|

| OMB APPROVAL | ||

|

| OMB Number: | 3235-0570 | |

|

| Expires: | August 31, 2011 | |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .18.9 | ||

| SECURITIES AND EXCHANGE COMMISSION |

| ||

| Washington, D.C. 20549 |

| ||

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8220 | ||||||||

| |||||||||

ING Variable Products Trust | |||||||||

(Exact name of registrant as specified in charter) | |||||||||

| |||||||||

7337 E. Doubletree Ranch Rd., Scottsdale, AZ |

| 85258 | |||||||

(Address of principal executive offices) |

| (Zip code) | |||||||

| |||||||||

CT Corporation System, 101 Federal Street, Boston, MA 02110 | |||||||||

(Name and address of agent for service) | |||||||||

| |||||||||

Registrant’s telephone number, including area code: | 1-800-992-0180 |

| |||||||

| |||||||||

Date of fiscal year end: | December 31 |

| |||||||

| |||||||||

Date of reporting period: | January 1, 2008 to December 31, 2008 |

| |||||||

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

December 31, 2008

Classes ADV, I and S

ING Variable Products Trust

Domestic Equity Growth Portfolios

n ING VP MidCap Opportunities Portfolio

n ING VP SmallCap Opportunities Portfolio

International Equity Portfolio

n ING VP International Value Portfolio

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds' investment objectives, risks, charges, expenses and other information. This information should be read carefully.

MUTUAL FUNDS

TABLE OF CONTENTS

| President's Letter | 1 | ||||||

| Market Perspective | 2 | ||||||

| Portfolio Managers' Reports | 4 | ||||||

| Shareholder Expense Examples | 10 | ||||||

| Report of Independent Registered Public Accounting Firm | 11 | ||||||

| Statements of Assets and Liabilities | 12 | ||||||

| Statements of Operations | 13 | ||||||

| Statements of Changes in Net Assets | 14 | ||||||

| Financial Highlights | 16 | ||||||

| Notes to Financial Statements | 18 | ||||||

| Portfolios of Investments | 32 | ||||||

| Tax Information | 40 | ||||||

| Trustee and Officer Information | 41 | ||||||

| Advisory Contract Approval Discussion | 46 | ||||||

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the ING Funds' website at www.ingfunds.com; and (3) on the U.S. Securities and Exchange Commission's ("SEC") website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the ING Funds' website at www.ingfunds.com and on the SEC's website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Portfolios' Forms N-Q are available on the SEC's website at www.sec.gov. The Portfolios' Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330; and is available upon request from the Portfolio by calling Shareholder Services toll-free at (800) 992-0180.

PRESIDENT'S LETTER

Dear Shareholders,

We are in the midst of one of the most challenging periods ever faced by investors, and we at ING Funds are aware of the anxiety that you may be feeling at this time.

I want to assure you that we are actively engaged in monitoring the situation and are committed to keeping you fully informed of how the rapidly unfolding events around us may impact your investments with our company.

We recognize that the confidence of many investors is being tested, perhaps as never before. It is understandable that some of you may be second guessing your investment strategy due to these recent events. We encourage you to work with your investment professional and seek out their advice about your portfolio in light of the current conditions. But we also urge investors not to make rash decisions. ING Funds still believes that a well-diversified, globally allocated portfolio remains the most effective investment strategy of all. We ask that investors not lose sight of their commitment to the long-term.

We thank you for your support and confidence and we look forward to continuing to do business with you in the future.

Sincerely,

Shaun Mathews

President & Chief Executive Officer

ING Funds

January 23, 2009

The views expressed in the President's Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice. Consider the fund's investment objectives, risks, and charges and expenses carefully before investing. The prospectus contains this information and other information about the fund.

International investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

1

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2008

In our semi-annual report, we described a failed second quarter rally that fizzled when investors realized that borderline recessionary conditions and a credit crunch had not gone away. By year-end, governments were committing previously unimaginable sums of taxpayer money to prevent systemic collapse. Global equities in the form of the MSCI World® Index(1) measured in local currencies, including net reinvested dividends ("MSCI" for regions discussed below) plunged 29.70% in the six months ended December 31, 2008 (down 38.70% for the entire fiscal year). (The MSCI World® Index plunged 40.71% for the entire fiscal year, measured in U.S. dollars.) In currencies, the dollar at first drifted near record lows against the euro. But the tide turned in mid-July and for the six months ended December 31, 2008, the dollar strengthened by 12.10% (4.50% for the entire fiscal year). The dollar also soared 37.80% against the pound for the six months ended December 31, 2008 (37.90% for the entire fiscal year). But the yen advanced as carry trades (essentially short yen positions) were unwound and the dollar fell 14.90% for the six months ended December 31, 2008 (down 19.60% for the entire fiscal year).

Even more dramatic was the price of oil which marched to an all-time high of around $147 per barrel in mid-July, only to lose more than two thirds of that price by December 31, 2008.

The economic statistics remained bleak. By the end of October, the Standard & Poor's ("S&P")/Case-Shiller National U.S. Home Price Index(2) of house prices had fallen a record 18% over the year. New home sales were at 1991 levels. Some 45% of existing home sales were distressed.

Payrolls declined in every month of 2008, as the number of people claiming unemployment reached 4.1 million, a 26-year high. Gross domestic product ("GDP") fell at an annualized rate of 0.50% in the third quarter, and the National Bureau of Economic Research announced that the recession had actually started in December 2007.

Yet these were side-shows to the fireworks display in the financial sector, where major institutions — hanging by a thread through problems rooted in unwise mortgage borrowing, lending and investment — met different fates in September 2008 at the hands of the U.S. government.

The Federal National Mortgage Association ("Fannie Mae") and the Federal Home Loan Mortgage Corporation ("Freddie Mac") were taken into "conservatorship." Merrill Lynch was acquired by the Bank of America with a wink from the authorities. AIG received an $85 billion loan from a reluctant government, which also took a 79.90% equity stake in AIG. But Lehman Brothers having sought capital, then a buyer, found neither and was left to file for Chapter 11 bankruptcy protection.

The U.S. government was now in the position of choosing winners and losers among financial institutions: none too successfully, for it quickly became obvious that by pointedly leaving Lehman Brothers to go under, a credit crisis had become a credit market collapse. Lending all but seized up.

Policy response was huge but at least initially muddled. A Troubled Asset Relief Plan ("TARP") would set up a $700 billion fund to buy illiquid mortgage securities from financial institutions. But on November 12, 2008 with half of the money already used to recapitalize banks, Treasury Secretary Paulson announced that the rest of the funds would not be used to buy illiquid mortgage securities after all. This merely renewed the pressure on the holders of such securities like Citigroup, which within two weeks received guarantees from the government against losses and another $20 billion in capital.

Other programs were of more practical use, like support for the commercial paper market and a guarantee facility for money market funds. Arguably the most effective measure was the announced intention to buy vast quantities of agency mortgage-backed securities and debentures. This had the effect of driving down rates on the 30-year mortgage towards 5.00%, a record low. In the meantime, the newly-elected president promised a stimulus package worth approximately $1 trillion. And by year end, the Federal Open Market Committee ("FOMC") reduced interest rates to a range of between 0% and 0.25%.

2008 ended with much gloom and bad news still to come, but the platform for recovery was perhaps taking shape.

In U.S. fixed-income markets, yields on the 90-day Treasury Bills briefly turned negative in December 2008, while the yield on the ten-year Treasury Note fell below 2.50%, something we had not seen in 50 years. The Barclays Capital U.S. Aggregate Bond Index(3), formerly known as the Lehman Brothers U.S. Aggregate Bond Index, of investment grade bonds returned 4.10% for the six months ended December 31, 2008, (5.20% for the entire fiscal year). By contrast, high yield bonds, represented by the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index(4), formerly known as

2

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2008

the Lehman Brothers High Yield Bond — 2% Issuer Constrained Composite Index, behaved more like a stock index and returned (25.10)% for the six months ended December 31, 2008 (down 25.90% for the entire fiscal year).

U.S. equities, represented by the S&P 500® Composite Stock Price ("S&P 500®") Index(5), including dividends, returned (28.50)% for the six months ended December 31, 2008, (down 37.00% for the entire fiscal year), increasingly unimpressed by sharply falling oil prices. Profits for S&P 500® Index companies suffered their fifth straight quarter of decline, led again by the financials sector, although taxpayer money was also potentially committed to save the big three auto makers from bankruptcy. On November 20, 2008, the S&P 500® Index plumbed a level not seen since April 1997, before a December recovery.

