OMB APPROVAL

OMB Number: 3235-0570

Expires: January 31, 2017

Estimated average burden

hours per response……20.6

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07986

The Alger Institutional Funds

(Exact name of registrant as specified in charter)

360 Park Avenue South New York, New York 10010

(Address of principal executive offices) (Zip code)

Mr. Hal Liebes

Fred Alger Management, Inc.

360 Park Avenue South

New York, New York 10010

(Name and address of agent for service)

Registrant's telephone number, including area code: 212-806-8800

Date of fiscal year end: October 31

Date of reporting period: April 30, 2016

ITEM 1. REPORT(S) TO STOCKHOLDERS.

Table of Contents

The Alger Institutional Funds

|

| Shareholders’ Letter | 1 |

| Fund Highlights | 11 |

| Portfolio Summary | 15 |

| Schedules of Investments | 16 |

| Statements of Assets and Liabilities | 37 |

| Statements of Operations | 41 |

| Statements of Changes in Net Assets | 43 |

| Financial Highlights | 47 |

| Notes to Financial Statements | 57 |

| Additional Information | 79 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online.

When documents such as prospectuses and annual and semi-annual reports are

available, we’ll send you an e-mail notification with a convenient link that will take you

directly to the fund information on our website. To sign up for this free service, simply

enroll at www.icsdelivery.com/alger.

Shareholders' Letter April 30, 2016

Dear Shareholders,

Investor Stampede Creates Risks and Opportunities

Gary Larson’s quirky cartoon series “The Far Side” draws chuckles by having animals

exhibit human-like behavior. In one popular cartoon, a massive bison stampede extends

to the horizon. One insightful bison quips to a neighboring beast “As if we all knew where

we’re going.” The six-month reporting period ended April 30 was notable as a period filled

with economic uncertainty, diverging global monetary policies, and significant pressure on

interest rates. As with the cartoon, where this takes us as investors is unclear, yet in such

periods of deep uncertainty we are reminded that the best decisions are those that are the

most thoughtful and not based upon emotion. Many investors, in an unquenchable thirst

for income (and a misguided flight to “safety”) have rushed to bond-like equities, that is,

equities that pay steady dividends. The end result was striking. While the S&P 500 index

gained 0.43%, the Telecomm, Utilities, and Consumer Staples sectors climbed 14.68%,

12.90%, and 6.02%, respectively. These sectors have some of the poorest long-term growth

prospects in the current economic environment. On the other hand, higher growth sectors

like Information Technology, Health Care, and Consumer Discretionary each sustained

losses.

We have learned in our 52 years of investing that there is no free lunch. Success in investing is

not achieved by considering one factor, such as dividend yield, but instead by understanding

companies, their management, their industries, and their competitors. It is with this more

complete view that high-quality companies with strong growth potential can be identified.

Such companies, we maintain, can potentially provide investors with wealth creation from

capital appreciation and with protection from the erosion of inflation upon their savings.

Stampedes, of course, can have dire consequences. The recent investor stampede, we believe,

is dangerous, as investors have increased their exposure to the risk of higher interest rates

and, at the same time, the relatively high valuations of stocks with generally poor growth

prospects. We think the opportunities, long term, lie in the opposite direction. In particular,

these investors may miss the attractive investment opportunities that can be found within the

most vibrant industries in the U.S. and the world. America is seen as a leader in innovation

in the Health Care and IT sectors, and has the richest and most diverse consumer market in

the world. We believe it is within these sectors that superior companies and investments for

long-term growth and capital appreciation can be found.

Investing in overseas markets is more challenging with different dynamics at play. The

widely followed MSCI ACWI ex USA and MSCI Emerging Markets indices declined 1.51%

and 0.01%, respectively, during the reporting period with concerns over commodity prices

contributing to weakening investor sentiment. In many overseas markets, this is entirely

logical as the economies of many countries are strongly tied to their roles as commodities

producers. As in the U.S., defensive sectors tended to outperform abroad. Nevertheless,

international markets also have sectors that offer strong potential for long-term growth.

The rising middle class in many international markets is creating increased demand for

goods and services, which in turn is creating opportunities for leading companies. Our

team of international and emerging markets portfolio managers and analysts has a depth of

- 1 -

experience in navigating foreign markets and identifying through fundamental research high-

quality growth companies across the globe. In these markets, diversification is paramount,

so our international funds are well diversified, typically owning companies across the globe

and across industries.

Oil and the U.S. Economy

From late 2013 until the start of the reporting period, the price of West Texas Intermediate

(WTI) fell from $110.62 a barrel to $46.12. It then declined to a low of $26.19 a barrel as

of February 11, which was a 43.20% drop. The decline was accompanied by an 11.43%

decline of the S&P 500. In both 2015 and early 2016, many investors misread the decline in

oil as a harbinger of a U.S. recession in 2016. We have consistently argued otherwise, noting

that while cheap oil prices would, not surprisingly, drive down earnings in the energy and

closely related sectors, there were broad benefits to the U.S. economy from lower energy

prices. Cheap oil has bolstered Americans’ finances by slashing energy costs and allowing

Americans to strengthen their personal balance sheets by increasing their savings. It has

also supported retail shopping and spending on homes. The U.S. housing market continues

to improve in a steady fashion. Many indicators of consumer spending like ecommerce,

travel, leisure, automotive, and home durables are quite healthy, despite the weakness

reported in headlines about department store sales and the sales of other “old” economy

retailers. Changing patterns of consumer preferences – largely based, in our view, on both

ecommerce technology and on the rise of younger generations of Americans (the X and Y

generations) as the baby boomers increasingly retire – is a large phenomenon that creates

challenges for companies that have failed to adapt to the “new” marketplace and great

opportunities for those that have helped define it in our time. Amazon.com, Inc., Netflix,

Inc., Alphabet, Inc. (formerly Google), and Apple, Inc. are all doing quite well in this new

American marketplace, while the landscape, especially in retail, is littered with companies,

once good or even great, but today struggling to adapt their business models to the new and

obvious reality.

So despite fears, corporate fundamentals are fine in the U.S. S&P 500 earnings ex-materials

and ex-energy grew a healthy 6.3% in 2015, despite the additional headwind of a strong U.S.

dollar weighing on both exports and foreign earnings. For the first quarter of 2016, overall

results for the S&P 500 slowed from that pace, but we expect continued growth in earnings

in 2016 (again, ex-materials and ex-energy, though these might actually contribute to

earnings growth on a reported basis through declining losses in these sectors). We note that

oil appears to have bottomed in February and has since rebounded to close the reporting

period at $45.98. Investor sentiment remains very cautious in our view, and indeed almost

bearish, but there has been a significant rally in equities of late, with the S&P 500 generating

a 13.39% return from February 12 to April 30.

Global Economy Weakens

Concerns over global economic growth continue. In early 2015, the International Monetary

Fund forecasted that the global economy would grow 3.3% in 2015 and 3.8% in 2016. In

October, it lowered those numbers to 3.1% for 2015 and 3.6% for this year. It maintained

its 2015 estimate in January, but lowered its 2016 estimate to 3.4%. Also during the reporting

period, estimates for global corporate earnings per share for the MSCI World Index were

revised downward each month, declining from $106.72 in November to $101.20 as of April

30.

- 2 -

We are encouraged by the actions of many central banks across the globe, including the Bank

of Japan (BOJ), the People’s Bank of China, and the European Central Bank, to provide

additional economic stimulus. The BOJ, for its part, joined a handful of other countries that

have maintained negative interest rates. Many central banks have also expressed a willingness

to provide additional stimulus, and in the U.S., the Federal Reserve is taking a cautious

approach to normalizing monetary policy after raising the fed funds rate in December.

We note, as we did in the fall of 2015 in an Alger market commentary, that monetary

policy is not sufficient to stimulate fundamental, lasting growth in any economy. We hope

to see future governmental actions to improve structural growth in Europe, Asia, and other

foreign markets, and certainly we see that austerity policies are fading globally.

Further, in the significant changes occurring in international markets and economies, we

see many opportunities for investors. Economic and political concerns have dominated

investors’ mindset for a significant time now. But, as in the U.S., there are many companies

forging ahead in their markets and globally, showing both solid earnings growth and strong

fundamentals. We are always on the lookout for companies that are disrupting traditional

business models by exploiting large-scale changes. The internet continues to be an investable

trend but, especially in emerging markets, adoption of Western technology and lifestyles

(whether directly or in copycat fashion) is meeting with notable success in many regions

and sectors.

The U.S. Dollar, Emerging Markets, and Interest Rates

The previous end of the U.S. asset buying program, or quantitative easing, combined with

the Federal Reserve’s start to raising interest rates and anticipation of domestic economic

growth, has supported a strong U.S. dollar, especially relative to countries that have been

increasing monetary stimulus. At the start of the reporting period, the U.S. Dollar Index,

which measures U.S. currency against currencies of trading partners, was at 96.89, up

considerably from 79.14 in early 2014. Later in the reporting period, the Federal Reserve

signaled that it would take a cautious approach to raising interest rates, which caused the

strengthening of the U.S. dollar to moderate slightly, and the U.S. Dollar Index closed the

reporting period at 93.80. As mentioned previously, investors have fretted over the impact

of a strong dollar on U.S. exports and foreign earnings. We think the strong dollar does pose

challenges to U.S. exporters, especially those of undifferentiated commodity-like products

or services. In the end, however, we think U.S. companies with value-added products

and service models that are differentiated from the competition will do fine. Since global

competition is fierce, foreign companies seeking to succeed will invest in superior products

and services that will help them obtain their goals. We think there are many U.S. companies

that offer highly competitive products and services to the global market, even with the

recent disadvantage of a stronger U.S. dollar.

