FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of February, 2012

Commission File Number: 001-12440

ENERSIS S.A.

(Translation of Registrant’s Name into English)

Santa Rosa 76

Santiago, Chile

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file

annual reports under cover of Form 20-F or Form 40-F:

Form 20-F [X] Form 40-F [ ]

Indicate by check mark if the registrant is submitting the Form 6-K

in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes [ ] No [X]

Indicate by check mark if the registrant is submitting the Form 6-K

in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes [ ] No [X]

Indicate by check mark whether by furnishing the information

ontained in this Form, the Registrant is also thereby furnishing the

information to the Commission

pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

Yes [ ] No [X]

If °;Yes” is marked, indicate below the file number assigned to the registrant

in connection with Rule 12g3-2(b): N/A

| PRESS RELEASE Year Ended 2011 |

ENERSIS

ANNOUNCES CONSOLIDATED RESULTS

FOR YEAR ENDED ON DECEMBER 31, 2011

| Highlights for the Period |

SUMMARY

Ø2011 confirmed the strong growth in demand for electricity in the countries where we operate, as a result of the dynamic economic activity in these markets.

ØRegarding distribution business, it is important to note the improvement in our Peruvian and Chilean operations, with growth in electricity demand of 7.3% and 4.6% respectively.

ØOur Bocamina I coal-fired thermal plant damaged by the Chilean earthquake in February 2010, restarted operations. This allowed us to provide the Chilean Central Interconnected System(“SIC”) with a stable andreliable source of energy during a dry year.

ØOur distribution business customer base increased by around 384,000 customers, which confirms the natural growth of this business, an important stabilizing factor for our cash flows.

ØIn the generation business, operating revenues fell 2.9% mainly due to lower average sales prices, partially offset by higher physical sales in Peru and Colombia.

ØEBITDA for the Enersis Group was very balanced in terms of business segment:

•Generation and Transmission: 56%

•Distribution: 44%

ØThe Company’s EBITDAdecreased by Ch$ 134,323 million, or 5.9%, primarily due to Ch$ 70,601 million in higher costs related to fuel consumption in the generation business, mainly in Argentina and Chile. Additionally, Enersis accounted for the full impact of the equity tax reform in Colombia, for taxes payable throughout the 2011-2014 period. This non-recurring factor affected operating income of our Colombian operations (both distribution and generation subsidiaries) by Ch$ 72,671 million. The aforementioned decreases were partially offset by better results in our Chilean and Peruvian distribution companies, together with our generation facilities in Peru and Brazil, as well as our transmission in Brazil.

ØOperating income for 2011 amounted to Ch$ 1,566,311 million, representing a decline of 8.1% compared to 2010. It is important to highlight the negative operating performance of our subsidiaries in Argentina because of a long-time postponement of tariff adjustments, due to the delay in the accomplishment of certain issues set by an act of agreement subscribed with the National Government of Argentina, which is affecting the financial equilibrium in Edesur.

ØBecause of the aforementioned, Enersis S.A., made some provisions for its subsidiaries Empresa Distribuidora Sur S.A., and Central Costanera S.A., that had an impact of Ch$ 106,750 million over Enersis’results. Without these provisions, results would have been similar to those obtained in 2010, despite the severe drought affecting Chile for the last 30 months. This ratifies the benefit of being properly diversified.

Pg. 1

| PRESS RELEASE Year Ended 2011 |

DISTRIBUTIONBUSINESS

Consolidated figures for the distribution businesses are detailed as follows:

ØOperating revenues rose by 1.2% to Ch$ 4,447,427 million.

ØProcurement and service costs were Ch$ 2,904,966 million, 1.5% lower than 2010.

ØEBITDA in 2011 amounted to Ch$ 939,597 million, a reduction of 4.4% compared to 2010, mainly due to the reduced results of our businesses in Argentina, Colombia and Brazil, partially compensated by improvements in Chile and Peru.

Factors influencing this lower distribution business EBITDA, as follows:

In Chile,EBITDA grew by Ch$ 12,538 million, mainly explained by:

ØBetter energy sales margin related to 4.6% higher energy demand, which was reflected in higher sales volume in almost every market segment.

ØLower personnel expenses for Ch$ 4,974 million.

In Peru,EBITDA rose by Ch$ 5,944 million as result of:

Ø7.3% increase in physical sales in every market segment.

ØLower procurement and services costs by Ch$ 3,182 million, mainly because of synergies in technology and information systems.

In Argentina,EBITDA decreased by Ch$ 36,245 million, mainly explained by:

ØCh$ 23,866 million increased in salaries under unions agreements, higher payroll and extra time payments.

ØLower sales margin mainly explained by 2.3% lower industrial sales, compensated by a 2.8% increase in sales volume related to a higher residential consumption, which reflects growth in the number of clients and lower temperatures during the winter season of 2011.

In Brazil,EBITDA decreased by Ch$ 4,217 million as result of:

ØLower energy sales revenues in Coelce, explained by lower average sales price related to a 6.4% drop in energy sales from the industrial segment.

ØThe above was partially compensated by higher energy sales volume in Ampla and Coelce.

In Colombia,EBITDA decreased by Ch$ 21,704 million, mostly as result of:

ØThe effect of the Colombian government equity tax reform, which implied recording in 2011 the entire tax payable during 2011-2014.

ØThe previous effect more than offset the positive operating margins registered in 2011, as result of 2.7% increase in energy sales in all the client segments.

Pg. 2

| PRESS RELEASE Year Ended 2011 |

GENERATION ANDTRANSMISSIONBUSINESS

ØConsolidated physical sales increased 2.2% to 64,840 GWh, explained by increases in all the countries where we operate, led by Peru, Colombia and Chile.

ØOperating revenues decreased 2.9% to Ch$ 2,700,026 million, mainly explained by lower average sales prices, more than offsetting the higher physical sales.

ØProcurement and services costs declined by 2.1% to Ch$ 1,272,985 million as a result of lower other variable costs and transportation expenses, partially offset by higher fuel consumption in Argentina and Chile.

ØEBITDA amounted to Ch$ 1,200,281 million, a decrease of 7.3% compared to the previous year.

ØConsolidated hydroelectric generation remained almost the same than in 2010, representing a 59% of total generation.

Factors affecting these results are:

In Chile,EBITDA decreased Ch$ 110,189 million, mainly due to:

ØDecrease in energy sales revenues explained by lower average price, due to lower water availability which impacted energy sales to the spot market. This was partially offset by a 1.0% increase in energy sales volume.

ØHigher energy purchase costs of Ch$ 66,320 million and higher fuel consumption of Ch$ 32,088 million linked to a poorer hydrological condition, partially offset by lower transport expenses of Ch$ 46,133 million.

In Colombia, EBITDA fell by Ch$ 7,283 million, mainly due to:

ØIncrease in other fixed operating costs of Ch$ 40,804 million, mainly explained by the non-recurring effect of the equity tax reform which implied the booking on January 1, 2011 of the full amount payable in the period 2011-2014.

ØReduced energy sales revenues of Ch$ 10,742 million due to a 4.0% lower average energy sale prices, partially compensated by an increase of 2.0% in physical sales.

ØReduction in energy cost purchases of Ch$ 43,256 million, explained by lower thermal dispatch because of higher hydro generation.

In Peru,EBITDA increased by Ch$ 32,851 million due to:

ØHigher energy sales revenues of Ch$ 31,049 million explained by higher generation from both thermal and hydro facilities, and also higher average price and a 9.9% increase in sales volume.

ØLower personnel expenses of Ch$ 8,819 million and a decrease in the energy purchase costs by Ch$ 1,691 million.

ØThe latter was partially offset by higher fuel consumption cost of Ch$ 3,913 million linked to higher thermal dispatch, and higher transport expenses by Ch$ 3,615 million.

In Argentina, EBITDA decreased by Ch$ 14,242 million due to:

ØHigher fuel consumption cost of Ch$ 40,195 million, increase in transport expenses of Ch$ 4,529 million related to higher thermal dispatch, and also higher energy purchases costs of Ch$ 4,444 million.

Pg. 3

| PRESS RELEASE Year Ended 2011 |

ØHigher personnel expenses of Ch$ 4,563 million, explained by increased wages under unions agreements.

ØThis was partially offset by higher energy sales of Ch$ 44,256 million, related to 12.8% increase in average energy sales price.

In Brazil, EBITDA increased by Ch$ 4,202 million due to:

ØIncrease of Ch$ 10,747 millionin Cachoeira Dourada’s contribution margin due to 5.3%increase in average sales price and 4.0% increase in physical sales.

ØHigher contribution margin of Ch$2,468 million in CIEN, due to its recognition as regulatory asset by the local authority since April 2011, permitting entrance of tolls according to RAP(permitted annual remuneration) system.

ØLower energy purchase costs of Ch$ 4,736 million and lower fuel consumption costs of Ch$ 1,771 million in Fortaleza, due to 37.9% lower generation. The latter caused an increase in spot market purchases, which allowed to maximize margin in a high hydrology and low prices scenario.

FINANCIALSUMMARY

ØThe average nominal interest rate increased from 8.5% up to 9.6%, mainly because of inflationary effects in Chile.

ØLiquidity, a key consideration in our financial management, continues to be in a very solid position, as shown below on a consolidated basis for Enersis:

·Cash and cash equivalents amount to US$ 2,350 million.

·Committed credit lines for US$ 818 million.

·Non-committed credit lines available for US$ 1,944 million.

ØIn this context, it is important to highlight the successful issuance of an unsecured bond in local currency by Emgesa in the international capital markets, for the Colombian peso equivalent of US$ 400 million. This break-through deal, the first bond issued in local currency by a privatesector Colombian company in the international markets, was rated “Investment Grade” by Fitch Ratings and Standard and Poor’s.

ØIn June 2011, Ampla successfully issued local bonds (debentures) for the equivalent of US$160 million, maturing in 5 and 7 years, allowing the extension of its debt’smaturity.

ØIn November, Coelce issued local bonds (debentures) for the equivalent of US$ 240 million, also maturing in 5 and 7 years.

