In February 2003, we amended and restated our Stockholder Rights Agreement and currently each share of our outstanding common stock is associated with one right. Each right entitles stockholders to purchase 1/100,000 share of our Series B Preferred Stock at an exercise price of $21.00.

The rights only become exercisable in certain limited circumstances following the tenth day after a person or group announces acquisition of or tender offers for 15% or more of our common stock. For a limited period of time following the announcement of any such acquisition or offer, the rights are redeemable by us at a price of $0.01 per right. If the rights are not redeemed, each right will then entitle the holder to purchase common stock having the value of twice the then-current exercise price. For a limited period of time after the exercisability of the rights, each right, at the discretion of our Board of Directors, may be exchanged for either 1/100,000 share of Series B Preferred Stock or one share of common stock per right. The rights expire on June 22, 2013.

Our Board of Directors has the authority to issue up to 499,999 shares of undesignated preferred stock and to determine the powers, preferences and rights and the qualifications, limitations or restrictions granted to or imposed upon any wholly unissued shares of undesignated preferred stock and to fix the number of shares constituting any series and the designation of such series, without the consent of our stockholders. The preferred stock could be issued with voting, liquidation, dividend and other rights superior to those of the holders of common stock.

The issuance of Series B Preferred Stock or any preferred stock subsequently issued by our Board of Directors, under some circumstances, could have the effect of delaying, deferring or preventing a change in control.

Some provisions contained in the rights plan, and in the equivalent rights plan that our subsidiary, JDS Uniphase Canada Ltd., has adopted with respect to our exchangeable shares, may have the effect of discouraging a third party from making an acquisition proposal for us and may thereby inhibit a change in control. For example, such provisions may deter tender offers for shares of common stock or exchangeable shares, which offers may be attractive to stockholders, or deter purchases of large blocks of common stock or exchangeable shares, thereby limiting the opportunity for stockholders to receive a premium for their shares of common stock or exchangeable shares over the then-prevailing market prices.

We are subject to the provisions of Section 203 of the Delaware General Corporation Law prohibiting, under some circumstances, publicly-held Delaware corporations from engaging in business combinations with some stockholders for a specified period of time without the approval of the holders of substantially all of our outstanding voting stock. Such provisions could delay or impede the removal of incumbent directors and could make more difficult a merger, tender offer or proxy contest involving us, even if such events could be beneficial, in the short-term, to the interests of the stockholders. In addition, such provisions could limit the price that some investors might be willing to pay in the future for shares of our common stock. Our certificate of incorporation and bylaws contain provisions relating to the limitations of liability and indemnification of our directors and officers, dividing our board of directors into three classes of directors serving three-year terms and providing that our stockholders can take action only at a duly called annual or special meeting of stockholders. These provisions also may have the effect of deterring hostile takeovers or delaying changes in control or management of us.

None.

ITEM 2. PROPERTIES

Our principal offices are located in Milpitas, California, United States. The table below summarizes the properties that we owned and leased as of June 30, 2006:

| Location | | | Square footage | | Location | | | Square footage |

| Leased Properties: | | | | | Leased Properties (cont.): | | | | |

| NORTH AMERICA: | | | | | APAC: | | | | |

| Canada: | | | | | Australia: | | | | |

| Mississauga, Ontario | | 1,056 | | | North Sydney | | 1,119 | | |

| Ottawa, Ontario | | 114,100 | (1) | | China: | | | | |

| Ottawa, Ontario | | 271,987 | | | Beijing | | 85,076 | | |

| | | | | | Guangzhou | | 2,085 | | |

| United States: | | | | | Hong Kong | | 770 | | |

| Allentown, Pennsylvania | | 30,000 | (2) | | Shanghai | | 1,717 | | |

| Atlanta, Georgia | | 16,468 | | | Shenzhen | | 468,707 | | |

| Bloomfield, Connecticut | | 60,000 | | | India: | | | | |

| Camarillo, California | | 17,370 | | | Alwar, Rajasthan | | 246 | | |

| Columbia, Maryland | | 994 | | | Andheri (E), Mumbai | | 1,143 | | |

| Commerce, California | | 27,136 | | | Bangalore | | 1,339 | | |

| Coral Springs, Florida | | 30,000 | | | New Delhi ,Delhi | | 4,600 | | |

| Eatontown, New Jersey | | 3,641 | | | Japan: | | | | |

| Ewing Township, New Jersey | | 30,000 | | | Tokyo | | 4,433 | | |

| Germantown, Maryland | | 160,141 | | | Naka-ku, Yokohama | | 2,368 | | |

| Horsham, Pennsylvania | | 126,500 | (1) | | Korea: | | | | |

| Indianapolis, Indiana | | 98,133 | | | Gangnam-gu, Seoul | | 5,521 | | |

| Lakewood, Colorado | | 4,773 | | | Malaysia: | | | | |

| Melbourne, Florida | | 11,700 | (2) | | Bukit Damansara, Kuala Lum | | 3,600 | | |

| Milpitas, California | | 240,210 | | | Singapore | | 21,806 | | |

| Morrisville, North Carolina | | 12,410 | | | Taiwan: | | | | |

| Palmdale, California | | 403 | | | Taipei | | 12,060 | | |

| Piscataway, New Jersey | | 132,650 | (1) | | | | | | |

| Richardson, Texas | | 10,071 | | | REST OF WORLD: | | | | |

| Salem, Virginia | | 19,800 | | | Brazil: | | | | |

| Santa Clara, California | | 46,338 | (1) | | Rio de Janeiro | | 2,055 | | |

| San Jose, California | | 22,750 | (1) | | Turkey: | | | | |

| San Jose, California | | 121,840 | | | Ankara | | 1,830 | | |

| Santa Barbara, California | | 24,453 | | | United Arab Emirates: | | | | |

| Santa Rosa, California | | 13,671 | | | Dubai | | 1,560 | | |

| Sarasota, Florida | | 2,500 | | | | | | | |

| Terre Haute, Indiana | | 12,600 | | | Total leased square footage: | | 2,491,129 | | |

| Van Nuys, California | | 2,632 | | | | | | | |

| Weston, Florida | | 316 | | | | | | | |

| |

| Mexico: | | | | | | | | | |

| Mexico City | | 7,535 | | | Owned Properties: | | | | |

| | | | | | NORTH AMERICA: | | | | |

| EUROPE: | | | | | Canada: | | | | |

| Austria: | | | | | Scarborough, Ontario | | 10,000 | (3) | |

| Leobersdorf | | 3,208 | | | United States: | | | | |

| Denmark: | | | | | Bloomfield, CT | | 24,000 | | |

| Glostrup | | 377 | | | Rochester, MN | | 40,500 | (2) | |

| France: | | | | | Santa Rosa, CA | | 492,117 | | |

| Plaisir | | 14,973 | | | | | | | |

| St. Etienne | | 23,293 | | | EUROPE: | | | | |

| Essone | | 2,874 | | | Germany: | | | | |

| Germany: | | | | | Eningen | | 303,941 | | |

| Berlin | | 545 | | | Italy: | | | | |

| Eningen | | 110,276 | | | Milan | | 12,378 | (3) | |

| Eching | | 5,666 | | | Switzerland: | | | | |

| Italy: | | | | | Bern | | 11,840 | | |

| Monza | | 2,454 | | | | | | | |

| Poland: | | | | | REST OF WORLD: | | | | |

| Warsaw | | 1,091 | | | Brazil: | | | | |

| Russia: | | | | | Cotia | | 64,583 | (3) | |

| Moscow | | 753 | | | Sao Paulo | | 2,583 | | |

| Spain: | | | | | | | | | |

| Madrid | | 15,069 | | | Total owned square footage: | | 961,942 | | |

| Sweden: | | | | | | | | | |

| Farsta | | 2,928 | | | Total leased and owned square footage: | | 3,453,071 | | |

| United Kingdom: | | | | | | | | | |

| Plymouth, Devon | | 2,852 | | | | | | | |

| Alsager, Cheshire | | 807 | | | | | | | |

| Basingstoke | | 7,480 | | | | | | | |

| Crane Meadow | | 270 | | | | | | | |

37

____________________

| (1) | | Operations have ceased and these properties have been vacated as part of our restructuring programs. |

| (2) | | Operations have ceased at these properties. We are in the process of vacating properties as part of our restructuring activities. |

| (3) | | These properties are under contract of sale and have been classified in our financial statements as “held for sale”. See “Note 8. Reduction of Other Intangibles and Other Long-Lived Assets” of the Notes to Consolidated Financial Statements. |

As part of our Global Realignment Program and subsequent restructuring programs, we have completed and approved restructuring plans to close sites, vacate buildings at closed sites as well as at continuing operations and consolidate excess facilities worldwide. Of the total leased and owned square footage as of June 30, 2006, approximately 422,000 square feet were related to properties included in our Global Realignment Program and subsequent restructuring programs identified as surplus to our needs. Please see the description of our manufacturing sites under the heading “Manufacturing” in Item 1.

