|

| OMB APPROVAL | ||

|

| OMB Number: | 3235-0570 | |

|

| Expires: | September 30, 2007 | |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .19.3 | ||

| SECURITIES AND EXCHANGE COMMISSION |

| ||

| Washington, D.C. 20549 |

| ||

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8220 | ||||||||

| |||||||||

ING Variable Products Trust | |||||||||

(Exact name of registrant as specified in charter) | |||||||||

| |||||||||

7337 E. Doubletree Ranch Rd., Scottsdale, AZ |

| 85258 | |||||||

(Address of principal executive offices) |

| (Zip code) | |||||||

| |||||||||

CT Corporation System, 101 Federal Street, Boston, MA 02110 | |||||||||

(Name and address of agent for service) | |||||||||

| |||||||||

Registrant’s telephone number, including area code: | 1-800-992-0180 |

| |||||||

| |||||||||

Date of fiscal year end: | December 31 |

| |||||||

| |||||||||

Date of reporting period: | January 1, 2006 to December 31, 2006 |

| |||||||

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Funds

Annual Report

December 31, 2006

Classes ADV, I and S

ING Variable Products Trust

Domestic Equity and Income Portfolio

n ING VP Real Estate Portfolio

Domestic Equity Growth Portfolios

n ING VP MidCap Opportunities Portfolio

n ING VP SmallCap Opportunities Portfolio

Domestic Equity Value Portfolios

n ING VP Financial Services Portfolio

Fixed-Income Portfolio

n ING VP High Yield Bond Portfolio

International Equity Portfolio

n ING VP International Value Portfolio

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds' investment objectives, risks, charges, expenses and other information. This information should be read carefully.

TABLE OF CONTENTS

| President's Letter | 1 | ||||||

| Market Perspective | 2 | ||||||

| Portfolio Managers' Reports | 4 | ||||||

| Shareholder Expense Examples | 16 | ||||||

| Report of Independent Registered Public Accounting Firm | 18 | ||||||

| Statements of Assets and Liabilities | 19 | ||||||

| Statements of Operations | 21 | ||||||

| Statements of Changes in Net Assets | 23 | ||||||

| Financial Highlights | 26 | ||||||

| Notes to Financial Statements | 32 | ||||||

| Portfolios of Investments | 46 | ||||||

| Tax Information | 61 | ||||||

| Trustee and Officer Information | 62 | ||||||

| Advisory Contract Approval Discussion | 66 | ||||||

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available (1) without charge, upon request, by calling Shareholder Services toll-free at 1-800-992-0180; (2) on the ING Funds' website at www.ingfunds.com; and (3) on the SEC's website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the ING Funds' website at www.ingfunds.com and on the SEC's website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Portfolios' Forms N-Q are available on the SEC's website at www.sec.gov. The Portfolios' Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330; and is available upon request from the Portfolio by calling Shareholder Services toll-free at 1-800-992-0180.

(THIS PAGE INTENTIONALLY LEFT BLANK)

PRESIDENT'S LETTER

Dear Shareholder,

In its recent meetings, the U.S. Federal Reserve Board (the "Fed") ceased what was a two-year trend. That trend — a string of 17 consecutive interest rate hikes that ended last fall — was seen by many analysts as a sign that the Fed was concerned about containing inflation.

Now, the Fed is neither raising nor lowering interest rates, which puts us in the midst of what economists refer to as a "plateau." Historically, there have been six similar plateaus since 1982 and during four of those periods the Standard & Poor's 500® Composite Stock Price Index(1) ("S&P 500® Index") rose significantly.

Of course, the Fed's actions impact economies and market performance around the world. For instance, the current interest rate climate has been cited as one reason for a decline in the value of the dollar. Last year, that drop in the dollar meant that international stocks — which are often determined in foreign currencies — generally experienced strong performance as foreign currencies climbed and world stock markets continued to produce strong results.

Meanwhile, here at home, 2006 was an interesting year for equity investors. In May of 2006, the S&P 500® Index hit a five-year high followed by a market correction and several months of non-directional returns. A strong rally occurred in the second half of the year driven in part by the aforementioned dollar decline and the interest rate plateau. The good news is many economists believe that these conditions may continue in the months to come.

At ING Funds, we are committed to providing you, the investor, with an array of investment choices that enables you to build a diversified portfolio across a variety of asset classes. We do so, with a view that the globalization of markets is an initial consideration in the products we offer.

We take the confidence you place in us with your investments very seriously — everyone in our firm is committed to renewing this trust each and every day.

Shaun Mathews

President

ING Funds

January 31, 2007

The views expressed in the President's Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

(1) The S&P 500® Index is an unmanaged index that measures the performance of the securities of approximately 500 of the largest companies in the U.S.

1

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2006

In our semi-annual report, we described how the feast of the first quarter had turned to famine in the second quarter for global equity markets on concerns that rising interest rates would freeze out global growth. Indeed as late as June 27, 2006, the year-to-date return on the Morgan Stanley Capital International ("MSCI") World IndexSM(1) measured in local currencies, including net reinvested dividends had been precisely 0%. However, the second half of the year ended December 31, 2006, was much healthier and the same index powered ahead 12.3% and for the year ended December 31, 2006, returned 20.07%. The return to dollar based in vestors was a little better at 13.2%, as late in the year a slowing economy and hints that central banks would be diversifying out of dollars weighed on that currency. For the six months ended December 31, 2006, the dollar fell 3.1% against the euro and 5.6% against the pound, but gained 4.1% on the yen due to stumbling growth and miniscule interest rates in Japan. For the year ended December 31, 2006, the dollar fell 10.6% against the euro and 12.4% against the pound, but gained 1.3% against the yen.

As the first half of 2006 ended, the Federal Open Market Committee ("FOMC") had just raised the federal funds rate for the seventeenth time since June 2004, to 5.25%. The relatively mild accompanying language led many in the fixed income market to hope that the tightening cycle was now over. Not everyone believed it, especially when new Middle East conflict pushed the price of oil to another record on July 14, 2006. But data, especially on housing, had mostly pointed to cooling demand and a tame employment report on August 4, 2006 probably decided the matter. Four days later the FOMC met and left rates unchanged. The booming housing market had been a powerful driver of growth in recent years through new construction and demand created by mortgage loan refinancing. This boom was deteriorating a ppreciably with housing prices and the key new building permits measure falling sharply. Only in the last few days of 2006 did the slump show some signs of bottoming out with unexpectedly good new and existing home sales figures reported, along with rebounding consumer confidence. For the six months ended December 31, 2006, the Lehman Brothers® Aggregate Bond ("LBAB") Index(2) of investment grade bonds gained 5.09% and for the year ended December 31, 2006 it gained 4.33%. The most important dynamic was the broad yield curve inversion, suggestive of an expected fall in interest rates and a further economic slow down. The ten-year Treasury yield fell 43 basis points (0.43%) to 4.71%, while the yield on the three-month Bill rose by 3 basis points (0.03%) to 4.89%. Since mid-August, with the exception of two days, bond investors had been prepare d to lend money to the government for ten years at a lower interest rate than for three months.

