MASSMUTUAL SELECT FUNDS

This Prospectus describes the following Funds:

| | |

Fixed Income | | Sub-Advised by: |

| MassMutual Select Strategic Bond Fund | | Western Asset Management Company/Western Asset Management Company Limited |

| |

Large Cap Value | | |

| MassMutual Select Diversified Value Fund | | AllianceBernstein L.P. |

| MassMutual Select Fundamental Value Fund | | Wellington Management Company, LLP |

| MassMutual Select Value Equity Fund | | Fidelity Management & Research Company |

| MassMutual Select Large Cap Value Fund | | Davis Selected Advisers, L.P. |

| |

Large Cap Core | | |

| MassMutual Select Indexed Equity Fund | | Northern Trust Investments, N.A. |

| MassMutual Select Core Opportunities Fund | | Victory Capital Management Inc. |

| |

Large Cap Growth | | |

| MassMutual Select Blue Chip Growth Fund | | T. Rowe Price Associates, Inc. |

| MassMutual Select Large Cap Growth Fund | | AllianceBernstein L.P. |

| MassMutual Select Growth Equity Fund | | Grantham, Mayo, Van Otterloo & Co. LLC |

| MassMutual Select Aggressive Growth Fund | | Sands Capital Management, LLC/Delaware Management Company |

| MassMutual Select OTC 100 Fund | | Northern Trust Investments, N.A. |

| |

Mid/Small Cap Value | | |

| MassMutual Select Focused Value Fund | | Harris Associates L.P./Cooke & Bieler, L.P. |

| MassMutual Select Mid-Cap Value Fund | | Cooke & Bieler, L.P. |

| MassMutual Select Small Cap Value Equity Fund | | SSgA Funds Management, Inc. |

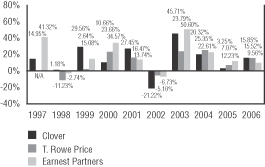

| MassMutual Select Small Company Value Fund | | Clover Capital Management, Inc./T. Rowe Price Associates, Inc./EARNEST Partners, LLC |

| |

Small Cap Core | | |

| MassMutual Select Small Cap Core Equity Fund | | Goldman Sachs Asset Management, L.P. |

| |

Mid/Small Cap Growth | | |

| MassMutual Select Mid Cap Growth Equity Fund | | Navellier & Associates, Inc. |

| MassMutual Select Mid Cap Growth Equity II Fund | | T. Rowe Price Associates, Inc. |

| MassMutual Select Small Cap Growth Equity Fund | | Waddell & Reed Investment Management Company/ Wellington Management Company, LLP |

| MassMutual Select Small Company Growth Fund | | Mazama Capital Management, Inc./Eagle Asset Management, Inc |

| MassMutual Select Emerging Growth Fund | | Delaware Management Company/Insight Capital Research & Management, Inc. |

| |

International/Global | | |

| MassMutual Select Diversified International Fund | | AllianceBernstein L.P. |

| MassMutual Select Overseas Fund | | Harris Associates L.P./Massachusetts Financial Services Company |

| |

Lifestyle/Asset Allocation | | |

| MassMutual Select Strategic Balanced Fund | | ClearBridge Advisors, LLC/Western Asset Management Company/Western Asset Management Company Limited |

| MassMutual Select Destination Retirement Income Fund | | |

| MassMutual Select Destination Retirement 2010 Fund | | |

| MassMutual Select Destination Retirement 2020 Fund | | |

| MassMutual Select Destination Retirement 2030 Fund | | |

| MassMutual Select Destination Retirement 2040 Fund | | |

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this Prospectus. Any statement to the contrary is a crime.

PROSPECTUS

April 2, 2007

– 1 –

| | |

| Table Of Contents | | Page |

| |

Summary Information | | 4 |

About the Funds | | |

MassMutual Select Strategic Bond Fund | | 6 |

MassMutual Select Strategic Balanced Fund | | 10 |

MassMutual Select Diversified Value Fund | | 14 |

MassMutual Select Fundamental Value Fund | | 16 |

MassMutual Select Value Equity Fund | | 20 |

MassMutual Select Large Cap Value Fund | | 22 |

MassMutual Select Indexed Equity Fund | | 26 |

MassMutual Select Core Opportunities Fund | | 28 |

MassMutual Select Blue Chip Growth Fund | | 30 |

MassMutual Select Large Cap Growth Fund | | 34 |

MassMutual Select Growth Equity Fund | | 38 |

MassMutual Select Aggressive Growth Fund | | 42 |

MassMutual Select OTC 100 Fund | | 46 |

MassMutual Select Focused Value Fund | | 48 |

MassMutual Select Mid-Cap Value Fund | | 52 |

MassMutual Select Small Cap Value Equity Fund | | 54 |

MassMutual Select Small Company Value Fund | | 56 |

MassMutual Select Small Cap Core Equity Fund | | 60 |

MassMutual Select Mid Cap Growth Equity Fund | | 62 |

MassMutual Select Mid Cap Growth Equity II Fund | | 66 |

MassMutual Select Small Cap Growth Equity Fund | | 70 |

MassMutual Select Small Company Growth Fund | | 74 |

MassMutual Select Emerging Growth Fund | | 78 |

MassMutual Select Diversified International Fund | | 82 |

MassMutual Select Overseas Fund | | 86 |

MassMutual Select Destination Retirement Funds | | 90 |

MassMutual Select Destination Retirement Income Fund | | 90 |

MassMutual Select Destination Retirement 2010 Fund | | 90 |

MassMutual Select Destination Retirement 2020 Fund | | 90 |

MassMutual Select Destination Retirement 2030 Fund | | 90 |

MassMutual Select Destination Retirement 2040 Fund | | 91 |

Summary of Principal Risks | | 100 |

About the Investment Adviser and Sub-Advisers | | |

Massachusetts Mutual Life Insurance Company | | 107 |

AllianceBernstein L.P. | | 107 |

ClearBridge Advisors, LLC | | 109 |

Clover Capital Management, Inc. | | 109 |

Cooke & Bieler, L.P. | | 110 |

Davis Selected Advisers, L.P. | | 111 |

Delaware Management Company | | 111 |

Eagle Asset Management, Inc. | | 113 |

EARNEST Partners, LLC | | 113 |

Fidelity Management & Research Company | | 113 |

Goldman Sachs Asset Management, L.P. | | 113 |

Grantham, Mayo, Van Otterloo & Co. LLC | | 114 |

Harris Associates L.P. | | 114 |

Insight Capital Research & Management, Inc. | | 115 |

Massachusetts Financial Services Company | | 115 |

Mazama Capital Management, Inc. | | 115 |

Navellier & Associates, Inc. | | 116 |

Northern Trust Investments, N.A. | | 116 |

Sands Capital Management, LLC | | 116 |

SSgA Funds Management, Inc. | | 117 |

T. Rowe Price Associates, Inc. | | 117 |

– 2 –

– 3 –

Summary Information

MassMutual Select Funds (the “Funds” or the “Trust”) provides a broad range of investment choices across the risk/return spectrum. The summary pages that follow describe each Fund’s:

| · | Principal Investment Strategies and Risks. A “Summary of Principal Risks” of investing in the Funds begins on page 100. |

| · | Investment return over the past ten years, or since inception if the Fund is less than ten years old. |

| · | Average annual total returns for the last one-, five- and ten-year periods (or, shorter periods for newer Funds) and how the Fund’s performance compares to that of a comparable broad-based index. |

A description of the Trust’s policies and procedures with respect to the disclosure of each Fund’s portfolio securities is available in the Funds’ Statement of Additional Information.

Past Performance is not an indication of future performance. There is no assurance that a Fund’s investment objective will be achieved, and you can lose money by investing in the Funds.

Important Notes about performance information for the Funds.

Where indicated, average annual total returns for Class A, Class L and Class Y shares of a Fund are based on the performance of Class S Shares, adjusted for class specific expenses, and average annual total returns for Class N shares of a Fund is based on the performance of Class A Shares, adjusted for class specific expenses.

