UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

ANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811- 07584

Rydex Series Funds

(Exact name of registrant as specified in charter)

805 King Farm Boulevard, Suite 600

Rockville, Maryland 20850

(Address of principal executive offices) (Zip code)

Amy J. Lee

Rydex Series Funds

805 King Farm Boulevard, Suite 600

Rockville, Maryland 20850

(Name and address of agent for service)

Registrant's telephone number, including area code: 1-301-296-5100

Date of fiscal year end: December 31

Date of reporting period: December 31, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

12.31.2014

Guggenheim Funds Annual Report

| Guggenheim Alternative Fund |

| Guggenheim Multi-Hedge Strategies Fund | | |

| Rydex Specialty Fund |

| Rydex Commodities Strategy Fund | | |

| RDXSGIALT-ANN-1214x1215 | guggenheiminvestments.com |

| DEAR SHAREHOLDER | 2 |

| ECONOMIC AND MARKET OVERVIEW | 4 |

| ABOUT SHAREHOLDERS’ FUND EXPENSES | 7 |

| ALTERNATIVE FUND | |

| MULTI-HEDGE STRATEGIES FUND | 10 |

| SPECIALTY FUND | |

| COMMODITIES STRATEGY FUND | 43 |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | 55 |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 78 |

| OTHER INFORMATION | 79 |

| INFORMATION ON BOARD OF TRUSTEES AND OFFICERS | 80 |

| GUGGENHEIM INVESTMENTS PRIVACY POLICIES | 84 |

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 1 |

Dear Shareholder:

Security Investors, LLC (the “Investment Adviser”) is pleased to present the annual shareholder report for two alternative strategy funds (the “Funds”) that are part of the Rydex Series Funds. This report covers performance of the Funds for the annual period ended December 31, 2014.

The Investment Adviser is a part of Guggenheim Investments, which represents the investment management businesses of Guggenheim Partners, LLC, a global, diversified financial services firm.

Guggenheim Funds Distributors, LLC is the distributor of the Funds. Guggenheim Funds Distributors, LLC is affiliated with Guggenheim Partners, LLC and Security Investors, LLC.

We encourage you to read the Economic and Market Overview section of the report, which follows this letter, and then the Performance Report and Fund profile for each Fund.

We are committed to providing innovative investment solutions and appreciate the trust you place in us.

Sincerely,

Donald C. Cacciapaglia

President

January 31, 2015

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objectives, risks, charges, expenses and other information, which should be considered carefully before investing. Obtain a prospectus and summary prospectus (if available) at guggenheiminvestments.com or call 800.820.0888.

| 2 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

The Multi-Hedge Strategies Fund is subject to a number of risks and may not be suitable for all investors. • The Fund’s use of derivatives such as futures, options and swap agreements may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. • The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. • The Fund’s use of short selling involves increased risks and costs. The Fund risks paying more for a security than it received from its sale. • The Fund’s investments in high yield securities and unrated securities of similar credit quality (“junk bonds”) may be subject to greater levels of interest rate, credit and liquidity risk than funds that do not invest in such securities. • The Fund’s fixed income investments will change in value in response to interest rate changes and other factors. • The Fund’s exposure to the commodity and currency markets may subject the Fund to greater volatility as commodity-and currency-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry, commodity or currency—such as droughts, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. The Fund may also incur transaction costs with the conversion between various currencies. • The Fund’s exposure to foreign currencies subjects the Fund to the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of short positions, that the U.S. dollar will decline in value relative to the currency being hedged. • These risks may cause the Fund to experience higher losses and/or volatility than a fund that does not invest in derivatives, use leverage or short sales or have exposure to high yield/fixed income securities, foreign currencies and/or securities. • This Fund is considered non-diversified and can invest a greater portion of its assets in securities of individual issuers than a diversified fund. As a result, changes in the market value of a single security could cause greater fluctuations in the value of fund shares than would occur in a more diversified fund. • Please read the prospectus for more detailed information regarding these and other risks.

The Commodities Strategy Fund is subject may not be suitable for all investors. • The Fund’s exposure to the commodity markets may subject the Fund to greater volatility as commodity-linked investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity—such as droughts, floods, weather, embargos, tariffs and international economic, political and regulatory developments. • To the extent that the Fund’s investments are concentrated in energy-related commodities, the Fund is subject to the risk that this sector will underperform the market as a whole. • The Fund’s use of derivatives, such as futures, options, structured notes and swap agreements, may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities or investments underlying those derivatives. • The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. • The Fund is subject to tracking error risks, which may cause the Fund’s performance not to match that of or be lower than the Fund’s underlying benchmark. • The Fund's investments in other investment companies subjects the Fund to those risks affecting the investment company, including the possibility that the value of the underlying securities held by the investment company could decrease. Moreover, the Fund will incur its pro rata share of the expenses of the underlying investment companies’ expenses. • This Fund is considered non-diversified and can invest a greater portion of its assets in securities of individual issuers than a diversified fund. As a result, changes in the market value of a single security could cause greater fluctuations in the value of fund shares than would occur in a more diversified fund. • See the prospectus for more information on these and additional risks.

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 3 |

ECONOMIC AND MARKET OVERVIEW (Unaudited) | December 31, 2014 |

The U.S. economy continued to grow throughout the 12 months ended December 31, 2014, despite some seasonal volatility in September and October that caused spreads in leveraged credit to widen and upward momentum in U.S. stocks to deteriorate. By the end of October, the spread widening had reversed and equities regained their footing, with some key indices shooting to new highs. Markets similarly overcame a weather-related winter soft patch in the first quarter of 2014. The benchmark U.S. 10-year Treasury rate declined from 3.03% to 2.17% over the period, a positive stimulant to continued economic expansion.

U.S. growth appears to have decoupled from the rest of the world. The third quarter’s 5% U.S. gross domestic product (GDP) growth—the fastest pace in 11 years—signals that the U.S. economy is doing very well. Deeming growth sustainable, the U.S. Federal Reserve (the “Fed”) formally ended its quantitative easing (QE) program in October, and all eyes are now on economic data—primarily inflation and employment figures—that would prompt the Fed to raise rates in 2015. Slowing global growth has translated into expectations of weaker demand for oil in an already oversupplied market, which contributed to oil’s 49% decline in the second half of the year, with West Texas Intermediate ending the year at a five-year low of $53 a barrel.

The bright side to declining energy prices is that it leaves more money for consumers to spend on other goods. Data are already confirming this, as American consumer confidence reached new post-recession highs, and fourth quarter retail spending posted solid gains. Overall, this should be positive for consumer-related companies with primarily domestic operations.

The U.S. added 246,000 jobs per month on average in 2014. Employment levels are transitioning from the recovery phase to the expansion phase, which typically coincides with accelerating economic activity. The downward trend in labor force participation has begun to flatten and, as fewer people leave the workforce, the rapid decline in the nation’s unemployment rate could begin to slow. Until unemployment falls below the natural rate of unemployment, it’s unlikely that the U.S. economy will experience the kind of meaningful wage pressure that would spur action by the Fed. An improving labor market, subdued mortgage rates, and tight housing inventory all point to a rebound in the housing market.

The battle against deflation in Europe forced the European Central Bank (ECB) to announce its own form of QE via purchases of asset-backed securities (ABS) and covered bonds. The consensus appears to be that in its current form, the program is insufficient to avert a slowdown. The next step for the ECB may be to buy sovereign bonds, which the ECB will decide on in the coming months. The only notable positive for Europe over the past year has been the devaluation of

| 4 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

ECONOMIC AND MARKET OVERVIEW (Unaudited)(continued) | December 31, 2014 |

the euro, which fell by 13% against the U.S. dollar between May and December. A weaker euro makes exports more competitive, but still will not be enough to boost inflation in the region.

While markets were already anxious over Europe’s struggles and the potential impact of a stronger dollar on U.S. company earnings, Japan relapsed into recession. This drove the Bank of Japan to announce it would expand its asset purchase program in 2015. China also faces slowing growth as financing costs remain high for smaller companies, forcing the People’s Bank of China (PBOC) to cut benchmark interest rates for the first time since July 2012.

From an investment standpoint, U.S. assets continue to look attractive. With global central banks easing or engaging in their form of QE, global yields remain anchored and are driving investors into U.S. markets. But we are wary of the potential for a setback in U.S. equities as certain factors, such as oil prices and currency fluctuations, drive markets to aggressively discount valuations for some sectors more than others.

For the year ended December 31, 2014, the Standard & Poor’s 500® (“S&P 500”) Index* returned 13.69%. The Morgan Stanley Capital International (“MSCI”) Europe-Australasia-Far East (“EAFE”) Index* returned -4.90%. The return of the MSCI Emerging Markets Index* was -2.19%.

In the bond market, the Barclays U.S. Aggregate Bond Index* posted a 5.97% return for the period, while the Barclays U.S. Corporate High Yield Index* returned 2.45%. The return of the Bank of America Merrill Lynch 3-Month U.S. Treasury Bill Index* was 0.04% for the 12-month period.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

*Index Definitions:

The following indices are referenced throughout this report. Indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees, or expenses.

Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS.

Barclays U.S. Corporate High Yield Index measures the market of U.S. dollar denominated, non-investment grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB +/BB + or below.

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 5 |

ECONOMIC AND MARKET OVERVIEW (Unaudited)(concluded) | December 31, 2014 |

Bank of America (“BofA”) Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada.

MSCI Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance in the global emerging markets.

S&P 500®Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad economy, representing all major industries and is considered a representation of the U.S. stock market.

S&P Goldman Sachs Commodity Index (“GSCI”)TM, a benchmark for investment performance in the commodity markets, measures investable commodity price movements and inflation in the world economy. The index is calculated primarily on a world production weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies, including, but not limited to, convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage and relative-value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry.

| 6 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) |

All mutual funds have operating expenses and it is important for our shareholders to understand the impact of costs on their investments. Shareholders of a Fund incur two types of costs: (i) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and exchange fees; and (ii) ongoing costs, including management fees, administrative services, and shareholder reports, among others. These ongoing costs, or operating expenses, are deducted from a fund’s gross income and reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets, which is known as the expense ratio. The following examples are intended to help investors understand the ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 made at the beginning of the period and held for the entire six-month period beginning June 30, 2014 and ending December 31, 2014.

The following tables illustrate a Fund’s costs in two ways:

Table 1. Based on actual Fund return. This section helps investors estimate the actual expenses paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. Investors may use the information here, together with the amount invested, to estimate the expenses paid over the period. Simply divide the Fund’s account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number provided under the heading “Expenses Paid During Period.”

