UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-7994 | |||||||

| ||||||||

Western Asset Global Partners Income Fund Inc. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

55 Water Street, New York, NY |

| 10041 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Robert I. Frenkel, Esq. Legg Mason & Co., LLC 100 First Stamford Place Stamford, CT 06902 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (888) 777-0102 |

| ||||||

| ||||||||

Date of fiscal year end: | August 31 |

| ||||||

| ||||||||

Date of reporting period: | August 31, 2009 |

| ||||||

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

ANNUAL REPORT / AUGUST 31, 2009

Western Asset Global Partners Income Fund Inc.

(GDF)

Managed by WESTERN ASSET

INVESTMENT PRODUCTS: NOT FDIC INSURED · NO BANK GUARANTEE · MAY LOSE VALUE

|

Fund objective

The Fund’s investment objective is to maintain a high level of current income. As a secondary objective, the Fund seeks capital appreciation.

What’s inside

Letter from the chairman | I |

|

|

Fund overview | 1 |

|

|

Fund at a glance | 7 |

|

|

Schedule of investments | 8 |

|

|

Statement of assets and liabilities | 27 |

|

|

Statement of operations | 28 |

|

|

Statements of changes in net assets | 29 |

|

|

Statement of cash flows | 30 |

|

|

Financial highlights | 31 |

|

|

Notes to financial statements | 32 |

|

|

Report of independent registered public accounting firm | 47 |

|

|

Additional information | 48 |

|

|

Annual chief executive officer and chief financial officer certifications | 54 |

|

|

Dividend reinvestment and cash purchase plan | 55 |

Legg Mason Partners Fund Advisor, LLC (“LMPFA”) is the Fund’s investment manager. Western Asset Management Company (“Western Asset”), Western Asset Management Company Pte. Ltd. (“Western Singapore”), Western Asset Management Company Ltd (“Western Japan”) and Western Asset Management Company Limited (“Western Asset Limited”) are the Fund’s subadvisers. LMPFA, Western Asset, Western Singapore, Western Japan and Western Asset Limited are wholly-owned subsidiaries of Legg Mason Inc.

Letter from the chairman

Dear Shareholder,

While the U.S. economy remained weak during the twelve-month reporting period ended August 31, 2009, there were indications that the worst may be over. Looking back, the U.S. Department of Commerce reported that third and fourth quarter 2008 U.S. gross domestic product (“GDP”)i contracted 2.7% and 5.4%, respectively. The economic contraction accelerated during the first quarter of 2009, as GDP fell 6.4%. However, the news was relatively better during the second quarter, as GDP declined 0.7%. The economy’s more modest contraction was due, in part, to smaller declines in both exports and business spending.

The U.S. recession, which began in December 2007, now has the dubious distinction of being the lengthiest since the Great Depression. Contributing to the economy’s troubles has been extreme weakness in the labor market. Since December 2007, approximately 7.4 million jobs have been shed and we have experienced twenty consecutive months of job losses. In addition, the unemployment rate, reported as 9.7% in August 2009, reached its highest level since June 1983.

Another strain on the economy, the housing market, may finally be getting closer to reaching a bottom. After plunging late in 2008, new single-family home starts have been fairly stable and sales of single-family homes increased for the fourth straight month in July 2009. In addition, while home prices have continued to fall, the pace of the decline has generally moderated. Other recent economic news also seemed to be “less negative” or, in some cases, actually positive. For example, job losses in August were 216,000, less than the 276,000 jobs shed the prior month and substantially lower than the monthly losses earlier in the year. Elsewhere, inflation remained low, manufacturing expanded in August for the first time in eighteen months and durable goods orders in July posted their largest increase in two years.

Ongoing issues related to the housing and subprime mortgage markets and seizing credit markets prompted the Federal Reserve Board (“Fed”)ii to take aggressive and, in some cases, unprecedented actions. After reducing the federal funds rateiii from 5.25% in August 2007 to a range of 0 to 1/4 percent

Western Asset Global Partners Income Fund Inc. |

| I |

Letter from the chairman continued

in December 2008—a historic low—the Fed has maintained this stance thus far in 2009. In conjunction with its August 2009 meeting, the Fed stated that it “will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

In addition to maintaining extremely low short-term interest rates, the Fed took several actions to improve liquidity in the credit markets. Back in September 2008, it announced an $85 billion rescue plan for ailing AIG and pumped $70 billion into the financial system as Lehman Brothers’ bankruptcy and mounting troubles at other financial firms roiled the markets. More recently, the Fed has taken additional measures to thaw the frozen credit markets, including the purchase of debt issued by Fannie Mae and Freddie Mac, as well as introducing the Term Asset-Backed Securities Loan Facility (“TALF”). In March 2009, the Fed continued to pursue aggressive measures as it announced its intentions to:

· Purchase up to an additional $750 billion of agency mortgage-backed securities, bringing its total purchases of these securities to up to $1.25 trillion in 2009.

· Increase its purchases of agency debt this year by up to $100 billion to a total of up to $200 billion.

· Buy up to $300 billion of longer-term Treasury securities over the next six months.

The U.S. Department of the Treasury has also taken an active role in attempting to stabilize the financial system, as it orchestrated the government’s takeover of mortgage giants Fannie Mae and Freddie Mac in September 2008. In October, the Treasury’s $700 billion Troubled Asset Relief Program (“TARP”) was approved by Congress and signed into law by former President Bush. Then, in March 2009, Treasury Secretary Geithner introduced the Public-Private Partnership Investment Program (“PPIP”), which is intended to facilitate the purchase of troubled mortgage assets from bank balance sheets. President Obama has also made reviving the economy a priority in his administration, the cornerstone thus far being the $787 billion stimulus package that was signed into law in February 2009.

During the twelve-month reporting period ended August 31, 2009, both short- and long-term Treasury yields experienced periods of extreme volatility. When the period began, two- and ten-year Treasury yields were 2.36% and 3.83%, respectively. While earlier in 2008 investors were focused on the subprime segment of the mortgage-backed market, these concerns broadened to include a wide range of financial institutions and markets. As a result, other fixed-income instruments also experienced increased price volatility. This unrest triggered several “flights to quality,” causing Treasury yields to move lower (and their prices higher), while riskier segments of the market saw their yields move higher (and their prices lower). This was particularly true toward

II |

| Western Asset Global Partners Income Fund Inc. |

the end of 2008, as the turmoil in the financial markets and sharply falling stock prices caused investors to flee securities that were perceived to be risky, even high-quality corporate bonds and high-grade municipal bonds. When the first half of the reporting period ended on February 28, 2009, two- and ten-year Treasury yields were 1.00% and 3.02%, respectively. During the second half of the period, Treasury yields generally moved higher (and their prices lower) until early June. Two- and ten-year yields peaked at 1.42% and 3.98%, respectively, before falling and ending the reporting period at 0.97% and 3.40%, respectively. In a reversal from 2008, investor risk aversion faded as the twelve-month reporting period progressed, driving spread sector (non-Treasury) prices higher. For the twelve-month period ended August 31, 2009, the Barclays Capital U.S. Aggregate Indexiv returned 7.94%.

The high-yield bond market produced positive results for the twelve months ended August 31, 2009. After generating extremely poor results from September through November 2008, the asset class posted positive returns during eight of the last nine months of the reporting period. This strong rally was due to a variety of factors, including the unfreezing of the credit markets, improving economic data and strong investor demand. All told, over the twelve months ended August 31, 2009, the Citigroup High Yield Market Indexv returned 5.31%.

After falling sharply in September and October 2008, emerging market debt prices rallied sharply—posting positive returns during nine of the last ten months of the reporting period. This was triggered by firming and, in some cases, rising commodity prices, optimism that the worst of the global recession was over and increased investor risk appetite. Over the twelve months ended August 31, 2009, the JPMorgan Emerging Markets Bond Index Global (“EMBI Global”)vi returned 5.37%.

A special note regarding increased market volatility

Dramatically higher volatility in the financial markets has been very challenging for many investors. Market movements have been rapid—sometimes in reaction to economic news, and sometimes creating the news. In the midst of this evolving market environment, we at Legg Mason want to do everything we can to help you reach your financial goals. Now, as always, we remain committed to providing you with excellent service and a full spectrum of investment choices. Rest assured, we will continue to work hard to ensure that our investment managers make every effort to deliver strong long-term results.

We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our enhanced website, www.leggmason.com/cef. Here you can gain immediate access to many special features to help guide you through difficult times, including:

· Fund prices and performance,

Western Asset Global Partners Income Fund Inc. |

| III |

Letter from the chairman continued

· Market insights and commentaries from our portfolio managers, and

· A host of educational resources.

During periods of market unrest, it is especially important to work closely with your financial advisor and remember that reaching one’s investment goals unfolds over time and through multiple market cycles. Time and again, history has shown that, over the long run, the markets have eventually recovered and grown.