Performance information provided for some of the Funds is based on either a composite of all portfolios managed by the Fund’s sub-adviser, or on a mutual fund managed by the Fund’s sub-adviser, with investment objectives, policies and investment strategies substantially similar to those of the Funds and without material client-imposed restrictions, and is provided solely to illustrate the sub-adviser’s performance in managing such a portfolio. In such cases, the performance provided does not show the particular Fund’s performance. For the composites, some of these portfolios are mutual funds registered with the Securities and Exchange Commission (“SEC”) and some are private accounts. The performance provided reflects the sub-adviser’s composite or mutual fund performance, adjusted for estimated expenses of each class of the relevant Fund. The investment returns assume the reinvestment of dividends and capital gains distributions. The performance provided does not reflect fees that may be paid by investors for administrative services or group annuity contract charges. The composites of portfolios were not subject to all of the investment restrictions to which the Funds will be subject, including restrictions imposed by the Investment Company Act of 1940 and the Internal Revenue Code of 1986, each as amended. No assurance can be given that the Funds’ performance would not have been lower had it been in operation during the periods for which composite or mutual fund performance is provided. The Funds’ performance may have differed due to factors such as differences in cash flows into and out of the Funds, differences in fees and expenses, and differences in portfolio size and investments. Prior performance of the sub-advisers is not indicative of future rates of return and is no indication of future performance of the Funds.

In all cases, investment returns assume the reinvestment of dividends and capital gains distributions. Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

– 4 –

Important Note about Fees and Expenses.

As an investor, you pay certain fees and expenses in connection with your investment. These fees and expenses will vary depending on the Fund in which you invest and the class of shares that you purchase. The fee tables shown on the following pages under “Expense Information” are meant to assist you in understanding these fees and expenses. Each fee table shows, in addition to any shareholder fees, a Fund’s “Total Annual Fund Operating Expenses” and, in some cases, “Net Fund Expenses.” These costs are deducted from a Fund’s assets, which means you pay them indirectly.

Important Information about the Focused Value Fund

Massachusetts Mutual Life Insurance Company (“MassMutual”) will gradually change the allocation of assets between the Focused Value Fund’s two sub-advisers, Harris Associates L.P. (“Harris”) and Cooke & Bieler, L.P. (“Cooke & Bieler”), with the ultimate goal of removing Cooke & Bieler as co-Sub-Adviser to the Fund. This action is intended to bring the Fund back to its original roots as a concentrated portfolio of securities that span the stock capitalization range, managed solely by Harris. While the investment objective of the Fund will not change, the removal of Cooke & Bieler may increase the volatility of the Fund because the Fund will ultimately hold fewer securities. Neither the Management Fees nor the Total Fund Expenses are expected to change due to this sub-adviser change.

– 5 –

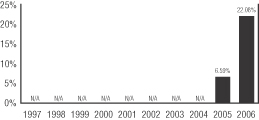

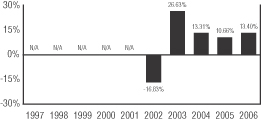

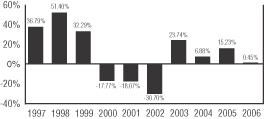

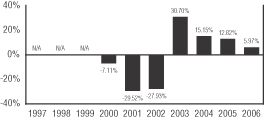

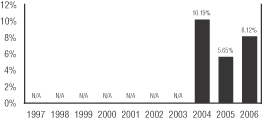

MassMutual Select Strategic Bond Fund

Investment Objective

This Fund seeks a superior total rate of return by investing in fixed income instruments.

Principal Investment Strategies and Risks

The Fund normally invests at least 80% of its net assets in U.S. dollar-denominated fixed income securities and other debt instruments of domestic and foreign entities, including corporate bonds, securities issued or guaranteed by the U.S. government, its agencies or instrumentalities, mortgage-backed securities and money market instruments. The Fund may invest up to 20% of its total assets in non-U.S. dollar-denominated securities.

The Fund’s Sub-Adviser, Western Asset Management Company’s (“Western Asset”) opportunistic approach seeks to capitalize on inefficiencies in fixed income markets to add incremental value to the Fund’s portfolio. Western Asset places significant emphasis on risk management since the general objective is to exceed benchmark returns while approximating benchmark risk. When making investment decisions, Western Asset focuses on such critical areas as sector allocation, issue selection, duration weighting and term structure. Western Asset Management Company Limited (“WAML”), an affiliate of Western Asset, has sub-advisory responsibility for Western Asset’s non-U.S. dollar denominated investments. Western Asset will determine the portion of the Fund’s assets to be allocated to non-U.S. dollar denominated securities from time to time. WAML will select the foreign country and currency composition based on its evaluation of relative interest rates, inflation rates, exchange rates, monetary and fiscal policies, trade and current account balances and any other specific factors WAML believes relevant.

The Fund emphasizes diversification, the use of multiple strategies and identification of long-term trends. The three key factors that determine the allocation decisions for the Fund are: the construction of an outlook for fundamental economic activity, the review of historical yield spreads or corporate debt versus Treasuries and the evaluation of changes in credit quality and its impact on prices.

The Fund’s target average modified duration is expected to range within 30% of the duration of the domestic bond market as a whole. “Duration” refers to the range within which the average modified duration of a portfolio is expected to fluctuate. Modified duration measures the expected sensitivity of market price to changes in interest rates, taking into account the effects of structural complexities (for example, some bonds can be prepaid by the issuer).

The Principal Risks of investing in the Fund are Market Risk, Credit Risk, Management Risk, Prepayment Risk, Liquidity Risk, Derivative Risk, Foreign Investment Risk, Emerging Markets Risk, Currency Risk, Leveraging Risk and Portfolio Turnover Risk.

These Risks are described beginning on page 100.

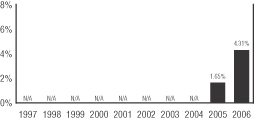

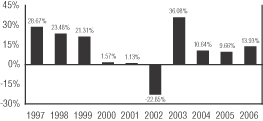

Annual Performance(1)

The bar chart shows the risks of investing in the Fund by showing changes in the Fund’s performance from year to year. Sales charges and taxes are not included in the calculations of returns in this bar chart. If those charges and taxes were included, the returns would be lower than those shown.

Class S Shares

During the period shown above, the highest quarterly return for the Fund was 4.30% for the quarter ended September 30, 2006 and the lowest quarterly return was -0.90% for the quarter ended March 31, 2006.

Average Annual Total Returns(1)

(for the periods ended December 31, 2006)

The table shows the risk of investing in the Fund by comparing the Fund’s returns with a broad measure of market performance over different time periods.

| | | | | |

| | | One

Year | | Since

Inception

(12/31/04) |

Return Before Taxes – Class S | | | 4.31% | | 2.97% |

Return After Taxes on Distributions – Class S | | | 2.91% | | 1.97% |

Return After Taxes on Distributions and Sale of Fund Shares – Class S | | | 2.81% | | 1.95% |

Return Before Taxes – Class Y | | | 4.38% | | 2.96% |

Return Before Taxes – Class L | | | 4.31% | | 2.93% |

Return Before Taxes – Class A+ | | - | 0.95% | | 0.20% |

Return Before Taxes – Class N+ | | | 2.73% | | 2.35% |

| | | | | | |

Lehman Brothers® Aggregate Bond Index^ | | | 4.33% | | 3.48% |

(1) Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

+ Performance for Class A and Class N shares of the Fund reflects any applicable sales charge.

^ The Lehman Brothers® Aggregate Bond Index is an unmanaged index of fixed rate investment grade securities with at least one year to maturity combining the Lehman Brothers Government/Credit Index and the Lehman Brothers Mortgage-Backed Securities Index. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes.

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

After-tax returns are shown for only Class S and after-tax returns for other classes will vary.