Table 2. Based on hypothetical 5% return. This section is intended to help investors compare a Fund’s cost with those of other mutual funds. The table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid during the period. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on the 5% return. Investors can assess a Fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 7 |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)(continued) |

The calculations illustrated above assume no shares were bought or sold during the period. Actual costs may have been higher or lower, depending on the amount of investment and the timing of any purchases or redemptions.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, and contingent deferred sales charges ("CDSC") on redemptions, if any. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

More information about a Fund’s expenses, including annual expense ratios for the past five years, can be found in the Financial Highlights section of this report. For additional information on operating expenses and other shareholder costs, please refer to the appropriate Fund prospectus.

| 8 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)(concluded) |

| | Expense Ratio1 | Fund Return | Beginning Account Value June 30, 2014 | Ending Account Value December 31, 2014 | Expenses Paid During Period2 |

Table 1. Based on actual Fund return3 | |

| | |

| Multi-Hedge Strategies Fund | | | | | |

| A-Class | 3.00% | 4.68% | $1,000.00 | $1,046.80 | $15.48 |

| C-Class | 3.76% | 4.26% | 1,000.00 | 1,042.60 | 19.36 |

| H-Class | 3.00% | 4.68% | 1,000.00 | 1,046.80 | 15.48 |

| Institutional Class | 2.75% | 4.80% | 1,000.00 | 1,048.00 | 14.20 |

| Commodities Strategy Fund | | | | | |

| A-Class | 1.56% | (36.85%) | 1,000.00 | 631.50 | 6.42 |

| C-Class | 2.34% | (37.03%) | 1,000.00 | 629.70 | 9.61 |

| H-Class | 1.60% | (36.76%) | 1,000.00 | 632.40 | 6.58 |

| |

| Table 2. Based on hypothetical 5% return (before expenses) |

| |

| Multi-Hedge Strategies Fund | | | | | |

| A-Class | 3.00% | 5.00% | $1,000.00 | $1,010.08 | $15.20 |

| C-Class | 3.76% | 5.00% | 1,000.00 | 1,006.25 | 19.01 |

| H-Class | 3.00% | 5.00% | 1,000.00 | 1,010.08 | 15.20 |

| Institutional Class | 2.75% | 5.00% | 1,000.00 | 1,011.34 | 13.94 |

| Commodities Strategy Fund | | | | | |

| A-Class | 1.56% | 5.00% | 1,000.00 | 1,017.34 | 7.93 |

| C-Class | 2.34% | 5.00% | 1,000.00 | 1,013.41 | 11.88 |

| H-Class | 1.60% | 5.00% | 1,000.00 | 1,017.14 | 8.13 |

1 | Annualized and excludes expenses of the underlying funds in which the Funds invest. This ratio represents net expenses, which include interest expense related to securities sold short. Excluding short interest expenses, the operating expense ratio of the Multi-Hedge Strategies Fund would be 1.44%, 2.19%, 1.44% and 1.18% for the A-Class, C-Class, H-Class and Institutional Class, respectively. |

2 | Expenses are equal to the Fund's annualized expense ratio, net of any applicable fee waivers, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

3 | Actual cumulative return at net asset value for the period June 30, 2014 to December 31, 2014. |

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 9 |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited) | December 31, 2014 |

MULTI-HEDGE STRATEGIES FUND

OBJECTIVE: Seeks long-term capital appreciation with less risk than traditional equity funds.

2014 was the fifth full fiscal year of performance since the Fund’s objective was changed from hedge fund replication to capital appreciation. The Fund seeks capital appreciation with low correlation to equity and fixed income markets, while doing so with low risk–typically in the 5.0% to 8.0% range. The risk-adjusted results for fiscal year 2014 were good for a fifth year, as the Fund’s H-Class shares generated a 4.77% return with only 3.3% annualized risk, resulting in a Sharpe ratio* of 1.42. In addition to generating a good Sharpe ratio, the Fund did so with correlation** of 48% to the S&P 500 Index and -17% to the Barclays U.S. Aggregate Bond Index over the course of the year.

The S&P 500 had four negative-return calendar months in 2014 and, in two of these months, Multi-Hedge Strategies produced positive returns; the Barclays U.S. Aggregate Bond Index had three negative-return calendar months and, in one of these months, Multi-Hedge Strategies produced a positive return.

The S&P 500 beta-adjusted performance (i.e., alpha) of the Fund’s H-Class shares for the year was 2.80% as the fund had a realized beta of 14%. These results demonstrate the Fund’s diversification benefits.

While no longer a replication product, the Fund still maintains the HFRX Global Hedge Fund Index as one of its benchmarks. This benchmark returned -0.58% for the year. In contrast to the diversification benefits provided by the Multi-Hedge Strategies Fund, the HFRX Global Hedge Fund Index had a correlation of 81% to the S&P 500 in 2014. In spite of the greater equity return contribution to the HFRX Global Hedge Fund performance, the Multi-Hedge Strategies Fund has outperformed this index by more than 8% (1.3% annualized), net of fees, since the Fund changed its investment objective on August 1, 2009.

All five of the hedge fund strategies used within the Fund contributed positively to gross fund returns in 2014.

The Fund’s Global Macro strategies contributed the most to gross fund returns with 2.56%. Within Global Macro, the Managed Futures models contributed 2.95%. The Managed Futures models seek to profit from global trends and reversions by trading commodity, currency, equity, and fixed income futures. The Volatility Arbitrage model contributed -0.38%; this strategy seeks to profit from relative value trades across the VIX futures curve.

| 10 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited)(continued) | December 31, 2014 |

The Equity Market Neutral strategies contributed 1.28% to gross fund returns. The Quantitative Market Neutral model contributed 1.12%; this model allocates to stocks resulting in a portfolio with tilts toward value and momentum characteristics while seeking equity beta neutrality. The Closed-end Arbitrage model contributed 0.16%; this strategy purchases closed-end funds trading at discounts while hedging the market-related risks associated with each fund.

The Long/Short Equity strategies contributed 0.97% to gross fund returns, with the Industry and Factor Rotation model contributing 0.54% and the Size model contributing 0.43%. The Industry and Factor Rotation model allocates to industries and risk factors based upon recent trends while typically maintaining a positive equity market beta. The Size model tactically trades the relative performance of large capitalization equities versus small capitalization equities.

The Merger Arbitrage strategy contributed 0.82% to gross fund returns; this strategy typically invests in definitive merger deals and makes allocations based upon the expected return and risk parameters of each trade.

The Treasury Flattener model is the only Fixed Income strategy currently being used and it contributed 0.52% to gross fund returns. The Treasury Flattener model purchases ten-year Treasury note futures and hedges with two-year Treasury note futures on a duration-neutral basis when the yield spread between the two representative bonds is attractive.

Performance displayed represents past performance which is no guarantee of future results.

| * | Sharpe Ratio: a risk-adjusted measure calculated using standard deviation and excess return to determine reward per unit of risk. The higher the Sharpe ratio, the better the fund’s historical risk-adjusted performance. |

| ** | Correlation is a measurement between -1 and 1, which indicates the linear relationship between two variables. If there is no relationship between two variables, the correlation coefficient is 0. If there is a perfect relationship, the correlation is 1. And if there is a perfect inverse relationship, the correlation is -1. |

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 11 |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited)(continued) | December 31, 2014 |

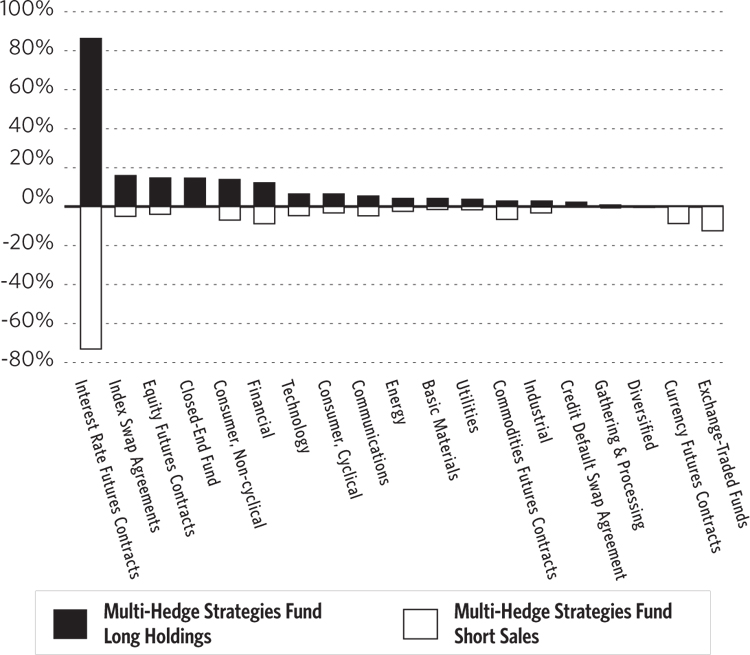

Consolidated Holdings Diversification

(Market Exposure as % of Net Assets)

“Consolidated Holdings Diversification (Market Exposure as % of Net Assets)” excludes any temporary cash investments or investments in Guggenheim Strategy Funds Trust mutual funds.

| Inception Dates: |

| A-Class | September 19, 2005 |

| C-Class | September 19, 2005 |

| H-Class | September 19, 2005 |

| Institutional Class | May 3, 2010 |

| Ten Largest Long Holdings (% of Total Net Assets) |

| TRW Automotive Holdings Corp. | 2.5% |

| Protective Life Corp. | 2.2% |

| Covance, Inc. | 2.1% |

| Time Warner Cable, Inc. | 2.1% |

| CareFusion Corp. | 2.0% |

| Covidien plc | 1.8% |

| Hudson City Bancorp, Inc. | 1.7% |

| Sigma-Aldrich Corp. | 1.6% |

| Dresser-Rand Group, Inc. | 1.5% |

| Lorillard, Inc. | 1.4% |

| Top Ten Total | 18.9% |

| | |

| “Ten Largest Long Holdings” exclude any temporary cash or derivative investments. |

| 12 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited)(continued) | December 31, 2014 |

