| > | | Continued pressure on the price of medicines. |

| > | | Higher regulatory hurdles for new medicines and new indications. |

| > | | Competition from research-based and, increasingly, generic pharmaceutical companies. |

PRICING PRESSURE

The growing demand for healthcare means ever-increasing pressure on healthcare budgets and, whilst payers recognise the need to reward innovation, they have a duty to spend their limited financial resources wisely. Cost-containment, including pharmaceutical spending, therefore continues to be a fundamental consideration. The current global economic downturn is likely to further constrain healthcare providers and those patients who pay directly for their medicines, and additional challenges may arise if suppliers and distributors face credit-related difficulties.

The research-based pharmaceutical industry’s challenge is to manage the associated downward pressure on the price of its products, whilst continuing to invest in the discovery, development, manufacturing and marketing of new medicines.

Most of our sales are generated in highly regulated markets where governments exert various levels of control on price and reimbursement. The network of pricing systems creates a complex matrix that must be managed to optimise revenues. This may be further complicated by currency fluctuations within regions. The principal aspects of price regulation in the major markets are described more in the Geographical Review from page 48.

Payers also increasingly require demonstration of the economic as well as therapeutic value of medicines. Meeting these needs across a diverse range of national and local reimbursement systems requires significant additional resources.

REGULATORY REQUIREMENTS

The pharmaceutical industry is one of the most regulated of all industries and, whilst efforts to harmonise regulations globally are increasing, the number and impact of these regulations continue to grow. Regulatory drug review and approval is a complex and time consuming process, typically taking between six months and two years. In recent years, regulatory processes have become subject to more conditions including patient risk management plans, patient registries, post-marketing requirements, and conditional and limited approvals.

Traditional clinical trials designed to establish safety and efficacy remain a core component of drug development programmes but regulators are increasingly requiring that programmes also clearly demonstrate the benefits and risks of new medicine in the context of other available therapies, as well as demonstrating long-term medical outcomes, such as survival and quality of life improvements.

In addition to safety and efficacy, pre-approval regulation covers every aspect of the product including the chemical composition, manufacturing, quality controls, handling, packaging, labelling, distribution, promotion and marketing. Post approval and launch, all aspects relating to a product’s safety, efficacy and quality must continue to meet regulatory requirements. See also Ensuring Product Quality (page 27).

COMPETITION

Our main competitors are other international, research-based pharmaceutical companies that sell innovative, patent-protected, prescription medicines. Following patent expiry, our products also compete with generic pharmaceuticals. Since generic manufacturers do not bear the same high costs of R&D, nor do they typically invest as significantly in safety monitoring or marketing, they typically adopt lower prices for their products.

The generic industry is increasingly challenging innovators’ patents and in the US, the world’s largest pharmaceutical market, many leading medicines have faced or are facing patent challenges from generic manufacturers. The research-based industry is also experiencing increased challenges elsewhere in the world, for example in Europe, Canada, Asia and Latin America. It is increasingly complex to enforce patent rights and other intellectual property in certain markets, especially those where practices are in place to encourage broad access to medicines. While there are few established regulatory systems for biosimilars of biological products, several markets, including the US, are considering regulatory structures that might allow for an abbreviated marketing approval mechanism akin to that for generic pharmaceuticals. Further information about the risk of the early loss and expiry of patents is explained in the Intellectual Property section on page 26.

Competition also comes from collaborations and partnerships between traditional pharmaceutical companies and smaller biotechnology and vaccine companies. Increasingly, as pharmaceutical companies seek to expand their pipeline, they are able to gain access to promising new product candidates by partnering with these smaller companies that may lack some of the infrastructure for growth that a larger company can provide. Competition for high quality collaborations is increasingly fierce as the major pharmaceutical companies frequently focus on the same opportunities to enhance their in-house capabilities.

Further information about the principal risks and uncertainties we face can be found in the Risk section from page 74.

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

| > | | Despite a continually challenging environment, including generic pressure, combined sales ofArimidex,Crestor,Nexium,SeroquelandSymbicortup 5% in the US – 65% of our total US sales. |

| > | | Maintained market position as the second largest brand name pharmaceutical company in Canada. |

| > | | Solid sales performance in the Rest of World, up 5%. |

| > | | Strong brand performance in Western Europe but intense competition and governmental controls over healthcare expenditure. |

| > | | Strong volume growth from key products,Crestor,LosecandSeroquelin Japan. |

| > | | Emerging Rest of World delivers strong sales growth, up 16% with Emerging Europe sales up 10% and Emerging Asia sales up 10%. |

| > | | Continued expansion in China, including continued sales growth up 31%. |

| > | | EU Commission of a Sectoral Inquiry into the pharmaceutical industry continues, with a final report expected in Spring 2009. |

For more information regarding our products please refer to the relevant sections of the Therapy Area Review from page 53. Details of relevant continuing litigation can be found in Note 25 to the Financial Statements (from page 144) and details of relevant risks are set out in the Principal Risks and Uncertainties section (from page 76).

For the AstraZeneca definition of markets please see the Glossary on page 199.

US

Despite full generic competition toToprol-XLand the growth in generic omeprazole, sales in the US increased 1% in 2008 to $13,510 million (2007: $13,366 million). Combined sales ofArimidex,Crestor,Nexium,Seroquel, andSymbicortwere up 5% to $8,803 million (2007: $8,414 million) – 65% of our total US sales. AstraZeneca is currently the third largest pharmaceutical company in the US, with a 5.6% share of US prescription pharmaceutical sales. Sales for Aptium Oncology and Astra Tech fell by 2% and rose by 33% to $395 million (2007: $402 million) and $80 million (2007: $60 million), respectively.

Nexiumcontinues to lead the branded proton pump inhibitor (PPI) market for new prescriptions, total prescriptions and total capsules dispensed. Generic pantoprazole showed strong growth after being introduced late in 2007 and together with generic omeprazole captured most of the market growth, resulting in price and share erosion across the entire branded PPI market. In the face of generic pressure,Nexiumcontinued to fare better than its branded competitors with sales in 2008 down 8% to $3,101 million (2007: $3,383 million). During the year, the US Food and Drug Administration (FDA) approved the use ofNexiumin children ages one to 11 years old for the short-term treatment of gastroesophageal reflux disease.

Seroquelmaintained its strong position as the number one prescribed atypical anti-psychotic on the market, with sales up 5% to $3,015 million (2007: $2,863 million). Seroquelposted total prescription growth of 6.6% with an increase of one million prescriptions, outpacing the rate of market growth for anti-psychotics by almost two points, leading the market in absolute total prescription growth. During the year, the FDA approvedSeroquelfor the maintenance of bipolar disorder as adjunct therapy to lithium or divalproex. The FDA also approvedSeroquel XRfor the depressive episodes of bipolar disorder, the manic or mixed episodes associated with bipolar I disorder (as either monotherapy or adjunct therapy to lithium or divalproex), and for maintenance treatment of bipolar disorder as adjunct therapy to lithium or divalproex.

Supplemental new drug applications (sNDAs) were submitted to the FDA for use ofSeroquel XRin adult patients for major depressive disorder (MDD) and generalised anxiety disorder (GAD). In December 2008, we received a Complete Response Letter from the FDA related to the MDD submission, while the GAD submission remains under review. We also submitted an sNDA to the FDA for use ofSeroquelfor treatment of schizophrenia in 13 to 17 year olds and for treatment of acute manic episodes of bipolar I disorder for 10 to 17 year olds. The US Prescribing Information forSeroquel andSeroquel XRis being updated to include new safety information regarding use in children and adolescents.SeroquelandSeroquel XRare not approved currently for use in paediatric patients under 18 years of age.

Crestorsales were up 18% to $1,678 million (2007: $1,424 million) with a total prescription growth of 10.8%, and was the only branded statin to grow in total prescriptions throughout 2008 despite generic pressure. The new indication to slow the progression of atherosclerosis in adult patients with elevated cholesterol, an important differentiator from other products in the cholesterol-lowering market, was successfully introduced and awareness amongst physicians is high. Under the terms of an agreement executed in November 2008, Abbott obtained the non-exclusive right to promoteCrestoralongside AstraZeneca in the US (excluding Puerto Rico) increasingCrestor‘s profile and share of voice. New data presented in November 2008 from the JUPITER study demonstrated thatCrestor20mg significantly reduced major cardiovascular (CV) events – defined by the study as the combined risk of myocardial infarction, stroke, arterial revascularisation, hospitalisation for unstable angina, or death from CV causes – by 44% compared to placebo among men and women with elevated hsCRP (high-sensitivity C-reactive protein) but low to normal cholesterol levels. hsCRP is a recognised marker of inflammation that is associated with an increased risk of atherosclerotic CV events. The JUPITER results also showed that for patients in the trial takingCrestor, the combined risk of heart attack, stroke or CV death was reduced by nearly half. We expect to file a regulatory submission with the FDA that includes the JUPITER data in the first half of 2009 and, if approved, will begin promotional activities within the approved labelling.

