UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811- 07584

Rydex Series Funds

(Exact name of registrant as specified in charter)

702 King Farm Boulevard, Suite 200

Rockville, Maryland 20850

(Address of principal executive offices) (Zip code)

Amy J. Lee

Rydex Series Funds

702 King Farm Boulevard, Suite 200

Rockville, Maryland 20850

(Name and address of agent for service)

Registrant's telephone number, including area code: (301) 296-5100

Date of fiscal year end: December 31

Date of reporting period: January 1, 2023 – June 30, 2023

Item 1. Reports to Stockholders.

The registrant’s semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

6.30.2023

Guggenheim Funds Semi-Annual Report

Guggenheim Alternative Fund |

Guggenheim Multi-Hedge Strategies Fund | | |

Rydex Commodities Fund |

Rydex Commodities Strategy Fund | | |

GuggenheimInvestments.com | RDXSGIALT-SEMI-0623x1223 |

| | |

DEAR SHAREHOLDER | 2 |

ECONOMIC AND MARKET OVERVIEW | 4 |

ABOUT SHAREHOLDERS’ FUND EXPENSES | 6 |

MULTI-HEDGE STRATEGIES FUND | 9 |

COMMODITIES STRATEGY FUND | 53 |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | 64 |

OTHER INFORMATION | 85 |

INFORMATION ON BOARD OF TRUSTEES AND OFFICERS | 99 |

GUGGENHEIM INVESTMENTS PRIVACY NOTICE | 108 |

LIQUIDITY RISK MANAGEMENT PROGRAM | 112 |

| | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 1 |

Dear Shareholder:

Security Investors, LLC (the “Investment Adviser”) is pleased to present the semi-annual shareholder report for two alternative strategy funds (each a “Fund”) that are part of the Rydex Series Funds. This report covers performance of the Funds for the semi-annual period ended June 30, 2023 (the “Reporting Period”).

The Investment Adviser is a part of Guggenheim Investments, which represents the investment management businesses of Guggenheim Partners, LLC (“Guggenheim”), a global, diversified financial services firm.

Guggenheim Funds Distributors, LLC is the distributor of the Funds. Guggenheim Funds Distributors, LLC is affiliated with Guggenheim and the Investment Adviser.

We encourage you to read the Economic and Market Overview section of the report, which follows this letter.

We are committed to providing innovative investment solutions and appreciate the trust you place in us.

Sincerely,

Security Investors, LLC

July 31, 2023

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objectives, risks, charges, expenses and other information, which should be considered carefully before investing. Obtain a prospectus and summary prospectus (if available) at guggenheiminvestments.com or call 800.820.0888.

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

2 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | |

The Multi-Hedge Strategies Fund is subject to a number of risks and may not be suitable for all investors. ● The Fund’s use of derivatives such as futures, options and swap agreements may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. ● The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. ● The Fund’s use of short selling involves increased risks and costs. The Fund risks paying more for a security than it received from its sale. ● The Fund’s investments in high yield securities and unrated securities of similar credit quality (“junk bonds”) may be subject to greater levels of interest rate, credit and liquidity risk than funds that do not invest in such securities. ● The Fund’s fixed income investments will change in value in response to interest rate changes and other factors. ● The Fund’s exposure to the commodity and currency markets may subject the Fund to greater volatility as commodity- and currency-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry, commodity or currency—such as droughts, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. The Fund may also incur transaction costs with the conversion between various currencies. ● The Fund’s exposure to foreign currencies subjects the Fund to the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of short positions, that the U.S. dollar will decline in value relative to the currency being hedged. ● These risks may cause the Fund to experience higher losses and/or volatility than a fund that does not invest in derivatives, use leverage or short sales or have exposure to high yield/fixed income securities, foreign currencies and/or securities. ● See the prospectus for more detailed information regarding these and additional risks.

The Commodities Strategy Fund is subject to a number of risks and may not be suitable for all investors. ● The Fund’s exposure to the commodity markets may subject the Fund to greater volatility as commodity-linked investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity—such as droughts, floods, weather, embargos, tariffs and international economic, political and regulatory developments. ● To the extent that the Fund’s investments are concentrated in energy-related commodities, the Fund is subject to the risk that this sector will underperform the market as a whole. ● The Fund’s use of derivatives, such as futures, options, structured notes and swap agreements, may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities or investments underlying those derivatives. ● The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. ● The Fund is subject to tracking error risks, which may cause the Fund’s performance not to match that of or be lower than the Fund’s underlying benchmark. ● The Fund’s investments in other investment companies subjects the Fund to those risks affecting the investment company, including the possibility that the value of the underlying securities held by the investment company could decrease. Moreover, the Fund will incur its pro rata share of the expenses of the underlying investment companies’ expenses. ●This Fund is considered non-diversified and can invest a greater portion of its assets in securities of individual issuers than a diversified fund. As a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a more diversified fund. ● See the prospectus for more detailed information on these and additional risks.

| | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 3 |

ECONOMIC AND MARKET OVERVIEW (Unaudited) | June 30, 2023 |

The fundamental backdrop we see for the economy is that inflation, while making some progress, continues to run well above target while the labor market appears overheated. As a result, the U.S. Federal Reserve (the “Fed”) is employing a deliberate and forceful strategy which has the effect of weakening the economy. The Fed believes this strategy is required to meaningfully reduce inflation. We expect Fed policymakers to deliver an additional rate hike in September 2023 as they try to limit an undue easing of financial conditions that could risk a resurgence in inflation. Quantitative tightening appears likely to continue at least into early 2024.

Despite the abrupt tightening of Fed policy seen over recent quarters, growth of real gross domestic product has been resilient, aided by a significant fiscal expansion and easing inflation pressures that have boosted real personal consumption. Indeed, headline personal consumption expenditures inflation has slowed to 2.5% on an annualized basis in the three months ended May 2023, down from 7.3% in the corresponding period a year earlier, helping to lift real income growth and support consumer spending.

Notwithstanding recent stronger-than-expected economic activity, we continue to believe the Fed’s policy measures will likely result in a higher unemployment rate and may ultimately lead to a recession. A range of leading indicators, including a low unemployment rate, an inverted yield curve, a declining leading economic index, and falling consumer confidence, suggest a downturn may be approaching.

While a recession understandably provokes fear among investors, in this environment it is arguably not the worst outcome from a medium-term perspective, as we see signs a recession could be moderate in its severity. Moreover, we expect inflation to be brought under control as spending and demand for labor cool, in turn allowing the Fed to start to ease its monetary policy stance as we progress through 2024.

For the Reporting Period, the S&P 500® Index* returned 16.89%. The MSCI Europe-Australasia-Far East (“EAFE”) Index* returned 11.67%. The return of the MSCI Emerging Markets Index* was 4.89%.

In the bond market, the Bloomberg U.S. Aggregate Bond Index* posted a 2.09% return for the Reporting Period, while the Bloomberg U.S. Corporate High Yield Index* returned 5.38%. The return of the ICE Bank of America (“BofA”) 3-Month U.S. Treasury Bill Index* was 2.27% for the Reporting Period.

4 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | |

ECONOMIC AND MARKET OVERVIEW (Unaudited)(concluded) | June 30, 2023 |

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

*Index Definitions:

The following indices are referenced throughout this report. Indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees, or expenses.

Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, mortgage-backed securities or “MBS” (agency fixed-rate and hybrid adjustable-rate mortgage, or “ARM”, pass-throughs), asset-backed securities (“ABS”), and commercial mortgage-backed securities (“CMBS”) (agency and non-agency).

Bloomberg U.S. Corporate High Yield Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB +/BB + or below.

HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies, including, but not limited to, convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage and relative-value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry.

ICE BofA 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada.

MSCI Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance in the global emerging markets.

S&P 500® Index is a broad-based index, the performance of which is based on the performance of 500 widely held common stocks chosen for market size, liquidity, and industry group representation.

S&P Goldman Sachs Commodity Index (S&P GSCI®), a benchmark for investment performance in the commodity markets, measures investable commodity price movements and inflation in the world economy. The index is calculated primarily on a world production weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

| | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 5 |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) |

All mutual funds have operating expenses, and it is important for our shareholders to understand the impact of costs on their investments. Shareholders of a fund incur two types of costs: (i) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, other distributions, and exchange fees, and (ii) ongoing costs, including management fees, administrative services, and shareholder reports, among others. These ongoing costs, or operating expenses, are deducted from a fund’s gross income and reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets, which is known as the expense ratio. The following examples are intended to help investors understand the ongoing costs (in dollars) of investing in a fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 made at the beginning of the period and held for the entire six-month period beginning December 31, 2022 and ending June 30, 2023.

The following tables illustrate the Funds’ costs in two ways:

Table 1. Based on actual Fund return: This section helps investors estimate the actual expenses paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fifth column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. Investors may use the information here, together with the amount invested, to estimate the expenses paid over the period. Simply divide the Fund’s account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number provided under the heading “Expenses Paid During Period.”

Table 2. Based on hypothetical 5% return: This section is intended to help investors compare a fund’s cost with those of other mutual funds. The table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid during the period. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on the 5% return. Investors can assess a fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

The calculations illustrated above assume no shares were bought or sold during the period. Actual costs may have been higher or lower, depending on the amount of investment and the timing of any purchases or redemptions.

