 million in 2003-04 and averaging $5 million over the remaining two years of the forward estimates period, as a result of the recently imposed smoking restrictions in gambling venues.

Investment income also has a significant impact on 2002-03 total revenue estimates, with a projected $103 million increase in investment income above the 2002-03 Budget. This movement is largely the result of additional dividend receipts from the metropolitan water sector and from the gas sector. However, partly offsetting this increase is a reduction in projected distributions from the Transport Accident Commission, reflecting reduced investment returns (averaging $64 million per annum between 2002-03 to 2004-05).

Other economic/demographic effects also reflect stronger than expected property market sales and prices with higher than projected revenue from the Land Titles Office in 2002-03 of $35 million.

Across the forward estimates period policy decisions account for approximately $1 million per annum reduction in projected taxation revenue since the 2002-03 Budget. This reduction reflects the Government's new policy of payroll tax exemption for paid maternity leave.

Other initiatives affecting revenue include revenue from property sales associated with the Flinders Street overpass project. Over the forward estimates period starting in 2003-04 these initiatives increase total revenue by $29 million per annum on average.

Commonwealth general purpose grants and specific purpose payments have been revised as a result of revisions to population growth assumptions. These population revisions arise from the 2001 Census and the incorporation of final 2002-03 Commonwealth Budget specific purpose payment projections, which includes grants for Roads of National Importance.

Administrative revenue variations are $125 million per annum on average over the forward estimates period above the 2002-03 Budget. These projections mainly reflect revisions to commercial and miscellaneous revenue.

Included in the operating revenue movements are changes since the release of the Pre-Election Budget Update on 15 November 2002. Since that date operating revenue for 2002-03 is projected to increase by approximately $95 million as a result of continued strength in the property market and revisions to Commonwealth Government general purpose grants. However, these grant revisions also result in a projected decline in operating revenue in 2003-04 by approximately $58 million. Over the remaining two years operating revenue is projected to increase by approximately $26 million per annum on average above Pre-Election Budget Update estimates.

Operating expenses

As reflected in Table 2.2 operating expenses are projected to be $680 million higher in 2002-03 and $427 million per annum on average over the remainder of the forward estimates higher than the 2002-03 Budget.

The movement in superannuation expense reflects the impact of poor equity market performance on superannuation funds in 2002-03. Over the remainder of the forward estimates period superannuation expense is projected to exceed the budget estimates by $97 million per annum on average. Equity market performance has a significant impact on the value of financial assets held by state superannuation funds and therefore on the State's unfunded superannuation liability and superannuation expense. The increase in superannuation expense in 2002-03 also reflects the effect of revised CPI projections on indexed superannuation benefits.

Since the 2002-03 Budget output policy decisions account for additional operating expenses of $181 million in 2002-03 (with the impact on operating expenses in this year offset by forward estimates contingency funding) and $161 million per annum on average between 2003-04 and 2005-06. These policy decisions include funding for the Melbourne Cricket Ground redevelopment, farm business support grants, the Government's Innovation Statement, the Metropolitan Fire and Emergency Services Board and Country Fire Authority enterprise bargaining agreement, franchise interim operating agreements for trains and trams, and additional funding provided for the Disabilities and Impairments program in government schools. Specific policy decisions since the 2002-03 Budget are summarised in Appendix A, Specific Policy Initiatives Affecting the Budget Position.

Changes to Commonwealth grants funding, in particular specific purpose payments in relation to the National Health Development Fund and Roads of National Importance, also impact on the Government's operating expenses. In 2002-03 these revisions are projected to increase operating expenses by approximately $25 million and approximately $4 million per annum on average over the remainder of the forward estimates period.

There are a number of industrial agreements under negotiation and the wage growth contingency variations reflect the projected outcomes of these negotiations.

Expenditure reclassifications are changes in the treatment of certain transactions (as more information becomes available) to better reflect accounting policies. The changes over the forward estimates period largely reflect the change in accounting policies for roads funding in reclassifying operating expenditure to capital expenditure.

There are a number of other administrative variations to operating expenses that are offset within existing contingency funding. In 2002-03 these variations are approximately $180 million and over the remainder of the forwards estimates period are $166 million per annum on average. Other administrative variations include:

- •

- increased hospital expenses funded by higher third party revenue sources ($70 million per annum); and

- •

- the impact of the finalisation of contracts for a number of major infrastructure projects, including conversion of expenditure associated with the Spencer Street Station project to reflect delivery under the Partnerships Victoria model.

The operating expenses also include adjustments since the release of the Pre-Election Budget Update on 15 November 2002. Since that date operating expenses are projected to increase by approximately $43 million in 2002-03, largely as a result of additional payments under the First Home Owners Grant program (matched by additional revenue received from the Commonwealth general purpose grants). Over the remainder of the forward estimates period total operating expenses are projected to decline by approximately $29 million per annum on average based on Pre-Election Budget Update estimates.

SUMMARY STATEMENT OF FINANCIAL POSITION

Table 2.3 provides a summary of the general government sector statement of financial position. A more detailed statement of financial position is provided in Chapter 4, Estimated Financial Statements and Notes.

