UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-7994 |

|

Salomon Brothers Global Partners Income Fund Inc. |

(Exact name of registrant as specified in charter) |

|

125 Broad Street, New York, NY | | 10004 |

(Address of principal executive offices) | | (Zip code) |

|

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

300 First Stamford Place, 4th Floor

Stamford, CT 06902 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (800) 725-6666 | |

|

Date of fiscal year end: | August 31 | |

|

Date of reporting period: | August 31, 2006 | |

| | | | | | | | |

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

| Salomon Brothers |

| Global Partners |

| Income Fund Inc. |

| |

| |

ANNUAL REPORT | | |

| | |

| | |

AUGUST 31, 2006 | | |

| | |

| | |

| | |

| | INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

| Salomon Brothers

Global Partners

Income Fund Inc. |

Annual Report • August 31, 2006

What’s Inside

Fund Objective

The Fund seeks to maintain a high level of current income by investing primarily in a portfolio of high-yield U.S. and non-U.S. corporate debt securities. As a secondary objective, the Fund seeks capital appreciation.

Letter from the Chairman | I |

| |

Fund Overview | 1 |

| |

Fund at a Glance | 4 |

| |

Schedule of Investments | 5 |

| |

Statement of Assets and Liabilities | 22 |

| |

Statement of Operations | 23 |

| |

Statements of Changes in Net Assets | 24 |

| |

Statement of Cash Flows | 25 |

| |

Financial Highlights | 26 |

| |

Notes to Financial Statements | 27 |

| |

Report of Independent Registered Public Accounting Firm | 35 |

| |

Board Approval of Management and Subadvisory Agreements | 36 |

| |

Additional Information | 39 |

| |

Annual Chief Executive Officer and Chief Financial Officer Certification | 42 |

| |

Dividend Reinvestment and Cash Purchase Plan | 43 |

“Smith Barney”, “Salomon Brothers” and “Citi” are service marks of Citigroup, licensed for use by Legg Mason as the names of funds and investment managers. Legg Mason and its affiliates, as well as the Fund’s investment manager, are not affiliated with Citigroup.

R. JAY GERKEN, CFA

Chairman, President and

Chief Executive Officer

Dear Shareholder,

While the U.S. economy continued to expand during the reporting period, it did so at an uneven pace. After expanding 4.1% in the third quarter of 2005, gross domestic product (“GDP”)i growth slipped to 1.7% during the fourth quarter. The economy then rebounded sharply in the first quarter of 2006, with GDP rising 5.6%, its best showing since the third quarter of 2003. However, the economy then took a step backwards in the second quarter of 2006, as GDP growth was 2.6%, according to final estimates released by the U.S. Bureau of Economic Analysis. The decline was largely attributed to lower consumer spending, triggered by higher interest rates and oil prices, as well as a cooling housing market. In addition, business spending fell during the quarter.

The Federal Reserve Board (“Fed”)ii continued to raise interest rates during most of the reporting period. Since it began its tightening campaign in June 2004, the Fed increased rates 17 consecutive times, bringing the federal funds rateiii from 1.00% to 5.25%. However, in August 2006, the Fed paused from raising rates. In its official statement, the Fed said, “...the Committee judges that some inflation risks remain. The extent and timing of any additional firming that may be needed to address these risks will depend on the evolution of the outlook for both inflation and economic growth, as implied by incoming information.”

Both short- and long-term yields rose over the reporting period. However, after peaking in late June — with two and 10 year Treasuries hitting 5.29% and 5.25%, respectively — rates fell sharply on hopes that the Fed would end its tightening cycle. Overall, during the 12 months ended August 31, 2006, two-year Treasury yields increased from 3.84% to 4.79%. Over the same period, 10-year Treasury

Salomon Brothers Global Partners Income Fund Inc. I

yields moved from 4.02% to 4.74%. Looking at the 12-month period as a whole, the overall bond market, as measured by the Lehman Brothers U.S. Aggregate Indexiv, returned 1.71%.

Given continued strong corporate profits and low default rates, high yield bonds generated positive returns during the reporting period. While there were notable company specific issues, mostly in the automobile industry, they were not enough to drag down the overall high yield market. During the 12-month period ended August 31, 2006, the Citigroup High Yield Market Indexv returned 5.06%.

Despite periods of weakness, emerging markets debt generated strong results over the 12-month period, as the JPMorgan Emerging Markets Bond Index Globalvi returned 9.02%. A strong global economy, solid domestic spending and high-energy prices supported many emerging market countries. We believe this was enough to overcome the negatives associated with rising global interest rates.

Please read on for a more detailed look at prevailing economic and market conditions during the Fund’s fiscal year and to learn how those conditions have affected Fund performance.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry (not directly affecting closed-end investment companies, such as this Fund) have come under the scrutiny of federal and state regulators. Affiliates of the Fund’s Manager have, in recent years, received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the open-end funds’ response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund is not in a position to predict the outcome of these requests and investigations, or whether these may affect the Fund.

II Salomon Brothers Global Partners Income Fund Inc.

Important information with regard to recent regulatory developments that may affect the Fund is contained in the Notes to Financial Statements included in this report.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you meet your financial goals.

Sincerely, |

|

| |

|

R. Jay Gerken, CFA |

Chairman, President and Chief Executive Officer |

September 28, 2006

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

i | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| |

ii | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| |

iii | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| |

iv | The Lehman Brothers U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| |

v | The Citigroup High Yield Market Index is a broad-based unmanaged index of high yield securities. |

| |

vi | The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds, and local market instruments. Countries covered are Algeria, Argentina, Brazil, Bulgaria, Chile, China, Colombia, Cote d’Ivoire, Croatia, Ecuador, Greece, Hungary, Lebanon, Malaysia, Mexico, Morocco, Nigeria, Panama, Peru, the Philippines, Poland, Russia, South Africa, South Korea, Thailand, Turkey and Venezuela. |

Salomon Brothers Global Partners Income Fund Inc. III

Fund Overview

Special Shareholder Notices

Following the purchase of substantially all of Citigroup’s asset management business in December 2005, Legg Mason, Inc. (“Legg Mason”) undertook an internal reorganization to consolidate the advisory services provided to the legacy Citigroup funds through a more limited number of advisers. As part of this reorganization, at a meeting held on June 26, 2006, the Fund’s Board approved a new management agreement with Legg Mason Partners Fund Advisor, LLC (“LMPFA”), under which LMPFA became the investment adviser for the Fund effective August 1, 2006.

Western Asset Management Company (“Western Asset”) became the subadviser for the Fund, under a new sub-advisory agreement between LMPFA and Western Asset, effective August 1, 2006. LMPFA and Western Asset are wholly-owned subsidiaries of Legg Mason. The portfolio managers who are responsible for the day-to-day management of the Fund remain the same immediately prior to and immediately after the date of these changes.

LMPFA provides administrative and certain oversight services to the Fund. LMPFA has delegated to the subadviser, the day-to-day portfolio management of the Fund. The management fee for the Fund remains unchanged.

In addition to these advisory changes, effective October 9, 2006, the Fund’s name is Western Asset Global Partners Income Fund Inc.

Q. What were the overall market conditions during the Fund’s reporting period?

A. The global bond market experienced periods of volatility over the last 12 months, but ultimately generated positive results. The global bond market’s ups and downs were particularly evident in more risky asset classes, such as high yield and emerging market debt. In both of these asset classes, periods of investor risk aversion led to periods of weakness. This was often tied to the actions of the Federal Reserve Board (“Fed”)i. However, looking at the period as a whole, both asset classes ultimately generated solid returns.

Performance Review

For the 12 months ended August 31, 2006, the Salomon Brothers Global Partners Income Fund Inc. returned 6.70%, based on its net asset value (“NAV”)ii and 0.08% based on its New York Stock Exchange (“NYSE”) market price per share. In comparison, the Fund’s unmanaged benchmarks, the Citigroup High Yield Market Indexiii and the JPMorgan Emerging Markets Bond Index Globaliv, returned 5.06% and 9.02%, respectively, for the same period. The Lipper Emerging Markets Debt Closed-End Funds Category Averagev increased 9.60% over the same time frame. Please note that Lipper performance returns are based on each fund’s NAV.

During the 12-month period, the Fund made distributions to shareholders totaling $0.9630 per share. The performance table shows the Fund’s 12-month total return based

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 1

on its NAV and market price as of August 31, 2006. Past performance is no guarantee of future results.

Performance Snapshot as of August 31, 2006 (unaudited)

Price Per Share | | | 12-Month

Total Return | |

| | | | |

$12.93 (NAV) | | 6.70% | |

$11.77 (Market Price) | | 0.08% | |

All figures represent past performance and are not a guarantee of future results.

Total returns are based on changes in NAV or market price, respectively. Total returns assume the reinvestment of all distributions in additional shares.

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. During the first half of the reporting period, the Fund’s performance was driven predominantly by strong industry and security selection in the high yield portion of the portfolio. Positive country selection in the emerging markets debt portion of the portfolio enhanced results as well. In particular, security selection in the tower and utilities industries and an underweight to automotive securities contributed to performance. From a country perspective, an underweight in Russia and an overweight in Argentina positively contributed to results. The use of leverage also supported the Fund’s performance.

During the second half of the reporting period, overweights in emerging market debt issued by Mexico and Brazil enhanced results. In the high yield portion of the portfolio, the Fund’s exposure to Ford and General Motors boosted returns, as they rebounded strongly. In addition, the Fund’s overweight position in a number of individual securities, including Newpage and Hawaiian Telcom benefited results.

Q. What were the leading detractors from performance?

A. During the first half of the reporting period, the Fund’s overall asset allocation positioning between high yield and emerging markets debt detracted slightly from performance. Security selection in Brazil and Argentina also was a negative to results. During the second half of the reporting period, the Fund’s overweight in the energy, gaming, and entertainment industries were negative contributors to performance.

Q. Were there any significant changes to the Fund during the reporting period?

A. Earlier in the period, we increased the Fund’s allocation to high yield securities over emerging markets debt in an effort to take advantage of more compelling valuations. This was accomplished by selling out of more liquid emerging credits like Brazil, Mexico and

2 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Russia. We also reinvested assets from a series of calls and tenders, primarily in the telecommunications sector, into automotive, healthcare and energy credits.

Looking for Additional Information?

