Item 1: Report to Shareholders

|

| Blue Chip Growth Fund | December 31, 2006 |

The views and opinions in this report were current as of December 31, 2006. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our E-mail Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Fellow Shareholders

Global stock markets and your fund rallied strongly in the six months ended December 31, 2006. Investors responded favorably to moderating inflation and interest rates, declining energy prices, and stronger corporate profits, which remained healthy despite the notable weakness in housing and manufacturing. We believe that continued earnings strength, coupled with stable interest rates and reasonable valuations, can produce favorable investment performance, particularly for large-cap growth stocks that have lagged the broad market.

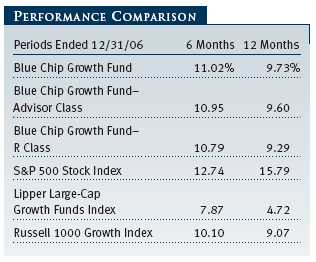

Your fund produced solid returns that outperformed the Lipper Large-Cap Growth Funds peer group and the style-specific Russell 1000 Growth Index for the six months and year ended December 31, 2006. However, large-cap growth stocks continued to underperform large-cap value shares and the broad market, as measured by the S&P 500 Index. (Results for the Advisor and R Class shares varied slightly, reflecting their different fee structures.)

The Blue Chip Growth Fund has delivered consistently strong long-term performance compared with its peer group. Lipper ranked the fund in the top 13% of its large-cap growth funds universe for the past one and five years and in the top quintile for the past 3- and 10-year periods ended December 31, 2006. (Based on cumulative total return, Lipper ranked the Blue Chip Growth Fund 89 out of 723, 109 out of 616, 63 out of 505, and 33 out of 186 funds for the 1-, 3-, 5-, and 10-year periods ended December 31, 2006, respectively. Past performance cannot guarantee future results.)

HIGHLIGHTS

• Global stock markets and your fund rallied strongly in the six-month period ended December 31, 2006.

• Large-cap growth stocks posted solid gains but trailed value shares for the past six and 12 months.

• After generating poor results in the first half, financials, health care, and information technology were the fund’s best contributors for the past six months.

• We think high-quality, consistent-growth companies appear attractive.

MARKET ENVIRONMENT

As we noted in our midyear letter, the market has faced some unique challenges that we felt would dissipate over time. The Federal Reserve did, in fact, stop increasing interest rates in June, after 17 quarter-point increases. There is now some debate as to whether the Fed will hold steady or perhaps even cut rates. However, moderation in economic growth, some weakness in manufacturing, and a continued housing slump have slowed inflation somewhat. We believe the Fed has a reasonable chance of controlling inflation while orchestrating a “soft landing.”

Energy and commodity prices corrected significantly in the fourth quarter; at the time of this writing, oil is priced below $55 per barrel. This generally makes the task of controlling inflation easier, helps consumer spending, and also provides a boost to corporate profits for companies that are heavy energy consumers. There are vexing geopolitical risks that have periodically unsettled global markets, but perhaps they will become less daunting as negotiations with North Korea take place and as progress will hopefully be made in the Middle East. The midterm elections yielded a change of leadership in the Congress, which initially unsettled investors. However, as we suspected, simply resolving the uncertainty was a favorable development for the market.

Ultimately, corporate earnings, interest rates, and valuations will be the primary determinants of the stock market’s performance. While corporate earnings and interest rates always play a key role, we believe we are at a pivotal point where discerning their direction is more challenging than usual. The economy has expanded for 60 straight months, and the S&P 500 has posted 18 consecutive quarters of double-digit earnings growth. On balance, we think corporate profits will be strong, particularly in some out-of-favor areas, such as health care. Inflation has eased a bit recently, but labor costs continue to escalate. Economic growth has moderated, and the housing slowdown may serve to dampen earnings and also interest rates. Despite the second-half rally, valuations are reasonable for many large-cap, consistent-growth companies.