– 6 –

Expense Information

| | | | | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | | Class A | | | Class N | |

Shareholder Fees

(fees paid directly from your investment) | | | | | | | | | | | | | |

Maximum Sales Charge (Load) on purchases (as a % of offering price) | | None | | None | | None | | | 4.75% | | | None | |

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | | None | | None | | None | | | None | (1) | | 1.00% | (2) |

| Annual Fund Operating Expenses (expenses that are deducted from Fund assets) (% of average net assets) | | | | | | | | | | | | | |

Management Fees | | .55% | | .55% | | .55% | | | .55% | | | .55% | |

Distribution and Service (Rule 12b-1) Fees | | None | | None | | None | | | .25% | | | .50% | |

Other Expenses(3) | | .10% | | .16% | | .31% | | | .31% | | | .36% | |

| Total Annual Fund Operating Expenses(4) | | .65% | | .71% | | .86% | | | 1.11% | | | 1.41% | |

| | | | | | | | | | | | | |

Less Expense Reimbursement | | — | | — | | (.11% | ) | | (.11% | ) | | (.11% | ) |

| Net Fund Expenses(5)(6) | | .65% | | .71% | | .75% | | | 1.00% | | | 1.30% | |

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in each share class of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. For Class A shares, the examples include the initial sales charge. The examples also assume that your investment earns a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class S | | $ | 66 | | $ | 208 | | $ | 362 | | $ | 810 |

Class Y | | $ | 73 | | $ | 227 | | $ | 395 | | $ | 883 |

Class L | | $ | 77 | | $ | 263 | | $ | 466 | | $ | 1,051 |

Class A | | $ | 572 | | $ | 801 | | $ | 1,047 | | $ | 1,753 |

Class N | | $ | 236 | | $ | 435 | | $ | 761 | | $ | 1,681 |

Except for Class N shares, the figures shown above would be the same whether you sold your shares at the end of a period or kept them. For Class N shares, you would pay the following expenses if you did not redeem your shares:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class N | | $ | 132 | | $ | 435 | | $ | 761 | | $ | 1,681 |

| (1) | | A contingent deferred sales charge may apply to shares redeemed within 18 months of purchase from initial investments of $1 million or more. |

| (2) | | Applies to shares redeemed within 18 months of purchase. |

| (3) | | Other Expenses include Acquired Fund fees and expenses, which represent approximate expenses borne indirectly by the Fund in its most recent fiscal year through investments in other pooled investment vehicles. The amount of Acquired Fund fees and expenses may change in the coming year due to a number of factors including, among others, a change in allocation of the Fund’s investments among other pooled investment vehicles. |

| (4) | | Because Total Annual Fund Operating Expenses include Acquired Fund fees and expenses, they may not correspond to the ratios of expenses to average daily net assets shown in the “Financial Highlights” tables in this prospectus, which reflect the operating expenses of the Fund and do not include Acquired Fund fees and expenses. |

| (5) | | The expenses in the above table reflect a written agreement by MassMutual to cap the fees and expenses of the Fund (other than extraordinary litigation and legal expenses, or other non-recurring or unusual expenses), excluding Acquired Fund fees and expenses, through March 31, 2008 to the extent that Net Fund Expenses would otherwise exceed .70%, .75%, .75%, 1.00% and 1.30% for classes S, Y, L, A and N, respectively. The agreement cannot be terminated unilaterally by MassMutual. |

| (6) | | Employee benefit plans which invest in the Fund through MassMutual separate investment accounts may pay additional charges under their group annuity contract or services agreement. Investors who purchase shares directly from the Fund may also be subject to charges imposed in their administrative services or other agreement with MassMutual or MassMutual affiliate. None of these charges are deducted from Fund assets. |

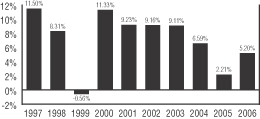

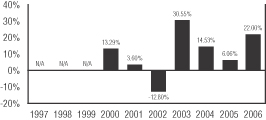

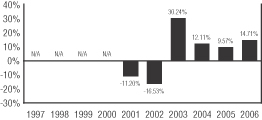

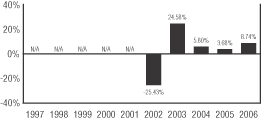

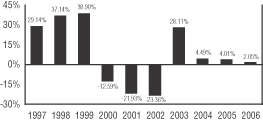

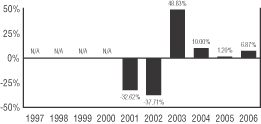

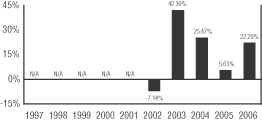

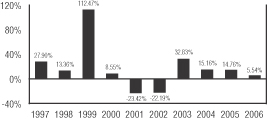

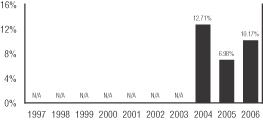

Western Asset Prior Performance for

Similar Accounts*

The bar chart illustrates the variability of returns achieved by Western Asset for all accounts with investment objectives, policies and investment strategies similar to that of the Fund. The composite performance does not represent the historical performance of the Fund and should not be interpreted as being indicative of future performance of the Fund.

During the periods shown above, the highest quarterly return was 4.40% for the quarter ended June 30, 2003 and the lowest was -2.18% for the quarter ended June 30, 2004.

– 7 –

Western Asset Average Annual Total Returns for

Similar Accounts*

(for the periods ended December 31, 2006)

The table compares Western Asset’s investment results for all accounts with investment objectives, policies and investment strategies similar to that of the Fund to an index measuring the broad market over different time periods.

| | | | | | | |

| | | One Year | | Five Years | | Ten Years |

Western Asset Composite | | | | | | | |

Class S* | | | 5.20% | | 6.42% | | 7.14% |

Class Y* | | | 5.15% | | 6.37% | | 7.09% |

Class L* | | | 5.14% | | 6.37% | | 7.09% |

Class A* | | - | 0.09% | | 5.09% | | 6.32% |

Class N* | | | 3.59% | | 5.82% | | 6.54% |

| | | | | | | | |

Lehman Brothers Aggregate

Bond Index^ | | | 4.33% | | 5.06% | | 6.24% |

* Western Asset’s Similar Account performance is a composite of all portfolios managed by Western Asset with substantially similar investment objectives, policies and investment strategies as the Fund, and without significant client-imposed restrictions, adjusted to reflect the fees and expenses of each of the Fund’s share classes, including sales loads. The bar chart is based on Class S expenses. The composite performance does not represent the historical performance of the MassMutual Select Strategic Bond Fund and should not be interpreted as being indicative of the future performance of the Fund. For additional information, please refer to “Investment Performance” in this Prospectus. Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

^ The Lehman Brothers Aggregate Bond Index is an unmanaged index of fixed rate investment grade securities with at least one year to maturity combining the Lehman Brothers Government/Credit Index and the Lehman Brothers Mortgage-Backed Securities Index. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

– 8 –

[THIS PAGE INTENTIONALLY LEFT BLANK]

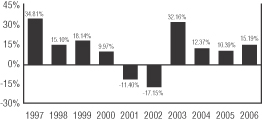

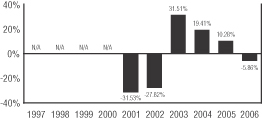

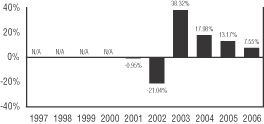

MassMutual Select Strategic Balanced Fund

Investment Objective

This Fund seeks long-term capital growth, consistent with preservation of capital and balanced by current income.

Principal Investment Strategies and Risks

To obtain its objective, the Fund takes a multi-managed approach whereby two Sub-Advisers independently manage their own portion of the Fund’s assets. ClearBridge Advisors, LLC (“ClearBridge”) manages the equity component and Western Asset Management Company (“Western Asset”) manages the fixed income component.

The equity component will invest primarily in common stocks and common stock equivalents, such as preferred stocks and securities convertible into common stocks, of companies that ClearBridge believes are undervalued in the marketplace. While ClearBridge selects investments primarily for their capital appreciation potential, secondary consideration is given to a company’s dividend record and the potential for an improved dividend return. The equity component generally invests in securities of large, well-known companies but may also invest a significant portion of its assets in securities of small to medium-sized companies when ClearBridge believes smaller companies offer more attractive value opportunities.

The fixed income component will invest in a wide variety of investment-grade fixed-income sectors, including government, corporate, mortgage-backed, asset-backed, and cash equivalents, in both U.S. dollars and local currencies. It also allows for opportunistic use of non-dollar, high-yield, and emerging market securities to enhance portfolio returns and lower volatility. Western Asset Management Company Limited (“WAML”), an affiliate of Western Asset, has sub-advisory responsibility for Western Asset’s non-U.S. dollar denominated investments. Western Asset will determine the portion of the Fund’s assets to be allocated to non-U.S. dollar denominated securities from time to time. WAML will select the foreign country and currency composition based on its evaluation of relative interest rates, inflation rates, exchange rates, monetary and fiscal policies, trade and current account balances and any other specific factors WAML believes relevant.

The Fund’s target allocation is 60% equity securities and 40% fixed income securities but may fluctuate based on cash-flow activity or market performance. Additionally, the Fund’s Adviser may change the allocation of the Fund’s assets between the Fund’s Sub-Advisers on a basis determined by the Fund’s Adviser to be in the best interest of shareholders. In unusual circumstances the Fund may, for temporary defensive purposes, invest up to 100% of its total assets in money market instruments.