In international markets, plainly entering recession, the MSCI Japan® Index(6) slumped 35.90% for the six months ended December 31, 2008, (down 42.60% for the entire fiscal year). The strengthening yen hit exports in an export-dependent economy even as global demand slowed for other reasons. The MSCI Europe ex UK® Index(7) sagged 29.40% for the six months ended December 31, 2008 (down 43.20% for the entire fiscal year), beset by sharply falling economic activity and a European Central Bank in denial that inflation was falling fast. Finally, rates were reduced by an unprecedented 175 basis points (or 1.75%) in two months near the end of the year while governments, one after the other, proposed large stimulus packages. In the UK, the MSCI UK® Index(8) fell 19.40% for the six months ended December 31, 2008 (down 28.50% for the entire fiscal year). The UK had allowed a bigger ho using bubble than the United States and deeper personal indebtedness in an economy more dependent on the financial sector. Rates were reduced to 1951 levels as venerable banks ceased to exist as independent entities.

(1) The MSCI World® Index is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

(2) The S&P/Case-Shiller National U.S. Home Price Index tracks the value of single-family housing within the United States. The index is a composite of single-family home price indices for the nine U.S. Census divisions and is calculated quarterly.

(3) The Barclays Capital U.S. Aggregate Bond Index is an unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

(4) The Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index is an unmanaged index that measures the performance of non-investment grade fixed-income securities.

(5) The S&P 500® Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the United States.

(6) The MSCI Japan® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(7) The MSCI Europe ex UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(8) The MSCI UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolios' performance is subject to change since the period's end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING's Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

ING VP MIDCAP OPPORTUNITIES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING VP MidCap Opportunities Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Uri Landesman, Senior Vice President and Head of International Equities* and Jeff Bianchi, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

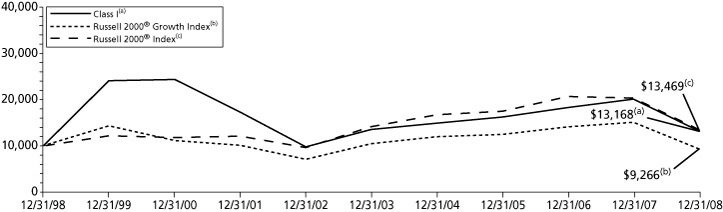

Performance: For the year ended December 31, 2008, the Portfolio's Class I shares provided a total return of (37.62)% compared to the Russell Midcap® Growth Index(1) and the Russell Midcap® Index(2), which returned (44.32)% and (41.46)%, respectively, for the same period.

Portfolio Specifics: The Russell Midcap® Growth Index declined steeply during the twelve months ended December 31, 2008. Needless to say, all economic sectors within the index experienced significant double-digit declines. The main causes were a global financial crisis unlike any other since the Great Depression and a subsequent global economic slowdown that has brought recessionary conditions to several regions of the world. In addition to plummeting equity market valuations, housing prices, oil and a broad range of other commodities fell precipitously, creating fears of deflation.

Given the weak pricing backdrop, coupled with demand destruction, the energy sector experienced the sharpest decline of 56%. The equipment and services and oil gas and consumable fuels sub-sectors were down roughly equivalent amounts. The utilities sector slid 53%, led lower by independent power producers. The financials sector was the third worst performer with a decline of 49%. The consumer finance industry was particularly weak.

Not surprisingly, defensive sectors had relatively better results. The consumer staples sector had the smallest decline, 29%, partially due to a moderate sell-off in the food products industry. The healthcare sector was off 33%, with biotechnology stocks being nearly flat. A 40% decline in the telecommunication services sector was still better than the performance of the Russell Midcap® Growth Index.

The Portfolio's excess return relative to the benchmark was entirely attributable to stock selection, which was especially strong in the information technology, healthcare, consumer staples, industrials, materials and financials sectors.

Millennium Pharmaceuticals, Inc. made a significant contribution to the relative return. During the second quarter, the stock was acquired by Takeda Pharmaceutical Co., Ltd. The Portfolio benefited from lower than benchmark exposure to Intuitive Surgical, Inc. The biggest net contribution to return was derived from not owning Electronic Arts, Inc.

Two energy stocks, Key Energy Services, Inc. ("Key Energy") and National Oilwell Varco, Inc. ("National Oilwell") hurt performance the most. Key Energy's 3rd Quarter 2008 earnings were disappointing due to hurricanes in the Gulf Coast. Also, because of market uncertainties, the company retracted 4th Quarter 2008 guidance and refused to confirm prior full-year guidance. Shares of National Oilwell were affected by weak commodity prices, resulting in fears of reduced drilling. Shares of SPX Corp., a diversified manufacturer, were impacted by concerns regarding lower power consumption and the credit crisis.

Current Strategy and Outlook: Although credit spreads have recently narrowed as governments have injected funds into banks and slashed interest rates, credit availability and counterparty risk aversion remain concerns. Meanwhile, the real economy seems likely to incur more damage than previously indicated. We believe stock market volatility will remain elevated. We believe stock picking will prove important in 2009. Many good companies with relatively strong business momentum were treated indifferently in the 2008 market. In addition, market sentiment seems to have been buoyed by the late November $800 billion lending program and massive stimulus plans of the incoming Obama administration.

Narrowing credit spreads could eventually lead to increased credit availability and improvement in perceived counterparty risk. We continuously seek companies that we believe exhibit strong business momentum and market recognition at appropriate valuation levels.

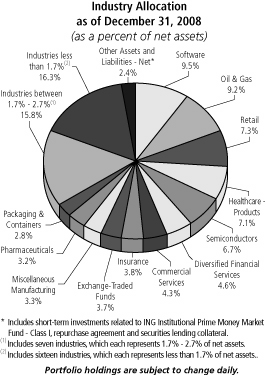

Top Ten Holdings*

as of December 31, 2008

(as a percent of net assets)

| iShares Russell Midcap Growth Index Fund | 3.7 | % | |||||

| St. Jude Medical, Inc. | 3.2 | % | |||||

| Invesco Ltd. | 2.3 | % | |||||

| Ecolab, Inc. | 2.0 | % | |||||

| Intuit, Inc. | 2.0 | % | |||||

| Fiserv, Inc. | 1.9 | % | |||||

| ITT Corp. | 1.9 | % | |||||

| BMC Software, Inc. | 1.9 | % | |||||

| Murphy Oil Corp. | 1.8 | % | |||||

| Ross Stores, Inc. | 1.8 | % | |||||

* Excludes short-term investments related to ING Institutional Prime Money Market Fund — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

* Effective August 13, 2008, Mr. Landesman replaced Richard Welsh as a portfolio manager to the Portfolio.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

4

PORTFOLIO MANAGERS' REPORT

ING VP MIDCAP OPPORTUNITIES PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2008 | |||||||||||||||||||||||

| 1 Year | 5 Year | Since Inception of Class ADV December 29, 2006 | Since Inception of Class I May 5, 2000 | Since Inception of Class S May 7, 2001 | |||||||||||||||||||

| Class ADV | (38.04 | )% | — | (11.95 | )% | — | — | ||||||||||||||||

| Class I | (37.62 | )% | 0.80 | % | — | (5.00 | )% | — | |||||||||||||||

| Class S | (37.72 | )% | 0.58 | % | — | — | (1.57 | )% | |||||||||||||||

| Russell Midcap® Growth Index(1) | (44.32 | )% | (2.33 | )% | (21.24 | )%(3) | (5.85 | )%(4) | (2.23 | )%(5) | |||||||||||||

| Russell Midcap® Index(2) | (41.46 | )% | (0.71 | )% | (21.38 | )%(3) | 1.14 | %(4) | 1.25 | %(5) | |||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP MidCap Opportunities Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolios, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Total returns reflect that the Investment Adviser may have waived or recouped fees and expenses otherwise payable by the Portfolio.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contract, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Russell Midcap® Growth Index is an unmanaged index that measures the performance of those companies included in the Russell Midcap® Index with relatively higher price-to-book ratios and higher forecasted growth values.