PORTFOLIO REVIEW

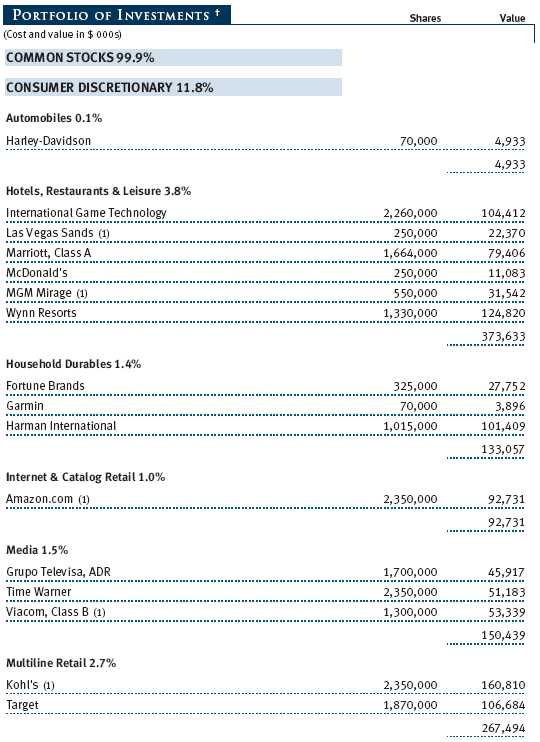

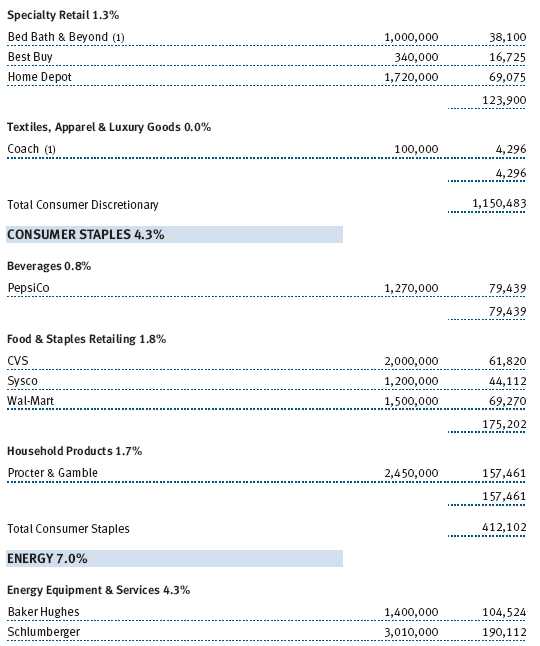

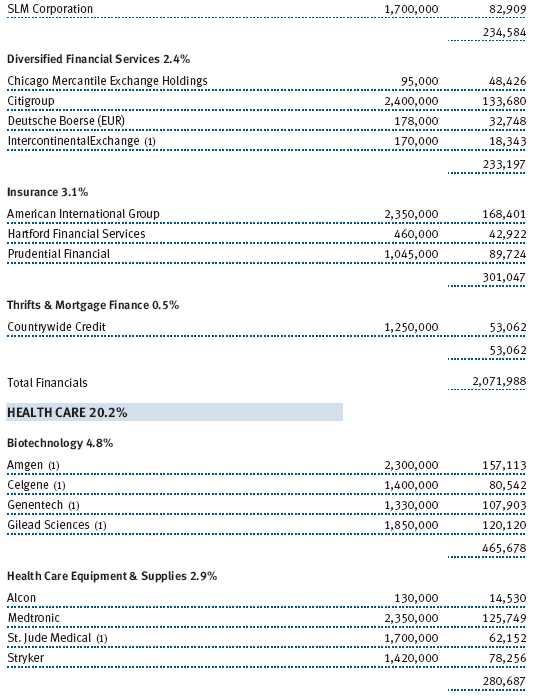

After a mixed performance in the first half of the year, the financials sector was the largest second-half contributor. Goldman Sachs, Merrill Lynch, and Morgan Stanley were stellar performers, benefiting from strong capital market conditions and a continued global boom in mergers and acquisitions. Franklin Resources, State Street, Charles Schwab, and Northern Trust also prospered in this environment as their asset management and securities processing businesses continued to thrive. Franklin Resources and State Street generated particularly strong growth from their international operations. Patience with insurance giants American International Group and Prudential and diversified financial services companies such as Citigroup and American Express also yielded solid gains. (Please refer to the portfolio of investments for a complete listing of holdings and the amount each represents in the portfolio.)

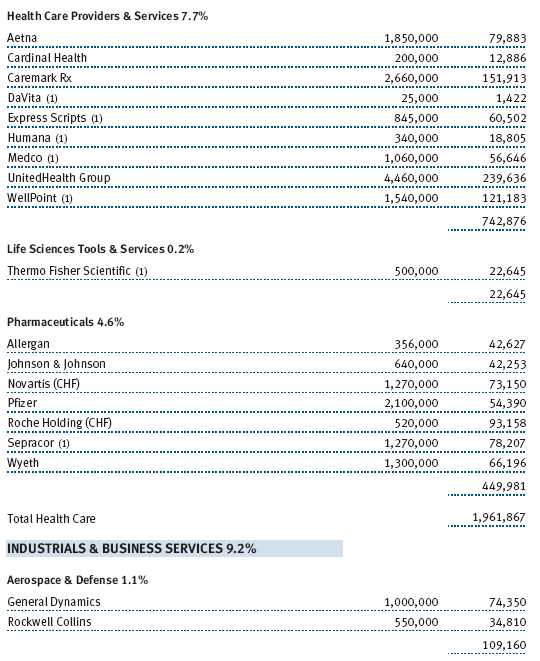

Despite the controversy surrounding health care’s fortunes under a Democratic Congress, the sector contained some major second-half winners for your fund. UnitedHealth Group recovered from its stock option-related woes after the dismissal of several managers and the implementation of stronger internal controls. Managed care stalwarts WellPoint and Aetna also performed well. Leading pharmaceutical benefit manager Caremark RX received competing buyout offers from CVS and then Express Scripts. We think either combination would be beneficial for shareholders. We also believe that Wal-Mart’s recent offering of certain generic drugs at $4 per prescription will not significantly damage the industry’s profitability.

Stryker, Medtronic, and, to a lesser extent, St. Jude Medical also rallied and overcame the mediocre performance that plagued many health care equipment stocks in the first half. In biotechnology, a new holding, Celgene, produced strong gains as its cancer treatments showed dynamic growth. Longtime holding Gilead Sciences, with its suite of market-leading HIV drugs, also generated superior returns.

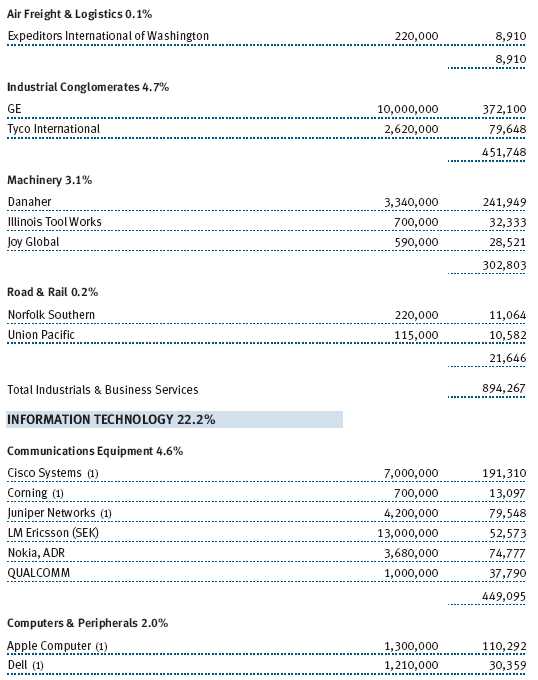

The information technology sector produced solid second-half results. Microsoft recovered as investors began to appreciate that 2007 could be a very good year, thanks to several important product launches in addition to its new operating system, Vista. Software leaders Oracle and Adobe Systems produced strong gains. Our patience with network equipment giant Cisco Systems began to pay off. The company benefited from sales of consumer-based equipment (under the Scientific-Atlanta and Linksys brands) as well as routers and other equipment used by corporations. Juniper Networks and LM Ericsson also produced good contributions. Automatic Data Processing, a payroll processor, continued to generate stable growth and earnings, which buoyed its shares. Internet leaders Google and Monster Worldwide were again among our best holdings. Conversely, Yahoo! and several semiconductor companies were major disappointments, which we address in a separate discussion below.

Hotels and gaming stocks were among the most consistently positive investments in 2006. Wynn Resorts, with its significant presence in China and Las Vegas, enjoyed explosive profit growth and stock performance, as did MGM Mirage and Las Vegas Sands. Gaming equipment maker International Game Technology and hotelier Marriott produced notable gains, and our analysts are bullish on their prospects for the next few years. Other strong contributors within the consumer discretionary sector included multiline retailer Kohl’s and media stocks Viacom and Grupo Televisa.