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

OUR FINANCIAL PERFORMANCE

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2008 | | 2007 | | 2006 | | 2008 compared to 2007 | | 2007 compared to 2006 | |

| | | | | | | | | | | Growth due | | | | | | | | | | | Growth due | | | | | | | | | | | | | | | | | |

| | | | | | | CER | | | to exchange | | | | | | | CER | | | to exchange | | | | | | | CER | | | Reported | | | CER | | | Reported | |

| | | Sales | | | growth | | | effect | | | Sales | | | growth | | | effect | | | Sales | | | growth | | | growth | | | growth | | | growth | |

| | | $m | | | $m | | | $m | | | $m | | | $m | | | $m | | | $m | | | % | | | % | | | % | | | % | |

| | |

| US | | | 13,510 | | | | 142 | | | | 2 | | | | 13,366 | | | | 917 | | | | – | | | | 12,449 | | | | 1 | | | | 1 | | | | 7 | | | | 7 | |

| | |

| Canada | | | 1,275 | | | | 95 | | | | 35 | | | | 1,145 | | | | 54 | | | | 60 | | | | 1,031 | | | | 8 | | | | 11 | | | | 5 | | | | 11 | |

| | |

North America | | | 14,785 | | | | 237 | | | | 37 | | | | 14,511 | | | | 971 | | | | 60 | | | | 13,480 | | | | 2 | | | | 2 | | | | 7 | | | | 8 | |

| | |

| Western Europe | | | 9,743 | | | | 55 | | | | 573 | | | | 9,115 | | | | 282 | | | | 760 | | | | 8,073 | | | | 1 | | | | 7 | | | | 3 | | | | 13 | |

| | |

| Japan | | | 1,957 | | | | 73 | | | | 223 | | | | 1,661 | | | | 170 | | | | (12 | ) | | | 1,503 | | | | 4 | | | | 18 | | | | 11 | | | | 11 | |

| | |

| Other Established ROW | | | 843 | | | | 107 | | | | 21 | | | | 715 | | | | 83 | | | | 77 | | | | 555 | | | | 15 | | | | 18 | | | | 15 | | | | 29 | |

| | |

Established ROW | | | 12,543 | | | | 235 | | | | 817 | | | | 11,491 | | | | 535 | | | | 825 | | | | 10,131 | | | | 2 | | | | 9 | | | | 5 | | | | 13 | |

| | |

| Emerging Europe | | | 1,215 | | | | 102 | | | | 85 | | | | 1,028 | | | | 102 | | | | 95 | | | | 831 | | | | 10 | | | | 18 | | | | 12 | | | | 24 | |

| | |

| China | | | 627 | | | | 136 | | | | 54 | | | | 437 | | | | 91 | | | | 18 | | | | 328 | | | | 31 | | | | 43 | | | | 28 | | | | 33 | |

| | |

| Emerging Asia Pacific | | | 802 | | | | 72 | | | | (19 | ) | | | 749 | | | | 62 | | | | 41 | | | | 646 | | | | 10 | | | | 7 | | | | 10 | | | | 16 | |

| | |

| Other Emerging ROW | | | 1,629 | | | | 247 | | | | 39 | | | | 1,343 | | | | 223 | | | | 61 | | | | 1,059 | | | | 18 | | | | 21 | | | | 21 | | | | 27 | |

| | |

Emerging ROW | | | 4,273 | | | | 557 | | | | 159 | | | | 3,557 | | | | 478 | | | | 215 | | | | 2,864 | | | | 16 | | | | 20 | | | | 17 | | | | 24 | |

| | |

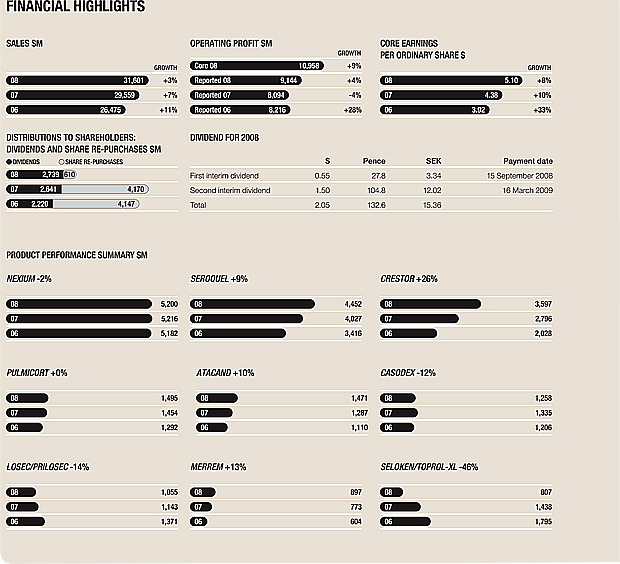

Total sales | | | 31,601 | | | | 1,029 | | | | 1,013 | | | | 29,559 | | | | 1,984 | | | | 1,100 | | | | 26,475 | | | | 3 | | | | 7 | | | | 7 | | | | 12 | |

| | |

In another agreement with Abbott, we are investigating the fixed dose combination of the active ingredients inCrestor(rosuvastatin calcium) and Trilipix™ (fenofibric acid) for the treatment of mixed dyslipidaemia. A Phase III trial in 2008 demonstrated that a combination of rosuvastatin calcium and fenofibric acid delivers greater improvements in treating all three key lipids (LDL, HDL and triglycerides) than the pre-specified monotherapy comparators. Currently, dyslipidaemia affects more than 100 million US residents and has been shown to play a pivotal role in the development of atherosclerosis and consequently, cardiovascular disease. Patients with mixed dyslipidaemia are expected to become more prominent segments of the dyslipidaemic population. Abbott obtained approval of Trilipix™ in December 2008 as the first and only fibrate labelled for use with a statin.

To maximise the value ofMerrem IVduring the year we announced an agreement with Cubist, who will provide promotional and scientific affairs support forMerrem IVin the US and Puerto Rico.

Arimidexcontinued to perform well with sales up 9% to $754 million (2007: $694 million) for the full year. Arimidexcontinues to be the market leader in new prescriptions for branded hormonal treatments for breast cancer in the US.

In September 2008, an additional six-month period of exclusivity was granted to marketCasodexfor its licensed advanced prostate cancer indication until 1 April 2009.

Pulmicort Respules, the only inhaled corticosteroid for the treatment of asthma approved in the US for children as young as 12 months, showed strong sales growth with sales up 2% to $982 million (2007: $964 million). On 23 September 2008, the US District Court for the District of New Jersey denied a motion filed by Teva Pharmaceuticals Ltd. for summary judgment of no infringement in thePulmicort Respulespatent litigation. On 19 November 2008, the same court awarded a temporary restraining order against Teva Pharmaceuticals after Teva launched its generic product ‘at risk’ on 18 November 2008. On 25 November 2008, the parties settled the matter and AstraZeneca granted Teva a licence to launch its generic product in late 2009.

In its first full year after launch in June 2007,Symbicort Rapihaler(pMDI) continued to deliver steady growth with sales up 410% to $255 million (2007: $50 million). Widespread physician experience and growing appreciation of the differentiating feature of control plus fast onset has led to the product surpassing a 10% new prescription share of the inhaled corticosteroid/long acting beta agonist market.Symbicortis now prescribed to one in five of all patients that are new to combination therapy.

In 2008, two sNDAs were submitted to the FDA: one for the use ofSymbicortin chronic obstructive pulmonary disease and another for its use in paediatric asthma for ages six to 12. In October 2008, the pMDI device was enhanced with an actuation counter.

Synagisis the only FDA-approved monoclonal antibody (MAb) to help protect high-risk babies against severe Respiratory Syncytial Virus (RSV) disease. In its first full year in AstraZeneca, sales in the US were $923 million.

In 2008, distribution agreements continued with Par Pharmaceutical for all available strengths of generic metoprolol succinate. Also, Ranbaxy Pharmaceuticals began distribution of authorised generics of both felodipine and 40mg omeprazole.

Currently, there is no direct government control of prices for commercial prescription drug sales in the US. However, some publicly funded programmes – such as Medicaid and TRICARE (Department of Veterans Affairs) – have statutorily mandated rebates that have the effect of price controls for these programmes. Additionally, pressure on pricing, availability and utilisation of prescription drugs for both commercial and public payers continues to increase, driven by, among other things, an increased focus on generic alternatives. Primary drivers of increased generic use are budgetary policies within healthcare systems and providers, including the use of “generics only” formularies, and increases in patient co-insurance or co-payments. While it is unlikely that there will be widespread adoption of a broad national price control scheme in the near term, there will continue to be increased attention to pharmaceutical prices and their impact on healthcare costs for the foreseeable future.