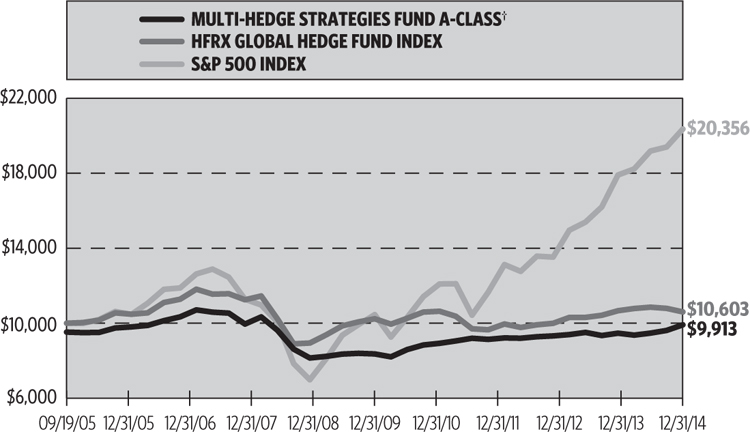

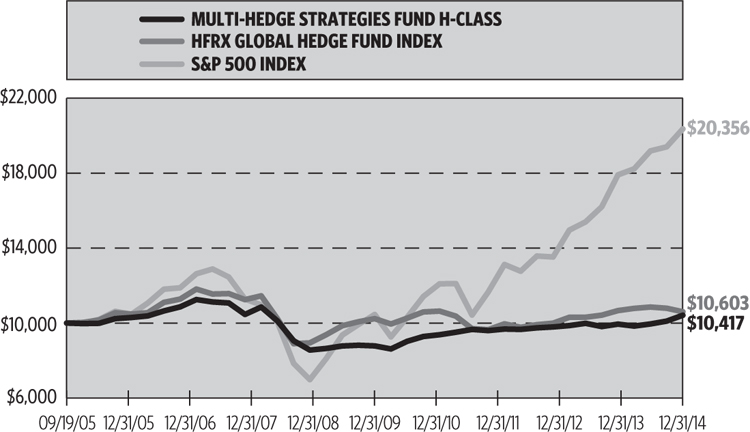

Cumulative Fund Performance*

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 13 |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited)(concluded) | December 31, 2014 |

Average Annual Returns*

Periods Ended December 31, 2014

| | 1 Year | 5 Year | Since Inception (09/19/05) |

| A-Class Shares | 4.73% | 3.39% | 0.43% |

A-Class Shares with sales charge† | -0.26% | 2.38% | -0.09% |

| C-Class Shares | 3.97% | 2.62% | -0.32% |

C-Class Shares with CDSC‡ | 2.97% | 2.62% | -0.32% |

| H-Class Shares | 4.77% | 3.39% | 0.44% |

| HFRX Global Hedge Fund Index | -0.58% | 1.04% | 0.63% |

| S&P 500 Index | 13.69% | 15.45% | 7.96% |

| | | | |

| | | 1 Year | Since Inception (05/03/10) |

| Institutional Class Shares | | 4.98% | 3.87% |

| HFRX Global Hedge Fund Index | | -0.58% | 0.61% |

| S&P 500 Index | | 13.69% | 14.65% |

| * | The performance data represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns are historical and include changes in principal and reinvested dividends and capital gains and do not reflect the effect of taxes. The HFRX Global Hedge Fund Index and the S&P 500 Index are unmanaged indices and, unlike the Fund, have no management fees or operating expenses to reduce their reported returns. The graphs are based on A-Class shares and H-Class shares only; performance for C-Class and Institutional Class shares will vary due to differences in fee structures. |

† | Fund returns are calculated using the maximum sales charge of 4.75%. |

‡ | Fund returns include a CDSC of 1% if redeemed within 12 months of purchase. |

| 14 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

| CONSOLIDATED SCHEDULE OF INVESTMENTS | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

COMMON STOCKS† - 60.2% | |

| | | | | | | | | |

| CONSUMER, NON-CYCLICAL - 13.9% | |

Covance, Inc.*,1 | | | 20,022 | | | $ | 2,079,084 | |

CareFusion Corp.*,1 | | | 33,555 | | | | 1,991,154 | |

Covidien plc1 | | | 17,232 | | | | 1,762,489 | |

Lorillard, Inc.1 | | | 23,249 | | | | 1,463,292 | |

| Cubist Pharmaceuticals, Inc.* | | | 11,581 | | | | 1,165,627 | |

Allergan, Inc.1 | | | 4,120 | | | | 875,872 | |

| Volcano Corp.* | | | 14,948 | | | | 267,270 | |

Gentiva Health Services, Inc.*,1 | | | 11,621 | | | | 221,380 | |

| Avanir Pharmaceuticals, Inc. — Class A* | | | 12,924 | | | | 219,062 | |

Kroger Co.1 | | | 3,297 | | | | 211,701 | |

Chiquita Brands International, Inc.*,1 | | | 14,612 | | | | 211,290 | |

Ingredion, Inc.1 | | | 2,342 | | | | 198,696 | |

Archer-Daniels-Midland Co.1 | | | 3,632 | | | | 188,864 | |

Tyson Foods, Inc. — Class A1 | | | 4,683 | | | | 187,741 | |

Molson Coors Brewing Co. — Class B1 | | | 2,509 | | | | 186,971 | |

Humana, Inc.1 | | | 1,242 | | | | 178,388 | |

Tornier N.V.*,1 | | | 6,894 | | | | 175,797 | |

Amgen, Inc.1 | | | 1,092 | | | | 173,945 | |

Pfizer, Inc.1 | | | 5,423 | | | | 168,926 | |

Cintas Corp.1 | | | 1,625 | | | | 127,465 | |

DENTSPLY International, Inc.1 | | | 2,365 | | | | 125,983 | |

DaVita HealthCare Partners, Inc.*,1 | | | 1,648 | | | | 124,820 | |

| Pilgrim’s Pride Corp.* | | | 3,154 | | | | 103,420 | |

Hill-Rom Holdings, Inc.1 | | | 2,174 | | | | 99,178 | |

Dr Pepper Snapple Group, Inc.1 | | | 1,338 | | | | 95,908 | |

Omnicare, Inc.1 | | | 1,314 | | | | 95,830 | |

Johnson & Johnson1 | | | 884 | | | | 92,440 | |

Charles River Laboratories International, Inc.*,1 | | | 1,433 | | | | 91,196 | |

Quanta Services, Inc.*,1 | | | 2,652 | | | | 75,290 | |

United Therapeutics Corp.*,1 | | | 526 | | | | 68,112 | |

JM Smucker Co.1 | | | 646 | | | | 65,233 | |

UnitedHealth Group, Inc.1 | | | 621 | | | | 62,777 | |

Apollo Education Group, Inc. — Class A*,1 | | | 1,816 | | | | 61,944 | |

DeVry Education Group, Inc.1 | | | 1,290 | | | | 61,236 | |

Constellation Brands, Inc. — Class A*,1 | | | 597 | | | | 58,607 | |

General Mills, Inc.1 | | | 1,052 | | | | 56,103 | |

Cooper Companies, Inc.1 | | | 335 | | | | 54,300 | |

Universal Health Services, Inc. — Class B1 | | | 478 | | | | 53,182 | |

Myriad Genetics, Inc.*,2 | | | 1,433 | | | | 48,808 | |

Biogen Idec, Inc.*,1 | | | 143 | | | | 48,541 | |

Anthem, Inc.1 | | | 383 | | | | 48,132 | |

Gilead Sciences, Inc.*,1 | | | 406 | | | | 38,270 | |

ManpowerGroup, Inc.1 | | | 526 | | | | 35,857 | |

| Herbalife Ltd. | | | 932 | | | | 35,136 | |

Eli Lilly & Co.1 | | | 478 | | | | 32,977 | |

United Rentals, Inc.*,1 | | | 263 | | | | 26,829 | |

Coca-Cola Enterprises, Inc.1 | | | 239 | | | | 10,569 | |

| Mallinckrodt plc* | | | 95 | | | | 9,408 | |

Edwards Lifesciences Corp.*,1 | | | 72 | | | | 9,171 | |

| Total Consumer, Non-cyclical | | | | | | | 13,844,271 | |

| | | | | | | | | |

| FINANCIAL - 12.2% | |

Protective Life Corp.1 | | | 31,983 | | | | 2,227,617 | |

Hudson City Bancorp, Inc.1 | | | 165,788 | | | | 1,677,775 | |

American Realty Capital Healthcare Trust, Inc.1 | | | 103,593 | | | | 1,232,757 | |

Aviv REIT, Inc.1 | | | 24,835 | | | | 856,311 | |

Susquehanna Bancshares, Inc.1 | | | 51,302 | | | | 688,986 | |

Glimcher Realty Trust1 | | | 28,045 | | | | 385,339 | |

Bank of Kentucky Financial Corp.1 | | | 7,865 | | | | 379,644 | |

Morgan Stanley1 | | | 5,423 | | | | 210,412 | |

SunTrust Banks, Inc.1 | | | 4,826 | | | | 202,209 | |

Bank of America Corp.1 | | | 11,254 | | | | 201,334 | |

Voya Financial, Inc.1 | | | 4,635 | | | | 196,432 | |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 15 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