The Principal Risks of investing in the Fund are Market Risk, Credit Risk, Management Risk, Prepayment Risk, Liquidity Risk, Derivative Risk, Foreign Investment Risk, Emerging Markets Risk, Currency Risk, Smaller Company Risk, Leveraging Risk and Portfolio Turnover Risk.

These Risks are described beginning on page 100.

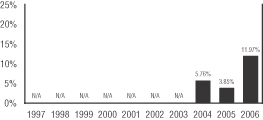

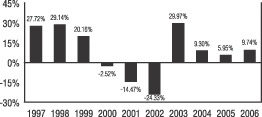

Annual Performance(1)

The bar chart shows the risks of investing in the Fund by showing changes in the Fund’s performance from year to year. Sales charges and taxes are not included in the calculations of returns in this bar chart. If those charges and taxes were included, the returns would be lower than those shown.

Class S Shares

During the periods shown above, the highest quarterly return for the Fund was 5.40% for the quarter ended December 31, 2006 and the lowest quarterly return was -2.19% for the quarter ended March 31, 2005.

Average Annual Total Returns(1)

(for the periods ended December 31, 2006)

The table shows the risk of investing in the Fund by comparing the Fund’s returns with a broad measure of market performance over different time periods.

| | | | |

| | | One

Year | | Since Inception (12/31/03) |

Return Before Taxes – Class S | | 11.97% | | 7.13% |

Return After Taxes on Distributions – Class S | | 11.14% | | 6.57% |

Return After Taxes on Distributions and Sale of Fund Shares – Class S | | 8.26% | | 5.91% |

Return Before Taxes – Class Y | | 11.90% | | 7.07% |

Return Before Taxes – Class L | | 11.73% | | 6.93% |

Return Before Taxes – Class A+ | | 5.13% | | 4.59% |

Return Before Taxes – Class N+ | | 10.21% | | 6.35% |

| | | | | |

Russell 3000® Index^ | | 15.72% | | 11.19% |

Lipper Balanced Fund Index^^ | | 11.60% | | 8.59% |

Lehman Brothers® Aggregate Bond Index^^^ | | 4.33% | | 3.73% |

– 10 –

(1) Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

+ Performance for Class A and Class N shares of the Fund reflects any applicable sales charge.

^ The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^^ The Lipper Balanced Fund Index is an unmanaged, equally weighted index of the 30 largest mutual funds within the Lipper Balanced Category. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^^^ The Lehman Brothers® Aggregate Bond Index is an unmanaged index of fixed rate investment grade securities with at least one year to maturity combining the Lehman Brothers Government/Credit Index and the Lehman Brothers Mortgage-Backed Securities Index. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes.

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

After-tax returns are shown for only Class S and after-tax returns for other classes will vary.

Expense Information

| | | | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | Class A | | | Class N | |

| Shareholder Fees (fees paid directly from your investment) | | | | | | | | | | | | |

Maximum Sales Charge (Load) on purchases (as a % of offering price) | | None | | None | | None | | 5.75% | | | None | |

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | | None | | None | | None | | None | (1) | | 1.00% | (2) |

Annual Fund Operating Expenses (expenses that are deducted from Fund assets) (% of average net assets) | | | | | | | | | | | | |

Management Fees | | .60% | | .60% | | .60% | | .60% | | | .60% | |

Distribution and Service (Rule 12b-1) Fees | | None | | None | | None | | .25% | | | .50% | |

Other Expenses(3) | | .18% | | .23% | | .38% | | .38% | | | .43% | |

| Total Annual Fund Operating Expenses(4)(5) | | .78% | | .83% | | .98% | | 1.23% | | | 1.53% | |

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in each share class of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. For Class A shares, the examples include the initial sales charge. The examples also assume that your investment earns a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class S | | $ | 80 | | $ | 249 | | $ | 433 | | $ | 966 |

Class Y | | $ | 85 | | $ | 265 | | $ | 460 | | $ | 1,025 |

Class L | | $ | 100 | | $ | 312 | | $ | 542 | | $ | 1,201 |

Class A | | $ | 693 | | $ | 943 | | $ | 1,212 | | $ | 1,978 |

Class N | | $ | 259 | | $ | 483 | | $ | 834 | | $ | 1,824 |

Except for Class N shares, the figures shown above would be the same whether you sold your shares at the end of a period or kept them. For Class N shares, you would pay the following expenses if you did not redeem your shares:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class N | | $ | 156 | | $ | 483 | | $ | 834 | | $ | 1,824 |

| (1) | | A contingent deferred sales charge may apply to shares redeemed within 18 months of purchase from initial investments of $1 million or more. |

| (2) | | Applies to shares redeemed within 18 months of purchase. |

| (3) | | Other Expenses include Acquired Fund fees and expenses, which represent approximate expenses borne indirectly by the Fund in its most recent fiscal year through investments in other pooled investment vehicles. The amount of Acquired Fund fees and expenses may change in the coming year due to a number of factors including, among others, a change in allocation of the Fund’s investments among other pooled investment vehicles. |

| (4) | | Because Total Annual Fund Operating Expenses include Acquired Fund fees and expenses, they may not correspond to the ratios of expenses to average daily net assets shown in the “Financial Highlights” tables in this prospectus, which reflect the operating expenses of the Fund and do not include Acquired Fund fees and expenses. |

| (5) | | Employee benefit plans which invest in the Fund through MassMutual separate investment accounts may pay additional charges under their group annuity contract or services agreement. Investors who purchase shares directly from the Fund may also be subject to charges imposed in their administrative services or other agreement with MassMutual or MassMutual affiliate. None of these charges are deducted from Fund assets. |

– 11 –

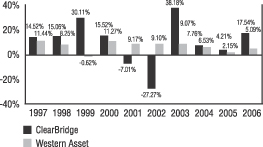

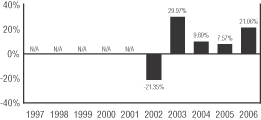

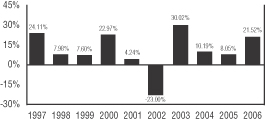

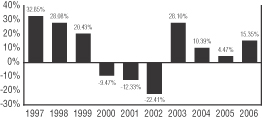

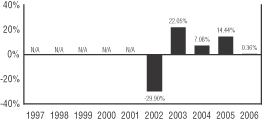

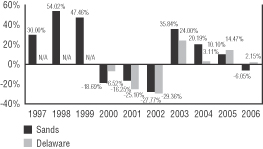

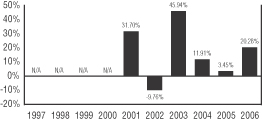

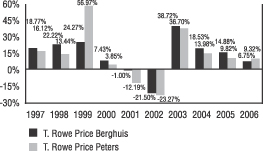

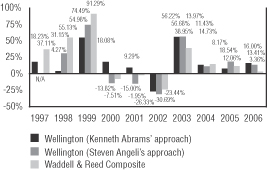

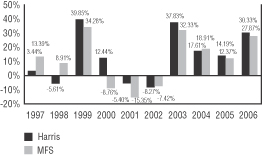

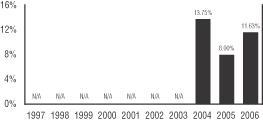

ClearBridge and Western Asset Prior Performance for Similar Accounts*

The bar chart illustrates the variability of returns achieved by each Sub-Adviser for accounts with investment objectives, policies and investment strategies similar to that of the portion of the Fund managed by each Sub-Adviser. The performance does not represent the historical performance of the Fund and should not be interpreted as being indicative of future performance of the Fund.

| | | | |

| | | Highest Quarter | | Lowest Quarter |

ClearBridge Mutual Fund | | 21.81%, 2Q 2003 | | -22.06%, 3Q 2002 |

Western Asset Composite | | 4.38%, 2Q 2003 | | -2.19%, 2Q 2004 |

ClearBridge and Western Asset Average Annual

Total Returns for Similar Accounts*

(for the periods ended December 31, 2006)

The table compares each Sub-Adviser’s investment results for accounts with investment objectives, policies and investment strategies similar to that of the portion of the Fund managed by each Sub-Adviser to an index measuring the broad market over different time periods.