ASTRAZENECA ANNUAL REPORT AND FOR M 20-F INFORMATION 2008

In the current political climate, policymakers are likely to consider healthcare reform a top priority. The reauthorisation of the State Childrens’ Health Insurance Program (SCHIP), a joint federal-state programme to expand healthcare coverage (including prescription drug coverage) for qualifying children, is poised to be one of the first healthcare reform proposals debated in the 111th Congress. A sustained focus on containing prescription drug costs is also likely, which could include proposals to allow the government to negotiate Medicare Part D prices directly with the pharmaceutical industry, increase manufacturers’ Medicaid drug rebate payments under the Medicaid drug rebate statute, and/or expand Medicaid rebates for patients who qualify for both Medicaid and Medicare (so-called ‘dual eligibles’). Additionally, there could be efforts to pass legislation implementing comparative effectiveness research requirements and/or legislation allowing for the commercial importation of drugs into the US from selected countries by certain individual consumers, pharmacies and drug wholesalers. Finally, proposals that would require disclosure of payments to healthcare professionals (eg for speaker contracts) are also being considered at the state and federal levels.

In its third year of operation, the Medicare Part D prescription drug programme maintained high levels of enrollment and beneficiary satisfaction, achieved prescription volume growth similar to other mature markets and provided access to our medicines for a large segment of the patient population. Through the AZ&Me Prescription Savings Programme for Patients with Medicare Part D, AstraZeneca provides prescription access to financially needy Medicare D beneficiaries. Although difficult to quantify, Medicare Part D has had an indirect effect on pricing in the broader US market. Despite the pricing challenges, overall access in key accounts was maintained or improved in 2008. It is difficult to predict fully the longer-term effects of this initiative on our business.

We continue to support My Medicare Matters, a community based outreach and education programme, in partnership with the National Council on Aging. Funding from AstraZeneca also supports MyMedicareCommunity.org, an on-line community for grass roots organisations serving people with Medicare. During 2007 and 2008, we supported a pilot grant programme focused on testing new approaches to finding and enrolling eligible people in the Medicare’s Low-Income Subsidy (LIS) programme. Over 40,000 LIS applications were submitted as a result of these demonstration projects.

Additionally, AstraZeneca has been providing patient assistance to the uninsured for 30 years and, in the last six years, has provided more than $3 billion in savings to more than one million patients in the US and Puerto Rico. Last year alone, we provided more than $612 million in savings to approximately 440,000 people without drug coverage (approximately 2.7 million prescriptions).

CANADA

Despite the entry of the generic forms ofSeroquel IR, sales in Canada increased by 8% (+11% reported) to $1,275 million (2007: $1,145 million). Combined sales ofCrestor,Nexium,SeroquelandAtacandwere up 18% to over $864 million (2007: $713 million) withCrestor,SeroquelandNexiumamong the top 20 prescription products in Canada by sales.

We remain the second largest brand name pharmaceutical company in Canada.Crestormaintained its number two ranking in the statin market and was the fastest-growing product in both new and total prescription segments (25.9% and 32.0% growth respectively).Crestoris also the third largest product in Canada by sales. Together,Seroquel XRandSeroquel IRremain the leaders in new and total prescriptions within the atypical anti-psychotics market.Atacandcontinues to outperform the anti-hypertensive market, with total prescription growth of over 15.0% compared with market growth of only 7.4%. Several key regulatory approvals were achieved in Canada in 2008. Canada was the first country in which we gained regulatory approval forSeroquel XRfor the treatment of bipolar mania, withSeroquel XRandSeroquel IRalso approved for the treatment of bipolar depression (approvals were received eight months and five months respectively ahead of standard Health Canada review timelines). In addition, a new tablet strength forAtacand(32mg) was approved by Health Canada.

Organisational efficiencies were gained with the closure of the Canadian packaging plant and transfer of product packaging to the Newark, Delaware facility, and further efficiencies were obtained through the movement to common North American technology platforms.

The Canadian government has instituted a Health Technology Assessment appraisal system through their Common Drug review process which rejects almost six out of 10 new medications. The Patented Medicine Prices Review Board has the role of setting

the maximum non-excessive price in the market. For patients to gain optimal access to medicines, they then need to be listed on provincial formularies. This long process means patients in Canada can typically wait over two years following the regulatory approval for access to be granted.

The different provinces have adopted different approaches to pharmaceutical funding, from one end of the continuum in Quebec with more open access to more restricted access, therapeutic substitution and price tendering on the horizon in British Colombia. The trend in Canada indicates provinces will increase their access restrictions and drive prices down while the complex reimbursement system will continue to result in access delays.

Sales in the rest of the world performed strongly in 2008, up 5% (+12% reported) to $16,816 million (2007: $15,048 million). Key products (Arimidex,Crestor,Nexium,SeroquelandSymbicort) delivered a strong performance, up 14% (+20% reported) with sales of $7,413 million (2007: $6,189 million). Latin America, the Middle East and Africa and Asia Pacific regions delivered particularly strong sales, up 13% (+19% reported) with sales of $5,858 million (2007: $4,906 million).

ESTABLISHED REST OF WORLD

Sales in our Established Rest of World Markets increased by 2% (+9% reported), with good growth fromCrestor,SeroquelandSymbicortand our oncology products, together withSynagis,offsetting declines in sales of our proton pump inhibitors in Western Europe.

WESTERN EUROPE

In Western Europe, we saw a flat market with overall growth of 1% (+7% reported). This reflected decreasing sales in France (down 1%, +7% reported), Germany (down 2%, +6% reported), Italy (down 6%, +2% reported) and Spain (down 8%, -1% reported), partly offset by strong growth in the UK (up 8%, +2% reported). Sales in established European markets were mainly impacted by the loss of patent/marketing exclusivity onCasodex, by government initiatives to contain drug expenditures and by the loss of sales due to an ageing portfolio of mature brands. These impacts were partly offset by continued strong performance of key products (mainlyCrestorandSeroquel).

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

We have continued with our programme of resource management in Western Europe and reduced costs by $159 million and headcount by 618 during 2008.

Overall our sales in France were down 1% (+7% reported) to $1,922 million (2007: $1,794 million). The strong performance ofCrestorandNexium, which gained significant market share from competitors, was offset by the loss of patent/marketing exclusivity expiry forCasodex.

In Germany, sales were down 2% (+6% reported) to $1,307 million (2007: $1,233 million), mainly due to theCasodexpatent/marketing exclusivity expiry and the government restriction on access toNexiumleading to a reduction in sales of 34% over last year. Seroquelcontinued to grow well with 27% growth (+38% reported) reaching 29.5% of the market for atypical anti-psychotics.

In the UK, sales were up 8% (+2% reported) to $1,020 million (2007: $1,004 million) driven bySymbicort(+34%, +25% reported),Seroquel(+32%, +22% reported), andArimidex(+8%, +1% reported). Many of our other brands also performed well withMerrem(+13%, +6% reported) being of particular note. Competition remained intense but our key brands gained market share in their respective segments. Especially strong wereSeroquelandSymbicortachieving gains of 2.4 and 1.3 percentage points respectively. The UK Government and pharmaceutical industry have entered into ‘terms of reference’ discussions concerning potential changes to the pricing and reimbursement scheme. The impact of these changes is likely to be $90 million in 2009.

In Italy,Crestorperformed strongly increasing its sales by 12% (+22% reported). The specialty care brands also showed good growth withSeroquelincreasing sales by 19% (+28% reported) with 32.9% of the market for atypical anti-psychotics andArimidexincreasing sales by 12% (+21% reported) with 32.0% of the market for aromatase inhibitors and tamoxifen. However, overall sales declined by 6% (+2% reported) to $1,323 million (2007: $1,294 million) as a result of reference pricing at the regional level on PPIs and measures to control their prescribing by physicians, combined withCasodexpatent/marketing exclusivity expiry.

In Spain, sales were down 8% (-1% reported) to $863 million (2007: $868 million) due toSymbicort (-7%, +1% reported) and generic competition forCasodexandArimidex.

Synagissales outside the US are undertaken through a subsidiary of Abbott Laboratories with revenue of $307 million ($169 million in the seven months from June to December 2007). We estimate that about 36% of sales arise in Western Europe, about 32% in Japan and over 7% in Canada. Strong growth has been recorded in Latin America in 2008.

Most governments in Europe directly intervene to control the price and reimbursement of medicines. The decision-making power of prescribers in Europe has been eroded in favour of a diverse range of payers. While the systems to control pharmaceutical spending vary, they all have had a noticeable negative impact on the uptake and availability of innovative medicines. Several governments have imposed price reductions and increased the use of generic medicines as part of healthcare expenditure control. Several countries are applying strict tests of cost-effectiveness of medicines, which has reduced access of European patients to medicines in areas of high unmet need. These and other measures all contribute to an increasingly tough environment for branded pharmaceuticals in Europe. However, the anticipated radical change in the UK pharmaceutical system towards direct government control of prices was abandoned. Parallel trading of branded pharmaceuticals continues to challenge the European pharmaceutical market; a report commissioned for the EU Commission acknowledged this and also highlighted the negative impact of parallel trading on patient safety.