Over the past six months, the portfolio’s top contributors came from a variety of industries. Conglomerates GE and Danaher provided strong results. The portfolio’s largest holding, ExxonMobil, outperformed the majority of energy stocks, which in general produced lackluster or negative stock returns in the second half. Aerospace and defense giant General Dynamics and biogenetic seed maker Monsanto continued to generate solid gains. Procter & Gamble also rebounded over the past six months.

Although we enjoyed a strong second half, we had several losers. Yahoo! was the major disappointment because it has had difficulty managing various business segments and dealing with aggressive competitors such as Google. Fortunately, we have maintained a larger investment in Google than Yahoo!. We reduced our stake in Yahoo! over the past six months, but we are comfortable with the current position size, given that the company made several management changes and its most important product introduction (paid search platform “Project Panama”) appears to be on schedule with revised guidelines.

Our semiconductor stocks continued to disappoint. Marvell Technology, Linear Technology, and Maxim Integrated Products were the most notable losers. We have pared some of our positions but continue to believe these companies are well managed. We think results are somewhat depressed on a cyclical basis and that long-term growth prospects are much better than the current prices imply. We intend to remain patient, but we are not going to add to these holdings unless we see specific product innovations or efficiency improvements indicating that earnings growth could accelerate.

Energy services companies, which have been among the strongest performers in the portfolio for several years, suffered a sharp correction in the second half. Schlumberger, Baker Hughes, and Smith International were among our largest detractors. We trimmed some of our holdings at higher prices, but much of the fourth-quarter weakness in these stocks was due to the extraordinarily mild winter in the Eastern U.S. We are mindful that energy prices could continue to correct, but we think these companies should continue to grow and appear reasonably valued.

STRATEGY

We target companies with durable, sustainable earnings and cash flow growth. The free cash flow we prize has become even more valuable now that tax laws treat dividends more favorably.

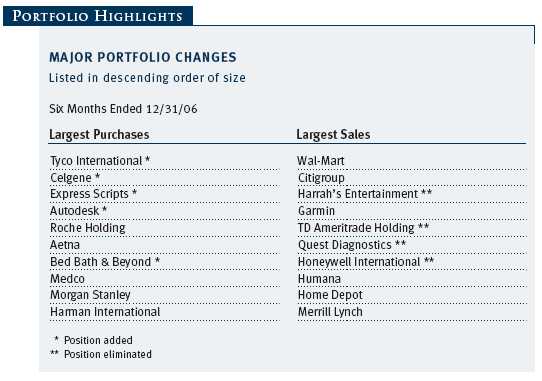

Additions to existing holdings such as Roche Holding, Aetna, Medco, Morgan Stanley, and Harman International were significant enough to be included in our table of largest purchases for the past six months. Tyco International was our largest purchase and a new holding for the portfolio in the second half. Although we previously owned and subsequently sold Tyco (after a crisis at the company), our industrials analyst now believes that the stock is particularly attractive. The company has announced that it will spin off several of its businesses, and we thought that the sum of those values exceeded our purchase price by a wide margin. Fundamentals at several of the businesses, including their industry-leading health care and electronics operations, are also improving. Bed Bath & Beyond is another of our analysts’ favorites. We are attracted to the company’s strong growth (despite the slowdown in housing), prodigious free cash flow, and its Christmas Tree Stores business.

Celgene, another significant second-half addition, has a good management team, a strong biotech product pipeline, and one of the fastest earnings growth rates among our holdings. We have spent significant time with management in our offices and at its headquarters, and the stock has done well due to the accelerating growth of several key products—particularly Revlimid, a cancer drug. We also initiated a position in Express Scripts, a fast-growing pharmaceutical benefit manager (PBM). As noted above, both Express Scripts and CVS have bid to acquire Caremark, another holding in the PBM area. We are confident that either deal will yield good results, but we think the Express Scripts bid is more attractive. We believe the entire PBM area should do well, despite concerns regarding pricing controls, competition from Wal-Mart, and the growth of mail order and generics.

We made significant Wal-Mart and Citigroup sales over the past six months, as it became apparent to us that the major reengineering of operations at both companies was proceeding more slowly than planned. However, we added back some Citigroup after the company made several management changes and renewed its effort to reign in expenses. Harrah’s was one of our most disappointing sales because the company received a takeover bid shortly after we sold. However, proceeds from our sale were reinvested in other gaming stocks such as MGM Mirage and Wynn, which performed well. We nearly eliminated Garmin, the leading maker of hand-held personal navigation devices. While we hate to sell a major winner that we think can continue to grow, it approached our price target and we became concerned about pricing pressure.

We sold Quest Diagnostics because it lost a major contract, and we believed that other health care companies had more attractive prospects. We reduced our stake in Humana because it is exposed to potential pricing actions and ramifications from the new Democratic majority in Congress. However, our health care analyst believes that the company could prosper if radical changes are not made to the Medicare program. Honeywell and First Data were eliminated as they approached price targets, and our analysts saw other opportunities with better return potential.

OUTLOOK

The stock market rallied over the past six months, but many large-cap growth stocks did not fully participate. Several issues concerned investors, including the sharp decline in housing prices, geopolitical events, the fixation on the Fed’s interest rate policy, and whether the economy will achieve a soft landing. The regulatory scrutiny of stock option practices has also weighed heavily on growth stocks in general, and technology companies in particular, throughout the year.

We have weighed these risks carefully. We think that the housing correction may be stubborn but not severely affect economic growth. On balance, we believe corporate profits will be relatively strong in 2007, particularly in some out-of-favor areas such as health care. More subdued commodity prices suggest that core inflation could moderate over time. Finally, we contend that valuation is often underestimated as a determinant of future stock performance. Valuations are not as supportive as they were at midyear—when we argued that stocks were quite compelling—and that makes us more cautious. However, we think high-quality, consistent-growth companies appear attractive. We believe a solid case can be made for investing in U.S. stocks for the following reasons:

1. Earnings growth remains strong at many high-quality U.S. companies, many of which do not need a robust economic recovery to produce strong profit growth.

2. The stocks of many consistent-growth companies remain reasonably valued despite the recent market rebound.

3. Many of the issues noted above, such as stock option regulatory concerns, are not likely to be long-term fundamental negatives.

4. Companies have reduced expenses significantly. Consequently, a continued pickup in revenue growth could result in strong profit growth.