ØCoverage and protection: In order to mitigate exchange rate and interest rate risks, Enersis has established strict internal rules to protect our cash flows and balance sheet from fluctuations in these variables.

·Our exchange rate policy is based on cash flows and we strive to maintain a balance between US dollar indexed flows, and assets and liabilities in such currency. In addition to this policy, we have contracted cross currency swaps for a total amount of US$ 1,379 million and forwards for US$ 105 million.

Pg. 4

| PRESS RELEASE Year Ended 2011 |

· In order to reduce financial results’ volatility due to changes in market interest rates, weseek to maintain an adequate balance in our debt structure. Thus, we have contracted interest rate swaps (from variable to fixed rates) for US$ 315 million.

MARKETSUMMARY

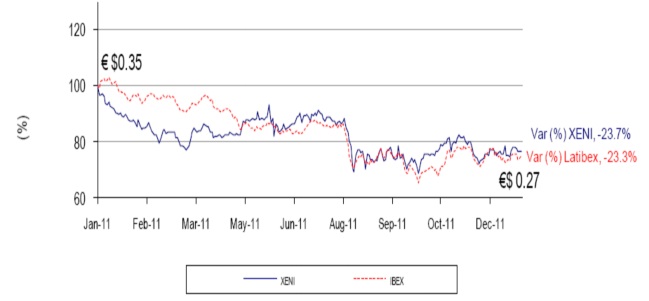

ØThe Chilean Stock Exchange’s main index, IPSA, showed an important decrease of 15.2% during 2011. This has been consistent with the global economic scenario and the behavior of the principal stock exchanges. In Latin America, all the countries where the group has presence have shown negative numbers: BOVESPA (Brazil): -18.1%; COLCAP (Colombia): -13.8%; MERVAL (Argentina): -30.1% and ISBVL (Peru): -14.7%. In developed countries, the stock exchanges showed mixed results: IBEX: -13.1%, UKX: -5.6%; FTSE 250: -12.6%; S&P 500: 0% and Dow Jones Industrial: +5.5%. All these stock performances are calculated in their domestic currency and are therefore not comparable.

ØIn line with that markets, Enersis’ share price decreased during last 12 months. The price as of December 31, 2011 was $182.6 which represents a 16.0% decrease in comparison with December 31, 2010 price, when it reached $217.4. This low performance is mainly explained by the negative global economic scenario and also by the drought affecting Chile for the last 30 months, reducing the results of its generation affiliates.

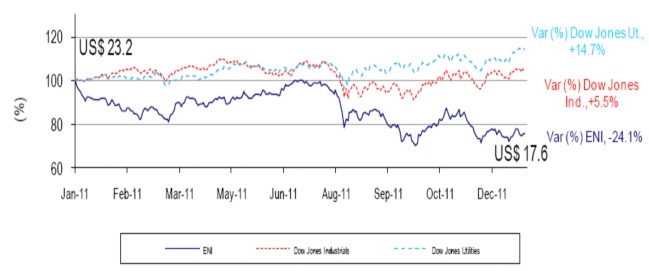

ØEnersis’ ADS lost 24.1% of its value during 2011. The price fell from US$23.2 on December 31, 2010, to US$17.6 on December 31, 2011. The global economic situation, together with a high volatility in the international equity markets, as well as the drought that affected the Chilean territory, impacted the equity’s value.

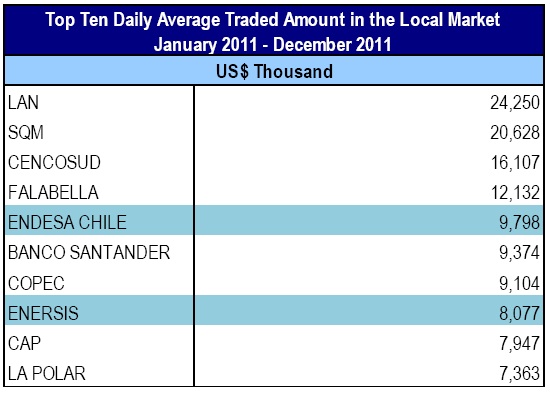

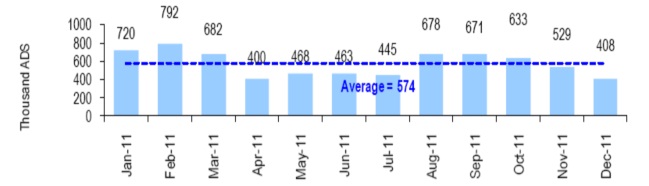

ØDuring 2011, Enersis was, again, among the most actively traded companies in the local market (Santiago Stock Exchange and Chilean Electronic Exchange), with a daily average trading volume of US$ 8.1 million.

|

| Source: Santiago Stock |

Pg. 5

| PRESS RELEASE Year Ended 2011 |

RISKRATINGCLASSIFICATIONINFORMATION

Enersis’current ratings are supported by its well diversified asset portfolio, strong credit metrics, adequate debt structure and solid liquidity.The Company’sgeographic diversification in Latin America provides a natural hedge against different regulations and weather conditions. Most ofEnersis’operating subsidiaries are financially strong and have leading market positions in the countries where Enersis operates.

Summarizing the main events occurred during 2011, we can highlight the following,

On April 25, 2011, Moody's upgraded the senior unsecured rating of Enersis from“Baa3”to“Baa2”,with stable outlook.

On July 15, 2011,Feller Rate confirmed the “AA” local rating of Enersis’bonds, shares and commercial papers program. Rating perspectives continue to be stable.

More recently, Standard & Poor’s (November 30, 2011) and Fitch Ratings (January 5, 2012) affirmed the international credit risk rating for Enersison “BBB+”, with stableoutlook.

The current international risk ratings are,

| Enersis | S&P | Moody’s | Fitch |

| Corporate | BBB+ / Stable | Baa2 / Stable | BBB+ / Stable |

The domestic ratings (for securities issued in Chile),

| Enersis | Feller Rate | Fitch |

| Shares | 1stClass Level 1 | 1stClass Level 1 |

| Bonds | AA / Stable | AA / Stable |

Pg. 6

| PRESS RELEASE Year Ended 2011 |

| TABLE OFCONTENTS | |

Summary | 1 |

Distribution Business | 2 |

Generation and Transmission Business | 3 |

Financial Summary | 4 |

Market Summary | 5 |

Risk Rating Classification Information | 6 |

TABLE OF CONTENTS | 7 |

| YEAR ENDED DECEMBER 31, 2011 | 9 |

| GENERAL INFORMATION | 9 |

SIMPLIFIED ORGANIZATIONAL STRUCTURE | 10 |

CONSOLIDATED INCOME STATEMENT ANALYSIS | 11 |

NET INCOME | 11 |

OPERATING INCOME | 11 |

NET FINANCIAL INCOME | 13 |

SALE OF ASSETS | 13 |

TAXES | 13 |

CONSOLIDATED BALANCE SHEET ANALYSIS | 14 |

ASSETS UNDER IFRS | 14 |

| BOOK VALUE AND ECONOMIC VALUE OF ASSETS | 16 |

| LIABILITIES AND SHAREHOLDERS’ EQUITY UNDER IFRS | 17 |

DEBT MATURITY WITH THIRD PARTIES, THOUSAND US$ | 19 |

DEBT MATURITY WITH THIRD PARTIES, MILLION CH$ | 19 |

EVOLUTION OF KEY FINANCIAL RATIOS | 20 |

UNDER IFRS | 21 |

CASH FLOW RECEIVED FROM FOREIGN SUBSIDIARIES BY ENERSIS, CHILECTRA AND ENDESA CHILE | 22 |

| THE PRINCIPAL RISKS ASSOCIATED TO THE ACTIVITIES OF THE ENERSIS GROUP | 23 |

| ARGENTINA | 28 |

GENERATION | 28 |

Endesa Costanera | 28 |

El Chocon | 29 |

DISTRIBUTION | 30 |

Edesur | 30 |

| BRAZIL | 31 |

ENDESA BRASIL | 31 |

GENERATION | 31 |

Cachoeira | 31 |

Fortaleza (cgtf) | 32 |

TRANSMISSION | 33 |

CIEN | 33 |

DISTRIBUTION | 34 |

Ampla | 34 |

Coelce | 35 |

| Pg. 7 | |

| PRESS RELEASE Year Ended 2011 |

| CHILE | 36 |

GENERATION | 36 |

Endesa Chile | 36 |

DISTRIBUTION | 37 |

Chilectra | 37 |

| COLOMBIA | 39 |

GENERATION | 39 |

Emgesa | 39 |

DISTRIBUTION | 40 |

Codensa | 40 |

GENERATION | 41 |

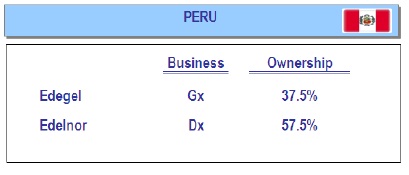

Edegel | 41 |

DISTRIBUTION | 42 |

Edelnor | 42 |

| MARKET INFORMATION | 44 |

EQUITY MARKET | 44 |

DEBT MARKET | 47 |

| CONFERENCE CALL INVITATION | 48 |

DISCLAIMER | 49 |

| Pg. 8 | |

| PRESS RELEASE Year Ended 2011 |

YEARENDEDDECEMBER31, 2011

GENERALINFORMATION

(Santiago, Chile, Tuesday, January 31, 2012.) Enersis S.A. (NYSE: ENI), announced today its consolidated financial results for the year ended December 31, 2011. All figures are in Chilean pesos (Ch$) and in accordance with International Financial Reporting Standards (IFRS). Variations refer to comparison between the year ended December 31, 2010 and December 31, 2011.

Figures as of December 31, 2011 are additionally translated into US$, merely as a convenience translation, using the exchange rate of US$ 1 = Ch$ 519.20 for the Balance Sheet, and the average exchange rate for the period of US$ 1 = Ch$ 483.57 for the Income Statement, Cash Flow Statements, Capex and Depreciation values.