6 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)(continued) |

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, and contingent deferred sales charges (“CDSC”) on redemptions, if any. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

More information about the Funds’ expenses, including annual expense ratios for periods up to five years (subject to the Fund’s inception date), can be found in the Financial Highlights section of this report. For additional information on operating expenses and other shareholder costs, please refer to the appropriate Fund prospectus.

| | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 7 |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)(concluded) |

| Expense

Ratio1 | Fund

Return | Beginning

Account Value

December 31,

2022 | Ending

Account Value

June 30,

2023 | Expenses

Paid During

Period2 |

Table 1. Based on actual Fund return3 |

Multi-Hedge Strategies Fund |

A-Class | 1.72% | 1.57% | $ 1,000.00 | $ 1,015.70 | $ 8.60 |

C-Class | 2.47% | 1.21% | 1,000.00 | 1,012.10 | 12.32 |

P-Class | 1.72% | 1.60% | 1,000.00 | 1,016.00 | 8.60 |

Institutional Class | 1.47% | 1.72% | 1,000.00 | 1,017.20 | 7.35 |

Commodities Strategy Fund |

A-Class | 1.54% | (8.68%) | 1,000.00 | 913.20 | 7.31 |

C-Class | 2.29% | (9.03%) | 1,000.00 | 909.70 | 10.84 |

H-Class | 1.55% | (8.66%) | 1,000.00 | 913.40 | 7.35 |

|

Table 2. Based on hypothetical 5% return (before expenses) |

Multi-Hedge Strategies Fund |

A-Class | 1.72% | 5.00% | $ 1,000.00 | $ 1,016.27 | $ 8.60 |

C-Class | 2.47% | 5.00% | 1,000.00 | 1,012.55 | 12.33 |

P-Class | 1.72% | 5.00% | 1,000.00 | 1,016.27 | 8.60 |

Institutional Class | 1.47% | 5.00% | 1,000.00 | 1,017.50 | 7.35 |

Commodities Strategy Fund |

A-Class | 1.54% | 5.00% | 1,000.00 | 1,017.16 | 7.70 |

C-Class | 2.29% | 5.00% | 1,000.00 | 1,013.44 | 11.43 |

H-Class | 1.55% | 5.00% | 1,000.00 | 1,017.11 | 7.75 |

1 | Annualized and excludes expenses of the underlying funds in which the Funds invest. This ratio represents net expenses which includes dividends on short sales and interest expenses. Excluding these expenses, the net expense ratio of the Multi-Hedge Strategies Fund would be 1.39%, 2.14%, 1.39% and 1.14% for the A-Class, C-Class, P-Class and Institutional Class, respectively. |

2 | Expenses are equal to the Fund’s annualized expense ratio, net of any applicable fee waivers, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

3 | Actual cumulative return at net asset value for the period December 31, 2022 to June 30, 2023. |

8 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND

OBJECTIVE: Seeks to provide long-term capital appreciation with less risk than traditional equity funds.

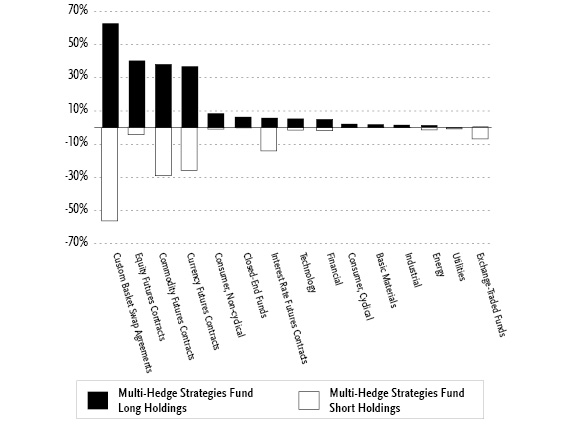

Consolidated Holdings Diversification (Market Exposure as % of Net Assets)

“Consolidated Holdings Diversification (Market Exposure as % of Net Assets)” excludes any temporary cash investments, investments in Guggenheim Strategy Funds Trust mutual funds, or investments in Guggenheim Ultra Short Duration Fund. Investments in those Funds do not provide “market exposure” to meet the Fund’s investment objective, but will significantly increase the portfolio’s exposure to certain other asset categories (and their associated risks), which may cause the Fund to deviate from its principal investment strategy, including: (i) high yield, high risk debt securities rated below the top four long-term rating categories by a nationally recognized statistical rating organization (also known as “junk bonds”); (ii) securities issued by the U.S. government or its agencies and instrumentalities; (iii) CLOs and similar investments; and (iv) other short-term fixed income securities.

| | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 9 |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited)(concluded) | June 30, 2023 |

Inception Dates: |

A-Class | September 19, 2005 |

C-Class | September 19, 2005 |

P-Class | September 19, 2005 |

Institutional Class | May 3, 2010 |

Ten Largest Holdings | % of Total Net Assets |

Guggenheim Ultra Short Duration Fund — Institutional Class | 7.5% |

Guggenheim Strategy Fund II | 7.5% |

Guggenheim Strategy Fund III | 2.2% |

VMware, Inc. — Class A | 2.1% |

Horizon Therapeutics plc | 1.8% |

ForgeRock, Inc. — Class A | 1.5% |

Focus Financial Partners, Inc. — Class A | 1.2% |

Radius Global Infrastructure, Inc. — Class A | 1.1% |

Syneos Health, Inc. | 1.1% |

Life Storage, Inc. | 1.0% |

Top Ten Total | 27.0% |

| | |

“Ten Largest Holdings” excludes any temporary cash or derivative investments. |

Average Annual Returns*

Periods Ended June 30, 2023

| 6 Month† | 1 Year | 5 Year | 10 Year |

A-Class Shares | 1.57% | (0.03%) | 3.38% | 2.08% |

A-Class Shares with sales charge‡ | (3.25%) | (4.78%) | 2.37% | 1.58% |

C-Class Shares | 1.21% | (0.80%) | 2.63% | 1.33% |

C-Class Shares with CDSC§ | 0.21% | (1.78%) | 2.63% | 1.33% |

P-Class Shares | 1.60% | (0.01%) | 3.39% | 2.10% |

Institutional Class Shares | 1.72% | 0.24% | 3.65% | 2.33% |

S&P 500 Index | 16.89% | 19.59% | 12.31% | 12.86% |

HFRX Global Hedge Fund Index | 0.63% | 1.31% | 1.71% | 1.51% |

* | The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns are historical and include changes in principal and reinvested dividends and capital gains and do not reflect the effect of taxes. The S&P 500 Index and the HFRX Global Hedge Fund Index are unmanaged indices and, unlike the Fund, have no management fees or operating expenses to reduce their reported returns. |

† | 6 month returns are not annualized. |

‡ | Fund returns are calculated using the maximum sales charge of 4.75%. |

§ | Fund returns include a CDSC of 1% if redeemed within 12 months of purchase. |

10 | THE GUGGENHEIM FUNDS SEMI-NNUAL REPORT | |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

COMMON STOCKS† - 24.4% |

| | | | | | | | | |

Consumer, Non-cyclical - 8.5% |

Horizon Therapeutics plc*,8 | | | 14,874 | | | $ | 1,529,791 | |

Syneos Health, Inc.* | | | 22,656 | | | | 954,724 | |

IVERIC bio, Inc.* | | | 21,233 | | | | 835,306 | |

Amedisys, Inc.*,8 | | | 8,570 | | | | 783,641 | |

Triton International Ltd.8 | | | 9,197 | | | | 765,742 | |

DICE Therapeutics, Inc.* | | | 15,449 | | | | 717,761 | |

NuVasive, Inc.* | | | 14,543 | | | | 604,843 | |

VectivBio Holding AG*,8 | | | 31,692 | | | | 534,644 | |

Chinook Therapeutics, Inc.* | | | 9,562 | | | | 367,372 | |

Seagen, Inc.*,8 | | | 1,594 | | | | 306,781 | |

Total Consumer, Non-cyclical | | | 7,400,605 | |

| | | | | | | | | |

Technology - 5.2% |

VMware, Inc. — Class A*,8 | | | 12,601 | | | | 1,810,506 | |

ForgeRock, Inc. — Class A* | | | 65,591 | | | | 1,347,239 | |

Tower Semiconductor Ltd.* | | | 22,123 | | | | 830,055 | |

Activision Blizzard, Inc.*,8 | | | 6,659 | | | | 561,354 | |

Total Technology | | | 4,549,154 | |

| | | | | | | | | |

Financial - 5.0% |

Focus Financial Partners, Inc. — Class A* | | | 19,855 | | | | 1,042,586 | |

Radius Global Infrastructure, Inc. — Class A*,8 | | | 66,769 | | | | 994,858 | |

Life Storage, Inc. REIT8 | | | 6,392 | | | | 849,880 | |

Lakeland Bancorp, Inc. | | | 36,286 | | | | 485,869 | |

Greenhill & Company, Inc. | | | 29,350 | | | | 429,978 | |

Urstadt Biddle Properties, Inc. — Class A REIT | | | 11,308 | | | | 240,408 | |

Argo Group International Holdings Ltd. | | | 5,511 | | | | 163,181 | |

Necessity Retail REIT, Inc. | | | 13,747 | | | | 92,930 | |

Total Financial | | | 4,299,690 | |

| | | | | | | | | |

Consumer, Cyclical - 2.1% |

Univar Solutions, Inc.*,8 | | | 18,233 | | | | 653,471 | |

iRobot Corp.* | | | 12,316 | | | | 557,299 | |

Spirit Airlines, Inc. | | | 21,083 | | | | 361,784 | |

NEOGAMES S.A.* | | | 9,427 | | | | 246,233 | |

Total Consumer, Cyclical | | | 1,818,787 | |

| | | | | | | | | |

Basic Materials - 1.7% |

Diversey Holdings Ltd.*,1 | | | 99,422 | | | | 834,150 | |

Arconic Corp.*,8 | | | 22,322 | | | | 660,285 | |

Total Basic Materials | | | 1,494,435 | |

| | | | | | | | | |

Industrial - 1.5% |

National Instruments Corp.8 | | | 14,539 | | | | 834,539 | |

Aerojet Rocketdyne Holdings, Inc.* | | | 8,700 | | | | 477,369 | |

Total Industrial | | | 1,311,908 | |

| | | | | | | | | |

Energy - 0.4% |

PDC Energy, Inc.8 | | | 5,547 | | | | 394,614 | |

| | | | | | | | | |

Total Common Stocks |

(Cost $21,197,389) | | | | | | | 21,269,193 | |

| | | | | | | | | |

MASTER LIMITED PARTNERSHIPS† - 0.6% |

Energy - 0.6% |

Magellan Midstream Partners, LP8 | | | 8,246 | | | | 513,891 | |

Total Master Limited Partnerships |

(Cost $515,606) | | | | | | | 513,891 | |

| | | | | | | | | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 11 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