Information about your fund

Please read on for a more detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

Important information with regard to recent regulatory developments that may affect the Fund is contained in the Notes to Financial Statements included in this report.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

September 30, 2009

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

i | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

ii | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

iii | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

iv | The Barclays Capital (formerly Lehman Brothers) U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

v | The Citigroup High Yield Market Index is a broad-based unmanaged index of high-yield securities. |

vi | The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds and local market instruments. |

IV |

| Western Asset Global Partners Income Fund Inc. |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund seeks to maintain a high level of current income. As a secondary objective, the Fund seeks capital appreciation. Under normal market conditions, the Fund will invest at least 33% of its total assets in securities of issuers that are, or are incorporated in or generate the majority of their revenue in, emerging market countries and at least 33% of its total assets in high-yield U.S. corporate debt securities. The Fund is also able to invest up to 33% of its total assets in a broad range of other U.S. and non-U.S. fixed-income securities, both investment grade and high-yield securities, including, but not limited to, corporate bonds, loans, mortgage- and asset-backed securities, preferred stocks and sovereign debt, derivative instruments of the foregoing securities and dollar rolls.

The Fund’s investment process assimilates top-down macroeconomic views with bottom-up credit analysts’ fundamental and relative value views regarding industry and issuer opportunities. As a firm, Western Asset Management Company (“Western Asset”), the Fund’s subadviser, aims to add value by exploiting inefficiencies in the fixed-income markets. A fundamental approach is used to identify these inefficiencies. The Fund diversifies its holdings across a range of securities, industries and maturity dates in an attempt to minimize the risk of any individual holding. We use various tools, both external and proprietary, to help identify, measure and manage portfolio risk. In particular, we look for companies that we believe have the ability to weather adverse economic conditions while providing moderate to high returns to bondholders, companies that are repositioning in the marketplace and that we believe are temporarily undervalued, and companies that demonstrate an ability to improve their financial condition where that improvement and positive trajectory have not yet been fully appreciated by rating agencies and the market. Often times, this strategy will result in a higher concentration of lower-rated securities in the portfolio versus the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Indexi. However, no assurance can be given that markets will perform as we predict, and a risk of loss exists.

At Western Asset, we utilize a fixed-income team approach, with decisions derived from interaction among various investment management sector specialists. The sector teams are comprised of Western Asset’s senior portfolio managers, research analysts and an in-house economist. Under this team approach, management of client fixed-income portfolios will reflect a consensus of interdisciplinary views within the Western Asset organization.

Western Asset Global Partners Income Fund Inc. | 1 |

Fund overview continued

Q. What were the overall market conditions during the Fund’s reporting period?

A. During the fiscal year, the global fixed-income market experienced periods of heightened volatility. Changing perceptions regarding the economy, deflation, inflation and future central bank monetary policy caused bond prices to fluctuate.

As the reporting period began, we were in the midst of a “flight to quality,” triggered by the seizing credit markets. Investor risk aversion intensified during the fourth quarter of 2008, given the severe disruptions in the global financial markets. At the epicenter of the turmoil was the September 2008 bankruptcy of Lehman Brothers. During this time, investors were drawn to the relative safety of shorter-term Treasuries, driving their yields down to historically low levels. In contrast, riskier portions of the fixed-income market generally performed poorly, as spreads in many sectors widened to record high levels.

Overall, Treasury yields moved higher from January 2009 through the end of the fiscal year, especially on the long end of the yield curveii. This was due to less demand for these securities as risk aversion abated and, in terms of longer-term Treasuries, because of concerns regarding the massive amount of new Treasury issuance that would be needed to fund the economic stimulus package. A return to more normal market conditions, including improved liquidity and signs that the economy might be bottoming, caused a sharp rebound in the spread sectors (non-Treasuries). Following their poor performance in 2008, many of the spread sectors recouped a large portion of their earlier losses over the last eight months of the reporting period.

Looking at high-yield bonds and emerging market debt, investors largely shunned these securities following the demise of Lehman Brothers in September 2008. Expectations for high-yield defaults moved sharply higher and emerging market debt prices were weighed down by rapidly falling commodity prices. However, as investor risk aversion abated and global economic conditions started to improve, emerging market debt and high-yield prices staged an impressive rally beginning in November and December 2008, respectively.

Q. How did we respond to these changing market conditions?

A. The first three months of the fiscal year were extremely challenging, as we continued to see forced selling by overly leveraged investors, a lack of liquidity and heightened risk aversion. Collectively, this triggered extensive spread widening, in many cases to levels that appeared to be both excessive and unsustainable. Rather than follow the herd and aggressively upgrade

2 | Western Asset Global Partners Income Fund Inc. |

the credit quality of the portfolio at the trough of the credit cycle, we maintained our lower-quality bias, where we opportunistically saw the most value. For more than thirty years, we have continued to follow our research-driven, long-term value oriented approach and emphasized the selection of securities that we believed to be attractively priced. As a consequence of maintaining our disciplined approach to investing, we were able to capitalize on the sustained market rally that began in December 2008 and continued up through the end of August 2009.

As a consequence of changing market conditions over the course of the Fund’s fiscal year, we made several adjustments to the Fund’s portfolio. We increased our exposure to Russia through the purchase of select corporate and quasi-sovereign names. At the same time, we reduced our emerging market currency exposure given the extreme volatility seen in those markets and the relative attractiveness of investments in hard currency corporate, sovereign and quasi-sovereign securities. Within the high-yield market, we emphasized more defensive non-cyclical areas, such as Utilities, and avoided Consumer Cyclicals1.

In the second half of the reporting period, we used interest rate swaps to maintain exposure to the Brazilian interest rate market while making a concurrent reduction in our exposure to the Brazilian real. This strategy was a contributor to performance during the second half of the fiscal year. In the fourth quarter of 2008, we utilized currency forwards to obtain short-dated exposure to the Russian ruble versus the U.S. dollar and the euro. This resulted in a modest reduction in the Fund’s performance. The Fund also used credit default swaps to increase its exposure to investment grade and high-yield bonds. This strategy was an overall positive contributor to performance.

Performance review

For the twelve months ended August 31, 2009, Western Asset Global Partners Income Fund Inc. returned 2.22% based on its net asset value (“NAV”)iii and 15.51% based on its New York Stock Exchange (“NYSE”) market price per share. The Fund’s unmanaged benchmarks, the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Index and the EMBI Global, returned 7.00% and 5.37%, respectively, for the same period. The Lipper Global Income Closed-End Funds Category Averageiv returned 4.28% over the same time frame. Please note that Lipper performance returns are based on each fund’s NAV.

1 Consumer Cyclicals consists of the following industries: Automotive, Entertainment, Gaming, Home Construction, Lodging, Retailers, Restaurants, Textiles and other consumer services.

Western Asset Global Partners Income Fund Inc. | 3 |

Fund overview continued

During the twelve-month period, the Fund made distributions to shareholders totaling $1.14 per share. The performance table shows the Fund’s twelve-month total return based on its NAV and market price as of August 31, 2009. Past performance is no guarantee of future results.

| PERFORMANCE SNAPSHOT as of August 31, 2009 (unaudited) |

|

|

| |

|

|

|

|

| |

| PRICE PER SHARE |

| 12-MONTH |

| |

| $10.06 (NAV) |

| 2.22 | % |

|

| $10.23 (Market Price) |

| 15.51 | % |

|

|

|

|

|

|

|

| All figures represent past performance and are not a guarantee of future results. |

|

|

|

|

|

|

|

|

|

|

* | Total returns are based on changes in NAV or market price, respectively. Total returns assume the reinvestment of all distributions in additional shares in accordance with the Fund’s Dividend Reinvestment Plan. | ||||

Q. What were the leading contributors to performance?

A. As discussed, the first three months of the fiscal year were extremely difficult and the Fund significantly lagged its benchmarks during that time. However, the same strategies that hurt performance during those three months were beneficial to the Fund’s performance as the reporting period progressed. This, in turn, helped the Fund recoup much of its earlier underperformance.

Our favoring of high-yield bonds was rewarded as their spreads significantly narrowed during the last nine months of the reporting period. In particular, our overweight positions versus the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Index in the more defensive Wireless1 and Health Care sectors were beneficial, as were our underweights to the Information Technology and Media — Non-Cable sectors. In terms of individual securities, overweights to Intelsat, Ford Motor Credit Co., Sprint Capital Corp., Harrah’s and Bank of America Corp. were all positive contributors to performance.

Looking at the Fund’s exposure to emerging market debt, security selection was the primary contributor to performance. Examples of strong holdings included Thailand Telecommunication Services company True Move Co., Ltd., as it rallied almost 50% during the fiscal year. The Fund’s exposure to Russia was also beneficial to performance during the fiscal year. In particular among Russian issues, the Fund’s increased exposure to quasi-sovereign banks, domestic oil and gas names and the Steel2 sector all benefitted performance.

