Exhibit 99.2

CANADA MORTGAGE AND HOUSING CORPORATION 2023 ANNUAL REPORT To request an alternate format, please contact us at: 1-800-668-2642 700 Montreal Road, contactcentre@cmhc.ca Ottawa, ON K1A 0P7 CMHC.ca

2023 Annual Report 2

4 2023 Highlights 5 National Housing Strategy (NHS) Highlights 6 Message From the Chair 8 Message From the President and CEO 10 Management Discussion and Analysis 11 Our Strategy 14 Our Performance 16 Data, Research and Insights 18 Reconciliation and Indigenous Relations 21 Anti-Racism and Equity 23 Our Culture 24 Our People 26 Business and Financial Highlights 26 Economic and Housing Environment 28 Consolidated Financial Highlights 31 Assisted Housing 35 Mortgage Insurance 39 Mortgage Funding 41 Capital Management 43 Risk Management 45 Climate-Related Financial Risk Disclosures 52 Looking Ahead to 2024 53 Consolidated Financial Statements 143 Corporate Governance 147 Appendix: OSFI Consultations and Guidelines 149 Glossary 152 Historical Information TABLE OF CONTENTS

2023 HIGHLIGHTS $29 billion of Affordability-Linked NHA Mortgage-Backed Securities were issued by Approved Issuers in 2023. More than 48,000 housing units were purchased across Canada with the help of our homeowner insurance products in 2023 (over 15% insured in rural areas). Of the 220,000-plus rental units insured in 2023 close to 40% were for new construction, adding new units to the marketplace. CMB program limit increase, providing funding for CMHC insured loans on multi-unit rental projects. Over 127,000 rental units insured in 2023 were for MLI Select, a mortgage loan insurance product that advances affordability and climate compatibility.

NHS HIGHLIGHTS NHS at a glance1 272,169 housing units repaired or committed (Target: 300,000 units) 345,377 community housing units protected (Target: 385,000 units) 134,707 new housing units created or committed (Target: 160,000 units) 31% committed funding towards the housing needs of women and their children (Target: 25%) $6.13 billion for the construction, repair and financial support of Indigenous and Northern housing 23,858 Indigenous and Northern units built, repaired or financially supported $2.5 billion committed in 2023 for the Housing Accelerator Fund to fast track 68,092 housing units. The Rapid Housing Initiative has supported the creation of 15,742 affordable units for those experiencing or at risk of homelessness, including 6,239 units for Indigenous peoples. Reduction or elimination of housing need for over 517,000 households with NHS commitments made to date. 1 NHS results are cumulative to date, and targets are cumulative until the program end date.

MESSAGE FROM THE CHAIR The year 2023 was one in which Canadians learned a lot about housing and the scale of our country’s housing shortage. Housing affordability led the news consistently. Experts, including many top minds from CMHC, were consulted on the challenge and on solutions. This national focus is a great source of strength as we work together, as a country, to make housing accessible.

Making progress Transforming that attention into roofs over heads doesn’t happen overnight. However, as you’ll see in the pages of this report, progress is being made. This includes real headway toward the ambitious targets set out in the federal government’s National Housing Strategy – which CMHC helps to deliver. CMHC’s industry-leading market intelligence and research work is giving us all a clearer picture, and guiding decision makers toward targeted solutions. Meanwhile, CMHC’s commercial operations – which are separate from government programming and pay dividends back to the federal government – continue to provide stability and liquidity to Canada’s housing system. People behind the numbers You’re going to see a lot of numbers in the following pages, but I ask to read through those to see the people behind them. For example, when you’re reading about the more than 192,700 housing units created and repaired by the Affordable Housing Fund2, know that one of those units is home to Robert in Edmonton, and it changed his life. The Fund supported the Salvation Army Grace Village, a 175-bed supportive housing facility for people like Robert, who need help making the move from chronic homelessness to permanent housing. I’ll speak for all my fellow Board members when I say that we work very hard to keep the Roberts of this country in mind as we oversee and guide CMHC’s work. Leadership changes We also keep in mind the people who produced CMHC’s results, and we said a fond farewell to one of them in 2023. President and CEO Romy Bowers, who left the organization in December, was a great leader for CMHC, and her influence will continue for years to come. I was pleased that Senior Vice-President Michel Tremblay, who’s already had a long career with CMHC, accepted the Board’s request to step in on an interim basis. His steady hands will guide us forward until the Governor in Council appoints a permanent successor, and we thank him for taking on this responsibility. Meanwhile, the government is also in the process of selecting five Board directors, and a new chair. It’s my honour and privilege to continue in the position until the new chair is named. I’ll speak, again, for my fellow Board members when I say it was also a privilege and an honour to be part of CMHC’s work in 2023. And I hope that, as you read through this report, you will see why. Derek Ballantyne Chair, CMHC Board of Directors 2 The 2023 Fall Economic Statement announced changes to the following program names: The Affordable Housing Fund (AHF), formerly known as the National Housing Co-Investment Fund (NHCF) and, The Apartment Construction Loan Program (ACLP), formerly known as the Rental Construction Financing Initiative (RCFi).

MESSAGE FROM THE PRESIDENT AND CEO It’s no understatement to say that 2023 brought significant housing challenges in Canada. Rising interest rates to tame inflation and labour shortages hindered the country’s ability to create much-needed housing supply. Many Canadians found it tough to pay their mortgage or rent, and far too many vulnerable people struggled to keep a roof over their heads.

Yet, even in these challenging times, CMHC continued to prove it’s a company that Canadians can count on. As this annual report shows, we made strong progress on our ambitious goals for 2023. This is the result of great work from our leadership and dedicated, expert staff – and the laser focus we gave to three pillars of work that will drive our strategy moving forward. Deliver Commercial Solutions Our commercial products continued to help stabilize the housing finance system in these uncertain economic times and incentivize more supply. Our team successfully met an unprecedented demand for MLI Select, part of our multi-unit mortgage loan insurance products. We also delivered an expansion of financing for purpose-built rentals through Canada Mortgage Bonds. In fact, loans insured by CMHC accounted for most of the urgently needed purpose-built rental apartment construction in the country. Build for the Future We were able to articulate the sheer scope of the country’s housing shortage. CMHC researchers found that Canada needs an additional 3.5 million homes beyond current projections to restore affordability. This one number raised awareness of all levels of government and the private and non-profit sectors to the magnitude of the efforts needed to overcome the current housing affordability crisis. CMHC will continue to be a leader in providing vital research and thought leadership through opportunities like our National Housing Conference in March 2024, where we highlighted cutting-edge innovation knowledge. Delivering Government Programs and Priorities In 2023, we also continued to deliver on federal government priorities for Canadians. There has been good progress on the National Housing Strategy targets, despite tough economic conditions. We reached agreements with 15 cities and the Province of Québec for the Housing Accelerator Fund, which will help these local governments get more housing built more quickly. In 2024, we will be extending proven supply-oriented programs, such as the Affordable Housing Fund and the Apartment Construction Loan program. We will also stand up newly announced initiatives, including consulting with the housing industry on a catalogue of homes to help accelerate construction. Creating impact amid change These accomplishments took place against the backdrop of significant changes for CMHC. We recalibrated our responsibilities with Infrastructure Canada, and they now lead on certain areas of housing policy advice, for example. This is an opportunity to align housing policies government-wide. The end of 2023 saw the departure of our former President and CEO, Romy Bowers. I would like to recognize Romy’s strong and steady leadership, which guided CMHC to reach the extraordinary achievements highlighted in this report. I would also like to thank our Chair, Derek Ballantyne, for his wise stewardship of CMHC since 2018. I have the utmost confidence in our skilled and dedicated senior leadership team and our employees across the country, who continue to deliver results for Canadians throughout these many changes. Canada’s housing challenges are serious, complex and urgent. However, I am optimistic that our country is united in facing them with strength and resolve – and CMHC is proud to be at the heart of this effort. Michel Tremblay Acting President and Chief Executive Officer

MANAGEMENT DISCUSSION AND ANALYSIS The following management discussion and analysis of the financial condition and results of operations was prepared for the year ended 31 December 2023 and approved by the Board of Directors on 20 March 2024. This section should be read in conjunction with the audited consolidated financial statements. Unless otherwise indicated, all financial information in this report has been prepared in accordance with International Financial Reporting Standards (IFRS) and all amounts are expressed in Canadian dollars. Forward-looking statements Our annual report contains forward-looking statements that include, but are not limited to: • the statements with respect to our outlook for the regulatory environment in which we operate • the outlook and priorities for each activity • the risk environment By their nature, forward-looking statements require us to make assumptions. They are subject to inherent risks and uncertainties that may cause actual results to differ materially from expectations expressed in the forward-looking statements. Non-IFRS measures We use a number of financial measures to assess our performance. Some of these measures are not calculated in accordance with IFRS and are not defined by IFRS, and do not have standardized meanings that would ensure consistency and comparability with other institutions. These non-IFRS measures are presented to supplement the information disclosed. They may be useful in analyzing performance and understanding the measures used by management in its financial and operational decision making. Where non-IFRS measures are used throughout the annual report, a definition of the term will be disclosed in the glossary for non-IFRS financial measures.

OUR STRATEGY Our strategy focuses our work on where we can improve the housing system and have the greatest possible impact on outcomes and results for Canadians. We work in close coordination and collaboration with many federal partners as well as other orders of government, Indigenous governments and partners, housing providers and stakeholders, and people with lived experience. Our enhanced collaboration with Infrastructure Canada will better link housing and infrastructure investments at the community level, better align housing with other federal policies and will improve housing outcomes.

Outcomes People in core housing need have equitable and reliable access to housing that is secure and affordable. Canada has the number of homes and mix of housing options to serve diverse needs. Canada’s housing system supports sustainability and stability. Strategic Results 1. Needs of households in core housing need are met through public policy measures. 2. Systemic racism, inequities and other barriers to access are removed. 3. Current and future housing needs and supply gaps are understood by system participants. 4. Barriers to access, building, or renovating housing are removed. 5. Current and future financial, environmental, and social vulnerabilities, including racism and discrimination, to the housing system are understood and tempered. 6. The housing system advances climate compatibility. 7. Housing is in the spirit of Reconciliation.

Our strategy focuses our work on where we can improve the housing system and have the greatest possible impact on outcomes and results for Canadians.