| | | | | | |

| | | One Year | | Five Years | | Ten Years |

ClearBridge Mutual Fund | | | | | | |

Class S* | | 17.54% | | 5.81% | | 9.34% |

Class Y* | | 17.49% | | 5.76% | | 9.29% |

Class L* | | 17.34% | | 5.61% | | 9.14% |

Class A* | | 10.36% | | 4.11% | | 8.24% |

Class N* | | 15.79% | | 5.05% | | 8.58% |

| | | | | | | |

Lipper Balanced Fund Index^ | | 11.60% | | 6.51% | | 7.44% |

Russell 3000 Index^^ | | 15.72% | | 7.17% | | 8.64% |

| | | | | | |

| | | One Year | | Five Years | | Ten

Years |

Western Asset Composite | | | | | | |

Class S* | | 5.09% | | 6.35% | | 7.08% |

Class Y* | | 5.04% | | 6.30% | | 7.03% |

Class L* | | 4.89% | | 6.15% | | 6.88% |

Class A* | | -1.38% | | 4.54% | | 5.79% |

Class N* | | 3.34% | | 5.72% | | 6.54% |

| | | | | | | |

Lipper Balanced Fund Index^ | | 11.60% | | 6.51% | | 7.44% |

Lehman Brothers Aggregate Bond Index^^^ | | 4.33% | | 5.06% | | 6.24% |

* Western Asset’s Similar Account performance is a composite of all portfolios managed by Western Asset with substantially similar investment objectives, policies and investment strategies as the portion of the Fund managed by Western Asset, and without significant client-imposed restrictions, adjusted to reflect the fees and expenses of each of the Fund’s share classes, including sales loads. ClearBridge’s Similar Account performance is from a mutual fund managed by ClearBridge (the Legg Mason Partners Fundamental Value Fund) with substantially similar investment objectives, policies and investment strategies as the portion of the Fund managed by ClearBridge, and without significant client-imposed restrictions, adjusted to reflect the fees and expenses of each of the Fund’s share classes. The bar chart is based on Class S expenses. Each Sub-Adviser’s Similar Account performance does not represent the historical performance of the MassMutual Select Strategic Balanced Fund and should not be interpreted as being indicative of the future performance of the Fund. For additional information, please refer to “Investment Performance” in this Prospectus. Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

^ The Lipper Balanced Fund Index is an unmanaged, equally weighted index of the 30 largest mutual funds within the Lipper Balanced Category. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^^ The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^^^ The Lehman Brothers Aggregate Bond Index is an unmanaged index of fixed rate investment grade securities with at least one year to maturity combining the Lehman Brothers Government/Credit Index and the Lehman Brothers Mortgage-Backed Securities Index. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

– 12 –

[THIS PAGE INTENTIONALLY LEFT BLANK]

MassMutual Select Diversified Value Fund

Investment Objective

This Fund seeks to achieve long-term growth of capital and income by investing primarily in a diversified portfolio of equity securities of larger, well-established companies.

Principal Investment Strategies and Risks

The Fund normally invests at least 80% of its net assets in stocks, securities convertible into stocks, and other securities, such as warrants and stock rights, whose value is based on stock prices.

The Fund’s Sub-Adviser, AllianceBernstein L.P. (“AllianceBernstein”) through the investment professionals of its Bernstein Investment Research and Management unit, takes a “bottom-up” investment approach that is value-based and price-driven, and it relies on the intensive fundamental research of its internal research staff to identify these buying opportunities in the marketplace. The investment process begins with a broad universe of about 650 stocks encompassing most of the S&P 500 and the Russell 1000® Value Index. AllianceBernstein will invest the Fund’s assets in the common stocks of large companies that it identifies as having earnings growth potential that may not be recognized by the market at large. AllianceBernstein seeks to identify compelling buying opportunities created when companies are undervalued on the basis of investor reactions to near-term problems or circumstances even though their long-term prospects remain sound. In addition, to moderate risk, AllianceBernstein may buy companies among the largest in the benchmark (the Russell 1000 Value Index) even if such companies are not attractive from a risk-adjusted return basis. In such cases, AllianceBernstein will underweight these companies versus their weight in the benchmark. Portfolio holdings will be primarily in U.S. issuers although ADRs and securities of foreign issuers that trade on domestic exchanges and in the over-the-counter markets also may be purchased. AllianceBernstein uses a risk factor model to control risk. This model includes broad industry sectors and various measures of financial and valuation characteristics. AllianceBernstein looks at a measure of earnings quality. The measure of earnings quality compares changes in the balance-sheet accrual component of reported earnings for each stock to the market average. All else being equal, AllianceBernstein prefers stocks with lower accruals. In addition, earnings revisions and momentum tools are incorporated into the portfolio management process to optimize the timing of purchases and sales. To limit stock-specific risk relative to the benchmark, AllianceBernstein employs constraints on security and sector over/underweights.

The Principal Risks of investing in the Fund are Market Risk, Credit Risk, Management Risk, Derivative Risk, Foreign Investment Risk, Value Company Risk and Leveraging Risk.

These Risks are described beginning on page 100.

Annual Performance(1)

The bar chart shows the risks of investing in the Fund by showing changes in the Fund’s performance from year to year. Sales charges and taxes are not included in the calculations of returns in this bar chart. If those charges and taxes were included, the returns would be lower than those shown.

Class S Shares

During the period shown above, the highest quarterly return for the Fund was 8.05% for the quarter ended December 31, 2006 and the lowest quarterly return was -0.27% for the quarter ended March 31, 2005.

Average Annual Total Returns(1)

(for the periods ended December 31, 2006)

The table shows the risk of investing in the Fund by comparing the Fund’s returns with a broad measure of market performance over different time periods.

| | | | |

| | | One

Year | | Since Inception (10/15/04) |

Return Before Taxes – Class S | | 22.08% | | 17.60% |

Return After Taxes on Distributions – Class S | | 21.24% | | 16.91% |

Return After Taxes on Distributions and Sale of Fund Shares – Class S | | 15.45% | | 15.09% |

Return Before Taxes – Class Y | | 21.92% | | 17.49% |

Return Before Taxes – Class L | | 21.82% | | 17.38% |

Return Before Taxes – Class A+ | | 14.43% | | 13.94% |

Return Before Taxes – Class N+ | | 20.11% | | 16.68% |

| | | | | |

Russell 1000® Value Index^ | | 22.25% | | 18.32% |

(1) Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

+ Performance for Class A and Class N shares of the Fund reflects any applicable sales charge.

^ The Russell 1000® Value Index is an unmanaged index representative of stocks with a greater than average value orientation among the stocks of the largest 1000 U.S. companies based on capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes.

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

After-tax returns are shown for only Class S and after-tax returns for other classes will vary.

– 14 –

Expense Information

| | | | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | Class A | | | Class N | |

| Shareholder Fees (fees paid directly from your investment) | | | | | | | | | | | | |

Maximum Sales Charge (Load) on purchases (as a % of offering price) | | None | | None | | None | | 5.75% | | | None | |

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | | None | | None | | None | | None | (1) | | 1.00% | (2) |

| Annual Fund Operating Expenses (expenses that are deducted from Fund assets) (% of average net assets) | | | | | | | | | | | | |

Management Fees | | .50% | | .50% | | .50% | | .50% | | | .50% | |

Distribution and Service (Rule 12b-1) Fees | | None | | None | | None | | .25% | | | .50% | |

Other Expenses(3) | | .08% | | .18% | | .29% | | .33% | | | .39% | |

| Total Annual Fund Operating Expenses(4)(5) | | .58% | | .68% | | .79% | | 1.08% | | | 1.39% | |

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in each share class of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. For Class A shares, the examples include the initial sales charge. The examples also assume that your investment earns a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class S | | $ | 59 | | $ | 186 | | $ | 324 | | $ | 726 |

