UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07874

JPMorgan Insurance Trust

(Exact name of registrant as specified in charter)

277 Park Avenue

New York, NY 10172

(Address of principal executive offices) (Zip code)

Gregory S. Samuels

277 Park Avenue

New York, NY 10172

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: December 31

Date of reporting period: January 1, 2020 through December 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Annual Report

JPMorgan Insurance Trust

December 31, 2020

JPMorgan Insurance Trust Core Bond Portfolio

| | | | |

NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

| | |  | |

CONTENTS

Investments in the Portfolio are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when the Portfolio’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of the Portfolio or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of the Portfolio.

This Portfolio is intended to be a funding vehicle for variable annuity contracts and variable life insurance policies (collectively “Policies”) offered by the separate accounts of various insurance companies. Portfolio shares may also be offered to qualified pension and retirement plans and accounts permitting accumulation of assets on a tax-deferred basis (“Eligible Plans”). Individuals may not purchase shares directly from the Portfolio.

Prospective investors should refer to the Portfolio’s prospectuses for a discussion of the Portfolio’s investment objective, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about the Portfolio, including management fees and other expenses. Please read it carefully before investing.

LETTER TO SHAREHOLDERS

February 4, 2021 (Unaudited)

Dear Shareholders,

The immense efforts of central banks, government and researchers in the public and private sectors appear to have shepherded the world through the most difficult days of a profound crisis caused by the pandemic. While the economic and health care challenges are not behind us, the uncertainty and turbulence of 2020 has abated.

| | |

| | “We believe the clear lesson is that investors who remained fully invested over the past year, in the face of uncertainty over the direction of the pandemic and the unprecedented responses to it, were likely rewarded for their resolve.” — Andrea L. Lisher |

The development of multiple vaccines against Covid-19 toward the end of 2020 provided hope that the pandemic would be halted and that economic and social activity could begin to resume in the year ahead. That optimism spread to global financial markets. While leading equity indexes fell by 20% or more in the first quarter of 2020, financial markets stabilized and equity markets largely rebounded — slowly at first and then rapidly the second half of the year. At the end of 2020, the S&P 500 Index had generated a total return of 18.10% for the full 12 months and 22.16% for the final six months of the year.

We believe the clear lesson is that investors who remained fully invested over the past year, in the face of uncertainty over the

direction of the pandemic and the unprecedented responses to it, were likely rewarded for their resolve.

Certainly, enormous challenges remain in both the implementation of global vaccinations and in the rebuilding of economies at the local, national and international levels. However, the advances in the fight against Covid-19 provide policymakers and investors with the opportunity to plan for the future and meet those challenges. J.P. Morgan Asset Management has thrived amid the many challenges presented by the pandemic. Moreover, our deep experience in risk management enabled us to better navigate increased volatility in global financial markets. Throughout 2020, we continued to seek to operate under the same fundamental practices and principles that have driven our success for more than a century with an unwavering focus on putting our clients at the center of everything we do.

On behalf of J.P. Morgan Asset Management, thank you for entrusting us to manage your investment. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

Andrea L. Lisher

Head of Americas, Client

J.P. Morgan Asset Management

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 1 |

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2020 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Portfolio (Class 1 Shares)* | | | 7.84% | |

| Bloomberg Barclays U.S. Aggregate Index | | | 7.51% | |

| |

| Net Assets as of 12/31/2020 (In Thousands) | | | $531,776 | |

| Duration as of 12/31/2020 | | | 5.9 years | |

INVESTMENT OBJECTIVE**

The JPMorgan Insurance Trust Core Bond Portfolio (the “Portfolio”) seeks to maximize total return by investing primarily in a diversified portfolio of intermediate- and long-term debt securities.

HOW DID THE MARKET PERFORM?

Global financial markets generally recovered from a sharp sell-off in the first quarter of 2020, led by a rally in equity markets in the second half of the year. Investor demand for equity was largely fueled by continued support from central banks, relief spending by governments across the globe and the development and approvals of the first vaccines against Covid-19.

In the first days of January 2020, financial markets largely shrugged off a brief flare-up in military tensions between the U.S. and Iran. However, the emergence and spread of Covid-19 fed increasing investor uncertainty and by early March, the novel coronavirus was declared a pandemic by the World Health Organization. The closure of large sectors of national economies on a global scale sparked a dramatic sell-off in financial markets. Yields on developed market sovereign bonds fell sharply and prices for commodity gold spiked. By the end of the first quarter of 2020, leading developed market equity indexes had lost 20% or more of their value from the start of the year. Corporate bond prices fell and the price of crude oil ended the first quarter down by 60%.

Leading central banks promptly responded with lower interest rates and/or asset purchasing programs, which helped to support asset price stability and head off a potential liquidity crunch in credit markets. Governments also responded with a range of fiscal stimulus or paycheck protection programs designed to cushion the economic impact of the pandemic. In the ensuing months, global equity markets staged a slow and uneven rebound, led by U.S. and emerging markets.

At the start of the second half of the year, U.S. equity led a broad rebound in both developed markets and emerging markets equity. The U.S. Federal Reserve (the “Fed”) signaled its continued support for asset purchases and low benchmark interest rates. While the spread of Covid-19 accelerated in the U.S., multiple candidate vaccines were being developed around the world and the number of hospitalizations at the end of the summer was relatively small compared with what was to come at the end of the year.

U.S. equity markets continued to outperformed bond markets in the final months of the year amid investor optimism following the U.S. Food and Drug Administration’s approval of the first vaccines against Covid-19. While the results of the U.S. presidential election were contested, President-elect Joe Biden’s early cabinet choices — including former Fed Chairwoman Janet Yellen — removed some investor uncertainty. The Fed kept interest rates and policies unchanged and Congressional negotiations over proposed relief and stimulus spending continued through the month.

WHAT WERE THE MAIN DRIVERS OF THE PORTFOLIO’S PERFORMANCE?

The Portfolio’s Class 1 shares outperformed the Bloomberg Barclays U.S. Aggregate Index (the “Benchmark”) for the twelve months ended December 31, 2020.

Relative to the Benchmark, the Portfolio’s overweight allocations to asset-backed securities and corporate credit were leading contributors to performance during the period. The Portfolio’s security selection in corporate credit also contributed to performance. The Portfolio’s slightly longer duration profile relative to the Benchmark, its overweight position in the 5-10 year portion of the yield curve and its underweight position in the 20-plus year portion of the yield curve also contributed to relative performance. Generally, bonds with longer duration will experience a greater increase in price as interest rates fall versus bonds with shorter duration. The yield curve shows the relationship between yields and maturity dates for a set of similar bonds at a given point in time.

The Portfolio’s overweight allocation to non- agency commercial mortgage-backed securities (CMBS) was the leading detractor from relative performance as CMBS generally underperformed other credit sectors during the year.

HOW WAS THE PORTFOLIO POSITIONED?

The Portfolio’s primary strategy was to focus on security selection and relative value, which seeks to identify undervalued bonds among individual securities and across market sectors. The portfolio managers used bottom-up fundamental research to construct what they believed to be a portfolio of undervalued fixed income securities.

| | | | | | | | | | |

| | | | | |

| 2 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

Relative to the Benchmark, the Portfolio ended the reporting period with an underweight position in U.S. Treasury securities and an overweight position in corporate credit and securitized debt sectors, including asset-backed securities, commercial mortgage-backed securities and mortgage-backed securities, which included both agency and non-agency debt. The Portfolio was overweight in the intermediate part of the yield curve, underweight in the long end of the yield curve and maintained a longer duration profile before finishing the year shorter in duration than the Benchmark.

| | | | |

PORTFOLIO COMPOSITION*** | |

| Corporate Bonds | | | 28.1 | % |

| Mortgage-Backed Securities | | | 20.1 | |

| U.S. Treasury Obligations | | | 18.3 | |

| Asset-Backed Securities | | | 9.5 | |

| Collateralized Mortgage Obligations | | | 6.3 | |

| Commercial Mortgage-Backed Securities | | | 4.6 | |

| Others (each less than 1.0%) | | | 0.7 | |

| Short-Term Investments | | | 12.4 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Portfolio’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2020. The Portfolio’s composition is subject to change. |

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 3 |

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2020 (Unaudited) (continued)

| | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2020 | |

| | | | |

| | | INCEPTION DATE OF

CLASS | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS 1 SHARES | | May 1, 1997 | | | 7.84 | % | | | 4.30 | % | | | 3.86 | % |

CLASS 2 SHARES | | August 16, 2006 | | | 7.68 | | | | 4.04 | | | | 3.61 | |

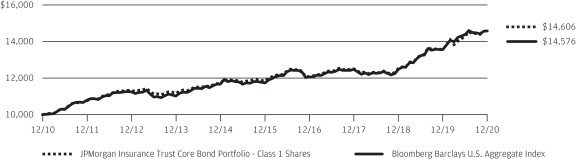

TEN YEAR PERFORMANCE 12/31/10 TO 12/31/20

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

The graph illustrates comparative performance for $10,000 invested in Class 1 Shares of the JPMorgan Insurance Trust Core Bond Portfolio and the Bloomberg Barclays U.S. Aggregate Index from December 31, 2010 to December 31, 2020. The performance of the Portfolio assumes reinvestment of all dividends and capital gain distributions, if any. The performance of the Bloomberg Barclays U.S. Aggregate Index does not reflect the deduction of expenses associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark,

if applicable. The Bloomberg Barclays U.S. Aggregate Index is an unmanaged index that represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Investors cannot invest directly in an index.

Portfolio performance does not reflect any charges imposed by the Policies or Eligible Plans. If these charges were included, the returns would be lower than shown. Portfolio performance may reflect the waiver of the Portfolio’s fees and reimbursement of expenses for certain periods. Without these waivers and reimbursements, performance would have been lower. The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | | | |

| | | | | |

| 4 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2020

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — 30.6% | |

|

Aerospace & Defense — 0.8% | |

| | |

Airbus Finance BV (France) 2.70%, 4/17/2023 (a) | | | 32 | | | | 34 | |

| | |

Airbus SE (France) 3.15%, 4/10/2027 (a) | | | 164 | | | | 178 | |

| | |

BAE Systems Holdings, Inc. (United Kingdom) 3.80%, 10/7/2024 (a) | | | 45 | | | | 50 | |

| | |

BAE Systems plc (United Kingdom)

1.90%, 2/15/2031 (a) | | | 200 | | | | 202 | |

| | |

5.80%, 10/11/2041 (a) | | | 51 | | | | 73 | |

| | |

Boeing Co. (The)

4.51%, 5/1/2023 | | | 513 | | | | 554 | |

| | |

1.95%, 2/1/2024 | | | 185 | | | | 191 | |

| | |

4.88%, 5/1/2025 | | | 125 | | | | 143 | |

| | |

2.75%, 2/1/2026 | | | 180 | | | | 189 | |

| | |

2.70%, 2/1/2027 | | | 640 | | | | 665 | |

| | |

5.15%, 5/1/2030 | | | 190 | | | | 230 | |

| | |

5.71%, 5/1/2040 | | | 175 | | | | 226 | |

| | |

L3Harris Technologies, Inc.

