SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| OR | |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended December 31, 2004 | |

| OR | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from__________ to __________ |

Commission file number 001-12440

ENERSIS S.A.

(Exact name of Registrant as specified in its charter)

| ENERSIS S.A. | CHILE | |

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organization) | |

| Avenida Santa Rosa 76,Santiago Santiago, Chile | ||

| (Address of principal executive offices) | ||

| Securities registered or to be registered pursuant to Section 12(b) of the Act: | ||

| Title of Each Class | Name of each exchange on which registered | |

| American Depositary Shares representing Common Stock | New York Stock Exchange | |

| Common Stock, no par value | New York Stock Exchange* | |

| U.S.$ 300,000,000 6.90% Notes due December 1, 2006 | New York Stock Exchange | |

| U.S.$ 350,000,000 7.40% Notes due December 1, 2016 | New York Stock Exchange | |

| U.S.$ 150,000,000 6.60% Notes due December 1, 2026 | New York Stock Exchange | |

| * | Listed, not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

U.S.$ 350,000,000 7.375% Notes due January 15, 2014

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: Shares of Common Stock: 32,651,166,465

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

YES ![]() NO

NO ![]()

Indicate by check mark which financial statements item the registrant has elected to follow:

| ITEM 17 | ITEM 18 | |

TABLE OF CONTENTS

i

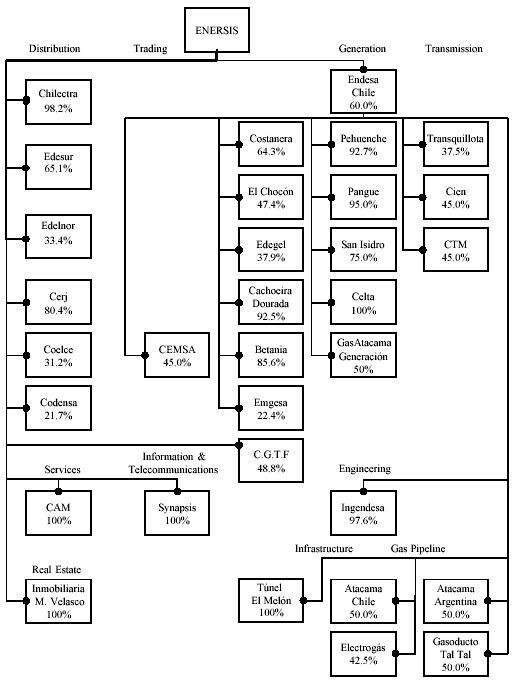

Enersis Simplified Corporate Structure

as of December 31, 2004*

| * | Percentages refer to economic interest in each one of our main operating entities. See “Introduction—Calculation of Economic Interest.” |

ii

INTRODUCTION

Financial Information

As used in this annual report on Form 20-F, first person personal pronouns such as “we,” “us” or “our” refers to ENERSIS S.A. (“Enersis”) and our consolidated subsidiariesunless the context indicates otherwise. Unless otherwise indicated, our interest in our principal subsidiaries and related companies is expressed in terms of our economic interest as of December 31, 2004.

In this annual report on Form 20-F, unless otherwise specified, references to “dollars,” “$,” “U.S. dollars” or “U.S.$ “ are to U.S. dollars, references to “pesos” or “Ch$ ” are to Chilean pesos, the legal currency of Chile, references to “Ar$” or “Argentine pesos” are to the legal currency of Argentina, references to “R$,” “reals” or “reais” are to Brazilian reals, the legal currency of Brazil, references to “soles” are to Peruvian soles, the legal currency of Peru, references to “CPs” or Colombian pesos are to the legal currency of Colombia and references to “UF” are to Unidades de Fomento. The Unidad de Fomento is a Chilean inflation-indexed, peso-denominated monetary unit. The UF rate is set daily in advance based on changes in the previous month’s inflation rate. As of December 31, 2004, 1 UF was equivalent to Ch$ 17,317.05. The U.S. dollar equivalent of 1 UF was U.S.$ 31.07 at December 31, 2004, using the Observed Exchange Rate reported by theBanco Central de Chile (the “Chilean Central Bank” or the “Central Bank”) as of December 31, 2004 of Ch$ 557.40 per U.S.$ 1.00. As of May 31, 2005, 1 UF was equivalent to Ch$ 17,407.28. The U.S. dollar equivalent of 1 UF was U.S.$ 29.86 as of May 31, 2005, using the Observed Exchange Rate reported by the Central Bank of Ch$ 583.00 per U.S.$ 1.00.

Our consolidated financial statements and, unless otherwise indicated, other financial information concerning us and our subsidiaries included in this annual report are presented in constant Chilean pesos in conformity with Chilean generally accepted accounting principles (“Chilean GAAP”) and the rules of theSuperintendencia de Valores y Seguros, or SVS. Our audited consolidated financial statements for the three fiscal years ended December 31, 2004 are expressed in constant Chilean pesos as of December 31, 2004. See note 2(c) to our consolidated financial statements. For Chilean accounting purposes, inflation adjustments are calculated based on a “one-month lag” convention using an inflation adjustment factor based on theIndice de Precios al Consumidor (Chilean consumer price index or “Chilean CPI”). The Chilean CPI is published by Chile’sInstituto Nacional de Estadísticas (the “National Bureau of Statistics”). For example, the inflation adjustment applicable for the 2004 calendar year is the percentage change between the November 2003 Chilean CPI and the November 2004 Chilean CPI, which was 2.5%. Chilean GAAP differs in certain important respects from accounting principles generally accepted in the United States (“U.S. GAAP”). See Note 36 to our consolidated financial statements contained elsewhere in this annual report for a description of the principal differences between Chilean GAAP and U.S. GAAP, as they relate to us, and for a reconciliation to U.S. GAAP of net income and stockholders’ equity for the period and as of the dates therein indicated. Certain amounts may not add up due to rounding.

Under Chilean GAAP, we consolidate the results from operations of a company defined as a “subsidiary” under Law No. 18,046 (the “Chilean Companies Act”). In order to consolidate a company, we must generally satisfy one of two criteria:

| • | control, directly or indirectly, more than a 50% voting interest in that company; or | |

| • | nominate or have the power to nominate a majority of the board of directors of that company if we control 50% or less of the voting interest of that company. |

As of December 31, 2004, we consolidated Endesa-Chile,Enersis Internacional, or Enersis Internacional,Chilectra S.A., or Chilectra,Inversiones Distrilima S.A. (which in turn consolidatedEmpresa de Distribución Eléctrica de Lima Norte S.A.A. or Edelnor),Empresa Distribuidora Sur S.A., or Edesur,Inmobiliaria Manso de Velasco Limitada, or IMV,Synapsis Soluciones y Servicios IT Ltda., or Synapsis,Compañía Americana de Multiservicios Ltda., or CAM,Companhia de Eletricidade do Rio de Janeiro S.A., or Cerj,Codensa S.A. E.S.P. or Codensa,Elesur S.A.or Elesur andInvestluz (which in turn consolidatedCompanhia Energética do Ceará S.A., or Coelce).

3

Endesa-Chile, in turn, consolidated all of its operational Chilean subsidiaries. In Argentina, Endesa-Chile consolidated the hydroelectric companyCentral Hidroeléctrica El Chocón S.A., or El Chocón, and thermoelectric companiesCentral Costanera S.A., or Costanera. In Colombia, Endesa-Chile consolidated generation companiesCentral Hidroeléctrica de Betania S.A. E.S.P., or Betania, andEmgesa S.A. E.S.P., or Emgesa. Endesa-Chile also consolidated the hydroelectric companyCachoeira Dourada S.A., or Cachoeira Dourada, in Brazil and the generation companyEdegel S.A.A., or Edegel, in Peru.

For the convenience of the reader, this annual report contains translations of certain Chilean peso amounts into U.S.$ at specified rates. Unless otherwise indicated, the U.S. dollar equivalent for information in Chilean pesos is based on the Observed Exchange Rate, as defined in “Item 3. Key Information—A. Selected Financial Data—Exchange Rates” at December 31, 2004. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos. No representation is made that the Chilean peso or U.S. dollar amounts shown in this annual report could have been or could be converted into U.S.$ or Chilean pesos, as the case may be, at such rate or at any other rate. See “Item 3. Key Information—A. Selected Financial Data—Exchange Rates.”