Table 2.3: General government summary statement of financial position as at 30 June

| | 2002 Actual | 2003 Revised | 2004 Estimate | 2005 Estimate | 2006 Estimate | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||||

| Current assets | 4 126.4 | 4 260.1 | 4 415.2 | 4 539.3 | 4 664.9 | |||||

| Non-current assets | 42 376.9 | 44 031.4 | 45 040.5 | 46 863.9 | 49 135.9 | |||||

| Total assets | 46 503.3 | 48 291.5 | 49 455.7 | 51 403.1 | 53 800.7 | |||||

Current liabilities | 3 817.9 | 4 421.5 | 4 177.1 | 3 989.3 | 4 417.1 | |||||

| Non-current liabilities | 20 840.7 | 20 992.3 | 21 742.8 | 22 695.8 | 23 152.5 | |||||

| Total liabilities | 24 658.6 | 25 413.8 | 25 919.9 | 26 685.1 | 27 569.6 | |||||

Net assets | 21 844.7 | 22 877.7 | 23 535.8 | 24 718.1 | 26 231.1 | |||||

Source: Department of Treasury and Finance

General government sector assets were $46.5 billion as at 30 June 2002 and are projected to be $53.8 billion in 30 June 2006, representing a projected growth of 15.7 per cent over the forward estimates period. This trend reflects the significant levels of capital investment expenditure by the Government over the forward estimates period in public infrastructure including roads, health, education and housing.

Table 2.4 shows general government net financial liabilities (excluding the Growing Victoria infrastructure reserve) are projected to increase over the forward estimates period from $15.8 billion as at 30 June 2002 to $16.9 billion as at 30 June 2006. This growth largely reflects the increase in the unfunded superannuation liability. However, as a proportion of GSP, net financial liabilities are projected to decline from 8.6 per cent as at 30 June 2002 to 7.5 per cent of GSP by 30 June 2006.

Table 2.4: General government net financial liabilities as at 30 June

| | 2002 Actual | 2003 Revised | 2004 Estimate | 2005 Estimate | 2006 Estimate | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||||

| Financial assets | ||||||||||

| Cash and deposits | 1 667 | 1 726 | 1 747 | 1 760 | 1 774 | |||||

| Advances paid | 237 | 237 | 171 | 124 | 81 | |||||

| Investments, loans and placements | 2 450 | 3 143 | 3 061 | 3 287 | 3 619 | |||||

| Growing Victoria | 1 363 | 715 | 61 | 5 | — | |||||

| Total | 5 717 | 5 821 | 5 040 | 5 176 | 5 475 | |||||

Financial liabilities | ||||||||||

| Deposits held | 434 | 434 | 434 | 434 | 434 | |||||

| Advances received | 2 | 2 | 1 | 1 | 1 | |||||

| Borrowings | 6 350 | 6 350 | 6 345 | 6 349 | 6 787 | |||||

| Total | 6 786 | 6 785 | 6 780 | 6 784 | 7 222 | |||||

Net debt | 1 069 | 965 | 1 739 | 1 608 | 1 747 | |||||

| Net debt (excl. Growing Victoria)(a) | 2 432 | 1 679 | 1 801 | 1 613 | 1 747 | |||||

Unfunded superannuation | 13 383 | 13 996 | 14 321 | 14 888 | 15 128 | |||||

Net financial liabilities | 14 452 | 14 961 | 16 060 | 16 496 | 16 876 | |||||

| Net financial liabilities (excl. Growing Victoria)(a) | 15 815 | 15 676 | 16 122 | 16 501 | 16 876 | |||||

Net financial liabilities to GSP (excl. Growing Victoria)—%(a) | 8.6 | 8.1 | 7.9 | 7.7 | 7.5 | |||||

| Net debt to GSP (excl. Growing Victoria) | 1.3 | 0.9 | 0.9 | 0.8 | 0.8 | |||||

Source: Department of Treasury and Finance

Note:

- (a)

- The Growing Victoria infrastructure reserve investments are not offset against gross debt on the grounds that these investments are earmarked for infrastructure projects and are therefore not available to redeem gross debt.

Consistent with this reduction in net financial liabilities as a proportion of GSP, over the forward estimates period is the reduction in net debt (excluding the Growing Victoria infrastructure reserve) over the same period. Net debt is projected to fall from 1.3 per cent of GSP as at 30 June 2002 to 0.8 per cent of GSP by 30 June 2006 (also refer to Table 2.5). The increase in net debt projected in 2005-06 reflects the statement of financial position impact flowing from the completion and handover to the State of the Partnerships Victoria Spencer Street Station project. The increase in net debt is matched by an increase in the State's non-current assets (Table 2.3).

OTHER BUDGET INDICATORS

The financial projections presented in Chapter 4, Estimated Financial Statements and Notes and summarised in Tables 2.1 and 2.3 are based on generally accepted accounting principles, in particular AAS31 "Financial Reporting by Governments'. An alternative method of presentation is the Government Finance Statistics (GFS) system employed by the Australian Bureau of Statistics. All jurisdictions are required to present information on this basis in budget papers, consistent with the Uniform Presentation Format agreement. Key GFS measures are shown in Table 2.5.

Table 2.5: GFS budget measures (excluding the Growing Victoria infrastructure reserve)

| | 2002-03 Budget | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||||

| Net operating balance (GFS) | 488.7 | 1 218.8 | 298.1 | 485.2 | 664.6 | |||||

| GFS net lending(a) | 162.6 | 935.7 | -150.6 | -415.5 | -109.9 | |||||

| GFS cash surplus(a) | 304.5 | 1 051.4 | 305.0 | 321.0 | 302.9 | |||||

Source: Department of Treasury and Finance

Note:

- (a)

- The table shows GFS net lending (+) / borrowing (-) and GFS cash surplus (+) / deficit (-) excluding drawdowns against the Growing Victoria infrastructure reserve. Growing Victoria infrastructure reserve investments (detailed in Table 2.4) are not offset against gross debt on the grounds that these investments are earmarked for infrastructure projects and are therefore not available to redeem gross debt.