The Fund is traded under the symbol “GDF” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under symbol XGDFX on most financial websites. Barron’s and The Wall Street Journal’s Monday edition both carry closed-end fund tables that provide additional information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites as well as www.leggmason.com/InvestorServices.

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102, Monday through Friday from 8:00 a.m. to 6:00 p.m. Eastern Time, for the Fund’s current NAV, market price and other information.

Thank you for your investment in the Salomon Brothers Global Partners Income Fund Inc. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company

September 28, 2006

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS: The Fund may invest in high-yield and foreign securities, including emerging markets, which involve risks beyond those inherent solely in higher-rated and domestic investments. High-yield bonds involve greater credit and liquidity risks than investment grade bonds. Investing in foreign securities is subject to certain risks not associated with domestic investing, such as currency fluctuations, and changes in political and economic conditions. These risks are magnified in emerging or developing markets. Derivatives, such as options or futures, can be illiquid and harder to value, especially in declining markets. A small investment in certain derivatives may have a potentially large impact on the Fund’s performance.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

i The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments.

ii NAV is calculated by subtracting total liabilities from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is at the Fund’s market price as determined by supply of and demand for the Fund’s shares.

iii The Citigroup High Yield Market Index is a broad-based unmanaged index of high yield securities.

iv The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds, and local market instruments. Countries covered are Algeria, Argentina, Brazil, Bulgaria, Chile, China, Colombia, Cote d’Ivoire, Croatia, Ecuador, Greece, Hungary, Lebanon, Malaysia, Mexico, Morocco, Nigeria, Panama, Peru, the Philippines, Poland, Russia, South Africa, South Korea, Thailand, Turkey and Venezuela.

v Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended August 31, 2006, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 13 funds in the Fund’s Lipper category.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 3

Fund at a Glance (unaudited)

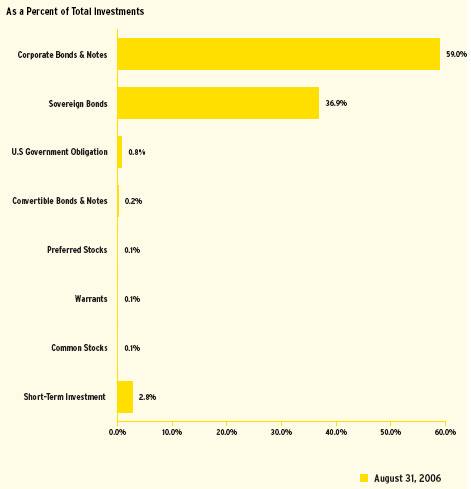

Investment Breakdown

4 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006)

SALOMON BROTHERS GLOBAL PARTNERS INCOME FUND INC.

Face

Amount

| | Security(a) | | Value | |

| | | | | |

CORPORATE BONDS & NOTES — 59.0% | | | |

Aerospace & Defense — 0.7% | | | |

$ | 275,000 | | Alliant Techsystems Inc., Senior Subordinated Notes, 6.750% due 4/1/16 | | $ | 268,125 | |

| | DRS Technologies Inc., Senior Subordinated Notes: | | | |

675,000 | | 6.875% due 11/1/13 | | 658,125 | |

65,000 | | 6.625% due 2/1/16 | | 63,537 | |

750,000 | | L-3 Communications Corp., Senior Subordinated Notes, 7.625% due 6/15/12 | | 772,500 | |

| | Total Aerospace & Defense | | 1,762,287 | |

| | | |

Airlines — 0.3% | | | |

275,000 | | American Airlines Inc., Pass-Through Certificates, Series 2001-02, Class C, 7.800% due 10/1/06 | | 275,172 | |

| | Continental Airlines Inc., Pass-Through Certificates: | | | |

61,582 | | Series 1998-1, Class C, 6.541% due 9/15/08 | | 58,915 | |

232,162 | | Series 2000-2, Class C, 8.312% due 4/2/11 | | 224,181 | |

265,000 | | Series 2001-2, Class D, 7.568% due 12/1/06 | | 264,747 | |

| | Total Airlines | | 823,015 | |

| | | |

Auto Components — 0.5% | | | |

420,000 | | Keystone Automotive Operations Inc., Senior Subordinated Notes, 9.750% due 11/1/13 | | 401,100 | |

| | TRW Automotive Inc.: | | | |

174,000 | | Senior Notes, 9.375% due 2/15/13 | | 186,615 | |

49,000 | | Senior Subordinated Notes, 11.000% due 2/15/13 | | 53,533 | |

| | Visteon Corp., Senior Notes: | | | |

560,000 | | 8.250% due 8/1/10 | | 551,600 | |

190,000 | | 7.000% due 3/10/14 | | 169,575 | |

| | Total Auto Components | | 1,362,423 | |

| | | |

Automobiles — 2.0% | | | |

| | Ford Motor Co.: | | | |

| | Debentures: | | | |

315,000 | | 8.875% due 1/15/22 | | 269,325 | |

175,000 | | 8.900% due 1/15/32 | | 157,937 | |

4,135,000 | | Notes, 7.450% due 7/16/31 | | 3,266,650 | |

| | General Motors Corp.: | | | |

| | Senior Debentures: | | | |

200,000 | | 8.250% due 7/15/23 | | 167,000 | |

1,030,000 | | 8.375% due 7/15/33 | | 867,775 | |

375,000 | | Senior Notes, 7.200% due 1/15/11 | | 337,969 | |

| | Total Automobiles | | 5,066,656 | |

| | | |

Beverages — 0.2% | | | |

515,000 | | Constellation Brands Inc., Senior Notes, 7.250% due 9/1/16 | | 520,150 | |

| | | |

Biotechnology — 0.0% | | | |

50,000 | | Angiotech Pharmaceuticals Inc., Senior Subordinated Notes, 7.750% due 4/1/14 (b) | | 49,000 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 5

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Building Products — 1.2% | | | |

| | | Associated Materials Inc.: | | | | |

$ | 1,445,000 | | Senior Discount Notes, step bond to yield 11.974% due 3/1/14 | | $ | 794,750 | |

20,000 | | Senior Subordinated Notes, 9.750% due 4/15/12 | | 19,700 | |

430,000 | | Jacuzzi Brands Inc., Secured Notes, 9.625% due 7/1/10 | | 457,950 | |

780,000 | | Nortek Inc., Senior Subordinated Notes, 8.500% due 9/1/14 | | 729,300 | |

820,000 | | NTK Holdings Inc., Senior Discount Notes, step bond to yield 11.263% due 3/1/14 | | 553,500 | |

650,000 | | Ply Gem Industries Inc., Senior Subordinated Notes, 9.000% due 2/15/12 | | 529,750 | |

| | Total Building Products | | 3,084,950 | |

| | | | | |

Capital Markets — 0.4% | | | |

423,000 | | BCP Crystal U.S. Holdings Corp., Senior Subordinated Notes, 9.625% due 6/15/14 | | 460,541 | |

| | E*TRADE Financial Corp., Senior Notes: | | | |

470,000 | | 7.375% due 9/15/13 | | 477,050 | |

200,000 | | 7.875% due 12/1/15 | | 209,000 | |

| | Total Capital Markets | | 1,146,591 | |

| | | | | |

Chemicals — 2.3% | | | |

370,000 | | Chemtura Corp., Notes, 6.875% due 6/1/16 | | 359,825 | |

500,000 | | Equistar Chemicals LP, Senior Notes, 10.625% due 5/1/11 | | 540,000 | |

685,000 | | Huntsman International LLC, Senior Subordinated Notes, 10.125% due 7/1/09 | | 702,125 | |

100,000 | | IMC Global Inc., Senior Notes, 10.875% due 8/1/13 | | 112,500 | |

525,000 | | Innophos Inc., Senior Subordinated Notes, 8.875% due 8/15/14 | | 527,625 | |

| | Lyondell Chemical Co., Senior Secured Notes: | | | |

147,000 | | 9.500% due 12/15/08 | | 152,145 | |

325,000 | | 11.125% due 7/15/12 | | 355,875 | |

450,000 | | Methanex Corp., Senior Notes, 8.750% due 8/15/12 | | 483,750 | |

790,000 | | Millennium America Inc., Senior Notes, 9.250% due 6/15/08 | | 811,725 | |

1,130,000 | | Montell Finance Co. BV, Debentures, 8.100% due 3/15/27 (b) | | 1,053,725 | |

| | Rhodia SA: | | | |

223,000 | | Senior Notes, 10.250% due 6/1/10 | | 245,857 | |

516,000 | | Senior Subordinated Notes, 8.875% due 6/1/11 | | 530,190 | |

| | Total Chemicals | | 5,875,342 | |

| | | | | |

Commercial Banks — 0.7% | | | |

1,620,000 | | Russian Agricultural Bank, Notes, 7.175% due 5/16/13 (b) | | 1,676,700 | |

| | | | | |

Commercial Services & Supplies — 1.0% | | | |

275,000 | | Allied Security Escrow Corp., Senior Subordinated Notes, 11.375% due 7/15/11 | | 272,938 | |

| | Allied Waste North America Inc., Senior Notes, Series B: | | | |

200,000 | | 9.250% due 9/1/12 | | 215,000 | |

175,000 | | 7.250% due 3/15/15 | | 172,813 | |

350,000 | | Brand Services Inc., Senior Notes, 12.000% due 10/15/12 | | 394,863 | |

639,000 | | DynCorp International LLC/DIV Capital Corporation, Senior Subordinated Notes, 9.500% due 2/15/13 | | 662,962 | |

2,000,000 | | Safety-Kleen Services Inc., Senior Subordinated Notes, 9.250% due 6/1/08 (c)(d) | | 2,000 | |

795,000 | | Windstream Corp., Senior Notes, 8.625% due 8/1/16 (b) | | 844,687 | |

| | Total Commercial Services & Supplies | | 2,565,263 | |

See Notes to Financial Statements.