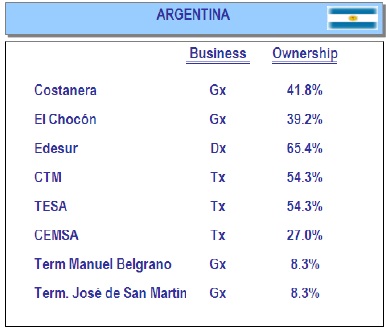

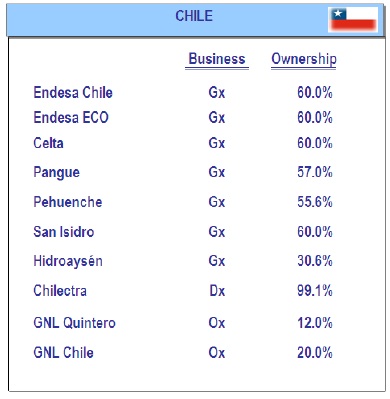

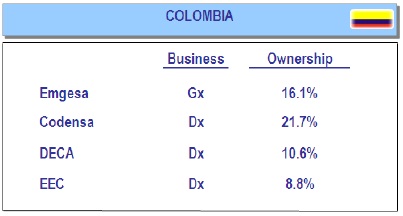

The consolidation includes the following investment vehicles and companies:

a) In Chile: Endesa Chile (NYSE: EOC)*, Chilectra, and Inmobiliaria Manso de Velasco.

b) Others than Chile: Distrilima (Peru), Endesa Brasil (Brazil)**, Edesur (Argentina) and Codensa (Colombia).

| * | Includes Endesa Chile Chilean subsidiaries (Celta, Pangue, Pehuenche, San Isidro, and Tunel El Melón), non Chilean subsidiaries (Endesa Costanera, El Chocon, Edegel and Emgesa) and jointly controlled companies (Gas Atacama, Transquillota and Hidroaysén.) |

| ** | Includes Endesa Fortaleza, CIEN, Cachoeira Dourada, Ampla and Coelce. |

Pg. 9

| PRESS RELEASE Year Ended 2011 |

SIMPLIFIEDORGANIZATIONALSTRUCTURE

| ||

|  | |

|

| |

| ||

Pg. 10

| PRESS RELEASE Year Ended 2011 |

CONSOLIDATEDINCOMESTATEMENTANALYSIS

NETINCOME

Enersis’ Net Income attributable to the owners of the controller for the cumulative period as of December 31, 2011 reached Ch$ 375,471 million, representing a 22.8% decrease over the same period 2010, which was Ch$ 486,227 million.

Under IFRS

Table 1 | ||||||

CONSOLIDATED INCOME STATEMENT | (Million Ch$) | (Thousand US$) | ||||

| 2010 | 2011 | Var 2010-2011 | Chg % | 2011 | |

Sales | 6,179,230 | 6,254,252 | 75,022 | 1.2% | 12,933,499 | |

Energy sales | 5,653,725 | 5,805,296 | 151,571 | 2.7% | 12,005,079 | |

Other sales | 50,571 | 31,746 | (18,825) | (37.2%) | 65,650 | |

Other services | 474,934 | 417,210 | (57,724) | (12.2%) | 862,770 | |

Other operating income | 384,351 | 280,628 | (103,723) | (27.0%) | 580,326 | |

Revenues | 6,563,581 | 6,534,880 | (28,701) | (0.4%) | 13,513,825 | |

Energy purchases | (1,554,715) | (1,762,818) | (208,104) | (13.4%) | (3,645,425) | |

Fuel consumption | (672,038) | (742,639) | (70,601) | (10.5%) | (1,535,743) | |

Transportation expenses | (405,983) | (393,991) | 11,992 | 3.0% | (814,755) | |

Other variable costs | (888,910) | (638,986) | 249,924 | 28.1% | (1,321,393) | |

Procurements and Services | (3,521,646) | (3,538,435) | (16,788) | (0.5%) | (7,317,316) | |

|

|

|

|

|

| |

Contribution Margin | 3,041,935 | 2,996,446 | (45,489) | (1.5%) | 6,196,508 | |

Other work performed by entity and capitalized | 44,869 | 50,173 | 5,304 | 11.8% | 103,756 | |

Employee benefits expense | (374,678) | (378,552) | (3,874) | (1.0%) | (782,828) | |

Other fixed operating expenses | (450,435) | (540,698) | (90,264) | (20.0%) | (1,118,139) | |

Gross Operating Income (EBITDA) | 2,261,691 | 2,127,368 | (134,323) | (5.9%) | 4,399,297 | |

Depreciation and amortization | (449,017) | (424,900) | 24,117 | 5.4% | (878,673) | |

Reversal of impairment profit (impairment loss) recognized in profit or loss | (108,373) | (136,157) | (27,784) | (25.6%) | (281,567) | |

Operating Income | 1,704,301 | 1,566,311 | (137,990) | (8.1%) | 3,239,057 | |

Net Financial Income | (270,605) | (236,585) | 34,020 | 12.6% | (489,247) | |

Financial income | 171,237 | 233,613 | 62,376 | 36.4% | 483,100 | |

Financial costs | (438,358) | (465,411) | (27,053) | (6.2%) | (962,449) | |

Gain (Loss) for indexed assets and liabilities | (15,056) | (25,092) | (10,036) | (66.7%) | (51,889) | |

Foreign currency exchange differences, net | 11,572 | 20,306 | 8,733 | 75.5% | 41,991 | |

Gains | 91,331 | 80,873 | (10,459) | (11.5%) | 167,241 | |

Losses | (79,759) | (60,567) | 19,192 | 24.1% | (125,250) | |

Share of profit (loss) of associates accounted for using the equity method | 1,016 | 8,466 | 7,450 | 733.5% | 17,507 | |

Net Income From Other Investments | 273 | 1,038 | 766 | 280.7% | 2,147 | |

Net Income From Sale of Assets | 11,711 | (5,853) | (17,563) | (150.0%) | (12,103) | |

Net Income Before Taxes | 1,446,695 | 1,333,377 | (113,318) | (7.8%) | 2,757,362 | |

Income Tax | (346,007) | (460,837) | (114,830) | (33.2%) | (952,989) | |

NET INCOME ATTRIBUTABLE TO: | 1,100,688 | 872,541 | (228,148) | (20.7%) | 1,804,373 | |

Owners of parent | 486,227 | 375,471 | (110,756) | (22.8%) | 776,457 | |

Non-controlling interest | 614,462 | 497,069 | (117,392) | (19.1%) | 1,027,916 | |

Earning per share (Ch$ /share and US$ / ADR) | 14.9 | 11.5 | (3.4) | (22.8%) | 1.2 | |

OPERATINGINCOME

Operating income decreased by Ch$ 137,990 million, or 8.1% when compared to 2010.

Below we present operating revenues and costs breakdown by business line for the period ending on December 31, 2010 and 2011:

Pg. 11

| PRESS RELEASE Year Ended 2011 |

Table 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income by Businesses | Generation and Transmission | Distribution | |||||||||||

Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ | |||

2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 | |

Operating Revenues | 2,780,604 | 2,700,026 |

| (2.9%) |

| 5,583,527 |

| 4,392,626 | 4,447,427 |

| 1.2% |

| 9,197,071 |

Operating Costs | (1,730,510) | (1,705,652) |

| (1.4%) |

| (3,527,209) |

| (3,700,891) | (3,854,905) |

| 4.2% |

| (7,971,762) |

Operating Income | 1,050,094 | 994,374 |

| (5.3%) |

| 2,056,318 |

| 691,735 | 592,522 |

| (14.3%) |

| 1,225,308 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income by Businesses | Eliminations and Others |

| Consolidated | ||||||||||

Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ | |||

2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 | |

Operating Revenues | (609,649) | (612,573) |

| 0.5% |

| (1,266,773) |

| 6,563,581 | 6,534,880 |

| (0.4%) |

| 13,513,825 |

Operating Costs | 572,121 | 591,988 |

| 3.5% |

| 1,224,203 |

| (4,859,280) | (4,968,570) |

| 2.2% |

| (10,274,768) |

Operating Income | (37,528) | (20,585) |

| (45.1%) |

| (42,569) |

| 1,704,301 | 1,566,311 |

| (8.1%) |

| 3,239,057 |

Operating income for generation and transmission business line, detailed by country is shown in the following table:

Table 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Generation & Transmission | Chile |

| Argentina |

| Brazil | |||||||||||||||

Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ | ||||

2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 | |

Operating Revenues | 1,345,371 | 1,257,995 |

| (6.5%) |

| 2,601,475 |

| 358,090 | 395,296 |

| 10.4% |

| 817,454 |

| 359,211 | 309,049 |

| (14.0%) |

| 639,099 |

% of consolidated | 48% | 47% |

|

|

| 47% |

| 13% | 15% |

|

|

| 15% |

| 13% | 11% |

|

|

| 11% |

Operating Costs | (832,601) | (859,191) |

| 3.2% |

| (1,776,766) |

| (311,379) | (361,383) |

| 16.1% |

| (747,322) |

| (200,399) | (105,556) |

| (47.3%) |

| (218,285) |

% of consolidated | 48% | 50% |

|

|

| 50% |

| 18% | 21% |

|

|

| 21% |

| 12% | 6% |

|

|

| 6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income | 512,769 | 398,804 |

| (22.2%) |

| 824,708 |

| 46,710 | 33,914 |

| (27.4%) |

| 70,132 |

| 158,812 | 203,493 |

| 28.1% |

| 420,814 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Generation & Transmission | Peru |

| Colombia |

| Consolidated | |||||||||||||||

Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ | ||||

2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 | |

Operating Revenues | 211,264 | 239,841 |

| 13.5% |

| 495,981 |

| 507,526 | 498,569 |

| (1.8%) |

| 1,031,017 |

| 2,780,604 | 2,700,026 |

| (2.9%) |

| 5,583,527 |

% of consolidated | 8% | 9% |

|

|

| 9% |

| 18% | 18% |

|

|

| 18% |

| 100% | 100% |

|

|

|

|

Operating Costs | (140,944) | (135,187) |

| (4.1%) |

| (279,560) |

| (246,044) | (245,061) |

| (0.4%) |

| (506,774) |

| (1,730,510) | (1,705,652) |

| (1.4%) |

| (3,527,209) |

% of consolidated | 8% | 8% |

|

|

| 8% |

| 14% | 14% |

|

|

| 14% |

| 100% | 100% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income | 70,319 | 104,655 |

| 48.8% |

| 216,421 |

| 261,482 | 253,508 |

| (3.0%) |

| 524,243 |

| 1,050,094 | 994,374 |

| (5.3%) |

| 2,056,318 |

Distribution businessshowed a Ch$ 99,213 million lower operating income, totaling Ch$ 592,522 million. Physical sales amounted to 69,552 GWh, representing an increase of 2,278 GWh, or 3.4%. Our customer base increased by 384 thousand of new clients approximately, amounting to 13.7 million customers.