5. Many of our holdings generate significant free cash flow, and free cash flow margins are at multi-decade highs. Shareholder-oriented management can use this cash to pay dividends, repurchase shares, or make value-added acquisitions.

We will continue to strive to enhance returns while managing risk by investing in quality companies with durable, sustainable earnings and cash flow growth. We appreciate your continued confidence in this endeavor.

Respectfully submitted,

Larry J. Puglia

President and chairman of the Investment Advisory Committee

January 9, 2007

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

RISKS OF STOCK INVESTING

The fund’s share price can fall because of weakness in the stock markets, a particular industry, or specific holdings. Stock markets can decline for many reasons, including adverse political or economic developments, changes in investor psychology, or heavy institutional selling. The prospects for an industry or company may deteriorate because of a variety of factors, including disappointing earnings or changes in the competitive environment. In addition, the investment manager’s assessment of companies held in a fund may prove incorrect, resulting in losses or poor performance even in rising markets. Growth stocks can be volatile because these companies usually invest a high portion of earnings in their businesses, and earnings disappointments often lead to sharply falling prices. The value approach carries the risk that a security’s intrinsic value may not be recognized for a long time or that the stock may actually be appropriately priced.

GLOSSARY

Dividend yield: The annual dividend of a stock divided by the stock’s price.

Free cash flow: The excess cash a company is generating from its operations that can be taken out of the business for the benefit of shareholders, such as dividends, share repurchases, investments, and acquisitions.

Lipper indexes: Fund benchmarks that consist of a small number (10 to 30) of the largest mutual funds in a particular category as tracked by Lipper Inc.

Price/book ratio: A valuation measure that compares a stock’s market price to its book value, i.e., the company’s net worth divided by the number of outstanding shares.

Price/earnings ratio (P/E): A valuation measure calculated by dividing the price of a stock by its current or projected earnings per share. This ratio gives investors an idea of how much they are paying for current or future earnings power.

Russell 1000 Growth Index: Market capitalization-weighted index of those firms in the Russell 1000 with higher price-to-book ratios and higher forecasted growth values.

S&P 500 Stock Index: An unmanaged index that tracks the stocks of 500 primarily large-cap U.S. companies.

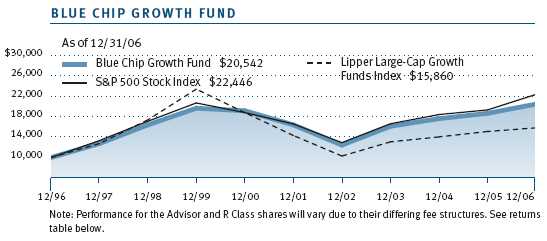

| GROWTH OF $10,000 |

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

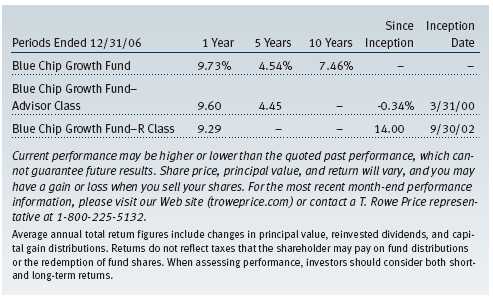

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

This table shows how the fund would have performed each year if its actual (or cumulative) returns had been earned at a constant rate.

| FUND EXPENSE EXAMPLE |

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Please note that the fund has three share classes: The original share class (“investor class”) charges no distribution and service (12b-1) fee; Advisor Class shares are offered only through unaffiliated brokers and other financial intermediaries and charge a 0.25% 12b-1 fee; R Class shares are available to retirement plans serviced by intermediaries and charge a 0.50% 12b-1 fee. Each share class is presented separately in the table.

Actual Expenses

The first line of the following table (“Actual”) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (“Hypothetical”) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual small-account maintenance fee of $10, generally for accounts with less than $2,000 ($500 for UGMA/UTMA). The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $25,000 or more, accounts employing automatic investing, and IRAs and other retirement plan accounts that utilize a prototype plan sponsored by T. Rowe Price (although a separate custodial or administrative fee may apply to such accounts). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