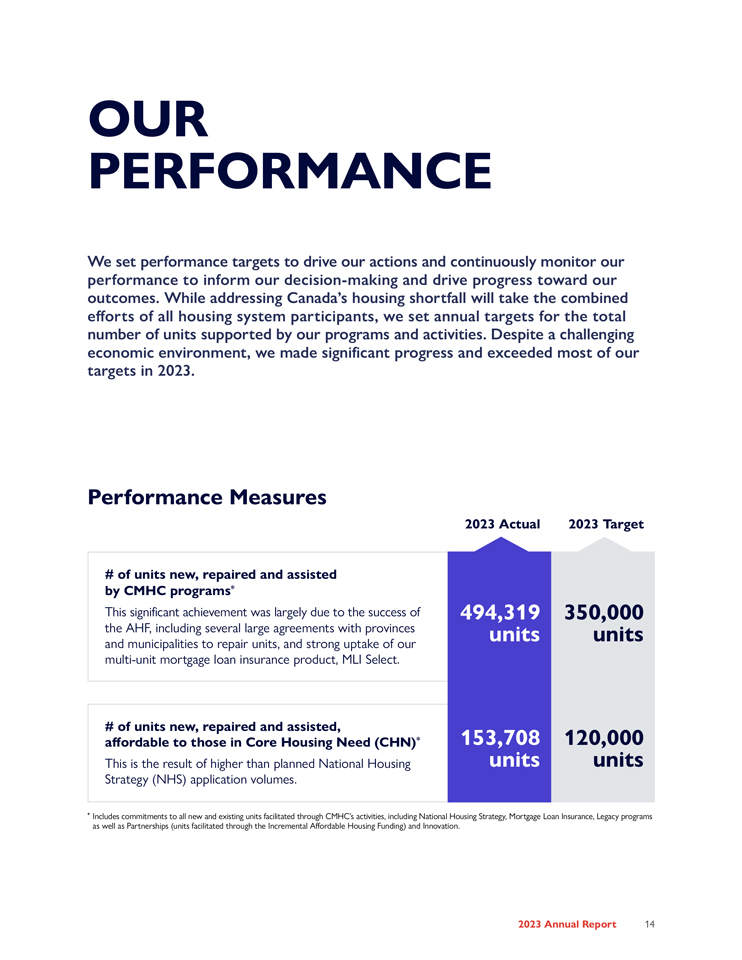

OUR PERFORMANCE We set performance targets to drive our actions and continuously monitor our performance to inform our decision-making and drive progress toward our outcomes. While addressing Canada’s housing shortfall will take the combined efforts of all housing system participants, we set annual targets for the total number of units supported by our programs and activities. Despite a challenging economic environment, we made significant progress and exceeded most of our targets in 2023. Performance Measures 2023 Actual 2023 Target # of units new, repaired and assisted by CMHC programs* This significant achievement was largely due to the success of 494,319 350,000 the AHF, including several large agreements with provinces units units and municipalities to repair units, and strong uptake of our multi-unit mortgage loan insurance product, MLI Select. # of units new, repaired and assisted, affordable to those in Core Housing Need (CHN)* 153,708 120,000 This is the result of higher than planned National Housing units units Strategy (NHS) application volumes. * Includes commitments to all new and existing units facilitated through CMHC’s activities, including National Housing Strategy, Mortgage Loan Insurance, Legacy programs as well as Partnerships (units facilitated through the Incremental Affordable Housing Funding) and Innovation.

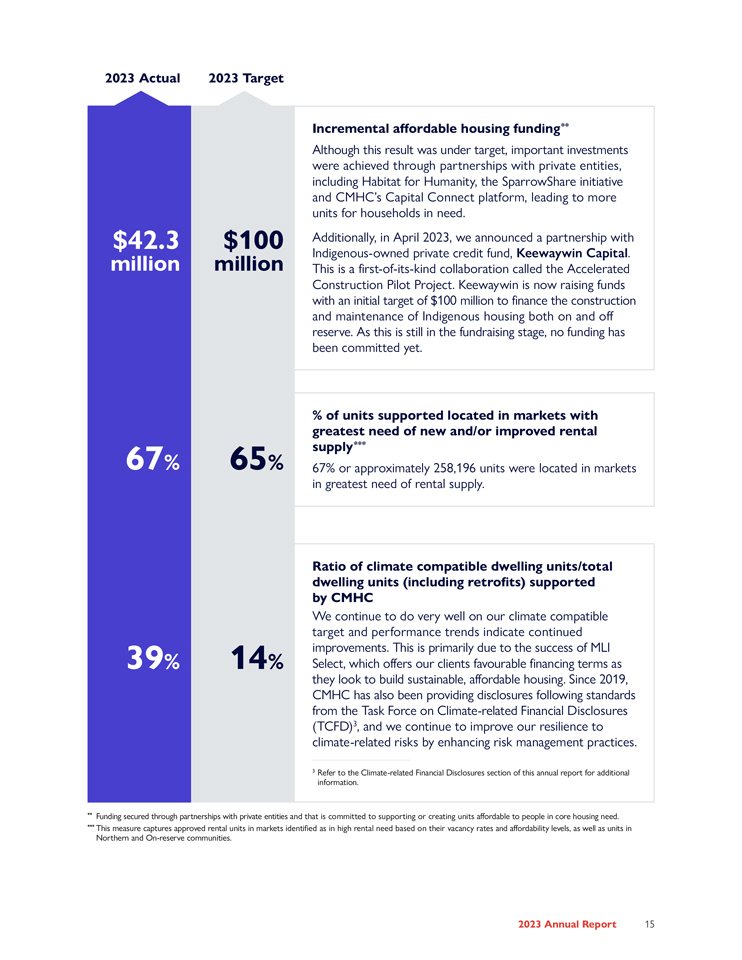

2023 Actual 2023 Target Incremental affordable housing funding** Although this result was under target, important investments were achieved through partnerships with private entities, including Habitat for Humanity, the SparrowShare initiative and CMHC’s Capital Connect platform, leading to more units for households in need. $42.3 $100 Additionally, in April 2023, we announced a partnership with million million Indigenous-owned private credit fund, Keewaywin Capital. This is a first-of-its-kind collaboration called the Accelerated Construction Pilot Project. Keewaywin is now raising funds with an initial target of $100 million to finance the construction and maintenance of Indigenous housing both on and off reserve. As this is still in the fundraising stage, no funding has been committed yet. % of units supported located in markets with greatest need of new and/or improved rental 67 supply*** % 65% 67% or approximately 258,196 units were located in markets in greatest need of rental supply. Ratio of climate compatible dwelling units/total dwelling units (including retrofits) supported by CMHC We continue to do very well on our climate compatible target and performance trends indicate continued improvements. This is primarily due to the success of MLI 39% 14% Select, which offers our clients favourable financing terms as they look to build sustainable, affordable housing. Since 2019, CMHC has also been providing disclosures following standards from the Task Force on Climate-related Financial Disclosures (TCFD)3, and we continue to improve our resilience to climate-related risks by enhancing risk management practices. 3 Refer to the Climate-related Financial Disclosures section of this annual report for additional information. ** Funding secured through partnerships with private entities and that is committed to supporting or creating units affordable to people in core housing need. *** This measure captures approved rental units in markets identified as in high rental need based on their vacancy rates and affordability levels, as well as units in Northern and On-reserve communities.

DATA, RESEARCH AND INSIGHTS Housing affordability and supply are complex issues driven by a web of financial, governance, fiscal, social, demographic and environmental factors. Broad research is needed to find root causes and potential solutions to tackle the biggest questions. • We conduct housing surveys, research and analysis to better understand current and future challenges of the housing system, barriers to housing affordability and households in core housing need, while recognizing the unique needs of Indigenous and vulnerable populations. • We strengthen CMHC’s leadership in the housing system by offering bold insights and thought leadership that influence others to act. • We work to deepen our understanding of the scale and factors behind households in core housing need and the social and economic arguments for additional investments. • We work to identify the systemic barriers that racialized Canadians face in securing and maintaining access to affordable, adequate housing, to ensure housing policies address inequity, bias and discrimination.

Our Research Hubs To help us respond to critical knowledge gaps, and further our understanding, raise awareness and influence decision makers around major areas of housing, we established working groups (HUBs) of cross-functional and multi-disciplinary experts from across the organization. We identified seven areas of focus: Core housing need Housing Supply finance gaps Racism Indigenous and systemic reconciliation barriers Policy Climate effectiveness change Broad research is needed to find root causes and potential solutions biggest to questions tackle the . Our accomplishments in 2023: Core housing need transitions of racialized Canadians4: Our research concluded that racialized groups face unique barriers in accessing housing that meets their needs. These include discriminatory barriers as well as heightened affordability challenges. Estimation that an additional 3.5 million homes are needed by 20305, above and beyond what is projected to restore affordability by 2030: Through effective modeling, we gained better sight of the magnitude of Canada’s housing supply shortages and a good understanding of the financial/capital needed to close that gap. Further work will include details across income groups, by market and by tenure type. Longitudinal study6 on the impacts of the NHS: We’re developing this study to characterize how NHS investments impact the lives of Canadians and the environment in which they live. Linking key surveys: We are developing an approach to link the Canadian Housing Survey7 and Census, and other existing data8 to assess the extent to which the NHS is achieving its targets to move persons out of core housing need and to provide affordable and inclusive housing to populations experiencing vulnerabilities. Research by Indigenous partners: With support from CMHC, the Assembly of First Nations is studying the transfer of care and control and finding capital to close the infrastructure gap on-reserve. Inuit Tapiriit Kanatami is developing research in support of the Inuit Nunangat Housing Strategy. Other research is being conducted on urban, rural and northern housing providers to address data gaps and needs. 4 https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-research/research-reports/housing-needs/ core-housing-need-transitions-racialized-communities-canada 5 https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-research/research-reports/accelerate-supply/ housing-shortages-canada-updating-how-much-we-need-by-2030 6 https://www.cmhc-schl.gc.ca/media-newsroom/news-releases/2023/research-grant-assessing-long-term-housing-outcomes 7 https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-research/surveys/canadian-housing-survey 8 https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-data

RECONCILIATION AND INDIGENOUS RELATIONS CMHC, is committed to closing the housing gap for Indigenous peoples. This cannot be accomplished without adopting reconciliation principles within our organization, including in our housing programs and policies. Our Reconciliation Action Plan In 2022, an Indigenous-led team began developing CMHC’s Reconciliation Action Plan (RAP). The RAP articulates the vision, goals, guiding principles and actions to advance meaningful reconciliation.

