As filed with the Securities and Exchange Commission on February 18, 2009.

| | Registration No. 333-________ |

| U.S. SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| |

| FORM N-14 |

| |

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X] |

| |

| [ ] Pre-Effective Amendment No. |

| [ ] Post-Effective Amendment No. |

| |

| PRINCIPAL FUNDS, INC. |

| f/k/a Principal Investors Fund, Inc. |

| (Exact name of Registrant as specified in charter) |

| |

| 680 8th Street, Des Moines, Iowa 50392-2080 |

| (Address of Registrant's Principal Executive Offices) |

| |

| 515-248-3842 |

| (Registrant's Telephone Number, Including Area Code) |

| |

| Michael D. Roughton |

| Counsel, Principal Funds, Inc. |

| 711 High Street, Suite 405 West |

| Des Moines, Iowa 50392-2080 |

| (Name and Address of Agent for Service) |

| |

| Copies of all communications to: |

| | John W. Blouch |

| Dykema Gossett PLLC |

| | 1300 I Street, N.W. |

| | Washington, D.C. 20005-3353 |

| | 202-906-8714; 202-906-8669 (Fax) |

| Approximate date of proposed public offering: As soon as practicable after this Registration Statement |

| becomes effective. |

| |

| Title of Securities Being Registered: Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional |

| Class Shares common stock, par value $.01 per share. |

| |

| No filing fee is due because an indefinite number of shares have been registered in reliance on Section 24(f) |

| under the Investment Company Act of 1940, as amended. |

| |

| It is proposed that this filing will become effective on March 20, 2009, pursuant to Rule 488. |

| PRINCIPAL FUNDS, INC. |

| 680 8th Street |

| Des Moines, Iowa 50392-2080 |

Dear Shareholder:

A Special Meeting of Shareholders of Principal Funds, Inc. (“PFI”) will be held at 680 8th Street, Des Moines, Iowa 50392-2080, on April 27, 2009 at 10 a.m., Central Time.

At the meeting, shareholders of the MidCap Growth Fund II (the “Acquired Fund”) will be asked to consider and approve a Plan of Acquisition (the “Plan”) providing for the reorganization of the MidCap Growth Fund II into the MidCap Growth Fund III (the “Acquiring Fund”). Each of these Funds is a separate series or fund of PFI.

Under the Plan: (i) the Acquiring Fund will acquire all the assets, subject to all the liabilities, of the Acquired Fund in exchange for shares of the Acquiring Fund; (ii) the Acquiring Fund shares will be distributed to the shareholders of the Acquired Fund; and (iii) the Acquired Fund will liquidate and terminate (the “Reorganization”). As a result of the Reorganization, each shareholder of the Acquired Fund will become a shareholder of the Acquiring Fund. The total value of all shares of the Acquiring Fund issued in the Reorganization will equal the total value of the net assets of the Acquired Fund. The number of full and fractional shares of the Acquiring Fund received by a shareholder of the Acquired Fund will be equal in value to the value of that shareholder’s shares of the Acquired Fund as of the close of regularly scheduled trading on the New York Stock Exchange (“NYSE”) on the closing date of the Reorganization. Holders of Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares of the Acquired Fund will receive, respectively, Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares of the Acquiring Fund. The Reorganization is expected to occur as of the close of regularly scheduled trading on the NYSE on May 1, 2009. All share classes of the Acquired Fund will vote in the aggregate and not by class with respect to the Reorganization.

The Board of Directors of PFI believes that the Reorganization will serve the best interests of shareholders of both the Acquired and Acquiring Funds. The Funds have the same investment objectives in that both Funds seek to provide long-term growth of capital. The Funds also have substantially the same principal policies and risks in that both invest in midcap growth securities. The Acquiring Fund has lower advisory fee rates on assets over $500 million and lower overall expense ratios than the Acquired Fund. Further, the Acquiring Fund has outperformed the Acquired Fund for each of the last two calendar years. Moreover, because the Acquiring Fund is much

larger than the Acquired Fund, the Reorganization may be expected to afford shareholders of the Acquired Fund on an ongoing basis greater prospects for growth and efficient management. Combining the Funds will not result in any dilution of the interests of existing shareholders of the Funds.

The value of your investment will not be affected by the Reorganization. Furthermore, in the opinion of legal counsel, no gain or loss will be recognized by any shareholder for federal income tax purposes as a result of the Reorganization.

Enclosed you will find a Notice of Special Meeting of Shareholders, a Proxy Statement/Prospectus, and a proxy card for shares of the Acquired Fund you owned as of February 27, 2009, the record date for the Meeting. The Proxy Statement/Prospectus provides background information and describes in detail the matters to be voted on at the Meeting.

The Board of Directors has unanimously voted in favor of the proposed Reorganization and recommends that you vote FOR the Proposal.

In order for shares to be voted at the Meeting, we urge you to read the Proxy Statement/Prospectus and then complete and mail your proxy card(s) in the enclosed postage-paid envelope, allowing sufficient time for receipt by us by April 26, 2009. As a convenience, we offer three options by which to vote your shares:

By Internet: Follow the instructions located on your proxy card.

By Phone: The phone number is located on your proxy card. Be sure you have your control number, as printed on your proxy card, available at the time you call.

By Mail: Sign your proxy card and enclose it in the postage-paid envelope provided in this proxy package.

We appreciate your taking the time to respond to this important matter. Your vote is important. If you have any questions regarding the Reorganization, please call our shareholder services department toll free at 1-800-222-5852.

| PRINCIPAL FUNDS, INC. |

| 680 8th Street |

| Des Moines, Iowa 50392-2080 |

|

| NOTICE OF SPECIAL MEETING OF SHAREHOLDERS |

To the Shareholders of the MidCap Growth Fund II:

Notice is hereby given that a Special Meeting of Shareholders (the “Meeting”) of the MidCap Growth Fund II, a separate series of Principal Funds, Inc. (“PFI”), will be held at 680 8th Street, Des Moines, Iowa 50392-2080, on April 27, 2009 at 10 a.m., Central Time. A Proxy Statement/ Prospectus providing information about the following proposal to be voted on at the Meeting is included with this notice. The Meeting is being held to consider and vote on such proposal as well as any other business that may properly come before the Meeting or any adjournment thereof:

| Proposal: | Approval of a Plan of Acquisition providing for the |

| | reorganization of the MidCap Growth Fund II (the “Fund”) |

| | into the MidCap Growth Fund III. |

The Board of Directors of PFI recommends that shareholders of the Fund vote FOR the Proposal.

Approval of the Proposal will require the affirmative vote of the holders of at least a “Majority of the Outstanding Voting Securities” (as defined in the accompanying Proxy Statement/Prospectus) of the Fund.

Each shareholder of record at the close of business on February 27, 2009 is entitled to receive notice of and to vote at the Meeting.

Please read the attached Proxy Statement/Prospectus.

| By order of the Board of Directors |

| |

| Nora M. Everett |

| President |

__________, 2009

Des Moines, Iowa |

| PRINCIPAL FUNDS, INC. |

| 680 8th Street |

| Des Moines, Iowa 50392-2080 |

| ————————— |

| PROXY STATEMENT/PROSPECTUS |

| SPECIAL MEETING OF SHAREHOLDERS |

| TO BE HELD APRIL 27, 2009 |

| RELATING TO THE REORGANIZATION OF: |

| THE MIDCAP GROWTH FUND II INTO |

| THE MIDCAP GROWTH FUND III |

This Proxy Statement/Prospectus is furnished in connection with the solicitation by the Board of Directors (the “Board” or “Directors”) of Principal Funds, Inc. (“PFI”) of proxies to be used at a Special Meeting of Shareholders of PFI to be held at 680 8th Street, Des Moines, Iowa 50392-2080, on April 27, 2009, at 10 a.m., Central Time (the “Meeting”).

At the Meeting, shareholders of the MidCap Growth Fund II (the “Acquired Fund”) will be asked to consider and approve a proposed Plan of Acquisition (the “Plan”) providing for the reorganization of the Acquired Fund into the MidCap Growth Fund III (the “Acquiring Fund”).