RIGHTS††† - 0.0% |

Consumer, Non-cyclical - 0.0% |

Lantheus Holdings, Inc.* | | | 42,000 | | | $ | — | |

Alexion Pharmaceuticals, Inc.* | | | 34,843 | | | | — | |

Viatris, Inc.* | | | 31,686 | | | | — | |

Johnson & Johnson* | | | 3,841 | | | | — | |

Total Consumer, Non-cyclical | | | — | |

| | | | | | | | | |

Total Rights |

(Cost $5,387) | | | | | | | — | |

| | | | | | | | | |

MUTUAL FUNDS† - 17.2% |

Guggenheim Ultra Short Duration Fund — Institutional Class2 | | | 674,462 | | | | 6,562,518 | |

Guggenheim Strategy Fund II2 | | | 269,618 | | | | 6,530,150 | |

Guggenheim Strategy Fund III2 | | | 79,031 | | | | 1,916,508 | |

Total Mutual Funds |

(Cost $15,386,814) | | | | | | | 15,009,176 | |

| | | | | | | | | |

CLOSED-END FUNDS† - 6.4% |

Nuveen California Quality Municipal Income Fund | | | 15,399 | | | | 168,157 | |

BlackRock MuniHoldings California Quality Fund, Inc. | | | 15,332 | | | | 166,352 | |

SRH Total Return Fund, Inc. | | | 12,448 | | | | 165,309 | |

Adams Diversified Equity Fund, Inc. | | | 9,810 | | | | 164,906 | |

Gabelli Dividend & Income Trust | | | 7,793 | | | | 164,666 | |

General American Investors Company, Inc. | | | 3,931 | | | | 164,001 | |

Nuveen New Jersey Quality Municipal Income Fund | | | 13,868 | | | | 159,066 | |

Tekla Life Sciences Investors | | | 11,633 | | | | 157,511 | |

Nuveen Real Asset Income and Growth Fund | | | 13,740 | | | | 156,911 | |

Nuveen Pennsylvania Quality Municipal Income Fund | | | 12,665 | | | | 142,355 | |

Ellsworth Growth and Income Fund Ltd. | | | 13,091 | | | | 112,583 | |

DWS Municipal Income Trust | | | 12,906 | | | | 111,121 | |

Clough Global Equity Fund | | | 17,457 | | | | 108,932 | |

Voya Infrastructure Industrials and Materials Fund | | | 10,483 | | | | 103,467 | |

BlackRock New York Municipal Income Trust | | | 9,653 | | | | 99,812 | |

Tekla Healthcare Investors | | | 5,842 | | | | 99,606 | |

BrandywineGLOBAL Global Income Opportunities Fund, Inc. | | | 9,164 | | | | 73,679 | |

Pioneer Municipal High Income Fund Trust | | | 8,497 | | | | 72,479 | |

Gabelli Healthcare & WellnessRx Trust | | | 6,833 | | | | 68,057 | |

Bancroft Fund Ltd. | | | 3,889 | | | | 66,463 | |

Western Asset Emerging Markets Debt Fund, Inc. | | | 7,592 | | | | 65,443 | |

Invesco Trust for Investment Grade New York Municipals | | | 6,338 | | | | 64,774 | |

12 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

Western Asset Inflation-Linked Opportunities & Income Fund | | | 7,180 | | | $ | 63,615 | |

Aberdeen Total Dynamic Dividend Fund | | | 7,613 | | | | 62,883 | |

AllianceBernstein National Municipal Income Fund, Inc. | | | 5,745 | | | | 61,644 | |

CBRE Global Real Estate Income Fund | | | 11,535 | | | | 60,328 | |

Mexico Fund, Inc. | | | 3,497 | | | | 58,680 | |

BNY Mellon Municipal Income, Inc. | | | 8,592 | | | | 54,044 | |

Swiss Helvetia Fund, Inc. | | | 6,017 | | | | 49,460 | |

Tortoise Power and Energy Infrastructure Fund, Inc. | | | 3,601 | | | | 47,569 | |

Invesco Pennsylvania Value Municipal Income Trust | | | 4,485 | | | | 44,222 | |

LMP Capital and Income Fund, Inc. | | | 3,360 | | | | 43,042 | |

MFS High Yield Municipal Trust | | | 12,937 | | | | 41,657 | |

Eaton Vance California Municipal Bond Fund | | | 4,485 | | | | 39,916 | |

abrdn Japan Equity Fund, Inc. | | | 6,477 | | | | 39,315 | |

Nuveen AMT-Free Quality Municipal Income Fund | | | 3,478 | | | | 38,015 | |

DWS Strategic Municipal Income Trust | | | 3,785 | | | | 32,116 | |

Blackstone Long-Short Credit Income Fund | | | 2,790 | | | | 31,639 | |

Principal Real Estate Income Fund | | | 3,031 | | | | 28,673 | |

First Trust Specialty Finance and Financial Opportunities Fund | | | 8,735 | | | | 28,476 | |

MFS Municipal Income Trust | | | 5,349 | | | | 27,280 | |

BNY Mellon High Yield Strategies Fund | | | 11,930 | | | | 26,485 | |

Neuberger Berman California Municipal Fund, Inc. | | | 2,440 | | | | 25,986 | |

Western Asset Municipal Partners Fund, Inc. | | | 2,139 | | | | 25,030 | |

John Hancock Tax-Advantaged Global Shareholder Yield Fund | | | 4,591 | | | | 21,532 | |

BlackRock California Municipal Income Trust | | | 1,740 | | | | 20,636 | |

Virtus Convertible & Income Fund | | | 5,683 | | | | 19,777 | |

Nuveen AMT-Free Municipal Credit Income Fund | | | 1,650 | | | | 19,305 | |

Nuveen Municipal Credit Income Fund | | | 1,652 | | | | 19,262 | |

Nuveen Quality Municipal Income Fund | | | 1,706 | | | | 19,227 | |

Nuveen Credit Strategies Income Fund | | | 3,585 | | | | 18,104 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 13 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

abrdn Global Dynamic Dividend | | | 1,857 | | | $ | 17,716 | |

BlackRock Municipal 2030 Target Term Trust | | | 832 | | | | 17,289 | |

BlackRock MuniYield Quality Fund III, Inc. | | | 1,558 | | | | 17,045 | |

Nuveen Floating Rate Income Fund/Closed-end Fund | | | 2,108 | | | | 16,632 | |

Virtus Convertible & Income Fund II | | | 5,181 | | | | 16,113 | |

Royce Global Value Trust, Inc. | | | 1,700 | | | | 15,708 | |

BlackRock MuniYield Quality Fund, Inc. | | | 1,357 | | | | 15,700 | |

BlackRock Municipal Income Fund, Inc. | | | 1,355 | | | | 15,501 | |

Nuveen Floating Rate Income Opportunity Fund | | | 1,945 | | | | 15,171 | |

Nuveen Dow 30sm Dynamic Overwrite Fund | | | 1,073 | | | | 15,140 | |

BlackRock MuniHoldings Fund, Inc. | | | 1,297 | | | | 15,084 | |

Nuveen New York Quality Municipal Income Fund | | | 1,374 | | | | 14,771 | |

abrdn Emerging Markets Equity | | | 2,803 | | | | 14,548 | |

BlackRock Municipal Income Trust | | | 1,459 | | | | 14,502 | |

Nuveen New York AMT-Free Quality Municipal Income Fund | | | 1,389 | | | | 14,376 | |

Nuveen California AMT-Free Quality Municipal Income Fund | | | 1,238 | | | | 14,287 | |

Putnam Municipal Opportunities Trust | | | 1,379 | | | | 14,080 | |

Allspring Income Opportunities | | | 2,180 | | | | 14,061 | |

BlackRock MuniHoldings New Jersey Quality Fund, Inc. | | | 1,230 | | | | 13,739 | |

BlackRock Municipal Income Trust II | | | 1,311 | | | | 13,648 | |

MFS Investment Grade Municipal Trust | | | 1,846 | | | | 13,577 | |

Putnam Managed Municipal Income Trust | | | 2,206 | | | | 13,435 | |

Neuberger Berman New York Municipal Fund, Inc. | | | 1,405 | | | | 13,390 | |

BlackRock MuniVest Fund, Inc. | | | 1,980 | | | | 13,325 | |

BlackRock MuniYield Fund, Inc. | | | 1,273 | | | | 13,290 | |

Blackrock Investment Quality Municipal Trust, Inc. | | | 1,137 | | | | 13,223 | |

BlackRock MuniYield New York Quality Fund, Inc. | | | 1,303 | | | | 13,199 | |

BlackRock Municipal Income Quality Trust | | | 1,159 | | | | 13,039 | |

Nuveen Senior Income Fund | | | 2,829 | | | | 12,957 | |

Nuveen Real Estate Income Fund | | | 1,737 | | | | 12,906 | |

Western Asset High Income Opportunity Fund, Inc. | | | 3,402 | | | | 12,860 | |

Herzfeld Caribbean Basin Fund, Inc. | | | 3,246 | | | | 12,788 | |

14 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

Allspring Multi-Sector Income | | | 1,369 | | | $ | 12,677 | |

BlackRock MuniAssets Fund, Inc. | | | 1,242 | | | | 12,644 | |

Western Asset Managed Municipals Fund, Inc. | | | 1,272 | | | | 12,631 | |

BNY Mellon Strategic Municipal Bond Fund, Inc. | | | 2,208 | | | | 12,586 | |

BlackRock MuniYield Michigan Quality Fund, Inc. | | | 1,137 | | | | 12,564 | |

BlackRock MuniHoldings Quality Fund II, Inc. | | | 1,276 | | | | 12,390 | |

Nuveen Short Duration Credit Opportunities Fund | | | 1,066 | | | | 12,312 | |

Voya Emerging Markets High Dividend Equity Fund | | | 2,347 | | | | 12,251 | |

BlackRock MuniHoldings New York Quality Fund, Inc. | | | 1,156 | | | | 12,115 | |

Allspring Global Dividend Oppo | | | 2,744 | | | | 11,936 | |

Nuveen California Municipal Value Fund, Inc. | | | 1,395 | | | | 11,927 | |

BlackRock MuniYield Quality Fund II, Inc. | | | 1,184 | | | | 11,911 | |

Nuveen AMT-Free Municipal Value Fund | | | 856 | | | | 11,753 | |

BlackRock MuniVest Fund II, Inc. | | | 1,105 | | | | 11,746 | |

Western Asset High Yield Defined Opportunity Fund, Inc. | | | 997 | | | | 11,715 | |