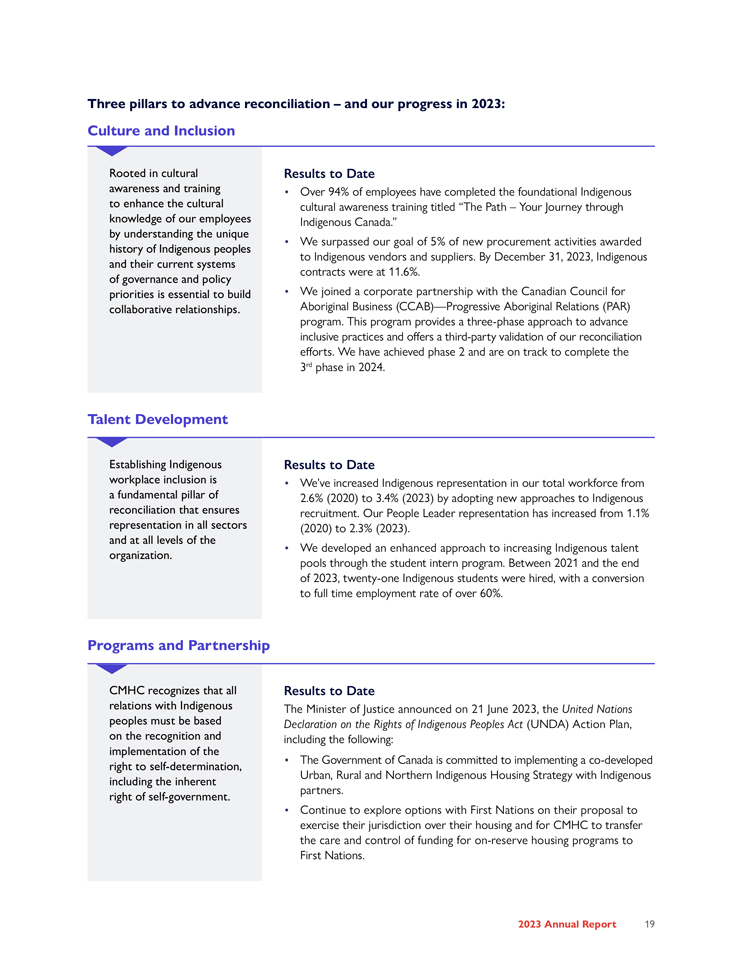

Three pillars to advance reconciliation – and our progress in 2023: Culture and Inclusion Rooted in cultural Results to Date awareness and training • Over 94% of employees have completed the foundational Indigenous to enhance the cultural cultural awareness training titled “The Path – Your Journey through knowledge of our employees Indigenous Canada.” by understanding the unique • We surpassed our goal of 5% of new procurement activities awarded history of Indigenous peoples to Indigenous vendors and suppliers. By December 31, 2023, Indigenous and their current systems contracts were at 11.6%. of governance and policy priorities is essential to build • We joined a corporate partnership with the Canadian Council for collaborative relationships. Aboriginal Business (CCAB)—Progressive Aboriginal Relations (PAR) program. This program provides a three-phase approach to advance inclusive practices and offers a third-party validation of our reconciliation efforts. We have achieved phase 2 and are on track to complete the 3rd phase in 2024. Talent Development Establishing Indigenous Results to Date workplace inclusion is • We’ve increased Indigenous representation in our total workforce from a fundamental pillar of 2.6% (2020) to 3.4% (2023) by adopting new approaches to Indigenous reconciliation that ensures recruitment. Our People Leader representation has increased from 1.1% representation in all sectors (2020) to 2.3% (2023). and at all levels of the • We developed an enhanced approach to increasing Indigenous talent organization. pools through the student intern program. Between 2021 and the end of 2023, twenty-one Indigenous students were hired, with a conversion to full time employment rate of over 60%. Programs and Partnership CMHC recognizes that all Results to Date relations with Indigenous The Minister of Justice announced on 21 June 2023, the United Nations peoples must be based Declaration on the Rights of Indigenous Peoples Act (UNDA) Action Plan, on the recognition and including the following: implementation of the • The Government of Canada is committed to implementing a co-developed right to self-determination, Urban, Rural and Northern Indigenous Housing Strategy with Indigenous including the inherent partners. right of self-government. • Continue to explore options with First Nations on their proposal to exercise their jurisdiction over their housing and for CMHC to transfer the care and control of funding for on-reserve housing programs to First Nations.

Working with Indigenous governments and organizations We are committed to a renewed nation-to-nation relationship with Indigenous peoples, guided by the principle that Indigenous nations are self-determining, self-governing, and rightfully aspire to having strong and healthy communities. The NHS recognizes that Indigenous peoples, wherever they reside, should have access to adequate, secure, and affordable housing. Many NHS programs prioritize funding for projects that serve Indigenous peoples and families. Proposals for projects supporting Indigenous peoples are reviewed through separate, more flexible processes to help reduce barriers and ensure that more projects serving these communities are funded. Affordable Housing Fund Of the $225 million available to ensure community housing providers can protect affordability for Indigenous families and undertake necessary repairs to their projects, $25 million is available through the Affordable Housing Fund to preserve units operated and administered by Indigenous organizations under long-term agreements. To date, 144 of 560 units have been committed through this funding stream. Indigenous Shelter and Transitional Housing Initiative At the end of 2023, $142.8 million has been conditionally or financially committed toward the construction of 11 shelters and 25 transitional homes, new safe spaces for Indigenous women, 2SLGBTQQIA+ people, and their children. Rapid Housing Initiative (RHI) 40% of all units created under RHI are for First Nations, Inuit, or Métis people, representing 6,239 units at the end of 2023. Federal Community Housing Initiative $1.9 million to maintain at least 170 urban, rural and northern units, is dedicated to helping ensure community housing providers can protect affordability and undertake necessary repairs for Indigenous peoples living in urban, rural and northern communities. Federal Lands Initiative (FLI) In 2021, the FLI introduced strategies to address barriers to participation and enhance engagement with Indigenous organizations. At the end of 2023, 25% of successful projects included Indigenous participation. Canada Greener Affordable Homes Program The program has committed funding to support 6 pre-retrofit applications from Indigenous proponents to date.

ANTI-RACISM AND EQUITY CMHC is committed in supporting populations in core housing need, and experiencing homelessness, which affect many equity-denied groups who continue to face barriers to accessing housing. We are committed to doing our part to build a more equitable housing system.

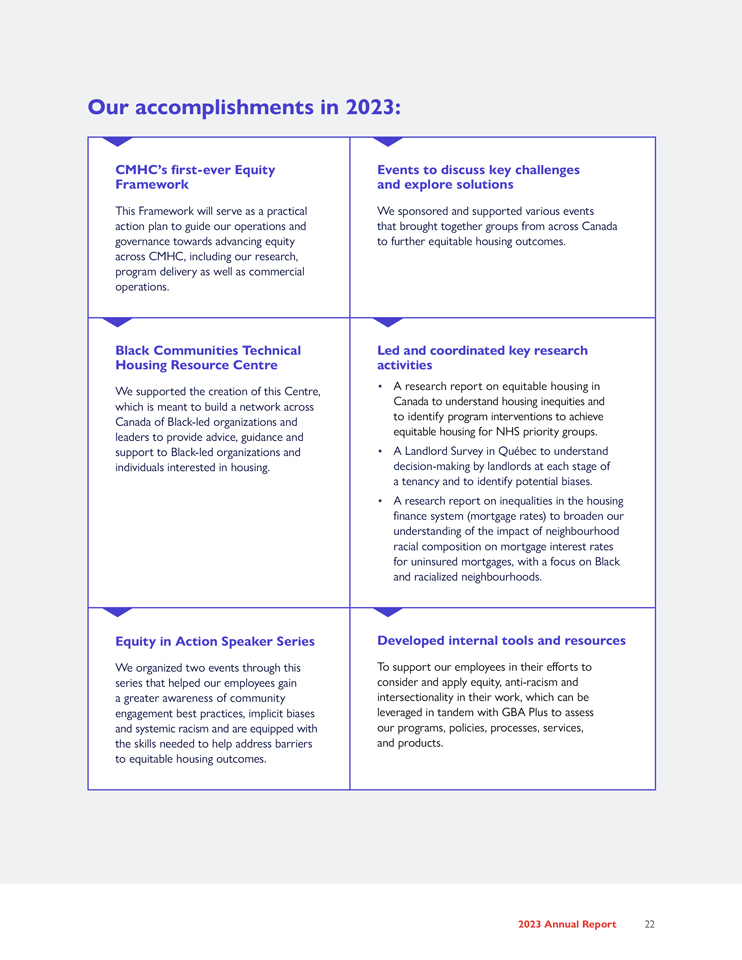

Our accomplishments in 2023: CMHC’s first-ever Equity Events to discuss key challenges Framework and explore solutions This Framework will serve as a practical We sponsored and supported various events action plan to guide our operations and that brought together groups from across Canada governance towards advancing equity to further equitable housing outcomes. across CMHC, including our research, program delivery as well as commercial operations. Black Communities Technical Led and coordinated key research Housing Resource Centre activities We supported the creation of this Centre, • A research report on equitable housing in which is meant to build a network across Canada to understand housing inequities and Canada of Black-led organizations and to identify program interventions to achieve leaders to provide advice, guidance and equitable housing for NHS priority groups. support to Black-led organizations and • A Landlord Survey in Québec to understand individuals interested in housing. decision-making by landlords at each stage of a tenancy and to identify potential biases. • A research report on inequalities in the housing finance system (mortgage rates) to broaden our understanding of the impact of neighbourhood racial composition on mortgage interest rates for uninsured mortgages, with a focus on Black and racialized neighbourhoods. Equity in Action Speaker Series Developed internal tools and resources We organized two events through this To support our employees in their efforts to series that helped our employees gain consider and apply equity, anti-racism and a greater awareness of community intersectionality in their work, which can be engagement best practices, implicit biases leveraged in tandem with GBA Plus to assess and systemic racism and are equipped with our programs, policies, processes, services, the skills needed to help address barriers and products. to equitable housing outcomes.

OUR CULTURE • If strategy is what we do, then culture is how we do it. When combined with strategy, culture accelerates execution and creates strategic advantage. Culture is created communally and is a key driver to influence meaningful change. Demonstrating our values is a shared accountability and our employee community is expected and motivated to do so every day. Our corporate values articulate how we want to think and act – Courage, Community and Impact. • Our approach to culture gives us the courage to do what is right – ask tough questions, try new things, and stand up for those who face housing challenges. As a community (inside and outside CMHC), we champion diversity and equity in our housing system and trust in one another. We are committed to building impactful solutions by focusing on the outcomes that matter the most as we strive toward a future where everyone in Canada has a place to call home. • While culture is a shared accountability for all employees, our People Leaders have enormous influence to set the organizational context for their teams by establishing clear goals, coaching and providing ongoing feedback, and making decisions on priorities – all while fostering an inclusive and collaborative environment. Courage Community Impact We have a bold aspiration and We are one diverse team, mutually We prioritize the results that must lead difficult but necessary trusting and supporting each other, have the most impact on changes to the housing system. and creating partnerships in the our aspiration. best interest of the communities that we serve.

OUR PEOPLE Workplace Diversity, Equity and Inclusion Our culture of inclusivity makes it possible for us to attract and retain top talent, foster innovation and growth, and deliver meaningful programs and services to the people we serve. Our 2023-2025 Workplace Diversity, Equity and Inclusion Framework guides our efforts to sustain a diverse workforce and cultivate an inclusive workplace culture. It is creating meaningful changes and greater shared accountability in advancing workplace diversity, equity and inclusion at CMHC, evident in our stable Inclusion Index at 82%. We improved our self-identification form and strengthened our workforce representation measurements. This ensures that we’re collecting reliable and inclusive data to inform our work. We made important progress in meeting our minimum workforce representation goals, including leadership representation. We remain committed to having a workforce that is representative of the Canadian population.

