| 56 | ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2006 |

FINANCIAL REVIEW CONTINUED

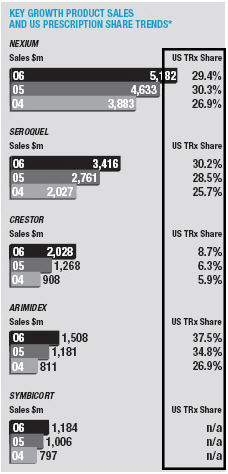

The Gastrointestinal portfolio grew for the second year in a row, up 4% asNexiumgrowth more than offset the continuing decline inLosec/Prilosec.Nexiumsales increased by 12% to $5,182 million. Sales in the US were up 13% to $3,527 million on continued strong volume growth offset by lower price realisation.Nexiumsales in other markets increased 10%, as good volume growth in France and Italy helped mitigate the significant price erosion in Germany.Losec/Prilosecsales were down 16% to $1,371 million with declines of 12% in the US and 17% elsewhere.

In Cardiovascular, sales grew by 15% to $6,118 million.Crestorsales exceeded $2 billion, reaching $2,028 million, up 59%. Sales in the US were up 57% to $1,148 million.Crestorshare of new prescriptions in the US statin market was 9.6% in December 2006 (compared with 6.9% at the beginning of 2006). Sales in other markets increased by 61% on good growth in Europe and the second half launch in Japan.Seloken/Toprol-XLsales increased by 3% to $1,795 million. US sales growth was restricted to 7% by the launch in November of genericToprol-XL25mg by Sandoz (formerly Eon Labs) and our move to recognising revenue conservatively as prescriptions are written (as opposed to on shipment). Sales were $1,382 million in the US. The performances ofCrestorandSeloken/Toprol-XLmore than offset declines inZestrilandPlendil, down by 7% and 24%, respectively.

Respiratory and Inflammation sales increased by 10% to $3,151 million.Symbicortsales were the main driver of this growth and increased 18% to $1,184 million. Sales ofSymbicortarise principally in Europe – the Company continues to plan for a US launch around the middle of 2007, although achieving this launch timeline is dependent upon successful transfer of technology and completion of the required validation batches. Elsewhere in the therapy area,Pulmicortsales rose by 11% with annual sales of $1,292 million, whilstRhinocortsales declined to $360 million, down by 7%.

Sales in the Oncology portfolio grew by 12% to $4,262 million.Arimidexsales increased 29% to $1,508 million, with growth rates in the US (up to $614 million) and other markets the same.Casodexsales grew by 9% to $1,206 million on strong performances outside the US andZoladexsales exceeded $1 billion for the second year in a row, again on good performance outside the US.Iressasales fell by 11% to $237 million, a slower decline than in 2005, as growth in Asia Pacific went some way to offset declines in the US.

Neuroscience sales grew by 16% to $4,704 million.Seroquelsales exceeded $3 billion to reach $3,416 million (up 24%). In the US,Seroquelshare of new prescriptions in the anti-psychotic market increased to over 30% in December. Sales in other markets increased by 23%.

We discuss the performances of the therapy areas and the individual products in those areas in more detail in the relevant sections of the Business Review.

Geographical Analysis

In the US, sales were up 16%. Sales growth forNexium,Seroquel,ArimidexandCrestoramounted to $1,441 million, whilst there were declines in products such asPrilosec.Toprol-XLgrew in the year although it faced generic competition from November. Adjusting sales to excludeToprol-XLsales from both 2006 and 2005, growth was 11%.

Revenue from outside the US now accounts for 53% of our sales. In Europe, sales increased by 6% for the full year, with good volume growth partially offset by lower realised prices. Sales for the five key growth products combined grew by 21%. However, performance was hindered by declines in Germany, where doctors have been encouraged to prescribe generics.

Sales in Japan increased by 5% as a result of good growth forCasodexandArimidextogether with the launch ofCrestor. Sales in China were up 19% to $328 million on the back of strong growth in all the major therapeutic areas, particularly Oncology.

We discuss the geographic performances in more detail in the appropriate sections of the Business Review on pages 33 to 36.