ITEM 3. LEGAL PROCEEDINGS

Pending Litigation

The Securities Class Actions:

Litigation under the federal securities laws has been pending against the Company and certain former and current officers and directors since March 27, 2002. On July 26, 2002, the Northern District of California consolidated all the securities actions then filed in or transferred to that court under the title In re JDS Uniphase Corporation Securities Litigation, Master File No. C-02-1486 CW, and appointed the Connecticut Retirement Plans and Trust Funds as Lead Plaintiff.

The complaint in In re JDS Uniphase Corporation Securities Litigation purports to be brought on behalf of a class consisting of those who acquired the Company’s securities from October 28, 1999, through July 26, 2001, as well as on behalf of subclasses consisting of those who acquired the Company’s common stock pursuant to its acquisitions of OCLI, E-TEK, and SDL. Plaintiffs allege that Defendants made material misstatements and omissions concerning demand for the company’s products, improperly recognized revenue, overstated the value of inventory, and failed to timely write down goodwill. The complaint seeks unspecified damages and alleges various violations of the federal securities laws, specifically Sections 10(b), 14(a), 20(a), and 20A of the Securities Exchange Act of 1934 and Sections 11, 12(a)(2), and 15 of the Securities Act of 1933. In January 2005, the Court denied the motion to dismiss claims against the Company, Jozef Straus, Anthony R. Muller, and Charles Abbe, and granted in part and denied in part the motion to dismiss claims against Kevin Kalkhoven. Defendants subsequently filed answers denying liability for the claims asserted against them.

On December 21, 2005, the Court granted Plaintiffs’ motion for class certification. On April 6, 2006, the Court granted Plaintiffs’ motion for approval of its proposed plan for providing notice of class certification to members of the Plaintiff class.

Discovery inIn re JDS Uniphase Corporation Securities Litigation is ongoing. Each party has noticed and taken depositions of both party and non-party witnesses. The deadline for fact discovery, except for depositions and discovery arising from new information obtained at depositions, is September 29, 2006. The closing date for completion of depositions and discovery arising from new information obtained at depositions is December 1, 2006. The closing date for expert discovery is March 19, 2007. The next case management conference is scheduled for May 4, 2007, and trial is scheduled for October 1, 2007.

A related securities case, Zelman v. JDS Uniphase Corp., No. C-02-4656 CW (N.D. Cal.), is purportedly brought on behalf of a class of purchasers of debt securities that were allegedly linked to the price of JDSU’s common stock. The Zelman complaint alleges that the debt securities were issued by an investment bank during the period from March 6, 2001 through July 26, 2001. The complaint names the Company and several of its former officers and directors as Defendants, alleges violations of the federal securities laws, specifically Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, and Rule 10b-5, and seeks unspecified damages. On August 26, 2005, Defendants

38

answered the complaint. On November 16, 2005, the Court granted Plaintiffs’ motion for class certification, which Defendants had not opposed. At a case management conference on November 18, 2005, the Court ordered that discovery in the Zelman action proceed according to the same schedule as discovery In re JDS Uniphase Corporation Securities Litigation. On January 9, 2006, the Court granted Plaintiffs’ motion for approval of their proposed form and method of class notice, which Defendants had not opposed. No trial date has been set.

The Derivative Actions:

Derivative actions purporting to be brought on the Company’s behalf have been filed in state and federal courts against several of the Company’s current and former officers and directors based on the same events alleged in the securities litigation. The complaint in Corwin v. Kaplan, No. C-02-2020 CW (N.D. Cal.), asserts state law claims for breach of fiduciary duty, misappropriation of confidential information, waste of corporate assets, indemnification, and insider trading. The complaint seeks unspecified damages. In January 2005, the Court stayed the action pending resolution of In re JDS Uniphase Corporation Securities Litigation. At the July 15, 2005 case management conference in that action, however, the Court suggested that any mediation of the federal securities action also should include the derivative action.

On November 28, 2005, another derivative action was filed against JDSU and certain of its current and former officers and directors in federal court. That action, titled Trasky v. Straus, No. C-05-4855 (N.D. Cal.), asserts claims for breach of fiduciary duty, abuse of control, gross mismanagement, unjust enrichment, insider trading, and constructive fraud, and seeks unspecified damages and equitable relief. On March 16, 2006, the Trasky action was consolidated with the Corwin action, which has been stayed since January 2005, as noted above.

In the California state derivative action, In re JDS Uniphase Corporation Derivative Litigation, Master File No. CV806911 (Santa Clara Super. Ct.), the complaint asserts claims for breach of fiduciary duty, waste of corporate assets, abuse of control, gross mismanagement, unjust enrichment, and constructive fraud purportedly on behalf of the Company and certain of its current and former officers and directors. The complaint also asserts claims for violation of California Corporations Code Sections 25402 and 25502.5 against defendants who sold the Company’s stock and asserts claims for breach of contract, professional negligence, and negligent misrepresentation against the Company’s former auditor, Ernst & Young LLP. The complaint seeks unspecified damages. On April 24, 2006, the Court approved the parties’ stipulation staying the California derivative action until January 16, 2007, subject to the parties’ rights to seek a lifting of the stay based on developments in the federal securities action. On April 24, 2006, the Court also approved the parties’ stipulation in the shareholder inspection demand action brought by the plaintiff in the California derivative action. Pursuant to that stipulation, the shareholder inspection demand action is stayed until January 16, 2007, subject to the parties’ rights to seek a lifting of the stay based on developments in the federal securities action.

No activity has occurred in Cromas v. Straus, Civil Action No. 19580 (Del. Ch. Ct.), the Delaware derivative action, since our last quarterly filing as of March 31, 2006.

The OCLI and SDL Shareholder Actions:

Plaintiffs purporting to represent the former shareholders of OCLI and SDL have filed suit against the former directors of those companies, asserting that they breached their fiduciary duties in connection with the events alleged in the securities litigation against the Company. Plaintiffs in the OCLI action, Pang v. Dwight, No. 02-231989 (Sonoma Super. Ct.), purport to represent a class of former shareholders of OCLI who exchanged their OCLI shares for JDSU shares when JDSU acquired OCLI. The complaint names the former directors of OCLI as Defendants, asserts causes of action for breach of fiduciary duty and breach of the duty of candor, and seeks unspecified damages. No activity has occurred in the OCLI action since our last filing. The Plaintiffs in the SDL action, Cook v. Scifres, Master File No. CV814824 (Santa Clara Super. Ct.), purport to represent a class of former shareholders of SDL who exchanged their SDL shares for JDSU shares when the Company acquired SDL. Plaintiffs filed an amended complaint on September 12, 2005. The complaint names the former directors of SDL as Defendants, asserts causes of action for breach of fiduciary duty and breach of the duty of disclosure, and seeks unspecified damages. Defendants demurred to the complaint on October 12, 2005. On August 16, 2006, the Court sustained the demurrer with leave to amend.

39

The deadline for Plaintiffs to file a second amended complaint is October 16, 2006. A case management conference is scheduled for October 24, 2006. Limited discovery in the SDL action has occurred. No trial date has been set in either the OCLI or SDL action.