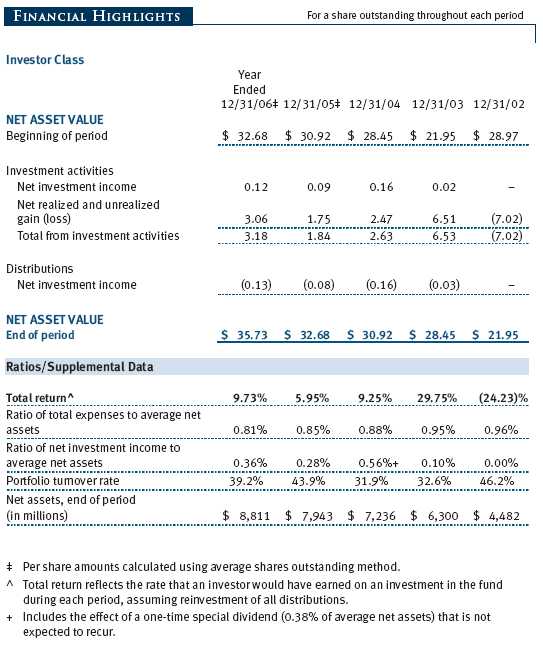

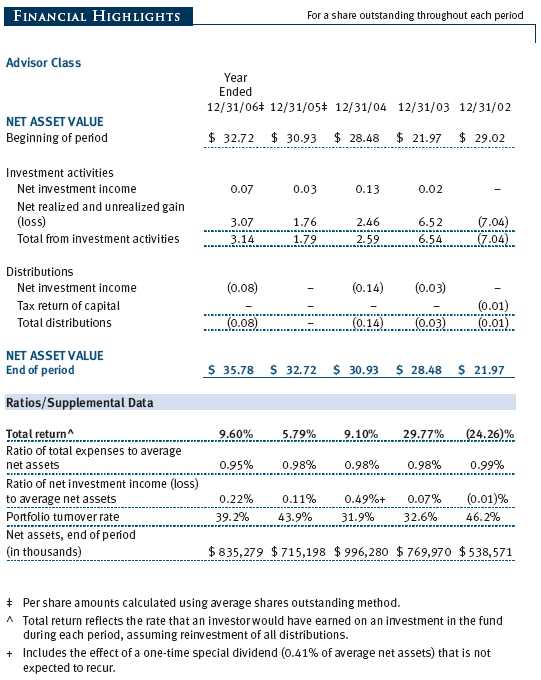

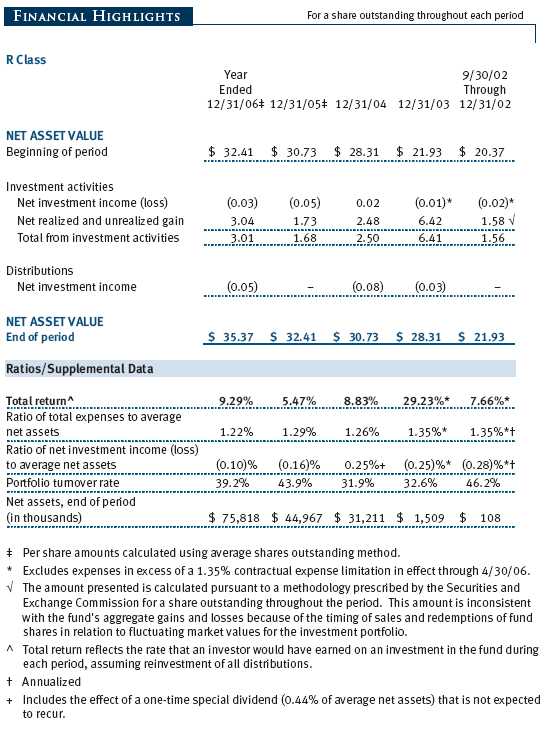

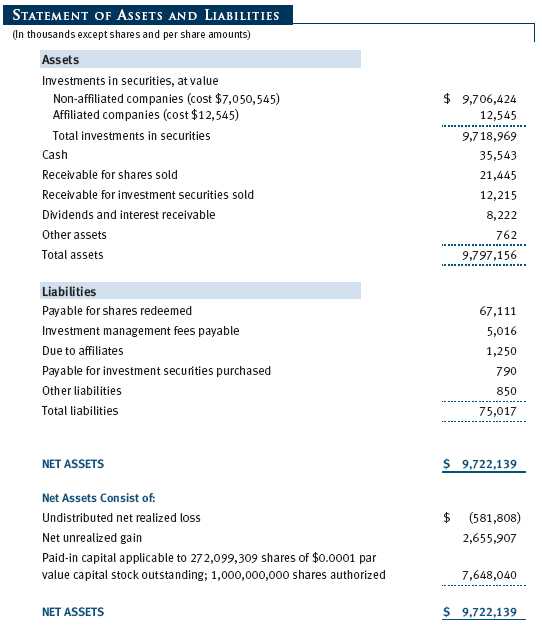

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| NOTES TO FINANCIAL STATEMENTS |

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

T. Rowe Price Blue Chip Growth Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund seeks to provide long-term capital growth. Income is a secondary objective. The fund has three classes of shares: the Blue Chip Growth Fund original share class, referred to in this report as the Investor Class, offered since June 30, 1993; the Blue Chip Growth Fund—Advisor Class (Advisor Class), offered since March 31, 2000; and the Blue Chip Growth Fund—R Class (R Class), offered since September 30, 2002. Advisor Class shares are sold only through unaffiliated brokers and other unaffiliated financial intermediaries, and R Class shares are available to retirement plans serviced by intermediaries. The Advisor Class and R Class each operate under separate Board-approved Rule 12b-1 plans, pursuant to which each class compensates financial intermediaries for distribution, shareholder servicing, and/or certain administrative services. Each class has exclusive voting rights on matters related solely to that class, separate voting rights on matters that relate to all classes, and, in all other respects, the same rights and obligations as the other classes.

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by fund management. Fund management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the fund ultimately realizes upon sale of the securities.

Valuation The fund values its investments and computes its net asset value per share at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day that the NYSE is open for business. Equity securities listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made, except for OTC Bulletin Board securities, which are valued at the mean of the latest bid and asked prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the latest bid and asked prices for domestic securities and the last quoted sale price for international securities.

Investments in mutual funds are valued at the mutual fund’s closing net asset value per share on the day of valuation.

Other investments, including restricted securities, and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors.

Most foreign markets close before the close of trading on the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, which in turn will affect the fund’s share price, the fund will adjust the previous closing prices to reflect the fair value of the securities as of the close of the NYSE, as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors. A fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. In deciding whether to make fair value adjustments, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund uses outside pricing services to provide it with closing market prices and information used for adjusting those prices. The fund cannot predict when and how often it will use closing prices and when it will adjust those prices to reflect fair value. As a means of evaluating its fair value process, the fund routinely compares closing market prices, the next day’s opening prices in the same markets, and adjusted prices.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Class Accounting The Advisor Class and R Class each pay distribution, shareholder servicing, and/or certain administrative expenses in the form of Rule 12b-1 fees, in an amount not exceeding 0.25% and 0.50%, respectively, of the class’s average daily net assets. Shareholder servicing, prospectus, and shareholder report expenses incurred by each class are charged directly to the class to which they relate. Expenses common to all classes, investment income, and realized and unrealized gains and losses are allocated to the classes based upon the relative daily net assets of each class.

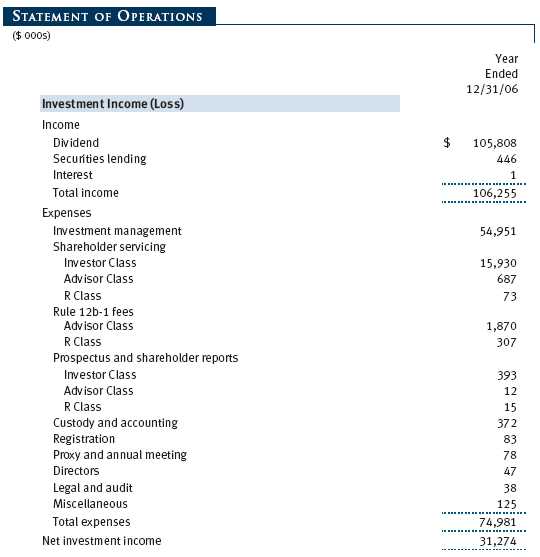

Rebates and Credits Subject to best execution, the fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the fund in cash. Commission rebates are reflected as realized gain on securities in the accompanying financial statements and totaled $73,000 for the year ended December 31, 2006. Additionally, the fund earns credits on temporarily uninvested cash balances at the custodian that reduce the fund’s custody charges. Custody expense in the accompanying financial statements is presented before reduction for credits.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared and paid by each class on an annual basis. Capital gain distributions, if any, are declared and paid by the fund, typically on an annual basis.