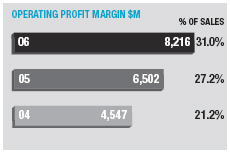

Operating Margin and Retained Profit

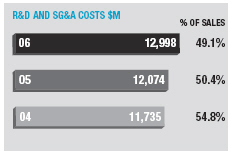

Operating margin increased by 3.8 percentage points from 27.2% to 31.0 %. Excluding the effects of currency and other income, underlying margin increased 2.9 percentage points for the full year.

Gross margin increased by 1.4 percentage points to 79.0% of sales. Slightly lower payments to Merck (4.7% of sales) benefited gross margin by 0.1 percentage points whilst currency and royalties reduced gross margin by 0.1 percentage points and 0.2 percentage points, respectively. Excluding the prior year costs for the early termination of the MedPointeZomigUS distribution agreement and manufacturing provisons (in total $137 million) and the 2006 provisions made in respect

ofToprol-XL, NXY-059 and manufacturing efficiencies (in total $215 million), underlying margin improved by 1.5 percentage points.

Research and development expenditure was up 16% to $3,902 million (14% excluding the Cambridge Antibody Technology investment) and increased by 0.6 percentage points to 14.7% of sales. Selling, general and administrative cost increases were restricted to 5% over the last year, reaching $9,096 million and adding 2.0 percentage points to operating margin.

Higher net other income and expense increased operating margin by 1.1 percentage points due principally to higher royalties, plus the $109 million gain recognised in the first half of the year from the divestment of the US anaesthetics and analgesic products to Abraxis BioSciences Inc., and the disposal of non-core products in Scandinavia ($32 million) in the final quarter.

Included within cost of sales is the movement in fair value of financial instruments used to manage our transactional currency exposures; the loss for the year, net of an exchange gain on the underlying exposures, was $11 million. Other fair value movements of $5 million are charged elsewhere in operating profit.

Net interest and dividend income for the year was $327 million (2005 $165 million). The increase over 2005 is primarily attributable to higher average investment balances and yields. The reported amounts include $43 million (2005 $15 million) arising from employee benefit fund assets and liabilities reported under IAS 19, “Employee Benefits”.

The effective tax rate for the twelve months was 29.0% (2005 29.1%) . The decrease compared to 2005 is the net effect of tax benefits arising from a different geographical mix of profits, tax deductions relating to share-based payments and the recognition of deferred tax assets in respect of tax credit carry forwards, offset by an increase in tax provisions principally in relation to global transfer pricing issues.

Earnings per share increased by 34% from $2.91 in 2005 to $3.86 for the current year. We estimate that the share re-purchase scheme has added 6 cents to earnings per share (after taking account of interest income foregone).

In 2006,Toprol-XLcontributed US sales of $1,382 million and earnings per share of 50 cents. Since the timing of approval and launch

| SHAREHOLDER INFORMATION | 171 |

DEFINITIONS AND INTERPRETATION

Figures in parentheses in tables and in the Financial Statements are used to represent negative numbers.

Except where otherwise indicated, figures included in this report relating to pharmaceutical product market sizes and market shares are obtained from syndicated industry sources, primarily IMS Health (IMS), a market research firm internationally recognised by the pharmaceutical industry. The 2006 market share figures included in this report are based primarily on data obtained from an online IMS database.

IMS data may differ from that compiled by the Group with respect to its own products. Of particular significance in this regard are the following: (1) AstraZeneca publishes its financial results on a financial year and quarterly interim basis, whereas IMS issues its data on a monthly and quarterly basis; (2) the online IMS database is updated quarterly and uses the average exchange rates for the relevant quarter; (3) IMS data from the US is not adjusted for Medicaid and similar state rebates; and (4) IMS sales data are compiled using actual wholesaler data and data from statistically representative panels of retail and hospital pharmacies, which data are then projected by IMS to give figures for national markets.