1 Wireless is included in the Telecommunication Services sector.

2 Steel is included in the Industrials sector.

4 | Western Asset Global Partners Income Fund Inc. |

Q. What were the leading detractors from performance?

A. Within high-yield, security selection was the most significant detractor from performance. In particular, the Fund’s overweight positions in Energy Future Holdings Corp., Chesapeake Energy Corp. and Edison Mission Energy meaningfully detracted from relative results. In terms of sector allocation, an overweight to the normally defensive Electric Utilities area was a detractor from performance. The Gaming1 sector, another area that is generally viewed as being defensive in nature, detracted given high levels of leverage in the space. Elsewhere, the Fund’s lower quality bias was, overall, a slight detractor from performance versus the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Index.

In terms of the Fund’s emerging market exposure, overweights to Venezuela and Argentina were detractors from results, as they lagged the EMBI Global during the fiscal year. As with most of the global Financials sector, the banking system in Kazakhstan came under significant pressure over the course of the reporting period. While the sector was able to withstand the storm and prices recovered in the second half of the reporting period, the sector as a whole underperformed the EMBI Global for the reporting period. As such, the Fund’s exposure to Kazakhstan banking sector holdings such as ATF Capital BV, HSBK Europe BV and TuranAlem Finance BV also detracted from performance. These positions were all eliminated from the Fund’s portfolio at the end of June. Elsewhere, currency selection was a detractor from performance. In particular, the Fund’s positions in the Russian ruble and Brazilian real underperformed, although the underperformance in the Brazilian real was largely offset by the strong rally in the front end of the Brazilian treasury curve.

Looking for additional information?

The Fund is traded under the symbol “GDF” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under the symbol “XGDFX” on most financial websites. Barron’s and The Wall Street Journal’s Monday edition both carry closed-end fund tables that provide additional information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites, as well as www.leggmason.com/cef.

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Standard Time, for the Fund’s current NAV, market price and other information.

1 Gaming is included in the Consumer Discretionary sector.

Western Asset Global Partners Income Fund Inc. | 5 |

Fund overview continued

Thank you for your investment in Western Asset Global Partners Income Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company

September 15, 2009

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of August 31, 2009 and are subject to change and may not be representative of the portfolio managers’ current or future investments. Please refer to pages 8 through 26 for a list and percentage breakdown of the Fund’s holdings.

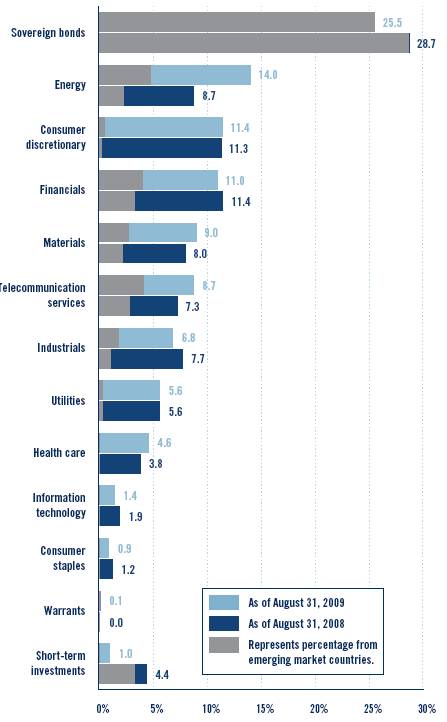

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of total investments) as of August 31, 2009 were: Sovereign Bonds (25.5%), Energy (14.0%), Consumer Discretionary (11.4%), Financials (11.0%) and Materials (9.0%). The Fund’s portfolio composition is subject to change at any time.

RISKS: The Fund may invest in high-yield and foreign securities, including emerging markets, which involve risks beyond those inherent in higher-rated and domestic investments. High-yield bonds involve greater credit and liquidity risks than investment grade bonds. Investing in foreign securities is subject to certain risks not associated with domestic investing, such as currency fluctuations, and changes in political and economic conditions. These risks are magnified in emerging or developing markets. Derivatives, such as options and futures, can be illiquid and harder to value, especially in declining markets. A small investment in certain derivatives may have a potentially large impact on the Fund’s performance.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

i | The Barclays Capital (formerly Lehman Brothers) U.S. Corporate High Yield 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Barclays Capital U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. |

ii | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

iii | Net asset value (“NAV”) is calculated by subtracting total liabilities and outstanding preferred stock (if any) from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

iv | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the twelve-month period ended August 31, 2009, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 16 funds in the Fund’s Lipper category. |

6 | Western Asset Global Partners Income Fund Inc. |

Fund at a glance† (unaudited)

INVESTMENT BREAKDOWN (%) As a percent of total investments

† The bar graphs above represent the composition of the Fund’s investments as of August 31, 2009 and August 31, 2008 and do not include derivatives. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 7 |

Schedule of investments

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

CORPORATE BONDS & NOTES — 71.2% |

|

|

| |||

CONSUMER DISCRETIONARY — 10.9% |

|

|

| |||

|

| Auto Components — 0.3% |

|

|

| |

110,000 |

| Affinia Group Inc., Senior Secured Notes, 10.750% due 8/15/16(a) |

| $ | 114,125 |

|

485,000 |

| Allison Transmission Inc., Senior Notes, 11.250% due 11/1/15(a)(b) |

| 409,825 |

| |

|

| Visteon Corp., Senior Notes: |

|

|

| |

159,000 |

| 8.250% due 8/1/10(c) |

| 10,335 |

| |

577,000 |

| 12.250% due 12/31/16(a)(c) |

| 41,833 |

| |

|

| Total Auto Components |

| 576,118 |

| |

|

| Automobiles — 0.2% |

|

|

| |

|

| General Motors Corp.: |

|

|

| |

930,000 |

| Notes, 7.200% due 1/15/11(c) |

| 141,825 |

| |

1,645,000 |

| Senior Debentures, 8.375% due 7/15/33(c) |

| 261,144 |

| |

|

| Total Automobiles |

| 402,969 |

| |

|

| Diversified Consumer Services — 0.5% |

|

|

| |

875,000 |

| Education Management LLC/Education Management Finance Corp., Senior Subordinated Notes, 10.250% due 6/1/16 |

| 919,844 |

| |

130,000 |

| Service Corp. International, Senior Notes, 7.500% due 4/1/27 |

| 110,500 |

| |

|

| Total Diversified Consumer Services |

| 1,030,344 |

| |

|

| Hotels, Restaurants & Leisure — 3.7% |

|

|

| |

355,000 |

| Ameristar Casinos Inc., Senior Notes, 9.250% due 6/1/14(a) |

| 364,762 |

| |

|

| Boyd Gaming Corp., Senior Subordinated Notes: |

|

|

| |

90,000 |

| 6.750% due 4/15/14 |

| 78,863 |

| |

100,000 |

| 7.125% due 2/1/16 |

| 83,750 |

| |

1,250,000 |

| Caesars Entertainment Inc., Senior Subordinated Notes, 8.125% due 5/15/11 |

| 1,156,250 |

| |

675,000 |

| Denny’s Holdings Inc., Senior Notes, 10.000% due 10/1/12 |

| 680,062 |

| |

425,000 |

| Downstream Development Quapaw, Senior Notes, 12.000% due 10/15/15(a) |

| 270,937 |

| |

|

| El Pollo Loco Inc.: |

|

|

| |

755,000 |

| Senior Notes, 11.750% due 11/15/13 |

| 649,300 |

| |

185,000 |

| Senior Secured Notes, 11.750% due 12/1/12(a) |

| 194,250 |

| |

180,000 |

| Harrah’s Operating Co. Inc., Senior Notes, 10.750% due 2/1/16 |

| 117,450 |

| |

660,000 |

| Harrahs Operating Escrow LLC/Harrahs Escrow Corp., Senior Secured Notes, 11.250% due 6/1/17(a) |

| 674,850 |

| |

440,000 |

| Indianapolis Downs LLC & Capital Corp., Senior Secured Notes, 11.000% due 11/1/12(a) |

| 314,600 |

| |

885,000 |

| Inn of the Mountain Gods Resort & Casino, Senior Notes, 12.000% due 11/15/10(c)(d) |

| 393,825 |

| |

See Notes to Financial Statements.