Faced with fading business activity, as the key housing engine seized up, and a yield curve inverted to the point of recession according to some commentators, investors in U.S. equities must have been in the mood to sell. Not so fast. Those investors saw things differently and indeed the apparent "disagreement" between the bond market and global stock markets was a well discussed feature of the second half of the year. For one thing, the oil price, having hit its record, fell back, as surly calm returned to the Middle East, as the summer driving and hurricane seasons came and went and as winter got off to a mild start in the key North East region. The price of oil averaged 22% less in the fourth quarter than at its peak, boosting consumers' spending power and confidence. And if longer-term int erest rates were falling then stocks looked more attractive as bonds provided less competition and the present value of future corporate profits rose. Speaking of which, Standard & Poor's 500® Composite Stock Price ("S&P 500®") Index(3) companies duly reported their 13th straight double-digit quarterly percentage earnings gain. Gross domestic product ("GDP") growth may have slowed, but the share of corporate profits, reported at 12.4%, was the highest since the 1950's. The next merger or acquisition to get investors in the mood never seemed far away. Five of them were even announced in one day on November 6, 2006, sending markets up about 1%. For the six months ended December 31, 2006, the S&P 500® Index, including dividends, rose 12.7% and for the year ended December 31, 2006, the S&P 500&r eg; Index, including dividends, rose 15.8%. All but 30 basis points (0.30%) of the gain came after August 8, 2006, making six-year highs as the year ended.

International markets, based on MSCI local currency indices, as in the U.S., finished near their best levels for the year. In Japan the market advanced 8.7%, in 2006, after a late surge. The long awaited increase in interest rates from 0.0% to 0.25% took place in July just as the economic recovery was losing impetus. Third quarter growth was estimated at only 0.8% and generated by exports and capital spending alone. Consumer spending was lagging despite low

2

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2006

unemployment and almost flat prices, yet business confidence remained high and profit growth healthy. Elsewhere, Asian markets ex Japan rose 28.2% in 2006, but with wide disparities, ranging from –2.0% in Thailand to 83.4% in China. In Thailand the uncertainty caused by a military coup was compounded when the junta imposed exchange controls to hold back the strong baht, only to rescind them the next day. China's market soared in surely speculative excess, and in the absence of attractive alternatives, as investors sought a piece of the world's fourth largest economy. By the end of 2006 the Chinese market had become the third biggest emerging market after South Korea and Taiwan. European ex UK markets surged 16.1%, in 2006. The Eurozone's GDP growth had recorded its best first half of a year since 2000, 1.7%, and the lowest unemployment rate, 7.8%, since the start of the Eurozone itself. But as the second half of 2006, wore on there were signs that the best news was behind it and the third quarter's annualized growth fell to 2.0%. Business confidence, however, stayed buoyant and cheered by extensive merger and acquisition activity despite headwinds in the form of a strengthening euro, a hawkish European Central Bank that raised rates three times and the looming rise in German sales tax. UK equities added 8.6% in the six months ended December 31, 2006. The Bank of England raised rates twice as GDP growth accelerated to 2.9% year over year, inflation climbed above target and house prices, an import ant demand generator, continued their recovery with average prices up more than 10% in 2006. Again, however, it was widespread, large scale mergers and acquisitions energizing the market.

(1) The MSCI World IndexSM is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

(2) The LBAB Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

(3) The S&P 500® Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the U.S.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolios' performance is subject to change since the period's end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of the Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

ING VP REAL ESTATE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

The ING VP Real Estate Portfolio (the "Portfolio") seeks total return. The Portfolio is managed by T. Ritson Ferguson, CFA, Chief Investment Officer and Managing Director and Joseph P. Smith, CFA, Managing Director, of ING Clarion Real Estate Securities L.P. — the Sub-Adviser.

Performance: For the year ended December 31, 2006, the Portfolio's Class I shares provided a total return of 36.17% compared to the Morgan Stanley Capital International ("MSCI") U.S. REIT® Index(1) and the Dow Jones Wilshire ("DJW") Real Estate Securities Index(2), which returned 35.92% and 35.88% for the same period.

Portfolio Specifics: The Portfolio's performance was driven by positive stock selection, especially in the office and mall sectors. The Portfolio's holdings in the office sector was the largest contributor to performance in 2006, as several of the Portfolio's investments in the office sector were targets of M&A activity, and were acquired at attractive premiums to their pre-announcement trading prices. An overweight in the office sector also added value for the year. Stock selection within the hotel sector, combined with the Portfolio's slight overweight to the hotel sector which underperformed the market during the second half of the year, detracted from relative performance.

Real estate asset values continued to grow in 2006 because of two factors — cash flow growth and cap rate compression. Buoyed by a strong economy, demand from tenants helped improve occupancies and rental rates, resulting in higher cash flows from real estate assets. Simultaneously, the desire by many investors to increase their exposure to the real estate asset class helped drive up the price paid for the real estate cash flows. In other words, investors were willing to accept lower initial yields (i.e., cap rates) and lower expected rates of return (IRR's) to invest in real estate. The combination of higher cash flows and lower yields helped explain both the growth in real asset values, as well as the outsized capital appreciation for REIT share prices in 2006.

Current Strategy and Outlook: We believe overall earnings growth for real estate companies to accelerate in 2007 to 9.5%, driven by improving real estate fundamentals. As with 2006, we believe, earnings growth will occur from increases in occupancy, rent gains and expense containment. We continue to favor property companies in the office and apartment sectors and maintain an underweight to the hotel, industrial, and retail sectors of the market. We continue to find value in companies across all sectors of the market, especially in companies that exhibit market leadership, are run by strong management teams and are able to consistently grow their earnings.

In our opinion, there are two broad fundamental reasons to stay positive about REIT return potential: 1) the economic forecast for the U.S. is for moderating economic growth with stable interest rates (i.e., real estate returns remain competitive versus other asset classes in a moderating economy), and 2) real estate stocks are priced at reasonable levels relative to private market values (i.e., net asset value ("NAV")), which historically has portended good relative returns for REITs.