(2) The Russell Midcap® Index is an unmanaged index that measures the performance of the 800 smallest companies in the Russell 1000® Index, which represent approximately 26% of the total market capitalization of the Russell 1000® Index.

(3) Since inception performance for the indices is shown from January 1, 2007.

(4) Since inception performance for the indices is shown from May 1, 2000.

(5) Since inception performance for the indices is shown from May 1, 2001.

5

ING VP SMALLCAP OPPORTUNITIES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING VP SmallCap Opportunities Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Steve Salopek and James Hasso*, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

Performance: For the year ended December 31, 2008, the Portfolio's Class I shares provided a total return of (34.48)%, compared to the Russell 2000® Growth Index(1) and the Russell 2000® Index(2), which returned (38.54)% and (33.79)%, respectively, for the same period.

Portfolio Specifics: Despite the recent rally of over 28% for the Russell 2000® Growth Index, it was down more than 38% for the year. This past year was the worst since 1973 for small-cap stocks. There were few places to hide and returns were negative across all sectors. Small-cap growth held up well relative to large-cap growth, underperforming by only 0.10% (as measured by the Russell 2000® Growth and Russell 1000® Growth, respectively). Energy was down almost 50% for the year due to the significant decline in the price of oil and the fact that the current economic environment is unfavorable for energy.

Stock selection within industrials, consumer discretionary, technology and utilities benefited the Portfolio during the period. Notable outperformance versus the benchmark within industrials was due to strong stock selection within commercial services and supplies, as well as our slight underweight in electrical equipment. Consumer discretionary benefited most from stock selection within hotels, restaurants and leisure.

Stock selection coupled with our slight underweight positions within energy and healthcare detracted most from performance. Within energy, a modest overweight in energy equipment and services negatively impacted performance. Underperformance in healthcare is attributable to our underweight in biotechnology as well as stock selection within the industry. Stock selection within pharmaceuticals also detracted from results.

Greatbatch, Inc. ("Greatbatch") and Capella Education Co. ("Capella Education") contributed significantly to performance over the period. Capella Education, an online post-secondary education company, outperformed due to the less cyclical nature of the education business, as the number of people going back to school increases during an economic downturn. Also, the company has had good execution, seen an increase in the student body and margins have improved.

Greatbatch is a leading developer and manufacturer of critical components used in medical devices for the cardiac rhythm management, neurostimulation, vascular and interventional radiology markets. The company executed well on its acquisition strategy, which helped it diversify from its Cardiac Rhythm Management franchise and provide greater stability/visibility to its operating earnings. Also, the street was initially skeptical of the company's ability to diversify and execute on the diversification strategy. As each quarter passed, the company's execution proved to be flawless and the firm gained substantial momentum as evidenced by increasing earnings and expanded margins.

Abritron, Inc. ("Arbitron") and Xyratex Ltd. ("Xyratex") were two of the largest detractors from performance over the period. Arbitron, which measures the listening audience for radio and provides this data to both radio stations and advertisers, recently lost market share to a competitor. We continue to hold this name, as the company remains the market leader, expectations have been reset and we believe the valuation is reasonable. Xyratex designs and manufactures technology that supports storage and data communication networks. The company provided guidance that revenue and earnings would be significantly below expectations for its November quarter, due to weakness in customer orders. We continue to hold the stock mainly due to valuation, as nearly 50% of its market cap is in cash.

Current Strategy and Outlook: We continue to focus on companies with strong balance sheets and cash flow generation capabilities. We are conscious of the difficulties in the current economic environment. We believe, however, that the economy will begin to improve in 2009 due to the massive amount of monetary stimulus being pumped into the system globally.

Accordingly, we have begun to increase our exposure to more early cyclical companies. Within financials, we continue to mitigate risk through diversification and are invested across the financial sector, in banks, diversified financials, insurance companies and real estate investment trusts ("REITS"). The banks that we own are typically over-capitalized and have higher reserves than industry averages. We continue to take advantage of the volatility in the market to acquire attractively valued companies whose share prices we believe are not trading on fundamentals.

Top Ten Holdings*

as of December 31, 2008

(as a percent of net assets)

| iShares Russell 2000 Growth Index Fund | 2.0 | % | |||||

| Waste Connections, Inc. | 1.3 | % | |||||

| Solera Holdings, Inc. | 1.3 | % | |||||

| Parametric Technology Corp. | 1.2 | % | |||||

| Chattem, Inc. | 1.2 | % | |||||

| WMS Industries, Inc. | 1.1 | % | |||||

| Bio-Rad Laboratories, Inc. | 1.1 | % | |||||

| Watson Wyatt Worldwide, Inc. | 1.1 | % | |||||

| Interwoven, Inc. | 1.1 | % | |||||

| Varian, Inc. | 1.1 | % | |||||

* Excludes short-term investments related to ING Institutional Prime Money Market Fund — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

* Mr. Hasso was added as portfolio manager to the Portfolio effective October 1, 2008.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

6

PORTFOLIO MANAGERS' REPORT

ING VP SMALLCAP OPPORTUNITIES PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2008 | |||||||||||||||||||||||

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV November 20, 2008 | Since Inception of Class S May 3, 2001 | |||||||||||||||||||

| Class ADV | — | — | — | 25.03 | % | — | |||||||||||||||||

| Class I | (34.48 | )% | (0.49 | )% | 2.79 | % | — | — | |||||||||||||||

| Class S | (34.59 | )% | (0.69 | )% | — | — | (5.51 | )% | |||||||||||||||

| Russell 2000® Growth Index(1) | (38.54 | )% | (2.35 | )% | (0.76 | )% | 5.42 | %(3) | (1.70 | )%(4) | |||||||||||||

| Russell 2000® Index(2) | (33.79 | )% | (0.93 | )% | 3.02 | % | 5.80 | %(3) | 1.68 | %(4) | |||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP SmallCap Opportunities Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolios, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contracts, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The Russell 2000® Growth Index is an unmanaged index that measures the performance of securities of smaller U.S. companies with greater-than-average growth orientation.

(2) The Russell 2000® Index is an unmanaged index that measures the performance of securities of small U.S. companies.

(3) Since inception performance for the indices is shown from December 1, 2008.

(4) Since inception performance for the indices is shown from May 1, 2001.

7

ING VP INTERNATIONAL VALUE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING VP International Value Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Philip A. Schwartz, CFA, Senior Vice President and Director of International Investment Strategy of ING Investment Management Co. — the Sub- Adviser.

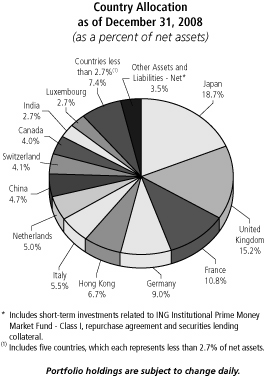

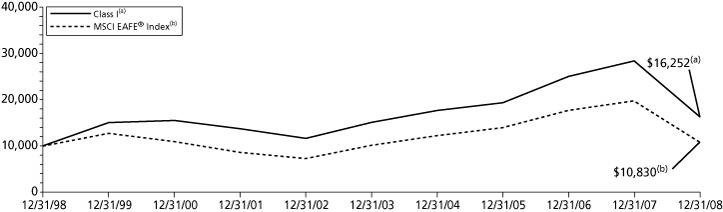

Performance: For the year ended December 31, 2008, the Portfolio's Class I shares provided a total return of (42.76)% compared to the Morgan Stanley Capital International — Europe, Australasia and Far East ("MSCI EAFE®") Index(1), which returned (43.38)% for the same period.

Portfolio Specifics: The year 2008 was underscored by a litany of issues, including an escalating financial crisis, rampant inflation, a possible war between Iran and Israel, a global recession, collapsing of storied companies, unparalleled levels of market volatility, threat of deflation and a credit crunch to boot. Certainly the times have tested the fortitude of investors worldwide, as trillions of dollars have been wiped out. However, one must not forget that chaos breeds opportunity. With massive monetary and fiscal actions taken around the world, we are optimistic about what the future may have in store.

Surprising though it may seem, selection within the financials sector bolstered the Portfolio's 2008 relative performance. Additionally, selection within the industrials sector added value. Regionally, our exposure to non-benchmark North America (Canada specifically) proved effective. The positive performance was offset most by an underweight and selection in consumer staples. Selection within the relatively weak materials sector coupled with selection in consumer discretionary detracted from results. From a regional standpoint our selection within Europe detracted.