Under the Plan: (i) the Acquiring Fund will acquire all the assets, subject to all the liabilities of the Acquired Fund in exchange for shares of the Acquiring Fund; (ii) the Acquiring Fund shares will be distributed to the Shareholders of the Acquired Fund; and (iii) the Acquired Fund will liquidate and terminate (the “Reorganization”). As a result of the Reorganization, each shareholder of the Acquired Fund will become a shareholder of the Acquiring Fund. The total value of all shares of the Acquiring Fund issued in the Reorganization will equal the total value of the net assets of the Acquired Fund. The number of full and fractional shares of the Acquiring Fund received by a shareholder of the Acquired Fund will be equal in value to the value of that shareholder’s shares of the Acquired Fund as of the close of regularly scheduled trading on the New York Stock Exchange (“NYSE”) on the closing date of the Reorganization. Holders of Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares will receive, respectively, Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares of the Acquiring Fund. If approved by shareholders of the Acquired Fund, the Reorganization is expected to occur immediately after the close of regularly scheduled trading on the NYSE on May 1, 2009 (the “Effective Time”). All share classes of the Acquired Fund will vote in the aggregate and not by class. The terms and conditions of the Reorganization are more fully described below in this Proxy Statement/Prospectus and the Form of Plan of Acquisition which is attached hereto as Appendix A.

This Proxy Statement/Prospectus contains information shareholders should know before voting on the Reorganization. Please read it carefully and retain it for future reference. The Annual and Semi-Annual Reports to

Shareholders of PFI contain additional information about the investments of the Acquired and Acquiring Funds, and the Annual Report contains discussions of the market conditions and investment strategies that significantly affected these Funds during the fiscal year ended October 31, 2008. Copies of these reports may be obtained at no charge by calling our shareholder services department toll free at 1-800-247-4123.

A Statement of Additional Information dated March 1, 2009 (the “Statement of Additional Information”) relating to this Proxy Statement/ Prospectus has been filed with the Securities and Exchange Commission (“SEC”) and is incorporated by reference into this Proxy Statement/ Prospectus. PFI’s Prospectus, dated March 1, 2009 and as supplemented (“PFI Prospectus”), and the Statement of Additional Information for PFI, dated March 1, 2009 and as supplemented (“PFI SAI”), have been filed with the SEC and, insofar as they relate to the MidCap Growth Fund II, are incorporated by reference into this Proxy Statement/Prospectus. Copies of these documents may be obtained without charge by writing to PFI at the address noted above or by calling our shareholder services department toll free at 1-800-222-5852. You may also call our shareholder services department toll fee at 1-800-222-5852 if you have any questions regarding the Reorganization.

PFI is subject to the informational requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940 (the “1940 Act”) and files reports, proxy materials and other information with the SEC. Such reports, proxy materials and other information may be inspected and copied at the Public Reference Room of the SEC at 100 F Street, N.E., Washington, D.C. 20549 (information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-202-551-5850). Such materials are also available on the SEC’s EDGAR Database on its Internet site at www.sec.gov, and copies may be obtained, after paying a duplicating fee, by email request addressed to publicinfo@sec.gov or by writing to the SEC’s Public Reference Room.

The SEC has not approved or disapproved these securities or passed upon the accuracy or adequacy of this Proxy Statement/Prospectus. Any representation to the contrary is a criminal offense.

The date of this Proxy Statement/Prospectus is __________, 2009.

2

| TABLE OF CONTENTS |

| | Page |

| |

| INTRODUCTION | 4 |

| THE REORGANIZATION | 5 |

| PROPOSAL: APPROVAL OF A PLAN OF ACQUISITION | |

| PROVIDING FOR THE REORGANIZATION OF | |

| THE MIDCAP GROWTH FUND II | |

| INTO THE MIDCAP GROWTH FUND III | 7 |

| Comparison of Acquired and Acquiring Funds | 7 |

| Comparison of Investment Objectives and Strategies | 13 |

| Fees and Expenses of the Funds | 13 |

| Comparison of Principal Investment Risks | 16 |

| Performance | 20 |

| INFORMATION ABOUT THE REORGANIZATION | 23 |

| Plan of Acquisition | 23 |

| Reasons for the Reorganization | 24 |

| Board Consideration of the Reorganization | 24 |

| Description of the Securities to Be Issued | 26 |

| Federal Income Tax Consequences | 26 |

| CAPITALIZATION | 28 |

| ADDITIONAL INFORMATION ABOUT THE FUNDS | 29 |

| Certain Investment Strategies and Related Risks of the Funds | 29 |

| Multiple Classes of Shares | 38 |

| Costs of Investing in the Funds | 38 |

| Distribution Plans and Additional Information Regarding | |

| Intermediary Compensation | 40 |

| Dividends and Distributions | 44 |

| Pricing of Fund Shares | 45 |

| Purchases, Redemptions, and Exchanges of Shares | 47 |

| Frequent Purchases and Redemptions | 49 |

| Tax Considerations | 50 |

| Portfolio Holdings Information | 51 |

| VOTING INFORMATION | 51 |

| OUTSTANDING SHARES AND SHARE OWNERSHIP | 53 |

| FINANCIAL HIGHLIGHTS | 54 |

| FINANCIAL STATEMENTS | 63 |

| LEGAL MATTERS | 63 |

| OTHER INFORMATION | 63 |

| APPENDIX A Form of Plan of Acquisition | A-1 |

| APPENDIX B Description of Indices | B-1 |

3

This Proxy Statement/Prospectus is being furnished to shareholders of the Acquired Fund to provide information regarding the Plan and the Reorganization.

Principal Funds, Inc. PFI is a Maryland corporation and an open-end management investment company registered with the SEC under the 1940 Act. PFI currently offers 72 separate series or funds (the “PFI Funds”), including the Acquired and Acquiring Funds. The sponsor of PFI is Principal Life Insurance Company (“Principal Life”), and the investment advisor to the PFI Funds is Principal Management Corporation (“PMC”). PFI has two underwriters: Principal Funds Distributor, Inc. (the “Distributor” or “PFD”) for all share classes, and Princor Financial Services Corporation (“Princor”), a co-distributor with PFD for Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 (sometimes collectively referred to as the “Retirement Class”), Class J, and Institutional Class shares. Principal Life, an insurance company organized in 1879 under the laws of Iowa, PMC, PFD, and Princor are indirect, wholly-owned subsidiaries of Principal Financial Group, Inc. (“PFG”). Their address is the Principal Financial Group, Des Moines, Iowa 50392-2080.

Investment Management. Pursuant to an investment advisory agreement with PFI with respect to the Acquired and Acquiring Funds, PMC provides investment advisory services and certain corporate administrative services to the Funds. As permitted by the investment advisory agreement, PMC has entered into sub-advisory agreements with respect to the Acquired and Acquiring Funds as follows:

| Acquired Fund | Sub-Advisors |

| MidCap Growth Fund II | Jacobs Levy Equity Management, Inc. |

| (“Jacobs Levy”) |

| | MacKay Shields LLC. (“MacKay Shields”) |

| Acquiring Fund | Sub-Advisors |

| MidCap Growth Fund III | Mellon Capital Management Corporation |

| | (“Mellon Capital”) |

| | Turner Investment Partners, Inc. (“Turner”) |

PMC and each sub-advisor are registered with the SEC as investment advisors under the Investment Advisers Act of 1940.

Jacobs Levy is located at 100 Campus Drive, Florham Park, NJ 07932-0650.

MacKay Shields is located at 9 West 57th Street, New York, NY 10019. Mellon Capital is located at 500 Grant Street, Suite 4200, Pittsburgh, PA 15258. Mellon Capital is a wholly owned subsidiary of Mellon Financial Corporation.

Turner is located at 1205 Westlakes Drive, Suite 100, Berwyn, PA 19312.

4

At its meeting held on December 19, 2008, the Board, including all the Directors who are not “interested persons” (as defined in the 1940 Act) of PFI (the “Independent Directors”), approved the Reorganization pursuant to the Plan providing for the combination of the Acquired Fund into the Acquiring Fund. The Board concluded that the Reorganization is in the best interests of the Acquired Fund and the Acquiring Fund and that the interests of existing shareholders of the Funds will not be diluted as a result of the Reorganization. The factors that the Board considered in deciding to approve the Reorganization are discussed below under “Information About the Reorganization – Board Consideration of the Reorganization.”

The Reorganization contemplates: (i) the transfer of all the assets, subject to all of the liabilities, of the Acquired Fund to the Acquiring Fund in exchange for shares of the Acquiring Fund; (ii) the distribution to Acquired Fund shareholders of the Acquiring Fund shares; and (iii) the liquidation and termination of the Acquired Fund. As a result of the Reorganization, each shareholder of the Acquired Fund will become a shareholder of the Acquiring Fund. In the Reorganization, the Acquiring Fund will issue a number of shares with a total value equal to the total value of the net assets of the Acquired Fund, and each shareholder of the Acquired Fund will receive a number of full and fractional shares of the Acquiring Fund with a value equal to the value of that shareholder’s shares of the Acquired Fund, as of the close of regularly scheduled trading on the NYSE on the closing date of the Reorganization (the “Effective Time”). The closing date of the Reorganization is expected to be May 1, 2009. Holders of Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares of the Acquired Fund will receive, respectively, Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares of the Acquiring Fund. The terms and conditions of the Reorganization are more fully described below in this Proxy Statement/Prospectus and in the Form of Plan of Acquisition, which is attached hereto as Appendix A.