3.83%, 4/27/2025 | | | 60 | | | | 67 | |

| | |

1.80%, 1/15/2031 | | | 220 | | | | 224 | |

| | |

Leidos, Inc. 2.30%, 2/15/2031 (a) | | | 120 | | | | 122 | |

| | |

Lockheed Martin Corp. 4.50%, 5/15/2036 | | | 70 | | | | 92 | |

| | |

Northrop Grumman Corp.

3.20%, 2/1/2027 | | | 76 | | | | 86 | |

| | |

3.25%, 1/15/2028 | | | 50 | | | | 56 | |

| | |

5.15%, 5/1/2040 | | | 140 | | | | 193 | |

| | |

Precision Castparts Corp. 3.25%, 6/15/2025 | | | 30 | | | | 33 | |

| | |

Raytheon Technologies Corp.

3.20%, 3/15/2024 | | | 28 | | | | 30 | |

| | |

4.50%, 6/1/2042 | | | 80 | | | | 104 | |

| | |

4.15%, 5/15/2045 | | | 138 | | | | 175 | |

| | |

3.75%, 11/1/2046 | | | 80 | | | | 95 | |

| | |

4.35%, 4/15/2047 | | | 90 | | | | 118 | |

| | | | | | | | |

| | |

| | | | | | | 4,130 | |

| | | | | | | | |

|

Airlines — 0.0% (b) | |

| | |

Continental Airlines Pass-Through Trust | | | | | | | | |

| | |

Series 2012-2, Class A Shares, 4.00%, 10/29/2024 | | | 16 | | | | 16 | |

| | | | | | | | |

|

Automobiles — 0.3% | |

| | |

BMW US Capital LLC (Germany) 2.25%, 9/15/2023 (a) | | | 45 | | | | 47 | |

| | |

General Motors Co. 6.13%, 10/1/2025 | | | 130 | | | | 158 | |

| | |

Hyundai Capital America

1.15%, 11/10/2022 (a) | | | 394 | | | | 396 | |

| | |

1.80%, 10/15/2025 (a) | | | 140 | | | | 143 | |

| | |

2.38%, 10/15/2027 (a) | | | 130 | | | | 134 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Automobiles — continued | |

| | |

Nissan Motor Co. Ltd. (Japan) 3.52%, 9/17/2025 (a) | | | 481 | | | | 515 | |

| | |

4.35%, 9/17/2027 (a) | | | 200 | | | | 221 | |

| | |

Volkswagen Group of America Finance LLC (Germany) 1.63%, 11/24/2027 (a) | | | 200 | | | | 202 | |

| | | | | | | | |

| | |

| | | | | | | 1,816 | |

| | | | | | | | |

|

Banks — 5.4% | |

| | |

ABN AMRO Bank NV (Netherlands) 4.75%, 7/28/2025 (a) | | | 200 | | | | 230 | |

| | |

AIB Group plc (Ireland) | | | | | | | | |

| | |

(ICE LIBOR USD 3 Month + 1.87%), 4.26%, 4/10/2025 (a) (c) | | | 250 | | | | 273 | |

| | |

ANZ New Zealand Int’l Ltd. (New Zealand)

3.45%, 1/21/2028 (a) | | | 200 | | | | 229 | |

| | |

2.55%, 2/13/2030 (a) | | | 200 | | | | 218 | |

| | |

ASB Bank Ltd. (New Zealand) 3.13%, 5/23/2024 (a) | | | 230 | | | | 248 | |

| | |

Banco Nacional de Panama (Panama) 2.50%, 8/11/2030 (a) | | | 300 | | | | 300 | |

| | |

Banco Santander SA (Spain)

2.75%, 5/28/2025 | | | 200 | | | | 214 | |

| | |

2.75%, 12/3/2030 | | | 200 | | | | 206 | |

| | |

Bank of America Corp. | | | | | | | | |

| | |

(ICE LIBOR USD 3 Month + 1.16%), 3.12%, 1/20/2023 (c) | | | 100 | | | | 103 | |

| | |

(ICE LIBOR USD 3 Month + 0.79%), 3.00%, 12/20/2023 (c) | | | 26 | | | | 27 | |

| | |

4.00%, 1/22/2025 | | | 114 | | | | 128 | |

| | |

Series L, 3.95%, 4/21/2025 | | | 92 | | | | 104 | |

| | |

(ICE LIBOR USD 3 Month + 0.81%), 3.37%, 1/23/2026 (c) | | | 100 | | | | 110 | |

| | |

4.45%, 3/3/2026 | | | 69 | | | | 81 | |

| | |

3.25%, 10/21/2027 | | | 514 | | | | 575 | |

| | |

(ICE LIBOR USD 3 Month + 1.51%), 3.71%, 4/24/2028 (c) | | | 260 | | | | 296 | |

| | |

(ICE LIBOR USD 3 Month + 1.04%), 3.42%, 12/20/2028 (c) | | | 408 | | | | 461 | |

| | |

(ICE LIBOR USD 3 Month + 1.07%), 3.97%, 3/5/2029 (c) | | | 280 | | | | 326 | |

| | |

(ICE LIBOR USD 3 Month + 0.99%), 2.50%, 2/13/2031 (c) | | | 525 | | | | 557 | |

| | |

(SOFR + 2.15%), 2.59%, 4/29/2031 (c) | | | 313 | | | | 335 | |

| | |

(SOFR + 1.53%), 1.90%, 7/23/2031 (c) | | | 150 | | | | 152 | |

| | |

(SOFR + 1.93%), 2.68%, 6/19/2041 (c) | | | 1,158 | | | | 1,205 | |

| | |

Bank of Montreal (Canada)

1.85%, 5/1/2025 | | | 200 | | | | 210 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 5 |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2020 (Unaudited) (continued)

(Amounts in thousands)

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Banks — continued | |

| | |

(USD Swap Semi 5 Year + 1.43%), 3.80%, 12/15/2032 (c) | | | 47 | | | | 53 | |

| | |

Bank of Nova Scotia (The) (Canada)

1.63%, 5/1/2023 | | | 680 | | | | 700 | |

| | |

4.50%, 12/16/2025 | | | 25 | | | | 29 | |

| | |

Banque Federative du Credit Mutuel SA (France) 2.38%, 11/21/2024 (a) | | | 254 | | | | 269 | |

| | |

Barclays plc (United Kingdom) | | | | | | | | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 0.80%), 1.01%, 12/10/2024 (c) | | | 369 | | | | 372 | |

| | |

3.65%, 3/16/2025 | | | 200 | | | | 220 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 1.90%), 2.64%, 6/24/2031 (c) | | | 440 | | | | 458 | |

| | |

BBVA USA 2.50%, 8/27/2024 | | | 250 | | | | 265 | |

| | |

BNP Paribas SA (France) | | | | | | | | |

| | |

(SOFR + 2.07%), 2.22%, 6/9/2026 (a) (c) | | | 525 | | | | 549 | |

| | |

(SOFR + 1.51%), 3.05%, 1/13/2031 (a) (c) | | | 320 | | | | 349 | |

| | |

BNZ International Funding Ltd. (New Zealand) 2.90%, 2/21/2022 (a) | | | 250 | | | | 257 | |

| | |

Citigroup, Inc.

2.90%, 12/8/2021 | | | 100 | | | | 102 | |

| | |

2.75%, 4/25/2022 | | | 200 | | | | 206 | |

| | |

(ICE LIBOR USD 3 Month + 0.72%), 3.14%, 1/24/2023 (c) | | | 74 | | | | 76 | |

| | |

(ICE LIBOR USD 3 Month + 0.90%), 3.35%, 4/24/2025 (c) | | | 90 | | | | 98 | |

| | |

4.40%, 6/10/2025 | | | 78 | | | | 89 | |

| | |

(SOFR + 2.75%), 3.11%, 4/8/2026 (c) | | | 380 | | | | 415 | |

| | |

3.40%, 5/1/2026 | | | 75 | | | | 85 | |

| | |

4.45%, 9/29/2027 | | | 210 | | | | 248 | |

| | |

(ICE LIBOR USD 3 Month + 1.39%), 3.67%, 7/24/2028 (c) | | | 250 | | | | 283 | |

| | |

(ICE LIBOR USD 3 Month + 1.34%), 3.98%, 3/20/2030 (c) | | | 220 | | | | 259 | |

| | |

(ICE LIBOR USD 3 Month + 1.17%), 3.88%, 1/24/2039 (c) | | | 50 | | | | 59 | |

| | |

8.13%, 7/15/2039 | | | 56 | | | | 100 | |

| | |

Citizens Financial Group, Inc.

2.38%, 7/28/2021 | | | 24 | | | | 24 | |

| | |

2.85%, 7/27/2026 | | | 200 | | | | 223 | |

| | |

Comerica, Inc. 4.00%, 2/1/2029 | | | 150 | | | | 179 | |

| | |

Commonwealth Bank of Australia (Australia) 2.85%, 5/18/2026 (a) | | | 80 | | | | 89 | |

| | |

Cooperatieve Rabobank UA (Netherlands) 3.75%, 7/21/2026 | | | 450 | | | | 509 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Banks — continued | |

| | |

Credit Agricole SA (France) (SOFR + 1.68%), 1.91%, 6/16/2026 (a) (c) | | | 650 | | | | 674 | |

| | |

Danske Bank A/S (Denmark) 2.00%, 9/8/2021 (a) | | | 200 | | | | 202 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 1.03%), 1.17%, 12/8/2023 (a) (c) | | | 480 | | | | 482 | |

| | |

Fifth Third Bancorp | | | | | | | | |

| | |

3.65%, 1/25/2024 | | | 90 | | | | 98 | |

| | |

HSBC Holdings plc (United Kingdom) | | | | | | | | |

| | |

(ICE LIBOR USD 3 Month + 0.99%), 3.95%, 5/18/2024 (c) | | | 229 | | | | 247 | |

| | |

4.38%, 11/23/2026 | | | 200 | | | | 231 | |

| | |

(SOFR + 1.95%), 2.36%, 8/18/2031 (c) | | | 300 | | | | 310 | |

| | |

6.50%, 9/15/2037 | | | 250 | | | | 365 | |

| | |

6.10%, 1/14/2042 | | | 120 | | | | 182 | |

| | |

Huntington Bancshares, Inc. 2.55%, 2/4/2030 | | | 315 | | | | 338 | |

| | |

ING Groep NV (Netherlands) 4.10%, 10/2/2023 | | | 200 | | | | 220 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 1.10%),

1.40%, 7/1/2026 (a) (c) | | | 210 | | | | 214 | |

| | |

3.95%, 3/29/2027 | | | 200 | | | | 231 | |

| | |

KeyCorp 4.15%, 10/29/2025 | | | 65 | | | | 76 | |

| | |

Lloyds Banking Group plc (United Kingdom) | | | | | | | | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 1.10%),

1.33%, 6/15/2023 (c) | | | 200 | | | | 202 | |

| | |

4.50%, 11/4/2024 | | | 220 | | | | 246 | |

| | |

4.58%, 12/10/2025 | | | 200 | | | | 229 | |

| | |

Mitsubishi UFJ Financial Group, Inc.