New Accounting Pronouncements In June 2006, the Financial Accounting Standards Board (“FASB”) issued FASB Interpretation No. 48 (“FIN 48”), Accounting for Uncertainty in Income Taxes, a clarification of FASB Statement No. 109, Accounting for Income Taxes. FIN 48 establishes financial reporting rules regarding recognition and measurement of tax positions taken or expected to be taken on a tax return. Management is evaluating the anticipated impact, if any, that FIN 48 will have on the fund upon adoption, which, pursuant to a delay granted by the U.S. Securities and Exchange Commission, is expected to be on the last business day of the fund’s semi-annual period, June 29, 2007.

In September 2006, the FASB released the Statement of Financial Accounting Standard No. 157 (“FAS 157”), Fair Value Measurements. FAS 157 clarifies the definition of fair value and establishes the framework for measuring fair value, as well as proper disclosure of this methodology in the financial statements. It will be effective for the fund’s fiscal year beginning January 1, 2008. Management is evaluating the effects of FAS 157; however, it is not expected to have a material impact on the fund’s net assets or results of operations.

NOTE 2 - INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

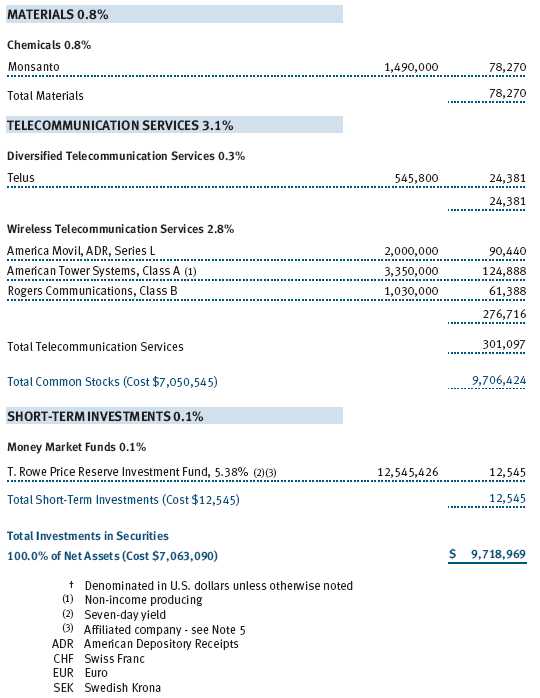

Securities Lending The fund lends its securities to approved brokers to earn additional income. It receives as collateral cash and U.S. government securities valued at 102% to 105% of the value of the securities on loan. Cash collateral is invested in a money market pooled trust managed by the fund’s lending agent in accordance with investment guidelines approved by fund management. Collateral is maintained over the life of the loan in an amount not less than the value of loaned securities, as determined at the close of fund business each day; any additional collateral required due to changes in security values is delivered to the fund the next business day. Although risk is mitigated by the collateral, the fund could experience a delay in recovering its securities and a possible loss of income or value if the borrower fails to return the securities. Securities lending revenue recognized by the fund consists of earnings on invested collateral and borrowing fees, net of any rebates to the borrower and compensation to the lending agent. At December 31, 2006, there were no securities on loan.

Other Purchases and sales of portfolio securities, other than short-term securities, aggregated $3,685,879,000 and $3,541,148,000, respectively, for the year ended December 31, 2006.

NOTE 3 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Federal income tax regulations differ from generally accepted accounting principles; therefore, distributions determined in accordance with tax regulations may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character. Financial records are not adjusted for temporary differences.

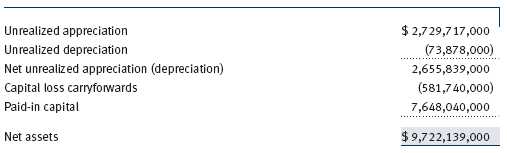

Distributions during the year ended December 31, 2006, totaled $34,067,000 and were characterized as ordinary income for tax purposes. At December 31, 2006, the tax-basis components of net assets were as follows:

The fund intends to retain realized gains to the extent of available capital loss carryforwards. During the year ended December 31, 2006, the fund utilized $317,127,000 of capital loss carryforwards. As of December 31, 2006, the fund had $581,740,000 of capital loss carryforwards, of which $338,447,000 expire in 2010, and $243,293,000 expire in 2011.

For the year ended December 31, 2006, the fund recorded the following permanent reclassifications to reflect tax character. Reclassifications to paid-in capital relate primarily to per share rounding of distributions. Reclassifications between income and gain relate primarily to the character of currency gains and losses. Results of operations and net assets were not affected by these reclassifications.

At December 31, 2006, the cost of investments for federal income tax purposes was $7,063,158,000.

NOTE 4 - ACQUISITION

On November 13, 2006, the fund acquired substantially all of the assets of the Bremer Growth Fund (the acquired fund), pursuant to the Agreement and Plan of Reorganization dated September 20, 2006, and approved by shareholders of the acquired fund on November 3, 2006. The acquisition was accomplished by a tax-free exchange of 1,655,855 shares of the fund (with a value of $57,491,000) for the 4,199,664 shares of the acquired fund outstanding on November 10, 2006. The net assets of the acquired fund at that date included $12,098,000 of unrealized appreciation. Net assets of the acquired fund were combined with those of the fund, resulting in aggregate net assets of $8,561,973,000 immediately after the acquisition.

NOTE 5 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (the manager or Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. The investment management agreement between the fund and the manager provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee and a group fee. The individual fund fee is equal to 0.30% of the fund’s average daily net assets up to $15 billion and 0.255% of the fund’s average daily net assets in excess of $15 billion; previously, through May 1, 2005, the individual fund fee had been a flat rate of 0.30% of the fund’s average daily net assets. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.29% for assets in excess of $160 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At December 31, 2006, the effective annual group fee rate was 0.31%.

In addition, the fund has entered into service agreements with Price Associates and two wholly owned subsidiaries of Price Associates (collectively, Price). Price Associates computes the daily share prices and provides certain other administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend disbursing agent. T. Rowe Price Retirement Plan Services, Inc., provides subaccounting and recordkeeping services for certain retirement accounts invested in the Investor Class and R Class. For the year ended December 31, 2006, expenses incurred pursuant to these service agreements were $84,000 for Price Associates, $3,961,000 for T. Rowe Price Services, Inc., and $7,165,000 for T. Rowe Price Retirement Plan Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

Additionally, the fund is one of several mutual funds in which certain college savings plans managed by Price Associates may invest. As approved by the fund’s Board of Directors, shareholder servicing costs associated with each college savings plan are borne by the fund in proportion to the average daily value of its shares owned by the college savings plan. For the year ended December 31, 2006, the fund was charged $808,000 for shareholder servicing costs related to the college savings plans, of which $626,000 was for services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At December 31, 2006, approximately 5% of the outstanding shares of the Investor Class were held by college savings plans.