USE OF CASH RESOURCES

Table 2.6 provides a summary of the application of cash resources for asset investment and the increase/decrease in net debt. Significant surpluses from operating activities, together with drawdown from the Growing Victoria infrastructure reserve, will be predominately applied to fund infrastructure investment.

Table: 2.6 Application of cash resources

| | 2002-03 Budget | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| | ($ million) | |||||||||

| Operating surplus | 521.8 | 593.9 | 316.6 | 515.4 | 684.1 | |||||

| Plus: Non-cash expenses (net)(a) | 1 074.7 | 1 717.6 | 1 457.8 | 1 790.2 | 1 534.3 | |||||

| Net cash flow from operating activities | 1 596.5 | 2 311.5 | 1 774.4 | 2 305.5 | 2 218.4 | |||||

Plus: Net drawdown of Growing Victoria infrastructure reserve | 570.0 | 648.3 | 653.2 | 56.9 | 4.5 | |||||

| Total cash available for asset investment | 2 166.5 | 2 959.8 | 2 427.6 | 2 362.4 | 2 222.9 | |||||

| Less: | ||||||||||

| Net investment in fixed assets(b) | 2 066.1 | 2 189.1 | 2 537.4 | 2 163.8 | 1 911.8 | |||||

| Other investment activities (net) | 13.5 | 17.6 | 11.8 | 10.9 | 445.7 | |||||

| Decrease/-increase in net debt (excluding Growing Victoria) | 87.0 | 753.1 | -121.6 | 187.8 | -134.5 | |||||

Source: Department of Treasury and Finance

Notes:

- (a)

- Includes depreciation and increases in the unfunded superannuation liability and liability for employee benefits.

- (b)

- Includes net contribution to other sectors of government.

CHAPTER 3: ECONOMIC CONDITIONS AND OUTLOOK

- •

- The global economic recovery has been more muted than expected at budget time.

- •

- Although housing and business investment show continued strength, growth in Victoria has moderated in response to the drought, the impact of international conditions on exports and a moderation in consumer spending.

- •

- Victorian economic growth is expected to be 3.25 per cent in 2002-03, rising to 3.75 per cent in 2003-04 as the economy emerges from the drought. Most other 2002-03 Budget forecasts remain unchanged.

- •

- Downside risks to the economic outlook include the overseas outlook, the failure of autumn rains, and a slowing of population growth. Upside risks include an unexpectedly strong construction sector.

THE ECONOMY SINCE THE BUDGET

World economic conditions

Since budget time, concerns have emerged about the pace of the global recovery, leading to a more moderate international outlook. According to the December 2002 Consensus Economics survey, world growth is expected to increase from 1.7 per cent in 2002 to 2.3 per cent in 2003, well down from the 3.0 per cent expected at budget time, largely reflecting a less optimistic outlook for the United States and Europe.

The US economic recovery appears to be slowing, with business investment remaining soft and signs of labour market weakness. Sentiment has been adversely affected by the ongoing stock market correction and uncertainty about developments in the Middle East, although there are more recent signs of a rebound in confidence. Tax cuts, increased defence spending and the large reduction in US interest rates in November should provide some support to activity. Economic conditions have worsened markedly in the large European economies, especially Germany, prompting the recent interest rate cut by the European Central Bank.

Despite a return to growth in the September quarter, Japanese economic conditions remain vulnerable. Unemployment remains historically high, consumer prices continue to decline and the outlook for industrial production is weakening.

Although growth prospects have weakened in the rest of East Asia, conditions remain relatively robust, particularly in China. While the aftermath of the Bali bombing is likely to damage the tourism industry, the impact may be confined largely to Indonesia.

Australia and Victoria

The Victorian economy grew by 4.9 per cent in 2001-02, above the budget estimate of 3.75 per cent, and more strongly than the national economy (3.9 per cent). Victorian gross state product (GSP) per head is now the second highest of the States, behind only Western Australia.

However, there were signs of moderation in the September quarter. National growth is being constrained by weaker global economic conditions, compounded by the drought. In Victoria, the September quarter saw a decline in international merchandise export volumes and weakness in consumer spending. The main impetus to growth came from business investment and dwelling construction.

The latest Australian Bureau of Agricultural and Resource Economics (ABARE) forecasts predict that Victorian winter crop production for 2002-03 will decline by 70 per cent, implying a more severe impact than nationally (down 56 per cent). However, because crop production represents a smaller share of agriculture in Victoria than in most other States, the overall impact of the drought is likely to be relatively smaller than nationally. Nevertheless, there are still likely to be significant adverse effects on Victorian livestock production, dairying, wool production and other agricultural activities. A complete recovery from the drought may take several seasons in the case of livestock industries. The value of Victorian dairy exports declined in the September quarter, due to price, rather than volume effects.

Victorian consumer spending grew by a relatively low 0.2 per cent in the September quarter and retail trade remained weak in the early part of the December quarter. Much of this weakness appears to reflect the unwinding of a surge in household goods and related purchases during the housing construction boom and weakness in hospitality and services, which may be associated with the introduction of the smoking ban at Victorian gaming venues.