(Japan) 3.00%, 2/22/2022 | | | 38 | | | | 39 | |

| | |

2.67%, 7/25/2022 | | | 80 | | | | 83 | |

| | |

3.76%, 7/26/2023 | | | 172 | | | | 187 | |

| | |

3.41%, 3/7/2024 | | | 170 | | | | 185 | |

| | |

2.19%, 2/25/2025 | | | 200 | | | | 211 | |

| | |

2.05%, 7/17/2030 | | | 340 | | | | 355 | |

| | |

3.75%, 7/18/2039 | | | 515 | | | | 626 | |

| | |

Mizuho Financial Group, Inc. (Japan) (ICE LIBOR USD 3 Month + 1.31%), 2.87%, 9/13/2030 (c) | | | 220 | | | | 239 | |

| | |

National Australia Bank Ltd. (Australia)

3.38%, 1/14/2026 | | | 300 | | | | 337 | |

| | |

2.33%, 8/21/2030 (a) | | | 250 | | | | 254 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 5 Year + 1.88%), 3.93%, 8/2/2034 (a) (c) | | | 440 | | | | 494 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| 6 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Banks — continued | |

| | |

Natwest Group plc (United Kingdom) | | | | | | | | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 2.55%), 3.07%, 5/22/2028 (c) | | | 440 | | | | 477 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 5 Year + 2.10%), 3.75%, 11/1/2029 (c) | | | 200 | | | | 213 | |

| | |

(ICE LIBOR USD 3 Month + 1.87%), 4.44%, 5/8/2030 (c) | | | 200 | | | | 238 | |

| | |

NatWest Markets plc (United Kingdom) 3.63%, 9/29/2022 (a) | | | 315 | | | | 332 | |

| | |

Regions Financial Corp. 3.80%, 8/14/2023 | | | 27 | | | | 29 | |

| | |

Royal Bank of Canada (Canada)

2.75%, 2/1/2022 | | | 66 | | | | 68 | |

| | |

3.70%, 10/5/2023 | | | 300 | | | | 327 | |

| | |

4.65%, 1/27/2026 | | | 30 | | | | 35 | |

| | |

Societe Generale SA (France)

3.88%, 3/28/2024 (a) | | | 380 | | | | 414 | |

| | |

2.63%, 10/16/2024 (a) | | | 200 | | | | 212 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 1.10%), 1.49%, 12/14/2026 (a) (c) | | | 260 | | | | 262 | |

| | |

3.00%, 1/22/2030 (a) | | | 331 | | | | 353 | |

| | |

Standard Chartered plc (United Kingdom) | | | | | | | | |

| | |

(ICE LIBOR USD 3 Month + 1.15%), 4.25%, 1/20/2023 (a) (c) | | | 220 | | | | 228 | |

| | |

(ICE LIBOR USD 3 Month + 1.91%), 4.30%, 5/21/2030 (a) (c) | | | 200 | | | | 234 | |

| | |

Sumitomo Mitsui Financial Group, Inc. (Japan)

2.44%, 10/19/2021 | | | 45 | | | | 46 | |

| | |

2.85%, 1/11/2022 | | | 130 | | | | 133 | |

| | |

2.78%, 10/18/2022 | | | 82 | | | | 85 | |

| | |

3.10%, 1/17/2023 | | | 55 | | | | 58 | |

| | |

3.94%, 10/16/2023 | | | 300 | | | | 329 | |

| | |

3.01%, 10/19/2026 | | | 25 | | | | 28 | |

| | |

3.04%, 7/16/2029 | | | 345 | | | | 382 | |

| | |

Toronto-Dominion Bank (The) (Canada) 3.25%, 3/11/2024 | | | 140 | | | | 152 | |

| | |

Truist Financial Corp.

2.70%, 1/27/2022 | | | 91 | | | | 93 | |

| | |

1.95%, 6/5/2030 | | | 140 | | | | 145 | |

| | |

US Bancorp

3.38%, 2/5/2024 | | | 120 | | | | 131 | |

| | |

7.50%, 6/1/2026 | | | 100 | | | | 132 | |

| | |

Wells Fargo & Co.

3.07%, 1/24/2023 | | | 245 | | | | 252 | |

| | |

3.75%, 1/24/2024 | | | 105 | | | | 115 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Banks — continued | |

| | |

3.30%, 9/9/2024 | | | 80 | | | | 88 | |

| | |

3.00%, 4/22/2026 | | | 284 | | | | 312 | |

| | |

4.10%, 6/3/2026 | | | 24 | | | | 27 | |

| | |

(ICE LIBOR USD 3 Month + 1.17%), 3.20%, 6/17/2027 (c) | | | 470 | | | | 521 | |

| | |

(SOFR + 2.10%), 2.39%, 6/2/2028 (c) | | | 400 | | | | 426 | |

| | |

(SOFR + 2.53%), 3.07%, 4/30/2041 (c) | | | 255 | | | | 277 | |

| | |

5.38%, 11/2/2043 | | | 200 | | | | 278 | |

| | |

4.40%, 6/14/2046 | | | 47 | | | | 59 | |

| | |

4.75%, 12/7/2046 | | | 53 | | | | 69 | |

| | |

Westpac Banking Corp. (Australia) | | | | | | | | |

| | |

2.85%, 5/13/2026 | | | 100 | | | | 111 | |

| | |

(USD ICE Swap Rate 5 Year + 2.24%), 4.32%, 11/23/2031 (c) | | | 140 | | | | 160 | |

| | |

4.42%, 7/24/2039 | | | 100 | | | | 127 | |

| | | | | | | | |

| | |

| | | | | | | 28,668 | |

| | | | | | | | |

|

Beverages — 0.9% | |

| | |

Anheuser-Busch Cos. LLC (Belgium)

4.70%, 2/1/2036 | | | 571 | | | | 724 | |

| | |

4.90%, 2/1/2046 | | | 260 | | | | 339 | |

| | |

Anheuser-Busch InBev Finance, Inc. (Belgium) 4.70%, 2/1/2036 | | | 120 | | | | 151 | |

| | |

Anheuser-Busch InBev Worldwide, Inc. (Belgium)

4.38%, 4/15/2038 | | | 150 | | | | 185 | |

| | |

4.35%, 6/1/2040 | | | 225 | | | | 276 | |

| | |

4.44%, 10/6/2048 | | | 130 | | | | 162 | |

| | |

4.50%, 6/1/2050 | | | 295 | | | | 371 | |

| | |

4.75%, 4/15/2058 | | | 95 | | | | 124 | |

| | |

4.60%, 6/1/2060 | | | 105 | | | | 134 | |

| | |

Coca-Cola Femsa SAB de CV (Mexico)

2.75%, 1/22/2030 | | | 155 | | | | 167 | |

| | |

1.85%, 9/1/2032 | | | 215 | | | | 214 | |

| | |

Constellation Brands, Inc.

4.40%, 11/15/2025 | | | 50 | | | | 58 | |

| | |

2.88%, 5/1/2030 | | | 420 | | | | 460 | |

| | |

5.25%, 11/15/2048 | | | 25 | | | | 35 | |

| | |

Diageo Capital plc (United Kingdom)

1.38%, 9/29/2025 | | | 350 | | | | 360 | |

| | |

2.00%, 4/29/2030 | | | 350 | | | | 365 | |

| | |

Fomento Economico Mexicano SAB de CV (Mexico) 3.50%, 1/16/2050 | | | 260 | | | | 288 | |

| | |

Keurig Dr Pepper, Inc.

3.13%, 12/15/2023 | | | 100 | | | | 108 | |

| | |

4.42%, 5/25/2025 | | | 30 | | | | 35 | |

| | |

3.43%, 6/15/2027 | | | 20 | | | | 23 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 7 |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2020 (continued)

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Beverages — continued | |

| | |

4.99%, 5/25/2038 | | | 43 | | | | 57 | |

| | |

4.42%, 12/15/2046 | | | 64 | | | | 81 | |

| | |

5.09%, 5/25/2048 | | | 60 | | | | 84 | |

| | | | | | | | |

| | |

| | | | | | | 4,801 | |

| | | | | | | | |

|

Biotechnology — 0.7% | |

| | |

AbbVie, Inc.

3.45%, 3/15/2022 | | | 52 | | | | 54 | |

| | |

2.80%, 3/15/2023 | | | 100 | | | | 105 | |

| | |

3.85%, 6/15/2024 | | | 42 | | | | 46 | |

| | |

3.20%, 11/21/2029 | | | 516 | | | | 578 | |

| | |

4.50%, 5/14/2035 | | | 100 | | | | 126 | |

| | |

4.05%, 11/21/2039 | | | 510 | | | | 615 | |

| | |

4.40%, 11/6/2042 | | | 370 | | | | 464 | |

| | |

4.85%, 6/15/2044 | | | 200 | | | | 264 | |

| | |

Amgen, Inc. 2.20%, 2/21/2027 | | | 120 | | | | 129 | |

| | |

Baxalta, Inc.