Technical Terms

References to “GW” and “GWh” are to gigawatts and gigawatt hours, respectively; references to “MW” and “MWh” are to megawatts and megawatt hours, respectively; references to “kW” and “kWh” are to kilowatts and kilowatt hours, respectively; and references to “kV” are to kilovolts. Unless otherwise indicated, statistics provided in this annual report with respect to electricity generation facilities are expressed in MW, in the case of the installed capacity of such facilities, and in GWh, in the case of the aggregate annual electricity production of such facilities. One GW = 1,000 MW, and one MW = 1,000 kW. Statistics relating to aggregate annual electricity production are expressed in GWh and are based on a year of 8,760 hours. Statistics relating to installed capacity and production of the electricity industry do not include electricity of self-generators. Statistics relating to our production do not include electricity consumed by our generators.

Energy losses are calculated by:

| • | subtracting the number of GWh of energy sold from the number of GWh of energy purchased and self-generated within a given period; and | |

| • | calculating the percentage that the resulting quantity bears to the aggregate number of GWh of energy purchased and self-generated within the same period. |

Calculation of Economic Interest

References are made in this annual report to the “economic interest” of Enersis in its subsidiaries or related companies. In circumstances where Enersis does not own its interest in a subsidiary or related company directly, the economic interest of Enersis in such ultimate subsidiary or related company is calculated by multiplying the percentage ownership interest of Enersis in a directly held subsidiary or related company by the percentage ownership interest of any entity in the chain of ownership of such ultimate subsidiary or related company. For example, if Enersis owns 60% of a directly held subsidiary and that subsidiary owns 40% of a related company, Enersis’ economic ownership interest in such related company would be 24%. References are also made in this annual report to the economic interest of Endesa-Chile in its subsidiaries and related companies. Calculation of Endesa-Chile’s economic interest is made based on the same method used to calculate the economic interest of Enersis.

Enersis, a holding company engaged in the generation, transmission and distribution of electricity in Chile, Argentina, Brazil, Colombia and Peru, beneficially owned as of the date of this annual report, directly or indirectly, 60.0% of Endesa-Chile’s outstanding capital stock. ENDESA, S.A. (“Endesa-Spain”), the largest electricity generation and distribution company in Spain, owned a 60.6% beneficial interest in Enersis as of December 31, 2004.

4

Forward-Looking Statements

This annual report contains statements that are or may constitute forward-looking statements. These statements appear throughout this annual report and include statements regarding our intent, belief or current expectations, including but not limited to any statements concerning:

| • | our capital investment program; | |

| • | trends affecting our financial condition or results from operations; | |

| • | our dividend policy; | |

| • | the future impact of competition and regulation; | |

| • | political and economic conditions in the countries in which we or our related companies operate or may operate in the future; | |

| • | any statements preceded by, followed by or that include the words “believes,” “expects,” “predicts,” “anticipates,” “intends,” “estimates,” “should,” “may” or similar expressions; and | |

| • | other statements contained or incorporated by reference in this annual report regarding matters that are not historical facts. |

Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to:

| • | changes in the regulatory environment in one or more of the countries in which we operate; | |

| • | changes in the environmental regulatory framework in one or more of the countries in which we operate; | |

| • | our ability to implement proposed capital expenditures, including our ability to arrange financing where required; | |

| • | the nature and extent of future competition in our principal markets; | |

| • | political, economic and demographic developments in the emerging market countries of South America where we conduct our business; and | |

| • | the factors discussed below under “Risk Factors.” |

You should not place undue reliance on such statements, which speak only as of the date that they were made. You should consider these cautionary statements together with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to forward-looking statements contained in this annual report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

For all these forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

5

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

| A. | Selected Financial Data. |

The following summary of consolidated financial data should be read in conjunction with, and is qualified in its entirety by reference to our audited consolidated financial statements including their notes, included elsewhere in this annual report. Our consolidated financial statements are prepared in accordance with Chilean GAAP and the related rules of the SVS, which together differ in certain important respects from U.S. GAAP. Note 36 to our consolidated financial statements provides a description of the principal differences between Chilean GAAP and U.S. GAAP and a reconciliation to U.S. GAAP of net income (loss) and shareholders’ equity for the periods and as of the dates therein indicated. Financial data as of or for each of the five years ended December 31, 2004 in the following table have been restated in constant Chilean pesos as of December 31, 2004. All data, except ratios and operating data, are in millions. For convenience purposes, all data presented in U.S.$ in the following summary as of or for the year ended December 31, 2004 are translated at the Observed Exchange Rate for December 31, 2004 of Ch$ 557.40 per U.S.$ 1.00. Such translations should not be construed as representing that the Chilean peso amounts actually represent, have been or could be converted into U.S.$ at the rates indicated or used herein or at all. For information concerning historical exchange rates, see “—Exchange Rates” below.

In 2003, we soldCompañía Eléctrica del Río Maipo or Río Maipo andInfraestructura Dos Mil S.A. or Infraestructura 2000, and, as a result, these companies ceased to be reflected in our financial statements with effect from January 1, 2003.

On May 27, 2004, we acquired 99.99% of Elesur S.A. and we have consolidated Elesur S.A. from that date.

The information detailed in the following table includes changes in certain accounting policies for the five years ended and as of December 31, 2004, which affect the comparability of the data presented below. See Note 3 to our consolidated financial statements for a further description of changes in our accounting policies.

6

| For the year ended December 31, | ||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| (millions of | ||||||||||||

| (millions of constant Ch$ of December 31, 2004) | U.S.$ )(1) | |||||||||||

| CONSOLIDATED INCOME | ||||||||||||

| STATEMENT DATA | ||||||||||||

| Chilean GAAP: | ||||||||||||

| Sales | 2,854,232 | 3,167,223 | 2,573,500 | 2,418,451 | 2,708,925 | 4,860 | ||||||

| Cost of operations | (1,961,835 | ) | (2,096,704 | ) | (1,791,035 | ) | (1,695,212 | ) | (1,898,088 | ) | (3,405 | ) |

| Administrative and selling expenses | (320,165 | ) | (289,377 | ) | (231,045 | ) | (173,741 | ) | (176,635 | ) | (317 | ) |

| Operating income | 572,232 | 781,142 | 551,420 | 549,498 | 634,202 | 1,138 | ||||||

| Equity in income (loss) of related | ||||||||||||

| Companies, net | 80 | (11,077 | ) | 8,556 | 17,955 | 31,145 | 56 | |||||

| Goodwill amortization | (74,242 | ) | (83,417 | ) | (524,192 | ) | (54,559 | ) | (53,201 | ) | (95 | ) |

| Interest (expense) income, net | (466,481 | ) | (410,174 | ) | (372,275 | ) | (362,027 | ) | (286,504 | ) | (514 | ) |

| Price-level restatement, net | (17,085 | ) | (29,368 | ) | (11,537 | ) | (10,818 | ) | 13,630 | 24 | ||

| Other non-operating income (expense), net | 382,344 | 11,145 | 74,841 | (56,832 | ) | (73,723 | ) | (132 | ) | |||

| Income before income taxes, minority | ||||||||||||

| interest and amortization of negative | ||||||||||||

| goodwill(2) | 396,848 | 258,251 | (273,187 | ) | 83,217 | 265,549 | 477 | |||||

| Income taxes | (151,481 | ) | (134,428 | ) | (68,344 | ) | (42,610 | ) | (137,241 | ) | (246 | ) |

| Extraordinary loss | — | — | (23,165 | ) | — | — | — | |||||

| Minority interest | (190,486 | ) | (129,565 | ) | 16,857 | (80,283 | ) | (101,107 | ) | (181 | ) | |

| Amortization of negative goodwill | 44,149 | 49,381 | 116,204 | 52,456 | 17,107 | 31 | ||||||

| Net Income (loss) | 99,030 | 43,639 | (231,635 | ) | 12,780 | 44,308 | 81 | |||||

| Net Income (loss) per Share | 14.56 | 5.26 | (27.94 | ) | 0.39 | 1.36 | n.a. | |||||

| Net Income (loss) per ADS | 728.16 | 263.17 | (1,396.90 | ) | 19.57 | 67.85 | n.a. | |||||

| U.S. GAAP (3): | ||||||||||||

| Operating Income | 795,191 | 832,342 | (223,671 | ) | 484,294 | 631,378 | 1,133 | |||||