ACE Ltd.1 | | | 1,696 | | | $ | 194,836 | |

Berkshire Hathaway, Inc. — Class B*,1 | | | 1,290 | | | | 193,694 | |

Hanover Insurance Group, Inc.1 | | | 2,700 | | | | 192,564 | |

Starwood Property Trust, Inc.1 | | | 8,148 | | | | 189,359 | |

PartnerRe Ltd.1 | | | 1,648 | | | | 188,086 | |

Wells Fargo & Co.1 | | | 3,417 | | | | 187,320 | |

Everest Re Group Ltd.1 | | | 1,099 | | | | 187,160 | |

MFA Financial, Inc.1 | | | 23,319 | | | | 186,319 | |

Two Harbors Investment Corp.1 | | | 18,541 | | | | 185,781 | |

Chimera Investment Corp.1 | | | 57,700 | | | | 183,486 | |

American Capital Agency Corp.1 | | | 8,291 | | | | 180,993 | |

Interactive Brokers Group, Inc. — Class A1 | | | 6,164 | | | | 179,742 | |

Air Lease Corp. — Class A1 | | | 5,065 | | | | 173,780 | |

AmREIT, Inc.1 | | | 6,349 | | | | 168,503 | |

Ameriprise Financial, Inc.1 | | | 1,242 | | | | 164,254 | |

PNC Financial Services Group, Inc.1 | | | 1,625 | | | | 148,249 | |

Allstate Corp.1 | | | 1,962 | | | | 137,831 | |

Capital One Financial Corp.1 | | | 1,529 | | | | 126,219 | |

| Hudson Valley Holding Corp. | | | 3,400 | | | | 92,344 | |

Reinsurance Group of America, Inc. — Class A1 | | | 1,004 | | | | 87,970 | |

CNA Financial Corp.1 | | | 2,174 | | | | 84,156 | |

Travelers Companies, Inc.1 | | | 764 | | | | 80,869 | |

Axis Capital Holdings Ltd.1 | | | 1,481 | | | | 75,664 | |

Taubman Centers, Inc.1 | | | 884 | | | | 67,555 | |

Navient Corp.1 | | | 2,628 | | | | 56,791 | |

Southside Bancshares, Inc.1 | | | 1,882 | | | | 54,411 | |

Annaly Capital Management, Inc.1 | | | 4,945 | | | | 53,455 | |

BioMed Realty Trust, Inc.1 | | | 2,270 | | | | 48,896 | |

Assurant, Inc.1 | | | 478 | | | | 32,710 | |

Huntington Bancshares, Inc.1 | | | 1,505 | | | | 15,833 | |

Legg Mason, Inc.1 | | | 238 | | | | 12,702 | |

Fifth Third Bancorp1 | | | 406 | | | | 8,272 | |

Jones Lang LaSalle, Inc.1 | | | 48 | | | | 7,197 | |

Unum Group1 | | | 48 | | | | 1,674 | |

| Total Financial | | | | | | | 12,207,491 | |

| | | | | | | | | |

| CONSUMER, CYCLICAL - 6.5% | |

TRW Automotive Holdings Corp.*,1 | | | 23,954 | | | | 2,463,669 | |

| PetSmart, Inc. | | | 13,076 | | | | 1,063,013 | |

| Brookfield Residential Properties, Inc.* | | | 11,052 | | | | 265,911 | |

Royal Caribbean Cruises Ltd.1 | | | 2,700 | | | | 222,561 | |

Alaska Air Group, Inc.1 | | | 3,489 | | | | 208,502 | |

Lowe’s Companies, Inc.1 | | | 3,011 | | | | 207,157 | |

CVS Health Corp.1 | | | 2,127 | | | | 204,851 | |

Whirlpool Corp.1 | | | 1,027 | | | | 198,971 | |

Foot Locker, Inc.1 | | | 3,417 | | | | 191,968 | |

Wyndham Worldwide Corp.1 | | | 2,222 | | | | 190,559 | |

PACCAR, Inc.1 | | | 2,771 | | | | 188,456 | |

Lear Corp.1 | | | 1,911 | | | | 187,431 | |

Macy’s, Inc.1 | | | 2,748 | | | | 180,681 | |

The Gap, Inc.1 | | | 2,963 | | | | 124,772 | |

PulteGroup, Inc.1 | | | 5,566 | | | | 119,446 | |

Carnival Corp.1 | | | 1,433 | | | | 64,958 | |

Deckers Outdoor Corp.*,1 | | | 693 | | | | 63,091 | |

Wendy’s Co.1 | | | 6,858 | | | | 61,928 | |

WABCO Holdings, Inc.*,1 | | | 526 | | | | 55,114 | |

Southwest Airlines Co.1 | | | 1,218 | | | | 51,546 | |

Visteon Corp.*,1 | | | 430 | | | | 45,950 | |

Dillard’s, Inc. — Class A1 | | | 286 | | | | 35,801 | |

Dolby Laboratories, Inc. — Class A1 | | | 764 | | | | 32,944 | |

Leggett & Platt, Inc.1 | | | 549 | | | | 23,393 | |

GameStop Corp. — Class A1 | | | 430 | | | | 14,534 | |

Ford Motor Co.1 | | | 884 | | | | 13,702 | |

Kohl’s Corp.1 | | | 191 | | | | 11,659 | |

General Motors Co.1 | | | 95 | | | | 3,316 | |

Walgreens Boots Alliance, Inc.1 | | | 24 | | | | 1,829 | |

Brinker International, Inc.1 | | | 24 | | | | 1,409 | |

| Total Consumer, Cyclical | | | | | | | 6,499,122 | |

| 16 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

| TECHNOLOGY - 6.5% | |

| Spansion, Inc. — Class A* | | | 41,436 | | | $ | 1,417,940 | |

International Rectifier Corp.*,1 | | | 27,913 | | | | 1,113,729 | |

Tokyo Electron Ltd. ADR1 | | | 53,832 | | | | 1,027,115 | |

Digital River, Inc.*,1 | | | 9,801 | | | | 242,378 | |

Oracle Corp.1 | | | 4,659 | | | | 209,516 | |

Hewlett-Packard Co.1 | | | 5,137 | | | | 206,148 | |

Intel Corp.1 | | | 5,328 | | | | 193,353 | |

Microsoft Corp.1 | | | 4,086 | | | | 189,794 | |

DST Systems, Inc.1 | | | 1,936 | | | | 182,274 | |

Broadridge Financial Solutions, Inc.1 | | | 3,752 | | | | 173,268 | |

Activision Blizzard, Inc.1 | | | 8,577 | | | | 172,826 | |

Western Digital Corp.1 | | | 1,433 | | | | 158,633 | |

Computer Sciences Corp.1 | | | 2,509 | | | | 158,192 | |

CA, Inc.1 | | | 5,065 | | | | 154,229 | |

Micron Technology, Inc.*,1 | | | 4,205 | | | | 147,217 | |

Brocade Communications Systems, Inc.1 | | | 12,066 | | | | 142,862 | |

Xerox Corp.1 | | | 9,844 | | | | 136,438 | |

QUALCOMM, Inc.1 | | | 1,744 | | | | 129,632 | |

Fidelity National Information Services, Inc.1 | | | 1,696 | | | | 105,491 | |

NVIDIA Corp.1 | | | 3,966 | | | | 79,518 | |

Pitney Bowes, Inc.1 | | | 2,820 | | | | 68,723 | |

Lam Research Corp.1 | | | 478 | | | | 37,925 | |

Skyworks Solutions, Inc.1 | | | 263 | | | | 19,123 | |

PTC, Inc.*,1 | | | 286 | | | | 10,482 | |

KLA-Tencor Corp.1 | | | 143 | | | | 10,056 | |

| Total Technology | | | | | | | 6,486,862 | |

| | | | | | | | | |

| COMMUNICATIONS - 5.4% | |

Time Warner Cable, Inc.1 | | | 13,634 | | | | 2,073,186 | |

DIRECTV*,1 | | | 10,793 | | | | 935,753 | |

Trulia, Inc.*,1 | | | 14,948 | | | | 688,056 | |

Sapient Corp.*,1 | | | 17,033 | | | | 423,780 | |

Time Warner, Inc.1 | | | 2,365 | | | | 202,018 | |

Liberty Interactive Corp. — Class A*,1 | | | 6,713 | | | | 197,496 | |

Gannett Company, Inc.1 | | | 5,973 | | | | 190,718 | |

Frontier Communications Corp.1,2 | | | 26,377 | | | | 175,935 | |

Yahoo!, Inc.*,1 | | | 3,249 | | | | 164,107 | |

IAC/InterActiveCorp1 | | | 1,601 | | | | 97,325 | |

Walt Disney Co.1 | | | 932 | | | | 87,785 | |

| Windstream Holdings, Inc. | | | 6,547 | | | | 53,947 | |

Cisco Systems, Inc.1 | | | 1,458 | | | | 40,554 | |

John Wiley & Sons, Inc. — Class A1 | | | 311 | | | | 18,424 | |

Harris Corp.1 | | | 24 | | | | 1,724 | |

T-Mobile US, Inc.*,1 | | | 48 | | | | 1,293 | |

| Total Communications | | | | | | | 5,352,101 | |

| | | | | | | | | |

| ENERGY - 4.2% | |

Dresser-Rand Group, Inc.*,1 | | | 18,548 | | | | 1,517,230 | |

Baker Hughes, Inc.1 | | | 19,325 | | | | 1,083,553 | |

| Talisman Energy, Inc. | | | 22,574 | | | | 176,755 | |

Chevron Corp.1 | | | 1,458 | | | | 163,559 | |

Devon Energy Corp.1 | | | 2,437 | | | | 149,170 | |

Murphy Oil Corp.1 | | | 2,891 | | | | 146,053 | |

Hess Corp.1 | | | 1,936 | | | | 142,916 | |

Murphy USA, Inc.*,1 | | | 2,054 | | | | 141,438 | |

ConocoPhillips1 | | | 2,007 | | | | 138,603 | |

Valero Energy Corp.1 | | | 2,031 | | | | 100,535 | |

Chesapeake Energy Corp.1 | | | 4,205 | | | | 82,292 | |

Unit Corp.*,1 | | | 2,222 | | | | 75,770 | |

Nabors Industries Ltd.1 | | | 4,587 | | | | 59,540 | |

Occidental Petroleum Corp.1 | | | 669 | | | | 53,928 | |

Denbury Resources, Inc.1 | | | 5,973 | | | | 48,560 | |

Helmerich & Payne, Inc.1 | | | 646 | | | | 43,553 | |

Apache Corp.1 | | | 526 | | | | 32,964 | |

Superior Energy Services, Inc.1 | | | 1,458 | | | | 29,379 | |

| Amec Foster Wheeler plc ADR | | | 1,285 | | | | 16,622 | |

California Resources Corp.*,1 | | | 267 | | | | 1,471 | |

| Total Energy | | | | | | | 4,203,891 | |

| | | | | | | | | |

| BASIC MATERIALS - 4.2% | |

Sigma-Aldrich Corp.1 | | | 11,809 | | | | 1,621,021 | |

Rockwood Holdings, Inc.1 | | | 18,373 | | | | 1,447,793 | |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 17 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