Western Asset Municipal High Income Fund, Inc. | | | 1,767 | | | | 11,574 | |

PIMCO California Municipal Income Fund II | | | 1,943 | | | | 11,561 | |

Western Asset Premier Bond Fund | | | 1,131 | | | | 11,525 | |

Cohen & Steers Infrastructure Fund, Inc. | | | 487 | | | | 11,503 | |

Western Asset Inflation - Linked Securities & Income Fund | | | 1,388 | | | | 11,465 | |

BlackRock Long-Term Municipal Advantage Trust | | | 1,183 | | | | 11,440 | |

MFS High Income Municipal Trust | | | 3,249 | | | | 11,307 | |

Western Asset Global High Income Fund, Inc. | | | 1,550 | | | | 11,300 | |

Royce Value Trust, Inc. | | | 814 | | | | 11,233 | |

Nuveen Global High Income Fund | | | 1,003 | | | | 11,203 | |

Lazard Global Total Return and Income Fund, Inc. | | | 713 | | | | 11,130 | |

Virtus Diversified Income & Co. | | | 557 | | | | 11,129 | |

Nuveen Arizona Quality Municipal Income Fund | | | 1,034 | | | | 11,115 | |

Neuberger Berman Real Estate Securities Income Fund, Inc. | | | 3,655 | | | | 11,111 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 15 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

Sprott Focus Trust, Inc. | | | 1,393 | | | $ | 11,088 | |

Nuveen Virginia Quality Municipal Income Fund | | | 1,027 | | | | 11,081 | |

Eaton Vance Enhanced Equity Income Fund II | | | 619 | | | | 11,074 | |

Delaware Investments National Municipal Income Fund | | | 1,102 | | | | 11,064 | |

Eaton Vance Tax-Managed Buy-Write Income Fund | | | 795 | | | | 11,043 | |

Royce Micro-Capital Trust, Inc. | | | 1,262 | | | | 11,043 | |

Eaton Vance Tax-Advantaged Dividend Income Fund | | | 483 | | | | 10,988 | |

BlackRock MuniYield Pennsylvania Quality Fund | | | 938 | | | | 10,965 | |

Nuveen Massachusetts Quality Municipal Income Fund | | | 1,047 | | | | 10,931 | |

John Hancock Hedged Equity & Income Fund | | | 1,012 | | | | 10,909 | |

PIMCO New York Municipal Income Fund II | | | 1,436 | | | | 10,899 | |

Allspring Utilities and High I | | | 1,077 | | | | 10,899 | |

Western Asset Investment Grade Income Fund, Inc. | | | 937 | | | | 10,897 | |

abrdn Global Premier Propertie | | | 2,778 | | | | 10,890 | |

abrdn Australia Equity Fund In | | | 2,526 | | | | 10,887 | |

Federated Hermes Premier Municipal Income Fund | | | 1,024 | | | | 10,885 | |

Eaton Vance Risk-Managed Diversified Equity Income Fund | | | 1,323 | | | | 10,875 | |

Gabelli Global Small and Mid Capital Value Trust | | | 907 | | | | 10,869 | |

New Germany Fund, Inc. | | | 1,210 | | | | 10,866 | |

Gabelli Global Utility & Income Trust | | | 764 | | | | 10,865 | |

Tri-Continental Corp. | | | 396 | | | | 10,858 | |

Eaton Vance Tax-Advantaged Global Dividend Income Fund | | | 650 | | | | 10,855 | |

Templeton Emerging Markets Fund/United States | | | 916 | | | | 10,845 | |

Voya Global Advantage and Premium Opportunity Fund | | | 1,269 | | | | 10,837 | |

BlackRock Floating Rate Income Trust | | | 929 | | | | 10,832 | |

Flaherty & Crumrine Preferred and Income Opportunity Fund, Inc. | | | 1,351 | | | | 10,822 | |

Cohen & Steers REIT and Preferred and Income Fund, Inc. | | | 569 | | | | 10,805 | |

First Trust Enhanced Equity Income Fund | | | 616 | | | | 10,798 | |

Western Asset Intermediate Muni Fund, Inc. | | | 1,415 | | | | 10,782 | |

BlackRock Debt Strategies Fund, Inc. | | | 1,101 | | | | 10,779 | |

16 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

Blackstone Strategic Credit Fund | | | 986 | | | $ | 10,777 | |

Eaton Vance Tax-Managed Buy-Write Opportunities Fund | | | 843 | | | | 10,774 | |

BlackRock Floating Rate Income Strategies Fund, Inc. | | | 881 | | | | 10,757 | |

Cohen & Steers Quality Income Realty Fund, Inc. | | | 926 | | | | 10,742 | |

BlackRock Corporate High Yield Fund, Inc. | | | 1,204 | | | | 10,740 | |

Apollo Senior Floating Rate Fund, Inc. | | | 831 | | | | 10,728 | |

BlackRock Enhanced Global Dividend Trust | | | 1,065 | | | | 10,725 | |

BlackRock Resources & Commodities Strategy Trust | | | 1,182 | | | | 10,721 | |

European Equity Fund, Inc. | | | 1,245 | | | | 10,719 | |

Tekla Healthcare Opportunities Fund | | | 562 | | | | 10,717 | |

MFS Charter Income Trust | | | 1,698 | | | | 10,714 | |

Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund | | | 466 | | | | 10,699 | |

RiverNorth Opportunities Fund, Inc. | | | 934 | | | | 10,685 | |

First Trust Senior Floating Rate Income Fund II | | | 1,078 | | | | 10,672 | |

PIMCO New York Municipal Income Fund III | | | 1,696 | | | | 10,668 | |

Nuveen Minnesota Quality Municipal Income Fund | | | 954 | | | | 10,666 | |

Miller/Howard High Dividend Fund | | | 1,052 | | | | 10,657 | |

Nuveen Select Maturities Municipal Fund | | | 1,182 | | | | 10,638 | |

First Trust High Income Long/Short Fund | | | 929 | | | | 10,628 | |

Invesco High Income Trust II | | | 1,011 | | | | 10,615 | |

Source Capital, Inc. | | | 277 | | | | 10,615 | |

BNY Mellon Strategic Municipals, Inc. | | | 1,706 | | | | 10,611 | |

Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund | | | 1,356 | | | | 10,577 | |

PGIM High Yield Bond Fund, Inc. | | | 850 | | | | 10,557 | |

Eaton Vance Tax Managed Global Buy Write Opportunities Fund | | | 1,284 | | | | 10,554 | |

Invesco Quality Municipal Income Trust | | | 1,104 | | | | 10,554 | |

Pioneer Municipal High Income Advantage Fund, Inc. | | | 1,335 | | | | 10,547 | |

Invesco Value Municipal Income Trust | | | 892 | | | | 10,543 | |

Neuberger Berman Municipal Fund, Inc. | | | 1,024 | | | | 10,527 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 17 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

BlackRock Limited Duration Income Trust | | | 817 | | | $ | 10,523 | |

BlackRock Enhanced International Dividend Trust | | | 1,934 | | | | 10,521 | |

Invesco California Value Municipal Income Trust | | | 1,098 | | | | 10,519 | |

Eaton Vance New York Municipal Bond Fund | | | 1,119 | | | | 10,519 | |

Eaton Vance Tax-Managed Global Diversified Equity Income Fund | | | 1,328 | | | | 10,518 | |

Eaton Vance Municipal Income Trust | | | 1,051 | | | | 10,457 | |

PGIM Global High Yield Fund, Inc. | | | 953 | | | | 10,454 | |

MFS Multimarket Income Trust | | | 2,316 | | | | 10,445 | |

Flaherty & Crumrine Preferred and Income Securities Fund, Inc. | | | 760 | | | | 10,442 | |

BNY Mellon Municipal Bond Infrastructure Fund, Inc. | | | 969 | | | | 10,436 | |

Franklin Limited Duration Income Trust | | | 1,687 | | | | 10,426 | |

Franklin Universal Trust | | | 1,548 | | | | 10,418 | |

Eaton Vance California Municipal Income Trust | | | 1,043 | | | | 10,414 | |

Eaton Vance Municipal Bond Fund | | | 1,044 | | | | 10,388 | |

Invesco Advantage Municipal Income Trust II | | | 1,234 | | | | 10,378 | |

Invesco Municipal Opportunity Trust | | | 1,097 | | | | 10,377 | |

Invesco Municipal Trust | | | 1,100 | | | | 10,373 | |

Invesco Trust for Investment Grade Municipals | | | 1,068 | | | | 10,370 | |

MFS Intermediate High Income Fund | | | 6,362 | | | | 10,370 | |

Flaherty & Crumrine Preferred & Income Fund, Inc. | | | 1,051 | | | | 10,363 | |

Virtus Total Return Fund, Inc. | | | 1,704 | | | | 10,360 | |

Pioneer High Income Fund, Inc. | | | 1,541 | | | | 10,356 | |

John Hancock Investors Trust | | | 819 | | | | 10,352 | |

DTF Tax-Free Income 2028 Term Fund, Inc. | | | 960 | | | | 10,339 | |

Flaherty & Crumrine Total Return Fund, Inc. | | | 717 | | | | 10,303 | |

Credit Suisse High Yield Bond Fund | | | 5,425 | | | | 10,253 | |

Invesco Bond Fund | | | 689 | | | | 10,252 | |

Insight Select Income Fund | | | 655 | | | | 10,243 | |

Neuberger Berman High Yield Strategies Fund, Inc.1 | | | 1,367 | | | | 10,239 | |