| Equity in Income (loss) of Related | ||||||||||||

| Companies | 80 | (29,169 | ) | 24,115 | 44,703 | 31,147 | 56 | |||||

| Income taxes | (240,520 | ) | (228,010 | ) | (2,853 | ) | (22,293 | ) | (127,835 | ) | (229 | ) |

| Net Income (loss) from continuing | ||||||||||||

| operations | 76,530 | (40,083 | ) | (341,711 | ) | 30,217 | 151,774 | 272 | ||||

| Income (loss) from discontinued | ||||||||||||

| operations net of tax and minority | ||||||||||||

| interest | 270 | 294 | 172 | 71 | — | — | ||||||

| Net Income (loss) | 76,798 | 2,938 | (341,539 | ) | 30,001 | 151,774 | 272 | |||||

| Net Income (loss) from continuing | ||||||||||||

| operations per Share | 10.66 | (4.85 | ) | (41.21 | ) | 1.48 | 4.65 | — | ||||

| Net Income (loss) from continuing | — | |||||||||||

| operations per ADS | 532.08 | (241.73 | ) | (2,060.76 | ) | 73.80 | 67.85 | — | ||||

| Net Income (loss) per Share | 10.66 | 0.38 | (41.21 | ) | 1.47 | 4.65 | — | |||||

| Net Income (loss) per ADS | 533.92 | 17.70 | (2,059.74 | ) | 73.29 | 67.85 | — | |||||

| Cash Dividends per share | — | 1.95 | — | — | — | |||||||

| Cash Dividends per ADS | — | 96.35 | — | — | — | |||||||

| Capital stock | 812,235 | 812,235 | 812,235 | 2,446,711 | 2,446,130 | 4,388 | ||||||

| Number of shares of common stock | ||||||||||||

| (thousands) | 6,800,000 | 8,291,020 | 8,291,020 | 32,651,166 | 32,651,166 | 58,578 | ||||||

| Number of American Depository Shares | ||||||||||||

| (thousands) | 21,019 | 14,892 | 6,578 | 55,111 | 66,345 | 119 | ||||||

7

| As at December 31, | ||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| (millions of | ||||||||||||

| (millions of constant Ch$ of December 31, 2004) | U.S.$ )(1) | |||||||||||

| CONSOLIDATED BALANCE SHEET DATA | ||||||||||||

| Chilean GAAP: | ||||||||||||

| Total assets | 12,169,731 | 13,209,583 | 13,056,307 | 10,982,893 | 10,507,525 | 18,851 | ||||||

| Long Term Debt | 5,408,966 | 6,037,954 | 5,594,683 | 3,782,448 | 3,804,155 | 6,825 | ||||||

| Minority interest | 3,862,233 | 4,217,165 | 4,193,387 | 3,433,014 | 3,125,006 | 5,606 | ||||||

| Shareholders’ equity | 1,209,960 | 1,257,376 | 1,041,027 | 2,612,102 | 2,559,553 | 4,592 | ||||||

| U.S. GAAP (3): | ||||||||||||

| Total assets | 12,265,727 | 13,568,929 | 12,764,812 | 10,826,515 | 10,556,885 | 18,940 | ||||||

| Long Term Debt | 5,663,768 | 6,634,789 | 5,389,355 | 3,901,670 | 3,994,458 | 7,166 | ||||||

| Minority Interest | 3,709,857 | 4,103,444 | 4,407,383 | 3,205,939 | 2,901,154 | 5,205 | ||||||

| Shareholders’ Equity | 1,175,467 | 1,199,434 | 886,229 | 2,575,334 | 2,634,544 | 4,726 | ||||||

| �� | ||||||||||||

| As of or for the year ended | ||||||||||||

| December 31, | ||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||

| (millions of constant Ch$ of December 31, 2004, | (millions of | |||||||||||

| except for ratios and operating data) | U.S.$ )(1) | |||||||||||

| OTHER CONSOLIDATED FINANCIAL DATA | ||||||||||||

| Chilean GAAP: | ||||||||||||

| Capital expenditures | 355,101 | 353,594 | 329,121 | 265,256 | 265,934 | 477 | ||||||

| Depreciation and amortization | 450,018 | 449,353 | 481,247 | 415,124 | 386,292 | 693 | ||||||

| U.S. GAAP(3): | ||||||||||||

| Capital expenditures | 355,101 | 353,594 | 329,121 | 265,256 | 265,934 | 477 | ||||||

| Depreciation and amortization | 506,140 | 513,260 | 1,073,868 | 414,542 | 366,751 | 658 | ||||||

| (1) | Solely for the convenience of the reader, Chilean peso amounts have been translated into dollars at the rate of Ch$ 557.40 per U.S. dollar, the Observed Exchange Rate for December 31, 2004. |

| (2) | “Income before income taxes, minority interest and amortization of negative goodwill” as shown in our audited consolidated income statement. |

| (3) | See “Item 5. Results from Operations for the Fiscal Years Ended December 31, 2003 and December 31, 2004 and Note 36 for a discussion of how our income statement and balance sheet can be impacted by accounting differences under Chilean and U.S. GAAP. The two most significant adjustments that result from reconciling our Chilean GAAP accounts to U.S. GAAP relate to accounting for amortization of goodwill discussed in paragraphs (i), (h) and (II-o) of Note 36 and accounting for derivative instruments discussed in paragraphs (t) and (II-j) of Note 36 to the audited consolidated financial statements. |

8

| As of or for the year ended December 31, | ||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | ||||||

| Operating Data of Subsidiaries | ||||||||||

| Chilectra | ||||||||||

| Electricity Sold (GWh) (1) | 8,854 | 9,585 | 9,952 | 10,518 | 11,317 | |||||

| Number of Customers (thousands) | 1,262 | 1,289 | 1,319 | 1,341 | 1,371 | |||||

| Total Energy Losses (%) (2) | 5.2 | 5.4 | 5.6 | 5.6 | 5.2 | |||||

| Río Maipo | ||||||||||

| Electricity Sold (GWh) | 1,191 | 1,245 | 1,274 | — | — | |||||

| Number of Customers (thousands) | 287 | 294 | 302 | — | — | |||||

| Total Energy Losses (%) (2) | 5.4 | 6.4 | 6.2 | — | — | |||||

| Edesur | ||||||||||

| Electricity Sold (GWh) | 12,597 | 12,909 | 12,138 | 12,656 | 13,322 | |||||

| Number of Customers (thousands) | 2,108 | 2,097 | 2,090 | 2,117 | 2,139 | |||||

| Total Energy Losses (%) (2) | 10.3 | 9.9 | 11.6 | 11.8 | 11.8 | |||||

| Cerj | ||||||||||

| Electricity Sold (GWh) | 7,656 | 6,739 | 7,145 | 7,276 | 7,628 | |||||

| Number of Customers (thousands) | 1,581 | 1,691 | 1,778 | 2,012 | 2,115 | |||||

| Total Energy Losses (%) (2) | 19.7 | 22.7 | 22.6 | 23.6 | 22.8 | |||||

| Coelce | ||||||||||

| Electricity Sold (GWh) | 5,894 | 5,352 | 5,558 | 5,905 | 6,141 | |||||

| Number of Customers (thousands) | 1,796 | 1,917 | 2,009 | 2,109 | 2,334 | |||||

| Total Energy Losses (%) (2) | 13.3 | 13.0 | 12.9 | 13.5 | 13.9 | |||||

| Codensa | ||||||||||

| Electricity Sold (GWh) | 8,776 | 8,673 | 9,015 | 9,254 | 9,656 | |||||

| Number of Customers (thousands) | 1,802 | 1,850 | 1,911 | 1,972 | 2,015 | |||||

| Total Energy Losses (%) (2) | 10.5 | 11.8 | 10.3 | 10.2 | 9.7 | |||||

| Edelnor | ||||||||||

| Electricity Sold (GWh) | 3,583 | 3,685 | 3,872 | 3,968 | 4,250 | |||||

| Number of Customers (thousands) | 852 | 867 | 871 | 892 | 912 | |||||

| Total Energy Losses (%) (2) | 9.9 | 8.9 | 8.5 | 8.4 | 8.4 | |||||

| Endesa-Chile | ||||||||||

| Installed capacity in Chile (MW) | 4,035 | 3,935 | 3,935 | 3,763 | 4,477 | |||||

| Installed capacity in Argentina(MW) | 3,622 | 3,622 | 3,622 | 3,622 | 3,623 | |||||

| Installed capacity in Colombia (MW) | 3,035 | 3,035 | 2,735 | 2,589 | 2,609 | |||||