3.60%, 6/23/2022 | | | 7 | | | | 7 | |

| | |

5.25%, 6/23/2045 | | | 3 | | | | 4 | |

| | |

Biogen, Inc. | | | | | | | | |

| | |

2.25%, 5/1/2030 | | | 289 | | | | 302 | |

| | |

3.15%, 5/1/2050 | | | 75 | | | | 77 | |

| | |

Gilead Sciences, Inc. 2.60%, 10/1/2040 | | | 310 | | | | 312 | |

| | |

Regeneron Pharmaceuticals, Inc. 1.75%, 9/15/2030 | | | 460 | | | | 453 | |

| | | | | | | | |

| | |

| | | | | | | 3,536 | |

| | | | | | | | |

|

Building Products — 0.1% | |

| | |

Lennox International, Inc. 1.35%, 8/1/2025 | | | 540 | | | | 552 | |

| | |

Masco Corp.

2.00%, 10/1/2030 | | | 90 | | | | 92 | |

| | |

6.50%, 8/15/2032 | | | 80 | | | | 107 | |

| | | | | | | | |

| | |

| | | | | | | 751 | |

| | | | | | | | |

|

Capital Markets — 2.3% | |

| | |

Bank of New York Mellon Corp. (The) 3.25%, 9/11/2024 | | | 100 | | | | 110 | |

| | |

BlackRock, Inc. 1.90%, 1/28/2031 | | | 189 | | | | 198 | |

| | |

Blackstone Holdings Finance Co. LLC 4.45%, 7/15/2045 (a) | | | 21 | | | | 27 | |

| | |

Brookfield Finance, Inc. (Canada)

3.90%, 1/25/2028 | | | 55 | | | | 63 | |

| | |

4.85%, 3/29/2029 | | | 54 | | | | 66 | |

| | |

4.70%, 9/20/2047 | | | 44 | | | | 56 | |

| | |

Charles Schwab Corp. (The)

0.90%, 3/11/2026 | | | 75 | | | | 76 | |

| | |

3.20%, 3/2/2027 | | | 100 | | | | 112 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Capital Markets — continued | |

| | |

Series H, (US Treasury Yield Curve Rate T Note Constant Maturity 10 Year + 3.08%), 4.00%, 12/1/2030 (c) (d) (e) | | | 190 | | | | 200 | |

| | |

CME Group, Inc. 3.00%, 3/15/2025 | | | 97 | | | | 106 | |

| | |

Credit Suisse Group AG (Switzerland)

3.80%, 6/9/2023 | | | 350 | | | | 377 | |

| | |

3.75%, 3/26/2025 | | | 250 | | | | 278 | |

| | |

(SOFR + 1.56%), 2.59%, 9/11/2025 (a) (c) | | | 250 | | | | 263 | |

| | |

(SOFR + 2.04%), 2.19%, 6/5/2026 (a) (c) | | | 250 | | | | 261 | |

| | |

Daiwa Securities Group, Inc. (Japan) 3.13%, 4/19/2022 (a) | | | 49 | | | | 51 | |

| | |

Deutsche Bank AG (Germany)

4.25%, 10/14/2021 | | | 100 | | | | 102 | |

| | |

3.30%, 11/16/2022 | | | 100 | | | | 104 | |

| | |

(SOFR + 2.16%), 2.22%, 9/18/2024 (c) | | | 380 | | | | 391 | |

| | |

(SOFR + 1.87%), 2.13%, 11/24/2026 (c) | | | 205 | | | | 210 | |

| | |

Goldman Sachs Group, Inc. (The) | | | | | | | | |

| | |

(ICE LIBOR USD 3 Month + 0.82%), 2.88%, 10/31/2022 (c) | | | 100 | | | | 102 | |

| | |

(ICE LIBOR USD 3 Month + 1.05%), 2.91%, 6/5/2023 (c) | | | 598 | | | | 619 | |

| | |

(ICE LIBOR USD 3 Month + 0.99%), 2.90%, 7/24/2023 (c) | | | 213 | | | | 221 | |

| | |

3.50%, 1/23/2025 | | | 100 | | | | 110 | |

| | |

(ICE LIBOR USD 3 Month + 1.20%), 3.27%, 9/29/2025 (c) | | | 137 | | | | 150 | |

| | |

4.25%, 10/21/2025 | | | 105 | | | | 121 | |

| | |

3.50%, 11/16/2026 | | | 142 | | | | 160 | |

| | |

3.85%, 1/26/2027 | | | 45 | | | | 51 | |

| | |

(ICE LIBOR USD 3 Month + 1.51%), 3.69%, 6/5/2028 (c) | | | 209 | | | | 241 | |

| | |

2.60%, 2/7/2030 | | | 400 | | | | 430 | |

| | |

6.75%, 10/1/2037 | | | 80 | | | | 122 | |

| | |

(ICE LIBOR USD 3 Month + 1.43%), 4.41%, 4/23/2039 (c) | | | 215 | | | | 275 | |

| | |

4.75%, 10/21/2045 | | | 400 | | | | 556 | |

| | |

Intercontinental Exchange, Inc. 4.00%, 10/15/2023 | | | 59 | | | | 65 | |

| | |

Invesco Finance plc

4.00%, 1/30/2024 | | | 29 | | | | 32 | |

| | |

3.75%, 1/15/2026 | | | 36 | | | | 40 | |

| | |

Jefferies Group LLC 6.45%, 6/8/2027 | | | 81 | | | | 103 | |

| | |

Macquarie Bank Ltd. (Australia) 4.00%, 7/29/2025 (a) | | | 100 | | | | 114 | |

| | |

Macquarie Group Ltd. (Australia) | | | | | | | | |

| | |

(ICE LIBOR USD 3 Month + 1.37%), 3.76%, 11/28/2028 (a) (c) | | | 145 | | | | 161 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| 8 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Capital Markets — continued | |

| | |

(ICE LIBOR USD 3 Month + 1.75%), 5.03%, 1/15/2030 (a) (c) | | | 220 | | | | 266 | |

| | |

Morgan Stanley

5.50%, 7/28/2021 | | | 35 | | | | 36 | |

| | |

2.63%, 11/17/2021 | | | 170 | | | | 173 | |

| | |

3.75%, 2/25/2023 | | | 142 | | | | 152 | |

| | |

4.10%, 5/22/2023 | | | 100 | | | | 109 | |

| | |

3.70%, 10/23/2024 | | | 69 | | | | 77 | |

| | |

4.00%, 7/23/2025 | | | 276 | | | | 316 | |

| | |

5.00%, 11/24/2025 | | | 70 | | | | 84 | |

| | |

3.88%, 1/27/2026 | | | 341 | | | | 391 | |

| | |

(SOFR + 1.99%), 2.19%, 4/28/2026 (c) | | | 980 | | | | 1,035 | |

| | |

4.35%, 9/8/2026 | | | 20 | | | | 24 | |

| | |

3.63%, 1/20/2027 | | | 159 | | | | 182 | |

| | |

(ICE LIBOR USD 3 Month + 1.34%), 3.59%, 7/22/2028 (c) | | | 222 | | | | 253 | |

| | |

(ICE LIBOR USD 3 Month + 1.14%), 3.77%, 1/24/2029 (c) | | | 96 | | | | 111 | |

| | |

(SOFR + 1.03%), 1.79%, 2/13/2032 (c) | | | 280 | | | | 282 | |

| | |

4.30%, 1/27/2045 | | | 85 | | | | 113 | |

| | |

Nomura Holdings, Inc. (Japan)

2.65%, 1/16/2025 | | | 212 | | | | 226 | |

| | |

2.68%, 7/16/2030 | | | 200 | | | | 212 | |

| | |

Northern Trust Corp.

1.95%, 5/1/2030 | | | 375 | | | | 390 | |

| | |

(ICE LIBOR USD 3 Month + 1.13%), 3.38%, 5/8/2032 (c) | | | 29 | | | | 32 | |

| | |

Nuveen LLC 4.00%, 11/1/2028 (a) | | | 160 | | | | 191 | |

| | |

S&P Global, Inc. 3.25%, 12/1/2049 | | | 150 | | | | 175 | |

| | |

TD Ameritrade Holding Corp. 2.95%, 4/1/2022 | | | 17 | | | | 17 | |

| | |

UBS AG (Switzerland) 1.75%, 4/21/2022 (a) | | | 200 | | | | 203 | |

| | |

UBS Group AG (Switzerland)

4.13%, 9/24/2025 (a) | | | 200 | | | | 229 | |

| | |

(US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 1.08%), 1.36%, 1/30/2027 (a) (c) | | | 200 | | | | 202 | |

| | | | | | | | |

| | |

| | | | | | | 12,205 | |

| | | | | | | | |

|

Chemicals — 0.8% | |

| | |

Air Products and Chemicals, Inc. 1.85%, 5/15/2027 | | | 310 | | | | 328 | |

| | |

Albemarle Corp. 5.45%, 12/1/2044 | | | 50 | | | | 60 | |

| | |

Celanese US Holdings LLC 3.50%, 5/8/2024 | | | 151 | | | | 163 | |

| | |

Chevron Phillips Chemical Co. LLC 5.13%, 4/1/2025 (a) | | | 485 | | | | 569 | |

| | |

Dow Chemical Co. (The)

4.55%, 11/30/2025 | | | 200 | | | | 234 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Chemicals — continued | |

| | |

3.60%, 11/15/2050 | | | 245 | | | | 275 | |

| | |

DuPont de Nemours, Inc. 5.32%, 11/15/2038 | | | 595 | | | | 805 | |

| | |

Eastman Chemical Co. 4.50%, 12/1/2028 | | | 220 | | | | 265 | |

| | |

Ecolab, Inc. 3.25%, 1/14/2023 | | | 90 | | | | 95 | |

| | |

International Flavors & Fragrances, Inc.

4.45%, 9/26/2028 | | | 45 | | | | 53 | |

| | |

5.00%, 9/26/2048 | | | 52 | | | | 70 | |

| | |

LYB International Finance III LLC

1.25%, 10/1/2025 | | | 80 | | | | 82 | |

| | |

3.38%, 5/1/2030 | | | 235 | | | | 263 | |

| | |

Nutrien Ltd. (Canada)

4.00%, 12/15/2026 | | | 70 | | | | 82 | |

| | |

4.20%, 4/1/2029 | | | 25 | | | | 30 | |

| | |

4.13%, 3/15/2035 | | | 90 | | | | 107 | |

| | |

5.00%, 4/1/2049 | | | 40 | | | | 55 | |

| | |

Nutrition & Biosciences, Inc.