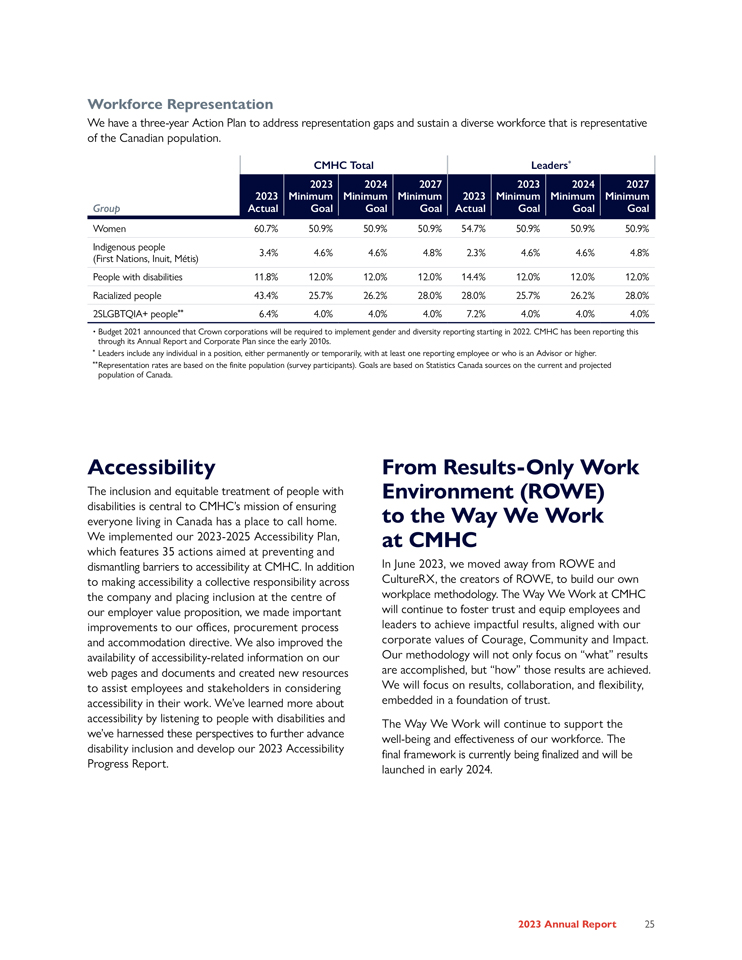

Workforce Representation We have a three-year Action Plan to address representation gaps and sustain a diverse workforce that is representative of the Canadian population. CMHC Total Leaders* 2023 2024 2027 2023 2024 2027 2023 Minimum Minimum Minimum 2023 Minimum Minimum Minimum Group Actual Goal Goal Goal Actual Goal Goal Goal Women 60.7% 50.9% 50.9% 50.9% 54.7% 50.9% 50.9% 50.9% Indigenous people 3.4% 4.6% 4.6% 4.8% 2.3% 4.6% 4.6% 4.8% (First Nations, Inuit, Métis) People with disabilities 11.8% 12.0% 12.0% 12.0% 14.4% 12.0% 12.0% 12.0% Racialized people 43.4% 25.7% 26.2% 28.0% 28.0% 25.7% 26.2% 28.0% 2SLGBTQIA+ people** 6.4% 4.0% 4.0% 4.0% 7.2% 4.0% 4.0% 4.0% • Budget 2021 announced that Crown corporations will be required to implement gender and diversity reporting starting in 2022. CMHC has been reporting this through its Annual Report and Corporate Plan since the early 2010s. * Leaders include any individual in a position, either permanently or temporarily, with at least one reporting employee or who is an Advisor or higher. ** Representation rates are based on the finite population (survey participants). Goals are based on Statistics Canada sources on the current and projected population of Canada. Accessibility The inclusion and equitable treatment of people with disabilities is central to CMHC’s mission of ensuring everyone living in Canada has a place to call home. We implemented our 2023-2025 Accessibility Plan, which features 35 actions aimed at preventing and dismantling barriers to accessibility at CMHC. In addition to making accessibility a collective responsibility across the company and placing inclusion at the centre of our employer value proposition, we made important improvements to our offices, procurement process and accommodation directive. We also improved the availability of accessibility-related information on our web pages and documents and created new resources to assist employees and stakeholders in considering accessibility in their work. We’ve learned more about accessibility by listening to people with disabilities and we’ve harnessed these perspectives to further advance disability inclusion and develop our 2023 Accessibility Progress Report. From Results-Only Work Environment (ROWE) to the Way We Work at CMHC In June 2023, we moved away from ROWE and CultureRX, the creators of ROWE, to build our own workplace methodology. The Way We Work at CMHC will continue to foster trust and equip employees and leaders to achieve impactful results, aligned with our corporate values of Courage, Community and Impact. Our methodology will not only focus on “what” results are accomplished, but “how” those results are achieved. We will focus on results, collaboration, and flexibility, embedded in a foundation of trust. The Way We Work will continue to support the well-being and effectiveness of our workforce. The final framework is currently being finalized and will be launched in early 2024.

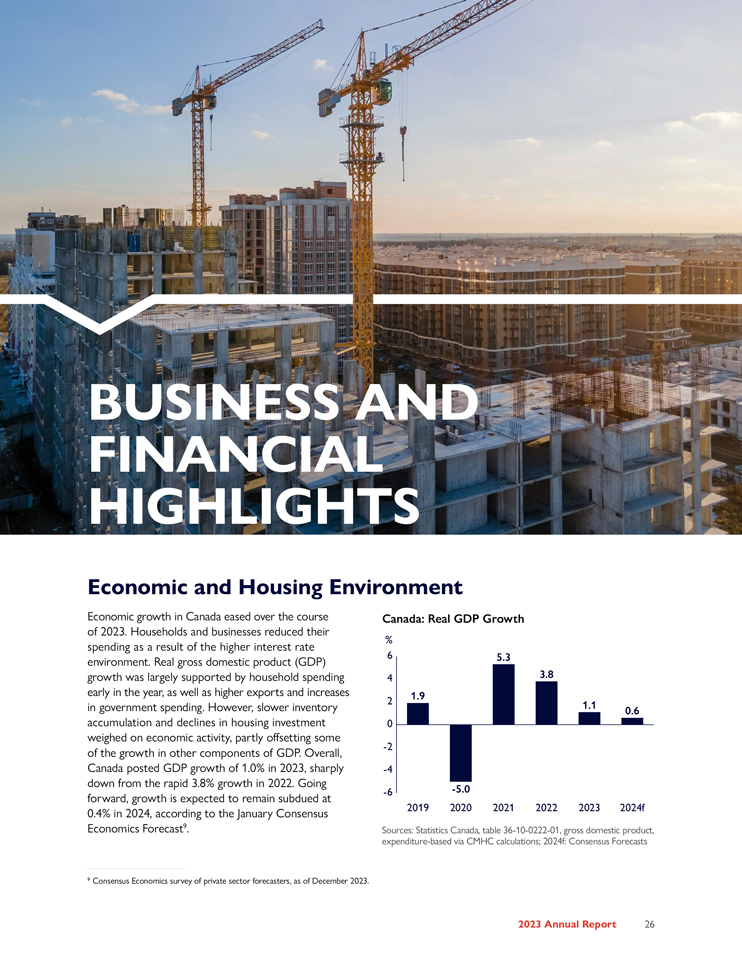

BUSINESS AND FINANCIAL HIGHLIGHTS Economic and Housing Environment Economic growth in Canada eased over the course Canada: Real GDP Growth of 2023. Households and businesses reduced their % spending as a result of the higher interest rate 6 5.3 environment. Real gross domestic product (GDP) growth was largely supported by household spending 4 3.8 early in the year, as well as higher exports and increases 1.9 2 1.1 in government spending. However, slower inventory 0.6 accumulation and declines in housing investment 0 weighed on economic activity, partly offsetting some -2 of the growth in other components of GDP. Overall, Canada posted GDP growth of 1.0% in 2023, sharply -4 down from the rapid 3.8% growth in 2022. Going -6 -5.0 forward, growth is expected to remain subdued at 0.4% in 2024, according to the January Consensus 2019 2020 2021 2022 2023 2024f Economics Forecast9. Sources: Statistics Canada, table 36-10-0222-01, gross domestic product, expenditure-based via CMHC calculations; 2024f: Consensus Forecasts 9 Consensus Economics survey of private sector forecasters, as of December 2023.

While headline inflation declined from its peak of 8.1% in 2022, its downward trend slowed over the first half of 2023 (reaching 3.4% in December). To bring inflation down, the Bank of Canada continued to raise its policy rate further throughout 2023, reaching 5% in July. Long-term bond yields rose sharply since July, reaching levels not recorded since the 2008-2009 recession. However, bond yields have fallen in recent months, roughly returning to the same levels at the start of the year, at 3.21%. Persistently higher bond yields are likely to constrain both investment and consumption in Canada. As the impacts of this uncertain environment spread throughout the economy, household consumption growth started to slow over the final three quarters of the year. Meanwhile, household disposable income continued to rise. As a result, the household savings rate moved slightly higher, to 5.6% in 2023, above its 3.4% average in the decade to 2020. Stronger disposable income was also a key factor contributing to a slight improvement in the ratio of household debt to disposable income. Disposable income was 1.0% higher in the third quarter of 2023 compared with the previous quarter, while debt edged up by 0.8%. Overall, the ratio fell to a seasonally adjusted 181.6% in the third quarter, from 181.9% in the second quarter. This means that for every dollar of disposable income, Canadians owed $1.82 in credit market debt. Looking ahead, however, the ratio is expected to edge higher before stabilizing, as the share of income spent on interest payments at current rates is expected to continue to rise as homeowners renew their mortgages. Thus, elevated household indebtedness remained a key vulnerability for the Canadian economy. Labour markets in Canada showed some resilience in 2023. However, the pace of employment growth started moderating during the first half of the year. While the unmet demand for labour started to ease, reports of shortages of skilled workers remained widespread. The unemployment rate rose throughout the year but remained low, rising from 5.0% in April to 5.8% in December. Wage growth stayed in the 4-5% range since 2022, considerably higher than the 2.3% average over the past decade. The series of mortgage rate hikes since mid-2022, combined with strict mortgage qualification criteria, limited the number of eligible homebuyers. Higher rates also pose potential challenges for mortgage renewals in the future. In 2023, Canada MLS® sales dropped 11% to 443,636 units relative to the previous year. This level was 33% below peak sales recorded in 2021. MLS® listings decreased by 8% as some sellers opted to wait for better housing conditions or couldn’t afford upgrades. This led to price declines. The average MLS® home price fell 4% in 2023 to $678,319, aligning closely with 2021 levels. Higher interest rates and persistent labour shortages hindered developers’ ability to increase housing supply. Nevertheless, new home construction almost hit multi-decade highs at 241,735 units, but fell short of the 2021-2022 levels of approximately 270,000 units. While high-rise starts peaked in 2023, low-rise sectors, notably single-detached and semi-detached homes, experienced declines. The intensified affordability issue prompted a shift in demand towards more affordable housing options. Furthermore, apartment projects often require an extended period, spanning several years between pre-selling and construction. Therefore, the surge in apartment starts might not entirely reflect the weakening of housing demand and might instead mirror pre-inflationary conditions. Strong demand for rentals persisted due to favourable job market conditions and demographic factors, such as immigration and population aging. The reduced opportunities for potential homebuyers also contributed to the increased rental demand. Despite substantial rental construction, the vacancy rate for rental apartments reached a new low of 1.5% in 2023. This led to record rent growth. The fixed-sample average 2-bedroom apartment rent in existing apartment structures grew by 8.0% to $1,359 in 2023. In the condominium market, average 2-bedroom rents reached $2,049 in 2023. This increased housing affordability challenges, particularly for low-income renters.

Consolidated Financial Highlights We deliver our mandate and pursue our strategy through three business activities—Assisted Housing, Mortgage Insurance and Mortgage Funding. Our consolidated results are provided in this section, which is followed by a description of each of our business activities and their results. IFRS 17 Insurance contracts – effective date of 1 January 2023 We adopted IFRS 17 Insurance contracts, which replaces IFRS 4 Insurance contracts on 1 January 2023. As the adoption of IFRS 17 has been applied retrospectively, we have restated the 2022 comparative results, where applicable. Financial statement line items on the consolidated balance sheet have changed with the provision for claims replaced by insurance contract liabilities, which now also includes unearned premiums and fees from insurance contracts. In addition, amounts related to deferred acquisition costs, deferred Government of Canada fees, estimated borrower judgment recoveries, and premiums receivable are now recorded within insurance contract liabilities instead of accounts receivable and other assets. Government of Canada fees payable, previously recorded in accounts payable and other liabilities, is also recorded in insurance contract liabilities. Financial statement line item descriptions on the consolidated statement of income and comprehensive income have changed with insurance claims expense removed and self-insurance service expense added. IFRS 17 also requires us to present the following financial statement line items: insurance revenue, insurance service expenses, insurance service result and insurance finance expense for contracts issued. With the adoption of IFRS 17, we have also adopted new performance metrics as follows: • Insurance service expense ratio: Replacing the loss ratio, this metric measures the ratio between insurance service expense over insurance revenues. • Contractual Service Margin (CSM): Represents the expected future profit of our insurance contract liabilities. • Initial CSM ratio: Represents the estimated embedded profit of premiums received on insurance contracts in the period. Our return on equity and return on required equity is 2%-5% lower on average subsequent to the adoption of IFRS 17, mainly due to slower recognition patterns of premiums received based on new recognition methodologies required by IFRS 17. For further details, refer to Note 3 of our Consolidated Financial Statements. Condensed Consolidated Balance Sheets Assisted Mortgage Mortgage Housing Insurance Funding Activity Activity Activity Eliminations Total (in millions) 2023 2022 2023 2022 2023 2022 2023 2022 (restated) 2023 2022 (restated) Cash, cash equivalents and 1 5,325 6,848 17,644 15,750 3,858 3,445 (728) (990) 26,099 25,053 investment securities Loans 13,110 10,262 56 62 257,996 259,352 — 271,162 269,676 All other assets 972 532 551 954 786 955 (1) (2) 2,308 2,439 Total assets 19,407 17,642 18,251 16,766 262,640 263,752 (729) (992) 299,569 297,168 Insurance contract liabilities — 7,079 6,405 — — 7,079 6,405 Borrowings 17,721 15,798 — 257,996 259,352 (741) (1,006) 274,976 274,144 Unearned premiums and fees — 278 214 2,498 2,390 — 2,776 2,604 All other liabilities 872 998 614 377 689 679 — 2,175 2,054 Total liabilities 18,593 16,796 7,971 6,996 261,183 262,421 (741) (1,006) 287,006 285,207 Total equity of Canada 814 846 10,280 9,770 1,457 1,331 12 14 12,563 11,961 1 Includes securities purchased under resale agreements.