Operating Income for distribution business line, detailed by country, is as follows:

Table 4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Distribution | Chile |

| Argentina |

| Brazil | |||||||||||||||

Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ | ||||

2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 | |

Operating Revenues | 1,016,997 | 1,046,191 |

| 2.9% |

| 2,163,474 |

| 295,538 | 279,725 |

| (5.4%) |

| 578,458 |

| 1,987,042 | 1,976,716 |

| (0.5%) |

| 4,087,755 |

% of consolidated | 23% | 24% |

|

|

| 24% |

| 7% | 6% |

|

|

| 6% |

| 45% | 44% |

|

|

| 44% |

Operating Costs | (905,231) | (926,506) |

| 2.4% |

| (1,915,971) |

| (291,594) | (416,895) |

| 43.0% |

| (862,119) |

| (1,683,188) | (1,622,070) |

| (3.6%) |

| (3,354,364) |

% of consolidated | 24% | 24% |

|

|

| 24% |

| 8% | 11% |

|

|

| 11% |

| 45% | 42% |

|

|

| 42% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income | 111,767 | 119,685 |

| 7.1% |

| 247,502 |

| 3,944 | (137,170) |

| (3578.0%) |

| (283,661) |

| 303,854 | 354,646 |

| 16.7% |

| 733,391 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Distribution | Peru |

| Colombia |

| Consolidated | |||||||||||||||

Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ |

| Million Ch$ |

| Chg% |

| Th. US$ | ||||

2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 |

| 2010 | 2011 |

|

|

| 2011 | |

Operating Revenues | 307,159 | 329,309 |

| 7.2% |

| 680,996 |

| 785,890 | 815,487 |

| 3.8% |

| 1,686,388 |

| 4,392,626 | 4,447,427 |

| 1.2% |

| 9,197,071 |

% of consolidated | 7% | 7% |

|

|

| 7% |

| 18% | 18% |

|

|

| 18% |

| 100% | 100% |

|

|

|

|

Operating Costs | (242,211) | (259,410) |

| 7.1% |

| (536,447) |

| (578,667) | (630,025) |

| 8.9% |

| (1,302,861) |

| (3,700,891) | (3,854,905) |

| 4.2% |

| (7,971,762) |

% of consolidated | 7% | 7% |

|

|

| 7% |

| 16% | 16% |

|

|

| 16% |

| 100% | 100% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income | 64,948 | 69,900 |

| 7.6% |

| 144,549 |

| 207,222 | 185,462 |

| (10.5%) |

| 383,527 |

| 691,735 | 592,522 |

| (14.3%) |

| 1,225,308 |

Pg. 12

| PRESS RELEASE Year Ended 2011 |

NETFINANCIALINCOME

The Company’s net financial income as of December 31, 2011 wasa loss of Ch$ 236,585 million, representing an improvement of 12.6% over 2010. The latter is mainly explained by higher financial income of Ch$ 62,376 million, mainly as a result of recognition of the agreement with CELG by Ch$ 35,181 million; the update on liabilities related to pension plans in Brazil and higher time deposits during the period mainly explained by Chilectra, CGTF and Enersis.

The latter was partially offset by higher financial expense by Ch$27,053 million, explained by the update on pensions in Brazil and a higher average cost of debt.

Additionally, during the period the Company registered a loss for indexed assets and liabilities of Ch$ 10,036 million, as a result of to the negative impact of inflation over U.F. denominated debt in Chile. The U.F., a non-transaction currency linked to the inflation in Chile, increased its value by 3.9% during 2011, when compared to the 2.5% increase registered during 2010.

SALE OFASSETS

The net income from sale of assets registered a decrease of Ch$ 17,564 million, explained by the recognition of the loss generated due to the sale of CAM.

TAXES

Income tax net expense increased by Ch$ 114,830 million at the end of December 2011. The latter is explained by increases in: Ampla by Ch$ 20,097 million; CIEN by Ch$ 19,333 million; Cachoeira Dourada by Ch$ 12,815 million; Edesur by Ch$ 11,613 million; Chilectra by Ch$ 10,213 million; Coelce by Ch$ 12,269 million; Endesa Chile by Ch$ 8,291 million; San Isidro by Ch$ 7,268 million; Edegel by Ch$ 6,812 million; Pangue by Ch$ 10,213 million; Codensa by Ch$ 5,757 million; Enersis by Ch$ 5,560 million and Emgesa by Ch$ 4,105 million.

The latter was partially offset by decreases in: Pehuenche by Ch$ 8,253 million; Celta by Ch$ 4,039 million and Gas Atacama by Ch$ 857 million

Pg. 13

| PRESS RELEASE Year Ended 2011 |

CONSOLIDATEDBALANCESHEETANALYSIS

ASSETSUNDERIFRS

Table 5 |

|

|

|

|

|

|

ASSETS | (Million Ch$) |

| (Thousand US$) | |||

| As of Dec 31, 2010 | As of December 31, 2011 | Var 2010-2011 | Chg % | As of December 31, 2011 | |

|

|

|

|

|

| |

CURRENT ASSETS |

|

|

|

|

|

|

Cash and cash equivalents | 961,355 | 1,219,921 | 258,566 | 26.9% |

| 2,349,617 |

Other current financial assets | 7,818 | 939 | (6,878) | (88.0%) |

| 1,809 |

Other current non-financial assets | 35,993 | 72,466 | 36,473 | 101.3% |

| 139,573 |

Trade and other current receivables | 1,038,098 | 977,602 | (60,496) | (5.8%) |

| 1,882,901 |

Accounts receivable from related companies | 20,472 | 35,283 | 14,811 | 72.3% |

| 67,956 |

Inventories | 62,652 | 77,926 | 15,274 | 24.4% |

| 150,088 |

Current tax assets | 137,987 | 141,828 | 3,840 | 2.8% |

| 273,166 |

Non-current assets (or disposal groups) classified as held for sale | 73,893 | - | (73,893) | (100.0%) |

| - |

Total Current Assets | 2,338,268 | 2,525,965 | 187,697 | 8.0% |

| 4,865,110 |

|

|

|

|

|

|

|

NON-CURRENT ASSETS |

|

|

|

|

|

|

Other non-current financial assets | 62,969 | 37,355 | (25,614) | (40.7%) |

| 71,947 |

Other non-current non-financial assets | 103,736 | 109,501 | 5,765 | 5.6% |

| 210,904 |

Trade accounts receivables and other receivables, net | 319,568 | 443,328 | 123,760 | 38.7% |

| 853,868 |

Investment accounted for using equity method | 14,102 | 13,193 | (908) | (6.4%) |

| 25,411 |

Intangible assets other than goodwill | 1,452,586 | 1,467,398 | 14,812 | 1.0% |

| 2,826,268 |

Goodwill | 1,477,022 | 1,476,404 | (618) | (0.0%) |

| 2,843,613 |

Property, plant and equipment, net | 6,751,941 | 7,242,731 | 490,790 | 7.3% |

| 13,949,790 |

Investment properties | 33,019 | 38,056 | 5,037 | 15.3% |

| 73,297 |

Deferred tax assets | 452,634 | 379,939 | (72,696) | (16.1%) |

| 731,777 |

Total Non-Current Assets | 10,667,577 | 11,207,906 | 540,329 | 5.1% |

| 21,586,875 |

|

|

|

|

|

|

|

TOTAL ASSETS | 13,005,845 | 13,733,871 | 728,026 | 5.6% |

| 26,451,985 |

Total Assetsincreased Ch$ 728,026 million, mainly due to:

ØCh$ 540,329 million increase in non-current assets, or 5.1%, as a result of:

vCh$ 490,790 million increase in Property, Plant and Equipment, explained by the net effect resulting from the translation of financial statements from local currencies to Chilean pesos by Ch$ 314,867 million, and additions for the period in approximately Ch$ 498,142 million. The latter was partially offset by the depreciation for the period of Ch$ 322,218 million.

vCh$ 14,812 million increase in intangible assets other than goodwill, due to additions for the period of Ch$ 191,072 million, partially offset by the depreciation for the period of Ch$ 102,682 million, the exchange rates variations and the translation effect of Ch$ 15,036 million and effects related to the application of IFRIC 12 by Ch$ 58,542 million.

vCh$ 123,760 million increase in trade accounts receivables and other receivables, mainly due to the increase in Ampla by Ch$ 62,736 million and Coelce by Ch$ 23,054 million, by the appliance of IFRIC 12 interpretation, related to service concession arrangements. Also due to increases in Costanera and Chocon for a total consideration of Ch$ 25,148 million due to FONINVEMEN II and Cachoeira Dourada due to the agreement with CELG by Ch$ 12,866 million. The latter was partially offset by the decrease in Chilectra by Ch$ 3,347 million and CIEN by Ch$ 2,263 million.

The latter was partially compensated by

Pg. 14

| PRESS RELEASE Year Ended 2011 |

vCh$ 72,696 million decrease in deferred taxes in: Codensa by Ch$ 30,704 million; Edesur by Ch$ 17,449 million; CIEN by Ch$ 15,550 million; Chilectra by Ch$ 8,870 million and Enersis by Ch$ 2,385 million.

vDecrease of Ch$ 25,614 million in other non-current financial assets, mainly explained by the drop in Endesa Chile by Ch$ 15,878 million, due to MTM of derivatives and reduction in Enersis by Ch$ 8,667 million in cash collateral.