The fund is also one of several mutual funds sponsored by Price Associates (underlying Price funds) in which the T. Rowe Price Spectrum Funds (Spectrum Funds) may invest. The Spectrum Funds do not invest in the underlying Price funds for the purpose of exercising management or control. Pursuant to a special servicing agreement, expenses associated with the operation of the Spectrum Funds are borne by each underlying Price fund to the extent of estimated savings to it and in proportion to the average daily value of its shares owned by the Spectrum Funds. Expenses allocated under this agreement are reflected as shareholder servicing expense in the accompanying financial statements. For the year ended December 31, 2006, the fund was allocated $808,000 of Spectrum Funds’ expenses, of which $580,000 related to services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At December 31, 2006, approximately 7% of the outstanding shares of the Investor Class were held by the Spectrum Funds.

The fund may invest in the T. Rowe Price Reserve Investment Fund and the T. Rowe Price Government Reserve Investment Fund (collectively, the T. Rowe Price Reserve Funds), open-end management investment companies managed by Price Associates and affiliates of the fund. The T. Rowe Price Reserve Funds are offered as cash management options to mutual funds, trusts, and other accounts managed by Price Associates and/or its affiliates, and are not available for direct purchase by members of the public. The T. Rowe Price Reserve Funds pay no investment management fees. During the year ended December 31, 2006, dividend income from the T. Rowe Price Reserve Funds totaled $1,100,000, and the value of shares of the T. Rowe Price Reserve Funds held at December 31, 2006, and December 31, 2005, was $12,545,000 and $56,348,000, respectively.

NOTE 6 - INTERFUND BORROWING

Pursuant to its prospectus, the fund may borrow up to 33 1/3% of its total assets. The fund is party to an interfund borrowing agreement between itself and other T. Rowe Price-sponsored mutual funds, which permits it to borrow or lend cash at rates beneficial to both the borrowing and lending funds. Loans totaling 10% or more of a borrowing fund’s total assets are collateralized at 102% of the value of the loan; loans of less than 10% are unsecured. During the year ended December 31, 2006, the fund had outstanding borrowings on 13 days, in the average amount of $9,854,000, and at an average annual rate of 5.40%. There were no borrowings outstanding at December 31, 2006.

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

To the Board of Directors and Shareholders of T. Rowe Price Blue Chip Growth Fund, Inc.

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of T. Rowe Price Blue Chip Growth Fund, Inc. (the “Fund”) at December 31, 2006, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the fiscal periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the auditing standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2006 by correspondence with the custodian and by agreement to the underlying ownership record for T. Rowe Price Reserve Investment Fund, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

February 12, 2007

| TAX INFORMATION (UNAUDITED) FOR THE TAX YEAR ENDED 12/31/06 |

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

For taxable non-corporate shareholders, $30,791,000 of the fund’s income represents qualified dividend income subject to the 15% rate category.

For corporate shareholders, $30,791,000 of the fund’s income qualifies for the dividends-received deduction.

| INFORMATION ON PROXY VOTING POLICIES, PROCEDURES, AND RECORDS |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information, which you may request by calling 1-800-225-5132 or by accessing the SEC’s Web site, www.sec.gov. The description of our proxy voting policies and procedures is also available on our Web site, www.troweprice.com. To access it, click on the words “Company Info” at the top of our homepage for individual investors. Then, in the window that appears, click on the “Proxy Voting Policy” navigation button in the top left corner.

Each fund’s most recent annual proxy voting record is available on our Web site and through the SEC’s Web site. To access it through our Web site, follow the directions above, then click on the words “Proxy Voting Record” at the bottom of the Proxy Voting Policy page.

| HOW TO OBTAIN QUARTERLY PORTFOLIO HOLDINGS |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s Web site (www.sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 450 Fifth St. N.W., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| ABOUT THE FUND’S DIRECTORS AND OFFICERS |

Your fund is governed by a Board of Directors that meets regularly to review a wide variety of matters affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and other business affairs. The Board of Directors elects the fund’s officers, who are listed in the final table. At least 75% of Board members are independent of T. Rowe Price Associates, Inc. (T. Rowe Price), and T. Rowe Price International, Inc. (T. Rowe Price International); “inside” or “interested” directors are officers of T. Rowe Price. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund directors and is available without charge by calling a T. Rowe Price representative at 1-800-225-5132.

| Independent Directors | |

| Name | |

| (Year of Birth) | Principal Occupation(s) During Past 5 Years and Directorships of |

| Year Elected * | Other Public Companies |

| Jeremiah E. Casey | Director, Allfirst Financial Inc. (previously First Maryland Bankcorp) |

| (1940) | (1983 to 2002); Director, National Life Insurance (2001 to 2005); |

| 2005 | Director, The Rouse Company, real estate developers (1990 to 2004) |

| Anthony W. Deering | Chairman, Exeter Capital, LLC, a private investment firm (2004 to |

| (1945) | present); Director, Vornado Real Estate Investment Trust (3/04 to |

| 2001 | present); Director, Mercantile Bankshares (4/03 to present); Member, |

| Advisory Board, Deutsche Bank North America (2004 to present); | |

| Director, Chairman of the Board, and Chief Executive Officer, The | |

| Rouse Company, real estate developers (1997 to 2004) | |

| Donald W. Dick, Jr. | Principal, EuroCapital Advisors, LLC, an acquisition and management |

| (1943) | advisory firm; Chairman, President, and Chief Executive Officer, |

| 1993 | The Haven Group, a custom manufacturer of modular homes (1/04 |

| to present) | |

| David K. Fagin | Chairman and President, Nye Corporation (6/88 to present); Director, |

| (1938) | Canyon Resources Corp., Golden Star Resources Ltd. (5/92 to present), |

| 1993 | and Pacific Rim Mining Corp. (2/02 to present) |

| Karen N. Horn | Director, Federal National Mortgage Association (9/06 to present); |