Class Y | | $ | 69 | | $ | 218 | | $ | 379 | | $ | 847 |

Class L | | $ | 81 | | $ | 252 | | $ | 439 | | $ | 978 |

Class A | | $ | 679 | | $ | 899 | | $ | 1,136 | | $ | 1,816 |

Class N | | $ | 245 | | $ | 440 | | $ | 761 | | $ | 1,669 |

Except for Class N shares, the figures shown above would be the same whether you sold your shares at the end of a period or kept them. For Class N shares, you would pay the following expenses if you did not redeem your shares:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class N | | $ | 142 | | $ | 440 | | $ | 761 | | $ | 1,669 |

| (1) | | A contingent deferred sales charge may apply to shares redeemed within 18 months of purchase from initial investments of $1 million or more. |

| (2) | | Applies to shares redeemed within 18 months of purchase. |

| (3) | | Other Expenses include Acquired Fund fees and expenses, which represent approximate expenses borne indirectly by the Fund in its most recent fiscal year through investments in other pooled investment vehicles. The amount of Acquired Fund fees and expenses may change in the coming year due to a number of factors including, among others, a change in allocation of the Fund’s investments among other pooled investment vehicles. |

| (4) | | Because Total Annual Fund Operating Expenses include Acquired Fund fees and expenses, they may not correspond to the ratios of expenses to average daily net assets shown in the “Financial Highlights” tables in this prospectus, which reflect the operating expenses of the Fund and do not include Acquired Fund fees and expenses. |

| (5) | | Employee benefit plans which invest in the Fund through MassMutual separate investment accounts may pay additional charges under their group annuity contract or services agreement. Investors who purchase shares directly from the Fund may also be subject to charges imposed in their administrative services or other agreement with MassMutual or MassMutual affiliate. None of these charges are deducted from Fund assets. |

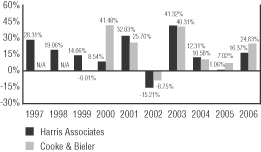

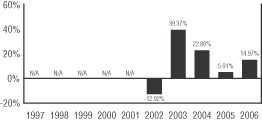

AllianceBernstein Prior Performance for Similar Accounts*

The bar chart illustrates the variability of returns achieved by AllianceBernstein for accounts with investment objectives, policies and investment strategies similar to that of the Fund. The composite performance does not represent the historical performance of the Fund and should not be interpreted as being indicative of future performance of the Fund.

During the periods shown above, the highest quarterly return was 16.48% for the quarter ended June 30, 2003 and the lowest was -18.82% for the quarter ended September 30, 2002.

AllianceBernstein Average Annual Total Returns for Similar Accounts*

(for the periods ended December 31, 2006)

The table compares AllianceBernstein’s investment results for accounts with investment objectives, policies and investment strategies similar to that of the Fund to an index measuring the broad market over different time periods.

| | | | | | |

| | | One

Year | | Five

Years | | Since

Inception

(4/1/99) |

AllianceBernstein Composite | | | | | | |

Class S* | | 22.00% | | 11.03% | | 9.46% |

Class Y* | | 21.90% | | 10.93% | | 9.36% |

Class L* | | 21.79% | | 10.81% | | 9.25% |

Class A* | | 14.51% | | 9.22% | | 8.12% |

Class N* | | 20.19% | | 10.21% | | 8.64% |

| | | | | | | |

Russell 1000 Value Index^ | | 22.25% | | 10.86% | | 7.81% |

* Performance shown is the composite of all portfolios with about 150 stocks managed by AllianceBernstein with substantially similar investment objectives, policies and investment strategies and without significant client-imposed restrictions, adjusted to reflect the fees and expenses of each of the Fund’s share classes, including sales loads. The bar chart is based on Class S expenses. The composite performance does not represent the historical performance of the MassMutual Select Diversified Value Fund and should not be interpreted as being indicative of the future performance of the Fund. For additional information, please refer to “Investment Performance” in this Prospectus. Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

^ The Russell 1000 Value Index is an unmanaged index representative of stocks with a greater than average value orientation among the stocks of the largest 1000 U.S. companies based on capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

– 15 –

MassMutual Select Fundamental Value Fund

Investment Objective

The Fund seeks long-term total return.

Principal Investment Strategies and Risks

Under normal circumstances, the Fund invests at least 80% of its net assets in equity securities. Although the Fund may invest in companies with a broad range of market capitalizations, the Fund will tend to focus on companies with large capitalizations (generally having market capitalizations above $2 billion). The Fund may invest up to 20% of its total assets in the securities of foreign issuers.

The investment approach of the Fund’s Sub-Adviser, Wellington Management Company, LLP (“Wellington Management”), is based on the fundamental analysis of companies with large market capitalizations and estimated below-average projected price-to-earnings ratio. Fundamental analysis involves the assessment of company-specific factors such as its business environment, management, balance sheet, income statement, cash flow, anticipated earnings, hidden or undervalued assets, dividends, and other related measures of value. The typical purchase candidate may be characterized as an overlooked or misunderstood company with sound fundamentals. Holdings are frequently in viable, growing businesses with good financial strength in industries that are temporarily out of favor and under-researched by institutions, but provide the potential for above-average total returns and which sell at estimated below-average price-to-earnings multiples. Portfolio construction is driven primarily by security selection. Market timing is not employed, and limited consideration is given to macroeconomic analysis in establishing sector and industry weightings. This process of stock selection is sometimes referred to as a “bottom-up” process and frequently leads to contrarian industry weightings. Existing holdings are sold as they approach their price targets.

The Principal Risks of investing in the Fund are Market Risk, Credit Risk, Management Risk, Liquidity Risk, Derivative Risk, Foreign Investment Risk, Emerging Markets Risk, Currency Risk, Value Company Risk and Leveraging Risk.

These Risks are described beginning on page 100.

Annual Performance(1)

The bar chart shows the risks of investing in the Fund by showing changes in the Fund’s performance from year to year. Sales charges and taxes are not included in the calculations of returns in this bar chart. If those charges and taxes were included, the returns would be lower than those shown.

Class S Shares

During the periods shown above, the highest quarterly return for the Fund was 17.18% for the quarter ended June 30, 2003 and the lowest quarterly return was -20.11% for the quarter ended September 30, 2002.

Average Annual Total Returns(1)

(for the periods ended December 31, 2006)

The table shows the risk of investing in the Fund by comparing the Fund’s returns with a broad measure of market performance over different time periods.

| | | | | | |

| | | One

Year | | Five Years | | Since Inception (12/31/01) |

Return Before Taxes – Class S | | 21.06% | | 7.89% | | 7.88% |

Return After Taxes on Distributions – Class S | | 19.39% | | 7.31% | | 7.31% |

Return After Taxes on Distributions and Sale of Fund Shares – Class S | | 15.75% | | 6.75% | | 6.74% |

Return Before Taxes – Class Y | | 21.05% | | 7.84% | | 7.83% |

Return Before Taxes – Class L | | 20.90% | | 7.69% | | 7.69% |

Return Before Taxes – Class A+ | | 13.61% | | 6.16% | | 6.16% |

Return Before Taxes – Class N+ | | 19.09% | | 7.12% | | 7.12% |

| | | | | | | |

Russell 1000® Value Index^ | | 22.25% | | 10.86% | | 10.70% |

S&P 500® Index^^ | | 15.78% | | 6.19% | | 5.94% |

(1) Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

+ Performance for Class A shares of the Fund reflects any applicable sales charge. Performance for Class N shares of the Fund prior to December 31, 2002 is based on Class A shares, adjusted to reflect Class N expenses, and also reflects any applicable sales charge.

^ The Russell 1000® Value Index is an unmanaged index representative of stocks with a greater than average value orientation among the stocks of the largest 1000 U.S. companies based on capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^^ The S&P 500® Index is a widely recognized, unmanaged index representative of common stocks of larger capitalized U.S. companies. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

Going forward, the Fund’s performance will be compared to the Russell 1000 Value Index rather than the S&P 500 Index because the Russell 1000 Value Index more closely represents the Fund’s investment strategy.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes.

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

After-tax returns are shown for only Class S and after-tax returns for other classes will vary.