| Installed capacity in Brazil (MW) (3) | 658 | 658 | 658 | 658 | 658 | |||||

| Installed capacity in Peru (MW) | 997 | 997 | 1,003 | 967 | 967 | |||||

| Production in Chile (GWh) (4) | 15,346 | 15,741 | 16,286 | 16,524 | 16,797 | |||||

| Production in Argentina (GWh) (4) | 10,129 | 9,948 | 7,167 | 7,997 | 11,290 | |||||

| Production in Colombia (GWh) (4) | 9,618 | 10,106 | 10,699 | 10,794 | 11,881 | |||||

| Production in Brazil (GWh) (4) | 3,406 | 2,256 | 2,467 | 3,024 | 3,262 | |||||

| Production in Peru (GWh) (4) | 3,623 | 4,176 | 4,141 | 4,287 | 4,136 | |||||

| (1) | Energy sold by Chilectra includes sales to Río Maipo up to 2003, year in which we sold this company. |

| (2) | Energy losses are calculated by (a) subtracting the number of GWh of energy sold from the aggregate GWh of energy purchased and self-generated within a period and (b) calculating the percentage that the resulting sum bears to the aggregate number of GWh of energy purchased and self-generated within the same period. Energy losses arise from illegally tapped energy as well as technical failures. |

| (3) | If Enersis’ investments in C.G.T. Fortaleza (319 MW) and in Cerj (62 MW) were included, total installed capacity in Brazil would be 1,039 MW as of December 31, 2004. See “Item 4. Information on the Company – D. Property, plants and equipment”. |

| (4) | Energy production is defined as total generation minus energy consumption and technical losses within our own power plants. |

9

EXCHANGE RATES

To the extent our financial liabilities are denominated in foreign currencies, fluctuations in the exchange rate between the Chilean peso and the foreign currencies may have a significant impact on our earnings.

Chile’sLey Orgánica del Banco Central de Chile No. 18,840, or the Central Bank Act, enacted in 1989, liberalized the ability to buy and sell foreign exchange in Chile. Prior to 1989, the law authorized the purchase and sale of foreign exchange only in those cases explicitly authorized by the Central Bank. The Central Bank Act currently provides that the Central Bank may require that certain purchases and sales of foreign exchange be carried out in theMercado Cambiario Formal, or the formal exchange market, a market formed by banks and other entities explicitly authorized by the Central Bank. Purchases and sales of foreign exchange which are generally permitted to be transacted outside the formal exchange market can be carried out in theMercado Cambiario Informal, or the informal exchange market, which is a recognized currency market in Chile. Both the formal and informal exchange markets are driven by free market forces.

For the purposes of the operation of the formal exchange market, the Central Bank sets a reference exchange rate (dólar acuerdo). The reference exchange rate is reset daily by the Central Bank, taking into account internal and external inflation and variations in parties between the Chilean peso and each of the U.S. dollar, the Japanese yen and the Euro in a ratio of 80:5:15, respectively. In order to keep the average exchange rate within certain limits, on rare occasions the Central Bank intervenes by buying or selling foreign exchange in the formal exchange market. The daily observed exchange rate (dólar observado) reported by the Central Bank and published daily in Chilean newspapers is computed by taking the weighted average of the previous business day’s transactions in the formal exchange market.

The informal exchange market reflects transactions carried out at informal exchange rates by entities not expressly authorized to operate in the formal exchange market (e.g., certain foreign exchange houses, travel agencies and others). There are no limits imposed on the extent to which the rate of exchange in the informal exchange market can fluctuate above or below the observed exchange rate. Since 1993, the observed exchange rate and the informal exchange rate have typically been within less than 1% of each other. On December 31, 2004, the informal exchange rate was Ch$ 556.00, or 0.25% lower than the published observed exchange rate of Ch$ 557.40 per U.S.$ 1.00. On May 31, 2005, the informal exchange rate was Ch$ 583.00 per U.S.$ 1.00, the same as the observed exchange rate corresponding to such date. Unless otherwise indicated, amounts translated to U.S. dollars were calculated based on the exchange rates in effect as of December 31, 2004.

The following table sets forth, for the periods and dates indicated, certain information concerning the observed exchange rate reported by the Central Bank. No representation is made that the Chilean peso or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or Chilean pesos, as the case may be, at the rates indicated or at any other rate. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

| Observed Exchange Rate (1) | |||||||||

| (Ch$ per U.S.$ ) | |||||||||

| Year | Low (2) | High (2) | Average (3) | Period-end | |||||

| 2000 | 501.04 | 580.37 | 542.08 | 573.65 | |||||

| 2001 | 557.13 | 716.62 | 637.57 | 654.79 | |||||

| 2002 | 641.75 | 756.56 | 692.32 | 718.61 | |||||

| 2003 | 593.10 | 758.21 | 686.89 | 593.80 | |||||

| 2004 | 557.40 | 649.45 | 611.11 | 557.40 | |||||

| Observed Exchange Rate (1) | |||||||||

| (Ch$ per U.S.$ ) | |||||||||

| Last six months | Low (2) | High (2) | Average | Period-end | |||||

| 2004 | |||||||||

| December | 557.40 | 597.27 | — | 557.40 | |||||

| Observed Exchange Rate (1) | |||||||||

| (Ch$ per U.S.$ ) | |||||||||

| Last six months | Low (2) | High (2) | Average | Period-end | |||||

| 2005 | |||||||||

| January | 560.30 | 586.18 | — | 585.40 | |||||

| February | 563.22 | 583.84 | — | 573.55 | |||||

| March | 578.60 | 591.69 | — | 585.93 | |||||

| April | 572.75 | 588.95 | — | 582.73 | |||||

| May | 570.83 | 583.59 | — | 583.00 | |||||

| Source: Central Bank. | |||||||||

| (1) | Reflects Chilean pesos at historical values rather than in constant Chilean pesos. |

| (2) | Exchange rates are the high and low, on a day-by-day basis, for each period. |

| (3) | The average of the exchange rates on the last day of each month during the period. |

10

| B. | Capitalization and indebtedness. |

| Not applicable. | |

| C. | Reasons for the offer and use of proceeds. |

| Not applicable. | |

| D. | Risk Factors. |

Risks Relating to Our Operations

Since our business depends heavily on hydrological conditions, drought conditions may hurt our profitability.

Approximately 69% of our consolidated installed capacity in Chile, Argentina, Brazil, Colombia and Peru is hydroelectric. Accordingly, adverse hydrological conditions affect our business and have a substantial influence over our results.

During periods of drought, thermal plants, including those that use natural gas, fuel oil or coal as a fuel, are dispatched more frequently. Our operating expenses increase during these periods and, depending on the size of our electricity commitments, we may have to buy electricity from other parties in order to meet these commitments. The cost of these electricity purchases in the spot market may exceed the price at which we committed to sell electricity, thus producing losses.

In 2000, our generation subsidiaries established a new commercial policy in order to mitigate the potential impact of interruptions to our ability to supply electricity, including those caused by droughts, interruptions in gas supply and prolonged plant stoppages. Pursuant to this policy, a volume of contracts is determined for each generation company that reduces the risks to acceptable levels, assured by a degree of statistical reliability of 95%. Any contracts for volumes that exceed this 95% level are required to include clauses transferring the risk of interruptions to the customers. However, there can be no assurance that this policy will shield us from the potential negative consequences of long droughts.

The Argentine natural gas crisis has increased the vulnerability of the electricity sector in Chile.

In Argentina, the low price imposed by regulators on natural gas has directly affected production and investment in natural gas fields, which has in turn impacted the short and medium-term availability of this fuel in Chile. A natural gas shortage may force electricity generation companies, including ours, to use more expensive fuel oil, thus substantially increasing production costs. Strong demand for electricity in Chile’s central region, which increased by 7.9% in 2004 and is expected to continue to increase significantly in the foreseeable future, combined with a low level of investment in the electricity sector, makes the Chilean electricity sector particularly exposed to the adverse effects of the Argentine natural gas crisis.

11

In Chile’s central region, Endesa-Chile’s thermal plants San Isidro and Taltal use natural gas for thermal generation and have take-or-pay gas contracts with Argentine suppliers. On March 26, 2004, the Argentine government announced a resolution allowing governmental authorities to partially suspend natural gas exports and giving the President of Argentina the power to temporarily suspend the long-term supply contracts of Argentine exporters. Since that date, Argentina has significantly curtailed its natural gas exports to Chile. As a result, the Chilean electricity sector is more vulnerable than in the past.

