OMB APPROVAL

OMB Number: 3235-0570

Expires: August 31, 2020

Estimated average burden

hours per response……20.6

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07986

The Alger Institutional Funds

(Exact name of registrant as specified in charter)

360 Park Avenue South New York, New York 10010

(Address of principal executive offices) (Zip code)

Mr. Hal Liebes

Fred Alger Management, Inc.

360 Park Avenue South

New York, New York 10010

(Name and address of agent for service)

Registrant's telephone number, including area code: 212-806-8800

Date of fiscal year end: October 31

Date of reporting period: April 30, 2018

ITEM 1. REPORT(S) TO STOCKHOLDERS.

Table of Contents

The Alger Institutional Funds

|

| Shareholders’ Letter | 1 |

| Fund Highlights | 11 |

| Portfolio Summary | 19 |

| Schedules of Investments | 20 |

| Statements of Assets and Liabilities | 37 |

| Statements of Operations | 41 |

| Statements of Changes in Net Assets | 43 |

| Financial Highlights | 47 |

| Notes to Financial Statements | 62 |

| Additional Information | 87 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online.

When documents such as prospectuses and annual and semi-annual reports are

available, we’ll send you an e-mail notification with a convenient link that will take you

directly to the fund information on our website. To sign up for this free service, simply

enroll at www.icsdelivery.com/alger.

Shareholders’ Letter April 30, 2018

Dear Shareholders,

Corporations Generate Stellar Earnings but Emotions Spark Volatility

After a nearly one-and-a-half-year period during which the S&P 500 Index didn’t experience

a single monthly decline, concerns about potential inflation caused the index to tumble

11.84% in late January and early February. We believe investors may have subsequently

determined that the decline was excessive when considering the strength of corporate

fundamentals and the potential for additional economic growth. The market selloff was

therefore short-lived. The combination of strong performance leading up to the January

peak and the 4.56% market gain after the market pullback resulted in the S&P 500 Index

advancing 3.82% during the six-month reporting period ended April 30, 2018.

Not surprisingly, the market decline, which lasted less than two weeks, prompted pundits

to renew their predictions that the ongoing bull market was ending. As evidenced by the

positive performance of equities during the reporting period, the renewed predictions were

a continuation of pundits being consistently wrong since the end of the Great Recession

with negative views, driven by what we believe has been market noise. In this letter, we urge

investors to focus on the strength of corporate fundamentals and economic growth. These

factors, we believe, can potentially support equity gains in the foreseeable future. We explain

why equities still carry potential for generating attractive returns despite concerns that we

believe are misguided about the length of the current bull market, potential for inflation,

and fears that President Donald Trump’s proposed tariffs could hinder global trade.

Market Overview

News that wages were 2.9% higher in January of 2018 than in January of 2017 strengthened

fears of inflation and ushered in market volatility. Some investors may also have believed

that market gains, equity valuations, and optimism were excessive relative to corporate

fundamentals and the potential benefits of lower taxes resulting from tax reform. Despite

those concerns, anticipation of strong first-quarter earnings helped reverse the decline. The

recovery in equity prices was further supported by corporations eventually reporting strong

earnings growth. Non-U.S. equities followed a similar pattern with the MSCI Emerging

Markets Index gaining 4.94% and the MSCI ACWI ex USA Index advancing 3.73% for the

six-month reporting period.

As growth equity investors, we are encouraged by the continuation of the multiyear

outperformance of growth stocks. The Russell 1000 Growth Index led with a 5.68% return

compared to 1.94% of its value-oriented counterpart during the six-month reporting period.

Growth outperformance also occurred with mid- and small-cap stocks. At the same time,

rising interest rates caused investors to continue dumping bond-like equities in favor of

growth equities, as illustrated by the Consumer Discretionary and Information Technology

sectors’ outperformance of the overall S&P 500 Index. Sectors such as Real Estate, Utilities,

and Consumer Staples that generally consist of companies that offer higher dividend yields

but less potential for earnings growth lagged with negative returns. At Alger, we have

previously written about the potential for investors to rapidly flee bond-like equities in favor

of growth stocks, so this development was no surprise to our firm.

- 1 -

The Importance of Earnings Growth and Innovation

At Alger, our in-depth research has led us to believe that corporate fundamentals are healthy

with businesses having strong potential for growing their earnings. Our research also points

to the economy being stronger than commonly believed and therefore highly supportive

of earnings growth. We have also maintained that earnings growth resulting from lower

corporate taxes could be stronger than commonly believed. While some observers have

focused on how tax reform has directly boosted earnings by cutting corporate expenses in

the form of taxes, we have also assessed the potential for businesses to use their tax savings

to increase their investments in growth initiatives. Tax reform is also supporting business

spending by allowing full expensing of capital expenditures. Banks’ increased willingness

to provide financing to corporations is an additional tailwind for business spending. This

increased spending, in turn, is providing opportunities for certain corporations to improve

their earnings by offering products and services that can help businesses grow and increase

productivity.

Our belief that corporate earnings would be stronger than expected was validated by first-

quarter results. As of the end of the six-month reporting period, 81% of S&P 500 companies

had reported first-quarter numbers. Of those, 78% reported positive earnings-per-share

(EPS) surprises and 77% reported positive sales surprises. At that pace, the percentage of

positive EPS surprises would be the highest since FactSet Research started tracking earnings

in the third quarter of 2008. Among companies that had reported, earnings grew 24.2%

compared to earlier estimates of 17.1%.

We believe that earnings growth drives long-term equity performance. On one hand,

companies with strong earnings can reward investors with stock buybacks and dividends.

Companies can also use profits to develop new and disruptive products and services that

can capture market share. Perhaps most importantly, earnings also support valuations.

Keeping the Economy in Perspective

Economists and investors frequently focus on monetary policy to gain insight into

economic cycles. Optimism often grows as the Federal Reserve cuts the fed funds rate and

pessimism spikes when the central bank begins tightening monetary policy. We agree that it

is important to understand the relationship of monetary tightening, the economy, and equity

performance, but in our view, Fed policy appears to be a long way from sparking a recession

or a bear market. Indeed, bull markets have traditionally persisted during fed rate increases

and recessions typically haven’t occurred until the real fed funds rate, which is the nominal

fed funds rate minus inflation, hits 2% or higher. With the real fed funds rate currently at

about 0% and the Federal Reserve expected to raise rates approximately 75 basis points a

year, we maintain that monetary policy is unlikely to kill the economic recovery or stifle the

equity market in the foreseeable future.1

We believe that bonds are a different matter. During periods of fed funds rate increases,

the 10-year Treasury bond has generated an average annual return of -2.7% compared to

the average annual return of 6.2% of the S&P 500 Index.2 We also believe that valuations

imply that earnings multiples may not suffer as rates rise, with the S&P 500 Index having

an EPS yield on April 30 that was approximately 328 bps higher than the yield of the 10-

year Treasury bond. While bonds are susceptible to monetary tightening, we believe the

economy is strong and can absorb the impact of fed rate increases.3

- 2 -

Outlook

In past years, economic growth has been driven primarily by consumer spending, but

business spending, which is growing at a faster rate than the nation’s gross domestic product,

is now playing a more significant role. In our view, business spending is likely to increase

in the coming months and provide additional support to the U.S. economy while helping

corporations boost productivity and earnings. Other indicators, such as the Conference

Board’s Leading Economic Index (LEI), are encouraging. The LEI typically leads S&P 500

Index earnings by 6 to 18 months, so its record high reading of 109.4 in April suggests that

the bull market still has a long runway.

We acknowledge that over the long term, monetary tightening, rising labor costs, and tariffs

leading to a potential trade war could be a headwind for equities. We think the best way

to address those risks is to invest in highly innovative companies that can disrupt their

industries by creating new products and services. During the global financial crisis, for

example, U.S. e-commerce and internet advertising spending grew 33% while total U.S.

retail sales increased only 1%. At the same time, we are experiencing unprecedented levels

of innovation, with artificial intelligence, cloud computing, internet connectivity, genome

sequencing, and novel drug developments allowing leading companies to disrupt their

respective industries with new products and business models.

In closing, we urge investors to focus on corporate fundamentals rather than react hastily

to what we believe are short-sighted views of market pundits. As an active, research-driven

investor, we intend to continue seeking out innovative companies that can grow their

earnings and revenues.

Portfolio Matters

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund returned 6.29% for the fiscal six-month

period ended April 30, 2018, compared to the 5.68% return of the Russell 1000 Growth

Index.

Contributors to Performance

During the reporting period, the largest sector weightings were Information Technology

and Consumer Discretionary. The largest sector overweight was Information Technology

and the largest underweight was Consumer Staples. The Consumer Discretionary and

Health Care sectors provided the greatest contributions to relative performance. Regarding

individual positions, Amazon.com, Inc.; Microsoft Corp.; Visa, Inc., Cl. A; UnitedHealth

Group, Inc.; and Netflix, Inc. were the top contributors to performance.

Amazon is well known as a leading U.S. online retailer. Its shares contributed to performance

as Amazon has enjoyed strong high unit volume growth, in large part driven by the company

continuing to take market share from traditional brick and mortar retailers. Its leadership in

the sizable and expanding web hosting industry also supported the performance of Amazon

shares.