– 16 –

Expense Information

| | | | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | Class A | | | Class N | |

| Shareholder Fees (fees paid directly from your investment) | | | | | | | | | | | | |

Maximum Sales Charge (Load) on purchases (as a % of offering price) | | None | | None | | None | | 5.75% | | | None | |

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | | None | | None | | None | | None | (1) | | 1.00% | (2) |

| Annual Fund Operating Expenses (expenses that are deducted from Fund assets) (% of average net assets) | | | | | | | | | | | | |

Management Fees | | .65% | | .65% | | .65% | | .65% | | | .65% | |

Distribution and Service (Rule 12b-1) Fees | | None | | None | | None | | .25% | | | .50% | |

Other Expenses(3) | | .14% | | .18% | | .33% | | .33% | | | .38% | |

Total Annual Fund Operating Expenses(4)(5) | | .79% | | .83% | | .98% | | 1.23% | | | 1.53% | |

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in each share class of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. For Class A shares, the examples include the initial sales charge. The examples also assume that your investment earns a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class S | | $ | 81 | | $ | 252 | | $ | 439 | | $ | 978 |

Class Y | | $ | 85 | | $ | 265 | | $ | 460 | | $ | 1,025 |

Class L | | $ | 100 | | $ | 312 | | $ | 542 | | $ | 1,201 |

Class A | | $ | 693 | | $ | 943 | | $ | 1,212 | | $ | 1,978 |

Class N | | $ | 259 | | $ | 483 | | $ | 834 | | $ | 1,824 |

Except for Class N shares, the figures shown above would be the same whether you sold your shares at the end of a period or kept them. For Class N shares, you would pay the following expenses if you did not redeem your shares:

| | | | | | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class N | | $ | 156 | | $ | 483 | | $ | 834 | | $ | 1,824 |

| (1) | | A contingent deferred sales charge may apply to shares redeemed within 18 months of purchase from initial investments of $1 million or more. |

| (2) | | Applies to shares redeemed within 18 months of purchase. |

| (3) | | Other Expenses include Acquired Fund fees and expenses, which represent approximate expenses borne indirectly by the Fund in its most recent fiscal year through investments in other pooled investment vehicles. The amount of Acquired Fund fees and expenses may change in the coming year due to a number of factors including, among others, a change in allocation of the Fund’s investments among other pooled investment vehicles. |

| (4) | | Because Total Annual Fund Operating Expenses include Acquired Fund fees and expenses, they may not correspond to the ratios of expenses to average daily net assets shown in the “Financial Highlights” tables in this prospectus, which reflect the operating expenses of the Fund and do not include Acquired Fund fees and expenses. |

| (5) | | Employee benefit plans which invest in the Fund through MassMutual separate investment accounts may pay additional charges under their group annuity contract or services agreement. Investors who purchase shares directly from the Fund may also be subject to charges imposed in their administrative services or other agreement with MassMutual or MassMutual affiliate. None of these charges are deducted from Fund assets. |

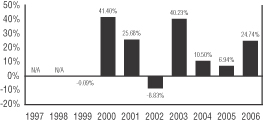

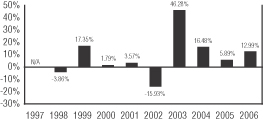

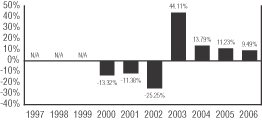

Wellington Management

Prior Performance for Similar Accounts*

The bar chart illustrates the variability of returns achieved by Wellington Management for accounts with investment objectives, policies and investment strategies similar to that of the Fund. The composite performance does not represent the historical performance of the Fund and should not be interpreted as being indicative of future performance of the Fund.

During the periods shown above, the highest quarterly return was 17.33% for the quarter ended June 30, 2003 and the lowest was -20.03% for the quarter ended September 30, 2002.

– 17 –

Wellington Management Average Annual Total

Returns for Similar Accounts*

(for the periods ended December 31, 2006)

The table compares Wellington Management’s investment results for accounts with investment objectives, policies and investment strategies similar to that of the Fund to an index measuring the broad market over different time periods.

| | | | | | |

| | | One Year | | Five Years | | Ten Years |

Wellington Management Composite | | | | | | |

Class S* | | 21.52% | | 7.69% | | 10.35% |

Class Y* | | 21.48% | | 7.65% | | 10.31% |

Class L* | | 21.33% | | 7.50% | | 10.16% |

Class A* | | 14.12% | | 5.98% | | 9.26% |

Class N* | | 19.78% | | 6.94% | | 9.60% |

| | | | | | | |

Russell 1000 Value Index^ | | 22.25% | | 10.86% | | 11.00% |

S&P 500 Index^^ | | 15.78% | | 6.19% | | 8.42% |

* Performance shown is the composite of all portfolios managed by Wellington Management with substantially similar investment objectives, policies and investment strategies and without significant client-imposed restrictions, adjusted to reflect the fees and expenses of each of the Fund’s share classes, including sales loads. The bar chart is based on Class S expenses. The composite performance does not represent the historical performance of the MassMutual Select Fundamental Value Fund and should not be interpreted as being indicative of the future performance of the Fund. For additional information, please refer to “Investment Performance” in this Prospectus. Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

^ The Russell 1000 Value Index is an unmanaged index representative of stocks with a greater than average value orientation among the stocks of the largest 1000 U.S. companies based on capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^ ^ The S&P 500 Index is a widely recognized, unmanaged index representative of common stocks of larger capitalized U.S. companies. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

– 18 –

[THIS PAGE INTENTIONALLY LEFT BLANK]

MassMutual Select Value Equity Fund

Investment Objective

The Fund seeks long-term growth of capital.

Principal Investment Strategies and Risks

The Fund’s Sub-Adviser, Fidelity Management & Research Company (“FMR”), invests in securities of companies that it believes are undervalued in the marketplace in relation to factors such as the company’s assets, sales, earnings, growth potential, or cash flow, or in relation to securities of other companies in the same industry. FMR considers traditional and other measures of value such as price/earnings (P/E), price/sales (P/S), or price/book (P/B) ratios, earnings relative to enterprise value (the total value of a company’s outstanding equity and debt), and the discounted value of a company’s projected future free cash flows. The types of companies in which the Fund may invest include companies experiencing positive fundamental change, such as a new management team or product launch, a significant cost-cutting initiative, a merger or acquisition, or a reduction in industry capacity that should lead to improved pricing; companies whose earnings potential has increased or is expected to increase more than generally perceived; and companies that have enjoyed recent market popularity but which appear to have temporarily fallen out of favor for reasons that are considered non-recurring or short-term.

FMR normally invests at least 80% of the Fund’s net assets in equity securities. FMR normally invests the Fund’s assets primarily in common stocks. FMR may invest the Fund’s assets in securities of foreign issuers in addition to securities of domestic issuers. In buying and selling securities for the Fund, FMR relies on fundamental analysis of each issuer and its potential for success in light of its current financial condition, its industry position, and economic and market factors. Factors considered include growth potential, earnings estimates, and management. FMR may use various techniques, such as buying and selling futures contracts and exchange traded funds, to increase or decrease the Fund’s exposure to changing security prices or other factors that affect security values. If FMR’s strategies do not work as intended, the Fund may not achieve its objective.

In response to market, economic, political or other conditions, FMR may temporarily use a different investment strategy for defensive purposes. If FMR does so, different factors could affect the Fund’s performance and the Fund may not achieve its investment objective.

The Principal Risks of investing in the Fund are Market Risk, Credit Risk, Management Risk, Liquidity Risk, Derivative Risk, Non-Diversification Risk, Foreign Investment Risk, Emerging Markets Risk, Currency Risk, Value Company Risk, Leveraging Risk and Portfolio Turnover Risk.

These Risks are described beginning on page 100.

Note that although the Fund was originally registered as a non-diversified fund, under a position of the SEC, the Fund is currently required to operate as a diversified fund and will not operate as a non-diversified fund in the future until it obtains any necessary shareholder approval.

Annual Performance(1)

The bar chart shows the risks of investing in the Fund by showing changes in the Fund’s performance from year to year. Sales charges and taxes are not included in the calculations of returns in this bar chart. If those charges and taxes were included, the returns would be lower than those shown.

Class S Shares

During the periods shown above, the highest quarterly return for the Fund was 15.56% for the quarter ended June 30, 2003 and the lowest quarterly return was -18.23% for the quarter ended September 30, 2002.

– 20 –

Average Annual Total Returns(1)

(for the periods ended December 31, 2006)

The table shows the risk of investing in the Fund by comparing the Fund’s returns with a broad measure of market performance over different time periods.

| | | | | | |

| | | One

Year | | Five

Years | | Since Inception (5/1/01) |

Return Before Taxes – Class S | | 13.40% | | 8.41% | | 6.20% |

Return After Taxes on Distributions – Class S | | 10.00% | | 7.09% | | 5.02% |

Return After Taxes on Distributions and Sale of Fund Shares – Class S | | 11.37% | | 6.91% | | 5.00% |

Return Before Taxes – Class Y | | 13.33% | | 8.35% | | 6.13% |

Return Before Taxes – Class L | | 13.06% | | 8.18% | | 5.97% |

Return Before Taxes – Class A+ | | 6.34% | | 6.63% | | 4.62% |

Return Before Taxes – Class N+ | | 11.63% | | 7.59% | | 5.42% |

| | | | | | | |

Russell 1000® Value Index^ | | 22.25% | | 10.86% | | 8.66% |

(1) Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

+ Performance for Class A shares of the Fund reflects any applicable sales charge. Performance for Class N shares of the Fund prior to December 31, 2002 is based on Class A shares, adjusted to reflect Class N expenses, and also reflects any applicable sales charge.