CF Industries Holdings, Inc.1 | | | 717 | | | $ | 195,411 | |

Dow Chemical Co.1 | | | 3,584 | | | | 163,466 | |

LyondellBasell Industries N.V. — Class A1 | | | 1,696 | | | | 134,645 | |

Freeport-McMoRan, Inc.1 | | | 5,376 | | | | 125,583 | |

Penford Corp.*,1 | | | 6,408 | | | | 119,766 | |

Cabot Corp.1 | | | 2,389 | | | | 104,782 | |

Domtar Corp.1 | | | 2,270 | | | | 91,299 | |

United States Steel Corp.1 | | | 3,058 | | | | 81,771 | |

Ashland, Inc.1 | | | 597 | | | | 71,497 | |

Westlake Chemical Corp.1 | | | 693 | | | | 42,335 | |

| Total Basic Materials | | | | | | | 4,199,369 | |

| | | | | | | | | |

| UTILITIES - 3.7% | |

Cleco Corp.1 | | | 24,148 | | | | 1,317,031 | |

Pepco Holdings, Inc.1 | | | 25,759 | | | | 693,690 | |

Ameren Corp.1 | | | 4,539 | | | | 209,384 | |

Great Plains Energy, Inc.1 | | | 7,239 | | | | 205,660 | |

Westar Energy, Inc.1 | | | 4,970 | | | | 204,963 | |

American Electric Power Company, Inc.1 | | | 3,249 | | | | 197,279 | |

Public Service Enterprise Group, Inc.1 | | | 4,731 | | | | 195,911 | |

DTE Energy Co.1 | | | 1,888 | | | | 163,067 | |

Xcel Energy, Inc.1 | | | 4,373 | | | | 157,078 | |

Atmos Energy Corp.1 | | | 2,605 | | | | 145,203 | |

AGL Resources, Inc.1 | | | 1,768 | | | | 96,374 | |

UGI Corp.1 | | | 1,864 | | | | 70,795 | |

Alliant Energy Corp.1 | | | 501 | | | | 33,276 | |

| Total Utilities | | | | | | | 3,689,711 | |

| | | | | | | | | |

| INDUSTRIAL - 2.9% | |

Republic Services, Inc. — Class A1 | | | 4,922 | | | | 198,111 | |

Sonoco Products Co.1 | | | 4,420 | | | | 193,155 | |

FedEx Corp.1 | | | 1,076 | | | | 186,857 | |

Ryder System, Inc.1 | | | 2,007 | | | | 186,350 | |

AMERCO1 | | | 646 | | | | 183,631 | |

GATX Corp.1 | | | 2,963 | | | | 170,491 | |

Caterpillar, Inc.1 | | | 1,816 | | | | 166,218 | |

Corning, Inc.1 | | | 6,976 | | | | 159,959 | |

Energizer Holdings, Inc.1 | | | 1,242 | | | | 159,672 | |

Dover Corp.1 | | | 2,127 | | | | 152,547 | |

Northrop Grumman Corp.1 | | | 1,027 | | | | 151,369 | |

Trinity Industries, Inc.1 | | | 4,898 | | | | 137,193 | |

Exelis, Inc.1 | | | 7,598 | | | | 133,193 | |

Alliant Techsystems, Inc.1 | | | 1,123 | | | | 130,549 | |

General Electric Co.1 | | | 4,373 | | | | 110,506 | |

Timken Co.1 | | | 2,222 | | | | 94,835 | |

Packaging Corporation of America1 | | | 1,147 | | | | 89,523 | |

Arrow Electronics, Inc.*,1 | | | 1,362 | | | | 78,846 | |

CSX Corp.1 | | | 1,648 | | | | 59,707 | |

| Garmin Ltd. | | | 812 | | | | 42,898 | |

Raytheon Co.1 | | | 358 | | | | 38,725 | |

Snap-on, Inc.1 | | | 191 | | | | 26,117 | |

Huntington Ingalls Industries, Inc.1 | | | 191 | | | | 21,480 | |

Norfolk Southern Corp.1 | | | 120 | | | | 13,153 | |

PerkinElmer, Inc.1 | | | 120 | | | | 5,248 | |

SPX Corp.1 | | | 48 | | | | 4,124 | |

Vishay Intertechnology, Inc.1 | | | 238 | | | | 3,368 | |

General Dynamics Corp.1 | | | 24 | | | | 3,303 | |

ITT Corp.1 | | | 72 | | | | 2,913 | |

| Total Industrial | | | | | | | 2,904,041 | |

| | | | | | | | | |

| GATHERING & PROCESSING - 0.4% | |

| Atlas Pipeline Partners, LP | | | 14,838 | | | | 404,484 | |

| | | | | | | | | |

| DIVERSIFIED - 0.3% | |

| Restaurant Brands International, Inc.* | | | 8,744 | | | | 341,367 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $54,631,820) | | | | | | | 60,132,710 | |

| | | | | | | | | |

CLOSED-END FUNDS† - 14.6% | |

Cohen & Steers REIT and Preferred Income Fund, Inc.1 | | | 29,266 | | | | 555,762 | |

AllianzGI Equity & Convertible Income Fund1 | | | 26,297 | | | | 543,822 | |

Adams Express Co.1 | | | 38,366 | | | | 524,848 | |

| 18 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

Western Asset/Claymore Inflation-Linked Opportunities & Income Fund1,2,3 | | | 42,994 | | | $ | 485,833 | |

Nuveen Dividend Advantage Municipal Income Fund1 | | | 29,006 | | | | 409,275 | |

Nuveen Maryland Premium Income Municipal Fund1 | | | 31,217 | | | | 394,895 | |

Alpine Total Dynamic Dividend Fund1 | | | 46,227 | | | | 392,467 | |

BlackRock Enhanced Equity Dividend Trust1 | | | 46,007 | | | | 373,578 | |

Gabelli Healthcare & WellnessRx Trust1 | | | 34,995 | | | | 364,649 | |

Tri-Continental Corp.1 | | | 16,527 | | | | 353,843 | |

BlackRock Core Bond Trust1 | | | 26,503 | | | | 349,839 | |

Morgan Stanley Emerging Markets Debt Fund, Inc.1 | | | 38,416 | | | | 349,201 | |

Western Asset/Claymore Inflation-Linked Securities & Income Fund1,3 | | | 28,621 | | | | 332,004 | |

GDL Fund1 | | | 28,773 | | | | 294,348 | |

General American Investors Company, Inc.1 | | | 8,131 | | | | 284,585 | |

Zweig Total Return Fund, Inc.1 | | | 19,794 | | | | 277,314 | |

BlackRock Credit Allocation Income Trust1 | | | 19,837 | | | | 256,294 | |

Swiss Helvetia Fund, Inc.1 | | | 22,252 | | | | 247,887 | |

Clough Global Opportunities Fund1 | | | 17,603 | | | | 225,670 | |

Neuberger Berman Real Estate Securities Income Fund, Inc.1 | | | 40,537 | | | | 214,441 | |

BlackRock Resources & Commodities Strategy Trust1 | | | 20,190 | | | | 196,044 | |

Clough Global Allocation Fund1 | | | 13,038 | | | | 192,441 | |

First Trust High Income Long/Short Fund1 | | | 11,584 | | | | 185,343 | |

Petroleum & Resources Corp.1 | | | 7,691 | | | | 183,353 | |

Advent Claymore Convertible Securities and Income Fund II1,3 | | | 27,025 | | | | 170,258 | |

BlackRock MuniYield Michigan Quality Fund II, Inc.1 | | | 12,262 | | | | 157,689 | |

Duff & Phelps Global Utility Income Fund, Inc.1 | | | 7,151 | | | | 154,747 | |

Madison Covered Call & Equity Strategy Fund1 | | | 18,832 | | | | 153,292 | |

Western Asset Worldwide Income Fund, Inc.1 | | | 11,879 | | | | 135,539 | |

First Trust Enhanced Equity Income Fund1 | | | 8,919 | | | | 127,898 | |

Cohen & Steers Infrastructure Fund, Inc.1 | | | 5,610 | | | | 127,459 | |

Morgan Stanley Income Securities, Inc.1 | | | 6,723 | | | | 120,543 | |

Central Securities Corp.1 | | | 4,995 | | | | 109,489 | |

Ellsworth Fund Ltd.1 | | | 12,425 | | | | 108,222 | |

Western Asset High Yield Defined Opportunity Fund, Inc.1 | | | 6,787 | | | | 107,031 | |

MFS InterMarket Income Trust I1 | | | 12,819 | | | | 106,782 | |

MFS Multimarket Income Trust1 | | | 16,107 | | | | 104,695 | |

Putnam High Income Securities Fund1,2 | | | 12,831 | | | | 104,059 | |

Boulder Total Return Fund, Inc.1 | | | 3,724 | | | | 103,267 | |

Bancroft Fund Ltd.1 | | | 5,140 | | | | 103,108 | |

Zweig Fund, Inc.1 | | | 6,564 | | | | 101,479 | |

Morgan Stanley India Investment Fund, Inc.1 | | | 3,722 | | | | 100,010 | |

New Ireland Fund, Inc.1 | | | 7,889 | | | | 99,559 | |

Eaton Vance Tax-Advantaged Dividend Income Fund1 | | | 4,497 | | | | 93,538 | |

Franklin Limited Duration Income Trust1 | | | 7,159 | | | | 87,268 | |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 19 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

LMP Real Estate Income Fund, Inc.1 | | | 6,951 | | | $ | 87,235 | |

Cohen & Steers Quality Income Realty Fund, Inc.1 | | | 7,131 | | | | 86,927 | |

First Trust Aberdeen Global Opportunity Income Fund1 | | | 7,156 | | | | 86,158 | |

RMR Real Estate Income Fund1 | | | 3,998 | | | | 83,238 | |

John Hancock Premium Dividend Fund1 | | | 6,029 | | | | 82,899 | |

China Fund, Inc.1 | | | 4,542 | | | | 82,801 | |

CBRE Clarion Global Real Estate Income Fund1 | | | 9,163 | | | | 82,375 | |

Nuveen New Jersey Dividend Advantage Municipal Fund1 | | | 6,097 | | | | 82,188 | |

Brookfield Global Listed Infrastructure Income Fund, Inc.1 | | | 3,892 | | | | 81,304 | |

Cohen & Steers Closed-End Opportunity Fund, Inc.1 | | | 6,097 | | | | 80,176 | |

Korea Equity Fund, Inc.1 | | | 10,366 | | | | 79,818 | |

Japan Smaller Capitalization Fund, Inc.1 | | | 8,839 | | | | 79,286 | |

MFS Charter Income Trust1 | | | 8,537 | | | | 78,455 | |

Boulder Growth & Income Fund, Inc.1 | | | 8,654 | | | | 78,319 | |

BlackRock Corporate High Yield Fund, Inc.1 | | | 6,640 | | | | 75,696 | |

Liberty All Star Equity Fund1 | | | 12,634 | | | | 75,551 | |

Western Asset Global Corporate Defined Opportunity Fund, Inc.1 | | | 4,093 | | | | 72,774 | |

Templeton Dragon Fund, Inc.1 | | | 2,978 | | | | 71,591 | |

Central Europe Russia and Turkey Fund, Inc.1 | | | 3,581 | | | | 70,832 | |

Gabelli Dividend & Income Trust1 | | | 3,261 | | | | 70,633 | |

Tortoise Energy Independence Fund, Inc.1 | | | 3,656 | | | | 69,281 | |

Cushing Renaissance Fund1 | | | 3,125 | | | | 66,625 | |

AllianceBernstein Income Fund, Inc.1 | | | 8,909 | | | | 66,550 | |

Delaware Investments National Municipal Income Fund1 | | | 5,003 | | | | 65,339 | |