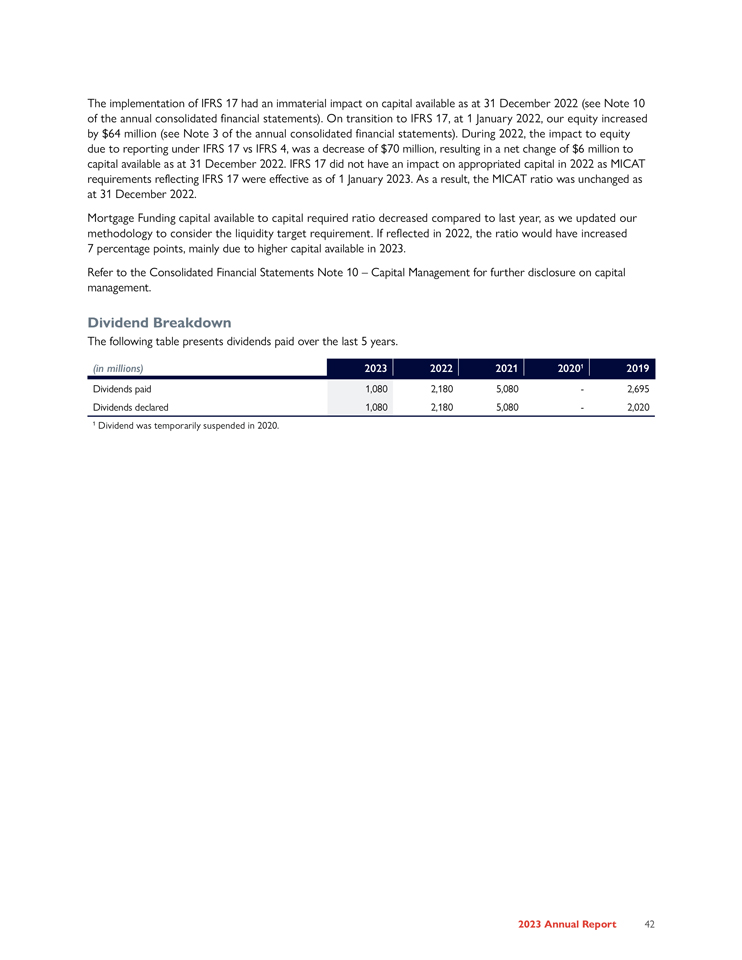

Financial Position In 2023, we declared dividends of $1,080 million, funded from our retained earnings from prior years and our 2023 net income of $1,310 million. We declare dividends after regulatory and other capitalization requirements are met ensuring that our Mortgage Insurance and Mortgage Funding activities are appropriately capitalized. Our total assets and liabilities increased throughout the year primarily due to increases in loans ($2,809 million) and borrowings ($2,078 million) at amortized cost in the Assisted Housing Activity due to additional loans under the Apartment Construction Loan Program (ACLP), the Affordable Housing Fund (AHF) and Canada Greener Homes Loans (CGHL). A decrease in interest rates and the suspension of the dividend in the Mortgage Insurance Activity, contributed to an increase of $1,046 million in cash, cash equivalents and investment securities. Insurance contract liabilities increased $674 million primarily attributed to new business underwritten outpacing our recognition of unearned profit. These increases in assets and liabilities were partially offset by decreases in both loans and borrowings at amortized cost of $1,356 million in the Mortgage Funding Activity as maturities of Canada Mortgage Bonds (CMB) exceeded new issuances and balances are decreasing under the Insured Mortgage Purchase Program (IMPP) as we are no longer issuing loans under the program. Condensed Consolidated Statements of Income and Comprehensive Income Assisted Mortgage Mortgage Housing Insurance Funding Activity Activity Activity Eliminations Total (in millions) 2023 2022 2023 2022 2023 2023 2022 2023 2022 (restated) 2022 (restated) Government funding 5,494 3,408 — — — 5,494 3,408 Housing programs expenses (5,114) (3,061) — — — (5,114) (3,061) Premiums and fees earned — 33 23 827 756 — 860 779 Insurance service result — 885 973 — — 885 973 Operating expenses (405) (361) (172) (177) (64) (68) — (641) (606) All other income1 5 204 160 153 97 53 12 23 274 433 Income (loss) before income taxes (20) 190 906 972 860 741 12 23 1,758 1,926 Income taxes—(50) (230) (245) (215) (185) (3) (6) (448) (486) Net income (loss) (20) 140 676 727 645 556 9 17 1,310 1,440 Other comprehensive income (loss) (12) 137 334 (573) 61 (160) (11) 23 372 (573) Comprehensive income (32) 277 1,010 154 706 396 (2) 40 1,682 867 1 Includes net interest income (loss), investment income, net gains (losses) on financial instruments, insurance finance expense for contracts issued, other income (loss) and self-insurance service income. Revenues and Expenses • In the Assisted Housing Activity, our revenues include government funding for the expenses we incur to deliver housing programs, resulting in no impact to net income. Government funding and housing programs expenses have increased in 2023, mainly due to the Housing Accelerator Fund (HAF), and increased activity in the Rapid Housing Initiative (RHI) and AHF. Related operating expenses also increased driven mainly by administration expenses to run CGHL and the third round of the RHI program, which were launched in the third quarter of 2022 and the first quarter of 2023, respectively. In 2023, our total income before income taxes decreased by $168 million (9%) mainly due to the following: • A decrease of $210 million (111%) in the Assisted Housing Activity, mainly due to an increase in net losses on financial instruments of $211 million (164%), primarily due to decreases in borrowing issuances for ACLP as we borrow at below market rates which leads to gains at the time of borrowing, as well as losses on loans issued

below market value in the CGHL portfolio, as more loans were issued in 2023 compared to 2022 for these programs. There was also a decrease in Other Income of $90 million (102%), primarily due to the valuation of our real estate inventory, which did not increase as significantly as compared to last year. This decrease was partially offset by an increase in net interest income of $102 million (785%) due to higher interest rates. • A decrease of $66 million (7%) in the Mortgage Insurance Activity, primarily due to a decrease of $88 million (9%) in the insurance service result due to higher claims expense as arrears rates increased this year, compared to prior year where lower arrears volume, better than expected economic conditions and updated model assumptions subsequent to the transition to IFRS 17 on 1 January 2022 led to a large release in the estimate of our liabilities for incurred claims. • The decrease was partially offset by an increase of $119 million (16%) in the Mortgage Funding Activity, primarily due to higher guarantee fees earned of $71 million (9%) as a result of pricing increases in recent years, as well as higher investment income of $41 million (84%) due to higher interest rates. Other Comprehensive Income Other comprehensive income (OCI), net of tax, increased by $945 million (165%) mainly due to the following: • An increase of $1,510 million (146%) in net unrealized gains from debt instruments held at fair value through other comprehensive income mostly due to decreases in bond yields in 2023, compared to the significant increases in bond yields in 2022 which resulted in large unrealized losses. • The increase is partially offset by an increase in remeasurement losses of the net defined benefit plans of $314 million (111%), mainly as a result of the decrease in the discount rate used to remeasure the pension obligation in 2023 compared to an increase in the discount rate in 2022. There was also an increase in insurance finance expense for insurance contracts issued of $251 million (143%) as interest rates decreased in the current year compared to an increase in the prior year. Financial Performance Against 2023 Plan 2023 (in millions) Actual Plan Total assets 299,569 298,333 Total liabilities 287,006 286,701 Total equity of Canada 12,563 11,632 Total revenues and government funding1 7,505 8,997 Total expenses2 5,747 6,806 Income taxes 448 547 Net income 1,310 1,644 Operating budget ratio (%) 9.1% 9.9% 1 Includes net interest income, insurance service result, net financial result, government funding, premiums and fees earned, and other income. 2 Includes housing programs expenses, operating expenses and self-insurance service income. Total equity was $931 million higher than plan mainly due to $700 million lower than planned dividends in 2023 to retain capital for higher than planned multi-unit insurance volumes. Total revenues and government funding were $1,492 million lower than planned due to lower than planned take-up of the One-time top up to the Canada Housing Benefit, and the timing of when government funding is required for the National Housing Strategy, particularly for Canada Greener Affordable Housing (CGAH) and RHI, for which the timing of expenses claimed were lower than planned in the year. Additionally, insurance service result was lower than planned as the actual claims release into revenue was slower than anticipated in the plan, which also contributed to the lower net income.

Assisted Housing What we do We help people living in Canada access housing that meets their needs and that they can afford. We achieve this through a range of programs and initiatives to support the construction of new housing supply, including affordable housing, and the repair, preservation and revitalization of existing affordable and community housing. How we do it We receive parliamentary appropriations and low-cost funding from the government to deliver housing programs that: • support the creation, repair and preservation of housing; • provide funding for affordability supports to housing proponents; • fund housing programs, including those in response to circumstances of critical national importance; • help Canadians acquire affordable housing, prioritizing target populations and those who have been made vulnerable and are facing housing challenges. We do this through our program delivery and partnerships with provinces, territories, municipalities, Indigenous governments and organizations, non-profit and co-operative housing organizations, and private sector companies. National Housing Strategy update We continue to deliver on the National Housing Strategy (NHS), which is giving more people in Canada a place to call home. We are currently on track to meet or exceed its targets for new units, repaired units, community housing units protected, as well as households for which housing need is reduced or eliminated. We are closely monitoring the potential impact of the current economic environment on our overall program outcomes for future years. Ongoing reporting for the NHS is available on the Place to Call Home website and includes achievements for all its initiatives (placetocallhome.ca). We help people living in Canada access housing that meets their needs and that they can afford.

Federal Budgets and 2023 Fall Economic Statement We were encouraged by additional housing investments announced in recent Federal Budgets and in the 2023 Fall Economic Statement (FES). We have worked diligently to ensure a timely launch of supporting initiatives. The following were launched in 2023: • Housing Accelerator Fund (HAF): Budget 2022 included $4 billion over five years, starting in 2022-2023, for a new Housing Accelerator Fund, that provides incentive funding to local governments encouraging initiatives aimed at increasing housing supply. The HAF was launched on 17 March 2023, the application portal opened on 4 July 2023 and has since closed. • Canada Greener Affordable Housing (CGAH): Announced in Budget 2021, an additional $458.5 million was allocated in Budget 2022 for this program. CGAH was launched on 26 May 2023 and the application portal opened on 1 June 2023. The following will have an impact starting in 2024: • Affordable Housing Fund (AHF) (formerly National Housing Co-Investment Fund (NHCF)): As announced in Budget 2022, funding was advanced so that all remaining funds will be committed by 2025-2026. This will accelerate the creation of up to 4,300 new units and the repair of up to 17,800 units for Canadians most in need. • Low-cost flood insurance program: Funding is provided for Public Safety Canada and CMHC to work with the Department of Finance Canada to establish this program, aimed at protecting households at high risk of flooding and without access to adequate insurance. • Reallocation of funding from the Affordable Housing Fund’s (AHF), repair stream to its new construction stream: This reallocation will be used, as needed, to boost the construction of new affordable homes for Canadians most in need.