References to prevalence of disease have been derived from a variety of sources and are not intended to be indicative of the current market or any potential market for AstraZeneca’s pharmaceutical products since, among other things, there may be no correlation between the prevalence of a disease and the number of individuals who are treated for such a disease.

| Terms used in the Annual Report | |

| and Form 20-F Information | US equivalent or brief description |

| Accruals | Accrued expenses |

|

|

| Allotted | Issued |

|

|

| Bank borrowings | Payable to banks |

|

|

| Called-up share capital | Issued share capital |

|

|

| Creditors | Liabilities/payables |

|

|

| Current instalments of loans | Long term debt due within one year |

|

|

| Debtors | Receivables and prepaid expenses |

|

|

| Earnings | Net income |

|

|

| Finance lease | Capital lease |

|

|

| Fixed asset investments | Non-current investments |

|

|

| Freehold | Ownership with absolute rights in perpetuity |

|

|

| Interest receivable | Interest income |

|

|

| Interest payable | Interest expense |

|

|

| Loans | Long term debt |

|

|

| Prepayments | Prepaid expenses |

|

|

| Profit | Income |

|

|

| Profit and loss account | Income statement/consolidated statement of income |

|

|

| Reserves | Retained earnings |

|

|

| Short term investments | Redeemable securities and short term deposits |

|

|

| Share premium account | Premiums paid in excess of par value of Ordinary Shares |

|

|

| Statement of recognised | |

| income and expense | Statement of comprehensive income |

|

|

GLOSSARY

The following abbreviations and expressions have the following meanings when used in this report:

ACE (Inhibitor)– Angiotensin-converting enzyme blocks the production of a hormone called angiotensin II. Angiotensin II narrows blood vessels and thereby raises blood pressure.

ACS– Acute Coronary Syndrome, an umbrella term used to cover any group of clinical symptoms compatible with acute myocardial ischemia.

Adjuvant– Assisting in the prevention, improvement or cure of disease.

ADP– Adenosine diphosphate attaches to receptors on the surface of platelets to form blood clots.

Adverse reaction– An unwanted, negative consequence associated with the use of a medicine.

Agonist– A substance capable of binding to a molecular target to initiate or enhance a physiological reaction.

Anaesthesia– The total or partial loss of sensation, especially in relation to pain.

Analgesia– The inability to feel pain.

Abbreviated New Drug Application (ANDA)–A marketing approval application for a generic drug submitted to the US Food and Drug Administration.

Antagonist– A substance capable of binding to a molecular target to neutralise or counteract a physiological reaction.

Anti-androgen– A drug that blocks the cellular uptake of testosterone by the prostate gland and used in the treatment of prostate cancer.

Anti-psychotic drug– For the treatment of the unrealistic ideas, delusions (false beliefs) and hallucinations (false perceptions) that can appear during depression or mania.

Aromatase inhibitor– A drug that inhibits the enzyme aromatase, which is involved in the production of the female sex hormone, oestrogen.

AstraZeneca or AstraZeneca Group– AstraZeneca PLC and its subsidiaries.

Atherosclerosis– Disease of the arteries linked to the build-up of lipids (fats) in the walls and the formation of atheromatous plaque, which contracts the lumen of these vessels.

Atrial fibrillation (AF)– Abnormal irregular heart rhythm with chaotic generation of electrical signals in the atria of the heart.

Atypical anti-psychotic drugs– Second generation drugs to treat psychosis with reduced likelihood to cause movement disorders.

Biomarker– A characteristic that is objectively measured and evaluated as an indicator of normal biological processes, pathogenic processes, or pharmacological responses to a therapeutic intervention.

Biopharmaceuticals/Biologics– A new class of systemic therapies that contain proteins (usually produced naturally by living organisms in response to disease, for example antibodies), as opposed to traditional pharmaceutical drugs that are made up of non-living chemicals.

Bipolar disorder– Any of several mood disorders characterised usually by alternating episodes of depression and mania or by episodes of depression alternating with mild non-psychotic excitement.

Bronchodilator– A drug that causes the widening of the bronchi (major air passages of the lungs).

Cardiovascular (CV)– Relating to the heart and blood vessels.

CAT– Cambridge Antibody Technology Group plc.

Candidate Drug (CD)– A drug to be taken into clinical concept testing phase.

CEE– Central and Eastern Europe.

CHF– Congestive Heart Failure. A condition in which the heart’s function as a pump (to circulate blood throughout the body) is inadequate to meet the body’s needs and leads to a poor blood supply, which may cause the body’s organ systems to fail.

Chronic Obstructive Pulmonary Disease (COPD)–Any disorder that persistently obstructs bronchial airflow, eg bronchitis.