Siemens AG, a German industrial corporation, had a sharp rally from its November 20 lows in reaction to President-elect Obama's plans to build out infrastructure. The position was initiated in the fourth quarter of 2008. ArcelorMittal, an Indian steel giant, was initiated in October (after the massive sell-off that commenced in June). The stock saw a bit of appreciation in the fourth quarter amidst a cut in production among steel producers. Nippon Telegraph and Telephone Corp. also contributed to results.

Swiss mining giant Xstrata PLC saw shares fall precipitously during the second half of the year amidst sliding commodity prices. Peugeot S.A., a French automaker was initiated in June; however, the stock followed a downward trend as weakened consumer spending and general malaise impacted the automotive industry.

Current Strategy and Outlook: We believe that we have been capitalizing upon opportunities that the downturn has provided. Despite abating inflationary concerns, risks to the upside remain, as investors gauge the level of systemic risk that is inherent in the global economy. On the upside, however, central banks have responded in a coordinated fashion, potentially mitigating a severe downturn. We will seek further opportunities across a wide array of markets.

Top Ten Holdings*

as of December 31, 2008

(as a percent of net assets)

| Siemens AG | 3.6 | % | |||||

| Tokyo Electron Ltd. | 3.1 | % | |||||

| Nippon Telegraph & Telephone Corp. | 3.0 | % | |||||

| E.ON AG | 3.0 | % | |||||

| Swire Pacific Ltd. | 3.0 | % | |||||

| Huaneng Power International, Inc. | 2.9 | % | |||||

| Total SA | 2.9 | % | |||||

| Canon, Inc. ADR | 2.9 | % | |||||

| ENI S.p.A. | 2.8 | % | |||||

| Terna S.p.A | 2.7 | % | |||||

* Excludes short-term investments related to securities lending collateral.

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

8

PORTFOLIO MANAGERS' REPORT

ING VP INTERNATIONAL VALUE PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2008 | |||||||||||||||||||||||

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV December 29, 2006 | Since Inception of Class S March 19, 2002 | |||||||||||||||||||

| Class ADV | (43.11 | )% | — | — | (19.88 | )% | — | ||||||||||||||||

| Class I | (42.76 | )% | 1.55 | % | 4.97 | % | — | — | |||||||||||||||

| Class S | (42.31 | )% | 1.41 | % | — | — | 1.78 | % | |||||||||||||||

| MSCI EAFE® Index(1) | (43.38 | )% | 1.66 | % | 0.80 | % | (20.66 | )%(2) | 3.46 | %(3) | |||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING VP International Value Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. For variable annuity contracts, please call (800) 992-0180 to get performance through the most recent month end. For variable universal life policies, please log on to www.ing.com/us to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The MSCI EAFE® Index is an unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East. It includes the reinvestment of dividends net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing.

(2) Since inception performance for the index is shown from January 1, 2007.

(3) Since inception performance for the index is shown from April 1, 2002.

Prior to July 1, 2002, the portfolio was sub-advised by a different sub-adviser.

9

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Portfolio, you incur two types of costs: (1) transaction costs, including redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Portfolio expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2008 to December 31, 2008. The Portfolios' expenses are shown without the imposition of any charges which are, or may be, imposed under your annuity contract. Expenses would have been higher if such charges were included.

Actual Expenses

The first section of the table shown, "Actual Portfolio Return," provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, "Hypothetical (5% return before expenses)," provides information about hypothetical account values and hypothetical expenses based on the Portfolio's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different mutual funds. In addition, if these transactional costs were included, your costs would have been higher.

| Actual Portfolio Return | Hypothetical (5% return before expenses) | ||||||||||||||||||||||||||||||||||

| ING VP MidCap Opportunities Portfolio | Beginning Account Value July 1, 2008 | Ending Account Value December 31, 2008 | Annualized Expense Ratio | Expenses Paid During the Period Ended December 31, 2008* | Beginning Account Value July 1, 2008 | Ending Account Value December 31, 2008 | Annualized Expense Ratio | Expenses Paid During the Period Ended December 31, 2008* | |||||||||||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 662.50 | 1.20 | % | $ | 5.01 | $ | 1,000.00 | $ | 1,019.10 | 1.20 | % | $ | 6.09 | |||||||||||||||||||

| Class I | 1,000.00 | 664.60 | 0.70 | 2.93 | 1,000.00 | 1,021.62 | 0.70 | 3.56 | |||||||||||||||||||||||||||

| Class S | 1,000.00 | 664.20 | 0.90 | 3.76 | 1,000.00 | 1,020.61 | 0.90 | 4.57 | |||||||||||||||||||||||||||

| ING VP SmallCap Opportunities Portfolio | |||||||||||||||||||||||||||||||||||

| Class ADV(1) | $ | 1,000.00 | $ | 1,250.30 | 1.40 | % | $ | 1.81 | $ | 1,000.00 | $ | 1,018.10 | 1.40 | % | $ | 7.10 | |||||||||||||||||||

| Class I | 1,000.00 | 690.00 | 0.90 | 3.82 | 1,000.00 | 1,020.61 | 0.90 | 4.57 | |||||||||||||||||||||||||||

| Class S | 1,000.00 | 689.70 | 1.10 | 4.67 | 1,000.00 | 1,019.61 | 1.10 | 5.58 | |||||||||||||||||||||||||||

| ING VP International Value Portfolio | |||||||||||||||||||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 646.60 | 1.50 | % | $ | 6.21 | $ | 1,000.00 | $ | 1,017.60 | 1.50 | % | $ | 7.61 | |||||||||||||||||||

| Class I | 1,000.00 | 648.20 | 1.00 | 4.14 | 1,000.00 | 1,020.11 | 1.00 | 5.08 | |||||||||||||||||||||||||||

| Class S | 1,000.00 | 652.70 | 1.20 | 4.99 | 1,000.00 | 1,019.10 | 1.20 | 6.09 | |||||||||||||||||||||||||||

* Expenses are equal to each Portfolio's respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/366 to reflect the most recent fiscal half-year.

(1) Commencement of operations was November 20, 2008. Expenses paid for the Actual Portfolio Return reflect the 42 day period ended December 31, 2008.

10

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Shareholders and Board of Trustees

ING Variable Products Trust

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of ING VP MidCap Opportunities Portfolio, ING VP SmallCap Opportunities Portfolio, and ING VP International Value Portfolio, each a series of ING Variable Products Trust, as of December 31, 2008, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2008, by correspondence with the custodian and brokers, or by other appropriate auditing procedures when replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the aforementioned portfolios as of December 31, 2008, and the results of their operations, the changes in their net assets, and the financial highlights for the periods specified in the first paragraph above, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

February 24, 2009

11

STATEMENTS OF ASSETS AND LIABILITIES AS OF DECEMBER 31, 2008

| ING VP MidCap Opportunities Portfolio | ING VP SmallCap Opportunities Portfolio | ING VP International Value Portfolio | |||||||||||||

| ASSETS: | |||||||||||||||

| Investments in securities at value+* | $ | 434,437,456 | $ | 107,873,662 | $ | 337,528,581 | |||||||||

| Short-term investments** | 12,116,164 | 11,999,372 | 15,260,091 | ||||||||||||

| Short-term investments in affiliates**** | 8,533,000 | 2,858,000 | 6,893,000 | ||||||||||||

| Short-term investments at amortized cost | 2,461,000 | — | 2,386,000 | ||||||||||||

| Cash | 7 | 379 | 29,063 | ||||||||||||

| Foreign currencies at value*** | 50,482 | — | 1,254,944 | ||||||||||||

| Receivables: | |||||||||||||||

| Investment securities sold | 7,025,212 | 1,163,239 | 4,480,209 | ||||||||||||

| Fund shares sold | 1,317,215 | 161,470 | 306,938 | ||||||||||||

| Dividends and interest | 310,040 | 58,269 | 572,296 | ||||||||||||

| Prepaid expenses | 1,981 | 688 | 2,072 | ||||||||||||

| Reimbursement due from manager | 155,940 | 5,911 | 47,760 | ||||||||||||

| Total assets | 466,408,497 | 124,120,990 | 368,760,954 | ||||||||||||

| LIABILITIES: | |||||||||||||||

| Payable for investment securities purchased | 8,183,632 | 1,139,075 | 2,667,684 | ||||||||||||