The Board of Directors of PFI believes that the Reorganization will serve the best interests of shareholders of both the Acquired and Acquiring Funds. The Funds have the same investment objectives in that both Funds seek to provide long-term growth of capital. The Funds also have substantially the same principal policies and risks in that both invest in midcap growth securities. The Acquiring Fund has lower advisory fee rates on assets over $500 million and lower overall expense ratios than the Acquired Fund. Further, the Acquiring Fund has outperformed the Acquired Fund for each of the last two calendar years. Moreover, because the Acquiring Fund is much larger than the Acquired Fund, the Reorganization may be expected to afford

5

shareholders of the Acquired Fund on an ongoing basis greater prospects for growth and efficient management. Combining the Funds will not result in any dilution of the interests of existing shareholders of the Funds.

In the opinion of legal counsel, the Reorganization will qualify as a tax-free reorganization and, for federal income tax purposes, no gain or loss will be recognized as a result of the Reorganization by the Acquired or Acquiring Fund shareholders. See “Information About the Reorganization – Federal Income Tax Consequences.”

The Reorganization will not result in any material change in the purchase and redemption procedures followed with respect to the distribution of shares. See “Additional Information About the Funds – Purchases, Redemptions and Exchanges of Shares.”

The Acquired Fund will pay all expenses and out-of-pocket fees incurred in connection with the Reorganization, including printing, mailing, and legal fees. These expenses and fees are expected to total $45,000.

6

PROPOSAL:

APPROVAL OF A PLAN OF ACQUISITION PROVIDING FOR THE REORGANIZATION OF THE

MIDCAP GROWTH FUND II

INTO THE MIDCAP GROWTH FUND III.

Shareholders of the MidCap Growth Fund II (the “Acquired Fund”) are being asked to approve the reorganization of the Acquired Fund into the MidCap Growth Fund III (the “Acquiring Fund.)

Comparison of Acquired and Acquiring Funds

The following table provides comparative information with respect to the Acquired and Acquiring Funds. The description below of the Acquiring Fund reflects of the appointment of Jacobs Levy as an additional sub-advisor to the Acquiring Fund and changes to its investment strategies to reflect Jacob Levy’s management style and the allocation of the Acquiring Fund’s assets between two sub-advisors. The appointment of Jacobs Levy as an additional sub-advisor and these changes in investment strategies will become effective at the Effective Time of the Reorganization.

| MidCap Growth Fund II | | | MidCap Growth Fund III |

| (Acquired Fund) | | | (Acquiring Fund) |

| |

| Approximate Net Assets as of October 31, 2008: |

| $205,666,000 | | | $529,818,000 |

| |

| Investment Advisor: PMC |

| Sub-Advisors and Portfolio Managers: |

Jacobs Levy Bruce Jacobs, Ph.D. Dr. Jacobs | Mellon Capital Adam T. Logan, CFA. Joining the |

| serves as co-chief investment officer, | company in 1998, Mr. Logan is a |

| portfolio manager, and co-director of | portfolio manager and Vice President |

| research. Prior to co-founding Jacobs | of Mellon Capital. Previously, he |

| Levy in 1986, Dr. Jacobs was Senior | performed duties as a financial analyst |

| Managing Director of a quantitative | in Mellon Financial Corporation’s |

| equity management affiliate of the | corporate finance department. He is |

| Prudential Insurance Company of | currently responsible for the |

| America. Dr. Jacobs earned a BA from | management of client portfolios with a |

| Columbia College, an MS in | specific focus on mid and small |

| Operations Research and Computer | capitalization securities. He earned a |

| Science from Columbia University, an | BA in Finance from Westminster |

| MSIA from Carnegie Mellon | College and an MBA from the Katz |

| University, and an MA in Applied | Graduate School of Business at the |

7

Economics and a Ph.D. in Finance from the University of Pennsylvania’s Wharton School. Ken Levy, CFA. Mr. Levy serves as co-chief investment officer, portfolio manager, and co-director of research. Prior to co-founding Jacobs Levy in 1986, Mr. Levy was Managing Director of a quantitative equity management affiliate of the Prudential Insurance Company of America. He earned a BA in Economics from Cornell University and an MBA and an MA in Business Economics from the University of Pennsylvania’s Wharton School. He has earned the right to use the Chartered Financial Analyst designation.

MacKay Shields Robert J. Centrella, CFA. Mr. Centrella is a Managing Director Portfolio Manager/Research Analyst Equity Division and joined MacKay Shields in 1996 as a Portfolio Manager/Research Analyst in the Equity Division. He received a BS in Accounting from the University of Scranton and an MBA in Finance from George Mason University. He has earned the right to use the Chartered Financial Analyst designation. Edmund C. Spelman. Mr. Spelman Senior Managing Director and Head of the Growth Equity Division; he leads the Partners MidCap Growth Fund II investment team. Mr. Spelman has worked for MacKay Shields since 1991. Mr. Spelman earned a BA and an MS from the University of Pennsylvania. | | University of Pittsburgh. He has earned the right to use the Chartered Financial Analyst designation. John O’Toole, CFA. Joining the company in 1990, Mr. O’Toole is a Senior Vice President and a principal of Mellon Capital. Mr. O’Toole holds an MBA in Finance from the University of Chicago and a BA in Economics from the University of Pennsylvania. He has earned the right to use the Chartered Financial Analyst designation. Turner Tara R. Hedlund, CFA, CPA. Ms. Hedlund joined Turner in 2000. Previously, she was an audit engagement senior at Arthur Andersen LLP. She has been in investment management since 1995. She earned a BBS in Accountancy from Villanova University. She has earned the right to use the Chartered Financial Analyst designation. Christopher K. McHugh. Mr. McHugh, Vice President and Senior Portfolio Manager, joined Turner in 1990. Prior to joining Turner, he was a performance specialist at Provident Capital Management. He earned a BS in Accounting from Philadelphia University and an MBA in Finance from St. Joseph’s University. Jason D. Schrotberger, CFA. Mr. Schrotberger joined Turner in 2001. Previously, he was an investment analyst at BlackRock Financial Management. He has been in investment management since 1994. He earned a BA in Economics from Denison University and an MBA in Finance from the University of Illinois. He has earned the right to use the Chartered Financial Analyst designation. |

| |

8

| | Jacobs Levy (will become an additional sub-advisor as of the Effective Time.) Bruce Jacobs, Ph.D. Ken Levy, CFA. (See portfolio manager biographical profiles under Acquired Fund above.) |

Investment Objective:

Both Funds seek long-term growth of capital.

Principal Investment Strategies: Under normal market conditions, the Fund invests at least 80% of its assets in common stocks of companies with medium market capitalizations (those with market capitalizations similar to companies in the Russell Midcap Growth Index) (as of December 31, 2008, this range was between approximately $0.02 billion and $14.9 billion at the time of purchase). Market capitalization is defined as total current market value of a company’s outstanding common stock Companies may range from the well- established and well-known to the new and unseasoned. Jacobs Levy selects stocks using a growth oriented investment approach based on proprietary research that attempts to detect and take advantage of market inefficiencies. Its approach combines human insight and intuition, finance and behavioral theory, and quantitative and statistical methods in a proprietary process it refers to as “disentangling.” The disentangling process evaluates various market inefficiencies simultaneously, isolating each potential source of return. Jacobs Levy believes that disentangling provides more reliable predictions of future stock price behavior than simple single-factor | | The Fund invests primarily in common stocks and other equity securities of U.S. companies with strong earningsgrowth potential. Under normal market conditions, the Fund invests at least 80% of its net assets (plus any borrowings for investment purposes) in common stocks of companies with medium market capitalizations (those with market capitalizations similar to companies in the Russell Midcap Growth Index (as of December 31, 2008, this range was between approximately $0.02 billion and $14.9 billion). Market capitalization is defined as total current market value of a company’s outstanding common stock. The Fund may purchase securities issued as part of, or a short period after, companies’ initial public offerings (“IPOs”) and may at times dispose of those shares shortly after their acquisition. The Fund may invest up to 25% of its net assets in securities of foreign companies, including securities of issuers in emerging countries and securities quoted in foreign currencies. Turner invests the assets allocated to it in securities of companies that are diversified across economic sectors. It |