The ERISA Actions:

A consolidated action entitledIn re JDS Uniphase Corporation ERISA Litigation, Case No. C-03-4743 WWS (MEJ), is pending in the District Court for the Northern District of California against the Company, certain of its former and current officers and directors, and certain other current and former JDSU employees on behalf of a purported class of participants in the 401(k) Plans of the Company and Optical Coating Laboratory, Inc. and the Plans themselves. On October 31, 2005, Plaintiffs filed an amended complaint. The amended complaint alleges that Defendants violated the Employee Retirement Income Security Act by breaching their fiduciary duties to the Plans and the Plans’ participants. The amended complaint alleges a purported class period from February 4, 2000, to the present and seeks an unspecified amount of damages, restitution, a constructive trust, and other equitable remedies. Certain individual Defendants’ motion to dismiss portions of the amended complaint was granted with prejudice on June 15, 2006.

Plaintiffs filed a second amended complaint on June 30, 2006. Defendants answered the complaint on July 6, 2006, and JDSU asserted counterclaims for breach of contract. Plaintiffs moved to dismiss JDSU’s counterclaims on August 4, 2006. Both sides have begun taking discovery. No trial date has been set.

The Company believes that the factual allegations and circumstances underlying these securities class actions, derivative actions, the OCLI and SDL class actions, and the ERISA class actions are without merit. The expense of defending these lawsuits has been costly, will continue to be costly, and could be quite significant and may not be covered by our insurance policies. The defense of these lawsuits could also result in continued diversion of our management’s time and attention away from business operations which could prove to be time consuming and disruptive to normal business operations. An unfavorable outcome or settlement of this litigation could have a material adverse effect on the Company’s financial position, liquidity or results of operations.

The Company is also subject to a variety of other claims and suits that arise from time to time in the ordinary course of our business. While management currently believes that resolving claims against the Company, individually or in aggregate, will not have a material adverse impact on its financial position, results of operations or statement of cash flows, these matters are subject to inherent uncertainties and management’s view of these matters may change in the future. Were an unfavorable final outcome to occur, there exists the possibility of a material adverse impact on the Company’s financial position, results of operations or statement of cash flows for the period in which the effect becomes reasonably estimable.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

40

PART II

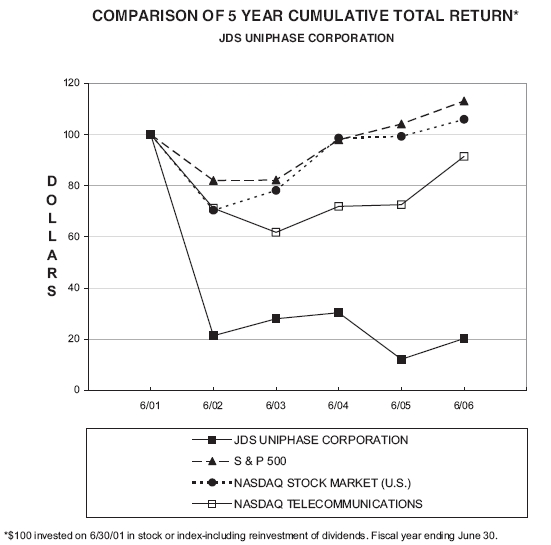

| ITEM 5. | | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

|

Our common stock is traded on the NASDAQ Stock Market under the symbol “JDSU” and our exchangeable shares of JDS Uniphase Canada Ltd. are traded on the Toronto Stock Exchange under the symbol “JDU.” Holders of exchangeable shares may tender their holdings for common stock on a one-for-one basis at any time. As of August 26, 2006, we had 1,688,154,805 shares of common stock outstanding, including 51,661,271 exchangeable shares. The closing price on August 26, 2006 was $2.58 for the common stock and Canadian $2.88 for the exchangeable shares. The following table summarizes the high and low closing sales prices for our common stock as reported on the NASDAQ Stock Market during fiscal 2006 and 2005:

| | | High | | Low |

| Fiscal 2006: | | | | | | |

| Fourth Quarter | | $ | 4.13 | | $ | 2.33 |

| Third Quarter | | | 4.18 | | | 2.42 |

| Second Quarter | | | 2.80 | | | 1.90 |

| First Quarter | | | 2.22 | | | 1.49 |

| Fiscal 2005: | | | | | | |

| Fourth Quarter | | $ | 1.66 | | $ | 1.36 |

| Third Quarter | | | 3.13 | | | 1.60 |

| Second Quarter | | | 3.56 | | | 3.03 |

| First Quarter | | | 3.56 | | | 2.97 |

As of August 26, 2006, we had 446 holders of record of our common stock and exchangeable shares. We have not paid cash dividends on our common stock and do not anticipate paying cash dividends in the foreseeable future.

ITEM 6. SELECTED FINANCIAL DATA

This table sets forth selected financial data of JDSU, in thousands, except share and per share amounts, for the periods indicated. This data should be read in conjunction with and is qualified by reference to “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of this Annual Report on Form 10-K and our audited consolidated financial statements, including the notes thereto and our independent registered public accounting firms’ reports thereon and the other financial information included in Item 8 of this Form 10-K. The selected data in this section are not intended to replace the consolidated financial statements included in this report.

| | | Years Ended June 30, |

| | | 2006(3) | | 2005 | | 2004 | | 2003(2)(4) | | 2002(1)(4) |

| Consolidated Statement of Operations Data: | | | | | | | | | | | | | | | | | | | | |

| Net revenue | | $ | 1,204.3 | | | $ | 712.2 | | | $ | 635.9 | | | $ | 675.9 | | | $ | 1,098.2 | |

| Gross profit (loss) | | | 340.5 | | | | 112.2 | | | | 135.9 | | | | 55.4 | | | | (72.9 | ) |

| Amortization of goodwill and other | | | | | | | | | | | | | | | | | | | | |

| intangibles (2) | | | 24.4 | | | | 6.4 | | | | 6.1 | | | | 19.8 | | | | 1,308.7 | |

| Acquired in-process research and development | | | 20.3 | | | | 1.1 | | | | 2.6 | | | | 0.4 | | | | 25.3 | |

| Reduction of goodwill and other long-lived | | | | | | | | | | | | | | | | | | | | |

| assets | | | 28.0 | | | | 85.3 | | | | 52.3 | | | | 393.6 | | | | 5,979.4 | |

| Restructuring charges | | | 35.0 | | | | 18.2 | | | | 11.5 | | | | 121.3 | | | | 260.0 | |

| Total operating expense | | | 588.5 | | | | 362.0 | | | | 316.7 | | | | 956.1 | | | | 8,211.1 | |

| Loss from operations | | | (248.0 | ) | | | (249.8 | ) | | | (180.8 | ) | | | (900.7 | ) | | | (8,284.0 | ) |

| Net loss | | | (151.2 | ) | | | (261.3 | ) | | | (115.5 | ) | | | (933.8 | ) | | | (8,738.3 | ) |

| Net loss per share-basic and diluted | | | (0.09 | ) | | | (0.18 | ) | | | (0.08 | ) | | | (0.66 | ) | | | (6.50 | ) |

41

| | | Years Ended June 30, |

| | | 2006(3) | | 2005 | | 2004 | | 2003 | | 2002(1) |

| Consolidated Balance Sheet Data: | | | | | | | | | | | | | | | | |

| Cash, cash equivalents, short-term investments, | | | | | | | | | | | | | | | | |

| and restricted cash. | | $ | 1,238.6 | | $ | 1,304.5 | | $ | 1,545.9 | | $ | 1,234.1 | | $ | 1,450.4 | |

| Working capital | | | 1,382.6 | | | 1,350.9 | | | 1,539.5 | | | 1,168.4 | | | 1,430.5 | |

| Total assets | | | 3,065.1 | | | 2,089.9 | | | 2,392.2 | | | 2,137.8 | | | 3,004.5 | |

| Long-term obligations | | | 1,059.1 | | | 519.4 | | | 508.9 | | | 16.3 | | | 8.9 | |

| Total stockholders’ equity | | | 1,583.6 | | | 1,329.7 | | | 1,571.1 | | | 1,671.1 | | | 2,471.4 | |