In January 2008 AstraZeneca, together with several other companies, was the subject of an unannounced inspection simultaneous with the launch by the EU Commission (Commission) of a Sectoral Inquiry (Inquiry) into the pharmaceutical industry. The Inquiry relates to the introduction of innovative and generic medicines and covers commercial and other practices, including the use of patents. On 28 November 2008 the Commission published its preliminary report. The report does not identify wrongdoing by any individual companies but is stated to provide a factual basis for further consideration. The Commission has stated that it will commence individual investigations where there are indications that competition rules have been breached. The preliminary report focuses on a number of issues relating to competition in the EU, referring to strategies which the Commission believes pharmaceutical companies use to block or delay generic entry. Such strategies include: patent filings and enforcement;

patent settlement agreements and other agreements; interventions before national regulatory authorities; and life-cycle management strategies.

A final report is expected in Spring 2009. AstraZeneca has been co-operating fully with the Commission and participating in European Federation for Pharmaceutical Industries and Associations activities.

JAPAN

In Japan, we were the fifth fastest-growing company amongst the top 15 pharmaceutical companies, maintaining our market ranking of number 12 in 2008. Strong volume growth from key products offset the biennial government review of downward drug prices to deliver sales up 4% (+18% reported) to $1,957 million (2007: $1,661 million). The key drivers of growth being the continued success ofCrestor(+93%, +118% reported), the continued growth ofLosec(+5%, +18% reported) and the increased penetration ofSeroquel(+10%, +24% reported).

In Japan, there is formal central government control of prices by the Ministry of Health, Labour and Welfare (MHLW) and the pricing and reimbursement system has remained largely stable in the last few years. As expected, pharmaceuticals were subject to price reductions in April 2008. The long-term objective of the Japanese government is to raise generic volume share from 18.7% in 2007 to 30% by 2012; recent reforms have supported this goal by making substitution of a generic product for a branded product easier.

In 2008, the MHLW continued their push towards the acceptance of non-Japanese Asian data as part of the regulatory approval package for Japanese patients. Despite increasing budgetary pressures associated with an ageing population, they also publicly recognised the importance of the pharmaceutical industry and their own drive to reward innovation better in the future.

OTHER ESTABLISHED REST OF WORLD

In Australia and New Zealand, we delivered a strong sales performance with sales up by 15% (+18% reported) to $843 million (2007: $715 million). Both our primary care and specialist care portfolios continued to grow, driven mainly by sales growth forCrestor,AtacandandNexiumin primary care and bySeroquelandArimidexin specialist care. On a CER basis, these five brands,Arimidex,Crestor,Seroquel,AtacandandNexium, grew by 33% (+37% reported).

ASTRAZENECA ANNUAL REPORT AND FOR M 20-F INFORMATION 2008

EMERGING REST OF WORLD

In the Emerging Rest of World regions, sales increased 16% (+20% reported) to $4,273 million for the full year (2007: $3,557 million), accounting for nearly 63% of total sales growth outside the US. Sales in Emerging Europe were up 10% (+18% reported) to $1,215 million (2007: $1,028 million). Sales in China increased 31% (+43% reported) to $627 million (2007: $437 million) and sales in Emerging Asia Pacific increased 10% (+7% reported) to $802 million (2007: $749 million).

As the pharmaceutical markets in Asia Pacific, Latin America and elsewhere develop, reforms in pricing and reimbursement will inevitably follow. As these markets become more important to our business, we have to consider carefully such factors when we develop brands. In many of the major markets, such as China, Brazil and Mexico, the patient pays directly for prescription medicines, and this will be an increasingly important issue for our business. Other growing markets, such as South Korea and Turkey are seeing more direct government intervention in pricing and reimbursement, more in line with the systems in Europe, Canada and Australia.

EMERGING EUROPE

Russia continued to enjoy strong sales growth driven bySymbicort,MerremandCrestorin 2008. Our business in Romania performed particularly well, almost doubling its size, primarily driven bySeroquel,NexiumandCrestor. Our continued expansion included the establishment of a local marketing presence in Ukraine and Kazakhstan.

CHINA

In China, in line with our growth and expansion strategy of the past four years, we have continued to build our presence and sales (including Hong Kong) were up 31% (+43% reported) to $627 million (2007: $437 million). We are the largest multinational pharmaceutical company in the prescription market in China, as surveyed by the Hong Kong Association of the Pharmaceutical Industry, with a growth rate for prescription sales of 28.8% (+40.2% reported). Our investment in China increased with further growth in the number of sales representatives, and continued to support our innovation discovery research centre in Shanghai and our several external collaborations, including a new clinical pharmacology unit in Peking University and a translational science laboratory in Guangdong Province People’s Hospital.

EMERGING ASIA PACIFIC

In the rest of the Emerging Asia Pacific region, overall sales were up 10% (+7% reported) to $802 million (2007: $749 million) by achieving strong growth in India, Indonesia, Singapore, Thailand and Vietnam, where market dynamics continue to be positive.

LATIN AMERICA

Latin America enjoyed strong sales performance up 18% (+22% reported) to $1,159 million (2007: $947 million), mainly driven by Mexico, Brazil, Venezuela, Central America and the Caribbean. As a result, our market share grew to 3% in the prescription market, improving our position from tenth to eighth in the prescription market ranking.

This reflects the investment made to develop our key products in fast-growing markets.Atacand,Crestor,Nexium,SeroquelandSymbicortall showed strong performance with overall sales up 33% (+38% reported) to $516 million (2007: $372 million). Nexiumis our best selling prescription product in Latin America with overall sales up 25% (+28% reported) to $185 million (2007: $144 million) and the fifth best selling prescription product in the Latin American market.Crestoris now our second best selling prescription product with overall sales up 46% (+52% reported) to $128 million (2007: $84 million) and is the eleventh best selling prescription product in the Latin American market.

Our top three largest markets in the region are now Brazil, Mexico and Venezuela. Brazil sales were up 21% (+33% reported) to $440 million (2007: $330 million), Mexico sales were up 6% (+6% reported) to $353 million (2007: $334 million) and Venezuela sales were up 37% (+37% reported) to $142 million (2007: $103 million).

MIDDLE EAST AND AFRICA

In 2008, the region again delivered a very strong double-digit growth, driven mainly byAtacand,Crestor,SeroquelandSymbicort, with particularly good performances in Gulf States, Levant, Egypt, South Africa and Maghreb. We have recently established a new marketing company in Israel as part of our investment plan in the region.

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

| > | | Crestorsales up 26% to $3.6 billion andCrestor is now approved in every EU country. |

| > | | Crestorstudy demonstrates significant reduction in major cardiovascular events (44% compared to placebo in men and women with elevated hsCRP but low/normal cholesterol levels). |

| > | | Atacandsales up 10% to $1.5 billion. |

| > | | Worldwide collaboration with Bristol-Myers Squibb to develop and commercialise dapagliflozin expanded to include Japan. |

| > | | US submission for fixed dose combination ofCrestorand Abbott’s Trilipix™, for the treatment of mixed dyslypidaemia, anticipated for third quarter 2009. |

| > | | Toprol-XLUS sales down 70% for the full year. |

OUR MARKETED PRODUCTS

Crestor1 (rosuvastatin calcium) is a statin for the treatment of dyslipidaemia and hypercholesterolemia, and to slow the progression of atherosclerosis.

Atacand2 (candesartan cilexetil) is an angiotensin II antagonist for the first-line treatment of hypertension and symptomatic heart failure.

Seloken/Toprol-XL(metoprolol succinate) is a once daily tablet for 24-hour control of hypertension and for use in heart failure and angina.

Tenormin(atenolol) is a cardioselective beta-blocker for hypertension, angina pectoris and other cardiovascular disorders.

Zestril3 (lisinopril dihydrate), an ACE inhibitor, is used for the treatment of a wide range of cardiovascular diseases, including hypertension.

Plendil(felodipine) is a calcium antagonist for the treatment of hypertension and angina.

| |

| 1 | Licensed from Shionogi & Co. Ltd. |

| |

| 2 | Licensed from Takeda Chemicals Industries Ltd. |

| |

| 3 | Licensed from Merck & Co., Inc. |

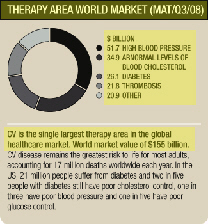

Backed by over 40 years’ experience, AstraZeneca is a world leader in cardiovascular (CV) medicines. We aim to build on our strong position, focusing on the growth areas of atherosclerosis (hardening of the arteries), thrombosis (blood clotting), diabetes and atrial fibrillation.