Boom conditions in the residential construction sector have persisted for longer than anticipated at budget time. In addition, business investment has grown more strongly than expected, reaching levels 16.8 per cent higher than a year earlier in trend terms (abstracting from major asset sales) in the September quarter. Non-residential building has been particularly strong since budget time.

The improvement in labour market conditions, which began in early 2002, has continued. Victorian employment grew by 1.1 per cent in 2001-02, in line with the budget estimate (1.25 per cent). During the six months ending November 2002, the trend measure of Victorian employment has grown at an annualised rate of 1.6 per cent, broadly in line with expectations at budget time. Full-time employment has been trending up and the Victorian unemployment rate has now been below 6 per cent for three consecutive months.

Migration from interstate has continued, although the net gains in June quarter 2002 were relatively modest. During 2001-02, Victoria gained over 6 200 migrants from interstate and Victoria's population grew by 1.3 per cent, compared with 1.1 per cent nationally.

ECONOMIC OUTLOOK

Revised projections for the Victorian economy are presented in Table 3.1.

The Commonwealth, in its Mid-Year Economic and Fiscal Outlook, released in late November, revised down its forecast for national growth in 2002-03 from 3.75 per cent at budget time to 3.0 per cent. This largely reflected the impact of the drought. The December Consensus Economics survey implies an average private sector forecast of 3.2 per cent.

The latest El Niño assessment by the Bureau of Meteorology indicates a likely return to "neutral" weather patterns by around autumn 2003. The Commonwealth has revised its forecast for national growth in 2003-04 upward from 3.5 per cent to 4.0 per cent to reflect the expected recovery in farm production and exports. The implied Consensus forecast currently is 3.5 per cent.

The forecast for GSP growth in 2002-03 has been revised down slightly to 3.25 per cent (3.50 per cent at the time of the 2002-03 Budget and the Pre-Election Budget Update). The contribution from state final demand growth has been revised upward because the unexpected strength of the housing sector and business investment is projected to outweigh the impact of more moderate growth in consumer spending. However, the drought and weaker international economy has led to a reduction in the forecast contribution to growth from net exports, and this more than outweighs the upward revision to forecast growth in state final demand.

For 2003-04, forecast Victorian GSP growth has been revised upward slightly to 3.75 per cent, capturing the expected effects of a sustained recovery in exports in line with the ending of the drought. With a smaller exposure to the drought than many other areas of Australia (notably New South Wales), the cyclical effects of the drought on the Victorian economy may be a little less pronounced.

During the course of 2003, the dwelling investment cycle is expected to finally turn down and business investment is anticipated to ease to more sustainable levels. This should moderate growth during the post-drought recovery.

Beyond 2003-04, Victorian GSP growth is projected to return to its long-run rate of 3.5 per cent per annum.

These forecasts differ slightly from those presented in the Pre-Election Budget Update in mid-November. Since then, ABARE released its first estimates of the impact of the drought on summer crops (cottonseed, sorghum and rice), and these are expected to decline by 59 per cent nationally. Although concentrated in New South Wales and Queensland, the large fall in summer crops is likely to have adverse indirect effects on incomes in other States, including Victoria.

There has been a slight upward revision to the population growth rate for 2002-03. In the forward years, population growth continues to be based on ABS Series R projections which assume net interstate migration gains of 2 000 persons per annum.

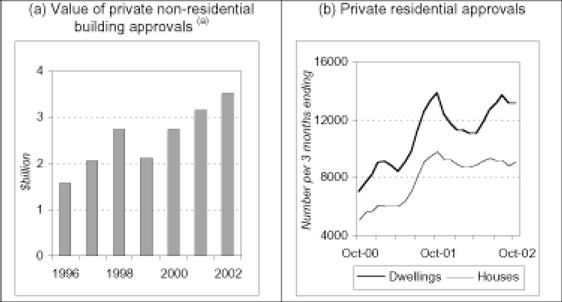

Otherwise, the economic forecasts for 2002-03 and beyond are unchanged since budget time. Forward indicators of the labour market, although softening in November, remain consistent with moderate jobs growth. Consumer and business sentiment continue to be generally positive. Forward indicators of overall Victorian construction sector activity remain strong (see Chart 3.1).

Chart 3.1: Victorian building construction forward indicators

Source: Australian Bureau of Statistics, Cat. No. 8731.0

Notes:

Table 3.1: Economic forecasts(a)

(Projections in 2002-03 Budget, where different, are in parentheses)

| | 2001-02 Actual | 2002-03 Forecast | 2003-04 Forecast | ||||

|---|---|---|---|---|---|---|---|

| Gross state product | 4.9 (3.75 | ) | 3.25 (3.50 | ) | 3.75 (3.50 | ) | |

| Employment | 1.1 (1.25 | ) | 1.50 | 1.50 | |||

| Unemployment rate (b) | 6.3 (6.25 | ) | 6.00 | 6.00 | |||

| Consumer price index | 2.8 (2.75 | ) | 2.75 (2.25 | ) | 2.25 | ||

| Wage cost index (c) | 3.5 (3.75 | ) | 3.50 | 3.50 | |||

| Population (d) | 1.3 (1.2 | ) | 1.1 (1.0 | ) | 1.0 |

Sources: Australian Bureau of Statistics; Department of Treasury and Finance

Notes:

- (a)

- Per cent change on preceding year unless otherwise indicated.