1.83%, 10/15/2027 (a) | | | 190 | | | | 196 | |

| | |

3.27%, 11/15/2040 (a) | | | 110 | | | | 118 | |

| | |

3.47%, 12/1/2050 (a) | | | 85 | | | | 92 | |

| | |

Sherwin-Williams Co. (The) 3.13%, 6/1/2024 | | | 29 | | | | 31 | |

| | |

Union Carbide Corp. 7.75%, 10/1/2096 | | | 80 | | | | 123 | |

| | | | | | | | |

| | |

| | | | | | | 4,096 | |

| | | | | | | | |

|

Commercial Services & Supplies — 0.1% | |

| | |

Brambles USA, Inc. (Australia) 4.13%, 10/23/2025 (a) | | | 70 | | | | 79 | |

| | |

Ford Foundation (The) Series 2020, 2.82%, 6/1/2070 | | | 90 | | | | 96 | |

| | |

Republic Services, Inc. 1.45%, 2/15/2031 | | | 230 | | | | 225 | |

| | | | | | | | |

| | |

| | | | | | | 400 | |

| | | | | | | | |

|

Construction & Engineering — 0.1% | |

| | |

Quanta Services, Inc. 2.90%, 10/1/2030 | | | 360 | | | | 386 | |

| | | | | | | | |

|

Construction Materials — 0.0% (b) | |

| | |

Martin Marietta Materials, Inc.

3.45%, 6/1/2027 | | | 52 | | | | 58 | |

| | |

3.50%, 12/15/2027 | | | 100 | | | | 114 | |

| | | | | | | | |

| | |

| | | | | | | 172 | |

| | | | | | | | |

|

Consumer Finance — 1.0% | |

| | |

AerCap Ireland Capital DAC (Ireland)

4.45%, 12/16/2021 | | | 150 | | | | 154 | |

| | |

4.13%, 7/3/2023 | | | 150 | | | | 161 | |

| | |

4.50%, 9/15/2023 | | | 600 | | | | 651 | |

| | |

3.15%, 2/15/2024 | | | 650 | | | | 681 | |

| | |

2.88%, 8/14/2024 | | | 150 | | | | 156 | |

| | |

American Express Co. 4.20%, 11/6/2025 | | | 150 | | | | 174 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 9 |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2020 (continued)

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Consumer Finance — continued | |

| | |

American Express Credit Corp. 2.25%, 5/5/2021 | | | 73 | | | | 73 | |

| | |

American Honda Finance Corp. 2.30%, 9/9/2026 | | | 17 | | | | 19 | |

| | |

Avolon Holdings Funding Ltd. (Ireland)

5.50%, 1/15/2023 (a) | | | 195 | | | | 207 | |

| | |

2.88%, 2/15/2025 (a) | | | 194 | | | | 198 | |

| | |

5.50%, 1/15/2026 (a) | | | 395 | | | | 447 | |

| | |

4.25%, 4/15/2026 (a) | | | 245 | | | | 264 | |

| | |

4.38%, 5/1/2026 (a) | | | 150 | | | | 163 | |

| | |

Capital One Financial Corp.

3.75%, 4/24/2024 | | | 130 | | | | 142 | |

| | |

4.20%, 10/29/2025 | | | 40 | | | | 46 | |

| | |

3.75%, 7/28/2026 | | | 196 | | | | 222 | |

| | |

John Deere Capital Corp. 2.25%, 9/14/2026 | | | 125 | | | | 135 | |

| | |

Park Aerospace Holdings Ltd. (Ireland)

5.25%, 8/15/2022 (a) | | | 995 | | | | 1,044 | |

| | |

4.50%, 3/15/2023 (a) | | | 475 | | | | 498 | |

| | |

5.50%, 2/15/2024 (a) | | | 160 | | | | 174 | |

| | | | | | | | |

| | |

| | | | | | | 5,609 | |

| | | | | | | | |

|

Containers & Packaging — 0.1% | |

| | |

Packaging Corp. of America 4.05%, 12/15/2049 | | | 155 | | | | 192 | |

| | |

WRKCo, Inc.

3.00%, 9/15/2024 | | | 80 | | | | 86 | |

| | |

3.90%, 6/1/2028 | | | 35 | | | | 41 | |

| | | | | | | | |

| | |

| | | | | | | 319 | |

| | | | | | | | |

|

Diversified Consumer Services — 0.1% | |

| | |

Emory University Series 2020, 2.14%, 9/1/2030 | | | 240 | | | | 252 | |

| | |

Pepperdine University Series 2020, 3.30%, 12/1/2059 | | | 110 | | | | 117 | |

| | |

University of Southern California Series A, 3.23%, 10/1/2120 | | | 110 | | | | 110 | |

| | | | | | | | |

| | |

| | | | | | | 479 | |

| | | | | | | | |

|

Diversified Financial Services — 0.4% | |

| | |

AIG Global Funding 1.90%, 10/6/2021 (a) | | | 100 | | | | 101 | |

| | |

Blackstone Secured Lending Fund 3.65%, 7/14/2023 (a) | | | 200 | | | | 208 | |

| | |

CK Hutchison International 16 Ltd. (United Kingdom) 1.88%, 10/3/2021 (a) | | | 200 | | | | 202 | |

| | |

GE Capital Funding LLC 4.40%, 5/15/2030 (a) | | | 445 | | | | 524 | |

| | |

GE Capital International Funding Co. Unlimited Co. 4.42%, 11/15/2035 | | | 600 | | | | 715 | |

| | |

GTP Acquisition Partners I LLC 3.48%, 6/16/2025 (a) | | | 67 | | | | 72 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Diversified Financial Services — continued | |

| | |

Mitsubishi UFJ Lease & Finance Co. Ltd. (Japan) 2.65%, 9/19/2022 (a) | | | 200 | | | | 206 | |

| | |

National Rural Utilities Cooperative Finance Corp. 2.95%, 2/7/2024 | | | 44 | | | | 47 | |

| | |

ORIX Corp. (Japan)

2.90%, 7/18/2022 | | | 40 | | | | 42 | |

| | |

3.25%, 12/4/2024 | | | 100 | | | | 109 | |

| | |

3.70%, 7/18/2027 | | | 100 | | | | 114 | |

| | | | | | | | |

| | |

| | | | | | | 2,340 | |

| | | | | | | | |

|

Diversified Telecommunication Services — 0.9% | |

| | |

AT&T, Inc.

2.30%, 6/1/2027 | | | 520 | | | | 554 | |

| | |

1.65%, 2/1/2028 | | | 255 | | | | 260 | |

| | |

4.30%, 2/15/2030 | | | 178 | | | | 213 | |

| | |

2.25%, 2/1/2032 | | | 430 | | | | 436 | |

| | |

3.50%, 6/1/2041 | | | 154 | | | | 166 | |

| | |

3.10%, 2/1/2043 | | | 645 | | | | 652 | |

| | |

3.50%, 9/15/2053 (a) | | | 436 | | | | 434 | |

| | |

Deutsche Telekom International Finance BV (Germany) 4.88%, 3/6/2042 (a) | | | 150 | | | | 199 | |

| | |

Telefonica Emisiones SA (Spain) 5.46%, 2/16/2021 | | | 19 | | | | 19 | |

| | |

Verizon Communications, Inc.

2.63%, 8/15/2026 | | | 12 | | | | 13 | |

| | |

3.88%, 2/8/2029 | | | 75 | | | | 88 | |

| | |

3.15%, 3/22/2030 | | | 40 | | | | 45 | |

| | |

4.50%, 8/10/2033 | | | 125 | | | | 158 | |

| | |

4.40%, 11/1/2034 | | | 209 | | | | 261 | |

| | |

4.27%, 1/15/2036 | | | 85 | | | | 105 | |

| | |

2.65%, 11/20/2040 | | | 260 | | | | 263 | |

| | |

4.86%, 8/21/2046 | | | 134 | | | | 181 | |

| | |

4.67%, 3/15/2055 | | | 340 | | | | 456 | |

| | |

2.99%, 10/30/2056 (a) | | | 82 | | | | 82 | |

| | | | | | | | |

| | |

| | | | | | | 4,585 | |

| | | | | | | | |

|

Electric Utilities — 1.6% | |

| | |

AEP Transmission Co. LLC 3.15%, 9/15/2049 | | | 35 | | | | 39 | |

| | |

Alabama Power Co. 6.13%, 5/15/2038 | | | 62 | | | | 92 | |

| | |

Avangrid, Inc. 3.15%, 12/1/2024 | | | 72 | | | | 78 | |

| | |

Baltimore Gas and Electric Co.

3.50%, 8/15/2046 | | | 47 | | | | 55 | |

| | |

2.90%, 6/15/2050 | | | 110 | | | | 118 | |

| | |

CenterPoint Energy Houston Electric LLC

3.95%, 3/1/2048 | | | 10 | | | | 12 | |

| | |

Series AD, 2.90%, 7/1/2050 | | | 200 | | | | 217 | |

| | |

China Southern Power Grid International Finance BVI Co. Ltd. (China) 3.50%, 5/8/2027 (a) | | | 200 | | | | 220 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| 10 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Electric Utilities — continued | |

| | |

Cleveland Electric Illuminating Co. (The)

3.50%, 4/1/2028 (a) | | | 95 | | | | 101 | |

| | |

4.55%, 11/15/2030 (a) | | | 65 | | | | 75 | |

| | |

Commonwealth Edison Co. 3.65%, 6/15/2046 | | | 30 | | | | 36 | |

| | |

Duke Energy Corp.

2.65%, 9/1/2026 | | | 100 | | | | 109 | |

| | |

3.40%, 6/15/2029 | | | 61 | | | | 69 | |

| | |

Duke Energy Indiana LLC 3.75%, 5/15/2046 | | | 60 | | | | 72 | |

| | |

Duke Energy Ohio, Inc. 3.70%, 6/15/2046 | | | 46 | | | | 54 | |

| | |

Duke Energy Progress LLC 3.70%, 10/15/2046 | | | 54 | | | | 65 | |

| | |

Duquesne Light Holdings, Inc.

3.62%, 8/1/2027 (a) | | | 160 | | | | 177 | |

| | |

2.53%, 10/1/2030 (a) | | | 210 | | | | 217 | |

| | |

Edison International

3.55%, 11/15/2024 | | | 284 | | | | 306 | |

| | |

4.13%, 3/15/2028 | | | 100 | | | | 111 | |

| | |

Emera US Finance LP (Canada) 4.75%, 6/15/2046 | | | 130 | | | | 166 | |

| | |

Enel Finance International NV (Italy) 3.63%, 5/25/2027 (a) | | | 220 | | | | 250 | |

| | |

Entergy Arkansas LLC 3.50%, 4/1/2026 | | | 22 | | | | 25 | |

| | |

Entergy Corp. 2.95%, 9/1/2026 | | | 21 | | | | 23 | |

| | |

Entergy Louisiana LLC

2.40%, 10/1/2026 | | | 59 | | | | 64 | |

| | |

3.05%, 6/1/2031 | | | 38 | | | | 43 | |

| | |

4.00%, 3/15/2033 | | | 40 | | | | 50 | |

| | |

2.90%, 3/15/2051 | | | 130 | | | | 138 | |

| | |

Entergy Mississippi LLC 3.85%, 6/1/2049 | | | 135 | | | | 164 | |

| | |

Evergy Metro, Inc.