Detractors from Performance

The Industrials and Real Estate sectors were among the sectors that detracted from results.

Regarding individual positions, Broadcom, Inc.; Facebook, Inc., Cl. A; Newell Brands, Inc.;

Equinix, Inc.; and Stanley Black & Decker, Inc. were the top detractors from performance.

- 3 -

Facebook operates the world’s largest social network. Facebook continues to take advertising

market share from print, radio, and television media because the social network offers

brands a robust return on digital advertising spending. Investors have been excited by the

growth of both Instagram, which is Facebook’s video and picture sharing platform, and

WhatsApp, which is the company’s texting and voice over internet protocol service. Shares

of the company underperformed when some measures of Facebook consumer engagement

deteriorated, which suggested user fatigue may be occurring. Facebook also endured a

public relations crisis as management tried to contain media and customer fallout about a

data breach that led to reservations about the company’s privacy safeguards.

Alger Capital Appreciation Focus Fund

The Alger Capital Appreciation Focus Fund returned 8.80% for the fiscal six-month period

ended April 30, 2018, compared to the 5.68% return of the Russell 1000 Growth Index.

Contributors to Performance

During the reporting period, the largest sector weightings were Information Technology

and Consumer Discretionary. The largest sector overweight was Information Technology

and the largest underweight was Consumer Staples. The Consumer Discretionary and

Health Care sectors provided the greatest contributions to relative performance. Regarding

individual positions, Amazon.com, Inc.; Microsoft Corp.; Red Hat, Inc.; Salesforce.com,

Inc.; and Visa, Inc., Cl. A were the top contributors to performance. Shares of Amazon

outperformed in response to developments identified in the Alger Capital Appreciation

Institutional Fund discussion.

Detractors from Performance

The Industrials and Real Estate sectors were among the sectors that detracted from results.

Regarding individual positions, Broadcom, Inc.; Facebook, Inc., Cl. A; Newell Brands, Inc.;

Equinix, Inc.; and Applied Materials, Inc. were the top detractors from performance. Shares

of Facebook underperformed in response to developments identified in the Alger Capital

Appreciation Institutional Fund discussion.

Alger Mid Cap Growth Institutional Fund

The Alger Mid Cap Growth Institutional Fund returned 3.46% for the fiscal six-month

period ended April 30, 2018, compared to the 5.16% return of the Russell Midcap Growth

Index. In January 2018, Dan Chung, CEO and CIO of Alger, joined Teresa McRoberts,

Senior Vice President, in managing the Fund. In managing his portion of the portfolio, Mr.

Chung coordinates and oversees portfolio management allocations among Alger analysts.

Portfolio allocations among the investment professionals are rebalanced by Mr. Chung on a

recurring basis. Alex Goldman and Chris Walsh, formerly Senior Vice Presidents at Alger,

were previously part of the Fund’s portfolio management team and are no longer affiliated

with the Fund or with Alger.

Contributors to Performance

During the reporting period, the largest sector weightings were Information Technology

and Health Care. The largest sector overweight was Health Care and the largest underweight

was Consumer Staples. The Health Care and Financials sectors provided the greatest

contributions to relative performance. Among individual positions, Abiomed, Inc.; Insulet

Corp.; Red Hat, Inc.; Splunk, Inc.; and Match Group, Inc. were the top contributors to

performance.

- 4 -

Insulet provides a continuous insulin delivery system for people with insulin-dependent

diabetes. Insulet’s proprietary Omnipod Insulin Management System is the only tubeless

insulin delivery device available. Insulet also works with global pharmaceutical and

biotechnology companies to tailor its Omnipod system for the delivery of subcutaneous

drugs across multiple therapeutic areas. Its stock performance benefited from news that

UnitedHealth Group, Inc., which is a managed health care organization with approximately

50 million members, will provide coverage for Omnipod. Only a small portion of the

organization’s members currently use the system.

Detractors from Performance

The Information Technology and Industrials sectors were among the sectors that detracted

from results. Regarding individual positions, TESARO, Inc.; Coherent, Inc.; Clovis Oncology,

Inc.; Lumentum Holdings, Inc.; and Universal Display Corp. were the top detractors from

results. Universal Display develops and manufactures organic light emitting diode (OLED)

technologies and materials for display screens in computers, smartphones, televisions, and

automobiles. The company’s unique positioning has allowed it to capitalize on the growing

use of OLED across a broad set of customers in multiple industries. The company provided

fiscal year-end revenue guidance that was below expectations, further fueling speculation

that growth may be peaking for Apple’s OLED-based IPhone X and that Apple may not

use OLED in its new low-end iPhone model. However, we believe guidance is more a result

of timing than structural changes in OLED adoption.

Alger Small Cap Growth Institutional Fund

The Alger Small Cap Growth Institutional Fund returned 6.54% for the fiscal six-month

period ended April 30, 2018, compared to the 5.46% return of the Russell 2000 Growth

Index.

Contributors to Performance

During the reporting period, the largest sector weightings were Health Care and Information

Technology. The largest sector overweight was Health Care and the largest underweight

was Industrials. The Health Care and Information Technology sectors provided the largest

contributions to relative performance. Among individual positions, Abiomed, Inc.; Quidel

Corp.; Insulet Corp.; Tyler Technologies, Inc.; and Proofpoint, Inc. were the top contributors

to performance. Shares of Insulet performed strongly in response to developments

described in the Alger Mid Cap Growth Institutional Fund discussion.

Detractors from Performance

The Financials and Industrials sectors were among sectors that detracted from results.

Regarding individual positions, LendingClub Corp.; WageWorks, Inc.; Cognex Corp.;

ACADIA Pharmaceuticals, Inc.; and Intarcia Therapeutics, Inc. were the top detractors

from results. WageWorks is the leading provider and administrator of consumer-directed,

tax-advantaged benefit accounts that employers provide to employees. It offers its services

through its software-as-a-service (SaaS) platform. These accounts include health and

dependent care, commuter benefits, and other employee programs such as COBRA. Its

stock performance weakened in March after the company filed for an SEC extension for

releasing quarterly results. In filing the extension, WageWorks said its auditor had not yet

completed the audit of its financial statements due primarily to issues such as “managing

change and assessing risk in the areas of non-routine complex transactions.”

- 5 -

I thank you for putting your trust in Alger.

Sincerely,

Daniel C. Chung, CFA

Chief Investment Officer

Fred Alger Management, Inc.

1 Dan Chung and Brad Neuman, Capital Markets: Observations and Insights: Party Without the Punch? Fred Alger Management,

Spring 2018.

2 Ibid.

3 Ibid.

Investors cannot invest directly in an index. Index performance does not reflect the

deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general

information of shareholders of the funds. This report is not authorized for distribution to

prospective investors in a fund unless preceded or accompanied by an effective prospectus

for the fund. Fund returns represent the fiscal six-month period return of Class I shares.

The performance data quoted represents past performance, which is not an

indication or guarantee of future results.

Standardized performance results can be found on the following pages. The investment

return and principal value of an investment in a fund will fluctuate so that an investor’s shares,

when redeemed, may be worth more or less than their original cost. Current performance

may be lower or higher than the performance quoted. For performance data current to the

most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the funds’ management in this report are as of the date of the

Shareholders’ Letter and are subject to change at any time subsequent to this date. There

is no guarantee that any of the assumptions that formed the basis for the opinions stated

herein are accurate or that they will materialize. Moreover, the information forming the

basis for such assumptions is from sources believed to be reliable; however, there is no

guarantee that such information is accurate. Any securities mentioned, whether owned in a

fund or otherwise, are considered in the context of the construction of an overall portfolio

of securities and therefore reference to them should not be construed as a recommendation

or offer to purchase or sell any such security. Inclusion of such securities in a fund and

transactions in such securities, if any, may be for a variety of reasons, including, without

limitation, in response to cash flows, inclusion in a benchmark, and risk control. The

reference to a specific security should also be understood in such context and not viewed as

a statement that the security is a significant holding in a fund. Please refer to the Schedules

of Investments for each fund that is included in this report for a complete list of fund

holdings as of April 30, 2018. Securities mentioned in the Shareholders’ Letter, if not found

in the Schedule of Investments, may have been held by the funds during the six-month

period.

- 6 -

Risk Disclosures

Alger Capital Appreciation Institutional Fund

Investing in the stock market involves gains and losses and may not be suitable for all

investors. The value of an investment may move up or down, sometimes rapidly and

unpredictably, and may be worth more or less than what you invested. Stocks tend to

be more volatile than other investments such as bonds. Growth stocks tend to be more

volatile than other stocks as the prices of growth stocks tend to be higher in relation to

their companies’ earnings and may be more sensitive to market, political, and economic

developments. The Fund may have a significant portion of its assets invested in securities

of companies conducting business in a related group of industries within a sector, which

may make the Fund more vulnerable to unfavorable developments in that sector than a fund

that has a more diversified portfolio. Many technology companies have limited operating

histories and prices of these companies’ securities have historically been more volatile

than other securities due to increased competition, government regulation, and risk of

obsolescence due to the progress of technological developments. Investing in companies

of small capitalizations involves the risk that such issuers may have limited product lines

or financial resources, lack management depth, or have more limited liquidity. The cost of

borrowing money to leverage may exceed the returns for the securities purchased or the

securities purchased may actually go down in value more quickly than if the Fund had not

borrowed.