HYPERTENSION, ATHEROSCLEROSIS AND DYSLIPIDAEMIA

High blood pressure (hypertension) and abnormal levels of blood cholesterol (dyslipidaemia) are well known to damage the arterial wall and thereby lead to atherosclerosis. CV events driven by atherosclerotic disease remain the leading cause of death in the western world. Lipid-modifying therapy, primarily statins, is a cornerstone of treating atherosclerotic risk. Within the lipid-modifying market, generics are taking a significant share of the market and it is anticipated that generic atorvastatin will be available late 2011. Recent studies of some competitor products created uncertainty about clinical efficacy leading to reduced sales of these products, whilst AstraZeneca’s study (see below) provided positive data on the effect of rosuvastatin.

OUR FOCUS

Our key marketed products

Since its launch in 2003, our statin,Crestor, has continued to gain market share, based on its differentiated profile in managing cholesterol levels and its unique recent label indication for treating atherosclerotic disease. Following new approvals during 2008 in Germany, Spain, Poland, Norway and Malta,Crestoris now approved in every EU country.

Less than half of the people thought to have high levels of low-density lipoprotein cholesterol (LDL-C) ‘bad cholesterol’ get diagnosed and treated and of those people, only about half reach their physician’s recommended cholesterol target using existing treatments.Crestoris the most effective statin in lowering LDL-C and the majority of patients reach their LDL-C goals using the usual 10mg starting dose.Crestoralso produces an increase in high-density lipoprotein cholesterol (HDL-C) ‘good cholesterol’, across a range of doses. At its usual 10mg starting dose,Crestorhas been shown, versus placebo, to reduce LDL-C by up to 52% and raise HDL-C by up to 14% with eight out of 10 patients reaching their lipid goals.

In the US,Crestoris also approved for use as an adjunct to diet for slowing the progression of atherosclerosis in patients with elevated cholesterol.Crestoris the only statin with an

atherosclerosis indication in the US which is not limited by disease severity or restricted to patients with coronary heart disease.

Atacand, first launched in 1997, is approved for the treatment of hypertension in over 100 countries and for symptomatic heart failure in over 70 countries. Angiotensin II antagonists are the fastest growing sector of the global hypertension market. Available as a once a day tablet, launches of the 32mg dosage strength outside the US continued during the year, and this dosage is now available in most Established Markets. In July 2008, we sought approval in Europe for two dose strengths ofAtacand Plus(candesartan cilexetil/hydrochlorothiazide) which is a fixed combination ofAtacandand the diuretic hydrochlorothiazide (HCTZ), indicated for the treatment of hypertension in patients who need more than monotherapy.

Clinical trial developments

GALAXY, our long-term global clinical research programme forCrestorinvestigating links between optimal lipid control, atherosclerosis and CV morbidity and mortality, has completed a number of studies involving over 69,000 patients in over 55 countries.

Data from the latest study, JUPITER, published in November 2008, demonstrated thatCrestor20mg significantly reduced major CV events (defined in this study as the combined risk of myocardial infarction, stroke, arterial revascularisation, hospitalisation for unstable angina, or death from CV causes) by 44% compared to placebo among men and women with elevated high-sensitivity C-reactive protein (hsCRP) (and other risk factors) but low to normal cholesterol levels. Results also showed that for patients takingCrestor, the combined risk of heart attack, stroke or CV death was reduced by nearly half, risk of heart attack was cut by more than half, risk of stroke was cut by nearly half and total mortality was significantly reduced by 20%.Crestor20mg was well tolerated in nearly 9,000 patients during the course of the study. There was no difference between treatment groups for major adverse events, including cancer or myopathy. There was a small increase in physician reported diabetes consistent with data from other large placebo controlled statin trials.

GISSI-HF, an investigator sponsored study published in September 2008, evaluatedCrestor10mg and placebo in a heart failure population and confirmed the results of our CORONA study in showing no difference between the treatments in the primary endpoints of death or CV hospitalisation in patients with heart failure, over and above optimised heart failure treatment. Both studies

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

ARRHYTHMIA AND THROMBOSIS

Atrial fibrillation (AF) is the most common cardiac arrhythmia. Rhythm-control therapy to control the symptoms of AF is dominated by generic amiodarone, which is effective at maintaining patients in normal heart rhythm, but very poorly tolerated. There remains an unmet need for a safe and tolerated therapy with effective symptom relief. Two competitor products are in late development for use in AF and recent data from an outcome study of one of them versus placebo in AF patients showed clinical benefit in addition to symptom relief – the first time for an anti-arrhythmic agent.

Patients surviving an acute coronary event are at increased risk from further thrombosis and treatment guidelines advocate anti-platelet therapy. New guidelines issued in 2007 by the European Society of Cardiology for the treatment of acute coronary syndrome (ACS), have highlighted the negative consequences of drug induced bleeding in conjunction with the treatment of ACS, reinforcing the need for new anti-thrombosis drugs with acceptable bleeding risk.

During the year, two new anti-coagulants (dabigatran and rivaroxaban) were approved in Europe for use in prevention of deep vein thrombosis in conjunction with orthopaedic surgery. No Phase III data are yet available for the ability of new anti-coagulants to prevent strokes in AF, the major chronic indication for anti-coagulants, without the risks and repeated monitoring of warfarin or other vitamin K antagonists.

OUR FOCUS

In the pipeline

Brilinta(ticagrelor AZD6140), the first reversible, oral, adenosine diphosphate (ADP) receptor antagonist, is being developed to reduce the risk of blood clots and thrombotic events in patients diagnosed with ACS. Ticagrelor is currently being studied in the Phase III PLATO clinical trial, involving over 18,000 ACS patients in 43 countries, to determine if it is superior to clopidogrel for reducing the risk of thrombotic events in ACS patients.

The effectiveness of AZD0837 (an oral, direct thrombin inhibitor) in preventing strokes and other embolic events in AF patients will be studied in more than 35 countries, using a once-daily extended release formulation that provides sustained anti-coagulation effect throughout the dosing interval. We anticipate starting these Phase III studies in 2009.

Our lead compound in the treatment of AF is AZD1305, a combined ion channel blocker, which has progressed into Phase IIa testing in both the IV and oral form.

In December 2007, we filed patent infringement actions against seven generic drug manufacturers in the US following receipt of notices of their intent to market generic copies ofCrestorbefore the 2016 expiry of our licensed patent covering the active ingredient inCrestor. In July 2008, we filed a patent infringement action against Teva Pharmaceuticals in the US following receipt of its notice of its intent to market generic copies ofCrestorbefore the 2016 expiry of our licensed patent covering the active ingredient inCrestor. These eight cases are proceeding as a consolidated action in US District Court, District of Delaware.

Also in the US, Teva Pharmaceuticals (Teva’s Israeli parent company) filed a patent infringement lawsuit concerningCrestoron 6 October 2008. Teva alleges thatCrestortablets infringe a recently re-issued Teva US patent that claims stabilised pharmaceutical compounds.

AstraZeneca has full confidence in itsCrestorproduct and the intellectual property protecting it, and will vigorously defend and enforce it.

Further information is set out in Note 25 to the Financial Statements on page 148.

FINANCIAL PERFORMANCE 2008/2007

PERFORMANCE 2008

Reported performance

CV sales were up 4% as reported to $6,963 million (2007: $6,686 million). Strong growth fromCrestor, fuelled by the promotion of the atherosclerosis indication and increased sales ofAtacand offset the continuing significant declines inSeloken/Toprol-XL.

Performance – CER growth rates

CV sales were unchanged from 2007 at CER.Crestorsales increased by 26% to $3,597 million. US sales forCrestorfor the full year increased by 18% to $1,678 million. Crestortotal prescription share in the US statin market increased to 9.9% in December 2008 from 8.6% in December 2007, and was the only branded statin to gain market share.Crestorsales in the Rest of World were up 34% for the full year to $1,919 million, over half of global sales for the product. Sales were up 16% in Western Europe to $836 million and 93% in Japan driving sales growth in the Established Markets and the Rest of World up 33% in total. Sales in Emerging Markets increased by 41%.

Toprol-XLand authorised generic sales of the drug in the US were down 70% for the full year to $295 million. For the full year,Selokensales in the Rest of World were up 1% to $512 million.

US sales forAtacandfor the full year increased 1% to $262 million. Sales in other markets were up 12% to $1,209 million, on a 10% increase in Established Markets and an 18% increase in Emerging Markets.

PERFORMANCE 2007

Reported performance

CV sales rose by 9% from $6,118 million in 2006 to $6,686 million in 2007. Continued strong growth fromCrestormore than offset the significant declines inSeloken/Toprol-XL.