Wells Fargo Advantage Multi-Sector Income Fund1 | | | 4,784 | | | | 65,206 | |

Voya Natural Resources Equity Income Fund1 | | | 7,843 | | | | 65,018 | |

BlackRock Multi-Sector Income Trust1 | | | 3,867 | | | | 64,850 | |

Morgan Stanley Asia-Pacific Fund, Inc.1 | | | 4,131 | | | | 61,345 | |

Western Asset Emerging Markets Income Fund, Inc.1 | | | 5,495 | | | | 60,170 | |

Royce Value Trust, Inc.1 | | | 4,192 | | | | 60,071 | |

Lazard Global Total Return and Income Fund, Inc.1 | | | 3,778 | | | | 59,730 | |

Ivy High Income Opportunities Fund1 | | | 3,751 | | | | 59,491 | |

Korea Fund, Inc.1 | | | 1,526 | | | | 57,256 | |

Strategic Global Income Fund, Inc.1 | | | 6,389 | | | | 54,179 | |

Clough Global Equity Fund1 | | | 3,675 | | | | 53,214 | |

Asia Tigers Fund, Inc.1 | | | 4,644 | | | | 51,688 | |

Royce Micro-Capital Trust, Inc.1 | | | 4,981 | | | | 50,208 | |

Macquarie Global Infrastructure Total Return Fund, Inc.1 | | | 2,022 | | | | 49,984 | |

Western Asset Emerging Markets Debt Fund, Inc.1 | | | 3,152 | | | | 49,676 | |

Nuveen Diversified Dividend & Income Fund1 | | | 3,859 | | | | 45,420 | |

Deutsche Global High Income Fund, Inc.1 | | | 5,758 | | | | 45,200 | |

| 20 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

Delaware Enhanced Global Dividend & Income Fund1 | | | 3,974 | | | $ | 44,787 | |

Global High Income Fund, Inc.1 | | | 5,023 | | | | 44,303 | |

Nuveen Build America Bond Opportunity Fund1 | | | 1,993 | | | | 43,746 | |

Source Capital, Inc.1 | | | 592 | | | | 42,700 | |

Gabelli Global Utility & Income Trust1 | | | 2,140 | | | | 41,516 | |

Nuveen S&P 500 Dynamic Overwrite Fund1 | | | 2,842 | | | | 40,641 | |

Cohen & Steers Total Return Realty Fund, Inc.1 | | | 3,052 | | | | 40,286 | |

LMP Capital and Income Fund, Inc.1 | | | 2,346 | | | | 39,319 | |

Virtus Global Multi-Sector Income Fund1 | | | 2,412 | | | | 38,230 | |

New America High Income Fund, Inc.1 | | | 4,150 | | | | 37,101 | |

First Trust Intermediate Duration Preferred & Income Fund1 | | | 1,622 | | | | 36,836 | |

First Trust Dividend and Income Fund1 | | | 3,869 | | | | 35,827 | |

Nuveen Build America Bond Fund1 | | | 1,631 | | | | 34,545 | |

Advent/Claymore Enhanced Growth & Income Fund1,3 | | | 3,863 | | | | 34,381 | |

India Fund, Inc.1 | | | 1,310 | | | | 33,811 | |

First Opportunity Fund, Inc.1 | | | 3,444 | | | | 32,890 | |

Aberdeen Greater China Fund, Inc.1 | | | 3,173 | | | | 31,477 | |

Alpine Global Dynamic Dividend Fund1 | | | 3,182 | | | | 31,311 | |

John Hancock Income Securities Trust1 | | | 2,074 | | | | 29,637 | |

Blackstone / GSO Strategic Credit Fund1 | | | 1,731 | | | | 28,527 | |

BlackRock Debt Strategies Fund, Inc.1 | | | 7,592 | | | | 28,242 | |

Royce Focus Trust, Inc.1 | | | 3,557 | | | | 25,859 | |

Nuveen Multi-Market Income Fund1 | | | 3,331 | | | | 25,549 | |

BlackRock Global Opportunities Equity Trust1 | | | 1,921 | | | | 25,223 | |

European Equity Fund, Inc.1 | | | 3,075 | | | | 25,215 | |

Cohen & Steers Limited Duration Preferred and Income Fund, Inc.1 | | | 1,021 | | | | 23,136 | |

Madison Strategic Sector Premium Fund1 | | | 1,898 | | | | 22,605 | |

First Trust Aberdeen Emerging Opportunity Fund1 | | | 1,337 | | | | 21,994 | |

Delaware Investments Dividend & Income Fund, Inc.1 | | | 2,182 | | | | 21,493 | |

Asia Pacific Fund, Inc.*,1 | | | 1,898 | | | | 21,390 | |

Aberdeen Singapore Fund, Inc.1 | | | 1,738 | | | | 20,717 | |

Nuveen Global Equity Income Fund1 | | | 1,570 | | | | 20,426 | |

Nuveen S&P 500 Buy-Write Income Fund1 | | | 1,635 | | | | 19,800 | |

New Germany Fund, Inc.1 | | | 1,405 | | | | 19,684 | |

MFS Intermediate High Income Fund1 | | | 7,331 | | | | 19,427 | |

Fort Dearborn Income Securities, Inc.1 | | | 1,333 | | | | 18,875 | |

BlackRock Utility and Infrastructure Trust1 | | | 892 | | | | 18,500 | |

Nuveen Tax-Advantaged Dividend Growth Fund1 | | | 1,029 | | | | 16,618 | |

Nuveen Pennsylvania Investment Quality Municipal Fund1 | | | 986 | | | | 13,538 | |

Managed High Yield Plus Fund, Inc.1 | | | 7,327 | | | | 13,189 | |

Mexico Equity & Income Fund, Inc.1 | | | 937 | | | | 11,666 | |

Nuveen Credit Strategies Income Fund1 | | | 1,309 | | | | 11,480 | |

Aberdeen Latin America Equity Fund, Inc.1 | | | 509 | | | | 11,402 | |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 21 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

Morgan Stanley Emerging Markets Fund, Inc.1 | | | 754 | | | $ | 10,971 | |

Transamerica Income Shares, Inc. — Class E1 | | | 506 | | | | 10,231 | |

Deutsche Strategic Income Trust1 | | | 830 | | | | 9,595 | |

Western Asset Income Fund1 | | | 664 | | | | 8,931 | |

JPMorgan China Region Fund, Inc.1 | | | 492 | | | | 8,310 | |

Denali Fund, Inc.1 | | | 355 | | | | 7,899 | |

Aberdeen Emerging Markets Smaller Company Opportunities Fund, Inc.1 | | | 526 | | | | 6,880 | |

Neuberger Berman High Yield Strategies Fund, Inc.1 | | | 553 | | | | 6,802 | |

Latin American Discovery Fund, Inc.1 | | | 544 | | | | 6,066 | |

Invesco Bond Fund1 | | | 242 | | | | 4,453 | |

BlackRock Income Trust, Inc.1 | | | 685 | | | | 4,384 | |

Taiwan Fund, Inc.1 | | | 219 | | | | 3,581 | |

Montgomery Street Income Securities, Inc.1 | | | 182 | | | | 2,988 | |

Deutsche High Income Trust1 | | | 327 | | | | 2,858 | |

Cutwater Select Income Fund1 | | | 76 | | | | 1,470 | |

Diversified Real Asset Income Fund1 | | | 84 | | | | 1,457 | |

Calamos Global Dynamic Income Fund1 | | | 156 | | | | 1,440 | |

| Total Closed-End Funds | | | | | | | | |

| (Cost $14,008,716) | | | | | | | 14,568,640 | |

| | | | | | | | | |

MUTUAL FUNDS†,3 - 0.0% | |

| Guggenheim Strategy Fund I | | | 788 | | | | 19,578 | |

| Guggenheim Strategy Fund II | | | 235 | | | | 5,833 | |

| Total Mutual Funds | | | | | | | | |

| (Cost $25,489) | | | | | | | 25,411 | |

| | | | | | | | | |

| | | Face

Amount | | | | |

| | | | | | | | | |

REPURCHASE AGREEMENTS††,4 - 18.3% | |

HSBC Group

issued 12/31/14 at 0.02%

due 01/02/15 | | $ | 11,842,089 | | | | 11,842,089 | |

RBC Capital Markets

issued 12/31/14 at 0.03%

due 01/02/15 | | | 6,397,604 | | | | 6,397,604 | |

| Total Repurchase Agreements | | | | | | | | |

| (Cost $18,239,693) | | | | | | | 18,239,693 | |

| | | | | | | | | |

SECURITIES LENDING COLLATERAL††,5 - 0.2% | |

| Repurchase Agreements | | | | | | | | |

HSBC Securities, Inc.

issued 12/31/14 at 0.06%

due 01/02/15 | | | 124,751 | | | | 124,751 | |

BNP Paribas Securities Corp.

issued 12/31/14 at 0.06%

due 01/02/15 | | | 50,420 | | | | 50,420 | |

Barclays Capital, Inc.