____________________

| (1) | | We acquired IBM’s optical transceiver business on December 28, 2001 in a transaction accounted for as a purchase. The Consolidated Statement of Operations for fiscal 2002 included the results of operations of the optical transceiver business subsequent to December 28, 2001 and the Consolidated Balance Sheet as of June 30, 2002 included the financial position of the optical transceiver business. |

| |

| (2) | | Commencing July 1, 2002, in accordance with SFAS 142, we no longer amortize goodwill, but test for impairment of goodwill on an annual basis and at any other time if events occur or circumstances indicate that the carrying amount of goodwill may not be recoverable. Fiscal years 2002 and 2001 include goodwill amortization as a component of the expense for amortization of goodwill and other intangibles. |

| |

| (3) | | (a) Effective July 3, 2005, the first day of fiscal 2006, we adopted Statement of Financial Accounting Standard No. 123, “Share-Based Payment (Revised 2004)” (“SFAS 123(R)”) on a modified prospective basis. As a result, we have included stock-based compensation costs in our results of operations for fiscal 2006. |

| |

| | | (b) On August 3, 2005, we acquired Acterna, Inc. (“Acterna”) in a transaction accounted for as a purchase. The Consolidated Statement of Operations for fiscal 2006 included the results of operations from Acterna subsequent to August 3, 2005 and the Consolidated Balance Sheet as of June 30, 2006 included the Acterna’s financial position. |

| |

| | | (c) On May 17, 2006, we completed an offering of $375 million aggregate principal amount of 1% Senior Convertible Notes due 2026. On June 5, 2006, we sold an additional $50 million aggregate principal amount of the notes which were issued upon the exercise by the initial purchasers of an over-allotment option granted by JDSU. The sale of the additional notes brought the total aggregate principal amount of 1% Senior Convertible Notes outstanding to $425 million. Both transactions are included in the Consolidated Balance Sheet as of June 30, 2006. |

| |

| (4) | | The Company has reclassified expenses related to amortization of acquired developed technology, losses related to the sale of assets and loss on sale of subsidiaries’ net assets in the Consolidated Statements of Operations. See “Note 1. Description of Business and Summary of Significant Accounting Policies” to the Notes of Consolidated Financial Statements for more information. These reclassifications are included in the table for fiscal years 2006, 2005 and 2004. The above reclassifications for fiscal years 2003 and 2002 are not reflected in the table as supporting information is not available. |

42

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONSOUR INDUSTRIES AND DEVELOPMENTS

We are committed to enabling broadband and optical innovation in the communications and commercial markets. We are also a leading provider of communications test & measurement solutions and optical products for telecommunications service providers, cable operators, and network equipment manufacturers. Furthermore, we are a leading provider of innovative optical solutions for medical/environmental instrumentation, semiconductor processing, display, brand authentication, aerospace, defense, and decorative applications. We currently employ 7,099 employees worldwide.

Our Optical Communications segment consists generally of:

- Optical components and modules sold to OEM suppliers of enterprise and storage solutions, such as Cisco, Sun Microsystems, Hewlett-Packard, Emulex, QLogic, McData and EMC.

- Optical components, modules and sub-systems sold to OEM providers to communications network carriers, such as Nortel, Lucent, Alcatel, Ciena, Cisco, Fujitsu, Siemens, and Huawei.

Our Communications Test & Measurement segment consists generally of:

- Manufacturing and lab test platforms used in the design, performance, and interoperability testing of network equipment for all major and emerging core, metro, cable, and access network technologies for customers such as Lucent, Nortel, Alcatel, Motorola, Siemens, and Cisco.

- Field test instrumentation and software used in the installation, provisioning, and maintenance of broadband voice, video, and data communication services for customers such as AT&T, Deutsche Telecom, Comcast, Telefonica, China Telecom and Verizon.

- Network and service assurance systems used to monitor and troubleshoot network performance and to optimize quality of service for customers such as British Telecom, Time Warner, Bell South and Bell Canada.

Our Advanced Optical Technologies segment consists generally of:

- Custom, high precision coated optics used in medical/environmental instrumentation, and optical sensors for aerospace and defense applications.

- Light interference pigment products utilized for security purposes in currencies and other documents, anti-counterfeiting devices and decorative surface treatments.

Our Lasers business unit consists generally of:

- Laser subsystems used in biotech instrumentation, semiconductor inspection, electronic material processing and precision machining.

- Our innovative Photonic Power delivery system used to drive sensors, gauges, actuators, low power communications devices, nanotechnology.

Overall, our optical communications markets are notable for, among other things, their high concentration of customers at each level of the industry, extremely long design cycles and increasing competition from Asian (principally China-based) suppliers. One consequence of a highly concentrated customer base and increasing Asian competition is systemic pricing pressure at each level of the industry. Large capital investment requirements, long return on investment periods, uncertain business models and complex and shifting regulatory hurdles, among other things, currently combine to limit opportunities for new carriers and their system suppliers to emerge. Thus, we expect that high customer concentration, attendant pricing pressure, and other effects on our communications markets will remain for the foreseeable future. Long design cycles mean that considerable resources must be spent to design and develop new products with limited visibility relative to the ultimate market opportunity for the products (pricing and volumes) or the timing thereof.

43

As a supplier of components and modules to this industry, we feel the effects most acutely, as system designs must first be initiated at the carrier level, communicated to the systems provider and then communicated to us and our competitors. During system design periods, shifts in economic, industry, customer or consumer conditions could and often do cause redesigns, delays or even cancellations to occur with their related costs to those involved. Communications industry design cycles are often challenging for companies without the financial and infrastructural resources to sustain the long periods between project initiation and revenue realization.

The advanced optical technologies markets and the laser business, while more diverse, share some of the customer concentration and design cycle attributes of our communications markets.

We are working aggressively on a strategy to expand our products, customers and distribution channels for several of our core competencies in these areas to, among other things, reduce our exposure to customer concentration and long design cycles across our company. As part of this strategy, we have expanded into the Communications Test & Measurement segment, which has expanded our customer base and distribution significantly.

On August 3, 2005, we completed the acquisition of privately held Acterna, Inc. (“Acterna”), a leading worldwide provider of broadband and optical test and measurement solutions for telecommunications and cable service providers and network equipment manufacturers. Beginning in the first quarter of fiscal 2006, the addition of Acterna formed a new reportable segment to our business: Communications Test & Measurement. One attribute of this segment is considerable seasonal revenue variability. We expect this seasonality to continue for the foreseeable future, impacting our Communications Test & Measurement financial results, our overall product mix, and financial performance.

On November 30, 2005, we completed the acquisition of Agility Communications, Inc. (“Agility”), a leading provider of widely tunable laser solutions for optical networks which is included in Optical Communications.

On May 4, 2006, we completed the acquisition of Test-Um Inc. (“Test-Um”), an industry-leading provider of home networking test instruments for the FTTx and digital cable markets which is included in Communications Test & Measurement.

Major business developments during fiscal 2006 include:

- Net revenue in fiscal 2006 increased 69%, or $492.1 million, to $1,204.3 million from $712.2 million in fiscal 2005. Net revenue in fiscal 2006 consisted of $470.5 million, or approximately 39% of net revenue, from Optical Communications, $494.5 million, or approximately 41% of net revenue, from Communications Test & Measurement, $162.8 million, or approximately 14% of net revenue, from Advanced Optical Technologies, and $80.5 million, or approximately 6% of net revenue, from Lasers.Communications Test & Measurement net revenue includes $4.0 million of deferred revenue that is eliminated from consolidated revenue as a result of purchase accounting adjustments.

- Gross margin in fiscal 2006 increased to 28% from 16% in fiscal 2005. The improvement in gross margin was primarily related to the addition of Communications Test & Measurement, an increase in Optical Communications’ sales volume, and the impact of our on-going manufacturing cost reduction programs.

- Our combined research and development (“R&D”) and selling, general and administrative (“SG&A”) expenses, as a percent of net revenue, increased to 40% in fiscal 2006, from 35% in fiscal 2005. The increase is primarily related to higher operating expenses associated with recent acquisitions and the inclusion of stock compensation expenses resulting from the adoption of Statement of Financial Accounting Standard No. 123, “Share-Based Payment (Revised 2004)”(“SFAS 123(R)”).

For fiscal 2006, we recorded adjustments related to the recognition of asset retirement obligations for several leased facilities, the recognition of deferred rent expense over the term of certain leases, license fees, restructuring charges, insurance recoveries, the initial market value of certain marketable equity securities not previously recorded and other expenses not previously recorded. The corrections resulted in additional net losses of $6.3 million ($7.7 million in operating losses and $1.4 million in gains on investments) related to prior years. Management and the Audit Committee believe that such amounts are not material to previously reported financial statements. There was no impact on net loss per share in fiscal 2006 from these adjustments.