Performance – CER growth rates

CV sales grew by 5% at CER.Crestorsales increased by 33% to $2,796 million. In the US,Crestor sales for the full year were $1,424 million, a 24% increase over 2006. Total prescriptions in the US statin market increased 8% for the year;Crestorprescriptions were up 22%. Sales outside the US for the full year increased 45% to $1,372 million, nearly half the total worldwide sales for the product. Sales were up 26% in Western Europe with good growth in France and Italy. Sales in Canada increased 43%.

Global sales ofSeloken/Toprol-XLfell by 22% to $1,438 million. US sales of theToprol-XLproduct range, which includes sales of the authorised generic were down 30% for the full year, as the full range of dosage strengths were subject to generic competition from August 2007. Sales ofSelokenin other markets were up 5% for the full year as a result of growth in Emerging Markets.

Atacandsales in the US were unchanged for the full year whilst sales in other markets increased 12%.

Continued small declines were seen inZestril(down 10% to $295 million) andPlendil(down 7% to $271 million), with general global falls compensated by increases in discrete markets.

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

| > | | Sales ofNexium$5.2 billion, down 2%. |

| > | | Nexiumsubmissions in the EU for the short-term maintenance of haemostasis and prevention of re-bleeding in patients with peptic ulcer bleeding following therapeutic endoscopy and in the US for use in patients with peptic ulcer bleeding following therapeutic endoscopy. |

| > | | In late 2008, a Complete Response Letter received from the FDA in connection with ourNexiumsubmission for peptic ulcer bleeding. |

| > | | Losec/Prilosec sales $1.05 billion declining in the EU and US due to continuous generic pressure including the recent patent expiry in Italy. Overall sales down 14%; Japan sales still growing, up 5%. |

| > | | Settlement of patent litigation in the US brought by AstraZeneca against Ranbaxy, with enforceability of disputedNexiumpatents conceded and an agreement for licensed sales of genericNexiumfrom May 2014. |

| > | | Other patent litigation continuing in the US against generic manufacturers following abbreviated new drug applications relating toNexium. |

Nexium(esomeprazole) is the first proton pump inhibitor (PPI) for the treatment of acid-related diseases to offer clinical improvements over other PPIs and other treatments.

Losec/Prilosec(omeprazole) is used for the short-term and long-term treatment of acid-related diseases.

Entocort(budesonide) is a locally acting corticosteroid for the treatment of inflammatory bowel disease (IBD).

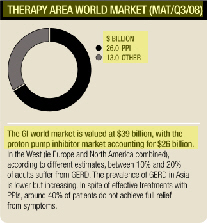

We aim to maintain our strong position in gastrointestinal (GI) treatments by continuing to focus on PPIs. NewNexiumline extensions include prevention of re-bleeding in patients with peptic ulcer bleeding, and prevention of low dose aspirin associated peptic ulcer. Our research and development is focused on finding new, innovative ways for treating acid reflux related disease.

GASTRO-OESOPHAGEAL

REFLUX DISEASE (GERD)

OUR FOCUS

Our key marketed products

Nexiumis an effective, long-term therapy for patients with GERD. For the treatment of active peptic ulcer disease, seven-dayNexiumtriple therapy (in combination with two antibiotics for the eradication of H.pylori) heals most patients without the need for follow-up anti-secretory therapy. Since it was first launched in 2000,Nexiumhas been used in the treatment of acid-related diseases in over one billion patient treatments.

Nexiumis available in approximately 100 countries for the treatment of acid-related diseases. In the US and EU,Nexiumis also approved for the treatment of children aged 12 to 17 years with GERD and in 2008 was approved for use in these countries in children aged one to 11 years old.Nexiumis also approved in the US, the EU, Canada and Australia for the treatment of patients with the rare gastric disorder, Zollinger-Ellison syndrome. In Europe,Nexiumis approved for the healing and prevention of ulcers associated with non-steroidal anti-inflammatory drug (NSAID) therapy including Cox2 inhibitors. In the US,Nexiumis approved for reducing the risk of gastric ulcers associated with continuous NSAID therapy in patients at risk of developing gastric ulcers.

Nexium IV, which is used when oral administration is not suitable for the treatment of GERD and upper GI side effects induced by NSAIDs, is approved in 86 countries including the US and all EU countries.

During 2008, we announced the submission of a supplemental new drug application (sNDA) to the FDA forNexium IV(esomeprazole sodium) injection, seeking approval for use in patients with peptic ulcer bleeding following therapeutic endoscopy. This was followed by an EU submission forNexium IV and tablets, seeking approval for the short-term maintenance of haemostasis and prevention of re-bleeding in patients with peptic ulcer bleeding following therapeutic endoscopy.

In late November 2008, we received the FDA Complete Response Letter regarding ourNexium IVsNDA for peptic ulcer bleed. The application has not received FDA approval in its present form. We are reviewing their comments and will respond in due course. The EU submission is still being reviewed by the European regulatory authorities.

Since its launch in 1988, we estimate that patients have benefited from over 900 million treatments withLosec/Prilosec. We continue to maintain patent property coveringLosec/ Prilosec. Further information about the status of omeprazole patents and patent litigation, including details of generic omeprazole launches, is set out in Note 25 to the Financial Statements on page 150.

Entocorthas better tolerability than other corticosteroids in inflammatory bowel disease and greater efficacy than aminosalicylic acid medicines. It is prescribed as first-line therapy for both acute treatment and maintenance of clinical remission of mild to moderate, active Crohn’s disease and is approved in more than 40 countries.

Clinical trial developments

Data from theNexium IVPeptic Ulcer Bleed study (a multinational, randomised trial of 767 patients with peptic ulcer bleeding) is the basis for submissions in the US and EU referred to above. The study shows that use ofNexium IVfor three days, followed by oralNexiumtherapy for 27 days, was statistically more effective in reducing gastric ulcers compared to placebo after both three and 30 days.

In the pipeline

Our activities focus on reflux inhibitors and hypersensitivity therapy. Our lead compound, AZD3355, is undergoing clinical trials. Follow-up compounds are in Phase I testing.

Non-GERD related GI projects were successfully transferred to the spin-out company Albireo, in which AstraZeneca holds a large minority stake.

In the US, we are continuing to pursue patent litigation against various generic manufacturers who have filed abbreviated new drug applications (ANDAs) and are seeking to market esomeprazole magnesium products before the expiration of certain of our patents relating toNexium.

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

OUR FINANCIAL PERFORMANCE

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2008 | | 2007 | | 2006 | | 2008 compared to 2007 | | 2007 compared to 2006 | |

| |

| | | | | | | | | | | Growth due | | | | | | | | | | | Growth due | | | | | | | | | | | | | | | | | |

| | | | | | | CER | | | to exchange | | | | | | | CER | | | to exchange | | | | | | | CER | | | Reported | | | CER | | | Reported | |

| | | Sales | | | growth | | | effect | | | Sales | | | growth | | | effect | | | Sales | | | growth | | | growth | | | growth | | | growth | |

| | | $m | | | $m | | | $m | | | $m | | | $m | | | $m | | | $m | | | % | | | % | | | % | | | % | |

| | |

Nexium | | | 5,200 | | | | (121 | ) | | | 105 | | | | 5,216 | | | | (104 | ) | | | 138 | | | | 5,182 | | | | (2 | ) | | | – | | | | (2 | ) | | | 1 | |

| | |

Losec/Prilosec | | | 1,055 | | | | (156 | ) | | | 68 | | | | 1,143 | | | | (277 | ) | | | 49 | | | | 1,371 | | | | (14 | ) | | | (8 | ) | | | (20 | ) | | | (17 | ) |

| | |

| Other | | | 89 | | | | 2 | | | | 3 | | | | 84 | | | | 2 | | | | 4 | | | | 78 | | | | 2 | | | | 6 | | | | 3 | | | | 8 | |

| | |

Total | | | 6,344 | | | | (275 | ) | | | 176 | | | | 6,443 | | | | (379 | ) | | | 191 | | | | 6,631 | | | | (4 | ) | | | (2 | ) | | | (6 | ) | | | (3 | ) |

| | |

On 15 April 2008, AstraZeneca announced it had settled itsNexiumpatent infringement litigation against Ranbaxy Pharmaceutical Industries and affiliates (Ranbaxy). As a consequence of the settlement, the patent litigation filed by AstraZeneca following Ranbaxy’s submission to the FDA of an ANDA for a generic version ofNexiumhas been dismissed. Under the settlement Ranbaxy concedes that all six patents asserted by AstraZeneca in the patent litigation are valid and enforceable. Ranbaxy also accepts that four of the patents would be infringed by the unlicensed sale of Ranbaxy’s proposed generic product. The settlement agreement allows Ranbaxy to commence sales of a generic version ofNexiumunder a licence from AstraZeneca from 27 May 2014, the expiry date of US Patent Numbers 5,877,192 and 6,875,872. We are co-operating fully with the Federal Trade Commission inquiry regarding this settlement.