^ The Russell 1000® Value Index is an unmanaged index representative of stocks with a greater than average value orientation among the stocks of the largest 1000 U.S. companies based on capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes.

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

After-tax returns are shown for only Class S and after-tax returns for other classes will vary.

Expense Information

| | | | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | Class A | | | Class N | |

| Shareholder Fees (fees paid directly from your investment) | | | | | | | | | | | | |

Maximum Sales Charge (Load) on purchases (as a % of offering price) | | None | | None | | None | | 5.75% | | | None | |

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | | None | | None | | None | | None | (1) | | 1.00% | (2) |

| | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | Class A | | Class N |

| Annual Fund Operating Expenses (expenses that are deducted from Fund assets) (% of average net assets) | | | | | | | | | | |

Management Fees | | .70% | | .70% | | .70% | | .70% | | .70% |

Distribution and Service (Rule 12b-1) Fees | | None | | None | | None | | .25% | | .50% |

Other Expenses(3) | | .16% | | .21% | | .36% | | .36% | | .41% |

| Total Annual Fund Operating Expenses(4)(5) | | .86% | | .91% | | 1.06% | | 1.31% | | 1.61% |

Examples

These examples are intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The examples assume that you invest $10,000 in each share class of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. For Class A shares, the examples include the initial sales charge. The examples also assume that your investment earns a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class S | | $ 88 | | $274 | | $ 477 | | $1,061 |

Class Y | | $ 93 | | $290 | | $ 504 | | $1,120 |

Class L | | $108 | | $337 | | $ 585 | | $1,294 |

Class A | | $701 | | $966 | | $1,252 | | $2,063 |

Class N | | $267 | | $508 | | $ 876 | | $1,911 |

Except for Class N shares, the figures shown above would be the same whether you sold your shares at the end of a period or kept them. For Class N shares, you would pay the following expenses if you did not redeem your shares:

| | | | | | | | |

| | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Class N | | $164 | | $508 | | $876 | | $1,911 |

| (1) | | A contingent deferred sales charge may apply to shares redeemed within 18 months of purchase from initial investments of $1 million or more. |

| (2) | | Applies to shares redeemed within 18 months of purchase. |

| (3) | | Other Expenses include Acquired Fund fees and expenses, which represent approximate expenses borne indirectly by the Fund in its most recent fiscal year through investments in other pooled investment vehicles. The amount of Acquired Fund fees and expenses may change in the coming year due to a number of factors including, among others, a change in allocation of the Fund’s investments among other pooled investment vehicles. |

| (4) | | Because Total Annual Fund Operating Expenses include Acquired Fund fees and expenses, they may not correspond to the ratios of expenses to average daily net assets shown in the “Financial Highlights” tables in this prospectus, which reflect the operating expenses of the Fund and do not include Acquired Fund fees and expenses. |

| (5) | | Employee benefit plans which invest in the Fund through MassMutual separate investment accounts may pay additional charges under their group annuity contract or services agreement. Investors who purchase shares directly from the Fund may also be subject to charges imposed in their administrative services or other agreement with MassMutual or MassMutual affiliate. None of these charges are deducted from Fund assets. |

– 21 –

MassMutual Select Large Cap Value Fund

Investment Objective

This Fund seeks both capital growth and income.

Principal Investment Strategies and Risks

The Fund seeks to achieve its investment objective by selecting businesses that possess characteristics that the Fund’s Sub-Adviser, Davis Selected Advisers, L.P. (“Davis”) believes foster the creation of long-term value, such as proven management, a durable franchise and business model, and sustainable competitive advantages. Davis will normally invest at least 80% of the Fund’s net assets in common stock of companies with market capitalizations, at the time of purchase, of at least $5 billion. The Fund’s investment strategy is to select these companies for the long-term. In the current market environment, we expect that current income will be low.

Using intensive research into company fundamentals, the Sub-Adviser looks for factors, both quantitative and qualitative, that it believes foster sustainable long-term business growth. While few companies will exhibit all of these qualities, the Sub-Adviser believes that nearly every company in which it invests has a majority and appropriate mix of these traits:

| · | First-Class Management: Proven track record; Significant personal ownership stake in business; Intelligent allocators of capital; Smart appliers of technology to improve business and lower costs; |

| · | Strong Financial Condition and Profitability: Strong balance sheets; Low cost structure/low debt; High after-tax returns on capital; High quality of earnings; |

| · | Strategic Positioning for the Long-Term: Non-obsolescent products/industries; Dominant position in a growing market; Global presence and brand names. |

The Fund may also invest in foreign securities and may, but generally does not, use derivatives as a hedge against currency risks.

The Principal Risks of investing in the Fund are Market Risk, Credit Risk, Management Risk, Derivative Risk, Foreign Investment Risk, Currency Risk, Value Company Risk and Leveraging Risk.

These Risks are described beginning on page 100.

Annual Performance(1)

The bar chart shows the risks of investing in the Fund by showing changes in the Fund’s performance from year to year. Sales charges and taxes are not included in the calculations of returns in this bar chart. If those charges and taxes were included, the returns would be lower than those shown.

Class S Shares

During the periods shown above, the highest quarterly return for the Fund was 17.32% for the quarter ended June 30, 2003 and the lowest quarterly return was -13.42% for the quarter ended September 30, 2001.

Average Annual Total Returns(1)

(for the periods ended December 31, 2006)

The table shows the risk of investing in the Fund by comparing the Fund’s returns with a broad measure of market performance over different time periods.

| | | | | | |

| | | One

Year | | Five

Years | | Since Inception (5/1/00) |

Return Before Taxes – Class S | | 14.71% | | 8.90% | | 4.71% |

Return After Taxes on Distributions – Class S | | 14.57% | | 8.73% | | 4.52% |

Return After Taxes on Distributions and Sale of Fund Shares – Class S | | 9.73% | | 7.68% | | 3.98% |

Return Before Taxes – Class Y | | 14.65% | | 8.81% | | 4.61% |

Return Before Taxes – Class L | | 14.42% | | 8.65% | | 4.45% |

Return Before Taxes – Class A+ | | 7.65% | | 7.13% | | 3.29% |

Return Before Taxes – Class N+ | | 12.87% | | 8.05% | | 3.87% |

| | | | | | | |

S&P 500® Index^ | | 15.78% | | 6.19% | | 1.30% |

Russell 1000® Value Index^^ | | 22.25% | | 10.86% | | 8.32% |

(1) Performance shown does not reflect fees that may be paid by investors for administrative services or group annuity contract charges.

+ Performance for Class A shares of the Fund reflects any applicable sales charge. Performance for Class N shares of the Fund prior to December 31, 2002 is based on Class A shares, adjusted to reflect Class N expenses, and also reflects any applicable sales charge.

^ The S&P 500® Index is a widely recognized, unmanaged index representative of common stocks of larger capitalized U.S. companies. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

^ ^ The Russell 1000® Value Index is an unmanaged index representative of stocks with a greater than average value orientation among the stocks of the largest 1000 U.S. companies based on capitalization. The Index does not incur expenses or reflect any deduction for taxes and cannot be purchased directly by investors.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes.

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

After-tax returns are shown for only Class S and after-tax returns for other classes will vary.

– 22 –

Expense Information

| | | | | | | | | | | | |

| | | Class S | | Class Y | | Class L | | Class A | | | Class N | |

| Shareholder Fees (fees paid directly from your investment) | | | | | | | | | | | | |

Maximum Sales Charge (Load) on purchases (as a % of offering price) | | None | | None | | None | | 5.75% | | | None | |

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | | None | | None | | None | | None | (1) | | 1.00% | (2) |

| Annual Fund Operating Expenses (expenses that are deducted from Fund assets) (% of average net assets) | | | | | | | | | | | | |

Management Fees | | .65% | | .65% | | .65% | | .65% | | | .65% | |

Distribution and Service (Rule 12b-1) Fees | | None | | None | | None | | .25% | | | .50% | |

Other Expenses(3) | | .11% | | .20% | | .35% | | .35% | | | .40% | |

| Total Annual Fund Operating Expenses(4)(5) | | .76% | | .85% | | 1.00% | | 1.25% | | | 1.55% | |

Examples