| Payable for fund shares redeemed | 65,728 | 52,578 | 503,249 | ||||||||||||

| Payable upon receipt of securities loaned | 12,494,193 | 12,133,632 | 15,329,004 | ||||||||||||

| Payable to affiliates | 346,830 | 83,640 | 269,976 | ||||||||||||

| Payable for directors fees | 5,412 | 6,590 | 5,904 | ||||||||||||

| Other accrued expenses and liabilities | 63,100 | 62,751 | 180,826 | ||||||||||||

| Total liabilities | 21,158,895 | 13,478,266 | 18,956,643 | ||||||||||||

| NET ASSETS | $ | 445,249,602 | $ | 110,642,724 | $ | 349,804,311 | |||||||||

| NET ASSETS WERE COMPRISED OF: | |||||||||||||||

| Paid-in capital | $ | 1,503,561,856 | $ | 163,109,709 | $ | 599,908,672 | |||||||||

| Undistributed net investment income | 140,380 | 4,255 | 357,245 | ||||||||||||

| Accumulated net realized loss on investments and foreign currency related transactions | (972,977,101 | ) | (19,363,145 | ) | (175,921,459 | ) | |||||||||

| Net unrealized depreciation on investments and foreign currency related transactions | (85,475,533 | ) | (33,108,095 | ) | (74,540,147 | ) | |||||||||

| NET ASSETS | $ | 445,249,602 | $ | 110,642,724 | $ | 349,804,311 | |||||||||

| + Including securities loaned at value | $ | 12,142,621 | $ | 12,088,921 | $ | 14,727,224 | |||||||||

| * Cost of investments in securities | $ | 519,535,175 | $ | 140,847,497 | $ | 411,986,324 | |||||||||

| ** Cost of short-term investments | $ | 12,494,193 | $ | 12,133,632 | $ | 15,329,004 | |||||||||

| *** Cost of foreign currencies | $ | 50,267 | $ | — | $ | 1,259,415 | |||||||||

| **** Cost of short-term investments in affiliates | $ | 8,533,000 | $ | 2,858,000 | $ | 6,893,000 | |||||||||

| Class ADV: | |||||||||||||||

| Net Assets | $ | 785 | $ | 3,751 | $ | 452 | |||||||||

| Shares authorized | unlimited | unlimited | unlimited | ||||||||||||

| Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | |||||||||

| Shares outstanding | 124 | 312 | 67 | ||||||||||||

| Net asset value and redemption price per share | $ | 6.32 | $ | 12.04 | $ | 6.74 | |||||||||

| Class I: | |||||||||||||||

| Net Assets | $ | 195,295,457 | $ | 56,475,894 | $ | 340,021,877 | |||||||||

| Shares authorized | unlimited | unlimited | unlimited | ||||||||||||

| Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | |||||||||

| Shares outstanding | 30,506,721 | 4,602,618 | 50,205,326 | ||||||||||||

| Net asset value and redemption price per share | $ | 6.40 | $ | 12.27 | $ | 6.77 | |||||||||

| Class S: | |||||||||||||||

| Net Assets | $ | 249,953,360 | $ | 54,163,079 | $ | 9,781,982 | |||||||||

| Shares authorized | unlimited | unlimited | unlimited | ||||||||||||

| Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | |||||||||

| Shares outstanding | 39,761,459 | 4,495,328 | 1,411,595 | ||||||||||||

| Net asset value and redemption price per share | $ | 6.29 | $ | 12.05 | $ | 6.93 | |||||||||

See Accompanying Notes to Financial Statements

12

STATEMENTS OF OPERATIONS FOR THE YEAR ENDED DECEMBER 31, 2008

| ING VP MidCap Opportunities Portfolio | ING VP SmallCap Opportunities Portfolio | ING VP International Value Portfolio | |||||||||||||

| INVESTMENT INCOME: | |||||||||||||||

| Dividends, net of foreign taxes withheld*(1) | $ | 3,411,441 | $ | 1,025,846 | $ | 15,343,596 | |||||||||

| Interest | 28,769 | 13,002 | 960,934 | ||||||||||||

| Securities lending income, net | 229,176 | 293,331 | 716,509 | ||||||||||||

| Total investment income | 3,669,386 | 1,332,179 | 17,021,039 | ||||||||||||

| EXPENSES: | |||||||||||||||

| Investment management fees | 3,144,773 | 1,166,075 | 4,026,991 | ||||||||||||

| Distribution and service fees: | |||||||||||||||

| Class ADV | 8 | 2 | 4 | ||||||||||||

| Class S | 593,826 | 202,898 | 31,862 | ||||||||||||

| Transfer agent fees | 1,216 | 758 | 1,122 | ||||||||||||

| Administrative service fees | 433,403 | 155,475 | 473,758 | ||||||||||||

| Shareholder reporting expense | 99,355 | 43,225 | 143,227 | ||||||||||||

| Registration fees | — | — | 398 | ||||||||||||

| Professional fees | 50,036 | 31,541 | 102,290 | ||||||||||||

| Custody and accounting expense | 48,910 | 30,076 | 216,722 | ||||||||||||

| Directors fees | 16,603 | 7,110 | 15,084 | ||||||||||||

| Miscellaneous expense | 11,812 | 8,408 | 20,842 | ||||||||||||

| Interest expense | 333 | 389 | 3,342 | ||||||||||||

| Total expenses | 4,400,275 | 1,645,957 | 5,035,642 | ||||||||||||

| Net waived and reimbursed fees | (905,412 | ) | (79,444 | ) | (261,553 | ) | |||||||||

| Net expenses | 3,494,863 | 1,566,513 | 4,774,089 | ||||||||||||

| Net investment income (loss) | 174,523 | (234,334 | ) | 12,246,950 | |||||||||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY RELATED TRANSACTIONS: | |||||||||||||||

| Net realized gain (loss) on: | |||||||||||||||

| Investments | (123,758,980 | ) | (18,380,769 | ) | (173,209,791 | ) | |||||||||

| Foreign currency related transactions | — | — | 1,700,435 | ||||||||||||

| Net realized loss on investments and foreign currency related transactions | (123,758,980 | ) | (18,380,769 | ) | (171,509,356 | ) | |||||||||

| Net change in unrealized appreciation or depreciation on: | |||||||||||||||

| Investments | (109,710,909 | ) | (44,168,656 | ) | (97,594,787 | ) | |||||||||

| Foreign currency related transactions | 305 | — | (10,544 | ) | |||||||||||

| Net change in unrealized appreciation or depreciation on investments and foreign currency related transactions | (109,710,604 | ) | (44,168,656 | ) | (97,605,331 | ) | |||||||||

| Net realized and unrealized loss on investments and foreign currency related transactions | (233,469,584 | ) | (62,549,425 | ) | (269,114,687 | ) | |||||||||

| Decrease in net assets resulting from operations | $ | (233,295,061 | ) | $ | (62,783,759 | ) | $ | (256,867,737 | ) | ||||||

| * Foreign taxes withheld | $ | 7,204 | $ | 2,172 | $ | 1,807,174 | |||||||||

| (1) Dividends from affiliates | $ | 286,817 | $ | 81,838 | $ | 532,775 | |||||||||