John Hancock Income Securities Trust | | | 947 | | | | 10,199 | |

MFS Intermediate Income Trust | | | 3,708 | | | | 10,160 | |

BlackRock Taxable Municipal Bond Trust | | | 612 | | | | 10,153 | |

18 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Value | |

Morgan Stanley Emerging Markets Debt Fund, Inc. | | | 1,574 | | | $ | 10,137 | |

Eaton Vance Municipal Income 2028 Term Trust | | | 576 | | | | 10,126 | |

MFS Government Markets Income Trust | | | 3,142 | | | | 10,086 | |

Saba Capital Income & Opportunities Fund | | | 1,306 | | | | 10,056 | |

Nuveen Preferred & Income Securities Fund | | | 1,391 | | | | 8,875 | |

Kayne Anderson Energy Infrastructure Fund | | | 1,079 | | | | 8,783 | |

Nuveen Municipal Value Fund, Inc. | | | 1,004 | | | | 8,735 | |

Nuveen California Select Tax-Free Income Portfolio | | | 566 | | | | 7,375 | |

BlackRock Enhanced Government Fund, Inc. | | | 752 | | | | 7,182 | |

Nuveen Preferred & Income Opportunities Fund | | | 968 | | | | 6,273 | |

Nuveen Multi-Market Income Fund | | | 1,011 | | | | 5,864 | |

BlackRock Virginia Municipal Bond Trust | | | 432 | | | | 4,632 | |

Kayne Anderson NextGen Energy & Infrastructure, Inc. | | | 564 | | | | 4,004 | |

Nuveen Missouri Quality Municipal Income Fund | | | 319 | | | | 3,177 | |

Nuveen Multi-Asset Income Fund | | | 267 | | | | 3,113 | |

Nuveen Preferred & Income Term Fund | | | 185 | | | | 3,106 | |

Putnam Premier Income Trust | | | 750 | | | | 2,640 | |

Barings Global Short Duration High Yield Fund | | | 200 | | | | 2,608 | |

Western Asset Mortgage Opportunity Fund, Inc. | | | 177 | | | | 1,873 | |

PIMCO California Municipal Income Fund | | | 175 | | | | 1,715 | |

Putnam Master Intermediate Income Trust | | | 304 | | | | 961 | |

Nuveen New York Municipal Value Fund | | | 76 | | | | 642 | |

Nuveen Preferred and Income Fund | | | 24 | | | | 387 | |

Nuveen Mortgage and Income Fund | | | 23 | | | | 371 | |

Nuveen New York Select Tax-Free Income Portfolio | | | 14 | | | | 166 | |

Nuveen Intermediate Duration Municipal Term Fund Liquidating Trust | | | 955 | | | | — | |

Total Closed-End Funds |

(Cost $5,425,833) | | | | | | | 5,619,587 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 19 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Face

Amount | | | Value | |

U.S. TREASURY BILLS†† - 10.6% |

U.S. Treasury Bills |

5.02% due 08/03/233 | | $ | 4,700,000 | | | $ | 4,679,304 | |

5.11% due 07/18/233,4,8 | | | 4,586,000 | | | | 4,576,402 | |

Total U.S. Treasury Bills |

(Cost $9,252,841) | | | | | | | 9,255,706 | |

| | | | | | | | | |

REPURCHASE AGREEMENTS††,5 - 27.2% |

J.P. Morgan Securities LLC

issued 06/30/23 at 5.05%

due 07/03/23 | | | 12,905,446 | | | | 12,905,446 | |

Barclays Capital, Inc.

issued 06/30/23 at 5.06%

due 07/03/23 | | | 5,677,745 | | | | 5,677,745 | |

BofA Securities, Inc.

issued 06/30/23 at 5.06%

due 07/03/23 | | | 5,161,587 | | | | 5,161,587 | |

Total Repurchase Agreements |

(Cost $23,744,778) | | | | | | | 23,744,778 | |

| | | Shares | | | | | |

SECURITIES LENDING COLLATERAL†,6 - 0.7% |

Money Market Fund |

First American Government Obligations Fund — Class X, 5.01%7 | | | 660,141 | | | | 660,141 | |

Total Securities Lending Collateral |

(Cost $660,141) | | | | | | | 660,141 | |

| | | | | | | | | |

Total Investments - 87.1% |

(Cost $76,188,789) | | | 76,072,472 | |

| |

COMMON STOCKS SOLD SHORT† - (5.2)% |

Utilities - (0.1)% |

Brookfield Infrastructure Corp. — Class A | | | 2,483 | | | | (113,175 | ) |

| | | | | | | | | |

Consumer, Non-cyclical - (0.7)% |

Globus Medical, Inc. — Class A* | | | 10,907 | | | | (649,403 | ) |

| | | | | | | | | |

Energy - (0.9)% |

ONEOK, Inc. | | | 5,500 | | | | (339,460 | ) |

Chevron Corp. | | | 2,573 | | | | (404,862 | ) |

Total Energy | | | (744,322 | ) |

| | | | | | | | | |

Technology - (1.6)% |

Broadcom, Inc. | | | 1,588 | | | | (1,377,479 | ) |

| | | | | | | | | |

Financial - (1.9)% |

Global Net Lease, Inc. | | | 9,196 | | | | (94,535 | ) |

Regency Centers Corp. | | | 3,833 | | | | (236,764 | ) |

Provident Financial Services, Inc. | | | 30,186 | | | | (493,239 | ) |

Extra Space Storage, Inc. | | | 5,721 | | | | (851,571 | ) |

Total Financial | | | (1,676,109 | ) |

| | | | | | | | | |

Total Common Stocks Sold Short |

(Proceeds $3,926,863) | | | | | | | (4,560,488 | ) |

| | | | | | | | | |

EXCHANGE-TRADED FUNDS SOLD SHORT† - (6.9)% |

SPDR Gold Shares — Class D | | | 20 | | | | (3,565 | ) |

iShares MSCI All Country Asia ex Japan ETF | | | 102 | | | | (6,777 | ) |

iShares Mortgage Real Estate ETF | | | 309 | | | | (7,292 | ) |

iShares 7-10 Year Treasury Bond ETF | | | 120 | | | | (11,592 | ) |

iShares Agency Bond ETF | | | 109 | | | | (11,659 | ) |

20 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | |

Value

| |

Financial Select Sector SPDR Fund | | | 371 | | | $ | (12,506 | ) |

Energy Select Sector SPDR Fund | | | 202 | | | | (16,396 | ) |

Utilities Select Sector SPDR Fund | | | 272 | | | | (17,800 | ) |

VanEck Gold Miners ETF | | | 595 | | | | (17,915 | ) |

iShares Latin America 40 ETF | | | 956 | | | | (25,975 | ) |

iShares MSCI Emerging Markets ETF | | | 694 | | | | (27,455 | ) |

iShares Preferred & Income Securities ETF | | | 1,644 | | | | (50,849 | ) |

iShares Floating Rate Bond ETF | | | 1,030 | | | | (52,345 | ) |

iShares iBoxx $ Investment Grade Corporate Bond ETF | | | 581 | | | | (62,829 | ) |

iShares Core High Dividend ETF | | | 654 | | | | (65,917 | ) |

iShares TIPS Bond ETF | | | 693 | | | | (74,581 | ) |

iShares Russell 1000 Growth ETF | | | 319 | | | | (87,782 | ) |

iShares MBS ETF | | | 964 | | | | (89,907 | ) |

SPDR S&P Biotech ETF | | | 1,219 | | | | (101,421 | ) |

iShares Russell 2000 Index ETF | | | 864 | | | | (161,801 | ) |

Schwab U.S. Aggregate Bond ETF | | | 4,032 | | | | (186,117 | ) |

Health Care Select Sector SPDR Fund | | | 1,417 | | | | (188,079 | ) |

SPDR Bloomberg Convertible Securities ETF | | | 2,742 | | | | (191,803 | ) |

iShares U.S. Real Estate ETF | | | 2,328 | | | | (201,465 | ) |

iShares JP Morgan USD Emerging Markets Bond ETF | | | 2,501 | | | | (216,437 | ) |

VanEck High Yield Muni ETF | | | 4,592 | | | | (235,753 | ) |

Invesco Senior Loan ETF | | | 12,080 | | | | (254,163 | ) |

SPDR Nuveen Bloomberg High Yield Municipal Bond ETF | | | 14,736 | | | | (368,547 | ) |

iShares National Muni Bond ETF | | | 3,668 | | | | (391,486 | ) |

iShares Russell 1000 Value ETF | | | 2,675 | | | | (422,195 | ) |

iShares MSCI EAFE ETF | | | 5,917 | | | | (428,982 | ) |

SPDR S&P 500 ETF Trust | | | 1,207 | | | | (535,039 | ) |

SPDR Nuveen Bloomberg Municipal Bond ETF | | | 15,653 | | | | (722,543 | ) |

iShares iBoxx High Yield Corporate Bond ETF | | | 10,451 | | | | (784,557 | ) |

Total Exchange-Traded Funds Sold Short |

(Proceeds $6,412,853) | | | | | | | (6,033,530 | ) |

| | | | | | | | | |

Total Securities Sold Short - (12.1)% |

(Proceeds $10,339,716) | | $ | (10,594,018 | ) |

Other Assets & Liabilities, net - 25.0% | | | 21,852,897 | |

Total Net Assets - 100.0% | | $ | 87,331,351 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 21 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

Futures Contracts |

Description | | Number of

Contracts | | | Expiration

Date | | | Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation)** | |

Interest Rate Futures Contracts Purchased† |

Canadian Government 10 Year Bond Futures Contracts | | | 25 | | | | Sep 2023 | | | $ | 2,312,868 | | | $ | 16,901 | |

U.S. Treasury 10 Year Note Futures Contracts | | | 16 | | | | Sep 2023 | | | | 1,797,000 | | | | 2,933 | |

Euro - OATS Futures Contracts | | | 5 | | | | Sep 2023 | | | | 700,829 | | | | 500 | |

| | | | | | | | | | | $ | 4,810,697 | | | $ | 20,334 | |

Commodity Futures Contracts Purchased† |

Live Cattle Futures Contracts | | | 123 | | | | Aug 2023 | | | $ | 8,704,710 | | | $ | 443,947 | |

Natural Gas Futures Contracts | | | 107 | | | | Aug 2023 | | | | 2,957,480 | | | | 123,427 | |

Cattle Feeder Futures Contracts | | | 8 | | | | Aug 2023 | | | | 989,200 | | | | 100,483 | |

Cocoa Futures Contracts | | | 38 | | | | Sep 2023 | | | | 1,275,660 | | | | 90,115 | |

Soybean Oil Futures Contracts | | | 22 | | | | Dec 2023 | | | | 778,404 | | | | 64,139 | |

NY Harbor ULSD Futures Contracts | | | 7 | | | | Jul 2023 | | | | 718,859 | | | | 10,512 | |

Brent Crude Futures Contracts | | | 9 | | | | Jul 2023 | | | | 677,790 | | | | 6,265 | |