All projections, apart from population, are rounded to the nearest 0.25 percentage point. - (b)

- Year average level, per cent.

- (c)

- Total hourly rate, excluding bonuses.

- (d)

- June quarter, per cent change on previous June quarter, based on ABS Series R projections.

ECONOMIC RISKS

Major risks to the economic outlook, both upside and downside, include:

- •

- stronger than expected construction activity. Relevant forward indicators are yet to show much evidence of the anticipated slowdown in this sector;

- •

- continuing softness in the global economy, particularly in the United States. Recent weakness in US employment growth and high profile bankruptcies highlight the risk that the recovery may stall for a protracted period, with potentially adverse implications for Australian and Victorian exports;

- •

- a continuation of the drought into next season, which would hamper export production and exacerbate downward pressure on farm incomes with indirect effects on the rest of the economy;

- •

- US and allied military action against Iraq with possible implications for oil prices, confidence, growth, and trade relations; and

- •

- a slowing of population growth, currently assumed to be at least 1.0 per cent per annum. The gain from net interstate migration in the June quarter 2002 (231 persons) was the lowest for almost four years. High levels of Victorian (and New South Wales) housing prices may encourage population movement to locations with relatively cheaper accommodation. If Victoria's population growth rate moderates, as occurred during the 1980s, the economic growth rate projections could be affected. Major revisions to the historical data for the components of population growth following the most recent Census are scheduled for release by the ABS in March 2003.

These issues are discussed in more detail in Chapter 5, Statement of Risks.

CHAPTER 4: ESTIMATED FINANCIAL STATEMENTS AND NOTES

Introduction

The Estimated Financial Statements in this chapter have been prepared in accordance with the provisions in the Financial Management Act 1994. This Act requires the Estimated Financial Statements to be based on generally accepted accounting principles (GAAP) and to be consistent with the Financial Policy Objectives and Strategies Statement (see Chapter 1, Financial policy objectives and strategies).

The purpose of the Estimated Financial Statements is to set out the forecast financial results for the Victorian budget sector referred to in these statements as the general government sector. Because of the prospective nature of these statements they reflect a number of professional judgements about the most likely operating and financial conditions for the Victorian general government sector. International developments and other risks to the national economy, from which Victoria would not be immune, may cause the general government actual result to differ from the projected result.

The accompanying notes to the Estimated Financial Statements provide details of material economic and other assumptions used and the specific forecast assumptions underlying material items in the financial statements. A number of these assumptions are subject to inherent uncertainties, which are outside the control of the Government.

ESTIMATED FINANCIAL STATEMENTS FOR THE VICTORIAN GENERAL GOVERNMENT SECTOR

Table 4.1: Estimated statement of financial performance for the year ending 30 June

| | Note | 2002-03 Budget | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | ($ million) | ||||||||||

| Revenue from ordinary activities | ||||||||||||

| Taxation | 2 | 8 802.7 | 9 213.5 | 9 123.5 | 9 375.3 | 9 564.2 | ||||||

| Fines and regulatory fees | 554.0 | 555.5 | 551.3 | 577.1 | 586.8 | |||||||

| Investment revenue | 3 | 1 061.6 | 1 164.4 | 946.6 | 996.9 | 1 158.3 | ||||||

| Grants revenue | 4 | 11 753.5 | 11 794.0 | 11 965.0 | 12 464.3 | 13 027.1 | ||||||

| Sale of goods and services | 2 049.9 | 2 086.6 | 2 084.0 | 2 115.3 | 2 148.8 | |||||||

| Gains (losses) on the disposal of physical assets | 19.6 | 19.6 | 9.0 | 9.2 | 9.3 | |||||||

| Fair value of assets received free of charge | 1.1 | 1.1 | 1.1 | 8.7 | 1.2 | |||||||

| Inter sector capital asset charge | 501.0 | 501.0 | 514.0 | 514.0 | 514.0 | |||||||

| Other revenue | 538.3 | 698.3 | 643.0 | 688.1 | 631.3 | |||||||

| Total revenue | 25 281.7 | 26 034.0 | 25 837.7 | 26 748.9 | 27 641.0 | |||||||

| Expenses from ordinary activities | ||||||||||||

| Employee benefits | 9 041.5 | 9 275.5 | 9 566.4 | 9 875.8 | 10 215.6 | |||||||

| Superannuation | 1 713.1 | 2 368.4 | 1 819.3 | 1 856.4 | 1 910.4 | |||||||

| Depreciation | 5 | 952.2 | 959.2 | 1 008.5 | 1 072.5 | 1 120.6 | ||||||

| Amortisation | 6 | 70.6 | 70.6 | 67.7 | 65.3 | 65.4 | ||||||

| Borrowing costs | 7 | 495.2 | 493.4 | 485.9 | 477.6 | 469.0 | ||||||

| Grants and transfer payments | 8 | 4 118.9 | 4 317.2 | 4 052.6 | 4 105.2 | 4 128.2 | ||||||

| Supplies and services | 8 299.9 | 7 887.2 | 8 451.1 | 8 708.8 | 8 978.8 | |||||||

| Other expenses | 68.6 | 68.6 | 69.6 | 71.9 | 68.8 | |||||||

| Total expenses | 9 | 24 760.0 | 25 440.1 | 25 521.1 | 26 233.5 | 26 956.8 | ||||||

| Net result | 521.8 | 593.9 | 316.6 | 515.4 | 684.1 | |||||||

Movements in asset revaluation reserve | 737.8 | 737.8 | 768.6 | 800.6 | 833.8 | |||||||

| Total changes in equity other than contributions to other sectors by the State in its capacity as owner | 1 259.6 | 1 331.7 | 1 085.2 | 1 316.0 | 1 517.9 | |||||||

The accompanying notes form part of these Estimated Financial Statements.