Low interest rates by historical standards and a moderately growing economy form an ideal environment for real estate investors. We look for another such year in 2007. The U.S. economy is making a graceful mid-business cycle transition from a period of above-average growth to more moderate and sustainable growth. Inflation is expected to settle down to about 2.5%, interest rates should stabilize at current levels, which represent a slightly restrictive monetary policy, and we believe GDP growth should slow to approximately 3%. Corporate profits are high, and consumers are still relatively well-off and confident, which bodes well for the demand side of the real estate equation.

Currently, we estimate that public company valuations represent a premium of only 2% to the private market values (i.e.,NAV) for equivalent real estate portfolios. Historically, REITs have traded in a band of -10% to +10%. The significant private market appetite for real estate, which led to a flurry of public company acquisition announcements throughout the year, suggests that our NAV estimates may be slightly conservative.

All-in-all, we expect a good backdrop for real estate again this year. In the assumed context of a growing economy and improving real estate market conditions, we expect investors to still embrace real estate. We believe earnings growth of 9.5% plus a dividend yield of 3.7% suggest low double-digit returns are possible. REITs are not unique in looking a bit expensive relative to historic valuation levels. With few, if any, obvious options for getting double-digit returns, investors are likely to maintain a positive view about investing in real estate, which bodes well for REITs holding their current multiples.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

Top Ten Holdings

as of December 31, 2006

(as a percent of net assets)

| Simon Property Group, Inc. | 6.4 | % | |||||

| Boston Properties, Inc. | 5.2 | % | |||||

| Equity Office Properties Trust | 5.0 | % | |||||

| Archstone-Smith Trust | 5.0 | % | |||||

| Vornado Realty Trust | 4.9 | % | |||||

| Prologis | 4.7 | % | |||||

| Equity Residential | 4.1 | % | |||||

| Public Storage, Inc. | 4.0 | % | |||||

| AvalonBay Communities, Inc. | 4.0 | % | |||||

| Host Hotels & Resorts, Inc. | 3.9 | % | |||||

Portfolio holdings are subject to change daily.

4

PORTFOLIO MANAGERS' REPORT

ING VP REAL ESTATE PORTFOLIO

Average Annual Total Returns for the Periods Ended December 31, 2006

| 1 Year | Since Inception of Class I May 3, 2004 | Since Inception of Class S May 13, 2005 | |||||||||||||

| Class I | 36.17 | % | 33.18 | % | — | ||||||||||

| Class S | 35.84 | % | — | 32.30 | % | ||||||||||

| MSCI U.S. REIT® Index(1) | 35.92 | % | 32.07 | %(3) | 30.29 | %(4) | |||||||||

| DJW Real Estate Securities Index(2) | 35.88 | % | 33.58 | %(3) | 31.54 | %(4) | |||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Real Estate Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expense. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contracts, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The MSCI U.S. REIT® Index is a free float-adjusted market capitalization weighted index that is comprised of equity real estate investment trusts that are included in the MSCI U.S. Investable Market 2500 Index (with the exception of specialty REITs that do not generate a majority of their revenue and income from real estate rental and leasing obligations). The Index represents approximately 85% of the U.S. REIT market. The MSCI U.S. REIT® Index more closely tracks the type of securities in which the Fund invests than the DJW Real Estate Securities Index.

(2) The DJW Real Estate Securities Index is an unmanaged, market capitalization weighted index of publicly traded real estate securities, such as REITs, real estate operating companies ("REOCs") and partnerships. The index is comprised of companies whose charter is the equity ownership and operation of commercial real estate.

(3) Since inception performance for the indices is shown from May 1, 2004.

(4) Since inception performance for the indices is shown from May 1, 2005.

5

ING VP MIDCAP OPPORTUNITIES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

The ING VP MidCap Opportunities Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Richard Welsh, Portfolio Manager and Jeff Bianchi, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2006, the Portfolio's Class I shares provided a total return of 7.79% compared to the Russell Midcap® Growth Index(1) and the Russell Midcap® Index(2), which returned 10.66% and 15.26%, respectively, for the same period.

Portfolio Specifics: The market responded favorably to stronger-than-expected economic and earnings growth. Valuations were helped during the latter half of the year by a sharp decline in commodity prices, which tempered inflation and interest rate fears.

All economic sectors, with the exception of energy, generated positive returns for the year. The market was led by sectors typically associated with value investing such as telecommunication services and financials. The energy sector performed the worst, reflecting ample oil and gas supplies as well as warmer-than-expected weather. Healthcare and information technology performed poorly as well. Mid-cap growth stocks generally underperformed mid-cap value stocks by almost 10%, which acted as a drag on the Portfolio's performance due to our overweight in growth stocks. We believe that as economic and earnings growth slows further, growth stocks will outperform value.

Sector Allocation accounted for the majority of the underperformance for the year, as our underweights in sectors that are not typically associated with growth, including energy, materials, and financials, hurt relative results.

Stock selection was least favorable in information technology and financials. Citrix Systems, Inc., a supplier of access information software and services, was one of our worst performing stocks last year, as it reported disappointing results due to weak licensing growth in its core presentation products. It was victim to a market that failed to reward companies with the highest expected growth. We sold our position in Citrix Systems, Inc. The shares of Micros Systems, Inc., which provides software solutions to the hospitality industry, underperformed. Slowing hotel software roll-out at a large customer as well as concerns about rising gasoline prices and weaker consumer spending trends hurting its restaurant software business pressured the stock. In financials, Legg Mason, Inc., a global asset manager, underperformed due to an earnings shortfall from weaker-than-expected asset flows and a delay in merger-related savings from the acquisition of Citigroup's asset management business. We also sold our Legg Mason, Inc. holding.

Stock selection within the energy and industrials sectors added the most to returns. Veritas DGC, Inc., a seismic data collection company for the discovery of oil, was acquired by a French company, Compagnie Generale de Geophysique-Veritas. In the industrials sector, Wesco International, Inc. and McDermott International, Inc. performed well. Wesco International, Inc., an electrical equipment distributor, was helped by strong demand from commercial construction, the utility industry and the overall industrial economy. McDermott International, Inc., which provides energy services, experienced stronger–than-expected bookings and as a result earnings expectations were revised significantly higher.