8 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Hotels, Restaurants & Leisure — 3.7% continued |

|

|

| |

|

| MGM MIRAGE Inc.: |

|

|

| |

20,000 |

| Senior Notes, 8.500% due 9/15/10 |

| $ | 19,500 |

|

|

| Senior Secured Notes: |

|

|

| |

40,000 |

| 10.375% due 5/15/14(a) |

| 42,300 |

| |

95,000 |

| 11.125% due 11/15/17(a) |

| 103,313 |

| |

840,000 |

| Senior Subordinated Notes, 8.375% due 2/1/11 |

| 716,100 |

| |

55,000 |

| Mohegan Tribal Gaming Authority, Senior Subordinated Notes, 6.875% due 2/15/15 |

| 38,225 |

| |

120,000 |

| Penn National Gaming Inc., Senior Subordinated Notes, 8.750% due 8/15/19(a) |

| 119,700 |

| |

440,000 |

| Pinnacle Entertainment Inc., Senior Notes, 8.625% due 8/1/17(a) |

| 435,600 |

| |

695,000 |

| Sbarro Inc., Senior Notes, 10.375% due 2/1/15 |

| 496,925 |

| |

|

| Snoqualmie Entertainment Authority, Senior Secured Notes: |

|

|

| |

290,000 |

| 4.680% due 2/1/14(a)(e) |

| 143,550 |

| |

10,000 |

| 9.125% due 2/1/15(a) |

| 5,550 |

| |

|

| Station Casinos Inc.: |

|

|

| |

|

| Senior Notes: |

|

|

| |

735,000 |

| 6.000% due 4/1/12(c)(d) |

| 236,119 |

| |

185,000 |

| 7.750% due 8/15/16(c)(d) |

| 58,506 |

| |

|

| Senior Subordinated Notes: |

|

|

| |

475,000 |

| 6.500% due 2/1/14(c)(d) |

| 19,000 |

| |

50,000 |

| 6.625% due 3/15/18(c)(d) |

| 2,000 |

| |

|

| Total Hotels, Restaurants & Leisure |

| 7,415,287 |

| |

|

| Household Durables — 0.6% |

|

|

| |

|

| American Greetings Corp., Senior Notes: |

|

|

| |

55,000 |

| 7.375% due 6/1/16 |

| 47,300 |

| |

15,000 |

| 7.375% due 6/1/16 |

| 11,550 |

| |

250,000 |

| K Hovnanian Enterprises Inc., Senior Notes, 11.500% due 5/1/13 |

| 243,125 |

| |

375,000 |

| Norcraft Cos. LP/Norcraft Finance Corp., Senior Subordinated Notes, 9.000% due 11/1/11 |

| 380,625 |

| |

695,000 |

| Norcraft Holdings LP/Norcraft Capital Corp., Senior Discount Notes, 9.750% due 9/1/12 |

| 667,200 |

| |

|

| Total Household Durables |

| 1,349,800 |

| |

|

| Leisure Equipment & Products — 0.1% |

|

|

| |

125,000 |

| WMG Acquisition Corp., Senior Secured Notes, 9.500% due 6/15/16(a) |

| 130,000 |

| |

|

| Media — 4.2% |

|

|

| |

|

| Affinion Group Inc.: |

|

|

| |

|

| Senior Notes: |

|

|

| |

370,000 |

| 10.125% due 10/15/13(a) |

| 369,537 |

| |

295,000 |

| 10.125% due 10/15/13 |

| 294,631 |

| |

See Notes to Financial Statements.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 9 |

Schedule of investments continued

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Media — 4.2% continued |

|

|

| |

935,000 |

| Senior Subordinated Notes, 11.500% due 10/15/15 |

| $ | 902,275 |

|

|

| CCH I LLC/CCH I Capital Corp.: |

|

|

| |

270,000 |

| Senior Notes, 11.000% due 10/1/15(c)(d) |

| 36,450 |

| |

1,989,000 |

| Senior Secured Notes, 11.000% due 10/1/15(c)(d) |

| 288,405 |

| |

38,000 |

| CCH II LLC/CCH II Capital Corp., Senior Notes, 10.250% due 10/1/13(d) |

| 42,418 |

| |

|

| Cengage Learning Acquisitions Inc.: |

|

|

| |

250,000 |

| Senior Notes, 10.500% due 1/15/15(a) |

| 228,750 |

| |

450,000 |

| Senior Subordinated Notes, 13.250% due 7/15/15(a) |

| 382,500 |

| |

130,000 |

| Charter Communications Holdings LLC, Senior Discount Notes, 12.125% due 1/15/12(c)(d) |

| 1,300 |

| |

160,000 |

| Charter Communications Holdings LLC/Charter Communications Holdings Capital Corp., Senior Discount Notes, 11.750% due 5/15/11(c)(d) |

| 1,000 |

| |

1,010,000 |

| Charter Communications Inc., Senior Secured Notes, 12.875% due 9/15/14(a)(d) |

| 1,100,900 |

| |

|

| CSC Holdings Inc., Senior Notes: |

|

|

| |

345,000 |

| 6.750% due 4/15/12 |

| 348,450 |

| |

560,000 |

| 8.500% due 6/15/15(a) |

| 568,400 |

| |

|

| DIRECTV Holdings LLC/DIRECTV Financing Co. Inc., Senior Notes: |

|

|

| |

75,000 |

| 8.375% due 3/15/13 |

| 77,250 |

| |

25,000 |

| 7.625% due 5/15/16 |

| 26,438 |

| |

|

| DISH DBS Corp., Senior Notes: |

|

|

| |

280,000 |

| 6.625% due 10/1/14 |

| 266,700 |

| |

45,000 |

| 7.750% due 5/31/15 |

| 44,325 |

| |

825,000 |

| 7.875% due 9/1/19(a) |

| 817,781 |

| |

520,000 |

| Globo Communicacoes e Participacoes SA, Bonds, 7.250% due 4/26/22(a) |

| 535,600 |

| |

440,000 |

| Grupo Televisa SA, Senior Notes, 6.625% due 3/18/25 |

| 442,647 |

| |

1,145,000 |

| Idearc Inc., Senior Notes, 8.000% due 11/15/16(c) |

| 93,031 |

| |

150,000 |

| R.H. Donnelley Corp., Senior Notes, 8.875% due 1/15/16(c) |

| 9,563 |

| |

400,000 |

| Sinclair Broadcast Group Inc., Senior Subordinated Notes, 8.000% due 3/15/12 |

| 331,000 |

| |

320,000 |

| Sun Media Corp., Senior Notes, 7.625% due 2/15/13 |

| 218,400 |

| |

540,000 |

| Univision Communications Inc., Senior Secured Notes, 12.000% due 7/1/14(a) |

| 569,700 |

| |

180,000 |

| UPC Holding BV, Senior Notes, 9.875% due 4/15/18(a) |

| 182,925 |

| |

|

| Virgin Media Finance PLC: |

|

|

| |

140,000 |

| Senior Bonds, 9.500% due 8/15/16 |

| 144,550 |

| |

150,000 |

| Senior Notes, 9.125% due 8/15/16 |

| 152,625 |

| |

|

| Total Media |

| 8,477,551 |

| |

See Notes to Financial Statements.

10 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Multiline Retail — 0.5% |