issued 12/31/14 at 0.05%

due 01/02/15 | | | 23,910 | | | | 23,910 | |

| Total Securities Lending Collateral | | | | | | | | |

| (Cost $199,081) | | | | | | | 199,081 | |

| | | | | | | | | |

| Total Investments - 93.3% | | | | | | | | |

| (Cost $87,104,799) | | | | | | $ | 93,165,535 | |

| 22 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

COMMON STOCKS SOLD SHORT† - (37.3)% | |

| | | | | | | | | |

| DIVERSIFIED - (0.4)% | |

| Restaurant Brands International, LP* | | | 87 | | | $ | (3,287 | ) |

| Leucadia National Corp. | | | 3,900 | | | | (87,438 | ) |

| Restaurant Brands International, Inc.* | | | 8,657 | | | | (337,952 | ) |

| Total Diversified | | | | | | | (428,677 | ) |

| | | | | | | | | |

| BASIC MATERIALS - (1.6)% | |

| Compass Minerals International, Inc. | | | 48 | | | | (4,168 | ) |

| Carpenter Technology Corp. | | | 95 | | | | (4,679 | ) |

| Tahoe Resources, Inc. | | | 1,220 | | | | (16,921 | ) |

| Airgas, Inc. | | | 192 | | | | (22,115 | ) |

| Sherwin-Williams Co. | | | 143 | | | | (37,615 | ) |

| PPG Industries, Inc. | | | 192 | | | | (44,381 | ) |

| Newmont Mining Corp. | | | 3,565 | | | | (67,379 | ) |

| Southern Copper Corp. | | | 2,847 | | | | (80,285 | ) |

| Ecolab, Inc. | | | 813 | | | | (84,975 | ) |

| Monsanto Co. | | | 718 | | | | (85,779 | ) |

| Praxair, Inc. | | | 718 | | | | (93,024 | ) |

| FMC Corp. | | | 1,675 | | | | (95,525 | ) |

| EI du Pont de Nemours & Co. | | | 1,292 | | | | (95,530 | ) |

| Allegheny Technologies, Inc. | | | 2,751 | | | | (95,652 | ) |

| WR Grace & Co.* | | | 1,005 | | | | (95,867 | ) |

| Valspar Corp. | | | 1,125 | | | | (97,290 | ) |

| Albemarle Corp. | | | 8,824 | | | | (530,587 | ) |

| Total Basic Materials | | | | | | | (1,551,772 | ) |

| | | | | | | | | |

| UTILITIES - (1.6)% | |

| NRG Energy, Inc. | | | 359 | | | | (9,675 | ) |

| American Water Works Company, Inc. | | | 215 | | | | (11,460 | ) |

| Exelon Corp. | | | 933 | | | | (34,596 | ) |

| PG&E Corp. | | | 1,340 | | | | (71,342 | ) |

| MDU Resources Group, Inc. | | | 3,724 | | | | (87,514 | ) |

| Calpine Corp.* | | | 4,163 | | | | (92,127 | ) |

| PPL Corp. | | | 2,560 | | | | (93,005 | ) |

| CenterPoint Energy, Inc. | | | 3,971 | | | | (93,041 | ) |

| OGE Energy Corp. | | | 2,632 | | | | (93,383 | ) |

| Sempra Energy | | | 861 | | | | (95,881 | ) |

| National Fuel Gas Co. | | | 1,388 | | | | (96,508 | ) |

| Aqua America, Inc. | | | 3,678 | | | | (98,202 | ) |

| NextEra Energy, Inc. | | | 933 | | | | (99,169 | ) |

| ITC Holdings Corp. | | | 2,464 | | | | (99,620 | ) |

| Dominion Resources, Inc. | | | 1,308 | | | | (100,585 | ) |

| Southern Co. | | | 2,057 | | | | (101,019 | ) |

| TECO Energy, Inc. | | | 4,952 | | | | (101,466 | ) |

| Questar Corp. | | | 4,018 | | | | (101,575 | ) |

| FirstEnergy Corp. | | | 2,655 | | | | (103,518 | ) |

| Total Utilities | | | | | | | (1,583,686 | ) |

| | | | | | | | | |

| ENERGY - (2.4)% | |

| Continental Resources, Inc.* | | | 48 | | | | (1,841 | ) |

| Amec Foster Wheeler plc ADR | | | 593 | | | | (7,673 | ) |

| Southwestern Energy Co.* | | | 310 | | | | (8,460 | ) |

| Williams Companies, Inc. | | | 335 | | | | (15,055 | ) |

| Frank’s International N.V. | | | 1,052 | | | | (17,495 | ) |

| Laredo Petroleum, Inc.* | | | 1,795 | | | | (18,578 | ) |

| WPX Energy, Inc.* | | | 2,225 | | | | (25,877 | ) |

| RPC, Inc. | | | 2,512 | | | | (32,756 | ) |

| Gulfport Energy Corp.* | | | 1,077 | | | | (44,954 | ) |

| MRC Global, Inc.* | | | 3,086 | | | | (46,753 | ) |

| Cheniere Energy, Inc.* | | | 790 | | | | (55,616 | ) |

| Concho Resources, Inc.* | | | 574 | | | | (57,257 | ) |

| Peabody Energy Corp. | | | 7,560 | | | | (58,514 | ) |

| Range Resources Corp. | | | 1,363 | | | | (72,852 | ) |

| Antero Resources Corp.* | | | 1,818 | | | | (73,774 | ) |

| Kosmos Energy Ltd.* | | | 8,947 | | | | (75,065 | ) |

| Cobalt International Energy, Inc.* | | | 8,756 | | | | (77,841 | ) |

| Dril-Quip, Inc.* | | | 1,028 | | | | (78,878 | ) |

| CONSOL Energy, Inc. | | | 2,345 | | | | (79,285 | ) |

| Oceaneering International, Inc. | | | 1,363 | | | | (80,158 | ) |

| FMC Technologies, Inc.* | | | 1,722 | | | | (80,659 | ) |

| Pioneer Natural Resources Co. | | | 550 | | | | (81,868 | ) |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 23 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