See Accompanying Notes to Financial Statements

13

STATEMENTS OF CHANGES IN NET ASSETS

| ING VP MidCap Opportunities Portfolio | ING VP SmallCap Opportunities Portfolio | ||||||||||||||||||

| Year Ended December 31, 2008 | Year Ended December 31, 2007 | Year Ended December 31, 2008 | Year Ended December 31, 2007 | ||||||||||||||||

| FROM OPERATIONS: | |||||||||||||||||||

| Net investment income (loss) | $ | 174,523 | $ | (481,868 | ) | $ | (234,334 | ) | $ | (110,075 | ) | ||||||||

| Net realized gain (loss) on investments and foreign currency related transactions | (123,758,980 | ) | 23,754,020 | (18,380,769 | ) | 29,418,968 | |||||||||||||

| Net change in unrealized appreciation or depreciation on investments and foreign currency related transactions | (109,710,604 | ) | 540,832 | (44,168,656 | ) | (9,571,655 | ) | ||||||||||||

| Increase (decrease) in net assets resulting from operations | (233,295,061 | ) | 23,812,984 | (62,783,759 | ) | 19,737,238 | |||||||||||||

| FROM DISTRIBUTIONS TO SHAREHOLDERS: | |||||||||||||||||||

| Net realized gains: | |||||||||||||||||||

| Class I | — | — | (12,294,247 | ) | — | ||||||||||||||

| Class S | — | — | (13,213,982 | ) | — | ||||||||||||||

| Total distributions | — | — | (25,508,229 | ) | — | ||||||||||||||

| FROM CAPITAL SHARE TRANSACTIONS: | |||||||||||||||||||

| Net proceeds from sale of shares | 243,250,863 | 22,816,062 | 22,773,411 | 15,326,085 | |||||||||||||||

| Proceeds from shares issued in merger (Note 12) | 376,785,676 | — | — | — | |||||||||||||||

| Payments by affiliates (Note 16) | 15,465 | — | 110,798 | — | |||||||||||||||

| Reinvestment of distributions | — | — | 25,508,229 | — | |||||||||||||||

| 620,052,004 | 22,816,062 | 48,392,438 | 15,326,085 | ||||||||||||||||

| Cost of shares redeemed | (66,458,733 | ) | (26,642,565 | ) | (38,364,302 | ) | (49,892,455 | ) | |||||||||||

| Net increase (decrease) in net assets resulting from capital share transactions | 553,593,271 | (3,826,503 | ) | 10,028,136 | (34,566,370 | ) | |||||||||||||

| Net increase (decrease) in net assets | 320,298,210 | 19,986,481 | (78,263,852 | ) | (14,829,132 | ) | |||||||||||||

| NET ASSETS: | |||||||||||||||||||

| Beginning of year | 124,951,392 | 104,964,911 | 188,906,576 | 203,735,708 | |||||||||||||||

| End of year | $ | 445,249,602 | $ | 124,951,392 | $ | 110,642,724 | $ | 188,906,576 | |||||||||||

| Undistributed net investment income at end of year | $ | 140,380 | $ | — | $ | 4,255 | $ | 10,722 | |||||||||||

See Accompanying Notes to Financial Statements

14

STATEMENTS OF CHANGES IN NET ASSETS

| ING VP International Value Portfolio | |||||||||||

| Year Ended December 31, 2008 | Year Ended December 31, 2007 | ||||||||||

| FROM OPERATIONS: | |||||||||||

| Net investment income | $ | 12,246,950 | $ | 9,089,975 | |||||||

| Net realized gain (loss) on investments and foreign currency related transactions | (171,509,356 | ) | 76,290,163 | ||||||||

| Net change in unrealized appreciation or depreciation on investments and foreign currency related transactions | (97,605,331 | ) | (22,053,258 | ) | |||||||

| Increase (decrease) in net assets resulting from operations | (256,867,737 | ) | 63,326,880 | ||||||||

| FROM DISTRIBUTIONS TO SHAREHOLDERS: | |||||||||||

| Net investment income: | |||||||||||

| Class ADV | (17 | ) | (13 | ) | |||||||

| Class I | (13,548,576 | ) | (8,825,087 | ) | |||||||

| Class S | (331,802 | ) | (162,420 | ) | |||||||

| Net realized gains: | |||||||||||

| Class ADV | (120 | ) | (178 | ) | |||||||

| Class I | (76,788,879 | ) | (83,156,172 | ) | |||||||

| Class S | (2,020,745 | ) | (1,777,328 | ) | |||||||

| Total distributions | (92,690,139 | ) | (93,921,198 | ) | |||||||

| FROM CAPITAL SHARE TRANSACTIONS: | |||||||||||

| Net proceeds from sale of shares | 154,981,343 | 67,884,934 | |||||||||

| Payments by affiliates (Note 16) | 729,720 | — | |||||||||

| Reinvestment of distributions | 92,690,003 | 93,921,002 | |||||||||

| 248,401,066 | 161,805,936 | ||||||||||

| Cost of shares redeemed | (78,590,732 | ) | (69,048,165 | ) | |||||||

| Net increase in net assets resulting from capital share transactions | 169,810,334 | 92,757,771 | |||||||||

| Net increase (decrease) in net assets | (179,747,542 | ) | 62,163,453 | ||||||||

| NET ASSETS: | |||||||||||

| Beginning of year | 529,551,853 | 467,388,400 | |||||||||

| End of year | $ | 349,804,311 | $ | 529,551,853 | |||||||

| Undistributed net investment income at end of year | $ | 357,245 | $ | 152,688 | |||||||

See Accompanying Notes to Financial Statements

15

FINANCIAL HIGHLIGHTS

Selected data for a share of beneficial interest outstanding throughout each year or period.

| Income (loss) from investment operations | Less distributions | ||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) | Total from investment operations | From net investment income | From net realized gains | Total distributions | Payments by affiliates (note 16) | Net asset value, end of year or period | Total Return(1) | ||||||||||||||||||||||||||||||||||

| Year or period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | |||||||||||||||||||||||||||||||||

| ING VP MidCap Opportunities Portfolio | |||||||||||||||||||||||||||||||||||||||||||

| Class ADV | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 10.20 | (0.03 | )• | (3.85 | ) | (3.88 | ) | — | — | — | 0.00 | * | 6.32 | (38.04 | )(a) | ||||||||||||||||||||||||||||

| 12-31-07 | 8.16 | (0.07 | ) | 2.11 | 2.04 | — | — | — | — | 10.20 | 25.00 | ||||||||||||||||||||||||||||||||

| 12-29-06(4)-12-31-06 | 8.16 | *† | (0.00 | )* | — | (0.00 | )* | — | — | — | — | 8.16 | (b) | — | |||||||||||||||||||||||||||||

| Class I | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 10.26 | 0.01 | (3.87 | ) | (3.86 | ) | — | — | — | 0.00 | * | 6.40 | (37.62 | )(a) | |||||||||||||||||||||||||||||

| 12-31-07 | 8.16 | (0.03 | ) | 2.13 | 2.10 | — | — | — | — | 10.26 | 25.74 | ||||||||||||||||||||||||||||||||

| 12-31-06 | 7.57 | (0.03 | ) | 0.62 | 0.59 | — | — | — | — | 8.16 | 7.79 | ||||||||||||||||||||||||||||||||

| 12-31-05 | 6.86 | (0.02 | ) | 0.73 | 0.71 | — | — | — | ��� | 7.57 | 10.35 | ||||||||||||||||||||||||||||||||

| 12-31-04 | 6.15 | (0.02 | ) | 0.73 | 0.71 | — | — | — | — | 6.86 | 11.54 | ||||||||||||||||||||||||||||||||

| Class S | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 10.10 | (0.00 | )* | (3.81 | ) | (3.81 | ) | — | — | — | 0.00 | * | 6.29 | (37.72 | )(a) | ||||||||||||||||||||||||||||

| 12-31-07 | 8.05 | (0.06 | ) | 2.11 | 2.05 | — | — | — | — | 10.10 | 25.47 | ||||||||||||||||||||||||||||||||

| 12-31-06 | 7.48 | (0.05 | ) | 0.62 | 0.57 | — | — | — | — | 8.05 | 7.62 | ||||||||||||||||||||||||||||||||

| 12-31-05 | 6.79 | (0.04 | ) | 0.73 | 0.69 | — | — | — | — | 7.48 | 10.16 | ||||||||||||||||||||||||||||||||

| 12-31-04 | 6.11 | (0.03 | ) | 0.71 | 0.68 | — | — | — | — | 6.79 | 11.13 | ||||||||||||||||||||||||||||||||

| ING VP SmallCap Opportunities Portfolio | |||||||||||||||||||||||||||||||||||||||||||

| Class ADV | |||||||||||||||||||||||||||||||||||||||||||

| 11-20-08(4)-12-31-08 | 9.63 | (0.01 | ) | 2.41 | 2.40 | — | — | — | 0.01 | 12.04 | 25.03 | (c) | |||||||||||||||||||||||||||||||

| Class I | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 21.98 | (0.01 | ) | (6.61 | ) | (6.62 | ) | — | 3.10 | 3.10 | 0.01 | 12.27 | (34.48 | )(c) | |||||||||||||||||||||||||||||