9

analyses. Security valuation entails sophisticated modeling of large numbers of stocks and proprietary factors based on reasonable, intuitive relationships. The firm examines a wide range of data, including balance sheets and income statements, analyst forecasts, corporate management signals, economic releases, and security prices. MacKay Shields invests in growth stocks by utilizing a bottom-up approach that combines time-tested fundamental multi-factor screens with hands-on fundamental research. MacKay Shields looks to capitalize on evolving growth trends while adhering to risk controls. As a result of its process, MacKay Shields seeks to invest primarily in companies with a history of increasing earnings and sales at a rate that is generally higher than that of average companies. MacKay Shields process leads to a diversified portfolio. The Fund may engage in the lending of portfolio securities and may invest in securities of foreign issuers. The Fund may also use various techniques, such as buying and selling exchange traded funds, to increase or decrease exposure to changing security prices or other factors that affect security value. MacKay Shields maintains a flexible approach toward investing in various types of companies as well as multiple types of securities, including common stocks, preferred stocks, warrants and other equity securities, depending upon the economic environment and the relative attractiveness of the various securities markets. MacKay Shields may invest in any securities that, in its judgment, are ready for a rise in price, or are expected to | | attempts to maintain sector concentrations that approximate those of its current benchmark, the Russell Midcap Growth Index. The Fund is not an index fund and does not limit its investment to the securities of issuers in the Russell Midcap Growth Index. Turner selects stocks that it believes have strong earnings growth potential. Turner invests assets allocated to it in companies with strong earnings dynamics, and sells those with deteriorating earnings prospects. Turner believes forecasts for market timing and sector rotation are unreliable and introduce an unacceptable level of risk. As a result, under normal market conditions, Turner’s portion of the Fund is fully invested. In the view of Mellon Capital, many medium-sized companies: • are in fast growing industries, • offer superior earnings growth potential, and • are characterized by strong balance sheets and high returns on equity.Mellon Capital may also hold assets allocated to it in investments in large and small capitalization companies,including emerging and cyclical growth companies. Mellon Capital uses valuation models designed to identify common stocks of companies that have demonstrated consistent earnings momentum and delivered superior results relative to market analyst expectations. Other considerations include profit margins, growth in cash flow and other standard balance sheet measures. Mellon Capital holds securities generally characterized by strong earnings momentum measures and higher expected earnings pershare growth. |

| |

| |

10

undergo an acceleration in growth of earnings. The latter could occur because of special factors, such as new management, new products, changes in consumer demand, and changes in the economy. MacKay Shields may sell a stock if the stock’s earnings growth rate decelerates, if its valuation is deemed too high in relation to its growth rate or to its peer group or if, in general, MacKay Shields does not believe that the security will help the Fund meet its investment objective. | | Mellon Capital’s valuation model incorporates information about the relevant criteria as of the most recent period for which data are available. Once ranked, the securities are categorized under the headings “buy,” “sell,” or “hold.” The decision to buy, sell or hold is made by Mellon Capital based primarily on output of the valuation model. However, that decision may be modified due to subsequently available or other specific relevant information about the security. In addition, Mellon Capital manages risk by diversifying across companies and industries, limiting the potential adverseimpact from any one stock or industry. Jacobs Levy selects stocks using a growth oriented investment approach based on proprietary research that attempts to detect and take advantage of market inefficiencies. Its approach combines human insight and intuition, finance and behavioral theory, and quantitative and statistical methods in a proprietary process it refers to as “disentangling.” The disentangling process evaluates various market inefficiencies simultaneously, isolating each potential source of return. Jacobs Levy believes that disentangling provides more reliable predictions of future stock price behavior than simple single-factor analyses. Security valuation entails sophisticated modeling of large numbers of stocks and proprietary factors based on reasonable, intuitive relationships. The firm examines a wide range of data, including balance sheets and income statements, analyst forecasts, corporate management signals, economic releases, and security prices. |

11

In July 2009, PMC will begin investing approximately 25% of the Acquiring Fund’s assets in common stocks in an attempt to match or exceed the performance of the Russell MidCap 2000 Growth Index. PMC’s strategy is an active quantitative approach to asset management which PMC refers to as “structured equity.” PMC’s structured equity strategy applies a risk-controlled investment process that slightly over/underweights individual stocks relative to their weight in the Russell 2000 Growth Index. Through the structured equity strategy, PMC expects the Fund to achieve returns in excess of those of the Russell 2000 Growth Index for performance with lower risk and improved predictability of returns for the entire Fund compared to the Russell 2000 Growth Index.

Cash Management Program

PMC has implemented a cash management program for Acquiring Fund. The Acquiring Fund has cash available in its portfolio to meet redemption requests and to pay expenses. Additionally, the Acquiring Fund receives cash flows when shareholders purchase shares. PMC will invest the cash, which comprises a very small portion of the funds’ portfolios, in money market investments and in stock index futures contracts based on the Fund’s market cap to gain exposure to the market. Stock index futures provide returns similar to those of common stocks. PMC believes that, over the long term, this strategy will enhance the investment performance of the Acquiring Fund.

Hedging and Other Strategies:

Each of the Funds may invest in inverse floating rate obligations, may engage in hedging transactions through the use of financial futures and options thereon and may also purchase and sell securities on a when-issued or forward commitment basis, invest in mortgage-backed securities, enter into repurchase agreements, invest in stand-by commitments, engage in swap agreements, and lend portfolio securities. Each of the Funds may invest in floating rate and variable rate obligations, including participation interests therein.

Temporary Defensive Investing:

For temporary defensive purposes in times of unusual or adverse market, economic, or political conditions, each Fund may invest up to 100% of its assets in cash and cash equivalents. In taking such defensive measures, either Fund may fail to achieve its investment objective.

Fundamental Investment Restrictions:

Each of the Funds is subject to the same fundamental investment restrictions which may not be changed without the approval of the shareholders of the Fund. These fundamental restrictions deal with such matters as the issuance of senior securities, purchasing or selling real estate or commodities, borrowing money, making loans, underwriting securities of

12

other issuers, diversification or concentration of investments, and short sales of securities. The fundamental investment restrictions of the Funds are described in the Statement of Additional Information.

Comparison of Investment Objectives and Strategies

The Funds have the same investment objectives in that both Funds seeks to provide long-term growth of capital. They also have substantially the same principal policies and risks in that both invest primarily in midcap growth securities. The Funds differ in that the Acquiring Fund but not the Acquired Fund participates in PMC’s cash management program, the Acquiring Fund gives greater emphasis to investing in initial public offerings and its investments in foreign securities may include those of emerging market issuers. Finally, as described above and beginning in July 2009, PMC is expected to begin to invest approximately 25% of the Acquiring Fund’s assets pursuant to its structured equity strategy.

The investment objective of each of the Funds may be changed by the Board without shareholder approval.

Additional information about the investment strategies and the types of securities in which the Funds may invest is discussed below under “Certain Investment Strategies and Related Risks of the Funds” as well as in the Statement of Additional Information.

The Statement of Additional Information provides further information about the portfolio manager(s) for each Fund, including information about compensation, other accounts managed and ownership of Fund shares.

| | Fees and Expenses of the Funds |

The tables below compare the fees and expenses of the shares of the Acquired and Acquiring Funds. In the Reorganization, the holders of Class R-1, Class R-2, Class R-3, Class R-4, Class R-5, and Institutional Class shares of the Acquired Fund will receive, respectively, Class R-1, Class R-2, Class R-3, Class R-4, Class R-5, and Institutional Class shares of the Acquiring Fund.

Fees and Expenses as a % of average daily net assets

The following table shows: (a) the ratios of expenses to average net assets of the Acquired Fund for the fiscal year ended October 31, 2008; (b) the ratios of expenses to average net assets of the Acquiring Fund for the fiscal year ended October 31, 2008; and (c) the pro forma expense ratios of the Acquiring fund for the fiscal year ending October 31, 2008 assuming that the Reorganization had taken place at the commencement of the fiscal year ended October 31, 2008.