| (1943) | Managing Director and President, Global Private Client Services, |

| 2003 | Marsh Inc. (1999 to 2003); Director, Georgia Pacific (5/04 to |

| 12/05), Eli Lilly and Company, and Simon Property Group | |

| Theo C. Rodgers | President, A&R Development Corporation |

| (1941) | |

| 2005 | |

| John G. Schreiber | Owner/President, Centaur Capital Partners, Inc., a real estate invest- |

| (1946) | ment company; Partner, Blackstone Real Estate Advisors, L.P. |

| 2001 |

| * Each independent director oversees 115 T. Rowe Price portfolios and serves until retirement, resignation, or |

| election of a successor. |

| Inside Directors | |

| Name | |

| (Year of Birth) | |

| Year Elected * | |

| [Number of T. Rowe Price | Principal Occupation(s) During Past 5 Years and Directorships of |

| Portfolios Overseen] | Other Public Companies |

| Edward C. Bernard | Director and Vice President, T. Rowe Price and T. Rowe Price Group, |

| (1956) | Inc.; Chairman of the Board, Director, and President, T. Rowe Price |

| 2006 | Investment Services, Inc.; Chairman of the Board and Director, |

| [115] | T. Rowe Price International, Inc., T. Rowe Price Retirement Plan |

| Services, Inc., T. Rowe Price Services, Inc., and T. Rowe Price Savings | |

| Bank; Director, T. Rowe Price Global Asset Management Limited and | |

| T. Rowe Price Global Investment Services Limited; Chief Executive | |

| Officer, Chairman of the Board, Director, and President, T. Rowe Price | |

| Trust Company; Chairman of the Board, all funds | |

| Brian C. Rogers, CFA, CIC | Chief Investment Officer, Director, and Vice President, T. Rowe Price |

| (1955) | and T. Rowe Price Group, Inc.; Vice President, T. Rowe Price Trust |

| 2006 | Company |

| [62] | |

| * Each inside director serves until retirement, resignation, or election of a successor. | |

| Officers | |

| Name (Year of Birth) | |

| Title and Fund(s) Served | Principal Occupation(s) |

| P. Robert Bartolo, CPA (1972) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Peter J. Bates, CFA (1974) | Vice President, T. Rowe Price; formerly intern, |

| Vice President, Blue Chip Growth Fund | T. Rowe Price (to 2004) and Vice President of |

| Finance, Rent-A-Center, Inc. (to 2003) | |

| Joseph A. Carrier, CPA (1960) | Vice President, T. Rowe Price, T. Rowe Price |

| Treasurer, Blue Chip Growth Fund | Group, Inc., T. Rowe Price Investment Services, |

| Inc., and T. Rowe Price Trust Company | |

| D. Kyle Cerminara, CFA (1977) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Donald J. Easley, CFA (1971) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Henry M. Ellenbogen (1971) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Roger L. Fiery III, CPA (1959) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc., T. Rowe Price International, Inc., |

| and T. Rowe Price Trust Company | |

| John R. Gilner (1961) | Chief Compliance Officer and Vice President, |

| Chief Compliance Officer, Blue Chip Growth Fund | T. Rowe Price; Vice President, T. Rowe Price |

| Group, Inc., and T. Rowe Price Investment | |

| Services, Inc. | |

| Gregory S. Golczewski (1966) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Trust Company |

| Henry H. Hopkins (1942) | Director and Vice President, T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Investment Services, Inc., T. Rowe Price Services, |

| Inc., and T. Rowe Price Trust Company; Vice | |

| President, T. Rowe Price, T. Rowe Price Group, | |

| Inc., T. Rowe Price International, Inc., and | |

| T. Rowe Price Retirement Plan Services, Inc. | |

| Thomas J. Huber, CFA (1966) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Kris H. Jenner, M.D., D. Phil. (1962) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Patricia B. Lippert (1953) | Assistant Vice President, T. Rowe Price and |

| Secretary, Blue Chip Growth Fund | T. Rowe Price Investment Services, Inc. |

| Jason Nogueira, CFA (1974) | Vice President, T. Rowe Price; formerly |

| Vice President, Blue Chip Growth Fund | Healthcare Equity Analyst, Putnam Investments |

| (to 2004); student, Harvard Business School | |

| (to 2003) | |

| Timothy E. Parker (1974) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Larry J. Puglia, CFA, CPA (1960) | Vice President, T. Rowe Price, T. Rowe Price |

| President, Blue Chip Growth Fund | Group, Inc., and T. Rowe Price Trust Company |

| Karen M. Regan (1967) | Vice President, T. Rowe Price |

| Vice President, Blue Chip Growth Fund | |

| Robert W. Sharps, CFA, CPA (1971) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc. |

| Robert W. Smith (1961) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc., and T. Rowe Price Trust Company |

| Joshua K. Spencer, CFA (1973) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Blue Chip Growth Fund | Group, Inc.; formerly Research Analyst and |

| Sector Fund Portfolio Manager, Fidelity | |

| Investments (to 2004) | |

| Julie L. Waples (1970) | Vice President, T. Rowe Price |

| Vice President, Blue Chip Growth Fund | |

| Unless otherwise noted, officers have been employees of T. Rowe Price or T. Rowe Price International for at | |

| least five years. | |

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors/Trustees has determined that Mr. Donald W. Dick Jr. qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. Dick is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed to the registrant for the last two fiscal years for professional services rendered by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable for 2006, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. Reclassification from tax fees to audit fees of fiscal 2005 amounts related to the auditing of tax disclosures within the registrant’s annual financial statements has been made in order to conform to fiscal 2006 presentation. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $1,401,000 and $883,000, respectively, and were less than the aggregate fees billed for those same periods by the registrant’s principal accountant for audit services rendered to the T. Rowe Price Funds. Preceding fiscal year amount reflects the reclassification of tax fees described in (a) – (d) above.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Schedule of Investments.

Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES | |

| Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment | |

| Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the | |

| undersigned, thereunto duly authorized. | |

| T. Rowe Price Blue Chip Growth Fund, Inc. | |

| By | /s/ Edward C. Bernard |

| Edward C. Bernard | |

| Principal Executive Officer | |

| Date | February 16, 2007 |

| Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment | |

| Company Act of 1940, this report has been signed below by the following persons on behalf of | |

| the registrant and in the capacities and on the dates indicated. | |

| By | /s/ Edward C. Bernard |

| Edward C. Bernard | |

| Principal Executive Officer | |

| Date | February 16, 2007 |

| By | /s/ Joseph A. Carrier |

| Joseph A. Carrier | |

| Principal Financial Officer | |

| Date | February 16, 2007 |