Funding retrofits for greener homes The Canada Greener Affordable Homes Program (CGAH) contributes to the decarbonization goals of Canada’s Green Buildings Strategy, to help meet net-zero emissions by 2050. There are two funding opportunities: 1. Retrofit funding for deep energy retrofits aims to reduce energy consumption and greenhouse gas emissions of rental buildings. This funding will allow affordable housing providers to make improvements to aging buildings that will improve energy efficiency and extend their lifespan. 2. Pre-Retrofit funding is available for various activities, including energy audits, energy modelling studies and building condition assessment reports, needed for a Retrofit Funding application. The levels of energy consumption and greenhouse gas reductions needed to be eligible for CGAH are significant. Achieving this deep level of energy retrofits is new for many eligible proponents and takes complex project planning. The success of a Retrofit Funding project depends on a building’s physical characteristics, such as age, structure, and heating source. In other words, it takes time to develop a comprehensive deep energy retrofit plan that includes professional reports detailing how a project can achieve climate objectives, documents the scope of retrofits, cost estimates, and expected timelines for completion. Here is how we aimed to make the process easier for proponents: • Following the program launch, we gave virtual information sessions to affordable housing providers, highlighting program features, clarifying proponent and project eligibility criteria, and documentation requirements. There are ongoing efforts to market the program to eligible proponents. • We developed the CGAH application process, drawing on the success and simplicity of the Rapid Housing Initiative implementation and delivery. We used best practices, such as reducing documentation needed to apply, and improving the application portal user experience. This has made the process simpler and has provided a more positive client experience, and faster application approvals. • The delivery team meets with clients prior to their application submission to help determine the qualification of candidates or whether other programs with a lower depth of requirement are more suitable. • The delivery team works directly with applicants who may not fully meet the energy reduction requirements to determine a pathway forward for their project. • The first application window for Pre-Retrofit Funding was competitive and oversubscribed, with nearly 250 applications totaling $34.2 million in requested funding. This demonstrates great interest in completing deep energy retrofits on affordable housing projects. As successful proponents complete the necessary pre-development work over the next few months, we expect to see an influx of Retrofit Funding applications. • As of December 31, there were sixty-three Pre-Retrofit Funding commitments, of which sixty-two files have started advancing, and 2 are fully funded. 6 Retrofit Funding projects are currently under review. The Canada Greener Homes Loan (CGHL) was launched in June 2022. The CGHL builds on the Canada Greener Homes Grant delivered by Natural Resources Canada and offers interest-free financing of up to $40,000 to homeowners who undertake retrofits identified through an authorized EnerGuide energy assessment. Budget 2021 had provided $4.4 billion over five years for the Canada Greener Homes Loan (CGHL), that also included a dedicated stream of funding for the Canada Greener Affordable Housing. At the end of 2023, the Canada Greener Homes Loan has committed over 48,000 loans for more than $1.1 billion. Approximately 55% of applicants have completed their retrofits and have received final loan funding. The most popular retrofits are heat pumps, with 45% of loans including funding for a heat pump, windows and solar panels.

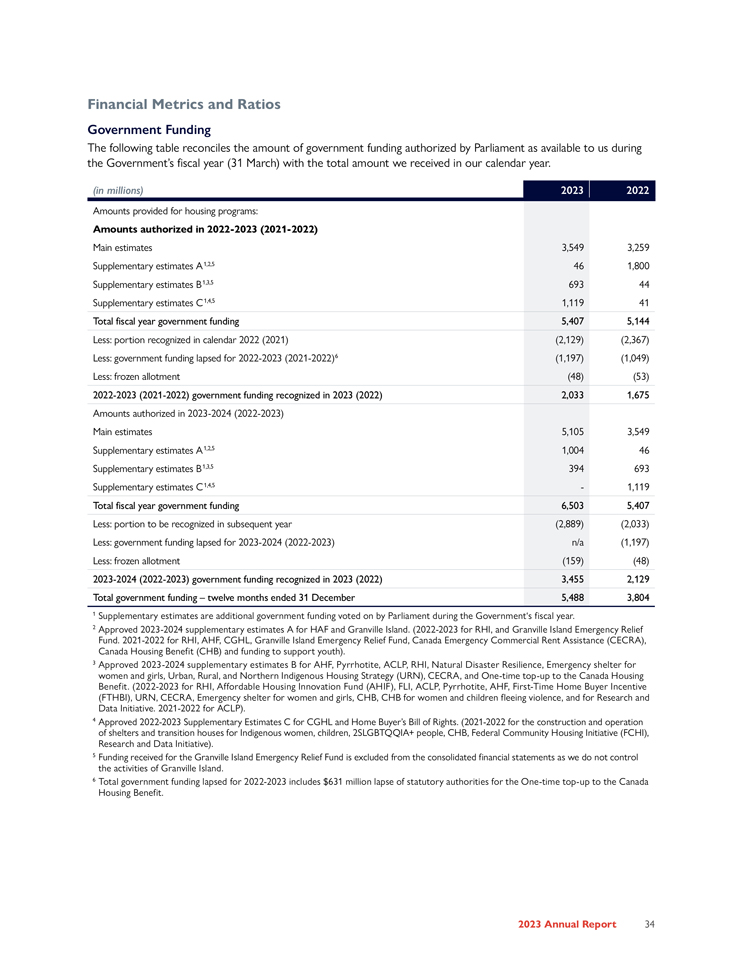

Financial Metrics and Ratios Government Funding The following table reconciles the amount of government funding authorized by Parliament as available to us during the Government’s fiscal year (31 March) with the total amount we received in our calendar year. (in millions) 2023 2022 Amounts provided for housing programs: Amounts authorized in 2022-2023 (2021-2022) Main estimates 3,549 3,259 Supplementary estimates A1,2,5 46 1,800 Supplementary estimates B1,3,5 693 44 Supplementary estimates C1,4,5 1,119 41 Total fiscal year government funding 5,407 5,144 Less: portion recognized in calendar 2022 (2021) (2,129) (2,367) Less: government funding lapsed for 2022-2023 (2021-2022)6 (1,197) (1,049) Less: frozen allotment (48) (53) 2022-2023 (2021-2022) government funding recognized in 2023 (2022) 2,033 1,675 Amounts authorized in 2023-2024 (2022-2023) Main estimates 5,105 3,549 Supplementary estimates A1,2,5 1,004 46 Supplementary estimates B1,3,5 394 693 Supplementary estimates C1,4,5—1,119 Total fiscal year government funding 6,503 5,407 Less: portion to be recognized in subsequent year (2,889) (2,033) Less: government funding lapsed for 2023-2024 (2022-2023) n/a (1,197) Less: frozen allotment (159) (48) 2023-2024 (2022-2023) government funding recognized in 2023 (2022) 3,455 2,129 Total government funding – twelve months ended 31 December 5,488 3,804 1 Supplementary estimates are additional government funding voted on by Parliament during the Government‘s fiscal year. 2 Approved 2023-2024 supplementary estimates A for HAF and Granville Island. (2022-2023 for RHI, and Granville Island Emergency Relief Fund. 2021-2022 for RHI, AHF, CGHL, Granville Island Emergency Relief Fund, Canada Emergency Commercial Rent Assistance (CECRA), Canada Housing Benefit (CHB) and funding to support youth). 3 Approved 2023-2024 supplementary estimates B for AHF, Pyrrhotite, ACLP, RHI, Natural Disaster Resilience, Emergency shelter for women and girls, Urban, Rural, and Northern Indigenous Housing Strategy (URN), CECRA, and One-time top-up to the Canada Housing Benefit. (2022-2023 for RHI, Affordable Housing Innovation Fund (AHIF), FLI, ACLP, Pyrrhotite, AHF, First-Time Home Buyer Incentive (FTHBI), URN, CECRA, Emergency shelter for women and girls, CHB, CHB for women and children fleeing violence, and for Research and Data Initiative. 2021-2022 for ACLP). 4 Approved 2022-2023 Supplementary Estimates C for CGHL and Home Buyer’s Bill of Rights. (2021-2022 for the construction and operation of shelters and transition houses for Indigenous women, children, 2SLGBTQQIA+ people, CHB, Federal Community Housing Initiative (FCHI), Research and Data Initiative). 5 Funding received for the Granville Island Emergency Relief Fund is excluded from the consolidated financial statements as we do not control the activities of Granville Island. 6 Total government funding lapsed for 2022-2023 includes $631 million lapse of statutory authorities for the One-time top-up to the Canada Housing Benefit.

Mortgage Insurance What we do We offer competitive mortgage insurance products to support homeownership financing and facilitate the construction, purchase, and refinance of multi-unit residential properties. These activities support the stability of the Canadian financial system. We operate these programs on a commercial basis with due regard for loss and without the need for government funding. How we do it We work with lenders to offer transactional homeowner and portfolio mortgage insurance products in all parts of Canada. We also offer multi-unit mortgage insurance, which provides access to preferred lenders’ interest rates for the construction, purchase and refinancing of multi-unit residential properties, including affordable rental housing. Our Products Transactional Homeowner Insurance Protects lenders against borrower default, enabling qualified borrowers, with a minimum down payment of 5% and less than 20%, to access mortgage financing at competitive rates for the purchase of 1-4 unit residential properties. Portfolio Insurance Allows lenders to pool low-ratio residential mortgages (i.e. mortgages on 1-4 unit residential properties with down payments of 20% or more) and insure these against borrower default, making them eligible for our securitization programs. Multi-Unit Residential Insurance Protects lenders against borrower default on loans for the construction, purchase and refinancing of multi-unit (5+ units) residential properties.