13

| Annual Fund Operating Expenses |

| |

| | | | | Total |

| | Management | 12b-1 | Other | Operating |

| Class | Fees | Fees | Expenses | Expenses |

| (a) MidCap Growth Fund II (Acquired Fund) | | |

| R-1 | 1.00% | 0.35% | 0.54% | 1.89% |

| R-2 | 1.00% | 0.30% | 0.46% | 1.76% |

| R-3 | 1.00% | 0.25% | 0.33% | 1.58% |

| R-4 | 1.00% | 0.10% | 0.29% | 1.39% |

| R-5 | 1.00% | N/A | 0.27% | 1.27% |

| Institutional | 1.00% | N/A | 0.04% | 1.04%(1) |

| |

| (b) MidCap Growth Fund III (Acquiring Fund) | | |

| R-1 | 0.99% | 0.35% | 0.54% | 1.88% |

| R-2 | 0.99% | 0.30% | 0.46% | 1.75% |

| R-3 | 0.99% | 0.25% | 0.33% | 1.57% |

| R-4 | 0.99% | 0.10% | 0.29% | 1.38% |

| R-5 | 0.99% | N/A | 0.27% | 1.26% |

| Institutional | 0.99% | N/A | 0.02% | 1.01%(1) |

| |

| (c) MidCap Growth Fund III (Acquiring Fund) | | |

| (Pro forma assuming Reorganization)(2) | | |

| R-1 | 0.99% | 0.35% | 0.54% | 1.88% |

| R-2 | 0.99% | 0.30% | 0.46% | 1.75% |

| R-3 | 0.99% | 0.25% | 0.33% | 1.57% |

| R-4 | 0.99% | 0.10% | 0.29% | 1.38% |

| R-5 | 0.99% | N/A | 0.27% | 1.26% |

| Institutional | 0.99% | N/A | 0.01% | 1.00% |

| (1) | Expense information has been restated to reflect current fees. Certain other operating expenses of the Funds have been increased effective March 1, 2009. |

| (2) | The pro forma figures do not reflect the costs associated with the Reorganization. |

14

Examples: The following examples are intended to help you compare the costs of investing in shares of the Acquired and Acquiring Funds. The examples assume that fund expenses continue at the rates shown in the table above, that you invest $10,000 in the particular fund for the time periods indicated, regardless of whether you redeem or continue to hold the shares at the end of the period, and that all dividends and distributions are reinvested. The examples also assume that your investment has a 5% return each year. The examples should not be considered a representation of future expenses of the Acquired or Acquiring fund. Actual expenses may be greater or less than those shown.

| | Number of Years You Own Your Shares |

| Share Class | 1 Year | 3 Years | 5 Years | 10 Years |

| MidCap Growth Fund II (Acquired Fund) | | |

| R-1 | $192 | $594 | $1,021 | $2,212 |

| R-2 | 179 | 554 | 954 | 2,073 |

| R-3 | 161 | 499 | 860 | 1,878 |

| R-4 | 142 | 440 | 761 | 1,669 |

| R-5 | 129 | 403 | 697 | 1,534 |

| Institutional | 106 | 331 | 574 | 1,271 |

| |

| MidCap Growth Fund III (Acquiring Fund) | | |

| R-1 | $191 | $591 | $1,016 | $2,201 |

| R-2 | 178 | 551 | 949 | 2,062 |

| R-3 | 160 | 496 | 855 | 1,867 |

| R-4 | 140 | 437 | 755 | 1,657 |

| R-5 | 128 | 400 | 692 | 1,523 |

| Institutional | 103 | 322 | 558 | 1,236 |

| |

| MidCap Growth Fund III (Acquiring Fund) | | |

| (Pro forma assuming Reorganization) | | |

| R-1 | $191 | $591 | $1,016 | $2,201 |

| R-2 | 178 | 551 | 949 | 2,062 |

| R-3 | 160 | 496 | 855 | 1,867 |

| R-4 | 140 | 437 | 755 | 1,657 |

| R-5 | 128 | 400 | 692 | 1,523 |

| Institutional | 102 | 318 | 552 | 1,225 |

15

Investment Management Fees/Sub-Advisory Arrangements

The Funds each pay their investment advisor, PMC, an advisory fee which for each Fund is calculated as a percentage of the Fund’s average daily net assets pursuant to the following fee schedules:

MidCap Growth Fund II (Acquired Fund)

1.00% for the first $500 million, .98% for the next $500 million, .96% for the next $500 million, and .95% on all assets over $1.5 billion.

MidCap Growth Fund III (Acquiring Fund)

1.00% for the first $500 million, .96% for the next $500 million, .94% for the next $500 million, and .92% on all assets over $1.5 billion.

As sub-advisors to the Funds, Jacobs Levy, MacKay Shields, Mellon Capital, and Turner are paid sub-advisory fees. These sub-advisory fees are paid by PMC, not by the Funds.

A discussion of the basis of the Board’s approval of the advisory and sub-advisory agreements with respect to the Acquired and Acquiring Funds is available in PFI’s Annual Report to Shareholders for the fiscal year ended October 31, 2008.

Comparison of Principal Investment Risks

In deciding whether to approve the Reorganization, shareholders should consider the amount and character of investment risk involved in the respective investment objectives and strategies of the Acquired and Acquiring Funds. Because the Funds have the same investment objectives and substantially the same principal policies, the Funds’ risks are substantially similar. As described below, the Funds also have some different risks.

Risks Applicable to both Funds:

Credit and Counterparty Risk. Each of the Funds is subject to the risk that the issuer or guarantor of a fixed-income security or other obligation, the counterparty to a derivatives contract or repurchase agreement, or the borrower of a portfolio’s securities will be unable or unwilling to make timely principal, interest, or settlement payments, or otherwise to honor its obligations.

Liquidity Risk. The Funds are exposed to liquidity risk when trading volume, lack of a market maker, or legal restrictions impair the Funds’ ability to sell particular securities or close derivative positions at an advantageous price.

Market Risk. The value of the Funds’ portfolio securities may go down in response to overall stock or bond market movements. Markets tend to move in cycles, with periods of rising prices and periods of falling prices. Stocks tend to go up and down in value more than bonds. If the Funds’

16

investments are concentrated in certain sectors, its performance could be worse than the overall market. It is possible to lose money when investing in the fund.

Active Trading Risk. The Funds may actively trades portfolio securities in an attempt to achieve their investment objective and, therefore, may have high portfolio turnover rates that may increase the fund’s brokerage costs, accelerate the realization of taxable gains, and adversely impact fund performance.

Management Risk. The Funds are actively managed by their investment advisor or sub-advisor(s). The performance of the Funds will reflect in part the ability of the advisor or sub-advisor(s) to make investment decisions that are suited to achieving the Funds’ investment objectives. If the advisor’s or sub-advisor(s)’ strategies do not perform as expected, the Funds could underperform other mutual funds with similar investment objectives or lose money.

Securities Lending Risk. To earn additional income, the Funds may lend portfolio securities to approved financial institutions. Risks of such a practice include the possibility that a financial institution becomes insolvent, increasing the likelihood that the Funds will be unable to recover the loaned security or its value. Further, the cash collateral received by the Funds in connection with such a loan may be invested in a security that subsequently loses value.

Equity Securities Risk. Equity securities include common, preferred, and convertible preferred stocks and securities the values of which are tied to the price of stocks, such as rights, warrants, and convertible debt securities. Common and preferred stocks represent equity ownership in a company. Stock markets are volatile, and the price of equity securities (and their equivalents) will fluctuate. The value of equity securities purchased by the Funds could decline if the financial condition of the companies in which the fund invests decline or if overall market and economic conditions deteriorate.

Foreign Securities Risk. Foreign securities carry risks that are not generally found in securities of U.S. companies. These risks include the loss of value as a result of political instability and financial and economic events in foreign countries. In addition, nationalization, expropriation or confiscatory taxation, and foreign exchange restrictions could adversely affect the Fund’s investments in a foreign country. Foreign securities may be subject to less stringent reporting, accounting, and disclosure standards than are required of U.S. companies, and foreign countries may also have problems associated with and causing delays in the settlement of sales.

17

Market Segment Risk. The Funds are subject to the risk that their principal market segment, mid capitalization, may underperform compared to other market segments or to the equity markets as a whole. The Funds’ strategy of investing in mid cap stocks carries the risk that in certain markets mid cap stocks will underperform small cap or large cap stocks.

Exchange Rate Risk. Because foreign securities are generally denominated in foreign currencies, the value of the net assets of a fund as measured in U.S. dollars will be affected by changes in exchange rates. To protect against future uncertainties in foreign currency exchange rates, the Funds are authorized to enter into certain foreign currency exchange transactions. In addition, the Funds’ foreign investments may be less liquid and their price more volatile than comparable investments in U.S. securities. Settlement periods may be longer for foreign securities and portfolio liquidity may be affected.