6 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Communications Equipment — 0.6% | | | |

$ | 1,725,000 | | Lucent Technologies Inc., Debentures, 6.450% due 3/15/29 | | $ | 1,479,187 | |

| | | |

Consumer Finance — 2.5% | | | |

| | Ford Motor Credit Co.: | | | |

| | Notes: | | | |

100,000 | | 7.875% due 6/15/10 | | 98,361 | |

830,000 | | 7.000% due 10/1/13 | | 775,687 | |

| | Senior Notes: | | | |

862,000 | | 10.486% due 6/15/11 (b)(e) | | 912,590 | |

90,000 | | 9.875% due 8/10/11 | | 94,123 | |

| | General Motors Acceptance Corp., Notes: | | | |

3,225,000 | | 8.000% due 11/1/31 | | 3,268,325 | |

1,300,000 | | 6.875% due 8/28/12 | | 1,270,594 | |

| | Total Consumer Finance | | 6,419,680 | |

| | | | | |

Containers & Packaging — 1.3% | | | |

525,000 | | Berry Plastics Corp., Senior Subordinated Notes, 10.750% due 7/15/12 | | 574,875 | |

660,000 | | Graham Packaging Co. Inc., Senior Subordinated Notes, 9.875% due 10/15/14 | | 638,550 | |

| | Graphic Packaging International Corp.: | | | |

195,000 | | Senior Notes, 8.500% due 8/15/11 | | 198,900 | |

555,000 | | Senior Subordinated Notes, 9.500% due 8/15/13 | | 560,550 | |

| | Owens-Brockway Glass Container Inc., Senior Notes: | | | |

75,000 | | 8.250% due 5/15/13 | | 76,312 | |

525,000 | | 6.750% due 12/1/14 | | 490,875 | |

175,000 | | Owens-Illinois Inc., Debentures, 7.500% due 5/15/10 | | 174,125 | |

260,000 | | Plastipak Holdings Inc., Senior Notes, 8.500% due 12/15/15 (b) | | 260,000 | |

130,000 | | Pliant Corp., Senior Secured Second Lien Notes, 11.125% due 9/1/09 | | 126,100 | |

325,000 | | Radnor Holdings Corp., Senior Notes, 11.000% due 3/15/10 (d) | | 79,625 | |

100,000 | | Tekni-Plex Inc., Senior Subordinated Notes, Series B, 12.750% due 6/15/10 | | 72,500 | |

| | Total Containers & Packaging | | 3,252,412 | |

| | | | | |

Diversified Consumer Services — 0.8% | | | |

345,000 | | Education Management LLC/Education Management Corp., Senior Notes,

8.750% due 6/1/14 (b) | | 343,275 | |

| | Hertz Corp.: | | | |

450,000 | | Senior Notes, 8.875% due 1/1/14 (b) | | 469,125 | |

1,170,000 | | Senior Subordinated Notes, 10.500% due 1/1/16 (b) | | 1,266,525 | |

| | Total Diversified Consumer Services | | 2,078,925 | |

| | | | | |

Diversified Financial Services — 2.2% | | | |

308,000 | | Alamosa Delaware Inc., Senior Notes, 11.000% due 7/31/10 | | 338,030 | |

450,000 | | Basell AF SCA, Senior Subordinated Notes, 8.375% due 8/15/15 (b) | | 452,812 | |

335,000 | | CCM Merger Inc., Notes, 8.000% due 8/1/13 (b) | | 322,438 | |

| | Citisteel USA Inc., Senior Secured Notes: | | | |

225,000 | | 12.490% due 9/1/10 (e) | | 232,313 | |

140,000 | | 15.000% due 10/1/10 (b)(f) | | 150,500 | |

490,000 | | El Paso Performance-Linked Trust, Notes, 7.750% due 7/15/11 (b) | | 501,637 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 7

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Diversified Financial Services — 2.2% (continued) | | | |

$ | 340,000 | | Hughes Network Systems LLC/HNS Finance Corp., Senior Notes,

9.500% due 4/15/14 (b) | | $ | 346,800 | |

315,000 | | Sarawak International Inc., Senior Bonds, 5.500% due 8/3/15 | | 303,886 | |

507,000 | | Targeted Return Index Securities (TRAINS), Secured Notes, Series HY-1-2006,

7.548% due 5/1/16 (b) | | 503,607 | |

760,000 | | TNK-BP Finance SA, 7.500% due 7/18/16 (b) | | 790,168 | |

230,000 | | UCAR Finance Inc., Senior Notes, 10.250% due 2/15/12 | | 242,650 | |

270,000 | | UGS Corp., Senior Subordinated Notes, 10.000% due 6/1/12 | | 291,600 | |

600,000 | | Vanguard Health Holdings Co. I LLC, Senior Discount Notes, step bond to yield

10.044% due 10/1/15 | | 435,000 | |

755,000 | | Vanguard Health Holdings Co. II LLC, Senior Subordinated Notes,

9.000% due 10/1/14 | | 736,125 | |

| | Total Diversified Financial Services | | 5,647,566 | |

| | | | | |

Diversified Telecommunication Services — 3.7% | | | |

| | Cincinnati Bell Inc.: | | | |

580,000 | | Senior Notes, 7.000% due 2/15/15 | | 568,400 | |

105,000 | | Senior Subordinated Notes, 8.375% due 1/15/14 | | 105,919 | |

35,000 | | Cincinnati Bell Telephone Co., Senior Debentures, 6.300% due 12/1/28 | | 30,100 | |

445,000 | | Citizens Communications Co., Senior Notes, 9.000% due 8/15/31 | | 471,700 | |

670,000 | | Hawaiian Telcom Communications Inc., Senior Subordinated Notes, Series B,

12.500% due 5/1/15 | | 688,425 | |

600,000 | | Insight Midwest LP/Insight Capital Inc., Senior Notes, 10.500% due 11/1/10 | | 633,000 | |

| | Intelsat Bermuda Ltd., Senior Notes: | | | |

485,000 | | 9.250% due 6/15/16 (b) | | 506,825 | |

975,000 | | 11.250% due 6/15/16 (b) | | 1,015,219 | |

230,000 | | Intelsat Ltd., Notes, 7.625% due 4/15/12 | | 200,675 | |

340,000 | | Nordic Telephone Co. Holdings, Senior Notes, 8.875% due 5/1/16 (b) | | 355,300 | |

310,000 | | NTL Cable PLC, Senior Notes, 9.125% due 8/15/16 | | 322,400 | |

195,000 | | PanAmSat Corp., Senior Notes, 9.000% due 8/15/14 | | 199,388 | |

| | Qwest Communications International Inc., Senior Notes: | | | |

60,000 | | 7.500% due 2/15/14 | | 59,775 | |

285,000 | | Series B, 7.500% due 2/15/14 | | 283,931 | |

| | Qwest Corp.: | | | |

1,460,000 | | Debentures, 6.875% due 9/15/33 | | 1,314,000 | |

995,000 | | Notes, 8.875% due 3/15/12 | | 1,082,062 | |

800,000 | | Southwestern Bell Telephone Co., Debentures, 7.000% due 11/15/27 | | 805,790 | |

845,000 | | Telcordia Technologies Inc., Senior Subordinated Notes, 10.000% due 3/15/13 (b) | | 678,112 | |

75,000 | | Wind Acquisition Finance SA, Senior Bond, 10.750% due 12/1/15 (b) | | 81,844 | |

| | Total Diversified Telecommunication Services | | 9,402,865 | |

| | | | | |

Electric Utilities — 0.8% | | | |

| | Enersis SA, Notes: | | | |

1,247,000 | | 7.375% due 1/15/14 | | 1,315,756 | |

472,000 | | 7.400% due 12/1/16 | | 501,479 | |

192,050 | | Midwest Generation LLC, Pass-Through Certificates, Series B, 8.560% due 1/2/16 | | 204,173 | |

| | Total Electric Utilities | | 2,021,408 | |

| | | | | | | |

See Notes to Financial Statements.

8 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Energy Equipment & Services — 0.4% | | | |

$ | 235,000 | | Allis-Chalmers Energy Inc., Senior Notes, 9.000% due 1/15/14 (b) | | $ | 240,288 | |

507,000 | | Dresser-Rand Group Inc., Senior Subordinated Notes, 7.375% due 11/1/14 | | 490,522 | |

100,000 | | GulfMark Offshore Inc., Senior Notes, 7.750% due 7/15/14 | | 100,000 | |

80,000 | | Pride International Inc., Senior Notes, 7.375% due 7/15/14 | | 81,800 | |

| | Total Energy Equipment & Services | | 912,610 | |

| | | | | |

Food Products — 0.5% | | | |

800,000 | | Dole Food Co. Inc., Senior Notes, 7.250% due 6/15/10 | | 754,000 | |

625,000 | | Pinnacle Foods Holding Corp., Senior Subordinated Notes, 8.250% due 12/1/13 | | 617,187 | |

| | Total Food Products | | 1,371,187 | |

| | | | | |

Health Care Providers & Services — 2.6% | | | |

600,000 | | AmeriPath Inc., Senior Subordinated Notes, 10.500% due 4/1/13 | | 637,500 | |

855,000 | | DaVita Inc., Senior Subordinated Notes, 7.250% due 3/15/15 | | 842,175 | |

210,000 | | Extendicare Health Services Inc., Senior Notes, 9.500% due 7/1/10 | | 220,500 | |

| | HCA Inc.: | | | |

| | Debentures: | | | |

400,000 | | 7.500% due 12/15/23 | | 307,696 | |

230,000 | | 7.500% due 11/15/95 | | 158,233 | |

110,000 | | Medium-Term Notes, 7.750% due 7/15/36 | | 82,474 | |

125,000 | | Notes, 7.690% due 6/15/25 | | 97,223 | |

| | Senior Notes: | | | |

875,000 | | 6.375% due 1/15/15 | | 697,813 | |

125,000 | | 6.500% due 2/15/16 | | 99,063 | |

975,000 | | IASIS Healthcare LLC/IASIS Capital Corp., Senior Subordinated Notes,

8.750% due 6/15/14 | | 933,562 | |

| | Tenet Healthcare Corp., Senior Notes: | | | |

750,000 | | 7.375% due 2/1/13 | | 671,250 | |

1,000,000 | | 9.875% due 7/1/14 | | 980,000 | |

370,000 | | 6.875% due 11/15/31 | | 282,125 | |

725,000 | | Triad Hospitals Inc., Senior Subordinated Notes, 7.000% due 11/15/13 | | 696,000 | |

| | Total Health Care Providers & Services | | 6,705,614 | |

| | | | | |

Hotels, Restaurants & Leisure — 4.2% | | | |

400,000 | | Boyd Gaming Corp., Senior Subordinated Notes, 6.750% due 4/15/14 | | 379,000 | |