Alger Capital Appreciation Focus Fund

Investing in the stock market involves gains and losses and may not be suitable for all

investors. The value of an investment may move up or down, sometimes rapidly and

unpredictably, and may be worth more or less than what you invested. Stocks tend to

be more volatile than other investments such as bonds. Growth stocks tend to be more

volatile than other stocks as the prices of growth stocks tend to be higher in relation to

their companies’ earnings and may be more sensitive to market, political, and economic

developments. The Fund may have a significant portion of its assets invested in securities

of companies conducting business in a related group of industries within a sector, which

may make the Fund more vulnerable to unfavorable developments in that sector than a fund

that has a more diversified portfolio. Many technology companies have limited operating

histories and prices of these companies’ securities have historically been more volatile

than other securities due to increased competition, government regulation, and risk of

obsolescence due to the progress of technological developments. Investing in companies

of all capitalizations involves the risk that smaller issuers may have limited product lines or

financial resources, lack management depth, or have more limited liquidity. The Fund may

have a more concentrated portfolio than other funds, so it may be more vulnerable to changes

in the market value of a single issuer and may be more susceptible to risks associated with

a single economic, political or regulatory occurrence than a fund that has a more diversified

portfolio. Active trading of portfolio securities may incur increased transaction costs and

brokerage commissions, and potentially increase taxes that a shareholder may pay, which can

lower the actual return on an investment.

Alger Mid Cap Growth Institutional Fund

Investing in the stock market involves gains and losses and may not be suitable for all

investors. The value of an investment may move up or down, sometimes rapidly and

unpredictably, and may be worth more or less than what you invested. Stocks tend to

- 7 -

be more volatile than other investments such as bonds. Growth stocks tend to be more

volatile than other stocks as the prices of growth stocks tend to be higher in relation to

their companies’ earnings and may be more sensitive to market, political, and economic

developments. Investing in companies of medium capitalizations involves the risk that such

issuers may have limited product lines or financial resources, lack management depth, or

have more limited liquidity. The Fund may have a significant portion of its assets invested

in securities of companies conducting business in a related group of industries within a

sector, which may make the Fund more vulnerable to unfavorable developments in that

sector than a fund that has a more diversified portfolio. Many technology companies have

limited operating histories and prices of these companies’ securities have historically been

more volatile than other securities due to increased competition, government regulation,

and risk of obsolescence due to the progress of technological developments. The Fund

may have a significant portion of its assets invested in securities of healthcare companies,

which may be significantly affected by intense competition, aggressive pricing, government

regulation, technological innovations, product obsolescence, patent considerations, product

compatibility and consumer preferences, and may be more volatile than the securities of

other companies. Foreign investing involves special risks including currency risk and risks

related to political, social, or economic conditions. Active trading of portfolio securities may

incur increased transaction costs and brokerage commissions, and potentially increase taxes

that a shareholder may pay, which can lower the actual return on an investment.

Alger Small Cap Growth Institutional Fund

Investing in the stock market involves gains and losses and may not be suitable for all

investors. The value of an investment may move up or down, sometimes rapidly and

unpredictably, and may be worth more or less than what you invested. Stocks tend to

be more volatile than other investments such as bonds. Growth stocks tend to be more

volatile than other stocks as the prices of growth stocks tend to be higher in relation to

their companies’ earnings and may be more sensitive to market, political, and economic

developments. Investing in companies of small capitalizations involves the risk that such

issuers may have limited product lines or financial resources, lack management depth, or

have more limited liquidity. The Fund may have a significant portion of its assets invested

in securities of companies conducting business in a related group of industries within a

sector, which may make the Fund more vulnerable to unfavorable developments in that

sector than a fund that has a more diversified portfolio. Many technology companies have

limited operating histories and prices of these companies’ securities have historically been

more volatile than other securities due to increased competition, government regulation,

and risk of obsolescence due to the progress of technological developments. The Fund

may have a significant portion of its assets invested in securities of healthcare companies,

which may be significantly affected by intense competition, aggressive pricing, government

regulation, technological innovations, product obsolescence, patent considerations, product

compatibility and consumer preferences, and may be more volatile than the securities of

other companies. Foreign investing involves special risks including currency risk and risks

related to political, social, or economic conditions.

For a more detailed discussion of the risks associated with a fund, please see the Prospectus.

- 8 -

Before investing, carefully consider a fund’s investment objective, risks, charges,

and expenses.

For a prospectus or a summary prospectus containing this and other information

about The Alger Institutional Funds call us at (800) 992-3863 or visit us at www.alger.

com. Read it carefully before investing.

Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Definitions:

• S&P 500 Index: An index of large company stocks considered representative

of the U.S. stock market.

• Russell 1000 Growth Index: An index of common stocks designed to track

performance of large-capitalization companies with greater than average

growth orientation.

• Russell 1000 Value Index: An index of common stocks designed to measures

the performance of those Russell 1000 companies with lower price/book

ratios and lower forecasted growth values.

• Morgan Stanley Capital International (MSCI) All Country World Index

(ACWI) ex USA: An unmanaged, market capitalization-weighted index de-

signed to provide a broad measure of equity market performance throughout

the world, including both developing and emerging markets, but excluding

the United States.

• MSCI Emerging Markets Index: A free float-adjusted market capitalization

index designed to measure equity market performance in the global emerging

markets.

• Russell Midcap Growth Index: An index of common stocks designed to

track performance of medium-capitalization companies with greater than

average growth orientation.

• Russell 2500 Growth Index: An index of common stocks designed to track

performance of small- and medium-capitalization companies with greater

than average growth orientation.

• Russell 2000 Growth Index: An index of common stocks designed to track

performance of small-capitalization companies with greater than average

growth orientation.

• The Conference Board’s Leading Economic Index: An index based on a va-

riety of economic data and is part of the Conference Board’s analytic system

that seeks to signal peaks and troughs in the business cycle.

• FactSet Research Systems provides data and research for investment manag-

ers, hedge funds, investment bankers and other financial professionals.

- 9 -

| | | | | | | | | |

| FUND PERFORMANCE AS OF 3/31/18 (Unaudited) |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | 1 | | 5 | | 10 | | SINCE | |

| | | YEAR | | YEARS | | YEARS | | INCEPTION | |

| Alger Capital Appreciation Institutional Class I (Inception | | | | | | | | | |

| 11/8/93) | 21.40 | % | 15.00 | % | 11.12 | % | 12.16 | % |

| Alger Capital Appreciation Institutional Class R (Inception | | | | | | | | | |

| 1/27/03)* | 20.85 | % | 14.45 | % | 10.58 | % | 11.60 | % |

| Alger Capital Appreciation Institutional Class Y (Inception | | | | | | | | | |

| 2/28/17) | 21.88 | % | n/a | | n/a | | 21.81 | % |

| Alger Capital Appreciation Institutional Class Z-2 | | | | | | | | | |

| (Inception 10/14/16) | | 21.78 | % | n/a | | n/a | | 22.94 | % |

| |

| Alger Capital Appreciation Focus Class A (Inception | | | | | | | | | |

| 12/31/12) | 18.87 | % | 15.18 | % | n/a | | 16.26 | % |

| Alger Capital Appreciation Focus Class C (Inception | | | | | | | | | |

| 12/31/12) | 23.45 | % | 15.56 | % | n/a | | 16.57 | % |

| Alger Capital Appreciation Focus Class I (Inception | | | | | | | | | |

| 11/8/93) | 25.47 | % | 16.53 | % | 9.44 | % | 9.15 | % |

| Alger Capital Appreciation Focus Class Y (Inception | | | | | | | | | |

| 2/28/17) | 25.99 | % | n/a | | n/a | | 25.98 | % |

| Alger Capital Appreciation Focus Class Z (Inception | | | | | | | | | |

| 12/31/12) | 25.82 | % | 16.83 | % | n/a | | 17.87 | % |

| |

| Alger Mid Cap Growth Institutional Class I (Inception | | | | | | | | | |

| 11/8/93) | 18.93 | % | 11.94 | % | 6.76 | % | 11.84 | % |

| Alger Mid Cap Growth Institutional Class R (Inception | | | | | | | | | |

| 1/27/03)* | 18.36 | % | 11.34 | % | 6.20 | % | 11.27 | % |

| Alger Mid Cap Growth Institutional Class Z-2 (Inception | | | | | | | | | |

| 10/14/16) | 19.27 | % | n/a | | n/a | | 23.64 | % |

| |

| Alger Small Cap Growth Institutional Class I | | | | | | | | | |

| (Inception 11/8/93) | | 22.61 | % | 10.49 | % | 8.96 | % | 9.47 | % |

| Alger Small Cap Growth Institutional Class R (Inception | | | | | | | | | |

| 1/27/03)* | 22.06 | % | 9.94 | % | 8.44 | % | 8.94 | % |

| Alger Small Cap Growth Institutional Class Z-2 (Inception | | | | | | | | | |

| 8/1/16) | 23.03 | % | n/a | | n/a | | 22.98 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future

results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and

capital gains.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R shares,

are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the higher

operating expenses of Class R shares.