44

RECENT ACCOUNTING PRONOUCEMENTS

SFAS No. 123(R)

Effective July 3, 2005, the first day of fiscal 2006, we adopted Statement of Financial Accounting Standard No. 123, “Share-Based Payment (Revised 2004)” (“SFAS 123(R)”) on a modified prospective basis. As a result, we have included stock-based compensation costs in our results of operations for the year ended June 30, 2006. See “Note 12. Stock-Based Compensation” of our Notes to Consolidated Financial Statements for more details.

SAB 107

In March 2005, the Securities Exchange Commission (“SEC”) issued Staff Accounting Bulletin No. 107, “Share-Based Payment,” (“SAB 107”). SAB 107 provides guidance regarding the interactions between SFAS 123(R) and certain SEC rules and regulations, including guidance related to valuation methods, the classification of compensation expense, non-GAAP financial measures, the accounting for income tax effects of share-based payment arrangements, disclosures in Management’s Discussion and Analysis (“MD&A”) subsequent to adoption of SFAS 123(R), and modifications of options prior to the adoption of SFAS 123(R). We began adhering to the guidance in SAB 107 upon the implementation of SFAS 123(R) starting the quarter ended September 30, 2005. See “Note 12. Stock-Based Compensation” of our Consolidated Financial Statements and “Employee Stock Options” in MD&A for more details.

SFAS No. 154

In June 2005, Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standard No. 154, “Accounting Changes and Error Corrections, a replacement of APB Opinion No. 20, Accounting Changes, and FASB Statement No. 3, Reporting Accounting Changes in Interim Financial Statements” (“SFAS 154”). The Statement applies to all voluntary changes in accounting principle, and changes the requirements for accounting for and reporting of a change in accounting principle. SFAS 154 requires retrospective application to prior periods’ financial statements of a voluntary change in accounting principle unless it is impracticable. SFAS 154 requires that a change in method of depreciation, amortization, or depletion for long-lived, nonfinancial assets be accounted for as a change in accounting estimate that is affected by a change in accounting principle. Opinion 20 previously required that such a change be reported as a change in accounting principle. SFAS 154 is effective for accounting changes and corrections of errors made in fiscal years beginning after December 15, 2005. The adoption of this pronouncement is not expected to have a material impact on our financial statements.

FIN 47

In March 2005, the FASB issued Interpretation No. 47, “Accounting for Conditional Asset Retirement Obligations” (“FIN 47”) which clarifies that the term “conditional asset retirement obligation” as used in Statement of Financial Accounting Standard No. 143, “Accounting for Asset Retirement Obligations” (“SFAS 143”), refers to a legal obligation to perform an asset retirement activity in which the timing and/or method of settlement are conditional on a future event that may or may not be within the control of the entity. However, the obligation to perform the asset retirement activity is unconditional even though uncertainty exists about the timing and/or method of settlement. FIN 47 requires that the uncertainty about the timing and/or method of settlement of a conditional asset retirement obligation be factored into the measurement of the liability when sufficient information exists. FIN 47 also clarifies when an entity would have sufficient information to reasonably estimate the fair value of an asset retirement obligation. FIN 47 is effective no later than the end of fiscal years ending after December 15, 2005. The adoption of this pronouncement did not have a material impact on our financial statements.

FIN 48

In June 2006, FASB issued interpretation No. 48, “Accounting for Uncertainty in Income Taxes-an interpretation of FASB Statement No. 109 (FAS No. 109)” (“FIN 48”). This interpretation prescribes a recognition threshold and measurement attribute for tax positions taken or expected to be taken in a tax return. This interpretation also provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods, disclosure and transition. The evaluation of a tax position in accordance with this interpretation is a two-step process. In the

45

first step, recognition, it is determined whether it is more-likely-than-not that a tax position will be sustained upon examination, including resolution of any related appeals or litigation processes, based on the technical merits of the position. The second step addresses measurement of a tax position that meets the more-likely-than-not criteria. The tax position is measured at the largest amount of benefit that is greater than 50 percent likely of being realized upon ultimate settlement. Differences between tax positions taken in a tax return and amounts recognized in the financial statements will generally result in a) an increase in a liability for income taxes payable or a reduction of an income tax refund receivable, b) a reduction in a deferred tax asset or an increase in a deferred tax liability or c) both a and b. Tax positions that previously failed to meet the more-likely-than-not recognition threshold should be recognized in the first subsequent financial reporting period in which that threshold is met. Previously recognized tax positions that no longer meet the more-likely-than-not recognition threshold should be de-recognized in the first subsequent financial reporting period in which that threshold is no longer met. Use of a valuation allowance as described in FAS No. 109 is not an appropriate substitute for the de-recognition of a tax position. The requirement to assess the need for a valuation allowance for deferred tax assets based on sufficiency of future taxable income is unchanged by this interpretation. This Interpretation is effective for fiscal years beginning after December 15, 2006. We are currently evaluating the impact FIN 48 will have to our consolidated balance sheet and statement of operations.

EITF 06-3

In March 2006, the Emerging Issues Task Force published Issue No. 06-3, “How Taxes Collected from Customers and Remitted to Governmental Authorities Should Be Presented in the Income Statement” (“EITF 06-3”) which requires a policy be adopted to present externally imposed taxes on revenue-producing transactions on either a gross or net basis. Gross or net presentation may be elected for each different type of tax, but similar taxes should be presented consistently. Taxes within the scope of this issue would include taxes that are imposed on a revenue transaction between a seller and a customer. EITF 06-3 is effective in interim and annual financial periods beginning after December 15, 2006. The adoption of EITF 06-3 will not have a material impact on our financial statements.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of our consolidated financial statements in conformity with accounting principles generally accepted in the United States requires us to make estimates and judgments that affect the reported amounts of assets and liabilities, net revenue and expenses, and the related disclosures. We base our estimates on historical experience, our knowledge of economic and market factors and various other assumptions that we believe to be reasonable under the circumstances. Estimates and judgments used in the preparation of our financial statements are, by their nature, uncertain and unpredictable, and depend upon, among other things, many factors outside of our control, such as demand for our products and economic conditions. Accordingly, our estimates and judgments may prove to be incorrect and actual results may differ, perhaps significantly, from these estimates under different estimates, assumptions or conditions. We believe the following critical accounting policies are affected by significant estimates, assumptions and judgments used in the preparation of our consolidated financial statements.

Revenue Recognition:We recognize revenue when it is realized or realizable and earned. We considers revenue realized or realizable and earned when it has persuasive evidence of an arrangement, delivery has occurred, the sales price is fixed or determinable, and collectibility is reasonably assured. Delivery does not occur until products have been shipped or services have been provided to the client, risk of loss has transferred to the client and client acceptance has been obtained, client acceptance provisions have lapsed, or we has objective evidence that the criteria specified in the client acceptance provisions have been satisfied. In situations where a formal acceptance is required but the acceptance only relates to whether the product meets its published specifications, revenue is generally recognized upon shipment provided all other revenue recognition criteria are met. The sales price is not considered to be fixed or determinable until all contingencies related to the sale have been resolved.

We reduce revenue for rebates and other similar allowances. Revenue is recognized only if these estimates can be reliably determined. We base our estimates on historical results taking into consideration the type of client, the type of transaction and the specifics of each arrangement.

In addition to the aforementioned general policies, the following are the specific revenue recognition policies for multiple-element arrangements and for each major category of revenue.

46

Hardware

Revenue from hardware sales is generally recognized when the product is shipped to the customer and when there are no unfulfilled company obligations that affect the customer’s final acceptance of the arrangement. Any cost of warranties and remaining obligations that are inconsequential or perfunctory are accrued when the corresponding revenue is recognized. Revenue from rentals and operating leases is recognized on a straight-line basis over the term of the rental or lease.

Multiple-Element Arrangements

We enter into multiple-element revenue arrangements, which may include any combination of hardware, software and services. Certain of our networking and communications products are integrated with software that is not considered essential to the functionality of the equipment. We believe that this equipment is not considered software related and would therefore be excluded from the scope of American Institute of Certified Public Accountants (AICPA) Statement of Position (SOP) No. 97-2, “Software Revenue Recognition” (“SOP 97-2”). Accordingly, we allocate the fair value of the equipment when sold with software according to the FASB Emerging Issues Task Force Abstracts No. 00-21, “Revenue Arrangements with Multiple Deliverables” (“EITF 00-21”). The value of the arrangement, less the allocated hardware is then considered within the scope of SOP 97-2.