Current Strategy and Outlook: We believe that economic growth will continue albeit at a moderating pace. We believe that inflation will remain in check and that should have favorable interest rate implications for equity valuations. Consistent with an economy transitioning to slower growth, we are focusing intently on companies whose business momentum prospects are both attractive and reasonably certain. We continue to concentrate on stocks with above average business momentum, market recognition and appropriate valuations.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

Top Ten Holdings*

as of December 31, 2006

(as a percent of net assets)

| Coach, Inc. | 3.2 | % | |||||

| Roper Industries, Inc. | 2.8 | % | |||||

| Cameron International Corp. | 2.6 | % | |||||

| Nordstrom, Inc. | 2.4 | % | |||||

| Gen-Probe, Inc. | 2.3 | % | |||||

| Akamai Technologies, Inc. | 2.3 | % | |||||

| Dun & Bradstreet Corp. | 2.2 | % | |||||

| Harman International Industries, Inc. | �� | 2.1 | % | ||||

| McDermott International, Inc. | 2.1 | % | |||||

| Digital River, Inc. | 2.1 | % | |||||

* Excludes short-term investments related to repurchase agreement and securities lending collateral.

Portfolio holdings are subject to change daily.

6

PORTFOLIO MANAGERS' REPORT

ING VP MIDCAP OPPORTUNITIES PORTFOLIO

Average Annual Total Returns for the Periods Ended December 31, 2006*

| 1 Year | 5 Year | Since Inception of Class I May 5, 2000 | Since Inception of Class S May 7, 2001 | ||||||||||||||||

| Class I | 7.79 | % | 6.09 | % | (2.98 | )% | — | ||||||||||||

| Class S | 7.62 | % | 5.91 | % | — | 2.25 | % | ||||||||||||

| Russell Midcap® Growth Index(1) | 10.66 | % | 8.22 | % | (0.67 | )%(3) | 5.52 | %(4) | |||||||||||

| Russell Midcap® Index(2) | 15.26 | % | 12.88 | % | 9.08 | %(3) | 10.71 | %(4) | |||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP MidCap Opportunities Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolios, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Total returns reflect that the Investment Adviser may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contract, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

* ADV Class commenced operations on December 29, 2006, therefore, there is no performance information for the period ended December 31, 2006.

(1) The Russell Midcap® Growth Index is an unmanaged index that measures the performance of those companies included in the Russell Midcap® Index with relatively higher price-to-book ratios and higher forecasted growth values.

(2) The Russell Midcap® Index is an unmanaged index that measures the performance of the 800 smallest companies in the Russell 1000® Index, which represent approximately 26% of the total market capitalization of the Russell 1000® Index.

(3) Since inception performance for the indices is shown from May 1, 2000.

(4) Since inception performance for the indices is shown from May 1, 2001.

7

ING VP SMALLCAP OPPORTUNITIES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

The ING VP SmallCap Opportunities Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Steve Salopek, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2006, the Portfolio's Class I shares provided a total return of 12.57%, compared to the Russell 2000® Growth Index(1) and the Russell 2000® Index(2), which returned 13.35% and 18.37%, respectively, for the same period.

Portfolio Specifics: Small-cap stocks generally performed well in 2006, out-performing both mid- and large-caps. The Russell 2000® Index gained 18.4% in 2006, outperforming the large-cap Russell 1000® Index for the seventh year out of eight. Economic strength propelled small-cap corporate earnings to record highs, and acquisitions of smaller firms by private equity buyers also aided results. Despite strong overall performance, this year proved to be a volatile ride for small-caps. During the first quarter, the market favored mid- and small-sized companies within the small-cap universe, and this trend continued as the market sold off during the summer. Larger sized companies declined, with the highest liquidity stocks selling down the most. Larger capitalization companies declined the most, with the highest liquidity stocks suf fering the most. During the third quarter, cyclical companies corrected significantly, affecting the transportation, energy and capital goods areas. During this sell-off, financials showed resiliency, which provided support for the Russell 2000® Index. Although volatility was at an all time low, it was a difficult year for stock selection, as the market did not differentiate between high- and low-quality companies.

Strong stock selection in industrials, materials and financials contributed most to results. Our overweight in industrials and underweight in health care also added to performance. Stock selection in health care, technology and consumer discretionary hurt results. Our underweight position in consumer staples and materials also negatively impacted performance.

Wesco International, Inc. and Albemarle Corp. added significantly to relative performance over the period. Wesco International, Inc., a distributor of electrical supplies and equipment and provider of procurement solutions, was the greatest contributor. Strength in Wesco International, Inc.'s commercial construction end markets, as well as utility company spending on the upgrading of electricity transmission and distribution (i.e., the power grid), helped fuel strong organic growth and margin performance. Albemarle Corp. is in the catalyst and specialty chemicals businesses. Favorable performance can be attributed to a significant improvement in the operations of both of these businesses, as well as leverage from increased pricing, which led to higher cash flow growth than was expected.

Chemed Corp. and Parallel Petroleum Corp. were two of the largest detractors from performance over the period. The former is primarily a hospice provider with meaningful exposure to Medicare reimbursement. Chemed Corp. lowered earnings estimates as a result of Medicare reimbursement issues that capped revenue from certain markets and the company was unable to offset this negative development with a reduction in costs to service patients. Parallel Petroleum Corp. is an exploration and production company with a focus on natural gas. The company's performance was negatively impacted by lower natural gas prices and missed production estimates during the third quarter. As a result, earnings estimates were cut and questions were raised about the value of the company's properties and their ability to develop and exploit them.

Current Strategy and Outlook: We believe that economic growth will continue to slow. We continue to focus on companies with strong balance sheets and cash flow generation capabilities that can show stable growth despite a moderating economy. Our largest overweight in the Portfolio is energy. The valuations of the companies in this sector are at or below long-term averages. Also, the implied volatility from futures contracts for oil and gas are low, which is beneficial for smaller, less liquid shares. Our largest underweight is consumer discretionary, as this sector is heavily reliant on consumer spending. Although the impact of rising interest rates and gas prices have been somewhat alleviated, we believe that the weakness in the housing market and the absence of mortgage equity withdrawals will continue to be a headwind for the consumer. In capital goods we have positioned the Portfolio away from deeply cyclical companies. We are likely to increase our weighting in consumer services, especially in companies that can show stable growth despite a slowing economy.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

Top Ten Holdings*

as of December 31, 2006

(as a percent of net assets)

| iShares Russell 2000 Growth Index Fund | 2.6 | % | |||||

| Ansys, Inc. | 1.5 | % | |||||

| Psychiatric Solutions, Inc. | 1.3 | % | |||||

| NewAlliance Bancshares, Inc. | 1.3 | % | |||||

| Toro Co. | 1.2 | % | |||||

| UAP Holding Corp. | 1.2 | % | |||||

| Valueclick, Inc. | 1.2 | % | |||||

| Micros Systems, Inc. | 1.2 | % | |||||

| Life Time Fitness, Inc. | 1.2 | % | |||||

| Entegris, Inc. | 1.1 | % | |||||

* Excludes short-term investments related to repurchase agreement and securities lending collateral.