- 10 -

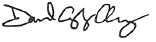

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2018 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital

Appreciation Institutional Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2018. Figures for the Alger Capital Appreciation Institutional Fund Class I

shares and the Russell 1000 Growth Index include reinvestment of dividends and capital gains. Performance for the

Alger Capital Appreciation Institutional Fund Class R, Class Y and Class Z-2 shares may vary from the results shown

above due to differences in expenses the class bears. Investors cannot invest directly in any index. Index performance

does not reflect deduction for fees, expenses, or taxes.

- 11 -

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2018 (Unaudited) (Continued)

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 04/30/18 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | 19.92 | % | 15.23 | % | 10.60 | % | 12.18 | % |

| Class R (Inception 1/27/03)* | 19.37 | % | 14.68 | % | 10.06 | % | 11.62 | % |

| Russell 1000 Growth Index | 18.96 | % | 15.13 | % | 10.81 | % | 9.35 | % |

| |

| |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 2/28/2017 | |

| Class Y (Inception 2/28/17) | 20.46 | % | n/a | | n/a | | 21.63 | % |

| Russell 1000 Growth Index | 18.96 | % | n/a | | n/a | | 19.48 | % |

| |

| |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 10/14/2016 | |

| Class Z-2 (Inception 10/14/16) | 20.33 | % | n/a | | n/a | | 22.74 | % |

| Russell 1000 Growth Index | 18.96 | % | n/a | | n/a | | 22.31 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R

shares, are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the

higher operating expenses of Class R shares.

- 12 -

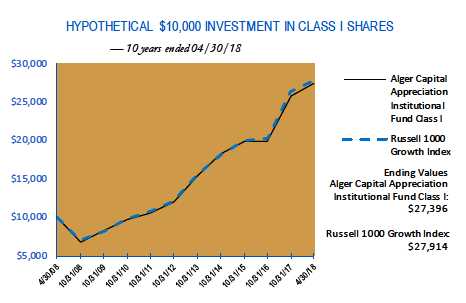

ALGER CAPITAL APPRECIATION FOCUS FUND

Fund Highlights Through April 30, 2018 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital

Appreciation Focus Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2018. Beginning December 31, 2012 Alger Capital Appreciation Focus

Fund changed its investment strategy to invest in a smaller number of issuers. The figures for the Alger Capital

Appreciation Focus Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends and

capital gains. Performance for the Alger Capital Appreciation Focus Fund Class A, Class C, Class Y and Class Z

shares may vary from the results shown above due to differences in expenses the class bears. Investors cannot invest

directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

- 13 -

ALGER CAPITAL APPRECIATION FOCUS FUND

Fund Highlights Through April 30, 2018 (Unaudited) (Continued)

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 04/30/18 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | 24.50 | % | 17.01 | % | 9.06 | % | 9.21 | % |

| Russell 1000 Growth Index | 18.96 | % | 15.13 | % | 10.81 | % | 9.35 | % |

| |

| |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 12/31/2012 | |

| Class A (Inception 12/31/12) | 17.92 | % | 15.65 | % | n/a | | 16.44 | % |

| Class C (Inception 12/31/12) | 22.51 | % | 16.03 | % | n/a | | 16.73 | % |

| Class Z (Inception 12/31/12) | 24.87 | % | 17.32 | % | n/a | | 18.03 | % |

| Russell 1000 Growth Index | 18.96 | % | 15.13 | % | n/a | | 16.56 | % |

| |

| |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 2/28/2017 | |

| Class Y (Inception 2/28/17) | 25.04 | % | n/a | | n/a | | 26.18 | % |

| Russell 1000 Growth Index | 18.96 | % | n/a | | n/a | | 19.48 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average

annual total returns include changes in share price and reinvestment of dividends and capital gains. Class A returns reflect the maximum

initial sales charge and Class C returns reflect the applicable contingent deferred sales charge. The chart and table above do not reflect the

deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return

and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance

may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call us at (800) 992-3863.

- 14 -

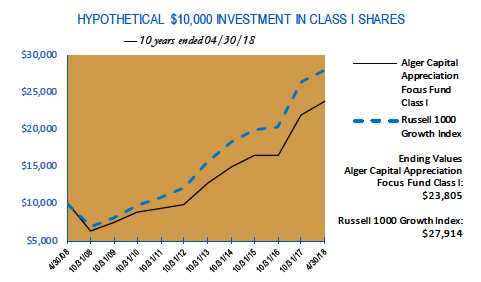

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2018 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Mid Cap

Growth Institutional Fund Class I shares and the Russell Midcap Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2018. Figures for the Alger Mid Cap Growth Institutional Fund Class I

shares and the Russell Midcap Growth Index include reinvestment of dividends and capital gains. Performance for

the Alger Mid Cap Growth Institutional Fund Class R and Class Z-2 shares may vary from the results shown above

due to differences in expenses the class bears. Investors cannot invest directly in any index. Index performance does

not reflect deduction for fees, expenses, or taxes.

- 15 -

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2018 (Unaudited) (Continued)

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 04/30/18 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | 16.60 | % | 11.71 | % | 6.07 | % | 11.77 | % |

| Class R (Inception 1/27/03)* | 16.05 | % | 11.12 | % | 5.51 | % | 11.21 | % |

| Russell Midcap Growth Index | 16.87 | % | 12.76 | % | 9.74 | % | 9.70 | % |

| |

| |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 10/14/2016 | |

| Class Z-2 (Inception 10/14/16) | 16.94 | % | n/a | | n/a | | 21.90 | % |

| Russell Midcap Growth Index | 16.87 | % | n/a | | n/a | | 19.37 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R

shares, are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the

higher operating expenses of Class R shares.

- 16 -

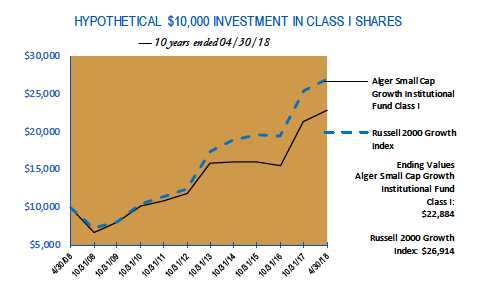

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2018 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Small Cap

Growth Institutional Fund Class I shares and the Russell 2000 Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2018. The figures for the Alger Small Cap Growth Institutional Fund Class

I shares and the Russell 2000 Growth Index include reinvestment of dividends and capital gains. Performance for

the Alger Small Cap Growth Institutional Fund Class R and Class Z-2 shares may vary from the results shown above

due to differences in expenses the class bears. Investors cannot invest directly in any index. Index performance does

not reflect deduction for fees, expenses, or taxes.

- 17 -

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2018 (Unaudited) (Continued)

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 04/30/18 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | 22.82 | % | 11.13 | % | 8.61 | % | 9.50 | % |

| Class R (Inception 1/27/03)* | 22.23 | % | 10.59 | % | 8.08 | % | 8.97 | % |

| Russell 2000 Growth Index | 16.60 | % | 13.07 | % | 10.41 | % | 7.68 | % |

| |

| |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since 8/1/2016 | |

| Class Z-2 (Inception 8/1/16) | 23.22 | % | n/a | | n/a | | 22.85 | % |

| Russell 2000 Growth Index | 16.60 | % | n/a | | n/a | | 17.50 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R

shares, are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the

higher operating expenses of Class R shares.

- 18 -

PORTFOLIO SUMMARY†

April 30, 2018 (Unaudited)

| | | | | | | | | | | | | |

| | | Alger Capital | | | | | | | | | | | |

| | | Appreciation Institutional | | | Alger Capital | | | Alger Mid Cap Growth | | | Alger Small Cap Growth | |

| SECTORS | | Fund | | | Appreciation Focus Fund | | | Institutional Fund | | | Institutional Fund | |

| Consumer Discretionary | | 16.2 | % | | 14.4 | % | | 14.9 | % | | 7.9 | % |

| Consumer Staples | | 0.8 | | | | 0.0 | | | 1.4 | | | 1.0 | |

| Energy | | 1.3 | | | | 0.7 | | | 1.3 | | | 1.5 | |

| Financials | | 6.9 | | | 10.1 | | | 5.8 | | | 3.7 | |

| Health Care | | 12.6 | | | 12.0 | | | 22.6 | | | 42.5 | |

| Industrials | | 8.3 | | | | 4.8 | | | 12.4 | | | 5.5 | |

| Information Technology | | 43.5 | | | 48.0 | | | 32.9 | | | 34.9 | |

| Materials | | 3.2 | | | | 1.8 | | | 4.5 | | | 1.6 | |

| Real Estate | | 2.3 | | | | 2.2 | | | 2.1 | | | 0.8 | |

| Short-Term Investments and | | | | | | | | | | | | | |

| Net Other Assets | | 4.9 | | | | 6.0 | | | 2.1 | | | 0.6 | |

| | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % |

† Based on net assets for each Fund.