Growth Stock Risk. Growth stocks typically trade at higher multiples of current earnings than other securities. Growth stocks are often more sensitive to market fluctuations than other securities because their market prices are highly sensitive to future earnings expectations. Similarly, because growth securities typically do not make dividend payments to shareholders, investment returns are based on capital appreciation, making returns more dependent on market increases and decreases. Growth stocks may therefore be more volatile than non-growth stocks. The Funds’ strategy of investing in growth stocks also carries the risk that in certain markets growth stocks will underperform value stocks.

Mid Cap Stock Risk. Medium capitalization companies may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, mid-size companies may pose greater risk due to narrow product lines, limited financial resources, less depth in management, or a limited trading market for their securities.

Risks Applicable to the Acquired Fund:

Exchange-Traded Funds (“ETFs”) Risk. To the extent that the Acquired Fund invests in ETFs, the Fund will be subject to substantially the same risks as those associated with the direct ownership of the securities comprising the index on which the ETF is based, and the value of the Fund’s investment will fluctuate in response to the performance of the underlying index. ETFs typically incur fees that are separate from those of the Fund. Accordingly, the Fund’s investments in ETFs will result in the layering of expenses such that shareholders will indirectly bear a proportionate share of the ETFs’ operating expenses, in addition to paying Fund expenses.

18

Risks Applicable to the Acquiring Fund:

Underlying Fund Risk. The Principal LifeTime Funds and the Strategic Asset Management (“SAM”) Portfolios operate as funds of funds and invest principally in other PFI Funds (“Underlying Funds”). From time to time, an Underlying Fund may experience relatively large investments or redemptions by a fund of funds due to the reallocation or rebalancing of its assets. These transactions may have adverse effects on Underlying Fund performance to the extent an Underlying Fund is required to sell portfolio securities to meet such redemptions, or to invest cash from such investments, at times it would not otherwise do so. This may be particularly important when a fund of funds owns a significant portion of an underlying fund. These transactions may also accelerate the realization of taxable income if sales of portfolio securities result in gains, and could increase transaction costs. In addition, when a fund of funds reallocates or redeems significant assets away from an Underlying Fund, the loss of assets to the Underlying Fund could result in increased expense ratios for that fund.

PMC is the advisor to the Principal LifeTime Funds and each of the Underlying Funds. Principal Global Investors, Inc. (“PGI”), an affiliate of PMC, is Sub-Advisor to these funds.The Acquiring Fund is among the Underlying Funds owned by the Principal LifeTime Funds. Principal and PGI are committed to minimizing the potential impact of underlying fund risk on Underlying Funds to the extent consistent with pursuing the investment objectives of the funds of funds which it manages. Each may face conflicts of interest in fulfilling its responsibilities to all such funds. The following table shows the percentage of the outstanding shares of the Acquiring Fund owned by the Principal LifeTime Funds as of October 31, 2008.

| Principal LifeTime Funds | MidCap Growth Fund III Acquiring Fund |

| Principal LifeTime 2010 | | 0.55% |

| Principal LifeTime 2015 | | 0.14% |

| Principal LifeTime 2020 | | 7.51% |

| Principal LifeTime 2025 | | 0.19% |

| Principal LifeTime 2030 | | 8.00% |

| Principal LifeTime 2035 | | 0.14% |

| Principal LifeTime 2040 | | 4.81% |

| Principal LifeTime 2045 | | 0.06% |

| Principal LifeTime 2050 | | 2.08% |

| Principal LifeTime 2055 | | 0.01% |

| Principal LifeTime Strategic Income | | 0.26% |

| Total | 23.75% |

19

Emerging Market Risk. Investments in emerging market countries involve special risks. Certain emerging market countries have historically experienced, and may continue to experience, certain economic problems. These may include: high rates of inflation, high interest rates, exchange rate fluctuations, large amounts of debt, balance of payments and trade difficulties, and extreme poverty and unemployment.

Initial Public Offerings (“IPOs”) Risk. There are risks associated with the purchase of shares issued in IPOs by companies that have little operating history as public companies, as well as risks inherent in those sectors of the market where these new issuers operate. The market for IPO issuers has been volatile and share prices of certain newly-public companies have fluctuated in significant amounts over short periods of time. The Acquiring Fund cannot guarantee continued access to IPO offerings and may at times dispose of IPO shares shortly after their acquisition.

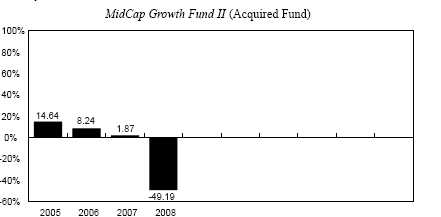

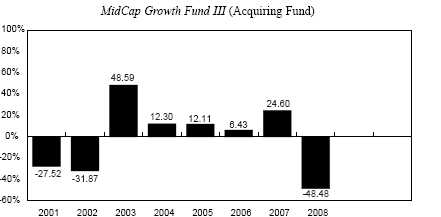

The bar charts below show how each Fund’s total return has varied year-by-year, while the tables below show each Fund’s performance over time (along with the returns of a broad-based market index and an index of funds with similar investment objectives for reference). A Fund’s past performance is not necessarily an indication of how the Fund will perform in the future.

Year-By-Year Total Returns (%) as of 12/31 Each Year (Institutional Class)

| Highest return for a quarter during | | |

| the period of the bar chart above: | Q1 ’06 | 10.87% |

| Lowest return for a quarter during | | |

| the period of the bar chart above: | Q4 ’08 | -29.05% |

The year-to-date return as of December 31, 2008 is -49.19% .

20

Year-By-Year Total Returns (%) as of 12/31 Each Year (Institutional Class)

| Highest return for a quarter during | | |

| the period of the bar chart above: | Q4 ’01 | 24.96% |

| Lowest return for a quarter during | | |

| the period of the bar chart above: | Q3 ’01 | -31.34% |

The year-to-date return as of December 31, 2008 is -48.48% .

Average Annual Total Returns (%) for periods ended December 31, 2008

| | | Life of |

| | 1 Year | Fund(1) |

| MidCap Growth Fund II | | |

| (Acquired Fund) | | |

| —Institutional Class (before taxes) | -49.19 | -10.48 |

| (after taxes on distributions)(2) | -49.19 | -11.70 |

| (after taxes on distributions and sale of shares) (2) | -31.97 | -8.82 |

| —R-1 Class | -49.60 | -11.35 |

| —R-2 Class | -49.55 | -11.24 |

| —R-3 Class | -49.46 | -11.08 |

| —R-4 Class | -49.36 | -10.93 |

| —R-5 Class | -49.32 | -10.82 |

| Russell Midcap Growth Index(3) | -44.32 | -2.19 |

| Morningstar Mid-Cap Growth Category Average | -43.77 | -3.23 |

21

| | | | Life of |

| | 1 Year | 5 Years | Fund(4) |

| MidCap Growth Fund III | | | |

| (Acquiring Fund) | | | |

| —Institutional Class (before taxes) (5) | -48.48 | -2.97 | -6.08 |

| (after taxes on distributions)(2) (5) | -48.48 | -3.26 | -6.25 |

| (after taxes on distributions and sale of shares)(2) (5) | -31.51 | -2.30 | -4.87 |

| —R-1 Class(6) | -48.84 | -3.82 | -6.73 |

| —R-2 Class | -48.81 | -3.71 | -6.77 |

| —R-3 Class | -48.67 | -3.50 | -6.43 |

| —R-4 Class | -48.62 | -3.35 | -6.42 |

| —R-5 Class | -48.56 | -3.20 | -6.26 |

| Russell Midcap Growth Index(3) | -44.32 | -2.33 | -3.77 |

| Morningstar Mid-Cap Growth Category Average | -43.77 | -2.44 | -4.64 |

| (1) | Lifetime results are measured from December 29, 2004. |

| |

| (2) | After-tax returns are calculated using the historical highest individual federal marginal income-tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor’s tax situation and may differ from those shown. The after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. |

| |

| (3) | Index performance does not reflect deductions for fees, expenses or taxes. For a description of the indices, see Appendix B to this Proxy Statement/ Prospectus. |

| |

| (4) | Lifetime results are measured from the date the R-3 Class shares were first sold (December 6, 2000). |

| |

| (5) | Institutional Class shares were first sold on March 1, 2001. The returns for the periods prior to that date are based on the performance of the R-3 Class shares adjusted to reflect the fees and expenses of Institutional Class shares. |

| |

| | The adjustments result in performance for such periods that is no higher than the historical performance of the R-3 Class shares. R-3 shares were first sold on December 6, 2000. |

| |

| (6) | The R-1 Class shares were first sold on November 1, 2004. For periods prior to the date on which the R-1 Class began operations, its returns are based on the performance of the Fund’s R-3 Class shares adjusted to reflect the fees and expenses of the R-1 Class. The adjustments result in performance (for the periods prior to the date the R-1 began operations) that is no higher than the historical performance of the R-3 Class shares. The Institutional Class shares were first sold on December 6, 2000. |

22

INFORMATION ABOUT THE REORGANIZATION

Plan of Acquisition

The terms of the Plan are summarized below. The summary is qualified in its entirety by reference to the Form of the Plan which is attached as Appendix A to this Proxy Statement/Prospectus.