|

|

| |

50,000 |

| Dollar General Corp., Senior Notes, 10.625% due 7/15/15 |

| $ | 55,750 |

|

|

| Neiman Marcus Group Inc.: |

|

|

| |

1,193,127 |

| Senior Notes, 9.000% due 10/15/15(b) |

| 894,845 |

| |

140,000 |

| Senior Secured Notes, 7.125% due 6/1/28 |

| 107,100 |

| |

|

| Total Multiline Retail |

| 1,057,695 |

| |

|

| Specialty Retail — 0.5% |

|

|

| |

540,000 |

| Blockbuster Inc., Senior Subordinated Notes, 9.000% due 9/1/12 |

| 284,850 |

| |

120,000 |

| Eye Care Centers of America, Senior Subordinated Notes, 10.750% due 2/15/15 |

| 124,350 |

| |

40,000 |

| Limited Brands Inc., Senior Notes, 8.500% due 6/15/19(a) |

| 40,588 |

| |

545,000 |

| Michaels Stores Inc., Senior Notes, 10.000% due 11/1/14 |

| 523,200 |

| |

|

| Total Specialty Retail |

| 972,988 |

| |

|

| Textiles, Apparel & Luxury Goods — 0.3% |

|

|

| |

630,000 |

| Oxford Industries Inc., Senior Secured Notes, 11.375% due 7/15/15 |

| 658,350 |

| |

|

| TOTAL CONSUMER DISCRETIONARY |

| 22,071,102 |

| |

CONSUMER STAPLES — 0.9% |

|

|

| |||

|

| Food Products — 0.3% |

|

|

| |

380,000 |

| Dole Food Co. Inc., Senior Notes, 7.250% due 6/15/10 |

| 380,000 |

| |

290,000 |

| Smithfield Foods Inc., Senior Secured Notes, 10.000% due 7/15/14(a) |

| 297,250 |

| |

|

| Total Food Products |

| 677,250 |

| |

|

| Household Products — 0.3% |

|

|

| |

300,000 |

| American Achievement Corp., Senior Subordinated Notes, 8.250% due 4/1/12(a) |

| 295,500 |

| |

325,000 |

| Visant Holding Corp., Senior Notes, 8.750% due 12/1/13 |

| 329,875 |

| |

|

| Total Household Products |

| 625,375 |

| |

|

| Tobacco — 0.3% |

|

|

| |

|

| Alliance One International Inc., Senior Notes: |

|

|

| |

310,000 |

| 10.000% due 7/15/16(a) |

| 307,675 |

| |

180,000 |

| 10.000% due 7/15/16(a) |

| 178,650 |

| |

|

| Total Tobacco |

| 486,325 |

| |

|

| TOTAL CONSUMER STAPLES |

| 1,788,950 |

| |

ENERGY — 13.8% |

|

|

| |||

|

| Energy Equipment & Services — 0.6% |

|

|

| |

380,000 |

| Basic Energy Services Inc., Senior Secured Notes, 11.625% due 8/1/14(a) |

| 389,500 |

| |

355,000 |

| Complete Production Services Inc., Senior Notes, 8.000% due 12/15/16 |

| 306,187 |

| |

425,000 |

| Key Energy Services Inc., Senior Notes, 8.375% due 12/1/14 |

| 386,750 |

| |

70,000 |

| Southern Natural Gas Co., Senior Notes, 8.000% due 3/1/32 |

| 81,443 |

| |

|

| Total Energy Equipment & Services |

| 1,163,880 |

| |

See Notes to Financial Statements.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 11 |

Schedule of investments continued

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Oil, Gas & Consumable Fuels — 13.2% |

|

|

| |

340,000 |

| Arch Coal Inc., Senior Notes, 8.750% due 8/1/16(a) |

| $ | 341,700 |

|

540,000 |

| Atlas Pipeline Partners LP, Senior Notes, 8.750% due 6/15/18 |

| 442,800 |

| |

1,675,000 |

| Belden & Blake Corp., Secured Notes, 8.750% due 7/15/12 |

| 1,507,500 |

| |

320,000 |

| Berry Petroleum Co., Senior Notes, 10.250% due 6/1/14 |

| 335,600 |

| |

|

| Chesapeake Energy Corp., Senior Notes: |

|

|

| |

990,000 |

| 6.625% due 1/15/16 |

| 904,613 |

| |

250,000 |

| 6.875% due 1/15/16 |

| 230,625 |

| |

410,000 |

| 7.250% due 12/15/18 |

| 377,200 |

| |

500,000 |

| Compagnie Generale de Geophysique SA, Senior Notes, 7.750% due 5/15/17 |

| 475,000 |

| |

1,152,077 |

| Corral Petroleum Holdings AB, Senior Secured Subordinated Bonds, 5.509% due 4/15/10 (a) (b) (e) |

| 887,099 |

| |

1,000,000 |

| Ecopetrol SA, Notes, 7.625% due 7/23/19(a) |

| 1,071,300 |

| |

|

| El Paso Corp.: |

|

|

| |

860,000 |

| Medium-Term Notes, 7.800% due 8/1/31 |

| 771,116 |

| |

635,000 |

| Notes, 7.875% due 6/15/12 |

| 653,831 |

| |

90,000 |

| Encore Acquisition Co., Senior Subordinated Notes, 9.500% due 5/1/16 |

| 91,350 |

| |

|

| Enterprise Products Operating LLP: |

|

|

| |

350,000 |

| Junior Subordinated Notes, 8.375% due 8/1/66(e) |

| 304,003 |

| |

260,000 |

| Subordinated Notes, 7.034% due 1/15/68(e) |

| 213,516 |

| |

805,000 |

| EXCO Resources Inc., Senior Notes, 7.250% due 1/15/11 |

| 792,925 |

| |

400,000 |

| Forest Oil Corp., Senior Notes, 8.500% due 2/15/14(a) |

| 404,000 |

| |

795,000 |

| International Coal Group Inc., Senior Notes, 10.250% due 7/15/14 |

| 675,750 |

| |

1,530,000 |

| KazMunaiGaz Finance Sub B.V., Senior Notes, 8.375% due 7/2/13(a) |

| 1,499,400 |

| |

|

| Mariner Energy Inc., Senior Notes: |

|

|

| |

260,000 |

| 7.500% due 4/15/13 |

| 247,000 |

| |

120,000 |

| 8.000% due 5/15/17 |

| 106,800 |

| |

330,000 |

| MarkWest Energy Partners LP/MarkWest Energy Finance Corp., Senior Notes, 8.750% due 4/15/18 |

| 315,150 |

| |

|

| OPTI Canada Inc., Senior Secured Notes: |

|

|

| |

375,000 |

| 7.875% due 12/15/14 |

| 241,875 |

| |

205,000 |

| 8.250% due 12/15/14 |

| 134,275 |

| |

140,000 |

| Parallel Petroleum Corp., Senior Notes, 10.250% due 8/1/14 |

| 96,600 |

| |

300,000 |

| Parker Drilling Co., Senior Notes, 9.625% due 10/1/13 |

| 295,500 |

| |

373,000 |

| Pemex Project Funding Master Trust, Senior Bonds, 6.625% due 6/15/35 |

| 341,587 |

| |

470,000 |

| Petrohawk Energy Corp., Senior Notes, 9.125% due 7/15/13 |

| 479,400 |

| |

4,280,000 |

| Petroleos Mexicanos, 8.000% due 5/3/19(a) |

| 4,836,400 |

| |

390,000 |

| Petroleum Co. of Trinidad & Tobago Ltd., Senior Notes, 9.750% due 8/14/19(a) |

| 425,588 |

| |

2,470,000 |

| Petronas Capital Ltd., 5.250% due 8/12/19(a) |

| 2,467,831 |

| |

See Notes to Financial Statements.

12 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Oil, Gas & Consumable Fuels — 13.2% continued |

|

|

| |

470,000 |

| Petroplus Finance Ltd., Senior Notes, 6.750% due 5/1/14(a) |

| $ | 430,050 |

|

325,000 |

| Plains Exploration & Production Co., Senior Notes, 10.000% due 3/1/16 |

| 346,125 |

| |

|

| Quicksilver Resources Inc., Senior Notes: |

|

|

| |

200,000 |

| 8.250% due 8/1/15 |

| 189,000 |

| |

240,000 |

| 11.750% due 1/1/16 |

| 255,600 |

| |

600,000 |

| Ras Laffan Liquefied Natural Gas Co., Ltd. III, Senior Secured Bonds, 5.500% due 9/30/14 (a) |

| 623,878 |

| |

|

| SandRidge Energy Inc., Senior Notes: |

|

|

| |

360,000 |

| 8.625% due 4/1/15(b) |

| 340,200 |

| |

790,000 |

| 8.000% due 6/1/18(a) |

| 718,900 |

| |

1,090,000 |

| SemGroup LP, Senior Notes, 8.750% due 11/15/15(a)(c)(d) |

| 70,850 |

| |

110,000 |

| Targa Resources Partners LP, Senior Notes, 8.250% due 7/1/16 |

| 99,000 |

| |

200,000 |

| Teekay Corp., Senior Notes, 8.875% due 7/15/11 |

| 200,000 |

| |

95,000 |

| Tennessee Gas Pipeline Co., Senior Notes, 8.000% due 2/1/16 |

| 107,068 |

| |

380,000 |

| VeraSun Energy Corp., Senior Notes, 9.375% due 6/1/17(c) |

| 55,100 |

| |

330,000 |

| W&T Offshore Inc., Senior Notes, 8.250% due 6/15/14(a) |

| 292,050 |

| |

725,000 |

| Whiting Petroleum Corp., Senior Subordinated Notes, 7.000% due 2/1/14 |

| 714,125 |

| |

185,000 |

| Williams Cos. Inc., Notes, 8.750% due 3/15/32 |

| 208,663 |

| |

|

| Total Oil, Gas & Consumable Fuels |

| 26,617,943 |

| |

|

| TOTAL ENERGY |

| 27,781,823 |

| |

FINANCIALS — 10.2% |

|

|

| |||

|

| Capital Markets — 0.0% |

|

|

| |

385,000 |

| Lehman Brothers Holdings Inc., Medium-Term Notes, Senior Notes, 5.250% due 2/6/12(c) |

| 69,300 |

| |

|

| Commercial Banks — 3.8% |

|

|

| |

300,000 |

| BAC Capital Trust VI, Capital Securities, Junior Subordinated Notes, 5.625% due 3/8/35 |

| 205,878 |

| |

|

| ICICI Bank Ltd., Subordinated Bonds: |

|

|

| |

186,000 |

| 6.375% due 4/30/22(a)(e) |

| 148,178 |

| |

130,000 |

| 6.375% due 4/30/22(a)(e) |

| 102,585 |

| |

390,000 |

| Rabobank Nederland NV, Junior Subordinated Notes, 11.000% due 6/30/19(a)(e)(f) |

| 461,928 |

| |

|

| Royal Bank of Scotland Group PLC, Subordinated Notes: |

|

|

| |

205,000 |

| 5.000% due 11/12/13 |

| 185,580 |

| |

90,000 |

| 5.050% due 1/8/15 |

| 79,852 |

| |

|

| RSHB Capital, Loan Participation Notes: |

|

|

| |

1,920,000 |

| Notes, 9.000% due 6/11/14(a) |

| 2,049,408 |

| |

|

| Secured Notes: |

|

|

| |

731,000 |

| 7.175% due 5/16/13(a) |

| 732,827 |

| |

See Notes to Financial Statements.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 13 |