425,000 | | Caesars Entertainment Inc., Senior Subordinated Notes, 8.875% due 9/15/08 | | 446,781 | |

125,000 | | Carrols Corp., Senior Subordinated Notes, 9.000% due 1/15/13 | | 123,125 | |

325,000 | | Choctaw Resort Development Enterprise, Senior Notes, 7.250% due 11/15/19 (b) | | 320,125 | |

675,000 | | Denny’s Holdings Inc., Senior Notes, 10.000% due 10/1/12 | | 683,437 | |

575,000 | | Herbst Gaming Inc., Senior Subordinated Notes, 7.000% due 11/15/14 | | 556,312 | |

550,000 | | Hilton Hotels Corp., Notes, 7.625% due 12/1/12 | | 584,267 | |

650,000 | | Inn of the Mountain Gods Resort & Casino, Senior Notes, 12.000% due 11/15/10 | | 659,750 | |

700,000 | | Isle of Capri Casinos Inc., Senior Subordinated Notes, 7.000% due 3/1/14 | | 668,500 | |

265,000 | | Kerzner International Ltd., Senior Subordinated Notes, 6.750% due 10/1/15 | | 284,875 | |

550,000 | | Las Vegas Sands Corp., Senior Notes, 6.375% due 2/15/15 | | 514,250 | |

| | MGM MIRAGE Inc., Senior Notes: | | | |

400,000 | | 6.750% due 9/1/12 | | 391,000 | |

300,000 | | 6.625% due 7/15/15 | | 283,875 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 9

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Hotels, Restaurants & Leisure — 4.2% (continued) | | | |

| | | Mohegan Tribal Gaming Authority, Senior Subordinated Notes: | | | | |

$ | 375,000 | | 7.125% due 8/15/14 | | $ | 367,500 | |

375,000 | | 6.875% due 2/15/15 | | 360,000 | |

700,000 | | Penn National Gaming Inc., Senior Subordinated Notes, 6.750% due 3/1/15 | | 677,250 | |

675,000 | | Pinnacle Entertainment Inc., Senior Subordinated Notes, 8.250% due 3/15/12 | | 681,750 | |

610,000 | | Pokagon Gaming Authority, Senior Notes, 10.375% due 6/15/14 (b) | | 648,125 | |

40,000 | | River Rock Entertainment Authority, Senior Notes, 9.750% due 11/1/11 | | 42,550 | |

525,000 | | Sbarro Inc., Senior Notes, 11.000% due 9/15/09 | | 534,188 | |

700,000 | | Starwood Hotels & Resorts Worldwide Inc., Senior Notes, 7.875% due 5/1/12 | | 761,250 | |

| | Station Casinos Inc.: | | | |

195,000 | | Senior Notes, 7.750% due 8/15/16 | | 202,069 | |

| | Senior Subordinated Notes: | | | |

475,000 | | 6.500% due 2/1/14 | | 445,313 | |

125,000 | | 6.625% due 3/15/18 | | 112,188 | |

| | Total Hotels, Restaurants & Leisure | | 10,727,480 | |

| | | | | |

Household Durables — 1.4% | | | |

55,000 | | American Greetings Corp., Senior Notes, 7.375% due 6/1/16 | | 55,619 | |

| | Beazer Homes USA Inc., Senior Notes: | | | |

50,000 | | 6.875% due 7/15/15 | | 44,750 | |

295,000 | | 8.125% due 6/15/16 (b) | | 283,200 | |

1,250,000 | | Holt Group Inc., Senior Notes, 9.750% due 1/15/06 (c)(d)(g) | | 0 | |

675,000 | | Interface Inc., Senior Subordinated Notes, 9.500% due 2/1/14 | | 696,937 | |

| | K Hovnanian Enterprises Inc., Senior Notes: | | | |

465,000 | | 7.500% due 5/15/16 | | 430,125 | |

615,000 | | 8.625% due 1/15/17 | | 603,469 | |

190,000 | | Norcraft Cos. LP/Norcraft Finance Corp., Senior Subordinated Notes,

9.000% due 11/1/11 | | 191,900 | |

295,000 | | Norcraft Holdings LP/Norcraft Capital Corp., Senior Discount Notes, step bond to yield

9.580% due 9/1/12 | | 240,425 | |

600,000 | | Sealy Mattress Co., Senior Subordinated Notes, 8.250% due 6/15/14 | | 609,000 | |

374,000 | | Tempur-Pedic Inc./Tempur Production USA Inc., Senior Subordinated Notes,

10.250% due 8/15/10 | | 393,635 | |

| | Total Household Durables | | 3,549,060 | |

| | | | | |

Household Products — 0.4% | | | |

| | Nutro Products Inc.: | | | |

75,000 | | Senior Notes, 9.230% due 10/15/13 (b)(e) | | 77,625 | |

205,000 | | Senior Subordinated Notes, 10.750% due 4/15/14 (b) | | 217,300 | |

| | Spectrum Brands Inc., Senior Subordinated Notes: | | | |

380,000 | | 8.500% due 10/1/13 | | 317,775 | |

107,000 | | 7.375% due 2/1/15 | | 83,460 | |

325,000 | | Visant Holding Corp., Senior Notes, 8.750% due 12/1/13 (b) | | 320,125 | |

| | Total Household Products | | 1,016,285 | |

See Notes to Financial Statements.

10 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Independent Power Producers & Energy Traders — 3.0% | | | |

$ | 155,000 | | AES China Generating Co., Ltd., Class A, 8.250% due 6/26/10 | | $ | 152,868 | |

| | AES Corp.: | | | |

| | Senior Notes: | | | |

400,000 | | 8.750% due 6/15/08 | | 418,000 | |

175,000 | | 9.500% due 6/1/09 | | 188,125 | |

300,000 | | 9.375% due 9/15/10 | | 325,500 | |

90,000 | | 8.875% due 2/15/11 | | 96,750 | |

370,000 | | 7.750% due 3/1/14 | | 382,950 | |

130,000 | | Senior Secured Notes, 9.000% due 5/15/15 (b) | | 140,888 | |

375,000 | | Calpine Generating Co. LLC, Senior Secured Notes, 14.120% due 4/1/11 (d)(e) | | 402,188 | |

| | Dynegy Holdings Inc., Senior Debentures: | | | |

800,000 | | 7.125% due 5/15/18 | | 710,000 | |

750,000 | | 7.625% due 10/15/26 | | 665,625 | |

| | Edison Mission Energy, Senior Notes: | | | |

1,100,000 | | 7.730% due 6/15/09 | | 1,130,250 | |

70,000 | | 7.500% due 6/15/13 (b) | | 70,350 | |

460,000 | | 7.750% due 6/15/16 (b) | | 462,300 | |

950,000 | | Mirant North America LLC, Senior Notes, 7.375% due 12/31/13 | | 945,250 | |

| | NRG Energy Inc., Senior Notes: | | | |

275,000 | | 7.250% due 2/1/14 | | 272,250 | |

1,355,000 | | 7.375% due 2/1/16 | | 1,338,062 | |

| | Total Independent Power Producers & Energy Traders | | 7,701,356 | |

| | | | | |

Industrial Conglomerates — 0.3% | | | |

342,000 | | Koppers Inc., Senior Notes, 9.875% due 10/15/13 | | 371,925 | |

500,000 | | Moll Industries Inc., Senior Subordinated Notes, 10.500% due 7/1/08 (c)(d)(g) | | 0 | |

450,000 | | Sequa Corp., Senior Notes, 9.000% due 8/1/09 | | 477,000 | |

| | Total Industrial Conglomerates | | 848,925 | |

| | | | | |

Insurance — 0.3% | | | |

770,000 | | Crum & Forster Holdings Corp., Senior Notes, 10.375% due 6/15/13 | | 770,000 | |

| | | | | |

Internet & Catalog Retail — 0.3% | | | |

115,000 | | Brookstone Co. Inc., Senior Secured Notes, 12.000% due 10/15/12 | | 105,225 | |

656,000 | | FTD Inc., Senior Subordinated Notes, 7.750% due 2/15/14 | | 642,880 | |

| | Total Internet & Catalog Retail | | 748,105 | |

| | | | | |

IT Services — 0.5% | | | |

| | Sungard Data Systems Inc.: | | | |

475,000 | | Senior Notes, 9.125% due 8/15/13 | | 492,813 | |

810,000 | | Senior Subordinated Notes, 10.250% due 8/15/15 | | 831,262 | |

| | Total IT Services | | 1,324,075 | |

| | | | | |

Leisure Equipment & Products — 0.1% | | | |

305,000 | | Warner Music Group, Senior Subordinated Notes, 7.375% due 4/15/14 | | 295,088 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 11

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Machinery — 0.5% | | | |

| | | Case New Holland Inc., Senior Notes: | | | | |

$ | 300,000 | | 9.250% due 8/1/11 | | $ | 319,500 | |

50,000 | | 7.125% due 3/1/14 | | 49,625 | |

235,000 | | Commercial Vehicle Group Inc., Senior Notes, 8.000% due 7/1/13 | | 225,013 | |

211,000 | | Invensys PLC, Senior Notes, 9.875% due 3/15/11 (b) | | 228,935 | |

130,000 | | Mueller Group Inc., Senior Subordinated Notes, 10.000% due 5/1/12 | | 142,350 | |

406,000 | | Mueller Holdings Inc., Discount Notes, step bond to yield 14.871% due 4/15/14 | | 359,310 | |

| | Total Machinery | | 1,324,733 | |

| | | | | |

Media — 6.8% | | | |

715,000 | | Affinion Group Inc., Senior Notes, 10.125% due 10/15/13 (b) | | 745,387 | |

| | AMC Entertainment Inc.: | | | |

80,000 | | Senior Notes, Series B, 8.625% due 8/15/12 | | 82,400 | |

810,000 | | Senior Subordinated Notes, 11.000% due 2/1/16 | | 883,912 | |

125,000 | | Barrington Broadcasting Group LLC/Barrington Broadcasting Capital Corp., Senior Subordinated Notes, 10.500% due 8/15/14 (b) | | 123,125 | |

525,895 | | CanWest Media Inc., Senior Subordinated Notes, 8.000% due 9/15/12 | | 511,433 | |