Low Sulphur Gas Oil Futures Contracts | | | 9 | | | | Aug 2023 | | | | 634,275 | | | | (3,265 | ) |

Hard Red Winter Wheat Futures Contracts | | | 23 | | | | Sep 2023 | | | | 912,237 | | | | (15,235 | ) |

WTI Crude Futures Contracts | | | 11 | | | | Jul 2023 | | | | 776,050 | | | | (16,418 | ) |

Silver Futures Contracts | | | 4 | | | | Sep 2023 | | | | 459,500 | | | | (26,972 | ) |

Soybean Meal Futures Contracts | | | 50 | | | | Mar 2024 | | | | 1,928,500 | | | | (40,595 | ) |

Gasoline RBOB Futures Contracts | | | 52 | | | | Sep 2023 | | | | 4,841,710 | | | | (42,842 | ) |

Coffee ‘C’ Futures Contracts | | | 9 | | | | Sep 2023 | | | | 536,625 | | | | (43,135 | ) |

Gold 100 oz. Futures Contracts | | | 5 | | | | Aug 2023 | | | | 963,900 | | | | (55,733 | ) |

Sugar #11 Futures Contracts | | | 254 | | | | Apr 2024 | | | | 6,164,682 | | | | (631,102 | ) |

| | | | | | | | | | | $ | 33,319,582 | | | $ | (36,409 | ) |

Currency Futures Contracts Purchased† |

Euro FX Futures Contracts | | | 50 | | | | Sep 2023 | | | $ | 6,846,875 | | | $ | 77,048 | |

British Pound Futures Contracts | | | 153 | | | | Sep 2023 | | | | 12,145,331 | | | | 45,435 | |

New Zealand Dollar Futures Contracts | | | 25 | | | | Sep 2023 | | | | 1,533,625 | | | | 6,014 | |

Canadian Dollar Futures Contracts | | | 74 | | | | Sep 2023 | | | | 5,592,920 | | | | (16,750 | ) |

Japanese Yen Futures Contracts | | | 69 | | | | Sep 2023 | | | | 6,049,144 | | | | (171,401 | ) |

| | | | | | | | | | | $ | 32,167,895 | | | $ | (59,654 | ) |

Equity Futures Contracts Purchased† |

Tokyo Stock Price Index Futures Contracts | | | 9 | | | | Sep 2023 | | | $ | 1,435,384 | | | $ | 89,216 | |

Nikkei 225 (OSE) Index Futures Contracts | | | 5 | | | | Sep 2023 | | | | 1,158,551 | | | | 78,537 | |

IBEX 35 Index Futures Contracts†† | | | 9 | | | | Jul 2023 | | | | 939,622 | | | | 29,452 | |

FTSE MIB Index Futures Contracts | | | 5 | | | | Sep 2023 | | | | 775,759 | | | | 27,133 | |

CAC 40 10 Euro Index Futures Contracts | | | 9 | | | | Jul 2023 | | | | 730,255 | | | | 19,142 | |

SPI 200 Index Futures Contracts | | | 9 | | | | Sep 2023 | | | | 1,077,638 | | | | 18,755 | |

OMX Stockholm 30 Index Futures Contracts†† | | | 31 | | | | Jul 2023 | | | | 666,870 | | | | 3,874 | |

Euro STOXX 50 Index Futures Contracts | | | 17 | | | | Sep 2023 | | | | 823,652 | | | | 2,158 | |

DAX Index Futures Contracts | | | 2 | | | | Sep 2023 | | | | 889,980 | | | | 1,951 | |

FTSE 100 Index Futures Contracts | | | 6 | | | | Sep 2023 | | | | 576,104 | | | | 1,465 | |

Russell 2000 Index Mini Futures Contracts | | | 30 | | | | Sep 2023 | | | | 2,854,650 | | | | (1,635 | ) |

22 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

Futures Contracts (continued) |

Description | | Number of

Contracts | | | Expiration

Date | | | Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation)** | |

Equity Futures Contracts Purchased† (continued) |

NASDAQ-100 Index Mini Futures Contracts | | | 15 | | | | Sep 2023 | | | $ | 4,599,375 | | | $ | (2,298 | ) |

Dow Jones Industrial Average Index Mini Futures Contracts | | | 30 | | | | Sep 2023 | | | | 5,194,200 | | | | (2,524 | ) |

S&P 500 Index Mini Futures Contracts | | | 25 | | | | Sep 2023 | | | | 5,608,125 | | | | (2,878 | ) |

CBOE Volatility Index Futures Contracts | | | 172 | | | | Sep 2023 | | | | 3,035,800 | | | | (196,399 | ) |

CBOE Volatility Index Futures Contracts | | | 247 | | | | Dec 2023 | | | | 4,730,050 | | | | (359,821 | ) |

| | | | | | | | | | | $ | 35,096,015 | | | $ | (293,872 | ) |

Equity Futures Contracts Sold Short† |

CBOE Volatility Index Futures Contracts | | | 256 | | | | Jul 2023 | | | $ | 3,840,000 | | | $ | 402,004 | |

S&P/TSX 60 IX Index Futures Contracts | | | 1 | | | | Sep 2023 | | | | 183,957 | | | | (2,345 | ) |

| | | | | | | | | | | $ | 4,023,957 | | | $ | 399,659 | |

Interest Rate Futures Contracts Sold Short† |

Long Gilt Futures Contracts†† | | | 47 | | | | Sep 2023 | | | $ | 5,689,590 | | | $ | 14,489 | |

Euro - Bund Futures Contracts | | | 12 | | | | Sep 2023 | | | | 1,752,063 | | | | (489 | ) |

Euro - BTP Italian Government Bond Futures Contracts†† | | | 14 | | | | Sep 2023 | | | | 1,774,678 | | | | (588 | ) |

U.S. Treasury Long Bond Futures Contracts | | | 3 | | | | Sep 2023 | | | | 381,375 | | | | (631 | ) |

Euro - 30 year Bond Futures Contracts | | | 6 | | | | Sep 2023 | | | | 914,997 | | | | (808 | ) |

Australian Government 10 Year Bond Futures Contracts | | | 7 | | | | Sep 2023 | | | | 542,952 | | | | (1,471 | ) |

U.S. Treasury Ultra Long Bond Futures Contracts | | | 9 | | | | Sep 2023 | | | | 1,229,344 | | | | (3,456 | ) |

| | | | | | | | | | | $ | 12,284,999 | | | $ | 7,046 | |

Currency Futures Contracts Sold Short† |

Australian Dollar Futures Contracts | | | 61 | | | | Sep 2023 | | | $ | 4,071,140 | | | $ | 56,081 | |

Swiss Franc Futures Contracts | | | 131 | | | | Sep 2023 | | | | 18,443,981 | | | | (77,669 | ) |

| | | | | | | | | | | $ | 22,515,121 | | | $ | (21,588 | ) |

Commodity Futures Contracts Sold Short† |

Sugar #11 Futures Contracts | | | 58 | | | | Sep 2023 | | | $ | 1,482,387 | | | $ | 185,634 | |

Corn Futures Contracts | | | 22 | | | | Sep 2023 | | | | 537,900 | | | | 136,136 | |

Sugar #11 Futures Contracts | | | 87 | | | | Feb 2024 | | | | 2,233,325 | | | | 91,219 | |

Wheat Futures Contracts | | | 38 | | | | Sep 2023 | | | | 1,228,350 | | | | 32,024 | |

LME Primary Aluminum Futures Contracts | | | 13 | | | | Aug 2023 | | | | 693,794 | | | | 23,883 | |

Copper Futures Contracts | | | 5 | | | | Sep 2023 | | | | 470,375 | | | | 15,022 | |

LME Nickel Futures Contracts | | | 3 | | | | Aug 2023 | | | | 368,064 | | | | 12,746 | |

LME Zinc Futures Contracts | | | 9 | | | | Aug 2023 | | | | 537,581 | | | | 1,626 | |

LME Lead Futures Contracts | | | 2 | | | | Aug 2023 | | | | 105,073 | | | | 371 | |

Soybean Futures Contracts | | | 14 | | | | Nov 2023 | | | | 939,750 | | | | 131 | |

Soybean Meal Futures Contracts | | | 2 | | | | Dec 2023 | | | | 79,320 | | | | (3,296 | ) |

Gasoline RBOB Futures Contracts | | | 11 | | | | Jul 2023 | | | | 1,176,945 | | | | (4,371 | ) |

Cotton #2 Futures Contracts | | | 15 | | | | Dec 2023 | | | | 603,150 | | | | (9,622 | ) |

Gasoline RBOB Futures Contracts | | | 21 | | | | Aug 2023 | | | | 2,171,660 | | | | (16,728 | ) |

Natural Gas Futures Contracts | | | 31 | | | | Jul 2023 | | | | 863,040 | | | | (36,039 | ) |

Lean Hogs Futures Contracts | | | 18 | | | | Aug 2023 | | | | 665,820 | | | | (50,137 | ) |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 23 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

Futures Contracts (continued) |

Description | | Number of

Contracts | | | Expiration

Date | | | Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation)** | |

Commodity Futures Contracts Sold Short† (continued) |

Live Cattle Futures Contracts | | | 110 | | | | Dec 2023 | | | $ | 8,069,600 | | | $ | (277,435 | ) |

Natural Gas Futures Contracts | | | 112 | | | | Sep 2023 | | | | 3,186,400 | | | | (323,175 | ) |

| | | | | | | | | | | $ | 25,412,534 | | | $ | (222,011 | ) |

Custom Basket Swap Agreements |

Counterparty | Reference

Obligation | Type | Financing

Rate | | Payment

Frequency | | | Maturity

Date | | | Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

OTC Custom Basket Swap Agreements†† |

Goldman Sachs International | GS Long/Short Equity Custom Basket | Pay | 5.52% (Federal Funds Rate + 0.45%) | | | At Maturity | | | | 05/06/24 | | | $ | 13,181,537 | | | $ | 905,553 | |

Morgan Stanley Capital Services LLC | MS Long/Short Equity Custom Basket | Pay | 5.47% (Federal Funds Rate + 0.40%) | | | At Maturity | | | | 08/31/23 | | | | 13,181,579 | | | | 897,005 | |