| 12-31-07 | 19.97 | 0.01 | 2.00 | 2.01 | — | — | — | — | 21.98 | 10.07 | |||||||||||||||||||||||||||||||||

| 12-31-06 | 17.74 | (0.07 | ) | 2.30 | 2.23 | — | — | — | — | 19.97 | 12.57 | ||||||||||||||||||||||||||||||||

| 12-31-05 | 16.26 | (0.08 | ) | 1.56 | 1.48 | — | — | — | — | 17.74 | 9.10 | ||||||||||||||||||||||||||||||||

| 12-31-04 | 14.76 | (0.09 | ) | 1.59 | 1.50 | — | — | — | — | 16.26 | 10.16 | ||||||||||||||||||||||||||||||||

| Class S | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 21.68 | (0.05 | ) | (6.49 | ) | (6.54 | ) | — | 3.10 | 3.10 | 0.01 | 12.05 | (34.59 | )(c) | |||||||||||||||||||||||||||||

| 12-31-07 | 19.74 | (0.03 | ) | 1.97 | 1.94 | — | — | — | — | 21.68 | 9.83 | ||||||||||||||||||||||||||||||||

| 12-31-06 | 17.57 | (0.11 | ) | 2.28 | 2.17 | — | — | — | — | 19.74 | 12.35 | ||||||||||||||||||||||||||||||||

| 12-31-05 | 16.14 | (0.12 | ) | 1.55 | 1.43 | — | — | — | — | 17.57 | 8.86 | ||||||||||||||||||||||||||||||||

| 12-31-04 | 14.68 | (0.11 | ) | 1.57 | 1.46 | — | — | — | — | 16.14 | 9.95 | ||||||||||||||||||||||||||||||||

| Ratios to average net assets | Supplemental data | ||||||||||||||||||||||||||

| Expenses before reductions/additions(2)(3) | Expenses net of fee waivers and/or recoupments, if any(2)(3) | Expenses net of all reductions/additions(2)(3) | Net investment income (loss)(2)(3) | Net assets, end of year or period | Portfolio turnover rate | ||||||||||||||||||||||

| Year or period ended | (%) | (%) | (%) | (%) | ($000's) | (%) | |||||||||||||||||||||

| ING VP MidCap Opportunities Portfolio | |||||||||||||||||||||||||||

| Class ADV | |||||||||||||||||||||||||||

| 12-31-08 | 1.38 | 1.20 | †† | 1.20 | †† | (0.40 | )†† | 1 | 191 | ||||||||||||||||||

| 12-31-07 | 1.39 | 1.40 | † | 1.40 | † | (0.79 | )† | 1 | 186 | ||||||||||||||||||

| 12-29-06(4)-12-31-06 | 1.45 | 1.40 | 1.40 | (1.40 | ) | 1 | 139 | ||||||||||||||||||||

| Class I | |||||||||||||||||||||||||||

| 12-31-08 | 0.88 | 0.70 | †† | 0.70 | †† | 0.11 | †† | 195,295 | 191 | ||||||||||||||||||

| 12-31-07 | 0.89 | 0.90 | † | 0.90 | † | (0.39 | )† | 91,459 | 186 | ||||||||||||||||||

| 12-31-06 | 0.95 | 0.90 | 0.90 | (0.32 | ) | 71,154 | 139 | ||||||||||||||||||||

| 12-31-05 | 0.97 | 0.90 | 0.90 | (0.31 | ) | 78,760 | 90 | ||||||||||||||||||||

| 12-31-04 | 0.96 | 0.94 | 0.94 | (0.47 | ) | 83,969 | 73 | ||||||||||||||||||||

| Class S | |||||||||||||||||||||||||||

| 12-31-08 | 1.13 | 0.90 | †† | 0.90 | †† | (0.02 | )†† | 249,953 | 191 | ||||||||||||||||||

| 12-31-07 | 1.14 | 1.10 | † | 1.10 | † | (0.59 | )† | 33,491 | 186 | ||||||||||||||||||

| 12-31-06 | 1.20 | 1.10 | 1.10 | (0.53 | ) | 33,810 | 139 | ||||||||||||||||||||

| 12-31-05 | 1.22 | 1.10 | 1.10 | (0.51 | ) | 41,989 | 90 | ||||||||||||||||||||

| 12-31-04 | 1.21 | 1.14 | 1.14 | (0.68 | ) | 42,808 | 73 | ||||||||||||||||||||

| ING VP SmallCap Opportunities Portfolio | |||||||||||||||||||||||||||

| Class ADV | |||||||||||||||||||||||||||

| 11-20-08(4)-12-31-08 | 1.43 | 1.40 | †† | 1.40 | †† | (0.93 | )†† | 4 | 148 | ||||||||||||||||||

| Class I | |||||||||||||||||||||||||||

| 12-31-08 | 0.93 | 0.90 | †† | 0.90 | †† | (0.04 | )†† | 56,476 | 148 | ||||||||||||||||||

| 12-31-07 | 0.90 | 0.90 | †† | 0.90 | †† | 0.07 | †† | 83,695 | 97 | ||||||||||||||||||

| 12-31-06 | 0.93 | 0.90 | 0.90 | (0.35 | ) | 81,210 | 84 | ||||||||||||||||||||

| 12-31-05 | 0.96 | 0.90 | 0.90 | (0.52 | ) | 81,155 | 83 | ||||||||||||||||||||

| 12-31-04 | 0.94 | 0.90 | 0.90 | (0.58 | ) | 86,218 | 67 | ||||||||||||||||||||

| Class S | |||||||||||||||||||||||||||

| 12-31-08 | 1.18 | 1.10 | †† | 1.10 | †† | (0.26 | )†† | 54,163 | 148 | ||||||||||||||||||

| 12-31-07 | 1.15 | 1.10 | †† | 1.10 | †† | (0.14 | )†† | 105,212 | 97 | ||||||||||||||||||

| 12-31-06 | 1.18 | 1.10 | 1.10 | (0.55 | ) | 122,526 | 84 | ||||||||||||||||||||

| 12-31-05 | 1.21 | 1.10 | 1.10 | (0.72 | ) | 118,854 | 83 | ||||||||||||||||||||

| 12-31-04 | 1.19 | 1.10 | 1.10 | (0.78 | ) | 109,246 | 67 | ||||||||||||||||||||

See Accompanying Notes to Financial Statements

16

FINANCIAL HIGHLIGHTS (CONTINUED)

Selected data for a share of beneficial interest outstanding throughout each year or period.

| Income (loss) from investment operations | Less distributions | ||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) | Total from investment operations | From net investment income | From net realized gains | Total distributions | Payments by affiliates (note 16) | Net asset value, end of year or period | Total Return(1) | ||||||||||||||||||||||||||||||||||

| Year or period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | |||||||||||||||||||||||||||||||||

| ING VP International Value Portfolio | |||||||||||||||||||||||||||||||||||||||||||

| Class ADV | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 14.21 | 0.22 | (5.67 | ) | (5.45 | ) | 0.25 | 1.78 | 2.03 | 0.01 | 6.74 | (43.11 | )(d) | ||||||||||||||||||||||||||||||

| 12-31-07 | 15.26 | 0.19 | 1.60 | 1.79 | 0.19 | 2.65 | 2.84 | — | 14.21 | 12.63 | |||||||||||||||||||||||||||||||||

| 12-29-06(4)-12-31-06 | 15.26 | † | (0.00 | )• | — | (0.00 | )• | — | — | — | — | 15.26 | (b) | — | |||||||||||||||||||||||||||||

| Class I | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 14.24 | 0.27 | (5.67 | ) | (5.40 | ) | 0.30 | 1.78 | 2.08 | 0.01 | 6.77 | (42.76 | )(d) | ||||||||||||||||||||||||||||||

| 12-31-07 | 15.26 | 0.28 | 1.62 | 1.90 | 0.27 | 2.65 | 2.92 | — | 14.24 | 13.44 | |||||||||||||||||||||||||||||||||

| 12-31-06 | 12.73 | 0.34 | 3.36 | 3.70 | 0.35 | 0.82 | 1.17 | — | 15.26 | 29.44 | |||||||||||||||||||||||||||||||||