ØCh$ 187,697 million increase in current assets or 8.0%, mainly due to:

vCh$ 258,566 million increase in Cash and Cash Equivalent, primarily explained by increases in: Enersis by Ch$ 266,013 million due to increases inrepos; higher amount of time deposits in Emgesa by Ch$ 61,676 million, Coelce by Ch$ 58,658 million, Codensa by Ch$ 55,608 million Cachoeira Dourada by Ch$ 41,348 million, CGTF by Ch$ 23,112 million, Edegel by Ch$ 18,899 million, Endesa Argentina by Ch$ 3,424 million and Endesa Chile by Ch$ 2,835 million. The latter was partially offset by decreases in Endesa Brasil by Ch$ 143,892 million explained by a payment made to IFC and dividends, Chilectra by Ch$ 80,239 million due to debt payment and dividends, Edesur by Ch$ 24,227 million due to decreases in time deposits, Edelnor by Ch$ 17,502 million and CIEN by Ch$ 11,421 million.

vIncrease in other current non-financial assets by Ch$ 36,473 million, mainly explained by prepayments of goods and services, mostly related to insurances.

vCh$ 73,893 million decrease in non-current assets classified as held for sell, related to the selling process of the former subsidiaries CAM and Synapsis, that took place in the first quarter of 2011.

vDecrease in trade and other accounts receivables by Ch$ 60,496 million mainly explained by: Coelce by Ch$ 41,821 million, Chilectra by Ch$ 32,779 million, Ampla by Ch$ 18,724 million, GasAtacama by Ch$ 7,947 million, CGTF by Ch$ 1,295 million and Codensa by Ch$ 975 million. The latter was partially compensated by increases in Endesa Chile by Ch$ 21,186 million, Pehuenche by Ch$ 19,352 million, Edelnor by Ch$ 12,688 million, Edegel by Ch$ 6,009 million and Pangue by Ch$ 3,946 million.

Pg. 15

| PRESS RELEASE Year Ended 2011 |

BOOKVALUE ANDECONOMICVALUE OFASSETS

Regarding the more important assets, the following should be mentioned:

Properties, Plants and Equipment are valued at their purchase cost, net of the corresponding accumulated depreciation and impairment loss they have been subject to. Properties, Plants and Equipment, net of their residual value, if applicable, are linearly depreciated by distributing the cost of their different elements along the estimated years of useful life, which is the period that the companies expect to use them. The useful life is reviewed regularly.

The goodwill value generated by consolidation represents the acquisition cost surplus on the Group’sstake in terms of the reasonable value of assets and liabilities, including the identifiable contingent liabilities of a subsidiary at the time of acquisition. Goodwill is not amortized. Instead, at the closing of each accounting period an assessment is made of whether any impairment has occurred during the period that could reduce its recoverable value to an amount below the registered net cost, proceeding in this event to make a timely impairment adjustment (See Note 3.e to the Consolidated Financial Statements).

Throughout the fiscal year and in particular at the date of closing, an assessment is made as to any indication of possible loss due to the impairment of any asset. In the event of any such indication, an estimate of the recoverable sum of said asset is made to determine, if applicable, the depreciated amount. If this involves identifiable assets that do not originate independent cash flows, the recoverability of the Cash Generating Unit that the asset belongs to is estimated, understanding as such the smaller group of identifiable assets that generate independent cash incomes.

Assets expressed in foreign currency are expressed at the prevalent exchange rate at the closing of the period.

Notes and accounts receivable from related companies are classified according to their short and long term maturities. These operations are adjusted according to prevalent market equity conditions.

In summary, assets are valued according to the International Financial Reporting Standards, whose criteria are expressed in Note 3 of the Consolidated Financial Statements.

Pg. 16

| PRESS RELEASE Year Ended 2011 |

Table 6 |

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS' EQUITY | (Million Ch$) |

| (Thousand US$) | |||

| As of Dec 31, 2010 | As of December 31, 2011 | Var 2010-2011 | Chg % | As of December 31, 2011 | |

|

|

|

|

|

|

|

CURRENT LIABILITIES |

|

|

|

|

|

|

Other current financial liabilities | 665,598 | 672,082 | 6,484 | 1.0% |

| 1,294,458 |

Trade and other current payables | 1,224,490 | 1,235,064 | 10,574 | 0.9% |

| 2,378,784 |

Accounts payable to related companies | 148,202 | 157,178 | 8,975 | 6.1% |

| 302,730 |

Other short-term provisions | 115,449 | 99,703 | (15,747) | (13.6%) |

| 192,031 |

Current tax liabilities | 147,667 | 235,853 | 88,187 | 59.7% |

| 454,263 |

Current provisions for employee benefits | 5,450 | - | (5,450) | (100.0%) |

| - |

Other current non-financial liabilities | 35,791 | 60,653 | 24,863 | 69.5% |

| 116,821 |

Liabilities (or disposal groups) classified as held for sale | 64,630 | - | (64,630) | (100.0%) |

| - |

Total Current Liabilities | 2,407,277 | 2,460,534 | 53,256 | 2.2% |

| 4,739,086 |

|

|

|

|

|

|

|

NON-CURRENT LIABILITIES |

|

|

|

|

|

|

Other non-current financial liabilities | 3,014,956 | 3,271,355 | 256,399 | 8.5% |

| 6,300,761 |

Non-current payables | 37,237 | 14,305 | (22,932) | (61.6%) |

| 27,551 |

Accounts payable to related companies | 1,084 | - | (1,084) | (100.0%) |

| - |

Other-long term provisions | 225,522 | 202,574 | (22,949) | (10.2%) |

| 390,165 |

Deferred tax liabilities | 555,924 | 508,438 | (47,485) | (8.5%) |

| 979,272 |

Non-current provisions for employee benefits | 215,819 | 277,526 | 61,707 | 28.6% |

| 534,526 |

Other non-current non-financial liabilities | 33,997 | 102,985 | 68,988 | 202.9% |

| 198,354 |

Total Non-Current Liabilities | 4,084,540 | 4,377,183 | 292,644 | 7.2% |

| 8,430,630 |

|

|

|

|

|

|

|

SHAREHOLDERS' EQUITY |

|

|

|

|

|

|

Issued capital | 2,824,883 | 2,824,883 | - | 0.0% |

| 5,440,838 |

Retained earnings (losses) | 2,103,690 | 2,232,969 | 129,279 | 6.1% |

| 4,300,788 |

Share premium | 158,760 | 158,760 | - | 0.0% |

| 305,777 |

Other equity changes | - | - | - |

|

| - |

Reserves | (1,351,787) | (1,320,883) | 30,905 | 2.3% |

| (2,544,073) |

|

|

| - |

|

|

|

Equity Attributable to Shareholders of the Company | 3,735,545 | 3,895,729 | 160,184 | 4.3% |

| 7,503,329 |

Equity Attributable to Minority Interest | 2,778,483 | 3,000,425 | 221,942 | 8.0% |

| 5,778,939 |

Total Shareholders' Equity | 6,514,028 | 6,896,154 | 382,126 | 5.9% |

| 13,282,269 |

|

|

|

|

|

|

|

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY | 13,005,845 | 13,733,871 | 728,026 | 5.6% |

| 26,451,985 |

TheCompany’s total liabilities and shareholders’ equity increased by Ch$ 728,026 million, whencompared to the period ended on December 31, 2010, due to Ch$ 382,126 million increase inshareholders’ equity, Ch$ 292,643 million increase in non-current liabilities and Ch$ 53,257 million increase of current liabilities. The detail is explained as follows:

ØNon-current liabilities increased by Ch$ 292,643 million, or 7.2%, mainly due to:

vOther non-current financial liabilities (financial debt and derivatives) increased by Ch$ 256,399 million, mainly due to increases in: Emgesa by Ch$ 147,029 million, due to the issuance of a bond in local currency in the international capital market; in Coelce by Ch$ 82,662 million due to higher amount of loans; in Endesa Chile by Ch$ 38,476 million, due to the effect of debt in US$ and UF; in Ampla by Ch$ 9,875 million due to exchange rate differences; in Codensa by Ch$ 18,636 million; in Chocon by Ch$ 17,138 million and Edesur by Ch$ 8,611 million. The latter was partially offset by CIEN by Ch$ 56,400 million, due to a loan payment.

vOther non-current non-financial liabilities increased by Ch$ 68,988 million, mainly in Emgesa and Codensa by Ch$ 22,026 million and Ch$ 14,519 million respectively, due to the recording of the equity tax impact as of January 2, 2011. Also due to increases in Endesa Chile by Ch$ 8,881 million, CIEN by Ch$ 4,461 million, Coelce by Ch$ 3,699 million, Cachoeira Dourada by Ch$ 3,501 million and in Ampla by Ch$ 2,147 million.

Pg. 17

| PRESS RELEASE Year Ended 2011 |

vIncrease in non-current provisions for employee benefits of Ch$ 61,707 million due to increases in Ampla by Ch$ 44,229 million; Emgesa by Ch$ 4,778 million; Edesur by Ch$ 4,009, Coelce by Ch$ 2,134 million; Codensa by Ch$ 1,692 million; Chilectra by Ch$ 1,527 million and Endesa Chile by Ch$ 714 million.

vDecreases in Other long term provisions by Ch$ 22,949 million due to lower provisions in CIEN by Ch$ 36,149; Edegel by Ch$ 8,617 million and Edesur by Ch$ 2,211 million, partially compensated by increases in Ampla of Ch$ 13,294 million; Coelce by Ch$ 9,212 million and Codensa by Ch$ 2,596 million.

vDecrease in non-current payable by Ch$ 22,932 million due to the decrease in Coelce by Ch$ 5,935 million; Cachoeira Dourada by Ch$ 4,700 million; CIEN by Ch$ 4,599 million and Ampla by Ch$ 3,965 million.