We are a holding company and depend on payments from our subsidiaries and related companies to meet our payment obligations.

We are a holding company with no significant assets other than the stock of our subsidiaries. To pay our obligations, we rely on cash from dividends, loans, interest payments, capital reductions and other distributions from our subsidiaries, as well as cash from proceeds of the issuance of our own capital stock or new debt. In addition, the ability of our subsidiaries to pay dividends, interest payments, loans and other distributions to us is subject to legal constraints such as dividend restrictions, fiduciary duties, contractual limitations and foreign exchange controls that may be imposed in any of the five countries where our subsidiaries operate, and to the operating results of our subsidiaries and equity affiliates. Our subsidiaries and equity affiliates may be additionally limited by their operating results.

We have generally been able to access the cash flows of our Chilean subsidiaries. We have not been similarly able to access the cash flows of our non-Chilean operating subsidiaries due to government regulations, strategic considerations, economic conditions, and credit restrictions. See “Item 5 — Operating and Financial Review and Prospects — Results from Operations for the years ended December 31, 2003 and 2004 — Liquidity and Capital Resources”.

Our future results from operations outside Chile may continue to be subject to greater economic and political uncertainties than what we have experienced in Chile, thereby reducing the likelihood that we will be able to rely on cash flow from operations in those entities to repay our debt.

Dividend Limits and Other Legal Restrictions. We and our Chilean subsidiaries are subject to customary legal restrictions limiting the amount of dividend distributions. Some of our non-Chilean subsidiaries are also subject to legal reserve requirements and other restrictions on dividend payments. In addition, the ability of any of our less-than-wholly-owned subsidiaries to upstream cash to us may be limited by the fiduciary duties of the directors of such subsidiaries to their minority shareholders. As a consequence of such duties, our subsidiaries could, under certain circumstances, be prevented from upstreaming cash to us.

Contractual Constraints. Upstreaming restrictions in our subsidiaries’ contractual agreements include:

| • | prohibitions against dividend distributions by Endesa-Chile in the case of default, and Pangue, our Chilean generation subsidiary, if it is not in compliance with certain debt to equity ratios and debt coverage ratios (each as defined in Pangue’s credit agreements); | |

| • | prohibitions against dividend distributions by Edelnor and Edegel in Peru, and Betania in Colombia in the case of default of certain loans; | |

| • | prohibitions against repayments by Betania of intercompany debt unless it raises additional funds from the sale of assets or capital reductions of Emgesa, and against payments of interest on intercompany debt if any scheduled payment of Betania’s syndicated loan is due and not paid; | |

| • | prohibitions against dividend distributions, capital reductions, intercompany interest payments and debt repayment by Cerj and Coelce in Brazil and Costanera in Argentina while certain of its debt is outstanding. |

We are not aware of any contractual limitations on our equity affiliates’ ability to pay dividends or other distributions to us.

12

Operating Results of Our Subsidiaries. The ability of our subsidiaries and equity affiliates to pay dividends or make loan payments or other distributions to us is limited by their operating results. To the extent that the cash needs at any of our subsidiaries exceed available cash, such subsidiary will not be able to make cash available to us.

Foreign Exchange Controls. The ability of our non-Chilean subsidiaries and equity affiliates to pay dividends and make loan payments or other distributions to us may be subject to emergency restrictions that may be imposed by Central Banks or other governmental authorities in the various jurisdictions in which we operate. For example, during the economic crisis in Argentina, the Central Bank of Argentina imposed restrictions on the transfer of funds outside of Argentina.

Chilean regulatory authorities may impose fines on our Chilean subsidiaries due to operational failures which affect the electricity system

In Chile, our electricity businesses may be subject to regulatory fines for any breach of current regulations, including energy supply failure. As of December 31, 2004, such fines may range from 1 Unidad Tributaria Mensual (“UTM”), equivalent to approximately U.S. $ 54, to 10,000 Unidades Tributarias Anuales (“UTA”), equivalent to approximately U.S.$ 6.5 million. Any electricity company supervised by the Chilean Superintendency of Electricity and Fuels, or SEF, may be subject to these fines, which apply in cases where, in the opinion of the SEF, operational failures that affect the regular energy supply to the system are the fault of such company. These fines are subject to appeal.

If rationing policies are imposed by any regulatory authority as a result of adverse hydrological conditions in the countries in which we operate, our business, financial condition and results from operations may be affected adversely in a material way. Rationing periods may occur in the future, and consequently our generation subsidiaries may be required to pay regulatory penalties if such subsidiaries fail to provide adequate service under such conditions.

Our subsidiaries may be subject to other significant regulatory fines.

Our generation and distribution subsidiaries may be required to pay fines or to compensate customers if those subsidiaries are unable to deliver electricity to them even if such failure is due to forces outside of our control. For example, in 1999 Argentine regulators required us to pay approximately U.S.$ 59 million in fines as a consequence of electricity outages resulting from a fire in one of our distribution substations belonging to Edesur. The imposition of these penalties in Argentina increased our operating costs significantly and was not accounted for under the tariff structure that determines our revenues. Although we received compensation from the contractor responsible for the fire, there can be no assurance that we will receive compensation from third parties in the event of any future delivery failure. See “Item 5 — Operating and Financial Review and Prospects — Results from Operations for the years ended December 31, 2003 and 2004.” Our profitability will be affected adversely if we are required to pay penalties and compensation.

On August 14, 2003, the SEF imposed fines on some of our Chilean generation subsidiaries in an aggregate amount of 5,330 UTA, equivalent to approximately U.S.$ 3.5 million, due to a failure in the transmission of energy in the Metropolitan Region on September 23, 2002. On April 27 and May 3, 2004, the SEF imposed fines on both Endesa-Chile and Chilectra in an aggregate amount of 2,030 UTA, equivalent to approximately U.S.$ 1.3 million, due to a black out that occurred in the Metropolitan Region on January 13, 2003. Our subsidiaries are currently appealing these fines, but these appeals may not be successful.

Governmental regulations may impose additional operating costs which may reduce our profits.

We are subject to extensive regulation of tariffs and other aspects of our business in the countries in which we operate, and these regulations may affect our profitability adversely. In addition, changes in the regulatory framework, including changes that if adopted would significantly affect our operations, are frequently submitted to the legislators and administrative authorities in the countries in which we operate, and could have a material adverse impact on our business.

13

Electricity rationing in Chile: If our Chilean generating subsidiaries cannot satisfy their contracts during electricity rationing periods, we may be exposed to higher costs of sales. In the event of droughts or prolonged shutdowns in the country’s thermal plants, the Chilean government may impose periods of electricity rationing, limiting the volume of electricity we can generate. If as a result of a rationing decree, we are unable to generate sufficient electricity to satisfy our contracts, we may be forced to buy electricity in the spot market at the corresponding node withdrawal price. The spot price can be significantly higher than our electricity generating costs and can be as high as the "failure cost" set by the National Energy Commission (NEC). The "failure cost" is determined by the NEC’s economic models as the highest cost of electricity not delivered during periods of energy deficits. If we cannot buy enough electricity in the spot market to meet all our contractual obligations, we would have to compensate our regulated customers, among others, for the volume not supplied at the “rationed end-consumer price”. If rationing policies are imposed by regulatory authorities in Chile, our business, financial conditions and results of operations may be affected adversely.

Water Rights. Approximately 76% of the installed capacity of our Chilean generation subsidiaries is hydroelectric. These generation companies own unlimited duration unconditional and absolute property water rights granted by the Chilean Water Authority. However, in March 2005, Chilean Congress approved a modification to the current laws governing unused water rights. Under the amended law, beginning on January 1, 2006, Chilean generation companies will have to pay an annual license for unused water rights. By the end of 2005, we will have to determine which water rights are likely to be eventually utilized for a hydroelectric project and which will not. If we determine that some water rights will not be used for a future project, we will abandon such water rights in order to avoid liability for license payments. We estimate that in the event that we do not abandon any water rights in the SIC, we will have to pay license fees aggregating no more than the equivalent of U.S.$ 4.0 million per year. When any future project commences operations, license fees paid for the corresponding water rights will be recovered retroactively through a tax credit, for a term of up to eight years before the start up of the project that utilizes the water rights.