Portfolio holdings are subject to change daily.

8

PORTFOLIO MANAGERS' REPORT

ING VP SMALLCAP OPPORTUNITIES PORTFOLIO

Average Annual Total Returns for the Periods Ended December 31, 2006

| 1 Year | 5 Year | 10 Year | Since Inception of Class S May 3, 2001 | ||||||||||||||||

| Class I | 12.57 | % | 1.13 | % | 9.49 | % | — | ||||||||||||

| Class S | 12.35 | % | 0.92 | % | — | (1.82 | )% | ||||||||||||

| Russell 2000® Growth Index(1) | 13.35 | % | 6.93 | % | 4.88 | % | 5.21 | %(3) | |||||||||||

| Russell 2000® Index(2) | 18.37 | % | 11.39 | % | 9.44 | % | 10.30 | %(3) | |||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP SmallCap Opportunities Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolios, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Total returns reflect that the Investment Adviser may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contracts, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Russell 2000® Growth Index is an unmanaged index that measures the performance of securities of smaller U.S. companies with greater-than-average growth orientation.

(2) The Russell 2000® Index is an unmanaged index that measures the performance of securities of small U.S. companies.

(3) Since inception performance for the indices is shown from May 1, 2001.

9

ING VP FINANCIAL SERVICES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

The ING VP Financial Services Portfolio (the "Portfolio") seeks long term capital appreciation. The Portfolio is managed by Steven L. Rayner, Portfolio Manager and Robert M. Kloss, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

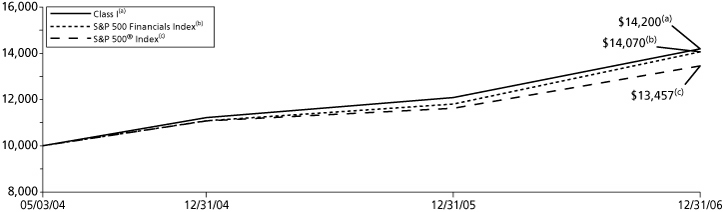

Performance: For the year ended December 31, 2006, the Portfolio's Class I shares provided a total return of 17.47% compared to the Standard & Poor's 500 Financials Index(1) ("S&P 500 Financials Index") and the Standard & Poor's 500® Composite Stock Price Index(2) ("S&P 500® Index"), which returned 19.21% and 15.79%, respectively, for the same period.

Portfolio Specifics: With the U.S. Federal Reserve Board ("Fed") on hold, the equity markets and financial stocks in general rallied during the second half of the year. A procession of mixed economic news kept investors hopeful that the Fed might even cut rates sometime in 2007. However, deterioration in the housing market, which took its toll on selected areas in financials, served to quell this thinking. Gross domestic product growth forecasts have also come down, but still imply a soft landing. The yield curve has remained flat or inverted, acting as a headwind for spread-based income.

Over the past twelve months, we have shifted the Portfolio's tilt from economically sensitive cyclical stocks to a more defensive stance. The shape of the yield curve and credit concerns have kept us underweight bank stocks, though we remain alert for the opportunity to take advantage of the Fed easing if and when it comes.

Capital markets stocks, including brokers, asset managers, and trust banks, were the largest contributors to performance for the period as both our overweight positioning and individual stock selection benefited the Portfolio. A variety of insurance stocks paid off, in terms of allocation and selection in part due to a benign hurricane season. In addition, a number of our life insurance companies produced solid earnings and proved more resilient to spread pressures than banks. Our underweight position in banks continued to benefit the Portfolio, as it underperformed.

Consolidation activity in the richly-valued real estate investment trust ("REIT") market continued to attract new money, and our valuation-driven underweight position acted as a drag even though the REIT names we did own performed well. The relatively small consumer finance industry group performed poorly. While we maintained a neutral weight, our individual stock selections were hurt by credit concerns, which produced slightly negative returns. REITs produced good absolute results, but underperformed the benchmark.

Merrill Lynch & Co., Inc., Morgan Stanley, and Goldman Sachs Group, Inc. all performed well. All three brokerages benefited from trading, merger and acquisition and security issuance activity. Strong equity markets and fund flows contributed to returns from asset managers Affiliated Managers Group and Franklin Resources. Capital markets and transaction flow exposure also aided JPMorgan Chase, Citigroup, and The Bank of New York. Strong pricing and a lack of catastrophes proved helpful for property/casualty holdings Axis Capital Holdings Ltd., Endurance Specialty Holdings Ltd., and St. Paul Travelers Co., Inc. Commercial banks Wells Fargo & Co., Bank of America Corp. and US Bancorp made positive contributions, as did REITs KKR Financial Corp. and Douglas Emmett, Inc.

In contrast, life/health insurer Conseco, Inc. did not earn the debt rating upgrade we expected, and the stock declined after a weak quarter, prompting the sale of our position. Credit card giant Capital One Financial Corp. fell on concerns of consumer credit and their acquisition of North Fork Bank. We continue to like the stock and believe investors will be well-rewarded as North Fork Bank is integrated and the market gains respect for the merged company's more stable risk profile.

Health insurer Aflac, Inc. was weak due to a sales shortfall in their key Japanese market. As the year progressed, we saw an increase in the risk level for many areas in financials, and reacted by positioning the Portfolio more defensively. This included reducing our broker overweight, toning down our property and casualty insurance allocation, as the stocks reacted positively to earnings, and eliminating positions in companies with weaker balance sheets.

Current Strategy and Outlook: In the face of an inverted yield curve and credit concerns, we remain underweight banks, though recent price weakening and the possibility of Fed easing in 2007 make us somewhat more constructive on this segment. We have also maintained our REIT underweight, though we continue to scour the group for opportunities that meet our valuation parameters.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

Top Ten Holdings*

as of December 31, 2006

(as a percent of net assets)

| Citigroup, Inc. | 6.0 | % | |||||

| Bank of America Corp. | 5.4 | % | |||||

| JPMorgan Chase & Co. | 4.8 | % | |||||

| American International Group, Inc. | 4.7 | % | |||||

| Wells Fargo & Co. | 4.5 | % | |||||

| US Bancorp. | 4.0 | % | |||||

| Bank of New York Co., Inc. | 3.4 | % | |||||

| Wachovia Corp. | 3.4 | % | |||||

| Merrill Lynch & Co., Inc. | 3.2 | % | |||||

| Affiliated Managers Group, Inc. | 3.0 | % | |||||

* Excludes short-term investments related to repurchase agreement.