Cognitive disorders– The class of disorders consisting of significant impairment of cognition or memory that represents a marked deterioration from a previous level of functioning.

CR– Corporate Responsibility.

Corticosteroid– Any of the steroid hormones made by the cortex (outer layer) of the adrenal gland.

CRC– Colo-rectal cancer.

Crohn’s disease– A chronic inflammatory disorder of the bowels.

Directors– The Directors of the Company.

Diabetes– A metabolic disorder characterised by hyperglycaemia (high glucose blood sugar), among other signs, or a variable disorder of carbohydrate metabolism usually characterised by inadequate secretion or utilisation of insulin.

Diuretic– A drug that causes the increased passing of urine.

Dopamine partial agonists– Mimic the effects of dopamine in the brain by stimulating dopamine receptors.

Double-blind study– A clinical study in which neither the subject, nor the investigator nor the research team interacting with the subject or data during the trial knows what treatment a subject is receiving.

Drug metabolism– The biochemical modification or degradation of drugs, usually through specialised enzymatic systems.

Dyslipidaemia– A condition marked by abnormal concentrations of lipids or lipoproteins in the blood.

EEA– European Economic Area.

Efficacy– The outcomes measured in Phase III clinical trials that indicate that the test drug has the intended benefit.

Epidermal Growth Factor (EGF) receptor– A protein found on the surface of some cells and to which epidermal growth factor binds, causing the cells to divide. It is found at abnormally high levels on the surface of many types of cancer cells, so these cells may divide excessively in the presence of epidermal growth factor.

EFPIA– European Federation for Pharmaceutical Industries and Associations.

EMEA– The European Medicines Agency.

Excipient– An inactive substance that serves as the vehicle or medium for a drug or other active substance.

Food and Drug Administration (FDA)– Part of the US Department of Health and Human Services Agency responsible for development, approval, manufacture, sale and use of all drugs, biologics, vaccines and medical devices in the US.

First-line therapy– Treatment given to a newly diagnosed patient, who has therefore not yet been treated.

First time in man– The first time that an experimental compound is administered to a human. It implies that the compound has passed ethical review bodies and passed formal regulatory toxicology studies.

Gastrointestinal (GI)– Relating to the stomach and intestines.

Generic– Drugs that are copies of brand-name drugs and have regulatory approval.

Gastro-oesophageal reflux disease (GERD)– A recurrent condition where gastric juices, containing acid, travel back from the stomach into the oesophagus.

Group– The Company and its subsidiaries.

Head-to-head study– A clinical trial in which two different medicines are directly compared with each other with respect to their effect on a marker of the disease or a specific event associated with the disease. (For drugs under development, this is often a comparison with a marketed drug that is seen to be the gold standard.)

Hydrofluoroalkanes (HFAs)– A new propellant for metered-dose inhalers that are more environmentally friendly than the current CFC-based inhalers.

High-density lipoprotein cholesterol (HDL-C)– HDL carries cholesterol in the blood, sometimes referred to as “good” cholesterol.

High-throughput screening– The process of using automated tests to search quickly through large numbers of substances for desired binding or activity characteristics.

Hormone– A chemical “signal” carried in the blood.

HKAPI– Hong Kong Association of the Pharmaceutical Industry.

Hypertension– High blood pressure.

IMS Health Inc.– Provider of pharmaceutical market data globally.

IR– Immediate release.

Ischaemic heart disease– A chronic disease caused by insufficient blood supply to the heart.

Leukotriene receptor antagonist– New type of asthma medication. They are non-steroidal medications, which are taken long term and have been shown to reduce reliever use and may also allow the asthmatic to reduce high doses of inhaled steroids.

Line extension– A new formulation, indication or presentation of a product that is already approved.

Lipid– Another word for “fat”. Lipids are one of the main constituents of plant and animal cells.

Low-density lipoprotein cholesterol (LDL-C)– LDL is the major carrier of cholesterol in the blood, sometimes referred to as “bad” cholesterol.

Luteinising hormone-releasing hormone (LHRH)– A naturally occurring hormone that controls sex hormones in both men and women.

LHRH agonist– A compound that is similar to LHRH in structure and is able to act like it.

Marketing Authorisation Application (MAA)– An application for authorisation to place medicinal products on the market. This is a specific term for the EU/EEA markets.