650,000 | | CCH I Holdings LLC/CCH I Holding Capital Corp., Senior Notes, 11.750% due 5/15/14 | | 445,250 | |

780,000 | | CCH I LLC/CCH Capital Corp., Senior Secured Notes, 11.000% due 10/1/15 | | 696,150 | |

680,000 | | CCH II LLC/CCH II Capital Corp., Senior Notes, 10.250% due 9/15/10 | | 691,900 | |

| | Charter Communications Holdings LLC/Charter Communications Holdings Capital Corp., Senior Notes: | | | |

220,000 | | 8.625% due 4/1/09 | | 201,850 | |

120,000 | | 10.750% due 10/1/09 | | 110,400 | |

240,000 | | Charter Communications Holdings LLC/Charter Communications Holdings II Capital Corp., Senior Notes, 9.625% due 11/15/09 | | 219,600 | |

300,000 | | Charter Communications Operating LLC, Second Lien Senior Notes, 8.375% due 4/30/14 (b) | | 304,500 | |

115,000 | | CMP Susquehanna Corp., Senior Subordinated Notes, 9.875% due 5/15/14 (b) | | 107,813 | |

| | CSC Holdings Inc.: | | | |

900,000 | | Debentures, Series B, 8.125% due 8/15/09 | | 933,750 | |

| | Senior Debentures: | | | |

70,000 | | 7.875% due 2/15/18 | | 71,925 | |

75,000 | | 7.625% due 7/15/18 | | 76,031 | |

| | Senior Notes: | | | |

50,000 | | Series B, 7.625% due 4/1/11 | | 51,375 | |

375,000 | | Series WI, 7.250% due 4/15/12 | | 370,313 | |

635,000 | | Dex Media West LLC/Dex Media Finance Co., Senior Subordinated Notes, Series B,

9.875% due 8/15/13 | | 685,006 | |

| | DIRECTV Holdings LLC/DIRECTV Financing Co. Inc., Senior Notes: | | | |

325,000 | | 8.375% due 3/15/13 | | 342,875 | |

495,000 | | 6.375% due 6/15/15 | | 465,300 | |

| | EchoStar DBS Corp., Senior Notes: | | | |

450,000 | | 6.625% due 10/1/14 | | 433,688 | |

1,290,000 | | 7.125% due 2/1/16 (b) | | 1,262,587 | |

See Notes to Financial Statements.

12 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Media — 6.8% (continued) | | | |

$ | 445,000 | | Houghton Mifflin Co., Senior Discount Notes, step bond to yield 11.202% due 10/15/13 | | $ | 374,913 | |

300,000 | | Interep National Radio Sales Inc., Senior Subordinated Notes, Series B, 10.000% due 7/1/08 | | 258,000 | |

395,000 | | Kabel Deutschland GMBH, Senior Notes, 10.625% due 7/1/14 (b) | | 424,625 | |

675,000 | | Lamar Media Corp., Senior Subordinated Notes, 6.625% due 8/15/15 | | 636,188 | |

650,000 | | LodgeNet Entertainment Corp., Senior Subordinated Notes, 9.500% due 6/15/13 | | 700,375 | |

50,000 | | Mediacom Broadband LLC/Mediacom Broadband Corp., Senior Notes, 8.500% due 10/15/15 | | 49,750 | |

455,000 | | Primedia Inc., Senior Notes, 8.875% due 5/15/11 | | 443,625 | |

200,000 | | Quebecor Media Inc., Senior Notes, 7.750% due 3/15/16 | | 199,000 | |

| | R.H. Donnelley Corp.: | | | |

| | Senior Discount Notes: | | | |

100,000 | | Series A-1, 6.875% due 1/15/13 | | 90,250 | |

200,000 | | Series A-2, 6.875% due 1/15/13 | | 180,500 | |

650,000 | | Senior Notes, Series A-3, 8.875% due 1/15/16 | | 643,500 | |

100,000 | | R.H. Donnelley Finance Corp. I, Senior Subordinated Notes, 10.875% due 12/15/12 (b) | | 110,000 | |

225,000 | | R.H. Donnelley Inc., Senior Subordinated Notes, 10.875% due 12/15/12 | | 247,500 | |

375,000 | | Radio One Inc., Senior Subordinated Notes, Series B, 8.875% due 7/1/11 | | 382,500 | |

| | Rainbow National Services LLC: | | | |

760,000 | | Senior Notes, 8.750% due 9/1/12 (b) | | 805,600 | |

100,000 | | Senior Subordinated Debentures, 10.375% due 9/1/14 (b) | | 111,875 | |

| | Rogers Cable Inc.: | | | |

260,000 | | Secured Notes, 5.500% due 3/15/14 | | 242,125 | |

200,000 | | Senior Secured Notes, 6.250% due 6/15/13 | | 195,750 | |

140,000 | | Senior Secured Second Priority Notes, 6.750% due 3/15/15 | | 139,650 | |

660,000 | | Sinclair Broadcast Group Inc., Senior Subordinated Notes, 8.000% due 3/15/12 | | 671,550 | |

90,000 | | Vertis Inc., Senior Secured Second Lien Notes, 9.750% due 4/1/09 | | 91,575 | |

125,000 | | Videotron Ltee., Senior Notes, 6.375% due 12/15/15 | | 117,656 | |

| | XM Satellite Radio Inc., Senior Notes: | | | |

150,000 | | 9.989% due 5/1/13 (b)(e) | | 140,625 | |

340,000 | | 9.750% due 5/1/14 (b) | | 321,300 | |

| | Total Media | | 17,395,002 | |

| | | | | |

Metals & Mining — 1.5% | | | |

50,000 | | Chaparral Steel Co., Senior Notes, 10.000% due 7/15/13 | | 55,500 | |

600,000 | | Corporacion Nacional del Cobre-Codelco, Notes, 5.500% due 10/15/13 (b) | | 595,238 | |

315,000 | | International Steel Group Inc., Senior Notes, 6.500% due 4/15/14 | | 300,825 | |

180,000 | | IPSCO Inc., Senior Notes, 8.750% due 6/1/13 | | 193,050 | |

910,000 | | Metals USA Inc., Senior Secured Notes, 11.125% due 12/1/15 (b) | | 1,007,825 | |

90,000 | | PNA Group Inc., Senior Notes, 10.750% due 9/1/16 (b) | | 92,250 | |

345,000 | | RathGibson Inc., Senior Notes, 11.250% due 2/15/14 (b) | | 357,075 | |

| | Vale Overseas Ltd., Notes: | | | |

450,000 | | 6.250% due 1/11/16 | | 448,875 | |

801,000 | | 8.250% due 1/17/34 | | 926,356 | |

| | Total Metals & Mining | | 3,976,994 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 13

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Multiline Retail — 0.6% | | | |

$ | 350,000 | | Harry & David Operations, Senior Notes, 9.000% due 3/1/13 | | $ | 322,000 | |

795,000 | | Neiman Marcus Group Inc., Senior Subordinated Notes, 10.375% due 10/15/15 | | 854,625 | |

225,000 | | Saks Inc., Notes, 9.875% due 10/1/11 | | 244,687 | |

| | Total Multiline Retail | | 1,421,312 | |

| | | | | |

Office Electronics — 0.3% | | | |

700,000 | | Xerox Capital Trust I Exchange Capital Securities, 8.000% due 2/1/27 | | 721,875 | |

| | | | | |

Oil, Gas & Consumable Fuels — 6.8% | | | |

735,000 | | Belden & Blake Corp., Secured Notes, 8.750% due 7/15/12 | | 757,050 | |

| | Chesapeake Energy Corp., Senior Notes: | | | |

1,390,000 | | 6.625% due 1/15/16 | | 1,341,350 | |

100,000 | | 6.875% due 1/15/16 | | 97,500 | |

170,000 | | 6.500% due 8/15/17 | | 158,525 | |

812,000 | | Cimarex Energy Co., Senior Notes, 9.600% due 3/15/12 | | 862,750 | |

120,000 | | Colorado Interstate Gas Co., Senior Notes, 6.800% due 11/15/15 | | 119,528 | |

165,000 | | Compagnie Generale de Geophysique SA, Senior Notes, 7.500% due 5/15/15 | | 165,000 | |

| | El Paso Corp.: | | | |

| | Medium-Term Notes: | | | |

675,000 | | 7.800% due 8/1/31 | | 680,062 | |

875,000 | | 7.750% due 1/15/32 | | 883,750 | |

825,000 | | Notes, 7.875% due 6/15/12 | | 855,937 | |

350,000 | | Enterprise Products Operating LP, Junior Subordinated Notes, 8.375% due 8/1/66 (e) | | 365,479 | |

670,000 | | EXCO Resources Inc., Senior Notes, 7.250% due 1/15/11 | | 654,925 | |

450,000 | | Hanover Equipment Trust, Secured Notes, 8.750% due 9/1/11 | | 470,250 | |

375,000 | | Inergy LP/Inergy Finance Corp., Senior Notes, 8.250% due 3/1/16 | | 387,188 | |

810,000 | | International Coal Group Inc., Senior Notes, 10.250% due 7/15/14 (b) | | 840,375 | |

260,000 | | Mariner Energy Inc., Senior Notes, 7.500% due 4/15/13 (b) | | 254,150 | |

70,000 | | Northwest Pipelines Corp., Senior Notes, 7.000% due 6/15/16 (b) | | 71,138 | |

75,000 | | OMI Corp., Senior Notes, 7.625% due 12/1/13 | | 75,375 | |

300,000 | | Parker Drilling Co., Senior Notes, 9.625% due 10/1/13 | | 328,500 | |

1,200,000 | | Pemex Project Funding Master Trust, 6.125% due 8/15/08 | | 1,207,800 | |

340,000 | | Petrohawk Energy Corp., Senior Notes, 9.125% due 7/15/13 (b) | | 347,650 | |

1,500,000 | | Petronas Capital Ltd., Notes, 7.875% due 5/22/22 (b) | | 1,793,832 | |

1,010,000 | | Petrozuata Finance Inc., 8.220% due 4/1/17 | | 1,015,050 | |

400,000 | | Pogo Producing Co., Senior Subordinated Notes, 7.875% due 5/1/13 (b) | | 410,000 | |

450,000 | | Quicksilver Resources Inc., Senior Subordinated Notes, 7.125% due 4/1/16 | | 432,000 | |

30,000 | | SESI LLC, Senior Notes, 6.875% due 6/1/14 (b) | | 29,550 | |

200,000 | | Swift Energy Co., Senior Subordinated Notes, 9.375% due 5/1/12 | | 212,000 | |

725,000 | | Whiting Petroleum Corp., Senior Subordinated Notes, 7.000% due 2/1/14 | | 717,750 | |

| | Williams Cos. Inc.: | | | |

| | Notes: | | | |

1,400,000 | | 7.875% due 9/1/21 | | 1,431,500 | |

260,000 | | 8.750% due 3/15/32 | | 281,450 | |

300,000 | | Senior Notes, 7.625% due 7/15/19 | | 306,000 | |

| | Total Oil, Gas & Consumable Fuels | | 17,553,414 | |

| | | | | | | |

See Notes to Financial Statements.