- 19 -

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited)

| | | | |

| COMMON STOCKS—92.0% | | SHARES | | VALUE |

| AEROSPACE & DEFENSE—2.2% | | | | |

| General Dynamics Corp. | | 67,789 | $ | 13,646,603 |

| The Boeing Co. | | 137,996 | | 46,029,946 |

| United Technologies Corp. | | 153,919 | | 18,493,368 |

| | | | | 78,169,917 |

| AIR FREIGHT & LOGISTICS—0.4% | | | | |

| FedEx Corp. | | 42,984 | | 10,625,645 |

| XPO Logistics, Inc. * | | 35,195 | | 3,419,546 |

| | | | | 14,045,191 |

| APPAREL ACCESSORIES & LUXURY GOODS—0.8% | | | | |

| Adidas AG | | 25,889 | | 6,363,253 |

| PVH Corp. | | 128,057 | | 20,446,861 |

| | | | | 26,810,114 |

| APPLICATION SOFTWARE—6.0% | | | | |

| Adobe Systems, Inc. * | | 228,384 | | 50,609,894 |

| Autodesk, Inc. * | | 337,873 | | 42,538,211 |

| salesforce. com, Inc. * | | 994,201 | | 120,288,379 |

| | | | | 213,436,484 |

| ASSET MANAGEMENT & CUSTODY BANKS—0.3% | | | | |

| BlackRock, Inc. , Cl. A | | 17,291 | | 9,017,256 |

| AUTO PARTS & EQUIPMENT—0.3% | | | | |

| Aptiv PLC. | | 111,418 | | 9,423,734 |

| BIOTECHNOLOGY—3.7% | | | | |

| AbbVie, Inc. | | 279,044 | | 26,941,698 |

| BioMarin Pharmaceutical, Inc. * | | 175,147 | | 14,626,526 |

| Celgene Corp. * | | 117,159 | | 10,204,549 |

| Exact Sciences Corp. * | | 225,449 | | 11,274,705 |

| Sarepta Therapeutics, Inc. * | | 263,420 | | 20,114,751 |

| Vertex Pharmaceuticals, Inc. * | | 323,064 | | 49,480,482 |

| | | | | 132,642,711 |

| CABLE & SATELLITE—0.6% | | | | |

| Charter Communications, Inc. , Cl. A* | | 28,361 | | 7,694,056 |

| Comcast Corp. , Cl. A | | 454,512 | | 14,267,131 |

| | | | | 21,961,187 |

| COMMUNICATIONS EQUIPMENT—0.3% | | | | |

| Palo Alto Networks, Inc. * | | 59,312 | | 11,418,153 |

| CONSTRUCTION MACHINERY & HEAVY TRUCKS—0.3% | | | | |

| Caterpillar, Inc. | | 74,130 | | 10,701,407 |

| CONSTRUCTION MATERIALS—1.0% | | | | |

| Vulcan Materials Co. | | 329,877 | | 36,843,962 |

| DATA PROCESSING & OUTSOURCED SERVICES—4.9% | | | | |

| Visa, Inc. , Cl. A | | 1,388,501 | | 176,173,007 |

| DIVERSIFIED BANKS—2.3% | | | | |

| Bank of America Corp. | | 2,043,184 | | 61,132,065 |

| Citigroup, Inc. | | 100,416 | | 6,855,400 |

- 20 -

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | |

| COMMON STOCKS—92.0% (CONT. ) | | SHARES | | VALUE |

| DIVERSIFIED BANKS—2.3% (CONT. ) | | | | |

| JPMorgan Chase & Co. | | 144,107 | $ | 15,675,960 |

| | | | | 83,663,425 |

| DIVERSIFIED CHEMICALS—0.3% | | | | |

| DowDuPont, Inc. | | 196,354 | | 12,417,427 |

| DIVERSIFIED SUPPORT SERVICES—0.5% | | | | |

| Cintas Corp. | | 111,457 | | 18,981,127 |

| FINANCIAL EXCHANGES & DATA—2.7% | | | | |

| Intercontinental Exchange, Inc. | | 817,507 | | 59,236,557 |

| S&P Global, Inc. | | 202,065 | | 38,109,459 |

| | | | | 97,346,016 |

| HEALTH CARE EQUIPMENT—3.9% | | | | |

| Boston Scientific Corp. * | | 1,090,862 | | 31,329,557 |

| Danaher Corp. | | 473,476 | | 47,499,112 |

| Intuitive Surgical, Inc. * | | 30,164 | | 13,295,688 |

| Medtronic PLC. | | 276,992 | | 22,195,369 |

| Zimmer Biomet Holdings, Inc. | | 235,578 | | 27,131,518 |

| | | | | 141,451,244 |

| HOME ENTERTAINMENT SOFTWARE—0.4% | | | | |

| Electronic Arts, Inc. * | | 120,914 | | 14,265,434 |

| HOME IMPROVEMENT RETAIL—2.6% | | | | |

| The Home Depot, Inc. | | 498,169 | | 92,061,631 |

| HOTELS RESORTS & CRUISE LINES—0.5% | | | | |

| Norwegian Cruise Line Holdings Ltd. * | | 329,433 | | 17,614,783 |

| HYPERMARKETS & SUPER CENTERS—0.2% | | | | |

| Walmart, Inc. | | 96,262 | | 8,515,337 |

| INDUSTRIAL CONGLOMERATES—2.3% | | | | |

| Honeywell International, Inc. | | 577,449 | | 83,545,321 |

| INDUSTRIAL GASES—1.0% | | | | |

| Air Products & Chemicals, Inc. | | 227,616 | | 36,939,801 |

| INDUSTRIAL MACHINERY—1.0% | | | | |

| Stanley Black & Decker, Inc. | | 262,917 | | 37,226,418 |

| INTERNET & DIRECT MARKETING RETAIL—10.0% | | | | |

| Amazon. com, Inc. * | | 211,232 | | 330,816,772 |

| Netflix, Inc. * | | 91,952 | | 28,731,322 |

| | | | | 359,548,094 |

| INTERNET SOFTWARE & SERVICES—12.3% | | | | |

| Alibaba Group Holding Ltd. #* | | 429,749 | | 76,727,386 |

| Alphabet, Inc. , Cl. C* | | 154,549 | | 157,227,334 |

| Altaba, Inc. * | | 601,133 | | 42,127,401 |

| Facebook, Inc. , Cl. A* | | 936,760 | | 161,122,720 |

| Palantir Technologies, Inc. , Cl. A*,@,(a) | | 239,030 | | 1,374,423 |

| Tencent Holdings Ltd. | | 37,111 | | 1,824,485 |

| | | | | 440,403,749 |

- 21 -

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | |

| COMMON STOCKS—92.0% (CONT. ) | | SHARES | | VALUE |

| INVESTMENT BANKING & BROKERAGE—0.8% | | | | |

| Morgan Stanley | | 533,921 | $ | 27,561,002 |

| IT CONSULTING & OTHER SERVICES—0.6% | | | | |

| Cognizant Technology Solutions Corp. , Cl. A | | 257,225 | | 21,046,150 |

| LEISURE FACILITIES—0.5% | | | | |

| Vail Resorts, Inc. | | 83,190 | | 19,076,299 |

| LIFE SCIENCES TOOLS & SERVICES—0.7% | | | | |

| Illumina, Inc. * | | 98,137 | | 23,644,147 |

| MANAGED HEALTH CARE—3.8% | | | | |

| UnitedHealth Group, Inc. | | 575,506 | | 136,049,618 |

| OIL & GAS EQUIPMENT & SERVICES—0.4% | | | | |

| Halliburton Co. | | 274,344 | | 14,537,489 |

| OIL & GAS EXPLORATION & PRODUCTION—0.9% | | | | |

| Pioneer Natural Resources Co. | | 157,483 | | 31,740,699 |

| PAPER PACKAGING—0.2% | | | | |

| International Paper Co. | | 118,938 | | 6,132,443 |

| PHARMACEUTICALS—0.4% | | | | |

| Allergan PLC. | | 43,015 | | 6,609,255 |

| Bristol-Myers Squibb Co. | | 117,896 | | 6,145,918 |

| | | | | 12,755,173 |

| PROPERTY & CASUALTY INSURANCE—0.3% | | | | |

| The Progressive Corp. | | 153,620 | | 9,261,750 |

| RAILROADS—1.4% | | | | |

| Union Pacific Corp. | | 373,658 | | 49,931,919 |

| RESTAURANTS—0.9% | | | | |

| McDonald's Corp. | | 188,559 | | 31,572,319 |

| SEMICONDUCTOR EQUIPMENT—1.5% | | | | |

| Applied Materials, Inc. | | 891,505 | | 44,281,053 |

| Lam Research Corp. | | 54,526 | | 10,090,582 |

| | | | | 54,371,635 |

| SEMICONDUCTORS—4.1% | | | | |

| Broadcom, Inc. | | 342,017 | | 78,465,540 |

| Cavium, Inc. * | | 112,088 | | 8,407,721 |