AstraZeneca’sNexiumpatent infringement litigation against Teva/IVAX and Dr Reddy’s Laboratories remains ongoing. No trial date has been set in either case.

During 2008, we received additional notices that patent challenges had been filed by generic drug manufacturers in respect of 20mg and 40mg delayed-release esomeprazole magnesium capsules. Details of these filings and of new and continuing litigation are set out in Note 25 to the Financial Statements on page 153.

The European Patent Office ruled in 2007 that the European process patent forNexiumand the European patent for the multiple unit pellet (MUPS) formulations of PPI, which expire in 2015, are valid in amended form following post-grant oppositions. These decisions are now subject to appeal proceedings.

Further, the European Patent Office granted a new European patent on 19 November 2008 for the MUPS formulations of esomeprazole and omeprazole, which expires in 2015.

We continue to have full confidence in our intellectual property protectingNexiumand will vigorously defend and enforce it.

The decision of the European Court of First Instance on our appeal against the European Commission’s Decision in 2005 to impose fines on us totalling€60 million ($75 million) for alleged infringements of European competition law relating to certain omeprazole intellectual property and regulatory rights is still pending. Further information about this case is set out in Note 25 to the Financial Statements on page 151.

In 2008 we filed complaints for patent infringement against two generic manufacturers (Barr Laboratories and Mylan Pharmaceuticals) in response to notices of ANDA submissions in respect of generic forms ofEntocort EC.

FINANCIAL PERFORMANCE 2008/2007

PERFORMANCE 2008

Reported performance

Sales for 2008 were down 2% on a reported basis to $6,344 million from $6,443 million in 2007.

Performance – CER growth rates

GI sales fell by 4% at CER. GlobalNexiumsales were down 2%, excluding the effects of exchange, to $5,200 million from $5,216 million the previous year. The decline was driven by the decrease in the US of 8% to $3,101 million, however this was largely mitigated by sales in other markets increasing by 9% to $2,099 million. In the US, dispensed retail tablet volumes increased by 2% andNexiumwas the only major PPI brand to do so in 2008 In the Rest of World, growth in Canada (9%), Japan (5%) and Emerging Markets (20%) more than offset the 5% decline in Western European sales.

For the full year, sales ofLosecfell 14% to $1,055 million.Prilosecsales in the US were down 25% as a result of generic competition for the 40mg dosage form in the second half of the year. In the Rest of World, sales declined by 11%, despite increases in China (19%) and Japan (5%).

PERFORMANCE 2007

Reported performance

GI sales fell by 3% to $6,443 million in 2007 from $6,631 million in the previous year.

Performance – CER growth rates

GI sales fell by 6% at CER. Worldwide,Nexiumsales fell by 2% to $5,216 million. In the US,Nexium sales for the full year were $3,383 million, down 4%. Estimated volume growth was 2% for the year. Nexiummarket share in the branded segment of the PPI market increased by 1.5 percentage points in 2007; however, generic omeprazole share of the prescription PPI market increased to 27.4% by December 2007, an increase of nearly 7 percentage points since December 2006. Realised prices declined by around 8% for the year.Nexiumsales in other markets were up 2% for the full year to $1,833 million, as growth in Emerging Markets more than offset the declines in Western Europe.

For the full year,Losecsales declined by 20% to $1,143 million.Prilosecsales in the US were down 3% to $226 million.Losecsales in other markets were down 24%, although sales increased in Japan and China; sales in these two markets accounted for almost 30% of the brand’s performance.

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

| > | | Merremsales of $897 million, up 13%. |

| > | | Strong reported growth forMerremof 16% globally; 39% in the US. |

| > | | Synagissales of $1.23 billion; in the US $923 million. |

| > | | Biologics Licence Application submitted for motavizumab, an improved anti-respiratory syncytial virus monoclonal antibody. A Complete Response Letter subsequently received from the FDA. |

| > | | Market authorisation application submitted to European Medicines Agency for Live Attenuated Influenza Vaccine. |

OUR MARKETED PRODUCTS

Synagis(palivizumab) is a humanised monoclonal antibody used for the prevention of serious lower respiratory tract disease caused by RSV in paediatric patients at high risk of acquiring RSV disease.

Merrem/Meronem1 (meropenem) is a carbapenem anti-bacterial used for the treatment of serious infections in hospitalised patients.

FluMist(Influenza Virus Vaccine Live, Intranasal) is a live, attenuated, trivalent influenza virus vaccine licensed in the US for active immunisation of people two to 49 years of age against influenza disease caused by influenza virus subtypes A and type B contained in the vaccine.

| |

| 1 | Licensed from Dainippon Sumitomo Pharma Co., Ltd. |

We aim to build a leading franchise in the treatment of infectious diseases through continued commercialisation of the in-line brands such asSynagis,MerremandFluMist, effective use of our structural and genomic-based discovery technologies and antibody platforms, and through continued research of novel approaches in areas of unmet medical need.

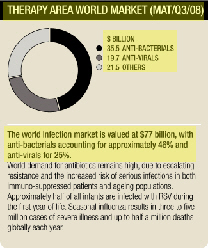

RESISTANT BACTERIAL INFECTIONS

World demand for antibiotics remains high, due to escalating resistance and the increased risk of serious infections in both immuno-suppressed patients and ageing populations. Many bacterial infections currently have few satisfactory treatment options prompting demand for new and better therapies.

OUR FOCUS

Our key marketed products

Merrem/Meronem(meropenem) is a carbapenem antibiotic, which is active against most bacteria that cause serious infections in hospitalised patients. Merremis the leading carbapenem and has a growing share of the intravenous antibiotic market because of its activity against bacteria resistant to many other agents. To meet the high and growing need for new and better therapies for resistant bacterial infections we have built an anti-bacterials discovery capability that places AstraZeneca among the industry leaders with the capability to create novel mechanism anti-bacterials.

RESPIRATORY SYNCYTIAL VIRUS (RSV)

Approximately half of all infants are infected with RSV during the first year of life and nearly all children in the US have been infected by the time they reach their second birthday. Unlike other viral infections, there is no complete and durable immunity created by RSV, so repeated infection is likely and common. Premature babies (earlier than 36 weeks gestational age, especially those less than 32 weeks) or babies with chronic lung disease or congenital heart disease are at an even greater risk of contracting severe RSV disease than full-term babies.

OUR FOCUS

Our key marketed products

Synagisis used for the prevention of serious lower respiratory tract disease caused by RSV in children at high risk of the disease. It was the first monoclonal antibody (MAb) approved in the US for an infectious disease and since its launch in 1998 it has become the standard of care for RSV prevention.Synagisremains the only immunoprophylaxis in the marketplace

indicated for the prevention of RSV in paediatric patients at high risk of RSV.Synagisis administered by intra-muscular injection.

In the pipeline

During 2008, we filed a biological licence application with the FDA for an improved anti-RSV MAb, motavizumab. We recently completed a Phase III study with motavizumab as a prophylaxis in infants with haemodynamically significant congenital heart disease. We are also conducting a Phase IIb study with motavizumab as a treatment for children hospitalised with severe RSV disease. In November 2008 we received a Complete Response Letter from the FDA asking for additional information on motavizumab which we are confident we can respond to and does not lead us to believe it is necessary to conduct further clinical trials.

In addition, three intranasal vaccines are being developed for the prevention of lower respiratory tract illness caused by RSV and parainfluenza virus-3 (PIV3): MEDI-559 (RSV), MEDI-560 (PIV3) and MEDI-534 (RSV-PIV3). We are conducting several Phase I and Phase I/II studies for these vaccines alone and in collaboration with the US National Institute of Allergy and Infectious Diseases under a Co-operative Research and Development Agreement.

Influenza is the most common vaccine-preventable disease in the developed world. According to World Health Organization estimates, seasonal influenza results in three to five million cases of severe illness and up to half a million deaths globally each year, primarily among the elderly. Rates of infection are highest among children, with school-aged children significantly contributing to the spread of the disease. Influenza also has socio-economic consequences related to both direct and indirect healthcare costs, including hospitalisations, work absence and loss of work productivity when either a caregiver or child is sick with influenza.