| Cabot Oil & Gas Corp. — Class A | | | 2,775 | | | $ | (82,168 | ) |

| Targa Resources Partners, LP | | | 8,674 | | | | (415,312 | ) |

| Halliburton Co. | | | 21,644 | | | | (851,259 | ) |

| Total Energy | | | | | | | (2,439,948 | ) |

| | | | | | | | | |

| INDUSTRIAL - (3.0)% | |

| Hexcel Corp.* | | | 167 | | | | (6,929 | ) |

| Fortune Brands Home & Security, Inc. | | | 192 | | | | (8,692 | ) |

| Vulcan Materials Co. | | | 143 | | | | (9,399 | ) |

| USG Corp.* | | | 360 | | | | (10,076 | ) |

| Roper Industries, Inc. | | | 72 | | | | (11,257 | ) |

| Tyco International plc | | | 263 | | | | (11,535 | ) |

| Teekay Corp. | | | 263 | | | | (13,384 | ) |

| Babcock & Wilcox Co. | | | 478 | | | | (14,483 | ) |

| Waste Management, Inc. | | | 287 | | | | (14,729 | ) |

| Clean Harbors, Inc.* | | | 359 | | | | (17,250 | ) |

| Martin Marietta Materials, Inc. | | | 167 | | | | (18,423 | ) |

| Genesee & Wyoming, Inc. — Class A* | | | 215 | | | | (19,333 | ) |

| Wabtec Corp. | | | 240 | | | | (20,854 | ) |

| KLX, Inc.* | | | 622 | | | | (25,658 | ) |

| Lincoln Electric Holdings, Inc. | | | 383 | | | | (26,461 | ) |

| Rockwell Collins, Inc. | | | 359 | | | | (30,328 | ) |

| Xylem, Inc. | | | 1,005 | | | | (38,260 | ) |

| Jacobs Engineering Group, Inc.* | | | 861 | | | | (38,478 | ) |

| Triumph Group, Inc. | | | 574 | | | | (38,584 | ) |

| Colfax Corp.* | | | 790 | | | | (40,740 | ) |

| Acuity Brands, Inc. | | | 311 | | | | (43,562 | ) |

| Waters Corp.* | | | 407 | | | | (45,877 | ) |

| Emerson Electric Co. | | | 790 | | | | (48,767 | ) |

| Chicago Bridge & Iron Company N.V. | | | 1,172 | | | | (49,201 | ) |

| Eagle Materials, Inc. | | | 837 | | | | (63,638 | ) |

| Manitowoc Company, Inc. | | | 2,943 | | | | (65,040 | ) |

| Donaldson Company, Inc. | | | 1,698 | | | | (65,594 | ) |

| B/E Aerospace, Inc.* | | | 1,244 | | | | (72,177 | ) |

| KBR, Inc. | | | 4,808 | | | | (81,496 | ) |

| Jabil Circuit, Inc. | | | 3,828 | | | | (83,565 | ) |

| SunPower Corp. — Class A* | | | 3,301 | | | | (85,265 | ) |

| Armstrong World Industries, Inc.* | | | 1,698 | | | | (86,802 | ) |

| Landstar System, Inc. | | | 1,212 | | | | (87,906 | ) |

| Graco, Inc. | | | 1,100 | | | | (88,198 | ) |

| SBA Communications Corp. — Class A* | | | 813 | | | | (90,047 | ) |

| Trimble Navigation Ltd.* | | | 3,421 | | | | (90,793 | ) |

| National Instruments Corp. | | | 2,966 | | | | (92,213 | ) |

| Nordson Corp. | | | 1,196 | | | | (93,240 | ) |

| Boeing Co. | | | 718 | | | | (93,326 | ) |

| Kansas City Southern | | | 765 | | | | (93,353 | ) |

| TransDigm Group, Inc. | | | 478 | | | | (93,855 | ) |

| Mettler-Toledo International, Inc.* | | | 311 | | | | (94,065 | ) |

| AptarGroup, Inc. | | | 1,435 | | | | (95,915 | ) |

| Expeditors International of Washington, Inc. | | | 2,153 | | | | (96,045 | ) |

| Stericycle, Inc.* | | | 742 | | | | (97,261 | ) |

| United Parcel Service, Inc. — Class B | | | 885 | | | | (98,385 | ) |

| CH Robinson Worldwide, Inc. | | | 1,315 | | | | (98,480 | ) |

| J.B. Hunt Transport Services, Inc. | | | 1,172 | | | | (98,741 | ) |

| Pall Corp. | | | 1,005 | | | | (101,716 | ) |

| Middleby Corp.* | | | 1,028 | | | | (101,875 | ) |

| Sealed Air Corp. | | | 2,464 | | | | (104,548 | ) |

| Total Industrial | | | | | | | (3,015,799 | ) |

| | | | | | | | | |

| CONSUMER, CYCLICAL - (3.2)% | |

| Domino’s Pizza, Inc. | | | 48 | | | | (4,520 | ) |

| Kate Spade & Co.* | | | 215 | | | | (6,882 | ) |

| Coach, Inc. | | | 215 | | | | (8,075 | ) |

| Taylor Morrison Home Corp. — Class A* | | | 527 | | | | (9,955 | ) |

| Hasbro, Inc. | | | 215 | | | | (11,823 | ) |

| World Fuel Services Corp. | | | 263 | | | | (12,343 | ) |

| Sally Beauty Holdings, Inc.* | | | 430 | | | | (13,218 | ) |

| McDonald’s Corp. | | | 167 | | | | (15,648 | ) |

| Spirit Airlines, Inc.* | | | 311 | | | | (23,505 | ) |

| Mattel, Inc. | | | 790 | | | | (24,446 | ) |

| 24 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

| BorgWarner, Inc. | | | 455 | | | $ | (25,002 | ) |

| Dollar General Corp.* | | | 478 | | | | (33,795 | ) |

| Ross Stores, Inc. | | | 383 | | | | (36,102 | ) |

| MSC Industrial Direct Company, Inc. — Class A | | | 455 | | | | (36,969 | ) |

| Scotts Miracle-Gro Co. — Class A | | | 598 | | | | (37,267 | ) |

| Rite Aid Corp.* | | | 5,071 | | | | (38,134 | ) |

| Cabela’s, Inc.* | | | 765 | | | | (40,323 | ) |

| Delta Air Lines, Inc. | | | 1,028 | | | | (50,567 | ) |

| L Brands, Inc. | | | 598 | | | | (51,757 | ) |

| DSW, Inc. — Class A | | | 1,435 | | | | (53,526 | ) |

| SeaWorld Entertainment, Inc. | | | 3,301 | | | | (59,088 | ) |

| Tesla Motors, Inc.* | | | 335 | | | | (74,507 | ) |

| Ralph Lauren Corp. — Class A | | | 407 | | | | (75,360 | ) |

| United Continental Holdings, Inc.* | | | 1,196 | | | | (80,001 | ) |

| Yum! Brands, Inc. | | | 1,148 | | | | (83,632 | ) |

| Tupperware Brands Corp. | | | 1,340 | | | | (84,420 | ) |

| Dunkin’ Brands Group, Inc. | | | 2,010 | | | | (85,727 | ) |

| Navistar International Corp.* | | | 2,608 | | | | (87,316 | ) |

| WW Grainger, Inc. | | | 343 | | | | (87,427 | ) |

| Tempur Sealy International, Inc.* | | | 1,603 | | | | (88,021 | ) |

| Toll Brothers, Inc.* | | | 2,583 | | | | (88,519 | ) |

| PVH Corp. | | | 693 | | | | (88,822 | ) |

| Target Corp. | | | 1,172 | | | | (88,967 | ) |

| Toro Co. | | | 1,435 | | | | (91,568 | ) |

| DreamWorks Animation SKG, Inc. — Class A* | | | 4,163 | | | | (92,960 | ) |

| LKQ Corp.* | | | 3,325 | | | | (93,499 | ) |

| Ulta Salon Cosmetics & Fragrance, Inc.* | | | 742 | | | | (94,857 | ) |

| Costco Wholesale Corp. | | | 670 | | | | (94,972 | ) |

| HD Supply Holdings, Inc.* | | | 3,253 | | | | (95,931 | ) |

| Choice Hotels International, Inc. | | | 1,746 | | | | (97,811 | ) |

| Tractor Supply Co. | | | 1,244 | | | | (98,052 | ) |

| Starbucks Corp. | | | 1,196 | | | | (98,132 | ) |

| Fastenal Co. | | | 2,081 | | | | (98,973 | ) |

| Panera Bread Co. — Class A* | | | 574 | | | | (100,335 | ) |

| GNC Holdings, Inc. — Class A | | | 2,153 | | | | (101,105 | ) |

| Goodyear Tire & Rubber Co. | | | 3,540 | | | | (101,138 | ) |

| Copart, Inc.* | | | 2,798 | | | | (102,099 | ) |

| CarMax, Inc.* | | | 1,698 | | | | (113,053 | ) |

| Lions Gate Entertainment Corp. | | | 3,764 | | | | (120,523 | ) |

| Total Consumer, Cyclical | | | | | | | (3,200,672 | ) |

| | | | | | | | | |

| TECHNOLOGY - (4.6)% | |

| salesforce.com, Inc.* | | | 95 | | | | (5,634 | ) |

| Accenture plc — Class A | | | 72 | | | | (6,430 | ) |

| Red Hat, Inc.* | | | 95 | | | | (6,568 | ) |

| Teradata Corp.* | | | 167 | | | | (7,295 | ) |

| International Business Machines Corp. | | | 48 | | | | (7,701 | ) |

| Jack Henry & Associates, Inc. | | | 143 | | | | (8,886 | ) |

| Solera Holdings, Inc. | | | 239 | | | | (12,232 | ) |

| VeriFone Systems, Inc.* | | | 598 | | | | (22,246 | ) |

| Veeva Systems, Inc. — Class A* | | | 957 | | | | (25,274 | ) |

| Linear Technology Corp. | | | 574 | | | | (26,174 | ) |

| IHS, Inc. — Class A* | | | 263 | | | | (29,950 | ) |

| SunEdison, Inc.* | | | 1,578 | | | | (30,787 | ) |

| athenahealth, Inc.* | | | 263 | | | | (38,319 | ) |

| Diebold, Inc. | | | 1,148 | | | | (39,767 | ) |

| Genpact Ltd.* | | | 2,583 | | | | (48,896 | ) |

| Informatica Corp.* | | | 1,340 | | | | (51,101 | ) |

| Allscripts Healthcare Solutions, Inc.* | | | 4,091 | | | | (52,242 | ) |

| Freescale Semiconductor Ltd.* | | | 2,655 | | | | (66,986 | ) |

| Cree, Inc.* | | | 2,201 | | | | (70,916 | ) |

| Stratasys Ltd.* | | | 909 | | | | (75,547 | ) |

| Rackspace Hosting, Inc.* | | | 1,675 | | | | (78,407 | ) |

| Workday, Inc. — Class A* | | | 1,028 | | | | (83,895 | ) |

| Zynga, Inc. — Class A* | | | 32,008 | | | | (85,141 | ) |

| Altera Corp. | | | 2,392 | | | | (88,360 | ) |

| SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 25 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

| Nuance Communications, Inc.* | | | 6,220 | | | $ | (88,759 | ) |

| SolarWinds, Inc.* | | | 1,795 | | | | (89,445 | ) |

| MSCI, Inc. — Class A | | | 1,962 | | | | (93,077 | ) |

| Paychex, Inc. | | | 2,033 | | | | (93,864 | ) |

| NCR Corp.* | | | 3,253 | | | | (94,792 | ) |

| Atmel Corp.* | | | 11,315 | | | | (94,989 | ) |

| Tableau Software, Inc. — Class A* | | | 1,148 | | | | (97,304 | ) |

| IPG Photonics Corp.* | | | 1,315 | | | | (98,520 | ) |

| NetSuite, Inc.* | | | 909 | | | | (99,236 | ) |

| ServiceNow, Inc.* | | | 1,507 | | | | (102,251 | ) |

| Leidos Holdings, Inc. | | | 2,392 | | | | (104,100 | ) |

| Applied Materials, Inc. | | | 43,739 | | | | (1,089,977 | ) |

| Cypress Semiconductor Corp. | | | 101,811 | | | | (1,453,862 | ) |

| Total Technology | | | | | | | (4,568,930 | ) |

| | | | | | | | | |

| COMMUNICATIONS - (4.7)% | |

| United States Cellular Corp.* | | | 335 | | | | (13,343 | ) |

| Alliance Data Systems Corp.* | | | 72 | | | | (20,596 | ) |

| CenturyLink, Inc. | | | 550 | | | | (21,769 | ) |

| DISH Network Corp. — Class A* | | | 311 | | | | (22,669 | ) |

| Charter Communications, Inc. — Class A* | | | 167 | | | | (27,826 | ) |

| Clear Channel Outdoor Holdings, Inc. — Class A | | | 2,798 | | | | (29,631 | ) |

| Verizon Communications, Inc. | | | 742 | | | | (34,711 | ) |

| HomeAway, Inc.* | | | 1,698 | | | | (50,566 | ) |

| Pandora Media, Inc.* | | | 3,421 | | | | (60,996 | ) |

| Netflix, Inc.* | | | 192 | | | | (65,589 | ) |

| Palo Alto Networks, Inc.* | | | 550 | | | | (67,413 | ) |

| Level 3 Communications, Inc.* | | | 1,389 | | | | (68,589 | ) |

| Discovery Communications, Inc. — Class A* | | | 2,416 | | | | (83,231 | ) |

| Splunk, Inc.* | | | 1,435 | | | | (84,593 | ) |

| Amazon.com, Inc.* | | | 287 | | | | (89,070 | ) |

| Motorola Solutions, Inc. | | | 1,460 | | | | (97,937 | ) |

| LinkedIn Corp. — Class A* | | | 430 | | | | (98,775 | ) |

| JDS Uniphase Corp.* | | | 7,201 | | | | (98,798 | ) |

| AMC Networks, Inc. — Class A* | | | 1,555 | | | | (99,162 | ) |

| Groupon, Inc. — Class A* | | | 12,894 | | | | (106,504 | ) |

| AT&T, Inc. | | | 15,000 | | | | (503,850 | ) |

| Zillow, Inc. — Class A* | | | 6,636 | | | | (702,686 | ) |

| Comcast Corp. — Class A | | | 39,197 | | | | (2,273,818 | ) |

| Total Communications | | | | | | | (4,722,122 | ) |

| | | | | | | | | |

| CONSUMER, NON-CYCLICAL - (7.0)% | |

| Medivation, Inc.* | | | 24 | | | | (2,391 | ) |

| Intercept Pharmaceuticals, Inc.* | | | 24 | | | | (3,744 | ) |

| Keurig Green Mountain, Inc. | | | 48 | | | | (6,355 | ) |

| Coty, Inc. — Class A* | | | 311 | | | | (6,425 | ) |

| ConAgra Foods, Inc. | | | 215 | | | | (7,800 | ) |

| Robert Half International, Inc. | | | 143 | | | | (8,348 | ) |

| Alnylam Pharmaceuticals, Inc.* | | | 95 | | | | (9,215 | ) |

| Clorox Co. | | | 95 | | | | (9,900 | ) |

| Moody’s Corp. | | | 120 | | | | (11,497 | ) |

| H&R Block, Inc. | | | 360 | | | | (12,125 | ) |

| Altria Group, Inc. | | | 263 | | | | (12,958 | ) |

| PepsiCo, Inc. | | | 167 | | | | (15,792 | ) |

| Kellogg Co. | | | 263 | | | | (17,211 | ) |

| Western Union Co. | | | 1,077 | | | | (19,289 | ) |

| Kraft Foods Group, Inc. | | | 311 | | | | (19,487 | ) |

| FleetCor Technologies, Inc.* | | | 215 | | | | (31,973 | ) |

| Bruker Corp.* | | | 1,938 | | | | (38,024 | ) |

| WhiteWave Foods Co. — Class A* | | | 1,100 | | | | (38,489 | ) |

| Incyte Corp.* | | | 574 | | | | (41,965 | ) |

| Gartner, Inc.* | | | 527 | | | | (44,379 | ) |

| Sysco Corp. | | | 1,244 | | | | (49,374 | ) |

| Kindred Healthcare, Inc. | | | 2,987 | | | | (54,304 | ) |

| CoStar Group, Inc.* | | | 311 | | | | (57,109 | ) |

| Intuitive Surgical, Inc.* | | | 120 | | | | (63,473 | ) |

| Hain Celestial Group, Inc.* | | | 1,100 | | | | (64,119 | ) |

| Bunge Ltd. | | | 718 | | | | (65,273 | ) |

| 26 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (continued) | December 31, 2014 |

| MULTI-HEDGE STRATEGIES FUND | |

| | | Shares | | | Value | |

| | | | | | | | | |

| Avon Products, Inc. | | | 7,176 | | | $ | (67,383 | ) |

| Catamaran Corp.* | | | 1,315 | | | | (68,051 | ) |

| Vertex Pharmaceuticals, Inc.* | | | 598 | | | | (71,042 | ) |

| Estee Lauder Companies, Inc. — Class A | | | 957 | | | | (72,923 | ) |

| Pharmacyclics, Inc.* | | | 670 | | | | (81,914 | ) |

| Seattle Genetics, Inc.* | | | 2,583 | | | | (82,992 | ) |

| Brown-Forman Corp. — Class B | | | 993 | | | | (87,225 | ) |

| Hertz Global Holdings, Inc.* | | | 3,517 | | | | (87,714 | ) |