Portfolio holdings are subject to change daily.

10

PORTFOLIO MANAGERS' REPORT

ING VP FINANCIAL SERVICES PORTFOLIO

Average Annual Total Returns for the Periods Ended December 31, 2006

| 1 Year | Since Inception of Class I and S May 3, 2004 | ||||||||||

| Class I | 17.47 | % | 14.07 | % | |||||||

| Class S | 17.11 | % | 13.80 | % | |||||||

| S&P 500 Financials Index(1) | 19.21 | % | 13.67 | %(3) | |||||||

| S&P 500® Index(2) | 15.79 | % | 11.78 | %(3) | |||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP Financial Services against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The S&P 500 Financials Index is a capitalization-weighted index of all stocks designed to measure the performance of the financial sector of the S&P 500® Index.

(2) The S&P 500® Index is an unmanaged index that measures the performance of the securities of approximately 500 of the largest companies in the U.S.

(3) Since inception performance for the indices is shown from May 1, 2004.

11

ING VP HIGH YIELD BOND PORTFOLIO

PORTFOLIO MANAGERS' REPORT

The ING VP High Yield Bond Portfolio (the "Portfolio") seeks to provide investors with a high level of current income and total return by investing at least 80% of its assets in high yield (high risk) bonds, that are unrated or rated below investment grade. The Portfolio is managed by Greg Jacobs*, Portfolio Manager and Kurt Kringelis*, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2006, the Portfolio's Class I shares provided a total return of 9.78% compared to the Lehman Brothers® High Yield Bond Index(1) and the Lehman Brothers® High Yield Bond Index-2% Issuer Constrained Composite Index(2), which returned 11.85% and 10.76%, respectively, for the same period.

Portfolio Specifics: 2006 was supposed to be the year that synchronized global growth led to capacity constraints in labor and manufacturing and rising commodity prices. This combination was expected to produce inflation rates that would have been unacceptable to the U.S. Federal Reserve Board ("Fed") and global investors in general. A repudiation of U.S. dollar-based assets and a Fed bent on draining liquidity from the market was expected to lead to rising interest rates and a decline in prices of high risk assets relative to their low risk counterparts. As the carry trade was unwound, volatility was expected to re-emerge. Investors were also expected to come to the realization that the Fed was behind this steepening of the yield curve and that it could not control inflation.

However, capital markets rarely serve up what is expected. Although, we did in fact experience the greatest surge in global growth since the 1970s, and the longest string of 6% plus gross domestic product ("GDP") growth since the 1980s, the economy could not deal with a simultaneous slowdown in housing and manufacturing. Even though there was a brief inflation scare as the core consumer price index reached a peak of 2.9%, a level not seen since 1996, unit labor cost increases were offset by falling goods prices. The market correctly predicted that growth and inflation would moderate and these robust economic statistics would be fleeting.

Overall, last year's high yield bond market can best be described as a battle of two halves. In the first half of 2006, the market faced inflation and oil fears, giving up most of its gains through April in the May-June period. In the second half of the year, investors shrugged off weakness in housing and focused on a benign Fed as sufficient reason to buy riskier assets. While the investment grade bond market worried about the re-levering of corporate balance sheets, the high yield market gladly financed these transactions and ended the year searching for similar deals.

Investing in riskier assets was the theme of 2006 as investors searched for yield and higher returns. The Portfolio underperformed its index in the first half of the year due to its conservative credit profile and underweight in the automotive sector. Performance rebounded in the second half as the Portfolio increased its overweight in single-B rated bonds and its exposure to Ford and General Motors Corp. On the strength of the performance in these two issuers, the automotive industry outperformed the benchmark by more than 11.0% for the year. An overweight in the cable industry acted as a positive contributor to performance, as it outperformed the benchmark by more than 8.0%.

Current Strategy and Outlook: Our basic outlook for high yield remains unchanged. Fundamentally, the outlook remains healthy, with strong profit growth and low interest rates, while the asset class continues to attract capital from investors searching for yield. While the strong second half 2006 returns certainly limit the potential upside for 2007, as long as defaults remain low and risk appetite is high, it is difficult to envision a meaningful reversal to this trend. As a result, we believe the market is likely to continue to outperform, with spreads remaining at historically tight levels. The increase in lower quality issuance over the past couple years will eventually cause an increase in defaults, but we continue to believe that occurrence is still several quarters away.

* Effective March 1, 2007, Randall Parrish will be named Portfolio Manager to the Portfolio and Greg Jacobs and Kurt Kringelis are removed as Portfolio Managers to the Portfolio.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

Industry Allocation

as of December 31, 2006

(as a percent of net assets)

| Diversified Financial Services | 13.3 | % | |||||

| Media | 13.2 | % | |||||

| Telecommunications | 8.4 | % | |||||

| Chemicals | 6.5 | % | |||||

| Retail | 5.6 | % | |||||

| Commercial Services | 5.4 | % | |||||

| Forest Products & Paper | 4.9 | % | |||||

| Healthcare-Services | 4.5 | % | |||||

| Oil & Gas | 4.2 | % | |||||

| Entertainment | 3.9 | % | |||||

| Electric | 2.9 | % | |||||

| Leisure Time | 2.2 | % | |||||

| Industries between 1.3% - 2.0%(1) | 12.8 | % | |||||

| Industries less than 1.3%(2) | 12.3 | % | |||||

| Other Assets and Liabilities, Net* | (0.1 | )% | |||||

| Net Assets | 100.0 | % | |||||

* Includes short-term investments related to repurchase agreement.

(1) Includes eight industries, which each represents 1.3% - 2.0% of net assets.