Under the Plan, the Acquiring Fund will acquire all the assets and assume all the liabilities of the Acquired Fund. We expect that the closing date will be May 1, 2009, or such earlier or later date as PMC may determine, and that the Effective Time of the Reorganization will be as of the close of regularly scheduled trading on the NYSE (normally 3:00 p.m., Central Time) on that date. Each Fund will determine its net asset values as of the close of trading on the NYSE using the procedures described in its then current prospectus (the procedures applicable to the Acquired Fund and the Acquiring Fund are identical). The Acquiring Fund will issue to the Acquired Fund a number of shares of each share class with a total value equal to the total value of the net assets of the corresponding share class of the Acquired Fund outstanding at the Effective Time.

Immediately after the Effective Time, the Acquired Fund will distribute to its shareholders Acquiring Fund shares of the same class as the Acquired Fund shares each shareholder owns in exchange for all Acquired Fund shares of that class. Acquired Fund shareholders will receive a number of full and fractional shares of the Acquiring Fund that are equal in value to the value of the shares of the Acquired Fund that are surrendered in the exchange. In connection with the exchange, the Acquiring Fund will credit on its books an appropriate number of its shares to the account of each Acquired Fund shareholder, and the Acquired Fund will cancel on its books all its shares registered to the account of that shareholder. After the Effective Time, the Acquired Fund will be dissolved in accordance with applicable law.

The Plan may be amended, but no amendment may be made which in the opinion of the Board would materially adversely affect the interests of the shareholders of the Acquired Fund. The Board may abandon and terminate the Plan at any time before the Effective Time if it believes that consummation of the transactions contemplated by the Plan would not be in the best interests of the shareholders of either of the Funds.

Under the Plan, the Acquired Fund will pay all expenses and out-of-pocket fees incurred in connection with the Reorganization.

If the Plan is not consummated for any reason, the Board will consider other possible courses of action.

23

Reasons for the Reorganization

The Board of Directors of PFI believes that the Reorganization will serve the best interests of shareholders of both the Acquired and Acquiring Funds. The Funds have the same investment objectives in that both Funds seek to provide long-term growth of capital. The Funds also have substantially the same principal policies and risks in that both invest in midcap growth securities. The Acquiring Fund has lower advisory fee rates on assets over $500 million and lower overall expense ratios than the Acquired Fund. Further, the Acquiring Fund has outperformed the Acquired Fund for each of the last two calendar years. Moreover, because the Acquiring Fund is much larger than the Acquired Fund, the Reorganization may be expected to afford shareholders of the Acquired Fund on an ongoing basis greater prospects for growth and efficient management. Combining the Funds will not result in any dilution of the interests of existing shareholders of the Funds.

Board Consideration of the Reorganization

The Board, including the Independent Directors, considered the Reorganization pursuant to the Plan at its meeting on December 19, 2008. The Board considered information presented by PMC, and the Independent Directors were assisted by independent legal counsel. The Board requested and evaluated such information as it deemed necessary to consider the Reorganization. At the meeting, the Board unanimously approved the Reorganization after concluding that participation in the Reorganization is in the best interests of the Acquired Fund and the Acquiring Fund and that the interests of existing shareholders of the Funds will not be diluted as a result of the Reorganization.

In determining whether to approve the Reorganization, the Board made inquiry into a number of matters and considered, among others, the following factors, in no order of priority:

(1) the same investment objectives and substantially the same principal investment strategies shared by the Funds;

(2) the absence of any substantial differences in the Funds’ fundamental investment restrictions;

(3) estimated trading costs associated with disposing of any portfolio securities of the Acquired Fund and reinvesting the proceeds in connection with the Reorganization;

(4) expense ratios and available information regarding the fees and expenses of the Funds;

(5) comparative investment performance of and other information pertaining to the Funds;

24

(6) the potential effect on the Acquired Fund’s shareholders of investing in a larger fund and the potential effect on the portfolio management of the Acquiring Fund of a larger asset base following the Reorganization;

(7) the prospects for growth of and for achieving economies of scale by the Acquired Fund in combination with the Acquiring Fund;

(8) the absence of any material differences in the rights of shareholders of the Funds;

(9) the financial strength, investment experience and resources of Mellon Capital and Turner, which currently serve as the sub-advisors to the Acquiring Fund, and Jacobs Levy which will become an additional sub-advisor to the Acquiring Fund at the Effective Time of the Reorganization;

(10)any direct or indirect benefits expected to be derived by PMC and its affiliates from the Reorganization;

(11) the direct or indirect federal income tax consequences of the Reorganization, including the expected tax-free nature of the Reorganization and the impact of any federal income tax loss carry forwards and the estimated capital gain or loss expected to be incurred in connection with disposing of any portfolio securities that would not be compatible with the investment objectives and strategies of the Acquiring Fund;

(12)the fact that the Reorganization will not result in any dilution of Acquired or Acquiring Fund shareholder values;

(13)the terms and conditions of the Plan; and

(14)possible alternatives to the Reorganization.

The Board’s decision to recommend approval of the Reorganization was based on a number of factors, including the following:

(1) it should be reasonable for shareholders of the Acquired Fund to have similar investment expectations after the Reorganization because the Funds have the same investment objectives and substantially similar principal investment strategies and risks;

(2) Mellon Capital, Turner, and Jacobs Levy as sub-advisors responsible for managing the assets of the Acquiring Fund may be expected to continue to provide high quality investment advisory services and personnel for the foreseeable future;

(3) lower advisory fees and overall expense ratios of the Acquiring Fund; and

(4) the combination of the Acquired Fund into the much larger Acquiring Fund may be expected to afford shareholders of the Acquired Fund on an ongoing basis greater prospects for growth and efficient management.

25

Description of the Securities to Be Issued

PFI is a Maryland corporation that is authorized to issue its shares of common stock in separate series and separate classes of series. Each of the Acquired and Acquiring Funds is a separate series of PFI, and the Class R-1, Class R-2, Class R-3, Class R-4, Class R-5 and Institutional Class shares of common stock of the Acquiring Fund to be issued in connection with the Reorganization represent interests in the assets belonging to that series and have identical dividend, liquidation and other rights, except that expenses allocated to a particular series or class are borne solely by that series or class and may cause differences in rights as described herein. Expenses related to the distribution of, and other identified expenses properly allocated to, the shares of a particular series or class are charged to, and borne solely by, that series or class, and the bearing of expenses by a particular series or class may be appropriately reflected in the net asset value attributable to, and the dividend and liquidation rights of, that series or class.

All shares of PFI have equal voting rights and are voted in the aggregate and not by separate series or class of shares except that shares are voted by series or class: (i) when expressly required by Maryland law or the 1940 Act and (ii) on any matter submitted to shareholders which the Board has determined affects the interests of only a particular series or class.

The share classes of the Acquired Fund have the same rights with respect to the Acquired Fund that the share classes of the Acquiring Fund have with respect to the Acquiring Fund.

Shares of both Funds, when issued, have no cumulative voting rights, are fully paid and non-assessable, have no preemptive or conversion rights and are freely transferable. Each fractional share has proportionately the same rights as are provided for a full share.

| | Federal Income Tax Consequences |

To be considered a tax-free “reorganization” under Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”), a reorganization must exhibit a continuity of business enterprise. Because the Acquiring Fund will use a portion of the Acquired Fund’s assets in its business and will continue the Acquired Fund’s historic business, the combination of the Acquired Fund into the Acquiring Fund will exhibit a continuity of business enterprise. Therefore, the combination will be considered a tax-free “reorganization” under applicable provisions of the Code. In the opinion of tax counsel to PFI, no gain or loss will be recognized by either of the Funds or their shareholders in connection with the combination, the tax cost basis of the Acquiring Fund shares received by shareholders of the Acquired Fund will equal the tax cost basis of their shares in the Acquired Fund, and their holding periods for the Acquiring Fund shares will include their holding periods for the Acquired Fund shares.