Schedule of investments continued

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Commercial Banks — 3.8% continued |

|

|

| |

810,000 |

| 7.125% due 1/14/14(a) |

| $ | 810,486 |

|

530,000 |

| 7.125% due 1/14/14(a) |

| 532,650 |

| |

100,000 |

| Senior Notes, 6.299% due 5/15/17(a) |

| 90,750 |

| |

|

| Senior Secured Notes: |

|

|

| |

120,000 |

| 7.175% due 5/16/13(a) |

| 120,696 |

| |

1,686,000 |

| 6.299% due 5/15/17(a) |

| 1,521,615 |

| |

600,000 |

| Wells Fargo Capital XIII, Medium-Term Notes, 7.700% due 3/26/13(e)(f) |

| 525,000 |

| |

170,000 |

| Wells Fargo Capital XV, Junior Subordinated Notes, 9.750% due 9/26/13(e)(f) |

| 173,400 |

| |

|

| Total Commercial Banks |

| 7,740,833 |

| |

|

| Consumer Finance — 3.1% |

|

|

| |

1,110,000 |

| FMG Finance Pty Ltd., Senior Secured Notes, 10.625% due 9/1/16(a) |

| 1,198,800 |

| |

|

| Ford Motor Credit Co.: |

|

|

| |

295,000 |

| Notes, 7.000% due 10/1/13 |

| 263,295 |

| |

|

| Senior Notes: |

|

|

| |

402,000 |

| 5.879% due 6/15/11(e) |

| 370,342 |

| |

240,000 |

| 9.875% due 8/10/11 |

| 237,563 |

| |

2,680,000 |

| 12.000% due 5/15/15 |

| 2,792,882 |

| |

325,000 |

| Ford Motor Credit Co., LLC, Senior Notes, 7.500% due 8/1/12 |

| 299,325 |

| |

|

| GMAC LLC: |

|

|

| |

1,409,000 |

| Senior Notes, 8.000% due 11/1/31(a) |

| 1,102,542 |

| |

43,000 |

| Subordinated Notes, 8.000% due 12/31/18(a) |

| 31,713 |

| |

|

| Total Consumer Finance |

| 6,296,462 |

| |

|

| Diversified Financial Services — 2.2% |

|

|

| |

310,000 |

| Capital One Capital V, Junior Subordinated Notes, Cumulative Trust Preferred Securities, 10.250% due 8/15/39 |

| 315,956 |

| |

630,000 |

| CCM Merger Inc., Notes, 8.000% due 8/1/13(a) |

| 513,450 |

| |

|

| CIT Group Inc., Senior Notes: |

|

|

| |

140,000 |

| 4.125% due 11/3/09 |

| 91,616 |

| |

480,000 |

| 0.759% due 3/12/10(e) |

| 300,600 |

| |

260,000 |

| Galaxy Entertainment Finance Co., Ltd., Senior Notes, 6.218% due 12/15/10(a)(e) |

| 253,500 |

| |

50,000 |

| JPMorgan Chase & Co., Junior Subordinated Notes, 7.900% due 4/30/18(e)(f) |

| 47,795 |

| |

|

| Leucadia National Corp., Senior Notes: |

|

|

| |

380,000 |

| 8.125% due 9/15/15 |

| 374,300 |

| |

140,000 |

| 7.125% due 3/15/17 |

| 129,150 |

| |

|

| TNK-BP Finance SA, Senior Notes: |

|

|

| |

560,000 |

| 7.500% due 7/18/16(a) |

| 529,200 |

| |

100,000 |

| 7.500% due 7/18/16(a) |

| 95,500 |

| |

See Notes to Financial Statements.

14 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Diversified Financial Services — 2.2% continued |

|

|

| |

1,160,000 |

| 7.875% due 3/13/18(a) |

| $ | 1,096,200 |

|

610,000 |

| Vanguard Health Holdings Co., I LLC, Senior Discount Notes, step bond to yield 10.998% due 10/1/15 |

| 616,100 |

| |

|

| Total Diversified Financial Services |

| 4,363,367 |

| |

|

| Insurance — 0.6% |

|

|

| |

|

| American International Group Inc.: |

|

|

| |

315,000 |

| Junior Subordinated Notes, 8.175% due 5/15/58(e) |

| 150,413 |

| |

|

| Medium-Term Senior Notes: |

|

|

| |

455,000 |

| 5.450% due 5/18/17 |

| 305,130 |

| |

170,000 |

| 5.850% due 1/16/18 |

| 113,449 |

| |

525,000 |

| Senior Notes, 8.250% due 8/15/18 |

| 421,062 |

| |

250,000 |

| MetLife Capital Trust IV, Junior Subordinated Notes, 7.875% due 12/15/37(a) |

| 223,750 |

| |

|

| Total Insurance |

| 1,213,804 |

| |

|

| Real Estate Investment Trusts (REITs) — 0.1% |

|

|

| |

120,000 |

| Host Hotels & Resorts, LP, Senior Notes, 6.375% due 3/15/15 |

| 113,100 |

| |

120,000 |

| Ventas Realty LP/Ventas Capital Corp., Senior Notes, 6.500% due 6/1/16 |

| 111,900 |

| |

|

| Total Real Estate Investment Trusts (REITs) |

| 225,000 |

| |

|

| Real Estate Management & Development — 0.4% |

|

|

| |

174,200 |

| Ashton Woods USA LLC, Ashton Woods Finance Co., Senior Subordinated Notes, step bond to yield 23.715% due 6/30/15(a)(d)(g) |

| 65,325 |

| |

20,000 |

| Forest City Enterprises Inc., Senior Notes, 7.625% due 6/1/15 |

| 12,650 |

| |

|

| Realogy Corp.: |

|

|

| |

590,000 |

| Senior Notes, 10.500% due 4/15/14 |

| 354,000 |

| |

640,000 |

| Senior Subordinated Notes, 12.375% due 4/15/15 |

| 262,400 |

| |

55,379 |

| Senior Toggle Notes, 11.000% due 4/15/14(b) |

| 27,690 |

| |

|

| Total Real Estate Management & Development |

| 722,065 |

| |

|

| TOTAL FINANCIALS |

| 20,630,831 |

| |

HEALTH CARE — 4.6% |

|

|

| |||

|

| Health Care Equipment & Supplies — 0.4% |

|

|

| |

|

| Biomet Inc., Senior Notes: |

|

|

| |

605,000 |

| Toggle 10.375% due 10/15/17(b) |

| 633,737 |

| |

85,000 |

| 11.625% due 10/15/17 |

| 90,313 |

| |

|

| Total Health Care Equipment & Supplies |

| 724,050 |

| |

|

| Health Care Providers & Services — 4.2% |

|

|

| |

310,000 |

| Community Health Systems Inc., Senior Notes, 8.875% due 7/15/15 |

| 312,713 |

| |

980,000 |

| CRC Health Corp., Senior Subordinated Notes, 10.750% due 2/1/16 |

| 666,400 |

| |

See Notes to Financial Statements.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 15 |