Morgan Stanley Capital Services LLC | MS Equity Market Neutral Custom Basket | Pay | 5.47% (Federal Funds Rate + 0.40%) | | | At Maturity | | | | 08/31/23 | | | | 14,204,022 | | | | 366,470 | |

Goldman Sachs International | GS Equity Market Neutral Custom Basket | Pay | 5.52% (Federal Funds Rate + 0.45%) | | | At Maturity | | | | 05/06/24 | | | | 14,204,030 | | | | 363,537 | |

| | | | | | | | | | | | | | $ | 54,771,168 | | | $ | 2,532,565 | |

24 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

Custom Basket Swap Agreements (concluded) |

Counterparty | Reference

Obligation | Type | Financing

Rate | | Payment

Frequency | | | Maturity

Date | | | Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

OTC Custom Basket Swap Agreements Sold Short†† |

Goldman Sachs International | GS Equity Market Neutral Custom Basket | Receive | 4.86% (Federal Funds Rate - 0.21%) | | | At Maturity | | | | 05/06/24 | | | $ | 14,999,612 | | | $ | 1,765,451 | |

Morgan Stanley Capital Services LLC | MS Equity Market Neutral Custom Basket | Receive | 4.75% (Federal Funds Rate - 0.32%) | | | At Maturity | | | | 08/31/23 | | | | 14,999,603 | | | | 1,756,605 | |

Goldman Sachs International | GS Long/Short Equity Custom Basket | Receive | 4.86% (Federal Funds Rate - 0.21%) | | | At Maturity | | | | 05/06/24 | | | | 9,422,430 | | | | (264,965 | ) |

Morgan Stanley Capital Services LLC | MS Long/Short Equity Custom Basket | Receive | 4.77% (Federal Funds Rate - 0.30%) | | | At Maturity | | | | 08/31/23 | | | | 9,527,904 | | | | (265,877 | ) |

| | | | | | | | | | | | | | $ | 48,949,549 | | | $ | 2,991,214 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 25 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

MS LONG/SHORT EQUITY LONG CUSTOM BASKET |

Consumer, Non-cyclical |

John B Sanfilippo & Son, Inc. | | | 560 | | | | 0.49 | % | | $ | 24,146 | |

Vertex Pharmaceuticals, Inc. | | | 176 | | | | 0.46 | % | | | 23,455 | |

Perdoceo Education Corp. | | | 8,233 | | | | 0.76 | % | | | 12,498 | |

Quanex Building Products Corp. | | | 2,181 | | | | 0.43 | % | | | 10,789 | |

Kimberly-Clark Corp. | | | 1,001 | | | | 1.05 | % | | | 10,007 | |

AMN Healthcare Services, Inc. | | | 433 | | | | 0.36 | % | | | 9,942 | |

Hackett Group, Inc. | | | 3,176 | | | | 0.54 | % | | | 9,839 | |

Viatris, Inc. | | | 14,597 | | | | 1.11 | % | | | 9,352 | |

USANA Health Sciences, Inc. | | | 1,049 | | | | 0.50 | % | | | 6,693 | |

Dynavax Technologies Corp. | | | 4,722 | | | | 0.46 | % | | | 6,436 | |

Exelixis, Inc. | | | 3,830 | | | | 0.56 | % | | | 6,360 | |

Innoviva, Inc. | | | 8,283 | | | | 0.80 | % | | | 4,458 | |

Edwards Lifesciences Corp. | | | 430 | | | | 0.31 | % | | | 4,456 | |

Vector Group Ltd. | | | 7,075 | | | | 0.69 | % | | | 4,384 | |

H&R Block, Inc. | | | 4,451 | | | | 1.08 | % | | | 3,341 | |

Johnson & Johnson | | | 268 | | | | 0.34 | % | | | 3,256 | |

Merck & Company, Inc. | | | 1,212 | | | | 1.06 | % | | | 2,077 | |

United Therapeutics Corp. | | | 455 | | | | 0.76 | % | | | 870 | |

Molina Healthcare, Inc. | | | 94 | | | | 0.21 | % | | | 838 | |

Quest Diagnostics, Inc. | | | 203 | | | | 0.22 | % | | | 808 | |

Perrigo Company plc | | | 836 | | | | 0.22 | % | | | 729 | |

Altria Group, Inc. | | | 1,135 | | | | 0.39 | % | | | 345 | |

Abbott Laboratories | | | 1,321 | | | | 1.09 | % | | | (293 | ) |

QIAGEN N.V. | | | 598 | | | | 0.20 | % | | | (547 | ) |

Moderna, Inc. | | | 228 | | | | 0.21 | % | | | (1,873 | ) |

Bristol-Myers Squibb Co. | | | 2,071 | | | | 1.00 | % | | | (2,320 | ) |

Vir Biotechnology, Inc. | | | 1,392 | | | | 0.26 | % | | | (3,103 | ) |

Neurocrine Biosciences, Inc. | | | 566 | | | | 0.40 | % | | | (3,808 | ) |

Supernus Pharmaceuticals, Inc. | | | 1,126 | | | | 0.26 | % | | | (4,072 | ) |

Hershey Co. | | | 527 | | | | 1.00 | % | | | (4,318 | ) |

Premier, Inc. — Class A | | | 1,588 | | | | 0.33 | % | | | (5,320 | ) |

Amgen, Inc. | | | 619 | | | | 1.04 | % | | | (5,704 | ) |

Grand Canyon Education, Inc. | | | 587 | | | | 0.46 | % | | | (6,311 | ) |

Gilead Sciences, Inc. | | | 1,296 | | | | 0.76 | % | | | (9,583 | ) |

Campbell Soup Co. | | | 1,080 | | | | 0.37 | % | | | (9,718 | ) |

Humana, Inc. | | | 128 | | | | 0.43 | % | | | (9,951 | ) |

Eagle Pharmaceuticals, Inc. | | | 1,569 | | | | 0.23 | % | | | (17,999 | ) |

Incyte Corp. | | | 2,071 | | | | 0.98 | % | | | (18,922 | ) |

Royalty Pharma plc — Class A | | | 2,620 | | | | 0.61 | % | | | (29,714 | ) |

Total Consumer, Non-cyclical | | | 21,523 | |

| | | | | | | | | | | | | |

Communications |

Yelp, Inc. — Class A | | | 2,779 | | | | 0.77 | % | | | 23,300 | |

Cisco Systems, Inc. | | | 2,725 | | | | 1.07 | % | | | 12,245 | |

Extreme Networks, Inc. | | | 1,367 | | | | 0.27 | % | | | 9,292 | |

26 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

InterDigital, Inc. | | | 639 | | | | 0.47 | % | | $ | 7,727 | |

Nexstar Media Group, Inc. — Class A | | | 437 | | | | 0.55 | % | | | 4,253 | |

Motorola Solutions, Inc. | | | 134 | | | | 0.30 | % | | | 1,046 | |

T-Mobile US, Inc. | | | 345 | | | | 0.36 | % | | | 831 | |

VeriSign, Inc. | | | 606 | | | | 1.04 | % | | | 291 | |

TEGNA, Inc. | | | 2,909 | | | | 0.36 | % | | | 32 | |

Verizon Communications, Inc. | | | 1,310 | | | | 0.37 | % | | | (183 | ) |

A10 Networks, Inc. | | | 4,747 | | | | 0.53 | % | | | (1,174 | ) |

Total Communications | | | 57,660 | |

| | | | | | | | | | | | | |

Consumer, Cyclical |

Allison Transmission Holdings, Inc. | | | 2,292 | | | | 0.98 | % | | | 43,496 | |

PulteGroup, Inc. | | | 1,586 | | | | 0.93 | % | | | 31,038 | |

DR Horton, Inc. | | | 792 | | | | 0.73 | % | | | 23,026 | |

MDC Holdings, Inc. | | | 2,520 | | | | 0.89 | % | | | 20,957 | |

Taylor Morrison Home Corp. — Class A | | | 1,342 | | | | 0.50 | % | | | 16,393 | |

Boyd Gaming Corp. | | | 1,151 | | | | 0.61 | % | | | 16,261 | |

Brunswick Corp. | | | 1,158 | | | | 0.76 | % | | | 14,479 | |

Patrick Industries, Inc. | | | 951 | | | | 0.58 | % | | | 12,707 | |

Tri Pointe Homes, Inc. | | | 3,552 | | | | 0.89 | % | | | 12,541 | |

MSC Industrial Direct Company, Inc. — Class A | | | 1,481 | | | | 1.07 | % | | | 12,500 | |

Meritage Homes Corp. | | | 378 | | | | 0.41 | % | | | 7,853 | |

NVR, Inc. | | | 8 | | | | 0.39 | % | | | 5,282 | |

Cavco Industries, Inc. | | | 173 | | | | 0.39 | % | | | 4,706 | |

Academy Sports & Outdoors, Inc. | | | 556 | | | | 0.23 | % | | | 3,094 | |

Green Brick Partners, Inc. | | | 556 | | | | 0.24 | % | | | 2,817 | |

Gentex Corp. | | | 4,411 | | | | 0.98 | % | | | 2,593 | |

Monarch Casino & Resort, Inc. | | | 884 | | | | 0.47 | % | | | 2,235 | |

Home Depot, Inc. | | | 94 | | | | 0.22 | % | | | 1,964 | |

Dolby Laboratories, Inc. — Class A | | | 1,151 | | | | 0.73 | % | | | 1,085 | |

Steven Madden Ltd. | | | 1 | | | | 0.00 | % | | | 16 | |

Buckle, Inc. | | | 1,425 | | | | 0.37 | % | | | (3,065 | ) |

PetMed Express, Inc. | | | 5,353 | | | | 0.56 | % | | | (4,947 | ) |

Total Consumer, Cyclical | | | 227,015 | |

| | | | | | | | | | | | | |

Industrial |

Standex International Corp. | | | 813 | | | | 0.87 | % | | | 42,906 | |

Vishay Intertechnology, Inc. | | | 3,159 | | | | 0.70 | % | | | 42,426 | |

Snap-on, Inc. | | | 529 | | | | 1.16 | % | | | 38,211 | |

Eagle Materials, Inc. | | | 558 | | | | 0.79 | % | | | 35,353 | |

Mueller Industries, Inc. | | | 1,429 | | | | 0.95 | % | | | 30,439 | |

Louisiana-Pacific Corp. | | | 1,087 | | | | 0.62 | % | | | 23,998 | |

Boise Cascade Co. | | | 1,304 | | | | 0.89 | % | | | 20,829 | |

Builders FirstSource, Inc. | | | 1,005 | | | | 1.04 | % | | | 20,805 | |

Fortive Corp. | | | 2,050 | | | | 1.16 | % | | | 19,921 | |

Simpson Manufacturing Company, Inc. | | | 650 | | | | 0.68 | % | | | 17,704 | |

SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | 27 |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

UFP Industries, Inc. | | | 1,360 | | | | 1.00 | % | | $ | 17,499 | |

Dorian LPG Ltd. | | | 1,262 | | | | 0.25 | % | | | 16,467 | |

ITT, Inc. | | | 1,676 | | | | 1.19 | % | | | 12,110 | |

Donaldson Company, Inc. | | | 1,628 | | | | 0.77 | % | | | 6,872 | |

Masco Corp. | | | 1,183 | | | | 0.51 | % | | | 6,745 | |

Landstar System, Inc. | | | 451 | | | | 0.66 | % | | | 6,575 | |

Armstrong World Industries, Inc. | | | 1,112 | | | | 0.62 | % | | | 6,178 | |

Dover Corp. | | | 832 | | | | 0.93 | % | | | 4,697 | |

Expeditors International of Washington, Inc. | | | 432 | | | | 0.40 | % | | | 2,946 | |

Keysight Technologies, Inc. | | | 240 | | | | 0.30 | % | | | 2,913 | |

International Seaways, Inc. | | | 1,015 | | | | 0.29 | % | | | 2,095 | |

Ardmore Shipping Corp. | | | 3,581 | | | | 0.34 | % | | | 1,068 | |

GrafTech International Ltd. | | | 6,080 | | | | 0.23 | % | | | 872 | |

Scorpio Tankers, Inc. | | | 928 | | | | 0.33 | % | | | 770 | |

Toro Co. | | | 481 | | | | 0.37 | % | | | 136 | |

Garmin Ltd. | | | 430 | | | | 0.34 | % | | | (519 | ) |

Argan, Inc. | | | 1,214 | | | | 0.36 | % | | | (1,696 | ) |

Golar LNG Ltd. | | | 2,904 | | | | 0.44 | % | | | (3,872 | ) |

Acuity Brands, Inc. | | | 566 | | | | 0.70 | % | | | (6,040 | ) |

Lindsay Corp. | | | 240 | | | | 0.22 | % | | | (7,352 | ) |

3M Co. | | | 1,379 | | | | 1.05 | % | | | (9,640 | ) |

Sturm Ruger & Company, Inc. | | | 1,693 | | | | 0.68 | % | | | (10,231 | ) |

Total Industrial | | | 341,185 | |

| | | | | | | | | | | | | |

Basic Materials |

NewMarket Corp. | | | 242 | | | | 0.74 | % | | | 20,530 | |

Livent Corp. | | | 1 | | | | 0.00 | % | | | 25 | |

CF Industries Holdings, Inc. | | | 642 | | | | 0.34 | % | | | (57 | ) |

LyondellBasell Industries N.V. — Class A | | | 541 | | | | 0.38 | % | | | (812 | ) |

Westlake Corp. | | | 761 | | | | 0.69 | % | | | (1,913 | ) |

AdvanSix, Inc. | | | 949 | | | | 0.25 | % | | | (4,303 | ) |

Olin Corp. | | | 1,314 | | | | 0.51 | % | | | (5,049 | ) |

Total Basic Materials | | | 8,396 | |

| | | | | | | | | | | | | |

Technology |

NetApp, Inc. | | | 1,688 | | | | 0.98 | % | | | 20,588 | |

Dropbox, Inc. — Class A | | | 4,706 | | | | 0.95 | % | | | 19,937 | |

Kulicke & Soffa Industries, Inc. | | | 1,904 | | | | 0.86 | % | | | 17,891 | |

KLA Corp. | | | 207 | | | | 0.76 | % | | | 13,666 | |

Diodes, Inc. | | | 735 | | | | 0.52 | % | | | 13,255 | |

Microsoft Corp. | | | 219 | | | | 0.57 | % | | | 12,417 | |

Teradata Corp. | | | 589 | | | | 0.24 | % | | | 11,379 | |

Teradyne, Inc. | | | 533 | | | | 0.45 | % | | | 10,100 | |

Photronics, Inc. | | | 1,958 | | | | 0.38 | % | | | 8,396 | |

Applied Materials, Inc. | | | 700 | | | | 0.77 | % | | | 7,708 | |

Cirrus Logic, Inc. | | | 562 | | | | 0.35 | % | | | 7,675 | |

Apple, Inc. | | | 441 | | | | 0.65 | % | | | 5,769 | |

Cognizant Technology Solutions Corp. — Class A | | | 1,028 | | | | 0.51 | % | | | 3,609 | |

QUALCOMM, Inc. | | | 240 | | | | 0.22 | % | | | 3,395 | |

Qualys, Inc. | | | 221 | | | | 0.22 | % | | | 1,923 | |

NetScout Systems, Inc. | | | 2,556 | | | | 0.60 | % | | | 1,712 | |

Veradigm, Inc. | | | 3,329 | | | | 0.32 | % | | | 347 | |

Akamai Technologies, Inc. | | | 710 | | | | 0.48 | % | | | (2,900 | ) |

Total Technology | | | 156,867 | |

| | | | | | | | | | | | | |

Financial |

MGIC Investment Corp. | | | 8,920 | | | | 1.07 | % | | | 13,844 | |

28 | THE GUGGENHEIM FUNDS SEMI-ANNUAL REPORT | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS. |

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited)(continued) | June 30, 2023 |

MULTI-HEDGE STRATEGIES FUND | |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

Essent Group Ltd. | | | 2,269 | | | | 0.81 | % | | $ | 12,813 | |

NMI Holdings, Inc. — Class A | | | 2,384 | | | | 0.47 | % | | | 12,609 | |

Weyerhaeuser Co. | | | 3,266 | | | | 0.83 | % | | | 12,547 | |

Radian Group, Inc. | | | 2,729 | | | | 0.52 | % | | | 9,108 | |

Evercore, Inc. — Class A | | | 487 | | | | 0.46 | % | | | 8,981 | |

Mr Cooper Group, Inc. | | | 1,433 | | | | 0.55 | % | | | 4,976 | |

Hilltop Holdings, Inc. | | | 921 | | | | 0.22 | % | | | 2,935 | |

Preferred Bank/Los Angeles CA | | | 1,826 | | | | 0.76 | % | | | 2,122 | |

SouthState Corp. | | | 2,077 | | | | 1.04 | % | | | 610 | |

SEI Investments Co. | | | 2,367 | | | | 1.07 | % | | | 430 | |

International Bancshares Corp. | | | 658 | | | | 0.22 | % | | | 407 | |

Raymond James Financial, Inc. | | | 1 | | | | 0.00 | % | | | 8 | |

Allstate Corp. | | | 249 | | | | 0.21 | % | | | (169 | ) |

Travelers Companies, Inc. | | | 157 | | | | 0.21 | % | | | (189 | ) |

S&T Bancorp, Inc. | | | 1,511 | | | | 0.31 | % | | | (1,396 | ) |

Equity Commonwealth | | | 6,680 | | | | 1.03 | % | | | (2,488 | ) |

Renasant Corp. | | | 1,565 | | | | 0.31 | % | | | (9,798 | ) |

FB Financial Corp. | | | 1,812 | | | | 0.39 | % | | | (15,398 | ) |

Total Financial | | | 51,944 | |

| | | | | | | | | | | | | |

Utilities |

MGE Energy, Inc. | | | 1,701 | | | | 1.02 | % | | | 11,708 | |

ONE Gas, Inc. | | | 1,488 | | | | 0.87 | % | | | 2,900 | |

Chesapeake Utilities Corp. | | | 520 | | | | 0.47 | % | | | 2,097 | |

Atmos Energy Corp. | | | 1,189 | | | | 1.05 | % | | | 1,912 | |

Ameren Corp. | | | 1,674 | | | | 1.04 | % | | | (433 | ) |

Consolidated Edison, Inc. | | | 972 | | | | 0.67 | % | | | (2,462 | ) |

Black Hills Corp. | | | 2,215 | | | | 1.01 | % | | | (3,698 | ) |

National Fuel Gas Co. | | | 1,500 | | | | 0.58 | % | | | (10,300 | ) |

OGE Energy Corp. | | | 3,849 | | | | 1.05 | % | | | (11,880 | ) |

Clearway Energy, Inc. — Class C | | | 2,806 | | | | 0.61 | % | | | (13,485 | ) |

Total Utilities | | | (23,641 | ) |

| | | | | | | | | | | | | |

Energy |

Marathon Petroleum Corp. | | | 1,268 | | | | 1.12 | % | | | 17,213 | |

Exxon Mobil Corp. | | | 1,302 | | | | 1.06 | % | | | 10,602 | |

REX American Resources Corp. | | | 1,379 | | | | 0.36 | % | | | 8,015 | |

California Resources Corp. | | | 1,214 | | | | 0.42 | % | | | 5,906 | |

SM Energy Co. | | | 1,208 | | | | 0.29 | % | | | 5,739 | |

PBF Energy, Inc. — Class A | | | 1,201 | | | | 0.37 | % | | | 5,303 | |

Cheniere Energy, Inc. | | | 566 | | | | 0.65 | % | | | 4,818 | |

Valero Energy Corp. | | | 1,202 | | | | 1.07 | % | | | 2,929 | |

Phillips 66 | | | 654 | | | | 0.47 | % | | | (588 | ) |

Occidental Petroleum Corp. | | | 690 | | | | 0.31 | % | | | (3,881 | ) |

Total Energy | | | 56,056 | |

Total MS Long/Short Equity Long Custom Basket | | | 897,005 | |

| | | | | | | | | |

MS LONG/SHORT EQUITY SHORT CUSTOM BASKET |

Consumer, Non-cyclical |

Driven Brands Holdings, Inc. | | | 4,340 | | | | (1.24 | )% | | | 10,664 | |