Medicaid– A US health insurance programme for individuals and families with low incomes and resources. It is jointly funded by the states and federal government, and is managed by the states.

Medicare– A US health insurance programme for US citizens aged 65 or older, US citizens under age 65 with certain disabilities, and US citizens of all ages with permanent kidney failure requiring dialysis or a kidney transplant. Recently, Medicare began offering prescription drug coverage under Part D of the Medicare Prescription Drug Benefit.

Metabolic syndrome– A combination of medical disorders that increase one’s risk for cardiovascular disease and diabetes.

MHLW– Japanese Ministry of Health, Labour and Welfare.

Monoclonal antibody– An antibody derived from a single clone of cells; all antibodies derived from such a group of cells have the same sequence of DNA.Monotherapy– Treatment where only one agent is given.

Myocardial infarction (MI)– A heart attack.

New Chemical Entity (NCE)– A new, pharmacologically-active chemical substance. The term is used to differentiate from line extensions and existing drug products.

NCI– US National Cancer Institute.

New Drug Application (NDA)– An application to the FDA for approval to market a drug product in the US.

Neuroscience– Sciences that deal with the structure or function of the nervous system and brain.

Normotensive– Indicating a normal arterial blood pressure.

NSAID– Non-steroidal anti-inflammatory drug.

NSCLC– Non-small cell lung cancer.

OA– Osteoarthritis.

Oncology– The study of diseases that cause cancer.

Odontology– A science dealing with the teeth, their structure and development, and their diseases.

Outcomes study– A large clinical trial in which the effect of a drug in preventing or delaying a specific and important medical event related to that disease area (eg the occurrence of a heart attack) is measured, rather than the effect on a marker of the disease (eg blood levels of certain enzymes).

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | Trade marks

Trade marks of the AstraZeneca group of companies appear throughout this document in italics. AstraZeneca, the AstraZeneca logotype and the AstraZeneca symbol are all trade marks of the AstraZeneca group of companies. Trade marks of companies other than AstraZeneca appear with a®or™ sign and include: Abraxane®, a registered trade mark of Abraxis BioScience, Inc.; Avastin™, a trade mark of Genentech, Inc.; Cubicin™, a trade mark of Cubist Pharmaceuticals, Inc.; CytoFab™, a trade mark of Protherics, Inc.; Herceptin™, a trade mark of Genentech, Inc.; Humira™, a trade mark of Abbott Laboratories, Inc.; Prinivil™, a trade mark of Merck & Co., Inc.; Taxotere™, a trade mark of Aventis Pharma S.A.; TriCor™, a trade mark of Fournier Industrie et Santé and Zocor™, a trade mark of Merck & Co., Inc. Use of terms

In this Annual Report and Form 20-F Information, unless the context otherwise requires, ‘AstraZeneca’, ‘the Group’, ‘the Company’, ‘we’, ‘us’ and ‘our’ refer to AstraZeneca PLC and its consolidated entities. | | Statements of competitive position

Except as otherwise stated, market information in this Annual Report and Form 20-F Information regarding the position of our business or products relative to its or their competition is based upon published statistical data for the 12 months ended 30 September 2006, obtained from IMS Health, a leading supplier of statistical data to the pharmaceutical industry. Except as otherwise stated, these market share and industry data from IMS Health have been derived by comparing our sales revenue to competitors’ and total market sales revenues for that period. For the purposes of this Annual Report and Form 20-F Information, references to the world pharmaceutical market or similar phrases are to 52 countries contained in IMS Health’s MIDAS Quantum database, which amount to approximately 95% (in value) of the countries audited by IMS Health. | | Statements of growth rates, sales and market data Except as otherwise stated, growth rates and sales in this Annual Report and Form 20-F Information are given at constant exchange rates (CER) to show underlying performance by excluding the effects of exchange rate movements. Market data are given in actual US dollars. Statements of dates

Except as otherwise stated, references to days and/or months in this Annual Report and Form 20-F Information are references to days and/or months in 2006. AstraZeneca websites

Information on or accessible through our websites, including astrazeneca.com, astrazenecaclinicaltrials.com, rosuvastatininformation.com and cambridgeantibody.com, does not form part of this document. | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |