| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | January 31, 2014 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .20.6 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07986 |

|

The Alger Institutional Funds |

(Exact name of registrant as specified in charter) |

|

111 Fifth Avenue New York, New York | | 10003 |

(Address of principal executive offices) | | (Zip code) |

|

Mr. Hal Liebes Fred Alger Management, Inc. 111 Fifth Avenue New York, New York 10003 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-806-8800 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | April 30, 2011 | |

| | | | | | | | |

ITEM 1. REPORT(S) TO STOCKHOLDERS.

The Alger Institutional Funds

SEMI-ANNUAL REPORT

April 30, 2011

(Unaudited)

Table of Contents

THE ALGER INSTITUTIONAL FUNDS

Letter to Our Shareholders | 1 |

| |

Fund Highlights | 9 |

| |

Portfolio Summary | 13 |

| |

Schedules of Investments | 14 |

| |

Statements of Assets and Liabilities | 38 |

| |

Statements of Operations | 40 |

| |

Statements of Changes in Net Assets | 42 |

| |

Financial Highlights | 44 |

| |

Notes to Financial Statements | 52 |

| |

Additional Information | 67 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we’ll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

Dear Shareholders, | | May 20, 2011 |

Indications that the economic recovery was gaining traction fueled a strong equity rally during the six-month period ended April 30, 2011, with the S&P 500 posting a 16.36% return. Market volatility was prevalent, however, as many investors feared that political turmoil in the Middle East and North Africa would disrupt global oil production and lead to higher energy prices. Concerns over the economic impact of the earthquake, tsunami and nuclear power plant accident in Japan also weighed heavily on investors. During the period, we maintained our focus on generating strong investment returns by conducting thoughtful, research-driven stock selection, while also assessing macro economic developments and the humanitarian impact of the Japan crisis.

Performance of the S&P 500 was virtually flat in November, but encouraging retail shopping trends and other upbeat news pushed the index into positive territory for December and January. Yet, by mid-February, investors’ fears over rising oil prices strengthened and equity markets started to perform in a manner that we have seen before—market returns became inversely correlated to the price of oil. Market volatility continued as investors focused on the implications of the Japan crisis, although a steady stream of encouraging economic data helped support the ongoing equity rally throughout the remainder of the six-month period.

Broadly speaking, market performance was consistent with our expectations. In our Winter 2010/2011 Market Commentary, we maintained that economic acceleration, strong corporate earnings, healthy balance sheets, job market improvements, and other developments would lead to further gains in U.S. equities this year. Yet, we cautioned that volatility would continue and markets would eventually struggle to maintain gains as weak real estate prices, high unemployment rates, and fears of potential global trade conflicts lingered.

The Recovery Strengthens

The six-month period was highlighted by a variety of encouraging developments. In January, for example, the Department of Labor announced that December unemployment dropped to 9.4%, down from 9.8% in November. The trend continued, with the rate dropping to 9.0% in January and to 8.9% in February—its lowest level since April of 2009. Also encouraging, applications for unemployment insurance declined by 22,000 to 391,000 for the week ended February 19, sparking optimism that job layoffs were slowing. In the corporate world, earnings growth continued with many of our holdings, like Apple, Inc., Oracle Corp., United Parcel Service, Inc., ConocoPhillips, Cliffs Natural Resources, Inc., and Aetna, Inc. contributing to optimism with earnings that outpaced analysts’ forecasts. In Detroit, Chrysler Group LLC’s January U.S. auto sales climbed 23% and General Motors Co. achieved its first annual profit since 2004.

The Conference Board, meanwhile, reported that its Consumer Confidence Index climbed to 70.4 in February, its highest level in three years. Also impressive was

1

Federal Reserve data showing annualized GDP growth of 2.8% for the fourth quarter, which while below analysts’ expectations, was still encouraging. The Federal Reserve also estimated that 2011 GDP would grow 3.4% to 3.9%, compared to a previous estimate of 3.0% to 3.6%.

Trouble Overseas

Investor optimism eventually waned and the S&P 500 tumbled approximately 6.41% during the three-and-a-half-week period ended March 18. While the end of earnings season may have naturally shifted investor attention from corporate fundamentals, turmoil in the Middle East and in North Africa clearly weighed heavily on markets by creating concerns over the possible economic implications of higher energy prices and the lack of decisive change in U.S. energy consumption and in U.S. energy policy. Rising prices for all types of commodities also continued to be a central issue. Indeed, escalating food prices and the economic challenges they created in many parts of the world were significant triggers to the anti-government protests in Tunisia that sparked rebellion across Bahrain, Yemen, Egypt, Algeria, and eventually Libya. In Egypt, where 40% of the nation lives in poverty, President Hosni Mubarak was forced to resign, which encouraged similar protests in other countries. Protestors in Libya eventually shut down an estimated 50% of the country’s daily oil production of 1.8 million barrels. Concerns over a tightening of oil supply drove prices of West Texas Intermediate Crude from $91.55 a barrel at the beginning of the year to $113.52 on April 29.

Investors became even more skittish in March when Japan was hit by a magnitude 8.9 earthquake—the strongest in the country’s history. The quake and resulting tsunami left a wake of despair, destroying entire towns and communities in a single day. Even more alarming, the earthquake damaged cooling systems at the Fukushima Daiichi nuclear power facility, and a series of explosions damaged the plant’s nuclear reactors, left fuel rods exposed, and released radiation into the atmosphere. U.S. officials urged expatriates to stay at least 50 miles from the facility as Japanese workers frantically struggled to stop the crisis from worsening. Investors, understandably, grew concerned: Japan is the world’s third-largest economy, so disruptions in manufacturing and consumption could have a considerable impact on global growth, at least in the near term. As we watch the disaster unfold, we feel confident that as the Japanese rebuild their nation, they will become stronger as a country, and they will eventually make many positive contributions to society and the global economy. In the meantime, we continue to admire their perseverance.

Investor Psychology and the Road Ahead

We still believe that equity markets have strong potential for generating attractive gains, although fears over oil prices and concerns over Japan’s impact on global economic growth will be significant challenges. Regarding oil, higher energy prices do not necessarily cause economic recession. Rather, it is the rate of change that is important. Oil price spikes must be drastic to cause an “oil shock” to the economy (we recognize that the fundamental strength of the economy at the time oil prices increase also matters, but we currently think the U.S. economy is stronger than most

2

believe). Generally speaking, past global recessions and cyclical bear markets triggered by oil have occurred only after prices increased by more than 100% in a short period, according to BCA Research, an independent economic research firm. We are not at that point yet. Disruptions in petroleum production, of course, could cause pain at the pump for American motorists, but in some ways, the U.S. is better prepared for price increases than in the past. Americans now spend just slightly more than 5% of their disposable income on energy, down from more than 8% in the 1980s, according to BCA. Oil’s role in America’s energy usage has also declined, accounting for only 37% of energy consumed in 2009, down from 44% in 1980, according to the U.S. Energy Information Administration. We also believe that the run up in oil prices that occurred from 2003 to 2008 succeeded in conditioning, at least partially, American consumers and businesses to potentially higher energy prices over the long term.

We believe that the development of a substantial oil shortage is unlikely. World oil production exceeds demand by an estimated three million to four million barrels per day, and many oil producing countries are capable of boosting output. Demand in the U.S. and developed economies has, in fact, been relatively flat, with emerging markets, especially China, driving recent oil demand growth. Additionally, consumption of oil in Japan, at least for the short term, has been crimped by the country’s crisis. An escalation of political turmoil in the Middle East and North Africa is still possible, but unless it affects oil production in Saudi Arabia, which is the world’s second-largest oil producer, it is unlikely to result in near-term supply shortages.

Regarding Japan, the impact of the country’s crisis on the global economy will be felt in coming months. Japan represents 6% to 8% of global GDP, and power outages have shut down many factories in the country. Supply chain disruptions, especially in the auto and technology industries, will occur as a result. These are short-term events that long-term investors should, and we think will, look beyond. Moreover, the massive rebuilding of Japan should eventually be a source of global economic stimulus. Finally, with an unreliable power supply in Japan, it is currently unknown if the country’s manufacturing capacity is significantly compromised even in the short term; however, much of the country’s industry infrastructure is state-of-the-art technology that minimizes damage from earthquakes, so it’s possible that manufacturing production will resume as soon as dependable electrical energy is restored.

We maintain that market resilience in the first quarter signals investors’ understanding of a vital fact: the U.S. economic recovery is strengthening. This has and will continue to support, we believe, a continuing rally in U.S. equities. Alger’s philosophy of “Investing in Positive Dynamic Change” has never been more appropriate than today. Change, whether from political events such as the uprisings in the Middle East or from the continuing impact of emerging markets across Asia and South America, has never been more evident. While change is almost always unsettling for some investors, we believe that it generates opportunities to buy attractively priced and well-run companies that have superior potential for growth. We continue to believe that research is the cornerstone of superior portfolio management, regardless of economic conditions and that our proven and disciplined process for identifying

3

companies experiencing Positive Dynamic Change will continue to produce superior long-term results for our clients.

Portfolio Matters

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund returned 19.35% for the fiscal six-month period ended April 30, 2011, compared to the Russell 3000 Growth Index return of 17.77%.

During the period, the largest portfolio weightings in the Alger Capital Appreciation Institutional Fund were in the Information Technology and Health Care sectors. The largest sector overweight for the period was in Financials and the largest sector underweight for the period was in Consumer Staples. Relative outperformance in the Information Technology and Energy sectors was the most important contributor to performance. Sectors that detracted from performance included Health Care and Consumer Staples.

Among the most important relative contributors were Patriot Coal Corp., Skyworks Solutions, Inc., Cliffs Natural Resources, Inc., Seagate Technology PLC, and Marvell Technology Group Ltd. Conversely, detracting from overall results on a relative basis were Brocade Communications Systems Inc., Oracle Corp., United Technologies Corp., Baxter International Inc., and International Business Machines Corp.

Alger Large Cap Growth Institutional Fund

The Alger Large Cap Growth Institutional Fund returned 14.38% for the fiscal six-month period ended April 30, 2011, compared with a return of 16.96% for the Russell 1000 Growth Index.

During the period, the largest portfolio weightings in the Alger Large Cap Growth Institutional Fund were in the Information Technology and Health Care sectors. The largest sector overweight for the period was in Energy and the largest sector underweight for the period was in Industrials. Relative outperformance in the Materials and Energy sectors was the most important contributor to performance. Sectors that detracted from performance included Health Care and Consumer Staples.

Among the most important relative contributors were Burlington Northern Santa Fe Railway, Boeing Co., Las Vegas Sands Corp., Lowe’s Cos., and Carnival Corp. Conversely, detracting from relative performance were United Technologies Corp., Oracle Corp., International Business Machines Corp., Medco Health Solutions, Inc., and Transocean Ltd.

4

Alger Mid Cap Growth Institutional Fund

The Alger Mid Cap Growth Institutional Fund returned 23.95% for the fiscal six-month period ended April 30, 2011, compared to the 22.62% return of the Russell Midcap Growth Index.

During the period, the largest portfolio weightings in the Alger Mid Cap Growth Institutional Fund were in the Information Technology and Consumer Discretionary sectors. The largest sector overweight for the period was in Information Technology and the largest sector underweight for the period was in Industrials. Relative outperformance in the Information Technology and Energy sectors was the most important contributor to performance. Sectors that detracted from the portfolio included Industrials and Consumer Staples.

Among the most important relative contributors were Cliffs Natural Resources, Inc., Skyworks Solutions, Inc., Human Genome Sciences, Inc., Atheros Communications Inc., and Mariner Energy Inc. Conversely, detracting from overall results on a relative basis were Brocade Communications Systems, Inc., Intuitive Surgical, Inc., SmartHeat, Inc., New York Times Co., and Select Medical Holdings Corporation.

Alger Small Cap Growth Institutional Fund

For the fiscal six-month period ended April 30, 2011, the Alger Small Cap Growth Institutional Fund returned 26.35%, compared to the Russell 2000 Growth Index, which returned 27.07%.

During the period, the largest portfolio weightings in the Alger Small Cap Growth Institutional Fund were in the Information Technology and Health Care sectors. The largest sector overweight for the period was in Industrials and the largest sector underweight for the period was in Information Technology. Relative outperformance in the Energy and Materials sectors was the most important contributor to performance. Sectors that detracted from the portfolio included Financials and Consumer Staples.

Among the most important relative contributors were Dollar Thrifty Automotive Group, Inc., Mariner Energy Inc., Dana Holding Corp., PAREXEL International Corp., and BE Aerospace, Inc. Conversely, detracting from overall results on a relative basis were Brocade Communications Systems, Inc., InterMune, Inc., PMI Group, Inc., Acorda Therapeutics, Inc., and Medivation, Inc.

As always, we strive to deliver consistently superior investment results for you, our shareholders, and we thank you for your business and your continued confidence in Alger.

Respectfully submitted,

Dan Chung, CFA

Chief Investment Officer

5

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Funds unless proceeded or accompanied by an effective prospectus for the Funds. Fund returns represent the fiscal six-month period return of Class I shares. The performance data quoted represents past performance, which is not an indication or guarantee of future results. Standardized performance results can be found on the following pages. The investment return and principal value of an investment in a fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the Funds’ management in this report are as of the date of the Shareholders letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable; however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities, if any, may be for a variety of reasons, including without limitation, in response to cash flows, inclusion in a benchmark, and risk control. The reference to a specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in a portfolio. Please refer to the Schedules of Investments for each fund that is included in this report for a complete list of fund holdings as of April 30, 2011. Securities mentioned in the Shareholders Letter, if not found in the Schedule of Investments, may have been held by the Funds during the six-month fiscal period.

A Word About Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends to be higher in relation to their companies’ earnings and may be more sensitive to market, political and economic developments. Investing in the stock market involves gains and losses and may not be suitable for all investors. Stocks of small and mid-sized companies are subject to greater risk than stocks of larger, more established companies owing to such factors as limited liquidity, inexperienced management, and limited financial resources. Funds that participate in leveraging, such as the Capital Appreciation Institutional Fund, are subject to the risk that borrowing money to leverage will exceed the returns for securities purchased or that the securities purchased may actually go down in value; thus, the Funds’ net asset

6

value can decrease more quickly than if the Funds had not borrowed. For a more detailed discussion of the risks associated with these Funds, please see the Funds’ Prospectus.

Before investing, carefully consider a Fund’s investment objective, risks, charges, and expenses.

For a prospectus or a summary prospectus containing this and other information about the Alger Institutional Funds call us at (800) 992-3863 or visit us at www.alger.com. Read it carefully before investing.

Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Index Definitions:

· Russell 3000 Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on the total market capitalization, which represents 98% of the U.S. Equity Market.

· Russell 1000 Growth Index is an unmanaged index designed to measure the performance of the largest 1,000 companies in the Russell 3000 Index with higher price-to-book ratios and higher forecasted growth values.

· Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell Midcap Index measures the performance of the mid-cap segment of the U.S. equity universe

· Russell 2000 Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe.

· The Standard & Poor’s 500 Index is an index of large-company common stocks and is considered to be representative of the U.S. stock market.

· Investors cannot invest directly in any index.

7

FUND PERFORMANCE AS OF 3/31/11 (Unaudited)

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | |

Alger Capital Appreciation Class I (Inception 11/8/93) | | 16.38 | % | 8.14 | % | 5.99 | % |

Alger Capital Appreciation Class R* (Inception 1/27/03) | | 15.75 | % | 7.58 | % | 5.45 | % |

| | | | | | | |

Alger Large Cap Growth Class I (Inception 11/8/93) | | 14.77 | % | 1.75 | % | 1.30 | % |

Alger Large Cap Growth Class R* (Inception 1/27/03) | | 14.02 | % | 1.19 | % | 0.77 | % |

| | | | | | | |

Alger Mid Cap Growth Class I (Inception 11/8/93) | | 23.17 | % | 2.14 | % | 5.70 | % |

Alger Mid Cap Growth Class R* (Inception 1/27/03) | | 22.49 | % | 1.62 | % | 5.17 | % |

| | | | | | | |

Alger Small Cap Growth Class I (Inception 11/8/93) | | 26.18 | % | 5.19 | % | 7.18 | % |

Alger Small Cap Growth Class R* (Inception 1/27/03) | | 25.55 | % | 4.68 | % | 6.68 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

8

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through April 30, 2011 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital Appreciation Institutional Fund Class I shares, the Russell 3000 Growth Index (an unmanaged indices of common stocks) and the Russell 1000 Growth Index (a unmanaged index of common stocks) for the ten years ended April 30, 2011. Figures for the Alger Capital Appreciation Institutional Fund Class I shares, the Russell 3000 Growth Index and the Russell 1000 Growth Index include reinvestment of dividends. Performance for the Alger Capital Appreciation Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 4/30/11

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since

11/8/1993 | |

Class I (Inception 11/8/93) | | 20.66 | % | 8.87 | % | 5.27 | % | 11.88 | % |

Class R* (Inception 1/27/03) | | 20.03 | % | 8.32 | % | 4.73 | % | 11.31 | % |

Russell 3000 Growth Index | | 21.62 | % | 5.05 | % | 2.38 | % | 7.44 | % |

Russell 1000 Growth Index | | 20.87 | % | 5.06 | % | 2.11 | % | 7.68 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

9

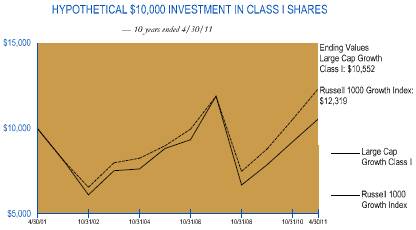

ALGER LARGE CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2011 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Large Cap Growth Institutional Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2011. The figures for the Alger Large Cap Growth Institutional Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Performance for the Alger Large Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 4/30/11

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since

11/8/1993 | |

Class I (Inception 11/8/93) | | 17.54 | % | 2.13 | % | 0.54 | % | 7.68 | % |

Class R* (Inception 1/27/03) | | 16.70 | % | 1.57 | % | 0.01 | % | 7.12 | % |

Russell 1000 Growth Index | | 20.87 | % | 5.06 | % | 2.11 | % | 7.68 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

10

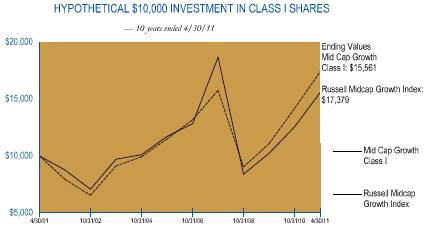

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2011 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2011. Figures for the Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index include reinvestment of dividends. Performance for the Alger Mid Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 4/30/11

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since

11/8/1993 | |

Class I (Inception 11/8/93) | | 25.77 | % | 2.96 | % | 4.52 | % | 12.89 | % |

Class R* (Inception 1/27/03) | | 25.08 | % | 2.43 | % | 4.00 | % | 12.33 | % |

Russell Midcap Growth Index | | 27.40 | % | 5.59 | % | 5.68 | % | 9.09 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

11

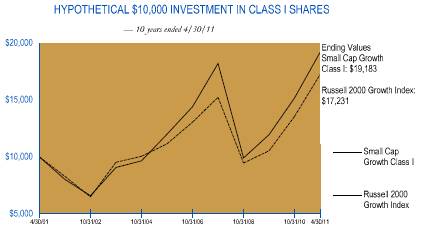

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through April 30, 2011 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index (an unmanaged index of common stocks) for the ten years ended April 30, 2011. The figures for the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index include reinvestment of dividends. Performance for the Alger Small Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 4/30/11

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | Since

11/8/1993 | |

Class I (Inception 11/8/93) | | 27.10 | % | 5.88 | % | 6.73 | % | 9.88 | % |

Class R* (Inception 1/27/03) | | 26.45 | % | 5.37 | % | 6.23 | % | 9.35 | % |

Russell 2000 Growth Index | | 30.29 | % | 5.14 | % | 5.59 | % | 6.47 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

12

PORTFOLIO SUMMARY*

April 30, 2011 (Unaudited)

SECTORS | | Alger Capital

Appreciation

Institutional Fund | | Alger Large Cap

Growth

Institutional Fund | | Alger Mid Cap

Growth

Institutional Fund | | Alger Small Cap

Growth

Institutional Fund | |

Consumer Discretionary | | 12.8 | % | 13.9 | % | 13.2 | % | 18.2 | % |

Consumer Staples | | 4.1 | | 7.5 | | 1.7 | | 2.2 | |

Energy | | 11.5 | | 11.0 | | 9.0 | | 5.8 | |

Financials | | 6.7 | | 5.4 | | 7.2 | | 4.0 | |

Health Care | | 10.7 | | 9.7 | | 13.0 | | 17.6 | |

Industrials | | 15.3 | | 11.1 | | 20.3 | | 15.7 | |

Information Technology | | 29.0 | | 27.8 | | 28.1 | | 26.6 | |

Materials | | 4.8 | | 4.7 | | 8.3 | | 5.2 | |

Telecommunication Services | | 0.5 | | 1.0 | | 0.0 | | 0.0 | |

Utilities | | 0.0 | | 0.0 | | 0.0 | | 1.1 | |

Short-Term Investments and Net Other Assets | | 4.6 | | 7.9 | | (0.8 | ) | 3.6 | |

| | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % |

* Based on net assets for each Fund.

13

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments‡ (Unaudited) April 30, 2011

| | SHARES | | VALUE | |

COMMON STOCKS—95.1% | | | | | |

ADVERTISING—1.7% | | | | | |

Focus Media Holding Ltd.#* | | 603,300 | | $ | 21,205,995 | |

| | | | | |

AEROSPACE & DEFENSE—0.8% | | | | | |

Goodrich Corp. | | 118,700 | | 10,489,519 | |

| | | | | |

AIR FREIGHT & LOGISTICS—2.7% | | | | | |

FedEx Corp. | | 114,600 | | 10,963,782 | |

United Parcel Service, Inc., Cl. B | | 309,200 | | 23,180,724 | |

| | | | 34,144,506 | |

AIRLINES—0.7% | | | | | |

United Continental Holdings, Inc.* | | 376,000 | | 8,580,320 | |

| | | | | |

APPAREL RETAIL—0.3% | | | | | |

Abercrombie & Fitch Co., Cl. A | | 61,300 | | 4,340,040 | |

| | | | | |

APPLICATION SOFTWARE—1.5% | | | | | |

Informatica Corp. * | | 153,200 | | 8,580,732 | |

Nice Systems Ltd. #* | | 153,000 | | 5,833,890 | |

Salesforce.com, Inc. * | | 35,900 | | 4,975,740 | |

| | | | 19,390,362 | |

ASSET MANAGEMENT & CUSTODY BANKS—0.9% | | | | | |

BlackRock, Inc. | | 56,500 | | 11,070,610 | |

| | | | | |

AUTO PARTS & EQUIPMENT—0.4% | | | | | |

Lear Corp. | | 111,800 | | 5,717,452 | |

| | | | | |

AUTOMOBILE MANUFACTURERS—1.4% | | | | | |

Bayerische Motoren Werke AG# | | 549,800 | | 17,236,230 | |

| | | | | |

BIOTECHNOLOGY—0.8% | | | | | |

Human Genome Sciences, Inc.* | | 326,100 | | 9,610,167 | |

| | | | | |

BROADCASTING & CABLE TV—0.3% | | | | | |

CBS Corp., Cl. B | | 149,900 | | 3,780,478 | |

| | | | | |

COAL & CONSUMABLE FUELS—1.0% | | | | | |

Peabody Energy Corp. | | 181,400 | | 12,121,148 | |

| | | | | |

COMMODITY CHEMICALS—0.6% | | | | | |

Celanese Corp. | | 153,100 | | 7,642,752 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—3.1% | | | | | |

Ciena Corp. * | | 180,500 | | 5,097,320 | |

Cisco Systems, Inc. | | 167,400 | | 2,939,544 | |

Corning, Inc. | | 248,700 | | 5,207,778 | |

Qualcomm, Inc. | | 381,400 | | 21,678,776 | |

Riverbed Technology, Inc. * | | 113,300 | | 3,981,362 | |

| | | | 38,904,780 | |

COMPUTER HARDWARE—6.5% | | | | | |

Apple, Inc. * | | 187,900 | | 65,432,416 | |

Hewlett-Packard Co. | | 442,700 | | 17,871,799 | |

| | | | 83,304,215 | |

COMPUTER STORAGE & PERIPHERALS—2.0% | | | | | |

EMC Corp. * | | 565,900 | | 16,037,606 | |

SanDisk Corp. * | | 103,200 | | 5,071,248 | |

| | | | | | |

14

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

COMPUTER STORAGE & PERIPHERALS—(CONT.) | | | | | |

Seagate Technology PLC | | 233,400 | | $ | 4,112,508 | |

| | | | 25,221,362 | |

CONSTRUCTION & ENGINEERING—0.1% | | | | | |

Chicago Bridge & Iron Co., NV# | | 31,800 | | 1,289,172 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—3.8% | | | | | |

Caterpillar, Inc. | | 124,500 | | 14,368,545 | |

Cummins, Inc. | | 134,000 | | 16,104,120 | |

Deere & Co. | | 83,100 | | 8,102,250 | |

WABCO Holdings, Inc. * | | 112,400 | | 8,300,740 | |

| | | | 46,875,655 | |

DATA PROCESSING & OUTSOURCED SERVICES—0.9% | | | | | |

Mastercard, Inc. | | 40,400 | | 11,145,956 | |

| | | | | |

DEPARTMENT STORES—0.7% | | | | | |

Kohl’s Corp. | | 162,600 | | 8,570,646 | |

| | | | | |

DIVERSIFIED BANKS—0.2% | | | | | |

Itau Unibanco Holding SA# | | 124,500 | | 2,956,875 | |

| | | | | |

DIVERSIFIED METALS & MINING—2.5% | | | | | |

Cliffs Natural Resources, Inc. | | 134,800 | | 12,633,456 | |

Freeport-McMoRan Copper & Gold, Inc. | | 132,700 | | 7,302,481 | |

Molycorp, Inc. * | | 146,300 | | 10,723,790 | |

| | | | 30,659,727 | |

DRUG RETAIL—0.8% | | | | | |

CVS Caremark Corp. | | 292,200 | | 10,589,328 | |

| | | | | |

ENVIRONMENTAL & FACILITIES SERVICES—0.6% | | | | | |

Republic Services, Inc. | | 255,900 | | 8,091,558 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.7% | | | | | |

Mosaic Co., /The | | 125,100 | | 9,364,986 | |

| | | | | |

FOOTWEAR—0.2% | | | | | |

NIKE Inc., Cl. B | | 37,800 | | 3,111,696 | |

| | | | | |

GOLD—0.4% | | | | | |

Yamana Gold, Inc. | | 446,000 | | 5,668,660 | |

| | | | | |

HEALTH CARE DISTRIBUTORS—0.5% | | | | | |

McKesson Corp. | | 74,600 | | 6,192,546 | |

| | | | | |

HEALTH CARE EQUIPMENT—1.6% | | | | | |

Covidien PLC | | 309,740 | | 17,249,421 | |

Insulet Corp. * | | 133,500 | | 2,868,915 | |

| | | | 20,118,336 | |

HEALTH CARE FACILITIES—0.7% | | | | | |

Universal Health Services, Inc., Cl. B | | 173,700 | | 9,515,286 | |

| | | | | |

HEALTH CARE SERVICES—0.8% | | | | | |

Express Scripts, Inc.* | | 184,600 | | 10,474,204 | |

| | | | | | |

15

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HOME IMPROVEMENT RETAIL—1.6% | | | | | |

Lowe’s Companies, Inc. | | 772,600 | | $ | 20,280,750 | |

| | | | | | |

HOTELS RESORTS & CRUISE LINES—0.5% | | | | | |

Wyndham Worldwide Corporation | | 192,800 | | 6,672,808 | |

| | | | | |

HOUSEHOLD APPLIANCES—0.4% | | | | | |

Stanley Black & Decker, Inc. | | 77,700 | | 5,644,905 | |

| | | | | |

HOUSEHOLD PRODUCTS—1.1% | | | | | |

Procter & Gamble Co., /The | | 203,000 | | 13,174,700 | |

| | | | | |

HUMAN RESOURCE & EMPLOYMENT SERVICES—0.4% | | | | | |

Towers Watson & Co. | | 91,170 | | 5,229,511 | |

| | | | | |

HYPERMARKETS & SUPER CENTERS—0.5% | | | | | |

Wal-Mart Stores, Inc. | | 114,410 | | 6,290,262 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—1.4% | | | | | |

3M Co. | | 65,400 | | 6,357,534 | |

Tyco International Ltd. | | 246,255 | | 12,002,469 | |

| | | | 18,360,003 | |

INDUSTRIAL MACHINERY—1.9% | | | | | |

Flowserve Corp. | | 61,900 | | 7,837,778 | |

Ingersoll-Rand PLC | | 333,800 | | 16,856,900 | |

| | | | 24,694,678 | |

INTEGRATED OIL & GAS—4.3% | | | | | |

Chevron Corp. | | 60,600 | | 6,632,064 | |

ConocoPhillips | | 309,800 | | 24,452,514 | |

Royal Dutch Shell PLC # | | 322,200 | | 24,964,056 | |

| | | | 56,048,634 | |

INTEGRATED TELECOMMUNICATION SERVICES—0.2% | | | | | |

Verizon Communications, Inc. | | 78,800 | | 2,977,064 | |

| | | | | |

INTERNET RETAIL—1.9% | | | | | |

Amazon.com, Inc. * | | 77,300 | | 15,189,450 | |

Expedia, Inc. | | 304,225 | | 7,614,752 | |

| | | | 22,804,202 | |

INTERNET SOFTWARE & SERVICES—5.6% | | | | | |

eBay, Inc. * | | 235,300 | | 8,094,320 | |

Google, Inc., Cl. A * | | 43,710 | | 23,782,610 | |

GSI Commerce, Inc. * | | 383,750 | | 11,232,363 | |

IAC/InterActiveCorp. * | | 224,300 | | 8,099,473 | |

Sina Corp. * | | 29,930 | | 4,033,068 | |

VistaPrint Ltd. * | | 171,200 | | 9,313,280 | |

Yahoo! Inc. * | | 363,800 | | 6,457,450 | |

| | | | 71,012,564 | |

INVESTMENT BANKING & BROKERAGE—1.1% | | | | | |

Goldman Sachs Group, Inc., /The | | 48,500 | | 7,323,985 | |

Lazard Ltd., Cl. A | | 120,800 | | 4,952,800 | |

LPL Investment Holdings, Inc. * | | 46,400 | | 1,701,952 | |

| | | | 13,978,737 | |

16

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

IT CONSULTING & OTHER SERVICES—2.0% | | | | | |

International Business Machines Corp. | | 146,800 | | $ | 25,041,144 | |

| | | | | | |

LEISURE PRODUCTS—1.6% | | | | | |

Hanesbrands, Inc. * | | 203,600 | | 6,619,036 | |

Phillips-Van Heusen Corp. | | 197,600 | | 13,913,016 | |

Warnaco Group Inc., /The * | | 4,800 | | 308,928 | |

| | | | 20,840,980 | |

LIFE & HEALTH INSURANCE—1.0% | | | | | |

MetLife, Inc. | | 266,600 | | 12,474,214 | |

| | | | | |

LIFE SCIENCES TOOLS & SERVICES—1.8% | | | | | |

Thermo Fisher Scientific, Inc.* | | 390,400 | | 23,420,096 | |

| | | | | |

MANAGED HEALTH CARE—1.4% | | | | | |

Aetna, Inc. | | 429,300 | | 17,764,434 | |

| | | | | |

MOVIES & ENTERTAINMENT—0.9% | | | | | |

Liberty Media Corp., Capital, Cl. A * | | 62,600 | | 5,150,102 | |

Walt Disney Co., /The | | 138,300 | | 5,960,730 | |

| | | | 11,110,832 | |

OIL & GAS EQUIPMENT & SERVICES—3.1% | | | | | |

Baker Hughes, Inc. | | 371,800 | | 28,781,038 | |

Halliburton Company | | 127,300 | | 6,426,104 | |

National Oilwell Varco, Inc. | | 58,300 | | 4,471,027 | |

| | | | 39,678,169 | |

OIL & GAS EXPLORATION & PRODUCTION—2.5% | | | | | |

Devon Energy Corp. | | 81,800 | | 7,443,800 | |

Newfield Exploration Co. * | | 89,000 | | 6,301,200 | |

Nexen, Inc. | | 506,100 | | 13,376,223 | |

Petrohawk Energy Corp. * | | 150,500 | | 4,065,005 | |

| | | | 31,186,228 | |

OIL, GAS & CONSUMABLE FUELS—0.6% | | | | | |

Williams Cos., Inc., /The | | 231,900 | | 7,692,123 | |

| | | | | |

OTHER DIVERSIFIED FINANCIAL SERVICES—2.9% | | | | | |

BM&F Bovespa SA | | 1,437,400 | | 10,785,066 | |

Citigroup, Inc. * | | 1,743,800 | | 8,004,042 | |

JPMorgan Chase & Co. | | 407,400 | | 18,589,662 | |

| | | | 37,378,770 | |

PHARMACEUTICALS—2.8% | | | | | |

Allergan, Inc. | | 153,900 | | 12,244,284 | |

Auxilium Pharmaceuticals, Inc. * | | 246,000 | | 5,992,560 | |

Johnson & Johnson | | 128,400 | | 8,438,448 | |

Pfizer, Inc. | | 382,200 | | 8,010,912 | |

| | | | 34,686,204 | |

PRECIOUS METALS & MINERALS—0.6% | | | | | |

Stillwater Mining Co.* | | 343,300 | | 7,830,673 | |

| | | | | |

RAILROADS—1.3% | | | | | |

CSX Corp. | | 210,100 | | 16,532,769 | |

17

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

RESEARCH & CONSULTING SERVICES—0.3% | | | | | |

Verisk Analytic, Inc., Cl. A* | | 99,500 | | $ | 3,273,550 | |

| | | | | | |

RESTAURANTS—0.9% | | | | | |

McDonald’s Corp. | | 147,600 | | 11,558,556 | |

| | | | | |

SEMICONDUCTOR EQUIPMENT—0.6% | | | | | |

Lam Research Corp.* | | 167,299 | | 8,082,215 | |

| | | | | |

SEMICONDUCTORS—3.9% | | | | | |

Altera Corp. | | 161,600 | | 7,869,920 | |

Avago Technologies Ltd. | | 280,600 | | 9,388,876 | |

Broadcom Corp., Cl. A * | | 94,600 | | 3,328,028 | |

NXP Semiconductor NV * | | 212,800 | | 7,107,520 | |

ON Semiconductor Corp. * | | 165,400 | | 1,738,354 | |

Skyworks Solutions, Inc. * | | 348,000 | | 10,948,080 | |

Texas Instruments, Inc. | | 276,600 | | 9,827,598 | |

| | | | 50,208,376 | |

SOFT DRINKS—1.0% | | | | | |

PepsiCo, Inc. | | 187,000 | | 12,882,430 | |

| | | | | |

SPECIALIZED FINANCE—0.6% | | | | | |

CME Group, Inc. | | 25,700 | | 7,601,289 | |

| | | | | |

SYSTEMS SOFTWARE—2.9% | | | | | |

Oracle Corp. | | 1,028,900 | | 37,091,845 | |

| | | | | |

TOBACCO—0.7% | | | | | |

Philip Morris International, Inc. | | 127,050 | | 8,822,352 | |

| | | | | |

TRUCKING—1.3% | | | | | |

Hertz Global Holdings, Inc.* | | 968,900 | | 16,674,769 | |

| | | | | |

WIRELESS TELECOMMUNICATION SERVICES—0.3% | | | | | |

SBA Communications Corp.* | | 101,300 | | 3,913,219 | |

| | | | | |

TOTAL COMMON STOCKS | | | | | |

(Cost $1,052,570,830) | | | | 1,210,298,622 | |

| | | | | |

CONVERTIBLE PREFERRED STOCK—0.3% | | | | | |

PHARMACEUTICALS—0.3% | | | | | |

Merrimack Pharmaceuticals, Inc., Series G, %, *,(L3),(a) | | | | | |

(Cost $3,475,570) | | 496,510 | | 3,475,570 | |

| | | | | |

Total Investments | | | | | |

(Cost $1,056,046,400)(b) | | 95.4 | % | 1,213,774,192 | |

Other Assets in Excess of Liabilities | | 4.6 | | 58,851,655 | |

| | | | | |

NET ASSETS | | 100.0 | % | $ | 1,272,625,847 | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

* | Non-income producing security. |

# | American Depository Receipts. |

18

(a) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $3,475,570 and represents 0.3% of the net assets of the Fund. |

(b) | At April 30, 2011, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $1,061,339,610 amounted to $152,434,582 which consisted of aggregate gross unrealized appreciation of $171,372,818 and aggregate gross unrealized depreciation of $18,938,236. |

(L3) | Security classified as Level 3 for ASC 820 disclosure purposes based on valuation inputs. |

See Notes to Financial Statements.

19

THE ALGER INSTITUTIONAL FUNDS | ALGER LARGE CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments‡ (Unaudited) April 30, 2011

| | SHARES | | VALUE | |

COMMON STOCKS—92.1% | | | | | |

AEROSPACE & DEFENSE—1.9% | | | | | |

Boeing Co., /The | | 3,100 | | $ | 247,318 | |

General Dynamics Corp. | | 3,100 | | 225,742 | |

| | | | 473,060 | |

AIR FREIGHT & LOGISTICS—2.1% | | | | | |

FedEx Corp. | | 2,550 | | 243,958 | |

United Parcel Service, Inc., Cl. B | | 3,250 | | 243,652 | |

| | | | 487,610 | |

AIRLINES—0.5% | | | | | |

Delta Air Lines, Inc.* | | 12,550 | | 130,269 | |

| | | | | |

APPLICATION SOFTWARE—1.6% | | | | | |

Adobe Systems, Inc. * | | 5,400 | | 181,170 | |

Salesforce.com, Inc. * | | 1,500 | | 207,900 | |

| | | | 389,070 | |

ASSET MANAGEMENT & CUSTODY BANKS—0.9% | | | | | |

BlackRock, Inc. | | 1,150 | | 225,331 | |

| | | | | |

AUTOMOBILE MANUFACTURERS—0.7% | | | | | |

General Motors Co.* | | 5,400 | | 173,286 | |

| | | | | |

BIOTECHNOLOGY—1.4% | | | | | |

Celgene Corp. * | | 2,100 | | 123,648 | |

Gilead Sciences, Inc. * | | 5,650 | | 219,446 | |

| | | | 343,094 | |

BREWERS—0.5% | | | | | |

Anheuser-Busch InBev NV# | | 1,950 | | 124,742 | |

| | | | | |

BROADCASTING & CABLE TV—0.6% | | | | | |

Discovery Communications, Inc., Series C* | | 3,650 | | 144,029 | |

| | | | | |

CABLE & SATELLITE—0.8% | | | | | |

Comcast Corporation, Cl. A | | 7,700 | | 202,048 | |

| | | | | |

CASINOS & GAMING—0.4% | | | | | |

Las Vegas Sands Corp.* | | 2,350 | | 110,474 | |

| | | | | |

COAL & CONSUMABLE FUELS—0.9% | | | | | |

Peabody Energy Corp. | | 3,500 | | 233,870 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—4.3% | | | | | |

Cisco Systems, Inc. | | 13,400 | | 235,304 | |

Corning, Inc. | | 12,600 | | 263,844 | |

Juniper Networks, Inc. * | | 2,200 | | 84,326 | |

Qualcomm, Inc. | | 8,250 | | 468,930 | |

| | | | 1,052,404 | |

COMPUTER HARDWARE—5.7% | | | | | |

Apple, Inc. * | | 3,350 | | 1,166,570 | |

Hewlett-Packard Co. | | 6,150 | | 248,275 | |

| | | | 1,414,845 | |

COMPUTER STORAGE & PERIPHERALS—1.3% | | | | | |

EMC Corp.* | | 11,350 | | 321,659 | |

| | | | | | |

20

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—1.7% | | | | | |

Caterpillar, Inc. | | 2,000 | | $ | 230,820 | |

Cummins, Inc. | | 1,600 | | 192,288 | |

| | | | 423,108 | |

CONSUMER FINANCE—0.6% | | | | | |

American Express Co. | | 2,800 | | 137,424 | |

| | | | | |

DATA PROCESSING & OUTSOURCED SERVICES—0.8% | | | | | |

Mastercard, Inc. | | 750 | | 206,918 | |

| | | | | |

DEPARTMENT STORES—0.8% | | | | | |

Kohl’s Corp. | | 3,950 | | 208,205 | |

| | | | | |

DIVERSIFIED CHEMICALS—0.8% | | | | | |

EI Du Pont de Nemours & Co. | | 3,300 | | 187,407 | |

| | | | | |

DIVERSIFIED METALS & MINING—1.7% | | | | | |

Cliffs Natural Resources, Inc. | | 2,500 | | 234,300 | |

Freeport-McMoRan Copper & Gold, Inc. | | 3,400 | | 187,102 | |

| | | | 421,402 | |

DRUG RETAIL—1.0% | | | | | |

CVS Caremark Corp. | | 6,650 | | 240,996 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—0.5% | | | | | |

Emerson Electric Co.* | | 2,000 | | 121,520 | |

| | | | | |

ENVIRONMENTAL & FACILITIES SERVICES—0.8% | | | | | |

Republic Services, Inc. | | 6,550 | | 207,111 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.6% | | | | | |

Mosaic Co., /The | | 2,100 | | 157,206 | |

| | | | | |

FOOTWEAR—0.9% | | | | | |

NIKE Inc., Cl. B | | 2,600 | | 214,032 | |

| | | | | |

GENERAL MERCHANDISE STORES—1.3% | | | | | |

Dollar General Corp. * | | 3,500 | | 114,065 | |

Target Corp. | | 4,150 | | 203,765 | |

| | | | 317,830 | |

GOLD—0.9% | | | | | |

Goldcorp, Inc. | | 3,800 | | 212,154 | |

| | | | | |

HEALTH CARE EQUIPMENT—1.0% | | | | | |

Covidien PLC | | 4,250 | | 236,683 | |

| | | | | |

HEALTH CARE SERVICES—1.1% | | | | | |

Medco Health Solutions, Inc. * | | 3,200 | | 189,856 | |

Quest Diagnostics, Inc. | | 1,300 | | 73,294 | |

| | | | 263,150 | |

HOME IMPROVEMENT RETAIL—0.9% | | | | | |

Lowe’s Companies, Inc. | | 8,900 | | 233,625 | |

| | | | | |

HOTELS RESORTS & CRUISE LINES—1.5% | | | | | |

Carnival Corp. | | 5,050 | | 192,254 | |

Marriott International, Inc., Cl. A | | 5,050 | | 178,265 | |

| | | | 370,519 | |

| | | | | | |

21

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HOUSEHOLD APPLIANCES—0.7% | | | | | |

Stanley Black & Decker, Inc. | | 2,450 | | $ | 177,993 | |

| | | | | | |

HOUSEHOLD PRODUCTS—1.2% | | | | | |

Procter & Gamble Co., /The | | 4,600 | | 298,540 | |

| | | | | |

HYPERMARKETS & SUPER CENTERS—1.2% | | | | | |

Wal-Mart Stores, Inc. | | 5,600 | | 307,888 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—1.8% | | | | | |

3M Co. | | 2,200 | | 213,862 | |

Tyco International Ltd. | | 4,550 | | 221,767 | |

| | | | 435,629 | |

INDUSTRIAL MACHINERY—0.8% | | | | | |

Illinois Tool Works, Inc. | | 3,550 | | 207,356 | |

| | | | | |

INTEGRATED OIL & GAS—5.4% | | | | | |

Chevron Corp. | | 4,850 | | 530,784 | |

Exxon Mobil Corp. | | 5,550 | | 488,400 | |

Royal Dutch Shell PLC # | | 3,750 | | 290,550 | |

| | | | 1,309,734 | |

INTERNET RETAIL—1.8% | | | | | |

Amazon.com, Inc. * | | 1,550 | | 304,574 | |

Expedia, Inc. | | 5,300 | | 132,659 | |

| | | | 437,233 | |

INTERNET SOFTWARE & SERVICES—4.4% | | | | | |

eBay, Inc. * | | 5,750 | | 197,800 | |

Google, Inc., Cl. A * | | 1,302 | | 708,417 | |

Yahoo! Inc. * | | 9,850 | | 174,838 | |

| | | | 1,081,055 | |

INVESTMENT BANKING & BROKERAGE—1.0% | | | | | |

Charles Schwab Corp., /The | | 6,350 | | 116,269 | |

Goldman Sachs Group, Inc., /The | | 850 | | 128,358 | |

| | | | 244,627 | |

IT CONSULTING & OTHER SERVICES—2.8% | | | | | |

Cognizant Technology Solutions Corp., Cl. A * | | 1,450 | | 120,205 | |

International Business Machines Corp. | | 3,400 | | 579,972 | |

| | | | 700,177 | |

LIFE SCIENCES TOOLS & SERVICES—1.1% | | | | | |

Thermo Fisher Scientific, Inc.* | | 4,350 | | 260,957 | |

| | | | | |

MANAGED HEALTH CARE—1.1% | | | | | |

Aetna, Inc. | | 6,650 | | 275,177 | |

| | | | | |

MOVIES & ENTERTAINMENT—0.7% | | | | | |

Walt Disney Co., /The | | 4,150 | | 178,865 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—2.2% | | | | | |

Baker Hughes, Inc. | | 2,800 | | 216,748 | |

Schlumberger Ltd. | | 3,550 | | 318,613 | |

| | | | 535,361 | |

OIL & GAS EXPLORATION & PRODUCTION—2.5% | | | | | |

Devon Energy Corp. | | 4,150 | | 377,650 | |

22

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

OIL & GAS EXPLORATION & PRODUCTION—(CONT.) | | | | | |

Nexen, Inc. | | 9,500 | | $ | 251,085 | |

| | | | 628,735 | |

OTHER DIVERSIFIED FINANCIAL SERVICES—2.4% | | | | | |

BM&F Bovespa SA | | 19,700 | | 147,813 | |

Citigroup, Inc. * | | 38,500 | | 176,715 | |

JPMorgan Chase & Co. | | 5,700 | | 260,090 | |

| | | | 584,618 | |

PACKAGED FOODS & MEATS—0.7% | | | | | |

Kraft Foods, Inc., Cl. A | | 5,450 | | 183,011 | |

| | | | | |

PAPER PRODUCTS—0.7% | | | | | |

International Paper Co. | | 6,000 | | 185,280 | |

| | | | | |

PHARMACEUTICALS—4.0% | | | | | |

Allergan, Inc. | | 2,150 | | 171,054 | |

Bristol-Myers Squibb Co. | | 6,600 | | 185,460 | |

Johnson & Johnson | | 4,050 | | 266,165 | |

Pfizer, Inc. | | 9,800 | | 205,408 | |

Teva Pharmaceutical Industries Ltd. # | | 3,900 | | 178,347 | |

| | | | 1,006,434 | |

RAILROADS—1.0% | | | | | |

CSX Corp. | | 3,150 | | 247,874 | |

| | | | | |

RESTAURANTS—2.1% | | | | | |

McDonald’s Corp. | | 4,150 | | 324,986 | |

Starbucks Corp. | | 5,350 | | 193,616 | |

| | | | 518,602 | |

SEMICONDUCTORS—2.7% | | | | | |

ARM Holdings PLC # | | 3,900 | | 122,694 | |

Broadcom Corp., Cl. A * | | 5,350 | | 188,213 | |

Intel Corp. | | 9,050 | | 209,870 | |

Texas Instruments, Inc. | | 4,400 | | 156,332 | |

| | | | 677,109 | |

SOFT DRINKS—2.9% | | | | | |

Coca-Cola Co., /The | | 4,750 | | 320,435 | |

PepsiCo, Inc. | | 5,450 | | 375,450 | |

| | | | 695,885 | |

SPECIALIZED FINANCE—0.5% | | | | | |

CME Group, Inc. | | 450 | | 133,097 | |

| | | | | |

SPECIALTY STORES—0.7% | | | | | |

Staples, Inc. | | 8,550 | | 180,747 | |

| | | | | |

SYSTEMS SOFTWARE—4.2% | | | | | |

Check Point Software Technologies Ltd. * | | 2,400 | | 131,832 | |

Microsoft Corp. | | 10,700 | | 278,414 | |

Oracle Corp. | | 13,850 | | 499,293 | |

VMware, Inc., Cl. A * | | 1,400 | | 133,602 | |

| | | | 1,043,141 | |

| | | | | | |

23

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

WIRELESS TELECOMMUNICATION SERVICES—1.0% | | | | | |

American Tower Corp., Cl. A* | | 4,700 | | $ | 245,857 | |

| | | | | |

TOTAL COMMON STOCKS | | | | | |

(Cost $19,694,848) | | | | 22,766,063 | |

| | | | | |

Total Investments | | | | | |

(Cost $19,694,848)(a) | | 92.1 | % | 22,766,063 | |

Other Assets in Excess of Liabilities | | 7.9 | | 1,947,791 | |

| | | | | |

NET ASSETS | | 100.0 | % | $ | 24,713,854 | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

| |

* | Non-income producing security. |

# | American Depository Receipts. |

(a) | At April 30, 2011, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $19,725,005 amounted to $3,041,058 which consisted of aggregate gross unrealized appreciation of $3,641,436 and aggregate gross unrealized depreciation of $600,378. |

See Notes to Financial Statements.

24

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments‡ (Unaudited) April 30, 2011

| | SHARES | | VALUE | |

COMMON STOCKS—99.3% | | | | | |

ADVERTISING—0.4% | | | | | |

Interpublic Group of Cos., Inc., /The | | 265,300 | | $ | 3,117,275 | |

| | | | | | |

AEROSPACE & DEFENSE—2.9% | | | | | |

Goodrich Corp. | | 89,400 | | 7,900,278 | |

Spirit Aerosystems Holdings, Inc., Cl. A * | | 506,800 | | 12,467,280 | |

| | | | 20,367,558 | |

AIRLINES—0.9% | | | | | |

United Continental Holdings, Inc.* | | 277,800 | | 6,339,396 | |

| | | | | |

APPAREL RETAIL—1.3% | | | | | |

Abercrombie & Fitch Co., Cl. A | | 73,700 | | 5,217,960 | |

Fast Retailing Co., Ltd. | | 23,200 | | 3,635,010 | |

| | | | 8,852,970 | |

APPLICATION SOFTWARE—4.7% | | | | | |

Adobe Systems, Inc. * | | 157,300 | | 5,277,415 | |

Cadence Design Systems, Inc. * | | 325,600 | | 3,379,728 | |

Informatica Corp. * | | 159,200 | | 8,916,792 | |

QLIK Technologies, Inc. * | | 95,355 | | 3,057,081 | |

RealPage, Inc. * | | 76,500 | | 2,440,350 | |

Salesforce.com, Inc. * | | 67,200 | | 9,313,920 | |

| | | | 32,385,286 | |

ASSET MANAGEMENT & CUSTODY BANKS—2.6% | | | | | |

Blackstone Group LP | | 278,100 | | 5,267,214 | |

KKR & Co., LP | | 360,900 | | 6,842,664 | |

T. Rowe Price Group, Inc. | | 96,200 | | 6,180,850 | |

| | | | 18,290,728 | |

AUTOMOTIVE RETAIL—1.0% | | | | | |

Carmax, Inc.* | | 207,400 | | 7,196,780 | |

| | | | | |

BIOTECHNOLOGY—1.8% | | | | | |

Human Genome Sciences, Inc. * | | 274,900 | | 8,101,303 | |

InterMune, Inc. * | | 43,900 | | 1,959,696 | |

Optimer Pharmaceuticals, Inc. * | | 189,559 | | 2,394,130 | |

| | | | 12,455,129 | |

BROADCASTING & CABLE TV—2.8% | | | | | |

CBS Corp., Cl. B | | 344,500 | | 8,688,290 | |

Discovery Communications, Inc., Series C * | | 261,400 | | 10,314,843 | |

| | | | 19,003,133 | |

CASINOS & GAMING—0.5% | | | | | |

Wynn Resorts Ltd. | | 23,900 | | 3,516,885 | |

| | | | | |

CHEMICALS—0.8% | | | | | |

Metabolix, Inc.* | | 656,860 | | 5,307,429 | |

| | | | | |

COAL & CONSUMABLE FUELS—1.3% | | | | | |

Arch Coal, Inc. | | 114,900 | | 3,941,070 | |

Patriot Coal Corp. * | | 210,100 | | 5,290,318 | |

| | | | 9,231,388 | |

COMMUNICATIONS EQUIPMENT—2.6% | | | | | |

Ciena Corp. * | | 195,400 | | 5,518,096 | |

25

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

COMMUNICATIONS EQUIPMENT—(CONT.) | | | | | |

Finisar Corp. * | | 255,000 | | $ | 7,162,950 | |

Riverbed Technology, Inc. * | | 152,200 | | 5,348,308 | |

| | | | 18,029,354 | |

COMPUTER HARDWARE—1.3% | | | | | |

Teradata Corp.* | | 165,500 | | 9,254,760 | |

| | | | | |

COMPUTER STORAGE & PERIPHERALS—1.2% | | | | | |

SanDisk Corp.* | | 169,300 | | 8,319,402 | |

| | | | | |

CONSTRUCTION & ENGINEERING—1.8% | | | | | |

Aecom Technology Corp. * | | 217,300 | | 5,923,598 | |

Chicago Bridge & Iron Co., NV # | | 165,800 | | 6,721,532 | |

| | | | 12,645,130 | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—3.7% | | | | | |

Cummins, Inc. | | 57,700 | | 6,934,386 | |

Joy Global, Inc. | | 141,700 | | 14,304,615 | |

Westport Innovations, Inc. * | | 165,300 | | 4,182,090 | |

| | | | 25,421,091 | |

DISTILLERS & VINTNERS—0.5% | | | | | |

Brown-Forman Corp., Cl. B | | 47,800 | | 3,434,908 | |

| | | | | |

DIVERSIFIED BANKS—0.7% | | | | | |

Comerica, Inc. | | 131,800 | | 4,999,174 | |

| | | | | |

DIVERSIFIED METALS & MINING—4.9% | | | | | |

Cliffs Natural Resources, Inc. | | 154,500 | | 14,479,740 | |

Ivanhoe Mines Ltd. * | | 138,600 | | 3,642,408 | |

Molycorp, Inc. * | | 89,000 | | 6,523,700 | |

Walter Energy, Inc. | | 70,200 | | 9,703,044 | |

| | | | 34,348,892 | |

EDUCATION SERVICES—0.5% | | | | | |

ITT Educational Services, Inc.* | | 49,500 | | 3,550,635 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—2.4% | | | | | |

AMETEK, Inc. | | 226,850 | | 10,444,174 | |

General Cable Corp. * | | 124,600 | | 6,043,100 | |

| | | | 16,487,274 | |

ELECTRONIC MANUFACTURING SERVICES—0.9% | | | | | |

Trimble Navigation Ltd.* | | 136,000 | | 6,370,240 | |

| | | | | |

ENVIRONMENTAL & FACILITIES SERVICES—1.0% | | | | | |

Stericycle, Inc.* | | 76,100 | | 6,946,408 | |

| | | | | |

FOOD RETAIL—0.5% | | | | | |

Whole Foods Market, Inc.* | | 55,500 | | 3,483,180 | |

| | | | | |

GENERAL MERCHANDISE STORES—1.0% | | | | | |

Dollar General Corp.* | | 215,200 | | 7,013,368 | |

| | | | | |

GOLD—1.6% | | | | | |

Yamana Gold, Inc. | | 885,100 | | 11,249,621 | |

| | | | | |

HEALTH CARE EQUIPMENT—0.9% | | | | | |

Hospira, Inc.* | | 112,400 | | 6,376,452 | |

| | | | | | |

26

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HEALTH CARE FACILITIES—1.0% | | | | | |

Universal Health Services, Inc., Cl. B | | 127,195 | | $ | 6,967,742 | |

| | | | | | |

HEALTH CARE SERVICES—0.5% | | | | | |

Quest Diagnostics, Inc. | | 57,400 | | 3,236,212 | |

| | | | | |

HEALTH CARE TECHNOLOGY—1.4% | | | | | |

Agilent Technologies, Inc. * | | 69,600 | | 3,473,736 | |

Allscripts Healthcare Solutions, Inc. * | | 288,500 | | 6,214,290 | |

| | | | 9,688,026 | |

HOTELS RESORTS & CRUISE LINES—1.2% | | | | | |

Interval Leisure Group * | | 92,300 | | 1,483,261 | |

Orient-Express Hotels Ltd., Cl. A * | | 140,200 | | 1,720,254 | |

Royal Caribbean Cruises Ltd. * | | 134,200 | | 5,343,844 | |

| | | | 8,547,359 | |

HOUSEHOLD PRODUCTS—0.7% | | | | | |

Church & Dwight Co., Inc. | | 58,500 | | 4,825,080 | |

| | | | | |

HUMAN RESOURCE & EMPLOYMENT SERVICES—1.0% | | | | | |

Robert Half International, Inc. | | 227,700 | | 6,906,141 | |

| | | | | |

INDUSTRIAL MACHINERY—4.0% | | | | | |

Flowserve Corp. | | 73,000 | | 9,243,260 | |

Pall Corp. | | 86,200 | | 5,037,528 | |

SPX Corp. | | 156,800 | | 13,555,360 | |

| | | | 27,836,148 | |

INTERNET RETAIL—1.1% | | | | | |

NetFlix, Inc. * | | 14,100 | | 3,280,647 | |

priceline.com, Inc. * | | 7,600 | | 4,157,276 | |

| | | | 7,437,923 | |

INTERNET SOFTWARE & SERVICES—4.9% | | | | | |

Ancestry.com, Inc. * | | 103,400 | | 4,725,380 | |

OpenTable, Inc. * | | 182,600 | | 20,321,554 | |

VistaPrint Ltd. * | | 162,500 | | 8,840,000 | |

| | | | 33,886,934 | |

INVESTMENT BANKING & BROKERAGE—1.4% | | | | | |

Greenhill & Co., Inc. | | 167,600 | | 9,888,400 | |

| | | | | |

IT CONSULTING & OTHER SERVICES—2.3% | | | | | |

Cognizant Technology Solutions Corp., Cl. A * | | 157,500 | | 13,056,750 | |

Gartner, Inc. * | | 64,100 | | 2,750,531 | |

| | | | 15,807,281 | |

LEISURE PRODUCTS—1.6% | | | | | |

Coach, Inc. | | 90,700 | | 5,424,767 | |

Polo Ralph Lauren Corp., Cl. A | | 40,600 | | 5,309,262 | |

| | | | 10,734,029 | |

LIFE SCIENCES TOOLS & SERVICES—0.5% | | | | | |

Waters Corp.* | | 35,400 | | 3,469,200 | |

| | | | | |

MANAGED HEALTH CARE—4.9% | | | | | |

Aetna, Inc. | | 242,100 | | 10,018,098 | |

CIGNA Corp. | | 303,100 | | 14,194,173 | |

27

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

MANAGED HEALTH CARE—(CONT.) | | | | | |

Humana, Inc. * | | 137,700 | | $ | 10,481,724 | |

| | | | 34,693,995 | |

MOTORCYCLE MANUFACTURERS—0.4% | | | | | |

Harley-Davidson, Inc. | | 81,400 | | 3,032,964 | |

| | | | | |

NETWORKING EQUIPMENT—0.7% | | | | | |

Fortinet, Inc.* | | 100,800 | | 4,908,960 | |

| | | | | |

OIL & GAS DRILLING—1.2% | | | | | |

Nabors Industries Ltd.* | | 263,800 | | 8,082,832 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—0.8% | | | | | |

Superior Energy Services, Inc.* | | 143,700 | | 5,520,954 | |

| | | | | |

OIL & GAS EXPLORATION & PRODUCTION—5.7% | | | | | |

Concho Resources, Inc., /Restricted * | | 33,100 | | 3,536,735 | |

Newfield Exploration Co. * | | 157,000 | | 11,115,600 | |

Nexen, Inc. | | 267,557 | | 7,071,532 | |

Petrohawk Energy Corp. *,^ | | 402,800 | | 10,879,628 | |

Pioneer Natural Resources Co. | | 69,500 | | 7,104,985 | |

| | | | 39,708,480 | |

OTHER DIVERSIFIED FINANCIAL SERVICES—0.5% | | | | | |

BM&F Bovespa SA | | 445,887 | | 3,345,569 | |

| | | | | |

PHARMACEUTICALS—0.5% | | | | | |

Medicis Pharmaceutical Corp., Cl. A | | 98,700 | | 3,499,902 | |

| | | | | |

PRECIOUS METALS & MINERALS—1.0% | | | | | |

Stillwater Mining Co.* | | 314,400 | | 7,171,464 | |

| | | | | |

RAILROADS—1.5% | | | | | |

Kansas City Southern* | | 179,700 | | 10,442,367 | |

| | | | | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—0.7% | | | | | |

BR Malls Participacoes SA | | 471,740 | | 4,963,160 | |

| | | | | |

REAL ESTATE SERVICES—1.3% | | | | | |

CB Richard Ellis Group, Inc.* | | 327,900 | | 8,758,209 | |

| | | | | |

RESEARCH & CONSULTING SERVICES—1.1% | | | | | |

Verisk Analytic, Inc., Cl. A* | | 235,000 | | 7,731,500 | |

| | | | | |

RESTAURANTS—0.4% | | | | | |

McCormick & Schmick’s Seafood Restaurants, Inc.* | | 292,976 | | 2,674,871 | |

| | | | | |

SEMICONDUCTOR EQUIPMENT—2.0% | | | | | |

Kla-Tencor Corp. | | 121,100 | | 5,316,290 | |

Lam Research Corp. * | | 177,000 | | 8,550,870 | |

| | | | 13,867,160 | |

SEMICONDUCTORS—6.7% | | | | | |

Altera Corp. | | 215,300 | | 10,485,110 | |

Avago Technologies Ltd. | | 200,500 | | 6,708,730 | |

Netlogic Microsystems, Inc. * | | 120,100 | | 5,179,913 | |

NVIDIA Corp. * | | 270,300 | | 5,406,000 | |

NXP Semiconductor NV * | | 150,800 | | 5,036,720 | |

ON Semiconductor Corp. * | | 512,400 | | 5,385,324 | |

| | | | | | |

28

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

SEMICONDUCTORS—(CONT.) | | | | | |

Skyworks Solutions, Inc. * | | 255,500 | | $ | 8,038,030 | |

| | | | 46,239,827 | |

SPECIALIZED CONSUMER SERVICES—0.5% | | | | | |

Sotheby’s | | 75,200 | | 3,799,104 | |

| | | | | |

SPECIALTY STORES—0.5% | | | | | |

L’Occitane International SA* | | 1,426,200 | | 3,423,042 | |

| | | | | |

SYSTEMS SOFTWARE—0.8% | | | | | |

Check Point Software Technologies Ltd.* | | 106,300 | | 5,839,059 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $614,316,914) | | | | 690,927,740 | |

| | | | | |

CONVERTIBLE PREFERRED STOCK—1.5% | | | | | |

BIOTECHNOLOGY—1.5% | | | | | |

Merrimack Pharmaceuticals, Inc., Series B-10, *,(L3),(a) | | 115,098 | | 1,240,756 | |

Merrimack Pharmaceuticals, Inc., Series B-3, *,(L3),(b) | | 11,510 | | 124,078 | |

Merrimack Pharmaceuticals, Inc., Series B-4, *,(L3),(c) | | 345,008 | | 3,719,186 | |

Merrimack Pharmaceuticals, Inc., Series B-7, *,(L3),(a) | | 115,098 | | 1,240,756 | |

Merrimack Pharmaceuticals, Inc., Series C-2, *,(L3),(d) | | 611,759 | | 4,282,314 | |

| | | | 10,607,090 | |

TOTAL CONVERTIBLE PREFERRED STOCK

(Cost $5,689,999) | | | | 10,607,090 | |

| | | | | |

Total Investments

(Cost $620,006,913)(e) | | 100.8 | % | 701,534,830 | |

Liabilities in Excess of Other Assets | | (0.8 | ) | (5,336,637 | ) |

| | | | | |

NET ASSETS | | 100.0 | % | $ | 696,198,193 | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

| |

^ | All or a portion of this security has been pledged as collateral for written call options. |

* | Non-income producing security. |

# | American Depository Receipts. |

(a) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $666,188 and represents 0.2% of the net assets of the Fund. |

(b) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $66,620 and represents 0.0% of the net assets of the Fund. |

(c) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $1,996,908 and represents 0.5% of the net assets of the Fund. |

(d) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $2,294,095 and represents 0.6% of the net assets of the Fund. |

29

(e) | At April 30, 2011, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $624,073,945 amounted to $77,460,885 which consisted of aggregate gross unrealized appreciation of $95,567,652 and aggregate gross unrealized depreciation of $18,106,767. |

(L3) | Security classified as Level 3 for ASC 820 disclosure purposes based on valuation inputs. |

See Notes to Financial Statements.