Homeowner Mortgage Loan Insurance (MLI) Homeowner mortgage loan insurance (MLI) is an important contributor to our affordability and stability objectives, and we continue to deliver on our commercial activities and seek an appropriate and diverse presence in the market. In 2023, our homeowner insurance products helped buyers purchase over 48,000 housing units across Canada, with just over 15% insured in rural areas of the country. CMHC also offers lenders default-management tools to help them assist borrowers who are facing difficulty in paying their insured mortgages. Energy-efficient housing is made more affordable with MLI. CMHC’s Eco Plus and Eco Improvement programs help reduce the impact of housing on climate change and contribute to the Government of Canada’s plan to achieve carbon neutrality by 2050. These programs offer a 25% partial insurance premium refund on the cost of mortgage loan insurance for those buying, building or improving homes for energy efficiency. As energy efficiency standards improve, so will the criteria for the Eco programs, which will see more certifications and ongoing alignment with Natural Resources Canada’s EnerGuide rating system. 187 loans benefitted from these programs in 2023. CMHC Connect is modernizing our homeowner mortgage loan insurance business by introducing enhanced technologies, processes and services that allow for faster decision-making and increased transparency. CMHC Connect is the umbrella platform that includes our insurance servicing, transactional homeowner MLI, portfolio insurance, and administration systems. Through this long-term project and investment, we are providing an improved client experience for lenders, which will ultimately better serve Canadians and build a strong foundation for the future. Significant components of our portfolio and claims, defaults and arrears functions have been modernized. Focus is on replacing and modernizing our transactional homeowner insurance underwriting system, emili, over the next few years. In the interim, we will continue to make investments in emili to ensure mortgage insurance risk is managed appropriately and that we deliver a positive experience to clients. Multi-Unit Mortgage Loan Insurance (MU MLI) Over 2023, uncertain economic conditions including high interest rates and increased construction costs continued to add pressure to the rental housing market, making it harder for multi-unit (MU) projects to be viable. Higher capital requirements for uninsured loans also incentivized lenders to send more loans to CMHC for MU MLI, allowing them to offer lower interest rates. Collectively, these conditions pushed demand for MU MLI to record-high levels. Focus on Underwriting Operations With the increased demand for MU MLI, CMHC undertook a composite plan focused on several key factors: augmented staffing resources, process and policy clarifications, and risk-based accelerated underwriting. The efficiency gained allowed us to succeed in processing the higher volume of applications received. These efforts have positioned our Underwriting Operations function well for 2024 as the evolution of our approach to underwriting continues. Enhanced GST Rental Rebate On 14 September 2023, the Prime Minister announced the introduction of legislation to enhance the Goods and Services Tax (GST) Rental Rebate for new purpose-built rental housing, to incentivize construction of much-needed rental housing. The legislation received Royal Assent on 15 December 2023. The enhanced GST rental rebate increases the GST rebate from 36% to 100% of the GST for new purpose-built rental housing, such as apartment buildings, student housing, and senior residences, built specifically for long-term rental accommodation. This enhancement is a temporary measure that will apply to purpose-built rental housing that qualify for the current rebate where the construction of the building or addition begins after 13 September 2023 and is substantially completed before 2036. Furthermore, certain harmonized provinces announced that they would match the enhanced GST rental rebate and remove fully or partially the provincial comment of the HST. The enhanced GST rental rebate is expected to increase volumes in our MLI business, however the impact is not yet known.

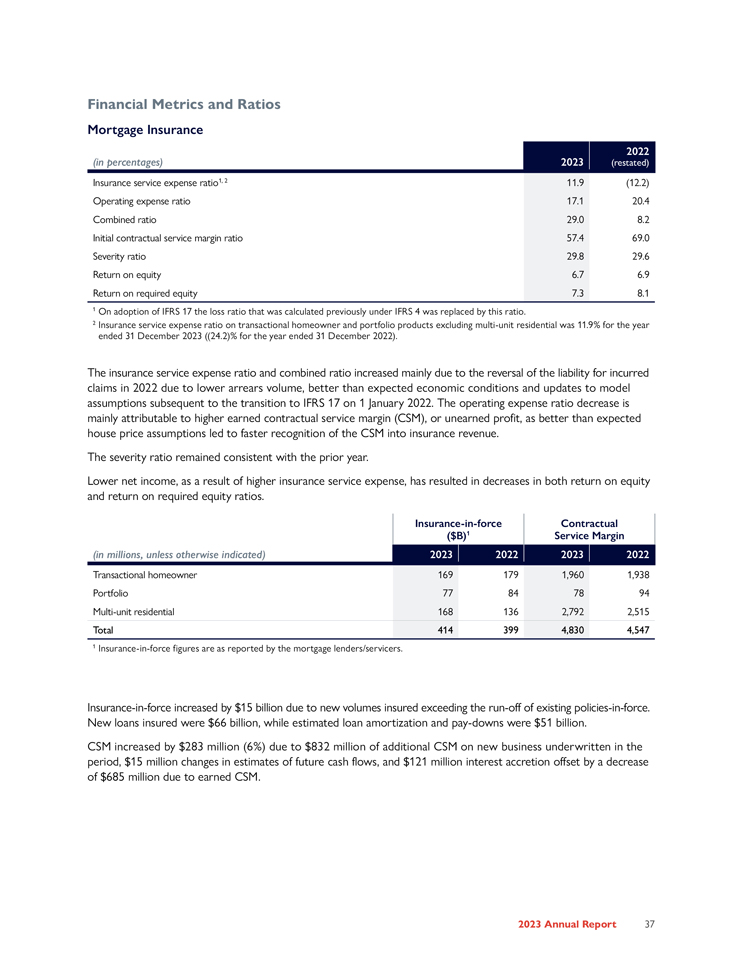

Financial Metrics and Ratios Mortgage Insurance percentages) 2023 2022 (in (restated) Insurance service expense ratio1, 2 11.9 (12.2) Operating expense ratio 17.1 20.4 Combined ratio 29.0 8.2 Initial contractual service margin ratio 57.4 69.0 Severity ratio 29.8 29.6 Return on equity 6.7 6.9 Return on required equity 7.3 8.1 1 On adoption of IFRS 17 the loss ratio that was calculated previously under IFRS 4 was replaced by this ratio. 2 Insurance service expense ratio on transactional homeowner and portfolio products excluding multi-unit residential was 11.9% for the year ended 31 December 2023 ((24.2)% for the year ended 31 December 2022). The insurance service expense ratio and combined ratio increased mainly due to the reversal of the liability for incurred claims in 2022 due to lower arrears volume, better than expected economic conditions and updates to model assumptions subsequent to the transition to IFRS 17 on 1 January 2022. The operating expense ratio decrease is mainly attributable to higher earned contractual service margin (CSM), or unearned profit, as better than expected house price assumptions led to faster recognition of the CSM into insurance revenue. The severity ratio remained consistent with the prior year. Lower net income, as a result of higher insurance service expense, has resulted in decreases in both return on equity and return on required equity ratios. Insurance-in-force Contractual ($B)1 Service Margin (in millions, unless otherwise indicated) 2023 2022 2023 2022 Transactional homeowner 169 179 1,960 1,938 Portfolio 77 84 78 94 Multi-unit residential 168 136 2,792 2,515 Total 414 399 4,830 4,547 1 Insurance-in-force figures are as reported by the mortgage lenders/servicers. Insurance-in-force increased by $15 billion due to new volumes insured exceeding the run-off of existing policies-in-force. New loans insured were $66 billion, while estimated loan amortization and pay-downs were $51 billion. CSM increased by $283 million (6%) due to $832 million of additional CSM on new business underwritten in the period, $15 million changes in estimates of future cash flows, and $121 million interest accretion offset by a decrease of $685 million due to earned CSM.

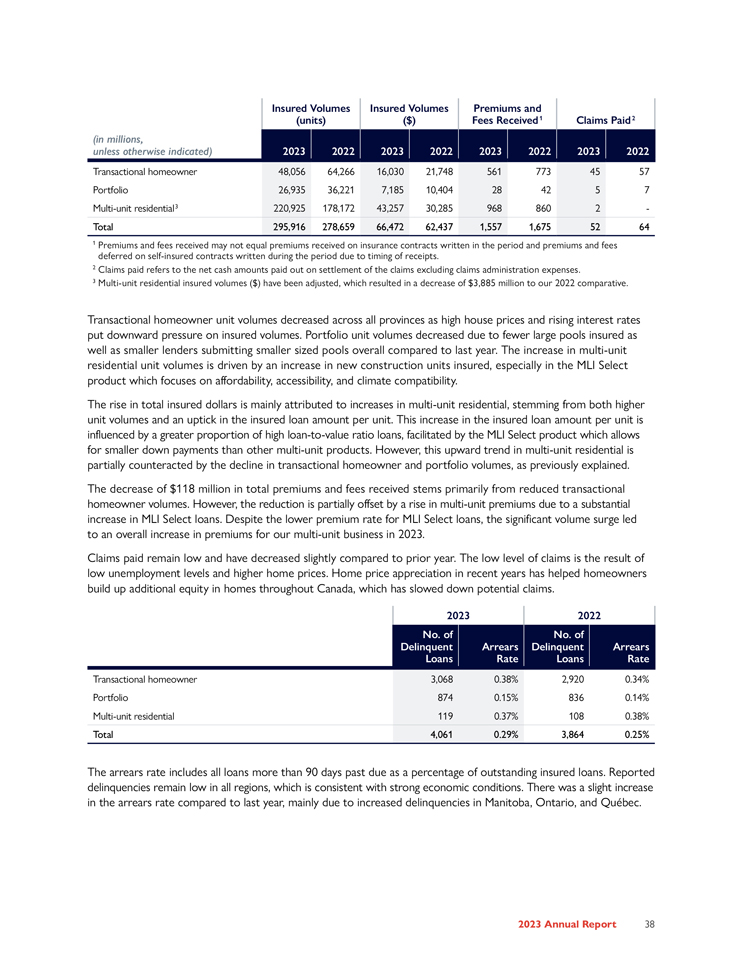

Insured Volumes Insured Volumes Premiums and (units) ($) Fees Received1 Claims Paid2 (in millions, unless otherwise indicated) 2023 2022 2023 2022 2023 2022 2023 2022 Transactional homeowner 48,056 64,266 16,030 21,748 561 773 45 57 Portfolio 26,935 36,221 7,185 10,404 28 42 5 7 Multi-unit residential3 220,925 178,172 43,257 30,285 968 860 2—Total 295,916 278,659 66,472 62,437 1,557 1,675 52 64 1 Premiums and fees received may not equal premiums received on insurance contracts written in the period and premiums and fees deferred on self-insured contracts written during the period due to timing of receipts. 2 Claims paid refers to the net cash amounts paid out on settlement of the claims excluding claims administration expenses. 3 Multi-unit residential insured volumes ($) have been adjusted, which resulted in a decrease of $3,885 million to our 2022 comparative. Transactional homeowner unit volumes decreased across all provinces as high house prices and rising interest rates put downward pressure on insured volumes. Portfolio unit volumes decreased due to fewer large pools insured as well as smaller lenders submitting smaller sized pools overall compared to last year. The increase in multi-unit residential unit volumes is driven by an increase in new construction units insured, especially in the MLI Select product which focuses on affordability, accessibility, and climate compatibility. The rise in total insured dollars is mainly attributed to increases in multi-unit residential, stemming from both higher unit volumes and an uptick in the insured loan amount per unit. This increase in the insured loan amount per unit is influenced by a greater proportion of high loan-to-value ratio loans, facilitated by the MLI Select product which allows for smaller down payments than other multi-unit products. However, this upward trend in multi-unit residential is partially counteracted by the decline in transactional homeowner and portfolio volumes, as previously explained. The decrease of $118 million in total premiums and fees received stems primarily from reduced transactional homeowner volumes. However, the reduction is partially offset by a rise in multi-unit premiums due to a substantial increase in MLI Select loans. Despite the lower premium rate for MLI Select loans, the significant volume surge led to an overall increase in premiums for our multi-unit business in 2023. Claims paid remain low and have decreased slightly compared to prior year. The low level of claims is the result of low unemployment levels and higher home prices. Home price appreciation in recent years has helped homeowners build up additional equity in homes throughout Canada, which has slowed down potential claims. 2023 2022 No. of No. of Delinquent Arrears Delinquent Arrears Loans Rate Loans Rate Transactional homeowner 3,068 0.38% 2,920 0.34% Portfolio 874 0.15% 836 0.14% Multi-unit residential 119 0.37% 108 0.38% Total 4,061 0.29% 3,864 0.25% The arrears rate includes all loans more than 90 days past due as a percentage of outstanding insured loans. Reported delinquencies remain low in all regions, which is consistent with strong economic conditions. There was a slight increase in the arrears rate compared to last year, mainly due to increased delinquencies in Manitoba, Ontario, and Québec.