In the case of water rights located in the extreme south of Chile (in particular, the eleventh and twelfth regions, outside the area comprised by the SIC), the license payments will be paid starting as of January 1, 2013, using the same tax refund regime mentioned above for the SIC.

Following the prolonged drought in 1999, the Electricity Law was amended pursuant to Article 99 bis to provide that a drought can no longer constitute a force majeure event and therefore cannot be invoked by hydroelectric generating companies as a basis for failure to deliver energy. Despite the fact that generation companies have changed their commercial strategies and have been more reluctant to enter into long-term contracts, any contractual shortfall caused by extreme droughts can no longer be invoked as an exception to our obligations.

Resolution 88. In May 2001, the Ministry of Economy issued Resolution 88, under which electricity generators such as Endesa-Chile and its Chilean subsidiaries are required to provide electricity to distribution companies that are not able to freely contract adequate supply to deliver to their customers. Under the terms of Resolution 88, each generator must supply energy to the distributors with deficit positions in proportion to the firm energy of each generator at a price equal to the node price. Firm energy is the estimated amount of energy that can be reliably delivered to an interconnected system during a given year by all generating units in that system, under certain assumptions. If Endesa-Chile and its Chilean subsidiaries cannot generate sufficient energy to supply their share of distribution companies’ needs, they will be required to purchase energy on the spot market, at prices that may be significantly higher than the price at which they would be required to sell to distributors, and accordingly they may incur losses. In addition, the requirement to sell to distributors limits Endesa-Chile’s ability to expand sales to non-regulated customers, who may be more profitable for us. For a more complete discussion of this topic, see “Item 4. Information on the Company—Electricity Industry Regulatory Framework”.

Environmental regulations in the countries in which we operate may increase our costs of operations.

Our operating subsidiaries are also subject to environmental regulations, which, among other things, require us to perform environmental impact studies for future projects and obtain permits from both local and national regulators. Approval of these environmental impact studies may be withheld by governmental authorities, public opposition may result in delays or modifications to any proposed project and laws or regulations may change or be interpreted in a manner that could adversely affect our operations or our plans for companies in which we holdinvestments. See “Item 4. Information on the Company—D. Property, plants and equipment—Environmental Issues”.

14

Construction of new facilities may be affected adversely by factors associated commonly with new construction projects.

Factors that may affect our ability to build new facilities include:

| • | delays in obtaining regulatory approvals, including environmental permits; | |

| • | shortages or changes in the prices of equipment, materials or labor; | |

| • | local opposition of political and ethnic groups; | |

| • | adverse changes in the political and regulatory environment in the countries where we and our related companies operate; | |

| • | adverse weather conditions, which may delay the completion of power plants or substations, or natural disasters, accidents or other unforeseen events; and | |

| • | the inability to obtain financing at affordable rates. |

Any of these factors may cause delays in the completion of all or part of our capital investments program and may increase the cost of the projects.

Foreign exchange risks may affect our results from operations and financial condition adversely.

The Chilean peso and the other South American currencies in which we and our subsidiaries operate have been subject to large devaluations and appreciations against the U.S. dollar in the past and may be subject to significant fluctuations in the future. Historically, a significant portion of our consolidated indebtedness has been denominated in U.S. dollars and, although a substantial portion of our revenues are linked in part to U.S. dollars, we generally have been and will continue to be materially exposed to fluctuations of our local currencies against the dollar because of time lags and other limitations in the indexation of our tariffs to the U.S. dollar.

Because of this exposure, the cash generated by us and our subsidiaries can be diminished materially when our local currencies devalue against the dollar. For example, in the case of our Argentine subsidiaries, regulatory changes introduced in 2002 eliminated dollar indexation of our tariffs altogether, which together with a devaluation of approximately 71% of the Argentine peso against the U.S. dollar and pesification of our contractual rates, resulted in a reduction of net cash generation. Future volatility in the exchange rate of the Chilean peso, and the other currencies in which we receive revenues or incur expenditures, to the U.S. dollar, may affect our financial condition and results from operations. For more information on the risks associated with foreign exchange rates, see “Item 11. Quantitative and Qualitative Disclosures About Market Risk.”

As of December 31, 2004, Enersis had total consolidated indebtedness (net of derivatives transactions) of U.S.$ 6,657 million, of which U.S.$ 3,560 million, or 53.5%, was denominated in U.S. dollars. The latter amount is net of a U.S./UF swap contract for U.S. $750 million. For the twelve-month period ended December 31, 2004, our revenues amounted to U.S.$ 5,476 million (before consolidation adjustments) of which U.S.$ 400 million, or 7.3%, were denominated in U.S. dollars, and U.S.$ 772 million, or 14.1% were linked in some way to the U.S. dollar. In aggregate, 21.4% of our revenues (before consolidation adjustments) were either in U.S. dollars or correlated to such currency through some form of indexation. On the other hand, the equivalent of U.S.$ 1,152 million were revenues in pesos, which represents 21.0% of our 2004 revenues (before consolidation adjustments).

In addition to the U.S. dollar and the Chilean peso, and as of December 31, 2004, our foreign-currency denominated consolidated indebtedness included the equivalent of U.S.$ 609 million in Brazilian reals (net of a U.S.$/R$ swap contract for U.S.$ 79 million), U.S.$ 697 million in Colombian pesos, U.S.$ 250 million in Peruvian soles, and U.S.$ 80 million in Argentine pesos, for an aggregate of U.S.$ 1,637 million in currencies other than Chilean pesos and U.S. dollars. At the same time, revenues before consolidation adjustments in these other currencies for the twelve-month period ended December 31, 2004, included the equivalent of U.S.$ 1,196 million in Brazilian reais, U.S.$ 927 million in Colombian pesos, U.S.$ 601 million in Argentine pesos, and U.S.$ 428 million in Peruvian soles. Despite the fact that we have both revenues and debt in these same currencies, we believe that we are exposed to risk in terms of our foreign exchange exposure to these four currencies. The most material case is that of Argentina, where most of our debt is denominated in U.S. dollars while our revenues are mostly in Argentine pesos, as discussed above.

15

The impact on the value of our assets of high levels of devaluation in the countries in which we operate outside Chile may not be reflected on our reported financial condition as a result of Chilean accounting treatment.

The manner in which we restate our foreign investments under Chilean GAAP requires us to translate non-monetary assets and non-monetary liabilities of our non-Chilean subsidiaries and equity affiliates into U.S. dollars at historical rates of exchange. This accounting treatment may have the effect of excluding from our reported balance sheet the effect of devaluation on our non-monetary assets in the countries in which our subsidiaries and investments are located because devaluations of the local currency against the dollar or the Chilean peso are not reflected. See “Item 5. Results from Operations for the Fiscal Years Ended December 31, 2003 and December 31, 2004—Critical Accounting Policies—Technical Bulletin No. 64”.

We and our subsidiaries may be subject to refinancing risk.

As of December 31, 2004, on a consolidated basis, we had U.S.$ 635 million of indebtedness maturing in 2005, U.S.$ 1,169 million in 2006, and U.S.$ 1,279 million of indebtedness maturing in the period 2007 through 2008 and U.S.$ 3,573 million maturing thereafter.

We may be unable to refinance our indebtedness or obtain such refinancing on terms acceptable to us. In the absence of such refinancing, we could be forced to dispose of assets in order to make up for any shortfall in the payments due on our indebtedness under circumstances that might not be favorable to obtaining the best price for such assets. Furthermore, assets may not be sold quickly enough, or for amounts sufficient to enable us to make such payments.

As of December 31, 2004, the debt of our Brazilian and Argentine operating subsidiaries amounted to approximately U.S.$ 999 million. U.S.$ 254 million of this amount is short-term debt due in 2005. As a matter of policy for all of our Brazilian and Argentine subsidiaries, we are primarily making interest payments when due, and we are negotiating extensions of the principal payment dates of most of our outstanding debt. Our international creditors have understood the extraordinary circumstances that have led us to take these steps and have accepted these financing arrangements. However, if our international creditors do not continue to accept rolling over debt principal when it becomes due, we may be unable to refinance our indebtedness on terms acceptable to us. Default under the indebtedness of our Argentine or Brazilian subsidiaries could trigger a cross-default under our other indebtedness. For further discussion of our short term debt obligations and their expected refinancing, see “Item 5 — Results from Operations for the years ended December 31, 2003 and 2004 — Liquidity and Capital Resources”.

We are subject to financial covenants under our existing indebtedness.