Table 4.2: Estimated statement of financial position as at 30 June

| | Note | 2003 Revised | 2004 Estimate | 2005 Estimate | 2006 Estimate | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| | | ($ million) | ||||||||

| Current assets | ||||||||||

| Cash assets | 1 725.6 | 1 747.2 | 1 760.4 | 1 774.4 | ||||||

| Other financial assets | 1 177.9 | 1 197.3 | 1 225.3 | 1 253.2 | ||||||

| Receivables | 1 155.3 | 1 269.4 | 1 352.2 | 1 435.7 | ||||||

| Prepayments | 41.4 | 41.5 | 41.5 | 41.5 | ||||||

| Inventories | 159.8 | 159.9 | 159.9 | 160.0 | ||||||

| Other assets | 13 | 0.0 | 0.0 | 0.0 | 0.0 | |||||

| Total current assets | 4 260.1 | 4 415.2 | 4 539.3 | 4 664.9 | ||||||

| Non-current assets | ||||||||||

| Other financial assets | 2 701.9 | 1 946.6 | 2 087.7 | 2 387.8 | ||||||

| Receivables | 347.2 | 296.7 | 266.5 | 245.6 | ||||||

| Inventories | 155.6 | 155.6 | 155.6 | 155.6 | ||||||

| Property, plant and equipment | 10 | 24 529.1 | 25 752.8 | 26 927.8 | 28 395.5 | |||||

| Roads and earthworks | 11 | 13 232.2 | 13 805.9 | 14 337.6 | 14 859.3 | |||||

| Other assets | 13 | 3 065.3 | 3 082.8 | 3 088.7 | 3 092.0 | |||||

| Total non-current assets | 44 031.4 | 45 040.5 | 46 863.9 | 49 135.9 | ||||||

| Total assets | 48 291.5 | 49 455.7 | 51 403.1 | 53 800.7 | ||||||

| Current liabilities | ||||||||||

| Payables | 1 535.5 | 1 534.4 | 1 530.1 | 1 533.8 | ||||||

| Interest-bearing liabilities | 125.1 | 128.7 | 142.1 | 158.1 | ||||||

| Employee benefits | 14 | 873.5 | 920.1 | 950.9 | 981.5 | |||||

| Superannuation | 15 | 1 518.9 | 1 242.7 | 1 016.4 | 1 395.2 | |||||

| Outstanding insurance claims | 11.9 | 10.9 | 9.9 | 8.9 | ||||||

| Other liabilities | 356.7 | 340.3 | 339.9 | 339.7 | ||||||

| Total current liabilities | 4 421.5 | 4 177.1 | 3 989.3 | 4 417.1 | ||||||

| Non-current liabilities | ||||||||||

| Payables | 8.8 | 8.7 | 8.6 | 8.6 | ||||||

| Interest-bearing liabilities | 6 234.3 | 6 225.3 | 6 216.3 | 6 638.4 | ||||||

| Employee benefits | 14 | 1 872.5 | 2 041.1 | 2 221.1 | 2 405.5 | |||||

| Superannuation | 15 | 12 477.5 | 13 078.3 | 13 871.3 | 13 733.2 | |||||

| Outstanding insurance claims | 97.6 | 94.6 | 91.6 | 88.6 | ||||||

| Other liabilities | 301.6 | 294.7 | 287.0 | 278.2 | ||||||

| Total non-current liabilities | 20 992.3 | 21 742.8 | 22 695.8 | 23 152.5 | ||||||

| Total liabilities | 25 413.8 | 25 919.9 | 26 685.1 | 27 569.6 | ||||||

| Net assets | 22 877.7 | 23 535.8 | 24 718.1 | 26 231.1 | ||||||

| Equity | ||||||||||

| Retained earnings | 13 336.1 | 13 502.9 | 13 685.8 | 14 196.4 | ||||||

| Reserves | 8 947.7 | 9 716.3 | 10 516.9 | 11 350.6 | ||||||

| Net result for year | 593.9 | 316.6 | 515.4 | 684.1 | ||||||

| Total equity | 16 | 22 877.7 | 23 535.8 | 24 718.1 | 26 231.1 | |||||

The accompanying notes form part of these Estimated Financial Statements.