30

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Options Written‡ (Unaudited) April 30, 2011

| | CONTRACTS | | SHARES

SUBJECT

TO PUT/

CALL | | VALUE | |

PUT OPTIONS WRITTEN | | | | | | | |

Petrohawk Energy Corp./ June/ 27 | | 600 | | 60,000 | | 107,400 | |

| | | | | | | |

TOTAL PUT OPTIONS WRITTEN | | | | | | | |

(Premiums Received $124,789) | | | | | | 107,400 | |

| | | | | | | |

CALL OPTIONS WRITTEN | | | | | | | |

Concho Resources, Inc./ May/ 105 | | 169 | | 16,900 | | $ | 57,460 | |

Petrohawk Energy Corp./ June/ 27 | | 600 | | 60,000 | | 105,600 | |

| | | | | | | |

TOTAL CALL OPTIONS WRITTEN | | | | | | | |

(Premiums Received $140,801) | | | | | | 163,060 | |

| | | | | | | |

TOTAL OPTIONS WRITTEN | | | | | | | |

(Premiums Received $265,590) | | | | | | $ | 270,460 | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

See Notes to Financial Statements.

31

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments‡ (Unaudited) April 30, 2011

| | SHARES | | VALUE | |

COMMON STOCKS—96.4% | | | | | |

AEROSPACE & DEFENSE—2.1% | | | | | |

AAR Corp. | | 534,800 | | $ | 13,926,192 | |

Esterline Technologies Corp. * | | 224,775 | | 16,138,845 | |

| | | | 30,065,037 | |

AIRLINES—0.5% | | | | | |

US Airways Group, Inc.* | | 745,650 | | 6,777,959 | |

| | | | | |

APPAREL RETAIL—2.6% | | | | | |

ANN Inc. * | | 538,350 | | 16,801,903 | |

Childrens Place Retail Stores, Inc., /The * | | 209,700 | | 11,149,748 | |

DSW Inc., Cl. A * | | 64,150 | | 3,045,842 | |

Express, Inc. | | 324,950 | | 7,015,671 | |

| | | | 38,013,164 | |

APPLICATION SOFTWARE—8.8% | | | | | |

BroadSoft, Inc. * | | 219,919 | | 9,995,319 | |

Cadence Design Systems, Inc. * | | 1,372,050 | | 14,241,879 | |

Concur Technologies, Inc. * | | 191,350 | | 11,073,425 | |

Nice Systems Ltd. #* | | 424,655 | | 16,192,094 | |

QLIK Technologies, Inc. * | | 478,700 | | 15,347,121 | |

RealPage, Inc. * | | 380,100 | | 12,125,190 | |

Solera Holdings, Inc. | | 241,600 | | 13,288,000 | |

Taleo Corp., Cl. A * | | 338,100 | | 12,262,887 | |

Ultimate Software Group, Inc. * | | 208,000 | | 11,648,000 | |

VanceInfo Technologies, Inc. #* | | 303,600 | | 9,763,776 | |

| | | | 125,937,691 | |

ASSET MANAGEMENT & CUSTODY BANKS—1.0% | | | | | |

Fortress Investment Group LLC, Cl. A* | | 2,362,950 | | 14,579,402 | |

| | | | | |

AUTO PARTS & EQUIPMENT—1.1% | | | | | |

Dana Holding Corp.* | | 879,900 | | 15,987,783 | |

| | | | | |

BIOTECHNOLOGY—2.9% | | | | | |

Cubist Pharmaceuticals, Inc. * | | 287,250 | | 9,723,413 | |

Incyte Corp., Ltd. * | | 310,500 | | 5,738,040 | |

InterMune, Inc. * | | 256,100 | | 11,432,303 | |

Onyx Pharmaceuticals, Inc. * | | 104,100 | | 3,911,037 | |

Optimer Pharmaceuticals, Inc. * | | 890,812 | | 11,250,956 | |

| | | | 42,055,749 | |

COAL & CONSUMABLE FUELS—0.6% | | | | | |

Patriot Coal Corp.* | | 343,350 | | 8,645,553 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—3.7% | | | | | |

Acme Packet, Inc. * | | 132,050 | | 10,908,651 | |

Aruba Networks, Inc. * | | 319,200 | | 11,468,856 | |

Ciena Corp. * | | 394,800 | | 11,149,152 | |

Finisar Corp. * | | 360,300 | | 10,120,827 | |

Riverbed Technology, Inc. * | | 292,600 | | 10,281,964 | |

| | | | 53,929,450 | |

CONSTRUCTION & ENGINEERING—0.7% | | | | | |

Aecom Technology Corp.* | | 351,450 | | 9,580,527 | |

| | | | | | |

32

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

DATA PROCESSING & OUTSOURCED SERVICES—2.0% | | | | | |

Jack Henry & Associates, Inc. | | 350,550 | | $ | 11,908,184 | |

Wright Express Corp. * | | 289,985 | | 16,334,855 | |

| | | | 28,243,039 | |

DISTRIBUTORS—0.8% | | | | | |

LKQ Corp.* | | 479,240 | | 12,086,433 | |

| | | | | |

DIVERSIFIED CHEMICALS—0.9% | | | | | |

Solutia, Inc.* | | 492,900 | | 12,987,915 | |

| | | | | |

EDUCATION SERVICES—0.5% | | | | | |

American Public Education, Inc.* | | 163,900 | | 6,924,775 | |

| | | | | |

ELECTRIC UTILITIES—1.1% | | | | | |

ITC Holdings Corp. | | 215,385 | | 15,277,258 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—2.1% | | | | | |

GrafTech International Ltd. * | | 664,300 | | 15,411,760 | |

Woodward Governor Co. | | 382,000 | | 14,153,100 | |

| | | | 29,564,860 | |

ELECTRONIC COMPONENTS—1.0% | | | | | |

Aeroflex Holding Corp. * | | 385,100 | | 6,816,270 | |

Fabrinet * | | 307,700 | | 7,092,485 | |

| | | | 13,908,755 | |

ENVIRONMENTAL & FACILITIES SERVICES—2.8% | | | | | |

Clean Harbors, Inc. * | | 149,500 | | 14,725,750 | |

Tetra Tech, Inc. * | | 432,650 | | 10,219,193 | |

Waste Connections, Inc. | | 533,400 | | 16,412,718 | |

| | | | 41,357,661 | |

FOOD DISTRIBUTORS—0.9% | | | | | |

United Natural Foods, Inc.* | | 308,850 | | 13,184,807 | |

| | | | | |

FOOD RETAIL—0.5% | | | | | |

Fresh Market, Inc., /The* | | 171,650 | | 7,178,403 | |

| | | | | |

GOLD—0.7% | | | | | |

Gammon Gold, Inc.* | | 879,600 | | 9,596,436 | |

| | | | | |

HEALTH CARE EQUIPMENT—3.0% | | | | | |

Arthrocare Corp. * | | 180,300 | | 6,369,999 | |

Insulet Corp. * | | 565,150 | | 12,145,073 | |

MAKO Surgical Corp. * | | 374,842 | | 10,296,910 | |

Sirona Dental Systems, Inc. * | | 159,300 | | 9,091,251 | |

Thoratec Corp. * | | 201,650 | | 6,190,655 | |

| | | | 44,093,888 | |

HEALTH CARE FACILITIES—1.5% | | | | | |

Healthsouth Corp. * | | 404,350 | | 10,363,491 | |

Kindred Healthcare, Inc. * | | 124,350 | | 3,136,107 | |

LifePoint Hospitals, Inc. * | | 180,200 | | 7,498,122 | |

| | | | 20,997,720 | |

HEALTH CARE SERVICES—2.3% | | | | | |

Catalyst Health Solutions, Inc. * | | 243,500 | | 14,502,860 | |

Gentiva Health Services, Inc. * | | 374,650 | | 10,490,200 | |

| | | | | | |

33

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HEALTH CARE SERVICES—(CONT.) | | | | | |

HMS Holdings Corp. * | | 110,000 | | $ | 8,658,100 | |

| | | | 33,651,160 | |

HEALTH CARE SUPPLIES—0.9% | | | | | |

Align Technology, Inc.* | | 512,300 | | 12,366,922 | |

| | | | | |

HEALTH CARE TECHNOLOGY—1.3% | | | | | |

MedAssets, Inc. * | | 289,650 | | 4,640,193 | |

Medidata Solutions, Inc. * | | 526,550 | | 13,516,539 | |

| | | | 18,156,732 | |

HOME FURNISHINGS—0.4% | | | | | |

Ethan Allen Interiors, Inc. | | 217,350 | | 5,235,962 | |

| | | | | |

HOTELS RESORTS & CRUISE LINES—1.5% | | | | | |

Gaylord Entertainment Co. * | | 289,050 | | 10,368,224 | |

Interval Leisure Group * | | 731,316 | | 11,752,248 | |

| | | | 22,120,472 | |

HOUSEHOLD APPLIANCES—0.6% | | | | | |

SodaStream International Ltd.* | | 173,450 | | 7,933,603 | |

| | | | | |

HOUSEWARES & SPECIALTIES—1.0% | | | | | |

Tupperware Brands Corp. | | 229,350 | | 14,602,715 | |

| | | | | |

INDUSTRIAL MACHINERY—3.9% | | | | | |

Actuant Corp., Cl. A | | 546,260 | | 15,164,178 | |

Barnes Group, Inc. | | 658,650 | | 16,295,001 | |

CLARCOR, Inc. | | 202,550 | | 9,153,235 | |

RBC Bearings, Inc. * | | 417,390 | | 16,386,730 | |

| | | | 56,999,144 | |

INTERNET RETAIL—1.2% | | | | | |

Shutterfly, Inc.* | | 291,400 | | 17,938,584 | |

| | | | | |