We are subject to certain fairly standard financial covenants related to maximum ratios of indebtedness to adjusted cash flow, indebtedness to EBITDA, debt to equity and minimum ratio of adjusted cash flow to interest expense. In addition, substantially all of our indebtedness contains cross-default provisions, generally triggered by default on other indebtedness in amounts exceeding U.S.$ 30 million on an individual basis. In the event that any of our cross-default provisions are triggered and our existing creditors demand immediate repayment, substantially all of our indebtedness will become due and we would be unable to pay such debt.

For more information on these credit facilities, see “Item 5 — Results from Operations for the years ended December 31, 2003 and 2004 — Liquidity and Capital Resources”.

16

We are currently involved in various litigation proceedings, which could result in unfavorable decisions or financial penalties for us, and we will continue to be subject to future litigation proceedings, which could have material adverse consequences to our business.

We are a party to a number of legal proceedings, some of which have been pending for several years. Some of these claims may be resolved against us. Our financial condition or results from operations could be affected adversely to a material extent if certain of these material claims are resolved against us. See “Item 8 - Legal Proceedings” and Note 30 to our consolidated financial statements included in this annual report.

There may be potential conflicts of interest with our affiliates which could adversely affect our business.

As of December 31, 2004 Endesa-Spain owned 60.6% of Enersis’ share capital. Therefore, Endesa-Spain has the power to determine the outcome of most material matters to be decided by a vote of our shareholders, such as the election of the majority of our board members and, subject to contractual and legal restrictions, the distribution of dividends. Endesa-Spain can also exercise influence over our operations and business strategies. Endesa-Spain conducts its business in South America through us and through affiliates not consolidated by us. To the extent any conflict arises between our interests and those of Endesa-Spain’s other businesses in any jurisdiction in South America, Endesa-Spain may have a conflict of interest, which could have an adverse effect on our business.

Certain of our directors are officers of Endesa-Spain and officers and directors of certain subsidiaries of Endesa-Spain. For more information about these directors please refer to “Item 6. Directors, Senior Management and Employees – Directors and Senior Management.”

Our subsidiaries sell electricity to other companies controlled by Endesa-Spain at regulated prices and have entered into contracts for other services with other companies controlled by Endesa-Spain, or the Endesa Group.

The values of our subsidiaries’ long-term energy supply contracts are subject to fluctuations in the market prices of certain commodities.

We have economic exposure to fluctuations in the market prices of certain commodities as a result of the long-term energy sales contracts we have entered into. Our subsidiaries have material obligations under long-term fixed-price electricity sales contracts, the values of which fluctuate with the market price of electricity. In addition, our generation subsidiaries have material obligations as selling parties under long-term energy supply contracts with prices that vary in accordance with the market price of electricity, water levels in our reservoirs, the market prices of primary materials such as natural gas, oil, coal and other energy-related products, as well as the exchange rate of the U.S. dollar. Changes in the market price of these commodities and in the exchange rate do not always correlate with changes in the market price of electricity or with our cost of production of electricity; accordingly, there may be times when the price paid to us under these contracts is less than our cost of production or acquisition of electricity. We do not carry out transactions in commodity derivative instruments to manage our exposure to commodity price fluctuations. Under Chilean GAAP, our income statement does not reflect fluctuations in the fair value of our long-term energy contracts, although we are required to do so under U.S. GAAP. Our policy is not to enter into supply contracts for amounts exceeding our firm capacity under adverse hydrological conditions. For further discussion, please refer to “Item 11. Quantitative and Qualitative Disclosures About Market Risk—Commodity Price Risk” in this annual report.

Risk Factors Relating to Chile

Our business is dependent on the Chilean economy and our revenues are sensitive to its performance.

A substantial portion of our assets and operations are located in Chile and, accordingly, our financial condition and results from operations are to a certain extent dependent upon economic conditions prevailing in Chile. In 2004, the Chilean economy grew by 6.1% compared to a 3.7% increase in 2003. The Central Bank recently reclassified its criteria for growth measurements. The latest Chilean Central Bank forecasts for GDP growths between 5.3% and 6.3% for 2005 and approximately 5% for 2006 (Central Bank, “Informe Política Monetaria,” May 2005). There is no assurance that such growth will be achieved, that the growth trend will continue in the future, or that future developments in the Chilean economy will not impair our ability to proceed with our strategic plans or impact our financial condition or results from operations adversely. Our financial condition and results from operations could also be affected by changes in economic or other policies of the Chilean government, which has exercised and continues to exercise a substantial influence over many aspects of the private sector. In addition, our financial condition and results from operations could also be affected by other political or economic developments in Chile, as well as regulatory changes or administrative practices of Chilean authorities, over which we have no control.

17

Increased inflation in Chile may affect our results from operations adversely.

Although Chilean inflation has been low in recent years, Chile experienced high levels of inflation in the past. High levels of inflation in Chile could affect the Chilean economy adversely and, indirectly, the value of shares of Enersis’ common stock and ADSs. The Chilean Consumer Price Index, or Chilean CPI, for the 12 months ended December 31, 2004, was 2.4%, and government officials expect Chilean CPI to be approximately 2.0% and 3.0% for 2005 and 2006, respectively. Historically, a substantial part of our expenses have been denominated in Chilean pesos, and future increases in Chilean inflation could cause our expenses to rise significantly. As a result, the level of Chilean inflation may affect our financial condition and results from operations.

We believe that moderate inflation will not materially affect our business in Chile. Electricity tariffs in Chile, both for generation and distribution, contain indexing mechanisms that are intended to neutralize the effects of inflation. However, we believe that the performance of the Chilean economy, our operating results, and the value of securities issued by us, could be affected adversely if inflation levels were to rise significantly.

Lawsuits against us brought outside Chile or complaints against us based on foreign legal concepts may be unsuccessful.

We are incorporated under the laws of Chile and substantially all of our assets are located in Chile or elsewhere in South America. All of our directors and officers reside outside the United States and most of their assets are located outside the United States as well. If any shareholder were to bring a lawsuit against our directors, officers or experts in the United States, it may be difficult for them to effect service of legal process within the United States upon these persons or to enforce against them, in United States courts or Chilean courts, judgments obtained in the United States courts based upon the civil liability provisions of the federal securities laws of the United States. In addition, there is doubt as to whether an action could be brought successfully in Chile on the basis of liability based solely upon the civil liability provisions of the United States federal securities laws.

Foreign exchange risks may affect the U.S. dollar amount of dividends payable to holders of Enersis’ ADSs adversely.

Chilean trading in the shares of common stock underlying the ADSs is conducted in pesos. Enersis’ depositary will receive cash distributions that we make with respect to the shares underlying the ADSs in pesos. The depositary will convert such pesos to U.S. dollars at the then-prevailing exchange rate to make dividend and other distribution payments in respect of ADSs. If the Chilean peso appreciates against the U.S. dollar, the value of the ADSs and any distributions ADS holders receive from the depositary may decrease.

The relative illiquidity and volatility of Chilean securities markets could affect the price of the Enersis ADSs and common stock adversely.

Chilean securities markets are substantially smaller and less liquid than the major securities markets in the United States. In addition, Chilean securities markets may be affected materially by developments in other emerging markets, particularly other countries in South America. The low liquidity of the Chilean market may impair the ability of holders of ADSs to sell shares of our common stock withdrawn from the ADS program into the Chilean market in the amount and at the price and time they wish to do so.

Risk Factors Relating to the Rest of South America.

South American economic fluctuations are likely to affect our results from operations.

All of our operations are located in South America. Although we originally operated only in Chile, we have, through strategic acquisitions and investments, expanded our operations throughout South America. In 2004, we generated 65% of our consolidated operating revenues and 62% of our consolidated operating income outside Chile (before consolidation adjustments). Accordingly, our consolidated revenues are sensitive to the performance of the South American economies as a whole. If local, regional or worldwide economic trends adversely affect the economy of any of the countries in which we have investments or operations, our financial condition and results from operations could be affected adversely.

18

The South American financial and securities markets are, to varying degrees, influenced by economic and market conditions in other emerging market countries. Although economic conditions are different in each country, investor reaction to developments in one country can have significant effects on the securities of issuers in other countries, including Chile. Chilean financial and securities markets may be affected adversely by events elsewhere, especially in other emerging markets, and such effects may affect the value of or the interest rate yields in the secondary markets for our debt securities. Moreover, Enersis and Endesa-Chile have significant investments in relatively risky non-Chilean countries such as Argentina, Brazil, Colombia and Peru. Generation and upstreaming of cash from subsidiaries in these countries have proven to be volatile.