ØCurrent liabilities increased by Ch$ 53,257 million, equivalent to 2,2%, mainly explained by the following changes:

vIncrease in current tax liabilities by Ch$ 88,187 million, explained by increases in Chilectra by Ch$ 15,833 million; Cachoeira Dourada by Ch$ 14,780 million; Emgesa by Ch$ 14,175 million; Edegel by Ch$ 14,056 million; San Isidro by Ch$ 5,740 million; Ampla by Ch$ 5,533 million and Pehuenche by Ch$ 4,804 million.

vIncrease in Other current non-financial liabilities by Ch$ 24,863 million, explained by increases in: Ampla by Ch$ 8,138 million; Edesur by Ch$ 6,612 million; Edelnor by Ch$ 3,445 million; Coelce by Ch$ 2,728 million; Codensa by Ch$ 1,425 million; Cachoeira Dourada by Ch$ 836 million and CGTF by Ch$ 715 million.

The above was partially offset by:

vReduction in liabilities included in groups of assets for disposal classified as held for sale, of Ch$64,630 million, as a result of the sale of the liabilities of CAM and Synapsis during the third quarter of 2011.

Equity increases by Ch$382,126 million with respect to 2010:

vThe equity attributable to owners of the controller increases by Ch$160,184 million, mainly explained by the effect of the comprehensive result for the period of Ch$ 368,569 million, primarily driven by the result of the dominant of Ch$ 375,471 million, positive translation reserves of Ch$ 60,107 million, negative hedge reserve of Ch$ 41,094 million and negative other reserves of Ch$ 25,916 million, less dividends of Ch$ 209,887 million.

vNon-controller participations increased by Ch$ 221,942 million, mainly explained by the effect of the comprehensive result for the period of Ch$ 602,765 million, principally driven by the result for the period of the non-controllers of Ch$ 497,069 million and other comprehensive results of the period of Ch$ 105,696 million, partially offset by the reduction in other equity movements of Ch$ 380,823 million.

Pg. 18

| PRESS RELEASE Year Ended 2011 |

Table 7 |

|

|

|

|

|

|

|

|

(Thousand US$) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Balance | TOTAL |

Chile | 108,829.1 | 423,483.2 | 736,635.3 | 223,650.4 | 426,470.4 | 17,622.3 | 1,074,414.4 | 3,011,105.0 |

Enersis | 4,492.9 | 4,751.2 | 551,142.6 | 5,313.3 | 412,063.1 | 5,941.9 | 32,118.8 | 1,015,823.8 |

Chilectra | 0.6 | - | - | - | - | - | - | 0.6 |

Endesa Chile | 104,335.6 | 418,731.9 | 185,492.7 | 218,337.0 | 14,407.3 | 11,680.3 | 1,042,295.7 | 1,995,280.6 |

Argentina | 170,558.8 | 106,393.4 | 60,023.8 | 35,065.6 | 17,077.1 | - | - | 389,118.8 |

Edesur | 41,828.9 | 42,946.4 | 6,988.0 | - | - | - | - | 91,763.3 |

Costanera | 98,247.6 | 34,996.2 | 27,958.6 | 27,341.9 | 17,077.1 | - | - | 205,621.3 |

Chocón | 30,207.3 | 28,450.8 | 25,077.2 | 7,723.8 | - | - | - | 91,459.1 |

Hidroinvest | 275.0 | - | - | - | - | - | - | 275.0 |

CTM | - | - | - | - | - | - | - | - |

TESA | - | - | - | - | - | - | - | - |

Peru | 115,630.2 | 110,663.4 | 107,015.5 | 83,759.3 | 88,965.9 | 84,269.0 | 141,167.3 | 731,470.7 |

Edelnor | 55,684.8 | 58,917.5 | 56,738.0 | 50,040.8 | 31,602.4 | 37,093.8 | 59,345.3 | 349,422.6 |

Edegel | 59,945.4 | 51,745.9 | 50,277.5 | 33,718.5 | 57,363.5 | 47,175.2 | 81,822.0 | 382,048.1 |

Brazil | 529,486.2 | 227,965.7 | 163,503.3 | 137,081.1 | 187,498.7 | 128,575.8 | 141,668.2 | 1,515,778.9 |

Endesa Brasil | - | - | - | - | - | - | - | - |

Coelce | 119,141.8 | 98,395.9 | 96,580.1 | 38,857.3 | 91,942.6 | 63,785.0 | 79,395.4 | 588,098.1 |

Ampla | 287,995.6 | 115,178.5 | 51,489.4 | 81,671.9 | 87,887.1 | 56,493.6 | 58,395.7 | 739,112.0 |

Cachoeira | - | - | - | - | - | - | - | - |

Cien | 108,929.4 | - | - | - | - | - | - | 108,929.4 |

Fortaleza | 13,419.3 | 14,391.4 | 15,433.8 | 16,551.9 | 7,669.0 | 8,297.1 | 3,877.0 | 79,639.5 |

Colombia | 174,359.9 | 41,179.8 | 284,480.4 | 128,686.9 | 74,638.4 | 289,030.7 | 689,813.1 | 1,682,189.2 |

Codensa | 17,357.3 | 41,179.8 | 211,561.2 | - | 74,638.4 | 201,523.7 | 41,179.8 | 587,440.2 |

Emgesa | 157,002.7 | - | 72,919.1 | 128,686.9 | - | 87,507.1 | 648,633.3 | 1,094,749.1 |

TOTAL | 1,098,864.3 | 909,685.5 | 1,351,658.2 | 608,243.3 | 794,650.5 | 519,497.8 | 2,047,063.1 | 7,329,662.7 |

DEBTMATURITY WITHTHIRDPARTIES, MILLIONCH$

Table 7.1 |

|

|

|

|

|

|

|

|

(Million Ch$) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Balance | TOTAL |

Chile | 56,504 | 219,872 | 382,461 | 116,119 | 221,423 | 9,149 | 557,836 | 1,563,366 |

Enersis | 2,333 | 2,467 | 286,153 | 2,759 | 213,943 | 3,085 | 16,676 | 527,416 |

Chilectra | 0 | - | - | - | - | - | - | 0 |

Endesa Chile | 54,171 | 217,406 | 96,308 | 113,361 | 7,480 | 6,064 | 541,160 | 1,035,950 |

Argentina | 88,554 | 55,239 | 31,164 | 18,206 | 8,866 | - | - | 202,030 |

Edesur | 21,718 | 22,298 | 3,628 | - | - | - | - | 47,644 |

Costanera | 51,010 | 18,170 | 14,516 | 14,196 | 8,866 | - | - | 106,759 |

Chocón | 15,684 | 14,772 | 13,020 | 4,010 | - | - | - | 47,486 |

Hidroinvest | 143 | - | - | - | - | - | - | 143 |

CTM | - | - | - | - | - | - | - | - |

TESA | - | - | - | - | - | - | - | - |

Peru | 60,035 | 57,456 | 55,562 | 43,488 | 46,191 | 43,752 | 73,294 | 379,780 |

Edelnor | 28,912 | 30,590 | 29,458 | 25,981 | 16,408 | 19,259 | 30,812 | 181,420 |

Edegel | 31,124 | 26,866 | 26,104 | 17,507 | 29,783 | 24,493 | 42,482 | 198,359 |

Brazil | 274,909 | 118,360 | 84,891 | 71,172 | 97,349 | 66,757 | 73,554 | 786,992 |

Endesa Brasil | - | - | - | - | - | - | - | - |

Coelce | 61,858 | 51,087 | 50,144 | 20,175 | 47,737 | 33,117 | 41,222 | 305,341 |

Ampla | 149,527 | 59,801 | 26,733 | 42,404 | 45,631 | 29,332 | 30,319 | 383,747 |

Cachoeira | - | - | - | - | - | - | - | - |

Cien | 56,556 | - | - | - | - | - | - | 56,556 |

Fortaleza | 6,967 | 7,472 | 8,013 | 8,594 | 3,982 | 4,308 | 2,013 | 41,349 |

Colombia | 90,528 | 21,381 | 147,702 | 66,814 | 38,752 | 150,065 | 358,151 | 873,393 |

Codensa | 9,012 | 21,381 | 109,843 | - | 38,752 | 104,631 | 21,381 | 304,999 |

Emgesa | 81,516 | - | 37,860 | 66,814 | - | 45,434 | 336,770 | 568,394 |

TOTAL | 570,530 | 472,309 | 701,781 | 315,800 | 412,583 | 269,723 | 1,062,835 | 3,805,561 |

Pg. 19

| PRESS RELEASE Year Ended 2011 |

EVOLUTIONOFKEYFINANCIALRATIOS

Table 8 |

|

|

|

|

|

Indicator | Unit | As of Dec 31, 2010 | As of December 31, 2011 | Var 2010-2011 | Chg % |

Liquidity | Times | 0.97 | 1.03 | 0.06 | 6.2% |

Acid ratio test * | Times | 0.94 | 0.98 | 0.04 | 4.3% |

Working capital | Million Ch$ | (69,010) | 65,431 | 134,441 | 194.8% |

Working capital | Thousand US$ | (132,915) | 126,023 | 258,939 | 194.8% |

Leverage ** | Times | 1.00 | 0.99 | (0.01) | (1.0%) |

Short-term debt | % | 37.0 | 36.0 | (1.00) | (2.7%) |

Long-term debt | % | 63.0 | 64.0 | 1.00 | 1.6% |

* (Current assets net of inventories and prepaid expenses) / Current liabilities |

|

|

| ||

** Total debt / (equity + minority interest) |

|

|

|

|

|

|

|

|

|

|

|

Table 8.1 |

|

|

|

|

|

Indicator | Unit | 2010 | 2011 | Var 2010-2011 | Chg % |

Financial expenses coverage * | Times | 5.12 | 4.52 | (0.59) | (11.6%) |

Op. income / Op. rev. | % | 25.97 | 23.97 | (2.00) | (7.7%) |

ROE ** | % | 13.41 | 9.84 | (3.57) | (26.6%) |

ROA ** | % | 8.40 | 6.53 | (1.87) | (22.3%) |

* EBITDA / Financial costs |

|

|

|

|

|

** Annualized figures |

|

|

|

|

|

The liquidity ratio at December 31, 2011 was 1.03:1, a slight increase of 0.06 times, equivalent to 6.2%, with respect to December 31, 2010. This reflects a company with a solid liquidity position, maintaining its bank debt, financing its investments with cash generation and a satisfactory debt maturity structure.

The leverage ratio is 0.99:1 as of December 31, 2011, reducing by 1.0% with respect to December 31, 2010.