Schedule of investments continued

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Health Care Providers & Services — 4.2% continued |

|

|

| |

|

| DaVita Inc.: |

|

|

| |

310,000 |

| Senior Notes, 6.625% due 3/15/13 |

| $ | 302,250 |

|

455,000 |

| Senior Subordinated Notes, 7.250% due 3/15/15 |

| 441,350 |

| |

|

| HCA Inc.: |

|

|

| |

400,000 |

| Debentures, 7.500% due 12/15/23 |

| 315,740 |

| |

4,000 |

| Senior Notes, 6.250% due 2/15/13 |

| 3,730 |

| |

|

| Senior Secured Notes: |

|

|

| |

230,000 |

| 9.250% due 11/15/16 |

| 233,450 |

| |

1,375,000 |

| 9.625% due 11/15/16(b) |

| 1,392,187 |

| |

420,000 |

| 7.875% due 2/15/20(a) |

| 410,550 |

| |

975,000 |

| IASIS Healthcare LLC/IASIS Capital Corp., Senior Subordinated Notes, 8.750% due 6/15/14 |

| 957,937 |

| |

|

| Tenet Healthcare Corp.: |

|

|

| |

|

| Senior Notes: |

|

|

| |

159,000 |

| 7.375% due 2/1/13 |

| 147,075 |

| |

412,000 |

| 9.000% due 5/1/15(a) |

| 424,360 |

| |

822,000 |

| 10.000% due 5/1/18(a) |

| 889,815 |

| |

11,000 |

| Senior Secured Notes, 8.875% due 7/1/19(a) |

| 11,330 |

| |

|

| Universal Hospital Services Inc., Senior Secured Notes: |

|

|

| |

130,000 |

| 4.635% due 6/1/15(e) |

| 105,950 |

| |

635,000 |

| 8.500% due 6/1/15(b) |

| 615,950 |

| |

962,000 |

| US Oncology Holdings Inc., Senior Notes, 7.654% due 3/15/12(b)(e) |

| 822,510 |

| |

445,000 |

| US Oncology Inc., Senior Secured Notes, 9.125% due 8/15/17(a) |

| 465,025 |

| |

|

| Total Health Care Providers & Services |

| 8,518,322 |

| |

|

| Pharmaceuticals — 0.0% |

|

|

| |

1,515,000 |

| Leiner Health Products Inc., Senior Subordinated Notes, 11.000% due 6/1/12(c)(d) |

| 7,575 |

| |

|

| TOTAL HEALTH CARE |

| 9,249,947 |

| |

INDUSTRIALS — 6.4% |

|

|

| |||

|

| Aerospace & Defense — 0.6% |

|

|

| |

1,321,000 |

| Hawker Beechcraft Acquisition Co., Senior Notes, 8.875% due 4/1/15(b) |

| 759,575 |

| |

400,000 |

| L-3 Communications Corp., Senior Subordinated Notes, 6.375% due 10/15/15 |

| 379,000 |

| |

|

| Total Aerospace & Defense |

| 1,138,575 |

| |

|

| Airlines — 0.9% |

|

|

| |

|

| Continental Airlines Inc., Pass-Through Certificates: |

|

|

| |

143,137 |

| 8.312% due 4/2/11 |

| 118,803 |

| |

230,000 |

| 7.339% due 4/19/14 |

| 177,100 |

| |

1,520,000 |

| DAE Aviation Holdings Inc., Senior Notes, 11.250% due 8/1/15(a) |

| 1,071,600 |

| |

See Notes to Financial Statements.

16 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Airlines — 0.9% continued |

|

|

| |

|

| Delta Air Lines Inc., Pass-Through Certificates: |

|

|

| |

310,000 |

| 7.711% due 9/18/11 |

| $ | 272,800 |

|

294,455 |

| 8.954% due 8/10/14 |

| 216,425 |

| |

|

| Total Airlines |

| 1,856,728 |

| |

|

| Building Products — 0.9% |

|

|

| |

|

| Associated Materials Inc.: |

|

|

| |

1,420,000 |

| Senior Discount Notes, 11.250% due 3/1/14 |

| 773,900 |

| |

170,000 |

| Senior Subordinated Notes, 9.750% due 4/15/12 |

| 153,000 |

| |

578,000 |

| GTL Trade Finance Inc., Senior Notes, 7.250% due 10/20/17(a) |

| 623,084 |

| |

250,000 |

| Nortek Inc., Senior Secured Notes, 10.000% due 12/1/13(d) |

| 233,750 |

| |

1,020,000 |

| NTK Holdings Inc., Senior Discount Notes, step bond to yield 24.194% due 3/1/14(d) |

| 51,000 |

| |

60,000 |

| USG Corp., Senior Notes, 9.750% due 8/1/14(a) |

| 61,950 |

| |

|

| Total Building Products |

| 1,896,684 |

| |

|

| Commercial Services & Supplies — 1.1% |

|

|

| |

|

| Altegrity Inc., Senior Subordinated Notes: |

|

|

| |

60,000 |

| 10.500% due 11/1/15(a) |

| 49,950 |

| |

750,000 |

| 11.750% due 5/1/16(a) |

| 575,625 |

| |

584,000 |

| DynCorp International LLC/DIV Capital Corp., Senior Subordinated Notes, 9.500% due 2/15/13 |

| 594,950 |

| |

|

| RSC Equipment Rental Inc.: |

|

|

| |

780,000 |

| Senior Notes, 9.500% due 12/1/14 |

| 702,000 |

| |

240,000 |

| Senior Secured Notes, 10.000% due 7/15/17(a) |

| 252,000 |

| |

|

| Total Commercial Services & Supplies |

| 2,174,525 |

| |

|

| Construction & Engineering — 0.2% |

|

|

| |

470,000 |

| Odebrecht Finance Ltd., 7.500% due 10/18/17(a) |

| 473,525 |

| |

|

| Machinery — 0.1% |

|

|

| |

170,000 |

| American Railcar Industries Inc., Senior Notes, 7.500% due 3/1/14 |

| 158,525 |

| |

90,000 |

| Terex Corp., Senior Notes, 10.875% due 6/1/16 |

| 94,725 |

| |

|

| Total Machinery |

| 253,250 |

| |

|

| Road & Rail — 1.7% |

|

|

| |

|

| Kansas City Southern de Mexico, Senior Notes: |

|

|

| |

1,095,000 |

| 9.375% due 5/1/12 |

| 1,084,050 |

| |

160,000 |

| 7.625% due 12/1/13 |

| 145,600 |

| |

25,000 |

| 7.375% due 6/1/14 |

| 22,250 |

| |

1,200,000 |

| 12.500% due 4/1/16(a) |

| 1,272,000 |

| |

75,000 |

| Kansas City Southern Railway, Senior Notes, 13.000% due 12/15/13 |

| 84,938 |

| |

850,000 |

| RailAmerica Inc., Senior Secured Notes, 9.250% due 7/1/17(a) |

| 882,937 |

| |

|

| Total Road & Rail |

| 3,491,775 |

| |

See Notes to Financial Statements.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 17 |

Schedule of investments continued

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Trading Companies & Distributors — 0.7% |

|

|

| |

390,000 |

| Ashtead Capital Inc., Notes, 9.000% due 8/15/16(a) |

| $ | 344,175 |

|

175,000 |

| Ashtead Holdings PLC, Senior Secured Notes, 8.625% due 8/1/15(a) |

| 154,437 |

| |

430,000 |

| H&E Equipment Services Inc., Senior Notes, 8.375% due 7/15/16 |

| 371,950 |

| |

1,160,000 |

| Penhall International Corp., Senior Secured Notes, 12.000% due 8/1/14(a)(d) |

| 469,800 |

| |

|

| Total Trading Companies & Distributors |

| 1,340,362 |

| |

|

| Transportation Infrastructure — 0.2% |

|

|

| |

|

| Swift Transportation Co., Senior Secured Notes: |

|

|

| |

190,000 |

| 8.190% due 5/15/15(a)(e) |

| 97,850 |

| |

375,000 |

| 12.500% due 5/15/17(a) |

| 208,125 |

| |

|

| Total Transportation Infrastructure |

| 305,975 |

| |

|

| TOTAL INDUSTRIALS |

| 12,931,399 |

| |

INFORMATION TECHNOLOGY — 1.3% |

|

|

| |||

|

| Communications Equipment — 0.3% |

|

|

| |

880,000 |

| Lucent Technologies Inc., Debentures, 6.450% due 3/15/29 |

| 602,800 |

| |

|

| IT Services — 0.8% |

|

|

| |

|

| Ceridian Corp., Senior Notes: |

|

|

| |

60,000 |

| 11.250% due 11/15/15 |

| 51,300 |

| |

445,000 |

| 12.250% due 11/15/15(b) |

| 353,775 |

| |

1,500,000 |

| First Data Corp., 5.625% due 11/1/11 |

| 1,207,500 |

| |

|

| Total IT Services |

| 1,612,575 |

| |

|

| Semiconductors & Semiconductor Equipment — 0.2% |

|

|

| |

|

| Freescale Semiconductor Inc.: |

|

|

| |

|

| Senior Notes: |

|

|

| |

320,000 |

| 8.875% due 12/15/14 |

| 217,600 |

| |

83,950 |

| 9.125% due 12/15/14(b) |

| 49,111 |

| |

280,000 |

| Senior Subordinated Notes, 10.125% due 12/15/16 |

| 156,800 |

| |

120,000 |

| Sensata Technologies B.V., Senior Notes, 8.000% due 5/1/14 |

| 103,200 |

| |

|

| Total Semiconductors & Semiconductor Equipment |

| 526,711 |

| |

|

| TOTAL INFORMATION TECHNOLOGY |

| 2,742,086 |

| |

MATERIALS — 8.7% |

|

|

| |||

|

| Chemicals — 0.5% |

|

|

| |

345,000 |

| Ashland Inc., Senior Notes, 9.125% due 6/1/17(a) |

| 363,113 |

| |

750,000 |

| FMC Finance III SA, Senior Notes, 6.875% due 7/15/17 |

| 712,500 |

| |

30,000 |

| Methanex Corp., Senior Notes, 8.750% due 8/15/12 |

| 29,700 |

| |

|

| Total Chemicals |

| 1,105,313 |

| |

|

| Containers & Packaging — 0.6% |

|

|

| |

200,000 |

| BWAY Corp., Senior Subordinated Notes, 10.000% due 4/15/14(a) |

| 208,500 |

| |

See Notes to Financial Statements.