Certain South American economies have been characterized by frequent and occasionally drastic intervention by governmental authorities, which may affect our business adversely.

Governmental authorities have often changed monetary, credit, tariff and other policies to influence the course of the economy of Argentina, Brazil, Colombia and Peru. These governments’ actions to control inflation and effect other policies have often involved wage, price and tariff rate controls as well as other interventionist measures, which have included freezing bank accounts and imposing capital controls. Changes in the policies of these governmental authorities with respect to tariff rates, exchange controls, regulations and taxation could affect our business and financial results adversely, as could inflation, devaluation, social instability and other political, economic or diplomatic developments, including the response by governments in the region to such circumstances. If governmental authorities intervene in any of the countries in which we operate, it could cause our business to be less profitable, and our results from operations may be affected adversely.

Risk Factors Related to Brazil

Energy losses in Brazil may affect our financial results adversely.

Our Brazilian distribution subsidiaries experience materially higher energy losses than occur in the rest of our distribution operations, with Coelce and Cerj experiencing loss rates for 2004 of 13.9% and 22.8%, respectively, compared with an average loss rate of 9.0% for the rest of our distribution operations. Elevated energy loss rates in our Brazilian distribution subsidiaries are due principally to energy theft, which is particularly acute in areas with high concentrations of low-income customers and in periods of economic downturn. Energy losses affect our financial results because lost energy could otherwise have been distributed to customers or sold to other distributors in return for payment.

Brazilian Energy Sector Reform could have an adverse effect on our business and operations in Brazil.

Following the electricity supply crisis in 2001, due to low rainfalls, the electricity committee of the Brazilian federal government announced various measures for revitalizing the energy sector and ensuring a high level of competition, attracting new investments and increasing the transparency of the rules governing these services.

In March 2004, Federal Laws Nº 10,847 and 10,848 were enacted in order to establish a new model for the Brazilian Electricity Sector. These laws were subsequently implemented by decrees and resolutions enacted by MME (Ministry of Mines and Energy) and ANEEL (the Brazilian National Agency of Electric Energy). Additionally, these resolutions will, among other things, determine how the inherent risks will be distributed among the different market participants (i.e. hydrological risk, market fluctuations and accounts receivable) and prohibit the participation of distribution companies in related activities like generation.

The new Brazilian model for the electricity sector creates a regulatory framework based on the principle of stability and low tariffs for consumers. It also seeks to guarantee the expansion of installed capacity to satisfy demand growth. Pursuant to this model, 100% of distributors’ forecasted energy demand must be satisfied through long-term contracts. Accordingly, several bidding processes have been and will be called by ANEEL and the Chamber of Energy Sales in advance of the expiration of current contracts in the regulated environment. Therefore, our distribution companies may end up bidding for either more or less than actual demand. For additional information, please refer to “Item 4. Information on the Company’s Operations in Brazil – Structure of the new Electricity Sector”.

19

Future governmental initiatives may affect our operations adversely.

Program for Regulatory Losses in Brazil.In connection with the next distribution tariff setting process in 2008, we expect the government to reduce the provision for energy losses in tariffs. This represents a risk for our companies, Cerj and Coelce, because tariffs today recognize a level of losses close to the real level of each company. Consequently, any future reduction will negatively affect Brazilian operations if we are not able to reduce the high level of energy theft.

Brazilian social low-income program. The Brazilian authorities have designed a program that will ensure electricity to those who cannot afford it. The program provides a subsidy to the distributor supply in order to allow residential consumers to pay a lower tariff for energy if they satisfy certain requirements. Consumers have faced difficulties enrolling in government programs of this kind. To solve this problem, ANEEL enacted Resolution No. 148/05, which allows consumers to enjoy the benefits of the government program by making a simple declaration agreeing to deliver the documentation that proves compliance with the applicable requirements of the program until February 2006. It is uncertain whether ANEEL will extend the deadline beyond such date, or whether consumers who have not delivered the required documentation by that date will lose the benefit of the electricity subsidy. Approximately 40% of Cerj’s customers require this benefit in order to pay their electricity bills. If these customers are unable to participate in this program, they may be unable to pay amounts owing to us in a timely manner, if at all, and electricity theft may increase, any of which may adversely affect our operating results.

Universalization Program in Brazil. We are currently participating in the creation of the “Universalization Program”, a governmental initiative to provide electricity in rural areas. This program will require us to make certain investments, and we are uncertain at this time as to the amounts of such required investments or how such investments will be financed.

Risk Factors Related to Argentina

The Central Bank of Argentina has recently lifted, but may reinstate, restrictions on the transfer of funds outside of Argentina that could prevent our Argentine subsidiaries from distributing dividends and paying principal on certain of their external debt as it comes due.

From December 3, 2001 to May 6, 2003, the Argentine government imposed a number of monetary and currency exchange control measures that included restrictions on the free transfer of funds deposited with banks and severe restrictions on transferring funds abroad (including payments of dividends, principal and interest on debt), with certain exceptions for transfers related to foreign trade and other authorized transactions. The restrictions, requiring the Argentine Central Bank’s prior authorization for the transfer of funds abroad in order to make payments of principal and/or interest, were gradually relaxed from January to May 2003.

Currently, funds may be transferred abroad without the prior authorization of the Argentine Central Bank in order to pay dividends corresponding to prior periods provided that independent accountants have certified the financial statements for such period.

There can be no assurance, however, that the Argentine Central Bank will not once again require its prior authorization for the transfer of funds abroad for principal and/or interest payments by any of our Argentine subsidiaries to their foreign creditors or for dividend payments by our Argentine subsidiaries to their shareholders.

Should the Argentine Central Bank reimpose restrictions on the transfer of funds outside of Argentina that prevent our Argentine subsidiaries from paying principal on certain of their external debt, a substantial portion of their debt obligations may become due and payable, unless new financing is funded outside Argentina and is available to our Argentine subsidiaries or they are able to renegotiate, or obtain a waiver with respect to the indebtedness that would be subject to such restrictions. If similar restrictions are imposed again, our Argentine subsidiaries may not be able to obtain new financing or be able to renegotiate or obtain waivers with respect to indebtedness subject to foreign exchange restrictions. In addition, such restrictions may impede the ability of our Argentine subsidiaries to make cash distributions to us.

20

As of December 31, 2004, the debt of our Argentine subsidiaries amounted to approximately U.S.$ 506 million. As a matter of policy for all of our Argentine subsidiaries, including generation and distribution companies, as long as the foreign currency restrictions remain in Argentina, and as long as fundamental issues concerning the electricity sector remain unresolved, we are primarily making interest payments when due, as permitted by the Argentine Central Bank, and we are rolling over most of our outstanding debt. On December 31, 2003, our Argentine subsidiaries’ total outstanding debt was U.S.$ 620 million, of which U.S.$ 393 million was due during 2004. We paid U.S.$ 113 million of principal and rolled over U.S.$ 280 million. Our international creditors have understood the extraordinary circumstances that have led us to take these steps and to date have accepted these refinancing arrangements. If our creditors do not continue to accept, or the Argentine Central Bank will not continue to permit, rolling over debt principal when it becomes due, we may be unable to refinance our indebtedness on terms acceptable to us.

Argentine authorities have implemented a number of monetary and currency-exchange control measures that have had, and may continue to have, an adverse effect on our results from operations and financial condition in Argentina.

The Economic Emergency Law has affected Edesur adversely by repealing the provisions of Edesur’s concession contract that permitted its distribution tariffs to be pegged to the dollar, and that provided for certain price indexation mechanisms. Since Edesur’s invoices to its clients are no longer pegged to the dollar, the dollar value of such receivables declined significantly in the wake of the devaluation of the Argentine peso. Because Edesur’s indebtedness is largely dollar-denominated, the above-mentioned factors have had, and may continue to have, a significant negative impact on Edesur’s net income.

The Economic Emergency Law also authorized the Argentine Federal Executive Branch to renegotiate all public service contracts, and establishes certain guidelines dealing with potential impacts on the Argentine domestic economy, quality of service and capital expenditure plans, consumer interests, the security of the systems, and the profitability of the companies providing such services. On March 20, 2002, the government listed the set of contracts to be renegotiated, as well as the general procedures to be used as guidance in such negotiations. Among these contracts is Edesur’s concession contract.