OUR FOCUS

Our key marketed products

FluMistis the first live, attenuated nasally delivered vaccine approved in the US for the prevention of disease caused by influenza A and B viruses in eligible children and adults, ages two to 49 years. In 2008, the US Centres for Disease Control and Prevention’s Advisory Committee on Immunization Practices voted to expand recommendations for routine seasonal influenza vaccination to include all school-age children up to the age of 18 years as soon as feasible but no later than the 2009/2010 influenza season. During the year,

ASTRAZENECA ANNUAL REPORT AND FOR M 20-F INFORMATION 2008

OUR FINANCIAL PERFORMANCE

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2008 | | | 2007 | | | 2006 | | | 2008 compared to 2007 | | | 2007 compared to 2006 | |

| | | | | | | | | | | Growth due | | | | | | | | | | | Growth due | | | | | | | | | | | | | | | | | |

| | | | | | | CER | | | to exchange | | | | | | | CER | | | to exchange | | | | | | | CER | | | Reported | | | CER | | | Reported | |

| | | Sales | | | growth | | | effect | | | Sales | | | growth | | | effect | | | Sales | | | growth | | | growth | | | growth | | | growth | |

| | | $m | | | $m | | | $m | | | $m | | | $m | | | $m | | | $m | | | % | | | % | | | % | | | % | |

| | |

Merrem | | | 897 | | | | 97 | | | | 27 | | | | 773 | | | | 121 | | | | 48 | | | | 604 | | | | 13 | | | | 16 | | | | 20 | | | | 28 | |

| | |

Synagis1 | | | 1,230 | | | | 612 | | | | – | | | | 618 | | | | 618 | | | | – | | | | – | | | | n/m | | | | n/m | | | | n/m | | | | n/m | |

| | |

FluMist1 | | | 104 | | | | 51 | | | | – | | | | 53 | | | | 53 | | | | – | | | | – | | | | n/m | | | | n/m | | | | n/m | | | | n/m | |

| | |

| Other | | | 220 | | | | (54 | ) | | | 4 | | | | 270 | | | | (12 | ) | | | 11 | | | | 271 | | | | (20 | ) | | | (19 | ) | | | (4 | ) | | | – | |

| | |

Total | | | 2,451 | | | | 706 | | | | 31 | | | | 1,714 | | | | 780 | | | | 59 | | | | 875 | | | | 41 | | | | 43 | | | | 89 | | | | 96 | |

| | |

we began rolling out the international marketing plan for our nasal spray influenza vaccine. The first milestone was the filing of a market authorisation application to the European Medicines Agency in late 2008.

HCV infects an estimated 170 million people worldwide and the current market for HCV therapy exceeds $2 billion annually. However, therapy for the strains that predominate in the US and Western Europe require 12 months’ treatment and produces a durable cure in only 50% of patients. Key opinion leaders expect the current standard of treatment (interferon plus ribavirin) to change to a form of combination therapy involving one or more new mechanism of action direct-acting anti-virals and there are several small and large pharmaceutical companies with varying HCV pipelines focused on such therapies. A future paradigm of combinations of anti-virals as standard care offers the opportunity for several new therapies to be widely used.

OUR FOCUS

In the pipeline

Projects in development include AZD7295, a novel HCV compound, currently in Phase II.

Sepsis is a life-threatening condition resulting from uncontrolled severe infections, which affects an estimated three million people a year worldwide. Few industry pipelines are focused on the development of products specifically for registration for the treatment of sepsis or septic shock.

OUR FOCUS

In the pipeline

The development programme for CytoFab™, our potential treatment for severe sepsis licensed from Protherics, continues in Phase II development. CytoFab™ has the potential to be one of a limited number of medicines specifically developed for such patients.

TB remains a worldwide threat and is newly diagnosed in over eight million people worldwide every year. It is one of the greatest causes of death from infectious disease in the developing world.

OUR FOCUS

As part of our commitment to making a contribution to improving health in the developing world, we are working to find a new, improved treatment for TB. We have a dedicated research facility in Bangalore, India that is focused on finding a treatment for TB that will act on drug-resistant strains, simplify the treatment regime (current regimes are complex and lengthy, meaning many patients give up before the infection is fully treated) and be compatible with HIV/AIDS therapies (TB and HIV/AIDS form a lethal combination, each speeding the other’s progress). Over 80 scientists in Bangalore work closely with our infection research centre in Boston, US as well as with academic leaders in the field, and they have full access to all AstraZeneca’s platform technologies, such as high throughput screening and compound libraries. It is a complex area of research, but we hope to have identified a candidate drug for testing in man within the next two to three years.

FINANCIAL PERFORMANCE 2008/2007

PERFORMANCE 2008

Reported performance

Total Infection sales increased on a reported basis by 43% to $2,451 million as a full year ofSynagisandFluMistsales were taken in the Group for the first time, andMerremsales enjoyed another year of good growth.

Performance – CER growth rates

Infection sales were up 41% at CER. For the full year,Synagissales were $1,230 million. Sales in 2007 were $618 million, but this only reflected sales since the acquisition of MedImmune in June 2007. Worldwide sales ofSynagisin the fourth quarter were $506 million, a 5% increase over the same period in 2007 when the product was included in sales.

FluMistsales were $104 million for the full year. In contrast to 2008, all of 2007FluMistsales of $53 million were realised in the fourth quarter as a result of the timing of regulatory approvals for the new formulation and expanded label.

PERFORMANCE 2007

Reported performance

Infection sales grew by 96% to $1,714 million from $875 million in 2006, driven by the inclusion of seven months ofSynagisandFluMistsales and an increase inMerremsales of 28%.

Performance – CER growth rates

Infection sales grew by 89%, after excluding the effect of exchange. CER growth of 20% fromMerrem, with sales of $773 million, and the inclusion ofSynagisandFluMistwere the principal drivers of this growth. Sales ofSynagistotalled $618 million for the period post-acquisition of MedImmune, with $480 million arising in the fourth quarter.Synagissales are highly seasonal, with the majority of sales recorded in the fourth and first quarters.

Sales ofFluMistwere $53 million for the full year, all of which were recorded in the fourth quarter. As withSynagis, there were no corresponding sales in the prior year period.

Sales ofMerremincreased by 20% to $773 million, with strong growth in the US (sales up 32% to $149 million) and Western Europe (sales up 20% to $307 million).

ASTRAZENECA ANNUAL REPORT AND FORM 20-F INFORMATION 2008

| > | | Seroquelsales up 9% to over $4.45 billion.

|

| |

| > | | Seroquel XRapproved in the US for acute bipolar depression, acute bipolar mania and bipolar maintenance.

|

| |

| > | | Seroquel XRapproved under the European Mutual Recognition Procedure for the treatment of acute bipolar depression and acute bipolar mania in October.Seroquelalso approved at the same time for the treatment of acute bipolar depression.

|

| |

| > | | FDA Complete Response Letter received onSeroquel XRfor Major Depressive Disorder in December.

|

| |

| > | | Regulatory submissions made forSeroquel XRfor the treatment of Major Depressive Disorder and for Generalised Anxiety Disorder in both the US and EU.

|

| |

| > | | Summary Judgment Motion granted to AstraZeneca in the patent infringement actions commenced against two generic drug manufacturers in the US following abbreviated new drug applications relating toSeroquel.

|

| |

| > | | Separate lawsuits filed in the US against third party manufacturers relating to infringement of theSeroquel XRpatents.

|

| |

| > | | Personal injury actions in the US and Canada involvingSeroquelbeing defended vigorously.

|

Seroquel(quetiapine fumarate) is an atypical anti-psychotic drug approved for the treatment of adult schizophrenia and bipolar disorder (mania, depression and maintenance).

Zomig(zolmitriptan) is for the treatment of migraine with or without aura.

Diprivan(propofol) is an intravenous general anaesthetic used in the induction and maintenance of anaesthesia, light sedation for diagnostic procedures and for intensive care sedation.

Naropin (ropivacaine) is a long-acting local anaesthetic, replacing the previous standard treatment of bupivacaine.

Xylocaine(lidocaine) is a widely used short-acting local anaesthetic.

EMLA(lidocaine + prilocaine) is a local anaesthetic for topical application.

We aim to strengthen our position in neuroscience through further growth of

SeroquelandSeroquel XRand by the successful introduction of a range of new medicines aimed at significant medical need in psychiatry, analgesia (pain control) and cognition (including Alzheimer’s disease and cognitive disorders in schizophrenia).

Most branded schizophrenia products will face generic competition in the period 2012 to 2015, with all current atypical anti-psychotic patents expiring by 2018. Future demand will be for products with significantly improved efficacy and tolerability.

The depression and anxiety markets are currently dominated by generic selective serotonin re-uptake inhibitors and serotonin norepinephrine re-uptake inhibitors. As growth in the US slows, the Japanese market continues to grow. Generic growth is anticipated over the next five years as patents expire.

OUR FOCUS

Our key marketed products

Seroquelis a leading atypical anti-psychotic treatment for adult schizophrenia and bipolar disorder.Seroquelremains the most commonly prescribed atypical anti-psychotic in the US, where it is the only atypical anti-psychotic approved as monotherapy treatment for both bipolar depression and bipolar mania as well as the leading atypical brand globally by sales value. Its clinical development programme was substantially completed during 2008 resulting in worldwide launches ofSeroquel XRfor schizophrenia. We have also made the associated regulatory submissions and data presentations in bipolar disorder, major depressive disorder (MDD) and generalised anxiety disorder (GAD).