The financial cost coverage shows a fall of 0.59 times, equivalent to 11.6%, passing from 5.12:1 at December 31, 2010 to 4.52:1 at December 31,2011. This is the result of the fall in the company’sEBITDA in 2011.

The profitability indicator, being operating income over ordinary revenues, declined 7.7% to 24.0% at December 31, 2011.

On the other hand, the annualized return on equity of the owners of the controller (dominant) is 9.8%, with a fall of 26.6% with respect to December 31, 2010 when it was 13.4%. This was the result of the lower result reported for the period, added to the increase of the equity of the owners.

The annualized return on assets passed from 8.4% as of December 31, 2010 to 6.5% in December 31, 2011 as a result of the decline in the result for the present period and the increase in assets.

Pg. 20

| PRESS RELEASE Year Ended 2011 |

Consolidated Statements of Cash Flows Analysis

UNDERIFRS

Table 9 | ||||||

Cash Flow | (Million Ch$) |

| (Thousand US$) | |||

| 2010 | 2011 | Var 2010-2011 | Chg % | 2011 | |

|

|

|

|

|

|

|

Net Income | 1,100,688 | 872,541 | (228,148) | (20.7%) | 1,804,373 | |

Adjustments to reconcile net income | ||||||

Income tax expense | 346,007 | 460,837 | 114,830 | 33.2% | 952,989 | |

Decrease (increse) in inventories | 13,375 | (9,319) | (22,694) | (169.7%) | (19,271) | |

Decrease (increase) in trade accounts receivable | (164,046) | (10,784) | 153,262 | 93.4% | (22,301) | |

Decrease (increase) in other operating accounts receivable | (171,237) | (233,613) | (62,376) | (36.4%) | (483,100) | |

Decrease (increase) in trade accounts payable | 128,805 | (179,340) | (308,144) | (239.2%) | (370,866) | |

Decrease (increase) in other operating accounts payable | 453,414 | 490,504 | 37,090 | 8.2% | 1,014,338 | |

Depreciation and amortization expense | 449,017 | 424,900 | (24,117) | (5.4%) | 878,673 | |

(Reversal of) Impairment losses | 108,373 | 136,157 | 27,784 | 25.6% | 281,567 | |

Provisions | (29,193) | (83,617) | (54,423) | (186.4%) | (172,915) | |

Unrealized foreign currency exchange differences | (11,572) | (20,306) | (8,733) | (75.5%) | (41,991) | |

Non-distributed gains from associates | (1,016) | (8,466) | (7,450) | (733.5%) | (17,507) | |

Minority interest | - | - | - | - | ||

Other non-cash | 71,286 | 242,958 | 171,672 | 240.8% | 502,425 | |

Total adjustments to Reconcile to Operating Income | 1,193,213 | 1,209,911 | 16,698 | 1.4% | 2,502,040 | |

Dividends paid | - | - | - | - | ||

Dividends received | - | - | - | - | ||

Payments of interest classified as operating | - | - | - | - | ||

Proceeds of interest received classified as operating | - | - | - | - | ||

Income taxes refund (paid) | (349,297) | (361,092) | (11,795) | (3.4%) | (746,721) | |

Other inflows (outflows) of cash | (1,189) | (22,913) | (21,724) | (1826.3%) | (47,384) | |

NET CASH FLOWS PROVIDED BY OPERATING ACTIVITIES | 1,943,415 | 1,698,446 | (244,969) | (12.6%) |

| 3,512,307 |

|

|

|

|

|

|

|

Net Cash Flows provided by (used in) Investing Activities |

|

|

|

|

|

|

Cash flows from loss of control of subsidiaries or other businesses. | - | 12,662 | 12,662 |

|

| 26,185 |

Acquisitions of associates | - | - | - |

|

| - |

Cash flows used for the purchase of non-controlling | - | - |

|

|

|

|

Loans to related companies | - | (26) | (26) |

|

| (53) |

Proceeds from sales of property, plant and equipment | 8,890 | 6,049 | (2,841) | (32.0%) |

| 12,509 |

Purchase of property, plant and equipment | (473,922) | (498,142) | (24,220) | (5.1%) |

| (1,030,134) |

Proceeds from sales of intangible assets | 1,425 | 8,966 | 7,541 | 529.3% |

| 18,540 |

Acquisitions of intangible assets | (227,419) | (187,864) | 39,555 | 17.4% |

| (388,494) |

Proceeds from other long term assets. | - | 41 | 41 |

|

| 85 |

Purchase of other long-term assets | - | - | - |

|

| - |

Proceeds from prepayments reimbursed and third party loans | - | - | - |

|

| - |

Prepayments and third party loans | - | (1,285) | (1,285) |

|

| (2,657) |

Dividends received | 3,279 | 4,025 | 746 | 22.8% |

| 8,324 |

Interest received | 6,808 | 19,612 | 12,804 | 188.1% |

| 40,556 |

Other inflows (outflows) of cash | (94,842) | 11,992 | 106,834 | 112.6% |

| 24,799 |

NET CASH FLOWS FROM (USED IN) INVESTING ACTIVITIES | (775,781) | (623,970) | 151,811 | 19.6% |

| (1,290,340) |

|

|

|

|

|

|

|

Cash Flows provided by (used in) Financing Activities |

|

|

|

|

|

|

Proceeds from shares issue | - | 97 | 97 |

|

| 201 |

Proceeds from long-term borrowings | 263,125 | 646,273 | 383,148 | 145.6% |

| 1,336,462 |

Repayments of borrowings | 822 | 9,129 | 8,307 | 1011.0% |

| 18,878 |

Payments of loans | (740,287) | (629,404) | 110,882 | 15.0% |

| (1,301,579) |

Payments of finance lease liabilities | (24,130) | (11,479) | 12,651 | 52.4% |

| (23,738) |

Repayment of loans to related companies | - | - | - |

|

| - |

Dividends paid | (556,087) | (648,107) | (92,020) | (16.5%) |

| (1,340,255) |

Interest paid | (244,596) | (248,097) | (3,501) | (1.4%) |

| (513,053) |

Other financing proceeds (payments) | 18,132 | (9,841) | (27,974) | (154.3%) |

| (20,351) |

NET CASH FLOWS PROVIDED BY (USED IN) FINANCING ACTIVITIES | (1,283,021) | (891,430) | 391,591 | 30.5% |

| (1,843,434) |

|

|

|

|

|

|

|

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS BEFORE EFFECTS OF EXCHANGE RATE | (115,387) | 183,047 | 298,434 | 258.6% |

| 378,533 |

|

|

|

|

|

|

|

Effect of exchange rate changes on cash and cash equivalents | (58,159) | 75,519 | 133,678 | 229.8% |

| 156,170 |

Net Increase (Decrease) in Cash and Cash Equivalents | (173,546) | 258,566 | 432,112 | 249.0% | 534,703 | |

Cash and cash equivalents at end of period | 1,134,901 | 961,355 | (173,546) | (15.3%) |

| 1,988,037 |

Ending Balance of Cash and Cash Equivalents | 961,355 | 1,219,921 | 258,566 | 26.9% |

| 2,522,740 |

Pg. 21

| PRESS RELEASE Year Ended 2011 |

The company generated a negative net cash flow during the period of Ch$ 183,047 million, comprising the following:

Operating activities for 2011 generated a net positive flow of Ch$ 1,698,447 million, a fall of 12.6% compared to the year before. This flow comprises mainly the earnings for the period of Ch$ 872,541 million, which is adjusted to reconcile the result of Ch$ 708,679 million. This adjustment includes the amortization, depreciation and impairment of assets of Ch$ 561,057 million and interest expenses of Ch$ 256,891 million. This is partly compensated by the reduction in working capital of Ch$ 107,436 million.

Investment activities generated a negative net cash flow of Ch$ 623,970 million, representing an increase in cash of 19.6% or Ch$ 151,811 million compared to the same period of 2010. These disbursements relate mainly to the acquisition of properties, plant and equipment of Ch$ 498,142 million and the incorporation of intangible assets (IFRIC 12) of Ch$187,864 million, compensated partly by the net cash flow from the sale of CAM and Synapsis of Ch$12,662 million and interests received of Ch$ 19,612 million.

Financing activities generated a net negative cash flow of Ch$ 891,430 million, principally the payment of dividends for Ch$ 648,107 million, loan repayments of Ch$ 629,404 million and interest payments of Ch$ 248,097 million. This is partially offset by loan drawings of Ch$ 646,273 million.

CASHFLOWRECEIVEDFROMFOREIGNSUBSIDIARIES BYENERSIS, CHILECTRA ANDENDESACHILE

Table 10 |

|

|

|

|

|

|

|

|

|

|

Cash Flow | Interest Received | Dividends Received | Capital Reductions | Others | Total Cash Received | |||||

(Thousand US$) | ||||||||||

| 2010 | 2011 | 2010 | 2011 | 2010 | 2011 | 2010 | 2011 | 2010 | 2011 |

Argentina | 1,586.2 | 1,503.3 | 8,772.2 | - | - | - | - | 101.8 | 10,358.5 | 1,605.1 |

Peru | - | - | 68,582.2 | 77,896.4 | - | - | - | - | 68,582.2 | 77,896.4 |

Brazil | - | - | 194,835.9 | 345,810.2 | - | - | - | - | 194,835.9 | 345,810.2 |

Colombia | - | - | 221,251.8 | 27,664.4 | 59,462.9 | - | - | - | 280,714.7 | 27,664.4 |

Others | - | - | - | - | - | - | - | - | - | - |

Total | 1,586.2 | 1,503.3 | 493,442.1 | 451,371.1 | 59,462.9 | - | - | 101.8 | 554,491.3 | 452,976.2 |