Finally, it’s important to note that the strong U.S. dollar has also driven periods of capital

outflows from countries with weaker currencies, especially emerging markets. We believe

the sensitivity of global markets to the U.S. dollar is likely to cause the Federal Reserve to

exercise extreme caution when normalizing monetary policy. At the same time, an estimated

$8 trillion in debt is trading globally with negative yields. When the Federal Reserve eventually

takes further actions to normalize policy, it’s likely that higher interest rates will attract even

more investors to U.S. debt, which could limit increases in yields here at home.

- 3 -

The Appeal of Growth Equities and the Downside of the Investor Stampede

We believe growth stocks are well positioned to outperform the market and especially bond-

like equites that have recently reached extreme valuations. The recent market action has

left traditional growth stocks at attractive valuations, especially when assessing PEG ratios.

PEG ratios are determined by dividing a company’s price-to-earnings ratio, or P/E, by its

expected earnings growth rate. As of April 30 of this year, the 12-month forward earnings

PEG for the Russell 1000 Growth Index was 42% lower than that of the Russell 1000 Value

Index. For most of 2016, the difference in PEGs has exceeded anything that has occurred

since at least 2002. In addition, bond-like sectors such as Utilities and Consumer Staples

are trading at over a 20% premium to their 20-year average P/E ratio while growth sectors

like Information Technology and Health Care are trading at double-digit discounts. From a

historical perspective, low P/E ratios have typically indicated strong potential for stocks to

outperform and we believe the current valuations of growth stocks are no exception.

Over the long term, equity returns are driven by corporate fundamentals, including earnings

and revenue growth. While dividend yields play an important role in the total return an

investor should expect from equities, it is a mistake, in our view, to focus solely, or overly, on

the dividend yield of a stock itself. It is, after all, a company’s fundamental success growing

its sales and profits that ultimately will deliver the cash flow to support dividends and

future dividend growth. The recent stampede into bond-like equities shows many signs of

investors’ failure to discriminate between companies with strong longer term fundamentals

and those that simply happen to pay a relatively higher dividend yield today. Much like

fixed-income securities, these bond-like equities will be very interest-rate sensitive. Even a

small change in interest rates or inflation could hurt the performance of bond-like stocks,

especially those trading at high valuations with poor growth prospects or leveraged balance

sheets.

Reasons for Optimism

Concerns over global growth are likely to drive market volatility, but we maintain that the

U.S. will continue to be an economic leader. April marked the 74th consecutive month of

private-sector job growth in the U.S., which is an unprecedented accomplishment. Over the

last year, the majority of those who have returned to the labor force have been from among

the long-term unemployed, which is a category of Americans that has traditionally faced

substantial challenges with finding work. In addition to steady job creation, the nation’s

5.0% unemployment rate implies that the job market is healthy. We continue to believe that

low oil prices combined with low inflation and the Federal Reserve’s cautious approach to

raising interest rates will continue to support the country’s economy.

Corporate America is also strong. In the fourth quarter, S&P 500 companies ex-financials

held $1.44 trillion in cash, according to FactSet Research Systems, Inc. The figure represents

a 0.5% year-over-year decline, but is still the third-highest level in 10 years. Fixed capital

expenditures during the quarter also declined when compared to the record level of outlays

during the same quarter of 2014. Yet, the $170.4 billion in outlays for the final quarter

of 2015 represented the third-highest level in 10 years, despite a 41% drop in capital

expenditures by energy companies. Corporations are also buying back stock at a rapid pace,

with approximately 30% of S&P 500 constituents having reduced their share count by at

least 4% during the first quarter, according to S&P Capital IQ.

- 4 -

We urge investors to carefully assess the appeal of growth equities and to evaluate the role

of bond-like equities in their investment strategies. We are in an era of rapid and dynamic

change. New technologies such as the internet, smartphones, ebooks, and social media have

reached 50% market penetration in a fraction of the time that older innovations such as

washing machines, dishwashers, and landline telephones required. Medical innovation in

orthopedic, cardiac, and cancer treatments (to name only a few) has advanced and will

continue to advance in ways that were unimaginable only a generation or so ago. We think

every prudent, long-term investor should have a portfolio “overweight” in the industries,

companies, and trends that are changing nearly every aspect of modern day life.

Portfolio Matters

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund returned -4.12% for the fiscal six-month

period ended April 30, 2016, compared to the -1.37% return of the Russell 1000 Growth

Index.

During the period, the largest sector weightings were Information Technology and

Consumer Discretionary. The largest sector overweight was Information Technology

and the largest sector underweight was Consumer Staples. Stock selection resulted in the

Consumer Discretionary sector contributing to relative performance, while other sectors

detracted from results.

Among the most important relative contributors were Apple, Inc.; Newell Brands, Inc.;

Honeywell International, Inc.; and Edwards Lifesciences Corp. Shares of social network

provider Facebook, Inc., Cl. A also contributed to performance. Facebook performed

strongly in response to the company’s social network continuing to take advertising market

share from print and television media. We believe investors were also encouraged by the

growth of Instagram, which is the company’s video- and photo-sharing network, and by the

potential for Facebook to further grow advertising revenues.

Conversely, detracting from overall results on a relative basis were Allergan PLC.; Vertex

Pharmaceuticals, Inc.; Norwegian Cruise Line Holdings Ltd.; and Anadarko Petroleum

Corp. Also detracting from performance were shares of LinkedIn Corporation Cl A. The

company operates the world’s largest social network for professionals and provides services

for recruiters and human resource professionals. LinkedIn also offers digital advertising and

premium memberships. During the first quarter, the company disclosed disappointing sales

and it provided weak profit guidance. It said Europe and Asia were weak areas.

Alger Capital Appreciation Focus Fund

The Alger Capital Appreciation Focus Fund returned -4.28% for the fiscal six-month period

ended April 30, 2016, compared to the -1.37% return of its benchmark, the Russell 1000

Growth Index.

During the reporting period, the largest sector weightings were Information Technology

and Health Care. The largest sector overweight was Information Technology and the largest

sector underweight was Consumer Staples. Relative outperformance in the Information

Technology and Industrials sectors was the most important contributor to performance,

while Health Care and Financials were among sectors that detracted from results.

- 5 -

Among the most important relative contributors were Apple, Inc.; Honeywell International,

Inc.; Newell Brands, Inc.; and HD Supply Holdings, Inc. Shares of social network provider

Facebook, Inc., Cl. A also contributed to performance. The stock performed strongly

in response to reasons identified in the Alger Capital Appreciation Institutional Fund

discussion.

Conversely, detracting from overall results on a relative basis were Norwegian Cruise Line

Holdings Ltd.; Vertex Pharmaceuticals, Inc.; Delphi Automotive PLC.; and Shire PLC. Shares

of Allergan PLC. also detracted from results. The company manufactures and distributes

both branded and generic pharmaceuticals globally. With an upcoming presidential

election, investors were concerned that increased government regulatory intervention could

negatively affect the company’s closing of a planned merger with Pfizer, Inc. The deal was

eventually halted by regulators.

Alger Mid Cap Growth Institutional Fund

The Alger Mid Cap Growth Institutional Fund returned -6.12% for the fiscal six-month

period ended April 30, 2016, compared to the -1.54% return of Russell Midcap Growth

Index.

During the reporting period, the largest sector weightings were Consumer Discretionary

and Information Technology. The largest sector overweight was Information Technology

and the largest sector underweight was Consumer Staples. Stock selection in the Consumer

Discretionary, Materials and Energy sectors contributed to relative performance, while

Health Care and Information Technology were among sectors that detracted from results.

Among the most important relative contributors were Newell Brands, Inc.; Broadcom Ltd.;

Coach, Inc.; and CBS Corp., Cl. B. Shares of HD Supply Holdings, Inc. also contributed to

performance. HD Supply Holdings is an industrial distributor of products for infrastructure,

housing, commercial buildings, and other construction applications. During the first quarter,

investors responded favorably to the healthy residential housing market and stronger-than-

expected guidance from the company. Investors also responded favorably to the company

refinancing expensive debt.

Conversely, detracting from overall results on a relative basis were NetScout Systems,

Inc.; Norwegian Cruise Line Holdings Ltd.; Portola Pharmaceuticals, Inc.; and DexCom,

Inc. Shares of Royal Caribbean Cruises Ltd. also detracted from results. Royal Caribbean

is a leading cruise operator. Investor concerns over the impact of a potential economic

slowdown on consumer cyclicals caused shares of Royal Caribbean to underperform.

We believe investors’ outlook for the economy has improved, but performance of Royal

Caribbean stock did not initially bounce back, perhaps because of concerns over terrorism.

Alger Small Cap Growth Institutional Fund

The Alger Small Cap Growth Institutional Fund returned -9.54% for the fiscal six-month

period ended April 30, 2016, compared to the -4.96 % return of the Russell 2000 Growth

Index.

During the period, the largest sector weightings were Information Technology and Health

Care. The largest sector overweight was Information Technology and the largest sector

underweight was Consumer Discretionary. The Energy and Health Care sectors provided

- 6 -

the largest contributions to relative performance, while Information Technology and

Consumer Discretionary were among sectors that detracted from results.

Among the most important relative contributors were CyrusOne, Inc.; PRA Health Sciences,

Inc.; Sun Hydraulics Corp.; and FEI Co. Shares of Burlington Stores, Inc. also contributed

to performance. Burlington Stores is a retailer of branded clothing and other apparel in

the U.S. The company’s off-price retail model has benefitted from a lackluster economic

environment highlighted by wages not keeping pace with increasing clothing prices. As a

result, Burlington reported revenues that were in line with expectations and earnings growth

for 2015 despite weak fourth-quarter margins due in part to mild fall and winter weather

hurting sales of warm clothing.

Conversely, detracting from overall results on a relative basis were WisdomTree Investments,

Inc.; Proofpoint, Inc.; and Incyte Corp. Shares of SPS Commerce, Inc. also detracted from

results. The company offers cloud-based software that enhances how suppliers, retailers,

and distributors manage and fulfill customer orders. The company reported fourth-quarter

earnings that were slightly above expectations, but it issued disappointing guidance for

2016. This past quarter, management said the company faced challenges in hiring additional

salespeople due to the improving labor market; therefore, SPS Commerce expects to ramp

up hiring this year, which could delay re-acceleration in recurring revenue growth.

I thank you for putting your trust in Alger.

Daniel C. Chung, CFA

Chief Investment Officer

Fred Alger Management, Inc.

As of April 30, 2016, the following companies represented the stated percentages of Alger

assets under management: Amazon.com, Inc., 3.56%; Netflix, Inc.; 0.27%; Alphabet, Inc.;

(formerly Google), 05.81%; and Apple, Inc., 4.15%.

Investors cannot invest directly in an index. Index performance does not

reflect the deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general

information of shareholders of the funds. This report is not authorized for distribution to

prospective investors in a fund unless preceded or accompanied by an effective prospectus

for the fund. Fund returns represent the fiscal period return of Class I shares.

The performance data quoted represent past performance, which is not an

indication or guarantee of future results.

Standardized performance results can be found on the following pages. The investment

return and principal value of an investment in a fund will fluctuate so that an investor’s shares,

when redeemed, may be worth more or less than their original cost. Current performance

- 7 -

may be lower or higher than the performance quoted. For performance data current to the

most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the funds’ management in this report are as of the date of the

Shareholders’ Letter and are subject to change at any time subsequent to this date. There

is no guarantee that any of the assumptions that formed the basis for the opinions stated

herein are accurate or that they will materialize. Moreover, the information forming the

basis for such assumptions is from sources believed to be reliable; however, there is no

guarantee that such information is accurate. Any securities mentioned, whether owned in a

fund or otherwise, are considered in the context of the construction of an overall portfolio

of securities and therefore reference to them should not be construed as a recommendation

or offer to purchase or sell any such security. Inclusion of such securities in a fund and

transactions in such securities, if any, may be for a variety of reasons, including, without

limitation, in response to cash flows, inclusion in a benchmark, and risk control. The

reference to a specific security should also be understood in such context and not viewed as

a statement that the security is a significant holding in a fund. Please refer to the Schedules

of Investments for each fund that is included in this report for a complete list of fund

holdings as of April 30, 2016. Securities mentioned in the Shareholders’ Letter, if not found

in the Schedule of Investments, may have been held by the funds during the six-month

period.

A Word about Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends

to be higher in relation to their companies’ earnings and may be more sensitive to market,

political and economic developments. Investing in the stock market involves gains and

losses and may not be suitable for all investors. Stocks of small- and mid-sized companies

are subject to greater risk than stocks of larger, more established companies owing to such

factors as limited liquidity, inexperienced management, and limited financial resources.

Funds that participate in leveraging, such as the Capital Appreciation Institutional Fund, are

subject to the risk that the cost of borrowing money to leverage will exceed the returns for

securities purchased or that the securities purchased may actually go down in value; thus, a

fund’s net asset value can decrease more quickly than if the fund had not borrowed.

A small investment in derivatives could have a potentially large impact on a fund’s

performance. When purchasing options, a fund bears the risk that if the market value of

the underlying security does not move to a level that would make exercise of the option

profitable, the option will expire unexercised. When a call option written by a fund is

exercised, the fund will not participate in any increase in the underlying security’s value

above the exercise price. When a put option written by a fund is exercised, the fund will

be required to purchase the underlying security at a price in excess of its market value. Use

of options on securities indexes is subject to the risk that trading in the options may be

interrupted if trading in certain securities included in the index is interrupted, the risk that

price movements in a fund’s portfolio securities may not correlate precisely with movements

in the level of an index, and the risk that Fred Alger Management, Inc. may not predict

correctly movements in the direction of a particular market or of the stock market generally.

- 8 -

Because certain options may require settlement in cash, a fund may be forced to liquidate

portfolio securities to meet settlement obligations. For a more detailed discussion of the

risks associated with these funds, please see the prospectus.

Before investing, carefully consider a fund’s investment objective, risks, charges,

and expenses. For a prospectus or a summary prospectus containing this and other

information about The Alger Institutional Funds call us at (800) 992-3863 or visit us

at www.alger.com. Read it carefully before investing.

Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext,

SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Definitions:

• S&P 500 index: An index of large company stocks considered representative

of the U.S. stock market.

• Morgan Stanley Capital International (MSCI) All Country World Index

(ACWI) ex USA is an unmanaged, market capitalization-weighted index de-

signed to provide a broad measure of equity market performance throughout

the world, including both developing and emerging markets, but excluding

the United States.

• MSCI Emerging Markets Index: A free float-adjusted market capitalization

index designed to measure equity market performance in the global emerging

markets.

• Russell 3000 Growth Index: An index of common stocks designed to track

performance of companies with greater than average growth orientation in

general.

• Russell 1000 Growth Index: An index of common stocks designed to track

performance of large-capitalization companies with greater than average

growth orientation.

• Russell 1000 Value Index: An index designed to track the performance of

large-capitalization stocks that have value characteristics.

• Russell Midcap Growth Index: An index of common stocks designed to

track performance of medium-capitalization companies with greater than

average growth orientation.

• Russell 2000 Growth Index: An index of common stocks designed to track

performance of small-capitalization companies with greater than average

growth orientation.

• The MSCI World Index: An index that captures large and mid cap repre-

sentation across 23 Developed Markets (DM) countries. The index covers

approximately 85% of the free float-adjusted market capitalization in each

country.

• FactSet Research Systems, Inc. is a multinational financial data and software

company.

• S&P Capital IQ provides research, data, and analysis on capital markets and

- 9 -

other topics for investment managers, investment banks, private equity funds,

advisory firms, corporations and universities.

• The U.S. Dollar Index measures US currency against currencies of trading

partners.

| | | | | | | | | |

| FUND PERFORMANCE AS OF 3/31/16 (Unaudited) |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | 1 | | 5 | | 10 | | SINCE | |

| | | YEAR | | YEARS | | YEARS | | INCEPTION | |

| Alger Capital Appreciation Class I (Inception 11/8/93) | | (2.10 | )% | 11.41 | % | 9.76 | % | 11.63 | % |

| Alger Capital Appreciation Class R (Inception 1/27/03)* | | (2.56 | )% | 10.86 | % | 9.21 | % | 11.07 | % |

| |

| Alger Capital Appreciation Focus Class A (Inception | | | | | | | | | |

| 12/31/12) | | (6.53 | )% | n/a | | n/a | | 13.67 | % |

| Alger Capital Appreciation Focus Class C (Inception | | | | | | | | | |

| 12/31/12) | | (3.03 | )% | n/a | | n/a | | 14.70 | % |

| Alger Capital Appreciation Focus Class I (Inception | | | | | | | | | |

| 11/8/93) | | (1.22 | )% | 10.49 | % | 6.03 | % | 8.18 | % |

| Alger Capital Appreciation Focus Class Z (Inception | | | | | | | | | |

| 12/31/12) | | (0.96 | )% | n/a | | n/a | | 16.03 | % |

| |

| Alger Mid Cap Growth Class I (Inception 11/8/93) | | (12.45 | )% | 6.51 | % | 4.30 | % | 11.28 | % |

| Alger Mid Cap Growth Class R (Inception 1/27/03)* | | (12.95 | )% | 5.95 | % | 3.76 | % | 10.72 | % |

| |

| Alger Small Cap Growth Class I (Inception 11/8/93) | | (17.72 | )% | 3.23 | % | 4.20 | % | 8.18 | % |

| Alger Small Cap Growth Class R (Inception 1/27/03)* | | (18.16 | )% | 2.71 | % | 3.69 | % | 7.66 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future

results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends

and capital gains.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R shares,

are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the higher

operating expenses of Class R shares.

- 10 -

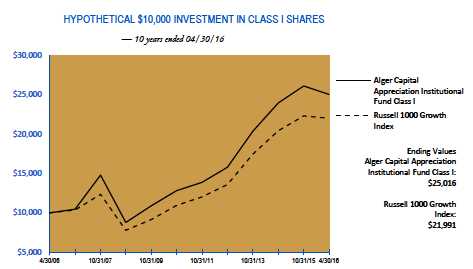

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2016 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital

Appreciation Institutional Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2016. Figures for the Alger Capital Appreciation Institutional Fund Class

I shares and the Russell 1000 Growth Index include reinvestment of dividends. Performance for the Alger Capital

Appreciation Institutional Fund Class R shares may vary from the results shown above due to differences in expenses

the class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees,

expenses, or taxes.

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 4/30/16 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARSr | | 11/8/1993 | |

| Class I (Inception 11/8/93) | (2.34 | )% | 10.34 | % | 9.60 | % | 11.53 | % |

| Class R (Inception 1/27/03)* | (2.82 | )% | 9.79 | % | 9.05 | % | 10.97 | % |

| Russell 1000 Growth Index | 1.07 | % | 11.44 | % | 8.20 | % | 8.51 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R

shares, are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the

higher operating expenses of Class R shares.

- 11 -

ALGER CAPITAL APPRECIATION FOCUS FUND

Fund Highlights Through April 30, 2016 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital

Appreciation Focus Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2016. Beginning December 31, 2012 Alger Capital Appreciation Focus

Fund changed its investment strategy to invest a substantial portion of its assets in a small number of issuers. The

figures for the Alger Capital Appreciation Focus Fund Class I shares and the Russell 1000 Growth Index include

reinvestment of dividends. Performance for the Alger Capital Appreciation Focus Fund Class A, Class C and Class Z

shares may vary from the results shown above due to differences in expenses the class bears. Investors cannot invest

directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 4/30/16 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | (2.67 | )% | 9.42 | % | 5.71 | % | 8.06 | % |

| Russell 1000 Growth Index | 1.07 | % | 11.44 | % | 8.20 | % | 8.51 | % |

| |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 12/31/2012 | |

| Class A (Inception 12/31/12) | (7.92 | )% | n/a | | n/a | | 12.69 | % |

| Class C (Inception 12/31/12) | (4.45 | )% | n/a | | n/a | | 13.68 | % |

| Class Z (Inception 12/31/12) | (2.40 | )% | n/a | | n/a | | 14.98 | % |

| Russell 1000 Growth Index | 1.07 | % | n/a | | n/a | | 14.99 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

- 12 -

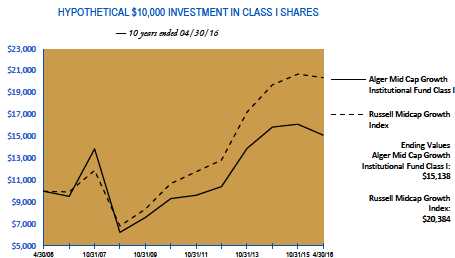

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2016 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Mid Cap

Growth Institutional Fund Class I shares and the Russell Midcap Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2016. Figures for the Alger Mid Cap Growth Institutional Fund Class I

shares and the Russell Midcap Growth Index include reinvestment of dividends. Performance for the Alger Mid Cap

Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses

the class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees,

expenses, or taxes.

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 4/30/16 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | (11.09 | )% | 5.53 | % | 4.23 | % | 11.21 | % |

| Class R (Inception 1/27/03)* | (11.54 | )% | 4.99 | % | 3.70 | % | 10.65 | % |

| Russell Midcap Growth Index | (4.13 | )% | 9.20 | % | 7.38 | % | 9.12 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R

shares, are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the

higher operating expenses of Class R shares.

- 13 -

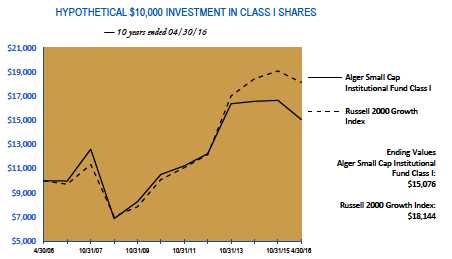

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2016 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Small Cap

Growth Institutional Fund Class I shares and the Russell 2000 Growth Index (an unmanaged index of common

stocks) for the ten years ended April 30, 2016. The figures for the Alger Small Cap Growth Institutional Fund Class

I shares and the Russell 2000 Growth Index include reinvestment of dividends. Performance for the Alger Small

Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses

the class bears. Investors cannot invest directly in any index. Index performance does not reflect deduction for fees,

expenses, or taxes.

| | | | | | | | |

| PERFORMANCE COMPARISON AS OF 4/30/16 |

| AVERAGE ANNUAL TOTAL RETURNS |

| | | | | | | | Since | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | 11/8/1993 | |

| Class I (Inception 11/8/93) | (13.72 | )% | 2.53 | % | 4.19 | % | 8.20 | % |

| Class R (Inception 1/27/03)* | (14.17 | )% | 2.03 | % | 3.68 | % | 7.68 | % |

| Russell 2000 Growth Index | (8.27 | )% | 7.15 | % | 6.14 | % | 6.62 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s

average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above

do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares.

Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost.

Current performance may be higher or lower than the performance quoted. For updated performance, visit us at www.alger.com or call

us at (800) 992-3863.

* Since inception performance is calculated from 11/08/93. Performance figures prior to 1/27/03, inception of Class R

shares, are those of the Fund's Class I Shares. The performance figures prior to 1/27/03 have been reduced to reflect the

higher operating expenses of Class R shares.

- 14 -

PORTFOLIO SUMMARY†

April 30, 2016 (Unaudited)

| | | | | | | | | | | | | |

| | | Alger Capital | | | | | | | | | | | |

| | | Appreciation Institutional | | | Alger Capital | | | Alger Mid Cap Growth | | | Alger Small Cap Growth | |

| SECTORS | | Fund | | | Appreciation Focus Fund | | | Institutional Fund | | | Institutional Fund | |

| Consumer Discretionary | | 18.4 | % | | 20.1 | % | | 27.1 | % | | 12.0 | % |

| Consumer Staples | | 8.2 | | | | 3.7 | | | 5.0 | | | 1.7 | |

| Energy | | 1.6 | | | | 1.4 | | | 1.0 | | | 1.6 | |

| Financials | | 3.1 | | | | 5.0 | | | 7.7 | | | 8.1 | |

| Health Care | | 18.3 | | | 18.0 | | | 15.7 | | | 28.7 | |

| Industrials | | 10.7 | | | | 8.3 | | | 15.9 | | | 10.3 | |

| Information Technology | | 33.1 | | | 36.8 | | | 22.4 | | | 31.7 | |

| Materials | | 1.2 | | | | 0.7 | | | 4.8 | | | 3.0 | |

| Telecommunication Services | 1.9 | | | | 1.5 | | | 0.0 | | | 0.0 | |

| Short-Term Investments and | | | | | | | | | | | | | |

| Net Other Assets | | 3.5 | | | | 4.5 | | | 0.4 | | | 2.9 | |

| | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % |

| |

| † Based on net assets for each Fund | | | | | | | | | | | |

- 15 -

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited)

| | | | | | |

| COMMON STOCKS—94.4% | | SHARES | | | | VALUE |

| ADVERTISING—0.0% | | | | | | |

| Choicestream, Inc.*,@,(a) | | 124,658 | $ | 52,356 |

| AEROSPACE & DEFENSE—5.1% | | | | | | |

| Honeywell International, Inc. | | 1,180,459 | | | 134,891,050 |

| Lockheed Martin Corp. | | 98,571 | | | | 22,905,929 |

| The Boeing Co. | | 175,763 | | | | 23,692,852 |

| TransDigm Group, Inc.* | | 15,600 | | | | 3,554,772 |

| | | | | | 185,044,603 |

| AIRLINES—1.2% | | | | | | |

| Delta Air Lines, Inc. | | 579,700 | | | | 24,156,099 |

| Southwest Airlines Co | | 424,500 | | | | 18,936,945 |

| Spirit Airlines, Inc.* | | 36,500 | | | | 1,603,445 |

| | | | | | 44,696,489 |

| ALTERNATIVE CARRIERS—0.6% | | | | | | |

| Level 3 Communications, Inc.* | | 416,109 | | | 21,745,856 |

| APPAREL ACCESSORIES & LUXURY GOODS—0.6% | | | | | | |

| Hanesbrands, Inc. | | 316,500 | | | | 9,187,995 |

| PVH Corp. | | 100,500 | | | | 9,607,800 |

| Under Armour, Inc., Cl. A* | | 59,500 | | | | 2,614,430 |

| | | | | | 21,410,225 |

| APPLICATION SOFTWARE—2.2% | | | | | | |

| Adobe Systems, Inc.* | | 357,554 | | | | 33,688,738 |

| salesforce.com, inc.* | | 625,234 | | | | 47,392,737 |

| | | | | | 81,081,475 |

| AUTO PARTS & EQUIPMENT—1.4% | | | | | | |

| Delphi Automotive PLC. | | 595,027 | | | | 43,811,838 |

| WABCO Holdings, Inc.* | | 60,300 | | | | 6,763,248 |

| | | | | | 50,575,086 |

| AUTOMOBILE MANUFACTURERS—0.1% | | | | | | |

| Tesla Motors, Inc.* | | 15,800 | | | | 3,804,008 |

| BIOTECHNOLOGY—4.7% | | | | | | |

| ACADIA Pharmaceuticals, Inc.* | | 286,100 | | | | 9,241,030 |

| Biogen, Inc.* | | 122,045 | | | | 33,561,155 |

| BioMarin Pharmaceutical, Inc.* | | 266,130 | | | | 22,535,888 |

| Celgene Corp.* | | 420,690 | | | | 43,503,553 |

| Gilead Sciences, Inc. | | 363,022 | | | | 32,022,171 |

| Incyte Corp.* | | 75,798 | | | | 5,477,921 |

| Vertex Pharmaceuticals, Inc.* | | 286,718 | | | | 24,181,796 |

| | | | | | 170,523,514 |

| BREWERS—1.5% | | | | | | |

| Molson Coors Brewing Co., Cl. B | | 571,576 | | | 54,659,813 |

| BROADCASTING—1.5% | | | | | | |

| CBS Corp., Cl. B | | 1,003,000 | | | 56,077,730 |

| BUILDING PRODUCTS—0.3% | | | | | | |

| Fortune Brands Home & Security, Inc. | | 183,497 | | | | 10,167,569 |

| Lennox International, Inc. | | 13,684 | | | | 1,846,656 |

| | | | | | 12,014,225 |

- 16 -

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | | VALUE |

| CABLE & SATELLITE—1.7% | | | | | | |

| Comcast Corporation, Cl. A | | 1,022,820 | $ | | 62,146,543 |

| CASINOS & GAMING—0.2% | | | | | | |

| Las Vegas Sands Corp. | | 120,700 | | | | 5,449,605 |

| COMMUNICATIONS EQUIPMENT—0.3% | | | | | | |

| Arista Networks, Inc.* | | 106,330 | | | | 7,083,705 |

| Cisco Systems, Inc. | | 144,400 | | | | 3,969,556 |

| | | | | | | 11,053,261 |

| CONSUMER FINANCE—0.1% | | | | | | |

| LendingClub Corp.* | | 397,300 | | | | 3,138,670 |

| DATA PROCESSING & OUTSOURCED SERVICES—4.0% | | | | | | |

| Alliance Data Systems Corp.* | | 18,427 | | | | 3,746,394 |

| Sabre Corp. | | 682,740 | | | | 19,765,323 |

| Visa, Inc., Cl. A | | 1,562,555 | | | 120,691,748 |

| | | | | | 144,203,465 |

| DIVERSIFIED CHEMICALS—0.2% | | | | | | |

| EI Du Pont de Nemours & Co. | | 118,400 | | | | 7,803,744 |

| DRUG RETAIL—1.5% | | | | | | |

| CVS Caremark Corp. | | 418,108 | | | | 42,019,854 |

| Walgreens Boots Alliance, Inc. | | 170,293 | | | | 13,500,829 |

| | | | | | 55,520,683 |

| ELECTRICAL COMPONENTS & EQUIPMENT—0.4% | | | | | | |

| Eaton Corp., PLC. | | 213,500 | | | 13,508,145 |

| ENVIRONMENTAL & FACILITIES SERVICES—0.4% | | | | | | |

| Stericycle, Inc.* | | 168,400 | | | 16,092,304 |

| FOOD RETAIL—0.6% | | | | | | |

| The Kroger Co. | | 575,252 | | | 20,358,168 |

| GENERAL MERCHANDISE STORES—0.9% | | | | | | |

| Dollar General Corp. | | 217,429 | | | | 17,809,609 |

| Dollar Tree, Inc.* | | 163,721 | | | | 13,050,201 |

| | | | | | 30,859,810 |

| HEALTH CARE EQUIPMENT—3.2% | | | | | | |

| Boston Scientific Corp.* | | 991,300 | | | | 21,729,296 |

| DexCom, Inc.* | | 188,100 | | | | 12,109,878 |

| Edwards Lifesciences Corp.* | | 273,000 | | | | 28,995,330 |

| Medtronic PLC. | | 234,900 | | | | 18,592,335 |

| STERIS PLC. | | 335,700 | | | | 23,723,919 |

| Stryker Corp. | | 111,300 | | | | 12,132,813 |

| | | | | | 117,283,571 |

| HEALTH CARE FACILITIES—0.7% | | | | | | |

| Acadia Healthcare Co., Inc.* | | 47,000 | | | | 2,969,930 |

| Amsurg Corp.* | | 120,300 | | | | 9,741,894 |

| HCA Holdings, Inc.* | | 170,047 | | | | 13,709,189 |

| | | | | | 26,421,013 |

| HOME ENTERTAINMENT SOFTWARE—1.0% | | | | | | |

| Activision Blizzard, Inc. | | 165,954 | | | | 5,720,434 |

| Electronic Arts, Inc.* | | 502,800 | | | | 31,098,180 |

| | | | | | 36,818,614 |

- 17 -

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | | VALUE |

| HOME IMPROVEMENT RETAIL—0.8% | | | | | | |

| The Home Depot, Inc. | | 220,807 | $ | | 29,563,849 |

| HOTELS RESORTS & CRUISE LINES—1.4% | | | | | | |

| Ctrip.com International Ltd.#* | | 299,894 | | | | 13,078,377 |

| Norwegian Cruise Line Holdings Ltd.* | | 486,000 | | | | 23,760,540 |

| Royal Caribbean Cruises Ltd. | | 189,300 | | | | 14,651,820 |

| | | | | | 51,490,737 |

| HOUSEWARES & SPECIALTIES—1.9% | | | | | | |

| Newell Brands, Inc. | | 1,534,493 | | | | 69,880,811 |

| HYPERMARKETS & SUPER CENTERS—0.5% | | | | | | |

| Costco Wholesale Corp. | | 123,000 | | | 18,219,990 |

| INDUSTRIAL CONGLOMERATES—0.8% | | | | | | |

| 3M Co. | | 70,100 | | | | 11,733,338 |

| General Electric Co. | | 584,189 | | | | 17,963,812 |

| | | | | | 29,697,150 |

| INDUSTRIAL GASES—0.2% | | | | | | |

| Air Products & Chemicals, Inc. | | 39,027 | | | | 5,693,649 |

| INTEGRATED OIL & GAS—0.3% | | | | | | |

| TOTAL SA# | | 207,400 | | | 10,525,550 |

| INTEGRATED TELECOMMUNICATION SERVICES—1.3% | | | | | | |

| AT&T, Inc. | | 661,400 | | | | 25,675,548 |

| Verizon Communications, Inc. | | 433,600 | | | | 22,087,584 |

| | | | | | 47,763,132 |

| INTERNET RETAIL—4.3% | | | | | | |

| Amazon.com, Inc.* | | 223,571 | | | 147,465,196 |

| NetFlix, Inc.* | | 99,996 | | | | 9,002,640 |

| The Priceline Group, Inc.* | | 1,400 | | | | 1,881,124 |

| | | | | | 158,348,960 |

| INTERNET SOFTWARE & SERVICES—12.8% | | | | | | |

| Alphabet, Inc., Cl. C* | | 352,219 | | | 244,091,289 |

| comScore, Inc.* | | 225,400 | | | | 6,901,748 |

| Facebook, Inc., Cl. A* | | 1,403,932 | | | 165,074,325 |

| LinkedIn Corp., Cl. A* | | 81,036 | | | | 10,154,621 |

| Palantir Technologies, Inc., Cl. A*,@ | | 239,030 | | | | 2,629,330 |

| Twitter, Inc.* | | 67,900 | | | | 992,698 |

| Yahoo! Inc.* | | 1,035,148 | | | | 37,886,417 |

| | | | | | 467,730,428 |

| INVESTMENT BANKING & BROKERAGE—0.5% | | | | | | |

| Morgan Stanley | | 543,430 | | | | 14,705,216 |

| The Goldman Sachs Group, Inc. | | 29,000 | | | | 4,759,190 |

| | | | | | 19,464,406 |

| LEISURE PRODUCTS—0.5% | | | | | | |

| Coach, Inc. | | 471,200 | | | 18,975,224 |

| LIFE SCIENCES TOOLS & SERVICES—2.1% | | | | | | |

| Thermo Fisher Scientific, Inc. | | 518,779 | | | 74,833,871 |

| MANAGED HEALTH CARE—2.3% | | | | | | |

| Aetna, Inc. | | 116,557 | | | | 13,085,854 |

| Humana, Inc. | | 50,200 | | | | 8,888,914 |

- 18 -

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | | VALUE |

| MANAGED HEALTH CARE—(CONT.) | | | | | | |