Table 4.3: Estimated statement of cash flows for the year ending 30 June

| | Note | 2002-03 Budget | 2002-03 Revised | 2003-04 Estimate | 2004-05 Estimate | 2005-06 Estimate | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | ($ million) | |||||||||||

| Cash flows from operating activities | |||||||||||||

| Receipts | |||||||||||||

| Taxation | 8 788.0 | 9 104.8 | 9 093.4 | 9 357.1 | 9 541.1 | ||||||||

| Fines and regulatory fees | 429.6 | 431.1 | 425.2 | 448.1 | 461.1 | ||||||||

| Grants | 11 752.0 | 11 792.5 | 11 965.0 | 12 464.4 | 13 027.2 | ||||||||

| Sale of goods and services | 2 052.0 | 2 112.5 | 2 079.5 | 2 112.4 | 2 146.1 | ||||||||

| Interest received | 338.1 | 314.8 | 338.9 | 325.6 | 343.1 | ||||||||

| Dividends received | 406.5 | 547.3 | 274.4 | 326.6 | 444.9 | ||||||||

| Capital asset charge received | 501.0 | 501.0 | 514.0 | 514.0 | 514.0 | ||||||||

| Other receipts | 842.4 | 1 064.2 | 926.4 | 998.7 | 964.5 | ||||||||

| Total receipts | 25 109.6 | 25 868.2 | 25 616.6 | 26 546.8 | 27 442.1 | ||||||||

| Payments | |||||||||||||

| Employee benefits | 8 844.4 | 9 075.7 | 9 351.2 | 9 665.1 | 10 000.5 | ||||||||

| Superannuation | 1 757.9 | 1 754.8 | 1 494.7 | 1 289.7 | 1 669.7 | ||||||||

| Grants and transfer payments | 4 117.2 | 4 315.5 | 4 050.9 | 4 103.4 | 4 126.4 | ||||||||

| Supplies and services(b) | 8 314.3 | 7 936.3 | 8 472.8 | 8 718.0 | 8 968.8 | ||||||||

| Interest paid | 479.3 | 474.3 | 472.6 | 465.1 | 458.3 | ||||||||

| Other payments | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | ||||||||

| Total payments | 23 513.1 | 23 556.7 | 23 842.3 | 24 241.3 | 25 223.6 | ||||||||

| Net cash flows from operating activities | 17 | 1 596.5 | 2 311.5 | 1 774.4 | 2 305.5 | 2 218.4 | |||||||

Cash flows from investing activities | |||||||||||||

| Net customer loans repaid | 1.8 | 0.1 | 65.9 | 47.0 | 43.0 | ||||||||

| Net disposal (purchase) of investments | 518.6 | (45.6 | ) | 735.8 | (169.1 | ) | (328.2 | ) | |||||

| (Net contribution to) other sectors of government | (218.0 | ) | (298.7 | ) | (427.1 | ) | (133.7 | ) | (4.8 | ) | |||

| Proceeds from sale of property, plant and equipment | 79.2 | 79.3 | 58.7 | 50.1 | 45.4 | ||||||||

| (Purchases of) property, plant and equipment | (1 927.3 | ) | (1 969.7 | ) | (2 169.0 | ) | (2 080.2 | ) | (1 952.4 | ) | |||

| Net cash flows from investing activities | (1 545.6 | ) | (2 234.6 | ) | (1 735.8 | ) | (2 285.8 | ) | (2 196.9 | ) | |||

Cash flows from financing activities | |||||||||||||

| Net drawdowns (repayments) of borrowings | (19.0 | ) | (19.0 | ) | (17.6 | ) | (5.8 | ) | (6.5 | ) | |||

| Net cash flows from financing activities | (19.0 | ) | (19.0 | ) | (17.6 | ) | (5.8 | ) | (6.5 | ) | |||

| Net increase in cash and deposits held | 31.9 | 57.9 | 21.0 | 13.9 | 15.1 | ||||||||

| Cash at beginning of reporting period | 1 663.2 | 1 663.2 | 1 721.1 | 1 742.1 | 1 756.0 | ||||||||

| Cash and deposits at end of reporting period | 1 695.1 | 1 721.1 | 1 742.1 | 1 756.0 | 1 771.0 | ||||||||

Notes:

- (a)

- Cash balances do not equal the Statement of Financial Position cash balances due to the inclusion of a bank overdraft facility.

- (b)

- Includes intragovernment purchase of services previously incorporated under other payments.

The accompanying notes form part of these Estimated Financial Statements.

NOTES TO THE ESTIMATED FINANCIAL STATEMENTS

Due to the possibility that circumstances or events outlined in the Estimated Financial Statements may not occur as expected, actual results may differ from those forecast and the difference may be material. Accordingly, no guarantee is given that the financial results will be achieved. However, the best professional judgement has been applied in preparing the Estimated Financial Statements.

Table of contents

| | | | ||

|---|---|---|---|---|

| Assumptions | ||||

| Note 1: | Statement of significant accounting policies and forecast assumptions | |||

| Note 2: | Taxation | |||

| Note 3: | Investment revenue | |||

| Note 4: | Grants revenue | |||

| Note 5: | Depreciation | |||

| Note 6: | Amortisation | |||

| Note 7: | Borrowing costs | |||

| Note 8: | Grants and transfer payments | |||

| Note 9: | Total expenses from ordinary activities by department | |||

| Note 10: | Property, plant and equipment | |||

| Note 11: | Roads and earthworks | |||

| Note 12: | Reconciliation of movements in fixed assets | |||

| Note 13: | Other assets | |||

| Note 14: | Employee benefits | |||

| Note 15: | Superannuation | |||

| Note 16: | Reconciliation of changes in equity | |||

| Note 17: | Cash flow information | |||

| Note 18: | General government sector entities | |||

The Estimated Financial Statements have been prepared using the material economic and other assumptions listed below.