14 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | | | |

Paper & Forest Products — 0.9% | | | |

$ | 125,000 | | Abitibi-Consolidated Inc., Notes, 7.750% due 6/15/11 | | $ | 115,938 | |

735,000 | | Appleton Papers Inc., Senior Subordinated Notes, Series B, 9.750% due 6/15/14 | | 729,487 | |

115,000 | | Domtar Inc., Notes, 5.375% due 12/1/13 | | 98,900 | |

| | NewPage Corp.: | | | |

115,000 | | Senior Secured Notes, 11.739% due 5/1/12 (e) | | 124,775 | |

300,000 | | Senior Subordinated Notes, 12.000% due 5/1/13 | | 311,250 | |

140,000 | | P.H. Glatfelter, Senior Notes, 7.125% due 5/1/16 (b) | | 138,710 | |

600,000 | | Smurfit Capital Funding PLC, Debentures, 7.500% due 11/20/25 | | 549,000 | |

| | Verso Paper Holdings LLC: | | | |

175,000 | | Senior Secured Notes, 9.125% due 8/1/14 (b) | | 175,000 | |

175,000 | | Senior Subordinated Notes, 11.375% due 8/1/16 (b) | | 174,125 | |

| | Total Paper & Forest Products | | 2,417,185 | |

| | | | | |

Personal Products — 0.1% | | | |

335,000 | | Playtex Products Inc., Senior Secured Notes, 8.000% due 3/1/11 | | 350,075 | |

| | | | | |

Pharmaceuticals — 0.6% | | | |

720,000 | | Leiner Health Products Inc., Senior Subordinated Notes, 11.000% due 6/1/12 | | 687,600 | |

775,000 | | Valeant Pharmaceuticals International, Senior Notes, 7.000% due 12/15/11 | | 732,375 | |

| | Total Pharmaceuticals | | 1,419,975 | |

| | | | | |

Real Estate Investment Trusts (REITs) — 0.7% | | | |

290,000 | | Felcor Lodging LP, Senior Notes, 8.500% due 6/1/11 | | 308,125 | |

20,000 | | Forest City Enterprises Inc., Senior Notes, 7.625% due 6/1/15 | | 20,250 | |

| | Host Marriott LP: | | | |

| | Senior Notes: | | | |

125,000 | | Series I, 9.500% due 1/15/07 | | 127,031 | |

1,025,000 | | Series O, 6.375% due 3/15/15 | | 989,125 | |

125,000 | | Series Q, 6.750% due 6/1/16 | | 121,875 | |

275,000 | | Kimball Hill Inc., Senior Subordinated Notes, 10.500% due 12/15/12 | | 237,188 | |

115,000 | | Ventas Realty LP/Ventas Capital Corp., Senior Notes, 6.500% due 6/1/16 | | 113,850 | |

| | Total Real Estate Investment Trusts (REITs) | | 1,917,444 | |

| | | | | |

Road & Rail — 0.4% | | | |

330,000 | | Avis Budget Car Rental LLC/Avis Budget Finance Inc., Senior Notes,

7.905% due 5/15/14 (b)(e) | | 324,225 | |

| | Grupo Transportacion Ferroviaria Mexicana SA de CV, Senior Notes: | | | |

100,000 | | 10.250% due 6/15/07 | | 102,500 | |

510,000 | | 9.375% due 5/1/12 | | 542,513 | |

30,000 | | 12.500% due 6/15/12 | | 33,450 | |

| | Total Road & Rail | | 1,002,688 | |

| | | | | |

Semiconductors & Semiconductor Equipment — 0.2% | | | |

620,000 | | MagnaChip Semiconductor, Senior Subordinated Notes, 8.000% due 12/15/14 | | 399,900 | |

| | | | | |

Software — 0.3% | | | |

335,000 | | Activant Solutions Inc., Senior Subordinated Notes, 9.500% due 5/1/16 (b) | | 315,738 | |

490,000 | | UGS Capital Corp. II, Senior Subordinated Notes, 10.380% due 6/1/11 (b)(e)(f) | | 496,125 | |

| | Total Software | | 811,863 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 15

Schedule of Investments (August 31, 2006) (continued)

Face

Amount

| | Security(a) | | Value | |

| | | |

Specialty Retail — 1.2% | | | |

| | AutoNation Inc., Senior Notes: | | | |

$ | 125,000 | | 7.507% due 4/15/13 (b)(e) | | $ | 126,250 | |

155,000 | | 7.000% due 4/15/14 (b) | | 153,644 | |

335,000 | | Blockbuster Inc., Senior Subordinated Notes, 9.000% due 9/1/12 | | 311,550 | |

575,000 | | Buffets Inc., Senior Subordinated Notes, 11.250% due 7/15/10 | | 609,500 | |

110,000 | | EPL Finance Corp., Senior Notes, 11.750% due 11/15/13 (b) | | 123,475 | |

230,000 | | Eye Care Centers of America, Senior Subordinated Notes, 10.750% due 2/15/15 | | 247,825 | |

450,000 | | Hines Nurseries Inc., Senior Notes, 10.250% due 10/1/11 | | 402,750 | |

326,000 | | Jafra Cosmetics International Inc., Senior Subordinated Notes, 10.750% due 5/15/11 | | 353,710 | |

375,000 | | PETCO Animal Supplies Inc., Senior Subordinated Notes, 10.750% due 11/1/11 | | 396,562 | |

490,000 | | Suburban Propane Partners LP/Suburban Energy Finance Corp., Senior Notes,

6.875% due 12/15/13 | | 471,625 | |

| | Total Specialty Retail | | 3,196,891 | |

| | | | | |

Textiles, Apparel & Luxury Goods — 0.7% | | | |

980,000 | | Levi Strauss & Co., Senior Notes, 9.750% due 1/15/15 | | 1,019,200 | |

325,000 | | Oxford Industries Inc., Senior Notes, 8.875% due 6/1/11 | | 329,875 | |

120,000 | | Russell Corp., Senior Notes, 9.250% due 5/1/10 | | 125,550 | |

425,000 | | Simmons Co., Senior Discount Notes, 9.995% due 12/15/14 | | 298,562 | |

| | Total Textiles, Apparel & Luxury Goods | | 1,773,187 | |

| | | | | |

Tobacco — 0.1% | | | |

320,000 | | Alliance One International Inc., Senior Notes, 11.000% due 5/15/12 | | 321,600 | |

| | | | | |

Trading Companies & Distributors — 0.7% | | | |

220,000 | | Ashtead Capital Inc., Notes, 9.000% due 8/15/16 (b) | | 225,500 | |

500,000 | | H&E Equipment Services Inc., Senior Notes, 8.375% due 7/15/16 (b) | | 510,000 | |

590,000 | | Penhall International Corp., Senior Secured Notes, 12.000% due 8/1/14 (b) | | 604,750 | |

410,000 | | Transdigm Inc., Senior Subordinated Notes, 7.750% due 7/15/14 (b) | | 408,975 | |

| | Total Trading Companies & Distributors | | 1,749,225 | |

| | | | | |

Wireless Telecommunication Services — 1.4% | | | |

200,000 | | American Tower Corp., Senior Notes, 7.500% due 5/1/12 | | 204,500 | |

2,060,000 | | Nextel Communications Inc., Senior Notes, Series D, 7.375% due 8/1/15 | | 2,121,775 | |

70,000 | | Rogers Wireless Communications Inc., Secured Notes, 7.250% due 12/15/12 | | 72,538 | |

190,000 | | Rogers Wireless Inc., Senior Subordinated Notes, 8.000% due 12/15/12 | | 199,500 | |

510,000 | | Rural Cellular Corp., Senior Notes, 9.875% due 2/1/10 | | 529,125 | |

500,000 | | UbiquiTel Operating Co., Senior Notes, 9.875% due 3/1/11 | | 546,250 | |

| | Total Wireless Telecommunication Services | | 3,673,688 | |

| | TOTAL CORPORATE BONDS & NOTES

(Cost — $155,034,676) | | 151,631,256 | |

| | | | | | | |

See Notes to Financial Statements.