26

Capital Loss Carryforward. As of October 31, 2008, the Acquired Fund had an accumulated capital loss carryforward of approximately $66,116,000 expiring in 2016. After the Reorganization, these losses will be available to the Acquiring Fund to offset its capital gains, although the amount of offsetting losses in any given year may be limited. As a result of this limitation, it is possible that the Acquiring Fund may not be able to use these losses as rapidly as the Acquired Fund might have, and part of these losses may not be useable at all. The ability of the Acquiring Fund to utilize the accumulated capital loss carryforward in the future depends upon a variety of factors that cannot be known in advance, including the existence of capital gains against which these losses may be offset. In addition, the benefits of any capital loss carryforward currently are available only to shareholders of the Acquired Fund. After the Reorganization, however, these benefits will inure to the benefit of all shareholders of the Acquiring Fund.

Distribution of Income and Gains. Prior to the Reorganization, the Acquired Fund, whose taxable year will end as a result of the Reorganization, will declare to its shareholders of record one or more distributions of all of its previously undistributed net investment income and net realized capital gain, including capital gains on any securities disposed of in connection with the Reorganization. Such distributions will be made to shareholders before the Reorganization. An Acquired Fund shareholder will be required to include any such distributions in such shareholder’s taxable income. This may result in the recognition of income that could have been deferred or might never have been realized had the Reorganization not occurred.

The foregoing is only a summary of the principal federal income tax consequences of the Reorganization and should not be considered to be tax advice. There can be no assurance that the Internal Revenue Service will concur on all or any of the issues discussed above. You may wish to consult with your own tax advisors regarding the federal, state, and local tax consequences with respect to the foregoing matters and any other considerations which may apply in your particular circumstances.

27

CAPITALIZATION

The following tables show as of October 31, 2008: (i) the capitalization of the Acquired Fund; (ii) the capitalization of the Acquiring Fund; and (iii), the pro forma combined capitalization of the Acquiring Fund, adjusted to reflect the estimated expenses of the Reorganization, as if the Reorganization had occurred as of that date. As of October 31, 2008, the Acquired Fund had outstanding six classes of shares: Institutional, R-1, R-2, R-3, R-4, and R-5. As of October 31, 2008, the Acquiring Fund had outstanding ten classes of shares: Class A, Class B, Class C, Class J, Institutional, R-1, R-2, R-3, R-4, and R-5.

The Acquired Fund will pay all expenses and out-of-pocket fees incurred in connection with the Reorganization including printing, mailing, and legal fees. The expenses and fees the Acquired Fund will pay are expected to total $45,000.

| | Net Asset | Shares |

| Share | Net Assets | Value | Outstanding |

Class | (000s) | Per Share | (000s) |

| MidCap Growth Fund II | | | |

| (Acquired Fund) | | | |

| Institutional | $191,051 | $5.71 | 33,454 |

| R-1 | 1,454 | 5.47 | 266 |

| R-2 | 1,150 | 5.50 | 209 |

| R-3 | 4,701 | 5.54 | 849 |

| R-4 | 5,183 | 5.58 | 929 |

| R-5 | 2,127 | 5.62 | 379 |

| | $205,666 | | 36,086 |

| MidCap Growth Fund III | | | |

| (Acquiring Fund) | | | |

| Class A | $ 21,252 | $6.20 | 3,425 |

| Class B | 5,477 | 6.04 | 907 |

| Class C | 778 | 6.15 | 126 |

| Class J | 20,178 | 5.94 | 3,399 |

| Institutional | 423,812 | 6.37 | 66,503 |

| R-1 | 775 | 6.13 | 126 |

| R-2 | 7,120 | 6.21 | 1,146 |

| R-3 | 23,848 | 6.41 | 3,719 |

| R-4 | 17,117 | 6.42 | 2,667 |

| R-5 | 9,461 | 6.51 | 1,453 |

| | $529,818 | | 83,471 |

28

| | | Net Asset | Shares |

| Share | Net Assets | Value | Outstanding |

| Class | (000s) | Per Share | (000s) |

| Reduction in net assets and decrease in | | |

| net asset values per share of the Acquired | | |

| Fund to reflect the estimated expenses | | |

| of the Reorganization. | | | |

| Institutional | $(42) | $0.00 | (7) |

| R-1 | * | ** | *** |

| R-2 | * | ** | *** |

| R-3 | (1) | 0.00 | *** |

| R-4 | (1) | 0.00 | *** |

| R-5 | (1) | 0.00 | *** |

| Decrease in shares outstanding of the | | |

| Acquired Fund to reflect the exchange | | |

| for shares of the Acquiring Fund. | | |

| Institutional | | | (3,461) |

| R-1 | | | (29) |

| R-2 | | | (24) |

| R-3 | | | (116) |

| R-4 | | | (122) |

| R-5 | | | (52) |

| * | Less than $500. |

| ** | Per share amount is less than $.005. |

| *** | Less than 500 shares. |

ADDITIONAL INFORMATION ABOUT THE FUNDS

Certain Investment Strategies and Related Risks of the Funds

This section provides information about certain investment strategies and related risks of the Funds. The Statement of Additional Information contains additional information about investment strategies and their related risks.

Some of the principal investment risks vary between the Funds and the variations are described above. The value of each Fund’s securities may fluctuate on a daily basis. As with all mutual funds, as the values of each Fund’s assets rise or fall, the Fund’s share price changes. If an investor sells Fund shares when their value is less than the price the investor paid, the investor will lose money. As with any security, the securities in which the Funds invest have associated risk.

Market Volatility

Equity securities include common stocks, preferred stocks, convertible securities, depositary receipts, rights, and warrants. Common stocks, the most familiar type, represent an equity (ownership) interest in a corporation. The value of a company’s stock may fall as a result of factors directly relating to

29

that company, such as decisions made by its management or lower demand for the company’s products or services. A stock’s value may also fall because of factors affecting not just the company, but also companies in the same industry or in a number of different industries, such as increases in production costs. The value of a company’s stock may also be affected by changes in financial markets that are relatively unrelated to the company or its industry, such as changes in interest rates or currency exchange rates. In addition, a company’s stock generally pays dividends only after the company invests in its own business and makes required payments to holders of its bonds and other debt. For this reason, the value of a company’s stock will usually react more strongly than its bonds and other debt to actual or perceived changes in the company’s financial condition or prospects. Stocks of smaller companies may be more vulnerable to adverse developments than those of larger companies.

Fixed-income securities include bonds and other debt instruments that are used by issuers to borrow money from investors. The issuer generally pays the investor a fixed, variable or floating rate of interest. The amount borrowed must be repaid at maturity. Some debt securities, such as zero coupon bonds, do not pay current interest, but are sold at a discount from their face values.

Fixed-income securities are sensitive to changes in interest rates. In general, fixed-income security prices rise when interest rates fall and fall when interest rates rise. Longer term bonds and zero coupon bonds are generally more sensitive to interest rate changes.

Fixed-income security prices are also affected by the credit quality of the issuer. Investment grade debt securities are medium and high quality securities. Some bonds, such as lower grade or “junk” bonds, may have speculative characteristics and may be particularly sensitive to economic conditions and the financial condition of the issuers.

Repurchase Agreements and Loaned Securities

The Funds may invest a portion of their assets in repurchase agreements, although this is not a principal investment strategy. Repurchase agreements typically involve the purchase of debt securities from a financial institution such as a bank, savings and loan association, or broker-dealer. A repurchase agreement provides that the Fund sells back to the seller and that the seller repurchases the underlying securities at a specified price on a specific date. Repurchase agreements may be viewed as loans by the Fund collateralized by the underlying securities. This arrangement results in a fixed rate of return that is not subject to market fluctuation while the Fund holds the security. In the event of a default or bankruptcy by a selling financial institution, the affected Fund bears a risk of loss. To minimize such risks, the Funds enter

30

into repurchase agreements only with large, well-capitalized and well-established financial institutions. In addition, the value of the securities collateralizing the repurchase agreement is, and during the entire term of the repurchase agreement remains, at least equal to the repurchase price, including accrued interest.

The Funds may lend their portfolio securities to unaffiliated broker-dealers and other unaffiliated qualified financial institutions. These transactions involve risk of loss to a fund if the counterparty should fail to return such securities to the fund upon demand or if the counterparty’s collateral invested by the fund declines in value as a result of investment losses.

Currency Contracts