| Marvell Technology Group Ltd. | | 333,413 | | 6,688,265 |

| Microchip Technology, Inc. | | 203,639 | | 17,036,439 |

| Micron Technology, Inc. * | | 241,253 | | 11,092,813 |

| NVIDIA Corp. | | 105,887 | | 23,813,986 |

| | | | | 145,504,764 |

| SPECIALTY CHEMICALS—0.7% | | | | |

| The Sherwin-Williams Co. | | 68,415 | | 25,153,459 |

| SYSTEMS SOFTWARE—10.0% | | | | |

| Microsoft Corp. | | 3,098,923 | | 289,811,279 |

| Red Hat, Inc. * | | 276,518 | | 45,089,025 |

| ServiceNow, Inc. * | | 78,649 | | 13,066,745 |

| Smartsheet, Inc. , Cl. A* | | 28,973 | | 559,179 |

- 22 -

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | | |

| COMMON STOCKS—92.0% (CONT. ) | | SHARES | | | VALUE |

| SYSTEMS SOFTWARE—10.0% (CONT. ) | | | | | |

| VMware, Inc. , Cl. A* | | 60,812 | | $ | 8,103,807 |

| | | | | | 356,630,035 |

| TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—3.2% | | | | | |

| Apple, Inc. | | 703,830 | | | 116,314,946 |

| TOBACCO—0.6% | | | | | |

| Philip Morris International, Inc. | | 267,337 | | | 21,921,634 |

| TRADING COMPANIES & DISTRIBUTORS—0.2% | | | | | |

| United Rentals, Inc. * | | 45,223 | | | 6,783,450 |

| TOTAL COMMON STOCKS | | | | | |

| (Cost $2,304,614,049) | | | | | 3,294,611,861 |

| PREFERRED STOCKS—0.3% | | SHARES | | | VALUE |

| INTERNET SOFTWARE & SERVICES—0.2% | | | | | |

| Palantir Technologies, Inc. , Cl. B*,@,(a) | | 974,841 | | | 5,605,336 |

| Palantir Technologies, Inc. , Cl. D*,@,(a) | | 127,007 | | | 730,290 |

| | | | | | 6,335,626 |

| PHARMACEUTICALS—0.1% | | | | | |

| Intarcia Therapeutics, Inc. , Series DD*,@,(a) | | 111,655 | | | 2,993,470 |

| TOTAL PREFERRED STOCKS | | | | | |

| (Cost $10,892,407) | | | | | 9,329,096 |

| MASTER LIMITED PARTNERSHIP—0.5% | | SHARES | | | VALUE |

| ASSET MANAGEMENT & CUSTODY BANKS—0.5% | | | | | |

| The Blackstone Group LP. | | 628,783 | | | 19,460,834 |

| (Cost $16,934,849) | | | | | 19,460,834 |

| REAL ESTATE INVESTMENT TRUST—2.3% | | SHARES | | | VALUE |

| SPECIALIZED—2.3% | | | | | |

| Equinix, Inc. | | 103,330 | | | 43,480,231 |

| SBA Communications Corp. , Cl. A* | | 249,566 | | | 39,987,960 |

| | | | | | 83,468,191 |

| TOTAL REAL ESTATE INVESTMENT TRUST | | | | | |

| (Cost $85,449,459) | | | | | 83,468,191 |

| Total Investments | | | | | |

| (Cost $2,417,890,764) | | 95.1 | % | $ | 3,406,869,982 |

| Unaffiliated Securities (Cost $2,417,890,764) | | | | | 3,406,869,982 |

| Other Assets in Excess of Liabilities | | 4.9 | % | | 175,887,858 |

| NET ASSETS | | 100.0 | % | $ | 3,582,757,840 |

# American Depositary Receipts.

(a) Security is valued in good faith at fair value determined using significant unobservable inputs pursuant to procedures established by the

Board.

* Non-income producing security.

- 23 -

THE ALGER INSTITUTIONAL FUNDS

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

@ Restricted security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to not be liquid

and may be sold only to qualified buyers.

| | | | | | | | | |

| | | | | % of net assets | | | | % of net assets | |

| | Acquisition | | Acquisition | (Acquisition | | | Market | as of | |

| Security | Date(s) | | Cost | Date) | | | Value | 4/30/2018 | |

| Intarcia Therapeutics, Inc. , Series | | | | | | | | | |

| DD | 03/27/14 | $ | 3,616,505 | 014 | % | $ | 2,993,470 | 0.08 | % |

| Palantir Technologies, Inc. , Cl. A | 10/07/14 | | 1,555,368 | 0.05 | % | | 1,374,423 | 0.04 | % |

| Palantir Technologies, Inc. , Cl. B | 10/07/14 | | 6,437,297 | 0.22 | % | | 5,605,336 | 0.16 | % |

| Palantir Technologies, Inc. , Cl. D | 10/14/14 | | 838,605 | 0.03 | % | | 730,290 | 0.02 | % |

| Total | | | | | | $ | 10,703,519 | 0.30 | % |

| | | | | | | | | | |

| See Notes to Financial Statements. | | | | | | | | |

- 24 -

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION FOCUS FUND

Schedule of Investments April 30, 2018 (Unaudited)

| | | | |

| COMMON STOCKS—91.3% | | SHARES | | VALUE |

| AIR FREIGHT & LOGISTICS—0.6% | | | | |

| XPO Logistics, Inc. * | | 11,229 | $ | 1,091,010 |

| APPAREL ACCESSORIES & LUXURY GOODS—0.5% | | | | |

| PVH Corp. | | 5,007 | | 799,468 |

| APPLICATION SOFTWARE—8.9% | | | | |

| Adobe Systems, Inc. * | | 14,818 | | 3,283,669 |

| Autodesk, Inc. * | | 23,571 | | 2,967,589 |

| salesforce. com, Inc. * | | 72,106 | | 8,724,105 |

| | | | | 14,975,363 |

| ASSET MANAGEMENT & CUSTODY BANKS—0.3% | | | | |

| BlackRock, Inc. , Cl. A | | 810 | | 422,415 |

| BIOTECHNOLOGY—2.0% | | | | |

| Exact Sciences Corp. * | | 5,324 | | 266,253 |

| Sarepta Therapeutics, Inc. * | | 11,618 | | 887,150 |

| Vertex Pharmaceuticals, Inc. * | | 14,516 | | 2,223,271 |

| | | | | 3,376,674 |

| CONSTRUCTION MACHINERY & HEAVY TRUCKS—0.3% | | | | |

| Caterpillar, Inc. | | 3,646 | | 526,337 |

| CONSTRUCTION MATERIALS—1.2% | | | | |

| Vulcan Materials Co. | | 18,852 | | 2,105,580 |

| DATA PROCESSING & OUTSOURCED SERVICES—5.1% | | | | |

| Visa, Inc. , Cl. A | | 68,181 | | 8,650,805 |

| DIVERSIFIED BANKS—2.7% | | | | |

| Bank of America Corp. | | 152,132 | | 4,551,789 |

| DIVERSIFIED SUPPORT SERVICES—0.7% | | | | |

| Cintas Corp. | | 6,958 | | 1,184,947 |

| FINANCIAL EXCHANGES & DATA—6.1% | | | | |

| Intercontinental Exchange, Inc. | | 89,381 | | 6,476,547 |

| S&P Global, Inc. | | 20,554 | | 3,876,485 |

| | | | | 10,353,032 |

| HEALTH CARE EQUIPMENT—5.0% | | | | |

| Boston Scientific Corp. * | | 79,675 | | 2,288,266 |

| Danaher Corp. | | 37,996 | | 3,811,759 |

| DexCom, Inc. * | | 9,845 | | 720,457 |

| Zimmer Biomet Holdings, Inc. | | 14,641 | | 1,686,204 |

| | | | | 8,506,686 |

| HOME ENTERTAINMENT SOFTWARE—0.3% | | | | |

| Electronic Arts, Inc. * | | 4,539 | | 535,511 |

| HOME IMPROVEMENT RETAIL—2.5% | | | | |

| The Home Depot, Inc. | | 22,646 | | 4,184,981 |

| INDUSTRIAL CONGLOMERATES—2.4% | | | | |

| Honeywell International, Inc. | | 27,817 | | 4,024,563 |

| INDUSTRIAL GASES—0.6% | | | | |

| Air Products & Chemicals, Inc. | | 6,208 | | 1,007,496 |

- 25 -

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION FOCUS FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | |

| COMMON STOCKS—91.3% (CONT. ) | | SHARES | | VALUE |

| INDUSTRIAL MACHINERY—0.8% | | | | |

| Stanley Black & Decker, Inc. | | 9,098 | $ | 1,288,186 |

| INTERNET & DIRECT MARKETING RETAIL—9.7% | | | | |

| Amazon. com, Inc. * | | 9,863 | | 15,446,740 |

| Netflix, Inc. * | | 3,272 | | 1,022,369 |

| | | | | 16,469,109 |

| INTERNET SOFTWARE & SERVICES—12.5% | | | | |

| Alibaba Group Holding Ltd. #* | | 30,319 | | 5,413,154 |

| Alphabet, Inc. , Cl. C* | | 7,249 | | 7,374,625 |

| Facebook, Inc. , Cl. A* | | 44,878 | | 7,719,016 |

| Tencent Holdings Ltd. | | 1,710 | | 84,069 |

| Wix. com Ltd. * | | 5,445 | | 447,851 |

| | | | | 21,038,715 |

| INVESTMENT BANKING & BROKERAGE—0.6% | | | | |

| Morgan Stanley | | 20,876 | | 1,077,619 |

| IT CONSULTING & OTHER SERVICES—1.2% | | | | |

| EPAM Systems, Inc. * | | 17,583 | | 2,010,616 |

| LEISURE FACILITIES—1.1% | | | | |

| Vail Resorts, Inc. | | 7,844 | | 1,798,708 |

| MANAGED HEALTH CARE—4.9% | | | | |

| UnitedHealth Group, Inc. | | 35,240 | | 8,330,736 |

| OIL & GAS EXPLORATION & PRODUCTION—0.7% | | | | |

| Pioneer Natural Resources Co. | | 6,038 | | 1,216,959 |

| SEMICONDUCTOR EQUIPMENT—2.3% | | | | |

| Applied Materials, Inc. | | 79,076 | | 3,927,705 |

| SEMICONDUCTORS—3.3% | | | | |

| Broadcom, Inc. | | 19,725 | | 4,525,309 |

| Marvell Technology Group Ltd. | | 47,963 | | 962,138 |

| | | | | 5,487,447 |

| SPECIALIZED CONSUMER SERVICES—0.6% | | | | |

| ServiceMaster Global Holdings, Inc. * | | 19,782 | | 1,000,969 |

| SYSTEMS SOFTWARE—11.4% | | | | |

| Microsoft Corp. | | 153,564 | | 14,361,305 |

| Red Hat, Inc. * | | 29,996 | | 4,891,148 |

| | | | | 19,252,453 |

| TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—3.0% | | | | |

| Apple, Inc. | | 30,948 | | 5,114,466 |

| TOTAL COMMON STOCKS | | | | |

| (Cost $132,541,163) | | | | 154,310,345 |

| PREFERRED STOCKS—0.1% | | SHARES | | VALUE |

| BIOTECHNOLOGY—0.1% | | | | |

| Prosetta Biosciences, Inc. , Series D*,@,(a),(b) | | 76,825 | | 230,475 |

| (Cost $345,713) | | | | 230,475 |

- 26 -

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION FOCUS FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | | |

| MASTER LIMITED PARTNERSHIP—0.4% | | SHARES | | | VALUE |

| ASSET MANAGEMENT & CUSTODY BANKS—0.4% | | | | | |

| The Blackstone Group LP. | | 21,687 | | $ | 671,213 |

| (Cost $688,672) | | | | | 671,213 |

| REAL ESTATE INVESTMENT TRUST—2.2% | | SHARES | | | VALUE |

| SPECIALIZED—2.2% | | | | | |

| Equinix, Inc. | | 7,172 | | | 3,017,906 |

| SBA Communications Corp. , Cl. A* | | 4,064 | | | 651,175 |

| | | | | | 3,669,081 |

| TOTAL REAL ESTATE INVESTMENT TRUST | | | | | |

| (Cost $3,968,269) | | | | | 3,669,081 |

| Total Investments | | | | | |

| (Cost $137,543,817) | | 94.0 | % | $ | 158,881,114 |

| Affiliated Securities (Cost $345,713) | | | | | 230,475 |

| Unaffiliated Securities (Cost $137,198,104) | | | | | 158,650,639 |

| Other Assets in Excess of Liabilities | | 6.0 | % | | 10,106,341 |

| NET ASSETS | | 100.0 | % | $ | 168,987,455 |

# American Depositary Receipts.

(a) Deemed an affiliate of the Alger fund complex during the year in accordance with Section 2(a)(3) of the Investment Company Act of

1940. See Affiliated Securities Note 11.

(b) Security is valued in good faith at fair value determined using significant unobservable inputs pursuant to procedures established by

the Board.

* Non-income producing security.

@ Restricted security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to not be liquid

and may be sold only to qualified buyers.

| | | | | | | | | |

| | | | | % of net assets | | | | % of net assets | |

| | Acquisition | | Acquisition | (Acquisition | | | Market | as of | |

| Security | Date(s) | | Cost | Date) | | | Value | 4/30/2018 | |

| Prosetta Biosciences, Inc. , Series D | 02/06/15 | $ | 345,713 | 0.80 | % | $ | 230,475 | 0.14 | % |

| Total | | | | | | $ | 230,475 | 0.14 | % |

| | | | | | | | | | |

| |

| |

| See Notes to Financial Statements. | | | | | | | | |

- 27 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited)