(2) Includes twenty nine industries, which each represents less than 1.3% of net assets.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2006

(as a percent of net assets)

| HCA, Inc., 9.250%, due 11/15/16 | 1.9 | % | |||||

| Ford Motor Credit Co., 9.750%, due 09/15/10 | 1.5 | % | |||||

| Ford Motor Credit Co., 9.875%, due 08/10/11 | 1.5 | % | |||||

| Charter Communications Operating, LLC, 8.375%, due 04/30/14 | 1.4 | % | |||||

| Ashtead Capital, Inc., 9.000%, due 08/15/16 | 1.3 | % | |||||

| CCH I, LLC, 11.000%, due 10/01/15 | 1.2 | % | |||||

| PolyOne Corp., 8.875%, due 05/01/12 | 1.1 | % | |||||

| Idearc, Inc., 8.000%, due 11/15/16 | 1.1 | % | |||||

| Lyondell Chemical Co., 8.000%, due 09/15/14 | 1.1 | % | |||||

| Neiman-Marcus Group, Inc., 9.000%, due 10/15/15 | 1.1 | % | |||||

Portfolio holdings are subject to change daily.

12

PORTFOLIO MANAGERS' REPORT

ING VP HIGH YIELD BOND PORTFOLIO

Average Annual Total Returns for the Periods Ended December 31, 2006*

| 1 Year | 5 Year | 10 Year | Since Inception of Class S April 29, 2005† | ||||||||||||||||

| Class I | 9.78 | % | 6.84 | % | 2.82 | % | — | ||||||||||||

| Class S | 9.60 | % | — | — | 8.20 | % | |||||||||||||

| Lehman Brothers® High Yield Bond Index(1) | 11.85 | % | 10.18 | % | 6.59 | % | 10.40 | %(3) | |||||||||||

| Lehman Brothers® High Yield Bond Index - 2% Issuer Constrained Composite Index(2) | 10.76 | % | 10.20 | % | 6.63 | % | 9.77 | %(3) | |||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP High Yield Bond Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contracts, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

* Class ADV commenced operations on December 29, 2006, therefore, there is no performance information for the period ended December 31, 2006. Class S commenced operations on April 29, 2005.

† On May 1, 2006, all outstanding shares of Class S were fully redeemed. On December 29, 2006, Class S recommenced operations. The returns for Class S include the performance of Class I, adjusted to reflect the higher expenses of Class S, for the period of May 2, 2006 to December 28, 2006.

(1) The Lehman Brothers® High Yield Bond Index is an unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment grade.

(2) The Lehman Brothers® High Yield Bond — 2% Issuer Constrained Composite Index is an unmanaged index that measures the performance of fixed-income securities. The Composite Index more closely tracks the types of securities in which the Fund invests than the Lehman Brothers High Yield Bond Index.

(3) Since inception performance of the index is shown from May 1, 2005.

13

ING VP INTERNATIONAL VALUE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

The ING VP International Value Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Philip A. Schwartz*, CFA, Senior Vice President and Director of International Investment Strategy of ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2006, the Portfolio's Class I shares provided a total return of 29.44% compared to the Morgan Stanley Capital International — Europe, Australasia and Far East ("MSCI EAFE®") Index(1), which returned 26.34% for the same period.

Portfolio Specifics: International markets got off to a great start during the first five months of the year, but certain markets corrected in May and June. In particular, emerging markets suffered as riskier assets sold off. Most of the losses were recovered during the third quarter amid an increase in merger and acquisition activity, a decline in oil prices and improved consumer sentiment across Europe. The resurgence of the markets continued through the end of the year and was driven by improved consumer spending and industrial production figures.

Stock selection helped performance overall, particularly in materials, financials, industrials and telecommunications services. Underweight positions in healthcare and energy, coupled with an overweight in telecommunications services and utilities contributed positively. An underweight position in Japan and an allocation to non-benchmark emerging markets also benefited the Portfolio.

In contrast, while security selection in materials boosted performance, an underweight allocation acted as a slight drag. Further, our holdings in energy and consumer staples negatively impacted the Portfolio. Our allocation to the European region and non-benchmark North America hurt the strategy.

China Mobile Ltd, a Hong Kong-based mobile phone service provider, rose due to a record number of subscribers. Severn Trent PLC, a UK waste, water and utilities service provider, benefited from increased profits and net income, both of which beat estimates. Heineken NV, a Dutch international beer brewer, performed well due to the introduction of new beers and their entry into the Russian market.

SGL Carbon AG, a German manufacturer of carbon and graphite materials, suffered from a decrease in cash flow from its operations. The German telecommunications provider, Deutsche Telekom AG was negatively impacted after several mid-year cuts to its ratings, which stemmed from disappointing first-half results. Swedish high tech engineering group Sandvik AB similarly suffered when several analysts cut their mid-year rating.

Current Strategy and Outlook: We remain positive about 2007. With growth well underpinned in foreign economies and retreating oil prices, the outlook for international markets has improved in recent months. Consequently we remain overweight emerging markets. We also increased our position in Japan, as positive economic growth and attractive values provide opportunities. We continue to maintain an underweight to consumer discretionary, a modest underweight in financials and an overweight in energy. Major risk factors include a potential slowdown in global growth, stemming from central banks further tightening, and a potential for investors to become more risk averse.

* Effective December 31, 2006, Richard T. Saler is no longer a portfolio manager to the Portfolio.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

Top Ten Holdings*

as of December 31, 2006

(as a percent of net assets)

| Bombardier, Inc. - Class B | 3.0 | % | |||||

| PetroChina Co., Ltd. | 2.9 | % | |||||

| Kirin Brewery Co., Ltd. | 2.8 | % | |||||

| Fortum OYJ | 2.6 | % | |||||

| Royal Bank of Scotland Group PLC | 2.6 | % | |||||

| Toyota Motor Corp. | 2.5 | % | |||||

| Yamaha Motor Co., Ltd. | 2.5 | % | |||||

| Vodafone Group PLC | 2.5 | % | |||||

| Allianz AG | 2.5 | % | |||||

| Nippon Telegraph & Telephone Corp. | 2.4 | % | |||||

* Excludes short-term investments related to repurchase agreement and securities lending collateral.

Portfolio holdings are subject to change daily.

14

PORTFOLIO MANAGERS' REPORT

ING VP INTERNATIONAL VALUE PORTFOLIO

Average Annual Total Returns for the Periods Ended December 31, 2006*

| 1 Year | 5 Year | Since Inception of Class I August 8, 1997 | Since Inception of Class S March 19, 2002 | ||||||||||||||||

| Class I | 29.44 | % | 12.80 | % | 12.25 | % | — | ||||||||||||

| Class S | 28.81 | % | — | — | 12.09 | % | |||||||||||||

| MSCI EAFE® Index(1) | 26.34 | % | 14.98 | % | 6.81 | %(2) | 15.70 | %(3) | |||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP International Value Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contracts, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

* ADV Class commenced operations on December 29, 2006, therefore, there is no performance information for the period ended December 31, 2006.