To the extent that a deliverable(s) in a multiple-element arrangement is subject to specific guidance (for example, software that is subject to SOP 97-2 on whether and/or how to separate multiple-deliverable arrangements into separate units of accounting (separability) and how to allocate value among those separate units of accounting (allocation), that deliverable(s) is accounted for in accordance with such specific guidance. A multiple-element arrangement is separated into more than one unit of accounting if all of the following criteria are met:

- The delivered item(s) has value to the client on a standalone basis.

- There is objective and reliable evidence of the fair value of the undelivered item(s).

- If the arrangement includes a general right of return relative to the delivered item(s), delivery or performance of the undelivered item(s) is considered probable and substantially in the control of us.

If these criteria are not met, revenue is deferred until the earlier of when such criteria are met or when the last undelivered element is delivered. If there is objective and reliable evidence of fair value for all units of accounting in an arrangement, the arrangement consideration is allocated to the separate units of accounting based on each unit’s relative fair value. There may be cases, however, in which there is objective and reliable evidence of fair value of the undelivered item(s) but no such evidence for the delivered item(s). In those cases, the residual method is used to allocate the arrangement consideration. Under the residual method, the amount of consideration allocated to the delivered item(s) equals the total arrangement consideration less the aggregate fair value of the undelivered item(s). The revenue policies described below are then applied to each unit of accounting, as applicable.

Services

Revenue from services and system maintenance is typically recognized on a straight-line basis over the term of the contract. Revenue from time and material contracts is recognized at the contractual rates as labor hours are delivered and direct expenses are incurred. Revenue related to extended warranty and product maintenance contracts is deferred and recognized on a straight-line basis over the delivery period. We also generate service revenue from hardware repairs and calibrations which is recognized as revenue upon completion of the service.

Software

Revenue from perpetually licensed software is recognized at the inception of the license term. Revenue from time based license arrangements is recognized on a subscription basis over the period that the customer is using the license. Revenue from maintenance, unspecified upgrades and technical support is recognized over the period such items are delivered. In multiple-element revenue arrangements that include software that is more than incidental to the products or services as a whole (software multiple-element arrangements), software and software-related

47

elements are accounted for in accordance with the following policies. Software-related elements include software products and services as well as any non-software deliverable(s) for which a software deliverable is essential to its functionality.

A software multiple-element arrangement is separated into more than one unit of accounting if all of the following criteria are met:

- The functionality of the delivered element(s) is not dependent on the undelivered element(s).

- There is vendor-specific objective evidence (VSOE) of fair value of the undelivered element(s).

- Delivery of the delivered element(s) represents the culmination of the earnings process for that element(s).

If these criteria are not met, the revenue is deferred until the earlier of when such criteria are met or when the last undelivered element is delivered. If there is VSOE for all units of accounting in an arrangement, the arrangement consideration is allocated to the separate units of accounting based on each unit's relative VSOE. There may be cases, however, in which there is VSOE of the undelivered item(s) but no such evidence for the delivered item(s). In these cases, the residual method is used to allocate the arrangement consideration. Under the residual method, the amount of consideration allocated to the delivered item(s) equals the total arrangement consideration less the aggregate VSOE of the undelivered elements. We limits its assessment of VSOE for each undelivered element is primarily determined via contract specific substantive renewal rates. Changes to the elements in an arrangement and our ability to establish vendor-specific objective evidence for those elements could affect the timing of the revenue recognition.

Allowances for Doubtful Accounts:We perform credit evaluations of our customers’ financial condition. We maintain allowances for doubtful accounts for estimated losses resulting from the inability of our customers to make required payments. We record our bad debt expenses as selling, general and administrative expenses. When we become aware that a specific customer is unable to meet its financial obligations to us, for example, as a result of bankruptcy or deterioration in the customer’s operating results or financial position, we record a specific allowance to reflect the level of credit risk in the customer’s outstanding receivable balance. In addition, we record additional allowances based on certain percentages of our aged receivable balances. These percentages are determined by a variety of factors including, but not limited to, current economic trends, historical payment and bad debt write-off experience. We are not able to predict changes in the financial condition of our customers, and if circumstances related to our customers deteriorate, our estimates of the recoverability of our trade receivables could be materially affected and we may be required to record additional allowances. Alternatively, if we provide more allowances than we need, we may reverse a portion of such provisions in future periods based on our actual collection experience.

Stock-based Compensation: We estimate the fair value of equity awards granted using the Black-Scholes-Merton option-pricing formula and a single option award approach. This option-pricing model requires the input of highly subjective assumptions, including the option’s expected life and the price volatility of the underlying stock. The expected stock price volatility assumption was determined using a combination of historical and implied volatility of our common stock. In addition, we are required to estimate the expected forfeiture rate and only recognize expense for those shares expected to vest. When estimating forfeitures, we consider voluntary termination behavior as well as future workforce reduction programs. Estimated forfeiture rates are trued-up to actual forfeiture results as the stock-based awards vest the forfeiture rate based on historical experience of our stock-based award that are granted, exercised and cancelled. Total fair value of the equity awards, net of forfeiture, is then amortized on a straight-line basis over the requisite service periods of the awards, which is generally the vesting period.

Investments:We hold equity interests in both publicly traded and privately held companies. When the carrying value of an investment exceeds its fair value and the decline in value is deemed to be other-than-temporary, we write down the value of the investment and establish a new cost basis. Fair values for investments in public companies are determined using quoted market prices. Fair values for investments in privately held companies are estimated based upon one or more of the following but not limited to: Assessment of the investees’ historical and forecasted financial condition; operating results and cash flows; the values of recent rounds of financing; and quoted market prices of comparable public companies. We regularly evaluate our investments based on criteria that include, but are not limited to, the duration and extent to which the fair value has been less than the carrying value, the current economic environment and the duration of any market decline, and the financial health and business outlook of the investees.

48

We generally believe an other-than-temporary decline occurs when the fair value of an investment is below the carrying value for six consecutive months. Future adverse changes in these or other factors could result in an other-than-temporary decline in the value of our investments, thereby requiring us to write down such investments. Our ability to liquidate our investment positions in privately held companies will be affected to a significant degree by the lack of an actively traded market, and we may not be able to dispose of these investments in a timely manner.

Inventory Valuation:We assess the value of our inventory on a quarterly basis and write-down those inventories which are obsolete or in excess of our forecasted usage to their estimated realizable value. Our estimates of realizable value are based upon our analysis and assumptions including, but not limited to, forecasted sales levels by product, expected product lifecycle, product development plans and future demand requirements. Our marketing department plays a key role in our excess review process by providing updated sales forecasts, managing product rollovers and working with manufacturing to maximize recovery of excess inventory. If actual market conditions are less favorable than our forecasts or actual demand from our customers is lower than our estimates, we may be required to record additional inventory write downs. If actual market conditions are more favorable than anticipated, inventory previously written down may be sold, resulting in lower cost of sales and higher income from operations than expected in that period.

Goodwill Valuation: We test goodwill for possible impairment on an annual basis and at any other time if events occur or circumstances indicate that the carrying amount of goodwill may not be recoverable. Circumstances that could trigger an impairment test include but are not limited to: a significant adverse change in the business climate or legal factors; an adverse action or assessment by a regulator; unanticipated competition; loss of key personnel; the likelihood that a reporting unit or significant portion of a reporting unit will be sold or otherwise disposed; results of testing for recoverability of a significant asset group within a reporting unit; and recognition of a goodwill impairment loss in the financial statements of a subsidiary that is a component of a reporting unit.

Thedetermination as to whether a write down of goodwill is necessary involves significant judgment based on the short-term and long-term projections of the future performance of the reporting unit to which the goodwill is attributed. The assumptions supporting the estimated future cash flows of the reporting unit, including the discount rate used and estimated terminal value reflect our best estimates.