Mortgage Funding What we do We promote stability in the Canadian financial system by providing access to funding for mortgages under all economic conditions. We do this by enabling approved financial institutions to pool eligible insured mortgages into marketable securities to be sold to investors. The sale of these securities generates funds for residential mortgage financing. How we do it We guarantee the timely payment of principal and interest of National Housing Act Mortgage-Backed Securities (NHA MBS) issued by approved financial institutions. We also guarantee Canada Mortgage Bonds (CMB) that are issued through the Canada Housing Trust. We are responsible for the administration of the covered bond legal framework, another source of mortgage funding that we administer on a cost-recovery basis. Our products National Housing Act Mortgage-Backed Securities Program Provides approved financial institutions with efficient access to mortgage financing in the form of amortizing securities. Canada Mortgage Bonds Program Provides approved financial institutions with efficient and stable access to mortgage funding through the issuance of marketable bullet bonds (principal paid at maturity). CMBs are issued through the Canada Housing Trust, with proceeds used to purchase NHA MBS. Canadian Registered Covered Bond Program Enables registered issuers to issue debt instruments backed by pools of uninsured Canadian residential mortgages to investors. Increased Annual Limit on Canada Mortgage Bond Program On 26 September 2023, the Deputy Prime Minister and Minister of Finance announced an increase to the annual limit for Canada Mortgage Bonds (CMB) from $40 billion to $45 billion in 2023 and up to $60 billion beginning 1 January 2024. The extra funding will be used to provide low-cost financing for multi-unit rental projects through CMHC-insured loans. The Minister of Finance authorized CMHC to provide up to $155 billion in 2023 and up to $170 billion of new guarantees of market NHA MBS annually, including $20 billion to support the special purpose guarantee in the CMB program, beginning 1 January 2024. National Housing Act Mortgage-Backed Securities In 2023, we continued to provide preferential guarantee fees for NHA MBS that contain social housing loans or multi-family loans insured under the MLI Multi-Unit Flex product or MLI Select product with the affordability commitment (“Affordability-Linked Pools”). These Affordability-Linked Pools supported the NHS by incentivizing lenders to provide cost-effective financing choices, helping increase the availability of affordable housing to people in Canada. The issuance of Affordability-Linked Pools totalled $29 billion in 2023, more than double the $12.6 billion issued in 2022.

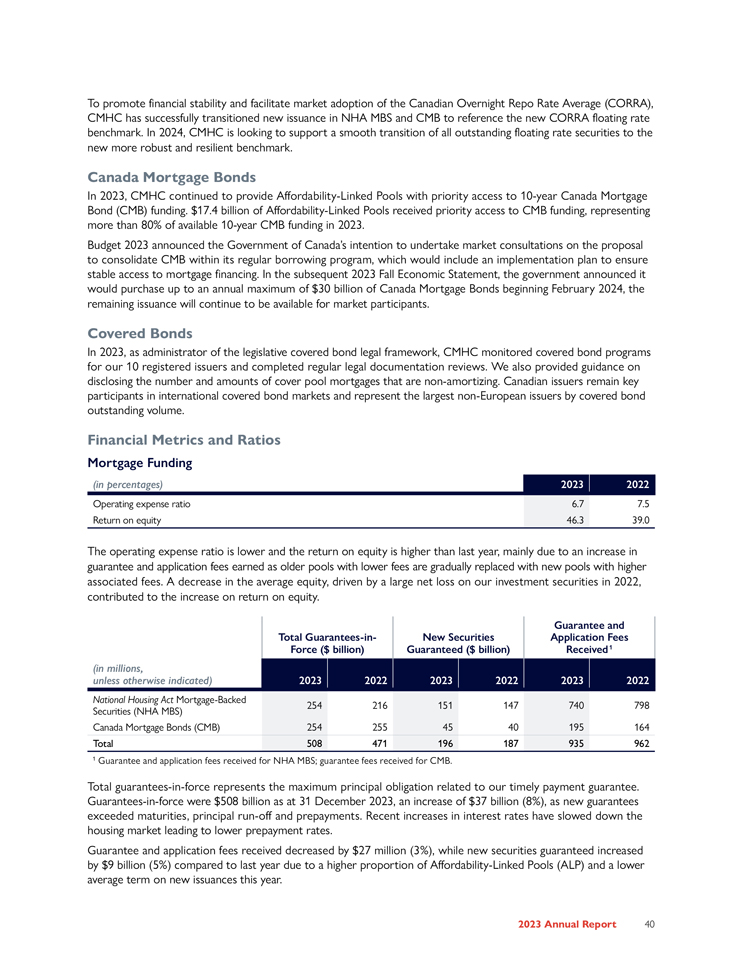

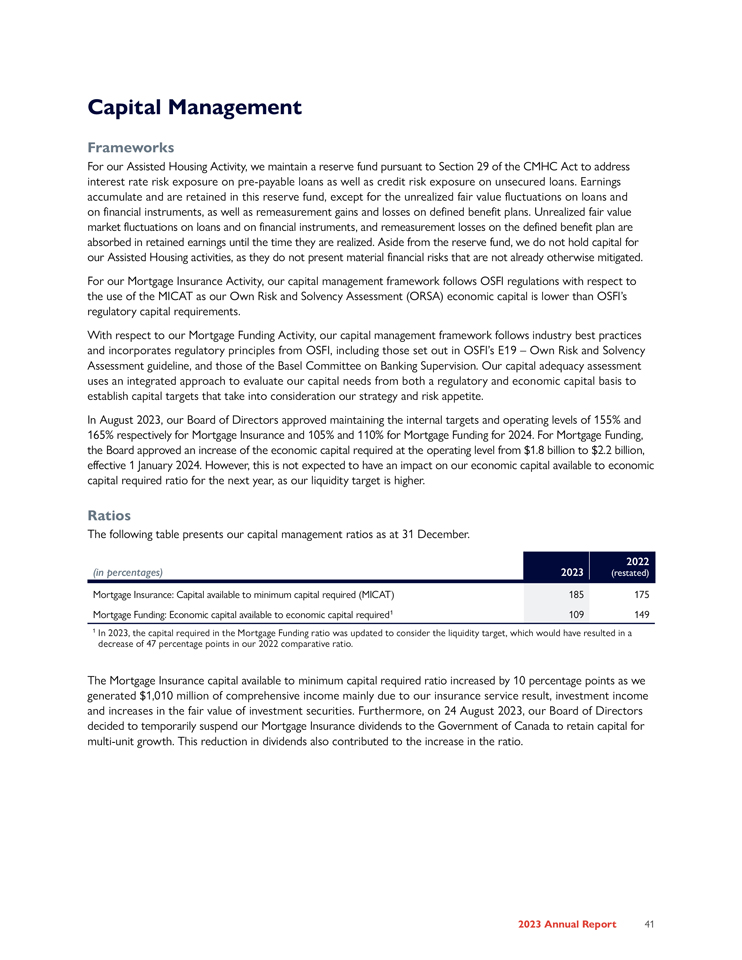

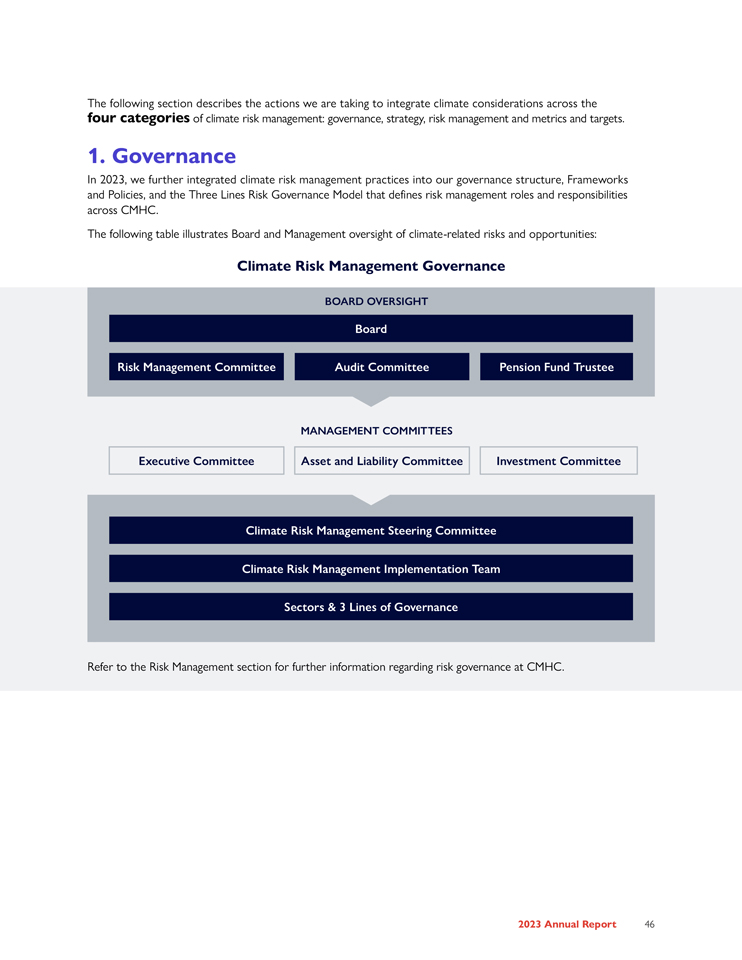

To promote financial stability and facilitate market adoption of the Canadian Overnight Repo Rate Average (CORRA), CMHC has successfully transitioned new issuance in NHA MBS and CMB to reference the new CORRA floating rate benchmark. In 2024, CMHC is looking to support a smooth transition of all outstanding floating rate securities to the new more robust and resilient benchmark. Canada Mortgage Bonds In 2023, CMHC continued to provide Affordability-Linked Pools with priority access to 10-year Canada Mortgage Bond (CMB) funding. $17.4 billion of Affordability-Linked Pools received priority access to CMB funding, representing more than 80% of available 10-year CMB funding in 2023. Budget 2023 announced the Government of Canada’s intention to undertake market consultations on the proposal to consolidate CMB within its regular borrowing program, which would include an implementation plan to ensure stable access to mortgage financing. In the subsequent 2023 Fall Economic Statement, the government announced it would purchase up to an annual maximum of $30 billion of Canada Mortgage Bonds beginning February 2024, the remaining issuance will continue to be available for market participants. Covered Bonds In 2023, as administrator of the legislative covered bond legal framework, CMHC monitored covered bond programs for our 10 registered issuers and completed regular legal documentation reviews. We also provided guidance on disclosing the number and amounts of cover pool mortgages that are non-amortizing. Canadian issuers remain key participants in international covered bond markets and represent the largest non-European issuers by covered bond outstanding volume. Financial Metrics and Ratios Mortgage Funding (in percentages) 2023 2022 Operating expense ratio 6.7 7.5 Return on equity 46.3 39.0 The operating expense ratio is lower and the return on equity is higher than last year, mainly due to an increase in guarantee and application fees earned as older pools with lower fees are gradually replaced with new pools with higher associated fees. A decrease in the average equity, driven by a large net loss on our investment securities in 2022, contributed to the increase on return on equity. Guarantee and Total Guarantees-in- New Securities Application Fees Force ($ billion) Guaranteed ($ billion) Received1 (in millions, unless otherwise indicated) 2023 2022 2023 2022 2023 2022 National Housing Act Mortgage-Backed 254 216 151 147 740 798 Securities (NHA MBS) Canada Mortgage Bonds (CMB) 254 255 45 40 195 164 Total 508 471 196 187 935 962 1 Guarantee and application fees received for NHA MBS; guarantee fees received for CMB. Total guarantees-in-force represents the maximum principal obligation related to our timely payment guarantee. Guarantees-in-force were $508 billion as at 31 December 2023, an increase of $37 billion (8%), as new guarantees exceeded maturities, principal run-off and prepayments. Recent increases in interest rates have slowed down the housing market leading to lower prepayment rates. Guarantee and application fees received decreased by $27 million (3%), while new securities guaranteed increased by $9 billion (5%) compared to last year due to a higher proportion of Affordability-Linked Pools (ALP) and a lower average term on new issuances this year.