| UnitedHealth Group, Inc. | | 470,204 | $ | | 61,916,463 |

| | | | | | 83,891,231 |

| MOVIES & ENTERTAINMENT—0.5% | | | | | | |

| The Walt Disney Co. | | 67,865 | | | | 7,007,740 |

| Time Warner, Inc. | | 127,952 | | | | 9,614,313 |

| | | | | | 16,622,053 |

| OIL & GAS EQUIPMENT & SERVICES—0.6% | | | | | | |

| Halliburton Company | | 294,991 | | | | 12,186,078 |

| Schlumberger Ltd. | | 41,400 | | | | 3,326,076 |

| Weatherford International PLC.* | | 694,900 | | | | 5,649,537 |

| | | | | | 21,161,691 |

| OIL & GAS EXPLORATION & PRODUCTION—0.7% | | | | | | |

| EOG Resources, Inc. | | 242,400 | | | | 20,027,088 |

| Pioneer Natural Resources Co. | | 35,100 | | | | 5,830,110 |

| | | | | | 25,857,198 |

| OTHER DIVERSIFIED FINANCIAL SERVICES—0.5% | | | | | | |

| Bank of America Corp. | | 1,301,243 | | | 18,946,098 |

| PACKAGED FOODS & MEATS—0.5% | | | | | | |

| Mead Johnson Nutrition Co., Cl. A | | 21,800 | | | | 1,899,870 |

| The Kraft Heinz Co. | | 194,000 | | | | 15,145,580 |

| TreeHouse Foods, Inc.* | | 25,500 | | | | 2,254,200 |

| | | | | | 19,299,650 |

| PHARMACEUTICALS—5.2% | | | | | | |

| Allergan PLC.* | | 365,010 | | | | 79,046,566 |

| Bristol-Myers Squibb Co. | | 837,940 | | | | 60,482,509 |

| Eli Lilly & Co. | | 207,900 | | | | 15,702,687 |

| Pacira Pharmaceuticals, Inc.* | | 305,694 | | | | 16,541,102 |

| Pfizer, Inc. | | 334,300 | | | | 10,934,953 |

| Shire PLC. | | 116,632 | | | | 7,278,817 |

| | | | | | 189,986,634 |

| RAILROADS—0.3% | | | | | | |

| Union Pacific Corp. | | 136,846 | | | | 11,937,077 |

| REGIONAL BANKS—0.2% | | | | | | |

| Citizens Financial Group, Inc. | | 350,000 | | | | 7,997,500 |

| RESEARCH & CONSULTING SERVICES—0.5% | | | | | | |

| Verisk Analytics, Inc., Cl. A* | | 244,800 | | | 18,991,584 |

| RESTAURANTS—1.4% | | | | | | |

| McDonald's Corp. | | 166,294 | | | | 21,034,528 |

| Starbucks Corp. | | 512,973 | | | | 28,844,472 |

| | | | | | 49,879,000 |

| SECURITY & ALARM SERVICES—0.6% | | | | | | |

| Tyco International PLC. | | 523,373 | | | 20,160,328 |

| SEMICONDUCTORS—2.5% | | | | | | |

| Broadcom Ltd. | | 274,560 | | | | 40,017,120 |

| Microsemi Corp.* | | 636,000 | | | | 21,490,440 |

| NXP Semiconductors NV* | | 350,397 | | | | 29,881,856 |

| | | | | | 91,389,416 |

- 19 -

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | | | VALUE |

| SOFT DRINKS—2.1% | | | | | | | |

| Monster Beverage Corp.* | | 59,900 | $ | | 8,638,778 |

| PepsiCo, Inc. | | 648,547 | | | | | 66,774,399 |

| The Coca-Cola Co. | | 39,400 | | | | | 1,765,120 |

| | | | | | 77,178,297 |

| SPECIALIZED CONSUMER SERVICES—0.6% | | | | | | | |

| ServiceMaster Global Holdings, Inc.* | | 531,000 | | | 20,347,920 |

| SPECIALIZED FINANCE—0.2% | | | | | | | |

| S&P Global, Inc. | | 68,566 | | | | | 7,326,277 |

| SPECIALTY CHEMICALS—0.8% | | | | | | | |

| PPG Industries, Inc. | | 131,869 | | | | | 14,557,019 |

| The Sherwin-Williams Co. | | 55,800 | | | | | 16,031,898 |

| | | | | | 30,588,917 |

| SPECIALTY STORES—0.7% | | | | | | | |

| Signet Jewelers Ltd. | | 218,293 | | | 23,697,888 |

| SYSTEMS SOFTWARE—5.4% | | | | | | | |

| Microsoft Corp. | | 3,252,219 | | | 162,188,162 |

| Oracle Corp. | | 181,900 | | | | | 7,250,534 |

| Red Hat, Inc.* | | 180,400 | | | | | 13,235,948 |

| ServiceNow, Inc.* | | 224,834 | | | | | 16,071,134 |

| | | | | | 198,745,778 |

| TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—4.6% | | | | | | | |

| Apple, Inc. | | 1,791,321 | | | 167,918,431 |

| TOBACCO—1.5% | | | | | | | |

| Altria Group, Inc. | | 532,194 | | | | | 33,373,886 |

| Philip Morris International, Inc. | | 220,900 | | | | | 21,674,708 |

| | | | | | 55,048,594 |

| TRADING COMPANIES & DISTRIBUTORS—0.9% | | | | | | | |

| HD Supply Holdings, Inc.* | | 997,656 | | | 34,199,648 |

| TOTAL COMMON STOCKS | | | | | | | |

| (Cost $3,152,285,223) | | | | | 3,445,701,943 |

| PREFERRED STOCKS—0.5% | | SHARES | | | | | VALUE |

| ADVERTISING—0.1% | | | | | | | |

| Choicestream, Inc., Cl. A*,@,(a) | | 1,074,935 | | | | | 451,473 |

| Choicestream, Inc., Cl. B*,@,(a) | | 2,500,538 | | | | | 1,050,226 |

| | | | | | | | 1,501,699 |

| INTERNET SOFTWARE & SERVICES—0.3% | | | | | | | |

| Palantir Technologies, Inc., Cl. B*,@ | | 974,841 | | | | | 10,723,251 |

| Palantir Technologies, Inc., Cl. D*,@ | | 127,007 | | | | | 1,397,077 |

| | | | | | 12,120,328 |

| PHARMACEUTICALS—0.1% | | | | | | | |

| Intarcia Therapeutics, Inc.*,@ | | 111,655 | | | | | 3,690,198 |

| TOTAL PREFERRED STOCKS | | | | | | | |

| (Cost $13,252,335) | | | | | | | 17,312,225 |

| MASTER LIMITED PARTNERSHIP—0.7% | | SHARES | | | | | VALUE |

| ASSET MANAGEMENT & CUSTODY BANKS—0.7% | | | | | | | |

| The Blackstone Group LP. | | 953,062 | | | 26,152,021 |

| (Cost $30,055,316) | | | | | | | 26,152,021 |

- 20 -

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | |

| REAL ESTATE INVESTMENT TRUST—0.9% | | SHARES | | | VALUE |

| MORTGAGE—0.6% | | | | | |

| Blackstone Mortgage Trust, Inc., Cl. A | | 833,840 | | $ | 22,913,923 |

| SPECIALIZED—0.3% | | | | | |

| Crown Castle International Corp. | | 144,700 | | | 12,571,536 |

| TOTAL REAL ESTATE INVESTMENT TRUST | | | | | |

| (Cost $36,699,515) | | | | | 35,485,459 |

| Total Investments | | | | | |

| (Cost $3,232,292,389)(b) | | 96.5 | % | | 3,524,651,648 |

| Other Assets in Excess of Liabilities | | 3.5 | % | | 126,528,597 |

| NET ASSETS | | 100.0 | % | $ | 3,651,180,245 |

# American Depositary Receipts.

(a) Deemed an affiliate of the Alger fund complex during the year for purposes of Section 2(a)(3) of the Investment

Company Act of 1940. See Affiliated Securities in Notes to Financial Statements.

(b) At April 30, 2016, the net unrealized appreciation on investments, based on cost for federal income tax purposes

of $3,293,870,885, amounted to $230,780,763 which consisted of aggregate gross unrealized appreciation of

$368,002,684 and aggregate gross unrealized depreciation of $137,221,921.

* Non-income producing security.

@ Restricted security - Investment in security not registered under the Securities Act of 1933. The investment is deemed

to not be liquid and may be sold only to qualified buyers.

| | | | | | | | | |

| | | | | % of net assets | | | | % of net assets | |

| | Acquisition | | | (Acquisition | | | Market | as of | |

| Security | Date(s) | | Cost | Date) | | | Value | 4/30/2016 | |

| Choicestream, Inc. | 03/14/14 | $ | 36,151 | 0.00 | % | $ | 52,356 | 0.00 | % |

| Choicestream, Inc., Cl. A | 12/17/13 | | 859,605 | 0.03 | % | | 451,473 | 0.01 | % |

| Choicestream, Inc., Cl. B | 07/10/14 | | 1,500,323 | 0.05 | % | | 1,050,226 | 0.03 | % |

| Intarcia Therapeutics, Inc. | 03/27/14 | | 3,616,506 | 0.14 | % | | 3,690,198 | 0.10 | % |

| Palantir Technologies, Inc., Cl. A | 10/07/14 | | 1,555,368 | 0.05 | % | | 2,629,330 | 0.07 | % |

| Palantir Technologies, Inc., Cl. B | 10/07/14 | | 6,437,297 | 0.22 | % | | 10,723,251 | 0.29 | % |

| Palantir Technologies, Inc., Cl. D | 10/14/14 | | 838,605 | 0.03 | % | | 1,397,077 | 0.04 | % |

| Total | | | | | | $ | 19,993,911 | 0.54 | % |

| | | | | | | | | | |

| See Notes to Financial Statements. | | | | | | | | | |

- 21 -

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION FOCUS FUND

Schedule of Investments April 30, 2016 (Unaudited)