Long-lived asset valuation (property, plant and equipment and intangible assets):

Long-lived assets held and used

We test long-lived assets or asset groups for recoverability when events or changes in circumstances indicate that their carrying amounts may not be recoverable. Circumstances which could trigger a review include, but are not limited to: Significant decreases in the market price of the asset; significant adverse changes in the business climate or legal factors; accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of the asset; current period cash flow or operating losses combined with a history of losses or a forecast of continuing losses associated with the use of the asset; and current expectation that the asset will more likely than not be sold or disposed of significantly before the end of its estimated useful life.

Recoverability is assessed based on the carrying amounts of the asset and its fair value which is generally determined based on the sum of the undiscounted cash flows expected to result from the use and the eventual disposal of the asset, as well as specific appraisals in certain instances. An impairment loss is recognized when the carrying amount is not recoverable and exceeds fair value.

Long-lived assets held for sale

We classify long-lived assets as held for sale when certain criteria are met, including: Management’s commitment to a plan to sell the assets; the availability of the assets for immediate sale in their present condition; whether an active program to locate buyers and other actions to sell the assets has been initiated; whether the sale of the assets is probable and their transfer is expected to qualify for recognition as a completed sale within one year; whether the assets are being marketed at reasonable prices in relation to their fair value; and how unlikely it is that significant changes will be made to the plan to sell the assets. Long-lived assets held for sale are classified as other current assets in the Consolidated Balance Sheet.

49

We measure long-lived assets to be disposed of by sale at the lower of carrying amounts or fair value less cost to sell. Fair value is determined using quoted market prices or the anticipated cash flows discounted at a rate commensurate with the risk involved.

Income Taxes: In accordance with Statement of Financial Accounting Standards No. 109, “Accounting for Income Taxes”(“SFAS 109”), we recognize income taxes using an asset and liability approach. This approach requires the recognition of taxes payable or refundable for the current year and deferred tax liabilities and assets for the future tax consequences of events that have been recognized in our consolidated financial statements or tax returns. The measurement of current and deferred taxes is based on provisions of the enacted tax law and the effects of future changes in tax laws or rates are not anticipated.

SFAS 109 provides for recognition of deferred tax assets if the realization of such deferred tax assets is more likely than not to occur. With the exception of certain international jurisdictions, we have determined that at this time it is more likely than not that deferred tax assets attributable to the remaining jurisdictions will not be realized, primarily due to uncertainties related to our ability to utilize our net operating loss carryforwards before they expire based on our recent years history of losses. Accordingly, we have established a valuation allowance for such deferred tax assets. If there is a change in our ability to realize our deferred tax assets, then our tax provision may decrease in the period in which we determine that realization is more likely than not.

We are subject to income tax audits by the respective tax authorities in all of the jurisdictions in which we operate. The determination of tax liabilities in each of these jurisdictions requires the interpretation and application of complex and sometimes uncertain tax laws and regulations. We recognize liabilities based on our estimate of whether, and the extent to which, additional tax liabilities are probable. If we ultimately determine that the payment of such a liability is not necessary, then we reverse the liability and recognize a tax benefit during the period in which the determination is made that the liability is no longer necessary.

The recognition and measurement of current taxes payable or refundable and deferred tax assets and liabilities requires that we make certain estimates and judgments. Changes to these estimates or a change in judgment may have a material impact on our tax provision in a future period.

Warranty Accrual:We provide reserves for the estimated costs of product warranties at the time revenue is recognized. We estimate the costs of our warranty obligations based on our historical experience of known product failure rates, use of materials to repair or replace defective products and service delivery costs incurred in correcting product failures. In addition, from time to time, specific warranty accruals may be made if unforeseen technical problems arise. Should our actual experience relative to these factors differ from our estimates, we may be required to record additional warranty reserves. Alternatively, if we provide more reserves than we need, we may reverse a portion of such provisions in future periods.

Restructuring Accrual:In April 2001, we began to implement formalized restructuring programs based on our business strategies and economic outlook and recorded significant charges in connection with our Global Realignment Program. In connection with these plans, we have recorded estimated expenses for severance and outplacement costs, lease cancellations, asset write-offs and other restructuring costs. In accordance with Statement of Financial Accounting Standard No. 146, “Accounting for Costs Associated with Exit or Disposal Activities” (“SFAS 146”), generally costs associated with restructuring activities initiated after December 31, 2002 have been recognized when they are incurred rather than at the date of a commitment to an exit or disposal plan. However, in the case of leases, the expense is estimated and accrued when the property is vacated. Given the significance of, and the timing of the execution of such activities, this process is complex and involves periodic reassessments of estimates made at the time the original decisions were made, including evaluating real estate market conditions for expected vacancy periods and sub-lease rents. In addition, post-employment benefits accrued for workforce reductions related to restructuring activities initiated after December 31, 2002 are accounted for under Statement of Financial Accounting Standards No. 112, “Employer’s Accounting for Post-employment Benefits” (“SFAS 112”). A liability for post-employment benefits is recorded when payment is probable, the amount is reasonably estimable, and the obligation relates to rights that have vested or accumulated. We continually evaluate the adequacy of the remaining liabilities under our restructuring initiatives. Although we believe that these estimates accurately reflect the costs of our restructuring plans, actual results may differ, thereby requiring us to record additional provisions or reverse a portion of such provisions.

50

Pension and Other Postretirement Benefits: The determination of our obligation and expense for pension and other postretirement benefits payable to employees and retirees is dependent on our selection of certain assumptions used by actuaries in calculating such amounts. Those assumptions include, among others, the discount rate, expected long-term rate of return on plan assets, compensation increases and mortality assumptions for the plan participants. Measurements of net periodic benefit costs are based on the assumptions used for the previous year end measurements of assets and obligations. We review our actuarial assumptions on an annual basis and, in consultation with our actuaries, make modifications to the assumptions based on current rates and trends when appropriate. In accordance with SFAS No. 87, “Employer’s Accounting for Pensions” (“SFAS 87”), and SFAS No. 106 “Employer’s Accounting for Postretirement Benefits Other than Pensions” (“SFAS 106”), actual results that differ from our assumptions are accumulated and amortized over future periods and, therefore, generally affect our recognized expense and recorded obligation in such future periods. While we believe that our assumptions are appropriate, significant differences in our actual experience or significant changes in our assumptions that may be required under new legislation, or accounting pronouncements, or otherwise may materially affect our pension and other post-retirement obligations and our future expense.

Loss Contingencies:We are subject to the possibility of various loss contingencies arising in the ordinary course of business. We consider the likelihood of loss or impairment of an asset or the incurrence of a liability, as well as our ability to reasonably estimate the amount of loss in determining loss contingencies. An estimated loss is accrued when it is probable that an asset has been impaired or a liability has been incurred and the amount of loss can be reasonably estimated. We regularly evaluate current information available to us to determine whether such accruals should be adjusted and whether new accruals are required.

RESULTS OF OPERATIONS

The results of operations for the current period are not necessarily indicative of results to be expected for future years. The following table sets forth the components of our Consolidated Statements of Operations as a percentage of net revenue:

| | | Years Ended June 30, |

| | | 2006 | | 2005 | | 2004 |

| Net revenue | | 100 | % | | 100 | % | | 100 | % |

| Cost of sales | | 69 | | | 82 | | | 77 | |

| Amortization of acquired developed technologies | | 3 | | | 2 | | | 2 | |

| Gross profit | | 28 | | | 16 | | | 21 | |

| Operating expenses: | | | | | | | | | |

| Research and development | | 13 | | | 13 | | | 16 | |

| Selling, general and administrative | | 27 | | | 22 | | | 23 | |

| Amortization of other intangibles | | 2 | | | 1 | | | 1 | |

| Acquired in-process research and development | | 2 | | | — | | | — | |

| Reduction of goodwill | | 2 | | | 8 | | | — | |

| Reduction of intangibles and loss on long-lived assets | | — | | | 4 | | | 8 | |

| Restructuring charges | | 3 | | | 3 | | | 2 | |

| Total operating expenses | | 49 | | | 51 | | | 50 | |

| Loss from operations | | (21 | ) | | (35 | ) | | (29 | ) |

| Interest and other, net | | 2 | | | (1 | ) | | 4 | |

| Gain on sale of investments | | 6 | | | 3 | | | 6 | |

| Reduction in fair value of investments | | — | | | (2 | ) | | (1 | ) |

| Loss on equity method investments | | — | | | (1 | ) | | (1 | ) |

| Loss before income taxes and cumulative effect of an accounting change | | (13 | ) | | (36 | ) | | (21 | ) |

| Provision of (benefit for) income taxes | | — | | | 1 | | | (3 | ) |

| Loss before cumulative effect of an accounting change | | (13 | ) | | (37 | ) | | (18 | ) |

| Cumulative effect of an accounting change | | — | | | — | | | — | |

| Net loss | | (13 | )% | | (37 | )% | | (18 | )% |

51

Financial Data for Fiscal 2006, 2005, and 2004:

The following table summarizes selected Consolidated Statement of Operations items (in millions, except for percentages):

| | | | | | | | Percentage | | | | | | | | | | | | | | Percentage |

| | 2006 | | 2005 | | Change | | Change | | 2005 | | 2004 | | Change | | Change |

| Net Revenue | $ | 1,204.3 | | | $ | 712.2 | | | $ | 492.1 | | | 69 | % | | $ | 712.2 | | | $ | 635.9 | | | $ | 76.3 | | | 12 | % |

| |

| Gross profit | | 340.5 | | | | 112.2 | | | | 228.3 | | | 203 | % | | | 112.2 | | | | 135.9 | | | | (23.7 | ) | | -17 | % |

| Percentage of net revenue | | 28 | % | | | 16 | % | | | | | | | | | | 16 | % | | | 21 | % | | | | | | | |

| |

| Research and development | | 155.5 | | | | 93.7 | | | | 61.8 | | | 66 | % | | | 93.7 | | | | 99.5 | | | | (5.8 | ) | | -6 | % |

| Percentage of net revenue | | 13 | % | | | 13 | % | | | | | | | | | | 13 | % | | | 16 | % | | | | | | | |

| |

| Selling, general and administrative | | 325.3 | | | | 157.3 | | | | 168.0 | | | 107 | % | | | 157.3 | | | | 144.7 | | | | 12.6 | | | 9 | % |

| Percentage of net revenue | | 27 | % | | | 22 | % | | | | | | | | | | 22 | % | | | 23 | % | | | | | | | |

| |

| Amortization of other intangibles | | 24.4 | | | | 6.4 | | | | 18.0 | | | 281 | % | | | 6.4 | | | | 6.1 | | | | 0.3 | | | 5 | % |

| Percentage of net revenue | | 2 | % | | | 1 | % | | | | | | | | | | 1 | % | | | 1 | % | | | | | | | |

| |

| Acquired in-process research and | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| development. | | 20.3 | | | | 1.1 | | | | 19.2 | | | 1745 | % | | | 1.1 | | | | 2.6 | | | | (1.5 | ) | | -58 | % |

| Percentage of net revenue | | 2 | % | | | — | | | | | | | | | | | — | | | | — | | | | | | | | |

| |

| Reduction of goodwill | | 22.4 | | | | 53.7 | | | | (31.3 | ) | | -58 | % | | | 53.7 | | | | — | | | | 53.7 | | | — | |

| Percentage of net revenue | | 2 | % | | | 8 | % | | | | | | | | | | 8 | % | | | — | | | | | | | | |

| |

| Reduction of other long-lived assets | | 5.6 | | | | 31.6 | | | | (26.0 | ) | | -82 | % | | | 31.6 | | | | 52.3 | | | | (20.7 | ) | | -40 | % |

| Percentage of net revenue | | — | | | | 4 | % | | | | | | | | | | 4 | % | | | 8 | % | | | | | | | |

| |

| Restructuring charges | | 35.0 | | | | 18.2 | | | | 16.8 | | | 92 | % | | | 18.2 | | | | 11.5 | | | | 6.7 | | | 58 | % |

| Percentage of net revenue | | 3 | % | | | 3 | % | | | | | | | | | | 3 | % | | | 2 | % | | | | | | | |

Net Revenue:

Net revenue in fiscal 2006 increased 69%, or $492.1 million, to $1,204.3 million from $712.2 million in fiscal 2005. The increase is primarily due to recent acquisitions and an increase in demand of our agile optical network (“AON”) products, including Reconfigurable Optical Add / Drop Multiplexers (ROADM), optical switches, blockers, and tunables. Recent acquisitions include Acterna in August 2005, Agility in November 2005, and Lightwave in May 2005. The increase in net revenue was partially offset by a decrease in net revenue in our custom optics business unit due to our decision to exit non-core and unprofitable product lines.

Our net revenue increased by $76.3 million from fiscal 2004 to fiscal 2005. The increase in net revenue between fiscal 2004 and 2005 is mainly related to higher demand for products in our Optical Communications segment which had net revenue increase by $104.8 million year over year. Specific products that grew were the wavelength blocker, switch products, and the optical pumps product. This increase in net revenue was partially offset by a $22.6 million decrease in our Advanced Optical Technologies segment net revenue. This decrease was primarily due to rapidly declining revenue during fiscal 2005 from our micro display window products. We have terminated these product lines and are not anticipating meaningful revenue from such products in the future.

Going forward, we expect to continue to encounter a number of industry and market structural risks and uncertainties that will limit our business climate and market visibility, and consequently, our ability to predict future revenue, profitability and general financial performance, and that could create quarter over quarter variability in one or more of our financial measures. These structural risks and uncertainties include: (a) strong pricing pressures, particularly within our Optical Communications markets, due to, among other things, a highly concentrated customer base, increasing Asian competition, excess device manufacturing capacity within the optical communications

52

industry and a general commoditization trend for many of our products; (b) high product mix variability, particularly in our Optical Communications products, which causes revenue variability, as well as gross profit variability due to, among other things, factory utilization fluctuations and inventory and supply chain management complexities; (c) seasonal buying patterns within our Communications Test & Measurement customers, which causes significant seasonal revenue variation within this high gross margin business unit; and (d) continuing service provider business model uncertainty, which causes demand, revenue and profitability measure unpredictability at each level of the communications industry. Moreover, the current trend of communications industry consolidations is expected to continue, directly affecting our Optical Communication’s and Communications Test & Measurement’s customer base and adding additional risk and uncertainty to our financial and business predictability.

Our program of North American assembly manufacturing transitions are entering their final phases, but until completed, these activities will continue to present additional supply chain and product delivery disruption risks, yield and quality concerns and increased cost risks. These risks, while expected to diminish over the next several quarters, also currently limit our ability to predict future revenue, profitability and general financial performance.

We operate primarily in three geographic regions: Americas, Europe and Asia. The following table presents net revenue by geographic regions (in millions):

| | | Years Ended June 30, |

| | | 2006 | | 2005 | | 2004 |

| Net revenue: | | | | | | | | | |

| Americas | | $ | 736.2 | | $ | 466.6 | | $ | 406.9 |

| Europe | | | 283.1 | | | 132.4 | | | 124.1 |

| Asia-Pacific | | | 185.0 | | | 113.2 | | | 104.9 |

| Total net revenue | | $ | 1,204.3 | | $ | 712.2 | | $ | 635.9 |

Net revenue from customers outside the Americas represented 39%, 34%, and 36% of net revenue for the fiscal years ended 2006, 2005, and 2004, respectively. Net revenue was assigned to geographic regions based on the customers’ shipment locations. We expect revenue from international customers to continue to be an important part of our overall net revenue and an increasing focus for net revenue growth.

During fiscal 2006, 2005, and 2004, no customer accounted for more than 10% of net revenue.

Gross Profit:

Gross profit in fiscal 2006 increased 203%, or $228.3 million, to $340.5 million from $112.2 million in fiscal 2005. The increase is primarily due to the addition of our Communications Test & Measurement segment, additional gross profit in Optical Communications primarily from an increase in sales volume and savings from our on-going manufacturing cost reduction programs. This increase in gross profit was partially offset by an increase in amortization expense of acquired developed technologies and purchase accounting adjustments due to the acquisitions of Acterna in August 2005 and Agility in November 2005. Gross profit excluding amortization expense of acquired developed technologies in fiscal 2006 increased 200%, or $251.3 million, to $376.9 million from $125.6 million in fiscal 2005. In addition, fiscal 2006 includes a stock compensation expense of $3.3 million related to the adoption of SFAS 123(R).