18 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Containers & Packaging — 0.6% continued |

|

|

| |

|

| Graham Packaging Co. L.P.: |

|

|

| |

125,000 |

| Senior Notes, 8.500% due 10/15/12 |

| $ | 125,625 |

|

220,000 |

| Senior Subordinated Notes, 9.875% due 10/15/14 |

| 220,000 |

| |

325,000 |

| Radnor Holdings Inc., Senior Notes, 11.000% due 3/15/10(c)(d)(g) |

| 0 |

| |

200,000 |

| Rock-Tenn Co., Senior Notes, 9.250% due 3/15/16 |

| 211,500 |

| |

410,000 |

| Solo Cup Co., Senior Secured Notes, 10.500% due 11/1/13(a) |

| 432,550 |

| |

|

| Total Containers & Packaging |

| 1,198,175 |

| |

|

| Metals & Mining — 5.3% |

|

|

| |

|

| Evraz Group SA, Notes: |

|

|

| |

940,000 |

| 8.875% due 4/24/13(a) |

| 863,625 |

| |

220,000 |

| 8.875% due 4/24/13(a) |

| 202,950 |

| |

470,000 |

| Metals USA Inc., Senior Secured Notes, 11.125% due 12/1/15 |

| 432,400 |

| |

1,445,313 |

| Noranda Aluminium Acquisition Corp., Senior Notes, 6.163% due 5/15/15(b)(e) |

| 888,868 |

| |

|

| Novelis Inc., Senior Notes: |

|

|

| |

815,000 |

| 7.250% due 2/15/15 |

| 664,225 |

| |

170,000 |

| 11.500% due 2/15/15(a) |

| 165,325 |

| |

260,000 |

| Rio Tinto Finance USA Ltd., Senior Notes, 9.000% due 5/1/19 |

| 311,948 |

| |

835,000 |

| Ryerson Inc., Senior Secured Notes, 12.000% due 11/1/15 |

| 772,375 |

| |

|

| Teck Resources Ltd., Senior Secured Notes: |

|

|

| |

180,000 |

| 9.750% due 5/15/14 |

| 195,300 |

| |

150,000 |

| 10.250% due 5/15/16 |

| 166,500 |

| |

120,000 |

| 10.750% due 5/15/19 |

| 137,250 |

| |

4,280,000 |

| Vale Overseas Ltd., Notes, 6.875% due 11/21/36(h) |

| 4,306,557 |

| |

1,530,000 |

| Vedanta Resources PLC, Senior Notes, 8.750% due 1/15/14(a) |

| 1,503,225 |

| |

|

| Total Metals & Mining |

| 10,610,548 |

| |

|

| Paper & Forest Products — 2.3% |

|

|

| |

1,490,000 |

| Abitibi-Consolidated Co. of Canada, Senior Secured Notes, 13.750% due 4/1/11(a)(c) |

| 1,422,950 |

| |

1,620,000 |

| Appleton Papers Inc., Senior Subordinated Notes, 9.750% due 6/15/14(d) |

| 739,125 |

| |

180,000 |

| Celulosa Arauco y Constitucion SA, Senior Notes, 7.250% due 7/29/19(a) |

| 194,359 |

| |

590,000 |

| Georgia-Pacific LLC, Senior Notes, 8.250% due 5/1/16(a) |

| 598,850 |

| |

|

| NewPage Corp., Senior Secured Notes: |

|

|

| |

1,075,000 |

| 6.733% due 5/1/12(e) |

| 464,937 |

| |

25,000 |

| 10.000% due 5/1/12 |

| 13,688 |

| |

658,129 |

| Newpage Holding Corp., Senior Notes, 8.579% due 11/1/13(b)(e) |

| 154,660 |

| |

150,000 |

| PE Paper Escrow GmbH, Senior Secured Notes, 12.000% due 8/1/14(a) |

| 154,032 |

| |

600,000 |

| Smurfit Capital Funding PLC, Debentures, 7.500% due 11/20/25 |

| 469,500 |

| |

See Notes to Financial Statements.

Western Asset Global Partners Income Fund Inc. 2009 Annual Report | 19 |

Schedule of investments continued

August 31, 2009

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE AMOUNT† |

| SECURITY |

| VALUE |

| |

|

| Paper & Forest Products — 2.3% continued |

|

|

| |

385,000 |

| Verso Paper Holdings LLC, Senior Secured Notes, 11.500% due 7/1/14(a) |

| $ | 379,225 |

|

|

| Total Paper & Forest Products |

| 4,591,326 |

| |

|

| TOTAL MATERIALS |

| 17,505,362 |

| |

TELECOMMUNICATION SERVICES — 8.8% |

|

|

| |||

|

| Diversified Telecommunication Services — 4.8% |

|

|

| |

|

| Axtel SAB de CV, Senior Notes: |

|

|

| |

70,000 |

| 11.000% due 12/15/13 |

| 72,450 |

| |

1,793,000 |

| 7.625% due 2/1/17(a) |

| 1,622,665 |

| |

100,000 |

| 7.625% due 2/1/17(a) |

| 90,750 |

| |

250,000 |

| CC Holdings GS V LLC, Senior Secured Notes, 7.750% due 5/1/17(a) |

| 253,750 |

| |

110,000 |

| Cincinnati Bell Telephone Co., Senior Debentures, 6.300% due 12/1/28 |

| 79,750 |

| |

405,000 |

| Hawaiian Telcom Communications Inc., Senior Subordinated Notes, 12.500% due |

| 506 |

| |

340,000 |

| Intelsat Bermuda Ltd., Senior Notes, 11.250% due 6/15/16 |

| 356,150 |

| |

690,000 |

| Intelsat Corp., Senior Notes, 9.250% due 8/15/14 |

| 703,800 |

| |

685,000 |

| Intelsat Intermediate Holding Co., Ltd., Senior Discount Notes, step bond to yield 10.415% due 2/1/15 |

| 671,300 |

| |

730,000 |

| Intelsat Jackson Holdings Ltd., Senior Notes, 11.500% due 6/15/16 |

| 746,425 |

| |

|

| Level 3 Financing Inc., Senior Notes: |

|

|

| |

430,000 |

| 12.250% due 3/15/13 |

| 421,400 |

| |

705,000 |

| 9.250% due 11/1/14 |

| 585,150 |

| |

675,000 |

| Nordic Telephone Co. Holdings, Senior Secured Bonds, 8.875% due 5/1/16(a) |

| 688,500 |

| |

615,000 |

| Qwest Communications International Inc., Senior Notes, 7.500% due 2/15/14 |

| 596,550 |

| |

480,000 |

| UBS Luxembourg SA for OJSC Vimpel Communications, Loan Participation Notes, 8.250% due 5/23/16(a) |

| 462,000 |

| |

520,000 |

| Vimpel Communications, Loan Participation Notes, 8.375% due 4/30/13(a) |

| 520,624 |

| |

248,000 |

| VIP Finance Ireland Ltd. for OJSC Vimpel Communications, Loan Participation Notes, Secured Notes, 8.375% due 4/30/13(a) |

| 249,618 |

| |

|

| Wind Acquisition Finance SA: |

|

|

| |

455,000 |

| Senior Bonds, 10.750% due 12/1/15(a) |

| 491,400 |

| |

360,000 |

| Senior Notes, 11.750% due 7/15/17(a) |

| 392,400 |

| |

580,000 |

| Windstream Corp., Senior Notes, 8.625% due 8/1/16 |

| 585,075 |

| |

|

| Total Diversified Telecommunication Services |

| 9,590,263 |

| |

|

| Wireless Telecommunication Services — 4.0% |

|

|

| |

420,000 |

| ALLTEL Communications Inc., Senior Notes, 10.375% due 12/1/17(a)(b) |

| 511,059 |

| |

See Notes to Financial Statements.

20 | Western Asset Global Partners Income Fund Inc. 2009 Annual Report |

WESTERN ASSET GLOBAL PARTNERS INCOME FUND INC.

FACE AMOUNT† |

| SECURITY |

| VALUE |

| |

|

| Wireless Telecommunication Services — 4.0% continued |

|

|

| |

700,000 |