| | | | | |

| COMMON STOCKS—91.6% | | SHARES | | | VALUE |

| AEROSPACE & DEFENSE—5.2% | | | | | |

| Honeywell International, Inc. | | 32,190 | $ | 3,678,351 |

| AIRLINES—1.1% | | | | | |

| Delta Air Lines, Inc. | | 18,060 | | | 752,560 |

| ALTERNATIVE CARRIERS—1.5% | | | | | |

| Level 3 Communications, Inc.* | | 20,060 | | | 1,048,336 |

| APPAREL ACCESSORIES & LUXURY GOODS—1.2% | | | | | |

| PVH Corp. | | 9,080 | | | 868,048 |

| APPLICATION SOFTWARE—2.6% | | | | | |

| Adobe Systems, Inc.* | | 8,550 | | | 805,581 |

| salesforce.com, inc.* | | 13,960 | | | 1,058,168 |

| | | | | | 1,863,749 |

| AUTO PARTS & EQUIPMENT—1.5% | | | | | |

| Delphi Automotive PLC. | | 14,000 | | | 1,030,820 |

| BIOTECHNOLOGY—5.0% | | | | | |

| Biogen, Inc.* | | 3,100 | | | 852,469 |

| BioMarin Pharmaceutical, Inc.* | | 6,350 | | | 537,718 |

| Celgene Corp.* | | 10,260 | | | 1,060,987 |

| Gilead Sciences, Inc. | | 6,830 | | | 602,474 |

| Vertex Pharmaceuticals, Inc.* | | 5,310 | | | 447,845 |

| | | | | | 3,501,493 |

| BREWERS—1.5% | | | | | |

| Molson Coors Brewing Co., Cl. B | | 10,840 | | | 1,036,629 |

| BROADCASTING—4.8% | | | | | |

| CBS Corp., Cl. B | | 60,690 | | | 3,393,178 |

| CABLE & SATELLITE—2.3% | | | | | |

| Comcast Corporation, Cl. A | | 26,630 | | | 1,618,039 |

| CASINOS & GAMING—0.9% | | | | | |

| Red Rock Resorts, Inc., Cl. A* | | 32,700 | | | 609,528 |

| DATA PROCESSING & OUTSOURCED SERVICES—3.9% | | | | | |

| Visa, Inc., Cl. A | | 35,490 | | | 2,741,248 |

| DRUG RETAIL—1.2% | | | | | |

| CVS Caremark Corp. | | 8,400 | | | 844,200 |

| HEALTH CARE EQUIPMENT—2.1% | | | | | |

| DexCom, Inc.* | | 7,080 | | | 455,810 |

| Edwards Lifesciences Corp.* | | 4,660 | | | 494,939 |

| STERIS PLC. | | 7,390 | | | 522,251 |

| | | | | | 1,473,000 |

| HOME ENTERTAINMENT SOFTWARE—2.3% | | | | | |

| Electronic Arts, Inc.* | | 25,880 | | | 1,600,678 |

| HOTELS RESORTS & CRUISE LINES—2.5% | | | | | |

| Norwegian Cruise Line Holdings Ltd.* | | 35,767 | | | 1,748,649 |

| HOUSEWARES & SPECIALTIES—1.8% | | | | | |

| Newell Brands, Inc. | | 27,825 | | | 1,267,151 |

- 22 -

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION FOCUS FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | | VALUE |

| INTERNET RETAIL—4.1% | | | | | | |

| Amazon.com, Inc.* | | 4,430 | $ | 2,921,984 |

| INTERNET SOFTWARE & SERVICES—14.9% | | | | | | |

| Alphabet, Inc., Cl. C* | | 6,851 | | | | 4,747,812 |

| comScore, Inc.* | | 10,190 | | | | 312,018 |

| Facebook, Inc., Cl. A* | | 27,530 | | | | 3,236,977 |

| Match Group, Inc.* | | 29,580 | | | | 337,212 |

| Stamps.com, Inc.* | | 11,620 | | | | 957,023 |

| Yahoo! Inc.* | | 26,230 | | | | 960,018 |

| | | | | | 10,551,060 |

| INVESTMENT BANKING & BROKERAGE—0.6% | | | | | | |

| Morgan Stanley | | 16,790 | | | | 454,337 |

| LIFE SCIENCES TOOLS & SERVICES—2.3% | | | | | | |

| Thermo Fisher Scientific, Inc. | | 11,280 | | | | 1,627,140 |

| MANAGED HEALTH CARE—2.7% | | | | | | |

| UnitedHealth Group, Inc. | | 14,710 | | | | 1,937,013 |

| OIL & GAS EQUIPMENT & SERVICES—0.3% | | | | | | |

| Weatherford International PLC.* | | 28,810 | | | | 234,225 |

| OIL & GAS EXPLORATION & PRODUCTION—1.1% | | | | | | |

| Anadarko Petroleum Corp. | | 15,129 | | | | 798,206 |

| OTHER DIVERSIFIED FINANCIAL SERVICES—1.0% | | | | | | |

| Bank of America Corp. | | 49,010 | | | | 713,586 |

| PACKAGED FOODS & MEATS—1.0% | | | | | | |

| Pinnacle Foods, Inc. | | 16,310 | | | | 694,643 |

| PHARMACEUTICALS—5.4% | | | | | | |

| Allergan PLC.* | | 8,760 | | | | 1,897,066 |

| Bristol-Myers Squibb Co. | | 22,380 | | | | 1,615,388 |

| Pacira Pharmaceuticals, Inc.* | | 6,020 | | | | 325,742 |

| | | | | | | 3,838,196 |

| SECURITY & ALARM SERVICES—0.7% | | | | | | |

| Tyco International PLC. | | 12,030 | | | | 463,396 |

| SEMICONDUCTORS—3.1% | | | | | | |

| Broadcom Ltd. | | 7,350 | | | | 1,071,262 |

| Microsemi Corp.* | | 13,460 | | | | 454,813 |

| NXP Semiconductors NV* | | 7,870 | | | | 671,154 |

| | | | | | | 2,197,229 |

| SPECIALTY CHEMICALS—0.7% | | | | | | |

| The Sherwin-Williams Co. | | 1,640 | | | | 471,188 |

| SPECIALTY STORES—1.0% | | | | | | |

| Signet Jewelers Ltd. | | 6,450 | | | | 700,212 |

| SYSTEMS SOFTWARE—5.3% | | | | | | |

| Microsoft Corp. | | 66,990 | | | | 3,340,791 |

| TubeMogul, Inc.* | | 32,630 | | | | 422,885 |

| | | | | | | 3,763,676 |

- 23 -

THE ALGER INSTITUTIONAL FUNDS | ALGER CAPITAL APPRECIATION FOCUS FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | | VALUE |

| TECHNOLOGY HARDWARE STORAGE & PERIPHERALS—4.7% | | | | | | |

| Apple, Inc. | | 35,711 | | $ | | 3,347,549 |

| TRADING COMPANIES & DISTRIBUTORS—1.3% | | | | | | |

| HD Supply Holdings, Inc.* | | 27,130 | | | | 930,016 |

| TOTAL COMMON STOCKS | | | | | | |

| (Cost $61,854,144) | | | | | | 64,719,313 |

| PREFERRED STOCKS—0.5% | | SHARES | | | | VALUE |

| BIOTECHNOLOGY—0.5% | | | | | | |

| Prosetta Biosciences, Inc.*,@,(a) | | 76,825 | | | | 347,249 |

| (Cost $345,713) | | | | | | 347,249 |

| MASTER LIMITED PARTNERSHIP—1.2% | | SHARES | | | | VALUE |

| ASSET MANAGEMENT & CUSTODY BANKS—1.2% | | | | | | |

| The Blackstone Group LP. | | 31,770 | | | | 871,769 |

| (Cost $945,997) | | | | | | 871,769 |

| REAL ESTATE INVESTMENT TRUST—2.2% | | SHARES | | | | VALUE |

| SPECIALIZED—2.2% | | | | | | |

| Crown Castle International Corp. | | 17,970 | | | | 1,561,234 |

| (Cost $1,521,597) | | | | | | 1,561,234 |

| Total Investments | | | | | | |

| (Cost $64,667,451)(b) | | 95.5 | % | | | 67,499,565 |

| Other Assets in Excess of Liabilities | | 4.5 | % | | | 3,151,188 |

| NET ASSETS | | 100.0 | % | $ | | 70,650,753 |

(a) Deemed an affiliate of the Alger fund complex during the year for purposes of Section 2(a)(3) of the Investment

Company Act of 1940. See Affiliated Securities in Notes to Financial Statements.

(b) At April 30, 2016, the net unrealized appreciation on investments, based on cost for federal income tax purposes

of $65,845,255, amounted to $1,654,310 which consisted of aggregate gross unrealized appreciation of

$4,623,399 and aggregate gross unrealized depreciation of $2,969,089.

* Non-income producing security.