3.15%, 3/15/2023 | | | 24 | | | | 25 | |

| | |

5.30%, 10/1/2041 | | | 50 | | | | 68 | |

| | |

4.20%, 3/15/2048 | | | 50 | | | | 65 | |

| | |

Evergy, Inc. 2.90%, 9/15/2029 | | | 170 | | | | 186 | |

| | |

Florida Power & Light Co. 5.40%, 9/1/2035 | | | 50 | | | | 71 | |

| | |

Fortis, Inc. (Canada) 3.06%, 10/4/2026 | | | 124 | | | | 136 | |

| | |

Hydro-Quebec (Canada) Series IO, 8.05%, 7/7/2024 | | | 100 | | | | 125 | |

| | |

Interstate Power and Light Co. 2.30%, 6/1/2030 | | | 315 | | | | 333 | |

| | |

ITC Holdings Corp. | | | | | | | | |

| | |

2.70%, 11/15/2022 | | | 100 | | | | 104 | |

| | |

2.95%, 5/14/2030 (a) | | | 100 | | | | 109 | |

| | |

Jersey Central Power & Light Co.

4.30%, 1/15/2026 (a) | | | 40 | | | | 45 | |

| | |

6.15%, 6/1/2037 | | | 30 | | | | 38 | |

| | |

Massachusetts Electric Co. 4.00%, 8/15/2046 (a) | | | 56 | | | | 68 | |

| | |

MidAmerican Energy Co. 3.50%, 10/15/2024 | | | 59 | | | | 65 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Electric Utilities — continued | |

| | |

Mid-Atlantic Interstate Transmission LLC 4.10%, 5/15/2028 (a) | | | 40 | | | | 45 | |

| | |

Nevada Power Co. Series CC, 3.70%, 5/1/2029 | | | 100 | | | | 117 | |

| | |

New England Power Co. (United Kingdom) 3.80%, 12/5/2047 (a) | | | 45 | | | | 53 | |

| | |

NextEra Energy Capital Holdings, Inc. 3.55%, 5/1/2027 | | | 27 | | | | 31 | |

| | |

Niagara Mohawk Power Corp.

3.51%, 10/1/2024 (a) | | | 19 | | | | 21 | |

| | |

1.96%, 6/27/2030 (a) | | | 250 | | | | 257 | |

| | |

NRG Energy, Inc.

2.00%, 12/2/2025 (a) | | | 185 | | | | 192 | |

| | |

2.45%, 12/2/2027 (a) | | | 210 | | | | 221 | |

| | |

4.45%, 6/15/2029 (a) | | | 110 | | | | 127 | |

| | |

Oncor Electric Delivery Co. LLC

5.75%, 3/15/2029 | | | 25 | | | | 33 | |

| | |

3.10%, 9/15/2049 | | | 215 | | | | 247 | |

| | |

Pacific Gas and Electric Co.

(ICE LIBOR USD 3 Month + 1.38%), 1.60%, 11/15/2021 (c) | | | 330 | | | | 330 | |

| | |

1.75%, 6/16/2022 | | | 320 | | | | 321 | |

| | |

3.45%, 7/1/2025 | | | 145 | | | | 157 | |

| | |

2.95%, 3/1/2026 | | | 90 | | | | 95 | |

| | |

3.75%, 8/15/2042 (f) | | | 33 | | | | 33 | |

| | |

4.30%, 3/15/2045 | | | 55 | | | | 59 | |

| | |

4.00%, 12/1/2046 | | | 230 | | | | 238 | |

| | |

PECO Energy Co. 2.80%, 6/15/2050 | | | 100 | | | | 106 | |

| | |

Pennsylvania Electric Co. 3.25%, 3/15/2028 (a) | | | 19 | | | | 20 | |

| | |

Potomac Electric Power Co. 6.50%, 11/15/2037 | | | 75 | | | | 114 | |

| | |

PPL Capital Funding, Inc.

3.40%, 6/1/2023 | | | 30 | | | | 32 | |

| | |

4.00%, 9/15/2047 | | | 20 | | | | 23 | |

| | |

Public Service Co. of Oklahoma Series G, 6.63%, 11/15/2037 | | | 175 | | | | 257 | |

| | |

Public Service Electric and Gas Co.

3.00%, 5/15/2025 | | | 83 | | | | 91 | |

| | |

5.38%, 11/1/2039 | | | 28 | | | | 39 | |

| | |

Southern California Edison Co. | | | | | | | | |

| | |

Series C, 3.50%, 10/1/2023 | | | 53 | | | | 57 | |

| | |

Series B, 3.65%, 3/1/2028 | | | 80 | | | | 90 | |

| | |

Series 05-B, 5.55%, 1/15/2036 | | | 80 | | | | 102 | |

| | |

4.05%, 3/15/2042 | | | 100 | | | | 114 | |

| | |

Tampa Electric Co. 4.45%, 6/15/2049 | | | 100 | | | | 131 | |

| | |

Toledo Edison Co. (The) 6.15%, 5/15/2037 | | | 50 | | | | 68 | |

| | |

Union Electric Co. 2.95%, 6/15/2027 | | | 36 | | | | 40 | |

| | |

Virginia Electric and Power Co. 6.35%, 11/30/2037 | | | 70 | | | | 106 | |

| | | | | | | | |

| | |

| | | | | | | 8,551 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 11 |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2020 (continued)

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Electronic Equipment, Instruments & Components — 0.1% | |

| | |

Arrow Electronics, Inc.

4.50%, 3/1/2023 | | | 8 | | | | 8 | |

| | |

3.25%, 9/8/2024 | | | 44 | | | | 48 | |

| | |

3.88%, 1/12/2028 | | | 22 | | | | 25 | |

| | |

Corning, Inc.

5.35%, 11/15/2048 | | | 110 | | | | 155 | |

| | |

3.90%, 11/15/2049 | | | 174 | | | | 213 | |

| | | | | | | | |

| | |

| | | | | | | 449 | |

| | | | | | | | |

|

Energy Equipment & Services — 0.2% | |

| | |

Baker Hughes a GE Co. LLC

3.14%, 11/7/2029 | | | 180 | | | | 198 | |

| | |

4.49%, 5/1/2030 | | | 115 | | | | 138 | |

| | |

Baker Hughes Holdings LLC 5.13%, 9/15/2040 | | | 40 | | | | 53 | |

| | |

Halliburton Co.

3.80%, 11/15/2025 | | | 4 | | | | 4 | |

| | |

4.85%, 11/15/2035 | | | 30 | | | | 35 | |

| | |

6.70%, 9/15/2038 | | | 60 | | | | 80 | |

| | |

National Oilwell Varco, Inc. 3.60%, 12/1/2029 | | | 200 | | | | 209 | |

| | |

Schlumberger Finance Canada Ltd. 1.40%, 9/17/2025 | | | 300 | | | | 308 | |

| | |

Schlumberger Holdings Corp.

3.75%, 5/1/2024 (a) | | | 55 | | | | 60 | |

| | |

3.90%, 5/17/2028 (a) | | | 62 | | | | 70 | |

| | | | | | | | |

| | |

| | | | | | | 1,155 | |

| | | | | | | | |

|

Entertainment — 0.1% | |

| | |

NBCUniversal Media LLC 5.95%, 4/1/2041 | | | 75 | | | | 114 | |

| | |

Walt Disney Co. (The) 7.30%, 4/30/2028 | | | 150 | | | | 207 | |

| | | | | | | | |

| | |

| | | | | | | 321 | |

| | | | | | | | |

|

Equity Real Estate Investment Trusts (REITs) — 1.7% | |

| | |

Alexandria Real Estate Equities, Inc.

3.80%, 4/15/2026 | | | 23 | | | | 26 | |

| | |

1.88%, 2/1/2033 | | | 140 | | | | 140 | |

| | |

4.00%, 2/1/2050 | | | 125 | | | | 155 | |

| | |

American Campus Communities Operating Partnership LP

3.63%, 11/15/2027 | | | 100 | | | | 110 | |

| | |

2.85%, 2/1/2030 | | | 190 | | | | 199 | |

| | |

American Tower Corp.

5.00%, 2/15/2024 | | | 71 | | | | 80 | |

| | |

3.38%, 10/15/2026 | | | 44 | | | | 49 | |

| | |

1.50%, 1/31/2028 | | | 325 | | | | 327 | |

| | |

2.90%, 1/15/2030 | | | 30 | | | | 33 | |

| | |

2.10%, 6/15/2030 | | | 150 | | | | 154 | |

| | |

1.88%, 10/15/2030 | | | 275 | | | | 277 | |

| | |

3.70%, 10/15/2049 | | | 230 | | | | 261 | |

| | |

2.95%, 1/15/2051 | | | 215 | | | | 215 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Equity Real Estate Investment Trusts (REITs) — continued | |

| | |

Boston Properties LP

3.13%, 9/1/2023 | | | 30 | | | | 32 | |

| | |

3.20%, 1/15/2025 | | | 61 | | | | 67 | |

| | |

3.65%, 2/1/2026 | | | 67 | | | | 76 | |

| | |

Brixmor Operating Partnership LP

3.65%, 6/15/2024 | | | 50 | | | | 54 | |

| | |

3.85%, 2/1/2025 | | | 50 | | | | 55 | |

| | |

Corporate Office Properties LP 2.25%, 3/15/2026 | | | 470 | | | | 490 | |

| | |

Crown Castle International Corp.