16 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount | | Security(a) | | Value | |

| | | |

ASSET-BACKED SECURITY — 0.0% | | | |

Diversified Financial Services — 0.0% | | | |

$ | 987,700 | | Airplanes Pass-Through Trust, Subordinated Notes, Series D,

10.875% due 3/15/19 (c)(d)(g)

(Cost — $987,334) | | $ | 0 | |

| | | |

CONVERTIBLE BONDS & NOTES — 0.2% | | | |

Semiconductors & Semiconductor Equipment — 0.1% | | | |

175,000 | | Amkor Technology Inc., Senior Subordinated Bond, 2.500% due 5/15/11 | | 149,406 | |

| | | | | |

Wireless Telecommunication Services — 0.1% | | | |

325,000 | | American Tower Corp., Notes, 5.000% due 2/15/10 | | 325,406 | |

| | TOTAL CONVERTIBLE BONDS & NOTES

(Cost — $348,975) | | 474,812 | |

| | | | | |

SOVEREIGN BONDS — 36.9% | | | |

Argentina — 1.7% | | | |

| | Republic of Argentina: | | | |

4,199,250 | | 5.590% due 8/3/12 (e) | | 3,908,587 | |

5,670,000 | | GDP Linked Securities, 0.000% due 12/15/35 (e) | | 544,320 | |

| | Total Argentina | | 4,452,907 | |

| | | | | |

Brazil — 7.8% | | | |

| | Federative Republic of Brazil: | | | |

3,824,000 | | 11.000% due 8/17/40 | | 4,997,012 | |

| | Collective Action Securities: | | | |

2,185,000 | | 8.750% due 2/4/25 | | 2,601,243 | |

11,184,000 | | Notes, 8.000% due 1/15/15 (h) | | 12,294,012 | |

| | Total Brazil | | 19,892,267 | |

| | | | | |

Colombia — 1.7% | | | |

| | Republic of Colombia: | | | |

1,775,000 | | 10.000% due 1/23/12 | | 2,071,425 | |

525,000 | | 10.750% due 1/15/13 | | 643,256 | |

1,000,000 | | 11.750% due 2/25/20 | | 1,405,000 | |

130,000 | | 10.375% due 1/28/33 | | 176,638 | |

| | Total Colombia | | 4,296,319 | |

| | | | | |

Ecuador — 0.7% | | | |

1,785,000 | | Republic of Ecuador, 10.000% due 8/15/30 | | 1,780,538 | |

| | | | | |

El Salvador — 0.8% | | | |

| | Republic of El Salvador: | | | |

1,555,000 | | 7.750% due 1/24/23 (b) | | 1,726,050 | |

330,000 | | 8.250% due 4/10/32 (b) | | 371,250 | |

| | Total El Salvador | | 2,097,300 | |

| | | | | |

Indonesia — 0.2% | | | |

500,000 | | Republic of Indonesia, 8.500% due 10/12/35 (b) | | 578,100 | |

| | | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 17

Schedule of Investments (August 31, 2006) (continued)

Face

Amount | | Security(a) | | Value | |

| | | |

Malaysia — 0.6% | | | |

$ | 352,000 | | Federation of Malaysia, 8.750% due 6/1/09 | | $ | 382,458 | |

1,092,000 | | Penerbangan Malaysia Berhad, 5.625% due 3/15/16 | | 1,089,172 | |

| | Total Malaysia | | 1,471,630 | |

| | | | | |

Mexico — 8.1% | | | |

| | United Mexican States: | | | |

800,000 | | 11.375% due 9/15/16 | | 1,145,000 | |

| | Medium-Term Notes: | | | |

8,330,000 | | 5.625% due 1/15/17 | | 8,240,453 | |

1,795,000 | | 8.300% due 8/15/31 | | 2,261,700 | |

| | Series A: | | | |

1,050,000 | | 6.375% due 1/16/13 | | 1,094,100 | |

1,972,000 | | 5.875% due 1/15/14 | | 2,009,961 | |

3,783,000 | | 6.625% due 3/3/15 | | 4,021,329 | |

1,355,000 | | 8.000% due 9/24/22 | | 1,631,081 | |

245,000 | | 7.500% due 4/8/33 | | 284,506 | |

| | Total Mexico | | 20,688,130 | |

| | | | | |

Panama — 1.8% | | | |

| | Republic of Panama: | | | |

300,000 | | 9.625% due 2/8/11 | | 342,225 | |

3,025,000 | | 7.250% due 3/15/15 | | 3,198,937 | |

243,000 | | 9.375% due 4/1/29 | | 309,825 | |

781,000 | | 6.700% due 1/26/36 | | 764,404 | |

| | Total Panama | | 4,615,391 | |

| | | | | |

Peru — 1.0% | | | |

| | Republic of Peru, PDI: | | | |

2,148,800 | | 5.000% due 3/7/17 (e) | | 2,124,626 | |

368,930 | | 5.000% due 3/7/17 (b)(e) | | 365,241 | |

| | Total Peru | | 2,489,867 | |

| | | | | |

Philippines — 0.5% | | | |

| | Republic of the Philippines: | | | |

850,000 | | 10.625% due 3/16/25 (h) | | 1,116,135 | |

195,000 | | 9.500% due 2/2/30 | | 238,144 | |

| | Total Philippines | | 1,354,279 | |

| | | | | |

Russia — 5.6% | | | |

| | Russian Federation: | | | |

1,455,000 | | 11.000% due 7/24/18 (b) | | 2,095,200 | |

540,000 | | 12.750% due 6/24/28 (b) | | 966,600 | |

10,110,540 | | 5.000% due 3/31/30 (b) | | 11,257,075 | |

| | Total Russia | | 14,318,875 | |

| | | | | |

South Africa — 0.7% | | | |

1,775,000 | | Republic of South Africa, 6.500% due 6/2/14 | | 1,855,949 | |

| | | | | | | |

See Notes to Financial Statements.

18 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Face

Amount | | Security(a) | | Value | |

| | | |

Turkey — 3.0% | | | |

| | Republic of Turkey: | | | |

$ | 350,000 | | 11.750% due 6/15/10 | | $ 411,250 | |

2,077,000 | | 11.500% due 1/23/12 | | 2,520,959 | |

205,000 | | 11.000% due 1/14/13 | | 248,050 | |

900,000 | | 7.250% due 3/15/15 | | 916,875 | |

128,000 | | 7.000% due 6/5/20 | | 126,400 | |

1,551,000 | | 11.875% due 1/15/30 (h) | | 2,318,745 | |

332,000 | | 8.000% due 2/14/34 | | 348,185 | |

| | Collective Action Securities, Notes: | | | |

463,000 | | 9.500% due 1/15/14 | | 531,292 | |

360,000 | | 7.375% due 2/5/25 | | 359,550 | |

| | Total Turkey | | 7,781,306 | |

| | | | | |

Uruguay — 0.5% | | | |

1,350,000 | | Republic of Uruguay, Benchmark Bonds, 7.250% due 2/15/11 | | 1,383,750 | |

| | | | | |

Venezuela — 2.2% | | | |

| | Bolivarian Republic of Venezuela: | | | |

3,575,000 | | 8.500% due 10/8/14 | | 4,006,681 | |

551,000 | | 5.750% due 2/26/16 | | 515,185 | |

233,000 | | 7.650% due 4/21/25 | | 249,427 | |

675,000 | | Collective Action Securities, Notes, 10.750% due 9/19/13 | | 829,406 | |

| | Total Venezuela | | 5,600,699 | |

| | TOTAL SOVEREIGN BONDS

(Cost — $88,720,771) | | 94,657,307 | |

| | | | | |

U.S. GOVERNMENT OBLIGATION — 0.8% | | | |

U.S. Treasury Obligation — 0.8% | | | |

1,990,000 | | U.S. Treasury Notes, 5.125% due 5/15/16 (Cost — $2,021,027) | | 2,047,135 | |

| | | | | |

Shares | | | | | |

| | | |

COMMON STOCKS — 0.1% | | | |

CONSUMER DISCRETIONARY — 0.0% | | | |

Household Durables — 0.0% | | | |

1,349,235 | | Home Interiors of Gifts Inc. (c)(g)* | | 13,492 | |

10,194 | | Mattress Discounters Corp. (c)(g)* | | 0 | |

| | TOTAL CONSUMER DISCRETIONARY | | 13,492 | |

| | | | | |

CONSUMER STAPLES — 0.0% | | | |

Food Products — 0.0% | | | |

688 | | Imperial Sugar Co. | | 21,163 | |

| | | | | |

INDUSTRIALS — 0.0% | | | |

Machinery — 0.0% | | | |

5 | | Glasstech Inc. (c)(g)* | | 0 | |

| | | | | | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 19

Schedule of Investments (August 31, 2006) (continued)

Shares | | Security(a) | | Value | |

| | | |

INFORMATION TECHNOLOGY — 0.0% | | | |

Computers & Peripherals — 0.0% | | | |

12,166 | | Axiohm Transaction Solutions Inc. (c)(g)* | | $ | 0 | |

| | | | | |

MATERIALS — 0.1% | | | |

Chemicals — 0.1% | | | |

12,121 | | Applied Extrusion Technologies Inc., Class A Shares * | | 78,787 | |

| | TOTAL COMMON STOCKS

(Cost — $1,577,994) | | 113,442 | |

| | | | | |

PREFERRED STOCKS — 0.1% | | | |

CONSUMER DISCRETIONARY — 0.0% | | | |

Textiles, Apparel & Luxury Goods — 0.0% | | | |

12 | | Anvil Holdings Inc., Class B, 13.000% (g)* | | 63 | |

| | | | | |

ENERGY — 0.1% | | | |

Oil, Gas & Consumable Fuels — 0.1% | | | |

828 | | Chesapeake Energy Corp., convertible 6.250% | | 222,318 | |

| | | | | |

FINANCIALS — 0.0% | | | |

Diversified Financial Services — 0.0% | | | |

6,800 | | Preferred Plus, Series FRD-1, 7.400% | | 124,372 | |

300 | | Saturns, Series F 2003-5, 8.125% | | 5,787 | |

4,091 | | TCR Holdings Corp., Class B Shares, 0.000% (c)(g)* | | 4 | |

2,250 | | TCR Holdings Corp., Class C Shares, 0.000% (c)(g)* | | 2 | |

5,932 | | TCR Holdings Corp., Class D Shares, 0.000% (c)(g)* | | 6 | |

12,271 | | TCR Holdings Corp., Class E Shares, 0.000% (c)(g)* | | 12 | |

| | TOTAL FINANCIALS | | 130,183 | |

| | | | | |

INDUSTRIALS — 0.0% | | | |

Machinery — 0.0% | | | |

5 | | Glasstech Inc., 0.000% (c)(g)* | | 0 | |

| | TOTAL PREFERRED STOCKS

(Cost — $319,562) | | 352,564 | |

| | | | | |

ESCROWED SHARES (g) — 0.0% | | | |

1,750,000 | | Breed Technologies Inc. (c)* | | 0 | |

625,000 | | Pillowtex Corp. * | | 0 | |

397,208 | | Vlasic Foods International Inc. (c)* | | 7,944 | |

| | TOTAL ESCROWED SHARES

(Cost — $0) | | 7,944 | |

| | | | | | |

See Notes to Financial Statements.

20 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Schedule of Investments (August 31, 2006) (continued)

Warrants | | Security(a) | | Value | |

| | | |

WARRANTS — 0.1% | | | |

9,125 | | Bolivarian Republic of Venezuela, Oil-linked payment obligations, Expires 4/15/20 | | $ | 337,625 | |

1,837,246 | | ContiFinancial Corp., Liquidating Trust, Units of Interest (Represents interest in a trust in the liquidation of ContiFinancial Corp. and its affiliates) (c)(g)* | | 6 | |

1,000 | | Mattress Discounters Co., Expires 7/15/07 (b)(c)(g)* | | 0 | |

4,202 | | Pillowtex Corp., Expires 11/24/09 (c)(g)* | | 0 | |

750 | | UbiquiTel Inc., Expires 4/15/10 (b)(c)(g)* | | 7 | |

| | TOTAL WARRANTS

(Cost — $44,998) | | 337,638 | |

| | | | | |

| | TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT

(Cost — $249,055,337) | | 249,622,098 | |

| | | | | |

Face

Amount | | | | | |

| | | |

SHORT-TERM INVESTMENT — 2.8% | | | |

Repurchase Agreement — 2.8% | | | |

$ | 7,251,000 | | Nomura Securities International, Inc. tri-party repurchase agreement dated 8/31/06, 5.240% due 9/1/06; Proceeds at maturity — $7,252,055; (Fully collateralized by various U.S. Treasury Notes and U.S government agency obligations, 0.000% to 5.250% due 10/25/06 to 4/18/16; Market value — $7,396,695 (Cost — $7,251,000) | | 7,251,000 | |

| | TOTAL INVESTMENTS — 100.0% (Cost — $256,306,337#) | | $ | 256,873,098 | |

| | | | | | | |

* Non-income producing security.

(a) All securities are segregated pursuant to a revolving credit facility and for reverse repurchase agreements.

(b) Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors, unless otherwise noted.

(c) Illiquid security.

(d) Security is currently in default.

(e) Variable rate security. Interest rate disclosed is that which is in effect at August 31, 2006.

(f) Payment-in-kind security for which part of the income earned may be paid as additional principal.

(g) Security is valued in good faith at fair value by or under the direction of the Board of Directors (See Note 1).

(h) All or a portion of this security is held by the counterparty as collateral for open reverse repurchase agreements.

# Aggregate cost for federal income tax purposes is $257,001,792.

Abbreviations used in this schedule:

GDP – Gross Domestic Product

PDI – Past Due Interest

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 21

Statement of Assets and Liabilities (August 31, 2006)

ASSETS: | | | |

Investments, at value (Cost — $256,306,337) | | $ | 256,873,098 | |

Cash | | 241,568 | |

Dividends and interest receivable | | 4,614,481 | |

Receivable for securities sold | | 378,491 | |

Prepaid expenses | | 16,110 | |

Total Assets | | 262,123,748 | |

LIABILITIES: | | | |

Loan payable | | 47,124,414 | |

Payable for open reverse repurchase agreements | | 14,243,246 | |

Distributions payable | | 1,207,888 | |

Interest payable | | 872,152 | |

Payable for securities purchased | | 631,670 | |

Investment management fee payable | | 174,887 | |

Directors’ fees payable | | 1,494 | |

Accrued expenses | | 144,320 | |

Total Liabilities | | 64,400,071 | |

Total Net Assets | | $ | 197,723,677 | |

| | | |

NET ASSETS: | | | |

Par value ($0.001 par value; 15,289,720 shares issued and outstanding; 100,000,000 shares authorized) | | $ | 15,290 | |

Paid-in capital in excess of par value | | 205,937,505 | |

Overdistributed net investment income | | (1,057,898 | ) |

Accumulated net realized loss on investments and swap contracts | | (7,737,981 | ) |

Net unrealized appreciation on investments | | 566,761 | |

Total Net Assets | | $ | 197,723,677 | |

| | | |

Shares Outstanding | | 15,289,720 | |

Net Asset Value | | $ | 12.93 | |

See Notes to Financial Statements.

22 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Statement of Operations (For the year ended August 31, 2006)

INVESTMENT INCOME: | | | |

Interest | | $ | 20,687,860 | |

Dividends | | 38,955 | |

Total Investment Income | | 20,726,815 | |

EXPENSES: | | | |

Interest expense (Notes 3 and 4) | | 4,017,683 | |

Investment management fee (Note 2) | | 2,068,775 | |

Shareholder reports | | 98,556 | |

Directors’ fees | | 70,967 | |

Audit and tax | | 56,520 | |

Custody fees | | 36,357 | |

Transfer agent fees | | 32,728 | |

Legal fees | | 21,771 | |

Stock exchange listing fees | | 19,603 | |

Loan fees | | 6,995 | |

Insurance | | 3,736 | |

Miscellaneous expenses | | 5,571 | |

Total Expenses | | 6,439,262 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | (4,385 | ) |

Net Expenses | | 6,434,877 | |

Net Investment Income | | 14,291,938 | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND SWAP CONTRACTS (NOTES 1 AND 3): | | | |

Net Realized Gain From: | | | |

Investment transactions | | 10,152,974 | |

Swap contracts | | 12,448 | |

Net Realized Gain | | 10,165,422 | |

Change in Net Unrealized Appreciation/Depreciation From: | | | |

Investments | | (11,597,552 | ) |

Swap contracts | | (109,920 | ) |

Change in Net Unrealized Appreciation/Depreciation | | (11,707,472 | ) |

Net Loss on Investments and Swap Contracts | | (1,542,050 | ) |

Increase in Net Assets From Operations | | $ | 12,749,888 | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 23

Statements of Changes in Net Assets (For the years ended August 31,)

| | 2006 | | 2005 | |

OPERATIONS: | | | | | |

Net investment income | | $ | 14,291,938 | | $ | 16,290,709 | |

Net realized gain | | 10,165,422 | | 10,356,507 | |

Change in net unrealized appreciation/depreciation | | (11,707,472 | ) | 5,096,351 | |

Increase in Net Assets From Operations | | 12,749,888 | | 31,743,567 | |

DISTRIBUTIONS TO SHAREHOLDERS FROM (NOTE 1): | | | | | |

Net investment income | | (14,723,997 | ) | (18,167,280 | ) |

Decrease in Net Assets From Distributions to Shareholders | | (14,723,997 | ) | (18,167,280 | ) |

FUND SHARE TRANSACTIONS: | | | | | |

Proceeds from shares issued on reinvestment of distributions (89,072 shares issued) | | — | | 1,185,386 | |

Increase in Net Assets From Fund Share Transactions | | — | | 1,185,386 | |

Increase (Decrease) in Net Assets | | (1,974,109 | ) | 14,761,673 | |

NET ASSETS: | | | | | |

Beginning of year | | 199,697,786 | | 184,936,113 | |

End of year* | | $ | 197,723,677 | | $ | 199,697,786 | |

| | | | | |

* Includes overdistributed net investment income of: | | $ | (1,057,898 | ) | $ | (1,192,662 | ) |

See Notes to Financial Statements.

24 Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report

Statement of Cash Flows (For the year ended August 31, 2006)

CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: | | | |

Interest and dividends received | | $ | 20,325,657 | |

Operating expenses paid | | (2,449,615 | ) |

Net purchases of short-term investments | | (519,000 | ) |

Realized gain on swap contracts | | 12,448 | |

Purchases of long-term investments | | (188,309,610 | ) |

Proceeds from disposition of long-term investments | | 204,230,087 | |

Interest paid | | (3,621,605 | ) |

Net Cash Provided By Operating Activities | | 29,668,362 | |

| | | |

CASH FLOWS USED BY FINANCING ACTIVITIES: | | | |

Cash distributions paid on Common Stock | | (14,831,119 | ) |

Cash paid on loan | | (12,000,000 | ) |

Cash paid on reverse repurchase agreements | | (2,596,129 | ) |

Net Cash Flows Used By Financing Activities | | (29,427,248 | ) |

Net Increase in Cash | | 241,114 | |

Cash, Beginning of year | | 454 | |

Cash, End of year | | $ | 241,568 | |

| | | |

RECONCILIATION OF INCREASE IN NET ASSETS FROM OPERATIONS TO NET CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: | | | |

Increase in Net Assets From Operations | | $ | 12,749,888 | |

Accretion of discount on investments | | (1,378,959 | ) |

Amortization of premium on investments | | 569,549 | |

Decrease in investments, at value | | 17,796,916 | |

Decrease in payable for securities purchased | | (3,493,806 | ) |

Decrease in interest receivable | | 408,252 | |

Decrease in receivable for securities sold | | 2,652,865 | |

Increase in prepaid expenses | | (3,170 | ) |

Increase in interest payable | | 396,078 | |

Decrease in accrued expenses | | (29,251 | ) |

Total Adjustments | | 16,918,474 | |

Net Cash Flows Provided By Operating Activities | | $ | 29,668,362 | |

See Notes to Financial Statements.

Salomon Brothers Global Partners Income Fund Inc. 2006 Annual Report 25

Financial Highlights

For a share of common stock outstanding throughout each year ended August 31:

| | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Net Asset Value, Beginning of Year | | $13.06 | | $12.17 | | $11.55 | | $8.88 | | $10.77 | |

Income (Loss) From Operations: | | | | | | | | | | | |

Net investment income | | 0.97 | | 1.07 | | 1.15 | | 1.30 | | 1.36 | |

Net realized and unrealized gain (loss) | | (0.14 | ) | 1.01 | | 0.89 | | 2.79 | | (1.83 | ) |

Total Income (Loss) From Operations | | 0.83 | | 2.08 | | 2.04 | | 4.09 | | (0.47 | ) |

Less Distributions From: | | | | | | | | | | | |

Net investment income | | (0.96 | ) | (1.19 | ) | (1.43 | ) | (1.43 | ) | (1.38 | ) |

Return of capital | | — | | — | | — | | — | | (0.05 | ) |

Total Distributions | | (0.96 | ) | (1.19 | ) | (1.43 | ) | (1.43 | ) | (1.43 | ) |

Increase in Net Asset Value Due to Shares Issued on Reinvestment of Distributions | | — | | — | | 0.01 | | 0.01 | | 0.01 | |

Net Asset Value, End of Year | | $12.93 | | $13.06 | | $12.17 | | $11.55 | | $ 8.88 | |

Market Price, End of Year | | $11.77 | | $12.78 | | $14.03 | | $13.11 | | $10.43 | |

Total Return, Based on NAV | | 6.70 | %(1) | 17.88 | % | 18.63 | % | 49.79 | % | (4.85 | )% |

Total Return, Based on Market Price Per Share(2) | | 0.08 | % | (0.39 | )% | 18.86 | % | 42.71 | % | (0.25 | )% |