(1) The MSCI EAFE® Index is an unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East. It includes the reinvestment of dividends net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing.

(2) Since inception performance for the index is shown from August 1, 1997.

(3) Since inception performance for the index is shown from April 1, 2002.

Prior to July 1, 2002, the portfolio was sub-advised by a different sub-adviser.

15

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Portfolio, you incur two types of costs: (1) transaction costs, including redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Portfolio expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2006 to December 31, 2006. The Portfolios' expenses are shown without the imposition of any charges which are, or may be, imposed under your annuity contract. Expenses would have been higher if such charges were included.

Actual Expenses

The first section of the table shown, "Actual Portfolio Return," provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, "Hypothetical 5% Return," provides information about hypothetical account values and hypothetical expenses based on the Portfolio's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different mutual funds. In addition, if these transactional costs were included, your costs would have been higher.

| ING VP Real Estate Portfolio | Beginning Account Value July 1, 2006 | Ending Account Value December 31, 2006 | Annualized Expense Ratio | Expenses Paid During the Six Months Ended December 31, 2006* | |||||||||||||||

| Actual Portfolio Return | |||||||||||||||||||

| Class I | $ | 1,000.00 | $ | 1,182.00 | 0.93 | % | $ | 5.11 | |||||||||||

| Class S | 1,000.00 | 1,180.90 | 1.18 | 6.49 | |||||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||||

| Class I | $ | 1,000.00 | $ | 1,020.52 | 0.93 | % | $ | 4.74 | |||||||||||

| Class S | 1,000.00 | 1,019.26 | 1.18 | 6.01 | |||||||||||||||

| ING VP MidCap Opportunities Portfolio | |||||||||||||||||||

| Actual Portfolio Return | |||||||||||||||||||

| Class ADV(a) | $ | 1,000.00 | $ | 1,000.00 | 1.40 | % | $ | 0.12 | |||||||||||

| Class I | 1,000.00 | 1,029.00 | 0.90 | 4.60 | |||||||||||||||

| Class S | 1,000.00 | 1,028.10 | 1.10 | 5.62 | |||||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 1,018.15 | 1.40 | % | $ | 7.12 | |||||||||||

| Class I | 1,000.00 | 1,020.67 | 0.90 | 4.58 | |||||||||||||||

| Class S | 1,000.00 | 1,019.66 | 1.10 | 5.60 | |||||||||||||||

* Expenses are equal to each Portfolio's respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/365 to reflect the most recent fiscal half-year (except "Actual Portfolio Return" information for all share classes footnoted above).

(a) Commencement of operations for Class ADV or Class S was December 29, 2006. Expenses paid reflect the three day period ended December 31, 2006 with 0.00% return.

16

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) (CONTINUED)

| ING VP SmallCap Opportunities Portfolio | Beginning Account Value July 1, 2006 | Ending Account Value December 31, 2006 | Annualized Expense Ratio | Expenses Paid During the Six Months Ended December 31, 2006* | |||||||||||||||

| Actual Portfolio Return | |||||||||||||||||||

| Class I | $ | 1,000.00 | $ | 1,063.90 | 0.90 | % | $ | 4.68 | |||||||||||

| Class S | 1,000.00 | 1,063.00 | 1.10 | 5.72 | |||||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||||

| Class I | $ | 1,000.00 | $ | 1,020.67 | 0.90 | % | $ | 4.58 | |||||||||||

| Class S | 1,000.00 | 1,019.66 | 1.10 | 5.60 | |||||||||||||||

| ING VP Financial Services Portfolio | |||||||||||||||||||

| Actual Portfolio Return | |||||||||||||||||||

| Class I | $ | 1,000.00 | $ | 1,149.70 | 0.80 | % | $ | 4.33 | |||||||||||

| Class S | 1,000.00 | 1,147.90 | 1.05 | 5.68 | |||||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||||

| Class I | $ | 1,000.00 | $ | 1,021.17 | 0.80 | % | $ | 4.08 | |||||||||||

| Class S | 1,000.00 | 1,019.91 | 1.05 | 5.35 | |||||||||||||||

| ING VP High Yield Bond Portfolio | |||||||||||||||||||

| Actual Portfolio Return | |||||||||||||||||||

| Class ADV(a) | $ | 1,000.00 | $ | 1,000.00 | 1.21 | % | $ | 0.10 | |||||||||||

| Class I | 1,000.00 | 1,076.30 | 0.72 | 3.77 | |||||||||||||||

| Class S(a) | 1,000.00 | 1,000.00 | 0.91 | 0.07 | |||||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 1,019.11 | 1.21 | % | $ | 6.16 | |||||||||||

| Class I | 1,000.00 | 1,021.58 | 0.72 | 3.67 | |||||||||||||||

| Class S | 1,000.00 | 1,020.62 | 0.91 | 4.63 | |||||||||||||||

| ING VP International Value Portfolio | |||||||||||||||||||

| Actual Portfolio Return | |||||||||||||||||||

| Class ADV(a) | $ | 1,000.00 | $ | 1,000.00 | 1.50 | % | $ | 0.12 | |||||||||||

| Class I | 1,000.00 | 1,165.00 | 1.00 | 5.46 | |||||||||||||||

| Class S | 1,000.00 | 1,161.40 | 1.20 | 6.54 | |||||||||||||||

| Hypothetical (5% return before expenses) | |||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 1,017.64 | 1.50 | % | $ | 7.63 | |||||||||||

| Class I | 1,000.00 | 1,020.16 | 1.00 | 5.09 | |||||||||||||||

| Class S | 1,000.00 | 1,019.16 | 1.20 | 6.11 | |||||||||||||||

* Expenses are equal to each Portfolio's respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/365 to reflect the most recent fiscal half-year (except "Actual Portfolio Return" information for all share classes footnoted above).

(a) Commencement of operations for Class ADV and Class S was December 29, 2006. Expenses paid reflect the three day period ended December 31, 2006 with 0.00% return.

17

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Shareholders and Board of Trustees

ING Variable Products Trust

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of ING VP Real Estate Portfolio, ING VP MidCap Opportunities Portfolio, ING VP SmallCap Opportunities Portfolio, ING VP Financial Services Portfolio, ING VP High Yield Bond Portfolio, and ING VP International Value Portfolio, each a series of ING Variable Products Trust, as of December 31, 2006, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2006 by correspondence with the custodian and brokers, or by other appropriate auditing procedures when replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.