5.25%, 1/15/2023 | | | 60 | | | | 66 | |

| | |

4.00%, 3/1/2027 | | | 24 | | | | 27 | |

| | |

2.25%, 1/15/2031 | | | 295 | | | | 306 | |

| | |

Digital Realty Trust LP 3.70%, 8/15/2027 | | | 31 | | | | 36 | |

| | |

Duke Realty LP

3.25%, 6/30/2026 | | | 18 | | | | 20 | |

| | |

2.88%, 11/15/2029 | | | 95 | | | | 105 | |

| | |

Equinix, Inc. 1.55%, 3/15/2028 | | | 285 | | | | 290 | |

| | |

Essex Portfolio LP

1.65%, 1/15/2031 | | | 200 | | | | 199 | |

| | |

2.65%, 3/15/2032 | | | 145 | | | | 155 | |

| | |

GAIF Bond Issuer Pty. Ltd. (Australia) 3.40%, 9/30/2026 (a) | | | 79 | | | | 85 | |

| | |

Goodman US Finance Three LLC (Australia) 3.70%, 3/15/2028 (a) | | | 43 | | | | 47 | |

| | |

Healthcare Trust of America Holdings LP

3.10%, 2/15/2030 | | | 310 | | | | 338 | |

| | |

2.00%, 3/15/2031 | | | 160 | | | | 160 | |

| | |

Healthpeak Properties, Inc.

3.88%, 8/15/2024 | | | 115 | | | | 127 | |

| | |

3.50%, 7/15/2029 | | | 132 | | | | 150 | |

| | |

3.00%, 1/15/2030 | | | 90 | | | | 98 | |

| | |

Kimco Realty Corp. 2.70%, 10/1/2030 | | | 320 | | | | 344 | |

| | |

Life Storage LP

4.00%, 6/15/2029 | | | 150 | | | | 175 | |

| | |

2.20%, 10/15/2030 | | | 300 | | | | 306 | |

| | |

Mid-America Apartments LP 1.70%, 2/15/2031 | | | 150 | | | | 149 | |

| | |

National Retail Properties, Inc.

3.60%, 12/15/2026 | | | 58 | | | | 64 | |

| | |

4.30%, 10/15/2028 | | | 150 | | | | 174 | |

| | |

Office Properties Income Trust 4.00%, 7/15/2022 | | | 78 | | | | 80 | |

| | |

Prologis LP

3.25%, 10/1/2026 | | | 19 | | | | 22 | |

| | |

1.25%, 10/15/2030 | | | 165 | | | | 163 | |

| | |

2.13%, 10/15/2050 | | | 150 | | | | 139 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| 12 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Equity Real Estate Investment Trusts (REITs) — continued | |

| | |

Realty Income Corp.

3.88%, 7/15/2024 | | | 20 | | | | 22 | |

| | |

3.88%, 4/15/2025 | | | 60 | | | | 67 | |

| | |

3.25%, 1/15/2031 | | | 170 | | | | 193 | |

| | |

4.65%, 3/15/2047 | | | 38 | | | | 52 | |

| | |

Regency Centers LP 2.95%, 9/15/2029 | | | 215 | | | | 230 | |

| | |

Scentre Group Trust 1 (Australia) 3.50%, 2/12/2025 (a) | | | 170 | | | | 182 | |

| | |

SITE Centers Corp. 3.63%, 2/1/2025 | | | 61 | | | | 63 | |

| | |

UDR, Inc.

2.95%, 9/1/2026 | | | 28 | | | | 31 | |

| | |

3.20%, 1/15/2030 | | | 150 | | | | 167 | |

| | |

3.00%, 8/15/2031 | | | 25 | | | | 27 | |

| | |

2.10%, 8/1/2032 | | | 160 | | | | 163 | |

| | |

1.90%, 3/15/2033 | | | 240 | | | | 240 | |

| | |

Ventas Realty LP

4.13%, 1/15/2026 | | | 34 | | | | 39 | |

| | |

3.85%, 4/1/2027 | | | 49 | | | | 55 | |

| | |

Vornado Realty LP 3.50%, 1/15/2025 | | | 60 | | | | 63 | |

| | |

Welltower, Inc.

2.70%, 2/15/2027 | | | 63 | | | | 69 | |

| | |

3.10%, 1/15/2030 | | | 85 | | | | 93 | |

| | |

6.50%, 3/15/2041 | | | 125 | | | | 175 | |

| | |

WP Carey, Inc. 4.25%, 10/1/2026 | | | 245 | | | | 282 | |

| | | | | | | | |

| | |

| | | | | | | 8,838 | |

| | | | | | | | |

|

Food & Staples Retailing — 0.3% | |

| | |

Alimentation Couche-Tard, Inc. (Canada)

2.95%, 1/25/2030 (a) | | | 90 | | | | 98 | |

| | |

3.80%, 1/25/2050 (a) | | | 230 | | | | 272 | |

| | |

Costco Wholesale Corp.

2.75%, 5/18/2024 | | | 21 | | | | 23 | |

| | |

1.38%, 6/20/2027 | | | 450 | | | | 463 | |

| | |

CVS Pass-Through Trust

7.51%, 1/10/2032 (a) | | | 68 | | | | 84 | |

| | |

5.93%, 1/10/2034 (a) | | | 74 | | | | 90 | |

| | |

Series 2013, 4.70%, 1/10/2036 (a) | | | 158 | | | | 178 | |

| | |

Kroger Co. (The)

2.20%, 5/1/2030 | | | 500 | | | | 525 | |

| | |

5.40%, 7/15/2040 | | | 18 | | | | 25 | |

| | | | | | | | |

| | |

| | | | | | | 1,758 | |

| | | | | | | | |

|

Food Products — 0.5% | |

| | |

Campbell Soup Co. 3.13%, 4/24/2050 | | | 47 | | | | 50 | |

| | |

Cargill, Inc.

3.25%, 3/1/2023 (a) | | | 25 | | | | 26 | |

| | |

2.13%, 4/23/2030 (a) | | | 291 | | | | 306 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Food Products — continued | |

| | |

Conagra Brands, Inc.

5.30%, 11/1/2038 | | | 35 | | | | 47 | |

| | |

5.40%, 11/1/2048 | | | 105 | | | | 149 | |

| | |

General Mills, Inc.

4.00%, 4/17/2025 | | | 60 | | | | 68 | |

| | |

4.15%, 2/15/2043 | | | 100 | | | | 125 | |

| | |

Kellogg Co. 2.10%, 6/1/2030 | | | 140 | | | | 147 | |

| | |

Mars, Inc. 1.63%, 7/16/2032 (a) | | | 390 | | | | 387 | |

| | |

McCormick & Co., Inc. 2.50%, 4/15/2030 | | | 342 | | | | 366 | |

| | |

Mead Johnson Nutrition Co. (United Kingdom) | | | | | | | | |

| | |

4.13%, 11/15/2025 | | | 27 | | | | 31 | |

| | |

Mondelez International, Inc. 1.50%, 5/4/2025 | | | 80 | | | | 83 | |

| | |

Smithfield Foods, Inc.

5.20%, 4/1/2029 (a) | | | 160 | | | | 190 | |

| | |

3.00%, 10/15/2030 (a) | | | 380 | | | | 402 | |

| | |

Tyson Foods, Inc.

4.88%, 8/15/2034 | | | 20 | | | | 26 | |

| | |

5.15%, 8/15/2044 | | | 90 | | | | 124 | |

| | |

4.55%, 6/2/2047 | | | 100 | | | | 133 | |

| | | | | | | | |

| | |

| | | | | | | 2,660 | |

| | | | | | | | |

|

Gas Utilities — 0.3% | |

| | |

Atmos Energy Corp.

4.13%, 10/15/2044 | | | 50 | | | | 63 | |

| | |

4.13%, 3/15/2049 | | | 155 | | | | 200 | |

| | |

Boston Gas Co. 4.49%, 2/15/2042 (a) | | | 22 | | | | 28 | |

| | |

Brooklyn Union Gas Co. (The) 4.27%, 3/15/2048 (a) | | | 80 | | | | 102 | |

| | |

Eastern Energy Gas Holdings LLC Series C, 3.90%, 11/15/2049 | | | 137 | | | | 161 | |

| | |

ONE Gas, Inc. 2.00%, 5/15/2030 | | | 200 | | | | 209 | |

| | |

Piedmont Natural Gas Co., Inc. 3.50%, 6/1/2029 | | | 200 | | | | 229 | |

| | |

Southern California Gas Co. Series XX, 2.55%, 2/1/2030 | | | 195 | | | | 211 | |

| | |

Southern Natural Gas Co. LLC

8.00%, 3/1/2032 | | | 53 | | | | 76 | |

| | |

4.80%, 3/15/2047 (a) | | | 26 | | | | 30 | |

| | |

Southwest Gas Corp. 3.80%, 9/29/2046 | | | 44 | | | | 51 | |

| | | | | | | | |

| | |

| | | | | | | 1,360 | |

| | | | | | | | |

|

Health Care Equipment & Supplies — 0.2% | |

| | |

Abbott Laboratories

1.15%, 1/30/2028 | | | 170 | | | | 172 | |

| | |

4.75%, 11/30/2036 | | | 130 | | | | 179 | |

| | |

Becton Dickinson and Co. 4.67%, 6/6/2047 | | | 160 | | | | 210 | |

| | |

Boston Scientific Corp.

4.00%, 3/1/2029 | | | 101 | | | | 119 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| DECEMBER 31, 2020 | | JPMORGAN INSURANCE TRUST | | | | | | | | 13 |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2020 (continued)

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Health Care Equipment & Supplies — continued | |

| | |

4.55%, 3/1/2039 | | | 100 | | | | 128 | |

| | |

DH Europe Finance II SARL 3.25%, 11/15/2039 | | | 184 | | | | 209 | |

| | |

Zimmer Biomet Holdings, Inc. 3.70%, 3/19/2023 | | | 27 | | | | 29 | |

| | | | | | | | |

| | |

| | | | | | | 1,046 | |

| | | | | | | | |

|

Health Care Providers & Services — 1.0% | |

| | |

Advocate Health & Hospitals Corp. Series 2020, 2.21%, 6/15/2030 | | | 130 | | | | 135 | |

| | |

Anthem, Inc.

3.30%, 1/15/2023 | | | 18 | | | | 19 | |

| | |

3.35%, 12/1/2024 | | | 70 | | | | 77 | |

| | |

4.10%, 3/1/2028 | | | 55 | | | | 65 | |

| | |

4.65%, 1/15/2043 | | | 18 | | | | 24 | |

| | |

4.65%, 8/15/2044 | | | 65 | | | | 85 | |

| | |

Ascension Health Series B, 2.53%, 11/15/2029 | | | 190 | | | | 208 | |

| | |

Children’s Hospital Series 2020, 2.93%, 7/15/2050 | | | 180 | | | | 180 | |

| | |

Cigna Corp. 4.50%, 2/25/2026 | | | 127 | | | | 149 | |

| | |

CommonSpirit Health

1.55%, 10/1/2025 | | | 145 | | | | 149 | |

| | |

2.78%, 10/1/2030 | | | 145 | | | | 153 | |

| | |

3.91%, 10/1/2050 | | | 140 | | | | 156 | |

| | |

CVS Health Corp.