| | | | |

| COMMON STOCKS—93.3% | | SHARES | | VALUE |

| AEROSPACE & DEFENSE—1.4% | | | | |

| HEICO Corp. | | 16,929 | $ | 1,487,213 |

| APPAREL ACCESSORIES & LUXURY GOODS—2.5% | | | | |

| PVH Corp. | | 9,532 | | 1,521,974 |

| Tapestry, Inc. | | 19,927 | | 1,071,475 |

| | | | | 2,593,449 |

| APPAREL RETAIL—2.4% | | | | |

| Burlington Stores, Inc. * | | 9,565 | | 1,299,405 |

| Ross Stores, Inc. | | 15,536 | | 1,256,086 |

| | | | | 2,555,491 |

| APPLICATION SOFTWARE—4.7% | | | | |

| ANSYS, Inc. * | | 3,266 | | 527,981 |

| Autodesk, Inc. * | | 14,722 | | 1,853,500 |

| Globant SA* | | 30,247 | | 1,361,417 |

| Splunk, Inc. * | | 12,064 | | 1,238,370 |

| | | | | 4,981,268 |

| ASSET MANAGEMENT & CUSTODY BANKS—0.7% | | | | |

| WisdomTree Investments, Inc. | | 74,123 | | 783,480 |

| AUTO PARTS & EQUIPMENT—1.1% | | | | |

| Aptiv PLC. | | 14,319 | | 1,211,101 |

| AUTOMOTIVE RETAIL—0.9% | | | | |

| AutoZone, Inc. * | | 1,549 | | 967,382 |

| BIOTECHNOLOGY—5.9% | | | | |

| Agios Pharmaceuticals, Inc. * | | 3,850 | | 323,054 |

| BeiGene Ltd. #* | | 1,949 | | 330,511 |

| BioMarin Pharmaceutical, Inc. * | | 7,298 | | 609,456 |

| Bluebird Bio, Inc. * | | 5,046 | | 858,577 |

| Clovis Oncology, Inc. * | | 12,338 | | 535,222 |

| Exact Sciences Corp. * | | 8,082 | | 404,181 |

| Halozyme Therapeutics, Inc. * | | 15,653 | | 296,311 |

| Immunomedics, Inc. * | | 19,451 | | 354,203 |

| Incyte Corp. * | | 1,310 | | 81,141 |

| Neurocrine Biosciences, Inc. * | | 6,942 | | 562,857 |

| Sage Therapeutics, Inc. * | | 2,867 | | 412,619 |

| Sarepta Therapeutics, Inc. * | | 13,832 | | 1,056,212 |

| TESARO, Inc. * | | 6,982 | | 355,454 |

| | | | | 6,179,798 |

| BUILDING PRODUCTS—1.2% | | | | |

| Lennox International, Inc. | | 6,805 | | 1,315,883 |

| COMMUNICATIONS EQUIPMENT—1.6% | | | | |

| Palo Alto Networks, Inc. * | | 8,773 | | 1,688,890 |

| CONSTRUCTION MACHINERY & HEAVY TRUCKS—0.9% | | | | |

| Wabtec Corp. | | 10,500 | | 932,505 |

| CONSTRUCTION MATERIALS—1.8% | | | | |

| Vulcan Materials Co. | | 16,718 | | 1,867,233 |

- 28 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | |

| COMMON STOCKS—93.3% (CONT. ) | | SHARES | | VALUE |

| DATA PROCESSING & OUTSOURCED SERVICES—6.9% | | | | |

| Alliance Data Systems Corp. | | 5,345 | $ | 1,085,303 |

| Fiserv, Inc. * | | 26,470 | | 1,875,664 |

| FleetCor Technologies, Inc. * | | 7,764 | | 1,609,322 |

| GDS Holdings Ltd. #* | | 37,207 | | 1,085,328 |

| Worldpay, Inc. , Cl. A* | | 20,259 | | 1,645,436 |

| | | | | 7,301,053 |

| DIVERSIFIED SUPPORT SERVICES—1.5% | | | | |

| Cintas Corp. | | 9,585 | | 1,632,326 |

| ELECTRICAL COMPONENTS & EQUIPMENT—2.3% | | | | |

| AMETEK, Inc. | | 16,713 | | 1,166,567 |

| Rockwell Automation, Inc. | | 7,409 | | 1,219,003 |

| | | | | 2,385,570 |

| ELECTRONIC EQUIPMENT & INSTRUMENTS—1.0% | | | | |

| Trimble, Inc. * | | 30,858 | | 1,067,687 |

| FERTILIZERS & AGRICULTURAL CHEMICALS—0.5% | | | | |

| FMC Corp. | | 6,715 | | 535,387 |

| FINANCIAL EXCHANGES & DATA—2.2% | | | | |

| Intercontinental Exchange, Inc. | | 13,279 | | 962,197 |

| MarketAxess Holdings, Inc. | | 6,597 | | 1,310,362 |

| | | | | 2,272,559 |

| GENERAL MERCHANDISE STORES—1.0% | | | | |

| Dollar Tree, Inc. * | | 11,146 | | 1,068,790 |

| HEALTH CARE EQUIPMENT—7.6% | | | | |

| ABIOMED, Inc. * | | 7,551 | | 2,272,473 |

| AxoGen, Inc. * | | 9,918 | | 394,736 |

| DexCom, Inc. * | | 8,517 | | 623,274 |

| Edwards Lifesciences Corp. * | | 7,125 | | 907,440 |

| IDEXX Laboratories, Inc. * | | 4,910 | | 954,946 |

| Insulet Corp. * | | 17,251 | | 1,483,586 |

| Masimo Corp. * | | 7,938 | | 712,277 |

| Penumbra, Inc. * | | 1,773 | | 220,473 |

| Zimmer Biomet Holdings, Inc. | | 3,619 | | 416,800 |

| | | | | 7,986,005 |

| HEALTH CARE SUPPLIES—1.2% | | | | |

| Align Technology, Inc. * | | 4,942 | | 1,234,759 |

| HEALTH CARE TECHNOLOGY—1.0% | | | | |

| Medidata Solutions, Inc. * | | 7,078 | | 505,086 |

| Veeva Systems, Inc. , Cl. A* | | 7,633 | | 535,302 |

| | | | | 1,040,388 |

| HOME ENTERTAINMENT SOFTWARE—1.5% | | | | |

| Electronic Arts, Inc. * | | 5,731 | | 676,143 |

| Take-Two Interactive Software, Inc. * | | 9,000 | | 897,390 |

| | | | | 1,573,533 |

| HOTELS RESORTS & CRUISE LINES—2.3% | | | | |

| Hilton Worldwide Holdings, Inc. | | 12,883 | | 1,015,696 |

- 29 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | |

| COMMON STOCKS—93.3% (CONT. ) | | SHARES | | VALUE |

| HOTELS RESORTS & CRUISE LINES—2.3% (CONT. ) | | | | |

| Norwegian Cruise Line Holdings Ltd. * | | 26,752 | $ | 1,430,429 |

| | | | | 2,446,125 |

| HOUSEHOLD PRODUCTS—0.9% | | | | |

| Church & Dwight Co. , Inc. | | 20,572 | | 950,426 |

| INDUSTRIAL CONGLOMERATES—1.8% | | | | |

| Roper Technologies, Inc. | | 7,272 | | 1,921,190 |

| INDUSTRIAL MACHINERY—2.7% | | | | |

| Fortive Corp. | | 24,942 | | 1,753,672 |

| Parker-Hannifin Corp. | | 3,277 | | 539,460 |

| Stanley Black & Decker, Inc. | | 3,714 | | 525,865 |

| | | | | 2,818,997 |

| INTERNET SOFTWARE & SERVICES—4.5% | | | | |

| Etsy, Inc. * | | 36,587 | | 1,095,415 |

| GrubHub, Inc. * | | 10,870 | | 1,099,392 |

| IAC/InterActiveCorp* | | 4,625 | | 749,897 |

| Match Group, Inc. * | | 12,706 | | 598,707 |

| Palantir Technologies, Inc. , Cl. A*,@,(a) | | 12,426 | | 71,450 |

| Yelp, Inc. , Cl. A* | | 24,138 | | 1,082,589 |

| | | | | 4,697,450 |

| IT CONSULTING & OTHER SERVICES—2.3% | | | | |

| EPAM Systems, Inc. * | | 11,898 | | 1,360,536 |

| Gartner, Inc. * | | 8,664 | | 1,050,857 |

| | | | | 2,411,393 |

| LEISURE FACILITIES—1.3% | | | | |

| Vail Resorts, Inc. | | 5,857 | | 1,343,069 |

| LIFE SCIENCES TOOLS & SERVICES—2.3% | | | | |

| Agilent Technologies, Inc. | | 10,241 | | 673,243 |

| Bio-Techne Corp. | | 1,856 | | 280,089 |

| Illumina, Inc. * | | 6,302 | | 1,518,341 |

| | | | | 2,471,673 |

| MANAGED HEALTH CARE—0.4% | | | | |

| WellCare Health Plans, Inc. * | | 2,119 | | 434,734 |

| METAL & GLASS CONTAINERS—0.8% | | | | |

| Ball Corp. | | 20,130 | | 807,012 |

| OIL & GAS EXPLORATION & PRODUCTION—1.3% | | | | |

| Encana Corp. | | 106,625 | | 1,330,680 |

| PACKAGED FOODS & MEATS—0.5% | | | | |

| Pinnacle Foods, Inc. | | 8,548 | | 516,299 |

| PAPER PACKAGING—0.9% | | | | |

| International Paper Co. | | 18,697 | | 964,017 |

| PHARMACEUTICALS—2.3% | | | | |

| Aerie Pharmaceuticals, Inc. * | | 16,369 | | 838,093 |

| GW Pharmaceuticals PLC. #* | | 5,031 | | 668,670 |

| Zoetis, Inc. , Cl. A | | 10,484 | | 875,204 |

| | | | | 2,381,967 |

- 30 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | |

| COMMON STOCKS—93.3% (CONT. ) | | SHARES | | VALUE |

| PROPERTY & CASUALTY INSURANCE—1.6% | | | | |

| The Progressive Corp. | | 28,415 | $ | 1,713,140 |

| REGIONAL BANKS—1.0% | | | | |

| Regions Financial Corp. | | 56,780 | | 1,061,786 |

| RESTAURANTS—1.9% | | | | |

| Chipotle Mexican Grill, Inc. , Cl. A* | | 1,868 | | 790,780 |

| Dunkin' Brands Group, Inc. | | 13,211 | | 805,343 |

| Restaurant Brands International, Inc. | | 7,910 | | 430,462 |

| | | | | 2,026,585 |

| SEMICONDUCTOR EQUIPMENT—2.2% | | | | |

| Lam Research Corp. | | 12,412 | | 2,296,965 |

| SEMICONDUCTORS—3.2% | | | | |

| Cavium, Inc. * | | 8,550 | | 641,335 |

| Marvell Technology Group Ltd. | | 37,235 | | 746,934 |

| Microchip Technology, Inc. | | 12,786 | | 1,069,677 |

| Skyworks Solutions, Inc. | | 11,071 | | 960,520 |

| | | | | 3,418,466 |

| SPECIALIZED CONSUMER SERVICES—1.5% | | | | |

| ServiceMaster Global Holdings, Inc. * | | 31,462 | | 1,591,977 |

| SPECIALTY CHEMICALS—0.5% | | | | |

| WR Grace & Co. | | 8,262 | | 565,451 |

| SYSTEMS SOFTWARE—4.7% | | | | |

| Proofpoint, Inc. * | | 11,539 | | 1,360,910 |

| Red Hat, Inc. * | | 12,485 | | 2,035,804 |

| ServiceNow, Inc. * | | 9,561 | | 1,588,464 |

| | | | | 4,985,178 |

| TRUCKING—0.6% | | | | |

| Old Dominion Freight Line, Inc. | | 4,322 | | 578,543 |

| TOTAL COMMON STOCKS | | | | |

| (Cost $91,043,431) | | | | 98,394,873 |

| PREFERRED STOCKS—0.9% | | SHARES | | VALUE |

| BIOTECHNOLOGY—0.4% | | | | |

| Prosetta Biosciences, Inc. , Series D*,@,(a),(b) | | 166,009 | | 498,027 |

| INTERNET SOFTWARE & SERVICES—0.3% | | | | |

| Palantir Technologies, Inc. , Cl. B*,@,(a) | | 50,675 | | 291,381 |

| PHARMACEUTICALS—0.2% | | | | |

| Intarcia Therapeutics, Inc. , Series DD*,@,(a) | | 7,588 | | 203,435 |

| TOTAL PREFERRED STOCKS | | | | |

| (Cost $1,327,445) | | | | 992,843 |

| RIGHTS—1.3% | | SHARES | | VALUE |

| BIOTECHNOLOGY—1.3% | | | | |

| Tolero CDR*,@,(a),(c) | | 422,928 | | 1,379,227 |

| (Cost $226,186) | | | | 1,379,227 |

- 31 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2018 (Unaudited) (Continued)

| | | | | |

| REAL ESTATE INVESTMENT TRUST—2.1% | | SHARES | | | VALUE |

| SPECIALIZED—2.1% | | | | | |

| CyrusOne, Inc. | | 19,723 | | $ | 1,056,956 |

| SBA Communications Corp. , Cl. A* | | 7,324 | | | 1,173,524 |

| | | | | | 2,230,480 |

| TOTAL REAL ESTATE INVESTMENT TRUST | | | | | |

| (Cost $2,045,688) | | | | | 2,230,480 |

| SPECIAL PURPOSE VEHICLE—0.3% | | SHARES | | | VALUE |

| CONSUMER FINANCE—0.3% | | | | | |

| JS Kred SPV I, LLC. *,@,(a) | | 240,362 | | | 294,540 |

| (Cost $240,362) | | | | | 294,540 |

| Total Investments | | | | | |

| (Cost $94,883,112) | | 97.9 | % | $ | 103,291,963 |

| Affiliated Securities (Cost $747,040) | | | | | 498,027 |

| Unaffiliated Securities (Cost $94,136,072) | | | | | 102,793,936 |

| Other Assets in Excess of Liabilities | | 2.10 | % | | 2,219,842 |

| NET ASSETS | | 100.0 | % | $ | 105,511,805 |

# American Depositary Receipts.

(a) Security is valued in good faith at fair value determined using significant unobservable inputs pursuant to procedures established by the

Board.

(b) Deemed an affiliate of the Alger fund complex during the year in accordance with Section 2(a)(3) of the Investment Company Act of

1940. See Affiliated Securities Note 11.

(c) Contingent Deferred Rights.