| 12-31-05 | 12.76 | 0.18 | • | 0.89 | 1.07 | 0.30 | 0.80 | 1.10 | — | 12.73 | 9.43 | ||||||||||||||||||||||||||||||||

| 12-31-04 | 11.01 | 0.16 | 1.74 | 1.90 | 0.15 | — | 0.15 | — | 12.76 | 17.41 | |||||||||||||||||||||||||||||||||

| Class S | |||||||||||||||||||||||||||||||||||||||||||

| 12-31-08 | 14.39 | 0.25 | (5.66 | ) | (5.41 | ) | 0.28 | 1.78 | 2.06 | 0.01 | 6.93 | (42.31 | )(d) | ||||||||||||||||||||||||||||||

| 12-31-07 | 15.41 | 0.23 | 1.64 | 1.87 | 0.24 | 2.65 | 2.89 | — | 14.39 | 13.06 | |||||||||||||||||||||||||||||||||

| 12-31-06 | 12.88 | 0.28 | 3.39 | 3.67 | 0.32 | 0.82 | 1.14 | — | 15.41 | 28.81 | |||||||||||||||||||||||||||||||||

| 12-31-05 | 12.92 | 0.13 | • | 0.92 | 1.05 | 0.29 | 0.80 | 1.09 | — | 12.88 | 9.04 | ||||||||||||||||||||||||||||||||

| 12-31-04 | 11.16 | 0.13 | 1.76 | 1.89 | 0.13 | — | 0.13 | — | 12.92 | 17.03 | |||||||||||||||||||||||||||||||||

| Ratios to average net assets | Supplemental data | ||||||||||||||||||||||||||

| Expenses before reductions/additions(2)(3) | Expenses net of fee waivers and/or recoupments, if any(2)(3) | Expenses net of all reductions/additions(2)(3) | Net investment income (loss)(2)(3) | Net assets, end of year or period | Portfolio turnover rate | ||||||||||||||||||||||

| Year or period ended | (%) | (%) | (%) | (%) | ($000's) | (%) | |||||||||||||||||||||

| ING VP International Value Portfolio | |||||||||||||||||||||||||||

| Class ADV | |||||||||||||||||||||||||||

| 12-31-08 | 1.56 | 1.50 | †† | 1.50 | †† | 2.06 | †† | 0 | ** | 207 | |||||||||||||||||

| 12-31-07 | 1.69 | 1.50 | †† | 1.50 | †† | 1.25 | †† | 1 | 202 | ||||||||||||||||||

| 12-29-06(4)-12-31-06 | 1.69 | 1.50 | †† | 1.50 | †† | (1.50 | )†† | 1 | 146 | ||||||||||||||||||

| Class I | |||||||||||||||||||||||||||

| 12-31-08 | 1.06 | 1.00 | †† | 1.00 | †† | 2.59 | †† | 340,022 | 207 | ||||||||||||||||||

| 12-31-07 | 1.19 | 1.00 | †† | 1.00 | †† | 1.77 | †† | 515,883 | 202 | ||||||||||||||||||

| 12-31-06 | 1.19 | 1.00 | †† | 1.00 | †† | 2.40 | †† | 460,381 | 146 | ||||||||||||||||||

| 12-31-05 | 1.22 | 1.00 | 1.00 | 1.50 | 348,326 | 125 | |||||||||||||||||||||

| 12-31-04 | 1.22 | 1.00 | 1.00 | 1.48 | 262,694 | 98 | |||||||||||||||||||||

| Class S | |||||||||||||||||||||||||||

| 12-31-08 | 1.31 | 1.20 | †† | 1.20 | †† | 2.35 | †† | 9,782 | 207 | ||||||||||||||||||

| 12-31-07 | 1.44 | 1.20 | †† | 1.20 | †† | 1.44 | †† | 13,668 | 202 | ||||||||||||||||||

| 12-31-06 | 1.44 | 1.20 | †† | 1.20 | †† | 2.00 | †† | 7,007 | 146 | ||||||||||||||||||

| 12-31-05 | 1.47 | 1.20 | 1.20 | 1.05 | 2,847 | 125 | |||||||||||||||||||||

| 12-31-04 | 1.47 | 1.20 | 1.20 | 1.14 | 1,225 | 98 | |||||||||||||||||||||

(1) Total return is calculated assuming reinvestment of all dividends and capital gain distributions at net asset value and does not reflect the effect of insurance contract charges. Total return for periods less than one year is not annualized.

(2) Annualized for periods less than one year.

(3) Expense ratios reflect operating expenses of a Portfolio. Expenses before reductions do not reflect amounts reimbursed by the Investment Adviser and/or Distributor or reductions from brokerage commis sion recapture arrangements or other expense offset arrangements and do not represent the amount paid by a Portfolio during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by the Investment Adviser or Distributor but prior to reductions from brokerage commission recapture arrangements or other expense offset arrangements. Expenses net of all reductions represent the net expenses paid by a Portfolio. Net investment income (loss) is net of all such additions or reductions.

(4) Commencement of operations.

• Calculated using average number of shares outstanding throughout the period.

* Amount is more than $(0.005), or less than $0.005

** Amount is less than $500.

† Impact of waiving the advisory fee for the ING Institutional Prime Money Market Fund holding has more than 0.005% impact on the expense ratio and net investment income or loss ratio.

†† Impact of waiving the advisory fee for the ING I nstitutional Prime Money Market Fund holding has less than 0.005% impact on the expense ratio and net investment income or loss ratio.

(a) In 2008, there was no impact on total return due to payment by affiliate.

(b) For ING VP MidCap Opportunities Portfolio amount was previously reported as $8.20 and has been corrected to reflect the actual NAV. For ING VP International Portfolio amount was previously reported as $15.38 and has been corrected to reflect the actual NAV.

(c) Excluding a paym ent by affiliate in 2008, VP Small Cap Opportunities total return would have been 24.72%, (34.52)% and (34.64)% for Classes ADV, I and S, respectively.

(d) Excluding a payment by affiliate in 2008, VP International Value total return would have been (43.18)%, (42.86)% and (42.43)% on Classes ADV, I and S, respectively.

See Accompanying Notes to Financial Statements

17

NOTES TO FINANCIAL STATEMENTS AS OF DECEMBER 31, 2008

NOTE 1 — ORGANIZATION

Organization. ING Variable Products Trust (the "Trust") is a business trust organized under the laws of the Commonwealth of Massachusetts on December 17, 1993 and registered under the Investment Company Act of 1940, as amended ("1940 Act"), as a diversified, open-end management investment company. There are three active investment series which comprise the Trust. The names of the Portfolios are: ING VP MidCap Opportunities Portfolio ("MidCap Opportunities"), ING VP SmallCap Opportunities Portfolio ("SmallCap Opportunities") and ING VP International Value Portfolio ("International Value"); each, a "Portfolio" and collectively, the "Portfolios."

Each Portfolio's investment objective is to seek long-term capital appreciation.

Each Portfolio offers Adviser Class ("ADV Class") shares, Class I shares and Class S shares. The classes differ principally in the applicable distribution and shareholder service fees. Shareholders of each class also bear certain expenses that pertain to that particular class. All shareholders bear the common expenses of the Portfolios and earn income and realized gains/losses from a Portfolio pro rata based on the average daily net assets of each class, without distinction between share classes. Dividends are determined separately for each class based on income and expenses allocable to each class. Common expenses of the Portfolios (including custodial asset-based fees, legal and audit fees, printing and mailing expenses, transfer agency out-of-pocket expenses, and fees and expenses of the independent trustees) are allocated to each Portfolio in proportion to its average net assets. Expenses directly attributable to a particular portfolio ( including advisory, administration, custodial transaction-based, registration, other professional, distribution and/or service fees, certain taxes, and offering costs) are charged directly to that Portfolio. Differences in per share dividend rates generally result from the differences in separate class expenses, including distribution and shareholder service fees, if applicable.

Shares of the Portfolios may be offered to separate accounts of insurance companies as investment options under variable annuity contracts and variable life insurance policies ("Variable Contracts"). Shares may also be offered to qualified pension and retirement plans outside the Variable Contract and to certain investment advisers and their affiliates. Class I shares may be made available to other investment companies, including series of the Trust under fund-of-funds arrangements.

Participating insurance companies and other designated organizations are authorized to receive purchase orders on each Portfolio's behalf.