@ Restricted security - Investment in security not registered under the Securities Act of 1933. The investment is deemed

to not be liquid and may be sold only to qualified buyers.

| | | | | | | | | |

| | | | | % of net assets | | | | % of net assets | |

| | Acquisition | | | (Acquisition | | | Market | as of | |

| Security | Date(s) | | Cost | Date) | | | Value | 4/30/2016 | |

| Prosetta Biosciences, Inc. | 02/06/15 | $ | 345,713 | 0.80 | % | $ | 347,249 | 0.49 | % |

| Total | | | | | | $ | 347,249 | 0.49 | % |

| | | | | | | | | | |

| |

| |

| See Notes to Financial Statements. | | | | | | | | | |

- 24 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited)

| | | | | |

| COMMON STOCKS—94.2% | | SHARES | | | VALUE |

| ADVERTISING—0.0% | | | | | |

| Choicestream, Inc.*,@,(a) | | 8,930 | $ | 3,750 |

| AEROSPACE & DEFENSE—2.4% | | | | | |

| Hexcel Corp. | | 26,800 | | | 1,213,236 |

| TransDigm Group, Inc.* | | 6,800 | | | 1,549,516 |

| | | | | | 2,762,752 |

| AIRLINES—1.9% | | | | | |

| Southwest Airlines Co | | 24,400 | | | 1,088,484 |

| Spirit Airlines, Inc.* | | 7,800 | | | 342,654 |

| United Continental Holdings, Inc.* | | 15,100 | | | 691,731 |

| | | | | | 2,122,869 |

| APPAREL ACCESSORIES & LUXURY GOODS—3.4% | | | | | |

| Hanesbrands, Inc. | | 48,900 | | | 1,419,567 |

| lululemon athletica, Inc.* | | 8,000 | | | 524,400 |

| PVH Corp. | | 10,500 | | | 1,003,800 |

| Under Armour, Inc., Cl. A* | | 11,800 | | | 518,492 |

| Under Armour, Inc., Cl. C* | | 10,600 | | | 432,480 |

| | | | | | 3,898,739 |

| APPAREL RETAIL—1.8% | | | | | |

| Burlington Stores, Inc.* | | 11,800 | | | 672,246 |

| Ross Stores, Inc. | | 24,500 | | | 1,391,110 |

| | | | | | 2,063,356 |

| APPLICATION SOFTWARE—0.5% | | | | | |

| Guidewire Software, Inc.* | | 3,300 | | | 188,001 |

| Intuit, Inc. | | 3,700 | | | 373,293 |

| | | | | | 561,294 |

| AUTO PARTS & EQUIPMENT—2.4% | | | | | |

| Delphi Automotive PLC. | | 20,950 | | | 1,542,548 |

| WABCO Holdings, Inc.* | | 10,000 | | | 1,121,600 |

| | | | | | 2,664,148 |

| AUTOMOBILE MANUFACTURERS—0.2% | | | | | |

| Tesla Motors, Inc.* | | 800 | | | 192,608 |

| AUTOMOTIVE RETAIL—0.9% | | | | | |

| O'Reilly Automotive, Inc.* | | 3,900 | | | 1,024,452 |

| BIOTECHNOLOGY—3.4% | | | | | |

| Anacor Pharmaceuticals, Inc.* | | 5,600 | | | 351,344 |

| BioMarin Pharmaceutical, Inc.* | | 8,000 | | | 677,440 |

| Bluebird Bio, Inc.* | | 5,100 | | | 226,185 |

| Incyte Corp.* | | 8,500 | | | 614,295 |

| Juno Therapeutics, Inc.* | | 2,500 | | | 105,225 |

| Portola Pharmaceuticals, Inc.* | | 11,600 | | | 275,616 |

| Ultragenyx Pharmaceutical, Inc.* | | 6,400 | | | 432,768 |

| United Therapeutics Corp.* | | 5,700 | | | 599,640 |

| Vertex Pharmaceuticals, Inc.* | | 6,300 | | | 531,342 |

| | | | | | 3,813,855 |

| BROADCASTING—1.2% | | | | | |

| CBS Corp., Cl. B | | 23,900 | | | 1,336,249 |

- 25 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | VALUE |

| BROADCASTING & CABLE TV—0.7% | | | | | |

| Discovery Communications, Inc., Series A* | | 30,200 | $ | 824,762 |

| BUILDING PRODUCTS—3.0% | | | | | |

| Allegion PLC. | | 25,000 | | | 1,636,250 |

| AO Smith Corp. | | 8,600 | | | 664,092 |

| Fortune Brands Home & Security, Inc. | | 20,300 | | | 1,124,823 |

| | | | | | 3,425,165 |

| CASINOS & GAMING—1.1% | | | | | |

| Penn National Gaming, Inc.* | | 44,200 | | | 712,946 |

| Red Rock Resorts, Inc., Cl. A* | | 30,100 | | | 561,064 |

| | | | | | 1,274,010 |

| COMMUNICATIONS EQUIPMENT—2.7% | | | | | |

| Arista Networks, Inc.* | | 9,200 | | | 612,904 |

| Ciena Corp.* | | 20,000 | | | 336,600 |

| F5 Networks, Inc.* | | 9,500 | | | 995,125 |

| Finisar Corp.* | | 20,800 | | | 342,368 |

| Lumentum Holdings, Inc.* | | 13,700 | | | 346,610 |

| Palo Alto Networks, Inc.* | | 3,200 | | | 482,784 |

| | | | | | 3,116,391 |

| CONSTRUCTION & FARM MACHINERY & HEAVY | | | | | |

| TRUCKS—0.6% | | | | | |

| Wabtec Corp. | | 8,300 | | | 688,319 |

| CONSUMER FINANCE—0.1% | | | | | |

| LendingClub Corp.* | | 18,900 | | | 149,310 |

| DATA PROCESSING & OUTSOURCED SERVICES—4.4% | | | | | |

| Alliance Data Systems Corp.* | | 3,800 | | | 772,578 |

| Fiserv, Inc.* | | 14,900 | | | 1,456,028 |

| MAXIMUS, Inc. | | 18,300 | | | 968,070 |

| Sabre Corp. | | 34,400 | | | 995,880 |

| Vantiv, Inc., CL. A* | | 14,500 | | | 790,830 |

| | | | | | 4,983,386 |

| DISTILLERS & VINTNERS—0.4% | | | | | |

| Constellation Brands Inc., Cl. A | | 2,700 | | | 421,362 |

| ENVIRONMENTAL & FACILITIES SERVICES—0.9% | | | | | |

| Stericycle, Inc.* | | 10,400 | | | 993,824 |

| FOOD RETAIL—0.8% | | | | | |

| The Kroger Co. | | 26,500 | | | 937,835 |

| GENERAL MERCHANDISE STORES—2.0% | | | | | |

| Dollar General Corp. | | 16,200 | | | 1,326,942 |

| Dollar Tree, Inc.* | | 12,500 | | | 996,375 |

| | | | | | 2,323,317 |

| HEALTH CARE EQUIPMENT—5.0% | | | | | |

| ABIOMED, Inc.* | | 11,800 | | | 1,146,252 |

| DexCom, Inc.* | | 21,600 | | | 1,390,608 |

| Edwards Lifesciences Corp.* | | 14,200 | | | 1,508,182 |

| Hologic, Inc.* | | 15,100 | | | 507,209 |

- 26 -

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments April 30, 2016 (Unaudited) (Continued)

| | | | | |

| COMMON STOCKS—(CONT.) | | SHARES | | | VALUE |

| HEALTH CARE EQUIPMENT—(CONT.) | | | | | |

| IDEXX Laboratories, Inc.* | | 10,100 | $ | 851,935 |

| STERIS PLC. | | 3,300 | | | 233,211 |

| | | | | | 5,637,397 |

| HEALTH CARE FACILITIES—3.9% | | | | | |

| Acadia Healthcare Co., Inc.* | | 16,400 | | | 1,036,316 |

| Amsurg Corp.* | | 11,700 | | | 947,466 |

| Universal Health Services, Inc., Cl. B | | 9,800 | | | 1,310,064 |

| VCA Antech, Inc.* | | 18,100 | | | 1,139,757 |

| | | | | | 4,433,603 |

| HEALTH CARE SERVICES—0.8% | | | | | |

| Adeptus Health, Inc., Cl. A* | | 8,700 | | | 592,644 |

| Diplomat Pharmacy, Inc.* | | 10,500 | | | 318,045 |

| | | | | | 910,689 |

| HOME ENTERTAINMENT SOFTWARE—0.7% | | | | | |

| Electronic Arts, Inc.* | | 13,500 | | | 834,975 |

| HOMEBUILDING—0.3% | | | | | |

| Toll Brothers, Inc.* | | 10,900 | | | 297,570 |

| HOTELS RESORTS & CRUISE LINES—5.9% | | | | | |

| Ctrip.com International Ltd.#* | | 6,400 | | | 279,104 |

| Diamond Resorts International, Inc.* | | 72,100 | | | 1,529,241 |

| Norwegian Cruise Line Holdings Ltd.* | | 54,300 | | | 2,654,727 |

| Royal Caribbean Cruises Ltd. | | 29,500 | | | 2,283,300 |

| | | | | | 6,746,372 |

| HOUSEHOLD PRODUCTS—1.1% | | | | | |

| Church & Dwight Co., Inc. | | 12,900 | | | 1,195,830 |

| HOUSEWARES & SPECIALTIES—2.4% | | | | | |

| Newell Brands, Inc. | | 59,096 | | | 2,691,232 |

| INDUSTRIAL GASES—0.5% | | | | | |

| Air Products & Chemicals, Inc. | | 4,000 | | | 583,560 |

| INDUSTRIAL MACHINERY—1.5% | | | | | |

| Colfax Corp.* | | 17,300 | | | 561,039 |

| Donaldson Co., Inc. | | 23,300 | | | 761,444 |

| Graco, Inc. | | 5,300 | | | 415,467 |

| | | | | | 1,737,950 |

| INTERNET SOFTWARE & SERVICES—2.9% | | | | | |

| comScore, Inc.* | | 21,300 | | | 652,206 |

| Cornerstone OnDemand, Inc.* | | 14,139 | | | 485,675 |

| Criteo SA#* | | 10,400 | | | 433,576 |

| LinkedIn Corp., Cl. A* | | 3,300 | | | 413,523 |

| Palantir Technologies, Inc., Cl. A*,@ | | 12,426 | | | 136,686 |

| SPS Commerce, Inc.* | | 10,500 | | | 534,765 |