Source: Internal Financial Report

Pg. 22

| PRESS RELEASE Year Ended 2011 |

Table 11 |

|

|

|

|

|

|

|

|

|

| Payments for Additions of Fixed Assets |

| Depreciation | ||||||

|

|

|

|

|

|

|

|

|

|

| Million Ch$ |

| Thousand US$ |

| Million Ch$ |

| Thousand US$ | ||

| 2010 | 2011 |

| 2011 |

| 2010 | 2011 |

| 2011 |

Endesa Chile | 254,872 | 264,883 |

| 547,766 |

| 175,068 | 170,051 |

| 351,657 |

Cachoeira | 4,668 | 686 |

| 1,419 |

| 7,383 | 7,280 |

| 15,055 |

Endesa Fortaleza | 1,870 | 7,530 |

| 15,572 |

| 7,999 | 8,051 |

| 16,649 |

Cien | 1,884 | 310 |

| 641 |

| 29,986 | 11,122 |

| 23,000 |

Chilectra S.A. | 31,148 | 19,947 |

| 41,249 |

| 21,191 | 21,777 |

| 45,034 |

Edesur | 58,221 | 82,014 |

| 169,601 |

| 14,279 | 13,244 |

| 27,388 |

Edelnor | 33,203 | 37,704 |

| 77,970 |

| 19,800 | 20,002 |

| 41,363 |

Ampla (*) | 120,785 | 131,519 |

| 271,975 |

| 44,976 | 56,424 |

| 116,682 |

Coelce (*) | 102,946 | 51,309 |

| 106,105 |

| 51,936 | 41,649 |

| 86,128 |

Codensa | 76,255 | 77,456 |

| 160,175 |

| 59,143 | 59,957 |

| 123,988 |

Cam Ltda.(**) | 1,148 | 46 |

| 95 |

| 1,774 | 294 |

| 608 |

Inmobiliaria Manso de Velasco Ltda. | 708 | 2,311 |

| 4,779 |

| 285 | 259 |

| 536 |

Synapsis (***) | 3,326 | 488 |

| 1,009 |

| 3,084 | 478 |

| 988 |

Enersis holding and investment companies | 388 | 991 |

| 2,049 |

| 1,080 | 1,208 |

| 2,498 |

Total | 691,422 | 677,194 |

| 1,400,405 |

| 437,984 | 411,796 |

| 851,575 |

(*) Includes concessions intangible assets. |

|

|

|

|

|

|

|

|

|

(**) Company sold on February 24th, 2011. | |||||||||

(***) Company sold on March 1st, 2011. | |||||||||

THEPRINCIPALRISKS ASSOCIATED TO THE ACTIVITIES OF THEENERSISGROUP

Commercial and Regulatory Risk

The Group’s activities are subject to a broad range of governmental standards and environmentalregulations. Any modification of such standards and regulations may affect the Group’s activities,economic situation and operating results.

The Group’s distribution activity is subject to a wide range of rulesregarding tariffs and other issues that govern their activities in each of the countries where it operates and which could modify distribution subsidiaries operating results.

The Group’s generation activity is subject to existing hydrological and weatherconditions in thegeographic zones in which the Group’s hydroelectric generating plants are located. Commercial policieshave been planned in order to moderate the possible impact of changes in these variables.

Group’s activities are subjectto certain environmental regulation which Enersis fulfills constantly. Modifications applied on such regulations may affect the operations, economic condition or the results of these operations.

Enersis and its operating subsidiaries are subject to environmental regulations which, among other things, require the company to conduct environmental impact studies for future projects, obtaining permits, licenses and other authorizations and the fulfillment of all requirements of those licenses, permits and norms. As any other regulated company, Enersis cannot guarantee:

·The approval from regulators of environmental impact studies.

Pg. 23

| PRESS RELEASE Year Ended 2011 |

·That public opposition may not cause delays or modifications to any proposed project and

·That laws or regulations may not change or be interpreted in a manner that could adversely affect the operations or the plans for companies in which Enersis or its subsidiaries hold investments.

The group’s commercial activity has been planned to moderate possible impacts resulting fromchanges in hydrological conditions.

Enersis group’s operations include hydroelectric generation and therefore depend on the hydrologicalconditions at any time in the broad geographical zones where its hydroelectric generation installations are located. If hydrological conditions produce droughts or other conditions that negatively affect hydroelectric generation, the results could be adversely affected. Enersis has therefore defined as an essential part of its commercial policy not to contract 100% of its total capacity. The electricity business is also affected by atmospheric conditions like average temperatures which govern consumption. The different weather conditions can produce differences in the margin obtained by the business.

Financial situation and the results from operations could be adversely affected if risk exposureweren’t efficiently managed in regards to interest rates, prices of commodities, and exchangerates.

Interest Rate Risk

Interest rate variations modify the fair value of those assets and liabilities that accrue a fixed interest rate, as well as the future flows of assets and liabilities pegged to a variable interest rate.

In compliance with our current interest rate hedging policy, the portion of fixed and/or hedged debt to the total net debt was 62% as of December 31, 2011 on a consolidated basis.

Depending on the Group’s estimates and debt structure objectives, hedging transactions take placehiring derivatives that mitigate these risks.

The structure of Enersis’ financial debt sort by fixed, protected and variable interest rate, and after derivatives, is as follows:

Net Position:

| Dec. 31 | Dec. 31 | |

| 2011 | 2010 | |

| % | % | |

| Fixed Interest Rate | 62% | 51% |

| Variable Interest Rate | 38% | 49% |

| Total | 100% | 100% |

Exchange Rate Risk

The exchange rate risks are mainly related to the following transactions:

·Foreign currency debts raised by Group’s companies.

·Payments to be made on international markets for the acquisition of projects related materials.

·Group companies’ incomes directly linked to the evolutionof the dollar, and

Pg. 24

| PRESS RELEASE Year Ended 2011 |

·Incoming cash flows from our subsidiaries abroad exposed to exchange rate fluctuations.

In order to mitigate exchange rate risks, Enersis’ exchange rate hedging policy is based on cash flowsand it strives to maintain a balance between dollar indexed flows and the asset and liability levels in such currency. Cross currency swaps and exchange rate forwards are the instruments currently used incompliance with this policy. Likewise, the policy looks to refinance debts in each company’s functional currency.

Commodities Risk

Enersis is exposed to the price fluctuation risk on some commodities, basically through

·Fuel purchases for the electricity generation and also,

·Energy transactions in the local markets.

In order to reduce risks in extreme drought conditions, the company has designed a trading policy thatdefines sales commitment levels consistent with its generating plants’ firm energy in a dry year, including risk mitigation clauses in some unregulated clients’ contracts.

In view of the operative conditions by the electricity generation market in Chile has experienced, like extreme drought and rising oil prices, the company has decided to hire a derivative to place a cap on the Brent price for consumption. As of December 31, 2011 there are no outstanding coverage instruments and instruments taken in the past have been specific and for no considerable monetary amounts. Market and operative conditions will be constantly analyzed to adjust the volume hedged or take new hedges for the following months.

Liquidity Risk

In engaging committed long term credit facilities and short term financial investments the Group maintains a consistent liquidity policy, for the amounts required to support projected needs for the period, contingent with the situation and the expectations in the debt and capital markets.

As of December 31, 2011, the Enersis Group held liquidity in the amount of Ch$ 1,217,904 million in Cash and Cash Equivalent and Ch$ 424,561 million in committed long term credit lines. As of December 31st, 2010, the Enersis Group held liquidity in the amount of Ch$ 961,355 million in Cash and Cash Equivalent and Ch$ 242,750 million in committed long term credit lines.

Credit Risk

Credit risk in accounts receivable, originating from trading activities, has been historically very limitedgiven that the short term collection conditions with customers doesn’t allow them to individuallyaccumulate significant amounts. Additionally, in the case of the so-called “unregulated clients” of ourelectricity generation and distribution business, a formal procedure is applied to control the credit risk, using a systematic evaluation of our counterparties, index definition and credit risk factors by virtue of which the contracts are approved or additional guarantee requirements are defined.

Furthermore, in our electricity generating business, in the event of non-payment, some countries allow power supply cut-offs, and in almost all contracts a lack of payment is established as cause for contract termination. For this purpose, credit risks are constantly monitored and the maximum amounts exposed to payment risks are measured, which are limited.

Pg. 25

| PRESS RELEASE Year Ended 2011 |

In turn, in our electricity distribution business, the energy supply cut-off is a power held by our companies in case of default by our customers, applied in accordance with the applicable regulation in each country, enabling the credit risk evaluation and control process, which is also limited.

Surplus cash flow investments are placed in prime national and foreign financial entities (with an investment grade equivalent risk rating) with limits set for each entity.

In the selection of banks for investment, the Group considers those that hold two investment grade classifications, according to the three main international risk agencies (Moody’s, S&P and FitchRatings).

Positions are backed up by treasury bonds from the country of operations and instruments issued by the most reputable banks, favoring, wherever possible, the first ones.

Derivatives are engaged with highly solvent entities; about 80% of operations are conducted with entities that hold an A- or higher rating.

Risk Measurement

The Enersis Group measures the Value at Risk (VaR) of its debt and financial derivatives positions in order to guarantee that the risk taken by the company remains consistent with the risk exposure defined by Management, thus restricting the volatility of its financial results.

The positions portfolio used in the calculations of the current Value at Risk is comprised of debt and financial derivatives.

The calculated Value at Risk represents the possible value loss of the aforementioned positions portfolio over one day time horizon with 95% of confidence.

The volatility of the risk variables that affect the value of the positions portfolio has been studied, including:

·The U.S. dollar Libor interest rate.

·The usual banking local indexes for debts, taking into account the different currencies our companies operate under, and

·The exchange rates of the different currencies involved in the calculation.

The calculation of VaR is based on generating possible future scenarios (at one day) of market values (both spot and term) for the risk variables, using Bootstrapping methodology. The number of scenarios generated ensures compliance with the simulation convergence criteria. A matrix of volatilities and correlations between the various risk variables calculated based on the historical values of the logarithmic price return, has been applied to simulate the future price scenario.

Once the price scenarios have been obtained, the fair value of the portfolio is calculated using such scenarios, obtaining a distribution of possible values at one day. The one-day 95% confidence VaR number is calculated as the 5% percentile of the potential increases in the fair value of the portfolio in one day.

The various debt positions and financial derivatives included in the calculation have been valued consistently using the financial capital calculation methodology reported to Management.

Pg. 26

| PRESS RELEASE Year Ended 2011 |