4.30%, 3/25/2028 | | | 54 | | | | 64 | |

| | |

3.25%, 8/15/2029 | | | 155 | | | | 175 | |

| | |

1.88%, 2/28/2031 | | | 312 | | | | 315 | |

| | |

2.70%, 8/21/2040 | | | 130 | | | | 132 | |

| | |

5.05%, 3/25/2048 | | | 323 | | | | 437 | |

| | |

Hackensack Meridian Health, Inc. Series 2020, 2.88%, 9/1/2050 | | | 230 | | | | 237 | |

| | |

HCA, Inc.

5.25%, 6/15/2026 | | | 340 | | | | 402 | |

| | |

5.13%, 6/15/2039 | | | 125 | | | | 160 | |

| | |

5.50%, 6/15/2047 | | | 245 | | | | 327 | |

| | |

Memorial Health Services 3.45%, 11/1/2049 | | | 245 | | | | 262 | |

| | |

MidMichigan Health Series 2020, 3.41%, 6/1/2050 | | | 80 | | | | 89 | |

| | |

Mount Sinai Hospitals Group, Inc. Series 2017, 3.98%, 7/1/2048 | | | 83 | | | | 94 | |

| | |

MultiCare Health System 2.80%, 8/15/2050 | | | 120 | | | | 124 | |

| | |

Providence St Joseph Health Obligated Group Series H, 2.75%, 10/1/2026 | | | 36 | | | | 39 | |

| | |

Quest Diagnostics, Inc.

3.45%, 6/1/2026 | | | 17 | | | | 19 | |

| | |

2.80%, 6/30/2031 | | | 95 | | | | 104 | |

| | |

Rush Obligated Group Series 2020, 3.92%, 11/15/2029 | | | 233 | | | | 275 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Health Care Providers & Services — continued | |

| | |

Texas Health Resources 2.33%, 11/15/2050 | | | 140 | | | | 132 | |

| | |

UnitedHealth Group, Inc.

4.63%, 7/15/2035 | | | 34 | | | | 46 | |

| | |

3.50%, 8/15/2039 | | | 160 | | | | 190 | |

| | |

Universal Health Services, Inc. 2.65%, 10/15/2030 (a) | | | 170 | | | | 177 | |

| | |

Yale-New Haven Health Services Corp.

Series 2020, 2.50%, 7/1/2050 | | | 200 | | | | 195 | |

| | | | | | | | |

| | |

| | | | | | | 5,395 | |

| | | | | | | | |

|

Hotels, Restaurants & Leisure — 0.0% (b) | |

| | |

McDonald’s Corp. 4.70%, 12/9/2035 | | | 60 | | | | 77 | |

| | |

Starbucks Corp. 2.55%, 11/15/2030 | | | 170 | | | | 184 | |

| | | | | | | | |

| | |

| | | | | | | 261 | |

| | | | | | | | |

|

Household Products — 0.0% (b) | |

| | |

Procter & Gamble — ESOP Series A, 9.36%, 1/1/2021 | | | 6 | | | | 6 | |

| | | | | | | | |

|

Independent Power and Renewable Electricity Producers — 0.2% | |

| | |

Alexander Funding Trust 1.84%, 11/15/2023 (a) | | | 200 | | | | 202 | |

| | |

Exelon Generation Co. LLC | | | | | | | | |

| | |

3.40%, 3/15/2022 | | | 50 | | | | 52 | |

| | |

4.25%, 6/15/2022 | | | 38 | | | | 40 | |

| | |

3.25%, 6/1/2025 | | | 250 | | | | 273 | |

| | |

6.25%, 10/1/2039 | | | 100 | | | | 120 | |

| | |

5.75%, 10/1/2041 | | | 29 | | | | 33 | |

| | |

PSEG Power LLC 4.15%, 9/15/2021 | | | 37 | | | | 38 | |

| | |

Southern Power Co. 5.15%, 9/15/2041 | | | 50 | | | | 61 | |

| | |

Tri-State Generation and Transmission Association, Inc. 4.25%, 6/1/2046 | | | 25 | | | | 29 | |

| | | | | | | | |

| | |

| | | | | | | 848 | |

| | | | | | | | |

|

Industrial Conglomerates — 0.3% | |

| | |

General Electric Co. | | | | | | | | |

| | |

3.45%, 5/1/2027 | | | 105 | | | | 119 | |

| | |

3.63%, 5/1/2030 | | | 160 | | | | 183 | |

| | |

5.88%, 1/14/2038 | | | 100 | | | | 135 | |

| | |

Honeywell International, Inc. | | | | | | | | |

| | |

1.35%, 6/1/2025 | | | 400 | | | | 414 | |

| | |

2.50%, 11/1/2026 | | | 150 | | | | 165 | |

| | |

Roper Technologies, Inc. | | | | | | | | |

| | |

1.40%, 9/15/2027 | | | 350 | | | | 354 | |

| | |

2.00%, 6/30/2030 | | | 160 | | | | 164 | |

| | | | | | | | |

| | |

| | | | | | | 1,534 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | | | |

| | | | | |

| 14 | | | | | | | | JPMORGAN INSURANCE TRUST | | DECEMBER 31, 2020 |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

Corporate Bonds — continued | |

|

Insurance — 0.9% | |

| | |

AIA Group Ltd. (Hong Kong) | | | | | | | | |

| | |

3.20%, 3/11/2025 (a) | | | 200 | | | | 215 | |

| | |

3.90%, 4/6/2028 (a) | | | 210 | | | | 239 | |

| | |

3.60%, 4/9/2029 (a) | | | 200 | | | | 225 | |

| | |

American Financial Group, Inc. 3.50%, 8/15/2026 | | | 100 | | | | 109 | |

| | |

American International Group, Inc. 3.88%, 1/15/2035 | | | 180 | | | | 216 | |

| | |

Assurant, Inc. 4.20%, 9/27/2023 | | | 85 | | | | 93 | |

| | |

Athene Global Funding | | | | | | | | |

| | |

2.75%, 6/25/2024 (a) | | | 155 | | | | 164 | |

| | |

2.95%, 11/12/2026 (a) | | | 410 | | | | 440 | |

| | |

Berkshire Hathaway Finance Corp. 4.30%, 5/15/2043 | | | 62 | | | | 82 | |

| | |

Brown & Brown, Inc. 2.38%, 3/15/2031 | | | 460 | | | | 481 | |

| | |

Chubb INA Holdings, Inc. | | | | | | | | |

| | |

2.88%, 11/3/2022 | | | 42 | | | | 44 | |

| | |

2.70%, 3/13/2023 | | | 120 | | | | 126 | |

| | |

CNA Financial Corp. 3.95%, 5/15/2024 | | | 44 | | | | 49 | |

| | |

Dai-ichi Life Insurance Co. Ltd. (The) (Japan) (ICE LIBOR USD 3 Month + 3.66%), 4.00%, 7/24/2026 (a) (c) (d) (e) | | | 200 | | | | 221 | |

| | |

Guardian Life Insurance Co. of America (The) | | | | | | | | |

| | |

4.85%, 1/24/2077 (a) | | | 21 | | | | 29 | |

| | |

Hanover Insurance Group, Inc. (The) 2.50%, 9/1/2030 | | | 120 | | | | 125 | |

| | |

Hartford Financial Services Group, Inc. (The) 4.30%, 4/15/2043 | | | 70 | | | | 88 | |

| | |

Intact US Holdings, Inc. 4.60%, 11/9/2022 | | | 100 | | | | 106 | |

| | |

Jackson National Life Global Funding | | | | | | | | |

| | |

3.88%, 6/11/2025 (a) | | | 87 | | | | 98 | |

| | |

3.05%, 4/29/2026 (a) | | | 104 | | | | 116 | |

| | |

Liberty Mutual Group, Inc. | | | | | | | | |

| | |

4.57%, 2/1/2029 (a) | | | 27 | | | | 33 | |

| | |

3.95%, 10/15/2050 (a) | | | 207 | | | | 248 | |

| | |

Lincoln National Corp. | | | | | | | | |

| | |

4.20%, 3/15/2022 | | | 20 | | | | 21 | |

| | |

4.00%, 9/1/2023 | | | 50 | | | | 54 | |

| | |

Manulife Financial Corp. (Canada) (USD ICE Swap Rate 5 Year + 1.65%), 4.06%, 2/24/2032 (c) | | | 100 | | | | 109 | |

| | |

Markel Corp. 3.63%, 3/30/2023 | | | 40 | | | | 43 | |

| | |

MetLife, Inc. 4.13%, 8/13/2042 | | | 28 | | | | 35 | |

| | |

New York Life Global Funding | | | | | | | | |

| | |

2.00%, 4/13/2021 (a) | | | 29 | | | | 29 | |

| | |

2.35%, 7/14/2026 (a) | | | 65 | | | | 70 | |

| | |

New York Life Insurance Co. 4.45%, 5/15/2069 (a) | | | 105 | | | | 141 | |

| | | | | | | | |

| INVESTMENTS | | PRINCIPAL

AMOUNT ($000) | | | VALUE ($000) | |

| | | | | | | | |

|

Insurance — continued | |

| | |

Pacific Life Insurance Co. (ICE LIBOR USD 3 Month + 2.80%), 4.30%, 10/24/2067 (a) (c) | | | 134 | | | | 152 | |

| | |

Principal Financial Group, Inc. | | | | | | | | |

| | |

3.13%, 5/15/2023 | | | 30 | | | | 32 | |

| | |

3.70%, 5/15/2029 | | | 30 | | | | 35 | |

| | |

Progressive Corp. (The) Series B, (ICE LIBOR USD 3 Month + 2.54%), 5.38%, 3/15/2023 (c) (d) (e) | | | 50 | | | | 52 | |

| | |

Prudential Financial, Inc. 3.91%, 12/7/2047 | | | 61 | | | | 73 | |

| | |

Prudential Insurance Co. of America (The) 8.30%, 7/1/2025 (a) | | | 150 | | | | 194 | |

| | |

Reliance Standard Life Global Funding II 3.85%, 9/19/2023 (a) | | | 105 | | | | 113 | |

| | |

Teachers Insurance & Annuity Association of America 4.27%, 5/15/2047 (a) | | | 50 | | | | 62 | |