Material economic and other assumptions(a)

| | 2002-03 | 2003-04 | 2004-05 | 2005-06 | ||||

|---|---|---|---|---|---|---|---|---|

| Gross state product | 3.25 | 3.75 | 3.50 | 3.50 | ||||

| Employment | 1.50 | 1.50 | 1.50 | 1.50 | ||||

| Consumer price index | 2.75 | 2.25 | 2.25 | 2.25 | ||||

| Wage cost index(b) | 3.50 | 3.50 | 3.50 | 3.50 | ||||

| Population(c) | 1.10 | 1.00 | 0.90 | 0.90 |

Source: Australian Bureau of Statistics, Department of Treasury and Finance

Notes:

- (a)

- Year-average per cent change on previous year unless otherwise indicated. All projections apart from population are rounded to the nearest 0.25 percentage point.

- (b)

- Total hourly rate excluding bonuses.

- (c)

- June quarter, per cent change on previous June quarter. Based on ABS Series R projections.

Note 1: Statement of significant accounting policies and forecast assumptions

In order to assist in understanding the financial information presented, the following summary presents the significant accounting policies and forecast assumptions which have been adopted in preparing and presenting the Estimated Financial Statements for the forecast period (which includes the budget year and the estimates for the three subsequent years).

A. Compliance framework

These Estimated Financial Statements have been prepared in accordance with sections 23H-23N of the Financial Management Act 1994 (the FMA) and are based on Australian GAAP. In accordance with the FMA, the information presented in the Estimated Financial Statements takes into account Government decisions and other circumstances that may have a material effect on the statements.

In accordance with Australian GAAP, all applicable pronouncements issued by the Australian Accounting Standards Board (AASB) and abstracts of the Urgent Issues Group have been applied in the preparation and presentation of the Estimated Financial Statements. However, as there is no specific AAS or other Australian authoritative pronouncements on the preparation and presentation of prospective financial statements, AAS 6 Accounting Policies permits the application of pronouncements of other national accounting standard setting bodies. Because Australian and New Zealand accounting standards are closely harmonised, the major requirements of New Zealand Financial Reporting Standard (FRS 29) Prospective Financial Information have been applied in presenting the Estimated Financial Statements. The requirements of FRS 29 have been modified to achieve presentation consistency with AASB 1018 Statement of Financial Performance, AAS 36 Statement of Financial Position and AAS 37 Financial Report Presentation and Disclosures.

Future reporting basis

The Financial Management Act 1994 requires the identification of the reporting basis on which subsequent government financial reports will be prepared.

Future Estimated Financial Statements are expected to be prepared on a consistent basis, except for any changes in reporting required by new or revised Australian Accounting Standards. The effect of the intended adoption in Australia of International Accounting Standards from 1 January 2005 is as yet uncertain, and no adjustment has been made for any consequent effect.

B. Basis of accounting and measurement

The accrual basis of accounting has been employed in the preparation of the Estimated Financial Statements whereby assets, liabilities, equity, revenues and expenses are recognised in the reporting period to which they were incurred, regardless of when cash is received or paid.

The opening balances of 1 July 2002 represent the actual audited values as at 30 June 2002 and are based on either a cost or fair value basis. Those items measured at valuation include:

- •

- non-current physical assets, other than plant and equipment, are measured at their fair value;

- •

- investments and productive trees in commercial native forests which are recognised at their net market value; and

- •

- certain liabilities (e.g. unfunded superannuation) which are calculated with regard to actuarial assessment.

The estimated impact of future revaluations of non-current physical assets is included in the forecasts at the total general government level.

Liabilities other than those actuarially determined do not include the impact of revaluations due to the inherent difficulties in identifying and forecasting these amounts.

C. Basis of consolidation

The Estimated Financial Statements include all reporting entities in the Victorian general government (budget) sector that are controlled by the Crown. Details of the entities included in the general government sector are shown in Note 18.

In the process of reporting the general government sector as a single economic entity, all material transactions and balances within the sector are eliminated.

D. Forecast reporting periods

The reporting period for the general government sector is the year ending 30 June. However, for those entities with a reporting period other than the year ending 30 June, the latest audited financial statements are used as the basis of the opening balance for 1 July 2002. For example, TAFE institutes have reporting periods ending 31 December.

E. Revenues

Taxation

Accounting policy

General government sector taxation and fee revenue is recognised upon the earlier of either the receipt by the State of a taxpayer's self-assessment or the time the taxpayer's obligation to pay arises, pursuant to the issue of an assessment.

The types of revenue included in the estimates are as follows:

- •

- payroll tax;

- •

- land tax;

- •

- stamp duties—including conveyancing, land transfers, and mortgages;

- •

- bank accounts debit tax;

- •

- gambling taxes—including private lotteries, electronic gaming machines, casino and racing;

- •

- insurance duty—compulsory third party, life and non-life; and

- •

- motor vehicle taxes—registration fees, stamp duty and driver licence fees.

Forecast assumption

The State's tax revenues are forecast by a process, which involves:

- •

- assessment of demand and supply conditions in the markets from which the taxes are sourced (e.g. in the case of payroll tax, assessment of employment and wages outlooks; in the case of motor vehicle fees, assessment of the outlook for demand for cars reflecting long-term underlying demand factors and cyclical demand factors);

- •

- analysis of historical information and relationships using econometric and other statistical methods;

- •

- application of the Department of Treasury and Finance's economic forecasts where there is a relationship between taxation variables and economic variables; and

- •

- consultation with private sector economists, industry associations, and relevant government authorities (e.g. State Revenue Office, Vic Roads, Office of Gambling Regulation).